Gold at (1:30 am est) $1174.10 down $1.10

silver at $16.82: up 7 cents

Access market prices:

Gold: 1170.25

Silver: 16.75

Another raid by our banker friends in gold and silver as they try desperately to keep a lid on the turmoil in the world. Last night, Italy voted “No” to reforms and as promised Renzi quit as PM. Italy has a huge problem with its banks. They have 360 billion euros of non performing loans on their books with little equity left. Most of the ownership of Italian bank bonds are owned by Italians (especially senior citizens and that is their entire wealth tied up with these bonds). If they bail in on the banks, then these guys suffer and that is exactly what Renzi tried to avoid. Now will the ECB bail in and create havoc in Italy..stay tuned

THE DAILY GOLD FIX REPORT FROM SHANGHAI AND LONDON

.

The Shanghai fix is at 10:15 pm est last night and 2:15 am est early this morning

The fix for London is at 5:30 am est (first fix) and 10 am est (second fix)

Thus Shanghai’s second fix corresponds to 195 minutes before London’s first fix.

And now the fix recordings:

MONDAY gold fix Shanghai

Shanghai morning fix Dec 5 (10:15 pm est last night): $ 1195.92

NY ACCESS PRICE: $1175.00 (AT THE EXACT SAME TIME)/premium $20.92

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Shanghai afternoon fix: 2: 15 am est (second fix/early morning):$ 1198.11

NY ACCESS PRICE: 1173.00 (AT THE EXACT SAME TIME/2:15 am)

HUGE SPREAD 2ND FIX TODAY!!: $25.11

China rejects NY pricing of gold as a fraud

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

London Fix: Dec 5: 5:30 am est: $1164.90 (NY: same time: $1164.90 5:30AM)

London Second fix Dec 5: 10 am est: $1162.60 (NY same time: $1162.10 10 AM)

It seems that Shanghai pricing is higher than the other two , (NY and London). The spread has been occurring on a regular basis and thus I expect to see arbitrage happening as investors buy the lower priced NY gold and sell to China at the higher price. This should drain the comex.

Also why would mining companies hand in their gold to the comex and receive constantly lower prices. They would be open to lawsuits if they knowingly continue to supply the comex despite the fact that they could be receiving higher prices in Shanghai.

end

For comex gold:

NOTICES FILINGS FOR DECEMBER CONTRACT MONTH: 216 NOTICE(S) FOR 21,600 OZ. TOTAL NOTICES SO FAR: 6723 FOR 672,300 OZ (20.91 TONNES)

For silver:

NOTICES FOR DECEMBER CONTRACT MONTH FOR SILVER: 407 NOTICE(s) OR 2,035,000 OZ. TOTAL NUMBER OF NOTICES FILED SO FAR; 1446 FOR 7,230,000 OZ

Let us have a look at the data for today

.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total open interest ROSE by 383 contracts UP to 159,474 with respect to FRIDAY’S trading. In ounces, the OI is still represented by just less THAN 1 BILLION oz i.e. .797 BILLION TO BE EXACT or 114% of annual global silver production (ex Russia & ex China).

FOR THE DECEMBER FRONT MONTH: 407 NOTICES FILED FOR 2,035,000 OZ.

In gold, the total comex gold ROSE by 1,447 contracts WITH THE RISE IN THE PRICE GOLD ($8.20 with FRIDAY’S trading ).The total gold OI stands at 399,442 contracts. The bankers have done a good job of eviscerating gold (and silver) longs. We are very close to the bottom with respect to OI. Generally 390,000 should do it.

we had a 216 notices filed upon for 21,600 oz of gold.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD:

We had a huge changes in tonnes of gold at the GLD, a SMALL withdrawal of .32 tonnes of gold. When you have a tiny amount, it generally is more fees like insurance and storage

Inventory rests tonight: 869.90 tonnes

.

SLV

we no changes in silver inventory tonight

THE SLV Inventory rests at: 345.955 million oz

.

First, here is an outline of what will be discussed tonight: Preliminary data

1. Today, we had the open interest in silver ROSE by 383 contracts UP to 159,474 despite the fact that the price of silver ROSE by $.32 with FRIDAY’S trading. The gold open interest ROSE by 1447 contracts UP to 399,442 DESPITE THE FACT THAT the price of gold ROSE BY $8.20 WITH FRIDAY’S TRADING.

(report Harvey).

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)Late SUNDAY night/MONDAY morning: Shanghai closed DOWN 29.13 POINTS OR 1.21%/ /Hang Sang closed DOWN 59.27 OR 0.26%. The Nikkei closed DOWN 151.09 OR 0.82%/Australia’s all ordinaires CLOSED DOWN 0.81% /Chinese yuan (ONSHORE) closed UP at 6.8836/Oil ROSE to 52.04 dollars per barrel for WTI and 54.73 for Brent. Stocks in Europe: ALL IN THE GREEN. Offshore yuan trades 6.8772 yuan to the dollar vs 6.8836 for onshore yuan.THE SPREAD BETWEEN ONSHORE AND OFFSHORE NARROWS HUGELY AGAIN AS CHINA ATTEMPTS TO STOP MORE USA DOLLARS LEAVING CHINA’S SHORES / CHINA SENDS A CLEAR MESSAGE TO THE USA AND JANET TO NOT RAISE RATES IN DECEMBER

REPORT ON JAPAN SOUTH KOREA NORTH KOREA AND CHINA

3a)THAILAND/SOUTH KOREA

none today

b) REPORT ON JAPAN

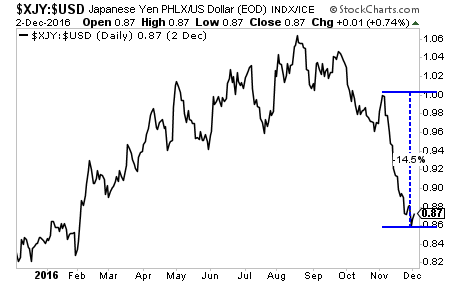

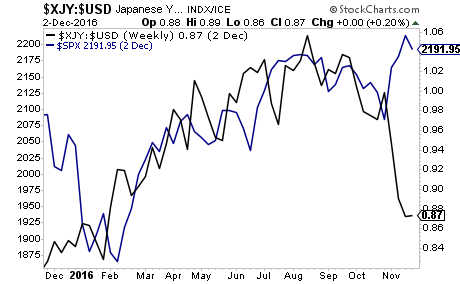

The collapsing yen!!:

( Graham Summers/Phoenix Research Capital)

c) REPORT ON CHINA

China is now rethinking investing in USA real estate. There is no doubt that China is worried about their rapidly sinking foreign exchange reserve of USA dollars. No doubt it is better to buy USA gold than USA properties

(courtesy zero hedge)

4 EUROPEAN AFFAIRS

i)Italy

Renzi loses the Italian referendum by a wide margin:

(zero hedge)

ii)Renzi will resign: the Euro tumbles

iv)Here is Goldman Sachs’ take on what will happen in the next few months in Italy. Although the situation is very fluid, they are probably correct:

(courtesy Goldman Sachs)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

i)Turkey

With the Turkish Lira falling and high interest rates, Turkey is now proposing tradw with Russia, China and Iran in their respective currencies bypassing the USA dollar.

It should help them..

( zero hedge)

ii)Monday:

The lira drops to 3.67 to the dollar but the real problem in Turkey is the shortage of dollars. They have a net deficit of 210 billion dollars of a deficit. ( Reserves – corporate borrowings in dollars)

6.GLOBAL ISSUES

Vancouver, Canada

Just looks what happens to an economy when China withdraws its cash: the entire Vancouver housing market freezes up as sales crash (up to 10% lower in one month and for sale signs proliferate the streets:

(courtesy Wolf Richter/WolfStreet)

7. OIL ISSUES

i)OPEC production rises to 34.19 million barrels per day. However the agreement is for 32.50 million barrels per day target. OPEC will need to find a cut of 1/2 million barrels in order to reach its quota for a cut: highly unlikely. No wonder the shale boys are rushing to hedge the price of oil

( zero hedge)

ii) USA shale companies are rushing in to hedge the higher oil prices and that in itself is OPEC’s biggest risk to the deal.

( zero hedge)

8. EMERGING MARKETS

A good snapshot as to what is going on in hyperflation torn Venezuela;

( mac Slavo/SHTFPlan.com)

9. PHYSICAL MARKETS

ia)Your crime scene early this morning with respect to gold:

( zero hedge)

i)Premiums in China for gold has skyrockets to a 3 year high. Noe the highest ever daily gold withdrawal (strictly physical) of 28 tonnes removed from the SGE (withdrawal equals demand)

( zero hedge)

ii)Deutsche bank settles to pay 60 million which will now open many more cases against these crooks: remember this is only on the fix/they have committed crimes in all aspects of gold/silver trading

(reuters)

iii)Koos Jansen totally makes fools out of GFM’s gold demand stats:

( Koos Jansen/Bullionstar)

iv)Jim Sinclair: capital markets have been destroyed, Capitalism is dead

I urge you to listen to the 33 minute tape

( Jim Sinclair/Greg Hunter/USAWatchdog)

10.USA STORIES

ia)Trading today from Europe and the uSA: total manipulation! The Italian banking system collapses despite Draghi’s largess: just take a look at Italian bank stocks and credit default spreads.

( zero hedge)

ib)According to Markit, the huge gain in Sept and October is tapering off but still the uSA economy jumps to 13th month highs. However new orders are also stalling.

( Markit/Services)

ic)the following is Janet Yellen’s favourite market condition index for labour: it is down for the 5th straight month:

ii)Over the weekend, we had a bit of diplomatic problem as Trump receives a call from Taiwanese President Tsai Ing-wen congratulating him on his victory. The problem is that USA does not officially recognize Taiwan as they stated in 1988 there is only one China and that is the government of Beijing. China got a little antsy but averted a diplomatic row by stating that the call was a “gimmick”

( zero hedge)

iii)How on earth can Trump save this company from moving to Mexico?

( zero hedge)

iv)The Kersten Institute reported on the pension study of public pensions and it is startling: The entire pension is unfunded by $1 trillion which averages about $93,000 per household in the USA (Dec 2015 figures) a rise from 77,700 per household in 2014.

( zerohedge)

Let us head over to the comex:

.

The total gold comex open interest ROSE BY 1447 CONTRACTS to an OI level of 399,442 AS THE PRICE OF GOLD ROSE $8.20 with FRIDAY’S trading. We are now in the contract month of December and it is the biggest of the year. here the front month of December showed a DECREASE of 989 contracts DOWN to 3272.We had 216 notices served upon yesterday we lost another 773 contracts or 77,300 oz will not stand for delivery and no doubt where paper settled. We should be coming to an end in this paper settlement in December as hedge funds will drain the comex gold and send it off to Shanghai.

For the next delivery month of January we had a GAIN of 78 contracts UP to 2546. For the next big active delivery month of February we had a GAIN of 2,064 contracts up to 275,782.

We had 1,612 notices filed upon today for 161,200 oz

And now for the wild silver comex results. Total silver OI ROSE by 383 contracts FROM 159,091 UP TO 159,474 as the price of silver ROSE BY $0.32 with FRIDAY’S trading. We are moving further from the all time record high for silver open interest set on Wednesday August 3/2016: (224,540). We are now in the next major delivery month of December and here it FELL BY 421 contracts DOWN to 2063 CONTRACTS . We had 407 notices served upon yesterday so we lost 14 contracts or an additional 70,000 oz will not stand for delivery.

The next non active delivery month is January and here the OI fell by 293 contracts down to 3422. This level seems highly elevated. Maybe we are going to see the same huge metals gains in silver as we have witnessed in gold.

The next big active delivery month is March and here the OI rose by 1084 contracts up to 130,085 contracts.

We had 23 notices filed for 115,000 oz for the December contract.

Eventually at the end of December 2015: 6.4512 tonnes of gold stood for delivery

Eventually at the end of December 2015: 18.84 million oz of silver stood for delivery

VOLUMES: for the gold comex

Today the estimated volume was 214,913 contracts which is fair.

Friday’s confirmed volume was 189,582 contracts which is fair

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz |

6,430.000 oz

Brinks

2,000 kilobars

|

| Deposits to the Dealer Inventory in oz | nil oz |

| Deposits to the Customer Inventory, in oz |

nil oz

|

| No of oz served (contracts) today |

216 notices

21600 oz

|

| No of oz to be served (notices) |

4045 contracts

404,500 oz

|

| Total monthly oz gold served (contracts) so far this month |

6723 notices

672,300 oz

20.91 tonnes

|

| Total accumulative withdrawals of gold from the Dealers inventory this month | nil oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | 3,433,916.7 oz |

For December:

Today, 0 notices were issued from JPMorgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equates to 1612 contract(s) of which 95 notices were stopped (received) by jPMorgan dealer and 655 notice(s) was (were) stopped/ Received) by jPMorgan customer account.

March 2015: 2.311 tonnes (March is a non delivery month)

| Silver | Ounces |

| Withdrawals from Dealers Inventory | nil |

| Withdrawals from Customer Inventory |

500,133.290 oz

CNT,

|

| Deposits to the Dealer Inventory |

nil OZ

|

| Deposits to the Customer Inventory |

498,133.470 oz

CNT

|

| No of oz served today (contracts) |

23 CONTRACT(S)

(115,000 OZ)

|

| No of oz to be served (notices) |

2040 contracts

(10,200,000 oz)

|

| Total monthly oz silver served (contracts) | 1469 contracts (7,345,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month | 975,923.7 oz |

end

end

NPV for Sprott and Central Fund of Canada

end

Major gold/silver stories for MONDAY

GOLDCORE/BLOG/MARK O’BYRNE

Potential “Systemic Crisis In Eurozone” After Italy Votes No, Renzi Resigns

Italy Votes No, Renzi Resigns – Potential “Systemic Crisis In Eurozone”

Italy’s Prime Minister Matteo Renzi has said he will officially resign Monday, after voters apparently rejected his proposals for constitutional reform. What should investors keep an eye out for after his defeat?

Although the referendum on Sunday was officially on Renzi’s plan for legislative overhaul, it was widely seen in Italy as a vote of confidence in the prime minister and his government. In voting “no” — projections suggest 59% of those in the ballot made that choice — the Italians have set the stage for an early election and perhaps given local populist parties the chance to deliver a Brexit- or Trump-style shake-up.

But if the political uncertainty lasts, the fallout from the vote could have an effect not only within Italy — on its already embattled banks, for instance — but also beyond the borders of the boot-shaped country.

The problems in Italy could — in theory — “spark a systemic crisis in the eurozone,” said Holger Schmieding, chief economist at Berenberg, in a recent note.

A “protracted period of political uncertainty after a ‘no’ vote could exacerbate the Italian banking issues, unsettle the Italian bond market and weigh on business and consumer confidence,” he said.

Over recent weeks, the spread between Italian and German 10-year government-bond yields has reached a two-year high, according to Dow Jones Newswires. That has been interpreted by some as a sign that the eurozone is at risk of a breakaway.

Even though markets have been anticipating a “no” vote in Italy, Italian sovereigns bond yields may continue to surge as investors will ask higher return for their risk…”

Real full article from Marketwatch here

Gold and Silver Bullion – News and Commentary

Euro Slips With Asian Stocks While Bonds Rise as Italy Votes No (Bloomberg.com)

Gold prices nudge up after Italian PM resigns (Reuters.com)

Gold Prices Ease, Surrender Gains On Dollar Strength (NDTV.com)

Euro Reaches 20-Month Low as Renzi Concedes Referendum Defeat (Bloomberg.com)

Renzi Quits as Italy Referendum Defeat Deepens Europe’s Turmoil (Bloomberg.com)

What to know now that Italy has voted ‘no,’ with Renzi set to step down (MarketWatch.com)

We Have Killed Capitalism – Jim Sinclair (USAWatchDog.com)

Donald Trump’s unhappy fate is to oversee a financial crisis far worse than the last (CityAM.com)

Platinum supply under extreme pressure – Dunne (MiningWeekly.com)

Gold Prices (LBMA AM)

05 Dec: USD 1,164.90, GBP 915.84 & EUR 1,095.36 per ounce

02 Dec: USD 1,171.65, GBP 929.00 & EUR 1,100.88 per ounce

01 Dec: USD 1,168.75, GBP 930.09 & EUR 1,099.68 per ounce

30 Nov: USD 1,187.40, GBP 952.06 & EUR 1,115.44 per ounce

29 Nov: USD 1,187.30, GBP 952.45 & EUR 1,119.98 per ounce

28 Nov: USD 1,189.10, GBP 956.51 & EUR 1,117.99 per ounce

25 Nov: USD 1,187.50, GBP 953.30 & EUR 1,121.83 per ounce

Silver Prices (LBMA)

05 Dec: USD 16.62, GBP 13.05 & EUR 15.54 per ounce

02 Dec: USD 16.35, GBP 12.95 & EUR 15.36 per ounce

01 Dec: USD 16.30, GBP 12.91 & EUR 15.35 per ounce

30 Nov: USD 16.67, GBP 13.39 & EUR 15.66 per ounce

29 Nov: USD 16.54, GBP 13.26 & EUR 15.61 per ounce

28 Nov: USD 16.68, GBP 13.45 & EUR 15.73 per ounce

25 Nov: USD 16.47, GBP 13.21 & EUR 15.55 per ounce

Recent Market Updates

– Gold and Silver Will Protect From Coming Financial Crash – Rickards

– RBS Fail Bank of England Stress Test

– Peak Silver – Supply Deficits Mean Higher Prices

– Bail In Risk – €4 Trillion Banking System In Italy Poses Contagion Risk as Referendum Looms

– Gold Down 13.5% In 13 Days – Trump Bearish For Gold?

– War On Cash Just Got Real – India and Citibank In Australia

– Russia Gold Buying In October Is Biggest Monthly Allocation Since 1998

– Stocks, Bonds, Pension Funds “Will Be Wiped Out…” – Rickards

– Physical Gold Is A “Long-Term Position” as “Hedge Against Governments”

– Gold Sell Off On Fed Noise – “Interesting Times” To “Support Gold”

– Islamic Gold – Vital New Dynamic In Physical Gold Market

– Peak Gold Globally – “Bullish For Gold”

– Gold Price Should Go Higher On Global Risks and Trump – Capital Economics

end

Your crime scene early this morning with respect to gold:

(courtesy zero hedge)

Gold Double-Slammed As ‘Traders’ Puke $3.5 Billion Notional Through Futures Markets

The Italian referendum’s “no” vote sparked the rational reach for safe-havens as the Euro-endgame became more questionable… but that lasted less than an hour and since the $1190 highs overnight, gold has been monkeyhammered to 10-month lows amid two legs lower (EU open and US open) with spikes in volume of around $3.5 billion notional…

end

Premiums in China for gold has skyrockets to a 3 year high. Noe the highest ever daily gold withdrawal (strictly physical) of 28 tonnes removed from the SGE (withdrawal equals demand)

(courtesy zero hedge)

Sudden Scramble For Gold In China Sends Premiums To 3 Year High

While paper gold traders can’t seem to dump the precious metal fast enough, physical gold demand is soaring around the world. India retail premiums are spiking (amid demonetization), local China premiums soar to a 3-year-high (as capital controls loom), and coin sales from the US Mint have risen for the 4th straight month, accelerating post-election to the highest since July 2015 since Trump’s victory at the election.

Following the initial panic-buying across India after Modi’s demonetization effort shook the nation’s faith in fiat currency (sending local gold premiums soaring), news of reported gold import curbs in China (and looming capital controls) has sent gold premiums in China near three-year highs amid limited supply of the precious metal (as Reuters reports)…

The import curbs may be part of China’s efforts to limit outflows of the yuan after the currency’s slide to its weakest in more than eight years, traders say. China allows only 15 banks to import gold, including three foreign lenders.

“There is severe restriction on the banks’ quota to import gold into China. Each one of them have to justify their need,” a Hong Kong-based banker said.

Gold was sold in China at about $24 an ounce above the international spot benchmark this week. Premiums went as high as $30 last week, the most since January 2014,according to Thomson Reuters data.

“Supply has been limited and so the premiums have held firm,” said Cameron Alexander, analyst with Thomson Reuters-owned metals consultancy GFMS.

And as Jesse’s Cafe Americain notes, yesterday saw over 28 tonnes of physical gold taken off the Shanghai Gold Exchange (in one day), easily the biggest day this year for physical gold withdrawals in Shanghai...

But it’t not just Asia.

In the US, physical gold demand has soared post-election in The United States as the paper prices was pummeled…

This is the 4th month in a row of rising physical gold demand, to the highest level since July 2015 (as China turmoil began to ripple through the world)…

So unlike with stocks where higher prices create higher demand, some level of economic rationality remains in precious metals as physical bullion demand reacts to take advantage of low prices to buy more.

end

Deutsche bank settles to pay 60 million which will now open many more cases against these crooks: remember this is only on the fix/they have committed crimes in all aspects of gold/silver trading

(reuters)

Deutsche Bank to pay $60 million to settle U.S. gold price-fixing case

Deutsche Bank AG has agreed to pay $60 million to settle private U.S. antitrust litigation by traders and other investors who accused the German bank of conspiring to manipulate gold prices at their expense.

The preliminary settlement was filed on Friday with the U.S. District Court in Manhattan, and requires a judge’s approval.

Deutsche Bank denied wrongdoing. The bank in October agreed to pay $38 million to settle similar litigation over alleged silver price manipulation.

Amanda Williams, a spokeswoman for the bank, declined to comment. Lawyers for the plaintiffs did not immediately respond to requests for comment.

The case is one of many in the Manhattan court in which investors accused banks of conspiring to rig rates and prices in financial and commodities markets.

Investors sued Deutsche Bank, Barclays Plc, Bank of Nova Scotia, HSBC Holdings Plc and Societe Generale in 2014, claiming that they conspired to fix gold prices from 2004 to 2013.

While the investors did not estimate the size of the banks’ gold portfolios, they said the gold derivatives market alone reached $650 billion during the class period.

Deutsche Bank had agreed to settle its part of the case in April, but the terms were not disclosed until now.

In an Oct. 3 decision, U.S. District Judge Valerie Caproni in Manhattan said investors could pursue much of their lawsuit against the other four banks.

Deutsche Bank has separately been in talks with U.S. authorities on a potential multibillion-dollar penalty related to mortgage securities.

The case is In re: Commodity Exchange Inc Gold Futures and Options Trading Litigation, U.S. District Court, Southern District of New York, No. 14-mc-02548.

(Reporting by Jonathan Stempel in New York; editing

end

zero hedge responds to the DB settlement:

(courtesy zero hedge)

Deutsche Bank Pays $60 Million To Settle Gold-Manipulation Lawsuit

2016 is shaping up as the year when countless conspiracy theories will be confirmed to be non-conspiracy fact: from central bank rigging of capital markets, to political rigging of elections, to media rigging of public sentiment, and now, commercial bank rigging of both silver and gold. In short, “tinfoil hat-wearing nutjobs living in their parents basement” were right all along.

In early October, we reported that “In A Major Victory For Gold And Silver Traders, Manipulation Lawsuit Against Gold-Fixing Banks Ordered To Proceed,” however one bank was exempt: Deutsche Bank. The reason why was known since April, when we first reported that Deutsche Bank had agreed to settle the class action lawsuit filed in July 2014 accusing a consortium of banks of plotting to manipulate gold and silver. Among the charges that Deutsche Bank effectively refused to contest were the following:

- employment of a manipulative device claims

- bid-rigging, and unjust enrichment.

- price fixing and unlawful restraint

- price manipulation claims

- aiding and abetting and principal-agent claims.

An affidavit filed in October shed more light on the settlement process:

The negotiations with Deutsche Bank over the material terms of the Settlement took place over several months starting in December 2015 and continuing until the Deutsche Bank Settlement Agreement was executed on September 6, 2016.

Following initial phone calls with Deutsche Bank’s counsel in December 2015, Lowey and Grant & Eisenhofer engaged in lengthy negotiations with Deutsche Bank’s counsel over the material terms of the settlement, including the amount of the settlement consideration, the scope of the cooperation to be provided by the Deutsche Bank Defendants, the scope of the releases, and the circumstances under which the parties would have the right to terminate the settlement.

During the course of the negotiations, Class Counsel presented what we perceived to be the strengths and weaknesses of the claims and defenses, as well as Deutsche Bank’s litigation exposure.

In February 2016, we reached an agreement with Deutsche Bank on the amount of the settlement, subject to the negotiation of other material terms of the deal. For example, given that this is the first settlement in the case, it was our view that the cooperation provisions of the deal were extremely important to our ability to maximize the overall recovery for the class against the Non-Settling Defendants. The negotiations as to the scope of the cooperation provisions continued for several months.

On April 13, 2016, counsel for Deutsche Bank and Class Counsel signed a Binding Settlement Term Sheet (“Term Sheet”). The Term Sheet set forth the terms on which the parties agreed, subject to the negotiation of a full Settlement Agreement, to settle Plaintiffs’ claims against Deutsche Bank. At the time the Term Sheet was executed, Class Counsel was well-informed about the legal risks, factual uncertainties, potential damages, and other aspects of the strengths and weaknesses of the claims and defenses asserted.

By letter dated April 13, 2016, the Parties reported to the Court via ECF that the Term Sheet had been executed, and advised the Court that the Term Sheet would be superseded by a formal settlement agreement. ECF No. 116.

The parties negotiated the Deutsche Bank Settlement Agreement over the course of the next several months. The negotiations over the terms of the Deutsche Bank Settlement Agreement included various material terms over which the parties had substantial disagreement, requiring significant give and take on both sides. To that end, drafts of the Deutsche Bank Settlement Agreement went back and forth between the parties, and numerous contested issues were raised, negotiated and resolved, including without limitation, continuing negotiations over the scope of Deutsche Bank’s cooperation (see ¶ 4(A)-(G)), the scope of the releases (see ¶ 12 (A)-(C)), and the circumstances under which the parties could terminate the Settlement (see ¶ 21).

Thus, the Deutsche Bank Settlement Agreement, which was executed (along with the Supplemental Agreement) on September 6, 2016, was the culmination of arm’s-length settlement negotiations that had extended over many months.

The Deutsche Bank Settlement was not the product of collusion. Before any financial numbers were discussed in the settlement negotiations and before any demand or counter-offer was ever made, we were well informed about the legal risks, factual uncertainties, potential damages, and other aspects of the strengths and weaknesses of the claims against Deutsche Bank.

The Deutsche Bank Settlement involves a structure and terms that are common in class action settlements in this District. The consideration that Deutsche Bank has agreed to pay is within the range of that which may be found to be fair, reasonable, and adequate at final approval.

There was just one thing missing: the settlement amount. Then, on October 17, the first part of the answer was revealed when according to court filings, Deutsche Bank had agreed to pay $38 million to settle the silver manipulation litigation.

The settlement, which was disclosed in papers filed in Manhattan federal court, concludes one of many recent lawsuits in which investors have accused banks of conspiring to rig the precious metal markets. However, until Deutsche Bank’s payment of $38 million to settle silver manipulation allegations, there was never any formal closure.

* * *

Then, last night, two months after the silver settlement, Deutsche Bank agreed to pay another $60 million to settle the other side of the antitrust litigation: that of rigging gold.

As Reuters first reported, the preliminary settlement was filed on Friday with the U.S. District Court in Manhattan, and requires a judge’s approval. As part of the settelement, Deutsche Bank has denied any wrongdoing, and with the two settlements, and some $98 million out of pocket, it is clear of any future liability regarding precious metals manipulation.

The case is one of many in the Manhattan court in which investors accused banks of conspiring to rig rates and prices in financial and commodities markets.

As we reported previously, in an Oct. 3 decision, U.S. District Judge Valerie Caproni in Manhattan said investors could pursue much of their lawsuit against the other four banks named in the anti-trust lawsuit which include Barclays, Bank of Nova Scotia, HSBC and Societe Generale.

In October, Vincent Briganti, a lawyer for the investors, said the silver settlement deal provides “substantial monetary compensation plus cooperation from Deutsche Bank in the continued prosecution of this important case against the non-settling defendants.” He has yet to comment on the gold settlement. Alas, as a result of the settlement, yet another discovery process has been scuttled, preventing the public from having a glimpse into what really went on in precious metal “markets.”

* * *

So who gets to benefit from the settlement? This is what the lawyer said on the silver settlement disclosed in early October:

We have reason to believe that there are at least hundreds of geographically dispersed persons and entities that fall within the Settlement Class definition. The Settlement Class includes traders of COMEX Silver Futures contracts, anyone who traded in physical silver based on the Silver Fix, and traders in various silver derivatives.

The same will likely be applicable to gold traders following Friday’s monetary settlement.

The other beneficiary, of course, is the class of investors, people and “conspiracy theorists” who claimed all along that gold and silver were subject to rigging in various forms throughout the years. Well, you were right. However, we wouldn’t hold much hope for getting any substantial monetary rewards. By the time the settlement is done, there will likely be at best a few hundred dollars left per claimant.

The good news is that this formal closure will open the door for other, similar lawsuits – for both silver and gold manipulation – now that the seal has been broken.

end

Koos Jansen totally makes fools out of GFM’s gold demand stats:

(courtesy Koos Jansen/Bullionstar)

Koos Jansen: Debunking GFMS’ gold demand statistics

Submitted by cpowell on Sat, 2016-12-03 16:07. Section: Daily Dispatches

By Koos Jansen

BullionStar.com, Singapore

Saturday, December 3, 2016

What came to light as on odd discrepancy between GFMS’ Chinese gold demand and “apparent supply” has proven to be a tenacious cover-up by the oldest consultancy firm in the gold market.

Not only does GFMS publish incomplete and misleading data on Chinese gold demand — all its supply-and-demand data is incomplete and misleading.

As a result, the vast majority of investors has been brainwashed to believe total gold supply and demand consists mainly of global mine output and jewelry demand. In reality, the supply-and-demand data GFMS publishes is just the tip of the iceberg. But the firm is reluctant to admit this, lest its business model be severely damaged.

GFMS has denied all allegations about its incomplete Chinese gold demand statistics by continuously making up false arguments. Therefore, BullionStar will debunk, once more, such arguments spread by GFMS. …

… For the remainder of the analysis:

https://www.bullionstar.com/blogs/koos-jansen/debunking-gfms-gold-demand…

end

Jim Sinclair: capital markets have beeen destroyed, Capitalism is dead

(courtesy Jim Sinclair/Greg Hunter/USAWatchdog)

I urge you to listen to the 33 minute tape

There are no markets anymore and capitalism is dead, Sinclair tells USA Watchdog

Submitted by cpowell on Sun, 2016-12-04 01:02. Section: Daily Dispatches

8p ET Saturday, December 3, 2016

Dear Friend of GATA and Gold:

Mining entrepreneur and gold advocate Jim Sinclair today tells USA Watchdog’s Greg Hunter that there are no markets anymore and that, since markets are the prerequisite of capitalism, capitalism is dead too. Whatever succeeds the current financial system, Sinclair predicts, will be based on gold, which is being acquired in bulk by Russia and China, countries that know that big changes are coming. Sinclair’s interview is 33 minutes long and can be heard at USA Watchdog here:

http://usawatchdog.com/we-have-killed-capitalism-jim-sinclair/#more-1820…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

Fake news = fake markets… (public article)

Here is Bill Holter with his public article:

(courtesy Bill Holter/Holter-Sinclair collaboration)

Growing up in the 1960’s, I can still remember hearing and reading about Russian propaganda. While I am certain some of what the Western press reported was “spun”, even a 10 year old could see through much of what Russia was trying to portray to its people.Fast forward to present day, we seem to have switched places. The current mainstream media reports defy nearly any and all logic on a daily basis. Reporting has obviously been very poor for many years and it really did not matter what the subject was. Economics, finance, geopolitics, home grown politics, it has not mattered, logic has been turned on its head. I could go through example after example but would now require a book …or more likely a “series” of books. Using just one example to illustrate the lunacy, the U.S. now has 95 million OUT OF THE WORKFORCE and thus no longer counted as “unemployed”! Where is the logic here? Mainstream media reports it (under their breath) while cheerleading the lowest unemployment rate in decades. The White House and Wall Street both report “strong” employment with glee. The fact remains, our true unemployment number as calculated back in the day of “Russian propaganda” is somewhere around 20% …We just had an election here in the U.S. that I’ve dubbed as a rejection “fake news”, fake polls, fake values, fake everything. My first thought was “hooray for the rule of law”! What is truly disturbing (especially after the election), theI say “disturbing” because the lame duck House of Representatives was elected two years ago to eviscerate Obaminationcare along with many other “executive orders” …and did absolutely none of what they promised. Why would the House pass this now? Why would they not wait until the newly elected Reps and Senators (not to mention new President) arrive? What can they possibly be thinking other than a failed (thwarted) arrival to Washington of Mr. Trump?Getting into the “meat” of what they are trying to pass, it is most obvious they are trying to legislate awayTRUTH! In essence, they are trying to say and I paraphrase, if you disagree with the official story, you are Russian propaganda. Never mind that these “propaganda sites” document, footnote and use rock solid logic in their work …they are “fake news” and should be ignored or worse, JAILED! What a travesty Mr. Paul Ryan!Reported today, the website www.nakedcapitalism.com is fighting back and is considering filing suit against and demanding retraction from the Washington Post“Fake News” Site Threatens Washington Post With Defamation Suit, Demands Retraction I find it beyond lame when the likes of WAPO and NY Times resort to labelling obvious truth as fake news. This is surreal on so many levels it is beyond words.Shifting gears but in keeping with the subject of “truth”, let’s look at just one market, gold. For years it has been said central banks have no reason to and would never manipulate gold. GATA has over the years posted reams of hard and easily connectible evidence showing this is not true. In fact, Deutsche Bank agreed to a wrist slap $60 million fine for doing just this, manipulating the gold markets. This will be followed by other firms and most likely larger fines (as DB rolled over first).An excellent article last week;http://www.zerohedge.com/news/2016-12-02/buy-dip-us-gold-coin-sales-soar-highest-16-months-china-premium-spikes-3-year-highs discusses gold demand. The below chart shows offtake from the Shanghai exchange.With just one month left in the year, Shanghai has withdrawn close to 2,200 tons (28 tons just this last Friday). If you take Chinese and Russian supply out of the equation as they do not export, total global production of gold is roughly 2,400 tons. Shanghai/China have been purchasing nearly all global production of gold over the past several years. This does not account for Indian demand which has historically been another 1,000 tons per year or thereabouts. Nor does it account for the rest of global demand which has been brisk from Europe, the U.S. and elsewhere. Where exactly is/has this excess demand being met with supply? From where is this gold coming from? The obvious answer, and one of common logic says it can only be coming from where it exists (existed), Western vaults!We could look at other markets like the credit markets where interest rates went negative …at a time debt ratios were never worse. Or, we could look at equity valuations at a 98 percentile in historic valuation levels. The point is this, markets do not make any sense from the standpoint of any fundamental logic in all of history!Many say that anyone claiming “manipulation” or “rigged markets” are just sore losers because they are wrong and need something to cover their errors. The tactic now by government/mainstream media/”official finance” is to label obvious truth as lies. MSM has become so desperate they start stories by claiming “fake news” as their proof and refutation of facts and logic. Government is apparently trying to legislate away “truth” if it does not agree with the official story by labeling websites as Russian propaganda. What proof has been offered showing any connection to any of these websites to Russia in any fashion? The answer of course there is none whatsoever other than being said “it is so”. This course of thought and action is no different than the child caught with his hand in the cookie jar asking “who are you going to believe, me or your own lying eyes”?To finish, and to pre answer the legion of trolls sure to jump on this article, please answer these questions. Do you believe mainstream media is or has been reporting news truthfully or in any fair or balanced way? Do you believe the media is separate and autonomous from government? I would remind you of the 10’s of 1,000’s of e-mails hacked from John Podesta. The only response to date has been “these were illegally stolen”, NEVER have they been claimed to be false. If the e-mails then are not false (several people have already resigned because of the revelations), then we know for an absolute fact that polls, debates, and other news to “affect perception” are outright bogus and propaganda!I would then ask, if there has been a coordinated effort to “shape” public consciousness, why would these people leave markets to their own to possibly discredit their desired stories? What good would it do to report economic growth, low interest rates, low unemployment and basically “economic and financial nirvana” if the Dow was trading at 6,000, interest rates at 7% or gold trading at $5,000 per ounce? I would suggest the “propaganda” was ramped up to unbelievable levels BECAUSE THEY HAD TO SUPPORT the picture of where markets were and are trading! I believe the “LIE” began in the markets and then had to be supported with the story, not the other way around.So there you have it, please explain why markets must be free, fair and unfettered if we know for a fact that mainstream media and government have massaged, spun and outright lied to the public in so many documented instances? If you do answer this, please do so as an adult. Do not reply saying “because” or “because they say so”.MSM, Washington and Wall Street have burned their credibility …yet people still ask why the Dow is 19,000, gold is $1,175 or the dollar still spends …? So simple a caveman could figure this one out!Standing watch and not being fooled,Bill HolterHolter-Sinclair collaborationComments welcome bholter@hotmail.com

end

Your early MONDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight

:

1 Chinese yuan vs USA dollar/yuan DOWN to 6.8836(SMALL REVALUATION NORTHBOUND /CHINA UNHAPPY TODAY CONCERNING USA DOLLAR RISE/MORE $ USA DOLLARS LEAVE CHINA/OFFSHORE YUAN NARROWS COMPLETELY TO 6.8772 / Shanghai bourse CLOSED DOWN 39.13 POINTS OR 1.21% / HANG SANG CLOSED DOWN 59.27 OR 0.26%

2. Nikkei closed DOWN 151.09 POINTS OR 1.21% /USA: YEN RISES TO 114.36

3. Europe stocks opened ALL IN THE GREEN ( /USA dollar index FALLS TO 100.65/Euro UP to 1.0697

3b Japan 10 year bond yield: RISES +.041%/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 113.01/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD FINALLY IN THE POSITIVE/BANK OF JAPAN LOSING CONTROL OF THEIR YIELD CURVE AS THEY PURCHASE ALL BONDS TO GET TO ZERO RATE!!

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 52.04 and Brent: 54.73

3f Gold DOWN/Yen DOWN

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil UP for WTI and UP for Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10 yr bund RISES TO +.341%/Italian 10 yr bond yield rises 11 full basis points to 202% from 1.91% on Friday.

3j Greek 10 year bond yield RISES to : 6.48%

3k Gold at $1168.15/silver $16.67(7:45 am est) SILVER BELOW RESISTANCE AT $18.50

3l USA vs Russian rouble; (Russian rouble UP 11/100 in roubles/dollar) 63/68-

3m oil into the 52 dollar handle for WTI and 54 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation (already upon us). This can spell financial disaster for the rest of the world/China forced to do QE!! as it lowers its yuan value to the dollar/GOT a SMALL REVALUATION UPWARD from POBC.

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 114.36 DESTROYING WHATEVER IS LEFT OF OUR YEN CARRY TRADERS

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 1.0094 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.0788 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT

3r the 10 Year German bund now POSITIVE territory with the 10 year RISES to +.345%

/German 9+ year rate BASICALLY negative%!!!

3s The Greece ELA NOW at 71.4 billion euros,AND NOW THE ECB WILL ACCEPT GREEK BONDS (WHAT A DISASTER)

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.419% early this morning. Thirty year rate at 3.09% /POLICY ERROR) GETTING DANGEROUSLY HIGH

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

(courtesy Jim Reid/Bloomberg/Deutsche bank/zero hedge)

European Stocks Soar, US Futures, Euro Jump After Failed Italian Referendum

Blink, and you missed the “sell off” from Italy’s failed referendum vote.

In the initial hours after yesterday’s vote which has cost Italy’s PM his job and ushered in a period of political limbo and potential chaos, markets were jolted by the scale of Renzi’s defeat which, as Reuters put it, “pointed to further turbulence and political crisis in the euro zone’s heavily indebted third-largest economy and particular uncertainty was focused on the country’s fragile banks.” The euro fell to a 20 month low, as low as $1.0508 and the Milan bourse shed as much as 2% while Italian bond yields spiked sharply higher.

As confirmed by the following headlines, there was a palpable sense of panic about how markets would react:

- Renzi Quits as Italy Referendum Defeat Deepens Europe’s Turmoil

- Shares of Monte Paschi, UniCredit don’t immediately set opening price, limit down

- Pop. Milano drops as much as 6%, Banco Popolare as much as 5.9%

- While ‘No’ outcome shouldn’t be major surprise, “margin of rejection and news of Renzi’s resignation will spook the markets”

- Spread on Italian government debt seen widening further when markets open, stock market down

- Italy ‘No’ a Lost Opportunity; Won’t Impact Utilities: Bernstein

- Markets to Correct on Italy Vote, EU Survival in Spotlight: Citi

And then, just before the European open, everything changed on a dime, or rather in “three minutes” as Guillermo Hernandez Sampere, head of trading at MPPM EK put it: “After Brexit, it took three days for markets to shake it off, with Trump it took three hours, with Italy it took three minutes.The fast money, who expected markets to fall further with this outcome, are now covering their positions.”

Well, maybe not exactly three minutes but, well see for yourselves: the rebound was enough to prompt questions if the ECB now has its own plunge protection team.

What happened was the following: after global stock futures slid on Sunday night, European equities shrugged off the outcome of the Italian referendum to rally the most since the U.S. election, with the Stoxx Europe 600 rising as much as 1.4% in early London. In fact, European shares soared the most since the Trump presidential victory, even as Italian banks sustained losses and the cost of insuring their bonds against default jumped. Gold erased earlier gains to head for the lowest close since February, while equity volatility indices slid in Europe and the US.

Italian financials rose 0.5 percent having fallen more than 4 percentand shares in the world’s oldest bank, Monte dei Paschi were flat on the day after being suspended at the opening.

Political risk from Italy hasn’t spread beyond its borders as markets were correctly positioned for the anti-establishment mood sweeping around the world. This was a departure from the Brexit referendum and Donald Trump’s surprise election, when traders were caught out by populist votes.

The Euro, likewise, after falling to 20 month lows, rebounded strongly, and was trading virtually unchanged from its Friday levels, as the dollar and gold sold off, while 10y Treasury futures dropped to session lows, with the March contract touching lows of 124-09+ after block trade.

To be sure, not everyone was a winner on the news associated with Italy’s political limbo, and Italian namls Banca Popolare di Milano Scarl and UniCredit SpA both slid at least 2% as the outcome of the referendum raised questions about the nation’s plans to plug holes in the banking sector. Renzi’s reforms were aimed at simplifying the legislative process in a nation that’s seen 63 governments since the end of World War II. However, even Italy’s banks seemed ready to forget anything ever happened on Sunday night and were poised to move into the green at the first possible opportunity.

Bonds remained under pressure though. Italy’s benchmark 10-year bond yield jumped 11 basis points (bps) to 2.01%, widening the premium investors demand for holding Italian bonds over safer German bonds to 175 bps, before easing slightly.

“What the market is watching for is not so much the vote itself,” but the potential fallout from a Renzi resignation, said Ric Spooner, chief market analyst in Sydney at CMC Markets Asia Pacific Ltd. Payrolls “showed an improvement in the U.S. labor market and it’s all moving in the right direction for the Fed to continue raising rates.”

This is where we stand as US traders walk in: The Stoxx Europe 600 Index climbed 1.3 percent at 10:05 a.m. in London. Italy’s FTSE MIB Index, one of the worst-performing stock indexes in the world this year, rose 0.3 percent. Futures on the S&P 500 Index were up 0.4 percent, after the underlying benchmark ended Friday up less than 0.1 percent.

Credit-default swaps on Italy jumped 14 basis points to 186 basis points, the highest since June. The cost of insuring Banca Monte dei Paschi SpA’s senior bonds against losses for five years jumped 27 basis points to 482 basis points, the highest since July, according to data compiled by CMA. Credit-default swap contracts insuring UniCredit’s senior bonds against losses rose 13 basis points to 224 basis points.

However, while there was some Italy-focused risk, 10Y Treasury yields rose two basis points to 2.40% after shedding seven basis points on Friday, as concerns about a short covering squeeze in US Treasuries quickly faded.

As a result of the price action, a favorable narrative was quickly spun: “Our base scenario is a caretaker government which could be in place before Christmas, and no new elections before 2018,” Indosuez Wealth Management chief economist Marie Owens Thomsen said. “If indeed things pan out according to our base scenario, there would be little reason for any broad-based turmoil. It is still utterly unlikely that Italy would leave the EU or the euro.”

Others jumped on the bullish bandwagon: “Rather than fretting about political risk, companies appear to be gearing up for further expansion. Employment is rising at one of the fastest rates seen over the past five years,” said Chris Williamson, chief economist at Markit.

In short, it is as if Italy’s referendum not only never happened, but was a good thing all along, and with that S&P is set to rise back to new all time highs.

Market Snapshot

- S&P 500 futures up 0.6% to 2205

- Stoxx 600 up 1.3% to 344

- FTSE 100 up 0.8% to 6788

- DAX up 1.8% to 10704

- German 10Yr yield up 3bps to 0.31%

- Italian 10Yr yield up 8bps to 1.99%

- Spanish 10Yr yield up 2bps to 1.57%

- S&P GSCI Index up 0.6% to 388.8

- MSCI Asia Pacific down 0.6% to 135

- Nikkei 225 down 0.8% to 18275

- Hang Seng down 0.3% to 22506

- Shanghai Composite down 1.2% to 3205

- S&P/ASX 200 down 0.8% to 5400

- US 10-yr yield up 2bps to 2.4%

- Dollar Index up 0.18% to 100.95

- WTI Crude futures up 0.6% to $52.00

- Brent Futures up 0.6% to $54.79

- Gold spot down 1.1% to $1,165

- Silver spot down 1% to $16.57

Bulletin Headline Summary from RanSquawk:

- European equities enter the North American crossover in positive territory despite the victory for the ‘No’ camp in the Italian referendum

- FX price action this morning has been all risk based, with the sharp comeback in equities after Italy’s referendum vote mirroring that seen in the wake of the US election result

- Looking ahead, highlights include UK and US Services PMI, ISM non-Manufacturing PMI, Fed’s Dudley, Evans, Bullard, Draghi

Top Global Headlines:

- Italy Sinks Into Political Limbo as Defeat Sweeps Renzi Away: Prime Minister Matteo Renzi announced his resignation, Finance minister cancels trip to Brussels as cabinet meets

- Trump Takes On China in Tweets on Currency, South China Sea: President-elect had been criticized after call with Taiwan, offshore yuan drops amid concern China to be named manipulator

- Trump Warns U.S. Companies Against ‘Very Expensive Mistake’

- Norwegian Surges After U.S. Approves Trans-Atlantic Expansion: Carrier’s Irish unit receives approval for U.S.- Europe routes

- Dakota Access Oil Pipeline in New Setback as U.S. Permit Denied: Analysis, exploration of alternative sites needed, Army says

- Citi Makes a Clarion Call for Commodity Bulls With 2017 View: Bank bullish on oil, copper, zinc on 6 to 12-month horizon

- Novartis CAR-T Has 82% Remission Rate in Pediatric Study

- Burberry Gains After FT Says Retailer Rejected Coach Approach

* * *

Asian stock markets, many of which were not open long enough to take advantage of Europe’s miraculous ramp, traded lower amid European political uncertainty after the Italian referendum in which PM Renzi lost and announced that he is to resign. This pressured Nikkei 225 (-0.8%) and ASX (-0.7%), alongside weakness in US equity futures. Chinese markets conformed to the negative tone with Shanghai Comp. (-1.3%) further weighed by a disappointing liquidity injection by the PBoC, while the launch of the Shenzhen-Hong Kong stock connect only briefly helped stem downside for the Hang Seng (-0.4%) and Shenzhen Comp. (-0.8%). 10yr JGBs traded higher as risk averse sentiment resulted in a flight to safety, although upside was limited after the BoJ’s buying operations were for a relatively paltry JPY 370bn of JGBs.

Top Asian News

- Billionaire Li Ka-Shing Offers $5.4 Billion for Australia’s Duet: Cheung Kong Infrastructure offers A$3 per share in cash

- Modi’s Cash Clampdown Set to Shrink India’s Key Services Sector: Nikkei Services PMI plunges to lowest since December 2013

- China Regulator Slams Leveraged Stock Acquirers as ‘Robbers’: CSRC chairman questions funding sources of some acquisitions

- New Zealand’s John Key to Step Down as Prime Minister: Key says he couldn’t commit to serving another full term

- Trump Takes On China in Tweets on Currency, South China Sea: President-elect had been criticized after call with Taiwan

- Man GLG Asia Hedge Fund Managers Walsh and Vidale Said to Leave: Departure came after April closure of a GLG Asian equity fund

- Shenzhen Opens Stock Market Up to the World, Is Little Noticed

In Europe, as noted above, it was a story of a major rebound, even as the Italian referendum has stolen the headlines so far this morning, with the week kicking off in a busy fashion. The price action seen across asset classes has been remarkably similar to that seen in the wake of the Brexit and Trump victories, with initial risk off sentiment dictating play, before a sense of calm returns to markets to see the entirety of the risk-off price action reversed. This sees equities trade firmly in the green by mid-morning, including the FTSE MIB (+0.4%). However it is worth noting that Italian banks remain the underperformers, with Unicredit lower by 4.7%. In terms of reasons behind the reversal, views vary across major banks with Nomura highlighting that the No vote was already priced in, however with the likes of Citi and MS suggesting that a correction could be seen due to political volatility in the form of the likelihood of elections and the possibility of an ‘Italexit’. Also of note BNP Paribas suggest that the ECB are less likely to announce a scaling back of QE at their meeting. Bunds opened higher this morning, before paring their opening gains and falling to see a total move of over a point, while the GE/IT spread widened this morning by approximately 6bps.

Top European News

- Aixtron Sees Slim Path to Save China Sale After Obama Order: Decision leaves door open for sale if U.S. unit is split off

- RBS Will Pay Up to $1 Billion Over 2008 Rights Issue Claims: The bank says the settlement covered by existing provisions

- $38 Billion Finnish Fund Moves Assets to U.S. as Europe Founders: Ilmarinen used to be underweight U.S. assets

- U.K. Supreme Court Brexit Hearing Moves EU Exit Decision Closer: All 11 judges to hear government case on triggering Brexit

- VW’s German Ranks Gird to Face Questions as U.S. Pursues Execs: Dozens hire lawyers as Justice Department seeks cooperators

In currencies, the euro was unchanged from Friday’s close 1.0674, paring a slump of as much as 1.5% earlier in the session. Polls show an early election in Italy would see the anti-euro Five Star Movement sweep into power. The offshore yuan lost 0.1 percent as Chinese shares declined. U.S. President-elect Trump rejected criticism of his decision to take a phone call from Taiwan’s president and reiterated concerns over China’s currency and trade policies to his 16.6 million Twitter followers. The kiwi weakened 0.6 percent as New Zealand Prime Minister John Key said he’ll stand down and backed Finance Minister Bill English to succeed him. The Bloomberg Dollar Spot Index, a gauge of the greenback against 10 major peers, jumped 0.3 percent following its first weekly retreat since Trump’s victory.

In commodities, gold swung fell 1 percent, extending a 0.5 percent decline last week that was its fourth straight weekly loss. Oil prices are also continuing higher, in line with risk sentiment, but driven by the coordinated intentions on production levels emanating from the OPEC meeting next week. Another OPEC meeting scheduled for the weekend ahead in Vienna. Base metals are also showing some modest gains in the early part of the week, with the risk on mood benefitting from growth/infrastructure spending prospects. Copper for three-month delivery rallied 1.6 percent, while zinc gained 1.8 percent and Nickel rallied 1.4 percent.

DB’s Jim Reid concludes the overnight wrap

Only one place to start this morning and that’s with the Italian referendum vote. With almost all votes accounted for, PM Renzi has formally announced defeat after a relatively wide margin of 60% versus 40% voted in favour of rejecting the reforms. Renzi has said that he will submit his resignation to Italy’s president, Sergio Mattarella, this afternoon and also said that he will not be available to lead a caretaker government. The reaction in markets has been fairly orderly so far although we may have to wait for the European open to see the full impact. The Euro is down a little over 1%, dragging a number of other European currencies with it. Equity markets in Asia are down anywhere from -0.50% to -1.50% while equity index futures are down -0.30% in the US. In rates 10y Treasury yields are just over 3bps lower.

The obvious question now is what next? Well clearly the immediate risk is political instability. We’ll refer back to DB’s Marco Stringa’s report from last week where he highlighted that the short term tail risk is an immediate election (not his base case but perhaps a higher risk with the large no vote yesterday). The trigger would be failure to form a new government due to unbridgeable divisions among traditional parties. A failure to find a compromise on a new electoral law could also have a similar impact but with a longer time horizon. All eyes would be on the banking sector in such a scenario and if a solution wasn’t found then stress could eclipse July 2016 levels. Marco’s central case is that a new government supported by a similar parliamentary majority to the current one, with a narrow objective – writing a new electoral law – and limited duration will be formed. This muddle through scenario means that Italy’s economy will continue to perform poorly in both absolute and relative terms and over the medium term there will have to been a convergence to either pro-reform government or a euro-sceptic government. So this is only the beginning of a long path ahead for Italy but expect swift political manoeuvrings this week as the country will need to try to find a solution quickly.

The other populist test this weekend was the Austria presidential election where the Green party backed independent candidate, Alexander Van der Bellen, came out on top versus the far right Freedom party candidate, Nobert Hofer, by a score of 53.3% to 46.7%. Hofer has since conceded defeat. As our economists highlight, despite this result, Austria still faces a complex political outlook. First, the populist FPO party is leading in the opinion polls by about 8pp and it will be interesting to see whether Hofer’s defeat narrows this lead. They note that at the moment, the FPO is heading towards the late 2018 parliamentary election in a position of strength. Secondly, Chancellor Kern, sitting atop a mainstream coalition of SPO/OVP, is struggling with his reforms. He rules out early elections, but there is nevertheless a non-negligible risk that his government collapses already in 2017, giving a second opportunity to test support for populism in Austria. For example, the longer the muddling-through of the grand coalition last and the stronger their underperformance in the polls, the more likely there will be an early election.

Continuing with the politics theme, the remaining weekend newsflow is focused on the latest round of comments from President-elect Trump. In a social media posting, Trump warned of heavy import tax tariffs for US companies moving production overseas and selling back into the US, suggesting a possible 35% tariff for those companies that do. Clearly the statement is pretty ambiguous for now and throws open a whole wide range of questions particularly for businesses with multiple entities and so forth. A wider question also might be how other countries respond to such possible tariffs. One to keep an eye on.

Switching over to this week’s main event, that being the ECB meeting this Thursday. As a base case our European economists expect the ECB to announce a 6-month extension of the current €80bn QE programme (an extension from March 2017 to September 2017). This is likely to be complemented by a move to improve the supply of eligible bonds, perhaps by the removal or softening of the yield floor. This would facilitate a steeper yield curve and incentive transmission. In an alternative scenario our economists believe that the market would react negatively to say a slowing in the pace of purchases to €60bn. Indeed our economists have derived three rules that need to be satisfied by spot and forward core inflation in order for the ECB to taper. The soonest these are likely to be satisfied is mid-2017. They go on to highlight that if the ECB’s above-consensus view on growth is correct, the euro exchange rate depreciates in line with DB’s house view and systematic financial crisis is avoided, tapering could be announced in June 2017. On the other hand if their below-consensus view on growth is correct and the growth/inflation relationship is weak, tapering could wait until end-2017. The last thing to note is today’s market reaction to the referendum result which also has the potential to influence Thursday’s meeting actions.

Wrapping up the rest of the markets in Asia this morning where the other focus in FX has been on the New Zealand Dollar which is down close to 1% following the unexpected resignation of the country’s Prime Minister, John Key. The PM has since backed his deputy for the role and said that he is stepping down for personal reasons. There’s also been a bit of data out of China this morning. The Caixin services PMI was reported as rising 0.7pts to 53.1 in November which is the highest level since July 2015. Combined with a weaker manufacturing reading however, the composite has held steady at 52.9.

A quick recap now of how we closed out Friday. For those that missed it, the focus in what was an otherwise fairly quiet session ahead of the weekend events, was on the US November employment report. In a nutshell it was a fairly mixed batch of data. The headline nonfarm payrolls gain of 178k pretty much matched expectations (180k) while cumulative net revisions amounted to a modest -2k drop. Most noteworthy was the unexpected drop in the unemployment rate from 4.9% to 4.6% (vs. 4.9% expected) and to the lowest level since August 2007. The broader U-6 measure also dipped two-tenths to 9.3% and to the lowest since April 2008. The interesting take on this came with the fact that the unemployment rate dipped as the labour force participation rate dropped one-tenth to 62.7%. Meanwhile the other interesting take away was the softness in average hourly earnings (-0.1% mom vs. +0.2% expected). It was actually the first monthly decline in earnings since December 2014 and had the effect of lowering the YoY rate to +2.5% from +2.8%.

Onto this week’s calendar now. This morning in Europe we’re kicking off the week with the remainder of the November PMI’s which includes the final services and composite revisions for the Euro area, Germany and France, as well as a first look at the data for the UK and non-core. Euro area retail sales data for the month of October is also out today. In the US this afternoon we’ll also get the remaining PMI’s as well as the ISM non-manufacturing print for November and labour market conditions index. Tuesday kicks off in Germany with the latest factory orders data before we then get the final Q3 GDP reading for the Euro area. In the US tomorrow we’ll get the October trade balance reading, Q3 unit labour costs and nonfarm productivity, October factory orders, December IBD/TIPP economic optimism reading and the final durable and capital goods orders revisions. Germany gets things going again on Wednesday when we’ll get the latest industrial production report. French trade data and UK industrial and manufacturing production will also be released. The only data due out in the US on Wednesday is JOLTS job openings and consumer credit for October. China will also release November foreign reserves data at some stage. The early data to get things going on Thursday comes from Japan where the final Q3 GDP reading will be released. China will then be following with important November trade data. There’s no data in Europe on Thursday but all eyes will be on the main event of the week, the ECB policy meeting outcome just after midday. The only data out of the US on Thursday will be initial jobless claims. We close out the week in Asia on Friday with the November CPI and PPI prints in China. In Europe we’ll get trade data in Germany, industrial production data in France and trade data in the UK. Over in the US we’ll get the final October wholesale inventories report along with a first look at the University of Michigan consumer sentiment report. Away from the data the Fedspeak this week all comes today with Dudley, Evans and Bullard scheduled.

end

3.REPORT ON JAPAN SOUTH KOREA NORTH KOREA AND CHINA

i)Late SUNDAY night/MONDAY morning: Shanghai closed DOWN 29.13 POINTS OR 1.21%/ /Hang Sang closed DOWN 59.27 OR 0.26%. The Nikkei closed DOWN 151.09 OR 0.82%/Australia’s all ordinaires CLOSED DOWN 0.81% /Chinese yuan (ONSHORE) closed UP at 6.8836/Oil ROSE to 52.04 dollars per barrel for WTI and 54.73 for Brent. Stocks in Europe: ALL IN THE GREEN. Offshore yuan trades 6.8772 yuan to the dollar vs 6.8836 for onshore yuan.THE SPREAD BETWEEN ONSHORE AND OFFSHORE NARROWS HUGELY AGAIN AS CHINA ATTEMPTS TO STOP MORE USA DOLLARS LEAVING CHINA’S SHORES / CHINA SENDS A CLEAR MESSAGE TO THE USA AND JANET TO NOT RAISE RATES IN DECEMBER.

3a)THAILAND/SOUTH KOREA/:

b) REPORT ON JAPAN

The collapsing yen!!:

(courtesy Graham Summers/Phoenix Research Capital)

Is the Bank of Japan TRYING to Crash the Markets?

Is the Bank of Japan is trying to crash the markets?

This is not conspiracy theory. In the last month the BoJ has devalued the Yen 14% against the $USD.

By any other measure this is a crash as far as currencies go. And it could lead to MAJOR issues for the financial system.

The last time the BoJ collapsed the Yen this aggressively the ENTIRE commodity markets imploded collapsing over 40%. Oil ended up collapsing from $60 to sub $48 in a matter of weeks.

Eventually this mess spilled over into stocks with China being forced to devalue the Yuan and the S&P 500 Crashing 10% in a few days as a result.

Here’s the Yen/$USD pair today with the S&P 500 (blue line)… this could get VERY ugly VERY fast.

Another Crisis is brewing… the time to prepare is now.

http://phoenixcapitalmarketing.com/Prepare1.html

Best Regards

Graham Summers

Chief Market Strategist

Phoenix Capital Research

end

c) Report on CHINA

China is now rethinking investing in USA real estate. There is no doubt that China is worried about their rapidly sinking foreign exchange reserve of USA dollars. No doubt it is better to buy USA gold than USA properties

(courtesy zero hedge)

Chinese Developers Rethink U.S. Real Estate Projects: “I See Danger…U.S. Real Estate Is Peaking”

For months we’ve been warning that real estate markets in NYC and San Francisco, among others, are getting ready to rollover as the market is about to be flooded with new supply of luxury apartments (see here and here). Real estate in both markets are just starting to show signs of cracking as the apartments sales cycle is getting stretched out and pricing growth has stalled.

Now, per an article from the Wall Street Journal, wealthy Chinese real estate investors are admitting that the jig is up in large cities like New York and are running for the hills. With a substantial amount of capacity expected to come online over the next several quarters and a growth cycle that is entering its 8th year, one Chinese real estate investor admits “you get a sense now that it’s peaking.”

Swelling supply of high-end New York condominiums could result in losses for some Chinese developers, analysts said. A push to partner with U.S. developers on other projects, meanwhile, has brought unexpected legal spats and other delays.

“I see a danger in the real-estate market in the U.S.,”said John Liang, Xinyuan Real Estate’s managing director of U.S. operations. “With its seven- to eight-year cycle, you get a sense now that it’s peaking.” He added that he sees value in middle-tier residential properties in Manhattan and Queens.

“Right now the prices are really high,” said Zhang Xin, chief executive of Soho China, whose family invested in a stake in Manhattan’s General Motors Building in 2013. “I would be very cautious if I were to make a large investment in New York’s real estate today.”

Of course, Manhattan isn’t the only Burrough experiencing a supply glut. Forest City Realty was just forced to take a $300mm impairment charge on a joint venture with a Shanghai-based development company after “unprecedented rental supply in downtown Brooklyn” forced the copanies to delay development.

CL Investment, which has three other high-end residential projects in Manhattan, plans to keep the office space as part of efforts to diversify, according to a person with knowledge of the matter.

In Brooklyn, N.Y., a deal between Shanghai-based, state-owned conglomerate Greenland Holding Group and Forest City Realty Trust on a 22-acre, 15-building mixed-use project in various stages of construction is facing stiff headwinds.

Forest City earlier this month said it took a $307.6 million impairment charge for the project, called Pacific Park Brooklyn, and said it plans “to delay future vertical development.”

“We revised the schedule due to a number of factors,including almost unprecedented concentrations of new rental supply in downtown Brooklyn, which will take time for the market to absorb,” said Forest City CEO David LaRue.

Just to add insult to injury, the softening real estate market is coming just as China is once again looking to tighten rules on capital investments outside of China.

The headwinds come at a time when Beijing once again is planning to tighten its rules on Chinese investment capital leaving the country.

The Chinese State Council is expected to soon announce new reviews of foreign acquisitions of $10 billion or more and property investments by state-owned firms of more than $1 billion, according to people with direct knowledge of the matter and documents reviewed by The Wall Street Journal.

Total Chinese direct investment in U.S. real-estate and hospitality assets is nearly $12.6 billion, accounting for nearly a fifth of total Chinese investment in the U.S.since 1990, according to a recent report from the Rhodium Group and the National Committee on U.S.-China Relations. Most of the activity has taken place since 2010 and is concentrated in areas such as New York, Los Angeles and San Francisco.

Of course, no matter what kind of capital controls are put in place, just like the Vancouver and Sydney real estate markets, we suspect that when Chinese money needs to be laundered, people will find a way. The only question is now that yet another bubble has run its course, where subsequent bubbles will emerge.

* * *

For those who missed it, below is what we recently wrote after 3Q16 apartment closings plunged 18.6% in NYC.

New York City apartment owners should take note of the latest 3Q16 “Elliman Report” on Manhattan real estate sales because the market looks to be in free fall. In fact, the number of apartment closings plunged 18.6% YoY while apartments sat on the market an average of 8.2% longer. Inventory also spiked with re-sale inventory up 8.2% YoY and new development inventory up a massive 27.2%.

“The number of re-sales has fallen year over year in each of the last four quarters at an increasing rate. Listing inventory reflected significant differences in the rate of growth between re-sale and new development. Re-sale inventory expanded 8.2% to 5,290 while new development inventory surged 27.2% to 973 respectively from the same period a year ago.“

Median sales prices did increase YoY by 7.6% but collapsed QoQ despite a massive surge in pricing on the luxury end of the market.

The re-sale market looks even more bleak, on a standalone basis, as the overall numbers above are skewed by sales of super-luxury new development units. The number of re-sale closings collapsed over 20% YoY while days on the market increased 7.5%

All segments of the market exhibited volume weakness with co-op sales down 17.1% YoY on a 14.1% increase in listing days and a modest 1.4% increase in median sales price.

Condo sales declined 20.1% YoY on a 2.4% increase in listing days and a 6.7% increase in median sales price. Meanwhile, condo inventory rose over 15%.

And, of course, the luxury market seemed to hold up the best in 3Q with volumes still weak at -18.6% but median pricing up 23.9% and listing inventory down YoY.

In conclusion, the lesson seems to be that the marginal New York City buyer has been priced out of the market (volume down 20%) while sellers have not yet accepted that the bubble has burst deciding instead to maintain listing prices while letting their apartments sit on the market longer amid growing inventory levels. Meanwhile, the luxury market is the only segment that seems to be holding up which only serves to prove that Chinese billionaires still have cash they would like to hide in the U.S.

end

4 EUROPEAN AFFAIRS

Italy

Renzi loses the Italian referendum by a wide margin:

(courtesy zero hedge)

Renzi Loses Italian Referendum By Wide Margin; “Northern League” Calls For Early Elections

Update #3: First Projections confirm exit polls – wide margin of victory for “no” defeat for Renzi…

* * *

Update #2: Following the exit polls and the market’s response, “Northern League” leader Salvini has called for early elections:

- SALVINI: NO VICTORY WOULD MEAN PEOPLE DEFEATING ESTABLISHMENT

- ITALY NORTHERN LEAGUE LEADER CALLS FOR EARLY ELECTIONS: MNI

* * *

Update #1: The Exit polls have begun:

- *ITALY REFERENDUM: ‘NO’ AT 55%-59% IN EMG EXIT POLL

- *ITALY REFERENDUM: ‘NO’ AT 55%-59% IN TECNE EXIT POLL

- *ITALY REFERENDUM: ‘NO’ AT 54%-58% IN RAI EXIT POLL

Exit polls have at times proved unreliable in Italy, underestimating Renzi’s 2014 victory in European elections by 10 percentage points, but for now, the market seems convinced…

EURUSD is tumbling…

Some comments from anti-establishmentarians have begin:

- LE PEN AIDE ON ITALIAN REFERENDUM RESULT TWEETS ‘IT’S A GREAT VICTORY FOR THE PEOPLE…IT’S FOR OTHER NATIONS TO BE SET FREE’

Hope the exit polls in Italy are right. This vote looks to me to be more about the Euro than constitutional change.

Turnout was high.

- *ITALY REFERENDUM: ITALIANS ABROAD TURNOUT 30.9%:FOREIGN OFFICE

So what happens next?We leave it to Doug Casey to sum it all up succinctly:

December 4 referendum fails >> M5S comes to power >> Italians vote to leave the euro currency >> European Union collapses

How did we get here? Here’s a quick timeline from Bloomberg’s Marco Bertacche

- April 15, 2014: The Senate approves first version of reform, backed by Renzi allies and Berlusconi’s party

- Jan. 31, 2015: Renzi’s candidate is elected president of the republic, prompting Berlusconi to withdraw support for reforms

- April 12, 2016: Lower house completes approval, lacking two-thirds majority needed to avoid referendum

- Aug. 4, 2016: Highest court accepts referendum request with more than 500,000 signatures from Yes campaign

- Sept. 26, 2016: Renzi’s cabinet calls for Dec. 4 referendum. Decision is binding

* * *