Gold at (1:30 am est) $1175.00 up $7.40

silver at $17.20: up 46 cents

Access market prices:

Gold: 1174.10

Silver: 17.15

THE DAILY GOLD FIX REPORT FROM SHANGHAI AND LONDON

.

The Shanghai fix is at 10:15 pm est last night and 2:15 am est early this morning

The fix for London is at 5:30 am est (first fix) and 10 am est (second fix)

Thus Shanghai’s second fix corresponds to 195 minutes before London’s first fix.

And now the fix recordings:

WEDNESDAY gold fix Shanghai

Shanghai morning fix Dec 7 (10:15 pm est last night): $ 1193.75

NY ACCESS PRICE: $1169.30 (AT THE EXACT SAME TIME)/premium $24.45

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Shanghai afternoon fix: 2: 15 am est (second fix/early morning):$ 1194.69

NY ACCESS PRICE: 1168.40 (AT THE EXACT SAME TIME/2:15 am)

HUGE SPREAD 2ND FIX TODAY!!: $26.29

China rejects NY pricing of gold as a fraud

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

London Fix: Dec 7: 5:30 am est: $1171.25 (NY: same time: $1171.95 5:30AM)

London Second fix Dec 7: 10 am est: $1177.65 (NY same time: $1178.70 10 AM)

It seems that Shanghai pricing is higher than the other two , (NY and London). The spread has been occurring on a regular basis and thus I expect to see arbitrage happening as investors buy the lower priced NY gold and sell to China at the higher price. This should drain the comex.

Also why would mining companies hand in their gold to the comex and receive constantly lower prices. They would be open to lawsuits if they knowingly continue to supply the comex despite the fact that they could be receiving higher prices in Shanghai.

end

For comex gold:

NOTICES FILINGS FOR DECEMBER CONTRACT MONTH: 16 NOTICE(S) FOR 1600 OZ. TOTAL NOTICES SO FAR: 8388 FOR 838,800 OZ (26.09 TONNES)

For silver:

NOTICES FOR DECEMBER CONTRACT MONTH FOR SILVER: 3 NOTICE(s) OR 15,000 OZ. TOTAL NUMBER OF NOTICES FILED SO FAR; 1524 FOR 7,620,000 OZ

Let us have a look at the data for today

.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total open interest FELL by 529 contracts DOWN to 159,337 with respect to YESTERDAY’S trading. In ounces, the OI is still represented by just less THAN 1 BILLION oz i.e. .796 BILLION TO BE EXACT or 114% of annual global silver production (ex Russia & ex China).

FOR THE DECEMBER FRONT MONTH: 3 NOTICES FILED FOR 15,000 OZ.

In gold, the total comex gold FELL by 1170 contracts WITH THE FALL IN THE PRICE GOLD ($6.40 with YESTERDAY’S trading ).The total gold OI stands at 393,524 contracts. The bankers have done a good job of eviscerating gold (and silver) longs. We are very close to the bottom with respect to OI. Generally 390,000 should do it.

we had a 16 notices filed upon for 1600 oz of gold.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD:

We had another huge change in tonnes of gold at the GLD, a massive withdrawal of 6.23 tonnes of gold and this gold is heading toward Shanghai

Inventory rests tonight: 863.67 tonnes

.

SLV

we no changes in silver inventory tonight

THE SLV Inventory rests at: 345.955 million oz

.

First, here is an outline of what will be discussed tonight: Preliminary data

1. Today, we had the open interest in silver FELL by 529 contracts DOWN to 159,337 as the price of silver FELL by $.08 with YESTERDAY’S trading. The gold open interest FELL by 1170 contracts DOWN to 393,524 as the price of gold FELL BY $6.40 WITH YESTERDAY’S TRADING.

(report Harvey).

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)Late TUESDAY night/WEDNESDAY morning: Shanghai closed UP 22.59 POINTS OR 0.71%/ /Hang Sang closed UP 125.77 OR 0.55%. The Nikkei closed UP 136.75 OR 0.74%/Australia’s all ordinaires CLOSED UP 0.89% /Chinese yuan (ONSHORE) closed DOWN at 6.8800/Oil ROSE to 50.96 dollars per barrel for WTI and 53.80 for Brent. Stocks in Europe: ALL IN THE GREEN. Offshore yuan trades 6.90321 yuan to the dollar vs 6.8800 for onshore yuan.THE SPREAD BETWEEN ONSHORE AND OFFSHORE WIDENS AGAIN AS MORE USA DOLLARS LEAVING CHINA’S SHORES / CHINA SENDS A CLEAR MESSAGE TO THE USA AND JANET TO NOT RAISE RATES IN DECEMBER.

REPORT ON JAPAN SOUTH KOREA NORTH KOREA AND CHINA

3a)THAILAND/SOUTH KOREA

none today

b) REPORT ON JAPAN

none today

c) REPORT ON CHINA

i)A huge commentary: This will no doubt be a black swan as Chinese official reserves (including FX changes) drops 69 billion USA, the biggest drop since last January. The new official reserves are 3.05 trillion and the part that is alarming is that the Chinese authorities are claiming the loss of dollars is starting to cause problems with the businesses and the issuance of dividends etc.

( zero hedge)

( zero hedge)

4 EUROPEAN AFFAIRS

i)Italy/Monte de Paschi

The fun begins: The Italian government prepares to nationalize Monte de Paschi.

Monte needs 5 billion euros by the end of December and if they cannot get it, they will be toast. For the Italian government is coming to the rescue to the tune of 2 billion euros out of 5 billion needed or 40% of the new company. The existing shareholders are now toast. The fun begins as the government will buy the junior bonds at face value and leave the senior bonds alone and not buying their notes. That should set a showdown in bankruptcy court. Then we have the new bail in rules which suggests that all holders, bond holders, equity holders and depositors must share in the loss and not taxpayers which is must Germany has been demanding . However they have problems with Deutsche bank and they will need a rescue. That is why I stated earlier today that the rescue of Monte de Paschi will no doubt cause contagion effects all over the place.

(courtesy zero hedge)

ii)Renzi resigns today after the approval of the budget bill. This may precipitate early elections:

( zero hedge)

iii)This ought to hurt: Moody’s has cut Italy’s senior unsecured government debt rating from stable to negative but leaving it at Baa2 for now. I guess that they are concerned with the Italian banks health.

(courtesy zero hedge)

iv)France:

A good snapshot as to what is happening on the ground in France today:

(courtesy Yes Mamou/Gatestone Institute)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

6.GLOBAL ISSUES

India

Modi was counting on 5 trillion of the total 15 trillion rupees outstanding would remain undeclared due to tax invasion. He was wrong. Already 82% of rupees have been deposited.

Today’s data shows a complete collapse in their composite PMI. Their economy is now in shambles and Modi has nothing to show for his stupid and senseless demonetization.

what a doorknob..

( zero hedge)

7. OIL ISSUES

i)The truth in oil production and why OPEC cheating will cap oil at 52.00 dollars . No doubt that oil will be heading southbound

( Nick Cunningham/Oil Price.com)

ii)Crude finally falls on news of the huge Cushing buildup

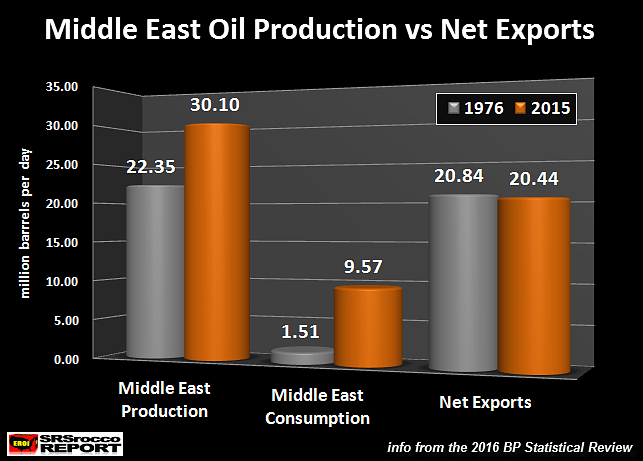

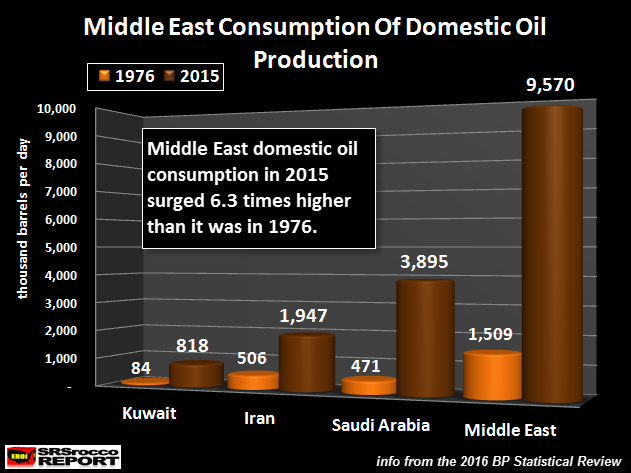

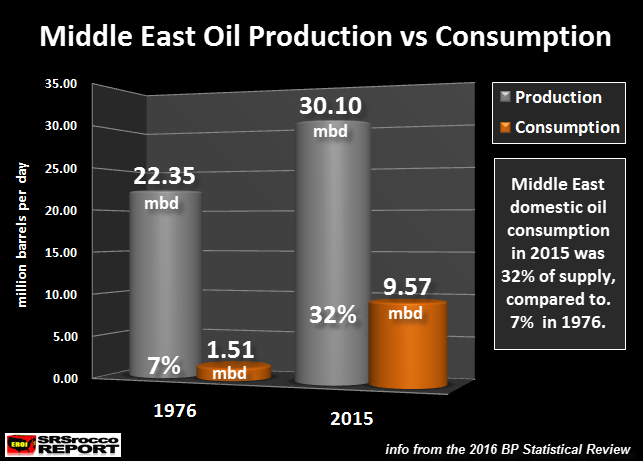

iii)I will bet that you did not know that Middle east countries have been consuming a lot more of their production? Guess again

8. EMERGING MARKETS

none today

9. PHYSICAL MARKETS

i)Position limits are now off the table on oil and gold and other commodities.They will leave it to the new administration and I am happy about that

( Wall Street Journal/GATA)

ii)The following is quite an understatement: “governments and the financial press falsify economic conditions”:

John Embry…

iii)Quite a report: Market rigging is striving to save a disintegrating Europe?

(the King report/GATA)

iv)These three kingpins are getting off lightly for rigging Euribor: HSBC, JPMorgan and Credit Agricole

( London’s Financial Times)

v)I warned you many times that this was happening in the settling process: gold in London and Hong Kong is used to settle upon comex contracts and that is why it takes so long to settle as they must wait for the gold to come:

(courtesy Koos Jansen/GATA)

10.USA STORIES

i)Continuing with our story from yesterday, the Mayor of Dallas has filed a lawsuit to block withdrawals from the Dallas police and firefighter pension fund. This is in response to a huge run on the bank in November and December. There have been huge contributions to the fund because of the guaranteed 8% return on their investment. Now the funds are fleeing. Will this be the first of many Ponzi schemes to go bust?

( zero hedge)

ii)Trump is on a roll: The huge electronic manufacturer Foxconn says it is in discussions to expand its USA operations. Foxconn chief and Softbank CEO Son are very close friends and this may be part of the 50 billion USA dollar investment talked about yesterday.

( zero hedge)

iii)Now Trump is on the warpath on pharmaceutical companies. It is going to bring drug prices down

(courtesy zero hedge)

iv) Janet’s favourite labour report is the JOLTS report which is simply hirings, firings and quits. If you study the data it sure looks like the job market is rolling over in the USA

(courtesy zero hedge/JOLTS)

v)A good choice for USA ambassador to China in the choosing of Iowa Governor Branstad . Iowa is the biggest producer of soybeans, corn and pigs and the state is the biggest exporter of the first two items to China. However the governor will have his work cut out for him on the dumping of steel and other products into the uSA

( zero hedge)

vi)This is an interesting choice: Oklahoma’s Attorney General Scott Pruitt who spent half his time suing the EPA is going to head it:

(courtesy zero hedge)

Let us head over to the comex:

.

The total gold comex open interest FELL BY 1170 CONTRACTS to an OI level of 393,524 AS THE PRICE OF GOLD FELL $6.40 with YESTERDAY’S trading. We are now in the contract month of December and it is the biggest of the year. Here the front month of December showed a DECREASE of 127 contracts DOWN to 1,463.We had 37 notices served upon yesterday so we lost another 90 contracts or 9000 oz will not stand for delivery and no doubt these were paper settled.

For the next delivery month of January we had a LOSS of 13 contracts DOWN to 2559. For the next big active delivery month of February we had a LOSS of 1977 contracts down to 269,789.

We had 16 notices filed upon today for 1600 oz

And now for the wild silver comex results. Total silver OI FELL by 529 contracts FROM 159,866 DOWN TO 159,337 as the price of silver FELL BY $0.08 with YESTERDAY’S trading. We are moving further from the all time record high for silver open interest set on Wednesday August 3/2016: (224,540). We are now in the next major delivery month of December and here it FELL BY 144 contracts DOWN to 1844 CONTRACTS . We had 52 notices served upon yesterday so we lost 92 contracts or an additional 460,000 oz will not stand for delivery.

The next non active delivery month is January and here the OI fell by 476 contracts down to 2665. This level seems highly elevated. Maybe we are going to see the same huge metals gains in silver as we have witnessed in gold.

The next big active delivery month is March and here the OI FELL by 3 contracts DOWN to 129,501 contracts.

We had 3 notices filed for 15,000 oz for the December contract.

Eventually at the end of December 2015: 6.4512 tonnes of gold stood for delivery

Eventually at the end of December 2015: 18.84 million oz of silver stood for delivery

VOLUMES: for the gold comex

Today the estimated volume was 138,226 contracts which is poor.

Friday’s confirmed volume was 146,975 contracts which is fair- to poor

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz |

34,547.075 oz

Scotia

|

| Deposits to the Dealer Inventory in oz | nil oz |

| Deposits to the Customer Inventory, in oz |

51,910.665 oz

Scotia

|

| No of oz served (contracts) today |

16 notices

1600 oz

|

| No of oz to be served (notices) |

1447 contracts

144,700 oz

|

| Total monthly oz gold served (contracts) so far this month |

8388 notices

838,800 oz

26.09 tonnes

|

| Total accumulative withdrawals of gold from the Dealers inventory this month | nil oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | 3,497,880.9 oz |

For December:

Today, 1 notice(s) were issued from JPMorgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equates to 16 contract(s) of which 0 notices were stopped (received) by jPMorgan dealer and 0 notice(s) was (were) stopped/ Received) by jPMorgan customer account.

March 2015: 2.311 tonnes (March is a non delivery month)

| Silver | Ounces |

| Withdrawals from Dealers Inventory | nil |

| Withdrawals from Customer Inventory |

434,345.109 oz

SCOTIA,

Brinks

|

| Deposits to the Dealer Inventory |

nil OZ

|

| Deposits to the Customer Inventory |

902,363.109 oz

jpm

scotia

|

| No of oz served today (contracts) |

3 CONTRACT(S)

(15,000 OZ)

|

| No of oz to be served (notices) |

1841 contracts

(9,205,000 oz)

|

| Total monthly oz silver served (contracts) | 1524 contracts (7,620,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month | 1,500,437.8 oz |

end

end

NPV for Sprott and Central Fund of Canada

end

Major gold/silver stories for WEDNESDAY

GOLDCORE/BLOG/MARK O’BYRNE

Buy Silver – May Replace Gold As Money In India

Buy Silver – May Replace Gold as Preferred Money of India

Silver replacing gold as India’s preferred investment option again after 100 years?

by Fergal O’Connor, Senior Lecturer in Finance, University of York

The Indian government has been trying to reduce its citizens’ demand for imported gold through a number of means over the last few years. This is part of a wider crackdown on currency used in the black market, that included the withdrawal and replacement of its two largest-denomination bank notes in early November. The strategy will likely have some unintended consequences if we take our cues from the events of 1910.

Growth in Indian gold and silver jewellery demand. Thomson Reuters GFMS Gold 2016 and Silver Survey 2016

Growth in Indian gold and silver jewellery demand. Thomson Reuters GFMS Gold 2016 and Silver Survey 2016

Indians’ famous love for gold has created serious and ongoing economic issues for the nation. In 2011, Australian investment bank Macquarie estimated that 78% of India’s household savings were held in gold.

In effect, this means that India has a dual currency system where people choose to save mostly in gold rather than rupees. This is unlike any other major economy and begs the question: how do you wean a population off a precious metal?

Bling and buy sale

Building up savings in gold rather than deposits in a bank creates a permanent drag on India’s growth. This happens because the savings do not increase the available funds for lending within the banking system. One reason it is so difficult to put this gold to work as investment capital is that 79% of it is bought as jewellery, rather than bars or coins.

Australian 2017 Silver Bullion Coin (1oz) now in stock

Australian 2017 Silver Bullion Coin (1oz) now in stock

India is the world’s largest consumer of gold jewellery at nearly 700 tonnes in 2015 according to the GFMS Gold Survey 2016. However, it mines less than two tonnes of gold a year. This means India must import gold worth US$25 billion each year, pushing up its current account deficit and pulling down the value of the rupee.

In 2015, prime minister Narendra Modi’s government introduced a Sovereign Gold Bond scheme which allowed gold holders to swap their gold for an interest-bearing bond. At the end of the bond’s life investors would effectively be returned the same amount of gold. This move reduced the minimum amount of gold necessary to participate in such a scheme to two grams. As of November 2016, 14 tonnes of gold had been subscribed to the two gold bond issues, with another five tonnes collected through the older gold monetisation scheme (which has a larger minimum deposit of 30 grams).

However, relative to India’s estimated privately held gold stock of 20,000 tonnes, these deposits represent tiny amounts and it still doesn’t seem like a solution.

Unintended consequences

An alternative would be to permanently reduce gold imports. To that end, in 2013, the government started to increase import taxes on gold imports to 6%; this now stands at 10%. However, falling gold prices during that period meant that there was still a 12% increase in gold imports in 2015 as consumers snapped up what they saw as bargain prices.

And here is where we go back more than 100 years to see how this all worked out last time. You see, India has battled precious metals imports for quite some time. In 1910 the government of India increased the import tariffs on silver from 5% to 11%. A market report in 1912, by Pixley & Abell, a gold wholesaler, pointed to a 28% fall in silver demand in the Indian bazaars in the three years following the increase. They attributed this to not just a fall in demand for silver due to tax increases, but also a substitution of gold for silver in people’s savings as gold became more attractive on a relative basis.

Between 1910 and 1930 net imports of silver in India fell from 98m ounces to 31m, according to British Geological Survey reports. After this time India gradually became the world’s largest gold consumer, a position it finally lost to China in 2015.

And it seems a return to silver as a major investment for consumers in India may be on the cards. Following the recent import tax hikes for gold, 2015 saw Indian silver imports grow to almost 8,000 tonnes, 14% up on the previous 2014 record. At the same time, demand for gold jewellery, which accounts for 75% of all Indian gold demand, is down 30% for the 12 months to the end of September 2016, according to the World Gold Council. This points to a possible shift back to silver as a more prominent investment in India.

Gold makes up the vast majority of Indian jewellery sales. But the graph below shows the rapid growth in silver jewellery demand in India, which is up over 600% in ten years, relative to marginal growth of only 25% in gold jewellery demand.

Of course silver is not the only precious metal investment option available. If investors want a more compact form of wealth, then platinum, worth 56 times more per ounce, might suit. But a swap to silver in India, as was the norm pre-World War I, seems more likely and could have a major effect on prices. For a sense of scale, the Indian gold jewellery market in 2015 was worth US$25 billion, while the total world silver jewellery market was worth only US$3.5 billion.

Conclusion

Even a small substitution from gold to silver would result in a massive increase in the price of silver. A 10% reallocation from gold jewellery investment to silver in India would nearly double world silver jewellery demand. Mines and other sources would not be able to fill the gap immediately; prices would rise, further fuelling demand and creating a new, shiny headache for those trying to marshal India’s unusual economy.

This article was originally published on The Conversation. Read the original article.

Gold and Silver Bullion – News and Commentary

Gold down on US rate hike expectations; ECB meeting in focus (MoneyControl.com)

Gold prices gain slightly in Asia with demand forces in focus (Investing.com)

Trade Deficit in U.S. Widened to a Four-Month High in October (Bloomberg.com)

UK manufacturing slides, as Italian bank rescue hopes build – business live (TheGuardian.com)

America’s relationship with China could get frosty under Trump (MoneyWeek.com)

Fake News = Fake Markets… (GoldSeek.com)

Market rigging strives to save disintegrating Europe (TheKingReport.com)

From Hot to Not, Investors Exit Gold Funds in Switch to Equities (Bloomberg.com)

Gold appetite hit a 5-year high in November as prices tumbled (MarketWatch.com)

Gold Prices (LBMA AM)

07 Dec: USD 1,171.25, GBP 929.62 & EUR 1,092.19 per ounce

06 Dec: USD 1,171.15, GBP 918.18 & EUR 1,086.94 per ounce

05 Dec: USD 1,164.90, GBP 915.84 & EUR 1,095.36 per ounce

02 Dec: USD 1,171.65, GBP 929.00 & EUR 1,100.88 per ounce

01 Dec: USD 1,168.75, GBP 930.09 & EUR 1,099.68 per ounce

30 Nov: USD 1,187.40, GBP 952.06 & EUR 1,115.44 per ounce

29 Nov: USD 1,187.30, GBP 952.45 & EUR 1,119.98 per ounce

Silver Prices (LBMA)

07 Dec: USD 16.77, GBP 13.32 & EUR 15.64 per ounce

06 Dec: USD 16.79, GBP 13.17 & EUR 15.63 per ounce

05 Dec: USD 16.62, GBP 13.05 & EUR 15.54 per ounce

02 Dec: USD 16.35, GBP 12.95 & EUR 15.36 per ounce

01 Dec: USD 16.30, GBP 12.91 & EUR 15.35 per ounce

30 Nov: USD 16.67, GBP 13.39 & EUR 15.66 per ounce

29 Nov: USD 16.54, GBP 13.26 & EUR 15.61 per ounce

Recent Market Updates

– Shariah Gold Standard Approved for $2 Trillion Islamic Finance Market

– Potential “Systemic Crisis In Eurozone” After Italy Votes No, Renzi Resigns

– Gold and Silver Will Protect From Coming Financial Crash – Rickards

– RBS Fail Bank of England Stress Test

– Peak Silver – Supply Deficits Mean Higher Prices

– Bail In Risk – €4 Trillion Banking System In Italy Poses Contagion Risk as Referendum Looms

– Gold Down 13.5% In 13 Days – Trump Bearish For Gold?

– War On Cash Just Got Real – India and Citibank In Australia

– Russia Gold Buying In October Is Biggest Monthly Allocation Since 1998

– Stocks, Bonds, Pension Funds “Will Be Wiped Out…” – Rickards

– Physical Gold Is A “Long-Term Position” as “Hedge Against Governments”

– Gold Sell Off On Fed Noise – “Interesting Times” To “Support Gold”

– Islamic Gold – Vital New Dynamic In Physical Gold Market

-END-

Gold/silver trading early this morning:

Gold & Silver Spike, Erase Italy Vote Losses

After puking over $30 from post-Italy vote highs, gold prices are jumping this morning and have erased the losses. Silver is soaring, breaking back above $17, well above pre-Italy levels…

As Bloomberg notes, some analysts aren’t convinced the rally is over.

More infrastructure spending in the U.S. and low global interest rates may accelerate the pace of inflation, which would renew demand for gold as an alternative asset, Commerzbank AG analysts led by Eugen Weinberg, wrote in a note dated Dec. 2.

Gold may rise to $1,300 in the fourth quarter of 2017 and may reach $1,400 in 2018, according to Commerzbank.

There’s also the possibility of a Trump-led trade war with China, uncertainty from elections in Europe, risks to market stability from the Italian banking sector and complications from Britain’s exit from the European Union. All those could revive the appeal of bullion.

The sell-off in gold “is a little bit too violent and too short-sighted,” said Chad Morganlander, a money manager at Stifel, Nicolaus & Co. in Florham Park, New Jersey, where he helps oversee about $172 billion. The fund hasn’t pared its positions in SPDR Gold, he said. “We’re expecting gold to start to move higher over the course of the next six to 12 months as interest rates stay anchored below expectations.”

And it seems the surge in physical demand that we have noted is catching up with paper prices…

Helped by a weakening dollar…

end

Position limits are now off the table on oil and gold and other commodities.They will leave it to the new administration and I am happy about that

(courtesy Wall Street Journal/GATA)

CFTC leaves shaping position limits rule to Trump administration

Submitted by cpowell on Tue, 2016-12-06 15:15. Section: Daily Dispatches

By Andrew Ackerman and Alexander Osipovich

The Wall Street Journal

Tuesday, December 6, 2016

WASHINGTON — U.S. regulators failed to put the finishing touches on a much-debated, long-delayed rule to limit speculation in commodities like oil and gold, opting instead to propose a scaled-back version that leaves its outcome in the hands of the Trump administration.

The Commodity Futures Trading Commission voted unanimously Monday to float, for the third time since 2011, a proposed rule that would cap the size of trading positions firms could take in more than two dozen core commodity contracts, including a variety of energy and precious-metals commodities, to curb any one trader’s influence.

The move punts a decision on the rule’s final contours to the Trump administration, which has pledged to dismantle the Dodd-Frank financial law that authorized the restrictions.

“I did not want to finalize a rule that next year the commission would choose not to defend or implement,” CFTC Chairman Timothy Massad said on a call with reporters.

Specifically, the latest proposal would restrict a firm from owning more than the equivalent of 25 percent of a commodity’s estimated “deliverable supply” in a given month. In some cases, however, it would effectively raise the position limits because it would increase the estimated supply of the commodities. Monday’s version also gives traders more leeway than prior iterations of the measure if they are managing business risks. …

… For the remainder of the report:

http://www.wsj.com/articles/cftc-to-repropose-position-limit-rules-14809

end

Quite a report: Market rigging is striving to save a disintegrating Europe?

(the King report/GATA)

King Report: Market rigging strives to save disintegrating Europe

Submitted by cpowell on Tue, 2016-12-06 15:23. Section: Daily Dispatches

From The King Report

Burr Ridge, Illinois

Tuesday, December 6, 2016

As always when a political event occurs, be alert for central bank intervention.

Someone intervened in European stocks before European bourses opened Monday. Unlike previous interventions, the Brexit and Italian referendum manipulations are intended to save the European Union, not just banks or stocks.

The severity of the situation across the pond cannot be understated. The EU and Europe itself are disintegrating. European nations are collapsing under the strain of busted banks and immigration that is accelerating the insolvency of welfare states.

Even worse, societal and cultural norms are collapsing. European elites’ response to increasing crime and disorder has been to allow refugee enclaves to become de-facto sovereign states that are not policed. …

… For the remainder of the report, subscribe here:

end

The following is quite an understatement: “governments and the financial press falsify economic conditions”:

John Embry…

Governments, financial press falsify economic conditions, Embry tells KWN

Submitted by cpowell on Tue, 2016-12-06 17:37. Section: Daily Dispatches

12:37p ET Tuesday, December 6, 2016

Dear Friend of GATA and Gold:

Governments and financial news organizations are falsifying the condition of the world’s economy, Sprott Asset Management’s John Embry tells King World News today, and the price action in the monetary metals is “ludicrous.” Embry’s comments are excerpted at KWN here:

http://kingworldnews.com/we-are-most-assuredly-headed-for-armageddon/

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

These three kingpins are getting off lightly for rigging Euribor: HSBC, JPMorgan and Credit Agricole

(courtesy London’s Financial Times).

Brussels to fine three banks over Euribor rate rigging

Submitted by cpowell on Tue, 2016-12-06 21:23. Section: Daily Dispatches

By Rochelle Toplensky and Martin Arnold

Financial Times, London

Tuesday, December 6, 2016

Brussels on Wednesday will hit HSBC, JPMorgan, and Credit Agricole with multimillion-euro fines for rigging the Euribor interest rate benchmark, closing a five-year cartel probe into a scandal that shook the financial world.

The three banks held out against a 2013 settlement with the European Commission that imposed almost E1 billion of fines on Deutsche Bank, Societe Generale, and Royal Bank of Scotland.

Margrethe Vestager, the EU’s competition commissioner, is expected to unveil fines on the trio of banks ranging from tens of millions of euros to the low hundreds, according to people familiar with the case.

The decision is an example of the long shadow that still hangs over the industry from alleged misconduct during the years of the financial boom. …

Ms. Vestager is still developing a cartel case against multiple banks for allegedly manipulating the $5.3 trillion forex market. Given the extent of evidence in the hands of investigators, officials expect any forex fines to exceed those imposed during the rate-rigging probes. …

… For the remainder of the report:

https://www.ft.com/content/c43c4f8e-bbd7-11e6-8b45-b8b81dd5d080

end

I warned you many times that this was happening in the settling process: gold in London and Hong Kong is used to settle upon comex contracts and that is why it takes so long to settle as they must wait for the gold to come:

(courtesy Koos Jansen/GATA)

Koos Jansen: Gold in London and Hong Kong is used to settle Comex futures

2:27p ET Wednesday, December 7, 2016

Dear Friend of GATA and Gold:

Gold researcher Koos Jansen shows today how gold futures contracts on the New York Commodities Exchange are being used to hedge and settle gold trades around the world, especially in London and Hong Kong. Jansen’s report is headlined “Gold in London and Hong Kong Is Used to Settle Comex Futures” and it’s posted at Bullion Star here:

https://www.bullionstar.com/blogs/koos-jansen/london-hong-kong-gold-used…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

I have now about seen everything. India is now confiscating gold, even jewellery in amounts greater than 250 grams as officials search out hidden money

No wonder the Indian economy is tanking like a lead balloon

(courtesy Mish Shedlock/Mishtalk)

India Confiscates Gold, Even Jewelry, In Raids On Hidden Money

Submitted by Michael Shedlock via MishTalk.com,

Global financial repression picks up steam, led by India. After declaring large denomination notes illegal, India now targets gold.

It’s not just gold bars or bullion. The government has raided houses, no questions asked, confiscating jewelry.

For background to this article, please see my November 27 article Cash Chaos in India, 86% of Money in Circulation Withdrawn; Cash Still King in Japan.

Large denomination means 500-rupee ($7.30) and 1,000-rupee notes ($14.60), which account for more than 85 percent of the money supply. They are no longer legal tender, effective immediately.

As one might imagine, chaos ensued. And it continues.

India Confiscates Gold

Picking up where we left off, please consider Message to Modi: Do No More Harm by Mihir Sharma.

The chaos accompanying “demonetization” hasn’t eased up noticeably. It seems likely the disruption to the economy, especially in cash-centric rural India, will hit growth sharply for at least a few quarters. It’s tough to say for how long and by how much; we are in uncharted territory here and guesses have varied widely. But many analysts agree with former Prime Minister Manmohan Singh, who’s predicting the new policy will knock 2 percentage points off that world-beating GDP growth rate.

Demonetization was originally sold as a “surgical strike on black money” — the illicit piles of cash many rich Indians have accumulated out of sight of the taxman. It’s now clear the policy has been anything but surgical. Worse, uncomfortable questions are being asked about whether the complicated rules and exemptions that have accompanied demonetization have allowed black-money holders to launder most of their cash. Of late, Modi’s chosen to focus instead on demonetization as means of advancing a cashless economy.

Yet the idea of a war on unaccounted-for wealth remains central to demonetization’s popular appeal, which means Modi will have to find other ways to keep that narrative going. So the government has now begun to push income-tax officials to conduct raids on those who might be concealing assets in forms other than cash, such as gold.

There’s already enough fear of such raids becoming common again that the government felt the need to step in to quell some of the anxiety. That didn’t help much. The government “clarified,” among other things, the rules governing when tax officials could seize gold: Nothing would happen “if the holding is limited to 500 grams per married woman, 250 grams per unmarried woman and 100 grams per male.” It also said that there would be no limits on jewelry “provided it is acquired… from inheritance.” Also, the “officer conducting [the] search has discretion to not seize [an] even higher quantity of gold jewelry.”

What this means, unfortunately, is that India’s income tax officers have just won the lottery. During a raid, they can, on the spot, decide whether or not to confiscate a family’s gold holdings. And remember, India has an enormous amount of gold — 20,000 metric tons, much of it inherited. (The rules governing simple searches are different, but few know that.) Rather than cleaning up tax administration, the government has handed tax officials more power than they’ve had for decades. The rich will pay what they need to escape harassment; the rest will suffer.

Rich Escape, Poor and Middle Class Suffer

The last line in the preceding article says all you need to know about what’s happening: “The rich will pay what they need to escape harassment; the rest will suffer.”

Evidence suggests the politically connected, and their friends, knew about the ban on cash and acted in advance. Everyone else is stuck.

India’s raid on gold reinforces its ban on cash. Short term aside, these kinds of actions will increase demand for gold.

What’s Next?

I keep wondering: what’s next? People pretend they know, I admit I do not. However, I am quite sure a currency crisis is coming. Where it strikes first is unknown, but the list of likely candidates increases every year.

My spotlight has been on Japan, China, and the EU. India caught me off guard, but it adheres to my general theory this pot will eventually boil over in a cascade from an unexpected place, outside the US.

US actions may cause a currency crisis, but I believe a crisis will hitelsewhere first. If I am correct, gold will be the safe haven, regardless of currency, but especially where the crisis hits.

end

Your early WEDNESDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight

1 Chinese yuan vs USA dollar/yuan DOWN to 6.88000(SMALL DEVALUATION SOUTHBOUND /CHINA UNHAPPY TODAY CONCERNING USA DOLLAR RISE/MORE $ USA DOLLARS LEAVE CHINA/OFFSHORE YUAN WIDENS COMPLETELY TO 6.90321 / Shanghai bourse CLOSED UP 22.59 POINTS OR 0.71% / HANG SANG CLOSED UP 125.77 OR 0.55%

2. Nikkei closed UP 136.75 POINTS OR 0.74% /USA: YEN FALLS TO 113.99

3. Europe stocks opened ALL IN THE GREEN ( /USA dollar index RISES TO 100.53/Euro UP to 1.0727

3b Japan 10 year bond yield: FALLS +.032%/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 113.01/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD FINALLY IN THE POSITIVE/BANK OF JAPAN LOSING CONTROL OF THEIR YIELD CURVE AS THEY PURCHASE ALL BONDS TO GET TO ZERO RATE!!

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 50.96 and Brent: 53.80

3f Gold UP/Yen UP

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil DOWN for WTI and UP for Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10 yr bund FALLS TO +.349%/Italian 10 yr bond yield FALLS 7 full basis points to 1.90%

3j Greek 10 year bond yield RISES to : 6.716%

3k Gold at $1173.60/silver $16.80(7:45 am est) SILVER BELOW RESISTANCE AT $18.50

3l USA vs Russian rouble; (Russian rouble UP 14/100 in roubles/dollar) 63.72-

3m oil into the 50 dollar handle for WTI and 53 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation (already upon us). This can spell financial disaster for the rest of the world/China forced to do QE!! as it lowers its yuan value to the dollar/GOT a SMALL DEVALUATION DOWNWARD from POBC.

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 113.99 DESTROYING WHATEVER IS LEFT OF OUR YEN CARRY TRADERS

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 1.0102 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.0836 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT

3r the 10 Year German bund now POSITIVE territory with the 10 year FALLS to +.349%

/German 9+ year rate BASICALLY negative%!!!

3s The Greece ELA NOW at 71.4 billion euros,AND NOW THE ECB WILL ACCEPT GREEK BONDS (WHAT A DISASTER)

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.367% early this morning. Thirty year rate at 3.054% /POLICY ERROR) GETTING DANGEROUSLY HIGH

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

(courtesy Jim Reid/Bloomberg/Deutsche bank/zero hedge)

Longest Winning Streak For Global Stocks Since September On Monte Paschi Bailout Hopes, ECB Optimism

Global stocks extended the longest winning streak since September, with Asia up 0.8% and Europe rising 0.7% while bonds and credit markets strengthened amid hopes that the European Central Bank will prolong quantitative easing, while optimism an Italian bailout of Monte Paschi will prevent European bank contagion, has pushed European financial stocks higher. US equity futures were little changed.

A note from Goldman’s David Kostin overnight perhaps summarized it best: “Large-cap fund managers embrace Hope over Fear.“ For now hope is certainly in the driver’s seat, leading European equities higher for a third day, with the Bloomberg World Banks Index trading at the highest level in more than a year. Bonds rose across the euro area, with the yield on the benchmark German bund falling from the highest in almost three weeks, while perceived investment-grade credit risk fell for a seventh day, the longest run since May. The pound fell after an unexpected decline in manufacturing output.

The Stoxx Europe 600 Index added 0.7% as of 10:46 a.m. in London as mining companies and banks rallied. Credit Suisse AG gained 8 percent, while Banca Monte Paschi rose 7.1 percent after La Stampa reported Italy will ask for a 15 billion euro ESM loan for the lender, among other banks.

(HARVEY: Monte de Paschi rises 7.1% with the bailout calling for the shareholders to get wiped out completely????)

Investors’ concerns were that a defeat for Renzi in a referendum on constitutional reforms could further undermine faith in the European Union – following Britain’s decision to quit the bloc – as well as confidence in the euro currency. Market reaction to Renzi’s defeat and his resignations was relatively muted, partly as a consequence of a pledge by the ECB to buy Italian government debt if markets became unsettled. “Despite the fact that the probability of early elections has risen, the market is focusing on the banking sector and the fact the government seems to be showing more urgency in dealing with that problem,” Mizuho strategist Antoine Bouvet said.

“People had gone into the referendum with a very pessimistic view and I think the last five years have taught us that, as far as the euro is concerned, political issues often don’t have a lasting impact,” DZ Bank currency analyst Sonja Marten said.

Ahead of tomorrow’s ECB announcement (previewed here), investors are positioned for an extension of monthly asset purchases of 80 billion euros ($86 billion) past March even as uncertainty lingers that Draghi may inject an element of hawkishness and hint at tapering or even ending QE at some point in the future. With overnight volatility on the euro at the highest since the U.K.’s vote to leave the European Union in June, traders are hedging bets that ECB President Mario Draghi will carry on with accommodative policies. Last year he defied weeks of anticipation for more support with underwhelming stimulus that sent bond yields and the euro surging.

“The base expectation is that we are going to get an extension of the stimulus program by another six to nine months,” said Michael Hewson, a market analyst at CMC Markets in London. “Broad sentiment is starting to turn around — we are getting some repositioning for a better 2017 in terms of growth.”

Japan’s Topix index gained 0.9% in Tokyo as the MSCI Asia Pacific Index added 0.4%. Futures on the S&P 500 Index were little changed after the measure posted a 0.3% advance on Tuesday. The Dow Jones Industrial Average rose 0.2 percent to close at another record.

Brent and WTI rose after the Kremlin said Russian President Vladimir Putin personally agreed to output cuts with the nation’s oil companies. Brent above $54/bbl, WTI above $51/bbl. “The headlines that Putin personally agreed to the oil output cut sent prices higher,” says Ole Hansen, head of commodity strategy at Saxo Bank. “This adds to the pressure on OPEC to deliver their own cuts.” “The market is taking that at face value and looking for at least half of the 600k b/d non-OPEC cut to be assured.” The one-minute trading volume in WTI hit day-high >1,900 lots at 9:17am London time, shortly after Russia headlines.

One of the biggest movers in the currency markets was the Australian dollar, down 0.4 percent after data showed the Australian economy shrank by 0.5 percent, its biggest contraction since 2008, in the third quarter. Australian stocks, however, closed 0.9 percent higher in anticipation of more fiscal and monetary stimulus. While rate futures imply scant chance of a Reserve Bank interest rate cut in the coming months, prospects of a hike vanished.

China’s foreign exchange reserves fell by more than expected last month to $3.05 trillion, their lowest since 2011, the central bank said. The yuan currency last stood at 6.8850 to the dollar compared to a mid-point of 6.8808 set by the central bank. The currency is down 5 percent so far this year.

In rates, Germany’s 10-year bond yield fell two basis points to 0.34 percent, after climbing to 0.38 percent, the highest since Nov. 14. The government plans to sell 3 billion euros of 2018 securities. Italian sovereign debt securities due in a decade advanced for a second day, almost erasing losses suffered in the aftermath of Sunday’s referendum. The nation’s 10-year bond yield fell four basis points to 1.91 percent, adding to a four-basis point drop from Tuesday. Portugal’s 10-year bond yield reached the lowest level since Nov. 15. Treasury 10-year note yields were little changed at 2.37 percent. The Markit iTraxx Europe Index of credit-default swaps on investment-grade companies dropped one basis point to 74 basis points, the lowest since Nov. 9. A gauge of swaps on junk-rated companies fell to a three-month low.

Market Snapshot

- S&P 500 futures up less than 0.1% to 2211

- Stoxx 600 up 0.7% to 347

- FTSE 100 down less than 0.1% to 6742

- DAX up 0.1% to 10698

- German 10Yr yield up less than 1bp to 0.34%

- Italian 10Yr yield down 7bps to 1.92%

- Spanish 10Yr yield down 6bps to 1.5%

- S&P GSCI Index down 0.1% to 389.6

- MSCI Asia Pacific up 0.8% to 136

- Nikkei 225 up 0.5% to 18361

- Hang Seng up 0.8% to 22675

- Shanghai Composite down 0.2% to 3200

- S&P/ASX 200 up 0.5% to 5429

- US 10-yr yield down 1bp to 2.38%

- Dollar Indexunchanged at 100.09

- WTI Crude futures down 0.4% to $51.59

- Brent Futures down less than 0.1% to $54.91

- Gold spot up 0.1% to $1,172

- Silver spot up 0.4% to $16.82

Global Headlines

- Credit Suisse Steps Up Cost Cuts as Revenue Eludes CEO Thiam: Lowers target for operating costs by 1 billion francs

- Linde Chairman Said to Pitch Praxair Merger Plan to Board: Jobs in Germany said part of deliberations about Praxair plan

- JPMorgan, HSBC, Credit Agricole Fined $521 Million Over Euribor: Banks fined by the European Commission for rigging the Euribor benchmark

- Shell and Total Said to Sign Initial Oil Deals With Iran: Deals for S. Azadegan, Yadavaran, Kish fields, oil official says

- Lilly Threatens Sanofi’s Dominance in Insulin With Knockoff Drug: Novo sees U.S. drugmaker as its ‘most formidable’ rival ahead

- Blackstone to Buy Solvay’s Acetow Business for $1.1 Billion: Buyout firm agreed to pay about seven times earnings for a business supplying materials for cigarette filters

- Western Digital in Samsung License Deal, Boosts 2Q Forecast: CFO Mark Long spoke in analyst day presentation

- FirstEnergy Seeks to Sell $885 Million Worth of Power Plants: AE Supply unit looking to sell gas-fired, hydro power plants

- Exxon Sees 175 Million Ton LNG Shortage by 2030 Without Spending: Financing challenges seen for new LNG developments

- Pfizer, Flynn Fined Record $113 Million Over Epilepsy Drug: U.K. CMA imposes record fines for abusing dominant position

Asian stocks markets traded mostly higher following a positive lead from Wall St where strength in financials and telecoms underpinned sentiment and resulted in the Dow posting a second consecutive record close. ASX 200 (+0.9%) outperformed despite a poor GDP release as the recent slew of weak data keeps prospects of future easing alive, while Nikkei 225 (+0.7%) was also higher led by SoftBank shares after reports it is to invest USD 50bIn in the US and create 50,000 US jobs. Markets in China conformed to the tone, although upside in the Shanghai Comp (+0.7%) was capped after the PBoC conducted a poor liquidity operation for the third consecutive day, while Jakarta stock markets were negative after Indonesia was hit by a magnitude 6.5 earthquake. 10yr JGBs traded with marginal gains despite the mostly heightened risk appetite in the region, as the BoJ were present in the market for over JPY 1.3trl under its bond buying program, while participants also digested unwaveringly dovish comments from BoJ Deputy Governor Iwata. PBoC injected CNY 30bIn 7-day reverse repos, CNY 20bIn in 14-day reverse repos and CNY 20bIn in 28-day reverse repos. PBoC set the mid-point at 6.8808 (Prey. 6.8575). BoJ Deputy Governor Iwata stated that the BoJ will continue to expand monetary base, while he also added that they will not hesitate to take further measures if required and that yield control can only be achieved by large JGB buying by the central bank.

- Asian Top News

- Hong Kong Faces Housing Risks as Fed Tightening Looms, IMF Says: Stretched property valuations mean Hong Kong’s economy is vulnerable if interest rates rise faster than expected

- Investors Lose 99% as Hong Kong Rights Offerings Go Badly Wrong: Repeat rights issuers under scrutiny as bourse link expands

- RBA Will Look Through Australia’s Economic Shocker, Traders Bet: Swaps still see more than 75% chance RBA on hold through 2017

- Chinese Regulators Fined Medtronic $17 Million for Price- Fixing: Penalties for fixing prices with dealers extending to 2014

- Jho Low Family Digs in to Stop 1MDB Asset Seizure by U.S.: Relatives seek to replace trustees who refused to fight U.S.

- Soros Alumnus Shiozumi Says Bears on Abenomics Have It All Wrong: Shiozumi, T. Rowe Price’s Ciganer see Japan stock rally

European stocks trade in positive territory this morning (Euro Stox: +1.2%) as Santa gives an early Christmas present to Banca Monte Paschi (+7.9%) in the form of source reports of the state taking a controlling stake in the Co. for EUR 2bIn as soon as this weekend. As such, the Italian bellwether lifted sentiment for financials across the continent. Material names were also among the best performers, while energy names outperformed amid positive reports suggesting Russia could be on board with the OPEC production cuts. Elsewhere, fixed income markets remain relatively muted, with the German 10Y continuing to hover just above the 160 level and trading in a tight range throughout the morning.

European Top News

• Ahold Delhaize Plans $1.1 Billion Buyback as Cash Piles Up: Europe’s top retailer forecasts 23% increase in free cash flow

• PostNL Rejects New Bpost Takeover Bid on Governance Concerns: Belgian state’s role prompted Dutch authorities’ objections

• U.K. Manufacturing Unexpectedly Drops Most in Eight Months: Total production falls, led by oil and gas extraction

In currencies, the Bloomberg Dollar Spot Index, which tracks the greenback against 10 major peers, was little changed. The pound dropped 0.6 percent to $1.2597 after industrial production in October fell 1.3 percent, driven by a slide in oil and gas extraction. The euro was little changed at $1.0726 after posting a 0.4 percent drop on Tuesday. Overnight volatility in the common currency versus its U.S. counterpart jumped to 23 percent, the most since June 23, based on closing prices. The Australian dollar traded as low as 74.17 U.S. cents before paring its drop to 0.1% after the statistics bureau said third-quarter gross domestic product decreased 0.5 percent from the prior quarter, the first contraction since 2011. The Reserve Bank of Australia on Tuesday kept interest rates unchanged and Governor Philip Lowe said “some slowing in the year-ended growth rate is likely.”

In commodities, oil traded near $51 a barrel amid speculation a production boost from U.S. shale producers will counter the first output cuts from OPEC in eight years. Copper gained 0.6%, recouping an earlier decline. Steel rebar in China climbed with iron ore to the highest in more than two years, as reports of a crackdown on illegal plants spurred speculation that the government is stepping up supply-side reforms. Spot gold was little changed at $1,171.62 an ounce.

Looking at the day ahead, we got the October industrial and manufacturing production reports for the UK, which both missed sharply printing -1.1% and -0.4% YoY, on expectations of a 0.5% and 0.2% rebound respectively. It’s fairly quiet in the US where we’ll get the October JOLTS job openings report along with the October consumer credit print. China released November foreign reserves which showed a surprisingly steep drop of $70 billion, the biggest since January. We’ll also get central bank decisions today from the Reserve Bank of India, which unexpectedly kept rates unchanged even as it warned the economy would slow down.

US Event Calendar

- 7am: MBA Mortgage Applications, Dec. 2 (prior -9.4%)

- 10am: JOLTS Job Openings, Oct. est. 5.50m (prior 5.486m)

- 10:30am: DOE Energy Inventories

- 3pm: Consumer Credit, Oct., est. $18.650b (prior $19.292b)

DB’s Jim Reid concludes the overnight wrap

Although there is little uncertainty in the alpine weather forecast this morning, I must admit to being quite confused by financial markets this week. In our 2017 credit outlook we suggested that we like European financial over non-financial credit as the outlook has changed markedly since the sector’s nadir in late summer where it priced in almost permanent negative yields and flat yield curves. Rising yields and a steeper yield curve partly due to Kuroda’s new policy framework helped. President-elect Trump has since given this trade a further boost with additional hopes on easier regulation ahead. However we’ve been struggling with reconciling our optimistic view with our thoughts that a ‘no’ was likely in the Italian referendum and a period of turbulence possible for the sector given the country’s banking sector problems. We thought it would be more difficult to solve them quickly and safely with a ‘no’. However we decided to ride out this expected volatility and take any near-term stresses and losses that this would entail. Given yesterday’s price action we needn’t have even bothered getting stressed as European financials saw a remarkable day in spite of (or perhaps strangely because of) the speculation of imminent government intervention in the sector that might be necessary after the ‘no’ vote.

Indeed the Stoxx 600 Banks index rallied to the tune of +5.61% yesterday for its biggest one-day gain since April. The main driver was that remarkable rebound for Italian Banks. Unicredit (+12.81%), Mediobanca (+9.94%), Unione di Banche Italiane (+9.70%), Banco Popolare di Milano (+9.03%), and Intesa Sanpaolo (+8.16%) all more than wiping out the previous day losses. With those moves the FTSE Italia All-Share Banks index rallied +8.97% and had its best day since July while the FTSE MIB closed up +4.15%. That compares to gains of +0.97% for the Stoxx 600 and +0.34% for the S&P 500.

It was much the same in credit markets. While the iTraxx Main index tightened an impressive 4bps, more eye catching were the moves for the iTraxx Senior and Sub Financials indices which ended the day 7bps and 7.5bps tighter respectively. Within the Sub-Fins constituents, spreads for Unicredit, Generali, Intesa and Mediobanca were 18bps, 16bps, 15bps and 7bps tighter respectively. There was a similar outperformance for BTP’s too where 10y yields ended the day just over 4bps lower at 1.940% which compared to a move of 4bps higher for 10y Bund yields. US Treasury yields on the other hand were little changed around 2.389%.

Although the above suits our sector view I’m still scratching my head this morning explaining the strength of the move given the week’s news. All help very welcome with aggressively short covering perhaps a big catalyst. For now then the political focus in Italy turns over to the elections and as DB’s Marco Stringa summarised yesterday in his report, the key question is not ‘when’ Italy goes to elections but ‘how’. In other words which electoral law. Since the weekend this has now become a focal point for investors and yesterday’s report from Marco has helped to summarise some of the key Q&A’s on the more specific details of the process.

Away from all things Italy related there was an important development to note on the Brexit front last night. Yesterday PM May accepted a Labour Party motion which will be debated in the House of Commons today, calling on the government to publish its plans for the leaving the EU prior to triggering Article 50. According to the BBC as many as 40 Tories were said to be prepared to support the Labour Party in demanding more parliamentary scrutiny of the government’s plans. One to watch.

To the latest in Asia now where for the most part bourses in Asia have strengthened and so following the generally positive sentiment over the last 24 hours. Indeed when will we start to hear talk of a Santa Claus rally? The Nikkei (+0.54%), Hang Seng (+0.35%), Shanghai Comp (+0.10%) and ASX (+0.87%) in particular are all firmer although the Kospi (-0.10%) is a touch weaker. Those moves have come despite WTI Oil retreating a further -0.65% this morning which follows the -1.66% decline yesterday and the first down day since the OPEC meeting last week. Meanwhile in FX markets the Aussie Dollar has weakened close to half a percent following a much weaker than expected Q3 GDP print (-0.5% qoq vs. -0.1% expected). In fact it was the first negative quarterly contraction since 2011 and the joint worst since 2008.

Moving on. Just as you might have expected primary issuance to slow down into year end, it was interesting to note the relatively busy day for issuance in the HY energy space yesterday. Indeed Chesapeake, Matador Resources, Rowan Companies and Parsley Energy priced deals after Cheniere Energy had priced a decent sized deal on Monday. The timing follows a decent rally in spreads following the OPEC meeting. Indeed based on DB pricing to the close on Monday, cash spreads for US HY energy are 32bps tighter at 510bps since OPEC. In fact that is now the tightest spread since November 2014 after spreads peaked above 1900bps back in February.

Elsewhere, with regards to the data yesterday, in the US the trade deficit was reported as widening to $42.6bn in October from $36.2bn in the month prior. That was as a result of a -1.8% mom drop in exports while imports were reported as rising +1.3% mom. Meanwhile factory orders rose a slightly above market +2.7% mom in October (vs. +2.6% expected) while durable goods orders were revised down to a still strong +4.6% mom from +4.8% in the initial flash estimate. Elsewhere nonfarm productivity was confirmed at +3.1% qoq in Q3 while unit labour costs were revised up to +0.7% qoq from +0.3%. Finally the IBD/TIPP economic optimism reading for December was reported as rising 3.4pts in December to 54.8. That’s actually the highest reading since November 2006. The Atlanta Fed did downgrade their Q4 GDP forecast to 2.6% from 2.9% yesterday although that reflected the employment and auto sales data last week.

As far as the data was concerned in Europe, Q3 GDP growth for the Euro area was confirmed at +0.3% qoq although the annual rate was revised up by one tenth to +1.7% yoy which left it unchanged versus Q2. The most eye catching print in Europe yesterday was the October factory orders reading in Germany where orders were reported as rising a bumper +4.9% mom (vs. +0.6% expected) and so helping to raise the YoY rate to +6.3% from +2.9%. That was the largest monthly jump since July 2014 although our European economists did warn that a combination of several factors likely overstates the underlying improvement. This includes a very large workday adjustment, the impact of the Paris autoshow during the month, and a post Brexit recovery.

In terms of the day ahead, this morning in Europe the early data comes from Germany where the October industrial production data is due (expected to rise +0.8% mom). Shortly after we’ll get the October trade data out of France before we then get the Halifax house price index data for the UK for last month. We’ll then get the October industrial and manufacturing production reports for the UK where both are expected to have risen +0.2% mom. It’s fairly quiet in the US this afternoon. We’ll get the October JOLTS job openings report along with the October consumer credit print. China is also due to release November foreign reserves data at some stage today. We’ll also get central bank decisions today from the Reserve Bank of India (expected to cut by 25bps) and Bank of Canada (expected to hold)

end

3.REPORT ON JAPAN SOUTH KOREA NORTH KOREA AND CHINA

i)Late TUESDAY night/WEDNESDAY morning: Shanghai closed UP 22.59 POINTS OR 0.71%/ /Hang Sang closed UP 125.77 OR 0.55%. The Nikkei closed UP 136.75 OR 0.74%/Australia’s all ordinaires CLOSED UP 0.89% /Chinese yuan (ONSHORE) closed DOWN at 6.8800/Oil ROSE to 50.96 dollars per barrel for WTI and 53.80 for Brent. Stocks in Europe: ALL IN THE GREEN. Offshore yuan trades 6.90321 yuan to the dollar vs 6.8800 for onshore yuan.THE SPREAD BETWEEN ONSHORE AND OFFSHORE WIDENS AGAIN AS MORE USA DOLLARS LEAVING CHINA’S SHORES / CHINA SENDS A CLEAR MESSAGE TO THE USA AND JANET TO NOT RAISE RATES IN DECEMBER.

3a)THAILAND/SOUTH KOREA/:

b) REPORT ON JAPAN

c) REPORT ON CHINA

A huge commentary: This will no doubt be a black swan as Chinese official reserves (including FX changes) drops 69 billion USA, the biggest drop since last January. The new official reserves are 3.05 trillion and the part that is alarming is that the Chinese authorities are claiming the loss of dollars is starting to cause problems with the businesses and the issuance of dividends etc.

(courtesy zero hedge)

Chinese Reserves Tumble By $69 Billion, Biggest Drop Since January

While in recent months, the PBOC had tried to mask the real pace of reserve outflows, covering up the accelerated selling of US-denominated assets to defend its rapidly devaluing currency, we noted in October that using more accurate calculations, China’s capital outflows are once again surging, having hit $78 billion in September. Overnight, China, unable to continue “covering up” its reserve state, disclosed that, as we warned, FX reserve liquidation had soared with total reserves falling by nearly $70 billion last month as the country’s central bank burned through more of its reserves in the fight to defend the renminbi from greater depreciation on the back of accelerating capital outflows. This was the largest decline since January.

PBOC’s total reserves declined by $69.1 billion to $3.051 trillion in November, a decline of 2.2 per cent from the previous month and the largest drop since January’s fall of 3 per cent. A median forecast from economists had predicted a fall of only 1.9 per cent from October.

After adjusting for currency valuation effects, the reserves fall would be about US$34bn.

As the FT notes, this “fifth consecutive monthly fall indicates growing difficulty for policymakers. Since the renminbi’s sharp depreciation in August 2015, Beijing has sought to combat more severe softening against the greenback by selling dollars from the central bank’s foreign exchange reserves.”

The yuan’s weakness has helped to continue driving the outflows that began plaguing China after the one-off devaluation in August 2015. In the first ten months of 2016 capital outflows from China rose to $530bn, with October’s level exceeding the year’s monthly average.

A separate dataset, called “PBOC’s FX position” (usually released around the middle of the month), would give a useful cross-check on PBOC’s FX sales net of valuation effects. This data shows the amount of PBOC’s FX assets at book value. Partly reflecting the uncertainty of the size of valuation effects, there is sometimes a significant gap between this data and the reserves data after adjusting for estimated currency valuation effects (e.g., in the last few months since June, the former suggests that the monthly average of PBOC’s FX sales was about US$25bn more than implied by the latter)

The latest reserve figure come amid signs that ramped-up efforts to curb heavy capital outflows have begun to interfere with foreign businesses in China. Several European firms have been unable to remit dividends due to new foreign exchange controls that the EU Chamber of Commerce in Beijing called “disruptive to business operations”.

Media reports over the past couple of weeks suggest that the authorities would be tightening outflows through administrative means, including on outbound FDI, gold imports and cross-border net RMB payments. The impact of such measures will not be fully visible until December forex levels are released, but after November’s drop they look unlikely to be the last.

There has not been any concrete official confirmation or detail of the reported rules and implementation, so it is difficult to assess the potential effectiveness. In general, a stronger capital control could help mitigate excessive volatility in outflows driven by temporary sentiment factors. However, outflows may also reflect structural diversification demand. We have previously estimated that there could be a substantial amount of Chinese wealth to be allocated to foreign assets over time given that Chinese residents have been under-diversified. To the extent that diversification is an important driver, control measures could be effective in dampening short-term outflows but may be less so in reducing the fundamental pent-up pressure on the exchange rate.

end

(courtesy zero hedge)

China Newspapers Blast “Diplomatic Rookie” Trump For “Inability To Keep His Mouth Shut”

It seems that Trump’s phone call with Taiwan’s president Tsai Ing-wen as well a recent pair of tweets from the president-elect blasting China for devaluing their currency, taxing U.S. imports and military provocations in the South China Sea have served their purpose of ruffling some feathers in Beijing.

Did China ask us if it was OK to devalue their currency (making it hard for our companies to compete), heavily tax our products going into..

their country (the U.S. doesn’t tax them) or to build a massive military complex in the middle of the South China Sea? I don’t think so!

While the “official reaction” out of Beijing to Trump’s “provocations and falsehoods” has been muted, newspapers across China, often viewed as a mouthpiece of the Communist Party, have spent the day lashing out at the “diplomatic rookie.”. Per Yahoo News, the People’s Daily accused Trump of “provoking friction and messing up China-US relations,” a move they say will not help “make America great again.”

Donald Trump is a “diplomatic rookie” who must learn not to cross Beijing on issues like trade and Taiwan, Chinese state media said Tuesday, warning America could pay dearly for his naivety.

Trump’s protocol-shattering call with Taiwan’s president and a subsequent Twitter tirade against Beijing’s policies could risk upending the delicate balance between the world’s two largest economies, major media outlets said.

“Provoking friction and messing up China-US relations won’t help ‘make America great again'”, said a front-page opinion piece in the overseas edition of Communist Party mouthpiece People’s Daily.

The Global Times blasted Trump’s “inability to keep his mouth shut” adding that Trump “doesn’t have sufficient resources” to be provocative with China.

The nationalist Global Times newspaper’s Chinese edition also ran a page-one story on Trump’s “inability to keep his mouth shut”, damning his “provocation and falsehoods”.

Noting that Sino-US relations had reached a delicate equilibrium thanks to years of careful management, an editorial in the paper warned that Trump “can make a lot of noise but that does not exempt him from the rules of the major power game,” adding that he “doesn’t have sufficient resources” to be provocative with China.

“Trump’s China-bashing tweet is just a cover for his real intent, which is to treat China as a fat lamb and cut a piece of meat off it,” it said.

“He is trying to pillage other countries for US prosperity,” it warned, but instead he will unwittingly “smash the current world economic order” of which the US is the “biggest beneficiary.”

A companion commentary warned that Trump “will in time learn not to cross China”, threatening “a fierce competition” with Beijing if the US increases arm sales to Taiwan.

Meanwhile, the China Daily noted that Beijing would likely remain somewhat muted in their response so long as Trump is “shooting from the hip” but warned that a failure to “moderate his behavior” after taking office would result in “costly troubles” for the United States.

Meanwhile the English-language China Daily newspaper warned that “diplomatic rookie” Trump needs to moderate his behaviour or he will create “costly troubles for his country”.

“As president-elect, Trump can expect some forgiveness even when he is shooting from the hip. But things will be different when he becomes president.”

“If Trump continues talking this way after taking office… China is going to have to make some adjustments in its thinking,” Jia Qingguo, professor at Peking University, told AFP, calling the comments “sobering”.

Well, this relationship certainly seems to be off to a fantastic start…should be full of very fun developments over the next four years

4 EUROPEAN AFFAIRS

Italy/Monte de Paschi

The fun begins: The Italian government prepares to nationalize Monte de Paschi.

Monte needs 5 billion euros by the end of December and if they cannot get it, they will be toast. For the Italian government is coming to the rescue to the tune of 2 billion euros out of 5 billion needed or 40% of the new company. The existing shareholders are now toast. The fun begins as the government will buy the junior bonds at face value and leave the senior bonds alone and not buying their notes. That should set a showdown in bankruptcy court. Then we have the new bail in rules which suggests that all holders, bond holders, equity holders and depositors must share in the loss and not taxpayers which is must Germany has been demanding . However they have problems with Deutsche bank and they will need a rescue. That is why I stated earlier today that the rescue of Monte de Paschi will no doubt cause contagion effects all over the place.

(courtesy zero hedge)

Italian Government Prepares To Nationalize Monte Paschi

After two previous taxpayer funded bailouts, and nearly five months of foreplay since the third largest Italian bank failed the latest European stress test at the end of July, in which the Italian government in September vow that “bailout for Italian banks has been ‘absolutely’ ruled out“, a third bailout, as we previewed earlier today, is now imminent.

According to Reuters, which cites two sources, Italy is preparing to take a €2 billion controlling stake in Monte Paschi as the bank’s hopes of a private funding rescue have faded after a fruitless five month search to secure an anchor investor, following Prime Minister Matteo Renzi’s decision to quit.

The government, which is already the ailing bank’s single largest shareholder with a four percent share, is planning do a debt-for-equity swap, and buy junior bonds held by ordinary Italians to take the stake up to 40%, the sources said. The bonds would then be equitized, converting the government’s bond stake into pure equity ownership, a troubling approach as it would effectively wipe out the existing equity tranche and position the bank for a potential bankruptcy fight in court where the government faces off with the equity committee.

This transaction would make the government by far the biggest shareholder, meaning the Treasury would be able to control Italy’s third biggest bank and its shareholder meetings, or in other words, the bank would be nationalized.

The sources said a government decree authorizing the deal, which would see the state buy the subordinated bonds from retail investors and convert them into shares, could be rushed through as early as this weekend. Italy’s treasury would buy the bonds held by around 40,000 retail investors at face value, the sources said.

It is unclear how the senior bondholders, who would not be made whole would feel about a government transaction which favors the juniors (who would get par) where the bulk of the retail investors are found, would feel about such a transaction which would bring memories of the US government’s “bailout” of GM which flipped the bankruptcy process on its head by prioritizing junior pensioners over senior creditors.

The way the transaction is structured, the government would ensure retail investors do not suffer any losses in the bank’s bailout, making it politically more palatable and staving off the risk of a run on deposits that could trigger a wider banking crisis.

The bank, which needs to raise €5 billion by the end of December or risk winding down, is set to raise 1 billion euros from a bond swap with institutional investors and Rome is hoping the 2 billion euros participation from the government could help persuade private investors to fill the 2 billion euros gap. Since any new equity investors would come in as the equivalent of post-petition equity, it would mean that existing equityholders, already a token amount, would be wiped out.

“It’s a de-facto nationalization with a strong presence by the state that can attract other investors and allow the transaction to be completed,” said one of the sources, speaking on condition of anonymity.

There is another problem: in the past both Merkel and Schauble, not to mention Djisselbloem, have made it expressly clear that a bail-in mechanism should be used to preserve insolvent banks, and a state-funded and taxpayer backed bailout/nationalization is no longer permitted. Allowing Italy to proceed with this transaction would make a mockery of Europe’s entire “bail-in” protocol, not to mention the European finance ministers’ resolve and ability to implement anything, which is why the European Commission would need to assess whether the government’s intervention is taking place at market prices or if it constitutes state aid, another source said.

However, since an Italian contagion wave would inevitably slam Deutsche Bank and Germany’s various other banks, Europe will find the deal to be “whatever it needs it to be, to make it possible.

Monte dei Paschi, rated the weakest lender in European stress tests this summer, had planned to arrange a private rescue, starting with a firm commitment from one or more anchor investors and then launching a share sale this week.

There is still some hope for a private rescue without a government intervention, but that is evaporating by the hour. According to Reuters, the chances of the privately backed deal going ahead as planned were now slim. A source close to Qatar’s cash-rich sovereign wealth fund said it could inject €1.4 billion in the bank but wanted to wait to see what kind of government would succeed Renzi. Other sources were more cautious on Qatar’s willingness to back the deal.

Monte Paschi’s bank’s chief executive, Marco Morelli, held talks with European Central Bank officials in Frankfurt on Tuesday to review its options. A meeting of the bank’s board is likely to take place on Wednesday. At that point it is likely to greenlight the first major European bank bailout in a year in which the G-20 leader previously declared that the global economy is fixed and is now reflating itself back to growth.

end

Renzi resigns today after the approval of the budget bill. This may precipitate early elections:

(courtesy zero hedge)

Italy PM Renzi To Resign Today After Approval Of Budget Bill

In what may be an unexpected development, following yesterday’s news that Renzi would hold off resigning for the immediate future as per the president’s request, moments ago the Italian prime minister tweeted that he would formally resign at 7pm local time, well ahead of expectations, following passage of the budget bill.

Legge di bilancio approvata. Alle 19 le dimissioni formali. Grazie a tutti e viva l’Italiahttp://www.governo.it/sites/governo.it/files/slide-leggebilancio2017.pdf …

The resignation may precipitate new elections, and potentially lead to an outcome in which the anti-Euro M5S party ends up in the driver’s seat, pushing Italy further into political limbo.

More as we see it.

end

This ought to hurt: Moody’s has cut Italy’s senior unsecured government debt rating from stable to negative but leaving it at Baa2 for now. I guess that they are concerned with the Italian banks health.

(courtesy zero hedge)

Moody’s Cuts Italy Ratings Outlook To Negative

Moody’s has cut Italy’s long-term senior unsecured government debt rating outlook from ‘stable’ to ‘negative’, leaving it at Baa2 for now. Citing “slow and halting progress” on economic and fiscal reform in Italy, noting that reduction in Italy’s large debt burden will be further postponed given subdued medium-term growth prospects, recent fiscal slippage.

The drivers for today’s rating action are:

(i) the slow and halting progress on economic and fiscal reform in Italy, the prospects for which have diminished further following the ‘no’ vote in Sunday’s constitutional referendum; and

(ii) the resulting rising risk that the reduction in Italy’s large debt burden will be further postponed given subdued medium-term growth prospects and recent fiscal slippage, thereby prolonging the sovereign’s exposure to unforeseen shocks.

Concurrently, Moody’s has today maintained the local-currency and foreign-currency bond ceilings at Aa2. The local-currency and foreign-currency deposit ceilings remain unchanged at Aa2. The short-term foreign-currency bond and deposit ceilings remain unchanged at P-1.

RATINGS RATIONALE – RATIONALE FOR CHANGING THE OUTLOOK TO NEGATIVE

FIRST DRIVER: DIMINISHED PROSPECTS FOR STRUCTURAL ECONOMIC AND FISCAL REFORM FOLLOWING THE REJECTION OF CONSITUTIONAL REFORM

The first driver of Moody’s decision to change the outlook on Italy’s Baa2 rating to negative relates to the diminished likelihood, following the ‘no’ vote in Sunday’s constitutional referendum, that the Italian government will make meaningful further progress on the structural economic and fiscal reforms needed in order to stabilise the government’s credit profile and improve its capacity to absorb shocks.