Gold at (1:30 am est) $1204.30 UP $3.40

silver at $17.00: UP 3 CENTS

Access market prices:

Gold: $1209.30

Silver: $17.10

THE DAILY GOLD FIX REPORT FROM SHANGHAI AND LONDON

.

The Shanghai fix is at 10:15 pm est last night and 2:15 am est early this morning

The fix for London is at 5:30 am est (first fix) and 10 am est (second fix)

Thus Shanghai’s second fix corresponds to 195 minutes before London’s first fix.

And now the fix recordings:

Shanghai FIRST morning fix Jan 20/17 (10:15 pm est last night): $ 1219.24

NY ACCESS PRICE: $1207.70 (AT THE EXACT SAME TIME)/premium $11.54

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Shanghai SECOND afternoon fix: 2: 15 am est (second fix/early morning):$ 1215.74

NY ACCESS PRICE: $1201.85 (AT THE EXACT SAME TIME/2:15 am)

THE SPREAD 2ND FIX TODAY!!: $7.61

China rejects NY pricing of gold as a fraud/arbitrage will now commence fully

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

London Fix: Jan 20/2017: 5:30 am est: $1199.10 (NY: same time: $1199.55 (5:30AM)

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

London Second fix Jan 20.2017: 10 am est: $1200.55 (NY same time: $1201.30 (10 AM)

It seems that Shanghai pricing is higher than the other two , (NY and London). The spread has been occurring on a regular basis and thus I expect to see arbitrage happening as investors buy the lower priced NY gold and sell to China at the higher price. This should drain the comex.

Also why would mining companies hand in their gold to the comex and receive constantly lower prices. They would be open to lawsuits if they knowingly continue to supply the comex despite the fact that they could be receiving higher prices in Shanghai.

end

For comex gold:

NOTICES FILINGS FOR JANUARY CONTRACT MONTH: 10 NOTICE(S) FOR 1000 OZ. TOTAL NOTICES SO FAR: 1185 FOR 118,500 OZ (3.6858 TONNES)

For silver:

NOTICES FOR JANUARY CONTRACT MONTH FOR SILVER: 2 NOTICE(s) FOR 10,000 OZ. TOTAL NUMBER OF NOTICES FILED SO FAR; 559 FOR 2,795,000 OZ

Let us have a look at the data for today

.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total open interest FELL by 1625 contracts DOWN to 172,592 with respect to YESTERDAY’S TRADING. In ounces, the OI is still represented by just less THAN 1 BILLION oz i.e. .862 BILLION TO BE EXACT or 123% of annual global silver production (ex Russia & ex China).

FOR THE JANUARY FRONT MONTH IN SILVER: 2 NOTICES FILED FOR 10,000 OZ.

In gold, the total comex gold ROSE BY 9,603 contracts DESPITE THE FALL IN THE PRICE GOLD ($10.40 with YESTERDAY’S trading ).The total gold OI stands at 475,227 contracts.

we had 10 notice(s) filed upon for 1000 oz of gold.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD:

We had no changes in tonnes of gold at the GLD

Inventory rests tonight: 807.96 tonnes

.

SLV

we had no changes in silver into the SLV:

THE SLV Inventory rests at: 338.356 million oz

.

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in silver FALL by 1625 contracts DOWN to 172,592 AS SILVER FELL 26 CENTS with YESTERDAY’S trading. The gold open interest ROSE by 9,603 contracts UP to 475,227 DESPITE THE FACT THAT THE PRICE OF GOLD FELL BY $10.40 WITH YESTERDAY’S TRADING

(report Harvey).

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

2c) COT report

Harvey

3. ASIAN AFFAIRS

REPORT ON JAPAN SOUTH KOREA NORTH KOREA AND CHINA

3a)THAILAND/SOUTH KOREA

b) RPORT ON JAPAN

c) REPORT ON CHINA

i)A very important commentary. Even though we know that the data is fudged, China has now released data to suggest that their growth is the slowest in 26 years at 6.8%

( zerohedge)

ii)This is a surprise move: the POBC cuts reserve ratios and then offers temporary funding and support for its largest banks. They wish to avoid a cash crunch!!

(courtesy zerohedge)

4 EUROPEAN AFFAIRS

As you can see, global growth is falling out of bed: today UK retail sales plunge 2% and this caused the Pound to contract but it later recovered a bit:

( zero hedge)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

none today

6.GLOBAL ISSUES

i)A good commentary on what 5 territorial disputes may influence gold and/or problems for the world authorities: the two biggest of course is the South Chinese Seas and the Israel/Palestine conflict.

( Barton Edgerton/GlobalRiskInsights.com)

ii)It seems that 22 Mexican pesos per dollar is the line in the sand. Former Mexican commerce secretary Gutierrez comments that Mexico must show a tough stance against trump. With that and intervention, the peso surged

( zero hedge)

7. OIL ISSUES

i)Rig count rises which will mean increase production. Oil after rising in the early part of the day, falters again

( zero hedge)

ii)A good look at the Saudi economy and how it will fare with oil below 60 dollars per barrel. The privatization of Aramco will surely provide enough capital to diversify this nation

( Gregory Brew/OilPrice.com)

8. EMERGING MARKETS

none today

9. PHYSICAL MARKETS

i)As we outlined yesterday, the POBC are investigating the Bitcoin platform which caused the price of Bitcoin to fall. This caused a flood of investors to enter physical gold and GOld ETF’s denominated in physical metal:

( zero hedge)

ii)Gold trading today: higher with the Trump rally faltering: money flowing into gold and bonds!

( zero hedge)

iii)Bill Murphy interviewed by Daily coin

( Bill Murphy/GATA)

iv)This is a good one: John Embry states that we should watch out when the world finally realizes all of the fake news, manipulated (and false data), all hell will break loose. He outlines the most important commentaries of this past week, that which I have also highlighted to you.

( Kingworldnews/John Embry)

v)Alasdair Macleod..why we should own and hold onto gold

( Alasdair Macleod)

vi)The new Sec Treasurer to be Mnuchin states that he believes in the long term the USA dollar is important but he backs boss Trump that the dollar should weaken and help USA exports

( GATA/Bloomberg)

10.USA STORIES

i)Trump is now the 45th President of the USA. His speech sends the Dow down as well as the Peso. The key sound bite: “we’re transferring power from Washington to “the people”

( zero hedge)

ib)Statement from President Trump: He wants to crate 25 million jobs, grow the economy by 4% and lower taxes for all Americans

( President Trump/zero hedge)

ii)Zero hedge comments on the Steve Mnuchin confirmation hearings. He in essence is echoing his boss where he states that the dollar is too high but in the long run he supports a “strong dollar”

( zero hedge)

iii)This should be fun: Trump team is preparing for dramatic cuts to spending and yet they need infrastructure spending. They will try and cut programs that nobody ever heard of:

( zero hedge)

Let us head over to the comex:

The total gold comex open interest ROSE BY 9,603 CONTRACTS UP to an OI level of 475,227 AS THE PRICE OF GOLD FELL $10.40 with YESTERDAY’S trading. We are now in the contract month of JANUARY and it is one of the poorest deliveries of the year.

With the front month of January we had a LOSS of 35 contract(s) DOWN to 72. We had 41 notices filed YESTERDAY so we GAINED 6 contract(s) or AN ADDITIONAL 600 oz WILL STAND for gold in this non active delivery month of January. For the next big active delivery month of February we had a LOSS of 8914 contracts DOWN to 193,356.(feb 2016: 201,000 contracts). March had a LOSS of 80 contracts as it’s OI is now 925. We are on a par with respect to OI when we compare data for open interest re the Feb 2016 contract.

We had 10 notice(s) filed upon today for 1000 oz

And now for the wild silver comex results. Total silver OI FELL by 1625 contracts FROM 174,217 DOWN TO 172,592 AS the price of silver FELL 26 CENTS with YESTERDAY’S trading. We are moving further from the all time record high for silver open interest set on Wednesday August 3/2016: (224,540).

We are now in the non active delivery month of January and here the OI FELL by 121 contract(s) FALLING TO 109. We had 122 notice(s) filed on yesterday so we gained 1 silver contracts or an additional 5,000 oz will stand in this delivery month of January. The next non active month of February saw the OI rise by 7 contract(s) RISING TO 261.

The next big active delivery month is March and here the OI FELL by 2595 contracts DOWN to 132,041 contracts.

We had 2 notice(s) filed for 10,000 oz for the January contract.

VOLUMES: for the gold comex

Today the estimated volume was 228,499 contracts which is good.

Yesterday’s confirmed volume was 283,375 contracts which is very good

volumes on gold are getting higher!

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz |

nil OZ

|

| Deposits to the Dealer Inventory in oz | nil oz

|

| Deposits to the Customer Inventory, in oz |

nil

|

| No of oz served (contracts) today |

10 notice(s)

1000 oz

|

| No of oz to be served (notices) |

62 contracts

6200 oz

|

| Total monthly oz gold served (contracts) so far this month |

1185 notices

118,500 oz

3.68584 tonnes

|

| Total accumulative withdrawals of gold from the Dealers inventory this month | 3000.000 oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | 4,806,084.1 oz |

Today, 0 notice(s) were issued from JPMorgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equates to 10 contract(s) of which 0 notices were stopped (received) by jPMorgan dealer and 0 notice(s) was (were) stopped/ Received) by jPMorgan customer account.

March 2015: 2.311 tonnes (March is a non delivery month)

| Silver | Ounces |

| Withdrawals from Dealers Inventory | nil |

| Withdrawals from Customer Inventory |

839,313.699 0z

Brinks

Delaware

Scotia

|

| Deposits to the Dealer Inventory |

nil oz

|

| Deposits to the Customer Inventory |

750,960.974 oz

JPM

|

| No of oz served today (contracts) |

2 CONTRACT(S)

(10,000 OZ)

|

| No of oz to be served (notices) |

107 contracts

(545,000 oz)

|

| Total monthly oz silver served (contracts) | 559 contracts (2,795,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month | 19,182,617.0 oz |

end

And now the Gold inventory at the GLD

Jan 20/no changes in gold inventory a the GLD/Inventory rests at 807.96 tonnes

Jan 19/no changes in gold inventory at the GLD/Inventory rests at 807.96 tonnes

Jan 18/no changes in gold inventory at the GLD/Inventory rests at 807.96 tonnes

Jan 17/17/a deposit of 2.96 tonnes of gold/inventory at the GLD rests at 807.96 tonnes. I guess there is no more gold inventory to sent to C+Shanghai

Jan 13/17/there were no changes in gold inventory at the GLD/Inventory rests at 805.00 tonnes

Jan 12/2017/no change in gold inventory at the GLD/Inventory rests at 805.00 tonnes

Jan 11/no change in gold inventory at the GLD/Inventory rests at 805.00 tonnes

JAN 10/no changes in gold inventory at the GLD/Inventory rests at 805.00 tonnes

JAN 9/A WITHDRAWAL OF 8.87 TONNES OF GOLD FROM THE GLD/INVENTORY RESTS AT 805.00 TONNES

end

NPV for Sprott and Central Fund of Canada

end

At 3:30 pm est we receive the COT report which gives position levels of our major players. For several weeks, the commercials were goading the specs to go short. That change last week and the commercials went net short and the specs net long.

Let us see what today brings:

First the gold COT

| Gold COT Report – Futures | ||||||

| Large Speculators | Commercial | Total | ||||

| Long | Short | Spreading | Long | Short | Long | Short |

| 218,144 | 111,103 | 104,399 | 101,399 | 224,510 | 423,942 | 440,012 |

| Change from Prior Reporting Period | ||||||

| 4,144 | 6,585 | 15,238 | 4,636 | 1,931 | 24,018 | 23,754 |

| Traders | ||||||

| 157 | 96 | 85 | 53 | 51 | 249 | 202 |

| Small Speculators | ||||||

| Long | Short | Open Interest | ||||

| 43,995 | 27,925 | 467,937 | ||||

| -82 | 182 | 23,936 | ||||

| non reportable positions | Change from the previous reporting period | |||||

| COT Gold Report – Positions as of | Tuesday, January 17, 2017 | |||||

Our large specs:

Interesting:

those large specs that have been long in gold added 4144 contracts to their long side those large specs that have been short in gold added 6585 contracts to their short side.

Our commercials

those large specs that have been long in gold added 4636 contracts to their long side.

those large specs that have been short in gold added a tiny 1931 contracts to their short side.

Our small specs:

those small specs that have been long in gold pitched a tiny 82 contracts from their long side.

those small specs that have been short in gold added a tiny 182 contracts.

Conclusions: commercials go net long changing direction from last week. They went net long by 2705 contracts. The large specs went net short by 2441 contracts and that is very bullish for gold.

And now for our silver COT

| Silver COT Report: Futures | |||||

| Large Speculators | Commercial | ||||

| Long | Short | Spreading | Long | Short | |

| 90,838 | 21,356 | 12,618 | 45,028 | 126,764 | |

| 2,408 | -2,473 | 2,082 | 3,603 | 6,402 | |

| Traders | |||||

| 95 | 36 | 39 | 32 | 38 | |

| Small Speculators | Open Interest | Total | |||

| Long | Short | 172,056 | Long | Short | |

| 23,572 | 11,318 | 148,484 | 160,738 | ||

| -1,077 | 1,005 | 7,016 | 8,093 | 6,011 | |

| non reportable positions | Positions as of: | 143 | 100 | ||

|

|

Tuesday, January 17, 2017 | © SilverSeek.com | |||

Our large specs:

Those large specs that have been long in silver added 2408 contracts to their long side

those large specs that have been short in silver pitched 2473 contracts from their short side.

Our commercials;

those commercials that have been long in silver added 3603 contracts to their long side.

those commercials that have been short in silver added 6402 contracts to their short side.

Our small specs;

Those small specs that have been long in silver pitched 1077 contracts from their long side.

those small specs that have been short in silver added 1005 contracts to their short side.

Conclusions:

large specs go net long by 4800 contracts; commercials go net short by 2799 contracts.

It sure looks like JPMorgan is controlling the silver comex market.

Major gold/silver trading/commentaries for FRIDAY

GOLDCORE/BLOG/MARK O’BYRNE

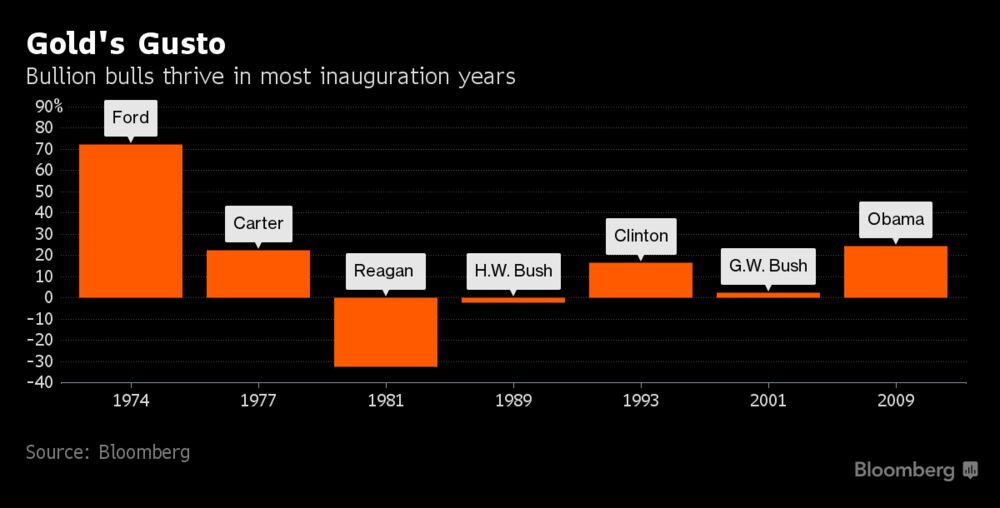

Gold’s Gains 15% In Inauguration Years Since 1974

– Gold’s average gains in inauguration years of 15% since 1974

– First year of new President frequently a time of increased uncertainties and risks

– Gold rose 30% in the 12 months after Obama inauguration

– Massive political uncertainty – President’s conflict with the CIA

– ‘Strong dollar policy’ to end as U.S. has $120 trillion plus debt

– Trump inherits Bush and Obama’s humongous debt

Gold performs well in inauguration years (see table) and has seen average gains of 15% in inaugural years since the 1970s.

Given the degree of uncertainty, divisiveness and conflict that Trump’s election has already created – both in America and internationally, it seems almost certain that the many risks as President Trump takes power will lead to higher gold prices.

Besides the myriad of risks today and arguable the most uncertain geo-political situation since World War II or the height of the Cold War, gold investors and buyers can look to Presidential history, as gold has recorded has average gains of 15% in inaugural years since 1974.

This may be due to the fact that the first year of many administrations is frequently a time of significant change and increased uncertainties and risks. Markets are concerned that the US presidential handover and advent of President Trump will lead to volatility and turmoil in 2017 which will likely impact risk assets such as stocks.

The price of gold has already gained 5% this year and appears to be consolidating just above US$1,200 an ounce today. Investors can take a look at history for signal and indications as to how gold and stocks might perform this year.

Bloomberg points out:

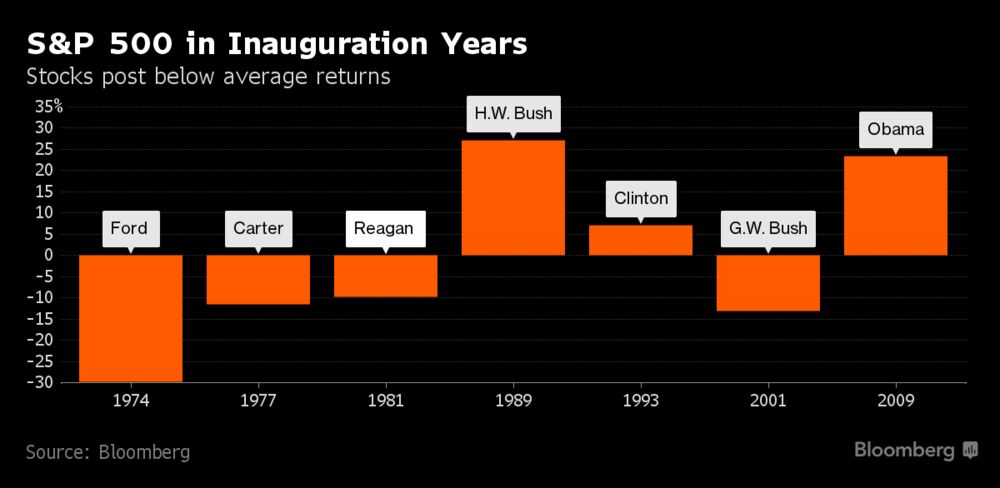

A look at recent presidential transitions supports optimism among traders over the metal’s prospects. Gold has averaged gains of almost 15 percent in years marking the inauguration of a new president since the 1970s, advancing in five of those seven years.

In contrast, the S&P 500 index of equities declined in four of those years for an average loss over the period of 0.9 percent.

From Presidents Gerald Ford to Barack Obama, bullion has often served as a haven in times of political flux.

The metal has climbed about 5 percent this year as questions over the possible economic impact of Donald Trump’s policies add to investor angst over Brexit and mounting trade frictions. Bulls reason that gold will extend its gain as scant details of Trump’s fiscal stimulus program and tensions with trading partners including China unnerve investors.

Axel Merk of Merk Investments LLC told Bloomberg that

“We have no idea what’s going to happen with some of Trump’s policies — everybody is a little nervous…”

“Gold is relatively undervalued and will push higher.”

Like Trump or loathe him, most would acknowledge that his recent press conference, ill judged tweets and recent transition to power has been a complete mess.

Trump time … Let the games begin

Today is “T day” or “Trump day” as the world awaits the inauguration and advent of Donald Trump as President of the United States. The eyes of the world are on Washington and traders and investors will be keeping an eye on the U.S. stock and bond markets, the dollar and gold.

Trump’s first speech as President, expected some time after his swearing in at 1700 GMT, may see President Trump offer more detail on his fiscal and economic policies, especially infrastructure spending and taxation, in addition to trade policy.

When Barack Obama was sworn in eight years ago, the dollar strengthened by more than 4% in a day. This reassured markets and lulled many investors into a false sense of security regarding the dollar and markets. In the subsequent month after Obama’s inauguration, gold was 16% higher and in the course of the following 12 months, gold rose by 30% and gold was 23.4% higher in the calendar year 2009.

Markets and the dollar are unlikely to welcome Trump’s inauguration with such enthusiasm today. However, there is that possibility but investors should fade the short term noise and focus on the fact that gold is likely to perform well in 2017 and in the coming years for some of the reasons outlined below.

Trump’s conflict with the CIA

Trump’s continuing spat with America’s top intelligence agencies including accusing them of Nazi like tactics shows the level of geo-political uncertainty and risk facing the U.S. and the world.

At his first news conference last week, he said

“I think it was disgraceful, disgraceful that the intelligence agencies allowed any information that turned out to be so false and fake out. I think it’s a disgrace, and I say that … that’s something that Nazi Germany would have done and did do,” Trump told a news conference in New York.

Trump has been smeared by senior elements in the CIA in another “dodgy dossier” akin to that of the “weapons of mass destruction” dossier which helped get the U.S. and the UK into the disastrous Iraq war. The tactics used in smearing Trump as a “sexual deviant” are akin to those used by FBI Director J. Edgar Hoover against politicians and others including Martin Luther King in the 1960s.

Martin Luther King was an outsider, a political activist, a civil rights activist and a man of peace who fought peacefully for the rights of the poor and the disenfranchised , especially the African-American community.

Trump is a maverick business man and today is set to become an insider and one of the most powerful men in the world. A civil war between a U.S. President and senior elements in the intelligence agencies will likely lead to political instability on a massive scale and is a recipe for disaster.

We do not like to have to consider the ‘assassination’ scenario but the precedent of JFK’s assassination looms large. Trump is hated by large sections of the American population and indeed by very powerful operators in the politics and intelligence circles in Washington D.C. and in the U.S. There are alas likely lots of willing patsies.

‘Strong dollar policy’ to end as U.S. has $100 trillion plus debt

The dollar was on the back foot again yesterday despite some strong data, most notably some strong numbers in the Philadelphia Fed Manufacturing Index and a very low initial jobless claims number.

New Treasury Secretary Steve Mnuchin sparred with Democratic lawmakers on various topics, and actually expressed support for a strong US dollar, placing him at odds with President Trump and attempting to clarify comments by the president-elect that hit the currency earlier this week.

Mnuchin, a former Goldman Sachs banker, told a Senate confirmation hearing yesterday that a strong currency remained important over the long-term, reflecting America’s attractions as an investment destination.

On Monday Trump appeared to break from decades of the strong dollar policy in the US by saying that the greenback’s strength is “killing us” and was preventing American companies from competing internationally and with China.

Trump and Mnuchin’s comments highlight the uncertainties and many conflicting signals over Trump’s financial and economic policies.

Will Trump’s speech today reignite the US dollar strength seen in late 2016 or will his speech lead to a sell off in the dollar and a surge in the gold price? We are living in a ‘Brave New Trump World’ and as Aldous Huxley said “You pays your money and you takes your choice.”

Now more than ever, the short term is nigh impossible to predict.

We believe that Trump will attempt to end the ‘strong dollar policy’ or at the very least will try and push the dollar lower in the short term in order to boost American exports and jobs in a desperate attempt to kick start the moribund U.S. economy.

There is also the somewhat important matter of the U.S.’ near bankruptcy with its $20 trillion nominal debt and over $100 trillion in unfunded liabilities (more on this below). The market will dictate the value of the dollar in the long term not the pronouncements of Trump or his Treasury Secretary.

Investors should fade the short term noise and focus on the diversification benefits that owning physical gold will provide in the coming months and years.

Trump inherits Bush and Obama’s humongous debt

Contrary to superficial figures and analysis, Obama has left Trump an enfeebled and massively indebted U.S. economy with some 95 million out of work. This accounts for Trump’s popularity among large sections of the working and middle classes.

President Obama is set to leave a massive near $20 trillion debt crisis for his successor.

The U.S. national debt reached $19.96 trillion last week and increased by roughly $1 trillion a year during Obama’s Presidency and during the so called fake news “recovery.” Obama and his government, like Bush before them, spent money like drunken sailors and pushed the U.S. closer to the brink of bankruptcy.

There is also the not insignificant matter of the between $100 trillion and $150 trillion in unfunded liabilities – for medicare, medicaid and social security as the baby boomers retire.

The U.S., like the EU and most western nations, is “kicking the can down the road.” Consequently, a U.S. and global debt crisis looks likely during the first term of President Trump.

This continuing surge in the U.S. national debt to the $20 trillion level means that the U.S. is now the largest debtor nation in the world – by a significant margin. Its total debt of over $120 trillion means it is the largest debtor nation the world has ever seen.

Donald Trump holds three gold bullion bars after accepting it as a security deposit for a 10 year lease for on the 50th floor of 40 Wall Street in New York City, a Trump owned property, during a news conference in New York, September 15, 2011. REUTERS/Mike Segar

This profligacy will be paid back by the people of the U.S., and most likely by people in all indebted western nations, in the form of higher taxes, higher interest rates, inflation, currency wars involving devaluations and almost certainly a currency crisis involving the dollar and other leading fiat currencies.

Owning gold coins and bars in your possession and owning bullion in allocated and most importantly in segregated accounts will continue to protect and grow wealth in the coming years.

As we outlined yesterday, the POBC are investigating the Bitcoin platform which caused the price of Bitcoin to fall. This caused a flood of investors to enter physical gold and GOld ETF’s denominated in physical metal:

(courtesy zero hedge)

Chinese Investors Exit Bitcoin, Flood Into Gold ETFs

Amid a weakening yuan and a tumbling Bitcoin (amid crackdowns on ‘virtual’ capital outflows from China), Chinese money is moving to bullion as investors seek an alternative to the ‘managed’ fiat paper offered by the PBOC. In the week through Monday, China attracted $52 million, the biggest inflow into commodity-linked exchange-traded funds of all countriestracked by Bloomberg.

As China cracks down on various Bitcoin exchanges, sparking an exodus from Bitcoin China platforms, gold has pushed higher…

As Bloomberg reports,Huaan Yifu Gold ETF, China’s largest ETF backed by raw materials, is getting all the attention, attracting almost $72 million last week.

“Chinese capital outflow has certainly elevated the risk to the financial system,” Chad Morganlander, a portfolio manager at Washington Crossing Advisors, which oversees $1.5 billion, said in a telephone interview. “It would be no surprise to me that Chinese gold ETF caught a bid under this elevated or increased concern about reserves, about the currency and about trade relations.”

Huaan Yifu attracted the third-biggest inflow into gold ETFs in the week through Monday, behind Frankfurt-listed Xetra-Gold, which got $172.9 million, and London-listed Source Physical ETF, which lured $73.6 million. ETF holders are bucking the trend in China’s jewelry market that saw the nation’s gold imports from Hong Kong fall in November to the lowest since January.

There are other troubles triggering capital flight and sending money to gold. The International Monetary Fund warned that China’s continued reliance on policy stimulus measures and the slow progress in addressing corporate debt raise the risk of a “sharper slowdown or disruptive adjustment.” The IMF issued the warning even as it raised the nation’s growth forecast for this year by 0.3 percentage points to 6.5 percent.

We will see shortly…

END

Gold trading today: higher with the Trump rally faltering: money flowing into gold and bonds!

(courtesy zero hedge)

Trump Rally Reverses: US Equity Outflows In 4 of Past 5 Weeks Offset By Gold, Bond Inflows

When looking at the latest weekly fund flows, it is clear that the Trump trade is over if only for the time being. As BofA reports, citing EPFR data, the last week saw the largest precious metal inflows in 5 months ($1.3bn), the 4th consecutive week of bond inflows ($4.5bn), and a week of modest $1.7bn equity inflows, however US stocks saw $2.5 billion in outflows, representing the 4th weekly outflow in the past 5 weeks.

Some highlights from BofA’s Michael Hartnett:

Election to Inauguration flows: since the US election, BofAML GWIM ETFs show private clients big buyers of Financials, Materials, Bank Loans, Industrials, TIPS, Value; big sellers of Low-Volatility & Precious Metals

Inauguration reversals: EPFR flows show partial profit-taking in these Trump reflation trades into the inauguration…1st outflows from financials in 17 weeks, 1st government bond inflows in 6 weeks (largest in 6 months), and 1st inflows to precious metals in 10 weeks; we also note 1st outflows from HY funds in 8 weeks; but we also see ongoing inflows to “inflation trades” of materials, TIPS, and (in particular) bank loans; so a “pause” in the Davos Man to Joe Six Pack rotation rather than major reversal

Post-inauguration tactics: meanwhile our Global Flow Trading Rule, which had flirted with a “sell” signal mid-Dec’16, has pulled back from the abyss (inflows to equities & HY currently below the 4-week “sell” threshold of 1.0% of AUM, and global PMIs continue to trend higher

Stick with Icarus Trade: our BofAML Bull & Bear Indicator also indicates more bullish sentiment (up to 3-month high of 4.9 – Chart 2) but remains some way below “sell” trigger of 8.0; Positioning, Profits & Policy make us stick with our Icarus Trade view… any Jan/Feb wobble to be followed by one last 10% melt-up in stocks & commodities in H1 before visible investor “hubris” on macro & markets signals the “Big Top”

And the details:

Asset Class Flows

- Equities: $1.7bn inflows ($1.7bn mutual fund outflows vs $3.4bn ETF inflows)

- Bonds: $4.5bn inflows (4 straight weeks)

- Precious metals: first inflows in 10 weeks ($1.3bn – largest in 5 months)

Fixed Income Flows

- First outflows from HY bond funds in 8 weeks ($0.3bn)

- First govt bond inflows in 6 weeks ($1.0bn – largest in 6 months)

- 4 straight weeks of IG bond inflows ($2.2bn)

- 10 straight weeks of inflows to bank loan funds ($0.7bn)

- 6 straight weeks of inflows to TIPS funds ($0.3bn)

- 3 straight weeks of inflows to EM debt funds ($0.4bn)

Equity Flows

- Japan: strong $2.5bn inflows

- Europe: $0.7bn outflows (largest in 6 weeks)

- EM: small inflows of $64mn (2 straight weeks)

- US: $2.5bn outflows (outflows in 4 of past 5 weeks)

- By sector: first outflows from financials in 17 weeks ($0.7bn); first outflows from tech in 6 weeks ($0.1bn); inflows to energy in 6 of past 7 weeks ($0.4bn); inflows to materials in 10 of past 11 weeks ($0.2bn)

end

Bill Murphy interviewed by Daily coin

(courtesy Bill Murphy/GATA)

(courtesy Kingworldnews/John Embry)

John Embry: Watch out when reality breaks through fake news, manipulated markets

Submitted by cpowell on Thu, 2017-01-19 18:17. Section: Daily Dispatches

1:17p ET Thursday, January 19, 2017

Dear Friend of GATA and Gold:

Sprott Asset Management’s John Embry tells King World News today that people are going to be horrified when reality breaks through fake news, manipulated markets, propaganda, and economic data that has been falsified by government. An excerpt from his interview is posted at KWN here:

http://kingworldnews.com/the-uninformed-public-will-be-horrified-by-what…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

Alasdair Macleod..why we should own and hold onto gold

(courtesy Alasdair Macleod)

Gold – a primer for 2017

You know when to buy gold: it’s when nearly every trader and commentator tells you that gold is going lower and you should sell it.

This is Harry Dent on 10th January: “I still see gold landing somewhere between $650 and $750 in the next year or so” i. Dent invokes Elliott Wave Theory. EWT states that a bull market is comprised of impulse waves of three separated by two corrective ones, totalling five all together. Bear markets are made up of three waves, two impulse in the direction of the bear trend, separated by one consolidating countertrend.

I am simplifying the theory considerably to make a point, but I do know my onions, having in the past taught, examined and lectured on EWT on behalf of the UK’s Society of Technical Analysts. Ralph Elliott only applied his theory to equity markets. Reflecting the greater value over time placed on stakes in human progress, it makes sense. It is modern chartists who have extended its use to other markets.

But money and currencies? The first decision you must make is which of the two variables in a price is in a bull market. It is commonly thought gold is the variable, but the chart below illustrates the problem is more likely fiat currencies priced in gold.

The four currencies shown, including the dollar, have been firmly in bear markets since the year before Bretton Woods was abandoned. Note also that the price scale in the chart is logarithmic, so these are enormous losses for fiat currencies. So, Dent and his fellow-travellers are effectively using a theory that was never intended to be used outside equity markets to recommend their clients and subscribers play a counter-trend rally that’s already over five years old.

Elliott theorists are also oblivious to a mathematical impossibility. If a currency is deemed to be in a bull market, it moves up in fives. If the other currency being measured against it, or commodity if you must, is in a bear market, it moves down in threes. How can one be moving in fives, while the other moves in threes? It cannot, it is a story of square pegs and round holes, and wholly disqualifies EWT applied to gold.

You cannot rule out the possibility that gold will go to Mr Dent’s $650 to $750, but for that to transpire I suggest two things would have to happen. Interest rates would have to be raised beyond the point where bad debts and falling bond prices break the banks, and the Fed would have to convincingly signal to markets that it is prepared to stand aside and let the banks fail. I believe these two conditions to be extremely unlikely. In the event of an interest-rate induced crisis, it is far more likely the Fed will repeat the successful formula (from the Fed’s point of view) of providing unlimited credit, as it did post-Lehman. A pathological fear of deflation ensures the outcome. And unlike the time of the Lehman crisis, investors will know the solution in advance, and their response will differ accordingly.

It was the post-election move in gold that wrong-footed everyone. A Trump victory was quickly turned from an event that brought with it heightened uncertainty, to one that promised higher interest rates, higher bond yields, and a strong dollar. The winners in this about-face, in the gold contract on Comex at least, were the bullion banks, which were very short. It suited them to drive gold and silver lower to close their short positions, and/or show favourable year-end book values. Amateurs in the game, who are nearly always caught out by the bullion banks’ periodic bear-raids, take the aggressive fall in prices as evidence that they should panic at what often ends up being the bottom of the market.

These banks are still short, having not managed to buy back all their positions, which is probably one reason why the current rally is so strong. And things are not looking good for the bullion banks, with prices running away from them with only a partial increase in open interest. As can be seen in the graph above, measured in gold the dollar has lost 97% of its value since 1969. If the dollar was a stock, informed opinion would be that it is bust and should not be bought. The same would be true of sterling, which has lost 98.5%, and the euro (including its components before 2001), down 98%. The legendary trader of yore, WD Gann, reckoned that any stock that fell to less than ten per cent of its high was probably bust, and should be avoided. It’s a good rule of thumb, and on that measure, not even the yen has a future.

The confusion for investors seeking guidance from so-called experts is they are always presented with charts showing gold priced in dollars. The immediate and unwritten assumption is that it’s the gold price that moves, and the currency is constant, overlooking the fact that the dollar persistently loses its purchasing power, confirmed by the almost continuous increase in the consumer price index. Showing gold priced in dollars, or any other currency for that matter, also encourages the myth that gold is an investment which either outperforms or underperforms cash. Technically, gold is not an investment. It is either a commodity, money or both, depending on your point of view and how you define things. Almost all financial commentators, including most gold bugs, make this very basic mistake.

Another myth that must be addressed is that gold is no longer money. For most of the world’s population, it most certainly is money, mainly because of its superior qualities as a store of value. Our second chart shows what has happened to selected Asian currencies over the same time-frame as the first chart, and includes the US dollar for comparison.

A Turkish national, holding on to his lira, has lost 99.99999% of his purchasing power measured in gold. An Indonesian has done somewhat better having lost 99.92565% on his rupiahs, but we are splitting hairs. The point is, does anyone seriously think the nearly two billion people behind this sample regard their governments’ fiat currencies as having any use beyond a means of rapid exchange?

Obviously not. Gold will always be regarded by all Asians as the preferred money, to be bought and held by selling the fiat. The only people who argue that gold is no longer money are Western-educated economists and their followers, having influence over an audience which mostly doesn’t care one way or another. These economists and their epigones probably number no more than a million or so, being a percentage of the global population that is not too remote from the percentage losses an Asian has suffered by holding on to his national currency.

The economists’ motivation is not so much a search for the truth, but more of a consequence of the sponsorship of their education by governments, and subsequent employment by both government agencies and a compliant financial establishment. Economists are like the three wise monkeys in their support for government currencies. The United States government does not want to see any challenge to its primacy over issuing the world’s reserve currency, and does everything to protect it, with a special dislike (or is it fear?) reserved for gold. Therefore, establishment economists dance to this tune, and are paid to do so.

The US Constitution explicitly states that gold and silver are money, yet since President Roosevelt banned the ownership of gold coin, gold bullion and gold certificates in 1933, US citizens have been denied this constitutional right. Few complain. Furthermore, when US citizens were once more permitted to own gold, any notional profits arising from the dollar’s debasement has been deemed profit and subject to tax on capital gainsii.

It is no coincidence that the dramatic declines in purchasing power for all fiat currencies, in addition to those illustrated in the two charts included in this article, stemmed from the time the dollar’s purchasing power could no longer be maintained at $35 to the ounce. The collapse in fiat currencies’ purchasing power since then has been in two broad moves, the first in the 1970s and the second from 2002 to 2011. Yet still, we have the establishment mainstream in financial markets claiming that gold is not money, and every time the dollar pathetically rallies from its deathbed against gold, they chorus “We told you so”.

Eurozone demand could be the surprise for 2017. The influence of Western-centric ignorance will probably be tested again later this year, as the Eurozone desperately tries to preserve its future and that of the euro. Only this week, President-elect Trump fired a starting gun on the EU’s political disintegration, by offering Britain and any other leavers quick and practical trade deals. This is a major about-turn from American post-war policy towards Europe. The change of policy is all fine and dandy, but it could be a trigger for the end-game of a financial mess in the Eurozone, whose resolution looks insoluble without massive monetary expansion. No wonder prescient Germans are already accumulating gold, and there can be little doubt that other EU nationals will increase their hedging against the euro’s ultimate failure as well, because that failure is becoming more likely by the day.

Sophisticated ignorance over gold goes one step deeper as well. Many commentators, knowingly or unknowingly, form a judgement based on their interpretation of the charts, and then select from a range of fundamental arguments to suit. Take India, where the currency has been mostly withdrawn. Recorded gold demand will presumably fall because there is little currency available to the unbanked masses for payment. This ignores unrecorded increases in smuggling, stimulated by the enhanced risk to the purchasing power of the rupee, already down 99.67% since 1969. Add to this stories that China has been restricting import licences for gold. For the chartist, the two largest sources of demand for physical gold are conveniently removed from the market. Throw in a strong dollar, and how could anyone argue against a falling gold price?

Except, since Harry Dent made his prediction on January 10th, gold has risen inexorably, despite these negatives. At the very least, he and his ursine tribe are being badly squeezed. What should worry these people even more is that the dollar’s falling purchasing power today against gold is driven by physical demand for bullion, and is despite the dollar’s strength against other fiat currencies.

Some important physical buyers appear to be waking up to the inflation and currency risks ahead. It should be clear to any intelligent observer that 1.3 billion Indians will chase up food prices later this year, because crops are not being planted through lack of cash. Monetary inflation in China is likely to lead to rising prices for a further 1.4 billion Chinese. Property bubbles abound throughout Asia, with new skyscrapers going up everywhere. It is redolent of the conditions that led to the Asian crisis in the late nineties, on a grander scale.

Crucially, measured in dollars the strength of energy and raw material prices throughout 2016 was an early warning of future price inflation everywhere, and expanding bank credit in America is fuelling the trend as well. The conditions for a reversal of the forty-year trend of declining price inflation are now in place, negating any bearish argument against gold. We don’t know who is actually buying physical gold, suffice to say the really big money has very little exposure. But now that the status quo is being challenged and price inflation is back on the agenda, central banks and other big buyers now find gold attractive.

I have written at length elsewhere about how price inflation is going to be a growing problem, and how restricted the Fed is in responding to it. The danger is increasingly being recognised by the other commentators. Additionally, Trump’s planned economic stimulus is unfortunately timed, coming on top of an economy that is being successfully inflated by expanding bank credit. Instead of declining, gold has every reason to go considerably higher, measured in those continually depreciating fiat currencies.

END

The new Sec Treasurer to be Mnuchin states that he believes in the long term the USA dollar is important but he backs boss Trump that the dollar should weaken and help USA exports

(courtesy GATA/Bloomberg)

Mnuchin says long-term strength of U.S. dollar is important

Submitted by cpowell on Fri, 2017-01-20 00:54. Section: Daily Dispatches

By Saleha Mohsin and Austin Weinstein

Bloomberg News

Thursday, January 19, 2017

Treasury Secretary nominee Steven Mnuchin told lawmakers today the long-term strength of the U.S. dollar is important and said President-elect Donald Trump’s comments that the currency was too high weren’t meant as a longer-run policy.

The dollar’s “long-term strength — over long periods of time — is important,” Mnuchin said in response to questions at his confirmation hearing before the Senate Finance Committee in Washington. “The U.S. currency has been the most attractive currency to be in for very, very long periods of time. I think that it’s important and I think you see that now more than ever.” …

… For the remainder of the report:

https://www.bloomberg.com/news/articles/2017-01-19/mnuchin-says-long-ter…

Your early FRIDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight

1 Chinese yuan vs USA dollar/yuan DOWN to 6.8785(SMALL DEVALUATION SOUTHBOUND /CHINA UNHAPPY TODAY CONCERNING USA DOLLAR RISE/MORE $ USA DOLLARS LEAVE CHINA/OFFSHORE YUAN NARROWS COMPLETELY BUT FALLS AS WELL TO 6.8539 / Shanghai bourse CLOSED UP 21.84 POINTS OR 0.71% / HANG SANG CLOSED DOWN 164.05 OR 0.71%

2. Nikkei closed UP 65.66 POINTS OR 0.34% /USA: YEN RISES TO 115.16

3. Europe stocks opened ALL MIXED ( /USA dollar index RISES TO 101.35/Euro DOWN to 1.0642

3b Japan 10 year bond yield: FALLS TO +.066%/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 115.16/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD FINALLY IN THE POSITIVE/BANK OF JAPAN LOSING CONTROL OF THEIR YIELD CURVE AS THEY PURCHASE ALL BONDS TO GET TO ZERO RATE!!

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 51.89 and Brent: 55.00

3f Gold UP/Yen DOWN

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil UP for WTI and UP for Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund RISES TO +.404%/Italian 10 yr bond yield UP to 2.015%

3j Greek 10 year bond yield RISES to : 7.11%

3k Gold at $1202.40/silver $16.96(8:15 am est) SILVER BELOW RESISTANCE AT $18.50

3l USA vs Russian rouble; (Russian rouble UP 4/100 in roubles/dollar) 59.85-

3m oil into the 51 dollar handle for WTI and 55 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation (already upon us). This can spell financial disaster for the rest of the world/China forced to do QE!! as it lowers its yuan value to the dollar/GOT a SMALL DEVALUATION DOWNWARD from POBC.

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 115.16 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 1.0076 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.0724 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT

3r the 10 Year German bund now POSITIVE territory with the 10 year RISES to +.404%

3s The Greece ELA NOW at 71.4 billion euros,AND NOW THE ECB WILL ACCEPT GREEK BONDS (WHAT A DISASTER)

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.50% early this morning. Thirty year rate at 3.068% /POLICY ERROR)GETTING DANGEROUSLY HIGH

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

(courtesy Jim Reid/Bloomberg/Deutsche bank/zero hedge)

S&P Futures, Dollar Rise As World Awaits Trump Inauguration Speech

Global shares were mixed, equity futures, the dollar and crude rose as investors focused their attention on today’s inauguration of Donald Trump as U.S. president. While the early tone is well bid, some traders anticipate a volatile session, with speculation that a bout of “sell the inauguration” could cap the aging Trump rally, which started with his inauguration.

Despite last night’s Yellen speech which was more dovish than her remarks just 24 hours earlier, and which suggested that the US economy is “not overheating”, the dollar managed to rebound from overnight losses and was trading 0.2% higher this morning. The early gains came after China reported its first economic expansion in 2 years (conveniently with president Xi in Davos) with GDP rising to 6.8% after quarters of decline.

However for the year, China’s GDP growth declined to the slowest pace in 26 years, despite a record debt load and record weak Yuan.

But it will be all about Trump today: tens of thousands of law enforcement officers and miles of barriers were in place in Washington D.C., as officials braced for hundreds of thousands of people planning to celebrate or protest the inauguration of Trump. The inauguration is “definitely a big moment for the markets,” said Neil Mellor, a London-based currency strategist at Bank of New York Mellon Corp. “We could get more clues about what Trump is planning today. If he ramps up the rhetoric the market will be concerned about building long dollar positions.”

“All eyes will be on the content and style of Trump’s inauguration speech,” Morgan Stanley’s Hans Redeker wrote in a note. “The more ‘Presidential’ this speech comes across, the better the outcome for markets.”

“[Trump is] likely to talk about job creation and unifying the U.S. and we may have to wait a bit longer for details on economic measures,” said Natixis fixed income strategist Cyril Regnat.

“It’s clear that investors have reached a level where they are prepared to wait and see what the Trump administration has to offer,” said Ric Spooner, chief market analyst at CMC Markets Asia Pacific Ltd. in Sydney.

Trump’s inauguration ceremony “will be followed by a speech that will be carefully decoded by those looking for signs of things to come in the new U.S. administration, an exercise that amounts to political astrology in an era characterized by a shakeup of the old rules of the game,” Citigroup’s chief global political analyst Tina Fordham wrote in note.

As Bloomberg notes, rallies in the dollar and equities are easing this week before Trump is sworn in as the 45th American president, with investors growing anxious for indications the administration will follow through on pro-growth campaign promises. Billionaire investor George Soros said the euphoria among stock investors since Trump’s victory will end as uncertainty takes over. The Dow Jones Industrial Average has churned in its tightest range ever over the past month.

European stocks opened weaker before recouping some losses to trade flat. Trading was choppy with mining shares, the biggest beneficiaries of the reflation rally spurred by Trump’s election win, the biggest drag on the indexes. The Stoxx Europe 600 Index was poised for its worst week since early December while the pound slid after a report showed U.K. retail sales fell at the fastest pace in almost five years last month. Gold headed for a fourth weekly advance.

Fund flows in the run-up to Friday’s inauguration indicate investors moving into less risky assets and locking in some profits in banking stocks and high-yield debt. Precious metals funds saw their first inflows in 10 weeks, according to data from fund tracker EPFR and Bank of America-Merrill Lynch while money was pulled from funds focused on financials stocks and high-yield bonds.

The Stoxx Europe 600 Index little changed as declines in miners offset gains in energy shares. Futures on the S&P 500 Index rose 0.2%. The S&P500 is heading for its biggest weekly drop of 2017. Contracts on the Dow Jones Industrial Average were little changed on Friday, and may be pressued by the disappointing earnings from both American Express and IBM.

10Y yields were flat at 2.5%, erasing previous declines. Government bonds retreated across the European Union.

* * *

Bulletin summary from RanSquawk

- Somewhat of a quiet affair this morning with European bourses failing to find any firm direction

- USD saw softness during Asian hours amid dovish interpretations of Yellen’s latest comments as well as ahead of Trump’s inauguration

- As well as Presidential Elect Trump’s Inauguration, today also see Canadian CPI and comments form Fed’s Harker and Williams

Market Snapshot

- S&P 500 futures up 0.2% to 2267

- Stoxx 600 down 0.1% to 362

- FTSE 100 down less than 0.1% to 7205

- DAX down less than 0.1% to 11595

- German 10Yr yield up 2bps to 0.4%

- Italian 10Yr yield up 3bps to 2.02%

- Spanish 10Yr yield up 2bps to 1.5%

- S&P GSCI Index up 0.5% to 396.9

- MSCI Asia Pacific down 0.1% to 140

- Nikkei 225 up 0.3% to 19138

- Hang Seng down 0.7% to 22886

- Shanghai Composite up 0.7% to 3123

- S&P/ASX 200 down 0.7% to 5655

- US 10-yr yield up 3bps to 2.5%

- Dollar Index up 0.16% to 101.31

- WTI Crude futures up 1.2% to $51.98

- Brent Futures up 1.2% to $54.79

- Gold spot down 0.3% to $1,201

- Silver spot down 0.9% to $16.87

Top Global News

- Trump Arrives for Inauguration With Promise to Unify the Nation: Addresses supporters on eve of swearing-in

- Yellen Says Fed Not Behind the Curve, Backs Gradual Rate Rises: Yellen sees risk in allowing the economy to run too hot

- Data showed U.K. retail sales fell at the fastest pace in almost five years in December

- China’s central bank said it provided a “temporary liquidity facility’’ to some major commercial banks for 28 days to help ease a cash crunch before the Lunar New Year holiday

- Soros Says Markets to Slump With Trump, EU Faces Disintegration: Says incoming U.S. president will fail

- JPMorgan Boosts CEO Dimon’s Annual Pay 3.7% to $28 Million: Bank awards $19 million compensation packages to four deputies

- IBM Margins Narrow While It Struggles to End Sales Slide: Revenue slips for 19th quarter, margins shrink for fifth

- American Express Profit Falls 8.2% as Expenses Top Estimates: Lender increases forecast for full-year earnings- per-share

- Deutsche Bank Burden in Mortgage Settlement Eased by Fine Print: German bank is the first to negotiate such a provision

- Heineken in Discussions With Kirin to Double Down in Brazil: Price would be less than a quarter of what it paid in 2011

- TPG’s Cushman & Wakefield Said to Have Held Early IPO Talks: Company said to hold informal meetings on listing soon as 3Q

* * *

Looking at regional markets, Asian stocks traded mixed following an uninspiring lead from Wall Street with participants cautious ahead of the US Presidential Inauguration and as the region digests Chinese GDP data. ASX 200 (-0.7%) lagged amid continued weakness in financials with mining names also pressured after iron ore prices fell over 1%. Conversely, Nikkei 225 (+0.3%) initially traded choppy alongside fluctuations in JPY, but was able to finish higher as JPY weakened slightly while Shanghai Comp (+0.7%) and Hang Seng (-0.6%) were mixed after a slew of tier-1 Chinese data including GDP in which the Y/Y figure beat expectations, although the pace of growth for 2016 was at its slowest in 26 years. Finally, 10yr JGBs traded higher amid a mostly cautious tone in the Asia-Pac region, while the BoJ were also in the market for a respectable JPY 1.12trl of JGBs ranging from 1yr-25yr-F maturities.

Chinese data

- Chinese GDP (Q4) Y/Y 6.8% vs. Exp. 6.7% (Prey. 6.7%)

- Chinese GDP YTD (Q4) Y/Y 6.7% vs. Exp. 6.7% (Prey. 6.7%): slowest yearly growth in 26 years.

- Chinese Industrial Production (Dec) Y/Y 6.0% vs. Exp. 6.1% (Prey. 6.2%); YTD (Dec) Y/Y 6.0% vs. Exp. 6.0% (Prey. 6.0%)

- Chinese Retail Sales (Dec) Y/Y 10.9% vs. Exp. 10.7% (Prey. 10.8%); Sales YTD (Dec) Y/Y 10.4% vs. Exp. 10.4% (Prey. 10.4%)

Top Asian News

- Mystery $9 Billion in Cash With Indians After Modi Shock Ban: Public withdrew more cash than currency in circulation: report

- Indonesia Tax Agency Demands Meeting With Top Google Executives: Google paid 5.2b rupiah in 2015 taxes: documents

- China Says It Offered Temporary Funding Support to Big Banks: ‘The central bank has a new liquidity tool,’ analyst says

- Mnuchin Says He’ll Tag China an FX-Manipulator If Warranted: Trump had backed away from pledge to add label immediately

In Europe, it has been a quiet morning with European bourses failing to find any firm direction, slight underperformance however has been observed in basis materials with Rio Tinto shares leading the FTSE 100 lower amid the declines in Iron prices.11 out of 19 Stoxx 600 sectors fall with basic resources, retail underperforming and oil & gas, construction & materials outperforming. 51% of Stoxx 600 members decline, 46% gain. While large UK supermarkets, Tesco’s and Sainsbury’s are soft today amid a negative note from Exane. Fixed income markets trade marginally in the red with Bunds lower by around 14 ticks, breaking below the 163.00 level, while slight outperformance in the curve has been notable in 5s and 10s.

Top European News

- U.K. Retail Sales Fall Most Since 2012 as Price Rises Bite: Sales drop 1.9% from November, decline 2% excluding auto fuel

- Lloyds Said to Shuffle Executives, Preparing for Strategy Review: CEO protege takes role examining group design, costs

- BofA, UBS Said to Lead Banks Sharing $427 Million UniCredit Fee: Fees represent about 3% of deal size vs 2% average

- Maersk IPO Plans Won’t Derail Bid for Dong’s $2.8 Billion Unit: Potential Dong bidders include DEA, PGNiG, BI analyst says

- Close Brothers Says Had Strong Performance at Start Fiscal Year: Confident of strong 1H result, good outcome for full 2017

- Tryg 4Q Net Misses Estimates; CEO Says 2017 on Track for Targets: Tryg 4Q profit after tax DKK560m vs est DKK664m

In currencies, the Bloomberg Dollar Spot Index was up 0.2 percent as of 10:38 a.m. in London after falling as much as 0.3 percent. The gauge is heading toward its first weekly advance since the period ending Dec. 23. The pound dropped 0.3 percent to $1.2301 and the euro retreated 0.3 percent to $1.0637. Nerves among USD longs were telling in late Asia and first thing in London were telling as the presidential inauguration ahead carries the ever-present risk of way lies ahead in terms of trade and currency policy in particular. This has since been reversed to some degree as UST yields push higher towards the highs seen at the very start of the year, but USD gains look a little more hesitant given events later in the day. USD/JPY is eyeing a return to the mid 115.00 highs seen yesterday, but notable was the EUFt/USD return to the upper 1.0600’s again despite was an unchanged status quo at the ECB Thursday, with tapering considerations dismissed out of hand to see the accommodative stance maintained despite rising headline inflation. For GBP, a softer than expect retail sales read in the UK for Dec has put a modest dent in the Pound based on the EUR/GBP upturn, which as yet struggles for momentum above the .8650 mark. Cable has slipped below 1.2300, but partly due to the broader USD impact. 1.2250 support has yet to be tested.

In commodities, the Trump inauguration ahead is prompting much caution across all asset classes, but given the prospective impact on infra structure spending and trade policy which has ramifications for China in particular, base metals in particular have been trading flat to marginally lower over the last 24-36 hours or so. Gold was finding a modest bid as the USD retreated a little this morning, but with US Treasuries pulling back again, we have seen the yellow metal slip back below USD1200.00, although it is likely that general risk sentiment will provide some support given today’s key events In Washington. Oil prices have stabilised after some notable losses in recent sessions, but the USD50.00 handle looks safe for now.

Government:

- 12pm: President-Elect Donald Trump takes oath of office

- Senate to hold confirmation votes on some Cabinet nominees

- 3pm: Congressional Hispanic Caucus holds news conference with House Democratic leaders on immigration policy

* * *

DB’s Jim Reid concludes the overnight wrap

In my 2017 outlook presentation in Paris I asked 4 questions where the audience were able to vote on the answer. The first was when will the next US recession occur? The audience voted 45% for 2019 and 45% for 2020 or beyond. The rest were 2017 and 2018. So they were pretty optimistic that the cycle will extend. When I asked this question to two big audiences on my travels last year around 70% answered 2017 or 2018 so expectations have seemingly changed. I also asked whether Italy will still be in the single currency in 5 years time. 91% said yes. Last year around 80% said yes in similar polls so again a more optimistic crowd. When asked whether the ECB will be fully out of QE by YE 2018 around 80% said no so it seems investors, although optimistic, still feel the ECB need to keep stimulus high over the next two years. Finally I asked what was the most likely event to occur out of the following four by the end of 2018? a) 10 year USTs above 5%, b) the S&P 500 trading below 1500, c) England winning the football World Cup or d) France electing Le Pen. Interestingly answer a) won with nearly 50% and the biggest shock was that England winning the World Cup scored 40% on this measure with the other two making up the last 10%. So only a few French investors thought a Le Pen victory was more likely than 5% yields, the S&P 500 below 1500 or England winning the World Cup.

So overall an optimistic crowd contrasting with surveys I did last year at various conferences. So there’s no doubt sentiment has changed in 2017 even if markets are in a bit of a lull. This should change soon one way or another as Donald Trump’s inauguration today marks the start of what promises to be a fascinating ride with a wide range of outcomes. Trump is set to speak at 2.30pm GMT and all we know right now is that Trump was said to have prepared the speech himself, with some advice and counsel from advisers as well as from some historians specifically regarding the length of the speech. Trump was also said to have told reporters that the speech will aim to unite America but we know little more than that at this stage. So it remains to be seen just how market moving this will be.

One topic which is certainly hogging the spotlight right now is the administration’s views on the US Dollar. Treasury secretary nominee Steven Mnuchin was the latest to address the currency debate yesterday and added to the confusion by saying that Trump’s observation on Monday that the Dollar is too strong was not meant as a “long-term comment”. Instead, Mnuchin said that “long-term strength over long periods of time is important” and that “I believe that’s a reflection of (the US having) the most attractive investment environment in the world”. Mnuchin also made comments about bank regulation, saying he supports the Volcker rule. On top of this he also said that he would look to raise the debt ceiling sooner rather than later, while also saying that he would label China a FX manipulator if warranted.

Over in markets, Dollar strength was again a theme yesterday after the USD index closed up +0.22% although it did pare earlier gains of as much as +0.80%. The other theme yesterday was the second successive day of Treasury yields climbing higher. In fact 10y Treasury yields closed up 4.4bps higher yesterday at 2.475% – which is a YTD high – and have all of a sudden risen 17bps from the intraday lows on Tuesday. The data helped at the margin but it appeared to be Yellen’s speech the day before and then those comments from Mnuchin which helped drive yields higher. The Fed Chair spoke again this morning but it seems to largely be a repeat of what she said previously, with little new information to highlight. Meanwhile US equity markets never really got going yesterday with the S&P 500 finishing -0.36% with rate sensitive sectors in particular underperforming.

Before we go any further we’re straight to China now where the latest monthly data dump is in. It has revealed that China’s economy grew 6.8% yoy in Q4 last year which was slightly more than the 6.7% expected by the market. For full year 2016, China reported growth of 6.7% which, while being the slowest pace since 1990, did end up right in the middle of the government’s official target. Meanwhile other activity indicators were mixed. Retail sales rose +10.9% yoy in December (vs. +10.7% expected) which is a tenth higher than that in November, although industrial production did slip two-tenths to +6.0% yoy (vs. +6.1% expected). Finally fixed asset investment was reported as rising +8.1% yoy for the full year (vs. +8.3% expected).

In terms of the market reaction Chinese equity markets are higher in response with the Shanghai Comp and CSI 300 +0.54% and +0.69% although a Bloomberg report suggesting that the China Financial Futures Exchange is to relax curbs on trading might also be helping the positive tone. Elsewhere it’s more mixed. The Nikkei is +0.14% although the Hang Seng (-0.58%), Kospi (-0.19%) and ASX (-0.58%) are down.

Moving on. The other focus for markets yesterday was the ECB meeting outcome. As we’d expected, a patient message was preached. Our European economists noted that the Bank is looking through the rise in headline inflation as the ECB’s patience and willingness to wait to extract the underlying trend from inflation was emphasized. Draghi said the Council will “continue to look through” HICP inflation “if judged to be transient and to have no implications for medium-term price stability”. The ECB President also outlined a framework for judging the “sustained adjustment” of inflation. In the view of our colleagues, “looking through” inflation implies less risk of an early tightening move in March. June is still the earliest timing for a tapering decision.

Away from that it was interesting to hear comments (Bloomberg) from hedge-fund manager George Soros yesterday in Davos. Speaking about Brexit he said that “it is unlikely that Prime Minister May is actually going to remain in power” and that Britons are in denial about what the economic impact of Brexit could be. When commenting about Europe Soros added that the laws that govern the EU are “not appropriate to the current circumstances” and that while he acknowledges it can still be saved, those making decisions in Brussels “know that Europe is not functioning”.

Before we look at the day ahead, it was an overall decent day for economic data in the US yesterday. Housing starts were reported as rising a bumper +11.3% mom (vs. +9.0% expected) in December while the November data was also revised up. Building permits (-0.2% mom vs. +1.1% expected) did miss but again we saw upward revisions to prior months. Meanwhile initial jobless claims declined to 234k from 249k which is the lowest since November. Finally the Philly Fed manufacturing survey ticked up 3.9pts to 23.6 (vs. 15.3 expected). That’s actually the highest level since November 2014 and more importantly, the detail revealed broad-based improvement which is indicative of a decent improvement in business spending this year according to our US economists.

Looking at today’s calendar, this morning in Europe the early data comes from Germany where the December PPI print will be released. Thereafter we’ll get retail sales numbers in the UK for the month of December which is expected to show a -0.4% mom decline excluding fuel. There’s nothing of note in the US this afternoon although we will hear from both the Fed’s Harker (2pm GMT) and Williams (6pm GMT). Of course the main event today will be Donald Trump’s inauguration as the 45th US President. The swearing-in ceremony is due at 2.30pm GMT. Before we wrap up, in addition to all things Trump related this weekend it’s also worth highlighting a couple of other potentially interesting events. French presidential candidate Marine Le Pen and Holland’s Freedom Party head Geert Wilders are amongst political leaders speaking at a rally of European nationalist parties in Germany tomorrow. Meanwhile on Sunday, France’s leftist parties are due to hold the first round of their primary. So worth keeping an eye on both those events.

END

i)Late THURSDAY night/FRIDAY morning: Shanghai closed UP 21.84 POINTS OR 0.71%/ /Hang Sang closed DOWN 164.05 OR 0.71%. The Nikkei closed UP 65.66 POINTS OR 0.34% /Australia’s all ordinaires CLOSED DOWN 0.62%/Chinese yuan (ONSHORE) closed DOWN at 6.8785/Oil ROSE to 51.89 dollars per barrel for WTI and 55.00 for Brent. Stocks in Europe ALL MIXED. Offshore yuan trades 6.8539 yuan to the dollar vs 6.8785 for onshore yuan.THE SPREAD BETWEEN ONSHORE AND OFFSHORE COMPLETELY NARROWS AS POBC ATTEMPTS TO STOP DOLLARS FROM LEAVING CHINA’S SHORES. HOWEVER BOTH CHINESE YUANS FALL WITH THE HIGHER DOLLAR

3a)THAILAND/SOUTH KOREA/:

END

b) REPORT ON JAPAN

none today

c) REPORT ON CHINA

A very important commentary. Even though we know that the data is fudged, China has now released data to suggest that their growth is the slowest in 26 years at 6.8%

(courtesy zerohedge)

China Grows At Slowest Pace In 26 Years Despite Record Debt, Currency Devaluation

Amid constant liquidity additions, record credit support, a devaluing currency, and admission that the last three years of macro data was fabricated; China ended 2016 with the worst economic growth since 1990…

China’s macro data avalanche was a mixed bag. The headline GDP grew more than expected (+6.8% YoY) but Industrial Production disappointed and while retail sales rose more than expected, fixed asset investment growth missed.

If debt is growth then China’s transmission mechanism is officially FUBAR as Q4 saw the largest surge in aggregate financing ever…

Credit expansion at close to twice the pace of GDP growth will be tough to sustain without putting financial stability at risk.

And a massive devaluation occurred in the yuan during Q4… (along with soaring bond yields and rising default risk)

And the result of all that…

- GDP (4Q): +6.8% BEAT +6.7% Exp

- Industrial Production (Dec.): +6.0% MISS +6.1% Exp

- Retail Sales (Dec.): +10.9% BEAT +10.7% Exp

- Fixed Assets Investments (YTD): +8.1% MISS +8.3% Exp

As Bloomberg notes,

“Stable growth has come at the expense of higher leverage and bubbles from bonds to bitcoin. A policy shift toward controlling financial risks and curbing housing prices will weigh on the economy in 2017.”

On a long-term horizon, the economy seems to be filled by ever-growing debt rather than investment or consumption.

“GDP beat market expectations. Mind you, China’s growth remains supported by massive government spending and record-setting bank lending which in itself continues to fuel asset bubble fears.”

* * *

As a reminder, Bloomberg notes that a shrinking working-age population, reduced scope for additions to the capital stock and diminished space for productivity gains mean that China’s potential growth is slowing. Bloomberg Intelligence estimates potential growth at 7.1% in 2016, down from 7.3% in 2015 and on a path to 6.5% by the end of the decade.

As Enda Curran, Bloomberg’s Chief Asia Economics Correspondent, concludes…

Of course, there is a cost to propping up GDP like this. And that’s debt.

It’s hard to look past the headline number without considering the gargantuan lending China’s banks were forced to pump into the economy to keep things chugging along. We know that policy makers are aware of this risk given the recent signals about prudent monetary policy and a tolerance for slower growth.

The initial fallout was a drop in the offshore Yuan rate (following Yuan strength going into the numbers thanks to Yellen’s dovish comments)…

END

This is a surprise move: the POBC cuts reserve ratios and then offers temporary funding and support for its largest banks. They wish to avoid a cash crunch!!

(courtesy zerohedge)

In “Strange Move”, PBOC Cuts Reserve Ratio, Offers Temporary Funding Support For Largest Banks

Overnight the PBOC injected another CNY95 billion into its banking system bringing the total weekly injection to a record CNY1.13 trillion.

However, it was not enough and overnight China allowed its five biggest banks to cut their reserve requirement ratio by 1% taking it down to 16% thus temporarily lowering the amount of money that they must hold as reserves to relieve pressure in its financial system as demand for cash surges ahead of the Lunar New Year holiday, Reuters reported. The banks affected by the move iclude ICBC, CCB, Bank of China, Bocom, and Agricultural Bank of China. The last time the central bank cut RRR was Feb. 29, 2016. The move is expected to release approximately 630 billion yuan in liquidity.

The dramatic moves come in a bid to avert a cash crunch heading into the country’s biggest holiday of the year.

Earlier in the week short-term funding costs had spiked to their highest levels in nearly 10 years on fears that liquidity was sharply tightening, sparking a jump in the yuan currency. But China watchers polled by Reuters had not expected a cut in RRR until the third quarter of 2017, as such a move would put more pressure on the ailing yuan. Following the massive central bank liquidity injections, key funding and money market rates showed signs of easing on Friday but remained well above normal levels.

But wait, that’s not all, because also overnight, the PBOC said it provided a “temporary liquidity facility” to some major commercial banks for 28 days to help ease a cash crunch before the Lunar New Year holiday. According to Bloomberg, the operation provides more effective liquidity transmission before the week-long break, the People’s Bank of China said in a statement Friday.

The PBOC said the new lending facility will have a funding cost for banks that’s around the same as open-market operations for a similar 28-day period, which is about 2.55 percent. That means the tool differs from cutting the ratio of deposits big banks must hold in reserve and suggests a fresh evolution of tools policy makers have been overhauling.

Commercial banks had 11 trillion yuan ($1.6 trillion) of sovereign and financial bonds outstanding as of December, Ming said, and have pledged about 43 percent of those to access funding through central bank open market operations, limiting room for further such operations.

The PBOC’s statement Friday didn’t say whether the temporary funding required collateral. Should none be required, that would be unusual because most such tools involve collateral.

The PBOC has shifted toward selective tightening after a two-year easing cycle. President Xi Jinping and other policy makers decided at their annual economic conference last month China should plan prudent and neutral monetary policy this year to prevent financial risks.

“It’s too premature to conclude that there’s a change in China’s monetary policy direction,” Raymond Yeung, chief greater China economist at Australia & New Zealand Banking Group Ltd. in Hong Kong, wrote in a note. “Liquidity management and leverage control seem to be more appropriate expressions to describe the policy direction of China’s central bank.”

“It’s likely the central bank will use temporary liquidity facility as a regular tool in the future to ease liquidity shortage before quarter-end or holidays,” said Xia Le, chief economist at Banco Bilbao Vizcaya Argentaria SA in Hong Kong. The PBOC is using a new tool because older ones offer funds at a high cost and longer duration than needed, and it’s wasteful for banks that need money for five days to have to borrow for a full year, Xia said.

While in the past the PBOC has engaged in similar moves ahead of the new year, the latest move suggested there were additional factors involved in draining liquidity: “Today’s move seems to suggest that liquidity conditions are tighter than authorities’ expectations, as capital outflows remain strong,” said Zhou Hau, senior emerging markets economist at Commerzbank in Singapore.

“But in the meantime, an outright easing will add pressure on the yuan exchange rate as well. That could be the reason behind today’s strange move.”

The central bank will restore the RRR for the five banks to the normal level at an appropriate time after the holiday, according to Reuters’ sources. “This is a temporary adjustment, and is mainly in response to the cash withdrawal, tax payment and reserve payment. (The RRR) will go back to the normal rate after the Lunar New Year holiday,” one source said.