Gold at (1:30 am est) $1234.20 UP $4.20

silver at $17.73: up 6 cents

Access market prices:

Gold: $1234.00

Silver: $17.70

THE DAILY GOLD FIX REPORT FROM SHANGHAI AND LONDON

.

The Shanghai fix is at 10:15 pm est last night and 2:15 am est early this morning

The fix for London is at 5:30 am est (first fix) and 10 am est (second fix)

Thus Shanghai’s second fix corresponds to 195 minutes before London’s first fix.

And now the fix recordings:

Shanghai FIRST morning fix Feb 7/17 (10:15 pm est last night): $ 1238.64

NY ACCESS PRICE: $1232.20 (AT THE EXACT SAME TIME)/premium $6.44

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Shanghai SECOND afternoon fix: 2: 15 am est (second fix/early morning):$ 1241.64

NY ACCESS PRICE: $1233.45 (AT THE EXACT SAME TIME/2:15 am)

SPREAD/ 2ND FIX TODAY!!: $8.19

China rejects NY pricing of gold as a fraud/arbitrage will now commence fully

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

London FIRST Fix: Feb7/2017: 5:30 am est: $1231.00 (NY: same time: $1229.50 (5:30AM)

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

London Second fix Feb 7.2017: 10 am est: $1231.00 (NY same time: $1231.60 (10 AM)

It seems that Shanghai pricing is higher than the other two , (NY and London). The spread has been occurring on a regular basis and thus I expect to see arbitrage happening as investors buy the lower priced NY gold and sell to China at the higher price. This should drain the comex.

Also why would mining companies hand in their gold to the comex and receive constantly lower prices. They would be open to lawsuits if they knowingly continue to supply the comex despite the fact that they could be receiving higher prices in Shanghai.

end

For comex gold:

FEBRUARY/

NOTICES FILINGS FOR FEBRUARY CONTRACT MONTH: 111 NOTICE(S) FOR 11100 OZ. TOTAL NOTICES SO FAR: 5116 FOR 511,600 OZ (15.912 TONNES)

For silver:

For silver: FEBRUARY

1 NOTICES FILED FOR 5,000 OZ/

TOTAL NO OF NOTICES FILED: 146 FOR 730,000 OZ

Let us have a look at the data for today

.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total open interest ROSE by 2869 contracts UP to 193,336 with respect to YESTERDAY’S TRADING. In ounces, the OI is still represented by just less THAN 1 BILLION oz i.e. .966 BILLION TO BE EXACT or 138% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT FEBRUARY MONTH: 1 NOTICE(S) FOR 5,000 OZ

In gold, the total comex gold ROSE BY 9534 contracts WITH THE RISE IN THE PRICE GOLD ($11.50 with YESTERDAY’S trading ).The total gold OI stands at 411,275 contracts

we had 111 notice(s) filed upon for 11,100 oz of gold.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD:

We had a huge change in tonnes of gold at the GLD/a deposit of 8.30 tonnes

Inventory rests tonight: 826.95 tonnes

.

SLV

we had no changes in silver into the SLV

THE SLV Inventory rests at: 334.713 million oz

end

.

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in silver RISE by 2869 contracts UP to 193,336 AS SILVER WAS UP 22 CENTS with YESTERDAY’S trading. The gold open interest ROSE by 9534 contracts UP to 411,275 WITH THE RISE IN THE PRICE OF GOLD OF $11.50 (YESTERDAY’S TRADING)

(report Harvey

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

)

3. ASIAN AFFAIRS

i)Late MONDAY night/TUESDAY morning: Shanghai closed DOWN 3.89 POINTS OR .12%/ /Hang Sang CLOSED DOWN 16.67 POINTS OR .07% . The Nikkei closed DOWN 65.93 POINTS OR 0.35% /Australia’s all ordinaires CLOSED UP 0.13%/Chinese yuan (ONSHORE) closed DOWN at 6.8840/Oil FELL to 52.79 dollars per barrel for WTI and 55.46 for Brent. Stocks in Europe ALL IN THE GREEN. Offshore yuan trades 6.8342 yuan to the dollar vs 6.8840 for onshore yuan.THE SPREAD BETWEEN ONSHORE AND OFFSHORE WIDENS QUITE A BIT AS DOLLARS ARE LEAVING CHINA’S SHORES. BOTH YUANS WEAKER COUPLED WITH THE STRONGER DOLLAR

REPORT ON JAPAN SOUTH KOREA NORTH KOREA AND CHINA

3a)THAILAND/SOUTH KOREA

b) REPORT ON JAPAN

c) REPORT ON CHINA

i)Chinese dollar reserves which include USA dollars, foreign currencies like the Euro and the pound along with gold, fell to below $3 trillion equivalent. You can bet that China will engage in capital controls to prevent more USA dollars from leaving

( zerohedge)

ii)China just received a shock with reports of a huge demand decline for cars as inventories climb. This was due to tax hikes:

4. EUROPEAN AFFAIRS

i)ITALY

Quite a story!! Unicredit is Italy’s largest bank and they are undergoing a rights offering such that there will be a 70% dilution. The bank suffered a loss of 11 billion euros in 2016 and they are trying to steer their ship northbound in profits. The problem is none of the shareholders with greater than 3% ownership is wishing to participate in the rights offering

(COURTESY Milan news)

ii)GREECE

Disagreements between the IMF and the Germans over Greek debt has caused the 2 yr Greek bond to skyrocket to over 10%. The iMF is stating that no new austerity is needed even though the Germans et al want more austerity. The IMF wants debt forgiveness something that Germany will not allow.

fun and games with Greece…

( zerohedge)

iii)GERMANY

Shock in Germany as Merkel is losing support to Martin Schultz. However the euroskeptic party is faltering. A coalition without Merkel’s party will have no real changes in political outlook

(courtesy zero hedge)

iv)GERMANY/ISRAEL/DEUTSCHE BANK

German CEO Schwartz arrested in Tel Aviv. The bank’s offices were raided yesterday and today Schwartz was arrested. It seems that they have avoided paying any of the value added taxes on their many transactions with clients.

( zerohedge)

v)This does not look good for Europe and the leader of European production Germany just saw their industrial production plunge by the most since 2009

( zero hedge)

vi) UK/trading today/ UK Pound/uSA)

Dollar retraces gains today with Cable (Pound/USA dollar) sharply higher on May’s Parliamentary victory with respect to the Brexit

( zero hedge)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

i)Iran

more war of words from Iran’s Ayatollah..he vows revenge!

( zerohedge)

ii)Did Iran blink first:

( zero hedge)

6.GLOBAL ISSUES

7. OIL ISSUES

i)The EIA forecasts record amounts of crude production for next year. Down goes oil again

( zero hedge)

ii)It plunges again after the second biggest crude inventory build in USA history

( zero hedge)

8. EMERGING MARKETS

9. PHYSICAL MARKETS

10.USA STORIES

i)For the full year the USA trade deficit rises to 500 billion dollars, the biggest in 4 years. This is a negative towards GDP growth calculations. December saw a slight improvement

( zero hedge)

ii)Janet’s favourite labour stat is the JOLTS report. Job openings are going nowhere

(zero hedge)

iii) Both Student debt (1.41 trillion USA) and Auto loan debt (1.1 trillion USA) increase again and as such they total over 2.5 trillion dollar, an all time high. the taxpayer is going to take a huge hit on this

( zero hedge)

Let us head over to the comex:

The total gold comex open interest ROSE BY 9,534 CONTRACTS UP to an OI level of 411,275 WITH THE RISE IN THE PRICE OF GOLD ( $11.50 with YESTERDAY’S trading). We are now in the contract month of FEBRUARY and it is one of the better delivery months of the year. In this next big active delivery month of February we had a LOSS of 419 contracts DOWN to 1773. We had 156 notices served upon yesterday and therefore we LOST 263 contracts or an additional 26,300 oz will NOT stand for delivery and these were cash settled for a fiat bonus. The next non active contract month of March saw it’s OI fall by 105 contracts DOWN to 2202.The next big active month is April and here the OI ROSE by 8220 contracts UP to 282,672.

We had 111 notice(s) filed upon today for 11,100 oz

And now for the wild silver comex results. Total silver OI rose by 2869 contracts FROM 190,467 up to 193,336 as the price of silver ROSE IN PRICE TO THE TUNE OF 22 CENTS with respect to YESTERDAY’S trading. We are moving further from the all time record high for silver open interest set on Wednesday August 3/2016: (224,540).

The active month of February saw the OI FALL by 2 contract(s) DOWN TO 163. We had 0 notices served upon yesterday so we lost 2 CONTRACTS or an additional 10,000 oz will not stand.

The next big active delivery month is March and here the OI increase by 1632 contracts up to 125,244 contracts. For comparison purposes last year on the same date only 101,229 contracts were standing.

We had 1 notice(s) filed for 5,000 oz for the FEBRUARY contract.

VOLUMES: for the gold comex

Today the estimated volume was 197,335 contracts which is FAIR.

Yesterday’s confirmed volume was 205,409 contracts which is good

volumes on gold are getting higher!

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz |

11,340.82 OZ

incl

123 kilobars

I -D

Brinks

Scotia

|

| Deposits to the Dealer Inventory in oz | 999.97 oz

brinks |

| Deposits to the Customer Inventory, in oz |

nil oz

|

| No of oz served (contracts) today |

111 notice(s)

11,100 oz

|

| No of oz to be served (notices) |

1662 contracts

166,200 oz

|

| Total monthly oz gold served (contracts) so far this month |

5116 notices

511,600 oz

15.912 tonnes

|

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | 112,989.8 oz |

Today, 0 notice(s) were issued from JPMorgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equates to 111 contract(s) of which 23 notices were stopped (received) by jPMorgan dealer and 0 notice(s) was (were) stopped/ Received) by jPMorgan customer account.

March 2016: 2.311 tonnes (March is a non delivery month)

| Silver | Ounces |

| Withdrawals from Dealers Inventory | nil |

| Withdrawals from Customer Inventory |

579,294.04 0z

CNT

Delaware

|

| Deposits to the Dealer Inventory |

nil oz

|

| Deposits to the Customer Inventory |

602,702,352 OZ

Delaware

Scotia

|

| No of oz served today (contracts) |

1 CONTRACT(S)

(5,000 OZ)

|

| No of oz to be served (notices) |

160 contracts

(800,000 oz)

|

| Total monthly oz silver served (contracts) | 146 contracts (730,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month | 4,230,952.0 oz |

end

And now the Gold inventory at the GLD

Feb 7/another huge fake deposit of 8.30 tonnes of gold into the GLD/the addition is a paper addition and no doubt not physical/ total inventory: 826.95 tonnes

FEB 6/a huge deposit of 7.43 tonnes of gold into the GLD/Inventory rests at 818.65 tonnes

FEB 3/no change in gold inventory at the GLD/Inventory rests at 811.22 tonnes

Feb 2/another huge deposit of 1.48 tonnes/inventory rests at 811.22 tonnes

Feb 1/a huge “deposit” of 10.67 tonnes of gold into the GLD/Inventory rests at 809.74 tonnes. this should stop GLD from sending gold to Shanghai.

JAN 31/no change in gold inventory at the GLD/Inventory rests at 799.07 tonnes

jan 30/no change in gold inventory at the GLD/Inventory rests at 799.07 tonnes

Jan 27/no changes at the GLD/Inventory rests at 799.07 tonnes

Jan 26/no changes at the GLD/Inventory rests at 799.07 tonnes/

jan 25/another exactly the same withdrawal as yesterday: 50.4 tonnes and again this was used in the whacking of gold today/inventory rests at 799.07 tonnes

jan 24/a huge withdrawal of 5.04 tonnes and probably this was used today in the whacking of gold/inventory rests at 804.11 tonnes

Jan 23/a big change/this time a deposit of 1.19 tonnes of gold into the GLD/inventory rests at 809.15 tonnes. The drainage of gold from the GLD to Shanghai has now stopped!

Jan 20/no changes in gold inventory a the GLD/Inventory rests at 807.96 tonnes

Jan 19/no changes in gold inventory at the GLD/Inventory rests at 807.96 tonnes

Jan 18/no changes in gold inventory at the GLD/Inventory rests at 807.96 tonnes

Jan 17/17/a deposit of 2.96 tonnes of gold/inventory at the GLD rests at 807.96 tonnes. I guess there is no more gold inventory to sent to C+Shanghai

Jan 13/17/there were no changes in gold inventory at the GLD/Inventory rests at 805.00 tonnes

Jan 12/2017/no change in gold inventory at the GLD/Inventory rests at 805.00 tonnes

Jan 11/no change in gold inventory at the GLD/Inventory rests at 805.00 tonnes

JAN 10/no changes in gold inventory at the GLD/Inventory rests at 805.00 tonnes

JAN 9/A WITHDRAWAL OF 8.87 TONNES OF GOLD FROM THE GLD/INVENTORY RESTS AT 805.00 TONNES

end

NPV for Sprott and Central Fund of Canada

end

Major gold/silver trading/commentaries for TUESDAY

GOLDCORE/BLOG/MARK O’BYRNE

Gold Prices Rising Mean “Impending Market Volatility”

-

Gold prices rising & up 6.6% YTD

-

Signal “impending market volatility”

-

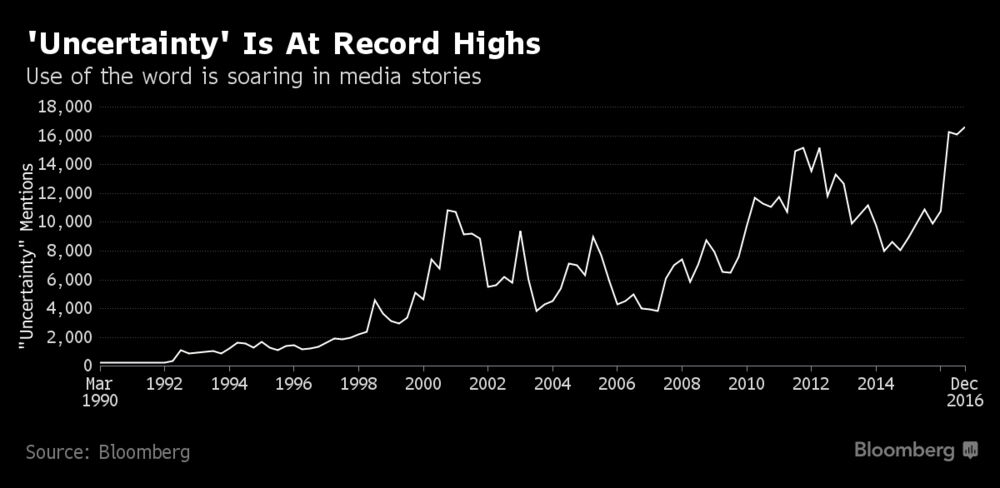

World has never been more uncertain (see chart)

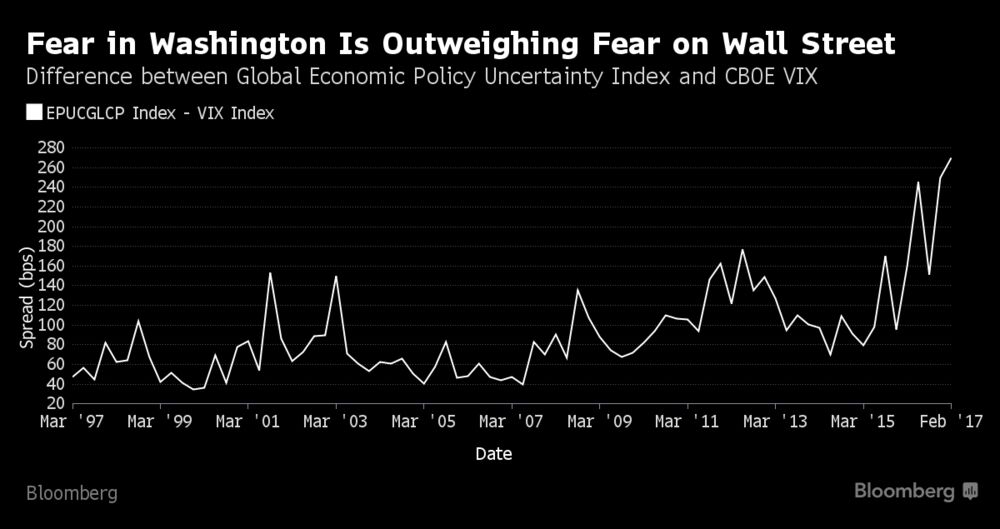

- Fear in Wall Street versus Fear in Washington

- Price of ‘plunge protection’ rising even as VIX remains low

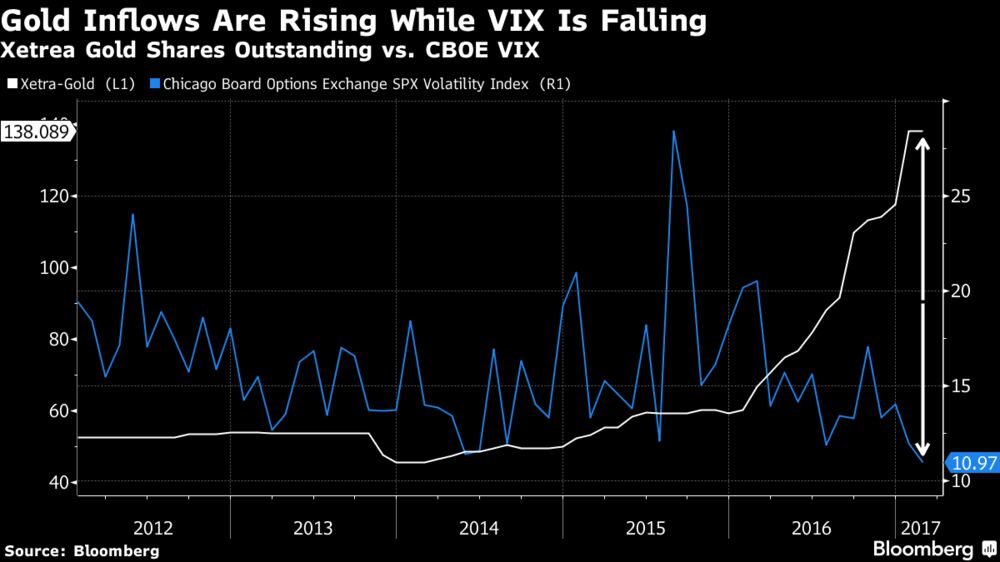

- Smart money diversifying into gold

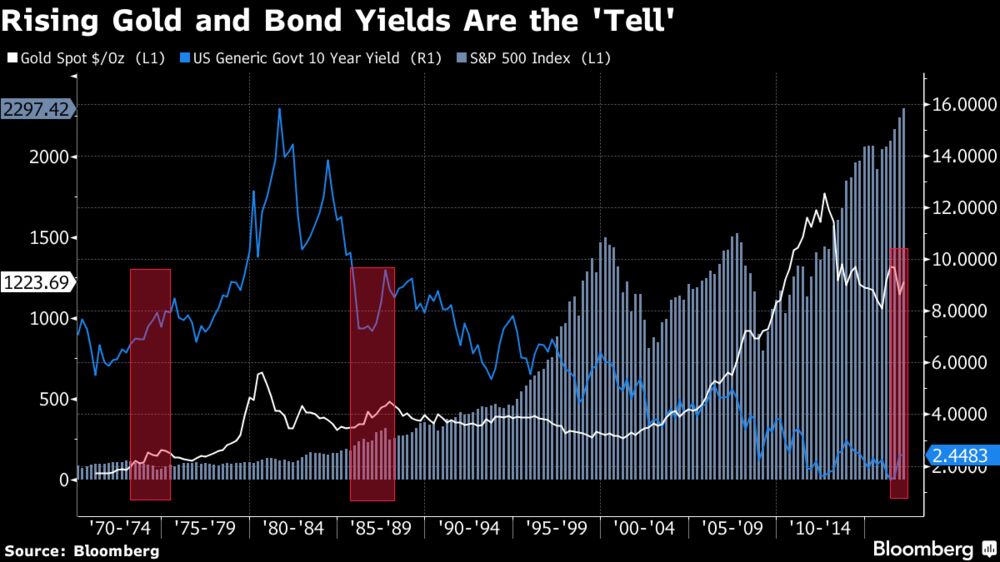

- Important to watch rising gold and rising bond yields

- Gold may prove the “tell”

Bloomberg have done an excellent article replete with five must see charts including gold charts that suggest that we are on the verge of significant market volatility and turmoil.

From Bloomberg:

“A former TV star as U.S. president doesn’t seem to have injected markets with much of a ‘‘fear factor.’’ But digging beneath the surface of an eight-year bull run exposes subtle signs that hint at an uneasy optimism.

The Dow Jones Industrial Average has sailed past 20,000 and the S&P 500 is nearing its life-time high set in January, indicating that investors have so far shrugged off the uncertainty brought by the new administration.

Here are five charts that suggest all is not well in markets:”

The article concludes by saying that it is important to watch rising bond yields and rising gold prices. We note that this was a toxic combination which was seen in the 1970s. The article concludes:

“Gold may prove the “tell,” according to Chris Flanagan, also at Bank of America. He advises investors to watch “for the combo of rising yields and rising gold prices to signal impending market volatility.” Three consecutive quarters of rising benchmark bond yields and gold prices preceded previous market falls including the 1973-1974 bond market crash and Black Monday in 1987, he says. The yield on the benchmark 10-year U.S. Treasury has risen to 2.44 percent from 1.77 percent since Trump’s election win. Gold has moved sideways.”

http://www.goldcore.com/us/gold-blog/gold-prices-rising-mean-impending-market-volatility/

END

Your early TUESDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight

1 Chinese yuan vs USA dollar/yuan WEAKER AT 6.8840(SMALL DEVALUATION SOUTHBOUND /OFFSHORE YUAN WIDENS TO 6.8342 / Shanghai bourse DOWN 3.89 POINTS OR .12% / HANG SANG CLOSED DOWN 16.67 POINTS OR .07%

2. Nikkei closed DOWN 65.931 POINTS OR 0.35% /USA: YEN RISES TO 112.42

3. Europe stocks opened ALL IN THE GREEN ( /USA dollar index RISES TO 100.57/Euro DOWN to 1.0677

3b Japan 10 year bond yield: RISES TO +.108%/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 112.42/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD FINALLY IN THE POSITIVE/BANK OF JAPAN LOSING CONTROL OF THEIR YIELD CURVE AS THEY PURCHASE ALL BONDS TO GET TO ZERO RATE!!

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 52.79 and Brent: 55.46

3f Gold DOWN/Yen DOWN

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil DOWN for WTI and DOWN for Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund FALLS TO +.381%/Italian 10 yr bond yield UP to 2.348%

3j Greek 10 year bond yield RISES to : 7.59%

3k Gold at $1230.90/silver $17.66(8:15 am est) SILVER BELOW RESISTANCE AT $18.50

3l USA vs Russian rouble; (Russian rouble DOWN 46/100 in roubles/dollar) 59.38-

3m oil into the 52 dollar handle for WTI and 55 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation (already upon us). This can spell financial disaster for the rest of the world/China forced to do QE!! as it lowers its yuan value to the dollar/GOT SMALL DEVALUATION SOUTHBOUND from POBC.

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 112.42 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 0.9988 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.0663 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT

3r the 10 Year German bund now POSITIVE territory with the 10 year FALLS to +.381%

3s The Greece ELA NOW at 71.4 billion euros,AND NOW THE ECB WILL ACCEPT GREEK BONDS (WHAT A DISASTER)

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.426% early this morning. Thirty year rate at 3.068% /POLICY ERROR)GETTING DANGEROUSLY HIGH

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

(courtesy Jim Reid/Bloomberg/Deutsche bank/zero hedge)

S&P Futures, European Stocks Bounce As Dollar Rises Most In Two Weeks; Gold, Yen Slide

The dollar rebounded from a key 200-DMA support level, strengthening against all major peers, pushing S&P futures higher as European shares rose, led by basic resources and real estate, while Asian stocks fall. Gold fell from its highest level since November as demand for some haven assets ebbed while global bonds declined. Oil dipped, pressured by a stronger dollar.

The Bloomberg Dollar Spot Index rose the most in almost two weeks, jumping against the offshore Chinese yuan on an unexpected fall in Beijing’s foreign exchange reserves below $3 trillion for the first time in six years, while a slumping euro benefited European stocks. “We think the dollar will go higher from here,” said Adam Cole, head of global foreign-exchange strategy in London at Royal Bank of Canada. “On balance Trump’s policies are dollar positive and that will win over the rhetoric.” The euro fell 0.8% to $1.0665, its biggest fall since Dec. 15 last year, while the dollar index was up over 0.7%, its biggest rise since Jan. 6.

European political jitters remained, and sent the spread between French and German 10-year bonds rose to 78 bps, the highest level since November 2012. It was 50 basis points only two weeks ago.

“The acceleration of the trend of wider spreads since the start of the year has been widespread and not just confined to France, where obviously the political tail risk is the greatest,” said Kenneth Broux, head of corporate research, FX and rates at Societe Generale.

Even as the main European indices advanced, banks posted the biggest declines on lackluster earnings and falling bond yields. European financial markets struggled with growing economic and political concerns involving the French and German elections on Tuesday as the euro neared its biggest fall this year and bond yield spreads over Germany reaching the widest in several years.

“The political calendar is likely to make some investors sit uneasy on some positions, particularly as the prevailing opinion remains that none of the anti-European parties will have a significant chance of getting close to power,” RBC Capital Markets strategists wrote in a note on Tuesday quoted by Reuters. “Whilst this is also our expectation, complacent markets will likely face at least one moment where the iron-clad view will be questioned.”

Among the rising political din, the markets broadly ignored a 3.0% plunge in German industrial output (exp.+0.3%), the biggest drop in 8 years, and yet another indication that the favorable global macro impulse driven mostly by China’s record credit injection in 2016 is fading fast.

European corporate earnings offered some cheer even though oil giant BP missed estimates, but failed to completely shrug off the unease fueled by the growing unpredictability of the French presidential election race. National Front Leader Marine Le Pen has vowed to fight globalization and take France out of the euro zone, while conservative candidate Francois Fillon on Monday vowed to fight on for the presidency despite a damaging scandal involving taxpayer-funded payments to his wife. Earlier on Tuesday, Emmanuel Macron, the independent centrist candidate and favorite to win the election, knocked down rumors he has a gay relationship outside his marriage since 2007.

Chipmaker AMS rose 16%, poised for its best-day ever after the company’s fourth-quarter revenue came in at the top end of the chipmaker’s expectations. BP was the biggest drag on the broader index, down 2.5%.

Elsewhere, MSCI’s index of Asia-Pacific ex-Japan fell 0.3% while Japan’s Nikkei closed down 0.35%, driven by a stronger Yen, although the USDJPY has since rebounded stronly. Chinese shares dropped 0.4%ahead of data that showed FX reserves fell for the seventh straight month in January and below $3 trillion for the first time in six years. The dollar rose 0.5 percent against the offshore yuan its biggest rise in three weeks. Concerns remain over the speed at which China has depleted its cash resources to defend the currency. Reserves were almost $4 trillion in mid-2014.

U.S. stock futures pointed to a 0.3% higher open, undoing all over Monday’s 0.2% drop.

Oil prices buckled under the dollar’s gains, extending their decline following the biggest one-day loss since Jan. 18 on Monday as worries about rising oil supply out of the United States tussled with optimism about output curbs elsewhere. U.S. crude fell 0.5% to $52.72 a barrel, after falling 1.5% on Monday. Brent fell 0.6% to $55.40, after sliding 1.9% on Monday.

Bulletin Headline Summary from RanSquawk

- European stocks trade with little direction in a similar fashion to their Asian counterparts amid light new fundamental news

- Energy underperforms in line with oil prices while soft BP earnings sees them lag in the FTSE 100

- A light economic calendar remains the case today, with highlights including US API crude oil inventories, comments from ECB’s Weidmann and earnings from Walt Disney

Market Snapshot

- S&P 500 futures up 0.3% to 2293

- Stoxx 600 up 0.4% to 363

- FTSE 100 up 0.6% to 7216

- DAX up 0.4% to 11557

- German 10Yr yield down 1bp to 0.36%

- Italian 10Yr yield down 3bps to 2.35%

- Spanish 10Yr yield down less than 1bp to 1.78%

- S&P GSCI Index up less than 0.1% to 396.9

- MSCI Asia Pacific down 0.3% to 142

- Nikkei 225 down 0.3% to 18911

- Hang Seng down less than 0.1% to 23332

- Shanghai Composite down 0.1% to 3153

- S&P/ASX 200 up 0.1% to 5622

- US 10-yr yield up less than 1bp to 2.42%

- Dollar Index up 0.77% to 100.68

- WTI Crude futures down 0.3% to $52.84

- Brent Futures down 0.3% to $55.53

- Gold spot down 0.5% to $1,229

- Silver spot down 0.8% to $17.60

Top Global News

- KKR to Combine Prisma With Paamco to Create $34 Billion Firm: Employees to own 60% of Paamco Prisma while KKR holds 40%

- Teva Loses CEO, Leaving Investors to Guess What’s Next: Board Chairman Peterburg will take over as interim CEO

- FXCM to Withdraw From U.S. After Probe, Sell Client Accounts: Gain Capital signs letter of intent to purchase U.S. accounts

- Philadelphia Fed’s Harker Says March Is on the Table for a Hike: Harker says it depends on how data shape up

- BP and Shell Hit After OPEC Output Cuts Halt Oil-Trading Bonanza: Oil traders benefited in 2015, 2016 from storage deals

- Trump Administration to Argue U.S. Faces Grave Peril Without Ban: Appellate judges will hear case Tuesday in San Francisco

- Bayer-Monsanto Seen Squeezing Brazil’s Farmers, Minister Says: ‘Only a small number of suppliers for a very large world’

Asian stocks dropped, pressured by a weak close in the US where the main indices were kept in check amid a lack of fundamental news and drivers, which resulted in the S&P 500 snapping a 3-day win streak. 7 out of 11 sectors retreat in the MSCI Asia Pacific Index with energy, consumer discretionary underperforming and utilities, real estate outperforming. ASX 200 (+0.1%) was initially lower with weakness in financials and consumer discretionary after Macquarie affirmed flat guidance Y/Y and reports that Tabcorp’s monopoly on in-venue betting was under threat by a potential Crown Resorts venture, although, the index then staged a late recovery into the close. Elsewhere, Nikkei 225 (-0.5%) suffered the brunt of a firmer JPY with mining and energy names weighed by declines seen in copper, iron ore and crude oil, while the Hang Seng (-0.1%) and Shanghai Comp (-0.4%) were dampened as participants digested the PBoC once again refraining from conducting open market operations due to high liquidity and reportedly urged banks to curb lending. Finally, 10yr JGBs traded marginally higher amid a risk averse tone in Japan, while mixed 10yr inflation-indexed auction results failed to spur any significant price action.

Top Asia News

- Top India Forecaster Sees Rate Pause in Break From Consensus: Would be helpful for economy, rupee “to stay pat”: BNP’s Hau

- India Said to Sell $993 Million ITC Stake to State-Owned LIC: Stake said to be sold for about 275.85 rupees a share

- China’s Central Bank Halts Gold Buying for Third Straight Month: Country’s foreign exchange reserves at lowest since ‘11

- Rio Gifts India Diamond Mine to Madhya Pradesh Government: Project hampered by delay in getting environmental permits

European equities traded mostly higher today, initially opening lower, before moving into modest positive territory throughout the European morning. 15 out of 19 Stoxx 600 sectors rise with basic resources, real estate outperforming and oil & gas, banks underperforming. 77% of Stoxx 600 members gain, 21% decline. Earnings continue to draw headlines, with BP (-2.4%) the worst performer in the FTSE after their report, while BNP Paribas (-4.3%) weigh on the CAC in the wake of their release. As such energy and financials are the worst performing sectors, with upside seen in materials so far this morning. Elsewhere, FTSE100 outperforms as exporters benefit once again from GBP softness French yields rose this morning as the political situation in the country intensifies, OAT’s trade higher by 0.65% slightly higher than the core regions this morning. Today supply is slightly heavier than average with the UK, ESM and the US all coming to market.

Top European News

- BNP Paribas Posts Net That Misses Estimates, Plans Cost Cuts: French consumer-banking earnings decline by 36% in quarter

- Statoil Vows to Keep Cutting Costs After Third Consecutive Loss: Company plans a further $1 billion of savings in 2017

- German Industrial Output Unexpectedly Falls Most in 8 Years: Output dropped 3% in December vs estimated 0.3% increase

- May Comfortably Sees Off First Attempts to Amend Brexit Bill: Commons lawmakers vote down series of opposition amendments

- Deutsche Boerse, LSE Submit Divestment Plans to Regulators: ormal remedy submitted to EC to ease antitrust concerns

In currencies, the JPY looks to be driving trade at present, and this has contributed to the USD/JPY move higher to 112.50 to spike through 111.75 initial support. Stronger levels seen below 111.50, and we have since recovered through 112.50 after hitting a 111.60 low. Elsewhere though, the USD has made good ground against the EUR, GBP and CAD as well as managing to pull the AUD and NZD back down to more familiar levels — the NZD after pushing to new cycle highs just shy of 0.7375. This has been facilitated by the loss of 120.00 in EUR/JPY, 140.00 in GBP/JPY and more modest JPY gains against the commodity currencies. EUR/USD has dropped down 1.0655 so far, and political tensions will be cited as a key driver, but this has not stopped EUR/GBP pushing back above 0.8600 again, resulting in a Cable move below notable support ahead of 1.2400. Brexit jitters allied with a significant fall in the BRC like for like sales over Jan have contributed to the latest round of losses here, but as the triggering of Article 50 nears, (GBP) longs are becoming nervous. The RBA overnight gave a balanced account of domestic and global prospects/risks whilst maintaining the cash rate at 1.50%, but despite a somewhat delayed move higher, failed to generate momentum for a fresh test on 0.7700. In contrast, the rise in NZ inflation expectations saw the recent 0.7350 highs stretched out by another 24-25 ticks, but this has since been reversed and we have since lost the 0.7300 handle. USD/CAD is now testing 1.3200 on the upside, dragged higher by the broader ‘USD’ move.

In commodities, there has been little of note in the commodities market over the last 24 hours, though Gold has dropped from the best levels in three months. Losses in USD/JPY highlight the risk skew to the moves in the yellow metal, but we have seen some resistance here through the USD1230.00 level. WTI has edged back under USD53.00, but limited emphasis on price action as long as we stay inside the USD50-55 range. Base metals trading sideways, but Copper has edged further away from USD2.70, but to a modest degree. Palladium the under-performer on the day so far, but little to note behind it as yet.

Looking at today’s calendar, this morning we kicked off in Germany where the December industrial production data was released and caused a mini shock when it showed a 3% plunge, the biggest in 8 years, on expectations of a modest rise. In the US the early release is the December trade balance reading, followed then by the latest JOLTS job openings print. Later we’ll get consumer credit for the month of December. Away from the data we are due to hear from the BoE’s Forbes this afternoon as well as the ECB’s Weidmann. The BoJ is also due to release minutes from the January meeting. Earnings wise there are 28 S&P 500 companies due to report including General Motors and Walt Disney.

US Event Calendar

- 8:30am: Trade Balance, Dec., est. -$45.0b (prior -$45.2b)

- 8:55am: Redbook weekly sales

- 10am: JOLTS Job Openings, Dec., est. 5.580m (prior 5.522m)

- 3pm: Consumer Credit, Dec., est. $20.0b (prior $24.532b)

- 4:30pm: API weekly oil inventories

US Government Docket

- Senate votes on nomination of Betsy DeVos for Education sec.

- House votes on measures to block Interior Dept and Education Dept regulations

- 10am: Andy Puzder, nominee for Labor sec., testifies before Senate Health, Education, Labor and Pensions Cmte

- 10am: House Armed Services Cmte holds full cmte hearing on the state of the military

- 10am: Senate Foreign Relations Cmte hearing on ‘‘The Plan to Defeat ISIS’’

- 10am: House Homeland Security Cmte hears from Homeland Security Sec. John Kelly on U.S. borders and the path to security

- 10:10am: Sen. Kirsten Gillibrand, D-N.Y., and Rep. Rosa DeLauro, D-Conn., hold press call to introduce ‘‘Family and Medical Insurance Leave Act”

- 2:30pm: House Democrats hold news conference on Obamacare

DB’s Jim Reid concludes the overnight wrap

I’ve been away for a long weekend and since I’ve last worked on the EMR before the break I have 35 new President Trump tweets to review. Indeed markets have started the week on the back foot with politics again the overriding theme for much of the past 24 hours. Indeed while various Trump developments continue to create headlines it was Europe’s turn to take the spotlight yesterday. Much of that can be attributed to France where Francois Fillon confirmed his intention to continue running for presidency despite pressure from his own party to step aside in the face of the scandal over his family’s employment. In a press conference yesterday Fillon continued to make the case for his continued candidacy while also expressing regret for the allegations put forward.

Together with Le Pen’s rally cry over the weekend, these developments put pressure on French assets from the get go yesterday. This was most notable in bonds where 10y OAT yields finished the day 5.9bps higher at 1.136% – compared to a 4.3bps rally for Bunds and 5.7bps rally for Treasuries – and to the highest since September 2015. It’s the spread over Bunds that we’ve been watching closely though and yesterday saw that 10y spread hit 77bps and the widest now since November 2012. That spread was as low as 45bps just four weeks ago and just 21bps in November last year. In fact it wasn’t just OATs which had a difficult day yesterday. Similar maturity yields in Italy (+10.7bps), Spain (+10.4bps) and Portugal (+7.5bps) all surged higher with the BTP-Bund spread also hitting a fresh three-year high at 200bps with looming banking sector concerns and potential elections also a focus for the market.

In equity markets it was the FTSE MIB (-2.21%) which drove losses in Europe with the banks in particular sharply lower. The Stoxx 600 edged down -0.68% while France’s CAC index finished the day -0.98% for its second worst-day of the year so far. The Euro also finished down -0.31% versus the Greenback. European credit markets weren’t immune to the risk off moves either with the iTraxx Main index ending the day some +3.5bps wider – the biggest move wider since September – while senior and sub financials sold off +5.0bps and +10.0bps respectively. The risk-off moves across the pond weren’t quite as exaggerated although the S&P 500 did still finish the day -0.21% and the Dow -0.09%.

There wasn’t much to drive markets in the US yesterday although one thing which caught our eye was the latest findings from the Fed’s Senior Loan Officer Survey. Regarding loans to large and mid-sized businesses, the survey revealed that banks net tightened standards by 1.4%, while standards were left unchanged for small firms. Although modest over the past couple of quarters, it is still worth noting that this is now the sixth quarter in succession that standards have tightened for large and medium sized firms. This usually only happens in recessions. Banks also reported that demand for C&I loans from large and middle-market firms, as well as small firms, was little changed. The most notable tightening in standards though was in consumer loans. During the quarter, banks reported an 8.3% net tightening in credit standards for credit cards and 11.6% net tightening for auto loans.

Refreshing our screens now, the broadly risk-off tone has continued in markets in Asia this morning, although this has been fairly modest for the most part. The Nikkei (-0.22%), Hang Seng (-0.16%), Shanghai Comp (-0.31%), Kospi (-0.12%) and ASX (-0.10%) are all in the red, while US equity index futures are little changed. Bonds are notably stronger with 10y yields in the antipodeans 7-8bps lower and yields in Hong Kong (-3.9bps), Singapore (-4.2bps) and China (-1.0bps) also lower. 10y JGB’s are unchanged at 0.092%. Meanwhile the US Dollar index has firmed another +0.22% this morning after the Fed’s Harker reiterated Williams’ comments from last week by saying that “March is on the table” for a possible Fed rate hike. Harker pointed towards the strong jobs numbers last week as well as “continued good news around GDP and GDP growth and continued signs that the labour market is strengthening”. Elsewhere this morning the Aussie Dollar is a touch firmer after the RBA left rates on hold as expected, with the broad policy stance remaining fairly neutral.

Coming back to politics briefly. France has rightly dominated much of the political focus in Europe lately but it was interesting to see the latest polls in Germany yesterday. An INSA poll for the Bild newspaper (of 2,042 people covering 3-6 February) revealed that support for the Social Democrats party has jumped ahead of Chancellor Merkel’s CDU party for the first time since 2010 according to Bloomberg. The poll put the Social Democrats at 31% versus 30% for CDU and 12% for the populist Alternative for Germany (AfD). The pollster highlighted that support for the Social Democrats was just 21% two weeks ago. The rising support for the Social Democrats comes following the appointment of Martin Schulz as the party’s leader so we’ll need to see if this support is maintained in the weeks and months ahead, rather than it being a temporary bounce. It’s worth keeping an eye on in any case.

Staying in Europe, yesterday we heard from ECB President Draghi. The overall tone felt mildly dovish with Draghi saying that “support from our monetary policy measures is still needed if inflation rates are to converge towards our objective with sufficient confidence and in a sustained manner” and that “underlying inflation pressures remain very subdued and are expected to pick up only gradually as we go on”. Draghi also defended the role of the Euro, calling it “irreversible” while also hitting back at the Trump administration comments about Germany being a currency manipulator. Draghi also highlighted that any relaxation of financial regulation “is very worrisome”.

Staying with the ECB, yesterday we got the latest CSPP holdings data. As of the 3rd of February, total holdings were reported at €60.98bn which implies net purchases settled last week of €2.17bn at an average daily run rate of €433m, ahead of the €365m average since the program started. Also released was the latest primary/secondary split. As of the end of January, 14.1% of purchases had been made in the primary market compared to 85.9% in the secondary. In January alone, there was a higher weight towards primary at 17.4% perhaps reflecting the strong start to the year for new corporate issuance.

Looking at today’s calendar, this morning we’re kicking off in Germany where the December industrial production data will be released. Thereafter we’ll get trade data in France followed by the latest house price data in the UK. This afternoon in the US the early release is the December trade balance reading, followed then by the latest JOLTS job openings print. Later on this evening we’ll get consumer credit for the month of December. Away from the data we are due to hear from the BoE’s Forbes this afternoon as well as the ECB’s Weidmann. The BoJ is also due to release minutes from the January meeting. Earnings wise there are 28 S&P 500 companies due to report including General Motors and Walt Disney. BP is among those reporting in Europe.

end

i)Late MONDAY night/TUESDAY morning: Shanghai closed DOWN 3.89 POINTS OR .12%/ /Hang Sang CLOSED DOWN 16.67 POINTS OR .07% . The Nikkei closed DOWN 65.93 POINTS OR 0.35% /Australia’s all ordinaires CLOSED UP 0.13%/Chinese yuan (ONSHORE) closed DOWN at 6.8840/Oil FELL to 52.79 dollars per barrel for WTI and 55.46 for Brent. Stocks in Europe ALL IN THE GREEN. Offshore yuan trades 6.8342 yuan to the dollar vs 6.8840 for onshore yuan.THE SPREAD BETWEEN ONSHORE AND OFFSHORE WIDENS QUITE A BIT AS DOLLARS ARE LEAVING CHINA’S SHORES. BOTH YUANS WEAKER COUPLED WITH THE STRONGER DOLLAR

3a)THAILAND/SOUTH KOREA/:

END

b) REPORT ON JAPAN

c) REPORT ON CHINA

Chinese dollar reserves which include USA dollars, foreign currencies like the Euro and the pound along with gold, fell to below $3 trillion equivalent. You can bet that China will engage in capital controls to prevent more USA dollars from leaving

(courtesy zerohedge)

Chinese Reserves Unexpectedly Drop Below $3 Trillion For The First Time Since 2011

Beijing surprised China-watchers this morning, when the PBOC announced that in January, China’s foreign-currency reserves dipped by $12.3 billion, below the key “psychological level” of $3 trillion, or $2.998 trillion to be exact, declining for the 7th consecutive month, and dropping to the lowest since early 2011. Consensus had expected a drop of $10.5 billion to just above $3 trillion.

According to the PBOC, holdings of SDRs decreased to 2.21 trillion from 2.24 trillion in December. Gold reserves remained at 59.24mm troy ounces, however rose in dollar terms due to the increase in the price of gold from $67.9BN to $71.3BN.

The central bank’s intervention in foreign-exchange markets drove the drop, as did seasonal factors such as high demand for other currencies during the week-long Lunar New Year holiday, the State Administration of Foreign Exchange said in a statement.

The January decline was much smaller than the $41 billion reported in December, and was the smallest in seven months, indicating China’s renewed crackdown on outflows appears to be working, at least for now. China has taken a raft of steps in recent months to make it harder to move money out of the country and reassert a firmer grip on its faltering currency, even as U.S. President Donald Trump steps up accusations that Beijing is keeping the yuan too cheap.

While the $3 trillion mark is not seen as a firm “line in the sand” for Beijing, concerns are swirling over the speed at which the country is depleting its reserves and how much longer it can afford to defend the currency. Some analysts estimate China needs to retain a minimum of $2.6 trillion to $2.8 trillion under the International Monetary Fund’s (IMF’s) adequacy measures, and fears of a devaluation would likely intensify capital flight.

The drop in January’s reserves could have been worse if not for a sudden reversal in the surging U.S. dollar in January, some analysts said. The softer dollar boosted the value of non-dollar currencies that Beijing holds. The yuan has gained nearly 1 percent against the dollar so far this year. But analysts expect downward pressure on the yuan to resume, especially if the U.S. continues to raise interest rates, which would likely trigger fresh capital outflows from emerging economies such as China and test its enhanced capital controls.

As Bloomberg adds, further erosion of the world’s largest stockpile may prompt policy makers again to tighten measures for controlling outflows and on companies transferring money to other countries. Authorities recently rolled out stricter requirements for citizens converting yuan into foreign currencies as the annual $50,000 foreign exchange quota for individuals reset Jan. 1.

Some analysts fear a heavy and sustained drain on reserves could prompt Beijing to devalue the yuan as it did in 2015, which would sow turmoil in global financial markets and likely stoke political tensions with the new U.S. administration.

Economists expect more forceful tightening of regulatory controls after Tuesday’s data, though China’s financial system is notoriously porous, with speculators quickly able to find new channels to get funds out of the country. Here are some thoughts from the economist community:

- “With FX reserves below $3 trillion, we can expect capital controls as well as tightening yuan liquidity to continue, as the authorities try to avoid a further drawdown,” said Chester Liaw, an economist at Forecast Pte Ltd in Singapore, referring the central bank’s surprise hike in short-term interest rates on Friday.

- “With reserves dropping below the psychologically important threshold of $3 trillion, this will further ramp up pressure on Chinese policy makers to prevent the further draining of reserves,” said Rajiv Biswas, Asia-Pacific chief economist at IHS Global Insight in Singapore. “The Chinese government and the PBOC are now facing a tremendous battle to stem further significant capital outflows while also trying to maintain confidence in the yuan.”

- “A combination of yuan strength, stricter capital controls and substantial valuation effects failed to arrest the slide,” Tom Orlik, chief Asia economist at Bloomberg Intelligence in Beijing, wrote in a report. “A seventh straight month of falling reserves, and a drop below the $3 trillion threshold, means no respite for China’s policy makers in their battle against capital outflows.”

- “The PBOC isn’t defending the $3 trillion threshold at all costs, as some thought,” said Harrison Hu, chief greater China economist at Royal Bank of Scotland Group Plc. in Singapore. “Reserves have showed signs of stabilization, and the momentum will continue.”

- “The breach of $3 trillion isn’t significant in the big picture,” said Jason Daw, head of emerging-market currency strategy in Singapore at Societe Generale SA. “It was only slightly lower than consensus and inevitable given the trend over the past couple of years.”

Chinese Auto Dealers Hit Panic Button As Tax Hike Triggers “Inventory Early Warning”

With the US automakers facing an “inventory bubble,” hope for any momentum rested squarely in the shoulders of China… until today. China Automobile Dealers Association just unleashed their “Inventory Early Warning Alert” for January 2017, citing sales-tax increase on small-engine cars and Chinese New Year holiday.

As we detailed previously, J.D.Power analyst Thomas King warned, 2016 ended with an inventory “bubble” that will require less production or more incentives to clear.

With near record high inventories of 3.9 million vehicles…

U.S. auto inventory finished 2016 at about 66 days supply, up from 60

days a year earlier. Inventory would last 2.23 months at the November

sales pace, according to the latest available data from the Census

Bureau. The stock-to-sales ratio in 2016 is extremely elevated compared

to historical norms…

And now China Auto Dealers issue a Vehicle Inventory Alert – the index soared most on record by 18.6 percentage points to 61.5%. (A reading above 50% indicates low market demand and high inventories)

The market demand index, average daily sales index, business conditions index chain decreased, of which the market demand index and the average daily sales index chain fell sharply, which is due to the December market overdraft.

The total market demand index was 23.0%, a decline of 51.6 percentage points, a substantial decline in market demand index.

Worse still, China Auto Dealers Association warns that further inventory pressure is expected in February due to holidays and fewer working days.

4. EUROPEAN AFFAIRS

ITALY

Quite a story!! Unicredit is Italy’s largest bank and they are undergoing a rights offering such that there will be a 70% dilution. The bank suffered a loss of 11 billion euros in 2016 and they are trying to steer their ship northbound in profits. The problem is none of the shareholders with greater than 3% ownership is wishing to participate in the rights offering

(COURTESY Milan news)

UniCredit begins $14 billion cash call against shaky backdrop

By Valentina Za | MILANMILAN UniCredit (CRDI.MI) was hit by a slump in Italian banking stocks on Monday as it began Italy’s biggest corporate share sale in an attempt to raise 13 billion euros ($14 billion) to rebuild its capital after a balance sheet clean up.

Italian banks are struggling to deal with bad loans left behind by a deep recession, leading to capital raisings and consolidation as Rome tried to steady confidence.

UniCredit’s shares held up relatively well after the bank launched its rights issue, but closed down 6.9 percent at 12.21 euros, while Italy’s banking index .FTIT8300 fell 4.7 percent.

The price of the rights to buy into the cash call CRDI.MI_r.MI, Europe’s largest since 2010, finished 18.85 percent lower, with traders saying they were moving in sync with the shares and there was no sign of speculative arbitrage.

Shareholders who do not want to “follow” their rights tend to sell in the first days of the process, traders said.

However, Monday’s losses were amplified by the spread between 10-year Italian and German government bonds hitting 200 basis points, its highest since mid-October 2014.

This was due to wider investor uncertainty about Europe’s future after France’s National Front leader Marine Le Pen pledged at the weekend to take her country out of the euro zone if she wins the presidential election.

Shares in UBI (UBI.MI) fell 5.5 percent, Banco BPM (BAMI.MI) shed 5.9 percent and Intesa Sanpaolo (ISP.MI) lost 2.4 percent.

UniCredit said last week it will post an 11.8 billion euros loss for 2016 due to one-off hits stemming mainly from loan writedowns, as it prepares to offload 17.7 billion euros in bad debts under a restructuring plan outlined in December.

This follows the hiring by Italy’s biggest bank by assets of French investment banker Jean Pierre Mustier as chief executive in July, with a brief to address concerns about UniCredit’s capital base.

INVESTOR SEARCH

Shareholders who do not exercise their rights face a dilution of more than 70 percent. UniCredit said on Friday that none of its shareholders with a stake of at least 3 percent had yet committed to buy into the share sale.

Its top shareholder is U.S. investment firm Capital Research and Management Company with 6.7 percent, followed by Abu Dhabi’s sovereign wealth fund Aabar and asset manager BlackRock (BLK.N) with a stake of about 5 percent each.

Sources told Reuters on Jan. 11 Aabar was set to buy into the share issue to keep its stake unchanged, but one source said last week this should not be taken for granted.

UniCredit is offering 13 new shares – at 8.09 euros each – for every five ordinary or savings shares, representing a 38 percent discount to the shares, excluding subscription rights.

The share offer – the bank’s second since 2012 when it tapped the market for 7.5 billion euros – is due to end by March 10, when a coupon payment is due on some high-risk bonds that UniCredit would not be able to honor without improving its capital ratio.

($1 = 0.9300 euros)

END

END

GREECE

Disagreements between the IMF and the Germans over Greek debt has caused the 2 yr Greek bond to skyrocket to over 10%. The iMF is stating that no new austerity is needed even though the Germans et al want more austerity. The IMF wants debt forgiveness something that Germany will not allow.

fun and games with Greece…

(courtesy zerohedge)

Fight Among Greek Creditors Over “Explosive” Debt Sends Greek Bond Yields Soaring

Greek 2Y bond yields soared, approaching 10% for the first time since September 2016, as an increasingly bitter fight between the nation’s creditors over its fiscal targets raised concerns it is running out of time to complete another review of its bailout program, and even sparked concerns a 4th Greek bailout may be in the offing. According to Bloomberg, the yield on Greek notes due in 2019 rose 79 basis points to 9.72% in afternoon trading in Athens. This particular issue was sold in April 2014 as part of a series of flagship sales that marked Greece’s “triumphal”, if brief, return from market exile.

The yield on the 2019 notes, which was below 4% in 2014, climbed to as much as 37% in 2015, when failed negotiations led to a referendum that threatened Greece’s position in the euro-area.

The reason for the latest selloff – which due to the illiquid nature of Greek bonds may well be just one holder selling oddlots – is the ongoing stand-off with European authorities over the terms and future of Greece’s bailout has led to a rare public split on the International Monetary Fund’s board, amid growing questions over the fund’s participation. European institutions and the IMF have for more than a year been at loggerheads over what the fund argues are far too stringent fiscal targets being demanded of Athens by its European creditors and calls by the IMF’s staff for Greece to receive more long-term debt relief, the FT writes.

As Bloomberg adds, the talks with creditors for the completion of the second review of Greece’s 86 billion-euro ($92 billion) bailout program has been stalled over significant differences between the IMF and euro area on projections for its economy, targets and debt sustainability. A deal between creditors is needed by a meeting of euro-area finance ministers in Brussels on Feb. 20, before the Dutch elections on March 15. After that, reaching a deal could become even trickier, with major maturities emerging which could force Greece into another technical default.

Greece won’t meet fiscal surplus targets set by its euro area creditors, the IMF warned on Monday, after executive directors met to discuss the fund’s annual assessment of the nation’s economy. The IMF’s assumptions aren’t based in reality and don’t take into account the reform of Greece’s public finances, according to a European Union official who spoke on condition of anonymity because the discussions are sensitive. To be sure, the IMF’s assumptions are rarely if ever “based in reality”, however markets are spooked by the increasingly acrimonious and public split among members of the Troika.

“It all hinges on talks with creditors which is typically a very difficult type of risk to price for investors,” Antoine Bouvet, Mizuho International interest rates strategist said by e-mail. “It is possible to imagine that some investors prefer waiting for the uncertainty to be resolved before re-investing this market.”

European institutions and the IMF have for more than a year been at loggerheads over what the fund argues are far too stringent fiscal targets being demanded of Athens by its European creditors and calls by the IMF’s staff for Greece to receive more long-term debt relief. The battle has raised questions over the IMF’s financial involvement in the current €86bn bailout, with German officials again on Monday saying that without the fund’s participation the rescue programme would end, potentially causing a new funding crisis for the government in Athens.

In an as-yet unpublished report on the Greek economy, the IMF’s staff argue that Greece’s debts are unsustainable and on an “explosive” path to reaching almost three times the country’s annual economic output by 2060. But that report, the FT writes, has been labelled overly gloomy by European officials. Moreover, after a meeting to discuss it on Monday the IMF issued an unusual statement conceding that its board was split over its findings.

“Most” of the 24 board members “agreed with the thrust of the staff appraisal” contained in its regular “Article 4” review of the Greek economy, the IMF said. However, “some . . . had different views on the fiscal path and debt sustainability”.

“Most directors agreed that Greece does not require further fiscal consolidation at this time, given the impressive adjustment to date which is expected to bring the medium-term primary fiscal surplus to around 1.5 percent of gross domestic product,” the IMF said. “The interesting thing was that ‘most’ directors didn’t ask for more austerity but just for a budget-neutral policy re-balancing,” said Thanassis Drogossis, an analyst at Athens-based Pantelakis Securities.

The IMF’s report is based on assumptions that are incorrect and misleading and would lead to the IMF having an inaccurate analysis of Greece’s debt sustainability, the EU official commented. Euro area considers the country’s debt to be sustainable after the implementation of the short-term debt measures decided by the Eurogroup.

On Tuesday, Greek government spokesman Dimitris Tzanakopoulos told reporters in Athens that Greece will only agree to bailout measures that are socially sustainable and will allow the country’s bonds to be admitted to the European Central Bank’s Quantitative Easing program. The IMF is causing needless delays, and the government will take initiatives in the coming days to try to bridge the differences between the sides, he said. The standoff is the latest in a long line of disputes that have buffeted Greek bonds since the nation regained market access.

“Despite Greece’s enormous sacrifices and European partners’ generous support, further relief may well be required to restore debt sustainability,” the IMF insists, adding that debt relief needs to be complemented with strong policy implementation to restore growth and sustainability.

As of this moment, there is little clarity on what happens next. A recent report from Credit Suisse laid out five possible scenarios, ranging from the benign to the horrific, as follows:

- Scenario 1:Quick resolution (in the coming days)

- Scenario 2: “We need more time” (March-April)

- Scenario 3: brinkmanship (July)

- Scenario 4: Early elections (before the summer)

- Scenario 5: Grexit? Oh pleeease!

A timeline of key events in the coming weeks will help investors as they gauge the risk of yet another Grexit:

END

GERMANY

Shock in Germany as Merkel is losing support to Martin Schultz. However the euroskeptic party is faltering. A coalition without Merkel’s party will have no real changes in political outlook

(courtesy zero hedgeL

Shock Poll Shows Merkel Losing Chancellorship If Elections Held Today; JPMorgan Stunned

Overnight we reported that Germany’s default swaps spiked to the highest level since Brexit as a recent poll showed that Merkel’s lead in the polls had slid to multi-year lows ahead of Germany’s elections later in the year, provoking some concerns that a formerly unthinkable “tail risk” outcome was becoming more likely. However, according to new data unveiled today, Merkel’s headaches are only just starting, because in a brand new poll released this afternoon, the CDU would get 30% of the vote, while the suddenly resurgent SPD would get 31%. This means that the SPD’s new head, Martin Schulz, would enter any coalition talks as the leader of the largest party, hence becoming Chancellor, leading to a stunned reaction by JPMorgan.

In a note released this afternoon by JPM’s Greg Fuzesi, the strategist writes that following the recent resignation of Sigmar Gabriel as leader and chancellor candidate of the SPD, there has been much attention on how his replacement Martin Schulz would perform. Having spent most of his career in the European Parliament, most recently as its president, and being relatively unknown in Germany, this is not easy to predict. In his first major TV interview, he was recently pressed to explain how exactly he differs from his predecessor Gabriel and also from Chancellor Merkel, and what his focus on fairness would mean in practice. This was not entirely straightforward for him.

Nevertheless, opinion polls were beginning to show a bounce last week and this appears to be continuing.

This afternoon, a new opinion poll from INSA showed the SPD gaining further support and overtaking the CDU/CSU for the first time in many years. If elections were held now, the INSA poll suggests that the CDU would get 30% of the vote, while the SPD would get 31%. This means that Schulz would enter any coalition talks as the leader of the largest party, hence becoming Chancellor.

It also means that a SPD-Green-Left coalition would currently win exactly 50% of seats, so that a government without the CDU/CSU could even be possible. In effect, the SPD has gained 10%-pts of support in past two (weekly) INSA polls, taking votes away from all other parties (see second chart below). Interestingly, the AfD has also suffered a significant decline.

Given that Schulz is relatively new to German politics, a novelty factor may be partly responsible for the jump in the polls. It is far too early to say whether this will endure, given that the election campaign has yet to properly begin. It will also be important to see whether other polls replicate the swing. The SPD has gained support in all recent polls, but these are all a week or more old and do not show the latest jump in the INSA poll. That said, there is no reason to dismiss the INSA poll. It is the newest organization and the only one to be done entirely online, but it (arguably) performed only marginally worse than other polls at the last Bundestag election.

A Schulz-led SPD-Green-Left coalition or a Schulz-led grand coalition would certainly be a huge event in German politics. Such possibilities no longer look like tail risks. A SPD-Green-Left coalition would bias German policymaking towards greater fiscal expenditure and investment, and center-left policies. But, even such a coalition would not mark a dramatic break with the past in many areas and would, we expect, continue Germany’s strong support of the EU and single currency.

In short, “Chancellor Schulz” may be just what Brussels, and to a lesser extent President Trump, ordered.

END

GERMANY/ISRAEL/DEUTSCHE BANK

German CEO Schwartz arrested in Tel Aviv. The bank’s offices were raided yesterday and today Schwartz was arrested. It seems that they have avoided paying any of the value added taxes on their many transactions with clients.

(courtesy zerohedge)

Deutsche Bank’s Office In Israel Raided, Managing Director Arrested Over Tax Violations

Define irony: just three days after Deutsche Bank took out a massive, full-page ad in German media to apologize for its market rigging “misconduct”, Deutsche Bank managing director, Boaz Schwartz, who is also the German lender’s chief executive officer in Israel, was arrested over alleged value-added-tax violations involving the company’s clients, in the latest setback in the German firm’s attempts to end years of legal issues and misconduct, prompting some to question the sincerity of DB’s solemn “apology.”

Schwartz, suspected of misreporting 550 million shekels ($146 million) of transactions, was arrested on Tuesday Bloomberg reported, a day after tax authorities raided the bank’s offices in Israel, seizing executives’ laptops and mobile phones, according to a statement from the Israel Tax Authority. He was freed under condition by Judge Karen Miller of the Jerusalem Magistrate’s Court. Israeli police had no comment on the executive’s arrest.

The Israel tax authority said that the alleged transactions were reported as if conducted by foreign residents and avoided Israel’s 17-percent VAT. In a statement, Deutsche Bank said it “acts in accordance with the law and strict legal advice both in Israel and abroad”, except when it gets caught?

The rest of the story is familiar: the arrest is the latest scandal to beset the lender struggling to settle lawsuits and rebuild confidence after misconduct costs helped tip Frankfurt-based Deutsche Bank into two years of losses. Legal cases that date back many years cost the company “reputation and trust” in addition to about 5 billion euros ($5.4 billion) since John Cryan took over as chief executive officer in July 2015, the CEO said in in advertisement in German newspapers this weekend, blaming the “misconduct of a few” employees for the transgressions.

Deutsche Bank had 9 million euros ($9.6 million) of revenue in Israel in 2015, which produced a pretax profit of 5 million euros, according to the lender’s annual report. The firm employed 11 workers in the country at the end of 2015, the report shows.

The fact that Israel is cracking down on the German lender, a bank which in the late 1990s admitted and regretted “dealing in nazi gold“, may be worth keeping an eye on.

end

This does not look good for Europe and the leader of European production Germany just saw their industrial production plunge by the most since 2009

(courtesy zero hedge)

German Industrial Production Plunges Most Since 2009

Just day after President Trump suggests Germany is a currency manipulator, and as Merkel looks set to lose her Chancellorship, Europe’s powerhouse economy just collapsed in December. Industrial production plunged 3.0% MoM in December – the biggest drop since Jan 2009 and over 8 standard deviations below expectations.

As Boomberg details, the figure excluding construction, which is comparable to the industrial production data reported by Eurostat, declined by an even greater 3.1%. The contraction was largely driven by capital goods, which subtracted 2 percentage points from the headline figure.

However, the losses were somewhat broad-based — the categories of non-durable consumer goods, intermediate goods and energy all subtracted from the headline figure.

For some context, this was 8 standard deviations below market expectations of a 0.3% rise…

The contraction in December will leave industry’s impact on 4Q GDP growth close to neutral. Germany is the first of the euro area’s four largest economies to report industrial production data for December.

Furthermore, Europe’s largest economy, the region’s growth driver, faces a series of risks that may damp output in the coming months. Protectionist trade policies under the new U.S. administration and complicated negotiations about the U.K.’s post-Brexit relationship with the European Union threaten to weigh on sentiment, just as a national election in September pits Chancellor Angela Merkel’s ruling party against a strengthening populist movement.

v) UK/trading today/ UK Pound/uSA)

Dollar retraces gains today with Cable (Pound/USA dollar) sharply higher on May’s Parliamentary victory with respect to the Brexit

(courtesy zero hedge)

Dollar Retraces Fed’s Harker ‘Hawkish’ Surge As Cable Spikes

We’re going to need another Fed speaker…

Harker comments overnight on March being live spiked the Dollar…

The USD plunge is being driven by Cable strength…ahead of The Commons Vote on Theresa May’s “take it or leave it” Brexit vote amendment.

- *U.K.’S MAY WINS COMMONS VOTE ON AMENDMENT TO BREXIT BILL

- *AMENDMENT DEMANDED U.K. PARLIAMENT APPROVE BREXIT DEAL

- *U.K.’S MAY WINS COMMONS VOTE ON AMENDMENT BY 326 TO 293

end

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

Iran

more war of words from Iran’s Ayatollah..he vows revenge!

(courtesy zerohedge)

Iran’s Ayatollah Vows Retaliation, Says Trump Exposes “Real Face” Of American Moral Corruption

Trump’s ongoing spat with Iran escalated on Tuesday, when Iran’s Supreme Leader, Ayatollah Ali Khamenei dismissed the US president’s warning to Iran to stop its missile tests, saying the new U.S. president had shown the “real face” of American corruption. “We are thankful to (Trump) for making our life easy as he showed the real face of America,” Khamenei said according to his website. He made the remarks in an address to the commanders of the Army Air Force on the verge of the Islamic Revolution’s victory anniversary which falls on February 10 this year.

“During his election campaign and after that, he confirmed what we have been saying for more than 30 years about the political, economic, moral and social corruption in the U.S. ruling system,” he added. It is unclear if Trump’s domestic opponents will be quick to agree with the Iranian.

Provocatively, the Supreme Leader once again alleged that it was the US that created ISIS:

“The new U.S. president says Iran should thank Obama! Why?! Should we thank him for [creating] ISIS, the ongoing wars in Iraq and Syria, or the blatant support for the 2009 sedition in Iran? He was the president who imposed paralyzing sanctions on the Iranian nation; of course, he did not achieve what he desired. No enemy can ever paralyze the Iranian nation.”

Quoted by Reuters, in his first speech since Trump’s inauguration, the Ayatollah called on Iranians to respond to Trump’s “threats” which failed to frighten Iranians, on the February 10th anniversary of the 1979 revolution.

“No enemy can paralyze the Iranian nation,” Khamenei said. “(Trump) says ‘you should be afraid of me’. No! The Iranian people will respond to his words on Feb. 10 and will show their stance against such threats.”

Report of the meeting and the full text of Ayatollah Khamenei’s speech, per IRNA, follows

The Iranian nation will respond to Trump’s words in a demonstration on February 10th: they will exhibit the stance the Iranian nation takes when threatened.

In this meeting the Leader of the Revolution stated: ‘The new U.S. president says Iran should thank Obama! Why?! Should we thank him for [creating] ISIS, the ongoing wars in Iraq and Syria, or the blatant support for the 2009 sedition in Iran? He was the president who imposed paralyzing sanctions on the Iranian nation; of course, he did not achieve what he desired. No enemy can ever paralyze the Iranian nation.’

Ayatollah Khamenei further tapped on Trump’s recent comment which involved ‘putting Iran on notice’. He added, ‘Trump says fear me! No. The Iranian nation will respond to your comments with a demonstration on the 10th of February: they will show others what kind of stance the nation of Iran takes when threatened.”

His Eminence stated: “We actually thank this new president [Trump]! We thank him, because he made it easier for us to reveal the real face of the United States. What we have been saying, for over thirty years, about political, economic, moral, and social corruption within the U.S. ruling establishment, he came out and exposed during the election campaigns and after the elections. Now, with everything he is doing—handcuffing a child as young as 5 at an airport—he is showing the reality of American human rights.’

Ayatollah Khamenei reminded the audience that, “The incident of the February 8, 1979 was unexpected for the regime and a blessing from God we were not counting upon. An unexpected provision should be hoped for in anything that the believing front does: it is true that logical and material calculations are necessary, but sometimes we should open up to counting on the supernatural too.’

He further added, “Such a blessing is achieved through endeavor and wisdom, accompanied by hope and trust in God; however, if we use wisdom and prudence along with trusting the Satan, the result will be a mirage. In any matter, including diplomacy and the country’s problems it is true that trusting demons and the materialistic power, which oppose your essence, leads to a mirage.”

We anticipate another prompt outburst from Trump’s twitter timeline, which will spark further concerns that the two nations are on collision course to at least terminating the Iran nuclear deal, if not more kinetic action. Keep an eye on US navy vessels in the gulf, and of course, the price of crude for hints if the market is getting nervous about the outcome.

end

Did Iran blink first:

(courtesy zero hedge)

Did Trump Scare Iran: Tehran Reportedly Pulls Missile From Launchpad Following Launch Prep

In what – if confirmed – may be the clearest indication that Trump’s Iranian escalation gambit has worked, Iran has allegedly removed a powerful missile from a launchpad east of Tehran within the past few days, Fox News reported, around the time the US imposed new sanctions on 25 Iranian individuals and entities, as U.S. and Iran continued trading public barbs about the Islamic Republic’s missile tests and nuclear ambitions.

Citing a satellite image taken on February 3 from ImageSat International and verified by U.S. officials, Iran was preparing a Safir missile for launch, the same type that Iran has previously used to put a satellite into space. The last time Iran launched a Safir missile was two years ago.

Satellite image from ImageSat International.

But in a surprising about face, Fox News learned Tuesday morning that Iran’s missile had been removed from the launchpad amid a flurry of activity on the launchpad which U.S. officials have been watching closely. It was not immediately clear why.

Satellite image from ImageSat International.

On Jan. 29, Iran launched a new type of medium-range ballistic missile prompting an emergency meeting of the U.N. Security Council on Jan. 31. A day later the White House issued a strongly worded statement from National Security Adviser Mike Flynn putting Iran “on notice.” Days later, American intelligence officials watched as Iran quickly cleaned up the site and prepared another missile on the same launch pad near Semnan, about 140 miles east of Tehran, before it was removed.

While it is unclear of Iran has taken the first step to de-escalate military tensions, it would come at a strange time. On Tuesday, Iran’s Supreme Leader issued a new warning to the White House about the coming 38th anniversary of Iran’s Revolution this Friday. “No enemy can paralyze the Iranian nation,” Khamenei said. “[Trump] says ‘you should be afraid of me’. No! The Iranian people will respond to his words on Feb. 10 and will show their stance against such threats,” as reported earlier.

On Sunday, Sen. Dianne Feinstein, D-Calif., called Iran’s recent ballistic missile launch “very dangerous” and said the launch “should not have happened,” and agreed with President Trump that new sanctions on the Islamic Republic were needed. Also Sunday, Iran fired off five advanced surface-to-air missiles as part of a military exercise Sunday. The Iranian Sayyad, or “Hunter”, missiles were launched from Dasht-e Kavir, a remote area 45 miles south of Semnan, the location of last week’s ballistic missile launch. Officials said the tests were successful.

If confirmed, expect much more “diplomatic” jawboning from Twitter Trump in the coming weeks, as the president’s policies of global intimidation seem to be bearing fruit.

6.GLOBAL ISSUES

7. OIL ISSUES

The EIA forecast record amounts of crude production for next year. Down goes oil:

(courtesy zero hedge)

Oil Slides After EIA Forecasts US Crude Output In 2018 Will Be The Highest Since 1970

Suggesting that the OPEC “production cut” gambit may soon backfire, on Tuesday the U.S. Energy Information Administration cut its 2017 world oil demand growth forecast by a fractional 10,000 barrels per day to 1.62 million bpd, and also cut its 2018 estimate by 50,000 bpd to 1.46 million bpd. At the same time, the EIA cut its U.S. crude output forecast for 2017 dractionally to 8.98mmbpd from its January 9 mmpd forecast – still 100,000 higher than 2016 – even as it aggressively boosted its 2018 US output forecast to 9.53 mmbpd from 9.30 mmbpd. If accurate, that would mark the highest US crude output since 1970, and indicate that US shale is indeed becoming a key global marginal oil producer.

“Global oil supply and demand is now expected to be largely in balance during 2017 as the gradual increase in world oil inventories that has occurred over the last few years comes to an end,” said Howard Gruenspecht, acting EIA administrator, in a statement.

While the EIA also forecast WTI would average $53.46 a barrel this year, up from the previous forecast for $52.50 and Brent at $54.54 this year, up from $53.50, the market’s kneejerk reaction was negative, with concerns about rising supply mounting, and as a result March West Texas Intermediate crude continued to trade lower, declining declined over 1%, to a 2-week low…

… dropping below its 50-day moving average, even as dollar gave up much of its intraday gains.

With CFTC reports showing that hedge fund net longs in crude are at all time highs, and conversely virtually all shorts have been blown out, the potential for a sharp reversal in WTI is on deck, with capitulatory selling possible should the declining trend continue. A key catalyst could be today’s API inventory report due at 4:30pm which over the past few weeks has shown a substantial increase in inventory, defying OPEC’s story about a market that is progressively shifting into equilibirium.

end

It plunges again after the second biggest crude inventory build in USA history

(courtesy zero hedge)

WTI/RBOB Plunge After 2nd Biggest Crude Inventory Build In US History

After a weak day in the energy complex driven by yuuge IEA output forecasts, and following last week’s continued trend of large inventory builds, API reported a shockingly massive 14.27 mm barrel build (2.5mm exp). This is the 2nd largest weekly build in US history. The reaction in WTI and RBOB futures was immediately obvious as the former plunged below $52 and the latter below $1.4750.

API

- Crude +14.27mm (+2.5mm exp)

- Cushing +624k

- Gasoline +2.903mm (+1.5mm exp)

- Distillates +1.373mm

The sixth weekly build in gasoline in a row… and a big build at Cushing…

But what really matters is the utterly massive build in crude inventories – the second bigest in history if the API data holds true for DOE data tomorrow

IEA forceasts sparked weakness into the API data all day (WTI dropped below is 50DMA and RBOB below its 200DMA)… and the API data sparked immediate selling pressure…

With WTI/Brent net positioning at record longs, we wish speculators luck.

end

8. EMERGING MARKETS

none today:

HUMOUR STORY

Your humour story of the day: