Gold at (1:30 am est) $1234.40 DOWN $0.70

silver was the star of the day: $17.19: UP 19 cents

Access market prices:

Gold: $1234.00

Silver: $17.96

THE DAILY GOLD FIX REPORT FROM SHANGHAI AND LONDON

.

The Shanghai fix is at 10:15 pm est last night and 2:15 am est early this morning

The fix for London is at 5:30 am est (first fix) and 10 am est (second fix)

Thus Shanghai’s second fix corresponds to 195 minutes before London’s first fix.

And now the fix recordings:

Shanghai FIRST morning fix Feb 10/17 (10:15 pm est last night): $ 1235.90

NY ACCESS PRICE: $1225.00.60 (AT THE EXACT SAME TIME)/premium $10.90

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Shanghai SECOND afternoon fix: 2: 15 am est (second fix/early morning):$ 1235.97

NY ACCESS PRICE: $1223.90 (AT THE EXACT SAME TIME/2:15 am)

SPREAD/ 2ND FIX TODAY!!: $12.07

China rejects NY pricing of gold as a fraud/arbitrage will now commence fully

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

London FIRST Fix: Feb 10/2017: 5:30 am est: $1225.75 (NY: same time: $1225.40 (5:30AM)

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

London Second fix Feb 10.2017: 10 am est: $1228.30 (NY same time: $1228.70

(10 AM)

It seems that Shanghai pricing is higher than the other two , (NY and London). The spread has been occurring on a regular basis and thus I expect to see arbitrage happening as investors buy the lower priced NY gold and sell to China at the higher price. This should drain the comex.

Also why would mining companies hand in their gold to the comex and receive constantly lower prices. They would be open to lawsuits if they knowingly continue to supply the comex despite the fact that they could be receiving higher prices in Shanghai.

end

For comex gold:

FEBRUARY/

NOTICES FILINGS FOR FEBRUARY CONTRACT MONTH: 3 NOTICE(S) FOR 300 OZ. TOTAL NOTICES SO FAR: 5122 FOR 512,200 OZ (15.931 TONNES)

For silver:

For silver: FEBRUARY

100 NOTICES FILED FOR 500,000 OZ/

TOTAL NO OF NOTICES FILED: 247 FOR 1,235,000 OZ

Let us have a look at the data for today

.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total open interest ROSE by 1,281 contracts UP to 192,661 with respect to YESTERDAY’S TRADING. In ounces, the OI is still represented by just less THAN 1 BILLION oz i.e. .963 BILLION TO BE EXACT or 138% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT FEBRUARY MONTH: THEY FILED: 100 NOTICE(S) FOR 500,000 OZ

In gold, the total comex gold FELL BY 6,954 contracts WITH THE FALL IN THE PRICE GOLD ($2.50 with YESTERDAY’S trading ).The total gold OI stands at 417,117 contracts

we had 3 notice(s) filed upon for 300 oz of gold.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD:

We had no changes in tonnes of gold at the GLD

Inventory rests tonight: 832.58 tonnes

.

SLV

we had no changes in silver into the SLV

THE SLV Inventory rests at: 334.713 million oz

end

.

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in silver RISE by 1281 contracts UP to 192,661 AS SILVER WAS UP 4 CENTS with YESTERDAY’S trading. The gold open interest FELL by 6,954 contracts DOWN to 417,117 WITH THE FALL IN THE PRICE OF GOLD OF $2.50 (YESTERDAY’S TRADING)

(report Harvey

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

2c) COT report

(Harvey)

3. ASIAN AFFAIRS

i)Late THURSDAY night/FRIDAY morning: Shanghai closed UP 13.52 POINTS OR .42%/ /Hang Sang CLOSED UP 49.84 POINTS OR .21% . The Nikkei closed UP 491.26 POINTS OR 2.49% /Australia’s all ordinaires CLOSED UP 0.84%/Chinese yuan (ONSHORE) closed DOWN at 6.8787/Oil ROSE to 53.73 dollars per barrel for WTI and 56.66 for Brent. Stocks in Europe MOSTLY IN THE GREEN. Offshore yuan trades 6.8703 yuan to the dollar vs 6.8787 for onshore yuan.THE SPREAD BETWEEN ONSHORE AND OFFSHORE WIDENS QUITE A BIT AGAIN AS DOLLARS ARE ATTEMPTING TO LEAVE CHINA’S SHORES. ONSHORE YUAN WEAKER AS IS OFFSHORE YUAN COUPLED WITH THE STRONGER DOLLAR

REPORT ON JAPAN SOUTH KOREA NORTH KOREA AND CHINA

3a)THAILAND/SOUTH KOREA

b) REPORT ON JAPAN

none today

c) REPORT ON CHINA

Trump learning to be a diplomat: he agrees to honour the ONE CHINA POLICY

(courtesy zero hedge)

4. EUROPEAN AFFAIRS

i)Greece

Greece lashes out at the IMF because they do not want them in the Troika. If the IMF bails then Germany also bails and thus Greece must leave the EU. As Mish states: this is nothing but a blame game

( Mish Shedlock/Mishtalk)

ii)They are all over the board with respect to Greece today. At first, there was a statement that the EU and the IMF agree on a common stance and then a Greek official blurted that no bailout deal is expected today

(courtesy zero hedge)

Schauble disparages Schultz as the SPD party is gaining in popular support against Merkel

( zerohedge)

iv/EU

We are starting to see stress in the system as investors are now shying away from safer bond issues:

( zerohedge)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

Huge rally in Tehran protesting Trump and celebrating the Islamic Revolution. Not good

( zero hedge)

6.GLOBAL ISSUES

7. OIL ISSUES

i)Oil jumps because the IEA reports 100% compliance on production cut:

( zero hedge)

ii)USA oil rigs continue to escalate in count which no doubt raises total crude production. What will OPEC do if the market does bit rebalance?

(courtesy zero hedge)

8. EMERGING MARKETS

9. PHYSICAL MARKETS

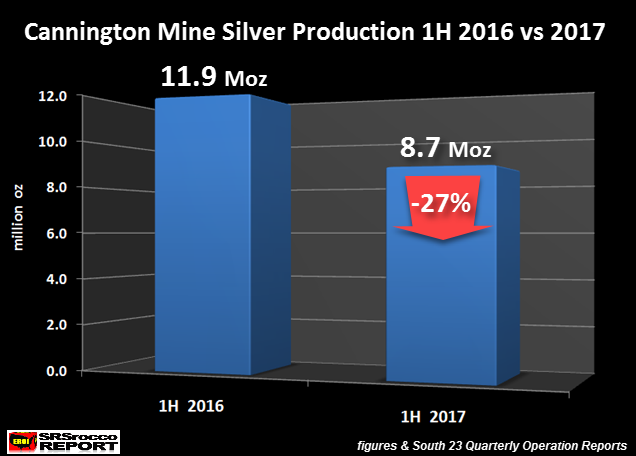

i)A great commentary from Steve St Angelo. The Cannington mine in Australia’s has always been a big producer of silver. This mine is now owned by South 32 having been spun out of BHP Billiton. We have seen silver production fall as base metal production falters. Now we are witnessing silver production falter as mining does deeper into the mines. Silver is lighter and generally floats to the surface while gold is denser. Thus as you go deeper into the lens silver values decrease. This is generally true in primary silver mines as well.

( Steve St Angelo/SRSRocco report)

ii)I brought this to your attention at the beginning of December. Grant Williams repeating this presentation last week. It is important as oil pricing is being positioned to the yuan and those that wish gold can purchase the gold from the SGE with their yuan

a must read..

( Grant Williams/GATA)

10.USA STORIES

i)The Court of Appeals unanimously rules against Trump. He now goes back to redrafting the executive order:

( zero hedge)

ii) he responds

(zero hedge)

iii)The wall will now cost $22 billion to build and it will take almost yrs to complete

( zero hedge)

iv)The important University of Michigan Consumer Confidence report plunges to near record lows as the “hope” component falters:

(c zero hedge)

(courtesy zero hedge)

vi) The only solution to the Dallas Pension mess is bankruptcy but that will hurt a lot of their pensioners

( Mish Shedlock/Mishtalk)

Let us head over to the comex:

The total gold comex open interest FELL BY 6954 CONTRACTS UP to an OI level of 417,117 WITH THE FALL IN THE PRICE OF GOLD ( $2.50 with YESTERDAY’S trading). We are now in the contract month of FEBRUARY and it is one of the better delivery months of the year. In this next big active delivery month of February we had a LOSS of 35 contracts DOWN to 1352. We had 0 notices served upon yesterday and therefore we LOST 35 contracts or an additional 3500 oz will NOT stand for delivery and these were cash settled for a fiat bonus. The next non active contract month of March saw it’s OI RISE by 75 contracts UP to 2154.The next big active month is April and here the OI FELL by 8587 contracts DOWN to 280,301.

We had 3 notice(s) filed upon today for 300 oz

And now for the wild silver comex results. Total silver OI ROSE by 1281 contracts FROM 191,380 UP TO 192,661 as the price of silver ROSE IN PRICE TO THE TUNE OF 4 CENTS with respect to YESTERDAY’S trading. We are moving further from the all time record high for silver open interest set on Wednesday August 3/2016: (224,540).

The active month of February saw the OI RISE by 106 contract(s) UP TO 285. We had 0 notice(s) served upon yesterday so we GAINED 106 CONTRACTS or an additional 530,000 oz will stand.

The next big active delivery month is March and here the OI decrease by 7397 contracts down to 106,030 contracts. For comparison purposes last year on the same date only 90,156 contracts were standing.

We had 100 notice(s) filed for 500,000 oz for the FEBRUARY contract.

VOLUMES: for the gold comex

Today the estimated volume was 224,836 contracts which is good.

Yesterday’s confirmed volume was 263,330 contracts which is very good

volumes on gold are getting higher!

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz |

NIL OZ

|

| Deposits to the Dealer Inventory in oz | nil oz |

| Deposits to the Customer Inventory, in oz |

NIL

|

| No of oz served (contracts) today |

3 notice(s)

300 oz

|

| No of oz to be served (notices) |

1349 contracts

134,900 oz

|

| Total monthly oz gold served (contracts) so far this month |

5122 notices

512,200 oz

15.931 tonnes

|

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | 121,574.9 oz |

Today, 0 notice(s) were issued from JPMorgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equates to 3 contract(s) of which 0 notices were stopped (received) by jPMorgan dealer and 1 notice(s) was (were) stopped/ Received) by jPMorgan customer account.

March 2016: 2.311 tonnes (March is a non delivery month)

| Silver | Ounces |

| Withdrawals from Dealers Inventory | nil |

| Withdrawals from Customer Inventory |

331,737.764 0z

DELAWARE

|

| Deposits to the Dealer Inventory |

nil oz

|

| Deposits to the Customer Inventory |

3011.100 oz

Delaware

|

| No of oz served today (contracts) |

100 CONTRACT(S)

(500,000 OZ)

|

| No of oz to be served (notices) |

185 contracts

(925,000 oz)

|

| Total monthly oz silver served (contracts) | 247 contracts (1,235,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month | 5,184,240.7 oz |

end

At 3:30 pm we receive the COT report which gives us position levels of our major players. Today is important because lately we have seen gold strengthening quite noticeably even at the comex table. Let us see if the banks are vacating their comex gold/silver shorts:

| Gold COT Report – Futures | ||||||

| Large Speculators | Commercial | Total | ||||

| Long | Short | Spreading | Long | Short | Long | Short |

| 216,408 | 99,259 | 51,747 | 106,024 | 240,170 | 374,179 | 391,176 |

| Change from Prior Reporting Period | ||||||

| 3,994 | 6,000 | 6,739 | 4,240 | 6,583 | 14,973 | 19,322 |

| Traders | ||||||

| 165 | 97 | 72 | 46 | 49 | 241 | 189 |

| Small Speculators | ||||||

| Long | Short | Open Interest | ||||

| 41,364 | 24,367 | 415,543 | ||||

| 2,137 | -2,212 | 17,110 | ||||

| non reportable positions | Change from the previous reporting period | |||||

| COT Gold Report – Positions as of | Tuesday, February 07, 2017 | |||||

end

Our large speculators:

those large specs that have been long in gold added 3994 contracts to their long side

those large specs that have been short in gold added 6000 contracts to their short side

Our commercials:

those commercials that have been long in gold added 4240 contracts to their long side

those commercials that have been short in gold added 6583 contracts to their short side.

Our small specs;

those small specs that have been long in gold added 2137 contracts to their long side

those small specs that have been short in gold covered 2212 contracts from their short side.

Conclusions: the commercials go net short by only 1243 contracts. However it looks like they are having trouble getting out of their massive shorts as they had to buy 4240 contracts

And now silver:

| Silver COT Report: Futures | |||||

| Large Speculators | Commercial | ||||

| Long | Short | Spreading | Long | Short | |

| 98,560 | 20,283 | 19,386 | 50,072 | 142,784 | |

| 1,651 | -652 | 2,886 | 807 | 4,106 | |

| Traders | |||||

| 97 | 35 | 45 | 34 | 36 | |

| Small Speculators | Open Interest | Total | |||

| Long | Short | 193,936 | Long | Short | |

| 25,918 | 11,483 | 168,018 | 182,453 | ||

| 1,753 | 757 | 7,097 | 5,344 | 6,340 | |

| non reportable positions | Positions as of: | 151 | 101 | ||

| Tuesday, February 07, 2017 | © SilverSeek.com | ||||

Our large specs:

Our large specs that have been long in silver added only 955 contracts to their long side.

Our large specs that have been short in silver covered 972 contracts from their short side.

Our commercials;

Those commercials that have been long in silver added 1414 contracts to their long side

those commercials that have been short in silver added 4538 contracts to their short side.

Our small specs:

those small specs that have been long in silver added 2087 contracts to their long side.

those small specs that have been short in silver added 890 contracts to their short side.

Conclusions;

the commercials go net short again by 3124 contracts. They seem emboldened again by continuing their supply of non backed silver paper.

And now the Gold inventory at the GLD

Feb 10/no changes at the GLD/Inventory rests at 832.58 tonnes

feb 9/no changes at the GLD/Inventory rests at 832.58 tonnes

Feb 8/another “deposit” of 5.63 tonnes of gold into the GLD/The addition is a paper addition/total inventory: 832.58 tonnes

Feb 7/another huge fake deposit of 8.30 tonnes of gold into the GLD/the addition is a paper addition and no doubt not physical/ total inventory: 826.95 tonnes

FEB 6/a huge deposit of 7.43 tonnes of gold into the GLD/Inventory rests at 818.65 tonnes

FEB 3/no change in gold inventory at the GLD/Inventory rests at 811.22 tonnes

Feb 2/another huge deposit of 1.48 tonnes/inventory rests at 811.22 tonnes

Feb 1/a huge “deposit” of 10.67 tonnes of gold into the GLD/Inventory rests at 809.74 tonnes. this should stop GLD from sending gold to Shanghai.

JAN 31/no change in gold inventory at the GLD/Inventory rests at 799.07 tonnes

jan 30/no change in gold inventory at the GLD/Inventory rests at 799.07 tonnes

Jan 27/no changes at the GLD/Inventory rests at 799.07 tonnes

Jan 26/no changes at the GLD/Inventory rests at 799.07 tonnes/

jan 25/another exactly the same withdrawal as yesterday: 50.4 tonnes and again this was used in the whacking of gold today/inventory rests at 799.07 tonnes

jan 24/a huge withdrawal of 5.04 tonnes and probably this was used today in the whacking of gold/inventory rests at 804.11 tonnes

Jan 23/a big change/this time a deposit of 1.19 tonnes of gold into the GLD/inventory rests at 809.15 tonnes. The drainage of gold from the GLD to Shanghai has now stopped!

Jan 20/no changes in gold inventory a the GLD/Inventory rests at 807.96 tonnes

Jan 19/no changes in gold inventory at the GLD/Inventory rests at 807.96 tonnes

Jan 18/no changes in gold inventory at the GLD/Inventory rests at 807.96 tonnes

Jan 17/17/a deposit of 2.96 tonnes of gold/inventory at the GLD rests at 807.96 tonnes. I guess there is no more gold inventory to sent to C+Shanghai

Jan 13/17/there were no changes in gold inventory at the GLD/Inventory rests at 805.00 tonnes

Jan 12/2017/no change in gold inventory at the GLD/Inventory rests at 805.00 tonnes

Jan 11/no change in gold inventory at the GLD/Inventory rests at 805.00 tonnes

JAN 10/no changes in gold inventory at the GLD/Inventory rests at 805.00 tonnes

JAN 9/A WITHDRAWAL OF 8.87 TONNES OF GOLD FROM THE GLD/INVENTORY RESTS AT 805.00 TONNES

end

NPV for Sprott and Central Fund of Canada

end

Major gold/silver trading/commentaries for FRIDAY

GOLDCORE/BLOG/MARK O’BYRNE

Gold Prices Up 5.8% YTD – Trump ‘Honeymoon’ Ends

Gold prices continued to shine this week reaching $1,244.70 per ounce and and has posted gains in five of the last six weeks. This week it reached a new three-month high – it’s highest since the Trump win and has climbed over 6% this year, beating the gains made in the same period in 2016.

The yellow metal has climbed 4.30% in the US dollar, 3.38% in the Euro and 1.35% in the sterling, in the last 30 days. This week gold is marginally higher in dollars and pounds but 1.5% higher in euro terms after the euro weakened on concerns of contagion due to the unresolved issues with Greece and other so called “PIIGS” nations and their still vulnerable banks and economies.

This performance has surprised many commentators and analysts as gold’s three month high has come at a time when stock prices are also breaking records.

When we are asked in years to come what we learnt from the Trump administration, the first thing that will come to mind is ‘Rules no longer applied.’

Whether you are for or against Trump, there is no denying that the rule book of what elected politicians should and should not do has been wholly torn to pieces and thrown out the window.

For starters, Trump appears to expect to be busy during his first 100 days putting in place exactly what he promised he would do, during his election campaign. This is almost unheard of. As Frank Holmes writes, the media took Trump literally but not seriously, his supporters took him seriously but not literally. The outcome of these expectations are showing themselves.

We take a brief look at what has driven gold this week and ask what the end of Trump’s honeymoon means for the gold price.

Strong stocks…strong dollar?

This week the gold price hit a three-month high and has surged over 7.5% so far this year. As we have shown in recent weeks, January saw gold post its biggest monthly gains since June 2016 (see table below) when surprise and uncertainty surrounding Brexit was driving the markets.

It may come as a surprise to some, but we are not just seeing reactions to everything that comes out of Trump’s mouth, office and Twitter feed at the moment. (Soon people will begin to realise that not every tweet can be seen as some kind of constitutional crisis). Attentions are beginning to refocus on the implications of what Trump may or may not succeed in doing, the wider US economy and, of course, what is happening elsewhere.

The gold price is being pushed upwards not only by the uncertainty surrounding Trump’s economic, foreign and domestic policies, a more dovish Fed, the growing populist movement in Europe, ongoing currency printing and debasement by central banks, growing inflation and the strength of the US dollar.

It is not just in Trump’s case that conventional rules no longer apply, they also appear to have been thrown out the window for precious metals in these first few weeks of 2017, namely that a strong US stock market means weak gold. Instead apparently strong economies, a record breaking stock market and recent highs for gold all seem to be able to exist in one realm of reality.

But this is a feat unlikely to last in the long-run, which only appears to be good for gold. As Frank Holmes points out in a recent piece, the rally on Wall Street is beginning to slow-down and investors are turning to gold.

Investors turn to gold at end of the honeymoon

Earlier this week we wrote about how you should really buy your loved one real gold this Valentine’s Day, by setting up a GoldSaver account, rather than waste money on the usual jewellery, chocolates and flowers.

As Frank Holmes explains it seems gold is also what we should turn to when the love affair is over, which is exactly what institutional investors are doing as the rose-tinted glasses and honeymoon with Trump disappears.

As we mentioned last week, the World Gold Council’s report for 2016 showed that gold demand climbed to it’s highest in four years, by 70%. Much of this was driven by ETF demand, which had their second-best year on record. Flows into gold ETFs have continued this year. Currently GLD holdings are 150 tonnes below their peak of 2016, but still at significant levels.

The inflows into GLD are perhaps having some effect on the gold price. These significant inflows are likely coming from institutional buyers which are indication of perhaps further gains in the gold price.

Holmes also highlights the growing demand for gold as a safe haven and hedge against uncertainty. He explains that as the world starts to get a proper feel for the Trump presidency, fund and investment managers have been ‘given a strong opportunity to demonstrate [their] value in the investment world.’

Institutional buying was no doubt influenced by leading hedge fund manager Stanley Druckenmiller who announced this week that he had bought gold in late December and January. Goldcore readers will remember that we wrote about Druckenmiller’s gold sales on the night of Trump’s victory. At the time he declared that he no longer saw the reasons to hold gold.

Today however he does, in an interview earlier this week he stated, “I wanted to own some currency and no country wants its currency to strengthen. Gold was down a lot so I bought it.” Quite the about turn!

It is likely that comments from the likes of Mario Draghi and Fed Chair Janet Yellen, that economic growth could be derailed, have encouraged Drukenmiller to buy back the gold he was so sure was right to sell

Uncertainty, gold’s best friend.

According to Bloomberg, Druckenmiller also pointed to the uncertainty over whether or not Trump will back the House Republican’s tax plan, as a reason for his precious metal’s purchase.

Holmes also points to this uncertainty as reason for the slow down in the Wall Street rally and gold’s climbs. Two campaign promises regarding infrastructure and tax reform, appear not to be moving anywhere. In fact, the chance of tax reform happening in the first 100 days days, even 200 days looks ‘less and less likely.’

Even though Trump has signed an executive order that is designed to reduce red-tape, companies, executives and shareholders seem increasingly lukewarm in their responses to Trump’s changes.

The most notorious of these was the Executive Order banning the immigration of citizens from seven countries. Holmes writes”

“…many in the business world have traditionally depended on foreign talent. That’s especially the case in Silicon Valley, where close to 40 percent of all workers are foreign-born, according to the 2016 Silicon Valley Index. (Around the same percentage of Fortune 500 companies were founded by immigrants or children of immigrants, including Steve Jobs, whose biological father was Syrian.) One of the more dramatic responses toward the travel ban was Uber CEO Travis Kalanick’s dropping out of Trump’s business advisory panel, following an outcry from users of the popular ride-sharing app who saw his participation with the president as an endorsement of his immigration policies.”

And whilst we may not all agree with Trump’s protectionism ideas and planned policies, Holmes argues that it is difficult not to see why US companies might feel like they need some level of protection. He refers to “China’s ascent as an economic and corporate juggernaut”.

“Take a look at the chart below, using data from Fortune Magazine’s annual list of the world’s 500 largest companies by revenue. Whereas the U.S. has lost ground globally over the past 20 years, China’s share of large companies has exploded, from having only three on the list in 1995 to 103 in 2015. The number of Japanese firms, meanwhile, has more than halved in that time.

But this, combined with how it is received across the various areas of US policy and lawmaking, is making predictions regarding the financial climate, so uncertain.

The weakening in the US dollar, something Trump has been pushing for since the week of his inauguration, combines with a dovish Federal Reserve, expectations of higher inflation and growing demand for a safe haven, have each helped to support the gold price.

The broken record of uncertainty

The most imminent threat of uncertainty comes from Trump. His proposals are running into problems and the new President’s reactions each time he realises the meaning of checks and balances are not even worthy of a prediction.

In turn, whilst Trump’s words to clearly have an impact, there is a wider world out there that is also trying to navigate financial crises, political changes and security issues. We have written before about ignoring the hype. Right now, it is difficult not to as one cannot disparage the thought that is the US-centric news that is supporting gold and will likely send it much higher.

But, the wider-outlook is what makes gold a good investment for the long-run. Presidents come and go, but their impact takes time to unfold and in the meantime there are decisions, trades, wars and elections going on across the world that also feed into the long-term gold trade.

Not too mention the looming milestone of a bankrupt America hitting the $20 trillion national debt mark in the coming weeks.

Gold as Druckenmiller alluded to, is a currency. But unlike sovereign currencies, it holds its value and does not rely on outside sources to maintain its value.

We’re starting to sound like broken records here but we strongly believe that the uncertainty and unpredictability that exists across much of the geopolitical sphere, but is exacerbated by Trump, makes being long-gold right now, an entirely logical and prudent decision. Providing it is owned in non digital, website, technology dependent formats of actual gold coins and bars that you can sell to many providers and take delivery with a phone call or a visit.

http://www.goldcore.com/us/gold-blog/gold-prices-5-8-ytd-trump-honeymoon-ends/

END

I brought this to your attention at the beginning of December. Grant Williams repeating this presentation last week. It is important as oil pricing is being positioned to the yuan and those that wish gold can purchase the gold from the SGE with their yuan

a must read..

(courtesy Grant Williams/GATA)

Grant Williams sees oil pricing transitioning to the yuan and gold

Submitted by cpowell on Fri, 2017-02-10 03:35. Section: Daily Dispatches

10:36p ET Thursday, February 9, 2017

Dear Friend of GATA and Gold:

Market analyst Grant Williams’ presentation at the Mines and Money conference in London in November, posted in the clear at Zero Hedge tonight, sees the end of the petrodollar system and its gradual replacement, already underway, with a Chinese yuan convertible into gold, transferring the gold pricing system to Asia:

http://www.zerohedge.com/news/2017-02-09/grant-williams-death-petrodolla…

Williams, publisher of the “Things That Make You Go Hmmm. …” letter, writes:

“If you are an oil producing country, do you:

“– Minimize your production in order to maximize your holdings of one of the most abundant and easily-produced commodities in the world — U.S. treasuries — as has been the case for the last 40 years, knowing full well that, with the level of entitlements due in the next decade, more will need to be printed like crazy? Or do you…

“– Maximize your production to gain the largest possible market share in the biggest oil market in the world and, through the ability to buy gold for yuan, thereby maximize your reserves of a scarce, physical commodity that is impossible to produce from thin air and that happens to be not only the most undervalued asset on the planet, but is trading at its most undervalued relative to U.S. treasuries in living memory?”

The problem with Williams’ conclusion is that gold is not really “impossible to produce from thin air.” Rather, central banks lease, swap, and sell gold nearly every day, causing it to be hypothecated and rehypothecated, creating vast imaginary supply, just as vast imaginary supply is created every day on futures exchanges.

Oil-producing governments acquiring gold should know this and should be insisting on delivery of real metal. But even if they are, they may be cooperating with the Western central banks that long have been undertaking leases, swaps, and sales to restrain the gold price, moderating and timing their acquisitions so a free-market price is delayed until the major governments and central banks are ready to transition as a group to a new world currency system.

Maybe, as Williams suggests, pricing oil in gold will be part of such a system. But that won’t be the key to such a system. The key will be the inability of governments, central banks, and their agents to keep producing the monetary metal “from thin air.”

What will cause that inability? If not international agreement — that is, the changed interests of governments and central banks — then only the wising up of gold investors and gold mining companies, which, as you may have noticed, has been taking quite a while.

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

A great commentary from Steve St Angelo. The Cannington mine in Australia’s has always been a big producer of silver. This mine is now owned by South 32 having been spun out of BHP Billiton. We have seen silver production fall as base metal production falters. Now we are witnessing silver production falter as mining does deeper into the mines. Silver is lighter and generally floats to the surface while gold is denser. Thus as you go deeper into the lens silver values decrease. This is generally true in primary silver mines as well.

(courtesy Steve St Angelo/SRSRocco report)

Production Plunged At The World’s Largest Primary Silver Mine

by SRSrocco on February 9, 2017

The largest primary silver mine in the world experienced a huge decline in its production due to falling ore grades. The Cannington Mine, now run by South 32 Ltd., suffered a huge drop in its silver production during its 1H 2017 reporting time-period. Some companies, such as South 32, start their fiscal new year in July. BHP Billiton, who owned the Cannington mine since its start-up in 1997, spun it off to South 32 back in 2015.

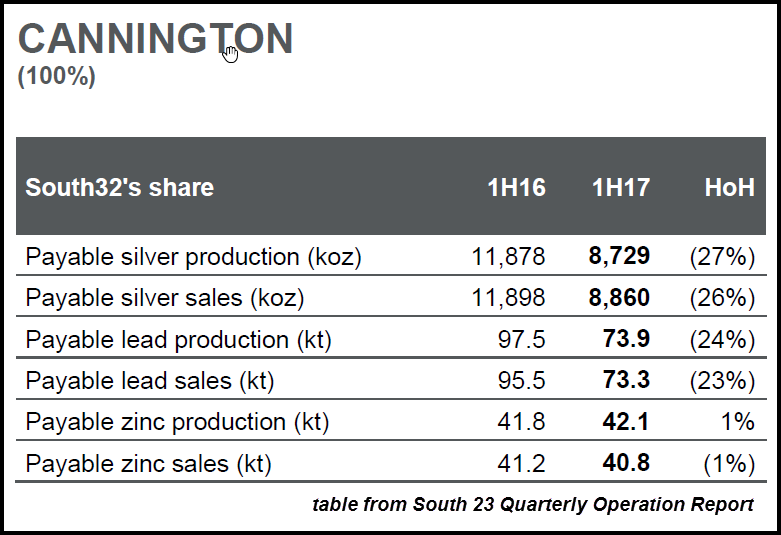

According to South 32’s production report, the Cannington Mine saw its silver production drop by a staggering 27% 1H 2017 versus 1H 2016:

Silver production at the Cannington Mine declined from 11.9 million oz (Moz) 1H 2016 to 8.7 Moz 1H 2017. Basically, these figures are comparing production from July-Dec 2015 versus July-Dec 2016. Again, the latter reporting period is stated as the first half of 2017 (1H 2017).

Regardless, this is a huge drop in silver production from the world’s largest primary silver mine located in Australia. Here is the actual table from the South 32 report:

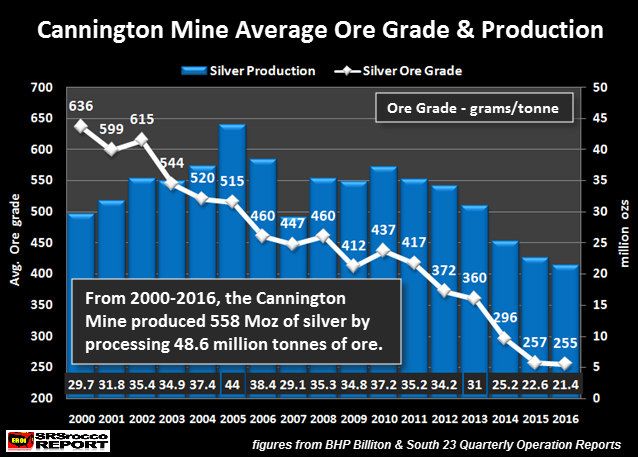

The reason for the big drop in silver production at Cannington was due to the huge decline in the silver ore grade at the mine. The average silver ore grade fell from 266 grams per tonne (g/t) 1H 2016 to 198 g/t in the 1H 2017. Falling silver ore grades are nothing new for Cannington, as it has been going on for quite some time. The world’s largest primary silver mine once produced silver at an average ore grade of 636 g/t… more than three times its current silver grade.

Here we can see that Cannington’s average silver ore grade declined from 636 g/t in 2000, to a low of 255 g/t in 2016. During its peak year in 2005, Cannington produced 44 Moz of silver at an average ore grade of 515 g/t. This one single mine produced more than half a billion ounces (558 Moz) of silver since 2000.

The chart above was one of 48 in published in my THE SILVER CHART REPORT. If you haven’t checked out the report, there is a lot of excellent information on the Silver Market and Industry not found in any other single publication on the internet.

The Silver Chart Report is a collection of my top silver charts from articles published over the past six years, and includes in-depth, never-before-seen charts and content that indicate that silver is on the rise. There are 48 charts in the report, broken down in five sections:

- Silver Production

- Mining & Falling Ore Grades

- Official Silver Coin Sales

- Silver Price

- The Silver Market

The charts in these five sections give the investor a broad background of the silver industry and market. Silver will likely be one of the most sought-after physical assets in the future. Why? There are several factors that will impact its price (value) in the future, and they are explained thoroughly in The Silver Chart Report.

Even though production has continued to decline at Cannington, it was still the largest primary silver mine in 2015:

This table from the Silver Institute, shows that the Cannington Mine ranked second in 2015, behind Polymetal’s Dukat Mine in Russia. However, revised data shows that the Cannington Mine actually produced 22.6 Moz of silver in 2015, not 22.2 Moz. So, when the Silver Institute publishes their updated primary silver mine data for 2016, they will put Cannington in the number one spot for 2015.

(Cannington Mine, North-west Queensland, Australia)

That being said, Cannington will fall to the number two spot in 2016, when all the data is finally released. According to the data released by the mining companies, here are the production results for 2016:

Top Four Primary Silver Mine Production In 2016:

1) Fresnillo’s Saucito Mine = 21.9 Moz

2) South 32’s Cannington Mine = 21.4 Moz

3) Tahoe’s Escobal Mine = 21.3 Moz

4) Polymetal’s Dukat = 19.3 Moz

Regardless, to see silver production fall 27% at the Cannington is quite amazing when we know its tremendous production history. South 23 states that the Cannington Mine will extract higher grade silver ores in the second half of the year, but production is estimated to only reach 19 Moz for the year.

When U.S. and global oil production starts to decline in a BIG WAY, silver production will feel it the most. Why? Because by-product silver supply from copper, zinc and lead production will fall precipitously as base metal demand plummets during the next financial and economic crisis.

The best time invest in physical silver is before supply evaporates or before its price or value heads towards Jupiter.

END

Your early FRIDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight

1 Chinese yuan vs USA dollar/yuan WEAKER AT 6.8787(SMALL DEVALUATION SOUTHBOUND /OFFSHORE YUAN WIDENS TO 6.8703 / Shanghai bourse UP 13.52 POINTS OR .42% / HANG SANG CLOSED UP 49.84 POINTS OR .21%

2. Nikkei closed UP 471.26 POINTS OR 2.49% /USA: YEN RISES TO 113.52

3. Europe stocks opened MOSTLY IN THE GREEN ( /USA dollar index RISES TO 100.85/Euro DOWN to 1.0634

3b Japan 10 year bond yield: FALLS TO +.092%/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 113.52/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD FINALLY IN THE POSITIVE/BANK OF JAPAN LOSING CONTROL OF THEIR YIELD CURVE AS THEY PURCHASE ALL BONDS TO GET TO ZERO RATE!!

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 53.73 and Brent: 56/66

3f Gold DOWN/Yen DOWN

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil UP for WTI and UP for Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund RISES TO +.331%/Italian 10 yr bond yield UP to 2.257%

3j Greek 10 year bond yield FALLS to : 7.463%

3k Gold at $1225.60/silver $17.61(8:15 am est) SILVER BELOW RESISTANCE AT $18.50

3l USA vs Russian rouble; (Russian rouble UP 31/100 in roubles/dollar) 58.61-

3m oil into the 53 dollar handle for WTI and 56 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation (already upon us). This can spell financial disaster for the rest of the world/China forced to do QE!! as it lowers its yuan value to the dollar/GOT SMALL DEVALUATION SOUTHBOUND from POBC.

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 113.52 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 1.0037 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.0668 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT

3r the 10 Year German bund now POSITIVE territory with the 10 year RISES to +.331%

3s The Greece ELA NOW at 71.4 billion euros,AND NOW THE ECB WILL ACCEPT GREEK BONDS (WHAT A DISASTER)

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.42% early this morning. Thirty year rate at 3.024% /POLICY ERROR)GETTING DANGEROUSLY HIGH

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

(courtesy Jim Reid/Bloomberg/Deutsche bank/zero hedge)

Futures Hit New Records, Global Stocks Rise On Strong Chinese Trade Data, Trump Tax Cut Hopes

S&P futures rose further into record territory, European shares rose to within striking distance of their highest levels in more than a year while bonds fell and the dollar rose as investors cheered a surge in Chinese trade data amid hopes of “phenomenal” tax cuts by Donald Trump, all of which have rekindled the Trumpflation trade.

The main economic release overnight was China’s trade data, which saw China post much stronger-than-expected exports and imports for January as demand picked up at home and abroad, however celebreations of a Chinese trade renaissance may be premature because as Goldman pointed out in a note, “the early Chinese New Year appears to have distorted January trade data (especially exports) on the upside.” Reuters agreed, noting that China watchers warned the long Lunar New Year holidays may have distorted the data to some degree, with companies pumping up production or rushing to build inventories before the break, which can last for weeks.

Concerns aside, China’s imports in January rose at the fastest pace since 2013, fueled by a continued construction boom which is boosting demand and global prices for resources from copper to steel, preliminary customs data showed on Friday. The 16.7% surge eclipsed the consensus estimate of 10.0%. China’s imports from the United States rose 23.4 percent in January, the fastest pace in at least a year, while its monthly trade surplus with the U.S. dipped to $21.37 billion. Led by electronics, China’s January exports climbed the most in almost a year, adding to evidence that Asia’s long trade recession may be bottoming out. January shipments rose 7.9 percent, more than twice as much as expected, after 2016 exports slumped nearly 8 percent.

China had been lagging a recent export recovery seen in Japan, South Korea and Taiwan, dragging on the regional supply chain. Its integrated circuit shipments rose 14.5 percent last month, while exports of mobile phones rose 7.9 percent. That left the country with a initial trade surplus of $51.35 billion for the month, the highest in a year. Customs is due to release updated data for trade on Feb. 23.

A quick summary of China’s trade data:

- Chinese Trade Balance (CNY) (Jan) 354.5bIn vs. bin Exp. 307.3bIn (Prey. 275.4bIn)

- Exports (CNY) (Jan) Y/Y 15.9% vs. Exp. 5.2% (Prey. 0.6%)

- Imports (CNY) (Jan) Y/Y 25.2% vs. Exp. 15.2% (Prey. 10.8%)

- Chinese Trade Balance (USD) (Jan) 51.35B vs. Exp. 48.50B (Prey. 40.82B)

- Exports (USD) (Jan) Y/Y 7.9% vs. Exp. 3.2% (Prey. -6.1%)

- Imports (USD) (Jan) Y/Y 16.7% vs. Exp. 10.0% (Prey. 3.1%)

“The export outlook for China is good, except for the potential risk of a Sino-U.S. trade war. The most important risk for China is what the Trump administration will do,” Jianguang Shen, chief economist at Mizuho Securities in Hong Kong.

China’s strong trade growth lifted shares of commodity-related sectors, in particular blue chip mining, across Europe helping regional indexes inch higher back towards last month’s peaks.

Aside from China, the positive tone was driven by a return of the “Trump reflation trade”, following Trump’s comments on Thursday that in coming weeks he would announce something “phenomenal” in terms of tax although he offered no further details. Renewed speculation that Trump’s economic policies will help boost economic growth and inflation pushed U.S. Treasury yields higher and lifted the dollar.

“President Trump promising tax reform in 2-3 weeks (potentially at the Feb 28 address to Congress) has added to risk bullish sentiment,” said Morgan Stanley strategists in a note to clients.

In early trading, Europe’s Stoxx 600 rose 0.2% and was poised to end the week about 1% higher helped by healthy corporate profits and a continued uptick in regional dealmaking which is seeing its strongest start to the year in more than a decade also helped underpin valuations.

Futures on Wall Street’s three main indexes all notched record highs overnight. As Bank of America highlighted overnight, the broad bullish sentiment was evident in investment flows too with investors pumping $13 billion into bonds, $6 billion into equities and even $2 billion into gold, in the past week according to latest data, although US equities continued to see outflows in 4 of the past 5 weeks.

As noted earlier, sentiment got a further boost on the political front when Trump seemed to change tack and said he would honor the longstanding “one China” policy during a phone call with China’s leader, a major diplomatic boost for Beijing which brooks no criticism of its claim to neighboring Taiwan.

Geopolitical focus now shifts to a meeting later on Friday between Trump and Japan’s Prime Minister Shinzo Abe in which Abe is expected to propose a new cabinet level framework for U.S.-Japan talks on trade, security and macroeconomic issues, including currencies.

The dollar was up 0.3 percent against the yen, up more than 1% for the week. The dollar index, which tracks the greenback against a basket of six major currencies, added 0.2 percent on the day to 100.8, on track to gain 0.8 percent for the week.

In commodities, oil jumped after the International Energy Agency said OPEC had achieved record initial compliance of 90 percent with their cuts agreement, while demand grew faster than expected. Futures gained as much as 1.1 percent in New York. In the first month of the Organization of Petroleum Exporting Countries’ agreement, key member Saudi Arabia reduced production by even more than it had committed, while higher demand is aiding the group’s bid to re-balance world markets, the IEA said.

* * *

Market Snapshot

- S&P 500 futures up 0.1% to 2,306.50

- STOXX Europe 600 down 0.07% to 366.53

- MXAP up 0.9% to 143.82

- MXAPJ up 0.4% to 460.74

- Nikkei up 2.5% to 19,378.93

- Topix up 2.2% to 1,546.56

- Hang Seng Index up 0.2% to 23,574.98

- Shanghai Composite up 0.4% to 3,196.70

- Sensex unchanged at 28,328.92

- Australia S&P/ASX 200 up 1% to 5,720.61

- Kospi up 0.5% to 2,075.08

- German 10Y yield rose 0.8 bps to 0.32%

- Euro down 0.09% to 1.0645 per US$

- Brent Futures up 1.1% to $56.23/bbl

- Italian 10Y yield fell 7.2 bps to 2.174%

- Spanish 10Y yield rose 3.1 bps to 1.656%

- Brent Futures up 1.1% to $56.23/bbl

- Gold spot down 0.2% to $1,225.53

- U.S. Dollar Index up 0.1% to 100.76

Top Headline News via BBG

- Trump Tells Xi He’ll Honor “One China,” Japan’s Shinzo Abe will try to convince Trump today that Japanese monetary policy isn’t aimed at manipulating the yen

- OPEC implemented 90% of promised output cuts in January, the first month of its agreement, as key member Saudi Arabia reduced production by even more than it had committed

- A federal appeals court unanimously refused to reinstate President Donald Trump’s ban on travel from seven Muslim- majority countries, issuing a sharp rebuke in a ruling likely destined for the U.S. Supreme Court

- Reckitt Benckiser Group Plc agreed to buy Mead Johnson Nutrition Co. for $16.6 billion, taking the U.K. consumer- products maker into the baby-formula market and providing a catalyst for growth as its sales momentum slows

- President Trump said a “phenomenal” plan to overhaul business taxes may be released within the next “two or three weeks,” heightening expectations as House Republican lawmakers are raising objections to their own leaders’ favored plan

- Western Gas to buy William Partners’ 50% non-operated interest in assets of Delaware Basin JV Gathering in exchange for WES’s 33.75% non-operated interest in two natural gas gathering systems in northern Penn. and $155m cash

- Walt Disney Co. plans to take full ownership of its ailing theme park in Paris to get the resort under control after 25 years of ups and downs at its first and only outlet in Europe

- The U.S. Senate confirmed Tom Price, a congressman and physician, to head the Department of Health and Human Services, a post where he’ll have a leading role in Republican efforts to dismantle Obamacare and implement its replacement, and oversee a budget of more than $1 trillion

- Ben Melkman, a former partner at Brevan Howard Asset Management, is receiving capital from billionaire Steven A. Cohen for the hedge fund he plans to start next month with more than $400 million under management, according to people with knowledge of the matter.

Asia equity markets carried over the momentum from the latest record day on Wall Street where the major indices printed fresh all-time highs as sentiment was underpinned by comments from US President Trump who will announce tax reforms in the upcoming 2-3 weeks. ASX 200 (+1.0%) was led by financial and energy names following similar outperformance in US, while Nikkei 225 (+2.6%) coat-tailed on the surge in USD/JPY which broke firmly above 113.00. Hang Seng (+0.6%) and Shanghai Comp (+0.4%). conformed to the widespread positive tone amid encouraging trade figures in which trade balance, exports and imports all beat estimates in both USD and CNY terms. 10yr JGBs saw spill-over selling from T-notes amid increases in global yields, although losses were stemmed after the BoJ raised the amount of JGB buying in the 10yr-25yr for today’s Rinban operations.

Top Asian News

- China Exports Surge Ahead of Trade Friction Risk With Trump

- Trapped China Cash Breathes Life Into Hong Kong Yuan Banking

- Hong Kong’s Biggest Arbitrage Trade Gets a Boost From China

- Asian Stocks Climb to 18-Month High on Trump’s Tax Revamp Plan

- Hong Kong Existing Home Prices Rise to Near Record High

- Top Indian Bank’s Profit Jumps on Insurance Unit Stake Sale

The final European session of the week has seen EU bourses supported by the strong lead from their US and Asian counterparts. Oil prices are at intra-day highs in the wake of the !EA monthly report, whereby they raised their global oil demand, while highlight that OPEC compliance is up to 90% with OECD stockpiles falling the most in 3-yrs. Elsewhere, the material sector outperforms amid China’s wider than expected trade surplus overnight, while firm earnings from ArcelorMittal has also supported the sector. Eurozone debt has been a touch softer across the board with bund prices flirting around 164.00 with the weakness led by the long of the curve, while the GE-FR 10yr spread back at 70bps having widened 3.2bps.

Top European News

- U.K. Industrial Output Posts Better Quarter Than First Estimated

- European Miners Surge After Earnings, Rebound in China Exports

- Brexit Gamble for Irish Funds Means Swapping U2 for Bankers

- Paschi’s Cash, Capital Crunch Adds Urgency to State Aid Plan

- UBS Counts on Russia Revival Even Without Trump-Putin Thaw

In currencies, the Bloomberg Dollar Spot Index rose less than 0.1 percent after Thursday’s 0.3 percent advance, and is poised to snap a six-week losing streak. The euro and British pound were both little changed. Citigroup Inc., the world’s largest foreign-exchange trading firm, sees the dollar rising this year even as the president talks the greenback down. Thin trading conditions still in evidence, with notable order levels intact as we head towards the weekend. In the lead USD pairings the recovery in the JPY spot rate has stalled ahead of initial resistance at 113.90-114.00, but the shallow pull-back suggests we are still well placed for an eventual test later in the session. Similarly in EUR/USD, pre 1.0616 bids continue to hold up a ‘much-anticipated’ downturn, but political risk seems to be tempered by German discord on how to accommodate the recent rise(s) in inflation. In the UK, strong manufacturing and industrial numbers beat expectations on all fronts, with the EU and non EU trade balances narrowing. GBP gains were muted however, though the data did manage to reverse some of the early morning weakness seen across the board. We continue to see sub 0.8500 demand holding up the EUR/GBP rate, while Cable through 1.2500 is finding it hard going, especially after coming against the strong resistance in the 1.2550-1.2600 zone.

In commodities, oil added 1 percent to $53.53 a barrel Friday after it climbed 1.3 percent the previous session. Gold fell 0.3 percent to $1,224.41 an ounce, after dropping 1.1 percent on Thursday. The metal, which is considered a haven asset, was at a three-month high earlier in the week. Iron ore futures jumped 3.8 percent in a fourth consecutive day of gains exceeding 1 percent. The !EA report dominated the headlines this morning, with 2017 Oil demand growth forecast to rise by 100k bpd. Production also fell by 1k in Jan to raise OPEC output (cut) compliance to 90% – 82% previously. This naturally saw WTI and Brent both rallying, but recent ranges look ‘safe’, with WTI through USD53.00 but still holding comfortably off the USD55.00 upper band. Notable losses in Gold after the moderate USD recovery and fresh record highs on Wall Street. Gains in the week stopped well short of key resistance at USD1250.00, moving down from USD1243 to USD1222.5 today. Strong gains in base metals on strong Chinese demand reported through Jan — Copper is back to USD2.70, but Zinc and Lead the out-performers — both gaining 2.5% on the day. !EA Monthly Report says they have raised their 2017 global oil demand growth forecast by 100,000bpd to 1.4mln bpd and estimate that OPEC are working with a 90% level of compliance to their output cut deal. OECD stock piles decline by 800,000bpd during Q4; most in three years.

Looking at today’s calendar, in the US the only data of note is the import price index reading for January, the flash University of Michigan consumer sentiment reading for this month, and then the January monthly budget statement later this evening. The only central bank speak comes from the ECB’s Mersch this morning, although Fed Vice-Chair Fischer will speak over the weekend. The other event to keep an eye on is the aforementioned meeting between President Trump and Japan PM Abe. Finally on the earnings front there are just 4 S&P 500 companies due to report.

* * *

US Event Calendar

- 8:30am: Import Price Index MoM, est. 0.3%, prior 0.4%; ex Petroleum MoM, prior -0.2%; YoY, est. 3.4%, prior 1.8%

- 10am: U. of Mich. Sentiment, est. 98, prior 98.5

- 10am: U. of Mich. Current Conditions, prior 111.3; Expectations, prior 90.3; 1 Yr Inflation, prior 2.6%; 5-10 Yr Inflation, prior 2.6%

- 2pm: Monthly Budget Statement, est. $45.0b, prior $27.5b deficit

DB’s Jim Reid concludes the overnight wrap

Metaphorically President Trump yesterday got his driver out and launched it high into the financial market fairway as he let the world know that there would be a “phenomenal” tax plan in the next two or three weeks in a meeting with US airline executives. During a press briefing later on in the day with White House Press Secretary Sean Spicer the question was asked whether or not this comment was corporate focused to which Spicer said it will be a “comprehensive” package and one “that will address both the business side of the tax ledger as well as the individual rates”. Trump also confirmed that he is working on seeking to roll back “burdensome regulations” and change the country’s “obsolete” infrastructure system.

With that in mind, today could be another day dominated by Trump headlines with the President due to meet with Japan PM Abe today in Washington. Ironically, they are also booked in for a round of golf tomorrow. While the scorecard may be of interest to some, markets will be more focused on the specifics that actually come out of the meeting. It should take on even more significance in light of Trump removing the US from the TPP, his comments about Japan being a currency manipulator and also accusations of Japan conducting unfair business practices. The suggestion is that today’s meeting will be about more than just two-way trade and should have a focus on a full range of economic ties with Abe supposedly planning to discuss creating jobs and also building infrastructure in the US. It’s worth also highlighting that overnight the Federal Appeals Court ruled against Trump’s executive order on the travel ban. Trump has since tweeted saying “see you in court” in reference to pursuing the appeal in the Supreme Court. So look out for any reaction to that today too.

Markets are certainly going into the end of the week in a better mood. The S&P 500 (+0.58%) and Dow (+0.59%) both hit fresh record highs last night with financials leading the charge on those Trump comments, as well as airlines. Interestingly Bloomberg ran a story overnight saying that DB’s Binky Chanda is now the most bullish US equity strategist of all the analysts they poll. Binky’s year end target is a lofty 2600 for the S&P500.

The Stoxx 600 (+0.78%) had also earlier rallied along with some of the peripheral bourses in Europe while this morning in Asia we’ve seen markets continue the positive momentum with bourses in Japan rallying hard (Nikkei +2.30%, Topix +2.04%), helped by a -1.50% decline for the Yen over the last two days. The Hang Seng (+0.58%), Shanghai Comp (+0.35%) and ASX (+0.83%) are also up in the early going.

Meanwhile credit also had a strong session yesterday with CDX IG and iTraxx Main indices ending 2.2bps tighter and 1.5bps tighter respectively. Indices in Asia and Australia are also a couple of basis points tighter this morning. In FX the Greenback firmed with the Dollar index closing +0.37%. That bounce means that the index has now closed higher for 7 consecutive sessions. At the other end of the risk spectrum we saw a decent reversal for Treasuries with 10y yields more or less completely undoing Wednesday’s rally after rising 5.9bps and back to 2.396%. Outside of Mr Trump, comments from the Fed’s Evans may have played a part after he said three rate hikes this year was not “unreasonable” although he did also say that he wasn’t sure what the right answer is on the balance sheet debate. The Fed’s Bullard did downplay the prospect of a March hike although that’s not surprising in the context of his call for just one rate hike over the next two years.

Meanwhile in Europe, bond markets were a bit more mixed yesterday. Bunds followed the moves in Treasuries with 10y yields up 1.6bps to 0.308% however there was a reasonable bounce for France (-1.9bps), Italy (-7.4bps), Spain (-7.4bps) and Portugal (-6.4bps). The exception to the moves in the periphery though came in Greece and most notably at the short end of the curve where 2y yields broke north of 10% yesterday, before settling to close at 9.816% but still up 64bps on the day. Yields are now up nearly 160bps this week alone as the continued deadlock around Greece’s debt talks continue to spook the market. It’s the standoff between the IMF and EU that is really the focus at the moment. Yesterday the IMF dug their heels in once again with spokesman Gerry Rice saying that the Fund stand by their analysis and reiterated their view that Greece should target a primary surplus target of 1.5% accompanied by significant debt relief. That contrasts to what the EU has been pushing for in no debt relief but more austerity and a primary surplus target of 3.5%. Interestingly a Bloomberg article broke last night suggesting that Greece’s creditors were readying a proposal, possibly as soon as today, on a framework of measures required to complete the bailout review. This apparently includes fiscal measures equal to about 2% of Greek GDP. So keep an eye on that this morning.

Coming back to the Asia session this morning where the latest trade data out of China was also released. In yuan terms, the trade surplus was reported as increasing more than expected in January (to 354bn yuan from 275bn; 307bn expected) thanks to a +15.9% yoy surge in exports (vs. +5.2% expected). That compares to a +0.6% yoy reading for exports in December. Imports also grew +25.2% yoy, jumping from +10.8% the month prior. In USD terms exports also surged 7.9% yoy (vs. +3.2% expected) from -6.2%.

Before we look at the day ahead, yesterday was another day of largely second tier data releases. In the US there was no change to the final wholesale inventories print of +1.0% mom in December, while initial jobless claims were reported as falling 12k last week to 234k, which in turn lowered the four-week average to just 244k. Prior to this in Germany the December trade surplus was reported as a narrower than expected €18.7bn (vs. €20.5bn expected), largely reflecting a -3.3% mom decline in exports. Imports were reported as being flat during the month.

Looking at today’s calendar, this morning in Europe we’ve got December industrial production reports due out of France, Italy and the UK, along with the latest trade balance reading in the latter. Over in the US this afternoon the only data of note is the import price index reading for January, the flash University of Michigan consumer sentiment reading for this month, and then the January monthly budget statement later this evening. The only central bank speak comes from the ECB’s Mersch this morning, although Fed Vice-Chair Fischer will speak over the weekend. The other event to keep an eye on is the aforementioned meeting between President Trump and Japan PM Abe. Finally on the earnings front there are just 4 S&P 500 companies due to report

end

i)Late THURSDAY night/FRIDAY morning: Shanghai closed UP 13.52 POINTS OR .42%/ /Hang Sang CLOSED UP 49.84 POINTS OR .21% . The Nikkei closed UP 491.26 POINTS OR 2.49% /Australia’s all ordinaires CLOSED UP 0.84%/Chinese yuan (ONSHORE) closed DOWN at 6.8787/Oil ROSE to 53.73 dollars per barrel for WTI and 56.66 for Brent. Stocks in Europe MOSTLY IN THE GREEN. Offshore yuan trades 6.8703 yuan to the dollar vs 6.8787 for onshore yuan.THE SPREAD BETWEEN ONSHORE AND OFFSHORE WIDENS QUITE A BIT AGAIN AS DOLLARS ARE ATTEMPTING TO LEAVE CHINA’S SHORES. ONSHORE YUAN WEAKER AS IS OFFSHORE YUAN COUPLED WITH THE STRONGER DOLLAR

3a)THAILAND/SOUTH KOREA/:

END

b) REPORT ON JAPAN

c) REPORT ON CHINA

Trump learning to be a diplomat: he agrees to honour the ONE CHINA POLICY

(courtesy zero hedge)

Trump Reverses, Agrees To Honor “One China” Policy In First Phone Call With Xi

In a major reversal to his stated foreign policy framework with China, in his first phone call held with China’s president Xi Jinping held on Thursday night, President Donald Trump agreed to honor the “one China” policy, easing a key source of diplomatic tension between the world’s two largest economies. The phone call came just one day after Trump sent Xi a letter stating he seeks a “constructive relationship” with China, took place hours after a US Appeals Court ruled against the Trump Administration’s executive order on immigration, and came ahead of Trump’s first official meeting with Japan’s PM Shinzo Abe.

In December, then president-elect Trump angered Beijing by talking to the president of Taiwan and saying the United States did not have to stick to the policy, under which Washington acknowledges the Chinese position that there is only one China and Taiwan is part of it. Trump later said the policy is “open to negotiation” putting further pressure on US-China relations. No issue is more sensitive to Beijing than Taiwan.

“The two leaders discussed numerous topics and President Trump agreed, at the request of President Xi, to honor our ‘One-China’ policy,” the White House said in a statement on Thursday night. “They also extended invitations to meet in their respective countries. President Trump and President Xi look forward to further talks with very successful outcomes.”

The White House statement described the call as “lengthy” and “extremely cordial,” providing no further details on what they discussed. Representatives from both sides would meet later to discuss and negotiate on “various issues of mutual interest,” it said.

The call came after U.S. and China military aircraft had an “unsafe” encounter over a disputed part of the South China Sea, the first publicly confirmed incident since May. The two surveillance planes flew within 1,000 feet of each other near the Scarborough Shoal, which is claimed by both China and the Philippines, a U.S. treaty ally.

Xi said it was necessary for both sides to increase cooperation, state-run China Central Television said. The Chinese president said his country was willing to boost ties with the U.S. on trade, investment, technology, energy and infrastructure. Xi also said the two countries should enhance communication in international and regional military affairs. “Facing an extremely complicated global situation and rising challenges, there’s a greater need for continuing to enhance cooperation between China and the U.S.,” Xi said, according to CCTV.

China and the United States also signaled that with the “one China” issue resolved, they could have more normal relations.

Below is a full timeline of Trump’s stance on the “One China” policy courtesy of Reuters.

- Dec 2 – Trump speaks by phone with President Tsai Ing-wen of Taiwan, a move that is likely to infuriate China, which considers the self-ruled island its own, and complicate U.S. relations with Beijing. China lodges swift protest, blaming Taiwan for the petty move.

- Dec 11 – Trump says the United States did not necessarily have to stick to its long-standing position that Taiwan is part of “one China,” questioning nearly four decades of U.S. policy.

- Dec 12 – China expresses “serious concern” after Trump said the United States did not necessarily have to stick to its long-held stance that Taiwan is part of “one China”.

- Dec 14 – In a veiled warning to Trump, China’s ambassador to the United States says Beijing will never bargain with Washington over issues involving its national sovereignty or territorial integrity.

- Jan 11 – Taiwan scrambles jets and navy ships after a group of Chinese warships, led by its sole aircraft carrier, sailed through the Taiwan Strait, the latest sign of heightened tension between Beijing and the island.

- Jan 12 – Trump’s then nominee for secretary of state, Rex Tillerson, says China should be denied access to islands it has built in the contested South China Sea, describing the placing of military assets there as “akin to Russia’s taking Crimea” from Ukraine.

- Feb 3 – China’s top diplomat, Yang Jiechi, tells Michael Flynn, Trump’s National Security Advisor, that China hopes it can work with the United States to manage and control disputes and sensitive problems.

- Feb 9 – Trump breaks the ice with Xi in a letter that says he looks forward to working with him to develop relations.

- Feb 9 – Trump changes tack and agrees to honor the “one China” policy during a phone call with Xi.

While Chinese Foreign Ministry spokesman Lu Kang also said the conversation was “very good” and “extensive,” he noted that “respect for the One-China policy is the obligation of the U.S. side.” The country’s dealing with Taiwan must come within that framework, Lu said at the ministry’s daily news briefing in Beijing. “The one China principle is the political foundation of the China-U.S. relationship,” he said. “From the phone call between the two presidents, we can see that the American government is committed to the One-China policy, and we appreciate that.”

Lu added that “ensuring this political basis does not waver is vital for the healthy, stable development of China-U.S. relations,” Lu said.

A spokesman for Taiwan President Tsai Ing-wen said in a statement it was in Taiwan’s interest to maintain good relations with the United States and China.

The U.S. and Chinese leaders had not spoken by telephone since Trump took office on Jan. 20. According to Reuters, diplomatic sources in Beijing said China had been nervous about Xi being left humiliated in the event a call with Trump went wrong and the details were leaked to the media.

In a separate statement carried by China’s Foreign Ministry, Xi said China appreciated Trump’s upholding of the “one China” policy. “I believe that the United States and China are cooperative partners, and through joint efforts we can push bilateral relations to a historic new high,” the statement quoted Xi as saying. “The development of China and the United States absolutely can complement each other and advance together. Both sides absolutely can become very good cooperative partners,” Xi said.

Taiwan’s top China policymaker, the Mainland Affairs Council, said it hoped for continued support from the United States and called on Beijing to adopt a “positive attitude” and “pragmatic communication” in resolving differences with Taiwan. China is deeply suspicious of Tsai, whose ruling Democratic Progressive Party espouses the island’s formal independence, a red line for Beijing, and has cut off a formal dialogue mechanism with the island. Tsai says she wants peace with China.

In a statement to Reuters, lawyer James Zimmerman, the former head of the American Chamber of Commerce in China, said Trump should have never raised the “one China” policy in the first place. “There is certainly a way of negotiating with the Chinese, but threats concerning fundamental, core interests are counterproductive from the get-go,” he said in an email.

“The end result is that Trump just confirmed to the world that he is a paper tiger, a ‘zhilaohu’ – someone that seems threatening but is wholly ineffectual and unable to stomach a challenge.”

Jia Qingguo, dean of the School of International Studies at Peking University and who has advised the government on foreign policy, said Trump had created a lot of uncertainty but was now back on track. “Trump has reassured people that he will be a responsible president,” he told Reuters. “…This is good news for China, because stable U.S.-China relations are good for China. Now we can do business.”

The White House described the call, which came hours before Trump plays host to Japanese Prime Minister Shinzo Abe, as “extremely cordial”, with both leaders expressing best wishes to their peoples. There was little or no mention in either the Chinese or U.S. statement of other contentious issues – trade and the disputed South China Sea – and neither matter has gone away. China on Friday reported an initial trade surplus of $51.35 billion for January, more than $21 billion of which was with the United States.

4. EUROPEAN AFFAIRS

Greece Lashes Out At IMF

Greece lashes out at the IMF because they do not want them in the Troika. If the IMF bails then Germany also bails and thus Greece must leave the EU. As Mish states: this is nothing but a blame game

(courtesy Mish Shedlock/Mishtalk)

Submitted by Mike Shedlock via MishTalk.com,

The game playing in Greece gets curiouser and curiouser.

German finance minister Wolfgang Schäuble went on TV saying the only way Greece can get a haircut is if it leaves the Eurozone.

The IMF reiterated that Greece will not be able to make its payments.

Greece insists the IMF is wrong, yet it wants credit relief.

The Financial Times reports Greeks Escalate Bailout Divisions by Lashing out at ‘Misleading’ IMF Report.

Greece’s finance minister has lashed out at the International Monetary Fund’s “misleading” analysis of the country’s economic health and debt trajectory, intensifying a rift between Athens and the Fund over its involvement in the country’s three-year bailout programme.

Responding to the IMF’s 91-page healthcheck of the Greek economy, Syriza’s Euclid Tsakalotos said the analysis gave an unfair and “insufficient” account of reform efforts undertaken by the left-wing government since the summer of 2015.

Mr Tsakalotos said the “overly pessimistic” account led the Fund to a wrong-headed assessment of the country’s debt dynamics, which the report says could reach “explosive” proportions above 200 per cent of GDP without major debt relief or bolder spending cuts and reforms.

Greece wants the IMF out of the troika so why does it insist its debt is sustainable? It makes no sense. If its debt was sustainable, the IMF would stay in.

I discussed this previously as a blame game scenario, with each party wanting to blame the others, but things have gotten so silly now I find it difficult to twist this pretzel in a way that fits.

Meanwhile, Greek unemployment is a “mere” 23%, despite the alleged Greek recovery.

Greece vs. US Great Depression

The IMF provided this comparison of Greece vs. the Great Depression.

Greece does not want the IMF in the troika but if the IMF leaves, Germany is set to pull the plug. There is obviously some sort of game here, but it is logically impossible for Greece to hold the conflicting positions it has.

The IMF is due to deliver a major decision on whether it will contribute to the country’s €86bn bailout when finance ministers meet in Brussels later this month.

Had Greece warmed up to the IMF, it could have blamed Germany and the IMF. Logically all it can do now is blame itself.

Enough of this nonsense, I repeat Dear IMF, Please Put Greece Out of Its Misery.

end

They are all over the board with respect to Greece today. At first, there was a statement that the EU and the IMF agree on a common stance and then a Greek official blurted that no bailout deal is expected today

(courtesy zero hedge)

Greek Bond Yields Tumble After Euro Zone, IMF Agree On “Common Stance”

Update: It appears expectations of an imminent deal may be premature, because this just hit the tape:

- GREEK OFFICIAL SAYS NO BAILOUT DEAL EXPECTED IN MEETING TODAY.

* * *

In a welcome sign the latest conflict between the troubled Greece’s lenders may be thawing, Reuters reports that Euro zone creditors and the International Monetary Fund have agreed between themselves to present a common stance to Greece later on Friday in talks on reforms and the fiscal path Athens must take, euro zone officials said.

As reported earlier this week, a united stance among the Troika would be a breakthrough because the two groups have differed for months on the need to reduce the “explosive” Greek debt burdern and the size of the primary surplus Greece should reach in 2018 and after. Those differences have hindered efforts to unlock further funding for Greece under its latest euro zone bailout program. The IMF hasn’t signed Greece’s third bailout package, but Germany-led eurozone lenders want the IMF to rejoin the bailout as a lender.

“There is agreement to present a united front to the Greeks,” a senior euro zone official quoted by Reuters said, adding that the outcome of Friday’s meeting with the Greeks was still unclear and it was unclear if Athens would accept the proposals. “What comes out of it, we will see,” the official said.

Jeroen Dijsselbloem, the chairman of euro zone finance ministers, said in The Hague that Friday’s meeting, in which Greek Finance Minister Euclid Tsakalotos will take part, was to discuss the size of Greece’s primary surplus. While the euro zone, or rather mostly Germany, wants Greece to reach a primary surplus of 3.5% of GDP and keep it there for many years, the IMF believes that with reforms in place now Greece will reach only 1.5% and has been pushing for Athens to legislate new measures that would safeguard the agreed euro zone targets.

Officials said the lenders would ask Greece to take 1.8 billion euros worth of new measures until 2018 and another 1.8 billion after 2018, focused on broadening the tax base and on pension cutbacks.

Meanwhile, the Greek Syriza government, elected to fight against lend-imposed austerity, has been loathe to make more cuts that will hit its battered citizens. Lenders have previously accused Greece of stalling on previously agreed upon reforms which, like in the past, have not been implemented.

As such, the Greek response remains the big wildcard. As the WSJ adds, if Greece accepts the proposal, representatives from the institutions could return to Athens as soon as next week and sort out the details, before a meeting of eurozone finance ministers on Feb. 20. Several Greek officials told the WSJ that the Greek government would be willing to make fiscal concessions for after 2018 if it misses fiscal targets.

But the Greeks want a “comprehensive agreement” that would include a clearer description of the country’s fiscal path, enough to make Greek bonds eligible for the ECB’s QE program. However, in an ongoing multivariable hurdle, the ECB has said Greek bonds would only be eligible for its quantitative-easing program if the current review of Greece’s bailout is completed and an agreement to restructure the eurozone’s loans to Athens removes concerns about the sustainability of the country’s high debts.

Until now, Germany has been insisting on a two-step sequence, in which Greece first signs up to more austerity before Berlin sits down with the IMF to see how much debt relief is still necessary.

Greece’s Economy Minister Dimitri Papadimitriou has called all sides to offer something at the same time, in order for an agreement to be reached. “Negotiation is like dancing the tango: you need both and who would make the first move is not clear,” he said.

The good news for Greece is that it doesn’t urgently need bailout cash until large debt falls due in July.

But all sides would prefer to reach an agreement before Europe’s attention shifts to its packed domestic political calendar, which includes elections in the Netherlands, France and Germany.

While the latest Greek crisis is still far from resolved, markets took heart from the news, and as a result Greece’s two-year bond yield tumbled 130 basis points to 8.7% after rising above the 10% mark on Thursday as worries about the bailout drove away buyers from Greece’s illiquid paper.

Finally, should negotiations fall apart, here again is a simply breakdown of the five scenarios facing Greece courtesy of Credit Suisse:

As of this moment, there is little clarity on what happens next. A recent report from Credit Suisse laid out five possible scenarios, ranging from the benign to the horrific, as follows:

- Scenario 1:Quick resolution (in the coming days)

- Scenario 2: “We need more time” (March-April)

- Scenario 3: brinkmanship (July)

- Scenario 4: Early elections (before the summer)

- Scenario 5: Grexit? Oh pleeease!

A timeline of key events in the coming weeks will help investors as they gauge the risk of yet another Grexit:

end

Schauble disparages Schultz as the SPD party is gaining in popular support against Merkel

(courtesy zerohedge)

The Knives Come Out: Schauble Says Martin Schulz Is The German Donald Trump

Earlier this week we reported that Germany’s default swaps spiked to the highest level since Brexit after a surprising new poll from INSA showed that Angela Merkel’s CDU would get only 30% of the vote, while the suddenly resurgent SPD would get 31% of the vote. This means that if the German elections were held today, the SPD’s new head, Martin Schulz, would enter any coalition talks as the leader of the largest party, hence becoming Chancellor.

It also means that a SPD-Green-Left coalition would currently win exactly 50% of seats, so that a government without the CDU/CSU could even be possible. In effect, the SPD has gained 10%-pts of support in past two (weekly) INSA polls, taking votes away from all other parties (see chart below). Interestingly, the AfD has also suffered a significant decline.