Gold at (1:30 am est) $1237.60 down $2.40

silver was : $18.02: down 4 CENTS

Access market prices:

Gold: $1235.50

Silver: $18.01

THE DAILY GOLD FIX REPORT FROM SHANGHAI AND LONDON

.

The Shanghai fix is at 10:15 pm est last night and 2:15 am est early this morning

The fix for London is at 5:30 am est (first fix) and 10 am est (second fix)

Thus Shanghai’s second fix corresponds to 195 minutes before London’s first fix.

And now the fix recordings:

Shanghai FIRST morning fix Feb 17/17 (10:15 pm est last night): $ 1248.41

NY ACCESS PRICE: $1238.25 (AT THE EXACT SAME TIME)/premium $10.16

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Shanghai SECOND afternoon fix: 2: 15 am est (second fix/early morning):$ 1248.41

NY ACCESS PRICE: $1238.20 (AT THE EXACT SAME TIME/2:15 am)

SPREAD/ 2ND FIX TODAY!!: 10.28

China rejects NY pricing of gold as a fraud/arbitrage will now commence fully

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

London FIRST Fix: Feb 17/2017: 5:30 am est: $1241.40 (NY: same time: $1241.20 (5:30AM)

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

London Second fix Feb 17.2017: 10 am est: $1241.95(NY same time: $1241.90 (10 am)

It seems that Shanghai pricing is higher than the other two , (NY and London). The spread has been occurring on a regular basis and thus I expect to see arbitrage happening as investors buy the lower priced NY gold and sell to China at the higher price. This should drain the comex.

Also why would mining companies hand in their gold to the comex and receive constantly lower prices. They would be open to lawsuits if they knowingly continue to supply the comex despite the fact that they could be receiving higher prices in Shanghai.

end

For comex gold:

FEBRUARY/

NOTICES FILINGS FOR FEBRUARY CONTRACT MONTH: 20 NOTICE(S) FOR 2000 OZ. TOTAL NOTICES SO FAR: 5145 FOR 514,500 OZ (16.003 TONNES)

For silver:

For silver: FEBRUARY

0 NOTICES FILED FOR nil OZ/

TOTAL NO OF NOTICES FILED: 406 FOR 2,030,000 OZ

Let us have a look at the data for today

.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total open interest ROSE by 5,314 contracts UP to 204,517 with respect to YESTERDAY’S TRADING. In ounces, the OI is still represented by just less THAN 1 BILLION oz i.e. 1.028 BILLION TO BE EXACT or 146% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT FEBRUARY MONTH: THEY FILED: 0 NOTICE(S) FOR nil OZ

In gold, the total comex gold ROSE BY A WHOPPING 9,001 contracts WITH THE RISE IN THE PRICE GOLD ($8.30 with YESTERDAY’S trading ).The total gold OI stands at 429,147 contracts

we had 20 notice(s) filed upon for 2000 oz of gold.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD:

We had another change in tonnes of gold at the GLD: this time a withdrawal of 2.37 tonnes of gold.

Inventory rests tonight: 841.17 tonnes

.

SLV

we had no changes in silver into the SLV

THE SLV Inventory rests at: 334.713 million oz

end

.

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in silver ROSE by 5314 contracts UP to 204,517 AS SILVER WAS UP 11 CENTS with YESTERDAY’S trading. The gold open interest ROSE by 11,944 contracts UP to 429,147 WITH THE RISE IN THE PRICE OF GOLD OF $8.30 (YESTERDAY’S TRADING)

(report Harvey

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

2c) COT report

(Harvey)

3. ASIAN AFFAIRS

i)Late THURSDAY night/FRIDAY morning: Shanghai closed DOWN 27.54 POINTS OR .85%/ /Hang Sang CLOSED DOWN 73.96 POINTS OR 0.58% . The Nikkei closed DOWN 112.91 POINTS OR 0.58% /Australia’s all ordinaires CLOSED DOWN 0.21%/Chinese yuan (ONSHORE) closed DOWN at 6.8678/Oil FELL to 53.13 dollars per barrel for WTI and 55.28 for Brent. Stocks in Europe ALL IN THE RED EXCEPT LONDON. Offshore yuan trades 6.8478 yuan to the dollar vs 6.8678 for onshore yuan.THE SPREAD BETWEEN ONSHORE AND OFFSHORE NARROWS WIDENS A BIT AS POBC ATTEMPTS TO STOP USA DOLLARS FROM LEAVING CHINA’S SHORES. ONSHORE YUAN WEAKER AS IS OFFSHORE YUAN COUPLED WITH THE STRONGER DOLLAR

REPORT ON JAPAN SOUTH KOREA NORTH KOREA AND CHINA

3a)THAILAND/SOUTH KOREA/NORTH KOREA

South Korea’s largest company Samsung has its Chief Executive Officer arrested for bribery perjury and embezzlement

( zero hedge)

b) REPORT ON JAPAN

c) REPORT ON CHINA

4. EUROPEAN AFFAIRS

This should be interesting: the two left wing candidates are to meet and decide on one candidate in the upcoming April elections. The combined vote may be enough for them to come in second place and thus remove the centrist candidates

( zero hedge)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

6.GLOBAL ISSUES

none today

7. OIL ISSUES

i)A great in depth analysis of the global oil market and why Berman believes that WTI is likely to be below 50 dollars than at 70 dollars

( Art Berman/Oil Price.com)

ii)Oil rigs continue to be utilized in the Permian basin which is causing a record amount of WTI oil glut

( zero hedge)

8. EMERGING MARKETS

none today

9. PHYSICAL MARKETS

i)Bloomberg also catches the above story

( Bloomberg/GATA)

ii)John Ing states that due to the world financial and political situation gold is the only vehicle that makes sense

( Ing/Kingworldnews)

iii)Lawrie Williams/ of Sharp’s Pixley gives his take on gold and silver. Both are rising despite some negative news:

( Lawrie Williams/Sharp’s Pixley

10.USA STORIES

i)All is not well in the auto loan department. The bubble seems to have burst in this 1.1 trillion USA market as subprime delinquencies (greater than 60 days) skyrocket. There are over 1 million auto loans borrowers that are behind greater than 60 days.

( zero hedge)

ii)This is a little troubling: Robert Harward has rejected Trump’s offer to becomes the next National Security Advisor. I guess it is David Patraeus or Keith Kellogg and nobody else can fill the roll:

( zero hedge)

iii)Trump tweets that General Keith Kellogg is in play for the NSA job

( zero hedge)

iv)This is interesting: farm incomes and equipment purchases are tanking while John Deere’s stock soars due to hedge fund purchases

( zerohedge)

( zero hedge)

a must read..

(courtesy Michael Snyder/Pepe Escobar)

(courtesy Pam Martens.Russ Martens/Wall Street on Parade)

viii)It starts; Chaffetz seeks charges against Hillary aid, Pagliano who decided not to show up to Congress once he was subpoenaed. He claims the 5th amendment but the FBI already had granted immunity to him so there was no reason for him not to testify.

( zerohedge)

ix)Pay attention to David Stockman as he outlines correctly what will happen in the next few months with respect to the USA economy:

( DailyReckoning/David Stockman)

x)The lawsuit has been going on for at least 5 years. The unsealing of the documents came last night as finally the government sues the largest USA Health Insurer on fraudulent overbilling

( zero hedge)

xi)The Senate confirmed Pruitt. He has been an very outspoken critic on global warming etc.

( zero hedge)

xii) This week’s wrap courtesy of Greg Hunter.

(Greg Hunter/USAWatchdog)

Let us head over to the comex:

The total gold comex open interest ROSE BY 9,001 CONTRACTS UP to an OI level of 429,147 WITH THE RISE IN THE PRICE OF GOLD ( $8.30 with YESTERDAY’S trading). We are now in the contract month of FEBRUARY and it is one of the better delivery months of the year. In this next big active delivery month of February we had a LOSS of 27 contracts DOWN to 903. We had 1 notice(s) served upon yesterday and therefore we LOST 26 contracts or an additional 2600 oz will not stand for delivery and NO DOUBT THEY WERE CASH SETTLED. The next non active contract month of March saw it’s OI FALL by 62 contracts DOWN TO 1960.The next big active month is April and here the OI ROSE by 6656 contracts UP to 281,772.

We had 20 notice(s) filed upon today for 2000 oz

And now for the wild silver comex results. Total silver OI ROSE by 5,314 contracts FROM 199,203 UP TO 204,517 AS THE PRICE OF SILVER ROSE TO THE TUNE OF 11 CENTS with respect to YESTERDAY’S trading. We are moving CLOSER TO the all time record high for silver open interest set on Wednesday August 3/2016: (224,540).

The active month of February saw the OI FALL by 8 contract(s) DOWN TO 140. We had 24 notice(s) served YESTERDAY so we GAINED 16 CONTRACTS or an additional 80,000 oz will stand for delivery.

The next big active delivery month is March and here the OI decrease by 4,939 contracts down to 75,387 contracts. For comparison purposes last year on the same date only 74,409 contracts were standing.

We had 0 notice(s) filed for 120,000 oz for the FEBRUARY contract.

VOLUMES: for the gold comex

Today the estimated volume was 159,278 contracts which is poor to fair.

Yesterday’s confirmed volume was 210,537 contracts which is good

volumes on gold are getting higher!

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz |

nil OZ

|

| Deposits to the Dealer Inventory in oz | 1999.900 oz

Brinks |

| Deposits to the Customer Inventory, in oz |

nil oz

|

| No of oz served (contracts) today |

20 notice(s)

2000 oz

|

| No of oz to be served (notices) |

883 contracts

88,300 oz

|

| Total monthly oz gold served (contracts) so far this month |

5145 notices

514,500 oz

16.003 tonnes

|

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | 207,001.3 oz |

Today, 0 notice(s) were issued from JPMorgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equates to 20 contract(s) of which 8 notices were stopped (received) by jPMorgan dealer and 0 notice(s) was (were) stopped/ Received) by jPMorgan customer account.

March 2016: 2.311 tonnes (March is a non delivery month)

| Silver | Ounces |

| Withdrawals from Dealers Inventory | nil |

| Withdrawals from Customer Inventory |

2837.100 0z

Brinks

|

| Deposits to the Dealer Inventory |

nil oz

|

| Deposits to the Customer Inventory |

873,830.260 oz

Brinks

CNT

|

| No of oz served today (contracts) |

0 CONTRACT(S)

(nil OZ)

|

| No of oz to be served (notices) |

140 contracts

(700,000 oz)

|

| Total monthly oz silver served (contracts) | 410 contracts (2,050,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month | 5,914,661.8 oz |

end

And now the Gold inventory at the GLD

feb 17/a withdrawal of 2.37 tonnes of gold from the GLD/Inventory rests at 841.17 tonnes

FEB 16/we had no changes in the GLD inventory today/Inventory rests at 843.54 tonnes

Feb 15./another deposit of 2.67 tonnes of gold into the GLD inventory despite another attempted whacking of gold/inventory rests at 843.54 tonnes

FEB 14/another deposit of 4.14 tonnes of gold into the GLD inventory/rests at 840.87 tonnes

FEB 13/another deposit of 4.15 tonnes of gold into the GLD/Inventory rests at 836.73 tonnes

Feb 10/no changes at the GLD/Inventory rests at 832.58 tonnes

feb 9/no changes at the GLD/Inventory rests at 832.58 tonnes

Feb 8/another “deposit” of 5.63 tonnes of gold into the GLD/The addition is a paper addition/total inventory: 832.58 tonnes

Feb 7/another huge fake deposit of 8.30 tonnes of gold into the GLD/the addition is a paper addition and no doubt not physical/ total inventory: 826.95 tonnes

FEB 6/a huge deposit of 7.43 tonnes of gold into the GLD/Inventory rests at 818.65 tonnes

FEB 3/no change in gold inventory at the GLD/Inventory rests at 811.22 tonnes

Feb 2/another huge deposit of 1.48 tonnes/inventory rests at 811.22 tonnes

Feb 1/a huge “deposit” of 10.67 tonnes of gold into the GLD/Inventory rests at 809.74 tonnes. this should stop GLD from sending gold to Shanghai.

JAN 31/no change in gold inventory at the GLD/Inventory rests at 799.07 tonnes

jan 30/no change in gold inventory at the GLD/Inventory rests at 799.07 tonnes

Jan 27/no changes at the GLD/Inventory rests at 799.07 tonnes

Jan 26/no changes at the GLD/Inventory rests at 799.07 tonnes/

jan 25/another exactly the same withdrawal as yesterday: 5.04 tonnes and again this was used in the whacking of gold today/inventory rests at 799.07 tonnes

jan 24/a huge withdrawal of 5.04 tonnes and probably this was used today in the whacking of gold/inventory rests at 804.11 tonnes

Jan 23/a big change/this time a deposit of 1.19 tonnes of gold into the GLD/inventory rests at 809.15 tonnes. The drainage of gold from the GLD to Shanghai has now stopped!

Jan 20/no changes in gold inventory a the GLD/Inventory rests at 807.96 tonnes

Jan 19/no changes in gold inventory at the GLD/Inventory rests at 807.96 tonnes

Jan 18/no changes in gold inventory at the GLD/Inventory rests at 807.96 tonnes

Jan 17/17/a deposit of 2.96 tonnes of gold/inventory at the GLD rests at 807.96 tonnes. I guess there is no more gold inventory to sent to C+Shanghai

Jan 13/17/there were no changes in gold inventory at the GLD/Inventory rests at 805.00 tonnes

Jan 12/2017/no change in gold inventory at the GLD/Inventory rests at 805.00 tonnes

Jan 11/no change in gold inventory at the GLD/Inventory rests at 805.00 tonnes

JAN 10/no changes in gold inventory at the GLD/Inventory rests at 805.00 tonnes

JAN 9/A WITHDRAWAL OF 8.87 TONNES OF GOLD FROM THE GLD/INVENTORY RESTS AT 805.00 TONNES

end

| Gold COT Report – Futures | ||||||

| Large Speculators | Commercial | Total | ||||

| Long | Short | Spreading | Long | Short | Long | Short |

| 212,259 | 102,507 | 57,432 | 105,674 | 233,462 | 375,365 | 393,401 |

| Change from Prior Reporting Period | ||||||

| -4,149 | 3,248 | 5,685 | -350 | -6,708 | 1,186 | 2,225 |

| Traders | ||||||

| 169 | 106 | 78 | 46 | 50 | 250 | 200 |

| Small Speculators | ||||||

| Long | Short | Open Interest | ||||

| 39,763 | 21,727 | 415,128 | ||||

| -1,601 | -2,640 | -415 | ||||

| non reportable positions | Change from the previous reporting period | |||||

| COT Gold Report – Positions as of | Tuesday, February 14, 2017 | |||||

Our Large Specs:

Those large specs that have been long in gold pitched 4149 contracts just as gold was about to rise??

those specs that have been short in gold added 3248 contracts to their short side??

Our commercials:

those commercials that have been long in gold pitched 350 contracts from their long side.

those commercials that have been short in gold covered in a hurry : 6708 contracts.

Our small specs:

those small specs that have been long in gold pitched 1601 contracts from their long side.

those small specs that have been short in gold covered 2640 contracts.

Conclusions:

strange COT: the commercials go net long by 6356 which is bullish.

| Silver COT Report: Futures | |||||

| Large Speculators | Commercial | ||||

| Long | Short | Spreading | Long | Short | |

| 104,765 | 19,953 | 16,346 | 48,659 | 147,686 | |

| 6,205 | -330 | -3,040 | -1,413 | 4,902 | |

| Traders | |||||

| 100 | 37 | 49 | 34 | 35 | |

| Small Speculators | Open Interest | Total | |||

| Long | Short | 195,338 | Long | Short | |

| 25,568 | 11,353 | 169,770 | 183,985 | ||

| -350 | -130 | 1,402 | 1,752 | 1,532 | |

| non reportable positions | Positions as of: | 159 | 106 | ||

| Tuesday, February 14, 2017 | © SilverSeek.com | ||||

Wow!! what a strange COT especially silver

Our large specs:

those large specs that have been long in silver added a whopping 6205 contracts to their long side and that is what we should have expected with a rising silver price.

those large specs who have been short in silver covered a tiny 330 contracts and they are certainly brave little souls.

Our commercials:

those commercials that have been long in silver pitched 1413 contracts from their long side.

those commercials that have been short in silver added a whopping 4902 contracts to their short side.

Our small specs;

those small specs that have been long in silver added 5995 contracts to their long side.

those small specs that have been short in silver covered a tiny 696 contracts.

Conclusions:

the commercials go net short by a rather large 6313 contracts with an advancing silver price.

Note the huge difference between silver and gold. Somebody is taking on the crooked banks in silver and in gold. In silver they are supplying the paper. In gold they are covering.

NPV for Sprott and Central Fund of Canada

end

Major gold/silver trading/commentaries for FRIDAY

GOLDCORE/BLOG/MARK O’BYRNE

Every Citizen Should Own 3.5 Ounces of Gold Bullion – Central Bank

- Central bank governor has “dream” for every citizen to own at least 100 grams of gold bullion

- Governor of Central Bank of Kyrgyzstan said the central bank had sold around 140 kilos of gold bullion to the domestic population already

- Central Asian country’s central bank continues to diversify into gold bullion

- “Gold can be stored for a long time … doesn’t lose its value for the population as a means of savings”

- “I’ll try to turn the dream into reality faster…”

The Governor of the Central bank of Kyrgyzstan has told Bloomberg News in an interview that it is his “dream” for every citizen in his country to own at least 100 grams (3.5 ounces) of gold as a way to protect their savings.

Diversifying one’s savings so that they are not solely held in fiat paper or electronic currencies in frequently vulnerable banks in a vulnerable banking and financial system is prudent advice in these uncertain times.

Indeed, there is a strong case to be made that the policies of most central banks in recent years have led to a massive debt bubble and the risk of another financial crisis, currency wars and currency debasement on a grand scale.

Hence, it was very refreshing to hear the actual governor of a central bank passionately advocate and proactively helping his fellow citizens to protect their savings by diversifying and having an allocation to physical gold.

From Bloomberg:

One of the first post-Soviet republics to adopt a new currency and let it trade freely, Kyrgyzstan’s central bank wants every citizen to diversify into gold. Governor Tolkunbek Abdygulov says his “dream” is for every one of the 6 million citizens to own at least 100 grams (3.5 ounces) of the precious metal, the Central Asian country’s biggest export.

“Gold can be stored for a long time and, despite the price fluctuations on international markets, it doesn’t lose its value for the population as a means of savings,” he said in an interview. “I’ll try to turn the dream into reality faster.”

In the two years that the central bank has offered bars directly to the population, about 140 kilograms of bullion have been sold, Abdygulov, 40, said by phone from the capital, Bishkek.

“We are hopeful that our country’s population will learn to diversify its savings into assets that are more liquid and — more importantly — capable of retaining their value,” he said. In rural areas, cattle is still the asset of choice for investors and savers, according to Abdygulov.

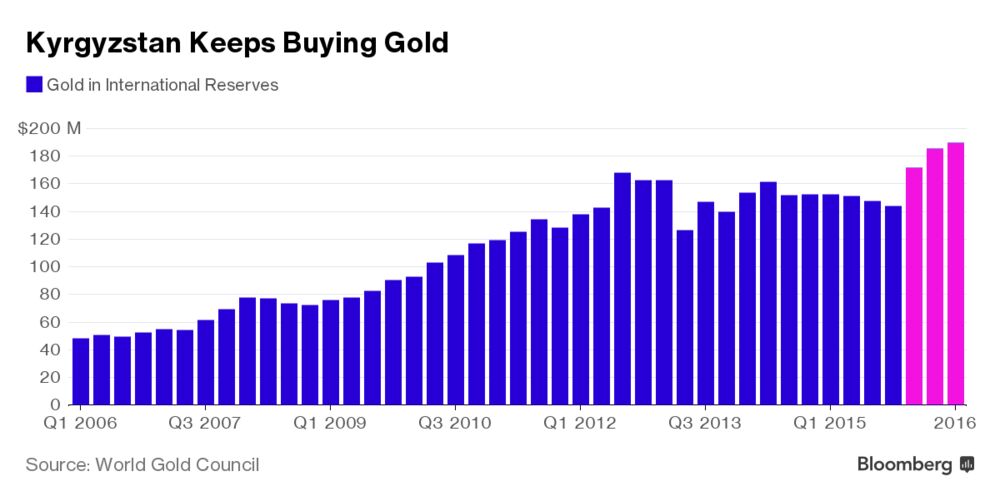

Kyrgyzstan has bucked a trend among central banks, the biggest owners of bullion, by stepping up buying even as its counterparts cut purchases in 2016 to a six-year low. Global combined bar and coin demand fell, according to the World Gold Council.

Across the emerging world, gold — often seen as the ultimate haven at times of upheaval — hardly needs any extra promotion. India, the world’s largest consumer after China, is in fact taking steps to curb imports of the precious metal by encouraging its citizens to deposit private gold holdings in banks.

In Turkey, where banks can use bullion as part of their reserve assets, President Recep Tayyip Erdogan last year called on people to convert their foreign-currency savings into liras and gold.

What makes Kyrgyzstan unique is the central bank’s effort to win converts by providing infrastructure for safe-keeping and investment. The central bank produces bars of different sizes, varying in weight from 1 to 100 grams.

The central bank governor believes his plan is realistic, even though it means the population would own about 600 tons of gold, equivalent to 30 times the nation’s current annual output. Abdygulov declined to specify the timeframe for when his goal of 100 grams per person can be met.

The options available for storage include safe deposit boxes at commercial lenders or with the central bank, he said. Some people opt to keep gold at home or possibly even bury it in the ground, according to Abdygulov.

With Kyrgyzstan enduring upheaval from economic crises in the early 1990s to bank failures during the last decade, gold is seen as a far safer bet than securities, he said.

“For Kyrgyzstan, gold is an alternative instrument of investment,” Abdygulov said. “The National Bank has ensured liquidity for gold — we aren’t only selling, but also buying back gold bars that we produced and sold.”

As Abdygulov took the reins of the central bank in 2014, Kyrgyz policy makers decided to raise gold’s share in its own reserves, now keeping about 10 percent of its $2 billion holdings in bullion. After years of capping the amount at 2.6 tons, the stockpile surged by more than 70 percent since 2012 to 4.5 tons at the end of the third quarter in 2016, according to the latest data compiled by the London-based World Gold Council.

With Kyrgyzstan’s output at about 20 tons a year, the central bank uses the national currency, the som, to buy gold mined locally, which can then be sold abroad if needed, according to Abdygulov. The governor said he’s counting on higher output in the future.

Abdygulov, who has masters degrees from Nagoya University in Japan and the University of North Texas, may be a gold enthusiast, but he’s no advocate for dislodging the dollar completely. His advice is based on the “rule of three” — splitting up savings between the som, foreign currency and gold.

As for the metal’s prospects, he’s upbeat, even after it surged the most in five years in 2016 and continued to post gains in 2017. Bullion has rallied more than 7 percent this year as concerns that Donald Trump’s policies on trade and immigration could derail U.S. growth boosted speculation that the Federal Reserve would be slow to raise borrowing costs.

End>

“Common sense is not so common” as Voltaire said. Financial and monetary common sense regarding gold and the importance of diversifying ones savings and investments is even more uncommon.

As one of the larger gold bullion delivery and storage specialists in the world and a vested commercial interest, GoldCore would obviously greatly welcome the central bank governors of Ireland, UK, U.S. and all western nations to urge their citizens to diversify their savings and own a small amount of gold.

As a specialist in the logistics of delivery and storage of physical gold, we can of course work with them and help them in this regard and we look forward to hearing from them.

We have long been passionate advocates of owning physical gold and have spent a lot of time educating about gold’s safe haven characteristics. This has been seen clearly in history and during the recent global financial crisis and indeed in the large body of new academic and independent research on gold in recent years.

The Governor clearly understands gold’s value and is acting accordingly in the interests of his fellow citizens.

Bravo Governor and Happy Friday folks !

end

Bloomberg also catches the above story

(courtesy Bloomberg/GATA)

Kyrgyzstan wants everyone to have 100 grams of gold

Submitted by cpowell on Thu, 2017-02-16 13:26. Section: Daily Dispatches

By Evgenia Pismennaya and Anna Andrianova

Bloomberg News

Thursday, February 15, 2017

A landlocked nation perched between China and Kazakhstan is embarking on an experiment with little parallel worldwide: shifting savings from cattle to gold.

One of the first post-Soviet republics to adopt a new currency and let it trade freely, Kyrgyzstan’s central bank wants every citizen to diversify into gold. Governor Tolkunbek Abdygulov says his “dream” is for every one of the 6 million citizens to own at least 100 grams (3.5 ounces) of the precious metal, the Central Asian country’s biggest export.

“Gold can be stored for a long time and, despite the price fluctuations on international markets, it doesn’t lose its value for the population as a means of savings,” he said in an interview. “I’ll try to turn the dream into reality faster.”

In the two years that the central bank has offered bars directly to the population, about 140 kilograms of bullion have been sold, Abdygulov, 40, said by phone from the capital, Bishkek. …

… For the remainder of the report:

https://www.bloomberg.com/politics/articles/2017-02-15/currency-pioneers…

END

John Ing states that due to the world financial and political situation gold is the only vehicle that makes sense

(courtesy Ing/Kingworldnews)

John Ing: The primary ‘Trump trade’ is to buy gold

Submitted by cpowell on Fri, 2017-02-17 03:39. Section: Daily Dispatches

10:40p ET Thursday, February 16, 2017

Dear Friend of GATA and Gold:

Canadian fund manager John Ing tonight gives King World News a comprehensive review of the world financial and political situation and concludes that the primary “Trump trade” is probably to buy gold. Ing’s commentary is posted at KWN here:

http://kingworldnews.com/man-asked-to-speak-to-chinese-officials-issues-…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

Lawrie Williams/ of Sharp’s Pixley gives his take on gold and silver. Both are rising despite some negative news:

(courtesy Lawrie Williams/Sharp’s Pixley)

LAWRIE WILLIAMS: Gold and silver defying HFT take-down efforts

17

The past few days have been somewhat encouraging for precious metals investors. Despite some seeming attempts, probably by the bullion banks, to bring gold and silver prices downwards, both made some significant recoveries. While the price recoveries may have been subsequently capped, with gold at around the $1,240 level and silver at around $18, this has to be seen as something of a victory for the gold bulls, although perhaps a pyrrhic one as the HF traders are probably not finished with their attacks yet.

Indeed this all happened in the light of some seemingly gold-negative news: An apparently slightly more hawkish Janet Yellen, some fairly positive U.S. economic data, news that long time gold supporter John Paulsen had liquidated some of his gold holdings in the GLD gold ETF and that George Soros had sold his Barrick Gold stock, taking some substantial profits. All seemingly bad news for gold, and by association for the other precious metals. Yet, despite all this gold has risen almost 8% year to date and silver around 13% and the major gold ETFs have been adding gold so far. The biggest of all, GLD, has added just short of 30 tonnes of gold this year, much of it in the past 2 weeks after seeing around 15 tonnes of sales in January.

This ‘safe haven’ gold demand seems to show few signs of diminishing, particularly given the apparent unpredictability of the USA’s new President and his unpopularity with much of the media, the self-styled intelligentsia, the intelligence community and the deep state. There is already talk of impeachment, but then there are major concerns about the kind of Administration a President Pence might preside over. Could be a case of ‘better the devil you know’!

If anything, silver has been performing better than gold with the Gold:Silver ratio (GSR) at around 69, down from around 72 at the beginning of the year. Indeed the GSR had been back at 68.6 during the past couple of days before coming back to just over 69 in today’s trading. Generally silver outperforms in a rising gold price scenario so if gold can break out above $1,250 there is a good chance the GSR will fall further. We have been predicting 65 as a likely level to be reached during the current year. Some consider this unrealistic but if anything we think a 65 level may prove to be conservative.

end

Your early FRIDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight

1 Chinese yuan vs USA dollar/yuan WEAKER AT 6.8678(SMALL DEVALUATION SOUTHBOUND /OFFSHORE YUAN WIDENS TO 6.8478 / Shanghai bourse DOWN 27.54 POINTS OR .85% / HANG SANG CLOSED DOWN 73.96 POINTS OR 0.31%

2. Nikkei closed DOWN 112.91 POINTS OR 0.58% /USA: YEN FALLS TO 112.83

3. Europe stocks opened ALL IN THE RED EXCEPT LONDON ( /USA dollar index RISES TO 100.61/Euro UP to 1.0654

3b Japan 10 year bond yield: FALLS TO +.094%/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 112.83/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD FINALLY IN THE POSITIVE/BANK OF JAPAN LOSING CONTROL OF THEIR YIELD CURVE AS THEY PURCHASE ALL BONDS TO GET TO ZERO RATE!!

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 53.13 and Brent: 55.28

3f Gold UP/Yen UP

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil DOWN for WTI and DOWN for Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund FALLS TO +.306%/Italian 10 yr bond yield DOWN to 2.178%

3j Greek 10 year bond yield RISES to : 7.85%

3k Gold at $1241.80/silver $18.03(8:15 am est) SILVER BELOW RESISTANCE AT $18.50

3l USA vs Russian rouble; (Russian rouble DOWN 52/100 in roubles/dollar) 58.14-

3m oil into the 53 dollar handle for WTI and 55 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation (already upon us). This can spell financial disaster for the rest of the world/China forced to do QE!! as it lowers its yuan value to the dollar/GOT SMALL DEVALUATION SOUTHBOUND from POBC.

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 112.83 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 0.9985 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.0638 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT

3r the 10 Year German bund now POSITIVE territory with the 10 year RISES to +.371%

3s The Greece ELA NOW at 71.4 billion euros,AND NOW THE ECB WILL ACCEPT GREEK BONDS (WHAT A DISASTER)

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.420% early this morning. Thirty year rate at 3.021% /POLICY ERROR)GETTING DANGEROUSLY HIGH

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

(courtesy Jim Reid/Bloomberg/Deutsche bank/zero hedge)

S&P Futures, Global Stocks Slide As European Political Fears Return; Gold Jumps

S&P equity futures followed Asian and European stocks lower, driven by weakness in French and Italian markets, as French political concerns returned; the pound tumbled after UK monthly retail sales unexpectedly dropped pushing the dollar higher and Euro lower.

About an hour after the European open, major indices experienced softness despite no fundamental catalyst to see Euro Stoxx 50 lower by 0.5%. The euro weakened and French bonds declined after the French Socialist Party’s presidential candidate, Benoit Hamon, said he’s in talks with far-left candidate Jean-Luc Melenchon about a single candidacy that would increase the likelihood of a stand -off with far-right front runner Marine le Pen, sending 10y OAT yields up 5bps and 6bps wider against Germany. Gold rebounded 0.2% as a quiet push into safe assets continued.

Global equity markets are set to end the week on a softer footing on Friday, after setting record highs in the previous two sessions, as investors looked for clarity on U.S. President Donald Trump’s policies on tax and trade. Confusion over US fiscal and monetary policy has grown as traders have gone back and forth assessing the prospects for President Donald Trump’s economics plans and the timing of U.S. interest-rate increases. Financial conditions have continued to tighten as March rate hike odds jumped after Yellen’s congressional testimony: the renewed uptick in 3M OIS and LIbor have yet to impact broader asset classes.

Trump’s plans last week to unveil a “phenomenal” tax policy spurred a rally in stocks, the dollar and emerging-market assets. In Congressional testimony this week, Yellen warned against waiting too long to tighten policy and said a healthier economy may warrant higher interest rates.

Speaking to Bloomberg, Naeem Aslam, chief market analyst at Think Markets said “many do believe that the market is getting ahead of itself and there is just too much optimism about how far Trump can go with his fiscal and tax plans as he still needs full approval from congress,” said “The chances of that are not that great and this is what makes some investors a little pessimistic.”

Much of the action was again in currencies, with the USDJPY sliding most of the overnight session, dragging global risk sentiment lower. Although the dollar was 0.3 percent firmer on the day, it was hovering near a one-week low against a basket of currencies .DXY and headed for its sixth week of losses in the last eight, as investors awaited substantive market-friendly news from President Donald Trump on tax reform. The greenback hit a one-month high on Wednesday after U.S. Federal Reserve Chair Janet Yellen supported a near-term rate hike due to signs of robust economic growth. Junichi Ishikawa, senior forex strategist at IG Securities in Tokyo said the dollar’s recent bounce lacked conviction.

“This shows that the market is still trying to work out the implication of President Trump’s policies, of which his approach to trade may not be supportive for the dollar,” he said.

The pound fell half a percent to $1.2427 after data showing retail sales in Britain fell shaprly 0.3% month-on-month last month, on expectations for a 0.9% rise.

The MSCI All-Country World index was headed for its fourth straight week of gains after hitting a record high on Thursday, but Asian and European markets eased as investors cashed in recent gains.

The MSCI’s index of Asia-Pacific shares outside Japan pulled back 0.2%, Tokyo stocks closed down 0.6 percent and the pan-European STOXX 600 index was 0.5 percent lower, although it remained near its highest level in 13 months.

Equities in Europe fell, paring a second weekly advance, led by commodity producers as prices of industrial metals were dragged down by further signs of tightening liquidity in China.

“It’s too soon to tell what divergent monetary policy will do to equity markets, but higher rates in the U.S. may help financials do better,” said Ramakrishnan.

In commodities, gold was set for its third week of gains as political uncertainty spurred demand for the safe haven precious metal. Spot gold was up 0.2% on the day. Brent crude futures were down 0.8%, paring back earlier gains. OPEC sources told Reuters the producers’ club could extend its output cut in order to rein in global oversupply. Copper was set to end the week lower as profit-taking pared back the price of the three-month copper contract, though concerns over supply from Chilean and Indonesian mines remained.

Bond yields slipped pretty much across the board. Yields on 10Y Treasuries hovered at 2.43% having crept higher during the week on U.S. rate hike speculation, while yields on Europe’s benchmark, German Bunds, were down 3 basis points at 0.32%. There has been a noticeable divide this week, with safe-haven Bunds and other core countries like France and Austria have seeing yields rise, while Spain and Italy have seen theirs fall for the first week in five, helped by some soothing noises from the European Central Bank. The ECB’s minutes on Thursday indicated little appetite for curbing stimulus, setting the scene for a divergence in central bank policy between the U.S. and Europe.

Market Snapshot

- S&P 500 futures down 0.3% to 2,339.00

- STOXX Europe 600 down 0.5% to 368.27

- German 10Y yield fell 3.0 bps to 0.319%

- Euro down 0.2% to 1.0650 per US$

- Brent Futures down 0.1% to $55.57/bbl

- Italian 10Y yield fell 8.6 bps to 2.156%

- Spanish 10Y yield rose 0.7 bps to 1.61%

- MXAP down 0.2% to 144.97

- MXAPJ down 0.3% to 466.19

- Nikkei down 0.6% to 19,234.62

- Topix down 0.4% to 1,544.54

- Hang Seng Index down 0.3% to 24,033.74

- Shanghai Composite down 0.9% to 3,202.08

- Sensex up 0.6% to 28,470.70

- Australia S&P/ASX 200 down 0.2% to 5,805.82

- Kospi down 0.06% to 2,080.58

- Brent Futures down 0.1% to $55.57/bbl

- Gold spot up 0.2% to $1,241.35

- U.S. Dollar Index up 0.2% to 100.67

Top Overnight News from BBG

- Mnuchin Warned by Japan, Germany as G-20 Sees New Economic Order

- Sage CEO Says Biotech Firm Has Received Takeover Interest

- U.S. House Steps Up Effort to Derail Exxon Climate Probe

- UnitedHealth Accused of Overcharging Medicare by Billions

- Trump’s Second Pick for Labor Differs More in Style Than Policy

- Boeing, SpaceX Safety Risks May Delay U.S. Astronaut Travel

- Macau Casino Stocks Flash Warnings That Preceded 2014 Crash

- U.K. Retail Sales Unexpectedly Decline as Inflation Bites

- Calpers, Others to Push Banks on Dakota Access Pipeline: FT

* * *

Asia equity markets traded negative following the subdued lead from the US, where the Nasdaq and S&P 500 ended their string of records, although the DJIA still edged a fresh all-time closing high with minimal gains of 0.04%. ASX 200 (-0.2%) was lower amid a lack of drivers with the index weighed down by the healthcare sector, whilst Nikkei 225 (-0.6%) was the laggard as exporters suffered from the recent JPY strength. China markets were also weak with the Shanghai Comp. (-0.9%) and Hang Seng (-0.4%) dampened after the PBoC’s liquidity operations amounted to a consecutive net weekly drain. 10yr JGBs were higher following advances in T-notes and amid the risk averse sentiment in Japan, while the curve was mixed with mild outperformance in the long-end. PBoC injected CNY 50bIn 7-day reverse repos, CNY 50bIn in 14-day reverse repos and CNY 50bIn in 28-day reverse repos for a net weekly drain of CNY 150bIn vs. Prev. CNY 625bn drain last week.

Top Asian News

- UOB Profit Declines as Bank Boosts Energy Loan Provisions

- Singapore’s Economy Expands at Fastest Pace in More Than 5 Years

- PBOC’s Cash Moves Act to Lower Banks’ Reserve Ratios, Data Show

- Coal-Loving Indonesian Investor Doubles Down After 39% Gain

- China’s H Shares Pare Weekly Advance as Banking Rally Stumbles

- Singapore, Hong Kong Restart Dual-Class Push to Snag IPOs

- China Futures Volume Surges as Brokers Climb on Looser Curbs

European stocks are also lower, with the Stoxx 600 down 0.5%, as this morning has seen a typically quiet Friday in terms of newsflow, however with price action garnering some attention. Around an hour into equity trade, major indices experiences softness amid no new fundamental catalyst to see Euro Stoxx 50 lower by 0.5%. In terms of a sector specific basis, energy is among the worst performers, while healthcare outperforms after Shire’s earnings yesterday and with AstraZeneca’s Lynparza met its primary endpoint. Elsewhere, the most notable earnings from the past 24 hours has come from Allianz, with an impressive beat and a share buyback program seeing Co. shares soar. In tandem with the downside seen in equities by mid-morning, fixed income markets pushed higher as Bunds retake the 164 level and retrace all the softness seen throughout the week. The US 10Y yield is also approaching pre-Yellen levels at around 2.64.

Top European News

- ECB Shows Readiness to Flex Rules If Inflation Goal’s at Stake

- Allianz Plans $3.2 Billion Share Buyback as Profit Climbs (3)

- U.K.’s Clark Meets PSA Chiefs to Make Case for Vauxhall

- Sprint by Turkish Stocks Leaves Fund Managers in Starting Blocks

- Swedish Muzak Startup Ditches Spotify in World Expansion Bid

In currencies, UK retail sales data was the only top tier release for the day, and came in far weaker than expected despite some correction expected due to the drop seen in the previous month. The Jan data missed on all counts, with headline M/M falling 0.3% vs a +0.9% rise expected. GBP was falling ahead of the release, with Cable trade above 1.2500 all too brief and followed up by a move through the 1.2400’s to retest the lows around 1.2385 seen earlier in the week. EUR/GBP raced up towards 0.8600 after a temporary dip towards 0.8500, but it looks as though heavy GBP/JPY sales provided just as much of the impetus as pre 142.00 trade earlier in the day led to an eventual drop below 140.00. The flow may well have been encouraged by the weakness in USD/JPY, which has now dropped below 113.00 putting the support from 112.50 back under threat as UST yields continue to struggle despite this week’s events/data.

In commodities, the Bloomberg Commodity Index fell 0.4 percent, heading for its fourth weekly drop in five. Oil declined 0.2 percent to $53.28 a barrel. Crude is heading for its first weekly decline in five weeks as expanding U.S. crude stockpiles countered output cuts from OPEC and other producing nations. Gold nudged 0.2 percent higher to $1,241.56 an ounce and is and is set for its seventh weekly gain in eight weeks. Front and centre at present is the rise in Gold, and despite the obvious negative correlation with the USD, the risk tone has turned a little to cause some wobbles on Wall Street. The Dow may have eked out some fresh record highs, but not after a confused start exacerbated by the rise in Treasuries. Base metals across the board have eased back off better levels on the week due to risk sentiment also, but minor outperformance seen in Platinum. USD weakness will also underpin Oil prices, but with the growth in inventories dismissed due to the future impact of the OPEC agreed productions, support in WTI looks well established and comfortably ahead of USD50.00, though little to prompt a move on USD55.00+ for now. Support in Brent comes in ahead of USD55.00.

Looking at the day ahead it looks set to be a fairly quiet end to the week. In Europe this morning the only data came from the UK where the January retail sales figures disappointed (-0.3%, Exp. 0.9%, last -1.9%) while in the US this we’ve got the Conference Board’s leading indicator for January. Earnings wise Allianz headlines a small list.

US Event Calendar

- 10am: Leading Index, est. 0.5%, prior 0.5%

- * * *

DB’s Jim Reid concludes the overnight wrap

On a relatively dull day markets wise the ECB minutes brought a little excitement to European bonds at least. The minutes said that implementing the planned QE programme would “inevitably” require “limited and temporary deviations” from the ECB’s capital key. Although ‘limited’ and ‘temporary’ don’t indicate anything substantial this was still enough to help peripherals rally strongly. Indeed 10y yields in Italy, Spain and Portugal finished -10.3bps, -8.9bps and -10.4bps lower respectively and so tightening their spreads to Bunds which ended -2.5bps on the day. 10y Treasury yields (-4.8bps to 2.445%) also finished lower for the first time since February 8th. Not even a bumper Philly Fed manufacturing index reading which saw the index surge nearly 20pts to 43.3 in February and the highest since 1984 could halt the reversal. The jump in the data was in fact the single biggest in a month since 2009 and came hot on the heels of a decent NY Fed manufacturing survey on Wednesday.

For the most part the reversal for bonds was also the case for risk assets. Despite staging a typical late bounce-back into the close the S&P 500 (-0.09%) finally snapped a run of 7 consecutive daily gains and finished lower for the first time since February 6th. The Dow (+0.04%) did manage to just eke out a small gain and extend the record high for another day although the runs did come to an end for the Nasdaq (-0.08%) and Russell 2000 (-0.36%) indices too. The overall tone in Europe had been relatively soft too (Stoxx 600 -0.37%) with Banks and Energy sectors under pressure. Oil was particularly volatile in the afternoon as we saw WTI touch as high at $53.59/bbl, before tumbling to $52.68/bbl, and then reverse again into the close to actually finish up +0.60% at around $53.36/bbl. A combination of growing US inventories following the latest EIA data and a Reuters report suggesting that OPEC could look to extend the six-month production cut both seemed to play their part.

Elsewhere there was a bit of excitement in the spike up in the VIX (+7.40%) to 12.86 in the early evening which saw it reach a new high for the month, only for the index to completely retrace into the close and end more or less flat. Currencies were a bit more one-way however with the Dollar index (-0.73%) down for the second day in a row following ten successive daily gains. The Yen (+0.81%) was a big beneficiary against that and we’re seeing that weigh on Japanese equities this morning with the Nikkei currently -0.55%. The Hang Seng (-0.15%), ASX (-0.14%) and Kospi (-0.17%) are also down while bourses in China were initially up helped by the news of the China futures exchange relaxing curbs on stock index futures trading, but are now down a similar amount.

Moving on. While there was some focus on the President Trump press conference yesterday, more so for its typical entertainment than any material updates for markets, House Speaker Ryan did emphasise separately that a tax reform “has to happen” and that following the President’s Day break on Monday, the House intends to “introduce legislation and repeal and replace Obamacare”. Ryan also said that a much anticipated border adjustment tax is needed to spur US manufacturing and that currency adjustment would occur with tax law harmonization.

Closer to home, time is ticking down now to the Eurogroup meeting on Monday and it seems that there is growing scepticism out there that a Greek deal will be struck in time. Germany parliamentary members stressed the need to have IMF participation yesterday which they also said is precisely the position taken by euro area finance ministers. The FT also ran an article downplaying hope of an agreement by next week, suggesting instead that a deal may be months away now. While Greece is likely able to stand on its own two feet until July (when heavy bond maturities are due) its looking like any progress will go on the backburner until the Dutch and first round of French elections are out of the way over the next couple of months.

Before we wrap up, the only other data yesterday in the US came in the housing sector where housing starts revealed a suspiring -2.6% mom decline in January (vs. 0.0% expected) but permits jumped a better than expected +4.6% mom (vs. +0.2% expected). Initial jobless claims rose 5k last week to 239k but remain at low levels still. Elsewhere, Fed Vice-Chair Fischer also spoke but didn’t give much away in terms of timing for the next rate hike while also declining to say whether or not he expects two or three moves this year.

While we’re on the Fed, it’s worth drawing your attention to our economists’ latest Global Economic Perspectives piece where they have taken a look at the looming leadership shake-up. They note that President Trump will have considerable scope to reshape the Fed. By April, there will now be at least three vacancies on the seven-seat Board of Governors (following Governor Tarullo’s resignation), whilst Fed Chair Janet Yellen’s term as Chair will end in January next year. They note that at this point there is substantial uncertainty about who could replace Chair Yellen – there has been little indication from the Trump administration about possible candidates. Our team discuss several of the candidates that have been mentioned (these include current Governor Jerome Powell, past Governor Kevin Warsh, and academic John Taylor). Based on Trump’s past comments, the makeup of his economic advisors and appointments, and the political leanings of Congressional Republicans, they argue that it would seem that Trump may prefer a candidate that: (1) has significant experience in markets and/or business (i.e., a market practitioner rather than an academic economist), (2) does not have strong hawkish leanings that would work against Trump’s growth agenda, and (3) does not forcefully reject greater Congressional oversight of the Fed. They write that who occupies the Chair’s seat would be critical for markets in any environment. But Yellen’s replacement could be even more important, as he or she may well preside over an economy that is near full employment and that is given a large dose of fiscal stimulus. This raises the risk that the Fed could fall behind the curve.

Looking at the day ahead it looks set to be a fairly quiet end to the week. In Europe this morning the only data comes from the UK where we’ll get the January retail sales figures (where a rebound is expected) while in the US this afternoon we’ve got the Conference Board’s leading indicator for January. Earnings wise Allianz headlines a small list

3. ASIAN AFFAIRS

i)Late THURSDAY night/FRIDAY morning: Shanghai closed DOWN 27.54 POINTS OR .85%/ /Hang Sang CLOSED DOWN 73.96 POINTS OR 0.58% . The Nikkei closed DOWN 112.91 POINTS OR 0.58% /Australia’s all ordinaires CLOSED DOWN 0.21%/Chinese yuan (ONSHORE) closed DOWN at 6.8678/Oil FELL to 53.13 dollars per barrel for WTI and 55.28 for Brent. Stocks in Europe ALL IN THE RED EXCEPT LONDON. Offshore yuan trades 6.8478 yuan to the dollar vs 6.8678 for onshore yuan.THE SPREAD BETWEEN ONSHORE AND OFFSHORE NARROWS WIDENS A BIT AS POBC ATTEMPTS TO STOP USA DOLLARS FROM LEAVING CHINA’S SHORES. ONSHORE YUAN WEAKER AS IS OFFSHORE YUAN COUPLED WITH THE STRONGER DOLLAR

3a)THAILAND/SOUTH KOREA/NORTH KOREA

South Korea’s largest company Samsung has its Chief Executive Officer arrested for bribery perjury and embezzlement

(courtesy zero hedge)

Samsung Chief Arrested For Bribery, Perjury And Embezzlement

Exactly one month ago, South Korea’s political crisis – recall that the country’s president Park Geun-hye was impeached last December – spilled over into the corporate sector when the country’s special prosecutor unexpectedly sought a warrant to arrest the head of Samsung, the country’s largest conglomerate, accusing him of paying multi-million dollar bribes to a friend of impeached President Park Geun-hye. On the night of January 16, investigators had grilled the head of Samsung, the world’s largest maker of smartphones, flat-screen TVs and memory chips, Jay Y. Lee for 22 straight hours last week as a suspect in a massive corruption scandal, which last month led to parliament impeaching president Park.

As a quick tangent, putting Samsung’s size and importance in context, the company generates $230 billion in annual revenue, equivalent to about 17% of South Korea’s export-oriented economy, the fourth largest in Asia.

The special prosecutor’s office had accused Lee of paying bribes total 43 billion won ($38 million) to organizations linked to Choi Soon-sil, a friend of the president who is at the center of the scandal, in order to secure the 2015 merger of two affiliates and cement his control of the family business. The 48-year-old Lee, who became the de facto head of the Samsung Group after his father, Lee Kun-hee, was incapacitated by a heart attack in 2014, was also accused of embezzlement and perjury. Prosecutors allege that Lee, 48, funded Park’s associates as he tried to consolidate control over the sprawling conglomerate founded by his grandfather.

But whereas on January 19 the court rejected a request from prosecutors to arrest Lee, one month later it changed its mind. Fast forward to today, when in denial of some cynics who suggested it would could not happen, Samsung chief Jay Y. Lee was formally arrested on allegations of bribery, perjury and embezzlement, “an extraordinary step that jeopardizes the executive’s ascent to the top role at the world’s biggest smartphone maker and the nation’s most powerful company.”

Samsung chief, Jay Y. Lee, leaves for the Seoul Central District Court,

February 16, 2017. Reuters

The Seoul Central District Court issued the warrant for Lee’s arrest early Friday and the 48-year-old Lee was taken into custody at the Seoul Detention Centre, where he had awaited the court’s decision following a day-long, closed-door hearing that ended on Thursday evening. According to Reuters, the judge’s decision was announced at about 5:30 a.m. (2030 GMT) on Friday, more than 10 hours after Lee, the sprawling conglomerate’s third-generation leader, had left the court. There’s a chance the suspect could destroy evidence or flee, so arresting him is appropriate, a court spokesperson said.

On Tuesday, the special prosecutor’s office had requested a warrant to arrest him and another executive, Samsung Electronics president Park Sang-jin, on bribery and other charges. The court rejected the request to arrest Park, who also heads the Korea Equestrian Federation, saying it was not needed given his “position, the boundary of his authority and his actual role”.

The court reversed its opinion because, as Reuters reports, the prosecution said it had secured additional evidence and brought more charges against Lee in the latest warrant request. “We acknowledge the cause and necessity of the arrest,” a judge said in his ruling, citing the extra charges and evidence.

When he testified at a parliamentary hearing in December, Lee said he never ordered donations to be made in return for preferential measures and rejected allegations he received wrongful government support to push through a merger of two Samsung affiliates in 2015. Still, Lee, who has been put under a travel ban, confirmed he had private meetings with Park and that Samsung had provided a horse worth 1 billion won that was used for equestrian lessons by Choi’s daughter.

That said, according to Bloomberg, when Including procedural steps and appeals, it may take as long as 18 months for a trial and verdict.

Meanwhile, a Samsung spokeswoman said no decision had been made about whether Lee’s arrest would be contested or whether bail would be sought.

Samsung and Lee have denied wrongdoing in the case. “We will do our best to ensure that the truth is revealed in future court proceedings,” the Samsung Group said in a brief statement after Lee’s arrest.

While Lee’s arrest is not expected to hamper day-to-day operation of Samsung Group companies, which are run by professional managers, experts have said it could affect strategic decision-making by South Korea’s biggest conglomerate. “There are more than 100,000 of us (in Samsung Electronics). It wouldn’t make sense for a company of that size to not function properly just because the owner is away. It’s business as usual for us,” said an engineer at Samsung Electronics, who declined to be identified.

Of course, when the boss of one of the world’s biggest companies is arrested for bribery, perjury and embezzlement, it is hardly ever a good thing.

To be sure, Lee’s arrest would have an impact on longer-term investment decisions, said Kim, now a professor at Sungkyunkwan University. “Samsung presidents are evaluated on an annual basis, so they cannot make bold bets about the future. They need a chairman when making long-term investment decisions,” he said.

Ultimately, Lee may be just a pawn, albeit very powerful, in the ongoing legal crusade against President Park and her close friend Choi Soon-sil, who is in detention and faces charges of abuse of power and attempted fraud. As reported last month, prosecutors focused their investigations on Samsung’s relationship with Park, 65, who was impeached by parliament in December and has been stripped of her powers while the Constitutional Court decides whether to uphold her impeachment.

They accused Samsung of paying bribes totaling 43 billion won ($37.74 million) to organizations linked to Choi to secure the government’s backing for a merger of two Samsung units. That funding includes Samsung’s sponsorship of the equestrian career of Choi’s daughter, who is in detention in Denmark, having been on a South Korean wanted list.

If parliament’s impeachment is upheld by the Constitutional Court, Park will become South Korea’s first democratically elected leader to be forced from office early. Park remains in office but stripped of her powers while she awaits the Constitutional Court’s decision.

“This is a painful event for Vice Chairman Lee,” said Kim Sang-jo, a shareholder activist and economics professor at Hansung University who was questioned by the special prosecutor as a witness in the probe. “But this will be an important opportunity for Samsung Group to sever ties with the past,” he said, referring to links between the government and the country’s conglomerates, also known as chaebol.

What happens to the company’s stock? It is unlikely that the market will be too excited about this rather unexpected outcome.

“In the short term, it could have an impact on the stock, only because of sentiment, and also because the stock has risen a lot recently,” Jung Sang-jin, a fund manager at Korea Investment Management, told Bloomberg. “In the long-term, there won’t be much impact on the stock, given previous times when other chaebol heads were arrested with few problems for their companies to keep running the business.”

Perhaps he is being too optimistic: keep an eye on the Kospi where trading may be more volatile than usual after today’s news. On the other hand, we are confident the fund manager is right: in the long run, it will most likely be business as usual.

END

b) REPORT ON JAPAN

c) REPORT ON CHINA

4. EUROPEAN AFFAIRS

This should be interesting: the two left wing candidates are to meet and decide on one candidate in the upcoming April elections. The combined vote may be enough for them to come in second place and thus remove the centrist candidates

(courtesy zero hedge)

French Bonds Tumble As Left-Wing Coalition Sparks More Le Pen Anxiety

The French presidential election campaign just proved that ‘two wrongs do not make a right’.

French bonds tumbled relative to Bunds as Bloomberg reports, Socialist Party presidential candidate Benoit Hamon said he’s holding further talks with far-left candidate Jean-Luc Melenchon about a potential single candidacy.

A merger could bring about a showdown with Marine Le Pen’s anti-euro National Front, with the latest polls showing the combined vote share of the two candidates would see them qualify for the second round of voting in May.

France, Opinion Way poll:

Le Pen (FN-ENF): 26%

Macron (EM-NI) 20% ↓

Fillon (LR-EPP): 20%

Hamon (PS-S&D) 16%

Mélenchon (FG-LEFT): 13% ↑

And Le Pen’s odds are rising on the news of the potential merger…

And the reaction is clear… French bond risk is resurging…

“This is clearly not a positive for French bonds,” said Kim Liu, a strategist at ABN Amro Bank.

“It increases the odds of a Le Pen victory, with French bonds already being very vulnerable to political risks. It’s too early to call if this is a game changer as we do not know how serious the merger talks are, but certainly this is not something the market is waiting for.”

end

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

6.GLOBAL ISSUES

none today

7. OIL ISSUES

A great in depth analysis of the global oil market and why Berman believes that WTI is likely to be below 50 dollars than at 70 dollars

(courtesy Art Berman/Oil Price.com)

Why Sub $50 Oil Is More Likely Than $70 Oil

Submitted by Arthur Berman via OilPrice.com,

It is more likely that oil prices will fall below $50 per barrel than that they will continue to rise toward $70. Prices have increased beyond supply and demand fundamentals because of premature expectations about the effects of an OPEC production cut on oil inventories.

Last week’s 13.8 million barrel addition to U.S. storage was the second largest in history. It moved U.S. crude oil inventories to new record high levels.

Meanwhile, 130 horizontal rigs have been added to tight oil drilling since the OPEC cut was first announced in September. That means that U.S. output will surge and will continue to be a drag on higher prices.

Comparative inventory analysis suggests that the current ~$53 per barrel WTI oil price is at least $6 per barrel too high. Don’t hold your breath for $70 oil prices.

Inventory Is The Key

Most analysts believe prices will increase steadily now that OPEC has decided to cut production. Their logic is that over-production caused lower oil prices and lower output should bring markets into production-consumption balance.

The problem is that production is not the same as supply and consumption is not the same as demand. Inventories lie in-between and modulate the flows from both sides of the production-consumption equation.

Inventory is clearly part of supply but is also a component of demand. Excess production goes into inventory when demand is less than supply. When consumption exceeds production, oil is withdrawn from inventory reflecting increased demand.

The International Energy Agency (IEA) reported last week that global liquids markets would move to a supply deficit by the first quarter of 2017 if OPEC production cuts take place as announced (Figure 1).

Figure 1. IEA Demand/Supply Balance until 2Q17. Source: IEA February 2017 Oil Market Report.

Yet the OECD inventories on which IEA’s forecast is based have increased and are now more than 400 million barrels above the 5-year average (Figure 2). In order for a supply deficit to develop in the first quarter of 2017, those stocks would have to be drastically reduced over the next 6 weeks. Comparative inventory analysis provides some context for the necessary magnitude of that reduction.

(Click to enlarge)

Figure 2. OECD Incremental Inventories Are At Record High Levels Although Absolute Inventories Have Flattened in Recent Months. Source: EIA and Labyrinth Consulting Services, Inc.

Comparative inventories index current storage levels against a moving average of values for the same calendar date over the previous 5 years. This provides the most reliable way of understanding oil-price trends by normalizing stock changes for seasonal variations and comparing them with 5-year average values.

Figure 3 shows that current OECD comparative inventories (C.I.) are at an all-time high level of more than 300 million barrels (absolute inventories are 3.1 billion barrels).

C.I. values around zero (+/- about 50 mmb) correspond to periods of high oil prices (>$80 per barrel) over the past decade. That suggests that comparative inventories need to fall approximately 200 to 300 million barrels to support $70 to $80 per barrel oil prices.

(Click to enlarge)

Figure 3. OECD Comparative Inventories Are At An All-Time High & Need to Fall 200-300 mmb To Support $70-$80 Per Barrel Oil Prices. Source: EIA STEO and Labyrinth Consulting Services, Inc.

What the IEA is apparently showing in Figure 1 as a “demand/supply balance” is really a demand/production balance. If OPEC cuts move forward as announced, consumption will exceed production in the first two quarters of 2017 and withdrawals from storage will occur. That is a legitimate demand increase.

The billions of barrels of working capacity remaining in inventory are not considered supply in this calculation of balance. That distorts the supply-demand relationship.* At the very least, it does not treat the ~550 million barrels of incremental inventory that has accumulated since December 2013 in Figure 2 as supply.

Inventory is like a savings account for oil. It may be in a separate account from checking but it is part of total available supply. This sort of confusion over definitions of supply and demand is easily avoided by considering comparative inventories. Related: Is $60 Oil Within Reach?

Figure 4 is a cross-plot of OECD comparative inventories and Brent prices. It shows that current prices of ~$55 per barrel are approximately $10 per barrel over-valued compared to the trend line. It further shows that comparative inventory levels must fall ~200 million barrels to support ~$70 per barrel oil prices.

(Click to enlarge)

Figure 4. OECD Comparative Inventories At Record Highs–Comparative Inventory Suggests That Current Prices Are ~$10/Barrel Over-Valued. Source: EIA and Labyrinth Consulting Services, Inc.

Movement toward market balance cannot help but accelerate as a result of OPEC production cuts. Still, the massive stock reductions necessary to support higher oil prices will only occur over a much longer period.

It will take at least a year to reduce OECD inventories 400 mmb down to the 5-year average. This assumes that all OPEC cuts take place as announced and continue beyond the 6-month term of those agreements. It also assumes that non-OPEC production declines or at least remains static.

U.S. Production Will Not Remain Static

It is worth recalling that over-production by the U.S. and Canada was the trigger for the global oil-price collapse in 2014 (Figure 5). These two countries accounted for almost half (44 percent) of the incremental increase in crude oil and lease condensate production in the world as of March 2015 peak production levels.

(Click to enlarge)

Figure 5. U.S. + Canada Incremental Ouput: The Major Contributor to Low Oil Prices. Source: EIA and Labyrinth Consulting Services, Inc.

U.S. production fell more than 1 million barrels per day (mmb/d) from April 2015 through September 2016 but is now recovering because of higher oil prices (Figure 6). EIA forecasts that field production will increase to 9.28 mmb/d by the end of 2017 and will reach almost 10 mmb/d by December 2018.

(Click to enlarge)

Figure 6. U.S. Crude Oil Production Has Increased 290 kb/d in The Last 4 Months After Falling 1.06 mmb/d From Apr 2015 to Sept 2016. Source: EIA February 2017 STEO and Labyrinth Consulting Services, Inc.Related: Energy Storage Set To Boom In 2017

EIA does not predict that WTI oil prices will exceed $60 per barrel throughout this 2-year period. It is interesting to note that EIA shows prices falling below $50 per barrel in February 2017 and remaining at that level through mid-year.

After OPEC announced that a production cut agreement was evolving in September 2016, the U.S. horizontal tight oil rig count accelerated. Since then, 130 rigs have been added and 67 percent have been in the Permian basin tight oil play (Figure 7). In recent weeks, the Eagle Ford play rig count has made impressive gains and the Bakken rig count has steadily increased also.

(Click to enlarge)

Figure 7. 130 Tight Oil Rigs Added Since Mid-Sept 2016: 67 percent Are In The Permian Basin. Source: Baker Hughes, EIA, Bloomberg and Labyrinth Consulting Services, Inc.

This reflects a massive flow of capital into these plays that will certainly result in production increases. Approximately $10 billion was spent in 2016 on Permian basin drilling and completion costs for horizontal tight oil wells. An additional $28 billion was spent on Permian land acquisitions.

Don’t Hold Your Breath for $70 Oil Prices

Traders, analysts and the press have consistently looked for every possible reason to anticipate higher prices since the collapse in 2014. Expectation of an OPEC production cut or freeze has provided an artificial lift to oil prices for at least a year and now, probably accounts for at least $6 per barrel of current $53 per barrel NYMEX futures prices.

A recent Wall Street Journal article noted a new record in long crude oil futures positions during the last week in January. It went on to speculate that this meant a possible end to the over-supply of oil and that prices should increase.

That observation is not supported by history. In fact, record long positions are commonly followed by a drop in oil prices. Notable examples shown in Figure 8 include price declines around the 2008 Financial Collapse, the 2014 world oil-price collapse, and the brief rally to $60 prices in the Spring of 2015.

(Click to enlarge)

Figure 8. Record Long Positions on Crude Oil Futures Suggests That Prices Will Fall. Source: CFTC, EIA and Labyrinth Consulting Services, Inc.

Inventory data provides compelling evidence that present oil prices are over-valued. Last week, 13.8 million barrels (mmb) were added to U.S. crude oil storage. That’s the second highest weekly addition ever–the highest was 14.2 mmb on October 28, 2016 when WTI prices were about $5 per barrel lower.

(Click to enlarge)

Figure 9. Crude Oil Inventories Are At Record Levels 140 mmb Above the 5-Year Average. Source: EIA and Labyrinth Consulting Services, Inc.

Comparative inventories are also near record highs (Figure 10). When C.I. was at this level in March 2016, WTI prices were around $39 per barrel. When C.I. was slightly lower in August 2016, prices were about $47 per barrel. The trend line in Figure 10 shows that oil prices are probably about $6 or $7 per barrel over-valued.

(Click to enlarge)

Figure 10. Comparative Inventories Near Record High Levels–Comparative Inventories Suggest Current Prices Are ~$7 Per Barrel Over-Valued. Source: EIA and Labyrinth Consulting Services, Inc.

Oil prices do not always reflect underlying fundamentals but markets eventually adjust because of them. Comparative inventory analysis suggests that current oil prices are over-valued. It is possible that markets have already priced in anticipated uplift from OPEC production cuts. If so, prices may not increase much beyond present levels and expectations of $70 prices any time soon are improbable.

OPEC cuts have almost certainly put a floor under oil prices but volatility will continue to characterize markets as it has for the past 2 years. U.S. production is a wild card that will almost certainly be a drag on upward price movement. My guess is that WTI prices are likely to move below $50 per barrel until effects of OPEC production cuts are reflected in falling global inventories.

*To its credit, IEA shows 2016 inventory declines reaching the maximum levels of the 2011-2015 average. That doesn’t change the fact that current stock levels are 400 mmb above the 2012-2016 5-year average. That’s why comparative inventories are essential.

end

Oil rigs continue to be utilized in the Permian basin which is causing a record amount of WTI oil glut

(courtesy zero hedge)

Permian Panic Continues As Rig Counts Rise Amid Record Glut In Crude

With a record glut of crude and gasoline, US crude production pushed to new cycle highs this week and continues to track lagged rig counts.

US crude inventories are at a new record high…

And so are Gasoline inventories…

And the rig ccount keeps rising with lagged oil prices…

- *U.S. OIL RIG COUNT UP 6 TO 597 , BAKER HUGHES SAYS :BHI US

Highest since October 2015

Production keeps rising, and has a long way to go to catch up to the lagged rig count…

And the oil algo idiocy from DOE data has been erased with RBOB back below $1.50…

The surge in rigs has been driven almost 100% in the Permian, but as OilPrice.com’s Nick Cunningham asks, how much longer that the Permian craze continue?

The two great dueling forces in the world oil market, OPEC and American production, have created an atmosphere of uncertainty, as prices hover above $50. Last week the EIA reported another record inventory and an increasing rig count, while analysts point to a possible crisis as a market held aloft by buoyant predictions of OPEC cuts slowly faces up to insufficient demand.

Crucial to this situation is the state of the U.S. patch, particularly the Permian Basin, which since late last year has been the focus of recovering production. The EIA data for the field is good, with new well production rising sharply and overall production of oil and gas rising sharply in 2017. While some speculate the bubble may burst, prospects for companies already invested in the Permian look positive, even if production costs are rising.

The Permian has seen the highest increase in rig count of any U.S. basin. Six of the twelve rigs added last week went up in the Permian, and its total now stands at 301 rigs, up from 172 a year ago, out of a total U.S. count of 741. In total the count is up 83 percent from May 2016, though it has yet to reach the booming numbers of 2013, when over two thousand rigs were in operation. Even 2015, as the U.S. sector was being squeezed by low prices, saw the total count hovering near two-thousand, according to Baker Hughes.

The increase is coming hot on the heels of the OPEC production deal, and seems to be in direct correlation with the OPEC announcement of nearly 900,000 bpd in cut production this month. For now, markets are happy, but underlying fundamentals remain as they were: cut production in Saudi Arabia and elsewhere will be made up by a resurgent American sector.

Last month, ExxonMobil paid $6.6 billion in order to double its exposure in the Permian, the single largest domestic U.S. oil deal since the price collapse in 2014, according to Forbes. Noble Energy announced in January 2017 it was acquiring Clayton Williams Energy for $2.7 billion, adding seventy-one thousand acres to its holdings in the Permian, specifically in the Southern Delaware Basin.

Austin-based Parsley Energy has been acquiring more acreage, amounting to $2.8 billion, and looks set to be a major Permian player, though its acquisitions came in at a steep $37,000/undeveloped acre.

That looks better when compared to other recent Permian purchases, where land is going for as much as $60,000/undeveloped acre, according to Bloomberg. Those prices are ten-times what drillers pay in the Bakken field in North Dakota, where oil production has fallen off, according to EIA data, and the rig count has fallen. Parsley got a better deal than Concho Resources Inc.’s acquisition last year from Reliance Energy, where the price averaged $45,000/undeveloped acre.

Bloomberg is predicting the steep prices in the Permian will drive away some investors and trigger a backlash. Companies without a foothold will look elsewhere. This thinking explains why Exxon and Parsley made such big grabs, before prices really got out of control.

But for those with the wherewithal, the Permian pays off better than any other field. Occidental Petroleum Corp., which thinks of the Permian as its “growth engine,” has indicated its keeping its primary focus on its 2.5 million acres there, where production costs are so low a price threshold below $40/barrel still assures profitability. The Permian’s so rich, one Occidental exec noted to Natural Gas Intel, “It is pretty hard to drill a dry hole there.” With that in mind, however, Occidental has looked to cut its costs in the Permian by as much as twenty-five percent, in order to make up for steep losses in 2016 Q4.

Other companies that are focused entirely on the Permian, like Diamondback Energy Inc., are not backing out. The company announced its production climbed thirty-eight percent, with Q4 production rising sixteen percent. The late-year boost, the result of the rise in prices on the back of the OPEC deal, helped out other Permian producers. But costs are rising, as running a well per-day rose from $13,900 to $16,000 in the space of a few months last year, according to CNBC.

The high price of getting into the Permian may be offset by the relatively low costs of producing there, as well as the abundance of oil and natural gas that await almost any driller who sinks a well. But if the land rush is in fact over, and attention swings elsewhere, the surge in Permian activity may slacken. That, of course, may be affected if the current bullish swing in prices comes to an end, and if analysts’ predictions of a sharp reduction in prices come to pass.