Gold at (1:30 am est) $1232.00 DOWN $5.50

silver was : $17.94: DOWN 5 CENTS

Access market prices:

Gold: $1237.90

Silver: $18.03

THE DAILY GOLD FIX REPORT FROM SHANGHAI AND LONDON

.

The Shanghai fix is at 10:15 pm est last night and 2:15 am est early this morning

The fix for London is at 5:30 am est (first fix) and 10 am est (second fix)

Thus Shanghai’s second fix corresponds to 195 minutes before London’s first fix.

And now the fix recordings:

Shanghai FIRST morning fix Feb 22/17 (10:15 pm est last night): $ 1245.45

NY ACCESS PRICE: $1236.40 (AT THE EXACT SAME TIME)/premium $9.05

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Shanghai SECOND afternoon fix: 2: 15 am est (second fix/early morning):$ 1246.39

NY ACCESS PRICE: $1235.00 (AT THE EXACT SAME TIME/2:15 am)

SPREAD/ 2ND FIX TODAY!!: 11.39

China rejects NY pricing of gold as a fraud/arbitrage will now commence fully

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

London FIRST Fix: Feb 22/2017: 5:30 am est: $1237.50 (NY: same time: $1237.40 (5:30AM)

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

London Second fix Feb 22.2017: 10 am est: $1236.65(NY same time: $1237.60 (10 am)

It seems that Shanghai pricing is higher than the other two , (NY and London). The spread has been occurring on a regular basis and thus I expect to see arbitrage happening as investors buy the lower priced NY gold and sell to China at the higher price. This should drain the comex.

Also why would mining companies hand in their gold to the comex and receive constantly lower prices. They would be open to lawsuits if they knowingly continue to supply the comex despite the fact that they could be receiving higher prices in Shanghai.

end

For comex gold:

FEBRUARY/

NOTICES FILINGS FOR FEBRUARY CONTRACT MONTH: 24 NOTICE(S) FOR 2400 OZ. TOTAL NOTICES SO FAR: 5315 FOR 531,500 OZ (16.530 TONNES)

For silver:

For silver: FEBRUARY

52 NOTICES FILED FOR 260,000 OZ/

TOTAL NO OF NOTICES FILED: 465 FOR 2,325,000 OZ

This is options expiry week for both the silver and gold contracts. First day notice is this Tuesday, Feb 28.2017. Options will expire on the comex on Thursday and on the OTC market in London, early Tuesday morning. For the first time comex has silver in backwardation February/March by 2 cents. The open interest on the silver comex is now over 1 billion oz and no doubt that the London OTC is multiples of that. We will be watching this week with open eyes.

As for Agnico eagle I phoned the company and got complete clarification on what is going on. The company produced record amounts of gold throughout the year and including the 4th quarter. However the last shipment out of Meadowbank could not leave because of inclement weather. Thus the profit which would have occurred in the last quarter will be included in this quarter. There is absolutely nothing wrong with the earnings side of things and the production side of things except the crooks are short selling the stock because they cannot get a hold of real metal to short.

Let us have a look at the data for today

.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total open interest ROSE by 2545 contracts UP to 208,147 with respect to YESTERDAY’S TRADING. In ounces, the OI is still represented by just less THAN 1 BILLION oz i.e. 1.041 BILLION TO BE EXACT or 149% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT FEBRUARY MONTH: THEY FILED: 24 NOTICE(S) FOR 2400 OZ

In gold, the total comex gold FELL BY 2843 contracts WITH THE FALL IN THE PRICE GOLD ($0.10 with YESTERDAY’S trading ).The total gold OI stands at 427,168 contracts

we had 24 notice(s) filed upon for 2400 oz of gold.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD:

We had no change in tonnes of gold at the GLD:

Inventory rests tonight: 841.17 tonnes

.

SLV

we had no changes in silver into the SLV:

THE SLV Inventory rests at: 335.281 million oz

end

.

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in silver ROSE by 2545 contracts UP to 208,147 AS SILVER WAS DOWN 3 CENTS with YESTERDAY’S trading. The gold open interest FELL by 2843 contracts DOWN to 428,168 WITH THE FALL IN THE PRICE OF GOLD OF $0.10 (YESTERDAY’S TRADING)

(report Harvey

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)Late TUESDAY night/WEDNESDAY morning: Shanghai closed UP 7.89 POINTS OR .241%/ /Hang Sang CLOSED UP 238.33 POINTS OR 0.99% . The Nikkei closed UP 1.56 POINTS OR 0.01% /Australia’s all ordinaires CLOSED UP 0.25%/Chinese yuan (ONSHORE) closed UP at 6.8780/Oil FELL to 53.90 dollars per barrel for WTI and 56.27 for Brent. Stocks in Europe ALL MIXED. Offshore yuan trades 6.8590 yuan to the dollar vs 6.8780 for onshore yuan.THE SPREAD BETWEEN ONSHORE AND OFFSHORE NARROWS A BIT AS POBC ATTEMPTS TO STOP USA DOLLARS FROM LEAVING CHINA’S SHORES. ONSHORE YUAN STRONGER AS IS OFFSHORE YUAN COUPLED WITH THE STRONGER DOLLAR

REPORT ON JAPAN SOUTH KOREA NORTH KOREA AND CHINA

3a)THAILAND/SOUTH KOREA/NORTH KOREA

none today

b) REPORT ON JAPAN

none today

c) REPORT ON CHINA

i)China is not happy that the USA carriers are patrolling the South China seas. This opens up a huge confrontation with China.

( zero hedge)

ii)China responds by deploying SAM batteries on the South China Sea islands..something that is annoying the Americans

( zero hedge)

4. EUROPEAN AFFAIRS

A flight to safety: German yields tumble especially on the 2yr and 10 yr as political fears grow. France: LePen, Germany: Schultz, and Holland: Wilder

( zero hedge)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

Now it is Iran’s turn to warn the USA: The enemy will receive a strong slap in the face. The uSA must be elated with the deal they have done with them;

( zero hedge)

6.GLOBAL ISSUES

A good look at what is going on inside Sweden. The author is stating that mainstream media is hiding the full picture and Trump is right about the immigrants. No doubt that the message is getting to France, Germany and Holland with their upcoming elections this year

( zero hedge)

7. OIL ISSUES

Oil rises a bit after a surprise inventory draw

( zero hedge)

8. EMERGING MARKETS

none today

9. PHYSICAL MARKETS

i)Fascinating: A Chinese firm Boyuan Mining company manufactured fake gold bars containing only 38% gold and the rest Tungsten. These bars were all used as collateral to get loans from several credit unions inside China. The total amount loaned out was 1.45 billion USA against this fake collateral

No gold entered the SGE which has strict rules on assays etc.

( Shanghai Daily/GATA)

ii)As I mentioned above, this is expiry option week. Options on the comex goes off the board on Thursday and on Tuesday morning for the OTC options. For the first time we are experiencing a 2 cent backwardation at the comex February over March. This means extreme shortage of metal. The open interest on the silver comex is now over 1 billion oz and the OTC levels are multiples of that. This is very dangerous as we will watch how this will play out this week.

a must read…

( James Turk/Kingworldnews)

iii)Craig Hemke details the silver fraud at the comex exactly the way I have described it to you over these past several months;

( Craig Hemke/TFMetals)

10.USA STORIES

i)The FOMC minutes hint at a hike fairly soon but they also warn that Trump’s policies may not materialize. They also claim that the VIX is too low.

March rate hike odds remained unchanged, the yield curve flattened and gold and silver rose

( zero hedge)

ii)The culture of banking officials for fraud strikes again. We now have 4 executives fired for the fake accounts scandal and no doubt there will be criminal charges especially now that the Trump administration has taken power in the USA

( Dugan)

iii)It sure looks like Trump wants to put more troops on the ground to defeat ISIS.

( Ron Paul)

iv)This is going to be exciting: James O’Keefe of Project Veritas is about to smoke CNN on Thursday:

( zero hedge)

v)This is a surprise; existing home sales jump a huge 3.3% well above the 1.1% estate despite rising rates: is the data cooked?

( zero hedge)

vi)My goodness: Trump calls the huge deficit spending by the USA has “out of control” and the pundits hardly flinched:

( zero hedge)

vii)This is what happens when you tax too much: that famous soda tax in Philadelphia has now caused a huge 30 to 50% plunge in sales and massive layoffs in the SUPERMARKET and other distributor sectors in the Philly area:

( zero hedge)

Let us head over to the comex:

The total gold comex open interest FELL BY 2,843 CONTRACTS UP to an OI level of 427,168 WITH THE FALL IN THE PRICE OF GOLD ( $0.10 with YESTERDAY’S trading). We are now in the contract month of FEBRUARY and it is one of the better delivery months of the year. In this next big active delivery month of February we had a LOSS of 187 contracts DOWN to 762. We had 146 notice(s) served upon yesterday and therefore we LOST 41 contracts or an additional 4100 oz will stand for delivery and IT LOOKS LIKE THE CASH SETTLEMENTS HAVE RESUMED FOR A FIAT PROFIT . The next non active contract month of March saw it’s OI FALL by 264 contracts DOWN TO 1616.The next big active month is April and here the OI FELL by 4102 contracts DOWN to 276,960.

We had 24 notice(s) filed upon today for 2400 oz

The active month of February saw the OI FALL BY 140 contract(s) DOWN TO 140. We had 3 notice(s) served YESTERDAY so we LOST 137 CONTRACTS or an additional 685,000 oz will NOT stand for delivery.

The next big active delivery month is March and here the OI decrease by 17,234 contracts down to 50,477 contracts. For comparison purposes last year on the same date only 43,487 contracts were standing.

We had 52 notice(s) filed for 260,000 oz for the FEBRUARY contract.

VOLUMES: for the gold comex

Today the estimated volume was 175,857 contracts which is fair.

Yesterday’s confirmed volume was 267,519 contracts which is very good

volumes on gold are getting higher!

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz |

62,823,054 OZ

HSBC

|

| Deposits to the Dealer Inventory in oz | nil oz |

| Deposits to the Customer Inventory, in oz |

nil oz

|

| No of oz served (contracts) today |

24 notice(s)

2400 oz

|

| No of oz to be served (notices) |

738 contracts

73,800 oz

|

| Total monthly oz gold served (contracts) so far this month |

5315 notices

5315 oz

16.530 tonnes

|

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | 287,058.4 oz |

Today, 0 notice(s) were issued from JPMorgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equates to 24 contract(s) of which 10 notices were stopped (received) by jPMorgan dealer and 0 notice(s) was (were) stopped/ Received) by jPMorgan customer account.

March 2016: 2.311 tonnes (March is a non delivery month)

| Silver | Ounces |

| Withdrawals from Dealers Inventory | nil |

| Withdrawals from Customer Inventory |

621,777.460 0z

CNT

Brinks

|

| Deposits to the Dealer Inventory |

nil oz

|

| Deposits to the Customer Inventory |

nil oz

|

| No of oz served today (contracts) |

52 CONTRACT(S)

(260,000 OZ)

|

| No of oz to be served (notices) |

121 contracts

(605,000 oz)

|

| Total monthly oz silver served (contracts) | 465 contracts (2,325,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month | 6,683,347.0 oz |

end

And now the Gold inventory at the GLD

FEB 22/no changes in gold inventory at the GLD/Inventory rests at 841.17 tonnes

FEB 21/no changes in gold inventory at the GLD/Inventory rests at 841.17 tonnes

feb 17/a withdrawal of 2.37 tonnes of gold from the GLD/Inventory rests at 841.17 tonnes

FEB 16/we had no changes in the GLD inventory today/Inventory rests at 843.54 tonnes

Feb 15./another deposit of 2.67 tonnes of gold into the GLD inventory despite another attempted whacking of gold/inventory rests at 843.54 tonnes

FEB 14/another deposit of 4.14 tonnes of gold into the GLD inventory/rests at 840.87 tonnes

FEB 13/another deposit of 4.15 tonnes of gold into the GLD/Inventory rests at 836.73 tonnes

Feb 10/no changes at the GLD/Inventory rests at 832.58 tonnes

feb 9/no changes at the GLD/Inventory rests at 832.58 tonnes

Feb 8/another “deposit” of 5.63 tonnes of gold into the GLD/The addition is a paper addition/total inventory: 832.58 tonnes

Feb 7/another huge fake deposit of 8.30 tonnes of gold into the GLD/the addition is a paper addition and no doubt not physical/ total inventory: 826.95 tonnes

FEB 6/a huge deposit of 7.43 tonnes of gold into the GLD/Inventory rests at 818.65 tonnes

FEB 3/no change in gold inventory at the GLD/Inventory rests at 811.22 tonnes

Feb 2/another huge deposit of 1.48 tonnes/inventory rests at 811.22 tonnes

Feb 1/a huge “deposit” of 10.67 tonnes of gold into the GLD/Inventory rests at 809.74 tonnes. this should stop GLD from sending gold to Shanghai.

JAN 31/no change in gold inventory at the GLD/Inventory rests at 799.07 tonnes

jan 30/no change in gold inventory at the GLD/Inventory rests at 799.07 tonnes

Jan 27/no changes at the GLD/Inventory rests at 799.07 tonnes

Jan 26/no changes at the GLD/Inventory rests at 799.07 tonnes/

jan 25/another exactly the same withdrawal as yesterday: 5.04 tonnes and again this was used in the whacking of gold today/inventory rests at 799.07 tonnes

jan 24/a huge withdrawal of 5.04 tonnes and probably this was used today in the whacking of gold/inventory rests at 804.11 tonnes

Jan 23/a big change/this time a deposit of 1.19 tonnes of gold into the GLD/inventory rests at 809.15 tonnes. The drainage of gold from the GLD to Shanghai has now stopped!

Jan 20/no changes in gold inventory a the GLD/Inventory rests at 807.96 tonnes

Jan 19/no changes in gold inventory at the GLD/Inventory rests at 807.96 tonnes

Jan 18/no changes in gold inventory at the GLD/Inventory rests at 807.96 tonnes

Jan 17/17/a deposit of 2.96 tonnes of gold/inventory at the GLD rests at 807.96 tonnes. I guess there is no more gold inventory to sent to C+Shanghai

end

NPV for Sprott and Central Fund of Canada

end

Major gold/silver trading/commentaries for WEDNESDAY

GOLDCORE/BLOG/MARK O’BYRNE

Gold To Rise – Inflation Rising and Real Chinese Gold Demand Higher Than “Official”

Frank Holmes joins Lawrie Williams, Koos Jansen and many others in questioning the “official” Chinese gold demand numbers. Real gold demand is likely much higher than the official numbers

by Frank Holmes

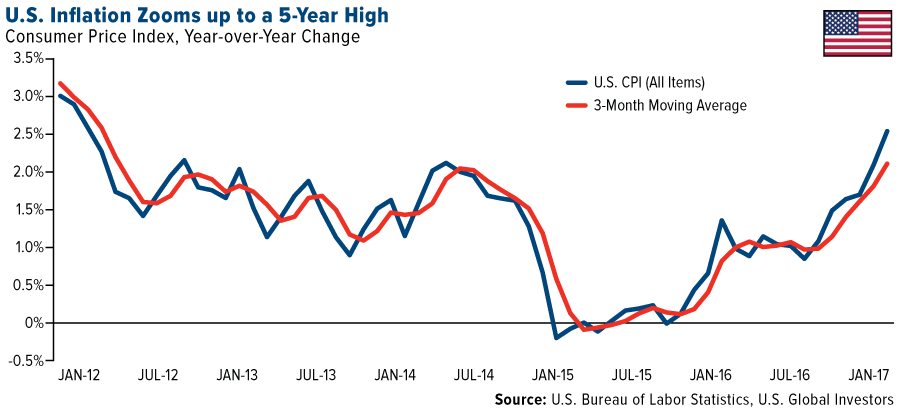

Inflation just got another jolt, rising as much as 2.5 percent year-over-year in January, the highest such rate since March 2012. Led by higher gasoline, rent and health care costs, consumer prices have now advanced for the sixth straight month. In addition, January is the second straight month for rates to be above the Federal Reserve’s target of 2 percent.

Air fares are also climbing, and speaking of air fares, billionaire investor Warren Buffett added to his domestic airline holdings, we learned last week. Buffett’s holding company, Berkshire Hathaway, is now the second-largest holder of American Airlines, with an 8.79 percent share of the company. It also increased its holdings in Delta Air Lines by over 800 percent, to 60 million shares. The company now owns 43.2 million shares of Southwest Airlines, and it increased its stake in United Continental to about 28 million shares.

A March rate hike now looks all but imminent. Many economists—including the Goldman Sachs economists I had the pleasure to hear speak this week—expect to see at least three such hikes this year alone.

Gold responded accordingly, closing above $1,240 for the first time since soon after the November election. Below you can see the gold price charted against the inflation-adjusted 10-year Treasury yield, which is now in subzero territory.

The question I have is: Why would an investor deliberately choose to lose money? But that’s precisely what’s happening now with inflation where it is.

| 2-Year | 3-Year | 10-Year | |

|---|---|---|---|

| Treasury Yield | 1.22% | 1.95% | 2.45% |

| Consumer Price Index | 2.50% | 2.50% | 2.50% |

| Real Yield | -1.28% | -0.55% | -0.05% |

|

As of February 16

|

Source: Federal Reserve, U.S. Global Investors

|

||

These were among some of the topics addressed by former Fed Chair Alan Greenspan, who spoke with the World Gold Council (WGC) for the winter edition of its “Gold Investor.”

|

“Significant increases in inflation will ultimately increase the price of gold,” Greenspan said. “Investment in gold now is insurance. It’s not for short-term gain, but for long-term protection.”

He also reiterated his view, which I share, that gold is much more than just a metal but a currency:

“I view gold as the primary global currency. It is the only currency, along with silver, that does not require a counterparty signature. Gold, however, has always been far more valuable per ounce than silver. No one refuses gold as payment to discharge an obligation. Credit instruments and fiat currency depend on the credit worthiness of a counterparty. Gold, along with silver, is one of the only currencies that has an intrinsic value. It has always been that way. No one questions its value, and it has always been a valuable commodity, first coined in Asia Minor in 600 BC.”

Although major stock indices continue to hit fresh all-time highs on hopes of tax reform and fiscal stimulus, it’s important to temper the exuberance with a little prudence. The bull market, currently in its eighth year, is facing some significant geopolitical and macroeconomic uncertainty, and we could be getting late in the economic cycle. This makes gold’s investment case even more attractive. For the 10-year period, the yellow metal has shown an inverse correlation to risk assets such as stocks and high-yield bonds.

It might be time to ensure that your portfolio has the recommended 10 percent in gold—that includes 5 percent in gold coins and jewelry, the other 5 percent in quality gold equities and mutual funds.

China and India to Lead World Economy by 2050

The long-term investment case for gold looks just as compelling following bullish reports last week from PricewaterhouseCoopers (PwC) and Morgan Stanley. China and India are the world’s top two consumers of gold, and both countries are expected to make huge economic gains in the next few decades. This is likely to boost gold demand even more, which has a high correlation with discretionary income growth.

China alone consumed approximately 2,000 metric tons in 2016, or roughly 60 percent of all the new gold that was mined during the year, according to veteran mining commentator Lawrie Williams, who based his estimates on calculations made by BullionStar’s Koos Jansen. The 2,000 metric tons is a much higher figure than what analysts and the media have been telling us, but I’ve always suspected China’s annual consumption to run higher than “official” numbers.

END

Fascinating: A Chinese firm Boyuan Mining company manufactured fake gold bars containing only 38% gold and the rest Tungsten. These bars were all used as collateral to get loans from several credit unions inside China. The total amount loaned out was 1.45 billion USA against this fake collateral

No gold entered the SGE which has strict rules on assays etc.

(courtesy Shanghai Daily/GATA)

Chinese firm said to have used tungsten to manufacture fake gold bars

Submitted by cpowell on Tue, 2017-02-21 12:52. Section: Daily Dispatches

Shanghai Gold Exchange Denies Connection with Fraudulent Manufacturer

By Leng Cheng

Shanghai Daily

Tuesday, February 21, 2017

The Shanghai Gold Exchange today denied a media report that it was connected with a supplier that has allegedly cheated loans with fake gold bars.

A Caijing magazine report on Monday accused Boyuan Mining Co., a metal producer based in Lingshan, Henan Province, which used to produce gold-plated tungsten bars, has caused loss of more than 10 billion yuan (US$1.45 billion) during the past decade through fraud.

The report referred the producer as one of the suppliers of Shanghai Gold Exchange since 2010 due to its expansion on assembly lines of gold production.

“Boyuan Mining Co. is not on the list of licensed suppliers,” said an announcement made by the exchange. “Gold ingots, gold bars, and silver ingots traded on the Shanghai Gold Exchange have gone through strict inspections.” …

The Caijing report said that Boyuan Mining Co. managed to produce a type of gold-plated tungsten bars weighing five kilograms with 62 percent tungsten and 38 percent gold since 2005. The bullion price surged more than 30 percent in 2007, marking its biggest rise since 1979.

Caijing said the company used those fake gold bars as collateral to obtain loans from several credit unions in both Henan Province and Shaanxi Province. Main suspects were detained by the police in May 2016, the report added. …

… For the remainder of the report:

http://www.shanghaidaily.com/business/Shanghai-Gold-Exchange-denies-conn…

END

As I mentioned above, this is expiry option week. Options on the comex goes off the board on Thursday and on Tuesday morning for the OTC options. For the first time we are experiencing a 2 cent backwardation at the comex February over March. This means extreme shortage of metal. The open interest on the silver comex is now over 1 billion oz and the OTC levels are multiples of that. This is very dangerous as we will watch how this will play out this week.

a must read…

(courtesy James Turk/Kingworldnews)

Turk sees indications of imminent short squeeze in silver

Submitted by cpowell on Tue, 2017-02-21 15:48. Section: Daily Dispatches

10:50a ET Tuesday, February 21, 2017

Dear Friend of GATA and Gold:

GoldMoney founder and GATA consultant James Turk, in comments posted today at King World News, describes indications of an imminent short squeeze in silver as investment banks that are short the metal struggle to keep it below $18. Turk’s comments are posted at KWN here:

http://kingworldnews.com/james-turk-warns-massive-short-squeeze-may-send…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

Craig Hemke details the silver fraud at the comex exactly the way I have described it to you over these past several months;

(courtesy Craig Hemke/TFMetals)

Metals Capped Into FOMC Minutes

An incredible amount of fraudulent, virtual silver is being created in order to cap price and paint the chart. Will JPM and the rest of The Evil Empire be successful once again in capping price and routing the Specs. The reaction to today’s FOMC minutes may help to determine the outcome.

Again, I can’t stress enough the devious and fraudulent nature of this latest attempt to contain and cap price. The past four days have seen the price of Comex Digital Silver pressing up against the key resistance of $18 and the 200-day moving average near $17.93. See below:

Over this same time period, the Comex Silver Banks led by JPM have increased the total supply of Comex silver contracts by 12,809 contracts. So, while price has been flat, total supply of Comex silver contracts has been increased by 6.5%. THIS is how you cap price and paint the chart!

Imagine for a moment where price would be this morning if total open interest was held flat for the past week. How much higher would price be if sellers of existing contracts needed to be found for the 12,809 contracts of buying pressure? On a larger scale, yes the price of Comex Digital Silver is up $2 year-to-date or about 13%, but how much higher would price be if The Banks hadn’t fraudulently added 44,000 new contracts since December 30?

Why do we always describe this as “fraud”? Two primary reasons:

- The Banks are selling something that they don’t have. Can you enter into a contract to sell a house or a car if you don’t actually own the house or car you are attempting to sell?

- The Banks create this new “silver” from whole cloth without depositing as collateral any additional silver into their Vaults.

Regarding point #2, see below. Note that at the beginning of 2017, total silver within the Comex vaulting structure was 181,903,037 ounces. Total Comex open interest that day was 163,812 contracts. With each contract representing 5,000 ounces of silver, this equates to a virtual exposure of 819,060,000 ounces.

As of last Friday, total open interest had grown to 205,602 contracts or 1,028,010,000 ounces or virtual silver yet the total amount of silver in the Comex vaults was stagnant at 184,088,021 ounces.

So, The Comex Silver Banks have increased the supply of virtual silver by 25% while only increasing the supply of physical silver in the vaults by 2%. This is fraud, this is a scam and this has absolutely ZERO connection to the supply/demand fundamentals of actual physical silver.

And what are The Banks attempting to accomplish in their aggressive efforts to cap price? Two things. First, maintaining price below the 200-day moving average is important in managing future Spec demand for additional Comex paper.

Second and perhaps more important is the chart-painting aspect of keeping price below $18. As you can see on this weekly chart, by capping price here, JPM et al are effectively attempting to paint a massive head-and-shoulder top onto the weekly chart.

So, once again, you must be alert and cautious here. The forces aligned against you in the Comex silver “market” are powerful and these criminals are doing everything in their collective power to rig price in their favor. Will they be successful (again)? That will depend upon a number of factors going forward. For today, at least, you’d be wise to not underestimate the collusive power of The Banks and the fraudulent nature of their paper derivative pricing scheme.

TF

end

Your early WEDNESDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight

1 Chinese yuan vs USA dollar/yuan STRONGER AT 6.8780(SMALL REVALUATION NORTHBOUND /OFFSHORE YUAN NARROWS TO 6.8590 / Shanghai bourse UP 7.89 POINTS OR .241% / HANG SANG CLOSED UP 238.33 POINTS OR 0.99%

2. Nikkei closed UP 1.56 POINTS OR 0.01% /USA: YEN FALLS TO 113.10

3. Europe stocks opened ALL MIXED ( /USA dollar index RISES TO 101.61/Euro DOWN to 1.0510

3b Japan 10 year bond yield: FALLS TO +.083%/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 113.10/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD FINALLY IN THE POSITIVE/BANK OF JAPAN LOSING CONTROL OF THEIR YIELD CURVE AS THEY PURCHASE ALL BONDS TO GET TO ZERO RATE!!

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 53.90 and Brent: 56.27

3f Gold UP/Yen UP

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil DOWN for WTI and DOWN for Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund FALLS TO +.256%/Italian 10 yr bond yield DOWN to 2.190%

3j Greek 10 year bond yield RISES to : 7.23%

3k Gold at $1238.25/silver $18.00(8:15 am est) SILVER BELOW RESISTANCE AT $18.50

3l USA vs Russian rouble; (Russian rouble UP 23/100 in roubles/dollar) 57.75-

3m oil into the 53 dollar handle for WTI and 56 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation (already upon us). This can spell financial disaster for the rest of the world/China forced to do QE!! as it lowers its yuan value to the dollar/GOT SMALL REVALUATION NORTHBOUND from POBC.

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 113.10 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 1.0126 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.0642 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT

3r the 10 Year German bund now POSITIVE territory with the 10 year RISES to +.324%

3s The Greece ELA NOW at 71.4 billion euros,AND NOW THE ECB WILL ACCEPT GREEK BONDS (WHAT A DISASTER)

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.411% early this morning. Thirty year rate at 3.021% /POLICY ERROR)GETTING DANGEROUSLY HIGH

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

(courtesy Jim Reid/Bloomberg/Deutsche bank/zero hedge)

European Rally Fizzles, S&P Futures Turn Red As USDJPY Slides, Bunds Strongly Bid

What started off in familiar fashion, with Asian stocks rising, and Europe hitting multi-month highs and US futures in record territory has stumbled in recent minutes following a continued rush for safety in short-dated German Bunds (the 2Y is now trading at -0.92%) and ongoing selling in the USDJPY, which has pushed Stoxx 600 back to unchanged, and S&P futures to modestly red for the session.

The exact catalyst is unclear although traders are citing continued French political risks, as the recent OAT selloff continued this morning on Le Pen fears.

Earlier in the session, global stocks hit record highs on Wednesday, pushing gains for the year above those for all of 2016, while the dollar rose before Federal Reserve minutes that will be scoured for clues on the timing of the next U.S. interest rate rise. MSCI’s main index of global stocks, which tracks share prices across 46 countries, hit a second successive record high. It has risen some 5.7 percent so far this year, beating the 5.6 percent gains of 2016. The MSCI Asia Pacific Index was at the highest level since July 2015 as Chinese shares traded in Hong Kong resumed a rally. Japanese equities managed to end higher even after fluctuations in the yen pressured the Topix.

European shares followed Asian bourses higher, buoyed by all main indexes on Wall Street touching record closing highs on Tuesday with Britain’s Lloyds Banking Group was up 3 percent after reporting its highest full-year profit in a decade, although that early optimism appears to have faded.

As a result, markets painted a mixed picture of investor sentiment on Wednesday, as political risk sent both the euro and German two-year bond yields lower while global equities tracked a U.S. rally. The dollar edged higher before the release of Fed minutes, up 0.3% at 101.64, gaining against the euro and sterling, pressuring oil lower.

The day’s most anticipated event for markets will be the release of the minutes of the Fed’s last policy meeting. Fed Chair Janet Yellen said last week it was likely the central bank would need to raise rates at an upcoming meeting. Markets have priced in only a slim chance of a rise next month but a much greater likelihood in May or June. The dollar rose 0.2 percent against a basket of major currencies and 0.3 percent versus the euro.

Economists expect to see further discussion in the minutes of the Fed’s balance sheet strategy given that many monetary policymakers have been publicly discussing the topic, even though it is clear that policymakers have not yet reached a consensus on the particulars of the Fed’s reinvestment policy. Additionally, DB economists expect the Fed to announce tapering of reinvestments this December, effective in January 2018. However they also expect a slower pace of tapering because the Fed will likely want to put as much distance between the Fed funds rate and the zero rate lower bound before risking greater disruptions to the long end of the Treasury curve. Thus, they still see the Fed hiking four times next year. Another key question many will hope to see some clarity on is whether March is “live” despite the Fed’s generally less than hawkish announcement: it is not clear how the Fed will bridge its actual dovish statement to hawkish minutes that suddenly make the March meeting in play.

Back to markets, where the Euro has dropped for a fourth day, dropping below 1.05 per dollar for the first time in more than six weeks. That lent early momentum to stocks, with the Stoxx Europe 600 Index advancing for a fourth session, however the rally has since fizzled. Germany’s Dax Index, already at an almost two-year high, briefly crossed the 12,000 level.

Technology stocks outperformed with Ericsson surging following an upbeat Bank of America-Merrill Lynch note. Basic resources sector fell, Goldman Sachs strategists wrote in a note commodity markets need proof of demand to rally further. Lloyds Banking Group Plc rose 3.7 percent as the mortgage lender swung to a quarterly profit and boosted its dividend. Futures on the S&P 500 were trading modestly in the red. The index added 0.6 percent Tuesday, with the Dow Jones Industrial Average, the Nasdaq Composite Index and the Russell 200 Index closing at all-time highs.

EU data saw the inflation rates as expected: core y/y unchanged at 0.9%. German IFO current conditions and expectations both exceeded consensus forecasts at 118.4 and 104 respectively.

European politics and the prospect of higher U.S. rates pushed the gap between short-dated U.S. and German benchmark government bond yields to its widest in nearly 17 years. German two-year yields hit a record low of minus 0.92 percent while U.S. equivalents touched 1.24 percent.

Oil prices dipped. Brent crude, the international benchmark, traded at $56.50 a barrel, down 17 cents. Copper also fell, as traders reduced their positions before the Fed minutes, though supply disruptions supported prices. The metal last traded at $6,030 a tonne, down 0.5 percent on the day. Gold edged up 0.1 percent to $1,236 an ounce.

On today’s calendar are the abovementioned minutes from the latest Fed meeting, which traders hope will provide details on whether March is indeed “live” as a bevy of recent Fed speakers have suggested.

Market Snapshot

- S&P 500 futures down 0.1% at 2,357.75

- STOXX Europe 600 down less than 0.1% to 373.33

- MXAP up 0.6% to 146.14

- MXAPJ up 0.6% to 470.46

- Nikkei down 0.01% to 19,379.87

- Topix up 0.1% to 1,557.09

- Hang Seng Index up 1% to 24,201.96

- Shanghai Composite up 0.2% to 3,261.22

- Sensex up 0.4% to 28,879.78

- Australia S&P/ASX 200 up 0.2% to 5,805.10

- Kospi up 0.2% to 2,106.61

- German 10Y yield fell 2.6 bps to 0.275%

- Euro down 0.3% to 1.0504 per US$

- Brent Futures down 0.6% to $56.32/bbl

- Italian 10Y yield rose 6.3 bps to 2.247%

- Spanish 10Y yield unchanged at 1.683%

- Brent Futures down 0.6% to $56.32/bbl

- Gold spot up 0.1% to $1,237.29

- U.S. Dollar Index up 0.3% to 101.64

Top Overnight News from BBG

- Fed’s $2.5 Trillion Hoard of Treasuries Seen Barely Shrinking

- McDonald’s to Cut Prices on Drinks as Fast-Food Industry Slumps

- Toll Brothers Beats Estimates as Company Delivers More Homes

- Facebook Said in Talks to Stream Major League Baseball Games

- Samsonite Says Mulling U.S. Manufacturing, But Not Due to Trump

- UPS Races to Cut Costs as E-Commerce Shifts Deliveries to Homes

- ConocoPhillips’ Reserves Drop to 15-Year Low as Oil- Sands Fade

- Ternium to Buy CSA Siderurgica do Atlantico From Thyssenkrupp

- Mexico and Canada Say Nafta Should Be Re-Negotiated Trilaterally

- Aramco Picks JPMorgan, HSBC, MS as Lead Underwriters

Asian markets traded mostly higher following the positive lead from Wall Street where all 3 major US indices posted gains of at least 0.5%. ASX 200 (+0.2%) saw mild upside amid buoyant consumer staples and healthcare sectors, however upside was limited by gold miners. Nikkei 225 (flat) initially declined amid the risk averse sentiment in the region alongside JPY strength, however double digit gains seen in Toshiba shares helped return the index to flat on the session. China was traded higher as Shanghai Comp. (+0.1%) initially lingered in the red following a weak liquidity injection by the PBoC but staged a late recovery, while Hang Seng (+0.8%) outperformed with properties leading the index as China Resources Land and China Overseas shares both surged more than 3%. 10yr JGBs traded higher amid the risk averse tone in the region, while the BoJ bond buying operation also provided support for the Japanese paper.

Top Asian News

- China’s $9 Trillion Moral Hazard Problem Grows Too Big to Ignore

- China Home Prices Rise in Fewest Cities in a Year Amid Curbs

- Petron Malaysia 4Q Net Income 112.6m Ringgit Vs 16.2m Rgt Y/y

- China Insurance Watchdog Vows to Severely Punish Speculators

- Anta Sports Proposes Higher Dividend; FY Net in Line With Est.

- Indonesia Debt Attractive for Manulife Even as Yield Gap Narrows

- China’s $9 Trillion Moral Hazard Grows Too Big to Ignore

European bourses have faded early gains, with Price action in equity markets has been dictated by the latest slew of earnings. UK financials have been led higher by Lloyds after the bank reported profits were ahead of analyst expectations, while the DAX broke above 12000 to touch its highest level since Apr’15 with Thyssenkrupp leading the index amid reports that they will divest assets of their Brazilian steel plant. Another day, another record low for the Schatz which is now yielding -0.9% amid signals that the ECB is buying German bonds, in particular those with a yield below the -0.4% deposit rate, which implies strong demand. While investors are seemingly holding off selling their short-end German debt as they are used as collateral to receive cash at the ECB, subsequently reigniting the fears of last year of a collateral squeeze which Draghi and Co. attempted to address in December. Additionally, the decline in the 2-yr yield has been much more pronounced (falling 13bps from Friday) since Le Pen’s significant narrowing in the Presidential poll seen at the back-end of last week (now over 40%).

Top European News

- German Business Sentiment Rises as Bundesbank Sees Growth Pickup

- Airbus Takes $2.3 Billion A400M Hit, Sees Profit Gain This Year

- RWE Writes Off 4.3 Billion Euros on Sliding Power Prices

- U.K. Gained Momentum at End of 2016 on Trade, Consumer Spending

- May Faces Calls to Tighten Takeover Rules After Kraft- Unilever

In currencies, the Bloomberg Dollar Spot Index rose 0.2 percent, reversing an earlier drop. The yen led advances in major currencies, strengthening 0.5 percent to 113.17 per dollar, following two days of declines. The British pound weakened 0.3 percent. The EUR is the big mover on the day as the fall out of the recent Le Pen gains (in the polls) continues. This has had a notable impact into short end German paper as investors are driven into ‘safe havens’ – precious metals also benefiting. EU/USD has now tested below 1.0500 and continues to do so, with the early drivers coming from EUR/GBP and EUR/JPY specifically. This looks set to continue as long as the polls remain where they are, and breaking some notable support levels, the cross rates in particular look vulnerable. EU data saw the inflation rates as expected — core y/y unchanged at 0.9%. German IFO current conditions and expectations both exceeded consensus forecasts at 118.4 and 104 respectively. Both Cable and USD/JPY have been impacted, with the former pushed up through 1.2500 in the early exchanges before 1.2500+ sellers overwhelmed. This pair remains range bound inside 1.2350-1.2600 for now, but the latest Q4 business investment figures disappointed — falling 0.9% vs +0.4% previously, though the GDP rate was revised up slightly to prompt some immediate algo driven buying. USD/JPY has now slipped back to 113.00 as a result, with lacklustre UST yields also playing their pair. The 10yr rate looks pretty stagnant inside the 2.30-2.55% range, but this translates into limited momentum in the spot rate either way

In commodities, gains in Gold (up 0.1% to $1,237) are perhaps more of a function of risk sentiment as the political arena in Europe grabs more of the attention. The polls show Le Pen making some notable gains, albeit still behind in the 2nd round, but enough to unnerve EUR holders at the very least if not investors globally. Safe haven flow has prompted significant moves in shorter end Bunds, but given the safe haven aspect, Gold has also benefited alongside Silver. Energy prices have seen some downside in European trade, paring some of yesterday’s gains which saw WTI fail to make a sustained break above USD 55.00/bbl. Furthermore, participants will likely be looking ahead to today’s rescheduled API release which has recently provided a slew of large builds.. Comments from Barkindo on further compliance have supported, but last night’s rhetoric from Iran suggested a move to $60.00 would hurt OPEC — in terms of deterring fresh production (Shale?). Inventory levels for Iron Ore in China are grabbing more of the headlines, and may put the brakes on some of the moves seen in base metals of late. On the day, Lead is the out-performer, while Copper gives back some of its recent gains, though holds comfortably above $2.70.

Looking at the day ahead, in the US the lone data release is January existing home sales. Later this evening we’ll get the FOMC minutes from the Jan 31st/Feb 1st meeting. Away from the data we’re due to hear from the Fed’s Powell at 6pm GMT, while BoE deputy governor Cunliffe is due to speak later this morning.

US Event Calendar

- 7am: MBA Mortgage Applications, prior -3.7%

- 10am: Existing Home Sales, est. 5.55m, prior 5.49m; MoM, est. 1.09%, prior -2.8%

- 1pm: Fed’s Powell Speaks on Economic Outlook in New York

- 2pm: FOMC Meeting Minutes

DB’s Jim Reid concludes the overnight wrap

Markets are in a celebratory mood at the moment with the flash European PMI’s for February lending further strength to the argument of an improving growth picture in Europe. Indeed the composite reading for the Euro area surged 1.6pts to 56.0 in February after the consensus was for broadly little change. That is the highest reading since April 2011 while the details revealed a 0.3pt rise in the manufacturing PMI to 55.5 and an even more significant 1.9pt jump in the services reading to 55.6. The country level breakdown also revealed an impressive 1.3pt jump in the composite for Germany to 56.1 and a 2.1pt jump in the composite for France to 56.2. So decent evidence that the European economy is showing signs of strong upward growth momentum in the first quarter of this year with growth also encouragingly broad-based by sector and country.

Significantly that data is also coming despite an increasingly uncertain political environment. Much has been made of the recent tightening in the French polls in favour of Le Pen versus Macron and Fillon. Yesterday we got more evidence of that with the release of another poll. The Elabe poll (covering 18-20 Feb) revealed first round support for Le Pen of 27.5% (up from 26% from the same pollster earlier this month) while support for Fillon actually rose 3 points to 20% and support for Macron fell about five points to 18.5%. In the second round a Le Pen – Fillon race has the latter coming out on top at 56% versus 44% which is unchanged, but a Le Pen – Macron race showed the margin of loss for Le Pen as tightening to 18% (59% versus 41%) from 26%. It’s worth noting that a live TV debate between Fillon, Hamon, Le Pen, Macron and Melenchon has been scheduled for March 20th, so that might be one to note in the calendar.

In terms of markets, French 10y OATs (+2.9bps to 1.080%) again underperform Bunds (+0.3bps to 0.296%) which in turn sent the spread between the two to a new four-and-a-bit year high of 79bps. The peripherals were also anywhere from 3bps to 7bps higher yesterday although in Greece 2y yields (-102bps) hit their lowest level since January following that news that Greece’s creditors are to return to continue discussions, suggesting a political framework is in place to allow an agreement to proceed.

Treasury yields also edged a bit higher with the 10y yield up 1.4bps to 2.429% although that was actually despite some disappointment in the latest PMI’s there (more on that below). Instead it was another day of familiar record highs for US equities which dominated the headlines with the S&P 500 (+0.60%), Dow (+0.58%), Nasdaq (+0.47%) and Russell 2000 (+0.75%) indices all notching up new all time highs. Better than expected results in the retail sector from Wal-Mart and Home Depot seemed to help, as did further gains for Oil with WTI finishing up +1.02% and back above $54/bbl.

Looking ahead to today, while there’s not a huge amount of data scheduled we will get the FOMC minutes later this evening from the Jan 31st/Feb 1st meeting. Our US economists noted in their daily that they expect to see further discussion in the minutes of the Fed’s balance sheet strategy given that many monetary policymakers have been publicly discussing the topic. They note though that it’s clear that policymakers have not yet reached a consensus on the particulars of the Fed’s reinvestment policy. Our economists have however re-evaluated the likely path of Fed balance sheet adjustments. They continue to expect the Fed to announce tapering of reinvestments this December, effective in January 2018. However they also expect a slower pace of tapering because the Fed will likely want to put as much distance between the Fed funds rate and the zero rate lower bound before risking greater disruptions to the long end of the Treasury curve. Thus, they still see the Fed hiking four times next year. Keep an eye on the minutes this evening for any more clues.

Back to markets where this morning in Asia it’s been a bit of a mixed start. While the Nikkei, Kospi and ASX are little changed, the Hang Seng is up +0.82% following stronger than expected GDP data out of Hong Kong (+1.2% qoq in Q4 versus +0.7% expected). On the other hand bourses in China are modestly in the red (Shanghai Comp -0.15%) following a strong start in the first two days of the week. In other markets the US Dollar is flat after the Fed’s Mester said that the Fed doesn’t want to surprise markets on possible future rate hikes. US equity index futures are also little changed Oil has continued to push on and bonds are mixed, albeit with modest moves.

Moving on. Trump related headlines may have abated somewhat in the last week or two but that’s not to say that this will continue. Our FX colleagues pointed out in a piece yesterday that two forthcoming events could bring more clarity to the border adjustment tax debate in particular. Trump is due to address a joint session of Congress on February 28th while the release of the White House’s “phenomenal” tax plan in the next fortnight or so could bring some clarity to the White House’s position. Both occasions could see a definitive endorsement or rejection of the Ryan-Brady BAT proposal and tip the balance in Congress. The team highlight that anecdotally, investors remain unconvinced that border adjustment will happen. Beyond this, it is impossible to derive a market-implied probability. But at least we can gauge the market’s fear of border adjustment from a number of instruments which would be idiosyncratically affected. Specifically, the discount of WTI over Brent futures has widened again since almost closing in early January. Since border adjustment would likely result in WTI trading at a premium, the oil market appears to increasingly discount the reform. The US retail sector, moreover, has almost fully closed its underperformance in the stock market since early January, also reflecting diminished fears of a BTA-driven rise in import costs. Lastly, the US breakeven curve still prices a higher risk of a nearterm, transient inflation shock than earlier this year, but this is probably consistent with lingering expectations of some protectionist measures, not just the BAT proposal. In conclusion our colleagues highlight then that the relevant principal component of these proxies suggests that the market has gradually discounted the border adjustment reform over the past three weeks, and expectations are now even below the peak of early January, prior to President Trump’s critical remarks in the Wall Street Journal on 15 January. Hence, while the market hasn’t fully priced it out, the risk is increasingly skewed toward Trump surprising the market with an endorsement of the Ryan-Brady proposal.

Wrapping up the remaining data yesterday, as noted earlier overall the PMI’s in the US were a little disappointing. Both the flash February services (-1.7pts to 53.9; 55.8 expected) and manufacturing (-0.7pts to 54.3; 55.4 expected) readings fell after expectations were for modest gains. That resulted in a dip in the composite to 54.3 from 55.8 although putting it in context that is still above the levels in 10 of the 12 months in 2016. There was also some Fedspeak to take stock of. Philadelphia Fed President Harker said that “at this point I would not take March off the table” while also highlighting that there is still important data to come. Meanwhile comments from BoE Governor Carney seemed to help Sterling to climb slightly after he said that if the Brexit process proceeds “relatively smoothly to an increasingly clear end-point” then that “would be consistent with a higher path of interest rates”.

Looking at the day ahead, this morning we’ll be kicking things off in Germany where the February IFO survey will be released. Shortly after that we get preliminary Q4 GDP in the UK with the various growth components also due to be released. The other data due out this morning will be the final January revisions for Euro area CPI. This afternoon in the US the lone data release is January existing home sales. Later this evening we’ll get the FOMC minutes from the Jan 31st/ Feb 1st meeting. Away from the data we’re due to hear from the Fed’s Powell at 6pm GMT, while BoE deputy governor Cunliffe is due to speak later this morning.

3. ASIAN AFFAIRS

i)Late TUESDAY night/WEDNESDAY morning: Shanghai closed UP 7.89 POINTS OR .241%/ /Hang Sang CLOSED UP 238.33 POINTS OR 0.99% . The Nikkei closed UP 1.56 POINTS OR 0.01% /Australia’s all ordinaires CLOSED UP 0.25%/Chinese yuan (ONSHORE) closed UP at 6.8780/Oil FELL to 53.90 dollars per barrel for WTI and 56.27 for Brent. Stocks in Europe ALL MIXED. Offshore yuan trades 6.8590 yuan to the dollar vs 6.8780 for onshore yuan.THE SPREAD BETWEEN ONSHORE AND OFFSHORE NARROWS A BIT AS POBC ATTEMPTS TO STOP USA DOLLARS FROM LEAVING CHINA’S SHORES. ONSHORE YUAN STRONGER AS IS OFFSHORE YUAN COUPLED WITH THE STRONGER DOLLAR

3a)THAILAND/SOUTH KOREA/NORTH KOREA

b) REPORT ON JAPAN

c) REPORT ON CHINA

China is not happy that the USA carriers are patrolling the South China seas. This opens up a huge confrontation with China.

(courtesy zero hedge)

China Opposes “Threatening And Damaging” US Carrier Patrols In South China Sea

One day after the US announced it had dispatched the USS Carl Vinson aircraft carrier group in the contested South Chine Sea on “routine” patrols (through a post on the aircraft carrier’s Facebook page), China responded and predictably, it wasn’t thrilled. In a statement by the foreign ministry, Beijing said on Tuesday that it opposed action by other countries “under the pretext of freedom of navigation” that could “threaten and damage” its sovereignty, a clear reference to US patrols in territory that China considers its own.

“China always respects the freedom of navigation and overflight all countries enjoy under international law,” Chinese foreign ministry spokesman Geng Shuang said at a daily news briefing. “But we are consistently opposed to relevant countries threatening and damaging the sovereignty and security of littoral countries under the flag of freedom of navigation and overflight,” Geng said in China’s first official comment on the latest U.S. patrol since it began.

Without explicitly naming the US, Geng said that “we hope relevant countries can do more to safeguard regional peace and stability.”

For the time being, the U.S. carrier strike group has not referred to its recent operations in the South China Sea as “freedom of navigation” patrols, although it will likely have to justify its presence in the region in the coming days, especially if confronted with Chinese naval forces. As Reuters adds, U.S. ships last year conducted several such patrols to counter any efforts to limit freedom of navigation in the strategic waters.

Meanwhile, China just wrapped up its own naval exercises in the South China Sea on Friday. War games involving its own aircraft carrier have unnerved neighbors with which it has long-running territorial disputes. Beijing most recently warned Washington against challenging its sovereignty in the South China Sea last week. It claims almost all of the resource-rich waters, through which about $5 trillion worth of trade passes each year.

At the same time, Brunei, Malaysia, the Philippines, Taiwan and Vietnam also claim parts of the South China Sea that command strategic sea lanes and have rich fishing grounds, along with oil and gas deposits.

The United States has criticized China’s construction of man-made islands and build-up of military facilities in the sea, and expressed concern they could be used to restrict free movement. Foreign ministers of the Association of South East Asian Nations (ASEAN) on Tuesday expressed concern over what they see as militarization in the South China Sea, Philippines Foreign Secretary Perfecto Yasay said after meeting with his ASEAN counterparts.

While tense relations between the Trump administration and Beijing have eased in recent weeks, following Trump’s concession that he would observe the “One China” policy, the long-running and on occasion violent tensions over the contested naval territories have little hope of resolution for the foreseeable future.

END

China responds by deploying SAM batteries on the South China Sea islands..something that is annoying the Americans

(courtesy zero hedge)

In Latest “Military Escalation” China Prepares Deployment Of SAM Batteries On South China Sea Islands

In China’s latest test of the US response to its escalating claims of islands in the South China Sea, Reuters reports that Beijing has “nearly finished building almost two dozen structures on artificial islands in the South China Sea that appear designed to house long-range surface-to-air missiles.” Predictably, such a development will likely raise questions about whether and how the United States will respond, given its vows to take a tough line on China in the South China Sea. The structures appear to be 20 meters (66 feet) long and 10 meters (33 feet) high.

Official cited by Reuters said the new structures were likely to house surface-to-air missiles that would expand China’s air defense umbrella over the islands. They did not give a time line on when they believed China would deploy missiles on the islands. “It certainly raises the tension,” Poling said. “The Chinese have gotten good at these steady increases in their capabilities.”

China’s Mischief Reef in the disputed Spratly Islands in the South China Sea

Building the concrete structures with retractable roofs on Subi, Mischief and Fiery Cross reefs, part of the Spratly Islands chain where China already has built military-length airstrips, could be considered a military escalation, the U.S. officials said in recent days, speaking on condition of anonymity. “It is not like the Chinese to build anything in the South China Sea just to build it, and these structures resemble others that house SAM batteries, so the logical conclusion is that’s what they are for,” said a U.S. intelligence official, referring to surface-to-air missiles.

Greg Poling, a South China Sea expert at the Center for Strategic and International Studies in Washington, said in a December report that China apparently had installed weapons, including anti-aircraft and anti-missile systems, on all seven of the islands it has built in the South China Sea.

On Tuesday, the Philippines said Southeast Asian countries saw China’s installation of weapons in the South China Sea as “very unsettling” and have urged dialogue to stop an escalation of “recent developments.” Philippine Foreign Secretary Perfecto Yasay did not say what provoked the concern but said the 10-member Association of South East Asian Nations, or ASEAN, hoped China and the United States would ensure peace and stability.

A Pentagon spokesman said the United States remained committed to “non-militarization in the South China Sea” and urged all claimants to take actions consistent with international law. In Beijing, Chinese Foreign Ministry spokesman Geng Shuang said on Wednesday he was aware of the report, though did not say if China was planning on placing missiles on the reefs. “China carrying out normal construction activities on its own territory, including deploying necessary and appropriate territorial defense facilities, is a normal right under international law for sovereign nations,” he told reporters.

Tillerson told the Senate Foreign Relations Committee that China’s building of islands and putting military assets on them was “akin to Russia’s taking Crimea” from Ukraine. In his written responses to follow-up questions, he softened his language, saying that in the event of an unspecified “contingency,” the United States and its allies “must be capable of limiting China’s access to and use of” those islands to pose a threat.

A U.S. intelligence official said that while the structures do not pose a significant military threat to U.S. forces in the region, given their visibility and vulnerability, the construction is a political test of how the Trump administration would respond, he said. “The logical response would also be political – something that should not lead to military escalation in a vital strategic area,” the official said.

Chas Freeman, a China expert and former assistant secretary of defense, said he was inclined to view such installations as serving a military purpose – bolstering China’s claims against those of other nations – rather than a political signal to the United States. “There is a tendency here in Washington to imagine that it’s all about us, but we are not a claimant in the South China Sea,” Freeman said. “We are not going to challenge China’s possession of any of these land features in my judgment. If that’s going to happen, it’s going to be done by the Vietnamese, or … the Filipinos … or the Malaysians, who are the three counter-claimants of note.”

He said it was an “unfortunate, but not (an) unpredictable development.”

The latest escalation over territorial claims in the contested area comes days after the US resumed “routine” aircraft carrier patrols in the South China Sea, a decision which China yesterday slammed as “threatening and dangerous.”

For now, the Trump administration – after vocally challenging China’s geopolitical ambitions in the contested maritime areas – has not provided a diplomatic response to China’s “tests” of its resolve.

END

4. EUROPEAN AFFAIRS

A flight to safety: German yields tumble especially on the 2yr and 10 yr as political fears grow. France: LePen, Germany: Schultz, and Holland: Wilder

(courtesy zero hedge)

Blow Out In German 2Y Bonds Sends Yield Crashing To Record Low As Political Fears Grow

The ongoing scramble for German safety away from French political uncertainty, has led to yet another blow out day for German 2 Year Schatz, with the yield tumbling to a fresh all time low of -0.92%, as Eurozone breakup concerns have spread from the bond market, and are now pressuring the euro sending the EURUSD below 1.05 for the first time in over a month.

The rush into German paper and out of France, means that the 10Y Greman-French spread has topped 0.8%, the widest in over four years, while the 2Y US-German spread is now well over 2%, the widest since at least 2000.

Granted, there was a brief moment of respite moments ago, when France 10Y Bonds briefly rallied after the latest OpinionWay poll found momentum for Le Pen stalling, sending French 10y bonds higher, and the yield lower as much as 5bps before paring loss to 2bps, although that burst of optimism appears to have quickly faded.

Adding to the German bid are signals that the ECB is buying German bonds, in particular those with a yield below the -0.4% deposit rate. With investors holding off selling their short-end German debt as they are used as collateral to receive cash at the ECB, fears have reignited of a collateral squeeze similar to late in 2016 which Draghi attempted, and failed, to address in the December ECB meeting.

Ironically, the rush into 2 Year paper took place even as Germany suffered another technically “failed” 30Y auction, in which the Bundesbank was forced to retain 41.8% of the auction as only €733 million bids were tendered for €1 billion in the offered 30Y paper at a yield of 1.04%.

The decline in the 2-Yr yield has been much more pronounced (falling 13bps from Friday) since Le Pen’s significant narrowing in the Presidential poll seen at the back-end of last week (now over 40%). The political uncertainty regarding the French Presidential election has filtered into FX markets, weighing on EUR, which is now hovering at 6-week lows having made a break below 1.0520, however the downside has been curbed at 1.0500 led by the upside in EUR/GBP.

As Bloomberg confirms in a note this morning, “German two-year yields are turning ever more negative in the build-up to France’s elections as demand for the securities saturates supply. It’s a reason for caution, and it’s weighing on the euro. ”

- Yield reached record-low of -0.915%; the notes are in a sweet spot should investors price in greater risk of a euro- area break-up and pile into securities closest to cash; French candidate Marine Le Pen has threatened to quit euro area

- German notes are also being supported because they’re the top assets for use as collateral in the euro area and ECB buying has made them more scarce.

- Bloomberg adds that central banks in Switzerland and the Czech Republic could also be mopping up German securities as part of their efforts to curb their currencies’ appreciation against the euro.

- France’s notes have been underperforming versus Germany; the two-year yield spread stands at close to 50bps, the widest since May 2012. The spread level is well above its five-year average, and statistical analysis shows it may have room to narrow back toward 36bps. But look to the April 2012 high of 83bps as a guide for how far the spread could go if risks escalate in as France’s election draws near

With US equities ignoring all adverse political news, keep an eye on the German bond market, where the 2Y has emerged as one of the last remaining barometers of political risk.

end

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

Now it is Iran’s turn to warn the USA: The enemy will receive a strong slap in the face. The uSA must be elated with the deal they have done with them;

(courtesy zero hedge)

Iran Warns US: “The Enemy Will Receive A Strong Slap In The Face”

This past Saturday, two weeks after the White House unveiled new sanctions on two dozen Iranian entities in retaliation for a recent ballistic missile test, Iran’s elite Revolutionary Guard announced it was set to conduct military drills this week despite warnings from the United States not to engage in such activity. General Mohammad Pakpour, commander of the force’s ground units, told a news conference that “the manoeuvres called ‘Grand Prophet 11’ will start Monday and last three days.” and warned that “rockets would be used” without specifying which kind.

Head of Iran’s Revolutionary guards ground forces Mohammad Pakpour (C) attends a funeral ceremony

Several days later, as Tehran concluded the previously announced war games, Iran retaliated in the ongoing escalation of sabre rattling, when the abovementioned General Mohammad Pakpour again took to the airwave, and said quoted by Reuters that the United States should expect a “strong slap in the face” if it underestimates Iran’s defensive capabilities, as Tehran concluded war games.

On Wednesday, the Revolutionary Guards concluded three days of exercises with rockets, artillery, tanks and helicopters, weeks after Trump warned that he had put Tehran “on notice” over the missile launch. “The message of these exercises … for world arrogance is not to do anything stupid,” said Pakpour, quoted by the semi-official news agency Tasnim.

“The enemy should not be mistaken in its assessments, and it will receive a strong slap in the face if it does make such a mistake,” said General Mohammad Pakpour, head of the Guards’ ground forces, quoted by the Guards’ website Sepahnews.

“Everyone could see today what power we have on the ground.” The Guards said they test-fired “advanced rockets” and used drones in the three-day exercises which were held in central and eastern Iran.

Meanwhile, as tensions also mount with Israel, a military analyst at Tasnim said that Iran-allied Hezbollah could use Iranian made Fateh 110 missiles to attack the Israeli nuclear reactor at Dimona from inside Lebanon. Hezbollah leader Sayyed Hassan Nasrallah said last Thursday that his group, which played a major role in ending Israel’s occupation of Lebanon, could strike Dimona.

“Since Lebanon’s Hezbollah is one of the chief holders of the Fateh 110, this missile is one of main alternatives for targeting the Dimona installations,” Hossein Dalirian said in a commentary carried by Tasnim.

In recent weeks, having been forced to concede geopolitically to China by dropping his demand to negotiate “One China”, Trump has pledged to get tough with Iran, warning the Islamic Republic after its ballistic missile test on Jan. 29 that it was playing with fire and all U.S. options were on the table. Just like China, which as reported earlier today has once again poked Trump by building SAM batteries on disputed islands in the South China Sea to see how far it can push the administration before retaliation, Iran is now engaging in exactly the same exercise, trying to gauge how much of Trump’s bluster will transform into actual actions. So far, Iran’s escalating actions have generated an eerie silence from the White House.

end

6.GLOBAL ISSUES

A good look at what is going on inside Sweden. The author is stating that mainstream media is hiding the full picture and Trump is right about the immigrants. No doubt that the message is getting to France, Germany and Holland with their upcoming elections this year

(courtesy zero hedge)

Swedish Mainstream Media Is “Hiding The Full Picture”: Trump Is Right About Immigrants

Authored by Chang Frick via Nyheter Idag,

Is it correct that Sweden got major problems handling the immigration? I would say yes. My grounds for claiming that is just by looking out the window where I live, inside a migrant dominated area. Almost every evening cars are set on fire and police officers are attacked by criminal gangs. But you don’t read very much about it in the Swedish main stream media.

There are lots of claims about what is going on in Sweden. On one side you have the Swedish main stream media that are very close to liberal press in the United States. We do not have anything like Fox News in Sweden, so there is not any big ”right-wing” media. Instead of Fox News, there is an ”alternative” scene with different kind of media outlets, some more serious than others. And some of them you can claim is based mostly in fake news.

But, you wont get the whole picture from the Swedish main stream media either. And you might just as well get fooled about specific claims about what is true and not.

My name is Chang Frick and i run this news outlet that you are reading right now. Ive been reporting a lot about whats going on in the suburbs in Sweden. When i work i am very often on the ground with my camera, taking photos and filming. So everything you see in the video above is produced by me. On top of that, i live in an area called ”Hallunda” in southern Stockholm. That is an heavily immigrant dominated area, mostly people from the middle east.

I see myself as a libertarian and if i could choose whoever president i would like to see in the United States it would be Ron Paul. Yeah, i am that kind of guy. But, whatever my personal political opinions are, i always put a big effort to report my stories correctly. When i do an article about something that happened in an immigrant area, i call the police and ask questions. I am always very carefully with presenting whom i talked to and i write down quotes word-by-word.

I talk to people on the ground, i ask what they have seen or heard. I never ask them what they think is going on, just what they know is going on. I also check how they know it, did they see it themselves and so on. That is basic journalism, you have to check stuff very carefully. I am not saying i am perfect, everyone can do a mistake, but i would say i put a lot of an effort to get my reporting correct.

My news outlet is not very big, but i get a lot of traffic in Sweden every time i report about what is going on in the suburbs. I would say my readers trust me a lot in my reporting, and a lot of my readers are politicians. At the same time, some critics claim that even I am producing fake news, but so far i have not seen anyone represent any evidence for it. But of course, anyone is more than welcome to look for wrongdoings from my side – that will just force me to become even better.

So, i will make some claims based on my experience of what is going on in Sweden. This is in the light of what Donald Trump recently said about Sweden.

1. You can’t get the whole picture reading Swedish MSM

The main stream media in Sweden is usually not lying or reporting fake news, even though it happens sometimes. But i would say it is mistakes and not anything that is done with purpose. A big news-outlet publishes lots and lots of stories every day, so of course you can find some wrongdoing once in a while. That does not mean the main stream media is a fake propaganda-machine. Mostly, what they claim, is usually true. There is references and all.

However, the mainstream media in Sweden is not giving you the whole picture. That is a claim I can make. You see, by not reporting some issues, you are not lying. And that, I would say, gives you a better understanding how it works. And it is because of that I built my own news outlet, where I try to fill in the blank spots that you cant find elsewhere from Sweden.

There is a lot going on in the Swedish suburbs that i would say is totally out of control. Ive seen it myself so many times, i have been talking to a lot of people living in these areas. After all, they are my neighbors.

2. No, we did not have any terror attack recently

Some people in social media even thinks that because of what Trump said, there have been a terror attack in Sweden. There have not been any such event in several years. It have happened once, but that was six years ago and nobody, except of the terrorist himself, got killed. What is true however is that Sweden got a lot of people who travel abroad to Syria and Irak to join ISIS.

Those guys get radicalized in Sweden and they also get recruited on Swedish soil. I dont know the numbers, but there is estimates of about a couple of hundreds. Lots of these guys return to Sweden after their participation in Syria and Iraq. So, are those people dangerous to Swedish society? Well, if you look at what happened in Nice or in Berlin, it is essentially enough with just one terrorist to create a lot of mess. And dead people.

3. Is there no go areas in Sweden? Well, it depends who you are…

Some claim that it is really dangerous to go to specific areas in Sweden. There is a term being used in Sweden that is ”no go zones”. I live in an area often described as that and well, i can go outside any time I want and walk around the area and nothing special will happen. But, at the same time, lots of people still does not feel safe in this area. Some of them is security personell and police officers.

And car owners. There is a lot of cars being set on fire. I have not a perfect answer yet to why this is happening. Some cars that are set on fire is about insurance fraud. I would say that more of those fires is about keeping the police busy. Just a few blocks away, there is lots of drugs being sold on the streets. If there is a police with resources to act, it means bad business for the local druglords. So lots of cars being set on fire is related to this, just to keep the police busy.

Some claim that cars being set on fire is about some muslim takeover or some kind of jihad. There is no evidence at all for that. I have never really seen anything than confirms such a claim.

But what is true is that the police get attacked in some of these no go zones. I have seen, and filmed that, myself. Immigrant kids throw rocks and even molotov-cocktails towards police officers during riots. The most known riots was those in Husby in northern Stockholm in 2013. Such riots does not happen very often, but there is definately tensions just below the surface in these areas, so we can most probably expect somewhat similar stuff going on in the future.

And working as a police officer in these areas means you often need back up from your colleagues. It happen more and more often that police officers are getting physical attacked. In an area nearby where i live someone threw a hand grenade towards the police who was sitting in a van. It was pretty much pure luck that they didn’t get injured. At other occasions there is molotov cocktails being thrown at the police and other stuff that can seriously harm, or even kill, a police officer.

So, well, you can’t totally deny that for some people these areas could be considered ”no go areas”. And, oh yes, some of these areas is pretty much ”no go” if you are trying to film or takes photos. There is a big chance that you will be attacked. It have happened to me and a lot of others as well.

4. Can Sweden handle the immigration?

This is a question where the answer is both yes and no. The migration, mainly from the middle east, is changing Sweden a lot. We have areas that are not even close to something we used to have. I am of course referring to the ”no go areas”. And those areas are growing, mostly because it is really hard to get a job if you are born outside Europe. To get a job you have to learn the language, you need education and you also need to understand the social codes in Sweden.

And by social codes i mean that swedes are not very tolerant at all. For example, when i was hanging out in New York i could talk to anyone in the subway. People are open minded and curious in New York, no matter who you are. It is not like that at all in Sweden. In the subway you will find most people being quiet or just talking to someone they already know. I am just trying to pinpoint a small example why it can be hard to ”get in” to the Swedish society. And to get a job, you need to know people.

So, lots of immigrants are living on social welfare. And they have nothing meaningful to do during the days. And the kids usually have their parents as role models, so you can figure out the rest.

This is the biggest problem Sweden is facing today. I base that claim on the political discussion but also where most of the government money is spent. Notice, the discussion about where tax money is going is a tricky one, so i am not presenting any exact numbers. What i am saying is that immigration is one of the biggest, if not the biggest, cost for tax payers in Sweden.

The effect on the society is that the whole society is changing from what it used to be. Not everything with the ”new” Sweden is bad, there are of course a lot of good examples, but as it is today – the sum of the effects – is going the wrong way. More and more people feel insecure, something i am pretty sure is related to immigration – even if i don’t have any scientific paper showing it.

5. Is Donald Trump correct about his claim about Sweden?

Well, the claim i am referring to is the tweet below, a tweet that i think sums it up what mr Trump have tried to say the latest days.