Gold at (1:30 am est) $1248.90 down $3.70

silver was : $18.44: UP 2 CENTS

Access market prices:

Gold: $1249.70

Silver: $18.45

For comex gold:

MARCH/

NOTICES FILINGS FOR MARCH CONTRACT MONTH: 23 NOTICE(S) FOR 2300 OZ. TOTAL NOTICES SO FAR: 24 FOR 100 OZ (0.0746 TONNES)

For silver:

For silver: MARCH

480 NOTICES FILED FOR 2,400,000 OZ/

Total number of notices filed so far this month: 829 for 4,145,000

For two weeks now, gold/silver equity shares have been whacked by our banker friends even though silver and gold metal have been on a tear for the past 8 weeks. To me, it seems that the equity shares are being hit trying to convince holders of real metal to sell their physical. I strongly believe that the comex has very little real gold/silver to serve gold/silver longs.

FEDERAL RESERVE BANK OF NEW YORK/GOLD MOVEMENT REPORT

In January reported that the total amount gold inventory at the FRBNY was 7,841 million dollars worth of gold valued at 42.21 dollars per oz.

In February: the total amount of gold inventory at the FRBNY remains at 7,841 million dollars valued at 42.21 dollar per oz

Thus movement is zero.

Let us have a look at the data for today

.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total open interest FELL by 1,939 contracts DOWN to 197,629 with respect to YESTERDAY’S TRADING. In ounces, the OI is still represented by just less THAN 1 BILLION oz i.e. 0.988 BILLION TO BE EXACT or 141% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT MARCH MONTH: THEY FILED: 480 NOTICE(S) FOR 2,400,000 OZ OF SILVER

In gold, the total comex gold FELL BY 6,282 contracts WITH THE FALL IN THE PRICE GOLD ($4.80 with YESTERDAY’S trading ).The total gold OI stands at 446,081 contracts.

we had 23 notice(s) filed upon for 2300 oz of gold.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD:

We had no change in tonnes of gold at the GLD:

Inventory rests tonight: 841.17 tonnes

.

SLV

we had no changes in silver into the SLV:

THE SLV Inventory rests at: 335.281 million oz

end

.

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in silver FELL by 1939 contracts DOWN to 197,629 DESPITE THE FACT THAT SILVER WAS UP 7 CENTS with YESTERDAY’S trading.WE MUST HAVE HAD CONSIDERABLE SHORT COVERING AGAIN. The gold open interest FELL by 6,282 contracts DOWN to 446,081 WITH THE FALL IN THE PRICE OF GOLD OF $4.80 (YESTERDAY’S TRADING)

(report Harvey

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

2C/ FEDERAL RESERVE BANK OF NY/GOLD MOVEMENT REPORT

(HARVEY)

3. ASIAN AFFAIRS

i)Late TUESDAY night/WEDNESDAY morning: Shanghai closed UP 5.20 POINTS OR .16%/ /Hang Sang CLOSED UP 35.76 POINTS OR 0.15% . The Nikkei closed UP 274.55 POINTS OR 1.44% /Australia’s all ordinaires CLOSED DOWN 0.18%/Chinese yuan (ONSHORE) closed DOWN at 6.8805/Oil ROSE to 54.12 dollars per barrel for WTI and 56.70 for Brent. Stocks in Europe ALL IN THE GREEN ..Offshore yuan trades 6.8724 yuan to the dollar vs 6.8805 for onshore yuan.THE SPREAD BETWEEN ONSHORE AND OFFSHORE NARROWS CONSIDERABLY AS POBC ATTEMPTS TO STOP USA DOLLARS FROM LEAVING CHINA’S SHORES. ONSHORE YUAN WEAKER AS IS OFFSHORE YUAN COUPLED WITH THE STRONGER DOLLAR

3a)THAILAND/SOUTH KOREA/NORTH KOREA

b) REPORT ON JAPAN

none today

c) REPORT ON CHINA

China backs Russia as it vetoes western backed UN sanctions against Syria:

( zerohedge)

4. EUROPEAN AFFAIRS

i)My goodness: Fillon is charged and yet he will stay in the French Presidential race

( zero hedge)

ii)The ECB now has a problem: German inflation jumps higher than the targeted 2.0% at 2.2%. This will heighten concerns that the ECB must stop it’s QE

( zerohedge)

iii)This is fascinating: the Euro Contagion Risk index authored by Sentix is exploding:

( Sentix/zero hedge)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

This is interesting: UAE a close ally of the USA signs a breakthrough military deal with Russia!!!..

( Korzun/StrategicCulture Foundation)

6.GLOBAL ISSUES

The Mexican Peso surges on word that the Fed will give it a helping hand. I wonder what Donald will think of the Fed helping the Meixcans?

(courtesy zerohedge)

7. OIL ISSUES

DOE reports a huge increase in crude inventories. The economy is just not performing well

( DOE/zero hedge)

8. EMERGING MARKETS

9. PHYSICAL MARKETS

I)This should hurt our banking cartel as gold supply in the world’s largest mine, Grasberg came to a screeching halt due to problems with the Indonesian government regulations. Freeport McMoRan the operator of the big mine has laid off thousands

( Varagur/Voice of America/GATA)

ii)For your interest: treasure hunters find an Iron age gold bracelet in a farm field. It is the earliest discovered gold in Britain

( Knapton/Telegraph/London/GATA)

iii)Demand for gold resumes in India. The latest figures show that India imported 50 tonnes of gold in February an increase of over 82% from a year ago. The fiasco of their removal of the two highest currency notes is over and gold will resume its normal northerly projection.

(courtesy Reuters/Mbumbai)

10.USA STORIES

i)Early trading:

The 30 yr yield rises above 3% as the march rate hike spikes above 80%. Remember that Stockman states that the rate hike will occur because the Fed has no choice with the huge inflationary pressures.

( zero hedge)

ii)Then bonds and gold were hammered on heavy short volume as the Dow approaches 21,000. Remember however March 15 is the debt ceiling official day as it “comes out of the closet”

( zero hedge)

iii)Incomes are rising faster than spending. However the gains in income is from the service sector and not from our “ordinary joe” on the assembly line. This is coupled with rising inflation and also our ordinary joes are having real trouble with rising inflationary pressures.

(courtesy zerohedge)

iv)Markit’s PMI in the uSA drops despite a surge in ISM new orders

( zero hedge)

v)USA construction spending tumbles on all fronts. This goes against “soft data” which suggests an economy booming along with the stock market.

( zero hedge)

vi)The analysts react to Trump’s presidential address yesterday. Great speech but no details. The fun will begin on March 15.

( zero hedge)

vii)New car sales are quite slow which forces one deal to rent extra space to house the overflow

(courtesy zero hedge)

viiii) Here is an update on the Dallas firefighter/police pension debacle. The recovery on the fraud on the purchase of real estate only recovers 2.2 million dollars out of a loss of 320 million

( zero hedge)

ix)Wow!! that did not take long: Goldman Sachs, the Atlanta Fed cut their estimate for the first quarter GDP to only 1.7%. JPMorgan cuts its estimate to 1.5% and Bank of American down to 1.3%. Great time for the Fed to raise rates!

( zero edge)

x)The Fed’s Beige Book notes a decline in optimism about the uSA economy. Also noted was a drop in BROADWAY attendance for NY shows.

( zero hedge/BeigeBook)

xi)Bloomberg is just received a document which outlines that Washington is preparing for a trade war and that they are not bound by WTO decisions as they never agreed to it when they entered the trade organization. It sure seems that Trump will do is border tax

( zero hedge/Bloomberg)

xii) Rob Kirby interviewed by Greg Hunter

Let us head over to the comex:

The total gold comex open interest FELL BY 6,282 CONTRACTS DOWN to an OI level of 4446,081 with THE FALL IN THE PRICE OF GOLD ( $4.80 with YESTERDAY’S trading). We are now in the contract month of MARCH and it is one of the poorer delivery months of the year. In this MARCH delivery month we had a LOSS of 517 contracts DOWN to 122. We had 1 contact(s) served upon yesterday, so we lost 516 CONTRACTS or 51,600 ounces will not stand for delivery. The next active contract month is April and here we saw it’s OI FALL by 10,758 contracts DOWN TO 280,881. The non active May contract month added 62 contracts and thus its OI is 62 contracts. The next big active month is June and here the OI ROSE by 2219 contracts up to 85,709.

We had 23 notice(s) filed upon today for 2300 oz

We are in the active delivery month is March and here the OI decreased by 3028 contracts down to 4271 contracts. We had 349 notices served upon yesterday so we lost 2679 contracts or an additional 13,395,000 oz will not stand for delivery. This is totally unbelievable. How could so many be late in rolling.

For historical reference: on the first day notice for the March/2016 silver contract: 19,020,000 oz. However the final amount standing at the end of March 2016: 6,755,000 oz as the banker boys were busy convincing holders of many silver contracts to cash settle just like they did today.

The April contract month gained 13 contracts to 953 contracts. The next active contract month is May and here the open interest gained 1166 contracts up to 154,914 contracts.

We had 480 notice(s) filed for 2,400,0000 oz for the MARCH 2017 contract.

VOLUMES: for the gold comex

Today the estimated volume was 297,403 contracts which is very good.

Yesterday’s confirmed volume was 254,273 contracts which is good

volumes on gold are getting higher!

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz |

nil OZ

|

| Deposits to the Dealer Inventory in oz | 1200.02 oz

Brinks |

| Deposits to the Customer Inventory, in oz |

nil

|

| No of oz served (contracts) today |

23 notice(s)

2300 oz

|

| No of oz to be served (notices) |

99 contracts

9,900 oz

|

| Total monthly oz gold served (contracts) so far this month |

24 notices

2400 oz

0.003 tonnes

|

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | oz |

Today, 0 notice(s) were issued from JPMorgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equates to 23 contract(s) of which 0 notices were stopped (received) by jPMorgan dealer and 0 notice(s) was (were) stopped/ Received) by jPMorgan customer account.

March 2016: 2.311 tonnes (March is a non delivery month)

| Silver | Ounces |

| Withdrawals from Dealers Inventory | nil |

| Withdrawals from Customer Inventory |

717,307.560 0z

Brinks

HSBC

|

| Deposits to the Dealer Inventory |

nil oz

|

| Deposits to the Customer Inventory |

815,013.702 oz

Scotia

JPM

Brinks

|

| No of oz served today (contracts) |

480 CONTRACT(S)

(2,400,000 OZ)

|

| No of oz to be served (notices) |

3791 contracts

(18,955,000 oz)

|

| Total monthly oz silver served (contracts) | 829 contracts (4,145,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month | 777,610.9 oz |

end

And now the Gold inventory at the GLD

March 1/no change in gold inventory at the GLD/Inventory rests at 841.17 tonnes

FEB 28/no changes in gold inventory at the GLD/Inventory rests at 841.17 tonnes

feb 27/no change in gold inventory at the GLD/Inventory rests at 841.17 tonnes

Feb 24/no changes in gold inventory at the GLD/Inventory rests at 841.17 tonnes

FEB 23/no changes in gold inventory at the GLD/Inventory rests at 841.17 tonnes

FEB 22/no changes in gold inventory at the GLD/Inventory rests at 841.17 tonnes

FEB 21/no changes in gold inventory at the GLD/Inventory rests at 841.17 tonnes

feb 17/a withdrawal of 2.37 tonnes of gold from the GLD/Inventory rests at 841.17 tonnes

FEB 16/we had no changes in the GLD inventory today/Inventory rests at 843.54 tonnes

Feb 15./another deposit of 2.67 tonnes of gold into the GLD inventory despite another attempted whacking of gold/inventory rests at 843.54 tonnes

FEB 14/another deposit of 4.14 tonnes of gold into the GLD inventory/rests at 840.87 tonnes

FEB 13/another deposit of 4.15 tonnes of gold into the GLD/Inventory rests at 836.73 tonnes

Feb 10/no changes at the GLD/Inventory rests at 832.58 tonnes

feb 9/no changes at the GLD/Inventory rests at 832.58 tonnes

Feb 8/another “deposit” of 5.63 tonnes of gold into the GLD/The addition is a paper addition/total inventory: 832.58 tonnes

Feb 7/another huge fake deposit of 8.30 tonnes of gold into the GLD/the addition is a paper addition and no doubt not physical/ total inventory: 826.95 tonnes

FEB 6/a huge deposit of 7.43 tonnes of gold into the GLD/Inventory rests at 818.65 tonnes

FEB 3/no change in gold inventory at the GLD/Inventory rests at 811.22 tonnes

Feb 2/another huge deposit of 1.48 tonnes/inventory rests at 811.22 tonnes

Feb 1/a huge “deposit” of 10.67 tonnes of gold into the GLD/Inventory rests at 809.74 tonnes. this should stop GLD from sending gold to Shanghai.

end

NPV for Sprott and Central Fund of Canada

end

Major gold/silver trading/commentaries for WEDNESDAY

GOLDCORE/BLOG/MARK O’BYRNE

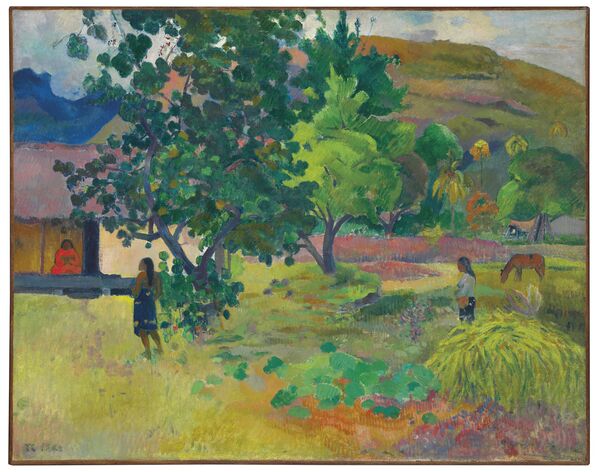

Art Market Bubble Bursting – Gauguin Priced At $85 Million Collapses 74%

– Art Market Bubble Bursting?

– Russian Billionaire Takes 74% Loss On “Investment”

– $85 Million Gauguin Bought By Dmitry Rybolovlev in 2008

– Christie’s auctioned the work at its evening sale in London

– Global art sales plummet, but China rises as ‘art superpower’

– China soon to dominates global art and gold market

– Art price volumes doubled since 2009

– As currencies debase super rich seek out stores of value

– Gold remains accessible store of value for all

– Stocks, bonds and many assets at record prices

– Gold half it’s real price in 1980

Te Fare by Paul Gauguin – Source: Christie’s

Russian billionaire Dmitry Rybolovlev paid €54 million or $85 million for a landscape by Paul Gauguin in a private transaction in June 2008. Yesterday, he incurred a whopping 74% loss on his store of value “investment” as reported by Bloomberg:

Gauguin’s 1892 landscape “Te Fare (La Maison)” fetched 20.3 million pounds ($25 million), including commission, at Tuesday evening’s sale of Impressionist and modern art at Christie’s in London. Rybolovlev will net about $22 million based on the hammer price. The auction house had estimated the value at $15 million to $22.4 million. The buyer was a client of Rebecca Wei, president of Christie’s Asia.

The Gauguin was one of four Rybolovlev pieces offered for sale on Tuesday. Another work, a Mark Rothko painting, will be auctioned March 7.

Rybolovlev — with a fortune of about $9.8 billion according to the Bloomberg Billionaires Index — invested about $2 billion in 38 works, from Leonardo da Vinci to Pablo Picasso. They were procured privately by Swiss art dealer Yves Bouvier, known for creating a network of tax-free art storage warehouses in Singapore and Luxembourg.

Two years ago, Rybolovlev sued Bouvier, alleging he was overcharged by as much as $1 billion, Bloomberg reported. Since then the Russian fertilizer magnate has been unloading works he acquired, some at record prices. He has already sold three for a loss totaling an estimated $100 million. The five works at Christie’s, all estimated below their purchase prices, were expected to deepen the loss.

The art industry is closely watching the London auctions running this week and next as the year’s first test of the global market following a significant contraction in 2016. Christie’s sales fell 17 percent to $4 billion pounds ($5.4 billion) last year, while Sotheby’s reported a 27 percent decline to $4.9 billion. Both houses saw steep declines in their two biggest categories: Impressionist and modern art, and postwar and contemporary art.

In May 2015, we warned about the bubble in the the fine art “investment market or indeed the Hyperinflation in Art Investment Market after a Picasso sold for $179 million.

William Banzai

William Banzai

At the time, we pointed out that ultra high net worth and family office buyers may be viewing the fine art market as a form of super safety deposit box and as a way to protect their wealth from market crashes, systemic risk and the risk of bail-ins and deposit confiscation today.

Since then global art sales plunged in 2016 as the number of high-value works of art sold dropped by half, while China regained its status as the world’s top market according to an annual report recently released by Artprice. Art auctions worldwide totalled $12.5 billion (11.8 billion euros) last year, down 22 percent from $16.1 billion in 2015, the report said.

The world’s biggest database for art prices and sales, working with Chinese partner Artron, attributed the drop to a plunge in the number of works worth more than $10 million each – from 160 in 2015 to just 80 last year. “On all continents, sellers are choosing a policy of ‘wait-and-see,’” Artprice CEO Thierry Ehrmann said.

In recent years, very wealthy art buyers may have believed art was less risky than holding increasingly debased digital currencies in banks that may be subject to deposit bail-ins.

As a diversification, art has some merit as it is not correlated with financial assets, but only as a very small part of an overall portfolio.

Given the scale of risks facing investors and savers today we are advising clients to increase allocations to gold from the standard 5% to 10% allocation to higher allocations of as much as 25% to 30%.

Most investors and savers cannot afford a Picasso or a Gauguin but the proven, timeless store of value that is physical gold remains accessible.

Gold in USD Adjusted for Inflation 1970-2017 – Macrotrends.net

Gold in USD Adjusted for Inflation 1970-2017 – Macrotrends.net

Not only is it accessible but it remains relatively cheap from a long term perspective, at nearly less than half its real price high of $2,200 price in 1980 when adjusted for the considerable inflation of the last 37 years.

Gold is also relatively cheap compared to most stock, bond and property markets, many of which are at all time record highs. These highs are in large part due to quantitative easing (QE), zero and negative percent interest rates and global currency debasement on a scale never seen in history.

END

This should hurt our banking cartel as gold supply in the world’s largest mine, Grasberg came to a screeching halt due to problems with the Indonesian government regulations. Freeport McMoRan the operator of the big mine has laid off thousands

(courtesy Varagur/Voice of America/GATA)

Showdown in Indonesia brings world’s biggest gold mine to standstill

Submitted by cpowell on Tue, 2017-02-28 12:52. Section: Daily Dispatches

By Krithika Varagur

Voice of America, Washington

Monday, February 27, 2017

JAKARTA, Indonesia — The American mining company Freeport-McMoRan has brought the world’s biggest gold mine, in the Indonesian province of West Papua, to a standstill. The corporation is butting heads with the Indonesian government over protectionist mining regulations. And now that Freeport has started to dismiss tens of thousands of workers, the local economy is poised to take a huge hit. In Mimika Regency, the West Papua province containing the Grasberg gold mine, 91 percent of the Gross Domestic Product is attributed to Freeport.

Freeport Indonesia abruptly stopped production on February 10 and laid off 10 percent of its foreign workers. It employs 32,000 people in Indonesia, about 12,000 of whom are full-time employees. The freeze was a reaction to a shakeup in Freeport’s 30-year contract with the Indonesian government, signed in 1991. Indonesia has tried to levy additional obligations from Freeport in an attempt to increase domestic revenue from its natural resources. Freeport retaliated last week by threatening to pursue arbitration and sue the government for damages. …

… For the remainder of the report:

http://www.voanews.com/a/showdown-in-indonesia-brings-gold-mine-to-stand…

END

For your interest: treasure hunters find an Iron age gold bracelet in a farm field. It is the earliest discovered gold in Britain

(courtesy Knapton/Telegraph/London/GATA)

Treasure hunters find Iron Age gold in farm field, earliest discovered in Britain

Submitted by cpowell on Tue, 2017-02-28 12:57. Section: Daily Dispatches

By Sarah Knapton

The Telegraph, London

Tuesday, February 28, 2017

Intricate jewellery found buried in a Staffordshire field is the earliest example of Iron Age gold ever found in Britain.

The collection, made up of four twisted metal neckbands, called torcs, and a bracelet, was discovered by two metal detectorists just before Christmas.

Experts say they would have been owned by wealthy powerful women who probably moved from continental Europe to marry rich Iron Age chiefs.

The pair who discovered the find had swept the field 20 years earlier and uncovered nothing. But after abandoning a fishing trip to go treasure hunting they came across the horde, which could be worth hundreds of thousands of pounds. …

… For the remainder of the report:

http://www.telegraph.co.uk/science/2017/02/28/iron-age-gold-found-farmer..

END

Demand for gold resumes in India. The latest figures show that India imported 50 tonnes of gold in February an increase of over 82% from a year ago. The fiasco of their removal of the two highest currency notes is over and gold will resume its normal northerly projection.

(courtesy Reuters/Mbumbai)

India’s February gold imports surge on pent-up demand – GFMS

India’s February gold imports surged to 50 tonnes, up more than 82 percent from a year ago, on pent-up jeweller demand and as retail consumers ramped up purchases for weddings, provisional data from consultancy GFMS showed on Wednesday.

The rise in imports by the world’s second-biggest consumer of the precious metal will support global prices that are trading near their highest level in 3-1/2 months, but could widen the South Asian country’s trade deficit.

“Pent-up demand on the ease of the cash crunch and wedding related demand lifted imports in February,” said Sudheesh Nambiath, a senior analyst at GFMS, a division of Thomson Reuters.

In November, Prime Minister Narendra Modi scrapped 500- and 1,000-rupee banknotes, notes that were 86 percent of the value of cash in circulation, as part of a crackdown on corruption, tax evasion and militant financing.

India’s gold imports had fallen to 27.4 tonnes in February 2016 as buyers postponed purchases in anticipation of a reduction in the import duty in the budget at the time.

This February, retail demand improved due to the wedding season and as cash supplies became normal, said Bachhraj Bamalwa, a jeweller based in the eastern Indian city of Kolkata.

But imports in March could fall as a recent rally in prices has started deterring buyers.

“Consumers are struggling to adjust with higher prices. They are postponing purchases expecting a correction in prices,” said Harshad Ajmera, the proprietor of JJ Gold House, a wholesaler based in Kolkata.

In the local market, gold futures were trading at 29,380 rupees ($439) per 10 grams on Wednesday, up more than 9 percent since falling to 26,862 rupees in December 2016, its lowest in 10 months.

India’s gold imports in 2016 had fallen nearly 44 percent versus 2015 to 510.4 tonnes, the lowest level in 13 years.

“Last year was an unusual year. This year consumption and imports will rise as jewellery demand has been recovering,” said Bamalwa.

(Reporting by Rajendra Jadhav; Editing by Christian Schmollinger)

END

A great commentary from Bill Holter tonight:

(courtesy Bill Holter/Holter-Sinclair collaboration)

They are playing with a revolution… by Joe six pack!

I had a long conversation with Jim Sundayevening regarding the increase in volume and pitch to sabotage President Trump. He asked that I write an article addressing the push/pull toward impeaching or at least neutering him. The “movement” to impeach him (even before taking office) has grown and now looks like there are actual odds the “left” will try in reality.

I wrote “the left” above but in reality it is not just the left as we have seen Paul Ryan, Darrell Issa and other so called conservatives begin to change colors. The reality is Donald Trump is up against a very powerful machine that is entrenched and sucking the life out of the country. This machine is not U.S. centric but in fact has tentacles all over the world with a stranglehold on many “not so sovereign” governments.

The story has been Russia, Russia, Russia, in a he said she said fashion. To this point there is and has been zero evidence directly tying Mr. Trump to Russia…but no matter, they may make some up. Michael Flynn did resign after admitting he spoke to a Russian minister though we still do not have transcripts. We believe Mr. Flynn most certainly asked Russia to not take the bait and retaliate at further U.S. sanctions after the election but before the inauguration. For this, Jim and I believe he should be given the medal of honor for averting WW III. We ask, where was the press, where were the left AND the right when president Obama was caught on a hot microphone in conversation with Russian president Medvedev saying “I will have more flexibility after the next election”? His statement of course fully understood and followed by Mr. Medvedev responding “I will inform Vladimir”. Where was the outrage then?!!!

As quipped above, we believe something will be “made up” in an effort to impeach President Trump. It is now most likely a “race” to get something started as fast as possible, prior to AG Jeff Sessions handing down any indictments. Please understand, this is a fight to the death between light and dark, and ANYTHING goes! Ask yourself this simple question, if President Trump was truly pulling the strings …and truly in bed with Russia, then why is it five Russian diplomats have recently been assassinated or had “untimely” heart attacks? https://www.youtube.com/watch?v=u73InAPFKqE These men were all long time personal friends of Mr. Putin, it certainly looks like he is being goaded into responding with force.

But why? Why does it (and has for several years) appear like the U.S. is trying to incite a war with Russia? This question I believe is most simple of all, the “deep state” either believes they can pull off another WWI or WWII where they pull the economy from the jaws of depression, …or more likely, they know the current system cannot continue and must kick the table over. I have been on the record for at least two years, “they must place blame” on something other than their Ponzi, blood sucking policies as reason for the collapse.

This is a very dangerous game both nationally and internationally. Internationally they are playing with human annihilation. Nationally they are playing with revolution, this needs a little explaining. If Mr. Trump is impeached, it will require votes from the right to do so …immediately after the people have spoken by taking both houses and 35 governorships. Should impeachment go forward, Joe six pack will take to the streets. Mr. six pack should not be confused with a bunch of delirious snowflakes carrying signs and backed up by paid vandals. No, Mr. six pack will be PACKING! He will be packing long arms and laden with full clips. Interestingly, there are many, and a majority of “law enforcement” named “JOE SIXPACK” who actually still believe in the rule of law.

Personally, as I hear of the prospects of impeachment, unless some “evidence”, REAL evidence, were to come out that actually makes sense and not a piece of Swiss cheese logic, I (and Jim) have personally decided to be Joe six packs. We are in a fight to retain, or to lose our country altogether. True Americans put up with huge transgressions over the past eight (and many prior) years. Like it or not, we were led by a Muslim president, probably not a natural born citizen and of questionable sexuality …but we did not riot, we did not destroy our neighbors businesses. No, we voted, because that is the “civilized” thing to do…

What I am arriving at is this, Joe six pack will not stand idly by when he is finally told “your vote does not matter”. Mr. six pack was fooled for many years when his “choices” were not really a choice, a vote for either one was a vote for “the machine”. Mr. six pack got wise to this and decided throw a monkey wrench into the machine. Joe can be told, and can accept many things. What he will not accept is “your vote does not count”! We hope it does not come to this but the road map shows that most all roads do lead to it. The odds, whether you like them or not, appear to favor an internal civil war unless the bastards get us nuked first.

Your early WEDNESDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight

1 Chinese yuan vs USA dollar/yuan WEAKER AT 6.8805(BIGGER DEVALUATION SOUHBOUND /OFFSHORE YUAN NARROWS TOWARDS ONSHORE TO 6.8724/ Shanghai bourse UP 5.20 POINTS OR .18% / HANG SANG CLOSED UP 35.76 POINTS OR 0.15%

2. Nikkei closed UP 274.55 POINTS OR 1.44% /USA: YEN FALLS TO 112.17

3. Europe stocks opened ALL IN THE GREEN ( /USA dollar index RISES TO 101.86/Euro DOWN to 1.0525

3b Japan 10 year bond yield: RISES TO +.065%/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 113.84/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD FINALLY IN THE POSITIVE/BANK OF JAPAN LOSING CONTROL OF THEIR YIELD CURVE AS THEY PURCHASE ALL BONDS TO GET TO ZERO RATE!!

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 54.12 and Brent: 56.70

3f Gold DOWN/Yen DOWN

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil UP for WTI and UP for Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund RISES TO +.268%/Italian 10 yr bond yield UP to 2.132%

3j Greek 10 year bond yield FALLS to : 6.97%

3k Gold at $1242.00/silver $18.33(8:15 am est) SILVER CLOSE TO RESISTANCE AT $18.50

3l USA vs Russian rouble; (Russian rouble UP 28/100 in roubles/dollar) 58.10-

3m oil into the 54 dollar handle for WTI and 56 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation (already upon us). This can spell financial disaster for the rest of the world/China forced to do QE!! as it lowers its yuan value to the dollar/GOT A BIGGER DEVALUATION SOUTHBOUND from POBC.

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 113.84 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 1.0111 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.0643 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT

3r the 10 Year German bund now POSITIVE territory with the 10 year RISES to +.268%

3s The Greece ELA NOW at 71.4 billion euros,AND NOW THE ECB WILL ACCEPT GREEK BONDS (WHAT A DISASTER)

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.440% early this morning. Thirty year rate at 3.034% /POLICY ERROR)GETTING DANGEROUSLY HIGH

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

(courtesy Jim Reid/Bloomberg/Deutsche bank/zero hedge)

Global Stocks, US Futures Surge, Bonds Tumble On “Presidential” Trump Speech, Hawkish Fed Speakers

While many Wall Street traders expecting Trump to unveil details of his economic plan went to bed empty handed last night, that was not enough to halt the market rally with the narrative shifting to Trump’s “measured”, “presidential” tone in which he offered an olive branch to both Democrats and Republicans in Congress while promising to make concessions and providing another round of grand visions for the US. Trump urged Americans to abandon conflict and help him remake the fabric of the country, a moment he hopes will turn the page on his administration’s chaotic beginning and bring clarity to his policy agenda. He offered few new proposals and made no suggestions on how he would pay for his plans, including a replacement of Obamacare, a tax overhaul including cuts for the middle class, $1 trillion in infrastructure investment and a large increase in defense spending.

“The market has been looking for reassurance that Trump intends to follow through on his campaign promises for fiscal spending, tax cuts and deregulation,” said James Woods, global investment analyst at Rivkin in Sydney. “He mentioned these policies but did not provide any actual details or time lines, which is what investors are looking for.”

For markets, the speech – either positive or negative – was overshadowed by comments from a handful of Federal Reserve policymakers, who suggested a March rate hike is live, contrary to market expectations. As a result, have tumbled, and global stocks surged following yesterday’s barrage of hawkish Fed speakers, especially Bill Dudley, who in the span of an hour managed to reprice March rate hike odds from just over 50% to 80%, meaning a March rate hike is now in play.

For those who missed it, here is a summary of Tuesday’s Fed talking heads, and what they said:

- Fed’s Dudley (Voter, Dove) said the case for rate hikes is more compelling.

- Fed’s Kaplan (Voter, Neutral) said the rate path is more important than timing of the next hike.

- Fed’s Williams (Non-Voter, Hawk) sees a March hike getting serious consideration. Williams also added he still is comfortable with 3 hikes this year and does not see need to delay rate hike.

- Fed’s Bullard (Non-Voter, Dove) stated that the Fed has essentially reached its dual mandate and should allow the balance sheet to normalize naturally. Bullard also added that the policy rate can stay relatively low over the horizon and that he still expects 2% growth, thus no reason to be aggressive on rate hikes

The most hawkish comments were out of both Dudley and Williams. In an interview with CNN, the usually dovish NY Fed President Dudley said that the case for tightening has become “a lot more compelling in recent months” and that “risks to the outlook are now starting to tilt to the upside”. Dudley was also quoted as saying that “animal spirits have been unleashed a bit post the election” and that “there’s no question sentiment has improved quite markedly”. He also said that 3-4% GDP growth in the medium term is possible should we see further improvement in productivity. Shortly before that San Francisco Fed President Williams said that a March hike is getting “serious consideration” given that the Fed is “very close” to achieving its dual mandate goals.

As expected, March hikes odds soared, rising as much as 80% after the barrage of hawks:

With March odds soaring to approximately 80% percent, they pushed the dollar higher and sent Treasuries lower.

Additionally, strong data out of China, where most PMIs came in better than expected, has eased concerns about China’s economy. The rundown:

- China’s Official Manufacturing PMI (Feb) 51.6 vs. Exp. 51.2 (Prey. 51.3).

- Chinese Non-Manufacturing PMI (Feb) 54.2 (Prey. 54.6);4-monthlow.

- Chinese Caixin Manufacturing PMI (Feb) 51.7 vs. Exp. 50.8 (Prey. 51.0).

Back to Trump: in a nutshell the long awaited Trump address had a familiar ‘America first’ theme throughout and plenty of echoes of his inaugural address. However the disappointment market wise has been the lack of detail. But there did seem to be a big effort to sound presidential. In terms of what we did get, the President returned again to the subject of rebuilding infrastructure, highlighting that he will be asking Congress to approve legislation that produces a $1tn investment financed through both public and private capital and guided by the principals of “hire American and buy American”. Trump also reconfirmed that he intends to repeal and replace Obamacare, increase defence spending, enforce immigration laws and also overhaul tax including cuts for the middle class. The tax subject was only really lightly touched. Trump said that his economic team is developing a “historic tax reform that will reduce the tax rate on our companies so that they can compete and thrive anywhere and with anyone” and also “at the same time provide massive tax relief for the middle class”. There was no specific mention whatsoever of the much anticipated border-adjusted tax. Another subject of much debate, bank regulation, was also avoided.

Overall, a speech that while disappointing on one hand (lack of specifics) was greeted as perhaps a return to Trump’s conciliatory, “presidential-sounding” roots. So as investors moved on from President Donald Trump’s address to Congress, shifting their focus to the timing of a U.S. rate increase as the dollar strengthened, stocks surged and bonds tumbled.

The Bloomberg Dollar Spot Index climbed the most in three weeks, the yield on 10-year Treasuries rose and European banking stocks gained after odds jumped for a Federal Reserve rate increase this month. Shares of commodity producers found support from a report indicating improving health for Chinese manufacturing which also helped prices for raw material exports.

“Fed speakers trump Trump,” Richard McGuire, the head of rates strategy at Rabobank International in London, wrote in a note. Trump’s speech lacked “fresh content for the market to trade off, with big tax cuts, deregulation and an infrastructure plan being mentioned but not supported by any details. Given this, all focus instead turned to the slew of hawkish rhetoric from Fed speakers.”

The dollar index climbed as much as 0.7 percent to its highest levels in seven weeks, having also been helped by data showing robust U.S. consumer spending.

“After dominating the markets since November, President Trump could now fade into the background as the focus shifts to the Fed and the prospect of rate increases,” said Kathleen Brooks, Research Director at City Index in London. “Fed members don’t just let words slip out when they speak to the press – this was a message for the markets, and the markets have duly reacted.”

European shares gained, with basic resources the top-performers on Trump’s promise of $1 trillion of infrastructure spending. The STOXX 600 index rose over 1 percent, with Germany’s DAX and France’s CAC 40 outperforming peers to climb 1.3 percent and 1.4 percent respectively, helped by strong company earnings reports. European stocks climbed the most since Feb. 1 as all industry sectors advanced. A gauge of banks gained 2 percent, leading the advance, while basic resources shares rose 1.9 percent.

Japan’s Topix index increased 1.2 percent, propelled by a weaker yen towards the the biggest rally in more than two weeks. The Shanghai Composite Index added 0.2 percent after data on the producer price rebound, giving top officials gathering in Beijing a solid economic backdrop as they seek to rein in financial risks.

The global MSCI ACWI index, which has risen more than 10 percent since Trump’s election in November, was flat, with gains in Europe offsetting earlier falls on Asian and U.S. bourses. The MSCI’s broadest index of Asia-Pacific shares outside Japan dipped 0.2 percent.

Futures on the S&P 500 Index added 0.5 percent, after the Dow Jones Industrial Average snapped a 12-day winning streak to close down 0.1 percent in the prior session. The S&P500 finished February with its best monthly gain since March, climbing 3.7

percent.

In commodity markets, crude oil prices lost more ground, with rising U.S. oil output adding pressure on the market, although OPEC production cuts continued to offer support. The stronger dollar weighed on gold, which dropped 0.3 percent to 1,244.36 an ounce, extending Tuesday’s decline.

2Y Treasury yields jumped to 1.304%, the highest since December, to match their highest levels since 2009. The gap between them and their German equivalents increased to its widest since 2000. Yields on 10-year Treasuries rose three basis points to 2.42 percent, climbing for a third straight day. Yields on benchmark German bonds climbed four basis points to 0.25 percent after a report showed unemployment continued to decline. Yields on French benchmarks and gilts both rose three basis points.

Market Snapshot

- S&P 500 futures up 0.5% to 2,375.50

- STOXX Europe 600 up 1% to 373.75

- MXAP down 0.3% to 144.70

- MXAPJ down 0.3% to 464.87

- Nikkei up 1.4% to 19,393.54

- Topix up 1.2% to 1,553.09

- Hang Seng Index up 0.2% to 23,776.49

- Shanghai Composite up 0.2% to 3,246.93

- Sensex up 0.9% to 28,990.65

- Australia S&P/ASX 200 down 0.1% to 5,704.80

- Kospi up 0.3% to 2,091.64

- Brent Futures up 0.5% to $56.81/bbl

- Gold spot down 0.3% to $1,244.68

- U.S. Dollar Index up 0.6% to 101.68

- US 10Y Yield

- German 10Y yield rose 4.1 bps to 0.249%

- Euro down 0.3% to 1.0540 per US$

- Brent Futures up 0.5% to $56.81/bbl

- Italian 10Y yield fell 4.8 bps to 2.086%

- Spanish 10Y yield rose 3.1 bps to 1.686%

Top Overnight News via BBG

- Trump’s Softer Tone Masks Hard Road Ahead for Agenda in Congress; Trump’s Scant Specifics Leave Questions on His Border-Tax Plans

- Comcast Targets Asia With Harry Potter-Featured Theme Park Deal

- Ahold Delhaize Profit Beats Analyst Estimates on Cost Cuts

- AMC Cinemas Beefs Up Marketing With Dine-In, Bottomless Popcorn

- Snap’s Investors Could Pile On Then Disappear After the IPO

- Hamilton Lane Prices 11.9m-Share IPO at $16: IPO Boutique

- Time Inc. Said to Ask Suitors to Submit Offers by Next Week

- TD Ameritrade Cuts Pricing Fee to $6.95 for Online Equity Trades

- World’s Second-Largest Copper Mine to Resume Some Operations

- Iberiabank Sees Sabadell United Deal 6% Accretive to 2018 EPS

- Apollo Commercial Got Justice Department Information Request

- Orexo Commences Patent Infringement Litigation Against Actavis

- Avianca Says It Hasn’t Been Notified of Lawsuit by Kingsland

- Femsa Sees Capex of About $1.3b in 2017

- Volkswagen Closes $256 Million Acquisition of Navistar Stake

- Euro-Area Manufacturing Picks Up as Inflation Pressures Build

- Toshiba Said to Seek Bids for Chip Unit at $13 Billion Value

Asia equity markets traded higher as the region digested a deluge of data including better than expected Chinese PMIs figures. Despite this, ASX 200 (-0.1%) was dampened by the negative lead from Wall St where the DJIA snapped a 12-day win streak, while better than expected Australian GDP also failed to inspire as the strong data also reduces prospects of future RBA action. Nikkei 225 (+1.4%) was underpinned by a weaker JPY, while Shanghai Comp (+0.3%) and Hang Seng (+0.2%) gained after the latest PMI figures in which the Official Manufacturing PMI and Caixin Manufacturing PMI surpassed estimates, although upside was capped on a weak PBoC liquidity operation and after Non-Manufacturing PMI fell to a 4-month low. 10yr JGBs saw spill-over selling from T-notes which were weakened following hawkish Fed comments that suggested a March hike was firmly on the table, while the BoJ’s Rinban announcement also added to the pressure as the central bank reduced its purchases in 1yr-3yr and 3yr-5yr government debt.

Top Asian News

- China Plans to Cut 500,000 Jobs This Year in Smokestack Sectors

- China’s Factory Gauge Strengthens as Producer Prices Rebound

- China’s Policy Balancing Act Faces Bumps as Bond Pain Swells

- Hedge Fund Oasis’s Wosner Named Director of Premier Foods

- Hong Kong Stocks Eke Out Gains as Galaxy Reports Higher Earnings

- Foxconn’s Gou Says Very Serious About Bid for Toshiba Chip Unit

- Being a Woman Means 43% Less Pay Than Men on Singapore Boards

- Stock Investors Have Seven Reasons to Be Cheerful: Markets Live

- Bouncing Back From Cash Ban, India Chasing V-Shaped Recovery

European bourses were also propelled higher, with the Stoxx 600 index rising more than 1%, after a barrage of hawkish comments from FOMC members yesterday has supported EU bourses in tandem with US equity futures with notable outperformance in financial names as the futures market raised the probability of a March hike (pricing stands at 80%). While markets were somewhat unresponsive to President Trumps speech in congress who failed to provide any significant surprises. Elsewhere, despite the build in API’s overnight, WTI and Brent crude futures are at elevated levels amid increased optimism over the prospects of the US economy. In fixed income markets, the overnight weakness in treasuries saw bunds opened lower, while the gains in equities have also weighed on prices. While the German curve has seen some notable bear steepening this morning, elsewhere the GE-FR spread is a touch tighter with reports that Presidential candidate Fillon called to speak to judges over probes in fake jobs. Additionally, he will give a speech at 1100GMT.

Top European News

- Euro-Area Manufacturing Picks Up as Inflation Pressures Build

- U.K. Manufacturing Growth Weakens as Price Pressures Slip

- German Unemployment Declines as Confidence in Economy Improves

- BP Targets $40 Break-Even Oil Price to Reassure Investors

- FCA to Overhaul IPO Information Flow Over Conflict Concerns

- CRH Capacity for Buys EU2b-EU3b in Next 18 Months, CEO Says

- London Home Price Cuts Spread and Deepen as Market Stagnates

- French Candidate Fillon Called in to Speak to Judges, JDD Says

- OATs Dip After Fillon Said to Continue Presidential Race

- European Miners Rebound as China Economic Data Spur Optimism

- Fillon Wife in Custody, Search Ongoing: Mediapart

- U.K. Consumer Borrowing Remains Below Average as Confidence Ebbs

In currencies, the Bloomberg Dollar Spot Index jumped 0.4 percent as of 9:53 a.m. in London, climbing for a fourth straight day and heading for the biggest advance since Feb. 7. The yen slumped 0.7 percent to 113.52 per dollar, for a third day of losses. The euro fell 0.3 percent to $1.0545 and the British pound was little changed at $1.2383 after slipping 0.5 percent Tuesday.FX markets have followed the lead set by Fed members Williams and Dudley yesterday, setting the USD free on the upside as has been threatening given the US rate profile. Along with hesitancy over president Trump’s general conduct and communication, the market has been split between the prospect of 2 or 3 rate hikes this year, but with March now firmly on the table, the short end of the Treasury yield curve has rallied, putting the 2yr back to the highs just shy of 1.30%. Gains in the belly look a little more reluctant, and the modest 5-6bp rise in the 10yr sees USD/JPY back in the mid 113.00’s, but struggling ahead of 114.00. EUR/USD has been pulled back into mid-low 1.0500’s, but sizeable expiries in the 1.0500-50 area look to be containing for now. German regional inflation rates are all higher, but within expectation levels, while unemployment was also largely as expected.

In commodities, gold dropped for a third day, falling 0.3 percent to $1,244.66 an ounce after completing a 3.1 percent gain in February. West Texas Intermediate Crude rose 0.5 percent to $54.26. Oil ended last month 2.3 percent higher. Copper added 1.7 percent, advancing for a fourth straight session. Oil prices have edged higher despite the impact of a stronger USD, but near term price action is all base on production cuts, with strong compliance to the agreement from OPEC members edging towards 95%. Non OPEC members are lagging according to the latest figures, but sources suggest the current path will lead to WTI rising to USD60.00. In light of this, hesitant gains through USD55.00 may be taking this into account, but price stability will clearly be welcomed all round. Precious metals have softened inversely with the USD, with Gold now trading just under USD1245.00, with Silver dipping to USD18.24/5 before finding support. Base metals find support from the latest China manufacturing stats — Copper rising close to 2% on the day, but Zinc outperforming 2.5% up on the day. Zinc prices still set to rise higher on mine closures, but the latest appointment of the environment minister has/is running into some opposition.

In terms of the day ahead, while the bulk of the attention will be on Trump’s speech there is still a reasonable amount of data to get through. Much of the focus will be on the January personal spending and income reports, alongside the core and deflator PCE readings. Also due out is the ISM manufacturing print for February as well as the final manufacturing PMI revision, while construction spending and vehicle sales round out the releases. If that wasn’t enough already, the Fed’s Beige Book is also due out this evening while Kaplan (6pm GMT) and Brainard (11pm GMT) are both due to speak.

US Event Calendar

- Wards Total Vehicle Sales, est. 17.7m, prior 17.5m; Wards Domestic Vehicle Sales, est. 13.7m, prior 13.6m

- 7am: MBA Mortgage Applications, prior -2.0%

- 8:30am: Personal Income, est. 0.3%, prior 0.3%; Personal Spending, est. 0.3%, prior 0.5%

- 8:30am: Real Personal Spending, est. -0.1%, prior 0.3%; PCE Deflator MoM, est. 0.5%, prior 0.2%; PCE Deflator YoY, est. 2.0%, prior 1.6%; PCE Core MoM, est. 0.3%, prior 0.1%; PCE Core YoY, est. 1.7%, prior 1.7%

- 9:45am: Markit US Manufacturing PMI, est. 54.5, prior 54.3

- 10am: ISM Manufacturing, est. 56.2, prior 56; ISM Prices Paid, est. 68, prior 69; ISM New Orders, prior 60.4; ISM Employment, prior 56.1

- 10am: Construction Spending MoM, est. 0.6%, prior -0.2%

- 1pm: Fed’s Kaplan Speaks in Dallas

- 2pm: U.S. Federal Reserve Releases Beige Book

- 2pm: U.S. Federal Reserve Releases Beige Book

- 6pm: Fed’s Brainard Speaks at Harvard

DB’s Jim Reid concludes the overnight wrap

Welcome to a new month and in reality only one place to start this morning and that is President Trump’s prime time address to Congress that started at 9pm EST last night. Before we delve into the details a reminder that as it’s the first of the month we’ll be doing our usual performance review at the end with all the tables and charts in the PDF. It’s our second performance review in a row as yesterday we looked back on 10 years of the EMR and looked at how assets have performed over what is essentially the period since the start of the financial crisis in February 2007. So if you missed it, see yesterday’s EMR at your leisure.

So in a nutshell the long awaited Trump address had a familiar ‘America first’ theme throughout and plenty of echoes of his inaugural address. However the disappointment market wise has been the lack of detail. But there did seem to be a big effort to sound presidential. In terms of what we did get, the President returned again to the subject of rebuilding infrastructure, highlighting that he will be asking Congress to approve legislation that produces a $1tn investment financed through both public and private capital and guided by the principals of “hire American and buy American”. Trump also reconfirmed that he intends to repeal and replace Obamacare, increase defence spending, enforce immigration laws and also overhaul tax including cuts for the middle class. The tax subject was only really lightly touched. Trump said that his economic team is developing a “historic tax reform that will reduce the tax rate on our companies so that they can compete and thrive anywhere and with anyone” and also “at the same time provide massive tax relief for the middle class”. There was no specific mention whatsoever of the much anticipated border-adjusted tax. Another subject of much debate, bank regulation, was also avoided.

Markets in Asia are mostly higher following Trump’s speech. The Nikkei (+1.03%), Hang Seng (+0.17%) and Shanghai Comp (+0.38%) are all up although the ASX (-0.13%) has struggled slightly. US equity index futures are also up +0.20% although they are little changed relative to the minutes prior to Trump speaking. Rates have crept higher however that may in part be to do with the Fedspeak late last night which we’ll touch on shortly. 2y yields are up +3.6bps and 10y yields up +2.9bps. The Dollar index is +0.45%, Gold (-0.42%) is weaker and other commodities little changed. We may have to wait for the European session to really kick in though for markets to digest the speech.

It would be fairly easy to wrap up here and move on to today’s calendar given that for the most part yesterday’s session was a fairly dull one and essentially just preparing the stage for Trump. However, there was some last minute month end excitement as after the US close we got some pretty hawkish comments out of both the Fed’s Dudley and Williams. In an interview with CNN, the usually dovish NY Fed President Dudley said that the case for tightening has become “a lot more compelling in recent months” and that “risks to the outlook are now starting to tilt to the upside”. Dudley was also quoted as saying that “animal spirits have been unleashed a bit post the election” and that “there’s no question sentiment has improved quite markedly”. He also said that 3-4% GDP growth in the medium term is possible should we see further improvement in productivity. Shortly before that San Francisco Fed President Williams said that a March hike is getting “serious consideration” given that the Fed is “very close” to achieving its dual mandate goals.

After trading fairly flat for much of the session short-end Treasury yields spiked in the last 30 minutes or so (and have continued to rise this morning as highlighted above). 2y yields closed 6.6bps higher at 1.260% and 5y yields finished 6.4bps higher at 1.929%. 10y yields also ended 2.5bps higher at 2.390%. Unsurprisingly Fed Funds contracts were also on the move with the March contract now at 0.750% (+3.5bps). It’s worth noting that one of the more dovish Fed officials, Lael Brainard, is due to speak this evening, while Fed Chair Yellen then speaks on Friday. The imperfect Bloomberg calculator (which overstates the chances but offers a good history of pricing) has also seen the March hike probability jump to 80% this morning from 52% yesterday and just 40% at the end of last week. Prior to that excitement, equity markets had largely limped through much of the session. The Dow (-0.12%) finally brought to an end a streak of 12 consecutive record highs while the S&P 500 (-0.26%) also finished in the red not helped by Senate Finance Chairman Orrin Hatch telling CNBC that he has real reservations about the border adjustment tax. In Europe the Stoxx 600 (+0.19%) recovered from a slow start. Commodities were generally a non-event for much of the session.

The rest of yesterday’s session was largely focused on the data. In the US the main release was the second estimate of Q4 GDP which came in at an unrevised +1.9% qoq annualized. The consensus had been for an upward revision to +2.1%. In the details growth in final sales was unrevised at +0.9% while personal consumption was revised up five-tenths to +3.0%. This was offset by a 1.1pt downward revision for business investment to +1.3% while the core PCE was also revised down one-tenth to +1.2%. Away from that there was some good news in the latest consumer confidence reading for February which was revealed as rising 3.2pts to 114.8 (vs. 111.0 expected) and the highest since July 2001. The Chicago PMI also surprised to the upside with the index up 7.1pts to 57.4 (vs. 53.5 expected) in February and the highest since January 2015. The Richmond Fed manufacturing index reading also rose 5pts to +17. Finally the advance goods trade balance reading in January revealed a wider than expected deficit ($69.2bn vs. $66.0bn expected). Over in Europe the only notable data came from France where headline CPI was revealed as rising a fairly benign +0.1% mom in February (vs. +0.4% expected). Q4 GDP did however come in as expected at +0.4% qoq.

Quickly coming back to Asia, this morning we also had some data out of China which very much played second fiddle to Trump. The official manufacturing PMI was confirmed as rising 0.3pts to 51.6 in February (vs. 51.2 expected) while the non-manufacturing PMI declined 0.4pts to 54.2. The Caixin manufacturing PMI also came in at 51.7 and up 0.7pts from January.

In terms of the day ahead, while the bulk of the attention will be on Trump’s speech there is still a reasonable amount of data to get through. The European session will also see a continuation of the February PMI releases with the final manufacturing prints to be confirmed alongside a first look at the data for the periphery and UK. We’ll also get the February CPI report in Germany as well money and credit aggregates data in the UK. It’s set to be another busy afternoon for data releases in the US again too. Much of the focus will be on the January personal spending and income reports, alongside the core and deflator PCE readings. Also due out is the ISM manufacturing print for February as well as the final manufacturing PMI revision, while construction spending and vehicle sales round out the releases. If that wasn’t enough already, the Fed’s Beige Book is also due out this evening while Kaplan (6pm GMT) and Brainard (11pm GMT) are both due to speak.

3. ASIAN AFFAIRS

i)Late TUESDAY night/WEDNESDAY morning: Shanghai closed UP 5.20 POINTS OR .16%/ /Hang Sang CLOSED UP 35.76 POINTS OR 0.15% . The Nikkei closed UP 274.55 POINTS OR 1.44% /Australia’s all ordinaires CLOSED DOWN 0.18%/Chinese yuan (ONSHORE) closed DOWN at 6.8805/Oil ROSE to 54.12 dollars per barrel for WTI and 56.70 for Brent. Stocks in Europe ALL IN THE GREEN ..Offshore yuan trades 6.8724 yuan to the dollar vs 6.8805 for onshore yuan.THE SPREAD BETWEEN ONSHORE AND OFFSHORE NARROWS CONSIDERABLY AS POBC ATTEMPTS TO STOP USA DOLLARS FROM LEAVING CHINA’S SHORES. ONSHORE YUAN WEAKER AS IS OFFSHORE YUAN COUPLED WITH THE STRONGER DOLLAR

3a)THAILAND/SOUTH KOREA/NORTH KOREA

b) REPORT ON JAPAN

none today

c) REPORT ON CHINA

China backs Russia as it vetoes western backed UN sanctions against Syria:

(courtesy zerohedge)

China Backs Russia To Veto Western-Backed UN Sanctions On Syria

The Trump administration’s early attempts to change, and restore, ties with Russia may be fading fast, but at least when it comes to relations between Russia and its western counterparts at the United Nations, absolutely nothing has changed. And, as has been the case for the past three years, the antagonism was on full front display when Russia, now without the recently deceased Vitaly Churkin, on Tuesday cast its seventh veto to protect the Syrian government from United Nations Security Council action, blocking an attempt by Western powers to impose yet another sanction over accusations of the recurring strawman, i.e., chemical weapons attacks, during the six-year Syrian conflict.

While the Russia vote was to be expected, what was surprising is that China once again backed Russia with its sixth veto on Syria according to Reuters, making it clear that at least when it comes to the UN and matters involving Syria, China is firmly in the Russia camp, and thus opposing the west.

Russian Deputy Ambassador to the United Nations Vladimir Safronkov

Russia had said the vote on the resolution, drafted by France, Britain and the United States, would harm U.N.-led peace talks between the warring Syrian parties in Geneva, which began last week. Nine council members voted in favor, Bolivia voted against, while Egypt, Ethiopia and Kazakhstan abstained. A resolution needs nine votes in favor and no vetoes by the United States, France, Russia, Britain or China to be adopted.

Russian President Vladimir Putin described the draft resolution on Tuesday as totally inappropriate. “As for sanctions against the Syrian leadership, I think the move is totally inappropriate now,” Putin said at a news conference. “It does not help, would not help the negotiation process. It would only hurt or undermine confidence during the process.”

Doing her best Samantha Power impression, the new US ambassador to the UN Nikki Haley told the council after the vote that ““For my friends in Russia, this resolution is very appropriate,” said US Ambassador to the United Nations Nikki Haley after the vote. “It is a sad day on the Security Council when members start making excuses for other member states killing their own people. The world is definitely a more dangerous place.”

The vote was one of the first confrontations at the United Nations between Russia and the United States since U.S. President Donald Trump took office in January, pledging to build closer ties with Moscow.

Russia’s Deputy U.N. Ambassador Vladimir Safronkov described the statements made against Moscow in the Security Council as “outrageous” and declared that “God will judge you.”

“Today’s clash or confrontation is not a result of our negative vote. It is a result of the fact that you decided on provocation while you knew well ahead of time our position,” said Safronkov. “The problem is that the basis of expert work on Syria come from dubious information submitted by the armed opposition, international NGOs sympathetic to it, the media and so-called ‘Friends of Syria’,” he argued.

“The co-sponsors [of the proposal] have chosen and odious and erroneous concept, which is totally unacceptable. The fact that the resolution wasn’t supported by six of the fifteen security council members should make the co-sponsors seriously think,” Safronkov said.

On the other hand, western powers put forward the resolution in response to the results of an investigation by the U.N. and the Organization for the Prohibition of Chemical Weapons (OPCW). The international inquiry “found” that as reported a month ago, Syrian government forces were responsible for three chlorine gas attacks and that Islamic State militants had used mustard gas. British U.N. Ambassador Matthew Rycroft told the council before the vote: “This is about taking a stand when children are poisoned. It’s that simple. It’s about taking a stand when civilians are maimed and murdered with toxic weapons.”

This reminds us of the first such fabricated attempt to start a war in Syria in the summer of 2013 when a produced YouTube clip was used as evidence of a chemical attack, only to be refuted several month later, although by then Russia and the US were already engaged in the Syrian proxy war.

To be sure, Syrian President Bashar al-Assad’s government has denied its forces have used chemical weapons. Russia has questioned the results of the U.N./OPCW inquiry and long said there was not enough proof for the Security Council to take any action.

French U.N. Ambassador Francois Delattre said the failure by the council to act would “send a message of impunity.”

Meanwhile China’s U.N. Ambassador Liu Jieyi said it was too early to act because the international investigation was still ongoing. “We oppose the use of chemical weapons,” he said.

* * *

And while the sanctions were being debated, a new round of UN-sponsored Syria peace talks between the warring sides kicked off in Geneva last week. Saying that he is not expecting a breakthrough, UN envoy Staffan de Mistura said he was nonetheless determined not to lose the momentum towards a resolution. Although the liberation of the city of Aleppo and the loss of key territories by Islamist rebels have tipped the balance in the Syrian conflict, potential disagreements could arise over the opposition’s continued insistence that the fate of the Syrian government of President Bashar Assad be settled as a precondition – something that is not currently on the table.

Russia announced that it has asked the Syrian government to halt all military operations for the duration of the talks, while other countries were expected to deliver the same message to the rebels. The last round of the Geneva talks was broken off nine months ago amid a sharp escalation in hostilities.

Bashar al-Jaafari, the Syrian government’s negotiator at the Geneva talks, warned on Saturday that Damascus will view opposition groups that refuse to condemn the deadly suicides attacks in Homs as accomplices of terrorists. In another comment on the attack, Jaafari said that “the terrorist explosions that hit Homs city are a message to Geneva from sponsors of terrorism, and we tell everyone that the message is received and this crime won’t pass unnoticed.”

end

4. EUROPEAN AFFAIRS

My goodness: Fillon is charged and yet he will stay in the French Presidential race

(courtesy zero hedge)

Defiant Fillon Reveals He Is Facing Criminal Charges, Will Stay In French Presidential Race

In yet another impromptu press conference delivered moments ago, French presidential contender Francois Fillon addressed the nation, and contrary to expectations the embattled candidate, fighting an escalating corruption probe, would announce he would drop out of the race, Fillon vowed to fight on, even as he revealed that judges planned to charge him with misuse of public funds.

Fillon confirmed that he was summoned to court on March 15 after earlier on Wednesday being questioned by magistrates investigating a ‘fake work’ scandal involving his wife. The summons prompted Fillon to cancell a campaign appearance at Paris’s farm show, triggering speculation he was preparing to pull out of the race. But at a press conference later in the morning, Fillon angrily denounced the investigation into the jobs affair, saying the probe was a challenge to the democratic process.

Fillon blasted the ongoing judicial inquiry as an attempt of “political assassination” directed at him. Having pleaded not guilty in the case of employment of his family members, Fillon will now have to prove it in court.

“I won’t give in, I won’t surrender, I won’t withdraw, I’ll fight to the end,” Fillon said ending his speech

Earlier, French media reported that Fillon’s presidential campaign director Patrick Stefanini had offered his resignation. There has been no confirmation yet.

Fillon, who was initially one of the pollsters’ favorites, saw his ratings drop after the scandal broke out in late January around his wife allegedly having been paid for jobs without exercising her duties. French media also questioned Fillon’s children’s employment as his parliamentary assistants between 2005 and 2007.

The French financial prosecutor’s office launched an official investigation on February, 24 into an allegedly fake employment of Fillon’s wife. The investigation is devoted to assignment of state funds, complicity, concealment of offenses and trading in influence.

French presidential elections are due to take place in two rounds on April 23 and May 7.

So far, French assets have reacted mutedly, with the French-German 2Y spread pushing modestly wider.

END

The ECB now has a problem: German inflation jumps higher than the targeted 2.0% at 2.2%. This will heighten concerns that the ECB must stop it’s QE

(courtesy zerohedge)

German Inflation Jumps 2.2%, Surpassing ECB Target And Highest Since 2012

Following a series of “hot” inflation prints from Germany’s states, moments ago German inflation rose more than expected, printing at 2.2% above the 2.1% consensus estimate, up from 1.9% in January and surpassing the ECB’s target of a rate just under 2 percent for the first time since August 2012, the peak of the Eurozone debt crisis.

With Germany headed for federal elections in September, the inflation figures will add more fuel to the debate about an end to the European Central Bank’s loose monetary policy.

Earlier on Wednesday, preliminary data from several German states showed that consumer price inflation accelerated across the country, mainly driven by higher food, energy and transportation costs. In the most populous state, North Rhine-Westphalia, annual inflation rose to 2.3 percent from 1.9 percent in January. It reached 2.5 percent in Hesse, 2.2 percent in Baden-Wuerttemberg, 2.1 percent in Bavaria, 2.0 percent in Brandenburg and 2.4 percent in Saxony.

The state readings, which are not harmonised to compare with other euro zone countries, fed into the just as hot nationwide inflation print released moments ago.

Yet not everyone was convinced Germany’s blistering headline inflation would be a hindrance to the ECB. Cited by Reuters, Capital Economics analyst Jennifer McKeown said the state readings supported the forecast, but German core inflation, which strips out volatile energy and food costs, was likely to remain weak in the coming months. “This should encourage the ECB to implement its asset purchases as planned,” McKeown said.

That said, a sustained rebound in German inflation would give Bundesbank President and ECB rate setter Jens Weidmann more grounds to argue for a reduction in the ECB’s bond-buying programme, a scheme that he has often criticised. The German central bank has warned that homes in large German cities are 15 to 30% overpriced, in a message that stoked further fears about the side-effects of the ECB’s stimulus.

The inflation rate for the entire euro zone is expected to rise to 2.0 percent in February from 1.8 percent in January, economists polled by Reuters said. Those figures are due on Thursday.

end

This is fascinating: the Euro Contagion Risk index authored by Sentix is exploding:

(courtesy Sentix/zero hedge)

Euro Breakup Contagion Risk Is Exploding

With existential elections looming, Sentix Euro Break-up Contagion Index – a market measure of the contagion risk from one or more countries leaving the euro area within the next 12 months period – has hit its post-2012 record recently…

As Sentix notes, the Eurocrisis is once again in the limelight. And this time the

drama consists of three main actors: Greece, Italy and France.

How dangerous this tendency for the cohesion of the eurozone could become is

a look at the index to the spreading risk, which has almost climbed to

the 50% mark – an all-time high!

France and Italy both seeing Euro-exit odds rising…

The Eurozone has now developed many more breaking points than just Greece. Although it has now been somewhat calmer about Italy, the euro exit probability remains almost unchanged at 13.9%. Added to this is the strong rise in the probability of exit from France. This is now 8.4% – compared to 5.7% in January! An all-time high.

end

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

This is interesting: UAE a close ally of the USA signs a breakthrough military deal with Russia!!!..

(courtesy Korzun/StrategicCulture Foundation)

Russia, UAE Sign Breakthrough Military Deal

Via Peter Korzun of The Strategic Culture Foundation,

The United Arab Emirates (UAE) has signed an outline agreement to buy Russian aircraft. It also plans to implement a joint project with Russia to develop a next-generation fighter that could enter service in seven or eight years.

According to Russian Industry and Trade Minister Denis Manturov, who led the Russian delegation at the IDEX 2017 exhibition, the UAE is to purchase a batch of advanced Sukhoi Su-35 Flanker-E fighters.

«We signed an agreement of intent for the purchase of the Su-35», Sergei Chemezov, CEO of Rostec Corporation, told Russian news agency TASS. He did not provide details about the deal. A total of 24 Su-35 fighters were sold to China under the first export contract.

The significance of signing ceremony was illustrated by the fact that it was attended by Sheikh Mohamed bin Zayed Al Nahyan, Crown Prince of Abu Dhabi and Deputy Supreme Commander of the UAE Armed Forces. As reported, the agreement «provides for procurement, development and partial manufacturing of advanced air, land and naval equipment to serve the requirements of the UAE armed forces».

According to The National Interest, «More troubling for the United States, the deal is an indication that the UAE—a long-time U.S. ally—is drifting into Moscow’s orbit».

According to Mr. Chemezov, work on the fifth generation joint light fighter is to start as early as 2018. The aircraft is expected to be a variation of the MiG-29 fighter jet. The future warplane proposed by Russia would be built in the UAE »full cycle» following completion of design work and the production of test aircraft. The memorandum of understanding between Russia and the UAE to jointly develop the fighter aircraft follows a similar fighter jet collaboration deal agreed between Russia and India last year.

The Su-35 is a multifunctional 4++ generation fighter, employing fifth-generation combat avionics. The one seater two-engine high-wing aircraft features a retractable tricycle-type landing gear and nose gear strut. Equipped with AL-41F1S turbojet engines with an afterburner and a controlled thrust vector, it is capable of «pivot turning» and deceiving enemy missiles.

The plane boasts a maximum speed of 2,400 km/h. Its maximum flying range is 3,600 km without external fuel tanks and 4,500 km with external fuel tanks. The service ceiling is 20,000 meters. The specifications allow it to easily outrun every Western fighter.

The aircraft has 12 external bays for precision missiles and air bombs and two bays for electronic warfare containers.

The armament includes 30mm guns, a huge number of missiles and rockets. The combat load is 8 tons. It has 12 hardpoints for carrying external weapons and stores. The aircraft would be launching its weapons from high supersonic speeds around Mach 1.5 at altitudes greater than 45,000 feet. This means the missiles could reach with their targets faster, giving opponents less time to maneuver or respond in kind.

Military experts are especially impressed with the Su-35’s sophisticated phased-array radar control system Irbis-E, which allows the plane to detect targets at distances of up to 400 kilometers. It can simultaneously track up to four ground targets or up to 30 airborne targets, as well as engage up to eight airborne targets at the same time. The radar has a friend-or-foe identification capability for aerial and maritime objects. It is capable of identifying the class and type of airborne targets and can take aerial photos of the ground. An oscillator with peak power output of 20 kW used in the passive phased array radar makes Irbis-E the most powerful radar control system on par with the best international designs, and ahead of most US and European active and passive phased array radars.

The aircraft is also equipped with «Khibiny-M» – a state-of-the-art electronic warfare equipment, which includes a radar warning system, radar jammer, co-operative radar jamming system, missile approach warner, laser warner and chaff and flare dispenser. A relatively small container in the shape of a torpedo is mounted on the wingtips of the aircraft to make the jets invulnerable to all modern means of defense and enemy fighters.

The pilot has two VHF/UHF encrypted radio communications systems and a jam-resistant military data link system between squadron aircraft and between the aircraft and ground control. The navigation system is based on a digital map display with a strapdown inertial navigation system and global positioning system.

High-strength, low-weight, composite materials have been used for non-structural items such as the radomes, nose wheel, door and leading-edge flaps. Some of the fuselage structures are of carbon fibre and aluminium lithium alloy.

The aircraft was deployed to Syria a year ago.

German magazine Stern stated that the Su-35 can be considered the world’s deadliest fighter jet other than the fifth-generation US F-22.

The UAE has already purchased Russian ground weapons, such as BMP-3 infantry combat vehicles and Pantsir S1 air-defense systems. The acquisition of the military aircraft is another big step on the way of developing military cooperation with Russia.

The Emirates is not the only Russian customer in the Persian Gulf. Russian Defense Minister Sergey Shoigu and Qatar’s State Minister for Defense Khalid bin Mohammad Al Attiyah signed a military cooperation agreement in September on the sidelines of the Army-2016 international military-technical forum in Kubinka near Moscow.

Kuwait and the UAE have purchased Russian infantry fighting vehicles.

Saudi Arabia has expressed interest in Russian “Iskander-E” short-range ballistic missiles, S-400 long-range air defense systems, missile patrol boats and medium landing ships. Saudi Arabia paid for Russian arms supplies to Egypt.