Gold: $1248.20 UP $1.30

Silver: $17.72 UP 16 cents

Closing access prices:

Gold $1245.60

silver: $17.80!!!

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

SHANGHAI GOLD FIX: FIRST FIX 10 15 PM EST (2:15 SHANGHAI LOCAL TIME)

SECOND FIX: 2:15 AM EST (6:15 SHANGHAI LOCAL TIME)

SHANGHAI FIRST GOLD FIX: 1253.52 DOLLARS PER OZ

NY PRICE OF GOLD AT EXACT SAME TIME: 1244.05

PREMIUM FIRST FIX: $9.47

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

SECOND SHANGHAI GOLD FIX: 1255.30

NY GOLD PRICE AT THE EXACT SAME TIME: 1242.85

Premium of Shanghai 2nd fix/NY:$12.45

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

LONDON FIRST GOLD FIX: 5:30 am est 1244.00

NY PRICING AT THE EXACT SAME TIME: 1243.65

LONDON SECOND GOLD FIX 10 AM: 1247.50

NY PRICING AT THE EXACT SAME TIME. 1246.80

For comex gold:

MARCH/

NOTICES FILINGS TODAY FOR MARCH CONTRACT MONTH: 10 NOTICE(S) FOR 1000 OZ. TOTAL NOTICES SO FAR: 82 FOR 8200 OZ (0.2550 TONNES)

For silver:

For silver: MARCH

137 NOTICES FILED TODAY FOR 685,000 OZ/

Total number of notices filed so far this month: 3646 for 18,230,000 oz

Today the markets reacted in horror with the failure of the House to pass the Trump Health bill (the Ryan bill). The Republicans are very divided and it is going to be impossible to pass anything exactly what David Stockman predicted.

We have now entered options expiry week so expect gold and silver to be subdued from today forward.

The comex options expiry is Tuesday March 28.

The OTC/LBMA options expiry is the morning of March 31.

Let us have a look at the data for today

.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total open interest ROSE BY 463 contracts UP to 191,977 with the TINY RISE IN PRICE ( 2 CENTS) WITH RESPECT TO YESTERDAY’S TRADING. In ounces, the OI is still represented by just less THAN 1 BILLION oz i.e. 0.960 BILLION TO BE EXACT or 137% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT MARCH MONTH: THEY FILED: 137 NOTICE(S) FOR 685,000 OZ OF SILVER

In gold, the total comex gold also ROSE BY STRONG 6232 contracts DESPITE THE FALL IN THE PRICE OF GOLD ($2.90 with YESTERDAY’S TRADING). The total gold OI stands at 459,089 contracts.

we had 10 notice(s) filed upon for 1000 oz of gold.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD:

We had another big change in tonnes of gold at the GLD: a withdrawal of 1.78 tonnes from the GLD. This gold is no doubt headed for Shanghai

Inventory rests tonight: 832.62 tonnes

.

SLV

We had no changes in inventory at the SLV/

THE SLV Inventory rests at: 332.504 million oz

end

.

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in silver ROSE BY 463 contracts UP TO to 191,977 AS SILVER WAS UP 2 CENT(S) with YESTERDAY’S trading. The gold open interest ROSE BY 6232 contracts UP to 459,089 DESPITE THE FALL IN THE PRICE OF GOLD OF $2.90 (YESTERDAY’S TRADING).

(report Harvey

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

2c) COT report

(Harvey)

3. ASIAN AFFAIRS

i)Late THURSDAY night/FRIDAY morning: Shanghai closed UP 20.85 POINTS OR .64%/ /Hang Sang CLOSED UP 30.57 POINTS OR 0.13% . The Nikkei closed UP 177.22 OR 0.93% /Australia’s all ordinaires CLOSED UP 0.73%/Chinese yuan (ONSHORE) closed UP at 6.8862/Oil ROSE to 47.93 dollars per barrel for WTI and 50.83 for Brent. Stocks in Europe ALL IN THE RED ..Offshore yuan trades 6.8741 yuan to the dollar vs 6.8862 for onshore yuan.THE SPREAD BETWEEN ONSHORE AND OFFSHORE NARROWS CONSIDERABLY AGAIN/ ONSHORE YUAN SLIGHTLY STRONGER BUT THE OFFSHORE YUAN IS SLIGHTLY WEAKER AND THIS IS COUPLED WITH THE SLIGHTLY WEAKER DOLLAR. CHINA SENDS HER DISPLEASURE SIGNAL TO WASHINGTON

3a)THAILAND/SOUTH KOREA/NORTH KOREA

b) REPORT ON JAPAN

none today

c) REPORT ON CHINA

Wow!! that happened fast! Huishan Dairy’s stock collapsed over 90 in minutes wiping out 4.2 billion in market value

( zerohedge)

4. EUROPEAN AFFAIRS

i)Switzerland

The Central Bank of Switzerland spent a mammoth 68 billion dollars worth of Euros in an attempt to keep the Swiss Franc from rising against the Euro.

( zero hedge)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

i)Russia/Norway

Norway is contemplating putting defense shields on its territory facing Russia. Russia warns Norway not to do it

( Gorka/StrategicCultureFoundation)

ii)RUSSIA

This is a surprise; Russia cuts interest rates by 25 basis points. What is more surprising is that the Rouble rose despite the fall in rates:

( zero hedge)

6.GLOBAL ISSUES

SWEDEN

Welcome to the new world. Sweden builds a police fortresss in Rinkeby, a suburb of Stockholm where many of the migrant (many Somalians) now live

( zero hedge)

7. OIL ISSUES

i)Trump approves the Trans Canada Keystone Pipeline project officially:

( zero hedge)

ii)USA rig counts up 10 weeks in a row and it is double the May 2016 lows. USA cured production is now at 13 month highs

( zero hedge)

8. EMERGING MARKETS

Venezuela is now in dire straits as it cannot pay for gasoline or other refined products. It will probably default later this year.

(courtesy Nick Cunningham/OilPrice.com)

9. PHYSICAL MARKETS

i)An extremely important paper from Ted Butler. You will note that I have been providing the managed money account for you on COT days. Basically Ted is stating that the non technical hedge funds have been accumulating silver and these guys do not budge on raid days. The long positions on these guys have been rising to around 80,000 contracts and this is coupled with small specs or non hedge funds who have accumulated another 30,000 contracts. Ted states that the 7 banks that hold 98,000 short positions are “dead men walking

( Ted Butler)

ii)A good look at mining in South Africa. At one time, South Africa produced over 1000 tonnes of gold, and that was about 90% of world production at that time

( Bloomberg/GATA)

iii)India last month received 37.2 tonnes from Switzerland in February which is terrific as India is now back into gold. If we extrapolate 37.2 tonnes x 12, India’s demand from Switzerland will exceed 446.4 tonnes. Switzerland is not the only source for India.

( Lawrie Williams/Sharp Pixley)

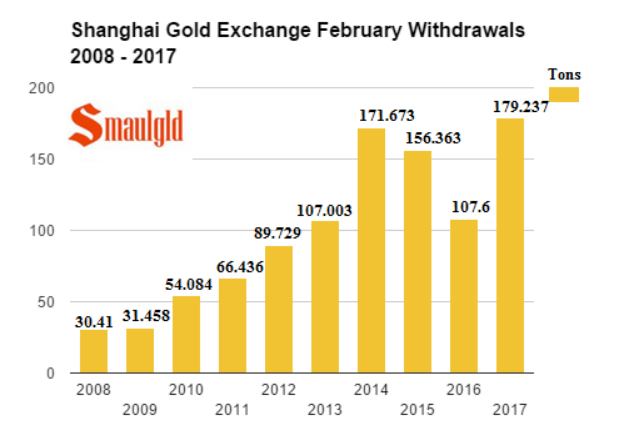

iv)We have already reported to you the huge withdrawals of gold from the Shanghai Gold Exchange and that generally equals demand. The total reported to you two weeks ago for February was 179 tonnes.

(Katchum/seeking Alpha)

10.USA STORIES

i)The CBO has now weighed in on the new Ryan proposals and they decided it was simply awful: it kept all the negatives and almost none of the positives. The new bill will not cover anybody new and while the original bill saved 337 billion over a 10 yr period, the new plan only saves 150 billion.

the conservatives will not like this at all..

( zero hedge)

ii)Trump issues an ultimatum: vote on Friday in the affirmative or Obamacare stays. The Freedom causes may capitulate:

( zerohedge)

iib) updates on the vote: Ryan claims that they do not have enough votes

(zero hedge)

ii c) Ryan pulls the Health Care bill

ii d) And now the last word on today’s debacle courtesy of David Stockman of Daily Reckoning/ContraCorner

iii)This will be explosive: the NSA is provide “smoking gun” proof that Obama spied on Trump during the 2016 election

( zero hedge)

iv)Nunes calls in Comey and Rogers for a closed session after he states that the intel is very concerning to him:

( zerohedge)

iv) OH OH!! something is up!!

FBI director Comey unexpectedly is called to the White House

( zero hedge)

v)Trump wins as a Virginia Judge correctly refuses to block the revised travel ban

( zero hedge)

vi)Hard data core durable goods shows that growth is very slow and the capital goods also declined:

( zero hedge)

vii)Even soft data USA services PMI, Manufacturing PMI’s both plunge to 6 month lows:

( zero hedge)

viii)the Fed continually claims that inflation is tiny. In reality it is rearing its ugly head.

Inflation is embedded in financial assets

(courtesy zero hedge)

ix)Here is why today’s debacle will make tax reform less likely exactly what David Stockman predicted:

( zerohedge)

x) Today’s wrap up courtesy of Greg Hunter of USAWatchdog

Let us head over to the comex:

The total gold comex open interest ROSE BY 6232 CONTRACTS UP to an OI level of 459,089 DESPITE THE FALL IN THE PRICE OF GOLD ( $2.90 with YESTERDAY’S trading).THE BANKERS SUPPLIED ALL THE NECESSARY CONTRACTS SHORT TO OUR NEWBIE LONGS. We are now in the contract month of MARCH and it is one of the poorer delivery months of the year. In this MARCH delivery month we had a GAIN of 6 contract(s) RISING TO 27. We had 0 contact(s) served UPON YESTERDAY, so we GAINED 6 CONTRACT(S) or AN ADDITIONAL 600 ounces will stand for delivery. The next active contract month is April and here we saw it’s OI LOST 3761 contracts DOWN TO 159,356 contracts.

For comparison purposes, the April 2016 contract at this time had an OI of 152,305 contracts. At the end of April/2016 only 12.3917 tonnes stood for physical delivery, although 21.306 tonnes stood initially at the beginning of April 2016.

The non active May contract month GAINED 92 contract(s) and thus its OI is 1312 contracts. The next big active month is June and here the OI ROSE by 9409 contracts up to 199,172.

We had 10 notice(s) filed upon today for 1009 oz

We are in the active delivery month is March and here the OI decreased by 88 contracts down to 335 contracts. We had 88 notices served upon yesterday so we LOST 0 CONTRACT(S) OR AN ADDITIONAL 0 OZ WILL STAND in this active delivery month of March.

For historical reference: on the first day notice for the March/2016 silver contract: 19,020,000 oz stood for delivery . However the final amount standing at the end of March 2016: 6,755,000 oz as the banker boys were busy convincing holders of many silver contracts to cash settle just like they did today.

The April/2017 contract month GAINED 5 contract(s) to 944 contracts. The next active contract month is May and here the open interest GAINED 174 contracts UP to 143,925 contracts.

FOR COMPARISON

Initially for the April 2016 contract, 1,180,000 oz stood for delivery. At the end of April 2016: 6,775,000 oz as bankers needed much silver to fill major holes elsewhere.

We had 137 notice(s) filed for 685,000 oz for the MARCH 2017 contract.

VOLUMES: for the gold comex

Today the estimated volume was 220, 225 contracts which is good.

Yesterday’s confirmed volume was 289,385 contracts which is very good.

volumes on gold are getting higher!

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz |

nil oz

|

| Deposits to the Dealer Inventory in oz | 999.98 oz

brinks |

| Deposits to the Customer Inventory, in oz |

nil oz

|

| No of oz served (contracts) today |

10 notice(s)

1000 oz

|

| No of oz to be served (notices) |

17 contracts

1700 oz

|

| Total monthly oz gold served (contracts) so far this month |

82 notices

8200 oz

0.2550 tonnes

|

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | 122,007.4 oz |

Today, 0 notice(s) were issued from JPMorgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equates to 10 contract(s) of which 0 notices were stopped (received) by jPMorgan dealer and 0 notice(s) was (were) stopped/ Received) by jPMorgan customer account.

March 2016: 2.311 tonnes (March is a non delivery month)

| Silver | Ounces |

| Withdrawals from Dealers Inventory | nil |

| Withdrawals from Customer Inventory |

121,780.369 oz

Brinks

Scotia

Delaware

|

| Deposits to the Dealer Inventory |

nil oz

|

| Deposits to the Customer Inventory |

nil oz

|

| No of oz served today (contracts) |

137 CONTRACT(S)

(685,000 OZ)

|

| No of oz to be served (notices) |

198 contracts

(990,000 oz)

|

| Total monthly oz silver served (contracts) | 3646 contracts (18,230,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month | 4,616,773.7 oz |

end

At 3:30 pm est we receive the COT report which gives us position levels of our major players.

Let us head over to the gold COT and see what gives!

| Gold COT Report – Futures | ||||||

| Large Speculators | Commercial | Total | ||||

| Long | Short | Spreading | Long | Short | Long | Short |

| 219,719 | 103,467 | 82,582 | 101,282 | 230,279 | 403,583 | 416,328 |

| Change from Prior Reporting Period | ||||||

| 9,404 | -810 | 13,494 | -1,253 | 4,457 | 21,645 | 17,141 |

| Traders | ||||||

| 161 | 95 | 90 | 46 | 50 | 245 | 202 |

| Small Speculators | ||||||

| Long | Short | Open Interest | ||||

| 43,297 | 30,552 | 446,880 | ||||

| -935 | 3,569 | 20,710 | ||||

| non reportable positions | Change from the previous reporting period | |||||

| COT Gold Report – Positions as of | Tuesday, March 21, 2017 | |||||

Interesting report!

Our Large Specs:

those large specs that have been long in gold added a huge 9404 contracts

those large specs that have been short in gold covered a tiny 810 contracts

Our commercials:

those commercials that have been long in gold pitched a tiny 1953 contracts

those commercials that have been short in gold added a small 4457 contracts (for them)

Our small specs:

those small specs that have been long in gold pitched 935 contracts from their long side

those small specs that have been short in gold added 3569 contracts to their short side.

Managed money ( a subset of large/small specs) generally referred to as hedge funds:

In gold; the hedge funds increased their managed money accts by 9080 contracts on the long side

and decreased by 741 contracts from their short side.

Conclusions:

commercials go net short by 5710 contracts which is bearish. The managed money (hedge funds) go net long by over 9100 contracts. They seem to remain resolute to what the commercials throw at them.

SILVER

| Silver COT Report: Futures | |||||

| Large Speculators | Commercial | ||||

| Long | Short | Spreading | Long | Short | |

| 100,337 | 21,225 | 17,362 | 48,468 | 142,202 | |

| -2,338 | 1,428 | 4,444 | 1,721 | -2,544 | |

| Traders | |||||

| 98 | 41 | 46 | 28 | 36 | |

| Small Speculators | Open Interest | Total | |||

| Long | Short | 190,819 | Long | Short | |

| 24,652 | 10,030 | 166,167 | 180,789 | ||

| 56 | 555 | 3,883 | 3,827 | 3,328 | |

| non reportable positions | Positions as of: | 146 | 109 | ||

| Tuesday, March 21, 2017 | |||||

And now the important COT report on silver and incorporating data form this morning’s Ted Butler commentary:

Our large specs:

Those large specs who have been long in silver pitched 2338 contracts from their long side.

those large specs that have been short in silver added 1428 contracts to their short side.

??

Our commercials:

those commercials that have been long in silver added 1721 contracts to their long side !!!!!

those commercials that have been short in silver pitched a huge 2544 contracts from their short side

wow!! commercials are capitulating!

Our small specs:

those small specs that have been long in silver added only 56 contracts to their long side

those small specs that have been short in silver added a tiny 555 contracts to their short side.

Managed money (hedge funds)

In Ted Butler’s paper released this morning (above) the managed money account which is a subset of the large/small specs had an open interest of 80,582 contracts at last weeks report

This week we saw a loss of only 1668 contracts from their long side and an increase of 1063 contracts from their short side for a net short position gain of 2731 contracts.

This subset is remaining very resolute and refusing to budge on commercial raids.

Conclusions:

commercials go net long 4265 contracts!!! and they also seem to be capitulating!

end

And now the Gold inventory at the GLD

March 24/another withdrawal of 1.78 tonnes from the GLD/Inventory rests at 832.62 tonnes

March 23/no change in gold inventory at the GLD/Inventory rests at 834.40 tonnes

March 22/no changes in gold inventory at the GLD/Inventory rests at 834.40 tonnes

March 21/a deposit of 4.15 tonnes of gold into the GLD/Inventory rests at 834.40 tonnes

March 20/WE HAD A MASSIVE 6.81 TONNE WITHDRAWAL FROM THE GLD/INVENTORY RESTS AT 830.25 TONNES/THIS GOLD MUST BE ON ITS WAY TO SHANGHAI. WITH GOLD RISING THESE PAST FEW DAYS, IT MAYS NO SENSE WHATSOEVER ON GOLD LIQUIDATION.

March 17/a huge withdrawal of 2.37 tonnes from the GLD/Inventory rests at 837.06 tonnes

March 16/no changes in gold inventory at the GLD/Inventory rests at 839.43 tonnes

March 15/ANOTHER HUGE DEPOSIT OF 4.44 TONNES/inventory rests at 839.43 tonnes

March 14/strange they whack gold and yet the GLD adds 2.93 tonnes of gold./inventory rests at 834.99 tonnes

March 13/a deposit of 6.78 tonnes of gold into the GLD/Inventory rests at 832.03 tonnes

March 10/ a withdrawal of 4.886 tonnes from the GLD/Inventory rests at 830.25

this tonnage no doubt is off to Shanghai

March 9/a withdrawal of 2.67 tonnes from the GLD/Inventory rests at 834.10

March 8/no change in gold inventory at the GLD/inventory rests at 836.77 tones

march 7/a huge withdrawal of 3.81 tonnes from the GLD inventory/inventory rests at 836.77 tonnes

March 6/No change in gold inventory at the GLD/Inventory rests at 840.58 tonnes

March 3/ a huge withdrawal of 2.96 tonnes of gold from the GLD/Inventory rests at 840.58 tonnes

March 2/a deposit of 2.37 tonnes of gold into the GLD/Inventory rests tat 843.54 tonnes

March 1/no change in gold inventory at the GLD/Inventory rests at 841.17 tonnes

FEB 28/no changes in gold inventory at the GLD/Inventory rests at 841.17 tonnes

feb 27/no change in gold inventory at the GLD/Inventory rests at 841.17 tonnes

Feb 24/no changes in gold inventory at the GLD/Inventory rests at 841.17 tonnes

FEB 23/no changes in gold inventory at the GLD/Inventory rests at 841.17 tonnes

FEB 22/no changes in gold inventory at the GLD/Inventory rests at 841.17 tonnes

FEB 21/no changes in gold inventory at the GLD/Inventory rests at 841.17 tonnes

feb 17/a withdrawal of 2.37 tonnes of gold from the GLD/Inventory rests at 841.17 tonnes

FEB 16/we had no changes in the GLD inventory today/Inventory rests at 843.54 tonnes

Feb 15./another deposit of 2.67 tonnes of gold into the GLD inventory despite another attempted whacking of gold/inventory rests at 843.54 tonnes

FEB 14/another deposit of 4.14 tonnes of gold into the GLD inventory/rests at 840.87 tonnes

FEB 13/another deposit of 4.15 tonnes of gold into the GLD/Inventory rests at 836.73 tonnes

Feb 10/no changes at the GLD/Inventory rests at 832.58 tonnes

feb 9/no changes at the GLD/Inventory rests at 832.58 tonnes

end

NPV for Sprott and Central Fund of Canada

will update later tonight the central fund of Canada figures

Sprott’s hostile 3.1 billion bid to take over Central Fund of Canada

(courtesy Sprott/GATA)

Sprott makes hostile $3.1 billion bid for Central Fund of Canada

Submitted by cpowell on Thu, 2017-03-09 01:19. Section: Daily Dispatches

From the Canadian Press

via Canadian Broadcasting Corp. News, Toronto

Wednesday, March 8, 2017

http://www.cbc.ca/news/canada/calgary/sprott-takeover-bid-central-fund-c…

Toronto-based Sprott Inc. said Wednesday it’s making an all-share hostile takeover bid worth $3.1 billion US for rival bullion holder Central Fund of Canada Ltd.

The money-management firm has filed an application with the Court of Queen’s Bench of Alberta seeking to allow shareholders of Calgary-based Central Fund to swap their shares for ones in a newly-formed trust that would be substantially similar to Sprott’s existing precious metal holding entities.

The company is going through the courts after its efforts to strike a friendly deal were rebuffed by the Spicer family that controls Central Fund, said Sprott spokesman Glen Williams.

“They weren’t interested in having those discussions,” Williams said.

Sprott is using the courts to try to give holders of the 252 million non-voting class A shares a say in takeover bids, which Central Fund explicitly states they have no right to participate in. That voting right is reserved for the 40,000 common shares outstanding, which the family of J.C. Stefan Spicer, chairman and CEO of Central Fund, control.

If successful through the courts, Sprott would then need the support of two-thirds of shareholder votes to close the takeover deal, but there’s no guarantee they will make it that far.

“It is unusual to go this route,” said Williams. “There’s no specific precedent where this has worked.”

Sprott did have success last year in taking over Central GoldTrust, a similar fund that was controlled by the Spicer family, after securing support from more than 96 percent of shareholder votes cast.

The firm says Central Fund’s shares are trading at a discount to net asset value and a takeover by Sprott could unlock US$304 million in shareholder value.

Central Fund did not have any immediate comment on the unsolicited offer. Williams said Sprott had not yet heard from Central Fund on the proposal but that some shareholders had already contacted them to voice their support.

Sprott’s existing precious metal holding companies are designed to allow investors to own gold and other metals without having to worry about taking care of the physical bullion.

end

Major gold/silver trading/commentaries for FRIDAY

GOLDCORE/BLOG/MARK O’BYRNEet.

Gold ETFs or Physical Gold? Hidden Dangers In GLD

By Mark O’Byrne March 24, 2017

by Olivier Garret on Forbes

Gold ETFs are rising in popularity due to their convenience. They’re easy to trade, there’s no need to store anything, and no one is going to break into your house to steal your GLD shares.

But there are a lot of hidden dangers inherent in the structure and operation of gold ETFs that few investors are aware of—and these risks are more pronounced than ever, as the threat of another financial crisis is always around the corner.

Considering the public’s waning trust in the banking system, many investors find themselves wondering how GLD stacks up to owning the real thing. When you look at both assets more closely, it’s clear that gold ETFs and gold bullion are very different investments.

Why GLD Is Not the Same as Gold

SPDR Gold Trust (GLD), the largest, most popular gold ETF, is an investment fund that holds physical gold to back its shares. The share price tracks the price of gold, and it trades like a stock, but the vast majority of investors don’t have a claim on the underlying gold.

The reason for this is that you can only request physical delivery of metal if you own a minimum of 100,000 GLD shares (most investors don’t: at $1,000 gold, 100,000 shares is more than a million dollars). Even if you do own enough shares, the GLD ETF reserves the right to settle your delivery request in cash.

So why is GLD appealing to investors if you never actually own any gold?

For one, the fund is both convenient and low cost. If you’re looking for an inexpensive way to invest in the direction of the gold price, GLD is ideal.

The other advantage is you can employ leverage with options, which can be risky, but it’s something you can’t do with gold bullion. If you’re an investor who doesn’t plan to take delivery and you’re comfortable with a higher degree of risk, GLD can be a good way to gain exposure to the price of gold.

Counterparty Risk on All Levels

While gold ETFs can be a fine investment, they come with a lot of counterparty risk inherent in their chain of custody. And this risk will only grow commensurately with systemic uncertainties.

Think about it: If you own GLD, you must rely on a counterparty to make good on your investment. If the fund’s management, structure, chain of custody, operational integrity, regulatory oversight, or delivery protocols break down, your investment is at risk.

It all raises too many questions. Can you be sure the bank doesn’t front-run its customers? How safe are the fund’s holdings? Is the fund protected by adequate insurance? Is the custodian bank trustworthy enough to safeguard the gold?

The best reason to own gold is as a hedge against risk. It can be your last line of defense in an economic crisis—a form of wealth insurance, if you will. But since gold ETFs are part of the very banking system you need protection from, you must ask yourself if they serve one of the primary purposes for owning gold.

In a period of financial crisis, the risks inherent in holding GLD would only rise. In fact, the frequency and severity of counterparty risks with gold ETFs are already rising.

When you consider how these ETFs function, the problem of counterparties quickly becomes apparent:

The Custodian

When you invest in GLD, you buy shares through an Authorized Participant, which is usually a large financial institution responsible for obtaining the underlying assets necessary to create ETF shares.

When it does so, it is buying shares in the fund’s trustee, the SPDR Gold Trust. The trustee then uses a custodian (HSBC) to source and store the gold for it.

Trust in the custodian is paramount: If you’re buying gold as a hedge against a failure in the financial system, you must be confident that the custodian would not be impaired if a crisis were to happen.

As HSBC is one of the world’s largest banks, you simply don’t have that assurance. If there’s a systemic disruption, your GLD shares would likely be negatively affected.

The Sub-Custodian

Custodians like HSBC can use sub-custodians, such as another bank, to source and store gold. So in addition to the risk you assume with the fund’s primary custodian, you’re now exposed to even more risk because it has added another counterparty.

The Trustee

There are no written contractual agreements between sub- custodians and the trustees or the custodians, which means if a sub-custodian drops the ball, the ability of the trustee or the custodian to take legal action is limited.

This leaves the trustee on the hook for any negligence. But trustees don’t insure the gold for gross negligence; they leave that to the custodian, who secures limited general insurance coverage for the contents of the vaults. The value of the gold in the vaults is likely to be much greater than this limited policy would cover.

What this all boils down to is that if anything happens to any of the counterparties, you’re the one who loses. And you have zero recourse.

http://www.goldcore.com/us/gold-blog/gold-etfs-physical- gold-hidden-dangers-gld/

-END-

END

An extremely important paper from Ted Butler. You will note that I have been providing the managed money account for you on COT days. Basically Ted is stating that the non technical hedge funds have been accumulating silver and these guys do not budge on raid days. The long positions on these guys have been rising to around 80,000 contracts and this is coupled with small specs or non hedge funds who have accumulated another 30,000 contracts. Ted states that the 7 banks that hold 98,000 short positions are “dead men walking

(courtesy Ted Butler)

Dead Men Walking?

|

March 23, 2017 – 10:48am

The narrative thus far – after decades of allowing themselves to be led in and out of COMEX silver futures contracts by their commercial counterparties, several managed money traders appear to have woken up to the fact they’ve been duped all along. A key component of the silver manipulation for the past 30 years has been the knee-jerk and mechanical reaction of the managed money traders to collectively sell whenever the commercials rigged prices lower beyond certain moving averages. Ditto for buying on rising prices.

The dependability of the managed money technical funds (Harvey: managed money = hedge funds) to obey commercially rigged price signals made the funds the true enablers of the manipulation. The commercials, mostly domestic and foreign banks, made their profits by getting the technical funds to buy high and sell low. Without the technical funds to maneuver at will, the commercials would have little reason to prolong the silver manipulation.

So obvious had become the continued whipsawing of the managed money traders by the commercials that a near-universal question emerged – “why are these technical funds engaging it such a bizarre and harmful (to their investors) game?” I’ve heard from more than one reader that there must be some kind of collusion between the technical funds and the commercials, featuring under the table payments to the technical funds by the commercials to continue deliberately losing. While I understand and empathize with the logic of such an explanation, given the nearly inexplicable behavior of the technical funds, I don’t see such collusion, as I’ve tried to explain over the years. I certainly see collusion, just not on the part of managed money traders to deliberately lose. (Harvey: he is wrong)

Nowhere is the price influence of the continuing contest between the managed money traders and the commercials more pronounced than it is in COMEX silver. That’s what led me to conclude the price of silver was manipulated more than 30 years ago. And while it is now true that this same price influence has come to infect just about all our markets, silver still maintains a unique role as being the most manipulated market of all. Not just because it was the first such market to be manipulated by futures positioning, but that has something to do with it. Being first means that silver has been manipulated in this manner for far longer than any other market and, as such, its price is necessarily more artificial. More to the point is that the objective relative measures involving actual production and consumption and real world supplies always feature silver at a much different level than any other commodity.

So extreme has become the size of the derivatives trade in silver compared to actual metal in the world and the fact that it has lasted so long (decades) that perhaps it’s no great surprise that, if the managed money traders were ever going to wake up to the realization they were being gamed; then they would likely first see it in silver. Should the managed money traders come to such a realization and radically alter their behavior, then there should be strong signs indicating such a change. Those strong signs abound and have been discussed on these pages.

First came the start of a buildup in core non-technical fund managed money long positions in COMEX silver, starting around three years ago. I define these positions as not being governed by price change, meaning such longs are not sold on price selloffs and, therefore, are not technical in nature. In simple terms, the core long position is the amount of long positions remaining after significant price declines. (Harvey: call these strong longs that refuse to budge not matter what criminal activity the banks throw at them) From the time the COT data started tracking managed money traders around 2009 until the fall of 2013, the long position of managed money traders in COMEX silver rarely fell below the 20,000 contract level at the depths of price declines. Again, what’s remaining long in the managed money category at the end of significant silver price declines is the core non-technical fund long position.

But starting in 2014, the core non-technical fund managed money long position began a years-long climb, first to 30,000 contracts, then 40,000 and finally this past December to nearly 60,000 contracts (56,000 contracts on Dec 6). This meant many more managed money longs remained long after selloffs. Then, on the $3 rally early this year, some 40,000 new managed money longs were added, as technical funds joined with their non-technical fund fellow managed money traders on the long side of COMEX silver futures, creating a combined managed money long position of 96,000 contracts on Feb 28. Part of me wants to apologize for throwing so many numbers at you, but I’m talking about the only numbers that matter. Every 10,000 contracts of COMEX silver is equal to 50 million oz of metal, so I am talking about the many hundreds of millions of oz that is setting the price of silver, so please bear with me (but certainly feel free to question me about any of this).

On the sharp $1.50 selloff thru the last COT report, some 16,000 managed money long positions were sold (presumably by technical funds), leaving over 80,000 contracts long in the managed money category. Prices moved higher since then, so there is little reason to suspect that the long position is lower as of yesterday’s cutoff date. If silver prices don’t get pushed below the recent lows ($16.75), then by my definition, the core non-technical fund long position in COMEX silver appears to be 80,000 contracts or 400 million oz, until proven otherwise. That is four times the 20,000 contract (100 million oz) core long position that existed prior to late 2013.

Not only is this a shocking and monumental increase in core long positions, I must remind you that it is unique to COMEX silver and this pattern of an exploding core non-technical managed money long position exists in no other market, gold included. Moreover, the stunning size of the core managed money long position in silver is also accompanied by at least another 30,000 contract core non-technical fund long position held by traders not in the managed money category. The bottom line, as I’ve indicated recently, is that there exists at least 110,000 contracts (550 million oz) of a core paper long position in COMEX silver futures not likely to be sold should silver prices get rigged lower.

Also as I’ve indicated previously, if this core long position is not about to be sold to the downside (as I believe), then it will only be sold to the upside. So here we have 550 million oz of paper silver held by a fairly diverse number of traders seemingly intent on holding until they can sell at what they conclude is a sufficiently high enough price. Because this huge core long silver position is held in paper contract or derivative form, there must be an equally huge corresponding short position. Thanks to exquisitely detailed government data (in the form of COT and Bank Participation Reports), we can pinpoint the huge short position in COMEX silver with even greater precision than the long side. That’s because, as large as the short position is in COMEX silver, it is held by far fewer traders than exist on the long side. Because the traders which hold the huge short position in COMEX silver are so very few in number, serious issues related to market concentration, position limits and collusion are raised, none of which I’ll go into today.

This issue today is that the core long position in COMEX silver is held by a diverse number of traders (into the hundreds), while nearly all of the short position is held by just 8 big commercial shorts. In last week’s COT report, these eight large traders held, essentially, the entire 98,000 contract (490 million oz) total commercial net short position. One of those 8 traders, JPMorgan, held around 27,000 contracts short, leaving the remaining 7 traders net short more than 70,000 contracts (350 million oz).

For the sake of brevity, let me quickly conclude that because the crooks and scoundrels at JPMorgan saw the need and wisdom to accumulate the many hundreds of millions of ounces of physical silver that they did acquire over the past six years, JPMorgan must be removed from any calculation of loss due to higher silver prices. The problem is that none of the crooks and scoundrels at the seven remaining big commercial shorts can be removed from such calculations because none bought actual silver. As such, I can’t help but think of these 7 big COMEX shorts as dead men walking – their financial fates sealed and with only the timing to be determined.

There are several forces that seal the fate of the seven big COMEX silver shorts. One, the unquestioned and documented buildup of core long positions, not about to be resolved by lower prices. Two, JPMorgan exiting the dead man fold, by virtue of snatching up every available ounce of actual silver for six years. Three, the growing awareness of the big seven’s predicament, including lawsuits hitting closer to home. Incredibly, these are self-reinforcing factors. For example, sensing the fate of the doomed 7 could and should have encouraged ever larger managed money core long positions.

Further, we know that the 7 big COMEX silver shorts are mostly foreign banks, speculating their butts off on the short side of silver and are not, repeat not, legitimately hedging in any way, just taking the other side of a speculative derivatives bet. Because there is no legitimate basis for why a Bank of Nova Scotia, for instance, would maintain a massive short position in COMEX silver, then, by definition, the basis for being short must be illegitimate. There is no way anyone could construct a legitimate economic motive behind the 7 big shorts’ massive and concentrated short position in COMEX silver; otherwise I would have heard it long ago. And not for a moment am I exempting JPMorgan in the legitimacy department, just in the 7 dead men’s fate.

What makes the 7 big traders dead men walking is that they can no longer resolve their fate profitably. It took years to create this very unique situation, but basically, they are trapped. There are only two ways for any short to get covered – by actual delivery or by buying back the short position. How the heck are the 7 big COMEX silver shorts going to secure 350 million ounces of physical silver in a hurry , with which to deliver against and close out their huge short position, when JPM has put a strangle hold on physical silver? Look at the current March silver delivery process – JPM has taken nearly all of the 15 million oz delivered this month. Any attempt by the big 7 to buy physical silver in any reasonable quantity would send the price soaring and financially cripple these traders.

Likewise, any attempt to buy back big quantities of COMEX paper futures contracts would also send prices soaring for the simple reason the big 7 (along with JPM) have been the sole sellers up until now. How can the former big short sellers simply turn around and begin to buy in earnest without causing prices to explode? In simple terms, they can’t. Sure, they can buy on lower prices as long as the core longs are willing to sell, but that’s the whole point – the evidence strongly suggests the core longs won’t sell on lower prices. This is what’s known as being between a rock and a hard place.

Of course, I can’t give you the exact timeline and sequence of events and if I tried to, you should reject that. No one can see the future with such clarity. I can’t tell you if the crooks at JPMorgan might not still continue to aid the 7 soon to be dead men by adding shorts for a while longer, but I don’t see JPMorgan bailing them out completely by donating the bank’s acquired physical silver of six years at low prices. My firm sense about JPMorgan and how they behave typically is that they would sooner rip your lungs out than look at you if there was a decent buck in it for them. Even if JPMorgan temporarily prolongs the silver manipulation, as they are certainly capable of doing that will only offer a brief stay of execution for the 7 walking dead.

What I can tell you is that when the time is up for the walking dead, it will be a time like no other in the history of silver. Prices can and will continue to muddle along as long as the 7 big shorts and JPMorgan continue to cap price rallies, but the moment the capping ends – either at the hands of JPM or the walking dead – the silver price landscape will be changed forever. None of us – myself included – will be able to fully comprehend the upcoming shock to the upside. This has little to do with price per se, just the mechanics of the market; but it will be seen most vividly in price. When the big shorts start to buy back their shorts to the upside, the world of silver will have changed.

Ted Butler

March 23, 2017

For subscription information please go to www.butlerresearch.com

END

A good look at mining in South Africa. At one time, South Africa produced over 1000 tonnes of gold, and that was about 90% of world production at that time

(courtesy Bloomberg/GATA)

Reviving South Africa’s gold industry means getting mine workers off their knees

Submitted by cpowell on Fri, 2017-03-24 01:45. Section: Daily Dispatches

By Kevin Crowley

Bloomberg News

Thursday, March 23, 2017

During his early years as a miner in South Africa, Joas Mahanuque spent six hours a day on his knees drilling for Impala Platinum Holdings Ltd. The dust-filled tunnels half a mile underground were too low for him to stand, and temperatures reached 105 degrees Fahrenheit (40 degrees Celsius).

Today he has essentially the same job 2.5 kilometers (1.5 miles) beneath the surface for Gold Fields Ltd. But unlike most of the precious-metals miners in the country, Mahanuque sits comfortably atop a new 7-ton vehicle, using a joystick to control an 8-foot drill as ventilated air blows behind him. …

If only it was that easy for the rest of the once dominant South African gold industry. After more than a century as the world’s top producer, the country has slipped to No. 7 over the past decade. Mines are deep, labor intensive and are being developed with mostly drill-and-blast methods little changed since the 1950s, which means costs have soared and output has dropped. …

… For the remainder of the report:

https://www.bloomberg.com/news/articles/2017-03-23/reviving-king-of-gold…

END

India last month received 37.2 tonnes from Switzerland in February which is terrific as India is now back into gold. If we extrapolate 37.2 tonnes x 12, India’s demand from Switzerland will exceed 446.4 tonnes. Switzerland is not the only source for India.

(courtesy Lawrie Williams/Sharp Pixley)

LAWRIE WILLIAMS: Swiss gold exports to India top the table in February

Gold exports from Switzerland are an excellent indicator of the strength of the gold flows from the West to the East and while the February overall figure was a low 88.7 tonnes, compared with total imports of 139 tonnes, the make-up of these totals in itself tells an interesting story.

The top recipient of Swiss gold exports in February was India – comfortably – with 37.2 tonnes confirming the reported pick-up in Indian gold demand so far this year as the populace got to grips with the withdrawal from circulation of Rupee 1,000 and 500 notes. India is very much a cash society and much of the gold buying pressures comes from individuals making small cash purchases when their financial situation makes this possible – and last year’s monsoon rains, and subsequent harvest, were good increasing gold demand from the enormous subsistence agricultural sector – which traditionally forms a very significant part of gold demand in the subcontinent.

And then the next biggest recipient of Swiss gold last month was mainland China with direct imports of 21.5 tonnes, dwarfing the 7.2 tonnes to Hong Kong. (Indeed Hong Kong was a substantial net exporter of gold back to Switzerland – more of which later). The direct flow of gold into mainland China again confirms that Hong Kong gold imports can very definitely no longer be considered a proxy for Chinese imports, nor flows from Hong Kong to the mainland be taken as anything more than an ever-decreasing indicator of overall Chinese gold consumption as more and more gold is taking the direct route. (See article: China 154, Hong Kong 39. Swiss Dec gold exports show remarkable gold flows which highlighted this situation with respect to a huge December figure for gold exports from Switzerland direct to mainland China).

A bar chart showing the breakdown of Swiss gold exports on a country-by country basis is shown below courtesy of Nick Laird’s www.goldchartsrus.com website:

The Swiss gold imports are interesting too in that although the UK is again the largest source of imported gold, accounting for a little over 30 tonnes, the second and third largest sources were Hong Kong (26.5 tonnes) and the United Arab Emirates (UAE) with 16.4 tonnes. Thailand also accounted for 9 tonnes of Swiss gold imports. All three of these are traditional gold consuming nations so the fact that Switzerland is importing gold from them suggests, perhaps, light demand and destocking by traders, perhaps coupled with some scrap. The higher gold price prevailing in February may also have stimulated some of these reverse flows. See chart below – again courtesy of www.goldchartsrus.com.

Most of the other sources of the Swiss gold imports are gold producing nations like the USA, Ghana, Burkina Faso, Argentina, Peru, Russia and South Africa, although one should perhaps see Germany and Italy as somewhat anomalous, although both were actually net importers of Swiss gold in February.

Switzerland is very much a conduit for gold flows from West to East, largely because of it being the location for four of the world’s largest independent gold refineries. (Swiss refineries are reported by www.bullionstar.com to account for 65-70% of world refined gold output). These refineries specialise in re-refining .995 London good delivery gold bars in 350-430 troy ounce sizes, and refining gold scrap, and producing the higher .999 purity and much smaller gold bars and wafers in demand in the East, as well as producing high purity gold coins for some nations. Upwards of 1,600 tonnes a year of gold passes through these Swiss refineries, which is around half global gold production. Indeed in 2013, when Chinese demand was booming and there were big liquidations out of the gold ETFs, it is reported that Swiss gold exports exceeded 2,500 tonnes (equivalent to nearly 80% of global new mined gold output that year).

So the importance of the Swiss gold import and export figures cannot be emphasised enough in terms of global gold flows and where they are coming from and going to. In the latest month’s figures almost 85% of the Swiss gold exports were headed for Asia. The West to East gold flows continue unabated.

23 Mar 2017

end

Your early FRIDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight

1 Chinese yuan vs USA dollar/yuan SLIGHTLY STRONGER AT 6.8862( SMALL REVALUATION NORTHBOUND /OFFSHORE YUAN MOVES WEAKER TO ONSHORE AT 6.8741/ Shanghai bourse UP 20.85 POINTS OR .64% / HANG SANG CLOSED UP 30.57 POINTS OR 0.13%

2. Nikkei closed UP 177.22 POINTS OR 0.93% /USA: YEN RISES TO 111.02

3. Europe stocks opened ALL IN THE RED ( /USA dollar index FALLS TO 99.69/Euro UP to 1.0802

3b Japan 10 year bond yield: RISES TO +.065%/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 111.02/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD FINALLY IN THE POSITIVE/BANK OF JAPAN LOSING CONTROL OF THEIR YIELD CURVE AS THEY PURCHASE ALL BONDS TO GET TO ZERO RATE!!

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 47.93 and Brent: 50.83

3f Gold DOWN/Yen DOWN

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil UP for WTI and UP for Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund RISES TO +.412%/Italian 10 yr bond yield UP to 2.255%

3j Greek 10 year bond yield FALLS to : 7.389%

3k Gold at $1245.70/silver $17.62(8:15 am est) SILVER RESISTANCE AT $18.50

3l USA vs Russian rouble; (Russian rouble UP 11/100 in roubles/dollar) 57.24-

3m oil into the 47 dollar handle for WTI and 50 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation (already upon us). This can spell financial disaster for the rest of the world/China forced to do QE!! as it lowers its yuan value to the dollar/GOT REVALUATION NORTHBOUND from POBC.

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 111.02 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 0.9920 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.0715 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT

3r the 10 Year German bund now POSITIVE territory with the 10 year RISES to +.412%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.421% early this morning. Thirty year rate at 3.032% /POLICY ERROR)GETTING DANGEROUSLY HIGH

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

(courtesy Jim Reid/Bloomberg/Deutsche bank/zero hedge)

All Eyes On Washington: US Futures Rise On Hope Healthcare Vote Will Pass

Asian shares and S&P futures rose on optimism that today’s rescheduled U.S. vote on health care will pass following Trump’s Ultimatum to the Freedom Caucus. European stocks gave up some of Thursday’s gains, falling for the fourth time in five days, and moving further away from a 15-month high reached a week ago while the yen weakened for the first time in nine days before the long awaited U.S. health-care vote that has dominated market sentiment this week. Oil was headed for a third weekly drop this month. Economic data include durable goods orders, Markit U.S. manufacturing PMI. Companies due to report earnings include Finish Line.

As Reuters notes, all eyes in global financial markets were fixed on stuttering Republican efforts to pass a replacement for Obamacare on Friday, with failure likely to undermine faith in Donald Trump’s promise to deliver a “phenomenal” U.S. tax reform. The White House’s ability to get legislation through Congress is crucial to “Trumpflation” bets on fiscal stimulus, tax cuts and capital repatriation that markets late last year assumed would drive inflation and growth higher. Below are the latest developments on the House vote on American Health Care Act, aka Trumpcare.

- The House delayed the vote on the AHCA bill amid doubts whether it could pass, with House GOP leaders later confirming the vote is to occur on Friday afternoon.

- President Trump reportedly warned House Republicans he would leave Obamacare in place and will move onto tax reform if the healthcare bill fails in today’s vote.

- US Freedom Caucus Chairman Meadows said the Freedom Caucus is to meet and discuss the revised health bill and that the bill has improved. Meadows also stated that he is a ‘no’ right now, but has not made the final decision.

- Congressional Budget Office released its scoring on the amended GOP healthcare bill which showed smaller savings over the next decade with the projected deficit reduction declining to USD 150bIn from USD 337b1n, while it maintained guidance that 14mln will lose coverage by 2018.

“No one has any idea what’s going to happen with this vote so they are sitting there waiting for actual information rather than theory,” said Ben Kumar, a London-based investment manager at Seven Investment Management, which oversees about 10 billion pounds ($12 billion). “In general you can ignore the politics and trade on the underlying fundamentals. The market is still fundamentally intact.”

“There is still a risk that the vote fails today, (and) there are numerous other uncertainties that suggest anything but a smooth course ahead for implementing the much anticipated tax reform reflation program,” said MUFG currency strategist Derek Halpenny, in London. “We still expect a much smaller tax cutting program simply due to the inability to agree on how a large program could be financed. The Trump reflation trade could still reverse course in a more meaningful way, resulting in dollar weakness.”

In Europe, the STOXX 600 Index dropped 0.5%, extending its weekly decline, with insurers and energy companies the biggest losers, as trading volumes dropped by almost a third from the previous week. The drop comes despite stronger than expected PMIs across the board for both Germany and France.

- France Manufacturing PMI, actual 53.4, est. 52.4, prior 52.2

- France Services PMI, actual 58.5, est. 56.1, prior 56.4

- Markit France Composite PMI, actual 57.6, est. 55.8, prior 55.9

- Germany Manufacturing PMI, actual 58.3, est. 56.5, prior 56.8

- Germany Services PMI, actual 55.6, est. 54.5, prior 54.4

- Germany Composite PMI, actual 57, est. 56, prior 56.1

The yen halted its longest rally since 2011 as U.S. lawmakers hurtled toward a vote on an amended health-care bill after a delay that fueled speculation President Donald Trump may struggle with other policies. Bonds were mixed, and oil rose for the first time this week even as a rotation out of growth sectors into safe utilities continued.

The Stoxx Europe 600 Index was down 0.5 percent as of 6:34 a.m., trimming the previous day’s brisk gains. Aegon NV weighed down insurers after it cut its Solvency II ratio. Japan’s Topix trimmed some losses for a week that included the biggest one-day drop since Trump’s election. The index finished with a 1.4 percent decline for the week. The MSCI Asia Pacific fared better, with a 0.1 percent decrease. Futures on the S&P 500 climbed 0.1 percent. The index fell 0.1 percent on Thursday.

The dollar recovered some ground against the yen, however, after U.S. Treasury yields inched higher in Asian time, halting an eight-day losing streak that is its worst since the end of 2010.

Bank of Japan Governor Haruhiko Kuroda told a Reuters event on Friday that there was “no reason” to raise the bank’s bond yield targets now with inflation so far from its 2 percent target.

A sell-off in a number of commodities markets has also been a factor in the weakness of share prices this week. Iron ore prices fell for a fourth day on Friday and are on course for their worst week since December. Crude inched higher, supported by a fall in Saudi exports to the United States, but remained under pressure from a glut of supply that OPEC curbs has broadly failed to stem. Thomson Reuters data shows OPEC shipments to Asia, the world’s biggest and fastest-growing oil-consuming region, are up more than 5 percent since January, suggesting the group of producers is shielding its main customers from the reductions. Unless OPEC extends the curbs beyond June or makes bigger cuts, traders say oil prices are at risk of falling further.

“OPEC’s goal of drawing down inventories to normal levels is not going to be reached before their agreement expires on June 30,” said U.S. investment bank Jefferies in a note to clients.

Leaders from European Union countries except the U.K. meet Saturday on the 60th anniversary of the bloc’s founding Treaty of Rome to discuss the way forward after Brexit. Meanwhile, representatives from five OPEC and non-OPEC members gather for a meeting of the Joint Ministerial Monitoring Committee to oversee oil production cuts.

* * *

Bulletin Headline Summary from RanSquawk

- Stocks reside modestly negative in Europe as participants await news regarding the litmus test of Trump’s power in the form of his healthcare bill

- EUR gains with Europe encouraged by strong PM! surveys

- Today’s highlights include Eurozone and US manufacturing and services PMIs, US Durable Goods Orders and comments from Fed’s Evans, Williams, Bullard and Dudley

House vote on American Health Care Act

Market Snapshot

- S&P 500 futures up 0.1% to 2,341.75

- STOXX Europe 600 down 0.5% to 375.7

- MXAP up 0.4% to 148.01

- MXAPJ up 0.08% to 478.73

- Nikkei up 0.9% to 19,262.53

- Topix up 0.9% to 1,543.92

- Hang Seng Index up 0.1% to 24,358.27

- Shanghai Composite up 0.6% to 3,269.45

- Sensex up 0.5% to 29,488.44

- Australia S&P/ASX 200 up 0.8% to 5,753.55

- Kospi down 0.2% to 2,168.95

- German 10Y yield rose 1.0 bps to 0.441%

- Euro up 0.1% to 1.0798 per US$

- Brent Futures up 0.3% to $50.69/bbl

- Italian 10Y yield rose 0.9 bps to 2.272%

- Spanish 10Y yield rose 2.2 bps to 1.753%

- Brent Futures up 0.3% to $50.69/bbl

- Gold spot down 0.2% to $1,242.62

- U.S. Dollar Index down 0.1% to 99.71

Top Overnight News via BBG

- Trump Dares GOP Into High-Stakes Vote on Troubled Health Bill

- Uber Rival Grab Said Raising $1.5 Billion in New Funding Round

- EU’s Juncker Says U.K.’s Brexit Bill Will Be Around $62 Billion

- Bayer Says Not Aware of Rejection of Monsanto Deal From India

- Monsanto Roundup Users to Question Ex-EPA Manager in Cancer Suit

- U.S. Equities See Biggest Outflows Since Brexit Vote: BofAML

- Watchmakers Like Mondaine Confront U.S. ‘Consumer Blockage’

- Euro-Area Economic Momentum Bodes Well for Wage Growth and Jobs

- Fed’s Kaplan Says MBS and Treasuries Should Both Be Rolled Off

- U.S. Biodiesel Producers File Trade Case Against Argentina

- Atanor Said to Sell Second Sugar Mill to Argentine Grocery Mogul

- Indonesian Govt Sees ‘Good Progress’ in Talks With Freeport

* * *

Asian markets trade mostly higher in the last day of the week as local stocks shrugged off a cautious tone on Wall Street where a delay in the healthcare bill vote dampened sentiment. ASX 200 (+0.8%) was led by the Healthcare and Financial sectors, while Nikkei 225 (+0.9%) benefited as USD/JPY recovered some ground. Elsewhere, Hang Seng (-0.1%) and Shanghai Comp. (+0.2%) traded choppy as participants digested earnings including CNOOC which posted its worst results in 5 years, while the PBoC also refrained from open market operations and stated that liquidity in China’s banking system is relatively high. Finally, 10yr JGBs were lower amid the increased risk appetite in Japan and after the latest weekly securities transactions data showed foreign investors upped their selling of Japanese bonds, while underperformance in the curve was seen in the belly.

Top Asian News

- BOJ Sells Bonds With Repurchase Agreements First Time Since 2008

- Kuroda Sees No Problems for BOJ Bond Purchases in the Future

- Huishan Dairy, Muddy Waters Target, Sinks 85% in Hong Kong

- Two-and-20 Era Cedes Way to No Fees Upfront as Hedge Funds Adapt

- Carlyle, Tiger Global Buy Stake in Delhivery for More Than $100m

- Nippon Yusen Cancels 2 Boeing 747 Airplane Orders

- Japan’s JR East Pitches Minimal Delays to Win U.K. Rail Bid

- Iron’s Rally Gives Way to Rout as China Futures Post Record Loss

Europe’s final session of the week kicked off with major bourses trading in the red, albeit modestly so, with risk mood steady as the US healthcare vote moved to late Friday. Newsflow throughout the European morning has been light, with energy names leading the way lower, while the material sector outperforms. In credit markets, price action is rather muted with the next focal point for the market being next week’s approach to quarter end, particularly given the recent squeeze in repos over year-end. Consequently, it is likely that positioning will take place ahead of this event.

Top European News

- Credit Suisse Increases Bonuses; Bank Said to Weigh Stock Sale

- Deutsche Bank Commits to London With New U.K. Headquarters

- German Output Growth Accelerates as Costs, Employment Spike

- French Companies Bet on Favorable Post-Election Business Outlook

- Fillon Accuses French President of Plot to Destroy His Candidacy

- U.K. Police Make Two More Arrests in London Terror Attack Probe

- End of Winter Pushes U.K. Natural Gas to Longest Slide in Decade

- Eni Becomes First Oil Major to Find Crude in Mexico Waters

- Schaeuble: Greece Can Only Stay in Euro If It Undertakes Reforms

- Nordea Cuts Correspondent Banking in Half as High Risk Area

- Biotest to Seek New Partner for Drug Rejected by ImmunoGen

Currency markets have been relatively subdued this morning, with traders looking for drivers given we must now wait until the end of Friday for the vote on healthcare in the US. This is set to resume just after the London close, so the JPY pairs in particular look set for some range bound trade ahead. USD/JPY continues to hold above 111.00, but is struggling for traction on the upside, despite US Treasury yields rising 3-4bps in the belly of the curve. EU PMIs came in strong this morning, and although much of this was to be assumed given the weakness of the EUR of late, traders bought the spot rate back up to 1.0800 in an isolated move, with USD/CHF moving the other way to suggest a USD based move. EUR/CHF was camped in the low 1.0700’s, though we did see some modest upside in EUR/GBP, which is back around the 0.8650 level. Cable is still struggling with selling interest through the 1.2500 mark, so the EUR/GBP reaction is partially a result of this, with next week’s triggering of Article 50 likely to limit the upside, but dip buying notable here in the wake of yesterday’s much stronger than expected retail sales release. Indeed at time of writing, the spot rate is still pushing for 1.2500+. but resistance ahead of 1.2600 is very strong.

Commodities traders will be looking to tonight’s vote on healthcare in the US as a measure of how president Trump’s spending plans will fare through Congress going forward. We see few material moves of note other than palladium, which has extended to near 2 year highs. Gold has come back in line with the USD, but is pushing higher —modestly — as the greenback trickles back, but US Treasuries seeing little movement against this. Interesting news for Copper as the strikes in the Escondida mine look to end of 43 day run of inactivity. This looks to be a temporary measure though as workers agree to extend current contracts. WTI is still struggling below the USD50.00 mark, with all eyes and ears on the OPEC meeting towards the end of May to see whether the production cut agreement can be extended.

Looking at the day ahead, in the US the main focus is likely to be on the February flash durable and capital goods orders data where market expectations is for a +1.3% mom rise in headline durable goods orders and +0.5% mom rise in core capex orders. The flash PMI’s will also be out in the US this afternoon. Away from the data there is plenty of Fedspeak with the Fed’s Evans (12pm GMT), Bullard (1.05pm GMT), Dudley (2pm GMT) and Williams (5.30pm GMT) scattered throughout the day. Of course the main focus will be on the healthcare bill developments.

US Event Calendar

- 8:30am: Durable Goods Orders, est. 1.3%, prior 2.0%;

- Durables Ex Transportation, est. 0.6%, prior 0.0%;

- Cap Goods Orders Nondef Ex Air, est. 0.5%, prior -0.1%

- 9:45am: Markit US Manufacturing PMI, est. 54.8, prior 54.2

- US Services PMI, est. 54, prior 53.8

- US Composite PMI, prior 54.1

- 10am: Revisions: Wholesale sales and inventories

Central Banks

- 8am: Fed’s Evans Speaks at Community Development Event

- 9:05am: Fed’s Bullard to Speak to Economic Club of Memphis

- 10am: Fed’s Dudley Speaks in New York at York College

- 1:30pm: Fed’s Williams Speaks in Q&A

* * *

DB’s Jim Reid concludes the overnight wrap

So it turns out we’ll have to wait a little bit longer for our first glimpse at how successful Mr Trump’s legislative agenda might be. The breaking news yesterday was that House GOP leaders postponed Thursday’s planned vote on the Obamacare replacement bill. Following a behind closed doors meeting late last night between Republican lawmakers the White House said that a vote is planning to go ahead this afternoon in Washington although there is still no suggestion that Trump has garnered sufficient support at this stage following the discussions last night. Indeed the most significant comment that we’ve heard came from Republican representative Chris Collins who confirmed that there will

be “no more negotiations” and that “if it loses, we just move on to tax reform”. In other words, it sounds like Trump has issued his final ultimatum.

According to various news reports centrist Republicans were said to have balked at proposed changes to the minimum insurance benefits which had been negotiated between the President and Freedom Caucus. At the same time the Freedom Caucus are also said to still be unhappy about some of the finer details. In another twist, the Congressional Budget Office announced last night that the latest version of the AHCA (as of March 22nd) is estimated to result in a reduction in the deficit of $150bn over the next 10 years which compares to the $337bn reduction in the original version. The plan is also estimated to still result in 24 million more people being uninsured in 2026. The scope of any last minute changes is clearly not reflected in these figures but nonetheless, it’s hard to see the results as boosting the GOP’s cause at what is clearly a very tense time for negotiations.

While the announcement of a delay to the vote caused a little bit of retracing for risk yesterday, the actual magnitude of the moves wasn’t particularly eye catching. The S&P 500 finished -0.11% with healthcare stocks underperforming after the index traded as high as +0.44% in the early going while the Dow closed -0.02% having also been up a similar amount. There’s no doubt that the intraday ranges have been a lot more exciting over the last few days however.

The average of the last 3 days has been a 1.03% swing in the high to low points which compares to an average of just 0.53% for the rest of the year to date. Meanwhile credit retraced just less than 1bp of the move tighter yesterday while Treasuries and the Greenback were actually fairly unperturbed. The 10y finished at 2.419% which was +1.4bps on the day while the intraday range was 5bps. The US Dollar index closed +0.08% although didn’t really budge much in and around the headlines. The VIX did however finish nearly 8% up from the day’s lows, closing at 13.12 and with that, closing at the highest level this year. In commodities Gold faded to end the day down -0.29% while WTI Oil finished below $48/bbl again after dipping -0.71%.

Before we look at how the Asia session has followed up, it’s worth noting that as well as the obvious focus on the healthcare bill developments, or lack thereof, the release of the global flash March PMI’s today should make for a bit of a welcome distraction. In Europe the consensus is for a modest tick lower in the composite Euro area reading to 55.8, albeit a level which would still suggest a possible uplift in growth from recent levels. In the US the consensus is for a lift in both the services (to 54.0 from 53.8) and manufacturing (54.8 from 54.2) readings. So keep an eye on those later today.

To Asia now then where for the most part it’s been a fairly mixed session again, although there are no obvious signs of concern ahead of the health bill vote later today. While there are decent gains for the Nikkei (+0.99%) and ASX (+0.99%), the Shanghai Comp and Kospi are both little changed while the Kospi (-0.32%) is down slightly. US equity index futures are a touch higher while Treasuries have weakened a bit further following comments from the Fed’s Kaplan who said that 3 hikes this year remains a “reasonable” baseline. Kaplan also said that the Fed should begin to roll off both mortgage backed securities and Treasury holdings when it begins the process of letting its balance sheet shrink.

Moving on. While markets were unsurprisingly occupied with the health care bill developments there was also some focus on the ECB’s TLTRO II auction. Take up was higher than expected at €233.5bn compared to the consensus forecast for €110bn. A total of 474 bidders also took part which compares to 200 bidders in December. While we didn’t get a country breakdown we did see equity markets in Europe strengthen following the news with the Stoxx 600 finishing up +0.85% and the peripherals up a little more. European Banks also rose +0.75% while bond yields generally finished higher (2y Bunds +2.9bps, 10y Bunds +2.3bps, 10y Peripherals +1bp to +5bps). Financials credit also tightened with the iTraxx Senior and Sub indices rallying 2bps and 5bps respectively, outperforming iTraxx Main which finished 1bp tighter.

Away from that the data in the US was once again fairly second tier in nature. New home sales were reported as rising +6.1% mom in February and more than the +1.6% expected by the market, perhaps reflecting the relatively mild winter. Initial jobless claims ticked up to 258k last week which was a rise of 18k, although the four-week average continues to hover around the 240k area. Meanwhile the Kansas City Fed’s manufacturing index rose 6pts to 20 in March which is in fact the highest reading since March 2011. Elsewhere, in Europe the European Commission’s flash consumer confidence reading rose 1.2pts to -5.0 in March which was a little better than expected. In the UK retail sales excluding fuel also surprised to the upside after printing at +1.3% mom (vs. +0.3% expected) in February. The CBI’s Distributive Trades Survey for March also revealed that 32% of respondents reported growth which was up from 27% in February.

There was also a little bit of Fedspeak yesterday although nothing that particularly moved the dial. Fed Chair Yellen didn’t touch on either monetary policy or the economy. San Francisco Fed President Williams did however and said that three “or maybe even more” rate increases this year makes sense, but depends on how the data comes in.

Looking at the day ahead, this morning in Europe we’re kicking off in France where the final revisions to Q4 GDP will be made. Thereafter we will get the aforementioned flash PMI’s for the Euro area, Germany and France. This afternoon in the US the main focus is likely to be on the February flash durable and capital goods orders data where market expectations is for a +1.3% mom rise in headline durable goods orders and +0.5% mom rise in core capex orders. The flash PMI’s will also be out in the US this afternoon. Away from the data there is plenty of Fedspeak with the Fed’s Evans (12pm GMT), Bullard (1.05pm GMT), Dudley (2pm GMT) and Williams (5.30pm GMT) scattered throughout the day. Of course the main focus will be on the healthcare bill developments.

3. ASIAN AFFAIRS

i)Late THURSDAY night/FRIDAY morning: Shanghai closed UP 20.85 POINTS OR .64%/ /Hang Sang CLOSED UP 30.57 POINTS OR 0.13% . The Nikkei closed UP 177.22 OR 0.93% /Australia’s all ordinaires CLOSED UP 0.73%/Chinese yuan (ONSHORE) closed UP at 6.8862/Oil ROSE to 47.93 dollars per barrel for WTI and 50.83 for Brent. Stocks in Europe ALL IN THE RED ..Offshore yuan trades 6.8741 yuan to the dollar vs 6.8862 for onshore yuan.THE SPREAD BETWEEN ONSHORE AND OFFSHORE NARROWS CONSIDERABLY AGAIN/ ONSHORE YUAN SLIGHTLY STRONGER BUT THE OFFSHORE YUAN IS SLIGHTLY WEAKER AND THIS IS COUPLED WITH THE SLIGHTLY WEAKER DOLLAR. CHINA SENDS HER DISPLEASURE SIGNAL TO WASHINGTON

3a)THAILAND/SOUTH KOREA/NORTH KOREA

b) REPORT ON JAPAN

c) REPORT ON CHINA

Wow!! that happened fast! Huishan Dairy’s stock collapsed over 90 in minutes wiping out 4.2 billion in market value

(courtesy zerohedge)

China’s Largest Dairy Operator Suddenly Crashes 90% To Record Low, Muddy Waters Says “Worth Close To Zero”

In December 2016, Muddy Waters’ Carson Block said China’s largest dairy farm operator, Hong-Kong listed China Huishan Dairy Holdings Co., is “worth close to zero” and questioned its profitability in a report. Today, with no catalyst, it suddenly almost is. The stock collapsed over 90% in minutes to a record low.

The sudden crash wiped out about $4.2 billion in market value in the stock, which is a member of the MSCI China Index.

In December, Muddy Waters alleged that Huishan had been overstating its spending on its cow farms by as much as 1.6 billion yuan to “support the company’s income statement.” The report also alleged that the company made an unannounced transfer of a subsidiary that owned at least four cow farms to an undisclosed related party and Muddy Waters concluded that Chairman Yang Kai controls the subsidiary and farms. Those findings came from several months of research including visits to 35 farms and five production facilities, drone flyovers of Huishan sites and interviews with alfalfa suppliers, according to the report. Muddy Waters said it has shorted Huishan’s stock.

“It will be even harder for Huishan to get funded in the capital market after the report, amid a couple of earlier allegations that have raised some red flags to investors,” said Robin Yuen, an analyst at RHB OSK Securities Hong Kong Ltd. Still, Huishan’s shares and operations are unlikely to “collapse” due to its high share concentration and sufficient cash flow generated by its dairy business, he said by telephone.

About 73 percent of Huishan’s shares are held by Champ Harvest Ltd., a company that’s in turn 90-percent owned by Yang. A buying spree by Yang had supported the shares last year, making it a painful trade for short sellers. A one-year rally of about 80 percent through a peak in June had made the shares expensive.

Well that is all over now!!

END

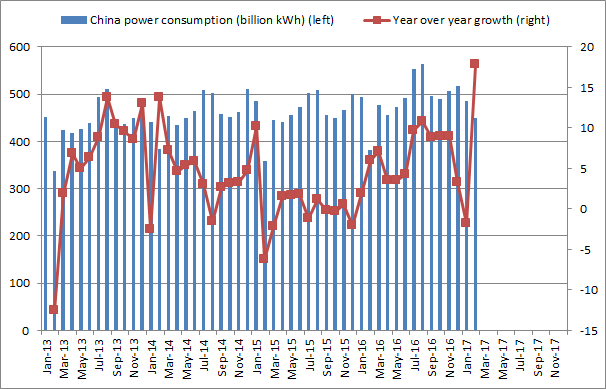

We have already reported to you the huge withdrawals of gold from the Shanghai Gold Exchange and that generally equals demand. The total reported to you two weeks ago for February was 179 tonnes.

However the following is very interesting: a huge increase in hydro consumption. That generally bodes well for commodities

(Katchum/seeking Alpha)

China’s Economy Explodes In February 2017

Mar. 24, 2017 5:23 AM ET

1 comment |Includes: SPDR Gold Trust ETF (GLD)

China’s February 2017 power consumption exploded. I have never seen such a large spike.

This means that there is a high probability that China’s GDP growth will accelerate and this will bode well for commodities. We’ll keep monitoring this trend.

This trend is confirmed by the record high Shanghai gold withdrawals in February 2017.

Something happened in February…

4. EUROPEAN AFFAIRS

Switzerland

The Central Bank of Switzerland spent a mammoth 68 billion dollars worth of Euros in an attempt to keep the Swiss Franc from rising against the Euro.

(courtesy zero hedge)

SNB Spent $68 Billion On Currency Manipulation In 2016

While Donald Trump has repeatedly expressed his displeasure with China for manipulating its currency, he appears to have recently figured out that over the past 2 years Beijing has been spending hundreds of billions in dollar to strengthen, not weaken, the Yuan and to halt the ~$1 trillion in capital flight from China. But while everyone knows that the biggest currency manipulation in the world, and perhaps the Milky Way galaxy is Japan, which now owns 40% of all JGBs in its ongoing attempt to pressure the Yen lower and explains why Abe was trembling when he met with Trump, terrified the US president would tell him to stop, one place where Trump may want to look is Europe’s famously “neutral” country, which however continues to be quite bellicose when it comes to currency warfare. Overnight, the SNB announced that in 2016 it spent 67.1 billion Swiss francs, or $67.6 billion, to purchase foreign currencies in an effort to weaken its currency.

The amount, published in the central bank’s annual report on Thursday, was roughly CHF20 billion lower than the 2015 total of 86.1 billion francs and a record of 188 billion spent in 2012. What is notable is that in 2015, the Swiss National Bank ended its 1.20 EURCHF peg, which ended up costing the SNB tens of billions in FX losses.

As shown in the chart below, the SNB has used interventions for the better part of a decade to keep the franc, Europe’s preeminent flight to safety currency, in check and lessen the risk of deflation. After it gave up its currency cap in early 2015, the SNB has also relied on a negative deposit rate to counter appreciation pressure. It reaffirmed that two-pillar policy stance last week.