Gold: $1275.30 UP $4.00

Silver: $18.28 UP 5 cents

Closing access prices:

Gold $1286.90

silver: $18.49!!!

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

SHANGHAI GOLD FIX: FIRST FIX 10 15 PM EST (2:15 SHANGHAI LOCAL TIME)

SECOND FIX: 2:15 AM EST (6:15 SHANGHAI LOCAL TIME)

SHANGHAI FIRST GOLD FIX: $1284.17 DOLLARS PER OZ

NY PRICE OF GOLD AT EXACT SAME TIME: 1277.50

PREMIUM FIRST FIX: $6.67

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

SECOND SHANGHAI GOLD FIX: $1284.60

NY GOLD PRICE AT THE EXACT SAME TIME: 1274.70

Premium of Shanghai 2nd fix/NY:$9.90

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

LONDON FIRST GOLD FIX: 5:30 am est 1272.30

NY PRICING AT THE EXACT SAME TIME: 1272.95

LONDON SECOND GOLD FIX 10 AM: 1274.30

NY PRICING AT THE EXACT SAME TIME. 1274.60

For comex gold:

APRIL/

NOTICES FILINGS TODAY FOR APRIL CONTRACT MONTH: 2 NOTICE(S) FOR 200 OZ.

TOTAL NOTICES SO FAR: 623 FOR 62,300 OZ (1.9378 TONNES)

For silver:

For silver: APRIL

0 NOTICES FILED TODAY FOR NIL OZ/

Total number of notices filed so far this month: 744 for 3,720,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

END

The open interest in silver continues to advance with today’s reading just over 220,000 contracts or about 4,000 contracts below the record set last year. The price of silver is a good $2.00 below the price when the record OI was set.

Late in the day, three important developments:

- Trump wanted a lower dollar with lower interest rates

- North Korea’s Kim stated that there is going to be a big event

- Talks with the Russia’s Lavrov and Putin did not go off too well

gold shot straight up to $1286.00 and silver is now trading at $18.49

The bankers sure have their work cut out for them. If they cannot contain gold and silver prices their derivatives will blow up!

Since gold and silver made their big move after the comex closed, I do not think that the OI’s for both gold and silver will advance to a higher degree. However I may be wrong. I will know let tonight…

Let us have a look at the data for today

.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total open interest ROSE BY ONLY 496 contracts UP to 220,172 DESPITE THE HUGE RISE IN PRICE ( 34 CENTS) WITH RESPECT TO YESTERDAY’S TRADING. THE HEDGE FUNDS (MANAGED MONEY) CONTINUE TO REMAIN STEADFAST WITH THEIR POSITIONS ON DOWNDRAFT DAYS WHILE SLOWLY ADDING TO THEIR LONGS ON GOOD DAYS. THE BANKERS ARE DESPERATELY TRYING TO COVER THEIR EVER BURGEONING SHORTS (OVER 555 MILLION OZ) BUT TO NO AVAIL. IT IS BECOMING ALMOST IMPOSSIBLE FOR THE BANKERS TO SUPPLY THE NECESSARY PAPER. In ounces, the OI is still represented by just OVER 1 BILLION oz i.e. 1.100 BILLION TO BE EXACT or 157% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT MARCH MONTH/ THEY FILED: 0 NOTICE(S) FOR NIL OZ OF SILVER

In gold, the total comex gold ROSE BY GIGANTIC 22,742 contracts WITH THE RISE IN THE PRICE OF GOLD ($20.00 with YESTERDAY’S TRADING). The total gold OI stands at 456,131 contracts.

we had 2 notice(s) filed upon for 200 oz of gold.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD:

We had no changes in tonnes of gold at the GLD:

Inventory rests tonight: 842.41 tonnes

.

SLV

We had no changes in silver inventory at the SLV today/

THE SLV Inventory rests at: 328.201 million oz

end

.

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in silver ROSE BY ONLY 496 contracts UP TO 220,172 DESPITE THE HUGE RISE IN SILVER YESTERDAY ( 34 CENTS). We no doubt had some attempted short covering but the longs keep piling on making it difficult for them to cover. Our managed money sector (the hedge funds) continue to remain steadfast in their conviction not to play (give up their longs) when the bankers decide to raid. On good days,like yesterday, they slowly add to their positions. Whereas the bankers could not supply the necessary silver paper they found no problem in supplying a massive 22,742 contracts as the gold OI rose to 456,131 WITH THE RISE IN THE PRICE OF GOLD ($20.00 YESTERDAY’S TRADING).

(report Harvey

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)Late TUESDAY night/WEDNESDAY morning: Shanghai closed DOWN 15.13 POINTS OR 0.460%/ /Hang Sang CLOSED UP 225.94 POINTS OR .93% . The Nikkei closed DOWN 195.26 OR 1.04% /Australia’s all ordinaires CLOSED UP 0.07%/Chinese yuan (ONSHORE) closed UP at 6.8938/Oil UP to 53.63 dollars per barrel for WTI and 56.44 for Brent. Stocks in Europe MOSTLY MIXED ..Offshore yuan trades 6.8989 yuan to the dollar vs 6.8938 for onshore yuan.FOR THE FIRST TIME IN OVER TWO MONTHS THE OFFSHORE IS WEAKER TO THE ONSHORE YUAN/ ONSHORE YUAN SLIGHTLY STRONGER AND THE OFFSHORE YUAN ALSO A LITTLE STRONGER AND THIS IS COUPLED WITH THE NO CHANGE ON THE DOLLAR.

3a)THAILAND/SOUTH KOREA/NORTH KOREA

b) REPORT ON JAPAN

JAPAN/NORTH KOREA/USA

The USA sends a nuclear sniffer aircraft that specializes in detecting radioactive debris after a detonation of a nuclear device to Okinawa Japan as the parties prepare for potential nuclear tests in the region. Tensions are coming to a boil

( zero hedge)

c) REPORT ON CHINA

i)CHINA/USA/NORTH KOREA

Trump calls Xi who tells him not to do anything unilaterally. Tensions boil

( zero hedge)

ii) China warns North Korea that they are at the tipping point and they threaten with ‘”never before seen measures”

( zero hedge)

4. EUROPEAN AFFAIRS

Mish Shedlock analyzes the upcoming French elections and it looks like it could be any combination that will win the first round and enter the final round

( Mish Shedlock/Mishtalk)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

i)SYRIA/RUSSIA/USA

Finally a refreshing candid discussion on what happened with the “chemical bomb”

there are two scenarios according to Peter Ford, British ambassador to Syria:

“What’s needed is an investigation, because there are two possibilities for what happened. One is the American version, that Assad dropped chemical weapons on this locality. The other version is that an ordinary bomb was dropped and it hit a munitions dump where jihadis were storing chemical weapons. We don’t know which of these two possibilities is the correct one. “

( yournewswire.com/BBC)

ii)RUSSIA/USA

Putin warns Trump as relations under the current uSA administration have collapsed. Tillerson gets a frigid reception

( zero hedge)

iii)Russia states that it will not back away from supporting Assad. Putin warns Tillerson that the USA must not strike Syria again

( zerohedge)

iv)Rex Tillerson is meeting Putin after the Russian President initially stated that he would not meet the Sec.of State

( zerohedge)

v)Lavrov speaks and he totally rejects the USA’s “hysterical campaign” of interventionism.

( zero hedge)

6 .GLOBAL ISSUES

CANADA

A good description of Toronto’s housing bubble and since this is my home town I can verify what is going on as foreign buyers snatch up homes. This past year the average price of a home in Toronto went up 30%.

( zero hedge)

7. OIL ISSUES

i)We have a secondary OPEC source which shows that Saudi oil production rose for the 2nd straight month.

( zerohedge)

ii)Oil drops as crude production hits a 20th month high and bottleneck occurring at Cushing Oklahoma

( zero hedge)

8. EMERGING MARKETS

9. PHYSICAL MARKETS

i)I saw this yesterday, but I thought the huge difference was a typo so I just took the actual trading price at 10 am as the fix. The fix was actually 12 dollars lower than what was trading and this cannot be explained

( zero hedge)

ii)Many of our readers are shareholders of Agnico Eagle, probably one of the better mining companies out there. JPMorgan has now upgraded their version of the company to overweight as they announced Meliadine into production with a 14 year lifespan.

( Toronto’s Financial Post)

iii)I rarely use technical analysis when I discuss the precious metals due to constant manipulation.. However if you use long term charts, then you can glean some interesting things

( Steve St Angelo/SRSRocco Report)

iv) Iron ore prices fall again in China as the glut of steel inside China is huge as these guys try to unload much of that commodity on the rest of the world:

( zero hedge)

v)March saw a huge jump in gold imports due to festival wedding demand. We will get official data shortly

( Bloomberg)

10. USA stories

i)THE BIG NEWS OF THE DAY: TRUMP CRASHES THE DOLLAR BY SAYING IT IS GETTING TOO STRONG!!

(courtesy zero hedge)

ii)TRUMP BACKTRACKS AGAIN: HEALTH CARE WILL COME BEFORE TAX REFORM

GOOD GRIEF!!

( zerohedge)

iii)Trump tells Bannon to straightened out your differences with Kushner or he will

( zero hedge)

iv)Trump reverses again on NATO: it is no longer obsolete:

( zero hedge)

Let us head over to the comex:

The total gold comex open interest ROSE BY 22,742 CONTRACTS UP to an OI level of 456,131 WITH THE RISE IN THE PRICE OF GOLD ( $20.00 with YESTERDAY’S trading). The bankers were certainly not shy in supplying the necessary paper to our newbie longs. We are now in the contract month of APRIL and it is one of the BETTER delivery months of the year. In this APRIL delivery month we had A GAIN OF 173 contract(s) RISING TO 1,922. We had 13 notices served yesterday so we GAINED 160 contracts or 16,000 oz will stand for delivery in the active delivery month of April.

At the end of April/2016 only 12.3917 tonnes stood for physical delivery, although 21.306 tonnes stood initially at the beginning of April 2016.

The non active May contract month GAINED 170 contract(s) and thus its OI is 2533 contracts. The next big active month is June and here the OI ROSE by 20,676 contracts UP to 328,857.

We had 2 notice(s) filed upon today for 200 oz

We are in the NON active delivery month is APRIL Here the open interest lost 96 contracts. We had 103 notices filed yesterday so we GAINED 7 contracts or an additional 35,000 oz will stand for delivery.

The next active contract month is May and here the open interest LOST 4535 contracts DOWN to 137.418 contracts which is astonishingly high. It is this front month that the crooked bankers are targeting as they must be frightened to see such a mammoth amount of contracts still standing for metal. The non active June contract GAINED 129 contracts to stand at 312. The next big active month will be July and here the OI gained 4394 contracts up to 52,833.

FOR COMPARISON SAKE, ON APRIL 12/2016 WE HAD 98,575 CONTRACTS STANDING FOR DELIVERY. SO YOU CAN VISUALIZE FOR YOURSELF THE HUGE DIFFERENCE BETWEEN 2016 AND THIS YEAR.

For those keeping score, the initial amount of silver oz that stood for delivery for the May 2016 contract month: 28.01 million oz. By conclusion of the month only 13.58 million oz stood and the rest was cash settled.(EFP ROUTE)

.

We had 0 notice(s) filed for NIL oz for the APRIL 2017 contract

VOLUMES: for the gold comex

Today the estimated volume was 112,960 contracts which is fair.

Yesterday’s confirmed volume was 300,367 contracts which is very good.

volumes on gold are STILL HIGHER THAN NORMAL!

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz |

11,721.496 oz

SCOTIA

|

| Deposits to the Dealer Inventory in oz | nil oz |

| Deposits to the Customer Inventory, in oz |

nil

|

| No of oz served (contracts) today |

2 notice(s)

200 OZ

|

| No of oz to be served (notices) |

1920 contracts

19,200 oz

|

| Total monthly oz gold served (contracts) so far this month |

623 notices

62,300 oz

1.93779 tonnes

|

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | 443,159.3 oz |

Today, 0 notice(s) were issued from JPMorgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equates to 2 contract(s) of which 0 notices were stopped (received) by jPMorgan dealer and 1 notice(s) was (were) stopped/ Received) by jPMorgan customer account.

March 2016: 2.311 tonnes (March is a non delivery month)

| Silver | Ounces |

| Withdrawals from Dealers Inventory | nil |

| Withdrawals from Customer Inventory |

1,267,401.980 oz

SCOTIA

CNT

DELAWARE

|

| Deposits to the Dealer Inventory |

nil oz

|

| Deposits to the Customer Inventory |

1,188,305.593 oz

JPMorgan

DELAWARE

|

| No of oz served today (contracts) |

0 CONTRACT(S)

(NIL OZ)

|

| No of oz to be served (notices) |

65 contracts

(325,000 oz)

|

| Total monthly oz silver served (contracts) | 744 contracts (3,720,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month | 6,524,172.0 oz |

FOR COMPARISON

Initially for the April 2016 contract, 1,180,000 oz stood for delivery. At the end of April 2016: 6,775,000 oz stood as bankers needed much silver to fill major holes elsewhere.

NPV for Sprott and Central Fund of Canada

will update later tonight the central fund of Canada figures

Sprott’s hostile 3.1 billion bid to take over Central Fund of Canada

(courtesy Sprott/GATA)

Sprott makes hostile $3.1 billion bid for Central Fund of Canada

Submitted by cpowell on Thu, 2017-03-09 01:19. Section: Daily Dispatches

From the Canadian Press

via Canadian Broadcasting Corp. News, Toronto

Wednesday, March 8, 2017

http://www.cbc.ca/news/canada/calgary/sprott-takeover-bid-central-fund-c…

Toronto-based Sprott Inc. said Wednesday it’s making an all-share hostile takeover bid worth $3.1 billion US for rival bullion holder Central Fund of Canada Ltd.

The money-management firm has filed an application with the Court of Queen’s Bench of Alberta seeking to allow shareholders of Calgary-based Central Fund to swap their shares for ones in a newly-formed trust that would be substantially similar to Sprott’s existing precious metal holding entities.

The company is going through the courts after its efforts to strike a friendly deal were rebuffed by the Spicer family that controls Central Fund, said Sprott spokesman Glen Williams.

“They weren’t interested in having those discussions,” Williams said.

Sprott is using the courts to try to give holders of the 252 million non-voting class A shares a say in takeover bids, which Central Fund explicitly states they have no right to participate in. That voting right is reserved for the 40,000 common shares outstanding, which the family of J.C. Stefan Spicer, chairman and CEO of Central Fund, control.

If successful through the courts, Sprott would then need the support of two-thirds of shareholder votes to close the takeover deal, but there’s no guarantee they will make it that far.

“It is unusual to go this route,” said Williams. “There’s no specific precedent where this has worked.”

Sprott did have success last year in taking over Central GoldTrust, a similar fund that was controlled by the Spicer family, after securing support from more than 96 percent of shareholder votes cast.

The firm says Central Fund’s shares are trading at a discount to net asset value and a takeover by Sprott could unlock US$304 million in shareholder value.

Central Fund did not have any immediate comment on the unsolicited offer. Williams said Sprott had not yet heard from Central Fund on the proposal but that some shareholders had already contacted them to voice their support.

Sprott’s existing precious metal holding companies are designed to allow investors to own gold and other metals without having to worry about taking care of the physical bullion.

end

And now the Gold inventory at the GLD

APRIL 12/no changes in gold inventory at the GLD/Inventory rests at 842.41 tonnes

April 11/a huge deposit of 4.12 tonnes into inventory/Inventory rests at 842.41 tonnes

this would no doubt be a paper gold entry. It would be difficult to find that amount of physical gold.

April 10/1.77 tonnes added into inventory at the GLD/inventory rests at 838.29 tonnes

April 7/a small withdrawal of .28 tonnes from the GLD/Inventory rests at 836.49 tonnes

April 6/no change in gold tonnage at the GLD/Inventory rests at 836.77 tonnes

April 5/no change in gold tonnage at the GLD/Inventory rests at 836.77 tonnes

April 4/no change in gold tonnage at the GLD/Inventory rests at 836.77 tonnes

April 3.2017: a huge deposit of 4.45 tonnes of gold into the GLD/Inventory rests at 836.77 tonnnes

March 31/another withdrawal of 1.19 tonnes of gold inventory fro the GLD/this inventory would no doubt be heading for Shanghai/GLD inventory: 822.32 tonnes

March 30/no changes in gold inventory at the GLD/Inventory rests at 833.51 tonnes

March 29/a withdrawal of 1.78 tonnes of gold out of the GLD/Inventory rests tongith at 833.51 tonnes

March 28/this is good!! A deposit of 2.67 tonnes of gold into the GLD/Inventory rests at 835.29 tonnes.

March 27/no changes in gold inventory at the GLD/Inventory rests at 832.62 tonnes

March 24/another withdrawal of 1.78 tonnes from the GLD/Inventory rests at 832.62 tonnes

March 23/no change in gold inventory at the GLD/Inventory rests at 834.40 tonnes

March 22/no changes in gold inventory at the GLD/Inventory rests at 834.40 tonnes

March 21/a deposit of 4.15 tonnes of gold into the GLD/Inventory rests at 834.40 tonnes

March 20/WE HAD A MASSIVE 6.81 TONNE WITHDRAWAL FROM THE GLD/INVENTORY RESTS AT 830.25 TONNES/THIS GOLD MUST BE ON ITS WAY TO SHANGHAI. WITH GOLD RISING THESE PAST FEW DAYS, IT MAYS NO SENSE WHATSOEVER ON GOLD LIQUIDATION.

March 17/a huge withdrawal of 2.37 tonnes from the GLD/Inventory rests at 837.06 tonnes

March 16/no changes in gold inventory at the GLD/Inventory rests at 839.43 tonnes

March 15/ANOTHER HUGE DEPOSIT OF 4.44 TONNES/inventory rests at 839.43 tonnes

March 14/strange they whack gold and yet the GLD adds 2.93 tonnes of gold./inventory rests at 834.99 tonnes

March 13/a deposit of 6.78 tonnes of gold into the GLD/Inventory rests at 832.03 tonnes

March 10/ a withdrawal of 4.886 tonnes from the GLD/Inventory rests at 830.25

this tonnage no doubt is off to Shanghai

March 9/a withdrawal of 2.67 tonnes from the GLD/Inventory rests at 834.10

March 8/no change in gold inventory at the GLD/inventory rests at 836.77 tones

end

Now the SLV Inventory

April 12/no changes in inventory at the SLV/Inventory rests at 328.201 million oz/

April 11/a paper deposit of 11.131 million oz into the SLV/no doubt yesterday’s entry of a withdrawal of 11.231 million oz was in error/328.201 million oz

April 10/ a paper withdrawal of 11.231 million oz of silver from the SLV and this silver was used in the raid today. Inventory rests at 317.231 million oz

April 7./ a withdrawal of 947,000 oz of silver from the SLV/Inventory rests at 328.201 million oz.

April 6/a tiny withdrawal of 136,000 oz of silver from the SLV/Inventory rests at 329.148 million oz

April 5/ a withdrawal of 1.042 million oz from the SLV/Inventory rests at 329.284 million oz

April 4/no change in inventory at the SLV/Inventory rests at 330.326 million oz/

April 3.2017; a withdrawal of 568,000 oz from the SLV/Inventory rests at 330.326

million oz/

Major gold/silver trading/commentaries for WEDNESDAY

GOLDCORE/BLOG/MARK O’BYRNE.

Gold Surges Above Key 200 Day Moving Average $1270 Level

– Gold price breaks above key 200-day moving average

– Gold hits 5-month high on back of investor nervousness

– Safe haven has 10% gains in 2017 after 9% gains in 2016

– Gold options signal more gains as ETF buying increases

– Geopolitical uncertainty over North Korea & Middle East

– Tensions high -World awaits US move & Russia response

– Russia says chemical attack was terrorist “false flag”

– Poor March jobs report shows US economy vulnerable

– French elections still tight and Le Pen still has chance

Gold prices surged another 2% to a five-month high above $1,270 amidst geopolitical uncertainty and weak US economic data.

The break above the 200-day moving average has cleared the way for a run towards $1,300/oz. It means that gold continues to be one of the best performing assets in 2017 with gains of 10.3% year to date building on the 9% gains in 2016.

Gold’s move was a traditional flight to safety following the US’ missile attack on Syria and Trump making aggressive sounds regarding intervention against North Korea including tweets.

The weak jobs report also prompted fears that future Fed interest rate hikes could be delayed or slowed and this has provided further support for the price of gold.

Tensions between Syria, Russia, North Korea and the US underline the serious geo-political risks. There is the real risk of a serious military confrontation. This is creating uncertainty which is an environment that serves gold best.

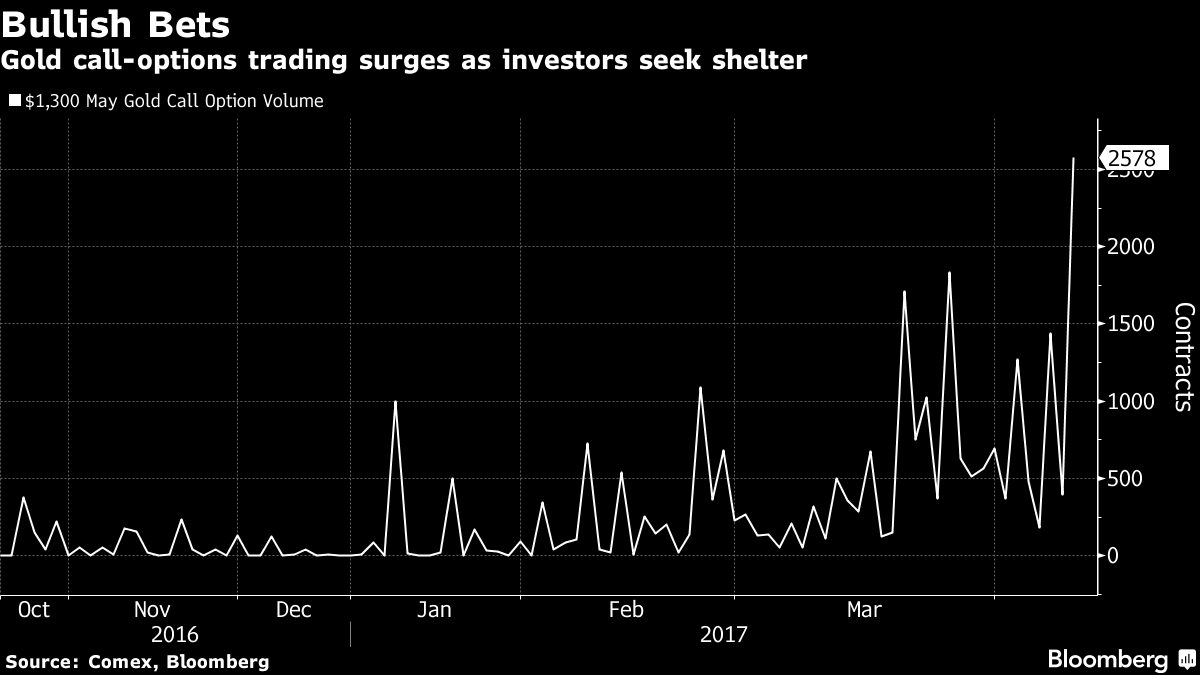

These risks have led to very bullish activity in the options market with a surge in call option gold buying and gold ETF buying.

As reported by Bloomberg:

Gold options are signaling there’s more room to run for bulls.

Prices and volumes surged Tuesday on calls giving holders the right to buy bullion at higher prices. As of 11:21 a.m. in New York, trading in the most-active option was 10 times Monday’s total, and price swings on options were at the highest in three months. Investors also returned to the biggest exchange-traded fund backed by the metal.

US TV hosts, Putin and Trump – all finger pointing

Since the chemical attack in Syria last week, finger pointing over who is responsible for the attack (and why) has been going strong.

Last week U.S. Senator and ex-Presidential candidate Ron Paul questioned the logic of an Assad-instructed chemical attack. With both ISIS and Al-Qaeda in retreat, what were Assad’s motives for making such a decision, asked Paul.

“It looks like maybe somebody didn’t like that so there had to be an episode,” said Paul, asking, “who benefits?”

“It doesn’t make any sense for Assad under these conditions to all of a sudden use poison gases – I think there’s zero chance he would have done this deliberately,” said Paul.

Prior to the chemical attacks it did appear that the US would be taking a side-seat when U.S. Secretary of State Rex Tillerson said, “The longer-term status of President Assad will be decided by the Syrian people.”

But then a chemical attack followed and theories abound on why it happened.

Following the chemical attack, last week, Putin called the US missile strike against Syria “an act of aggression against a sovereign state delivered in violation of international law under a far-fetched pretext.” By Friday afternoon Russian warships were headed toward the U.S. Navy warships that launched missiles.

The FT and the Guardian report today that Putin has claimed that Russia has evidence that the chemical attack was opposition rebel or terrorist led and designed to frame Syria’s President and to entice the United States into the war.

“We have information from different sources that these provocations – I cannot call them otherwise – are being prepared in other regions of Syria, including in the southern suburbs of Damascus where there are plans to throw some substance and accuse the official Syrian authorities.”

Putin also dismissed claims by the US that they attacked a Syrian air base due to presence of weapons of mass destruction, saying that we have seen such claims already in Iraq in 2003.

Bobble heads and TV hosts

In his disgust that NATO had not ruled that the US missile attack was a breach of international law, Putin called them “bobble heads.”

Last night the White house went on to accuse Moscow of releasing “false narratives” to mislead the world about the chemical attack in Syria last week.

Elsewhere in the US, MSNBC’s Lawrence O’Donnell told viewers a rumour he’d heard that Putin had told Assad to carry out the chemical attack in order to provoke a military reposes from Trump. Thereby, dispelling rumours that the US President and Putin are too close.

His evidence for this? He has none:

“It’s perfect, what you won’t hear is proof that that scenario that I have just outlined is impossible, because with Donald Trump anything is possible.”

Later today Russian Foreign Minister Sergey Lavrov will meet Mr Tillerson, US Secretary of State. Some hope should be taken from the fact that Tillerson is heading to Russia although he is unlikely to persuade Putin to distance himself from Assad.

Both the US and UK have failed to persuade G7 foreign ministers to impose new sanctions on Russia and Syria.

North Korean posturing and peacocking

If events in Syria means that you have missed what has been happening with North Korea then the following Trump tweets that North Korea was “looking for trouble” and that the United States would “solve the problem” with or without China’s help, will give you some indication.

Chinese government-influenced Global Times said Beijing would support stiffer UN sanctions, including “strictly limiting” oil exports to North Korea should it conduct a nuclear test. “China, too, can no longer stand the continuous escalation of the North Korean nuclear issue at its doorstep,” the newspapers editorial said. “Instead of accepting a situation that continues to worsen, putting an end to this is more in line with the wish of the Chinese public.”

For now, the world’s eyes are on Syria, with some reassurance about Trump’s upcoming conversation with China. However, it is right be nervous of macho strong men who have access to nuclear weapons.

War! What is it good for? Absolute uncertainty!

Whilst the North Korea situation is perhaps being handled with slightly more measure than the Middle East, someone is going to war and it is on everyone’s minds.

This Google Trends charts shows the ‘interest over time’ in the phrase ‘going to war’, one can clearly see the spike in interest in recent months.

Whichever theory is correct over who is provoking who in Syria (and there is probably some truth in them all) it all serves one purpose in the wider world – to build up the uncertainty felt across the globe.

We are seeing a rise in risk aversion across markets. Politicians should be working to reduce risk, however they are all working to their own agendas and, as a result, the levels of risk in the economy are growing.

In recent months we have mentioned uncertainty in relation to European elections, the Brexit vote, and the turbulent Trump Administration. We have also mentioned activity in Syria, North Korea and relations with Russia and in the last week it has all seemingly started to come to a head.

There have long been bad jobs reports or options about what the Fed may or not do. However war in the Middle East, with Russia on the opposite side, whilst the prospect of nuclear war in the background, is not something that we or governments can just push to one side or begin to predict the outcome of.

There is so much that is out of not only our hands but also politicians’ that we know more about what we don’t know than what we do. In times such as these we need to consider our portfolios and ask what we do know about investments.

What has history shown time and time again?

History has shown that in times of both peace and war, there is little we can rely on that will not be manipulated or debased in order to pay for war. However, gold and silver have long been able to hold their own in the backdrop of warring countries, posturing politicians and extreme uncertainty and conflict – indeed they tend to thrive in such conditions.

Gold is performing well and will continue to do so as investors know that it is a hedge and a safe haven when we are uncertain what lies on the horizon.

Those who began to buy gold this week are becoming increasingly aware of this, and this is why we advise you to own some physical gold in a safe jurisdiction in allocated and segregated storage.

END

I saw this yesterday, but I thought the huge difference was a typo so I just took the actual trading price at 10 am as the fix. The fix was actually 12 dollars lower than what was trading and this cannot be explained

(courtesy zero hedge)

Something Strange Happened During Yesterday’s London PM Gold Fix

Something strange happened during yesterday’s afternoon London fix: as gold was surging on a spike in geopolitical fears, which slammed the USDJPY below 110 and sent traders scrambling into safe assets such as TSYs, London’s gold price benchmark waterfalled lower before fixed some $12 below the spot price on Tuesday afternoon as “the auction appeared to become locked in a downward spiral”, according to Reuters.

From an initial $1,265.75, close to the spot price at 3pm London time, the auction price ratcheted steadily lower, with the gold price sliding by roughly $1-$2 increments every 30 seconds, before fixing at $1,252.90 in the ninth and final round. From the fifth round to the eighth the bid and offer volumes remained frozen, unable to match.

As Reuters notes, and as shown in the table below taken from the website of the auction’s administrator, Intercontinental Exchange, only five banks took part in the auction on Tuesday afternoon, out of 14

officially accredited participants.

The dramatic divergence between the spot price and the London fixing for Tuesday and several prior days is shown in the chart below.

A chart of recent divergences between the PM fix and spot prices shows that yesterday’s event is not isolated, and has in fact taken place on several occasions in the past, if not to the same extent.

The fat finger, or perhaps simple manipulation for which the London Fix has received so much media scrutiny over the past 4 years and prompted a thorough overhaul of the gold fixing process, came a day after ICE introduced clearing for the LBMA Gold Price auction, which sets the benchmark used by gold consumers and producers worldwide, before several participating banks had the necessary systems in place. As a result, China Construction Bank, Societe Generale, Standard Chartered and UBS are yet to confirm a date for their participation in the cleared auction, according to a notice on the LBMA’s website.

So what caused the waterfall selling during the PM Fix, which could have been a simple fat finger, or alternatively a coordinated attempt to prevent the fix from hitting a certain threshold price which would havestopped out one or moreLondon fix members from existing stop positions? It is unclear: according to Reuters, the ICEdeclined to comment. The LBMA, which owns the intellectual property rights to the auction, was not immediately available to comment. We don’t expect this particular gold pricing “incident” to get much media focus.

end

Many of our readers are shareholders of Agnico Eagle, probably one of the better mining companies out there. JPMorgan has now upgraded their version of the company to overweight as they announced Meliadine into production with a 14 year lifespan.

(courtesy Toronto’s Financial Post)

Agnico Eagle Mines Ltd upgraded, ‘well positioned for the new world of gold’

Agnico Eagle Mines Ltd. was upgraded to overweight from neutral at J.P. Morgan following a pullback in the stock that came despite ongoing progress in the company’s reserve replacement program.

“North American precious metals equities seem conflicted,” analyst John Bridges said in a research note.

He pointed out that some investors fear we may be in the midst of a 2016 reprise, when gold stocks began the year weak due to fears about rising interest rates, and then rallied as these concerns dissipated.

Others are worried that after many miners reported reserve declines at the end of the year, the impressive run of cost performance may be coming to an end.

While Bridges found more evidence of the long-term challenges miners face at the recent PDAC conference in Toronto, the analyst believes Agnico Eagle deserves more attention.

That stems from its well-established track record of finding new gold reserves at reasonable costs, as demonstrated by its modest 225 million share count and disciplined dividend payments.

“Agnico is well positioned for the new world of gold,” Bridges said. “The company has several long-life assets, and its overall production rate should be sustainable and could grow.”

end

I rarely use technical analysis when I discuss the precious metals due to constant manipulation.. However if you use long term charts, then you can glean some interesting things

(courtesy Steve St Angelo/SRSRocco Report)

CRITICAL SHORT-TERM SILVER PRICE TREND: Put into Perspective

By SRSROCCO April 11, 2017

The current silver price trend is once again at a critical juncture. It has been four years since the price of silver crossed an important trend line. However, the present setup will result in either another correction lower, or a much higher price.

This is a ten-year chart which shows the current trading setup for silver:

The blue line represents the 50 month moving average,and the red line, the 200 month moving average. Since the price of silver fell below the blue line at the beginning of 2013, its support has been the red line. It did not fall below the red line at its low in the beginning of 2016 and has bounced twice off the blue line, which is now acting as resistance by traders.

Currently, the silver price is hitting up against the 200 month moving average blue resistance line. If the silver price breaks above and closes above it, we could see a much higher silver price. However, if does not, then we could experience another short-term correction.

Looking at the current silver COT REPORT, there is a record commercial short position against silver. The Commercial short positions are from the large bullion banks:

The red lines at the bottom of the chart represent the total Commercial net short positions in silver. As we can see, it is at a record high. This high Commercial net short silver position normally means the silver price will likely head lower…. over the short term.

That being said, I have become less concerned about the SHORT-TERM silver price movement. While some investors are able to trade and make money trading silver, I am not one of them. My focus on silver is to hold onto it for the LONGER-TERM. Short term silver price movements are not a concern when we focus on the disintegrating energy and economic fundamentals.

Some precious metals investors have become frustrated or complacent due to the low silver price. This is understandable because some may have purchased silver at a higher price and feel as if they made the wrong investment decision. However, acquiring physical silver should be done over a period of time and be held as a SAFE HAVEN for the future…. just like any other retirement plan.

The BIG difference between owning physical silver and most paper retirement plans, is that the value of most retirement assets will likely plunge in value in the future while the price of silver will likely be much higher. Unfortunately, most investors are either too impatient, fickle or lack the ability to understand this LONG-TERM fundamental setup.

Lastly, if Americans who are mainly invested in STOCKS, BONDS and REAL ESTATE, diversified into a small 2-5% allocation of physical gold and silver, it would totally overwhelm the market…. forget about the rest of the 7 billion people in the world.

Which is precisely why the MANIPULATION of gold and silver has been done mainly through psychology, rather than price. Why? Because the current algorithm pricing mechanism for gold and silver is based on their cost of production. So, to see a current $18 silver price and $1,275 is not that ridiculous if it is based upon what it cost to produce them.

But, gold and silver behave much differently than most commodities, energy, good and services. While most commodities and energy are consumed, a lot of gold and silver are saved. So, gold and silver must be valued differently. If individuals realized the dire energy predicament we are facing in the future, they would realize it would be prudent to own some physical gold and silver. However, they are being mislead by the Mainstream media, so they cannot really be blamed.

When the markets finally crack…. the Fed and Central Banks may have one last RABBIT to pull out of the hat, and that would be a HYPERINFLATIONARY event. Unfortunately, this will not last long and will end quite badly.

Thus, when we reach this point… there is NO GOING BACK. The United States and world will look like a much different place and at that point, it will be too late to sell paper and buy gold and silver.

END

March saw a huge jump in gold imports due to festival wedding demand. We will get official data shortly

(courtesy Bloomberg)

India Gold Imports Said to Jump 582% on Festival, Wedding Demand

Bloomberg

* Consumption has been recovering from seven-year low in 2016

*Purchases from overseas fall 20% in the year ended March 31

Gold imports by India are said to have jumped almost seven-fold in March from a year earlier as jewelers stocked up anticipating a demand recovery during the wedding season that began this month and the auspicious Hindu gold-buying day of Akshaya Tritiya.

Shipments advanced 582.5 percent to 120.8 metric tons last month from a year earlier, according to a person familiar with provisional data from the finance ministry, who asked not to be identified as the data aren’t public. Imports dropped 20 percent to 716.4 tons in the year ended March 31. Finance Ministry spokesman D. S. Malik declined to comment on the data.

Consumption in India, the world’s second-biggest gold buyer, has been recovering after a falling to the lowest level in seven years in 2016. A strike in March last year after a levy was introduced on jewelry produced and sold in India reduced consumption that was further dented by the government’s decision to withdraw high-denomination currency notes. March usually sees a spurt in gold imports due to warehouse clearance and re-stocking, the person said.

“Imports were down till January due to demonetization, so now people are re-stocking,” Mehul Choksi, chairman of jewelry store chain Gitanjali Gems Ltd., said by phone from Mumbai.

Trade data in India has been encouraging so far and suggests that the challenges to purchases due to demonetization are probably fading faster than initially anticipated, UBS AG said in a report on April 5. Purchases are expected to pick up heading into the Akshaya Tritiya festival that falls toward the end of April this year, while import data for the next couple of months will be a good gauge of underlying demand, according to the report.

Indians buy gold during festivals and for marriages as part of the bridal trousseau or as gifts, and the nation imports almost all the gold it consumes.

-END-

Iron ore prices fall again in China as the glut of steel inside China is huge as these guys try to unload much of that commodity on the rest of the world:

(courtesy zero hedge)

Commodity Carnage Crushes Trumpflation Hopes: “Everyone’s Nervous The Bottom Is Falling Out”

Another night of ugliness in Asia as the ‘froth’ is blasted out of the exuberant hot-money-chased commodity markets. Chinese steel and iron ore futures tumbled on Wednesday to the lowest prices in months as market sentiment turned bearish on the demand outlook.

As Reuters reports, China’s producer price inflation cooled for the first time in seven months in March, pressured by fears that Chinese steel production is higher than demand, leaving a glut of the metal later this year.

“We’re not seeing much interest on the buy side, everyone is nervous that the bottom is falling out,” said a commodities trader in Perth, Australia, who closely monitors activity on China’s Dalian and Shanghai Futures Exchanges for overseas clients.

The most active rebar contract on the Shanghai Futures Exchange settled 3.5 percent down at 2,893 yuan ($420), the lowest since Feb. 2. The sharp decline in steel futures has tamed buying interest in the physical market as well. Iron ore for delivery to China’s Qingdao port has swung into a bear market, with the price sinking more than 20 percent from its 2017 high in February to $74.38 a tonne, according to Metal Bulletin.

It seems the hopes of Trumpflation (and the fading China credit impulse) has erased growth hope…

END

Your early WEDNESDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight

1 Chinese yuan vs USA dollar/yuan STRONGER 6.8938( REVALUATION NORTHBOUND /OFFSHORE YUAN MOVES STRONGER TO ONSHORE AT 6.8989/ Shanghai bourse DOWN 15.13 POINTS OR 0.60% / HANG SANG UP 225.94 POINTS OR .93%

2. Nikkei closed DOWN 195.26 POINTS OR 1.04% /USA: YEN RISES TO 109.64

3. Europe stocks opened MOSTLY MIXED ( /USA dollar index FALLS TO 100.71/Euro DOWN to 1.0598

3b Japan 10 year bond yield: FALLS TO +.029%/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 109.64/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD FINALLY IN THE POSITIVE/BANK OF JAPAN LOSING CONTROL OF THEIR YIELD CURVE AS THEY PURCHASE ALL BONDS TO GET TO ZERO RATE!!

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 53.63 and Brent: 56.44

3f Gold UP/Yen DOWN

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil UP for WTI and UP for Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund RISES TO +.208%/Italian 10 yr bond yield UP to 2.2311%

3j Greek 10 year bond yield FALLS to : 6.688%

3k Gold at $1274.15/silver $18.36 (8:15 am est) SILVER RESISTANCE AT $18.50

3l USA vs Russian rouble; (Russian rouble DOWN 10/100 in roubles/dollar) 57.07-

3m oil into the 53 dollar handle for WTI and 56 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation (already upon us). This can spell financial disaster for the rest of the world/China forced to do QE!! as it lowers its yuan value to the dollar/GOT SMALL REVALUATION NORTHBOUND

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 109.64 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 1.0078 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.0681 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017 (TODAY)

3r the 10 Year German bund now POSITIVE territory with the 10 year FALLS to +.208%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.296% early this morning. Thirty year rate at 2.930% /POLICY ERROR)GETTING DANGEROUSLY HIGH

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

(courtesy Jim Reid/Bloomberg/Deutsche bank/zero hedge)

Traders “Swoop” On Stocks, Oil Rises For 8th Day But Bonds Still Don’t Buy It

S&P futures are unchanged and Asian stocks closed mixed, however European stocks rebounded for first time this week, led by auto stocks after Daimler’s quarterly profit, as a break in alarming political news prompted traders to “swoop” – as Reuters puts it – on equities, cooling a safe-haven rally that saw the yen and gold at five-month highs and global government bond yields to drop their lowest this year.

Still, with many geopolitical unknowns in the days ahead as well as potential military escalation in North Korea, the mood remained “skittish”, and meant that what looked set to be oil’s longest winning run since August – up for 8 consecutive days, its longest streak in 2017 – has largely gone under the radar.

As DB’s Jim Reid puts it, it has felt quite quiet and orderly this week considering the risk-off tendencies and relatively big spike in volatility. However that might be because of a lack of activity given the pending Easter break. So poor liquidity is probably exacerbating the moves. Add to this the rising geopolitics tensions (North Korea, Syria), slow burning ongoing concerns about Trump trades post the healthcare debacle, and a steady increase of support for Melenchon in the recent French polls making it less certain who’ll contest the final round run-off. For now equity and credit markets remain fairly resilient which reduces the immediate worry but if vol remains elevated at these levels for a few days expect weakness.

This morning in Asia we got the latest inflation data out of China. In terms of the numbers, PPI in March has moderated somewhat after dipping two-tenths to +7.6% yoy (vs. +7.5% expected) following a bit of a levelling out in commodity prices. That said it also marks the seventh consecutive monthly positive print after 54 months of deflation in prices at the factory gate. Meanwhile CPI has edged up one-tenth to +0.9% yoy although did miss slightly relative to expectations for +1.0%, with a -4.4% yoy decline in food prices in particular having an impact.

Bourses in China are a touch weaker although that is the case for much of Asia this morning, if not the rest of the world. Global markets halted their recent declines with an early 0.3 percent rise for Europe’s STOXX 600 share index put it on course for its best day of the month. The rise in oil underpinned energy stocks while banks and carmakers also made ground. MSCI’s broadest index of Asia-Pacific shares outside Japan saw a late rally though Shanghai closed down 0.4 percent as China reported a slight slowdown in producer price inflation. South Korean stocks and the won gained for the first time in seven days. Hong Kong equities erased losses to rally in late trading. The yield on 10-year U.S. notes rose after closing Tuesday below 2.3 percent for the first time in four months. Oil extended its longest winning streak since December. Japan’s Topix fell to the lowest level of the year after the yen breached 110 yen per dollar for the first time since November on Tuesday. A quick breakdown from Bloomberg:

- The Stoxx Europe 600 rose 0.3 percent, with automakers leading gains as Daimler AG’s first-quarter profit almost doubled. Daimler shares rose 1.6 percent.

- Korea’s Kospi rose 0.2 percent, after dropping 2 percent over the previous six sessions. Japan’s Topix fell 1 percent, led by declines in banks, autos and other exporters. South Australia’s S&P/ASX 200 index gained less than 0.1 percent.

- The Hang Seng China Enterprises Index climbed 0.3 percent and the Hang Seng Index jumped 0.6 percent, wiping out earlier losses at the end of the trading day. The Shanghai Composite fell 0.5 percent. Data showed China’s producer price gains slowed last month from a peak in February, tempering the global inflation outlook.

At the same time, volatility is easing after the VIX climbed to a level unseen since November on Tuesday amid escalating global tensions.

“It is a modest rebound,” said Rabobank strategist Philip Marey. “We have discounted much of the news like the conflict between the Americans and the Russian on Syria and Trump’s tweets on North Korea, so maybe its time to move on.”

S&P500 futures are unchanged, having spent the Asian session in the red. Japan’s Nikkei had slid just over 1 percent as a rising yen weighed on exporters’ shares.

However, while stock traders are hoping to BTD, the allure of save havens persists with gold climbing as far as $1,280.30 at one stage, its highest since Nov. 10, while the 10Y TSY was at 2.30% at last check, flirting with the key support ling that has emerged since the Trump election, after dropping to 2.28% overnight.

“A degree of uncertainty has found its way into previously seemingly bulletproof financial markets,” wrote analysts at ANZ. “There is clearly some nervousness out there, with tensions around North Korea ratcheting higher and adding to an already heightened geopolitical environment. Global cyclical assets have not yet responded, but that can’t last.”

In geopolitics, Chinese President Xi Jinping on Wednesday stressed the need for a peaceful solution for the Korean peninsula on a call with U.S President Donald Trump. North Korea has warned of a nuclear attack on the United States at any sign of aggression as a U.S. Navy strike group steamed toward the Korean peninsula – a force Trump described as an “armada”. Japan’s navy also plans joint drills with the U.S. force, sources told Reuters. Trump said in a Tweet that North Korea was “looking for trouble” and the U.S. would “solve the problem” with or without China’s help.

The bellicose language has dragged South Korean stocks and the won to four-week lows and caused jitters across Asia. At the same time, U.S. Secretary of State Rex Tillerson was in Moscow to denounce Russian support for Syria’s Bashar al-Assad, raising the stakes in the Middle East. A joint news conference by Trump and NATO Secretary General Jens Stoltenberg was also likely to generate headlines.

In currencies, the yen, a favoured harbor in times of stress due to Japan’s position as the world’s largest creditor nation, also cooled in Europe after having surged over 1.2 percent against the dollar on Tuesday. The dollar huddled at 109.70 yen, having been as low as 109.35 at one stage. Dealers warned there was little in the way of chart support until the 200-day moving average at 108.72.

The euro steadied too, having dropped to its lowest in five months at 115.91 yen. It was looking to snap 11 straight sessions of losses, a record for the single currency. It was shade higher on the dollar at $1.0618. Political uncertainty in France added to the euro’s woes as hard-left candidate Jean-Luc Melenchon surged in the polls ahead of the May presidential election.

All this unease boosted bonds with yields on 10-year Treasuries US10YT=RR boasting their lowest close of the year on Tuesday. Yields were last at 2.30% and testing a hugely important barrier on the charts. European yields nudged only cautiously upwards despite the easier mood in other assets, as nearly 16 billion euros of upcoming debt sales weighing on risk-averse, holiday-thinned markets.

Meanwhile, US traders are looking for an upbeat earnings season set to kick off tomorrow with a handful of banks reporting Q1 results. Analysts expect earnings for all S&P 500 companies to have risen 10 percent in the first quarter from a year ago, according to Thomson Reuters data.

Oil’s winning streak got an added lift from reports Saudi Arabia was lobbying OPEC and other producers to extend a production cut beyond the first half of 2017. Global benchmark Brent edged up 30 cents to $56.53 a barrel, while U.S. crude added 25 cents to $53.66. If sustained, this would be the longest stretch of gains since August 2016.

Bulletin Headline Summary from RanSquawk

- European indices have remained afloat with oil prices rising amid a drawdown in last nights API report, while Saudi support of extension to cuts also keeps oil elevated.

- GBP undecided after mixed jobs report where importantly wage inflation is now below CPI.

- Looking ahead, highlights include DoE and Bank of Canada rate decision.

Market Snapshot

- S&P 500 futures up 0.1% to 2,353.00

- STOXX Europe 600 up 0.5% to 382.98

- MXAP down 0.08% to 146.72

- MXAPJ up 0.5% to 479.87

- Nikkei down 1% to 18,552.61

- Topix down 1% to 1,479.54

- Hang Seng Index up 0.9% to 24,313.50

- Shanghai Composite down 0.5% to 3,273.83

- Sensex down 0.3% to 29,685.83

- Australia S&P/ASX 200 up 0.08% to 5,933.96

- Kospi up 0.2% to 2,128.91

- German 10Y yield unchanged at 0.204%

- Euro up 0.1% to 1.0616 per US$

- Italian 10Y yield rose 3.9 bps to 1.986%

- Spanish 10Y yield rose 0.3 bps to 1.647%

- Brent Futures up 0.5% to $56.49/bbl

- Gold spot down 0.1% to $1,273.27

- U.S. Dollar Index down 0.07% to 100.64

Top Overnight News From Bloomberg

- Amazon Said to Mull Whole Foods Bid Before Jana Stepped In

- Meredith Said in Late-Stage Talks for Time Inc. Takeover

- Xi Urges North Korea Talks in Trump Call as Tensions Mount

- Oil Extends Longest Gain of 2017 as Saudis Seen Extending Curbs

- Tillerson, Lavrov Meet in Moscow as U.S. Blasts Russia on Syria

- BHP CEO Rejects Oil Spinoff for Third Time After Singer Demand

- Neurocrine Wins FDA Approval on Drug for Movement Disorder

- Arista Networks Says Ruling Allows for Product Imports Into U.S.

- Daimler’s First-Quarter Earnings Surge on Mercedes Success

- NuStar to Buy Navigator in $1.5 Billion Bet on Permian Pipelines

Asian markets were weighed by geopolitical concerns with the Nikkei 225 (-1%) the underperformer amid JPY strength. The downbeat tone was evident across the region, with the Shanghai Composite (-0.4%) finding itself in negative territory not helped by the 0.90%, vs. Exp. 1.00% CPI Y/Y miss, while ASX 200 (+0.1%) was also subdued, although strength in the materials sector and mining names stemmed downside. Finally, JGBs followed European and US fixed income markets, finding bullish pressure throughout the session. Noticeably, the BoJ lowered its 3yr-5yr purchases by JPY 30bIn which had no effect on the 10yr or the flight to safety, with the 10yr JGB Jun’17 contract higher by around 20 ticks. Chinese CPI (Mar) Y/Y 0.9% vs. Exp. 1.0% (Prey. 0.8%); – PPI (Mar) Y/Y 7.6% vs. Exp. 7.6% (Prey. 7.8%). PBoC refrained from open market operations again for a net daily drain of CNY 40bIn. BoJ Governor Kuroda stated BoJ easing is not targeting an FX level and that JPY weakness could help inflation reach target quicker. Kuroda further stated that he sees no problem with asset purchases or expansion of monetary base.

Top Asian News

- China Producer Price Reflation Moderates as Commodities Cool Off

- Xi, Trump Exchange Views on Issues Including North Korea Today

- China Says Escalating Korean Situation ’Irresponsible, Dangerous’

- Cathay Promotes Operating Chief Rupert Hogg to CEO After Loss

- Qantas Stops Selling Tickets in Zimbabwe Amid Cash Shortage

In Europe the risk off sentiment doesn’t last long with the markets shrugging off yesterday’s concerns to see equities trade higher again this morning. Energy names are leading the charge, with the sector benefitting as WTI trades above USD 533.50/bbl in the wake of reports of Saudi Arabia want OPEC to extend production cuts and is pushing for a six-month extension. Elsewhere this morning, Tesco’s earnings failed to lift the company, with concerns remaining after profits were weighed on by the 2014 accounting scandal. Fixed income markets have traded in a tighter range for much of the morning amid the slew of supply. Additionally, gilt prices notched lower in the wake of a relatively soft 2065 auction in which the tail had notably widened by some 1.7bps.

Top European News

- Tesco Lays Down Price Gauntlet to Rivals as Pressure Grows

- U.K. Households Facing Biggest Earnings Squeeze Since 2014

- EU Won’t Back Trade Deal If U.K. Chooses ‘Singapore-on- Thames’

- Puma Raises 2017 Earnings Forecast as Turnaround Progresses

- Swedish Elk-Hunt Bribery Case Widens to Handelsbanken Chairman

- Banco Popular Rises Most in Three Months on Takeover Speculation

- Melenchon Crashes Front-Runners’ Party as French Risks Rise

- German Economy Saw ‘Vigorous’ Expansion in 1Q 2017: Government

In currencies, the yen fell less than 0.1 percent to 109.70 against the dollar as of 8:44 a.m. in London, erasing an earlier gain of 0.2 percent. The currency jumped 1.2 percent on Tuesday for the biggest increase since January. The Bloomberg Dollar Spot Index fell 0.1 percent. The South Korean won rose 0.4 percent, after six days of declines. The euro added 0.1 percent to $1.0620, gaining for a third day. Focus in the FX markets has been on the JPY, as it gains across the board on geopolitical fears. We have finally broken through the 110.00 on the downside, tripping stops through 109.50 but with limited momentum though here as some had feared. Tensions over North Korea and Syria are unlikely to go away any time soon, so expect JPY demand to continue in the meantime. We see the EUR benefiting from times of risk off, but there is no relief for the single unit as the French elections continue to unnerve the market — there seems to be little confidence in the polls which continue to see Le Pen lagging. EUR/USD tested through 1.0600 yesterday and today, but struggles ahead of the first point of resistance at 1.0650. We saw EUR/JPY dipping under 116.00 in late Asia, but demand noted below here.

In commodities, oil climbed 0.4 percent to $53.61 a barrel, after advancing for six straight sessions. Saudi Arabia is likely to support extending OPEC output cuts into the second half of 2017 in an effort to boost oil prices, according to a person familiar with the kingdom’s internal discussions. Gold fell 0.1 percent to $1,273.70 an ounce, after jumping 1.6 percent on Tuesday to the highest since Nov. 9. The flight to safety has seen Gold on the ramp again in recent sessions, tipping USD1280.00 alongside the drop in the USD which has seen the JPY take out 110.00. Silver is now back above USD18.00 as a result, as precious metals have been the obvious trade in the last few days. Oil prices have pushed higher also as Saudi Arabia wants OPEC to extend the production cuts by another 6 months, with the API’s showing a drawdown to add impetus to the WTI rise through USD53.00. Brent is now pushing into the upper USD56.00’s. Base metals naturally suffer with the risk off tone as, with Copper now back under USD2.60, but techs note some near term support on the horizon. Zinc has been underperforming as supply picks up, but also stabilises to a modest degree today.

Looking at the day ahead, it’s quiet again in the US with just the March import price index reading and monthly budget statement due out. Away from the data the BoE’s Carney is due speak this morning, while the IMF’s Lagarde is also scheduled to speak at a conference in the next few hours. The Fed’s Kaplan then speaks this afternoon at 3pm BST. As highlighted earlier, expect politics to also remain a focus with Tillerson’s visit to Russia one to watch.

US Event Calendar

- 7am: MBA Mortgage Applications, prior -1.6%

- 8:30am: Import Price Index MoM, est. -0.2%, prior 0.2%; YoY, est. 3.95%, prior 4.6%; Import Price Index ex Petroleum MoM, est. 0.0%, prior 0.3%

- 8:30am: Export Price Index MoM, est. 0.0%, prior 0.3%; 8:30am: Export Price Index YoY, prior 3.1%

- 10am: Fed’s Kaplan Speaks in Fort Worth

- 2pm: Monthly Budget Statement, est. $169.0b deficit, prior $108.0b deficit

* * *

DB’s Jim Reid concludes the overnight wrap

So far this week vol has been spiking up like Sergey after he’s planted his pole at the end of the runway. Given the moves it’s got us asking the question as to whether this is the rise in vol we’ve been waiting for? Last night the VIX closed (15.07) at the highest level since the US election with European VSTOXX (22.95) also at the highs over the same period and just over double the all-time lows seen just over 3 weeks ago. Simultaneously Gold (+1.61%) hit 5 month highs last night and 10yr Treasury yields hit a 5 month low after falling 7bps to 2.296%. 10y Bund yields also held steady at 0.201% and continue to hover a shade above the 2017 low of 0.179% made intraday back in February.

It has felt quite quiet and orderly this week considering the risk-off tendencies and relatively big spike in volatility. However that might be because of a lack of activity given the pending Easter break. So poor liquidity is probably exacerbating the moves. Add to this the rising geopolitics tensions (North Korea, Syria), slow burning ongoing concerns about Trump trades post the healthcare debacle, and a steady increase of support for Melenchon in the recent French polls making it less certain who’ll contest the final round run-off. For now equity and credit markets remain fairly resilient which reduces the immediate worry but if vol remains elevated at these levels for a few days expect weakness.

In terms of the actual geopolitical developments yesterday, it was President Trump’s latest tweeting around North Korea which initially saw vol spike higher midway through the afternoon. Trump tweeted that “North Korea is looking for trouble” and that the US “will solve the problem” with or without the help of China – reiterating comments he has made previously. Overnight in an interview with Fox News, Trump also said that “we are sending an armada” to the North Korean peninsula. In addition to this and ahead of his visit to Russia, secretary of state Rex Tillerson was fairly blunt in his comments about Russia’s involvement in Syria. Speaking at the G-7 summit, Tillerson said that Russia had aligned itself with an “unreliable partner” in Syria’s al-Assad and urged Russia to abandon its support. Tillerson has travelled to Moscow and is due to meet foreign minister Sergei Lavrov. There’s also some chatter that he could meet President Putin although that is still to be confirmed. Putin had said yesterday that the recent chemical attacks in Syria were “provocations”.

So expect there to be plenty more headlines around this today. While safe havens rallied and volatility spiked higher yesterday it was notable that risk assets actually stayed relatively resilient all things considered. The S&P 500 pared a loss of as much as -0.85% to finish the day down only a modest -0.14%. The percentage loss for the Dow (-0.03%) was even smaller while the Stoxx 600 was -0.02% by the closing bell, despite the obvious moves in vol. In fact in the last six sessions, the Stoxx 600 hasn’t moved up or down by more than 0.20%. Meanwhile credit was a bit weaker at the margin (CDX IG +1bp, iTraxx Main +0.5bps, Crossover +3bps) but again the moves were pretty modest in reality.

This morning in Asia we’ve had the welcome distraction of the latest inflation data out of China. In terms of the numbers, PPI in March has moderated somewhat after dipping two-tenths to +7.6% yoy (vs. +7.5% expected) following a bit of a levelling out in commodity prices. That said it also marks the seventh consecutive monthly positive print after 54 months of deflation in prices at the factory gate. Meanwhile CPI has edged up one-tenth to +0.9% yoy although did miss slightly relative to expectations for +1.0%, with a -4.4% yoy decline in food prices in particular having an impact. Bourses in China are a touch weaker although that is the case for much of Asia this morning. The Shanghai Comp and CSI 300 are -0.32% and -0.04% respectively while the ASX and Hang Seng are -0.17% and -0.15%. In Japan the Nikkei (-1.24%) has notably underperformed reflecting the rally for the Yen (+1.04%) over the past 24 hours. US equity index futures are down about -0.20%.

Moving on. It was another fairly quiet day for macro data yesterday although we did get the first of a number of inflation reports during the week. In the UK headline CPI was reported as rising a higher than expected +0.4% mom in March (vs. +0.3% expected) which had the effect of holding the annual rate unchanged at +2.3%. However the core rate fell a little more than expected to +1.8% yoy from +2.0% although still remains well above the levels of 2015 and 2016. Headline RPI was a little softer than expected (+0.3% mom vs. +0.4% expected) however PPI output rose +0.4% mom and well ahead of the consensus estimate for +0.1%. Sterling (+0.61%) closed higher for the second day in succession yesterday.

Elsewhere in Europe there was some disappointment in the February industrial production print for the Euro area which came in at -0.3% mom (vs. +0.1% expected). More disappointing however was the six-tenths of a percent downward revision to the January data to +0.3%. Our European economists note that if industrial production remains unchanged in March, it will have fallen marginally in Q1 versus the strong +0.9% qoq growth in Q4. This lends some support to their view that the hard data is limiting upside in growth in Q1 despite the strong survey data. On that note, the German ZEW survey was upbeat in April with the current situations index rising 2.8pts to 80.1 and to the highest since July 2011, while the expectations index surged to 19.5 from 12.8. The data in the US yesterday was a bit of a non-event. The BLS JOLTS report revealed that job openings rose to 5.74m in February from 5.63m with both the quits rate and hiring rate edging down one-tenth. Meanwhile the NFIB small business sentiment index nudged down 0.6pts to 104.7 in March, although remains nearly 10pts above its pre-election level. Elsewhere there was a bit of Fedspeak yesterday although nothing that really moved the dial with San Francisco Fed President John Williams reiterating this view that three to four rate hikes this year seems appropriate.

Before we move on to today’s calendar, it’s worth highlighting yesterday’s report by our FX strategy team in which they look at how an exit from unconventional ECB policy would impact the euro. They find that “not all tightenings are created equal” and argue that it is the sequencing of the exit, rather than the overall monetary policy stance, that will determine whether the euro appreciates. A policy focused on an early exit from negative rates would be very bullish for the euro. The report shows that FX is far more sensitive to front-end rather than back-end yields and that this sensitivity has dramatically increased after the 2008 financial crisis. The report also shows that the effects of negative rates are highly non-linear, so that an early ECB hiking cycle will have a disproportionately positive impact on FX. In contrast, a policy focused on a tapering of the ECB’s PSPP program would not be bullish for the euro. QE operates via signaling effects on the short-term rate path as well as by depressing term premia. If the ECB is able to keep the front-end anchored, a rise in term premia alone could have bearish implications for the EUR via reduced demand for European fixed income. Similar effects were observed around the Fed taper tantrum.

Looking at the day ahead, this morning in Europe the main focus is likely to be on the UK again where we’ll get the March and February employment data. The consensus is for no change in the ILO unemployment rate at 4.7% and a slight dip in weekly earnings ex bonus to +2.1% yoy. It’s quiet again in the US this afternoon with just the March import price index reading and monthly budget statement

due out. Away from the data the BoE’s Carney is due speak this morning, while the IMF’s Lagarde is also scheduled to speak at a conference in the next few hours. The Fed’s Kaplan then speaks this afternoon at 3pm BST. As highlighted earlier, expect politics to also remain a focus with Tillerson’s visit to Russia one to watch.

END

3. ASIAN AFFAIRS

i)Late TUESDAY night/WEDNESDAY morning: Shanghai closed DOWN 15.13 POINTS OR 0.460%/ /Hang Sang CLOSED UP 225.94 POINTS OR .93% . The Nikkei closed DOWN 195.26 OR 1.04% /Australia’s all ordinaires CLOSED UP 0.07%/Chinese yuan (ONSHORE) closed UP at 6.8938/Oil UP to 53.63 dollars per barrel for WTI and 56.44 for Brent. Stocks in Europe MOSTLY MIXED ..Offshore yuan trades 6.8989 yuan to the dollar vs 6.8938 for onshore yuan.FOR THE FIRST TIME IN OVER TWO MONTHS THE OFFSHORE IS WEAKER TO THE ONSHORE YUAN/ ONSHORE YUAN SLIGHTLY STRONGER AND THE OFFSHORE YUAN ALSO A LITTLE STRONGER AND THIS IS COUPLED WITH THE NO CHANGE ON THE DOLLAR.

3a)THAILAND/SOUTH KOREA/NORTH KOREA

b) REPORT ON JAPAN

JAPAN/NORTH KOREA/USA

The USA sends a nuclear sniffer aircraft that specializes in detecting radioactive debris after a detonation of a nuclear device to Okinawa Japan as the parties prepare for potential nuclear tests in the region. Tensions are coming to a boil

(courtesy zero hedge)

US Deploys “Nuclear Sniffer” Plane To Japan As North Korea Tensions Come To A Boil

As tensions over North Korea’s nuclear program mount, the United States Air Force has deployed a WC-135 (a.k.a. the “Nuclear Sniffer”), an aircraft that specializes in detecting radioactive debris after the detonation of a nuclear device, to Okinawa, Japan to assist with monitoring for potential nuclear tests in the region. The aircraft was deployed to Kadena Air Base, Okinawa, as confirmed by the Nikkei media outlet reported based on talks with a senior Japan Self Defense Forces official.

According to The Aviationist, the WC-135 can be used to capture atmospheric samples and analyze the fallout residue in real-time to help confirm the characteristics of any nuclear warhead used.

Constant Phoenix flies in direct support of the U.S. Atomic Energy Detection System, a global network of nuclear detection sensors that monitor underground, underwater, space-based or atmospheric events. As the sole agency in the Department of Defense tasked with this mission, AFTAC’s role in nuclear event detection is critical to senior decision makers in the U.S. government, says the Air Force.

“Our aircraft is equipped with external flow devices that allow us to collect airborne particulate on filter paper and a compressor system for whole air samples,” said Tech. Sgt. Matthew Wilkens, a 9S100 and airborne operations section chief in a recent release. “The particulate samples are collected using a device that works like an old Wurlitzer jukebox. An arm grabs the paper from its slot and moves it to the exterior of the fuselage. After exposure, it is returned to the filter magazine where a new paper is selected for use. It’s a simple, yet very effective, concept.”

Effluent gasses are gathered by two scoops on the sides of the fuselage, which in turn trap fallout particles on filters. The mission crews have the ability to analyze the fallout residue in real-time, helping to confirm the presence of nuclear fallout and possibly determine the characteristics of the warhead involved.

The aircraft was supposed to arrive at its Forward Operating Base last month but it was forced to perform an emergency landing at Sultan Iskandar Muda airport in Banda Aceh, Indonesia, on its way to Japan, on Mar. 24, following an engine failure.

There are two WC-135 Constant Phoenix aircraft in service today which are operated by the 45th Reconnaissance Squadron from Offutt Air Force Base, with mission crews staffed by Detachment 1 from the Air Force Technical Applications Center.

Of course, this latest news follows an order revealed earlier this week from Pacific Command to turn the USS Carl Vinson strike group toward waters near the Korean peninsula for the second time in recent months, rather than onward to Australia for planned port visits.

Moreover, as we noted this morning, it also follows an unexpected call from Trump to Chinese President Xi this morning to discuss the rapidly developing situation on the peninsula.

“China insists on realizing the denuclearization of the peninsula, insists on maintaining peace and stability on the peninsula, and advocates resolving the problem through peaceful means,” Xi was quoted as saying in the call according to Chinese state broadcaster CCTV said.

Chinese Foreign Ministry spokesman Lu Kang, who said Trump had initiated the call, urged everyone to lower the tension. “We hope that the relevant parties do not adopt irresponsible actions. Under the current circumstances, this is very dangerous,” Lu told reporters at a regular press briefing. Kang also said Wednesday at a regular briefing in Beijing that it was a “good thing” that the two leaders were in touch again days after meeting in Florida.

Translation: Trump is strongly urged not to launch a unilateral strike on North Korea as he did on Syria without express Chinese prior approval.

end

Gold rises as North Korea tells foreign journalists to prepare for a “big event” tomorrow:

(courtesy zero hedge)

North Korea Tells Foreign Journalists To Prepare For “Big” Event On Thursday

In a potentially concerning geopolitical development, Reuters reports that foreign journalists visiting North Korea have been told to prepare for a “big and important event” on Thursday, although the wire service says there were “no indications it was directly linked to tensions in the region over the isolated state’s nuclear weapons program.”

According to Channel News Asia reported Jeremy Koh, “we’ve been told to be ready to move out at 620am, but no idea why. Also, no cell phones allowed.”

We’ve been told to be ready to move out at 620am, but no idea why. Also, no cell phones allowed. #Pyongyang#Dprk

As a reminder, April 15 marks the nation’s 105th birthday of founding president Kim Il Sung, North Korea’s biggest national day called “Day of the Sun”, and around 200 foreign journalists are in Pyongyang to cover it, however why North korea would urge particular attention to a day that falls two days earlier was unclear, although there is precedent: In April, 2012, North Korea attempted to launch a long-range rocket ahead of the 100th Day of the Sun. State media later confirmed the launch had failed.

The mystery grew when officials gave no details as to the nature of the event or where it would take place. That said, similar announcements in the past have been linked to relatively low-key set pieces. In 2016, Reuters adds, foreign journalists underwent hours of investigation by North Korean officials ahead of what turned out to be a pop concert to mark the finale of a ruling Workers’ Party congress.

Meanwhile, tensions are running high, with a U.S. Navy strike group steaming toward the western Pacific in a show of force and North Korea warning of a nuclear attack on the United States at any sign of American aggression.

Visits by foreign journalists to North Korea are rare and tightly coordinated, Reuters adds, and security checks at events attended by leader Kim Jong Un are especially rigorous. North Korea often uses such visits to showcase new construction projects. In recent weeks workers have been putting the finishing touches to the skyscraper-lined “Ryomyong” street in central Pyongyang.

Kim has made frequent visits to the street to inspect construction work there, according to state media. North Korea has in the past marked its April 15 holiday with tightly choreographed military parades.

Separately, in an unconfirmed report issued by Pravdareport.ru, “Kim Jong-un has ordered 25 percent of Pyongyang residents to leave the city immediately.”

In accordance with the order, 600,000 people should be urgently evacuated. Experts note that the evacuation will most likely be conducted due to extremely strained tensions in relations with the United States of America.

Reportedly, Pyongyang’s bomb shelters will not be able to accommodate the entire population of the North Korean capital. Therefore, 600,000 people – mostly individuals with criminal records – will have to leave Pyongyang to let others use bomb shelters.

We would not give this particular report much credibility, although with the information blackout out of North Korea it is impossible to confirm either way.

With market liquidity already thin, and desks barely staffed ahead of Friday’s holiday, will the market take the risk of another “irrational” demonstration of technological advancement by Kim over the next 24 hours, especially with Trump – and China – both making it abundantly clear any further provocations by North Korea’s regime would be met with retaliation, and hold stocks overnight? The answer will be revealed shortly.

c) REPORT ON CHINA

CHINA/USA/NORTH KOREA

Trump calls Xi who tells him not to do anything unilaterally. Tensions boil

(courtesy zero hedge)

Trump Unexpectedly Calls China’s President To Discuss North Korea

With the Carl Vinson carrier group steaming toward the Korean Penninsula (it is expected to arrive some time over the weekend), in an unexpected overnight development less than a week after his first meeting with China’s president, Donald Trump called President Xi on the phone to discuss trade and the developing North Korean situation. According to China’s state television, Xi stuck with his objective of “denuclearization” of the Korean Peninsula, and called for a peaceful resolution of rising tension.