Gold: $1255.10 UP 1.80

Silver: $16.83 up 1 cent(s)

Closing access prices:

Gold $1256.90

silver: $16.83!!!

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

SHANGHAI GOLD FIX: FIRST FIX 10 15 PM EST (2:15 SHANGHAI LOCAL TIME)

SECOND FIX: 2:15 AM EST (6:15 SHANGHAI LOCAL TIME)

SHANGHAI FIRST GOLD FIX: $1268.32 DOLLARS PER OZ

NY PRICE OF GOLD AT EXACT SAME TIME: 1257.25

PREMIUM FIRST FIX: $11.07

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

SECOND SHANGHAI GOLD FIX: $1266.95

NY GOLD PRICE AT THE EXACT SAME TIME: 1255.80

Premium of Shanghai 2nd fix/NY:$11.15

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

LONDON FIRST GOLD FIX: 5:30 am est $1255.80

NY PRICING AT THE EXACT SAME TIME: $1255.10

LONDON SECOND GOLD FIX 10 AM: $1255.45

NY PRICING AT THE EXACT SAME TIME. $1254.85

For comex gold:

MAY/

NOTICES FILINGS TODAY FOR APRIL CONTRACT MONTH: 8 NOTICE(S) FOR 800 OZ.

TOTAL NOTICES SO FAR: 35 FOR 3500 OZ (.1088 TONNES)

For silver:

For silver: MAY

535 NOTICES FILED TODAY FOR 2,675,000 OZ/

Total number of notices filed so far this month: 2713 for 13,565,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

FEDERAL RESERVE EAR MARKED GOLD REPORT for April

In Feb we had $7,841,000 worth of gold housed at the FRBNY valued at 42.21 dollars per oz

Last month: we had the same; $7,841,000 of gold valued at 42.21

thus 0 oz of gold moved out.

END

The key event today is the rising amount of silver that is standing for metal at the comex. It has now risen above what was standing on day one, April 30. On that day 16.8 million oz stood for delivery and for two consecutive days it has risen to close to 18.2 million oz. We have not seen that before.

Let us have a look at the data for today

.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total open interest FELL BY ONLY 1892 contracts DOWN to 194,123 WITH THE LOSS IN PRICE ( 38 CENTS) SILVER TOOK WITH RESPECT TO YESTERDAY’S TRADING. FOR THE PAST FEW YEARS WE HAVE NOTICED THAT THE OPEN INTEREST IN AN ACTIVE MONTH COLLAPSES AS WE APPROACH FIRST DAY NOTICE. WE NOW KNOW THAT THE MAJORITY OF THE LIQUIDATION RECEIVE AN EFP CONTRACT IN A FUTURE MONTH PLUS FIAT BONUS. WE HAVE BEEN WITNESSING THIS SAME PATTERN NOW FOR AT LEAST THE LAST COUPLE OF YEARS. In ounces, the OI is still represented by just UNDER 1 BILLION oz i.e. 0.970 BILLION TO BE EXACT or 142% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT MAY MONTH/ THEY FILED: 535 NOTICE(S) FOR 2,713,000 OZ OF SILVER

In gold, the total comex gold FELL BY 5,451 contracts WITH THE FALL IN THE PRICE OF GOLD ($11.80 with YESTERDAY’S TRADING). The total gold OI stands at 465,336 contracts.

we had 8 notice(s) filed upon for 800 oz of gold.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD:

We had no changes in tonnes of gold at the GLD:

Inventory rests tonight: 853.36 tonnes

.

SLV

Strange!!! We had another huge change in silver inventory at the SLV today..a massive deposit of 3,502 million oz with silver in the doldrums these past few days??????)

THE SLV Inventory rests at: 334.921 million oz

end

.

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in silver FELL BY ONLY 1,892 contracts DOWN TO 194,123, (AND NOW FURTHER FROM THE NEW COMEX RECORD SET ON FRIDAY/APRIL 21 AT 234,787), WITH THE FALL IN PRICE FOR SILVER ON FRIDAY (38 CENTS). It sure looks like we are witnessing the power of that obscure EFP contract. For the past few years, strangely we have seen the open interest collapse as we enter first day notice. The EFP allows the longs to liquidate his delivery contract month for a fiat bonus and the receipt of a future contract month once first day notice has occurred.

(report Harvey

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

2c) Federal Reserve Bank ear marked gold movement

(Harvey)

3. ASIAN AFFAIRS

i)Late MONDAY night/TUESDAY morning: Shanghai closed DOWN 10.95 POINTS OR .35% OR / /Hang Sang CLOSED UP 81.00 PONTS OR .33% . The Nikkei closed UP 135.18 OR 0.70% /Australia’s all ordinaires CLOSED DOWN .08%/Chinese yuan (ONSHORE) closed DOWN at 6.8953/Oil UP to 49.25 dollars per barrel for WTI and 52.03 for Brent. Stocks in Europe OPENED IN THE GREEN ..Offshore yuan trades 6.8920 yuan to the dollar vs 6.8953 for onshore yuan. NOW THE OFFSHORE IS A LITTLE WEAKER TO THE ONSHORE YUAN/ ONSHORE YUAN SLIGHTLY WEAKER (TO THE DOLLAR) AND THE OFFSHORE YUAN A LITTLE STRONGER TO THE DOLLAR AND THIS IS COUPLED WITH THE WEAKER DOLLAR. CHINA IS HAPPY

3a)THAILAND/SOUTH KOREA/NORTH KOREA

i)NORTH KOREA

More rhetoric from Kim as he is furious after the USA and Sout Korea deployed lancer bombers in war exercises conducted off the Korean peninsula

( zero hedge)

b) REPORT ON JAPAN

c) REPORT ON CHINA

i)CHINA/SOUTH KOREA/USA

China angry at the USA deployment of the THAAD anti missile defense system in South Korea. They warned of consequences

( zero hedge)

ii)NORTH KOREA//CHINA

China unleash an oil embargo on North Korea which would cripple the country:

(Calcuttawala/OilPrice.com)

4. EUROPEAN AFFAIRS

i)ITALY/Air Alitalia

It does not look good for Itays national carrier as they have filed for bankruptcy protection for the 2nd time in 9 years. Nobody is setting up to the plate to provide financing for the airline

( zero hedge)

ib)The Italian Government approves the Alitalia bankruptcy as it bonds collapse into the teens. A complete liquidation will cause 12,000 people to lose their jobs as well as a big hit the Italy’s GDP

this will be a continuing story..

(courtesy zero hedge)

ii)GREECE

Greece is going to be raped some more as they settle for more austerity measures in return for bailout money. Why they do not leave the EU is beyond me!

(zero hedge)

iii)GERMANY

Non Germans make up 10% of the population yet they account for 30.5% of all crimes in the country in 2016

( Kern/Gatestone Institute)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

Russia/USA

Putin and Trump hold their phone call and both are asking for restraint in dealing with Syria and North Korea;

( zero hedge)

6 .GLOBAL ISSUES

i)The run on Home Capital has now spread to another Canadian Mortgage lender, Equitable Group

( zero hedge)

ii)At the end of today, Apple reported:

They missed on revenue due to declining sales in China. This should have a damper effect on global trading for tomorrow

(courtesy zero hedge)

7. OIL ISSUES

i)Saudi Prince sends crude tumbling below $47.50

( zerohedge)

ii)It now seems that the OPEC production cut deal has backfired as the Saudis lose more market share to Iran and Iraq

( Paraskova/OilPrice.com)

iii)Then at the end of the day we got a surprise drawdown on crude and gasoline and this caused both to rise in price

(courtesy zero hedge)

8. EMERGING MARKETS

9. PHYSICAL MARKETS

i)USA GOLD news and views on gold’s undervaluation

( Mike Kosares/USAGold/GATA)

ii)Data from Switzerland shows that India is now again showing its love for gold having imported 55.6 tonnes in March. They may overtake China as the number one consumer of gold. I would also like to point out that these numbers do not include smuggled gold into India.

(Lawrie Williams/Sharp’s Pixley)

10. USA stories

i)The Republicans are at least one vote shy from failure to repealing Obamacare with many on the sidelines

It looks like it will fail for the 3rd time

( zero hedge)

ii)The hawks in Washington will be visibly upset as the Senate drops the new Russian sanctions bill;

( zero hedge)

iii) trading in NY/30 yr bond yield drops below 3% due to the auto bloodbath!

iv)The auto bloodbath which caused the markets in the uSA to tumble

(courtesy zerohedge)

Let us head over to the comex:

The total gold comex open interest FELL BY 5,451 CONTRACTS DOWN to an OI level of 464,123 WITH THE FALL IN THE PRICE OF GOLD ( $11.80 with YESTERDAY’S trading). The longs still continue to remain stoic as they refused to liquidate any of their contracts despite the constant torment experienced yesterday. However we may have had some banker short covering. We are now in the contract month of MAY and it is one of the POORER delivery months of the year. In this MAY delivery month we had A LOSS OF 17 contract(s) FALLING TO 418. We had 12 notices filed yesterday so we again lost 5 contracts or an additional 500 oz were cash settled through the EFP route where they receive a cash bonus plus a future gold contract.

The next big active month is June/2017 and here the OI LOST 6,381 contracts DOWN to 323,713. The non active July contract gained another 9 contracts to stand at 34 contracts. The next big active month is August and here the OI gained 599 contracts up to 55,254.

We had 8 notice(s) filed upon today for 800 oz

The non active June contract GAINED 203 contracts to stand at 1017. The next big active month will be July and here the OI SURPRISINGLY GAINED 1920 contracts UP to 151,200.

For those keeping score, the initial amount of silver oz that stood for delivery for the May 2016 contract month: 28.01 million oz. By conclusion of the month only 13.58 million oz stood and the rest was cash settled.(EFP ROUTE)

The line in the sand is $18.50 for silver and again it has been defended by the criminal bankers. Once this level is pierced, the monstrous billion oz of silver shorts will blow up. The bankers are defending the Alamo with their last stand at the $18.50 mark. THE NEW RECORD HIGH IN OPEN INTEREST WAS SET FRIDAY APRIL 21/2017 AT: 234,787.

We had 535 notice(s) filed for 2,675,000 oz for the MAY 2017 contract

VOLUMES: for the gold comex

Today the estimated volume was 171,263 contracts which is fair.

Yesterday’s confirmed volume was 209,781 contracts which is good.

volumes on gold are STILL HIGHER THAN NORMAL!

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz |

nil oz

|

| Deposits to the Dealer Inventory in oz | nil oz |

| Deposits to the Customer Inventory, in oz |

3,665.214 oz

Brinks

|

| No of oz served (contracts) today |

8 notice(s)

800 OZ

|

| No of oz to be served (notices) |

410 contracts

41000 oz

|

| Total monthly oz gold served (contracts) so far this month |

35 notices

3500 oz

.1088 tonnes

|

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | 23,338.2 oz |

Today, 0 notice(s) were issued from JPMorgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equates to 8 contract(s) of which 0 notices were stopped (received) by jPMorgan dealer and 0 notice(s) was (were) stopped/ Received) by jPMorgan customer account.

March 2016: 2.311 tonnes (March is a non delivery month)

| Silver | Ounces |

| Withdrawals from Dealers Inventory | nil |

| Withdrawals from Customer Inventory |

30,038.200 oz

Scotia

24,852.140 oz

CNT

total: 54,890.340 oz

|

| Deposits to the Dealer Inventory |

499,033.580 oz

CNT

|

| Deposits to the Customer Inventory |

0 oz

JPMorgan

101,625.287 oz

CNT

998.000 oz ???

Delaware

total: 102,623.287 oz

|

| No of oz served today (contracts) |

535 CONTRACT(S)

(2,675,000 OZ)

|

| No of oz to be served (notices) |

929 contracts

( 4,645,000 oz)

|

| Total monthly oz silver served (contracts) | 2713 contracts (13,565,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month | 1,908,422.1 oz |

i) Out of Scotia: 40,175.02 oz

NPV for Sprott and Central Fund of Canada

Sprott’s hostile 3.1 billion bid to take over Central Fund of Canada

(courtesy Sprott/GATA)

Sprott makes hostile $3.1 billion bid for Central Fund of Canada

Submitted by cpowell on Thu, 2017-03-09 01:19. Section: Daily Dispatches

From the Canadian Press

via Canadian Broadcasting Corp. News, Toronto

Wednesday, March 8, 2017

http://www.cbc.ca/news/canada/calgary/sprott-takeover-bid-central-fund-c…

Toronto-based Sprott Inc. said Wednesday it’s making an all-share hostile takeover bid worth $3.1 billion US for rival bullion holder Central Fund of Canada Ltd.

The money-management firm has filed an application with the Court of Queen’s Bench of Alberta seeking to allow shareholders of Calgary-based Central Fund to swap their shares for ones in a newly-formed trust that would be substantially similar to Sprott’s existing precious metal holding entities.

The company is going through the courts after its efforts to strike a friendly deal were rebuffed by the Spicer family that controls Central Fund, said Sprott spokesman Glen Williams.

“They weren’t interested in having those discussions,” Williams said.

Sprott is using the courts to try to give holders of the 252 million non-voting class A shares a say in takeover bids, which Central Fund explicitly states they have no right to participate in. That voting right is reserved for the 40,000 common shares outstanding, which the family of J.C. Stefan Spicer, chairman and CEO of Central Fund, control.

If successful through the courts, Sprott would then need the support of two-thirds of shareholder votes to close the takeover deal, but there’s no guarantee they will make it that far.

“It is unusual to go this route,” said Williams. “There’s no specific precedent where this has worked.”

Sprott did have success last year in taking over Central GoldTrust, a similar fund that was controlled by the Spicer family, after securing support from more than 96 percent of shareholder votes cast.

The firm says Central Fund’s shares are trading at a discount to net asset value and a takeover by Sprott could unlock US$304 million in shareholder value.

Central Fund did not have any immediate comment on the unsolicited offer. Williams said Sprott had not yet heard from Central Fund on the proposal but that some shareholders had already contacted them to voice their support.

Sprott’s existing precious metal holding companies are designed to allow investors to own gold and other metals without having to worry about taking care of the physical bullion.

end

And now the Gold inventory at the GLD

May 2/no change in inventory at the GLD/Inventory rests at 853.36 tonnes

May 1/ no changes in inventory at the GLD/inventory rests at 853.36 tonnes

April 28/no changes in inventory at the GLD/Inventory rests at 853.36 tonnes

April 27/a small withdrawal of .89 tonnes/Inventory is now at 853.36 tonnes

APRIL 26/we had no changes at the GLD/Inventory rests at 854.25 tonnes

April 25/2017/A WITHDRAWAL OF 5.92 TONNES OF GOLD FROM THE GLD/INVENTORY RESTS AT 854.25 TONNES

April 24/a deposit of 1.48 tonnes of gold into the GLD/inventory rests at 860.17 tonnes

April 21/A DEPOSIT OF 4.44 TONNES OF GOLD INTO THE GLD/INVENTORY RESTS AT 858.69 TONNES

APRIL 20/A WITHDRAWAL OF 6.51 TONNES FROM THE GLD/INVENTORY RESTS AT 854.25 TONNES

April 19/ A DEPOSIT OF 11.84 TONNES INTO THE GLD/INVENTORY RESTS AT 860.76 TONNES

April 18/no changes at the GLD/Inventory remains at 848.92 tonnes

April 17/no changes at the GLD/Inventory remains at 848.92 tonnes

April 13/a deposit of 6.51 tonnes into the GLD/Inventory rests at 848.92 tonnes

this no doubt is a paper deposit/

APRIL 12/no changes in gold inventory at the GLD/Inventory rests at 842.41 tonnes

April 11/a huge deposit of 4.12 tonnes into inventory/Inventory rests at 842.41 tonnes

this would no doubt be a paper gold entry. It would be difficult to find that amount of physical gold.

April 10/1.77 tonnes added into inventory at the GLD/inventory rests at 838.29 tonnes

April 7/a small withdrawal of .28 tonnes from the GLD/Inventory rests at 836.49 tonnes

April 6/no change in gold tonnage at the GLD/Inventory rests at 836.77 tonnes

April 5/no change in gold tonnage at the GLD/Inventory rests at 836.77 tonnes

April 4/no change in gold tonnage at the GLD/Inventory rests at 836.77 tonnes

April 3.2017: a huge deposit of 4.45 tonnes of gold into the GLD/Inventory rests at 836.77 tonnnes

March 31/another withdrawal of 1.19 tonnes of gold inventory fro the GLD/this inventory would no doubt be heading for Shanghai/GLD inventory: 822.32 tonnes

March 30/no changes in gold inventory at the GLD/Inventory rests at 833.51 tonnes

March 29/a withdrawal of 1.78 tonnes of gold out of the GLD/Inventory rests tongith at 833.51 tonnes

March 28/this is good!! A deposit of 2.67 tonnes of gold into the GLD/Inventory rests at 835.29 tonnes.

March 27/no changes in gold inventory at the GLD/Inventory rests at 832.62 tonnes

March 24/another withdrawal of 1.78 tonnes from the GLD/Inventory rests at 832.62 tonnes

March 23/no change in gold inventory at the GLD/Inventory rests at 834.40 tonnes

March 22/no changes in gold inventory at the GLD/Inventory rests at 834.40 tonnes

March 21/a deposit of 4.15 tonnes of gold into the GLD/Inventory rests at 834.40 tonnes

March 20/WE HAD A MASSIVE 6.81 TONNE WITHDRAWAL FROM THE GLD/INVENTORY RESTS AT 830.25 TONNES/THIS GOLD MUST BE ON ITS WAY TO SHANGHAI. WITH GOLD RISING THESE PAST FEW DAYS, IT MAYS NO SENSE WHATSOEVER ON GOLD LIQUIDATION.

March 17/a huge withdrawal of 2.37 tonnes from the GLD/Inventory rests at 837.06 tonnes

March 16/no changes in gold inventory at the GLD/Inventory rests at 839.43 tonnes

March 15/ANOTHER HUGE DEPOSIT OF 4.44 TONNES/inventory rests at 839.43 tonnes

end

Now the SLV Inventory

May 2/extremely strange again/a huge 3.502 million oz deposit into the SLV despite silver being in the toilet for the past several trading days.

may 1/extremely strange/with silver being walloped these past several days, the inventory rises again by a huge 1.136 million oz/(maybe someone can explain this phenomena??)

April 28/Strange again!! no change in inventory at the SLV/Inventory remains at 330.283 million oz (no liquidation with a drop in silver price??)

April 27.2017/Strange!! no change in inventory at the SLV/Inventory remains at 330.283 million oz (no liquidation???)

APRIL 26/2017/another huge deposit of 2.934 million oz into the SLV/Inventory rests at 330.283 million oz

April 25/a huge deposit of 1.98 million of into inventory/inventory rests at 327.349 million oz/

April 24/no changes in inventory at the SLV/Inventory rests at 325.361 million oz/

April 21/A WITHDRAWAL OF 719,000 OZ OF SILVER AT THE SLV/INVENTORY RESTS AT 325.361 MILLION OZ/

APRIL 20/NO CHANGES IN INVENTORY AT THE SLV/INVENTORY RESTS AT 326.308 MILLION OZ

April 19/a withdrawal of 1.893 million oz/inventory rests at 326.308 million oz/

April 18/no changes in inventory at the SLV/Inventory rests at 328.201 million oz

April 17/no changes in inventory at the SLV/Inventory rests at 328.201 million oz

April 13/no changes in inventory at the SLV/Inventory rests at 328.201 million oz

April 12/no changes in inventory at the SLV/Inventory rests at 328.201 million oz/

April 11/a paper deposit of 11.131 million oz into the SLV/no doubt yesterday’s entry of a withdrawal of 11.231 million oz was in error/328.201 million oz

April 10/ a paper withdrawal of 11.231 million oz of silver from the SLV and this silver was used in the raid today. Inventory rests at 317.231 million oz

April 7./ a withdrawal of 947,000 oz of silver from the SLV/Inventory rests at 328.201 million oz.

April 6/a tiny withdrawal of 136,000 oz of silver from the SLV/Inventory rests at 329.148 million oz

April 5/ a withdrawal of 1.042 million oz from the SLV/Inventory rests at 329.284 million oz

April 4/no change in inventory at the SLV/Inventory rests at 330.326 million oz/

April 3.2017; a withdrawal of 568,000 oz from the SLV/Inventory rests at 330.326

million oz/

Major gold/silver trading/commentaries for TUESDAY

GOLDCORE/BLOG/MARK O’BYRNE.

London Property Bubble Vulnerable To Crash

– London property market vulnerable to crash

– House prices in London are falling

– London property up 84% in 10 years (see chart)

– House prices have risen over 450% in 20 years

– Brexit tensions as seen over weekend and outlook for U.K. economy to impact property

– Global property bubble fragile – Risks to global economy

– Gold bullion a great hedge for property investors

by Jan Skoyles, Editor Mark O’Byrne

For the bargain price of 36 AED (£5) I can buy Global Property Scene magazine, here in Dubai. This month it is running the headline ‘ Could Brexit be the making of the UK Property market?’

Property here in Dubai is a big deal, everywhere you look there are cranes and in the middle of the Malls developers have spent a small fortune placing a stand with a 3D model of their latest development.

The Emirate is looking to position itself as the financial safe haven of the Middle East and with that, they know, comes a solid property market.

London property has long been the poster child for countries such as the UAE who are looking to develop what has for a while appeared to be an indestructible real estate market.

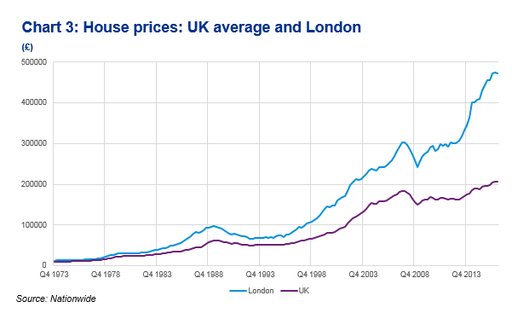

Since 2011 London house prices have climbed by 65%. Between 2006 and 2016, average house prices in the capital grew from £257,000 to £474,000 or by a very substantial 84.4%. These large gains were ‘built’ on the back of the very large appreciation that was seen in prices between 1996 and 2006 (see chart below).

Average house prices in London in 1997 were below £85,000 meaning that in 20 years prices have risen over 450%.

This has created an air around the city’s property markets – residential and commercial – that they are invincible and that they are a safe haven.

House Prices: UK & London Average (KPMG, March 2017)

House Prices: UK & London Average (KPMG, March 2017)

But London property values might not be as invincible as the world thinks.

UK’s Land Registry data for three London boroughs shows transaction volumes in London — the number of houses being bought and sold — are at an all-time low. Back in December asking prices in London dropped 4.3% in December with inner London down 6%, more exclusive areas dropped by as much as 10%.

The slump continued into the first quarter this year, a survey by the Royal Institution of Chartered Surveyors found that more agents than not reported price drops in March. London is now one of the five-slowest growing cities in the UK.

London property has for some time had many of the signs of a bubble. However, it is always very hard to pinpoint when a bubble might burst. We are certainly seeing signs that the overheated market is beginning to cool. Of course, all ‘good’ things must come to an end, but what is driving this particular scenario?

In a world of uncertainty what is tipping which scale can be confusing, but there are some factors at play here that are most likely responsible for the downturn we are witnessing.

Does a downturn or bursting of the London property market matter for the wider UK, or the world? Certainly, as with previous bubble bursts, these things are mere tips of much more dangerous icebergs.

Is the market even affordable?

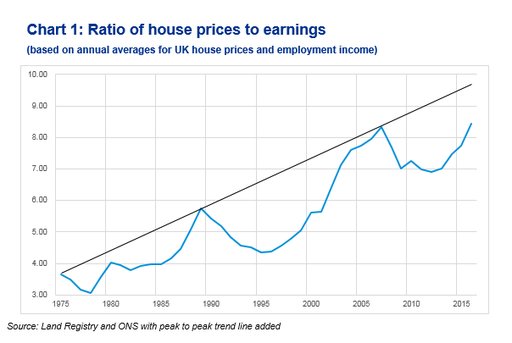

UK house prices are nearly 8.5 times average earnings, a level that the ratio has not been seen at since the last property boom. Yet, on average it has never been financially easier to get a mortgage – with interest rates at record lows in recent years debt servicing levels remain affordable… for now

House Prices to Earnings (KPMG, March 2017)

While KPMG’s research suggests that the house-price-to-earnings ratio is currently below the peak-to-peak trend, it is concerning that it has reached now back at all time record highs.

So as long as interest rates stay ultra ultra low, new borrowing could keep the property market going and keep UK house prices buoyant at least for a while longer.

Since 2013 the average value of London property has risen rapidly relative to rents. For first time buyers and working immigrants the decision to buy comes down to rent prices versus the cost of borrowing, this drives house prices.

So when buyers are optimistic about future house prices, they are generally happy to cover more expensive interest rate payments over rent, if they expect to see a return. This, combined with dinner party conversation over the infallibility in the London housing market, pushes buyers to buy property today terrified in the belief that prices will only get higher.

If record high rents begin to fall – which seems probable given the many global geo-political, financial and economic risks and indeed the risks posed by Brexit to the UK economy – then first time buyers and indeed buy to let investors might decide to hold off buying.

Also, as earnings are not increasing in line with ether inflation or house prices, factors such as Brexit and interest rates (both of which are wrapped up in uncertainty) are beginning to cast a shadow over the London property market. Something which could be disastrous for the UK economy.

Brexit blues dim London property

During the UK’s EU referendum, there were lots of on-the-street interviews with voters arguing that a post-Brexit world would impact the country’s property market. Post-Referendum we are still in a weird limbo as we await to see the result of Brexit negotiations.

In the meantime the rest of world’s financial markets and investors speculate over various uncertainties. This in turn will inevitably impact real estate prices.

The most immediate data we have that shows the impact of Brexit is the slowing of immigration into the UK by those looking to study or work. This was the case even in the run up to the referendum.

This fact is one of the contributors to the cooling off in London house prices. There is a slow-down in demand for not only property to buy but also to rent. Potential buy-to-let purchasers are seeing a slow-down in demand, which reduces the return on their investments.

But international investors (as opposed to immigrants) might not be put off just yet by the London property market. To those holding US dollars or euro, the capital’s real estate might seem to be quite the bargain. In dollar terms property is 16% cheaper 11% so for euro buyers than they were before the referendum due to the sharp fall in sterling. Providing they are comfortable with the considerable currency risk.

As was seen over the weekend and still very high tensions between the May government and the EU, Brexit uncertainties are set to continue. It is the impact of these, and likely further weakening in the pound, which may create further issues for the UK economy.

Is Brexit really an issue?

There is no doubt that Brexit has created some uncertainty in the UK housing market. The recent property prices speak for themselves. Should the Conservatives win the majority in the June election there could be less uncertainty although the negotiations with the EU are likely to be long and hard. There is no guarantee that they will be successfully wound up in even two years time and there is the real risk that they lead to a significant deterioration in relations between the UK and EU powers and leading EU nations.

A bigger concern for the UK housing market is interest rates. The cost of borrowing has been at record lows for several years. Central banks’ easy money policies, including the Bank of England, have meant that we have seen property prices increase around the world.

The era of record low interest rates was always going to come to an end and the finale is now on the horizon. The Bank of England warned back in February that the post-Brexit value of the sterling which is expected to send inflation to 2.7% this year, will prompt a hike in interest-rates.

If it costs more for buyers to borrow money then this quite simply means that there is less money to be spent on property. The market is already built on the sandy foundations of massive debt suggesting that this is a house of cards that can’t take another layer.

Even where there is real money playing a role, the amount required for a deposit is rapidly becoming unobtainable. First-time buyers are dropping like flies given the increase in deposit amounts; first-time buyer deposits have reached £34,000 across the UK, and nearly £100,000 in London.

In the last few years buyers (both property investors and first-time buyers) have been enjoying the merry-dance of borrow money at a low yield and spending it on the higher-yielding property market. And this isn’t just happening in London, it is happening across the global property market.

The dance has been going on for some time, but it looks as though the jig is about to come to an end, soon these same savvy investors might find themselves with an expensive lump of debt to service, a falling yield on rents and an asset which is worth far less than they had expected.

A problem only to be borne by foreign investors?

Back in January Catherine Mann, the OECD’s chief economist, spoke of vulnerabilities in asset markets. In regard to the UK property market she said this would be good for the country if the fall in prices was borne by foreign investors.

“[What’s] interesting in terms of the implications for the UK economy is who bears the burden – who bears the adjustment cost. If it’s a non-resident then lower house prices could actually be good for the UK.”

However, it is next to impossible that the UK will not feel the pain of the property bubble bursting. Aside from those buyers who will likely be left facing negative equity, unserviceable levels of debt and possible bankruptcy we also need to consider the impact of those who are still borrowing to buy property.

Local councils in the UK aren’t known for their investing prowess.

You just need to look at the Icelandic banking scandal that resulted in UK council being bailed out, for an example. This time around the councils have decided that their local property markets are ones worthy of a punt or two. They may well have been witnessing the optimism that remains amongst estate agents, with more respondents to the RICS survey than not saying they expect prices to climb in the next year.

Local councils are so confident about the strength of the property market that they are borrowing from the Public Works Loan Board (part of the Treasury). Most recently the Isle of Wight has borrowed a whopping £100 million in order to bet on property. Lord Oakshott, Chairman of Olim Property told the Financial Times, “English councils punting on property is an accident waiting to happen.”

“There are real echoes here of Northern Rock, where many punters were lent all the purchase price of a property, and the Icelandic bank scandals, where councils played a market they didn’t understand for short-term income gain.”

Councils overextending themselves (as we saw with Iceland) is not a cost that is later borne by foreign investors. It is borne by those who have to bail them out – the tax payer. We have been here before.

What about supply?

The RICS Chief Economist referred to the ‘flat trend in transaction levels.’ We can spend as much time as we want referring to buyers’ deposits, cost of borrowing and the impact of Brexit but we only do so in reference to demand. This over-heated market was also driven by levels of supply.

A small drop in prices, at levels mentioned in the beginning, means that supply is also likely to slow-down as owners fear they won’t get much return on their investment if they sell now, instead hoping to sit it out and wait for a correction.

Hometrack data shows supply is not keeping pace with sales in Birmingham and Manchester, despite prices set to increase. In London, a stall in prices is more or less inevitable as buyers aren’t purchasing houses at the same rate they’re being put on the market.

A brief check on a major property website by ZeroHedge found that there might be call for nervousness among sellers and estate agents. Despite discounts on Kensington and Chelsea properties by as much as 40% on those that have been listed for over a year, the number of listings appears to have doubled and little seems to be shifting.

Conclusion – Gold good hedge for property investors

Since the Second World War, UK house prices have only crashed three times, the second time was just ten years ago, then again in 2009 when they hit rock bottom. Since 2013 they have been unstoppable, especially in London.

The belief that they are unstoppable comes from the same drunken optimism the credit crisis came from – one of immortality and the mass delusion at nothing could threaten the property boom we were seeing. Data is now slowly revealing a different picture from the one so many people have been imagining for the last few years.

The property market is certainly seeing a serious cooling down and the question is whether this is the start of serious correction or a crash.

This is not just an event that will be kept local to London. Other “international cities” and major property markets such as Singapore and New York looks bubbly and vulnerable to sharp corrections.

Now would be a pertinent time for investors to review their portfolio allocation to property markets. Even if you do not hold property other than your own home, the bursting of the bubble will no doubt impact the global financial system, not to mention the national economies to which they are so intrinsically tied.

If property market corrects sharply or crashes, companies, councils and irresponsible lenders will need to be bailed out. Who will be footing the bill? We will. For reasons already explained by events played out during the financial crisis, it would be prudent for readers to consider how much exposure they have to not only the property market but also the banking system and the banks that have considerable exposures to property markets.

It is difficult to hedge property investments effectively. However, in our modern globalised world where interest rates and economic cycles are increasingly correlated, gold will likely become an excellent hedge for property investors in the coming years.

Property prices look over valued in many markets internationally today and in the event of price falls, gold is likely to act as a hedge and preserve wealth as it has done throughout history.

Investors should decide on a reasonable allocation to gold bullion, held in allocated and segregated storage in less debt laden jurisdictions.

Owning these assets outside of the digital and the financial system, away from the shaky, debt-fuelled banking system funding the overheated property markets will soon be seen as prudent

END

USA GOLD news and views on gold’s undervaluation

(courtesy Mike Kosares/USAGold/GATA)

USAGold’s News & Views for May notes gold’s undervaluation

Submitted by cpowell on Mon, 2017-05-01 17:16. Section: Daily Dispatches

1:15p ET Monday, May 1, 2017

Dear Friend of GATA and Gold:

USAGold’s News & Views letter for May, written and edited by proprietor Mike Kosares and published today, provides interesting data about what seems like gold’s substantial undervaluation, at least by the standards that applied before surreptitious intervention in the gold market by central banks became pervasive.

Indeed, it’s disappointing if no longer so surprising that the gold mining industry, financial journalists, and market analysts who disparage gold for its failing to keep up with inflation decline to inquire into the causes of gold’s seeming undervaluation. They might find an important story.

The May letter is posted at USAGold here:

http://www.usagold.com/publications/NewsViewsMay2017.html

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

Data from Switzerland shows that India is now again showing its love for gold having imported 55.6 tonnes in March. They may overtake China as the number one consumer of gold. I would also like to point out that these numbers do not include smuggled gold into India.

(Lawrie Williams/Sharp’s Pixley)

LAWRIE WILLIAMS: March Swiss gold exports show India no.1 again

The latest export figures for gold for the month of March from the Swiss Customs Administration show that India, once again, was easily the top recipient, taking 55.6 tonnes – more than gold flows from Switzerland to Hong Kong and China combined. Hong Kong imported 24.3 tonnes and the Chinese Mainland 24.0 tonnes directly. These latter figures confirm our now oft-stated observation that Hong Kong gold flows can no longer be considered a proxy for total Chinese imports with perhaps 40-50% now flowing directly into the Chinese Mainland by avoiding Hong Kong altogether.

See the excellent chart below from www.goldchartsrus.com which sets out the principal recipients of the Swiss gold exports on a country- by-country basis. Note also that India, Hong Kong and China alone accounted for around 74% of Switzerland’s total gold exports, while Asia and the Middle East accounted for just under 88%, emphasising the continuing flows of gold from West to East.

As for India itself, this is very much a continuation of the pattern seen earlier in the year suggesting that gold demand in the country, which used to be the world’s No. 1 consumer, is picking up significantly from the very low levels of a year ago when they were affected by a prolonged jewellers strike and the withdrawal of 100 and 50 rupee notes (India is very much a country which runs on cash). March is the third month in a row where India has topped the list of recipients of Swiss gold exports and has taken in 119 tonnes of Swiss gold in the first quarter of the year. (See: Over 80% of Switzerland January gold exports headed to Asia and Middle Eastand Swiss gold exports to India top the table in February).

While we may well see a reduction in Indian gold imports from Switzerland in April now that the Akshaya Tritya Festival (seen as a particularly auspicious time to buy gold) is behind us, wedding demand will probably mean that imports will remain at a positive level.

Also note that we reported that official figures from India itself also support the premise that its gold imports are indeed running stronger – See: Indian gold imports picking up?. This latter article showed that total February gold imports totaled over 89 tonnes in February. With only 37.2 tonnes being sourced from Switzerland that meant that nearly 60% of Indian gold imports were sourced from countries other than Switzerland during that month which puts an additional new complexion on likely total Indian gold imports for the year.

Indeed, in the rather restricted way that specialist precious metals consultancies like GFMS calculate gold consumption, India could well be rated by them as the world’s No.1 gold consumer again this year. Metals Focus, the other big London precious metals consultancy, follows a somewhat similar line to GFMS, although has been a bit more positive on China’s consumption, and with it providing data to the World Gold Council it will be interesting to see what position the latter takes in its next Gold Demand Trends report. The media tends to hang on the WGC figures as definitive and this could easily also suggest that India is back in first place among global gold consumers. But we will still reckon on China being No.1 regardless as the major consultancies do not seem to rate gold consumption by the financial sector as being relevant, while we do in terms of overall gold flows.

02 May 2017

https://www.sharpspixley.com/articles/law rie-williams-march-swiss-gold-exports-show-india-no1- again_266934.html

-END-

Your early TUESDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight

1 Chinese yuan vs USA dollar/yuan SLIGHTLY WEAKER 6.8953( DEVALUATION SOUTHBOUND /OFFSHORE YUAN MOVES STRONGER TO ONSHORE AT 6.8920/ Shanghai bourse CLOSED DOWN 10.95 POINTS OR .35% / HANG SANG CLOSED UP 81.00 POINTS OR .33%

2. Nikkei closed UP 135.18 POINTS OR 0.70% /USA: YEN RISES TO 112.21

3. Europe stocks OPENED ALL IN THE GREEN ( /USA dollar index FALLS TO 99.04/Euro UP to 1.0913

3b Japan 10 year bond yield: RISES TO +.021%/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 112.21/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD FINALLY IN THE POSITIVE/BANK OF JAPAN LOSING CONTROL OF THEIR YIELD CURVE AS THEY PURCHASE ALL BONDS TO GET TO ZERO RATE!!

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 49.25 and Brent: 52.03

3f Gold DOWN/Yen DOWN

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil UP for WTI and UP for Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund FALLS TO +.338%/Italian 10 yr bond yield DOWN to 2.328%

3j Greek 10 year bond yield FALLS to : 6.116%

3k Gold at $1255.80/silver $16.95 (8:15 am est) SILVER ABOVE RESISTANCE AT $18.50

3l USA vs Russian rouble; (Russian rouble DOWN 4/100 in roubles/dollar) 57.03-

3m oil into the 49 dollar handle for WTI and 52 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation (already upon us). This can spell financial disaster for the rest of the world/China forced to do QE!! as it lowers its yuan value to the dollar/GOT SMALL DEVALUATION SOUTHBOUND

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 112.21 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning .9946 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.0853 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now POSITIVE territory with the 10 year RISES to +.338%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.336% early this morning. Thirty year rate at 3.017% /POLICY ERROR)GETTING DANGEROUSLY HIGH

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

(courtesy Jim Reid/Bloomberg/Deutsche bank/zero hedge)

Global Stocks Hit All Time High As Fed Meeting Begins

With the Fed set to begin its latest 2-day meeting (no rate hike is expected), S&P futures are little changed with European and Asian stocks higher after the VIX dropped to a 10 year low and the Nasdaq rose to record highs, sending the MSCI All-Country Index back to all time highs, as global markets reopen after holiday with investors focusing on stronger corporate earnings, while ignoring weaker than expected “hard” economic data and geopolitical concerns. The yen extended losses, with the USDJPY rising to the highest since March 21; gold slid and WTI crude futures rose while Treasury yields climbed after Steven Mnuchin said it “could absolutely make sense” for the U.S. to sell ultra-long bonds.

The MSCI All-Country World Index was poised for another all time high, as global market cap once again rose above $50 trillion. European shares advanced after the May 1 holiday, as BP jumped after posting stronger than expected earnings. European government bonds fell across the board. The Nasdaq Composite index hit a record high on Monday as the world’s five largest companies by market capitalization — Apple, Alphabet, Microsoft, Amazon and Facebook — all hit intraday or closing highs.

“Risk assets are performing well and investors are clearly bullish,” Claudio Piron, strategist at Bank of America Merrill Lynch wrote in a client note. “Nevertheless, we advise caution and this month is especially notorious for its refrain to ’Sell in May’,” he added, although lately it appears that nothing can dent the bullish mood on Wall Street, where the VIX “fear gauge” closed at its lowest since before the global financial crisis on Monday.

The MSCI All-Country World Index rose 0.1 percent as of 10:35 a.m. in London.

The Stoxx Europe 600 Index increased 0.2 percent, with BP climbing 1.6 percent, and the banking sub-index was up 0.4 percent, showing no reaction to comments from U.S. President Donald Trump, who told Bloomberg Television he was actively considering breaking up big banks.

The Topix index rose 0.7 percent to the highest since March 21 as the yen weakened. Japanese markets will be closed for holidays over the next three days. MSCI’s broadest index of Asia-Pacific shares outside Japan gained 0.5 percent to its highest level since June 2015, as many of the region’s markets also reopened after a long holiday weekend. Japan’s Nikkei rose 0.7 percent after some robust earnings. South Korea paced gains, with the Kospi briefly topping its 2011 peak.

Much of the market’s attention has fallen on forecast-beating corporate earnings which have helped push shares higher across the globe this year. First-quarter profits at S&P 500 companies are expected to rise 13.6 percent, the strongest rise since 2011, according to Thomson Reuters I/B/E/S. European equivalents are seen up 13.9 percent.

“Higher corporate earnings and tax reform seem to be more important to the market than any off-the-cuff remark from Trump. That means people are not buying protection in the options market to protect themselves from a drop in the market,” said Neil Wilson, senior market analyst at ETX Capital.

Strong earnings have outweighed concern over patches of weak economic data. An official survey on Tuesday showed Chinese factory activity growth slowed more than expected in April.

The ISM measure of U.S. manufacturing activity also undershot forecasts on Monday.

“Soft” data in Europe was better with Euro-area factories expanding output at the fastest pace since 2011. The Markit Manufacturing PMI gauge rose to 56.7 in April from 56.2 the previous month, IHS Markit reported on Tuesday. An April 21 preliminary estimate was for an increase to 56.8. “Companies are benefiting from the historically weak euro, improved growth in key export markets, rising domestic demand and ongoing central-bank stimulus including record-low interest rates,” said Chris Williamson, chief economist at IHS Markit. “Optimism about the year ahead, meanwhile, appears unaffected by political worries.”

The dollar hit a one-month high against the safe-haven Japanese yen on some signs of easing tensions over North Korea and as U.S. bond yields rose after U.S. Treasury Secretary Steven Mnuchin said the government was looking into issuing ultra-long debt of maturities in excess of 30 years. Greek government bond yields fell after Greece and its lenders reached a long-awaited deal on reforms required to release further bailout funds.

U.S. 30-year Treasury yield were 1 basis point higher at 3.02 percent, just below Monday’s three-week high, after Mnuchin told Bloomberg issuing ultra-long bonds “can absolutely make sense”. “Mnuchin’s comments have at least stabilized the long end of the curve,” said Lee Hardman, a currency economist with Japan’s MUFG. “But the dollar is still on the defensive in the near term. The data from the U.S. has been coming in on the disappointing side and the Fed is likely to acknowledge that at this week’s meeting.”

The yield on 10-year Greek government bonds fell 30 basis points to 6.18 percent, their lowest since October 2014, after the deal with its lenders, which followed half a year of talks. Oil prices rose as investors weighed rising production in Libya and elsewhere and expectations that the OPEC producers group and others will extend output curbs. Brent crude last traded 29 cents higher at $51.81.

Companies due to report earnings include Apple, Pfizer, Merck and Aetna. Wards total vehicle sales may rise.

Global Market Snapshot

- S&P 500 futures down 0.1% to 2,384.75

- MXAP up 0.4% to 150.04

- MXAPJ up 0.6% to 490.83

- Nikkei up 0.7% to 19,445.70

- Topix up 0.7% to 1,550.30

- Hang Seng Index up 0.3% to 24,696.13

- Shanghai Composite down 0.4% to 3,143.71

- Sensex up 0.02% to 29,924.82

- Australia S&P/ASX 200 down 0.1% to 5,950.37

- Kospi up 0.7% to 2,219.67

- STOXX Europe 600 up 0.2% to 387.44

- German 10Y yield rose 1.2 bps to 0.329%

- Euro up 0.2% to 1.0915 per US$

- Brent Futures up 0.6% to $51.81/bbl

- Italian 10Y yield rose 3.7 bps to 1.987%

- Spanish 10Y yield rose 2.2 bps to 1.67%

- Brent Futures up 0.6% to $51.81/bbl

- Gold spot down 0.1% to $1,255.34

- U.S. Dollar Index down 0.02% to 99.05

Bulletin Headline Summary from RanSquawk

- European equities trade modestly higher with BP earnings helping to lift the FTSE 100

- GBP finds support after surprise rise in UK Mfg. PMI

- Looking ahead, highlights include US vehicle sales data

Top Overnight News From Bloomberg

- Trump Says He’d Meet North Korea’s Kim If Conditions Right

- Trump Weighs Breaking Up Wall Street Banks, Raising Gas Tax

- Barclays Falls for Third Day as Trump Suggests Bank Breakup

- IAC to Buy Angie’s List in Deal Valued at Over $500 Million

- Soros Says It’s ‘Disappointed’ by Terms of Proposed KWE Deal

- Euro-Area Manufacturing Expands at Fastest Pace in Six Years

- Monsanto Abandons Deal With Deere as Merger With Bayer Looms

- Boeing Had 15 Orders Incl. 13 for 737s in Week Ended April 30

- McDonald’s Japan Says ‘Gran’ Burger, McFlurry Drove April Sales

- Discovery, ProSiebenSat.1 Start Joint German Streaming Service

- Infosys Plans to Hire 10,000 American Workers Over Next 2 Years

- AstraZeneca Approval Unlikely a Big Commercial Opportunity: JPM

- Liberty Interactive Buying HSN May Lead to 10% Accretion: BofAML

Asian equities traded mixed as the majority of the region returned from public holiday and digested the weaker than expected Chinese PMI data. ASX 200 (-0.3%) was led lower by miners and financials after gold prices declined and following earnings from Big 4 bank ANZ Bank which missed expectations despite showing H1 cash earnings rose 23%. Nikkei 225 (+0.7%) traded positive on a weaker currency, while Shanghai Comp. (-0.3%) and Hang Seng (+0.3%) were mixed with the mainland bourse pressured after the PBoC refrained from open market operations and as participants mulled over the latest PMI data in which the Official and Caixin Manufacturing PMIs missed estimates to print 6-month and 7-month lows, respectively. 10yr JGBs traded flat with slightly weaker demand seen in today’s enhanced-liquidity auction for 2yr, 5yr, 10yr and 20yr JGBs, while the curve was mixed with mild underperformance seen in the long-end. RBA kept the Cash Rate unchanged at 1.50% vs. Exp. 1.50% (Prey. 1.50%), while it reiterated that unchanged policy is consistent with sustainable growth and achieving inflation target. RBA also commented that higher commodity prices give significant support to Australia’s national income and that a broad-based pick up was seen globally since last year.

Top Asian News

- China’s $11 Trillion Economy and Markets Are in a Tug of War

- DBS Profit Beats Forecasts, Helped by Wealth-Management Fees

- Pimco Warns of Credit Risks as Asia Bond Sales at Record

- Guangzhou R&F Halted Pending 1Q Results Release

- Hong Kong Stocks Fluctuate; Belle Surges While Developers Drop

- India’s Sensex Holds Close to Record; Reliance, Tata Motors Fall

- Asia’s FX Laggards Turn Leaders of Pack as Ringgit Rebounds

- Modi Adviser Says Bad Bank Not Needed to Solve Loan Mess

- Japan Stocks Rise to 6-Week High as Yen Weakens Before Holiday

- RBA Statement’s Unwritten Line: Baton Handed to Fiscal Stimulus

European equities have started the holiday-shortened week on the front-foot in the wake of the largely positive sentiment seen on Wall Street yesterday. More specifically, the FTSE 100 (+0.5%) outperforms its peers as a positive earnings update from BP (+1.4%) props up energy names across the continent with gains otherwise relatively broad-based in what has otherwise been a relatively light morning for stock specific newsflow. Fixed income markets trade modestly lower alongside some of the upside seen in European bourses with prices also relatively unreactive to the latest slew of largely in-line core Eurozone manufacturing PMIs. More specifically, French paper has been relatively steady as Macron continues to maintain his lead over Le Pen ahead of tomorrow’s televised debate and Sunday’s election results. Elsewhere, peripheral focus has been on Greece with a notable decline in yields after the Greek government has managed to strike a deal with creditors regarding austerity measures.

Top European News

- Greek Debt-Relief Talks Move Closer After Late-Night Athens Deal

- May Says Juncker Clash Shows Brexit Talks Will ‘Not Be Easy’

- Italian Joblessness Unexpectedly Increases as More Seek Work

- U.K. Manufacturing Growth Surges to Fastest in Three Years

- Soros Says It’s ‘Disappointed’ by Terms of Proposed KWE Deal

- Macron Tells Le Pen, Melenchon Voters He Hears Their Anger

- A $1 Trillion Asset Management Boom Is a Guide to Nordic Banking

In currencies, the yen slid 0.3 percent to 112.21 per dollar, the lowest since March 21, following a 0.3 percent slide on Monday. The euro rose 0.2 percent to $1.0917, while the British pound was little changed. The Bloomberg Dollar Spot Index was flat. The early price action in London this morning favoured the USD despite some data misses reported in yesterday’s holiday thinned markets. USD personal income and spending and ISM manufacturing PMIs all came in softer than expected, buy we saw the greenback on the front foot against a selection of currencies. USD/JPY was standout as we broke above 112.00, with some suggesting this was partly in the short term plug in the US finding gap, though we prefer the correlation to equities. UST yields still looking buoyed to maintain support through the figure, but upside momentum is clearly lacking. Gains also seen against the CAD and GBP, but Oil prices have recovered modestly to fend off a move to 1.3700 for now, but the spot rate remains poised for another push higher. GBP was trading on the backfoot as all things Brexit are back at the fore. Cable had slipped below 1.2880 from the mid-upper 1.2900’s seen late last week, but was given a boost this morning from the much better than expected UK manufacturing PMIs — at 57.3.

In commodities, West Texas Intermediate crude rose 0.4 percent to $49.04, erasing earlier losses. Oil fell 1 percent Monday as Libyan output surged, more rigs were added in the U.S. and Saudi Arabia cut prices to Asian customers. Oil prices initially took another dip, and any support coming in for WTI and Brent at predominantly based on hopes of the production cut agreement being extended into H2. Plenty of talk that there is strong intent, but we are unlikely to see a notable pick up until this is rubber stamped. Copper prices have risen on fresh strikes in Indonesia, with supply concerns outweighing demand issues emanating from the softer China PMIs. Nickel and Zinc keeping up with Copper this morning. Gold will likely find some support as the market looks to the French election this weekend, but little negative impact on the EUR as Le Pen softens her tone on the single unit.

Looking at the day ahead, this morning in Europe we’ll get the final April manufacturing PMI readings along with a first look at the data for the UK and the periphery. We’ll also get the Euro area wide unemployment rate for March. The only data due out in the US this evening is vehicle sales data for April. Away from the data the ECB’s Nouy is set to speak at two separate events today while Nowotny also speaks this evening. Germany’s Merkel is also due to meet Russia’s Putin which might be worth keeping an eye on. On the earnings front we’ve got 43 S&P 500 companies reporting including Merck, Pfizer (both at the open) and Apple (after the close).

US Event Calendar

- Wards Total Vehicle Sales, est. 17.1m, prior 16.5m

- Wards Domestic Vehicle Sales, est. 13.3m, prior 13m

DB’s Jim Reid concludes the overnight wrap

Perhaps the highlight of a light US session last night was the VIX closing at the lowest level since February 16th 2007, a span of nearly 123 months. The index closed at 10.11 which compares to the close on Friday of 10.82. It did actually touch an intraday low of 9.90 yesterday which is only the second time this year that the index has fallen below 10.00 (it touched 9.97 intraday in early February). To put yesterday’s closing level in context, in the 6871 business days since the inception of the VIX (going back to 1990) we have only ever seen the index close lower than last night’s level on 14 occasions. Quite impressive stats.

Given the holidays around the globe it won’t come as a surprise to hear then that price action in US equities wasn’t hugely exciting yesterday. The S&P 500 (+0.17%) and Dow (-0.13%) both faded into the close despite the Nasdaq (+0.73%) notching up a new record high. Initially sentiment was boosted by that news of a tentative agreement by Congress on a near $1.2tn spending bill, which is likely to be voted on in the coming days. In fact politics largely dominated yesterday’s session with banks under the spotlight after President Trump said in an interview with Bloomberg News that he is actively considering a breakup of Wall Street Banks and specifically calling for a “21st century” version of the 1933 Glass-Steagall law. Any weakness in bank stocks was short lived however with JP Morgan (+0.10%), Morgan Stanley (+0.88%) and Bank of America (+1.24%) all finishing up. In addition to the bank comments, Trump also added that he is open to increasing the US gasoline tax rate with additional revenues to be used to fund infrastructure development.

Away from this Treasury yields crept higher as the session progressed with the curve steepening too. 10y yields finished the day up 3.8bps at 2.319% while 30y yields rose a little over 5bps to close back above 3.000% again. Much of that move reflected comments from Treasury Secretary Steven Mnuchin who said that ultralong bond issuance “could absolutely make sense”. He added that the Treasury currently “have a working group looking at it”. Meanwhile, following the soft Q1 GDP print last week the Atlanta Fed released their initial first estimate of Q2 growth which they have pegged at 4.3%.

Staying with the macro, the main focus of the data yesterday was the ISM manufacturing reading which came in at a slightly disappointing 54.8 for April (vs. 56.5 expected) from 57.2 in March. At face value the index still remains firmly in expansion territory and points to much stronger growth than what the initial Q1 real GDP figures suggest. However there were some disappointing aspects within the details of the report. Ahead of payrolls this week the employment component tumbled 6.9pts to 52.0 which is essentially the biggest one-month decline since July 2011 when there were concerns about the US debt ceiling. The new orders component was soft too, falling 7.0pts to 57.5, albeit still at an elevated level. There was however some improvement seen in components for production and exports.

In terms of other data, the final manufacturing PMI for April was confirmed at 52.8 which was unchanged relative to the flash reading. Away from that personal spending in March came in flat after consensus was for a +0.2% mom rise. The February reading was also revised down a tenth while personal income was also below market (+0.2% mom vs. +0.3% expected). Meanwhile, as expected the PCE deflator (-0.2% mom) fell while the PCE core (-0.1% mom) was also down and in line with expectations. That has pushed the YoY rate down two-tenths to +1.6%.

This morning in Asia and with the exception of China we’ve seen most major bourses advance in early trading. The Nikkei (+0.70%), Hang Seng (+0.27%) and Kospi (+0.84%) are all up with the latter briefly edging above its all time record close at one stage. In China the Shanghai Comp (-0.35%) is in the red perhaps in response to a disappointing run of data in recent days. After the official PMIs were confirmed as weakening in April over the weekend this morning we saw the Caixin manufacturing PMI come in at 50.3 for April which is both down from 51.2 the month prior and also well below expectations for 51.3. Meanwhile in Australia the Aussie Dollar (+0.34%) is firmer after the RBA left rates on hold as expected.

Moving on. Today brings the latest monthly ECB purchasing data where hopefully we’ll get a much better guide to how the ECB is splitting their taper between corporate and government bonds. April was full of holidays which distorted the weekly data but viewed over the month we should get some guidance. Given the bank holidays yesterday in Europe we thought it would be worth quickly recapping some of the main news from the weekend which we touched on in yesterday’s EMR. In Italy former PM Renzi won the Democratic Party Primary with over 70% of votes which will likely be seen as a strong mandate ahead of next year’s general election. In France recent polls still point to a 20pp lead for Macron over Le Pen ahead of this weekend’s second round election. Finally the European Council released the guidelines intended to govern the EU’s Brexit negotiations with the UK after they were unanimously backed in Brussels. EU President Tusk noted that the unanimous support gives the EU a “strong political mandate for negotiations”. We also had a wrap up of what has been a decent earnings season so far on both sides of the pond.

Looking at the day ahead, this morning in Europe we’ll get the final April manufacturing PMI readings along with a first look at the data for the UK and the periphery. We’ll also get the Euro area wide unemployment rate for March. The only data due out in the US this evening is vehicle sales data for April. Away from the data the ECB’s Nouy is set to speak at two separate events today while Nowotny also speaks this evening. Germany’s Merkel is also due to meet Russia’s Putin which might be worth keeping an eye on. On the earnings front we’ve got 43 S&P 500 companies reporting including Merck, Pfizer (both at the open) and Apple (after the close).

In terms of the remainder of this week, kicking things off tomorrow will be Germany where the April unemployment numbers are due to be released. Shortly after that we’ll get Euro area PPI for March and then the advanced Q1 GDP report for the Euro area. In the US tomorrow we’ll get the ADP employment change report in April and the final April PMIs and ISM non-manufacturing reading. In the evening on Wednesday all eyes then turn over to the Fed meeting. In Asia on Thursday the early data is out of China with the remaining April Caixin PMIs. In Europe we’ll also get the remaining April services and composite PMIs as well as Euro area retail sales in March and UK money and credit aggregates data. In the US on Thursday the data includes initial jobless claims, Q1 nonfarm productivity and unit labour costs, March trade balance, March factory orders and the final revisions to March durable and capital goods orders. With little of note in Europe on Friday the main focus will be on the US where we’ll get the April employment report including nonfarm payrolls.

Away from the data, this week’s Fedspeak is reserved for Friday when we’ll hear separately from Fischer, Williams and Yellen, as well as a panel debate with Rosengren, Evans and Bullard. Over at the ECB, in the remainder of this week we are due to hear from Lautenschlaeger, Praet, Draghi and Mersch on Thursday. Other important events this week include Wednesday’s live televised debate between French presidential candidates Macron and Le Pen, Wednesday’s meeting between President Trump and Palestinian Authority President Abbas and UK local elections on Thursday. Finally, on the earnings front a total of 131 S&P 500 companies report this week and 85 Stoxx 600 companies report. Amongst those still to report from tomorrow are BNP Paribas, Facebook, Tesla, Time Warner, HSBC, BMW, Shell and VW.

3. ASIAN AFFAIRS

i)Late MONDAY night/TUESDAY morning: Shanghai closed DOWN 10.95 POINTS OR .35% OR / /Hang Sang CLOSED UP 81.00 PONTS OR .33% . The Nikkei closed UP 135.18 OR 0.70% /Australia’s all ordinaires CLOSED DOWN .08%/Chinese yuan (ONSHORE) closed DOWN at 6.8953/Oil UP to 49.25 dollars per barrel for WTI and 52.03 for Brent. Stocks in Europe OPENED IN THE GREEN ..Offshore yuan trades 6.8920 yuan to the dollar vs 6.8953 for onshore yuan. NOW THE OFFSHORE IS A LITTLE WEAKER TO THE ONSHORE YUAN/ ONSHORE YUAN SLIGHTLY WEAKER (TO THE DOLLAR) AND THE OFFSHORE YUAN A LITTLE STRONGER TO THE DOLLAR AND THIS IS COUPLED WITH THE WEAKER DOLLAR. CHINA IS HAPPY

3a)THAILAND/SOUTH KOREA/NORTH KOREA

NORTH KOREA

More rhetoric from Kim as he is furious after the USA and Sout Korea deployed lancer bombers in war exercises conducted off the Korean peninsula

(courtesy zero hedge)

Furious North Korea Threatens “Final Doom” After US Deploys Strategic Bombers

Another day, another jawboning escalation out of North Korea, which on Tuesday accused the US of pushing the Korean peninsula “to the brink of nuclear war” after two strategic U.S. bombers flew training drills with the South Korean and Japanese air forces in another show of strength. As Reuters reports, the two supersonic B-1B Lancer bombers were deployed amid rising tensions over North Korea’s pursuit of its nuclear and missile programs.

North Korea said the bombers conducted “a nuclear bomb dropping drill against major objects” in its territory at a time when Trump and “other U.S. warmongers are crying out for making a preemptive nuclear strike” on the North.

“The reckless military provocation is pushing the situation on the Korean peninsula closer to the brink of nuclear war,” the North’s official KCNA news agency said on Tuesday.

“Any military provocation against the DPRK will precisely mean a total war which will lead to the final doom of the US.”

A pair of B-1B Lancer bombers

The US air force said in a statement the bombers had flown from Guam to conduct training exercises with the South Korean and Japanese air forces.

The DoDBuzz website first reported yesterday that two Air Force B-1B Lancer bombers flew near the Korean Peninsula Monday, just days after North Korea conducted another failed ballistic missile launch.

The bombers departed Andersen Air Force Base, Guam, to conduct “bilateral training missions with their counterparts from the Republic of Korea and Japanese air forces,” said Lt Col Lori Hodge, PACAF public affairs deputy director. Hodge did not specify how close the bombers flew to the Korean Demilitarized Zone, known as the DMZ, but said they were escorted by South Korean fighter jets.

When asked if the bombers were carrying weapons, the command wouldn’t disclose, citing standard operating policy. In September, the service put on a similar show of force over South Korea, deploying B-1B bombers alongside South Korean fighter jets after another nuclear test from North Korea. The U.S. military has maintained a deployed strategic bomber presence in the Pacific since 2004.

While Hodge said the training was routine, the recent flyover marks another in a series of events the U.S. has taken to deter North Korea’s Kim Jong Un from additional ballistic missile tests — the latest which occurred April 28.

Ironically, the flight of the two bombers on Monday took place roughly at the same time as Donald Trump said he would be “honored” to meet North Korean leader Kim Jong Un in the right circumstances, and as his CIA director landed in South Korea for talks. South Korean Defense Ministry spokesman Moon Sang-gyun told a briefing in Seoul that Monday’s joint drill was conducted to deter provocations by the North.

Also overnight, Reuters reported that the U.S. military’s THAAD anti-missile defense system has reached operational capacity in South Korea, although they added that it would not be fully operational for some months. China has repeatedly expressed its opposition to the system, whose powerful radar it fears could reach inside Chinese territory. Foreign Ministry spokesman Geng Shuang again denounced THAAD on Tuesday.

“We will resolutely take necessary measures to defend our interests,” Geng said, without elaborating.

Asked about Trump’s suggestion he could meet Kim, Geng said China had noted U.S. comments that it wanted to use peaceful means to resolve the issue. Trump has been recently been full of praise of Chinese President Xi Jinping’s efforts to rein in its neighbor. “China has always believed that using peaceful means via dialogue and consultation to resolve the peninsula’s nuclear issue is the only realistic, feasible means to achieve denuclearisation of the peninsula and maintain peace and stability there, and is the only correct choice,” Geng told a daily news briefing.

It was widely feared North Korea could conduct its sixth nuclear test on or around April 15 to celebrate the anniversary of the birth of the North’s founding leader, Kim Il Sung, or on April 25 to coincide with the 85th anniversary of the foundation of its Korean People’s Army. The North has conducted such tests or missile launches to mark significant events in the past. Instead, North Korea conducted an annual military parade, featuring a display of missiles on April 15 and then a large, live-fire artillery drill 10 days later.

So far the joint US-Chinese deterrence appears to be having an effect on the Kim regime.

end

NORTH KOREA//CHINA

China unleash an oil embargo on North Korea which would cripple the country:

(Calcuttawala/OilPrice.com)

Further North Korea Nuclear Testing May Goad China Into Oil Embargo

Authored by Zainab Calcuttawala via OilPrice.com,

Chinese diplomatic analysts believe further nuclear tests by North Korea could push Beijing over the edge, prompting an oil embargo that would deal a devastating blow to Pyongyang’s stability.

US Secretary of State Rex Tillerson told Fox News that he had been informed that “China would be taking sanctions actions on their own,” should Pyongyang conduct another nuclear test.

“Crude oil is very likely to be included as part of new U.N. sanctions if North Korea continues with its provocative nuclear tests, and China will almost certainly endorse such an effort,” Sun Xingjie, an expert on North Korea from Jilin University said on the matter.

International sanctions against North Korea have been in place for the past several years, with the most recent United Nations-backed round targeting the country’s shipping network. A Chinese oil embargo would likely debilitate Kin Jong-un’s government.

“Instead of an oil embargo of just one or two months, which is unlikely to have a major impact on North Korea’s strategic oil reserves, we are talking about a halt in Chinese crude oil supplies for at least six months. That would be a real nightmare for Kim,” said Sun.

The expert said Beijing would likely require a mandate from the U.N. to take new actions against Pyongyang absent further nuclear activity.

Gasoline prices in North Korea jumped by as much as 83 percent this week on the back of reports that China is mulling over crude sanctions for the unruly neighbor.

While China has historically supported—above all—the stability of the Pyongyang regime as a means of avoiding a refugee crisis should the political system there collapse, now it is putting equal weight on regime stability and the denuclearization of that same regime.

end

b) REPORT ON JAPAN

none today

c) REPORT ON CHINA

CHINA/SOUTH KOREA/USA

China angry at the USA deployment of the THAAD anti missile defense system in South Korea. They warned of consequences

(courtesy zero hedge)

China Demands “Immediate Halt” Of US Missile Shield Deployment In South Korea

As we pointed out earlier today, Reuters cited US military officials who said that the U.S. military’s THAAD anti-missile defense system has “reached initial intercept capability” in South Korea, although they added that it would not be fully operational for some months. Just hours after the announcement, Beijing lashed out at DC and demanded an “immediate halt” to the controversial US missile shield. China’s Foreign Ministry spokesperson Geng Shuang voiced the government’s position against the move during a briefing on Tuesday.

“We oppose the deployment of the US missile system to South Korea and call on all parties to immediately stop this process. We are ready to take necessary measures to protect our interests,” he said according to AFP, adding that “China’s position on the THAAD issue has not changed.”

THAAD missile captured during launch

As Reuters noted earlier, the spokesperson didn’t specify what “necessary measures” China had in mind. However, responding to the THAAD installation, last week China announced on Thursday that it will stage live-fire exercises and test new weapons to protect its security.

Curiously, while on one hand Beijing lashed out at the shield’s deployment, on the other, the foreign ministry expressed support for US President Donald Trump’s surprise comments that he would be “honored” to meet North Korean leader Kim Jong-Un under the right conditions.

Asked about Trump’s remarks, Geng said that China “has always believed that dialogue and consultation… is the only realistic and viable way to achieve denuclearisation.”

“We also said many times that the US and DPRK… should make political decisions at an early date, take action and show good faith so that we can create a better atmosphere for resuming the peace talks and settling the issue,” he added.

Beijing has previously expressed loud concerns over the THAAD system and joint US-South Korean drills near the Korean Peninsula, consistently urging all the parties involved to find a peaceful solution to the volatile situation in the region. Backed by Russia, it also proposed a halt to military drills in exchange for an end to Pyongyang’s missile and nuclear tests during a United Nations Security Council (UNSC) session held in New York on Friday.

Moscow likewise considers the stationing of the THAAD system to be an “additional destabilizing factor for the region” amid alarmingly increasing tensions. It has called on Washington and Seoul to reconsider the decision.

Beijing has imposed a host of measures seen as economic retaliation against the South for the THAAD deployment, including a ban on tour groups. Retail conglomerate Lotte, which previously owned the golf course, has also been targeted, with 85 of its 99 stores in China shut down, while South Korea’s biggest automaker Hyundai Motor has said its Chinese sales have fallen sharply. The THAAD deployment comes as tension soars on the Korean peninsula following a series of missile launches by the North and warnings from the administration of US President Donald Trump that military action is an “option on the table.”

Further complicating matters, Trump stunned Seoul last week when he suggested South Korea should pay for the $1 billion THAAD system. “I informed South Korea it would be appropriate if they paid. It’s a billion-dollar system,” Trump was quoted as saying in a published report. “It’s phenomenal, shoots missiles right out of the sky.”

Seoul retorted that under the Status of Forces Agreement that governs the US military presence in the country, the South would provide the THAAD site and infrastructure while the US would pay to deploy and operate it.

Meanwhile, Thomas Karako, the director of the Missile Defense Project at the Center for Strategic and International Studies, noted that South Korea’s sole THAAD battery does not quite have the range to cover the entire country. But he called it an important first step. “This is not about a having a perfect shield, this is about buying time and thereby contributing to the overall credibility of deterrence,” Karako told AFP.

“South Korea with THAAD helps communicate to the North that today is not a good day to attack. It doesn’t mean that they could not do a lot of damage — they would — but it strengthens the overall posture.”