Gold: $1226.50 DOWN 19.90

Silver: $16.24 DOWN 28 cent(s)

Closing access prices:

Gold $1237.50

silver: $16.48!!!

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

SHANGHAI GOLD FIX: FIRST FIX 10 15 PM EST (2:15 SHANGHAI LOCAL TIME)

SECOND FIX: 2:15 AM EST (6:15 SHANGHAI LOCAL TIME)

SHANGHAI FIRST GOLD FIX: $1252.89 DOLLARS PER OZ

NY PRICE OF GOLD AT EXACT SAME TIME: 1241.-0

PREMIUM FIRST FIX: $11.89

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

SECOND SHANGHAI GOLD FIX: $1245.35

NY GOLD PRICE AT THE EXACT SAME TIME: 1236.30

Premium of Shanghai 2nd fix/NY:$9.05

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

LONDON FIRST GOLD FIX: 5:30 am est $1235.85

NY PRICING AT THE EXACT SAME TIME: $1235.80

LONDON SECOND GOLD FIX 10 AM: $1228.45

NY PRICING AT THE EXACT SAME TIME. $1228.60

For comex gold:

MAY/

NOTICES FILINGS TODAY FOR APRIL CONTRACT MONTH: 8 NOTICE(S) FOR 800 OZ.

TOTAL NOTICES SO FAR: 35 FOR 3500 OZ (.1088 TONNES)

For silver:

For silver: MAY

535 NOTICES FILED TODAY FOR 2,675,000 OZ/

Total number of notices filed so far this month: 2713 for 13,565,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

FEDERAL RESERVE EAR MARKED GOLD REPORT for April

In Feb we had $7,841,000 worth of gold housed at the FRBNY valued at 42.21 dollars per oz

Last month: we had the same; $7,841,000 of gold valued at 42.21

thus 0 oz of gold moved out.

END

The key event today is the rising amount of silver that is standing at the comex. It has now risen above what was standing on day one, first day notice, April 30. On that day 16.8 million oz stood for delivery and for 3 consecutive days it has risen to 19.1 million oz. We have not seen that before.

As far as the raid today, most of the damage has been done in the access market. They are afraid to whack during regular comex hours where physical transactions can occur.

Let us have a look at the data for today

.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total open interest ROSE BY 1,238 contracts UP to 190,478 DESPITE THE HUGE FALL IN PRICE ( 34 CENTS) SILVER TOOK WITH RESPECT TO YESTERDAY’S TRADING. NOBODY BUDGED!!. In ounces, the OI is still represented by just UNDER 1 BILLION oz i.e. 0.952 BILLION TO BE EXACT or 136% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT MAY MONTH/ THEY FILED: 600 NOTICE(S) FOR 3,000,000 OZ OF SILVER

In gold, the total comex gold FELL BY ONLY 2,638 contracts DESPITE THE CONTINUAL FALL IN THE PRICE OF GOLD ($8.70 with YESTERDAY’S TRADING). The total gold OI stands at 459,267 contracts.

we had 166 notice(s) filed upon for 16,600 oz of gold.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD:

We had a tiny changes in tonnes of gold at the GLD: a withdrawal of .28 tonnes to pay for fees

Inventory rests tonight: 853.08 tonnes

.

SLV

Strange!!! We had a tiny change in silver inventory at the SLV today..despite the huge drop in silver price (to pay for fees)..the withdrawal 144,000 oz/

THE SLV Inventory rests at: 334.777 million oz

end

.

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in silver ROSE BY 1,238 contracts UP TO 190,478, (AND NOW CLOSER TO THE NEW COMEX RECORD SET ON FRIDAY/APRIL 21 AT 234,787), DESPITE THE FALL IN PRICE FOR SILVER ON YESTERDAY (34 CENTS). Again, we must have had some considerable bank short covering.

(report Harvey

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

2c) Federal Reserve Bank ear marked gold movement

(Harvey)

3. ASIAN AFFAIRS

Late WEDNESDAY night/THURSDAY morning: Shanghai closed DOWN 7.97 POINTS OR .25% OR / /Hang Sang CLOSED DOWN 12.25 POINTS OR .05% . The Nikkei closed UP 135.15 POINT OR .70%/Australia’s all ordinaires CLOSED DOWN .26%/Chinese yuan (ONSHORE) closed DOWN at 6.8958/Oil DOWN to 47.28 dollars per barrel for WTI and 50.15 for Brent. Stocks in Europe OPENED IN THE GREEN ..Offshore yuan trades 6.8952 yuan to the dollar vs 6.8958 for onshore yuan. NOW THE OFFSHORE IS A LITTLE WEAKER TO THE ONSHORE YUAN/ ONSHORE YUAN SLIGHTLY WEAKER (TO THE DOLLAR) AND THE OFFSHORE YUAN: WEAKER TO THE DOLLAR AND THIS IS COUPLED WITH THE WEAKER DOLLAR. CHINA IS HAPPY

3a)THAILAND/SOUTH KOREA/NORTH KOREA

i)NORTH KOREA/USA

b) REPORT ON JAPAN

c) REPORT ON CHINA

i)I brought this important commentary/video to you earlier in the week. Kyle Bass warns that there are huge problems facing China especially with their WMP’s (WealthManagementProduct). In China these total over 4 trillion dollars worth of assets many of which are non performing. The total of all assets: 34 billion so these products represent around 10% of total assets. If you recall in the tape he warned us to watch for a rise in the overnight yuan inter banking rate.

lo and behold: it rose hugely last night

( Bloomberg/zero hedge)

ii)Last night the inter banking rate rose in China signaling lending problems inside their banks. Chinese commodities are crashing limit down as witnessed by the huge collapse in iron ore. Also the issuance of Wealth Management Products is well down which is signaling a liquidity problem in China

( zero hedge

iii)The war of words continue! China blast North Korea’s”irrational logic”

( zero hedge)

iv)I brought this important article to you on the weekend but it is worth repeating

a must read.

(courtesy Alasdair Macleod/Mises Institute)

4. EUROPEAN AFFAIRS

There was a huge debate last night between marine le Pen and Macron. Le Pen states that if she loses, France will be governed by Merkel. The polls seems to suggest a Macron victory on Sunday but he will not be able to pass much legislation

( Mish Shedlock/Mishtalk)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

I guess this is as good a reason for gold to fall as it gets: Iran attempts a missile launch from a submarine but it too fails like China’s attempt

( zero hedge)

6 .GLOBAL ISSUES

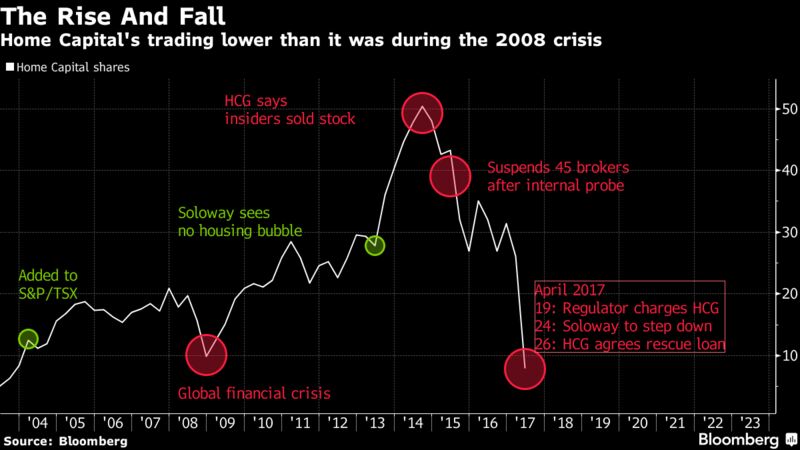

i)This is getting a little scary for Canada: BlackRock warns that it would be “folly” to ignore Home Capital woes

( Onosko/Bloomberg)

ii)RBC’s Charlie McElligott: “someone is blowing up”

7. OIL ISSUES

i)Crude oil drops on Russian comments that they may not extend cuts to production. Also noted is sliding demand

( zero hedge)

ii)Bloodbath in the oil sector as crude oil (WTI) drops into the 45 dollar handle;

( zero hedge)

8. EMERGING MARKETS

9. PHYSICAL MARKETS

The GFMS reports that scrap metal is down to only 58 tonnes. You can probably discount that number further as these guys are perennially wrong in their numbers especially on world scrap.

a must read..

( Steve St Angelo/SRSRocco report)

iv)Bitcoin now over 300 dollars above gold as we witness relentless Japanese buying frenzy

( zero hedge)

10. USA stories

i)this is bad for Janet and her data dependent data: USA productivity plunges in Q1

( zero hedge)

ii)This is not necessarily a good thing as the March trade deficit shrank by a little over 1 billion dollars. The reason was lower imports and less exports. The lower dollar did not help the export sector much

( zero hedge)

iii)Not good: USA factory orders tumble the most for 13 months. For data dependent Janet, this may deter her from raising rates

( zero hedge)

iv)Another Obamacare implosion: the last major healthcare provider in Iowa pulls out leaving no options in 2018. What is going to happen to those who receive subsidies for healthcare in Iowa? What a mess..

( zero hedge)

v)The bill passed the House. It is now up to the Senate to negate it

( zero hedge)

Let us head over to the comex:

The total gold comex open interest FELL BY ONLY 2638 CONTRACTS DOWN to an OI level of 459,267 DESPITE THE FALL IN THE PRICE OF GOLD ( $8.70 with YESTERDAY’S trading). The longs still continue to remain stoic as they refused to liquidate any of their contracts despite the constant torment. We are now in the contract month of MAY and it is one of the POORER delivery months of the year. In this MAY delivery month we had A LOSS OF 117 contract(s) FALLING TO 218. We had 131 notices filed yesterday so we GAINED 14 contracts or an additional 1400 oz are standing for delivery and no contracts were cash settled through the EFP route where they receive a cash bonus plus a future gold contract.

The next big active month is June/2017 and here the OI LOST 8305 contracts DOWN to 308,963. The non active July contract gained another 48 contracts to stand at 144 contracts. The next big active month is August and here the OI gained 5821 contracts up to 63,071.

We had 166 notice(s) filed upon today for 16600 oz

The non active June contract GAINED 19 contracts to stand at 931. The next big active month will be July and here the OI lost 25 contracts down to 147,073.

For those keeping score, the initial amount of silver oz that stood for delivery for the May 2016 contract month: 28.01 million oz. By conclusion of the month only 13.58 million oz stood and the rest was cash settled.(EFP ROUTE)

The line in the sand is $18.50 for silver and again it has been defended by the criminal bankers. Once this level is pierced, the monstrous billion oz of silver shorts will blow up. The bankers are defending the Alamo with their last stand at the $18.50 mark. THE NEW RECORD HIGH IN OPEN INTEREST WAS SET FRIDAY APRIL 21/2017 AT: 234,787.

We had 600 notice(s) filed for 3,000,000 oz for the MAY 2017 contract

VOLUMES: for the gold comex

Today the estimated volume was 326,604 contracts which is very good

Yesterday’s confirmed volume was 268,418 contracts which is good.

volumes on gold are STILL HIGHER THAN NORMAL!

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz |

13,262.22 oz

Manfra

Brinks

|

| Deposits to the Dealer Inventory in oz | nil oz |

| Deposits to the Customer Inventory, in oz |

16,814.98 oz

Manfra

HSBC

|

| No of oz served (contracts) today |

166 notice(s)

16,600 OZ

|

| No of oz to be served (notices) |

52 contracts

5200 oz

|

| Total monthly oz gold served (contracts) so far this month |

332 notices

33,200 oz

1.0326 tonnes

|

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | 41,325.9 oz |

Today, 0 notice(s) were issued from JPMorgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equates to 166 contract(s) of which 0 notices were stopped (received) by jPMorgan dealer and 0 notice(s) was (were) stopped/ Received) by jPMorgan customer account.

March 2016: 2.311 tonnes (March is a non delivery month)

| Silver | Ounces |

| Withdrawals from Dealers Inventory | nil |

| Withdrawals from Customer Inventory |

602,600.671 oz

CNT

90,201.260 oz

Scotia

total:

692,801.931 oz

|

| Deposits to the Dealer Inventory |

nil oz

|

| Deposits to the Customer Inventory |

237,913.930 oz

JPMorgan

400,350.700 oz

Scotia

total:

638,264.630 oz

|

| No of oz served today (contracts) |

600 CONTRACT(S)

(3,000,000 OZ)

|

| No of oz to be served (notices) |

438 contracts

( 2,190,000 oz)

|

| Total monthly oz silver served (contracts) | 3626 contracts (18,130,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month | 2,601,224.0 oz |

NPV for Sprott and Central Fund of Canada

Sprott’s hostile 3.1 billion bid to take over Central Fund of Canada

(courtesy Sprott/GATA)

Sprott makes hostile $3.1 billion bid for Central Fund of Canada

Submitted by cpowell on Thu, 2017-03-09 01:19. Section: Daily Dispatches

From the Canadian Press

via Canadian Broadcasting Corp. News, Toronto

Wednesday, March 8, 2017

http://www.cbc.ca/news/canada/calgary/sprott-takeover-bid-central-fund-c…

Toronto-based Sprott Inc. said Wednesday it’s making an all-share hostile takeover bid worth $3.1 billion US for rival bullion holder Central Fund of Canada Ltd.

The money-management firm has filed an application with the Court of Queen’s Bench of Alberta seeking to allow shareholders of Calgary-based Central Fund to swap their shares for ones in a newly-formed trust that would be substantially similar to Sprott’s existing precious metal holding entities.

The company is going through the courts after its efforts to strike a friendly deal were rebuffed by the Spicer family that controls Central Fund, said Sprott spokesman Glen Williams.

“They weren’t interested in having those discussions,” Williams said.

Sprott is using the courts to try to give holders of the 252 million non-voting class A shares a say in takeover bids, which Central Fund explicitly states they have no right to participate in. That voting right is reserved for the 40,000 common shares outstanding, which the family of J.C. Stefan Spicer, chairman and CEO of Central Fund, control.

If successful through the courts, Sprott would then need the support of two-thirds of shareholder votes to close the takeover deal, but there’s no guarantee they will make it that far.

“It is unusual to go this route,” said Williams. “There’s no specific precedent where this has worked.”

Sprott did have success last year in taking over Central GoldTrust, a similar fund that was controlled by the Spicer family, after securing support from more than 96 percent of shareholder votes cast.

The firm says Central Fund’s shares are trading at a discount to net asset value and a takeover by Sprott could unlock US$304 million in shareholder value.

Central Fund did not have any immediate comment on the unsolicited offer. Williams said Sprott had not yet heard from Central Fund on the proposal but that some shareholders had already contacted them to voice their support.

Sprott’s existing precious metal holding companies are designed to allow investors to own gold and other metals without having to worry about taking care of the physical bullion.

end

And now the Gold inventory at the GLD

May 4/A tiny change in inventory at the GLD /a withdrawal of .28 tonnes to pay for fees/inventory rests at 853.08 tonnes

May 3/no change in inventory at the GLD/Inventory rest at 853.36 tonnes

May 2/no change in inventory at the GLD/Inventory rests at 853.36 tonnes

May 1/ no changes in inventory at the GLD/inventory rests at 853.36 tonnes

April 28/no changes in inventory at the GLD/Inventory rests at 853.36 tonnes

April 27/a small withdrawal of .89 tonnes/Inventory is now at 853.36 tonnes

APRIL 26/we had no changes at the GLD/Inventory rests at 854.25 tonnes

April 25/2017/A WITHDRAWAL OF 5.92 TONNES OF GOLD FROM THE GLD/INVENTORY RESTS AT 854.25 TONNES

April 24/a deposit of 1.48 tonnes of gold into the GLD/inventory rests at 860.17 tonnes

April 21/A DEPOSIT OF 4.44 TONNES OF GOLD INTO THE GLD/INVENTORY RESTS AT 858.69 TONNES

APRIL 20/A WITHDRAWAL OF 6.51 TONNES FROM THE GLD/INVENTORY RESTS AT 854.25 TONNES

April 19/ A DEPOSIT OF 11.84 TONNES INTO THE GLD/INVENTORY RESTS AT 860.76 TONNES

April 18/no changes at the GLD/Inventory remains at 848.92 tonnes

April 17/no changes at the GLD/Inventory remains at 848.92 tonnes

April 13/a deposit of 6.51 tonnes into the GLD/Inventory rests at 848.92 tonnes

this no doubt is a paper deposit/

APRIL 12/no changes in gold inventory at the GLD/Inventory rests at 842.41 tonnes

April 11/a huge deposit of 4.12 tonnes into inventory/Inventory rests at 842.41 tonnes

this would no doubt be a paper gold entry. It would be difficult to find that amount of physical gold.

April 10/1.77 tonnes added into inventory at the GLD/inventory rests at 838.29 tonnes

April 7/a small withdrawal of .28 tonnes from the GLD/Inventory rests at 836.49 tonnes

April 6/no change in gold tonnage at the GLD/Inventory rests at 836.77 tonnes

April 5/no change in gold tonnage at the GLD/Inventory rests at 836.77 tonnes

April 4/no change in gold tonnage at the GLD/Inventory rests at 836.77 tonnes

April 3.2017: a huge deposit of 4.45 tonnes of gold into the GLD/Inventory rests at 836.77 tonnnes

March 31/another withdrawal of 1.19 tonnes of gold inventory fro the GLD/this inventory would no doubt be heading for Shanghai/GLD inventory: 822.32 tonnes

March 30/no changes in gold inventory at the GLD/Inventory rests at 833.51 tonnes

March 29/a withdrawal of 1.78 tonnes of gold out of the GLD/Inventory rests tongith at 833.51 tonnes

March 28/this is good!! A deposit of 2.67 tonnes of gold into the GLD/Inventory rests at 835.29 tonnes.

March 27/no changes in gold inventory at the GLD/Inventory rests at 832.62 tonnes

March 24/another withdrawal of 1.78 tonnes from the GLD/Inventory rests at 832.62 tonnes

March 23/no change in gold inventory at the GLD/Inventory rests at 834.40 tonnes

March 22/no changes in gold inventory at the GLD/Inventory rests at 834.40 tonnes

end

Now the SLV Inventory

May 4/a very tiny withdrawal of 144,000 oz to pay for fees/inventory rests tonight at 334.777 million oz/

May 3/strange!! with the drop in price of silver we had no change in inventory at the SLV/inventory rests at 334.921 million oz

May 2/extremely strange again/a huge 3.502 million oz deposit into the SLV despite silver being in the toilet for the past several trading days.Inventory 334.921 million oz

may 1/extremely strange/with silver being walloped these past several days, the inventory rises again by a huge 1.136 million oz/(maybe someone can explain this phenomena??)

April 28/Strange again!! no change in inventory at the SLV/Inventory remains at 330.283 million oz (no liquidation with a drop in silver price??)

April 27.2017/Strange!! no change in inventory at the SLV/Inventory remains at 330.283 million oz (no liquidation???)

APRIL 26/2017/another huge deposit of 2.934 million oz into the SLV/Inventory rests at 330.283 million oz

April 25/a huge deposit of 1.98 million of into inventory/inventory rests at 327.349 million oz/

April 24/no changes in inventory at the SLV/Inventory rests at 325.361 million oz/

April 21/A WITHDRAWAL OF 719,000 OZ OF SILVER AT THE SLV/INVENTORY RESTS AT 325.361 MILLION OZ/

APRIL 20/NO CHANGES IN INVENTORY AT THE SLV/INVENTORY RESTS AT 326.308 MILLION OZ

April 19/a withdrawal of 1.893 million oz/inventory rests at 326.308 million oz/

April 18/no changes in inventory at the SLV/Inventory rests at 328.201 million oz

April 17/no changes in inventory at the SLV/Inventory rests at 328.201 million oz

April 13/no changes in inventory at the SLV/Inventory rests at 328.201 million oz

April 12/no changes in inventory at the SLV/Inventory rests at 328.201 million oz/

April 11/a paper deposit of 11.131 million oz into the SLV/no doubt yesterday’s entry of a withdrawal of 11.231 million oz was in error/328.201 million oz

April 10/ a paper withdrawal of 11.231 million oz of silver from the SLV and this silver was used in the raid today. Inventory rests at 317.231 million oz

April 7./ a withdrawal of 947,000 oz of silver from the SLV/Inventory rests at 328.201 million oz.

April 6/a tiny withdrawal of 136,000 oz of silver from the SLV/Inventory rests at 329.148 million oz

April 5/ a withdrawal of 1.042 million oz from the SLV/Inventory rests at 329.284 million oz

April 4/no change in inventory at the SLV/Inventory rests at 330.326 million oz/

April 3.2017; a withdrawal of 568,000 oz from the SLV/Inventory rests at 330.326

million oz/

Major gold/silver trading/commentaries for THURSDAY

GOLDCORE/BLOG/MARK O’BYRNE.

GOLD/SILVER

Irish Property Bubble – 38pc Believe Housing Market Will Crash

Irish Property Bubble? Central Bank Governor Denies Is Bubble

Central Bank of Ireland governor Philip Lane yesterday rejected suggestions of an Irish property bubble and that the economy is on the brink of another housing bubble and said the recent increase in house prices is not indicative of a property bubble forming.

Minister for Finance Noonan & Governor of the Central Bank Lane. Source: RTE

Minister for Finance Noonan & Governor of the Central Bank Lane. Source: RTE

However, this optimism is not shared by a large part of the Irish people as there are very high levels of concern about the risk of another property bubble and property crash according to the latest Sunday Independent/Kantar Millward Brown poll:

“A quite astonishing 38pc of people believe that the housing market is destined to collapse as it did during the last recession. That is a much larger share than those who believe the contrary.

Growing fears about another property crash are reflected in another question put by the pollsters – “Is this a good time to buy a house?”

Five years ago, when the recovery hadn’t got going and property prices were on the floor, an overwhelming majority thought it a good time to buy. Now less than half do.

The fear of history repeating itself with another crash in house prices could well explain why, despite high and rising levels of optimism, spending in the shops is not rising at the same pace.”

The risks of a new Irish property bubble and another housing bubble comes at a time of considerable economic uncertainty due to the increasing likelihood of a ‘Hard Brexit.’ There are also the considerable risks from continuing uncertainty due to the Trump Presidency and contagion in the Eurozone.

Separately, news today comes that Irish executives increasingly expect a ‘Hard Brexit’ and are preparing accordingly.

The news comes on the same day that one of the largest retailers of food and meat in the UK, the Co-op, has announced it will sell only British beef and meat.

It publicly called on other UK retailers to “back home-grown goods” from the UK. Sainsbury and Tescos are major sellers of Irish beef and any knock-on change of policy would be hugely damaging to Irish farmers and the wider Irish economy.

The Dublin housing market is showing real signs of over heating and becoming a bubble again – particularly at the middle to higher end of the market.

Real diversification and an allocation to physical gold will protect from another new Irish property bubble and property crash.

Sources

Property crash in Ireland – 38pc believe housing market will collapse

No housing bubble – Central Bank of Ireland (RTE)

Central Bank governor rejects suggestions of new property bubble (Irish Times)

Brexit blockade: UK giant wants ban on Irish meat (Irish Independent)

Irish executives expect a hard Brexit (Irish Times)

‘I hate people talking down the property bubble’ – Ross O’Carroll Kelly

Related Content

Property Bubble In Dublin Housing Market Developing

Property Bubble In Ireland Developing Again

London Property Bubble Vulnerable To Crash

Veteran coin and bullion dealer ‘shocked’ by ‘panic selling’

Submitted by cpowell on Thu, 2017-05-04 00:11. Section: Daily Dispatches

8:11p ET Wednesday, May 3, 2017

Dear Friend of GATA and Gold:

Accumulation may be taking place in Asia, but in North America there is “panic selling” of gold and silver at the retail level, veteran coin and bullion dealer Bill Haynes of CMI Gold & Silver in Phoenix, Arizona, tells King World News today. “I am shocked at how bad the sentiment is in the gold and silver space,” Haynes says. “It’s worse than what we saw at the end of the brutal five-year gold and silver bear market that bottomed at the beginning of 2016.” An excerpt from the interview is posted at KWN here:

http://kingworldnews.com/alert-44-year-market-veteran-says-panic-selling…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

An in depth look at the market for iron ore and why its prices are tumbling.

(courtesy Axiom)

“A Nightmarish Picture For Iron Ore Prices” Has Emerged, Axiom Warns

As noted earlier, while European stocks and US equity markets have ignored the commodity crash in China, which in addition to iron ore plunging limit down, also saw rubber tumble 7% lower, and steel rebar, coke, coking coal plunge over 6% …

… Axiom’s Gordon Johnson warns (as we did a month ago) that the worst is yet to come, and in fact, the “backdrop of near-record/record iron ore inventories and aggressive domestic and seaborne iron ore supply, paints a nightmarish picture for iron ore prices over the coming months.“

* * *

Here are the choice excerpts from his overnight note “Why We Feel Iron Ore Prices Are Slated For a Sharp N-Term Fall (Even From Here) & Why Iron Ore Stocks (FMG; RIO; CLF; X) Are Attractive Shorts Right Now“

SUMMING THE BELOW ANALYSIS UP: With China’s April PMIs disappointing, suggesting China’s tightening measures are beginning to take hold (i.e., demand for steel in China is now weakening), we expect steel supply in China to begin to moderate imminently; stated differently, this suggests iron ore demand is in the process of waning, which, against a backdrop of near-record/record iron ore inventories and aggressive domestic and seaborne iron ore supply, paints a nightmarish picture for iron ore prices over the coming months. On this trend, we would be adding to shorts in FMG, CLF, RIO, and X.

SO WHY THE IRON ORE PRICE PESSIMISM & CONFIDENCE ON THE FMG, RIO, CLF, and X SHORTS?: We believe, when looking at the data, iron ore prices are on the precipice of a “spectacular decline”. As detailed below, iron ore imports into China were up 11.4% y/y to 95.6mt in March, and YTD were up 12.2% y/y to 271mt. In our view, due to what is expected to be a 1%-2%% fall in y/y crude steel production in China in 2017, which is below the +1.04% y/y growth seen in 2016, we believe elevated imports through March point to continued inventory build, as well as a lack of seaborne-supply-discipline to falling iron ore prices (iron ore prices fell 11.9% through March).

Exhibit 1: Despite Waning Crude Steel Output in China, Import

Growth Y/Y is Strong than Ever

Source: General Customs Administration, Axiom Capital Research.

Furthermore, moving to the domestic production of iron ore in China this year, it’s clear that momentum is picking up in a very rapid manner (a troubling trend if you’re an iron ore bull). That is, of the 266 domestic Chinese iron ore mines Mysteel tracks, capacity utilization has risen from 62% as of mid-April 2016, to 69.5% as of mid-April 2017; stated differently, domestic iron ore production is up 21.4% y/y to 45.6mt YTD. This stellar growth, we believe, is a byproduct of higher prices driven, we believe, not by fundamentals, but rather the “financialization” of the futures trading market in bulk commodity materials in China (where traders have to constantly speculate, in the overnight markets, on the daily directional shifts in commodity prices – due to the duration mismatch in assets vs. liabilities in the ~$4tn off-balance-sheet Wealth Management Products market). Yet, with the cash cost of iron ore production in China at ~$57.8/mt, until prices fall below this level, we would expect the “rising tide” of supply to continue to be a headache for the iron ore bulls.

Exhibit 2: Domestic China Iron Ore Supply is Growing Sharply Despite

Record Inventories and Record Seaborne Imports

Source: Mysteel.net, Axiom Capital Research.

WHAT ABOUT INVENTORIES? In addition to the above, as can be seen in Exhibits 3-4 below, inventories at both the Chinese ports and steel mills are at/near record highs. That is, looking first to major Chinese ports’ iron ore inventories, we note that inventory has increased by 15% thus far this year, and is 33% higher than at the same time last year; in fact, there is enough iron ore inventory sitting at the ports in China to construct 13,000 of Eiffel towers (that’s a hell of a lot of iron ore). Furthermore, while they have come down off their peaks experienced this year, steel mills’ iron ore inventories in China are also still high when compared to historical levels. Yet, despite these high inventory levels, iron ore prices remain above our $40/mt target for April; in short, we believe this dynamic is a byproduct of both: (a) stellar margins for steel mills earlier this year, pushing them to prefer higher-grade iron ore in the face of higher coking coal prices, and (b) the aforementioned preference for higher-grade iron ore, in the face of bloated coking coal prices, enabling elevated production rates at Chinese steel mills. However, based on the sharp fall in Chinese steel mill profitability (discussed below), we believe both of these dynamics have come to an abrupt end (a problem if you are an iron ore bull).

Exhibit 3: Chinese Ports’ Iron Ore Inventory is Sitting Near

Record Highs

Source: Shanghai Steelhome, Steel Business Briefing, Axiom Capital Research.

Exhibit 4: While Off Their Highs, Days of Imported Iron Ore Inventory

at China’s Steel Mills Remain High on a Relative Basis

Source: Mysteel.net, Axiom Capital Research.

AND SPREADS? Moving on to price trends, we note that steel prices in China have been in sharp correction territory for some time now; and, with Cyclone Debbie in Australia pushing coking coal prices higher, steel mill profit margins have deteriorated. This, in turn, caused a shift in approach from the steel mills in China. More specifically, instead of opting for the higher-grade version of iron ore, in an effort to shift costs lower, mills in China instead moved toward the lower-end version of iron ore (due to its ready supply at both the ports, and at the domestic mills in China) – this trend, which remains intact today (and is an outsized, yet underappreciated, in our view, risk to seaborne iron ore prices), is evidenced by the sharp fall in the premium of 62% Fe grade iron ore when compared to 58% Fe grade iron ore (see Exhibit 6).

Exhibit 5: China’s Blast Furnaces’ Cash Margins Have Come Down

Considerably From the Highs

Source: Bloomberg, Axiom Capital Research.

Exhibit 6: High-Grade Iron Ore Premium is in Full

Correction Mode

Source: Metal Bulletin, Beijing CUSTEEL E-commerce Co., Axiom Capital Research.

CONCLUSION: With the above as a backdrop, as we have warned for some time now, the recent correction in steel prices in China should come as no surprise. Why? Well, as detailed below (Exhibit 7), with China continuing to pump out record levels of crude steel output (i.e., supply), despite an aggressive push by the PBoC to clamp down on property speculation, as well as elevated interbank lending rates (suggesting liquidity has tightened) – Exhibit 8 – it seems, currently, supply is outstripping demand (a recipe for disaster for prices). Furthermore, as detailed below in Exhibit 9, given expectations of steel demand coming into 2017 in China were elevated (on expectations of a Trump-driven rally, as well as reflation in China), aggressive inventory building defined the better part of C1Q17 in China. Consequently, with China’s April PMIs disappointing, suggesting China’s tightening measures are beginning to take hold (i.e., demand for steel in China is now weakening), we expect steel supply in China to begin to moderate imminently; stated differently, this suggests iron ore demand is in the process of waning, which, against a backdrop of near-record/record iron ore inventories and aggressive domestic and seaborne iron ore output, paints a nightmarish picture for prices over the coming months. On this, we would be adding to shorts in FMG, CLF, RIO, and X.

Exhibit 7: CISA Members’ Daily Crude Steel Output

Source: China Iron & Steel Association (CISA), Axiom Capital Research.

Exhibit 8: Interbank Lending Rates in China Have Moved Structurally

Higher… Suggesting PBoC Tightening is “On the Menu”

Source: Bloomberg.

end

An excellent article from Steve St Angelo as he comments on the drying up of scrap gold. Americans have pawned off their gold to pay off debt or going further into debt

The GFMS reports that scrap metal is down to only 58 tonnes. You can probably discount that number further as these guys are perennially wrong in their numbers especially on world scrap.

a must read..

(courtesy Steve St Angelo/SRSRocco report)

U.S GOLD SCRAP MARKET DRYING UP: Americans Pawned Off Their Best Asset To Go Further Into Debt

by SRSrocco, May 2, 2017

After the U.S. economy disintegrated in 2008, due to the Banking and Housing crisis, Americans pawned off a record amount of gold. How much gold? Nearly, 32 million oz (1,000 metric tons). That’s one heck of a lot of gold. Matter-a-fact, U.S. gold scrap supply at its peak of 160 metric tons (mt) in 2011, was more than any other country in the world, even India and China.

It is quite unfortunate that Americans have pawned off their best asset only to go further into debt. Thus, enabling them to buy more garbage and trinkets they really don’t need. This is quite the opposite of Americans who become being extremely frugal and financially responsible after the 1930’s Great Depression. Today, banks have made it easy for Americans to BUY NOW and PAY LATER.

The consequences of this “Buy now, pay later” economic model is explained in this recent zerohedge article, 45% Of Americans Spend Up To Half Their Income Repaying Credit Card Debts:

First, roughly 50% of Americans have debt balances, excluding mortgages mind you, of over $25,000, with the average person owing over $37,000, versus a median personal income of just over $30,000.

Therefore, it’s not difficult to believe, as Northwestern Mutual points out, that 45% of Americans spend up to half of their monthly take home pay on debt service alone….which, again, excludes mortgage debt.

Because 45% of Americans are paying up to half of their monthly income to pay down credit cards and debt, they can’t use this income to purchase new goods and services. Thus, a staggering amount of the U.S. Gross Domestic Product (GDP) has been brought forward… thanks to easy credit and credit cards.

And, This is what Americans spent the most money on in the first quarter:

But that doesn’t mean that Americans stopped spending completely, quite the contrary. According to the BEA’s “goalseeked” models, even as retail sales tumbled, as Obamacare continued to drain disposable income away from other discretionary purchases, Americans – who spent far less on cars, clothing and housing in the first quarter than in Q4 – were scrambling to buy… recreational vehicles!?

When I travel up and down on the interstate where I live, I see a lot of these Recreational Vehicles (RVs), especially on the weekends. What is even more hilarious, is to see a huge 4X4 truck pulling a large RV, which is also pulling a smaller trailer behind it with two ATV’s on it. All of these vehicles consume one hell of a lot of fuel.

This sudden motivation for Americans to get into a RV and leave the RAT RACE (for a weekend), makes perfect sense to me. This is an extremely important indicator showing how Americans would rather go further into debt up to their eyeballs…. just to GET AWAY from it all. Americans spending a record percentage of their funds on RV’s to escape the insanity, suggests that the economy is getting ready to roll over and fall off a cliff.

Of course, Americans always want to do everything BIG. So, if you have the money (or credit) and a very large truck, you can pull one of these babies down the highway:

Most of the RV’s I see, have two axles. However, this one has four axles and more square feet than some small homes in older areas surrounding big cities. Unfortunately, RV’s will be one of the first items that will go extinct in the United States when the domestic oil industry disintegrates.

Regardless, let’s get back to the drying up of the U.S. secondary gold supply market.

U.S. Gold Scrap Supply Declines To The Lowest Level In Recent History

According to the data put out in the GFMS 2017 World Gold Survey, U.S. gold scrap supply fell to a low of 58.7 metric tons (1.9 million oz) in 2016 versus a record 160 metric tons (5.1 million oz) in 2011:

What is interesting to see in this chart is that U.S. gold scrap supply in 2016 (58.7 metric tons) is nearly two and a half times less than it was in 2010 (143 metric tons) while the gold price was even higher. Thus, Americans pawned off a great deal more gold in 2010 when the price was lower at $1,225 compared to $1,267 in 2016. Which means, the U.S. gold scrap supply market is drying up.

This can be more clearly seen in the following chart below:

Not only has the U.S. gold scrap supply fallen 2.5 times from its peak in 2011, it is also less than it was in 2003 when the gold price was 3.5 times less. Americans pawned 67.6 metric tons (mt) of gold in 2003 when the price was $363 on ounce. However, with the gold price at a much higher level of $1,267 last year, U.S. gold scrap supply fell to a low of 58.7 mt.

Again, the data implies that the U.S. secondary gold scrap supply market is likely drying up.

As was stated in the beginning of the article, total U.S. gold scrap supply equaled nearly 1,000 mt from 2008 to 2016 (actual figure was 982 mt). What is even more interesting, is if we compare U.S. jewelry demand versus gold scrap versus China & India.

When the gold price reached a peak of $1,900 in 2011, U.S. jewelry demand was 60.3 mt. Again, this is the year U.S. gold scrap supply reached a record 160 mt. We must remember, most of gold scrap comes from recycled gold jewelry. Which means, Americans pawned 266% more gold than their gold jewelry demand in 2011.

Here are the 2011 Gold figures for the U.S., China & India:

2011 U.S. Gold Scrap 160 mt / 60.3 mt Gold Jewelry Demand = 266%

2011 Chinese Gold Scrap 144 mt / 547 mt Gold Jewelry Demand = 26%

2011 Indian Gold Scrap 58 mt / 667 mt Gold Jewelry Demand = 9%

As we can see, Americans pawned off 266% more gold than their annual gold jewelry demand in 2011, versus 26% for the Chinese and only 9% for Indians. While some Chinese and Indians were selling their gold jewelry as scrap in 2011, the majority were holding on to it, especially in India. Of course, this is no secret as India tradition is to build their wealth by acquiring gold jewelry.

Americans are in serous trouble as they have sold off the family’s gold jewels to go further into debt, while the Asians and Indians continue to acquire the yellow precious metal. When the markets finally crack, very few Americans will be holding gold. Unfortunately, the majority of Americans will see their highly inflated investments of STOCKS, BONDS and REAL ESTATE collapse while the value-price of gold skyrockets.

end

Bitcoin now over 300 dollars above gold as we witness relentless Japanese buying frenzy

(courtesy zero hedge)

Bitcoin Soars Above $1,600 On Relentless Japanese Buying Frenzy

Four days ago we reported that bitcoin has surged above $1,400, hitting a new lifetime high, while rising above $1,500 on certain Chinese exchanges. Since then, bitcoin’s latest exponential rise has only accelerated, and moments ago the price of the cryptocurrency surged as high as $1,600 on the Coinbase exchange, rising as high as $1,655 on the troubled Bitfinex exchange.

What is prompting this relentless surge in Bitcoin?

Several things.

The first, as we noted on Monday, was “plain old supply and demand.” While unclear if the result of a regulatory crackdown seen recently in Chinese-based exchanges, Hong-Kong based Bitfinex and some other crypto exchanges in the industry “have been dealing with liquidity and withdrawal issues the past few weeks.” Specifically, Bitfinex had trouble processing transactions after the Taiwanese banks that handle them started blocking requests. That’s part of a trend where some banks are pulling out of sectors they deem risky. A representative from the exchange had confirmed to the WSJ that the inability of investors to withdraw bitcoin is affecting the price. Perversely, instead of forcing the price of bitcoin lower, the liquidity squeeze was forcing traders to offer higher bids to get their bitcoin out, which is subsequently forcing the price up.

Then, there is Japan.

As we observed previously, according to Japan’s Nikkei more than 10 Japanese companies are launching exchanges for bitcoin and other virtual currencies, with an eye to tap growing demand after legal changes that make such trades cheaper and easier in the country. As discussed previously, starting July, Japan’s consumption tax will no longer apply to purchases of virtual currencies. Exchanges in Japan have also been required since April to obtain a special license, which has requirements for finances and asset management structures, from the Finance Ministry.

One example: SBI Holdings has set up SBI Virtual Currencies, an exchange between the yen and cryptocurrencies like bitcoin and that of the Ethereum platform. The GMO Internet group is also establishing its own company, with plans to increase the number of digital currencies it trades based on demand. Kabu.com Securities and foreign exchange trader Money Partners Group plan to enter the field as well.

While the Bitfinex issue my be localized, Japan’s demand has been clearly confirmed by capital flows on various exchanges. Alex Sunnarborg, a CoinDesk research analyst, pointed to a spike in global trading volume, especially from Japan and its bitFlyer bitcoin exchange.

As the chart below shows, Japan’s currency JPY has been responsible for more than half, or 52.35% of bitcoin trading volume in the recent 24 hours, followed by the USD at 28.12%, CNY 8.23%, EUR 4.92% and KRW 2.9%. The rise in value shows a surge in trading activity, nearly $700 million in bitcoin according to CoinMarketCap. The trading is markedly led by Japanese markets

As Cryptocoinsnews adds, the Yen-bitcoin trading is all the more notable given that Japan continues to impose an 8% consumption rate tax on purchasing bitcoin through exchanges. Toward the end of 2016, Japanese officials took the call to formally end this tax tariff, a move that will go into effect in July this year.

Finally, there is the recent spike in demand for all other alt-coins.

As we further noted on Monday, there has been ongoing investor interest in other cryptocurrencies such as Ethereum which today also reached record highs, rising above $90, further boosting demand, according to Sunnarborg. These alternative digital currencies are usually bought and sold with bitcoin, requiring traders to buy bitcoin.

The Ripple network is experiencing adoption by a large number of financial institutions to process domestic and cross-border payments. This, in turn, has sparked interest in Ripple’s digital currency, which has had an impressive rally in the last two months, increasing from $0.0054 on March 1 to $0.054 on May 1.

We summarized the ongoing bitcoin frenzy as follows on Monday: “just as the Chinese bubble frenzy in bitcoin is fading, it may be replaced with a new one, in which thousands of Mrs. Watanabe traders shift their attention away from the FX market and toward digital currencies” and added that “If the transition is seamless, there is no telling just how far this particular bubble can grow.”

Four days later and $200 dollar higher, we are observing first hand just how accurate this predication may have been.

end

Your early THURSDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight

1 Chinese yuan vs USA dollar/yuan SLIGHTLY WEAKER 6.8958( DEVALUATION SOUTHBOUND /OFFSHORE YUAN MOVES WEAKER TO ONSHORE AT 6.8952/ Shanghai bourse CLOSED DOWN 7.97 POINTS OR .25% / HANG SANG CLOSED DOWN 12.25 OINTS OR .05%

2. Nikkei closed UP 135.15 POINTS OR .70% /USA: YEN RISES TO 112.87

3. Europe stocks OPENED ALL IN THE GREEN ( /USA dollar index RISRS TO 99.11/Euro DOWN to 1.0908

3b Japan 10 year bond yield: RISES TO +.021%/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 112871/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD FINALLY IN THE POSITIVE/BANK OF JAPAN LOSING CONTROL OF THEIR YIELD CURVE AS THEY PURCHASE ALL BONDS TO GET TO ZERO RATE!!

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 47.28 and Brent: 50.15

3f Gold DOWN/Yen DOWN

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil DOWN for WTI and DOWN for Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund RISES TO +.377%/Italian 10 yr bond yield DOWN to 2.254%

3j Greek 10 year bond yield FALLS to : 6.00%

3k Gold at $1233.40/silver $16.46 (8:15 am est) SILVER ABOVE RESISTANCE AT $18.50

3l USA vs Russian rouble; (Russian rouble DOWN 57/100 in roubles/dollar) 57.84-

3m oil into the 47 dollar handle for WTI and 50 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation (already upon us). This can spell financial disaster for the rest of the world/China forced to do QE!! as it lowers its yuan value to the dollar/GOT SMALL DEVALUATION SOUTHBOUND

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 112.87 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning .9926 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.0844 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now POSITIVE territory with the 10 year RISES to +.377%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.342% early this morning. Thirty year rate at 2.983% /POLICY ERROR)GETTING DANGEROUSLY HIGH

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

(courtesy Jim Reid/Bloomberg/Deutsche bank/zero hedge)

S&P Futures Jump Ahead Of GOP Healthcare Vote, Ignore China Commodity Crash

S&P futures rose on hopes a successful Republican healthcare vote on Thursday will unlock the Trump fiscal agenda, while European shares jumped to a 20 month high on signs Macron is poised to win Sunday’s French election coupled with reassuring corporate results, including strong earnings from HSBC, even as Chinese and Australian stocks fell as commodities, and iron ore futures particularly, tumbled. Oil also declined while the Bloomberg Dollar spot index fell 0.1% in London morning trading, after gaining 0.4% Wednesday. It weakened against all but two of its Group of 10 peers.

As reported overnight, Iron ore traded in China plunged limit down (-8%) in the afternoon session, with Rubber also limit down (7% lower), and steel rebar, coke, coking coal tumbling over 6% on concerns a crackdown on Wealth Management Products and shadow banking in general – in addition to the worst service sector PMI print in nearly a year – could result in a hard-landing for the Chinese economy (something both PIMCO and Kyle Bass warned about in the past 24 hours). Of note: the drop in iron ore prices was the biggest so far this year.

Concerns about a crackdown of credit in China also dragged 10-yr treasury futures lower, down 0.44% at the close, while the 21st Century Business Herald reported that Chinese borrowing costs in April surged with the average coupon rate up near 200bp.

Chinese worries however were lost on Europe, if only for the time being, after Europe reported a stronger than expected Service PMI print, rising to 56.4 from 56.0, beating expectations of 56.2, the 46th consecutive month of expansion and the highest reading since April 2011. Of note: Italy posted a nearly 10 year ago on its composite PMI category.

Helping European risk sentiment, a poll showing Macron had outperformed far-right candidate Marine Le Pen in a televised debate sent short-term French bond yields to their lowest in five months, with encouraging euro zone data also helping the mood. The most recent Oddschecker data showed that the market now gives Macron a 90% probability of victory.

Additionally, a flurry of stronger than expected earnings updates in Europe sent the STOXX 600 up 0.4% to its highest since August 2015, gaining for the day in a row, and included a smaller-than-feared fall in bank giant HSBC’s profits which sent its shares up more than 3%. The Stoxx Europe 600 and FTSE 100 also headed higher. Oil and gas stocks were also up 1.1 percent following robust updates from both Statoil and Royal Dutch Shell, which rose 3 percent and 2.3 percent respectively.

A rebounding European economy and a string of upbeat earnings are prompting firms from Morgan Stanley to Deutsche Asset Management to boost allocations to the region’s stocks. After trailing for most of last year, the Stoxx Europe 600 Index has outpaced the S&P 500 Index.

“There are a number of things playing out at the moment. Traditionally in May there is a strong dollar effect and that is adding to the pressure on the commodity bloc,” said Unicredit’s head of FX Strategy Vasileios Gkionakis. “In Europe it is slightly different. There is what is going on with the French election and we have been seeing some strong data.”

“We see more value in Europe versus the U.S.,” Deutsche Asset’s global head of research Phil Poole said in an interview with Bloomberg TV’s Mark Barton. The investment arm of Deutsche Bank AG increased allocation to Europe in its multi-asset portfolios from the lowest on record in the past quarter, Poole said. “Valuations are attractive, the European economy is growing. We feel there’s too much optimism priced into the Trump stimulus program.”

In the US, S&P 500 futures climbed on hopes Obamacare will get repealed giving a fresh boost to the Trump fiscal agenda and as investors awaited earnings reports from companies including Kellogg and Chesapeake. Futures on the S&P 500 Index expiring in June climbed 0.3 percent ot 6.75 to 2.390 at 6:40 am in New York. The benchmark hasn’t posted gains or losses exceeding 0.2% for six straight sessions, and has struggled to top a record last seen on March 1. Contracts on the Dow Jones Industrial Average added 52 points to 20,931 on Thursday.

At the end of its two-day meeting, the Fed kept its benchmark interest rate steady, as expected, but downplayed weak first-quarter economic growth and emphasized the strength of the labor market, a sign it was still on track for two more rate increases this year. Futures traders are now pricing in a 72 percent chance of a June rate hike, from 63 percent before the Fed’s statement, according to the CME Group’s FedWatch Tool. Attention now turns to U.S. non-farm payrolls for March, due on Friday, after separate data showed private employers added 177,000 jobs in April. That was higher than expected but the smallest increase since October.

After the dollar had risen across the board after the Fed’s meeting on Wednesday, the dollar index which measures it against the top six world currencies, was modestly lower, erasing some gains. It was, however, well higher at 113.00 yen. The euro meanwhile drew some support from Macron’s performance ahead of Sunday’s election run-off, and was barely budged at $1.0876.

In commodities, oil fell for a third session in four to leave it near its lowest since late March at $50.50 after the China services wobble and supply data had shown a smaller than expected decline in U.S. inventories. Bellwether industrial metal copper was also teetering near a four month low on what traders said was China-based selling and on expectations that two U.S. rate rises this year could curb interest in dollar-denominated metals. Iron-ore futures slid 5.3 percent. Copper futures dropped 0.4 percent extending Wednesday’s worst tumble since 2015. Oil declined 0.7 percent to $47.46 a barrel.

“Later today there is a mass of U.S. data including key employment numbers, durable goods and factory orders and if these also fall below expectations it would be reasonable to expect another wave of selling,” Kingdom Futures said in a note.

Occidental, Regeneron, Activision Blizzard among companies reporting earnings. Factory orders and durable goods orders due. U.S. MARKETS

Bulletin Headline Summary

- European equities trade modestly higher with Shell leading energy names higher

- EUR on the front foot as Macron clears TV hurdle, alongside firm Eurozone PMI figures

- Looking ahead, highlights include US trade balance, factory orders and a slew of ECB speakers

Market Snapshot

- S&P 500 futures up 0.2% to 2,387.75

- STOXX Europe 600 up 0.3% to 390.62

- MXAP down 0.4% to 149.04

- MXAPJ down 0.3% to 487.33

- Nikkei up 0.7% to 19,445.70

- Topix up 0.7% to 1,550.30

- Hang Seng Index down 0.05% to 24,683.88

- Shanghai Composite down 0.3% to 3,127.37

- German 10Y yield rose 3.8 bps to 0.364%

- Euro up 0.3% to 1.0918 per US$

- Brent Futures down 0.6% to $50.48/bbl

- Italian 10Y yield fell 4.4 bps to 1.967%

- Spanish 10Y yield fell 1.0 bps to 1.602%

- Sensex up 0.8% to 30,132.08

- Australia S&P/ASX 200 down 0.3% to 5,876.37

- Kospi up 1% to 2,241.24

- Gold spot down 0.2% to $1,236.22

- U.S. Dollar Index down 0.04% to 99.17

Top Overnight News

- China’s risk crackdown is rattling its municipal bond market, with yield premium over Chinese sovereign debt widening to a record

- In ultra-long Treasury debate, bond analysts find little to like, with strategists say stick with 10- and 30-year auction process as TBAC floats 20-year bond, 50-year zero coupons as alternatives

- Le Pen unleashed a barrage of attacks on Macron in TV debate as she tried to close a gap of some 20 percentage points in the only head-to-head debate of the French election campaign

- HSBC Shares Rise on Surprise Revenue Gain as Trading Tops Rivals

- Boeing to Start Production With JV Partner Tata This Year

- General Motors China April Vehicle Sales Fall 1.9% on Year

- Google Says Gmail Phishing Scam Affected Less Than 0.1% of Users

- Tesla Assures Model 3 on Time as Musk’s Cash Burn Continues

- WhatsApp Says Access Issue Fixed for Worldwide Users

- Shell Pumps a Torrent of Cash as Takeover, Cost Cuts Pay Off

- Big Beer Is Back as AB InBev, Carlsberg Beat Sales Estimates

- Facebook’s Social Network Fuels Growth as Ad Slowdown Looms

Asian equity markets traded mostly lower after weakness across the commodities complex and as participants digested the latest FOMC which spurred expectations for a June hike. ASX 200 (-0.5%) declined as materials names felt the brunt of the losses in the metals complex, while Shanghai Comp. (-0.3%) and Hang Seng (-0.4%) were pressured as commodity prices in China slumped in which Dalian iron ore futures hit limit down shortly after the open. Downside was also attributed to recent deleveraging in shadow banking, an increase in Chinese short-term money market rates and after Caixin Services and Composite PMI data fell to 11-month and 10-month lows respectively. However, heading into EU trade, the Shanghai Comp staged a modest recovery. As a reminder, Japanese markets remained closed for Greenery Day.

Top Asian News

- Asian Stocks Decline as Iron Ore Futures Tumble: Markets Wrap

- China Bonds Seen Extending Drop as PBOC Keeps Tight Rein on Cash

- China’s Belt-Road Plan May Top $500 Billion, Credit Suisse Says

- China H Shares Drop Most in Two Weeks Amid Deleveraging Concerns

- China’s Economy Shaping Up for Positive 2018, Rio Tinto Says

- Glencore Sees Trading Profit Boost, Enhancing Dividend Outlook

- Phone Betting Lifts Money Laundering Risk at Manila Casinos

- Australian Equity Movers: Corporate Travel, Fortescue, Eclipx

- Beijing Sandstorm Prompts Pollution Warning for Some 22 Million

European bourses are higher this morning as price action has been dictated by the latest slew of large cap earnings. The energy sector outperforms amid gains seen in Shell after they announced profits beat analyst estimates, however FTSE 100 slightly lags its counterparts despite the upside in Shell and HSBC shares, with the index hampered by the upside in GBP, while retail names slip following poor results from Next. In fixed income markets, EGBs trade lower amid the upside in equities, alongside the fall out of the FOMC meeting last night, while various issuance from the likes of Spain and France also kept prices subdued with Bund lower by 45 ticks. Elsewhere, the German/French spread is tighter after polls suggested Macron produced a stronger performance than Le Pen in the TV Presidential debate. The French Presidential candidates conducted a live TV debate in which Macron was seen to have performed better, as an Elabe poll showed that 63% thought Macron won the debate vs. 34% for Le Pen with the rest undecided.

Top European News

- U.K. Economy Rebounds in April With Unexpected Services Strength

- Euro-Area Growth Gathers Speed as Top Three Economies Converge

- BNP Stock Sale Managers Said to Be Left Holding Unsold Shares

- European Miners Drop to Lowest This Year as Iron Ore Tumbles

- Buyout Funds in ‘Shock’ as Swedish Tax Nightmare Becomes Reality

- Swiss Re Profit Drops to Lowest Since 2011 on Cyclone Claims

- SocGen Profit Drops After $1 Billion Libya Legal Settlement

- Siemens Is ‘Well-Advanced’ on Health-Care Unit Carve Out

- Rosneft Claims May Force Sistema to Give Up MTS Control: Citi

- Norges Bank to Raise Number of Policy Meetings, Publish Minutes

In currencies, the Bloomberg Dollar Spot Index fell 0.1 percent as of 10:33 a.m. in London, after gaining 0.4 percent Wednesday. It weakened against all but two of its Group of 10 peers; the euro added 0.4 percent to $1.0927, while the pound gained 0.3 percent; the yen lost 0.1 percent to 112.75 per dollar. It has been a choppy session seen in FX this morning, and we can assume the modest excitement in the aftermath of the FOMC statement release has played out. The USD saw a very modest rally after traders focused on the pricing for a Jun hike on what was effectively a `stand pat’ on policy, with the rate path still leaving room for 1 or 2 rate hikes this year. USD/JPY continues to run into resistance ahead of 113.00, and as Yellen and Co continually reiterate, constant data monitoring will determine the pace of rate move. As such, we may need a healthy jobs report tomorrow to see a sustained move above the figure, with techs pointing to resistance circa 113.25-30. USD/CHF has been notably quiet. EUR/USD is where the bulk of action is going through, and we see little sign of any defensive positioning ahead of this weekend’s election run off in France. Indeed, the market is still pushing for a move on 1.0950, as traders seen keen to take advantage of any gap should Macron win this weekend as the polls are suggesting, and a little more so in the wake of last night’s TV debate.

In commodities, further losses in Copper today to the detriment of the AUD, but the 2017 range is still intact as the lower band at USD2.50-45 holds for now. No disputing that the China PMIs have been a major contributor to this weakness, and to metals across the board, whilst supply concerns have been a constant weight through the year so far. This has also been an issue dampening Oil prices, where we now see Brent testing the USD50.000 mark, while WTI grapples with range traders coming in ahead of USD47.00 amid hopes of a production cut extension into H1 as OPEC and non OPEC members have been talking of late. Safe haven demand for Gold is minimal and this is all down to the heightened expectations/polls pointing to a Macron win this weekend. If he does, then Gold heads lower still. We have dipped under USD1235 this morning. Silver holding above mid USD16.00’s after recent slide.

Looking at today’s calendar, we’ll get a first look at the Q1 nonfarm productivity and unit labour costs data, as well as the latest weekly initial jobless claims print, March trade balance, March factory orders and final revisions to the March durable and capital goods orders data. Away from the data there are a number of ECB speakers on the cards for today including President Draghi at 4.30pm BST when he is due to speak in Switzerland. Lautenschlaeger, Praet and Mersch are also due. Away from this, UK local elections are scheduled today with polls closing at 10pm BST. We should have an idea of some of the results early tomorrow morning and they are worth keeping an eye given the proximity to next month’s General Election. Earnings wise today the headliners are AB Inbev, BMW and Shell.

US Event Calendar

- 7:30am: Challenger Job Cuts YoY, prior -2.0%

- 8:30am: Trade Balance, est. $44.5b deficit, prior $43.6b deficit

- 8:30am: Nonfarm Productivity, est. -0.1%, prior 1.3%; Unit Labor Costs, est. 2.7%, prior 1.7%

- 8:30am: Initial Jobless Claims, est. 248,000, prior 257,000; Continuing Claims, est. 1.99m, prior 1.99m

- 9:45am: Bloomberg Consumer Comfort, prior 50.8

- 10am: Factory Orders, est. 0.4%, prior 1.0%; Factory Orders Ex Trans, prior 0.4%

- 10am: Durable Goods Orders, est. 0.7%, prior 0.7%; Durables Ex Transportation, prior -0.2%

- 10am: Cap Goods Orders Nondef Ex Air, prior 0.2%; Cap Goods Ship Nondef Ex Air, prior 0.4%

Db’s Jim Reid concludes the overnight wrap

On your long but fulfilling DB powered commute this morning the main stories overnight revolve around the FOMC, the final French Presidential TV debate and plans to avoid the imminent potential US government shutdown. Overnight we can also report the breaking news that House Republicans will today vote on the GOP health care bill. Majority Leader Kevin McCarthy said that the Republican bill will have the votes required to push through so we’ll see how that goes today.

In terms of the Fed yesterday, as expected there were no real surprises to come from the decision to keep rates unchanged or out of the post meeting FOMC statement but there was just about enough for the market to ramp up the odds for another tightening next month. Indeed Bloomberg’s calculator (which overstates a little) now has the probability of a hike at 90% which compares to 67% this time yesterday. With regards to the statement itself the FOMC acknowledged the soft quarter for growth in Q1 and also softness in consumer spending but also emphasised the need to look through it and that the slowdown is likely to be transitory. There was a reference to fundamentals underpinning consumer spending remaining solid and the Committee generally sounded more upbeat on business fixed investment. On the labour market the Fed said that job gains were solid in recent months. The Committee also acknowledged the drop in core inflation in March and that while market-based measures of inflation compensation remain lower, survey-based measures of longer-term inflation expectations are little changed on balance. So all-in-all more of the same. Tomorrow’s Fedspeak could well be more interesting particularly for any snippets around the balance sheet. For now our US economists continue to expect the next rate hike to come in June with high conviction for this view.

A few hours after the Fed and post the US close we then learned that the House had finally approved a $1.17tn spending bill by a majority of 309-118 votes, moving a step closer to avoiding a government shutdown this Saturday. The bill will now pass over to the Senate where it is expected that a vote will be held today. According to the WSJ the bill supposedly excluded a number of Trump’s top priorities including a smaller than expected increase in military spending. The other main event after the US close was the live French presidential debate which finished up at 10.30pm BST last night having been going for about 2 hours. In terms of the outcome a snap Elabe poll out just after the debate showed that Macron won by a score of 63% to 34% over Le Pen. As expected there were the usual fiery exchanges but nothing that really moved the dial. Instead the general feeling was that Macron solidified his position and lead. Le Pen was questioned intensely about her plans for a dual-currency regime for the franc and euro while the FT also summarised that Macron focused routinely on the contradictions and inaccuracies in Le Pen’s plan to exit the EU. Le Pen on the other hand spent a great deal of time portraying Macron as an elitist. The Euro traded in a tight range through much of the debate and finished up little changed compared to where it was when the debate started.

With regards to markets yesterday, in what was another otherwise subdued day of price action, the most notable moves came in Treasuries following the FOMC. 2y and 10y yields ended the day up +3.6bps and +3.8ps respectively, although 30y yields ended up little changed with the US Treasury Borrowing Committee warning against possible issuance of long-dated bonds. The Greenback also firmed up with the Dollar index up about +0.45% versus this time yesterday. Gold and Silver sold off -1.48% and -2.14% respectively. Meanwhile price action in US equities remains incredibly dull. The S&P 500 did recover from Apple-driven heavier losses at the open but still finished down a small -0.13%. To put it in perspective the last six daily closing changes for the S&P have been -0.13%, +0.12%, +0.17%, -0.19%, +0.06% and -0.05%.

It wasn’t much more exciting in Europe yesterday where the Stoxx 600 closed -0.04%. European credit did outperform however led by financials with Senior and Sub Fins iTraxx indices ending 1bp and 7.5bps tighter respectively. One asset class which did see a decent move yesterday was base metals with Copper (-3.48%) in particular suffering its biggest-one day decline since 2015 following bearish stockpiles data.

That weakness in commodities coupled with further softening data in China this morning has seen most bourses in Asia edge lower in the early going. As we go to print the Hang Seng (-0.52%), Shanghai Comp (-0.25%) and ASX (-0.52%) are all in the red, although the Kospi (+0.57%) has gone against the grain. On that data, China’s Caixin services PMI in April declined 0.7pts to 51.5 which has left the composite reading at 51.2 versus 52.1 in March. The Aussie Dollar is also weaker this morning with the moves in commodities.

Moving on. In terms of the economic data in the US yesterday the April ADP print came in more or less in line with the consensus at 177k (vs. 175k expected). That follows a slightly downwardly revised 255k in March. It’s worth adding that the consensus for Friday’s NFP is hovering around 190k at present. Away from that the headline ISM non-manufacturing for April rose a solid 2.3pts to 57.5 (vs. 55.8) which is a smidgen below the YTD high made in February. At the same time the services PMI was also revised up 0.6pts to 53.1. Interestingly in the details of the ISM, the new orders component rose to a new 12-year high of 63.2 however the employment component edged down another 0.2pts to a fairly low 51.4. Remember also that the employment component in the ISM manufacturing softened so that may sound some caution ahead of payrolls.

In Europe yesterday the main report of note was the Q1 GDP print for the Euro area which revealed that the economy grew +0.5% qoq in Q1 which was in line with the market and one-tenth ahead of what our European team had pegged. Away from that, PPI in the Euro area was reported as falling -0.3% mom in March, while unemployment in Germany held steady at 5.8% in April.

Before we look at the day ahead its worth noting that yesterday Puerto Rico officially filed for protection from its creditors in what is being called by numerous press outlets the largest debt restructuring filing by a local government or US state ever. According to Bloomberg the debt amount is around $74bn which the commonwealth is asking a federal court to force creditors to take losses on.

Looking at today’s calendar, this morning in Europe the main focus will be on the final April PMI revisions where we’ll get the services and composite readings and also a first look at the data for the UK and periphery. Also due out this morning is money and credit aggregates data for the UK for March, and retail sales data for the Euro area. In the US this afternoon we’ll get a first look at the Q1 nonfarm productivity and unit labour costs data, as well as the latest weekly initial jobless claims print, March trade balance, March factory orders and final revisions to the March durable and capital goods orders data. Away from the data there are a number of ECB speakers on the cards for today including President Draghi at 4.30pm BST when he is due to speak in Switzerland. Lautenschlaeger, Praet and Mersch are also due. Away from this, UK local elections are scheduled today with polls closing at 10pm BST. We should have an idea of some of the results early tomorrow morning and they are worth keeping an eye given the proximity to next month’s General Election. Earnings wise today the headliners are AB Inbev, BMW and Shell.

3. ASIAN AFFAIRS

i)Late WEDNESDAY night/THURSDAY morning: Shanghai closed DOWN 7.97 POINTS OR .25% OR / /Hang Sang CLOSED DOWN 12.25 POINTS OR .05% . The Nikkei closed UP 135.15 POINT OR .70%/Australia’s all ordinaires CLOSED DOWN .26%/Chinese yuan (ONSHORE) closed DOWN at 6.8958/Oil DOWN to 47.28 dollars per barrel for WTI and 50.15 for Brent. Stocks in Europe OPENED IN THE GREEN ..Offshore yuan trades 6.8952 yuan to the dollar vs 6.8958 for onshore yuan. NOW THE OFFSHORE IS A LITTLE WEAKER TO THE ONSHORE YUAN/ ONSHORE YUAN SLIGHTLY WEAKER (TO THE DOLLAR) AND THE OFFSHORE YUAN: WEAKER TO THE DOLLAR AND THIS IS COUPLED WITH THE WEAKER DOLLAR. CHINA IS HAPPY

3a)THAILAND/SOUTH KOREA/NORTH KOREA

NORTH KOREA/USA

b) REPORT ON JAPAN

c) REPORT ON CHINA

I brought this important commentary/video to you earlier in the week. Kyle Bass warns that there are huge problems facing China especially with their WMP’s (WealthManagementProduct). In China these total over 4 trillion dollars worth of assets many of which are non performing. The total of all assets: 34 billion so these products represent around 10% of total assets. If you recall in the tape he warned us to watch for a rise in the overnight yuan inter banking rate.

lo and behold: it rose hugely last night

(courtesy Bloomberg/zero hedge)

a must view

Kyle Bass Warns “All Hell Is About To Break Loose” In China

China’s credit system expanded “too recklessly and too quickly,” and “it’s beginning to unravel,” warns Hayman Capital’s Kyle Bass.

Crucially, Bass notes that ballooning assets in Chinese wealth management products are another sign of a looming credit crisis in the nation.

“Some of the longer-term assets aren’t doing very well,” Bass said on Bloomberg TV from the annual Milken Institute Global Conference in Beverly Hills, California. “As soon as liabilities have problems – meaning the depositors decide to not roll their holdings – all hell breaks loose.”

The wealth management products, or WMPs, have swelled to $4 trillion in assets in the last few years, he said., on a $34 trillion banking system…

“think about this – in the US, our asset-liability mismatch at the peak of our subprime greatness was around 2%! … China’s mismatch is more than 10% of the system.”

Must Watch simplification of the next stage of the credit cycle in China…

https://www.bloomberg.com/api/embed/iframe?id=b00cebb6-70c5-455a-8d89-bd7551a30959

Timing the drop is hard, Bass notes, reminding Bloomberg’s Erik Schatzker that “in the US, the first bumps in the road hit in early 2007, and we didn’t start to really accelerate until mid 2008… even a large unraveling takes a while.“

Bass has been sounding the alarm for some time that debt-burdened Chinese banks need to be restructured…

“What you see when the liquidity dries up is people start going down… and this is the beginning of the Chinese credit crisis.”

And judging by the collapse in both Chinese stocks and bonds, the deleveraging is accelerating…

And liquidity is getting desperate again…

END

Last night the inter banking rate rose in China signaling lending problems inside their banks. Chinese commodities are crashing limit down as witnessed by the huge collapse in iron ore. Also the issuance of Wealth Management Products is well down which is signaling a liquidity problem in China

(courtesy zero hedge

Chinese Commodities Crash Limit-Down As Wealth Management Product Issuance Collapses

It seems Kyle Bass’ warning was extremely timely. The deleveraging of China’s $4 trillion shadow banking system just accelerated massively as Bank Wealth Product Issuance crashes 15% month-over-month. With stocks and bonds already plunging, commodities joined the ugliness tonight with Dalian Iron Ore limit down (8%) at the open (not helped by tumbling auto demand).

As Bloomberg reports, China April Bank Wealth Product Issuance Falls 15% M/m

Number of wealth management products issued by banks fell to 10,038 from 11,823 in March, 21st Century Business Herald reports, citing citing Wind Info data. The decline came after regulator tightens regulation on macro-prudential assessment and interbank business. Among top ten banks by wealth product sales, nine sold less than previous month (with the Agricultural Bank coillapsing 48%) only Minsheng Bank issued more.

And it’s weighing on the economy al;ready as China PMIs are all plunging (with Caixin Services tonight) – Activity in China’s services sector grew at its weakest rate in 11 months, a survey sponsored by Caixin showed on Thursday, in a further sign the world’s second-largest economy is losing some steam. The Caixin China General Services Business Activity Index fell for the fourth straight month to 51.5 in April, down from 52.2 in March and the lowest since May 2016’s 51.2, according to the poll compiled by international information and data analytics provider IHS Markit.

As Bass concluded so ominously:

“What you see when the liquidity dries up is people start going down… and this is the beginning of the Chinese credit crisis.”

And that’s what we are seeing…

Commodities…

Are following Bonds…

And stocks…

And as PIMCO noted earlier, the China credit impulse is now running in reverse…

The question now is not if China slows, but rather how fast. Equally important perhaps is the extent to which commodity prices will correct lower, especially in light of the current enthusiasm about the potential strength of the global growth cycle. The impending slowdown in China could be compounded by ongoing government efforts to rein in shadow bank credit; the cost of policy mistakes rises once the credit impulse goes into reverse.

END

I brought this important article to you on the weekend but it is worth repeating

a must read.

(courtesy Alasdair Macleod/Mises Institute)

China’s Plan To Subvert The Global Dollar Standard

Authored by Alasdair Macleod via The Mises Institute,

If nothing else, the Chinese have a sense of history and destiny. They have had a glorious past, stretching back millennia, and once controlled most of the Asian heartland in the days of Genghis and Kublai Khan. But even then, China was essentially inward-looking, protecting her own cultural values. Trade with Europeans in the centuries following Marco Polo’s visit was mostly at the behest of European travelers, not the Chinese. She exported her art and culture to visitors, and did not import European values.

This was a mistake, implicitly recognized by China’s current leadership. This time, China has embraced Western thinking and technology to further her own progress. The development of the Shanghai Cooperation Organization in recent years is the platform for China in partnership with Russia to embrace the Asian continent through peaceful trade, improving the lives of all the citizens of the many nations who are and will become members. The SCO promises a revolution in the wealth and living standards of over 40% of the world’s population, and associated benefits for its supplier-nations on the other continents.