GOLD: $1268.50 down $7.80

Silver: $17.19 down 20 cent(s)

Closing access prices:

Gold $1294.30

silver: $17.68

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

SHANGHAI GOLD FIX: FIRST FIX 10 15 PM EST (2:15 SHANGHAI LOCAL TIME)

SECOND FIX: 2:15 AM EST (6:15 SHANGHAI LOCAL TIME)

SHANGHAI FIRST GOLD FIX: $1282.60 DOLLARS PER OZ

NY PRICE OF GOLD AT EXACT SAME TIME: $1274.75

PREMIUM FIRST FIX: $7.85

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

SECOND SHANGHAI GOLD FIX: $1281.00

NY GOLD PRICE AT THE EXACT SAME TIME: $1274.25

Premium of Shanghai 2nd fix/NY:$6.75

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

LONDON FIRST GOLD FIX: 5:30 am est $1274.25

NY PRICING AT THE EXACT SAME TIME: $1274.55

LONDON SECOND GOLD FIX 10 AM: $1266.55

NY PRICING AT THE EXACT SAME TIME. $1266..60

For comex gold:

JUNE/

NOTICES FILINGS TODAY FOR APRIL CONTRACT MONTH: 13 NOTICE(S) FOR 1300 OZ.

TOTAL NOTICES SO FAR: 2118 FOR 211,800 OZ (6.5878 TONNES)

For silver:

For silver: JUNE

84 NOTICES FILED TODAY FOR 420,000 OZ/

Total number of notices filed so far this month: 783 for 3,915,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

END

Another raid as the bankers are determined to bury those who play the paper gold and paper silver game.

Over at the comex, the amount standing for the silver metal again rose in similar fashion to what we witnessed last month and also in April. It is up for the 7th consecutive day. We certainly have a determined entity trying to get its hands on whatever silver is available.

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

This is where we are heading: (JB Slear/Jim Sinclair)

According to JB Slear, this is what the future holds. Why should I write words. Get into the cellar as fast as you can!

Jim

In silver, the total open interest FELL BY 922 contract(s) DOWN to 205,319 WITH THE FALL IN PRICE OF SILVER THAT TOOK PLACE WITH YESTERDAY’S TRADING (DOWN 19 CENT(S). In ounces, the OI is still represented by just OVER 1 BILLION oz i.e. 1.0260 BILLION TO BE EXACT or 147% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT MAY MONTH/ THEY FILED: 84 NOTICE(S) FOR 420,000 OZ OF SILVER

In gold, the total comex gold FELL BY 8,583 contracts WITH THE GOOD SIZED WHACKING GOLD TOOK ($13.80 with YESTERDAY’S TRADING). The total gold OI stands at 488,383 contracts.

we had 13 notice(s) filed upon for 1300 oz of gold.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD:

We had no changes in tonnes of gold at the GLD:

Inventory rests tonight: 867.00 tonnes

.

SLV

Today: no changes in inventory/

THE SLV Inventory rests at: 339.605 million oz

end

.

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in silver FELL BY 922 contracts DOWN TO 205,319 (AND now A LITTLE FURTHER FROM THE NEW COMEX RECORD SET ON FRIDAY/APRIL 21/2017 AT 234,787), WITH THE FALL IN PRICE FOR SILVER WITH YESTERDAY’S TRADING ( DOWN 19 CENTS). NO QUESTION THAT WE AGAIN HAD CONTINUED FAILED SHORT COVERING BY THE BANKERS ALONG WITH CONSIDERABLE BANKER DELTA HEDGING AS SILVER IS GIVING THEM NIGHTMARES

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)Late THURSDAY night/FRIDAY morning: Shanghai closed UP 8.06 POINTS OR 0.26% / /Hang Sang CLOSED DOWN 32.77 POINTS OR 0.13% The Nikkei closed UP 104.00 POINTS OR 0.52%/Australia’s all ordinaires CLOSED UP 0.01%/Chinese yuan (ONSHORE) closed DOWN at 6.7971/Oil UP to 45.70 dollars per barrel for WTI and 47.94 for Brent. Stocks in Europe OPENED MIXED ..Offshore yuan trades 6.7913 yuan to the dollar vs 6.7971 for onshore yuan. NOW THE OFFSHORE IS MUCH WEAKER TO THE ONSHORE YUAN/ ONSHORE YUAN A LITTLE WEAKER (TO THE DOLLAR) AND THE OFFSHORE YUAN IS MUCH WEAKER TO THE DOLLAR AND THIS IS COUPLED WITH THE MUCH STRONGER DOLLAR. CHINA NOT HAPPY WITH THE NEWS THAT ITS DEBT HAS BEEN DOWNGRADED

3a)THAILAND/SOUTH KOREA/NORTH KOREA

i)NORTH KOREA

A little background on those 4 anti ship missiles fired by North Korea. It was a test for precise accuracy and it is alarming to the west

( Mac Slavo/SHTFPlan)

b) REPORT ON JAPAN

c) REPORT ON CHINA

Whenever you see the Chinese 5 year/10 yr invert , then recession is flashing red!! Actually everything is inverting!

( zerohedge)

4. EUROPEAN AFFAIRS

i)UK

Theresa May wins 318 seats and falls short of a majority. She will hook up with the Irish right wing Democratic Unionist Party to allow her to govern:

( zerohedge)

ii)An important lesson for us all. A must read…

( Simon Black/SovereignMan.com)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

6 .GLOBAL ISSUES

Mexican Industrial production simply crashes in April

( zero hedge)

7. OIL ISSUES

rig counts rise for the 21 st consecutive week

( zero hedge)

8. EMERGING MARKET

9. PHYSICAL MARKETS

i)Trading today in gold:

the Crooks are at it again:

( zero hedge)

ii)Mexico owes Canadian miners more than 360 million dollars with Goldcorp the lions share at 230 million

( Reuters/GATA)

iii)Chris Powell comments on the huge raid we have been experiencing this past two days:

( Chris Powell/GATA)

iv)A great reason to whack gold today: Gold imports jump 400% as the increase in GST tax fear as spurred stocking of gold

( Bloomberg)

v)totally absurd: Jim Cramer discusses bitcoin and highlights that it may hit 1 million dollars.

( Mish Shedlock/Mishtalk)

10. USA Stories

i)Trump accuses Comey of being a “leaker” and a liar and also he claims total and complete vindication

( zerohedge)

ii)Trump is set to file a complaint against Comey for leaking the memos to the New York Times and CNN

( zerohedge)

iib)Lawyer Kasowitz produces the May 11 New York Times article which clearly shows that someone leaked the memo prior to Trump’s tweet on the 12 of May

Perjury?…

( zero hedge)

iic)In a press conference Trump hints that he has the Comey tapes and he then tells the press that they are going to be very disappointed..

(courtesy zero hedge)

ii d)that did not take long!! The House Intelligence Committee demanded from Trump the tapes, if they exist..

iii)Not a good sign for the economy: credit card defaults surge the most since 2009:

( zero hedge)

iv)A huge drop in auto inventories will cause the revised 2nd quarter GDP to fall further

( zero hedge)

v)The list of retails in danger of bankruptcy now climb to 22

( zero hedge)

vi)Again Alan Dershowitz states that there is no obstruction case and was glad when Comey stated that yes, the President can say who will be prosecuted and who will not be prosecuted.

( the Fly)

Let us head over to the comex:

The total gold comex open interest FELL BY A GOOD SIZED 8.583 CONTRACTS DOWN to an OI level of 488,383 WITH THE FALL(WHACK) IN THE PRICE OF GOLD ($13.80 with YESTERDAY’S trading). The bankers were expecting more gold leaves to fall from the gold tree and as such they could not cover as much as they wanted.

We are now in the contract month of JUNE and it is one of the BETTER delivery months of the year. In this JUNE delivery month we had A LOSS OF 84 contract(s) FALLING TO 1997. We had 57 notices filed yesterday so we LOST ANOTHER 27 contracts or an additional 2700 oz will NOT stand for delivery in this very active delivery month of June AND WITHOUT A SHADOW OF DOUBT THESE 27 CONTRACTS RECEIVED AN EFP CONTRACT WHICH ENTITLES THEM TO A FIAT BONUS PLUS A FUTURE GOLD CONTRACT/OR A LONG CALL OR MOST LIKELY A LONDON BASED FORWARD GOLD CONTRACT. THESE EFP’S ARE PRIVATE OFF COMEX TRANSACTIONS. THE STUBBORN LONGS WHO ARE REMAINING STOIC ARE SO FAR REFUSING THAT FIAT BONUS

The non active July contract LOST 69 contracts to stand at 2,258 contracts. The next big active month is August and here the OI LOST 9019 contracts DOWN to 363,535.

We had 13 notice(s) filed upon today for 1300 oz

The next big active month will be July and here the OI LOST 4242 contracts DOWN to 122,456 as we start to wind down before first day notice Friday, June 30. July will be interesting to watch in silver as we witness fewer players pitching for EFP contracts than with gold.

The month of August, a non active month picked up 4 contracts to stand at 28. The next big active delivery month for silver will be September and here the OI already jumped by another 3049 contracts up to 43,021.

I will give you a snapshot as to what happened last year at the exact number of days before first day notice:

June 9.2016: 103,688 contracts were still outstanding vs 122,456 contracts June 9.2017

At the conclusion of June, the final standing for physical silver was 3,080,000 oz and we have already surpassed that number this year (3,945,000 oz).

The line in the sand is $18.50 for silver and again it has been defended by the criminal bankers. Once this level is pierced, the monstrous billion oz of silver shorts will blow up. The bankers are defending the Alamo with their last stand at the $18.50 mark. THE NEW RECORD HIGH IN OPEN INTEREST WAS SET FRIDAY APRIL 21/2017 AT: 234,787.

We had 84 notice(s) filed for 420,000 oz for the June 2017 contract

VOLUMES: for the gold comex

Today the estimated volume was 200,263 contracts which is GOOD

Yesterday’s confirmed volume was 264,414 contracts which is GOOD

volumes on gold are STILL HIGHER THAN NORMAL!

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz |

27,352.819 oz

Brinks

|

| Deposits to the Dealer Inventory in oz | nil oz

|

| Deposits to the Customer Inventory, in oz |

nil oz

|

| No of oz served (contracts) today |

13 notice(s)

1300 OZ

|

| No of oz to be served (notices) |

1984 contracts

198,400 oz

|

| Total monthly oz gold served (contracts) so far this month |

2118 notices

211800 oz

6.5878 tonnes

|

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | 143,815.8 oz |

Today, 0 notice(s) were issued from JPMorgan dealer account and 2 notices were issued from their client or customer account. The total of all issuance by all participants equates to 13 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 7 notice(s) was (were) stopped/ Received) by j.P.Morgan customer account.

| Silver | Ounces |

| Withdrawals from Dealers Inventory | nil |

| Withdrawals from Customer Inventory |

nil oz

|

| Deposits to the Dealer Inventory |

NIL oz

|

| Deposits to the Customer Inventory |

nil oz

|

| No of oz served today (contracts) |

84 CONTRACT(S)

(420,000 OZ)

|

| No of oz to be served (notices) |

7 contracts

( 35,000 oz)

|

| Total monthly oz silver served (contracts) | 783 contracts (3,915,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month | 2,295,343.5 oz |

NPV for Sprott and Central Fund of Canada

Sprott’s hostile 3.1 billion bid to take over Central Fund of Canada

(courtesy Sprott/GATA)

Sprott makes hostile $3.1 billion bid for Central Fund of Canada

Submitted by cpowell on Thu, 2017-03-09 01:19. Section: Daily Dispatches

From the Canadian Press

via Canadian Broadcasting Corp. News, Toronto

Wednesday, March 8, 2017

http://www.cbc.ca/news/canada/calgary/sprott-takeover-bid-central-fund-c…

Toronto-based Sprott Inc. said Wednesday it’s making an all-share hostile takeover bid worth $3.1 billion US for rival bullion holder Central Fund of Canada Ltd.

The money-management firm has filed an application with the Court of Queen’s Bench of Alberta seeking to allow shareholders of Calgary-based Central Fund to swap their shares for ones in a newly-formed trust that would be substantially similar to Sprott’s existing precious metal holding entities.

The company is going through the courts after its efforts to strike a friendly deal were rebuffed by the Spicer family that controls Central Fund, said Sprott spokesman Glen Williams.

“They weren’t interested in having those discussions,” Williams said.

Sprott is using the courts to try to give holders of the 252 million non-voting class A shares a say in takeover bids, which Central Fund explicitly states they have no right to participate in. That voting right is reserved for the 40,000 common shares outstanding, which the family of J.C. Stefan Spicer, chairman and CEO of Central Fund, control.

If successful through the courts, Sprott would then need the support of two-thirds of shareholder votes to close the takeover deal, but there’s no guarantee they will make it that far.

“It is unusual to go this route,” said Williams. “There’s no specific precedent where this has worked.”

Sprott did have success last year in taking over Central GoldTrust, a similar fund that was controlled by the Spicer family, after securing support from more than 96 percent of shareholder votes cast.

The firm says Central Fund’s shares are trading at a discount to net asset value and a takeover by Sprott could unlock US$304 million in shareholder value.

Central Fund did not have any immediate comment on the unsolicited offer. Williams said Sprott had not yet heard from Central Fund on the proposal but that some shareholders had already contacted them to voice their support.

Sprott’s existing precious metal holding companies are designed to allow investors to own gold and other metals without having to worry about taking care of the physical bullion.

end

At 3:30 pm we receive the COT which gives position levels of our major players. However because of the EFP’s issued, makes this report totally distorted

The report encompasses May 31, first day notice. You will recall we had a massive obliteration of open interest on the day but since then more paper gold has been added.

what an absolute fraud!

First the Gold COT:

| Gold COT Report – Futures | ||||||

| Large Speculators | Commercial | Total | ||||

| Long | Short | Spreading | Long | Short | Long | Short |

| 312,240 | 107,775 | 29,475 | 108,298 | 324,652 | 450,013 | 461,902 |

| Change from Prior Reporting Period | ||||||

| 61,698 | 24,323 | -6,074 | 4,547 | 37,682 | 60,171 | 55,931 |

| Traders | ||||||

| 188 | 96 | 78 | 48 | 59 | 268 | 206 |

| Small Speculators | ||||||

| Long | Short | Open Interest | ||||

| 44,028 | 32,139 | 494,041 | ||||

| -376 | 3,864 | 59,795 | ||||

| non reportable positions | Change from the previous reporting period | |||||

| COT Gold Report – Positions as of | Tuesday, June 6, 2 | |||||

OUR LARGE SPECS

those large specs that have been long in gold added an unheard 61,698 contracts

those large specs that have been short in gold added 24,323 contracts to their short list

OUR COMMERCIALS

those commercials that have been long in gold added 4547 contracts to their long side

those commercials that have been short in gold added a whopping 37,682 contracts.

OUR SMALL SPECS

those small specs that have been long in gold pitched 376 contracts to their long side

those small specs that have been short in gold added 3864 contracts to their short side.

Conclusion:

there is only one word to describe this: fraud!

Onto silver: note the difference between gold and silver

| Silver COT Report – Futures | ||||||

| Large Speculators | Commercial | Total | ||||

| Long | Short | Spreading | Long | Short | Long | Short |

| 101,713 | 35,772 | 31,973 | 52,429 | 128,053 | 186,115 | 195,798 |

| 5,145 | 618 | -158 | -432 | 4,110 | 4,555 | 4,570 |

| Traders | ||||||

| 95 | 48 | 59 | 35 | 38 | 159 | 123 |

| Small Speculators | ||||||

| Long | Short | Open Interest | ||||

| 22,852 | 13,169 | 208,967 | ||||

| -823 | -838 | 3,732 | ||||

| non reportable positions | Change from the previous reporting period | |||||

| COT Silver Report – Positions as of | Tuesday, June 6, 2017 | |||||

OUR LARGE SPECS

those large specs that have been long in silver added 5145 contracts to their long side

those large specs that have been short in silver added 618 contracts to their short side

OUR COMMERCIALS

those commercials that have been long in silver covered a tiny 432 contracts from their long side

those commercials that have been short in silver added only 4110 contracts to their short side

OUR SMALL SPECS

those small specs that have been long in silver covered 564 contracts to their long side

those small specs that have been short in silver covered 570 contracts.

Conclusions:

note the difference between gold and silver. Do not read anything into these figures as everything is paper. there is no physical settlement as EFP’s distort especially in gold.

And now the Gold inventory at the GLD

June 9/no change in inventory at the GLD/Inventory rests at 867.00 tonnes

June 8/AN ADDITION OF 3.07 TONNES OF GOLD ADDED TO THE GLD/INVENTORY RESTS AT 867.00 TONNES

June 7 a huge change in inventory/a deposit of 13.93 tonnes/inventory rests at 864.93 tonnes

June 6/ no changes in inventory at the GLD/Inventory remains at 851.00 tonnes

June 5.2017/no changes at the GLD/Inventory remain at 851.00 tonnes

June 2/2017/a huge deposit of 3.55 tonnes of gold into the GLD/Inventory rests at 851.00 tonnes

June 1/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 847.45 TONNES

May 31./ no change in gold inventory at the GLD/Inventory rests at 847.45 tonnes

May 30/no change in gold inventory at the GLD/Inventory rests at 847.45 tonnes

May 26./no change in inventory at the GLD/Inventory rests at 847.45 tonnes

May 25./no change in inventory at the GLD/Inventory rests at 847.45 tonnes

May 24/no change in inventory at the GLD/inventory rests at 847.45 tonnes

May 23/a paper withdrawal of 5.03 tonnes of gold from the GLD/Inventory rests at 847.45 tonnes

May 22/A DEPOSIT OF 1.77 TONNES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 852.48 TONNES

May 19/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 850.71 TONNES

May 18/a withdrawal of 1.18 tonnes of gold from the GLD/Inventory rests at 850.71

May 17/no change in the GLD inventory/inventory rests at 851.89 tonnes

May 16./ no change in the GLD inventory/inventory rests at 851.89 tonnes

May 15/no change in the GLD inventory/inventory rests at 851.89 tonnes

May 12/no changes in GLD/inventory rests at 851.89 tonnes

may 11/no changes in GLD inventory/inventory rests at 851.89 tonnes

May 10/no changes in GLD inventory/inventory rests at 851.89 tonnes/

May 9/a withdrawal of 1.19 tonnes from the GLD/Inventory rests tonight at 851.89 tonnes

May 8/no change in inventory at the GLD/Inventory rests at 853.08 tonnes

May 5/no changes in inventory at the GLD/Inventory rests at 853.08 tonnes

May 4/A tiny change in inventory at the GLD /a withdrawal of .28 tonnes to pay for fees/inventory rests at 853.08 tonnes

May 3/no change in inventory at the GLD/Inventory rest at 853.36 tonnes

May 2/no change in inventory at the GLD/Inventory rests at 853.36 tonnes

May 1/ no changes in inventory at the GLD/inventory rests at 853.36 tonnes

end

Now the SLV Inventory

June 9/no change in silver inventory at the SLV/Inventory rests at 339.605 million oz/

June 8/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 339.605 MILLION OZ/

June 7/no change in inventory at the SLV/inventory rests at 339.605 million oz/

June 6/no change in inventory at the SLV/Inventory rests at 339.605 million oz.

June 5/a huge change at the SLV/a withdrawal of 1.371 million oz /inventory rests at 339.605 million oz/

June 2/no change in silver inventory at the SLV/Inventory rests at 340.976 million oz/

June 1/NO CHANGE IN INVENTORY AT THE SLV/INVENTORY RESTS AT 340.976 MILLION OZ

May 31./ no change in silver inventory at the SLV/inventory rests at 340.976 million oz/

May 30/no change in silver inventory at the SLV/inventory rests at 340.976 million oz

May 26/another paper withdrawal of 946,000 oz of silver from the SLV with silver rising/inventory rests at 340.976 million oz

May 25/no change in silver inventory at the SLV/Inventory rests at 341.922 million oz

May 24./a “paper” withdrawal of 1.893 million oz from the SLV/inventory rests tonight at 341.922 million oz

May 23/no change in silver inventory at the SLV/inventory rests at 343.815 million oz

May 19/no change in silver inventory at the SLV/Inventory rests at 343.815 million oz.

may 18/2017/another big deposit of 1.42 million oz added to the SLV/inventory rests at 343.815 million oz.

may 17/no change in silver inventory at the SLV/Inventory rests at 342.395 million oz/

May 16./we had a huge addition of 1.416 million oz of silver into the SLV/inventory rests at 342.395 million oz

May 15/no changes in silver inventory/inventory rests at 340.979 million oz/

May 12/a huge change in silver: a deposit of 2.369 million oz/inventory rests at 340.979 million oz

May 11/no changes in silver inventory at the SLV/Inventory rests at 338.610 million oz

May 10/ a gigantic 3.833 million oz of silver added to the SLV and this occurred with the constant whacking of silver for the past 17 trading sessions/inventory rests at 338.610 million oz

may 9Again, no movement of inventory at the SLV. Inventory rests at 334.777 million oz

May 8/no change in silver inventory at the SLV/inventory rests at 334.777 million oz/

May 5/Strange!! no change in silver inventory at the SLV/Inventory rests tonight at 334.777 million oz

May 4/a very tiny withdrawal of 144,000 oz to pay for fees/inventory rests tonight at 334.777 million oz/

May 3/strange!! with the drop in price of silver we had no change in inventory at the SLV/inventory rests at 334.921 million oz

May 2/extremely strange again/a huge 3.502 million oz deposit into the SLV despite silver being in the toilet for the past several trading days.Inventory 334.921 million oz

may 1/extremely strange/with silver being walloped these past several days, the inventory rises again by a huge 1.136 million oz/(maybe someone can explain this phenomena??)

The actual figures can be found on our home page https://monetary-metals.com/

with this box in the left side

6 month: 1.26%

12 month: 1.43%

| BRON SUCHECKI | VP Operations |

|

| Unlocking the Productivity of Gold |

| MONETARY METALS & CO |

| M: +61 4 1210 1912 | bron@monetary-metals.com |

| Skype: bron.suchecki |

| Twitter: @bronsuchecki |

| Website: monetary-metals.com |

| Use this link to encrypt and safely send confidential documents to Monetary Metals® |

| https://cloud.sookasa.com/upload_page/f840a3c3-54e5-42b0-85b4-15c9e94ea5e |

end

Major gold/silver trading/commentaries for FRIDAY

GOLDCORE/BLOG/MARK O’BYRNE.

GOLD/SILVER

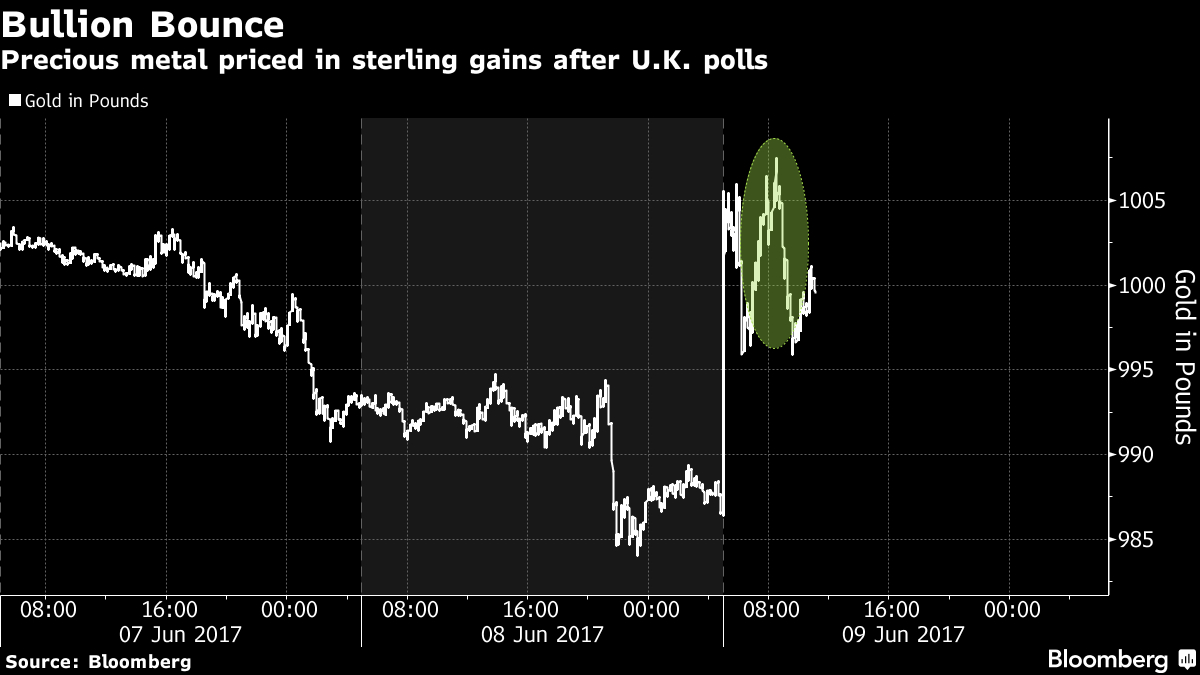

Gold in Pounds Surges 1.5% To £1,001/oz – UK Political Turmoil Likely

– Gold in pounds rises 1.5% from £986/oz to £1,001/oz after shock UK election result

– Gold reaches 7 week high and surges 6% in the last 30 days from £942/oz to £1,001/oz

Gold in pounds – 1 month

Gold in pounds – 1 month

– Very robust gold sales experienced by gold brokers, including GoldCore, in the UK this week and today

– May’s ruling Conservative party loses overall majority and prospect of hung U.K. parliament

– PM May vulnerable from within Tory Party and Corbyn has called for her to resign

– Corbyn and Labour party on the rise which may pose risks to vulnerable London property market and UK economy as investor sentiment towards UK sours further

– Vote set to boost political turmoil in UK, complicate Brexit talks with EU whose hand is strengthened

As reported by Bloomberg News this morning:

Gold priced in sterling surged to the highest level in more than seven weeks as Prime Minister Theresa May failed to win an overall majority in the U.K. election, signaling further political turmoil less than a year after Britain voted to leave the European Union.

The outcome throws into doubt May’s future as prime minister just days before negotiations are due to start on the country’s exit from the EU.

Instead of increasing her majority to strengthen her hand in talks with European leaders, May has lost seats and the Conservative Party has fallen short of an absolute majority in parliament.

“The weakness in the pound has pushed up gold prices in sterling,” said Madhavi Mehta, an analyst at Kotak Commodity Services Pvt in Mumbai. “The pound has weakened amid prospects that the Brexit negotiations will be long and arduous.”

Spot gold rose as much as 2.2 percent to £1,007.52 pounds an ounce before trading at 1,002.34 pounds by 3:32 p.m. in Singapore. Bullion in the U.S. currency retreated 0.4 percent to $1,272.93 an ounce, extending its decline from a seven-month high of $1,296.15. It’s heading for the first weekly drop since early May.

The Conservative Party was on course to win 318 seats, down from 330 held at the start of the campaign and short of the 326 seats needed for an overall majority. Jeremy Corbyn’s Labour Party will take 261 seats, a gain of 29 seats, according to BBC projections.

The shock results came after a day when the European Central Bank kept interest rates unchanged and former FBI Director James Comey gave testimony to a Senate panel about meetings with President Donald Trump that centered on whether the president sought to quash part of a federal probe into Russian meddling in the 2016 election.

While bullion prices in dollar terms have come off seven-month highs, assets in the SPDR Gold Trust, the largest exchange-traded fund backed by the metal, have expanded to 867 metric tons, the highest level since December.

News and Commentary

Gold in Pounds Rises to Seven-Week High on Hung U.K. Parliament (Bloomberg.com)

Sterling Falls Sharply On Hung Parliament In UK General Election (Investing.com)

Gold Imports by India Jump Fourfold as Tax Fear Spurred Stocking (Bloomberg.com)

Banco Popular faced eurozone’s first large-scale bank run – ECB (Reuters.com)

With gold mining activity nearing pre-boom levels, is this the end of the downturn? (ABC.net)

Source: Zero Hedge

Someone Just Dumped $4 Billion Of Gold Futures Ahead Of Comey Testimony (ZeroHedge.com)

40.5 Tonnes Of Paper Gold Dumped In 4 Minutes (InvestmentResearchDynamics.com)

The World’s Most And Least Peaceful Countries (Statista.com)

Spain’s Banco Popular Bailed In, Acquired By Santander For €1.00 (ZeroHedge.com)

India’s Tax Change Will Increase Gold Demand To 950 Tonnes By 2020 (Barrons.com)

END

Trading today in gold:

the Crooks are at it again:

(courtesy zero hedge)

UK Election Chaos Sparks Selling Spree In Bonds & Bullion

Because nothing says sell safe-havens like a shocking election result in the nation at the center of European Union chaos…

Exit Polls signal May failure… sell Gold

At least bonds initial reaction made some sense… but since then it’s been Sell the dip in yields and buy stocks… because more QE will paper over any political cracks, we’re sure…

Some have suggested that this is due to the May coalition implying a ‘softer’ Brexit, implying less global turmoil, implying less need for safety? We remind those ‘thinkers’, like pregnancy, there’s no half-Brexit.

end

Mexico owes Canadian miners more than 360 million dollars with Goldcorp the lions share at 230 million

(courtesy Reuters/GATA)

Mexico owes Canadian miners more than $360 million, Reuters says

Reuters

Thursday, June 8, 2017Mexico’s tax agency is holding more than $360 million in tax rebates owed to six Canadian miners, including $230 million to Goldcorp Inc., according to sources and official documents seen by Reuters, escalating the situation into a showdown between the Mexican government and Canadian mining firms operating in Mexico.In a string of meetings, Canadian officials have pressed Mexico to fix the problem, which hamstrings mining companies’ ability to invest in operations and is particularly difficult for smaller, cash-strapped miners and explorers, people familiar with the matter said.Vancouver-based Goldcorp declined to comment on its outstanding refund, which represents 142 percent of its 2016 net profit and 6 percent of its full-year revenue.Goldcorp, the world’s No. 3 gold miner by market value, is owed the largest amount, according to documents seen by Reuters, followed by Torex Gold Resources, a small, Toronto-based miner that began commercial production at its Mexico mine last year and is waiting on a refund of some $66.5 million. …… For the remainder of the report:http://www.reuters.com/article/us-mexico-mining-tax-exclusive-idUSKBN18Z…

* * *

END

Chris Powell comments on the huge raid we have been experiencing this past two days:

(courtesy Chris Powell/GATA)

Gold’s counterintuitive movement is an old story but it can’t be told

Submitted by cpowell on Thu, 2017-06-08 15:45. Section: Daily Dispatches

11:54a ET Thursday, June 8, 2017

Dear Friend of GATA and Gold:

Dave Kranzler of Investment Research Dynamics reports that a huge amount of “paper” gold was dumped on the futures exchange in New York today, apparently in connection with the anticipated congressional testimony of former FBI Director James Comey:

http://investmentresearchdynamics.com/40-5-tonnes-of-paper-gold-dumped-i…

Kranzler writes: “One/some/several ‘entities’ decided at 9:38 this morning that it was necessary to dump 14,315 contracts of paper gold. This is just the August contract. In total a lot more was unloaded. This represents 1.43 million ounces of gold. The Comex is showing only 900,000 ounces of ‘gold’ as ‘registered,’ or available for delivery in June, July, and August (assuming all of that gold is actually sitting physically in the Comex vaults as reported). If we make that generous assumption, 531,000 ounces of paper gold were naked-shorted.”

The counterintuitive movement of the gold price long has been one of GATA’s major points. It came to the attention of the Bank of Russia back in 2004, when the bank’s deputy chairman, Oleg V. Mozhaiskov, cited it in remarks to the London Bullion Market Association meeting in Moscow.

Mozhaiskov said: “The statistical correlation between the market prices of dollar and gold is obvious. For the problem we discuss today it means specifically that gold, in addition to its unique physical and chemical properties used in industry, has retained its particular monetary attractiveness for cautious financial investors, and its market price is still heavily influenced by the state of the international monetary system.

“This dualism in gold price formation distinguishes it from other commodities and makes the movements in the price sometimes so enigmatic that market analysts need to invent fantastic intrigues to explain price dynamics. Many have heard of the group of economists who came together in the society known as the Gold Anti-Trust Action Committee and started a number of lawsuits against the U.S. government, accusing it of organizing an anti-gold conspiracy. They believe that with the assistance of a number of major financial institutions (they mention in particular the Bank for International Settlements, J.P. Morgan Chase, Citigroup, Deutsche Bank, and others), some senior officials have been manipulating the market since 1994. As a result, the price dropped below US$300 an ounce at a time when it should, if it had kept pace with inflation, have reached US$740-760.

“I prefer not to comment on this information but dare assume that the specific facts included in the lawsuits might have given ground to suspicion that the real forces acting on the gold market are far from those of classic textbooks that explain to students how prices are born in a free market.”

Mozhaiskov’s address is posted at GATA’s internet site here:

GATA often has quoted the incisive remark of South African gold advocate Peter George on the eve of GATA’s conference in Dawson City, Yukon, in August 2005, a remark captured at the 35-second mark in the first video frame at GATA’s Internet site here:

George said: “In the last 10 years the central banks have effectively shown that when there is a real crisis, gold actually goes down. And it’s so blatant, it’s a joke.”

Your secretary/treasurer has put it more sardonically, as in a dispatch in 2012:

http://www.gata.org/node/11426

“If the Northern Hemisphere was destroyed in a nuclear war, the Federal Reserve, JPMorganChase, and HSBC would get some brokers to Sydney, Rio de Janeiro, and Johannesburg to sell gold futures massively and drive the price down by at least 5 percent. Kitco market analyst Jon Nadler would crawl out from the rubble and opine to the cockroaches that the gold price had fallen because so many gold buyers had been killed, as he always had predicted would happen. CPM Group’s Jeff Christian would telephone New Zealand not to worry because he was flying down with reams of gold-colored paper that would work just as well in Wellington as it did in New York as long as nobody asked what was behind it. And the World Gold Council would console itself with whatever high-fashion models could be found wearing nose rings in French Polynesia.”

Mainstream financial news organizations know all about this but are not likely to find it curious while JPMorganChase, HSBC, and other bullion and investment banks remain among their largest advertisers and while their organizations are owned by large multi-media corporations heavily regulated by governments. For as Upton Sinclair observed in 1934 as he tried to break through the media oligopoly of his time in his campaign for governor of California, “It is difficult to get a man to understand something when his salary depends upon his not understanding it.”

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

A great reason to whack gold today: Gold imports jump 400% as the increase in GST tax fear as spurred stocking of gold

(courtesy Bloomberg)

Gold imports by India jump fourfold as tax fear spurred stocking

Bloomberg News

Thursday, June 8, 2017India, which vies with China as the world’s top gold consumer, saw a fourfold increase in imports of the precious metal in May as traders stocked up fearing that the government would fix a higher rate for jewelry under a new national goods tax to be implemented from next month.Overseas purchases advanced to 126 metric tons in May from 31.5 tons a year earlier, according to a person familiar with provisional data from the finance ministry, who asked not to be identified as the data aren’t public. Finance Ministry spokesman D. S. Malik declined to comment on the data.India fixed the goods and services tax for gold at 3 percent, effective from July 1. The rate is lower than expected, Ketan Shroff, joint secretary at the India Bullion and Jewellers Association Ltd. said on Monday. The duty will replace more than a dozen domestic levies including excise tax and state tariffs, making India a common market for the first time. …… For the remainder of the report:https://www.bloomberg.com/news/articles/2017-06-08/gold-imports-by-india…

* * *

END

totally absurd: Jim Cramer discusses bitcoin and highlights that it may hit 1 million dollars.

(courtesy Mish Shedlock/Mishtalk)

Jim Cramer Goes Batty: “Bitcoin May Hit $1,000,000”; Act Now Before It’s Too Late!

Authored by Mike Shedlock via MishTalk.com,

It’s hard to know when bubbles will end but when analysis goes ape-sh*t batty, it’s easy to know the bubble exists.

Jim Cramer’s analysis of Bitcoin provides a perfect example.

CNBC reports Cramer says it’s possible bitcoin could reach $1 million one day.

The price of digital currency stockpiled by companies to pay off potential cyberthreats could reach $1 million one day, CNBC’s Jim Cramer said Wednesday.

Cramer was responding to a recent comment by Business Insider CEO Henry Blodget, who said bitcoin could go to $1 million.

“I think it could because the European banks are frantically trying to buy them so they can pay off ransomware. It’s a short-term way to be able to deal with cybersecurity. It is the way to pay off the bad guys,” Cramer said on “Squawk on the Street.”

“When you get hit and you’re not sure how to do bitcoin, these cyberattackers have customer service desks,” Cramer said.

What Blodget Really Said

Blodget also mentioned the downside: “Bitcoin could go to $1 million (or fall to $0),” said Blodget maintains the view that “ultimately, Bitcoin has no intrinsic value.”

New Target $1,000,000

The Coin Telegraph reports Bitcoin Price Can Reach $1 Mln: CNBC’s Jim Cramer.

On the CNBC show “Squawk on the Street,” Cramer stated that the demand toward Bitcoin is rapidly increasing and because of Bitcoin’s decentralized nature, its price could potentially enter the $1 mln region, which would bring the market cap of Bitcoin to tens of trillions of dollars.

However, Cramer’s reasoning behind his Bitcoin price prediction was fundamentally flawed as he failed to grasp the core purpose of Bitcoin and why investors are starting to purchase Bitcoin.

“I think it could because the European banks are frantically trying to buy them so they can pay off ransomware. It’s a short-term way to be able to deal with cybersecurity. It is the way to pay off the bad guys.”

Such claim is evidently non-factual because the European Bitcoin exchange market only accounts for nine percent of the global Bitcoin exchange market and it is behind the US, Japan, China and South Korea in trading volumes.

More importantly, Cramer’s statement fails to consider the fact that Bitcoin is being utilized as a currency and safe haven asset more than it is being used as a lifeline to feed ransomware developers.

In the case of WannaCry ransomware, the biggest ransomware attack in history, the distributors earned less than $100,000. That is only 0.0012 percent of the European Bitcoin exchange market. Thus, to say that Bitcoin price is rising because of 0.0012 percent of traders from the fifth largest Bitcoin exchange market is not an accurate depiction of the surging Bitcoin price.

Regardless, Cramer believes that Bitcoin price will reach $1 mln one day due to its rapidly increasing trading volumes and demand from investors.

Frantically “Trying” to Buy Bitcoins?!

The idea that banks need to “try” to buy Bitcoins is absurd.

Do. Or do not. There is no try.

Customer Service Desks

Cyberattackers have “customer service desks”? really? And they can be trusted? And banks don’t have backups? So banks need to “try” to stockpile Bitcoins as a precaution? And that will push the price to $1,000,000?

At least Henry Blodget discussed the downside without absurd hype.

Action to Take

If you think Bitcoin has any chance of hitting $1,000,000 then buy one for $2,725 or so and relax. Bitcoin is a life-long insurance policy.

Unlike term insurance, Bitcoin never expires. And unlike real estate, it’s easily divisible.

So buy one, put it in your will, and pass it to your kids. But make them promise to hold on to it. After all, a single Bitcoin may very well be worth $1 billion someday!

Why not? Why not $10 billion?

Even at $1 million, the world would be flooded with tens-of-thousands or hundreds-of-thousands of dollar “billionaires”.

Hyperinflation Anyone?

Back in the real world, please think of what it would take for Bitcoin to hit $1,000,000. The answer is hyperinflation. The US dollar would essentially go to zero vs everything.

So when Cramer or anyone else discusses the possibility of $1,000,000 Bitcoins, they are really discussing the possibility of hyperinflation in US dollars.

Act Now Before It’s Too Late

This setup reminds me of a post I did in 2005: It’s Too Late.

I think it’s too late.

In fact I know it’s too late.

How do I know?

The following Email I received tonight should explain it nicely.

When you see stuff like this, not only is it too late, it’s way too late.

As a practical matter, and without all the hype, I will stick with gold even as I wish I had taken out some Bitcoin insurance at $1, $10, $100, or even $1,000.

Supposedly, it’s still not too late.

end

Your early FRIDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight

1 Chinese yuan vs USA dollar/yuan WEAKER 6.7971(DEVALUATION SOUTHBOUND /OFFSHORE YUAN MOVES WEAKER TO ONSHORE AT 6.7913/ Shanghai bourse CLOSED UP 8.06 POINTS OR 0.26% / HANG SANG CLOSED DOWN 32.77 POINTS OR 0.13%

2. Nikkei closed UP 104.00 POINTS OR 0.52% /USA: YEN RISES TO 110.39

3. Europe stocks OPENED MIXED ( /USA dollar index RISES TO 97.38/Euro DOWN to 1.1179

3b Japan 10 year bond yield: FALLS TO +.056%/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 110.13/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD FINALLY IN THE POSITIVE/BANK OF JAPAN LOSING CONTROL OF THEIR YIELD CURVE AS THEY PURCHASE ALL BONDS TO GET TO ZERO RATE!!

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 45.78 and Brent: 47.94

3f Gold DOWN/Yen DOWN

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil UP for WTI and UP for Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund FALLS TO +.260%/Italian 10 yr bond yield DOWN to 2.10%

3j Greek 10 year bond yield FALLS to : 6.01???

3k Gold at $1273.00 silver at:17.35 (8:15 am est) SILVER BELOW RESISTANCE AT $18.50

3l USA vs Russian rouble; (Russian rouble DOWN 4/100 in roubles/dollar) 56.95-

3m oil into the 45 dollar handle for WTI and 47 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation (already upon us). This can spell financial disaster for the rest of the world/China forced to do QE!! as it lowers its yuan value to the dollar/GOT A SMALL SIZED DEVALUATION SOUTHBOUND

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 110.39 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 0.9714 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.0861 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now POSITIVE territory with the 10 year FALLS to +0.260%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.204% early this morning. Thirty year rate at 2.861% /POLICY ERROR)GETTING DANGEROUSLY HIGH

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

(courtesy Jim Reid/Bloomberg/Deutsche bank/zero hedge)

S&P Futures At Record High After “Shocking” UK Election Result

“Triple Threat Thursday” is now a distant memory, with both the ECB and Comey testimony “non-events” for the market, although the UK general election was a shocker in which contrary to expectations, Theresa May lost her majority in Parliament, sending sterling tumbling overnight and prompting even more confusion about the UK’s political fate and the future of Brexit. That however did not spook risk assets, and on Friday morning, European stocks gained with Asian stocks little changed, while S&P500 futures were set for new all time highs. Just like after Brexit, it was U.K. stocks that rallied the most among developed markets as the pound fell.

With the majority of seats counted, May’s Conservatives had no way to win an outright majority in parliament. That raised fears the political turmoil could delay and confound talks on leaving the European Union, which are due to start in less than two weeks, and the pound shed over 2 percent against the dollar.

Sterling dropped as low as $1.2636 in early London trading, before clawing back some ground. Yields on 10-year gilts fell 3 basis points to 1.00 percent. However, the damage contained, with S&P futures edging up 0.2 percent to 2,434, and just shy of record highs.

“The uncertainty is bad news for sterling,” said Bank of America, Merrill Lynch European equity & cross-asset strategist James Barty. “I think for the global market it doesn’t matter. Unlike Brexit, which at the time had a spillover into other markets, this is a very UK-specific thing.”

Most impacted by the UK result was the pound, which plunged the most in eight months as the election intended to strengthen Prime Minister Theresa May’s hand in negotiations with the European Union instead cast doubt over her future. The currency’s retreat gave British stocks a boost, but the election’s impact beyond the U.K. was muted.

The euro extended losses to three days, and the Stoxx Europe 600 Index swung. Fears of a supply glut continue to weigh on oil, but it managed to reverse an earlier decline.

“For now, the results of U.K. elections do not appear to be threatening the global growth story,” Mark Haefele, global chief investment officer at UBS Group AG, said in a note to clients. But for Britain,“political uncertainty is likely to more than offset any benefit from a marginally weaker pound,” he said.

The FTSE 100 Index jumped 0.8 percent. The Stoxx Europe 600 Index swung before trading little changed. Futures on the S&P 500 rose 0.1 percent. The underlying gauge advanced less than one point on Thursday, for a second day of gains.

In other overnight news, there was muted reaction to China inflation report as producer prices missed expectations, and eased further; PBOC reverse repos close to maturities; overnight Hibor falls for sixth day; Shanghai Composite closed modestly higher.

Overnight, Wall Street had also seemingly judged that the testimony of former FBI director James Comey was not life-threatening for the administration of President Donald Trump. Comey accused Trump of firing him to try to undermine the investigation into possible collusion by his campaign team with Russia’s alleged efforts to influence the 2016 election.

“I think the market is taking less of an alarmist review of this situation because there is no smoking gun here,” said Jefferies & Co money market economist Thomas Simons. “So it’s not particularly impactful for thinking about … Trump’s economic agenda to go through.”

In commodity markets, spot gold was 0.3% lower at $1,274.20 an ounce. Oil prices remained subdued, wit Brent having settled at its lowest since Nov. 29, the eve of an OPEC production cut deal.

Bulletin Headline Summary from RanSquawk

- UK PM May’s Conservative Party failed to win a majority in the UK general election although are still the largest party in government

- The Northern Irish DUP are expected to support the Conservatives in a “confidence and supply” arrangement, not a formal coalition

- Theresa May is now scheduled to head to Buckingham Palace to request to form a government

Market Snapshot

- S&P 500 futures up 0.2% to 2,434.25

- STOXX Europe 600 down 0.1% to 388.76

- MXAP down 0.03% to 155.14

- MXAPJ unchanged at 505.75

- Nikkei up 0.5% to 20,013.26

- Topix up 0.08% to 1,591.66

- Hang Seng Index down 0.1% to 26,030.29

- Shanghai Composite up 0.3% to 3,158.40

- Sensex down 0.06% to 31,193.17

- Australia S&P/ASX 200 up 0.02% to 5,677.80

- Kospi up 0.8% to 2,381.69

- German 10Y yield unchanged at 0.257%

- Euro down 0.3% to 1.1178 per US$

- Brent Futures down 0.4% to $47.69/bbl

- Italian 10Y yield fell 12.1 bps to 1.884%

- Spanish 10Y yield fell 2.8 bps to 1.448%

- Brent Futures down 0.3% to $47.70/bbl

- Gold spot down 0.3% to $1,274.34

- U.S. Dollar Index up 0.5% to 97.43

Top Overnight News

- May’s Bet Fails, Pound Falls as Government Loses Majority; House Passes Dodd-Frank Rollback Bill; FDA Toughens Stance on Opioids

- Theresa May’s future as Britain’s prime minister was thrown into doubt after her gamble to call an early election backfired spectacularly, casting uncertainty over the government’s make-up as well as the direction and timing of negotiations on leaving the European Union

- Ousted FBI chief James Comey and President Donald Trump accused each other of lying about their private encounters in the wake of dramatic Senate testimony that centered on whether the president sought to quash part of a federal probe into Russian meddling in the 2016 election

- Dish Network, Amazon considering extending their partnership or potentially merging sometime in the next few months

- Saudi Arabia dwarfs Qatar on almost any measure, yet there are plenty of ways the tussle between the Gulf neighbors could end up hurting the world’s biggest oil exporter — even if it wins

- Central banks are poised to start rowing in the one direction again

Asian equities have been somewhat unreactive to this hurdle for PM May and the uncertainty now surrounding the UK political front, with Asian bourses as well as US equity futures relatively mixed. Nikkei 225 (+0.7%) has been the outperformer thus far following the softness in the JPY, which had been looking to test yesterday’s high around 110.40. Shanghai Comp (+0.2%). and Hang Seng (-0.1 %) struggled to find any firm direction, while the marginal gains in the ASX 200 (+0.2%) were led by the rise in miners. Finally, 10yr JGB traded marginally higher as yields trickled lower throughout the session, with JGB’s also supported by the BoJ’s rinban operation.

- Chinese CPI (May) Y/Y 1.5% vs. Exp. 1.5% (Prey. 1.2%).

- Chinese PPI (May) Y/Y 5.5% vs. Exp. 5.6% (Prey. 6.4%)

Top Asian News

- China’s Factory Inflation Eases as Raw Material Prices Decline

- Philippines Suspends Resorts World Manila’s Casino Permit: BTVPh

- Great Wall Motor Gains as Strong Pre-Orders Seen for New Model

- Li Ka-Shing’s Firms Slump as Falling Pound Hurts Profit Outlook

- Hong Kong Stocks Retreat From 2015 High Amid Overheating Signs

- Dalian Iron Ore Caps Third Weekly Drop on Steel Market Outlook

- SoftBank Boosts Japan Stocks, Beating Impact of ‘Super Thursday’

- Little Impact Seen From U.K. Vote, ECB Meet, Comey: Asian NDFs

In European trading, the weaker GBP has benefitted UK equities with the FTSE 100 opening higher by over 1% before paring some of the gains amid the political uncertainty over what comes next. Utility companies led the way higher with SSE and Centrica both near the top of the FTSE, while large multinationals were helped by the depreciation in the GBP. Unsurprisingly, banking names such as Lloyds and RBS, declined while homebuilders also fell as the increased uncertainty could ultimately slow house purchases. Defensive sectors drove gains in other European equity markets with health care stocks performing well across the region. Gilts opened lower but recovered as UK equity markets reversed some of the gains. The UK data had little impact on UK asset classes despite industrial output rising less than expected in April, after declining for the previous three months.

Top European News

- Young Seek Revenge on Old as Divided Britain Upends its Politics

- Airbus Warns U.K. Government: Retain Labor Mobility to Save Jobs

- U.K. Heads for Hung Parliament as May’s Election Gamble Fails

- U.K. Industrial Output, Manufacturing Rise Less Than Forecast

- DUP Said to Consider Arrangement to Ensure May Has Support: Sky

- M&G Bond Manager Says Election Could Lead to Second Brexit Vote

In currencies, the initial reaction was seen in the GBP after the exit poll released on Thursday evening, which showed the Conservatives would fall short of a majority. GBP/USD then dropped to its lowest level in 7 weeks as reports emerged that Theresa May would not resign, although some profit taking saw GBP/USD bounce a little off its lowest levels. Other FX markets have been relatively unreactive with JPY weakness observed amid USD/JPY demand at the Tokyo fix. Today sees large options (2.1 bIn) expire at today’s 1000am NY cut. The pound weakened 1.7 percent to $1.2732 at 10:58 a.m. in London.

The yen retreated 0.3 percent to 110.35 per dollar. The euro slipped 0.3 percent to $1.1181. The Bloomberg Dollar Spot Index added 0.4 percent, gaining for a third day.

In commodities, WTI and Brent crude futures both stabilised after the large declines seen in the early part of the week and since the OPEC meeting in early June. The market has largely shrugged off the geopolitical tensions in the Middle-East with Qatar and other Gulf countries. West Texas oil gained 0.5 percent to $45.89 a barrel, after two days of losses. Crude has slumped this week as an unexpected increase in U.S. crude stockpiles cast doubt on OPEC’s ability to rebalance world crude markets. Gold fell 0.3 percent to $1,274.18 an ounce, declining a third day.

Looking at the day ahead, while the fallout from the UK election will no doubt be front and centre, there is also a little bit of data to get through. This morning in Europe we get more hard data points with more industrial production prints due in France and the UK along with trade data out of Germany and also the UK. In the US we are due to receive the wholesale trade report. The EU/NATO Conference is also due today. It’s worth also noting that this Sunday France begins the two-step process to elect a new National Assembly with polls due to close on Sunday evening. The second round is on June 18th.

US Event Calendar

- 10am: Wholesale Inventories MoM, est. -0.3%, prior -0.3%

- 10am: Wholesale Trade Sales MoM, est. 0.2%, prior 0.0%

* * *

DB’s Jim Reid concludes the overnight wrap

You’ll wake up to shock and chaos this morning here in the UK. In numbers terms this election result is a bigger surprise than Brexit or Trump if not quite on the same scale in terms of wider global market implications.

I say wake up as if you’re like me you haven’t been to bed yet so forgive my rambling. With 516 out of 650 seats declared at 4.25am the BBC/ITV forecasts are that the ruling Conservative party will fall a handful of seats short of an overall majority. They may be able to form a working majority with the help of the Northern Irish Unionist Parties (who may win around 10 seats) but if so this would still be a very weak government and PM Theresa May might be vulnerable given she staked her reputation on holding this very early election when her party had a 10-20% lead in the polls. Another election is possible at any time really. How this leaves the Brexit negotiations is a complete mystery. The range of eventual outcomes are now much wider on this front. Hard line Brexit Tories will hold more power in a weak Tory administration of some form but the possibility of fresh elections relatively soon and an alternative more soft line approach is also a possibility. Given we’re on a tight Brexit timetable this is not great news for the UK. The Europeans must be watching with some amusement. Overall it’s going to be constitutional chaos in the UK for the foreseeable future. Ironically the Conservative Party look set to win around 44% of the vote and increase their share – an impressive number in the context of recent decades. However as we discussed yesterday the return to a two party state hasn’t allowed them to run away with things.

In markets Sterling immediately tumbled -1.96% as soon as the exit poll hit the screens, touching a low of $1.2709. It’s recovered a little but is still down -1.62% versus yesterday’s close. The moves have mostly been contained in the currency. FTSE 100 futures are -0.20% while S&P 500 futures are actually up slightly. Safe havens like Gold (-0.60%) and the Yen (-0.26%) are weaker and Treasuries are flat. Bourses in Asia are generally flat to up +0.90% too.

Whatever the overall results of this election some of the stats about potential age demographics of the voters is very interesting. Sky did a poll on election day and found amongst 18-34 year olds Labour were on 63% and Conservatives 27%. With 35-54 year olds both were on 43% and over 55 year olds Labour on 23% and Conservatives on 59%. Labour made a huge push for the young who don’t normally vote in high numbers and the Conservative Party actually proposed policies that worked against their natural older vote perhaps thinking their early lead in the polls gave them an opportunity to try to balance the books more. So were the young more motivated than normal and were the elderly less motivated? It’s fascinating as this shows the dilemma a lot of politicians have around the world. We generally have a wealth divide where the older generation (who normally vote) have a high proportion of it relative to the young who are generally in debt and/or in many countries unemployed. It feels this divide is at the higher end of the historical range.

Are the young starting to rebel more and are looking for hope? Can you politically afford to attack the wealthier older voter to help redistribution? One of the big themes of our long-term study last year was that we thought we were at the end of a 35 year super cycle of policy, politics and with it interest rates and asset prices. Our argument was that the Trump and Brexit vote marked the turning point when the disenfranchised were starting to actually win elections/ referendums. If policy wasn’t increasingly calibrated to these ‘forgotten’ people then the incumbents would get voted out. What we felt was that this would mean more fiscal spending, bigger deficits and less reliance on monetary policy at least until fixed income markets rebelled and then you’d probably get central banks forced to monetise that debt. This was our slow roadmap for the future and nights like last night may be another inching towards that. As Mr Trump has discovered it’s not easy to increase spending though but I think the trend will be up in the years to come.

There’s no doubt that this will dominate the rest of Friday for markets but investors have also got the ECB to mull over following an overall fairly dovish outcome from yesterday’s policy meeting. The most significant part of the statement and as largely expected was the removal of the “or lower” rates guidance and also upgrading economic growth forecasts by 0.1pp. Mario Draghi also said that risks to the growth outlook are now “broadly balanced” which represented an upgrade to neutral. However, the inflation tone was distinctly dovish. Draghi described the outlook for core inflation for the rest of the year as “low and flat” which as our European economists aptly put is “insufficient”. Core inflation forecasts for 2018 and 2019 were revised lower by 0.1pp to 1.4% and 1.7%. Our colleagues note that these numbers are still consistent with a gradual exit but the ECB can afford to take it slowly. Our team highlight another two important points from the meeting. The first is that there was not a single hint of the ECB preparing the ground for tapering or a phasing out of QE and the second is that the Council is cautious about wage inflation. As a result, our economists have now pushed back their timing of exit. They had expected a taper pre-announcement decision in September and one-off depo hike in December. However they now expect a six-month extension of QE to be announced in December at a slower pace of €40bn. QE will likely continue in H2 2018 at a slower pace still and a oneoff depo rate hike cannot be excluded in mid-2018 if further concessions need to be made to the hawks. In summary the start of the policy rate tightening cycle is more likely to be mid-2019 than end 2018. You can find more in our economists’ report here.

Markets reacted swiftly to the ECB with the Euro edging lower initially before consolidating into the close to finish -0.38%, although it is down another -0.27% this morning and below $1.120. Benchmark Bund (-1.3bps) and OAT (-4.8bps) yields were both lower although it was the periphery which stood out with yields down 5bps to 13bps although as you’ll see shortly for reasons as much linked to Italian politics. 10y Treasury yields were actually a little higher (+1.6bps to 2.189%) while the S&P 500, despite getting a decent boost from Banks, limped to a +0.03% close. The James Comey testimony ended up being mostly a nonevent with both sides trading blows and accusing each other of lying, but as we had seen on Wednesday there was no silver bullet to really get markets excited about. It’s worth noting that late last night the House Republicans passed a bill to dismantle parts of the Dodd-Frank Act following a 233-to-186 majority. The Bill passes to the Senate now however it’s not expected to have much chance of passing in its current form.

Staying with markets, as noted above the standout mover in European bond markets yesterday was BTPs. 10y yields fell 12.8bps to 2.154% and the most since March 2016. This followed lawmakers in the ruling Democratic Party saying that the push to reform the country’s electoral law was “dead” which in turn lowered the probability of a snap election as early as this autumn. This followed the far right anti-establishment 5SM rejecting the proposal in a parliament debate yesterday. The FT suggested that the PD and 5SM could still go back to the drawing board in the coming days however so it might not be the last we hear of it. Led by Banks, the FTSE MIB also rallied to the tune of +1.46% yesterday which was in the context of the Stoxx 600 (-0.01%) closing more or less flat.

Back to Asia this morning where inflation reports have also been released in China. Headline CPI for May has nudged up three-tenths to +1.5% yoy, matching market expectations, however PPI slipped a little more than expected to +5.5% yoy (vs. +5.6% expected) from +6.4% in April. That makes it three straight monthly declines in the annual PPI reading although as a reminder that does follow 14 straight months of acceleration.

With regards to the remaining data yesterday, in the US the sole release was the latest weekly initial jobless claims print which came in at 245k and which has left the four-week moving average at a still low 242k. In Europe the main focus was on the final Q1 GDP revision for the Euro area which was revised up onetenth to +0.6% qoq after expectations were for no change. That also saw the annual rate notched up two-tenths to +1.9% yoy and the highest since Q4 2015. Away from that Germany reported a better than expected +0.8% mom uplift in industrial production in April (vs. +0.5% expected). That has lifted annual growth to +2.9% yoy from +2.2%.

Looking at the day ahead, while the fallout from the UK election will no doubt be front and centre, there is also a little bit of data to get through. This morning in Europe we get more hard data points with more industrial production prints due in France and the UK along with trade data out of Germany and also the UK. In the US we are due to receive the wholesale trade report. The EU/NATO Conference is also due today. It’s worth also noting that this Sunday France begins the two-step process to elect a new National Assembly with polls due to close on Sunday evening. The second round is on June 18th

3. ASIAN AFFAIRS

i)Late THURSDAY night/FRIDAY morning: Shanghai closed UP 8.06 POINTS OR 0.26% / /Hang Sang CLOSED DOWN 32.77 POINTS OR 0.13% The Nikkei closed UP 104.00 POINTS OR 0.52%/Australia’s all ordinaires CLOSED UP 0.01%/Chinese yuan (ONSHORE) closed DOWN at 6.7971/Oil UP to 45.70 dollars per barrel for WTI and 47.94 for Brent. Stocks in Europe OPENED MIXED ..Offshore yuan trades 6.7913 yuan to the dollar vs 6.7971 for onshore yuan. NOW THE OFFSHORE IS MUCH WEAKER TO THE ONSHORE YUAN/ ONSHORE YUAN A LITTLE WEAKER (TO THE DOLLAR) AND THE OFFSHORE YUAN IS MUCH WEAKER TO THE DOLLAR AND THIS IS COUPLED WITH THE MUCH STRONGER DOLLAR. CHINA NOT HAPPY WITH THE NEWS THAT ITS DEBT HAS BEEN DOWNGRADED

3a)THAILAND/SOUTH KOREA/NORTH KOREA

i)NORTH KOREA

A little background on those 4 anti ship missiles fired by North Korea. It was a test for precise accuracy and it is alarming to the west

(courtesy Mac Slavo/SHTFPlan)

WW3 Approaches, North Korea Launches 4 Anti-Ship Missiles

MacSlavo

SHTFplan.com

North Korea fired four anti-ship missiles into the sea east of the Korean Peninsula Thursday. The South Korean military said this new test was intended to demonstrate North Korea’s advancements in “precise targeting capability.”

As tensions continue to rise between the United States and the rogue nation of North Korea, the missile tests conducted also continue. This is now Kim Jong-Un’s fourth missile test in one month, as the volatile North Korean dictator continues to balk at the United Nations sanctions against his country. In fact, this is the nation’s first missile test since the UN implemented more, harsher, sanctions on the fascist nation.

South Korea’s joint chiefs said the projectiles, launched near the eastern port city of Wonsan, were believed to be surface-to-ship cruise missiles. “We assess that North Korea intended to show off its various missile capabilities, display its precise targeting capability, in the form of armed protests against ships in regard to US Navy carrier strike groups and joint naval drills,” Roh Jae-cheon, a spokesman for South Korea’s Joint Chiefs of Staffs told reporters.

Analysts say each launch, regardless of its success, improves missile technology for the dictatorship. The tests also ultimately provide information that will bring North Korea closer to its goal of building a missile that could reach the US. The launch comes one day after South Korea’s government suspended the deployment of a controversial US missile defense system which had strained relations with China and angered North Korea.

As North Korea continues to push the limits of it’s neighboring nations and the United States, it certainly seems like WW3 is becoming inevitable.

end

b) REPORT ON JAPAN

c) REPORT ON CHINA

Whenever you see the Chinese 5 year/10 yr invert , then recession is flashing red!! Actually everything is inverting!

(courtesy zerohedge)

“Historic” Chinese Yield Curve Inversion Flashes Recession

A month ago, China 5s10s curve inverted for the first time ever, flashing warning signs of an imminent recession(but technical, liquidity factors were offered as excuses for this shift in the belly of the curve). The curve then double-inverted (with 3s10s inverting) seemingly confirming fundamental fears. And now, China’s yield curve is inverted from 1Y to 10Y for the second time in history.

China’s $1.7 trillion government-bond market is turning curiouser and curiouser…

The yield on China’s one-year government bond climbs 6 basis points to 3.66%, rising above the 10-year yield of 3.65%, ChinaBond data show.

This is only the second time that the yield curve has inverted in data going back to 2006, with the first coming during a record cash crunch in June 2013.

As The Wall Street Journal recently wrote, such a “yield-curve inversion” defies normal market logic that bonds requiring a longer commitment should compensate investors with a higher return. It usually reflects investor pessimism about a country’s long-term growth and inflation prospects.

Perplexed traders and analysts offered up many excuses…

“Many of us are scratching our heads for an explanation because this kind of curve inversion is absolutely not normal,” said Wang Ming, a partner at Shanghai Yaozhi Asset Management Co., a bond fund that manages 2 billion yuan ($289.66 million) in assets.

“The inversion is a form of mispricing in the bond market,” said Liu Dongliang, senior analyst at China Merchants Bank . “The fact that no one is taking the bargain despite the higher yield on the five-year bond just shows how depressed investors’ mood is.”

“It’s really difficult to predict when the selloff or such anomalies will end because China’s bond market is reacting to the regulatory crackdown only and is no longer reflecting economic fundamentals,” said China Merchants Bank’s Mr. Liu.

But of course, the reality is – without massive and continued credit creation, there are very large questions about just how ‘dynamic’ Chinese growth could be and while technical flows are certainly part of the reasoning for short-end yields rising, the question is, why wouldn’t the rest of the world pile in to ‘reach for yield’… unless the fundamentals really did have them worried?

The nature of the inversion (higher yields, higher funding costs, and leverage pressure) is starting to reflexively impact the real economy (and hence the chances of dramatically lower growth/recession), as The FT reportsChinese corporate bond financing hit a record low in May, as a market rout discouraged new issuance while a wave of previously issued notes came due.

The combination of tight liquidity and a regulatory crackdown on leveraged investment in bonds has hammered China’s debt market in recent months.

Net corporate bond financing — new issuances less maturities — totalled negative Rmb217bn ($31bn) in May, well below the previous record low of negative Rmb89bn in February, according to data from Wind Information.

A “regulatory windstorm” led by China’s ambitious new banking regulator, Guo Shuqing, has targeted banks’ use of borrowed money to invest in bonds. The People’s Bank of China has also drained liquidity from the money market, making it more expensive for banks to borrow from each other to fund bond purchases.

“Banks’ demand for bonds has drastically reduced. The shock has been pretty large,” said Xu Hanfei, chief fixed-income analyst at China Merchants Securities in Shanghai. “Pressure has spread from the liabilities side to the asset side,” he said, referring to the impact of higher funding costs on demand for bonds.

“In the context of the increasing financing difficulty for bonds and non-standard (shadow bank) products, issuers of low quality are more severely impacted, and the corresponding credit risks tend to increase,” Haitong chief economist at Jiang Chao wrote this week.

Investors are also nervous about rising credit risk.

According to a survey of investors by Haitong Securities, only 5 per cent of bond investors are “optimistic” about low-rated corporate bonds. Companies cancelled or postponed 400 planned bond sales worth Rmb390bnbn in the year to May, up from Rmb286bn in cancellations a year earlier, according to Wind data.

But apart from that, we are sure everything is fine in the world’s biggest/second-biggest economy.

end

4. EUROPEAN AFFAIRS

UK

Theresa May wins 318 seats and falls short of a majority. She will hook up with the Irish rightwing Democratic Unionist Party to allow her to govern:

(courtesy zerohedge)

Theresa May Says She Will Form A Government With Support Of DUP Party

In a last ditch Hail Mary effort to avoid resignation and new snap elections, Theresa May arrived at Buckingham Palace earlier to meet with the Queen where she will attempt to cling to power by linking her Conservative party with Northern Ireland’s rightwing Democratic Unionist Party (DUP) following the disastrous election that left her short of a governing majority.

As noted earlier, May has reached an understanding with Northern Ireland’s Democratic Unionist Party to form a coalition U.K. Government. With 649 of 650 seats declared, the Conservatives had won 318 seats and Labour 261. 326 seats are needed for majority. The DUP, which took 10 seats, was considering an arrangement which would involve it supporting a Conservative minority government on key votes in parliament but not forming a formal coalition, Sky said.

“If … the Conservative Party has won the most seats and probably the most votes then it will be incumbent on us to ensure that we have that period of stability and that is exactly what we will do,” a grim-faced May said after winning her own parliamentary seat of Maidenhead, near London.

The prime minister is headed back to Downing 10 after meeting with the Queen shortly after midday to seek permission from the Queen to form a new government despite the Tories winning just 318 seats in Thursday’s general election, eight short of the 326 needed to secure a majority on their own. The support of the 10 members of parliament elected for the DUP, the more hardline of the two traditional pro-British parties in Northern Ireland, would put Mrs May just over the threshold to form a government.

According to the FT, the DUP has not agreed formally to join a coalition with the Tories, though such arrangements could be agreed later. Regardless, the deal means Mrs May will govern over a union of highly disparate interests. The Tories’ surprising expansion in Scotland means her new parliamentary party will include several MPs with strong pro-EU credentials, while the DUP is a fierce supporter of departure from the EU — even though Northern Ireland voted to remain.

In addition, she will face fierce resistance from opposition parties at Westminster. Leaders of the three largest, including Labour’s second-place finisher Jeremy Corbyn, all called for her to resign.

Nicola Sturgeon, the Scottish first minister and head of the Scottish National party, said Mrs May had “lost all authority and credibility” while Liberal Democrat leader Tim Farron said she “should be ashamed” and should resign “if she has an ounce of self respect”.

While the DUP is not a perfect match for the Tories ideologically — they are further left on public spending but more hardline on social issues such as gay marriage and abortion — the party is opposed Mr Corbyn, who expressed support for Irish nationalism during the 1980s.

“The two parties have worked well together for two years; there’s no reason to suppose they won’t continue to do so in the future,” said one DUP official. “But the point made time after time to Labour MPs remains: for as long as you allow yourselves to be led by an IRA cheerleader, you exclude yourselves from entering Number 10.”

Upon return to Downing 10, Theresa May said that she will “now form a government” as she seeks to govern with the support of the Northern Irish DUP party. She also adds that Brexit talks will start in 10 days as scheduled.

Earlier in the day, European Union leaders expressed fears that May’s shock loss of her majority would delay the Brexit talks, due to begin on June 19, and so raise the risk of negotiations failing.

As Reuters reported, May’s Labour rival Jeremy Corbyn, once written off by his opponents as a no-hoper, said May should step down and he wanted to form a minority government.

“We need a government that can act,” EU Budget Commissioner Guenther Oettinger told German broadcaster Deutschlandfunk. “With a weak negotiating partner, there’s a danger that the (Brexit) negotiations will turn out badly for both sides.”

The EU’s chief negotiator said the bloc’s stance on Brexit and the timetable for the talks were clear, but the divorce negotiations should only start when Britain is ready. “Let’s put our minds together on striking a deal,” Michel Barnier said.

But there was little sympathy from some other Europeans. “Yet another own goal, after Cameron now May, will make already complex negotiations even more complicated,” tweeted Guy Verhofstadt, the former Belgian premier who is the European Parliament’s point man for the Brexit process.

END

An important lesson for us all. A must read…

(courtesy Simon Black/SovereignMan.com)

This Is How A “Bail-Out” Becomes A “Bail-In”

Authored by Simon Black via SovereignMan.com,

Here’s the perfect example of how insane our financial system has become.

It was announced yesterday that, after a 24-hour white-knuckled ride, Spanish banking giant Banco Popular had been sold to Banco Santander for the price of just 1 euro.

Note- that’s 1 euro in TOTAL. Not 1 euro per share.

Banco Popular had once been one of Spain’s largest banks.

But just as certain banks tend to do from time to time, Popular sacrificed responsibility and good conduct for quick profits.

They spent years gambling their depositors’ savings away on idiotic, dangerous, pitiful loans. And those bad loans eventually came back to bite them.