GOLD: $1215.60 UP $1.50

Silver: $15.78 UP 7 cent(s)

Closing access prices:

Gold $1217.50

silver: $15.87

SHANGHAI GOLD FIX: FIRST FIX 10 15 PM EST (2:15 SHANGHAI LOCAL TIME)

SECOND FIX: 2:15 AM EST (6:15 SHANGHAI LOCAL TIME)

SHANGHAI FIRST GOLD FIX: $1221.84 DOLLARS PER OZ

NY PRICE OF GOLD AT EXACT SAME TIME: $1211.70

PREMIUM FIRST FIX: $10.14

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

SECOND SHANGHAI GOLD FIX: $1222.70

NY GOLD PRICE AT THE EXACT SAME TIME: $1212.20

Premium of Shanghai 2nd fix/NY:$10.80

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

LONDON FIRST GOLD FIX: 5:30 am est $1211.90

NY PRICING AT THE EXACT SAME TIME: $1211.35

LONDON SECOND GOLD FIX 10 AM: $1211.05

NY PRICING AT THE EXACT SAME TIME. $1211.30

For comex gold:

JULY/

NOTICES FILINGS TODAY FOR APRIL CONTRACT MONTH: 1 NOTICE(S) FOR 100 OZ.

TOTAL NOTICES SO FAR: 63 FOR 6300 OZ (.1959 TONNES)

For silver:

JULY

289 NOTICES FILED TODAY FOR

1,445,000 OZ/

Total number of notices filed so far this month: 2612 for 13,060,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

end

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total open interest ROSE BY ONLY 6 contract(s) UP to 207,952 DESPITE THE NICE RISE IN PRICE THAT SILVER TOOK WITH YESTERDAY’S TRADING (UP 28 CENT(S). WE AGAIN MOST HAVE HAD CONTINUAL NEW SPECS GOING SHORT WITH THE COMMERCIALS BOTH COVERING AND ALSO GOING LONG. THE NET EFFECT A TINY GAIN IN OI.

In ounces, the OI is still represented by just OVER 1 BILLION oz i.e. 1.039 BILLION TO BE EXACT or 149% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT MAY MONTH/ THEY FILED: 289 NOTICE(S) FOR 1,445,000 OZ OF SILVER

In gold, the total comex gold ROSE BY 4,372 CONTRACTS WITH THE RISE IN THE PRICE OF GOLD ($3.50 with YESTERDAY’S TRADING). The total gold OI stands at 481,624 contracts.

we had 1 notice(s) filed upon for 100 oz of gold.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD:

Strange!! had a huge changes in tonnes of gold at the GLD/a withdrawal of 2.96 tonnes of gold with gold rises today??

Inventory rests tonight: 832.39 tonnes

.

SLV

Today: STRANGE: AFTER AN EARLY HIT ON SILVER THIS MORNING, WE HAD ANOTHER HUGE RISE IN INVENTORY OF 2.364 MILLION OZ/

INVENTORY RESTS AT 347.026 MILLION OZ

Please note the difference between gold and silver with respect to the GLD and SLV inventory changes

end

.

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in silver ROSE BY 6 contracts UP TO 207,952 (AND now A LITTLE CLOSER FROM THE NEW COMEX RECORD SET ON FRIDAY/APRIL 21/2017 AT 234,787), DESPITE THE NICE RISE IN PRICE FOR SILVER WITH YESTERDAY’S TRADING (UP 28 CENTS ).We SEEM TO HAVE LOST NOBODY AS EVERYBODY remains firm and determined.

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)Late MONDAY night/TUESDAY morning: Shanghai closed DOWN 9.59 POINTS OR 0.30% / /Hang Sang CLOSED UP 377.58 POINTS OR 1.48% The Nikkei closed UP 114.50 POINTS OR 0.57%/Australia’s all ordinaires CLOSED UP 0.10%/Chinese yuan (ONSHORE) closed UP at 6.8015/Oil DOWN to 43.91 dollars per barrel for WTI and 46.36 for Brent. Stocks in Europe OPENED RED,, Offshore yuan trades 6.8055 yuan to the dollar vs 6.8015 for onshore yuan. NOW THE OFFSHORE IS A TOUCH WEAKER TO THE ONSHORE YUAN/ ONSHORE YUAN STRONGER (TO THE DOLLAR) AND THE OFFSHORE YUAN IS WEAKER TO THE DOLLAR AND THIS IS COUPLED WITH THE STRONGER DOLLAR. CHINA IS NOT HAPPY TODAY

3a)THAILAND/SOUTH KOREA/NORTH KOREA

i)NORTH KOREA

b) REPORT ON JAPAN

c) REPORT ON CHINA

More regulation and tighter money has now put an end to China’s second housing bubble. The first bubble burst in 2014 and now the second seems to have blown this market again

( Valentin Schmid/EpochTimes)

4. EUROPEAN AFFAIRS

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

Russia’s patience with Trump has run out: Russia is not set to expel 30 USA diplomats and seize USA assets in Russia

( zero hedge)

6 .GLOBAL ISSUES

7. OIL ISSUES

I)Goldman Sachs warns that oil could plunge below 40 dollars per barrel. The reasons are obvious as increasing supply from all avenues are just too great to handle the decreasing demand for oil

( zero hedge/Goldman Sachs)

ii)Down goes WTI back into the 43 dollar handle with news that the Saudis have breached their own OPEC agreement:

( zero hedge)

iii)Geopolitical events may cause the oversupply to under supply which could force oil to over 120 dollars per barrel.

(Nick Cunningham/OilPrice.com)

8. EMERGING MARKET

Sugar utopia in Venezuela

( zero hedge)

9. PHYSICAL MARKETS

i)Seems that we may be having a civil war between two computer factions in Bitcoin and that is sending crypto currencies spiraling southbound. The world is latching onto the ABX crypto system which is fully backed by gold and silver.

( zero hedge)

ii)A must read..the flash crash in silver was 100% orchestrated by government. That is why the regulators refused to investigate the raid

( zero hedge)

iii)The new LME contract sees a lackluster launch due to the fact that the gold is unallocated. The world is moving to the ABX system backed by real metal.

( zero hedge)

iv)Lynn Fisher correctly states that the flash crash in silver (twice) was meant to scare investors away from the precious metals and to hold only fiat. It is not working: gold and silver are deeply in backwardation in the physical markets in London

( zero hedge)

v)Jim Sinclair is not at all bothered by the actions of Tanzania. The government wants its fair share of the revenue

( GATA/Tanzania Royalty)

vi)A must listen to audio from Andrew Maguire taped last week:

( Kingworldnews/Andrew Maguire

10. USA Stories

i)Soaring premiums has now resulted in at least 2 million Americans ditching their health coverage. The biggest group of course is the 18 to 34 yr old group as there is really no need for them to fund the aging population

( zero hedge)

ii)Not good: wholesale inventories rise but wholesales sales tumble for the third straight month as unsold inventories climb:

this will be a negative to GDP

( zero hedge)

( zero hedge)

iv)Senate Republicans have canceled their first two weeks of their August recess to work on legislation. They still will not come up with anything

( zerohedge)

v)A good commentary tonight from Dave Kranzler of IRD: it is not just Illinois that is on the brink..it is the whole country

( Dave Kranzler/IRD)

Let us head over to the comex:

The total gold comex open interest ROSE BY 4,372 CONTRACTS up to an OI level of 479,667 WITH THE RISE IN THE PRICE OF GOLD ($3.50 with YESTERDAY’S trading). An open interest of around 390,000 to 400,000 is core and nothing will move these guys from their contracts. it sure looks like the supplier of the comex gold paper are the specs, and the purchasers going long are the commercials.

We are now in the contract month of JULY and it is one of the POORER delivery months of the year. .

The non active July contract LOST 5 contract(s) to stand at 79 contracts. We had only 1 notices filed YESTERDAY morning, so we LOST 4 contracts or an additional 40o oz that will NOT stand in this non active month of July. Thus 4 EFP notices were given which gives the long holder a fiat bonus plus a futures contract for delivery and most likely these are London based forwards. The contracts are private so we do not get to see all the particulars. The next big active month is August and here the OI LOST 9571 contracts DOWN to 272,047, as the bankers trying to keep this month down to manageable size. The next non active contract month is September and here they LOST another 26 contracts to stand at 430. The next active delivery month is October and here we gained 1343 contracts up to 20,033. October is the poorest of the active gold delivery months as most players move right to December.

We had 1 notice(s) filed upon today for 300 oz

For those keeping score: in the upcoming front delivery month of August:

On July 11.2016: open interest for the front month: 415,860 contracts compared to July 11.2017: 272,947.

However last yr at this time we had a record OI in gold at 655,000 contract for the entire complex.

We are now in the next big active month will be July and here the OI GAINED 135 contracts UP to 405. We had 61 notices served yesterday so we gained 196 notices or an additional 980,000 oz will stand at the comex, and 0 EFP contracts were issued which entitles them to receive a fiat bonus and a future delivery contract (which no doubt is a London based forward).

The month of August, a non active month gained 43 contracts to stand at 725. The next big active delivery month for silver will be September and here the OI already LOST ANOTHER 501 contracts DOWN to 157,626.

The line in the sand is $18.50 for silver and again it has been defended by the criminal bankers. Once this level is pierced, the monstrous billion oz of silver shorts will blow up. The bankers are defending the Alamo with their last stand at the $18.50 mark. THE NEW RECORD HIGH IN OPEN INTEREST WAS SET FRIDAY APRIL 21/2017 AT: 234,787.

As for the July contracts:

Initial amount that stood for silver for the July 2016 contract: 14.785 million oz

Final standing JULY 2016: 12.370 million with the difference being EFP’s taking delivery in London. Thus we are basically on par to what happened a year ago as to the total amount of silver ounces standing.

We had 292 notice(s) filed for 1445,000 oz for the June 2017 contract

VOLUMES: for the gold comex

Today the estimated volume was 94,993 contracts which is POOR/

Yesterday’s confirmed volume was 281,526 contracts which is excellent

volumes on gold are STILL HIGHER THAN NORMAL!

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz |

12.344/488 oz

Brinks

Delaware

|

| Deposits to the Dealer Inventory in oz | NIL oz |

| Deposits to the Customer Inventory, in oz |

NIL oz

|

| No of oz served (contracts) today |

1 notice(s)

100 OZ

|

| No of oz to be served (notices) |

78 contracts

7800 oz

|

| Total monthly oz gold served (contracts) so far this month |

63 notices

6300 oz

.1959 tonnes

|

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | 15,521.900 oz |

ii) Out of Delaware: 101.91 oz

Today, 0 notice(s) were issued from JPMorgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equates to 1 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped/ Received) by j.P.Morgan customer account.

| Silver | Ounces |

| Withdrawals from Dealers Inventory | nil |

| Withdrawals from Customer Inventory |

20,013.82 oz

HSBC

|

| Deposits to the Dealer Inventory |

nil oz

|

| Deposits to the Customer Inventory |

1,202,404.09 oz CNT

Delaware

JPMorgan

|

| No of oz served today (contracts) |

292 CONTRACT(S)

(1,445,000 OZ)

|

| No of oz to be served (notices) |

113 contracts

( 565,000 oz)

|

| Total monthly oz silver served (contracts) | 2612 contracts (13,060,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month | 512,483.4 oz |

NPV for Sprott and Central Fund of Canada

Sprott’s hostile 3.1 billion bid to take over Central Fund of Canada

(courtesy Sprott/GATA)

Sprott makes hostile $3.1 billion bid for Central Fund of Canada

Submitted by cpowell on Thu, 2017-03-09 01:19. Section: Daily Dispatches

From the Canadian Press

via Canadian Broadcasting Corp. News, Toronto

Wednesday, March 8, 2017

http://www.cbc.ca/news/canada/calgary/sprott-takeover-bid-central-fund-c…

Toronto-based Sprott Inc. said Wednesday it’s making an all-share hostile takeover bid worth $3.1 billion US for rival bullion holder Central Fund of Canada Ltd.

The money-management firm has filed an application with the Court of Queen’s Bench of Alberta seeking to allow shareholders of Calgary-based Central Fund to swap their shares for ones in a newly-formed trust that would be substantially similar to Sprott’s existing precious metal holding entities.

The company is going through the courts after its efforts to strike a friendly deal were rebuffed by the Spicer family that controls Central Fund, said Sprott spokesman Glen Williams.

“They weren’t interested in having those discussions,” Williams said.

Sprott is using the courts to try to give holders of the 252 million non-voting class A shares a say in takeover bids, which Central Fund explicitly states they have no right to participate in. That voting right is reserved for the 40,000 common shares outstanding, which the family of J.C. Stefan Spicer, chairman and CEO of Central Fund, control.

If successful through the courts, Sprott would then need the support of two-thirds of shareholder votes to close the takeover deal, but there’s no guarantee they will make it that far.

“It is unusual to go this route,” said Williams. “There’s no specific precedent where this has worked.”

Sprott did have success last year in taking over Central GoldTrust, a similar fund that was controlled by the Spicer family, after securing support from more than 96 percent of shareholder votes cast.

The firm says Central Fund’s shares are trading at a discount to net asset value and a takeover by Sprott could unlock US$304 million in shareholder value.

Central Fund did not have any immediate comment on the unsolicited offer. Williams said Sprott had not yet heard from Central Fund on the proposal but that some shareholders had already contacted them to voice their support.

Sprott’s existing precious metal holding companies are designed to allow investors to own gold and other metals without having to worry about taking care of the physical bullion.

end

And now the Gold inventory at the GLD

July 11/strange!@! we had a big withdrawal of 2.96 tonnes despite gold’s advance today/inventory rests tonight at 832.39 tonnes

July 10/no changes in gold inventory at the GLD/inventory rests at 835.35 tonnes

July 7/a massive withdrawal of 5.32 tonnes of paper gold were removed and this was used in the attack today/inventory rests at 835.35 tonnes

July 6/no changes in tonnage at the GLD/Inventory rests at 840.67 tonnes

July 5/A MASSIVE 5.62 TONNES OF GOLD LEFT THE GLD AND NO DOUBT WAS USED IN THE RAID THIS MORNING/INVENTORY REST

July 3/ A MASSIVE 7.37 TONNES OF GOLD LEAVE THE GLD/INVENTORY RESTS AT 846.29 TONNES

June 30/no change in gold inventory at the GLD/Inventory rests at 853.66 tonnes

June 29/no change in inventory at the GLD/inventory rests at 853.66 tonnes

June 28/no change in inventory at the GLD/Inventory rests at 853.66 tonnes

June 27.2017/a deposit of 2.64 tonnes into the GLD/inventory rests at 853.66 tonnes

June 26/a withdrawal of 2.66 tonnes from the GLD and this gold no doubt was part of the raid/Inventory rests at 851.02

June 23/no change in gold inventory at the GLD/Inventory rests at 853.68 tonnes

June 22/no change in gold inventory at the GLD/Inventory rests at 853.68 tonnes

June 21/no change in gold inventory at the GLD/Inventory rests at 853.68 tonnes

June 20/no change in gold inventory at the GLD//Inventory rests at 853.68 tonnes

June 19/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 853.68 TONNES

June 16/no changes in gold inventory at the GLD/Inventory rests at 853.68 tonnes

June 15/ a monstrous “paper” withdrawal of 13.32 tonnes/Inventory rests at 853.68 tonnes

June 14./NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 867.00 TONNES

June 13. No change in gold inventory at the GLD/Inventory rests at 867.00 tonnes

June 12/No change in gold inventory at the GLD/Inventory rests at 867.00 tonnes

June 9/no change in inventory at the GLD/Inventory rests at 867.00 tonnes

June 8/AN ADDITION OF 3.07 TONNES OF GOLD ADDED TO THE GLD/INVENTORY RESTS AT 867.00 TONNES

June 7 a huge change in inventory/a deposit of 13.93 tonnes/inventory rests at 864.93 tonnes

June 6/ no changes in inventory at the GLD/Inventory remains at 851.00 tonnes

June 5.2017/no changes at the GLD/Inventory remain at 851.00 tonnes

June 2/2017/a huge deposit of 3.55 tonnes of gold into the GLD/Inventory rests at 851.00 tonnes

June 1/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 847.45 TONNES

end

Now the SLV Inventory

July 11/ANOTHER MASSIVE INCREASE OF 2.364 MILLION OZ into the SLV inventory/inventory rests at 347.026 million oz

July 10/ A HUGE INCREASE OF 2.931 MILLION OZ OF SILVER DESPITE THE EARLY HIT ON SILVER THIS MORNING/INVENTORY RESTS AT 344.662 MILLION OZ.

July 7/Strange: no change in inventory (compare that with gold) Inventory rests at 341.731 million oz

July 6/ANOTHER MASSIVE DEPOSIT OF 2.126 MILLION OZ INTO THE SLV INVENTORY/INVENTORY RESTS AT 341.731 MILLION OZ.

July 5/STRANGE! NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 339.605 MILLION OZ

July 3/strange! with the huge whacking of silver we got an increase of 379,000 oz into inventory.

June 30/no change in silver inventory at the SLV/Inventory rests at 339.226 million oz

June 29/no change in silver inventory at the SLV/Inventory rests at 339.226 million oz/

June 28/ a small withdrawal of 662,000 oz form the SLV/Inventory rests at 339.226 million oz/

June 27/no change in the silver inventory at the SLV/Inventory rests at 339.888 million oz/

June 26/no change in the silver inventory at the SLV/Inventory rests at 339.888 million oz/

June 23/no change in silver inventory at the SLV/Inventory rests at 339.888 million oz

June 22/ a big change; a huge deposit of 2.175 million oz into the SLV/Inventory rests at 339.888 million oz

June 21/no change in silver inventory at the SLV/inventory rests at 337.713 million oz

June 20/a deposit of 1.513 million oz/inventory rests at 337.713 million oz/.

June 19/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 336.200 MILLION OZ

June 16/no changes in inventory at the SLV/inventory rests at 336.200 million oz

June 15/ a massive “paper withdrawal” of 3.405 million oz of silver/Inventory rests at 336.200 million oz/

June 14/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 339.605 MILLION OZ/

June 13/no change in silver inventory at the SLV/Inventory rests at 339.605 million oz

June 12/no change in silver inventory at the SLV/Inventory rests at 339.605 million oz/

June 9/no change in silver inventory at the SLV/Inventory rests at 339.605 million oz/

June 8/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 339.605 MILLION OZ/

June 7/no change in inventory at the SLV/inventory rests at 339.605 million oz/

June 6/no change in inventory at the SLV/Inventory rests at 339.605 million oz.

June 5/a huge change at the SLV/a withdrawal of 1.371 million oz /inventory rests at 339.605 million oz/

June 2/no change in silver inventory at the SLV/Inventory rests at 340.976 million oz/

June 1/NO CHANGE IN INVENTORY AT THE SLV/INVENTORY RESTS AT 340.976 MILLION OZ

-

Indicative gold forward offer rate for a 6 month duration+ 1.12%

Indicative gold forward offer rate for a 6 month duration+ 1.12% -

+ 1.42%

end

Major gold/silver trading/commentaries for TUESDAY

GOLDCORE/BLOG/MARK O’BYRNE.

GOLD/SILVER

“Silver’s Plunge Is Nearing Completion”

“Silver’s Plunge Is Nearing Completion”

– Silver’s plunge is nearing completion – Bloomberg analyst

– Silver’s 10% sharp fall in seconds remains “mystery”

– Plunge despite anemic global supply and strong demand

– Total silver supply declined in ’16 – lowest level since ’13

– Silver mine production down in ’16, first time in 14 years

– Total silver supply decreased by 32.6 Mln Ozs in 2016

– Supply deficit in 2016- fourth consecutive year (see table)

– “Falling knife” caution but opportunity presenting itself

Silver has had a torrid time of late with a the “flash crash” seeing a massive $450 million silver futures sell order pushing silver 10% lower in seconds and follow through selling later Friday after the better than expected U.S. jobs number.

Silver has had a torrid time of late with a the “flash crash” seeing a massive $450 million silver futures sell order pushing silver 10% lower in seconds and follow through selling later Friday after the better than expected U.S. jobs number.

The electronic futures silver and gold exchanges continue to ‘wag the dog’ of the global silver and gold markets … for now.

If one had just looked at the short-term trends of silver at the end of 2016, you would have thought we would be mad to predict that 2017 would be a bearish year.

At the time it appeared as though silver was in a new bull market and in the early months of 2017 the price climbed by around 9%. But since April silver has handed back its gains and some and it is now down 3% for the year.

This has been counter intuitive to gold and silver investors alike who are looking at an economy filled with macroeconomic, geopolitical and indeed monetary uncertainty and central banks who appear increasingly fallible as the months go on.

Some were left wondering how much lower silver could go when last Wednesday it fell through the important $16 level for the first time in 2017.

In addition, the silver price weakness was given an extra push two days later when it collapsed by 10% in a matter of seconds. The reasons why this happened are still unknown, if it was a mistake then no-one is owning up to it and if it was a result of a desire to shift off $450 million worth of silver futures in minute then we will never know.

But their might be a (silver-powered) light at the end of the tunnel. Some silver market and industry experts are forecasting the silver plunge to be coming to an end.

A justified plunge ended by global yields

Bloomberg’s Michael Cudmore believes that the plunge in silver was justified

‘Gold and silver have a particularly strong correlation with real rates since the metals provide no yield, and hence demand is inversely related to the opportunity cost of speculation.

An environment in which global bond yields are rising in the absence of significant inflationary pressures is about as bad as it gets for speculative precious metals, so the move makes sense.’

But, Cudmore argues, it won’t stay like this forever.

‘If the rise in global yields persists, then severe spillover effects in other asset markets could prompt a bid for precious metal havens again. So we are approaching the point where both higher yields and lower yields have the potential to boost the asset class.’

New diversified industrial demand

But for many investors, talk of very short term yield hikes are about as handy as a wet finger in the air. Is the picture still as bullish when you look at the basic fundamentals of physical silver demand and silver supply?

According to the Silver Institute around 55% of all silver consumed is for industrial use. The remainder is taken up by jewellery, coin, bullion and silverware. As a result of this dual demand, one can understandably get distracted by figures that suggest investment demand is down and therefore the price outlook is bearish.

But, on the other side of the demand coin things are not only looking positive but the face of industrial demand for silver is also changing. This is an indicator of a market which is able to be agile in the face of changing times. Something which cannot be said for other markets so involved in technology.

Bearish commentators like to refer to the falling in use for silver in the field of photography, once a big source of demand. However, the Silver Institute remind us that this has been the case for many years and is unlikely to be impacting upon demand figures now,

‘Photographic demand fell by just 3 percent in 2016 to 45.2 Moz, representing the lowest percentage decline since 2004, potentially indicating that the bulk of structural change in the photography market is over and that current fabrication volumes may be largely sustainable.’

In the meantime, bears would be wise to remember that there are several other applications for industrial silver and they are growing.

In the 2017 silver survey data showed new highs were recorded for silver’s growing use in the photovoltaic (solar energy) and ethylene oxide (essential ingredients in plastics) sectors. These are two major and growing sectors for industrial silver.

By way of example, photovoltaic demand climbed by another 34% in 2016, the strongest growth in six years thanks to a 49% increase in demand for solar panels. In all it appears that the physical demand for industrial use silver is still at a strong level.

Declining supply?

As readers know silver has a dual role: it is a precious metal and an industrial one. This means that when one might expect it to react to monetary events such as a rate hike, it doesn’t because other factors are also at the forefront of traders’ minds.

For silver the weak performance of both gold and base metals in the last few months has weighed down on the price, an almost double whammy if you will.

In 2016 the total demand for silver decreased marginally to 1.028 billion ounces, but declining supply meant that importantly 2016 was the fourth consecutive year with a supply deficit.

Scrap supply has been falling for some time and posted its lowest level since 1996. Meanwhile in 2016 global silver mine production recorded its first decline since 2002. When added to declining silver scrap supply and a contraction in producer hedging, total silver supply decreased by 32.6 million ounces last year.

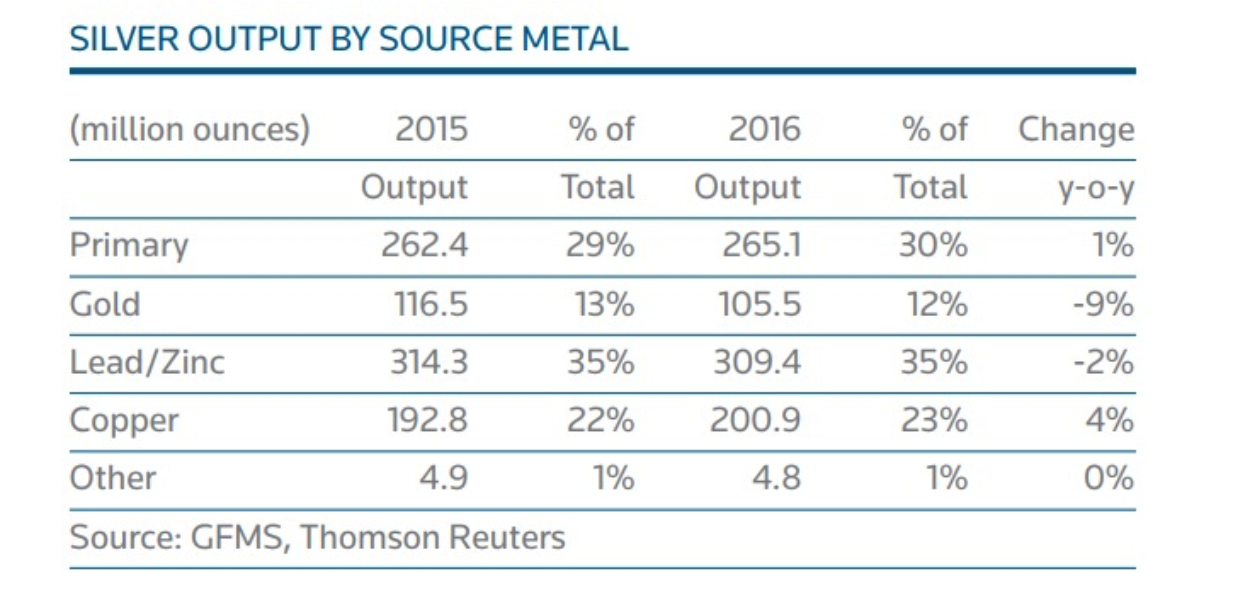

It does not appear as though the mining figures are set to improve. The Silver Survey 2017 report shows that the total silver mined in 2016 fell by 0.6% to 885.8 million oz. A large proportion of the drop was attributable to the lower output from the lead, zinc and gold sectors.

According to the Silver Institute 2017 survey, only 30% of the mined silver comes from mines whose primary metal is silver. 12% comes from primary gold mines and 23% is mined as part of primary copper deposit.

Given current gold and copper prices, it is not impossible to imagine further pressure on silver’s supply side given very few new mines will be developed in the current price environment.

“Falling knife” caution but buying opportunity presenting itself

The commentary space has generally been quiet about the price of silver. Instead, the behaviour of gold in relation to the geopolitical sphere has been the main topic of interest.

However, we appear to be close to a bottom in silver. This is in relation to both very positive supply demand fundamentals but also the likelihood of continuing robust investment demand as evidenced in robust silver ETF holdings.

In the short term, no one really knows where the price is headed to and silver looks vulnerable to further selling in the very short term.

During similar price falls over the years we have warned not to “catch a falling knife” on many occasions and this was echoed by Cudmore in his Bloomberg piece (on the terminal) as published on Zero Hedge.

However, one thing is for sure, silver remains great value given the still very strong fundamentals and when compared to valuations in stock and bond markets.

Silver and gold buyers should use the most recent bout of “mystery” selling as an opportunity to stack up on silver coins and bars in order to get long term exposure and financial insurance at short-term, discounted prices.

News and Commentary

Gold inches lower as market awaits rate hike cues (Reuters.com)

Gold, Silver Stable After Recent Beatdown (LSE.co.uk)

U.S. Stocks Rise on Tech Bounce, Commodities Gain (Bloomberg.com)

LME launches bid for slice of $5 trillion London gold market (Reuters.com)

U.S. ready for unilateral sanctions against North Korea (MarketWatch.com)

Exclusive: Aztec golden wolf sacrifice yields rich trove in Mexico City (Reuters.com)

Why One Trader Thinks “Silver’s Plunge Is Nearing Completion” (ZeroHedge.com)

Silver Flash-Crash – “There’s No Such Thing As A Bad Tick” (ZeroHedge.com)

Recent gold decline means cusp of move higher (AveryBGoodMan.com)

Deutsche Bundesbank gold reserves shrink 45 tons over the past ten years (SmaulGLD.com)

Bankers’ Endgame and the Rise of Gold and Silver (GoldSeek.com)

Gold Prices (LBMA AM)

11 Jul: USD 1,211.90, GBP 938.98 & EUR 1,063.68 per ounce

10 Jul: USD 1,207.55, GBP 938.63 & EUR 1,060.11 per ounce

07 Jul: USD 1,220.40, GBP 944.47 & EUR 1,068.95 per ounce

06 Jul: USD 1,224.30, GBP 946.14 & EUR 1,077.51 per ounce

05 Jul: USD 1,221.90, GBP 945.87 & EUR 1,078.45 per ounce

04 Jul: USD 1,224.25, GBP 947.32 & EUR 1,078.81 per ounce

03 Jul: USD 1,235.20, GBP 952.09 & EUR 1,085.00 per ounce

Silver Prices (LBMA)

11 Jul: USD 15.51, GBP 12.02 & EUR 13.61 per ounce

10 Jul: USD 15.22, GBP 11.82 & EUR 13.36 per ounce

07 Jul: USD 15.84, GBP 12.29 & EUR 13.88 per ounce

06 Jul: USD 16.01, GBP 12.36 & EUR 14.09 per ounce

05 Jul: USD 15.95, GBP 12.36 & EUR 14.09 per ounce

04 Jul: USD 16.15, GBP 12.48 & EUR 14.23 per ounce

03 Jul: USD 16.48, GBP 12.72 & EUR 14.49 per ounce

Recent Market Updates

– China, Russia Alliance Deepens Against American Overstretch

– Silver Prices Bounce Higher After Futures Manipulated 7% Lower In Minute

– Precious Metals Are “Best Defence” Against Bail-ins In Economic Crisis

– Buy Gold Near $1,200 “As Insurance” – UBS Wealth

– UK House Prices ‘On Brink’ Of Massive 40% Collapse

– Gold Up 8% In First Half 2017; Builds On 8.5% Gain In 2016

– Pensions Timebomb In America – “National Crisis” Cometh

– London Property Bubble Bursting? UK In Unchartered Territory On Brexit and Election Mess

– Shrinkflation – Real Inflation Much Higher Than Reported

– Goldman, Citi Turn Positive On Gold – Despite “Mysterious” Flash Crash

– Worst Crash In Our Lifetime Coming – Jim Rogers

– Go for Gold – Win a beautiful Gold Sovereign coin

– Only Gold Lasts Forever

end

Seems that we may be having a civil war between two computer factions in Bitcoin and that is sending crypto currencies spiraling southbound. The world is latching onto the ABX crypto system which is fully backed by gold and silver.

(courtesy zero hedge)

Looming Crypto ‘Civil War’ Sends Virtual Currencies Crashing, Ethereum Below $200

Chaos is back in cryptocurrencies with both Ethereum and Bitcoin collapsing in the last few hours as it appears concerns over the so-called ‘Bitcoin civil war’ are coming to a head.

As Bloomberg reports, it’s time for bitcoin traders to batten down the hatches.

The notoriously volatile cryptocurrency, whose 160 percent surge this year has captivated everyone from Wall Street bankers to Chinese grandmothers, could be headed for one of its most turbulent stretches yet.

Blame the bitcoin civil war. After two years of largely behind-the-scenes bickering, rival factions of computer whizzes who play key roles in bitcoin’s upkeep are poised to adopt two competing software updates at the end of the month. That has raised the possibility that bitcoin will split in two, an unprecedented event that would send shockwaves through the $41 billion market.

While both sides have big incentives to reach a consensus, bitcoin’s lack of a central authority has made compromise difficult. Even professional traders who’ve followed the dispute’s twists and turns aren’t sure how it will all pan out. Their advice: brace for volatility and be ready to act fast once a clear outcome emerges.

“It’s a high-stakes game of chicken,” said Arthur Hayes, a former market maker at Citigroup Inc. who now runs BitMEX, a bitcoin derivatives venue in Hong Kong. “If you’re a trader, there’s a lot of uncertainty as to what happens. Once there’s a definitive signal about what will be done, the price could move very quickly.”

All the largest market cap coins are getting slammed…

Ethereum plunged to as low as $189 before ripping back above $200…

Aside from Ether’s flash-crash, these are the lowest levels since May…

Bitcoin was battered below $2300 – its lowest since June 15th…

Bloomberg points out that behind the conflict is an ideological split about bitcoin’s rightful identity…

The community has bitterly argued whether the cryptocurrency should evolve to appeal to mainstream corporations and become more attractive to traditional capital, or fortify its position as a libertarian beacon;whether it should act more as an asset like gold, or as a payment system.

The seeds of the debate were planted years ago: To protect from cyber attacks, bitcoin by design caps the amount of information on its network, called the blockchain. That puts a ceiling on how many transactions it can process — the so-called block size limit — just as the currency’s growing popularity is boosting activity. As a result, transaction times and processing fees have soared to record levels this year, curtailing bitcoin’s ability to process payments with the same efficiency as services like Visa Inc.

To address this problem, two main schools of thought emerged.

- On one side are miners, who deploy costly computers to verify transactions and act as the backbone of the blockchain. They’re proposing a straightforward increase to the block size limit.

- On the other is Core, a group of developers instrumental in upholding bitcoin’s bug-proof software. They insist that to ease blockchain’s traffic jam, some of its data must be managed outside the main network. They claim that not only would it reduce congestion, but also allow other projects including smart contracts to be built on top of bitcoin.

But moving data off the blockchain effectively diminishes the influence of miners, the majority of whom are based in China and who have invested millions on giant server farms. Not surprisingly, Core’s proposal, called SegWit, has garnered resistance from miners, the most vocal being Wu Jihan, co-founder of the world’s largest mining organization Antpool.

“SegWit is itself a great technology, but the reason it hasn’t taken off is because its interest doesn’t align with miners,” Wu said.

Still, after previous counter-proposals championed by Wu fell through, miners last month agreed to compromise and support SegWit, in exchange for increasing the block size. Wu says the plan will alleviate short-to-medium term congestion and give Core enough time to flesh out a long-term solution. That proposal is what is known as SegWit2x, which implements SegWit and doubles the block size limit.

“You can think of the SegWit2x proposal as an olive branch,” said Wu.

Support for SegWit2x has reached levels unseen for previous solutions. About 85 percent of miners have signaled they are willing to run the software once it’s released on July 21, and some of bitcoin’s largest companies have also jumped on board. The unprecedented level of endorsement is partly prompted by anxiety of bitcoin losing its dominant status to ethereum, a newer cryptocurrency whose popularity has soared thanks to its ability to run smart contracts and its more corporate-friendly approach.

Below is an outline of the main events that could unify or divide bitcoin:

By July 21: SegWit2x software is released and supporters begin using it.

July 21 to July 31: The community monitors how many miners deploy SegWit2x:

If more than 80 percent deploy it consistently, that should signal community-wide adoption of SegWit and the avoidance of a split, at least for now.

But if a majority do not deploy, expect anxiety within the community to grow as the focus shifts to the Aug. 1 deadline.

Aug. 1: UASF is deployed by its supporters, who begin checking if bitcoin transactions are compliant with SegWit.

If a majority of miners still do not deploy SegWit2x or otherwise accept SegWit, and if UASF supporters do not back down, then two versions of bitcoin’s blockchain could come into existence: a UASF-backed one where only SegWit transactions are recognized, and another where all trades — SegWit and non-SegWit — are recognized.

If a split occurs, bitcoin will likely begin existing on both blockchains in parallel, resulting in two versions of the cryptocurrency. Expect traders to quickly re-price the value of both, likely leading to massive volatility.

“It’s moderates versus extremists,” said Atlanta-based Stephen Pair, chief executive officer of BitPay, one of the world’s largest bitcoin wallets. “It depends on how much a person values the majority of people staying on one chain at least for a little while longer, versus splitting and allowing each pursuing their own vision for scaling.”

As a reminder, investing legend Michgael Novogratz recently noted, that he’s looking to add more ether if it falls between $200 and $150… and more bitcoin if it falls to $2,000.

end

A must read..the flash crash in silver was 100% orchestrated by government. That is why the regulators refused to investigate the raid

(courtesy zero hedge)

Last week’s flash crash in silver was a government operation, Turk tells KWN

Submitted by cpowell on Mon, 2017-07-10 17:02. Section: Daily Dispatches

1p ET Monday, July 10, 2017

Dear Friend of GATA and Gold:

Last week’s flash crash in silver was obviously a government operation, which is why market regulators have declined to track down its perpetrators, though they easily could do so, GoldMoney founder and GATA consultant James Turk tells King World News today.

Turk adds: “Why did this last so-called flash crash happen to occur the moment Tokyo opened? The timing was purposefully chosen. It was all paper. No physical metal traded. The manipulators couldn’t risk starting a flash crash during normal market hours when the physical market is trading because they did not want the risk of having to fill orders from buyers of physical metal during the flash crash. Whenever the manipulators fill orders, the risk is that they reduce their available inventory of physical metal.”

The objective of these flash crashes, Turk says, is to scare investors away from the monetary metals.

Turk’s interview is excerpted at KWN here:

http://kingworldnews.com/james-turk-this-is-the-real-reason-the-governme…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

The new LME contract sees a lackluster launch due to the fact that the gold is unallocated. The world is moving to the ABX system backed by real metal.

(courtesy zero hedge)

New LME gold contract sees lackluster launch

Submitted by cpowell on Mon, 2017-07-10 18:21. Section: Daily Dispatches

By Henry Sanderson

Financial Times, London

Monday, July 10, 2017

An attempt by the London Metal Exchange and a group of banks including Goldman Sachs to grab a chunk of London’s $5 trillion-a-year gold market through a new futures contract got off to a lacklustre start today.

A total of $56 million worth of the yellow metal changed hands on the launch day, compared with $24 billion in the most active Comex gold futures contract in the United States, as the London Metals Exchange has yet to attract the big bullion banks JPMorgan and HSBC.

The two banks are supporting a rival initiative backed by the London Bullion Market Association to improve transparency following pressure from regulators. …

… For the remainder of the report:

https://www.ft.com/content/cfbd9b16-6554-11e7-8526-7b38dcaef614

end

Lynn Fisher correctly states that the flash crash in silver (twice) was meant to scare investors away from the precious metals and to hold only fiat. It is not working: gold and silver are deeply in backwardation in the physical markets in London

(courtesy zero hedge)

Lynn Fisher: Flash crash in silver was meant to scare investors

Submitted by cpowell on Mon, 2017-07-10 18:41. Section: Daily Dispatches

2:45p ET Monday, July 10, 2017

Dear Friend of GATA and Gold:

Lynn Fisher of Fisher Precious Metals in Deerfield Beach, Florida, writes today that last week’s flash crash in silver was clearly manipulation arising from the desperation of governments to discourage investment in the monetary metals. Fisher adds that “the bullion banks would not be cycling out of massive numbers of short positions if they thought the price was going to go down significantly.” Her commentary is headlined “Ongoing Flash Crash Speculation” and it’s posted at the company’s internet site here:

https://fisherpreciousmetals.com/ongoing-flash-crash-speculation/

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

Jim Sinclair is not at all bothered by the actions of Tanzania. The government wants its fair share of the revenue

(courtesy GATA/Tanzania Royalty)

Tanzania’s demands of mining industry don’t bother Sinclair

Submitted by cpowell on Tue, 2017-07-11 01:17. Section: Daily Dispatches

9:20p ET Monday, July 10, 2017

Dear Friend of GATA and Gold:

Tanzania’s demand for a greater share of revenue from mining operations in the country is causing alarm throughout the industry but it doesn’t bother Tanzanian Royalty Exploration Corp. and its executive chairman, James E. Sinclair.

In a statement last week Sinclair said: “The proposed changes appear to be an action to gain a fair share of the financial rewards for the people and nation of Tanzania while still providing incentives to the investors. The proposed legislation is not nationalization.”

Sinclair noted that his company already has granted a 45-percent interest to Tanzania’s state mining company.

Tanzania Royalty Exploration’s statement is posted at its internet site here:

http://www.tanzanianroyalty.com/wp-content/uploads/2017/07/170705TNXNR.p…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

A must listen to audio from Andrew Maguire taped last week:

(courtesy Kingworldnews/Andrew Maguire

KWN has also released the extremely important and timely audio interview with London metals trader Andrew Maguire and you can listen to it by CLICKING HERE OR ON THE IMAGE BELOW.

Your early TUESDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight

1 Chinese yuan vs USA dollar/yuan STRONGER 6.8015(REVALUATION NORTHBOUND /OFFSHORE YUAN MOVES WEAKER TO ONSHORE AT 6.8044/ Shanghai bourse CLOSED DOWN 9.59 POINTS OR 0.30% / HANG SANG CLOSED UP 377.58 POINTS OR 1.48%

2. Nikkei closed UP 114.50 POINTS OR 0.57% /USA: YEN RISES TO 114.34

3. Europe stocks OPENED MIXED TO RED ( /USA dollar index RISES TO 96.11/Euro UP to 1.1397

3b Japan 10 year bond yield: RISES TO +.096%/ GOVERNMENT INTERVENTION !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 114.34/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD FINALLY IN THE POSITIVE/BANK OF JAPAN LOSING CONTROL OF THEIR YIELD CURVE AS THEY PURCHASE ALL BONDS TO GET TO ZERO RATE!!

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 43.91 and Brent: 46.36

3f Gold DOWN/Yen DOWN

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil DOWN for WTI and DOWN for Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund RISES TO +.552%/Italian 10 yr bond yield UP to 2.30%

3j Greek 10 year bond yield FALLS to : 5.399???

3k Gold at $1210.05 silver at:15.53 (8:15 am est) SILVER BELOW RESISTANCE AT $18.50

3l USA vs Russian rouble; (Russian rouble DOWN 63/100 in roubles/dollar) 60.88-

3m oil into the 43 dollar handle for WTI and 46 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation (already upon us). This can spell financial disaster for the rest of the world/China forced to do QE!! as it lowers its yuan value to the dollar/GOT A SMALL SIZED REVALUATION NORTHBOUND

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 114.34 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 0.9684 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1038 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now POSITIVE territory with the 10 year RISING to +0.552%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.3890% early this morning. Thirty year rate at 2.9391% /POLICY ERROR)GETTING DANGEROUSLY HIGH

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

(courtesy Jim Reid/Bloomberg/Deutsche bank/zero hedge)

Bond Selloff Returns As EM Fears Rise; Oil Slides; BOJ Does Not Intervene

U.S. index futures point slightly lower open. Asian shares rose while stocks in Europe fell as energy producers got caught in a downdraft in oil prices and reversed an earlier gain after Goldman unexpectedly warned that WTI could slide below $40 absent “show and awe” from OPEC. The dollar rose, hitting a four-month high against the yen and bonds and top emerging market currencies were back under pressure on Tuesday, following last week’s hawkish rhetoric from central bankers.

Nonetheless, driven by expectations for solid earnings growth, MSCI’s 46-country All World share index was up for a third day running, although it started to slip as Europe’s bourses lost their footing early on. According to Bloomberg, the early European focus was on the overnight rally in USD/JPY toward 114.50 after tripping stops through 114.37 high from May; strong 5Y JGB auction also supports as curve steepens. The USD held small gains against G-10 through the European morning, GBP/USD pushes higher through 1.29 in thin liquidity; EMFX underperforms markedly. USTs sell off in tandem with the move in USD/JPY and see further pressure after bund and gilt futures open. European equity markets open higher before reversing; FTSE 100 underperforms with retail sector lagging after Marks and Spencer (-3.8%) trading update. Auto sector rallies after latest China vehicle sales numbers.

Overnight, all eyes were on the BOJ, and whether it would intervene again as it did on Friday for longer-term debt maturities, to stem the ongoing rise in JGB yields following a five-year bond auction. However, Kuroda was spared intervention for the second time in one week after the five-year bond auction saw a jump in buy side demand in the form of the highest bid-to-cover ratio since August 2014. Still, the Japanese currency dropped to 114.48 per dollar, its weakest level since mid-March. According to the Deutsche Bank Trade Weighted Index, the yen stands at its lowest since February 2016, a reflection of Japan’s monetary policy divergence versus other major central banks, according to traders in Europe. According to Bloomberg, while the yen’s haven status keeps it in vogue in the longer-term, as shown by risk reversals, the fact that the BOJ looks behind the curve compared to other major central banks in normalizing policy is sending the currency into defensive mode.

Also overnight, China’s central bank resumed its open-market operations for the first time in 13 days, ending the longest pause since April, offering 40 billion yuan in reverse repos. The net effect on the financial system was neutral, as the amount of injections matched maturities for the day. The PBOC hasn’t added cash on a net basis for 16 days in a row. The weighted average 7- day repo rate climbed 8 basis points to 2.80% as of 5:30 p.m. in Shanghai; the overnight cost rises 9 basis points to 2.62%. Japan’s Topix Index climbed 0.7 percent. Hong Kong’s Hang Seng Index strengthened 1.6 percent, heading for its first back-to-back gain in three weeks. The Hang Seng China Enterprises Index soared 2.1 percent, its biggest advance since March 16. The Shanghai Composite Index was down 0.3 percent after a short-lived advance mid-afternoon local time. Other indexes on the mainland were also lower.

Meanwhile, the bond selloff continued with bunds opening lower following Treasuries, as Germany’s 10-year yield edged up 2 basis points to 0.56% having more than doubled over the last few weeks, with losses extending as gilts slumped before the 2056 I/L syndication; bonds touched day’s low as bidding opened on the Netherlands 30y sale, before paring losses after the sale. Bund futures dipped to day’s low of 160.48 (46 ticks) as bidding opened on the Netherlands 01/2047. Long-end French bonds outperformed core, with OAT/bund spread tighter by 1-1.5bps across the curve. The outperforming 15-20y sector has previously been highlighted as the preferred spot for domestic real money investors.

Roger Webb, Head of European Credit at Aberdeen Asset Management said the slightly stronger-than-expected global growth numbers had boosted expectations of higher interest rates.

“I think the increased hawkishness we have seen from the central banks has led to a fear that we could see a mini-taper tantrum. I don’t think there is too much alarm. I think the move to slightly higher yields in Europe and the U.S., UK and elsewhere is probably understandable.”

The shift in sentiment was enough to propel the dollar higher against the basket of currencies including hitting a four-month high of 114.43 yen on the back of the past fortnight’s 25 basis-point rise in 10-year U.S. government bond yields. The pound added 0.3 percent to $1.2917 while the euro traded little changed. The New Zealand dollar fell to its lowest since June 23 meanwhile after an earthquake hit the country’s South Island. The Canadian dollar was down slightly too against its U.S. counterpart as investors awaited a Bank of Canada interest rate decision on Wednesday. The South African rand, Turkish lira and Russia rouble all dropped around 0.8 percent as the emerging market selling resumed too.

In commodities, crude oil slipped back after pushing higher overnight in Asia. Increased drilling activity in the United States and uncertainty over Libyan and Nigerian production cuts clouded the future supply outlook, leaving U.S. crude down a third of a dollar at $44.13 a barrel and Brent at $46.57. A bearish Goldman note did not help. Spot gold edged lower too, dipping to $1,212.13 an ounce and back near a four-month low touched in the previous session. Spring wheat rose 1.6 percent to $8.1250 a bushel on the Minneapolis Grain Exchange, surging 51% this year amid concerns drought in U.S. Northern Plains will curb output to a 15-year low.

More ominously, the one thing that has kept stocks near all time highs even as the global economic outlook has grown increasingly cloudly, corporate earnings appears to be turning over. Following recent mixed macro data and a drop in commodity prices, analysts have started to cut their forecasts for company earnings, raising concerns over elevated valuations and prices near all-time highs.

Bulletin Headline Summary from RanSquawk

- Asian equities traded with little in the way of firm direction, filtering into European trade, with energy underperforming

- FX markets saw USD/JPY continue its ascent, reaching 4-month highs as GBP position taking is evident ahead of delayed BoE speakers

- Looking ahead, highlights include US JOLTS, APIs, BoE’s Haldane, Broadbent, ECB’s Coeure, Constancio, Fed’s Brainard and Kashkari

Market Snpashot

- S&P 500 futures down 0.03% to 2,423.00

- STOXX Europe 600 down 0.2% to 380.79

- MXAP up 0.7% to 154.41

- MXAPJ up 0.8% to 506.52

- Nikkei up 0.6% to 20,195.48

- Topix up 0.7% to 1,627.14

- Hang Seng Index up 1.5% to 25,877.64

- Shanghai Composite down 0.3% to 3,203.04

- Sensex up 0.4% to 31,825.40

- Australia S&P/ASX 200 up 0.08% to 5,728.93

- Kospi up 0.6% to 2,396.00

- US 10Y yield rose

- German 10Y yield rose 2.0 bps to 0.56%

- Euro down 0.03% to 1.1396 per US$

- Italian 10Y yield fell 6.2 bps to 1.985%

- Spanish 10Y yield rose 0.9 bps to 1.68%

- Brent Futures down 0.6% to $46.59/bbl

- Gold spot down 0.2% to $1,211.43

- U.S. Dollar Index up 0.09% to 96.11

Top Overnight News

- Trump will nominate Randal Quarles Fed vice chair of supervision

- Trump Jr. was told before meeting of Kremlin effort to aid campaign: NYT

- Oil erased earlier gains to trade near $44 a barrel in New York after Goldman warned it could drop below $40

- F-35 Program Costs Jump to $406.5 Billion in Latest Estimate

- Trump Will Nominate Quarles as Fed’s Top Wall Street Regulator

- Trump’s FBI Pick Faces Questions on Independence Versus Loyalty

- Trump’s Son Sucked Into Russia Probe After Meeting With Lawyer

- U.K. June BRC like-for-like retail sales 1.2% vs 0.8% estimate

- China should keep interest rates stable in 2H: Securities Journal

- Australia June NAB business conditions index highest since 2008

- Banks Heed Carney’s Call to Tackle Risks of Climate Change

- Fed’s Williams says forecasts of one more 2017 rate hike seem reasonable

- Sanofi to Buy U.S. Vaccine Maker for Up to $750 Million

- Worldwide Semiconductor Revenue to Reach $400b in ’17: Gartner

- BioMarin Hemophilia Therapy Reduces Bleeding in Phase 1/2 Study

- Google-Backed Mobvoi Aiming for U.S. or HK IPO Within Two Years

- Cigna Names Arthur Cozad as CEO of Zurich Insurance Middle East

- Microsoft Funds Faster Internet for U.S. Heartland to Bridge Gap

- Getty Realty Prices 4.1m Shares at $23.15 Each

- Delta Cancels Flights Amid Air Traffic Control Center Evacuation

- AAR Names Michael Milligan CFO, Succeeds Timothy Romenesko

- Citrix Names Henshall CEO as Tatarinov Leaves; Reaffirms 2Q

- Venezuelan Prosecutor Charges Two Over PDVSA Contracting

- J.C. Penney Names Interim CFO After Edward Record Steps Down

- Alexander & Baldwin Names James Mead CFO, Succeeds Paul Ito

- Myokardia Files 9.2m- Share Shelf for Holder Third Rock Ventures

- Cypress Semiconductor Says Director Resigned Over Disagreement

Asian equities saw a lack of firm direction overnight amid quiet newsflow. This was despite a resumption in the PBoC’s open market operations with a CNY 40bIn injection for the first time in 13 days (however, was net neutral with CNY 40bIn of prior injections maturing). The Nikkei 225 (+0.4%) failed to find any firm direction, while ASX 200 (-0.1%) was choppy and failed to hold on to the early material and energy led advances. Chinese bourses yet again traded in mixed fashion with broad based gains keeping the Hang Seng (+1.0%) afloat, while the Shanghai Comp (-0.2%) treaded water. In fixed income markets, the Japanese 10Y held around 0.1%, owing to last week’s pledge by the BoJ to buy unlimited amounts in the 10yr and cap yields. However, further upside in yields could test the BoJ’s tolerance, and a slight concession was seen in the Japanese 5Y, subsequently leading to its outperformance amid today’s auction. PBoC injected CNY 30bIn and CNY 10bIn through 7-day and 14-day reverse repos; first injection for 13 days. PBoC set the CNY mid-point at 6.7983 vs. Prey. 6.7964. Chinese vehicle sales rose 4.6% for June according to the Chinese Passenger Car Association

Top Asian News

- China Hedge Funds Return 13% to Rank Near the Top Globally

- Pakistan’s Key Stock Index Heads for Biggest Drop Since 2009

- Foreign Banks Said to Seek Relief From India’s Derivatives Rule

- China Likely to Extend Tax Exemption for Electric Cars: CAAM

- China’s ‘Hottest Commodity’ Surges as Steel Seizes the Limelight

- HSBC Upgrades China, Russia to Overweight, Cuts Turkey Exposure

- China Is Likely to Extend Tax Break on Electric Cars, Group Says

- Korea Aerospace Wins 641.2b Won Order From Boeing

The majority of European bourses trade lower, following a slightly higher open, with the materials sector the only Stoxx 600 sector trading in the green. M&S lag amid misses in its Q2 food, clothing and home LFL sales. However, positive broker moves for UK grocers/retailers; Tesco & Morrisons have provided some reprieve for the supermarket names, both trading up in early market trade. The Dax does trade in the green however, as ThyssenKrupp (TKA GY) leads, following a decision to reduce up to 2500 admin jobs in a move that could save EUR 400mln. European paper has grinded lower throughout the session, slowly chipping away at yesterday’s marginal games, with range bound trade evident, as participants await a week of speech, with Yellen the highlight tomorrow. News does remain light in markets, with the break of 0.50% bund yield seen last week now acting as support for the yield.

Top European News

- Pearson to Sell 22% Stake in Penguin Random House to Bertelsmann

- Italy’s Production Rises More Than Expected, Boosting Outlook

- Italian Banks’ Big vs Small Divide to Widen, Goldman Sachs Says

- Italy May Industrial Production +0.7% M/m; Est. +0.5%

- M&S Quarterly Sales Dip in Setback to Rowe’s Turnaround Plan

- Thyssenkrupp to Cut Up to 2,500 Staff to Help Meet Profit Target

- BlueCrest Fund Manager Shorting U.K. Property Tips Spanish Peers

- Glencore Is Said to Draw Liberty House Bid for Australian Mine

In currencies, FX markets have been subdued with all anticipation on central bank speech, with Yellen the headlight tomorrow and Kashkari and Brainard expected today. BoE speech will be the key risk event for the day, with a GBP bid being seen early in the session, as investors will await Haldane and Broadbent. Hawkish positioning, accompanied by hawkish speech, could potentially spark some direction into the GBP. GBP/USD has indicated a bearish trend of late, after the rejection of the 1.3140 area, however, clear bids at the bottom of the range (1.27 — 1.28) do indicate buyers in the market, a break through 1.3140 will indicate a change in direction in the pair and could push us toward august 2016 levels. Overnight, movement was seen in NZD, the widely touted ‘over-valued’ currency did lose some ground, NZD/USD was the main catalyst of the move, after selling renewed in NZD/USD, tripping stops through 0.7250. JPY also continued to lower against its major counterparts, as USD/JPY did trade through the key 114.38 level, now residing around this resistance level, as a mini bidders vs. sellers battle is clear. A risk tone has been clear in currencies, with a weaker JPY being joined by a weaker CHF. EUR has benefited, with EUR/JPY firmly through 130.00 and EUR/CHF finding some early buyers as it looks like the pair will see its 13th green day in two weeks, likely to test the 1.11 area seen in April 2016.

In commodities, oil continues to highlight the commodities sector, seeing selling pressure following the European open, once again WTI rejecting the USD 44.90 area, looking to retest USD 43.60. Fundamental factors do continue to weigh on oil, with supply continuing to pick up, as Nigeria and Libya are now producing an additional 1mIn BPD between them, a huge dent in the 1.8mln combined OPEC agreement. The countries may be asked to cap their oil output following the slowdown of rebel problems resulting in a ramp, however, with Nigeria and Libyan officials not potentially attending the meeting, this could pave difficult. Reports early in Asia did state that Libyan and Nigerian officials may attend the joint meeting between OPEC and non-OPEC nations later this month as oil producers look for ways to cap rising production, however, with Barkindo stating that further cuts will not be discussed, source reports did state this could be in November, the agenda does remain unclear. Precious metals have suffered throughout Asian and European trade, all down for the session, Gold grinds lower, looking increasingly bearish, a break below July’s low (1204.87) is likely to lead to a test of 1195.00. Copper has seen some slight reprieve, following hitting a two-week low being hit on an inventory rise and Chinese data yesterday. Metals suffered late yesterday, with small bounces clear, likely profit taking, as Aluminium also saw its biggest intra-day drop in over two months. Iran said it is currently producing 3.8mln bpd of oil, according to its Deputy Oil Minister.

Look at today’s events, it is another quiet day: we will only see the NFIB small business optimism number for June (103.8, below the 104.4 expected vs. 104.5 previous) followed by JOLTS job openings and final wholesale inventories data for May (no revision expected ). In terms of Fedspeak, we will hear from Williams and Brainard speak today. The calm before the potential storm with Yellen scheduled to speak over the next two days.

US Event Calendar

- 6am: NFIB Small Business Optimism, est. 104.4, prior 104.5

- 10am: JOLTS Job Openings, est. 5,950, prior 6,044

- 10am: Wholesale Inventories MoM, est. 0.3%, prior 0.3%; Wholesale Trade Sales MoM, prior -0.4%

- 12:30pm: Fed’s Brainard Speaks on Monetary Policy in New York

DB’s Jim Reid concludes the overnight wrap

After a very dull 24 hours I thought it might be an opportune moment to recap our bigger picture thoughts on government bond yields given the sell-off of the last two weeks. As we discussed in our Long-Term Study last September we think 2016 will likely be seen as the inflection point and the end of the 35 year bull market for bonds. It won’t be a straight line reversal and perhaps the issue will eventually be more for future real returns over nominal returns. The reason for picking out 2016 was that this was the year that 1) voters in the bottom half of the income scale effectively won two landmark national votes and 2) endless extreme monetary policy for the first time started to impact the plumbing of the financial system. The impact of the first point is that it likely means politicians now have to steer policy specifically to this poorer income group to ensure that their electoral chances are enhanced. This likely means more fiscal policy and less austerity. The recent UK election reinforces this theme here and we think the theme will slowly spread.

With regards to the second point, 2016 was the year that negative rates cascaded like wildfire along the government bond curve in Europe. The problem being that the correlation between falling yields and poor EU bank equity performance is very strong and the correlation between bank equity and bank lending suggests that had the trends of 2016 continued much further then the real economy could have actually suffered by the negative yields actually aimed to support growth. However the fact that the BoJ and ECB pulled back from full-on QE in the last 4 months of last year suggested they appreciated that monetary policy had perhaps gone too far for now and was having some negative consequences. As such a slow reversal of the ultra low yield environment should have and should continue to follow. The risk being that at some point a government spends big and yields start to rise faster. This could still be many quarters ahead but if and when it does happen central banks might have to intervene and cap nominal yields to avoid carnage in a heavily indebted world. Then we move towards helicopter money – a story for another day. The problem with this view is that it’s as much to do with gut feel, a change in the political wind, and second guessing policy makers as it is to do with spreadsheet based analysis of the current available facts. As such it makes it much more difficult to prove! Anyway this is likely to be a slow moving story for now but generally since last year we’ve thought the general bias on yields is higher.

Yesterday wasn’t the day for this trend to continue though as government bond markets saw some relief as yields dropped after the big sell-off over the past 2 weeks. US Treasuries (2Y: -1bp; 10Y: -1bp) and German Bunds (2Y: -1bp; 10Y -3bp) saw yields fall across all maturities. UK Gilts (2Y: -3bps; 10Y: -3bps), French OATs (2Y: -1bps; 10Y: -3bps) and Italian BTPs (2Y: -2bps; 10Y: -7bps) saw similar moves lower.

With limited newsflow and data yesterday, global risk markets exhibited a mild risk-on tone. Equity markets were broadly positive as the US (S&P500 +0.1%) and Europe (STOXX +0.4%) ticked up, with technology stocks among the top gainers in both indices. In the UK the FTSE gained +0.3% on the day, while German (DAX +0.5%), French (CAC +0.4%) and Italian (FTSE MIB +0.8%) equities posted even higher returns. Currencies, credit and commodities were fairly range bound. Asian equities are generally following the firmer picture, again on low volumes. The Hang Seng is 1.1%, the Nikkei +0.5% but with Chinese equities a little more mixed (Shanghai Comp -0.2%). Treasury yields are back up 1bps and pretty much where they were this time yesterday now.

Taking a look at yesterday’s calendar, it was a fairly quiet day in terms of data. In Europe we saw German trade numbers for May where both the current account surplus and trade surplus came in above expectations at 17.3bn (vs. 15.4bn expected) and 22bn (vs. 18.7bn expected). Both exports and imports grew more than expected at 1.4% (vs. 0.3% expected; 0.9% previous) and +1.2% (vs. 0.3% expected; 1.2% previous). Following that we saw some sentiment data with the latest Bank of France business sentiment reading that disappointed at 103 for June (vs. 106 expected) and the July Sentix investor confidence reading for the Eurozone that clocked a tick above expectations at 28.3 (vs. 28.1 expected).

Over in the US it remained quiet post-payrolls with the only data of note being the June labour market conditions index that rose by 1.5 points in June but still disappointed relative to expectations of a 2.5 point increase. Consumer credit numbers were slightly higher than expected but didn’t really move the dial. Of more interest was Mr Trump’s intention to nominate Randal Quarles to be the banking watchdog at the Fed. This was anticipated but the feeling is that this will ease regulation for the sector.

Perhaps more interesting was the latest ECB CSPP data out yesterday. It was a strong week for the CSPP programme as purchases settled last week (€2.29bn) implied an average daily run rate of € 457mn, which was well above the average since inception of €366mn. With PSPP purchases at a more lowly €14bn, the CSPP/PSPP ratio was 16.3% which is above the average of 13.6% in Q2 (post QE trimming) and well above the pre-April average of 11.6%. Further on this the average monthly run rate (assuming 21 business days per month) of CSPP since April 2017 (after QE was trimmed) has been €7.7bn (vs. €7.7bn before April). The numbers have been all over the place of late and the ECB may be front-loading and preparing for illiquid summer credit markets but at face value we now have to think about as to whether the CSPP has been tapered at all so far.

Today’s calendar is also very quiet with no major releases of note in Europe. Over in the US we will only see the NFIB small business optimism number for June (104.4 expected vs. 104.5 previous) followed by JOLTS job openings and final wholesale inventories data for May (no revision expected ). In terms of Fedspeak, we will hear from Williams and Brainard speak today. The calm before the potential storm with Yellen scheduled to speak over the next two days.

3. ASIAN AFFAIRS

i)Late MONDAY night/TUESDAY morning: Shanghai closed DOWN 9.59 POINTS OR 0.30% / /Hang Sang CLOSED UP 377.58 POINTS OR 1.48% The Nikkei closed UP 114.50 POINTS OR 0.57%/Australia’s all ordinaires CLOSED UP 0.10%/Chinese yuan (ONSHORE) closed UP at 6.8015/Oil DOWN to 43.91 dollars per barrel for WTI and 46.36 for Brent. Stocks in Europe OPENED RED,, Offshore yuan trades 6.8055 yuan to the dollar vs 6.8015 for onshore yuan. NOW THE OFFSHORE IS A TOUCH WEAKER TO THE ONSHORE YUAN/ ONSHORE YUAN STRONGER (TO THE DOLLAR) AND THE OFFSHORE YUAN IS WEAKER TO THE DOLLAR AND THIS IS COUPLED WITH THE STRONGER DOLLAR. CHINA IS NOT HAPPY TODAY

3a)THAILAND/SOUTH KOREA/NORTH KOREA

NORTH KOREA

end

b) REPORT ON JAPAN

end

c) REPORT ON CHINA

More regulation and tighter money has now put an end to China’s second housing bubble. The first bubble burst in 2014 and now the second seems to have blown this market again

(courtesy Valentin Schmid/EpochTimes)

.

Is This The End Of China’s Second Housing Bubble?

Authored by Valentin Schmid via The Epoch Times,

When the economy started to cool in the beginning of 2016, China opened up the debt spigots again to stimulate the economy. After the failed initiative with the stock market in 2015, Chinese central planners chose residential real estate again.

And it worked. As mortgages made up 40.5 percent of new bank loans in 2016, house prices were rising at more than 10 percent year over year for most of 2016 and the beginning of 2017. Overall, they got so expensive that the average Chinese would have had to spend more than 160 times his annual income to purchase an average housing unit at the end of 2016.

Because housing uses a lot of human resources and raw material inputs, the economy also stabilized and has been doing rather well in 2017, according to both the official numbers and unofficial reports from organizations like the China Beige Book (CBB), which collects independent, on-the-ground data about the Chinese economy.

“China Beige Book’s new Q2 results show an economy that improved again, compared to both last quarter and a year ago, with retail and services each bouncing back from underwhelming Q1 performances,” states the most recent CBB report.

However, because Beijing’s central planners must walk a tightrope between stimulating the economy and exacerbating a financial bubble, they tightened housing regulations as well as lending in the beginning of 2017.

Has the Bubble Burst?

Research by TS Lombard now suggests the housing bubble may have burst for the second time after 2014.

“We expect the latest round of policy tightening in the property sector to drive down housing sales significantly over the next six months,” states the research firm, in its latest “China Watch” report.

One of the major reasons for the concern is increased regulation. Out of the 55 cities measured in the national property price index, 25 have increased regulation on housing purchases.

In Beijing, for example, some owners of residential real estate can no longer sell their apartments to private buyers—instead, they have to sell to businesses, because their apartment has been marked for business use by the authorities.

Other measures include higher down payments, price controls, and increasing the time until the unit can be sold again.

“First- and second-tier cities have enacted such draconian measures that it is nigh impossible to buy or sell a property,” states the report.

Credit Tightening

Although the central bank left its benchmark mortgage lending rate unchanged at 4.9 percent, banks have increased the rates they charge on mortgages to as high as 6 percent and, in some cases, have stopped giving out mortgages altogether because they have used up their quotas set by regulators.

The People’s Bank of China wants to lower the share of mortgage lending to 30 percent of new loans, which should influence new demand for housing.

“Unlike 10 years ago, when most Chinese households made a 50 to 70 percent down payment to buy a new apartment, more than 80 percent of borrowers in the past two years have put down 30 percent or less. With reduced mortgage funding availability, we believe it is unlikely that households will be able to finance their purchase through savings,” states the TS Lombard report.

So far, the slowdown in larger cities has been offset by more activity in smaller cities, which haven’t implemented as many tightening measures.

“Overall revenues and profits plunged in Tier 1 cities, with the slowdown concentrated primarily in the Beijing and Shanghai regions. Hiring stagnated, while cash ?ow worsened across the board,” the China Beige Book says.

However, TS Lombard expects smaller cities to follow the bigger cities with more restrictive measures for property buying, which will ultimately lead to a decline in housing transactions, if not prices outright.

“Property sales will decelerate notably in [the second half of 2017], with the monthly number of new residential housing transactions set to drop by 10 percent year-on-year, compared with a year-on-year rise of 8.3 percent in May.”

end

4. EUROPEAN AFFAIRS

end

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

Russia’s patience with Trump has run out: Russia is not set to expel 30 USA diplomats and seize USA assets in Russia

(courtesy zero hedge)

“We Are Forced To Strike Back”: Russia Set To Expel 30 US Diplomats, Seize US Assets

When Obama announced the expulsion of 35 Russian diplomats and the seizure of Russian diplomatic compounds in Maryland last December in response to alleged Russian interference in the election, Putin just smiled and said Russia would not retaliate, expecting that relations between Russia and the US would normalize under president Trump. Six months later, relations have not only not normalized but have deteriorated further following the latest round of sanctions against Russia despite daily allegations that Trump colluded with the Kremlin to convince several million Americans to vote against Hillary.

And, as a result, Putin’s patience appears to have run out, and according to Russian newspaper Izvestiya, the Kremlin is set to expel around 30 US diplomats and freeze some US assets in a retaliatory move against Washington.

Moscow may expel about 30 US diplomats, freeze some US assets in Russia https://sptnkne.ws/eSg6 #USRussia

Quoting a Foreign Ministry source, the Izvestiya newspaper says the move is due to the failure to reach an agreement on two Russian diplomatic compounds in the US seized by the outgoing Obama administration in December last year.

“There is a preliminary agreement on holding a meeting between Russian Deputy Prime Minister Sergey Ryabkov and US Under Secretary of State Thomas Shannon in St. Petersburg. If the compromise is not found there, we will have to take such measures,” a source in the Russian Foreign Ministry told the Izvestiya newspaper.

Izvestiya also cited Andrey Klimov, a senator in the upper house of Russia’s parliament, who said that “Russia had already waited more than six months for the Trump administration to improve the relationship between the two countries” and was now forced to strike back.

“We are forced to draw a line and answer in a similar way,” Klimov told Izvestiya. “These moves are not meant as our attempts to show our negative attitudes toward the Trump administration but rather as evidence of the fact that Russia is a strong nation that deserves respectable treatment.”

The Russian newspaper adds that the decision came after Trump and Putin’s first meeting at the G20 Summit in Germany failed to produce an agreement on the lightening of US sanctions against Russia. The issue of the Russian diplomatic compounds was also raised at the Putin-Trump meeting in Hamburg, according to the Russian press reports.

And, as Trump and his family face fresh claims of collusion with the Kremlin, Putin’s patience over the non-return of the Russian compounds has run out.

According to the newspaper, while the administration plans to seize the American summer house in a forest region outside of Moscow and a warehouse in the center of the city, it will not touch the residence of the American ambassador and the American international school in St. Petersburg.

end

6 .GLOBAL ISSUES

Why Did Ukraine Nationalize Its Largest Private Bank?

Authored by John Mills via The Mises Institute,