GOLD: $1268.70 DOWN $3.65

Silver: $16.64 DOWN 10 cent(s)

Closing access prices:

Gold $1268.60

silver: $16.68

SHANGHAI GOLD FIX: FIRST FIX 10 15 PM EST (2:15 SHANGHAI LOCAL TIME)

SECOND FIX: 2:15 AM EST (6:15 SHANGHAI LOCAL TIME)

SHANGHAI FIRST GOLD FIX: $1268.88 DOLLARS PER OZ

NY PRICE OF GOLD AT EXACT SAME TIME: $1263.50

PREMIUM FIRST FIX: $5.38

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

SECOND SHANGHAI GOLD FIX: $1266,17

NY GOLD PRICE AT THE EXACT SAME TIME: $1262.30

Premium of Shanghai 2nd fix/NY:$3.47

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

LONDON FIRST GOLD FIX: 5:30 am est $1261.80

NY PRICING AT THE EXACT SAME TIME: $1262.25

LONDON SECOND GOLD FIX 10 AM: $1268.10

NY PRICING AT THE EXACT SAME TIME. $1267.35

For comex gold:

AUGUST/

NOTICES FILINGS TODAY FOR APRIL CONTRACT MONTH: 73 NOTICE(S) FOR 7,300 OZ.

TOTAL NOTICES SO FAR: 3212 FOR 321,200 OZ (9.990 TONNES)

For silver:

AUGUST

2 NOTICES FILED TODAY FOR

10,000 OZ/

Total number of notices filed so far this month: 413 for 2,065,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

end

Last night, the crooks engineered another flash crash at 7:06 pm est which forced gold down to 1256. However, as in other days, gold/silver slowly recover on the day. The crooks only weapon now is the shorting of gold/silver equity shares trying to contain the actual metals price rise.

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total open interest FELL BY A TINY 1023 contracts from 207,258 DOWN TO 206,233 WITH THE FALL IN THE PRICE THAT SILVER TOOK WITH RESPECT TO YESTERDAY’S TRADING (DOWN 5 CENT(S). WHEN YOU COMPARE THE HUGE GAIN IN OI FOR GOLD THEN YOU MUST ADMIT THAT IT SURE LOOKS LIKE BOTH THE SPECULATOR SHORTS AND THE BANKER SHORTS ARE HAVING SEVERE PROBLEMS TRYING TO COVER THEIR SHORTFALL WHICH CANNOT COME TO FRUITION. THE LONGS REMAIN STOIC AND NOTHING WILL BUDGE OUR SILVER LEAVES FROM DEPARTING OUR SILVER TREE. YESTERDAY’S TRADING IS EVIDENCE OF THAT.

In ounces, the OI is still represented by just OVER 1 BILLION oz i.e. 1.030 BILLION TO BE EXACT or 147% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT MAY MONTH/ THEY FILED: 2 NOTICE(S) FOR 10,000 OZ OF SILVER

In gold, the open interest ROSE by A MONSTROUS 6,896 despite the FALL in price of gold ($0.65 yesterday.) The new OI for the gold complex rests at 455,605. Yesterday we had the bankers supplying a major amount of short paper to newbie longs who entered the arena again like gangbusters. The specs shorts covered what they could. .No wonder a flash crash was orchestrated at 7.01 pm last night with the intention of cooling gold’s jets. It seems that the raid failed again. The bankers are losing control over the precious metal markets

we had: 73 notice(s) filed upon for 7300 oz of gold.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD:

Today, no changes in gold inventory

Inventory rests tonight: 791.88 tonnes

IN THE LAST 15 DAYS: GLD SHEDS 45.62 TONNES YET GOLD IS HIGHER BY $45.20 . GO FIGURE!!

SLV

Today: : WE ANOTHER HUGE CHANGES IN SILVER INVENTORY TONIGHT: A WITHDRAWAL OF 1,181,000 OZ FROM THE SLV

INVENTORY RESTS AT 340.551 MILLION OZ

end

.

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in silver FALL BY A TINY 1023 contracts from 207,258 down to 206,233 (AND now A LITTLE FURTHER FROM THE NEW COMEX RECORD SET ON FRIDAY/APRIL 21/2017 AT 234,787). THE FALL IN OPEN INTEREST WAS ACCOMPANIED BY A SMALL LOSS IN PRICE FOR SILVER WITH RESPECT TO YESTERDAY’S TRADING (DOWN 5 CENTS ). WHEN WE SEE THE MASSIVE RISE IN GOLD OPEN INTEREST YESTERDAY, WE NO DOUBT WITNESSED MORE SPEC LONGS ENTER THE ARENA (with political unrest) WITH THE MAJORITY OF THE SPEC LONGS AGAIN BASICALLY REMAINING STOIC. THE SPEC LONGS SEEM TO BE TAKING ON THE BANKERS. THE SPEC SHORTS ARE DESPERATE TO COVER THEIR SHORTFALL BUT THEY ARE COMING IN CONTACT WITH A LARGE NUMBER OF NEW SPEC LONGS . THE BANKERS HAD NO CHOICE BUT TO COVER SOME OF THEIR MASSIVE SHORT PAPER WITH THE 5 CENT LOSS FROM SILVER. THE NET RESULT: A COMEX SILVER OPEN INTEREST SLIGHT DECREASE AND THE REASON FOR LAST NIGHT’S ATTEMPTED FLASH CRASH.

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)Late WEDNESDAY night/THURSDAY morning: Shanghai closed DOWN 12.13 POINTS OR 0.37% / /Hang Sang CLOSED DOWN 76.37 POINTS OR 0.28% The Nikkei closed DOWN 50.78 POINTS OR .25%/Australia’s all ordinaires CLOSED DOWN 0.37%/Chinese yuan (ONSHORE) closed UP at 6.7222/Oil UP to 49.61 dollars per barrel for WTI and 52.34 for Brent. Stocks in Europe OPENED MIXED , Offshore yuan trades 6.7283 yuan to the dollar vs 6.7222 for onshore yuan. NOW THE OFFSHORE IS WEAKER TO THE ONSHORE YUAN/ ONSHORE YUAN STRONGER (TO THE DOLLAR) AND THE OFFSHORE YUAN IS MUCH WEAKER TO THE DOLLAR AND THIS IS COUPLED WITH THE SLIGHTLY STRONGER DOLLAR. CHINA IS NOT HAPPY TODAY

3a)THAILAND/SOUTH KOREA/NORTH KOREA

i)NORTH KOREA//USA

b) REPORT ON JAPAN

c) REPORT ON CHINA

i)CHINA/INDIA

Last week we brought you the story about a spat between India and China concerning lands on their border.

China lambastes India claiming that they had better leave Chinese land or face war

( zero hedge)

ii)CHINA USA

4. EUROPEAN AFFAIRS

i)UK/BANK OF ENGLAND

The pound plunges after the Bank of England votes to keep rates unchanged and at record lows. However the Bank cut growth forecast.

( zero hedge)

ii)EURO/EU

The euro continues to strengthen and this is certainly not what Europe wants as the higher euro hurts their competitiveness. If tomorrow’s job report is weak, then they expect the Euro to top 1.20 to the dollar and this would be good for our precious metals

( zero hedge)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

Hillary Clinton’s intervention in Libya has created a huge emergency as 1.3 Libyans are in need of assistance as their economy grinds to a halt

( zero hedge)

6 .GLOBAL ISSUES

Toronto, Ontario Canada

Home prices fall by almost 5% and what is far worse: volume dropped over 40%. The provincial tax on home purchases was a mainstay of the Ontario Government which needs that revenue badly. Ontario has the worst debt structure from any sub sovereign anywhere in the world.

(courtesy zerohedge)

7. OIL ISSUES

8. EMERGING MARKET

INDIA

seems that the new GST tax introduced by Modi is killing their economy. New PMI down to recession like 46.

9. PHYSICAL MARKETS

i)Another flash crash in gold at exactly 7:06 last evening as the crooks try to influence gold and silver. All night gold and silver was down but as soon as we approached physical time zones, the metals rebound..they are losing control

( zero hedge)

ib)Flash crash fails! Let’s see what happens tonight at 7:06

( zero hedge)

ii)No transparency whatsoever at the LBMA London’s vaults

( Ronan Manly/Bullionstar/GATA)

iii)Kaminska talks about the splitting of the Bitcoin cryptocurrency and how this a mirroring a pre crash banking system

( Kaminska/London’s Financial times/GATA)

iv)A must read interview of John Embry talking to Kingworldnews. Embry discusses how gold and silver are gaining traction as the dollar loses its reserves currency status

( John Embry/Kingworldnews)

10. USA Stories

i)A study on USA public pension funds show a return of a measly .6% instead of the 7.6% assumption. This has creates massive liabilities and will no doubt bankrupt them

( zero hedge)

ii)What a joke: we have two service PMI:

1/ USA PMI

2. ISM service PMI

and both provided polar opposite results.

However what is clear, is that we are starting to see a fall in soft data reporting. Hard data continually falters

( zero hedge)

iii)An excellent commentary explaining why the USA may be in a technical default come Sept 29 or early October once they reach their debt limit;

( zero hedge)

It begins: Trump to launch a trade war with China on intellectual property and then probably on steel and aluminium/

( zerohedge)

( zero hedge)

v)In case you missed this yesterday; Seymour Hersh reveals the truth behind Russia gate:

( Seymour Hersh./zero hedge)

vi)This is the reason that gold spiked up 3 dollars in the access market this afternoon:

Mueller impanels a grand jury into the Russian probe:

( zerohedge)

Let us head over to the comex:

The total gold comex open interest ROSE BY A MONSTROUS 6,896 CONTRACTS UP to an OI level of 455,605 DESPITE THE FALL IN THE PRICE OF GOLD ($0.65 with YESTERDAY’S trading). We had a huge number of newbie longs enter the gold area to which our crooked bankers were more than happy to comply. The specs shorts covered as fast as their feet could carry them. The excitement in gold forced our crooks to engineer another flash crash at 7:06 pm last night in an attempt to cool gold/silver’s jets. The price slowly recovered as we entered the physical time zones. The crooks are losing control over the pricing of these precious metals.

We are now in the contract month of August and it is the 3rd best of the delivery months after December and June.

The active August contract LOST 220 contract(s) to stand at 2752 contracts. We had 193 notices filed upon yesterday so we lost 27 contracts or an additional 2700 oz will not stand at the comex and 27 EFP’s were issued which entitles the long holder to a fiat bonus plus a futures contract and most probably that would be a London based forward.

The non active September contract month saw it’s OI gain by 53 contracts up to 1920.

The next active contract month is Oct and here we saw a loss of 97 contracts down to 48,233.

The very big active December contract month saw it’s OI rise by 96904 contracts up to 351,330.

We had 73 notice(s) filed upon today for 7,300 oz

For those keeping score: in the upcoming front delivery month of August:

LAST YEAR WE HAD A MONSTROUS 44.7 TONNES OF GOLD INITIALLY. BY THE CONCLUSION OF THE AUGUST CONTRACT MONTH 44.358 TONNES STOOD FOR DELIVERY.

We are now in the next big non active silver contract month of August and here the OI FELL BY 105 contracts. We had 107 notices filed yesterday. Thus we gained 2 contracts or an additional 10,000 oz will stand. We are proceeding again where we left off last month (July) and the month before that (June), and finally the month before that(May), where the amount standing increases as the month proceeds and it begins right on day 2.

The next active contract month is September (and the last active month until December) saw it’s OI fall by 969 contacts down to 137,445. The next non active contract month for silver after September is October and here the OI LOST 2 contacts DOWN TO 18. After October, the big active contract month is December and here the OI FELL by 55 contracts DOWN to 59,199 contracts.

We had 2 notice(s) filed for 10,000 oz for the AUGUST 2017 contract

VOLUMES: for the gold comex

Today the estimated volume was 117,256 contracts which is POOR/

Yesterday’s confirmed volume was 219,750 contracts which is GOOD

volumes on gold are STILL HIGHER THAN NORMAL!

August 3/2017.

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz |

nil oz

|

| Deposits to the Dealer Inventory in oz | oz |

| Deposits to the Customer Inventory, in oz |

nil oz

|

| No of oz served (contracts) today |

73 notice(s)

7300 OZ

|

| No of oz to be served (notices) |

2679 contracts

(267,900 oz)

|

| Total monthly oz gold served (contracts) so far this month |

3212 notices

321,200 oz

9.990 tonnes

|

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | nil oz |

Today, 0 notice(s) were issued from JPMorgan dealer account and 5 notices were issued from their client or customer account. The total of all issuance by all participants equates to 73 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 4 notice(s) was (were) stopped/ Received) by j.P.Morgan customer account.

| Silver | Ounces |

| Withdrawals from Dealers Inventory | nil |

| Withdrawals from Customer Inventory |

40,445.890 oz

CNT

|

| Deposits to the Dealer Inventory |

nil oz

|

| Deposits to the Customer Inventory |

nil

oz

|

| No of oz served today (contracts) |

2 CONTRACT(S)

(10,000 OZ)

|

| No of oz to be served (notices) |

209 contracts

( 1,045,000 oz)

|

| Total monthly oz silver served (contracts) | 413 contracts (2,065,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month | 231,126.0 oz |

NPV for Sprott and Central Fund of Canada

Sprott’s hostile 3.1 billion bid to take over Central Fund of Canada

(courtesy Sprott/GATA)

Sprott makes hostile $3.1 billion bid for Central Fund of Canada

Submitted by cpowell on Thu, 2017-03-09 01:19. Section: Daily Dispatches

From the Canadian Press

via Canadian Broadcasting Corp. News, Toronto

Wednesday, March 8, 2017

http://www.cbc.ca/news/canada/calgary/sprott-takeover-bid-central-fund-c…

Toronto-based Sprott Inc. said Wednesday it’s making an all-share hostile takeover bid worth $3.1 billion US for rival bullion holder Central Fund of Canada Ltd.

The money-management firm has filed an application with the Court of Queen’s Bench of Alberta seeking to allow shareholders of Calgary-based Central Fund to swap their shares for ones in a newly-formed trust that would be substantially similar to Sprott’s existing precious metal holding entities.

The company is going through the courts after its efforts to strike a friendly deal were rebuffed by the Spicer family that controls Central Fund, said Sprott spokesman Glen Williams.

“They weren’t interested in having those discussions,” Williams said.

Sprott is using the courts to try to give holders of the 252 million non-voting class A shares a say in takeover bids, which Central Fund explicitly states they have no right to participate in. That voting right is reserved for the 40,000 common shares outstanding, which the family of J.C. Stefan Spicer, chairman and CEO of Central Fund, control.

If successful through the courts, Sprott would then need the support of two-thirds of shareholder votes to close the takeover deal, but there’s no guarantee they will make it that far.

“It is unusual to go this route,” said Williams. “There’s no specific precedent where this has worked.”

Sprott did have success last year in taking over Central GoldTrust, a similar fund that was controlled by the Spicer family, after securing support from more than 96 percent of shareholder votes cast.

The firm says Central Fund’s shares are trading at a discount to net asset value and a takeover by Sprott could unlock US$304 million in shareholder value.

Central Fund did not have any immediate comment on the unsolicited offer. Williams said Sprott had not yet heard from Central Fund on the proposal but that some shareholders had already contacted them to voice their support.

Sprott’s existing precious metal holding companies are designed to allow investors to own gold and other metals without having to worry about taking care of the physical bullion.

end

And now the Gold inventory at the GLD

August 3/no change in gold inventory at the GLD/Inventory rests at 791.88 tonnes

August 2/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 791.88 TONNES

Aug 1/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 791.88 TONNES

July 31/NO CHANGES AT THE GLD/INVENTORY RESTS AT 791.88 TONNES

July 28/ANOTHER MASSIVE WITHDRAWAL OF 3.54 TONNES OF GOLD WITH GOLD UP $9.15/INVENTORY RESTS AT 791.88 TONNES

July 27/LATE LAST NIGHT, A HUGE WITHDRAWAL OF 5.03 TONNES WITH GOLD UP $10.45 ON THE DAY/INVENTORY RESTS AT 795.42 TONNES

July 26/NO CHANGE IN GLD INVENTORY WITH GOLD DOWN $2.55/INVENTORY RESTS AT 800.45 TONNES

July 25/A MASSIVE 9.17 TONNES OF GOLD WITHDRAWN FROM THE GLD/INVENTORY RESTS AT 800.45 TONNES

July 24/A massive 9.62 tonnes withdrawal and yet the price remains constant (down only 25 cents)..inventory drops to 809.62 tonnes

July 21/with gold up $8.75 again, we had no changes in gold inventory at the GLD/inventory rests at 816.13 tonnes

July 20/WITH GOLD UP AGAIN TODAY ($3.50) WE HAD NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 816.13 TONNES

jULY 19/STRANGE!! AGAIN WITH GOLD UP $0.50 WE HAD ANOTHER HUGE 5.32 TONNES WITHDRAWAL FROM THE GLD/INVENTORY RESTS AT 816.13 TONNES THIS GOLD IS HEADING TO SHANGHAI

July 18/STRANGE AGAIN/WITH GOLD UP $7.50 WE HAD ANOTHER HUGE 5.62 TONNES WITHDRAWAL FROM THE GLD/INVENTORY RESTS AT 821.45 TONNES

July 17/strange again! with gold up $4.20 we had another huge withdrawal of 1.77 tonnes/inventory rests at 827.07 tonnes

July 14/strange@!!with gold up $12.00 today, we had a huge withdrawal of 3.55 tonnes/inventory rests at 828.84 tonnes

July 13/no change in gold inventory at the GLD/inventory rests at 832.39 tonnes

JULY 12/no change in gold inventory at the GLD/inventory rests at 832.39 tonnes

July 11/strange!@! we had a big withdrawal of 2.96 tonnes despite gold’s advance today/inventory rests tonight at 832.39 tonnes

July 10/no changes in gold inventory at the GLD/inventory rests at 835.35 tonnes

July 7/a massive withdrawal of 5.32 tonnes of paper gold were removed and this was used in the attack today/inventory rests at 835.35 tonnes

July 6/no changes in tonnage at the GLD/Inventory rests at 840.67 tonnes

July 5/A MASSIVE 5.62 TONNES OF GOLD LEFT THE GLD AND NO DOUBT WAS USED IN THE RAID THIS MORNING/INVENTORY REST

July 3/ A MASSIVE 7.37 TONNES OF GOLD LEAVE THE GLD/INVENTORY RESTS AT 846.29 TONNES

end

Now the SLV Inventory

August 3/A WITHDRAWAL OF 1,181,000 OZ FROM THE SLV/INVENTOR RESTS AT 340.551 MILLION OZ/

August 2/NO CHANGES IN SILVER INVENTORY AT THE SLV

INVENTORY RESTS AT 341.732 MILLION OZ/

August 1/A HUGE WITHDRAWAL OF 945,000 OZ/INVENTORY RESTS AT 341.732 MILLION OZ/

July 31/no change in silver inventory at the SLV/inventory rests at 342.677 million oz

July 28/ A HUGE WITHDRAWAL OF 1.15 MILLION OZ OF SILVER LEAVES THE SLV DESPITE SILVER BEING UP 11 CENTS TODAY/INVENTORY RESTS AT 342.677 MILLION OZ

July 27/NO CHANGE IN SILVER INVENTORY/INVENTORY RESTS AT 343.812 MILLION OZ WITH SILVER UP 13 CENTS TODAY.

July 26/NO CHANGE IN SILVER INVENTORY/INVENTORY RESTS AT 343.812 MILLION OZ

July 25/A MASSIVE 3.309 MILLION OZ OF INVENTORY WITHDRAWN FROM THE SLV DESPITE SILVER’S 10 CENT RISE TODAY.

July 24/no change in silver inventory despite its 4 cent drop/inventory remains at 347.121 million oz

July 21/STRANGE! WITH SILVER UP AGAIN TODAY (11 CENTS), NO CHANGE IN SILVER INVENTORY AT THE SLV/inventory 347.121 million oz/

July 20/STRANGE! WITH SILVER UP AGAIN TODAY, THE SLV INVENTORY LOWERS BY 945,000 OZ/INVENTORY RESTS AT 347.121 MILLION OZ/

July 19/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 348.066 MILLION OZ

July 18/a huge 946,000 oz withdrawal from the SLV despite silver’s 16 cent gain!

Inventory rests at 348.066 million oz

July 17/no change in silver inventory at the SLV/Inventory rests at 349.012 million oz

July 14/no change in silver inventory/inventory rests at 349.012 million oz/

July 13/no change in silver inventory/inventory at the SLV rests at 349.012 million oz/

JULY 12/another massive 1.986 million oz of silver added into the SLV/inventory rests at 349.012 million oz/the last 3 days saw 7.281 million oz added into the SV

July 11/ANOTHER MASSIVE INCREASE OF 2.364 MILLION OZ into the SLV inventory/inventory rests at 347.026 million oz

July 10/ A HUGE INCREASE OF 2.931 MILLION OZ OF SILVER DESPITE THE EARLY HIT ON SILVER THIS MORNING/INVENTORY RESTS AT 344.662 MILLION OZ.

July 7/Strange: no change in inventory (compare that with gold) Inventory rests at 341.731 million oz

July 6/ANOTHER MASSIVE DEPOSIT OF 2.126 MILLION OZ INTO THE SLV INVENTORY/INVENTORY RESTS AT 341.731 MILLION OZ.

July 5/STRANGE! NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 339.605 MILLION OZ

July 3/strange! with the huge whacking of silver we got an increase of 379,000 oz into inventory.

August 3.2017:

-

Indicative gold forward offer rate for a 6 month duration+ 1.28%

Indicative gold forward offer rate for a 6 month duration+ 1.28% -

+ 1.45%

end

END

Major gold/silver trading/commentaries for THURSDAY

GOLDCORE/BLOG/MARK O’BYRNE.

GOLD/SILVER

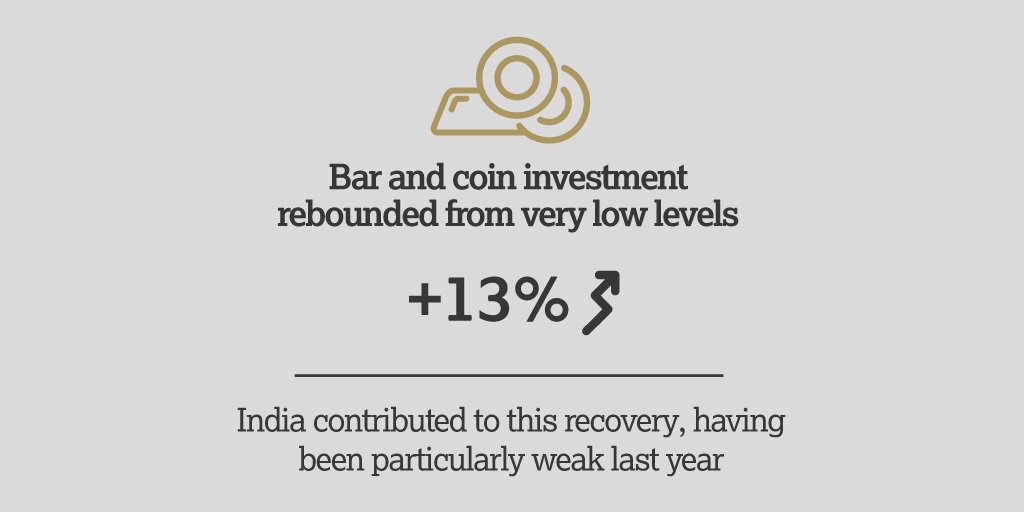

Gold Coins and Bars See Demand Rise of 11% in H2, 2017

– Gold coins, bars see demand rise of 11% in H2, 2017 to 532 tonnes according to WGC Gold Demand Trends

– Gold investment demand strong in China, India & Turkey

– Demand in Turkey surges on double digit inflation

– Total gold demand declines in Q2 on slower U.S. ETF inflows

– Gold held in ETFs in Europe reached all time high of 978t

– U.S. ETF inflows slowed from last year’s record

– Central banks continue to buy – 94t of declared purchases

– Turkey joined Kazakhstan & Russia in buying gold

– Well balanced market: ETF inflows continue and jewellery, technology and bar & coin demand up

– Important to note this is all official, transparent and recorded demand. There is demand and flows of gold that cannot be and are not recorded – especially into the Middle East, India, Russia and of course China

Key findings included in the Gold Demand Trends Q2 2017 report are as follows:

- Overall demand was 953t, a fall of 10% compared with 1,056t in Q2 2016

- Total consumer demand rose by 9% to 722t, from 660t in the same period last year

- Total investment demand (ETFs) fell 34% to 297t compared with 450t in Q2 2016

- Gold coins and bars rebounded 13% in H1

- Global jewellery demand grew 8% to 481 TONNES, from 447 TONNES in the same period last year

- Central bank demand climbed 20% to 94t compared with 78t in Q2 2016

- Demand in the technology sector increased 2% to 81t compared with 80t in Q2 2016

- Total supply was down 8% to 1,066t, from 1,160t in the same period last year (HARVEY: EQUALS 2,200 TONNES PER YEAR)

- Recycling fell 18% to 280t compared with 343t in Q2 2016

The Gold Demand Trends Q2 2017 report, which includes comprehensive data provided by Metals Focus, can be viewed at Gold Demand Trends.

News and Commentary

Dow has its first close above 22,000 (Yahoo.com)

Trump Signs Russia Sanctions Bill, But Lays Out His Concerns About the Law (Bloomberg.com)

Man claims to have found first silver piece minted by the U.S. (CTVNews.ca)

Source: Palisade via GoldCore

Turks Panic-Buy The Most Gold Ever In July (ZeroHedge.com)

What Is It About 1906ET That Spooks Precious Metals ‘Traders’? (ZeroHedge.com)

Dollar And Equities Will Plunge Together – While Gold Spikes (DollarCollapse.com)

Wont Be Long Now – Amazon and the New Tech Crash (DailyReckoning.com)

Crypto-currencies are mirroring pre-crash banking systems – Kaminska (FT.com)

Gold Prices (LBMA AM)

03 Aug: USD 1,261.80, GBP 952.41 & EUR 1,064.96 per ounce

02 Aug: USD 1,266.65, GBP 956.83 & EUR 1,069.56 per ounce

01 Aug: USD 1,267.05, GBP 957.76 & EUR 1,072.30 per ounce

31 Jul: USD 1,266.35, GBP 965.59 & EUR 1,079.06 per ounce

28 Jul: USD 1,259.60, GBP 961.96 & EUR 1,075.45 per ounce

27 Jul: USD 1,262.05, GBP 960.29 & EUR 1,076.53 per ounce

26 Jul: USD 1,245.40, GBP 956.72 & EUR 1,071.29 per ounce

Silver Prices (LBMA)

03 Aug: USD 16.47, GBP 12.50 & EUR 13.91 per ounce

02 Aug: USD 16.67, GBP 12.60 & EUR 14.09 per ounce

01 Aug: USD 16.74, GBP 12.67 & EUR 14.17 per ounce

31 Jul: USD 16.76, GBP 12.77 & EUR 14.29 per ounce

28 Jul: USD 16.56, GBP 12.66 & EUR 14.15 per ounce

27 Jul: USD 16.79, GBP 12.77 & EUR 14.34 per ounce

26 Jul: USD 16.37, GBP 12.54 & EUR 14.06 per ounce

Recent Market Updates

– Greenspan Warns Stagflation Like 1970s “Not Good For Asset Prices”

– What Investors Can Learn From the Japanese Art of Kintsukuroi

– Bitcoin, ICO Risk Versus Immutable Gold and Silver

– This Is Why Shrinkflation Is Making You Poor

– Gold A Good Store Of Value – Protect From $217 Trillion Global Debt Bubble

– Why Surging UK Household Debt Will Cause The Next Crisis

– Gold Seasonal Sweet Spot – August and September – Coming

– Commercial Property Market In Dublin Is Inflated and May Burst Again

– Gold Hedges Against Currency Devaluation and Cost Of Fuel, Food, Beer and Housing

– Millennials Can Punt On Bitcoin, Own Gold and Silver For Long Term

– “Time To Position In Gold Is Right Now” says Jim Rickards

– Bloomberg Silver Price Survey – Median 12 Month Forecast Of $20

– “Bigger Systemic Risk” Now Than 2008 – Bank of England

end

Another flash crash in gold at exactly 7:06 last evening as the crooks try to influence gold and silver. All night gold and silver was down but as soon as we approached physical time zones, the metals rebound..they are losing control

(courtesy zero hedge)

It’s 7pm In New York, Do You Know Where Your Precious Metals Manipulators Are?

It appears the machines have found a new pattern to follow…

Last night we pointed out the ‘odd’ – in the sense that nothing amazes us anymore, but still, behavior in precious metals futures markets.

At 1906 ET last night, Silver futures flash-smashed higher, running the day’s high-stops, before plunging back to earth…

Gold futures also followed suit tonight…

This would normally be shrugged off as just another example of the utter farce that global capital markets have become. However, a glance back in recent history at the silver market’s most recent chaos moment – on July 6th – and a ‘funny’ thing stood out!!!

Gold also followed suit that night too…

At exactly 1906 ET on July 6th, Silver futures flash-crashed (some say over 10%, though many data feeds have been subsequently ‘cleansed’ of that sin), before normalizing.

* * *

And sure enough, tonight, at exactly 1906ET once again, ‘someone’ went to town on Silver & Gold futures…

And it even looks like the machines tried to front-run each other a little into the 1906ET mini-flash-crash

So, we ask again, what is it about 1906ET that sends the algos in overdrive? Or is it all just coincidence? Probably nothing, right?

It’s now deja deja vu all over again…

END

Flash crash fails! Let’s see what happens tonight at 7:06

(courtesy zero hedge)

Gold Erases Flash-Crash Losses As Dollar, Bond Yields Slide After Dismal ISM Data

When even the ‘soft’ survey data is disappointing – catching down to collapsing ‘hard’ data – it seems markets can’t ignore reality any longer. While stocks are marginally lower following the collapse in ISM Services, Bond yields and the dollar are tumbling as gold lifts…

The Dolar Index is testing yesterday’s lows (and cycle lows)…

And the 30Y yield is back at two week lows…

And gold has erased all of its flash crash losses overnight…

So let’s see what happens at 1906ET tonight?

end

No transparency whatsoever at the LBMA London’s vaults

(courtesy Ronan Manly/Bullionstar)

Ronan Manly: Little transparency in LBMA’s London vault report

Submitted by cpowell on Wed, 2017-08-02 11:45. Section: Daily Dispatches

7:45a ET Wednesday, August 2, 2017

Dear Friend of GATA and Gold:

This week’s report by the London Bullion Market Association about the gold and silver held in London-area vaults brings little transparency to the issue and even contradicts itself, gold researcher Ronan Manly writes today.

Manly concludes: “The amount of gold in the London LBMA gold vaults (including the Bank of England’s) that is not central bank gold, that is not exchange-traded fund gold, and that is not institutional allocated gold is quite a low number. The actual number is difficult to determine because a) the LBMA will not produce a proper vault report that shows ownership of gold by category of holder, and b) neither will the Bank of England in its gold vault reporting provide a breakdown between the gold owned by central banks and the gold owned by bullion banks.

“So there is still no real transparency in this area — just a faint chink of light into a dark cavern.

“On the topic of London-vaulted silver, there appears to be a lot more silver in the LBMA vaults than even GFMS thought there was. It will be interesting to see how GFMS and the LBMA will resolve their apparent contradiction on the amount of silver stored in the London LBMA vaults.”

Manly’s analysis is headlined “LBMA Gold Vault Data — How Low Is the London Gold Float?” and it’s posted at Bullion Star here:

https://www.bullionstar.com/blogs/ronan-manly/lbma-gold-vault-data-relea…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

Kaminska talks about the splitting of the Bitcoin cryptocurrency and how this a mirroring a pre crash banking system

(courtesy Kaminska/London’s Financial times)

Izabella Kaminska: Crypto-currencies are mirroring pre-crash banking systems

Submitted by cpowell on Wed, 2017-08-02 13:46. Section: Daily Dispatches

By Izabella Kaminska

Financial Times, London

Tuesday, August 1, 2017

https://www.ft.com/content/9b464912-76ae-11e7-90c0-90a9d1bc9691

When bitcoin, the crypto currency, first arrived on the scene in 2009 it sold itself on a simple principle.

Unlike central bank money, the supply of which could be expanded on the whim of a non-democratically elected committee, bitcoin’s supply would remain capped at 21 million coins at any cost. This would be effected by way of a decentralised protocol, making it theoretically impossible for any single authority to override or control it.

This, ultimately, was bitcoin’s promise to the world: a currency manufactured and supported by the users for the users, which no single entity could manipulate, and which no third party was required to intermediate. Understandably the pledge appealed most to those who might describe themselves as hard-money enthusiasts. Their view was that uncontrolled money creation was the probable cause of most economic instability in the world and must therefore be constrained. Bitcoin offered them the perfect conduit for this vision.

More than eight years after bitcoin’s arrival, most of these principles have fallen by the wayside. Bitcoin spawned a litany of copycat systems — each with its own profiteering opportunity for early adopters. It no longer matters, for example, that the system is being engulfed by rogue and untethered private-money creation. Nor does it seem to matter that it’s been a long time since bitcoin could be honestly described as a decentralised system, free of intermediaries

Economies of scale, as is their habit, have ensured only a handful of professional mining outfits and pools control the bitcoin production scene — they can collude oligopolistically if they want. What matters is that the crypto scene’s popularity and profitability are soaring, especially for those who have become the new bitcoin power elite.

Even bitcoin is succumbing to the pressure. As of Tuesday a bitter ideological dispute over how the protocol should scale in the future has led to a breakaway version of the original currency. Because of the way bitcoin is designed, if this breakaway copy gains traction with miners, corporations and users — something we could know within a few hours or days — it could immediately expand bitcoin’s lifetime money supply to 42 million from 21 million.

Dubbed “bitcoin cash,” this money-creating breakaway ironically owes its existence to the more puritanical part of the community, who insist that replica bitcoin systems (known as sidechains) should never be allowed to tie themselves to the core system without limit; that would replicate the conventional and inflationary banking system.

Unsurprisingly, it is the miners, corporations, and intermediaries who support these sidechains: Only by forgoing some of their core principles can they remain profitable in this sector. Bitcoin purists tend to be the staunchest critics of the expanded crypto scene, pointing out that almost every day a new token or coin is being issued into the market on the flawed assumption that full convertibility and liquidity can be guaranteed.

Today’s crypto system is beginning to replicate the pre-crisis financial system of the United Kingdom, when banks — as long as they had acceptable assets to pledge at the central bank — could receive whatever official liquidity they demanded. For everything else, such as self-created assets, there was the wholesale funding market. We know many of these assets were self-valued at entirely fantastical rates. When the wholesale market froze up, only the central bank had the capacity to support them. The purists understand that the crypto scene will not have that saving grace.

That makes the bitcoin fork a judgment-of-Solomon moment. Only a decisive win by either side will prevent bitcoin from splitting itself apart. Who, if anyone, gives way in the event of a standoff will be a telling indicator of what really motivates the community.

END

A must read interview of John Embry talking to Kingworldnews. Embry discusses how gold and silver are gaining traction as the dollar loses its reserves currency status

(courtesy John Embry/Kingworldnews)

Dollar’s loss of reserve status will goose monetary metals, Embry tells KWN

Submitted by cpowell on Wed, 2017-08-02 23:38. Section: Daily Dispatches

7:40p ET Wednesday, August 2, 2017

Dear Friend of GATA and Gold:

Sprott Asset Management’s John Embry tells King World News today that the U.S. dollar may become the primary cause of breakouts in gold and silver as the dollar gradually loses its status as the world reserve currency. Embry’s comments are excerpted at KWN here:

http://kingworldnews.com/john-embry-we-are-about-to-enter-a-period-that-…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

Your early THURSDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight

1 Chinese yuan vs USA dollar/yuan STRONGER 6.7222(REVALUATION NORTHBOUND /OFFSHORE YUAN MOVES WEAKER TO ONSHORE AT 6.7283/ Shanghai bourse CLOSED DOWN 12.13 POINTS OR 0.37% / HANG SANG CLOSED DOWN 76,37 POINTS OR 0.28%

2. Nikkei closed DOWN 50.78 POINTS OR .25% /USA: YEN FALLS TO 110.48

3. Europe stocks OPENED MIXED TO RED ( /USA dollar index RISES TO 93.02/Euro DOWN to 1.1838

3b Japan 10 year bond yield: FALLS TO +.069%/ GOVERNMENT INTERVENTION !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 114.34/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD FINALLY IN THE POSITIVE/BANK OF JAPAN LOSING CONTROL OF THEIR YIELD CURVE AS THEY PURCHASE ALL BONDS TO GET TO ZERO RATE!!

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 49.61 and Brent: 52/34

3f Gold DOWN/Yen UP

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil UP for WTI and UP for Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund FALLS TO +.485%/Italian 10 yr bond yield DOWN to 2.016%

3j Greek 10 year bond yield FALLS to : 5.483???

3k Gold at $1267.00 silver at:16.54 (8:15 am est) SILVER BELOW RESISTANCE AT $18.50

3l USA vs Russian rouble; (Russian rouble DOWN 2/100 in roubles/dollar) 60.58-

3m oil into the 49 dollar handle for WTI and 52 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation (already upon us). This can spell financial disaster for the rest of the world/China forced to do QE!! as it lowers its yuan value to the dollar/GOT A SMALL SIZED REVALUATION NORTHBOUND

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 110.48 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 0.9696 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1477 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now POSITIVE territory with the 10 year FALLING to +0.483%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.2549% early this morning. Thirty year rate at 2.8390% /POLICY ERROR)GETTING DANGEROUSLY HIGH

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

(courtesy Jim Reid/Bloomberg/Deutsche bank/zero hedge)

Tech Stumble Drags Global Markets Lower; All Eyes On The BOE

E-mini futures are fractionally lower this morning (0.08%) after Apple’s surge helped the DJIA climb above 22,000 for the first time on Wednesday; Global shares declined for the first time in 4 days pressured by tech stocks: Asian shares fell, while Europe pared opening losses to trade unchanged.

Global markets fell on Thursday, as the MSCI All-Country World Index declined for the first time in four days, led by a tumble in tech shares as investors locked in recent gains after Wall Street’s Dow Jones Industrial Average broke the 22,000 barrier for the first tim. Despite the Dow’s record close above 22,000, caution crept into Asian trading as the MSCI’s index of Asia-Pacific shares ex-Japan fell 0.7%, with China, HK, Japan and Australia all down, while South Korean stocks plunged 1.7%, the biggest drop since November on plans to raise taxes for big corporations. The Kospi index fell as much as 2.2 percent, the most since Nov. 9. Samsung Electronics Co., which has the largest weighting on the index, dropped 2.5 percent. Japan’s Topix index closed little changed near a two-year high as investors parse through recent earnings results. Australia’s S&P/ASX 200 Index lost 0.2 percent as Rio Tinto shares tracked their London stock lower. Hong Kong’s Hang Seng Index was down 0.3 percent and the Shanghai Composite Index fell 0.4 percent.

“We haven’t seen a major correction in tech shares so far this year so they may be hitting a speed bump,” said Nobuhiko Kuramochi, chief strategist at Mizuho Securities.

In Europe, stock markets opened broadly lower, with Germany’s DAX slipping 0.6 percent and France’s CAC 0.4 percent lower, however initial losses have been since recouped with energy shares dragging as investors digested a rebound in American oil output that had crude prices fluctuating. Germany’s DAX falls 0.5%, testing 3-month lows hit on Tuesday, with heavyweight Siemens dropping 2.8% after posting mixed quarterly results. Furthermore, Germany’s July composite PMI slid to 54.7, the lowest since September, vs the flash reading of 55.1, well below the euro-area July composite PMI at 55.7. Data show Germany trailed euro-area peers for first time in 12 years. Technology stocks in Europe slipped 0.3 percent. “I don’t see too much in the way of downside for European stocks because economic data is strong – take a look at the Italian data today,” said Michael Hewson, chief market analyst at CMC Markets. The British pound strengthened before a rates decision.

The Bloomberg Dollar Spot index held near a 15-month low ahead of Friday’s U.S. payrolls data. In the overnight session, both the Aussie and Kiwi slid against the dollar as investors prepared for the RBA statement Friday, and RBNZ meeting on Aug. 10, as the dollar keeps trying to recover from a 31-month low against euro. In Europe, the pound rose to the highest level since September against the dollar amid bets for a hawkish tilt in BOE’s rates outlook. The dollar inched away from a 15-month low versus a basket of currencies, but was still looking wobbly due to doubts about whether there will be another U.S. interest rate rise this year. The dollar index, which measures the greenback’s value against a basket of six major currencies, rose about 0.12 percent to 92.951. On Wednesday, it slid to 92.548, its weakest level since May 2016.

Of note, the ruble extended its drop against the dollar to a sixth day as oil fell and U.S. President Donald Trump signed into law Russian sanctions aimed at squeezing financing of the country’s energy industry. The Russian currency dropped 0.2% to 60.72 per dollar, taking losses over the past six sessions to 2.4%. While immediate market impact of the new law is “negligible,” and most of the longer term impacts are “theoretical and debatable,” some negative market impact due to worsened perceptions of Russian political risk for international investors is still possible, Sberbank CIB analysts Cole Akeson and Andrey Kuznetsov write in research note.

European government bond yields edged slightly higher, with Germany’s 10-year yield rising less than one basis point to 0.49% . The yield on 10-year Treasuries dipped one basis point to 2.26%. The U.K.’s FTSE 100 Index gained less than 0.1 percent.

As Bloomberg notes, while corporate results have been largely dominating sentiment this week, Friday’s report on the U.S. employment market may provide the next inflection point. Investors are looking for clues on the strength of the world’s largest economy and the Federal Reserve’s next policy move, not least to see if the dollar will get any respite.

“Despite the recent pull back, the dollar remains broadly overvalued, and the starting point matters,” UBS strategists including Manik Narain wrote in a client note. “Expensive valuation reduces the likelihood of a further broad dollar rally.”

Today’s main event is the BoE inflation report and rate decision (no change overwhelmingly expect). The focus is likely to be on how the members voted and clues on inflation and rates outlook. Back in the June meeting, the 5-3 vote was more hawkish than expected, partly given growing concerns that the inflation overshoot was more pronounced than expected. Since then, macro data has not changed much, but Q2 CPI was actually more in-line with the BOE May inflation report, which should partly reduce the weight of the hawkish argument on inflation. Further, the composition of the committee is also changing, with Silvana Tenreyro now replacing Kisten Forbes who previously favoured a hike. For now, analysts do not expect BOE to tighten rates until Brexit related uncertainties have been sufficiently reduced. We shall get more clues shortly.

In commodities, West Texas Intermediate crude increased 0.4 percent to $49.78 a barrel after falling as much as 1 percent. Gold fell 0.3 percent to $1,263.44 an ounce, heading for a fourth day of declines after a second day in a row of slamdowns just after 7pm ET.

Today’s economic data include initial jobless claims, durable goods orders, Markit PMI readings. Earnings from Kraft Heinz, Allergan, Viacom Inc. and Yum! Brands , Duke Energy are due.

Bulletin Headline Summary from RanSquawk

- European bourses pare opening losses to trade relatively mixed.

- GBP rises after better than expected Services PMI.

- Looking ahead, highlights include the BoE QIR.

Market Snapshot

- S&P 500 futures down 0.2% to 2,469.75

- STOXX Europe 600 down 0.2% to 377.93

- MSCI Asia down 0.6% to 160.49

- MSCI Asia ex Japan down 0.7% to 527.52

- Nikkei down 0.3% to 20,029.26

- Topix down 0.03% to 1,633.82

- Hang Seng Index down 0.3% to 27,531.01

- Shanghai Composite down 0.4% to 3,272.93

- Sensex down 0.4% to 32,337.95

- Australia S&P/ASX 200 down 0.2% to 5,735.12

- Kospi down 1.7% to 2,386.85

- German 10Y yield rose 0.9 bps to 0.495%

- Euro down 0.2% to 1.1837 per US$

- Italian 10Y yield fell 0.4 bps to 1.723%

- Spanish 10Y yield rose 2.1 bps to 1.479%

- Gold spot down 0.4% to $1,261.58

- Brent Futures unchanged at $52.36/bbl

- U.S. Dollar Index up 0.2% to 92.97

Top Headlines

- Germany’s economy slowed more than initially estimated at the start of the third quarter, leaving it trailing the euro region’s other large nations

- Britain’s economy has moved into a phase of “steady but sluggish” growth and is at risk of a further slowdown, according to IHS Markit.

- Iceland’s central bank is ready and willing to lower its guard against fast cash with the country’s balance sheet on a firm footing and a stimulus unwinding underway in global capital markets

- China Tries to Calm U.S. Trade Spat While Readying Retaliation

- Fed Front-Runner Cohn Could Be Trump’s Bulldog in Egghead World

- Tronox Sells Alkali Chemicals to Genesis Energy for $1.325B

- Guggenheim Is Said to Be in Fund Sale Talks With Invesco

- Costco July Comp Sales up 6.2%, Est. Up 5%

- GM China July Vehicle Sales Rise 6.3% on Year

- Venator Materials Prices IPO at $20.00/Share: Huntsman Corp

- Glaxosmithkline Moves China Neuroscience Research to U.S

- Fox Is Said in Talks With Ion Media to Operate Local TV Stations

- Goldman Highlights Call Strategy That Has Done ‘Unusually Well’

- Sibanye May Cut 7,400 Jobs as It Restructures Gold Operations

- U.K. Shows ‘Steady But Sluggish’ Growth as Services Expand

The momentum from the DJIA’s 22,000 milestone was lost on Asia as the region traded negative across the board, with sentiment dampened amid earnings and a miss by the Chinese Caixin Services PMI:

- Chinese Caixin Services PMI (Jul) 51.5 vs. Exp. 51.9 (Prey. 51.6). (Newswires)

ASX 200 (-0.16%) was subdued by commodity names with Rio Tinto (-2.49%) shares down after the Co. missed on H1 underlying profit, while Nikkei 225 (-0.25%) was also lower and eyed a test of the 20,000 level to the downside. KOSPI (-1.68%) was the worst performer on tighter regulation to cool the housing sector, coupled with continued geopolitical concerns after the US told its citizens to leave North Korea by September 1st amid a travel ban and reports the US tested an intercontinental ballistic missile from California, which officials denied was in response to provocation from North Korea. Hang Seng (-0.28%) and Shanghai Comp (-0.37%) also conformed to the down beat tone following the miss on Chinese Services PMI and the PBoC cutting its liquidity injection by half. Finally, 10yr JGBs only saw minimal gains despite the dampened risk sentiment in the region, with upside capped by a weaker 10yr inflation-indexed auction.

Top Asian News

- The Conglomerate That Troubles China

- Korea Stocks Slump Most This Year as Rally Wanes on Moon Reforms

- Copper’s Rally Has Room to Run as Chinese Demand Accelerates

- Taiwan Futures Plunge 10 Percent After Brokerage’s Algo Error

- Global Bond Selloff Risk Puts Japan’s Chiba Bank on Defense

- Hong Kong’s Tiny Flats Pile Up as Property Market Dangers Grow

- Kishida Exits Japan Cabinet, Paving Way for Him to Challenge Abe

- Macquarie, GIC Bid $1.3 Billion for Philippine Renewable Stake

European bourses trade mixed. Sector specific energy continues to lag despite the recent bullish pressure in oil, with European equity earnings being the large driver in markets. The Dax companies highlighted the morning, with earnings form the likes of Deutsche Telekom, Siemens and Adidas all influencing the continued to see down days, with a test of 1255.00 seen overnight. German major. Deutsche Telekom’s beat in Adj. EBITA and revenues leave the telecoms giant to outperform in the Dax, however, a weak report from Siemens leaves the Dax in the red. European Composite and Services PMI data has largely been ignored by markets, with EGBs finding little direction. Peripheral debt have recovered following firm results in today’s Spanish auction with the GE/ES spread tightening slightly.

Top European News

- Macron Vows Millionaire Minister Will Cut Worker Protection

- UniCredit CEO Defies Doubters With Surprise Profit Surge

- French Budget Minister Rejoices at Neymar’s Taxes Prospect

- ECB Says Incoming Data Point to Solid, Broad-Based Growth Ahead

- Nomura’s Buckley Sees Multiple Reasons for BOE Rate Hike

- Next’s Shares Surge as Sales Rebound Unnerves Short Sellers

In currencies, the lack of price action from today’s European services and composite data is evident in the anticipation on the BoE. FX trade has been subdued through the European morning, with much of the volatility seen overnight and through yesterday’s US trade. GBP did see a slight bid following the slightly higher than expected Market Services and PMI data, aided by the +0.30% GDP growth. GBP/USD broke through yesterday’s high tripping some stops on the way through.

In comodities, a recent bid has been seen in WTI and Brent crude futures with no fundamental news. However, the price has broken yesterday’s high of 49.65 getting closer towards the USD 50/barrel, which may be a target to test. Global demand for gold fell 14% in the first half of this year, largely due to a decline in the purchasing of the yellow metal by exchange traded funds.

Looking at the day ahead, Thursday’s will round out July PMI data for the week. In Europe we get the final July services and composite PMIs for France , Germany and the Eurozone as well as a first look at UK’s service and composite PMI and other European countries. Thereafter, focus should shift to the BoE policy meeting (no change expected). Over in the US we should also get jobless claims data followed by the ISM non-manufacturing composite for July (56.9 expected). Thereafter we will get factory orders data as well as the final readings for durable and capital goods orders for June. Onto other events, the ECB will publish its economic bulletin. Notable US companies reporting include: Allergan, Viacom, Aetna, Kraft, Kellogg and ICE. Notable European companies reporting include: Siemens, Deutsche Telecom, ING and Adidas

US Event Calendar

- 7:30am: Challenger Job Cuts YoY, prior -19.3%

- 8:30am: Initial Jobless Claims, est. 243,000, prior 244,000; Continuing Claims, est. 1.96m, prior 1.96m

- 9:45am: Bloomberg Consumer Comfort, prior 48.6

- 9:45am: Markit US Services PMI, est. 54.2, prior 54.2; Markit US Composite PMI, prior 54.2

- 10am: ISM Non-Manf. Composite, est. 56.9, prior 57.4

- 10am: Factory Orders, est. 3.0%, prior -0.8%; Factory Orders Ex Trans, prior -0.3%

- Durable Goods Orders, est. 0.0%, prior 6.5%; Durables Ex Transportation, prior 0.2%

- Cap Goods Orders Nondef Ex Air, prior -0.1%; Cap Goods Ship Nondef Ex Air, prior 0.2%

DB’s Jim Reid concludes the overnight wrap

In the first 41 years of my life I bought one car at a total cost of around £12k. When I saw some of my peers and colleagues spend multiples of that on a regular basis I shook my head and wondered why you ever needed anything more extravagant to get you from A to B. I also made a mental note to rub it into these people when I retired many years before they did due to my frugal car habit. Then I got married, then I got a dog, then I had my first child and now the twins are coming in the next month. As a result yesterday saw me buy my second car in two years!! One for me and now a big family one. In doing so I broke another of my golden rules and that is to never buy a brand new car. Sigh! Part of the reason is that there is only one car we like with 3 isofixes in one row and that’s the Audi Q7. However only the latest model has this configuration so it could only be around 18 months old max. We did look at second hand ones but then a dealer gave us a spectacular deal if we took out finance on a new one! To be honest it was so crazy that it makes me particular worried about how easy and cheap it is to buy a car on credit in this country. It really does leave you a little worried about consumer debt. Anyway let’s hope I’m 3 and done. I’ll leave it to you to decide whether I mean kids or cars. On balance I think my wife would want it to be the first and me the second.

Maybe one shouldn’t be so worried about cheap and plentiful credit when the US equity market is setting a new record of some kind virtually every day. Or maybe that’s when you should be worried. Yesterday saw the Dow (+0.3%) clear 22000 for the first time, meaning that Mr Trump can now add it to his collection of stock market landmarks on his watch. The Dow first touched 19000 just over a week after his election victory. The S&P 500 (+0.05%) edged higher but both were slightly flattered by Apple (+4.73%) after its optimistic guidance the previous evening. Of the S&P 500, 299 stocks actually declined.

Interesting Bloomberg reported that yesterday marked 3 months (70 trading sessions) since the S&P 500 increased by more than 1% in any one day. So this leg of the rally has been pretty steady but relentless. This is the longest such stretch since the 79-day stretch back between November 2006 – March 2007. As we’ll see below, European equities aren’t quite keeping up at the moment and this morning our European equity strategist Sebastian Raedler highlights that European equities have fallen by around 5% from their May peak. He expects the tactical pull-back to continue to 360 on the Stoxx 600 (around 5% below current levels), as Euro area PMIs fade from elevated levels and euro strength weighs on European earnings. He re-iterates his long-standing year-end target of 375 on the Stoxx 600 (around 1% below current levels), as lower projected EPS growth (8% versus the previous forecast of 10% and consensus at 12.5%) is offset by a higher P/E target (14.6x, up from the previous target of 14.2x, due to our economists’ recent growth upgrade). He also lowers his FTSE 100 target (from 7,750 to 7,500, 1% upside from current levels) and raises his DAX target (from 11,800 to 12,400, 1% above current levels). See the following link for more details.

Moving onto today, we have the services PMIs and ISM to look forward to (preview at the end). Elsewhere we have the BoE inflation report and rate decision (no change overwhelmingly expect). The focus is likely to be on how the members voted and clues on inflation and rates outlook. Back in the June meeting, the 5-3 vote was more hawkish than expected, partly given growing concerns that the inflation overshoot was more pronounced than expected. Since then, macro data has not changed much, but Q2 CPI was actually more in-line with the BOE May inflation report, which should partly reduce the weight of the hawkish argument on inflation. Further, the composition of the committee is also changing, with Silvana Tenreyro now replacing Kisten Forbes who previously favoured a hike. For now, DB’s strategist do not expect BOE to tighten rates until Brexit related uncertainties have been sufficiently reduced. We shall get more clues this afternoon.

Onto the markets, US bourses continue to edge ahead as noted earlier. Within the S&P, losses in telco (-1.3%) and real estate (-0.5%) were broadly offset by gains in the IT, utilities and industrials sectors. The Stoxx 600 fell 0.4%, impacted by the rising EUR as well as weakness in materials and banks (StanChart -6%; SocGen -4% after results). Across the region, markets also softened, with the DAX (-0.6%), FTSE 100 (-0.2%), CAC (-0.4%) and Italian FTSE MIB (-0.2%). Turning to currency, the Euro continues to strengthen against the greenback, up 0.5% yesterday to another 30 month high. Sterling gained 0.2%, while the US dollar index continues to fall (-0.2%).

Government bond yields were little changed post Tuesday’s larger moves lower. USTs (2Y: unch; 10Y: -1bps), Bunds (2Y: +1bp; 10Y: -1bps), BTPs (2Y: unch; 10Y: unch) and OATs (2Y: unch; 10Y: unch) were broadly flat although Gilt yields were slightly higher (2Y: +2bp; 10Y: +2bps).

In commodities, WTI oil gained 0.9%, following the latest EIA report pointing to lower US crude inventories. This somewhat contradicts reports of higher oil supply from the American Petroleum Institute report and Reuters July survey the day before. As we type, oil has dipped 0.3% this morning. Elsewhere, precious metals were broadly unchanged (Gold -0.2%; Silver -0.1%) while industrial metals were slightly higher (Copper +0.1%; Aluminium +1%).

Away from the markets, two Fed Chiefs have updated the market on their latest thinking. San Francisco Fed Chief Williams has said overnight that inflation should close in on the Fed’s 2% target “within the next year or two”, while Cleveland’s Fed Chief Mester sees it approaching that level “over the next year”, but wanted to see more data (on Fed’s preferred measure, the PCE deflator, inflation is 1.4% currently). On balance sheet unwind, Williams acknowledged that to keep the economy on a sustainable path of growth, we need to gradually reduce the monetary stimulus and that it will be appropriate to start unwinding the balance sheet this autumn, noting the normalisation process should take four years. On the interest rates outlook, both reiterated the gradual path FOMC has communicated is appropriate and Williams thought the ‘new normal’ interest rate is around 2.5%.

Elsewhere, on the US debt ceiling, a leading House conservative has backed away from his earlier demands that any increase should be paired with steep spending cuts. Now, Republican Meadows just wants to “get it done sooner rather than later”. Turning to tax reform, expect the news-flow to slowly build but in an interview yesterday, representative Yoho said “there is no detail (on the tax reform)…it is a problem…”. For now, we wait and see. The market will hope it doesn’t end up being a replica of the healthcare bill in terms of ability to pass.

This morning Asian equity markets have broadly softened, the Kospi fell 1.5% impacted by Samsung (-3%) and property shares given additional government measures to cool the housing market. Elsewhere, the Nikkei (-0.3%), Hang Seng (-0.2%) and two of the Chinese bourses were down ~0.2%.

Before we take a look at today’s calendar, we wrap up with other data releases from yesterday. In the US, the headline ADP employment change for July was lower than expectations at 178k (vs. 190k expected), although the underlying trends are still solid given the June figure has been revised upwards by 33k. With US growth having picked up in 2Q, but inflation continuing to disappoint, DB’s Peter Hooper updated his outlook for the US economy and sees growth ahead slightly softer than prior expectations and the pace of rate hikes slightly slower. More details here. Over in Europe, the Eurozone PPI for June was in line with expectations at -0.1% mom (vs. -0.1% expected) and 2.5% yoy (vs. 2.5% expected). However, UK’s CIPS construction PMI for July missed expectations at 51.9 (vs. 54 expected), partly reflecting the uncertainty associated with Brexit.

Looking at the day ahead, Thursday’s will round out July PMI data for the week. In Europe we get the final July services and composite PMIs for France (55.7 expected for composite), Germany (55.1 expected for composite) and the Eurozone (55.8 expected for composite) as well as a first look at UK’s service and composite PMI (53.6 and 53.8 expected respectively) and other European countries. Thereafter, focus should shift to the BoE policy meeting (no change expected). Over in the US we should also get jobless claims data followed by the ISM non-manufacturing composite for July (56.9 expected). Thereafter we will get factory orders data as well as the final readings for durable and capital goods orders for June. Onto other events, the ECB will publish its economic bulletin. Notable US companies reporting include: Allergan, Viacom, Aetna, Kraft, Kellogg and ICE. Notable European companies reporting include: Siemens, Deutsche Telecom, ING and Adidas

3. ASIAN AFFAIRS

i)Late WEDNESDAY night/THURSDAY morning: Shanghai closed DOWN 12.13 POINTS OR 0.37% / /Hang Sang CLOSED DOWN 76.37 POINTS OR 0.28% The Nikkei closed DOWN 50.78 POINTS OR .25%/Australia’s all ordinaires CLOSED DOWN 0.37%/Chinese yuan (ONSHORE) closed UP at 6.7222/Oil UP to 49.61 dollars per barrel for WTI and 52.34 for Brent. Stocks in Europe OPENED MIXED , Offshore yuan trades 6.7283 yuan to the dollar vs 6.7222 for onshore yuan. NOW THE OFFSHORE IS WEAKER TO THE ONSHORE YUAN/ ONSHORE YUAN STRONGER (TO THE DOLLAR) AND THE OFFSHORE YUAN IS MUCH WEAKER TO THE DOLLAR AND THIS IS COUPLED WITH THE SLIGHTLY STRONGER DOLLAR. CHINA IS NOT HAPPY TODAY

3a)THAILAND/SOUTH KOREA/NORTH KOREA

NORTH KOREA/USA

b) REPORT ON JAPAN

end

c) REPORT ON CHINA

CHINA/INDIA

Last week we brought you the story about a spat between India and China concerning lands on their border.

China lambastes India claiming that they had better leave Chinese land or face war

(courtesy zero hedge)

China Threatens India Over Border: “Leave Chinese Land Or Face War”

While the world’s eyes are focused on Syria, Russia, Ukraine, and North Korea; there is another – much more tense – fight between two nuclear powers that is getting far too little attention. The world’s two most populous nations, China and India, have been engaged in a border dispute for decades but in recent months it has flared once again with a Chinese Ministry of Defense official now warning explicitly that Indian troops must leave the contested Doklam area if they do not want war.

The latest standoff started more than a month ago after Chinese troops started building a road on a remote plateau, which is disputed by China and Bhutan. Indian troops countered by moving to the flashpoint zone to halt the work, with China accusing them of violating its territorial sovereignty and calling for their immediate withdrawal.

China then added a large number of troops to the region:

“The crossing of the mutually recognised national borders on the part of India… is a serious violation of China’s territory and runs against the international law,” Chinese defence ministry spokesman Wu Qian told a press conference quoted by AFP, adding that “the determination and the willingness and the resolve of China to defend its sovereignty is indomitable, and it will safeguard its sovereignty and security interests at whatever cost.”

He also said that “border troops have taken emergency response measures in the area and will further step up deployment and trainings in response to the situation,” without giving any details about the deployment.

And now, as RT reports, during a heated TV debate between a retired Indian Army major general and now defense commentator, Ashok Mehta, and the director of the Chinese Defense Ministry’s Center for International Security Cooperation, Senior Colonel Zhou Bo; tempers frayed.

Speaking first, Mehta fired off a lengthy yet passionate tirade, accusing the Chinese of fanning anti-Indian sentiments in an overly aggressive way.

“Chinese media, think tanks, Xinhua, Global Times, PLA Daily have written the most aggressive and most belligerent stories about threatening India, taking India to war, opening a two-front conflict, teaching India a lesson,” the former general complained.

“I mean, that kind of language is not being used in India!” Mehta added.

Asked by the news anchor if he could provide any proof and name specific Chinese articles featuring warmongering rhetoric, the Indian expert failed to cite any, but instead recalled his professional background.

Zhao interrupted…

“General, you have been talking too much! This is not the right way of having this conversation,”

“Let me just use a few seconds – you [Indian troops] are on Chinese territory, so if you do not want a war, you’ve got to go away from Chinese territory,” the senior colonel remarked.

In a statement on Wednesday, Beijing said Indian troops were still present on Chinese territory, and that China had acted cautiously, demanding that Delhi pull out its forces.

“But the Indian side not only has not taken any actual steps to correct its mistake, it has concocted all sorts of reasons that don’t have a leg to stand on, to make up excuses for the Indian military’s illegal crossing of the border,” the Chinese Foreign Ministry said, as cited by Reuters.

As we noted previously, this isn’t the first time that these two nations have been at each other’s throats over their borders. In 1962 their armies clashed, leading to defeat of the Indian army, and thousands of casualties on both sides. Based on the rhetoric coming out of Beijing’s state sponsored media, it appears that China is willing to replicate that conflict.

An Angry Beijing Responds: “We Will Never Dance To Trump’s Tune”

With just one day to go until the Trump administration launches the first salvo in what could develop into a full-scale trade war between the US and China, there is the issue of a diplomatic (hopefully) resolution of escalating situation in North Korea, one which Citi today said is “increasingly likely” to involve military action. On this issue, China is becoming increasingly displeased with Trump’s relentless twitter badgering, and as AFP reports, “Trump-style outbursts are no way to get China to bend to the US’s will.”

The animosity between D.C. and Beijing has been building up for months, as the two capitals have long traded blame over the failure to rein in the North, but last week’s breakthrough in North Korean missile technology has raised the specter of a strike by Pyongyang on American cities, escalating the rhetoric.

“I am very disappointed in China,” President Donald Trump tweeted after the North boasted last week that the entire mainland US was within range of its intercontinental ballistic missiles. “Our foolish past leaders have allowed them to make hundreds of billions of dollars a year in trade, yet they do NOTHING for us with North Korea, just talk.”

While China – North Korea’s main trade partner and ally – has repeatedly countered that it does not hold the key to the crisis and has rejected Trump’s attempts to link the issue to the trade relationship, keeping official responses to Trump’s 140-character outbursts restrained, state media has been less muted.

“Trump is quite a personality,” an opinion piece published Monday by the Xinhua state news agency said. “But emotional venting cannot become a guiding policy for solving the nuclear issue … and even less should (the US) stab China in the back.”

It’s not just Trump who has repeatedly urged China to use its economic sway over North Korea to curb the regime’s nuclear program, even as Beijing insists dialogue is the only practical way forward. Recently Rex Tillerson derided China and Russia as “economic enablers” that bear “unique and special responsibility” for the growing threat posed by the North. And the US’s ambassador to the United Nations, Nikki Haley, spurned a UN response to the latest ICBM launch in favor of bomber flights and missile-defense-system tests, saying the time for talk on North Korea was “over.”

Such admonishments will not change the way China operates, analysts say.

“Trump might be brash and have an ‘in your face’ blunt style, but Beijing’s approach to Washington stays relatively the same,” Xu Guoqi, a China-US relations expert at the University of Hong Kong, told AFP.

“While Trump tweets his positions to the world, Beijing keeps its cards closer to its chest. (China) will never dance to Trump’s tune.” And with “today’s America weaker and more isolated in the world,” China has even less reason to respond, he said.

Meanwhile, Beijing authorities have reacted with caution to Trump’s unpredictable remarks, which have ranged from describing the country as a “currency manipulator” to calling President Xi Jinping “a very good man.” Relations had warmed following Trump’s pledge to honor the key “One China” policy and Xi’s visit to Trump’s Mar-a-Lago estate in Florida this April, but they have since soured again over North Korea.

Worse, if the US does not ease off against an implacable China, observers believe a deterioration is inevitable. “If the Americans continue to blame China while shifting away from its own obligation to defuse the crisis, the two powers are likely to have more quarrels,” said Zhong Zhenming, a China-US relations expert at Shanghai’s Tongji University. “(This is) exactly the result Pyongyang hopes to see,” he told AFP.

* * *

And while we await for the official announcement of Trump’s trade probe into China’s intellectual property and trade practices, it already took steps to further antagonize Beijing when in June the US slapped unprecedented sanctions on a Chinese bank accused of laundering North Korean cash after Trump tweeted that China’s efforts to curtail North Korea’s nuclear program had “not worked out.”

Still, some analysts believe Trump would stop short of following through on repeated threats to start a trade war, his main and perhaps last bargaining chip: “Neither China nor America could afford a trade war,” Zhong said.

Perhaps, but to the increasingly irrational White House, this may be the only option. An editorial in the state-run Global Times, a nationalistic tabloid, warned that the US would lose in a trade dispute with China, which as the top holder of US Treasury bonds “is actually supporting the dollar.”

“Washington had better not threaten China with trade since China has the tools to safeguard its economic interests,” it said.

4. EUROPEAN AFFAIRS

UK/BANK OF ENGLAND

The pound plunges after the Bank of England votes to keep rates unchanged and at record lows. However the Bank cut growth forecast.

(courtesy zero hedge)

Pound Plunges After BOE Votes 6-2 To Keep Rates Record Low, Cuts Growth Forecast

The whispers about a potential rate hike by the recently hawkish BOE ended up being wrong, when moments ago the Bank of England announced that in a 6-2 decision it kept rates unchanged at 0.25%, largely as expected. Saunders and McCafferty dissented in favor of an immediate interest-rate increase, with Haldane refusing to join the dissenters.

In separate unanimous decisions, the central bank also kept its bond purchase programs unchanged at GBP10BN and GBP435BN for corporate and government bonds respectively.

MPC holds #BankRate at 0.25%, maintains government bond purchases at £435bn and corporate bond purchases at £10bn.

The pound tumbled on the news…

… sliding as low as 1.3158, a 0.5% drop, as did 10Y Gilt yileds.

While the decision was largely as expected, what has mostly hit the pound is the BOE’s cut of its 2017 GDP forecast to 1.7%, and the trim of 2018 from 1.7% to 1.6%. It also slashed wage forecasts – the bank now sees 2018 wage growth at 3% now (vs. 3.5% in May).

The BOE also announced that it would end term funding drawdown in February 2018 – this may have a small impact upon long term OIS.

As the cable plunged, the FTSE 100 index rose as much as 0.5%, testing its 50-DMA, on the back of the BOE’s dovish U-turn.

The BOE did caution again, however, that “if the economy follows a path broadly consistent with the August central projection, then monetary policy could need to be tightened by a somewhat greater extent over the forecast period than the path implied by the yield curve underlying the August projections.” So far that’s not happening.

The monetary policy statement is below:

The Bank of England’s Monetary Policy Committee (MPC) sets monetary policy to meet the 2% inflation target, and in a way that helps to sustain growth and employment. At its meeting ending on 2 August 2017, the MPC voted by a majority of 6-2 to maintain Bank Rate at 0.25%. The Committee voted unanimously to maintain the stock of sterling non-financial investment-grade corporate bond purchases, financed by the issuance of central bank reserves, at £10 billion. The Committee voted unanimously to maintain the stock of UK government bond purchases, financed by the issuance of central bank reserves, at £435 billion. The Committee voted unanimously to close the drawdown period for the Term Funding Scheme (TFS) on 28 February 2018, as envisaged when the scheme was introduced.

The MPC’s overall assessment of the outlook for inflation and activity in the August Inflation Report is broadly similar to that in May. In the MPC’s central forecast, GDP growth remains sluggish in the near term as the squeeze on households’ real incomes continues to weigh on consumption. Growth then picks up to just above its reduced potential rate over the balance of the forecast period. Net trade and business investment firm up, and consumption growth recovers in line with modestly rising household incomes. Net trade is bolstered by strong global growth and the past depreciation of sterling. The combination of high rates of profitability, especially in the export sector, the low cost of capital and limited spare capacity supports investment by UK firms over the forecast period, offsetting the effect of continued uncertainties around Brexit.

CPI inflation rose to 2.6% in June from 2.3% in March, as expected. The MPC expects inflation to rise further in coming months and to peak around 3% in October, as the past depreciation of sterling continues to pass through to consumer prices. Conditional on the current market yield curve, inflation is projected to remain above the MPC’s target throughout the forecast period. This overshoot reflects entirely the effects of the referendum-related falls in sterling. As the effect of rising import prices on inflation diminishes, domestic inflationary pressures gradually pick up over the forecast period. As slack is absorbed, wage growth is projected to recover. In addition, margins in the consumer sector, having been squeezed by the pickup in import prices, are projected to be rebuilt. Consequently, inflation remains at a level slightly above the 2% target.

As in previous Reports, the MPC’s projections are conditioned on the average of a range of possible outcomes for the United Kingdom’s eventual trading relationship with the European Union. The projections also assume that, in the interim, households and companies base their decisions on the expectation of a smooth adjustment to that new trading relationship. Other important judgements include: that the lower level of sterling continues to boost consumer prices broadly as projected, and without adverse consequences for inflation expectations further ahead; that regular pay growth remains modest in the near term but picks up over the forecast period; and that subdued household spending growth is largely balanced by a pickup in other components of demand.

Monetary policy cannot prevent either the necessary real adjustment as the United Kingdom moves towards its new international trading arrangements or the weaker real income growth that is likely to accompany that adjustment over the next few years. Attempting to offset fully the effect of weaker sterling on inflation would be achievable only at the cost of higher unemployment and, in all likelihood, even weaker income growth. For this reason, the MPC’s remit specifies that, in exceptional circumstances, the Committee must balance any trade-off between the speed at which it intends to return inflation sustainably to the target and the support that monetary policy provides to jobs and activity. Through most of the forecast period, the economy operates with a small degree of spare capacity and CPI inflation is well above the target. By the end of the forecast, that trade-off is eliminated. Spare capacity is fully absorbed, and inflation remains above the target.

The Committee judges that, given the assumptions underlying its projections including the closure of the drawdown period of the TFS, and allowing for the effects of the recent prudential decisions of the Financial Policy Committee and the Prudential Regulation Authority, some tightening of monetary policy would be required to achieve a sustainable return of inflation to the target. Specifically, if the economy follows a path broadly consistent with the August central projection, then monetary policy could need to be tightened by a somewhat greater extent over the forecast period than the path implied by the yield curve underlying the August projections.