GOLD: $1275.40 DOWN $4.75

Silver: $16.95 DOWN 27 cents

Closing access prices:

Gold $1275.40

silver: $16.95

SHANGHAI GOLD FIX: FIRST FIX 10 15 PM EST (2:15 SHANGHAI LOCAL TIME)

SECOND FIX: 2:15 AM EST (6:15 SHANGHAI LOCAL TIME)

SHANGHAI FIRST GOLD FIX: $1293.86 DOLLARS PER OZ

NY PRICE OF GOLD AT EXACT SAME TIME: $1279.85

PREMIUM FIRST FIX: $14.01(premiums getting smaller)

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

SECOND SHANGHAI GOLD FIX: $1285.00

NY GOLD PRICE AT THE EXACT SAME TIME: $1279.00

Premium of Shanghai 2nd fix/NY:$6.00 PREMIUMS GETTING smaller)

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

LONDON FIRST GOLD FIX: 5:30 am est $1276.35

NY PRICING AT THE EXACT SAME TIME: $1276.30

LONDON SECOND GOLD FIX 10 AM: $1275.60

NY PRICING AT THE EXACT SAME TIME. 1276.95 ??

For comex gold:

NOVEMBER/

NOTICES FILINGS TODAY FOR OCT CONTRACT MONTH: 110 NOTICE(S) FOR 11000 OZ.

TOTAL NOTICES SO FAR: 966 FOR 96,600 OZ (3.004TONNES)

For silver:

NOVEMBER

7 NOTICE(S) FILED TODAY FOR

35,000 OZ/

Total number of notices filed so far this month: 863 for 4,315,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: $7174 bid /$7199 offer up $244.00 (MORNING)

BITCOIN CLOSING;$7099 BID:7124. OFFER down $124.00

end

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total open interest ROSE BY A HUGE 3562 contracts from 204 ,938 DOWN TO 208,500 WITH YESTERDAY’S TRADING IN WHICH SILVER ROSE BY A CONSIDERABLE 37 CENTS. THE CROOKS NO DOUBT ARE PULLING THEIR HAIR AS THEY ARE STILL HAVING AN AWFUL TIME TRYING TO COVER THEIR MASSIVE SILVER SHORTS. THEY TRY TO CONTINUE WITH THEIR TORMENT WITH NO APPRECIABLE FALL IN SILVER OI.YESTERDAY HUGE NUMBERS OF NEWBIE SPEC LONGS ENTERED THE SILVER ARENA TO WHICH OUR BANKERS DUTIFULLY SUPPLIED.

RESULT: A HUGE SIZED RISE IN OI COMEX WITH THE CONSIDERABLE 37 CENT PRICE GAIN. NEWBIE SPEC LONGS ENTERED THE ARENA AND THESE GUYS WERE DUTIFULLY SUPPLIED BY OUR CROOKED BANKERS. THERE WAS NO SHORTCOVERING YESTERDAY.

In ounces, the OI is still represented by just OVER 1 BILLION oz i.e. 1.042 BILLION TO BE EXACT or 149% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT OCT MONTH/ THEY FILED: 7 NOTICE(S) FOR 35,000 OZ OF SILVER

In gold, the open interest ROSE BY A LARGER THAN EXPECTED 8303 CONTRACTS WITH THE GOOD SIZED RISE IN PRICE OF GOLD ($11.25) WITH YESTERDAY’S TRADING . The new OI for the gold complex rests at 537,727. NEWBIE LONGS RE-ENTERED THE ARENA TO WHICH THE BANKERS DUTIFULLY SUPPLIED THE NECESSARY SHORT PAPER..

NO EFP’S WERE ISSUED FOR THE NOVEMBER CONTRACT MONTH.

Result: A GOOD SIZED INCREASE IN OI WITH THE RISE IN PRICE IN GOLD ($11.25). WE HAD ZERO BANK SHORT COVERING AS ANY OF OUR NEWBIE LONGS RE-ENTERED THE GOLD COMEX AREA TO WHICH OUR BANKERS DUTIFULLY SUPPLIED THE NECESSARY SHORT PAPER.

we had: 110 notice(s) filed upon for 11,000 oz of gold.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD:

A huge change in gold inventory at the GLD/ a withdrawal of 1.48 tonnes

Inventory rests tonight: 844.27 tonnes.

SLV

TODAY WE HAD NO CHANGE IN SILVER INVENTORY AT THE SLV

INVENTORY RESTS AT 319.018 MILLION OZ

end

.

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in silver ROSE BY A HUGE 3562 contracts from 204,938 UP TO 208,500 (AND now A LITTLE CLOSER TO THE NEW COMEX RECORD SET ON FRIDAY/APRIL 21/2017 AT 234,787) WITH THE CONSIDERABLE RISE IN SILVER PRICE (RISE OF 37 CENTS). OUR BANKERS WERE AGAIN UNSUCCESSFUL IN THEIR ATTEMPT TO COVER MUCH OF THEIR SILVER SHORTS. NEWBIE LONGS IN SILVER RE-ENTERED THE ARENA TO WHICH THE BANKERS DUTIFULLY SUPPLIED THE NECESSARY SHORT PAPER.

RESULT: A GOOD SIZED INCREASE IN SILVER OI AT THE COMEX WITH THE 37 CENT RISE IN PRICE (WITH RESPECT TO YESTERDAY’S TRADING). OUR BANKER FRIENDS WERE UNSUCCESSFUL IN THEIR ATTEMPT TO COVER ANY OF THEIR HUGE BURGEONING SILVER SHORTS . .NO EFP’S WERE ISSUED FOR THE UPCOMING NOVEMBER CONTRACT. NEWBIE LONGS RE=ENTERED THE SILVER ARENA TO WHICH OUR BANKERS DUTIFULLY SUPPLIED THE NECESSARY SHORT PAPER.

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)Late MONDAY night/TUESDAY morning: Shanghai closed UP 25.40 points or .75% /Hang Sang CLOSED UP 397.54 pts or 1.39% / The Nikkei closed UP 389.25 POINTS OR 1.73%/Australia’s all ordinaires CLOSED UP 1.00%/Chinese yuan (ONSHORE) closed DOWN at 6.635/Oil UP to 57.26 dollars per barrel for WTI and 63.99 for Brent. Stocks in Europe OPENED RED . ONSHORE YUAN CLOSED DOWN AGAINST THE DOLLAR AT 6.638. OFFSHORE YUAN CLOSED STRONGER TO THE ONSHORE YUAN AT 6.635 //ONSHORE YUAN WEAKER AGAINST THE DOLLAR/OFF SHORE WEAKER TO THE DOLLAR/. THE DOLLAR (INDEX) IS STRONGER AGAINST ALL MAJOR CURRENCIES. CHINA IS NOT VERY HAPPY TODAY.

3a)THAILAND/SOUTH KOREA/NORTH KOREA

i)North Korea//South Korea

b) REPORT ON JAPAN

c) REPORT ON CHINA

4. EUROPEAN AFFAIRS

( Mish Shedlock/Mishtalk)

ii)Giulio Meotti of the Gatestone Institute discusses that the European migrant crisis is the equivalent to the USA 9/11

(Meotti/Gatestone Institute)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

i)Saudi Arabia

ii)Obviously Lebanon did not declare war on Saudi Arabia. However deep seated animosity for the Shiites may bring about war as the Sunnis are extremely worried about Iran’s growing strength

( zerohedge)

iii)Yemen/Saudi Arabia

The Shiites from Yemen now are threatening Saudi ports and airports..

( zerohedge)

iv)Israel/Saudi Arabia/Hezbolloh

A leaked document confirms the co ordination between Saudi Arabia and Israel as both have a sworn enemy in Lebanon’s Hezbolloh

( zerohedge)

6 .GLOBAL ISSUES

7. OIL ISSUES

Nick Cunningham believes that the oil market has overreacted to the Saudi purge. It was far more important to see a drop in rigs than the purge in Saudi Arabia which will not change the policy directive

( Nick Cunningham,/Oil Price.com)

8. EMERGING MARKET

Goldman Sachs takes a big hit on bonds that it purchased in May of 2017

( zerohedge)

9. PHYSICAL MARKETS

i)The following is a superb article explaining how the Deep State has controlled the price of gold for over 40 years

a must read..

Electronic Gold: The Deep State’s Corrupt Threat to Human Prosperity and Freedom

Stewart Dougherty

ii)Funny story: Bitcoin rebounds sharply after Dennis Gartman predicts a wicked fall from Bitcoin.

( zerohedge)

10. USA stories which will influence the price of gold/silver

i)David Stockman discusses two important points:

- the bet of the USA is out of control

- the tax reform bill will solve nothing

( David Stockman)

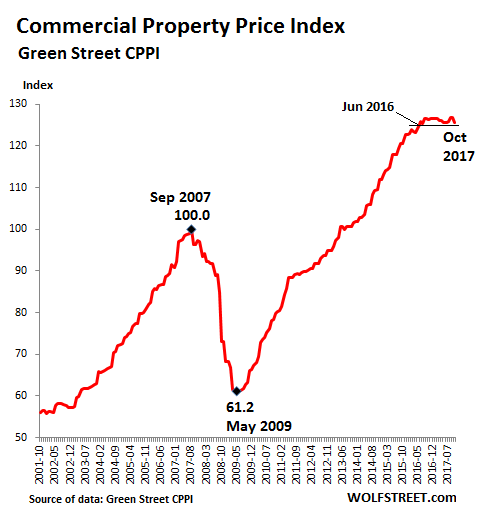

ii)Our resident expert on bricks and mortar operations in the USA reports on sinking property prices

Let us head over to the comex:

The total gold comex open interest ROSE BY A GREATER THAN EXPECTED 8,303 CONTRACTS UP to an OI level of 537,427 WITH THE GOOD SIZED RISE IN THE PRICE OF GOLD ($11.25 GAIN IN YESTERDAY’S TRADING). SOME NEWBIE LONGS RE ENTERED THE GOLD ARENA WITH THE BANKERS VERY SO EAGER TO SUPPLY THE NECESSARY PAPER.

NO EFP’S WERE ISSUED FOR NOVEMBER YESTERDAY.

Result: a GREATER THAN EXPECTED open interest INCREASE WITH THE CONSIDERABLE RISE IN THE PRICE OF GOLD ($11.25.) WE HAD ZERO BANKER SHORT COVERING. NEWBIE LONGS RE ENTERED THE ARENA TO WHICH OUR BANKER FRIENDS WERE MORE THAN WILLING TO SUPPLY THE NECESSARY SHORT PAPER.

.

We have now entered the NON active contract month of NOVEMBER.HERE WE HAD A GAIN OF 48 CONTRACT(S) UP TO 188. We had 27 notices filed YESTERDAY so surprisingly we again gained 75 contracts or 7500 additional oz will stand for delivery in this non active month of November. TO SEE BOTH GOLD AND SILVER RISE IN AMOUNT STANDING (QUEUE JUMPING) IS A GOOD INDICATOR OF PHYSICAL SHORTNESS FOR BOTH OF OUR PRECIOUS METALS.

The very big active December contract month saw it’s OI LOSS 219 contracts DOWN to 359,661. January saw its open interest rise by 329 contracts up to 442. FEBRUARY saw a gain of 7423 contacts up to 114,580.

.

We had 110 notice(s) filed upon today for 11000 oz

VOLUME FOR TODAY (PRELIMINARY) NOT AVAILABLE

CONFIRMED VOLUME YESTERDAY: 377,874

We had 7 notice(s) filed for 35,000 oz for the OCT. 2017 contract

Nov 7/2017.

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz |

29,312.128

oz

BRINKS

JPMORGAN

|

| Deposits to the Dealer Inventory in oz | nil oz |

| Deposits to the Customer Inventory, in oz |

NIL oz

|

| No of oz served (contracts) today |

110 notice(s)

11,000 OZ

|

| No of oz to be served (notices) |

78 contracts

(7800 oz)

|

| Total monthly oz gold served (contracts) so far this month |

966 notices

96,600 oz

3.004 tonnes

|

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

Today, 0 notice(s) were issued from JPMorgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equates to 110 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 53 notice(s) was (were) stopped/ Received) by j.P.Morgan customer account.

| Silver | Ounces |

| Withdrawals from Dealers Inventory | nil |

| Withdrawals from Customer Inventory |

209,236.140 oz

CNT

Delaware

Scotia

|

| Deposits to the Dealer Inventory |

nil oz

|

| Deposits to the Customer Inventory |

nil

oz

|

| No of oz served today (contracts) |

7 CONTRACT(S)

(35,000,OZ)

|

| No of oz to be served (notices) |

3 contract

(15,000 oz)

|

| Total monthly oz silver served (contracts) | 863 contracts

(4,315,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month | xx oz |

NPV for Sprott and Central Fund of Canada

Sprott WINS hostile 3.1 billion bid to take over Central Fund of Canada

(courtesy Sprott/GATA)

Sprott Inc. to take control of rival gold holder Central Fund of Canada

Posted Oct 2, 2017 8:43 am PDT

Last Updated Oct 2, 2017 at 9:20 am PDT

TORONTO – Sprott Inc. (TSX:SII) says it has struck a deal to take control of rival gold-holding firm Central Fund of Canada Ltd. (TSX:CEF.A) after a protracted takeover effort.

Toronto-based Sprott said Monday it will pay $120 million in cash and stock for Central Fund of Canada Ltd.’s common shares and for the right to administer and manage the fund’s assets.

The deal, which requires approval from Central Fund shareholders, would see its class A shareholders transferred to a new Sprott Physical Gold and Silver Trust.

Sprott says the deal would add $4.3 billion to its assets under management, which are focused largely on holding physical precious metals on behalf of clients, and 90,000 investors to its client base.

In March, Sprott tried to go through the Court of Queen’s Bench of Alberta to allow Central Fund’s class A shareholders to swap their shares to Sprott after the family that controls Central Fund rebuffed their attempt to make a deal.

Last year Sprott took over Central GoldTrust, a similar fund controlled by the same family, after securing support from more than 96 per cent of shareholder votes cast.

END

And now the Gold inventory at the GLD

Nov 7/a huge withdrawal of 1.48 tonnes of gold from the GLD/Inventory rests at 844.27 tonnes

NOV 6/ a tiny withdrawal of .29 tonnes to pay for fees etc/inventory rests at 845.75 tonnes

Nov 3/no change in gold inventory at the GLD/Inventory rests at 846.04 tonnes

NOV 2/STRANGE!!! WE HAD ANOTHER WITHDRAWAL OF 3.55 TONNES FROM THE GLD DESPITE GOLD’S RISE OF $6.60 YESTERDAY AND $1.55 TODAY/INVENTORY RESTS AT 846.04 TONNES

Nov 1/a withdrawal of 1.18 tonnes of gold from the GLD/Inventory rests at 849.59 tonnes

OCT 31/no change in gold inventory at the GLD/Inventory rests at 850.77 tonnes

Oct 30/STRANGE WITH GOLD UP THESE PAST TWO TRADING DAYS, THE GLD HAS A WITHDRAWAL OF 1.18 TONNES FROM ITS INVENTORY/INVENTORY RESTS AT 850.77 TONES

Oct 27/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 851.95 TONNES

Oct 26./A WITHDRAWAL OF 1.18 TONNES OF GOLD FROM THE GLD/INVENTORY RESTS AT 851.95 TONNES

Oct 25/NO CHANGE (SO FAR) IN GOLD INVENTORY/INVENTORY RESTS AT 853.13 TONNES

Oct 24./no change in gold inventory at the GLD/inventory rests at 853.13 tonnes

OCT 23./NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY REMAINS AT 853.13 TONNES

OCT 20/NO CHANGE IN GOLD INVENTORY AT THE GLD/ INVENTORY REMAINS AT 853.13 TONNES

oCT 19/NO CHANGE/853.13 TONNES

Oct 18 /no change in gold inventory at the GLD/ inventory rests at 853.13 tonnes

Oct 17./no change in gold inventory at the GLD/inventory rests at 853.13 tonnes

Oct 16/A HUGE WITHDRAWAL OF 5.32 TONNES FROM THE GLD/INVENTORY RESTS AT 853.13 TONNES

0CT 13/ NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 858.45 TONNES

Oct 12/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 858.45 TONNES

Oct 10/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 858.45 TONNES

Oct 9/ANOTHER DEPOSIT OF 4.43 TONNES INTO GLD/INVENTORY RESTS AT 858.45 TONNES

Oct 6/A DEPOSIT OF 2.96 TONNES OF GOLD INVENTORY INTO THE GLD/TONIGHT IT RESTS AT 854.02 TONNES

Oct 5/A LOSS OF 3.24 TONNES OF GOLD INVENTORY FROM THE GLD/INVENTORY RESTS AT 851.06 TONNES

Oct 4/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 854.30 TONNES

oCT 3/ A HUGE WITHDRAWAL OF 10.35 TONNES FROM THE GLD/INVENTORY RESTS AT 854.30 TONNES

Oct 2/STRANGE/WITH GOLD’S CONTINUAL WHACKING WE GOT A BIG FAT ZERO OZ LEAVING THE GLD/INVENTORY RESTS AT 864.65 TONNES

end

Now the SLV Inventory

Nov 7/a huge withdrawal of 9440,000 oz from the SLV/inventory rests at 318.074 million oz/

NOV 6/no change in silver inventory at the SLV/Inventory rests at 319.018 million oz/

Nov 3/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS TONIGHT AT 319.018 MILLION OZ.

NOV 2/A TINY LOSS OF 137,000 OZ BUT THAT WAS TO PAY FOR FEES LIKE INSURANCE AND STORAGE/INVENTORY RESTS AT 319.018 MILLION OZ/

Nov 1/STRANGE! WITH SILVER’S HUGE 48 CENT GAIN WE HAD NO GAIN IN INVENTORY AT THE SLV/INVENTORY RESTS AT 319.155 MILLION OZ/

Oct 31/no change in silver inventory at the SLV/Inventory rests at 319.155 million oz

Oct 30/STRANGE!WITH SILVER UP THESE PAST TWO TRADING DAYS, WE HAD A HUGE WITHDRAWAL OF 1.133 MILLION OZ FROM THE SLV/INVENTORY RESTS AT 319.155 MILLION OZ/

Oct 27/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 320.288 MILLION OZ

Oct 26/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 320.288 MILLION OZ/

Oct 25/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 320.288 MILLION OZ

Oct 24/no change in inventory at the SLV/inventory rests at 320.288 million oz/

oCT 23./STRANGE!!WITH SILVER RISING TODAY WE HAD A HUGE WITHDRAWAL OF 1.039 MILLION OZ/inventory rests at 320.288 million oz/

OCT 20NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 321.327 MILLION OZ

oCT 19/INVENTORY LOWERS TO 321.327 MILLION OZ

Oct 18 no change in silver inventory at the SLV/inventory rest at 322.271 million oz

Oct 17/ A MONSTROUS WITHDRAWAL OF 3.494 MILLION OZ FROM THE SLV/INVENTORY RESTS AT 322.271 MILLION OZ

Oct 16/ NO CHANGES IN SILVER INVENTORY AT THE SLV.INVENTORY RESTS AT 325.765 MILLION OZ

oCT 13/ NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 325.765 MILLION OZ

Oct 12/THE LAST TWO DAYS WE LOST 1.113 MILLION OZ FROM THE SLV/INVENTORY RESTS AT 325.765 MILLION OZ

Oct 10/NO CHANGE IN INVENTORY AT THE SLV/INVENTORY RESTS AT 326.898 MILLION OZ/

Oct 9/A HUGE DEPOSIT OF 1.227 MILLION OZ INTO THE INVENTORY OF THE SLV/INVENTORY RESTS AT 326.898 MILLION OZ

Oct 6/NO CHANGE IN SILVER INVENTORY/ INVENTORY RESTS AT 325.671 MILLON OZ

Oct 5/ANOTHER WITHDRAWAL OF 944,000 OZ FROM THE SLV/INVENTORY RESTS AT 325.671 MILLION OZ

OCT 4/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 326.615 MILLION Z

Oct 3/A TINY WITHDRAWAL OF 143,000 FROM THE SLV FOR FEES/INVENTORY RESTS AT 326.615 MILLION OZ

Oct 2/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 326,757 MILLION OZ

Nov 7/2017:

-

Indicative gold forward offer rate for a 6 month duration+ 1.41%

Indicative gold forward offer rate for a 6 month duration+ 1.41% -

+ 1.64%

end

Major gold/silver trading/commentaries for TUESDAY

GOLDCORE/BLOG/MARK O’BYRNE.

GOLD/SILVER

Peak Gold – Another Sign As Chinese Gold Production Falls 10%

World’s Largest Gold Producer China Sees Production Fall 10%

– Gold mining production in China fell by 9.8% in H1 2017

– Decreasing mine supply in world’s largest gold producer and across the globe

– GFMS World Gold Survey predicts mine production to contract year-on-year

– Peak gold production being seen in Australia, world’s no 2 producer

– Peak gold production globally while global gold demand remains robust

Editor Mark O’Byrne

Gold production in the world’s largest gold producer and buyer fell by nearly 10% in the first half of 2017 in what may be another indication of peak gold.

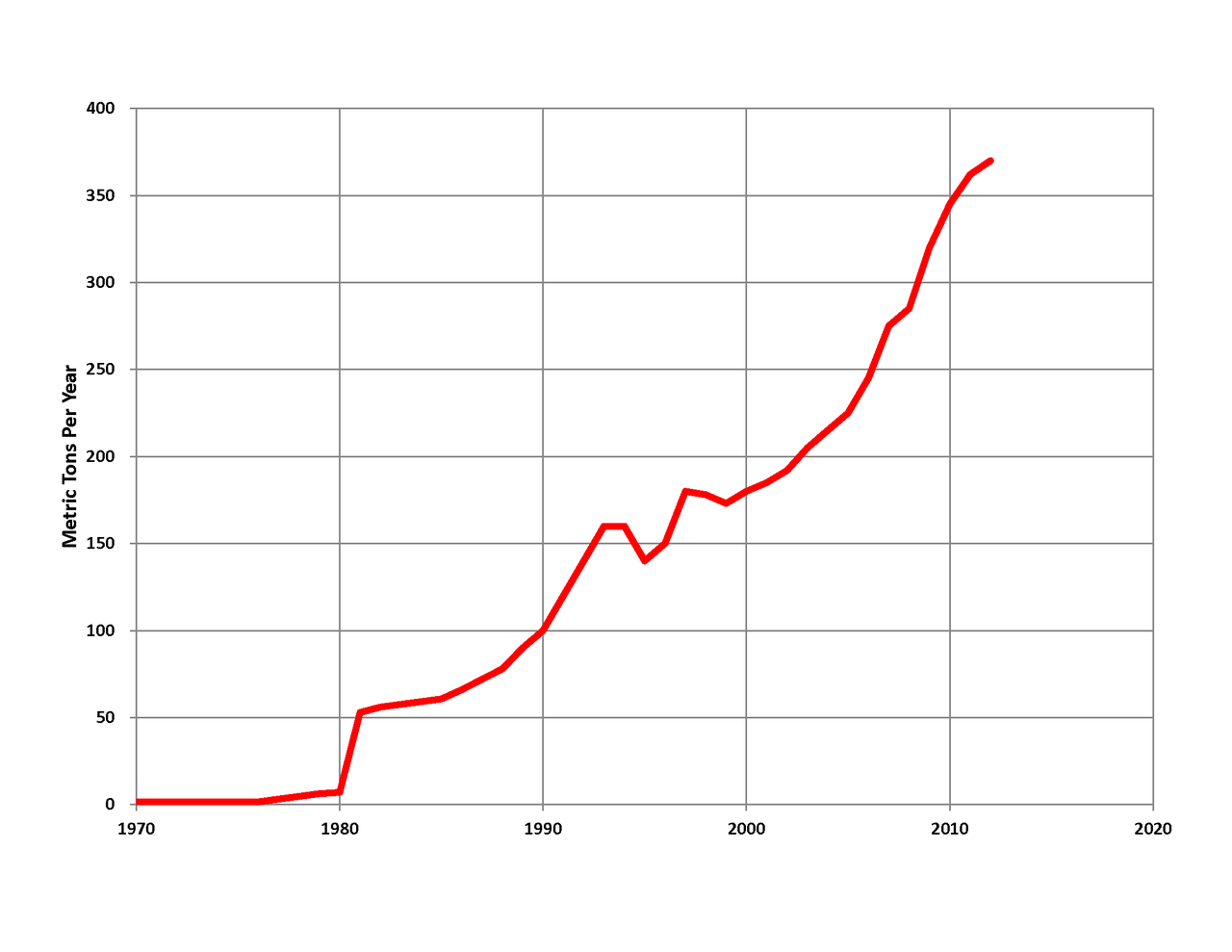

Chinese mine production registered the largest drop globally to total 207 tonnes in the first half of 2017, down 23 tonnes, or 9.8% year-on-year. In the same period last year the country produced 230 metric tons. China mined production of gold (Wikipedia)

China mined production of gold (Wikipedia)

The issue of declining gold supply in China is not expected to improve. The GFMS World Gold Survey expects Chinese gold supply to fall by 14% this year from the 2014 peak. Their latest update explains:

Based on limited updated quarterly production reports and annual production guidance, we expect mine production to contract year-on-year in Q3 2017. We expect losses in China to accelerate as capacity is curtailed further. Industry consensus points to a considerable drop in Chinese mine production for the year as a whole.

This fall in supply could have significant implications for global gold supply given the country’s leading role in the gold market. In 2016 the country produced 453t, 160t or 56% more than the second highest gold producing nation of Australia. It also leads global gold demand, beating India in the last five years.

These numbers could be an indication that we are reaching peak gold, if we haven’t already. Given the country relies heavily on domestic gold supply – a shortage of gold supply at home will force the country to import more from abroad, putting pressure on global supply with a likely rise in prices. A situation made worse by the fact that many other gold producing nations are also suffering from falling production levels – including world’s no 2 gold producer Australia.

Not just a crack in the China

In the first quarter of the year the ten largest Chinese gold mining companies accounted for 41.4% of the country’s total production. China is very reliant on their domestic gold supply and points to problems further down the line of meeting its high levels of gold demand.

At the beginning of the year China was the only major gold mining nation to have increased production in recent years, now it has joined its contemporaries in seeing falling production. The main reason for the fall in China’s gold supply isn’t on account of falling demand or prices:

The government’s escalating efforts to fight pollution and increase attention to environmental protection. As a result, output from the country’s nonferrous smelters fell by 30% or 14 tonnes in tandem with a 2% drop in ‘mine-produced gold’ to total 65 tonnes.

Declining supply is not a problem unique to China. It is a common problem in gold producing nations. At the beginning of the year GFMS noted that global mine supply in the first quarter of the year reached a total of 756 tonnes, one tonne below the same period in 2016.

The largest drop was in South America and Asia, which slipped by a combined 4% with China, Mongolia, and Peru suffering the top three country-level decreases. Oceania posted a fractional drop following severe weather conditions in Australia.

This is not a new problem. Just a quick glance at South Africa’s mining figures and one can see why it has has been a key point of concern for those monitoring global gold supply. It was once the leading producer, accounting for more than 40% of the total mined gold on earth.

We have been warning that it is the ‘canary in the gold mine’ as its 80% plunge in production point to a future of gold shortages and peak gold.

Earlier this quarter the Chairman of the World Gold Council Randall Oliphant expressed concern that the world might have already produced the most gold in a year that it ever will, on account of increasing gold demand and declining supply.

“We’re not going to fall off a cliff in the near term, but in the same time it’s really hard to see how we’re going to produce enough gold to meet all this demand.”

Peak gold here as uncertainties reach peak levels

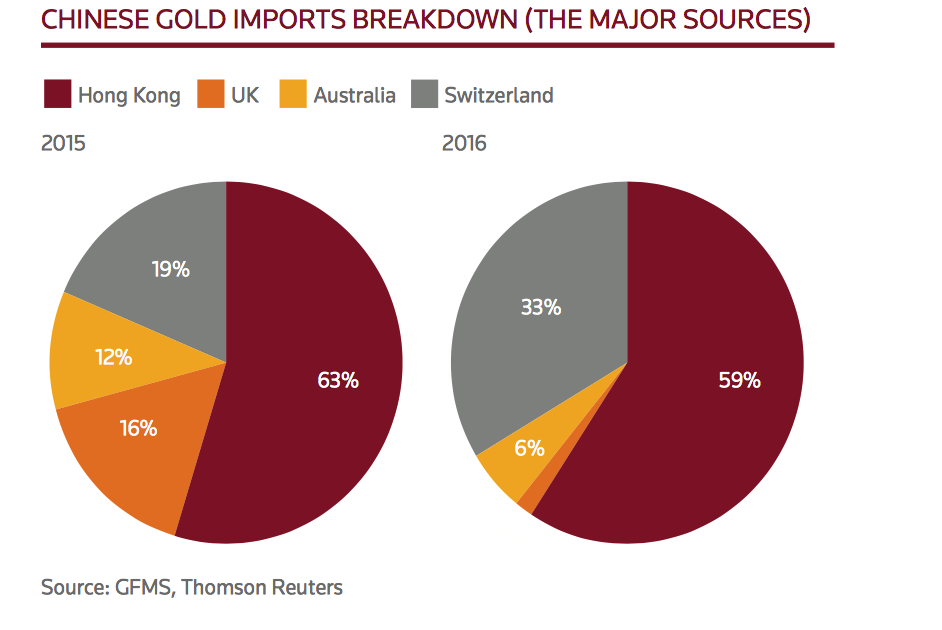

China does not export any of its domestically produced gold, but even this is not enough to satisfy demand from both investors and the official sector. Last year the country imported 1,281 tonnes of gold, from four key countries.

In the short term, China may well be able to increase imports in order to satisfy domestic demand. It may struggle to increase its own production. However, in the long-term this is not a sustainable solution. Gold mines are finite and supply relies on an ever-growing number of new mines being discovered. Something which we can no longer rely on, as Pierre Lassonde recently explained:

If you look back to the 70s, 80s and 90s, in every one of those decades, the industry found at least one 50+ million ounce gold deposit, at least ten 30+ million ounce deposits and countless 5 to 10 million ounce deposits. But if you look at the last 15 years, we found no 50 million ounce deposit, no 30 million ounce deposit and only very few 15 million ounce deposits.

Gold demand shows no sign of abating. As uncertainties increase across the world demand for physical gold increases. It is because of uncertainties that Oliphant believes that there will not be enough gold to satisfy demand. He sees risks in the political and economic system, combined with robust demand from India and China as the key drivers for increased gold demand and higher prices.

“All this uncertainty seems very fertile ground for people to get into gold.”

Diversify into actual physical gold before peak gold sees gold surge like bitcoin

We are at a key inflection point in gold history. There is an unstoppable force of global gold demand hurtling towards the inevitable and immovable object that is finite and diminishing gold supply.

Who wins? Gold investors. Gold will always be in demand for as long as governments cause uncertainties both politically and economically. Short of alchemy there is nothing anyone can do to discover more gold as quickly as governments can destroy our confidence in the system and the value of our savings.

Important developments such as these highlight the importance of not investing in paper, ETF or digital gold but buying actual gold bullion and ensuring that you own allocated and segregated physical gold bars and coins. If we have reached or are close to peak gold, investors do not want to find themselves on the wrong side of an ETF or digital gold redemption gone wrong.

RELATED CONTENT

Peak Gold – Did Gold Production Peak in 2015

Peak Gold Globally – “Bullish For Gold”

‘Peak Gold’ – Gold Production Collapse Continues In South Africa

News and Commentary

Gold dips amid firmer Asian stocks (Reuters.com)

Gold jumps more than 1 percent on geopolitical risks (Reuters.com)

‘Panic’ could set in after Saudi purge nabs ‘Warren Buffett of the Middle East’ (MarketWatch.com)

Stock market inches higher to fresh records (MarketWatch.com)

Stocks Mixed as Banks Retreat; Bonds, Oil Climb (Bloomberg.com)

Time To Break Up The EU and Its “Dysfunctional Currency”? (MoneyWeek.com)

What the purge in Saudi Arabia means for the price of oil (MoneyWeek.com)

On The Verge Of Catastrophe: Saudi Arabia Says Lebanon Declared War (ZeroHedge.com)

Bitcoin & Blockchain – “A Digital Wild West … Will Be Winners and Losers” (Bloomberg.com)

BITCOIN vs. GOLD: Which One’s A Bubble & How Much Energy Do They Really Consume (SRSRoccoReport.com)

Gold Prices (LBMA AM)

07 Nov: USD 1,276.35, GBP 970.92 & EUR 1,103.28 per ounce

06 Nov: USD 1,271.60, GBP 969.72 & EUR 1,095.61 per ounce

03 Nov: USD 1,275.30, GBP 976.24 & EUR 1,094.59 per ounce

02 Nov: USD 1,276.40, GBP 965.09 & EUR 1,095.92 per ounce

01 Nov: USD 1,279.25, GBP 961.48 & EUR 1,099.52 per ounce

31 Oct: USD 1,274.40, GBP 964.21 & EUR 1,095.60 per ounce

30 Oct: USD 1,272.75, GBP 966.91 & EUR 1,093.80 per ounce

Silver Prices (LBMA)

07 Nov: USD 17.01, GBP 12.95 & EUR 14.70 per ounce

06 Nov: USD 16.92, GBP 12.90 & EUR 14.59 per ounce

03 Nov: USD 17.09, GBP 13.05 & EUR 14.67 per ounce

02 Nov: USD 17.08, GBP 12.98 & EUR 14.66 per ounce

01 Nov: USD 16.94, GBP 12.74 & EUR 14.55 per ounce

31 Oct: USD 16.82, GBP 12.72 & EUR 14.45 per ounce

30 Oct: USD 16.74, GBP 12.69 & EUR 14.39 per ounce

Recent Market Updates

– German Investors Now World’s Largest Gold Buyers

– Gold Price Reacts as Central Banks Start Major Change

– Why Switzerland Could Save the World and Protect Your Gold

– Invest In Gold To Defend Against Bail-ins

– Stumbling UK Economy Shows Importance of Gold

– Wozniak and Thiel Fuel Bitcoin-Gold Debate: Gold Comes Out On Top

– Russia Buys 34 Tonnes Of Gold In September

– Gold Will Be Safe Haven Again In Looming EU Crisis

– Gold Is Valuable Due to “Extreme Rarity” – Must See CNN Video

– Gold Is Better Store of Value Than Bitcoin – Goldman Sachs

– Next Wall Street Crash Looms? Lessons On Anniversary Of 1987 Crash

– Key Charts: Gold is Cheap and US Recession May Be Closer Than Think

– Gold Up 74% Since Last Market Peak 10 Years Ago

END

The following is a superb article explaining how the Deep State has controlled the price of gold for over 40 years

a must read..

Electronic Gold: The Deep State’s Corrupt Threat to Human Prosperity and Freedom

by Stewart Dougherty

here is the article in the clear:

Electronic Gold: The Deep State’s Corrupt Threat to Human Prosperity and Freedom

Posted with permission and written by Stewart Dougherty, Inferential Analytics

“There are crooks everywhere you look now. The situation is desperate.” Final blog entry by Daphne Caruana Galizia, 53, renowned Maltese investigative reporter who specialized in exposing state corruption; posted on 16 October 2017, one day before she and her vehicle were blown to bits by a car bomb in Bidnija, Malta

In 2011, gold pulled a “Bitcoin” before anyone even knew what Bitcoin was: its price went vertical to $1,900 per ounce. Inflation-adjusted, the price was still far below its 1980 all-time high, and from all indications, it was going to keep heading north toward its free market print.

In surging, gold blurted out the Deep State Central Planners’ strategy for dealing with the Great Financial Crisis: the hyperinflation of bond, equities and real estate prices via the hyperinflation of both official and totally clandestine, off-the-books money supply, in order to create the hyperinflation of tax revenues desperately required by the government to forestall its fiscal collapse. Gold’s exposure of the Deep State Central Planners’ secret strategy was absolutely unacceptable to them, and had to be stopped.

Worse, gold’s price breakout interfered with the continuation of the largest and most profitable financial crime in history: gold price manipulation. As we have outlined in previous articles, including “Gold and Silver Price Manipulation: The Biggest Financial Crime in History,” from its commencement in 1980, this crime has netted its perpetrators more than $1 trillion in criminal, Mafia-style profits. The epic scale of this crime is exactly why it continues unabated to this day. (While the gold price rigging crime is virtually identical to the manipulation of silver prices, in the interests of brevity, we will solely focus on gold in this article.)

The weapon used in the gold price manipulation crime is paper, or, better stated, electronic gold in five distinct forms: gold futures; gold options on futures; bullion-bank controlled, deliberately audit-proof gold ETFs; gold EFPs (Exchanges for Physical); and the equities of bullion bank-controlled major mining companies. (The major miners serve the bullion banks, not their shareholders, and have actively participated in gold’s price destruction for years, starting with the “hedging” campaign that handed guaranteed profits to the banks and pitiful share prices to the stakeholders.)

These electronic (in other words, non-physical and unreal) gold products are used by Deep State financial insiders to misdirect funds intended by investors to flow into gold, away from gold. Those who “invest” in electronic gold are, in fact, aiding and abetting the exact financial criminals who are stealing from them. The Deep State financial elite is laughing itself sick that suckers still fall for the electronic gold scam nearly four decades after they first hatched it and after already having stolen $1 trillion from their marks. Proof that many people in our world never learn.

Simplified, the gold price rigging scam works by the orchestrators allowing natural market forces to increase the price in roughly $50 – 100 increments, whereupon they unleash massive, synchronized, simultaneous, shock-and-awe-style naked short sales, unbacked by any physical gold they actually own, that take the price right back down by $50 to $100 in a matter of minutes to a few days. This forces the price-attacked longs to dump their losing positions, enabling the shorts to cover at an illegal profit. Each such large-scale price raid produces hundreds of millions of dollars in profits for the criminal orchestrators, not just from the futures market, but from the companion options, swaps and equities markets, all of which act in unison, and in a price-predictable up or down manner. This identical wash, rinse, repeat cycle has occurred literally hundreds of times over the past 38 years, with no serious investigations or prosecutions whatsoever in that this is official,

state-sponsored, for-profit corruption.

For any one of hundreds of reasons, gold should be in a raging bull market at this time. Given that its price remains lackluster and greatly disappointing, rich gallows humor has emerged as a form of therapy for those attempting to deal with the irrationality of it all.

One gallows joke that made the rounds was that if nuclear war were declared, gold’s price would go down and the DJIA would go up. While this was a funny take on the absurdity of the situation, it seemed a bit far-fetched.

In an October 20, 2017 podcast interview, Mr. James Rickards, a leading public commentator on gold, stated that he had spent the previous day in an extremely exclusive national intelligence planning session overseen by CIA Director Mike Pompeo and National Security Advisor H.R. McMaster. Rickards reported that Pompeo told him, categorically, that military action will be taken against North Korea within 5 months, or by March 20, 2018. Rickards also reported that the group was informed that the assassination of Kim Jong Un is one U.S. military option officially on the table.

In the trading days after Mr. Rickards made that public announcement, the price of gold declined and the DJIA hit record highs.

In the practice of Inferential Analytics, the forecasting method we developed and use, we pay rapt attention when gallows humor becomes gallows fact, because it invariably signals that something is seriously wrong.

As practitioners and students of professional, CIA-style human manipulation, mind control and propaganda campaigns know, they are driven by misdirection, reverse psychology, twisted narratives, head fakes, false flags, imposters, blind alleys, Judas goats, projections, and the invention and dissemination of elaborate lies, told by professional liars, that are the exact opposite of reality. Such techniques are now being used to keep the gold price manipulation and electronic gold frauds alive, well and gushing profits for the insider looters.

The challenge faced by those who conduct professional swindles and stings is that such schemes burn through victims. The defrauded either go bankrupt, or wake up and get out. Therefore, con artists must constantly trawl for new suckers to screw.

In the case of the gold price manipulation swindle, the insider con men must find ways to lure new, naïve, outsider money onto the insider-controlled Gold Looting Field, in order for there to be fresh market liquidity for the insiders to sell into and plunder. This is becoming increasingly difficult, given that the insider criminals have been systematically screwing investors for nearly 40 years, have destroyed the gold market’s reputation, and have ravaged the prospect base of patsies.

Therefore, the gold market price wreckers are now in the paradoxical situation of needing to make, via controlled spokespersons and/or by riding on the coattails of independent, non-aligned commentators, a high-profile, bullish case for gold.

The rigging of gold persists without regulatory or legal interference because it is based on a straightforward deal between the profiteering Deep State financial elite, and the western governments they control: the criminals are allowed to manipulate the gold market however brazenly they wish and keep whatever sums they steal, as long as they keep the gold price under control. Gold price control is critical to states’ official monetary, fiscal and economic narratives, all of which are false. If the gold price were to get out of control, as it started to do in earnest in 2011, this would fatally contradict the states’ false narratives. Freed at this juncture, gold could easily ascend to $10,000 per ounce, which would announce to the people that reality is not what they are being told.

Mr. Rickards has been an unrelenting gold bull for several years. His first book was published in 2011, not long after the gold price had taken on momentum, and he has been a highly-visible pundit ever since. He expresses his views on all of the major business networks, in hundreds of radio and podcast interviews, and in articles and newsletters distributed all over the world.

Mr. Rickards positions himself as an “Insider’s Insider,” repeatedly referencing his connections to and interactions with the intelligence community and financial elite. Additionally, he has publicly stated that he has coordinated and participated in simulated financial war games developed for high level government, intelligence community, academician and private commercial sector participants. The purpose of these financial war games is to simulate the means by which nations might attack one another financially, as opposed to militarily, as the so-called art of war evolves.

Mr. Rickards states his views clearly and with conviction, and he can be quite convincing. Despite his compelling forecasts between 2011 and now for a surging gold price (he has stated that $10,000 per ounce gold is likely), the price has, in fact, plunged from $1,900 to $1,280 today, while virtually every other asset class, including stocks, bonds, real estate and even ethereal cryptocurrencies has surged.

Some of Rickards’s recent and current predictions include these:

1) Kevin Warsh would be named Chairman of the

Federal Reserve. Such a development would have been bullish for gold, because Warsh is said to oppose the exact kind of market manipulation that has been practiced by the Fed and that has criminalized the gold market for years. As we now know, this prediction was wrong, and subsequent to Powell’s nomination, the price of gold went down.

2) He categorically asserts that there will be no Federal Reserve rate hike in December, 2017. Obviously, this would be extremely bullish for gold, and anyone who believes the prediction should aggressively buy it at this time. The problem is that, barring some kind of extraordinary exogenous event, it is highly likely to be wrong. Interest rates will almost certainly be raised in December, regardless of economic conditions. If they are not, the Fed’s economic narrative will unravel and its credibility will be shredded, something that no central bank can allow to happen.

3) A new prediction is that there will be a government shut down this December, due to federal debt limit increase disputes among politicians. This would be bullish for gold and bearish for financial markets. In our view, this prediction is also destined to be wrong. With Republicans in control of the House, Senate and White House, they would totally “own” such a shutdown, which citizens detest, and this could only hurt them in the November, 2018 elections. We doubt they will allow this to happen.

4) The prediction that war with North Korea and/or the possible assassination of Kim Jong Un will occur by March 20, 2018 remains on the table. It is hard to imagine a story line more bullish for gold, given that such a war will almost certainly be nuclear and could swiftly morph into World War III. The global “rush to safety” in such a situation would be historic.

Over the past several years, Rickards has made literally dozens of similar, gold-bullish predictions, and yet the gold price has gone down to nowhere during the same period. As we can see, even excellent rationales for a rising price of gold, along with basic common sense, do nothing to create that outcome. The reason for this is simple: the gold market has been completely corrupted.

By publicly revealing specific content from the Pompeo / McMaster planning session, Rickards indicated that he is an official spokesperson for the Central Intelligence Agency and the national security complex. Because if the meeting Mr. Rickards reported upon actually occurred and if he actually attended it (and Mr. Rickards is a credible figure whose veracity we have no reason whatsoever to doubt), we simply cannot believe that he could have publicly revealed what transpired at it without the direct, formal authorization of Messrs. Pompeo and McMaster, its hosts. Further, we would think that Pompeo and McMaster would have required President Trump’s authorization to facilitate the public release, via Rickards or anyone else, of the timeline for war with North Korea and the nation’s active assassination options. If correct, this would mean that Rickards is a direct spokesperson for the CIA, the National Security Advisor, and by extension, President Trump.

Therefore, we are faced with an extremely curious situation where a direct consultant to and spokesperson for the Director of the Central Intelligence Agency, the National Security Advisor and the President of the United States is also one of the most high profile cheerleaders in the world for gold.

This is an extraordinary paradox, because we know that the Federal Reserve, U.S. Treasury, banks, brokerage houses, insurance companies, mutual fund corporations, pension fund managers and virtually every other participant in the United States financial services juggernaut have absolutely no interest in or anything whatsoever to gain from the people finally waking up to and acting upon the astoundingly bullish case for gold.

So we ask ourselves: Why would the government wish to align with someone who popularizes a point of view (“buy gold because it is going to $10,000 per ounce”) that is a direct threat to it and to the Deep State financial elite it serves? This would be like the Fed hiring Ron Paul, who wrote a book entitled “End the Fed,” to become one of its official champions and spokespersons. Can anyone imagine that happening? As we can see, this is a very complex and confusing situation.

While the bullish case for gold is directly contrary to the interests of the financial establishment generally, it is of extreme interest and benefit to the subset of the establishment that has made more than $1,000,000,000,000.00 in illegal profits over the past forty years by rigging the gold market, and that wishes to steal as much additional money as they can get away with.

No matter who writes them, gold-bullish commentaries are extremely helpful to the gold price rigging cartel, which needs constant capital injections into the electronic gold market in order to keep its looting spree going. By making his particularly cogent and compelling bullish arguments for gold, and given his stature, credibility and connections, Rickards is a God send to the price riggers. Over the years his work must certainly have heightened investor interest in gold and resulted in sizable fresh flows of investment capital pouring onto the electronic gold Looting Field.

It is likely that people at the highest levels of the Deep State financial elite fully realize that a large migration of the people’s money into precious metals is virtually inevitable, given the government’s urgent need to hyper-inflate money supply and massively stimulate the economy in order to hyper-inflate tax receipts, the only way it can avoid collapse. Ultimately, this is guaranteed to create severe, generalized consumer price inflation. Historically, hyperinflation has always resulted in a significantly higher gold price.

With massive and increasing structural deficits; exploding debt in all sectors; hostile demographics; social and political fracturing and disintegration; grotesque wealth inequality; extraordinary global trade competition; a complete collapse of respect for vital government organizations such as the Justice Department and FBI, which the people now realize have gone rogue; an extremely complex and corrosive global geopolitical environment; the real prospect of war, potentially nuclear and worldwide; not to mention numerous additional factors, we can only point to few other times in history more dangerous to the people’s financial welfare, and therefore more overall bullish for gold, one of the only financial sanctuaries proven to work in times of dislocation.

If a large move into precious metals is going to happen whether the Deep State financial elite likes it or not, they realize they must at least do everything possible to control where those funds go, while they still can. This means they must ensure that as much money as possible flows into electronic gold products controlled by them, and not into physical gold privately owned and controlled by citizens.

In our consumer research, we have found that the average U.S. citizen is literally clueless when it comes to gold. They are almost completely unaware of the gold products available to them, the prices of those products, or even where to buy them. After two generations of being deliberately educated in total ignorance about gold, none of this should come as a surprise. Knowing next to nothing about physical gold or the mechanics of buying it, they feel intimidated by the subject. Therefore, the simple fact is that if they do decide to buy gold, the path of least resistance leads them to electronic gold.

Financial services industry employees are trained to talk customers out of buying gold. They do this by pointing out its price volatility and riskiness. (The public has no idea that the gold price is manipulated, and fake.) If the customer still wants to buy it, then the broker steers them into electronic gold, such as bullion bank-controlled ETFs and major mining company equities.

This sterilizes the investor’s funds, and prevents them from being used to buy physical precious metals, which would interfere with the price rigging crime by increasing physical demand for and the price of gold, given its consistently tight supplies. It would also lessen capital flows onto the Gold Looting Field, the exact opposite of the Deep State manipulators’ agenda.

Over the past several years, there have been many, highly sensationalized mainstream media reports about counterfeit gold, such as the report last year about a few ten ounce PAMP gold bars with tungsten cores. To listen to the MSM, one would think that all of the physical investment gold in the world is fake. The fact is that the overwhelming majority of physical investment gold is genuine. Counterfeit gold hysteria is yet another spoke of the anti-physical gold propaganda wheel whose function is to scare people away from real physical gold personally owned and controlled by them, and into fake electronic gold controlled by the Deep State financial elite.

The Deep State financial elite fully understands that it cannot prevent all investment funds from reaching physical gold. But they do not need to in order to maintain their price rigging scheme, or to continue making significant profits from the electronic gold products they distribute and manage.

In fact, just as they benefit from the bullish case for gold that results in funds continuing to flow onto the Gold Looting Field, they also benefit when commentators speak about the virtues of personally owned physical gold. They fully realize that any commentator who recommends gold but also says that people should not personally own any of it would lose credibility. So it is completely fine with them when a gold booster such as Mr. Rickards makes positive comments about, for example, gold Maple Leafs, which he has done. They realize that as a practical matter, the average person is going to find the purchase of physical investment gold too difficult and intimidating to pursue, and will gravitate to electronic gold, even though some of them might buy some Maple Leafs. Apple does not need 100% smart phone market share to be enormously profitable, and neither does the Deep State financial elite need 100% gold market share to make massive gold profits, which they do.

The larger purpose behind the Deep State’s electronic gold products, beyond current profits, is to concentrate investment gold in a select number of locations that will be easy to control and raid when the time comes. When the gold price is reset, most likely by China and an outcome we view as inevitable, western governments will move fast to prohibit its private ownership. The Deep State elite, which for decades has exhibited an endless lust for other people’s money and greed that is beyond biblical, is simply not going to allow every day citizens to benefit from gold holdings that have surged in value. Therefore, when the Deep State elite realize that they have lost control and the price is about to be reset, they will pre-emptively cash-settle their electronic gold products in fiat currencies that will subsequently plunge in value, and abscond with the physical gold that backs such products. For investors, electronic gold is nothing but modern day Fools’ gold. For the Deep State, it is a free ride, on investors’ backs, to the most massive physical gold theft of all times.

Taken together, we believe these factors present a compelling argument why investors should exit all of the electronic gold products specified at the beginning of this article, and convert the proceeds into physical gold and/or non-Deep State-controlled equities of companies in which they have full confidence that managements are working for them, not the bullion banks. The fact is that the Deep State manipulation of the gold price is never going to end until people stop buying electronic gold and providing the liquidity the Deep State needs to continue perpetrating the gold price rigging crime.

More than 100 years ago, Dostoyevsky wrote: “Money is coined liberty, and so it is ten times dearer to the man who is deprived of freedom. If money is jingling in his pocket, he is half consoled, even if he cannot spend it. But money can always and everywhere be spent, and, moreover, forbidden fruit is sweetest of all.” When honest money is attacked, so is human freedom. Because it is impossible for human beings to be free if their currency is a fraud and they are at the same time prohibited from owning honest money. The gold price is, in fact, a barometer of human liberty. When it is fake, there is slavery; when it is honest, there is freedom.

Thanks to the Deep State financial elitists, for whom fraud and plunder are a way of life, the gold market has been a cesspool of corruption for nearly forty years. And as we can see, corruption has metastasized throughout the world. “There are crooks everywhere you look now. The situation is desperate,” said Daphne Caruana Galizia, prior to being assassinated for her work and courage. May she rest in peace. In the coming hurricane, the rest of us are going to need to exhibit her same bravery to fight the crooks who have corrupted our world and our futures with their nauseating arrogance, greed, and immorality.

Funny story: Bitcoin rebounds sharply after Dennis Gartman predicts a wicked fall from Bitcoin.

(courtesy zerohedge)

Bitcoin Rebounds Sharply After Gartman Predicts Drop

Having tumbled from record highs near $7600 to $6900 in the last two days, Bitcoin is rebounding this morning, back to $7250 following condemnation from Dennis Gartman and blessing from ‘father of financial futures’ Leo Melamed.

Gartman issued the following statement overnight…

BITCOIN: A Bubble Bursting… Maybe?: Our antipathy toward Bitcoin specifically and toward the crypto-currencies generically is widely known but yesterday’s action does look like a “reversal” to the downside… finally.

And Bitcoin surged…

But on the positive side, Reuters reports that Leo Melamed, 85, said while he was initially skeptical about bitcoin he sees similarities between it and International Monetary Market currency futures trading, which he launched as chairman of the Chicago exchange in 1972.

“The world in the 1970s didn’t look at currency trading as a valid instrument of finance. I too went from not believing (in bitcoin) to wanting to know more,” he said.

He says bitcoin could go beyond being a crypto-currency and represent a new asset class based on blockchain technology.

“My whole life is built abound new technology. I never said no to technology. People who say no to technology are soon dead. I’m still that same guy who believes in, at least examining change. That’s what bitcoin represents,” he also said.

Melamed said he expects major investors to take part in bitcoin futures, which the exchange plans to start by the end of year.

“That’s a very important step for bitcoin’s history… We will regulate, make bitcoin not wild, nor wilder. We’ll tame it into a regular type instrument of trade with rules.”

Finally, we note that as the cryptocurrency has surged in recent months, searches for “buy bitcoin” have overtaken “buy gold” dramatically

“With the U.S. stock market setting fresh all-time highs day after day, it’s no surprise gold prices have retreated,”Adrian Ash, research director at London-based BullionVault, said in a report.

“Some investors are also being distracted by the noise around Bitcoin and other cryptocurrencies. Altogether, that’s madeinterest from new gold investors the weakest since the metal’s half-decade price lows of end-2015.”

Your early TUESDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

2. Nikkei closed UP 389.25 POINTS OR 1.73% /USA: YEN RISES TO 114.12

3. Europe stocks OPENED RED /USA dollar index RISES TO 95.09/Euro DOWN TO 1.1565

3b Japan 10 year bond yield: RISES TO . +.032/ GOVERNMENT INTERVENTION !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 114.07/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD FINALLY IN THE POSITIVE/BANK OF JAPAN LOSING CONTROL OF THEIR YIELD CURVE AS THEY PURCHASE ALL BONDS TO GET TO ZERO RATE!!

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 57.26 and Brent: 63.99

3f Gold DOWN/Yen DOWN

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil UP for WTI and UP FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund RISES TO +.344%/Italian 10 yr bond yield DOWN to 1.735% /SPAIN 10 YR BOND YIELD DOWN TO 1.441%

3j Greek 10 year bond yield FALLS TO : 5.126???

3k Gold at $1276.90 silver at:17.05: 6 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble DOWN 64/100 in roubles/dollar) 58.91

3m oil into the 57 dollar handle for WTI and 63 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation (already upon us). This can spell financial disaster for the rest of the world/China forced to do QE!! as it lowers its yuan value to the dollar/GOT A GOOD SIZED DEVALUATION SOUTHBOUND

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 114.12 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 0.9996 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1554 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now POSITIVE territory with the 10 year RISING to +0.342%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.325% early this morning. Thirty year rate at 2.799% /

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

(courtesy Jim Reid/Bloomberg/Deutsche bank/zero hedge)

Global Stock Meltup Sends Nikkei To 25 Year High

The global risk levitation continues, sending Asian stocks just shy of records, to the highest since November 2007 and Japan’s Nikkei topped 22,750 – a level last seen in 1992 – while European shares and US equity futures were mixed, and the dollar rose across the board, gains accelerating through the European session with EURUSD dumping below 1.16 shortly German industrial output shrank more than forecast, eventually dropping to the lowest point since last month’s ECB meeting. Meanwhile soaring iron-ore prices couldn’t provide relief to the Aussie as the RBA held rates unchanged as expected; Oil traded unchanged at 2.5 year highs, while TSY 10-year yields rose while the German curve bear steepened, both driven by selling from global investors.

The Stoxx Europe 600 Index edged lower, erasing an early advance, despite earlier euphoria in stocks from Japan to Sydney, which reached fresh milestones. Disappointing reports from BMW AG and Associated British Foods Plc weighed on the European index as third-quarter earnings season continued. Earlier, the Stoxx Europe 600 Index rose as much as 0.3%, just shy of a 2-year high it reached last week. Maersk was among the worst performers after posting a quarterly loss, saying a cyberattack in the summer cost more than previously predicted. Spain’s IBEX 35 gains crossed back above its 200 day moving average. European bank stocks trimmed gains after European Central Bank President Mario Draghi said that the problem of non-performing loans isn’t solved yet, though supervision has improved the resilience of the banking sector in the euro region. Draghi was speaking at a conference in Frankfurt.

Over in Asia, equities rose to a decade high, with energy and commodities stocks leading gains as oil and metals prices rallied. The MSCI Asia Pacific Index gained 0.8 percent to 171.40, advancing for a second consecutive session. Oil-related shares advanced the most among sub-indexes as Inpex Corp. rose 3.7 percent and China Oilfield Services Ltd. added 4.6 percent. The MSCI EM Asia Index climbed to a fresh record. The Asia-wide gauge has risen 27 percent this year, outperforming a measure of global markets. The regional index is trading at the highest level since November 2007. Hong Kong’s equity benchmark was at its highest since December 2007 as Tencent Holdings Ltd. advanced for an eighth session. Australia’s S&P/ASX 200 index closed at its highest level since the financial crisis.

Japanese stocks climbed, bolstered by strong corporate earnings, with the Nikkei 225 Stock Average closing 1.7% higher at 22,937.60 at 3pm in Tokyo, climbing for 23 out of the past 25 trading sessions. Japan’s main stock index has gained 20% this year with Tokyo Electron, Fanuc, SoftBank and Kyocera providing the biggest boosts, as the Topix index rises 1.2% to 1,813.29 from Monday, pushing it up +19% YTD.

“Oil and other commodities’ fundamentals are improving amid OPEC’s efforts, stagnating U.S. production and stable growth in China are positive for most Asian markets,” said Hans Goetti, founder of HG Research, referring to output caps put in place by the Organization of Petroleum Exporting Countries. “Economic growth differentials also are in favor of Asian markets, so the rally should continue.”

The euro declined to a four-month low and bund yields nudged higher after German industrial production fell more than expected in September. WTI crude hovered near the highest since January as political upheaval in Saudi Arabia reverberated through the market. Yen traded at 113.99 per dollar from 113.71 on Monday; currency +2.6% YTD.

In rates, the yield on 10Y TSYs rose two basis points to 2.33%; Germany’s 10-year gained 1 bp to 0.34%; Britain’s 10-year yield rose 1 basis point to 1.263% while Japan’s 10-year yield advanced one basis point to 0.032%.

Investors’ focus returned to geopolitics as Trump continued his tour of Asia, while Saudi Arabia launched a crackdown on corruption. Speaking next to South Korean President Moon Jae-in in Seoul, Trump said he saw some progress on North Korea, said that now is the time to act with urgency and determination with North Korea, and called on the rogue state to “come to the table”. He added that the U.S. and South Korea will act together to confront North Korea’s actions, and the U.S. stands ready to use its full range of military capabilities “if need be.” Meanwhile, the South Korean President Moon says that he and Trump reaffirmed resolve to peacefully end N. Korean nuclear standoff.

Bulletin Headline Summary from RanSquawK

- European equities have struggled to maintain the Asian and American impetus

- RBA stood pat on rates as expected. RBNZ act looks to maximise employment as a goal

- Looking ahead, highlights include US APIs and comments from Fed’s Yellen and BoC’s Poloz

Market Snapshot

- S&P 500 futures little changed at 2,589

- STOXX Europe 600 up 0.04% to 396.73

- MSCI Asia up 0.8% to 171.40

- MSCI Asia ex Japan up 0.6% to 560.95

- Nikkei up 1.7% to 22,937.60

- Topix up 1.2% to 1,813.29

- Hang Seng Index up 1.4% to 28,994.34

- Shanghai Composite up 0.8% to 3,413.58

- Sensex down 0.9% to 33,424.09

- Australia S&P/ASX 200 up 1% to 6,014.34

- Kospi down 0.2% to 2,545.44

- German 10Y yield rose 1.3 bps to 0.349%

- Euro down 0.3% to $1.1574

- Italian 10Y yield fell 0.7 bps to 1.52%

- Spanish 10Y yield fell 0.9 bps to 1.459%

- Brent futures down 0.3% at $64.11/bbl

- Gold spot down 0.4% at $1,276.47

- U.S. Dollar Index up 0.3% at 95.04

Top Overnight News

- President Donald Trump again showed how quickly his tweets can outrun U.S. foreign-policy planning, after he backed Saudi Arabia’s king and crown prince over the arrests of dozens of officials before the State Department had completed its review of the moves

- U.S. President Donald Trump said that North Korea should “come to the table” and make a deal on its missile and nuclear programs

- ECB Executive Board member Sabine Lautenschlaeger would have “liked to see a clear exit” from the ECB’s asset- purchase program, she tells Bloomberg TV

- A ninth straight annual advance for emerging-market macro hedge funds doesn’t mean investors are expecting an exodus as the world’s central bankers start turning off the taps; demand remains so brisk that some are turning new money away

- German industrial production dropped 1.6% in September from August, when it surged 2.6 percent, the fastest pace in six years

- There are continued signs that French bonds could be one of the big winners from the ECB’s extension of stimulus; the bank set a new record in buying the country’s securities, purchasing 1.70 billion euros ($2 billion) relative to its capital key for October, compared with 1.57 billion a month earlier

- Saudi Arabia’s anti-corruption crackdown is expanding beyond the list of princes, billionaires and officials already arrested

- Multinational companies including Apple Inc., Pfizer Inc. and Ford Motor Co. would face a new tax on payments they make to offshore affiliates under the House Republicans’ tax bill — a surprise provision that has stunned tax experts

- Broadcom Ltd. is using a tactic popularized by corporate raiders in the 1980s to convince Qualcomm Inc. and its shareholders that it has the means to complete the biggest tech deal ever

- Biggest Danish Mortgage Bank Cancels IPO After Private Offer

Asian bourses higher across the board, having drawn encouragement from the close on Wall Street, where all three major indices touched yet more record highs over the surge in energy names amid rising oil prices. ASX 200 (+1.0%) briefly pushed through the key 6000 level for the first time since 2008 as miners lifted shares in Australia with iron prices continuing to rise. Similarly, the Nikkei 225 (+1.6%) traded at better levels, making fresh 25yr highs after topping 22,750. While, Chinese markets also eked out gains this morning with Evergrande the notable outperformer in China after the company stated that they were to sell CNY 60bln of property assets. In credit markets, across the Japanese curve, the short end outperformed with the curve somewhat steeper. JGBs had been tracking lower, in tandem with USTs as equities continue to reach new highs.

Top Asian News

- Razer Is Said to Raise $529 Million in IPO Priced Near Top End

- China Firms Have Found a Way to Cut Debt, at Least on Paper

- India’s Sensex Falls from Record as Drugmakers, Oil Shares Drop

- Hong Kong Traders Get Vertigo as Stocks Whipsaw to Decade- High

- Tencent’s Honour Loses Top Spot in China After Year-Long Run

- Lupin Gets FDA Warning Letter on Goa, Indore Plants; Shares Fall

- Bank of Korea Board Split on Timing of Rate Hike, Minutes Show

European equities have followed the theme across the globe, with the majority of bourses trading in the green. Sectors see energy leading the charge once again, as oil continues to drive the unit over 1%. The Dax sees another record and is only seeing weight from BMW following their earnings – Earnings do continue to drive with the biggest moves seen in Maersk, Dialog, Siemens Gamesa and Zalando all suffering after disappointing updates. Treasuries trade near session lows, as some selling volume has helped the marginal bearish push. US 2/10s have flattened to a new low around 70bps, with the curve not seeing levels like that since Nov 2007.

Top European News

- Fortum CEO Seeks Talks With Uniper Head as Germany Approves Bid

- Credit Agricole Unit Agrees to buy Italy Wealth Manager Leonardo

- U.K. Retail Sales Weaken as Cash-Strapped Consumers Hold Back

- German Industrial Output Drops as Manufacturing Takes Breather

- SocGen Faces French Criminal Probe Into Suspected Libya Bribery

- Draghi Says Banks’ Non-Performing-Loans Problem Isn’t Solved Yet

- Serbs Mull New IMF Deal as Weak Growth Mars Healthier Budget

- Siemens Is Said to Ready Job Cuts Amid Slump in Power Orders

In FX, USD A second wave of USD buying has been evident in European trade, with a push clear in USD/JPY, as Monday’s 114.73 how is set to behave as the next resistance level. Focus remains political, with eyes on the GOP tax bill, coinciding with President Trump’s visit of South Korea and later comments expected from current Fed Chair Yellen. The Kiwi was one of the movers overnight, finding volatility as the New Zealand PM outlined the review of RBNZ act, which will include maximising employment as a goal, however, further stated that there is no desire to have the exchange rate in the review. The initial spike higher in the NZD retraced through the Asian session and opened Europe back below pre-announcement levels. Australian RBA Cash Rate (Nov) 1.50% vs. Exp. 1.50% (Prev. 1.50%). RBA says forecasts are largely unchanged with the forecast remaining that inflation will pick up. Higher currency would slow the economy, adding that it is restraining price pressures. Labour market has continued to strengthen, although inflation remains low and will likely do so for some time. New Zealand Financial Minister stated that they will retain the 1-3% inflation target for RBNZ. There is no desire to have NZD included in the RBNZ review. The RBNZ review to include maximising employment as their goal.

In commodities, Oil continued to gain through yesterday’s session continuing to print fresh highs, the next clear resistance is likely to be 2015 highs, just through 60.00/bbl. Precious metals have been pushed lower, led by gold, largely in line with the bullish pressure seen in the USD this morning

Looking at the day ahead, datawise we’ll get Germany industrial production for September, Euro area retail sales for September and September JOLTS and October consumer credit in the US. The holds a forum on Banking Supervision which will include a speech from President Draghi. The Fed’s Quarles is also due to speak in the evening at the Clearing House annual conference. The OPEC world oil outlook will also be presented.

US Event Calendar

- 10am: JOLTS Job Openings, est. 6,075, prior 6,082

- 12:35pm: Fed’s Quarles Speaks at Clearing House Conference

- 2:30pm: Yellen to Receive Award for Ethics in Government

- 3pm: Consumer Credit, est. $17.5b, prior $13.1b

DB’s Jim Reid concludes the overnight wrap

Given the fairly light calendar elsewhere it feels like developments in and around Washington will likely hog the spotlight this week. With that in mind it was interesting to hear the latest view of DB’s Washington specialist Frank Kelly yesterday on his conference call. Unsurprisingly Frank thinks that the tax bill has little chance of passing in its current form. He made the point that the bill is likely to face an extraordinary amount of lobbying and noted three very powerful groups in the association of homebuilders, realtors and independent businesses. So the current House version is seen as more of an opening bid but as the days go on the lobbying will ramp up intensely. What is hugely important in Frank’s view though is the parallel developments in the Senate. Indeed early next week, or possibly late this week, the Senate Republicans will unveil a plan of their own which is likely to look very different to the current House bill legalisation, certainly in being a lot less sweeping. This morning, Bloomberg noted that the Senate’s tax plan may keep the mortgage interest deduction limit at $1m instead. Politico also ran an article yesterday saying that reconciling the difference between the two chambers could end up being the biggest hurdle. So keep an eye on that as the next important event in addition to any press snippets in terms of mark ups on the current House version.

In terms of timing Frank thinks that it’s very unlikely that we get the bill passed before Thanksgiving. Instead we might see something around the Holiday Season or possibly as late as early next year depending on how contentious it is. Frank is a bit more upbeat about getting something however given the health reform debacle. So all in all expect this to rumble on for some time.

Unlike politics, markets have had a slightly less complicated start to the week. Having dipped into the red at the open following the Saudi Arabia, China and Trump headlines from the weekend, equity markets largely closed on the front foot last night. In Europe the Stoxx 600 finished +0.13% while across the pond the S&P 500 also eked out a +0.13% gain by the end of play – the 5th day in a row it has closed higher – helped by a decent rally for energy stocks after WTI rose +3.07% and to the highest in two years on the back of those Saudi developments. The broader move higher was also despite the telecom sector doing its best to drag the index down after the news that Sprint and T-Mobile were officially ending merger talks. In fact M&A has been a bit of a theme over the last 24 hours particularly in the tech sector.

Bond markets were slightly firmer yesterday too. Bunds ended the session 2.8bps lower at 0.332% while Treasuries were 1.4bp lower to 2.316%. The Treasury curve was actually a bit flatter yesterday with the 2s10s curve dipping below 70bps intraday and to the lowest since early November 2007. It’s hard to know if the latest leg had anything to do with the weekend news of the NY Fed’s Dudley announcing his plan to retire by the middle of next year and before the end of his term in 2019. The board of the NY Fed will now choose the next President. The announcement means that the last member of the Yellen-Fischer- Dudley triumvirate will now step down and at face value one would think that this makes ‘continuity’ under Powell certainly more of a challenge given that Yellen was seen as having significant support from both Fischer and Dudley. So the decks have certainly been cleared for a Fed leadership change which is something to keep in mind as we approach 2018.

Back to bond markets briefly, it’s worth pointing out that the latest ECB PSPP and CSPP data was released yesterday. Significantly, with regards to the former, the ECB announced that there will be €124bn of reinvestments from January to October 2018 (so an average of €12bn a month). The pace will however be slower for the first three months of next year at just €23bn total for those months before ramping up from April. So that means that the pace of QE plus reinvestments following the taper announcement nearly two weeks ago will be around €38bn for January to March and closer to €45bn from April to October. In terms of CSPP, what was most interesting from the latest data was confirmation that next year’s CSPP redemptions are a lot smaller than would be implied by the eligible universe because purchases have been concentrated in liquid new-ish issues.

The data suggest that the average monthly CSPP redemptions over the next 12 months will only be €273m (2.7% pa of the current holdings versus close to 8% in the eligible universe). The data backs up the view of DB’s Michal Jezek as per his note here from mid-October.

Turning now to markets in Asia this morning where the rally for Oil is helping equity bourses to post decent gains. The Nikkei (+1.57%) in particular is at a new 25-year high while the Hang Seng (+1.22%), ASX 200 (+1.02%) and Shanghai Comp (+0.63%) are also up. There hasn’t been any notable updates from Trump’s Asia tour while this morning we also had the RBA meeting where policy was left unchanged, as expected.

Moving on. There were a few central bank speakers yesterday but in truth there wasn’t much in it to move the dial. The Fed’s Dudley spoke post his resignation announcement and said that “…there’s not a lot of discord going into this (Fed) transition…so I think it’s going to be a very, very smooth transition” and that the Fed vacancies “has no implication whatsoever for policy right now”. Further, he added that Governor Powell and Chair Yellen “are very well aligned, so I think this is going to be very evolutionary”.

Meanwhile the ECB’s Praet sounded a bit dovish, noting that “a substantial amount of monetary accommodation continues to be necessary…” and that “overall, inflation developments, despite the solid growth, have remained subdued”. In the details, he noted 3 factors were considered when ECB recalibrated its policy on QE back in October, including: i) pace – was reduced because “the brighter economic prospects have increased our confidence” on a gradual rise in inflation, ii) horizon – was extended because ECB “has always emphasized monetary policy needs to be persistent and patient for underlying inflation pressure to gradually build up” and iii) optionality – as retaining the option to recalibrate the APP if warranted is consistent with the forward guidance on the APP.

Before we take a look at today’s calendar, we wrap up with other data releases from yesterday. In the US, the Fed’s latest senior loan officer opinion survey was released. In the details, respondents indicated that bank’s lending

standards was i) eased for commercial and industrial loans (C&I), ii) broadly unchanged for most commercial (CRE) and residential real estate (RRE) loans, but iii) tightened for credit cards and auto loans. Conversely, in terms of demand, a) RRE and credit card lending was broadly unchanged, but b) demand for C&I and CRE loans was weaker.

In the Eurozone, the final reading for the October PMI was revised 0.1pts higher, with the services PMI now at 55.0 and composite PMI at 56.0. Overall, our economists believe that if this level is sustained, 4Q GDP growth could be closer to 0.7% qoq rather than the 0.5% qoq that they currently expect. Across the bloc in terms of composite PMI, France’s PMI was revised 0.1pt lower to 57.4, Germany’s PMI was revised 0.3pts lower to 56.6 and Spain’s PMI fell 1.3pts to a still solid 55.1 this month, albeit the lowest reading since February. Elsewhere, Italy’s flash PMI was lower than expectations at 52.1 (vs. 52.9 expected) and composite PMI was 53.9 (vs. 54.3 expected).

Elsewhere Germany’s September factory orders were above expectations at +1.0% mom (vs. -1.1% expected) and +9.5% yoy (vs. +7.1% expected). Excluding the volatile ‘other transport’ sector, manufacturing orders were still up +8.9% yoy. Elsewhere, the Eurozone’s September PPI was above consensus at +0.6% mom (vs. +0.4% expected) and +2.9% yoy (vs. +2.7% expected), while the November Sentix investor confidence also beat at 34 (vs. 31 expected) – now slightly lower than the pre-GFC high.

Looking at the day ahead, datawise we’ll get Germany industrial production for September, Euro area retail sales for September and September JOLTS and October consumer credit in the US. The ECB is due to hold a forum on Banking Supervision which will include a speech from President Draghi. The Fed’s Quarles is also due to speak in the evening at the Clearing House annual conference. The OPEC world oil outlook will also be presented.

3. ASIAN AFFAIRS

i)Late MONDAY night/TUESDAY morning: Shanghai closed UP 25.40 points or .75% /Hang Sang CLOSED UP 397.54 pts or 1.39% / The Nikkei closed UP 389.25 POINTS OR 1.73%/Australia’s all ordinaires CLOSED UP 1.00%/Chinese yuan (ONSHORE) closed DOWN at 6.635/Oil UP to 57.26 dollars per barrel for WTI and 63.99 for Brent. Stocks in Europe OPENED RED . ONSHORE YUAN CLOSED DOWN AGAINST THE DOLLAR AT 6.638. OFFSHORE YUAN CLOSED STRONGER TO THE ONSHORE YUAN AT 6.635 //ONSHORE YUAN WEAKER AGAINST THE DOLLAR/OFF SHORE WEAKER TO THE DOLLAR/. THE DOLLAR (INDEX) IS STRONGER AGAINST ALL MAJOR CURRENCIES. CHINA IS NOT VERY HAPPY TODAY.

3a)THAILAND/SOUTH KOREA/NORTH KOREA

NORTH KOREA//SOUTH KOREA

3b) REPORT ON JAPAN

3C CHINA REPORT.

4. EUROPEAN AFFAIRS

Italy/EU

Target 2 imbalances rise again for Italy as it hits a record 433 billion euros to Northern European nations. Germany has a net credit of 879 billion euros. It means that Italian and other southern European citizens are moving their euros to Northern block countries. This debt which is guaranteed by central banks can never be paid.

(courtesy Mish Shedlock/Mishtalk

Italy Target2 Imbalance Hits Record €432.5 Billion As Dwindling Trust In Banks Plunges

Authored by Mike Shedlock via www.themaven.net/mishtalk,

Contrary to ECB propaganda, Target2 imbalances are a direct result an unsustainable balance of payment system. The imbalances represent both capital flight and debts that can never be paid back. If you think Italy can pay German and other creditors a record €432.5 Billion, you are in Fantasyland.

The interesting aspect of Italy’s new record Target2 Imbalance is that it comes just as Dwindling Trust in Italian Banks is on the rise.