GOLD: $1266.15 up $5.00

Silver: $16.21 UP 8 cents

Closing access prices:

Gold $1265.80

silver: $16.20

SHANGHAI GOLD FIX: FIRST FIX 10 15 PM EST (2:15 SHANGHAI LOCAL TIME)

SECOND FIX: 2:15 AM EST (6:15 SHANGHAI LOCAL TIME)

SHANGHAI FIRST GOLD FIX: $1275.42 DOLLARS PER OZ

NY PRICE OF GOLD AT EXACT SAME TIME: $1264.00

PREMIUM FIRST FIX: $11.42

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

SECOND SHANGHAI GOLD FIX: $1277.71

NY GOLD PRICE AT THE EXACT SAME TIME: $1263.70

Premium of Shanghai 2nd fix/NY:$14.01

SHANGHAI REJECTS NY /LONDON PRICING OF GOLD

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

LONDON FIRST GOLD FIX: 5:30 am est $1265.95

NY PRICING AT THE EXACT SAME TIME: $1266.00

LONDON SECOND GOLD FIX 10 AM: $1264.55

NY PRICING AT THE EXACT SAME TIME. 1263.40??

For comex gold:

DECEMBER/

NUMBER OF NOTICES FILED TODAY FOR DECEMBER CONTRACT: 246 NOTICE(S) FOR 24600 OZ.

TOTAL NOTICES SO FAR: 8809 FOR 880,900 OZ (27.39 TONNES),

For silver:

DECEMBER

8 NOTICE(S) FILED TODAY FOR

40,000 OZ/

Total number of notices filed so far this month: 6235 for 31,175,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: BID $17,333/OFFER $17,480 UP $416 (morning)

BITCOIN : BID $16,338 : OFFER 16,499 down $584 (CLOSING)

end

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total open interest SURPRISINGLY FELL BY A GOOD SIZED 3572 contracts from 207,275 FALLING TO 203,703 DESPITE YESTERDAY’S 1 CENT FALL IN SILVER PRICING. WE HAD CONSIDERABLE COMEX LIQUIDATION BUT WE WERE AGAIN NOTIFIED THAT WE HAD ANOTHER GOOD SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP ROUTE: A RESPECTABLE 2867 EFP’S FOR MARCH (AND ZERO FOR DEC AND OTHER MONTHS) AND THUS TOTAL ISSUANCE OF 2867 CONTRACTS. HOWEVER THE MOVEMENT ACROSS TO LONDON IS NOT AS SEVERE AS IN GOLD AS THERE SEEMS TO BE A MAJOR PLAYER TAKING ON THE BANKS AT THE COMEX. STILL, WITH THE TRANSFER OF 2867 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. YESTERDAY WITNESSED 1089 EFP’S FOR SILVER ISSUED. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24 HRS IN THE ISSUING OF EFP’S.

ACCUMULATION FOR EFP’S/SILVER/ STARTING FROM FIRST DAY NOTICE/FOR MONTH OF DECEMBER:

40,365 CONTRACTS (FOR 14 TRADING DAYS TOTAL 40,365 CONTRACTS OR 201.82 MILLION OZ: AVERAGE PER DAY: 2,883 CONTRACTS OR 14.416 MILLION OZ/DAY)

RESULT: A GOOD SIZED FALL IN OI COMEX DESPITE THE TINY 1 CENT FALL IN SILVER PRICE. WE HAD CONSIDERABLE COMEX SILVER LIQUIDATION BUT WE ALSO HAD A FAIR SIZED SIZED EFP ISSUANCE OF 2864 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS: FROM THE CME DATA 2864 EFP’S WERE ISSUED TODAY (FOR MARCH EFP’S) FOR A DELIVERABLE CONTRACT OVER IN LONDON WITH A FIAT BONUS. WE REALLY LOST 705 OI CONTRACTS i.e. 2864 open interest contracts headed for London (EFP’s) TOGETHER WITH A DECREASE OF 3572 OI COMEX CONTRACTS. AND ALL OF THIS HAPPENED WITH THE FALL IN PRICE OF SILVER BY 1 CENT AND A CLOSING PRICE OF $16.13 WITH RESPECT TO YESTERDAY’S TRADING. YET WE STILL HAVE A MASSIVE AMOUNT OF SILVER STANDING AT THE COMEX.

In ounces AT THE COMEX, the OI is still represented by just OVER 1 BILLION oz i.e. 1.018 BILLION TO BE EXACT or 146% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT DECEMBER MONTH/ THEY FILED: 8 NOTICE(S) FOR 40,000 OZ OF SILVER

In gold, the open interest FELL BY A TINY 18 CONTRACTS DOWN TO 453,395 DESPITE THE SMALL SIZED FALL IN PRICE OF GOLD YESTERDAY ($1.45). HOWEVER, THE TOTAL NUMBER OF GOLD EFP’S ISSUED YESTERDAY FOR TODAY TOTALED A CONSIDERABLE 8815 CONTRACTS OF WHICH THE MONTH OF DECEMBER SAW 0 CONTRACTS AND FEB SAW THE ISSUANCE OF 8815 CONTRACTS. The new OI for the gold complex rests at 453,395. DEMAND FOR GOLD INTENSIFIES GREATLY AS WE CONTINUE TO WITNESS THE HUMONGOUS NUMBER OF EFP TRANSFERS TOGETHER WITH THE MASSIVE AMOUNT OF GOLD OUNCES STANDING FOR DECEMBER. EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES. IN ESSENCE WE HAVE A HUGE GAIN OF 8797 OI CONTRACTS: 18 OI CONTRACTS DECREASED AT THE COMEX AND A GOOD SIZED 8815 OI CONTRACTS WHICH NAVIGATED OVER TO LONDON.

FRIDAY, WE HAD 9150 EFP’S ISSUED.

ACCUMULATION OF EFP’S/ GOLD(EXCHANGE FOR PHYSICAL) FOR THE MONTH OF DECEMBER STARTING WITH FIRST DAY NOTICE: 179,361 CONTRACTS OR 17.936 MILLION OZ OR 557.88 TONNES (14 TRADING DAYS AND THUS AVERAGING: 12,881 EFP CONTRACTS PER TRADING DAY OR 1.2881 MILLION OZ/DAY)

Result: A TINY SIZED DECREASE IN OI DESPITE THE SMALL SIZED RISE IN PRICE IN GOLD TRADING YESTERDAY ($1.45). WE HAD A GOOD SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 8815. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX AND YET WE REACHED THE HUGE DELIVERY MONTH OF DECEMBER. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 8815 EFP CONTRACTS ISSUED, WE HAD A NET GAIN IN OPEN INTEREST OF 8,797 contracts:

8815 CONTRACTS MOVE TO LONDON AND A 18 CONTRACTS DECREASED AT THE COMEX. (in tonnes, the gain yesterday equates to 27.36)

we had: 246 notice(s) filed upon for 24,600 oz of gold.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD:

Today, VERY STRANGE!! WITH GOLD ADVANCING UP TO $1266., THE CROOKS DECIDED TO RAID THE COOKIE JAR AGAIN/ WE HAD A GOOD SIZED WITHDRAWAL OF 1.18 TONNES in gold inventory at the GLD.

Inventory rests tonight: 836.02 tonnes.

SLV

NOTE: THEY DO NOT RAID SILVER BECAUSE THERE IS NO PHYSICAL INVENTORY TO RAID AT THE SLV:

NO CHANGE IN SILVER INVENTORY AT THE SLV:

INVENTORY RESTS AT 326.337 MILLION OZ/

end

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in silver FELL BY A GOOD SIZED 3572 contracts from 207,945 DOWN TO 203,703 (AND now A LITTLE CLOSER TO THE NEW COMEX RECORD SET ON FRIDAY/APRIL 21/2017 AT 234,787) DESPITE THE TINY FALL IN PRICE OF SILVER OF 1 CENT YESTERDAY . HOWEVER,OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE ANOTHER 2867 PRIVATE EFP’S FOR MARCH (WE DO NOT GET A LOOK AT THESE CONTRACTS AS IT IS PRIVATE BUT THE CFTC DOES AUDIT THEM). EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. WE HAD CONSIDERABLE COMEX SILVER COMEX LIQUIDATION. BUT, IF WE TAKE THE OI LOSS AT THE COMEX OF 3572 CONTRACTS TO THE 2867 OI TRANSFERRED TO LONDON THROUGH EFP’S WE OBTAIN A SMALL LOSS OF 705 OPEN INTEREST CONTRACTS, AND YET WE STILL HAVE A HUGE AMOUNT OF SILVER OUNCES THAT ARE STANDING FOR METAL IN DECEMBER (SEE BELOW). THE NET LOSS TODAY IN OZ: 3.525 MILLION OZ!!!

RESULT: A FAIR SIZED DECREASE IN SILVER OI AT THE COMEX DESPITE THE 1 CENT FALL IN PRICE (WITH RESPECT TO YESTERDAY’S TRADING). BUT WE ALSO HAD ANOTHER 2867 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON . TOGETHER WITH THE HUGE AMOUNT OF SILVER OUNCES STANDING FOR DECEMBER, DEMAND FOR PHYSICAL SILVER INTENSIFIES DESPITE THE CONSTANT RAIDS.

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)Late TUESDAY night/WEDNESDAY morning: Shanghai closed DOWN 8.93 points or 0.27% /Hang Sang CLOSED DOWN 23.72 pts or 0.27% / The Nikkei closed UP 23.72 POINTS OR 0.10%/Australia’s all ordinaires CLOSED UP 0.08%/Chinese yuan (ONSHORE) closed UP at 6.5780/Oil UP to 57.76 dollars per barrel for WTI and 63.84 for Brent. Stocks in Europe OPENED MOSTLY IN THE RED . ONSHORE YUAN CLOSED WELL UP AGAINST THE DOLLAR AT 6.5780. OFFSHORE YUAN CLOSED DOWN AGAINST THE ONSHORE YUAN AT 6.5790 //ONSHORE YUAN STRONGER AGAINST THE DOLLAR/OFF SHORE STRONGER TO THE DOLLAR/. THE DOLLAR (INDEX) IS SLIGHTLY STRONGER AGAINST ALL MAJOR CURRENCIES. CHINA IS NOT SO HAPPY TODAY.(WEAKER MARKETS)

3a)THAILAND/SOUTH KOREA/NORTH KOREA

i)North Korea

North Korea is reported testing anthrax tipped ICBM’s!!

( zerohedge)

ii)According to London’s Telegraph, the uSA is preparing for a “bloody nose’ military attack on North Korea

( Telegraph)

( zerohedge)

b) REPORT ON JAPAN

3 c CHINA

4. EUROPEAN AFFAIRS

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

6 .GLOBAL ISSUES

i)SWEDEN

A key development: The Swedish central bank (Riksbank) has ended QE. Thus it will no longer add to its burgeoning balance sheet. However interest rate is to remain at negative 0.5%. Inflation is getting a strong foothold in Sweden.

( zerohedge)

ii) SOUTH AFRICA

Oh Boy!! this is not good. The South African rand tumbles as the ANC now decides to nationalize its Central bank and confiscate land a la Rhodesia (Zimbabwe)

( zerohedge)

7. OIL ISSUES

Oil and Gas data seems to confuse our traders. We had a good gasoline build, on top of production jumps. However also a good crude draw done was recorded. The key number: a huge production jump

( zerohedge)

8. EMERGING MARKET

9. PHYSICAL MARKETS

( zerohedge)

iii)Craig Hemke reminds us of a cable sent to NY where the author claims that the futures market in gold/silver will suppress the spot price

iv)This would be another deadly blow to the USA dollar as countries seek the use of the yuan to replace the dollar

( Gul/Voice of America/Washington)

10. USA stories which will influence the price of gold/silver

i)Existing home sales surge to 11 year highs despite mortgage application tumble

(courtesy zerohedge)

ii) the tax reform bill passes 51 to 48. Now the fun begins as the cost of this program adds 1.5 trillion dollars of debt.

( zerohedge)

iii)A must read…the upcoming fiscal derailment in the USA. David Stockman explains why FY 2019 will sink the USA economy

iv)SWAMP NEWS

v)Michael Snyder comments on the Washington Post story on “Fedcoin”. He figures that this is how the big boys are going to get rid of paper money

Let us head over to the comex:

The total gold comex open interest FELL BY A VERY TINY 18 CONTRACTS DOWN to an OI level of 453,395 DESPITE THE FALL IN THE PRICE OF GOLD ($1.45 LOSS WITH RESPECT TO YESTERDAY’S TRADING). WE DID HAVE MINIMAL COMEX GOLD LIQUIDATION BUT WE DID HAVE A HUGE GAIN IN TOTAL OPEN INTEREST AS WE HAD ANOTHER STRONG COMEX TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS. THE CME REPORTS THAT 0 EFPS WERE ISSUED FOR DECEMBER AND 8815 EFP’S WERE ISSUED FOR FEBRUARY FOR A TOTAL OF 8815 CONTRACTS. THE OBLIGATION STILL RESTS WITH THE BANKERS ON THESE TRANSFERS.

ON A NET BASIS IN OPEN INTEREST WE GAINED TODAY: 8,797 OI CONTRACTS IN THAT 8815 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE LOST 18 COMEX CONTRACTS. NET GAIN: 8797 contracts OR 879,700 OZ OR 27.36 TONNES

Result: AN SMALL SIZED INCREASE IN COMEX OPEN INTEREST DESPITE THE FALL IN THE PRICE OF GOLD TRADING YESTERDAY ($1.45.) WE HAD NO REAL GOLD LIQUIDATION . TOTAL OPEN INTEREST GAIN ON THE TWO EXCHANGES: 8797 OI CONTRACTS…

We have now entered the active contract month of DECEMBER. The open interest for the front month of December saw it’s open interest FELL by 1422 contracts DOWN to 471. We had 1469 notices filed upon yesterday so we GAINED 47 COMEX contracts or an additional 4700 oz will stand for delivery AT THE COMEX in this active delivery month of December as queue jumping returns. Bankers are still in need of physical.

January saw its open interest LOSS OF 65 contracts DOWN to 1456. FEBRUARY saw a loss of 1369 contacts down to 332,929.

We had 246 notice(s) filed upon today for 24,600 oz

PRELIMINARY VOLUME TODAY ESTIMATED; 193,434

FINAL NUMBERS CONFIRMED FOR YESTERDAY: 216,333

comex gold volumes are increasing dramatically

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

And now for the wild silver comex results.

Total silver OI FELL BY A considerable 3572 CONTRACTS FROM 207,275 DOWN TO 203,703 DESPITE YESTERDAY’S TINY 1 CENT LOSS IN PRICE . HOWEVER, WE DID HAVE ANOTHER GOOD SIZED 2869 EMERGENCY EFP’S FOR MARCH ISSUED BY OUR BANKERS (ZERO FOR DECEMBER) TO COMEX LONGS WHO RECEIVED A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON.THE TOTAL EFP’S ISSUED: 2869. IT SURE LOOKS LIKE THE SILVER BOYS HAVE STARTED TO MIGRATE TO LONDON FROM THE START OF DELIVERY MONTH AND CONTINUING RIGHT THROUGH UNTIL FIRST DAY NOTICE JUST LIKE WE ARE WITNESSING TODAY. USUALLY WE NOTED THAT CONTRACTION IN OI OCCURRED ONLY DURING THE LAST WEEK OF AN UPCOMING ACTIVE DELIVERY MONTH. THIS PROCESS HAS JUST BEGUN IN EARNEST IN SILVER STARTING IN SEPTEMBER. HOWEVER, IN GOLD, WE HAVE BEEN WITNESSING THIS FOR THE PAST 2 YEARS. WE HAD NO LONG SILVER LIQUIDATION AS DEMAND FOR PHYSICAL SILVER INTENSIFIES ESPECIALLY AS WE WITNESS A HUGE AMOUNT OF SILVER OUNCES STANDING FOR METAL IN DECEMBER AS WELL AS THAT CONTINUAL MIGRATION OF EFPS OVER TO LONDON. ON A PERCENTAGE BASIS THERE ARE MORE EFP’S ISSUED FOR GOLD THAN SILVER AS IT SEEMS THAT A MAJOR PLAYER WISHES TO TAKE ON THE CROOKED COMEX SHORTS. ON A NET BASIS WE LOST 705 OPEN INTEREST CONTRACTS:

3572 CONTRACTS LOSS AT THE COMEX WITH THE ADDITION OF 2867 OI CONTRACTS NAVIGATING OVER TO LONDON.

NET LOSS: 705 CONTRACTS

We are now in the big active delivery month of December and here the OI FELL by 297 contracts DOWN to 667. We had 297 notice filed UPON YESTERDAY so we LOST 0 contract or an additional NIL oz will stand in this active COMEX delivery month of December.

The January contract month ROSE by 0 contracts UP to 1324. February saw a gain OF 3 OI contract RISING TO 38. The March contract LOST 3323 contracts DOWN to 164,251.

We had 8 notice(s) filed for 40,000 oz for the DECEMBER 2017 contract

INITIAL standings for DECEMBER

Dec 20/2017.

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz |

6815.800 oz

212 kilobars

|

| Deposits to the Dealer Inventory in oz | nil oz |

| Deposits to the Customer Inventory, in oz |

nil oz

|

| No of oz served (contracts) today |

246 notice(s)

24600 OZ

|

| No of oz to be served (notices) |

225 contracts

(22,500 oz)

|

| Total monthly oz gold served (contracts) so far this month |

8809 notices

880,900 oz

27.39 tonnes

|

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

WE HAD nil DEALER DEPOSIT:

total dealer deposits: nil oz

We had nil dealer withdrawals:

total dealer withdrawals: nil oz

we had 0 customer deposit(s):

total customer deposits nil oz

We had 1 customer withdrawal(s)

i) Into Scotia: 6815.800 oz (212 kilobars)

Total customer withdrawals: 6815.8000 oz

we had 0 adjustment(s)

For DECEMBER:

Today, 0 notice(s) were issued from JPMorgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equates to 246 contract(s) of which 138 notices were stopped (received) by j.P. Morgan dealer and 34 notice(s) was (were) stopped/ Received) by j.P.Morgan customer account.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

To calculate the INITIAL total number of gold ounces standing for the DECEMBER. contract month, we take the total number of notices filed so far for the month (8809) x 100 oz or 880,900 oz, to which we add the difference between the open interest for the front month of DEC. (471 contracts) minus the number of notices served upon today (246 x 100 oz per contract) equals 902,400 oz, the number of ounces standing in this active month of DECEMBER

Thus the INITIAL standings for gold for the DECEMBER contract month:

No of notices served (8809) x 100 oz or ounces + {(471)OI for the front month minus the number of notices served upon today (246) x 100 oz which equals 902,400 oz standing in this active delivery month of DECEMBER (28.07 tonnes). THERE IS 33.4 TONNES OF REGISTERED GOLD AVAILABLE FOR DELIVERY SO FAR.

WE GAINED 47 COMEX CONTRACTS STANDING OR AN ADDITIONAL 4700 OZ WILL STAND AT THE COMEX

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

ON FIRST DAY NOTICE FOR DECEMBER 2016, THE INITIAL GOLD STANDING: 39.038 TONNES STANDING

BY THE END OF THE MONTH: FINAL: 29.791 TONNES STOOD FOR COMEX DELIVERY AS THE REMAINDER HAD TRANSFERRED OVER TO LONDON FORWARDS.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Total dealer inventory 1,070,309.229 or 33.29 tonnes (dealer gold continues to disappear)

Total gold inventory (dealer and customer) = 9,152,440.023 or 284.67 tonnes

I have a sneaky feeling that these withdrawals of gold in kilobars are being used in the hypothecating process and are being used in the raiding of gold!

The gold comex is an absolute fraud. The use of kilobars and exact weights makes the data totally absurd and fraudulent! To me, the only thing that makes sense is the fact that “kilobars: are entries of hypothecated gold sent to other jurisdictions so that they will not be short with their underwritten derivatives in that jurisdiction. This would be similar to the rehypothecated gold used by Jon Corzine at MF Global.

IN THE LAST 14 MONTHS 69 NET TONNES HAS LEFT THE COMEX.

end

And now for silver

AND NOW THE DECEMBER DELIVERY MONTH

DECEMBER INITIAL standings

| Silver | Ounces |

| Withdrawals from Dealers Inventory | nil oz |

| Withdrawals from Customer Inventory |

1,252,579.926 oz

brinks

Delaware

CNT

HSBC

|

| Deposits to the Dealer Inventory |

nil oz

|

| Deposits to the Customer Inventory |

599,962.600 oz

HSBC

|

| No of oz served today (contracts) |

8

CONTRACT(S)

(40,000 OZ)

|

| No of oz to be served (notices) |

362 contract

(1,810,000 oz)

|

| Total monthly oz silver served (contracts) | 6235 contracts

(31,175,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

today, we had 0 deposit(s) into the dealer account:

total dealer deposit: nil oz

we had 0 dealer withdrawals:

total dealer withdrawals: nil oz

we had 4 customer withdrawal(s):

i) Out of CNT: 609,606.616 oz

ii) out of Delaware: 511,526.990 oz

iii) Out of Brinks: 25,273.680 oz

iv) Out of HSBC: 106,172.640 oz

TOTAL CUSTOMER WITHDRAWAL 1,252,579.926 oz

We had 1 Customer deposit(s):

i) Into HSBC: 599,962.600 oz

***deposits into JPMorgan have stopped again

In the month of March and February, JPMorgan stopped (received) almost all of the comex silver contracts.

why is JPMorgan bringing in so much silver??? why is this not criminal in that they are also the massive short in silver

total customer deposits: 599,962.600 oz

we had 0 adjustment(s)

The total number of notices filed today for the DECEMBER. contract month is represented by 8 contract(s) FOR 40,000 oz. To calculate the number of silver ounces that will stand for delivery in DECEMBER., we take the total number of notices filed for the month so far at 6235 x 5,000 oz = 31,175,0000 oz to which we add the difference between the open interest for the front month of DEC. (370) and the number of notices served upon today (8 x 5000 oz) equals the number of ounces standing.

.

Thus the INITIAL standings for silver for the DECEMBER contract month: 6235 (notices served so far)x 5000 oz + OI for front month of DECEMBER(370) -number of notices served upon today (8)x 5000 oz equals 33,035,000 oz of silver standing for the DECEMBER contract month. This is EXCELLENT for this active delivery month of November.

WE LOST 0 CONTRACTS OR NIL OZ THAT WILL NOT STAND AT THE COMEX

ON FIRST DAY NOTICE FOR THE DECEMBER 2016 CONTRACT WE HAD 15.282 MILLION OZ STAND.

THE FINAL STANDING: 19.900 MILLION OZ AS QUEUE JUMPING INTENSIFIED.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

ESTIMATED VOLUME FOR TODAY: 59,104

CONFIRMED VOLUME FOR FRIDAY: 61,229 CONTRACTS

YESTERDAY’S CONFIRMED VOLUME OF 61,229 CONTRACTS EQUATES TO 306 MILLION OZ OR 43.7% OF ANNUAL GLOBAL PRODUCTION OF SILVER

COMMODITY LAW SUGGESTS THAT OPEN INTEREST SHOULD NOT BE MORE THAN 3% OF ANNUAL GLOBAL PRODUCTION. THE CROOKS ARE SUPPLYING MASSIVE PAPER TRYING TO KEEP SILVER IN CHECK.

Total dealer silver: 57.344 million

Total number of dealer and customer silver: 238.468 million oz

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price at that day at $18.42

The previous record was 224,540 contracts with the price at that time of $20.44

end

NPV for Sprott and Central Fund of Canada

1. Central Fund of Canada: traded at Negative 2.3 percent to NAV usa funds and Negative 2.0% to NAV for Cdn funds!!!!

Percentage of fund in gold 63.1%

Percentage of fund in silver:36.6%

cash .+.3%( Dec 20/2017)

2. Sprott silver fund (PSLV): NAV RISES TO -0.97% (Dec 20 /2017)

3. Sprott gold fund (PHYS): premium to NAV RISES TO -0.65% to NAV (Dec 20 /2017 )

Note: Sprott silver trust back into NEGATIVE territory at -0.97%-/Sprott physical gold trust is back into NEGATIVE/ territory at -0.65%/Central fund of Canada’s is still in jail but being rescued by Sprott.

Sprott WINS hostile 3.1 billion bid to take over Central Fund of Canada

(courtesy Sprott/GATA)

END

And now the Gold inventory at the GLD

Dec 20/DESPITE THE GOOD ADVANCE IN PRICE TODAY/THE CROOKS RAIDED THE COOKIE JAR TO THE TUNE OF 1.18 TONNES/INVENTORY RESTS AT 836.02 TONNES

Dec 19/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 837.20 TONNES

Dec 18 SHOCKINGLY AFTER TWO GOOD GOLD TRADING DAYS, THE CROOKS RAID THE COOKIE JAR BY THE SUM OF 7.09 TONNES/INVENTORY RESTS AT 837.20 TONNES

Dec 15/NO CHANGES IN GOLD INVENTORY/RESTS AT 844.29 TONNES.

Dec 14/a good sized gain of 1.48 tonnes of gold into the GLD/inventory rests at 844.29 tones

Dec 13/no changes in gold inventory at the GLD/inventory rests at 842.81 tonnes

Dec 12/SURPRISINGLY NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 842.81 TONNES

Dec 11/SURPRISINGLY NO CHANGES IN GOLD INVENTORY AT THE GLD DESPITE THE CONSTANT RAIDS ON GOLD/INVENTORY RESTS AT 842.81 TONNES

Dec 8/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 842.81 TONNES

Dec 7/A BIG WITHDRAWAL OF 2.66 TONNES FROM THE GLD/INVENTORY RESTS AT 842.81 TONNES

Dec 6/No changes in GOLD inventory at the GLD/Inventory rests at 845.47 tonnes

Dec 5/A WITHDRAWAL OF 2.64 TONNES FROM THE GLD/INVENTORY RESTS AT 845.47 TONNES

Dec 4/A MASSIVE DEPOSIT OF 8.56 TONNES OF GOLD INTO THE GLD/THE BLEEDING OF GLD GOLD HAS STOPPED/INVENTORY RESTS TONIGHT AT 848.11 TONNES

Dec 1/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 839.55 TONNES

Nov 30/no change in gold inventory at the GLD. Inventory rests at 839.55 tonnes

Nov 29/a withdrawal of 2.66 tonnes at the GLD/Inventory rests at 839.55 tonnes

NOV 28/ no change in gold inventory at the GLD/inventory rests at 842.21 tonnes

Nov 27 Strange!! we gold up by $6.40 today, we had a good sized withdrawal of 1.18 tonnes from the GLD. Here is something that is also strange: we have had exactly 1.18 tonnes of gold withdrawn from the comex on 5 separate occasions in the past 30 days..explanation?

Nov 24/no change in gold inventory at the GLD/Inventory rests at 843.09 tonnes

Nov 22/no change in gold inventory at the GLD/Inventory rests at 843.39 tonnes

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

Dec 120/2017/ Inventory rests tonight at 836.02 tonnes

*IN LAST 295 TRADING DAYS: 104.93 NET TONNES HAVE BEEN REMOVED FROM THE GLD

*LAST 230 TRADING DAYS: A NET 52.35 TONNES HAVE NOW BEEN ADDED INTO GLD INVENTORY.

*FROM FEB 1/2017: A NET 21.24 TONNES HAVE BEEN ADDED.

end

Now the SLV Inventory

Dec 20/INVENTORY REMAINS CONSTANT AT 326.337 MILLION OZ (COMPARE WITH GLD)

Dec 19/SILVER INVENTORY REMAINS CONSTANT AT 326.337 MILLION OZ

Dec 18.2017//SILVER INVENTORY CONTINUES TO REMAIN PAT./INVENTORY REMAINS AT 326.337 MILLION OZ/

INVENTORY RESTS AT 326.337 TONNES

Dec 15/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 326.337 MILLION OZ/

Dec 14/a small withdrawal of 377,000 oz and that usually means to pay for fees./inventory rests at 326.337 million oz/

Dec 13/no change in silver inventory at the SLV/Inventory rests at 326.714 million oz/

Dec 12/WOW!ANOTHER STRANGE ONE: SILVER HAS BEEN DOWN FOR 10 CONSECUTIVE DAYS, YET THE SLV ADDS ANOTHER 1.415 MILLION OZ TO ITS INVENTORY. IN THAT 10 DAY PERIOD, SLV ADDS 9.584 MILLION OZ/

INVENTORY RESTS AT 326.714 MILLION OZ

Dec 11/WOW!! ANOTHER STRANGE ONE: SILVER DESPITE BEING DOWN FOR 9 CONSECUTIVE TRADING DAYS ADDS ANOTHER 944,000 OZ TO ITS INVENTORY. FROM NOV 30 UNTIL TODAY SILVER HAS BEEN DOWN EVERY DAY. HOWEVER THE INVENTORY OF SILVER HAS RISEN 8.169 MILLION OZ.

Dec 8/A HUGE DEPOSIT OF 2.642 MILLION OZ/INVENTORY RESTS AT 324.355 MILLION OZ/

Dec 7/strange!! with the continual whacking of silver, no change in silver inventory at the SLV/Inventory rests at 321.713

Dec 6/no change in silver inventory at the SLV/Inventory remains at 21.713 million oz.

Dec 5/THIS ONE HIT ME LIKE A TON OF BRICKS: SLV ADDS 2.507 MILLION OZ DESPITE THE HUGE DRUBBING SILVER TOOK TODAY. (PRICE DISCOVERY?)

Dec 4/NO CHANGE IN SILVER INVENTORY AT THE SLV

INVENTORY RESTS AT 319.207 MILLION OZ/

Dec 1/VERY STRANGE!! WITH SILVER IN THE DUMPSTER THESE PAST FEW DAYS, SLV ADDS 2.076 MILLION OZ/???

INVENTORY 319.207 MILLION OZ/

Nov 30/no changes in silver inventory despite the huge drop in price/inventory rests at 317.130 million oz

Nov 29/no changes in silver inventory at the SLV/Inventory rests at 317.130 million oz/strange!! at drop of 32 cents and no change in inventory?

Nov 28/no change in silver inventory at the SLV/Inventory rests at 317.130 million oz.

Nov 27/NO CHANGE IN SILVER INVENTORY DESPITE A ZERO GAIN IN PRICE /QUITE OPPOSITE TO GOLD WHICH SAW 1.18 TONNES OF GOLD WITHDRAWN DESPITE A RISE IN PRICE OF $6.40

Nov 24/A WITHDRAWAL OF 944,000 OZ OF SILVER FROM THE SLV//INVENTORY RESTS AT 317.130 MILLION OZ

Nov 22/no change in silver inventory at the SLV/Inventory rests at 318.074 million oz.

Dec 19/2017:

Inventory 326.337 million oz

end

6 Month MM GOFO

Indicative gold forward offer rate for a 6 month duration

+ 1.80%

12 Month MM GOFO

+ 1.95%

30 day trend

end

end

Major gold/silver trading /commentaries for WEDNESDAY

GOLDCORE/BLOG/MARK O’BYRNE.

GOLD/SILVER

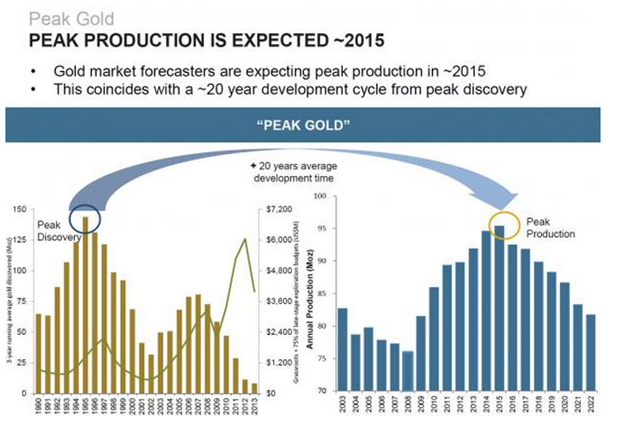

What Peak Gold, Interest Rates And Current Geopolitical Tensions Mean For Gold in 2018

What Peak Gold, Interest Rates And Current Geopolitical Tensions Mean For Gold in 2018

– Peak gold will be a major driver, gold over $5,000/oz ‘not beyond the realms of possibility’

– Relationship between interest rates and inflation are one of the key catalysts for price

– Geopolitical uncertainty will continue to play a key role in determining the price of gold

– What happens when the unstoppable force of robust global demand for gold meets the immovable object of a small, finite, rare and dwinding supply of physical gold?

The editors over at The Daily Reckoning have taken some time to speak to gold market experts about their thoughts and expectations for the precious metal in the new year.

There were two main catalysts mentioned by both the experts and the editors; the relationship between interest rates and inflation, and mounting geopolitical tensions.

Within these factors peak gold was of particular interest. Goldcore’s Mark O’Byrne told the Daily Reckoning:

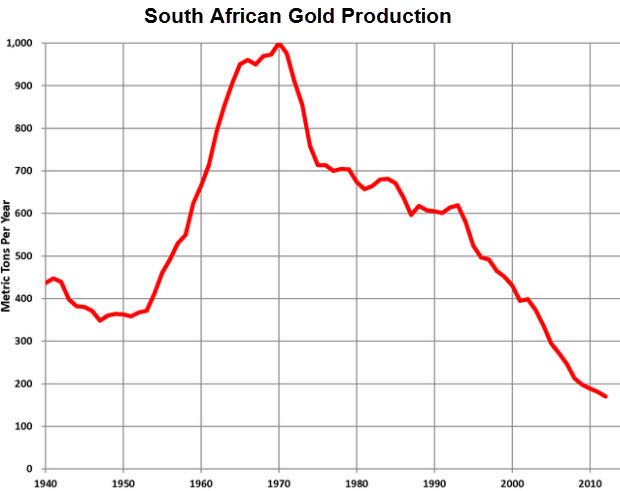

“We are on the cusp of peak gold production…Gold production in South Africa has already fallen over 75% and it is the canary in the gold mine so to speak.

All the data is suggesting this and leading people in the gold mining industry itself to say we are on the verge of a gold peak.”

According to Mark, “Uber-bull predictions of gold at over $5,000 per ounce are not beyond the realms of possibility…”

Peak gold has been an area of rising interest in recent years. The risk of falling gold production and a consequent reduction in supply are issues the mainstream are becoming slowly aware of. Some are already asking whether 2015 or 2016 marked the year of peak gold production.

As Mark mentioned in his interview with The Daily Reckoning the gold supply from South Africa has seen a dramatic fall of late. In 1970 South Africa produced over 1,000 tonnes of gold but this has since fallen to below 250 tonnes in recent years (see chart above).

Levels this low have not been seen since 1922, a year which did not have the advantage of the massive technological advances of recent years and more intensive mining practices.

As Mark asked at the beginning of the year: What happens when the unstoppable force of robust global demand for gold meets the immovable object of a small, finite, rare and dwinding supply of physical gold?

Below we bring you the rest of the Daily Reckoning’s piece entitled ‘Gold round-up: what our editors think about the yellow metal‘

The key to understanding gold price

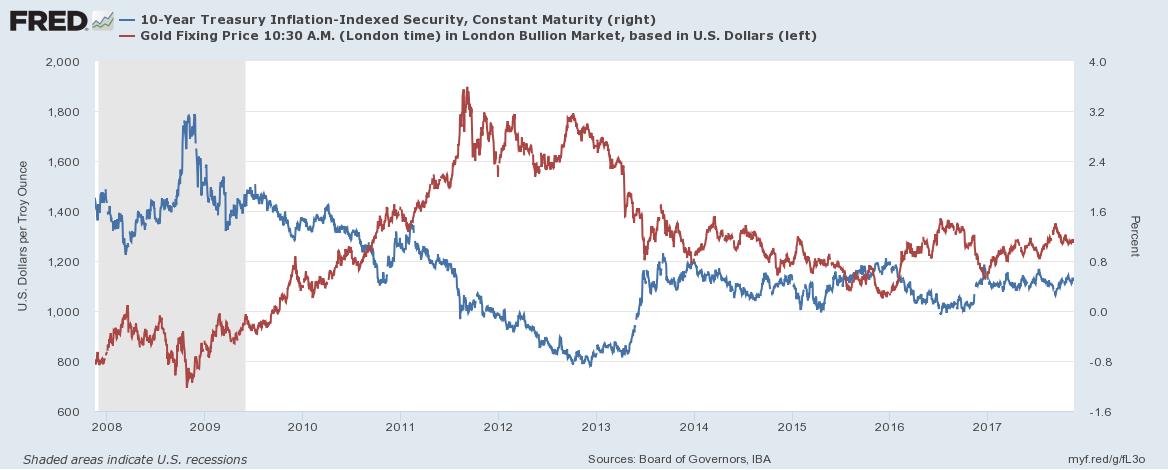

Let’s start with our growth expert, Sean Keyes, who thinks the key to understanding gold, and predicting future price hikes, lies in interest rates and inflation:

“When real rates are high gold goes down. Then real rates are low it goes up. It doesn’t really matter what’s causing real rates to change — it could be inflation or interest rates, or both together — what matters is the combination of the two.”

As Sean says here, in the past, the real interest rate has mirrored the gold price.

This, according to Sean, is the green light investors should look out for when trying to spot an incline in price.

David Stevenson agrees.

He kicked off the gold theme last week by deconstructing the popular view that interest rates could be harmful for bullion, and that inflation alone would improve value.

Both, according to David, are only partly right.

He reckons the true driver of the gold price is US real interest rate, saying:

Gold only comes under pressure when nominal rates rise faster than increases in the consumer price index.Further, before the great financial crisis that began a decade ago, the real interest rate was also viewed as being roughly equivalent to the real economic growth rate.

Now the US economy has been expanding someway faster than 0.5% in recent years. For example, 2017 Q3 annualised real growth was 3%.

So you see, according to David, negative interest rates could be a key facilitator for a rise in gold price.

But why would negative interest rates be a problem now?

In David’s view, the post-financial crisis is “very long in the tooth,” and at this point, recession looks more likely than inflation.

An obvious catalyst

So, with stock prices and junk bonds appearing more vulnerable to significant falls, central banks are likely to rely on negative interest rates to patch-up the wounds.

And this could be excellent news for the gold price:

In the next financial crisis, central banks could engineer even larger negative numbers that could lead to a gold price well in excess of $2,000 per ounce.

Gold’s time to shine

You’ve probably heard of Jim Rickards before.

Famously bullish about gold, Jim recently stated in an article for The Daily Reckoning that:

“The crisis in North Korea is not getting any better; it’s actually getting worse. Syria, Iran and the South China Sea are additional flashpoints. The headlines may fade in any given week, but geopolitical shocks will return when least expected and send gold soaring in a flight to safety.

Finally, the Fed will not raise rates in December, contrary to market expectations.

As market probabilities catch up with reality, the dollar will sink and gold will rally.”

You can read Jim’s full article here.

Should these events play out, investors may flock to gold as a safe-haven asset, and Jim’s $10,000 per ounce prediction could become a reality a lot sooner than anticipated.

Related reading

Peak Gold – Biggest Gold Story Not Being Reported

An Interview with GoldCore Founder, Mark O’Byrne

China, Russia Alliance Deepens Against American Overstretch

Gold Could Surge To $8,000/oz On Negative Interest Rates – Lassonde

News and Commentary

Gold prices little changed as dollar holds steady on tax bill hopes (Reuters.com)

Asia Stocks Mixed as Tax Vote Awaits; Yields Climb (Bloomberg.com)

U.S. stocks retreat from records (MarketWatch.com)

Single-family housing starts, permits hit 10-year high (Reuters.com)

Where Janet Yellen has fallen short as head of the Federal Reserve (MarketWatch.com)

Central banks, trade and bubbles threaten the 2018 status quo (Reuters.com)

Gold Prices (LBMA AM)

20 Dec: USD 1,265.95, GBP 944.27 & EUR 1,068.21 per ounce

19 Dec: USD 1,263.10, GBP 944.93 & EUR 1,070.10 per ounce

18 Dec: USD 1,258.65, GBP 943.11 & EUR 1,067.71 per ounce

15 Dec: USD 1,257.25, GBP 937.41 & EUR 1,065.52 per ounce

14 Dec: USD 1,255.60, GBP 935.67 & EUR 1,062.49 per ounce

13 Dec: USD 1,241.60, GBP 929.96 & EUR 1,056.97 per ounce

12 Dec: USD 1,243.40, GBP 933.92 & EUR 1,056.27 per ounce

Silver Prices (LBMA)

20 Dec: USD 16.19, GBP 12.09 & EUR 13.67 per ounce

19 Dec: USD 16.16, GBP 12.08 & EUR 13.68 per ounce

18 Dec: USD 16.09, GBP 12.04 & EUR 13.64 per ounce

15 Dec: USD 15.99, GBP 11.93 & EUR 13.55 per ounce

14 Dec: USD 16.01, GBP 11.92 & EUR 13.54 per ounce

13 Dec: USD 15.71, GBP 11.76 & EUR 13.38 per ounce

12 Dec: USD 15.78, GBP 11.82 & EUR 13.40 per ounce

Recent Market Updates

– New Rules For Cross-Border Cash and Gold Bullion Movements

– ‘Gold Strengthens Public Confidence In The Central Bank’ – Bundesbank

– WGC: 2018 Set To Be A Positive Year For Price of Gold and Investors

– Year-end Rate Hike Once Again Proves To Be Launchpad For Gold Price

– UK Stagflation Risk As Inflation Hits 3.1% and House Prices Fall

– Buy Gold, Silver Time After Speculators Reduce Longs and Banks Reduce Shorts

– Bitcoin – Plan Your Exit Strategy Now – Maybe With Gold

– Gold Demand Increases Along with Uncertainty Thanks to Trump, Brexit and North Korea

– UK Pensions Risk – Time to Rebalance and Allocate to Cash and Gold

– Bailins Coming In EU – 114 Italian Banks Have NP Loans Exceeding Tangible Assets

– Silver’s Positive Fundamentals Due To Strong Demand In Key Growth Industries

– An Interview with GoldCore Founder, Mark O’Byrne

– Risk Of Online Accounts Seen As One of Largest Brokerages In World Halts Online Trading After “Glitch”

JMcShirley.

This is very unusual for silver. Silver has been comatose in price for quite a while even though its volume is increasing. With the huge EFP’s issued, the bankers are getting nervous as their huge burgeoning shortfall is now weighing on them.

This is a very important development. I have never seen this happen twice in a week with no change in price.

end

Crypto Chaos – Bitcoin Spikes Back Above $17,000 After Flash-Crash, Bitcoin Cash Up 60%

Well that didn’t take long – Bitcoin is back at $17,000; Bitcoin Cash +60% at $3,500….

There is some logic as the forked currency gains over $1000 so the original Bitcoin loses that ‘dividend’…

Bitcoin rebounded earlier…

After futures were briefly halted on a crircuit-breaker…

For now the catalyst for the move appears to be a wave of selling from Coinbase HODLers as the exchange began allowing sends and receives in Bitcoin Cash(which split off from the original bitcoin on Aug. 1 after a group of developers decided to try to improve bitcoin transaction speeds and costs).

Investors in bitcoin at the time of the split should have received an equivalent amount of bitcoin cash, but Coinbase did not immediately do so, and said it would provide support by January. On Tuesday, Coinbase said all customers at the time of the split would have bitcoin cash.

The announcement follows news in the last few days that a large bitcoin payments processor BitPay and major cryptocurrency storage company Blockchain would support bitcoin cash.

Roger Ver (aka Bitcoin Jesus), an outspoken and early bitcoin investor, is a major supporter of bitcoin cash.

Additionally, some chatter that Tezos escaping an asset freeze of its $1.2 billion funds put some additional pressure on bitc55oin.

San Francisco federal judge refused to temporarily freeze $1.2 billion in cryptocurrency and other funds related to the Tezos Foundation and the block chain startup in a dispute between an investor and Tezos founders.

Investor Bruce MacDonald accused Tezos of engaging in the unlicensed sale of securities and use of a Swiss-based entity in an attempt to evade U.S. securities laws

* * *

Update: The entire Crypto space is under pressure as Asia opens…

Bitcoin is tumbling…

BTC flash crashed to $14,000 on GDAX…

Except Bitcoin Cash (which is up over 50% as Coinbase added the forked currency and it appears traders are rotating into it)…

* * *

Update: Bitcoin spot and futures are bid and have reebounded notably off the after-hours lows…

* * *

As we detailed earlier, shortly after the US equity market closed this evening, someone decided it was time to dump a few hundred Bitcoin, sending the price plunging below $17,000…

Did another HODLer just fold?

Potential investors in bitcoin should steer clear of a dangerous gamble and not complain to financial regulators if things do go wrong, Denmark’s central bank governor warned.

“You should stay away (from bitcoin). It is deadly,” central bank head Lars Rohde said in an interview with state broadcasterDR published online on Monday.

Additionally, CoinTelegraph reports that, according to Bitcoin.com co-founder and CTO Emil Oldenburg, Bitcoin is “useless” and has no future as a tradeable currency, citing high transaction fees and long lead times. In an interview with Swedish tech site Breakit, Oldenburg said that he had sold all of his Bitcoin and switched to Bitcoin Cash, a hard fork of Bitcoin created in August 2017.

Oldenburg justifies his actions, saying:

“An investment in Bitcoin right now I would say is the most risky investment one can make. It is extremely high-risk. I’ve actually sold all of my Bitcoins recently and switched to Bitcoin Cash.”

Despite the fact that Oldenburg’s company is in fact a Bitcoin wallet, the CTO says that he has become disenchanted with Bitcoin due to its high transaction fees and slow confirmation time, saying Bitcoin’s current performance is “completely unreasonable.”

Increased transaction speed and lower costs are the main features supporters of Bitcoin Cash point to when comparing the two coins.

Ethereum is also being sold but remain positive on the day…

Bitcoin futures are bid now…

end

Then to add to the ridiculousness of the situation, the other Bitcoin is halted on an “insider” trading probe

(courtesy zerohedge)

Bitcoin Cash Briefly Spikes To $8,500 After Massive Glitch; Trading Halted On “Insider Trading” Probe

Update: Just as we saw last night ahead of Bitcoin Cash’s release on GDAX, so this morning’s re-opening (reportedly at 12ET), Bitcoin is being dumped and Bitcoin Cash is surging…

* * *

As we detailed earlier, hours after announcing support for Bitcoin Cash, crypto-exchange Coinbase suffered a massive glitch which saw prices for the forked-cryptocurrency hit $8,500 for about an hour – around 250% higher than ‘normal’. It is unclear if any trades were executed during the spike, as trading was disabled for much of the anomaly.

As The Wall Street Journal reports, the company halted trading of the currency four minutes after trading began.

Hours later, Coinbase announced an investigation into whether any employees, contractors or their friends and family used confidential information about its plans to trade Bitcoin Cash before its announcement.

“It appears the price of bitcoin cash on other exchanges increased in the hours before our announcement… [while there’s] no indication of any wrongdoing at this time, we will be conducting an investigation…”

Coinbase in a blog post said it “maintains a strict trading policy and internal guidelines for employees.”

In bold font, the company added: “Coinbase employees have been prohibited from trading in Bitcoin Cash for several weeks.”

Noting the price increase of Bitcoin Cash in the hours before the announcement, Mr. Armstrong said Coinbase will be conducting an investigation into the matter.

“If we find evidence of any employee or contractor violating our policies—directly or indirectly—I will not hesitate to terminate the employee immediately and take appropriate legal action,” he wrote.

“Insider trading of crypto is so obvious,” Brian Hoffman, the chief executive of Open Bazaar, an online retail site that uses bitcoin, wrote on Twitter. Bitcoin Cash “skyrockets … hours later Coinbase rolls it out,” he noted.

In response, Coinbase confirms that sends and receives are still functional but trading on coinbase to resume once there is sufficient liquidity in GDAX.

[status] Monitoring: All BCH books will enter cancel-only mode, and all existing orders will be cleared. While in c… http://stspg.io/9dfaf0c30

An update on Bitcoin Cash for our customers: sends and receives are functional.

Buys and sells on http://Coinbase.com and in our mobile apps will be available to all customers once there is sufficient liquidity on GDAX. We anticipate that this will happen tomorrow. https://twitter.com/GDAX/status/943331326874214400 …

Coinbase – Buy/Sell Digital Currency

Coinbase is a secure online platform for buying, selling, transferring, and storing digital currency.

coinbase.com

Bitcoin Cash was added to both exchanges simultaneously on Tuesday. As TechCrunch‘s Fitz Tepper notes:

This is important to note because the liquidity (and price quotes) to buy and sell cryptocurrency on Coinbase come from GDAX, its sister exchange. So essentially a stable order book is needed on GDAX before Coinbase buy and sells can be functional.

This is why in the past the company has added assets (like Litecoin) to GDAX months before being added on Coinbase, so there could be sufficient liquidity at launch. On Twitter, Coinbases Ex-Director of Engineering Charlie Lee clarified that its operationally very hard to add an asset to both platforms at the same time.

To those saying I bought BCH with insider news, please stop. I had no info. I sold all the BCH I can the moment it was tradable on exchanges. And j just sold my 2 stuck BCH on Coinbase at $5000 each. Good riddance!

In hindsight, Coinbase should have listened to me. It was operationally very hard to launch on Coinbase and GDAX at the same time. Now with GDAX halted and Coinbase never opened, everyone is seeing a ridiculous price of $9500.

tons of support tickets and upset customers.

While the “Flash Spike” in Bitcoin Cash was happening, a flash crash was also taking place in Bitcoin, which tanked to the tune of $3,000 before recovering 60% to $17,000 and change.

BTC flash crashed to $14,000 on GDAX…

Prices are still volatile this morning with Bitcoin Cash moving back towards its record highs and Bitcoin fading…

Finally here is GDAX’s latest update:

We wanted to provide our customers with an update on Bitcoin Cash (BCH) trading on GDAX.

At 4:00pm PST on December 19, 2017, we launched three BCH order books on GDAX. All BCH order books opened in post-only mode, allowing customers to place open orders and establish liquidity.

At 5:20pm PST, we enabled trading on the BCH-USD book. The BCH-EUR and BCH-BTC books remained in post-only mode.

At 5:22pm PST, we paused trading in the BCH-USD order book due to significant volatility. Once paused, we cancelled resting orders and cleared all BCH order books. We made this decision to ensure a fair and orderly market.

BCH order books will reopen on December 20th at 9:00am PST. All BCH order books will open in post-only mode for a minimum of one hour to establish liquidity. We will continue to closely monitor market activity.

In a separate trading hiccup, another large cryptocurrency exchange, Gemini, was unable to transact bitcoin temporarily on Tuesday evening.

The New York-based exchange, whose bitcoin prices are referenced by futures contracts offered by Cboe Global Markets, said it couldn’t process trades temporarily because of problems on the blockchain, the technology underpinning the cryptocurrency. The outage, which lasted about 15 minutes, didn’t affect customers’ assets, the exchange said.

(courtesy zerohedge)

Litecoin Founder Cashes Out, Sells Entire Stake After 9,300% Rally

Charlie Lee, the creator of the world’s fifth-biggest cryptocurrency, Litecoin, announced shortly after midnight that he was cashing in his profits after a torrid, 9,300% rally in the past 12 months. In a post on reddit, the San Francisco-based software engineer who founded litecoin in 2013, said that he sold and donated all of his holdings over the past few days.

“Litecoin has been very good for me financially, so I am well off enough that I no longer need to tie my financial success to Litecoin’s success. For the first time in 6+ years, I no longer own a single LTC that’s not stored in a physical Litecoin” Lee said in the post.

Lee explained that his liquidation was aimed at preventing a “conflict of interest” when the creator of what is known as “Bitcoin Silver” makes comments on twitter about the digital currency – something he tends to do with chronic zeal – that could influence its price, he said. That said, Lee declined to comment in the post on how many coins he sold or at what price, and asked readers to please “don’t ask me how many coins I sold or at what price. I can tell you that the amount of coins was a small percentage of GDAX’s daily volume and it did not crash the market.”

Litecoin, which was trading at $3.67 on December 20, 2016, and $4.40 at the start of the year, has climbed 9,300% in the past 12 month. It tumbled on Wednesday, following most digital currencies lower after a flash crash in bitcoin after Coinbase announced it would finally transact in Bitcoin Cash which led to a brief avalanche of selling as traders repositioned.

However, Lee insisted in his post that his sale wasn’t a sign that he has lost faith in the cryptocurrency: “I will still spend all my time working on litecoin,” he said. “When litecoin succeeds, I will still be rewarded in lots of different ways, just not directly via ownership of coins.”

How does it feel to take profits on a high from the crypto boom that has been described as the biggest financial bubble of all time? “Weird” but also “somehow refreshing,” Lee wrote.

His full post below:

Litecoin price, tweets, and conflict of interest self

Over the past year, I try to stay away from price related tweets, but it’s hard because price is such an important aspect of Litecoin growth. And whenever I tweet about Litecoin price or even just good or bads news, I get accused of doing it for personal benefit. Some people even think I short LTC! So in a sense, it is conflict of interest for me to hold LTC and tweet about it because I have so much influence. I have always refrained from buying/selling LTC before or after my major tweets, but this is something only I know. And there will always be a doubt on whether any of my actions were to further my own personal wealth above the success of Litecoin and crypto-currency in general.

For this reason, in the past days, I have sold and donated all my LTC. Litecoin has been very good for me financially, so I am well off enough that I no longer need to tie my financial success to Litecoin’s success. For the first time in 6+ years, I no longer own a single LTC that’s not stored in a physical Litecoin. (I do have a few of those as collectibles.) This is definitely a weird feeling, but also somehow refreshing. Don’t worry. I’m not quitting Litecoin. I will still spend all my time working on Litecoin. When Litecoin succeeds, I will still be rewarded in lots of different ways, just not directly via ownership of coins. I now believe this is the best way for me to continue to oversee Litecoin’s growth.

Please don’t ask me how many coins I sold or at what price. I can tell you that the amount of coins was a small percentage of GDAX’s daily volume and it did not crash the market.

UPDATE: I wrote the above before the recent Bcash on GDAX/Coinbase fiasco. As you can see, some people even think I’m pumping Bcash for my personal benefit. It seems like I just can’t win.

On Wednesday morning, Lee was busy on twitter where he had dozens of posts defending his sale:

in a biz ppl put their money in what they have faith in. You believe in yourself right?

This is not business for me. It’s my life. I’m dedicated to Litecoin.

He also responded to a question by Mike Novogratz whether “@SatoshiLite selling all his $ltc is bullish or bearish? If @VitalikButerin or @ethereumJoseph sold all of their $eth I’d be worried.”

Is @SatoshiLite selling all his $ltc bullish or bearish? If @VitalikButerin or @ethereumJoseph sold all of their $eth I’d be worried.

I think it’s extremely bullish!

In a sense he is right, as there is no more whale overhang that can be sold at a moment’s notice.

He left off with a challenge to Satoshi Nakamoto, the creator of bitcoin, to do the same:

Craig Hemke reminds us of a cable sent to NY where the author claims that the futures market in gold/silver will suppress the spot price

(courtesy Craig Hemke)

Craig Hemke: It is what it is but it’s not what it seems

Submitted by cpowell on Tue, 2017-12-19 23:06. Section: Daily Dispatches

6:11p Tuesday, December 19, 2017

Dear Friend of GATA and Gold:

Craig Hemke of the TF Metals Report, writing today for Sprott Money, recalls the cable sent December 31, 1974, from the U.S. embassy in London to the State Department in Washington, conveying the assurances of London bullion banks that the gold futures market about to open in the United States would suppress demand for real metal. Hemke’s commentary is headlined “It Is What It Is But It’s Not What It Seems” and it’s posted at Sprott Money here:

https://www.sprottmoney.com/Blog/it-is-what-it-is-but-its-not-what-it-se…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

This would be another deadly blow to the USA dollar as countries seek the use of the yuan to replace the dollar

(courtesy Gul/Voice of America/Washington)

Pakistan examines Chinese proposal to replace dollar with yuan

Submitted by cpowell on Tue, 2017-12-19 23:25. Section: Daily Dispatches

By Ayaz Gul

Voice of America, Washington

Tuesday, December 19, 2017

ISLAMABAD, Pakistan — Officials in Pakistan say a Chinese proposal to replace the U.S. dollar with yuan for bilateral trade is under consideration.

Beijing has already committed to investing around $60 billion in the country by 2030 under a long-term plan of development cooperation with Islamabad, known as the China Pakistan Economic Corridor, or CPEC.

Bilateral trade between the two countries stood at around $14 billion in 2015 to 2016. Officials anticipate the trade volume is likely to increase significantly under ongoing CPEC cooperation.

Pakistan Interior Minister Ahsan Iqbal, who has also been overseeing CPEC implementation, revealed this week China is seeking bilateral trade in its own currency, known as renminbi, RMB, or yuan.

“We are examining the use of RMB instead of the U.S. dollar for trade between the two countries,” Iqbal said, adding that the use of Chinese currency would benefit Pakistan. But he went on to explain that the Pakistani currency would be used domestically.

The State Bank of Pakistan has already declared yuan as an approved foreign exchange for all purposes in the country. …

… For the remainder of the report:

https://www.voanews.com/a/pakistan-examines-chinese-proposal-to-replace-…

…

Hugo Salinas Price: Wild speculation in bitcoin

Submitted by cpowell on Wed, 2017-12-20 00:02. Section: Daily Dispatches

7:02p ET Tuesday, December 19, 2017

Dear Friend of GATA and Gold:

Hugo Salinas Price of the Mexican Civic Association for Silver writes today that the price of bitcoin is rising not because the cryptocurrency has any practical use but just because it is rising and that when people start taking profits, the price will fall just because it is falling. Salinas Price’s commentary is headlined “Wild Speculation in Bitcoin” and it’s posted at the association’s internet site, Plata.com.mx, here:

http://plata.com.mx/enUS/More/335?idioma=2

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

Your early WEDNESDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

i) Chinese yuan vs USA dollar/CLOSED UP AT 6.5780 /shanghai bourse CLOSED DOWN AT 8.93 POINTS 0.27% / HANG SANG CLOSED DOWN 19.57 POINTS OR 0.07%

2. Nikkei closed UP 23.72 POINTS OR 0.10% /USA: YEN RISES TO 113.19

3. Europe stocks OPENED MOSTLY RED /USA dollar index RISES TO 93.47/Euro RISES TO 1.1836

3b Japan 10 year bond yield: RISES TO . +.060/ GOVERNMENT INTERVENTION !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 113.19/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD FINALLY IN THE POSITIVE/BANK OF JAPAN LOSING CONTROL OF THEIR YIELD CURVE AS THEY PURCHASE ALL BONDS TO GET TO ZERO RATE!!

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 57.76 and Brent: 63.84

3f Gold UP/Yen DOWN

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil UP for WTI and UP FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund RISES TO +.400%/Italian 10 yr bond yield UP to 1.917% /SPAIN 10 YR BOND YIELD UP TO 1.487%

3j Greek 10 year bond yield RISES TO : 4.122?????????????????

3k Gold at $1265.90 silver at:16.23: 6 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble UP 12/100 in roubles/dollar) 58.65

3m oil into the 57 dollar handle for WTI and 63 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/China forced to do QE!! as it lowers its yuan value to the dollar/GOT A HUGE SIZED REVALUATION NORTHBOUND

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 113.19 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 0.9879 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1693 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now POSITIVE territory with the 10 year RISING to +0.400%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.465% early this morning. Thirty year rate at 2.834% /

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

(courtesy Jim Reid/Bloomberg/Deutsche bank/zero hedge)

Dow 25,000 In Sight As Tax Cuts Are “Priced In” One Last Time

Dow futures are up some 80 points this morning after early on Wednesday morning the Senate passed the Tax Reform bill in a party-line vote, and is now set to become law after a follow-up vote in the House and Trump’s signature some time on Wednesday afternoon. The good news is that the biggest political drama of 2017 will then be over. The bad news is that once the bill becomes law, the market will no longer be able to “price it in” every single day as it has for the past year.

As reported overnight, and as expected, the Senate approved the tax-cut legislation in a 51-48 party line vote, bringing President Donald Trump to the brink of his first major legislative victory. The bill now moves to the House of Representatives for a final vote Wednesday. With corporate and individual tax rates set to drop, the measures are largely anticipated to add to growth over the next year or two, though they will also swell the budget deficit.

And while S&P 500 futures extended modest gains on the bill news, they have so far fallen short of yesterday’s high, in somewhat tepid reaction to the passage of the U.S. tax bill in the Senate, suggesting there is only so many times an endlessly regurgitated piece of news can be “priced in for the first time.” MSCI’s world equity index was little changed and holding just below record highs hit on Monday.

Overnight, European bonds were mixed as U.S. Treasury yields edged lower after yesterday’s jump, sparked by hawkish comments from central bankers…

… and recovered from a brief dip following the Senate tax news, while the U.S. dollar comes under renewed pressure versus its G-10 peers as investors await a second House vote on the bill.

“Last week the reaction of bond markets was one of ambivalence about the likelihood of these measures getting passed,” said Michael Hewson, chief market analyst at CMC Markets in London. “However, U.S. yields have jumped sharply higher in the last two days as the prospect of higher inflation and growth prompted some positioning adjustments in anticipation that the measures, if passed, could prompt conditions that might see rates have to rise faster than expected next year.”

In global equities, the feel-good factor from U.S. tax reform faded in Europe on Wednesday, with stocks struggling for traction after a mixed session in Asia and the dollar trading little changed.

Most European stocks weakened, led by Spain ahead of a regional Catalan election on Thursday. Basic resources sector among the biggest gainers as industrial metals rebound in London trading. German debt again leads core euro-area government bonds lower, with notable underperformance in the front end driving yield curve bear-flattening.

Europe’s Stoxx 600 Index drifted little changed, down fractionally, with Spanish equities underperforming before tomorrow’s Catalan poll. Utilities and telecoms dropped, while miners gained as the Bloomberg Commodity Index advanced for a sixth day. Steinhoff shares crashed 30% after the furniture retailer said lenders have started to cut off support as reported yesterday. RWE leads Germany’s DAX Index higher after the departure of Innogy’s CEO sparked speculation around the company’s strategy

Earlier, Japan’s Topix index closed at its highest level since November 1991, while stocks in Hong Kong and China declined. ASX 200 (+0.1%) and Nikkei 225 (+0.1%) eventually traded positive on what was a choppy session with corporate scandals clouding over Japan including the maglev bid collusion, while Subaru was the worst performer after allegations it may have falsified mileage data. Chinese stock markets fared no better as both Hang Seng (-0.1%) and Shanghai Comp. (-0.3%) traded with a lacklustre tone, amid mild profit taking from recent gains. Finally, 10yr JGBs were flat as prices failed to benefit from the sombre risk tone or Rinban announcement valued at JPY 840bln in maturities across the curve, as the BoJ also kick-started its 2-day policy meeting today.

The euro got a lift from higher euro zone rates, gaining 0.5 percent on Tuesday, when central bank governors of Estonia, Slovakia and Germany all discussed the need to shift the debate from bond purchases to other tools such as interest rates.

“That’s re-igniting the debate about ECB tightening, so despite the outlook for the U.S. tax bill passage, euro-dollar is strong right now,” Masafumi Yamamoto, chief currency strategist for Mizuho Securities in Tokyo.

Against a basket of six rival currencies, the dollar was a touch lower on the day at 93.418 . The greenback edged down 0.2 percent to 113.11 yen, while the euro was a touch firmer at $1.1850.

Elsewhere, U.S. crude oil futures extended gains, helped by a North Sea pipeline outage, OPEC-led supply cuts and expectations that U.S. crude inventories had fallen for a fifth week. WTI and Brent crude futures remain supported by the larger than expected drawdown in crude stockpiles via last night’s API release (-5.22mln vs. Exp. -3.5mln). Elsewhere, the latest reports suggest that Ineos are pressing ahead with repairs on the Forties crude pipeline with their preferred repair option. In metals markets, gold was marginally higher on a tepid greenback, while copper was uneventful overnight and held near this month’s highs. Elsewhere, Chinese iron ore futures were seen lower by 1% overnight after steel prices hit a two-week low.

Market Snapshot

- S&P 500 futures up 0.3% to 2,692.25

- Brent Futures up 0.05% to $63.83/bbl

- MSCI Asia Pacific up 0.08% to 171.74

- MSCI Asia Pacific ex Japan down 0.01% to 558.57

- Nikkei up 0.1% to 22,891.72

- Topix up 0.3% to 1,821.16

- Hang Seng Index down 0.07% to 29,234.09

- Shanghai Composite down 0.3% to 3,287.61

- Sensex down 0.02% to 33,830.46

- Australia S&P/ASX 200 up 0.06% to 6,075.62

- Kospi down 0.3% to 2,472.37

- Gold spot up 0.2% to $1,264.57

- U.S. Dollar Index up 0.01% to 93.45

- STOXX Europe 600 down 0.1% to 390.63

- German 10Y yield fell 0.5 bps to 0.374%

- Euro up 0.03% to $1.1843

- Brent Futures up 0.05% to $63.83/bbl

- Italian 10Y yield rose 10.9 bps to 1.646%

- Spanish 10Y yield fell 4.2 bps to 1.443%

Top Overnight Headlines from BBG

- Senate Republicans passed the most extensive rewrite of the U.S. tax code in more than 30 years, a bill that delivers a deep, permanent tax cut for corporations and shorter-term relief for individuals

- Before reaching President Trump’s desk, the bill must return to the House for one final vote Wednesday. After that, the president said, he’ll hold a news conference at the White House

- European Commission says the U.K. will be a third country as of March 30, 2019 and transition period to end Dec. 31, 2020; U.K. officials fear Spain will threaten to veto a Brexit transition phase if the British prime minister refuses to negotiate a separate deal with the government in Madrid that covers the disputed territory of Gibraltar

- Sweden’s central bank formally ended a program of bond purchases after almost three years, but pledged continued support for the nation’s benchmark debt market into 2019 in a step designed to ensure a smooth retreat from record stimulus

- With elections in Catalonia on Thursday seen unlikely to give a clear majority to the separatist bloc demanding the region’s secession, bargain hunters are being lured to Spanish shares as the IBEX 35 Index trades near its cheapest relative to the Euro Stoxx 50 Index in more than seven years

- Uber Technologies Inc. lost a battle over its stance that it differs from traditional taxis, after the EU Court of Justice said the car-hailing app should be regulated as a transport service. The ruling can’t be appealed

- Bonds and equities in developing countries will continue to streak ahead in 2018, outpacing their developed-nation peers into next year, according to a Bloomberg survey of 20 investors, traders and strategists while currencies could struggle

- China says monetary policy will be prudent and neutral next year while fiscal policy will be proactive; will keep basic yuan stability at reasonable level, according to statement from Xinhua News released after top officials’ planning meeting

- BOE Agents’ Summary 4Q: pay growth edged up, expected to be higher in 2018; manufacturing supported by past decline in sterling

Asia equity markets traded with an indecisive tone after the Santa rally stalled on Wall St. where the majors retreated from record highs as participants sold the news of the House passing the tax reform bill, although the passage was later nullified after some provisions broke Senate rules. ASX 200 (+0.1%) and Nikkei 225 (+0.1%) eventually traded positive on what was a choppy session with corporate scandals clouding over Japan including the maglev bid collusion, while Subaru was the worst performer after allegations it may have falsified mileage data. Chinese stock markets fared no better as both Hang Seng (-0.1%) and Shanghai Comp. (-0.3%) traded with a lacklustre tone, amid mild profit taking from recent gains. Finally, 10yr JGBs were flat as prices failed to benefit from the sombre risk tone or Rinban announcement valued at JPY 840bln in maturities across the curve, as the BoJ also kick-started its 2-day policy meeting today.

Top Asian News

- China Reiterates Prudent, Neutral Monetary Policy

- Noble Group Is Said to Seek RCF Waiver Extension to May

- Bank of India Placed Under Corrective Action Plan; Shares Drop

- Fosun to Buy Asahi Stake in Tsingtao for $847m

- Only Thing Yen Experts Agree On Is U.S. Rates Will Drive It

European equities trade modestly lower as US tax optimism fails to make its way into Europe after the Senate approved the Republican tax bill with the House due to re-vote on the issue later today. As has been the case throughout the week, European macro newsflow remains particularly light as traders eye the festive period. Sector specific moves have been relatively broad-based with little in the way of outliers. Individual movers include Stada (+8.9%) at the top of the Stoxx 600 after signing an agreement with Bain/Cinven, with troubled German-listed Steinhoff (-30.0%) at the bottom of the pile after reports that lenders have severed credit lines to the Co. Bunds were already on the turn as Gilts re-joined the fray, but it was the scale of the gap down in UK bonds and follow-through selling off the Liffe open that appeared to catch the Eurex benchmark cold and nudge it to a fresh 162.20 low (-18 ticks vs +10 ticks at best). The 10 year UK debt future slumped to 124.51 (-45 ticks), partly in corrective trade given due to different closing times, before dip buyers stepped in to push prices back up to 124.85, and this looks like some psychological resistance in the cash market ahead of the 1.25% marker. However, bears or vigilantes are still directing moves at the current juncture amidst more curve re-steepening, while seasonally light volumes are also exacerbating price action with market contacts noting that a mere 200 lot sale in Bunds pushed the contract down 3 ticks.

Top European news

- Billionaire Niel Takes Iliad to Ireland With Eir Takeover

- Steinhoff Slumps to New Lows After Investors Sue in Germany

- Italy Elections Projected to Produce Hung Parliament: Corriere

- As Shell Gambles on Gas, Leaks Loom Over Clean Credentials

- SEB Says Riksbank’s First Rate Hike Now More Likely In 3Q

- New Areva Seeks Nuclear ‘El Dorado’ in Asia as Europe Declines

- Don’t Fear Amazon, Say Backers of Revival for European Grocers

In FX markets, SEK has been a key focus in European trade following a well-managed release by the RIksbank which initially saw pressure on EUR/SEK after the Bank announced their plans to bring forward reinvestment of redemptions. Thereafter, the cross returned to unchanged levels as the Riksbank left the door open to further easing; other key aspects of the release included the Bank maintaining their repo path. Elsewhere, the USD-index trade flat despite events Stateside with the DXY unable to breach the 93.50 level with some analysts attributing upside in USD/JPY to spread widening between USTs and JGBs. Elsewhere, the remainder of FX markets trade with little in the way of notable direction as volumes continue to recede.

In commodities, WTI and Brent crude futures remain supported by the larger than expected drawdown in crude stockpiles via last night’s API release (-5.22mln vs. Exp. -3.5mln). Elsewhere, the latest reports suggest that Ineos are pressing ahead with repairs on the Forties crude pipeline with their preferred repair option. In metals markets, gold was marginally higher on a tepid greenback, while copper was uneventful overnight and held near this month’s highs. Elsewhere, Chinese iron ore futures were seen lower by 1% overnight after steel prices hit a two-week low.

Looking at the day ahead, expect Brexit headlines to continue with the European Commission due to publish its directives for the Brexit transition phase and heads of mission from EU member states due to meet to discuss Brexit. Away from that, data releases include November PPI in Germany, December CBI retail sales in the UK and November existing home sales in the US.

US Event Calendar

- 7am: MBA Mortgage Applications, prior -2.3%

- 10am: Existing Home Sales, est. 5.53m, prior 5.48m

- 10am: Existing Home Sales MoM, est. 0.91%, prior 2.0%

DB’s Jim Reid concludes the overnight wrap

One can’t wind down too much though as a lot happened yesterday and the rest

of the week still has important news-flow ahead. Not only did the tax reform bill

take another big step forward but we saw a huge sell off in Government bond

yields around the globe, making it one of the worse days of the year for fixed

income.

Firstly on US tax reforms. As we type, the Senate has just passed the bill by

51-48 in a post midnight US vote. Earlier the House voted 227-203 to pass it.

However, later on, the House Majority Leader McCarthy noted the House may

have to vote again on Wednesday morning (US time), as the Senate found three

provisions in the House bill that don’t comply with the Chamber’s budget rules.

This is not expected to change the outcome though and with the Senate news

just in, today should be the day that the bill progresses towards Mr Trump’s desk.

Before this, yesterday was all about the moves in bonds. This was led by a sudden

sell-off in Europe. 10 year Bunds (+6.9bp) and BTPs (+10.8bp) both had their

worst day for 5.5 months while OATs (+7.5bp) had the worst for c1 month.

Treasuries (+7.0bp) and Gilts (+5.7bp) were also higher with 10yr Treasuries

(2.464%) at their highest yield since March 17.

There seemed to be several contributing causes that encouraged the sell-off.

i) Firstly the hawkish comments from three ECB central bankers. The ECB’s

Makuch said ECB “discussions are increasingly moving from asset purchases

to the eventual future use of interest rates to regulate the economy”. Then the

Bundesbank’s Weidmann reiterated his call for a definitive end date for QE, he

noted “a faster conclusion of net asset purchases and a clearly communicated

end date would have been reasonable” and that increased capacity utilisation will

lead to “somewhat higher wage pressure”. Finally, the ECB’s Hansson noted that

it’s important the ECB “moves gradually when adjusting policy guidance”, but

should consider moving to communication that draws attention to multi-faceted

aspect of monetary policy in 1H. ii) Secondly, the German Finance Agency Head

Tammo Diemer has confirmed that Germany will issue more long debt issuance

and some investors are also expecting increased supply of US government bonds

next year, which appears to be weighing on bonds, and finally iii) the less liquid

pre-Christmas trading period may have also exaggerated the moves.

Following on, the US 2s10 has steepened from its record low of 51.6bp, rising

9.4bp over the past two days to 61bp, which marks the largest consecutive

increase since President Trump was elected. On the topic of yield curves, our

US economists recently took a different approach to investigate the relationship

between the yield curve slope and future growth. They note that more than half

of the flattening this year has been driven by the term premium and that their

results suggest that the yield curve is signaling only a modest slowdown in the

year ahead. Overall, they do not think the yield curve flattening should be a source

of great consternation, at least not yet.

This morning in Asia, markets are mixed but little changed. The Nikkei (+0.19%),

Kospi (-0.27%), Hang Seng (-0.07%) and China’s CSI 300 (-0.28%) are trading

sideways. Treasuries are slightly firmer with UST 10y yields down 1.6bp this

morning.

Now recapping other markets performance from yesterday. US equities

softened from record highs as investors awaited the full passage of the tax bill.

The S&P (-0.32%), Dow (-0.15%) and Nasdaq (-0.44%) all traded modestly lower.

Within the S&P, losses were led by the real estate (-1.89%) and utilities sector,

with partial offsets from consumer staples and energy stocks. European markets

were broadly lower, partly reversing the prior day’s gains, with the Stoxx 600

(-0.42%) and DAX (-0.72%) lower while the FTSE bucked the trend and rose

+0.09%. The VIX rose for the second consecutive day and was up 5.3% to be

above 10 again (10.03).

Turning to currencies, the US dollar index weakened 0.25%, while Sterling was

broadly flat and the Euro gained 0.49%. In commodities, WTI oil rose 0.59% ahead

of API data expected to show a fifth consecutive week of shrinking US crude

inventories.

Away from the market and onto Fed speak. The Fed’s Kaplan has also cautioned

on the flattening yield curve, he noted that “it limits the Fed’s operating flexibility…in terms of how fast and how much we can raise rates”. He also added that the history of inversions tends to be a pretty reliable forward indicator of recessions, while this time may be different, but he “wouldn’t count on it”. Elsewhere, the Fed’s Kashkari noted that only a few contacts in his district suggest the upcoming tax reforms will lead to substantial changes in business behaviour, so for him the tax bill is not expected to result in a dramatic gain in investment or hiring.

Turning back to Brexit, the UK’s PM May has confided with her cabinet and then reiterated her desire for a bespoke trade deal after Brexit even though EU Chief negotiator Barnier noted earlier there should be no “cherry picking” of rules. Her office released a statement noting “we should be creative in designing our (Brexit) proposal” and that the UK would be seeking a “significantly more ambitious deal than the EU’s agreement with Canada”.

Finally over at Italy, President Mattarella is expected to dissolve parliament midnext week and call for a general election on 4th or 11th of March next year, as per an unnamed government official who spoke to Bloomberg. The timing is broadly in line with prior press reports.

Before we take a look at today’s calendar, we wrap up with other data releases from yesterday. In the US, the November housing starts were above market (1,297k vs. 1,250k expected), with this month’s rise led by a 5.9% mom increase in single family starts to the highest level since 2007. Housing permits also slight beat at 1,298k (vs. 1,270k expected). Elsewhere, the 3Q US current account deficit was slightly narrower than expected at -$110.6bln (vs. -$116.2bln). As a proportion of GDP, the deficit in 3Q amounts to 2.1%.