GOLD: $1288.00 up $5.05

Silver: $16.71 up 17 cents

Closing access prices:

Gold $1288.50

silver: $16.73

For comex gold:

DECEMBER/

NUMBER OF NOTICES FILED TODAY FOR DECEMBER CONTRACT: 33 NOTICE(S) FOR 3300 OZ.

TOTAL NOTICES SO FAR: 9056 FOR 905,600 OZ (28.30 TONNES),

For silver:

DECEMBER

8 NOTICE(S) FILED TODAY FOR

40,000 OZ/

Total number of notices filed so far this month: 6403 for 32,015,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: BID $15,775/OFFER $15,900 up $98 (morning)

BITCOIN : BID $14,994/OFFER $15,099 /DOWN $709 CLOSING

end

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total open interest SURPRISINGLY FELL BY A CONSIDERABLE 1462 contracts from 201,783 FALLING TO 200,321 DESPITE YESTERDAY’S GOOD 17 CENT RISE IN SILVER PRICING. WE HAD SOME COMEX LIQUIDATION AND WITHOUT A DOUBT WE MUST HAVE HAD SOME BANK SHORT- COVERING. HOWEVER, WE WERE AGAIN NOTIFIED THAT WE HAD ANOTHER FAIR SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP ROUTE: A RESPECTABLE 840 EFP’S FOR MARCH (AND ZERO FOR DEC AND OTHER MONTHS) AND THUS TOTAL ISSUANCE OF 840 CONTRACTS. HOWEVER THE MOVEMENT ACROSS TO LONDON IS NOT AS SEVERE AS IN GOLD AS THERE SEEMS TO BE A MAJOR PLAYER TAKING ON THE BANKS AT THE COMEX. STILL, WITH THE TRANSFER OF 840 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. YESTERDAY WITNESSED 1760 EFP’S FOR SILVER ISSUED. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24 HRS IN THE ISSUING OF EFP’S. I BELIEVE THAT WE MUST HAVE HAD SOME BANKER SHORT COVERING

ACCUMULATION FOR EFP’S/SILVER/ STARTING FROM FIRST DAY NOTICE/FOR MONTH OF DECEMBER:

45,351 CONTRACTS (FOR 18 TRADING DAYS TOTAL 45,351 CONTRACTS OR 226.755 MILLION OZ: AVERAGE PER DAY: 2,550 CONTRACTS OR 12.750 MILLION OZ/DAY)

TO GIVE YOU AN IDEA OF THE SIZE OF “PHYSICAL” TRANSFERRED TO LONDON: 222.755 MILLION OZ/700 MILLION OZ (EX CHINA EX RUSSIA) = 31.8% OF ANNUAL GLOBAL SILVER PRODUCTION

RESULT: A CONSIDERABLE SIZED LOSS IN OI COMEX DESPITE THE GOOD 18 CENT RISE IN SILVER PRICE WHICH INDICATES SOME BANKER SHORT-COVERING. WE HAD SOME COMEX SILVER LIQUIDATION . WE ALSO HAD A FAIR SIZED SIZED EFP ISSUANCE OF 840 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS: FROM THE CME DATA 840 EFP’S WERE ISSUED TODAY (FOR MARCH EFP’S) FOR A DELIVERABLE CONTRACT OVER IN LONDON WITH A FIAT BONUS. WE REALLY LOST 582 OI CONTRACTS i.e. 840 open interest contracts headed for London (EFP’s) TOGETHER WITH A DECREASE OF 1462 OI COMEX CONTRACTS. AND ALL OF THIS HAPPENED WITH THE RISE IN PRICE OF SILVER BY 18 CENTS AND A CLOSING PRICE OF $16.54 WITH RESPECT TO YESTERDAY’S TRADING. YET WE STILL HAVE A MASSIVE AMOUNT OF SILVER STANDING AT THE COMEX.

In ounces AT THE COMEX, the OI is still represented by just OVER 1 BILLION oz i.e. 1.001 BILLION TO BE EXACT or 143% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT DECEMBER MONTH/ THEY FILED: 8 NOTICE(S) FOR 40,000 OZ OF SILVER

In gold, the open interest ROSE BY A SMALL SIZED 313 CONTRACTS UP TO 456,470 DESPITE THE GOOD SIZED RISE IN PRICE OF GOLD WITH YESTERDAY’S TRADING ($7.10). HOWEVER, THE TOTAL NUMBER OF GOLD EFP’S ISSUED YESTERDAY FOR TODAY TOTALED 2056 CONTRACTS OF WHICH THE MONTH OF DECEMBER SAW 0 CONTRACTS AND FEB SAW THE ISSUANCE OF 2056 CONTRACTS. The new OI for the gold complex rests at 456,470. DEMAND FOR GOLD INTENSIFIES GREATLY AS WE CONTINUE TO WITNESS A HUGE NUMBER OF EFP TRANSFERS TOGETHER WITH THE MASSIVE AMOUNT OF GOLD OUNCES STANDING FOR DECEMBER. EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES. IN ESSENCE WE HAVE A GOOD GAIN OF 2369 OI CONTRACTS: 313 OI CONTRACTS INCREASED AT THE COMEX AND A GOOD SIZED 2056 OI CONTRACTS WHICH NAVIGATED OVER TO LONDON.

YESTERDAY, WE HAD 9906 EFP’S ISSUED.

ACCUMULATION OF EFP’S/ GOLD(EXCHANGE FOR PHYSICAL) FOR THE MONTH OF DECEMBER STARTING WITH FIRST DAY NOTICE: 203,067 CONTRACTS OR 20.3067 MILLION OZ OR 631.41 TONNES (18 TRADING DAYS AND THUS AVERAGING: 11,280 EFP CONTRACTS PER TRADING DAY OR 1.1271 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE AMOUNT OF “PHYSICAL’ TRANSFERRED: SO FAR 671 TONNES/2200 TONNES ) = 30.50% OF ANNUAL GLOBAL PRODUCTION OF GOLD. THIS IS IMPOSSIBLE AND EXPLAINS FULLY THE FRAUD!!

Result: A SMALL SIZED INCREASE IN OI DESPITE THE GOOD SIZED RISE IN PRICE IN GOLD TRADING ON YESTERDAY ($7.10). WE HAD A GOOD SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 2056. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX AND YET WE REACHED THE HUGE DELIVERY MONTH OF DECEMBER. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 2056 EFP CONTRACTS ISSUED, WE HAD A NET GAIN IN OPEN INTEREST OF 2369 contracts:

2056 CONTRACTS MOVE TO LONDON AND 313 CONTRACTS INCREASED AT THE COMEX. (in tonnes, the gain in total oi equates to 11.7 TONNES)

we had: 33 notice(s) filed upon for 3300 oz of gold.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD:

Today, NO CHANGES IN GOLD INVENTORY AT THE GLD

Inventory rests tonight: 837.50 tonnes.

SLV/

THIS MAKES A LOT OF SENSE: SILVER UP 17 CENTS AGAIN TODAY:

ANOTHER CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 802,000 OZ

INVENTORY RESTS AT 324.710 MILLION OZ/

end

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in silver FELL BY A CONSIDERABLE SIZED 1462 contracts from 201,783 DOWN TO 200,321 (AND now A LITTLE FURTHER FROM THE NEW COMEX RECORD SET ON FRIDAY/APRIL 21/2017 AT 234,787) DESPITE THE GOOD SIZED RISE IN PRICE OF SILVER TO THE TUNE OF 17 CENTS ON YESTERDAY . HOWEVER,OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE ANOTHER 840 PRIVATE EFP’S FOR MARCH (WE DO NOT GET A LOOK AT THESE CONTRACTS AS IT IS PRIVATE BUT THE CFTC DOES AUDIT THEM). EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. WE HAD ZERO COMEX SILVER COMEX LIQUIDATION. BUT, IF WE TAKE THE OI LOSS AT THE COMEX OF 1462 CONTRACTS TO THE 840 OI TRANSFERRED TO LONDON THROUGH EFP’S WE OBTAIN A LOSS OF 582 OPEN INTEREST CONTRACTS, AS WE MUST HAVE HAD SOME BANKER SHORT COVERING. WE STILL HAVE A HUGE AMOUNT OF SILVER OUNCES THAT ARE STANDING FOR METAL IN DECEMBER (SEE BELOW). THE NET LOSS TODAY IN OZ: 2.910 MILLION OZ!!!

RESULT: A SMALL SIZED DECREASE IN SILVER OI AT THE COMEX DESPITE THE GOOD SIZED RISE OF 18 CENTS IN PRICE (WITH RESPECT TO YESTERDAY’S TRADING). BUT WE ALSO HAD ANOTHER 840 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON . TOGETHER WITH THE HUGE AMOUNT OF SILVER OUNCES STANDING FOR DECEMBER, DEMAND FOR PHYSICAL SILVER INTENSIFIES

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

3a)THAILAND/SOUTH KOREA/NORTH KOREA

i)North Korea

b) REPORT ON JAPAN

3 c CHINA

4. EUROPEAN AFFAIRS

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

6 .GLOBAL ISSUES

7. OIL ISSUES

8. EMERGING MARKET

9. PHYSICAL MARKETS

10. USA stories which will influence the price of gold/silver

Let us head over to the comex:

The total gold comex open interest ROSE BY A SMALL 313 CONTRACTS UP to an OI level of 456,470 DESPITE THE GOOD SIZED RISE IN THE PRICE OF GOLD ($7.10 GAIN WITH RESPECT TO YESTERDAY’S TRADING). WE NOT ONLY HAD ZERO COMEX GOLD LIQUIDATION BUT WE ALSO HAVE ANOTHER GAIN IN TOTAL OPEN INTEREST AS WE HAD ANOTHER GOOD COMEX TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS. THE CME REPORTS THAT 0 EFPS WERE ISSUED FOR DECEMBER AND 2036 EFP’S WERE ISSUED FOR FEBRUARY FOR A TOTAL OF 2036 CONTRACTS. THE OBLIGATION STILL RESTS WITH THE BANKERS ON THESE TRANSFERS.

ON A NET BASIS IN OPEN INTEREST WE GAINED TODAY: 2,369 OI CONTRACTS IN THAT 2036 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE GAINED 313 COMEX CONTRACTS. NET GAIN: 2,369 contracts OR 236,900 OZ OR 7.368 TONNES

Result: AN SMALL SIZED INCREASE IN COMEX OPEN INTEREST WITH THE GOOD RISE IN THE PRICE OF YESTERDAY’S GOLD TRADING ($7.10.) WE HAD NO GOLD LIQUIDATION ANYWHERE. TOTAL OPEN INTEREST GAIN ON THE TWO EXCHANGES: 2369 OI CONTRACTS…

We have now entered the active contract month of DECEMBER. The open interest for the front month of December saw it’s open interest FALL by 26 contracts DOWN to 120. We had 44 notices filed upon yesterday so we GAINED 18 COMEX contracts or an additional 1800 oz will stand for delivery AT THE COMEX in this active delivery month of December , AS QUEUE JUMPING INTENSIFIES

January saw its open interest LOSE 127 contracts DOWN to 860. FEBRUARY saw a LOSS of 116 contacts DOWN to 331,420

We had 33 notice(s) filed upon today for 3300 oz

PRELIMINARY VOLUME TODAY ESTIMATED; 126,412

FINAL NUMBERS CONFIRMED FOR YESTERDAY: 207,169

comex gold volumes are slowing down

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

And now for the wild silver comex results.

Total silver OI FALL BY A CONSIDERABLE 1462 CONTRACTS FROM 201,783 UP TO 200,321 DESPITE YESTERDAY’S GOOD 18 CENT RISE IN PRICE WHICH SEEMS TO INDICATE WE HAD ANOTHER ROUND OF BANKER SHORT-COVERING. HOWEVER, WE DID HAVE ANOTHER MEDIUM SIZED 840 EMERGENCY EFP’S FOR MARCH ISSUED BY OUR BANKERS (ZERO FOR DECEMBER) TO COMEX LONGS WHO RECEIVED A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON.THE TOTAL EFP’S ISSUED: 840. IT SURE LOOKS LIKE THE SILVER BOYS HAVE STARTED TO MIGRATE TO LONDON FROM THE START OF DELIVERY MONTH AND CONTINUING RIGHT THROUGH UNTIL FIRST DAY NOTICE JUST LIKE WE ARE WITNESSING TODAY. USUALLY WE NOTED THAT CONTRACTION IN OI OCCURRED ONLY DURING THE LAST WEEK OF AN UPCOMING ACTIVE DELIVERY MONTH. THIS PROCESS HAS JUST BEGUN IN EARNEST IN SILVER STARTING IN SEPTEMBER. HOWEVER, IN GOLD, WE HAVE BEEN WITNESSING THIS FOR THE PAST 2 YEARS. WE HAD CONSIDERABLE LONG COMEX SILVER LIQUIDATION AS WELL AS TOTAL SILVER OI LIQUIDATION AS IT SEEMS THAT WE ARE HAVING SOME BANKER SHORT-COVERING. WE ARE ALSO WITNESSING A HUGE AMOUNT OF SILVER OUNCES STANDING FOR COMEX METAL IN DECEMBER AS WELL AS THAT CONTINUAL MIGRATION OF EFPS OVER TO LONDON. ON A PERCENTAGE BASIS THERE ARE MORE EFP’S ISSUED FOR GOLD THAN SILVER AS IT SEEMS THAT A MAJOR PLAYER WISHES TO TAKE ON THE CROOKED COMEX SHORTS. ON A NET BASIS WE LOST 582 OPEN INTEREST CONTRACTS:

1462 CONTRACTS LOSS AT THE COMEX WITH THE ADDITION OF 840 OI CONTRACTS NAVIGATING OVER TO LONDON.

NET LOSS: 582 CONTRACTS

We are now in the big active delivery month of December and here the OI GAIN by 24 contracts UP to 232. We had 0 notices filed ON YESTERDAY so we GAINED 24 contract or an additional 120,000 oz will stand in this active COMEX delivery month of December QUEUE jumping intensifies

The January contract month FELL by 687 contracts DOWN to 688. February saw a gain OF 24 OI contract RISING TO 83. The March contract LOST 1023 contracts DOWN to 159,589.

We had 8 notice(s) filed for 40,000 oz for the DECEMBER 2017 contracts

INITIAL standings for DECEMBER

Dec 27/2017.

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz |

N/A oz

|

| Deposits to the Dealer Inventory in oz | nil oz |

| Deposits to the Customer Inventory, in oz |

nil oz

|

| No of oz served (contracts) today |

33 notice(s)

3300 OZ

|

| No of oz to be served (notices) |

87 contracts

(8700 oz)

|

| Total monthly oz gold served (contracts) so far this month |

9056 notices

905600 oz

28.30 tonnes

|

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

For DECEMBER:

Today, 0 notice(s) were issued from JPMorgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equates to 33 contract(s) of which 8 notices were stopped (received) by j.P. Morgan dealer and 1 notice(s) was (were) stopped/ Received) by j.P.Morgan customer account.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

To calculate the INITIAL total number of gold ounces standing for the DECEMBER. contract month, we take the total number of notices filed so far for the month (9056) x 100 oz or 905,600 oz, to which we add the difference between the open interest for the front month of DEC. (120 contracts) minus the number of notices served upon today (33 x 100 oz per contract) equals 914,300 oz, the number of ounces standing in this active month of DECEMBER

Thus the INITIAL standings for gold for the DECEMBER contract month:

No of notices served (9056) x 100 oz or ounces + {(120)OI for the front month minus the number of notices served upon today (33) x 100 oz which equals 914,300 oz standing in this active delivery month of DECEMBER (28.402 tonnes). THERE IS 33.29 TONNES OF REGISTERED GOLD AVAILABLE FOR DELIVERY SO FAR.

WE GAINED 18 COMEX CONTRACTS STANDING OR AN ADDITIONAL 1800 OZ WILL STAND AT THE COMEX AND QUEUE JUMPING INTENSIFIES

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

ON FIRST DAY NOTICE FOR DECEMBER 2016, THE INITIAL GOLD STANDING: 39.038 TONNES STANDING

BY THE END OF THE MONTH: FINAL: 29.791 TONNES STOOD FOR COMEX DELIVERY AS THE REMAINDER HAD TRANSFERRED OVER TO LONDON FORWARDS.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Total dealer inventory 1,070,309.229 or 33.29 tonnes (dealer gold continues to disappear)

Total gold inventory (dealer and customer) = 9,143,181.135 or 284.39 tonnes

I have a sneaky feeling that these withdrawals of gold in kilobars are being used in the hypothecating process and are being used in the raiding of gold!

The gold comex is an absolute fraud. The use of kilobars and exact weights makes the data totally absurd and fraudulent! To me, the only thing that makes sense is the fact that “kilobars: are entries of hypothecated gold sent to other jurisdictions so that they will not be short with their underwritten derivatives in that jurisdiction. This would be similar to the rehypothecated gold used by Jon Corzine at MF Global.

IN THE LAST 14 MONTHS 70 NET TONNES HAS LEFT THE COMEX.

end

And now for silver

AND NOW THE DECEMBER DELIVERY MONTH

DECEMBER INITIAL standings

| Silver | Ounces |

| Withdrawals from Dealers Inventory | nil oz |

| Withdrawals from Customer Inventory |

N/A oz

|

| Deposits to the Dealer Inventory |

nil

oz

|

| Deposits to the Customer Inventory |

N/A oz

Scotia

|

| No of oz served today (contracts) |

8

CONTRACT(S)

(40,000 OZ)

|

| No of oz to be served (notices) |

224 contract

(1,120,000 oz)

|

| Total monthly oz silver served (contracts) | 6403 contracts

(32,015,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

CANNOT RETRIEVE COMEX INVENTORY DATA

The total number of notices filed today for the DECEMBER. contract month is represented by 8 contract(s) FOR 40,000 oz. To calculate the number of silver ounces that will stand for delivery in DECEMBER., we take the total number of notices filed for the month so far at 6403 x 5,000 oz = 32,015,000 oz to which we add the difference between the open interest for the front month of DEC. (232) and the number of notices served upon today (8x 5000 oz) equals the number of ounces standing.

.

Thus the INITIAL standings for silver for the DECEMBER contract month: 6403 (notices served so far)x 5000 oz + OI for front month of DECEMBER(232) -number of notices served upon today (8)x 5000 oz equals 33,135,000 oz of silver standing for the DECEMBER contract month. This is EXCELLENT for this active delivery month of November.

WE GAINED 24 CONTRACTS OR 120,000 additional OZ THAT WILL STAND AT THE COMEX AND QUEUE JUMPING INTENSIFIES.

ON FIRST DAY NOTICE FOR THE DECEMBER 2016 CONTRACT WE HAD 15.282 MILLION OZ STAND.

THE FINAL STANDING: 19.900 MILLION OZ AS QUEUE JUMPING INTENSIFIED.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

ESTIMATED VOLUME FOR TODAY: 41,446

CONFIRMED VOLUME FOR FRIDAY: 55,406 CONTRACTS

YESTERDAY’S CONFIRMED VOLUME OF 55046 CONTRACTS EQUATES TO 275 MILLION OZ OR 38.2% OF ANNUAL GLOBAL PRODUCTION OF SILVER

COMMODITY LAW SUGGESTS THAT OPEN INTEREST SHOULD NOT BE MORE THAN 3% OF ANNUAL GLOBAL PRODUCTION. THE CROOKS ARE SUPPLYING MASSIVE PAPER TRYING TO KEEP SILVER IN CHECK.

Total dealer silver: 59.182 million

Total number of dealer and customer silver: 240.232 million oz

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price at that day at $18.42

The previous record was 224,540 contracts with the price at that time of $20.44

end

NPV for Sprott and Central Fund of Canada

1. Central Fund of Canada: traded at Negative 1.3 percent to NAV usa funds and Negative 1.3% to NAV for Cdn funds!!!!

Percentage of fund in gold 63.0%

Percentage of fund in silver:36.7%

cash .+.3%( Dec 27/2017)

2. Sprott silver fund (PSLV): NAV RISES TO -1.03% (Dec 26 /2017)??????????????????????????????

3. Sprott gold fund (PHYS): premium to NAV FALLS TO -0.66% to NAV (Dec 26 /2017 )

Note: Sprott silver trust back into NEGATIVE territory at -1.03%-/Sprott physical gold trust is back into NEGATIVE/ territory at -0.66%/Central fund of Canada’s is still in jail but being rescued by Sprott.

Sprott WINS hostile 3.1 billion bid to take over Central Fund of Canada

(courtesy Sprott/GATA)

END

And now the Gold inventory at the GLD

Dec 27/NO CHANGES IN GOLD INVENTORY AT THE GLD/ INVENTORY RESTS AT 837.50 TONNES

Dec 26/no change in gold inventory at the GLD

Dec 22/ A DEPOSIT OF 1.48 TONNES OF GOLD INTO GLD INVENTORY/INVENTORY RESTS AT 837.50 TONNES

Dec 21′ NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 836.02 TONNES

Dec 20/DESPITE THE GOOD ADVANCE IN PRICE TODAY/THE CROOKS RAIDED THE COOKIE JAR TO THE TUNE OF 1.18 TONNES/INVENTORY RESTS AT 836.02 TONNES

Dec 19/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 837.20 TONNES

Dec 18 SHOCKINGLY AFTER TWO GOOD GOLD TRADING DAYS, THE CROOKS RAID THE COOKIE JAR BY THE SUM OF 7.09 TONNES/INVENTORY RESTS AT 837.20 TONNES

Dec 15/NO CHANGES IN GOLD INVENTORY/RESTS AT 844.29 TONNES.

Dec 14/a good sized gain of 1.48 tonnes of gold into the GLD/inventory rests at 844.29 tones

Dec 13/no changes in gold inventory at the GLD/inventory rests at 842.81 tonnes

Dec 12/SURPRISINGLY NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 842.81 TONNES

Dec 11/SURPRISINGLY NO CHANGES IN GOLD INVENTORY AT THE GLD DESPITE THE CONSTANT RAIDS ON GOLD/INVENTORY RESTS AT 842.81 TONNES

Dec 8/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 842.81 TONNES

Dec 7/A BIG WITHDRAWAL OF 2.66 TONNES FROM THE GLD/INVENTORY RESTS AT 842.81 TONNES

Dec 6/No changes in GOLD inventory at the GLD/Inventory rests at 845.47 tonnes

Dec 5/A WITHDRAWAL OF 2.64 TONNES FROM THE GLD/INVENTORY RESTS AT 845.47 TONNES

Dec 4/A MASSIVE DEPOSIT OF 8.56 TONNES OF GOLD INTO THE GLD/THE BLEEDING OF GLD GOLD HAS STOPPED/INVENTORY RESTS TONIGHT AT 848.11 TONNES

Dec 1/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 839.55 TONNES

Nov 30/no change in gold inventory at the GLD. Inventory rests at 839.55 tonnes

Nov 29/a withdrawal of 2.66 tonnes at the GLD/Inventory rests at 839.55 tonnes

NOV 28/ no change in gold inventory at the GLD/inventory rests at 842.21 tonnes

Nov 27 Strange!! we gold up by $6.40 today, we had a good sized withdrawal of 1.18 tonnes from the GLD. Here is something that is also strange: we have had exactly 1.18 tonnes of gold withdrawn from the comex on 5 separate occasions in the past 30 days..explanation?

Nov 24/no change in gold inventory at the GLD/Inventory rests at 843.09 tonnes

Nov 22/no change in gold inventory at the GLD/Inventory rests at 843.39 tonnes

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

Dec 27/2017/ Inventory rests tonight at 837.50 tonnes

*IN LAST 299 TRADING DAYS: 103.45 NET TONNES HAVE BEEN REMOVED FROM THE GLD

*LAST 234 TRADING DAYS: A NET 53.83 TONNES HAVE NOW BEEN ADDED INTO GLD INVENTORY.

*FROM FEB 1/2017: A NET 212.72 TONNES HAVE BEEN ADDED.

end

Now the SLV Inventory

Dec 27/WITH SILVER UP AGAIN BY 17 CENTS, WE LOST ANOTHER 802,000 OZ OF SILVER INVENTORY/WHAT CROOKS/INVENTORY RESTS AT 324.780 MILLION OZ/

Dec 26/no change in silver inventory at the SLV./Inventory rests at 325.582

Dec 21/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 326.227 MILLION OZ/

Dec 20/INVENTORY REMAINS CONSTANT AT 326.337 MILLION OZ (COMPARE WITH GLD)

Dec 19/SILVER INVENTORY REMAINS CONSTANT AT 326.337 MILLION OZ

Dec 18.2017//SILVER INVENTORY CONTINUES TO REMAIN PAT./INVENTORY REMAINS AT 326.337 MILLION OZ/

INVENTORY RESTS AT 326.337 TONNES

Dec 15/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 326.337 MILLION OZ/

Dec 14/a small withdrawal of 377,000 oz and that usually means to pay for fees./inventory rests at 326.337 million oz/

Dec 13/no change in silver inventory at the SLV/Inventory rests at 326.714 million oz/

Dec 12/WOW!ANOTHER STRANGE ONE: SILVER HAS BEEN DOWN FOR 10 CONSECUTIVE DAYS, YET THE SLV ADDS ANOTHER 1.415 MILLION OZ TO ITS INVENTORY. IN THAT 10 DAY PERIOD, SLV ADDS 9.584 MILLION OZ/

INVENTORY RESTS AT 326.714 MILLION OZ

Dec 11/WOW!! ANOTHER STRANGE ONE: SILVER DESPITE BEING DOWN FOR 9 CONSECUTIVE TRADING DAYS ADDS ANOTHER 944,000 OZ TO ITS INVENTORY. FROM NOV 30 UNTIL TODAY SILVER HAS BEEN DOWN EVERY DAY. HOWEVER THE INVENTORY OF SILVER HAS RISEN 8.169 MILLION OZ.

Dec 8/A HUGE DEPOSIT OF 2.642 MILLION OZ/INVENTORY RESTS AT 324.355 MILLION OZ/

Dec 7/strange!! with the continual whacking of silver, no change in silver inventory at the SLV/Inventory rests at 321.713

Dec 6/no change in silver inventory at the SLV/Inventory remains at 21.713 million oz.

Dec 5/THIS ONE HIT ME LIKE A TON OF BRICKS: SLV ADDS 2.507 MILLION OZ DESPITE THE HUGE DRUBBING SILVER TOOK TODAY. (PRICE DISCOVERY?)

Dec 4/NO CHANGE IN SILVER INVENTORY AT THE SLV

INVENTORY RESTS AT 319.207 MILLION OZ/

Dec 1/VERY STRANGE!! WITH SILVER IN THE DUMPSTER THESE PAST FEW DAYS, SLV ADDS 2.076 MILLION OZ/???

INVENTORY 319.207 MILLION OZ/

Nov 30/no changes in silver inventory despite the huge drop in price/inventory rests at 317.130 million oz

Nov 29/no changes in silver inventory at the SLV/Inventory rests at 317.130 million oz/strange!! at drop of 32 cents and no change in inventory?

Nov 28/no change in silver inventory at the SLV/Inventory rests at 317.130 million oz.

Nov 27/NO CHANGE IN SILVER INVENTORY DESPITE A ZERO GAIN IN PRICE /QUITE OPPOSITE TO GOLD WHICH SAW 1.18 TONNES OF GOLD WITHDRAWN DESPITE A RISE IN PRICE OF $6.40

Nov 24/A WITHDRAWAL OF 944,000 OZ OF SILVER FROM THE SLV//INVENTORY RESTS AT 317.130 MILLION OZ

Nov 22/no change in silver inventory at the SLV/Inventory rests at 318.074 million oz.

Dec 27/2017:

Inventory 324.780 million oz

end

6 Month MM GOFO

Indicative gold forward offer rate for a 6 month duration

+ 2.11%

12 Month MM GOFO

+ 2.11%

30 day trend

end

A

Major gold/silver trading /commentaries for WEDNESDAY

GOLDCORE/BLOG/MARK O’BYRNE.

GOLD/SILVER

Gold, Bitcoin and the Blockchain Replaces the Banks – Realists Guide To The Future

Gold, Bitcoin and the Blockchain Replaces the Banks – Realists Guide To The Future

– Futurist guide to 2028 shows a world of uncertainty and disruption

– One scenario suggests cybersecurity attacks will result in bitcoin and blockchain’s dominance of financial systems

– Cybersecurity threat will still loom large and wreak havoc. Gold, silver and other real assets will benefit.

– Adoption of cryptocurrencies and blockchain will send gold price soaring

– Use of cryptocurrencies to take advantage of world systems will see investors turn to safe havens such as gold bullion and coins

The media is filled with predictions for 2018. Will Trump survive another year? How will Brexit negotiations play out? Can bitcoin recover from its recent fall? What fake news will create the next disruption to the apparent status quo?

No one knows the answers to any of theses questions. If the past year to eighteen months has taught us anything it is that the polls and predictions are almost a waste of time. Arguably it is better to look further into the future and at a range of scenarios so one can consider the opportunities and threats that may lie ahead.

Bloomberg has done just this, with their ‘Pessimists Guide to 2028‘. In it the authors consider eight scenarios. Each scenario could very easily begin to take place in 2018, but the full impact will play out over the following decade.

The scenarios put forth are:

Scenario 1

Trump wins second term

Scenario 2

Fake news kills Facebook

Scenario 3

Bitcoin replaces the banks

Scenario 4

North Korea launches an attack

Scenario 5

Corbyn makes socialism great again

Scenario 6

Generational Warfare Destroys Europe

Scenario 7

China begins a trade war

Scenario 8

Electric Cars end the oil era

Below we bring you the Scenario 3: Bitcoin replaces the banks

Each scenario is deserving of attention in its own right but it is the third one which we believe is the most pertinent and arguably realistic. This is the assumption that bitcoin will replace the banks and gold will benefit. Arguably gold would benefit as a result of many of the scenarios put forward. But, given the interest in bitcoin this year it is an important reminder that both bitcoin’s growth and weaknesses will see gold and other real assets shine.

Visualizing The Future Of Shipping: Green & Autonomous

Space travel may be exciting, and self-driving cars certainly get a lot of hype. However, there remains a good…

2018

A U.S. regional lender announces that its systems have been taken down in a cyberattack and all its deposits have vanished. Regulators around the world reassure account holders that their deposits are safe. Bitcoin jumps to $40,000 as deep fears set in about the safety of the financial system. Gold surges too, but by less.

2021

China’s Alibaba adopts its own cryptocurrency for use inside its vast e-commerce network, establishing the mass-market viability of digital money. Following Venezuela’s lead, Greece and a few African countries adopt bitcoin, which hits $100,000.

2023

Rogue coders inside a regulatory-compliance software company inject a Trojan malware program called Worm Hole into scores of banks around the world. Undetected, it siphons data and cash from accounts in fractional increments.

2026

A 10-year-old schoolgirl in Pittsburgh discovers Worm Hole and exposes it on social media, triggering a run on the global banking system. Shares in Old Wall Street crash as major central banks embrace blockchain technology, bypassing the banks, and issue digital money directly to households.

2028

Many commercial lenders break apart. The global financial system gives way to a fragmented patchwork of digital currencies and payment systems dominated by such players as Alipay and Amazon.com. Bitcoin hits $1 million.

In light of this scenario’s end, Bloomberg offers Nightberg’s advice for the investor:

Vanished bank deposits would likely drive a major disbelief in all things digital, even bitcoin. Owning real physical assets, such as gold, luxury real estate for high net worth individuals, artwork, and safety vault producers in general as individuals seek to store more of their wealth within their private residences. The cyber-insurance sector would benefit as the world would scramble to find a solution to decimated trust in the financial sector. Nightberg macro research.

Bloomberg’s analysis and Nightberg’s conclusion bring up a fear which is not just for the future but is a very real one today: cybersecurity attacks. the scenario begins because of a cybersecurity attack and it this issue is still not resolved ten years into the future.

Cyber attacks are not something which can be overcome by cybersecurity. Like any form of attack there will be new approaches and strategies. The year of 2017 has been a very serious wake-up call as to how cyber power can flip the status quo on its head. Consider the apparent meddling by Russia in Western politics or North Korea’s (occasionally successful) attempts to steal bitcoin.

The invisible threat is very much on our doorstep.

This Christmas weekend HMS St Albans was forced to shadow a Russian warship in the North Sea. According to reports the warship was showing interest in ‘areas of national interest’. What is there apart from oil? The UK’s communication cables.

Air Chief Marshal Sir Stuart Peach, the chief of the UK’s defence staff, has recently expressed concerns over the security of the cables. Should they be cut (or service disrupted) then the damage would “immediately and potentially catastrophically” hit the economy.

Prepare for uncertainty, not the rise of bitcoin

This weekend’s posturing by the Russians or Bloomberg’s scenario planning should serve as a timely reminder as to what can and will survive such times. Physical gold cannot be made to disappear at the touch of a few buttons or by the cutting of cables. Should there be a global cyberattack on the financial system, the primary wealth would no longer be primarily digital (bitcoin, cash, stocks and bonds etc).

Gold and silver allocated and segregated bullion is important because of both its tangible nature and its role as a safe haven in times of geopolitical upset. Bitcoin, or any other cryptocurrency, cannot be considered safe when cyberattacks are a daily reality. They are also new and still untrusted by the majority of the system.

When seeking to diversify your portfolio in order to protect from uncertain scenarios you should consider the risks posed to digital gold providers who do not allow clients to interact and trade on the phone and are solely reliant for pricing and liquidity from online portals and online trading platforms.

Those who have outright legal ownership of physical gold and silver coins and bars outside the banking system will be far better prepared for cybersecurity attacks and uncertain times.

You can read more on the other seven scenarios here. Whilst reading them it is worth reminding oneself of how easily the world can change and how uncertain we are as to whether they may or may not happen.

Related reading

http://www.goldcore.com/ie/gold-blog/cyber-wars-crash-markets-threat-hum…

http://www.goldcore.com/us/gold-blog/cyber-attacks-show-vulnerability-di…

http://www.goldcore.com/us/gold-blog/cyberwar-risk-u-s-navy-victim-hacki…

News and Commentary

Gold eases from 3-week top as dollar holds steady (Reuters.com)

Gold Miners ETFs Set to Bounce Back in 2018 (ETFTrends.com)

Bitcoin $1 million, Amazon $1 trillion: Bold calls of 2017 are worth watching now (MarketWatch.com)

Oil prices slip away from 2015 highs, but market remains tight (Reuters.com)

Apple and its suppliers weigh on Wall Street (Reuters.com)

Source: Bloomberg

First English gold coin worth just a penny will sell for unbelievable amount (Mirror.co.uk)

Sudan sharply devalues its pound against U.S. dollar (Xinhuanet.com)

Israeli regulator seeks to ban cryptocurrency firms from stock exchange (Reuters.com)

Let regions go bankrupt, Chinese central bank official says (Bloomberg.com)

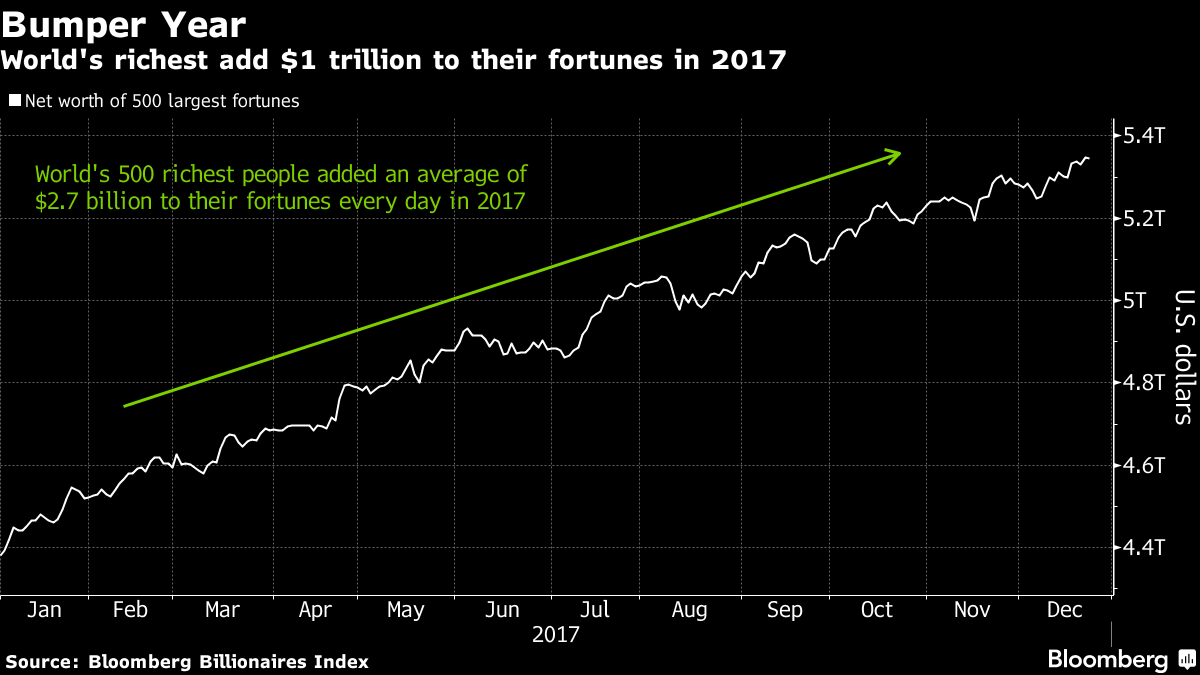

World’s Wealthiest Became $1 Trillion Richer in 2017 (Bloomberg.com)

Gold Prices (LBMA AM)

27 Dec: USD 1,285.40, GBP 958.78 & EUR 1,081.54 per ounce

22 Dec: USD 1,268.05, GBP 947.74 & EUR 1,069.85 per ounce

21 Dec: USD 1,265.85, GBP 945.97 & EUR 1,065.09 per ounce

20 Dec: USD 1,265.95, GBP 944.27 & EUR 1,068.21 per ounce

19 Dec: USD 1,263.10, GBP 944.93 & EUR 1,070.10 per ounce

18 Dec: USD 1,258.65, GBP 943.11 & EUR 1,067.71 per ounce

15 Dec: USD 1,257.25, GBP 937.41 & EUR 1,065.52 per ounce

Silver Prices (LBMA)

27 Dec: USD 16.50, GBP 12.30 & EUR 13.87 per ounce

22 Dec: USD 16.18, GBP 12.08 & EUR 13.65 per ounce

21 Dec: USD 16.15, GBP 12.08 & EUR 13.61 per ounce

20 Dec: USD 16.19, GBP 12.09 & EUR 13.67 per ounce

19 Dec: USD 16.16, GBP 12.08 & EUR 13.68 per ounce

18 Dec: USD 16.09, GBP 12.04 & EUR 13.64 per ounce

15 Dec: USD 15.99, GBP 11.93 & EUR 13.55 per ounce

Recent Market Updates

– Goldnomics Podcast – Gold, Stocks, Bitcoin in 2018. Everything Bubble Bursts?

– What Peak Gold, Interest Rates And Current Geopolitical Tensions Mean For Gold in 2018

– New Rules For Cross-Border Cash and Gold Bullion Movements

– ‘Gold Strengthens Public Confidence In The Central Bank’ – Bundesbank

– WGC: 2018 Set To Be A Positive Year For Price of Gold and Investors

– Year-end Rate Hike Once Again Proves To Be Launchpad For Gold Price

– UK Stagflation Risk As Inflation Hits 3.1% and House Prices Fall

– Buy Gold, Silver Time After Speculators Reduce Longs and Banks Reduce Shorts

– Bitcoin – Plan Your Exit Strategy Now – Maybe With Gold

– Gold Demand Increases Along with Uncertainty Thanks to Trump, Brexit and North Korea

– UK Pensions Risk – Time to Rebalance and Allocate to Cash and Gold

– Bailins Coming In EU – 114 Italian Banks Have NP Loans Exceeding Tangible Assets

– Silver’s Positive Fundamentals Due To Strong Demand In Key Growth Industries

end

Gold trading this morning!

(courtesy zerohedge)

Gold Jumps To Key Technical Level As VIX Collapses

Traders are dumping equity protection and buting chaos protection as VIX tumbles near the year’s lows and Gold jumps back towards its 100-day moving average – and its highest level in a month.

Gold is up 9 of the last 10 days, at its highest since early Dec and testing its 100DMA… ($1292)

And while Bitcoin has stabilized, the divergence between the alt-currencies is closing…

end

Your early WEDNESDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

Global Stocks Rise, Copper Soars In Thin Holiday Volumes

European stocks are steady in post-Christmas trading if struggling for traction after a mixed session in Asia, amid trading thinned by a holiday-shortened week and ongoing worries about the tech sector; however a strong rally in commodities – including copper and oil – buoyed expectations for a strong 2018 and helped offset concerns over the technology sector triggered by reports of soft iPhone X demand.

U.S. equity futures nudged higher while the dollar weakened against most G-10 peers as investors await the release of U.S. consumer-confidence data, with much of the spotlight falling on commodity currencies. The OZ dollar holds onto gains as copper surges to a three-year high; oil retreats after reaching the highest close in more than two years following a pipeline explosion in Libya on Tuesday. Treasuries and core European core bond yields are a touch lower.

The Stoxx Europe 600 Index edged lower, with tech stocks hit for the third day amid rumors of weak iPhone demand and leading the decline as chipmakers slumped after analysts lowered iPhone X shipment projections, sending the Nasdaq Composite Index lower overnight. While mining and oil stocks strengthened due to a surge in copper prices to a 3.5 year high (see below), the European STOXX 600 index slipped 0.1% as European tech stocks tumbled on reports that demand for Apple’s iPhone X may be weaker than expected. The equity benchmark index is poised for an annual gain of 8.1%, the best advance in four years. Elsewhere, Volvo rose as China’s Geely bought Cevian’s stake in the truckmaker, making it Volvo AB’s largest stakeholder. IWG surged the most since 2009 after confirming it has received a a non-binding takeover offer from a consortium backed by Brookfield Asset Management and Onex.

In Asia earlier Japanese equity benchmarks posted slight gains, Australian stocks were flat and China’s domestic shares dropped. Asian shares climbed 0.3% to near a recent one-month high, though it was more of a mixed picture in European stock markets. Shares of China’s new-energy automakers surged after the government announced it will extend purchase-tax exemption for another three years, through Dec. 31, 2020. BYD climbed as much as 5.9% on the mainland to the highest since Nov. 24; Zhongtong Bus & Holding Co. rises by 10% daily limit.

As the chart below shows, the recent dip in Emerging Asian stocks has been largely bought, and the selloff gap has been mostly filled.

In commodities, oil and copper prices rocketed to multi-year highs, pushing the MSCI world equity index 0.1% higher. While oil prices were strengthened largely because of an attack on a crude pipeline in Libya, the surge in copper was particularly eye-catching as the metal is seen as a proxy for global growth. Miners gained as copper climbed to a three-year high after China ordered its top producer to halt output to combat winter pollution.

“The rally in copper supports expectations that 2018 is going to be a strong year for synchronised global growth,” said Greg McKenna, chief strategist at AxiTrader. That, or at least until the artificial production shortage is resolved.

Visualizing The Future Of Shipping: Green & Autonomous

Space travel may be exciting, and self-driving cars certainly get a lot of hype. However, there remains a good…

Meanwhile, rising oil prices – WTI hit $60 a barrel for the first time since mid-2015 – boosted currencies that trade in line with commodities prices.

In currencies, the dollar eased against a basket of currencies and fell against the euro on Wednesday in thin holiday trading, while a rally in commodity prices helped push the Canadian and Australian dollars to their highest levels in two months. The EUR/USD made a session high after London came into the market, with the pair remaining above the 21-DMA; the USD/JPY is little changed while USD/JPY cross- currency basis swaps hit widest spread in more than a year. Cable rose to a one-week high amid broad dollar weakness while Aussie extended opening gains buoyed by flows against kiwi, which itself rose on outright short-covering against the U.S. dollar; traders report that ranges extended on thinning year-end liquidity.

As Reuters points out, while world stocks were up on the day, there was still an undercurrent of nervousness in the market which saw some safe haven flows into high-rated euro zone government bonds, pushing their yields a touch lower. “Geo-political risks have notched a little higher, supporting rates markets,” said Mizuho’s head of rates Peter Chatwell, referring in particular to a renewal in tensions around North Korea.

The United States announced sanctions on two North Korean officials behind their country’s ballistic missile program on Tuesday after the U.N. Security Council unanimously imposed new sanctions on North Korea last week. “The North Korean statement that U.N. sanctions are an act of war is, as tends to be the case, an exaggeration, but nevertheless the market has no choice but to price it. Some safe haven positioning is a natural reaction,” said Chatwell.

Today investors await the release of U.S. consumer-confidence and pending home sales data.

Market Snapshot

- S&P 500 futures up 0.07% to 2,689

- US 10Y yield down 0.1 bp to 2.47%

- STOXX Europe 600 down 0.02% to 390.22

- German 10Y yield fell 1.4 bps to 0.406%

- Euro up 0.2% to $1.1880

- Brent Futures down 1% to $66.37/bbl

- Italian 10Y yield rose 0.6 bps to 1.645%

- Spanish 10Y yield unchanged at 1.473%

- Brent Futures down 1% to $66.37/bbl

- Gold spot up 0.2% to $1,285.23

- U.S. Dollar Index down 0.1% to 93.13

- MSCI Asia Pacific up 0.3% to 172.69

- MSCI Asia Pacific ex Japan up 0.3% to 562.82

- Nikkei up 0.08% to 22,911.21

- Topix up 0.2% to 1,829.79

- Hang Seng Index up 0.07% to 29,597.66

- Shanghai Composite down 0.9% to 3,275.78

- Sensex down 0.3% to 33,905.60

- Australia S&P/ASX 200 unchanged at 6,069.87

- Kospi up 0.4% to 2,436.67

Overnight Media Digest

- Copper in London surged to the highest level since 2014 after China ordered its top producer to halt output to combat winter pollution, adding further impetus to a rally that’s been driven by optimism about demand as well as supply disruptions at mines

- ETFs linked to raw materials attracted about $450 million this month as of Dec. 21, on track for a third straight annual inflow, as investors are betting on synchronized global growth to improve the outlook for commodities from copper to natural gas in 2018

- Recent economic data offer a “warning for 2018” now that Chinese leaders are less motivated to prop up growth in the wake of their Congress in October, according to the China Beige Book

- German Social Democratic Party won’t agree to renew coalition with Chancellor Angela Merkel unless she backs EU reform, acting Foreign Minister Sigmar Gabriel quoted as saying in interview with Bild newspaper

- Spain November seasonally adjusted retail sales rose 2% y/y vs est. +0.8% y/y

- The United States imposed sanctions Tuesday on two North Korean officials who are considered key to their country’s development of ballistic missiles.

- A pipeline blast in Libya and a bullish budget forecast in Saudi Arabia boosted crude prices to levels not seen since mid-2015.

- Recent economic data offer a “warning for 2018” now that Chinese leaders are less motivated to prop up growth in the wake of their Congress in October, according to the China Beige Book.

- Fitch Downgrades AXA Financial, Inc.; Removes Ratings from Watch

- Daily Mail & General Trust Cut to Junk by S&P

In Asian markets, Japanese equity benchmarks posted slight gains, Australian stocks were flat and China’s domestic shares dropped. Asian shares climbed 0.3% to near a recent one-month high, though it was more of a mixed picture in European stock markets. Shares of China’s new-energy automakers surged after the government announced it will extend purchase-tax exemption for another three years, through Dec. 31, 2020. BYD climbed as much as 5.9% on the mainland to the highest since Nov. 24; Zhongtong Bus & Holding Co. rises by 10% daily limit.

Top Asian News

- Nomura Says Japanese Investors Should Buy Unhedged Dollar Bonds

- India Is Said to Propose Easing Rules on Debt Default Disclosure

- China to Discuss Changing Constitution for First Time Since 2004

- WeWork’s Chinese Rival Nixes ‘UrWork’ Label in Global Makeover

- Prosecutors Affirm Push for Samsung Heir to Get 12-Year Sentence

- DBS Hires Andy Yung as Vice President at Loans Team in Hong Kong

- 1MDB Makes Final Payment to IPIC in $1.2 Billion Settlement

In Europe, the Stoxx Europe 600 Index edged lower, with tech stocks hit for the third day amid rumors of weak iPhone demand and leading the decline as chipmakers slumped after analysts lowered iPhone X shipment projections, sending the Nasdaq Composite Index lower overnight. While mining and oil stocks strengthened due to a surge in copper prices to a 3.5 year high (see below), the European STOXX 600 index slipped 0.1% as European tech stocks tumbled on reports that demand for Apple’s iPhone X may be weaker than expected. The equity benchmark index is poised for an annual gain of 8.1%, the best advance in four years. Elsewhere, Volvo rose as China’s Geely bought Cevian’s stake in the truckmaker, making it Volvo AB’s largest stakeholder. IWG surged the most since 2009 after confirming it has received a a non-binding takeover offer from a consortium backed by Brookfield Asset Management and Onex

Top European News

- IWG Soars After Bid Approach From Canada’s Onex, Brookfield

- Russia Nuclear Power Output Reaches Post-Soviet Record This Year

- Bank of Spain Sees Growth Continuing But Losing Intensity

- Norway Oil Fund Says Taxes Should Be Paid Where Value Generated

In FX, the Bloomberg Dollar Spot Index decreased 0.2 percent to the lowest in almost two weeks, in thin holiday trading, while a rally in commodity prices helped push the Canadian and Australian dollars to their highest levels in two months. The EUR/USD made a session high after London came into the market, with the pair remaining above the 21-DMA and advancing 0.2% to $1.1884, the strongest in almost four week; the USD/JPY is unchanged at 113.25 per dollar, the strongest in more than a week while the USD/JPY cross- currency basis swaps hit widest spread in more than a year. Cable rose to a one-week high amid broad dollar weakness while Aussie extended opening gains buoyed by flows against kiwi, which itself rose on outright short-covering against the U.S. dollar; traders report that ranges extended on thinning year-end liquidity.

In commodities, WTI dropped 0.6% to $59.59 a barrel, the first retreat in more than a week and the biggest dip in two weeks. Gold increased 0.2% to $1,286.01 an ounce, hitting the highest in more than four weeks with its sixth consecutive advance. LME copper advanced 0.8 percent to $7,185.00 per metric ton, reaching the highest in about four years on its ninth consecutive advance and the biggest gain in a week.

US Event Calendar

- 10pm: U.S. Conf. Board Consumer Confidence, Dec., est. 128, prior 129.5; Present Situation, Dec., no est., prior 153.9; Expectations, Dec., no est., prior 113.3

end

3. ASIAN AFFAIRS

3 a NORTH KOREA/USA

NORTH KOREA/

Trump and the UN will not like this as Chinese ships have been caught through spy satellites selling oil to North Korea illegally

(courtesy zerohedge)

US Spy Satellites Catch Chinese Ships Illegally Selling Oil To North Korea

According to South Korea’s Chosun Ilbo, U.S. recon satellites have photographed around 30 illegal transactions involving Chinese vessels selling oil to North Korea on the West Sea in October. The images allegedly showed large Chinese and North Korean ships transacting in oil in a part of the West Sea closer to China than South Korea. The satellite pictures even showed the names of the ships.

A government source said, “We need to focus on the fact that the illicit trade started after a UN Security Council resolution in September drastically capped North Korea’s imports of refined petroleum products.” Meanwhile, on paper, China’s trade with North has recently collapsed after U.S. President Donald Trump unleashed a barrage of sanctions in September targeting North Korea’s imports of refined petroleum products.

Back in November, the US. Treasury Department sanctioned an additional six North Korean shipping and trading companies and 20 of their ships after the satellite pictures surfaced. In the above picture, the North Korean ship named Ryesonggang 1, was easily identified and connected to the illegal sale of oil from China.

According to Chosun Media, “the department noted that the two ships appeared to be illegally trading in oil from ship to ship to bypass sanctions.”

Ship-to-ship trade with North Korea on the high seas is forbidden in UNSC Resolution 2375 adopted in September, but such violations are nearly impossible to detect unless China aggressively cracks down on smuggling.

Last month, the Communist Party spokespeople slammed new US sanctions targeting Chinese traders doing business with North Koreans, calling them “wrong”. At this point, it’s still unknown if the Chinese government is turning a blind eye to the illegal open sea transactions with North Korea, but as of today it seems as a blatant snub to the Trump administration.

Meanwhile, as President Trump and the US celebrate last week’s latest round of new sanctions for North Korea at the UN, the likelihood of illegal smuggling routes between the two countries will surely expand. The question then is with all diplomatic avenues exhausted and China violating a UNSC resolution, what happens next?

end

my goodness. It has now been discovered that the latest North Korea defector has carried the anthrax antibodies. It is feared that North Korea is trying to develop warheads with the anthrax on them

(courtesy zerohedge)

Scientists Discovered North Korean Defector Carried Anthrax Antibodies

As we’ve reported here and here, there have been several high-profile defections this year involving Korean soldiers sprinting across the heavily fortified border between the two Koreas – a feat that had not been previously accomplished since 2007. In the first incident, the soldier was shot seven times as he staged a daring escape that ended with him being dragged to safety by American and South Korean forces. That incident was caught on video, which can be viewed below.

In the second incident, a North Korean soldier simply walked across.

Two other soldiers also escaped in incidents that apparently weren’t picked up by the western media.

Now, doctors examining one of the soldiers have reportedly discovered that he possesses antibodies to Anthrax – a potent chemical weapon that was notoriously used in the 2001 Anthrax attacks in the US. According to the New York Post, a South Korean intelligence official who spoke on condition of anonymity did not say which of the four soldiers who fled the hermit kingdom this year had the antibodies in his system. But the discovery is causing concern in Seoul because, once the bacterium is released, it can kill 80% of those infected within 24 hours unless antibiotics are taken or vaccination is available.

And while the US has stockpiles of the vaccine, South Korea has yet to produce it.

Defense Ministry spokeswoman Choi Hyun-soo said an anthrax “vaccine is expected to be developed by the end of 2019,” but likely not before then.

The restive North Korean regime has been suspected of developing biological weapons after publicizing the works of the Pyongyang Biological Technology Research Institute in 2015. The institute is run by the North Korean army.

Pyongyang claimed the facility specializes in pesticide research, but analysts have said its dual-use equipment suggests biological weapons are being manufactured in North Korea.

North Korea’s neighbors fear Pyongyang is conducting illegal biological weapons tests to see if anthrax-laden warheads can be loaded onto its missiles, the Sun of the UK reported. Media reports earlier this year suggested that North Korea had begun to test loading anthrax onto them.

The report said the US is aware of the tests, which are meant to ascertain whether the anthrax bacteria could survive reentry into the Earth’s atmosphere – as we pointed out last week.

Seoul believes North Korea has a chemical weapons stockpile of up to 5,000 tons and can produce biological warfare agents such as anthrax and smallpox. Also last week, the White House pointed to the dangers posed by North Korea in the National Security Strategy released by President Trump.

“North Korea – a country that starves its own people – has spent hundreds of millions of dollars on nuclear, chemical and biological weapons that could threaten our homeland,” read the report.

“[North Korea is] pursuing chemical and biological weapons which could also be delivered by missile.”

Pyongyang denied the Asahi report through the state media Korean Central News Agency.

“As a state party to the Biological Weapons Convention (BWC), [North Korea] maintains its consistent stand to oppose development, manufacture, stockpiling and possession of biological weapons,” the KCNA reported.

3 b JAPAN AFFAIRS

c) REPORT ON CHINA

It is when the company (NHA) states that one should not panic that is exactly what you must do: panic. NHA has 100 billion of debt in which 25% is due in 2018. NHA owns a lot of Deutsche bank shares. If DB suffers another meltdown this could cause the meltdown of NHA and lead the other 3 Chinese conglomerates into a full blown panic

(courtesy zerohedge)

To Avoid Liquidation Panic, HNA Assures Deutsche Shareholders It’s A “Long-Term Investor”

The notoriously acquisitive Chinese conglomerate HNA – which recently had a sharp falling out with Beijing resulting in a margin call “shocksave” – is facing a serious cash crunch in 2018 as nearly a quarter of its $100 billion in debt – a large chunk of which was accumulated during a multi-year buying spree that saw it become a major shareholder in Deutsche Bank, Hilton Worldwide and a large portfolio of international holdings – comes due.

But even as the company resorted to loaning out shares and entering into arcane derivative financing agreements to finance its debt-service payments, it is quickly finding that traditional avenues of financing are disappearing or becoming too costly.

Despite being one of China’s largest conglomerates, HNA has been shut out of stock and bond markets as lenders worry about its outsized debt load, forcing the company to pledge some of its core holdings as collateral for short-term loans, as the Wall Street Journal reported earlier this month.

This has forced the conglomerate to explore other options. To wit, the bank recently pledged some of its Deutsche Bank shares to UBS as collateral for a loan worth roughly $117. It also executed an options strategy known as a collar. This strategy involves purchasing out-of-the-money puts to protect against a large drop in the stock while simultaneously selling out-of-the money calls to offset the cost of the puts.

On Dec. 20, HNA’s unit entered into a new series of collar transactions with Swiss bank UBS Group AG, and pledged its Deutsche Bank shares to UBS in exchange for a total of 2.36 billion euros (US$2.8 billion) in net financing. It also has a margin loan from UBS and ICBC Standard Chartered PLC. In all, the new total amount of financing was about 99 million euros (US$117.6 million) higher than what was disclosed in a similar filing in May.

The additional collar financing disclosed this week should help protect HNA’s position in Deutsche Bank shares from margin calls in the future, according to people close to the companies. The new collar financing extends to 2020, longer than before, and gives HNA additional protection against volatility in Deutsche Bank shares, they said.

With memories of last fall’s dramatic plunge in Deutsche Bank shares still fresh – a selloff that was triggered by the DOJ’s decision to slap the already shaky German lender with a $14 billion fine – HNA assured its fellow shareholders that it is a “long-term investor” in Germany’s largest bank. The comment is, of course, self-serving: Though it has purchased downside protection to protect against a large drop in DB’s shares, a substantial decline in the company’s valuation could be the straw that pushes the conglomerate into bankruptcy, and potentially triggers China’s “Minsky moment.”

For context, HNA owns about $4 billion in DB shares, roughly equivalent to a 10% stake, as shown in the Bloomberg chart below and according to Reuters.

Concerns about HNA’s financial position intensified since it issued a bond last year with less than one year to maturity. The bond carried the extortionately high coupon of 9%, prompting us to wonder if the demise of one of China’s “Big Four” conglomerates might be rapidly approaching.

HNA has borrowed $40 billion since 2015 to finance its world-wide buying spree. But in some cases, it’s already getting buyers remorse. About a month ago, its chief executive acknowledged a shift in strategy, saying HNA was looking to sell assets it deemed noncore. For example, it is exploring a group of foreign commercial properties it owns.

As reported by Reuters, Alexander Schuetz, HNA’s representative on DB’s board, made the comments during an interview with German newspaper Handelsblatt. The comments were later picked up by Reuters and Bloomberg. Schultz specifically emphasized that HNA has “no interest in a sale” of its DB holdings.

Schuetz sought to dismiss any lingering speculation that HNA would sell its stake in the German lender, which is just under 10 percent and valued at around 3.3 billion euros ($3.9 billion). “We want to show that this is totally wrong,” he was quoted as saying.

HNA’s $50 billion worth of deal-making over the past two years has sparked intense scrutiny of its opaque ownership and use of leverage.

In the interview, Schuetz pointed to a new financing structure with derivatives – with a three-year maturity – that insure against a drop in the bank’s share price. “This shows that HNA is focused on the long-term and has no interest in a sale,” Schuetz said.

Late last month, S&P downgraded HNA’s credit rating by one notch from B+ to B, five notches below investment grade as a result of its “aggressive financial policy” and tightening liquidity amid looming debt maturities. Even before that, some of the conglomerate’s largest subsidiaries were issuing bonds with interest rates far higher than their credit ratings would seem to suggest.

To be sure, despite its reassurances, if HNA is still struggling to raise the capital needed to make its $28 billion debt-service payment at the end of June, it’s likely even core assets might be put on the chopping block.

4. EUROPEAN AFFAIRS

END

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

Russia is carrying out these new missile defense tests with more frequency.

(courtesy zerohedge)

Russia Tests Powerful ICBM Capable Of Overcoming Missile-Defense Systems

As North Korea vociferously condemns the US and the United Nations after the Security Council passed yet another round of sanctions against the restive regime, Russia is continuing to test ICBMs in preparation for a violent conflict on the neighboring Korean Peninsula while simultaneous calling for both sides to seek mediation.

Last night, Russia’s Strategic Missile Force tested the RS-12M Topol intercontinental ballistic missile (ICBM) at the Kapustin Yar practice range in the southern Astrakhan Region, the TASS News Agency reported Tuesday.

“On December 26, 2017, a combat team of the Strategic Missile Force test-fired an RS-12M Topol intercontinental ballistic missile from the Kapustin Yar state central combined arms training range in the Astrakhan Region,” Russia’s Defense Ministry said.

“The launch was aimed at testing perspective armament for intercontinental ballistic missiles,” the ministry said.

“During the tests, specialists obtained experimental data that will be used in the interests of developing effective means of overcoming anti-ballistic missile defense and equipping the perspective grouping of Russian ballistic missiles with them,” the Defense Ministry said.

As we explained last week, the latest round of sanctions aims to curb the North Korean energy trade – something both China and Russia have been reluctant to sign off on in the past. This suggests that two of the North’s erstwhile benefactors are becoming increasingly concerned about the possibility that a deadly, destabilizing conflict could erupt on the peninsula.

The new restrictions are meant to slash North Korea’s imports of refined petroleum products, further restrict shipping and impose a 12-month deadline for expatriate North Korean workers to be sent home, according to Bloomberg.

“Under the new sanctions, oil exports will be limited to their current level, which has already begun to result in shortages around the country,” the NY Times added. “Countries around the world will be ordered to expel North Korean workers, a key source of hard currency. Nations would also be urged to inspect all North Korean shipping and halt ship-to-ship transfers of fuel, which the North has used to evade sanctions.”

In response, the North (once again) swiftly condemned the sanctions as an “act of war”, and threatened to “further consolidate its self-defensive nuclear deterrence.”

Circling back to the launch, RS-12M Topol intercontinental ballistic missile (ICBM) at the Kapustin Yar practice range in the southern Astrakhan Region, the Defense Ministry reported on Tuesday.

According to TASS, the Kapustin Yar practice range was chosen because it allows testing perspective armaments capable of overcoming anti-ballistic missile defenses – a tacit reference to the US ABM systems that dot Eastern Europe and South Korea.

After the North’s latest ICBM test, Russia announced on Wednesday that North Korea’s latest intercontinental ballistic missile launch constituted a “provocative act”. Though Russia also called on both sides to “stay calm.” Russia has carried out ICBM tests with increasing frequency in recent months, while also deploying troops to its border to act as a bulwark should an armed conflict break out.

end

Turkey’s Main Opposition Party Threatens To “Come And Take Back 18 Islands Owned By Greece”

The leader of Turkey’s main opposition party Republican People’s Party (CHP), Kemal Kilicdaroglu, threatened to come and take back a total of 18 islands occupied by Greece.

No worries. The leader of Kemalist CHP will not come in the next days, weeks or months. He will come in 2019, after his party will win the general elections of Turkey scheduled to take place in the same year.

As KeepTalkingGreece.com reports, lashing out at the Greek defense minister’s remarks on the Aegean islands who a few days ago told Turkey “Molon Labe ” – meaning “come and take [them]” is a classical expression of defiance. According to Plutarch, Xerxes I, king of the Achaemenid Empire, demanded that the Spartans surrender their weapons and King Leonidas I responded with this phrase. It is an exemplary use of a laconic phrase –Kilicdaroglu said speaking at a party event in the northwestern province of Kocaeli…

“The Greek Defense minister says ‘Come and get it.’ I will come and take all of those islands back.

Why am I saying this? They said ‘Come and get it’ for Cyprus back in the day. What did Ecevit (former prime minister) do? He went there and took it back,”

The debate over the Aegean islands sparked when the CHP leader criticized President Recep Tayyip Erdogan on Dec. 11 over his failure to raise the issue of “18 occupied islands” during his visit to the country.

“Why did not you talk about 18 occupied islands? Article 12 and Article 18 of the Lausanne Treaty were clearly violated. There are 13,000 military units and nearly 5,000 Greek troops on the islands,” Kiliçdaroglu said.

The question is – what will Merkel do?

end

6. GLOBAL ISSUES

Argentina

“This Could Not Have Been Suicide” – Judge Agrees That Argentine Prosecutor Was Murdered

After a team of forensic experts ruled in September that the 2015 shooting death of Argentine prosecutor Alberto Nisman was, indeed, murder – not suicide as the authorities had initially ruled – a federal judge has validated those findings in a lengthy ruling that seems to point the finger at former Argentine President Cristina Fernandez de Kirchner.

The ruling is the latest blow to Fernandez, who won her bid for a senate seat in October. Though Fernandez has publicly said her decision to run is part of a political comeback, others have speculated that she ran for her senate seat to help insulate herself from accusations of money laundering and corruption, as well as her suspected work to cover up Iran’s role in financing the 1994 bombing of a Jewish community center in Buenos Aires – a bombing that killed 85 people.

Alberto Nisman

Years later, Nisman was assigned to investigate a possible cover-up of Iranian officials’ role in the bombing. But he was found dead of a gunshot wound to the head in January 2015, hours before he was due to testify against former President Fernandez The ruling comes after a prosecutor recommended last year that the case be investigated as a murder.

In another stunning decision, Tuesday’s ruling by the Argentine judge also charged that Diego Lagomarsino, a former employee of Nisman’s, was an accessory to his murder, after a gun owned by Lagomarsino was found near Nisman’s body, as Reuters reported.

In a 656-page ruling, judge Julian Ercolini said there was sufficient proof to conclude that the shot to the head that killed Nisman in January 2015 was not self-inflicted. That marked the first time any judge has said the case was a murder.

Fernandez and others had suggested the death was a suicide, but a prosecutor investigating the case last year recommended it be pursued as a murder probe.

“Nisman’s death could not have been a suicide,” Ercolini wrote in Tuesday’s ruling, which also charged Diego Lagomarsino, a former employee of Nisman‘s, with accessory to murder.

Lagomarsino has acknowledged lending Nisman the gun that killed him the day before he was to appear before Congress to detail his allegation against Fernandez. But he has said Nisman asked him for the gun to protect himself and his family.

Earlier this month, Fernandez was formally charged with treason by a federal judge, and a federal judge called for her arrest. But before her arrest, Congress would have to vote to strip Fernandez of her immunity.

Meanwhile, her former Foreign Minister, Hector Timerman, was placed under arrest and confined to his home, where he wrote this New York Times op-ed professing his innocence and claiming to be a political prisoner.

In an unrelated case, Fernandez and her two children were indicted back in April on corruption charges related to deals involving a family owned real-estate company.

After leaving office in December 2015 following eight years in power – a period where Argentina’s economy experienced continued decline.

Her successor, the center-right former Mayor of Buenos Aires Mauricio Macri, has swiftly implemented pro-growth economic reforms like abolishing the country’s capital controls and reaching a settlement with a group of US hedge funds led by Paul Singer’s Elliott Management Corporation.

Now, the possibility that Fernandez will be held accountable for her actions is looking increasingly likely.

end

Israel

Israel braces for indictments against Netanyahu

(courtesy zerohedge)

Israel Braces For “Earth Shattering” Indictments Against Netanyahu

As Israeli police conclude their corruption investigation of Prime Minister Benjamin Netanyahu, former advisor to the force, Lior Chorev, says the indictments to follow will be “earth-shattering” and will result in early elections – possibly as soon as May 2018, which would end the political career of the longest-serving Israeli leader since founding father David Ben-Gurion.

Israeli Prime Minister Benjamin Netanyahu (photo credit: AMIR COHEN/REUTERS)

Chorev, who resigned last month under pressure from Netanyahu’s allies, told The Jerusalem Post “When they [the recommendations] will be announced, they will have information such as the specific charges and a complete list of the people involved,” he said, adding “Netanyahu is not running a campaign for his innocence but a campaign to keep the coalition intact. It is a political campaign, not a legal one, and so far he is succeeding. He is keeping his coalition in one piece despite very complicated investigations.”

The indictment recommendations will bear “a lot of information that we didn’t know – and it will cause an earthquake here.”

While police recommendations in Israel aren’t binding, and prosecutors can choose to proceed with indictments, an official recommendation to indict would turn Israel’s political landscape on its head. Netanyahu has been questioned seven times by investigators in connection with two corruption cases.

Israel police claims that Chorev, as an external investigator, wouldn’t have access to information on the Netanyahu investigation:

“In these sensitive subjects, the Israel Police is providing information to the public via official statements that are released in accordance with the attorney-general and the state’s attorney,” the police said. “We are asking the public to focus only on official statement… Not once was the police blamed for leaking information by ‘different entities,’ but what they said was completely false.”

In response to the police wrap-up, Netanyahu’s allies in parliament are pushing through a bill that would forbid police from submitting written recommendations to the state prosecutor’s office on whether to indict a suspect – in what critics are calling a tool to silence investigators and interfere with police work.

“It’s ludicrous legislation because there’s no precedent for legislating those two complementing law enforcement agencies,” said Yohanan Plesner, president of the Israel Democracy Institute research center, referring to police and prosecutors. “There’s no logic to it unless one wants to create some sort of deterrence vis-a-vis the police.” –Bloomberg

Relations between Netanyahu and police have grown sour throughout the investigations, nearly a year after they became public knowledge. As Bloomberg reports, the prime minister and his supporters have accused police of deliberately leaking information about the investigations to Israeli media, claiming he’s the target of an organized campaign by the press and left-wing opponents to unseat him. Thousands of Israelis have taken to the streets in recent weekends, rallying against government corruption and calling on Netanyahu to step down.

Sara Netanyahu

According to a Justice Ministry announcement, between 2010 and 2013, Sara Netanyahu colluded with Seidoff “to create a false impression that the prime minister’s official residence on Balfour Street in Jerusalem does not employ a cook, despite the fact that throughout the entire period they employed cooks.” This was done, allegedly, to bypass a procedure that forbids ordering meals from restaurants and hiring chefs who cook at the residence when cooks are on hand. –Jewishpress.com

In a third case, 24 year old Shira Raban claims that Netanyahu incessantly insulted her while she worked for a cleaner at their residence for one month. Raban is seeking $64,000 for “verbal abuse and unreasonable requests” by Sara Netanyahu, and says she feared for her safety. Netanyahu allegedly forbade Raban from eating, drinking or resting, and required that she change her clothes dozens of times per day. Raban claims she was also required to wash her hands about 100 times a day with hot water, drying them on a separate towel from the Netanyahu family.

Several other former employees have claimed mistreatment by Sara Netanyahu, with one caretaker receiving an award of around $43,000 last year for mistreatment.

7. OIL ISSUES

end

8. EMERGING MARKET

(courtesy zerohedge)

Venezuelans Abandon Bolivar – Merchants Insist On Being Paid In Dollars

Venezuelans are struggling to carry out basic transactions like purchasing food as the value of their currency, the bolivar, has plunged against the dollar amid the country’s worsening economic collapse.

According to Reuters, over the past year, Venezuela’s currency weakened 97.5% against the greenback: Put another way, $1,000 of local currency purchased in early January would be worth just $25 now. The annual inflation rate in 2017 could reach $2,000. Though at least one other estimate puts the real rate of inflation closer to 2,800%.

Of course, President Maduro has blamed websites like DolarToday – which publishes the closest thing to an official black-market rate by surveying clandestine exchanges in Caracas and other cities – for the spread of black-market activity, part of a conspiracy organized by Washington and his local political opponents to force him from power.

One of the unintended consequences of the bolivar’s collapse has been a social experiment of sorts in the use of digital currencies: As we noted back in October, as many as 100,000 people are now mining digital currencies in Venezuela, defying a government crackdown that’s seen many of them thrown in prison.

But for those who can’t or haven’t resorted to transacting in bitcoin, an increasingly scarce supply of dollars is creating intractable problems for millions of Venezuelans, Reuters reported.

For many, simple purchases like a new tire for their car are simply out of reach.

There was no way Jose Ramon Garcia, a food transporter in Venezuela, could afford new tires for his van at $350 each.

Whether he opted to pay in U.S. currency or in the devalued local bolivar currency at the equivalent black market price, Garcia would have had to save up for years.

Though used to expensive repairs, this one was too much and put him out of business. “Repairs cost an arm and a leg in Venezuela,” said the now-unemployed 42-year-old Garcia, who has a wife and two children to support in the southern city of Guayana.

“There’s no point keeping bolivars.”

A practice that was initially adopted by shops catering to wealthy and middle-class Venezuelans is spreading to merchants selling everything from foodstuffs to medicine. Food sellers, dental and medical clinics, and others are starting to charge in dollars or their black-market equivalent – putting many basic goods and services out of reach for a growing number of Venezuelans.

“I can’t think in bolivars anymore, because you have to give a different price every hour,” said Yoselin Aguirre, 27, who makes and sells jewelry in the Paraguana peninsula and has recently pegged prices to the dollar. “To survive, you have to dollarize.”

The socialist government of the late president Hugo Chavez in 2003 brought in the strict controls in order to curb capital flight, as the wealthy sought to move money out of Venezuela after a coup attempt and major oil strike the previous year.

Oil revenue was initially able to bolster artificial exchange rates, though the black market grew and now is becoming unmanageable for the government.

Still, President Nicolas Maduro has maintained his predecessor, the late Hugo Chavez’s policies on capital controls, even as the spread between the official rate – some 10 bolivars per dollar – and the black market rate – of around 110,000 per dollar – is now huge.

The trend is angering Venezuelans who don’t have access to dollars. As Reuters pointed out, it also dampened Christmas celebrations this year due to a shortage of pine trees, toys, meat, chicken, cornmeal…the list goes on.

While sellers see a shift to hard currency as necessary, buyers sometimes blame them for speculating.

Rafael Vetencourt, 55, a steel worker in Ciudad Guayana, needed a prostate operation priced at $250.

“We don’t earn in dollars. It’s abusive to charge in dollars!” said Vetencourt, who had to decimate his savings to pay for the surgery.

Most Venezuelans, earning just $5 a month at the black-market rate, are nowhere near being able to save hard currency.

“How do I do it? I earn in bolivars and have no way to buy foreign currency,” said Cristina Centeno, a 31-year-old teacher who, like many, was seeking remote work online before Christmas in order to bring in some hard currency.

While many have begun mining bitcoin, purchasing the digital currency is also out of reach for many, since they would need to first convert their bolivars into dollars.

As the bolivar has continued to plummet, some communities have begun experimenting with alternative currencies that derive their value from a limited supply. In one Caracas neighborhood, several shops have started accepting the panal, one such alternative currency.

With the supply of dollars drying up since Maduro announced that the state-owned oil company would no longer settle payments for oil exports in greenbacks, it’s likely only a matter of time before more of these alternative paper currencies start springing up.

That is, unless the price of oil – which broke above $60 today – makes a surprising and altogether unlikely comeback.

end

And now your more important USA stories which will influence the price of gold/silver

DOW: UP 28.09 OR .11%

NASDAQ UP 3.09 OR .04%

TRADING IN GRAPH FORM FOR THE DAY

Yield Curve Collapses To 10 Year Lows, Stocks Stumble Amid “Unprecedented” Bullish Sentiment

Bonds and Bullion are bid and the yield curve crashed as the Santa Claus rally fails to appear for a second day…

Gold’s gains are S&P’s losses as the two converge for the month of December…

For the second day in a row, stocks went nowhere despite the promise of the Santa Claus rally… (NOTE the somewhat ridicluous instaramp in the last 2 minutes to get stocks green)

Futures show the week so far better – Nasdaq (green), Dow (blue), S&P (red) (note AAPL was down again today, testing its 50DMA)…