GOLD: $1336.75 UP $2.30

Silver: $17.20 UP 5 cents

Closing access prices:

Gold $1338.50

silver: $17.20

SHANGHAI GOLD FIX: FIRST FIX 10 15 PM EST (2:15 SHANGHAI LOCAL TIME)

SECOND FIX: 2:15 AM EST (6:15 SHANGHAI LOCAL TIME)

SHANGHAI FIRST GOLD FIX: $1348.63 DOLLARS PER OZ

NY PRICE OF GOLD AT EXACT SAME TIME: $1341.00

PREMIUM FIRST FIX: $7.63

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

SECOND SHANGHAI GOLD FIX: $1346.42

NY GOLD PRICE AT THE EXACT SAME TIME: $1339.32

Premium of Shanghai 2nd fix/NY:$7.16

SHANGHAI REJECTS NY /LONDON PRICING OF GOLD

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

LONDON FIRST GOLD FIX: 5:30 am est $1334.95

NY PRICING AT THE EXACT SAME TIME: $1334.65

LONDON SECOND GOLD FIX 10 AM: $1333.85

NY PRICING AT THE EXACT SAME TIME. $1333.10

For comex gold:

JANUARY/

NUMBER OF NOTICES FILED TODAY FOR JANUARY CONTRACT: 12 NOTICE(S) FOR 1200 OZ.

TOTAL NOTICES SO FAR: 449 FOR 44900 OZ (1.3965 TONNES),

For silver:

jANUARY

31 NOTICE(S) FILED TODAY FOR

155,000 OZ/

Total number of notices filed so far this month: 573 for 2,865,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: BID $12,319/OFFER $12,429 DOWN $1225 (morning)

Bitcoin: BID 10,480/OFFER $10,586 DOWN $3086(CLOSING)

end

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total open interest ROSE BY A HUGE 3979 contracts from 196,444 RISING TO 200,423 WITH FRIDAY’S 20 CENT RISE IN SILVER PRICING. WE HAD NO COMEX LIQUIDATION BUT WITHOUT A DOUBT WE WITNESSED ANOTHER FAILED MAJOR BANK SHORT- COVERING OPERATION ON FRIDAY. NOT ONLY THAT , WE WERE AGAIN NOTIFIED THAT WE HAD ANOTHER SMALL SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP ROUTE: 483 EFP’S FOR MARCH AND ZERO FOR OTHER MONTHS AND THUS TOTAL ISSUANCE OF 483 CONTRACTS. HOWEVER THE MOVEMENT ACROSS TO LONDON IS NOT AS SEVERE AS IN GOLD AS THERE SEEMS TO BE MAJOR PLAYERS WILLING TO TAKE ON THE BANKS AT THE COMEX. STILL, WITH THE TRANSFER OF 483 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24 HRS IN THE ISSUING OF EFP’S.

ACCUMULATION FOR EFP’S/SILVER/ STARTING FROM FIRST DAY NOTICE/FOR MONTH OF JANUARY:

24,244 CONTRACTS (FOR 11 TRADING DAYS TOTAL 24,244 CONTRACTS OR 121.220 MILLION OZ: AVERAGE PER DAY: 2204 CONTRACTS OR 11.020 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH: 121.220 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 19.04% OF ANNUAL GLOBAL PRODUCTION

RESULT: A HUGE SIZED GAIN IN OI COMEX WITH THE GOOD 20 CENT RISE IN SILVER PRICE WHICH USUALLY INDICATES ANOTHER FAILED BANKER SHORT-COVERING. WE ALSO HAD A SMALL SIZED EFP ISSUANCE OF 483 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS WERE MORE INTERESTED IN ATTACKING THE SILVER COMEX INSTEAD OF MOVING THEIR LONGS TO LONDON. FROM THE CME DATA 484 EFP’S WERE ISSUED FOR TODAY FOR A DELIVERABLE FORWARD CONTRACT OVER IN LONDON WITH A FIAT BONUS. WE REALLY GAINED 4462 OI CONTRACTS i.e. 483 open interest contracts headed for London (EFP’s) TOGETHER WITH A INCREASE OF 3979 OI COMEX CONTRACTS. AND ALL OF THIS HAPPENED WITH THE RISE IN PRICE OF SILVER OF 20 CENTS AND A CLOSING PRICE OF $17.15 WITH RESPECT TO FRIDAY’S TRADING. YET WE STILL HAVE A GOOD AMOUNT OF SILVER STANDING AT THE COMEX.

In ounces AT THE COMEX, the OI is still represented by just OVER 1 BILLION oz i.e. 1.0020 BILLION TO BE EXACT or 140% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT JANUARY MONTH/ THEY FILED: 31 NOTICE(S) FOR 155000 OZ OF SILVER

In gold, the open interest ROSE BY A CONSIDERABLE 10,992 CONTRACTS UP TO 574,992 WITH THE SOLID RISE IN PRICE OF GOLD WITH FRIDAY’S TRADING ($11.65). IT LOOKS LIKE OUR BANKERS STARTED TO COVER THEIR GOLD SHORTS IN A SIMILAR FASHION TO WHAT WE ARE WITNESSING IN SILVER. IN ANOTHER HUGE DEVELOPMENT, WE RECEIVED THE TOTAL NUMBER OF GOLD EFP’S ISSUED FRIDAY FOR MONDAY AND IT TOTALED A GOOD SIZED 7163 CONTRACTS OF WHICH THE MONTH OF FEBRUARY SAW 7163 CONTRACTS AND APRIL SAW THE ISSUANCE OF 0 CONTRACTS The new OI for the gold complex rests at 574,992. DEMAND FOR GOLD INTENSIFIES GREATLY AS WE CONTINUE TO WITNESS A HUGE NUMBER OF EFP TRANSFERS TOGETHER WITH THE MASSIVE INCREASE IN GOLD COMEX OI TOGETHER WITH THE TOTAL AMOUNT OF GOLD OUNCES STANDING FOR JANUARY COMEX. EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER (BIG RISE IN BOTH GOFO AND SIFO) AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES. IN ESSENCE WE HAVE ANOTHER GOOD GAIN OF 18,155 OI CONTRACTS: 10,992 OI CONTRACTS INCREASED AT THE COMEX AND A GOOD SIZED 7163 OI CONTRACTS WHICH NAVIGATED OVER TO LONDON.

FRIDAY, WE HAD 11170 EFP’S ISSUED.

ACCUMULATION OF EFP’S/ GOLD(EXCHANGE FOR PHYSICAL) FOR THE MONTH OF JANUARY STARTING WITH FIRST DAY NOTICE: 98,765 CONTRACTS OR 9.8765 MILLION OZ OR 307.20 TONNES (11 TRADING DAYS AND THUS AVERAGING: 8,978 EFP CONTRACTS PER TRADING DAY OR 8,978 OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SIZE OF THESE EFP TRANSFERS : SO FAR THIS MONTH IN 11 TRADING DAYS: IN TONNES: 307 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2017, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 2200 TONNES

THUS EFP TRANSFERS REPRESENTS 307/2200 TONNES = 13.95% OF GLOBAL ANNUAL PRODUCTION SO FAR IN JANUARY ALONE.

Result: A CONSIDERABLE SIZED INCREASE IN OI AT THE COMEX DESPITE THE SOLID RISE IN PRICE IN GOLD TRADING ON YESTERDAY ($11.65). WE HAD ANOTHER FAIR SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 7163. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX AND YET WE ALSO OBSERVED A HUGE DELIVERY MONTH FOR THE MONTH OF DECEMBER. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 7163 EFP CONTRACTS ISSUED, WE HAD A NET GAIN IN OPEN INTEREST OF 18,155 contracts ON THE TWO EXCHANGES:

7163 CONTRACTS MOVE TO LONDON AND 10,992 CONTRACTS INCREASED AT THE COMEX. (in tonnes, the gain in total oi equates to 56.47 TONNES)

we had: 12 notice(s) filed upon for 1200 oz of gold.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD

With gold up again today, we had no changes in inventory from the GLD:

Inventory rests tonight: 828.96 tonnes.

SLV/

NO CHANGES IN SILVER INVENTORY AT THE SLV/

INVENTORY RESTS AT 316.348 MILLION OZ/

end

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in silver ROSE BY A CONSIDERABLE 3979 contracts from 196,444 UP TO 200,423 (AND now A LITTLE CLOSER TO THE NEW COMEX RECORD SET ON FRIDAY/APRIL 21/2017 AT 234,787) WITH THE GOOD RISE IN PRICE OF SILVER TO THE TUNE OF 20 CENTS WITH RESPECT TO FRIDAY’S TRADING. WE HAD WITHOUT A DOUBT ANOTHER FAILED SHORT COVERING FROM OUR BANKERS AS THEY HAVE CAPITULATED.HOWEVER THIS TIME THEY WERE JOINED BY GOLD. NOT ONLY THAT BUT OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE ANOTHER SMALL 483 PRIVATE EFP’S FOR MARCH (WE DO NOT GET A LOOK AT THESE CONTRACTS AS IT IS PRIVATE BUT THE CFTC DOES AUDIT THEM) AND 0 EFP’S FOR ALL OTHER MONTHS . EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. WE HAD NO COMEX SILVER COMEX LIQUIDATION. IF WE TAKE THE OI GAIN AT THE COMEX OF 43979 CONTRACTS TO THE 483 OI TRANSFERRED TO LONDON THROUGH EFP’S WE OBTAIN A GAIN OF 4462 OPEN INTEREST CONTRACTS IN CONJUNCTION WITH ANOTHER FAILED BANKER SHORT COVERING. WE STILL HAVE A GOOD AMOUNT OF SILVER OUNCES THAT ARE STANDING FOR METAL IN JANUARY (SEE BELOW). THE NET GAIN TODAY IN OZ ON THE TWO EXCHANGES: 22.31 MILLION OZ!!!

RESULT: A STRONG SIZED INCREASE IN SILVER OI AT THE COMEX WITH THE SOLID RISE OF 20 CENTS IN PRICE (WITH RESPECT TO FRIDAY’S TRADING). BUT WE ALSO HAD ANOTHER 483 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE GOOD SIZED AMOUNT OF SILVER OUNCES STANDING FOR JANUARY, DEMAND FOR PHYSICAL SILVER INTENSIFIES AS WE WITNESS MAJOR BANK SHORT COVERING ACCOMPANIED BY INCREASES IN GOFO AND SIFO RATES INDICATING SCARCITY.

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)Late MONDAY night/TUESDAY morning: Shanghai closed UP 26.11 points or 0.77% /Hang Sang CLOSED UP 565.88 pts or 1.87% / The Nikkei closed UP 236.93 POINTS OR 1.00%/Australia’s all ordinaires CLOSED DOWN 0.35%/Chinese yuan (ONSHORE) closed WELL UP at 6.4422/Oil UP to 63.95 dollars per barrel for WTI and 69.38 for Brent. Stocks in Europe OPENED GREEN EXCEPT LONDON. ONSHORE YUAN CLOSED UP AGAINST THE DOLLAR AT 6.4422. OFFSHORE YUAN CLOSED UP AGAINST THE ONSHORE YUAN AT 6.4388 //ONSHORE YUAN MUCH STRONGER AGAINST THE DOLLAR/OFF SHORE STRONGER TO THE DOLLAR/. THE DOLLAR (INDEX) IS MUCH WEAKER AGAINST ALL MAJOR CURRENCIES. CHINA IS STILL HAPPY TODAY.(GOOD MARKETS )

3a)THAILAND/SOUTH KOREA/NORTH KOREA

i)/South Korea/North Korea

Tillerson breaks with Trump as he rejects a freeze of military exercises near North Korea for a freeze of their nuclear activities

( zerohedge)

b) REPORT ON JAPAN

i)Foreign exchange hedge costs have skyrocketed for Japanese investors and that is the reason for their purchase of USA treasuries to tumble.

( zerohedge)

ii)This is a must read…Albert Edwards speculates that it will be Japan that will trigger the global unwind. Why? because he believes Japan is finally heating up economically and that the central bank of Japan will have to cool their jets. This will force the shorts to cover their massive USA/Yen short and thus end the huge yen carry trade

3 c CHINA

i)Chinese rating agency, Dagong downgrades USA sovereign credit rating from A minus to BBB plus and they warn that a USA insolvency would detonate the next crisis

( zerohedge)

ii)Trump warns China that the USA trade deficits are getting worse and are “not sustainable”

4. EUROPEAN AFFAIRS

ii)England

( zerohedge)

(courtesy zerohedge)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

( zerohedge)

ii)NATO ally Turkey is threatening a massive invasion in northwest Syria trying to dislodge the kurds from AFRIN. Syria.

6 .GLOBAL ISSUES

1/3 of Canadians cannot pay their monthly bills as interest rates set to rise

( Globe and Mail)

7. OIL ISSUES

Russia, upon seeing a high value for oil, may decide to exit from the OPEC deal.

( Z. Calcuttawala/OilPrice.com)

8. EMERGING MARKET

9. PHYSICAL MARKETS

( Ted Butler)

ii)Saturday

( zero hedge)

iii)Sunday night: Cryptos originally slide and then rebound:

( zerohedge)

iv)Monday night/Tuesday morning:

Cryptos slide after another South Korean shutdown by the Finance Ministry.

( zerohedge)

v)Bitcoin just crashed below 12,000 dollars (down over 20%) amid growing fears of a crackdown

( zerohedge)

vi)Another crypto exchange, Kraken went offline last night at 9 pm est and that is getting users very nervous

( Bloomberg/GATA)

vii)A terrific interview of Eric Sprott as he talks about the huge numbers of EFP’s issued. I have been commenting that for gold this phenomenon has been going on for two years.

Nick Laird has graphed the totals issued for gold and for 2017: 6600 tonnes have transferred to London. Sprott agrees with me that the comex is a fraud vs the real market for gold.

( Hemke/Sprott/Gata)

viii)Only Libor? Nine banks have been accused of rigging the key Libor lending rates

( McLannahan/London Financial Times)

10. USA stories which will influence the price of gold/silver

ii)Soft data, Empire manufacturing falters to 6 month lows as orders and work hours plunge( zerohedge)

iii)This does not look good: Bellwether GE tumbles badly after a massive finance arm charge

(courtesy zerohedge)

iv)SWAMP STORIES

On Friday, we had a 11 count indictment against Mark Lambert who was the transportation specialist for moving the Uranium out of the USA and onto Russian shores. Lambert engaged in multiple bribes and money laundering with Russian officials. This is not the first indictment against individuals in the Uranium one deal. Back in 2009 or so there were 4 convictions but they were very light. The prosecutors: Rod Rosenstein and Mueller with McCabe fully aware as to what was going on

( zerohedge)

v)More fun in the swamp: Mueller subpoenas Bannon in the Russian probe

( zerohedge)

vi)Pam and Russ talk about Nomi Prins latest book: Collusion: How Central banks rigged the world.

Let us head over to the comex:

The total gold comex open interest ROSE BY A CONSIDERABLE 10,992 CONTRACTS UP to an OI level of 574,992 WITH THE SOLID RISE IN THE PRICE OF GOLD ($11.65 GAIN WITH RESPECT TO FRIDAY’S TRADING). WE HAD ZERO COMEX GOLD LIQUIDATION AND NO DOUBT WE WITNESSED SOME GOLD SHORT COVERING AT THE COMEX. WE ALSO WITNESSED ANOTHER STRONG COMEX TRANSFER THROUGH THE EFP ROUTE. THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS. THE CME REPORTS THAT 7163 EFP’S WERE ISSUED FOR FEBRUARY , 0 EFP’s FOR APRIL, AND 0 FOR DECEMBER: TOTAL 7163 CONTRACTS. THE OBLIGATION STILL RESTS WITH THE BANKERS ON THESE TRANSFERS.

ON A NET BASIS IN OPEN INTEREST WE GAINED TODAY: 18155 OI CONTRACTS IN THAT 7163 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE GAINED 10,992 COMEX CONTRACTS. NET GAIN ON THE TWO EXCHANGES: 18,155 contracts OR 1.8155 MILLION OZ OR 56.46 TONNES

Result: A CONSIDERABLE INCREASE IN COMEX OPEN INTEREST WITH THE RISE IN THE PRICE YESTERDAY’S GOLD TRADING ($11.65.) WE HAD NO GOLD LIQUIDATION AT THE COMEX. HOWEVER WE, NO DOUBT WE HAD ANOTHER FAILED BANKER SHORT COVERING AS THE BANKERS WERE CAUGHT OFF GUARD ON FRIDAY’S BIG PRICE RISE.. TOTAL OPEN INTEREST GAIN ON THE TWO EXCHANGES: 18,155 OI CONTRACTS…

We have now entered the active contract month of JANUARY. The open interest for the front month of JANUARY saw it’s open interest FALL by 180 contracts DOWN to 40. We had 181 notices served upon yesterday so we gained 1 contract or an additional 100 oz of gold will stand AT THE COMEX in this non active month of January.

FEBRUARY saw a LOSS of 6704 contacts DOWN to 324,958. March saw a loss of 209 contracts down to 492. April saw a GAIN of 12.223 contracts UP to 140,073.

We had 12 notice(s) filed upon today for 1200 oz

PRELIMINARY VOLUME TODAY ESTIMATED; 508,049

FINAL NUMBERS CONFIRMED FOR YESTERDAY: 429,668

comex gold volumes are RISING AGAIN

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

And now for the wild silver comex results.

Total silver OI rose BY A huge 3,979 CONTRACTS FROM 196,660 UP TO 200,423 WITH FRIDAY’S STRONG 20 CENT GAIN. AGAIN WE HAD CONTINUED FAILED BANKER SHORT COVERING. NOT ONLY THAT, WE HAD ANOTHER SMALL SIZED 483 EMERGENCY EFP’S FOR MARCH ISSUED BY OUR BANKERS (AND ZERO FOR ALL OTHER MONTHS) TO COMEX LONGS WHO RECEIVED A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON: THE TOTAL EFP’S ISSUED: 484. IT SURE LOOKS LIKE THE SILVER BOYS HAVE STARTED TO MIGRATE TO LONDON FROM THE START OF DELIVERY MONTH AND CONTINUING RIGHT THROUGH UNTIL FIRST DAY NOTICE JUST LIKE WE ARE WITNESSING TODAY. USUALLY WE NOTED THAT CONTRACTION IN OI OCCURRED ONLY DURING THE LAST WEEK OF AN UPCOMING ACTIVE DELIVERY MONTH. THIS PROCESS HAS JUST BEGUN IN EARNEST IN SILVER STARTING IN SEPTEMBER. HOWEVER, IN GOLD, WE HAVE BEEN WITNESSING THIS FOR THE PAST 2 YEARS. WE HAD ZERO LONG COMEX SILVER LIQUIDATION BUT A RISE IN TOTAL SILVER OI. WE ARE ALSO WITNESSING A FAIR AMOUNT OF SILVER OUNCES STANDING FOR COMEX METAL IN THIS NON ACTIVE JANUARY AS WELL AS THAT CONTINUAL MIGRATION OF EFPS OVER TO LONDON. ON A PERCENTAGE BASIS THERE ARE MORE EFP’S ISSUED FOR GOLD THAN SILVER. ON A NET BASIS WE GAINED 4462 OPEN INTEREST CONTRACTS:

3797 CONTRACT GAIN AT THE COMEX COMBINING WITH THE ADDITION OF 483 OI CONTRACTS NAVIGATING OVER TO LONDON.

NET GAIN TWO EXCHANGES: 4462 CONTRACTS

We are now in the poor non active delivery month of January and here the OI GAINED 39 contracts RISING TO 110. We had 0 notices served on Friday, so we GAINED 39 contracts or an additional 195,000 oz will stand for delivery AT THE COMEX AS QUEUE JUMPING INTENSIFIES

February saw a LOSS OF 2 OI contracts FALLING TO 379. The March contract LOST 793 contracts DOWN to 144,571.

We had 31 notice(s) filed for NIL 155,000 for the January 2018 contract for silver

INITIAL standings for JANUARY

Jan 16/2018.

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz |

nil oz

|

| Deposits to the Dealer Inventory in oz | nil oz |

| Deposits to the Customer Inventory, in oz |

nil oz

|

| No of oz served (contracts) today |

12 notice(s)

1200 OZ

|

| No of oz to be served (notices) |

28 contracts

(2800 oz)

|

| Total monthly oz gold served (contracts) so far this month |

449 notices

44900 oz

1.3965 tonnes

|

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

For JANUARY:

Today, 0 notice(s) were issued from JPMorgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equates to 12 contract(s) of which 9 notices were stopped (received) by j.P. Morgan dealer and 2 notice(s) was (were) stopped/ Received) by j.P.Morgan customer account.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

To calculate the INITIAL total number of gold ounces standing for the JANUARY. contract month, we take the total number of notices filed so far for the month (449) x 100 oz or 44900 oz, to which we add the difference between the open interest for the front month of JAN. (40 contracts) minus the number of notices served upon today (12 x 100 oz per contract) equals 47,700 oz, the number of ounces standing in this active month of JANUARY

Thus the INITIAL standings for gold for the JANUARY contract month:

No of notices served (449 x 100 oz or ounces + {(40)OI for the front month minus the number of notices served upon today (12 x 100 oz which equals 47,700 oz standing in this active delivery month of JANUARY (1.4836 tonnes). THERE IS 18.245 TONNES OF REGISTERED GOLD AVAILABLE FOR DELIVERY SO FAR.

WE GAINED 1 CONTRACT OR AN ADDITIONAL 100 OZ WILL STAND IN THIS NON ACTIVE DELIVERY MONTH OF JANUARY

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

ON FIRST DAY NOTICE FOR JANUARY 2017, THE INITIAL GOLD STANDING: 3.904 TONNES STANDING

BY THE END OF THE MONTH: FINAL: 3.555 TONNES STOOD FOR COMEX DELIVERY AS THE REMAINDER HAD TRANSFERRED OVER TO LONDON FORWARDS.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

I have a sneaky feeling that these withdrawals of gold in kilobars are being used in the hypothecating process and are being used in the raiding of gold!

The gold comex is an absolute fraud. The use of kilobars and exact weights makes the data totally absurd and fraudulent! To me, the only thing that makes sense is the fact that “kilobars: are entries of hypothecated gold sent to other jurisdictions so that they will not be short with their underwritten derivatives in that jurisdiction. This would be similar to the rehypothecated gold used by Jon Corzine at MF Global.

IN THE LAST 14 MONTHS 68 NET TONNES HAS LEFT THE COMEX.

end

And now for silver

AND NOW THE DECEMBER DELIVERY MONTH

DECEMBER FINAL standings

| Silver | Ounces |

| Withdrawals from Dealers Inventory | nil oz |

| Withdrawals from Customer Inventory |

70,391.030 oz

Brinks

Delaware

|

| Deposits to the Dealer Inventory |

nil

oz

|

| Deposits to the Customer Inventory |

nil oz

|

| No of oz served today (contracts) |

31

CONTRACT(S)

(155,000 OZ)

|

| No of oz to be served (notices) |

79 contract

(395,000 oz)

|

| Total monthly oz silver served (contracts) | 573 contracts

(2,865,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

we had no inventory movement at the dealer side of things

total inventory movement dealer: nil oz

we had 0 inventory deposits into the customer account

i

total inventory deposits: nil oz

we had 2 withdrawals from the customer account;

i) out of Brinks; 66,378.230 oz

ii) Out of Delaware: 3,922.800 oz

total withdrawals; 70,301.030oz

we had 0 adjustments

total dealer silver: 45.456 million

total dealer + customer silver: 246.485 million oz

The total number of notices filed today for the JANUARY. contract month is represented by 31 contract(s) FOR 155,000 oz. To calculate the number of silver ounces that will stand for delivery in JANUARY., we take the total number of notices filed for the month so far at 542 x 5,000 oz = 2,710,000 oz to which we add the difference between the open interest for the front month of JAN. (110) and the number of notices served upon today (31 x 5000 oz) equals the number of ounces standing.

.

Thus the INITIAL standings for silver for the JANUARY contract month: 573(notices served so far)x 5000 oz + OI for front month of JANUARY(110) -number of notices served upon today (31)x 5000 oz equals 3,260,000 oz of silver standing for the JANUARY contract month. This is VERY GOOD for this NONACTIVE delivery month of JANUARY. WE GAINED 28 CONTRACTS OR AN ADDITIONAL 140,000 OZ WILL STAND FOR DELIVERY IN THIS NON ACTIVE DELIVERY MONTH OF JANUARY AND QUEUE JUMPING INTENSIFIES.

ON FIRST DAY NOTICE FOR THE JANUARY 2017 CONTRACT WE HAD 3,790 MILLION OZ STAND.

THE FINAL STANDING: 3,730 MILLION OZ

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

ESTIMATED VOLUME FOR TODAY: 172,325

CONFIRMED VOLUME FOR FRIDAY: 129,518 CONTRACTS

YESTERDAY’S CONFIRMED VOLUME OF 129,518 CONTRACTS EQUATES TO 647.5 MILLION OZ OR 92.5% OF ANNUAL GLOBAL PRODUCTION OF SILVER

COMMODITY LAW SUGGESTS THAT OPEN INTEREST SHOULD NOT BE MORE THAN 3% OF ANNUAL GLOBAL PRODUCTION. THE CROOKS ARE SUPPLYING MASSIVE PAPER TRYING TO KEEP SILVER IN CHECK.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price at that day at $18.42

The previous record was 224,540 contracts with the price at that time of $20.44

end

NPV for Sprott and Central Fund of Canada

1. Central Fund of Canada: traded at Negative 3.0 percent to NAV usa funds and Negative 3.0% to NAV for Cdn funds!!!!

Percentage of fund in gold 63.0%

Percentage of fund in silver:36.8%

cash .+.2%( Jan 15/2018)

2. Sprott silver fund (PSLV): NAV FALLS TO -2.44% (Jan 15/2018)

3. Sprott gold fund (PHYS): premium to NAV FALLS TO -0.65% to NAV (Jan 15/2018 )

Note: Sprott silver trust back into NEGATIVE territory at -2.44%-/Sprott physical gold trust is back into NEGATIVE/ territory at -0.65%/Central fund of Canada’s is still in jail but being rescued by Sprott.

Sprott WINS hostile 3.1 billion bid to take over Central Fund of Canada

(courtesy Sprott/GATA)

END

And now the Gold inventory at the GLD

Jan 16/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 828.96 TONNES

Jan 12/no changes in inventory at the GLD despite the rise in gold price/inventory rests at 828.96 tonnes

Jan 11/ANOTHER IDENTICAL WITHDRAWAL OF 2.95 TONNES FROM THE GLD INVENTORY/INVENTORY RESTS AT 828.96 TONNES

Jan 10/with gold up today, a strange withdrawal of 2.95 tonnes/inventory rests at 831.91 tonnes

Jan 9/no changes in gold inventory at the GLD/Inventory rests at 834.88 tonnes

Jan 8/with gold falling by a tiny $1.40 and this being after 12 consecutive gains, today they announce another 1.44 tonnes of gold withdrawal from the GLD/

Jan 5/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 836.32 TONNES

Jan 4/2018/no change in gold inventory at the GLD/Inventory rests at 836.32 tonnes

Jan 3/a huge withdrawal of 1.18 tonnes of gold from the GLD/Inventory rests at 836.32 tonnes

Jan 2/2018/no changes in gold inventory at the GLD/inventory rests at 837.50 tonnes

Dec 29/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 837.50 TONNES

Dec 28/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 837.50 TONNES

Dec 27/NO CHANGES IN GOLD INVENTORY AT THE GLD/ INVENTORY RESTS AT 837.50 TONNES

Dec 26/no change in gold inventory at the GLD

Dec 22/ A DEPOSIT OF 1.48 TONNES OF GOLD INTO GLD INVENTORY/INVENTORY RESTS AT 837.50 TONNES

Dec 21′ NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 836.02 TONNES

Dec 20/DESPITE THE GOOD ADVANCE IN PRICE TODAY/THE CROOKS RAIDED THE COOKIE JAR TO THE TUNE OF 1.18 TONNES/INVENTORY RESTS AT 836.02 TONNES

Dec 19/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 837.20 TONNES

Dec 18 SHOCKINGLY AFTER TWO GOOD GOLD TRADING DAYS, THE CROOKS RAID THE COOKIE JAR BY THE SUM OF 7.09 TONNES/INVENTORY RESTS AT 837.20 TONNES

Dec 15/NO CHANGES IN GOLD INVENTORY/RESTS AT 844.29 TONNES.

Dec 14/a good sized gain of 1.48 tonnes of gold into the GLD/inventory rests at 844.29 tones

Dec 13/no changes in gold inventory at the GLD/inventory rests at 842.81 tonnes

Dec 12/SURPRISINGLY NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 842.81 TONNES

Dec 11/SURPRISINGLY NO CHANGES IN GOLD INVENTORY AT THE GLD DESPITE THE CONSTANT RAIDS ON GOLD/INVENTORY RESTS AT 842.81 TONNES

Dec 8/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 842.81 TONNES

Dec 7/A BIG WITHDRAWAL OF 2.66 TONNES FROM THE GLD/INVENTORY RESTS AT 842.81 TONNES

Dec 6/No changes in GOLD inventory at the GLD/Inventory rests at 845.47 tonnes

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

Jan 15/2018/ Inventory rests tonight at 828.96 tonnes

*IN LAST 309 TRADING DAYS: 111.99 NET TONNES HAVE BEEN REMOVED FROM THE GLD

*LAST 244 TRADING DAYS: A NET 45.32 TONNES HAVE NOW BEEN ADDED INTO GLD INVENTORY.

end

Now the SLV Inventory

Jan 16/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 316.348 MILLION OZ

Jan 12/no changes in silver inventory at the SLV/inventory rests at 316.348 million oz/

Jan 11/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 316.348 MILLION OZ/

Jan 10/with silver up again, we had a huge withdrawal of 1.227 million oz from the SLV/inventory rests at 316.348 million oz

Jan 9/a withdrawal of 848,000 oz from the SLV/Inventory rests at 317.575 million oz/

jan 8/no change in silver inventory at the SLV/Inventory rests at 318.423 million oz/

Jan 5/DESPITE NO CHANGE IN SILVER PRICING, WE HAD A HUGE WITHDRAWAL OF 2.026 MILLION OZ/INVENTORY RESTS AT 318.423 MILLION OZ.

Jan 4.2018/a slight withdrawal of 180,000 oz and this would be to pay for fees/inventory rests at 320.449 million oz/

Jan 3/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 320.629 MILLION OZ.

Jan 2/WITH SILVER UP DRAMATICALLY THESE PAST 4 TRADING DAYS, THE FOLLOWING MAKES NO SENSE: WE HAD A WITHDRAWAL OF 2.83 MILLION OZ FROM THE SLV

INVENTORY RESTS AT 320.629 MILLION OZ/

Dec 29/no changes in silver inventory at the SLV/inventory rests at 323.459 million oz/

Dec 28/DESPITE THE RISE IN SILVER AGAIN BY 13 CENTS, WE LOST ANOTHER 1,251,000 OZ OF SILVER FROM THE SILVER.

Dec 27/WITH SILVER UP AGAIN BY 17 CENTS, WE LOST ANOTHER 802,000 OZ OF SILVER INVENTORY/WHAT CROOKS/INVENTORY RESTS AT 324.780 MILLION OZ/

Dec 26/no change in silver inventory at the SLV./Inventory rests at 325.582

Dec 21/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 326.227 MILLION OZ/

Dec 20/INVENTORY REMAINS CONSTANT AT 326.337 MILLION OZ (COMPARE WITH GLD)

Dec 19/SILVER INVENTORY REMAINS CONSTANT AT 326.337 MILLION OZ

Dec 18.2017//SILVER INVENTORY CONTINUES TO REMAIN PAT./INVENTORY REMAINS AT 326.337 MILLION OZ/

INVENTORY RESTS AT 326.337 TONNES

Dec 15/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 326.337 MILLION OZ/

Dec 14/a small withdrawal of 377,000 oz and that usually means to pay for fees./inventory rests at 326.337 million oz/

Dec 13/no change in silver inventory at the SLV/Inventory rests at 326.714 million oz/

Dec 12/WOW!ANOTHER STRANGE ONE: SILVER HAS BEEN DOWN FOR 10 CONSECUTIVE DAYS, YET THE SLV ADDS ANOTHER 1.415 MILLION OZ TO ITS INVENTORY. IN THAT 10 DAY PERIOD, SLV ADDS 9.584 MILLION OZ/

INVENTORY RESTS AT 326.714 MILLION OZ

Dec 11/WOW!! ANOTHER STRANGE ONE: SILVER DESPITE BEING DOWN FOR 9 CONSECUTIVE TRADING DAYS ADDS ANOTHER 944,000 OZ TO ITS INVENTORY. FROM NOV 30 UNTIL TODAY SILVER HAS BEEN DOWN EVERY DAY. HOWEVER THE INVENTORY OF SILVER HAS RISEN 8.169 MILLION OZ.

Dec 8/A HUGE DEPOSIT OF 2.642 MILLION OZ/INVENTORY RESTS AT 324.355 MILLION OZ/

Dec 7/strange!! with the continual whacking of silver, no change in silver inventory at the SLV/Inventory rests at 321.713

Dec 6/no change in silver inventory at the SLV/Inventory remains at 21.713 million oz.

Jan 15/2017:

Inventory 316.348 million oz

end

THIS IS HUGE/A BIG JUMP IN GOFO RATES

6 Month MM GOFO

Indicative gold forward offer rate for a 6 month duration

+ 1.80%

12 Month MM GOFO

+ 2.11%

30 day trend

end

Major gold/silver trading /commentaries for TUESDAY

GOLDCORE/BLOG/MARK O’BYRNE.

GOLD/SILVER

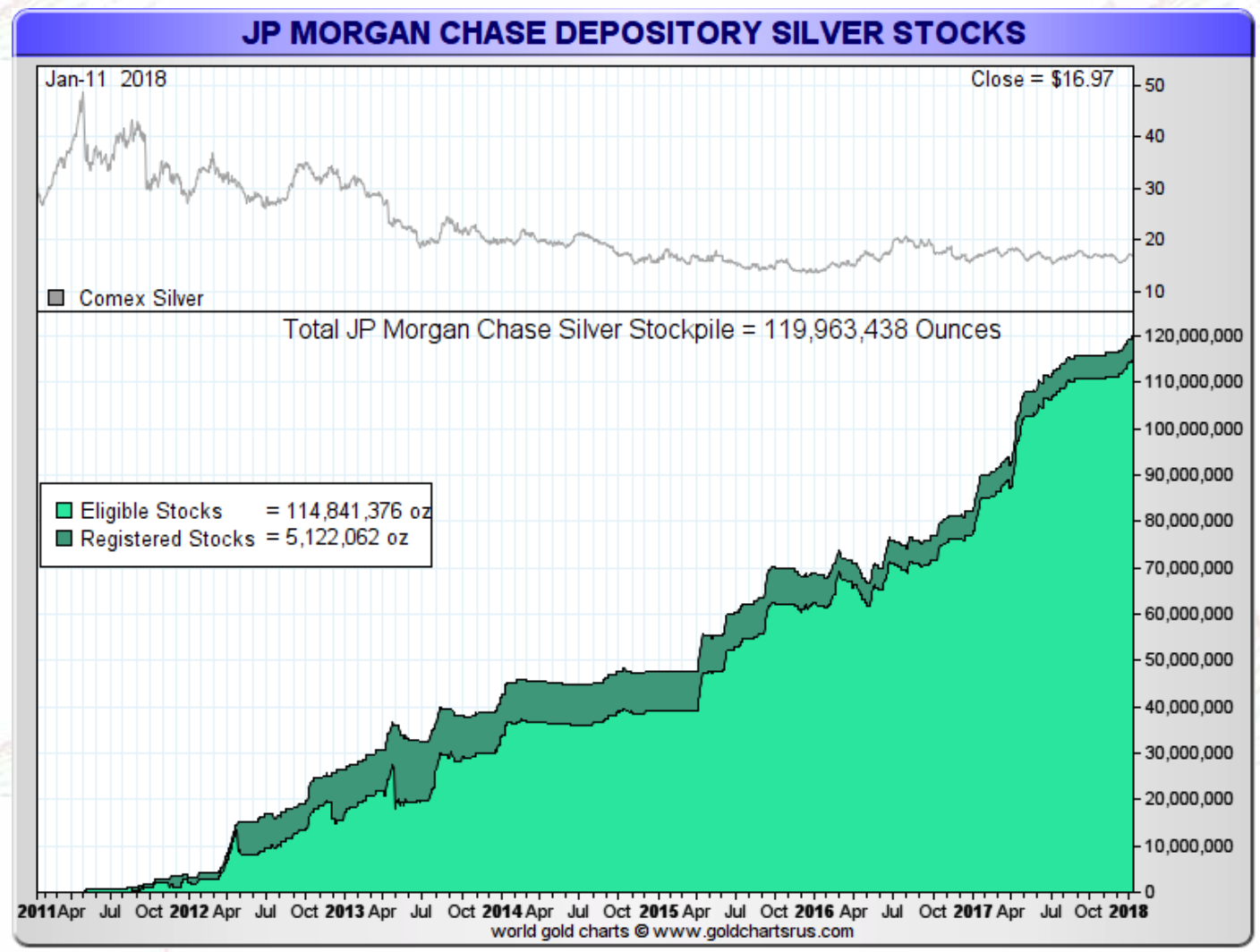

Silver Prices To Surge – JP Morgan Has Acquired A “Massive Quantity of Physical Silver”

Silver Prices To Surge – JP Morgan Has Acquired A “Massive Quantity of Physical Silver”

– JP Morgan continues to accumulate the biggest stockpile of physical silver in history

– “JPM now holds more than 133m oz -more than was held by the Hunt Bros” – Butler

– Silver hoard owned by JPM has increased from Zero ozs in 2011 to 120m ozs today

– Money managers showing more optimism towards silver through record buying

– “Near impossible to rule out an upside price surprise at any moment”

Editor: Mark O’Byrne

- Source: Sharelynx

Money managers are feeling increasingly optimistic about silver, against a backdrop of cautiousness regarding gold according to the latest Commitment of Traders (COT) report.

There has been some record buying in the last fortnight. The report shows some impressive moves given just under a month ago the silver market was net short. Last week speculative gross long positions in Comex silver futures rose by 11,920 contracts to 66,224. Whilst short positions fell by 10,379 contracts to 28,122. Silver’s net long positions now stand at 38,102 contracts.

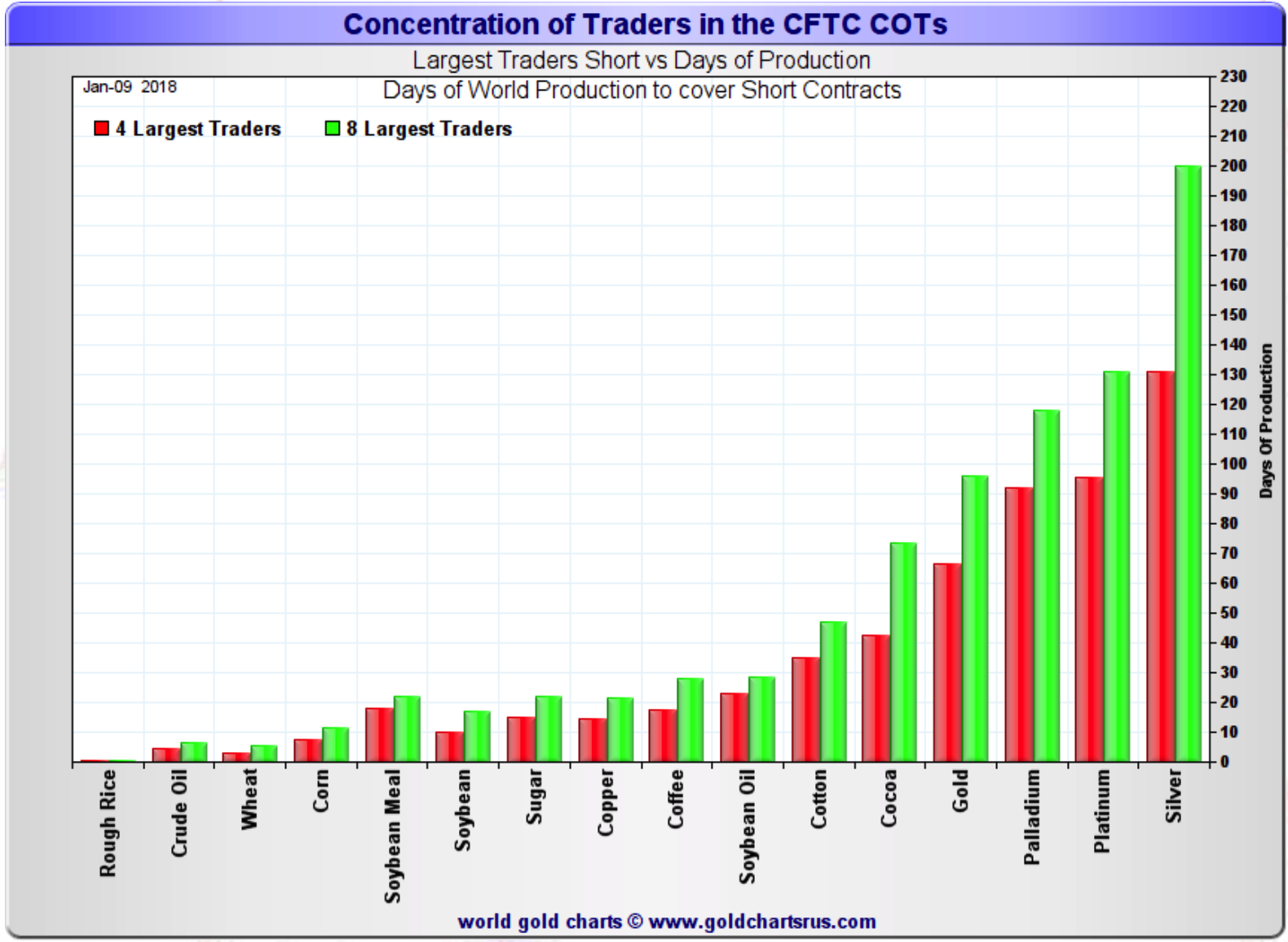

For the current week’s reporting, the four largest traders are short 130 days of world silver production-and the ‘5 through 8’ large traders are short an additional 70 or so days of world silver production-for a total of 200 days. This is around seven months of global silver production.

JP Morgan are out Hunting the silver market

Much of this is attributed to JP Morgan, who according to respected silver analyst Ted Butler, is responsible for the ‘third great investment accumulation of physical silver’.

The silver market has been closely monitoring JP Morgan’s activities for some time. Since April 2011 the powerful bank has been accumulating silver at a quite a rate. It has taken its position from zero to nearly 120m ounces this month, less than six years later.

Butler explains:

‘Just about every ounce moved into the JPMorgan COMEX warehouse over the past 7 years has come from futures deliveries stopped (taken) by JPM in its own name. JPMorgan took delivery of 14 million ounces in December and so far, 13 million ounces have remained in the warehouses from which the metal was delivered. So this means that JPMorgan now holds more than 133 million ounces of silver in COMEX warehouses, or more than was held by the Hunt Bros or by Berkshire Hathaway at their peaks. There was a lot more silver in the world in 1980 and 1998 than there is today, meaning that JPMorgan’s accumulation is much more of an accomplishment than previous silver acquisitions.’

Why would JP Morgan be stockpiling silver? As we pointed out a few years ago, it may be the case that they are anticipating geopolitical and financial turmoil?

This would not come as a surprise to JP Morgan shareholders who have previously received such warnings from CEO Jamie Dimon who has stated ‘there will be another crisis’.

Dimon has even admitted that the trigger for the next crisis may not be the same trigger as the last one – but there will be another crisis:

“Triggering events could be geopolitical (the 1973 Middle East crisis), a recession where the Fed rapidly increases interest rates (the 1980-1982 recession), a commodities price collapse (oil in the late 1980s), the commercial real estate crisis (in the early 1990s), the Asian crisis (in 1997),so-called “bubbles” (the 2000 Internet bubble and the 2008 mortgage/housing bubble), etc. While the past crises had different roots (you could spend a lot of time arguing the degree to which geopolitical, economic or purely financial factors caused each crisis), they generally had a strong effect across the financial markets.”

JP Morgan’s silver accumulation in the face of upcoming turmoil may lead some to ask why not go for gold? It’s likely that the depressed price is the deciding factor here.

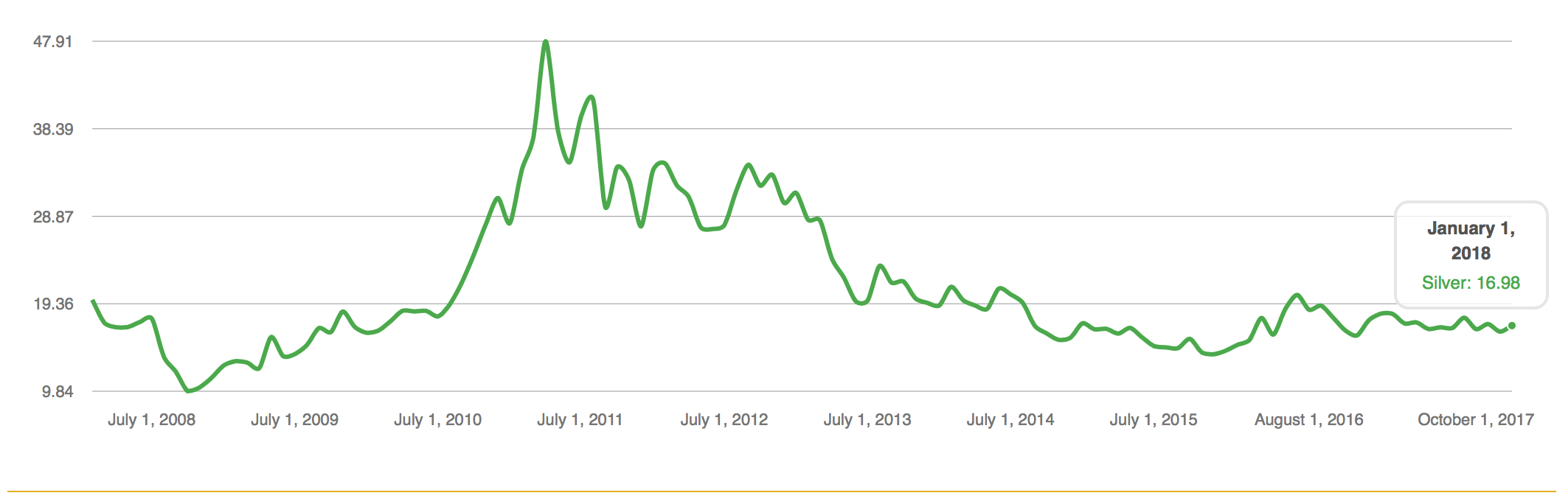

- Silver USD, Jan 2007 – Jan 2017, Goldcore.com

The bank is often compared to the Hunt brothers when it comes to cornering of the silver market, but in truth the bank has been much savvier and is set to make far more. After all, the Hunt’s accumulated primarily paper silver, JP Morgan are going after the hard stuff. Had the Hunt brothers, bought more physical silver bullion and less paper silver in the form of futures, they would likely have made even more money than they could imagine.

More silver bullion than we know?

Butler believes that ‘JPMorgan holds at least 675 million ounces of actual silver. Simply put, JPMorgan has acquired six times as much metal as bought by the Hunts or Berkshire Hathaway. If this really is the case then it would account for ‘nearly 45% of the 1.5 billion ounces of silver bullion in the form of industry standard 1,000 ounces bars in the world’.

The ability to accumulate so much physical silver whilst at the same time sell short huge quantities of paper derivatives or futures contracts could be the poster child for market manipulation. After all, the selling results in lower prices which then paves they way for more physical buying by the bank.

Butler again:

It couldn’t possibly be legitimate and that makes JPMorgan a market crook and manipulator. It also makes the federal regulator, the CFTC, and the self-regulating CME Group, incompetent, corrupt, or both. This takes a special kind of market manipulator, one most likely operating under some type of agreement with the regulators.

To what end are JP Morgan pursuing this path of silver hoarding?

That intent is to sell at as large a profit as possible. No one buys any investment asset with the intention of losing money, least of all JPMorgan. They didn’t spend the last seven years accumulating physical silver to sell that silver at anything but the highest price possible. I can’t tell you when JPM will let the price of silver fly, but I am certain that that day is coming.

Silver prices looks particularly undervalued right now. Last year it gained just 1.6%, compared to 11.5% for gold and 48% for palladium. Yet we (and big banks such as JP Morgan) remain bullish. We have previously written about our forecast that silver prices will surpass its nominal high of $50 per ounce and its inflation adjusted high of $150 per ounce in the coming years.

The fundamental reasons for our very bullish outlook on silver is very reasonable. There are increasing global macroeconomic, systemic, geopolitical and monetary risks. Silver’s historic role as money and a store of value has already been identified time and time again in the past and history is repeating itself. It is also worth considering the declining and very small supply of silver, not to mention increasing investment demand from one of the world’s most powerful banks and other contrarian investors.

We should see JP Morgan’s accumulation as not just a sign to buy physical silver but also that the next financial crisis is coming and its time to diversify into physical gold and silver bullion coins and bars.

Related Reading

JP Morgan To Corner Silver Market?

Silver Bullion Has Key New Player – China Replaces JP Morgan

Silver’s Positive Fundamentals Due To Strong Demand In Key Growth Industries

News and Commentary

Gold holds near 4-mth peak, buoyed by weaker dollar (Reuters.com)

Gold jumps to fresh 4-month high as dollar slide deepens (MarketWatch.com)

China Escalates Crackdown on Cryptocurrency Trading (Bloomberg.com)

Carillion’s Collapse Could Affect Companies From Madrid to Texas (Bloomberg.com)

Six banks accused of rigging key Canada lending rate (Bloomberg.com)

Bundesbank will add China’s yuan to currency reserves (Bloomberg.com)

Source: Bloomberg

Metals Power Higher as Sickly Dollar Spurs Copper-to-Gold Rally (Bloomberg.com)

What investors can learn from Carillion’s collapse (MoneyWeek.com)

Merkel could join Macron in Davos for epic clash with Trump (Reuters.com)

As Petro-Yuan Looms, Bundesbank Adds Renminbi To Currency Reserves (ZeroHedge.com)

2018 – Year of the Octopus – Mauldin (MauldinEconomics.com)

Gold Prices (LBMA AM)

16 Jan: USD 1,334.95, GBP 970.38 & EUR 1,091.32 per ounce

15 Jan: USD 1,343.00, GBP 971.93 & EUR 1,092.93 per ounce

12 Jan: USD 1,332.90, GBP 978.75 & EUR 1,099.78 per ounce

11 Jan: USD 1,319.85, GBP 978.14 & EUR 1,104.45 per ounce

10 Jan: USD 1,321.65, GBP 976.96 & EUR 1,103.31 per ounce

09 Jan: USD 1,314.95, GBP 972.01 & EUR 1,102.19 per ounce

Silver Prices (LBMA)

16 Jan: USD 17.10, GBP 12.43 & EUR 13.99 per ounce

15 Jan: USD 17.12, GBP 12.58 & EUR 14.14 per ounce

12 Jan: USD 17.12, GBP 12.56 & EUR 14.12 per ounce

11 Jan: USD 17.01, GBP 12.64 & EUR 14.24 per ounce

10 Jan: USD 17.13, GBP 12.64 & EUR 14.27 per ounce

09 Jan: USD 17.05, GBP 12.60 & EUR 14.30 per ounc

END

How JPMorgan acquired a massive 675 million oz of physical silver as they wait to profit from it

(courtesy Ted Butler)

The Last Great Silver Buy

January 12, 2018 – 1:44pm

In the annals of silver in the modern age, there have been two well-known instances of very large investor accumulations of the metal. First came the purchase by the Hunt Brothers and their associates in early 1980, followed by the purchase by Warren Buffett’s Berkshire Hathaway, 17 years later. The Hunts were said to control around 100 million ounces of actual metal (plus another 100 million ounces in long paper futures contracts), while Berkshire held as many as 129 million ounces.

Now there is compelling evidence of a third great investment accumulation of physical silver by none other than JPMorgan, one of the most powerful and connected banks in the world. This accumulation can be dated from the price peak of April 2011, after silver began what is now a near seven-year price decline. From zero in April 2011, the amount of silver in the JPMorgan COMEX warehouse has increased to 120 million ounces. Just about every ounce moved into the JPMorgan COMEX warehouse over the past 7 years has come from futures deliveries stopped (taken) by JPM in its own name. JPMorgan took delivery of 14 million ounces in December and so far, 13 million ounces have remained in the warehouses from which the metal was delivered. So this means that JPMorgan now holds more than 133 million ounces of silver in COMEX warehouses, or more than was held by the Hunt Bros or by Berkshire Hathaway at their peaks. There was a lot more silver in the world in 1980 and 1998 than there is today, meaning that JPMorgan’s accumulation is much more of an accomplishment than previous silver acquisitions.

JPMorgan’s COMEX warehouse silver holdings are only the tip of the iceberg. Beneath the surface, the true extent of JPMorgan’s physical silver accumulation is nothing short of mind-boggling. All told, including the verifiable 133 million ounces held in its own and other COMEX warehouses, JPMorgan holds at least 675 million ounces of actual silver. Simply put, JPMorgan has acquired six times as much metal as bought by the Hunts or Berkshire Hathaway. How is it possible that JPMorgan, could acquire such a massive quantity of physical silver, with no general awareness that it was doing so? More importantly, how did they do it while silver prices steadily declined over the entire time of JPM’s accumulation?

Common sense would dictate that such a large acquisition as JPM’s 675 million ounces (nearly 45% of the 1.5 billion ounces of silver bullion in the form of industry standard 1,000 ounces bars in the world), could not be bought by any entity without driving prices sharply higher. So how could JPMorgan do so without it being noticed and without driving prices sharply higher? The answer is that in addition to being the biggest physical silver accumulator in history, JPMorgan has simultaneously been the largest short seller in COMEX silver futures for the entire time since it acquired Bear Stearns in early 2008. JPMorgan has pulled off something that couldn’t possibly be replicated not just in silver but in any other world commodity. Never again will any one entity be able to accumulate 45% of the world’s supply of a commodity. JPMorgan’s accumulation is more bullish for silver than any other single consideration by a factor of 1,000.

How legitimate is it that a large financial entity could sell short massive quantities of paper derivatives contracts which result in lower prices, and then use those lower prices to accumulate silver on the cheap? It couldn’t possibly be legitimate and that makes JPMorgan a market crook and manipulator. It also makes the federal regulator, the CFTC, and the self-regulating CME Group, incompetent, corrupt, or both. This takes a special kind of market manipulator, one most likely operating under some type of agreement with the regulators.

As I have explained in past articles, 150 million ounces of silver was acquired by JPMorgan through buying 100 million Silver Eagles from the U.S. Mint, plus another 50 million Silver Maple Leafs from the Royal Canadian Mint. All these coins were melted into industry standard 1,000 ounce bars since as there’s no way anyone to unload 150 million Silver Eagles and Maple Leafs. In 2013 record sales of these silver coins conflicted strongly with reports from retail dealers of weak demand. By process of elimination, if it wasn’t the guy on the street buying all these coins, it had to be someone big. Based upon a variety of other supporting evidence that JPMorgan was the absolute king of the silver market, the most plausible explanation was that JPMorgan was Mr. Big when it came to buying Eagles and Maple Leafs. JPMorgan’s cessation in buying these coins a year or so ago is the only explanation for why sales then fell off a cliff. JPM controlled the price at which the mints sold and JPMorgan bought. It was a particularly clever and deceitful means by which JPM acquired 150 million ounces of silver at give-away prices.

At the exact time that silver topped out in April of 2011, JPMorgan opened its COMEX silver warehouse and began its epic accumulation of silver. Another almost impossible to explain phenomenon started then and continues to this day – an unusually large and persistent physical movement of silver brought into and taken out from the COMEX silver warehouses. Over the past near 7 years, there has been an average weekly movement of around 4.5 million ounces of physical silver turning over in the COMEX silver warehouses, far higher than ever before. In total, some 1.4 billion ounces of physical silver were moved in and out of the COMEX warehouses. This physical movement of silver in the COMEX warehouses is highly unique to silver, as no other commodity has seen any unusual turnover in exchange-approved warehouse inventories – just COMEX silver. I believe this unusual turnover was created by JPMorgan gobbling up all available silver in industry standard 1,000 ounce bars. JPM has been able to “skim off” 150 to 200 million ounces, which when combined with the 150 million ounces that JPM accumulated in mint-issued coins, brings to 300 to 350 million ounces of the 550 million ounces JPMorgan holds outside its COMEX warehouse holdings.

However, the main means by which JPMorgan has accumulated its massive hoard of physical silver is by continuously converting shares of the big silver ETF, SLV, into metal. All told, JPMorgan has acquired 250 to 300 million ounces of physical silver by this means. By converting shares of SLV into physical silver bullion, a large buyer can convert shares of SLV, (ownership of shares must be publicly-reported at certain SEC-mandated thresholds), into physical metal with no disclosure reporting requirements. It is the perfect means for someone big to acquire significant quantities of physical silver on the sly and no entity in the world is more qualified to do this than JPMorgan. That’s because JPMorgan is not only the largest Authorized Participant (market maker) in SLV, it is also the sole official custodian, which means it is in charge of all physical metal that moves in and out of the trust. Any time you see what looks like a highly counterintuitive redemption of metal from the SLV on rising prices, which has happened quite frequently over the past 7 years, dollars to donuts it is the handiwork of JPMorgan converting shares to metal.

With the publically disclosed 133 million ounces JPM holds in the COMEX warehouses, JPM’s total holdings are 675 million ounces at a minimum. For those who would contend that JPMorgan would have to report such holdings publicly, I say poppycock – JPMorgan reports what it wants to report and its vast army of accountants, lawyers and lobbyists are the main parties which determine what has to be reported publicly. Truth be told, JPMorgan could own a fleet of aircraft carriers and keep them off its public reporting books, if it so desired. Who would stop them? The CFTC? That JPMorgan has accumulated at least 675 million ounces of silver appears clear to me. More to the point is what JPMorgan intends to do with its epic physical silver holdings. The bank has maintained its death-grip on lower silver prices for so long it feels like it will do so forever.

However, I remain convinced that JPMorgan has the same intent as did the two previous great physical accumulators of investment silver, the Hunt Bros. and Warren Buffet. That intent is to sell at as large a profit as possible. No one buys any investment asset with the intention of losing money, least of all JPMorgan. They didn’t spend the last seven years accumulating physical silver to sell that silver at anything but the highest price possible. I can’t tell you when JPM will let the price of silver fly, but I am certain that that day is coming. And considering the means and deception with which it has accumulated the physical silver it holds, watching JPMorgan distribute its holdings at the highest prices it can attain will be one for the history books. That’s what these guys do for a living.

Given the clear evidence of the historic and epic accumulation by JPMorgan of physical silver in amounts so massive it’s near impossible to rule out an upside price surprise at any moment. That certainly includes a possible double cross by JPMorgan of its fellow big silver shorts. An email exchange with a subscriber this week prompted me to think back to the time when JPMorgan acquired Bear Stearns nearly ten years ago. Looking back over what has transpired since then, it’s now very easy for me to imagine JPMorgan playing a previously undisclosed role in Bear’s demise at the time. Who would put it past JPM to have exploited Bear Stearns’ vulnerability as the largest COMEX silver and gold short, at the time by helping to goose prices higher so that it could acquire Bear on the cheap and usurp the role of Mr. Big in matters silver and gold? Not me.

Ted Butler

January 12, 2018

end

Saturday

(courtesy zero hedge)

Cryptocurrencies Surge As South Korea Backs Off Crypto Ban

On Wednesday night, bitcoin and the entire crypto sector tumbled more than 10%, following reports that the Ministry of Justice in South Korea – one of the world’s most active cryptocurrency markets – said it was preparing legislation to close the country’s online exchanges amid a speculative boom in cryptocurrencies. That shot across the bow was paired with the news that tax authorities were investigating at least some of the exchanges in Korea.

In a statement, South Korea Attorney General Park Sang-ki said: “The South Korean Ministry of Justice is considering the closure of cryptocurrency trading to bring cryptocurrency mania and speculation under control for investor protection.”

However, confusion quickly erupted just hours later when following the surprise announcement, South Korea’s Ministry of Strategy and Finance, a key member of the country’s cryptocurrency task force, said that it does not agree with the “premature statement of the Ministry of Justice about a potential cryptocurrency trading ban.”

In a press conference, the South Korean Ministry of Strategy and Finance told local reporters that it had first heard of the Ministry of Justice’s cryptocurrency trading ban through media reports. The cryptocurrency task force participated by the central bank, MInistry of Finance, Ministry of Justice, and other agencies have not agreed upon the proposal.

“We do not share the same views as the Ministry of Justice on a potential cryptocurrency exchange ban,” MSF said according to the local Naver website.

Kim Dong-yeon, S.Korea Minister of Finance and Economy.

Adding to the confusion is that in addition to the ouctry from the Finance Ministry, the proposed ban drew swift pushback from within the South Korean government – the president’s office, in particular, said no move is “finalized” as of yet – as well as cryptocurrency supporters and traders in the country who cried foul as the statements sparked a fall in cryptocurrency prices.

Heading into the weekend, the public backlash against the proposed move was accelerating. On the Korean president’s Blue House website, more than 4,000 petitions have been filed related to “virtual currencies” since Jan. 10, CoinDesk reported.

As Coindesk further notes, one petition asking the Minister of Justice to step down in the aftermath of his proposed ban received more than 30,000 signatures on its own. Reuters reports that one petition alone has attracted more than 100,000 signatures and the website became inaccessible due to excess traffic. At last check the petition had over 153,000 signatures and rising fast.

As Coindesk further notes, one petition asking the Minister of Justice to step down in the aftermath of his proposed ban received more than 30,000 signatures on its own. Reuters reports that one petition alone has attracted more than 100,000 signatures and the website became inaccessible due to excess traffic. At last check the petition had over 153,000 signatures and rising fast.

Comments on the government’s website included a petition from a user who claimed to have lost money due to the Justice Ministry’s saber-rattling. Another petition compared cryptocurrency trading with the stock market, but claimed the latter is much more speculative. Yet another petition struck a supportive note on the development of new rules but called for the government to consult with the wider cryptocurrency community before implementing any such rules.

Angry South Koreans took to the streets to protest the uncoordinated ban announcement:

Jan 13 Myeongdong Seoul, busiest part of Korea.

This is the mess former (impeached) president left Korea with.

Current gov’t infuriated over a million people with #bitcoin trading ban fiasco.#Cryptocurrency market is fine. Fix the country first. Leave #bitcoin alone.

The bizarre unilateral decision by the country’s Justice Ministry sparked even more outrage: in addition to the government, and the broader public, Korea’s daily newspaper The Hankyoreh wrote that leaders of several opposition parties are moving to criticize what they deem a unilateral crackdown without any discussion or debate. One opposition lawmaker said the ban was not a government position, but rather one that the Ministry of Justice and, possibly the president, hold themselves.

“The government announcement should be based on detailed reviews and coordination. If there is a problem, we should warn and prepare in advance.”

Others politicians quickly piled on:

Jang Je Won, spokesperson for an opposition party (Jayoo Party), stated:

“South Korean government made the public to see its people as uninformed gamblers with a premature statement on #cryptocurrency trading ban. It’s not able to read the global trend in finance market.”

Yoo Eu Dong, spokesperson for an opposition party (Bareun Party) stated:

“The Justice Ministry’s premature statement on #cryptocurrency trading ban was a mockery of the Korean people. President should apologize to the people and have Justice Minister take responsibility of it.

In other words, from merely a daytrading infatuation, the fate of cryptocurrency trading has rapidly emerged as one of the most politically sensitive and socially polarizing issues within South Korean society, where as we previously reported, nothing short of crypto-mania is raging as “bitcoin zombies”, millions of mostly young people, spend their every hour daytrading cryptocurrencies.

Back in November, Prime Minister Lee Nak-yeon warned that “there are cases in which young Koreans including students are jumping in to make quick money and virtual currencies are used in illegal activities like drug dealing or multi-level marketing for frauds.” And in an attempt to limit what the South Korean government has called a dangerous obsession, the government has made efforts to crackdown on what it refers to as speculation surrounding cryptocurrencies.

Efforts included new regulations for banks conducting transactions with cryptocurrency exchanges. On Jan. 8, regulators inspected six banks to ensure compliance with the new regulations, which included strict know-your-customer identification rules, among other measures.

However, as confusion over the fate of crypto trading has grown, rather than comply with the new rules, some banks said they would simply cease trading with cryptocurrency exchanges altogether, according to the Korea Times, only to reverse shortly after.

On Friday, South Korea’s largest bank, Shinhan Bank, said that it would be closing down the virtual currency accounts it offers in order to comply with new regulations surrounding their use. The bank said it would ban customers from putting money into their virtual accounts that have been used for trading cryptocurrencies starting Jan. 15, according to Bloomberg. The bank would also delay issuing new virtual accounts for trading cryptocurrencies until the system for preventing money laundering is normalized.

Other banks jumped on board with the Industrial Bank of Korea said it would gradually close down accounts that were issued previously for trading cryptocurrencies, according to Yonhap. IBK also made a decision to not operate a real-name account system for trading cryptocurrencies, as did KEB Hana Bank.

* * *

However, overnight, in an indication that the South Korean purge launched by the Justice Ministry may be ending, and that a cryptocurrency ban will likely not happen following the public outcry, South Korea’s Chosun Ilbo reported that “the country will have no issues setting up a real-name cryptocurrency account system by end-January”, according to an unidentified official at Financial Services Commission.

Why “real name” accounts? Well, South Korea’s financial authorities asked banks to adopt real-name cryptocurrency account system earlier this month, with Yonhapn noting that the system will reflect the anti-money laundering guideline which is currently being worked on by financial authorities.

In other words, there will be no need to ban cryptocurrency trading as the danger of money laundering will be eliminated, as all accounts trading cryptos will henceforth be under real names, no longer “virtual.”

According to Chosun, the commission held a meeting with banks, including Kookmin, Shinhan, KEB Hana, NH and IBK, on Friday to conduct joint inspection over establishing a real-name account system. The article adds that while South Korea is technically prepared to create the system, but banks said the govt needs to give clear stance on its regulations over cryptocurrency trading.

Finally, in the most notable U-turn, while Shinhan Bank earlier said it will delay issuing new real-name accounts for trading cryptocurrencies, an unidentified official at Shinhan told the S.Korean daily that the bank still plans to launch the system after setting up anti- money laundering guidelines.

The news that South Korea appears to be rapidly shifting away from a bitcoin ban posture and toward one of regulation, sent the crypto space much higher overnight…

… as it suggests that instead of banning crypto trading outright, the government will instead allow the local trading frenzy to grow, however while extracting its pound of flesh in the form of transaction fees and capital gain taxes.

Incidentally, if the emerging South Korean model of quasi-approval spreads to other nations, it would be another implicit stamp of approval and regulatory validation of cryptocurrencies, for which the biggest, existential threat, is an outright government ban. However, that is unlikely if instead of shutting it down, governments decide to share the upside through taxation. It would also be the catalyst for the next, and even sharper move higher in cryptocurrency prices.

END

Sunday night: Cryptos originally slide and then rebound:

(courtesy zerohedge)

Cryptocurrencies Are Sliding Again

Crypto bulls rejoiced on Saturday when a report in South Korea’s Chosun Ilbo repudiated the Justice Ministry’s warning that it would seek to stifle digital-currency trading in South Korea, and instead, the country is planning to implement a real-name accounting system. The news effectively put an end to the confusion surrounding the future of cryptocurrency policy in one of bitcoin’s most active markets.

Alas, the relief rally was short-lived.

Cryptocurrencies are sliding again on Sunday, with only 2 of the top 20 currencies trading in the green, according to CryptoCompare.

Of course, South Korea isn’t the only country rushing to create a regulatory framework that would presumably help bring digital currencies into the mainstream: Treasury Secretary Steven Mnuchin said this week that US regulators are forming a cryptocurrency working group.

The selloff appears to have coincided with the Central Bank of Indonesia issuing a press release warning its citizens against the use of selling, buying or trading cryptocurrency and reiterating that virtual currencies are vulnerable to bubbles and manipulation, which is why they’re not legally recognized within Indonesia.

“Virtual currencies are vulnerable to bubble risks and susceptible to be used for money laundering and terrorism financing, therefore can potentially impact financial system stability and cause financial harm to society.”

Ripple Labs shot higher earlier this week after payments service MoneyGram said it would use Ripple Labs’ technology in its product.

But it unwound some of those gains this weekend after MoneyGram clarified that it is only using Ripple’s tech in a pilot program.

To be sure, the market wasn’t totally lacking in good news. As CoinTelegraph reports, the Russian Ministry of Finance has drafted a bill to legalize the trading of cryptocurrencies on approved exchanges, removing the threat of a crackdown that had once been raised by Deputy Finance Minister Alexei Moiseev.

* * *

Meanwhile, some believe that bitcoin’s comparatively lackluster start to 2018 is a sign that the pioneering currency is headed lower – potentially much lower – according to Academy Securities’ Peter Tchir. Tchir elaborated in a piece for Forbes “Bitcoin Is Headed Lower – For Now.”

Bitcoin, which hit a high of almost $19,000 on December 18, 2017 is headed lower – possibly much lower, for now.

This isn’t the end of Bitcoin, just a view that in the near term, the price of Bitcoin will continue lower (it may bounce, but the highs are in, for now). It is not the end of cryptocurrencies either, in fact the rise of other cryptocurrencies is part of the reason Bitcoin is due to continue its recent pullback.

While not a ‘perfect storm’ for Bitcoin – many factors have aligned against it in recent weeks

The ‘adoption’ story is fading. This was my view that futures and ETFs and ETNs would allow an increasing number of ‘mainstream’ buyers to enter the market. There are three reasons that story is over, for now.

- ‘Owning’ Bitcoin directly has been made easier as services like http://www.coinbase.com and have improved. Friends and colleagues on forbes.com and @reformedbroker have helped explain it to more people (link). The ‘problem’ with this is it has made the adoption trade less necessary as more people already own Bitcoin.

- Futures have been a failure in terms of generating real interest and demand and may have created a way for ‘pros’ to short Bitcoin at the expense of some retail investors.

- After futures were ‘rushed’ to the market, it seems as though ETFs and ETNs will have more difficulty arriving – delaying the single best source of new mainstream investor adoption (link).

The ‘competition’ story is heating up.

- There is rapidly growing interest in other forms of cryptocurrency which are now competing for investor attention and resources.

- Whether it is Litecoin, Ethereum, Ripple, or some other cryptocurrency you have barely announced, or some public company announced the launch of, there is growing competition for crypto investments.

- Some of this money, I think is merely chasing ‘lower priced’ offerings so they can own more coins (bubble behavior) but some is also looking for rational reasons to pick a ‘technology’ that overcomes some of Bitcoin’s shortcomings.

- Sites like http://www.coindesk.com have shifted their attention from what struck me as overly bitcoin focused a year ago – to much more broadbased coverage of crytpocurrencies and the businesses around them.

The ‘scalability’ issue is finally attracting attention. Real issues about potential growth rather than silly tulip analogies.

- Growing concern about the electricity costs required to mine bitcoin are becoming a real concern for many. The speed at which Bitcoin transactions can be processed is another. Many people found the fact that a Miami Bitcoin Conference Stopped Accepting Bitcoin due to fees and congestion as amusing, if not symbolic of some real issues facing Bitcoin’s ability to grow.

The ‘government’ or ‘crackdown’ risk is increasing.

- Korea seems to be announcing some new form of crackdown on an almost daily basis.

- Regulators seem to be commenting more and more about the risks posed by cryptocurrencies and the need to regulate them.

- FedCoin is a topic discussed more and more in circles plugged into D.C. which would be competition in a different form (to some hardcore cryptocurrency users – government backed crypto is an abomination of what crypto is meant to be – but for a lot of mainstream users – it has a certain appeal).

Some of these issues impact all cryptocurrencies as they have all benefited from the adoption phase and all will be hurt by increased government intervention. Other issues are Bitcoin specific.

For those of you about to enter the fifth stage of Not Owning Bitcoin Grief you may have time to take a deep breath and be patient.

end

Monday night/Tuesday morning: Cryptos slide after another South Korean shutdown by the Finance Ministry.

(courtesy zerohedge)

Cryptos Slide After Yet Another South Korean Shutdown Headline

Cryptocurrencies are sliding once again as Asia opens following headlines from South Korea’s finance ministry that a cryptocurrency exchange shutdown is still an option (but admittedly it needs “serious” discussion among ministries first).

While all of the main South Korean ministries agree that there is irrational speculation in cryptocurrency and rational regulation are needed to curb the speculation, only the Justice Ministry has said the shut down of cryptocurrency exchanges is needed as other ministries are concerned about side effects.

As Yonhap reports again, The Office for Government Policy Coordination made the announcement, downplaying the justice minister’s remark last week that the government is working on legislation to close all virtual currency exchanges to tackle speculation.

“The proposed shutdown of exchanges that the justice minister recently mentioned is one of the measures suggested by the justice ministry to curb speculation. A government-wide decision will be made in the future after sufficient consultation and coordination of opinions,” the office said in a statement.

Ripple is leading the overnight slam (down around 10%)…

Which leaves Ripple down 25% year-to-date (while Ethereum remains up around 65%)…

Bitcoin just broke back below $13,000 having tested above $14,000 during the day…

The irony is that all of this ‘news’ hit last night (and has done numerous times) but keeps getting regurgitated as new headlines that take the cryptos down briefly.

end

Bitcoin just crashed below 12,000 dollars (down over 20%) amid growing fears of a crackdown

(courtesy zerohedge)

Bitcoin Crashes 20% Amid Growing Fears Of Crypto Crackdown

As first discussed last night, the selling in bitcoin and across cryptocurrencies – which began as Asia opened, and appeared to be catalyzed by headlines from South Korea’s finance ministry that a cryptocurrency exchange shutdown is still an option…

… accelerated overnight with bitcoin plunging as much as 20% as the prospect of regulatory crackdowns appeared to spread across Asia. Having traded just above $11,000 this morning, the lowest level since late December, and down more than 40% from its all-time high of $20,000 set just a month ago, bitcoin fell 12.3% to $12,130 as at 7:30am ET.

As bitcoin halted a two-day rally, rival cryptocurrencies also plunged, and the losses in bitcoin are largely in line with those seen across the cryptocurrency space. As of writing, Ripple (XRP), stellar lumens (STR) and cardano (ADA) are down at least 25 percent on the day each. Ethereum’s ether (ETH) token has shed 18 percent in value in the last 24 hours.

As discussed last night, traders continue to focus largely on South Korea, one of the busiest markets around the globe for cryptocurrencies, where finance minister Kim Dong-yeon said overnight that shutting down cryptocurrency exchanges is still an option, but in what appeared a backtracking from last week’s vow to crack down on bitcoin by the Justice Ministry, Kim said that measures first need “serious” discussion among ministries, holding out hope for traders that a crackdown won’t go that far. Kim said there’s irrational speculation and that rational regulation was needed.

“The finance minister made it clear they’re definitely considering banning crypto trading – and it’s probably the third-largest market,” said Neil Wilson, senior market analyst in London for online trading platform ETX Capital. “The news is hitting prices and broader sentiment, and it follows China’s move to shutter mines.”

Meanwhile, according to Bloomberg, China – which first began targeting the industry last year – is escalating its clampdown on cryptocurrency trading, particularly online platforms and mobile apps that offer exchange-like services, although with China no longer a notable player in the crypto space, it is unclear what if any impact further halts of China’s already halted exchanges will have, besides just making cryptos that much more attractive of course.

As Reuters adds, a report today says that a PBoC official has said that centralized trading of virtual currencies should be banned, as well as individuals and businesses that provide related services. This is according to an internal memo that refers to PBoC Vice Governor Pan Gongsheng who reportedly said the government would continue to apply pressure to the virtual currency trade and prevent the build up of risks in that market.

“We’ve heard reports that South Korea, China and Japan have considered a shared approach, a path, to regulation,” ETX’s Wilson said, also citing a challenge to digital coins from a bill in the U.S Senate. “It looks like the light touch that has allowed the crypto-boom to explode may be coming to an end,” he wrote in a note to investors.

Also on Monday night, Steven Maijoor, chairman of the European Securities and Markets Authority, said investors “should be prepared to lose all their money” in bitcoin, in a Bloomberg TV interview in Hong Kong. “It has an extremely volatile value, which undermines its use as a currency,” he said. “It’s also not broadly accepted.”

What he really meant is that unlike stocks, traders should not expect a central bank bailout on their crypto investment when things turn rough. Which, of course, is the biggest part of the attraction.

So to summarize the speculated catalysts behind the selloff from CoinDesk:

- Firstly, comments on social media indicate there is unease in the investor community over talk of a cryptocurrency trading ban in South Korea and further possible crackdowns on trading and mining in China.

- And secondly, BTC futures contracts are trading at a discount to bitcoin’s global average calculated by CoinMarketCap. The January expiry futures contract on the CBOE is trading at $11,510 and CME’s is changing hands at $11,530. Meanwhile, BTC spot is trading at $11,816. The discount (futures price lower than spot price) indicates that the market participants are bearish on the underlying asset (BTC).

For the technicians, the chart analysis indicates scope for a drop to below $10,000 levels if the bulls can’t muster a response today.

The above chart (prices as per Coinbase) shows:

- The rising trendline (blue line) has been breached.

- A downside break of the triangle pattern, indicating the sell-off from the record high of $19,891.99 9 (Dec. 17 high) has resumed.

- The relative strength index (RSI) has turned bearish (below 50.00), indicating scope for further losses.

- The 50-day moving average (MA) has shed bullish bias (flattened).

- The 5-day and 10-day MAs carry a strong bearish bias (downward sloping).

* * *

Finally, the selling wasn’t confined to tokens: U.S. stocks with exposure to cryptocurrencies also plunged in pre-market trading:

- Riot Blockchain, a diagnostic machinery maker that rebranded as a blockchain company in October, falls 8.1% pre- market

- Overstock.com, which has a blockchain subsidiary called Medici Ventures, falls 7.5%

- Kodak, which said this month it’s working with WENN Digital to offer a blockchain-based service for paying photographers, drops 8.7%

- Metropolitan Bank, the issuing bank for a bitcoin debit card called Shift Card, is down 4.5%. On Jan. 14, Fortune reported that the bank halted all cryptocurrency-related international wires, citing an unidentified Metropolitan customer

- Seven Stars Cloud Group, which operated as an on-demand video service in China before buying a 51% stake in a blockchain company in June, drops 3.4%

- Square, which has a bitcoin service on its Square Cash app, falls 2.6%

Other cryptocurrency-exposed stocks to watch, according to Bloomberg, include: OTIV, SRAX, XNET, CRCW, RCGR, AMD, NVDA, MARA, MGTI.

end

Another crypto exchange, Kraken went offline last night at 9 pm est and that is getting users very nervous

(courtesy Bloomberg/GATA)

Big crypto exchange goes dark and users are getting nervous

Submitted by cpowell on Sat, 2018-01-13 00:09. Section: Daily Dispatches

By Camila Russo

Bloomberg News

Friday, January 12, 2018

One of the biggest cryptocurrency exchanges has been down for hours and its clients are starting to freak out.

Kraken went offline at 9 p.m. Pacific Time Wednesday for maintenance that was initially scheduled to last two hours, plus an additional two to three hours for withdrawals, according to an announcement on the San Francisco-based company’s website.

“We are still working to resolve the issues that we have identified and our team is working around the clock to ensure a smooth upgrade,” according to a status update on Kraken’s website posted seven hours ago. “This means it may still take several hours before we can relaunch the site.” …

… For the remainder of the report:

https://www.bloomberg.com/news/articles/2018-01-12/crypto-exchange-krake…

END

then another barrage of negative news on cryptos with one central banker stating what I have been telling you: be prepared for your crypto to go to zero

Crypto Carnage Continues – Ripple Now Down 40% Year-To-Date

Overnight reports from South Korea started it; European regulator comments extended it this morning; and Shanghai “scrutiny” headlines just sparked another slam as cryptocurrencies are getting hammered today…

We detailed the anxiety over a more widespread crackdown on crypto-trading overnight, and since the US came back from its MLK-Day vacation, things have got worse.

It started with a repeat of South Korean finance ministry shutdown headlines.

Then Steven Maijoor, chairman of the European Securities and Markets Authority, said investors “should be prepared to lose all their money” in bitcoin, in a Bloomberg TV interview in Hong Kong. “It has an extremely volatile value, which undermines its use as a currency,” he said. “It’s also not broadly accepted.”

That was followed by warnings from Germany’s Central Bank – Joachim Wuermeling, a member of the board of Germany’s Bundesbank, has suggested that any attempt to regulate cryptocurrencies would require international cooperation. Speaking at an event in Frankfurt on Jan. 15, the director told listeners: “Effective regulation of virtual currencies would therefore only be achievable through the greatest possible international cooperation, because the regulatory power of nation states is obviously limited.”

Then China headlines hit: Shanghai Stock Exchange has taken actions including suspending shares, requiring company clarification and asking for risk disclosure against some stocks amid speculation of blockchain concept, Shanghai Securities News reports, citing the bourse.

Shanghai-listed Easysight Supply Chain Management said in filingsthat co. will halt trading pending checks related to blockchain concept and warned investors again that blockchain business wouldn’t have significant impact on current earnings.

The reaction is not pretty as Ripple leads the collapse…

This leaves Ripple down 40% in 2018 and Bitcoin down almost 20% YTD…

There was one glimpse of silver-lining as CoinTelegraph reports that Mark Cuban, billionaire tech investor and owner of the NBA team The Dallas Mavericks tweeted on Tuesday, Jan. 16 that starting next season, it will be possible to buy tickets to the team’s games with Bitcoin.

end

A terrific interview of Eric Sprott as he talks about the huge numbers of EFP’s issued. I have been commenting that for gold this phenomenon has been going on for two years.

Nick Laird has graphed the totals issued for gold and for 2017: 6600 tonnes have transferred to London. Sprott agrees with me that the comex is a fraud vs the real market for gold.

(Courtesy Hemke/Sprott/Gata)

Comex’s ‘exchange for physicals’ mystify gold market, Sprott says

Submitted by cpowell on Mon, 2018-01-15 17:27. Section: Daily Dispatches

12:28p ET Monday, January 15, 2018

Dear Friend of GATA and Gold:

Interviewed by Craig Hemke of the TF Metals Report for Sprott Money News, mining entrepreneur Eric Sprott discusses the “exchange for physicals” mechanism that is moving gold futures delivery off the New York Commodities Exchange to secretive resolution in London.

“It makes you think that the comex is a fraud vis-a-vis the real market for gold,” Sprott says. “So I think the exchange for physical is just part of the whole thing. Move it off, get rid of it, put it under some carpet somewhere, so nobody sees what’s going on.”

The interview is 10 minutes long and can be heard and read at the Sprott Money internet site here: