GOLD: $1334.40 DOWN $10.50

Silver: $16.77 down 43 cents

Closing access prices:

Gold $1333.20

silver: $16.60

SHANGHAI GOLD FIX: FIRST FIX 10 15 PM EST (2:15 SHANGHAI LOCAL TIME)

SECOND FIX: 2:15 AM EST (6:15 SHANGHAI LOCAL TIME)

SHANGHAI FIRST GOLD FIX: $1356.09 DOLLARS PER OZ

NY PRICE OF GOLD AT EXACT SAME TIME: $1348.00

PREMIUM FIRST FIX: $8.09

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

SECOND SHANGHAI GOLD FIX: $1354.87

NY GOLD PRICE AT THE EXACT SAME TIME: $1348.70

Premium of Shanghai 2nd fix/NY:$6.17

SHANGHAI REJECTS NY /LONDON PRICING OF GOLD

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

LONDON FIRST GOLD FIX: 5:30 am est $1345.00

NY PRICING AT THE EXACT SAME TIME: $1345.65

LONDON SECOND GOLD FIX 10 AM: $1331.15

NY PRICING AT THE EXACT SAME TIME. $1330.75

For comex gold:

FEBRUARY/

NUMBER OF NOTICES FILED TODAY FOR FEBRUARY CONTRACT: 196 NOTICE(S) FOR 19600 OZ.

TOTAL NOTICES SO FAR: 871 FOR 87100 OZ (2.709 TONNES),

For silver:

jANUARY

0 NOTICE(S) FILED TODAY FOR

nil OZ/

Total number of notices filed so far this month: 124 for 620,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: BID $7,598/OFFER $7,695:DOWN $1424(morning)

Bitcoin: BID/ $8528/offer $8,628: down $490 (CLOSING/5 PM)

end

In case you missed this yesterday:

From the CBO:

it now looks like Congress will run out of money by the first half of March instead of late March or April

the way that the Democrats are acting, it does not look good for them to raise the debt ceiling!!

CBO>>

“Congress urged to take action on debt ceiling ahead of deadline: A Bloomberg report notes on Wednesday the CBO revised its estimate on when the Treasury Department will exhaust extraordinary measures to avoid debt default, with the expected deadline now in the first half of March (vs prior estimate for late March/early April). The Treasury Department separately urged Congress to “act promptly” amid its own estimated deadline at the end of February. According to the memo released by the CBO, the passage of tax reform legislation was a primary driver of the revised deadline amid changes to tax revenue projections. The updated timelines from the CBO and Treasury come as Congress continues to negotiate a government funding agreement following last month’s short- term stopgap bill.”

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total open interest ROSE BY HUGE 4770 contracts from 198,036 RISING TO 202,806 DESPITE YESTERDAY’S 7 CENT FALL IN SILVER PRICING. WE OBVIOUSLY HAD NO COMEX LIQUIDATION. HOWEVER, WE WERE AGAIN NOTIFIED THAT WE HAD ANOTHER GOOD SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP ROUTE: 1884 EFP’S FOR MARCH AND AND ZERO FOR ALL OTHER MONTHS AND THUS TOTAL ISSUANCE OF 1884 CONTRACTS. HOWEVER THE MOVEMENT ACROSS TO LONDON IS NOT AS SEVERE AS IN GOLD AS THERE SEEMS TO BE MAJOR PLAYERS WILLING TO TAKE ON THE BANKS AT THE COMEX. STILL, WITH THE TRANSFER OF 1884 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24 HRS IN THE ISSUING OF EFP’S.

ACCUMULATION FOR EFP’S/SILVER/ STARTING FROM FIRST DAY NOTICE/FOR MONTH OF FEBRUARY:

6546 CONTRACTS (FOR 3 TRADING DAYS TOTAL 6546 CONTRACTS OR 32.73 MILLION OZ: AVERAGE PER DAY: 2182 CONTRACTS OR 10.010 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH: 32.73 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 4.67% OF ANNUAL GLOBAL PRODUCTION

ACCUMULATION IN YEAR 2018 TO DATE SILVER EFP’S: 267.7 MILLION OZ.

ACCUMULATION FOR JAN 2018: 236.879 MILLION OZ

RESULT: A HUGE SIZED GAIN IN OI COMEX DESPITE THE 7 CENT FALL IN SILVER PRICE. WE HOWEVER HAD A GOOD SIZED EFP ISSUANCE OF 1884 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER . FROM THE CME DATA 1884 EFP’S FOR MARCH WERE ISSUED FOR TODAY FOR A DELIVERABLE FORWARD CONTRACT OVER IN LONDON WITH A FIAT BONUS. WE REALLY GAINED 6654 OI CONTRACTS i.e. 1884 open interest contracts headed for London (EFP’s) TOGETHER WITH A INCREASE OF 4770 OI COMEX CONTRACTS. AND ALL OF THIS HAPPENED WITH THE FALL IN PRICE OF SILVER OF 7 CENTS AND A CLOSING PRICE OF $17.20 WITH RESPECT TO YESTERDAY’S TRADING. YET WE STILL HAVE A GOOD AMOUNT OF SILVER STANDING AT THE COMEX.

In ounces AT THE COMEX, the OI is still represented by just OVER 1 BILLION oz i.e. 1.0040 BILLION TO BE EXACT or 145% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT FEBRUARY MONTH/ THEY FILED: 0 NOTICE(S) FOR NIL OZ OF SILVER

In gold, the open interest FELL BY 1427 CONTRACTS DOWN TO 550,608 DESPITE THE GOOD SIZED RISE IN PRICE OF GOLD WITH YESTERDAY’S TRADING ($8.00). IN ANOTHER DEVELOPMENT, WE RECEIVED THE TOTAL NUMBER OF GOLD EFP’S ISSUED FOR TODAY AND IT TOTALED A GOOD SIZED 6579 CONTRACTS OF WHICH APRIL SAW THE ISSUANCE OF 6579 CONTRACTS AND ALL OTHER MONTHS ZERO. The new OI for the gold complex rests at 550,608. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. DUE TO THE DELAY IN THE RELEASE OF YESTERDAY’S DATA YOU CAN BET THE FARM THAT THEY HAVE DELAYED THE RELEASE OF MANY EFPS. DEMAND FOR GOLD INTENSIFIES GREATLY AS WE CONTINUE TO WITNESS A HUGE NUMBER OF EFP TRANSFERS TOGETHER WITH THE MASSIVE INCREASE IN GOLD COMEX OI TOGETHER WITH THE TOTAL AMOUNT OF GOLD OUNCES STANDING FOR JANUARY COMEX. EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER (BIG RISE IN BOTH GOFO AND SIFO) AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES. IN ESSENCE TODAY WE HAVE A GAIN OF 5152 CONTRACTS: 1427 OI CONTRACTS DECREASED AT THE COMEX AND A STRONG SIZED 6579 OI CONTRACTS WHICH NAVIGATED OVER TO LONDON.

YESTERDAY, WE HAD 8262 EFP’S ISSUED.

ACCUMULATION OF EFP’S/ GOLD(EXCHANGE FOR PHYSICAL) FOR THE MONTH OF FEBRUARY STARTING WITH FIRST DAY NOTICE: 29,212 CONTRACTS OR 2,921,200 OZ OR 90.86 TONNES (3 TRADING DAYS AND THUS AVERAGING: 9,737 EFP CONTRACTS PER TRADING DAY OR 973,700 OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SIZE OF THESE EFP TRANSFERS : SO FAR THIS MONTH IN 2 TRADING DAYS: IN TONNES: 90.86 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2017, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 2200 TONNES

THUS EFP TRANSFERS REPRESENTS 90.86/2200 x 100% TONNES = 4.13% OF GLOBAL ANNUAL PRODUCTION SO FAR IN FEBRUARY ALONE.

ACCUMULATION OF GOLD EFP’S YEAR 2018 TO DATE: 743.17 TONNES

ACCUMULATION OF GOLD EFP’S FOR JANUARY 2018: 653.22 TONNES

Result: A FAIR SIZED DECREASE IN OI AT THE COMEX DESPITE THE GOOD SIZED RISE IN PRICE IN GOLD TRADING YESTERDAY ($8.00). IT IS WITHOUT A DOUBT THAT MANY OF THE DEPARTED COMEX LONGS ARE WAITING TO RECEIVE A PRIVATE EFP CONTRACT FOR EITHER FEBRUARY OR APRIL AND THESE GUYS ARE STILL NEGOTIATING THEIR DEAL. WE HAD ANOTHER GOOD SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 6579 AS THESE HAVE ALREADY BEEN NEGOTIATED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX AND YET WE ALSO OBSERVED A HUGE DELIVERY MONTH FOR THE MONTH OF DECEMBER. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 6579 EFP CONTRACTS ISSUED, WE HAD A NET GAIN IN OPEN INTEREST OF 95152 contracts ON THE TWO EXCHANGES:

6579 CONTRACTS MOVE TO LONDON AND 1427 CONTRACTS DECREASED AT THE COMEX. (in tonnes, the GAIN in total oi equates to 16.02 TONNES).

we had: 196 notice(s) filed upon for 19600 oz of gold.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD

No change in gold inventory at the GLD/

Inventory rests tonight: 841.35 tonnes.

SLV/

HUGE CHANGES IN SILVER INVENTORY AT THE SLV/ A WITHDRAWAL OF 982,000 OZ INVENTORY RESTS AT 312.914 MILLION OZ/

end

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in silver ROSE BY A HUGE 4770 contracts from 198,036 UP TO 202,806 (AND now A LITTLE FURTHER FROM THE NEW COMEX RECORD SET ON FRIDAY/APRIL 21/2017 AT 234,787) DESPITE THE FALL IN PRICE OF SILVER (7 CENTS WITH RESPECT TO YESTERDAY’S TRADING). OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE ANOTHER GOOD 1884 PRIVATE EFP’S FOR MARCH (WE DO NOT GET A LOOK AT THESE CONTRACTS AS IT IS PRIVATE BUT THE CFTC DOES AUDIT THEM) AND 0 EFP’S FOR ALL OTHER MONTHS . EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. WE HAD MINIMAL COMEX SILVER COMEX LIQUIDATION. IF WE TAKE THE OI GAIN AT THE COMEX OF 4770 CONTRACTS TO THE 1884 OI TRANSFERRED TO LONDON THROUGH EFP’S WE OBTAIN A GAIN OF 6546 OPEN INTEREST CONTRACTS. WE STILL HAVE A GOOD AMOUNT OF SILVER OUNCES THAT ARE STANDING FOR METAL IN JANUARY (SEE BELOW). THE NET GAIN TODAY IN OZ ON THE TWO EXCHANGES: 32.73 MILLION OZ!!!

RESULT: A HUGE SIZED INCREASE IN SILVER OI AT THE COMEX DESPITE THE SMALL SIZED FALL OF 7 CENTS IN PRICE (WITH RESPECT TO YESTERDAY’S TRADING). BUT WE ALSO HAD ANOTHER GOOD 1884 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE GOOD SIZED AMOUNT OF SILVER OUNCES STANDING FOR FEBRUARY, DEMAND FOR PHYSICAL SILVER INTENSIFIES AS WE WITNESS MAJOR BANK SHORT COVERING ACCOMPANIED BY INCREASES IN GOFO AND SIFO RATES INDICATING SCARCITY.

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)Late THURSDAY night/FRIDAY morning: Shanghai closed UP 15.10 points or 0.44% /Hang Sang CLOSED DOWN 40.31 or 0.12% / The Nikkei closed DOWN 2111.58 POINTS OR 0.90%/Australia’s all ordinaires CLOSED UP 0.50%/Chinese yuan (ONSHORE) closed UP at 6.2870/Oil UP to 65.76 dollars per barrel for WTI and 69.31 for Brent. Stocks in Europe OPENED RED . ONSHORE YUAN CLOSED DOWN AGAINST THE DOLLAR AT 6.2870. OFFSHORE YUAN CLOSED UP AGAINST THE ONSHORE YUAN AT 6.2922//ONSHORE YUAN MUCH STRONGER AGAINST THE DOLLAR/OFF SHORE MUCH STRONGEER TO THE DOLLAR/. THE DOLLAR (INDEX) IS MUCH STRONGER AGAINST ALL MAJOR CURRENCIES. CHINA IS HAPPY TODAY.(WEAKER CURRENCY BUT STRONG MARKETS )

3a)THAILAND/SOUTH KOREA/NORTH KOREA

i)North Korea

b) REPORT ON JAPAN

The Bank of Japan realized yesterday that they were in trouble as their long 10 yr bond yield hit .10%. They announced another round of QE buying. This time they are buying any bond any time the yield hits .11% on an unlimited basis as well as boosting POMO in a panic response to its surging rates

( zerohedge)

3 c CHINA

i)Chinese stocks tumble especially the Hang Sang. Hong Kong officials are now monitoring a surge in ATM withdrawals a citizens expect a big devaluation

( zerohedge)

( Investing In Chinese Stocks blog)

4. EUROPEAN AFFAIRS

i)Italy

Italian banks are dumping Italian sovereign bond debt by the bucketful. The only buyer: the ECB

( zerohedge)

ii)Germany/Deutsche Bank)

( zerohedge)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

( zerohedge)

6 .GLOBAL ISSUES

7. OIL ISSUES

8. EMERGING MARKET

9. PHYSICAL MARKETS

ii)Russian banks accumulated 205 tonnes of gold as official reserves last year

iii)LBMA always promises transparency but it never delivers upon that promise( Ronan Manly/Bullionstar/GATA)

Two commentaries: Chris Powell on Ted Butler/Ted Butler GATA)

v)Almost 1000 miners trapped in an underground mine, Sibanye in South Africa/the rescued

two commentaries

( Business Day/J’berg/GATA)

vi)Bitcoin crashes

( zerohedge)

vii)Bank of America and JPMorgan both bar crypto purchases on credit cards

10. USA stories which will influence the price of gold/silver

iii b)Here is where the jobs went in January: who is hiring and who is not

vi)This is not suppose to happen in a booming economy: core capital goods orders tumble the most in over a year

vii)All USA companies report a slump in January car sales

( zerohedge)

viii)My goodness: NEWSWEEK publisher caught defrauding the Government Agency in an ad revenue scheme

( zerohedge)

The memo is released and everything that we speculated on has proven to be true

I outlined the key points in red.

( zerohedge)

b)New text messages between our love birds discussed evading new security and monitoring issues and legal discovery( zero hedge)

c)Trump blasts the FBI leadership in their roll with respect to the issuing of FISA warrants, illegally spying on USA citizens

( zerohedge)

d)The Obama State department under the stewardship of John Kerry secretly distributed its own

“dossier” leaking it to Sen Cardin, a democrat from Maryland in an attempt to undermine Trump once he assumed the Presidency. This is according to new Freedom of Information documents

( zero hedge)

Let us head over to the comex:

The total gold comex open interest SURPRISINGLY FELL BY A CONSIDERABLE 1427 CONTRACTS DOWN to an OI level 550,608 DESPITE THE GOOD SIZED RISE IN THE PRICE OF GOLD ($8.00 GAIN WITH RESPECT TO YESTERDAY’S TRADING). WE HAD CONSIDERABLE COMEX GOLD LIQUIDATION. HOWEVER THE CME REPORTS THAT THE BANKERS ISSUED ANOTHER STRONG COMEX TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS. WE HAD A GOOD SIZED 6579 EFP’S ISSUED FOR APRIL AND 0 EFP’s FOR ALL OTHER MONTHS: TOTAL 6579 CONTRACTS. THE OBLIGATION STILL RESTS WITH THE BANKERS ON THESE TRANSFERS. ALSO REMEMBER THAT THERE IS NO DOUBT A HUGE DELAY IN THE ISSUANCE OF EFP’S AND IT PROBABLY TAKES AT LEAST 48 HRS AFTER LONGS GIVE UP THEIR COMEX CONTRACTS FOR THEM TO RECEIVE THEIR EFP’S AS THEY ARE NEGOTIATING THIS CONTRACT WITH THE BANKS FOR A FIAT BONUS PLUS THEIR TRANSFER TO A LONDON FORWARD… THE COMEX IS NOW AN ABSOLUTE FRAUD!!

ON A NET BASIS IN OPEN INTEREST WE GAINED TODAY: 5152 OI CONTRACTS IN THAT 6579 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE LOST 1427 COMEX CONTRACTS.

NET GAIN ON THE TWO EXCHANGES: 5152 contracts OR 515,200 OZ OR 16.02 TONNES,

Result: A STRONG DECREASE IN COMEX OPEN INTEREST DESPITE THE GOOD SIZED GAIN IN YESTERDAY’S GOLD TRADING ($8.00.) WE HAD CONSIDERABLE COMEX GOLD LIQUIDATION. TOTAL OPEN INTEREST GAIN ON THE TWO EXCHANGES: 5152 OI CONTRACTS..

We have now entered the active contract month of FEBRUARY where we lost 737 contracts to 2897 contracts. We had 223 notices filed upon yesterday, so we lost 514 contracts or 51,400 oz will not stand in this active contract month of February AND THESE WERE MORPHED INTO LONDON BASED FORWARDS.

March saw a GAIN of 33 contracts UP to 2078. April saw a LOSS of 1314 contracts DOWN to 397,395.

We had 196 notice(s) filed upon today for 19600 oz

PRELIMINARY VOLUME TODAY ESTIMATED; 280,450

FINAL NUMBERS CONFIRMED FOR YESTERDAY: 395,706

comex gold volumes are RISING AGAIN

Here is a summary of the latest gold trading volumes at the Comex per year

certainly the introduction of EFP’s has certainly had an effect:

Trading Volumes on the COMEX

Meanwhile, gold-trading volumes on the COMEX have never been higher:

end

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

And now for the wild silver comex results.

Total silver OI ROSE BY A HUGE 4770 CONTRACTS FROM 198,036 UP TO 202,806 DESPITE YESTERDAY’S 7 CENT LOSS. WE WERE ALSO INFORMED THAT WE HAD ANOTHER FAIR SIZED 1884 EMERGENCY EFP’S FOR MARCH ISSUED BY OUR BANKERS (WITH 0 EFP CONTRACTS FOR ALL OTHER MONTHS TO COMEX LONGS WHO RECEIVED A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON: THE TOTAL EFP’S ISSUED: 1884. THE SILVER BOYS HAVE STARTED TO MIGRATE TO LONDON FROM THE START OF DELIVERY MONTH AND CONTINUING RIGHT THROUGH UNTIL FIRST DAY NOTICE JUST LIKE WE ARE WITNESSING TODAY. USUALLY WE NOTED THAT CONTRACTION IN OI OCCURRED ONLY DURING THE LAST WEEK OF AN UPCOMING ACTIVE DELIVERY MONTH AS WE HAVE JUST SEEN IN GOLD TODAY. THIS PROCESS HAS JUST BEGUN IN EARNEST IN SILVER STARTING IN SEPTEMBER 2017. HOWEVER, IN GOLD, WE HAVE BEEN WITNESSING THIS FOR THE PAST 2 YEARS. NICK LAIRD WAS KIND ENOUGH TO SUPPLY US THE TOTAL FOR 2017 GOLD EFP’S AND IT WAS 6600 TONNES FOR THE ENTIRE YEAR. WE OBVIOUSLY HAD ZERO LONG COMEX SILVER LIQUIDATION AND A HUGE SIZED GAIN IN TOTAL SILVER OI. WE ARE ALSO WITNESSING A FAIR AMOUNT OF SILVER OUNCES STANDING FOR COMEX METAL IN THIS NON ACTIVE JANUARY AS WELL AS THAT CONTINUAL MIGRATION OF EFPS OVER TO LONDON. ON A PERCENTAGE BASIS THERE ARE MORE EFP’S ISSUED FOR GOLD THAN SILVER. ON A NET BASIS WE GAINED 6546 SILVER OPEN INTEREST CONTRACTS:

4770 CONTRACT GAIN AT THE COMEX COMBINING WITH THE ADDITION OF 1884 OI CONTRACTS NAVIGATING OVER TO LONDON.

NET GAIN TWO EXCHANGES: 6546 CONTRACTS

We are now in the poor non active delivery month of FEBRUARY and here the front month lost 8 contracts DOWN TO 3 contracts. We had 8 notices filed upon yesterday so we LOST 0 contracts or NIL ADDITIONAL oz will stand for delivery.

The March contract LOST 40 contracts DOWN to 126,457.

We had 0 notice(s) filed for NIL NIL for the FEBRUARY 2018 contract for silver

INITIAL standings for FEBRUARY

Feb2/2018.

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz |

nil oz

|

| Deposits to the Dealer Inventory in oz | nil oz |

| Deposits to the Customer Inventory, in oz |

7523.100

oz Scotia

|

| No of oz served (contracts) today |

196 notice(s)

19600 OZ

|

| No of oz to be served (notices) |

2701 contracts

(270,100 oz)

|

| Total monthly oz gold served (contracts) so far this month |

871 notices

87100 oz

2.709 tonnes

|

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

For FEBRUARY:

Today, 0 notice(s) were issued from JPMorgan dealer account and 182 notices were issued from their client or customer account. The total of all issuance by all participants equates to 196 contract(s) of which 153 notices were stopped (received) by j.P. Morgan dealer and 41 notice(s) was (were) stopped/ Received) by j.P.Morgan customer account.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

To calculate the INITIAL total number of gold ounces standing for the FEBRUARY. contract month, we take the total number of notices filed so far for the month (871) x 100 oz or 87,100 oz, to which we add the difference between the open interest for the front month of FEB. (2897 contracts) minus the number of notices served upon today (196 x 100 oz per contract) equals 357,200 oz, the number of ounces standing in this active month of FEBRUARY

Thus the INITIAL standings for gold for the FEBRUARY contract month:

No of notices served (871 x 100 oz or ounces + {(2897)OI for the front month minus the number of notices served upon today (196 x 100 oz )which equals 357,200 oz standing in this active delivery month of February (11.110 tonnes). THERE IS 13.463 TONNES OF REGISTERED GOLD AVAILABLE FOR DELIVERY SO FAR.

WE LOST 514 CONTRACTS OR AN ADDITIONAL 51,400 OZ WILL NOT STAND BUT THEY WILL JOIN OTHER LONGS AS THEY HAVE BEEN TRANSFERRED TO A LONDON BASED FORWARD THROUGH THE EFP ROUTE.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

IN THE LAST 17 MONTHS 66 NET TONNES HAS LEFT THE COMEX.

end

And now for silver

AND NOW THE DECEMBER DELIVERY MONTH

FEBRUARY FINAL standings

| Silver | Ounces |

| Withdrawals from Dealers Inventory | nil oz |

| Withdrawals from Customer Inventory |

352,369.800 oz

CNT

|

| Deposits to the Dealer Inventory |

nil

oz

|

| Deposits to the Customer Inventory |

591,161.460 OZ

JPMORGAN

|

| No of oz served today (contracts) |

0

CONTRACT(S)

(NIL OZ)

|

| No of oz to be served (notices) |

3 contracts

(15,000 oz)

|

| Total monthly oz silver served (contracts) | 124 contracts

(620,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

we had no inventory movement at the dealer side of things

total inventory movement dealer: nil oz

we had 1 inventory deposits into the customer account

i) into JPMORGAN: 591,161.460 oz

total inventory deposits: 591,161.460 oz

JPMORGAN CONTINUES TO ADD TO ITS INVENTORY DESPITE BEING THE BIGGEST SHORT AT THE COMEX. ACCORDING TO BUTLER JPMORGAN HAS AMASSED IN 2 YRS: 700 MILLION OZ PHYSICAL SILVER. THIS COULD EASILY BE PROVEN. THIS BEHAVIOUR IS TOTALLY CRIMINAL

we had 1 withdrawals from the customer account;

i) out of CNT: 352,369.800 oz

total withdrawals; 352,369.800 oz

we had 0 adjustment

i

total dealer silver: 43.131 million

total dealer + customer silver: 246.260 million oz

The total number of notices filed today for the FEBRUARY. contract month is represented by 0 contract(s) FOR NIL oz. To calculate the number of silver ounces that will stand for delivery in FEBRUARY., we take the total number of notices filed for the month so far at 124 x 5,000 oz = 640,000 oz to which we add the difference between the open interest for the front month of FEB. (3) and the number of notices served upon today (0 x 5000 oz) equals the number of ounces standing.

.

Thus the INITIAL standings for silver for the FEB contract month: 124(notices served so far)x 5000 oz + OI for front month of FEBRUARY(3) -number of notices served upon today (0)x 5000 oz equals 635,000 oz of silver standing for the FEBRUARY contract month.

WE LOST 0 CONTRACTS OR AN ADDITIONAL NIL OZ WILL STAND AT THE COMEX

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

ESTIMATED VOLUME FOR TODAY: 87,093

CONFIRMED VOLUME FOR YESTERDAY: 114,604 CONTRACTS

YESTERDAY’S CONFIRMED VOLUME OF 114,604 CONTRACTS EQUATES TO 573 MILLION OZ OR 81.8% OF ANNUAL GLOBAL PRODUCTION OF SILVER

COMMODITY LAW SUGGESTS THAT OPEN INTEREST SHOULD NOT BE MORE THAN 3% OF ANNUAL GLOBAL PRODUCTION. THE CROOKS ARE SUPPLYING MASSIVE PAPER TRYING TO KEEP SILVER IN CHECK.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price at that day at $18.42

The previous record was 224,540 contracts with the price at that time of $20.44

end

NPV for Sprott

1. Sprott silver fund (PSLV): NAV RISES TO -2.24% (FEB 1/2018)

2. Sprott gold fund (PHYS): premium to NAV FALLS TO -0.65% to NAV (FEB 1/2018 )

Note: Sprott silver trust back into NEGATIVE territory at -2.24%-/Sprott physical gold trust is back into NEGATIVE/ territory at -0.65%/Central fund of Canada’s is still in jail but being rescued by Sprott.

Sprott WINS hostile 3.1 billion bid to take over Central Fund of Canada

(courtesy Sprott/GATA)

3.SPROTT CEF.A FUND (FORMERLY CENTRAL FUND OF CANADA): NAV FALLS TO -3.49%: NAV 13.77/TRADING 13.30//DISCOUNT 3.49%

END

And now the Gold inventory at the GLD/

Feb 2/no change in gold inventory at the GLD/Inventory rests at 841.35 tonnes

Feb 1/with gold up by $8.00/the crooks decided not to add any new physical gold metal into the GLD./inventory rests at 841.35 tonnes

Jan 31/with gold up $3.15 today, GLD shed another 5.32 tonnes of gold from its inventory/inventory rests at 841.35 tonnes

jan 30/with gold down by $4.85/GLD shed another 1.47 tonnes of gold from its inventory/inventory rests at 846.67 tonnes

JAN 29/with gold down $11.25, the GLD shed 1.18 tonnes of gold/inventory rests at 848.14 tonnes

jan 26/2018/no changes in gold inventory at the GLD/inventory rests at 849.32 tonnes

jan 25/no changes in gold inventory at the GLD/inventory rests at 849.32 tonnes

Jan 24/A HUGE DEPOSIT OF 2.65 TONNES OF GOLD INTO GLD/INVENTORY RESTS AT 849.32 TONNES

Jan 23/NO CHANGE IN GOLD INVENTORY DESPITE GOLD’S RISE/INVENTORY RESTS AT 846.67 TONNES

Jan 22/a huge deposit of 5.71 tonnes of gold despite a drop in price/inventory rests at 846.67 tonnes. In 3 trading days, the GLD has added 17.71 tonnes/the bankers are now in trouble!!

Jan 19/no change in gold inventory at the GLD/Inventory rests at 840.76 tonnes

Jan 18/SHOCKINGLY A HUGE DEPOSIT OF 11.80 TONNES WITH GOLD DOWN ALMOST $12.00/INVENTORY RESTS AT 840.76

Jan 17/no changes in gold inventory at the GLD/inventory rests at 828.96 tonnes

Jan 16/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 828.96 TONNES

Jan 12/no changes in inventory at the GLD despite the rise in gold price/inventory rests at 828.96 tonnes

Jan 11/ANOTHER IDENTICAL WITHDRAWAL OF 2.95 TONNES FROM THE GLD INVENTORY/INVENTORY RESTS AT 828.96 TONNES

Jan 10/with gold up today, a strange withdrawal of 2.95 tonnes/inventory rests at 831.91 tonnes

Jan 9/no changes in gold inventory at the GLD/Inventory rests at 834.88 tonnes

Jan 8/with gold falling by a tiny $1.40 and this being after 12 consecutive gains, today they announce another 1.44 tonnes of gold withdrawal from the GLD/

Jan 5/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 836.32 TONNES

Jan 4/2018/no change in gold inventory at the GLD/Inventory rests at 836.32 tonnes

Jan 3/a huge withdrawal of 1.18 tonnes of gold from the GLD/Inventory rests at 836.32 tonnes

Jan 2/2018/no changes in gold inventory at the GLD/inventory rests at 837.50 tonnes

Dec 29/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 837.50 TONNES

Dec 28/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 837.50 TONNES

Dec 27/NO CHANGES IN GOLD INVENTORY AT THE GLD/ INVENTORY RESTS AT 837.50 TONNES

Dec 26/no change in gold inventory at the GLD

Dec 22/ A DEPOSIT OF 1.48 TONNES OF GOLD INTO GLD INVENTORY/INVENTORY RESTS AT 837.50 TONNES

Dec 21′ NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 836.02 TONNES

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

Feb 2/2018/ Inventory rests tonight at 841.35 tonnes

*IN LAST 318 TRADING DAYS: 99.80 NET TONNES HAVE BEEN REMOVED FROM THE GLD

*LAST 252 TRADING DAYS: A NET 57.51 TONNES HAVE NOW BEEN ADDED INTO GLD INVENTORY.

end

Now the SLV Inventory

Feb 2/we lost 982,000 oz from the SLV inventory /inventory rests at 313.896 million oz/

Feb 1/no change in silver inventory at the SLV/Inventory rests at 313.896 million oz/

Jan 31/ no change in inventory at the slv in total contrast to gold/inventory rests at 313.896 million oz/

Jan 30/no change in inventory/SLV inventory rests at 313.896 million oz/

Jan 29/no change in inventory/SLV inventory rests at 313.896 million oz/

Jan 26.2018/inventory rests at 313.896 million oz

Jan 25/with silver up today and yesterday, the SLV could only muster a gain of 848,000 oz

Inventory rests at 313.896 oz

jan 24/NO CHANGE IN SILVER INVENTORY DESPITE THE GOOD ADVANCE IN PRICE/INVENTORY RESTS AT 313.048 MILLION OZ/

Jan 23/ANOTHER HUGE WITHDRAWAL OF 1.131 MILLION OZ OF SILVER DESPITE THE TINY LOSS/THE CROOKS ARE USING THE INVENTORY TO RAID ON SILVER.

JAN 22.2018/with silver down by 5 cents/ the crooks at the SLV liquidate 1.321 million oz of silver/inventory rests at 314.179 million oz/

Jan 19/ no changes in silver inventory at the SLV/inventory rests at 315.500 million oz/

jan 18/A WITHDRAWAL OF 848,000 OZ OF SILVER FROM THE SLV/INVENTORY RESTS AT 315.500 MILLION OZ/

Jan 17/no changes in silver inventory at the SLV/inventory rests at 316.348 million oz/

Jan 16/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 316.348 MILLION OZ

Jan 12/no changes in silver inventory at the SLV/inventory rests at 316.348 million oz/

Jan 11/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 316.348 MILLION OZ/

Jan 10/with silver up again, we had a huge withdrawal of 1.227 million oz from the SLV/inventory rests at 316.348 million oz

Jan 9/a withdrawal of 848,000 oz from the SLV/Inventory rests at 317.575 million oz/

jan 8/no change in silver inventory at the SLV/Inventory rests at 318.423 million oz/

Jan 5/DESPITE NO CHANGE IN SILVER PRICING, WE HAD A HUGE WITHDRAWAL OF 2.026 MILLION OZ/INVENTORY RESTS AT 318.423 MILLION OZ.

Jan 4.2018/a slight withdrawal of 180,000 oz and this would be to pay for fees/inventory rests at 320.449 million oz/

Jan 3/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 320.629 MILLION OZ.

Jan 2/WITH SILVER UP DRAMATICALLY THESE PAST 4 TRADING DAYS, THE FOLLOWING MAKES NO SENSE: WE HAD A WITHDRAWAL OF 2.83 MILLION OZ FROM THE SLV

INVENTORY RESTS AT 320.629 MILLION OZ/

Dec 29/no changes in silver inventory at the SLV/inventory rests at 323.459 million oz/

Dec 28/DESPITE THE RISE IN SILVER AGAIN BY 13 CENTS, WE LOST ANOTHER 1,251,000 OZ OF SILVER FROM THE SILVER.

Dec 27/WITH SILVER UP AGAIN BY 17 CENTS, WE LOST ANOTHER 802,000 OZ OF SILVER INVENTORY/WHAT CROOKS/INVENTORY RESTS AT 324.780 MILLION OZ/

Dec 26/no change in silver inventory at the SLV./Inventory rests at 325.582

Dec 21/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 326.227 MILLION OZ/

.

Feb 2/2017:

Inventory 312.914 million oz

end

6 Month MM GOFO

Indicative gold forward offer rate for a 6 month duration

+ 1.70%

12 Month MM GOFO

+ 2.12%

end

At 3:30 pm we receive the COT report. With new revelations on the use of EFP’s which transfer longs to London, this report is totally useless. But for completeness sake, I am including it in my reporting to you

First/ gold COT

| Gold COT Report – Futures | ||||||

| Large Speculators | Commercial | Total | ||||

| Long | Short | Spreading | Long | Short | Long | Short |

| 298,327 | 91,065 | 57,648 | 154,690 | 379,766 | 510,665 | 528,479 |

| Change from Prior Reporting Period | ||||||

| -7,485 | -63 | -6,875 | -6,768 | -16,244 | -21,128 | -23,182 |

| Traders | ||||||

| 182 | 86 | 73 | 45 | 56 | 262 | 185 |

| Small Speculators | ||||||

| Long | Short | Open Interest | ||||

| 48,667 | 30,853 | 559,332 | ||||

| -1,961 | 93 | -23,089 | ||||

| non reportable positions | Change from the previous reporting period | |||||

| COT Gold Report – Positions as of | Tuesday, January 30, 2018 | |||||

OUR LARGE SPECULATORS

those large speculators that have been long in gold pitched a very large 7485 contracts from their long side and no doubt many are on their way to London

those large specs who have been short in gold covered a very tiny 63 contracts from their short side

OUR COMMERCIALS

those commercials who have been long in gold pitched a huge 6768 contracts from their long side

those commercials who have been short in gold covered a huge 16,244 contracts. (at the comex their obligation ends but in London on EFP transfers it begins.

commercials go net long by 9476 contracts

OUR SMALL SPECULATORS

those small specs who have been long in gold pitched 1961 contracts from their long side and these guys also morphed into London forwards.

those small specs who have been short in gold added 93 contracts to their short side.

| Silver COT Report: Futures | |||||

| Large Speculators | Commercial | ||||

| Long | Short | Spreading | Long | Short | |

| 72,145 | 39,723 | 30,601 | 68,278 | 115,569 | |

| -4,048 | -7,389 | 5,985 | -3,808 | 1,986 | |

| Traders | |||||

| 103 | 52 | 44 | 42 | 40 | |

| Small Speculators | Open Interest | Total | |||

| Long | Short | 198,358 | Long | Short | |

| 27,334 | 12,465 | 171,024 | 185,893 | ||

| 244 | -2,209 | -1,627 | -1,871 | 582 | |

| non reportable positions | Positions as of: | 163 | 121 | ||

| Tuesday, January 30, 2018 | © SilverSeek.c | ||||

OUR LARGE SPECULATORS

those large speculators who have been long in silver pitched a huge 4048 contracts from their long side these figures are net. Many longs in silver morphed into EFP contracts acquiring London based forwards.

those large speculators who are short in silver covered a huge 7389 contracts from their short side

OUR COMMERCIALS

those commercials who have been long in silver pitched 3803 contracts from their long side and maybe they were morphed into London based forwards.

those commercials who have been short in silver added a net 1986 contracts to their short side

OUR SMALL SPECULATORS

those small specs who have been long in silver added a tiny 286 contracts to their long side

those small specs who have been short in silver covered a huge 2347 contracts from their short side.

end.

Major gold/silver trading /commentaries for FRIDAY

GOLDCORE/BLOG/MARK O’BYRNE.

GOLD/SILVER

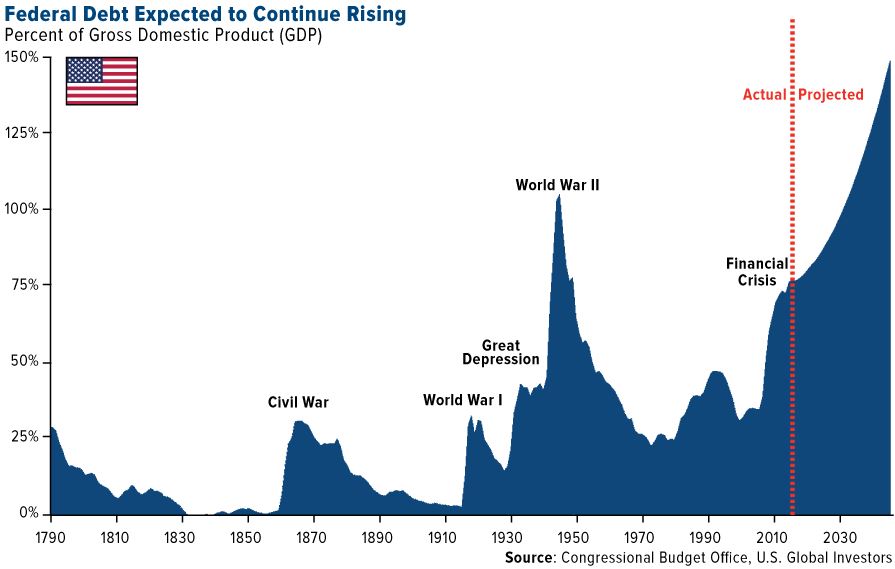

U.S. Debt Is “Extraordinarily High” and Are Stock And Bond Bubbles – Greenspan

– “We have a stock market bubble” warns Greenspan

– “Bond bubble will be the big issue” he tells Bloomberg TV (see video)

– “Fiscally unstable long-term outlook in which inflation will take hold”

– “Ratio of federal debt to GDP which is extraordinarily high” (see chart)

– Higher interest rates, inflation and stagflation coming

– Gold is the “ultimate insurance policy” – Greenspan

Source: US Funds

The man who made the term “irrational exuberance” famous says investors are at it again.

“There are two bubbles: We have a stock market bubble, and we have a bond market bubble,” Alan Greenspan, 91, said Wednesday on Bloomberg Television with Tom Keene and Scarlet Fu. Greenspan, who led the Federal Reserve from 1987 until 2006, memorably used the phrase to describe asset values during the 1990’s dot-com bubble.

Greenspan’s comments come as stock indexes remain near record highs, despite selling off in recent days, and as the yields on government notes and bonds hover not far from historic lows. Interest rates are expected to move up in coming years as the Fed continues with a campaign to gradually tighten monetary policy.

“At the end of the day, the bond market bubble will eventually be the critical issue, but for the short term it’s not too bad,” Greenspan said. “But we’re working, obviously, toward a major increase in long-term interest rates, and that has a very important impact, as you know, on the whole structure of the economy.”

The Fed on Wednesday opted to leave rates unchanged and markets are pricing in an increase at the central bank’s March meeting.

Greenspan sounded an alarm on forecasts that the U.S. government deficit will continue to climb as a share of gross domestic product. He said he was “surprised” that President Donald Trump didn’t specify how he would fund new government initiatives in Tuesday’s State of the Union speech. The president last month signed into law about $1.5 trillion in tax cuts that critics say will further balloon the budget gap.

U.S. Raises Longer-Term Debt Sales as Budget Deficit Worsens

Greenspan blamed the growing fiscal shortfall for his bond call.

“What’s behind the bubble? Well the fact, that, essentially, we’re beginning to run an ever-larger government deficit,” Greenspan said. As a share of GDP, “debt has been rising very significantly” and “we’re just not paying enough attention to that.”

End

Editors Note

Greenspan laughed when asked “what is behind the bubble” and explained that the deteriorating U.S. budget deficits are not sustainable and his comments in this regard are important to note:

“Essentially, we are beginning to run ever larger government deficits. Remember, that we are talking about deficits going to a trillion dollars.

But, debt has been rising very significantly and we are in fact – if you want to take the Congressional budget office figures at face value – we are going to run through the peaks of where we were during World War II on the ratio of federal debt to GDP which is extraordinarily high.

I think that we are not paying enough attention to that.”

As we noted in our recent podcasts, the total debt position of the U.S. is completely unsustainable and Trump’s irresponsible fiscal policies may speed up the slow bankruptcy of the U.S.

Last February, Greenspan said that gold is the “ultimate insurance policy” and “the primary global currency.”

He warned that “the eurozone isn’t working” and has “grave concerns about the euro.”

“Investment in gold now is insurance…”

Related reading

Greenspan Says Gold “Ultimate Insurance Policy” as has “Grave Concerns About Euro”

Greenspan Warns Stagflation Like 1970s “Not Good For Asset Prices”

News and Commentary

Gold likely to trade in an average of $1,410 by Q4 2018 (ScrapRegister.com)

Asia Stocks Slide; Rising Yields Spur BOJ to Act (Bloomberg.com)

Tech Selloff Accelerates as Treasury Rout Deepens (Bloomberg.com)

Chinese gold demand returns to growth as appetite for jewellery soars (SCMP.com)

China’s Gold Buying Rises 9.41% in 2017 (Xinhuanet.com)

Perth Mint’s Jan gold sales surges 38 pct m/m, silver jumps 22 pct (Reuters.com)

Source: SoundingLine

Gold Price To Rise Nearly 5% in 2018 – LBMA Forecast (LMBA.org)

Russian banks increase gold purchases at record pace (RT.com)

These are 5 finance terms you might be using incorrectly (StansBerryChurcHouse.com)

Bitcoin Is Just the Latest in the Trend Toward Decentralization (GoldSeek.com)

This Isn’t a Drill Mortgage Rates Hit Highest Level Since May 2014 (TheMaven.net)

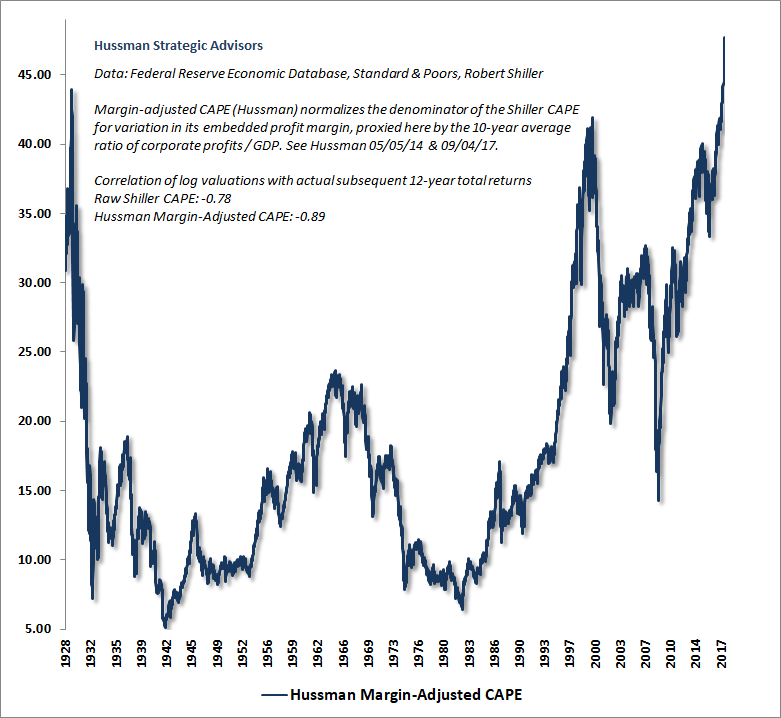

Crash ‘Risk’ Is Soaring: “This Is Where They Lost Their Minds” Hussman (ZeroHedge.com)

Gold Prices (LBMA AM)

02 Feb: USD 1,345.00, GBP 946.48 & EUR 1,077.61 per ounce

01 Feb: USD 1,341.10, GBP 941.99 & EUR 1,077.98 per ounce

31 Jan: USD 1,343.35, GBP 950.29 & EUR 1,078.98 per ounce

30 Jan: USD 1,345.70, GBP 954.37 & EUR 1,083.56 per ounce

29 Jan: USD 1,348.40, GBP 955.07 & EUR 1,085.46 per ounce

26 Jan: USD 1,354.35, GBP 950.21 & EUR 1,087.41 per ounce

25 Jan: USD 1,360.25, GBP 954.35 & EUR 1,095.27 per ounce

Silver Prices (LBMA)

02 Feb: USD 17.14, GBP 12.05 & EUR 13.72 per ounce

01 Feb: USD 17.19, GBP 12.09 & EUR 13.82 per ounce

31 Jan: USD 17.23, GBP 12.17 & EUR 13.84 per ounce

30 Jan: USD 17.30, GBP 12.24 & EUR 13.91 per ounce

29 Jan: USD 17.34, GBP 12.33 & EUR 13.99 per ounce

26 Jan: USD 17.40, GBP 12.21 & EUR 13.99 per ounce

25 Jan: USD 17.52, GBP 12.29 & EUR 14.12 per ounce

Gold & Silver Hammered As BLS Jobs Report Hits Tape

Nearly $2,000,000,000 of gold “sold” in two minutes, and silver hammered under $17. Here’s an update…

Today is one of the cartel’s favorite days to smash.

Gold & silver were hit hard as soon as the jobs report hit the tape:

In the first two minutes, 14,000 gold contracts were “sold” into the “news”.

For anybody doing the math, that’s $1,890,000,000 notional value of gold sold in two minutes, and it created less than a $10 move in the price of gold.

Silver was hit too as you can see. Right now, they have even managed to get silver under $17.

As to no surprise, the dollar shot straight up like a rocket ship.

Russian banks increase gold purchases at record pace

Submitted by cpowell on Thu, 2018-02-01 20:51. Section: Daily Dispatches

From Russia Today, Moscow

Thursday, February 1, 2018

The Russian government has purchased two-thirds of all the gold mined in country, buying it from local banks to add to reserves as the Kremlin sees the precious metal as a safe haven at a time of geopolitical turbulence.

“For banks this is good business. They credit mining companies, which return the loan with the gold they extracted. Then banks sell it to the central bank,” according to the Russian Finance Ministry, quoted by the Prime news agency.

Russia is the largest gold buyer in the world, and purchases by Russian banks have increased substantially in recent years.

Last year Russian banks bought 205.155 tons of gold, which is 4.7 percent more than in 2016 (195.89 tons), and approximately 67 percent of all gold produced in Russia. This is also a 13 percent increase compared to 2013.

The biggest buyers are VTB24, Sberbank, and Gazprombank. All three banks have registered at the Shanghai precious metals exchange. In April VTB announced plans to sell up to 100 tons of gold to China annually. …

… For the remainder of the report:

https://www.rt.com/business/417592-russian-banks-gold-purchases

END

LBMA always promises transparency but it never delivers upon that promise

(courtesy Ronan Manly/Bullionstar/GATA)

Ronan Manly: LBMA promises transparency but never delivers

Submitted by cpowell on Thu, 2018-02-01 21:21. Section: Daily Dispatches

4:23p ET Thursday, February 1, 2018

Dear Friend of GATA and Gold:

Gold researcher Ronan Manly today examines the years-long racket of the London Bullion Market Association’s promising greater transparency in the gold market while always failing to deliver. Manly’s analysis is headlined “What’s Happening (or Not) at the LBMA: Some Updates” and it’s posted at Bullion Star here:

https://www.bullionstar.com/blogs/ronan-manly/whats-happening-not-lbma-u…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

Ted Butler has been banging the table, screaming at the CFTC as they allow JPMorgan to acquire huge amounts of silver and now gold. JPMorgan is now up to 700 million oz of silver and they still are the largest silver short on the planet.

Two commentaries: Chris Powell on Ted Butler/Ted Butler GATA)

Ted Butler: CFTC’s long silver investigation missed what the agency just fined

Submitted by cpowell on Thu, 2018-02-01 21:47. Section: Daily Dispatches

4:48p ET Thursday, February 1, 2018

Dear Friend of GATA and Gold:

Rather than congratulate the U.S. Commodity Futures Trading Commission for taking note last week of the manipulation of the monetary metals futures markets, silver market rigging whistleblower Ted Butler today notes acerbically that the violations just cited by the commission took place during its interminable investigation of the silver market, which found … nothing at all!

Now, Butler writes, what about JPMorganChase’s domination of the silver market? Will the CFTC examine that?

Butler’s commentary is headlined “Unfinished Business” and it’s posted at GoldSeek’s companion site, SilverSeek, here —

http://silverseek.com/commentary/unfinished-business-17082

— and at 24hGold here:

http://www.24hgold.com/english/news-gold-silver-unfinished-business.aspx…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

Unfinished Business

|

February 1, 2018 – 11:23am

The big news this week was the filing of charges and settlements for price manipulation and “spoofing” brought by the CFTC, in conjunction with the DOJ and FBI, against three banks and a half dozen individual traders; mostly involving illegal trading activities in COMEX gold and silver futures. The announcement set off a debate about whether the filing proved the allegations that gold and silver prices were manipulated as many, certainly including me, have maintained.

http://www.cftc.gov/PressRoom/PressReleases/pr7682-18

Put simply, the filings do not prove that silver and gold have been manipulated lower in price over the years. But then again, neither do the filings show that prices have not been manipulated in the manner I contend. What the charges do prove is that spoofing is a corrupt and illegal practice that should not exist in any form and on that basis. My immediate reaction is what the heck took the CFTC this long to act? Regular readers know I have railed against spoofing for many years as being completely devoid of any redeeming or legitimate features while the CFTC stood by. The practice of placing phony orders to influence price should have been outlawed from day one.

That said, I suppose it is good that the agency finally took action, under the kindest interpretation of the cliché of it’s better late than never. Certainly, those banks and traders accused of the practice will likely not do so in the future. And seeing the CFTC actually use the word manipulation in connection with COMEX gold and silver can’t be considered bad. Beyond that, unfortunately, the charges and settlements are troubling in that they only scratch the surface of whether silver and gold prices are manipulated.

Truth be told, if the regulators were out to clean up what ails silver and gold pricing, then they didn’t come close with these filings. If the CFTC was intending that this week’s announcements showed that it was truly cracking down on bad actors in silver and gold, then it failed. I would remind you that many of the violations announced took place while the CFTC was in the midst of its infamous five year silver “investigation”.

Think I’m being too hard on the CFTC? Then try explaining how the agency has managed to ignore the activities of the most prominent gold and silver market crook of all – JPMorgan. It’s not as if the agency hasn’t been given ample evidence of JPMorgan’s dominant role in manipulating prices ever since the bank took over Bear Stearns in 2008. I know because I’ve done nothing but make the case against JPMorgan for nearly all that time.

And I must say, I am disappointed in the actions, or lack thereof, of the Enforcement Director, James McDonald. Privately, I’m still assured that McDonald is a straight arrow, although lately the question has come up whether what JPMorgan is doing is really illegal if higher ups in the government pecking order have ordered McDonald to keep off JPM’s case. To that I say balderdash – in matters silver and gold, JPMorgan is a stone cold crook and no order from above supersedes McDonald’s oath to uphold the Constitution and the law of the land. It’s disturbing that the agency seems to be going after the little fish, while the biggest market crook of them all, JPMorgan, gets a pass.

It’s not as if I haven’t gone out of my way to present the case against JPMorgan to McDonald, starting on his first day on the job last April 10. I spelled out in great detail how JPMorgan had never taken a loss on any short position it ever added in COMEX silver in nearly 10 years; a trading record that would be impossible if JPMorgan wasn’t rigging prices. And get this – since I wrote to McDonald last year, JPMorgan has added and bought back silver shorts on four separate occasions for more than 10,000 net contracts on each occasions, making close to $500 million in total trading profits. As a reminder, I base all my calculations on the data published by the agency.

http://silverseek.com/commentary/another-opportunity-16489

In that public letter last year, I even spelled out the rationale for why JPMorgan was manipulating silver (and gold) prices, namely, to allow this crooked bank in acquiring as much physical metal as it could get at the lowest prices it could rig. This is the means, motive, opportunity and intent behind JPMorgan’s manipulation – to pick up as much cheap metal as it possibly could. In the last 10 months, in addition to racking up massive profits in paper COMEX trading, JPMorgan has added another 100 million oz of silver to a hoard now measuring nearly 700 million oz. And as I have written recently, JPMorgan has been doing the exact same thing in gold, namely, making enormous paper profits by being the largest short in COMEX gold, while picking up boatloads of physical gold on the cheap – at least 20 million oz over the past 5 years.

You can lead a horse to water but you can’t force it to drink. I can lay out the crimes of JPMorgan, using the agency’s data and taking the risk of publicly accusing the nation’s largest bank of criminality, but I can’t force to the CFTC to do its job. After all, the easiest way to dismiss these very serious allegations would be to openly address them. To be fair, should the CFTC ever get around to cracking down on the crooks at JPMorgan, I will happily eat my words and sing the regulators’ praises.

Ted Butler

February 1, 2018

Questions or comments? info@butlerresearch.com

END

Almost 1000 miners trapped in an underground mine, Sibanye in South Africa

(courtesy Business Day/J’berg/GATA)

Nearly a thousand gold miners trapped underground in South Africa

Submitted by cpowell on Thu, 2018-02-01 22:08. Section: Daily Dispatches

Central banks and bullion banks are working hard to keep them trapped.

* * *

By Allan Seccombe

Business Day, Johannesburg

Thursday, February 1, 2018

About 950 workers are trapped underground at Sibanye-Stillwater’s Beatrix gold mine in the Free State, after an overnight power failure cause by a lightning strike.

Rescue efforts are under way, the Association of Mineworkers and Construction Union (AMCU) said this afternoon.

At least 40 workers had been brought back to the surface at the gold mine, with 950 miners still below ground at 3 Shaft at Beatrix, the union said.

Sibanye said a power pylon had been knocked over during a storm Wednesday night, cutting power to 4 Shaft and the main Beatrix operations of 2 and 3 Shafts. Power had since been restored to 4 Shaft and people hauled to surface.

Power was restored to 2 Shaft and workers were hoisted to the surface there today.

Sibanye wanted 950 workers at 3 Shaft to wait there until the winder serving the shaft was back in working order, rather than have hundreds of people walking for four hours to 2 Shaft, company spokesperson James Wellsted said.

No one had been injured, he said, and the company was supplying food and water to the workers trapped underground at 3 Shaft by deploying a capsule down the shaft, he said. The professional rescue team was with the trapped miners, he said.

There was no immediate timeline of when the workers would be returned to surface, he said. …

… For the remainder of the report:

https://www.businesslive.co.za/bd/companies/mining/2018-02-01-at-least-9…

* * *

END

All miners rescued

News 24 J’Berg/GATA)

All trapped gold miners in S. Africa rescued unhurt

Submitted by cpowell on Fri, 2018-02-02 12:11. Section: Daily Dispatches

By Jeanette Chabalala

News24, Johannesburg

Friday, February 2, 2018

WELKOM, South Africa — The National Union of Mineworkers confirmed today that all 955 Sibanye Gold mine workers who were trapped underground have been resurfaced.

“The mine workers were rescued at around 6:30 this morning,” the union’s national spokesperson, Livhuwani Mammburu, confirmed to News24.

“They are currently getting medical checkups. No injuries were sustained. They are just exhausted.”

A meeting was set to be held later at the mine’s training centre with management after all the workers had been attended to medically.

Sibanye Gold spokesperson James Wellsted also confirmed that the miners had been brought to the surface and that there were no serious injuries. …

… For the remainder of the report:

https://www.news24.com/SouthAfrica/News/rescued-sibanye-gold-miners-rece…

Bitcoin crashes

(courtesy zerohedge)

Bitcoin Bounces Hard But Cryptocarnage Remains

Update 0815ET: Just as we saw at yesterday’s US stock market close, dip-buyers just stepped in to Bitcoin in a significant way, lifting the crypto currency over $1000 off the lows and back above $8000…

But the carnage remains… for now…

Notably, another exchange – BitMEX is down…

* * *

It seemed like just yesterday that every cryptocurrency bloodbath would be promptly bought, often sending the price of bitcoin and its peers to new record highs. Those days appear to be over, at least for now.

So far this year, cryptocurrencies have been beset with bad news: Bitfinex, by some accounts the world’s largest exchange, was recently subpoenaed by the CFTC, along with Tether, a separate corporate entity that involves many of the same people from Bitfinex, as questions mount about the authenticity of its tether token. Tethers, which are widely used by crypto traders to quickly move in and out of different crypto pairs, are supposed to be backed by dollars, with one tether = one dollar. But Tether’s decision to fire its auditor appears to validate the concerns of the exchange’s critics.

Raising fears about another massive, Mt. Gox-like hack, Coincheck, a mid-sized Japanese exchange, reported this month that it suffered “the biggest crypto theft in its history” when hackers made off with $400 million worth of NEM tokens. On Friday, Bloomberg reported that Japan’s Financial Services Agency raided Coincheck’s offices a week after the hack, hauling out documents and computers as evidence.

The inspection was conducted to ensure security for users, Finance Minister Taro Aso said. On Friday morning, 10 FSA officials entered Coincheck’s premises to gain a better understanding of how the exchange is operating in light of the regulator’s business improvement order imposed earlier this week, an agency official told reporters in Tokyo. The exchange has until Feb. 13 to produce a report detailing the causes of the incident.

And as if the threat of cybertheft wasn’t enough to scare off the marginal buyer, the threat of regulators trying to ban crypto – much like China did – has become a major concern. Regulators in India said explicitly declared yesterday that bitcoin is not legal tender and said it would take “all measures to eliminate their use,”foreshadowing a coming crackdown in a market that many hoped would one day grow to one of bitcoin’s largest. After a weekslong will-they-won’t-they back and forth, South Korea‘s Ministry of Justice announced revealed that it had abandoned a proposal to ban crypto outright, but instead seek to regulate it, requiring exchanges to obtain details about customer identities.

After bitcoin’s worst month in years, it dipped below $8,000 Friday morning in the US to levels it hasn’t seen since November while Ethereum, Ripple and Litecoin all took double-digit beatings.

Meanwhile, as Bloomberg points out, bitcoin’s rough month was even worse in South Korea. As of Friday morning ET, bitcoin has dropped more than 60% from its January high in Korea as South Korea struggles with how to prevent money laundering and tax evasion without throttling the ecosystem.

The selloff has many Korea traders fearing the worst.

“The bubble in cryptocurrencies has burst” in Korea, said Yeol-mae Kim, an analyst at Eugene Investment & Securities Co. in Seoul. Because of the intense demand from retail buyers, bitcoin trades at what’s called “the kimchi premium” on SK exchanges. In January, the premium stretched to its widest level on record when bitcoin traded at $22,525 in Korea, $7,500 higher than the composite price at the time.

Bank Of America, JP Morgan Bar Crypto Purchases On Credit Card

The latest crackdown against cryptos was unveiled on Thursday when the largest US bitcoin exchange, Coinbase, sent out notices to clients, informing them that purchasing cryptocurrencies on credit would now be prohibitively expensive, if not impossible, as banks have started to process payments for bitcoin et al as “cash advances”, which tend to come with extremely high interest rates:

Dear Coinbase Customer

We’re writing because you have a credit card on file and want to inform you of a recent change that may increase the cost of purchasing digital currency with a credit card.

Recently, the MCC code for digital currency purchases was changed by a number of the major credit card networks. The new code will allow banks and card issuers to charge additional “cash advance” fees. These fees are not charged or collected by Coinbase. These additional fees will show up as a separate line item on your card statement.

The move came as a number of bank and card issuers announced that they would be reviewing changes to their policies around the purchases of crypto assets using credit cards.

Then, last Thursday the Wall Street Journal reported that Capital One banned customers from using credit cards to purchase bitcoin or coins on the Ethereum blockchain, citing “limiting mainstream acceptance and the elevated risks of fraud, loss and volatility.” Discover Financial announced it would likewise block bitcoin transactions.

Then yesterday, MarketWatch reported that Bank of America and other major lenders are assessing the use of credit cards to purchase bitcoin and other virtual currencies, which could result in restrictions or limits.

Today that was confirmed when Bank of America became the largest U.S. lender yet to bar customers from using their credit cards to buy cryptocurrencies.

According to an internal memo to employees obtained by Bloomberg, the second largest US bank said it “will begin declining credit card transactions with known cryptocurrency exchanges” starting today. It said the policy will apply to all personal and business credit cards issued by the bank.

Betty Riess, a spokeswoman for the Charlotte, North Carolina-based bank, confirmed the bank will no longer allow the transactions.

And then, moments later, JPM joined the fray too:

- JPMORGAN TO HALT CRYPTO PURCHASES ON SATURDAY, SPOKESWOMAN SAYS

As a reminder, a recent LendEdu survey revealed that just over 18% of bitcoin purchases were made using a credit card.

The good news: 82% of all crypto purhcases were not made using a credit card.

Your early FRIDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

i) Chinese yuan vs USA dollar/CLOSED UP AT 6.2844 /shanghai bourse CLOSED UP AT 15.10 POINTS 0.44% / HANG SANG CLOSED DOWN 40.31 POINTS OR 0.12%

2. Nikkei closed DOWN 211.58 POINTS OR 0.90% /USA: YEN RISES TO 109.88

3. Europe stocks OPENED RED /USA dollar index RISES TO 88.85/Euro FALLS TO 1.2490

3b Japan 10 year bond yield: RISES TO . +.085/ (CENTRAL BANK INTERVENTION THIS MORNING) GOVERNMENT INTERVENTION !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 109.88/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD FINALLY IN THE POSITIVE/BANK OF JAPAN LOSING CONTROL OF THEIR YIELD CURVE AS THEY PURCHASE ALL BONDS TO GET TO ZERO RATE!!

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 65.76 and Brent: 69.31

3f Gold UP/Yen DOWN

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil UP for WTI and UP FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund RISES TO +.734%/Italian 10 yr bond yield DOWN to 2.002`% /SPAIN 10 YR BOND YIELD UP TO 1.433%

3j Greek 10 year bond yield FALLS TO : 3.668?????????????????

3k Gold at $1346.30 silver at:17.18: 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble DOWN 35/100 in roubles/dollar) 56.31

3m oil into the 65 dollar handle for WTI and 69 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 109.88 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 0.9245 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1597 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now POSITIVE territory with the 10 year RISING to +0.734%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.7844% early this morning (THIS IS DEADLY TO ALL MARKETS). Thirty year rate at 3.032% /

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

(courtesy Jim Reid/Bloomberg/Deutsche bank/zero hedge)

“Sea Of Red”: Stocks, Futures Plunge Amid Soaring Yields

The last day of an already tumultuous week is shaping up as a bloodbath for investors across the globe as the following market snapshot of global stocks and futures shows.

European equity markets and U.S. equity futures sold off sharply, however as Bloomberg notes, the traditional pre-NFP lack of market activity has so far mitigated large cross-asset reaction. S&P futures were down as much as 20 points and flirting with the 2,800 level.

Equities were tested by the surge in bond yields, with some fund managers saying anything between 2.7% and 3% on the 10Y TSY would signal a bond bear market. The level is seen by many stock-watchers as a potential trigger for a correction in equities.

To be sure, the correlation between higher yields and lower equities continued overnight in a particularly aggressive manner. The silver lining is that as the US 10y tests 2.80% and the US 30y at 3.04%, the USD at least appears to have found a bottom, for now. Overnight German Bund yields also reached a two-year high as core European bonds fell along with gilts.

As we pointed out last night, the risk off sentiment took shape in Asia, with Chinese stocks continuing their recent plunge…

… as core yields weighed on the EM FX space as a whole. “Markets are increasingly choppy and price action increasingly unpredictable” Citi’s FX desk notes.

There was nothing obvious to trigger the move: some attributed the risk off mode to a report that 18 people were injured when a van intentionally hit pedestrians in central Shanghai, China. Additionally, WSJ reports, “Chinese stocks had their worst week since 2016, with fresh concerns about Beijing’s campaign to cut financial risk and predictions of a slowing economy…” The BoJ also knocked JPY back after it took action against the rising JGB 10y yield by announcing it would buy unlimited amounts of 10y JGBs at 11bps.

Meanwhile, Europe was a bloodbath largely due to to the previously discussed poor result from Deutsche Bank which sent the German lender’s stock tumbling. The weakness quickly spread to German stocks with the DAX turning negative for 2018, giving up an advance that had reached 5%, as the DAX slides for a fifth straight day. This was the worst weekly drop for the DAX since November 2016, down 3.5%

The DAX weakness sent the broader Eurostoxx Index dropped for a 5th day, the longest losing streak since November, and sliding below its 200-DMA.

In FX, the USD/JPY rallied further toward 110 after BOJ acted to control the yield curve by placing a cap on yields as it offered to buy an unlimited amount in 10yr JGBs at a yield of 0.110%. The BoJ also announced to buy JPY 450bln in 5yr-10yr, more than the prior JPY 410bln operation.

The Bloomberg Dollar Spot Index snapped a three-day decline and headed for its biggest gain since November as stretched short positioning called for caution ahead of the U.S. payrolls report. The yen was set for its worst week in 3 1/2 months as the BOJ further damped speculation about normalizing its policy anytime soon. Monetary policy prospects weighed on Antipodean currencies as well, while the euro and the pound also came under pressure. European bonds and equities traded in the red. USD strength was particularly evident against EMFX, with USD/ZAR trading back above 12.00.

Elsewhere, core yields edge higher but without much momentum, while credit spreads widen, iTraxx Crossover through 200-DMA. As Bloomberg highlights, a hawkish Euribor put trade targeting ~80bps of ECB hikes by end-2019 caught attention; crude and metals weighed by USD move, another bitcoin selloff of more than 10%.

Looking at today’s busy calendar, the highlight will obviously be the employment report. Average hourly earnings have taken over from the headline number as the key focus of the report at the moment. And while economists are strongly of the view that wages are going up this will not be seen in today’s report, where monthly income growth is expected to tick down a tenth (+0.2% vs. +0.3%) but the year-over-year trend may round up a tenth to 2.6%. For the headline number consensus expects a gain in payrolls (+180k vs. +148k) which should keep the unemployment rate steady at 4.1%. So far this week the employment and wages data has generally been positive. The latest evidence was 4Q unit labour costs yesterday which were above market at 2% (vs. 0.9% expected).

Elsewhere, oil traded near its highest level since 2015 in New York as forecasters paint a rosier picture for supply and demand. WTI and Brent crude futures have modestly extended on the prior day’s gains, albeit off best levels with WTI back below USD 66/bbl and Brent retreating from USD 70/bbl with energy newsflow otherwise relatively light ahead of the Baker Hughes rig count and earnings from Exxon and Chevron (keep an eye out for CAPEX plans). In metals markets, Gold has traded relatively sideways ahead of NFP, whilst Chinese steel futures were seen higher overnight amid ongoing speculation over further extensions to domestic steel production curbs.

Finally, Bitcoin continues to slide after a miserable January, dropping below $8,000 in early trading.

Market Snapshot

- S&P 500 futures down 0.7% to 2,803.75

- STOXX Europe 600 down 0.8% to 390.55

- MSCI Asia Pacific down 0.7% to 183.03

- MSCI Asia Pacific ex Japan down 0.7% to 599.58

- Nikkei down 0.9% to 23,274.53

- Topix down 0.3% to 1,864.20

- Hang Seng Index down 0.1% to 32,601.78

- Shanghai Composite up 0.4% to 3,462.08

- Sensex down 2.3% to 35,099.20

- Australia S&P/ASX 200 up 0.5% to 6,121.39

- Kospi down 1.7% to 2,525.39

- German 10Y yield rose 2.0 bps to 0.741%

- Euro down 0.2% to $1.2484

- Italian 10Y yield fell 6.3 bps to 1.697%

- Spanish 10Y yield rose 1.4 bps to 1.423%

- Brent futures up 0.2% to $69.78/bbl

- Gold spot down 0.2% to $1,346.44

- U.S. Dollar Index up 0.2% to 88.87

Top Overnight News

- Chancellor Angela Merkel’s bloc and Germany’s Social Democrats secured an agreement on education even as “large” policy differences remain, a top party official said as parties near a self-imposed weekend deadline

- The U.K. must not enter into a new customs union with the European Union after it leaves the bloc, Trade Secretary Liam Fox said, setting a new red line for Theresa May’s negotiations with Brussels and her own party on Brexit

- Riksbank Deputy Governor Martin Floden says “there are risks to the rate path, inflation in particular is unusually uncertain,” according to an interview with Market News International

- Japan’s government will likely present to Parliament its nominees of BOJ governor and deputy governors around mid- to late February at the earliest, Reuters reports, citing unidentified people familiar with the matter

- BofAML says “massive” equity inflows last week helped trigger a sell signal triggered Jan 30th via record equity inflows, bullish hedge fund risk appetite indicator and global equity index breadth measure

- U.K. Jan. Construction PMI 50.2 vs 52.2 est; housing activity lowest since Jul. 2016

- BOJ took action today after large increase in JGB yields: senior official

- Strong chance that BOJ’s Kuroda will be reappointed, according to people familiar, Reuters reports

- China to allow overseas investors to trade iron ore futures on Dalian exchange

Asia equity markets traded broadly lower with sentiment in the region dampened amid a lack of catalysts and following the indecisive lead from Wall St. where most major indices finished negative and the Nasdaq 100 underperformed. ASX 200 (+0.5%) and Nikkei 225 (-0.8%) were mixed with Australia kept afloat by financials and energy, while the Japanese benchmark was the laggard and saw nearly all the prior day’s gains wiped out. Elsewhere, Shanghai Comp. (-0.4%) and Hang Seng (-0.1%) were downbeat amid Shenzhen volatility, while continued inaction by the PBoC also resulted to a weekly net liquidity drain of CNY 760bln. Finally, 10yr JGBs reversed the initial spill-over selling from US, with support from a risk averse tone and after the BoJ Rinban announcement in which it increased purchases in the 5yr-10yr range. Furthermore, the BoJ also effectively placed a cap on yields as it offered to buy an unlimited amount in 10yr JGBs at a yield of 0.110%. BoJ announced to buy JPY 450bln in 5yr-10yr (Prev. JPY 410bln), JPY 190bln in 10yr-25yr and JPY 80bln in 25yr+ JGBs, while it also announced a special bond operation to buy an unlimited amount of 10yr JGBs at a yield of 0.110%. However, there were no takers for the fixed rate operation and the BoJ stated it took the steps after a surge in yields and that it is adhering to policy of keeping 10yr yield near 0%. PBoC skipped open market operations for a net weekly drain of JPY 760bln vs. Prev. JPY 320bln drain W/W.

Top Asia News

- Dollar Slide Spurs Yuan Forecast Revisions, Worry on Speed

- Foreign Funds Poured $13 Billion Into Chinese Shares in January

- Fosun’s $1.5 Billion Biotech Arm Is Said to Mull Hong Kong IPO

- HNA-Like Debt Pileups Raise Risk of Forced Asset Sales in China

- What’s on the Block in China’s Potential Sale of the Century?

- World’s Biggest Pension Fund Gains $55 Billion as Stocks Climb

- Mitsui & Co Surges to Highest Since 2008 on Share Buyback

European equities (Eurostoxx 50 -0.6%) are trading lower across the board following a downbeat session overnight in Asia-Pac and the US. Underperformance has been seen in the DAX (-1.1%) with the index dragged lower by Deutsche Bank (-6.1%) after reporting a larger than expected quarterly loss; Commerzbank (-1.5%) also seen lower but little contagion seen in the broader European banking sector. Elsewhere, energy names are the only sector trading higher in Europe alongside firmer energy prices, telecoms underperform with BT (-5.5%) at the bottom of the FSTE 100 following their latest earnings update.

Top European News

- Germany DAX Gives Up Year’s Gain in Worst Selloff Since 2016

- ECB Official Warns Markets Are Unprepared for Inflation Bogeyman

- Czechs Signal Pause in Rate Hikes and Bet on Currency Gains

- Wereldhave Slumps On 2018 Profit Guidance Miss, Dividend Cut

In FX, the DXY remains weak overall as its 2018 (and late 2017) bear trend continues, but the index is holding in above 88.500 and some key support levels ahead of the 88.000 level. In fact, the Dollar is firmer vs all G10 rivals as US Treasury yields continue their ascent and some benchmark maturities hit key or psychological levels (long bond over 3% for example). EUR/USD is pivoting around 1.2500, Cable still finding it tough on advances beyond 1.4200, USD/Cad sticky circa 1.2300 and similarly USD/CHF bouncing back towards 0.9300 after forays below. USD/JPY is still gradually firming within a wide 109.00-110.00 range, and sniffing out layered offers up to the top of that band, with a 50% Fib at 109.88 also providing some resistance. JPY undermined by more aggressive BoJ buying of JGBs overnight, NZD by weak building permits and the AUD extending recent losses/underperformance on disappointing data and rolled out RBA rate expectations. Ahead, NFP the main Friday focus.

In commodities, WTI and Brent crude futures have modestly extended on the prior day’s gains, albeit off best levels with WTI back below USD 66/bbl and Brent retreating from USD 70/bbl with energy newsflow otherwise relatively light ahead of the Baker Hughes rig count and earnings from Exxon and Chevron (keep an eye out for CAPEX plans). In metals markets, Gold has traded relatively sideways ahead of NFP, whilst Chinese steel futures were seen higher overnight amid ongoing speculation over further extensions to domestic steel production curbs.

US Event Calendar

- 8:30am: Change in Nonfarm Payrolls, est. 180,000, prior 148,000

- Unemployment Rate, est. 4.1%, prior 4.1%

- Average Hourly Earnings MoM, est. 0.2%, prior 0.3%; Average Hourly Earnings YoY, est. 2.6%, prior 2.5%

- 10am: U. of Mich. Sentiment, est. 95, prior 94.4; Current Conditions, prior 109.2; Expectations, prior 84.8

- 5%

- 10am: Factory Orders, est. 1.5%, prior 1.3%; Factory Orders Ex Trans, prior 0.8%

- 10am: Durable Goods Orders, prior 2.9%; Durables Ex Transportation, prior 0.6%

- 10am: Cap Goods Orders Nondef Ex Air, prior -0.3%

DB’s Jim Reid concludes the overnight wrap

Today’s highlight will obviously be the employment report. Average hourly earnings have taken over from the headline number as the key focus of the report at the moment. DB are strongly of the view that wages are going up but we are not convinced you’ll see that in this report. They expect the number to tick down a tenth (+0.2% vs. +0.3% – consensus 0.2%) but the year-over-year trend may round up a tenth to 2.6%. For the headline number they expect a healthy gain in payrolls (+210k vs. +148k – consensus 180k) which should keep the unemployment rate steady at 4.1%. So far this week the employment and wages data has generally been positive. The latest evidence was 4Q unit labour costs yesterday which were above market at 2% (vs. 0.9% expected).

The employment report comes at a time of a continued sell off in US treasuries. UST 10y yields jumped the most in 12 months, rising 8.5bp to 2.791% and making a fresh high since April 2014. The UST 30y also closed above 3% for the first time since May 17 (3.025%) while the 2s10s steepened 6.5bp back to the highest since mid-December. The weakness seemed to have several contributing factors, such as a perception of it being a hawkish FOMC statement the night before, more data that supports the view that inflation is firming (the highest ISM prices paid reading since May 2011), and the UCL data discussed above. Over in Europe, changes in core 10y bond yields were more modest, with Bunds and Gilts up c2bp and OATs up 0.8bp. Peripherals actually outperformed, with yields down 2-6bp, in part supported by successful debt auctions in Spain.

Staying with US equities, the S&P 500 initially traded higher yesterday post Facebook’s results (shares +3.3%) but pared back gains to be marginally lower (-0.06%) while other bourses were mixed (Dow +0.14%; Nasdaq -0.35%). European markets were broadly lower, with the Stoxx 600 (-0.50%), FTSE (-0.57%) and DAX (-1.41%) down to a c4 week low. The pull back in the DAX was broad based with all sectors in the red, particularly industrials, real estate and healthcare stocks. The VIX was little changed at 13.47 (-0.5%).

After the bell, Amazon’s share price jumped c6% after reporting the strongest holiday quarter sales growth in eight years, while Apple’s shares recovered to be up c3%, in part as the CFO guided to >10% growth in iphone sales for the current quarter and investors took note of Apple’s higher average selling price for iPhone (+14% on pcp) as a potential sign of solid demand for its iPhone X after earlier reports to the contrary. Elsewhere, Alphabet is down c2% after its 4Q results missed estimates.

This morning in Asia, markets are broadly lower. The Nikkei (-0.85%), Kospi (-1.62%) and China’s CSI300 (-0.20%) are all down while the Hang Seng is up modestly (+0.13%) as we type. Elsewhere, the BOJ has announced its first unlimited fixed rate bond purchase operation since July, while also offering to buy more (40bn Yen; $365m) 5-10 year bonds at its regular operation this morning.