GOLD: $1328.00 UP $3.40

Silver: $16.57 DOWN 3 cents

Closing access prices:

Gold $1329.50

silver: $16.57

SHANGHAI GOLD FIX: FIRST FIX 10 15 PM EST (2:15 SHANGHAI LOCAL TIME)

SECOND FIX: 2:15 AM EST (6:15 SHANGHAI LOCAL TIME)

SHANGHAI FIRST GOLD FIX: $1324.85 DOLLARS PER OZ

NY PRICE OF GOLD AT EXACT SAME TIME: $1323.60

PREMIUM FIRST FIX: $1.25

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

SECOND SHANGHAI GOLD FIX: $1334.47

NY GOLD PRICE AT THE EXACT SAME TIME: $13235.40

Premium of Shanghai 2nd fix/NY:$9.07

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

LONDON FIRST GOLD FIX: 5:30 am est $1329.40

NY PRICING AT THE EXACT SAME TIME: $1329.90

LONDON SECOND GOLD FIX 10 AM: $1325.35

NY PRICING AT THE EXACT SAME TIME. $1326.00

For comex gold:

FEBRUARY/

NUMBER OF NOTICES FILED TODAY FOR FEBRUARY CONTRACT: 0 NOTICE(S) FOR NIL OZ.

TOTAL NOTICES SO FAR:1783 FOR 178300 OZ (5.458 TONNES),

For silver:

FEBRUARY

89 NOTICE(S) FILED TODAY FOR

445,000 OZ/

Total number of notices filed so far this month: 215 for 1,075,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: BID $8508/OFFER $8576: DOWN $351(morning)

Bitcoin: BID/ $8602/offer $8671: DOWN $255 (CLOSING/5 PM)

end

There are 4 tools used by the manipulators to raise stock prices while stocking down gold and silver:

- increasing the value of the USA dollar index

- shorting yen (buying usa/yen) which is your carry trade ie. buy stocks, short yen gold

- hammer vix (the volatility index) which states that everything is OK. ie. short volatility and gold buy stocks

- contain the 10 yr USA treasury yield below 2.80%

we are beginning to see fractures in all of them. today it was the yen that rose and that drove gold/silver higher.

Let us have a look at the data for today\

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total open interest FELL BY A TINY SIZED 453 contracts from 195,964 FALLING TO 195,511 DESPITE YESTERDAY’S SOLID 40 CENT GAIN IN SILVER PRICING. WE HAD MINIMAL COMEX LIQUIDATION. HOWEVER, WE WERE AGAIN NOTIFIED THAT WE HAD ANOTHER GOOD SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP ROUTE: 1862 EFP’S FOR MARCH AND AND 0 EFP’S FOR MAY AND ZERO FOR ALL OTHER MONTHS AND THUS TOTAL ISSUANCE OF 1864 CONTRACTS. WITH THE TRANSFER OF 1862 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24 HRS IN THE ISSUING OF EFP’S. THE 1862 CONTRACTS TRANSLATES INTO 9.32 MILLION OZ. WITH THE HUGE DROP IN OPEN INTEREST AT THE COMEX. WE SHOULD EXPECT BIGGER GAINS IN EFP TRANSFERS IN THE NEXT FEW DAYS WITH THE LARGE LOSS AT THE COMEX AS LONGS GAVE UP SEEKING METAL AT THIS EXCHANGE.

ACCUMULATION FOR EFP’S/SILVER/ STARTING FROM FIRST DAY NOTICE/FOR MONTH OF FEBRUARY:

32,254 CONTRACTS (FOR 10 TRADING DAYS TOTAL 32,254 CONTRACTS OR 161.270 MILLION OZ: AVERAGE PER DAY: 3225 CONTRACTS OR 16.125 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH: 161.3 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 23.0% OF ANNUAL GLOBAL PRODUCTION

ACCUMULATION IN YEAR 2018 TO DATE SILVER EFP’S: 409.6 MILLION OZ.

ACCUMULATION FOR JAN 2018: 236.879 MILLION OZ

RESULT: A TINY SIZED GAIN IN OI SILVER COMEX DESPITE THE SOLID 40 CENT GAIN IN SILVER PRICE. WE HOWEVER HAD A GOOD SIZED EFP ISSUANCE OF 1862 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER . FROM THE CME DATA 1862 EFP’S FOR MONTHS MARCH AND MAY WERE ISSUED FOR MONDAY FOR A DELIVERABLE FORWARD CONTRACT OVER IN LONDON WITH A FIAT BONUS. WE GAINED 1883 OI CONTRACTS i.e. 1862 open interest contracts headed for London (EFP’s) TOGETHER WITH A INCREASE OF 21 OI COMEX CONTRACTS. AND ALL OF THIS HAPPENED WITH THE CONSIDERABLE RISE IN PRICE OF SILVER OF 40 CENTS AND A CLOSING PRICE OF $16.60 WITH RESPECT TO YESTERDAY’S TRADING. YET WE STILL HAVE A FAIR AMOUNT OF SILVER STANDING AT THE COMEX.

In ounces AT THE COMEX, the OI is still represented by just UNDER 1 BILLION oz i.e. 0.980 BILLION TO BE EXACT or 140% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT FEBRUARY MONTH/ THEY FILED: 89 NOTICE(S) FOR 445,000 OZ OF SILVER

In gold, the open interest FELL BY A TINY 590 CONTRACTS DOWN TO 510.150 DESPITE THE GOOD SIZED RISE IN PRICE OF GOLD WITH YESTERDAY’S TRADING ($12.00). HOWEVER, IN ANOTHER DEVELOPMENT, WE RECEIVED THE TOTAL NUMBER OF GOLD EFP’S ISSUED FOR MONDAY AND IT TOTALED A FAIR SIZED 3381 CONTRACTS OF WHICH APRIL SAW THE ISSUANCE OF 3381 CONTRACTS AND JUNE SAW THE ISSUANCE OF 0 CONTRACTS AND THEN ALL OTHER MONTHS ZERO. The new OI for the gold complex rests at 510,150. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. DEMAND FOR GOLD INTENSIFIES GREATLY AS WE CONTINUE TO WITNESS A HUGE NUMBER OF EFP TRANSFERS TOGETHER WITH THE MASSIVE INCREASE IN GOLD COMEX OI TOGETHER WITH THE TOTAL AMOUNT OF GOLD OUNCES STANDING FOR FEBRUARY COMEX. EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER (BIG RISE IN BOTH GOFO AND SIFO) AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES. IN ESSENCE TODAY DESPITE YESTERDAY’S TRADING IN GOLD, WE HAVE A GAIN OF 2791 CONTRACTS: 590 OI CONTRACTS DECREASED AT THE COMEX AND A FAIR SIZED 3381 OI CONTRACTS WHICH NAVIGATED OVER TO LONDON.(2791 oi gain in CONTRACTS EQUATES TO 8.68 TONNES)

FRIDAY, WE HAD 6968 EFP’S ISSUED.

ACCUMULATION OF EFP’S/ GOLD(EXCHANGE FOR PHYSICAL) FOR THE MONTH OF FEBRUARY STARTING WITH FIRST DAY NOTICE: 102,277 CONTRACTS OR 10,227,700 OZ OR 318.10 TONNES (10 TRADING DAYS AND THUS AVERAGING: 10,227 EFP CONTRACTS PER TRADING DAY OR 1,022,700 OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SIZE OF THESE EFP TRANSFERS : SO FAR THIS MONTH IN 9 TRADING DAYS: IN TONNES: 318.10 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2017, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 2200 TONNES

THUS EFP TRANSFERS REPRESENTS 318.10/2200 x 100% TONNES = 14.5% OF GLOBAL ANNUAL PRODUCTION SO FAR IN FEBRUARY ALONE.

ACCUMULATION OF GOLD EFP’S YEAR 2018 TO DATE: 951.63 TONNES

ACCUMULATION OF GOLD EFP’S FOR JANUARY 2018: 653.22 TONNES

Result: A TINY SIZED DECREASE IN OI AT THE COMEX DESPITE THE STRONG SIZED GAIN IN PRICE IN GOLD TRADING YESTERDAY ($12.00). IT IS WITHOUT A DOUBT THAT MANY OF THE DEPARTED COMEX LONGS RECEIVED THEIR PRIVATE EFP CONTRACT FOR EITHER APRIL OR JUNE. HOWEVER, WE HAD ANOTHER GOOD SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 3381 AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX AND YET WE ALSO OBSERVED A HUGE DELIVERY MONTH FOR THE MONTH OF DECEMBER. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 3381 EFP CONTRACTS ISSUED, WE HAD A NET GAIN IN OPEN INTEREST OF 2791 contracts ON THE TWO EXCHANGES:

3381 CONTRACTS MOVE TO LONDON AND 590 CONTRACTS DECREASED AT THE COMEX. (in tonnes, the GAIN in total oi equates to 8.68 TONNES).

we had: 0 notice(s) filed upon for NIL oz of gold.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD

WITH GOLD UP $3.40 TODAY, THE CROOKS DECIDED NOT THE RAID THE COOKIE JAR/INVENTORY REMAINS CONSTANT/

Inventory rests tonight: 820.71 tonnes.

SLV/

NO CHANGES IN SILVER INVENTORY AT THE SLV/ AGAIN WITH TODAY’S HUGE RISE IN SILVER PRICE: NO CHANGE IN INVENTORY

/INVENTORY RESTS AT 314.045 MILLION OZ/

can someone please explain why GLD behaves differently to SLV????

end

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in silver FELL BY A TINY 453 contracts from 195,964 UP TO 195,511 (AND now A LITTLE FURTHER TO THE NEW COMEX RECORD SET ON FRIDAY/APRIL 21/2017 AT 234,787) DESPITE THE STRONG SIZED RISE IN PRICE OF SILVER (40 CENTS WITH RESPECT TO YESTERDAY’S TRADING). OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE ANOTHER GOOD 1862 PRIVATE EFP’S FOR MARCH AND 0 EFP CONTRACTS OR MAY (WE DO NOT GET A LOOK AT THESE CONTRACTS AS IT IS PRIVATE BUT THE CFTC DOES AUDIT THEM) AND 0 EFP’S FOR ALL OTHER MONTHS . EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. WE HAD SOME COMEX SILVER COMEX LIQUIDATION. IF WE TAKE THE OI LOSS AT THE COMEX OF 453 CONTRACTS TO THE 1862 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A GAIN OF 1409 OPEN INTEREST CONTRACTS . WE STILL HAVE A GOOD AMOUNT OF SILVER OUNCES THAT ARE STANDING FOR METAL IN JANUARY (SEE BELOW). THE NET GAIN TODAY IN OZ ON THE TWO EXCHANGES: 7.04 MILLION OZ!!!

RESULT: A TINY SIZED DECREASE IN SILVER OI AT THE COMEX DESPITE THE CONSIDERABLE SIZED RISE OF 40 CENTS IN PRICE (WITH RESPECT TO YESTERDAY’S TRADING ). BUT WE ALSO HAD ANOTHER GOOD 1862 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE GOOD SIZED AMOUNT OF SILVER OUNCES STANDING FOR FEBRUARY, DEMAND FOR PHYSICAL SILVER INTENSIFIES AS WE WITNESS MAJOR BANK SHORT COVERING ACCOMPANIED BY INCREASES IN GOFO AND SIFO RATES INDICATING SCARCITY.

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)Late MONDAY night/TUESDAY morning: Shanghai closed UP 30.83 points or 0.93% /Hang Sang CLOSED UP 379.90 or 1.29% / The Nikkei closed DOWN 137.94 POINTS OR .65%/Australia’s all ordinaires CLOSED UP 0.63%/Chinese yuan (ONSHORE) closed DOWN at 6.3448/Oil DOWN to 59.08 dollars per barrel for WTI and 62.49 for Brent. Stocks in Europe OPENED DEEPLY IN THE RED EXCEPT LONDON . ONSHORE YUAN CLOSED DOWN AGAINST THE DOLLAR AT 6.3448. OFFSHORE YUAN CLOSED UP AGAINST THE ONSHORE YUAN AT 6.3395//ONSHORE YUAN A LOT WEAKER AGAINST THE DOLLAR/OFF SHORE A LOT STRONGER TO THE DOLLAR/. THE DOLLAR (INDEX) IS MUCH WEAKER AGAINST ALL MAJOR CURRENCIES INCLUDING ON SHORE CHINA YUAN. CHINA IS HAPPY TODAY STRONGER MARKETS IN CHINA

3a)THAILAND/SOUTH KOREA/NORTH KOREA

i)North Korea

b) REPORT ON JAPAN

3 c CHINA

4. EUROPEAN AFFAIRS

England/Ecuador embassy

The judge rejects Assange’s bid to drop his UK arrest warrant and now he is still stick inside the embassy

( zerohedge)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

i)SYRIA/RUSSIA/USA

( zerohedge)

ii)Not good: Iran unveils two nuclear capable ballistic missiles right after Israel’s attack on Syria

( zerohedge)

iii)TURKEY/CYPRUS/ISRAEL

A little background to this story: A few years ago Israel discovered natural gas off the coast of Israel (off of Haifa) and the gas field headed right into Cyprus waters. Israel told the Cyprus government of their find and from that day forward, both Israel and Cyprus started to develop these fields. You will recall that Cyprus is divided into two sections: The Greek side to the south and the Turkish side is to the north. In the 197o’s civil war broke out between the two sides and bad blood exists between the two ever since.

Turkey is not happy that the southern side has discovered riches and they are doing everything in their power to block development of Cypriot gas fields

( zerohedge)

iv)ISRAEL

Israeli police after a long investigation has now recommended that Prime Minister Metanyahu be indicted for bribery

( zerohedge)

6 .GLOBAL ISSUES

7. OIL ISSUES

i)Basket case Venezuela must now import crude oil from Russia as its production continues to cascade

( Z. Calcuttawala/OilPrice.com)

ii)Crude oil and gasoline drop after bigger and expected buildup

8. EMERGING MARKET

SOUTH AFRICA

Zuma has been ordered to resign/the rand falls

( zerohedge)

9. PHYSICAL MARKETS

i)Giant Barrick is facing a grilling from its shareholders and they deserve to be at the bottom of the pack

( GATA/Bloomberg)

ii)You need a whistleblower to tell the CFTC that the VIX causes manipulation in the markets?

( Bloomberg/GATA)

iii)No wonder the price of gold is being capped: Robert Lambourne reports on a huge increase in gold swaps in January.

total bank exposure 580 tonnes which is huge!

(courtesy Robert Lambourne/GATA)

10. USA stories which will influence the price of gold/silver

( zerohedge)

ii)Interesting: nobody is reporting their crypto profits to the IRS

( zerohedge)

iii)Trump threatens a reciprocal tax on imported goods (border tax adjustments). However White House officials denies if they are pursuing this

( zerohedge)

iv)The White House will now add Pakistan to its list of terror financing nations

(courtesy zerohedge)

v)A must read..how the rise in the 10 yr treasury yield will kill off much of Wall Street

(courtesy David Stockman)

vi)Interbank lending plummets: banks are refusing to lend to one another. Why? Answer: the rise in the 10 yr interest rate as the Fed rolls off maturing bonds.

a very important read..

( MishShedlock/Mishtalk)

vi)SWAMP STORIES

a)Pay attention to this story. A former Federal prosecutor and husband of Victoria Toensing, a lawyer representing Campbell, the Russian informant on the Uranium one scandal states that the Schiff memo is blocked not because of Trump but because the DOJ and the FBI are under ‘criminal’ investigation. That makes sense. Also it sure looks like Priestap is the deep throat providing all the information to Jeff Sessions (USA Attorney General)

( zerohedge)

( zerohedge)

c)and the next one to go will be General Kelly

(courtesy zerohedge)

d)Very strange indeed!! Susan rise emails herself an email on a secret meeting held on Jan 5.2017, two weeks before inauguration. In that meeting there was Susan Rice, Obama, James Comey, Assist Deputy Attorney General Sally Yates and Joe Biden. What was this meeting all about..unmasking? Grassley wants to know…

(courtesy zerohedge)

PRELIMINARY COMEX VOLUME FOR TODAY: 197,095 contracts

CONFIRMED COMEX VOL. FOR YESTERDAY: 225,883 CONTRACTS

comex gold volumes are RISING AGAIN

Here is a summary of the latest gold trading volumes at the Comex per year

certainly the introduction of EFP’s has certainly had an effect:

Trading Volumes on the COMEX

Meanwhile, gold-trading volumes on the COMEX have never been higher:

end

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

And now for the wild silver comex results.

Total silver OI FELL BY A TINY SIZED 590 CONTRACTS FROM 195,964 UP TO 195,511 DESPITE YESTERDAY’S STRONG SIZED 40 CENT RISE IN TRADING). HOWEVER,WE WERE ALSO INFORMED THAT WE HAD ANOTHER FAIR SIZED 1862 EMERGENCY EFP’S FOR MARCH ISSUED BY OUR BANKERS (WITH 0 EFP CONTRACTS FOR MAY AND ZERO FOR ALL OTHER MONTHS) TO COMEX LONGS WHO RECEIVED A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON: THE TOTAL EFP’S ISSUED: 1862. THE SILVER BOYS HAVE STARTED TO MIGRATE TO LONDON FROM THE START OF DELIVERY MONTH AND CONTINUING RIGHT THROUGH UNTIL FIRST DAY NOTICE JUST LIKE WE ARE WITNESSING TODAY. USUALLY WE NOTED THAT CONTRACTION IN OI OCCURRED ONLY DURING THE LAST WEEK OF AN UPCOMING ACTIVE DELIVERY MONTH AS WE HAVE JUST SEEN IN GOLD TODAY. THIS PROCESS HAS JUST BEGUN IN EARNEST IN SILVER STARTING IN SEPTEMBER 2017. HOWEVER, IN GOLD, WE HAVE BEEN WITNESSING THIS FOR THE PAST 2 YEARS. NICK LAIRD WAS KIND ENOUGH TO SUPPLY US THE TOTAL FOR 2017 GOLD EFP’S AND IT WAS 6600 TONNES FOR THE ENTIRE YEAR. WE OBVIOUSLY HAD MINIMAL LONG COMEX SILVER LIQUIDATION AND A GOOD SIZED GAIN IN TOTAL SILVER OI. WE ARE ALSO WITNESSING A FAIR AMOUNT OF SILVER OUNCES STANDING FOR COMEX METAL IN THIS NON ACTIVE JANUARY AS WELL AS THAT CONTINUAL MIGRATION OF EFPS OVER TO LONDON. ON A PERCENTAGE BASIS THERE ARE MORE EFP’S ISSUED FOR GOLD THAN SILVER. ON A NET BASIS WE GAINED 1409 SILVER OPEN INTEREST CONTRACTS:

453 CONTRACT LOSS AT THE COMEX COMBINING WITH THE ADDITION OF 1862 OI CONTRACTS NAVIGATING OVER TO LONDON.

NET GAIN TWO EXCHANGES: 1409 CONTRACTS

We are now in the poor non active delivery month of FEBRUARY and here the front month LOST 15 contracts DOWN TO 142 contracts. We had 16 notices filed upon yesterday so we GAINED 1 contract or 5,000 ADDITIONAL oz will stand for delivery at the comex

The March contract lost 3942 contracts DOWN to 92,463

April GAINED 38 contracts UP to 99 .

.

We had 89 notice(s) filed for 80,000 OZ for the FEBRUARY 2018 contract for silver

INITIAL standings for FEBRUARY

Feb 13/2018.

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz |

49,820.411 oz

Brinks

JPMorgan

|

| Deposits to the Dealer Inventory in oz | nil oz |

| Deposits to the Customer Inventory, in oz |

76,864.602 oz

JPMorgan

|

| No of oz served (contracts) today |

0 notice(s)

NIL OZ

|

| No of oz to be served (notices) |

1148 contracts

(114,800 oz)

|

| Total monthly oz gold served (contracts) so far this month |

1783 notices

178300 oz

5.5458 tonnes

|

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

For FEBRUARY:

Today, 0 notice(s) were issued from JPMorgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equates to 0 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped/ Received) by j.P.Morgan customer account.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

To calculate the INITIAL total number of gold ounces standing for the FEBRUARY. contract month, we take the total number of notices filed so far for the month (1783) x 100 oz or 178,300 oz, to which we add the difference between the open interest for the front month of FEB. (1148 contracts) minus the number of notices served upon today (0 x 100 oz per contract) equals 293,100 oz, the number of ounces standing in this active month of FEBRUARY

Thus the INITIAL standings for gold for the FEBRUARY contract month:

No of notices served (1783 x 100 oz or ounces + {(1148)OI for the front month minus the number of notices served upon today (0 x 100 oz )which equals 293,100 oz standing in this active delivery month of February (9.116 tonnes). THERE IS 12.08 TONNES OF REGISTERED GOLD AVAILABLE FOR DELIVERY SO FAR.

WE LOST 1 CONTRACT OR AN ADDITIONAL 100 OZ WILL NOT STAND IN THIS ACTIVE DELIVERY MONTH OF FEBRUARY.

THE COMEX IS NOW UNDER STRESS AS THE REGISTERED GOLD FALLS BELOW 13 TONNES AS WELL AS HUGE NUMBER OF TONNES LEAVING THE CUSTOMER ACCOUNT

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

IN THE LAST 17 MONTHS 70 NET TONNES HAS LEFT THE COMEX.

end

And now for silver

AND NOW THE DECEMBER DELIVERY MONTH

FEBRUARY FINAL standings

| Silver | Ounces |

| Withdrawals from Dealers Inventory | nil oz |

| Withdrawals from Customer Inventory |

928,298.505 oz

Brinks

CNT

Scotia

|

| Deposits to the Dealer Inventory |

443,526.420

oz

Brinks

|

| Deposits to the Customer Inventory |

658,702.116 OZ

JPM

CNT

|

| No of oz served today (contracts) |

89

CONTRACT(S

(445,000 OZ)

|

| No of oz to be served (notices) |

53 contracts

(265,000 oz)

|

| Total monthly oz silver served (contracts) | 304 contracts

(1,520,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

we had one inventory movement at the dealer side of things

i) into Brinks: 443,526.420 oz

total inventory movement dealer: 443,526.420 oz

we had 2 inventory deposits into the customer account

i) into J.P.MORGAN:655,789.316 oz ***

ii) into CNT:: 2812,800 oz

total inventory deposits: 658,702.116 oz

*** JPMorgan is continually adding to its inventory almost every single day.

we had 3 withdrawals from the customer account;

i) Out of Brinks: 5010.635 oz

ii) Out of CNT: 384m686,290

iii) Out of Scotia: 528,601.580

total withdrawals; 928,298.505 oz

we had 0 adjustment

total dealer silver: 43.384 million

total dealer + customer silver: 251.591 million oz

The total number of notices filed today for the FEBRUARY. contract month is represented by 89 contract(s) FOR 445,000 oz. To calculate the number of silver ounces that will stand for delivery in FEBRUARY., we take the total number of notices filed for the month so far at 304 x 5,000 oz = 1,520,000 oz to which we add the difference between the open interest for the front month of FEB. (142) and the number of notices served upon today (89 x 5000 oz) equals the number of ounces standing.

.

Thus the INITIAL standings for silver for the FEB contract month: 304(notices served so far)x 5000 oz + OI for front month of FEBRUARY(142) -number of notices served upon today (89)x 5000 oz equals 1,785,000 oz of silver standing for the FEBRUARY contract month.

WE GAINED 1 CONTRACT OR AN ADDITIONAL 5,000 OZ WILL STAND AT THE COMEX

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

ESTIMATED VOLUME FOR TODAY: 83,107 CONTRACTS

CONFIRMED VOLUME FOR YESTERDAY: 95,227 CONTRACTS

YESTERDAY’S CONFIRMED VOLUME OF 95,2278 CONTRACTS EQUATES TO 476 MILLION OZ OR 68.0% OF ANNUAL GLOBAL PRODUCTION OF SILVER

COMMODITY LAW SUGGESTS THAT OPEN INTEREST SHOULD NOT BE MORE THAN 3% OF ANNUAL GLOBAL PRODUCTION. THE CROOKS ARE SUPPLYING MASSIVE PAPER TRYING TO KEEP SILVER IN CHECK.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price at that day at $18.42

The previous record was 224,540 contracts with the price at that time of $20.44

end

NPV for Sprott

1. Sprott silver fund (PSLV): NAV RISES TO -1.98% (FEB 13/2018)

2. Sprott gold fund (PHYS): premium to NAV RISES TO -0.03% to NAV (FEB 13/2018 )

Note: Sprott silver trust back into NEGATIVE territory at -1.98%-/Sprott physical gold trust is back into NEGATIVE/ territory at -0.03%/Central fund of Canada’s is still in jail but being rescued by Sprott.

Sprott WINS hostile 3.1 billion bid to take over Central Fund of Canada

(courtesy Sprott/GATA)

3.SPROTT CEF.A FUND (FORMERLY CENTRAL FUND OF CANADA): NAV FALLS TO -4.46%: NAV 13.74/TRADING 13.12//DISCOUNT 4.41%

END

And now the Gold inventory at the GLD/

Feb 13/WITH GOLD UP $3.40 WE HAD NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY REMAINS AT 820.71 TONNES

Feb 12/STRANGE!!WITH GOLD RISING BY 12.00 DOLLARS, THE CROOKS DECIDED AGAIN TO WITHDRAW 5.6 TONNES OF GOLD FOR EMERGENCY USE ELSEWHERE/INVENTORY RESTS AT 820.71 TONNES

Feb 9/AGAIN WITH HUGE TURMOIL ON THE MARKETS, THE CROOKS WITHDREW 2 TONNES OF GOLD FROM THE GLD INVENTORY/INVENTORY RESTS AT 826.31 TONNES

Feb 8/DESPITE THE GOOD GAIN IN PRICE FOR GOLD TODAY/THE CROOKS REMOVED .96 TONNES FROM THE GLD INVENTORY/INVENTORY RESTS AT 828.31 TONNES

FEB 7/AN UNBELIEVABLE 12.08 TONNES WAS REMOVED BY THE CROOKED BANKERS AND THIS GOLD WAS USED IN THE ASSAULT THESE PAST FEW DAYS/INVENTORY RESTS AT 829.27 TONNES

Feb 6/AGAIN VERY STRANGE: WITH TODAY’S TURMOIL, THE CROOKS DID NOT ADD ANY GOLD INVENTORY INTO THE GLD/INVENTORY REMAINS AT 841.35 TONNES

Feb 5 Strange,with all of today’s turmoil, the crooks at the GLD decided to add zero ounces into GLD inventory/inventory rests at 841.35 tonnes

Feb 2/no change in gold inventory at the GLD/Inventory rests at 841.35 tonnes

Feb 1/with gold up by $8.00/the crooks decided not to add any new physical gold metal into the GLD./inventory rests at 841.35 tonnes

Jan 31/with gold up $3.15 today, GLD shed another 5.32 tonnes of gold from its inventory/inventory rests at 841.35 tonnes

jan 30/with gold down by $4.85/GLD shed another 1.47 tonnes of gold from its inventory/inventory rests at 846.67 tonnes

JAN 29/with gold down $11.25, the GLD shed 1.18 tonnes of gold/inventory rests at 848.14 tonnes

jan 26/2018/no changes in gold inventory at the GLD/inventory rests at 849.32 tonnes

jan 25/no changes in gold inventory at the GLD/inventory rests at 849.32 tonnes

Jan 24/A HUGE DEPOSIT OF 2.65 TONNES OF GOLD INTO GLD/INVENTORY RESTS AT 849.32 TONNES

Jan 23/NO CHANGE IN GOLD INVENTORY DESPITE GOLD’S RISE/INVENTORY RESTS AT 846.67 TONNES

Jan 22/a huge deposit of 5.71 tonnes of gold despite a drop in price/inventory rests at 846.67 tonnes. In 3 trading days, the GLD has added 17.71 tonnes/the bankers are now in trouble!!

Jan 19/no change in gold inventory at the GLD/Inventory rests at 840.76 tonnes

Jan 18/SHOCKINGLY A HUGE DEPOSIT OF 11.80 TONNES WITH GOLD DOWN ALMOST $12.00/INVENTORY RESTS AT 840.76

Jan 17/no changes in gold inventory at the GLD/inventory rests at 828.96 tonnes

Jan 16/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 828.96 TONNES

Jan 12/no changes in inventory at the GLD despite the rise in gold price/inventory rests at 828.96 tonnes

Jan 11/ANOTHER IDENTICAL WITHDRAWAL OF 2.95 TONNES FROM THE GLD INVENTORY/INVENTORY RESTS AT 828.96 TONNES

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

Feb 13/2018/ Inventory rests tonight at 820.71 tonnes

*IN LAST 324 TRADING DAYS: 120.44 NET TONNES HAVE BEEN REMOVED FROM THE GLD

*LAST 258 TRADING DAYS: A NET 36.87 TONNES HAVE NOW BEEN ADDED INTO GLD INVENTORY.

end

Now the SLV Inventory

Feb 13./NO CHANGE IN SILVER INVENTORY TODAY/INVENTORY RESTS AT 314.045 MILLION OZ/

Feb 12/AGAIN, WITH TODAY’S HUGE RISE IN SILVER PRICE, IN TOTAL CONTRAST TO GOLD: NO CHANGE IN SILVER INVENTORY/INVENTORY RESTS AT 314.045 MILLION OZ/

Feb 9/AGAIN WITH TURMOIL ON THE MARKETS, STRANGELY IN TOTAL CONTRAST TO GOLD: NO CHANGE IN SILVER INVENTORY/INVENTORY RESTS AT 314.045 MILLION OZ/

Feb 8/DESPITE THE TURMOIL TODAY AND A PRICE RISE: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 314.045 MILLION OZ/

FEB 7/no change in silver inventory at the SLV/Inventory rests at 314.045 million oz/

Feb 6/WITH ALL OF TODAY’S TURMOIL/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 314.045 MILLION OZ/

Feb 5/ we had HUGE change in silver inventory at the SLV/ A DEPOSIT OF 1.131 MILLION OZ INTO THE SLV/Inventory rests at 314.045 million oz/

Feb 2/we lost 982,000 oz from the SLV inventory /inventory rests at 312.914 million oz/

Feb 1/no change in silver inventory at the SLV/Inventory rests at 313.896 million oz/

Jan 31/ no change in inventory at the slv in total contrast to gold/inventory rests at 313.896 million oz/

Jan 30/no change in inventory/SLV inventory rests at 313.896 million oz/

Jan 29/no change in inventory/SLV inventory rests at 313.896 million oz/

Jan 26.2018/inventory rests at 313.896 million oz

Jan 25/with silver up today and yesterday, the SLV could only muster a gain of 848,000 oz

Inventory rests at 313.896 oz

jan 24/NO CHANGE IN SILVER INVENTORY DESPITE THE GOOD ADVANCE IN PRICE/INVENTORY RESTS AT 313.048 MILLION OZ/

Jan 23/ANOTHER HUGE WITHDRAWAL OF 1.131 MILLION OZ OF SILVER DESPITE THE TINY LOSS/THE CROOKS ARE USING THE INVENTORY TO RAID ON SILVER.

JAN 22.2018/with silver down by 5 cents/ the crooks at the SLV liquidate 1.321 million oz of silver/inventory rests at 314.179 million oz/

Jan 19/ no changes in silver inventory at the SLV/inventory rests at 315.500 million oz/

jan 18/A WITHDRAWAL OF 848,000 OZ OF SILVER FROM THE SLV/INVENTORY RESTS AT 315.500 MILLION OZ/

Jan 17/no changes in silver inventory at the SLV/inventory rests at 316.348 million oz/

Jan 16/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 316.348 MILLION OZ

Jan 12/no changes in silver inventory at the SLV/inventory rests at 316.348 million oz/

Feb 13/2017:

Inventory 314.045 million oz

end

6 Month MM GOFO

Indicative gold forward offer rate for a 6 month duration

+ 1.69%

12 Month MM GOFO

+ 2.09%

end

Major gold/silver trading /commentaries for TUESDAY

GOLDCORE/BLOG/MARK O’BYRNE.

GOLD/SILVER

Sovereign Wealth Funds Investing In Gold For “Long Term Returns” – PwC – GoldCore

January 13

February 2018

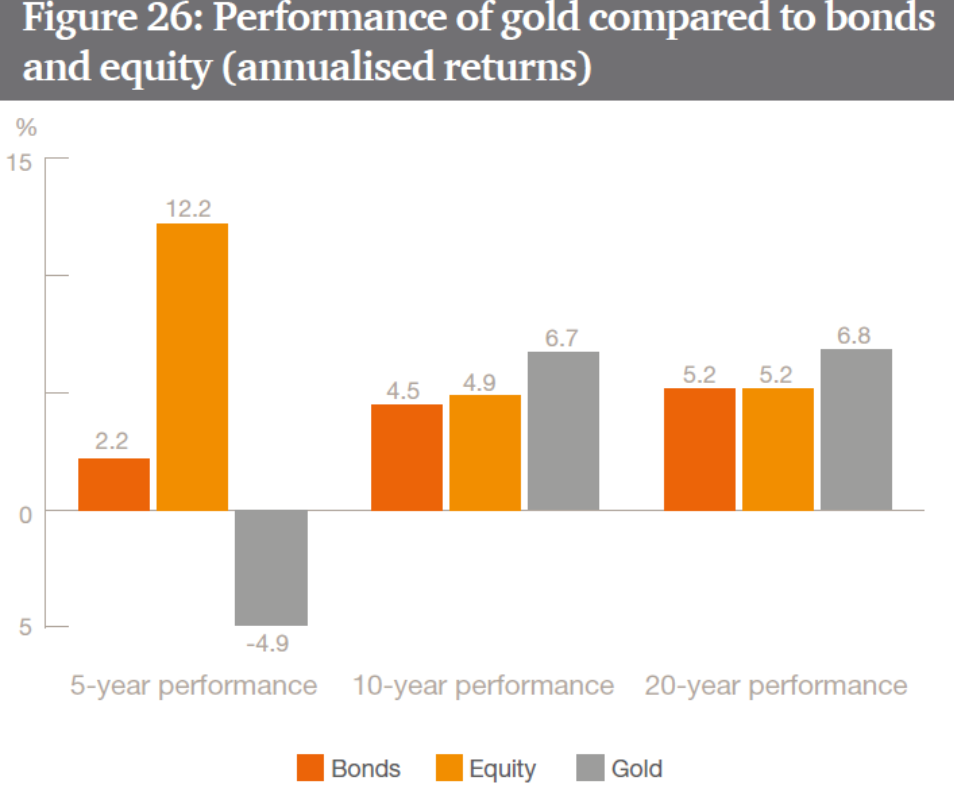

– Gold has outperformed equities and bonds over the long term – PwC Research

– Gold is up 6.7% and 6.8% per annum over 10 and 20 year periods; Stocks and bonds returned less than 5.2% respectively over same period (see PwC table)

– From 1971 to 2016 (45 years), “gold real returns were approximately 10% while inflation increased 4%”

– Gold also valuable due to lack of correlation and hedge against inflation, currency devaluation and uncertainty

– Sovereign wealth funds investing 23% of assets under management to alternative investments including gold

– Gold being diversified into by HNW, family offices, institutions, pensions, sovereign wealth funds and central banks

Source: PwC Research via Bloomberg and WGC data

In new research, entitled ‘The rising attractiveness of alternative asset classes for Sovereign Wealth Funds‘ PwC explain how gold is viewed as an important diversifier by sovereign wealth funds, as both an important hedge and for long term returns.

PwC now class gold as a ‘re-emerging asset class’ on the basis of its long-term out performance of stocks and bonds, low correlation with traditional assets, resilience and high liquidity.

Gold along with private equity, real estate and infrastructure now accounts for 23% of a total $7.4 trillion of assets under management by sovereign wealth funds.

The report notes that from a peak of 40% in 2013, sovereign wealth funds’ investment into fixed income instruments such as government bonds declined to 30% by 2016. Due to record low bond yields, the funds decided to turn their attention to alternative assets to enhance returns.

The report notes the impressiveness of both gold’s long-term performance and low correlation to other assets in the long-term, compared to other alternatives. In the short- term the benefit of gold’s liquidity is noted:

“[It] has one of the highest rates of daily volumes exchanged and can provide protection against short and medium term market corrections.”

The 23% allocation is expected to increase going forward, despite slight increases in rates recently and because of the likelihood of continuing very low interest rates.

This report comes at a time when we are seeing a growing interest by both large institutions and family offices in gold investment.

Like sovereign wealth funds, they are encouraged by gold’s long-term returns, high liquidity and resilience against economic shocks.

Long term outperformance to traditional asset classes

As we have seen in recent years gold, like all assets, has periods when it underperforms. This has been in the short-term in the last 3 to 5 years, but in the long-term – such as a 10, 20 or 40 year period, it is an entirely different story.

Indeed, gold’s recent underperformance, makes its long term outperformance all the more impressive.

The report shows that in the last ten years, gold delivered returns of 6.7% per annum, outperforming equities and bonds which returned just 4.9% and 4.5% respectively. This return was slightly greater over a 20-year period when gold returned 6.8% per annum, compared to equities and bonds which returned just 5.2% and 5.2%.

Over the long term, gold is one of the top three performing assets along with real estate and private equity.

“Gold’s long- term performance is attributed to three factors: increased demand from emerging markets, central banks becoming net buyers, and the emergence of new products, such as gold- based ETFs, which have simplified investing and made the material more accessible.” – PwC

PwC also note the importance of gold when it comes to protecting against currency devaluation:

“By introducing alternatives into the portfolio, the value of investments can be protected against a possible decrease in purchasing power of the currency the investments are denominated in. This can be done through instruments whose returns are somehow linked to inflation or have perceived intrinsic value. Assets with perceived intrinsic value, such as commodities, should increase in price alongside CPI. In cases of extreme inflation for example, gold has historically performed well, outpacing that inflation by 10%…gold performed well during inflationary periods. For example, from 1971 to 2016, gold real returns were approximately 10% while inflation increased 4% year- over-year.”

Gold doesn’t follow: Low correlation with traditional asset classes

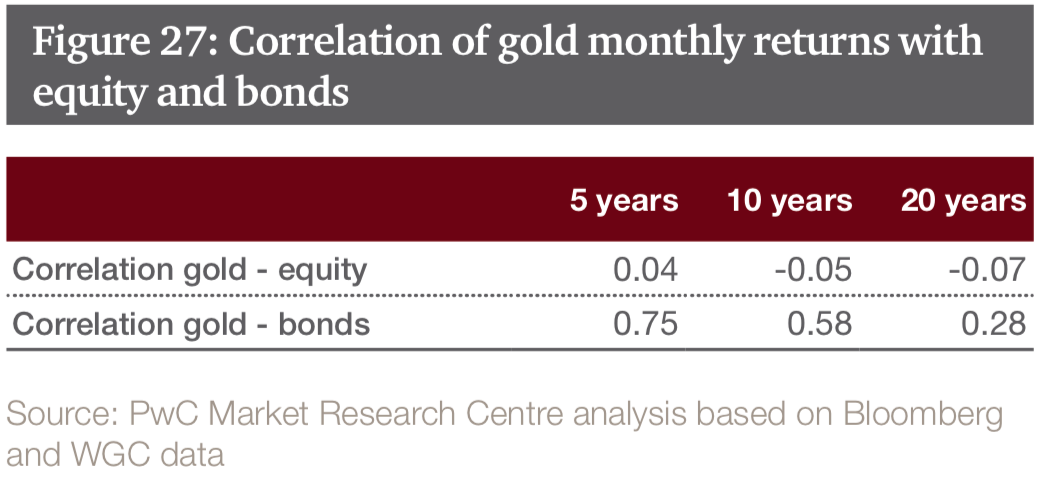

“Gold can be a useful addition to investment portfolios compared to other commodities, due to lower correlation with traditional asset classes. Between June 1997 and June 2017, the correlation between gold and equity returns was close to zero (-0.07), thus showing its diversification benefit. The asset class maintains only a negative correlation over a ten-year period as well, standing at -0.05. Gold is more correlated with bond returns, standing at 0.58 on a ten-year basis, and at 0.28 on a twenty-year correlation (see Figure 27)…Gold has, over all considered time periods, no statistically significant correlation with hedge funds, private equity, infrastructure, and real estate.”

As with the other factors discussed by PwC this is pertinent for all considering investing in gold, from retail and pension investors, larger institutions and family offices. Much of gold’s low correlation is due to the fact that it is less affected by economic cycles and geo-political risks than other financial assets. This means it shows resilience at times when others are showing weakness.

This has been seen in recent days when stock markets saw massive volatility and very sharp corrections and gold was essentially flat. Year to date in 2018, gold is nearly 1.7% higher while many stock indices are down sharply – Euro Stoxx 50 is down more than 4% year to date.

Resilient asset class during crises and instability

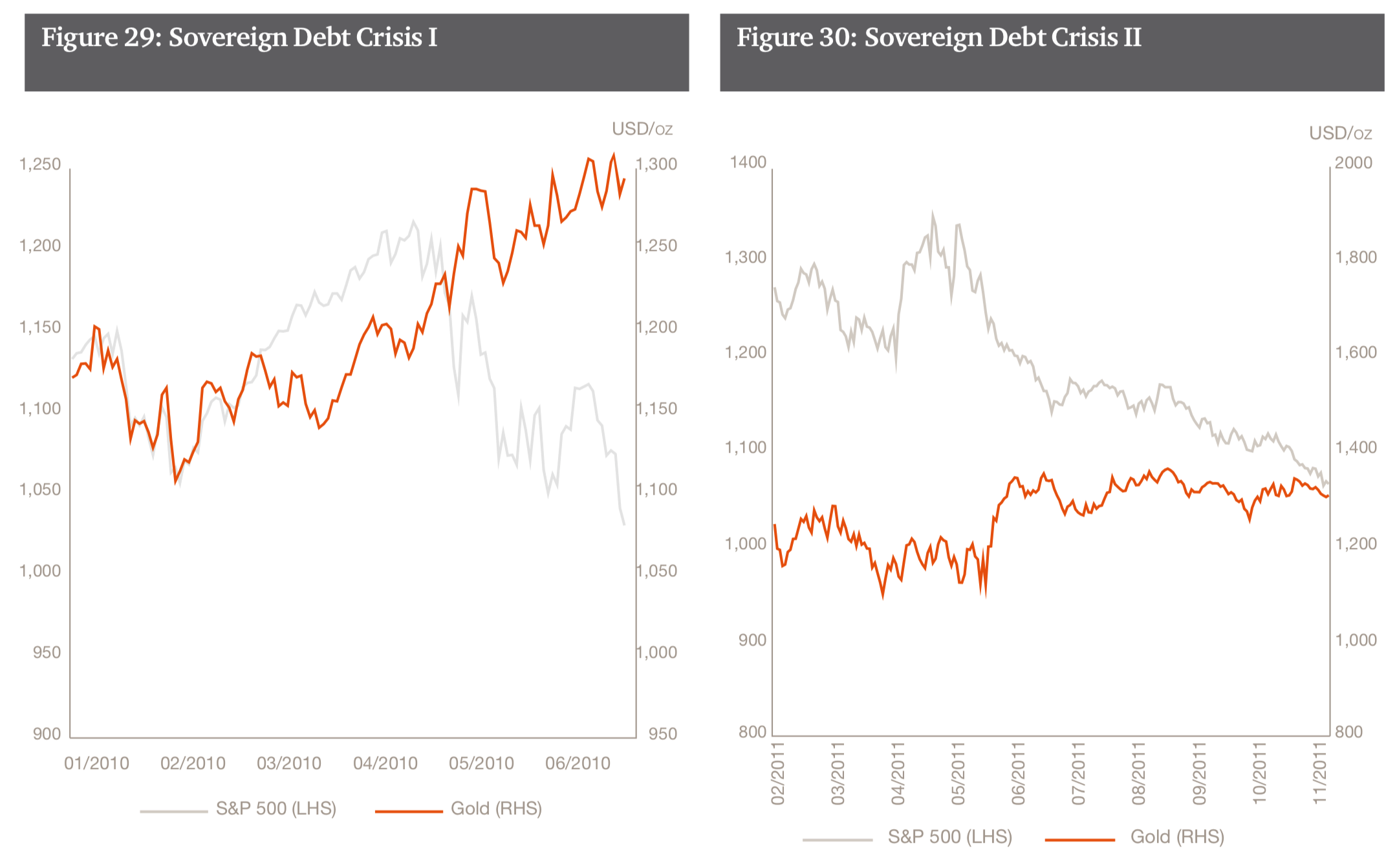

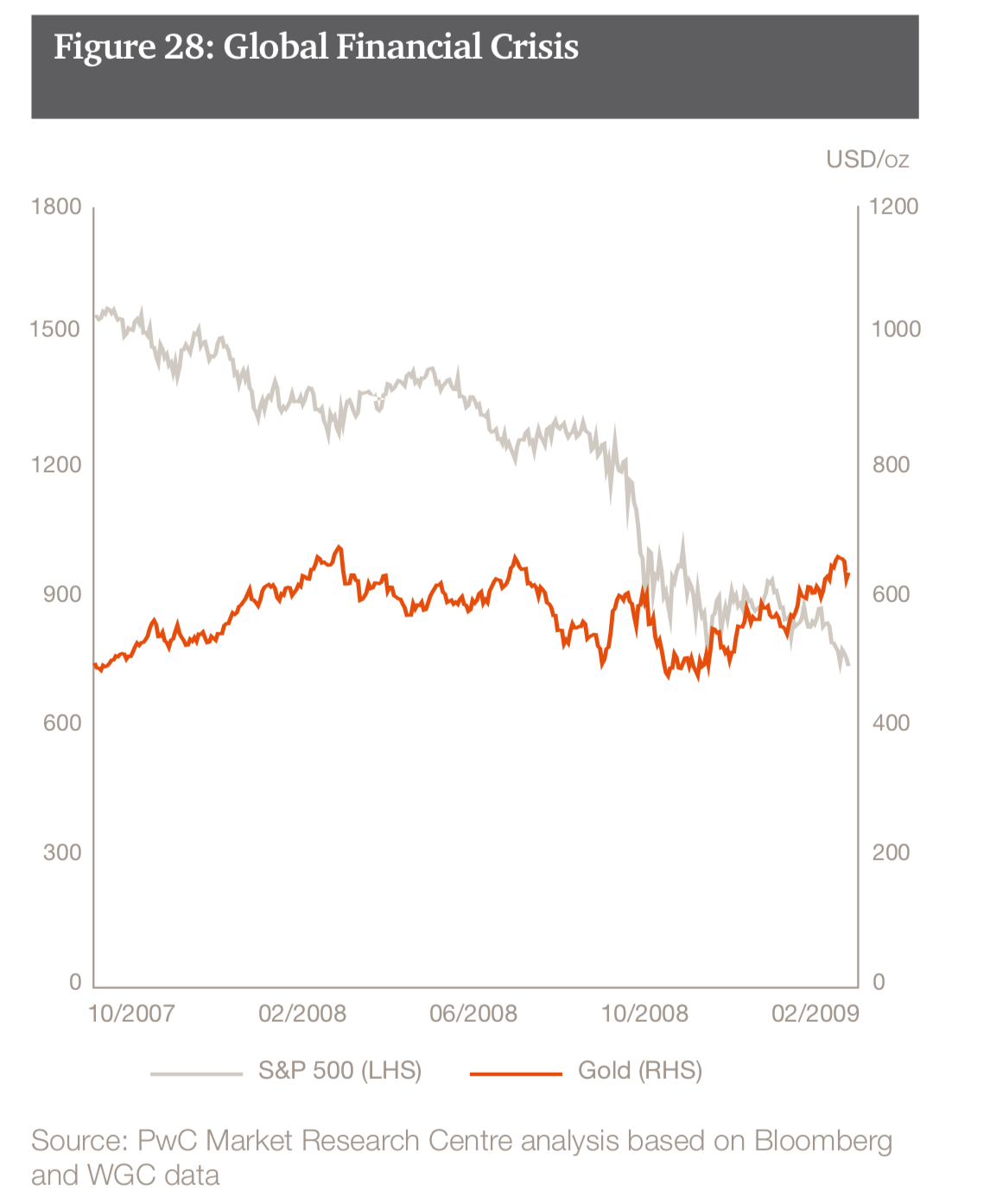

The gold price performs well in times of financial crises and extreme market events. During these times the correlation benefits become even more important, so it can provide portfolio insurance since it minimises portfolio losses. PwC explain that this is what distinguishes gold from other assets:

“Gold has delivered negatively correlated returns when equity indices, such as S&P 500, have plummeted. Figure 28, 29, and 30 show gold’s performance during episodes of acute market crisis (GFC and the Sovereign Debt Crisis I and II). In these cases, the gold price started to rise significantly as the S&P 500 index decreased. Generally speaking, the gold price per ounce rose as investors perceived uncertainty in the stock markets, and decreased as these markets gave signs of normalisation.”

After the bloodbath of the last week, S&P500 investors will be interested to hear how gold correlates to the market”

“Among alternatives, when examining the correlation of returns with the S&P 500 index, gold is an excellent diversifier presenting the lowest correlation on a five-, ten-, and twenty- year basis (0.04, -0.05, -0.07 respectively).”

Liquid gold

The asset is particularly liquid in contrast to many of the other assets considered by SWFs, this is something very beneficial according to PwC:

” Stabilization funds may, in particular, benefit from adding gold among their holdings as they are required to hold highly liquid assets to counter the effects of sudden macroeconomic shocks.

Gold has distinguished itself from other alternative asset classes as it has been more liquid, with USD 224 bn traded on average on a daily basis in 2016?.

Conclusion: Investment and pension case for gold is strong

PwC do not beat about the bush when it comes to their positivity towards gold as an investment. They synopsise and elucidate many of gold’s benefits which we have long been highlighting in recent years:

“All these features suggest that gold as an investment class can offer reliable support, not only during uncertain market and political conditions, such as periods of high inflation, stock market crashes, and geopolitical instability, but also under normal market conditions.”

They clearly see gold as playing a crucial role in the portfolios of sovereign wealth funds and indeed the majority of investors across the spectrum.

“The investment case for gold, during periods of market uncertainty, has proven to be strong, with the price of gold having surged rapidly and having countered the negative effects of adverse market conditions. Hence, investors can consider gold for diversification and long-term performance.”

Pwc Report on gold can be accessed here

Watch the PwC World Gold Council interview about the report here

-END-

END

Giant Barrick is facing a grilling from its shareholders and they deserve to be at the bottom of the pack

(courtesy GATA/Bloomberg)

Gold giant Barrick faces grilling after fall to the bottom of the pack

Submitted by cpowell on Mon, 2018-02-12 16:39. Section: Daily Dispatches

By Danielle Bochove

Bloomberg News

Monday, February 12, 2018

Barrick Gold Corp. executives will have some explaining to do when the company releases full-year results Wednesday.

Even with rising gold prices and a strengthened balance sheet, the world’s largest gold producer left shareholders with the worst returns among its top North American peers last year and the third-worst performance in the 15-company BI Global Senior Gold Valuation Peers index.

That’s a sharp reversal of the heady gains a year earlier when the Toronto-based company appeared unable to put a foot wrong. In 2016 Barrick’s Canadian shares soared 110 percent as it unveiled a sweeping plan to streamline the company. That same year its biggest rival, Newmont Mining Corp., rose 89 percent.

Notwithstanding the recent global stock rout that has sunk equities globally, Colorado-based Newmont’s shares have gained, while Barrick has stumbled. …

… For the remainder of the report:

https://www.bloomberg.com/news/articles/2018-02-12/gold-giant-to-face-gr…

END

You need a whistleblower to tell the CFTC that the VIX causes manipulation in the markets?

(courtesy Bloomberg/GATA)

VIX manipulation costs investors billions, whistle-blower tells CFTC

Submitted by cpowell on Tue, 2018-02-13 01:53. Section: Daily Dispatches

Think how easy it is for central banks themselves to do this stuff, easier still since mainstream financial news organizations will never question them about their market interventions.

* * *

By Brian Louis and Nikolaj Gammeltoft

Bloomberg News

Monday, February 12, 2018

A whistle-blower today told U.S. regulators that a scheme to manipulate the VIX, the volatility gauge thrust into the spotlight last week during a wild trading session, costs investors hundreds of millions of dollars a month.

A Washington-based lawyer told the Securities and Exchange Commission and Commodity Futures Trading Commission — the nation’s top markets regulators — in a letter today that his client found a flaw that allows traders “with sophisticated algorithms to move the VIX up or down by simply posting quotes on S&P options and without needing to physically engage in any trading or deploying any capital.” Billions in purportedly ill-gotten profits have been scooped up by “unethical electronic option market makers,” according to the letter.

The client wasn’t identified by name. He has held “senior positions at some of the largest investment firms in the world,” according to the letter written by Jason Zuckerman of Zuckerman Law, who has appeared on Washingtonian magazine’s list of top whistle-blower lawyers in the nation’s capital. …

… For the remainder of the report:

https://www.bloomberg.com/news/articles/2018-02-13/vix-manipulation-cost…

END

No wonder the price of gold is being capped: Robert Lambourne reports on a huge increase in gold swaps in January.

total bank exposure 580 tonnes which is huge!

(courtesy Robert Lambourne/GATA)

(GATA) Robert Lambourne: Gold market intervention by BIS increased substantially in January

Submitted by cpowell on 03:08PM ET Tuesday, February 13, 2018. Section: Daily Dispatches

By Robert Lambourne

Tuesday, February 13, 2018

The Bank for International Settlements substantially increased its use of gold swaps and other gold-related derivatives during January, according to the bank’s statement of account for the month:

https://www.bis.org/banking/balsheet/statofacc180131.pd f

This increase follows a large decline in the bank’s gold swaps in December. In recent months the BIS has been actively trading gold derivatives.

The information provided in the BIS monthly statement of account is not sufficient to calculate a precise amount of gold-related derivatives, including swaps, but it appears that the bank’s total exposure as of January 31, 2018, was 580 tonnes of gold. This compares to estimates of 450 tonnes, 600 tonnes, and 570 tonnes, respectively, at the December, November, and October month-ends and an audited swaps figure of 438 tonnes as of March 31, 2017.

When it comes to its activities in the gold market, the BIS provides little information on what it is doing. The lack of transparency fuels suspicion that this activity is related to official efforts to suppress the gold price.

END

Your early TUESDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

i) Chinese yuan vs USA dollar/CLOSED DOWN AT 6.3448 /shanghai bourse CLOSED UP AT 30.83 POINTS 0.98% / HANG SANG CLOSED UP 379.90 POINTS OR 1.29%

2. Nikkei closed DOWN 137.94 POINTS OR .65% /USA: YEN FALLS TO 107.46/DEADLY AS YEN CARRY TRADERS DISINTEGRATE

3. Europe stocks OPENED DEEPLY IN THE RED /USA dollar index FALLS TO 89.68/Euro RISES TO 1.2348

3b Japan 10 year bond yield: RISES TO . +.071/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 107.46/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD FINALLY IN THE POSITIVE/BANK OF JAPAN LOSING CONTROL OF THEIR YIELD CURVE AS THEY PURCHASE ALL BONDS TO GET TO ZERO RATE!!

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 59.08 and Brent: 62.49

3f Gold UP/Yen UP

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil DOWN for WTI and DOWN FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund FALLS TO +.731%/Italian 10 yr bond yield UP to 2.048% /SPAIN 10 YR BOND YIELD UP TO 1.487%

3j Greek 10 year bond yield RISES TO : 4.34?????????????????

3k Gold at $1328.20 silver at:16.62 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble UP 40/100 in roubles/dollar) 57.97

3m oil into the 60 dollar handle for WTI and 63 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 107.46 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 0.9328 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1521 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now POSITIVE territory with the 10 year RISING to +0.731%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.8276% early this morning (THIS IS DEADLY TO ALL MARKETS). Thirty year rate at 3.11910% /BOTH STILL DEADLY

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

(courtesy Jim Reid/Bloomberg/Deutsche bank/zero hedge)

Futures Slide As Global Stock Rally Fizzles Hit By Soaring Yen

Is the dead cat bounce over?

European shares rolled over this morning after a late downswing in Asia as markets struggled to find stability despite Monday’s frenzied rally, with futures this morning a bit of a mess.

“I think what we are seeing is a little bit of a consolidation,” said DZ Bank strategist Christian Lenk. “Given the pace of the move so far, we had to take a break somewhere and we have reached that region now.”

While there has been no specific driver, USD weakness for the third day in a row, and a consequent selloff in USD/JPY – which tumbled shortly before midnight ET – was the main focus in European session.

The resultant surge in the yen, which climbed to the highest since November 2016 pushing the USDJPY as low as 107.40, slammed the Nikkei after the midday break in Asia, with Trump comments on reciprocal tax yesterday also potentially having an influence on USD. Whatever the reason, Japanese stocks pared morning gains with Topix erasing 1.1% advance to trade 0.9% lower on the day. And with the USDJPY nearing the 2017 low of 107.32, Nikkei futures sold off further after the cash close.

At the same time, the EUR/USD lifted to 1.2350 mainly due to move in USD, while the British pound was briefly jolted to a session high of $1.3924 after headline annual UK inflation came in at 3.0%, a tenth of a point above forecasts and holding close to its highest level in nearly six years. In South Africa, the ZAR dipped briefly after President Zuma was said to refuse ANC’s resignation call.

Pressured by the weaker dollar and sliding European stocks, S&P 500 futures pointed to a drop for U.S. stocks at the market open after two days of gains.

The 10-year Treasury yield fell back to 2.83% after touching 2.902% on Monday. The general risk-off lifted core fixed income, U.S 2s10s flatten away from 200DMA after testing level for third day.

German bonds were also back in demand as recent multi-year highs on yields on both sides of the Atlantic proved attractive for some investors. Germany’s 10-year yield fell by almost 2 basis points to 0.73 as it retreated further from the 2-1/2 year high of 0.81 percent hit last week.

Hedge funds and other large speculators have boosted bets on Treasury futures to a record, indicating they expect the 2018 bond-market rout will resume in the days ahead. An investor at Goldman Sachs Asset Management warned Treasury 10-year yields could rise to as high as 3.5% in the next six months as the market prices in a steeper pace of Federal Reserve tightening.

All eyes will be on tomorrow’s CPI report. “The (U.S.) consumer prices numbers (on Wednesday) bear close watching as if it shows a strong rise, that could rattle U.S. long-term yields,” and currencies and stocks said Koji Fukaya, president of FPG Securities in Tokyo.

Meanwhile, in global stocks, a jump in global equities yesterday wasn’t enough to put traders’ minds at ease that the volatility that wiped $2 trillion from U.S. stocks last week has come to an end. Consumer-price data due Wednesday could give some clues on direction, given that pressure on equities has been emanating from the outlook for inflation.

European equities opened on the back foot (Eurostoxx 50 -0.3%) compared to the positive trading session in Asia (ex-Japan), with virtually all bourses in the red. Materials stand out as an outperforming sector amid the US infrastructure plans released yesterday whilst metals are extending gains. Telecoms underperform with BT (-1.2%) at the bottom of the FTSE 100 awaiting news from the Premier League TV rights.

While European equities declined and the Swiss franc gained alongside Treasuries and core euro-area bonds, there has been no clear shift toward haven demand as the kiwi rallied and EMFX rose a third day. European equity markets grind lower, while peripheral equity markets and export stocks underperformed.

Commodities found support from the weaker dollar, with metals higher, and bullion set for back-to-back gains. Copper prices on the London Metal Exchange extended an overnight rally to trade 1.4% higher at $6,927.00 per tonne. A report from the EIA yesterday noted that shale production for crude is to rise by 100k bbls in March, while another report this morning from the IEA expects US supply to grow more than demand in 2018, with US seen topping Russian production at year-end; as such both WTI and Brent have been pressured throughout the morning with the former briefly slipping below $59bbl. In metals markets, gold prices are near one-week highs amid the softer USD which has dictated a bulk of the price action for precious metals. Elsewhere, China have voiced concerns over US protectionism over steel, whilst aluminium prices have been pressured by building stockpiles. IEA have upgraded their forecast for global oil demand growth to 1.4mln bpd in 2018 from 1.3mln, however they say Non-OPEC supply, led by US, which is likely to grow more than demand in 2018.

On today’s calendar, U.S. sells 4-week bills; small business optimism index, which rose from 104.90 to 106.90, but below the 108.50 consensus. Starting Feb 15, Lunar new year celebrations for the Year of the Dog begin, affecting China, Hong Kong, Taiwan, Singapore, Malaysia and Indonesia. Chinese mainland markets are closed Feb. 15-21. India is out Tuesday for a public holiday.

Bulletin headline summary from Ransquawk

- European equities lower across the board after a mixed session overnight which saw the Nikkei 225 (-0.7%)

- hampered by the firmer JPY

- In FX markets, USD softer against its peers. GBP firmer as UK inflation exceeds expectations (3.0% Y/Y vs. Exp.

- 2.9%)

- Looking ahead, highlights include APIs, Japanese GDP and Fed’s Mester

Market Snapshot

- S&P 500 futures down 0.6% to 2,638.25

- MXAP up 0.6% to 172.27

- MXAPJ up 0.9% to 563.36

- Nikkei down 0.7% to 21,244.68

- Topix down 0.9% to 1,716.78

- Hang Seng Index up 1.3% to 29,839.53

- Shanghai Composite up 1% to 3,184.96

- Sensex up 0.9% to 34,300.47

- Australia S&P/ASX 200 up 0.6% to 5,855.90

- Kospi up 0.4% to 2,395.19

- Brent Futures down 0.4% to $62.35/bbl

- Gold spot up 0.5% to $1,328.85

- U.S. Dollar Index down 0.4% to 89.84

Top Overnight News

- The People’s Bank of China appointed JPMorgan Chase Bank N.A. as a yuan clearing bank in the U.S., the first non-Chinese lender for such a role globally and a further step to promote international use of the currency

- A whistle-blower told U.S. regulators that a scheme to manipulate the VIX, the volatility gauge thrust into the spotlight last week during a wild trading session, costs investors hundreds of millions of dollars a month

- OPEC and its allies have almost achieved their goal of clearing an oil glut, but their efforts could be derailed by rising supplies from the U.S. and other rivals, the International Energy Agency said

- South Africans awoke to find their nation in limbo after President Jacob Zuma’s refusal to obey his ruling African National Congress’s request to resign voluntarily prompted its top leadership to order his removal from office

- Cleveland Fed President Loretta Mester (voter) speaks; she holds a hawkish approach, looks for three hikes this year

In Asia, stocks traded mostly higher as the region cheered the continued rebound in the US, where all majors finished with firm gains and the S&P 500 posted its best 2-day performance in over 2 years. ASX 200 (+0.6%) and Nikkei 225 (-0.7%) both opened higher in which mining-related sectors led in Australia, while Japanese stocks were initially outperformed buoyed as participants played catch up on return from holiday, although a firmer currency later saw gains wiped out. Elsewhere, Shanghai Comp. (+1%) and Hang Seng (+1.3%) were jubilant heading closer to the Lunar New Year holidays and after the PBoC announced to lend CNY 393bln through the 1yr Medium-term Lending Facility. Furthermore, there was a decline in money market rates in which the 1-week CNH HIBOR fell by the most so far in 2018, and the latest Chinese lending data also showed both New Yuan Loans and Aggregate Financing surged from prior. Finally, 10yr JGBs were flat amid similar range-bound trade overnight in T-notes and although the BoJ were present in the market under its bond-buying program, this was kept at a reserved amount. Japanese PM Abe said he is undecided on the next BoJ Governor, while Abe also stated that it is up to the BoJ to decide specific monetary policy measures and that he expects the BoJ to continue taking bold measures to achieve price stability.

Top Asian News

- China Is Said to Plan Blocks on Take-Two’s Grand Theft Auto

European equities this morning opened on the back foot (Eurostoxx 50 -0.3%) compared to the positive trading session in Asia (ex-Japan) and the US. Materials stand out as an outperforming sector amid the US infrastructure plans released yesterday whilst metals are extending gains: Gold (+0.4%), Silver (+0.1%), Copper (+0.8%). Telecoms underperform with BT (-1.2%) at the bottom of the FTSE 100 awaiting news from the Premier League TV rights.

Top European News

- Greece Launches Tender for 5% Hellenic Telecom Stake Sale

- BHP Expects $1.8b Income Tax Expense Due to U.S. Reforms

- U.K. Inflation Holds Steady After BOE Warns of More Rate Hikes

In currencies, Yen strength is the main overnight and early European theme, as Usd/Jpy breached last Friday’s 108.05 low to the downside before overcoming barrier and psychological support at 108.00 on its way to fresh 5 month lows around 107.55. Bids reportedly in the 107.70 area were also filled in pretty short order as risk aversion ratcheted higher, but it remains unclear whether heightened demand for the Jpy (and Chf to a lesser degree) was prompted by the Nikkei’s failure to maintain catch-up gains after Japan’s long holiday weekend or vice-versa. 107.50-45 next in sight for Usd/Jpy, with buying interest not really seen until the low 107.30 area (including last year’s 107.32 low), while cross demand is also rife as Gbp/Jpy falls below the 150.00 handle. GBP firmer after higher than expected inflation figures (3.0 vs. Exp. 2.9% Y/Y), however the rise had been short-lived, given that the headline figure had been in line with the BoE’s forecast. Nzd another noted beneficiary of US Dollar weakness as the Index loses grip of 90.000 again, with the Kiwi reclaiming 0.7300 status and in part also gaining some impetus from Aud underperformance amidst mixed sentiment readings overnight and RBA rhetoric – Aud/Usd above 0.7850, but Aud/Nzd back under 1.0800. Other Usd/G10 major pairings more contained, albeit still showing a generally softer Greenback, with Eur/Usd regaining 1.2300, Cable around 1.3850 eyeing UK inflation data and Usd/Cad sub-1.2600. Elsewhere, Usd/Zar still in focus and testing recent lows (currently circa 11.9000) ahead of an ANC briefing at 12GMT, with President Zuma still resisting efforts to remove him from office

In commodities, the theme continues for the oil markets, more supply is set to come from US shale producers. A report from the EIA yesterday noted that shale production for crude is to rise by 100k bbls in March, while another report this morning from the IEA expects US supply to grow more than demand in 2018, with US seen topping Russian production at year-end; as such both WTI and Brent have been pressured throughout the morning with the former briefly slipping below USD 59.00bbl. In metals markets, gold prices are near one-week highs amid the softer USD which has dictated a bulk of the price action for precious metals. Elsewhere, China have voiced concerns over US protectionism over steel, whilst aluminium prices have been pressured by building stockpiles. IEA have upgraded their forecast for global oil demand growth to 1.4mln bpd in 2018 from 1.3mln, however they say Non-OPEC supply, led by US, which is likely to grow more than demand in 2018. Iraq oil minister states that there is no current discussion over exiting supply cut agreement Russian Energy Minister Novak stated that OPEC and Non-OPEC allies need to act very cautiously and avoid knee-jerk reactions in respect of new decisions

Looking ahead, the January CPI/PPI/RPI report in the UK is the main focus. In the US, the January NFIB small business optimism print will be released. Away from data, the Fed’s Mester is due to speak in the afternoon on monetary policy and the economic outlook. Pepsico will release earnings.

US Event Calendar

- 6am: NFIB Small Business Optimism, est. 105.3, prior 104.9

- 8am: Fed’s Mester to Discuss Monetary Policy and Economic Outlook

DB’s Jim Reid concludes the overnight wrap

Welcome to US CPI eve. All has seemed a bit quiet over the last 24 hours which probably partly reflects half-term (the rush hour trains were lovely and quiet yesterday), partly that the peak position squaring from last week’s vol spike has seemingly passed for now and also that markets are building up to tomorrow’s big US number. Maybe traders and investors were also buying Valentine’s Day cards and presents as well. I’ll be making my annual trip to Hotel Chocolat later today to buy overpriced chocolates in a nice (but far too big for the amount of produce inside them) package. Given my wife is full time feeding for her plus two ravenous boys, her chocolate intake at the moment is something to admire.

Ahead of tomorrow’s number we have an interesting CPI dress rehearsal today in the UK. This has been made more interesting by the hawkish BoE meeting last week and also two hawkish BoE speakers yesterday. Vlieghe suggested that 3 BoE hikes still leaves some excess demand and wouldn’t get inflation fully back to target. McCafferty said that rates will have to go up slightly earlier and fractionally more than the bank previously expected.

For today, markets are expecting a CPI print of -0.6% mom and 2.9% yoy (2.6% yoy for core) and a PPI reading of 3.0% yoy.

Before that, global equities continue to rebound. US bourses were all higher for the second consecutive day (S&P +1.39%; Dow +1.70%; Nasdaq +1.56%), with all sectors in the S&P up and gains led by the materials, tech and energy stocks. The VIX also traded 11.9% lower to 25.61. Since the beat on US wage growth, the S&P is now down 5.9% overall, but is up 4.9% from the intra-day lows. Similarly the VIX has jumped 90% since 1 February, but is 49% lower than the intra-day highs of 50.30 over the past seven trading days. Key European markets also advanced yesterday, with the Stoxx 600 (+1.17%), DAX (+1.45%) and FTSE (+1.19%) all higher, while the VSTOXX fell 18.9% to 28.16.

This morning in Asia, markets are rallying on the positive lead from the US. The Kospi (+0.68%), Hang Seng (+1.55%) and China’s CSI 300 (+1.23%) are all up as we type but the Nikkei has given up gains of >1% to trade lower for the day. Datawise, Japan’s January PPI was broadly in line at 0.3% mom and 2.7% yoy while China’s monthly net new loans were higher than expected at RMB$2,900bn (vs. $2,050bn expected).

In the US, President Trump has proposed a $4.4trn federal budget for 2019 that seeks to reduce domestic programs such as Medicare in favour of higher spending on the military and immigration enforcements. The plans will see the deficit almost double in FY19 to $984bln and rise $7.1trn over the next decade.

Mr Trump said he would push for a “reciprocal tax” on imports against higher tariff countries without providing details and reiterated his $1.5trn infrastructure plan of which $200bln federal funds will act as seed funds to incentivise further spending by state and local government as well as the private sector. Notably, both Reuters and NY Times noted Presidential budgets are rarely enacted by the Congress. The budget director Mulvaney called the plans as a “messaging document”, so we’ll wait and see if these messages will translate into any reality.

Yesterday we published a note using our fair value model between credit and volatility to assess where credit spreads should trade if and when the VIX (for US credit) or VStoxx (for European credit) stabilise at various levels. Spikes in vol are rarely sustained outside of a crisis so the fact that the current difference between actual and modeled spreads (see graphs in the note) are at one of the widest points on record isn’t necessarily a cause for major alarm yet. However to cite examples in the note, if equity vol settles at 15, Euro IG and HY should settle 15bps and 68bps wider. For the US, these numbers 24bps and 61bps wider all other things being equal. For vol at 20, these numbers are +27bps, +107bps, +43bps and +145bps respectively. See the full note here for more on this. A reminder that yesterday morning we also put out a quick note comparing this current sell-off across various assets to that seen during the 34 day taper tantrum in May 2013 and the 60 day risk sell-off after the surprise Fed hike in February 1994. All of them having a rates/yield/inflation related catalyst.

Back to credit, the latest ECB CSPP holdings data was released yesterday. The CSPP/PSPP ratio was 18.4% (28.1% over last 4 weeks). Before Apr 2017 when we were still at full QE the ratio was 11.5%. In the first taper (Apr-Dec 2017) the ratio edged up to 12.7% and since Jan 2018 it has increased to 24.8%. So far this year, QE purchases have been in line with our long-standing expectation that the CSPP/PSPP ratio would move to around 20% after the January taper.

Now recapping other markets performance from yesterday. Government bonds weakened slightly, with core 10y bond yields up 1-3bp. The UST 10y yields rose 0.7bp and Bunds up 1.2bp while Gilts underperformed (+3.1bp), partly weighed down by the hawkish BOE speak. Turning to currencies, the US dollarindex retreated 0.32% yesterday but is still up c1.7% since the beat on wage growth, while the Euro and Sterling gained 0.32% and 0.08% respectively. In commodities, WTI oil rose for the first time in seven days (+0.15%), in part as OPEC has revised up its demand forecasts and expect global demand to outpace the growth in US shale supply. Elsewhere, precious metals strengthened c1% (Gold +0.46%; Silver +1.16%) and other base metals were broadly higher (Copper +0.45%; Aluminium +1.02%; Zinc -0.38%).

Away from the markets and onto Germany, the latest Sonntagstrend survey showed 57% of Germans want the SPD members to vote and approve a coalition with Ms Merkel’s bloc. The support level is higher amongst SPD and CDU voters, at 85% and 87% respectively.

Elsewhere, our asset allocation strategist Binky Chadha has taken a closer look at the potential causes for the recent pullback in equities. Overall, the team concludes that a long overdue pullback on extended positioning was amplified in US equities by structured products. But despite the size of the pullback it was still just that and likely more to do with the need for liquidity and quick risk reduction. The team also noted 10% corrections in US equities are very rare outside recessions, with only 15 such selloffs since 1950. Further, they are normally associated with a clear unexpected catalyst such as oil price collapse, China devaluation and Russia LTCM. Refer to their note for more details.

In the UK, according to documents sighted by Bloomberg, EU officials will hold a discussion this Thursday on the options for a future trade deal with the UK post Brexit. The meeting looks to discuss the mobility of workers and how cars, chemicals and food safety are regulated in the internal market.

Before we take a look at today’s calendar, we wrap up with other data releasesfrom yesterday. In the US, the monthly federal budget surplus was $49.2bln(vs. $51bln expected) in January. The NY Fed survey of consumer expectations showed median one year ahead inflation expectations fell to 2.71% in January (vs.2.82% previous). Notably, respondents expect wage growth to be 2.73% in the coming year, the highest since the data series began in 2013. In the UK, Acadata noted London house prices fell 4.3% in 4Q17, the largest fall since 2009.

Looking ahead, the January CPI/PPI/RPI report in the UK is the main focus. In the US, the January NFIB small business optimism print will be released. Away from data, the Fed’s Mester is due to speak in the afternoon on monetary policy and the economic outlook. Pepsico will release earnings.

3. ASIAN AFFAIRS

i)Late MONDAY night/TUESDAY morning: Shanghai closed UP 30.83 points or 0.93% /Hang Sang CLOSED UP 379.90 or 1.29% / The Nikkei closed DOWN 137.94 POINTS OR .65%/Australia’s all ordinaires CLOSED UP 0.63%/Chinese yuan (ONSHORE) closed DOWN at 6.3448/Oil DOWN to 59.08 dollars per barrel for WTI and 62.49 for Brent. Stocks in Europe OPENED DEEPLY IN THE RED EXCEPT LONDON . ONSHORE YUAN CLOSED DOWN AGAINST THE DOLLAR AT 6.3448. OFFSHORE YUAN CLOSED UP AGAINST THE ONSHORE YUAN AT 6.3395//ONSHORE YUAN A LOT WEAKER AGAINST THE DOLLAR/OFF SHORE A LOT STRONGER TO THE DOLLAR/. THE DOLLAR (INDEX) IS MUCH WEAKER AGAINST ALL MAJOR CURRENCIES INCLUDING ON SHORE CHINA YUAN. CHINA IS HAPPY TODAY STRONGER MARKETS IN CHINA

3 a NORTH KOREA/USA

/NORTH KOREA

3 b JAPAN AFFAIRS

c) REPORT ON CHINA

4. EUROPEAN AFFAIRS

England/Ecuador embassy

The judge rejects Assange’s bid to drop his UK arrest warrant and now he is still stick inside the embassy

(courtesy zerohedge)

Judge Rejects Julian Assange’s Bid To Drop UK Arrest Warrant

In a pivotal moment for Wikileaks’ founder Julian Assange’s long-running legal battle to regain his freedom after spending the last six years without sunlight at the Ecuadorian Embassy in London, a UK judge delivered a disappointing ruling for Assange’s defense team.

After repudiating Assange’s lawyers characterization of the circumstances of his confinement, the judge has rejected his bid to have the warrant dropped, upholding the state’s case against the renown political dissident – who violated the terms of his bail in 2012 to show up at the Ecuadorian embassy disguised as a motorcycle courier.

Judge refuses to withdraw Julian Assange arrest warrant. https://www.theguardian.com/media/2018/feb/13/judge-refuses-to-withdraw-julian-assange-arrest-warrant?CMP=twt_gu …

Judge refuses to withdraw Julian Assange arrest warrant

WikiLeaks founder continues to face arrest if he leaves Ecuadorian embassy as judge rejects request to quash warrant

theguardian.com

Though the process isn’t over yet, the judge’s ruling that he had no reason to fear extradition to the US is a huge blow to his case for having the UK warrant dropped. In particular, the judge said Assange could leave the embassy whenever he liked, could have unlimited visitors, could choose when he eats and sleeps and exercises and even had access to sunlight via a balcony. Assange’s lawyers had also argued that his years inside the embassy were “adequate” punishment for any crimes he may or may not have committed.

Gasps in public gallery as judge says Assange can ‘leave the (Ecuadorian Embassy) whenever he likes, have unlimited visitors unsupervised, can choose when he eats, sleeps and exercises’. She’s knocking down most of Assange case to have arrest warrant dropped #Assange #wikileaks

Sweden dropped rape charges against Assange nearly 10 months ago, but the UK has refused to let him off the hook. In fact, reporters discovered that Sweden wanted to drop its pursuit years ago, but was persuaded to continue by Assange…

According tothe Guardian, Assange also suspects there is a secret US grand jury indictment against him and American authorities will seek his extradition.

Jonathan Cook: The UK’s hidden role in Assange’s detention https://www.jonathan-cook.net/blog/2018-02-12/the-uks-hidden-role-in-assanges-detention/ …

It appears as if the UK arrest warrant will be left in place, as Assange suggested in a tweet.

Not looking good. So far, judge is just defending UK state actions.

A bid to lift the arrest warrant last week was rejected when Judge Emma Arbuthnot rejected the notion that Sweden’s dropping of the case against Assange meant that the British authorities should no longer want him in custody. His defense team is arguing that Assange’s further detention would not serve justice. Assange has argued that if he hadn’t fled to the embassy, he would have been extradited to the US to face an unfair trial for his work, which he believes is essentially not different from investigative journalism.

In December, Assange received Ecuadorian citizenship, but the UK indicated it would not recognize his diplomatic status if requested by the Latin American nation, denying Assange the diplomatic immunity that would’ve allowed him to leave.

The UN has twice ruled that Assange is being improperly detained in the UK, and investigative work done by an Italian journalist uncovered malfeasance at the Crown Prosecution Service.

The judge also said that, if extradition motions were taken against Assange, he would be able to contest those.

To be sure, the process isn’t over yet. Assange noted that even if he loses the first point, the hearing may immediately continue on another…

Today, 2pm GMT, 9am EST, judge rules on whether to lift my UK arrest warrant following revelations of improper conduct by the UK government. Note that a win is a win, but even if we lose the first point today the hearing may immediately continue on another https://www.theguardian.com/media/2018/feb/13/julian-assange-saga-judge-to-rule-on-arrest-warrant …

Julian Assange saga: judge to rule on arrest warrant

After six years holed up in Ecuadorian embassy, WikiLeaks founder faces a pivotal moment

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

We now hear that two Russian fighters were killed last week in the uSA led attack in the Deir al Zor province, in the north west part of the country. Let us see if Russia has restraint on this one!

(courtesy zerohedge)

Russian Fighters Killed In Clash With US-Led Coalition Forces In Syria

With the calm of global capital markets shattered in the past two weeks, the ongoing military conflict in the Middle East has taken an understandable back seat to monetary matters. And yet, tensions involving Syria, Iran and Israel continue to escalate, most notably with this weekend’s outright attack by Israel on Syria, allegedly in retaliation for an Iranian drone launch from a Syrian army base, and which led to the first downing of an Israeli F-16 jet in decades.

Yet what has so far prevented the proxy way from spinning out of control, was that Putin – as guarantor of the Syria-Iran axis on one hand, and Netanyahu as his nemesis on the other, had expressed restraint. For now.

That may change, however, following a Reuters report that Russian fighters were among those killed when U.S.-led coalition forces clashed with pro-government forces in Syria earlier this month.

While Russia’s Defense Ministry said at the time that pro-government militias involved in the incident had been carrying out reconnaissance “and no Russian servicemen had been in the area”, the story changed on Monday when it emerged that at least two Russian men fighting informally with pro-government forces were killed in the incident in Deir al-Zor province, their associates told Reuters.

One of the dead was named as Vladimir Loginov, a Cossack from Russia’s Kaliningrad exclave. Maxim Buga, a leader of the Cossack community there, said Loginov had been killed around Feb. 7 along with “dozens” of other Russian fighters.

The other man killed was named as Kirill Ananiev, described as a radical Russian nationalist. Alexander Averin, a spokesman for the nationalist party he was linked to, told Reuters Ananiev had been killed in shelling in the same fighting on Feb. 7.

If the deaths are confirmed, it could turn into a political scandal for Putin, with the public demanding why the government is keeping military deaths under wraps. Already Grigory Yavlinsky, a veteran liberal politician who is running for president in elections next month, has called on Putin to disclose how many Russians had been killed in Syria and in what circumstances.

“If there was large-scale loss of life of Russian citizens, the relevant officials, including the commander-in-chief of our armed forces (Putin), are obliged to tell the country about it and decide who carries responsibility for this,” Yavlinsky said in a statement released by his Yabloko party.

Of course, if indeed Russian soldiers were killed while fighting under covert circumstances – in the same way as killed US “military advisors” are kept under seal – that is the last thing Moscow would like to publicize. Unless of course the political calculus shifts, and Putin decides that it is time for a full-blown military escalation, in which case the deaths will be used as the justification behind any armed conflict.

end

Not good: Iran unveils two nuclear capable ballistic missiles right after Israel’s attack on Syria

(courtesy zerohedge)

Iran Unveils Two Nuclear-Capable Ballistic Missiles After Israel Attack On Syria

Following Israel’s dramatic airstrikes on Syria on Saturday, seen by many as a “dramatic escalation” in regional tensions, and the most direct threat against Tehran in years, over the weekend Iran unveiled a series of new homemade nuclear-capable ballistic missiles during military parades, in a move that experts said was a bid to bolster the hardline ruling regime while cautioning Israel against any further escalation.

Describing the missile, Iran’s state-run Fars news agency described one of the rockets, the Ghadr , as a 2000km-range, liquid-fuel and ballistic missile which can reach territories as far as Israel.

The missile can carry different types of ‘Blast’ and ‘MRV’ (Multiple Reentry Vehicle) payloads to destroy a range of targets.

Meanwhile, the new version of the Qadr H ballistic missile “can be launched from mobile platforms or silos in different positions and can escape missile defense shields due to their radar-evading capability.”

As the Washington Free Beacon adds, Iranian military leaders rolled out the latest ballistic missile technology, which includes a nuclear-capable medium-range missile that appears to share similarities with North Korean technology on the heels of an encounter between what Israel claimed was an Iranian drone and Israeli forces.

The missiles are capable of reaching Israel even when fired from Iranian territory, raising concerns about an impending conflict between Tehran and the Jewish state that could further inflame the region.

While it was meant to deter further aggression by Israel, the demonstration of nuclear force by Iran could further inflame tensions between the two countries. Concerns that this nuclear-capable technology could be shared by Iran with its terrorist proxies are fueling longstanding concerns among the Israelis that an attack is imminent.

Iran’s ruling regime continues to invest millions of dollars it received as part of the landmark nuclear deal with the United States on its military technology, specifically ballistic missiles, which are subject to a ban under international statutes, even as Iranian dissidents continue to protest over the country’s ailing economy. According to conservative estimates, the Iranian regime has spent at least $16 billion in recent years on its military buildup and rogue operations in Syria, as well as other countries.

Some more details on the newly unveiled weapons: the two new nuclear-capable missiles unveiled over the weekend by Iran include the Ghadr missile, a medium-range rocket that was recently modified and upgraded by the Islamic Republic.