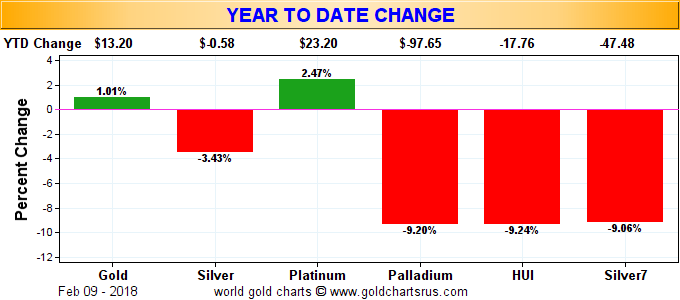

GOLD: $1324.60 UP $12.00

Silver: $16.60 UP 40 cents

Closing access prices:

Gold $1323.00

silver: $16.56

SHANGHAI GOLD FIX: FIRST FIX 10 15 PM EST (2:15 SHANGHAI LOCAL TIME)

SECOND FIX: 2:15 AM EST (6:15 SHANGHAI LOCAL TIME)

SHANGHAI FIRST GOLD FIX: $1331.29 DOLLARS PER OZ

NY PRICE OF GOLD AT EXACT SAME TIME: $1324.00

PREMIUM FIRST FIX: $7.90

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

SECOND SHANGHAI GOLD FIX: $1326.24

NY GOLD PRICE AT THE EXACT SAME TIME: $1323.90

Premium of Shanghai 2nd fix/NY:$2.34

SHANGHAI REJECTS NY /LONDON PRICING OF GOLD

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

LONDON FIRST GOLD FIX: 5:30 am est $1321.70

NY PRICING AT THE EXACT SAME TIME: $1321.00

LONDON SECOND GOLD FIX 10 AM: $1322.30

NY PRICING AT THE EXACT SAME TIME. $1321.10

For comex gold:

FEBRUARY/

NUMBER OF NOTICES FILED TODAY FOR FEBRUARY CONTRACT: 50 NOTICE(S) FOR 5000 OZ.

TOTAL NOTICES SO FAR:1783 FOR 178300 OZ (5.458 TONNES),

For silver:

FEBRUARY

16 NOTICE(S) FILED TODAY FOR

80,000 OZ/

Total number of notices filed so far this month: 215 for 1,075,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: BID $8692/OFFER $8763: up $381(morning)

Bitcoin: BID/ $8311/offer $8845: UP $463 (CLOSING/5 PM)

end

Let us have a look at the data for today\

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total open interest ROSE BY A CONSIDERABLE SIZED 2828 contracts from 193,135 RISING TO 196,163 DESPITE FRIDAY’S GOOD 18 CENT LOSS IN SILVER PRICING. WE HAD ZERO COMEX LIQUIDATION. HOWEVER, WE WERE AGAIN NOTIFIED THAT WE HAD ANOTHER HUGE SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP ROUTE: 2694 EFP’S FOR MARCH AND AND 139 EFP’S FOR MAY AND ZERO FOR ALL OTHER MONTHS AND THUS TOTAL ISSUANCE OF 2833 CONTRACTS. WITH THE TRANSFER OF 2833 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24 HRS IN THE ISSUING OF EFP’S. THE 2833 CONTRACTS TRANSLATES INTO 14.16 MILLION OZ. WITH THE HUGE DROP IN OPEN INTEREST AT THE COMEX. WE SHOULD EXPECT BIGGER GAINS IN EFP TRANSFERS IN THE NEXT FEW DAYS WITH THE LARGE LOSS AT THE COMEX AS LONGS GAVE UP SEEKING METAL AT THIS EXCHANGE.

ACCUMULATION FOR EFP’S/SILVER/ STARTING FROM FIRST DAY NOTICE/FOR MONTH OF FEBRUARY:

30,392 CONTRACTS (FOR 9 TRADING DAYS TOTAL 30,392 CONTRACTS OR 151.960 MILLION OZ: AVERAGE PER DAY: 3376 CONTRACTS OR 16.884 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH: 151.96 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 21.7% OF ANNUAL GLOBAL PRODUCTION

ACCUMULATION IN YEAR 2018 TO DATE SILVER EFP’S: 381.9 MILLION OZ.

ACCUMULATION FOR JAN 2018: 236.879 MILLION OZ

RESULT: A GOOD SIZED GAIN IN OI SILVER COMEX DESPITE THE CONSIDERABLE 18 CENT LOSS IN SILVER PRICE. WE HOWEVER HAD A GOOD SIZED EFP ISSUANCE OF 2833 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER . FROM THE CME DATA 2833 EFP’S FOR MONTHS MARCH AND MAY WERE ISSUED FOR MONDAY FOR A DELIVERABLE FORWARD CONTRACT OVER IN LONDON WITH A FIAT BONUS. WE GAINED 5523 OI CONTRACTS i.e. 2833 open interest contracts headed for London (EFP’s) TOGETHER WITH A INCREASE OF 2829 OI COMEX CONTRACTS. AND ALL OF THIS HAPPENED WITH THE CONSIDERABLE FALL IN PRICE OF SILVER OF 18 CENTS AND A CLOSING PRICE OF $16.20 WITH RESPECT TO YESTERDAY’S TRADING. YET WE STILL HAVE A FAIR AMOUNT OF SILVER STANDING AT THE COMEX.

In ounces AT THE COMEX, the OI is still represented by just UNDER 1 BILLION oz i.e. 0.980 BILLION TO BE EXACT or 140% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT FEBRUARY MONTH/ THEY FILED: 16 NOTICE(S) FOR 80,000 OZ OF SILVER

In gold, the open interest FELL BY ANOTHER CONSIDERABLE 6,968 CONTRACTS DOWN TO 510,740 WITH THE FAIR SIZED FALL IN PRICE OF GOLD WITH FRIDAY’S TRADING ($4.70). HOWEVER, IN ANOTHER DEVELOPMENT, WE RECEIVED THE TOTAL NUMBER OF GOLD EFP’S ISSUED FOR MONDAY AND IT TOTALED A FAIR SIZED 7526 CONTRACTS OF WHICH APRIL SAW THE ISSUANCE OF 7526 CONTRACTS AND JUNE SAW THE ISSUANCE OF 0 CONTRACTS AND THEN ALL OTHER MONTHS ZERO. The new OI for the gold complex rests at 510,740. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. DEMAND FOR GOLD INTENSIFIES GREATLY AS WE CONTINUE TO WITNESS A HUGE NUMBER OF EFP TRANSFERS TOGETHER WITH THE MASSIVE INCREASE IN GOLD COMEX OI TOGETHER WITH THE TOTAL AMOUNT OF GOLD OUNCES STANDING FOR FEBRUARY COMEX. EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER (BIG RISE IN BOTH GOFO AND SIFO) AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES. IN ESSENCE TODAY DESPITE YESTERDAY’S TRADING IN GOLD, WE HAVE A GAIN OF 658 CONTRACTS: 6968 OI CONTRACTS DECREASED AT THE COMEX AND A STRONG SIZED 7526 OI CONTRACTS WHICH NAVIGATED OVER TO LONDON.(658 oi gain in CONTRACTS EQUATES TO 2.046 TONNES)

FRIDAY, WE HAD 14,716 EFP’S ISSUED.

ACCUMULATION OF EFP’S/ GOLD(EXCHANGE FOR PHYSICAL) FOR THE MONTH OF FEBRUARY STARTING WITH FIRST DAY NOTICE: 98,896 CONTRACTS OR 9,889,600 OZ OR 307.60 TONNES (9 TRADING DAYS AND THUS AVERAGING: 10,988 EFP CONTRACTS PER TRADING DAY OR 1,098,800 OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SIZE OF THESE EFP TRANSFERS : SO FAR THIS MONTH IN 9 TRADING DAYS: IN TONNES: 307.60 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2017, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 2200 TONNES

THUS EFP TRANSFERS REPRESENTS 307.6/2200 x 100% TONNES = 13.98% OF GLOBAL ANNUAL PRODUCTION SO FAR IN FEBRUARY ALONE.

ACCUMULATION OF GOLD EFP’S YEAR 2018 TO DATE: 941.12 TONNES

ACCUMULATION OF GOLD EFP’S FOR JANUARY 2018: 653.22 TONNES

Result: A CONSIDERABLE SIZED DECREASE IN OI AT THE COMEX DESPITE THE FAIR SIZED FALL IN PRICE IN GOLD TRADING FRIDAY ($4.70). IT IS WITHOUT A DOUBT THAT MANY OF THE DEPARTED COMEX LONGS RECEIVED THEIR PRIVATE EFP CONTRACT FOR EITHER APRIL OR JUNE. HOWEVER, WE HAD ANOTHER GOOD SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 7526 AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX AND YET WE ALSO OBSERVED A HUGE DELIVERY MONTH FOR THE MONTH OF DECEMBER. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 7526 EFP CONTRACTS ISSUED, WE HAD A NET GAIN IN OPEN INTEREST OF 658 contracts ON THE TWO EXCHANGES:

7526 CONTRACTS MOVE TO LONDON AND 6968 CONTRACTS DECREASED AT THE COMEX. (in tonnes, the GAIN in total oi equates to 2.045 TONNES).

we had: 50 notice(s) filed upon for 5000 oz of gold.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD

WITH GOLD UP $12.00 TODAY, THE CROOKS WITHDREW ANOTHER 5.6 TONNES OF GOLD FROM THE GLD/INVENTORY RESTS AT 820.71

Inventory rests tonight: 820.71 tonnes.

SLV/ (IN TOTAL CONTRAST TO GOLD)

NO CHANGES IN SILVER INVENTORY AT THE SLV/ AGAIN WITH TODAY’S HUGE RISE IN SILVER PRICE: NO CHANGE IN INVENTORY

/INVENTORY RESTS AT 314.045 MILLION OZ/

can someone please explain why GLD behaves differently to SLV????

end

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in silver ROSE BY A CONSIDERABLE 2829 contracts from 193,135 UP TO 195,964 (AND now A LITTLE CLOSER TO THE NEW COMEX RECORD SET ON FRIDAY/APRIL 21/2017 AT 234,787) DESPITE THE GOOD SIZED FALL IN PRICE OF SILVER (18 CENTS WITH RESPECT TO FRIDAY’S TRADING). OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE ANOTHER GOOD 3215 PRIVATE EFP’S FOR MARCH AND 0 EFP CONTRACTS OR MAY (WE DO NOT GET A LOOK AT THESE CONTRACTS AS IT IS PRIVATE BUT THE CFTC DOES AUDIT THEM) AND 0 EFP’S FOR ALL OTHER MONTHS . EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. WE HAD SOME COMEX SILVER COMEX LIQUIDATION. IF WE TAKE THE OI GAIN AT THE COMEX OF 2829 CONTRACTS TO THE 2833 OI TRANSFERRED TO LONDON THROUGH EFP’S, SURPRISINGLY WE OBTAIN A GAIN OF 5523 OPEN INTEREST CONTRACTS DESPITE FRIDAY’S DRUBBING IN SILVER PRICE. WE STILL HAVE A GOOD AMOUNT OF SILVER OUNCES THAT ARE STANDING FOR METAL IN JANUARY (SEE BELOW). THE NET GAIN TODAY IN OZ ON THE TWO EXCHANGES: 27.61 MILLION OZ!!!

RESULT: A GOOD SIZED INCREASE IN SILVER OI AT THE COMEX DESPITE THE CONSIDERABLE SIZED FALL OF 18 CENTS IN PRICE (WITH RESPECT TO FRIDAY’S TRADING ). BUT WE ALSO HAD ANOTHER GOOD 2833 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE GOOD SIZED AMOUNT OF SILVER OUNCES STANDING FOR FEBRUARY, DEMAND FOR PHYSICAL SILVER INTENSIFIES AS WE WITNESS MAJOR BANK SHORT COVERING ACCOMPANIED BY INCREASES IN GOFO AND SIFO RATES INDICATING SCARCITY.

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)Late SUNDAY night/MONDAY morning: Shanghai closed UP 24.27 points or 0.78% /Hang Sang CLOSED DOWN 47.79 or 0.16% / The Nikkei closed HOLIDAY/Australia’s all ordinaires CLOSED UP 0.30%/Chinese yuan (ONSHORE) closed DOWN at 6.3286/Oil DOWN to 60.26 dollars per barrel for WTI and 63.65 for Brent. Stocks in Europe OPENED DEEPLY IN THE GREEN . ONSHORE YUAN CLOSED DOWN AGAINST THE DOLLAR AT 6.3286. OFFSHORE YUAN CLOSED DOWN AGAINST THE ONSHORE YUAN AT 6.3346//ONSHORE YUAN A LOT WEAKER AGAINST THE DOLLAR/OFF SHORE A LOT WEAKER TO THE DOLLAR/. THE DOLLAR (INDEX) IS MUCH WEAKER AGAINST ALL MAJOR CURRENCIES EXCEPT CHINA YUAN. CHINA IS HAPPY TODAY STRONGER MARKETS IN CHINA

3a)THAILAND/SOUTH KOREA/NORTH KOREA

i)North Korea

b) REPORT ON JAPAN

3 c CHINA

4. EUROPEAN AFFAIRS

GREAT BRITAIN

An excellent commentary from Alasdair Macleod as he correctly states that Great Britain should leave the EU at no cost to them and then have free trade with the rest of Europe. He explains why:

(/Alasdir Macleod)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

( zerohedge)

6 .GLOBAL ISSUES

( zerohedge)

7. OIL ISSUES

8. EMERGING MARKET

9. PHYSICAL MARKETS

i)As I explained below, the Fed has only two choices, rates or stocks. With Trump’s new spending initiate rates are heading higher and this will certainly cause stocks to flounder

( Eric Sprott/)

ii)Mike Kosares explains the meaning of volatility and how it usually presages a downward blast in the stockmarket and a rise in the price of gold

a must read..

( Michael Kosares/GATA)

iii)I wonder what gave this away: the Economist states that insider trading has been rife on Wall Steet

( the Economist/London)

10. USA stories which will influence the price of gold/silver

iv)Gold gets a boost with Trump’s huge infrastructure plan: 1 1.5 trillion spending boost:

v)Rand Paul over the weekend accuses correctly that many of the GOP of hypocrisy for agreeing to the bipartisan budget deal and the huge increase in spending.( zerohedge)

vi)It begins tonight: a free for all debate on immigration..should be fun

vii)SWAMP STORIES

a)Trump blocks the Democratic memo on national security concerns and states that they should remove sources and methods of how surveillance of citizens is applied

( zerohedge)

b)Rachel Brand, next in line after Rod Rosenstein at the Dept of Justice is leaving to become an executive at WalMart. It was also revealed that Rod Rosenstein signed one of the FISA warrants and thus the committee wants to speak to him again on this matter.

c)Is Counterintelligence chief Bill Priestap co-operating with the authorities and giving details on Comey, Strzok, Page, Hillary et al? No question about it: Bill Priestap is the deep throat and will down everyone associated with this mess!!

a must read..

(courtesy the ConservativeTreeHouse.com)

Let us head over to the comex:

The total gold comex open interest FELL BY A CONSIDERABLE 6968 CONTRACTS DOWN to an OI level 510,740 DESPITE THE FAIR SIZED FALL IN THE PRICE OF GOLD ($4.70 LOSS WITH RESPECT TO FRIDAY’S TRADING). WE HAD CONSIDERABLE COMEX GOLD LIQUIDATION. HOWEVER THE CME REPORTS THAT THE BANKERS ISSUED ANOTHER STRONG COMEX TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS. WE HAD A HUGE SIZED 7526 EFP’S ISSUED FOR APRIL AND 0 EFP’s FOR JUNE AND ZERO FOR ALL OTHER MONTHS: TOTAL 7526 CONTRACTS. THE OBLIGATION STILL RESTS WITH THE BANKERS ON THESE TRANSFERS. ALSO REMEMBER THAT THERE IS NO DOUBT A HUGE DELAY IN THE ISSUANCE OF EFP’S AND IT PROBABLY TAKES AT LEAST 48 HRS AFTER LONGS GIVE UP THEIR COMEX CONTRACTS FOR THEM TO RECEIVE THEIR EFP’S AS THEY ARE NEGOTIATING THIS CONTRACT WITH THE BANKS FOR A FIAT BONUS PLUS THEIR TRANSFER TO A LONDON FORWARD… THE COMEX IS NOW AN ABSOLUTE FRAUD!!

ON A NET BASIS IN OPEN INTEREST WE GAINED TODAY: 658 OI CONTRACTS IN THAT 7526 LONGS WERE TRANSFERRED AS FORWARDS TO LONDON AND WE LOST 6968 COMEX CONTRACTS.

NET GAIN ON THE TWO EXCHANGES: 658 contracts OR 65800 OZ OR 2.046 TONNES, AND THIS WAS ACCOMPLISHED WITH A FALL IN PRICE OF GOLD

Result: A HUGE SIZED DECREASE IN COMEX OPEN INTEREST DESPITE THE FAIR SIZED LOSS IN FRIDAY’S GOLD TRADING ($4.70.) WE HAD CONSIDERABLE COMEX GOLD LIQUIDATION. TOTAL OPEN INTEREST GAIN ON THE TWO EXCHANGES: 658 OI CONTRACTS..

We have now entered the active contract month of FEBRUARY where we lost 110 contracts to 1199 contracts. We had 141 notices filed upon yesterday, so we gained 31 contracts or an additional 3100 oz will stand in this active contract month of February

March saw a GAIN of 94 contracts UP to 2091. April saw a LOSS of 6967 contracts DOWN to 353,850. MARCH BECOMES THE FRONT MONTH FOR GOLD

We had 50 notice(s) filed upon today for 5000 oz

PRELIMINARY COMEX VOLUME FOR TODAY: 207,408 contracts

CONFIRMED COMEX VOLUME FOR YESTERDAY: 366,130 CONTRACTS

comex gold volumes are RISING AGAIN

Here is a summary of the latest gold trading volumes at the Comex per year

certainly the introduction of EFP’s has certainly had an effect:

Trading Volumes on the COMEX

Meanwhile, gold-trading volumes on the COMEX have never been higher:

end

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

And now for the wild silver comex results.

Total silver OI ROSE BY A CONSIDERABLE SIZED 2829 CONTRACTS FROM 193,135 UP TO 195,964 DESPITE FRIDAY’S GOOD SIZED 18 CENT DROP IN TRADING). HOWEVER,WE WERE ALSO INFORMED THAT WE HAD ANOTHER LARGE SIZED 2694 EMERGENCY EFP’S FOR MARCH ISSUED BY OUR BANKERS (WITH 139 EFP CONTRACTS FOR MAY AND ZERO FOR ALL OTHER MONTHS) TO COMEX LONGS WHO RECEIVED A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON: THE TOTAL EFP’S ISSUED: 2833. THE SILVER BOYS HAVE STARTED TO MIGRATE TO LONDON FROM THE START OF DELIVERY MONTH AND CONTINUING RIGHT THROUGH UNTIL FIRST DAY NOTICE JUST LIKE WE ARE WITNESSING TODAY. USUALLY WE NOTED THAT CONTRACTION IN OI OCCURRED ONLY DURING THE LAST WEEK OF AN UPCOMING ACTIVE DELIVERY MONTH AS WE HAVE JUST SEEN IN GOLD TODAY. THIS PROCESS HAS JUST BEGUN IN EARNEST IN SILVER STARTING IN SEPTEMBER 2017. HOWEVER, IN GOLD, WE HAVE BEEN WITNESSING THIS FOR THE PAST 2 YEARS. NICK LAIRD WAS KIND ENOUGH TO SUPPLY US THE TOTAL FOR 2017 GOLD EFP’S AND IT WAS 6600 TONNES FOR THE ENTIRE YEAR. WE OBVIOUSLY HAD ZERO LONG COMEX SILVER LIQUIDATION AND A GOOD SIZED GAIN IN TOTAL SILVER OI. WE ARE ALSO WITNESSING A FAIR AMOUNT OF SILVER OUNCES STANDING FOR COMEX METAL IN THIS NON ACTIVE JANUARY AS WELL AS THAT CONTINUAL MIGRATION OF EFPS OVER TO LONDON. ON A PERCENTAGE BASIS THERE ARE MORE EFP’S ISSUED FOR GOLD THAN SILVER. ON A NET BASIS WE GAINED 5523 SILVER OPEN INTEREST CONTRACTS:

2829 CONTRACT GAIN AT THE COMEX COMBINING WITH THE ADDITION OF 2833 OI CONTRACTS NAVIGATING OVER TO LONDON.

NET GAIN TWO EXCHANGES: 5523 CONTRACTS DESPITE THE DRUBBING SILVER TOOK IN PRICE WITH RESPECT TO FRIDAY’S TRADING

We are now in the poor non active delivery month of FEBRUARY and here the front month GAINED 16 contracts UP TO 157 contracts. We had 60 notices filed upon yesterday so we GAINED 76 contracts or 380,000 ADDITIONAL oz will stand for delivery at the comex as somebody was in urgent need of silver over at state side (NY)

The March contract lost 4696 contracts DOWN to 96,405

April lost 13 contracts down to 61 .

.

We had 16 notice(s) filed for 80,000 OZ for the FEBRUARY 2018 contract for silver

INITIAL standings for FEBRUARY

Feb 12/2018.

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz |

183,144.973 oz

Scotia

Delaware

I.Delaware

JPMorgan

|

| Deposits to the Dealer Inventory in oz | nil oz |

| Deposits to the Customer Inventory, in oz |

nil oz

|

| No of oz served (contracts) today |

50 notice(s)

5000 OZ

|

| No of oz to be served (notices) |

1149 contracts

(114,900 oz)

|

| Total monthly oz gold served (contracts) so far this month |

1783 notices

178300 oz

5.5458 tonnes

|

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

For FEBRUARY:

Today, 0 notice(s) were issued from JPMorgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equates to 50 contract(s) of which 49 notices were stopped (received) by j.P. Morgan dealer and 1 notice(s) was (were) stopped/ Received) by j.P.Morgan customer account.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

To calculate the INITIAL total number of gold ounces standing for the FEBRUARY. contract month, we take the total number of notices filed so far for the month (1783) x 100 oz or 178,300 oz, to which we add the difference between the open interest for the front month of FEB. (1199 contracts) minus the number of notices served upon today (50 x 100 oz per contract) equals 293,200 oz, the number of ounces standing in this active month of FEBRUARY

Thus the INITIAL standings for gold for the FEBRUARY contract month:

No of notices served (1783 x 100 oz or ounces + {(1199)OI for the front month minus the number of notices served upon today (50 x 100 oz )which equals 293,300 oz standing in this active delivery month of February (9.119 tonnes). THERE IS 12.08 TONNES OF REGISTERED GOLD AVAILABLE FOR DELIVERY SO FAR.

WE GAINED 31 CONTRACTS OR AN ADDITIONAL 3100 OZ WILL STAND IN THIS ACTIVE DELIVERY MONTH OF FEBRUARY.

THE COMEX IS NOW UNDER STRESS AS THE REGISTERED GOLD FALLS BELOW 13 TONNES AS WELL AS HUGE NUMBER OF TONNES LEAVING THE CUSTOMER ACCOUNT

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

IN THE LAST 17 MONTHS 71 NET TONNES HAS LEFT THE COMEX.

end

And now for silver

AND NOW THE DECEMBER DELIVERY MONTH

FEBRUARY FINAL standings

| Silver | Ounces |

| Withdrawals from Dealers Inventory | nil oz |

| Withdrawals from Customer Inventory |

54,585.481 oz

DELAWARE

I.DELAWARE

|

| Deposits to the Dealer Inventory |

nil

oz

|

| Deposits to the Customer Inventory |

1,202,371.700 OZ

JPM

Delaware

|

| No of oz served today (contracts) |

16

CONTRACT(S

(80,000 OZ)

|

| No of oz to be served (notices) |

141 contracts

(705,000 oz)

|

| Total monthly oz silver served (contracts) | 215 contracts

(1,075,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

we had no inventory movement at the dealer side of things

total inventory movement dealer: nil oz

we had 2 inventory deposits into the customer account

i) into J.P.MORGAN:1,201,401.200 oz

ii) into Delaware: 970.500 oz

total inventory deposits: 1,202,371.7000oz

we had 2 withdrawals from the customer account;

i Out of DELAWARE: 3965.500 OZ

ii) Out of International Delaware: 50,619.981 oz

total withdrawals; 54,585.481 oz

we had 0 adjustment

total dealer silver: 43.384 million

total dealer + customer silver: 251.417 million oz

The total number of notices filed today for the FEBRUARY. contract month is represented by 16 contract(s) FOR 80,000 oz. To calculate the number of silver ounces that will stand for delivery in FEBRUARY., we take the total number of notices filed for the month so far at 215 x 5,000 oz = 1,075,000 oz to which we add the difference between the open interest for the front month of FEB. (157) and the number of notices served upon today (16 x 5000 oz) equals the number of ounces standing.

.

Thus the INITIAL standings for silver for the FEB contract month: 215(notices served so far)x 5000 oz + OI for front month of FEBRUARY(157) -number of notices served upon today (16)x 5000 oz equals 1,780,000 oz of silver standing for the FEBRUARY contract month.

WE GAINED 16 CONTRACTS OR AN ADDITIONAL 80,000 OZ WILL STAND AT THE COMEX AS SOMEBODY WAS IN GREAT NEED OF SILVER STATE SIDE.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

ESTIMATED VOLUME FOR TODAY: 89,325 CONTRACTS

CONFIRMED VOLUME FOR YESTERDAY: 108,959 CONTRACTS

YESTERDAY’S CONFIRMED VOLUME OF 108,959 CONTRACTS EQUATES TO 544 MILLION OZ OR 77.8% OF ANNUAL GLOBAL PRODUCTION OF SILVER

COMMODITY LAW SUGGESTS THAT OPEN INTEREST SHOULD NOT BE MORE THAN 3% OF ANNUAL GLOBAL PRODUCTION. THE CROOKS ARE SUPPLYING MASSIVE PAPER TRYING TO KEEP SILVER IN CHECK.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price at that day at $18.42

The previous record was 224,540 contracts with the price at that time of $20.44

end

NPV for Sprott

1. Sprott silver fund (PSLV): NAV RISES TO -2.25% (FEB 12/2018)

2. Sprott gold fund (PHYS): premium to NAV FALLS TO -0.45% to NAV (FEB 8/2018 )

Note: Sprott silver trust back into NEGATIVE territory at -2.25%-/Sprott physical gold trust is back into NEGATIVE/ territory at -0.45%/Central fund of Canada’s is still in jail but being rescued by Sprott.

Sprott WINS hostile 3.1 billion bid to take over Central Fund of Canada

(courtesy Sprott/GATA)

3.SPROTT CEF.A FUND (FORMERLY CENTRAL FUND OF CANADA): NAV FALLS TO -4.11%: NAV 13.68/TRADING 13.11//DISCOUNT 4.11%

END

And now the Gold inventory at the GLD/

Feb 12/STRANGE!!WITH GOLD RISING BY 12.00 DOLLARS, THE CROOKS DECIDED AGAIN TO WITHDRAW 5.6 TONNES OF GOLD FOR EMERGENCY USE ELSEWHERE/INVENTORY RESTS AT 820.71 TONNES

Feb 9/AGAIN WITH HUGE TURMOIL ON THE MARKETS, THE CROOKS WITHDREW 2 TONNES OF GOLD FROM THE GLD INVENTORY/INVENTORY RESTS AT 826.31 TONNES

Feb 8/DESPITE THE GOOD GAIN IN PRICE FOR GOLD TODAY/THE CROOKS REMOVED .96 TONNES FROM THE GLD INVENTORY/INVENTORY RESTS AT 828.31 TONNES

FEB 7/AN UNBELIEVABLE 12.08 TONNES WAS REMOVED BY THE CROOKED BANKERS AND THIS GOLD WAS USED IN THE ASSAULT THESE PAST FEW DAYS/INVENTORY RESTS AT 829.27 TONNES

Feb 6/AGAIN VERY STRANGE: WITH TODAY’S TURMOIL, THE CROOKS DID NOT ADD ANY GOLD INVENTORY INTO THE GLD/INVENTORY REMAINS AT 841.35 TONNES

Feb 5 Strange,with all of today’s turmoil, the crooks at the GLD decided to add zero ounces into GLD inventory/inventory rests at 841.35 tonnes

Feb 2/no change in gold inventory at the GLD/Inventory rests at 841.35 tonnes

Feb 1/with gold up by $8.00/the crooks decided not to add any new physical gold metal into the GLD./inventory rests at 841.35 tonnes

Jan 31/with gold up $3.15 today, GLD shed another 5.32 tonnes of gold from its inventory/inventory rests at 841.35 tonnes

jan 30/with gold down by $4.85/GLD shed another 1.47 tonnes of gold from its inventory/inventory rests at 846.67 tonnes

JAN 29/with gold down $11.25, the GLD shed 1.18 tonnes of gold/inventory rests at 848.14 tonnes

jan 26/2018/no changes in gold inventory at the GLD/inventory rests at 849.32 tonnes

jan 25/no changes in gold inventory at the GLD/inventory rests at 849.32 tonnes

Jan 24/A HUGE DEPOSIT OF 2.65 TONNES OF GOLD INTO GLD/INVENTORY RESTS AT 849.32 TONNES

Jan 23/NO CHANGE IN GOLD INVENTORY DESPITE GOLD’S RISE/INVENTORY RESTS AT 846.67 TONNES

Jan 22/a huge deposit of 5.71 tonnes of gold despite a drop in price/inventory rests at 846.67 tonnes. In 3 trading days, the GLD has added 17.71 tonnes/the bankers are now in trouble!!

Jan 19/no change in gold inventory at the GLD/Inventory rests at 840.76 tonnes

Jan 18/SHOCKINGLY A HUGE DEPOSIT OF 11.80 TONNES WITH GOLD DOWN ALMOST $12.00/INVENTORY RESTS AT 840.76

Jan 17/no changes in gold inventory at the GLD/inventory rests at 828.96 tonnes

Jan 16/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 828.96 TONNES

Jan 12/no changes in inventory at the GLD despite the rise in gold price/inventory rests at 828.96 tonnes

Jan 11/ANOTHER IDENTICAL WITHDRAWAL OF 2.95 TONNES FROM THE GLD INVENTORY/INVENTORY RESTS AT 828.96 TONNES

Jan 10/with gold up today, a strange withdrawal of 2.95 tonnes/inventory rests at 831.91 tonnes

Jan 9/no changes in gold inventory at the GLD/Inventory rests at 834.88 tonnes

Jan 8/with gold falling by a tiny $1.40 and this being after 12 consecutive gains, today they announce another 1.44 tonnes of gold withdrawal from the GLD/

Jan 5/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 836.32 TONNES

Jan 4/2018/no change in gold inventory at the GLD/Inventory rests at 836.32 tonnes

Jan 3/a huge withdrawal of 1.18 tonnes of gold from the GLD/Inventory rests at 836.32 tonnes

Jan 2/2018/no changes in gold inventory at the GLD/inventory rests at 837.50 tonnes

Dec 29/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 837.50 TONNES

Dec 28/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 837.50 TONNES

Dec 27/NO CHANGES IN GOLD INVENTORY AT THE GLD/ INVENTORY RESTS AT 837.50 TONNES

Dec 26/no change in gold inventory at the GLD

Dec 22/ A DEPOSIT OF 1.48 TONNES OF GOLD INTO GLD INVENTORY/INVENTORY RESTS AT 837.50 TONNES

Dec 21′ NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 836.02 TONNES

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

Feb 12/2018/ Inventory rests tonight at 820.71 tonnes

*IN LAST 323 TRADING DAYS: 120.44 NET TONNES HAVE BEEN REMOVED FROM THE GLD

*LAST 257 TRADING DAYS: A NET 36.87 TONNES HAVE NOW BEEN ADDED INTO GLD INVENTORY.

end

Now the SLV Inventory

Feb 12/AGAIN, WITH TODAY’S HUGE RISE IN SILVER PRICE, IN TOTAL CONTRAST TO GOLD: NO CHANGE IN SILVER INVENTORY/INVENTORY RESTS AT 314.045 MILLION OZ/

Feb 9/AGAIN WITH TURMOIL ON THE MARKETS, STRANGELY IN TOTAL CONTRAST TO GOLD: NO CHANGE IN SILVER INVENTORY/INVENTORY RESTS AT 314.045 MILLION OZ/

Feb 8/DESPITE THE TURMOIL TODAY AND A PRICE RISE: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 314.045 MILLION OZ/

FEB 7/no change in silver inventory at the SLV/Inventory rests at 314.045 million oz/

Feb 6/WITH ALL OF TODAY’S TURMOIL/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 314.045 MILLION OZ/

Feb 5/ we had HUGE change in silver inventory at the SLV/ A DEPOSIT OF 1.131 MILLION OZ INTO THE SLV/Inventory rests at 314.045 million oz/

Feb 2/we lost 982,000 oz from the SLV inventory /inventory rests at 312.914 million oz/

Feb 1/no change in silver inventory at the SLV/Inventory rests at 313.896 million oz/

Jan 31/ no change in inventory at the slv in total contrast to gold/inventory rests at 313.896 million oz/

Jan 30/no change in inventory/SLV inventory rests at 313.896 million oz/

Jan 29/no change in inventory/SLV inventory rests at 313.896 million oz/

Jan 26.2018/inventory rests at 313.896 million oz

Jan 25/with silver up today and yesterday, the SLV could only muster a gain of 848,000 oz

Inventory rests at 313.896 oz

jan 24/NO CHANGE IN SILVER INVENTORY DESPITE THE GOOD ADVANCE IN PRICE/INVENTORY RESTS AT 313.048 MILLION OZ/

Jan 23/ANOTHER HUGE WITHDRAWAL OF 1.131 MILLION OZ OF SILVER DESPITE THE TINY LOSS/THE CROOKS ARE USING THE INVENTORY TO RAID ON SILVER.

JAN 22.2018/with silver down by 5 cents/ the crooks at the SLV liquidate 1.321 million oz of silver/inventory rests at 314.179 million oz/

Jan 19/ no changes in silver inventory at the SLV/inventory rests at 315.500 million oz/

jan 18/A WITHDRAWAL OF 848,000 OZ OF SILVER FROM THE SLV/INVENTORY RESTS AT 315.500 MILLION OZ/

Jan 17/no changes in silver inventory at the SLV/inventory rests at 316.348 million oz/

Jan 16/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 316.348 MILLION OZ

Jan 12/no changes in silver inventory at the SLV/inventory rests at 316.348 million oz/

Jan 11/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 316.348 MILLION OZ/

Jan 10/with silver up again, we had a huge withdrawal of 1.227 million oz from the SLV/inventory rests at 316.348 million oz

Jan 9/a withdrawal of 848,000 oz from the SLV/Inventory rests at 317.575 million oz/

jan 8/no change in silver inventory at the SLV/Inventory rests at 318.423 million oz/

Jan 5/DESPITE NO CHANGE IN SILVER PRICING, WE HAD A HUGE WITHDRAWAL OF 2.026 MILLION OZ/INVENTORY RESTS AT 318.423 MILLION OZ.

Jan 4.2018/a slight withdrawal of 180,000 oz and this would be to pay for fees/inventory rests at 320.449 million oz/

Jan 3/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 320.629 MILLION OZ.

Jan 2/WITH SILVER UP DRAMATICALLY THESE PAST 4 TRADING DAYS, THE FOLLOWING MAKES NO SENSE: WE HAD A WITHDRAWAL OF 2.83 MILLION OZ FROM THE SLV

INVENTORY RESTS AT 320.629 MILLION OZ/

Dec 29/no changes in silver inventory at the SLV/inventory rests at 323.459 million oz/

Dec 28/DESPITE THE RISE IN SILVER AGAIN BY 13 CENTS, WE LOST ANOTHER 1,251,000 OZ OF SILVER FROM THE SILVER.

Dec 27/WITH SILVER UP AGAIN BY 17 CENTS, WE LOST ANOTHER 802,000 OZ OF SILVER INVENTORY/WHAT CROOKS/INVENTORY RESTS AT 324.780 MILLION OZ/

Dec 26/no change in silver inventory at the SLV./Inventory rests at 325.582

Dec 21/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 326.227 MILLION OZ/

.

Feb 12/2017:

Inventory 314.045 million oz

end

6 Month MM GOFO

Indicative gold forward offer rate for a 6 month duration

+ 1.65%

12 Month MM GOFO

+ 2.07%

end

Major gold/silver trading /commentaries for MONDAY

GOLDCORE/BLOG/MARK O’BYRNE.

GOLD/SILVER

“This Is Where They Completely Lost Their Minds” – Hussman

“This Is Where They Completely Lost Their Minds” – Hussman

– Hussman warns ‘the S&P 500 to lose approximately two-thirds of its value over the completion of this cycle’

– ‘the market has lost value, even since 2009, when overvalued, overbought, overbullish conditions were joined by divergent internals’

– Believes the market is going to learn lessons about the crash ‘the hard way’

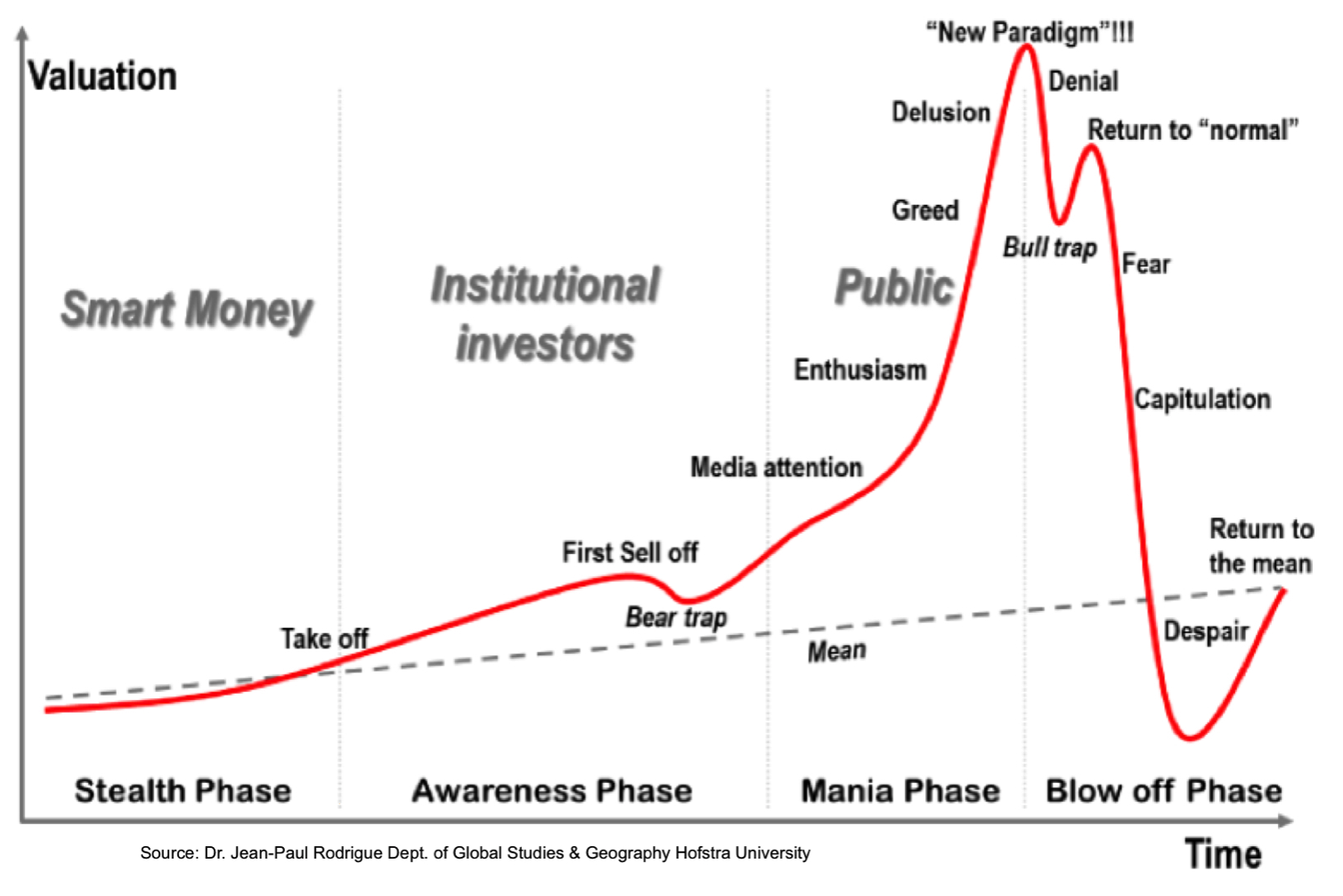

In an almost prophetic blog post from John Hussman last week, we are warned about the bubble waiting to collapse in the US equity market and the hard lesson investors are about to learn.

Drawing on both his own experience and the work of the much revered Didier Sornette, Hussman looks at the current state of the US equity market, where it sits in its cycle and how it compares to history.

The prognosis is not good. Hussman warns that ” the market has lost value, even since 2009, when overvalued, overbought, overbullish conditions were joined by divergent internals…I expect the S&P 500 to lose approximately two-thirds of its value over the completion of this cycle.”

Of course, the lesson may have finally begun. On Monday February 5th the Dow Jones dropped over 1,000 points, the largest single day drop ever, on a points-basis. Meanwhile, also on the 5th, the S&P500 went negative for 2018 closing down more than 7 percent from a record set in January. Similar action was repeated on the 8th February, with many traders declaring they’d never seen anything like it.

Of course, the lesson may have finally begun. On Monday February 5th the Dow Jones dropped over 1,000 points, the largest single day drop ever, on a points-basis. Meanwhile, also on the 5th, the S&P500 went negative for 2018 closing down more than 7 percent from a record set in January. Similar action was repeated on the 8th February, with many traders declaring they’d never seen anything like it.

Gold performed well following the rout and we believe gold prices may rise further as the drama leads period of risk aversion and a new found appreciation by investors looking for gold’s hedging and safe haven attributes.

You can hear more about our bubble crash predictions in our Goldnomics podcast. Here we take a look at one of the important financial questions of our day – is this the greatest stock market bubble in history?

Excerpts taken from ‘Measuring the Bubble’ on 1st February 2018

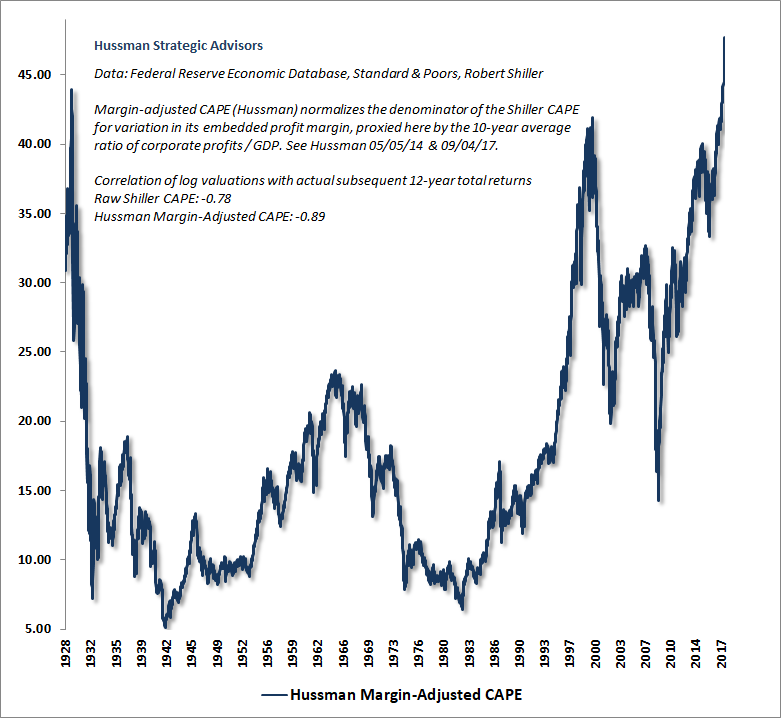

Last week, the U.S. equity market climbed to the steepest valuation level in history, based on the valuation measures most highly correlated with actual subsequent S&P 500 10-12 year total returns, across a century of market cycles

As Didier Sornette correctly observed in Why Markets Crash,

“The collapse is fundamentally due to the unstable position; the instantaneous cause of the crash is secondary.”

My sense is that investors are going to learn this again the hard way.

On the accelerating slope of the current advance

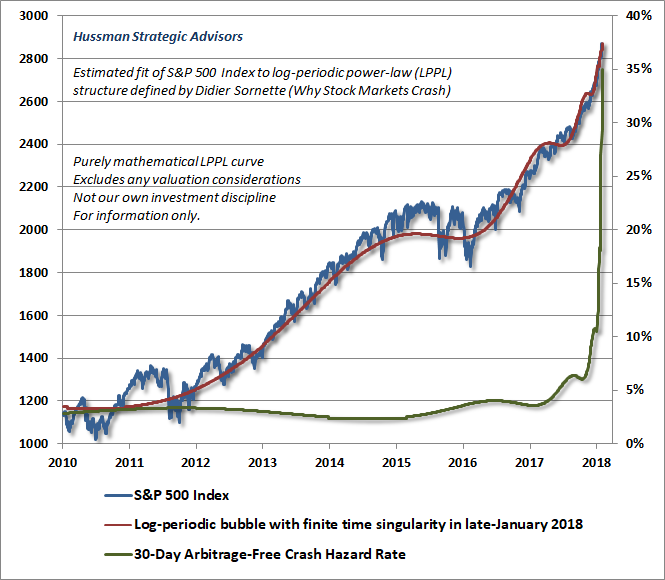

Speaking of Didier Sornette, I’ve periodically discussed his concept of “log periodic power-law” price behavior, which has accompanied speculative episodes in numerous markets and often precedes inflection points or collapses. This structure is based on a purely mathematical fit to price behavior, and does not reflect any valuation considerations. It’s not part of our own investment discipline, but we occasionally fit the log-periodic structure to price behavior when market movements are particularly extreme.

In recent years, those structures have generally identified inflection points of flat or correcting prices, but certainly not crashes in the S&P 500. Given the increasingly steep slope of the current market advance, along with the most extreme valuations in history and the most lopsided bullish sentiment in more than three decades, it’s quite possible that this instance will be different. In any event, the underlying “arbitrage” considerations described by Sornette are worth reviewing here.

In 2000, as the tech bubble was peaking, Nobel laureate Franco Modigliani observed that the late stages of a bubble can be “rational” in a certain sense, provided that investors are inclined to self-reinforcing behavior.

Imagine a market that you fully believe to be overvalued and at risk of a market crash. Indeed, let’s say that there is a defined probability of a crash, which increases rapidly as the pitch of the market advance becomes more extreme. Should you sell? Well, it depends. Given that an immediate crash is not certain, a speculator must, in each period, weigh the potential gain from holding a bit longer against the potential loss from overstaying. Sornette uses a similar argument to describe a speculative bubble advancing toward its peak (italics mine):

“Since the crash is not a certain deterministic outcome of the bubble, it remains rational for investors to remain in the market provided they are compensated by a higher rate of growth of the bubble for taking the risk of a crash, because there is a finite probability of ‘landing smoothly,’ that is, of attaining the end of the bubble without crash.”

“This line of reasoning provides us with the following important result: the market return from today to tomorrow is proportional to the crash hazard rate. In essence, investors must be compensated by a higher return in order to be induced to hold an asset that might crash. As the price variation speeds up, the no-arbitrage conditions, together with rational expectations, then imply that there must be an underlying risk, not yet revealed in the price dynamics, which justifies this apparent free ride and free lunch. The fundamental logic here is that the no-arbitrage condition, together with rational expectations, automatically implies a dramatic increase of a risk looming ahead each time the price appreciates significantly, such as in a speculative frenzy or in a bubble. This is the conclusion that rational traders will reach.”

The chart below shows our current best-fit parameterization of Sornette’s log-periodic structure, applied to the S&P 500 Index. Notably, unless we allow for the slope of the current market advance to become quite literally infinite, it’s impossible to closely fit the current price advance without setting the “finite-time singularity” – the point at which instability typically emerges – within a few days of the present date. Notably, the singularity is not the date of a crash. Rather, it’s the point where the pitch of the advance reaches an extreme, which may simply be an inflection point (as has been the case for other structures in recent years) or a pre-crash peak.

The collapse is fundamentally due to the unstable position; the instantaneous cause of the crash is secondary.

– Didier Sornette

If you want my opinion (which we don’t trade on and neither should you), my opinion is that this singularity will prove to be more than an inflection point.

Though nearly every morning prompts the phrase “Yup, they’re actually going to do this again,” the steepening pitch of this ascent – coupled with record valuation extremes, record overbought extremes, and the most lopsided bullish sentiment in over three decades – now produces the most extreme “overvalued, overbought, overbullish” moment in history. In prior cycles across history, similar syndromes were either joined or quickly followed by deterioration in market internals. In this cycle, it has been essential to wait for explicit deterioration in market internals before establishing a negative outlook. Notably, the market has lost value, even since 2009, when overvalued, overbought, overbullish conditions were joined by divergent internals.

I expect the S&P 500 to lose approximately two-thirds of its value over the completion of this cycle.

My impression is that future generations will look back on this moment and say “… and this is where they completely lost their minds.”

As I’ve regularly noted in recent months, our immediate outlook is essentially flat neutral for practical purposes, though we’re partial to a layer of tail-risk hedges, such as out-of-the-money index put options, given that a market decline on the order of even 5% would almost certainly be sufficient to send our measures of market internals into a negative condition. It’s best not to rely on the ability to execute sales into a falling market, because the range-expansion we’ve recently seen on the upside may very well have a mirror-image on the downside. As usual, we’ll respond to new evidence as it emerges.

END

Bitcoin and Crypto Prices Being Manipulated Like Precious Metals?

Bitcoin and Crypto Prices Being Manipulated Like Precious Metals? – FSN Interview GoldCore

Kerry Lutz of the Financial Survival Network (FSN) interviewed GoldCore’s Mark O’Byrne about the outlook for crypto currencies, financial markets and precious metals.

– Are bitcoin and crypto prices being manipulated like precious metals?

– Is there a coordinated backlash against bitcoin from JPM and powerful interests?

– 95% of cryptocurrencies and ICOs will likely go to zero

– Good cryptos will thrive, most will disappear in “massive creative destruction”

– Ponzi like nature of financial markets and fiat monetary system

– Fundamentals do not justify the massive gains in US stocks in recent years (near parabolic rise of over 300% in the S&P 500 since 2009)

– Is Plunge Protection Team (PPT) active in supporting markets?

– Retail investors including millennials piling into markets near top

– Smart money is reducing allocations to stocks and bonds; diversifying into gold

– Bitcoin is just nine years old and not proven store of value

– Gold proven store of value as seen in data, history and experience

– Gold backed crypto, crypto bullion, “digital gold” and “gold on the blockchain” has huge potential

– Perth Mint, Royal Mint, Royal Canadian Mint, LBMA and many others looking at blockchain

– Important blockchain solutions have full backing, transparency, security, stop the fraud and have customers interest at heart

– Important to own hard assets including physical gold and silver outside our digital financial and banking systems

Listen/ Watch To FSN GoldCore Interview On YouTube Here

News and Commentary

Gold edges up as dollar eases; eyes on US inflation data (Reuters.com)

Asia Stocks Rise With S&P Futures; Dollar Declines (Bloomberg.com)

Holiday drives up Chinese gold demand (GlobalTimes.cn)

Gold prices remain up on sustained jewellers’ buying in India (Livemint.com)

Bitcoin Finds a Bottom as Risk Aversion Grips Global Markets (Bloomberg.com)

Moody’s Threatens US Downgrade Due To Soaring Debt, “Fiscal Deterioration” (ZeroHedge.com)

Source: Goldchartsrus via Goldseek

Eight signals to watch that the U.S. stock rout is over (Reuters.com)

What America’s Super Bowl says about Asia’s stocks (StansBerryChurcHouse.com)

Where Will The U.S. Get the Cash? – Mauldin (GoldSeek.com)

Except For Gold…The Big 6 Commodities Were Closed Lower Again – Ed Steer (GoldSeek.com)

Granddaddy of all Bubbles Has Been Pierced – Doug Noland (CreditBubbleBulletin.blogspot.ie)

How China Is About to Shake Up the Oil Futures Market (Bloomberg.com)

Gold Prices (LBMA AM)

12 Feb: USD 1,321.70, GBP 955.19 & EUR 1,077.45 per ounce

09 Feb: USD 1,316.05, GBP 945.58 & EUR 1,072.84 per ounce

08 Feb: USD 1,311.05, GBP 944.87 & EUR 1,071.13 per ounce

07 Feb: USD 1,328.50, GBP 956.12 & EUR 1,075.95 per ounce

06 Feb: USD 1,344.65, GBP 962.50 & EUR 1,083.52 per ounce

05 Feb: USD 1,337.10, GBP 947.20 & EUR 1,072.49 per ounce

Silver Prices (LBMA)

12 Feb: USD 16.43, GBP 11.86 & EUR 13.39 per ounce

09 Feb: USD 16.36, GBP 11.83 & EUR 13.37 per ounce

08 Feb: USD 16.35, GBP 11.70 & EUR 13.36 per ounce

07 Feb: USD 16.69, GBP 12.02 & EUR 13.52 per ounce

06 Feb: USD 16.81, GBP 12.07 & EUR 13.59 per ounce

05 Feb: USD 16.88, GBP 12.01 & EUR 13.56 per ounce

Recent Market Updates

– “This Is Where They Completely Lost Their Minds” – Hussman

– Brexit Risks Increase – London Property Market and Pound Vulnerable

– Peak Gold: Global Gold Supply Flat In 2017 As China Output Falls By 9%

– Crypto Currency Backlash Sees Flight From Cryptos and Bitcoin

– Gold Rises As Global Stocks Plunge and Bitcoin Crashes 70%

– Shrinkflation Intensifies – Stealth Inflation As Thousands of Food Products Shrink In Size, Not Price

– U.S. Debt Is “Extraordinarily High” and Are Stock And Bond Bubbles – Greenspan

– Gold Bullion Price Suppression To End? Bullion Bank Traders Arrested For Manipulating Market

– ATMs Hit By Malware “Jackpotting” Attacks That Dispense All Cash In Minutes

– London Property Market Tumbles As Glut of Luxury Apartments Grows To 3,000

– Silver Bullion: Once and Future Money

– Greatest Stock Bubble In History? GoldNomics Podcast Transcript

– Davos – My Personal Experience of the $100,000 Event, $60 Burgers, Massive Inequality and the Blockchain Revolution

As I explained below, the Fed has only two choices, rates or stocks. With Trump’s new spending initiate rates are heading higher and this will certainly cause stocks to flounder

(courtesy Eric Sprott/)

Fed will have to choose between rates and stocks, Sprott says

Submitted by cpowell on Fri, 2018-02-09 22:22. Section: Daily Dispatches

5:23p ET Friday, February 9, 2018

Dear Friend of GATA and Gold:

Mining entrepreneur and Sprott Asset Management founder Eric Sprott, interviewed by the TF Metals Report’s Craig Hemke for the Sprott Money weekly wrapup, says the Federal Reserve soon may have to make a choice between letting interest rates rise or crashing the stock and housing markets. Under the circumstances this week, Sprott says, the monetary metals have not done badly. The interview is 12 minutes long and can be heard and read at Sprott Money here:

https://www.sprottmoney.com/Blog/the-natural-instinct-should-be-to-buy-g…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

Mike Kosares explains the meaning of volatility and how it usually presages a downward blast in the stockmarket and a rise in the price of gold

a must read..

(courtesy Michael Kosares/GATA)

Mike Kosares: The anatomy of volatility and what it means for gold

Submitted by cpowell on Sat, 2018-02-10 23:17. Section: Daily Dispatches

6:19p ET Saturday, February 10, 2018

Dear Friend of GATA and Gold:

USAGold’s Mike Kosares today cites a Swiss Finance Institute study concluding that market crashes tend to follow a period of low volatility, that volatility can spike for months, and that “in recent history volatility has preceded upward movement in the gold price.”

Kosares adds that while volatility may not always spike before a crash, “it most certainly has surged in the past before an increase in the price of gold.”

Kosares’ commentary is headlined “The Anatomy of Volatility and What It Means for Gold” and it’s posted at USAGold here:

http://www.usagold.com/cpmforum/2018/02/10/the-anatomy-of-volatility-and…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

I wonder what gave this away: the Economist states that insider trading has been rife on Wall Steet

(courtesy the Economist/London)

The Economist: Insider trading has been rife on Wall St., academics conclude

Submitted by cpowell on Mon, 2018-02-12 12:28. Section: Daily Dispatches

From The Economist, London

Saturday, February 10, 2018

Insider-trading prosecutions have netted plenty of small fry. But many grumble that the big fish swim off unharmed. That nagging fear has some new academic backing, from three studies. One argues that well-connected insiders profited even from the financial crisis. The others go further still, suggesting the entire share-trading system is rigged.

What is known about insider trading tends to come from prosecutions. But these require fortuitous tipoffs and extensive, expensive investigations, involving the examination of complex evidence from phone calls, e-mails, or informants wired with recorders. The resulting haze of numbers may befuddle a jury unless they are leavened with a few spicy details—exotic code words, say, or (even better) suitcases filled with cash.

The papers make imaginative use of pattern analysis from data to find that insider trading is probably pervasive. The approach reflects a new way of analysing conduct in the financial markets. It also raises questions about how to treat behaviour if it is systemic rather than limited to the occasional rogue trader. …

… For the remainder of the report:

https://www.economist.com/news/finance-and-economics/21736561-one-study-…

END

Interview of Bill Holter

Is Rothschild Going To Tank The Market To Punish Trump? — Bill Holter

Attachments areaPreview YouTube video Is Rothschild Going To Tank The Market To Punish Trump? — Bill Holter

Is Rothschild Going To Tank The Market To Punish Trump? — Bill Holter

Your early MONDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

i) Chinese yuan vs USA dollar/CLOSED DOWN AT 6.3246 /shanghai bourse CLOSED UP AT 24.27 POINTS 0.78% / HANG SANG CLOSED DOWN 47.79 POINTS OR 0.16%

2. Nikkei closed HOLIDAY /USA: YEN FALLS TO 108.68

3. Europe stocks OPENED DEEPLY IN THE GREEN /USA dollar index RISES TO 90.45/Euro FALLS TO 1.2236

3b Japan 10 year bond yield: FALLS TO . +.066/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 108.97/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD FINALLY IN THE POSITIVE/BANK OF JAPAN LOSING CONTROL OF THEIR YIELD CURVE AS THEY PURCHASE ALL BONDS TO GET TO ZERO RATE!!

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 60.26 and Brent: 63.65

3f Gold UP/Yen UP

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil DOWN for WTI and DOWN FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund RISES TO +.764%/Italian 10 yr bond yield UP to 2.039% /SPAIN 10 YR BOND YIELD UP TO 1.460%

3j Greek 10 year bond yield RISES TO : 4.167?????????????????

3k Gold at $1319.70 silver at:16.42 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble UP 40/100 in roubles/dollar) 57.97

3m oil into the 60 dollar handle for WTI and 63 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 108.68 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 0.9383 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1504 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now POSITIVE territory with the 10 year RISING to +0.764%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.8803% early this morning (THIS IS DEADLY TO ALL MARKETS). Thirty year rate at 3.17610% /BOTH DEADLY

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

(courtesy Jim Reid/Bloomberg/Deutsche bank/zero hedge)

US Futures Surge After Sharp Rebound In Asia And Europe; China “Plunge Protectors” Activated

Despite a very explicit warning by Goldman’s co-head of equity trading that the “regime has changed” and that instead of “buying the dip”, investors should be “selling-the-rip”, so far this morning a global BTFD relief rally from Asia to Europe has welcomed a rare respite from volatility as U.S. stock futures surged after a week that saw two of the biggest single-day percentage drops in seven years, with the Dow set to open some 300 points higher after Friday’s torrid last hour surge.

And as investors await today’s revised monthly budget statement, one which reportedly will no longer balance over the next 10 years, sending the dollar sliding in the process, S&P futures are about 30 handles higher, flirting with 2,650, some 100 points higher from the lows observed around noon on Friday.

S&P 500 futures jumped 1.2%, following a weekly decline that at one point was the largest since the financial crisis. Futures on the Dow Jones Industrial Average added 1.3 percent, while those on the Nasdaq 100 Index were up 1 percent. Meanwhile, the VIX fell 11% extending its drop to a second day after JPM wrote on Friday that the worst of the vol spike “unwind” by CTAs, risk parities and vol-targeting funds is behind us.

Traders have been on edge following tumultuous moves in equities last week, which saw the S&P 500 post its worst week in two years with a 5.2% decline on fears over interest rate hikes, ending a stretch of 588 days without a 5% drop.

However, what has been most surprising about today’s session is that Ten-year Treasury yields climbed on Monday, touching a fresh four-year high amid growing inflation fears, worries about the surging US deficit, and concerns the Federal Reserve may accelerate its rate-hike schedule even as it continues to shrink its balance sheet. The 10Y yield rose as high as 2.8930%, yet unlike last week this has – so far – not been enough to dent the equity enthusiasm.

The Treasury curve flattened, with futures edging further lower led by belly, EGB peripheral spreads see minor tightening given general risk-on; iTraxx Crossover also tightens ~12bps. Germany’s 10-year yield increased three basis points to 0.77 percent, the highest in more than two years. Britain’s 10-year yield rose five basis points to 1.605 percent, the highest in almost 22 months.

European equities rebounded on Monday from the worst weekly sell-off in two years with share prices firming in opening trading. Europe’s Stoxx 50 index climbed some 1.9%, led by miners as European bourses catch up with the gains seen late on Wall Street on Friday with macro newsflow otherwise light in the region. Sector wise, material names outperform i nfitting with some of the price action seen in the complex during Asia-Pac trade, energy names are also higher as energy prices continue to retrace some of the losses seen on Friday. In terms of stock specifics, Heineken (-4.2%) are seen lower after their earnings report was clouded by currency effects, Akzo Nobel (+1.7%) have been in focus today after reports in the FT suggesting the Co.’s chemicals unit has been subject to PE interest, Barclays (+1%) have been charged by the SFO regarding their Qatari loans and Airbus (-1.2%) are lower amid reports that they have stopped delivering A320neo jets due to issues with Pratt &Whitney engines.

Asia similarly surged, with South Korean equities and the won rose after North Korean leader Kim Jong Un invited his counterpart to meet. Vice President Mike Pence told the Washington Post the U.S. is ready to engage in talks about North Korea’s nuclear program, signaling a shift in policy. The won outperformed major currencies. Japan’s markets are closed for a holiday. Elsewhere, Hang Seng (-0.2%) and Shanghai Comp. (+0.8%) were positive ahead of this week’s Lunar New Year celebrations, while most of the Asia peripheries traded with cautious gains amid a lack of drivers and with various holiday closures scheduled through to next week.

China’s ChiNext index of small-cap and tech shares jumped after the government was said to call on companies and mutual funds to boost the stock market. The ChiNext rose 3.5% in Shenzhen, its biggest gain since July 27, after falling to a three-year low Friday. “The news about government support eased some worries,” said Shen Zhengyang, Shanghai-based strategist with Northeast Securities Co. “People are hunting for bargains, especially smaller companies that fell too much in the recent rout”

Others were more cautious: “Futures can move around quite a bit, but what I will be watching for is a stable ‘green’ in the futures coming into tomorrow,” BB&T’s Walter “Bucky” Hellwig told Bloomberg. ““This will show that the S&P didn’t hold on to its 200-day moving average by accident, and this confidence is going to pull more buyers into the market.”

To be sure, with Japan closed for holiday, and virtually no economic events and market drivers so far on Monday (this will change with Wednesday’s CPI release) has led to an extremely muted European session.

Meanwhile, the USD is weaker across the board after Sunday reports that the Trump budget to be released today will not only increase the US deficit but – for the first time under a Republican president – won’t balance over 10 years.

Other major currencies were rangebound, USD/ZAR drifts lower in anticipation of Zuma departure, RUB rallies with crude. Some other pairs from Bloomberg:

- EUR/USD rises as much as 0.4% to 1.2297 before paring as take-profit offers cap pair for now, volumes relatively muted amid Japan holiday

- GBP/USD edges up as as U.K. Prime Minister Theresa May embarks this week on a push to bring her divided Cabinet together and flesh out a Brexit strategy

- USD/JPY falls modestly

- AUD/NZD rises as cross bounces off 1.0750 area for the fifth time in as many days helped by macro flows

The dollar’s decline supported commodities, with metals higher and crude oil halting a six-day selloff. Both WTI and Brent crude futures have continued to retrace Friday’s losses despite Friday’s Baker Hughes rig count showing a climb of 26 oil rigs. In terms of energy newsflow, UAE energy minister stated the energy market is to balance this year with shale oil output to be absorbed by rising 2018 demand. In metals markets, spot gold is seen higher alongside the softer USD, although gains are likely being capped by this morning’s risk environment. Elsewhere, copper prices have recovered from their two month lows during London trade while Chinese iron ore futures were seen lower overnight after recent rampant gains ahead of the Lunar New Year which kicks off this Thursday.

And while there are few notable economic releases today, looking ahead investors will await U.S. consumer-price data on Wednesday with some trepidation. Pressure on equities has been emanating from the Treasury market and in the outlook for inflation, and any upside surprises will likely resume the positive correlation between bond and stock prices.

In geopolitical developments, North Korea invited South Korean President Moon for talks in Pyongyang, while President Moon stated that they should make preparations to realize the meeting. At the same time, a US official stated that there is no differences between US, South Korea and Japan on need to isolate North Korea until it gives up its nuclear weapons program.

There were also some notable central bank comments overnight, with BoE’s Haldane saying that minor interest rate increases are likely to be introduced later this year, while he also stated that inflation is currently running above target and that’s one of the factors interest rates were hiked last year. BoE Vlieghe said that if there are less credit headwinds, this may signal that the UK is ready for higher rates, there is increased evidence that a tight labour market is having upward effects on wages, also stating that rise in UK debt burden not sustainable if continues for many years.

ECB’s Nowotny said that the ECB is concerned regarding US attempts to politically influence FX rates. Nowotny also added that said that EU inflation still has room to increase so the ECB is still on the careful side, although that certainly won’t last forever and that there will be a need for higher interest rates in the foreseeable future. ECB’s Visco said ECB will be patient on pursuit of its inflation goal and that it has been challenging to push up inflation

expectations.

This week earnings season continues in full swing with reports from Bunge, TripAdvisor, SunPower, Con Edison, Bombardier, Heineken, Loews, Michelin, PepsiCo, MetLife,Cisco, Japan Post Bank, Credit Suisse, Nestle, Airbus, Allianz, Telstra, Coca-Cola, Deere, Eni, Credit Agricole and Campbell Soup.

Bulletin Headline Summary from RanSquawk

- European bourses catch up to the gains seen late Friday on Wall Street

- A relatively quiet start to the week in FX, partly due to Japan’s market holiday, but also as many participants simply take some time out after the hectic sessions of late

- Looking ahead, today sees a lack of tier 1 highlights

Market Snapshot

- S&P 500 futures up 1.2% to 2,649.25

- Brent Futures up 2.2% to $64.18/bbl

- Gold spot up 0.4% to $1,321.31

- U.S. Dollar Index down 0.3% to 90.21

- STOXX Europe 600 up 1.6% to 374.31

- MXAP up 0.4% to 171.13

- MXAPJ up 0.6% to 557.88

- Nikkei down 2.3% to 21,382.62

- Topix down 1.9% to 1,731.97

- Hang Seng Index down 0.2% to 29,459.63

- Shanghai Composite up 0.8% to 3,154.13

- Sensex up 1% to 34,329.57

- Australia S&P/ASX 200 down 0.3% to 5,820.70

- Kospi up 0.9% to 2,385.38

- German 10Y yield rose 3.7 bps to 0.782%

- Euro up 0.2% to $1.2271

- Brent Futures up 2.2% to $64.18/bbl

- Italian 10Y yield rose 5.4 bps to 1.779%

- Spanish 10Y yield fell 0.4 bps to 1.476%

Top Overnight News from Bloomberg

- President Trump will seek billions of dollars in new spending to build a border wall, improve veterans’ health care and combat opioid abuse in a budget proposal that’s likely to get little traction in a Republican Congress that has its own, very different spending priorities

- OMB’s Mulvaney: U.S. will post a larger budget deficit this year and could see a “spike” in interest rates as a result

- In a break from a longstanding Republican goal, the plan won’t balance the budget in 10 years, according to a person familiar with the proposal

- The U.S. is ready to engage in talks about North Korea’s nuclear program even as it maintains pressure on Kim Jong Un’s regime, Vice President Mike Pence said, signaling a shift in American policy

- The U.K. economy is ready for slightly higher rates, BOE’s Vlieghe says on a panel in London

- Reports of Prime Minister Shinzo Abe’s plan to nominate Haruhiko Kuroda for another term as chief of the Bank of Japan is seen as easing pressure on the yen

- BOE’s Vlieghe: U.K. economy ready for slightly higher rates

- ECB’s Nowotny says euro-area inflation has room to move higher so ECB is still on the careful side; Visco says risk of deflation averted, forex volatility seen as main risk for inflation

- German Chancellor Angela Merkel said she’s determined to serve another full term, rebuffing party critics who say she sold out to the Social Democrats to extend her 12 years in office

- China Jan. M2 Money Supply: 8.6% vs 8.2% est; New Yuan Loans 2.9t vs 2.1t est; Agg. Financing 3.1t vs 3.2t est.

Asia equity markets began a holiday-quietened week mostly positive in which the region got a mild lift as US equity futures extended on Friday’s late rebound. However, upside was contained with Japan away in observance of National Founding Day, while the ASX 200 (-0.3%) was the laggard as energy names reeled from last week’s drop in crude prices and with financials subdued as the Royal Banking Commission started its inquiry into the industry. Elsewhere, Hang Seng (-0.2%) and Shanghai Comp. (+0.8%) were positive ahead of this week’s Lunar New Year celebrations, while most of the Asia peripheries traded with cautious gains amid a lack of drivers and with various holiday closures scheduled through to next week. PBoC skipped open market operations.

Top Asian News

- China Is Said to Call on Companies, Mutual Funds to Boost Stocks

- China New Loans Hit Record on Seasonal Boost, Shadow Bank Curbs

- Chinese Tourists Are Taking Over the Earth, One Selfie at a Time

- Singapore Seen Leading Race to Tax $38 Billion Shopping Boom

- China’s Jan. New Loans 2.9T Yuan; Est. 2.05T Yuan

European equities have kicked the week off on the front foot (Eurostoxx 50 +1.9%) as European bourses catch up with the gains seen late on Wall Street on Friday with macro newsflow otherwise light in the region. Sector wise, material names outperform infitting with some of the price action seen in the complex during Asia-Pac trade, energy names are also higher as energy prices continue to retrace some of the losses seen on Friday. In terms of stock specifics, Heineken (-4.2%) are seen lower after their earnings report was clouded by currency effects, Akzo Nobel (+1.7%) have been in focus today after reports in the FT suggesting the Co.’s chemicals unit has been subject to PE interest, Barclays (+1%) have been charged by the SFO regarding their Qatari loans and Airbus (-1.2%) are lower amid reports that they have stopped delivering A320neo jets due to issues with Pratt &Whitney engines.

Top European News

- Barclays Bank Unit Charged by SFO Over 2008 Qatar Loan Deal

- ECB’s Nowotny Says Central Banks’ Task Isn’t to Satisfy Markets

- TDC Withdraws Recommendation of MTG Transaction After Bid999

- Kazakh Halyk Bank Weighs Dividend as CEO Predicts Excess Capital

- Berlusconi Papers Over Cracks in Alliance: Italy Campaign Trail

In FX, a relatively quiet start to the week, partly due to Japan’s market holiday, but also as many participants simply take some time out after the hectic sessions of late. The Usd is modestly weaker vs all its G10 peers bar the Kiwi, and then only just as Nzd/Usd nestles around 0.7250 and Aud/Nzd remains below 1.0800 – Aud/Usd maintaining 0.7800+ status. Cable has ticked up towards the top of a 1.3810-1.3875 range on little obvious Sterling supportive news or factors aside from further BoE rhetoric underscoring more policy tightening (albeit gradual), while Eur/Usd is mid-way between 1.2245-95 parameters amidst more qualms registered by ECB’s Nowotny about the US exerting political influence on exchange rates. Usd/Jpy even more contained within a 108.50-108.95 band, as are Usd/Chf and Usd/Cad in 0.9370-0.9400 and 1.2600-1.2555 ranges awaiting more direction – via stock market developments and US CPI data for example. The Dollar index is keeping its head above the 90.000 level with the latest weekly CFTC reports on spec positioning showing a slightly less short Greenback base, along with the Jpy, while Eur and Gbp longs lighten up a bit and Loonie longs increase their Cad holdings. In terms of option expiries, nothing really of note or in size for today’s NY cut.

In commodities, both WTI and Brent crude futures have continued to retrace Friday’s losses despite Friday’s Baker

Hughes rig count showing a climb of 26 oil rigs. In terms of energy newsflow, UAE energy minister stated the energy market is to balance this year with shale oil output to be absorbed by rising 2018 demand. In metals markets, spot gold is seen higher alongside the softer USD, although gains are likely being capped by this morning’s risk environment. Elsewhere, copper prices have recovered from their two month lows during London trade while Chinese iron ore futures were seen lower overnight after recent rampant gains ahead of the Lunar New Year which kicks off this Thursday. North Sea Forties pipeline is now said to be in full operation, according to sources. Phillips 66 reports a unit upset at wood river, Illinois refinery; the refinery has a crude capacity of 314K bpd.

With data fairly thin on Monday all eyes will instead be on the White House with President Trump expected to release a $1.5tn infrastructure plan, along with his 2019 budget blueprint. Away from that the only data of note is the January monthly budget statement in the US.

US Event Calendar

- 2pm: Monthly Budget Statement, est. $51.0b, prior $51.3b

DB’s Jim Reid concludes the overnight wrap

Are we potentially set for a Valentine’s Day sell-off on Wednesday for markets or will Cupid fire some dovish arrows for the market. Indeed we can’t remember a more eagerly anticipated number than the US CPI release on the most romantic day of the year. It’s near impossible to predict one number but our bias continues to be for higher inflation than expected in 2018. This number has been slightly complicated as the BLS have recently made some seasonal adjustments. Before this, January’s print (i.e. this week’s number) had consistently exceeded expectations in the last 25 years and February’s had consistently missed. So all a bit uncertain. Our economists also think we should watch healthcare inflation which is due some upside surprise soon. We’ll fully preview on Wednesday but that’ll be the focal point for the week and the focal point for pretty much every month this year in our opinion.

Other data will pale into insignificance this week but you can see what’s in store at the end of this report. It’s also worth mentioning that today President Trump is expected to release a $1.5tn infrastructure plan (which will kick off the process for producing legislation) and also his 2019 budget blueprint. Given the tax reform, the recent budget concessions to keep the government open, and this infrastructure plan, it’s no surprise to see investors looking at whether government bond yields are too low regardless of inflation. It’s also worth noting that it’s a half-term week in the UK and parts of Europe so that could add to the liquidity fun and games in either direction. On a similar vein Chinese New Year kicks off on Thursday, with mainland markets subsequently shut until February 21st.

Now recapping equities performance from Friday. European bourses were all lower after the negative leads from Asia, with key bourses down 1-1.5% (Stoxx 600 -1.45%; DAX -1.25%; FTSE -1.09%). Across the pond, the S&P exhibited large swings with a peak to trough intraday range of 4.1% before recovering throughout the day and closing 1.49% higher. The Dow (+1.38%) and Nasdaq (+1.44%) also advanced. Within the S&P, all sectors excluding energy were in the green, with gains led by the tech, real estate and utilities sectors. Elsewhere, the VIX also traded in a large range of c13pt (27.7 to 41.1) before closing 4.4pt lower to 29.06 (-13.2%).

Over the weekend, the Nikkei reported Japan’s PM Abe intends to nominate Kuroda for a second five year term as BOJ Governor. Our Japanese strategist Yamashita expect the near term market impacts to be limited, in part as consensus was broadly expecting a reappointment. Looking ahead, he expects the current monetary easing framework to remain in the short term, but a normalisation bias is more likely down the track, albeit with actual action likely to be made on the condition of inflation reaching +1% and the government declaring a victory over deflation. If normalisation occurs, he expects a hike in the 10y JGB yield target to be the BOJ’s first move towards normalization. ETF purchases are also likely to be scaled back sooner rather than later, although domestic stock prices will probably need to move back into an uptrend trend before that can happen. Refer to his note for more details.

Following on, Nick Burns from my team has examined the potential headwinds for HY credit due to the spike higher in equity market volatility. We believe there will likely be a reversal from the current levels of equity market volatility, but credit spreads will likely come under pressure unless equity market volatility falls towards the lows seen during 2017. Further, he has also looked at how the technicals seem to be less supportive in the early stages of 2018 than they have been in recent years. Refer to his note for more details.

This morning in Asia, markets are modestly higher. The Hang Seng (+0.58%), Kospi (+1.18%) and China’s CSI 300 (+0.81%) are all up while the ASX 200 is down 0.30% as we type. Elsewhere, the Japanese market is closed today for a holiday and WTI is rebounding c1%.

Now recapping other market’s performance from Friday. In government bonds, earlier risk aversion seemed to help core European 10y bond yields to fall 2-5bp (Bunds -1.8bp; Gilts -4.6bp) while peripherals yields rose 3-7bp. Turning to currencies, the US dollar index strengthened 0.24% while the Euro was broadly flat and Sterling fell 0.62%, weighed down by the softer than expected prints on IP and trade deficits. In commodities, WTI oil fell 3.19%, in part as the Baker Hughes US rig count posted its biggest weekly increase in more than year. Elsewhere, precious metals softened (Gold -0.16%; Silver -0.34%) and other base metals also weakened (Copper -1.41%; Zinc -0.69%; Aluminium -0.81%).

Away from markets, the US Budget director Mulvaney noted that rising budgets deficits are “a very dangerous idea, but it’s the world we live in” and the “US will post a larger deficit this year and could see a spike in interest rates, but lower deficit are possible over time given sustained economic growth”. Elsewhere, Congress has officially passed the two year spending deal with our US economists expecting the c$300bln increase in spending to potentially add several tenths to their 2018 and 2019 growth forecasts of 2.6% and 2.1% (Q4/Q4) respectively, subject to more details from the deal.

Over in Germany, the BamS has reported the SPD leader Martin Schulz will be replaced on Tuesday when the SPD leadership meets. The BamS did not say how it got the information but noted Andrea Nahles will be appointed as acting party Head. Earlier on Friday, Mr Schulz has “declared his withdrawal from a (proposed) role in the federal government” but said he wanted party members to vote in favour of the coalition government with Ms Merkel’s bloc. Elsewhere, Ms Merkel noted that it’s acceptable to give the finance ministry post to the SPD and that “a finance minister can’t just do what he wants”.

Finally onto central banks commentaries. The ECB’s Nowotny noted the recent equities sell off as “a normalisation” and that “…the task of central banks isn’t to satisfy markets but to ensure economic stability. So if necessary, rates will have to rise and markets will have to adapt to that”. On QE, he said “…I don’t think we will need it (after September), at least not in its current form”. On inflation, he noted it still has room to move higher, so the ECB is still on the careful side, but that won’t last forever, as “in the foreseeable future there will be a need for the ECB to raise rates…”

In the UK, the BOE’s Haldane said “some further tightening of policy might be needed over the period ahead”, but the BOE is “in no rush” to do so. He added rates in the UK “won’t remotely go back to levels we’ve seen in the past, but nonetheless keeping the cost of living under control is….the single best and most important thing we can do to help the economy”.

We wrap up with other data releases from Friday. In the US, the final reading of the December wholesale inventories was revised upward to 0.4% mom (vs. 0.2% expected). Overall,the Atlanta Fed’s GDPNow model now estimate that the US economy will grow 4.0% saar in 1Q, while the NY Fed’s estimate is c3.4% saar. In Europe, both France and Italy’s December IP was above market, at 4.5% yoy (vs. 3.5% expected) and 4.9% (vs. 1.9% expected) respectively. Conversely, a fall in output in the oil and gas and mining sectors contributed to a lower than expected December IP in the UK, at -1.3% mom (vs. -0.9%) and 0% yoy (vs 0.4%), while its December trade deficit widened to -£4.9bln (vs. -£2.4bln expected). Exports for the month rose 0.8% mom, while imports rose an even stronger 3.0% mom.

With data fairly thin on Monday all eyes will instead be on the White House with President Trump expected to release a $1.5tn infrastructure plan, along with his 2019 budget blueprint. Away from that the only data of note is the January monthly budget statement in the US. Heineken will report earnings.

3. ASIAN AFFAIRS

i)Late SUNDAY night/MONDAY morning: Shanghai closed UP 24.27 points or 0.78% /Hang Sang CLOSED DOWN 47.79 or 0.16% / The Nikkei closed HOLIDAY/Australia’s all ordinaires CLOSED UP 0.30%/Chinese yuan (ONSHORE) closed DOWN at 6.3286/Oil DOWN to 60.26 dollars per barrel for WTI and 63.65 for Brent. Stocks in Europe OPENED DEEPLY IN THE GREEN . ONSHORE YUAN CLOSED DOWN AGAINST THE DOLLAR AT 6.3286. OFFSHORE YUAN CLOSED DOWN AGAINST THE ONSHORE YUAN AT 6.3346//ONSHORE YUAN A LOT WEAKER AGAINST THE DOLLAR/OFF SHORE A LOT WEAKER TO THE DOLLAR/. THE DOLLAR (INDEX) IS MUCH WEAKER AGAINST ALL MAJOR CURRENCIES EXCEPT CHINA YUAN. CHINA IS HAPPY TODAY STRONGER MARKETS IN CHINA

3 a NORTH KOREA/USA

/NORTH KOREA

3 b JAPAN AFFAIRS

c) REPORT ON CHINA

4. EUROPEAN AFFAIRS

GREAT BRITAIN

An excellent commentary from Alasdair Macleod as he correctly states that Great Britain should leave the EU at no cost to them and then have free trade with the rest of Europe. He explains why:

(courtesy/Alasdair Macleod)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

A major escalation as Syria shoots down an F 16 jet on Israeli soil. Israel launches a large scale attack inside Syria wiping out huge weapon facilities

(courtesy zerohedge)