GOLD: $1330.95 UP $0.90

Silver: $16.62 DOWN 1 cent

Closing access prices:

Gold $1332.50

silver: $16.63

SHANGHAI GOLD FIX: FIRST FIX 10 15 PM EST (2:15 SHANGHAI LOCAL TIME)

SECOND FIX: 2:15 AM EST (6:15 SHANGHAI LOCAL TIME)

SHANGHAI FIRST GOLD FIX: $XXXX DOLLARS PER OZ

NY PRICE OF GOLD AT EXACT SAME TIME: $XXXX

PREMIUM FIRST FIX: $xxx

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

SECOND SHANGHAI GOLD FIX: $XXXX

NY GOLD PRICE AT THE EXACT SAME TIME: $xxx

discount of Shanghai 2nd fix/NY:$

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

LONDON FIRST GOLD FIX: 5:30 am est $1323.50

NY PRICING AT THE EXACT SAME TIME: $1323.45

LONDON SECOND GOLD FIX 10 AM: $1339.85

NY PRICING AT THE EXACT SAME TIME. $1340.30

For comex gold:

FEBRUARY/

NUMBER OF NOTICES FILED TODAY FOR FEBRUARY CONTRACT: 0 NOTICE(S) FOR nil OZ.

TOTAL NOTICES SO FAR:1784 FOR 178400 OZ (5.5489 TONNES),

For silver:

FEBRUARY

0 NOTICE(S) FILED TODAY FOR

nil OZ/

Total number of notices filed so far this month: 386 for 1,930,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: BID $10,246/OFFER $10,311: DOWN $173(morning)

Bitcoin: BID/ $9,952/offer $10,022: DOWN $468 (CLOSING/5 PM)

end

Let us have a look at the data for today\

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total open interest FELL BY A CONSIDERABLE SIZED 1683 contracts from 203,629 FALLING TO 201,946 DESPITE YESTERDAY’S 15 CENT GAIN IN SILVER PRICING. WE HAD CONSIDERABLE COMEX LIQUIDATION. HOWEVER, WE WERE AGAIN NOTIFIED THAT WE HAD ANOTHER FAIR SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP ROUTE: 1088 EFP’S FOR MARCH AND AND 111 EFP’S FOR MAY AND ZERO FOR ALL OTHER MONTHS AND THUS TOTAL ISSUANCE OF 1199 CONTRACTS. WITH THE TRANSFER OF 1199 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24 HRS IN THE ISSUING OF EFP’S. THE 1199 CONTRACTS TRANSLATES INTO 5.995 MILLION OZ DESPITE WITH THE CONTINUAL DROP IN OPEN INTEREST IN SILVER AT THE COMEX.

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF FEBRUARY:

41,468 CONTRACTS (FOR 16 TRADING DAYS TOTAL 41,468 CONTRACTS OR 207.345 MILLION OZ: AVERAGE PER DAY: 2591 CONTRACTS OR 12.958 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH: 207.345 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 29.57% OF ANNUAL GLOBAL PRODUCTION

ACCUMULATION IN YEAR 2018 TO DATE SILVER EFP’S: 455.87 MILLION OZ.

ACCUMULATION FOR JAN 2018: 236.879 MILLION OZ

RESULT: A CONSIDERABLE SIZED LOSS IN OI SILVER COMEX DESPITE THE 15 CENT GAIN IN SILVER PRICE. WE ALSO HAD A GOOD SIZED EFP ISSUANCE OF 1199 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER . FROM THE CME DATA 1199 EFP’S FOR MONTHS MARCH AND MAY WERE ISSUED FOR TODAY FOR A DELIVERABLE FORWARD CONTRACT OVER IN LONDON WITH A FIAT BONUS. WE LOST 484 OI CONTRACTS i.e. 1199 open interest contracts headed for London (EFP’s) TOGETHER WITH A DECREASE OF 1683 OI COMEX CONTRACTS. AND ALL OF THIS HAPPENED WITH THE RISE IN PRICE OF SILVER OF 15 CENTS AND A CLOSING PRICE OF $16.63 WITH RESPECT TO YESTERDAY’S TRADING. YET WE STILL HAVE A FAIR AMOUNT OF SILVER STANDING AT THE COMEX.

In ounces AT THE COMEX, the OI is still represented by just OVER 1 BILLION oz i.e. 1.0097 BILLION TO BE EXACT or 144% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT FEBRUARY MONTH/ THEY FILED: 0 NOTICE(S) FOR NIL OZ OF SILVER

In gold, the open interest FELL BY A SMALL 3705 CONTRACTS DOWN TO 524,449 DESPITE THE TINY RISE IN PRICE OF GOLD WITH YESTERDAY’S TRADING ($0.90). HOWEVER, IN ANOTHER DEVELOPMENT, WE RECEIVED THE TOTAL NUMBER OF GOLD EFP’S ISSUED FOR THURSDAY AND IT TOTALED AN HUGE SIZED 9751 CONTRACTS OF WHICH APRIL SAW THE ISSUANCE OF 9751 CONTRACTS AND JUNE SAW THE ISSUANCE OF 0 CONTRACTS AND THEN ALL OTHER MONTHS ZERO. The new OI for the gold complex rests at 524,449. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. DEMAND FOR GOLD INTENSIFIES GREATLY AS WE CONTINUE TO WITNESS A HUGE NUMBER OF EFP TRANSFERS TOGETHER WITH THE MASSIVE INCREASE IN GOLD COMEX OI TOGETHER WITH THE TOTAL AMOUNT OF GOLD OUNCES STANDING FOR FEBRUARY COMEX. EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER (BIG RISE IN BOTH GOFO AND SIFO) AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES. IN ESSENCE TODAY DESPITE YESTERDAY’S TRADING IN GOLD, WE HAVE A GAIN OF 6046 CONTRACTS: 3705 OI CONTRACTS DECREASED AT THE COMEX AND A GOOD SIZED 9751 OI CONTRACTS WHICH NAVIGATED OVER TO LONDON.(6046 oi gain in CONTRACTS EQUATES TO 18.92TONNES)

YESTERDAY, WE HAD 13,134 EFP’S ISSUED.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF FEBRUARY STARTING WITH FIRST DAY NOTICE: 181,973 CONTRACTS OR 18,197,300 OZ OR 566.00 TONNES (16 TRADING DAYS AND THUS AVERAGING: 11,373EFP CONTRACTS PER TRADING DAY OR 1,137,300 OZ/ TRADING DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SIZE OF THESE EFP TRANSFERS : SO FAR THIS MONTH IN 16 TRADING DAYS: IN TONNES: 566.00 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2017, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 2200 TONNES

THUS EFP TRANSFERS REPRESENTS 566.00/2200 x 100% TONNES = 25.72% OF GLOBAL ANNUAL PRODUCTION SO FAR IN FEBRUARY ALONE.

ACCUMULATION OF GOLD EFP’S YEAR 2018 TO DATE: 1199.40 TONNES

ACCUMULATION OF GOLD EFP’S FOR JANUARY 2018: 653.22 TONNES

Result: A GOOD SIZED DECREASE IN OI AT THE COMEX WITH THE TINY RISE IN PRICE IN GOLD TRADING YESTERDAY ($0.90). HOWEVER, WE HAD ANOTHER GOOD SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 9751 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX AND YET WE ALSO OBSERVED A HUGE DELIVERY MONTH FOR THE MONTH OF DECEMBER. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 9751 EFP CONTRACTS ISSUED, WE HAD A NET GAIN IN OPEN INTEREST OF 6046 contracts ON THE TWO EXCHANGES:

9751 CONTRACTS MOVE TO LONDON AND 3705 CONTRACTS DECREASED AT THE COMEX. (in tonnes, the GAIN in total oi equates to 23.02 TONNES).

we had: 0 notice(s) filed upon for NIL oz of gold.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD

WITH GOLD UP $0.90 /NO CHANGE IN GOLD INVENTORY AT THE GLD/

Inventory rests tonight: 827.79 tonnes.

SLV/

WITH SILVER DOWN 1 CENT TODAY:

NO CHANGES IN SILVER INVENTORY AT THE SLV/

/INVENTORY RESTS AT 315.271 MILLION OZ/

end

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in silver FELL BY AN EXPECTED 1683 contracts from 203,629 DOWN TO 201,946 (AND now A LITTLE FURTHER FROM THE NEW COMEX RECORD SET ON FRIDAY/APRIL 21/2017 AT 234,787) DESPITE THE FAIR SIZED RISE IN PRICE OF SILVER (15 CENTS WITH RESPECT TO YESTERDAY’S TRADING). OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE ANOTHER GOOD 1293 PRIVATE EFP’S FOR MARCH AND 28 EFP CONTRACTS OR MAY (WE DO NOT GET A LOOK AT THESE CONTRACTS AS IT IS PRIVATE BUT THE CFTC DOES AUDIT THEM) AND 0 EFP’S FOR ALL OTHER MONTHS . EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. WE HAD SOME COMEX SILVER COMEX LIQUIDATION. IF WE TAKE THE OI LOSS AT THE COMEX OF 1683 CONTRACTS TO THE 1199 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A SMALL LOSS OF 484 OPEN INTEREST CONTRACTS . WE STILL HAVE A GOOD AMOUNT OF SILVER OUNCES THAT ARE STANDING FOR METAL IN JANUARY (SEE BELOW). THE NET GAIN TODAY IN OZ ON THE TWO EXCHANGES: 2.42 MILLION OZ!!!

RESULT: A FAIR SIZED DECREASE IN SILVER OI AT THE COMEX DESPITE THE RISE OF 15 CENTS IN PRICE (WITH RESPECT TO YESTERDAY’S TRADING ). BUT WE ALSO HAD ANOTHER GOOD 1199 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE GOOD SIZED AMOUNT OF SILVER OUNCES STANDING FOR FEBRUARY, DEMAND FOR PHYSICAL SILVER INTENSIFIES AS WE WITNESS MAJOR BANK SHORT COVERING ACCOMPANIED BY INCREASES IN GOFO AND SIFO RATES INDICATING SCARCITY.

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)Late WEDNESDAY night/THURSDAY morning: Shanghai closed UP 69.40 POINTS OR 2.17% /Hang Sang CLOSED DOWN 466.21 POINTS OR 1.48% / The Nikkei closed DOWN 234.37 POINTS OR 1.07%/Australia’s all ordinaires CLOSED UP 0.17%/Chinese yuan (ONSHORE) closed DOWN at 6.3527/Oil DOWN to 61.28 dollars per barrel for WTI and 65.20 for Brent. Stocks in Europe OPENED DEEPLY IN THE RED EXCEPT SPAIN . ONSHORE YUAN CLOSED 6.3527 AGAINST THE DOLLAR AT 6.3527. OFFSHORE YUAN STILL CLOSED AGAINST THE ONSHORE YUAN AT 6.3527//ONSHORE YUAN TRADING/OFFSHORE YUAN NOT TRADING

3a)THAILAND/SOUTH KOREA/NORTH KOREA

i)North Korea

b) REPORT ON JAPAN

This is a biggy!!: Nippon Life Insurance, Japan’s largest life insurer will now become a seller of stocks as they believe that the bubble will burst. They also believe that the dollar is fall to below 105. This should end the advance of stocks basically around the world. He also states that the bubble in their bond market will also burst

( zerohedge)

3 c CHINA

i)Quite a story. Chinese companies have for several years have offered employees a deal: buy their company stock while at the same time guaranteeing any losses. That worked fine as long as the stock market rose. The reason for this deal: to prevent the stock falling and forcing mammoth loan margins calls by the upper management. Now Chinese companies have now been forced to halt trading in their company while they sort out the avalanche of margin calls they are receiving.

China returns today for trading

( zerohedge)

ii)China now crackdowns on anything that would resemble a selloff. So what did they do; they halted their own version of VIX

(courtesy zerohedge)

4. EUROPEAN AFFAIRS

ECB

The minutes of the ECB described a rather bullish tone for the Euro as it initially rose but then readers noticed sections where members were very concerned on the weakness of the USA dollar and also the thought that the USA was intentionally lowering its value. This would bring currency wars and after noticing this, the Euro fell. However cooler heads prevailed and the Euro continued its advance subject to the bullish tone by the ECB governors.

( zerohedge)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

6 .GLOBAL ISSUES

7. OIL ISSUES

WTI and gasoline pop after the DOE confirms the API report yesterday of a surprise crude drawdown. Rig counts increase and USA production slowed a bit

( zerohedge)

8. EMERGING MARKET

I)SOUTH AFRICA

My goodness: Ramaphosa is better than Zuma? He is now contemplating confiscating land from white farmers and handing it over to blacks

( Simon Black/SovereignMan.com)

ii)VENEZUELA

After a successful release of his crypto based, oil backed Petro, Maduro now hints at a gold backed Petro Oro. One small problem…he sold all of his gold.

(courtesy Molly Jane Zuckerman/CoinTelegraph.com

9. PHYSICAL MARKETS

Very interesting: FDIC is suing 16 banks alleging LIBOR manipulation in the big bank in Puerto Rico, Doral Bank

( Reuters/GATA)

10. USA stories which will influence the price of gold/silver

i)EARLY THIS MORNING/JAMES BULLARD CALMS THE MARKET:

( zerohedge)

ii)We now know what triggered the collapse of the Dow, the wipe out of XIV. It was a small firm called Catalyst whose betting strategy went haywire

( zerohedge)

iii)SWAMP STORIES

a)Another former Trump adviser is to meet Mueller

( zero hedge)

c)Mueller files new charges against Manafort: tax and bank fraud charges( zerohedge)

PRELIMINARY COMEX VOLUME FOR TODAY: 208,638 contracts

CONFIRMED COMEX VOL. FOR YESTERDAY: 263,094 CONTRACTS

comex gold volumes are RISING AGAIN

Here is a summary of the latest gold trading volumes at the Comex per year

certainly the introduction of EFP’s has certainly had an effect:

Trading Volumes on the COMEX

Meanwhile, gold-trading volumes on the COMEX have never been higher:

end

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

And now for the wild silver comex results.

Total silver OI FELL BY AN UNEXPECTED 1683 CONTRACTS FROM 203,629 DOWN TO 201,946 DESPITE YESTERDAY’S FAIR SIZED 15 CENT GAIN IN TRADING). HOWEVER,WE WERE ALSO INFORMED THAT WE HAD ANOTHER GOOD SIZED 1088 EMERGENCY EFP’S FOR MARCH ISSUED BY OUR BANKERS (WITH 111 EFP CONTRACTS FOR MAY AND ZERO FOR ALL OTHER MONTHS) TO COMEX LONGS WHO RECEIVED A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON: THE TOTAL EFP’S ISSUED: 1199. THE SILVER BOYS HAVE STARTED TO MIGRATE TO LONDON FROM THE START OF DELIVERY MONTH AND CONTINUING RIGHT THROUGH UNTIL FIRST DAY NOTICE JUST LIKE WE ARE WITNESSING TODAY. USUALLY WE NOTED THAT CONTRACTION IN OI OCCURRED ONLY DURING THE LAST WEEK OF AN UPCOMING ACTIVE DELIVERY MONTH AS WE HAVE JUST SEEN IN GOLD TODAY. THIS PROCESS HAS JUST BEGUN IN EARNEST IN SILVER STARTING IN SEPTEMBER 2017. HOWEVER, IN GOLD, WE HAVE BEEN WITNESSING THIS FOR THE PAST 2 YEARS. NICK LAIRD WAS KIND ENOUGH TO SUPPLY US THE TOTAL FOR 2017 GOLD EFP’S AND IT WAS 6600 TONNES FOR THE ENTIRE YEAR. WE OBVIOUSLY HAD SOME LONG COMEX SILVER LIQUIDATION AND A SMALL SIZED LOSS IN TOTAL SILVER OI. WE ARE ALSO WITNESSING A FAIR AMOUNT OF SILVER OUNCES STANDING FOR COMEX METAL IN THIS NON ACTIVE JANUARY AS WELL AS THAT CONTINUAL MIGRATION OF EFPS OVER TO LONDON. ON A PERCENTAGE BASIS THERE ARE MORE EFP’S ISSUED FOR GOLD THAN SILVER. ON A NET BASIS WE LOST 484 SILVER OPEN INTEREST CONTRACTS:

1683 CONTRACT LOSS AT THE COMEX COMBINING WITH THE ADDITION OF 1199 OI CONTRACTS NAVIGATING OVER TO LONDON.

NET LOSS ON THE TWO EXCHANGES: 484 CONTRACTS

We are now in the poor non active delivery month of FEBRUARY and here the front month LOST 76 contracts LOWERING TO 0 contracts. We had 76 notices filed upon yesterday so we GAINED 0 contract or NIL ADDITIONAL oz will stand for delivery at the comex

The March contract lost 9879 contracts DOWN to 53,370

April GAINED 32 contracts UP to 197 .

.

We had 0 notice(s) filed for NIL OZ for the FEBRUARY 2018 contract for silver

INITIAL standings for FEBRUARY

Feb 22/2018.

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz |

788.235 oz

HSBC

|

| Deposits to the Dealer Inventory in oz | nil oz |

| Deposits to the Customer Inventory, in oz | nil

|

| No of oz served (contracts) today |

0 notice(s)

NIL OZ

|

| No of oz to be served (notices) |

1107 contracts

(110,700 oz)

|

| Total monthly oz gold served (contracts) so far this month |

1784 notices

178400 oz

5.5489 tonnes

|

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

For FEBRUARY:

Today, 0 notice(s) were issued from JPMorgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equates to 0 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped/ Received) by j.P.Morgan customer account.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

To calculate the INITIAL total number of gold ounces standing for the FEBRUARY. contract month, we take the total number of notices filed so far for the month (1784) x 100 oz or 178,300 oz, to which we add the difference between the open interest for the front month of FEB. (1107 contracts) minus the number of notices served upon today (0 x 100 oz per contract) equals 289,100 oz, the number of ounces standing in this active month of FEBRUARY

Thus the INITIAL standings for gold for the FEBRUARY contract month:

No of notices served (1784 x 100 oz or ounces + {(1107)OI for the front month minus the number of notices served upon today (0 x 100 oz )which equals 289,100 oz standing in this active delivery month of February (8.99 tonnes). THERE IS 12.52 TONNES OF REGISTERED GOLD AVAILABLE FOR DELIVERY SO FAR.

WE LOST 24 CONTRACTS OR AN ADDITIONAL 2400 OZ WILL NOT STAND IN THIS ACTIVE DELIVERY MONTH OF FEBRUARY.

THE COMEX IS NOW UNDER STRESS AS THE REGISTERED GOLD FALLS BELOW 13 TONNES AS WELL AS HUGE NUMBER OF TONNES LEAVING THE CUSTOMER ACCOUNT

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

IN THE LAST 17 MONTHS 70 NET TONNES HAS LEFT THE COMEX.

end

And now for silver

AND NOW THE DECEMBER DELIVERY MONTH

FEBRUARY FINAL standings

| Silver | Ounces |

| Withdrawals from Dealers Inventory | nil oz |

| Withdrawals from Customer Inventory |

467,363.140 oz

Brinks

HSBC

Scotia

|

| Deposits to the Dealer Inventory |

nil

oz

|

| Deposits to the Customer Inventory |

nil oz

|

| No of oz served today (contracts) |

0

CONTRACT(S

(NIL OZ)

|

| No of oz to be served (notices) |

0 contracts

(385,000 oz)

|

| Total monthly oz silver served (contracts) | 386 contracts

(1,930,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

we had 0 inventory movement at the dealer side of things

total inventory movement dealer: nil oz

we had 0 inventory deposits into the customer account

total inventory deposits: nil oz

*** JPMorgan is continually adding to its inventory almost every single day.

JPMorgan now has 136 million oz of total silver inventory or 55% of all official comex silver.

JPMORGAN TOOK A BREAK TODAY IN NOT ADDING TO ITS OFFICIAL INVENTORY COUNT.

we had 3 withdrawals from the customer account;

iii) Out of Brinks:: 4993.150 oz

ii) Out of HSBC:: 211,427.160 oz

iii) out of Scotia: 250,942,230 oz

total withdrawals; 467,363.140 oz

we had 0 adjustments

total dealer silver: 45.329 million

total dealer + customer silver: 246.405 million oz

The total number of notices filed today for the FEBRUARY. contract month is represented by 76 contract(s) FOR 380,000 oz. To calculate the number of silver ounces that will stand for delivery in FEBRUARY., we take the total number of notices filed for the month so far at 386 x 5,000 oz = 1,930,000 oz to which we add the difference between the open interest for the front month of FEB. (0) and the number of notices served upon today (0 x 5000 oz) equals the number of ounces standing.

.

Thus the INITIAL standings for silver for the FEB contract month: 386(notices served so far)x 5000 oz + OI for front month of FEBRUARY(0) -number of notices served upon today (0)x 5000 oz equals 1,930,000 oz of silver standing for the FEBRUARY contract month.

WE GAINED 0 CONTRACT OR AN ADDITIONAL NIL OZ WILL STAND AT THE COMEX

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

ESTIMATED VOLUME FOR TODAY: 109,780 CONTRACTS

CONFIRMED VOLUME FOR YESTERDAY: 131,218 CONTRACTS

YESTERDAY’S CONFIRMED VOLUME OF 131,218 CONTRACTS EQUATES TO 656 MILLION OZ OR 93.7% OF ANNUAL GLOBAL PRODUCTION OF SILVER

COMMODITY LAW SUGGESTS THAT OPEN INTEREST SHOULD NOT BE MORE THAN 3% OF ANNUAL GLOBAL PRODUCTION. THE CROOKS ARE SUPPLYING MASSIVE PAPER TRYING TO KEEP SILVER IN CHECK.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price at that day at $18.42

The previous record was 224,540 contracts with the price at that time of $20.44

end

NPV for Sprott

1. Sprott silver fund (PSLV): NAV FALLS TO -2.35% (FEB 21/2018)

2. Sprott gold fund (PHYS): premium to NAV RISES TO -0.47% to NAV (FEB 20/2018 )

Note: Sprott silver trust back into NEGATIVE territory at -2.35%-/Sprott physical gold trust is back into NEGATIVE/ territory at -0.47%/Central fund of Canada’s is still in jail but being rescued by Sprott.

Sprott WINS hostile 3.1 billion bid to take over Central Fund of Canada

(courtesy Sprott/GATA)

3.SPROTT CEF.A FUND (FORMERLY CENTRAL FUND OF CANADA): NAV RISES TO -3.30%: NAV 13.68/TRADING 13.33//DISCOUNT 3.30.

END

And now the Gold inventory at the GLD/

FEB 22/WITH GOLD UP 90 CENTS AGAIN TODAY, WE HAD NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 827.79 TONNES

FEB 21/ WITH THE 90 CENT GAIN WE HAD ANOTHER DEPOSIT OF 3.15 TONNES OF GOLD INTO THE GLD INVENTORY/INVENTORY RESTS TONIGHT AT 827.79 TONNES

Feb 20/WITH GOLD DOWN BY $24.25, THE CROOKS DECIDED THAT THEY HAD BETTER RETURN (DEPOSIT) 3.34 TONNES OF GOLD INTO THE GLD/INVENTORY RESTS TONIGHT AT 824,64 TONNES

Feb 16/WITH GOLD UP BY 25 CENTS, THE CROOKS DECIDED AGAIN TO RAID THE COOKIE JAR BY WITHDRAWING 2.36 TONNES OF GOLD FROM THE GLD/INVENTORY RESTS AT 821.30 TONNES

Feb 15/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 823.66 TONNES

Feb 14/AN ADDITIONAL OF 2.95 TONNES OF GOLD INTO GLD WITH THE HUGE GAIN OF 27.40 IN PRICE/INVENTORY RESTS AT 823.66 TONNES

Feb 13/WITH GOLD UP $3.40 WE HAD NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY REMAINS AT 820.71 TONNES

Feb 12/STRANGE!!WITH GOLD RISING BY 12.00 DOLLARS, THE CROOKS DECIDED AGAIN TO WITHDRAW 5.6 TONNES OF GOLD FOR EMERGENCY USE ELSEWHERE/INVENTORY RESTS AT 820.71 TONNES

Feb 9/AGAIN WITH HUGE TURMOIL ON THE MARKETS, THE CROOKS WITHDREW 2 TONNES OF GOLD FROM THE GLD INVENTORY/INVENTORY RESTS AT 826.31 TONNES

Feb 8/DESPITE THE GOOD GAIN IN PRICE FOR GOLD TODAY/THE CROOKS REMOVED .96 TONNES FROM THE GLD INVENTORY/INVENTORY RESTS AT 828.31 TONNES

FEB 7/AN UNBELIEVABLE 12.08 TONNES WAS REMOVED BY THE CROOKED BANKERS AND THIS GOLD WAS USED IN THE ASSAULT THESE PAST FEW DAYS/INVENTORY RESTS AT 829.27 TONNES

Feb 6/AGAIN VERY STRANGE: WITH TODAY’S TURMOIL, THE CROOKS DID NOT ADD ANY GOLD INVENTORY INTO THE GLD/INVENTORY REMAINS AT 841.35 TONNES

Feb 5 Strange,with all of today’s turmoil, the crooks at the GLD decided to add zero ounces into GLD inventory/inventory rests at 841.35 tonnes

Feb 2/no change in gold inventory at the GLD/Inventory rests at 841.35 tonnes

Feb 1/with gold up by $8.00/the crooks decided not to add any new physical gold metal into the GLD./inventory rests at 841.35 tonnes

Jan 31/with gold up $3.15 today, GLD shed another 5.32 tonnes of gold from its inventory/inventory rests at 841.35 tonnes

jan 30/with gold down by $4.85/GLD shed another 1.47 tonnes of gold from its inventory/inventory rests at 846.67 tonnes

JAN 29/with gold down $11.25, the GLD shed 1.18 tonnes of gold/inventory rests at 848.14 tonnes

jan 26/2018/no changes in gold inventory at the GLD/inventory rests at 849.32 tonnes

jan 25/no changes in gold inventory at the GLD/inventory rests at 849.32 tonnes

Jan 24/A HUGE DEPOSIT OF 2.65 TONNES OF GOLD INTO GLD/INVENTORY RESTS AT 849.32 TONNES

Jan 23/NO CHANGE IN GOLD INVENTORY DESPITE GOLD’S RISE/INVENTORY RESTS AT 846.67 TONNES

Jan 22/a huge deposit of 5.71 tonnes of gold despite a drop in price/inventory rests at 846.67 tonnes. In 3 trading days, the GLD has added 17.71 tonnes/the bankers are now in trouble!!

Jan 19/no change in gold inventory at the GLD/Inventory rests at 840.76 tonnes

Jan 18/SHOCKINGLY A HUGE DEPOSIT OF 11.80 TONNES WITH GOLD DOWN ALMOST $12.00/INVENTORY RESTS AT 840.76

Jan 17/no changes in gold inventory at the GLD/inventory rests at 828.96 tonnes

Jan 16/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 828.96 TONNES

Jan 12/no changes in inventory at the GLD despite the rise in gold price/inventory rests at 828.96 tonnes

Jan 11/ANOTHER IDENTICAL WITHDRAWAL OF 2.95 TONNES FROM THE GLD INVENTORY/INVENTORY RESTS AT 828.96 TONNES

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

Feb 22/2018/ Inventory rests tonight at 827,79 tonnes

*IN LAST 328 TRADING DAYS: 113.36 NET TONNES HAVE BEEN REMOVED FROM THE GLD

*LAST 258 TRADING DAYS: A NET 43.95 TONNES HAVE NOW BEEN ADDED INTO GLD INVENTORY.

end

Now the SLV Inventory

fEB 22.2018/WITH SILVER DOWN 1 CENT TODAY, WE HAD NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 215.271 MILLION OZ/

FEB 21/WITH SILVER UP 15 CENTS TODAY, WE HAD A GOOD SIZED INVENTORY ADDITION OF 1.226 MILLION OZ/INVENTORY RESTS AT 215.271 MILLION OZ/

Feb 20/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 314.045 MILLION OZ

Feb 16/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 314.045 MILLION OZ/

Feb 15/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 314.045 MILLION OZ/

Feb 14./NO CHANGE IN SILVER INVENTORY DESPITE THE HUGE RISE IN PRICE/INVENTORY RESTS AT 314.045 MILLION OZ

Feb 13./NO CHANGE IN SILVER INVENTORY TODAY/INVENTORY RESTS AT 314.045 MILLION OZ/

Feb 12/AGAIN, WITH TODAY’S HUGE RISE IN SILVER PRICE, IN TOTAL CONTRAST TO GOLD: NO CHANGE IN SILVER INVENTORY/INVENTORY RESTS AT 314.045 MILLION OZ/

Feb 9/AGAIN WITH TURMOIL ON THE MARKETS, STRANGELY IN TOTAL CONTRAST TO GOLD: NO CHANGE IN SILVER INVENTORY/INVENTORY RESTS AT 314.045 MILLION OZ/

Feb 8/DESPITE THE TURMOIL TODAY AND A PRICE RISE: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 314.045 MILLION OZ/

FEB 7/no change in silver inventory at the SLV/Inventory rests at 314.045 million oz/

Feb 6/WITH ALL OF TODAY’S TURMOIL/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 314.045 MILLION OZ/

Feb 5/ we had HUGE change in silver inventory at the SLV/ A DEPOSIT OF 1.131 MILLION OZ INTO THE SLV/Inventory rests at 314.045 million oz/

Feb 2/we lost 982,000 oz from the SLV inventory /inventory rests at 312.914 million oz/

Feb 1/no change in silver inventory at the SLV/Inventory rests at 313.896 million oz/

Jan 31/ no change in inventory at the slv in total contrast to gold/inventory rests at 313.896 million oz/

Jan 30/no change in inventory/SLV inventory rests at 313.896 million oz/

Jan 29/no change in inventory/SLV inventory rests at 313.896 million oz/

Jan 26.2018/inventory rests at 313.896 million oz

Jan 25/with silver up today and yesterday, the SLV could only muster a gain of 848,000 oz

Inventory rests at 313.896 oz

jan 24/NO CHANGE IN SILVER INVENTORY DESPITE THE GOOD ADVANCE IN PRICE/INVENTORY RESTS AT 313.048 MILLION OZ/

Jan 23/ANOTHER HUGE WITHDRAWAL OF 1.131 MILLION OZ OF SILVER DESPITE THE TINY LOSS/THE CROOKS ARE USING THE INVENTORY TO RAID ON SILVER.

JAN 22.2018/with silver down by 5 cents/ the crooks at the SLV liquidate 1.321 million oz of silver/inventory rests at 314.179 million oz/

Jan 19/ no changes in silver inventory at the SLV/inventory rests at 315.500 million oz/

jan 18/A WITHDRAWAL OF 848,000 OZ OF SILVER FROM THE SLV/INVENTORY RESTS AT 315.500 MILLION OZ/

Jan 17/no changes in silver inventory at the SLV/inventory rests at 316.348 million oz/

Jan 16/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 316.348 MILLION OZ

Jan 12/no changes in silver inventory at the SLV/inventory rests at 316.348 million oz/

Feb 22/2017:

Inventory 315.271 million oz

end

HUGE SCARCITY OF GOLD IN LONDON AS THE GOLD LENDING RATE SURPASSES 2.27%

6 Month MM GOLD LENDING RATE 1.86/ and libor 6 month duration 2.13

Indicative gold forward offer rate for a 6 month duration/calculation:

GLR+ 1.86%

libor 2.13

gofo: .27%

12 Month MM GOLD LENDING RATE

+ 2.27%

GOFO = LIBOR – GOLD LENDING RATE

GOFO = 2.41 – 2.27 = .140

GOLD IS NOW EXTREMELY SCARCE.

end

Major gold/silver trading /commentaries for THURSDAY

GOLDCORE/BLOG/MARK O’BYRNE.

GOLD/SILVER

GoldCore

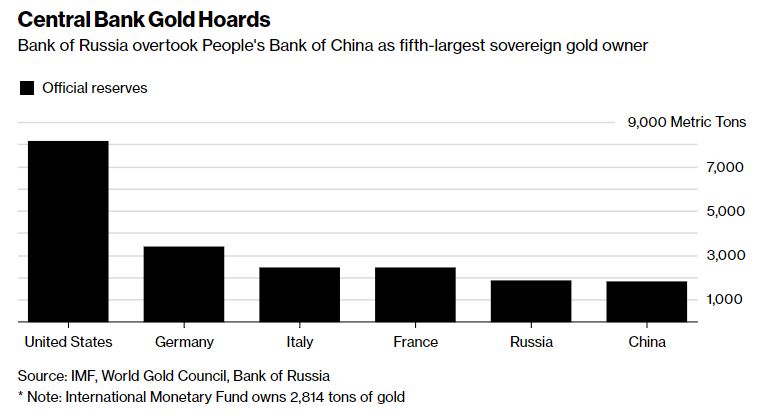

Russian Central Bank Buys Gold – 600,000 Ounces Or 18.7 Tons In January As Venezuela Launches ‘Petro Gold’

– Russian central bank buys gold – large 600,000 ounces or 18.7 tons of gold in January

– Russia increased its holdings to 1,857 tons, topping the People’s Bank of China’s ‘reported’ 1,843 tons

– Russia surpasses China as 6th largest holder of gold reserves – after U.S., Germany, IMF, Italy and France

– Turkish central bank added 205 tons “over 13 consecutive months” – Commerzbank

– Meanwhile, Russian ally Venezuela is launching a new gold-backed cryptocurrency next week

Russia has overtaken China as the fifth-biggest sovereign holder of gold, allowing it to diversify its foreign currency holdings amid a deepening rift with the US, Bloomberg News’ Eddie van der Walt reported overnight.

The Bank of Russia increased its holdings in January by almost 20 metric tons to 1,857 tons, topping the People’s Bank of China’s reported 1,843 tons. While Russia has increased its holdings every month since March 2015, China last reported buying gold in October 2016. The U.S. is still the largest owner of gold, with 8,134 tons, much of it stored in Fort Knox.

Russia’s central bank continues to add gold to reserves while the People’s Bank of China remains on hold, pointed out Commerzbank.

Analysts cited news that the Russian central bank bought 600,000 ounces, or 18.7 tons, of gold in January as it continued to diversify its reserves. Analysts cite IMF data showing that Turkey also bought large quantities of gold in January at 560,000 ounces or 17.4 tons.

“Thus the Turkish central bank has topped up its gold reserves by a total of 205 tonnes over 13 consecutive months,” Commerzbank added.

Kazakhstan continues to buy gold in small quantities, as it has been doing steadily for years.

This goes some way to plugging the gap left by the Chinese central bank. The PBOC, meanwhile, has not reported the purchase of gold for 15 months in a row.

Venezuelan President Nicolas Maduro said yesterday that his government was preparing to launch a new gold-backed cryptocurrency token next week as reported by Reuters.

![]()

Venezuela is preparing a new cryptocurrency called “petro gold” that will be backed by precious metals, Maduro said yesterday, a day after launching an oil-backed token.

“I don’t want to get ahead of things, but we have prepared a surprise, a gold-backed ‘petro,’ which will have the same parameters as the oil-backed ‘petro.’ This topic will be raised next week,” Maduro said.

Related Content

Russia Gold Rush Sees Record Reserves For Putin Era

Own Gold Bullion To “Support National Security” – Russian Central Bank

News and Commentary

Stocks Turn Lower, Dollar Rises After Fed Minutes (Bloomberg.com)

Venezuela’s Maduro Announces Another Cryptocurrency, Now Gold-Backed (SputnikNews.com)

Gold prices flat, U.S. interest rate outlook weighs (Reuters.com)

FDIC sues 16 banks alleging LIBOR manipulation in Doral Bank collapse (Reuters.com)

U.K. Economic Growth Revised Down as Consumers Hit by Inflation (Bloomberg.com)

Source: Bloomberg

Ireland – Worst Property Crisis in Western Europe Is Still Affecting Business (Bloomberg.com)

This Is Where The Next US Debt Crisis Is Hiding (ZeroHedge.com)

South Africa’s Brand New President Wants To Confiscate Land From White Farmers (ZeroHedge.com)

Meet the Italian government’s Orwellian new automated tax snitch (SovereignMan.com)

City should fear Corbyn much more than Brexit (CityAM.com)

Gold Prices (LBMA AM)

20 Feb: USD 1,337.40, GBP 955.97 & EUR 1,083.83 per ounce

19 Feb: USD 1,347.40, GBP 961.10 & EUR 1,085.47 per ounce

16 Feb: USD 1,358.60, GBP 964.61 & EUR 1,086.47 per ounce

15 Feb: USD 1,353.70, GBP 962.21 & EUR 1,084.45 per ounce

14 Feb: USD 1,330.75, GBP 959.74 & EUR 1,077.77 per ounce

13 Feb: USD 1,329.40, GBP 955.04 & EUR 1,077.61 per ounce

12 Feb: USD 1,321.70, GBP 955.19 & EUR 1,077.45 per ounce

Silver Prices (LBMA)

20 Feb: USD 16.57, GBP 11.85 & EUR 13.42 per ounce

19 Feb: USD 16.72, GBP 11.92 & EUR 13.46 per ounce

16 Feb: USD 16.84, GBP 11.97 & EUR 13.49 per ounce

15 Feb: USD 16.83, GBP 11.98 & EUR 13.49 per ounce

14 Feb: USD 16.58, GBP 11.97 & EUR 13.43 per ounce

13 Feb: USD 16.61, GBP 11.94 & EUR 13.46 per ounce

12 Feb: USD 16.43, GBP 11.86 & EUR 13.39 per ounce

Recent Market Updates

– Bitcoin or British Pound ‘Pretty Much Failed’ As Currency?

– Bank Bail-In Risk In European Countries Seen In 5 Key Charts

– US-China Trade War Escalates As Further Measures Are Taken

– Gold Up 3.8% In Week – If Closes Above $1,360/oz Will Be Biggest Weekly Gain In Nearly 2 Years

– Is The Gold Price Heading Higher? IG TV Interview GoldCore

– Global Debt Crisis II Cometh

– Sovereign Wealth Funds Investing In Gold For “Long Term Returns” – PwC

– Bitcoin and Crypto Prices Being Manipulated Like Precious Metals?

– “This Is Where They Completely Lost Their Minds” – Hussman

– Brexit Risks Increase – London Property Market and Pound Vulnerable

– Peak Gold: Global Gold Supply Flat In 2017 As China Output Falls By 9%

– Crypto Currency Backlash Sees Flight From Cryptos and Bitcoin

– Gold Rises As Global Stocks Plunge and Bitcoin Crashes 70%

Call for Gold Sovereigns at Ultra Low 4% Premium For Storage in London or Insured Delivery

END

Very interesting: FDIC is suing 16 banks alleging LIBOR manipulation in the big bank in Puerto Rico, Doral Bank

(courtesy Reuters/GATA)

FDIC sues 16 banks alleging LIBOR manipulation in Doral Bank collapse

Submitted by cpowell on Wed, 2018-02-21 14:03. Section: Daily Dispatches

From Reuters

Tuesday, February 20, 2018

A U.S. regulator on Tuesday filed a lawsuit against 16 U.S. and international banks alleging they had manipulated bbaLIBOR, which is a series of interest-rate benchmarks, leading to the collapse of Puerto Rico’s Doral Bank.

The Federal Deposit Insurance Corp., which brought the suit in its capacity as receiver for Doral Bank, alleged that the rate rigging harmed Doral by causing substantial losses with regard to its loan portfolio and derivative holdings.

The suit is the latest in a long line of lawsuits in the U.S. District Court in Manhattan targeting the alleged rigging by banks of one interest rate benchmark, market, or commodity or another. …

… For the remainder of the report:

https://www.reuters.com/article/us-usa-fdic-banks/us-fdic-sues-16-banks-.

Your early THURSDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

i) Chinese yuan vs USA dollar/CLOSED 6.3527 /shanghai bourse CLOSED UP 69.40 POINTS OR 2.17% / HANG SANG CLOSED DOWN 466.21 POINTS OR 1.48%

2. Nikkei closed DOWN 234.37 POINTS OR 1.07% /USA: YEN FALLS TO 107.35/ STILL DEADLY AS YEN CARRY TRADERS DISINTEGRATE

3. Europe stocks OPENED DEEPLY IN THE RED EXCEPT SPAIN /USA dollar index RISES TO 90.04/Euro RISES TO 1.2293

3b Japan 10 year bond yield: FALLS TO . +.056/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 107.48/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD FINALLY IN THE POSITIVE/BANK OF JAPAN LOSING CONTROL OF THEIR YIELD CURVE AS THEY PURCHASE ALL BONDS TO GET TO ZERO RATE!!

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 61.28 and Brent: 65.20

3f Gold DOWN/Yen UP

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil DOWN for WTI and DOWN FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund RISES TO +.711%/Italian 10 yr bond yield DOWN to 2.050% /SPAIN 10 YR BOND YIELD DOWN TO 1.505%

3j Greek 10 year bond yield RISES TO : 4.378?????????????????

3k Gold at $1322.40 silver at:16.46 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble DOWN 4/100 in roubles/dollar) 56.79

3m oil into the 61 dollar handle for WTI and 64 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 107.35 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 0.9379 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1522 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now POSITIVE territory with the 10 year RISING to +0.711%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

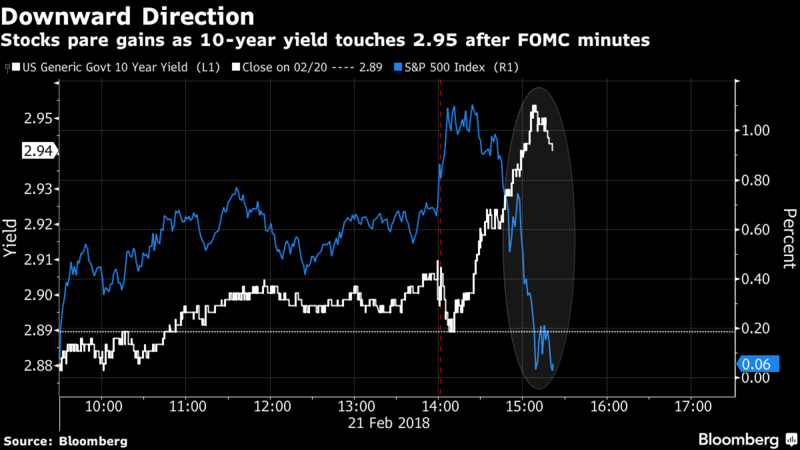

4. USA 10 year treasury bond at 2.9244% early this morning (THIS IS DEADLY TO ALL MARKETS). Thirty year rate at 3.2045% /BOTH VERY DEADLY

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

(courtesy Jim Reid/Bloomberg/Deutsche bank/zero hedge)

S&P Futures Rebound As Dollar Rally Ends, Yields Drop

Global stocks took another leg down during the early part of Thursday’s session, sliding to one-week lows in the wake of Wednesday’s unexpectedly market-moving FOMC minutes which confirmed the Fed was on track to raise interest rates several times this year, sending bond yields to new multi-year highs amid prospects for 4 rate hikes on deck (and according to Goldman, even 5 possible).

However, after sliding initially, S&P futures have since staged a rebound, rising as much as 20 points from session lows, and are currently back in the green, modestly above 2,700.

The rebound was helped by the end of the USD rally, as the dollar’s boost following the Fed minutes proved short-lived as the U.S. currency struggled to gain for a fifth day. Meanwhile, the euro was unfazed by a miss in German IFO data, finding support from broad dollar selling after the London open in a rather slow session. The dollar weakness sent EURUSD back to 1.23, while GBP underperforms after a disappointing GDP revision and the ongoing Brexit saga

In other key FX pairs, per BBG:

- USD/JPY declines 0.4% as a slide in local stocks spurs demand for haven assets

- EUR/USD edges up; premium to hedge political risks rising, with two-week smile flattening as demand for low-delta puts remains strong amid higher volatility in the front end

- GBP/USD resumes its slide, trades 0.2% lower, after data showed that the U.K. economy expanded less than previously estimated in 4Q as consumers and businesses absorbed faster price increases

Three rate rises are now almost fully priced in for 2018, compared with two as recently as December, and some analysts are even contemplating the possibility of as many as five rate hikes in 2018.

And while 10Y TSY yields have traded rangebound within 2 bps of 2.93%, German bunds have unwound the sell-off seen post-FOMC Minutes, following disappointing German IFO data after Wednesday’s weaker-than-forecast European PMIs. The “transatlantic spread” between German and U.S. 10-year borrowing costs widened to near a year high at 220 bps, reflecting the diverging monetary policy expectations between the two countries.

The 3% level on 10Y TSY yields is seen as a huge psychological milestone for bulls and bears alike. In the meantime though the yield, which hit four-year highs around 2.96 percent after the minutes, retreated to 2.93%. Two-year yields touched new nine-year peaks.

A break in the U.S. 10- year treasury above the psychological level of 3% may prove sufficiently attractive to spur demand among foreign investors. This would support the dollar against CEEMEA currencies, Rabobank EMFX strategist Piotr Matys writes in a note to clients.

The next hurdle for markets will be minutes from the European Central Bank’s last meeting at 1230 GMT, with investors keen to see if there was more talk of an eventual unwinding of stimulus. One school of thought says that shifting perceptions about the ECB’s policy outlook had a significant role to play in the surge in U.S. Treasury yields that began in September and picked up speed last month, roiling global stocks.

European equities followed Asia peers lower: the Stoxx Europe 600 Index slid as all the major national equity gauges in the region fell. In terms of sector specific moves, material names modestly lag their peers following price action in the complex as well as a disappointing earnings update from Anglo American (-4%) which has sent their shares near the bottom of the FSTE 100; with the index also hampered by lacklustre earnings from the likes of British American Tobacco (-4.6%), Barratt Developments (-4.0%) and BAE systems. However, losses for UK stocks have been capped by a well-received earnings report from Barclays (+5.1%) which allied with upside in AXA shares (+1.2%) post-earnings has also supported the financial sector.

Earlier in Asia most shares retreated, though China’s market bucked the trend as it reopened after a holiday. The Nikkei (-1.1%) and Hang Seng (-1.5%) saw losses of over 1%, while ASX 200 (+0.1%) saw initial 0.4% gains trimmed, with price action in Australia largely dictated by the slew of earnings.

“The market is pricing in the possibility of a tighter Fed over time,” Evan Brown, director at UBS Asset Management, who previously worked on the open market trading desk at the New York Fed, told Bloomberg TV in New York. On a day-to-day basis “you’re going to see volatility, you’re going to see equities get a little skittish when yields are rising, but as you look over the long term, fundamentals on the economy are very strong.”

However, for now Bloomberg notes that markets remain fragile as February is shaping up as one of the worst months for global equities in more than a year as concerns about a pick-up in inflation and expensive stock prices outweigh evidence of a buoyant U.S. economy. With recent data underpinning the view that inflation is no longer lagging, the OIS space shows traders pricing in just shy of three U.S. rate hikes over the next 12 months.

Elsewhere, gold retreated alongside most commodities. WTI and Brent crude trade lower albeit off worst levels after falling victim to the firmer USD despite last night’s unexpected build in the API report. As a reminder, due to the President’s Day Holiday on Monday the weekly DoE report will be released today. In metals markets, gold prices have also been hampered by the firmer USD, however, the move to the downside has perhaps been contained due to the price action seen in EU stocks this morning. Elsewhere, steel prices were seen lower during Asia-Pac trade as Chinese participants slowly returned from holiday, with a bulk of the market not expected to fully return until next week.

Bulletin headline summary from RanSquawk

- European equities (-1%) have kicked the session off on the back-foot as European participants digest the fall-out of yesterday’s FOMC minutes

- The DXY has nailed 90.000 with the aid of hawkish FOMC minutes, but Usd/Jpy continues to buck the broader trend amidst the ongoing global stock market retracement

- Looking ahead, highlights ECB minutes, US weekly jobs, DoEs and a slew of speakers

Market Snapshot

- S&P 500 futures down 0.3% to 2,691.50

- MSCI Asia Pacific down 0.8% to 175.69

- MSCI Asia Pacific ex Japan down 1% to 575.54

- Nikkei down 1.1% to 21,736.44

- Topix down 0.9% to 1,746.17

- Hang Seng Index down 1.5% to 30,965.68

- Shanghai Composite up 2.2% to 3,268.56

- Sensex unchanged at 33,846.31

- Australia S&P/ASX 200 up 0.1% to 5,950.88

- Kospi down 0.6% to 2,414.28

- STOXX Europe 600 down 0.9% to 377.57

- German 10Y yield fell 0.9 bps to 0.712%

- Euro up 0.02% to $1.2286

- Brent Futures down 0.6% to $65.00/bbl

- Italian 10Y yield fell 2.0 bps to 1.78%

- Spanish 10Y yield fell 1.2 bps to 1.501%

- Brent Futures down 0.6% to $65.00/bbl

- Gold spot down 0.1% to $1,322.89

- U.S. Dollar Index up 0.07% to 90.06

Top Overnight News

- Fed’s Quarles says the natural rate of interest is increasing in the U.S. and that the economy is in the best shape that it has been since the crisis

- U.K. GDP growth in 2017 was revised down to 1.7% from 1.8%, the weakest since 2012, as price rises led to household budgets being squeezed leading to slowing growth in a number of consumer-facing industries

- U.K. Prime Minister Theresa May will shut her most senior cabinet ministers away in a room until late Thursday night in an effort to force them to agree what kind of Brexit they want. But officials warn in private that the most divisive decisions may get kicked down the road

- The U.S. Treasury Department sold $35 billion of five-year notes at a yield of 2.658 percent. Bid/cover ratio fell to 2.44 from 2.48, indicating weaker demand

- U.S. central bankers sent a strong message Wednesday that an expansion with “substantial underlying economic momentum” could sustain more rate hikes; Treasuries sold off aggressively into the 3pm ET settlement as gains sparked by minutes of FOMC’s Jan. 31 meeting were quickly faded

- Federal Reserve Bank of Minneapolis President Neel Kashkari said the central bank’s symmetric approach to its 2% inflation target means “the math says we should be able to tolerate 2.5 percent for five years,” after running at 1.5 percent for five years

- Euro bulls are struggling to push the currency above $1.25 this year, just as the $1.20 level proved a blocking point in 2017

- Do 10-year Treasury yields hit 3 percent and retreat, or does positioning signal a sharp move higher? Open interest on 10-year Treasury futures suggests 3 percent may not be the crucial level after all

Asian markets trading broadly in the red with exception of the Shanghai Comp (+2.2%) which outperforms are participants plays catch up from their elongated break. The prospect of ‘further’ gradual rate hikes as noted in the most recent FOMC minutes boosted speculation that 4 rate hikes could be on the table particularly that these minutes were before the strong wage data in the most recent NFP and inflation data last week, which had subsequently pushed bond yields higher with the US 10yr yield hitting 2.95%, while equities slumped late in the US session. This transpired in Asia, with the Nikkei (-1.1%) and Hang Seng (-1.5%) seeing losses of over 1%, while ASX 200 (+0.1%) saw initial 0.4% gains trimmed, with price action in Australia largely dictated by the slew of earnings. In credit markets, the belly of the curve underperformed, with JGB 10yr yields tracking UST yields higher, while a firm 20yr JGB auction supported longer dated debt. Japan PM Abe Adviser Hamada says the BoJ should consider buying foreign bonds. PBoC sets CNY mid-point at 6.3530 (Prev. 6.3428).

Top Asian News

- China’s VIX Stops Updating Amid Government Scrutiny of Options

- Indonesia Sees Jump in 10-Year Bond Yield as ‘Temporary’

- India Releases Plan to Strengthen State Telecom Cos; MTNL Surges

- China Junk Bonds Show More Resilience on Local Investor Support

- Sembcorp Marine Extends Loss by Most Since 2008 After Earns Miss

European equities (-1%) have kicked the session off on the back-foot as European participants digest the fall-out of yesterday’s more hawkish than anticipated FOMC minutes which saw rate-setters take a confident view on the growth and inflation outlook. In terms of sector specific moves, material names modestly lag their peers following price action in the complex as well as a disappointing earnings update from Anglo American (-4%) which has sent their shares near the bottom of the FSTE 100; with the index also hampered by lacklustre earnings from the likes of British American Tobacco (-4.6%), Barratt Developments (-4.0%) and BAE systems. However, losses for UK stocks have been capped by a well-received earnings report from Barclays (+5.1%) which allied with upside in AXA shares (+1.2%) post-earnings has also supported the financial sector.

Top European news

- Neo-Fascist Beaten to a Pulp in Sicily: Italy Campaign Trail

- HSBC Chairman Is Said to Prepare Board Reduction: Sky

- Fosun Buys Controlling Stake in Lanvin

- FCA Probing Barclays Bank’s Treatment of Clients in Default

- German Business Confidence Slips as Companies Face Bottlenecks

In currencies, the DXY has nailed 90.000 with the aid of hawkish FOMC minutes, but Usd/Jpy continues to buck the broader trend amidst the ongoing global stock market retracement and heightened volatility. Flow-wise, heavy supply at and just ahead of 108.00 is still capping the pair, while 108.02 represents Fib resistance and the headline looks increasingly toppy given lower peaks since the recent 107.90 high. Hence, the broader Dollar and index is struggling to maintain gains and mount a challenge of the next upside technical objective at 90.886 despite reclaiming more lost ground vs other G10 rivals. Eur/Usd has lost grip of the 1.2300 handle and could see more downside on the back of a significantly weaker than expected German Ifo survey, especially as the technical picture also looks bearish below its 1.2319 Fib level and with little in the way of support until 1.2206. Cable is testing bids under 1.3900 amidst latest Brexit-related UK political accusations aimed at PM May, but holding above chart support seen around 1.3830. As per the single currency, Sterling may be prone to further losses in wake of a data miss as UK Q4 GDP was downgraded on zero business investment during the quarter (again likely as a result of Brexit). Elsewhere, Usd/majors fairly flat as the DXY hovers just above the 90.000 level.

In the commodities complex, WTI and Brent crude trade lower albeit off worst levels after falling victim to the firmer USD despite last night’s unexpected build in the API report. As a reminder, due to the President’s Day Holiday on Monday the weekly DoE report will be released today at the rescheduled time of 1600GMT. In metals markets, gold prices have also been hampered by the firmer USD, however, the move to the downside has perhaps been contained due to the price action seen in EU stocks this morning. Elsewhere, steel prices were seen lower during Asia-Pac trade as Chinese participants slowly returned from holiday, with a bulk of the market not expected to fully return until next week.

US Event Calendar

- 8:30am: Initial Jobless Claims, est. 230,000, prior 230,000; Continuing Claims, est. 1.93m, prior 1.94m

- 10am: Leading Index, est. 0.7%, prior 0.6%

- 11am: Kansas City Fed Manf. Activity, est. 18, prior 16

- 10am: Fed’s Dudley to Speak at New York Fed Briefing on Puerto Rico

- 12:10pm: Fed’s Bostic Speaks at Banking Conference in Atlanta

- 3:30pm: Fed’s Kaplan Speaks on Trade Panel in Vancouver

DB’s Jim Reid concludes the overnight wrap

The main thing that jumped yesterday was US yields after the FOMC minutes. Not long after the release yields were actually flat and the S&P 500 up around 1%. However then 10 yr US yields reacted and rose 6bps to 2.951% and the S&P 500 closed -0.55% – the lowest level in a week.

The minutes indicated that “a majority of participants noted that a stronger outlook for economic growth raised the likelihood that further gradual policy firming would be appropriate”. On the economy, it noted that “a number of participants indicated that they had marked up their forecasts for economic growth in the near term relative to …the December meeting” and that “several others suggested that the upside risks to the near-term outlook for economic activity may have increased.” On inflation,”almost all participants who commented agreed that a Phillips curve type inflation framework remained useful…”. Elsewhere, some participants said that they saw an appreciable risk that inflation would continue to fall short of the Fed’s objective, but overall inflation is expected to “move up” this year and stabilise around 2% over the medium term. On wage gains, “a number of participants judged that the continued tightening in labour markets was likely to translate into faster wage increases at some point”.

Notably, the relatively hawkish minutes was before the January wage growth and CPI / PPI prints, so it seems reasonable to assume that if the Fed was getting more confident in their growth and inflation outlook at their meeting, the subsequent data releases would have only added to their views.

Staying in the US, the flash February PMIs were all above market, with the composite PMI at 55.9 (vs. 53.8 previous), services at 55.9 (vs. 53.7 expected) and manufacturing PMI at 55.9 (vs. 55.5 expected). Conversely, Europe’s flash PMIs were a fair bit below expectations but remain at solid levels. The Euro area’s composite PMI came in at 57.5 (vs. 58.4 expected), while the services PMI was 56.7 (vs. 57.6 expected) and manufacturing PMI at 58.5 (vs. 59.2 expected).

Across the region, Germany’s composite PMI was 57.4 (vs. 58.5 expected) and France’s composite PMI was 57.8 (vs. 59.2 expected), with both countries’ services and manufacturing PMI also lower than expectations.

Given the weaker European PMI numbers yesterday I made a point of speaking to our head Euro Economist Mark Wall last night about his views on them. He was relatively relaxed as his forecasts always assumed some moderation in growth which the PMIs would have to eventually acknowledge if he were to be correct. He said that the momentum in recent months was implying 0.9% qoq GDP growth compared to a DB forecast of 0.6% qoq in H1. Yesterday’s numbers narrows these upside risks in H1. In H2 he continues to see a loss of momentum as capacity bites, credit conditions get capped and competitiveness erodes, etc.

He does think the recent financial conditions shock was too fleeting to believe it was the obvious culprit for the weaker numbers though. Even at 0.6%, GDP growth is above trend and despite the weaker PMIs, Mark believes that capacity will continue to be absorbed and the economy tighten. In fact he cited the fact that PMI delivery times lengthened in February, implying a further acceleration in underlying PPI inflation over the next 6-9 months and potential upside risks to inflation in H2.

Turning to news on the Brexit transition period where the EU had previously suggested an end date of December 2020. However, according to a draft UK government legal proposal obtained by Bloomberg, it suggests the actual date may be up for some debate. The document indicated “the UK believes the period’s duration should be determined simply by how long it will take to prepare and implement the new processes….that will underpin the future partnership” and that “the UK agrees this points to…around two years, but wishes to discuss with the EU the assessment that supports its prosed end date”. Later on, the Chief of Staff for Brexit Secretary Mr Jackson noted the UK has not changed its transition plans, which is “around two years”. Elsewhere, the EC’s Juncker “still believes that (both sides) should be able to agree (on the withdrawal agreement) by October and agree on the final terms…”

Staying in the UK, the December unemployment rate edged up from its c42 year low and rose for the first time since July last year to 4.4% (vs. 4.3% expected), while the average weekly earnings growth was in line and steady mom at 2.5% yoy. Speaking in front of the Treasury Committee, the BOE’s Haldane noted “…the pick-up in wages is starting to take root” and that “intelligence from our agents suggests wage settlements this year were going to pick up, perhaps with a number with a three in front of it….” Further, he added risks for the UK economy were “to the upside”.

Elsewhere, the BOE Governor Carney reiterated that cash rates need to rise in the “coming months” but it would be ‘gradual and limited” and refrained from providing guidance on potential timing. The implied Bloomberg odds of a May rate hike rose c4ppt to 61.5%.

This morning in Asia, markets are broadly lower with the Nikkei (-1.25%), Hang Seng (-0.98%) and Kospi (-0.58%) all down as we type. Elsewhere, UST 10y yield is down c1bp while the three key Chinese bourses are up 1.8%-2.1% after trading resumed following the New Year holidays.

Now recapping other market performance from yesterday. US bourses reversed earlier gains to close modestly lower (S&P -0.55%; Dow -0.67%; Nasdaq -0.22%). Within the S&P, all sectors fell with losses led by the real estate, energy and telco stocks. European markets were mixed but little changed as they closed well before the FOMC minutes were released. The Stoxx 600 edged up 0.16% while the FTSE rose 0.48% but the DAX dipped 0.14%. The VIX fell for the first time in three days to 20.02 (-2.8%).

Over in government bonds, core European 10y bond yields fell 1-3bp (Bunds & OATs -1.3bp; Gilts -3.1bp), with the latter partly impacted by the unemployment print. In the US, the treasury sold $35bn of five year notes at a yield of 2.658% with a bid-to-cover ratio of 2.44x (vs. 2.48x previous). Elsewhere, the UST 2y, 5y, 10y yields rose 4.7bp, 4.1bp and 6bp respectively. Turning to currencies, the US dollar index rose for the third trading day (+0.47%), while the Euro and Sterling fell 0.43% and 0.56% respectively. In commodities, WTI oil rose 0.39% to $61.79/ bbl while precious metals were little changed (Gold -0.34%; Silver +0.36%).

Away from the markets and onto three Fed speakers overnight. The Fed’s Kashkari said “Wall Street overreacts to everything….we can’t make policy based on market blips up and down”. On rates, he noted, “we debate each word change in the (FOMC) statement…a lot of debate goes into those…and I think (the word) “further” (in the last statement) was intended to say continuing the current path we’re on”. Elsewhere, the Fed’s Harker reiterated his views of two rate hikes in 2018 and unemployment falling to 3.6% by mid-2019 while the Fed’s Kaplan reaffirmed his call for “gradual and patient” tightening and expects an unemployment rate of 3.6% by year end. Notably, none of the three speakers are policy voters this year.

Before we take a look at today’s calendar, we wrap up with other data releases from yesterday. In the US, the January existing home sales was below expectations at 5.38m (vs. 5.6m) and down 4.8% yoy. Notably, the number of homes available for sale fell 9.5% yoy, partly continuing the upward pressure on home prices where the median selling price was up 5.8% yoy. Elsewhere, the UK’s January public sector net borrowing was broadly in line at -£11.6bln (vs. – £11.4bln expected).

Looking at the day ahead, the February confidence indicators and the final January CPI report in France are due, followed by the Germany’s IFO survey for February and the second estimate of Q4 GDP in the UK. In the US, data releases include initial jobless claims, the January leading indicators index and the February Kansas City Fed manufacturing activity index print. Japan’s CPI report for January will be out in the late evening. Away from the data, the Fed’s Dudley and Bostic are due to speak.

3. ASIAN AFFAIRS

i)Late WEDNESDAY night/THURSDAY morning: Shanghai closed UP 69.40 POINTS OR 2.17% /Hang Sang CLOSED DOWN 466.21 POINTS OR 1.48% / The Nikkei closed DOWN 234.37 POINTS OR 1.07%/Australia’s all ordinaires CLOSED UP 0.17%/Chinese yuan (ONSHORE) closed DOWN at 6.3527/Oil DOWN to 61.28 dollars per barrel for WTI and 65.20 for Brent. Stocks in Europe OPENED DEEPLY IN THE RED EXCEPT SPAIN . ONSHORE YUAN CLOSED 6.3527 AGAINST THE DOLLAR AT 6.3527. OFFSHORE YUAN STILL CLOSED AGAINST THE ONSHORE YUAN AT 6.3527//ONSHORE YUAN TRADING/OFFSHORE YUAN NOT TRADING

3 a NORTH KOREA/USA

/NORTH KOREA

3 b JAPAN AFFAIRS

This is a biggy!!: Nippon Life Insurance, Japan’s largest life insurer will now become a seller of stocks as they believe that the bubble will burst. They also believe that the dollar is fall to below 105. This should end the advance of stocks basically around the world. He also states that the bubble in their bond market will also burst

(courtesy zerohedge)

“Goldilocks Is Over”: Japan’s Largest Life Insurer Is Now Selling Rallies

While stocks are having second thoughts this morning as euphoria appears to have returned to markets for the time being, yesterday’s abrupt reversal in the S&P to the FOMC Minutes revealed that for many, the era of goldilocks may be ending ending. This morning, none other than Japan’s largest life insurer, Nippon Life Insurance, confirmed as much, saying that it will sell Japanese shares when they rise further, as the rally in risk assets driven by expectations of a “Goldilocks” scenario continuing is nearing an end, its chief investment officer told Reuters on Thursday.

Nippon CIO, Hiroshi Ozeki also said that the insurer expects the dollar to soften further against the yen but it is ready to buy the U.S. currency when it falls below 105 yen.

Agreeing with Nomura, which last week said that investors will have another chance to buy lower, Ozeki said that although global shares have bounced back in the past week or so, Nippon Life expects risk assets will be pummeled again.

But his most notably observation was that the era of “Goldilocks” is on its last breath: the CIO said market expectations of a scenario that is neither too hot nor too cold are based on the assumption of three “moderations”: moderate economic growth, moderate inflation and a moderate rise in asset prices.

“When any of those three disappear, there will be market corrections,” he said. ”Since Abenomics began (in 2012), our stance on Japanese stocks has been to ‘buy-on-dips’.

“But with their valuations at lofty levels” he said “we are no longer increasing our stock portfolio.”

Instead “As the end of Goldilocks markets approaches, we have to prepare ourself for tumbles in share prices,” he said.

Separately, FX traders who frontrun Japan’s insurance fund purchases will be happy to know that while Nippon Life expects the dollar could fall further against the yen, the insurer is now ready to buy dollars below 105 yen, Ozeki said as the greenback is “approaching levels in line with its fair value in purchasing power parity terms.”

Back to equity markets, Ozeki said that while the company does not expect a major market crash yet, he expects a real test for markets to come when the combined balance sheet of the world’s three biggest central banks – the Federal Reserve, the European Central Bank and the Bank of Japan – start to shrink.

Of course, as of this moment while the Fed started to trim its balance sheet, the ECB and the BOJ are still gobbling up bonds. But that is expected to change by early 2019 when all three central banks are expected to start withdrawing liquidity from the market.

Finally, Ozeki opined on what he believes is the biggest bubble: “everybody is trying to see if any bubbles are formed anywhere…I would think government bonds are the most expensive and what comes next will be a burst of the government bond bubble, even if not right away” he added.

Which, for his native Japan, where the 10Y yields below 0.1% only due to the constant intervention of the BOJ, will be a very big problem.

c) REPORT ON CHINA

Quite a story. Chinese companies have for several years have offered employees a deal: buy their company stock while at the same time guaranteeing any losses. That worked fine as long as the stock market rose. The reason for this deal: to prevent the stock falling and forcing mammoth loan margins calls by the upper management. Now Chinese companies have now been forced to halt trading in their company while they sort out the avalanche of margin calls they are receiving.

China trading begins today.

(courtesy zerohedge)

Chinese Companies Forced To Halt Trading Amid Avalanche Of Stock Loan Margin Calls

Back in the summer of 2017, just when we thought there were no more surprises left in the arsenal of the world’s foremost incubator of “financial engineering” – i.e., China – we got a stark lesson in never underestimating Chinese market manipulating ingenuity. The reason, as readers may recall, is that last June we reported, that according to Caixin, over two dozen Chinese companies had offered their employees a deal: buy company shares while guaranteeing that any losses would be covered.

The reason was simple: company founders and major shareholders had found themselves engaging in partial cash outs by pledging large batches of their stock as loan collateral and pocketing (and spending) the loan proceeds immediately, a practice that according to Reuters’ estimates had quadrupled in China over the past two years, and which worked great as long as stocks were rising, but once they started falling – as Chinese equities did early last summer – those who had taken out stock-collateralized loans were subject to escalating margin calls, forcing them to liquidate. Or rather, liquidating would have been the honorable thing to do, what they did instead was the most unethical and illegal option: shareholders and management encouraged their own employees to bail them out by buying the stock while guaranteeing to cover the downside – pushing the stock price higher, boosting the value of the pledged underlying asset, and stopping the margin calls if only briefly.

As we also noted at the time, while employees were lied to believe they were getting an unbeatable deal – who can say no when your own employer guarantees you all the upside and no downside if you just buy the company stock – the reality is that participants in such scheme were merely locking in their fates with that of their soon to be insolvent employers, who desperately needed to raise the price of their stock to fend off terminal margin calls. Furthermore, as analysts noted at the time, the promise to take any losses wasn’t legally binding and depended on big shareholders’ “virtue” which in China does not exist.

Calling this process yet another bootstrapped ponzi scheme, we said that it unveiled a deeper threat facing China’s smaller publicly-traded companies:

If markets continue to slide, there could be a surge in margin calls on these loans, potentially triggering a vicious cycle of share selling, increasing the risk of broader financial instability. “If stock prices fall, but shareholders don’t have enough capital to replenish their collateral, the pledged shares would face forced selling,” said Meng Shen, director of Chanson & Co, a Beijing-based boutique investment bank. “That would develop into a negative spiral; as the more you sell, the lower the stock price, which would then trigger more forced selling.”

Fast forward to today, and that’s pretty much where we are.

And while regulators have long since halted the practice of management being able to ask employees for a bailout, the problem with Chinese loans pledged against stock has only deteriorated, and as the FT reports, “listed Chinese companies are being forced to halt trading as their owners attempt to unwind risky bets they have made pledging company stock for loans.”

This is precisely the contingency that we said would happen if the broader Chinese market did not rebound sharply. Well, it did not, and in fact Chinese stocks – especially in recent weeks – have been some of the worst performers in the world. The result now is a brewing market crisis, as countless shareholders face self-reinforcing margin calls, which force liquidations, which send stocks lower, which prompt even more liquidations, which send stocks even lower, and so on.

The basis for this toxic loop first emerged in early 2017, when China tightened access to credit to address its mounting corporate debts; finding many of their traditional “shadow funding” pathways blocked, controlling shareholders in many smaller listed companies used their shares as collateral for credit. Then, following the market swoon late last spring, we got the first indication of just how bad the pledged loan problem could get in China, when the story described above took place.

It is now time for round 2, because just like last June, market jitters since the start of this month have pushed companies to warn their shareholders that they could face margin calls as share prices fall.

And since this time around, no simple “100% guaranteed” Ponzi schemes are available to bail shareholders out, companies are doing the only thing they can: halting trading to avoid further liquidations and even more margin calls.

That’s what happened to Shenzhen-listed Shenwu Environmental Technology, which is one of at least 20 groups in February that has stopped trading because of the risk of a margin call, where a share price decline triggers a demand to top up any money borrowed to buy the stock.

Some statistics from the FT:

China’s tighter controls over credit last year led to a wave of share pledges by listed groups: as of mid-December, shareholders in 317 Shanghai and Shenzhen-listed companies had pledged at least 40 per cent of their stock, compared with 224 companies a year earlier.

But why engage in such risky behavior as pledging shares? Mostly because as a result of Beijing’s crackdown on shadow banking, there are few other unregulated ways of extracting cash that do not involve actual selling.

The FT confirms as much, noting that “pledged shares for loans is one means that the companies have to access funding outside the traditional banking sector. Many others have borrowed from “shadow” lenders, often at high costs.”

“This is all part of the deleveraging campaign,” said Hong Hao, head of research in Bocom International in Hong Kong. “The owners of these companies have had to pledge shares just to get access to capital.”

In the case of the abovementioned Shenwu, the company announced that its controlling shareholder has pledged more than 40% of the group’s shares and was now in discussion with the margin lender.

* * *

Meanwhile, almost a year after we first warned that the practice of extensive stock pledging would have an unhappy ending, China’s securities regulator has finally started looking into the use of stock as collateral for loans, the Securities Times reported. In some cases, companies have simply noted in regulatory filings that the securities regulator is investigating the shareholders that have pledged the stock.

Making matters worse are two tangential issues:

- Fisrt, many of the smaller listed companies in China – those where share pledging dominates – are facing a slowdown in growth, alongside that of China itself, which due to its aggressive deleveraging campaign will see its GDP decline to in 2018, a factor that has weighed on the performance of many of Shenzhen’s small-cap companies;

- Second, whether due to liquidations – or their frontrunning – Shenzhen’s tech-focused ChiNext index has been falling gradually since 2015, but fell around 12% between January 25 and February 9. And as a result of the declining collateral value, the Loan To Value on the pledged loan keeps rising until it hits and/or surpasses 100%, at which point it’s game over.

“Some of these companies are heading toward dangerous territory,” a Shanghai-based analyst at a global bank told the FT, adding that it was not normal for companies to halt trading because they faced the risk of margin calls, and yet that’s precisely what is going on.

Still, some managed to find a silver lining: Bocom’s Hong said that the halting of trading to deal with problems could be a good sign. You see, he explained “in the past, shareholders facing margin calls would likely have been forced to sell off the stake without warning, he said. But China’s securities regulator has recently given companies permission to allow shareholders to work through problems with debtors instead of selling up to pay back loans.”

Which of course, is an odd definition of a “good sign”: because instead of facing reality, and selling, the entire market simply becomes hijacked by a handful of greedy executives. Meanwhile, the money of anyone who invested alongside them, well, as South Park put it best “it’s gone… it’s all gone.

end

China now crackdowns on anything that would resemble a selloff. So what did they do; they halted their own version of VIX

(courtesy zerohedge)

China Shuts Down Its VIX To Halt Market Turbulence

While most of the world saw regional equity markets covered in red overnight, China’s Shanghai Composite rebounded, rising 2.2% for two reasons: i) a delayed reaction to global equity prices after the country’s 5-day Lunar New Year holiday and ii) China’s latest crackdown on anything that can precipitate a selloff, like a high VIX for example.

And so, just like on August 24, 2015 when the US market crashed so hard in the pre-market, the VIX briefly “went offline” as input signals went haywire, China also decided to stop updating its local version of the VIX Index, taking its latest step to discourage speculation in equity-linked options after authorities tightened trading restrictions last week.

As Bloomberg first reported, China’s state-run Securities Index Co. didn’t publish a value for the SSE 50 ETF Volatility Index on its website Thursday. An employee who answered a Bloomberg phone call said the company stopped updating the measure to work on an upgrade, however according to “people familiar”, the move was designed to curb activity in the options market.

It’s unclear when the index will resume.

Just like the US VIX, the SSE 50 volatility index is the most widely-followed indicator of Chinese investor anxiety. Which is a problem because also just like the VIX, the index doubled in the span of a few days earlier this month. And the last thing Beijing wants is nervous investors thinking that other investors are nervous… and selling in a blind panic.

So what to do? Why shut it down of course, just like all global equity markets will be shut down once the real selling begins.

According to Bloomberg, the decision to stop publishing the index forms part of a broad effort by Chinese officials to contain market turbulence.

Other measures this month have included volume limits on active options traders and informal directives encouraging some major stockholders to purchase more shares. Chinese leaders have in the past faced criticism for meddling too much in markets, particularly during the nation’s 2015 equity crash.

The VIX blackout follows tighter curbs on options traders unveiled from Feb. 12, people familiar with the matter said last week, in part because they were alarmed by a gain of as much as 2,250 percent in the price of one bearish contract on the SSE 50 ETF (also known as the China 50 ETF). The fund is China’s only equity-linked product with options.

Demonstrating surprising wisdom, unlike the U.S., China has avoided approving derivatives and funds tied to its volatility gauge. And while it won’t have its own homegrown XIV collapse, China has more than enough potential candidates that will unleash the next crisis: just last night we reported that while China may not have inverse VIX ETFs, it has another, far more serious problem – pervasive stock loans, hundreds of which have seen margin calls in recent days, forcing dozens of companies to simply halt trading.

In fact, a pattern is emerging in China: any time there is a problem with any one asset, or any one indicator… why, just turn it off.

For now these “solutions” are working: volume in the SSE 50 ETF options was about 40% lower than the 20-day average on Thursday, according to data compiled by Bloomberg. What traders are more interested in is what happens when the volume hits 0% and nobody trades anymore, and – tied to that – what happens when China’s creeping admission that its capital markets are broken finally seeps through.

4. EUROPEAN AFFAIRS

ECB