GOLD: $1304.40 down $12.30

Silver: $16.27 down11 cents

Closing access prices:

Gold $1317.00

silver: $16.48

SHANGHAI GOLD FIX: FIRST FIX 10 15 PM EST (2:15 SHANGHAI LOCAL TIME)

SECOND FIX: 2:15 AM EST (6:15 SHANGHAI LOCAL TIME)

SHANGHAI FIRST GOLD FIX: $1323.53 DOLLARS PER OZ

NY PRICE OF GOLD AT EXACT SAME TIME: $1315.140

PREMIUM FIRST FIX: $8.13

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

SECOND SHANGHAI GOLD FIX: $1318.13

NY GOLD PRICE AT THE EXACT SAME TIME: $1314.40

PREMIUM SECOND FIX /NY:$3.73

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

LONDON FIRST GOLD FIX: 5:30 am est $1311.25

NY PRICING AT THE EXACT SAME TIME: $1311.20

LONDON SECOND GOLD FIX 10 AM: $1307.95

NY PRICING AT THE EXACT SAME TIME. $1307.70

For comex gold:

MARCH/

NUMBER OF NOTICES FILED TODAY FOR MARCH CONTRACT: 0 NOTICE(S) FOR NIL OZ.

TOTAL NOTICES SO FAR:2749 FOR 274900 OZ (8.5505 TONNES),

For silver:

MARCH

351 NOTICE(S) FILED TODAY FOR

1,755,000 OZ/

Total number of notices filed so far this month: 3858 for 19,290,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: BID $10,634/OFFER $10,713: UP $365(morning)

Bitcoin: BID/ $10,965/offer $11,040: UP $695 (CLOSING/5 PM)

end

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total open interest FELL BY A CONSIDERABLE SIZED 1333 contracts from 193,343 FALLING TO 192,010 DESPITE YESTERDAY’S TINY 5 CENT FALL IN SILVER PRICING. WE HAD SOME COMEX LIQUIDATION. HOWEVER, WE WERE AGAIN NOTIFIED THAT WE HAD ANOTHER STRONG SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP ROUTE: 0 EFP’S FOR MARCH AND AND 1849 EFP’S FOR MAY AND ZERO FOR ALL OTHER MONTHS AND THUS TOTAL ISSUANCE OF 1849 CONTRACTS. WITH THE TRANSFER OF 1849 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24 HRS IN THE ISSUING OF EFP’S. THE 1849 CONTRACTS TRANSLATES INTO 9.245 MILLION OZ DESPITE WITH THE CONTINUAL DROP IN OPEN INTEREST IN SILVER AT THE COMEX.

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF MARCH:

1849 CONTRACTS (FOR 1 TRADING DAYS TOTAL 1849 CONTRACTS OR 9.245 MILLION OZ: AVERAGE PER DAY: 1849 CONTRACTS OR 9.245 MILLION OZ/DAY

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH: 9.245 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 1.31% OF ANNUAL GLOBAL PRODUCTION

ACCUMULATION IN YEAR 2018 TO DATE SILVER EFP’S: 502.72 MILLION OZ.

ACCUMULATION FOR JAN 2018: 236.879 MILLION OZ

ACCUMULATION FOR MONTH OF FEBRUARY: 244.945 MILLION OZ

RESULT: WE HAD SOME LOSS IN COMEX OI SILVER COMEX WITH THE 5 CENT LOSS IN SILVER PRICE. WE ALSO HAD A GOOD SIZED EFP ISSUANCE OF 1849 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER . FROM THE CME DATA 1849 EFP’S FOR MONTHS MARCH AND MAY WERE ISSUED FOR A DELIVERABLE FORWARD CONTRACT OVER IN LONDON WITH A FIAT BONUS. WE GAINED 516 OI CONTRACTS i.e. 1849 open interest contracts headed for London (EFP’s) TOGETHER WITH A DECREASE OF 1333 OI COMEX CONTRACTS. AND ALL OF THIS HAPPENED WITH THE FALL IN PRICE OF SILVER OF 5 CENTS AND A CLOSING PRICE OF $16.38 WITH RESPECT TO YESTERDAY’S TRADING. YET WE STILL HAVE A FAIR AMOUNT OF SILVER STANDING AT THE COMEX.

In ounces AT THE COMEX, the OI is still represented by just UNDER 1 BILLION oz i.e. 0.960 BILLION TO BE EXACT or 137% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT FEBRUARY MONTH/ THEY FILED: 351 NOTICE(S) FOR 1,755,000 OZ OF SILVER

In gold, the open interest FELL BY A CONSIDERABLE 5048 CONTRACTS FALLING TO 527,812 DESPITE THE TINY FALL IN PRICE OF GOLD WITH RESPECT TO YESTERDAY’S TRADING ($0.70). HOWEVER, IN ANOTHER DEVELOPMENT, WE RECEIVED THE TOTAL NUMBER OF GOLD EFP’S ISSUED FOR THURSDAY AND IT TOTALED AN HUGE SIZED 9,903 CONTRACTS OF WHICH APRIL SAW THE ISSUANCE OF 9903 CONTRACTS AND JUNE SAW THE ISSUANCE OF 0 CONTRACTS AND THEN ALL OTHER MONTHS ZERO. The new OI for the gold complex rests at 527,812. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. DEMAND FOR GOLD INTENSIFIES GREATLY AS WE CONTINUE TO WITNESS A HUGE NUMBER OF EFP TRANSFERS TOGETHER WITH THE MASSIVE INCREASE IN GOLD COMEX OI TOGETHER WITH THE TOTAL AMOUNT OF GOLD OUNCES STANDING FOR FEBRUARY COMEX. EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER (BIG RISE IN BOTH GOFO AND SIFO) AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES. IN ESSENCE WE HAVE A GAIN OF 4855 CONTRACTS: 5048 OI CONTRACTS DECREASED AT THE COMEX AND A STRONG SIZED 9903 OI CONTRACTS WHICH NAVIGATED OVER TO LONDON.(4855 oi gain in CONTRACTS EQUATES TO 15.10TONNES)

YESTERDAY, WE HAD 13581 EFP’S ISSUED.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF MARCH : 9903 CONTRACTS OR 990,300 OZ OR 30.802 TONNES (1 TRADING DAY AND THUS AVERAGING: 9903EFP CONTRACTS PER TRADING DAY OR 990,300 OZ/ TRADING DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SIZE OF THESE EFP TRANSFERS : SO FAR THIS MONTH IN 1 TRADING DAY: IN TONNES: 30.82 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2017, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 2200 TONNES

THUS EFP TRANSFERS REPRESENTS 30.82/2200 x 100% TONNES = 1.40% OF GLOBAL ANNUAL PRODUCTION SO FAR IN MARCH ALONE.

ACCUMULATION OF GOLD EFP’S YEAR 2018 TO DATE: 1283.01 TONNES

ACCUMULATION OF GOLD EFP’S FOR JANUARY 2018: 653.22 TONNES

ACCUMULATION OF GOLD EFP’S FOR FEBRUARY: 649.45 TONNES

Result: A STRONG SIZED DECREASE IN OI AT THE COMEX DESPITE THE TINY FALL IN PRICE IN GOLD TRADING YESTERDAY ($0.70). HOWEVER, WE HAD ANOTHER GOOD SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 9903 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX AND YET WE ALSO OBSERVED A HUGE DELIVERY MONTH FOR THE MONTH OF DECEMBER. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 9903 EFP CONTRACTS ISSUED, WE HAD A NET GAIN IN OPEN INTEREST OF 4855 contracts ON THE TWO EXCHANGES:

9903 CONTRACTS MOVE TO LONDON AND 5048 CONTRACTS DECREASED AT THE COMEX. (in tonnes, the GAIN in total oi equates to 15.10 TONNES).

we had: 0 notice(s) filed upon for NIL oz of gold.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD

WITH GOLD DOWN $12.30 : a HUGE CHANGE IN GOLD INVENTORY AT THE GLD OF GOLD INTO THE GLD/ A DEPOSIT OF 2.96 TONNES

Inventory rests tonight: 833.98 tonnes.

SLV/

WITH SILVER DOWN 11 CENTS TODAY:

NO CHANGES IN SILVER INVENTORY AT THE SLV

/INVENTORY RESTS AT 316.590 MILLION OZ/

end

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in silver FELL BY 1333 contracts from 193,343 DOWN TO 192,010 (AND now A LITTLE FURTHER FROM THE NEW COMEX RECORD SET ON FRIDAY/APRIL 21/2017 AT 234,787) WITH THE FALL IN PRICE OF SILVER (5 CENTS WITH RESPECT TO YESTERDAY’S TRADING). OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE ANOTHER 0 PRIVATE EFP’S FOR MARCH AND 1849 EFP CONTRACTS OR MAY (WE DO NOT GET A LOOK AT THESE CONTRACTS AS IT IS PRIVATE BUT THE CFTC DOES AUDIT THEM) AND 0 EFP’S FOR ALL OTHER MONTHS . EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. WE HAD CONSIDERABLE COMEX SILVER COMEX LIQUIDATION. IF WE TAKE THE OI LOSS AT THE COMEX OF 1333 CONTRACTS TO THE 1849 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A GAIN OF 516 OPEN INTEREST CONTRACTS DESPITE THE RAID . WE STILL HAVE A STRONG AMOUNT OF SILVER OUNCES THAT ARE STANDING FOR METAL IN MARCH (SEE BELOW). THE NET GAIN TODAY IN OZ ON THE TWO EXCHANGES: 2.580 MILLION OZ!!!

RESULT: A CONSIDERABLE SIZED DECREASE IN SILVER OI AT THE COMEX DESPITE THE TINY FALL OF 5 CENTS IN PRICE (WITH RESPECT TO YESTERDAY’S TRADING ). BUT WE ALSO HAD ANOTHER GOOD 1849 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE GOOD SIZED AMOUNT OF SILVER OUNCES STANDING FOR MARCH, DEMAND FOR PHYSICAL SILVER INTENSIFIES AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)Late THURSDAY MORNING/WEDNESDAY NIGHT: Shanghai closed UP 14.34 POINTS OR 0.44% /Hang Sang CLOSED UP 199.53 POINTS OR 0.65% / The Nikkei closed DOWN 343.77 POINTS OR 1.56%/Australia’s all ordinaires CLOSED DOWN 0.68%/Chinese yuan (ONSHORE) closed DOWN at 6.3493/Oil DOWN to 61.26 dollars per barrel for WTI and 64.06 for Brent. Stocks in Europe OPENED DEEPLY IN THE RED . ONSHORE YUAN CLOSED DOWN AT 6.3493 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.3543 /ONSHORE YUAN TRADING STRONGER AGAINST OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING MUCH WEAKER AGAINST THE DOLLAR AND ALL OTHER CURRENCIES. CHINA IS HAPPY TODAY (WEAK CURRENCY AND GOOD CHINESE MARKETS/ BUT POOR GLOBAL MARKETS)

3a)THAILAND/SOUTH KOREA/NORTH KOREA

i)North Korea

b) REPORT ON JAPAN

3 c CHINA

i)China is definitely slowing down: the following will not help as Chinese giant HNA will planning to axe 100,000 jobs or 1/4 of its workforce

(SouthChinaMorningPost/Hong Kong)

4. EUROPEAN AFFAIRS

Great Britain/WPP

WPP is a Bellwether on the global economy..a rise in its stock means the global economy is growing and a drop in its value means contraction. Their stock fell 19% overnight as its chairman stated that he sees little growth. What does this mean to ad dependent Google, Facebook etc.

(courtesy zerohedge)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

(courtesy zerohedge)

6 .GLOBAL ISSUES

7. OIL ISSUES

8. EMERGING MARKET

South Africa

We highlighted this to you over the past few weeks. It looks like South Africa will confiscate White Owned land with zero compensation. This will surely bankrupt the country. Over 73% of all agricultural land in South Africa is owned by Whites.

(courtesy zerohedge)

9. PHYSICAL MARKETS

i)A good commentary today from Chris Powell on an interview Pierre Lassonde did with Kitco

( Chris Powell/GATA)

ii)We have been telling you that Libor has been rising for quite some time. It is now at dangerous levels as the global economy just cannot handle the higher rates. The reason for libor rising is due to the huge dollar repatriation which caused a scarcity of dollars in Europe. The banks which had previously levered their dollar deposits with exotic derivatives are now having difficulty due to the drain on their disappearing USA dollar deposits, the dollars that was used to lever in the first place. Because of the loss of those dollars, the banks are now afraid to loan to one another as they fear the banks will implode with their exotic derivatives and nothing to hold them up with.

THIS IS A MUST READ…

(courtesy Ambrose Evans Pritchard/UKTelegaph)

iii)My goodness Sheila Bair said a mouthful today: “We should not bank Bitcoin..the green Bills in your pocket do not have intrinsic value either”

(courtesy zerohedge/Barrons)

10. USA stories which will influence the price of gold/silver

i)USA Markets today

a)Early this morning, Powell flip flops

(courtesy zerohedge)

b)Then, strangely,on a report that the ECB will delay the end of its QE,, the Euro rises and the dollar tumbles

c)Fed’s Dudley sinks stocks when he signals that the 4 rate hikes are still gradual..

ii)Not good for GDP numbers: real personal spending drops the most in 2 years as saving rate jumbs.

( zerohedge)

(courtesy zerohedge)

iii b) The hardest hit country for tariffs on steel: Canada. China did not make the top 10 although it is the largest supplier of Aluminum

iv)Manhattan landlords are now feeling the pinch: they are slashing rents to fill vacant storefronts

(courtesy zerohedge)

v)Our good friends over at Wells Fargo are hit again after the Dept of Justice orders an investigation into the Wealth Management Division

c)The Mooch says that Kelly has blacklisted him form the West Wing. He also states that many more personnel will leave the wing:

( zero hedge)

d)the revolving door continues to operate at full speed as it looks like National Security Advisor McMaster is being pushed out the door

comex gold volumes are RISING AGAIN

Here is a summary of the latest gold trading volumes at the Comex per year

certainly the introduction of EFP’s has certainly had an effect:

Trading Volumes on the COMEX

PRELIMINARY COMEX VOLUME FOR TODAY: 383,498 contracts

CONFIRMED COMEX VOL. FOR YESTERDAY: 294,958 CONTRACTS

comex gold volumes are RISING AGAIN

Here is a summary of the latest gold trading volumes at the Comex per year

certainly the introduction of EFP’s has certainly had an effect:

Meanwhile, gold-trading volumes on the COMEX have never been higher:

end

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

And now for the wild silver comex results.

Total silver OI ROSE BY A CONSIDERABLE 1333 CONTRACTS FROM 193,343 DOWN TO 192,010 DESPITE YESTERDAY’S TINY 5 CENT FALL IN TRADING). HOWEVER,WE WERE ALSO INFORMED THAT WE HAD 0 EMERGENCY EFP’S FOR MARCH ISSUED BY OUR BANKERS (WITH 1849 EFP CONTRACTS FOR MAY AND ZERO FOR ALL OTHER MONTHS) TO COMEX LONGS WHO RECEIVED A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON: THE TOTAL EFP’S ISSUED: 1849. THE SILVER BOYS HAVE STARTED TO MIGRATE TO LONDON FROM THE START OF DELIVERY MONTH AND CONTINUING RIGHT THROUGH UNTIL FIRST DAY NOTICE JUST LIKE WE ARE WITNESSING TODAY. USUALLY WE NOTED THAT CONTRACTION IN OI OCCURRED ONLY DURING THE LAST WEEK OF AN UPCOMING ACTIVE DELIVERY MONTH AS WE HAVE JUST SEEN IN GOLD TODAY. THIS PROCESS HAS JUST BEGUN IN EARNEST IN SILVER STARTING IN SEPTEMBER 2017. HOWEVER, IN GOLD, WE HAVE BEEN WITNESSING THIS FOR THE PAST 2 YEARS. NICK LAIRD WAS KIND ENOUGH TO SUPPLY US THE TOTAL FOR 2017 GOLD EFP’S AND IT WAS 6600 TONNES FOR THE ENTIRE YEAR. WE OBVIOUSLY HAD CONSIDERABLE LONG COMEX SILVER LIQUIDATION BUT WE ALSO HAD A SMALL SIZED GAIN IN TOTAL SILVER OI FROM OUR TWO EXCHANGES. WE ARE ALSO WITNESSING A FAIR AMOUNT OF SILVER OUNCES STANDING FOR COMEX METAL IN THIS NON ACTIVE JANUARY AS WELL AS THAT CONTINUAL MIGRATION OF EFPS OVER TO LONDON. ON A PERCENTAGE BASIS THERE ARE MORE EFP’S ISSUED FOR GOLD THAN SILVER. ON A NET BASIS WE GAINED 516 SILVER OPEN INTEREST CONTRACTS

1333 CONTRACT LOSS AT THE COMEX COMBINING WITH THE ADDITION OF 1849 OI CONTRACTS NAVIGATING OVER TO LONDON.

NET GAIN ON THE TWO EXCHANGES: 516 CONTRACTS

We are now in the active delivery month of MARCH and here the front month LOST 3417 contracts FALLING TO 1517 contracts. We had 3507 contracts filed upon yesterday, so we GAINED 90 contracts or an additional 450,000 will stand in this active delivery month of March.

April lost 10 contracts down to 414 .

The next big active delivery month for silver will be May and here the OI lost by 460 contracts down to 149,945

We had 351 notice(s) filed for 1755,000 OZ for the MARCH 2018 contract for silver

INITIAL standings for MARCH

MARCH 1/2018.

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz |

nil oz

|

| Deposits to the Dealer Inventory in oz | 788.235 oz

Brinks |

| Deposits to the Customer Inventory, in oz | nil |

| No of oz served (contracts) today |

0 notice(s)

NIL OZ

|

| No of oz to be served (notices) |

665 contracts

(66,500 oz)

|

| Total monthly oz gold served (contracts) so far this month |

0 notices

|

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

For MARCH:

Today, 0 notice(s) were issued from JPMorgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equates to 0 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped/ Received) by j.P.Morgan customer account.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

To calculate the INITIAL total number of gold ounces standing for the MARCH. contract month, we take the total number of notices filed so far for the month (0) x 100 oz or 0 oz, to which we add the difference between the open interest for the front month of FEB. (665 contracts) minus the number of notices served upon today (0 x 100 oz per contract) equals 66,500 oz, the number of ounces standing in this nonactive month of MARCH (2.0684 tonnes)

Thus the INITIAL standings for gold for the MARCH contract month:

No of notices served (0 x 100 oz or ounces + {(665)OI for the front month minus the number of notices served upon today (0 x 100 oz )which equals 66,500 oz standing in this nonactive delivery month of March . THERE IS 10.556 TONNES OF REGISTERED GOLD AVAILABLE FOR DELIVERY SO FAR.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

IN THE LAST 17 MONTHS 70 NET TONNES HAS LEFT THE COMEX.

end

And now for silver

AND NOW THE DECEMBER DELIVERY MONTH

MARCH INITIAL standings

| Silver | Ounces |

| Withdrawals from Dealers Inventory | nil oz |

| Withdrawals from Customer Inventory |

150,299.000 oz

Scotia

|

| Deposits to the Dealer Inventory |

211,427,160

oz

brinks

|

| Deposits to the Customer Inventory |

985.560 oz

Delaware

|

| No of oz served today (contracts) |

351

CONTRACT(S

(1,755,000 OZ)

|

| No of oz to be served (notices) |

1166 contracts

(5,830,000 oz)

|

| Total monthly oz silver served (contracts) | 3858 contracts

(19,290,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

we had 1 inventory movement at the dealer side of things

we had 1 inventory deposits into the dealer account

i) Into Brinks: 211,427.160 oz

total inventory deposits into dealer: 211,427.160 oz

we had 1 deposits into the customer account

i) into Delaware:

985.560 oz was deposited into the customer account of Delaware

ii) JPMorgan: zero

*** JPMorgan for most of 2017 and in 2018 has adding to its inventory almost every single day.

JPMorgan now has 135 million oz of total silver inventory or 54% of all official comex silver.

total deposits customer account: 985.560 oz

we had 1 withdrawals from the customer account;

i) Out of Scotia: 150,299.000??? exact weight???

total withdrawals; 150,299.000 oz

we had 1 adjustments

i) out of CNT: 422,735.150 oz was adjusted out of the customer is this landed into the dealer account of CNT

total dealer silver: 56.193 million

total dealer + customer silver: 251,382 million oz

The total number of notices filed today for the March. contract month is represented by 351 contract(s) FOR 1,755,000 oz. To calculate the number of silver ounces that will stand for delivery in March., we take the total number of notices filed for the month so far at 3858 x 5,000 oz = 19,290,000 oz to which we add the difference between the open interest for the front month of Mar. (1517) and the number of notices served upon today (351 x 5000 oz) equals the number of ounces standing.

.

Thus the INITIAL standings for silver for the March contract month: 3507(notices served so far)x 5000 oz + OI for front month of March(1517) -number of notices served upon today (351)x 5000 oz equals 25,120,000 oz of silver standing for the March contract month.

We gained an additional 90 contracts or 450,000 additional silver oz will stand for delivery at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

ESTIMATED VOLUME FOR TODAY: 90,847 CONTRACTS

CONFIRMED VOLUME FOR YESTERDAY: 65,888 CONTRACTS

YESTERDAY’S CONFIRMED VOLUME OF 65,888 CONTRACTS EQUATES TO 329 MILLION OZ OR 47.0% OF ANNUAL GLOBAL PRODUCTION OF SILVER

COMMODITY LAW SUGGESTS THAT OPEN INTEREST SHOULD NOT BE MORE THAN 3% OF ANNUAL GLOBAL PRODUCTION. THE CROOKS ARE SUPPLYING MASSIVE PAPER TRYING TO KEEP SILVER IN CHECK.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price at that day at $18.42

The previous record was 224,540 contracts with the price at that time of $20.44

end

NPV for Sprott

1. Sprott silver fund (PSLV): NAV FALLS TO -1.57% (MARCH 1/2018)

2. Sprott gold fund (PHYS): premium to NAV RISES TO -0.42% to NAV (MARCH 12018 )

Note: Sprott silver trust back into NEGATIVE territory at -1.57%-/Sprott physical gold trust is back into NEGATIVE/ territory at -0.42%/Central fund of Canada’s is still in jail but being rescued by Sprott.

Sprott WINS hostile 3.1 billion bid to take over Central Fund of Canada

(courtesy Sprott/GATA)

3.SPROTT CEF.A FUND (FORMERLY CENTRAL FUND OF CANADA): NAV RISES TO -3.66%: NAV 13.62/TRADING 13.153//DISCOUNT 3.66.

END

And now the Gold inventory at the GLD/

March 1/WITH GOLD DOWN ANOTHER $12.30/A HUGE CHANGE IN GOLD INVENTORY/ A DEPOSIT OF 2.96 TONNES/INVENTORY RESTS AT 833.98 TONNES

FEB 28/WITH GOLD DOWN ANOTHER 70 CENTS/NO CHANGE IN GOLD INVENTORY/INVENTORY RESTS AT 831.03 TONNES/.

feb 27/WITH GOLD DOWN $13.80 WE HAD NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 831.03 TONNES

FEB 26/WITH GOLD UP $2.40/WE HAD ANOTHER INVENTORY GAIN/THIS TIME 1.77 TONNE ADDITION TO THE GLD INVENTORY/INVENTORY RESTS AT 831.03 TONNES/WE HAVE HAD 5 INCREASES IN THE PAST 6 TRADING GOLD SESSIONS/

FEB 23/WITH GOLD DOWN $1.15, WE HAD A GOOD INVENTORY GAIN OF 1.47 TONNES OF GOLD INTO THE GLD/INVENTORY RESTS AT 829.26 TONNES

FEB 22/WITH GOLD UP 90 CENTS AGAIN TODAY, WE HAD NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 827.79 TONNES

FEB 21/ WITH THE 90 CENT GAIN WE HAD ANOTHER DEPOSIT OF 3.15 TONNES OF GOLD INTO THE GLD INVENTORY/INVENTORY RESTS TONIGHT AT 827.79 TONNES

Feb 20/WITH GOLD DOWN BY $24.25, THE CROOKS DECIDED THAT THEY HAD BETTER RETURN (DEPOSIT) 3.34 TONNES OF GOLD INTO THE GLD/INVENTORY RESTS TONIGHT AT 824,64 TONNES

Feb 16/WITH GOLD UP BY 25 CENTS, THE CROOKS DECIDED AGAIN TO RAID THE COOKIE JAR BY WITHDRAWING 2.36 TONNES OF GOLD FROM THE GLD/INVENTORY RESTS AT 821.30 TONNES

Feb 15/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 823.66 TONNES

Feb 14/AN ADDITIONAL OF 2.95 TONNES OF GOLD INTO GLD WITH THE HUGE GAIN OF 27.40 IN PRICE/INVENTORY RESTS AT 823.66 TONNES

Feb 13/WITH GOLD UP $3.40 WE HAD NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY REMAINS AT 820.71 TONNES

Feb 12/STRANGE!!WITH GOLD RISING BY 12.00 DOLLARS, THE CROOKS DECIDED AGAIN TO WITHDRAW 5.6 TONNES OF GOLD FOR EMERGENCY USE ELSEWHERE/INVENTORY RESTS AT 820.71 TONNES

Feb 9/AGAIN WITH HUGE TURMOIL ON THE MARKETS, THE CROOKS WITHDREW 2 TONNES OF GOLD FROM THE GLD INVENTORY/INVENTORY RESTS AT 826.31 TONNES

Feb 8/DESPITE THE GOOD GAIN IN PRICE FOR GOLD TODAY/THE CROOKS REMOVED .96 TONNES FROM THE GLD INVENTORY/INVENTORY RESTS AT 828.31 TONNES

FEB 7/AN UNBELIEVABLE 12.08 TONNES WAS REMOVED BY THE CROOKED BANKERS AND THIS GOLD WAS USED IN THE ASSAULT THESE PAST FEW DAYS/INVENTORY RESTS AT 829.27 TONNES

Feb 6/AGAIN VERY STRANGE: WITH TODAY’S TURMOIL, THE CROOKS DID NOT ADD ANY GOLD INVENTORY INTO THE GLD/INVENTORY REMAINS AT 841.35 TONNES

Feb 5 Strange,with all of today’s turmoil, the crooks at the GLD decided to add zero ounces into GLD inventory/inventory rests at 841.35 tonnes

Feb 2/no change in gold inventory at the GLD/Inventory rests at 841.35 tonnes

Feb 1/with gold up by $8.00/the crooks decided not to add any new physical gold metal into the GLD./inventory rests at 841.35 tonnes

Jan 31/with gold up $3.15 today, GLD shed another 5.32 tonnes of gold from its inventory/inventory rests at 841.35 tonnes

jan 30/with gold down by $4.85/GLD shed another 1.47 tonnes of gold from its inventory/inventory rests at 846.67 tonnes

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

MARCH 1/2018/ Inventory rests tonight at 833.98 tonnes

*IN LAST 333 TRADING DAYS: 107,16 NET TONNES HAVE BEEN REMOVED FROM THE GLD

*LAST 263 TRADING DAYS: A NET 50.14 TONNES HAVE NOW BEEN ADDED INTO GLD INVENTORY.

end

Now the SLV Inventory

March 1/WITH SILVER DOWN 11 CENTS TODAY/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 316.590 MILLION OZ./

FEB 28/WITH SILVER DOWN 5 CENTS TODAY/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 316.590 MILLION OZ/

feb 27/WITH SILVER DOWN 17 CENTS/NO CHANGE IN SILVER INVENTORY/INVENTORY RESTS AT 316.590 MILLION OZ

FEB 26/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 316.590 MILLION OZ/

FEB 23/WITH SILVER DOWN 10 CENTS TODAY, WE HAD ANOTHER HUGE ADDITION OF 1.315 MILLION OZ/INVENTORY RESTS AT 316.590 MILLION OZ/

fEB 22.2018/WITH SILVER DOWN 1 CENT TODAY, WE HAD NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 315.271 MILLION OZ/

FEB 21/WITH SILVER UP 15 CENTS TODAY, WE HAD A GOOD SIZED INVENTORY ADDITION OF 1.226 MILLION OZ/INVENTORY RESTS AT 315.271 MILLION OZ/

Feb 20/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 314.045 MILLION OZ

Feb 16/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 314.045 MILLION OZ/

Feb 15/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 314.045 MILLION OZ/

Feb 14./NO CHANGE IN SILVER INVENTORY DESPITE THE HUGE RISE IN PRICE/INVENTORY RESTS AT 314.045 MILLION OZ

Feb 13./NO CHANGE IN SILVER INVENTORY TODAY/INVENTORY RESTS AT 314.045 MILLION OZ/

Feb 12/AGAIN, WITH TODAY’S HUGE RISE IN SILVER PRICE, IN TOTAL CONTRAST TO GOLD: NO CHANGE IN SILVER INVENTORY/INVENTORY RESTS AT 314.045 MILLION OZ/

Feb 9/AGAIN WITH TURMOIL ON THE MARKETS, STRANGELY IN TOTAL CONTRAST TO GOLD: NO CHANGE IN SILVER INVENTORY/INVENTORY RESTS AT 314.045 MILLION OZ/

Feb 8/DESPITE THE TURMOIL TODAY AND A PRICE RISE: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 314.045 MILLION OZ/

FEB 7/no change in silver inventory at the SLV/Inventory rests at 314.045 million oz/

Feb 6/WITH ALL OF TODAY’S TURMOIL/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 314.045 MILLION OZ/

Feb 5/ we had HUGE change in silver inventory at the SLV/ A DEPOSIT OF 1.131 MILLION OZ INTO THE SLV/Inventory rests at 314.045 million oz/

Feb 2/we lost 982,000 oz from the SLV inventory /inventory rests at 312.914 million oz/

Feb 1/no change in silver inventory at the SLV/Inventory rests at 313.896 million oz/

Jan 31/ no change in inventory at the slv in total contrast to gold/inventory rests at 313.896 million oz/

Jan 30/no change in inventory/SLV inventory rests at 313.896 million oz/

MARCH 1/2018: NO CHANGES TO SILVER INVENTORY/

Inventory 316.590 million oz

end

6 Month MM GOFO 1.93/ and libor 6 month duration 2.22

Indicative gold forward offer rate for a 6 month duration/calculation:

G0FO+ 1.93%

libor 2.22 FOR 6 MONTHS/

GOLD LENDING RATE: .290%

12 Month MM GOFO

+ 2.38%

LIBOR FOR 12 MONTH DURATION: 2.500

GOFO = LIBOR – GOLD LENDING RATE

GOLD LENDING RATE = .120

end

Major gold/silver trading /commentaries for THURSDAY

GOLDCORE/BLOG/MARK O’BYRNE.

GOLD/SILVER

GoldCore

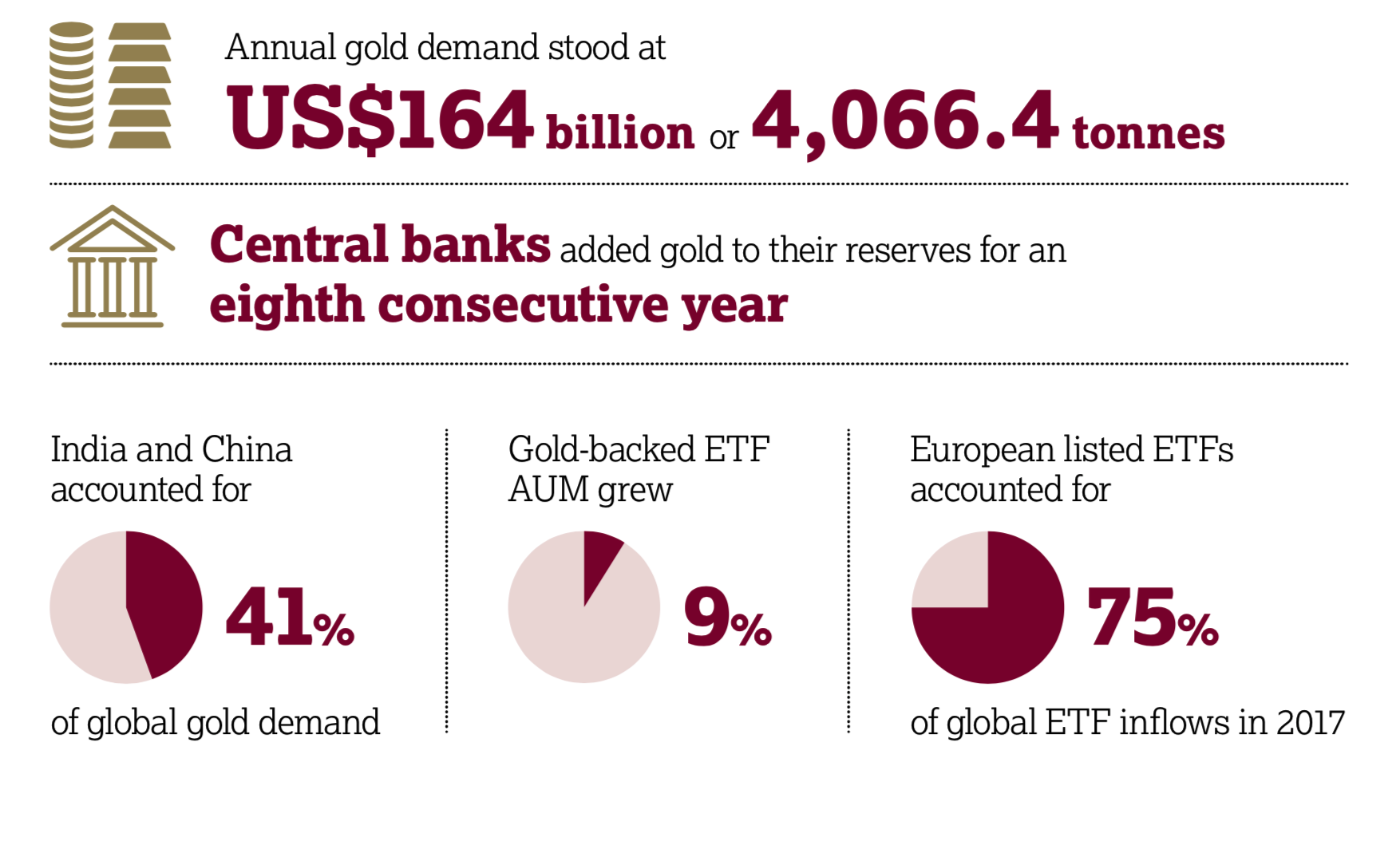

Four Key Themes To Drive Gold Prices In 2018 – World Gold Council

– Four key themes to drive gold prices in 2018 – World Gold Council annual review

– Monetary policies, frothy asset prices, global growth and demand and increasing market access important in 2018

– Weak US dollar in 2017 saw gold price up 13.5%, largest gain since 2010

– “Strong gold price performance was a positive for investors and producers, and was symptomatic of a more profound shift in sentiment: a growing recognition of gold’s

role as a wealth preservation and risk mitigation tool”

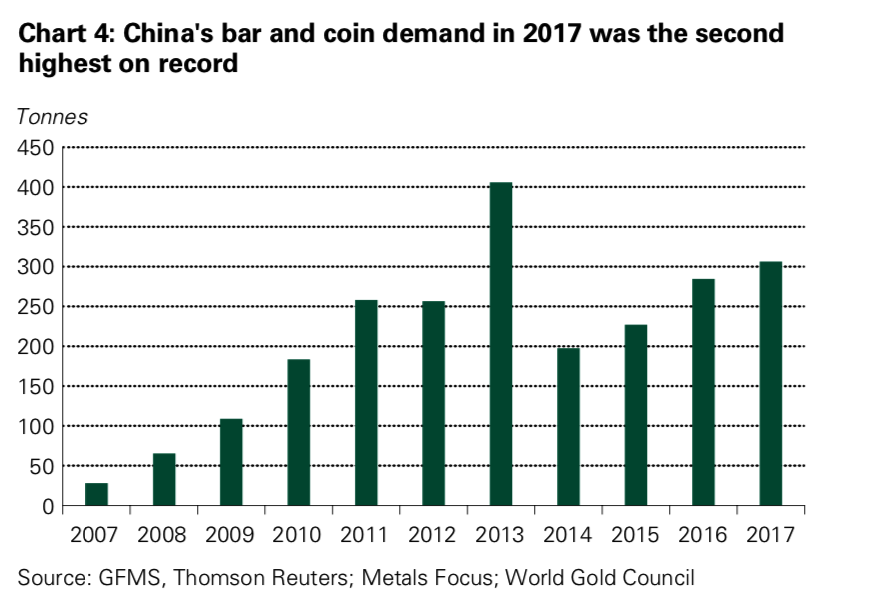

– China’s gold coins and bars market recorded its second-best year ever

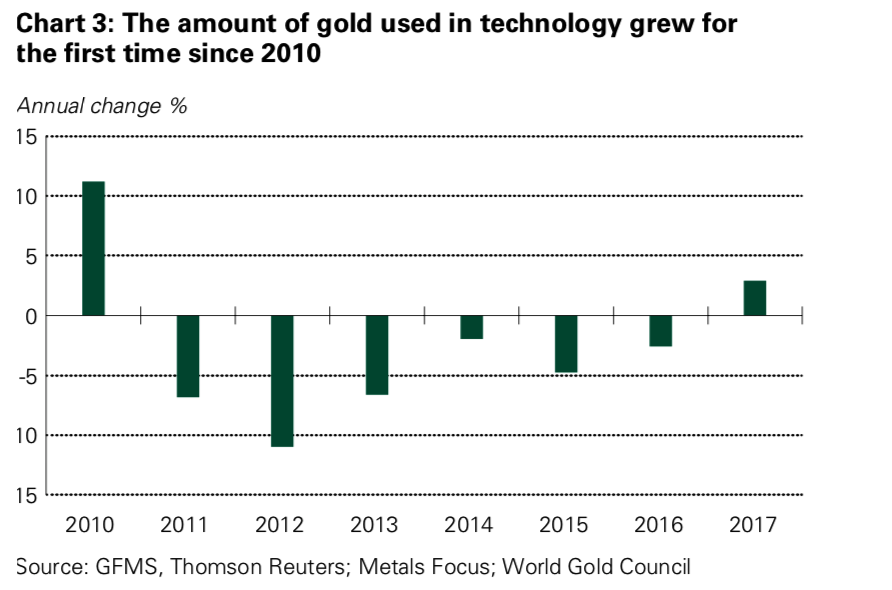

– German, central bank and technological demand supporting gold prices

– Latest Goldnomics podcast explores these and other themes

Editor: Mark O’Byrne

Annual Review 2017 has just been released by the World Gold Council (WGC) and it’s annual report on the gold market and the outlook for gold prices is fact based, comprehensive and well worth a read – especially the section ‘Market Outlook for 2018’.

2017 was a relatively quiet one for gold prices, which was surprising given the increasing tensions and turbulence going on in the rest of the financial and particularly political spheres. The World Gold Council’s comprehensive analysis strongly suggests that the set up for gold is very positive and we are on the verge of further gains in the coming years.

This is also our own view which we expanded upon in the just released latest Goldnomics podcast (Episode 3).

Gold demand fell slightly but supply was also down

2017 was a challenging year for gold demand: it fell to its lowest level since 2009. Investment and central bank demand accounted for most of the decline.

There were two interesting positive increases in gold demand in 2017; central banks and the technology industry. Whilst central bank demand did decline from the previous year, it was still notable.

According to the World Gold Council we are set to see both of these factors rise in 2018 which bodes well for gold prices.

Central banks continue buying as tensions rise between West and East

Last year made for the eighth consecutive year that central banks added to their gold reserves. As mentioned in our latest podcast this demand is high, but it could increase even more given the level of foreign exchange reserves.

Just this last week the news broke that the Russian central bank added a further 18 tonnes to their gold reserves. By way of reminder this is the bank that last year said it was stocking up on gold in order to “beef up national security.”

2017’s most notable central banks buying gold were Russia, Turkey and Kazakhstan. The former two having made some bold statements in recent times about protecting themselves from US dollar hegemony.

China, Russia, Iran and more recently Turkey have made no secret of their desire to operate outside of the financial and monetary control mechanisms the U.S. has managed to control for so long. China (another major central bank buyer) is the most important in this regard but each of these countries have actively encouraged private gold ownership as well as national, in order to reduce their reliance on and exposure to the US dollar.

Interestingly, the WGC highlight China’s phenomenal gold buying record which rose again once again in 2017 to the second highest level on record.

Geopolitical changes are seen as driving factors for the 2018 gold price by both the WGC and ourselves.

The WGC draw particular attention to the sabre-rattling between North Korea and the United States. Whilst in our latest podcast we do touch on North Korea we also consider a number of factors including the ‘massive’ destabilisation of the Middle East. We discuss rising political tensions as well as what uncertainty and war mean for the gold price. Hint … increased safe haven demand.

Tech demand for gold

In 2017 demand for gold in technology increased for the first time since 2010. The WGC expects this to be an ongoing trend as both the semi-conductor sector and gold nanoparticle-based technologies grow in popularity.

After contracting year after year since 2010, we expect technology demand to stabilise and, in some areas, grow over the coming years.

Back to Basics: Supply and Demand

The WGC look to synchronised global economic growth, monetary policy, frothy asset prices and market transparency and access including Sharia gold demand to drive the gold market into 2018.

Monetary policy and frothy asset prices are those grabbing the headlines of late. It may be surprising to many investors but higher interest rates are good news for gold (as discussed here) whilst frothy asset prices could lead to yet another stock market crash and indeed another financial crisis. Investors should realise that cash can quickly turn to trash and how bail-ins are a very real threat today.

However, it is the basics of supply and demand which are key to the price of gold in the long-term.

The underlying fundamentals of gold, particularly on the supply side, and the advent of peak gold, help to underpin gold’s likely rise to $10,000 in the long term.

Most commentators focus on the demand side of the gold market but we consider the supply side to be just as important. As discussed in our podcast we are seeing supply drop. According to this latest report from the WGC ‘Total supply [in 2017] fell 4% compared to 2016. Declines in recycling and hedging activity offset a modest rise in mine production.’

It is increasingly expensive to mine gold and there have been no major gold discoveries in recent years. How will this play out in the long term when gold demand has been increasing on average by 18% per year in recent years?

Elon Musk’s grand plans to mine in space gets lots of headlines and uninformed press which misguided gold bears use to bolster their weak central thesis. In truth, mining gold on asteroids or on Mars is fake gold news.

There is no real threat here to the gold market. Indeed, the notion of mining on other planets is laughable nonsense. It is not feasible today and if it does become feasible, the cost per ounce of “space gold” or “asteroid gold” will be hundreds of thousands of dollars if not million of dollars per ounce.

We discuss many of the 2018 factors raised by the WGC in Goldnomics but expand into other areas, notably the key decisions and lessons investors must take in the current environment when it comes to protecting their assets and the importance of owning gold in the safest way possible. Not all types of gold are made equal.

Annual Review 2017 and Outlook 2018 can be accessed via the World Gold Council here

Listen to Goldnomics (Ep. 3) on SoundCloud , Blubrry & iTunes. Watch on YouTube below

Listen to the full episode or skip directly to a key discussion point here

News and Commentary

Gold suffers first monthly loss since October (MarketWatch.com)

February U.S. Mint American Eagle gold, silver coin sales fall (Reuters.com)

Nationwide weakness: Pending home sales drop 4.7 percent in U.S. in January (CNBC.com)

Foxtons profits plunge over London housing market slump (TheGuardian.com)

Retail job losses may reach 15,000 as industry strains under cost pressures (CityAM.com)

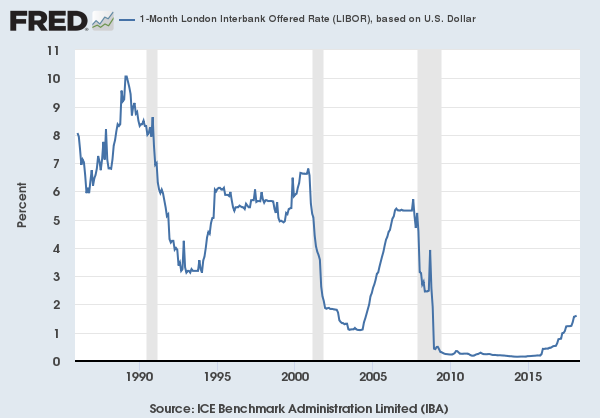

Source: St Louis Fed

Libor surge is nearing danger level for debt-drenched world (Telegraph.co.uk)

Tycoons fold on old-economy assets (MoneyWeek.com)

Lessons from Buffett’s latest letter: stay patient and avoid debt (MoneyWeek.com)

Europe’s leaders brace for the climax to Italy’s opera of an election (Telegraph.co.uk)

The World’s Cobalt Supply Is in Jeopardy (GoldSeek.com)

Gold Prices (LBMA AM)

01 Mar: USD 1,311.25, GBP 953.80 & EUR 1,075.75 per ounce

28 Feb: USD 1,320.30, GBP 951.14 & EUR 1,080.53 per ounce

27 Feb: USD 1,332.75, GBP 954.78 & EUR 1,081.26 per ounce

26 Feb: USD 1,339.05, GBP 953.00 & EUR 1,085.30 per ounce

23 Feb: USD 1,328.90, GBP 951.09 & EUR 1,079.20 per ounce

22 Feb: USD 1,323.50, GBP 952.66 & EUR 1,076.40 per ounce

21 Feb: USD 1,328.60, GBP 952.87 & EUR 1,078.16 per ounce

Silver Prices (LBMA)

01 Mar: USD 16.32, GBP 11.87 & EUR 13.39 per ounce

28 Feb: USD 16.44, GBP 11.88 & EUR 13.45 per ounce

27 Feb: USD 16.61, GBP 11.91 & EUR 13.48 per ounce

26 Feb: USD 16.67, GBP 11.88 & EUR 13.52 per ounce

23 Feb: USD 16.61, GBP 11.88 & EUR 13.50 per ounce

22 Feb: USD 16.47, GBP 11.86 & EUR 13.40 per ounce

21 Feb: USD 16.44, GBP 11.80 & EUR 13.35 per ounce

Recent Market Updates

– Is The Gold Price Going To $10,000? (Goldnomics Podcast 3)

– Gold Corridor From Dubai to China Sought By China

– Digital Gold Provide the Benefits Of Physical Gold?

– Weekly Briefing: Currency Wars – ECB Warns Re Trump, Russia and Turkey Buy Gold and BOE Bitcoin Warning

– Russian Central Bank Buys Gold – 600,000 Ounces Or 18.7 Tons In January As Venezuela Launches ‘Petro Gold’

– Bitcoin or British Pound ‘Pretty Much Failed’ As Currency?

– Bank Bail-In Risk In European Countries Seen In 5 Key Charts

– US-China Trade War Escalates As Further Measures Are Taken

– Gold Up 3.8% In Week – If Closes Above $1,360/oz Will Be Biggest Weekly Gain In Nearly 2 Years

– Is The Gold Price Heading Higher? IG TV Interview GoldCore

– Global Debt Crisis II Cometh

– Sovereign Wealth Funds Investing In Gold For “Long Term Returns” – PwC

– Bitcoin and Crypto Prices Being Manipulated Like Precious Metals?

Andrew Maguire’s Kinesis money which is a “bitcoin” but backed 100% by allocated gold and silver is set to go.

it think it would be a great idea to look at this!

please read at: https://kinesis.money/#/

(Andrew Maguire)

|

2:57 PM (1 hour ago) | ||

|

|||

Harvey

Here It is my friend! https://kinesis.money/#/ Please let everyone know.

Let catch up on Monday if you have time. We have billions in the hopper ready to be allocated on the 1st day of trading. The paper market days are over.

Warm regards

Andy

end

A good commentary today from Chris Powell on an interview Pierre Lassonde did with Kitco

(courtesy Chris Powell/GATA)

Lassonde likes the gold price with central banks rigging the market

Submitted by cpowell on Thu, 2018-03-01 05:12. Section: Daily Dispatches

12:18a ET Thursday, March 1, 2018

Dear Friend of GATA and Gold:

Oh, for a journalist who would put a few serious questions to Franco-Nevada Chairman Pierre Lassonde, former chairman of the World Gold Council, when he says, as he told Daniela Cambone of Kitco News this week, that “gold is well-priced” and “where it should be.”

http://www.kitco.com/news/video/show/BMO-Conference-2018/1869/2018-02-28…

Does Lassonde mean that gold is doing as well as it could against the daily gold derivatives trading by central banks?

After all, what is the Bank for International Settlements doing with those 600 or so tonnes’ worth of gold derivatives issued on behalf of its member central banks?http://www.gata.org/node/18041

Does Lassonde mean that the manipulative trading in gold recently admitted by three investment banks —

http://www.gata.org/node/18004

— has done no particular harm to gold investors?

Is Lassonde certain that the 15-percent discount given by CME Group, operator of the major U.S. futures exchanges, to governments and central banks for their surreptitious trading of gold futures —

http://www.gata.org/node/17976

— is part of an entirely innocent enterprise?

Or by asserting that gold is “where it should be” does Lassonde mean that he approves of the surreptitious rigging of the gold market by central banks?

Four years ago, when he was still a member of the World Gold Council’s Board of Directors, Lassonde told Cambone that central banks “spend no time whatsoever thinking about gold”:

http://www.gata.org/node/13683

Simultaneously the gold council was advertising a seminar for central bankers about trading, clearing, and vaulting gold and accounting for gold reserves:

http://www.gata.org/node/13851

In his interview with Kitco News this week Lassonde added that he doesn’t think gold is going anywhere this year. If gold does go anywhere, it sure won’t be with any help from this supposed leader of the gold industry. He well may be the favorite gold mining executive of central bankers.

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

We have been telling you that Libor has been rising for quite some time. It is now at dangerous levels as the global economy just cannot handle the higher rates. The reason for libor rising is due to the huge dollar repatriation which caused a scarcity of dollars in Europe. The banks which had previously levered their dollar deposits with exotic derivatives are now having difficulty due to the drain on their disappearing USA dollar deposits, the dollars that was used to lever in the first place. Because of the loss of those dollars, the banks are now afraid to loan to one another as they fear the banks will implode with their exotic derivatives and nothing to hold them up with.

THIS IS A MUST READ…

(courtesy Ambrose Evans Pritchard/UKTelegaph)

Ambrose Evans-Pritchard: Libor surge nears danger level for debt-drenched world

Submitted by cpowell on Thu, 2018-03-01 05:41. Section: Daily Dispatches

By Ambrose Evans-Pritchard

The Telegraph, London

Wednesday, February 28, 2018

The stress signals of the global credit system are flashing amber. The offshore dollar funding markets that lubricate world finance are facing an incipient squeeze.

The “Libor-OIS spread,” watched carefully by traders, has risen to levels reached during the onset of the Chinese currency crisis in early 2016 and during the onset of the Italian and Spanish funding crisis in late 2011

The three-month rate for dollar Libor (London Interbank Offered Rate) used to price a vast nexus of financial contracts around the world has spiked to a 10-year high of 2 percent this week. A third of all U.S. business loans are linked to Libor, as are most student loans, and 90 percent of the leverage loan market.

The U.S. can doubtless handle the sixfold rise in Libor costs over the last two years since it is a reflection of economic recovery itself. America needs tighter money: The economy is on the cusp of overheating, with a double blast of irresponsible fiscal stimulus coming from the Trump tax cuts and Republican pork barrel spending.

Whether the rest of the world can handle it is less clear. The Libor spike is transmitted almost instantly through global finance. The Bank for International Settlements says any rise in short-term borrowing costs on dollar markets resets rates on $5 trillion (L3.6 trillion) of dollar bank loans.

It tightens the whole credit structure in Asia and emerging markets regardless of what currency it is in. The Libor-OIS spread measures the extra cost that banks charge each other for short-term “unsecured” dollar loans on the London interbank market. It basically takes the pulse of the lending markets. …

… For the remainder of the report:

https://www.telegraph.co.uk/business/2018/02/28/libor-surge-nearing-dang…

* * *

The stress signals of the global credit system are flashing amber. The offshore dollar funding markets that lubricate world finance are facing an incipient squeeze.

The “Libor-OIS spread’ – watched carefully by traders – has risen to levels reached during the onset of the Chinese currency crisis in early 2016, and during the onset of the Italian and Spanish funding crisis in late 2011.

The three-month rate for dollar Libor (London Interbank Offered Rate) used to price a vast nexus of financial contracts around the world has spiked to a 10-year high of 2pc this week. A third of all US business loans are linked to Libor, as are most student loans, and 90pc of the leverage loan market.

The US can doubtless handle the sixfold rise in Libor costs over the last two years since it is a reflection of economic recovery itself. America needs tighter money: the economy is on the cusp of over-heating, with a double blast of irresponsible fiscal stimulus coming from the Trump tax cuts and Republican pork barrel spending.

Whether the rest of the world can handle it is less clear. The Libor spike is transmitted almost instantly through global finance. The Bank for International Settlements says any rise in short-term borrowing costs on dollar markets resets rates on $5 trillion (£3.6 trillion) of dollar banks loans.

It tightens the whole credit structure in Asia and emerging markets regardless of what currency it is in. The Libor-OIS spread measures the extra cost that banks charge each other for short-term “unsecured” dollar loans on the London interbank market. It basically takes the pulse of the lending markets.

Patrick Perret-Green from the hedge fund AdMacro says US companies are starting to repatriate their vast cash holdings abroad to comply with president Trump’s tax changes. This is being drained from the pool of available lending. “It is reducing offshore liquidity. US entities have little incentive to lend that money back out internationally because of risk weightings and capital charges,” he said.

US corporations have some $2.5 trillion in liquid assets offshore, led by the tech giants Apple with $257bn, Alphabet (Google) with $126bn, and Microsoft with $84bn. Much of the money is already in US dollar assets so there is no currency exchange when it returns to the US. The problem is that it vanishes from the dollar-based funding markets in the City or hubs such as Singapore. It rations credit for Asia, Latin America, Russia, and the Middle East.

Borrowers can suddenly find it harder to roll over three-month dollar loans. This is what happened in 2007 and 2008 when offshore markets seized up and threatened to bring down the European banking system.

The scale is epic. BIS data show that offshore dollar credit has ballooned from $2 trillion to $11.6 trillion in fifteen years, turbo-charged by leakage from the Fed’s QE. The BIS has identified a further $13 to $14 trillion in disguised lending through derivatives contracts that are “functionally equivalent”.

Dollar liabilities on this scale are unprecedented and leave the world financial system more vulnerable than ever before to rising US rates.This is the sharp edge of a bigger problem: the $70 trillion edifice of global bonds is built on the assumption of a deflationary global liquidity trap lasting deep into the 21st century. Almost $10 trillion is still trading at negative yields. The structure cannot withstand a sudden shift to a reflation psychology. This week’s Libor spike was driven by the hawkish debut of Fed chairman, Jay Powell, keen to show that he is no White House poodle – no Trumpian “Arthur Burns” – by bravely flagging four interest rate rises this year.

Michael Hartness from Bank of America says the ‘Powell Put’ is set at a lower strike price than the old “Fed Puts” of the Bernanke and Yellen eras, meaning that Mr Powell will not come to the rescue of asset markets until they have suffered.

This should give rise to pause since the US Treasury’s own watchdog (OFR) warns that broker margin debt is dangerously high and that Wall Street pricing is at its “97th percentile relative to the last 130 years”. Bank of America says the profits cycle for US equities has peaked. Its “Bull & Bear” indicator is at extreme levels of investor optimism, still issuing a sell alert despite the mini-crash in early February

The buy-to-dip reflex remains powerful. Veteran value investor Warren Buffet is rare in standing coolly on the sidelines, keeping his powder dry, accumulating $116bn in short-term Treasury notes and cash assets in order to better survive what he calls ‘economic discontinuities’. He has displaced China and Japan as the chief buyer at Treasury sales.

Mr Buffett insists that “history” is on his side, and the next crisis may come like a thief in the night. “If you want to be able to acquire the highest quality assets when prices crash, you have to be liquid,” he said.

For now the story is in the bond markets. The 10-year US Treasury yield has jumped 50 basis points to 2.9pc since the start of the year, driven both by rising inflation and the prospect of Mr Trump’s fiscal deficits topping $1 trillion at the top of the cycle – and therefore $2 trillion in a bad recession.

The buyer of last resort for this debt is currently adding to supply instead. The Fed will be selling down its $4.4 trillion stockpile of bonds at a pace of $50bn a month by the end of the year (though Citigroup warns that the Fed will be forced to carry out a volte-face and resume QE by 2020). In parallel, the European Central Bank will have tapered its asset purchases to zero by September.

A vast shift in the balance of the global bond supply and demand is underway. It is this that lies behind the wild ructions across global bourses this year. My own view is that rising US rates will hit just as the China and Europe come off the boil later this year, creating an unpredictable “scissor” action through currency and credit markets.

China’s slowdown is already crystallizing. The fiscal blitz before last autumn’s Communist Party Congress is fading. Credit growth – when measured properly – keeps slipping. The official PMI gauge of manufacturing fell to a 19-month low of 50.3 in February.

Data from Janus Henderson shows that a key measure of money growth – six-month real M1 – has dropped to the lowest level since the Great Recession in the biggest G7 and E7 economies combined. This is chiefly driven by China and the eurozone, including France and Spain. The data leads the real economy by six to nine months.

Asia and Europe are likely to look very different in late 2018. Far from seeing synchronized global growth in all regions – as the markets expect – we could instead see major tectonic plates moving against each other. In that context, surging dollar Libor rates and a hawkish Fed could prove inflammatory. It is not hard to imagine fresh currency flight from China and radical repricing of Italian sovereign debt.

The Fed likes to tell us that extracting the world from nine years of zero rates and QE will be a dull as “watching paint dry”. The coming drama is more likely to be a spine-shivering thriller

end

My goodness Sheila Bair said a mouthful today: “We should not bank Bitcoin..the green Bills in your pocket do not have intrinsic value either”

(courtesy zerohedge/Barrons)

Sheila Bair on Bitcoin: “We Shouldn’t Ban It: The Green Bills In Your Pocket Don’t Have Intrinsic Value, Either”

In a surprisingly forthright and honest interview between Barrons and Sheila Bair, the former FDIC chair who was responsible for big banks avoiding bank runs in the aftermath of the Lehman bankruptcy, discussed what she sees as the trigger for the next financial crisis, her thoughts on China’s record leverage (and the recent promotion of Xi Jinping to emperor), how she views the current economy, on $1.3 trillion in student debt, and finally on bitcoin.

While we will focus on the latter, here are some excerpts on the other key points. First, here is Bair on what she thinks will trigger the next crisis:

I’d keep an eye on credit-card debt. Subprime auto has been a problem for a couple years, and valuations on loans used to finance leveraged buyouts are high. Any type of secured lending backed by an asset that is overvalued should be a concern. That is what happened with housing. Corporate debt also has not gotten as much attention as it should. It is market-funded, rather than bank-funded, but the banks still have exposure. Then there’s cyber-risk. It took us so long to get around to the reforms postcrisis that we got a little behind on systemic cyber-risk, but regulators are very focused on it now.

On China’s risk to the global financial system:

We look at their debt and wag our fingers and tsk, tsk. It is high. But they realize it is a threat to financial stability and are dealing with it. Last month, regulators took over privately held Anbang Insurance to keep it from collapsing. It is a sign they are continuing to crack down on reckless growth and excessive leverage.

On Student Debt:

That debt is all on the government’s balance sheet, so no, not a market crisis. But there are parallels to 2008: There are massive amounts of unaffordable loans being made to people who can’t pay them, and the easy availability of those loans is leading to asset inflation. In 2008, that was reflected in housing prices. Today, that’s tuition. It’s too easy to raise tuition because kids will borrow to pay for it. If the loan defaults, the primary beneficiaries — educational institutions — have no skin in the game, like in the mortgage crisis.

How record student debt promotes inequality:

Student-loan stories always feature someone who borrowed $90,000 to go to grad school or med school. But those people generally get jobs and have earnings potential, and debt-forgiveness programs disproportionately help them. The distress and high default rates are among the kids borrowing $10,000 to go to a for-profit school and dropping out; $10,000 may not sound like a lot to you and me, but for a first-generation student or someone without a college degree, that’s a lot of money. Student debt also suppresses small-business formation. Kids who would have started a business in their parents’ garage can’t do that now because they owe $50,000. Beyond that, it’s just a terrible financial burden for our kids that didn’t exist 20 years ago.

And finally, and most importantly, is Bair’s tacit endorsement of bitcoin. By saying that “we should not ban it”, Bair has effectively become the highest ranked current or former administration official to recommend keeping bitcoin while pointing out that – just like the dollar – its value is only what someone else would be willing to pay for it.

Here is Bair’s view on cryptocurrencies.

Don’t put any money into bitcoin that you can’t afford to lose. But I don’t think we should ban it — the green bills in your pocket don’t have an intrinsic value, either. The value is based on what others think is its value. That’s true of any currency. Regulation should be focused on good disclosure, education, warding off fraud, and making sure it is not used for illicit activities. Let the market figure out what it’s worth. That is what it is doing now.

Source: Barrons

Your early THURSDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

i) Chinese yuan vs USA dollar/CLOSED DOWN 6.3493 /shanghai bourse CLOSED UP 14.34 POINTS OR 0.44% / HANG SANG CLOSED UP 199.53 POINTS OR 0.65%

2. Nikkei closed DOWN 343.77 POINTS OR 1.56% /USA: YEN RISES TO 106.69/ STILL DEADLY AS YEN CARRY TRADERS DISINTEGRATE

3. Europe stocks OPENED DEEPLY IN THE RED /USA dollar index RISES TO 90.76/Euro FALLS TO 1.2177

3b Japan 10 year bond yield: FALLS TO . +.043/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 106.69/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD FINALLY IN THE POSITIVE/BANK OF JAPAN LOSING CONTROL OF THEIR YIELD CURVE AS THEY PURCHASE ALL BONDS TO GET TO ZERO RATE!!

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 61.26 and Brent: 64.06

3f Gold DOWN/Yen UP

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil DOWN for WTI and DOWN FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund FALLS TO +.625%/Italian 10 yr bond yield DOWN to 1.970% /SPAIN 10 YR BOND YIELD DOWN TO 1.520%

3j Greek 10 year bond yield RISES TO : 4.475?????????????????

3k Gold at $1308.40 silver at:16.29 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble DOWN 49/100 in roubles/dollar) 56.83

3m oil into the 61 dollar handle for WTI and 64 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 106.69 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 0.9463 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1517 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now POSITIVE territory with the 10 year FALLING to +0.625%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.8220% early this morning (THIS IS DEADLY TO ALL MARKETS). Thirty year rate at 3.103% /BOTH VERY DEADLY

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

(courtesy Jim Reid/Bloomberg/Deutsche bank/zero hedge)

Risk-Off: Global Stock Rout Accelerates, Futures Slide Below 2700 Before Powell Part 2

With the worst month for global markets in two years now in the history books, world stocks entered March with shaky knees as global equity markets and US futures are a sea of red this morning, as European shares drop the most since a global rout three weeks ago following sharp declines in the U.S. and Asia ahead of Powell’s second testimony, and amid talk that Trump is ready to announce steep tariffs on steel and aluminum imports.

After attempting a breakout above the unchanged line overnight, S&P 500 Index futures have drifted lower, and the selloff has accelerated in recent minutes, sliding below 2700.

Today’s main event for markets will be Fed Chairman Jerome Powell’s appearance before the Senate Banking Committee following his comments Tuesday that spurred speculation the U.S. central bank might raise rates four times this year. Chinese purchasing managers’ indexes missed estimates on Wednesday, while President Donald Trump warned the U.S. would use “all available tools” to pressure the nation on trade.

Philip Shaw, chief economist at Investec in London said Powell’s testimony was unlikely to change from the one he delivered on Tuesday, putting the focus on the question and answer session.

“He (Powell) appears to have got an easy ride from lawmakers in the sense that the technical questioning on Tuesday wasn’t too heavy,” Shaw said. “He may not have such an easy time today with the Senate Banking Committee.”

Confirming the risk-off mood, the U.S. dollar rose to six-week highs against G-10 currencies while the gap between short-dated U.S. and German bond yields was at its widest since 1997. MSCI’s all-country equity benchmark fell 0.4% after snapping a record 15-month long winning streak in February, while European stocks lost almost 1 percent

Asian equity markets were hit hard after the S&P 500 and DJIA posted their worst monthly performance in over 2 years. This weighed on the Asia-Pac majors from the open with ASX 200 (-0.7%) led lower by weakness in energy names after similar underperformance of the sector in US due to declines in crude, while Nikkei 225 (-1.6%) suffered broad losses amid a firmer JPY. Chinese bourses outperformed, Hang Seng (+0.7%) and Shanghai Comp. (+0.4%) with pressure somewhat alleviated following better than expected Chinese Caixin Manufacturing PMI data and the resumption of PBoC liquidity operations.

Europe was also hit hard, with the Stoxx 50 down over -1%, as retailers and media companies were among the biggest losers in the Stocks Europe 600 Index as some earnings missed estimates and manufacturing data showed mounting signs growth momentum may have peaked. In terms of sector specific moves, losses are relatively broad-based with all ten sectors trading with losses; minor underperformance in the IT sector with Dialog Semiconductor paring back some of yesterday’s earnings-inspired gains. Ultimately, this morning’s trade has been one dominated by earnings with notable movers including: Cobham (+11.6%), Peugeot (+6.6%), AB Inbev (+5.3%), Eiffage (+2%), WPP (-13.2%), Adecco (-8.5%), Carrefour (-6.5%), Beiersdorf (-3.4%).

“A simultaneous sell-off in equity and bond markets, higher U.S. yields and concerns of possible outflows continue to buttress USD/Asia,” says Andy Ji, Asian currency strategist at Commonwealth Bank of Australia in Singapore. China’s faltering manufacturing PMI has stoked worries of weaker growth momentum, he says.

Ahead of Powell, Treasury yields fell to a two-week low despite surging earlier in the week on his comments which riled markets earlier this week. . Treasuries began unwinding Wednesday’s strong month-end related buying with 10-year futures edging lower from the open.

In global macro, the Bloomberg Dollar Spot Index rose to a six-week high before Powell’s Senate testimony, and preparations for trade wars as Trump is set to unveil steep tariffs on steel and aluminum imports, hurting EM exporters. Traders will watch for consistency in Powell’s message earlier this week on faster pace of tightening. The greenback’s major peers failed to sustain Asia-session gains even as month-end flows that had been supporting the dollar have ended.

The Aussie dollar dropped to a two-month low after disappointing capital expenditure data encouraged leveraged funds to add to short positions. Asia’s emerging currencies fell after a drop in U.S. stocks damped appetite for risk and the dollar kept rising. The region’s sovereign notes were mixed, while most stock markets rose.

Elsewhere, the U.K. pound extended a decline after the European Union published a draft Brexit treaty, squaring off with Prime Minister Theresa May.

Aluminum headed lower with President Donald Trump set to announce steep import tariffs on Thursday. West Texas Intermediate crude retreated for a third day, with oil futures seeing very little in the way of price action during Asia-Pac and European trade following yesterday’s DoE-inspired sell-off with newsflow today otherwise particularly light. In metals markets, spot gold has been unable to benefit from the risk aversion seen in European equity markets as the firmer USD supresses prices and extends on recent losses. Elsewhere, Chinese steel futures were seen higher overnight as the prospects of additional output cuts supports prices, whilst copper prices endured another session of losses despite encouraging Chinese Caixin Manufacturing PMI.

Key events include Powell’s comments, Trump’s announcement of trade sanctions, the ISM and vehicle data and reports from companies including Nordstrom and Kohl’s

Market Snapshot

- S&P 500 futures down 0.2% at 2,709.25

- STOXX Europe 600 down 0.5% to 377.58

- MXAP down 0.8% to 176.01

- MXAPJ down 0.2% to 576.93

- Nikkei down 1.6% to 21,724.47

- Topix down 1.6% to 1,740.20

- Hang Seng Index up 0.7% to 31,044.25

- Shanghai Composite up 0.4% to 3,273.76

- Sensex down 0.4% to 34,045.30

- Australia S&P/ASX 200 down 0.7% to 5,973.34

- Kospi down 1.2% to 2,427.36

- German 10Y yield fell 1.9 bps to 0.637%

- Euro down 0.06% to $1.2187

- Italian 10Y yield fell 3.0 bps to 1.706%

- Spanish 10Y yield fell 1.4 bps to 1.525%

- Brent Futures down 1.8% to $64.60/bbl

- Gold spot down 0.6% to $1,310.89

- U.S. Dollar Index up 0.1% to 90.73

Bulletin Headline Summary from RanSquawk

- European bourses have followed on from performance in their US and Asia-Pac counterparts (Eurostoxx 50 – 1.1%) to trade lower across the board

- Core bonds are gradually building on earlier positive momentum and advancing further amidst what appears to be heightened risk-off or averse sentiment

- Looking ahead, highlights include US manufacturing PMI, US PCE, US manufacturing ISM and a slew of speakers including Fed’s Powell

Top Overnight News

- Euro-area factory output continues to expand at a robust pace but with mounting signs that growth momentum may have peaked. The manufacturing gauge’s decline since the end of 2017 was the steepest in two years, reinforced by a slowdown in export orders across the region

- U.K. manufacturing lost a bit of steam last month, with growth slipping to an eight-month low

- EU officials were fairly sure the draft Brexit deal they published on Wednesday would be unacceptable to Theresa May. It’s part of their strategy to pressure the British government so that it decides to keep the U.K. as close to the EU as possible, according to three people familiar

- U.S. President Donald Trump is set to announce steep tariffs on steel and aluminum imports Thursday, people familiar with the matter said, in what would be one of his toughest actions yet to implement a hawkish trade agenda that risks antagonizing friends and foes alike

- Fed Chair Jerome Powell, who delivers his second round of semi-annual testimony to Congress on Thursday, told lawmakers on Tuesday the next two years will be “good” ones for the economy. If he’s right, he’ll be at the controls when the current U.S. expansion becomes the longest on record

- China’s rubber-stamp parliament is expected to enact sweeping legislative changes in a two-week session starting Monday that would allow President Xi to rule indefinitely and give him greater control over the levers of money and power

Asian equity markets were mostly lower as the downbeat tone rolled over from the US, where the S&P 500 and DJIA posted their worst monthly performance in over 2 years following the market turmoil seen in early February. This weighed on the Asia-Pac majors from the open with ASX 200 (-0.7%) led lower by weakness in energy names after similar underperformance of the sector in US due to declines in crude, while Nikkei 225 (-1.6%) suffered broad losses amid a firmer JPY. Chinese bourses outperformed, Hang Seng (+0.7%) and Shanghai Comp. (+0.4%) with pressure somewhat alleviated following better than expected Chinese Caixin Manufacturing PMI data and the resumption of PBoC liquidity operations. Finally, 10yr JGBs were subdued with prices contained after yesterday’s reduced-Rinban-induced selling, while a 10yr auction also failed to spur firm demand as the results were mixed with b/c slightly softer and accepted prices higher than prior. Chinese Caixin Manufacturing PMI (Feb) 51.6 vs. Exp. 51.3 (Prev. 51.5). PBoC injected CNY 100bln via 7-day reverse repos, CNY 30bln via 28-day reverse repos & CNY 20bln via 63-day reverse repos.

Top Asian News

- Xi Set to Pass Last Hurdle in Bid for Power to Reshape China

- BOJ’s Kataoka Urges More Stimulus, Says Tightening Long Way Off

- Exxon’s PNG LNG Project Seen Shut for Six Weeks After Quake

- Singapore Freezes World-Leading Ministerial Salaries For Now

European bourses have followed on from performance in their US and Asia-Pac counterparts (Eurostoxx 50 -1.1%) to trade lower across the board. In terms of sector specific moves, losses are relatively broad-based with all ten sectors trading with losses; minor underperformance in the IT sector with Dialog Semiconductor paring back some of yesterday’s earnings-inspired gains. Ultimately, this morning’s trade has been one dominated by earnings with notable movers including: Cobham (+11.6%), Peugeot (+6.6%), AB Inbev (+5.3%), Eiffage (+2%), WPP (-13.2%), Adecco (-8.5%), Carrefour (-6.5%), Beiersdorf (-3.4%).

Top European News

- Euro-Area Factories’ Slowing Pace Seen Hinting at Growth Peak

- U.K. Manufacturing Comes Further Off the Boil Amid Brexit Worry

- Germany Feb. Manufacturing PMI 60.6 vs Flash Reading 60.3

- France Feb. Manufacturing PMI 55.9 vs Flash Reading 56.1

- Italian Jobless Rate Rises as More People Seek Employment

In FX, the DXY has cleared another chart hurdle having climbed above 90.500-600 resistance on Wednesday, and has maintained positive momentum to edge towards the next upside technical objective around 90.886 (Fib level) despite Usd/Jpy and the Jpy in general bucking the overall trend (on safe-haven grounds). Eur/Usd is retesting sub-1.2200 bids around 1.2180 ahead of Fib support at 1.2173, and with decent option expiries between 1.2150 and 1.2200 (1 bn and 2 bn respectively) also in the mix. Cable continues to weaken on Brexit-related factors and trending even lower under 1.3750, while Eur/Gbp has breached 0.8850 even though the single currency is relatively soft independently (more long liquidation and political premium ahead of Italian and German votes on Sunday). On that note, Eur/Jpy is hovering just above 130.00 having dipped below overnight, and back on track to hit TOTW profit targets for a couple of major banks. The Aud is underperforming G10 peers again, and heading for a 0.7700 test after significantly weaker than forecast Aussie Capex data. Having breached key support at 0.7759, bears will be eyeing 0.7695, while Nzd/Usd is only just holding above 0.7200. Usd/Cad hovering around 1.2850 ahead of Canadian current account data and

In commodities, WTI and Brent crude futures have seen very little in the way of price action during Asia-Pac and European trade following yesterday’s DoE-inspired sell-off with newsflow today otherwise particularly light. In metals markets, spot gold has been unable to benefit from the risk aversion seen in European equity markets as the firmer USD supresses prices and extends on recent losses. Elsewhere, Chinese steel futures were seen higher overnight as the prospects of additional output cuts supports prices, whilst copper prices endured another session of losses despite encouraging Chinese Caixin Manufacturing PMI. North Sea Buzzard oil field production is still restricted; according to sources

Looking at the day ahead, a range of data will be out, including: January Core PCE, February ISM manufacturing index, personal income and spending, weekly initial jobless claims and continuing claims and total vehicle sales. Onto other events, the Fed’s Powell is back again in front of the US Senate while the US Transportation Secretary Ms Chao also testifies before the Senate on Trump’s infrastructure plan. The ECB’s Nouy and Lane will also speak. Finally senior officials from Euro area finance ministries will discuss the banking union and the future role of the ESM.

US Event Calendar

- 8:30am: Personal Income, est. 0.3%, prior 0.4%; Personal Spending, est. 0.2%, prior 0.4%; Real Personal Spending, est. -0.1%, prior 0.3%

- 8:30am: PCE Deflator MoM, est. 0.4%, prior 0.1%; PCE Deflator YoY, est. 1.7%, prior 1.7%;

- 8:30am: PCE Core MoM, est. 0.3%, prior 0.2%; PCE Core YoY, est. 1.5%, prior 1.5%

- 8:30am: Initial Jobless Claims, est. 225,000, prior 222,000; Continuing Claims, est. 1.93m, prior 1.88m

- 9:45am: Bloomberg Consumer Comfort, prior 56.6;

- 9:45am: Markit US Manufacturing PMI, est. 55.9, prior 55.9

- 10am: Construction Spending MoM, est. 0.3%, prior 0.7%

- 10am: ISM Manufacturing, est. 58.7, prior 59.1

- Wards Domestic Vehicle Sales, est. 13.3m, prior 13.1m; Total Vehicle Sales, est. 17.2m, prior 17.1m

DB’s Jim Reid concludes the overnight wrap

If you’re in Europe I hope your encounters with “The Beast from the East” weather system are going as well as can be expected. London saw some heavy snow yesterday – a rare sight. I was somewhat alarmed to read that meanwhile the Arctic is seeing a heatwave. Siberia is seeing temperatures 35 degrees C above averages at the moment and Greenland is having some of its hottest days for the time of year on record. There are always exceptions and extremes but I’ve seen a lot of stories suggesting that scientists are worried that global warming is causing this weather shift and that there is some evidence that climate could change more quickly in the future than even the most extreme forecasters have previously suggested. Food for thought.

Talking of which a turbulent February is now behind us and that’s just the markets. At the end today we’ll do our normal performance review but the highlight is that the record 15 month successive positive run for S&P 500 total returns are over. Interestingly yesterday was the fourth successive plus or minus 1% move day (in either direction) for the S&P 500 (-1.11%). February actually had 12 such days after the 13 months from the start of 2017 to January 2018 had just 10. An impressive stat.

Today we’ll see all the usual first of the month PMIs which are as important as ever, especially as its’ been a week of largely disappointing global data. We also have the all-important Fed preferred core US PCE inflation number. We’ll preview later but first today sees the fourth part of our series on the impact of rising yields and discusses the rising incidence of zombie firms in recent years (link).

Bottom-up data of some 3,000 companies in the FTSE All World index show that the percentage of zombie firms more than tripled to 2.0% of firms in 2016 from 0.6% in 1996. That matters because zombie firms are linked to fading business dynamism and because years of low interest rates should have led to fewer such firms, not more. There are early signs we are at a turning point, however. The numbers for 2017, with two-thirds of firms reporting, suggest that zombie firm incidence declined sharply last year. If this proves to be a real trend, it may give central banks confidence that continuing to raise rates and pull away from unconventional monetary policy will have some advantages. As a recap on Monday we outlined the macro reasons why yields are rising and why they will continue to (link). On Tuesday we looked at the relationship between yields and credit through history (link) and yesterday the same with equities (link) with lots of trade ideas. So feel free to dip back in.

Onto today, as discussed we have the potentially market sensitive January PCE data. The consensus is for a +0.3% mom core reading and +1.5% yoy reading (which would be unchanged versus December). As a reminder the big pickup in medical services inflation in the January CPI report and healthcare industries series in the PPI report should read-through positively to today’s PCE. Our US economists also expect a +0.3% mom print. It’s worth also highlighting that Fed Chair Powell will also testify again today (in front of the Senate this time) however its highly unlikely to differ much from Tuesday’s speech so shouldn’t be much of a game changer. This morning we’ve also got the final manufacturing PMIs in Europe which means a first look at the data for the periphery also.

This morning in Asia, markets are broadly lower with the Nikkei (-1.84%) and Hang Seng (-0.40%) both down following the late US sell-off while China’s CSI300 (+0.31%) is up. The Kospi is closed today. Datawise, China’s February Caixin manufacturing PMI was slightly above market at 51.6 (vs. 51.3 expected) while Japan’s 4Q capital spending also beat at 4.3% yoy (vs. 3%) and the final reading of the Nikkei manufacturing PMI was revised up by 0.1 to 54.1. Elsewhere, President Trump has warned China that the US will use “all available tools” to prevent it from undermining global competition.

Risk assets were soft yesterday with European bourses ending lower after a late day sell-off (Stoxx 600 -0.71%) with the S&P 500 reversing earlier gains to close -1.11% with all sectors in the red and losses led by energy and material stocks.

Elsewhere, WTI oil dropped 2.32% following a higher than expected build up in US crude inventories while the VIX rose 7% to 19.85. Yields in Europe fell between 2 and 3bps while 10y Treasuries ended 3.2bps lower – albeit still c2bps above Tuesday’s lows.