GOLD: $1319.00 DOWN $4.10

Silver: $16.39 DOWN 11 CENTS

Closing access prices:

Gold $1320.10

silver: $16.43

SHANGHAI GOLD FIX: FIRST FIX 10 15 PM EST (2:15 SHANGHAI LOCAL TIME)

SECOND FIX: 2:15 AM EST (6:15 SHANGHAI LOCAL TIME)

SHANGHAI FIRST GOLD FIX: $1333.90 DOLLARS PER OZ

NY PRICE OF GOLD AT EXACT SAME TIME: $1325.55

PREMIUM FIRST FIX: $8.35

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

SECOND SHANGHAI GOLD FIX: $1332.39

NY GOLD PRICE AT THE EXACT SAME TIME: $1325.50

PREMIUM SECOND FIX /NY:$6.87

SHANGHAI REJECTS NY PRICING OF GOLD.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

LONDON FIRST GOLD FIX: 5:30 am est $1326.30

NY PRICING AT THE EXACT SAME TIME: $1325.80

LONDON SECOND GOLD FIX 10 AM: $1320.40

NY PRICING AT THE EXACT SAME TIME. $1320.60

For comex gold:

MARCH/

NUMBER OF NOTICES FILED TODAY FOR MARCH CONTRACT: 0 NOTICE(S) FOR NIL OZ.

TOTAL NOTICES SO FAR:2749 FOR 274900 OZ (8.5505 TONNES),

For silver:

MARCH

143 NOTICE(S) FILED TODAY FOR

715,000 OZ/

Total number of notices filed so far this month: 4205 for 21,025,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: BID $11,514/OFFER $11,584: UP $486(morning)

Bitcoin: BID/ $11,535/offer $11,602: UP $507 (CLOSING/5 PM)

end

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total open interest FELL BY A CONSIDERABLE SIZED 1,702 contracts from 192,332 FALLING TO 190,630 DESPITE FRIDAY’S STRONG 23 CENT RISE IN SILVER PRICING. WE HAD SOME COMEX LIQUIDATION. HOWEVER, WE WERE AGAIN NOTIFIED THAT WE HAD ANOTHER GOOD SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP ROUTE: 0 EFP’S FOR MARCH, 1316 EFP’S FOR MAY AND ZERO FOR ALL OTHER MONTHS AND THUS TOTAL ISSUANCE OF 1316 CONTRACTS. WITH THE TRANSFER OF 1316 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 1316 CONTRACTS TRANSLATES INTO 6.580 MILLION OZ DESPITE WITH THE CONTINUAL DROP IN OPEN INTEREST IN SILVER AT THE COMEX.

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF MARCH:

5686 CONTRACTS (FOR 3 TRADING DAYS TOTAL 5686 CONTRACTS OR 28.430 MILLION OZ: AVERAGE PER DAY: 1895 CONTRACTS OR 6.476 MILLION OZ/DAY

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH: 28.43 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 4.06% OF ANNUAL GLOBAL PRODUCTION

ACCUMULATION IN YEAR 2018 TO DATE SILVER EFP’S: 521.905 MILLION OZ.

ACCUMULATION FOR JAN 2018: 236.879 MILLION OZ

ACCUMULATION FOR MONTH OF FEBRUARY: 244.945 MILLION OZ

RESULT: WE HAD SOME LOSS IN COMEX OI SILVER COMEX DESPITE THE 23 CENT GAIN IN SILVER PRICE. WE ALSO HAD A GOOD SIZED EFP ISSUANCE OF 1316 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER . FROM THE CME DATA 1316 EFP’S FOR MONTHS MARCH AND MAY WERE ISSUED FOR A DELIVERABLE FORWARD CONTRACT OVER IN LONDON WITH A FIAT BONUS. WE LOST 356 OI CONTRACTS i.e. 1316 open interest contracts headed for London (EFP’s) TOGETHER WITH A DECREASE OF 1702 OI COMEX CONTRACTS. AND ALL OF THIS HAPPENED WITH THE RISE IN PRICE OF SILVER OF 23 CENTS AND A CLOSING PRICE OF $16.50 WITH RESPECT TO YESTERDAY’S TRADING. YET WE STILL HAVE A FAIR AMOUNT OF SILVER STANDING AT THE COMEX.

In ounces AT THE COMEX, the OI is still represented by just UNDER 1 BILLION oz i.e. 0.953 BILLION TO BE EXACT or 136% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT FEBRUARY MONTH/ THEY FILED: 143 NOTICE(S) FOR 715,000 OZ OF SILVER

In gold, the open interest FELL BY A CONSIDERABLE 4448 CONTRACTS FALLING TO 505451 . DESPITE THE HUGE RISE IN PRICE ON FRIDAY ($18.70) HOWEVER FOR MONDAY, THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED AN FAIR SIZED 5140 CONTRACTS OF WHICH MARCH SAW THE ISSUANCE OF 55 CONTRACTS, APRIL SAW THE ISSUANCE OF 5085 CONTRACTS , JUNE SAW THE ISSUANCE OF 0 CONTRACTS AND THEN ALL OTHER MONTHS ZERO. The new OI for the gold complex rests at 505,451. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. DEMAND FOR GOLD INTENSIFIES GREATLY AS WE CONTINUE TO WITNESS A HUGE NUMBER OF EFP TRANSFERS TOGETHER WITH THE MASSIVE INCREASE IN GOLD COMEX OI TOGETHER WITH THE TOTAL AMOUNT OF GOLD OUNCES STANDING FOR FEBRUARY COMEX. EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES. IN ESSENCE WE HAVE A GAIN OF 692 CONTRACTS: 4448 OI CONTRACTS DECREASED AT THE COMEX AND A FAIR SIZED 5140 OI CONTRACTS WHICH NAVIGATED OVER TO LONDON.(692 oi gain in CONTRACTS EQUATES TO 2.15TONNES)

FRIDAY, WE HAD 20,030 EFP’S ISSUED.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF MARCH : 35,073 CONTRACTS OR 3,507,300 OZ OR 109.09 TONNES (3 TRADING DAYS AND THUS AVERAGING: 11,691EFP CONTRACTS PER TRADING DAY OR 1,169,100 OZ/ TRADING DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SIZE OF THESE EFP TRANSFERS : SO FAR THIS MONTH IN 3 TRADING DAYS IN TONNES: 109.09 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2017, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 2555 TONNES

THUS EFP TRANSFERS REPRESENTS 109.09/2200 x 100% TONNES = 4.26% OF GLOBAL ANNUAL PRODUCTION SO FAR IN MARCH ALONE.

ACCUMULATION OF GOLD EFP’S YEAR 2018 TO DATE: 1361.29 TONNES

ACCUMULATION OF GOLD EFP’S FOR JANUARY 2018: 653.22 TONNES

ACCUMULATION OF GOLD EFP’S FOR FEBRUARY: 649.45 TONNES

Result: A STRONG SIZED DECREASE IN OI AT THE COMEX DESPITE THE CONSIDERABLE RISE IN PRICE IN GOLD TRADING YESTERDAY ($18.70). HOWEVER, WE HAD ANOTHER FAIR SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 5140 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX AND YET WE ALSO OBSERVED A HUGE DELIVERY MONTH FOR THE MONTH OF DECEMBER. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 5140 EFP CONTRACTS ISSUED, WE HAD A NET GAIN IN OPEN INTEREST OF 692 contracts ON THE TWO EXCHANGES:

5140 CONTRACTS MOVE TO LONDON AND 4448 C ONTRACTS DECREASED AT THE COMEX. (in tonnes, the GAIN in total oi equates to 2.15 TONNES).

we had: 0 notice(s) filed upon for NIL oz of gold.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD

WITH GOLD DOWN $4.10 : NO CHANGES IN GOLD INVENTORY AT THE GLD /

Inventory rests tonight: 833.98 tonnes.

SLV/

WITH SILVER DOWN 11 CENTS TODAY:

NO CHANGES IN SILVER INVENTORY AT THE SLV/

/INVENTORY RESTS AT 318.069 MILLION OZ/

end

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in silver FELL BY 1702 contracts from 192,332 DOWN TO 190,630 (AND now A LITTLE FURTHER FROM THE NEW COMEX RECORD SET ON FRIDAY/APRIL 21/2017 AT 234,787) DESPITE THE RISE IN PRICE OF SILVER (23 CENTS WITH RESPECT TO FRIDAY’S TRADING). OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE ANOTHER 1316 EFP CONTRACTS FOR MAY (WE DO NOT GET A LOOK AT THESE CONTRACTS AS IT IS PRIVATE BUT THE CFTC DOES AUDIT THEM) AND 0 EFP’S FOR ALL OTHER MONTHS . EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. WE HAD CONSIDERABLE COMEX SILVER COMEX LIQUIDATION. IF WE TAKE THE OI LOSS AT THE COMEX OF 1702 CONTRACTS TO THE 1316 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A SMALL LOSS OF 356 OPEN INTEREST CONTRACTS WE STILL HAVE A STRONG AMOUNT OF SILVER OUNCES THAT ARE STANDING FOR METAL IN MARCH (SEE BELOW). THE NET LOSS TODAY IN OZ ON THE TWO EXCHANGES: 1.780 MILLION OZ!!!

RESULT: A CONSIDERABLE DECREASE IN SILVER OI AT THE COMEX DESPITE THE RISE OF 23 CENTS IN PRICE (WITH RESPECT TO FRIDAY’S TRADING ). BUT WE ALSO HAD ANOTHER FAIR 1316 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE GOOD SIZED AMOUNT OF SILVER OUNCES STANDING FOR MARCH, DEMAND FOR PHYSICAL SILVER INTENSIFIES AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)MONDAY MORNING/LATE SUNDAY NIGHT: Shanghai closed DOWN 2.39 POINTS OR 0.07% /Hang Sang CLOSED DOWN 697.06 POINTS OR2.28% / The Nikkei closed DOWN 139.55 POINTS OR 0.53%/Australia’s all ordinaires CLOSED DOWN 0.53%/Chinese yuan (ONSHORE) closed UP at 6.3400/Oil UP to 61.35 dollars per barrel for WTI and 64.44 for Brent. Stocks in Europe OPENED DEEPLY IN THE RED . ONSHORE YUAN CLOSED DOWN AT 6.3400 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.3395 /ONSHORE YUAN TRADING STRONGER AGAINST OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING MUCH STRONGER AGAINST THE DOLLAR . CHINA IS NOT HAPPY TODAY (STRONGER CURRENCY BUT TERRIBLE CHINESE MARKETS/ )

3a)THAILAND/SOUTH KOREA/NORTH KOREA

i)North Korea

b) REPORT ON JAPAN

3 c CHINA

China confirms 2018 slowdown

( zerohedge)

4. EUROPEAN AFFAIRS

i)The real reason for the closing of the Latvian bank and it is not the dubious money laundering charge. The reason is that after the collapse of Cyprus in 2010, Russian oligarchs needed another country to park its European/USA funds and in 2014 they found one in new EU member Latvia. The USA’s simple motive was to hurt Russia where it hurts the most ..in the pocketbook

( William Enghahl/Neo.org)

ii)Last night/Italy

The Euro slides as the anti-establishment vote surges

( zerohedge)

iii)And the results so far: strong anti-establishment performance/hung parliament is the probable result.

( zerohedge)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

( zerohedge)

6 .GLOBAL ISSUES

( zerohedge)

ii)Canadian dollar weakens terribly as Trump responds that tariffs will not come off until a new and “fair NAFTA agreement is signed. It looks like NAFTA is dead in the water.

(courtesy zerohedge)

iii)As promised to you: NAFTA is dead in the water. The loonie tumbles again late this afternoon when USA trade representative Lighthizer stated that discussions fell short of expectations and that time is running out.

( zerohedge)

7. OIL ISSUES

8. EMERGING MARKET

India

Quite a scam: the crooks used gold and diamonds to bribe a banker in this 2 billion dollar fraud at PNB. All of the crooks escaped India and are probably in Hong kong

( zerohedge)

9. PHYSICAL MARKETS

i)A very important video for you to see. Alasdair Macleod explains the significance of the March 26 oil futures contract which will inevitably be settled in gold. He explains that the uSA was not happy with this and was probably the reason that Trump initiated tariffs on aluminum and steel.

a must view

( Alasdair Macleod)

ii)An acknowledgement of central bank manipulation in the gold market but I agree with C Powell that it is not for desperate dollar liquidity but to store value to currencies

( C Powell/GATA)

10. USA stories which will influence the price of gold/silver

A. Economic data:

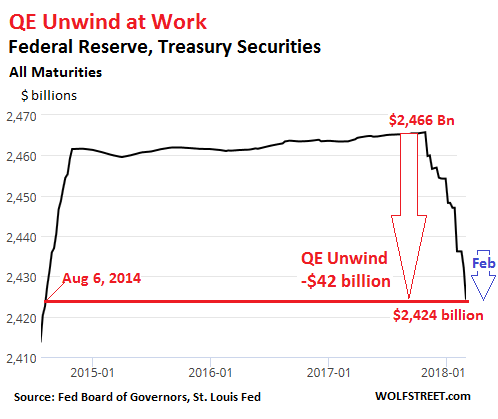

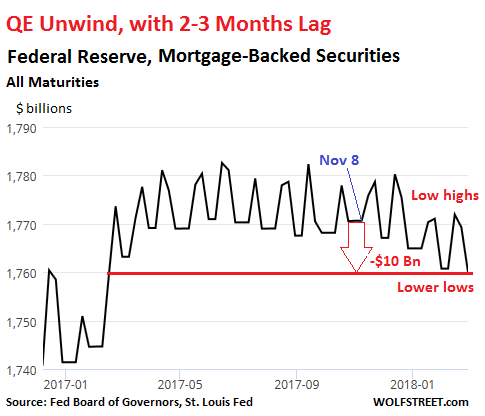

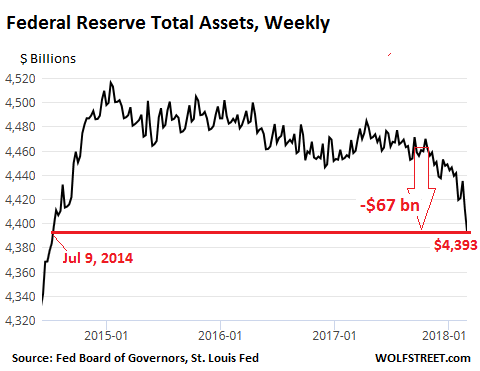

ii)The real story on the Fed unwind. Wolf Richter has it right: the Fed is unwinding QE perfectly to their plan( Wolf Richter/Wolfstreet)

Now the second problem is the trade war initiated by Trump in order to save its economy. He now plans a retaliatory tax…i.e. whatever tax Europe applies, so will the USA. The EU adds considerably more taxes on products than the USA(it is more protectionist that the uSA) so a tax by Trump will certainly hurt products coming into the USA and that will hurt stock markets from around the world. It will also be hugely inflationary in the USA and again that will cause costs to rise and break valuations causing severe hardship to its economy.

vi)Paul Ryan and for that matter, many Republicans are asking Trump to kill the proposed tariffs on steel and aluminum/ If not they may respond in kind. Interestingly enough the stock market did not go down as scheduled with the tariffs( zerohedge)

vi b)Ryan is rejected by Trump. The markets believe Trump is bluffing. Trump may be at war with his own party.

( zerohedge)

viii)Trump offers no tariff exemptions with regard to tariffs that he will implement. Due to the tariffs on aluminum and steel and both products are exported from Canada, you can assume that NAFTA is officially dead..

( zerohedge)

ix) Republican Senator Cochran to resign next month due to health reasons

( zerohedge)

x)I doubt this will happen but we had better report on it: the USA is said to consider a new military action against Syria as there are claims that Assad used chemical weapons

( zerohedge)

a)Eric Holder believes that Mueller will hit Trump with obstruction charges. I do not think so…it is his constitutional authority to fire Comey and his actions were not criminal in any way

( zero hedge)

b)Trump on the war path this morning as he slams the Obama administration for trying to discredit the Trump candidacy and then his presidency

comex gold volumes are RISING AGAIN

Here is a summary of the latest gold trading volumes at the Comex per year

certainly the introduction of EFP’s has certainly had an effect:

Trading Volumes on the COMEX

PRELIMINARY COMEX VOLUME FOR TODAY: 220,550 contracts

CONFIRMED COMEX VOL. FOR YESTERDAY: 281,421 CONTRACTS

comex gold volumes are RISING AGAIN

Here is a summary of the latest gold trading volumes at the Comex per year

certainly the introduction of EFP’s has certainly had an effect:

Meanwhile, gold-trading volumes on the COMEX have never been higher:

end

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

And now for the wild silver comex results.

Total silver OI FELL BY A CONSIDERABLE 1702 CONTRACTS FROM 192,332 DOWN TO 190,630 DESPITE FRIDAY’S 23 CENT RISE IN TRADING). HOWEVER,WE WERE ALSO INFORMED THAT WE HAD 1316 EMERGENCY EFP’S FOR MAY ISSUED BY OUR BANKERS AND ZERO FOR ALL OTHER MONTHS TO COMEX LONGS WHO RECEIVED A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON: THE TOTAL EFP’S ISSUED: 1316. THE SILVER BOYS HAVE STARTED TO MIGRATE TO LONDON FROM THE START OF DELIVERY MONTH AND CONTINUING RIGHT THROUGH UNTIL FIRST DAY NOTICE JUST LIKE WE ARE WITNESSING TODAY. USUALLY WE NOTED THAT CONTRACTION IN OI OCCURRED ONLY DURING THE LAST WEEK OF AN UPCOMING ACTIVE DELIVERY MONTH AS WE HAVE JUST SEEN IN GOLD TODAY. THIS PROCESS HAS JUST BEGUN IN EARNEST IN SILVER STARTING IN SEPTEMBER 2017. HOWEVER, IN GOLD, WE HAVE BEEN WITNESSING THIS FOR THE PAST 2 YEARS. NICK LAIRD WAS KIND ENOUGH TO SUPPLY US THE TOTAL FOR 2017 GOLD EFP’S AND IT WAS 6600 TONNES FOR THE ENTIRE YEAR. WE OBVIOUSLY HAD NO LONG COMEX SILVER LIQUIDATION BUT WE ALSO HAD A GOOD SIZED GAIN IN TOTAL SILVER OI FROM OUR TWO EXCHANGES. WE ARE ALSO WITNESSING A FAIR AMOUNT OF SILVER OUNCES STANDING FOR COMEX METAL IN THIS NON ACTIVE JANUARY AS WELL AS THAT CONTINUAL MIGRATION OF EFPS OVER TO LONDON. ON A PERCENTAGE BASIS THERE ARE MORE EFP’S ISSUED FOR GOLD THAN SILVER. ON A NET BASIS WE LOST 356 SILVER OPEN INTEREST CONTRACTS

1702 CONTRACT LOSS AT THE COMEX COMBINING WITH THE ADDITION OF 1316 OI CONTRACTS NAVIGATING OVER TO LONDON.

NET LOSS ON THE TWO EXCHANGES:356 CONTRACTS

AMOUNT STANDING FOR SILVER AT THE COMEX

We are now in the active delivery month of MARCH and here the front month LOST 216 contracts FALLING TO 1041 contracts. We had 204 contracts filed upon yesterday, so we LOST 16 contracts or an additional 80,000 will NOT stand in this active delivery month of March.

April GAINED 4 contracts RISING AT 418 .

The next big active delivery month for silver will be May and here the OI lost by 1747 contracts down to 147,117

We had 143 notice(s) filed for 715,000 OZ for the MARCH 2018 contract for silver

INITIAL standings for MARCH/GOLD

MARCH 5/2018.

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz |

nil oz

|

| Deposits to the Dealer Inventory in oz | NIL oz |

| Deposits to the Customer Inventory, in oz | nil |

| No of oz served (contracts) today |

0 notice(s)

NIL OZ

|

| No of oz to be served (notices) |

672 contracts

(67200 oz)

|

| Total monthly oz gold served (contracts) so far this month |

0 notices

|

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

For MARCH:

Today, 0 notice(s) were issued from JPMorgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equates to 0 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped/ Received) by j.P.Morgan customer account.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

To calculate the INITIAL total number of gold ounces standing for the MARCH. contract month, we take the total number of notices filed so far for the month (0) x 100 oz or 0 oz, to which we add the difference between the open interest for the front month of FEB. (672 contracts) minus the number of notices served upon today (0 x 100 oz per contract) equals 67,200 oz, the number of ounces standing in this nonactive month of MARCH (2.0902 tonnes)

Thus the INITIAL standings for gold for the MARCH contract month:

No of notices served (0 x 100 oz or ounces + {(672)OI for the front month minus the number of notices served upon today (0 x 100 oz )which equals 67,200 oz standing in this nonactive delivery month of March . THERE IS 10.556 TONNES OF REGISTERED GOLD AVAILABLE FOR DELIVERY SO FAR.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

IN THE LAST 17 MONTHS 70 NET TONNES HAS LEFT THE COMEX.

end

And now for silver

AND NOW THE DECEMBER DELIVERY MONTH

MARCH INITIAL standings/SILVER

| Silver | Ounces |

| Withdrawals from Dealers Inventory | nil oz |

| Withdrawals from Customer Inventory |

14,913.410 oz

DELAWARE

|

| Deposits to the Dealer Inventory |

nil

oz

|

| Deposits to the Customer Inventory |

NIL oz

|

| No of oz served today (contracts) |

143

CONTRACT(S

(715,000 OZ)

|

| No of oz to be served (notices) |

898 contracts

(4490,000 oz)

|

| Total monthly oz silver served (contracts) | 4205 contracts

(21,025,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

we had 0 inventory movement at the dealer side of things

total inventory deposits/withdrawals/ into dealer: nil oz

we had 0 deposits into the customer account

ii) JPMorgan: zero

*** JPMorgan for most of 2017 and in 2018 has adding to its inventory almost every single day.

JPMorgan now has 135 million oz of total silver inventory or 54% of all official comex silver.

total deposits customer account: NIL oz

JPMorgan did not add any silver into its warehouses (official) today.

we had 3 withdrawals from the customer account;

i) Out of Delaware: 25,300.750 oz

ii) Out of CNT: 599,138.810 oz

iii) Out of Brinks: 199,270.757 oz

total withdrawals; 823,719.300 oz

we had 1 adjustments

i) out of CNT: 603,196.330 oz was adjusted out of the customer is this landed into the dealer account of CNT

total dealer silver: 57,444 million

total dealer + customer silver: 251.779 million oz

The total number of notices filed today for the March. contract month is represented by 143 contract(s) FOR 715,000 oz. To calculate the number of silver ounces that will stand for delivery in March., we take the total number of notices filed for the month so far at 4205 x 5,000 oz = 21,025,000 oz to which we add the difference between the open interest for the front month of Mar. (1257) and the number of notices served upon today (143 x 5000 oz) equals the number of ounces standing.

.

Thus the INITIAL standings for silver for the March contract month: 4205(notices served so far)x 5000 oz + OI for front month of March(1257) -number of notices served upon today (143)x 5000 oz equals 25,515,000 oz of silver standing for the March contract month.

We LOST an additional 16 contracts or 80,000 additional silver oz will NOT stand for delivery at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

ESTIMATED VOLUME FOR TODAY: 54.428 CONTRACTS

CONFIRMED VOLUME FOR YESTERDAY: 79,045 CONTRACTS

YESTERDAY’S CONFIRMED VOLUME OF 79,045 CONTRACTS EQUATES TO 395 MILLION OZ OR 56.5% OF ANNUAL GLOBAL PRODUCTION OF SILVER

COMMODITY LAW SUGGESTS THAT OPEN INTEREST SHOULD NOT BE MORE THAN 3% OF ANNUAL GLOBAL PRODUCTION. THE CROOKS ARE SUPPLYING MASSIVE PAPER TRYING TO KEEP SILVER IN CHECK.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price at that day at $18.42

The previous record was 224,540 contracts with the price at that time of $20.44

end

NPV for Sprott

1. Sprott silver fund (PSLV): NAV RISES TO -1.66% (MARCH 5/2018)

2. Sprott gold fund (PHYS): premium to NAV RISES TO -0.38% to NAV (March 5/2018 )

Note: Sprott silver trust back into NEGATIVE territory at -1.66%-/Sprott physical gold trust is back into NEGATIVE/ territory at -0.38%/Central fund of Canada’s is still in jail but being rescued by Sprott.

Sprott WINS hostile 3.1 billion bid to take over Central Fund of Canada

(courtesy Sprott/GATA)

3.SPROTT CEF.A FUND (FORMERLY CENTRAL FUND OF CANADA): NAV RISES TO -2.95%: NAV 13.63/TRADING 13.23//DISCOUNT 2.95.

END

And now the Gold inventory at the GLD/

March 5/WITH GOLD DOWN $4.10/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 833.98 TONNES

MARCH 2/WITH GOLD UP $18.70/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 833.98 TONNES

March 1/WITH GOLD DOWN ANOTHER $12.30/A HUGE CHANGE IN GOLD INVENTORY/ A DEPOSIT OF 2.96 TONNES/INVENTORY RESTS AT 833.98 TONNES

FEB 28/WITH GOLD DOWN ANOTHER 70 CENTS/NO CHANGE IN GOLD INVENTORY/INVENTORY RESTS AT 831.03 TONNES/.

feb 27/WITH GOLD DOWN $13.80 WE HAD NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 831.03 TONNES

FEB 26/WITH GOLD UP $2.40/WE HAD ANOTHER INVENTORY GAIN/THIS TIME 1.77 TONNE ADDITION TO THE GLD INVENTORY/INVENTORY RESTS AT 831.03 TONNES/WE HAVE HAD 5 INCREASES IN THE PAST 6 TRADING GOLD SESSIONS/

FEB 23/WITH GOLD DOWN $1.15, WE HAD A GOOD INVENTORY GAIN OF 1.47 TONNES OF GOLD INTO THE GLD/INVENTORY RESTS AT 829.26 TONNES

FEB 22/WITH GOLD UP 90 CENTS AGAIN TODAY, WE HAD NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 827.79 TONNES

FEB 21/ WITH THE 90 CENT GAIN WE HAD ANOTHER DEPOSIT OF 3.15 TONNES OF GOLD INTO THE GLD INVENTORY/INVENTORY RESTS TONIGHT AT 827.79 TONNES

Feb 20/WITH GOLD DOWN BY $24.25, THE CROOKS DECIDED THAT THEY HAD BETTER RETURN (DEPOSIT) 3.34 TONNES OF GOLD INTO THE GLD/INVENTORY RESTS TONIGHT AT 824,64 TONNES

Feb 16/WITH GOLD UP BY 25 CENTS, THE CROOKS DECIDED AGAIN TO RAID THE COOKIE JAR BY WITHDRAWING 2.36 TONNES OF GOLD FROM THE GLD/INVENTORY RESTS AT 821.30 TONNES

Feb 15/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 823.66 TONNES

Feb 14/AN ADDITIONAL OF 2.95 TONNES OF GOLD INTO GLD WITH THE HUGE GAIN OF 27.40 IN PRICE/INVENTORY RESTS AT 823.66 TONNES

Feb 13/WITH GOLD UP $3.40 WE HAD NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY REMAINS AT 820.71 TONNES

Feb 12/STRANGE!!WITH GOLD RISING BY 12.00 DOLLARS, THE CROOKS DECIDED AGAIN TO WITHDRAW 5.6 TONNES OF GOLD FOR EMERGENCY USE ELSEWHERE/INVENTORY RESTS AT 820.71 TONNES

Feb 9/AGAIN WITH HUGE TURMOIL ON THE MARKETS, THE CROOKS WITHDREW 2 TONNES OF GOLD FROM THE GLD INVENTORY/INVENTORY RESTS AT 826.31 TONNES

Feb 8/DESPITE THE GOOD GAIN IN PRICE FOR GOLD TODAY/THE CROOKS REMOVED .96 TONNES FROM THE GLD INVENTORY/INVENTORY RESTS AT 828.31 TONNES

FEB 7/AN UNBELIEVABLE 12.08 TONNES WAS REMOVED BY THE CROOKED BANKERS AND THIS GOLD WAS USED IN THE ASSAULT THESE PAST FEW DAYS/INVENTORY RESTS AT 829.27 TONNES

Feb 6/AGAIN VERY STRANGE: WITH TODAY’S TURMOIL, THE CROOKS DID NOT ADD ANY GOLD INVENTORY INTO THE GLD/INVENTORY REMAINS AT 841.35 TONNES

Feb 5 Strange,with all of today’s turmoil, the crooks at the GLD decided to add zero ounces into GLD inventory/inventory rests at 841.35 tonnes

Feb 2/no change in gold inventory at the GLD/Inventory rests at 841.35 tonnes

Feb 1/with gold up by $8.00/the crooks decided not to add any new physical gold metal into the GLD./inventory rests at 841.35 tonnes

Jan 31/with gold up $3.15 today, GLD shed another 5.32 tonnes of gold from its inventory/inventory rests at 841.35 tonnes

jan 30/with gold down by $4.85/GLD shed another 1.47 tonnes of gold from its inventory/inventory rests at 846.67 tonnes

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

MARCH 5/2018/ Inventory rests tonight at 833.98 tonnes

*IN LAST 335 TRADING DAYS: 107,16 NET TONNES HAVE BEEN REMOVED FROM THE GLD

*LAST 265 TRADING DAYS: A NET 50.14 TONNES HAVE NOW BEEN ADDED INTO GLD INVENTORY.

end

Now the SLV Inventory

March 5/WITH SILVER DOWN 11 CENTS/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 318.069 MILLION OZ/

MARCH 2/WITH SILVER UP 23 CENTS: A HUGE 1.479 MILLION OZ WAS ADDED TO SILVER’S INVENTORY/INVENTORY RESTS AT 318.069 MILLION OZ/

March 1/WITH SILVER DOWN 11 CENTS TODAY/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 316.590 MILLION OZ./

FEB 28/WITH SILVER DOWN 5 CENTS TODAY/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 316.590 MILLION OZ/

feb 27/WITH SILVER DOWN 17 CENTS/NO CHANGE IN SILVER INVENTORY/INVENTORY RESTS AT 316.590 MILLION OZ

FEB 26/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 316.590 MILLION OZ/

FEB 23/WITH SILVER DOWN 10 CENTS TODAY, WE HAD ANOTHER HUGE ADDITION OF 1.315 MILLION OZ/INVENTORY RESTS AT 316.590 MILLION OZ/

fEB 22.2018/WITH SILVER DOWN 1 CENT TODAY, WE HAD NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 315.271 MILLION OZ/

FEB 21/WITH SILVER UP 15 CENTS TODAY, WE HAD A GOOD SIZED INVENTORY ADDITION OF 1.226 MILLION OZ/INVENTORY RESTS AT 315.271 MILLION OZ/

Feb 20/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 314.045 MILLION OZ

Feb 16/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 314.045 MILLION OZ/

Feb 15/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 314.045 MILLION OZ/

Feb 14./NO CHANGE IN SILVER INVENTORY DESPITE THE HUGE RISE IN PRICE/INVENTORY RESTS AT 314.045 MILLION OZ

Feb 13./NO CHANGE IN SILVER INVENTORY TODAY/INVENTORY RESTS AT 314.045 MILLION OZ/

Feb 12/AGAIN, WITH TODAY’S HUGE RISE IN SILVER PRICE, IN TOTAL CONTRAST TO GOLD: NO CHANGE IN SILVER INVENTORY/INVENTORY RESTS AT 314.045 MILLION OZ/

Feb 9/AGAIN WITH TURMOIL ON THE MARKETS, STRANGELY IN TOTAL CONTRAST TO GOLD: NO CHANGE IN SILVER INVENTORY/INVENTORY RESTS AT 314.045 MILLION OZ/

Feb 8/DESPITE THE TURMOIL TODAY AND A PRICE RISE: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 314.045 MILLION OZ/

FEB 7/no change in silver inventory at the SLV/Inventory rests at 314.045 million oz/

Feb 6/WITH ALL OF TODAY’S TURMOIL/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 314.045 MILLION OZ/

Feb 5/ we had HUGE change in silver inventory at the SLV/ A DEPOSIT OF 1.131 MILLION OZ INTO THE SLV/Inventory rests at 314.045 million oz/

Feb 2/we lost 982,000 oz from the SLV inventory /inventory rests at 312.914 million oz/

Feb 1/no change in silver inventory at the SLV/Inventory rests at 313.896 million oz/

Jan 31/ no change in inventory at the slv in total contrast to gold/inventory rests at 313.896 million oz/

Jan 30/no change in inventory/SLV inventory rests at 313.896 million oz/

MARCH 5/2018: NO CHANGES TO SILVER INVENTORY/

Inventory 318.069 million oz

end

6 Month MM GOFO 1.94/ and libor 6 month duration 2.03

Indicative gold forward offer rate for a 6 month duration/calculation:

G0FO+ 1.94%

libor 2.23 FOR 6 MONTHS/

GOLD LENDING RATE: .29%

XXXXXXXX

12 Month MM GOFO

+ 2.36%

LIBOR FOR 12 MONTH DURATION: 2.50

GOFO = LIBOR – GOLD LENDING RATE

GOLD LENDING RATE = +.140

end

Major gold/silver trading /commentaries for MONDAY

GOLDCORE/BLOG/MARK O’BYRNE.

GOLD/SILVER

Silver bullion will likely outperform gold bullion going forward

by John Rubino of Dollar Collapse

Normally the action in the gold and silver futures markets tends to be pretty similar, since the same general forces affect both precious metals. When inflation or some other source of anxiety is ascendant, both metals rise, and vice versa.

But lately – perhaps in a sign of how confused the world is becoming – gold and silver traders have diverged. Taking gold first, the speculators – who tend to be wrong at major inflection points – remain extremely bullish. Commercial traders, meanwhile – who tend to be right when speculators are wrong – are extremely bearish, with short positions more than double their longs. Historically that’s been a setup for a big drop in gold’s price.

Viewed as a chart with the gray bars representing speculators and red bars the commercials, and where divergence is bearish and convergence bullish, the result is pretty ugly.

But now check out silver. Where gold futures speculators’ long positions are three times their short bets, silver speculators are actually more short than long. In other words, the people who are usually wrong are bearish. The commercials, meanwhile, are almost in balance, which is usually bullish for silver’s subsequent action.

Shown graphically, speculators and commercials are meeting the middle at zero, something that’s both very rare and very positive.

What does this mean? One possible explanation is that silver has gotten too cheap relative to gold and needs to be revalued. That could happen in several ways, with both metals rising but silver rising more, or both falling but silver falling less. Or with gold dropping while silver rises, as improbable as that seems.

As the chart below illustrates, gold has recently been rising relative to silver (or silver has been falling relative to gold) with the gold/silver ratio now close to 80, meaning that it takes 80 ounces of silver to buy one ounce of gold. It’s been there two other times in the past decade and both times gold subsequently rose while silver rose a lot more.

Based on this (admittedly short) bit of recent history, an interesting trade might be to short gold and go long silver on the assumption that silver bullion will outperform gold bullion going forward. Or just stack more silver than usual for a while.

With the world’s mines producing only about 10 times as much silver as gold while silver stockpiles are dwarfed by those of gold because so much silver is used and then lost in industrial applications, this might be a trade that works for years rather than months.

News and Commentary

Stocks Mixed Amid Trade Fears; Italian Bonds Drop: Markets Wrap (Bloomberg)

Gold prices gain as dollar weakens amid trade war fears (Reuters)

Gold snaps multiday skid on trade-war fears, but logs weekly loss (Marketwatch)

Texas endowment “in no rush to sell” $1 billion gold position – New CEO says (Gata)

Ex–FDIC chief Sheila Bair says bitcoin’s like dollars — neither has intrinsic value (Marketwatch)

Source: Bloomberg

U.S. dollar outlook darkens as trade war looms (Reuters)

New analysis sees return of trillion-dollar budget deficits (CNBC)

Dumping U.S. debt may become a weapon in global trade war (Reuters)

Why South Africa Is Ripping Up Its Mining Rules Again (Bloomberg)

’Flation Is Gone. Inflation Is Back (Moneyweek)

Gold Prices (LBMA AM)

05 Mar: USD 1,326.30, GBP 958.78 & EUR 1,075.63 per ounce

02 Mar: USD 1,316.75, GBP 955.70 & EUR 1,071.04 per ounce

01 Mar: USD 1,311.25, GBP 953.80 & EUR 1,075.75 per ounce

28 Feb: USD 1,320.30, GBP 951.14 & EUR 1,080.53 per ounce

27 Feb: USD 1,332.75, GBP 954.78 & EUR 1,081.26 per ounce

26 Feb: USD 1,339.05, GBP 953.00 & EUR 1,085.30 per ounce

Silver Prices (LBMA)

05 Mar: USD 16.51, GBP 11.95 & EUR 13.42 per ounce

02 Mar: USD 16.45, GBP 11.92 & EUR 13.36 per ounce

01 Mar: USD 16.32, GBP 11.87 & EUR 13.39 per ounce

28 Feb: USD 16.44, GBP 11.88 & EUR 13.45 per ounce

27 Feb: USD 16.61, GBP 11.91 & EUR 13.48 per ounce

26 Feb: USD 16.67, GBP 11.88 & EUR 13.52 per ounce

Recent Market Updates

– Trump Risks Trade and Currency Wars – Protectionism and Economic War Loom

– Four Key Themes To Drive Gold Prices In 2018 – World Gold Council

– Is The Gold Price Going To $10,000? (Goldnomics Podcast 3)

– Gold Corridor From Dubai to China Sought By China

– Digital Gold Provide the Benefits Of Physical Gold?

– Weekly Briefing: Currency Wars – ECB Warns Re Trump, Russia and Turkey Buy Gold and BOE Bitcoin Warning

– Russian Central Bank Buys Gold – 600,000 Ounces Or 18.7 Tons In January As Venezuela Launches ‘Petro Gold’

– Bitcoin or British Pound ‘Pretty Much Failed’ As Currency?

– Bank Bail-In Risk In European Countries Seen In 5 Key Charts

– US-China Trade War Escalates As Further Measures Are Taken

Andrew Maguire’s Kinesis money which is a “bitcoin” but backed 100% by allocated gold and silver is set to go.

it think it would be a great idea to look at this!

please read at: https://kinesis.money/#/

(Andrew Maguire)

|

2:57 PM (1 hour ago) | ||

|

|||

Harvey

Here It is my friend! https://kinesis.money/#/ Please let everyone know.

Let catch up on Monday if you have time. We have billions in the hopper ready to be allocated on the 1st day of trading. The paper market days are over.

Warm regards

Andy

end.

A very important video for you to see. Alasdair Macleod explains the significance of the March 26 oil futures contract which will inevitably be settled in gold. He explains that the uSA was not happy with this and was probably the reason that Trump initiated tariffs on aluminum and steel.

a must view

(Alasdair Macleod)

Alasdair Macleod: The yuan oil futures contract’s implications for gold

Submitted by cpowell on Sat, 2018-03-03 15:43. Section: Daily Dispatches

10:43a ET Saturday, March 3, 2018

Dear Friend of GATA and Gold:

In a three-minute video posted at YouTube yesterday, GoldMoney research director Alasdair Macleod explains the connection between gold and the oil futures contract priced in yuan that China will begin offering on March 26. The contract, Macleod explains, is part of the general movement away from the U.S. dollar by China, Russia, and other Asian countries. The video is headlined “Oil-Yuan Futures to Start Later in the Month — Implications For Gold” and can be seen here:

https://www.youtube.com/watch?v=UYHb76Oo1RE&t=14s

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

An acknowledgement of central bank manipulation in the gold market but I agree with C Powell that it is not for desperate dollar liquidity but to store value to currencies

(courtesy C Powell/GATA)

A new theory about ‘gold pukes’: Banks desperate for dollar liquidity

Submitted by cpowell on Mon, 2018-03-05 03:22. Section: Daily Dispatches

10:30p ET Sunday, March 4, 2018

Dear Friend of GATA and Gold:

Zero Hedge tonight calls attention to an interview done with Jeffrey Snider, chief investment strategist and head of global research at Alhambra Investment Partners in Palmetto Bay, Florida, by hedge fund manager Erik Townsend at his MacroVoices internet site. Snider acknowledges that central banks are active in the gold market through leases and swaps but argues that their primary objective is not to suppress the gold price in defense of government currencies but to provide emergency liquidity and collateral to investment and commercial banks at times of market stress.

“Gold pukes,” Snider says, are desperate grabs for dollar liquidity by the private-sector banks selling collateral that happens to be handy.

Of course Snider’s theory does not match the accounts provided by central bank records themselves, which emphasize currency defense as the objective of intervention in the gold market. Nor does Snider’s theory explain the suddenness of the “gold pukes,” since no one who was more interested in getting a decent price for gold than in driving gold’s price down would sell so much in a few minutes. He would spread his sales out over at least a full day.

Even so, Snider faults the surreptitiousness of central bank activity in the gold market and the dishonesty of central bank balance sheets in regard to gold. That’s more than readers will ever get from the Financial Times and Wall Street Journal.

A transcript of Townsend’s interview with Snider is posted at MacroVoices here:

https://www.macrovoices.com/macro-voices-research/podcast-transcripts/16…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

The world is producing approximately 3260 tonnes per year, of which China is now 430 tonnes (dropping from 460) and Australia rising to 301 tonnes and Russia at 274 tonnes. I will use from now one: 3260 – 430 -275 = 2555 as gold production (ex China ex Russia)

Peak gold maybe but Australian and Russian output still rising

March 4, 2018lawrieongold

Now March is with us we are beginning to receive reasonably accurate figures on 2017 gold production around the world and the bi g question is is peak gold here or not. The answer is maybe. According to the World Gold Council’s figures, global gold output actually increased in 2017, but by such a small margin that it should probably be considered flat at 3,267 tonnes – as compared with 3,260 tonnes a year earlier – a tiny 0.2% increase and with global output continuing to trend downwards we can probably assume that 2017 was indeed the year of peak gold.

But, there is much variation between national outputs. While the world’s largest gold producer – China – is estimated to have seen its gold output fall by 9-10%, the world’s second, third and fourth largest miners – Australia, Russia and the USA have reportedly seen their annual gold production increase, but perhaps by not as much in combination as the fall in Chinese output.

As to the actual figures it all comes down to the accuracy of those reporting. China’s output reportedly fell to 430 tonnes from over 460 tonnes in 2017.

There is an argument ongoing as to which nation is currently the world’s second largest gold producer. In 2016 it was Australia with 287 tonnes while Russia was in 3rd place with 274 tonnes. Australian consultancy, Surbiton Associate which tends to produce very accurate figures on Australia reports 2017 Australian production at 301 tonnes, a good increase on 2016, and avers Australia remains the world’s second largest producer of gold. However, as we reported here three weeks ago (See: Russia may now be World No. 2 Gold Miner), the Russian Finance Ministry stated that Russian gold output in 2017 was a little over 306 tonnes which would put it ahead of Australia as the World No.2. Reports also suggest that gold output from other top producers Canada and Peru grew in 2017, while that of the former No.1 gold miner, South Africa continued to fall by nearly 4% last year according to that country’s Bureau of Statistics.

But the actual league table of producers is probably immaterial – it is the overall figure which counts and that does suggest that global gold production has, at the very least, plateaued. Cutbacks on gold exploration and big new capital projects, as the lower gold prices after the 2012 peak caused the big mining companies to rethink their expansion plans and capital expenditures, are taking their toll. Most of the big miners are predicting short term production falls after a number of years of ‘growth at any cost’.

Back to Australia and the latest Surbiton Associates assessment though: Australian gold mine production in calendar 2017 resultedin the highest annual output since 1999. Total gold mine output in 2017 reached 301 tonnes or almost 9.7 million ounces, up three tonnes on calendar 2016. Production in the December quarter 2017 totalled some 80 tonnes, up six tonnes on the previous quarter.

“At the average gold price for 2017, the 301 tonnes was worth almost A$16 billion,” said Dr Sandra Close, a Surbiton Associates’ director. “Australian gold production is still trending upwards and the next few years look promising.”

“The higher output in the December quarter was due to a number of factors including the strong recovery at Newcrest’s Cadia East mine near Orange, NSW which was almost 60,000 ounces higher,” Dr Close said. “Other operations with higher output included the Super Pit’s increase of 28,000 ounces, Peak up 21,000 ounces and Tropicana up 19,000 ounces.

“Further out, development of the Gold Fields and Gold Road Resources’ Gruyere joint venture in WA is one- third complete, with the start of mining scheduled for late this year,” Dr Close said. “The operation will commence in early 2019 at a rate of around 270,000 ounces of gold per year when in full production.”

The only closure of note was Doray Minerals’ Andy Well mine. It commenced production in 2013 and was placed on care and maintenance in early November, after producing about 40,000 ounces in 2017.

“Given the number of projects coming on stream and with few closures anticipated, it would not be surprising to see another 20 tonnes of production added to Australia’s annual output,” Dr Close said. “This suggests that Australia’s all-time record annual gold production of 314 tonnes recorded in 1997 might well be exceeded.”

She said however, that despite the generally upward trend anticipated, production will probably decline in the March quarter 2018 due to wet weather in Western Australia which is a common occurrence early in the year.

As noted above, Surbiton estimates thst Australia remains the world’s second largest gold producer behind China which produced an estimated 4300 tonnes in 2017.

Australia’s largest gold producers for the 2017 year were:

https://lawrieongold.com/2018/03/04/peak-gold-maybe- but-australian-and-russian-output-still-rising/

-END-

THE FOLLOWING CAME FROM KOOS JANSEN:

YOU WILL NOTE THAT FOR THE FIRST TIME EVER CHINA EXPORTED GOLD TO LONDON.

THE QUESTION IS WHY?

I ASKED MY GOOD FRIEND REG HOWE FOR HIS THOUGHTS ON THIS AND WE AGREE THAT THERE ARE TWO POSSIBILITIES: 1) THAT THERE IS EXTREME SHORTAGE IN LONDON AND A MAJOR BANK COULD NOT DELIVER UPON ALONG OVER THERE.. CHINA WOULD BE ASKING FOR A BIG QUID PRO QUO FOR PROVIDING THE NECESSARY PHYSICAL. (IT MAKES SENSE IN THE FACT THAT GOLD IS IN BACKWARDATION IN LONDON)

2. TO HELP IN THE FACILITATION OF THE NEW OIL FOR YUAN FOR GOLD NEW FORMAT OR SOME FUTURE MEASURE THAT CHINA WILL REQUIRE OR AT LEAST BENEFIT FROM ADDITION PHYSICAL LIQUIDITY IN LONODN..

REGARDLESS, IT SHOWS SCARCITY OVER THERE.

FROM REG HOWE TO ME:

“Have read speculation that it may have to do with the mechanics of settling the new oil and gold contracts in physical. More generally, I would guess it’s one of two things: (1) Chinese help in containing some serious stress in the gold market due to lack of physical, e.g., some central bank or major bullion bank unable to deliver, in which case there is likely a big quid pro quo; or (2) a positioning to facilitate some (other) future measure by China that will require or at least benefit from additional physical liquidity in London. In any event, seems to be more evidence of severe shortage of physical in London, otherwise they would just buy it there at today’s suppressed prices.”

END

Your early MONDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

i) Chinese yuan vs USA dollar/CLOSED UP 6.3400 /shanghai bourse CLOSED DOWN 2.39 POINTS OR 0.07% / HANG SANG CLOSED DOWN 697.06 POINTS OR 2.28%

2. Nikkei closed DOWN 139.55 POINTS OR 0.66% /USA: YEN FALLS TO 105.64/ STILL DEADLY AS YEN CARRY TRADERS DISINTEGRATE

3. Europe stocks OPENED DEEPLY IN THE GREEN EXCEPT ITALY /USA dollar index RISES TO 90.08/Euro FALLS TO 1.2299

3b Japan 10 year bond yield: FALLS TO . +.043/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 105.64/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD FINALLY IN THE POSITIVE/BANK OF JAPAN LOSING CONTROL OF THEIR YIELD CURVE AS THEY PURCHASE ALL BONDS TO GET TO ZERO RATE!!

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 61.35 and Brent: 64.44

3f Gold UP/Yen UP

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil UP for WTI and UP FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund RISES TO +.633%/Italian 10 yr bond yield UP to 2.03% /SPAIN 10 YR BOND YIELD UP TO 1.513%

3j Greek 10 year bond yield FALLS TO : 4.36?????????????????

3k Gold at $1323.50 silver at:16.52 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble DOWN 31/100 in roubles/dollar) 57.12

3m oil into the 61 dollar handle for WTI and 63 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 105.64 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 0.9384 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1545 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now POSITIVE territory with the 10 year RISING to +0.633%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.844% early this morning (THIS IS DEADLY TO ALL MARKETS). Thirty year rate at 3.0128% /BOTH VERY DEADLY

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

(courtesy Jim Reid/Bloomberg/Deutsche bank/zero hedge)

Jittery Markets Rebound From Sharp Losses, Italy Slumps On Anti-Establishment Surge

What started off as a sea of red, with S&P futures tumbling as much as -25 points ahead of the European open, on fears of trade wars and concerns about the surge in Italy’s anti-establishment parties, has managed to rebound notable and stabilize, with most Asian and European markets now green. The dollar was steady and Treasuries gained, while Italian bonds dropped as the nation headed toward a hung parliament

For those who missed it, Italian election results pointed to a hung parliament with anti-establishment 5-Star Movement as the largest single party and the Centre-Right seen as the leading coalition, with far-right junior coalition partner Northern League having possibly outperformed Berlusconi’s Forza Italia. Following the results, Italian League Head Salvini says the party is not available for bizarre coalitions, adding that the centre right coalition has won and can govern, adding that he is open to talks with all parties but rules out a broad coalition. Meanwhile, in Germany, Chancellor Angela Merkel is set to form her fourth government after the SPD voted in favour of another grand coalition. Merkel is set to be sworn in for her fourth term on 14th March.

As BBG notes, the Italian election result and Germany’s move toward a coalition kick off a busy week for macro events. Both the Bank of Japan and European Central Bank will meet to decide on interest rate policy, while China hosts its National People’s Congress. Overshadowing it all, however, will be the next developments on global trade after U.S. President Donald Trump riled markets with his proposed tariffs last week.

There’s a “lot of politics this week with Italy elections and NPC in China, also trade measures,” Frank Benzimra, head of Asia equity strategy at Societe Generale SA in Hong Kong, said. “The return of volatility we have seen since the end of January will probably remain.”

On Monday morning, Europe’s Stoxx 600 was up 0.6%, rebounding after closing in the red in the past four sessions, even as Italian stocks drop after a tremendous showing by anti-establishment groups in Sunday’s election, assuring a hung parliament and further chaos.

Surprisingly, in a day many expected a European bloodbath, almost all Stoxx 600 industry groups rise; carmakers pare an earlier drop of 1.4% to trade little changed; the sector fell at the open after U.S. President Donald Trump upped the ante on import tariffs, threatening taxes on cars from Europe that “freely pour into the U.S.”

Meanwhile, equity gauges from Tokyo to Sydney slumped during the Asian trading session amid worries about the implications of U.S. tariffs for the world’s economy. Italy’s stocks and bonds were the standout losers as Italy’s FTSE MIB Index remained in the red, dropping around 1%, after paring an earlier drop of as much as 2%.

Italian bonds, however, are slower to respond to this morning’s relief rally, and at last check were trading north of 2%.

As noted above, US index futures rebounded sharply from a much weaker open, and have declined only fractionally after a wave of buying was unleashed withe the European open.

Shares in Shanghai bucked regional weakness as China kept its 2018 growth target of around 6.5 percent. Newly added stocks accounted for six out of 10 worst performers on Hang Seng China Enterprises Index, as the big-cap gauge extended losses after its worst month since January 2016. China Gas tumbles as much as 5.2% to lead declines on HSCEI, which slides 1.8%; China Mobile drops 3.3% to head for its weakest finish since April 2014; ZhongAn Online P&C Insurance and Cnooc dropped more than 3%. The stocks were weighed down by declines in the broad market, said Ken Chen, Shanghai-based analyst with KGI Securities.

In macro, the yen initially gained, supported by populist parties’ surge in Italian elections, talk on trade wars and a BOJ looking toward the exit of its stimulus program; it strengthened as much as 0.4% to 105.35 per dollar, nearing a fresh 16-month high, before paring almost gains; Japan’s bonds advance as traders buy back after selling heavily last Friday following BOJ Governor Kuroda’s comments on monetary exit.

Meanwhile, the euro took a hit after Tokyo fix as investors were unclear over Italy’s future political direction, but wasn’t knocked down, managing to rebound strongly above 1.23 handle. The Euro holds little changed after rising above the 21-DMA, while risk reversals for the pair gain in the front-end, with one-week remaining in negative territory ahead of the ECB policy decision on Thursday.

The pound reversed an earlier drop after stronger-than- forecast U.K. PMIs

The Bloomberg Dollar Spot Index is steady and the Treasury curve bull flattens. Bund futures rose and BTPs slipped from the open, while European equities outside Italy traded in the green. The dollar steadied even as Treasuries advanced.

Elsewhere, China is reportedly seeking high level meetings with US in an effort to diffuse trade tensions and has asked for a list of US demands. Over the weekend, White House officials stated that President Trump plans to apply steel and aluminium tariffs globally and will not exempt allies such as Canada and Europe. In related news, EU’s Juncker said on Friday the EU will respond to US steel action which may involve tariffs on motorcycles, while there were also source reports that EU duties of about USD 3.5bln are to be considered if the US goes ahead with its tariff plan.

US President Trump also tweeted that the US could apply tax to cars from the EU.

In the latest Brexit developments, the EU is reportedly set to uncover differences with the UK in draft Brexit guidelines with the proposals to be vague to force UK to explain what it is seeking, according to reports. Elsewhere, EU negotiators will this week offer a Canada-style trade deal putting pressure on Theresa May’s Brexit ‘red lines’. Further reports suggest, the European Commission is preparing to take a hard line over plans to “roll over” 50 EU free trade agreements during the Brexit transition period, in a threat to British exports.

Looking ahead, highlights include US services PMI, ISM non-mfg PMI, Fed’s Quarles and Evans, as well as earnings from YY and Gibson Energy.

Bulletin headline summary from RanSquawk

- Italian election results pointed to a hung parliament with anti-establishment 5-Star Movement as the largest single party

- White House officials stated that President Trump plans to apply steel and aluminium tariffs globally and will not exempt allies such as Canada and Europe

- Looking ahead, highlights include US services PMI, ISM non-mfg PMI, Fed’s Quarles and Evans

Market Snapshot

- S&P 500 futures down 0.2% to 2,685.25

- STOXX Europe 600 up 0.2% to 367.92

- German 10Y yield fell 2.6 bps to 0.625%

- MSCI Asia Pacific down 1% to 172.68

- MSCI Asia Pacific ex Japan down 1.2% to 564.41

- Nikkei down 0.7% to 21,042.09

- Topix down 0.8% to 1,694.79

- Hang Seng Index down 2.3% to 29,886.39

- Shanghai Composite up 0.07% to 3,256.93

- Sensex down 0.9% to 33,754.18

- Australia S&P/ASX 200 down 0.6% to 5,895.03

- Kospi down 1.1% to 2,375.06

- Euro up 0.02% to $1.2319

- Italian 10Y yield rose 2.3 bps to 1.702%

- Spanish 10Y yield fell 3.2 bps to 1.518%

- Brent futures up 0.5% to $64.71/bbl

- U.S. Dollar Index little changed at 89.96

Top Overnight News from BBG

- Projections based on ballot-counting on Monday morning, following Italy’s vote on Sunday, suggested the two forces with the most gains, the euroskeptic Five Star Movement and the anti- migrant League, could reach a majority in at least one of the houses of the Rome-based parliament should they join forces

- China stepped up its push to curb financial risk, cutting its budget deficit target for the first time since 2012, to 2.6 percent of GDP from 3 percent, and setting a growth goal of around 6.5 percent that omitted last year’s aim for a faster pace if possible

- Chinese lawmakers will vote to appoint a new PBOC governor on March 19, according to a National People’s Congress agenda; while current bank regulatory chief Guo Shuqing and Hubei provincial party chief Jiang Chaoliang have both been tipped for the post, President Xi Jinping’s top economic policy adviser and Politburo member Liu He has recently been named by analysts in connection with the top monetary policy job and a vice premier position

- Trump administration shows scant sign of watering down its plan to impose stiff tariffs on steel and aluminum imports with carve-outs for specific countries, despite opposition from U.S. allies and Republican lawmakers.

- Tariffs would have “devastating effects on Europe, but also on the U.S. and the rest of the world,” EU Trade Commissioner Cecilia Malmstrom says to Swedish broadcaster SVT

- German Chancellor Angela Merkel says her government must begin its work “quickly” after Social Democrat vote to join coalition, citing global trade and competitiveness with China as urgent issues

Asian equity markets began a risk-packed week with a downbeat tone as region digested Italian elections, China economic announcements and continued trade war concerns. This ongoing political uncertainty and rise of the Euro sceptics dampened the risk tone with ASX 200 (-0.6%) and Nikkei 225 (-0.7%) negative throughout the session, while Japanese steel names and automakers remained pressured on lingering tariff/trade war concerns. Elsewhere, Hang Seng (-2.3%) underperformed and Shanghai Comp. (+0.1%) bucked the trend as participants contemplated over China’s economic work report in which the official GDP growth target was maintained at 6.5% as widely expected, before disappointing Chinese Caixin Services and Composite PMI data. Finally, 10yr JGBs were higher and reclaimed the 151.00 level, amid a rebound in Tnotes and a flight-to-quality due to the subdued risk tone. Chinese Premier Li delivered the Economic Work Report at the NPC in which he announced that China maintained GDP growth target at about 6.5% this year but dropped reference to ‘higher if possible’. Premier Li further stated that China will keep prudent monetary policy neutral and maintain proactive fiscal policy, while China will also take further measures to lower tax burden for companies.

Top Asian News

- China Turns Fiscal Screws While Targeting GDP Growth Around 6.5%

- China’s Top Tech Firms Heed the Call to Bring Listings Home

- Go-Jek Explores First IPO of a Billion-Dollar Indonesian Startup

- HSBC Is Said to Poach Morgan Stanley’s Top Indonesia Dealmaker

Amidst the prospects of ongoing global ‘trade wars’ and the political uncertainty stemming from the Italian elections, European equities saw a pessimistic open following a similar tone in the Asia-Pac session. As of now, major bourses have pared back earlier losses (Eurostoxx 50 +0.3%) with the exception of FTSE MIB (-1.2%) as a clear underperformer. Financials lag with banks amongst the worst performers on the FTSE MIB with BPER Banca (-7.3%), Banco BPM (-6.2%), Ubi Banca (-4.6%) seen at the foot of the index dragged down by the Italian elections. The Berlusconi-controlled Mediaset (-5.4%) are also lower following projections showing the centre-right coalition fronted by the former PM falling short of an absolute majority. Following US President Trump’s latest threat to hike tariffs in EU auto imports, German auto names are underperforming with DAX 30 heavyweights BMW (-1.1%) and Daimler (-0.4%) seen lower.

Top European News

- BMW May Have Most to Lose in Autos Trade War, Evercore Says

- U.K. Services Prop Up Economy on Better-Than-Forecast Growth

- Euro-Area Economy Looked a Little Less Buoyant in February

- May Secures Temporary Cease-Fire in U.K. Tory-Brexit Infighting

- Amid China M&A Drive, EU Rushes for Investment-Screening Deal

In FX, the DXY has given up 90.000 status after last week’s roller-coaster ride when the index almost recovered to 91.000 before recoiling on US President Trump’s plans to slap import tariffs on steel and aluminium that sparked another wave of global trade war and protectionism jitters. However, a recovery in the EUR has moved EUR/USD back above 1.2300 and moved the DXY back into negative territory for the session. Meanwhile, Eur/Jpy initially breached strong technical support at 129.50 before reclaiming 130.00 amid the recent EUR strength. Elsewhere, the Nzd, Aud and Cad are G10 underperformers after Chinese PMI misses and a general risk-off tone on the Trump proposals and pledges of retaliation, with the Kiwi extending gains above 0.7200 vs the Greenback, Aud/Usd trading around 0.7750 and Usd/Cad just off fresh 2018 highs but back below 1.2900 and just shy of key resistance in the 1.2915-25 area. The Jpy and Chf are both benefiting from their safe-haven appeal, with the former around 105.50 vs the Usd (strong barriers still reported at 105.00) and the latter within a 0.9750-85 range vs its US counterpart. Cable at session highs above 1.3800 and Eur/Gbp still above 0.8900 between 0.8905-50 with Sterling continuing to be hampered by Brexit uncertainty amidst more reports about the EU’s hard-line stance on transition terms and conditions.

In commodities, WTI and Brent crude futures traded higher despite the firmer USD as Libyan supply disruptions provide some reprieve after Libya’s Sharara oil field (largest in the nation) has halted pumping crude amid domestic protests. However, it was then later reported that production has resumed at the oil field. In terms of other energy newsflow, the IEA have upgraded their US oil output growth estimates by over 2mln bpd through 2023. Focus ahead will be on any comments from the meeting between OPEC and US shale producers as both sides look to address the ongoing global oil glut. In metals markets, gold prices remain modestly supported by the general risk tone with gains capped by the firmer USD. Elsewhere, Chinese steel futures were seen lower for a second consecutive session as demand in the region remains soft and despite China announcing that they will reduce around 30mln tonnes of steel capacity this year. Focus going forward will be on how Trump views/responds to threats made by the EU and Canada over counter-measures to last week’s tariff announcements.

Politics should dominate the start to the week for markets. In China the National People’s Congress is due to begin in Beijing, with Premier Li due to present a draft of his work plan for 2018 (continues to March 20th). Away from politics, the main data releases on Monday will be the final February services and composite PMIs around the globe, along with Euro area retail sales for January, the Sentix investor confidence reading for March and the February ISM non-manufacturing in the US. Elsewhere BOJ Deputy Governor nominee’s confirmation hearing will begin, while the Fed’s Quarles is also due to speak. It’s worth also highlighting that EU Council President Donald Tusk may circulate draft negotiating guidelines about the future relationship between the EU and UK on Monday.

US Event Calendar

- 9:45am: Markit US Services PMI, est. 55.9, prior 55.9; Composite PMI, prior 55.9

- 10am: ISM Non-Manf. Composite, est. 59, prior 59.9

- 1:15pm: Fed’s Quarles Speaks on Foreign Bank Regulation

DB’s Jim Reid concludes the overnight wrap

What’s the toughest business out there? After this weekend it’s definitely “snowbiz”. After a deluge of snow late Friday afternoon we made a big family snowman. By Saturday night after an incredibly quick melt it was as good as gone. I now know how mayflies feel.

Through history snowmen have lived as precarious as an existence as Italian Governments and as we bring news of yesterday’s election it’s worth remembering that they have seen around 90 governments since the start of the twentieth century. Counting is still underway, but initial results suggest there is no clear majority with a hung parliament very likely, while the Five Star Movement will likely be the most popular single party with c32% share of

the votes (up 6ppt vs. 2013 elections), as per RaiNews24, and better than final opinions polls suggested. RaiNews24 further notes that the Berlusconi led center-right coalition could achieve 35.5% of votes but still short of the 40% needed to avoid a hung parliament. However the League (c.16%) look set to beat Forza Italia (c.14%) which makes the centre-right look more anti immigration and euro sceptic. The center-left group led by Renzi could achieve c.23% of the votes. If the projections are true, it could lead to months of uncertainty until a coalition government could be formed. DB’s Mark Wall noted that an important lesson from the various political events over the last couple of years in the euro area is that unless there is a clear threat to euro area membership, there is little lasting impact on market sentiment. Further, it appeared all Euro sceptic parties had softened their stance on euro exit before the election. As long as the market remains convinced of this, he believes calmness should prevail. However for us there’s no doubting that populist parties have done better than expected and Italy is going to struggle to get a reforming agenda after these results.

In contrast, in Germany the political stalemate has ended after the SPD voted in favour (66% to 34%) of forming a new coalition government with Ms Merkel’s bloc, paving the way for her to be re-inaugurated as Chancellor by mid-March. Mark believes the appearance of a post-Schaeuble pro-European policy stance by Germany is a buffer against the potential risks from Italy. This morning, the Euro initially strengthened on Germany’s developments but pared back gains to be marginally lower following news from Italy.

In Asia, markets are broadly lower with the Nikkei (-0.71%), Kospi (-0.92%), Hang Seng (-1.26%) and China’s CSI 300 (-0.15%) all down as we type, while the UST 10y yield is down c2.5bp. Datawise, China’s February Caixin composite PMI (53.3 vs. 53.7 previous) and Japan’s Nikkei composite PMI (52.2 vs. 52.8 previous) were both softer than the prior month’s reading. Elsewhere, China has set an economic growth target of “around 6.5%” for 2018 but did not include the comment of “higher if possible in practice” as it did in 2017. Notably, the c6.5% target is in line with DB’s expectations.

Looking forward it’s a big week ahead macro wise with the back end where most of the action will come. On Friday, 5 weeks on from the average hourly earnings shock that caused the vol quake, we’ll see the latest US payroll report with all focus on this month’s wages number. The consensus is for another strong +0.3% mom number in February however base effects mean that the YoY rate would hold at +2.8% (in line with DB) if that is the case.

Before that we have the ECB meeting on Thursday and the BoJ on Friday. No change in policy is expected at either. For the ECB though, our economists expect the ECB to redefine the QE reaction function, reducing the likelihood that the ECB responds to economic and financial shocks with QE. The current forward guidance links the potential for an extension or expansion of QE to shocks to the economy and/or financial conditions. Our team expect the ECB to say that it will respond to shocks with the monetary policy stance more generally rather than QE specifically. By redefining the reaction function, this will set the ground for a June announcement that net asset purchases will end in December. The BoJ meeting should be a less exciting affair with the status quo maintained. Perhaps of most interest will be whether or not policy board member Goushi Kataoka officially puts forward his proposal for another easing. After we went to print on Friday Mr Kuroda caused a little bit of a stir though by suggesting that “Of course we will be considering and debating an exit [around fiscal year 2019].” This ends in March 2020 and is someway off but it’s a further sign that the bias for global QE continues to be for it to be wound down (for now).

Also this week China’s NPC starts today and continues through to March 20th with headlines already coming out as we discussed above. Our economists have also published a preview of the event which you can find here. For the rest of the week ahead see the day by day guide at the end. Watch out today for the final February services and composite PMIs released around the globe. The slowing Euro PMI manufacturing numbers of late have been a big market driver recently Of more unpredictable timing will be the next round in the latest trade rhetorics around the world after Thursday’s steel/aluminium tariffs announcement from the US President. Friday initially saw a big risk off/flight to quality when Mr Trump tweeted that “trade wars are good, and easy to win,”. EC President Juncker said Europe was prepared to respond forcefully to the developments by targeting imports of Harley-Davidson, Levi Strauss, and bourbon whiskey from the US.

Mr Trump didn’t let this topic stay quiet and tweeted on Saturday that “If the E.U. wants to further increase their already massive tariffs and barriers on U.S. companies doing business there, we will simply apply a Tax on their Cars which freely pour into the U.S.”

As the war of words was escalating, the European session was very weak on Friday before a US rally restored some stability into the market. The Stoxx 600 (-2.09%) and DAX (-2.27%) both fell the most since early February, while the FTSE was the relative outperformer (-1.47%). In the US, the S&P initially traded 1.1% down but closed 0.51% higher, in part as tech stocks rallied and investors seemed to have toned down the potential for a large scale trade war. Elsewhere, the Nadaq was up 1.08% while the Dow and the VIX (19.59) was down 0.29% and 12.8% respectively.

Over in government bonds, UST 10y yields initially traded 1.6bp lower but weakened throughout the day to close 5.6bp higher to 2.865%, effectively reversing Thursday’s gains. Some suggests the weakness was amplified due to rate-lock selling ahead of this week’s large IG credit issuances but the swings said much about confusion as to whether protectionism is likely to cause riskoff (lower yields) or higher global prices (higher yields). Elsewhere, core European 10y bond yields were little changed and rose c1bp (Bunds and Gilts +0.7bp; OAT +1.1bp).

Away from the markets and back onto President Trump’s tariff proposals. DB’s Brett Ryan believes the tariffs would have a negligible impact on the US trade deficit as imports of steel and aluminum account for 2% of all goods imports. On inflation, he believes the impact should be limited as cost increases are unlikely to be fully passed on to end customers. Overall, he believes it is the second order impacts of retaliatory measures undertaken by trading partners that could come with more substantial costs for the US and its trading partners further down the line. Our Chinese economists suggests the actual impact of the trade measures on China will also be relatively small – China exports only small shares of US steel (2%) and aluminum imports (11%). Further, with a senior advisor to President Xi (Liu He) visiting the US this week, they believe this indicates China is wanting to negotiate rather than retaliate (Link). Notably, this is consistent with comments by China’s Vice Foreign Minister Zhang over the weekend where he noted “China does not want to fight a trade war with the US, but we absolutely will not sit by and watch as China’s interest are damaged”.

Over in the UK, on Friday the UK PM May reiterated that the UK intends to leave the Single market and Customs unions as well as impose an end to freedom of movement. However, DB’s Oliver Harvey believes there were shifts in tone, particularly to the importance of trade and services. Overall, he believes the EU will welcome the level of detail in her speech, but he is sceptical whether it can form the basis of negotiations on a future trade deal. Much will depend on the response of the EU leadership in the coming days. Refer to his note for more details.

Finally on credit, Michal in my team has just published the monthly “IG Strategy: Issuance and Fund Flows” which provides commentary and data charts on the IG corporate bond market size, issuance and fund flows. This comprehensive report covers EUR, GBP and USD markets, including both DM and EM. It also puts both issuance and fund flows in the IG space into a broader global context. You can download the full report here.

We wrap up with other data releases from Friday. In the US, the final reading for the February Uni. of Michigan’s consumer sentiment was revised up by 0.2pts to 99.7. In the details, both 1 and 5 year-ahead inflation expectations were unrevised at 2.7% and 2.5% respectively. Back in Europe, the Euro area’s January PPI was in line at 0.4% mom, but prior revisions means the annual rate was softer than expectations at 1.5% yoy (vs. 1.6%). The final reading for Italy’s 4Q GDP was unrevised at 0.3% qoq and 1.6% yoy. Elsewhere, Germany’s January retail sales was below market at -0.7% mom and 2.3% yoy (vs. 3% expected), although the prior annual reading was revised up by 1.7ppt.

Politics should dominate the start to the week for markets. In China the National People’s Congress is due to begin in Beijing, with Premier Li due to present a draft of his work plan for 2018 (continues to March 20th). Away from politics, the main data releases on Monday will be the final February services and composite PMIs around the globe, along with Euro area retail sales for January, the Sentix investor confidence reading for March and the February ISM non-manufacturing in the US. Elsewhere BOJ Deputy Governor nominee’s confirmation hearing will begin, while the Fed’s Quarles is also due to speak. It’s worth also highlighting that EU Council President Donald Tusk may circulate draft negotiating guidelines about the future relationship between the EU and UK on Monday.

end

3. ASIAN AFFAIRS

i)MONDAY MORNING/LATE SUNDAY NIGHT: Shanghai closed DOWN 2.39 POINTS OR 0.07% /Hang Sang CLOSED DOWN 697.06 POINTS OR2.28% / The Nikkei closed DOWN 139.55 POINTS OR 0.53%/Australia’s all ordinaires CLOSED DOWN 0.53%/Chinese yuan (ONSHORE) closed UP at 6.3400/Oil UP to 61.35 dollars per barrel for WTI and 64.44 for Brent. Stocks in Europe OPENED DEEPLY IN THE RED . ONSHORE YUAN CLOSED DOWN AT 6.3400 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.3395 /ONSHORE YUAN TRADING STRONGER AGAINST OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING MUCH STRONGER AGAINST THE DOLLAR . CHINA IS NOT HAPPY TODAY (STRONGER CURRENCY BUT TERRIBLE CHINESE MARKETS/ )

3 a NORTH KOREA/USA

/NORTH KOREA

3 b JAPAN AFFAIRS

end

c) REPORT ON CHINA

China confirms 2018 slowdown

(courtesy zerohedge)

China Confirms Further Economic Slowdown: Highlights From 2018 Government Work Report

In the latest confirmation that as part of its grand deleveraging campaign, China’s economy is set to slow further in the current year, Beijing has set a 2018 growth target of around 6.5%, omitting an intention to hit “a faster pace if possible”, as the world’s largest nation continues its push to ensure financial stability. While the target of 6.5% is the same as last year, Bloomberg notes that the statement excludes an objective for output growth to be “higher if possible in practice” as it did in 2017.

“The omission from the GDP growth target of ‘higher if possible’ and the new lower budget deficit target suggest slower growth and a fiscal drag,” said Eurasia’s Callum Henderson. “This makes sense for China in the context of the new focus on financial de-risking, poverty alleviation and environment clean-up, but is less good news at the margin for those economies that have high export exposure to China.”

China’s newly downgraded growth target was released Monday ahead of Premier Li Keqiang’s report to the National People’s Congress gathering in Beijing.

While China’s GDP surpassed 2017’s target with 6.9% growth, the first acceleration since 2010, economists forecast a moderation to 6.5% this year amid the ongoing deleveraging drive and trade tensions with the Trump administration. To be sure President – or rather Emperor – Xi Jinping has made it clear he will accept slower growth in his push to curb pollution, poverty and debt risk at a time when the world’s second-largest economy is on a long-term growth slowdown. As a result, numerical GDP targets have been de-emphasized in favor of higher-quality expansion since last year, according to Bloomberg.

The government also signaled its intent to continue efforts to slow debt growth, and set the budget deficit target markedly lower, at 2.6% of GDP, down from 3% in the past two years; news of the proposed reduction in borrowing sent 10-year sovereign bonds futures higher last week after Bloomberg reported the plan to reduce the budget deficit target.