GOLD: $1325.75 DOWN $1.55

Silver: $16.54 DOWN 8 CENTS

Closing access prices:

Gold $1325.30

silver: $16.55

SHANGHAI GOLD FIX: FIRST FIX 10 15 PM EST (2:15 SHANGHAI LOCAL TIME)

SECOND FIX: 2:15 AM EST (6:15 SHANGHAI LOCAL TIME)

SHANGHAI FIRST GOLD FIX: $1336.22 DOLLARS PER OZ

NY PRICE OF GOLD AT EXACT SAME TIME: $1327.95

PREMIUM FIRST FIX: $8.27

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

SECOND SHANGHAI GOLD FIX: $1334.58

NY GOLD PRICE AT THE EXACT SAME TIME: $1327.90

PREMIUM SECOND FIX /NY:$8.68

SHANGHAI REJECTS NY PRICING OF GOLD.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

ON APRIL 1 2018 I WILL NO LONGER PROVIDE THE LONDON FIXES AS THEY ARE MANIPULATED AND THEY WILL BE PROVIDED 36 HRS AFTER THE FACT AND THUS TOTALLY USELESS TO US!!

LONDON FIRST GOLD FIX: 5:30 am est $1324.95

NY PRICING AT THE EXACT SAME TIME: $1325.40

LONDON SECOND GOLD FIX 10 AM: $1323.75

NY PRICING AT THE EXACT SAME TIME. $1323.80

For comex gold:

MARCH/

NUMBER OF NOTICES FILED TODAY FOR MARCH CONTRACT: 0 NOTICE(S) FOR nil OZ.

TOTAL NOTICES SO FAR:4 FOR 400 OZ

For silver:

MARCH

6 NOTICE(S) FILED TODAY FOR

30,000 OZ/

Total number of notices filed so far this month: 4834 for 24,170,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: BID $8647/OFFER $8,717: DOWN $459(morning)

Bitcoin: BID/ $8250/offer $8320: DOWN $853 (CLOSING/5 PM)

end

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total open interest ROSE BY A SMALL SIZED 910 contracts from 199,184 RISING TO 200,094 WITH YESTERDAY’S 10 CENT RISE IN SILVER PRICING. WE OBVIOUSLY HAD ZERO COMEX LIQUIDATION. HOWEVER, WE WERE AGAIN NOTIFIED THAT WE HAD ANOTHER STRONG SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP : 1323 EFP’S FOR MAY AND ZERO FOR ALL OTHER MONTHS AND THUS TOTAL ISSUANCE OF 1323 CONTRACTS. WITH THE TRANSFER OF 1323 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 1323 CONTRACTS TRANSLATES INTO 6.615 MILLION OZ WITH THE RISE IN OPEN INTEREST IN SILVER AT THE COMEX.

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF MARCH:

22,384 CONTRACTS (FOR 10 TRADING DAYS TOTAL 22,384 CONTRACTS OR 122.92 MILLION OZ: AVERAGE PER DAY: 2238 CONTRACTS OR 11.190 MILLION OZ/DAY

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH: 122.92 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 17.56% OF ANNUAL GLOBAL PRODUCTION

ACCUMULATION IN YEAR 2018 TO DATE SILVER EFP’S: 599.395 MILLION OZ.

ACCUMULATION FOR JAN 2018: 236.879 MILLION OZ

ACCUMULATION FOR MONTH OF FEBRUARY: 244.945 MILLION OZ

RESULT: WE HAD A SMALL SIZED GAIN IN COMEX OI SILVER COMEX OF 910 WITH THE 10 CENT RISE IN SILVER PRICE. WE ALSO HAD A GOOD SIZED EFP ISSUANCE OF 1323 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER . FROM THE CME DATA 1323 EFP’S FOR THE MONTH OF MAY WERE ISSUED FOR A DELIVERABLE FORWARD CONTRACT OVER IN LONDON WITH A FIAT BONUS. WE GAINED 2233 OI CONTRACTS i.e. 1323 open interest contracts headed for London (EFP’s) TOGETHER WITH A INCREASE OF 910 OI COMEX CONTRACTS. AND ALL OF THIS HAPPENED WITH THE RISE IN PRICE OF SILVER OF 10 CENTS AND A CLOSING PRICE OF $16.72 WITH RESPECT TO YESTERDAY’S TRADING. YET WE STILL HAVE A GOOD AMOUNT OF SILVER STANDING AT THE COMEX.

In ounces AT THE COMEX, the OI is still represented by just OVER 1 BILLION oz i.e. 1.001 BILLION TO BE EXACT or 142% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT MARCH MONTH/ THEY FILED: 248 NOTICE(S) FOR 1,240,000 OZ OF SILVER

In gold, the open interest ROSE BY AN ATMOSPHERIC SIZED 20,771 CONTRACTS UP TO 528,118 DESPITE THE FAIR SIZED RISE IN PRICE YESTERDAY ( GAIN OF ONLY $6.25) HOWEVER FOR TODAY, THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED AN STRONG SIZED 6784 CONTRACTS : APRIL SAW THE ISSUANCE OF 6784 CONTRACTS, JUNE SAW THE ISSUANCE OF 0 CONTRACTS AND THEN ALL OTHER MONTHS ZERO. The new OI for the gold complex rests at 528,118. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. DEMAND FOR GOLD INTENSIFIES GREATLY AS WE CONTINUE TO WITNESS A HUGE NUMBER OF EFP TRANSFERS TOGETHER WITH THE MASSIVE INCREASE IN GOLD COMEX OI TOGETHER WITH THE TOTAL AMOUNT OF GOLD OUNCES STANDING FOR FEBRUARY COMEX. EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES. IN ESSENCE WE HAVE A HUMONGOUS OI GAIN IN CONTRACTS: 20,771 OI CONTRACTS INCREASED AT THE COMEX AND A STRONG SIZED 6784 OI CONTRACTS WHICH NAVIGATED OVER TO LONDON.THUS TOTAL OI GAIN: 27555 CONTRACTS OR 2,755,000 OZ =85.69 TONNES

YESTERDAY, WE HAD 4161 EFP’S ISSUED.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF MARCH : 86,588 CONTRACTS OR 8,658,800 OZ OR 269.32 TONNES (10 TRADING DAYS AND THUS AVERAGING: 8659 EFP CONTRACTS PER TRADING DAY OR 865,900 OZ/ TRADING DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SIZE OF THESE EFP TRANSFERS : SO FAR THIS MONTH IN 10 TRADING DAYS IN TONNES: 269.32 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2017, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 2555 TONNES

THUS EFP TRANSFERS REPRESENTS 269.32/2550 x 100% TONNES = 10.56% OF GLOBAL ANNUAL PRODUCTION SO FAR IN MARCH ALONE.

ACCUMULATION OF GOLD EFP’S YEAR 2018 TO DATE: 1519.66 TONNES

ACCUMULATION OF GOLD EFP’S FOR JANUARY 2018: 653.22 TONNES

ACCUMULATION OF GOLD EFP’S FOR FEBRUARY: 649.45 TONNES

Result: AN ATMOSPHERIC SIZED INCREASE IN OI AT THE COMEX DESPITE THE SMALL RISE IN PRICE IN GOLD TRADING YESTERDAY ($6.25 GAIN). HOWEVER, WE HAD ANOTHER STRONG SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 6784 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX AND YET WE ALSO OBSERVED A HUGE DELIVERY MONTH FOR THE MONTH OF DECEMBER. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 6784 EFP CONTRACTS ISSUED, WE HAD A NET GAIN IN OPEN INTEREST OF 27,555 contracts ON THE TWO EXCHANGES:

6784 CONTRACTS MOVE TO LONDON AND 20,771 CONTRACTS INCREASED AT THE COMEX. (in tonnes, the GAIN in total oi equates to 85.69 TONNES).

we had: 2 notice(s) filed upon for 200 oz of gold.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD

WITH GOLD DOWN $1.55 : NO CHANGES IN GOLD INVENTORY AT THE GLD /

Inventory rests tonight: 833.73 tonnes.

SLV/

WITH SILVER DOWN 8 CENTS TODAY:

NO CHANGES IN SILVER INVENTORY AT THE SLV/

/INVENTORY RESTS AT 319.012 MILLION OZ/

end

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in silver ROSE BY A FAIR 910 contracts from 199,184 UP TO 200,094 (AND now A LITTLE CLOSER TO THE NEW COMEX RECORD SET ON FRIDAY/APRIL 21/2017 AT 234,787) DESPITE THE RISE IN PRICE OF SILVER (10 CENT GAIN WITH RESPECT TO YESTERDAY’S TRADING). OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE ANOTHER 1323 EFP CONTRACTS FOR MAY (WE DO NOT GET A LOOK AT THESE CONTRACTS AS IT IS PRIVATE BUT THE CFTC DOES AUDIT THEM) AND 0 EFP’S FOR ALL OTHER MONTHS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. WE HAD SOME COMEX SILVER COMEX LIQUIDATION. IF WE TAKE THE OI GAIN AT THE COMEX OF 910 CONTRACTS TO THE 1328 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A GAIN OF 2233 OPEN INTEREST CONTRACTS WE STILL HAVE A STRONG AMOUNT OF SILVER OUNCES THAT ARE STANDING FOR METAL IN MARCH (SEE BELOW). THE NET GAIN TODAY IN OZ ON THE TWO EXCHANGES: 11.16 MILLION OZ!!!

RESULT: A FAIR SIZED INCREASE IN SILVER OI AT THE COMEX WITH THE RISE IN SILVER PRICING YESTERDAY (10 CENTS GAIN IN PRICE) . BUT WE ALSO HAD ANOTHER GOOD SIZED 1323 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR MARCH, DEMAND FOR PHYSICAL SILVER INTENSIFIES AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)WEDNESDAY MORNING/TUESDAY NIGHT: Shanghai closed DOWN 18.86 POINTS OR 0.57% /Hang Sang CLOSED DOWN 166/44 POINTS OR 0.53% / The Nikkei closed DOWN 190.81 POINTS OR 0.87%/Australia’s all ordinaires CLOSED DOWN 0.57%/Chinese yuan (ONSHORE) closed UP at 6.3146/Oil UP to 61.09 dollars per barrel for WTI and 65.08 for Brent. Stocks in Europe OPENED GREEN EXCEPT LONDON . ONSHORE YUAN CLOSED UP AT 6.3268 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.3054 /ONSHORE YUAN TRADING STRONGER AGAINST OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING STRONGER AGAINST THE DOLLAR . CHINA IS NOT VERY HAPPY TODAY (STRONGER CURRENCY BUT WEEK CHINESE MARKETS/AND TRUMP TARIFFS INITIATED/ )

3a)THAILAND/SOUTH KOREA/NORTH KOREA

i)North Korea

b) REPORT ON JAPAN

3 c CHINA

i)China overproduces on steel which saved this country from further economic problems but still is facing a credit impulse collapse: as retail sales plunge

( zerohedge)

4. EUROPEAN AFFAIRS

SLOVAKIA

Murder and protests are rocking this small European nation of Slovakia. The government under Robert Fico is corrupt and he is now fighting for his political future

( zerohedge)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

i) Russia: UK

ii) The town of Salisbury is in total lockdown as the army investigates the Russian spy poisoning. The situation is escalating(courtesy zerohedge)

iii)The Russian response: this action is unacceptable. So far only words from Russia

(courtesy zerohedge)

6 .GLOBAL ISSUES

7. OIL ISSUES

ii)Oil is down by gasoline is up as crude builds but gasoline has a huge draw. Crude again is at record production

(courtesy zerohedge)

8. EMERGING MARKET

9. PHYSICAL MARKETS

i)In order to save itself they are advocating Venezuela to adopt the USA dollar

( Gillespie/CNN/GATA)

ii)Bitcoin sinks as google moves to ban all crypto advertising in June

( zerohedge)

10. USA stories which will influence the price of gold/silver

i)Instead of a gain of .3% the all important retail sales dropped for the 2nd straight month at .1% month/month.

This is a hard data report and certainly signals some problems in the economy

( zerohedge)

ii)This is not what the USA needs: the smell of stagflation. After reporting stagnant retail sales, the core PPI registered its biggest gain since 2014 coming in at .4% month/month instead of an expected print of .2%. This means input costs are on the rise which will hurt margins

( zerohedge)

iii)Business inventories jump in January (probably in anticipation of higher sales which did not happen) coupled with a sales drop, the highest in 18 months.

seems all of the hard data reports which January was not good for the USA

(courtesy zerohedge)

iv)New Jersey is second only to Illinois with the worst ratings of any state. Now the Governor of New Jersey is set to raise taxes on just about everything as they near financial disaster

( zerohedge)

v)A good commentary by Krieger on what Pompeo stands for.

( Mike Krieger/Liberty Blitzkrieg blog)

vi)That did not take long: The Atlanta Fed slashes its forecast for Q1 to below 2.0% at 1.9%,…so much for Trump`s 3.0% growth

vii) SWAMPVILLE

a)We are now witnessing Democrats being furious over Hillary Clinton`s latest comments on how she lost the elction

( zerohedge)

b)New York Times is reporting that Andrew Mccabe is to be fired days before his official retirement

( zerohedge)

c)Vanity Fair reports that Trump is planning to fire Attorney General Jeff Sessions and replacing him with EPA cabinet minister Pruitt, as well as removing McMaster as National Security Advisor. If this happens expect the market to tumble another 1000 points

(courtesy zerohedge)

Trading Volumes on the COMEX

PRELIMINARY COMEX VOLUME FOR TODAY: 282,592 contracts

CONFIRMED COMEX VOL. FOR YESTERDAY: 380,470 CONTRACTS

comex gold volumes are RISING AGAIN

Here is a summary of the latest gold trading volumes at the Comex per year

certainly the introduction of EFP’s has certainly had an effect:

Meanwhile, gold-trading volumes on the COMEX have never been higher:

end

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

And now for the wild silver comex results.

Total silver OI ROSE BY A FAIR SIZED 910 CONTRACTS FROM 199,184 UP TO 200,094 WITH OUR 10 CENT GAIN IN YESTERDAY’S TRADING). HOWEVER,WE WERE ALSO INFORMED THAT WE HAD 1323 EMERGENCY EFP’S FOR MAY ISSUED BY OUR BANKERS AND ZERO FOR ALL OTHER MONTHS TO COMEX LONGS WHO RECEIVED A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON: THE TOTAL EFP’S ISSUED: 1323. THE SILVER BOYS HAVE STARTED TO MIGRATE TO LONDON FROM THE START OF DELIVERY MONTH AND CONTINUING RIGHT THROUGH UNTIL FIRST DAY NOTICE JUST LIKE WE ARE WITNESSING TODAY. USUALLY WE NOTED THAT CONTRACTION IN OI OCCURRED ONLY DURING THE LAST WEEK OF AN UPCOMING ACTIVE DELIVERY MONTH AS WE HAVE JUST SEEN IN GOLD TODAY. THIS PROCESS HAS JUST BEGUN IN EARNEST IN SILVER STARTING IN SEPTEMBER 2017. HOWEVER, IN GOLD, WE HAVE BEEN WITNESSING THIS FOR THE PAST 2 YEARS. NICK LAIRD WAS KIND ENOUGH TO SUPPLY US THE TOTAL FOR 2017 GOLD EFP’S AND IT WAS 6600 TONNES FOR THE ENTIRE YEAR. WE OBVIOUSLY HAD ZERO LONG COMEX SILVER LIQUIDATION BUT WE ALSO HAD A HUGE SIZED GAIN IN TOTAL SILVER OI FROM OUR TWO EXCHANGES. WE ARE ALSO WITNESSING A STRONG AMOUNT OF SILVER OUNCES STANDING FOR COMEX METAL IN THIS NON ACTIVE JANUARY AS WELL AS THAT CONTINUAL MIGRATION OF EFPS OVER TO LONDON. ON A PERCENTAGE BASIS THERE ARE MORE EFP’S ISSUED FOR GOLD THAN SILVER. ON A NET BASIS WE GAINED 2233 SILVER OPEN INTEREST CONTRACTS AS WE OBTAINED A 910 CONTRACT GAIN AT THE COMEX COMBINING WITH THE ADDITION OF 1323 OI CONTRACTS NAVIGATING OVER TO LONDON.

NET GAIN ON THE TWO EXCHANGES:2233 CONTRACTS

AMOUNT STANDING FOR SILVER AT THE COMEX

We are now in the active delivery month of MARCH and here the front month GAINED 3 contracts RISING TO 402 contracts. We had 6 contracts filed upon yesterday, so we GAINED 9 contract or an additional 45,000 will stand in this active delivery month of March.(AS SOMEBODY IS IN URGENT NEED OF CONSIDERABLE PHYSICAL SILVER)

April LOST 10 contracts FALLING TO 433 .

The next big active delivery month for silver will be May and here the OI LOST 221 contracts DOWN to 143,589

We had 248 notice(s) filed for 1,240,000,000 OZ for the MARCH 2018 contract for silver

INITIAL standings for MARCH/GOLD

MARCH 14/2018.

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz |

nil oz

|

| Deposits to the Dealer Inventory in oz | NIL oz |

| Deposits to the Customer Inventory, in oz | nil OZ |

| No of oz served (contracts) today |

2 notice(s)

200 OZ

|

| No of oz to be served (notices) |

535 contracts

(53500 oz)

|

| Total monthly oz gold served (contracts) so far this month |

6 notices

600 oz

|

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

For MARCH:

Today, 0 notice(s) were issued from JPMorgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equates to 2 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped/ Received) by j.P.Morgan customer account.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

To calculate the INITIAL total number of gold ounces standing for the MARCH. contract month, we take the total number of notices filed so far for the month (6) x 100 oz or 0 oz, to which we add the difference between the open interest for the front month of FEB. (537 contracts) minus the number of notices served upon today (2 x 100 oz per contract) equals 54100 oz, the number of ounces standing in this nonactive month of MARCH (1.6821 tonnes)

Thus the INITIAL standings for gold for the MARCH contract month:

No of notices served (6 x 100 oz or ounces + {(537)OI for the front month minus the number of notices served upon today (2 x 100 oz )which equals 54100 oz standing in this nonactive delivery month of March . THERE IS 10.556 TONNES OF REGISTERED GOLD AVAILABLE FOR DELIVERY SO FAR.

WE LOST 0 CONTRACTS OR AN ADDITIONAL NIL OZ WILL STAND FOR DELIVERY IN THIS NON ACTIVE DELIVERY MONTH OF MARCH.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

IN THE LAST 18 MONTHS 70 NET TONNES HAS LEFT THE COMEX.

end

And now for silver

AND NOW THE DECEMBER DELIVERY MONTH

MARCH INITIAL standings/SILVER

| Silver | Ounces |

| Withdrawals from Dealers Inventory | nil oz |

| Withdrawals from Customer Inventory |

34,678.01 oz

Malca

|

| Deposits to the Dealer Inventory |

nil

oz

|

| Deposits to the Customer Inventory |

444,877.400 oz

Scotia

|

| No of oz served today (contracts) |

248

CONTRACT(S

(1,240,000 OZ)

|

| No of oz to be served (notices) |

154 contracts

(770,000 oz)

|

| Total monthly oz silver served (contracts) | 5082 contracts

(25,410,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

we had 0 inventory movement at the dealer side of things

total inventory deposits/withdrawals/ into dealer: nil oz

we had 1 deposits into the customer account

i) Scotia: 444,877.400 oz

ii) Into JPMorgan: zero

*** JPMorgan for most of 2017 and in 2018 has adding to its inventory almost every single day.

JPMorgan now has 135 million oz of total silver inventory or 54% of all official comex silver.

JPMorgan did not add any silver into its warehouses (official) today.

total deposits today: 444,877.400 oz

we had 1 withdrawals from the customer account;

i) Out of Malca 34,678.01 oz

total withdrawals; 34,678.01 oz

we had 1 adjustments

i) out of JPMorgan; 20,195.460 oz was removed from the customer account

total dealer silver: 59.419 million

total dealer + customer silver: 253.703 million oz

The total number of notices filed today for the March. contract month is represented by 248 contract(s) FOR 1,240,000 oz. To calculate the number of silver ounces that will stand for delivery in March., we take the total number of notices filed for the month so far at 5082 x 5,000 oz = 25,410,000 oz to which we add the difference between the open interest for the front month of Mar. (402) and the number of notices served upon today (248 x 5000 oz) equals the number of ounces standing.

.

Thus the INITIAL standings for silver for the March contract month: 5082(notices served so far)x 5000 oz + OI for front month of March(402) -number of notices served upon today (248)x 5000 oz equals 26,180,000 oz of silver standing for the March contract month.

We GAINED an additional 9 contracts or 45,000 additional silver oz will stand for delivery at the comex as somebody was in urgent need of physical silver.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

ESTIMATED VOLUME FOR TODAY: 62,963 CONTRACTS

CONFIRMED VOLUME FOR YESTERDAY: 74,979 CONTRACTS

YESTERDAY’S CONFIRMED VOLUME OF 72,979 CONTRACTS EQUATES TO 364 MILLION OZ OR 52.1% OF ANNUAL GLOBAL PRODUCTION OF SILVER

COMMODITY LAW SUGGESTS THAT OPEN INTEREST SHOULD NOT BE MORE THAN 3% OF ANNUAL GLOBAL PRODUCTION. THE CROOKS ARE SUPPLYING MASSIVE PAPER TRYING TO KEEP SILVER IN CHECK.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price at that day at $18.42

The previous record was 224,540 contracts with the price at that time of $20.44

end

NPV for Sprott

1. Sprott silver fund (PSLV): NAV RISES TO -2.32% (MARCH 14/2018)

2. Sprott gold fund (PHYS): premium to NAV RISES TO -0.53% to NAV (March 14/2018 )

Note: Sprott silver trust back into NEGATIVE territory at -2.32%-/Sprott physical gold trust is back into NEGATIVE/ territory at -0.653%/Central fund of Canada’s is still in jail but being rescued by Sprott.

Sprott WINS hostile 3.1 billion bid to take over Central Fund of Canada

(courtesy Sprott/GATA)

3.SPROTT CEF.A FUND (FORMERLY CENTRAL FUND OF CANADA): NAV RISES TO -2.78%: NAV 13.69/TRADING 13.30//DISCOUNT 2.78.

END

And now the Gold inventory at the GLD/

MARCH 14/WITH GOLD DOWN $1.55/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 833.73 TONNES

MARCH 13/WITH GOLD UP $6.25/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 833.73 TONNES

MARCH 12/WITH GOLD DOWN $3.00/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 833.73 TONNES

MARCH 9/WITH GOLD UP $2.25/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 833.73 TONNES

March 8/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 833.73 TONNES

MARCH 7/WITH GOLD DOWN 8.00/A SLIGHT CHANGE IN GOLD INVENTORY AT THE GLD/A WITHDRAWAL OF .25 TONNES TO PAY FOR FEES//INVENTORY RESTS AT 833.73 TONNES

MARCH 6/WITH GOLD UP $15.60/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 833.98 TONNES

March 5/WITH GOLD DOWN $4.10/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 833.98 TONNES

MARCH 2/WITH GOLD UP $18.70/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 833.98 TONNES

March 1/WITH GOLD DOWN ANOTHER $12.30/A HUGE CHANGE IN GOLD INVENTORY/ A DEPOSIT OF 2.96 TONNES/INVENTORY RESTS AT 833.98 TONNES

FEB 28/WITH GOLD DOWN ANOTHER 70 CENTS/NO CHANGE IN GOLD INVENTORY/INVENTORY RESTS AT 831.03 TONNES/.

feb 27/WITH GOLD DOWN $13.80 WE HAD NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 831.03 TONNES

FEB 26/WITH GOLD UP $2.40/WE HAD ANOTHER INVENTORY GAIN/THIS TIME 1.77 TONNE ADDITION TO THE GLD INVENTORY/INVENTORY RESTS AT 831.03 TONNES/WE HAVE HAD 5 INCREASES IN THE PAST 6 TRADING GOLD SESSIONS/

FEB 23/WITH GOLD DOWN $1.15, WE HAD A GOOD INVENTORY GAIN OF 1.47 TONNES OF GOLD INTO THE GLD/INVENTORY RESTS AT 829.26 TONNES

FEB 22/WITH GOLD UP 90 CENTS AGAIN TODAY, WE HAD NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 827.79 TONNES

FEB 21/ WITH THE 90 CENT GAIN WE HAD ANOTHER DEPOSIT OF 3.15 TONNES OF GOLD INTO THE GLD INVENTORY/INVENTORY RESTS TONIGHT AT 827.79 TONNES

Feb 20/WITH GOLD DOWN BY $24.25, THE CROOKS DECIDED THAT THEY HAD BETTER RETURN (DEPOSIT) 3.34 TONNES OF GOLD INTO THE GLD/INVENTORY RESTS TONIGHT AT 824,64 TONNES

Feb 16/WITH GOLD UP BY 25 CENTS, THE CROOKS DECIDED AGAIN TO RAID THE COOKIE JAR BY WITHDRAWING 2.36 TONNES OF GOLD FROM THE GLD/INVENTORY RESTS AT 821.30 TONNES

Feb 15/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 823.66 TONNES

Feb 14/AN ADDITIONAL OF 2.95 TONNES OF GOLD INTO GLD WITH THE HUGE GAIN OF 27.40 IN PRICE/INVENTORY RESTS AT 823.66 TONNES

Feb 13/WITH GOLD UP $3.40 WE HAD NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY REMAINS AT 820.71 TONNES

Feb 12/STRANGE!!WITH GOLD RISING BY 12.00 DOLLARS, THE CROOKS DECIDED AGAIN TO WITHDRAW 5.6 TONNES OF GOLD FOR EMERGENCY USE ELSEWHERE/INVENTORY RESTS AT 820.71 TONNES

Feb 9/AGAIN WITH HUGE TURMOIL ON THE MARKETS, THE CROOKS WITHDREW 2 TONNES OF GOLD FROM THE GLD INVENTORY/INVENTORY RESTS AT 826.31 TONNES

Feb 8/DESPITE THE GOOD GAIN IN PRICE FOR GOLD TODAY/THE CROOKS REMOVED .96 TONNES FROM THE GLD INVENTORY/INVENTORY RESTS AT 828.31 TONNES

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

MARCH 14/2018/ Inventory rests tonight at 833.73 tonnes

*IN LAST 342 TRADING DAYS: 107,41 NET TONNES HAVE BEEN REMOVED FROM THE GLD

*LAST 272 TRADING DAYS: A NET 48.89 TONNES HAVE NOW BEEN ADDED INTO GLD INVENTORY.

end

Now the SLV Inventory

MARCH 14/WITH SILVER DOWN 8 CENTS/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.012 MILLION OZ/

MARCH 13/WITH SILVER UP 10 CENTS/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.012 MILLION OZ/

MARCH 12/WITH SILVER DOWN 8 CENTS/A BIG CHANGES IN SILVER INVENTORY AT THE SLV/ A DEPOSIT OF 943,000 OZ/INVENTORY RESTS AT 319.012 MILLION OZ/

MARCH 9/WITH SILVER UP 21 CENTS, NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 318.069 MILLION OZ/

March 8/WITH SILVER DOWN 1 CENT TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 318.069 MILLION OZ/

MARCH 7/WITH SILVER DOWN 27 CENTS/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 318.069 MILLION OZ/

MARCH 6/WITH SILVER UP 38 CENTS/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 318.069 MILLION OZ/

March 5/WITH SILVER DOWN 11 CENTS/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 318.069 MILLION OZ/

MARCH 2/WITH SILVER UP 23 CENTS: A HUGE 1.479 MILLION OZ WAS ADDED TO SILVER’S INVENTORY/INVENTORY RESTS AT 318.069 MILLION OZ/

March 1/WITH SILVER DOWN 11 CENTS TODAY/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 316.590 MILLION OZ./

FEB 28/WITH SILVER DOWN 5 CENTS TODAY/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 316.590 MILLION OZ/

feb 27/WITH SILVER DOWN 17 CENTS/NO CHANGE IN SILVER INVENTORY/INVENTORY RESTS AT 316.590 MILLION OZ

FEB 26/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 316.590 MILLION OZ/

FEB 23/WITH SILVER DOWN 10 CENTS TODAY, WE HAD ANOTHER HUGE ADDITION OF 1.315 MILLION OZ/INVENTORY RESTS AT 316.590 MILLION OZ/

fEB 22.2018/WITH SILVER DOWN 1 CENT TODAY, WE HAD NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 315.271 MILLION OZ/

FEB 21/WITH SILVER UP 15 CENTS TODAY, WE HAD A GOOD SIZED INVENTORY ADDITION OF 1.226 MILLION OZ/INVENTORY RESTS AT 315.271 MILLION OZ/

Feb 20/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 314.045 MILLION OZ

Feb 16/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 314.045 MILLION OZ/

Feb 15/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 314.045 MILLION OZ/

Feb 14./NO CHANGE IN SILVER INVENTORY DESPITE THE HUGE RISE IN PRICE/INVENTORY RESTS AT 314.045 MILLION OZ

Feb 13./NO CHANGE IN SILVER INVENTORY TODAY/INVENTORY RESTS AT 314.045 MILLION OZ/

Feb 12/AGAIN, WITH TODAY’S HUGE RISE IN SILVER PRICE, IN TOTAL CONTRAST TO GOLD: NO CHANGE IN SILVER INVENTORY/INVENTORY RESTS AT 314.045 MILLION OZ/

Feb 9/AGAIN WITH TURMOIL ON THE MARKETS, STRANGELY IN TOTAL CONTRAST TO GOLD: NO CHANGE IN SILVER INVENTORY/INVENTORY RESTS AT 314.045 MILLION OZ/

Feb 8/DESPITE THE TURMOIL TODAY AND A PRICE RISE: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 314.045 MILLION OZ/

MARCH 14/2018: NO CHANGES TO SILVER INVENTORY/

Inventory 319.012 million oz

end

6 Month MM GOFO 1.97/ and libor 6 month duration 2.30

Indicative gold forward offer rate for a 6 month duration/calculation:

G0FO+ 1.97%

libor 2.30 FOR 6 MONTHS/

GOLD LENDING RATE: .33%

XXXXXXXX

12 Month MM GOFO

+ 2.39%

LIBOR FOR 12 MONTH DURATION: 2.58

GOFO = LIBOR – GOLD LENDING RATE

GOLD LENDING RATE = +.19

GOLD LENDING RATES FALLING TO APPROACH ZERO AS PHYSICAL GOLD IS SCARCE/GOFO RATES RISING

end

Major gold/silver trading /commentaries for WEDNESDAY

GOLDCORE/BLOG/MARK O’BYRNE.

GOLD/SILVER

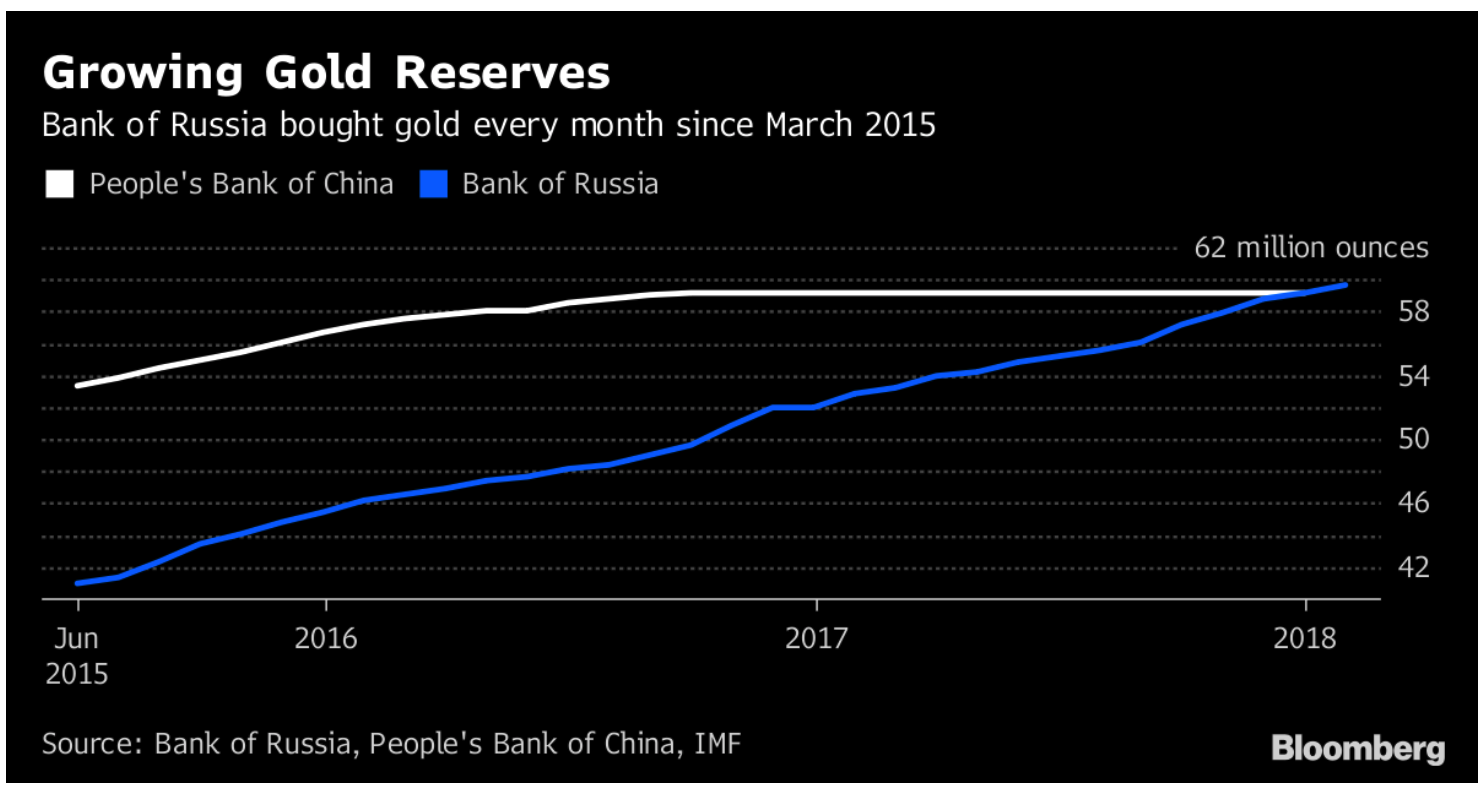

Hungary’s Gold Repatriation Adds To Growing Protest Against US Dollar Hegemony

Hungary’s Gold Repatriation Adds To Growing Protest Against US Dollar Hegemony

– Hungarian National Bank (MNB) to repatriate 100,000 ounces gold from Bank of England

– Follows trend of Netherlands, Germany, Austria and Belgium each looking to bring gold back to home soil

– Hungary one of the smallest gold owners amongst central banks, with just 5 tonnes

– Central bank gold purchases continue to be major drivers of gold market

– Russian central bank gold reserves now exceed those of China

– Decisions to repatriate and increase gold reserves come as rifts between East and West widen

A country’s sovereignty is becoming the driving force of so many changes in the geopolitical sphere, today. Whether it is Brexit, surprise electoral victories in central Europe or a change in trade deals, sovereignty is at the forefront of so many of these decisions.

One of the first indicators that there was a change in the water when it comes to globalisation and international cooperation was through central bank gold buying and repatriation.

For some time now many central banks have been working on building up their gold reserves and ensuring they are stored on soil it believes to be safe and trustworthy.

The most recent central bank to make this change is that of Hungary. Last week it was announced that it intends to bring 100,000 ounces of its very limited 5 tonnes gold reserves, back home from the Bank of England.

This is not an unusual move. In recent years we have seen the likes of Germany, Venezuela and the Netherlands each repatriate their gold from various locations. The pace does appear to have been picking up since the late Hugo Chavez decided to bring home 180 tonnes of gold in 2011.

Furthermore, huge central banks namely Russia and China have been adding to their gold hoards, one more publicly than the other. Both have also been encouraging the use of gold as a means of payment in international trade as a means of avoiding US dollar hegemony.

The decision to place more focus on gold reserves is a statement by central banks and their governments to reduce the counterparty risk on their reserve assets. When holding another country’s currency you are vulnerable, the same applies to when a third-party holds your gold at a time when their own assets are perhaps more exposed than you’re comfortable with.

Russia, China and Turkey leading the gold rush

Hungary’s decision on gold repatriation was not something that made the mainstream news. After all, 100,000 ounces is very little when you consider than Russia increased its physical gold exposure by 20 tons in January 2018 alone.

Hungary decision is, however, a major comment on the current mindset of countries that feel they need to start working to protect their finances and borders. Hungary’s political changes are widely known and have been criticised extensively by both the EU and wider Western world.

The decision to bring gold home is a statement that says Prime Minister Viktor Orban would rather have the country’s assets close to home rather than in the hands-off a country that perhaps does not have his own best interests at heart.

This is a common theme, not just reflected in gold repatriation decisions but also in gold purchases.

Russia, China and Turkey have each materially increased their gold reserves in recent years. Since March 2015 Russia has bought gold every single month. January’s purchase took their reserves above those of China, a level which had previously been monitored as an example of the East’s great interest in moving away from US dollar dominance.

China has been famously coy about its gold reserves. apart from the period from July 2015 to October 2016, China only reported its gold reserve increases at various multi-year intervals. Most recently it has been reporting zero additions to the IMF.

Russia’s reasons for buying so much gold is akin to those of China, Turkey and smaller countries such as Kazakhstan. Gold gives each of these countries independence from the US dollar amid financial sanctions, trade wars and ongoing posturing by the West.

The West is also full of gold bugs

Whilst many in the West are dismissive about gold, the behaviour of central banks suggests quite a different mindset. The top four holders of gold are all from the West. Germany, the second largest has been making big strides of late to show their interest and faith in gold.

Not only did they make the decision to repatriate a late proportion of their gold back to home soil but they also recognised that transparency when it came to the country’s gold reserves was paramount.

‘…another milestone and a global first, an additional fourth step towards increasing transparency was taken with the publication of a list of all German gold bars, totalling around 270,000 in number. The Bundesbank has now published this roughly 2,400-page list three times since October 2015, even though it involved a series of significant challenges. There is no ‘blueprint’ for inventory lists of gold holdings and, in 2015, virtually no central bank in the world had ever released such a list.’

Act like a central bank

Gold cannot be devalued as the euro, dollar, sterling and all fiat currencies currently are. It cannot be confiscated as can deposits through bank bail-ins and it is extremely difficult to confiscate gold coins and bars if owned in allocated and segregated storage in safe vaults in the safest jurisdictions in the world.

Gold is a borderless money that acts as the ultimate reserve and safe haven in a diversified portfolio. This is something central banks are strongly aware of. The difference between the East and West banks is that the East is making big strides to bring gold to the forefront of their international affairs.

By adding gold to their reserves they are gaining equal footing with Western banks who have so far tried to dominate under a US-centric financial system.

Much of the above may sound as though it does not apply to the everyday saver and investor, but that couldn’t be further from the truth. The decision to move assets into physical gold is a decision to take control of your portfolio and to reduce the counterparty risk to which it is exposed. This is no different whether you are a bank with billions or a person with a few thousand.

Recommended reading

Turkey, Gold and the End of US Dollar Hegemony

News and Commentary

Gold prices edge higher as dollar sags (Reuters.com)

Asian Stocks Mixed Ahead of U.S. Data; Yen Higher (Bloomberg.com)

U.S. February budget report shows first sign of wider deficits to come (MarketWatch.com)

Stocks Retreat Before Price Data; Dollar Drops (Bloomberg.com)

Here’s the ideal amount of gold to keep in your investment portfolio (MarketWatch.com)

Source: Gadfly, Bloomberg.

Jim Grant: “Uncomfortable Shocks” Lie Ahead As The Great Bond Bear Market Begins (ZeroHedge.com)

Sea Change Is Underway in Money Markets for Banks, Investors (Bloomberg.com)

Central Banks Are Looking for New Ways to Meet Inflation Targets (Bloomberg.com)

Gary North on central banking, gold, federal debt, and Keynesianism (Barbarous-Relic)

Getting the Cartier Crowd Hooked on Cheap Credit (Bloomberg.com)

Gold Prices (LBMA AM)

13 Mar: USD 1,318.70, GBP 948.94 & EUR 1,069.60 per ounce

12 Mar: USD 1,317.25, GBP 950.66 & EUR 1,069.87 per ounce

09 Mar: USD 1,319.35, GBP 955.21 & EUR 1,072.50 per ounce

08 Mar: USD 1,325.40, GBP 955.08 & EUR 1,070.39 per ounce

07 Mar: USD 1,332.50, GBP 960.07 & EUR 1,071.86 per ounce

06 Mar: USD 1,324.95, GBP 957.01 & EUR 1,074.00 per ounce

05 Mar: USD 1,326.30, GBP 958.78 & EUR 1,075.63 per ounce

Silver Prices (LBMA)

13 Mar: USD 16.51, GBP 11.88 & EUR 13.38 per ounce

12 Mar: USD 16.46, GBP 11.88 & EUR 13.39 per ounce

09 Mar: USD 16.49, GBP 11.92 & EUR 13.40 per ounce

08 Mar: USD 16.48, GBP 11.89 & EUR 13.31 per ounce

07 Mar: USD 16.65, GBP 12.01 & EUR 13.42 per ounce

06 Mar: USD 16.62, GBP 11.96 & EUR 13.41 per ounce

05 Mar: USD 16.51, GBP 11.95 & EUR 13.42 per ounce

Recent Market Updates

– Stock Market Selloff Showed Gold Can Reduce Portfolio Risk

– Gold Protects As Cashless Society Threatens Vulnerable

– Women’s Pension Crisis Highlights Dangers To Savers

– London Property Sees Brave Bet By Norway As Foxtons Profits Plunge

– Gold Does Not Fear Interest Rate Hikes

– RaboDirect Closing – Gold May Protect From Irish Banks Going “Belly Up Again” – Finuncane

– Silver bullion will likely outperform gold bullion going forward

– Gold $10,000? Goldnomics Podcast Quotations and Transcript

– Trump Risks Trade and Currency Wars – Protectionism and Economic War Loom

– Four Key Themes To Drive Gold Prices In 2018 – World Gold Council

– Is The Gold Price Going To $10,000? (Goldnomics Podcast 3)

– Gold Corridor From Dubai to China Sought By China

– Digital Gold Provide the Benefits Of Physical Gold?

Andrew Maguire’s Kinesis money which is a “bitcoin” but backed 100% by allocated gold and silver is set to go.

it think it would be a great idea to look at this!

please read at: https://kinesis.money/#/

(Andrew Maguire)

|

2:57 PM (1 hour ago) | ||

|

|||

Harvey

Here It is my friend! https://kinesis.money/#/ Please let everyone know.

Let catch up on Monday if you have time. We have billions in the hopper ready to be allocated on the 1st day of trading. The paper market days are over.

Warm regards

Andy

end.

END

In order to save itself they are advocating Venezuela to adopt the USA dollar

(courtesy Gillespie/CNN/GATA)

Venezuela urged to save itself by becoming a U.S. colony

Submitted by cpowell on Tue, 2018-03-13 22:28. Section: Daily Dispatches

Why not switch its currency to gold? Venezuela has plenty of it in the ground.

* * *

One Idea to Stop Venezuela’s Downward Spiral: Switch to the U.S. Dollar

By Patrick Gillespie

CNN, Atlanta

Tuesday, March 13, 2018

Venezuela’s currency, the bolivar, lost nearly all its value last year as the country spiraled into an economic crisis. One solution gaining popularity: Get rid of the bolivar and replace it with the U.S. dollar.

The idea is called dollarization. Ecuador, El Salvador, and some small island nations have done it. Now it could be coming to Venezuela, widely considered the world’s worst economy not mired in an armed conflict.

Venezuela has a presidential election this spring, and Henri Falcon is seen as the top opposition candidate to the incumbent, Nicolas Maduro. Francisco Rodriguez, a former Wall Street economist who advises Falcon, says he would shift the nation to the dollar to cure its biggest problem, soaring inflation. …

… For the remainder of the report:

http://money.cnn.com/2018/03/13/news/economy/us-dollar-venezuela/index.h…

end

Bitcoin sinks as google moves to ban all crypto advertising in June

(courtesy zerohedge)

Bitcoin Sinks As Google Moves To Ban All Crypto, ICO Ads In June

Mimicking its biggest rival for ad dollars – Facebook – Google will ban online advertisements promoting cryptocurrencies and initial coin offerings, and “other speculative financial instruments” starting in June.

Some aggressive businesses found a loophole: purposely misspelling words like “bitcoin” in their ads. A Google spokeswoman said the company’s policies will try to anticipate workarounds like this.

The reaction was immediate across the crypto space but for now is somewhat subdued…

Alphabet’s Google said the new policy will become effective in June across ads bought on its search and display-advertising network, as well as its YouTube unit.

But, as The Wall Street Journal reports, the policy also will restrict ads for nontraditional methods of wagering on the future movements of stock prices and foreign-exchange, such as binary options and financial spread-betting, Google said.

Google said last year it removed more than 130 million ads that were used by hackers to mine for cryptocurrency. That is a very small percentage of the ads run on Google’s ad network.

The company’s director of sustainable ads, Scott Spencer, declined to comment on how much potential ad revenue the company would be turning away by enacting the new policy, saying the decision was made to prevent consumer harm.

One wonders when the crackdown will start on inverse VIX ETFs, or just S&P ETFs, or brokerages? Aren’t they all capable of doing consumers “harm”?

As a reminder, here is Facebook’s justification:

We want people to continue to discover and learn about new products and services through Facebook ads without fear of scams or deception. That said, there are many companies who are advertising binary options, ICOs and cryptocurrencies that are not currently operating in good faith.

This policy is intentionally broad while we work to better detect deceptive and misleading advertising practices, and enforcement will begin to ramp up across our platforms including Facebook, Audience Network and Instagram. We will revisit this policy and how we enforce it as our signals improve.

We also understand that we may not catch every ad that should be removed under this new policy, and encourage our community to report content that violates our Advertising Policies. People can report any ad on Facebook by clicking on the upper right-hand corner of the ad.

This policy is part of an ongoing effort to improve the integrity and security of our ads, and to make it harder for scammers to profit from a presence on Facebook.

Which roughly translated is “because we know what’s best for you!”

Your early TUESDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

i) Chinese yuan vs USA dollar/CLOSED UP 6.3146 /shanghai bourse CLOSED DOWN 18.86 POINTS OR 0.57% / HANG SANG CLOSED DOWN 166.44 POINTS OR 0.53%

2. Nikkei closed DOWN 190.81 POINTS OR 0.87% /USA: YEN FALLS TO 106.48/

3. Europe stocks OPENED DEEPLY IN THE GREEN /USA dollar index RISES TO 89.77/Euro FALLS TO 1.2371

3b Japan 10 year bond yield: FALLS TO . +.05O/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 106.48/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD FINALLY IN THE POSITIVE/BANK OF JAPAN LOSING CONTROL OF THEIR YIELD CURVE AS THEY PURCHASE ALL BONDS TO GET TO ZERO RATE!!

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 61.09 and Brent: 65.08

3f Gold DOWN/Yen UP

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil UP for WTI and UP FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund FALLS TO +.624%/Italian 10 yr bond yield UP to 2.016% /SPAIN 10 YR BOND YIELD UP TO 1.413%

3j Greek 10 year bond yield RISES TO : 4.162?????????????????

3k Gold at $1325.65 silver at:16.59 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble UP 24/100 in roubles/dollar) 56.82

3m oil into the 61 dollar handle for WTI and 65 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 106.48 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 0.9451 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1696 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now POSITIVE territory with the 10 year FALLING to +0.624%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.846% early this morning (THIS IS DEADLY TO ALL MARKETS). Thirty year rate at 3.091% /

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

(courtesy Jim Reid/Bloomberg/Deutsche bank/zero hedge)

Futures Rebound Sharply Despite Ongoing Trump Cabinet, Trade War Turmoil

After two consecutive days of failed S&P ignition attempts, in which US stocks opened sharply higher only to close near the lows, on Wednesday the algos will try for the third consecutive time to escape the recent late-day selloff funk. S&P futures are higher after declining on Tuesday following a fresh personnel shakeup in the Trump administration and renewed US trade war speculation with China dampened investor sentiment.

European stocks rose modestly led by mining shares even as Asian shares fell despite stronger than expected Chinese economic data.

Equity markets were attempting to recover after Tuesday’s hefty losses, encouraged by stronger than expected Chinese factory data, but struggled to overcome fears of a global trade war as well as the prospect of political uncertainty in the United States. “As long as the threat of protectionism and a trade war remains, markets will remain vigilant,” Rabobank analysts told clients according to Reuters.

The latest set of tariffs, reportedly targeting Chinese tech, electronics and telecoms, were revealed by sources hours after Trump abruptly fired Secretary of State Rex Tillerson. Tillerson’s exit follows that of economic advisor Gary Cohn, a strong free trade proponent. Since Trump took office in 2017 as many as 35 senior officials from his administration have walked out, including Tillerson, according to Citi.

“The market probably correctly viewed this move as weakening internal White House opposition to some of Trump’s less market-friendly policies, in particular the President’s trade policy,” Daiwa strategist Mantas Vanagas said, quoted by Reuters.

The negative momentum faded somewhat in Europe, with a pan-European equity index up 0.24% after falling 1% on Tuesday. That left MSCI’s all-country equity index down 0.12% its second day in the red, although a rebound in the US will likely push it back in the green.

European stocks rose modestly after opening in the red after Tuesday’s plunge as traders assess the implications of a shakeup in the Trump administration amid corporate updates from companies including Inditex SA and Prudential Plc. The Stoxx Europe 600 Index rises 0.3%, with all major sectors with the exception of utilities are trading higher in the Euro Stoxx, while much of the morning stock movers have been dictated by company earnings, with Adidas (+9%) shares sitting at the top of DAX. Elsewhere, the IBEX underperforms its counterparts as index heavyweight Inditex (-3%) slipped after highlighting concerns over FX headwinds. Zara owner Inditex drops after reporting a slowdown in sales and its weakest profitability in a decade, while U.K. insurer Prudential rises after saying it divested 12 billion pounds ($16.7 billion) of annuities from its U.K. portfolio and plans to spin off its M&G Prudential unit. Miners were the best-performing industry group after Goldman Sachs analysts said the sector is enjoying robust global demand and after China reported strong economic data overnight.

There was no bounce earlier in Asia, where markets followed the negative US lead with the Nikkei (-0.9%), Kospi (-0.3%), Hang Seng (-0.5%) and Shanghai Comp (-0.6%) all down. The latest batch of mixed activity indicators were released in China early this morning. Industrial production in February rose unexpectedly to +7.2% ytd yoy (vs. +6.2% expected; +6.6% previously), as did fixed asset investment (+7.9% yoy vs. +7.0% expected; +7.2% previously) while retail sales were slightly below expectations at +9.7% yoy (vs. +9.8%) from +10.2% in the month prior. As shown in the chart below, Chinese macro data has been disappointing in recent months so the modest upside surprise in factory orders was a welcome change.

In global FX, the dollar pared an early decline as the euro felt some heat from another Draghi reference to the exchange rate, while the Yen rose following continued focus on the Moritomo scandal that has again rocked the Abe administration. A lackluster London session saw the pound shedding gains ahead of a May speech over the U.K.’s relationship with Russia. Bloomberg breaks down the latest overnight FX action:

- The euro set a day low of $1.2364 in early London trading after ECB President Draghi said in a speech that adjustments to monetary policy will remain predictable as policy makers look for further evidence that inflation dynamics are moving in the right direction

- He also said the central bank needs to monitor developments in the common currency closely as its appreciation since the beginning of the year cannot be explained solely by economic expansion

- AUD/USD saw leveraged demand on stronger-than- expected gains in China’s factory output and investment growth

- Kiwi shook off weaker-than-estimated 4Q current-account balance to climb on global fund demand to buy New Zealand’s bonds after Tuesday’s issuance

Treasuries and euro-area bonds were little changed. German 10-year government bond yields approached one-month lows and currently stand 20 basis points below this year’s peak at 0.60 percent, following a soft 30Year debt auction.

Economic data include retail sales and PPI. Williams-Sonoma and Signet Jewelers are among companies due to release results

Market Snapshot

- S&P 500 futures up 0.3% to 2,776.00

- STOXX Europe 600 up 0.3% to 376.55

- MXAP down 0.5% to 178.18

- MXAPJ down 0.4% to 587.85

- Nikkei down 0.9% to 21,777.29

- Topix down 0.5% to 1,743.21

- Hang Seng Index down 0.5% to 31,435.01

- Shanghai Composite down 0.6% to 3,291.38

- Sensex down 0.4% to 33,720.90

- Australia S&P/ASX 200 down 0.7% to 5,935.31

- Kospi down 0.3% to 2,486.08

- German 10Y yield fell 1.0 bps to 0.609%

- Euro down 0.2% to $1.2370

- Brent Futures down 0.2% to $64.51/bbl

- Italian 10Y yield fell 0.9 bps to 1.737%

- Spanish 10Y yield rose 0.8 bps to 1.405%

- Brent Futures down 0.2% to $64.51/bbl

- Gold spot down 0.2% to $1,324.41

- U.S. Dollar Index up 0.2% to 89.83

Top Overnight News

- ECB’s Praet says the central bank’s forward guidance on the path of policy rates will have to be further specified and calibrated as appropriate for inflation to remain on the sustained adjustment path toward levels below, but close to, 2% over the medium term

- The special election in southwestern Pennsylvania remained too close to call with all precincts reporting results. House seat in Pennsylvania may be a bellwether for the fall elections that will decide control of Congress

- Theresa May will meet with her national security and intelligence chiefs Wednesday to assess whether Russia has given a credible answer to her charge that it was behind the poisoning of Sergei and Yulia Skripal in Salisbury. She will then update Parliament on her response.

- China’s factory output and investment growth unexpectedly accelerated in the first two months of the year amid robust global demand

- U.S. Trade Representative Robert Lighthizer presented President Donald Trump with package of tariffs targeting equivalent of $30b a year in Chinese imports, but Trump urged him to aim for higher number, Politico reports, citing three unidentified people familiar with discussions

- Japanese Prime Minister Shinzo Abe and his finance minister denied ordering officials to tamper with documents at the center of a scandal rocking his administration.

- German Chancellor Angela Merkel was formally elected to a fourth term in a parliamentary vote, extending her 12 years in office at the helm of Europe’s biggest economy

- Germany may be ready to sacrifice Jens Weidmann in the contest of becoming the next head of the ECB in a trade for more influence on French President Emmanuel Macron’s push to create closer ties among euro countries

European equities are trading in the green this morning, subsequently pairing the initial losses that stemmed from Asian and US bourses, which saw risk-sentiment soured by reports of Secretary of State Tillerson being fired and increased caution over trade wars. All major sectors with the exception of utilities are trading higher in the Euro Stoxx, while much of the morning stock movers have been dictated by company earnings, with Adidas (+9%) shares sitting at the top of DAX. Elsewhere, the IBEX underperforms its counterparts as index heavyweight Inditex (-3%) slipped after highlighting concerns over FX headwinds.

Top European News

- Germany Ready to Sacrifice Weidmann as a Pawn in EU Chess Match

- Draghi Says Policy Adjustments to Proceed at Measured Pace

- Corin’s Billionaire Owners Said to Mull Sale of Orthopedic Firm

- Volvo Venture Seeks Top Self-Driving Role Angling for More Deals

- May Plots to Punish Russia as Crisis Over Poisoned Spy Deepens

In Asia, equity markets were negative across the board as the region tracked the losses on Wall St, where sentiment was dampened after another high-profile departure from the administration in which President Trump fired Secretary of State Rex Tillerson, while trade war concerns were also stoked by reports the US is looking to impose tariffs on Chinese goods. ASX 200 (-0.7%) and Nikkei 225 (-0.9%) were negative with financials pressured amid the ongoing royal commission hearings in which NAB employees were said to knowingly approved fake loans to reach targets, while Nikkei 225 was pressured by a firmer JPY and with some analysts also noting ‘Abexit’ worries in the wake of the land-sale/cronyism scandal. Shanghai Comp. (-0.4%) and Hang Seng (-1.4%) conformed to the weakness with tech and telecom names weighed as the US seeks to impose tariffs of USD 60bln on Chinese goods, which would target tech and telecom products as a punishment for intellectual property infringement. Although, losses in the mainland were somewhat stemmed by mixed data including higher than expected Industrial Production and Fixed Asset Investments. Finally, 10yr JGBs were flat despite the weakness in stocks, with an uneventful BoJ minutes release and unchanged BoJ Rinban operation amount for 1yr-10yr maturities also ensured quiet price action. BoJ Minutes from the January 22nd-23rd meeting stated it is appropriate to pursue powerful easing and that price momentum to reach target is maintained.

Top Asian News

- China’s Factory Output, Investment Rise on Robust Global Demand

- China Imposes Record $870 Million Fine for Stock Manipulation

- Noble Group Seeks to Sweeten Disputed Debt Deal After Backlash

- Toyota Offers Bigger Raises as Japan Pushes for Inflation

- Not Even Trump Can Slow Vietnam’s Economy, Official Says

In FX, USD weakness amidst ongoing global trade war and White House personnel concerns remains the principle theme, as the DXY continues to reject advances towards the 90.000 level and beyond, which in turn is shifting the technical outlook more bearish. However, EURUSD and single currency crosses have been knocked back to an extent by comments from ECB President Draghi and Chief Economist Praet, reiterating that inflation is still below target and therefore policy needs to stay ‘patient, persistent and prudent’. Key downside risks were highlighted – FX and the aforementioned potentially adverse trade developments due to US President Trump’s import tariff proposals. Eur/Usd is back below 1.2400, but holding above the 30 DMA at 1.2345, and also eyeing decent expiry interest from 1.2390-1.2405 (around 1 bn). Conversely, Aud/Usd is testing resistance either side of the 0.7900 handle again and recent peaks just below the big figure, aided by some Chinese data beats overnight and more balanced rather than dovish/cautious RBA rhetoric via Assistant Governor Kent. Chart-wise, yesterday’s 0.7898 high forms the first/nearest bullish target and offers are touted around 0.7925, if 0.7900 is breached. Cable looks capped by the 1.4000 level, and Usd/Cad by 1.3000, while Usd/Jpy is back in the 106.50 area after a further retreat from 107.00+ peaks late last week and earlier this week with the 10 DMA at 106.31 holding in for now. Elsewhere, Eur/Sek just a fraction softer after broadly as forecast Swedish CPI data that will underscore growing calls for the Riksbank to refrain from tightening for longer.

In commodities, oil prices are trading slightly higher with prices finding some slight reprieve from yesterday’s smaller than expected build in the latest API report, alongside the improvement in risk sentiment, which has seen WTI retest USD 61/bbl

Looking at the day ahead, it looks set to be another important day of data with February retail sales and PPI, followed by January business inventories. It’s worth also highlighting that the European Commission is expected to make comments on US steel and aluminium tariffs to the European Parliament.

US Event Calendar

- 7am: MBA Mortgage Applications, prior 0.3%

- 8:30am: Retail Sales Advance MoM, est. 0.3%, prior -0.3%

- Retail Sales Ex Auto MoM, est. 0.4%, prior 0.0%

- Retail Sales Ex Auto and Gas, est. 0.32%, prior -0.2%

- Retail Sales Control Group, est. 0.4%, prior 0.0%

- 8:30am: PPI Final Demand MoM, est. 0.1%, prior 0.4%

- PPI Ex Food and Energy MoM, est. 0.2%, prior 0.4%

- PPI Ex Food, Energy, Trade MoM, est. 0.2%, prior 0.4%

- 8:30am: PPI Final Demand YoY, est. 2.8%, prior 2.7%

- 8:30am: PPI Ex Food and Energy YoY, est. 2.6%, prior 2.2%

- 8:30am: PPI Ex Food, Energy, Trade YoY, prior 2.5%

- 10am: Business Inventories, est. 0.6%, prior 0.4%

DB’s Craig Nicol concludes the overnight wrap

Picking the right moment to run out and grab lunch is something of a fine art working in markets. Indeed, anyone who was out for the 12 minutes between 12.30pm GMT and 12.42pm GMT yesterday probably felt like they’d been gone a lot longer when they returned to their screens. It takes something fairly significant to overshadow US inflation data at the moment however the shock news that President Trump had ousted now former US Secretary of State Rex Tillerson was certainly enough to do just that.

The announcement came via a tweet from the President and it also included confirmation that CIA Director Mike Pompeo would take over the role. Trump confirmed with reporters that Tillerson “had a different mindset” relative to the President with the Iran nuclear deal named as an example. It was no secret that Tillerson’s tenure had been somewhat rocky however it’s fair to say that markets were still caught off guard, despite his clock probably ticking. Indeed Politico also reported that Tillerson had no plans to leave and was also unsure why he had been let go. There were suggestions that Tillerson’s vocal statements on Monday about condemning the Russian government about its alleged role in the Russian spy incident in the UK could have played a part however that remains to be seen. Various news outlets also confirmed that Trump wanted a new team in place ahead of talks with North Korea and also ongoing trade talks.

It’s not the first time that Trump has moved quickly in his administration without warning, with Reince Priebus and James Comey two other such examples. In fact, the NY Times also reported that Trump’s personal assistant, John McEntee, was let go on Monday and escorted from the White House, while another headline from the Times suggested that there would be more staff shifts this week. The bottom line for us is that all these moves show that the President is certainly moving a lot closer to his anti-globalist policy agenda. On that point, the view on Pompeo is that he and Trump are a lot closer aligned and that Pompeo is more likely to have the President’s ear. On a related note, it also appears that Larry Kudlow is now the favourite to replace Gary Cohn based on comments from the President yesterday. That’s perhaps more interesting given that Kudlow and Trump have clashed in the past over tax reform and also the recent tariff announcements.

Aside from the 12 minutes of a slightly more positive risk environment following the US CPI report (more on that below), the Tillerson news certainly more than played its part in equity markets dropping from early highs. The S&P 500 finished -0.64% last night after being up as much as +0.67% at one stage. A Reuters story suggesting that Trump was seeking for tariffs of up to $60bn a year on China imports seemed to just extend selling pressure into the evening. Meanwhile the previously untouchable Nasdaq (-1.02%) snapped its 7-day winning run while in Europe the big mover was the export-heavy DAX which tumbled to a -1.59% loss. Moves for bonds were actually a bit more contained. The high-to-low range on 10y Treasuries was 6bps and the yield did fall to the lowest in over a week (2.828%) at one point, however by the end of play they were just 2.6bps lower at 2.843%. The 30y auction was also relatively solid with the highest award to direct bidders since October 2015. In Europe bond markets were broadly 1-2bps lower while the Greenback was well offered with the Dollar index falling -0.26%. Gold (+0.26%) also seemed to benefit from a flight to quality bid.

With regards to the CPI data, that in-line +0.2% mom core print meant that the annual rate also held at +1.8% yoy for the third consecutive month. The unrounded reading was +0.182%, so the overall feeling was that it largely mirrored the marginally softer earnings number on Friday. However, momentum is still favouring the hawks with the three-month annualized rate now up to +3.1% and the highest since 2007. The six-month annualized rate is also at a

robust +2.5%. That should be comforting to a Fed which is targeting the gradual approach for now though. As a reminder that is the last CPI report that the Fed will see prior to the FOMC meeting next week however they will benefit from the release of the February PPI data today. Expectations for that is also for a +0.2% mom core reading while the headline is expected to show a +0.1% mom rise in producer prices.

Here in the UK there were no huge surprises to come from Chancellor Hammond’s Spring Statement. As widely expected the borrowing numbers for the current fiscal year and also the next were revised down. This year was revised down from £50bn to £45bn while next year was revised down from £40bn to £37bn. Headroom relative to the 2% cyclically adjusted borrowing to GDP target by 2020-21 is more or less unchanged versus the November estimate at around £15bn, so not a huge amount more fiscal room. Finally GDP forecasts remain fairly lacklustre and included a cut to the 2021-22 forecast. The 2018 forecast was however revised up one-tenth to 1.5%. Sterling closed up +0.40% last night versus the USD but that appeared to be more USD weakness related to the Tillerson news than anything else. Indeed versus the Euro, Sterling was closer to unchanged. Gilt yields also finished more or less unchanged by the end of play.

This morning in Asia, markets have largely followed the negative US lead with the Nikkei (-0.83%), Kospi (-0.51%), Hang Seng (-1.30%) and Shanghai Comp (-0.60%) all down as we type. The latest batch of activity indicators were released in China early this morning. Industrial production in February rose unexpectedly to +7.2% ytd yoy (vs. +6.2% expected; +6.6% previously), as did fixed asset investment (+7.9% yoy vs. +7.0% expected; +7.2% previously) while retail sales were slightly below expectations at +9.7% yoy (vs. +9.8%) from +10.2% in the month prior. The combined Jan and Feb data is meant to smooth out the effects of the Lunar New Year. Meanwhile, the Pennsylvania Congressional District special election in the US is appearing to head for a neck and neck finish.

Bloomberg is reporting that Democrat Conor Lamb holds a tiny lead of 579 votes over Republican Rich Sacconne, out of about 227,000 votes cast. Finally in Japan, the BOJ minutes showed most board members believe the bank must “persistently” pursue powerful easing. Notably, during Q&A BOJ Governor Kuroda noted “by combining various tools, it’s possible to shrink the BOJ’s balance sheet at an appropriate pace while keeping markets stable”.

Turning back to Europe, another Politico article yesterday suggested that the Bundesbank’s Weidmann is the favourite to replace Mario Draghi as ECB President from October 2019. However the story also suggested that his support was receiving pushback, in part given Weidmann’s vocal opposition to Draghi’s QE policy and his strict enforcement of the EU’s fiscal policies. Other potential German candidates touted include Klaus Regling (current head of the ESM) and Marcel Fratscher (Head of the research institute DIW Berlin). Notably, the swing factor for the candidacy likely depends on the relative support of French President Macron, who has been relatively quiet on this topic.

In other news, the OECD has upgraded its forecasts on global economic growth by 0.2-0.3ppt to 3.9% for both 2018 and 2019, with “private investment and trade picking up on the back of strong business and household confidence”. Across countries, growth in the US has been lifted to 2.9% for 2018 (+0.4ppt) and 2.8% for 2019 (+0.7ppt) in part due to the tax cuts and new fiscal spending increases, while the UK’s growth was revised slightly higher to 1.3% in 2018 and 1.1% in 2019. Notably, the agency also warned on protectionism and noted that “an escalation of trade tensions would be damaging for growth and jobs” and that countries should “avoid escalation and rely on global solutions to solve steel excess capacity”.

Before we take a look at today’s calendar, we wrap up with other data releases from yesterday. In the US, the February NFIB small business optimism index was above market at 107.6 (vs. 107.1 expected) and marked a fresh high since 1983. The survey also showed that c.1/3 of owners reported raising compensation to retain or attract workers in the month, the largest share in 17 years. In Europe, Italy’s Q4 unemployment rate was in line at 11% and the final reading of Spain’s February CPI was confirmed at 1.2% yoy. Elsewhere, France’s Q4 total payrolls was up +0.3% qoq (vs. +0.2% expected).

Looking at the day ahead, we’ll get final revisions to February CPI in Germany along with January industrial production and Q4 employment data for the Euro area. ECB President Draghi is scheduled to speak in the morning (8am London time), as well as the ECB’s Coeure, Praet Constancio and then Bank of France’s Governor Villeroy. In the US, it looks set to be another important day of data with February retail sales and PPI, followed by January business inventories. It’s worth also highlighting that the European Commission is expected to make comments on US steel and aluminium tariffs to the European Parliament.

end

3. ASIAN AFFAIRS

i)WEDNESDAY MORNING/TUESDAY NIGHT: Shanghai closed DOWN 18.86 POINTS OR 0.57% /Hang Sang CLOSED DOWN 166/44 POINTS OR 0.53% / The Nikkei closed DOWN 190.81 POINTS OR 0.87%/Australia’s all ordinaires CLOSED DOWN 0.57%/Chinese yuan (ONSHORE) closed UP at 6.3146/Oil UP to 61.09 dollars per barrel for WTI and 65.08 for Brent. Stocks in Europe OPENED GREEN EXCEPT LONDON . ONSHORE YUAN CLOSED UP AT 6.3268 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.3054 /ONSHORE YUAN TRADING STRONGER AGAINST OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING STRONGER AGAINST THE DOLLAR . CHINA IS NOT VERY HAPPY TODAY (STRONGER CURRENCY BUT WEEK CHINESE MARKETS/AND TRUMP TARIFFS INITIATED/ )

3 a NORTH KOREA/USA

/NORTH KOREA/USA

3 b JAPAN AFFAIRS

c) REPORT ON CHINA

China overproduces on steel which saved this country from further economic problems but still is facing a credit impulse collapse: as retail sales plunge

(courtesy zerohedge)

Steel Output Surge Saves Chinese Economy Despite Credit Impulse Collapse

Despite all the discontinuities that the lunar new year causes in China’s macro data, the global synchronous recovery narrative is fading fast, but while retail sales missed, China’s Industrial Production surged in February (thanks to Steel production up 5.9% YoY).

China’s macro data has been disappointing for a couple of months…

And as Bloomberg’s Enda Curran notes, it’s China data day, but with a catch.

Today’s numbers will cover a period when the economy more or less shut down for the annual New Year holidays which means it’s a tricky time of the year for gauging the economy’s true strength. We’ll have to wait for the March and April numbers to get a better handle.

And so what did the data look like…

- Retail Sales YTD YoY MISS +9.7% vs 9.8% exp vs 10.2% prior

- Industrial Production YTD YoY HUGE BEAT +7.2% vs 6.2% exp vs 6.6% prior

- Fixed Asset Investment YTD YoY HUGE BEAT +7.9% vs 7.0% exp vs 7.2% prior

Amid all the tariffs, it seems Steel saved China…

- China Jan.-Feb. Steel Product Output Rises 4.6% to 159.03M Tons

- China Jan.-Feb. Crude Steel Output Rises 5.9% to 136.82M Tons

And Iron Ore inventories are surging..

.

Iris Pang at ING has some interesting observations on industrial production. Even though factories were closed, the tech boom boosted output. Here’s some numbers:

“That growth will probably come from high-tech sectors, including industrial robots (+68.1 percent in 2017), new energy cars (+51.1 percent) and integrated circuits (+18.2 percent).

The cold winter is also likely to increase production of electricity. These areas will probably cushion the loss of production from capacity-cuts in cement, coke and crude oil.”

The figures do somewhat cut against the overarching narrative of a slowdown in the old-industrial drivers and a switch to consumption.

Meanwhile, Chinese stocks managed to scramble back into the green for the year after the lunar new year’s celebration, but are rolling over once again…

As foreign investors fled in February…

All of which happening as the lagged impact of the collapse of China’s credit impulse filters through…

And don’t expect it to resurge anytime soon as Xi – now emperor for life – cracks down on leverage and debt across society (for now).

Of course, as Bloomberg’s Chris Anstey concludes, from a financial-market perspective, it’s been some time since investors agonized over Chinese indicators. Most are comfortable that the hard-landing fears are in the rear-view mirror now, and have become accustomed to the idea that China is in a gradual transition from focus on quantity of growth to quality.

Of course, that complacency is there until something (like Anbang) goes boom..

Here Comes The Main Event: Trade War With China, And What Is Section 301

The recently announced global steel and aluminum tariffs (with various exemptions) by the Trump administration were just a (Section 232) preview of the main event: Trump’s imminent trade war with China, which as Credit Suisse previews, will be unveiled any moment in the form of tariffs and restrictions on trade with China, reportedly in retaliation for Chinese IP violations.

First, a reminder on the all-important Section 301:

- What is Section 301? Section 301 of the 1974 Trade Act allows the President to, among other things, “impose duties or other import restrictions on the products of [a] foreign country,” if the President determines that that country is violating a trade agreement or “engages in discriminatory or other acts or policies which are unjustifiable or unreasonable and which burden or restrict United States commerce.“ The U.S. relied heavily on the provision during the Reagan era (an administration in which the current USTR Robert Lighthizer served as Deputy USTR) into the early 1990s, but it has been used infrequently since the World Trade Organization was formed in 1995 and provided a forum for dispute resolution.

How will Section 301 figure in the upcoming US-Chinese trade war, and what are the key points:

- Last August, President Trump instructed his U.S. Trade Representative Robert Lighthizer to initiate a Section 301 investigation into China’s forced technology transfer policies.

- While the results of the 301 investigation are not due until August 2018, the President appears poised to act on the issue in the coming weeks.

- The President is reported to be seriously considering a package of tariffs on Chinese imports (targeting between $30BN and $60BN worth).

- Reports have stated that Administration officials have used China’s manufacturing roadmap, “Made in China 2025,” in deciding what goods to impose tariffs on. This will likely further concern Chinese leaders.

- In addition, the Administration has discussed rescinding licenses for Chinese businesses and employing other such methods to restrict Chinese investment in the United States. The President’s recent decision to block a Singaporean company’s bid to takeover a U.S. company underscores his aversion to Chinese direct investment (the company had Chinese affiliations).

- As part of the 301 action, the Administration has also reportedly discussed visa restrictions and a mandate that U.S. stock exchanges limit who can list in a U.S. market. It remains unclear whether the restrictions will go this far, but the President has, to date, been hawkish in his trade policy and there seem to be fewer and fewer moderating voices in the White House.

- The 301 investigation and potential actions resulting from it seem to complement congressional efforts to restrict Chinese investment through legislation broadening the jurisdiction of the Committee on Foreign Investment in the United States (CFIUS). We believe this legislation is on track to be signed into law in Q3 2018.

What to expect? here are some high-level thoughts from Credit Suisse:

- The Chinese will likely respond in kind, beginning a succession of tit-for-tat trade policies between the two countries.

- The United States has the option to take a multilateral approach and work with allied nations to initiate their own WTO dispute regarding Chinese technology transfer policies. However, at this point, the U.S. appears more likely to instead take unilateral retaliatory action without WTO authorization, which may run afoul of the U.S.’s WTO obligations.

- If the U.S. acts unilaterally (as it appears it will), China will likely bring a challenge before the World Trade Organization (WTO).

- The President appears committed to maintaining his “tough on China” stance. Even after losing top advisor Gary Cohn after the imposition of steel and aluminum tariffs, the President appears steadfast in his campaign against China’s trade practices and Chinese investment in the U.S, and we expect continued restrictive trade policies with respect to China.

- The President’s actions may not receive the congressional backlash that his steel and aluminum tariffs did. Many U.S. corporations are frustrated with China’s policy requiring foreign companies to turn over source code and other proprietary technology in exchange for access to the Chinese market. However, if the President takes this as far as he currently seems to be planning to, punitive measures by China coupled with the chilling of foreign investment could be a major concern for U.S. corporations.

In terms of specifics, the US trade deficit last year hit an all time high of $375BN.

The Trump administration is planning imposing tariffs on up to $60bn of Chinese goods, or roughly 13% of goods import from China ($505BN), and 2.75% of total US goods import according to Danske Bank; the tariffs will target tech products, telecoms & clothing.

A snapshot of the key aspect of the US-China trade relationship:

- the US exports soybeans, pharmaceuticals, vehicles and aircraft.

- the US imports textiles,clothing, manufactures of metals,electronics and toys.

How to trade it?