GOLD: $1326.75 UP $6.25

Silver: $16.62 UP 10 CENTS

Closing access prices:

Gold $1326.50

silver: $16.61

SHANGHAI GOLD FIX: FIRST FIX 10 15 PM EST (2:15 SHANGHAI LOCAL TIME)

SECOND FIX: 2:15 AM EST (6:15 SHANGHAI LOCAL TIME)

SHANGHAI FIRST GOLD FIX: $1330.53 DOLLARS PER OZ

NY PRICE OF GOLD AT EXACT SAME TIME: $1323.35

PREMIUM FIRST FIX: $7.18

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

SECOND SHANGHAI GOLD FIX: $1328.77

NY GOLD PRICE AT THE EXACT SAME TIME: $1320.50

PREMIUM SECOND FIX /NY:$8.27

SHANGHAI REJECTS NY PRICING OF GOLD.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

ON APRIL 1 2018 I WILL NO LONGER PROVIDE THE LONDON FIXES AS THEY ARE MANIPULATED AND THEY WILL BE PROVIDED 36 HRS AFTER THE FACT AND THUS TOTALLY USELESS TO US!!

LONDON FIRST GOLD FIX: 5:30 am est $1318.70

NY PRICING AT THE EXACT SAME TIME: $1317.75 ??

LONDON SECOND GOLD FIX 10 AM: $1322.75

NY PRICING AT THE EXACT SAME TIME. $1326.80???

For comex gold:

MARCH/

NUMBER OF NOTICES FILED TODAY FOR MARCH CONTRACT: 0 NOTICE(S) FOR nil OZ.

TOTAL NOTICES SO FAR:4 FOR 400 OZ

For silver:

MARCH

6 NOTICE(S) FILED TODAY FOR

30,000 OZ/

Total number of notices filed so far this month: 4834 for 24,170,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: BID $8934/OFFER $9,003: DOWN $155(morning)

Bitcoin: BID/ $9023/offer $9093: DOWN $65 (CLOSING/5 PM)

end

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total open interest ROSE BY A CONSIDERABLE SIZED 2228 contracts from 196,956 RISING TO 199,184 DESPITE YESTERDAY’S SMALL 8 CENT FALL IN SILVER PRICING. WE OBVIOUSLY HAD ZERO COMEX LIQUIDATION. HOWEVER, WE WERE AGAIN NOTIFIED THAT WE HAD ANOTHER SMALL SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP : 598 EFP’S FOR MAY AND ZERO FOR ALL OTHER MONTHS AND THUS TOTAL ISSUANCE OF 598 CONTRACTS. WITH THE TRANSFER OF 598 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 598 CONTRACTS TRANSLATES INTO 2.990 MILLION OZ WITH THE RISE IN OPEN INTEREST IN SILVER AT THE COMEX.

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF MARCH:

20,061 CONTRACTS (FOR 9 TRADING DAYS TOTAL 20,061 CONTRACTS OR 100.305 MILLION OZ: AVERAGE PER DAY: 2229 CONTRACTS OR 11.145 MILLION OZ/DAY

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH: 100.305 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 14.28% OF ANNUAL GLOBAL PRODUCTION

ACCUMULATION IN YEAR 2018 TO DATE SILVER EFP’S: 592.78 MILLION OZ.

ACCUMULATION FOR JAN 2018: 236.879 MILLION OZ

ACCUMULATION FOR MONTH OF FEBRUARY: 244.945 MILLION OZ

RESULT: WE HAD A CONSIDERABLE SIZED GAIN IN COMEX OI SILVER COMEX OF 2228 DESPITE THE SMALL 8 CENT FALL IN SILVER PRICE. WE ALSO HAD A SMALL SIZED EFP ISSUANCE OF 598 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER . FROM THE CME DATA 598 EFP’S FOR THE MONTH OF MAY WERE ISSUED FOR A DELIVERABLE FORWARD CONTRACT OVER IN LONDON WITH A FIAT BONUS. WE GAINED 2826 OI CONTRACTS i.e. 598 open interest contracts headed for London (EFP’s) TOGETHER WITH A INCREASE OF 2228 OI COMEX CONTRACTS. AND ALL OF THIS HAPPENED WITH THE FALL IN PRICE OF SILVER OF 8 CENTS AND A CLOSING PRICE OF $16.62 WITH RESPECT TO YESTERDAY’S TRADING. YET WE STILL HAVE A GOOD AMOUNT OF SILVER STANDING AT THE COMEX.

In ounces AT THE COMEX, the OI is still represented by just UNDER 1 BILLION oz i.e. 0.998 BILLION TO BE EXACT or 142% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT FEBRUARY MONTH/ THEY FILED: 6 NOTICE(S) FOR 30,000 OZ OF SILVER

In gold, the open interest ROSE BY A HUGE SIZED 10,222 CONTRACTS UP TO 505,991 DESPITE THE FALL IN PRICE YESTERDAY ( LOSS OF$3.00) HOWEVER FOR TODAY, THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED AN GOOD SIZED 4161 CONTRACTS : APRIL SAW THE ISSUANCE OF 4161 CONTRACTS, JUNE SAW THE ISSUANCE OF 0 CONTRACTS AND THEN ALL OTHER MONTHS ZERO. The new OI for the gold complex rests at 505,991. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. DEMAND FOR GOLD INTENSIFIES GREATLY AS WE CONTINUE TO WITNESS A HUGE NUMBER OF EFP TRANSFERS TOGETHER WITH THE MASSIVE INCREASE IN GOLD COMEX OI TOGETHER WITH THE TOTAL AMOUNT OF GOLD OUNCES STANDING FOR FEBRUARY COMEX. EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES. IN ESSENCE WE HAVE A GOOD OI GAIN IN CONTRACTS: 10,222 OI CONTRACTS INCREASED AT THE COMEX AND A GOOD SIZED 4161 OI CONTRACTS WHICH NAVIGATED OVER TO LONDON.THUS TOTAL OI GAIN: 14,383 CONTRACTS OR 1,438,300 OZ =44.73 TONNES

YETERDAY, WE HAD 6847 EFP’S ISSUED.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF MARCH : 79,804 CONTRACTS OR 7,980,400 OZ OR 248.22 TONNES (9 TRADING DAYS AND THUS AVERAGING: 8867 EFP CONTRACTS PER TRADING DAY OR 886,700 OZ/ TRADING DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SIZE OF THESE EFP TRANSFERS : SO FAR THIS MONTH IN 9 TRADING DAYS IN TONNES: 248.22 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2017, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 2555 TONNES

THUS EFP TRANSFERS REPRESENTS 248.22/2550 x 100% TONNES = 9.73% OF GLOBAL ANNUAL PRODUCTION SO FAR IN MARCH ALONE.

ACCUMULATION OF GOLD EFP’S YEAR 2018 TO DATE: 1498.56 TONNES

ACCUMULATION OF GOLD EFP’S FOR JANUARY 2018: 653.22 TONNES

ACCUMULATION OF GOLD EFP’S FOR FEBRUARY: 649.45 TONNES

Result: A HUGE SIZED INCREASE IN OI AT THE COMEX DESPITE THE FALL IN PRICE IN GOLD TRADING YESTERDAY ($3.00 LOSS). HOWEVER, WE HAD ANOTHER FAIR SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 4161 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX AND YET WE ALSO OBSERVED A HUGE DELIVERY MONTH FOR THE MONTH OF DECEMBER. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 4161 EFP CONTRACTS ISSUED, WE HAD A NET GAIN IN OPEN INTEREST OF 14,383 contracts ON THE TWO EXCHANGES:

4161 CONTRACTS MOVE TO LONDON AND 10,222 CONTRACTS INCREASED AT THE COMEX. (in tonnes, the GAIN in total oi equates to 44.73 TONNES).

we had: 0 notice(s) filed upon for nil oz of gold.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD

WITH GOLD UP $6.25 : NO CHANGES IN GOLD INVENTORY AT THE GLD /

Inventory rests tonight: 833.73 tonnes.

SLV/

WITH SILVER UP 10 CENTS TODAY:

NO CHANGES IN SILVER INVENTORY AT THE SLV/

/INVENTORY RESTS AT 319.012 MILLION OZ/

end

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in silver ROSE BY A CONSIDERABLE 2228 contracts from 196,956 UP TO 199,184 (AND now A LITTLE CLOSER TO THE NEW COMEX RECORD SET ON FRIDAY/APRIL 21/2017 AT 234,787) DESPITE THE FALL IN PRICE OF SILVER (8 CENT LOSS WITH RESPECT TO YESTERDAY’S TRADING). OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE ANOTHER 598 EFP CONTRACTS FOR MAY (WE DO NOT GET A LOOK AT THESE CONTRACTS AS IT IS PRIVATE BUT THE CFTC DOES AUDIT THEM) AND 0 EFP’S FOR ALL OTHER MONTHS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. WE HAD SOME COMEX SILVER COMEX LIQUIDATION. IF WE TAKE THE OI GAIN AT THE COMEX OF 2228 CONTRACTS TO THE 598 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A GAIN OF 2826 OPEN INTEREST CONTRACTS WE STILL HAVE A STRONG AMOUNT OF SILVER OUNCES THAT ARE STANDING FOR METAL IN MARCH (SEE BELOW). THE NET GAIN TODAY IN OZ ON THE TWO EXCHANGES: 14.130 MILLION OZ!!!

RESULT: A CONSIDERABLE SIZED INCREASE IN SILVER OI AT THE COMEX DESPITE THE FALL IN SILVER PRICING YESTERDAY (8 CENTS LOSS IN PRICE) . BUT WE ALSO HAD ANOTHER SMALL SIZED 598 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR MARCH, DEMAND FOR PHYSICAL SILVER INTENSIFIES AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)TUESDAY MORNING/MONDAY NIGHT: Shanghai closed DOWN 16.46 POINTS OR 0.49% /Hang Sang CLOSED UP 7.12 POINTS OR 0.02% / The Nikkei closed UP 144.07 POINTS OR 0.66%/Australia’s all ordinaires CLOSED DOWN 0.40%/Chinese yuan (ONSHORE) closed UP at 6.3268/Oil UP to 61.47 dollars per barrel for WTI and 64.86 for Brent. Stocks in Europe OPENED GREEN EXCEPT LONDON . ONSHORE YUAN CLOSED UP AT 6.3268 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.3287 /ONSHORE YUAN TRADING STRONGER AGAINST OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING STRONGER AGAINST THE DOLLAR . CHINA IS VERY HAPPY TODAY (STRONGER CURRENCY GOOD CHINESE MARKETS/BUT TRUMP TARIFFS INITIATED/ )

3a)THAILAND/SOUTH KOREA/NORTH KOREA

i)North Korea

b) REPORT ON JAPAN

3 c CHINA

4. EUROPEAN AFFAIRS

Brexit and the media are blamed as London house prices plunge the greatest since 2009

( zerohedge)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

After Tillerson was fired, he responds that Moscow was clearly behind the Skripal poisoning and it will trigger a response

( zerohedge)

ii)Russia/UK

Russia refuses to respond to the UK ultimatum until it receives nerve toxin samples

( zerohedge)

iib)RUSSIA/UK

Russia to the UK: “One does not give 24 hours notice to a nuclear power”..the situation escalates

( zerohedge)

(courtesy zerohedge)

6 .GLOBAL ISSUES

7. OIL ISSUES

8. EMERGING MARKET

9. PHYSICAL MARKETS

i)Congressman criticized the USA mint for inaction on the counterfeiting of gold/silver coins. The mint states that it is not significant enough to warrant action

( GATA./Ein Presswire.com)

ii)Although tiny in numbers, the Hungarian Central Bank must have been reading Nicholas B. as they now wish to repatriate their entire 3 tonnes of gold held in London

( GoldBroker.com)

10. USA stories which will influence the price of gold/silver

i)Big news of the day: Trump fires Rex Tillerson and replaces him with the man he always wanted there: Mike Pompeo

( zero hedge)

ii)Then stocks gain as Trump says that Kudlow has a very good chance.

( zerohedge)

iii)Then Trump fires his personal assistant, John McEntee who was escorted out of the White House yesterday. Reasons given: security issues.

( zerohedge)

iii b)Trump fires the top deputy, Steve Goldstein as he cleans house

(COURTESY ZEROHEDGE)

iv)Quite a stat: The Trump White House is losing one senior staff member every 17 days

( zerohedge)

v)Confidence level for ‘Main Street’ is humming again as small business confidence surges to its highest level since 1983

( zero hedge)

vi)Not what Jay Powell wants to see: USA consumer prices slow in February. He wants consumer prices to rise to force labour rates higher

(courtesy Reuters)

vii)China is not going to like this: the trade war escalates as trump demands broader tariffs against China

( zerohedge)

viii)SWAMP STORIES

a)The House Intelligence Committee after 14 months of hearings is ending the Russian probe and finds no collusion

( zerohedge)

comex gold volumes are RISING AGAIN

Here is a summary of the latest gold trading volumes at the Comex per year

certainly the introduction of EFP’s has certainly had an effect:

Trading Volumes on the COMEX

PRELIMINARY COMEX VOLUME FOR TODAY: 356,814 contracts

CONFIRMED COMEX VOL. FOR YESTERDAY: 264,844 CONTRACTS

comex gold volumes are RISING AGAIN

Here is a summary of the latest gold trading volumes at the Comex per year

certainly the introduction of EFP’s has certainly had an effect:

Meanwhile, gold-trading volumes on the COMEX have never been higher:

end

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

And now for the wild silver comex results.

Total silver OI ROSE BY A CONSIDERABLE 2228 CONTRACTS FROM 196,956 UP TO 199,184 DESPITE YESTERDAY’S 8 CENT LOSS IN YESTERDAY’S TRADING). HOWEVER,WE WERE ALSO INFORMED THAT WE HAD 598 EMERGENCY EFP’S FOR MAY ISSUED BY OUR BANKERS AND ZERO FOR ALL OTHER MONTHS TO COMEX LONGS WHO RECEIVED A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON: THE TOTAL EFP’S ISSUED: 598. THE SILVER BOYS HAVE STARTED TO MIGRATE TO LONDON FROM THE START OF DELIVERY MONTH AND CONTINUING RIGHT THROUGH UNTIL FIRST DAY NOTICE JUST LIKE WE ARE WITNESSING TODAY. USUALLY WE NOTED THAT CONTRACTION IN OI OCCURRED ONLY DURING THE LAST WEEK OF AN UPCOMING ACTIVE DELIVERY MONTH AS WE HAVE JUST SEEN IN GOLD TODAY. THIS PROCESS HAS JUST BEGUN IN EARNEST IN SILVER STARTING IN SEPTEMBER 2017. HOWEVER, IN GOLD, WE HAVE BEEN WITNESSING THIS FOR THE PAST 2 YEARS. NICK LAIRD WAS KIND ENOUGH TO SUPPLY US THE TOTAL FOR 2017 GOLD EFP’S AND IT WAS 6600 TONNES FOR THE ENTIRE YEAR. WE OBVIOUSLY HAD ZERO LONG COMEX SILVER LIQUIDATION BUT WE ALSO HAD A HUGE SIZED GAIN IN TOTAL SILVER OI FROM OUR TWO EXCHANGES. WE ARE ALSO WITNESSING A STRONG AMOUNT OF SILVER OUNCES STANDING FOR COMEX METAL IN THIS NON ACTIVE JANUARY AS WELL AS THAT CONTINUAL MIGRATION OF EFPS OVER TO LONDON. ON A PERCENTAGE BASIS THERE ARE MORE EFP’S ISSUED FOR GOLD THAN SILVER. ON A NET BASIS WE GAINED 2826 SILVER OPEN INTEREST CONTRACTS AS WE OBTAINED A 2228 CONTRACT GAIN AT THE COMEX COMBINING WITH THE ADDITION OF 598 OI CONTRACTS NAVIGATING OVER TO LONDON.

NET GAIN ON THE TWO EXCHANGES:2826 CONTRACTS

AMOUNT STANDING FOR SILVER AT THE COMEX

We are now in the active delivery month of MARCH and here the front month LOST 100 contracts FALLING TO 399 contracts. We had 101 contracts filed upon yesterday, so we GAINED 1 contract or an additional 5,000 will stand in this active delivery month of March.(AS SOMEBODY IS STILL IN GREAT NEED OF PHYSICAL SILVER)

April GAINED 16 contracts RISING TO 443 .

The next big active delivery month for silver will be May and here the OI GAINED 565 contracts UP to 143,810

We had 6 notice(s) filed for 30,000 OZ for the MARCH 2018 contract for silver

INITIAL standings for MARCH/GOLD

MARCH 13/2018.

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz |

nil oz

|

| Deposits to the Dealer Inventory in oz | NIL oz |

| Deposits to the Customer Inventory, in oz | nil OZ |

| No of oz served (contracts) today |

0 notice(s)

400 OZ

|

| No of oz to be served (notices) |

543 contracts

(54300 oz)

|

| Total monthly oz gold served (contracts) so far this month |

4 notices

400 oz

|

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

For MARCH:

Today, 0 notice(s) were issued from JPMorgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equates to 0 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped/ Received) by j.P.Morgan customer account.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

To calculate the INITIAL total number of gold ounces standing for the MARCH. contract month, we take the total number of notices filed so far for the month (4) x 100 oz or 0 oz, to which we add the difference between the open interest for the front month of FEB. (543 contracts) minus the number of notices served upon today (0 x 100 oz per contract) equals 54700 oz, the number of ounces standing in this nonactive month of MARCH (1.7013 tonnes)

Thus the INITIAL standings for gold for the MARCH contract month:

No of notices served (4 x 100 oz or ounces + {(543)OI for the front month minus the number of notices served upon today (0 x 100 oz )which equals 54700 oz standing in this nonactive delivery month of March . THERE IS 10.556 TONNES OF REGISTERED GOLD AVAILABLE FOR DELIVERY SO FAR.

WE LOST 0 CONTRACTS OR AN ADDITIONAL NIL OZ WILL STAND FOR DELIVERY IN THIS NON ACTIVE DELIVERY MONTH OF MARCH.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

IN THE LAST 18 MONTHS 70 NET TONNES HAS LEFT THE COMEX.

end

And now for silver

AND NOW THE DECEMBER DELIVERY MONTH

MARCH INITIAL standings/SILVER

| Silver | Ounces |

| Withdrawals from Dealers Inventory | nil oz |

| Withdrawals from Customer Inventory |

24,053.720 oz

HSBC

CNT

|

| Deposits to the Dealer Inventory |

nil

oz

|

| Deposits to the Customer Inventory |

1.227.412.748 oz

JPM

Brinks

|

| No of oz served today (contracts) |

6

CONTRACT(S

(30,000 OZ)

|

| No of oz to be served (notices) |

393 contracts

(1,965,000 oz)

|

| Total monthly oz silver served (contracts) | 4834 contracts

(24,170,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

we had 0 inventory movement at the dealer side of things

total inventory deposits/withdrawals/ into dealer: nil oz

we had 2 deposits into the customer account

i) JPMorgan: 602,667.500 oz

*** JPMorgan for most of 2017 and in 2018 has adding to its inventory almost every single day.

JPMorgan now has 135 million oz of total silver inventory or 54% of all official comex silver.

JPMorgan added silver into its warehouses (official) today.

ii) into Brinks: 624,745.248 oz

total deposits today: 1,227,412.748 oz

we had 2 withdrawals from the customer account;

i) Out of HSBC 20,022.32 oz

ii) Out of CNT:: 4,031.400 oz

total withdrawals; 24,053.720 oz

we had 0 adjustments

total dealer silver: 59.419 million

total dealer + customer silver: 253.313 million oz

The total number of notices filed today for the March. contract month is represented by 6 contract(s) FOR 30,000 oz. To calculate the number of silver ounces that will stand for delivery in March., we take the total number of notices filed for the month so far at 4834 x 5,000 oz = 24,170,000 oz to which we add the difference between the open interest for the front month of Mar. (399) and the number of notices served upon today (6 x 5000 oz) equals the number of ounces standing.

.

Thus the INITIAL standings for silver for the March contract month: 4834(notices served so far)x 5000 oz + OI for front month of March(399) -number of notices served upon today (6)x 5000 oz equals 26,135,000 oz of silver standing for the March contract month.

We GAINED an additional 1 contract or 5,000 additional silver oz will stand for delivery at the comex as somebody was in urgent need of physical silver.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

ESTIMATED VOLUME FOR TODAY: 69,286 CONTRACTS

CONFIRMED VOLUME FOR YESTERDAY: 57,590 CONTRACTS

YESTERDAY’S CONFIRMED VOLUME OF 57,590 CONTRACTS EQUATES TO 287 MILLION OZ OR 41.1% OF ANNUAL GLOBAL PRODUCTION OF SILVER

COMMODITY LAW SUGGESTS THAT OPEN INTEREST SHOULD NOT BE MORE THAN 3% OF ANNUAL GLOBAL PRODUCTION. THE CROOKS ARE SUPPLYING MASSIVE PAPER TRYING TO KEEP SILVER IN CHECK.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price at that day at $18.42

The previous record was 224,540 contracts with the price at that time of $20.44

end

NPV for Sprott

1. Sprott silver fund (PSLV): NAV FALLS TO -2.49% (MARCH 13/2018)

2. Sprott gold fund (PHYS): premium to NAV FALLS TO -0.66% to NAV (March 13/2018 )

Note: Sprott silver trust back into NEGATIVE territory at -2.49%-/Sprott physical gold trust is back into NEGATIVE/ territory at -0.66%/Central fund of Canada’s is still in jail but being rescued by Sprott.

Sprott WINS hostile 3.1 billion bid to take over Central Fund of Canada

(courtesy Sprott/GATA)

3.SPROTT CEF.A FUND (FORMERLY CENTRAL FUND OF CANADA): NAV RISES TO -3.27%: NAV 13.72/TRADING 13.28//DISCOUNT 3.27.

END

And now the Gold inventory at the GLD/

MARCH 13/WITH GOLD UP $6.25/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 833.73 TONNES

MARCH 12/WITH GOLD DOWN $3.00/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 833.73 TONNES

MARCH 9/WITH GOLD UP $2.25/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 833.73 TONNES

March 8/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 833.73 TONNES

MARCH 7/WITH GOLD DOWN 8.00/A SLIGHT CHANGE IN GOLD INVENTORY AT THE GLD/A WITHDRAWAL OF .25 TONNES TO PAY FOR FEES//INVENTORY RESTS AT 833.73 TONNES

MARCH 6/WITH GOLD UP $15.60/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 833.98 TONNES

March 5/WITH GOLD DOWN $4.10/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 833.98 TONNES

MARCH 2/WITH GOLD UP $18.70/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 833.98 TONNES

March 1/WITH GOLD DOWN ANOTHER $12.30/A HUGE CHANGE IN GOLD INVENTORY/ A DEPOSIT OF 2.96 TONNES/INVENTORY RESTS AT 833.98 TONNES

FEB 28/WITH GOLD DOWN ANOTHER 70 CENTS/NO CHANGE IN GOLD INVENTORY/INVENTORY RESTS AT 831.03 TONNES/.

feb 27/WITH GOLD DOWN $13.80 WE HAD NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 831.03 TONNES

FEB 26/WITH GOLD UP $2.40/WE HAD ANOTHER INVENTORY GAIN/THIS TIME 1.77 TONNE ADDITION TO THE GLD INVENTORY/INVENTORY RESTS AT 831.03 TONNES/WE HAVE HAD 5 INCREASES IN THE PAST 6 TRADING GOLD SESSIONS/

FEB 23/WITH GOLD DOWN $1.15, WE HAD A GOOD INVENTORY GAIN OF 1.47 TONNES OF GOLD INTO THE GLD/INVENTORY RESTS AT 829.26 TONNES

FEB 22/WITH GOLD UP 90 CENTS AGAIN TODAY, WE HAD NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 827.79 TONNES

FEB 21/ WITH THE 90 CENT GAIN WE HAD ANOTHER DEPOSIT OF 3.15 TONNES OF GOLD INTO THE GLD INVENTORY/INVENTORY RESTS TONIGHT AT 827.79 TONNES

Feb 20/WITH GOLD DOWN BY $24.25, THE CROOKS DECIDED THAT THEY HAD BETTER RETURN (DEPOSIT) 3.34 TONNES OF GOLD INTO THE GLD/INVENTORY RESTS TONIGHT AT 824,64 TONNES

Feb 16/WITH GOLD UP BY 25 CENTS, THE CROOKS DECIDED AGAIN TO RAID THE COOKIE JAR BY WITHDRAWING 2.36 TONNES OF GOLD FROM THE GLD/INVENTORY RESTS AT 821.30 TONNES

Feb 15/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 823.66 TONNES

Feb 14/AN ADDITIONAL OF 2.95 TONNES OF GOLD INTO GLD WITH THE HUGE GAIN OF 27.40 IN PRICE/INVENTORY RESTS AT 823.66 TONNES

Feb 13/WITH GOLD UP $3.40 WE HAD NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY REMAINS AT 820.71 TONNES

Feb 12/STRANGE!!WITH GOLD RISING BY 12.00 DOLLARS, THE CROOKS DECIDED AGAIN TO WITHDRAW 5.6 TONNES OF GOLD FOR EMERGENCY USE ELSEWHERE/INVENTORY RESTS AT 820.71 TONNES

Feb 9/AGAIN WITH HUGE TURMOIL ON THE MARKETS, THE CROOKS WITHDREW 2 TONNES OF GOLD FROM THE GLD INVENTORY/INVENTORY RESTS AT 826.31 TONNES

Feb 8/DESPITE THE GOOD GAIN IN PRICE FOR GOLD TODAY/THE CROOKS REMOVED .96 TONNES FROM THE GLD INVENTORY/INVENTORY RESTS AT 828.31 TONNES

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

MARCH 13/2018/ Inventory rests tonight at 833.73 tonnes

*IN LAST 341 TRADING DAYS: 107,41 NET TONNES HAVE BEEN REMOVED FROM THE GLD

*LAST 271 TRADING DAYS: A NET 48.89 TONNES HAVE NOW BEEN ADDED INTO GLD INVENTORY.

end

Now the SLV Inventory

MARCH 13/WITH SILVER UP 10 CENTS/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.012 MILLION OZ/

MARCH 12/WITH SILVER DOWN 8 CENTS/A BIG CHANGES IN SILVER INVENTORY AT THE SLV/ A DEPOSIT OF 943,000 OZ/INVENTORY RESTS AT 319.012 MILLION OZ/

MARCH 9/WITH SILVER UP 21 CENTS, NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 318.069 MILLION OZ/

March 8/WITH SILVER DOWN 1 CENT TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 318.069 MILLION OZ/

MARCH 7/WITH SILVER DOWN 27 CENTS/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 318.069 MILLION OZ/

MARCH 6/WITH SILVER UP 38 CENTS/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 318.069 MILLION OZ/

March 5/WITH SILVER DOWN 11 CENTS/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 318.069 MILLION OZ/

MARCH 2/WITH SILVER UP 23 CENTS: A HUGE 1.479 MILLION OZ WAS ADDED TO SILVER’S INVENTORY/INVENTORY RESTS AT 318.069 MILLION OZ/

March 1/WITH SILVER DOWN 11 CENTS TODAY/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 316.590 MILLION OZ./

FEB 28/WITH SILVER DOWN 5 CENTS TODAY/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 316.590 MILLION OZ/

feb 27/WITH SILVER DOWN 17 CENTS/NO CHANGE IN SILVER INVENTORY/INVENTORY RESTS AT 316.590 MILLION OZ

FEB 26/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 316.590 MILLION OZ/

FEB 23/WITH SILVER DOWN 10 CENTS TODAY, WE HAD ANOTHER HUGE ADDITION OF 1.315 MILLION OZ/INVENTORY RESTS AT 316.590 MILLION OZ/

fEB 22.2018/WITH SILVER DOWN 1 CENT TODAY, WE HAD NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 315.271 MILLION OZ/

FEB 21/WITH SILVER UP 15 CENTS TODAY, WE HAD A GOOD SIZED INVENTORY ADDITION OF 1.226 MILLION OZ/INVENTORY RESTS AT 315.271 MILLION OZ/

Feb 20/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 314.045 MILLION OZ

Feb 16/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 314.045 MILLION OZ/

Feb 15/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 314.045 MILLION OZ/

Feb 14./NO CHANGE IN SILVER INVENTORY DESPITE THE HUGE RISE IN PRICE/INVENTORY RESTS AT 314.045 MILLION OZ

Feb 13./NO CHANGE IN SILVER INVENTORY TODAY/INVENTORY RESTS AT 314.045 MILLION OZ/

Feb 12/AGAIN, WITH TODAY’S HUGE RISE IN SILVER PRICE, IN TOTAL CONTRAST TO GOLD: NO CHANGE IN SILVER INVENTORY/INVENTORY RESTS AT 314.045 MILLION OZ/

Feb 9/AGAIN WITH TURMOIL ON THE MARKETS, STRANGELY IN TOTAL CONTRAST TO GOLD: NO CHANGE IN SILVER INVENTORY/INVENTORY RESTS AT 314.045 MILLION OZ/

Feb 8/DESPITE THE TURMOIL TODAY AND A PRICE RISE: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 314.045 MILLION OZ/

MARCH 13/2018: NO CHANGES TO SILVER INVENTORY/

Inventory 319.012 million oz

end

6 Month MM GOFO 2,01/ and libor 6 month duration 2.29

Indicative gold forward offer rate for a 6 month duration/calculation:

G0FO+ 2.01%

libor 2.29 FOR 6 MONTHS/

GOLD LENDING RATE: .28%

XXXXXXXX

12 Month MM GOFO

+ 2.41%

LIBOR FOR 12 MONTH DURATION: 2.56

GOFO = LIBOR – GOLD LENDING RATE

GOLD LENDING RATE = +.17

GOLD LENDING RATES FALLING TO APPROACH ZERO AS PHYSICAL GOLD IS SCARCE/GOFO RATES RISING

end

Major gold/silver trading /commentaries for TUESDAY

GOLDCORE/BLOG/MARK O’BYRNE.

GOLD/SILVER

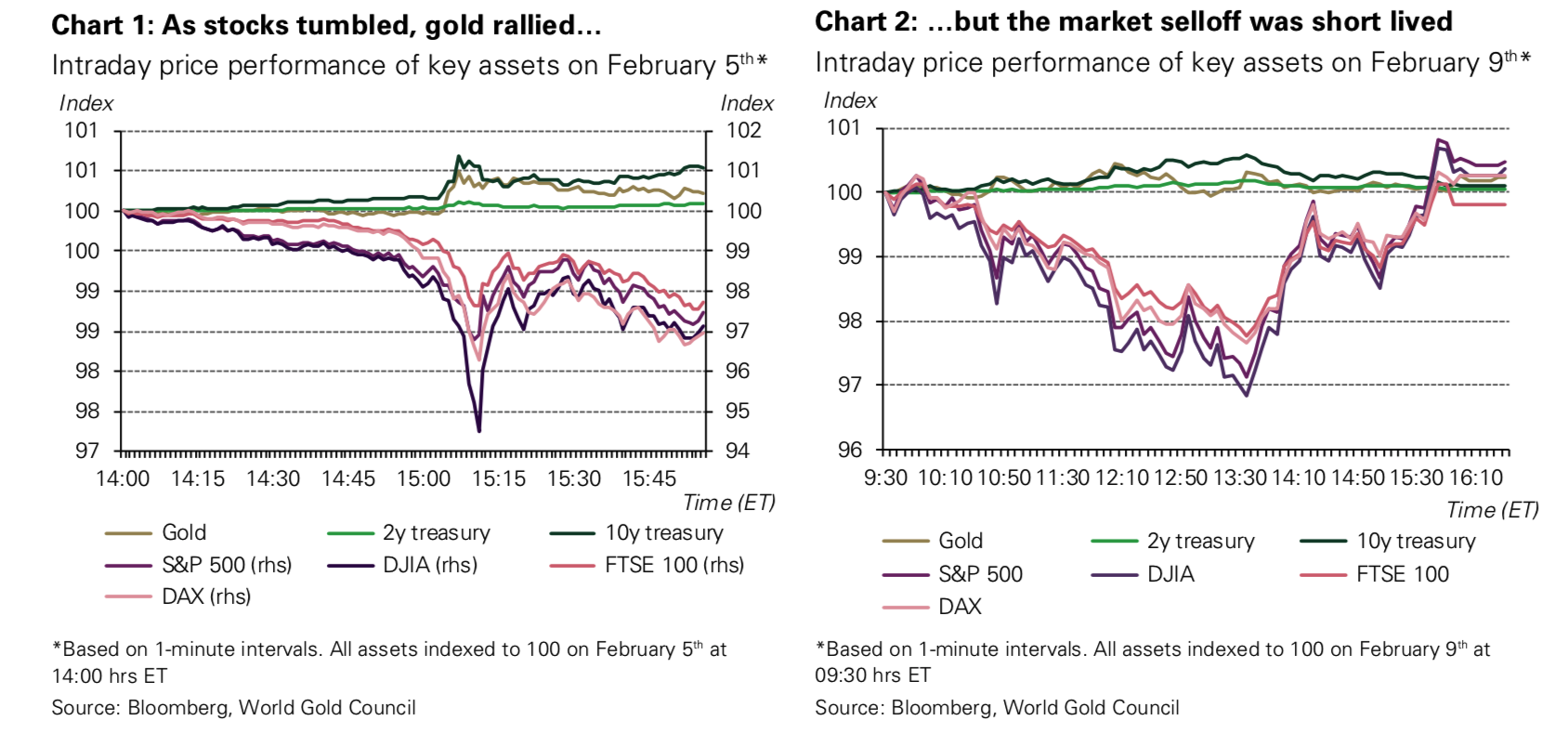

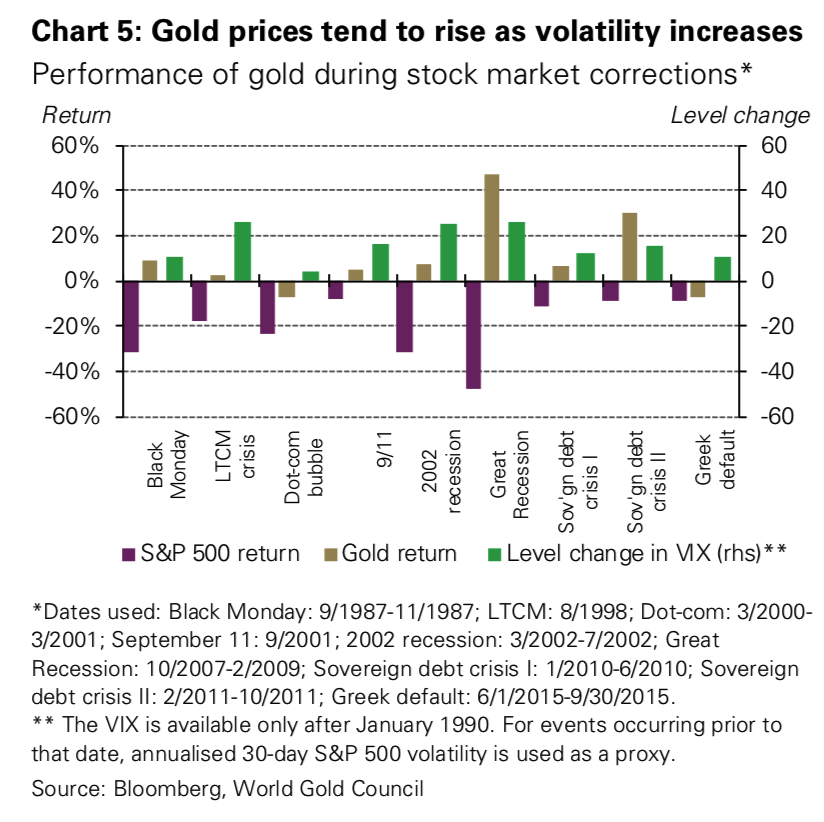

Stock Market Selloff Showed Gold Can Reduce Portfolio Risk

Stock Market Selloff Showed Gold Can Reduce Portfolio Risk

– Recent stock market selloff showed gold can deliver returns and reduce portfolio risk

– Gold’s performance during stock market selloff was consistent with historical behaviour

– Gold up nearly 10% in last year but performance during recent selloff was short-lived

– The stronger the market pullback, the stronger gold’s rally

– WGC: ‘a good time for investors to consider including or adding gold as a strategic component to their portfolios.’

– Gold remains one of the best assets outperforming treasuries and corporate bonds

A recent World Gold Council (WGC) study has concluded that the market selloff on February 5th made the case for gold as both a diversifier and an asset that protects portfolios during market downturns.

The stock market selloff of early February saw stocks tumble. But, whilst it was sharp it was also short-lived. Many watching the gold price were disappointed to see gold lose around 0.8% of its USD price between February 5th and February 12th, when both the Dow Jones and European stocks and begun to recover losses.

Yet to judge gold on its price performance alone is to misunderstand gold (or, in fact any asset’s) role in a portfolio. In order to appreciate it’s performance one must compare it to other assets as well as it’s long-term behaviour.

Gold’s protection was stronger than you realise

Whilst gold did drop by nearly 1% in USD terms it was a different story for other currencies (which account for 90% of gold demand). This was particularly the case in Europe where currencies weakened against the dollar, increasing gold prices. In euro terms old rallied by 0.9% and 1.8% in sterling, between Friday February 2nd and Monday February 12th.

The 0.8% overall drop in the gold price over the beginning and end of the stock market selloff was not reflective of gold’s performance during the period:

‘[Gold] still outperformed most assets on the week (other than treasuries) and reduced portfolio losses, providing liquidity to investors as market volatility rose.’

“Gold’s effectiveness as a hedge increases with systemic risks”

Gold and stocks are inversely correlated in market downturns. This is thanks to the behaviour of investors who typically show a ‘flight-to-quality’ behaviour.

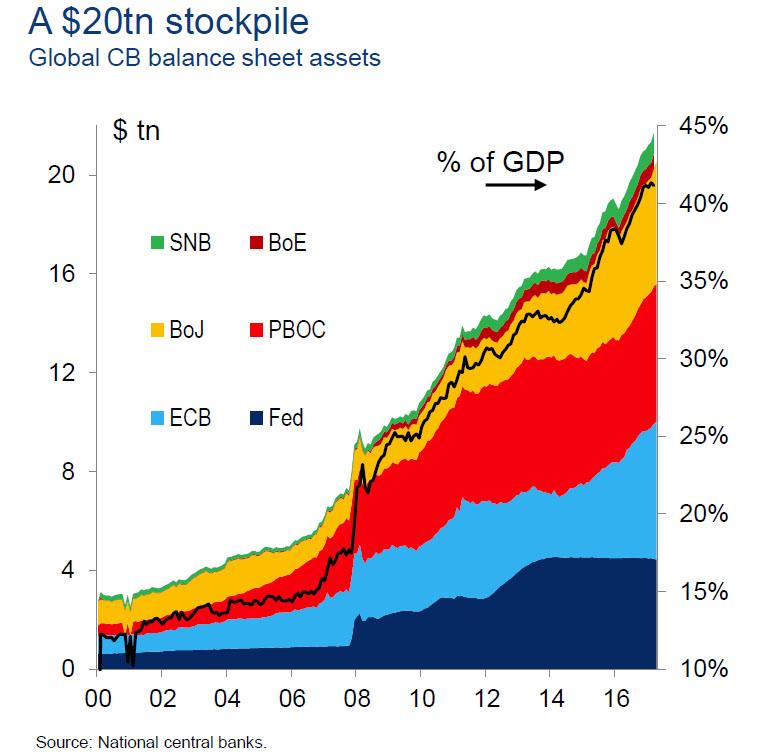

This benefit of gold is better seen when market crises are broader or last longer than the stock market correction we saw in February.

Examples include Black Monday, the 2008–2009 financial crisis and the European sovereign debt crisis (Chart 5). But there are exceptions.

Gold has been more effective as a hedge when a market correction has been broader (i.e. affects more than one sector or region) or lasted longer.

During the 2001 dot-com bubble burst, the risk was mainly centred around tech stocks and was not enough to elicit a strong reaction from gold; it was not until the broader US economy fell into recession that the gold price responded more sharply. Similarly, investors outside of Europe discounted the possibility of a spill-over from the 2015 Greek default. In recent pullback, as stocks quickly rebounded, gold’s reaction was more muted.

However, taking a longer, more strategic view, is quite relevant.

Looking beyond the short-term stock market selloff

As we often discussed, mainstream media and market commentary have a strong bias towards short-term views. This leads to a very blinkered approach and often an all-too-easy dismissal of gold as a worthy investment.

There has been talk of a stock-market correction for a long-while. Frothy asset prices, pumped-up valuations and the ongoing uptick in stock market prices appeared to be just asking for a market selloff. We finally saw a selloff last month when the DJIA had it’s biggest drop in history. Was this the end of the bubble? Prices did recover but that doesn’t mean it wasn’t the final bell in what has been a long run.

An environment is now forming where a number of corrections are becoming more likely in the near-future. Interest rates are slowly being hiked up, how markets and economies will cope with this after a record-long period of ultra-low interest rates is something we are just beginning to get a taste of.

Trade wars are looming, inflation levels are climbing and political sabre-rattling is growing stronger. With this in mind the World Gold Council reminds us of gold’s ‘four key roles in a portfolio’:

– delivering positive long-term returns

– improving diversification

– providing liquidity, especially in downturns

– enhancing portfolio performance through higher risk-adjusted returns

So far, 2018 has been a good case in point of gold’s role as a strategic asset. It has been one of the best-performing asset classes year-to-date, besting treasuries and corporate bonds (Chart 6). It has served as a diversifier and liquidity source as stock markets tumbled. Thus, gold helped investors improve their portfolios’ performance.

‘Consider including or adding gold as a strategic component to portfolios.’

The World Gold Council notes that there has been an increase in bullish positioning in gold options. ‘In our view, this type of bullish positioning suggests that investors may be increasing their portfolio protection against further market downturns…this is as good a time as any for investors to consider including or adding gold as a strategic component to their portfolios.’

You can find out more about investing in gold as part of a diversified portfolio in our Comprehensive Guide to Investing in Gold.

All quotes and charts taken from the World Gold Council.

Recommended Reading

Gold Rises As Global Stocks Plunge and Bitcoin Crashes 70%

Buy Gold, ‘Get Out Of The Stock Market’ Warns Druckenmiller

Invest In Gold Now As Stock Market To Crash – Faber

News and Commentary

Gold slips as dollar holds steady (Reuters.com)

Stocks in Asia Rally After U.S. Jobs; Yen Advances (Bloomberg.com)

S.Africa gold miners’ silicosis lawsuit settlement expected within 6 weeks (Reuters.com)

Worry about rising inflation? Sure, but there’s no reason to be scared (MarketWatch.com)

Gundlach Says Volatility ‘Genie’ May Not Be Back in Its Bottle (Bloomberg.com)

Source: Zerohedge

In Debt and in Demand: Europe’s Most-Leveraged Stocks Surge (Bloomberg.com)

Another Very Interesting COT Report (GoldSeek.com)

ICTA wins another one for coin buyers (NumismaticNews.net)

The Amazing Amount of Gold The U.S. Exported Since 2000 (GoldSeek.com)

Gold Prices (LBMA AM)

12 Mar: USD 1,317.25, GBP 950.66 & EUR 1,069.87 per ounce

09 Mar: USD 1,319.35, GBP 955.21 & EUR 1,072.50 per ounce

08 Mar: USD 1,325.40, GBP 955.08 & EUR 1,070.39 per ounce

07 Mar: USD 1,332.50, GBP 960.07 & EUR 1,071.86 per ounce

06 Mar: USD 1,324.95, GBP 957.01 & EUR 1,074.00 per ounce

05 Mar: USD 1,326.30, GBP 958.78 & EUR 1,075.63 per ounce

Silver Prices (LBMA)

12 Mar: USD 16.46, GBP 11.88 & EUR 13.39 per ounce

09 Mar: USD 16.49, GBP 11.92 & EUR 13.40 per ounce

08 Mar: USD 16.48, GBP 11.89 & EUR 13.31 per ounce

07 Mar: USD 16.65, GBP 12.01 & EUR 13.42 per ounce

06 Mar: USD 16.62, GBP 11.96 & EUR 13.41 per ounce

05 Mar: USD 16.51, GBP 11.95 & EUR 13.42 per ounce

Recent Market Updates

– Gold Protects As Cashless Society Threatens Vulnerable

– Women’s Pension Crisis Highlights Dangers To Savers

– London Property Sees Brave Bet By Norway As Foxtons Profits Plunge

– Gold Does Not Fear Interest Rate Hikes

– RaboDirect Closing – Gold May Protect From Irish Banks Going “Belly Up Again” – Finuncane

– Silver bullion will likely outperform gold bullion going forward

– Gold $10,000? Goldnomics Podcast Quotations and Transcript

– Trump Risks Trade and Currency Wars – Protectionism and Economic War Loom

– Four Key Themes To Drive Gold Prices In 2018 – World Gold Council

– Is The Gold Price Going To $10,000? (Goldnomics Podcast 3)

– Gold Corridor From Dubai to China Sought By China

– Digital Gold Provide the Benefits Of Physical Gold?

– Weekly Briefing: Currency Wars – ECB Warns Re Trump, Russia and Turkey Buy Gold and BOE Bitcoin Warning

Andrew Maguire’s Kinesis money which is a “bitcoin” but backed 100% by allocated gold and silver is set to go.

it think it would be a great idea to look at this!

please read at: https://kinesis.money/#/

(Andrew Maguire)

|

2:57 PM (1 hour ago) | ||

|

|||

Harvey

Here It is my friend! https://kinesis.money/#/ Please let everyone know.

Let catch up on Monday if you have time. We have billions in the hopper ready to be allocated on the 1st day of trading. The paper market days are over.

Warm regards

Andy

end.

END

Congressman criticized the USA mint for inaction on the counterfeiting of gold/silver coins. The mint states that it is not significant enough to warrant action

(courtesy GATA./Ein Presswire.com)

Congressman criticizes U.S. Mint for inaction on counterfeit precious metal coins

Submitted by cpowell on Mon, 2018-03-12 23:02. Section: Daily Dispatches

From EIN Presswire.com

via WVUE-TV8, New Orleans

Monday, March 12, 2018

WASHINGTON — U.S. Rep. Alex Mooney, R-West Virginia, criticized the United States Mint for its “disappointing and concerning” lack of awareness or action on the growing problem of high-quality counterfeits of U.S. precious-metals coins entering the country from China and elsewhere.

In a letter dated March 6, Rep. Mooney took the U.S. Mint to task on its perfunctory one-page response to a prior letter that he and Rep. Frank Lucas sent last October asking for information as to whether and to what extent the U.S. Mint has taken steps to protect the integrity of America’s minted coins, including reviewing and implementing the anti-counterfeiting measures already put in place by certain foreign government and private mints.

“The U.S. Mint’s response dated November 17, 2017, seemed to suggest a belief that the problem was not significant,” Mooney wrote in his March 6 letter.

“However, the U.S. Secret Service has since briefed my office about the extent of this activity and its frustration with a lack of supportive actions by other agencies, including the U.S. Mint.” …

… For the remainder of the report:

http://www.fox8live.com/story/37704978/congressman-criticizes-us-mint-fo…

end

Although tiny in numbers, the Hungarian Central Bank must have been reading Nicholas B. as they now wish to repatriate their entire 3 tonnes of gold held in London

(courtesy GoldBroker.com)

Hungary’s Central Bank To Repatriate Its Gold From London

The leadership of the Hungarian National Bank (MNB) has decided to bring back home Hungary’s gold reserves.

Up to now, 100,000 ounces (3 tons) of the precious metal were stored in London, which is in total worth some 33 billion forint ($130 million) at current gold prices.

The decision seems to be in line with international trends as storage of gold reserves out of the country is now considered risky by more and more central banks. Austrian, German, and Dutch central banks are among those who have recently decided to repatriate their gold reserves. According to MNB, this may also further strengthen market confidence towards Hungary.

MNB has been holding gold reserves since its foundation in 1924. Towards the end of World War II, it had been transported to Austria on the famous Gold Train, captured by the Americans, then repatriated in full in 1946.

The highest amount Hungary has ever had was around 65-70 tons at the beginning of the 70s. At the end of the 1980s, however, a decision was made to decrease gold reserves to the lowest possible level and rather to invest in sovereign debts, which as a consequence of the collapse of the Bretton Woods system are considered safer, more liquid and potentially of higher yields. At the beginning of 2010 this tendency changed again and central banks started to accumulate gold as a potential response to the financial crisis.

The Largest gold reserves in the world belong to the US and Germany, while in comparison to other Central-European countries Hungary has one of the tiniest amounts of the precious metal; for instance, Romania and Poland both have 103 tons, and Serbia has 13 tons. Since 1992, Hungary’s activity has remained steady, as the MNB hasn’t bought or sold any of its gold reserves.

end

Your early TUESDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

i) Chinese yuan vs USA dollar/CLOSED UP 6.3268 /shanghai bourse CLOSED DOWN 16.46 POINTS OR 0.49% / HANG SANG CLOSED UP 7.12 POINTS OR 0.02%

2. Nikkei closed UP 144.07 POINTS OR 0.66% /USA: YEN RISES TO 107.23/

3. Europe stocks OPENED DEEPLY IN THE GREEN EXCEPT LONDON /USA dollar index RISES TO 90.02/Euro FALLS TO 1.2335

3b Japan 10 year bond yield: FALLS TO . +.053/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 106.53/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD FINALLY IN THE POSITIVE/BANK OF JAPAN LOSING CONTROL OF THEIR YIELD CURVE AS THEY PURCHASE ALL BONDS TO GET TO ZERO RATE!!

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 61.47 and Brent: 64.86

3f Gold DOWN/Yen DOWN

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil UP for WTI and DOWN FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund FALLS TO +.624%/Italian 10 yr bond yield DOWN to 1.987% /SPAIN 10 YR BOND YIELD DOWN TO 1.377%

3j Greek 10 year bond yield FALLS TO : 4.147?????????????????

3k Gold at $1318.82 silver at:16.51 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble DOWN 2/100 in roubles/dollar) 56.93

3m oil into the 61 dollar handle for WTI and 64 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 106.53 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 0.9477 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1688 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now POSITIVE territory with the 10 year FALLING to +0.636%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.87% early this morning (THIS IS DEADLY TO ALL MARKETS). Thirty year rate at 3.133% /

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

(courtesy Jim Reid/Bloomberg/Deutsche bank/zero hedge)

Global Stocks, Futures Rise Ahead Of Key Inflation Report

After yesterday’s aborted market liftoff, which saw the S&P spike at the open then fizzle lower amid easing trade tensions and a goldilocks US economy, today world stocks are going for it again, with European stocks climbing following a mostly green Asian session.

The MSCI All-Country World index of stocks was up less than 0.1%, and has recovered about half its losses from the February correction.

S&P futures were trading at session highs while the dollar strengthened with less than 90 minutes to go until the much anticipate U.S. inflation report which will provide more clues on the pace of Fed tightening. Treasury yields were fractionally higher as oil slipped.

It’s all about the CPI print today, and as Deutsche Bank notes, “will we see yields march up today or will the latest batch of US inflation data disappoint? We’ll know the answer to that with the release of the February CPI report in the US. As a reminder, market expectations for the data is for a +0.2% mom headline and core reading. Should we see that then the annual rate should nudge up one tenth at the headline to +2.2% yoy while the core should hold at +1.8% yoy. One interesting point our colleagues make is that the annual growth rate of core CPI will mechanically rise by around 20bps in the March data release just from annualizing the -10% decline in wireless telephone services. In our economists’ view this should help core CPI to exceed +2.0% yoy in March, before then rising further to +2.3% yoy by the end of this year.”

Others chimed in: “Today’s CPI inflation data is likely to add further color to the US inflation picture, however it probably won’t add any further clarity to the overall inflation outlook puzzle, given that the Fed doesn’t use CPI as its inflation benchmark,” Michael Hewson, chief markets analyst at CMC Markets in London, told Reuters. “Nonetheless it is still a useful gauge in establishing when and how the price pressures we’ve been seeing build up in US supply chains start to filter down into the wider economy.”

That said, while the CPI is closely watched by traders, it is not the primary gauge the Fed uses to determine whether it is meeting its mandate of price stability. Instead, the Fed uses the personal consumption expenditure (PCE) index, or as UBS’ Paul Donovan puts it:

US consumer price inflation is due. Markets focus on this price measure. It matters to inflation-linked US government bonds. The Federal Reserve does not focus on this price measure. A relatively large part of US consumer price inflation is prices people do not pay in the real world. These prices may start adding to inflation this year.

Back to markets where the Stoxx Europe 600 Index rose for a seventh day in Europe’s longest run since October, led by oil and mining shares. Italian and Spanish stocks rose 0.3 to 0.4 percent, while Britain’s FTSE was a laggard, down 0.1 percent, and in early trading triggered a “death cross.”

MSCI’s Asia-Pacific shares ex-Japan index rose 0.2% after spending much of the day swerving in and out of negative territory, and after surging 1.5% on Monday. Japanese stocks fluctuated before closing higher, while Hong Kong and Chinese shares slipped. The yen weakened as investors digested the political fallout from a scandal embroiling Japanese Finance Minister Taro Aso, and decided – for now – that it won’t rock the Abe administration materially.

However both Asian and European trading has been muted, with modest volumes as most are waiting for U.S. CPI report. According to Bloomberg, a figure that misses or meets estimates is likely to reaffirm the case for just three rate hikes this year and give the green light to fresh appetite for risk assets.

Politics also remain in focus after President Donald Trump issued an unexpected executive order blocking Broadcom Ltd. from acquiring Qualcomm Inc., scuttling the $117 billion hostile takeover which would have been the biggest tech deal in history, and had been the subject of scrutiny over the deal’s threat to U.S. national security.

In FX, the Bloomberg Dollar Spot Index pared Monday’s drop ahead of the CPI reports as investors covered dollar-yen shorts after Aso refused to resign as part of the Moritomo scandal. Volatility remains in defensive mode with buyers yet to surface, while most major currencies stay in tight ranges in an overall quiet session. Pound traders stay sidelined, looking for headlines on Brexit and Hammond’s Spring Statement.

Overnight FX recap from Bloomberg:

- The euro was steady against the dollar with the pair hovering below the 21-DMA resistance, while the Treasury curve bear- steepened modestly

- The pound edged lower, slipping for the first time in three days and after failing to break the 21-DMA resistance; U.K. Chancellor Philip Hammond’s Spring Statement is seen more likely to give impetus to gilts as issuance is forecast to decline to the lowest in more than a decade

- The yen was the worst Group-of-10 performer, with USD/JPY rising as much as 0.8% to 107.22 as gains in Japanese equities spurred traders to cover short positions and the looming U.S. inflation data drew traders’ attention from the land-sale scandal with links to Japanese Prime Minister Abe

- New Zealand’s dollar climbed against all of its G-10 peers after the nation’s syndicated sale of April 2029 government bonds drew demand that was more than twice the expected range; NZD/USD rises as much as 0.5% to 0.7333, highest since Feb. 26

“The broader story remains that of U.S. monetary policy normalization in the backdrop of an improving economy and a further decline in currency market volatility would only fuel more risk taking appetite,” said Commerzbank’s FX strategist Thu Lan Nguyen.

The yen tends to suffer in an environment when riskier and higher-yielding assets are bid but Morgan Stanley strategists said in a note that a further deterioration in the political situation that affected the position of Abe, could see the yen“forcefully return towards its previous upward trend.”

The U.S. 10-year yield inched up to 2.88 percent after Monday’s Treasury auction was broadly in line with expectations. Gold retreated for a second day.

In Europe, Slovakia’s 10-year bond yield rose as much as five basis points and the cost of insuring exposure to its debt hit the highest in almost three months as the country’s government inched towards collapse. Slovak Prime Minister Robert Fico’s government moved closer to collapse on Monday after his junior coalition partner called for early elections amid a political crisis sparked by the killing of a journalist.

In commodities, crude oil prices staged a recovery after sliding on concerns over rising U.S. output. U.S. crude futures were up 0.2 percent to $61.51 per barrel. Brent also rose 0.2 percent to $65.08 per barrel. Spot gold fell 0.2 percent to $1,318 per ounce

Bulletin Headline Summary from RanSquawk

- European bourses marginally in the green with newsflow relatively quiet.

- JPY weakens across the board, USD/JPY back above 107.00

- Looking ahead, highlights include US CPI, UK Spring Statement and a speech from BoC Governor Poloz

Market Snapshot

- S&P 500 futures up 0.2% to 2,795

- STOXX Europe 600 up 0.07% to 379.48

- MXAP up 0.2% to 178.92

- MXAPJ up 0.2% to 590.82

- Nikkei up 0.7% to 21,968.10

- Topix up 0.6% to 1,751.03

- Hang Seng Index up 0.02% to 31,601.45

- Shanghai Composite down 0.5% to 3,310.24

- Sensex down 0.3% to 33,808.49

- Australia S&P/ASX 200 down 0.4% to 5,974.71

- Kospi up 0.4% to 2,494.49

- German 10Y yield unchanged at 0.632%

- Euro down 0.04% to $1.2329

- Brent Futures down 0.3% to $64.78/bbl

- Italian 10Y yield fell 0.7 bps to 1.746%

- Spanish 10Y yield fell 1.5 bps to 1.39%

- Brent futures up 0.2% to $61.1/bbl

- Gold spot down 0.4% to $1,317.70

- U.S. Dollar Index up 0.2% to 90.07

Top Overnight News

- The EU could get an exemption from U.S. steel and aluminum tariffs if the union was to be considered a reliable partner in fighting over capacities, among other criteria, Politico reports, citing three unidentified people

- Italy’s League senior lawmaker Giancarlo Giorgetti tells state television network RAI that the chance that the nation will have to hold a second elction this year is “more than 50%”

- Japanese Finance Minister Taro Aso says it seems the documents were changed to fit the parliamentary testimony of a MOF official. On being asked why we won’t resign he replied that he feels it’s his responsibility to find out what happened and prevent a repeat incident

- CNBC personality Larry Kudlow has emerged as President Donald Trump’s favorite to replace Gary Cohn, the outgoing director of the White House National Economic Council, two people familiar with the matter said

- Treasury’s $28 billion three-year note sale, which was $4 billion larger than two months ago, offered the highest yield for that maturity at auction since 2007, while the strength of demand as measured by the bid-to-cover ratio dipped to the lowest since November. Purchasers of the $21 billion in 10-year debt demanded a rate unseen since 2014, and the appetite for that auction was around the average for the past two years

- With his swift rejection of Broadcom Ltd.’s hostile takeover ofQualcomm Inc., Trump sent a clear signal to overseas investors: Any deal that could give China an edge in critical technology will be swatted down in the name of national security

- China is giving its central bank the power to write the rules for the financial sector, as part of a sweeping overhaul aimed at closing regulatory loopholes and curbing risk in the $43 trillion banking and insurance industries. The China Banking Regulatory Commission and the China Insurance Regulatory Commission will be merged in the biggest industry overhaul since 2003

- Trade wars are bad but President Donald Trump’s steel and aluminum tariffs won’t have much direct impact on the U.S. economy unless the situation escalates, according to a new survey conducted by Bloomberg News. Roughly two-thirds of the 35 economists polled by Bloomberg expect the tariffs that Trump signed last week would cause a small decrease in jobs and a small drop in U.S. economic growth

- Prime Minister Theresa May publicly accused Russia of a chemical weapon attack on British soil and warned of retaliatory measures that will further strain relations between the West and the Kremlin

Asia stocks were mixed following a similar varied lead from Wall St where S&P 500 and DJIA finished negative as Trump tariff overhang weighed heavily on industrials, while the Nasdaq outperformed amid tech resilience to post a 7th consecutive gain and fresh record high. Furthermore, trade across the Asia-Pac region was quiet in which stocks lacked any significant drivers for price action. As such, ASX 200 (-0.4%) was subdued as mining and commodity-related stocks dragged on Australia, while the largest weighted financials sector was also lower as the royal commission began hearings on mortgage fraud. Nikkei 225 (+0.7%) spent most the session in negative territory, but later coat-tailed on a rebound in USD/JPY. Elsewhere, Hang Seng (-0.1%) and Shanghai Comp. (-0.2%) were choppy with trade indecisive after the PBoC kept its liquidity efforts tepid. Sector-wise, the Hang Seng Telecom Index underperformed following some downward broker moves, while banking names benefitted from proposals to consolidate regulatory agencies and after ‘Big 4’ AgBank reported preliminary earnings as well as a private placement to raise as much as USD 15.8bln. Finally, 10yr JGBs lack demand and retreated below the 151.00 level amid a late recovery in Japanese stocks and following mixed 5yr auction results which attracted reduced interest than prior. PBoC injected CNY 30bln via 7-day reverse repos and CNY 30bln via 28-day reverse repos.

Top Asian News

- China’s Central Bank Gains More Power in Xi’s Regulatory Shuffle

- $103 Billion Quant Firm Piles Into China as Foreigners Welcomed

- Billionaire Agarwal’s Vedanta Jumps After Record Dividend Payout

- Qatar Stocks Surge Amid Steps to Raise Foreign Ownership Limit

European equity open followed the mixed sentiment seen in Asia as investors focus on the pending US inflation data. Sectors are mixed with energy among the outperformers as oil prices recover from yesterday’s losses, despite the rise in US crude output whilst sector heavyweight Total (+1.4%) at the top of the CAC 40 following an upgrade at Barclays. Likewise, BP (+0.9%) and Royal Dutch Shell (+0.6%) are moving in sympathy. Telecom sector is underperforming after France’s Iliad (-5.7%) slumped after the company FY 2017 results miss forecast, whilst Mediaset (-3.1%) is at the foot of the FTSE MIB following a downgrade at JP Morgan. Elsewhere, German utilities company E.ON (+5.7%) is again performing strong amid reports of the company expecting as many as 5000 job cuts and EUR 600mln to EUR 800mln of synergies as part of its asset swaps with RWE (+1.3%).

Top European News

- Steinhoff Seeks About $322 Million From KAP Share Placement

- Greencore Will Miss Profit Expectations as U.S. Woes Grow

- Paschi Names Rovellini CFO After Mele Unexpectedly Resigns

- French Connection Says No Formal Offer After Approach Last Year

- German Utility Deal Turns Coal Veteran Into Green Giant; EON to Cut 5,000 Jobs in Deal to Overhaul German Utilities

In FX, the DXY is still straddling 90.000, with the Usd largely rangebound vs G10 majors aside from the Jpy and Nzd that have broken out of Monday’s narrow bands in opposite directions. Usd/Jpy saw importer demand in the low 106.20 area and then short covering from leveraged accounts on the way up towards offers at 106.90 before eclipsing yesterday’s peak and retesting highs just over 107.00 seen after Friday’s NFP release. Follow through buying pushed the pair up to and just over nearest resistance around 107.20. Conversely, the Kiwi is looking to consolidate and build on gains above 0.7300 with the aid of some upbeat minor NZ data overnight (land prices), and ahead of tonight’s top tier Q4 GDP and current account updates. Aud/Usd continues to encounter resistance/offers in advance of 0.7900, and will look for further direction from RBA Assistant Governor Kent later. Eur/Usd remains in a tight band above 1.2300, and with a key Fib still limiting dips below the handle (1.2266), while the 30 DMA (1.2350) provides a near term cap. Cable is sticking close to the 1.3900 handle awaiting the UK Budget and any further Brexit news after some positive reports about transition implementation on Monday, while Usd/Cad is slightly firmer above 1.2850 after comments from Canada’s PM claiming that exemptions of US import tariffs are not contingent on NAFTA negotiations. Note, BoC Governor Poloz is due to speak this afternoon, and staying with Central Banks the January BoJ minutes will be released shortly before midnight.

In commodities, oil prices are taking a breather, with WTI and Brent trading with marginal gains, the latter back above USD 65/bbl from the sell-off seen yesterday fuelled by a Genscape build in stockpiles and the relentless rise in US Crude output reported by EIA. US April shale output is expected to hit record highs at 6.95mln bpd. In the metals complex, Iron ore continued the longest stretch of losses since 2016 whereas gold prices are creeping lower awaiting the US CPI data to gauge the outlook for inflation.

US Event Calendar

- 6am: NFIB Small Business Optimism, est. 107.1, prior 106.9

- 8:30am: US CPI MoM, est. 0.2%, prior 0.5%; Ex Food and Energy MoM, est. 0.2%, prior 0.3%

- 8:30am: US CPI YoY, est. 2.2%, prior 2.1%; Ex Food and Energy YoY, est. 1.8%, prior 1.8%

- 8:30am: Real Avg Weekly Earnings YoY, prior 0.44%; YoY, prior 0.8%

DB’s Jim Reid concludes the overnight wrap

Will we see yields march up today or will the latest batch of US inflation data disappoint? We’ll know the answer to that in about six hours with the release of the February CPI report in the US. As a reminder, market expectations for the data is for a +0.2% mom headline and core reading. Should we see that then the annual rate should nudge up one tenth at the headline to +2.2% yoy while the core should hold at +1.8% yoy. Our US economists are slightly below market on the headline reading at +0.1% mom however also expect a +0.2% core print. As we also noted in yesterday’s EMR, one interesting point our colleagues make is that the annual growth rate of core CPI will mechanically rise by around 20bps in the March data release just from annualizing the -10% decline in wireless telephone services. In our economists’ view this should help core CPI to exceed +2.0% yoy in March, before then rising further to +2.3% yoy by the end of this year.

This will also be the last CPI report that the Fed will see before the March FOMC meeting next week. So potentially an opportunity for officials to sharpen their pencils with the big debate being whether or not the median dot moves from 3 to 4 rate hikes. We’ll also have the PPI report tomorrow to digest. If you’re one for excitement, then one thing we would note is that recent evidence suggest that the CPI print tends to surprise one way or another. Indeed, for the core mom reading, the actual reading has differed from the consensus in 9 out of the last 13 months (69%) since the start of 2017. So the consensus estimate has only been right on 4 occasions in that time. Most of those have been a downside miss too (7 times) but remember that last month was a rare beat and the strongest monthly reading since 2005 (+0.35% vs. 0.2% expected). In the 2 and 3 years prior to that period, economists got it wrong just 29% and 36% of the time respectively.

As we head into that big data release, markets have largely spent the last 24 hours twiddling their thumbs with newsflow pretty light on Monday. After opening up on the front foot risk assets quickly seemed to take some chips off the table. Indeed, the S&P 500 ended -0.13% last night and the Dow -0.62%. However the seemingly unbreakable Nasdaq notched up another +0.36% gain which means it’s now closed higher for 7 consecutive sessions – the longest streak since last October. In Europe markets also faded from highs but for the most part stayed just above water. The Stoxx 600 in particular finished +0.25% and up for the sixth straight day.

Meanwhile rates markets were well offered to kick start the day however by the end of play yields ended lower across the board. 10y Treasuries ended the day down 2.6bps at 2.869% after trading as high as 2.909% earlier in the session. The double auction of 3y and 10y Treasuries proved to be no hurdle in the end with solid enough demand at both. While we’re on bonds it’s worth adding that the Treasury curve has flattened substantially since the recent highs, with the 5s30s and 2s10s at 49.4bp and 60.6bp respectively and c.12bp and c.18bp flatter than the February wides.

This morning in Asia, markets are mixed with the Kospi (+0.1%) and Nikkei (+0.51%) both firmer, while the Hang Seng (-0.27%), Shanghai Comp (-0.23%) and ASX (-0.36%) are all in the red. The most interesting overnight news is the announcement by President Trump that he has issued an executive order blocking Broadcom from acquiring Qualcomm. The President stated that “there is credible evidence that leads me to believe that Broadcom’s (takeover) might take actions that threaten to impair the national security of the US”. This of course follows the President’s toughened stance of foreign takeovers of US technology companies.

Moving on. Failing to break from tradition, headlines that we did get yesterday were mostly of a political nature. One of those was a WSJ story suggesting that President Trump’s lawyers were trying to negotiate a deal with special counsel Robert Mueller “that uses an interview with the president as leverage to spur a conclusion to the Russia investigation”. The article mentioned that Trump would agree to an interview so long as Mueller commits to a date for finishing at least the Trump-related portion of the investigation”. A separate Bloomberg report suggested that Mueller was likely to refuse this while he concludes other parts of the probe.

Staying with the US, President Trump confirmed yesterday that Secretary of Commerce Wilbur Ross will speak with EU representatives about limiting tariffs and barriers used against the US. To be honest there weren’t any real developments on the trade front yesterday aside from some retaliatory comments out of the EU. Also worth noting from the White House yesterday was a Politico article suggesting that Trump had narrowed down Gary Cohn’s successor to either former GM and Microsoft CEO Chris Liddell or current NEC deputy Shahira Knight. The article suggested that Cohn favoured Knight (who is also said to be a tax expert) however unnamed sources mentioned that she wasn’t necessarily interested in the job.

Closer to home we heard from Junior Brexit Minister Robin Walker yesterday. Robin said that the UK and EU are “very close to a deal” on a Brexit implementation period. Sterling actually dipped slightly following the comments – before recovering – although the comments seemed to be largely ignored in the end with no official statements from either the UK or EU to back it up. While we’re on the UK, another reminder that today we have the Chancellor’s Spring Statement. Our UK strategists aren’t expecting any policy announcements however they expect the market reaction to be focused on the publication of the 2018-2019 Gilt remit. You can find a preview note to the Statement here.

Earlier yesterday, the ECB’s Coeure noted that Euro area economic growth “is strong and well distributed” but it is still too dependent on monetary policy with at least 50bp of Euro area growth due to monetary policy. Elsewhere, he noted “inflation is not yet where we want it” and interest rates “will remain low long after the end” of QE.

Before we look at the day ahead, it was a very light day for economic data yesterday. In Europe we had the latest ECB CSPP data. The CSPP/PSPP ratio was 26.8% (27.9% over last 4 weeks). As a reminder, before Apr 2017 when QE was still €80bn/m the ratio was 11.5%. Between Apr-Dec 2017 (QE €60bn/m) the ratio edged up to 12.7% but since Jan 2018 (QE €30bn/m) the ratio is now 26%. Indeed, the strength of corporate vs. government purchases as proxied by the CSPP/PSPP ratio has so far surpassed our expectations of “roughly 20%”. In the US, the February monthly budget statement deficit was slightly better than expected at -$215bn (vs. -$216bn expected). Notably, the impact of recent changes in the tax code was evident in the revenue data, with net receipts down 9.4% yoy. Elsewhere, the NY Fed February survey of consumer expectations noted median one-year ahead inflation expectations rose to 2.83% from 2.71% in January, the highest reading in 12 months.

Looking at the day ahead, a reminder of the Special Congressional election in Pennsylvania which will likely be seen as a decent bellwether for the prospect of Republicans holding onto majorities in the House and Senate at the November midterms. Datawise, the big highlight is of course the February CPI report in the US, due out shortly after lunchtime. Away from that, we’ll also receive the February NFIB small business optimism reading. In Europe, the only data of note is wages data for France for Q4, while late in the evening in Japan the latest BoJ meeting minutes are due out. In the UK, Chancellor Hammond will deliver the Spring Statement at just after midday. Elsewhere, there is the European Council and European Commission statements on Brexit.

end

3. ASIAN AFFAIRS

i)TUESDAY MORNING/MONDAY NIGHT: Shanghai closed DOWN 16.46 POINTS OR 0.49% /Hang Sang CLOSED UP 7.12 POINTS OR 0.02% / The Nikkei closed UP 144.07 POINTS OR 0.66%/Australia’s all ordinaires CLOSED DOWN 0.40%/Chinese yuan (ONSHORE) closed UP at 6.3268/Oil UP to 61.47 dollars per barrel for WTI and 64.86 for Brent. Stocks in Europe OPENED GREEN EXCEPT LONDON . ONSHORE YUAN CLOSED UP AT 6.3268 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.3287 /ONSHORE YUAN TRADING STRONGER AGAINST OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING STRONGER AGAINST THE DOLLAR . CHINA IS VERY HAPPY TODAY (STRONGER CURRENCY GOOD CHINESE MARKETS/BUT TRUMP TARIFFS INITIATED/ )

3 a NORTH KOREA/USA

/NORTH KOREA/USA

3 b JAPAN AFFAIRS

c) REPORT ON CHINA

4. EUROPEAN AFFAIRS

Brexit and the media are blamed as London house prices plunge the greatest since 2009

(courtesy zerohedge)

Brexit, Media Blamed As London House Prices Plunge Most Since 2009

After a decade of soaring prices, spurred on by hot money flows from Russia and China, London’s 2017 property slowdown is accelerating in 2018 as Bloomberg reports house prices are falling at the fastest pace since the depths of the recession almost a decade ago, with the capital’s most expensive areas seeing the biggest declines.

Average prices fell 2.6% to 593,396 pounds ($820,000) in January, according to a report published by Acadata on Monday. That’s the most since August 2009.

London’s highest-priced boroughs were the biggest losers over the last year, while the largest single drop was recorded in Wandsworth, down almost 15 percent.

Wandsworth and Southwark are home to huge speculative property developments facing on to the River Thames – including the Battersea Power Station development – but the market for £1m-plus one-bed properties has shrivelled in recent years.

But, as Bloomberg reports, anecdotally it’s considerably worse according to realtors:

Business has been slow in “a lot” of offices since the start of the year, though there are more deals being done in some central outlets, Simon Aldous, a director at Savills, said in a survey published last week by the Royal Institution of Chartered Surveyors.

Offers for homes are often more than 10 percent below asking prices, James Gubbins, a partner at Dauntons in Pimlico, said in the poll.

“Uncertainty over Brexit is the issue,” Gubbins said.

Media coverage of the slowdown, including headlines about falling house prices, is making consumers nervous and holding back demand. New buyers registering with real-estate agents fell for an 11th month in February, RICS said last week.

The slump in London home prices has weighed on national prices too as home price inflation has dropped to its lowest since Feb 2012:

Increased taxes on landlords and loan limits in Singapore have also helped to damp demand from overseas, and as Lucian Cook, head of residential research at broker Savills Plc, warns, a decade of soaring prices means London’s more exposed to political and economic uncertainty, the prospect of interest rate increases and mortgage loan limits.

Interestingly, the north-west of England has now replaced the capital as the fastest-growing property market in the UK. Top of the league for price growth is Blackburn, which recorded average prices ahead by 16.4% over the last 12 months.

Ironically, especially compared to the US, with the most recent official data showing earnings growth averaging 2.5%, that means that unusually, wages are currently outpacing house prices.

END

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

Russia/USA

After Tillerson was fired, he responds that Moscow was clearly behind the Skripal poisoning and it will trigger a response

(courtesy zerohedge)

Tillerson: Moscow “Clearly” Behind Skripal Poisoning, “Will Trigger A Response”

U.S. Secretary of State Rex Tillerson told reporters Monday evening poisoning of former Russian double agent Sergei Skripal “clearly came from Russia” and “certainly will trigger a response.”

Tillerson noted that he didn’t know whether the Kremlin knew about the “really egregious” March 4 attack on Skripal, 66, and his daughter Yulia,33, but that the poison – which is “only in the hands of a very, very limited number of parties,” could not have come from anywhere else.

“There is never a justification for this type of attack – the attempted murder of a private citizen on the soil of a sovereign nation – and we are outraged that Russia appears to have again engaged in such behavior,” Tillerson said in a statement. “From Ukraine to Syria – and now the U.K. – Russia continues to be an irresponsible force of instability in the world, acting with open disregard for the sovereignty of other states and the life of their citizens.”

Lashing out at Russia for what the US and its allies are now framing as Moscow’s “destabilizing role” in world affairs, Tillerson said “and now in the UK,” Moscow “continues to be an irresponsible force of instability in the world, acting with open disregard for the sovereignty of other states and the life of their citizens.”

The White House took a softer tone, declining to name Russia as the likely culprit.

“The use of a highly lethal nerve agent against UK citizens on UK soil is an outrage,” said Press Secretary Sarah Sanders. “Right now, we are standing with our UK ally,” Sanders said, adding “I think they’re still working through even some of the details of that, and we’re going to continue to work with the UK.”

Tillerson’s comments came hours after British Prime Minister Theresa May told the House of Commons that the Kremlin was “highly likely” to be responsible for the attack in the southwestern city of Salisbury, and the UK government would consider it an “unlawful use of force.”

May fleshed out the evidence that the UK has gathered to make its determination, while insisting that actions would be taken to hold the regime accountable – raising the possibility of more sanctions against Russia.

Hedging her bets

Instead of outright declaring that Russian President Vladimir Putin authorized the attack, May said UK intelligence have come up with two possibilities of the origin of nerve agent: The attack was either ordered by Putin, or Russia lost control of the nerve agent used against Skripal.

“Russia has previously produced this agent, and the government has concluded that it is highly likely that Russia was responsible,” May said.

May said that the attack happened “against a backdrop of Russian state agression,” citing the annexation of Crimea four years ago and unrest in the Donbas region. She also brought up election meddling.

May has given Russia 36 hours to explain how the exotic nerve agent wound up poisoning Skripal, or face “extensive measures.”

Break: Theresa May gives Russian ambassador 36 hour ultimatum to explain how state developed nerve agent used in Salisbury, or face “extensive measures”.

“I share the impatience of this house and the country at large to bring those responsible to justice and take a full range of appropriate responses….but as a nation that believes in justice and the rule of law it’s right we proceed in the right way,” said May, adding “There can be no question of business as usual with Russia.”

end

Russia/UK

Russia refuses to respond to the UK ultimatum until it receives nerve toxin samples

(courtesy zerohedge)

Russia Refuses To Respond To UK “Ultimatum” Until It Receives Nerve Toxin Samples

Russia has refused to respond to the British “ultimatum” about a clandestine Soviet chemical weapon allegedly used in an ex-double agent’s poisoning until a sample of the agent is provided, the Russian foreign minister said. As reported on Monday, British PM Theresa May said a chemical weapon developed under a secret Soviet program dubbed Novichok was used in the poisoning of Sergei Skripal. May demanded that Russia provide details of the program, saying otherwise London would consider the poisoning an attack directed by the Russian government.

On Tuesday, Moscow balked at this demand, with the Russian Foreign Ministry saying that it had summoned British Ambassador to Moscow Laurie Bristow.

“We have certainly heard the ultimatum voiced in London,” Russia’s top diplomat Sergey Lavrov said. “The spokesperson for the Foreign Ministry has commented on our attitude to this,” he added referring to Maria Zakharova branding of May’s appearance in Parliament as a “circus.”

Lavrov said that a case of alleged use of chemical weapons should be handled through the proper channel, being the Organization for the Prohibition of Chemical Weapons of which both Russia and Britain are members.

“As soon as the rumors came up that the poisoning of Skripal involved a Russia-produced agent, which almost the entire English leadership has been fanning up, we sent an official request for access to this compound so that our experts could test it in accordance with the Chemical Weapons Convention [CWC],” Lavrov said. So far the request has been ignored by the British side, he added.

The minister assured that Russia has nothing to do with the poisoning of Skripal and would assist Britain in the investigation, provided that London meets its own obligations as to how such probes are to be handled.

The OPCW rules allow Britain in this case to send a request to Russia on the suspected Russian-made chemical weapon and expect a response within 10 days, Lavrov explained. If the response is not satisfactory, Britain would have to file a complaint with the organization’s executive council and the conference of CWC member-states, he said.

* * *

Russia’s diplomatic sparring aside, according to BlueBay Asset Management’s Timothy Ash, U.K. “countermeasures” mentioned in Prime Minister Theresa May’s statement likely mean new sanctions.