GOLD: $1316.50 DOWN $ 4.70 (COMEX TO COMEX CLOSINGS)

Silver: $16.52 DOWN 2 CENTS (COMEX TO COMEX CLOSINGS)

Closing access prices:

Gold $1317.30

silver: $16.52

For comex gold:

APRIL/

NUMBER OF NOTICES FILED TODAY FOR APRIL CONTRACT:117 NOTICE(S) FOR 11700 OZ.

TOTAL NOTICES SO FAR 1086 FOR 108,600 OZ (3.3779 tonnes)

THE COMEX IS OUT OF GOLD

For silver:

APRIL

15 NOTICE(S) FILED TODAY FOR

75,000 OZ/

Total number of notices filed so far this month: 497 for 2,485,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: BID $8780/OFFER $8882: DOWN $23(morning)

Bitcoin: BID/ $8998/offer $9098: UP $192 (CLOSING/5 PM)

end

First Shanghai gold fix comes at 10 pm est

The second Shanghai gold fix: 2:15 pm

First Shanghai gold fix gold: 10 pm est: 1331.25

NY price at the same time: 1324.40

PREMIUM TO NY SPOT: $6.85

ss

Second gold fix early this morning: 1331.93

USA gold at the exact same time: 1323.00

PREMIUM TO NY SPOT: $7.93

AGAIN, SHANGHAI REJECTS NEW YORK PRICING.

WE WILL NOT PROVIDE LONDON FIXES AS THEY ARE NOT ACCURATE AS TO WHAT IS GOING ON AT THE SAME TIME FRAME.

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total OPEN INTEREST FELL BY 5159 CONTRACTS FROM 201,707 FALLING TO 196,548 ACCOMPANYING YESTERDAY’S 18 CENT FALL IN SILVER PRICING. AFTER A STRING OF 4 CONSECUTIVE OI GAINS, WE NOW REGISTER 4 CONSECUTIVE DROPS IN OI. WE ARE NOW WITNESSING OUR USUAL AND CUSTOMARY COMEX LONG LIQUIDATION AS WE HEAD INTO THE ACTIVE DELIVERY MONTH OF MAY AS LONGS PACK THEIR BAGS AND MIGRATE OVER TO LONDON. WE WERE NOTIFIED THAT WE HAD AN STRONG SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP : 0 EFP CONTRACTS FOR APRIL, 3902 EFP’S FOR MAY , 782 EFP’S FOR JULY AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE OF 4684 CONTRACTS. WITH THE TRANSFER OF 4684 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 4684 EFP CONTRACTS TRANSLATES INTO 23.420 MILLION OZ ACCOMPANYING 1.THE FALL IN SILVER PRICE (18 CENTS) AT THE COMEX AND 2. THE STRONG AMOUNT OF SILVER OUNCES STANDING FOR APRIL COMEX DELIVERY.

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF APRIL:

73,158 CONTRACTS (FOR 19 TRADING DAYS TOTAL 73,158 CONTRACTS) OR 357.90 MILLION OZ: AVERAGE PER DAY: 3850 CONTRACTS OR 19.252 MILLION OZ/DAY

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH: 357.90 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 51.128% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)

ACCUMULATION IN YEAR 2018 TO DATE SILVER EFP’S: 1.0838 BILLION OZ.

ACCUMULATION FOR JAN 2018: 236.879 MILLION OZ

ACCUMULATION FOR FEB 2018: 244.95 MILLION OZ

ACCUMULATION FOR MARCH 2018: 236.67 MILLION OZ

RESULT: WE HAD A LARGE SIZED FALL IN COMEX OI SILVER COMEX OF 5159 WITH THE 18 CENT LOSS IN SILVER PRICE AS OUR CUSTOMARY COMEX LONG MIGRATION INTO LONDON BASED FORWARDS COMMENCED IN EARNEST AS WE ARE APPROACHING THE NEW ACTIVE MONTH OF MAY. THE CME NOTIFIED US THAT IN FACT WE HAD AN HUGE SIZED EFP ISSUANCE OF 4684 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) . FROM THE CME DATA: 0 CONTRACTS WERE ISSUED FOR APRIL, 3902 EFP’S WERE ISSUED FOR THE MONTH OF MAY, AND 782 EFP CONTRACTS FOR JULY, FOR A DELIVERABLE FORWARD CONTRACT OVER IN LONDON WITH A FIAT BONUS (TOTAL: 4684). TODAY WE LOST 475 TOTAL OI CONTRACTS ON THE TWO EXCHANGES: i.e. 4684 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH AN DECREASE OF 5159 OI COMEX CONTRACTS. AND ALL OF THIS HAPPENED WITH THE FALL IN PRICE OF SILVER OF 18 CENTS AND A CLOSING PRICE OF $16.54 WITH RESPECT TO YESTERDAY’S TRADING. YET WE STILL HAVE A STRONG AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY IN THIS NON ACTIVE APRIL DELIVERY MONTH.

In ounces AT THE COMEX, the OI is still represented by UNDER 1 BILLION oz i.e. .982 MILLION OZ TO BE EXACT or 140% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT APRIL MONTH/ THEY FILED: 15 NOTICE(S) FOR 15,000 OZ OF SILVER

IN SILVER, WE HAVE NOW SET THE NEW RECORD OF OPEN INTEREST AT 243,411 AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $16.51 ON APRIL 9.2018.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH 27 MILLION OZ AND APRIL 1.8 MILLION OZ)

- HUGE RECORD OPEN INTEREST IN SILVER 243,411 CONTRACTS (OR 1.217 BILLION OZ/ SET APRIL 9/2018

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017

- RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 357.9 MILLION OZ/ (SO FAR)

AND YET WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT). IT ALSO LOOKS LIKE BANKER CAPITULATION IN SILVER AS THEY STRUGGLE TO REMOVE SOME OF THEIR HUGE OBLIGATIONS.

In gold, the open interest ROSE BY 373 CONTRACTS UP TO 506,783 DESPITE THE FALL IN PRICE/YESTERDAY’S TRADING ( FALL OF $9.80). WE ARE NOW IN THE ACTIVE DELIVERY MONTH OF APRIL HEADING INTO THE NON ACTIVE MONTH OF MAY. THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A GIGANTIC SIZED 12,209 CONTRACTS : JUNE SAW THE ISSUANCE OF 11,659 CONTRACTS , MAY SAW THE ISSUANCE OF 400 CONTRACTS AND AUGUST SAW THE ISSUANCE OF: 150 CONTRACTS (REPORTED LATE YESTERDAY) WITH ALL OTHER MONTHS ZERO. The new OI for the gold complex rests at 506,783. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. DEMAND FOR GOLD INTENSIFIES GREATLY AS WE CONTINUE TO WITNESS A HUGE NUMBER OF EFP TRANSFERS TOGETHER WITH THE MASSIVE INCREASE IN GOLD COMEX OI TOGETHER WITH THE TOTAL AMOUNT OF GOLD OUNCES STANDING FOR FEBRUARY COMEX. EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE A LARGE SIZED OI GAIN IN CONTRACTS ON THE TWO EXCHANGES: 373 OI CONTRACTS INCREASED AT THE COMEX AND AN GIGANTIC SIZED 12,209 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON.THUS TOTAL OI GAIN: 12,582 CONTRACTS OR 1,258,200 OZ = 39.135 TONNES.

YESTERDAY, WE HAD 8946 EFP’S ISSUED.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF APRIL : 212,950 CONTRACTS OR 21,295,000 OZ OR 662.36 TONNES (19 TRADING DAYS AND THUS AVERAGING: 11,207 EFP CONTRACTS PER TRADING DAY OR 1,120,700 OZ/ TRADING DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SIZE OF THESE EFP TRANSFERS : SO FAR THIS MONTH IN 19 TRADING DAYS IN TONNES: 662.36 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2017, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 2555 TONNES

THUS EFP TRANSFERS REPRESENTS 662.36/2550 x 100% TONNES = 25.97% OF GLOBAL ANNUAL PRODUCTION SO FAR IN MARCH ALONE.*** THE ACCUMULATION OF EFP CONTRACTS IS RISING PER MONTH.

ACCUMULATION OF GOLD EFP’S YEAR 2018 TO DATE: 2,702.063* TONNES *SURPASSED ANNUAL PROD’N

ACCUMULATION OF GOLD EFP’S FOR JANUARY 2018: 653.22 TONNES

ACCUMULATION OF GOLD EFP’S FOR FEBRUARY 2018: 649.45 TONNES

ACCUMULATION OF GOLD EFP’S FOR MARCH 2018: 741.89 TONNES

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: AN INCREASE IN OI AT THE COMEX OF 373 DESPITE THE FALL IN PRICE // GOLD TRADING YESTERDAY ($9.80 LOSS). WE ALSO HAD A GIGANTIC SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 12,209 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 12,209 EFP CONTRACTS ISSUED, WE HAD A STRONG SIZED NET GAIN OF 12,209 CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

12,209 CONTRACTS MOVE TO LONDON AND 373 CONTRACTS INCREASED AT THE COMEX. (in tonnes, the GAIN in total oi equates to 39.135 TONNES).

we had:117 notice(s) filed upon for 11700 oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD…

WITH GOLD DOWN $4.90 /NO CHANGE IN GOLD INVENTORY AT THE GLD

Inventory rests tonight: 871.20 tonnes.

SLV/

WITH SILVER DOWN 2 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/

/INVENTORY RESTS AT 316.899 MILLION OZ/

end

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER FELL BY 5159 CONTRACTS from 201,707 DOWN TO 196,548 (AND FURTHER FROM THE NEW COMEX RECORD SET /APRIL 9/2017 AT 243,411). THE PREVIOUS RECORD OTHER THAN WAS ESTABLISHED AT: 234,787, SET ON APRIL 21.2017 ALMOST ONE YEAR AGO. THE PRICE OF SILVER ON THAT DAY: $17.89. AFTER WE HAVE HAD FOUR CONSECUTIVE OI GAINS WE NOW HAVE FOUR CONSECUTIVE OI DROPS AS OUR CUSTOMARY MIGRATION OF COMEX LONGS MORPH INTO LONDON FORWARDS HAVING COMMENCED WITH OUR MARCH INTO THE UPCOMING ACTIVE MAY DELIVERY MONTH (AT THE COMEX). TRUE TO FORM OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE: 0 EFP CONTRACTS FOR APRIL, 3902 EFP CONTRACTS FOR MAY (WE DO NOT GET A LOOK AT THESE CONTRACTS AS IT IS PRIVATE BUT THE CFTC DOES AUDIT THEM), AND 782 EFP’S FOR JULY AND ALL OTHER MONTHS ZERO. TOTAL EFP ISSUANCE: 4684 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI LOSS AT THE COMEX OF 5159 CONTRACTS TO THE 4684 OI TRANSFERRED TO LONDON THROUGH EFP’S, SURPRISINGLY WE OBTAIN A TINY LOSS OF 475 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES: 2.375 MILLION OZ!!! AND THIS OCCURRED DESPITE A FALL IN PRICE OF 18 CENTS. THE BANKERS ORCHESTRATED THEIR RAID ON MONDAY TO DESPERATELY TRY AND PARE THEIR GIGANTIC OPEN INTEREST SHORT ON BOTH EXCHANGES BUT TO NO AVAIL. JUDGING BY THE RECORD NUMBER OF ISSUANCE DURING THIS MONTH OF APRIL AT 357.4 MILLION OZ. I DO NOT THINK THAT OUR BANKERS HAVE BEEN TOO SUCCESSFUL. PLEASE REMEMBER THAT THERE CAN BE DELAY OF 24 TO 48 HOURS IN THE ISSUANCE OF THESE EFP’S, SO EXPECT THE NUMBERS ANNOUNCED (EFP’S) WILL INCREASE STEADILY AS WE HEAD INTO FIRST DAY NOTICE THIS MONDAY APRIL 30.

RESULT: A LARGE SIZED DECREASE IN SILVER OI AT THE COMEX WITH THE FALL IN SILVER PRICING / YESTERDAY (18 CENTS/) . BUT WE ALSO HAD ANOTHER HUMONGOUS SIZED 4684 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR APRIL, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON. EXPECT EFP ISSUANCE TO INCREASE DURING THIS WEEK AS WE HEAD INTO THE ACTIVE DELIVERY MONTH OF MAY.

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)THURSDAY MORNING/WEDNESDAY NIGHT: Shanghai closed DOWN 42.94 POINTS OR 1.38% /Hang Sang CLOSED DOWN 320.47 POINTS OR 1.06% / The Nikkei closed UP 104.29 POINTS OR 0.47%/Australia’s all ordinaires CLOSED UP .56% /Chinese yuan (ONSHORE) closed DOWN at 6.3238/Oil DOWN to 68.45 dollars per barrel for WTI and 74.53 for Brent. Stocks in Europe OPENED DEEPLY IN THE GREEN. ONSHORE YUAN CLOSED DOWN AT 6.3238 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.3179/ONSHORE YUAN TRADING WEAKER AGAINST OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING MUCH STRONGER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW LOOKS LIKE A FULL TRADE WAR IS BEGINNING/

/NORTH KOREA/SOUTH KOREA

i)North Korea/

b) REPORT ON JAPAN

3 c CHINA

i)China’s big worry: North Korea unifies with the South and becomes a strong USA ally with missiles pointing toward Beijing

( zerohedge)

ii)China is planning to lower the auto tariffs from 25% to either 15% or 10%. However cars manufactured in the uSA will still have its 25% tariff as Xi is still dueling with Trump

( zerohedge)

iii)USA top admiral warns that China now controls the South China Sea

( zerohedge)

4. EUROPEAN AFFAIRS

i)European ECB report to Europe/Press conference

Optimism from Draghi has he downplays soft economic data sends the Euro higher along with gold/silver

( zerohedge)

ii)Germany/Deutsche bank

World’s largest derivative bank and player reports disastrous results as it totally retreats from USA banking:

( zerohedge)

iib)the massive layoffs begin as Deutsche bank fires 400 USA bankers. It is these guys that we need to testify in the gold/silver manipulation

(courtesy zerohedge)

iii)Bill Blain correctly states that the reason millenials are not buying cars or home is simple: lack of money and huge amounts of debt

( Bill Blain/Mint partners)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

This is deadly: Russia has decided to send the new advanced S 300 anti aircraft missiles to Syria. This is a red line for Israel as they warn of catastrophic consequences.

( zerohedge)

ii)Iran/USA

More threats: this time the Iranian Naval Commander has threatened to sink USA ships in the Gulf and create a catastrophic situation if Trump kills the deal. If the deal is dropped, then Iran loses 1 million barrels of oil per day on top of other sanctions

( zerohedge)

the rhetoric intensifies: Israel claims that the Iranian regime is in its final days economically and militarily

( zerohedge)

6 .GLOBAL ISSUES

Why Canada is heading down the same path as other countries with no gold

( Alex Deluce/GoldTelegraph.com

7. OIL ISSUES

8. EMERGING MARKET

i)Venezuela

9. PHYSICAL MARKETS

iii)Simon Black comments on gold:

- very few gold discoveries in this last decade so supply of gold diminishes

- inflation is raring its ugly read

( Simon Black/SovereignMan.com)

10. USA stories which will influence the price of gold/silver

i)This morning’s early trading:

ii)This morning’s reports:

First: initial claims drop but durable goods also disappoint

( zerohedge)

iii)SWAMP STORIES

a)Giuliani has met Mueller and surprisingly he is discussing the upcoming Trump interview

( zerohedge)

Trading Volumes on the COMEX

PRELIMINARY COMEX VOLUME FOR TODAY:280,880 contracts

CONFIRMED COMEX VOL. FOR YESTERDAY: 283,076 contracts

comex gold volumes are RISING AGAIN

Here is a summary of the latest gold trading volumes at the Comex per year

certainly the introduction of EFP’s has certainly had an effect:

Meanwhile, gold-trading volumes on the COMEX have never been higher:

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

And now for the wild silver comex results.

Total silver OI FELL BY A CONSIDERABLE 5159 CONTRACTS FROM 201,707 DOWN TO 196,548 (AND FURTHER FROM THE NEW RECORD OI FOR SILVER SET APRIL 9.2018/ 243,411 CONTRACTS) WITH THE 18 CENT FALL IN SILVER PRICING. SINCE WE ARE HEADING INTO AN ACTIVE DELIVERY MONTH OF MAY, WE HAVE NOW WITNESSED OUR USUAL AND CUSTOMARY COMEX LIQUIDATION AND WE SHOULD SEE A GREATER MIGRATION OVER TO LONDON DURING THIS WEEK. AS A MATTER OF FACT, WE WERE INFORMED THAT WE HAD A GIGANTIC 3902 EFP CONTRACTS ISSUED FOR MAY, A SMALLER 782 EFP CONTRACT ISSUANCE FOR JULY AND ZERO FOR ALL OTHER MONTHS. THESE EFPS WERE ISSUED TO COMEX LONGS WHO RECEIVED A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. THE TOTAL EFP’S ISSUED: 4684. ON A NET BASIS WE LOST 475 SILVER OPEN INTEREST CONTRACTS AS WE OBTAINED A 5159 CONTRACT LOSS AT THE COMEX COMBINING WITH THE ADDITION OF 4684 OI CONTRACTS NAVIGATING OVER TO LONDON. DUE TO THE FACT THAT THE BOYS WERE VERY BUSY NEGOTIATING LONG COMEX CONTRACTS EMIGRATING TO LONDON,(AND WAITING FOR THEIR PASSPORTS) DO NOT BE SURPRISED TO SEE A HUGE ISSUANCE OVER THIS WEEK AS THE DELAY IN ISSUANCE CAN BE IN EXCESS OF 24 TO 48 HRS.

NET LOSS ON THE TWO EXCHANGES: 475 CONTRACTS

AMOUNT STANDING FOR SILVER AT THE COMEX

We are now in the non active delivery month of April and here the front month LOST 5 contracts FALLING TO 15 contracts. We had 5 notices filed upon so in essence we LOST 0 contracts or NIL additional ounces of silver will stand for delivery in this non active delivery month of April .

The next big active delivery month for silver will be May and here the OI LOST 10,522 contracts DOWN to 30,394. June saw a GAIN of 145 contracts to stand at 533. The next big delivery month for silver is July and here the OI ROSE by 5136 contracts UP to 117,341.

We had 15 notice(s) filed for 75,000 OZ for the APRIL 2018 contract for silver

INITIAL standings for APRIL/GOLD

APRIL 26/2018.

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz |

NIL OZ

|

| Deposits to the Dealer Inventory in oz | NIL oz |

| Deposits to the Customer Inventory, in oz | nil OZ |

| No of oz served (contracts) today |

117 notice(s)

11,700 OZ

|

| No of oz to be served (notices) |

408 contracts

(40,800 oz)

|

| Total monthly oz gold served (contracts) so far this month |

1086 notices

108600 OZ

3.3779 TONNES

|

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

For APRIL:

Today, 0 notice(s) were issued from JPMorgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equates to 117 contract(s) of which 2 notices were stopped (received) by j.P. Morgan dealer and 117 notice(s) was (were) stopped/ Received) by j.P.Morgan customer account.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

To calculate the INITIAL total number of gold ounces standing for the APRIL. contract month, we take the total number of notices filed so far for the month (1086) x 100 oz or 108,600 oz, to which we add the difference between the open interest for the front month of APRIL. (525 contracts) minus the number of notices served upon today (117 x 100 oz per contract) equals 149,400 oz, the number of ounces standing in this active month of APRIL (4.646 tonnes)

Thus the INITIAL standings for gold for the APRIL contract month:

No of notices served (969 x 100 oz or ounces + {(525)OI for the front month minus the number of notices served upon today (117 x 100 oz )which equals 149,400 oz standing in this active delivery month of APRIL . THERE IS 12.003 TONNES OF REGISTERED GOLD AVAILABLE FOR DELIVERY SO FAR.

WE LOST 1 COMEX OI CONTRACTS OR 100 OZ OF GOLD WILL STAND

IN THE LAST 18 MONTHS 73 NET TONNES HAS LEFT THE COMEX.

end

And now for silver

AND NOW THE APRIL DELIVERY MONTH

APRIL INITIAL standings/SILVER

| Silver | Ounces |

| Withdrawals from Dealers Inventory | nil oz |

| Withdrawals from Customer Inventory |

616,534.730 oz

CNT

|

| Deposits to the Dealer Inventory |

691,565.04

SCOTIA

Brinks

oz

|

| Deposits to the Customer Inventory |

302,394.200 oz

DELAWARE

MALCA

691,565

|

| No of oz served today (contracts) |

15

CONTRACT(S)

(75,000 OZ)

|

| No of oz to be served (notices) |

0 contracts

(0 oz)

|

| Total monthly oz silver served (contracts) | 497 contracts

(2,485,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

we had 2 inventory movement at the dealer side of things

i) Into dealer Scotia: 591,435,100 oz

ii) Into dealer Brinks: 89,275.900 oz

total dealer deposits: 691,565.041 oz

we had 3 deposits into the customer account

i) Into JPMorgan: nil oz

*** JPMorgan for most of 2017 and in 2018 has adding to its inventory almost every single day.

JPMorgan now has 140 million oz of total silver inventory or 53.4% of all official comex silver. (140 million/263 million)

JPMorgan did not deposit into its warehouses (official) today.

ii) Delaware: 1081.10: OZ

iii) Into Malca: 299,327.300

iv) Into Scotia: 1985.800

total deposits today: 302,394.200 oz

we had 1 withdrawals from the customer account;

i) Out of CNT 616,534.730 oz

total withdrawals; 616,534.730 oz

we had 0 adjustment

.

total dealer silver: 63.884 million

total dealer + customer silver: 261.417 million oz

The total number of notices filed today for the APRIL. contract month is represented by 15 contract(s) FOR 75,000 oz. To calculate the number of silver ounces that will stand for delivery in APRIL., we take the total number of notices filed for the month so far at 497 x 5,000 oz = 2,485,000 oz to which we add the difference between the open interest for the front month of April. (15) and the number of notices served upon today (15 x 5000 oz) equals the number of ounces standing.

.

Thus the INITIAL standings for silver for the APRIL contract month: 497(notices served so far)x 5000 oz + OI for front month of April(15) -number of notices served upon today (15)x 5000 oz equals 2,485,000 oz of silver standing for the April contract month

WE LOST 0 SILVER CONTRACT OR NIL ADDITIONAL OUNCES WILL STAND IN THIS NON ACTIVE DELIVERY MONTH OF APRIL

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

CRIMINALS!!

ESTIMATED VOLUME FOR TODAY: 116,079 CONTRACTS (WOW) 626 MILLION OZ OR 89% OF ANNUAL PRODUCTION.

CONFIRMED VOLUME FOR YESTERDAY: 137,751 CONTRACTS (my goodness)

YESTERDAY’S CONFIRMED VOLUME OF 137,751 CONTRACTS EQUATES TO 688 MILLION OZ (0..688 billion oz) OR 133% OF ANNUAL GLOBAL PRODUCTION OF SILVER

COMMODITY LAW SUGGESTS THAT OPEN INTEREST SHOULD NOT BE MORE THAN 3% OF ANNUAL GLOBAL PRODUCTION. THE CROOKS ARE SUPPLYING MASSIVE PAPER TRYING TO KEEP SILVER IN CHECK.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price at that day at $18.42

The previous record was 224,540 contracts with the price at that time of $20.44

end

NPV for Sprott

1. Sprott silver fund (PSLV): NAV FALLS TO -1.95% (APRIL 26/2018)

2. Sprott gold fund (PHYS): premium to NAV FALLS TO -0.61% to NAV (APRIL 26/2018 )

Note: Sprott silver trust back into NEGATIVE territory at -1.95%-/Sprott physical gold trust is back into NEGATIVE/ territory at -0.61%/Central fund of Canada’s is still in jail but being rescued by Sprott.

Sprott WINS hostile 3.1 billion bid to take over Central Fund of Canada

(courtesy Sprott/GATA)

3.SPROTT CEF.A FUND (FORMERLY CENTRAL FUND OF CANADA): NAV FALLS TO -1.95%: NAV 13.62/TRADING 13.35//DISCOUNT 1.95.

END

And now the Gold inventory at the GLD/

APRIL 26/WITH GOLD DOWN $4.90/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 871.20 TONNES

APRIL 25/AFTER 9 CONSECUTIVE DAYS OF NO MOVEMENT OF GOLD INTO OUT OF THE GLD, WE HAD A HUGE DEPOSIT OF 5.31 TONNES OF GOLD INTO THE GLD/INVENTORY RESTS AT 871.20 TONNES.

APRIL 24./WITH GOLD UP $9.90, WE HAD NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 865.89 TONNES/

APRIL 23.2018/WITH GOLD DOWN $14.00/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 865.89 TONNES.

APRIL 20/WITH GOLD DOWN $10.20: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 865.89 TONNES

APRIL 19/WITH GOLD DOWN $4.25: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 865.89 TONNES/

APRIL 18/WITH GOLD UP $3.65: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 865.89 TONNES

APRIL 17/WITH GOLD DOWN $1.00 NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 865.89 TONNES/

April 16/WITH GOLD UP$2.80/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 865.89 TONNES/

April 13/WITH GOLD UP $6.15, A HUGE DEPOSIT OF 5.90 TONNES INTO THE GLD INVENTORY/INVENTORY RESTS AT 865.89 TONNES

April 12/WITH GOLD DOWN $17.40/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 859.99 TONNES

April 11/WITH GOLD UP $13.85/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 859,99 TONNES

APRIL 10/WITH GOLD UP $5.25/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 859.99 TONNES

APRIL 9/WITH GOLD UP$4.50/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 859.99 TONNES

APRIL 6/WITH GOLD UP $7.50 ,A HUGE CHANGE IN INVENTORY AT THE GLD/ A DEPOSIT OF 5.90 TONNES/INVENTORY RESTS AT 859.99 TONNES

APRIL 5/WITH GOLD DOWN $8.20 WE HAD TWO ENTRIES: 1) TINY WITHDRAWAL OF .28 TONNES TO PAY FOR FEES AND 2) A DEPOSIT OF 2.06 TONNES//INVENTORY RESTS AT 854.09 TONNES

April 4/WITH GOLD UP $2.90 WE HAD NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 852.31 TONNES

APRIL 3./WITH GOLD DOWN $9.30 WE HAD NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 852.31 TONNES

APRIL 2/WITH GOLD UP $19.50, WE HAD A BIG CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF 6.19 TONNES/INVENTORY RESTS AT 852.31 TONNES

MARCH 29/WITH GOLD DOWN $3.20 AND OPTIONS EXPIRY FINISHED, WE HAD NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS A 846.12 TONNES

March 28/WITH GOLD DOWN $16.70, ANOTHER RAID ORCHESTRATED, AGAIN NO SURPRISES AS WE WITNESS ANOTHER 1.18 TONNES OF GOLD REMOVED/INVENTORY RESTS AT 846.12 TONNES

MARCH 27/WITH GOLD DOWN $11.70 AND A RAID INITIATED, IT WAS NO SURPRISE TO SEE THAT A MASSIVE WITHDRAWAL OF 3.24 TONNES WAS USED IN THE ABOVE RAID/INVENTORY RESTS AT 847.30 TONNES

MARCH 26./WITH GOLD UP $4.60/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 850.54 TONNES

MARCH 23/WITH GOLD UP $23.30/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 850.54 TONNES

MARCH 22.WITH GOLD UP $5.90, NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 850.54 TONNES/

MARCH 21/WITH GOLD UP $9.65 NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 850.54 TONNES

March 20/WITH GOLD DOWN $5.75, A SURPRISING HUMONGOUS DEPOSIT OF 10.32 TONNES OF GOLD INTO THE GLD/INVENTORY RESTS AT 850.64 TONNES/

SO FAR, FOR THE MONTH OF MARCH, THE GLD HAS ADDED 19.61 TONNES WITH A NET LOSS OF $17.45

March 19/WITH GOLD UP $5.25: ANOTHER HUGE DEPOSIT OF GOLD TO THE TUNE OF 2.07 TONNES/GOLD INVENTORY RESTS TONIGHT AT 840.22 TONNES

MARCH 16/WITH GOLD DOWN $5.65/OUR CROOKS DEPOSITED ANOTHER 4.42 TONNES INTO GLD INVENTORY/INVENTORY RESTS AT 838.15 TONNES

FOR THE WEEK: GOLD LOST $11.80, BUT GOLD INVENTORY ADVANCED:4.42 TONNES

MARCH 15/WITH GOLD DOWN $7.85, NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 833.73 TONNES

MARCH 14/WITH GOLD DOWN $1.55/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 833.73 TONNES

MARCH 13/WITH GOLD UP $6.25/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 833.73 TONNES

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

APRIL 26/2018/ Inventory rests tonight at 871.20 tonnes

*IN LAST 370 TRADING DAYS: 69.84 NET TONNES HAVE BEEN REMOVED FROM THE GLD

*LAST 320 TRADING DAYS: A NET 86.46 TONNES HAVE NOW BEEN ADDED INTO GLD INVENTORY.

end

Now the SLV Inventory/

APRIL 26/WITH SILVER DOWN 2 CENT/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 316,899 MILLION OZ/

APRIL 25./WITH SILVER DOWN 18 CENTS/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 316.899 MILLION OZ/

APRIL 24./WITH SILVER UP 8 CENTS/SOMETHING SPOOKED OUR CROOKS TO ADD SOME PAPER SILVER: A DEPOSIT OF 1.601 MILLION OZ/INVENTORY RESTS AT 316.899 MILLION OZ/

APRIL 23.2018/WITH SILVER DOWN 50 CENTS, ANOTHER HUGE WITHDRAWAL FROM THE SLV INVENTORY: A WITHDRAWAL OF 1.413 MILLION OZ/INVENTORY RESTS AT 315.298 MILLION OZ.

APRIL 20/WITH SILVER DOWN 11 CENTS: ANOTHER HUGE CHANGE IN SILVER INVENTORY: A WITHDRAWAL OF 1.13 MILLION OZ//SLV RESTS TONIGHT AT 316.711 MILLION OZ/

APRIL 19/WITH SILVER UP 3 CENTS TODAY: WE HAD A BIG CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.355 MILLION OZ/ MAKES ABSOLUTELY NO SENSE!!/INVENTORY RESTS AT 317.841 MILLION OZ

APRIL 18/WITH SILVER UP 44 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 320.196 MILLION OZ

APRIL 17/WITH SILVER UP 10 CENTS TODAY/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 320.196 MILLION OZ

April 16/WITH SILVER UP 7 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 320.196 MILLION OZ/

April 13/WITH SILVER UP 17 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 320.196 MILLION OZ.

April 12/WITH SILVER DOWN 27 CENTS/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 320.196 MILLION OZ/

April 11/2018/WITH SILVER UP 16 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 320.196 MILLION OZ/

APRIL 10/WITH GOLD UP 8 CENTS/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 320.196 MILLION OZ/

APRIL 9/WITH SILVER UP 12 CENTS/WE HAD NO CHANGES IN SILVER INVENTORY/INVENTORY RESTS AT 320.196 MILLION OZ/

APRIL 6/WITH SILVER UP 4 CENTS, WE HAD A HUGE DEPOSIT OF 1.319 MILLION OZ INTO THE SLV INVENTORY/INVENTORY RESTS AT 320.196 MILLION OZ

APRIL 5/WITH SILVER UP 6 CENTS/NO CHANGES IN INVENTORY AT THE SLV/INVENTORY RESTS AT 318.877 MILLION OZ/

April 4/WITH SILVER DOWN 11 CENTS/A SMALL CHANGE IN SILVER INVENTORY AT THE SLV/ A WITHRAWAL OF 135,000 OZ AND THIS IS PROBABLY TO PAY FOR FEES/INVENTORY RESTS AT 318.877 MILLION OZ/

APRIL 3./WITH SILVER DOWN 16 CENTS/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.012 MILLION OZ/

APRIL 2/WITH SILVER UP 34 CENTS/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.012 MILLION OZ/

MARCH 29/WITH SILVER UP 6 CENTS, THE CROOKS DECIDED THAT THEY HAD BETTER ADD SOME 943,000 PAPER OZ TO THEIR INVENTORY/INVENTORY RESTS AT 319.012 MILLION OZ

March 28/WITH SILVER DOWN 27 CENTS/AGAIN NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 318.069 MILLION OZ

MARCH 27/WITH SILVER DOWN 14 CENTS/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 318.069 MILLION OZ/

WITH SILVER UP 11 CENTS/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 318.069 MILLION OZ/

MARCH 23/WITH SILVER UP 19 CENTS, A HAD A BIG WITHDRAWAL OF 1.602 MILLION OZ.INVENTORY RESTS AT 318.069 MILLION OZ/

MARCH 22/WITH SILVER DOWN ONE CENT, NO CHANGE IN SLV INVENTORY/INVENTORY RESTS AT 319.671 MILLION OZ/

March 21/WITH SILVER UP 21 CENTS/NO CHANGE IN SLV INVENTORY/INVENTORY RESTS AT 319.671 MILLION OZ/

March 20/WITH SILVER DOWN 13 CENTS/NO CHANGE IN SLV INVENTORY/INVENTORY RESTS AT 319.671 MILLION OZ/

March 19/WITH SILVER UP 5 CENTS, THE SLV ADDS A SMALL 659,000 OZ TO ITS INVENTORY/INVENTORY RESTS AT 319.671 MILLION OZ/

MARCH 16/WITH SILVER DOWN 15 CENTS/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.012 MILLION OZ.

FOR THE WEEK; SILVER IS DOWN 42 CENTS YET ADDS 943,000 OZ OF SILVER INTO THE SLV/

MARCH 15/WITH SILVER DOWN 11 CENTS/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.012 MILLION OZ/

MARCH 14/WITH SILVER DOWN 8 CENTS/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.012 MILLION OZ/

MARCH 13/WITH SILVER UP 10 CENTS/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.012 MILLION OZ/

HAD ANOTHER HUGE ADDITION OF 1.315 MILLION OZ/INVENTORY RESTS AT 316.590 MILLION OZ/

APRIL 26/2018: NO CHANGES IN SILVER INVENTORY:

Inventory 316.899 million oz

end

6 Month MM GOFO 2.03/ and libor 6 month duration 2.52

Indicative gold forward offer rate for a 6 month duration/calculation:

G0FO+ 2.03%

libor 2.52 FOR 6 MONTHS/

GOLD LENDING RATE: .49%

XXXXXXXX

12 Month MM GOFO

+ 2.77%

LIBOR FOR 12 MONTH DURATION: 2.51

GOFO = LIBOR – GOLD LENDING RATE

GOLD LENDING RATE = +.26

end

Major gold/silver trading /commentaries for THURSDAY

GOLDCORE/BLOG/MARK O’BYRNE.

GOLD/SILVER

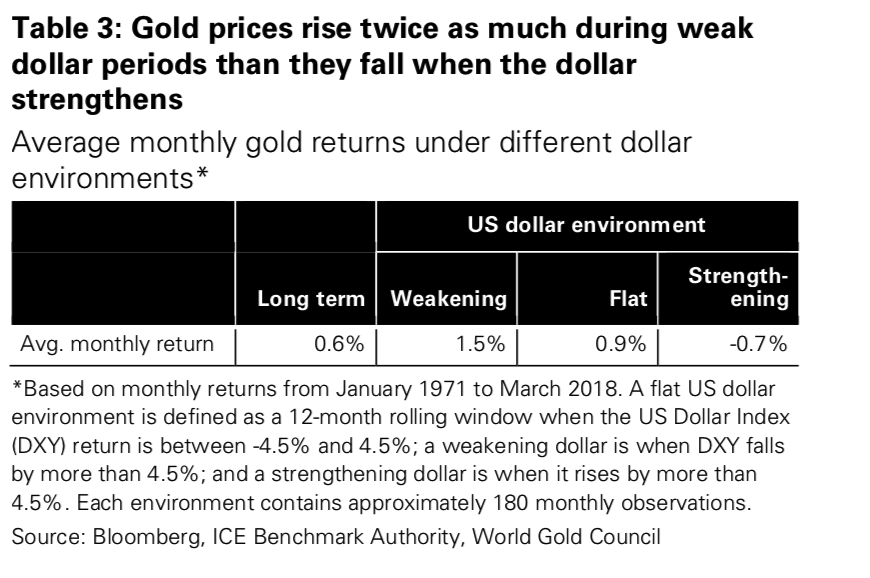

Gold Price Increasingly Influenced By Declining Dollar Rather Than Interest Rates

Gold Price Gains Due To Declining Dollar Rather Than Interest Rates

– Investors should not be put off by higher interest rates, World Gold Council research finds they do not always have a negative impact on gold

– Only short-term movements in gold are ‘heavily influenced by US interest rates’

– Correlation between US interest rates and gold is waning, with US dollar a better indicator of short-term gold price

– New findings will reassure gold investors that there is no single driver of the gold price including interest rates and the myth of the “all powerful” central bank

Editor: Mark O’Byrne

What drives the gold price? There is no single answer to that question. It is a multiple of factors, all of which vary in their influence depending on an even greater number of factors.

According to latest research from the World Gold Council, there are two factors in the short and medium-term that attract investors’ attention the most: the US dollar and US interest rates.

One overriding belief by gold market commentators and observers is that the direction of the US dollar carries a greater impact on the gold price than US interest rates.

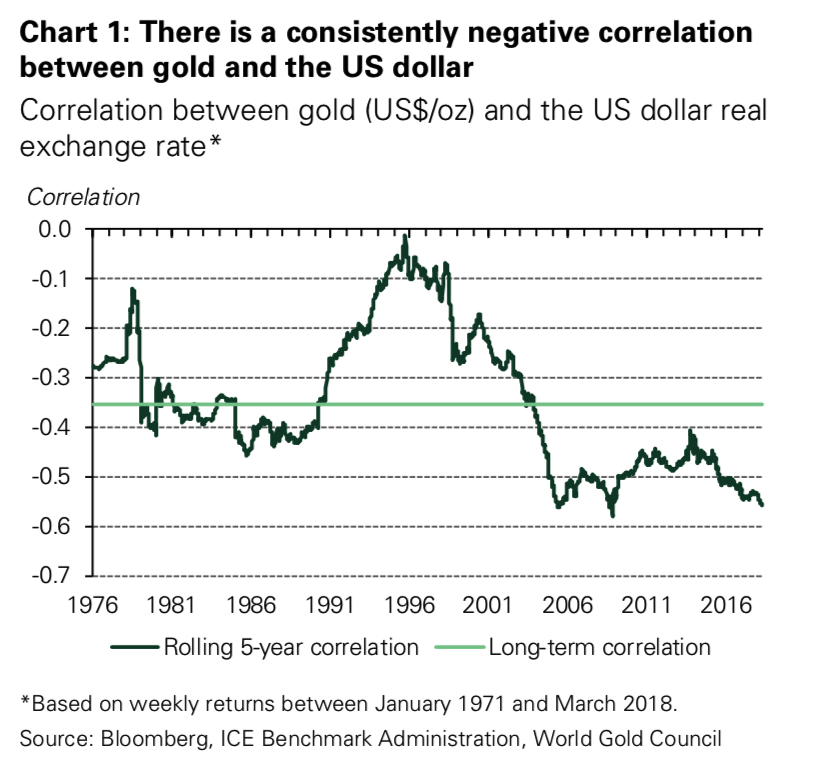

This is understandable given gold’s consistently negative correlation to the US dollar.

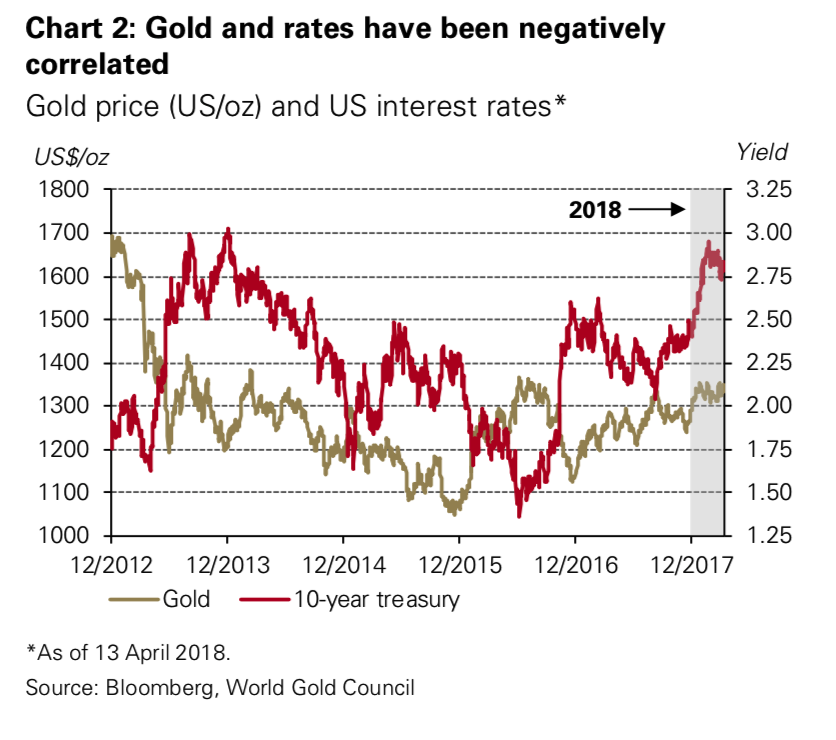

However, we have all noticed how gold has only reacted positively since the Federal Reserve has been hiking rates since last December – increasing by 8.5%.

So should we therefore assume that US interest rates do in fact matter more to the direction of the gold price?

There is no straight forward answer says the World Gold Council. ‘Generally’ the US dollar matters most to the precious metal’s price movements, ‘but there are exceptions to this rule’.

Gold and interest rates: a negative correlation

It makes sense that gold and interest rates should be negatively correlated. One is seen as the opportunity cost of another. Between 2013 and 2017 the negative correlation was strong:

‘[This] was likely a result of the strong influence that US monetary policy was exerting across global markets. This period coincided with a shift in investor expectations of US monetary policy from being very accommodative to moving towards normalisation.’

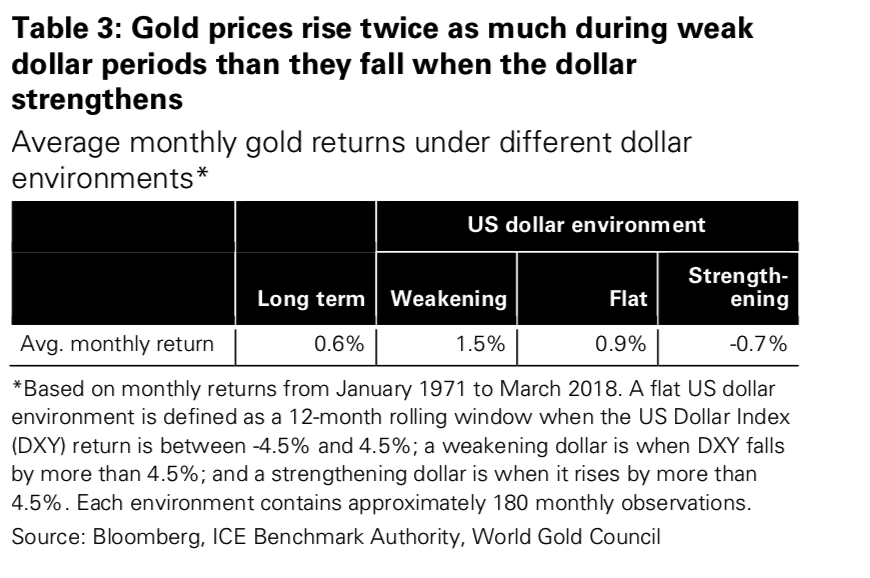

Conversely, higher rates are not always linked to higher prices

We are always quick to assume that US interest rate changes will begin to affect the price of gold. But consider the variety of demands involved in the gold market: jewellery, or technological demands- are they all influenced by US interest rates? The chances are, no.

‘US interest rates do not necessarily influence the behaviour of global consumers of gold jewellery or of technology demand. Nor do they affect the behaviour of investors outside the US for whom local interest rates matter more than US rates’

Interestingly the WGC research finds that whilst gold does react best to negative US interest rates, they can remain below 2.5% (significantly higher than today) and average gold returns remain positive.

‘Falling rates are generally linked to higher gold prices; yet rising rates are not always linked to lower prices.’

Take the above with a pinch of salt

These findings with a pinch of salt. There are so many factors that affect the price of gold that investors should not focus on the policies and currency of one country to determine their buying and selling decisions.

The WGC finds four broad categories which affect the price of gold. It is interactions between these categories that affect the performance of the precious metal.

Wealth and economic expansion: periods of growth are very supportive of jewellery, technology, and long-term savings

Market risk and uncertainty: market downturns often boost investment demand for gold as a safe haven

Opportunity cost: the price of competing assets such as bonds (through interest rates), currencies and other assets influence investor attitudes towards gold

Momentum and positioning: capital flows and price trends can ignite or dampen gold’s performance.

When it comes to gold’s long-term trend, the lobbying group finds that:

‘drivers related to wealth and economic expansion are generally more relevant for gold’s long-term trend. And drivers linked to the other three categories play a significant role in gold’s countercyclical behaviour.’

The US dollar will overtake rates when it comes to influence on gold price

In our view, one of the reasons the dollar will overtake rates to explain the direction of the gold price, is that movements in the dollar already reflect inflation expectations of monetary policy in the US. At the same time, they also reflect expectations of interest rate differentials between the US and major economies, as well as investors’ views on trade imbalances – all factors that are currently relevant for gold.

There is an ‘asymmetric correlation’ between gold prices and the US dollar. Why? Because not everyone pays for their gold in US dollars. Local currency movements impact demand more.

Thus, gold’s behaviour is best understood as a broad fiat currency hedge rather than simply a dollar hedge. This is apparent in periods when major currencies weaken, and investors buy gold to hedge that risk – for example, during the European sovereign debt crisis. In such instances, gold and the dollar have tended to move in sync, with both benefiting from safe haven inflows.

This further explains why the uncertain times ahead due to heightened geopolitical risk are likely to see further gold price gains. Even if the dollar strengthens on announcement of war in Syria (for example) we may still see the price of gold rise.

Read the original research here.

Recommended reading

Four Key Themes To Drive Gold Prices In 2018 – World Gold Council

Stock Market Selloff Showed Gold Can Reduce Portfolio Risk

Gold Does Not Fear Interest Rate Hikes

News and Commentary

Gold hovers near 5-wk lows amid dollar pressure, rising yields (Reuters.com)

Asian Stocks Mixed as Tech Rises; Dollar Steady (Bloomberg.com)

Gold prices could ‘test five year highs’ later this year: Researcher (CNBC.com)

Ex-UBS Metals Trader Beats Spoofing Conspiracy Charge (Bloomberg.com)

Deutsche Bank to Reduce Investment Banking in Focus on Europe (Bloomberg.com)

Central Bankers Can’t Agree on Cryptocurrencies (Bloomberg.com)

Debt-Enabled Asset-Bubbles Are On A Crash With Demographics (ZeroHedge.com)

It’s 2-Year Yields, Not 10-Years, We Worry About Most (ZeroHedge.com)

Gold prices could ‘test five year highs’ later this year (CNBC.com)

ABN Amro: Geo-politics and sanctions support commodities (Abnamro.nl)

Andrew Maguire’s Kinesis money which is a “bitcoin” but backed 100% by allocated gold and silver is set to go.

it think it would be a great idea to look at this!

please read at: https://kinesis.money/#/

(Andrew Maguire)

|

2:57 PM (1 hour ago) | ||

|

|||

Harvey

Here It is my friend! https://kinesis.money/#/ Please let everyone know.

Let catch up on Monday if you have time. We have billions in the hopper ready to be allocated on the 1st day of trading. The paper market days are over.

Warm regards

Andy

END

Movement of earmarked gold and no doubt that the gold is heading to Turkey

(Harvey)

Federal reserve bank of NY earmarked gold departures:

Ex-UBS metals trader beats spoofing conspiracy charge

Submitted by cpowell on Wed, 2018-04-25 16:13. Section: Daily Dispatches

By Christie Smythe

Bloomberg News

Wednesday, April 25, 2018

If anything is more precious than gold, it might be an acquittal.

A former UBS Group AG precious metals trader was found not guilty on Wednesday of scheming to manipulate futures markets through a practice known as spoofing.

Andre Flotron, 54, was cleared by a federal jury in New Haven, Connecticut, of a single count of conspiracy to engage in commodities fraud. It was the first acquital in a spoofing-related case. He could have faced as long as 25 years in prison if convicted.

“We’re extremely pleased with the jury’s verdict,” Flotron’s defense attorney Marc Mukasey said. “Justice has been done.” …

… For the remainder of the report:

https://www.bloomberg.com/news/articles/2018-04-25/ex-ubs-metals-trader-…

Craig Hemke at Sprott Money: The soaring dollar crushes the commodity rally

Submitted by cpowell on Wed, 2018-04-25 20:41. Section: Daily Dispatches

By Craig Hemke

Sprott Money, Toronto

Wednesday, April 25, 2018

Just last week it appeared that a general rally in commodities was underway.

Gold, silver, the base metals, and crude oil were all soaring. But now, less than one week later, prices are falling sharply. And why?

Blame the high-frequency traders who trade the digital derivative contracts.

They’ve “seen” the sudden, sharp rally in the U.S. dollar and they have been quick to dump their metals exposure as quickly as they bought it last week. …

… For the remainder of the analysis:

https://www.sprottmoney.com/Blog/the-soaring-dollar-crushes-the-commodit…

end

Simon Black comments on gold:

- very few gold discoveries in this last decade so supply of gold diminishes

- inflation is raring its ugly read

(courtesy Simon Black/SovereignMan.com)

Simon Black On “The Coming Boom In Gold Prices…”

Authored by Simon Black via SovereignMan.com,

In June 1884, a local farmer named Jan Gerritt Bantjes discovered gold on his property in a quiet corner of the South African Republic.

Though no one had any idea at the time, Bantjes’ farm was located on a vast geological formation known as the Witwatersrand Basin… which just happens to contain the world’s largest known gold reserves.

Within a few months, other local farmers started discovering gold… kicking off a full-fledged gold rush.

Just over a decade later, South Africa became the largest gold producer in the world… and the city of Johannesburg grew from absolutely nothing to a thriving boomtown.

This area is singlehandedly responsible for 40% of all the gold discovered in human history – some 2 billion ounces (or $2.6 trillion of wealth at today’s gold price).

And while the Witwatersrand Basin is still being mined to this day, it’s not as active as it used to be.

Gold production in Witwatersrand peaked in 1970, when miners pulled a whopping 1,000 metric tons of gold out of the ground.

A few decades later in 2016, the same area produced just 166 tonnes– a decline of 83%.

That’s not unusual in the natural resource business.

Whereas it takes nature hundreds of millions of years to deposit minerals deep in the earth’s crust, human beings only require a few decades to pull most of it out.

This creates the constant need for mining companies to explore for more and more major discoveries.

Problem is– that’s not happening. Mining companies aren’t finding anymore vast deposits.

According to Pierre Lassonde, founder of the gold royalty giant Franco-Nevada and former head of Newmont Mining–

If you look back to the 70s, 80s and 90s, in every one of those decades, the industry found at least one 50+ million-ounce gold deposit, at least ten 30+ million ounce deposits, and countless 5 to 10 million ounce deposits.

But if you look at the last 15 years, we found no 50-million-ounce deposit, no 30 million ounce deposit and only very few 15 million ounce deposits.

So where are those great big deposits we found in the past? How are they going to be replaced? We don’t know.

Bottom line: gold discoveries are dwindling.

Part of the reason for this is that mining companies aren’t investing as much money in exploration.

According to S&P Global Market Intelligence, major mining companies (excluding those in the iron ore business) have been cutting their exploration budgets for years.

By the end of 2016, exploration budgets hit an 11-year low.

And this has clearly had an effect on new discoveries.

This is all because the gold price has been relatively flat for the past several years.

Investors have lost interest. And the mining companies, eager to cut costs, have pared back their exploration budgets as a result.

But this is where it gets interesting: natural resources are cyclical. They go through extreme periods of BOOM and BUST.

When gold prices are high, major mining companies scramble for new discoveries.

Eventually when they start mining those deposits, though, the supply of gold increases, pushing prices down.

As the price falls, the miners’ profit margins fall, which causes investors to lose interest and the miners to reduce production.

This causes supply to fall, prices to increase, and the cycle starts all over again.

In a way it’s almost comical. And that brings us to today. Well, technically yesterday.

We’ve been seeing for more than a year that interest rates have been rising.

Yesterday afternoon the yield on the 10-year US Treasury note surpassed 3% for the first time since 2014.

And oil prices have been rising steadily as well.

Financial markets don’t like this combination– it means that inflation is coming. Big time. And stocks plummeted worldwide as a result.

Now, that immediate reaction was probably a bit too panicky.

But the deep concern that inflation is coming (or has already arrived) is completely valid.

Inflation is a HUGE problem. And the traditional hedge in times of inflation is GOLD.

But remember– new gold discoveries have collapsed in the past 15 years.

And, as Lassonde said above, there are few discoveries on the horizon to make up the difference.

These companies can’t just go out and start a new mine, either. Even if they found a promising deposit, with all of the bureaucratic red tape, it would take seven to nine years to start producing gold.

So when demand for gold really starts to heat up, the supply won’t be there.

And this could really cause the gold price to soar. (Silver could rise even more… but we’ll save that for another time.)

Now, there are plenty of small, highly speculative companies, known as ‘junior miners’ who specialize in exploring for new deposits.

And when the gold market is in a frenzy, juniors with great deposits tend to be acquired at ridiculous prices by the major miners.

Now, I’m not suggesting you load up on junior miners– you can make a lot of money if you know what you’re doing, and LOSE a lot of money if you don’t know what you’re doing.

These are tiny, extremely high-risk companies often run by sharks and con-men.

As Doug Casey writes in his novel Speculator, they’re great and taking YOUR money and THEIR dream, and turning it into THEIR money and YOUR dream.

Fortunately there are safer ways to take advantage of this looming imbalance between supply and demand in the gold market.

Physical coins are an easy option.

Gold coins typically sell at a price that’s higher than the market price of gold– to account for the work involved in minting the coin.

This price difference is known as the ‘premium’.

And when gold becomes popular, the premiums often increase too.

This means you can make money both from the rise in gold prices, as well as the increased premiums.

Avoid anything obscure– stick to the most popular gold coins like Canadian Maple Leafs.

And to continue learning how to ensure you thrive no matter what happens next in the world, I encourage you to download our free Perfect Plan B Guide.

Your early THURSDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

i) Chinese yuan vs USA dollar/CLOSED DOWN 6.3238 /shanghai bourse CLOSED DOWN 42.94 POINTS OR 1.38% / HANG SANG CLOSED DOWN 104.29 POINTS OR 0.47%

2. Nikkei closed UP 104.29 POINTS OR 0.47%/ /USA: YEN FALLS TO 109.20/

3. Europe stocks OPENED GREEN /USA dollar index FALLS TO 91.10/Euro RISES TO 1.2182

3b Japan 10 year bond yield: FALLS TO . +.06/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 109.10/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD FINALLY IN THE POSITIVE/BANK OF JAPAN LOSING CONTROL OF THEIR YIELD CURVE AS THEY PURCHASE ALL BONDS TO GET TO ZERO RATE!!

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 68.45 and Brent: 74.53

3f Gold UP/Yen UP

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil UP for WTI and UP FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund FALLS TO +.61%/Italian 10 yr bond yield DOWN to 1.76% /SPAIN 10 YR BOND YIELD DOWN TO 1.28%

3j Greek 10 year bond yield FALLS TO : 3.94?????????????????

3k Gold at $1325.20 silver at:16.58 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble DOWN 39/100 in roubles/dollar) 62.05

3m oil into the 68 dollar handle for WTI and 74 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 109.10 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 0.9832 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1977 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now POSITIVE territory with the 10 year FALLING to +0.61%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 3.00% early this morning (THIS IS DEADLY TO ALL MARKETS). Thirty year rate at 3.19% /

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

(courtesy Jim Reid/Bloomberg/Deutsche bank/zero hedge)

Stocks Rebound As 10Y Slides Back Under 3%; All Eyes On Draghi

Markets have slowed down modestly ahead of today’s key event, the ECB’s monetary policy decision and Draghi press conference, which will likely feature repeated versions of the same question: how worried is the ECB president? From sagging business confidence to falling industrial output, the region seems to be losing economic momentum after the best performance in a decade last year. We did a full ECB preview overnight; the summary scenario analysis of what to expect is shown below:

Meanwhile, despite generally muted volumes, there has been a lot of action with European stocks rising after an early drop amid a deluge of earnings, while Asian stocks were mixed led lower by selling out of China as investors digested the latest flood of company earnings, including a blockbuster beat by Facebook overnight.

The Stoxx 600 was up 0.5%%, nearing its 200-DMA which was tested earlier this week. Energy stocks gained ground, helped by rising oil prices and good quarterly results from a number of companies. Utilities showing strength (+0.9%) with the energy sector underperforming (-0.5%) following Shell earnings (-2.5%). Conversely with positive results for Total (+0.6%), Telefonica (+0.1%) and Volkswagen (+3%) but negative results for Deutsche Bank (+0.3%) and Roche (-0.1%%).

Asian stocks were generally downbeat, despite strength from the Nikkei 225 (+0.5%) which was underpinned by recent JPY weakness while the KOSPI (+1.1%) was the biggest gainer amid optimism ahead of tomorrow’s inter-Korean summit and after tech giant Samsung Electronics released its Q1 final results. Elsewhere, the Shanghai Comp. (-1.3%) and Hang Seng (-1.0%) were downbeat amid the backdrop of rising money market rates and another substantial consecutive net liquidity drain of CNY 150bln by the PBoC while tech stocks continued to reel from an FBI probe into Huawei.

Despite yesterday’s huge beat by Facebook, which sent its share 7% higher after hours, US equity futures were only modestly in the green.

The big story of the early half of the week, the level of the benchmark 10Y Treasury, fluctuated and recently dipped back under 3% as oil climbed. As Bloomberg adds, TSY futures rallied after early block trades, similar seen in bund futures as curves flatten; Open Interest changes hint that yesterdays huge German/UST 5s10s box trade was a new risk trade.

Meanwhile, the dollar hovered at a three-month high, although it has followed the 10Y lower and was trading at session lows. The biggest decliner versus the greenback was the krona after the Riksbank delayed its tightening; the Swedish currency touched its weakest level since December 2009 against the euro after the decision (more below).

In other FX news, the euro halted the previous day’s decline versus the dollar and inched higher from an almost two-month low. The common currency has weakened on each of the past four Draghi press conferences, and charts and trader positioning suggest it may do so again on Thursday on a dovish tone; ECB President will speak at 2:30pm Frankfurt time.

In notable central bank announcements, the Swedish Riksbank kept its overnight Rate unchanged at -0.50% as expected, however it surprised the market by announcing the rate will begin to increase towards the end of the year which is somewhat later than forecast previously. Underlying inflation has been somewhat lower than expected recently, which raises questions regarding the strength of the development in inflation. Deputy Ohlsson dissented at keeping the interest rate unchanged, advocating a hike to -0.25%

In key geopolitical news overnight, South Korea said that President Moon will meet with North Korea leader Kim at the border on Friday at 0930 local time In related news, there were also comments from a BoK official that any economic cooperation with North Korea will bolster South Korean consumer sentiment. Separately, French President Macron said he thinks US President Trump will not want US to remain in Iran nuclear deal based on prior statements.

In Brexit news, UK PM May is said to issue a wish list of her trade demands for a Brexit trade deal. UK PM May has held a cabinet meeting with Conservative Brexiteers whereby she was asked to stick to her plan of making a clean

break from the EU.

WTI and Brent crude futures sit in modest positive territory, continuing yesterday’s recovery. Prices remain firmer in spite of the latest DoE release which had an overall bearish impact on the market as traders continue to assess the plausibility of the US re-imposing sanctions upon Iran as well as declines in Venezuelan oil output. In metals markets, spot gold trades with little in the way of firm direction and in close proximity to 5-week lows as a firmer USD keeps a lid on gains for the precious metal. Elsewhere, aluminium has continued to face selling pressure in London amid the fallout from the latest updates for Rusal, whilst Chinese steel futures were supported overnight by domestic construction demand.

Economic data on Thursday include initial jobless claims, durable goods orders. PepsiCo, Bristol-Myers Squibb, General Motors and Intel are among companies due to release results.

Bulletin Headline Summary from RanSquawk

- Equity markets largely subdued after negative trading on Wednesday ahead of ECB’s rate decision

- SEK at eight year lows, however, following Riksbank rolling back rate hike expectations

- Looking ahead, highlights include, ECB’s rate decision and press conference, US durables, weekly jobs,

- advanced goods trade balance and a slew of earnings

Market Snapshot

- S&P 500 futures down 0.06% to 2,643.00

- STOXX Europe 600 up 0.5% to 381.95

- MXAP down 0.06% to 171.77

- MXAPJ down 0.2% to 556.79

- Nikkei up 0.5% to 22,319.61

- Topix up 0.3% to 1,772.13

- Hang Seng Index down 1.1% to 30,007.68

- Shanghai Composite down 1.4% to 3,075.03

- Sensex up 0.3% to 34,593.88

- Australia S&P/ASX 200 down 0.2% to 5,910.77

- Kospi up 1.1% to 2,475.64

- German 10Y yield fell 1.5 bps to 0.619%

- Euro up 0.1% to $1.2177

- Brent Futures up 0.5% to $74.33/bbl

- Italian 10Y yield rose 1.0 bps to 1.523%

- Spanish 10Y yield fell 1.1 bps to 1.291%

- Brent Futures up 0.5% to $74.33/bbl

- Gold spot up 0.03% to $1,323.59

- U.S. Dollar Index up 0.03% to 91.20

Top Overnight News from Bloomberg

- Mario Draghi’s press conference on Thursday may well feature repeated versions of the same question: how worried is he? From sagging business confidence to falling industrial output, the region seems to be losing economic momentum after the best performance in a decade last year

- French President Emmanuel Macron said he thinks U.S. President Donald Trump will withdraw from the Iran nuclear accord, dealing a blow to the six-nation agreement reached in 2015 and endorsed by world powers

- Fox News says Trump will join “Fox & Friends” at 8:00 a.m. New York time for an interview

- The European Union will begin surveillance of aluminum imports as part of a plan for possible curbs resulting from the controversial U.S. tariff imposed last month

- Brexit-backing Conservatives held private talks with U.K. PM Theresa May to demand that she sticks to her plan for a clean break with the EU; At the Tuesday meeting, May reassured euroskeptics she will deliver the kind of Brexit they want, according to two people familiar with the conversation

- The Riksbank again pushed back a plan to raise interest rates, announcing on Thursday they don’t see a tightening until “towards the end of the year,” while also holding their key rate at minus 0.5%

- This was a delay from their previous assessment that they could see tighter policy by the second half of this year

- China is considering proposals to cut import duty on passenger cars by about half, according to people with direct knowledge of the matter, a move that’s set to give a lift particularly to luxury-car makers such as BMW AG and Toyota Motor Corp.’s Lexus unit

- Deutsche Bank AG’s new chief executive officer can claim his first success. The European Central Bank has granted Germany’s largest lender an exemption from rules limiting how it can use funds at its Postbank retail subsidiary, a bank spokesman confirmed on Wednesday

The major Asia-Pac bourses traded mixed as markets failed to fully benefit from a mild tailwind after the gains in Wall St and as focus across global stock markets turned to a deluge of earnings. Nikkei 225 (+0.5%) was underpinned by recent JPY weakness and with Tokyo Electron the outperformer after its FY net firmly topped estimates, while the KOSPI (+1.1%) was the biggest gainer amid optimism ahead of tomorrow’s inter-Korean summit and after tech giant Samsung Electronics released its Q1 final results. Elsewhere, ASX 200 (-0.2%) was indecisive as Australia also reflected on the broad weakness during the prior day’s holiday closure, while Shanghai Comp. (-1.3%) and Hang Seng (-1.0%) were downbeat amid the backdrop of rising money market rates and another substantial consecutive net liquidity drain of CNY 150bln by the PBoC. Finally, 10yr JGBs were quiet with markets focused on earnings releases and amid a lack of Rinban announcement. Furthermore, the BoJ also kick-started its 2-day policy meeting today in which the central bank is expected to maintain policy settings, while focus would also be on the forecasts in the Outlook Report and whether there will be any changes to inflation estimates with the inclusion of the newly appointed Deputy Governors including known-reflationist Wakatabe. China MOFCOM repeated its opposition to unilateralism and protectionism, while it added that some Chinese firms have given up on the US market amid uncertainty. In other news, a China MIIT official said China is working on a significant tariff reduction for auto imports, while there were also reports that China is mulling lowering car import tariffs to 10% or 15% from the current 25%, with a decision possibly as early as next month

Top Asian News

- Komatsu Full Year Operating Income Forecast Misses Estimates

- Nomura Holdings 4Q Net Income 22.7b Yen

- Nippon Steel’s Operating Profit Misses Estimate, Stock Drops

- Philippine Bank of Communications Elects New Treasurer

- Tencent Wipeout Topping $118 Billion Reveals Depth of Tech Gloom

- SoftBank Names Ex-Goldman, Japan Post Bank Executive to Board

European equities (Eurostoxx 50+0.2%, DAX flat) trade with little in the way of firm direction as traders await today’s ECB meeting (albeit fireworks expected from the event); IBEX (+0.4%) and FTSE MIB (+0.5%) outperform. Utilities showing strength (+0.9%) with the energy sector underperforming (-0.5%) following Shell earnings (-2.5%). Conversely with positive results for Total (+0.6%), Telefonica (+0.1%) and Volkswagen (+3%) but negative results for Deutsche Bank (+0.3%) and Roche (-0.1%%). Looking ahead for Shire at 12:00 today, which may give some indication on the Takeda news

Top European News

- Iberdrola Turns a Takeover War With Enel Into an EU Problem

- BP Brings in Former BG Boss Lund to Succeed Svanberg as Chairman

- Lufthansa Falls on Fare Drop, Cost of Assets From Air Berlin

- Barclays Trading Gives Staley Momentum, But Misconduct Bites

- Telefonica First-Quarter Sales Drop as Spain Recovery Not Enough

- Nokia Sales Miss Estimates as Network Market Slump Persists

In currencies, the DXY continues to grind higher above the 91.000 level and eke out more fresh multi-month highs amidst widespread Dollar gains vs counterparts. 91.300 or so is the latest peak, as the DXY inches closer to then next upside technical targets circa 91.500 and then 91.750. CHF/GBP/CAD/NZD/AUD: All softer vs the Greenback, with Usd/Chf only a few pips below 0.9850 resistance, while Cable has breached the top of a support zone straddling 1.3900 to extend its sharp reversal from April highs (1.4377) and further undermine bullish seasonal dynamics, plus M&A factors that had been boosting the Pound. Usd/Cad towards the upper end of a relatively tight 1.2825-60 range with overriding Dollar strength marginally outweighing Loonie support from near term NAFTA deal expectations. Nzd/Usd looking more vulnerable just above 0.7050 as the Aud/Nzd cross climbs over 1.0700 and Aud/Usd derives a degree of traction from above forecast Aussie export/import price data overnight. EUR/JPY: The single currency has survived a stern test of support vs the Usd around 1.2155 to trade back up near the top of its trading parameters (1.2190), awaiting fresh/independent impetus from the ECB and still gleaning some direction from mega 1.2200 option expiries that run off later today. Usd/Jpy firmer above 109.00 between 109.25-50 amidst latest month end rebalancing models indicating a Jpy sell signal and with the BoJ not seen altering its easy/dovish stance at the culmination of the 2-day meeting early Friday

In commodities, WTI and Brent crude futures sit in modest positive territory (albeit off best levels) broadly continuing yesterday’s recovery. Prices remain firmer in spite of the latest DoE release which had an overall bearish impact on the market as traders continue to assess the plausibility of the US re-imposing sanctions upon Iran as well as declines in Venezuelan oil output. In metals markets, spot gold trades with little in the way of firm direction and in close proximity to 5-week lows as a firmer USD keeps a lid on gains for the precious metal. Elsewhere, aluminium has continued to face selling pressure in London amid the fallout from the latest updates for Rusal, whilst Chinese steel futures were supported overnight by domestic construction demand.

Looking at the day ahead, the highlight will be the ECB meeting just after midday followed by President Draghi’s media briefing shortly after. The BOE’s Brazier and ECB’s Nouy will also speak. Data due out includes Germany consumer confidence for May and US initial jobless claims, March advance goods trade balance and flash durable and capital goods orders data for March. Amazon, Microsoft, Total, Intel, Royal Dutch Shell and Volkswagen are notable earnings releases due out.

US Event Calendar

- 8:30am: Initial Jobless Claims, est. 230,000, prior 232,000; Continuing Claims, est. 1.85m, prior 1.86m

- 8:30am: Durable Goods Orders, est. 1.6%, prior 3.0%; Durables Ex Transportation, est. 0.5%, prior 1.0%

- 8:30am: Cap Goods Orders Nondef Ex Air, est. 0.46%, prior 1.4%; Cap Goods Ship Nondef Ex Air, est. 0.3%, prior 1.4%

- 8:30am: Retail Inventories MoM, prior 0.4%, revised 0.4%; Wholesale Inventories MoM, est. 0.65%, prior 1.0%

- 9:45am: Bloomberg Consumer Comfort, prior 58.1

- 11am: Kansas City Fed Manf. Activity, est. 17, prior 17

DB’s Jim Reid concludes the overnight wrap

Morning from Helsinki, it’s been a busy tour of the region but I did manage to watch the astonishing game of football on Tuesday night. I’m still recovering. Meanwhile bond markets aren’t really recovering even with what has been a negative risk reaction this week to the rising yield environment. Obviously our pieces highlighted at the top give chapter and verse on this theme so we won’t go into detail here but it is quite clear in 2018 that US treasuries are struggling to rally in risk off environments. That I think shows the direction of travel at the moment. The US 10y held above 3% yesterday and ended the day at 3.027% (just above 3.03% in Asia) with the latest move meaning that yields have risen for seven consecutive sessions which is the joint longest run since mid-April 2016.

Yields are up 29bps since early April and as discussed it appears that equity and credit markets are struggling a bit in the face of that. Having said that the Dow (+0.25%) climbed back into the close to rise for the first time in six days yesterday. The reaction to what is a good headline US earnings season continued to be mixed with Twitter (-2.4%) lower although Boeing rose +4.2% after it raised this year’s earnings forecasts. However, in after hours trading Facebook jumped around 7% after its results, while Visa and Qualcomm was up c3% and c2% respectively following their above market quarterly results.

Before these late results the S&P 500 also recovered from earlier losses to close slightly higher (+0.18%), but is comfortably in the red YTD (-1.28%) again after this past week. The Nasdaq (-0.05% yesterday) is still holding its head above water for 2018. European bourses weakened further yesterday (Stoxx -0.77%; DAX -1.02%; FTSE -0.62%) and EM equities also appeared to be showing signs of stress with the MSCI EM index closing last night -1.21% down. The US dollar index firmed 0.45% to a fresh 3 month high while the Euro and Sterling fell -0.59% and -0.33% respectively. Elsewhere, Gold (-0.54%) and the Yen (-0.56%) seemed to be absent from any safe haven flows. Credit indices widened modestly in Europe but tightened in the US (Main +1bp; CDX IG -0.7bp) reflecting the late day rebound in equities.

This morning in Asia, markets are trading mixed with the Kospi up +1.25% as Samsung’s result beat expectations, while the Nikkei is up +0.59% and Hang Seng (-0.70%) and Shanghai Comp. (-0.92%) are both down as we type. The futures on the S&P are up c0.3%.

The next test for the bond market will likely come with this afternoon’s ECB meeting, followed closely by President Draghi’s press conference. Our European economists (link) expect the “dovish exit” strategy to remain intact. They expect the ECB to retain confidence in the above-trend growth despite the recent loss of momentum (although the PMIs and Bank Lending survey this week should install confidence) and they expect the optimism – which increasingly extends to inflation – to remain conditional on the ECB being patient, persistent and prudent with stimulus. They also expect the ECB to signal ample monetary stimulus after QE ends.

In light of a core unchanged message then, the risk is that Draghi errs on the side of caution today. As our colleagues point out, the ECB is already highlighting the relative importance of policy rates and guidance post-QE. Draghi recently said that policy adjustments would proceed at a “measured pace” and conditional on the scale of the inflation gap and the uncertainties around the output gap and wages. The team expects Draghi to repeat this in the Q&A, but a more dovish outcome would be inserting “measured pace” into the press statement to strengthen forward guidance. Another dovish move would be recognition of risks by “monitoring” economic developments. Our economists still expect the ECB to pre-announce in June that QE will end in December after a taper in Q4, but the risk is that the ECB waits until July to announce something. A one-month delay shouldn’t impact the prospect of a likely Q4 taper though. Beyond this and as a reminder, DB’s base case is for the first policy rate hike to come in June 2019 – a 20bp deposit rate hike and 25bp refi rate hike. A second hike is forecast for December 2019. Today’s ECB meeting outcome is at 12.45pm BST and Draghi is due to speak at 1.30pm BST.

Ahead of today’s ECB meeting, two policy makers were quoted yesterday as sounding fairly upbeat despite some signs of softer data in recent weeks. The comments, published by Eurofi, came from Board Member Mersch and Governing Council member Vasiliauskas. Mersch was quoted as saying that “confidence has recently risen and convergence is being confirmed – partly because the temporary decline in the inflation rate has been weaker than our internal calculations had predicted”. Vasiliauskas was also noted as saying that “we have witnessed the strengthening of broad-based growth and steadily declining unemployment, providing conditions for inflation convergence to our objective” and that “this has increased my confidence that it is time to transition from the APP”.

Closer to home, Brexit headlines are likely to be back in vogue today with the UK government facing a motion vote in the House of Commons called by senior MPs on the UK’s future participation in the EU customs union. The motion calls for the government to change its position to seek an effective customs union with the EU27 after Brexit. DB’s Oliver Harvey highlighted in his report yesterday that the vote is non-binding and a government defeat does not represent a no confidence vote and will not result in a resignation from PM May. He highlights however that if the government were to lose, it may cast doubt on its ability to proceed with the legislation necessary to implement Brexit, in particular amendments to the UK withdrawal bill made by the House of Lords this week, and the government’s Trade and Customs Bill which is set to be voted on next month. So worth keeping an eye on. See Oli’s report for a lot more detail on the latest Brexit news.

Turning to trade, the FT reported President Trump will dispatch Treasury Secretary Mnuchin and Trade representative Lighthizer to China next week to discuss trade relations. Trump noted there was a “very good chance of making a deal” but warned that he would continue with plans for new tariffs if no progress was made.

Finally, our European team now believe the Euro area GDP has grown 0.4% qoq in Q1, rather than the 0.6% qoq growth they had pencilled in previously. While growth was expected to lose momentum in 2018 and 2019, they argue that temporary factors such as adverse weather conditions might have added some volatility in Q1. In order to map the signals coming from high-frequency monthly data into a real time estimate of GDP growth, they have built several “Now-Casting” models. These point to growth in the range of 0.4-0.5% qoq in Q1. Please see their note for more details. There were limited data releases from yesterday. In France, the April consumer confidence edged up 1pt mom to 101 (vs. 100 expected).

Looking at the day ahead, the highlight will be the ECB meeting just after midday followed by President Draghi’s media briefing shortly after. The BOE’s Brazier and ECB’s Nouy will also speak. Data due out includes Germany consumer confidence for May and US initial jobless claims, March advance goods trade balance and flash durable and capital goods orders data for March. Amazon, Microsoft, Total, Intel, Royal Dutch Shell and Volkswagen are notable earnings releases due out.

3. ASIAN AFFAIRS

i)THURSDAY MORNING/WEDNESDAY NIGHT: Shanghai closed DOWN 42.94 POINTS OR 1.38% /Hang Sang CLOSED DOWN 320.47 POINTS OR 1.06% / The Nikkei closed UP 104.29 POINTS OR 0.47%/Australia’s all ordinaires CLOSED UP .56% /Chinese yuan (ONSHORE) closed DOWN at 6.3238/Oil DOWN to 68.45 dollars per barrel for WTI and 74.53 for Brent. Stocks in Europe OPENED DEEPLY IN THE GREEN. ONSHORE YUAN CLOSED DOWN AT 6.3238 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.3179/ONSHORE YUAN TRADING WEAKER AGAINST OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING MUCH STRONGER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW LOOKS LIKE A FULL TRADE WAR IS BEGINNING/

3 a NORTH KOREA/USA

North Korea/South Korea

Leaders to meet tomorrow

(courtesy zerohedge)

Leaders Of Two Koreas Will Meet Friday Morning At The DMZ

In a meeting that’s widely viewed as a preamble to a historic summit involving President Trump and North Korean leader Kim Jong Un, the leaders of the two Korea’s – North Korean leader Kim Jong Un and South Korean President Moon Jae-in – are preparing to meet at the border at 9:30 am local time on Friday.

Friday’s summit will take place in the Peace House in in the border town of Panmunjom, located in the heart of the demilitarized zone.

Im Jong-seok, the chief of staff for President Moon, provided a full itinerary of the meeting – which will involve the ceremonial planting of a pine tree on the border – to Bloomberg:

- Kim to walk across border to South

- Kim to review South Korean military’s honor guard after walking together with Moon

- Moon, Kim to start summit at 10:30am local time Friday

- Moon, Kim to have lunch separately after morning meeting

- Moon, Kim to plant pine tree on border after lunch

- Moon, Kim to walk together around border before afternoon session

- Two Koreas to sign, announce agreements after summit

- Moon to host banquet for Kim from 6:30pm at peace house

- No Plan to extend summit to Saturday for now

- S. Korea: undecided whether Kim’s wife will accompany; hopes Kim’s wife to join dinner

- Kim Jong Un’s sister part of North Korean delegation

- S. Korea says issues related to denuclearization can’t be fully resolved at the inter-Korean summit; S. Korea would consider the summit a success if the North’s intention of denuclearization is included in the agreement

Meanwhile, South Korean Foreign Minister Kang Kyung-wha credited President Trump with bringing the two Korean leaders together for Friday’s summit during an interview with CNN’s Christiane Amanpour that’s slated to air Thursday night.