GOLD: $1322,20 UP $ 9.60 (COMEX TO COMEX CLOSINGS)

Silver: $16.74 UP 22 CENTS (COMEX TO COMEX CLOSINGS)

Closing access prices:

Gold $1321.25

silver: $16.71

For comex gold:

MAY/

NUMBER OF NOTICES FILED TODAY FOR MAY CONTRACT:165 NOTICE(S) FOR 16500 OZ.

TOTAL NOTICES SO FAR 613 FOR 61300 OZ (1.9066 tonnes)

For silver:

MAY

146 NOTICE(S) FILED TODAY FOR

730,000 OZ/

Total number of notices filed so far this month: 5664 for 28,320,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: BID $9278/OFFER $9378: UP $25(morning)

Bitcoin: BID/ $9121/offer $9221: DOWN $231 (CLOSING/5 PM)

end

First Shanghai gold fix comes at 10 pm est

The second Shanghai gold fix: 2:15 pm

First Shanghai gold fix gold: 10 pm est: 1322.18

NY price at the same time: 1314.85

PREMIUM TO NY SPOT: $7.33

ss

Second gold fix early this morning: 1320.69

USA gold at the exact same time: 1313.65

PREMIUM TO NY SPOT: $7.04

AGAIN, SHANGHAI REJECTS NEW YORK PRICING.

WE WILL NOT PROVIDE LONDON FIXES AS THEY ARE NOT ACCURATE AS TO WHAT IS GOING ON AT THE SAME TIME FRAME.

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total OPEN INTEREST FELL BY A SMALL 929 CONTRACTS FROM 195,865 FALLING TO 194,936 DESPITE YESTERDAY’S 6 CENT GAIN IN SILVER PRICING. WE ARE NOW WITNESSING OUR USUAL AND CUSTOMARY COMEX LONG LIQUIDATION AS WE ENTERED INTO THE ACTIVE DELIVERY MONTH OF MAY AS LONGS PACK THEIR BAGS AND MIGRATE OVER TO LONDON. WE WERE NOTIFIED THAT WE HAD A TINY SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP : 2033 EFP’S FOR JULY AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE OF 2033 CONTRACTS. WITH THE TRANSFER OF 2033 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 2033 EFP CONTRACTS TRANSLATES INTO 10.16 MILLION OZ ACCOMPANYING:

1.THE 6 CENT RISE IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES STANDING FOR MAY COMEX DELIVERY. (29.8 MILLION OZ)

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF APRIL: (FINAL)

12,935 CONTRACTS (FOR 8 TRADING DAYS TOTAL 12,935 CONTRACTS) OR 64.675 MILLION OZ: AVERAGE PER DAY: 1616 CONTRACTS OR 8.084 MILLION OZ/DAY

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH: 64.675 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 9.239% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)

ACCUMULATION IN YEAR 2018 TO DATE SILVER EFP’S: 1,210.1 MILLION OZ.

ACCUMULATION FOR JAN 2018: 236.879 MILLION OZ

ACCUMULATION FOR FEB 2018: 244.95 MILLION OZ

ACCUMULATION FOR MARCH 2018: 236.67 MILLION OZ

ACCUMULATION FOR APRIL 2018: 385.75 MILLION OZ

RESULT: WE HAD A SMALL SIZED DECREASE IN COMEX OI SILVER COMEX OF 929 DESPITE THE 6 CENT GAIN IN SILVER PRICE. WE HAVE NOW ENTERED THE NEW ACTIVE MONTH OF MAY. THE CME NOTIFIED US THAT IN FACT WE HAD AN STRONG SIZED EFP ISSUANCE OF 2033 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) . FROM THE CME DATA: 2033 EFP CONTRACTS FOR JULY, AND ZERO FOR ALL OVER MONTHS FOR A DELIVERABLE FORWARD CONTRACT OVER IN LONDON WITH A FIAT BONUS (TOTAL: 2033). TODAY WE GAINED 1104 TOTAL OI CONTRACTS ON THE TWO EXCHANGES: i.e. 2033 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH AN DECREASE OF 929 OI COMEX CONTRACTS. AND ALL OF THIS HAPPENED WITH THE RISE IN PRICE OF SILVER OF 6 CENTS AND A CLOSING PRICE OF $16.51 WITH RESPECT TO YESTERDAY’S TRADING. YET WE STILL HAVE A STRONG AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY IN THIS ACTIVE MAY DELIVERY MONTH. IT SURE SEEMS THAT WE MUST HAVE HAD SOME BANKER SHORT COVERING ON BOTH EXCHANGES.

In ounces AT THE COMEX, the OI is still represented by UNDER 1 BILLION oz i.e. .974 MILLION OZ TO BE EXACT or 139% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT MAY MONTH/ THEY FILED AT THE COMEX: 146 NOTICE(S) FOR 730,000 OZ OF SILVER

IN SILVER, WE HAVE NOW SET THE NEW RECORD OF OPEN INTEREST AT 243,411 AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $16.51 ON APRIL 9.2018.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH: 27 MILLION OZ , APRIL: 2.485 MILLION OZ AND MAY: 29.8 MILLION OZ )

- HUGE RECORD OPEN INTEREST IN SILVER 243,411 CONTRACTS (OR 1.217 BILLION OZ/ SET APRIL 9/2018

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017

- RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ (FINAL)

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT). IT ALSO LOOKS LIKE BANKER CAPITULATION IN SILVER AS THEY STRUGGLE TO REMOVE SOME OF THEIR HUGE OBLIGATIONS.

In gold, the open interest ROSE BY A CONSIDERABLE 3753 CONTRACTS UP TO 495,151 DESPITE THE FALL IN THE GOLD PRICE/YESTERDAY’S TRADING (LOSS OF $0.55). WE ARE NOW IN THE NON ACTIVE DELIVERY MONTH OF MAY. THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A HUGE SIZED 11,948 CONTRACTS : JUNE SAW THE ISSUANCE OF 9848 CONTRACTS , MAY SAW THE ISSUANCE OF 0 CONTRACTS AND AUGUST SAW THE ISSUANCE OF: 2100 CONTRACTS WITH ALL OTHER MONTHS ZERO. The new OI for the gold complex rests at 495,151. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE A GOOD SIZED OI GAIN IN CONTRACTS ON THE TWO EXCHANGES: 3753 OI CONTRACTS INCREASED AT THE COMEX AND AN CONSIDERABLE SIZED 11,948 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON.THUS TOTAL OI GAIN: 15,701 CONTRACTS OR 1,570,100 OZ = 48.83 TONNES. AND ALL OF THIS OCCURRED WITH A LOSS OF $0.55

YESTERDAY, WE HAD 11535 EFP’S ISSUED.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF MAY : 77,186 CONTRACTS OR 7,718,600 OZ OR 240.08 TONNES (8 TRADING DAYS AND THUS AVERAGING: 9,648 EFP CONTRACTS PER TRADING DAY OR 964,800 OZ/ TRADING DAY),,

TO GIVE YOU AN IDEA AS TO THE HUGE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 7 TRADING DAYS IN TONNES: 240.08 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2017, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 2555 TONNES

THUS EFP TRANSFERS REPRESENTS 240.08/2550 x 100% TONNES = 9.41% OF GLOBAL ANNUAL PRODUCTION SO FAR IN APRIL ALONE.*** THE ACCUMULATION OF EFP CONTRACTS IS RISING PER MONTH.

ACCUMULATION OF GOLD EFP’S YEAR 2018 TO DATE: 2,998.02* TONNES *SURPASSED ANNUAL PROD’N

ACCUMULATION OF GOLD EFP’S FOR JANUARY 2018: 653.22 TONNES

ACCUMULATION OF GOLD EFP’S FOR FEBRUARY 2018: 649.45 TONNES

ACCUMULATION OF GOLD EFP’S FOR MARCH 2018: 741.89 TONNES (22 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR APRIL 2018: 713.84 TONNES (21 TRADING DAYS)

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A CONSIDERABLE SIZED INCREASE IN OI AT THE COMEX OF 3753 DESPITE THE 55 CENT FALL IN PRICE // GOLD TRADING YESTERDAY ($0.55 LOSS). HOWEVER WE ALSO HAD A GIGANTIC SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 11,948 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 11,948 EFP CONTRACTS ISSUED, WE HAD A HUMONGOUS SIZED NET GAIN OF 15,701 CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

11,948 CONTRACTS MOVE TO LONDON AND 3753 CONTRACTS DECREASED AT THE COMEX. (in tonnes, the GAIN in total oi equates to 48.83 TONNES). ..AND ALL OF THESE OCCURRED AT THE COMEX WITH A LOSS OF 55 CENTS IN TRADING.

we had: 165 notice(s) filed upon for 16500 oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD…

WITH GOLD UP $9.60 /A HUGE CHANGE IN GOLD INVENTORY: A WITHDRAWAL OF 1.17 TONNES FROM THE GLD??

Inventory rests tonight: 862.96 tonnes.

SLV/

WITH SILVER UP 22 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV

/INVENTORY RESTS AT 323.263 MILLION OZ/

end

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER FELL BY A SMALL SIZED 929 CONTRACTS from 195,865 UP TO 194,936 (AND, CLOSER TO THE NEW COMEX RECORD SET /APRIL 9/2017 AT 243,411/SILVER PRICE AT THAT DAY: $16.53). THE PREVIOUS RECORD OTHER THAN WAS ESTABLISHED AT: 234,787, SET ON APRIL 21.2017 OVER ONE YEAR AGO. THE PRICE OF SILVER ON THAT DAY: $17.89. OUR CUSTOMARY MIGRATION OF COMEX LONGS MORPH INTO LONDON FORWARDS CONTINUES AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE: 0 EFP CONTRACTS FOR APRIL, 0 EFP CONTRACTS FOR MAY (WE DO NOT GET A LOOK AT THESE CONTRACTS AS IT IS PRIVATE BUT THE CFTC DOES AUDIT THEM), AND 2033 EFP’S FOR JULY AND ALL OTHER MONTHS ZERO. TOTAL EFP ISSUANCE: 2033 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI LOSS AT THE COMEX OF 929 CONTRACTS TO THE 2033 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A GAIN OF 1104 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES: 5.520 MILLION OZ!!! AND THIS OCCURRED WITH ONLY A 6 CENT RISE IN PRICE . THE BANKERS ORCHESTRATED THEIR RAID THROUGHOUT LAST WEEK DESPERATELY TRYING TO PARE THEIR GIGANTIC OPEN INTEREST SHORT ON BOTH EXCHANGES BUT TO NO AVAIL. JUDGING BY THE RECORD NUMBER OF EFP ISSUANCE DURING LAST MONTH OF APRIL AT 385.75 MILLION OZ AND THE TOTAL OI GAIN ON THE TWO EXCHANGES, I DO NOT THINK THAT OUR BANKERS HAVE BEEN TOO SUCCESSFUL. THE CONSTANT RAIDS ARE NOW BEING CALLED UPON BY OUR BANKER FRIENDS ARE DONE IN AN ATTEMPT TO SHAKE AS MANY SILVER LEAVES FROM THE SILVER TREE AS POSSIBLE.

RESULT: A SMALL SIZED DECREASE IN SILVER OI AT THE COMEX WITH THE 6 CENT RISE IN SILVER PRICING YESTERDAY. BUT WE ALSO HAD ANOTHER STRONG SIZED 2033 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR APRIL, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

)THURSDAY MORNING/WEDNESDAY NIGHT: Shanghai closed UP 15.26 points or 0 .48% /Hang Sang CLOSED UP 273.08 points or 0.89% / The Nikkei closed UP 88.30 POINTS OR .39% /Australia’s all ordinaires CLOSED UP .18% /Chinese yuan (ONSHORE) closed UP at 6.3503/Oil UP to 71.51 dollars per barrel for WTI and 77.38 for Brent. Stocks in Europe OPENED MIXED/RED. ONSHORE YUAN CLOSED DOWN AT 6.3438 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.3503/ONSHORE YUAN TRADING WEAKER AGAINST OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING MUCH STRONGER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW LOOKS LIKE A FULL TRADE WAR IS BEGINNING/

/NORTH KOREA/SOUTH KOREA

i)North Korea/South Korea/USA

Trump and Kim will meet in Singapore on June 12

(Fabian/the HILL)

b) REPORT ON JAPAN

3 c CHINA

South China Morning Post

Conglomerate Anbang’s ex chief Wu sentenced to 18 years behind bars for fraud and embezzlement

(courtesy South China Morning post)

4. EUROPEAN AFFAIRS

i)UK

The Bank of England leaves unchanged but with two voting in the negative. The pound plummets on the huge dovish inflation outlook

( zerohedge)

ii) Italy

The EU and ECB are not too happy with this development: both Euroskeptic parties will become the government after Berlusconi agreed not to partake in the government. These two parties love to spend and will no doubt break the 3% guideline putting it in direct confrontation with the EU. Remember that the Italy has a huge 360 billion euros of non performing loans on its books. Every Tom Dick and Harry are dumping Italian bonds with the only purchaser: the ECB

fun times again in Italy

( zerohedge)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

last night: a major escalation as Israel retaliates against Iranian shelling out of Syria

(zerohedge)

( zerohedge)

( zerohedge)

a must read…

( Tom Luongo)

(courtesy zerohedge)

6 .GLOBAL ISSUES

Nomi Prins is one smart girl.

a great book/and great commentary

( NomiPrins)

7. OIL ISSUES

8. EMERGING MARKET

Venezuela

9. PHYSICAL MARKETS

10. USA stories which will influence the price of gold/silver

ii)This morning’s data:

a)It seems that the Fed is not keeping the inflation it desires

( zerohedge)

b)This does not look good for Ford: it halts all production of its most profitable F series truck and lays off almost 8,000 staff

( zerohedge)

iv)SWAMP STORIES

Trading Volumes on the COMEX

PRELIMINARY COMEX VOLUME FOR TODAY: 371,048 contracts

CONFIRMED COMEX VOL. FOR YESTERDAY: 430,929 contracts

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

And now for the wild silver comex results.

Total silver OI FELL BY A SMALL SIZED 929 CONTRACTS FROM 195,865 DOWN TO 194,936 (AND CLOSER TO THE NEW RECORD OI FOR SILVER SET APRIL 9.2018/ 243,411 CONTRACTS) DESPITE THE 6 CENT GAIN IN SILVER PRICING. SINCE WE ARE NOW INTO THE ACTIVE DELIVERY MONTH OF MAY. WE WERE INFORMED THAT WE HAD A STRONG SIZED 2033 EFP CONTRACT ISSUANCE FOR JULY AND ZERO FOR ALL OTHER MONTHS. THESE EFPS WERE ISSUED TO COMEX LONGS WHO RECEIVED A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. THE TOTAL EFP’S ISSUED: 2033. ON A NET BASIS WE GAINED 1104 SILVER OPEN INTEREST CONTRACTS AS WE OBTAINED A 929 CONTRACT LOSS AT THE COMEX COMBINING WITH THE ADDITION OF 2033 OI CONTRACTS NAVIGATING OVER TO LONDON. DUE TO THE FACT THAT THE BOYS WERE VERY BUSY NEGOTIATING LONG COMEX CONTRACTS EMIGRATING TO LONDON,(AND WAITING FOR THEIR PASSPORTS)

NET GAIN ON THE TWO EXCHANGES: 1104 CONTRACTS

AMOUNT STANDING FOR SILVER AT THE COMEX

We are now in the active delivery month of MAY and here the front month LOST 5 contracts FALLING TO 448 contracts. We had 59 notices filed upon yesterday so we SURPRISINGLY AGAIN GAINED 54 contracts or 270,000 additional ounces will stand for delivery in this active delivery month of May AS SOMEBODY AGAIN WAS DESPERATE FOR PHYSICAL SILVER..

June saw a LOSS of 15 contracts to stand at 782 The next big delivery month for silver is July and here the OI FELL by 1709 contracts DOWN to 139,250. The next active delivery month after July for silver is September and here the OI ROSE by 575 contracts UP to 22,931

We had 146 notice(s) filed for 730,000 OZ for the MAY 2018 contract for silver

INITIAL standings for MAY/GOLD

MAY 10/2018.

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz |

21,735.675 OZ

Brinks

|

| Deposits to the Dealer Inventory in oz | NIL oz |

| Deposits to the Customer Inventory, in oz | 21,735.675 OZ

jpm |

| No of oz served (contracts) today |

165 notice(s)

16500 OZ

|

| No of oz to be served (notices) |

103 contracts

(10300 oz)

|

| Total monthly oz gold served (contracts) so far this month |

613 notices

61300 OZ

1.9066 TONNES

|

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

For MAY:

Today, 0 notice(s) were issued from JPMorgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equates to 165 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 120 notice(s) was (were) stopped/ Received) by j.P.Morgan customer account.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

To calculate the INITIAL total number of gold ounces standing for the MAY. contract month, we take the total number of notices filed so far for the month (613) x 100 oz or 61300 oz, to which we add the difference between the open interest for the front month of MAY. (268 contracts) minus the number of notices served upon today (165 x 100 oz per contract) equals 71,600 oz, the number of ounces standing in this active month of APRIL (2.227 tonnes)

Thus the INITIAL standings for gold for the MAY contract month:

No of notices served (613 x 100 oz) + {(268)OI for the front month minus the number of notices served upon today (165 x 100 oz )which equals 71,600 oz standing in this active delivery month of MAY . THERE ARE 9.954 TONNES OF REGISTERED GOLD AVAILABLE FOR DELIVERY SO FAR.

WE GAINED 6400 OZ OF GOLD (64 CONTRACTS) STANDING IN THIS NON ACTIVE DELIVERY MONTH OF MAY AS SOMEBODY BADLY NEEDED PHYSICAL GOLD AT THIS SIDE OF THE POND..

IN THE LAST 18 MONTHS 73 NET TONNES HAS LEFT THE COMEX.

end

And now for silver

AND NOW THE APRIL DELIVERY MONTH

MAY INITIAL standings/SILVER

| Silver | Ounces |

| Withdrawals from Dealers Inventory | nil oz |

| Withdrawals from Customer Inventory |

nil oz

|

| Deposits to the Dealer Inventory |

614,504.400

oz

CNT

|

| Deposits to the Customer Inventory |

nil oz

|

| No of oz served today (contracts) |

146

CONTRACT(S)

(730,000 OZ)

|

| No of oz to be served (notices) |

302 contracts

(1,510,000 oz)

|

| Total monthly oz silver served (contracts) | 5664 contracts

(28,320,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

we had 1 inventory movement at the dealer side of things

i) Into CNT: 614,504.400 oz

total dealer deposits: 614,504.400 oz

we had 0 deposits into the customer account

i) Into JPMorgan: nil oz

*** JPMorgan for most of 2017 and in 2018 has adding to its inventory almost every single day.

JPMorgan now has 140 million oz of total silver inventory or 53.4% of all official comex silver. (140 million/263 million)

JPMorgan did not deposit into its warehouses (official) today.

ii) Into everybody else: 0

total customer deposits today: 0 oz

we had 0 withdrawals from the customer account;

i

total withdrawals; nil oz

we had 0 adjustment

total dealer silver: 69.425 million

total dealer + customer silver: 268,647million oz

The total number of notices filed today for the MAY. contract month is represented by 146 contract(s) FOR 730,000 oz. To calculate the number of silver ounces that will stand for delivery in MAY., we take the total number of notices filed for the month so far at 5664 x 5,000 oz = 28,320,000 oz to which we add the difference between the open interest for the front month of MAY. (646) and the number of notices served upon today (164 x 5000 oz) equals the number of ounces standing.

.

Thus the INITIAL standings for silver for the MAY contract month: 5664(notices served so far)x 5000 oz + OI for front month of MAY(448) -number of notices served upon today (164)x 5000 oz equals 29,830,000 oz of silver standing for the MAY contract month

WE GAINED 54 CONTRACTS OR AN ADDITIONAL 270,000 OZ WILL STAND AT THE COMEX AS SOMEBODY WAS IN URGENT NEED OF PHYSICAL SILVER ON THIS SIDE OF THE POND.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

ESTIMATED VOLUME FOR TODAY: 83612 CONTRACTS

CONFIRMED VOLUME FOR YESTERDAY: 77960 CONTRACTS

YESTERDAY’S CONFIRMED VOLUME OF 77960 CONTRACTS EQUATES TO 389 MILLION OZ OR 55.68% OF ANNUAL GLOBAL PRODUCTION OF SILVER

COMMODITY LAW SUGGESTS THAT OPEN INTEREST SHOULD NOT BE MORE THAN 3% OF ANNUAL GLOBAL PRODUCTION. THE CROOKS ARE SUPPLYING MASSIVE PAPER TRYING TO KEEP SILVER IN CHECK.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price at that day at $18.42

The previous record was 224,540 contracts with the price at that time of $20.44

end

NPV for Sprott

1. Sprott silver fund (PSLV): NAV FALLS TO -1.83% (MAY10/2018)

2. Sprott gold fund (PHYS): premium to NAV FALLS TO -0.43% to NAV (MAY 10/2018 )

Note: Sprott silver trust back into NEGATIVE territory at -1.83%-/Sprott physical gold trust is back into NEGATIVE/ territory at -0.43%/Central fund of Canada’s is still in jail but being rescued by Sprott.

Sprott WINS hostile 3.1 billion bid to take over Central Fund of Canada

(courtesy Sprott/GATA)

3.SPROTT CEF.A FUND (FORMERLY CENTRAL FUND OF CANADA): NAV FALLS TO -2.31%: NAV 13.71/TRADING 13.38//DISCOUNT 2.31.

END

And now the Gold inventory at the GLD/

MAY 10/WITH GOLD UP $9.60/A WITHDRAWAL OF 1.17 TONNES FROM THE GLD/INVENTORY RESTS AT 862.96 TONNES/SUCH CROOKS

MAY 9/WITH GOLD DOWN $0.55/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 864.13 TONNES

MAY 8/WITH GOLD DOWN $0.10/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 864.13 TONNES

MAY 7/WITH GOLD DOWN $0.55/ANOTHER WITHDRAWAL OF 1.47 TONNES OF GOLD FROM THE GLD/INVENTORY RESTS AT 864.13 TONNES

MAY 4/WITH GOLD UP $2.05/A WITHDRAWAL OF 1.13 TONNES OF GOLD FROM THE GLD/INVENTORY RESTS AT 865.60 TONNES

MAY 3/WITH GOLD UP $7.05/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 866.77 TONNES

MAY 2/WITH GOLD DOWN $1.15/ A HUGE WITHDRAWAL OF 4.43 TONNES FROM THE GLD/INVENTORY RESTS AT 866.77 TONNES

MAY 1/WITH GOLD DOWN $12.15/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 871.20 TONNES

APRIL 30/WITH GOLD DOWN $4.05/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 871.20 TONNES.

APRIL 27./WITH GOLD UP $5.90/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 871.20 TONNES/

APRIL 26/WITH GOLD DOWN $4.90/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 871.20 TONNES

APRIL 25/AFTER 9 CONSECUTIVE DAYS OF NO MOVEMENT OF GOLD INTO OUT OF THE GLD, WE HAD A HUGE DEPOSIT OF 5.31 TONNES OF GOLD INTO THE GLD/INVENTORY RESTS AT 871.20 TONNES.

APRIL 24./WITH GOLD UP $9.90, WE HAD NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 865.89 TONNES/

APRIL 23.2018/WITH GOLD DOWN $14.00/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 865.89 TONNES.

APRIL 20/WITH GOLD DOWN $10.20: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 865.89 TONNES

APRIL 19/WITH GOLD DOWN $4.25: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 865.89 TONNES/

APRIL 18/WITH GOLD UP $3.65: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 865.89 TONNES

APRIL 17/WITH GOLD DOWN $1.00 NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 865.89 TONNES/

April 16/WITH GOLD UP$2.80/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 865.89 TONNES/

April 13/WITH GOLD UP $6.15, A HUGE DEPOSIT OF 5.90 TONNES INTO THE GLD INVENTORY/INVENTORY RESTS AT 865.89 TONNES

April 12/WITH GOLD DOWN $17.40/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 859.99 TONNES

April 11/WITH GOLD UP $13.85/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 859,99 TONNES

APRIL 10/WITH GOLD UP $5.25/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 859.99 TONNES

APRIL 9/WITH GOLD UP$4.50/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 859.99 TONNES

APRIL 6/WITH GOLD UP $7.50 ,A HUGE CHANGE IN INVENTORY AT THE GLD/ A DEPOSIT OF 5.90 TONNES/INVENTORY RESTS AT 859.99 TONNES

APRIL 5/WITH GOLD DOWN $8.20 WE HAD TWO ENTRIES: 1) TINY WITHDRAWAL OF .28 TONNES TO PAY FOR FEES AND 2) A DEPOSIT OF 2.06 TONNES//INVENTORY RESTS AT 854.09 TONNES

April 4/WITH GOLD UP $2.90 WE HAD NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 852.31 TONNES

APRIL 3./WITH GOLD DOWN $9.30 WE HAD NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 852.31 TONNES

APRIL 2/WITH GOLD UP $19.50, WE HAD A BIG CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF 6.19 TONNES/INVENTORY RESTS AT 852.31 TONNES

MARCH 29/WITH GOLD DOWN $3.20 AND OPTIONS EXPIRY FINISHED, WE HAD NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS A 846.12 TONNES

March 28/WITH GOLD DOWN $16.70, ANOTHER RAID ORCHESTRATED, AGAIN NO SURPRISES AS WE WITNESS ANOTHER 1.18 TONNES OF GOLD REMOVED/INVENTORY RESTS AT 846.12 TONNES

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

MAY 10/2018/ Inventory rests tonight at 862.96tonnes

*IN LAST 380 TRADING DAYS: 78.04 NET TONNES HAVE BEEN REMOVED FROM THE GLD

*LAST 330 TRADING DAYS: A NET 78,26 TONNES HAVE NOW BEEN ADDED INTO GLD INVENTORY.

end

Now the SLV Inventory/

MAY 10/WITH SILVER UP 22 CENTS/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 323.263 MILLION OZ/

MAY 9/WITH SILVER UP 6 CENTS/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 323.263 MILLION OZ/

MAY 8/WITH SILVER DOWN 2 CENTS:NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 323.263 MILLION OZ.

MAY 7/WITH SILVER FLAT: A BIG CHANGE IN SILVER INVENTORY AT THE SLV// A WITHDRAWAL OF 942,000 OZ OF SILVER FROM THE SLV INVENTORY/INVENTORY RESTS AT 323.263 MILLION OZ/

MAY4/WITH SILVER UP 5 CENTS/A BIG CHANGES IN SILVER INVENTORY AT THE SLV/ A DEPOSIT OF 1.224 MILLION OZ/INVENTORY RESTS AT 324.205 MILLION OZ/

MAY 2/WITH SILVER UP 24 CENTS/A HUGE CHANGE IN SILVER INVENTORY AT THE SLV// A DEPOSIT OF 6.082 MILLION OZ INTO THE SLV/INVENTORY RESTS AT 322.981 MILLION OZ/

MAY 1/WITH SILVER DOWN 24 CENTS/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 316.899 MILLION OZ/

APRIL 30/WITH SILVER DOWN 11 CENTS/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 316.899 MILLION OZ/

APRIL 27/WITH SILVER DOWN 5 CENTS/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 316.899 MILLION OZ/

APRIL 26/WITH SILVER DOWN 2 CENT/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 316,899 MILLION OZ/

APRIL 25./WITH SILVER DOWN 18 CENTS/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 316.899 MILLION OZ/

APRIL 24./WITH SILVER UP 8 CENTS/SOMETHING SPOOKED OUR CROOKS TO ADD SOME PAPER SILVER: A DEPOSIT OF 1.601 MILLION OZ/INVENTORY RESTS AT 316.899 MILLION OZ/

APRIL 23.2018/WITH SILVER DOWN 50 CENTS, ANOTHER HUGE WITHDRAWAL FROM THE SLV INVENTORY: A WITHDRAWAL OF 1.413 MILLION OZ/INVENTORY RESTS AT 315.298 MILLION OZ.

APRIL 20/WITH SILVER DOWN 11 CENTS: ANOTHER HUGE CHANGE IN SILVER INVENTORY: A WITHDRAWAL OF 1.13 MILLION OZ//SLV RESTS TONIGHT AT 316.711 MILLION OZ/

APRIL 19/WITH SILVER UP 3 CENTS TODAY: WE HAD A BIG CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.355 MILLION OZ/ MAKES ABSOLUTELY NO SENSE!!/INVENTORY RESTS AT 317.841 MILLION OZ

APRIL 18/WITH SILVER UP 44 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 320.196 MILLION OZ

APRIL 17/WITH SILVER UP 10 CENTS TODAY/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 320.196 MILLION OZ

April 16/WITH SILVER UP 7 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 320.196 MILLION OZ/

April 13/WITH SILVER UP 17 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 320.196 MILLION OZ.

April 12/WITH SILVER DOWN 27 CENTS/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 320.196 MILLION OZ/

April 11/2018/WITH SILVER UP 16 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 320.196 MILLION OZ/

APRIL 10/WITH GOLD UP 8 CENTS/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 320.196 MILLION OZ/

APRIL 9/WITH SILVER UP 12 CENTS/WE HAD NO CHANGES IN SILVER INVENTORY/INVENTORY RESTS AT 320.196 MILLION OZ/

APRIL 6/WITH SILVER UP 4 CENTS, WE HAD A HUGE DEPOSIT OF 1.319 MILLION OZ INTO THE SLV INVENTORY/INVENTORY RESTS AT 320.196 MILLION OZ

APRIL 5/WITH SILVER UP 6 CENTS/NO CHANGES IN INVENTORY AT THE SLV/INVENTORY RESTS AT 318.877 MILLION OZ/

April 4/WITH SILVER DOWN 11 CENTS/A SMALL CHANGE IN SILVER INVENTORY AT THE SLV/ A WITHRAWAL OF 135,000 OZ AND THIS IS PROBABLY TO PAY FOR FEES/INVENTORY RESTS AT 318.877 MILLION OZ/

APRIL 3./WITH SILVER DOWN 16 CENTS/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.012 MILLION OZ/

APRIL 2/WITH SILVER UP 34 CENTS/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.012 MILLION OZ/

MARCH 29/WITH SILVER UP 6 CENTS, THE CROOKS DECIDED THAT THEY HAD BETTER ADD SOME 943,000 PAPER OZ TO THEIR INVENTORY/INVENTORY RESTS AT 319.012 MILLION OZ

March 28/WITH SILVER DOWN 27 CENTS/AGAIN NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 318.069 MILLION OZ

MAY 10/2018:

Inventory 323.263 million oz

end

6 Month MM GOFO 2.07/ and libor 6 month duration 2.52

Indicative gold forward offer rate for a 6 month duration/calculation:

G0FO+ 2.08%

libor 2.52 FOR 6 MONTHS/

GOLD LENDING RATE: .45%

XXXXXXXX

12 Month MM GOFO

+ 2.77%

LIBOR FOR 12 MONTH DURATION: 2.54

GOFO = LIBOR – GOLD LENDING RATE

GOLD LENDING RATE = +.23

end

Major gold/silver trading /commentaries for THURSDAY

GOLDCORE/BLOG/MARK O’BYRNE.

GOLD/SILVER

Iran’s Gold Demand May Surge On Trump Sanctions

by Claudia Carpenter, Bloomberg

Iran’s gold demand will probably be “strong” for the next few months and then gradually decline as U.S. sanctions start to take effect, according to the researcher who covers the country for Metals Focus Ltd.

After a previous set of sanctions was imposed on Iran in 2012, it took two years for the country’s gold demand to start falling, according to data from the World Gold Council. It sank to only 45.1 tons by 2016, the lowest in at least six years and 65 percent lower than in 2013, according to gold council data. It rose to 64.5 tons last year.

“What’s going to happen initially, people will try to convert whatever they have into dollars or gold or whatever is of value that’s not going to depreciate,” Cagdas Kucukemiroglu, an analyst at London-based Metals Focus, said Wednesday by phone. “Then next year the demand will gradually start to go down but it’s not going to be drastic. The base is already very low.”

U.S. sanctions on Iran’s gold trade will be re-imposed after 90 days, according to the U.S. Department of the Treasury. President Donald Trump said Tuesday that the U.S. will withdraw from a landmark accord to curb Iran’s nuclear program and that he would re-instate financial restrictions on the country. The U.S. will be instituting the “highest level” of sanctions against Iran, Trump said.

What’s different this time for Iran’s gold demand is the weakening local currency rial, according to Kucukemiroglu, who supplies quarterly gold demand data for the Middle East to the producer-funded World Gold Council. The nation’s gold coin and bar demand more than tripled in the first quarter when the rial hit several record lows against the U.S. dollar.

Gold traders in Turkey may also be reluctant to supply metal to Iran because of a U.S. sanctions case against a Turkish banker involving gold, he said. The banker was convicted earlier this year of helping Iran evade U.S. financial sanctions. Iran mostly gets it gold from Turkey and the United Arab Emirates.

A weak rial and slowing economic growth may even cause Iranians to start selling their gold, Kucukemiroglu said. “If sanctions stay, the economy will get poorer. Gold is a good way to get cash when you need it.”

Source: Bloomberg

Listen on SoundCloud , Blubrry & iTunes. Watch on YouTube

News and Commentary

Iran’s Gold Demand Set for Spurt Before Trump Sanctions Bite (Bloomberg.com)

Dollar Drops as Treasuries Climb; Oil Extends Gain: Markets Wrap (Bloomberg.com)

Gold edges down on firm dollar, US bond yields (Reuters.com)

Gold recovers a major part of early losses to 200-DMA support (FXStreet.com)

Oil soars after Trump nixes Iran nuclear deal, stocks rally (Reuters.com)

Month of May Has Been a Great Time to Buy Gold (Goldseek.com)

Is the Supply of Gold Depleting? (GoldTelegraph.com)

Gold Mining Supply Is Collapsing (TheDailyCoin.com)

Gold Prices (LBMA AM)

09 May: USD 1,306.85, GBP 965.11 & EUR 1,102.07 per ounce

08 May: USD 1,310.05, GBP 969.44 & EUR 1,101.88 per ounce

04 May: USD 1,309.35, GBP 965.78 & EUR 1,094.09 per ounce

03 May: USD 1,313.30, GBP 966.19 & EUR 1,094.64 per ounce

02 May: USD 1,310.75, GBP 960.52 & EUR 1,091.99 per ounce

01 May: USD 1,309.20, GBP 956.37 & EUR 1,087.68 per ounce

30 Apr: USD 1,316.25, GBP 958.62 & EUR 1,087.62 per ounce

Silver Prices (LBMA)

09 May: USD 16.44, GBP 12.12 & EUR 13.84 per ounce

08 May: USD 16.45, GBP 12.17 & EUR 13.85 per ounce

04 May: USD 16.42, GBP 12.10 & EUR 13.72 per ounce

03 May: USD 16.47, GBP 12.12 & EUR 13.74 per ounce

02 May: USD 16.35, GBP 11.98 & EUR 13.62 per ounce

01 May: USD 16.25, GBP 11.87 & EUR 13.51 per ounce

30 Apr: USD 16.38, GBP 11.93 & EUR 13.54 per ounce

Recent Market Updates

– “Money Is Gold — and Nothing Else”

– U.K. Home Prices Plunge 3.1% In April – Largest Monthly Drop Since Financial Crisis In 2011

– Weekly Gold Update – Gold In Dollars Lower Despite Poor US Jobs and Other Data

– Own Some Gold and Avoid Overvalued Assets

– Gold Demand Falls In Q1 Despite Robust Central Bank and Investment Demand and Surging Demand In Turkey and Iran

– Smart Money Diversifying Into Gold – One Billionaire Invests Half His Net Worth

– “Blood In The Streets” Of U.S. Gold Bullion Market As Sale Of Gold Coins Collapse

– Most Important Chart Of The Century For Investors?

– Gold Mining Shares Are Speculative Making Gold Bullion A Better Investment

– Gold Price Increasingly Influenced By Declining Dollar Rather Than Interest Rates

– Cash “Vanishes” From Bank Accounts In Ireland

– Russia Buys 300,000 Ounces Of Gold In March – Nears 2,000 Tons In Gold Reserves

– Family Offices and HNWs Invest In Gold Again

Andrew Maguire’s Kinesis money which is a “bitcoin” but backed 100% by allocated gold and silver is set to go.

it think it would be a great idea to look at this!

please read at: https://kinesis.money/#/

(Andrew Maguire)

|

2:57 PM (1 hour ago) | ||

|

|||

Harvey

Here It is my friend! https://kinesis.money/#/ Please let everyone know.

Let catch up on Monday if you have time. We have billions in the hopper ready to be allocated on the 1st day of trading. The paper market days are over.

Warm regards

Andy

Chinese Gold Demand Off To A Hot Start In 2018

Gold was up half a percent year-to-date through last Friday.

This doesn’t sound very exciting, but over the same period, the S&P 500 Index was in the red – the first time in nearly a decade that stocks have been negative for the year through the beginning of May. The yellow metal is doing the one thing for which many investors have it in their portfolio – namely, it’s trading inversely to the market. This highlights its longstanding role as an attractive diversifier and store of value.

Gold has been under pressure from a strengthening U.S. dollar, and May has historically delivered lower prices. As I’ve pointed out before, this makes it an ideal entry point in anticipation of a late summer rally before Diwali and the Indian wedding season, during which gifts of gold jewelry are considered auspicious. Demand in China for the remainder of the year also looks promising.

India Gold Demand Weakened, but a Healthy Monsoon Could Help Reverse That

India’s demand for gold jewelry in the first quarter was down 12 percent from the same period last year, according to the latest report from the World Gold Council (WGC). Consumption fell to 87.7 metric tons, compared to 99.2 tons in the first three months of 2017. Contributing to this weakness was the fact that there were fewer auspicious days in the first quarter than in the same period of the past three years, according to the WGC.

However, this followed a monumental fourth quarter 2017, when gold demand in the world’s second-largest consumer was 189.6 metric tons – an all-time record – so a decline was expected.

Looking ahead, it’s estimated that India will have a “normal” monsoon season this summer. This is good news for gold’s Love Trade. A third of India’s gold demand comes from rural farmers, whose crop revenues depend on the rains from a healthy monsoon. When the subcontinent experiences a drought, as it did in 2014 and 2015, gold consumption suffers.

The India Meteorological Department (IMD) reports that its forecasts suggest “maximum probability for normal monsoon rainfall” and “low probability for deficient rainfall during the season.”

Chinese Bullion Demand Off to a Good Start in 2018

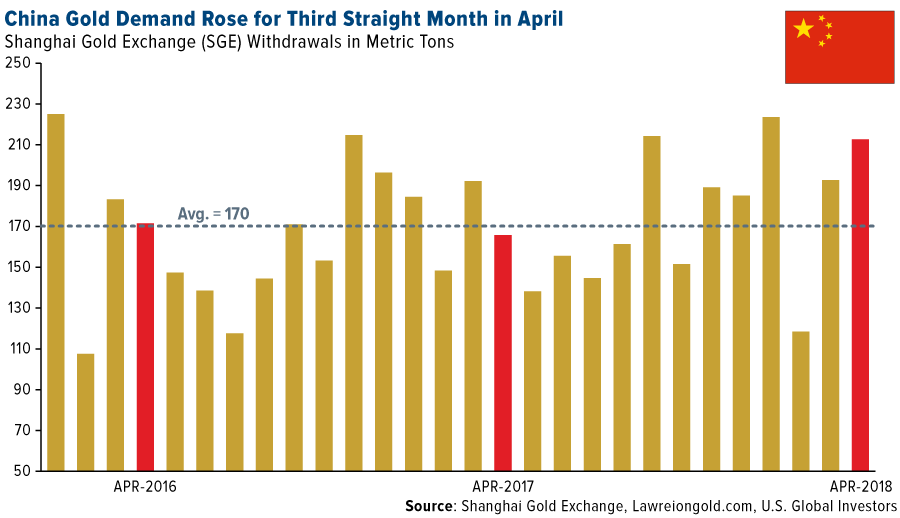

In China, the world’s largest importer of gold, jewelry demand rose 7 percent in the first quarter to 187.7 metric tons, a three-year high. According to the WGC, Chinese retailers are working on improving the customer experience, providing consumers with “a more holistic retail solution.” The industry is expecting a strong 2018 after a relatively subdued 2017.

Except for a weak February, demand so far this year has been particularly strong, with monthly withdrawals from the Shanghai Gold Exchange (SGE) above the two-year average of 170 metric tons. April represented the third straight month of rising demand. Withdrawals were 28 percent higher than in the same month in 2017, according to veteran precious metals commentator Lawrie Williams.

Williams writes that fears of a potential trade war with the U.S. could be driving Chinese investors into safe haven assets, including gold bars and coins. Indeed, the WGC reports that bullion demand in the first quarter finished at 78 metric tons, above the three- and five-year averages.

I believe this all bodes well for the Love Trade going forward, meaning it might be an opportune time for investors to consider increasing their exposure to gold and gold mining stocks. As always, I recommend a 10 percent weighting, with 5 percent in bars, coins and jewelry, and 5 percent in high-quality gold stocks, mutual funds and ETFs.

end

Your early THURSDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

i) Chinese yuan vs USA dollar/CLOSED UP 6.3503 /shanghai bourse CLOSED UP 15.26 POINTS OR 0 .48% / HANG SANG CLOSED UP 273.08 POINTS OR 0.89%

2. Nikkei closed UP 88.30 POINTS OR .39% / /USA: YEN FALLS TO 109.65/

3. Europe stocks OPENED MIXED/RED /USA dollar index FALLS TO 92.91/Euro RISES TO 1.1884

3b Japan 10 year bond yield: RISES TO . +.05/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 109.65/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD FINALLY IN THE POSITIVE/BANK OF JAPAN LOSING CONTROL OF THEIR YIELD CURVE AS THEY PURCHASE ALL BONDS TO GET TO ZERO RATE!!

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 71.51 and Brent: 77.38

3f Gold UP/Yen UP

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil UP for WTI and UP FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund RISES TO +.57%/Italian 10 yr bond yield UP to 1.85% /SPAIN 10 YR BOND YIELD DOWN TO 1.29%

3j Greek 10 year bond yield FALLS TO : 4.11?????????????????

3k Gold at $1317.82 silver at:16.463 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble UP 107/100 in roubles/dollar) 62.00

3m oil into the 71 dollar handle for WTI and 77 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 109.65 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 1.0023 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1914 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now POSITIVE territory with the 10 year FALLING to +0.54%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.97% early this morning (THIS IS DEADLY TO ALL MARKETS). Thirty year rate at 3.14%

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

(courtesy Jim Reid/Bloomberg/Deutsche bank/zero hedge)

Futures Flat After Barrage Of Overnight News; CPI Looms

US futures are flat, and European stocks are little changed after their longest winning streak since mid-March following a barrage of overnight news, including a dramatic escalation in fighting between Israel and Syria/Iran, a shocking election victory in Malaysia where opposition leader Mahathir Mohamad ended the six-decade rule of Najib Razak’s party sending more shock waves among emerging markets, and the blessing by Bersluconi of a new, anti-establishment, populist government in Italy.

The busy news agenda offers no respite to investors this week, with tension between Israel and Iran mounting just days after U.S. President Donald Trump roiled the international community with his decision to ditch a nuclear accord with the Islamic Republic. Meanwhile, the stage is set for a populist government to form in Italy, and traders are rapidly coming to terms with an election upset in Malaysia. Many will now be looking to American inflation data as a welcome diversion.

Meanwhile, it is Ascension Day holiday across several European countrie, leading to even poorer volumes, while the biggest economic catalyst of the week looms in the face of today’s US CPI print due in under 2 hours.

While the latest burst higher in US equities may have taken a breather, overnight Asian shares advanced, largely tracking oil as WTI crude rose to the highest since 2014, topping $71 on rising middle-eastern geopolitical fears. Having breached 3% for the second time in 2 week, 10Y Treasury yields, which have been driving up the greenback and exacting pain on emerging markets, dipped back under 3% to push the dollar toward its first drop in five days.

Europe’s Stoxx Europe 600 Index drifted lower on what is a public holiday in various parts of the region, with markets closed in countries including Switzerland, Sweden, and Austria. The main risk overnight was that Italy’s 5 Star and League have made significant steps to form a government, and expect to finalize everything in a short time. Looking at Brexit, EU officials suggest that the EU is looking to find a way forward to maintain trade between the UK and EU post-Brexit despite having reservations about PM May’s current plans.

Earlier, the MSCI Asia Index rose 0.5%, thanks to broad-based gains in stocks around the region. The Shanghai Comp. (+0.5%) and Hang Seng (+0.9%) shrugged off another liquidity drain by the PBoC to trade positive in which Hong Kong resumed its recent trend of outshining its regional peers, while participants also digested mixed Chinese inflation figures that showed CPI missed estimates at 1.8% vs. Exp. 1.9% although PPI growth gathered pace for the 1st time in 7-months to 3.4% as expected

- Chinese CPI (Apr) Y/Y 1.8% vs. Exp. 1.9% (Prev. 2.1%).

- Chinese PPI (Apr) Y/Y 3.4% vs. Exp. 3.4% (Prev. 3.1%)

The big story out of Asia was the shocking outcome of the Malaysian elections, where opposition leader Mahathir Mohamad’s surprise victory ended the six-decade rule of Najib Razak’s party and has investors bracing for further jolts across the EM space. While Malaysian markets were closed, trading in non-deliverable forwards suggested the ringgit will tumble Monday in the wake of the surprise ouster of the country’s ruling party. The 2045-maturity dollar bond also declined. The dip in the dollar, however, stabilized developing markets which signaled stability after days of losses, and the MSCI Emerging Market Index rallied for a fourth day.

Elsewhere in FX, the dollar fell alongside Treasury yields ahead of U.S. CPI data and an auction of 30-year debt on Thursday. The pound edged up ahead of the Bank of England policy decision, while the New Zealand dollar slipped to a five-month low after its central bank left the door open for a possible cut. The Bloomberg Dollar spot index fell for the first time in five days as the dollar slid against most of its G-10 peers, with the biggest gains seen in the Canadian dollar; benchmark Treasury yields slipped below the 3 percent level

“We find the reasons of the rally temporary in nature and by looking at past experience from dollar-depreciation cycles, we conclude that, as long as global growth holds up well, then the greenback should resume weakening on a multi-quarter basis,” according to Vasileios Gkionakis, head of currency strategy research at UniCredit Bank

Elsewhere, looking at today’s BOE decision, “what matters for the pound is whether Governor Carney is a man with or without conviction over future rate hikes,” according to ING Groep NV’s currency strategist Viraj Patel. A 7-2 split, Patel’s base-case scenario, would see sterling climb toward $1.36.

In geopolitics, the White House commented that the US is preparing to add additional sanctions on Iran as soon as next week. Overnight, the main event was the Israel Defense Forces conducting operations on Iran targets in Syria overnight.

Elsewhere, Deputy head of Iran’s revolutionary guards Salami said Europe cannot confront the US in the nuclear accord, adds diplomacy cannot help Iran, the only way is confrontation.

In commodities, energy prices are currently coming off overnight highs in which crude prices extended on the advances as traders adjust to supply disruption concerns in the wake of the US withdrawal from the Iran nuclear agreement. Following this withdrawal, Israeli military have increased the number of strikes targeted at dozens of Iranian facilities in retaliation to an Iranian rocket attack on the occupied Golan Heights, signalling a continued escalation of geopolitical tensions in the region. Yesterday’s DOE printed a larger than expected drawdown, providing some support to the complex. WTI (+0.7%) and Brent (+0.6%) crude prices are firmly above the USD 71.00/bbl and USD 77.00/bbl respectively. UBS expects Brent to trade at USD 80/bbl in 6 months (prior forecast at USD 65/bbl) and WTI to trade at a USD 5/bbl discount to Brent (prior USD 4/bbl discount). Elsewhere, gold prices are trading flat amid a slight easing of the greenback, while London copper saw modest gains on the back of lower inventories.

Economic data on Thursday include initial jobless claims and CPI. Nvidia, Telus and News Corp. are among companies due to release results

Market Snapshot

- S&P 500 futures up 0.2% to 2,701.00

- STOXX Europe 600 down 0.04% to 392.29

- MXAP up 0.5% to 173.78

- MXAPJ up 0.7% to 568.54

- Nikkei up 0.4% to 22,497.18

- Topix up 0.3% to 1,777.62

- Hang Seng Index up 0.9% to 30,809.22

- Shanghai Composite up 0.5% to 3,174.41

- Sensex up 0.05% to 35,335.91

- Australia S&P/ASX 200 up 0.2% to 6,118.75

- Kospi up 0.8% to 2,464.16

- German 10Y yield rose 0.2 bps to 0.561%

- Euro up 0.2% to $1.1871

- Italian 10Y yield rose 1.6 bps to 1.626%

- Spanish 10Y yield rose 0.4 bps to 1.308%

- Brent Futures up 0.6% to $77.69/bbl

- Gold spot up 0.03% to $1,313.11

- U.S. Dollar Index down 0.06% to 92.99

Top Overnight News from Bloomberg

- Trump personally welcomed home three Americans released from detention in North Korea, as he prepares for a landmark summit with Kim Jong Un

- Israel said it’s carrying out attacks inside Syria after Iranian forces based in that country fired a barrage of missiles at the Golan Heights

- Italian bonds slid after four-times premier Silvio Berlusconi dropped his opposition to a tie-up, giving the chances of a populist government ruling Italy a sizable boost

- Oil extended gains above $71 a barrel as a conflict between Israel and Iran ratcheted up, increasing prospects for tighter global supply after the U.S. renewed sanctions on OPEC’s third-largest producer

- With corporate-debt defaults on the rise, China’s securities regulator will probe bond funds to ensure that they have proper risk controls in place, according to people familiar with the matter

- Japanese investors sold U.S. sovereign bonds for a sixth month in March, while they added to holdings of French and German debt, according to the Ministry of Finance’s balance- of-payments data released Thursday

- Mahathir Mohamad’s surprise victory in Malaysia’s election ended the six-decade rule of Najib Razak’s party and has investors are bracing for further jolts as this news comes at a time when emerging markets are already under attack globally

- While money markets are betting officials will stay on hold this month, investors will look for any split among Bank of England’s MPC members to determine the chances of a rate increase this year

- Oil extended gains above $71 a barrel on the risk of supply disruptions as a conflict between Israel and Iran ratcheted up

Asian stocks traded positive across the board following the energy-fuelled upside on Wall St, where oil names outperformed as crude gained in the wake of Trump’s withdrawal from the Iran nuclear agreement and DoEs. As such, ASX 200 (+0.2%) was led by the energy sector as oil edged fresh multi-year highs last seen in 2014 and with RBOB also at its best levels since mid-2015, while Nikkei 225 (+0.4%) was also marginally higher amid earnings and with Mitsubishi Motors shares outpacing the broader market after it beat on its FY net and guided sales higher. Shanghai Comp. (+0.5%) and Hang Seng (+0.9%) shrugged off another liquidity drain by the PBoC to trade positive in which Hong Kong resumed its recent trend of outshining its regional peers, while participants also digested mixed Chinese inflation figures that showed CPI missed estimates at 1.8% vs. Exp. 1.9% although PPI growth gathered pace for the 1st time in 7-months to 3.4% as expected. Finally, 10yr JGBs were flat with demand lacking amid gains in riskier assets while a 10yr inflation-indexed auction was also largely ignored and failed to spur price action.

Top Asian News

- Mahathir Set to Become Malaysian Prime Minister After Shock Win

- Li Ka-shing to Retire Today, Ending Storied Career of Top Tycoon

- Bank of China, JD.com to Promote Cooperation on Fintech

- Malaysia’s 1MDB Spurs Voter Backlash, Global Probes: QuickTake

- Philippines Raises Benchmark Rate as Inflation Battle Heats Up

European equites trading mostly lower (Eurostoxx 50 -0.4%) ahead of the BoE rate decision, with the energy and telecoms sectors underperforming (-1.1% and -1.3% respectively). This resulting from Randgold Resources and BT’s (-8.2% and -9.0% respectively) uninspiring earnings, as well as BT’s announcement of job cuts. Financials are lower by 0.3% while RBS’s (+4.3%) lower than expected pay-out on MBS sales during the financial crisis, and UniCredit’s (+0.9%) positive financial results. Italy’s FTSE MIB is underperforming on the recent Italian political developments. In stock specific news Next (+6.2%) raised guidance on warm weather boosting sales, and Alstom (+0.9%) announced a USD 3bln agreement with GE to exit multiple energy joint ventures.

Top European News

- Italian Production Rises in Positive Sign for Economic Output

- U.K. Construction Slumped in March as Snow Stalled Projects

- RBS Clears Path to Award Dividends After $4.9 Billion DOJ Deal

- UniCredit Pushes on Costs, Asset Quality to Affirm Leadership

- ITV’s Online Ad Sales and Production Boost McCall as TV Weakens

In FX, DXY is Losing a bit more impetus below 93.000 and looking for some support from US CPI data amidst expectations for firmer headline and core prints, but softer leads via PPI in the run up. NZD/AUD: A very dovish hold from the RBNZ last night has hit the Kiwi hard, as the Central Bank signalled an even more prolonged period of unchanged policy and 50-50 odds that the next move in the OCR could be up or down. Nzd/Usd subsequently dived from a recovery high not far from 0.7000 to within a few pips of 0.6900, while the Aud/Nzd cross catapulted to just over 1.0800 from circa 1.0700 and lower in recent sessions. Conversely and consequently, Aud/Usd has continued its rebound from near 0.7400 lows towards 0.7500, but could be capped by mega option expiry interest at the big figure spread over the next few days (5 bn in total from today to May 16). CAD: The Loonie continues to outperform G10 counterparts and climb alongside oil prices that have extended to the upside on the US-Iran nuclear deal breakdown and with draws in US crude inventories adding to supply concerns. Usd/Cad is now bids/support around 1.2775 vs peaks earlier in the week just over 1.3000 and may derive further direction from Canadian new house price data later (although the US inflation data is likely to be more influential for the pair).

In commodities, energy prices are currently coming off overnight highs in which crude prices extended on the advances as traders adjust to supply disruption concerns in the wake of the US withdrawal from the Iran nuclear agreement. Following this withdrawal, Israeli military have increased the number of strikes targeted at dozens of Iranian facilities in retaliation to an Iranian rocket attack on the occupied Golan Heights, signalling a continued escalation of geopolitical tensions in the region. Yesterday’s DOE printed a larger than expected drawdown, providing some support to the complex. WTI (+0.7%) and Brent (+0.6%) crude prices are firmly above the USD 71.00/bbl and USD 77.00/bbl respectively. UBS expects Brent to trade at USD 80/bbl in 6 months (prior forecast at USD 65/bbl) and WTI to trade at a USD 5/bbl discount to Brent (prior USD 4/bbl discount). Elsewhere, gold prices are trading flat amid a slight easing of the greenback, while London copper saw modest gains on the back of lower inventories.

US Event Calendar

- 8:30am: Initial Jobless Claims, est. 219,000, prior 211,000; Continuing Claims, est. 1.8m, prior 1.76m

- 8:30am: US CPI MoM, est. 0.3%, prior -0.1%

- US CPI Ex Food and Energy MoM, est. 0.2%, prior 0.2%

- US CPI YoY, est. 2.5%, prior 2.4%

- US CPI Ex Food and Energy YoY, est. 2.2%, prior 2.1%

- US CPI Index NSA, est. 250.7, prior 249.6

- US CPI Core Index SA, prior 256.2

- Real Avg Weekly Earnings YoY, prior 0.94%; Real Avg Hourly Earning YoY, prior 0.4%

- 9:45am: Bloomberg Consumer Comfort, prior 56.5

- 2pm: Monthly Budget Statement, est. $212.0b, prior $208.7b deficit

3. ASIAN AFFAIRS

i)THURSDAY MORNING/WEDNESDAY NIGHT: Shanghai closed UP 15.26 points or 0 .48% /Hang Sang CLOSED UP 273.08 points or 0.89% / The Nikkei closed UP 88.30 POINTS OR .39% /Australia’s all ordinaires CLOSED UP .18% /Chinese yuan (ONSHORE) closed UP at 6.3503/Oil UP to 71.51 dollars per barrel for WTI and 77.38 for Brent. Stocks in Europe OPENED MIXED/RED. ONSHORE YUAN CLOSED DOWN AT 6.3438 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.3503/ONSHORE YUAN TRADING WEAKER AGAINST OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING MUCH STRONGER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW LOOKS LIKE A FULL TRADE WAR IS BEGINNING/

3 a NORTH KOREA/USA

North Korea/South Korea/usa

Trump and Kim will meet in Singapore on June 12

(Fabian/the HILL)

Trump says he will meet Kim on June 12 in Singapore

END.

3 b JAPAN AFFAIRS

end

c) REPORT ON CHINA/HONG KONG

South China Morning Post

Conglomerate Anbang’s ex chief Wu sentenced to 18 years behind bars for fraud and embezzlement

(courtesy South China Morning post)

Anbang’s ex-chief Wu Xiaohui sentenced to 18 years behind bars for US$12 billion fraud, embezzlement

Prison term completes the downfall of one of China’s most famous tycoons and closes another chapter in Beijing’s crackdown on high-level fraud and corruption

He will also have assets worth 10.5 billion yuan (US$1.65 billion) confiscated, Xinhua, China’s official state news agency, reported on Thursday.

Wu, who was once at the helm of one of China’s most aggressive asset buyers, was put on trial in the No.1 Intermediate People’s Court in Shanghai in late March, charged with illegal fundraising, fraud worth 65.2 billion yuan (US$10.24 billion) and embezzling 10 billion yuan from Anbang’s insurance premium income.

Anbang, founded in 2004, has grown from a seller of car insurance into one of China’s largest insurance providers, holding nearly 2 trillion yuan in assets. The Beijing-based insurer was known for an aggressive global buying spree in recent years, which included the acquisition of the New York’s Waldorf Astoria hotel in 2014 for almost US$2 billion.

Prosecutors in the case said Wu had severely harmed “the safety of investors’ capital” and “crushed national financial security”.

The top banking and insurance regulator said in April that it will inject 60.8 billion yuan into the beleaguered insurer to ensure its solvency.

The Chinese government seized control of the company in February.

Thursday’s sentencing closes a key chapter in a series of investigations into several of China’s biggest overseas asset buyers – known in China as “crocodiles” – since June 2017, in a government programme to pare back leveraged buyouts and rein in financial malfeasance.

It also completes the spectacular fall from grace of a man who once seemed to have it all.

Partnered with the son of a marshal who had helped found Communist China, married to the granddaughter of the country’s former paramount leader, and backed by China’s most powerful state firms and the industry’s top regulator, Wu was once the country’s most feted business tycoon. He was famous for his hard-handed business manner, his single-minded will to get ahead and willingness to confront anyone who got in his way.

Born into an ordinary family in a village in east China’s Zhejiang province in 1966, Wu started from scratch and eventually built a business empire holding 1.97 trillion yuan (US$310.9 billion) in assets and ranked 139th on the 2017 Global Fortune 500 list.

Backed by enormous capital power, he led his company on a wide-ranging global shopping spree, snapping up property landmarks like the Waldorf Astoria hotel in New York, and mounting a takeover battle against the Marriott Group with a US$14 billion bid to buy Starwood Hotels.

Iconic Waldorf Astoria hotel is part of China’s US property fire sale – but don’t expect a bargain

Between 2012 and 2016, Anbang WAS involved in 14 acquisitions valued at US$25.22 billion.

Wu also talked with US President Donald Trump’s son-in-law, Jared Kushner, about buying into a skyscraper project in Manhattan in 2016.

But the fame and fortune he built over decades came crashing down with remarkable speed.

On March 28, clad in a dark blue suit, the 52-year-old showed up to a court in Shanghai. Weeping in front of the China Central Television camera, the disgraced tycoon said he “regretted his mistakes”, and begged for a lenient sentence.

By that time Wu had seen Anbang Group taken over by the authorities, while he himself faced charges of fraud and embezzlement that could have put him in prison for life.

His rise was closely tied to what were once some of the biggest names in China’s political circles. His fall also tracked the decline of those once-celebrated families, and the reshuffle of the country’s ruling elite.

“Wu is smart and hardworking. But he tended to forget about his identity of late. He forgot he was the senior manager chosen by a powerful group to make money, and mistook himself as the power itself. That’s what caused this tragedy,” said a long-time business partner of Wu and Anbang, who asked to remain anonymous.

Wu’s early life has left few traces. Sources said he started out as a civil servant in his hometown in the early 1990s, but left for a business career a few years later.

Sino-Ocean first to swoop on Anbang assets since state takeover

By the early 2000s when he met Deng Zhuorui, granddaughter of former Chinese leader Deng Xiaoping, he was already a successful car salesman and into his second marriage.

It was his then business partner Chen Xiaolu, a son of marshal Chen Yi, a member of China’s first communist ruling generation, who introduced him to Deng.

The marriage was kept extremely low key, so that few people even knew when the wedding took place.

Even the man who had brought the two together in the first place “was not invited to their wedding and did not know of their marriage beforehand”, a personal friend close to Chen said.

When Chen asked Wu why he had not been told about the marriage, Wu said he had felt “ashamed” because he was a married man when he first met Deng.

Chinese media outlets Caixin and Southern Weekly reported that the marriage took place in 2004, after Wu had divorced his second wife, herself the relative of a Hangzhou mayor.

Anbang Group filed a statement in early 2017 denying Caixin’s report on Wu’s marital status, describing it as defamatory.

True or not, the year 2004 was certainly an important milestone in Wu’s business career. It saw the founding of a company called Anbang Property Insurance in Zhejiang province by seven shareholders including state-owned SAIC Motor, which took up a 20 per cent controlling stake.

Murky waters surrounding Wu Xiaohui and Anbang

The second biggest shareholder, holding 18 per cent, was Shanghai Standard Infrastructure Group, a subsidiary of a company registered as 40 per cent owned by Chen and 60 per cent by Deng.

A year later, another state-owned giant, Sinopec, bought up 20 per cent of Anbang Property Insurance for 340 million yuan, becoming the joint-biggest shareholder with SAIC.

Sinopec’s chairman at the time, Chen Tonghai, was sentenced to death in 2009 in what was believed to be the country’s biggest bribery case but was later granted a reprieve.

The fall of Chen did not bother Wu, or indeed Anbang.

By the time Anbang Property Insurance was restructured into Anbang Group in 2011, the firm was a financial conglomerate on the ascent, already strong enough to acquire a commercial bank in Chengdu for 5.6 billion yuan, and to see off China’s best-connected property developers when competing for land in Beijing’s Central Business District (CBD).

Conflicts erupted from time to time, particularly when other powerful business magnates were involved. But more often than not, Wu emerged as the victorious party.

A consortium that included China International Capital Corporation (CICC) won a bid for a land plot for 2.5 billion yuan in 2010, but was then not allowed to start developing the site. Late last year a source involved in the case told the Post that was because Anbang would not submit the land plot back to Beijing’s municipal government after first-stage development.

CICC is China’s most powerful investment bank, once headed by Levin Zhu, the son of former premier Zhu Rongji.

“We have been in dispute with Anbang for about seven years regarding handing over a land plot in CBD. They would just ignore requests to fulfil legal procedures, not only from us, but also from the Beijing municipal government,” said a source familiar with the dispute.

“There is simply no way to argue with Wu. He shies away from us, claiming to be busy, while the government seems to have no binding power over him.”

According to the prosecutor in Wu’s trial, he had increased his control of the company through three major capital injections in 2011 and 2014, ending up owning 98.2 per cent of Anbang Group.

In the process, Anbang’s registered capital swelled from 5.1 billion yuan to 61.9 billion yuan, giving it the capacity to issue more aggressive insurance policies and carry out more mergers and acquisitions.

However, the prosecutors said capital injection worth around 50 billion yuan had come from insurance premiums, which is against rules set by the China Insurance Regulatory Commission (CIRC).

The growth of Anbang’s income from insurance premiums became the stuff of legend in the industry. The group’s flagship Anbang Life Insurance unit, for instance, more than quadrupled its premiums income to 40.5 billion yuan in 2014. The premium income of the group as a whole surged by almost 39 times to 52.9 billion yuan in the year to 2014, thrashing all competitors.

The strong backing of then CIRC chairman Xiang Junbo played a key role, industry insiders say.

More than 96 per cent of the premiums income under Anbang Life came from banking channels between 2012 and 2014, compared to an industry average of less than 40 per cent, according to a report issued by state-owned Dagong Global Credit Rating.

Xiang was placed under a corruption probe in April 2017, and expelled from the Communist Party in September. A preliminary investigation found he had abused the power to supervise and approve, according to the party’s anti-graft watchdog.

“It is easy to hold a corrupted official accountable for wrongdoings. But if the problem with Xiang himself could lead to such big financial risks, it is more important to review the whole regulatory system, otherwise it would not solve the problem thoroughly,” said Professor Sun Wujun from the Nanjing University Business School.

“In the past decade, as financial innovation flourished amid ample liquidity, regulators failed to catch up and see through risks hidden by complicated structuring of financial products and heavy cross-investment. It is a key area that Beijing is pursuing and has been tightening,” he added.

4. EUROPEAN AFFAIRS

UK

The Bank of England leaves unchanged but with two voting in the negative. The pound plummets on the huge dovish inflation outlook

(courtesy zerohedge)

BOE Keeps Rates Unchanged In 7-2 Vote; Cable Plunges On Dovish Inflation Outlook

As was widely anticipated following the recent disappointing economic data out of the UK, the Bank of England announced it kept rates unchanged at 0.5% in a 7-2 vote, with Saunders and McCafferty dissenting (some more hawkish commentators were hoping for a 6-3 split).

Bank of England

✔@bankofengland

We have kept interest rates at 0.5%. Find out more at: https://b-o-e.uk/2IpQapv #InflationReport

As also expected, the BOE Committee also voted unanimously to keep its various QE programs unchanged.

However, the reason for the sharp kneejerk reaction lower in cable, which plunged as much as 100 pips on the report, was the sharp dovish language on inflation, with the key sentence the following: “Taking external and domestic influences together, CPI inflation is projected to fall back slightly more quickly than in February, reaching the target in two years.”

“The inflation rates of the most import-intensive components of the CPI appear to have peaked. The MPC judges that the impact of the past depreciation of sterling on CPI inflation, while remaining significant, is likely to fade a little faster than previously thought. Taking external and domestic influences together, CPI inflation is projected to fall back slightly more quickly than in February, reaching the target in two years. These projections are conditioned on a gently rising path for Bank Rate over the next three years.”

The BOE also trimmed its economic outlook: BOE’s growth and inflation outlooks. The preliminary estimate of GDP growth in the first quarter was 0.1%, 0.3 percentage points lower than expected in February. According to the BOE, This is likely in part to have reflected adverse weather in late February and early March.” However, the Committee also believes that the slowing in Q1 GDP growth has been overstated in the prelim release and believe that over time Q1 will be revised higher to 0.3% and thereafter look for 0.4% in Q2.

Of greater importance was the BOE’s view on Inflation, which is now seen as cooling faster than previously expected: the 2.5% CPI in March was lower than expected in the Feb QIR. Inflation rates of the most import-intensive components of CPI appear to have peaked. Impact of GBP depreciation while remains significant, is likely to fade a little faster than previously thought. CPI target is expected to be met in two years.

Other key observations:

- Rates: No mention of the historical guidance of: rates will need to rise at a somewhat faster pace and greater extent than markets are currently pricing in. Reiterated that any future rate increases were likely to be at a gradual pace and to a limited extent.

- Brexit: Minutes offer no new view by the MPC on the matter

- Wages: Wage growth are firming gradually and broadly as expected.

- Labour market: Hiring intentions remain strong and the unemployment rate has fallen slightly further over the past 3 months.

- Slack: MPC continues to judge that the UK economy has a limited degree of slack

- Case for unchanged: Members saw value in seeing how data unfolded in the coming months and to see whether softness in Q1 would persist.

- Case for lifting rates: Saw Q1 GDP as erratic and due to temp factors. Placed more weight on labour data and business surveys. Reduction in pass-through of GBP on inflation would not materially impact the inflation profile in the medium term.

Separately, looking at the Quarterly Inflation Report, the BoE forecasts three rate hikes over three years. As such the UK rates markets is pricing in a more dovish path of BoE hikes.

report, while the 2018 GDP forecast was cut (2019 and 2020 maintained), the 2018, 2019, 2020 inflation all lowered. Key forecasts:

- GDP Growth: 2018 Q2: 1.4% (Prev.1.8 %), 2019 Q2: 1.7% (Prev. 1.7%), 2020 Q2: 1.7% (Prev. 1.7%), 2021 Q2: 1.7%

- CPI Inflation: 2018 Q2: 2.4% (Prev. 2.7%), 2019 Q2: 2.1% (Prev. 2.2%), 2020 Q2: 2.0% (Prev. 2.1%), 2021 Q2: 2.0%

- Unemployment Rate: 2018 Q2: 4.1% (Prev. 4.2%), 2019 Q2: 4.0% (Prev. 4.2%), 2020 Q2 4.0% (Prev. 4.1%), 2021 Q2: 4.0%

- Average Weekly Earnings: 2018: 2.75% (Prev. 3.0%), 2019: 3.25% (Prev. 3.25%), 2020: 3.5% (Prev. 3.5%)

- Above forecasts are based on the path for the Bank Rate implied by forward market interest rates. The implied Bank Rate at the time of the report by the end of the forecast period was 1.2%

In summary, while the BOE is certainly not ending its tightening yet, it is hardly in a rush to hike. In kneejerk response, cable has tumbled by 100 pips…

… and gilts are rallying as UK money markets price out any further rate hikes by the BOE in 2018 as the global dovish wave returns.

end

The EU and ECB are not too happy with this development: both Euroskeptic parties will become the government after Berlusconi agreed not to partake in the government. These two parties love to spend and will no doubt break the 3% guideline putting it in direct confrontation with the EU. Remember that the Italy has a huge 360 billion euros of non performing loans on its books. Every Tom Dick and Harry are dumping Italian bonds with the only purchaser: the ECB

fun times again in Italy

(courtesy zerohedge)

Italian Bonds, Stocks Slide As Populist Parties On Verge Of Forming Euroskeptic Government

Chaos has returned to Italy and, appropriately, it has once again started with the bad boy of Italian politics, Silvio Berlusconi, the same flamboyant playboy-cum-former prime minister who back in 2011 nearly withdrew Italy from the Eurozone and only a flagrant political intervention by the ECB prevented the collapse of the European experiment.

As we reported yesterday, in a statement published late on Wednesday night in Italy, Berlusconi changed his long-standing position, and said he’d be open to an agreement between the League and the Five-Star Movement (otherwise known as M5S) to form a ruling coalition that wouldn’t include his center-right party, Forza Italia. And so, with his blessing, on Thursday the anti-establishment Five Star Movement and the far-right League were on the verge of forming a Euroskeptic government in which Europe’s third largest economy would be the latest to succumb to the populist wave unleashed by a decade of central bank errors and record income and wealth disparity.

The two leaders wasted no time, and Luigi Di Maio, the Five Star leader, and Matteo Salvini, the League leader, promptly met to try to iron out details of a potential agreement, including who become next prime minister. Key cabinet positions, including the finance ministry and foreign ministry, were also being discussed according to the FT.

In a joint statement after meeting on Thursday, Di Maio and Salvini described a “positive climate to define the government’s agenda and priorities” and said “technical” meetings among staff would begin in the afternoon. “In terms of the composition of the executive, and the premier, significant steps forward were taken amid constructive collaboration on all sides, with the aim of quickly giving an answer and a political government to the country,” they said.

To be sure, the two had held infrequent talks for the past few weeks, with no concrete outcomes decided due to the veto power bestowed upon Bunga Bunga; however with the Berlusconi blessing, the probability of a government becomes a virtual certainty. The reason: the 81-year-old Berlusconi had previously ruled out offering his support to a Five Star-League government unless his party was fully represented in the executive. At the same time, Five Star had vowed not to govern with Mr Berlusconi’s Forza Italia party, seeing it as part of the traditional political class it has been trying to unseat. This changed on Wednesday night when as we reported, the octogenrian playboy gave an green light to a deal, saying that while Forza Italia would vote against a Five Star-League government in parliament, this would not jeopardise his alliance with Mr Salvini on a local and regional level, where they rely on each other in many municipal and regional councils.

“If a centre-right political force takes on the responsibility of creating a government with Five Star we note that with respect,” Mr Berlusconi said in a tweet. “We will evaluate the government that is created, supporting any measures that are useful for Italians.”