GOLD: $1320,55 DOWN $ 1,75 (COMEX TO COMEX CLOSINGS)

Silver: $16.72 DOWN 2 CENTS (COMEX TO COMEX CLOSINGS)

Closing access prices:

Gold $1318.50

silver: $16.65

For comex gold:

MAY/

NUMBER OF NOTICES FILED TODAY FOR MAY CONTRACT:5 NOTICE(S) FOR 500 OZ.

TOTAL NOTICES SO FAR 618 FOR 61800 OZ (1.9066 tonnes)

For silver:

MAY

173 NOTICE(S) FILED TODAY FOR

865,000 OZ/

Total number of notices filed so far this month: 5837 for 29,185,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: BID $8648/OFFER $8748: DOWN $316(morning)

Bitcoin: BID/ $8383/offer $8483: DOWN $578 (CLOSING/5 PM)

end

First Shanghai gold fix comes at 10 pm est

The second Shanghai gold fix: 2:15 pm

First Shanghai gold fix gold: 10 pm est: 1325.88

NY price at the same time: 1320.10

PREMIUM TO NY SPOT: $5.78

ss

Second gold fix early this morning: 1329.07

USA gold at the exact same time: 1319.80

PREMIUM TO NY SPOT: $9.27

AGAIN, SHANGHAI REJECTS NEW YORK PRICING.

WE WILL NOT PROVIDE LONDON FIXES AS THEY ARE NOT ACCURATE AS TO WHAT IS GOING ON AT THE SAME TIME FRAME.

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total OPEN INTEREST ROSE BY A CONSIDERABLE 3339 CONTRACTS FROM 194,936 RISING TO 198,275 WITH YESTERDAY’S 22 CENT GAIN IN SILVER PRICING. WE ARE NOW WITNESSING OUR USUAL AND CUSTOMARY COMEX LONG LIQUIDATION AS WE ENTERED INTO THE ACTIVE DELIVERY MONTH OF MAY AS LONGS PACK THEIR BAGS AND MIGRATE OVER TO LONDON. WE WERE NOTIFIED THAT WE HAD A GIGANTIC SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP : 3261 EFP’S FOR JULY AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE OF 3261 CONTRACTS. WITH THE TRANSFER OF 3261 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 3261 EFP CONTRACTS TRANSLATES INTO 16.31 MILLION OZ ACCOMPANYING:

1.THE 22 CENT RISE IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES STANDING FOR MAY COMEX DELIVERY. (29.95 MILLION OZ)

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF APRIL: (FINAL)

16,196 CONTRACTS (FOR 9 TRADING DAYS TOTAL 16,196 CONTRACTS) OR 80.98 MILLION OZ: AVERAGE PER DAY: 1799 CONTRACTS OR 8.997 MILLION OZ/DAY

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH: 80.98 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 11.568% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)

ACCUMULATION IN YEAR 2018 TO DATE SILVER EFP’S: 1,226.4 MILLION OZ.

ACCUMULATION FOR JAN 2018: 236.879 MILLION OZ

ACCUMULATION FOR FEB 2018: 244.95 MILLION OZ

ACCUMULATION FOR MARCH 2018: 236.67 MILLION OZ

ACCUMULATION FOR APRIL 2018: 385.75 MILLION OZ

RESULT: WE HAD A HUGE SIZED INCREASE IN COMEX OI SILVER COMEX OF 3339 WITH THE 22 CENT GAIN IN SILVER PRICE. WE HAVE NOW ENTERED THE NEW ACTIVE MONTH OF MAY. THE CME NOTIFIED US THAT IN FACT WE HAD AN GIGANTIC SIZED EFP ISSUANCE OF 3261 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) . FROM THE CME DATA: 3261 EFP CONTRACTS FOR JULY, AND ZERO FOR ALL OVER MONTHS FOR A DELIVERABLE FORWARD CONTRACT OVER IN LONDON WITH A FIAT BONUS (TOTAL: 3261). TODAY WE GAINED 6600 TOTAL OI CONTRACTS ON THE TWO EXCHANGES: i.e. 3261 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH AN INCREASE OF 3339 OI COMEX CONTRACTS. AND ALL OF THIS HAPPENED WITH THE RISE IN PRICE OF SILVER OF 22 CENTS AND A CLOSING PRICE OF $16.73 WITH RESPECT TO YESTERDAY’S TRADING. YET WE STILL HAVE A STRONG AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY IN THIS ACTIVE MAY DELIVERY MONTH. IT SURE SEEMS THAT WE MUST HAVE HAD SOME BANKER SHORT COVERING ON BOTH EXCHANGES.

In ounces AT THE COMEX, the OI is still represented by UNDER 1 BILLION oz i.e. .991 MILLION OZ TO BE EXACT or 142% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT MAY MONTH/ THEY FILED AT THE COMEX: 146 NOTICE(S) FOR 730,000 OZ OF SILVER

IN SILVER, WE HAVE NOW SET THE NEW RECORD OF OPEN INTEREST AT 243,411 AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $16.51 ON APRIL 9.2018.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH: 27 MILLION OZ , APRIL: 2.485 MILLION OZ AND MAY: 29.95 MILLION OZ )

- HUGE RECORD OPEN INTEREST IN SILVER 243,411 CONTRACTS (OR 1.217 BILLION OZ/ SET APRIL 9/2018

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017

- RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ (FINAL)

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT). IT ALSO LOOKS LIKE BANKER CAPITULATION IN SILVER AS THEY STRUGGLE TO REMOVE SOME OF THEIR HUGE OBLIGATIONS.

In gold, the open interest ROSE BY A HUGE 11,165 CONTRACTS UP TO 506,316 WITH THE GAIN IN THE GOLD PRICE/YESTERDAY’S TRADING (GAIN OF $9.60). WE ARE NOW IN THE NON ACTIVE DELIVERY MONTH OF MAY. THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A LARGE SIZED 8945 CONTRACTS : JUNE SAW THE ISSUANCE OF 8945 CONTRACTS , MAY SAW THE ISSUANCE OF 0 CONTRACTS AND AUGUST SAW THE ISSUANCE OF: 0 CONTRACTS WITH ALL OTHER MONTHS ZERO. The new OI for the gold complex rests at 506,316. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE A HUMONGOUS SIZED OI GAIN IN CONTRACTS ON THE TWO EXCHANGES: 11,165 OI CONTRACTS INCREASED AT THE COMEX AND AN LARGE SIZED 8945 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON.THUS TOTAL OI GAIN: 20,110 CONTRACTS OR 20,110,000 OZ = 62.55 TONNES. AND ALL OF THIS OCCURRED WITH A GAIN OF $9.60

YESTERDAY, WE HAD 11948 EFP’S ISSUED.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF MAY : 86,131 CONTRACTS OR 8,613,100 OZ OR 267.90 TONNES (9 TRADING DAYS AND THUS AVERAGING: 9,570 EFP CONTRACTS PER TRADING DAY OR 957,000 OZ/ TRADING DAY),,

TO GIVE YOU AN IDEA AS TO THE HUGE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 9 TRADING DAYS IN TONNES: 267.90 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2017, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 2555 TONNES

THUS EFP TRANSFERS REPRESENTS 267.90/2550 x 100% TONNES = 10.50% OF GLOBAL ANNUAL PRODUCTION SO FAR IN APRIL ALONE.*** THE ACCUMULATION OF EFP CONTRACTS IS RISING PER MONTH.

ACCUMULATION OF GOLD EFP’S YEAR 2018 TO DATE: 3,025.84* TONNES *SURPASSED ANNUAL PROD’N

ACCUMULATION OF GOLD EFP’S FOR JANUARY 2018: 653.22 TONNES

ACCUMULATION OF GOLD EFP’S FOR FEBRUARY 2018: 649.45 TONNES

ACCUMULATION OF GOLD EFP’S FOR MARCH 2018: 741.89 TONNES (22 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR APRIL 2018: 713.84 TONNES (21 TRADING DAYS)

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A CONSIDERABLE SIZED INCREASE IN OI AT THE COMEX OF 11,165 WITH THE $9.60 RISE IN PRICE // GOLD TRADING YESTERDAY ($9.60 GAIN). HOWEVER WE ALSO HAD A LARGE SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 8945 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 8945 EFP CONTRACTS ISSUED, WE HAD A HUMONGOUS SIZED NET GAIN OF 20,110 CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

8945 CONTRACTS MOVE TO LONDON AND 11,165 CONTRACTS INCREASED AT THE COMEX. (in tonnes, the GAIN in total oi equates to 67.59 TONNES). ..AND ALL OF THESE OCCURRED AT THE COMEX WITH A GAIN OF $9.60 IN TRADING.

we had: 5 notice(s) filed upon for 500 oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD…

WITH GOLD DOWN $1.75 /NO CHANGES IN GOLD INVENTORY AT THE GLD

Inventory rests tonight: 862.96 tonnes.

SLV/

WITH SILVER DOWN 2 CENTS TODAY: THIS MAKES NO SENSE!! THE CROOKS AT THE SLV WITHDREW A HUGE 2.824 MILLION OZ FROM THE SLV INVENTORY

/INVENTORY RESTS AT 320.439 MILLION OZ/

end

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER ROSE BY A CONSIDERABLE SIZED 3339 CONTRACTS from 194,936 UP TO 198,275 (AND, CLOSER TO THE NEW COMEX RECORD SET /APRIL 9/2017 AT 243,411/SILVER PRICE AT THAT DAY: $16.53). THE PREVIOUS RECORD OTHER THAN WAS ESTABLISHED AT: 234,787, SET ON APRIL 21.2017 OVER ONE YEAR AGO. THE PRICE OF SILVER ON THAT DAY: $17.89. OUR CUSTOMARY MIGRATION OF COMEX LONGS MORPH INTO LONDON FORWARDS CONTINUES AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE: 0 EFP CONTRACTS FOR APRIL, 0 EFP CONTRACTS FOR MAY (WE DO NOT GET A LOOK AT THESE CONTRACTS AS IT IS PRIVATE BUT THE CFTC DOES AUDIT THEM), AND 3261 EFP’S FOR JULY AND ALL OTHER MONTHS ZERO. TOTAL EFP ISSUANCE: 3261 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI GAIN AT THE COMEX OF 3339 CONTRACTS TO THE 3261 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A GAIN OF 6600 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES: 33.00 MILLION OZ!!! AND THIS OCCURRED WITH ONLY A 22 CENT RISE IN PRICE . THE BANKERS ORCHESTRATED THEIR RAID THROUGHOUT LAST WEEK DESPERATELY TRYING TO PARE THEIR GIGANTIC OPEN INTEREST SHORT ON BOTH EXCHANGES BUT TO NO AVAIL. JUDGING BY THE RECORD NUMBER OF EFP ISSUANCE DURING LAST MONTH OF APRIL AT 385.75 MILLION OZ AND THE TOTAL OI GAIN ON THE TWO EXCHANGES, I DO NOT THINK THAT OUR BANKERS HAVE BEEN TOO SUCCESSFUL. THE CONSTANT RAIDS ARE NOW BEING CALLED UPON BY OUR BANKER FRIENDS ARE DONE IN AN ATTEMPT TO SHAKE AS MANY SILVER LEAVES FROM THE SILVER TREE AS POSSIBLE.

RESULT: A GOOD SIZED INCREASE IN SILVER OI AT THE COMEX WITH THE 22 CENT RISE IN SILVER PRICING YESTERDAY. BUT WE ALSO HAD ANOTHER STRONG SIZED 3261 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR APRIL, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)FRIDAY MORNING/THURSDAY NIGHT: Shanghai closed DOWN 11.15 points or 0 .35% /Hang Sang CLOSED UP 312.84 points or 1.02% / The Nikkei closed UP 261.30 POINTS OR 1.16% /Australia’s all ordinaires CLOSED UP .01% /Chinese yuan (ONSHORE) closed UP at 6.3329/Oil DOWN to 71.39 dollars per barrel for WTI and 77.22 for Brent. Stocks in Europe OPENED RED. ONSHORE YUAN CLOSED UP AT 6.3329 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.3250/ONSHORE YUAN TRADING WEAKER AGAINST OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING MUCH STRONGER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW LOOKS LIKE A FULL TRADE WAR IS BEGINNING/

/NORTH KOREA/SOUTH KOREA

i)North Korea/South Korea/USA

b) REPORT ON JAPAN

3 c CHINA

4. EUROPEAN AFFAIRS

i)EU

Europe is not happy with Trump’s new Iranian sanctions/ two commentaries

( Mish Shedlock/Mishtalk)

ii)Europe ends on a high note and extends its longest winning streak since 2015 despite poor economic data

(courtesy zerohedge)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

It seems that the USA/Israeli plan is to assassinate Iran’s chief revolutionary guard commander, Soleimani. It seems that Israel had him in their sights but Obama negated the attack

( zerohedge)

( zerohedge)

iv)Turkey

The Turkish lira plummets again as Erdogan states that he will begin to target interest rates

( zerohedge)

6 .GLOBAL ISSUES

7. OIL ISSUES

8. EMERGING MARKET

ARGENTINA

i)The Argentine Peso just fell to 23 Pesos per dollar despite a 40% interest rate. JPMorgan warns of disorder as 30 billion USA dollars of bonds come due. This is becoming the kiss of death to Argentina who has a huge amount of external debt denominated in currencies other than the Peso.

( zerohedge)

ii)Panic in Argentina as the Peso hits 24.25 to the dollar. No doubt the central bank of Argentina must come in and raise rates again

( zerohedge)

EMERGING MARKETS

Very important: the higher uSA dollar is playing havoc with our emerging markets, together with the higher price of oil. This is creating a tightening effect with our emerging markets causing funds to flee. Watch for the Brazilian real to reach 4..then we will witness panic in these markets which may cause contagion throughout the globe

( zerohedge)

9. PHYSICAL MARKETS

i)Emerging markets actually have two worries: a strong USA dollar and a weaker Chinese yuan

( Verma/Bloomberg/GATA)

ii)No doubt that Iran will use the purchase of gold to offset its problems of scarcity of dollars.

(Carpenter/Bloomberg)

iii)Interesting: Putin wants to break with the USA but instead of dumping dollars, he dumped Euros

( Andrianova/Bloomberg/GATA)

10. USA stories which will influence the price of gold/silver

ii)HAWAII rocked by a huge 6.9 magnitude earthquake. Toxic gas surfaces and fears mount as lava approaches a Hawaii power plant

(courtesy zerohedge)

iii)SWAMP STORIES

Trading Volumes on the COMEX

PRELIMINARY COMEX VOLUME FOR TODAY: 264,953 contracts

CONFIRMED COMEX VOL. FOR YESTERDAY: 399,496 contracts

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

And now for the wild silver comex results.

Total silver OI ROSE BY A LARGE SIZED 3339 CONTRACTS FROM 194,936 UP TO 198,275 (AND CLOSER TO THE NEW RECORD OI FOR SILVER SET APRIL 9.2018/ 243,411 CONTRACTS) WITH THE 22 CENT GAIN IN SILVER PRICING. SINCE WE ARE NOW INTO THE ACTIVE DELIVERY MONTH OF MAY. WE WERE INFORMED THAT WE HAD A STRONG SIZED 3261 EFP CONTRACT ISSUANCE FOR JULY AND ZERO FOR ALL OTHER MONTHS. THESE EFPS WERE ISSUED TO COMEX LONGS WHO RECEIVED A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. THE TOTAL EFP’S ISSUED: 3261. ON A NET BASIS WE GAINED 6600 SILVER OPEN INTEREST CONTRACTS AS WE OBTAINED A 3339 CONTRACT GAIN AT THE COMEX COMBINING WITH THE ADDITION OF 3261 OI CONTRACTS NAVIGATING OVER TO LONDON. DUE TO THE FACT THAT THE BOYS WERE VERY BUSY NEGOTIATING LONG COMEX CONTRACTS EMIGRATING TO LONDON,(AND WAITING FOR THEIR PASSPORTS)

NET GAIN ON THE TWO EXCHANGES: 6600 CONTRACTS

AMOUNT STANDING FOR SILVER AT THE COMEX

We are now in the active delivery month of MAY and here the front month LOST 122 contracts FALLING TO 326 contracts. We had 146 notices filed upon yesterday so we SURPRISINGLY AGAIN GAINED 24 contracts or 120,000 additional ounces will stand for delivery in this active delivery month of May AS SOMEBODY AGAIN WAS DESPERATE FOR PHYSICAL SILVER..

June saw a LOSS of 35 contracts to stand at 747 The next big delivery month for silver is July and here the OI ROSE by 1647 contracts UP to 140,897. The next active delivery month after July for silver is September and here the OI ROSE by 1213 contracts UP to 24,144

We had 173 notice(s) filed for 865,000 OZ for the MAY 2018 contract for silver

INITIAL standings for MAY/GOLD

MAY 11/2018.

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz |

nil OZ

|

| Deposits to the Dealer Inventory in oz | NIL oz |

| Deposits to the Customer Inventory, in oz | nil OZ |

| No of oz served (contracts) today |

5 notice(s)

500 OZ

|

| No of oz to be served (notices) |

101 contracts

(10100 oz)

|

| Total monthly oz gold served (contracts) so far this month |

618 notices

61800 OZ

1.922 TONNES

|

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

For MAY:

Today, 0 notice(s) were issued from JPMorgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equates to 5 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 4 notice(s) was (were) stopped/ Received) by j.P.Morgan customer account.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

To calculate the INITIAL total number of gold ounces standing for the MAY. contract month, we take the total number of notices filed so far for the month (618) x 100 oz or 61800 oz, to which we add the difference between the open interest for the front month of MAY. (106 contracts) minus the number of notices served upon today (5 x 100 oz per contract) equals 71,900 oz, the number of ounces standing in this active month of APRIL (2.227 tonnes)

Thus the INITIAL standings for gold for the MAY contract month:

No of notices served (618 x 100 oz) + {(106)OI for the front month minus the number of notices served upon today (5 x 100 oz )which equals 71,900 oz standing in this active delivery month of MAY . THERE ARE 9.954 TONNES OF REGISTERED GOLD AVAILABLE FOR DELIVERY SO FAR.

WE GAINED 300 OZ OF GOLD (3 CONTRACTS) STANDING IN THIS NON ACTIVE DELIVERY MONTH OF MAY AS SOMEBODY BADLY NEEDED PHYSICAL GOLD AT THIS SIDE OF THE POND..

IN THE LAST 18 MONTHS 73 NET TONNES HAS LEFT THE COMEX.

end

And now for silver

AND NOW THE APRIL DELIVERY MONTH

MAY INITIAL standings/SILVER

| Silver | Ounces |

| Withdrawals from Dealers Inventory | nil oz |

| Withdrawals from Customer Inventory |

nil oz

|

| Deposits to the Dealer Inventory |

nil

oz

|

| Deposits to the Customer Inventory |

nil oz

|

| No of oz served today (contracts) |

173

CONTRACT(S)

(865,000 OZ)

|

| No of oz to be served (notices) |

153 contracts

(765,000 oz)

|

| Total monthly oz silver served (contracts) | 5837 contracts

(29,185,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

we had 0 inventory movement at the dealer side of things

i

total dealer deposits: nil oz

we had 0 deposits into the customer account

i) Into JPMorgan: nil oz

*** JPMorgan for most of 2017 and in 2018 has adding to its inventory almost every single day.

JPMorgan now has 140 million oz of total silver inventory or 53.4% of all official comex silver. (140 million/263 million)

JPMorgan did not deposit into its warehouses (official) today.

ii) Into everybody else: 0

total customer deposits today: 0 oz

we had 2 withdrawals from the customer account;

i) out of Brinks; 32711.03 oz

ii) Out of Scotia: 80,380.120 oz

total withdrawals; 113,091.150 oz

we had 2 adjustments

i) Out of CNT: 259,354.572 oz was adjusted out of the dealer and this landed into the customer account of CNY’

ii) Out of Delaware: 4887.134 oz was adjusted out of the dealer and this landed into the customer account of Delaware

total dealer silver: 69.161 million

total dealer + customer silver: 268,536 million oz

The total number of notices filed today for the MAY. contract month is represented by 173 contract(s) FOR 865,000 oz. To calculate the number of silver ounces that will stand for delivery in MAY., we take the total number of notices filed for the month so far at 5837 x 5,000 oz = 29,185,000 oz to which we add the difference between the open interest for the front month of MAY. (326) and the number of notices served upon today (173 x 5000 oz) equals the number of ounces standing.

.

Thus the INITIAL standings for silver for the MAY contract month: 5837(notices served so far)x 5000 oz + OI for front month of MAY(326) -number of notices served upon today (173)x 5000 oz equals 29,950,000 oz of silver standing for the MAY contract month

WE GAINED 24 CONTRACTS OR AN ADDITIONAL 120,000 OZ WILL STAND AT THE COMEX AS SOMEBODY WAS IN URGENT NEED OF PHYSICAL SILVER ON THIS SIDE OF THE POND.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

ESTIMATED VOLUME FOR TODAY: 55,386 CONTRACTS

CONFIRMED VOLUME FOR YESTERDAY: 91,807 CONTRACTS

YESTERDAY’S CONFIRMED VOLUME OF 71,897 CONTRACTS EQUATES TO 459 MILLION OZ OR 65.55% OF ANNUAL GLOBAL PRODUCTION OF SILVER

COMMODITY LAW SUGGESTS THAT OPEN INTEREST SHOULD NOT BE MORE THAN 3% OF ANNUAL GLOBAL PRODUCTION. THE CROOKS ARE SUPPLYING MASSIVE PAPER TRYING TO KEEP SILVER IN CHECK.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price at that day at $18.42

The previous record was 224,540 contracts with the price at that time of $20.44

end

NPV for Sprott

1. Sprott silver fund (PSLV): NAV RISES TO -1.57% (MAY11/2018)

2. Sprott gold fund (PHYS): premium to NAV RISES TO -0.32% to NAV (MAY 11/2018 )

Note: Sprott silver trust back into NEGATIVE territory at -1.57%-/Sprott physical gold trust is back into NEGATIVE/ territory at -0.32%/Central fund of Canada’s is still in jail but being rescued by Sprott.

Sprott WINS hostile 3.1 billion bid to take over Central Fund of Canada

(courtesy Sprott/GATA)

3.SPROTT CEF.A FUND (FORMERLY CENTRAL FUND OF CANADA): NAV RISES TO -2.14%: NAV 13.67/TRADING 13.37//DISCOUNT 2.14.

END

And now the Gold inventory at the GLD/

MAY 11/WITH GOLD DOWN $1.75/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 862.96 TONNES/

MAY 10/WITH GOLD UP $9.60/A WITHDRAWAL OF 1.17 TONNES FROM THE GLD/INVENTORY RESTS AT 862.96 TONNES/SUCH CROOKS

MAY 9/WITH GOLD DOWN $0.55/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 864.13 TONNES

MAY 8/WITH GOLD DOWN $0.10/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 864.13 TONNES

MAY 7/WITH GOLD DOWN $0.55/ANOTHER WITHDRAWAL OF 1.47 TONNES OF GOLD FROM THE GLD/INVENTORY RESTS AT 864.13 TONNES

MAY 4/WITH GOLD UP $2.05/A WITHDRAWAL OF 1.13 TONNES OF GOLD FROM THE GLD/INVENTORY RESTS AT 865.60 TONNES

MAY 3/WITH GOLD UP $7.05/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 866.77 TONNES

MAY 2/WITH GOLD DOWN $1.15/ A HUGE WITHDRAWAL OF 4.43 TONNES FROM THE GLD/INVENTORY RESTS AT 866.77 TONNES

MAY 1/WITH GOLD DOWN $12.15/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 871.20 TONNES

APRIL 30/WITH GOLD DOWN $4.05/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 871.20 TONNES.

APRIL 27./WITH GOLD UP $5.90/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 871.20 TONNES/

APRIL 26/WITH GOLD DOWN $4.90/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 871.20 TONNES

APRIL 25/AFTER 9 CONSECUTIVE DAYS OF NO MOVEMENT OF GOLD INTO OUT OF THE GLD, WE HAD A HUGE DEPOSIT OF 5.31 TONNES OF GOLD INTO THE GLD/INVENTORY RESTS AT 871.20 TONNES.

APRIL 24./WITH GOLD UP $9.90, WE HAD NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 865.89 TONNES/

APRIL 23.2018/WITH GOLD DOWN $14.00/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 865.89 TONNES.

APRIL 20/WITH GOLD DOWN $10.20: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 865.89 TONNES

APRIL 19/WITH GOLD DOWN $4.25: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 865.89 TONNES/

APRIL 18/WITH GOLD UP $3.65: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 865.89 TONNES

APRIL 17/WITH GOLD DOWN $1.00 NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 865.89 TONNES/

April 16/WITH GOLD UP$2.80/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 865.89 TONNES/

April 13/WITH GOLD UP $6.15, A HUGE DEPOSIT OF 5.90 TONNES INTO THE GLD INVENTORY/INVENTORY RESTS AT 865.89 TONNES

April 12/WITH GOLD DOWN $17.40/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 859.99 TONNES

April 11/WITH GOLD UP $13.85/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 859,99 TONNES

APRIL 10/WITH GOLD UP $5.25/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 859.99 TONNES

APRIL 9/WITH GOLD UP$4.50/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 859.99 TONNES

APRIL 6/WITH GOLD UP $7.50 ,A HUGE CHANGE IN INVENTORY AT THE GLD/ A DEPOSIT OF 5.90 TONNES/INVENTORY RESTS AT 859.99 TONNES

APRIL 5/WITH GOLD DOWN $8.20 WE HAD TWO ENTRIES: 1) TINY WITHDRAWAL OF .28 TONNES TO PAY FOR FEES AND 2) A DEPOSIT OF 2.06 TONNES//INVENTORY RESTS AT 854.09 TONNES

April 4/WITH GOLD UP $2.90 WE HAD NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 852.31 TONNES

APRIL 3./WITH GOLD DOWN $9.30 WE HAD NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 852.31 TONNES

APRIL 2/WITH GOLD UP $19.50, WE HAD A BIG CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF 6.19 TONNES/INVENTORY RESTS AT 852.31 TONNES

MARCH 29/WITH GOLD DOWN $3.20 AND OPTIONS EXPIRY FINISHED, WE HAD NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS A 846.12 TONNES

March 28/WITH GOLD DOWN $16.70, ANOTHER RAID ORCHESTRATED, AGAIN NO SURPRISES AS WE WITNESS ANOTHER 1.18 TONNES OF GOLD REMOVED/INVENTORY RESTS AT 846.12 TONNES

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

MAY 11/2018/ Inventory rests tonight at 862.96tonnes

*IN LAST 381 TRADING DAYS: 78.04 NET TONNES HAVE BEEN REMOVED FROM THE GLD

*LAST 331 TRADING DAYS: A NET 78,26 TONNES HAVE NOW BEEN ADDED INTO GLD INVENTORY.

end

Now the SLV Inventory/

MAY 11/WITH SILVER DOWN 2 CENTS/THE CROOKS WITHDREW A MONSTROUS 2.824 MILLION OZ FROM THE SLV INVENTORY/INVENTORY RESTS AT 320.439 MILLION OZ/

MAY 10/WITH SILVER UP 22 CENTS/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 323.263 MILLION OZ/

MAY 9/WITH SILVER UP 6 CENTS/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 323.263 MILLION OZ/

MAY 8/WITH SILVER DOWN 2 CENTS:NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 323.263 MILLION OZ.

MAY 7/WITH SILVER FLAT: A BIG CHANGE IN SILVER INVENTORY AT THE SLV// A WITHDRAWAL OF 942,000 OZ OF SILVER FROM THE SLV INVENTORY/INVENTORY RESTS AT 323.263 MILLION OZ/

MAY4/WITH SILVER UP 5 CENTS/A BIG CHANGES IN SILVER INVENTORY AT THE SLV/ A DEPOSIT OF 1.224 MILLION OZ/INVENTORY RESTS AT 324.205 MILLION OZ/

MAY 2/WITH SILVER UP 24 CENTS/A HUGE CHANGE IN SILVER INVENTORY AT THE SLV// A DEPOSIT OF 6.082 MILLION OZ INTO THE SLV/INVENTORY RESTS AT 322.981 MILLION OZ/

MAY 1/WITH SILVER DOWN 24 CENTS/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 316.899 MILLION OZ/

APRIL 30/WITH SILVER DOWN 11 CENTS/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 316.899 MILLION OZ/

APRIL 27/WITH SILVER DOWN 5 CENTS/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 316.899 MILLION OZ/

APRIL 26/WITH SILVER DOWN 2 CENT/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 316,899 MILLION OZ/

APRIL 25./WITH SILVER DOWN 18 CENTS/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 316.899 MILLION OZ/

APRIL 24./WITH SILVER UP 8 CENTS/SOMETHING SPOOKED OUR CROOKS TO ADD SOME PAPER SILVER: A DEPOSIT OF 1.601 MILLION OZ/INVENTORY RESTS AT 316.899 MILLION OZ/

APRIL 23.2018/WITH SILVER DOWN 50 CENTS, ANOTHER HUGE WITHDRAWAL FROM THE SLV INVENTORY: A WITHDRAWAL OF 1.413 MILLION OZ/INVENTORY RESTS AT 315.298 MILLION OZ.

APRIL 20/WITH SILVER DOWN 11 CENTS: ANOTHER HUGE CHANGE IN SILVER INVENTORY: A WITHDRAWAL OF 1.13 MILLION OZ//SLV RESTS TONIGHT AT 316.711 MILLION OZ/

APRIL 19/WITH SILVER UP 3 CENTS TODAY: WE HAD A BIG CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.355 MILLION OZ/ MAKES ABSOLUTELY NO SENSE!!/INVENTORY RESTS AT 317.841 MILLION OZ

APRIL 18/WITH SILVER UP 44 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 320.196 MILLION OZ

APRIL 17/WITH SILVER UP 10 CENTS TODAY/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 320.196 MILLION OZ

April 16/WITH SILVER UP 7 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 320.196 MILLION OZ/

April 13/WITH SILVER UP 17 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 320.196 MILLION OZ.

April 12/WITH SILVER DOWN 27 CENTS/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 320.196 MILLION OZ/

April 11/2018/WITH SILVER UP 16 CENTS: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 320.196 MILLION OZ/

APRIL 10/WITH GOLD UP 8 CENTS/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 320.196 MILLION OZ/

APRIL 9/WITH SILVER UP 12 CENTS/WE HAD NO CHANGES IN SILVER INVENTORY/INVENTORY RESTS AT 320.196 MILLION OZ/

APRIL 6/WITH SILVER UP 4 CENTS, WE HAD A HUGE DEPOSIT OF 1.319 MILLION OZ INTO THE SLV INVENTORY/INVENTORY RESTS AT 320.196 MILLION OZ

APRIL 5/WITH SILVER UP 6 CENTS/NO CHANGES IN INVENTORY AT THE SLV/INVENTORY RESTS AT 318.877 MILLION OZ/

April 4/WITH SILVER DOWN 11 CENTS/A SMALL CHANGE IN SILVER INVENTORY AT THE SLV/ A WITHRAWAL OF 135,000 OZ AND THIS IS PROBABLY TO PAY FOR FEES/INVENTORY RESTS AT 318.877 MILLION OZ/

APRIL 3./WITH SILVER DOWN 16 CENTS/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.012 MILLION OZ/

APRIL 2/WITH SILVER UP 34 CENTS/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.012 MILLION OZ/

MARCH 29/WITH SILVER UP 6 CENTS, THE CROOKS DECIDED THAT THEY HAD BETTER ADD SOME 943,000 PAPER OZ TO THEIR INVENTORY/INVENTORY RESTS AT 319.012 MILLION OZ

March 28/WITH SILVER DOWN 27 CENTS/AGAIN NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 318.069 MILLION OZ

MAY 11/2018:

Inventory 320.439 million oz

end

6 Month MM GOFO 2.09/ and libor 6 month duration 2.54

Indicative gold forward offer rate for a 6 month duration/calculation:

G0FO+ 2.09%

libor 2.54 FOR 6 MONTHS/

GOLD LENDING RATE: .45%

XXXXXXXX

12 Month MM GOFO

+ 2.77%

LIBOR FOR 12 MONTH DURATION: 2.54

GOFO = LIBOR – GOLD LENDING RATE

GOLD LENDING RATE = +.23

end

At 3:30 pm we receive a totally useless report, the COT which gives position levels of our major players at the comex. Due to the fact that

many transfer their holdings (liabilities) to London this report has no value whatsoever.

First gold COT

| Gold COT Report – Futures | ||||||

| Large Speculators | Commercial | Total | ||||

| Long | Short | Spreading | Long | Short | Long | Short |

| 198,548 | 91,108 | 57,613 | 181,586 | 316,570 | 437,747 | 465,291 |

| Change from Prior Reporting Period | ||||||

| -11,029 | -11,690 | -8,543 | 1,851 | 4,963 | -17,721 | -15,270 |

| Traders | ||||||

| 187 | 83 | 86 | 49 | 53 | 282 | 184 |

| Small Speculators | ||||||

| Long | Short | Open Interest | ||||

| 53,651 | 26,107 | 491,398 | ||||

| 1,363 | -1,088 | -16,358 | ||||

| non reportable positions | Change from the previous reporting period | |||||

| COT Gold Report – Positions as of | Tuesday, May 8, 2018 | |||||

OUR LARGE SPECULATORS

those large speculators who have been long in gold pitched (transferred) 11,029 contracts from their long side

those large speculators who have been short in gold covered (transferred) 11,690 contracts from their short side

OUR COMMERCIALS

those commercials who have been long in gold added 1861 contracts to their long side.

those commercials who have been short in gold added 4963 contracts to their short side

OUR SMALL SPECULATORS

those small specs who have been long in gold added 1363 contracts to their long side

those small specs who have been short in gold covered (transferred) 1088 contracts from their short side.

And now for our useless COT silver report

| Silver COT Report: Futures | |||||

| Large Speculators | Commercial | ||||

| Long | Short | Spreading | Long | Short | |

| 72,713 | 72,834 | 15,233 | 77,127 | 94,204 | |

| 4,185 | -2,890 | -170 | -884 | 4,215 | |

| Traders | |||||

| 105 | 60 | 41 | 34 | 32 | |

| Small Speculators | Open Interest | Total | |||

| Long | Short | 195,865 | Long | Short | |

| 30,792 | 13,594 | 165,073 | 182,271 | ||

| -1,951 | 25 | 1,180 | 3,131 | 1,155 | |

| non reportable positions | Positions as of: | 155 | 12 | ||

OUR LARGE SPECULATORS

those large speculators that have been long in silver added 4185 contracts to their long side

those large speculators that have been short in silver pitched (transferred) 2890 contracts from their short side

OUR COMMERCIALS

those commercials that have been long in silver pitched (transferred) 884 contracts from their long side

those commercials that have been short in silver added 4215 contracts to their short side

OUR SMALL SPECULATORS

those small specs that have been long in silver pitched (transferred) 1951 contracts from their long side

those small specs that have been short in silver added 25 contracts to their long side.

end

Major gold/silver trading /commentaries for FRIDAY

GOLDCORE/BLOG/MARK O’BYRNE.

GOLD/SILVER

Gold Mining Supply Looks Set To Decline

- Global demand for gold is increasing while new discoveries of gold remain small

- Gold mining output in Australia is forecast to decrease by 50% in the next eight years

- Decline in global gold mining supply makes a price increase almost certain

Gold nugget (placer gold) from Colorado, USA. Source: Commons.wikimedia.org

Gold nugget (placer gold) from Colorado, USA. Source: Commons.wikimedia.org

by Lawrence Thomas, Gold Telegraph

The demand for gold is increasing, yet new discoveries of the precious metal have not kept pace with the demand. Funds for exploration are historically high, $54.3 billion, up 60 percent over the past 18 years.

The increased spending, however, has not produced the equivalent in new gold discoveries. During the past decade, 41 discoveries have resulted in a mere 215.5 million ounces of the precious metal. Even counting recently discovered but unexplored mines, which may hold as-yet major discoveries, the total available amount of gold in these discoveries are not expected to surpass 363 million ounces over the next ten years.

Gold discoveries have followed a predictable pattern. 263 major gold discoveries have been made in the past 28 years, but half of those discoveries happened in the 1990s. This boom lasted until the turn of the century when the rate of discovery began to decline. Only 16 discoveries were reported from 2000 to 2002, which produced 108.3 ounces of gold. That amount was below the average finds of the 1990s. This decline has continued, with both new discoveries and the amount of gold mined decreasing steadily. By 2010, only 18.6 million ounces of gold was discovered, a severe drop from the 61.5 ounces found in 2009.

Old sectors are being depleted, while active exploration for new discoveries has been slow. The amount of available gold has not met expectation and remains far below the 2009 high.

The lack of new discoveries is not the result of funding. $54.3 billion has been allocated to exploration during the past decade. Part of the problem is that the time span between discovery and production is around 20 years. Unless significant new discoveries are made, the amount of available gold could decrease in the near future, raising the demand for the metal even further. Scarcity invariably results in higher prices, and the decline in global gold makes a price increase almost certain.

Continued gold exploration has become critical. In 2018, Colorado-based Newmont Mining Corp., one of the world largest gold explorers, has allocated $1.3 billion to expand its current projects, an increase of $300 million from the previous year.

Much of the available gold in Australia’s northern Goldfield has been depleted, and companies are drilling to unprecedented depths of 3 kilometers below the surface hoping for new discoveries as new finds are becoming rarer and more expensive to pursue.

According to Richard Schodde, managing director of MinEx, Australia gold mining output could decrease by 50 percent over the next eight years, with only four mines remaining open by 2057.

The need to drill deeper will make gold harder to find and more expensive to produce.

Listen on SoundCloud , Blubrry & iTunes. Watch on YouTube

News and Commentary

PRECIOUS-Gold eases on firmer dollar; but eyes first weekly gain in four (Reuters.com)

Gold steady as dollar hovers below 2018 peak (Reuters.com)

Bottom in place? Gold jumped to 10-day high (FXStreet.com)

U.K. House-Price Gauge Drops to 5 1/2-Year Low as London Slumps (Bloomberg.com)

London house prices predicted to keep falling (CityAM.com)

Source: US Funds

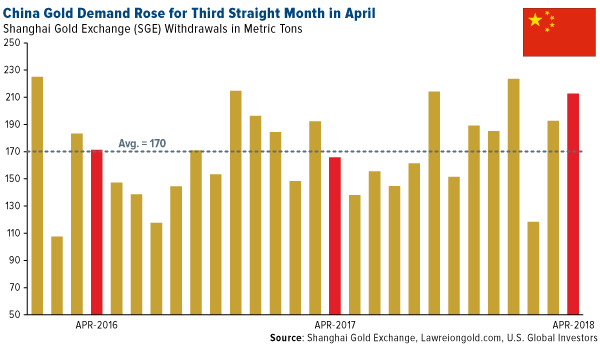

Gold Love Trade Looks Promising in India and China (USFunds.com)

The Wealthy Are Hoarding $10 Billion of Bitcoin in Bunkers (Bloomberg.com)

Gold Gets a Lifeline From a Surprising Source: Cheap Flights and Cars (Bloomberg.com)

Putin Wants to `Break’ With the Dollar But Dumps Euros Instead (Bloomberg.com)

The 1970s All Over Again? Part 1: The Middle East Explodes (GoldSeek.com)

Central Banks: The Great Experiment Has Failed (DailyReckoning.com)

Listen on SoundCloud , Blubrry & iTunes. Watch on YouTube below

Gold Prices (LBMA AM)

10 May: USD 1,314.80, GBP 969.27 & EUR 1,106.80 per ounce

09 May: USD 1,306.85, GBP 965.11 & EUR 1,102.07 per ounce

08 May: USD 1,310.05, GBP 969.44 & EUR 1,101.88 per ounce

04 May: USD 1,309.35, GBP 965.78 & EUR 1,094.09 per ounce

03 May: USD 1,313.30, GBP 966.19 & EUR 1,094.64 per ounce

02 May: USD 1,310.75, GBP 960.52 & EUR 1,091.99 per ounce

Silver Prices (LBMA)

10 May: USD 16.60, GBP 12.24 & EUR 13.97 per ounce

09 May: USD 16.44, GBP 12.12 & EUR 13.84 per ounce

08 May: USD 16.45, GBP 12.17 & EUR 13.85 per ounce

04 May: USD 16.42, GBP 12.10 & EUR 13.72 per ounce

03 May: USD 16.47, GBP 12.12 & EUR 13.74 per ounce

02 May: USD 16.35, GBP 11.98 & EUR 13.62 per ounce

Recent Market Updates

– Gold Mining Supply Globally Looks Set To Decline

– Gold Bullion Demand In Iran May Surge On Trump Sanctions

– “Money Is Gold — and Nothing Else”

– U.K. Home Prices Plunge 3.1% In April – Largest Monthly Drop Since Financial Crisis In 2011

– Weekly Gold Update – Gold In Dollars Lower Despite Poor US Jobs and Other Data

– Own Some Gold and Avoid Overvalued Assets

– Gold Demand Falls In Q1 Despite Robust Central Bank and Investment Demand and Surging Demand In Turkey and Iran

– Smart Money Diversifying Into Gold – One Billionaire Invests Half His Net Worth

– “Blood In The Streets” Of U.S. Gold Bullion Market As Sale Of Gold Coins Collapse

– Most Important Chart Of The Century For Investors?

– Gold Mining Shares Are Speculative Making Gold Bullion A Better Investment

– Gold Price Increasingly Influenced By Declining Dollar Rather Than Interest Rates

– Cash “Vanishes” From Bank Accounts In Ireland

Andrew Maguire’s Kinesis money which is a “bitcoin” but backed 100% by allocated gold and silver is set to go.

it think it would be a great idea to look at this!

please read at: https://kinesis.money/#/

(Andrew Maguire)

|

2:57 PM (1 hour ago) | ||

|

|||

Harvey

Here It is my friend! https://kinesis.money/#/ Please let everyone know.

Let catch up on Monday if you have time. We have billions in the hopper ready to be allocated on the 1st day of trading. The paper market days are over.

Warm regards

Andy

end

Emerging markets actually have two worries: a strong USA dollar and a weaker Chinese yuan

(courtesy Verma/Bloomberg/GATA)

Your early FRIDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

i) Chinese yuan vs USA dollar/CLOSED UP 6.3329 /shanghai bourse CLOSED DOWN 11.15 POINTS OR 0 .35% / HANG SANG CLOSED UP 312.84 POINTS OR 1.02%

2. Nikkei closed UP 261.30 POINTS OR 1.16% / /USA: YEN FALLS TO 109.32/

3. Europe stocks OPENED RED /USA dollar index FALLS TO 92.54/Euro RISES TO 1.1931

3b Japan 10 year bond yield: RISES TO . +.05/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 109.65/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD FINALLY IN THE POSITIVE/BANK OF JAPAN LOSING CONTROL OF THEIR YIELD CURVE AS THEY PURCHASE ALL BONDS TO GET TO ZERO RATE!!

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 71.39 and Brent: 77.22

3f Gold UP/Yen UP

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil UP for WTI and UP FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund RISES TO +.56%/Italian 10 yr bond yield UP to 1.87% /SPAIN 10 YR BOND YIELD DOWN TO 1.28%

3j Greek 10 year bond yield FALLS TO : 4.04?????????????????

3k Gold at $1325.10 silver at:16.79 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble UP 11/100 in roubles/dollar) 61.64

3m oil into the 71 dollar handle for WTI and 77 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 109.32 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 0.9998 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1933 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now POSITIVE territory with the 10 year RISING to +0.56%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.96% early this morning (THIS IS DEADLY TO ALL MARKETS). Thirty year rate at 3.11%

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

(courtesy Jim Reid/Bloomberg/Deutsche bank/zero hedge)

“Goldilocks Is Back”: Futures Spike As Dollar Tumbles; Curve Flattening Accelerates

Following several days of torrid newsflow, which markets digested without a glitch and continued their recent grind higher, the overnight session has been relatively quiet, and while trading was subdued post the European open, a burst of buying was observed in generally illiquid conditions as US traders walked in, sending S&P futures sharply to session highs as volatility continues to dip with the VIX now erasing its elevated level seen in 1Q.

Global equities are generally in the green this morning, with some exceptions across Europe.

There was no immediate catalyst for the move, although an acceleration in the slide of the dollar may have been the catalyst: after hitting a 2018 high on Wednesday, the BBDXY has been sliding since, dropping the most since March on Thursday, and then once again accelerating on the downside during the overnight session.

Aside from the recent burst in US buying, it was a lackluster European session as most markets drift with little momentum; earlier Asian stocks jumped after a disappointing US CPI print eased some pressure from the Fed to step up the pace of monetary tightening.

Europe’s Stoxx 600 Index erased an early advance, as a result of the sharp jump in the EURUSD this morning pressuring European exporters, although the index is still headed for its seventh week of increases, the longest streak in more than three years. In addition to exporter weakness, declines in the healthcare sector weighed on by a string of negative drug-trial results offset gains for basic resources as commodities, and oil in particular, continued to rise. After yesterday’s drubbing, Italian banks were supported by good earnings from Monte Dei Paschi (+13.5%),

As Bloomberg notes, investors have been weighing most recent economic data releases to judge the most likely path for global interest rates: in this regard Thursday’s U.S. CPI miss, which came as U.K. money markets priced out a hike this year after the Bank of England forecast slower price rises, suggests fears about accelerating tightening may have been premature, which in turn reincarnates the goldilocks “buy everything” thesis. Comments from European Central Bank Governor Mario Draghi at a conference in Italy will be the focus later.

Easing geopolitical fears also helped, and aided gains in Asian stocks after Trump and Kim set for their landmark meeting in Singapore on June 12. Meanwhile, Malaysian assets trading offshore began to stabilize after the shock election win for the opposition. Emerging-market stocks headed for the best week since February and most developing-nation currencies extended a rebound from the past month’s selloff, thanks to the sharp move lower in the dollar in the past 2 days.

While 10-Year TSY yields remained below 3%, the continued flattening in the curve after yesterday’s unexpectedly strong 30Y auction has put some traders on edge: this morning the 5s30s curve has flattened to the lowest level since August 2007, breaking 30bps to trade at 27bps now, a level technicians have predicted would lead to an acceleration in the move, especially if some of the record short overhang decides to finally cover. Meanwhile, 10s30s swaps are on the verge of inversion with the move continuing in Europe trading.

Some believe it’s only a matter of time before yields and the dollar resume their rise: the “mismatch between higher U.S rate differentials and a weaker USD is starting to reverse,” as the Fed looks likely to match its “dots,” while other central banks across G-10 face challenges to begin or extend their tightening process, David Bloom and Paul Mackel, strategists at HSBC Holdings. Needless to say, unless US yields resume their move higher, dollar gains may be capped for the time being.

And with the dollar sliding, WTI found new bids this morning, now on the verge of $72, and heading for a second week of gains after the U.S. pulled out of the Iran nuclear deal.

In metals, gold is currently trading flat on the day, with aluminum witnessing a slide for the second session in a row. Copper also slipping on the day, after peaks on Thursday due to shortened inventories, but still set to close positively for the week. Steel in the green for the day on growing Chinese demand.

In geopolitical developments, the 5 Star Movement and League government may be formed next week, and the parties will pass a flat tax and citizens income in 2019. Meanwhile, a top 5 Star member said the next Italian PM could be an independent figure who is not part of either 5 Star or League. Elsewhere, Iran Foreign Minister Zarif is to meet with Chinese Foreign Minister Wang on Sunday, Russian Foreign Minister Lavrov on Monday and EU officials on Tuesday to discuss preserving nuclear agreement.

Ten companies are on the earnings list on Friday, while macro investors can look forward to Michigan sentiment and data on import and export price indexes.

Bulletin Headline Summary from RanSquawk

- Major FX pairs trading within short ranges. EM currencies finding some respite

- European bourses flat on thin news flow ahead of the weekend

- Looking ahead, highlights include Canadian jobs report, Uni of Michigan, Baker Hughes, Fed’s Bullard and ECB’s Draghi

Market Snapshot

- S&P 500 futures up 0.3% to 2,726.25

- STOXX Europe 600 down 0.01% to 391.95

- MXAP up 1% to 175.74

- MXAPJ up 0.9% to 573.81

- Nikkei up 1.2% to 22,758.48

- Topix up 1% to 1,794.96

- Hang Seng Index up 1% to 31,122.06

- Shanghai Composite down 0.4% to 3,163.26

- Sensex up 0.4% to 35,382.05

- Australia S&P/ASX 200 down 0.04% to 6,116.19

- Kospi up 0.6% to 2,477.71

- German 10Y yield fell 1.4 bps to 0.543%

- Euro up 0.07% to $1.1923

- Italian 10Y yield rose 5.2 bps to 1.678%

- Spanish 10Y yield fell 2.0 bps to 1.293%

- Brent Futures unchanged at $77.47/bbl

- Gold spot up 0.1% to $1,323.34

- U.S. Dollar Index down 0.02% to 92.63

Top Overnight News from Bloomberg

- Trump: Administration will have “great health plans” coming out within four weeks; plans to release a proposal to bring down U.S. drug prices

- BOE’s Broadbent: 1Q weakness partly due to weather, still seen as temporary

- Corriere: if Five Star/Northern League talks go well, new government would be sworn in by end of next week

- As President Trump games out a historic summit with North Korea’s Kim Jong Un in Singapore next month, he is gambling he can construct a complicated pact to dismantle Pyongyang’s nuclear program. This is even though Trump’s track record shows he’s better at breaking than making deals

- The Treasury yield curve from 5 to 30 years flattened Thursday to the lowest level since August 2007, as a combination of weaker-than-expected U.S. inflation and solid demand for a record bond auction bolstered investor confidence in owning long-dated securities

- The global backlash against wages and migrants has hits the heart of Europe with Italy’s anti-establishment Five Star Movement and anti-immigrant League now taking until Monday to finish their plan to form a government in Rome

- Russia’s president, Putin said a “break” from the dollar is necessary to bolster the nation’s “economic sovereignty,” especially in light of recent penalties. But data show his central bank’s dollar reserves are rising, while the euro’s share is sliding

- Mark Carney’s window to raise interest rates before Brexit is closing. As the U.K. draws nearer to its divorce from the EU at the end of March with little certainty as to the economic repercussions, BOE policy makers with a benchmark interest rate of just 0.5 percent could be left with limited room to cut should they need to act

- Emerging markets with the weakest financial metrics, especially those with high inflation, tend to be the worst affected by U.S. interest-rate shocks, according to a study by Federal Reserve Board economists

- The lightest part of the refinery barrel may be the hardest hit by U.S. sanctions on Iran. Asian buyers have been scrambling to get both condensate and naphtha this year amid speculation that Iran sanctions will be renewed

- Former U.K. Prime Minister John Major said Theresa May’s quest for a post-Brexit alternative to the European Union’s Customs Union that provides for frictionless trade is one that’s doomed to fail

- United Nations Secretary-General Antonio Guterres said he’s optimistic that the U.S. and North Korea can reach a historic nuclear deal, crediting a toughened sanctions regime pushed by President Donald Trump at the UN Security Council for the isolated country’s willingness to negotiate

- The U.K. government has asked business groups to map their supply chains to flag the areas of the economy most at risk if Brexit imposes additional trading costs on exporters, two people familiar with the matter said

- Squeezed by ever-expanding U.S. sanctions, Vladimir Putin says he wants to dump the dollar. His central bank has been doing just the opposite

Asian stocks traded mostly positive after sentiment rolled over from the US where soft CPI data spurred hopes the Fed may have to slow the pace of hikes, while all sectors in the S&P 500 finished in the green with gains led by tech, telecoms and pharmaceuticals, which in turn underpinned NDX outperformance. ASX 200 (+0.2%) and Nikkei 225 (+1.0%) were positive with earnings also a key driver of price action and the top performing stocks in Japan spurred by corporate updates including KDDI, Panasonic and Suzuki. Hang Seng (+1.5%) and Shanghai Comp. (-0.2%) were mixed as Hong Kong sustained its outperformance streak, while the mainland lagged after the PBoC refrained from open market operations and widened the amount of liquidity it drained for the week. Finally, 10yr JGBs were quiet amid similar flat trade witnessed in T-notes and heightened appetite for riskier assets, while the BoJ’s rinban announcement also failed to spur demand with the amounts kept unchanged and at paltry JPY 285bln total for the day. PBoC skipped open market operations for a net weekly drain of CNY 140bln vs. last week’s net drain of CNY 110bln.

Top Asian News

- Hong Kong 1Q GDP Expands 2.2% Q/q; Est. 0.8%

- Q Technology Slumps by Record After Warning Its Profit May Halve

- Singapore Regulator Fines Ex-Genting Exec for Insider Trading

- Sri Lanka Holds Benchmark Rates as Consumer Prices Ease

European equities are mixed (Eurostoxx 50 -0.2%) with the exception of Spain’s IBEX (+0.2%). Looking at the sectors, health care is a noticeable underperformer amid negative drug updates from AstraZeneca (-0.3%) and Roche (-1.7%), subsequently dragging other health names across Europe (Novartis -0.7%, GSK -0.8%, Merck -0.9%) in sympathy. On the flip side, material names outperform following strong earnings from the world’s largest steelmaker ArcelorMittal (+1.7%) as it lifts the likes of Thyssenkrupp (+1.2%) with it. Elsewhere, Sika (+10%) rose to the top of the Stoxx 600 after striking a deal with France’s Saint Gobain (+2.4%) who are also seen higher on the news

Top European News

- Silver Lake Agrees to Buy Property Portal ZPG for $3 Billion

- Sika, Saint-Gobain Reach Deal to End Bitter Takeover Battle

- Interserve’s Woes Deepen as U.K. Watchdog Opens Probe

- AstraZeneca’s Fasenra Fails in Trial of Severe Lung Disease

In FX, the Greenback is down vs G10 rivals and the index rangebound between 92.630-840 after its retracement from new ytd highs just shy of 93.500 to around 92.500 in wake of some softer than expected components in the latest CPI release and ahead of more price indicators via import/export data and inflation expectations in the Michigan survey. AUD: A marginal outperformer, with Aud/Usd back up near 0.7550 and Aud/Nzd seemingly forming a more solid base above 1.0800. No lasting adverse effects on the back of weak housing data overnight as the broader risk tone remains relatively positive, while OTM option bids and hedge fund buying interest has been reported on dips; GBP/EUR/JPY/CHF: All slightly stronger vs the Dollar, with Cable sustaining recovery gains above 1.3500 in consolidative trade after initial post-BoE super Thursday losses and getting another M&A boost from US-based Silver Lake’s purchase of Zoopla (Gbp2.2 bn deal). Eur/Usd looks hemmed in between 1.1900-50 amidst heavy expiry option interest at either strike and 1.1925 (3.8 bn in total) and awaiting a speech from ECB President Draghi. Usd/Jpy has retreated a bit further from recent 110.00 or so multi-top peaks, but appears supported just ahead of 109.00, while Usd/Chf has also slipped back towards the base of a 1.0000-50 band after briefly touching parity on Thursday.

In commodities, oil is seeing profit taking heading into weekend as both WTI and Brent come off of recent highs, currently both down 0.3% and 0.1% respectively with newsflow relatively muted ahead of today’s Baker Hughes rig count. In the metals scope, gold is currently trading flat on the day, with aluminium witnessing a slide for the second session in a row. Copper also slipping on the day, after peaks on Thursday due to shortened inventories, but still set to close positively for the week. Steel in the green for the day on growing Chinese demand.

US Event Calendar

- 8:30am: Import Price Index MoM, est. 0.5%, prior 0.0%; Import Price Index ex Petroleum MoM, est. 0.2%, prior 0.1%

- Export Price Index MoM, est. 0.35%, prior 0.3%; Export Price Index YoY, prior 3.4%

- 10am: U. of Mich. Sentiment, est. 98.3, prior 98.8; Current Conditions, prior 114.9; Expectations, prior 88.4

- U. of Mich. 1 Yr Inflation, prior 2.7%; U. of Mich. 5-10 Yr Inflation, prior 2.5%

DB’s Jim Reid concludes the overnight wrap

So populism is back. The people have spoken and will continue to do so in Europe over the next 36 hours. Many behind the scenes deals will be struck and old tensions will resurface. Political bloc voting will dominate as will glitter! Yes tomorrow sees the 63rd annual Eurovision Song Contest – the largest singing (if you can call it that) competition in the world and one watched by hundreds of millions of people on TV worldwide.

It seems like the favourites are Cyprus, Norway and Israel. I’ve seen Cyprus’s entry and it reminds me of being in Ibiza circa 1992. The lead singer has very very big hair and a tight five piece dance troop behind her. In fact as I was watching I was petrified that one of the dancers would be slightly out of sync as slipping one beat behind could ensure being lassoed by the singer’s hair and having their eye taken out. Anyway one to watch if you have nothing better to do tomorrow night across Europe (and Australia).

Staying with the popular vote, it’s looking increasingly likely that Northern League and Five Star will form an anti-euro, anti-austerity full on populist coalition in Italy perhaps over the weekend, per Bloomberg. This is a pretty monumental political moment but its impact is likely more slow burning than immediate. In terms of implications, the shock value has been limited by the fact that neither campaigned to leave the Euro. However their fiscal pledges – if pursued – will put them on a collision course with the EU as will their desire to reverse pension and labour market reforms. So we’ll see if they can make good on their populists promises or whether they get watered down by the realities of power. It will also be interesting to see how it politicises the ECB end of QE decision. So lots to consider.

See DB’s Clemente De Lucia note from last night for more info (Link). For now, Italian risk is a bit soft. The MIB -0.96% underperformed a risk-on market yesterday and BTP 10yr yields rose +5.2bp on a day of falling yields (US 10yr -4.2bps) due to soft US inflation and a BoE hold that clearly wasn’t fully priced into 10yr Gilts (-2.7bps).

The core US CPI was on the softer side in April at +0.1% mom (vs. +0.2% expected). The unrounded number was +0.098% so it was also a genuine miss as opposed to just rounding. The monthly reading also meant that the annual rate remained unchanged at +2.1% yoy after expectations were for a lift to +2.2%, while the 6-month annualized rate nudged down to +2.35%. The details of the data showed that weakness was fairly broad based across core goods and core services with the biggest declines coming in airfares and car inflation. It’s worth noting that following the average hourly earnings miss in last week’s payrolls report, that now means that we’ve had two softer than expected US inflation prints in close succession. Combined with the healthcare component of the PPI on Wednesday, the read through for core PCE also looks soft for later this month. We still think higher inflation is inevitable in the US this year but there’s no doubt that the last week increases the risks to our view.

The weaker inflation helped risk and reduce vol with all US bourses ending higher (S&P +0.94%, Dow +0.80%; Nasdaq +0.89%). The S&P is now at the highest since mid-March, with all sectors up yesterday and gains led by the telco, utilities and tech stocks. Apple’s share price rose +1.43% to a record high while the VIX is below its 200 days moving average for the first time since mid-January.

In Europe, the DAX (+0.62%) and FTSE (+0.50%) also firmed but the Stoxx 600 dipped -0.12%, weighed down by the Italian MIB (-0.96%) as Italy’s Five Star and League parties said they’ve taken “significant steps forward” to form a new government.

In FX, the USD dollar index pared back losses to end -0.42% lower while the Euro jumped 0.54%. The Sterling fluctuated within a 1.2% intraday range before closing -0.21% lower after the dovish BOE meeting. Emerging markets benefited from the USD weakness and risk on tone too, with the 10y bond yields for Turkey (-12bp), Argentina (-20bp) and Russia (-23bp) all down. In commodities, WTI oil firmed +0.31% while precious metals also advanced (Gold +0.68%; Silver +1.38%).

This morning in Asia, markets are following US markets higher with the Nikkei (+0.90%), Kospi (+0.61%) and Hang Seng (+1.28%) all up, while the Shanghai Comp. is down -0.13%. Elsewhere, President Trump has confirmed that he and North Korea’s Kim Jong-Un will meet in Singapore on 12 June and he has high hopes of “doing something very meaningful” on denuclearisation.

Moving back to the BoE yesterday. The bank kept rates on hold as widely expected, but the vote was not unanimous (7-2), with both Saunders and McCafferty dissenting as they did in February. Our UK economists noted that the meeting brought out mixed messages from the BoE. On the one hand, the Bank retained its hawkish rhetoric by remaining relatively upbeat in its forecasts for growth in the medium term and likened the weakening in Q1 to noise.

Furthermore, the Bank was relatively sanguine on the softer wage growth to date emphasizing the continued erosion in slack, which will lift inflation in the forecast horizon. On the other hand, the BoE revised down its inflation forecasts both in the short and medium term, while reducing growth this year by 40bps. Later on, BoE’s Carney told the BBC that a rate hike was “likely by the end of the year”. Following all the above, the Bloomberg implied odds of a rate hike in the August meeting fell 12ppt to 42%. Overall, our UK team noted that given the lower urgency for a rate hike due to the need for “limited tightening” over the forecast horizon, they see an increase in rates contingent on growth bouncing back and negotiations on the Brexit front staying positive, while their call for an August rate hike stands.

Turning to US equities, DB’s Binky Chadha noted that equity markets are broadly flat post corporate results despite reporting the strongest earnings session in 8 years as investors’ focus shifts to rising cost pressure and its impacts on margins. He argued that cost pressures do not rise in isolation. Corporates respond through pricing and productivity measures, which combined with operating leverage to sales growth have historically more than offset rising costs. Overall, his team see the recent rise in cost pressures as a natural late cycle phenomenon while corporates can employ several levers in response as they have done historically. They believe that its much too early to be pricing in peak earnings and reiterate their S&P target of 3,000 by the end of 2018 (+10% from current levels)

Our European equity strategist Sebastian Raedler highlights that European equities have rebounded by 8% since late March even as European growth momentum has continued to soften. The main reason for the rebound is the weakness in the euro, with the EUR/USD falling by 5% over the same period. The team sees only marginal further EUR downside over the coming months however, in line with our FX strategists’ tactically neutral stance. In combination with the assumption of a continued fade in the Euro area PMI, this would imply a level of around 390 for the Stoxx 600 by end-Q2 (in line with current levels) before a decline to below 360 by end-Q3 (8% below current levels). The main upside risk for European equities is a further fall in the EUR. If the EUR/USD were to decline below 1.10, as implied by the recent moves in Euro area versus US PMIs, this would push up the implied fair-value for the Stoxx 600 to 415 by early Q3 (6% above current levels).

Before we take a look at today’s calendar, let’s wrap up with other data releases from yesterday. In the US, the weekly initial jobless claims (211k vs. 219k expected) and continuing claims (1,790k vs. 1,800k expected) were both lower than consensus. The four week moving average for the former is now the lowest for 49 years. Elsewhere, the April monthly budget surplus was slightly above expectations ($214bln vs. $212bln expected) and also the highest monthly print on record.

In the UK, the March IP was below consensus at 2.9% yoy (vs 3.1% expected) while manufacturing production was in line at 2.9% yoy. The March trade deficit widened more than expected to -£3.1bln (vs. -£2bln), partly due to a stronger rebound in imports. The RICS house price balance fell to -8 in April, which is the weakest since November 2012. On balance, surveyors expect prices to continue to decline over the next three months despite fewer reporting declining buyer interest. Finally, Italy’s March IP was above expectations at 1.2% mom (vs. 0.5%).

Looking at the day ahead, the only significant data coming from the US will be the April import price index and preliminary May University of Michigan consumer sentiment report. Elsewhere, the Spanish April CPI print is also due. ECB President Draghi will address an audience at the ADEMU conference in Florence.

3. ASIAN AFFAIRS

i)FRIDAY MORNING/THURSDAY NIGHT: Shanghai closed DOWN 11.15 points or 0 .35% /Hang Sang CLOSED UP 312.84 points or 1.02% / The Nikkei closed UP 261.30 POINTS OR 1.16% /Australia’s all ordinaires CLOSED UP .01% /Chinese yuan (ONSHORE) closed UP at 6.3329/Oil DOWN to 71.39 dollars per barrel for WTI and 77.22 for Brent. Stocks in Europe OPENED RED. ONSHORE YUAN CLOSED UP AT 6.3329 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.3250/ONSHORE YUAN TRADING WEAKER AGAINST OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING MUCH STRONGER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW LOOKS LIKE A FULL TRADE WAR IS BEGINNING/

3 a NORTH KOREA/USA

North Korea/South Korea/usa

END.

3 b JAPAN AFFAIRS

end

c) REPORT ON CHINA/HONG KONG

4. EUROPEAN AFFAIRS

EU

Europe is not happy with Trump’s new Iranian sanctions/ two commentaries

(courtesy Mish Shedlock/Mishtalk)

Europe’s Shakespearean Response To Iran Sanctions: New Word “Unisolationism”

Authored by Mike Shedlock via MishTalk,

Europe is huffing and puffing and full of fury over Trump’s Iran decision. The French even coined a new word.

Trump’s decision to re-impose sanctions means a blanket ban on all new business with Iran, effective immediately. Existing operations have three to six months to be wound down.

The US’s new ambassador to Germany, Richard Grenell, wasted no time poking a finger in the eyes of his host.

END

Merkel: “Trump’s Decision Damages Trust In The International Order”

One day after Angela Merkel said Europe can no longer rely on the US “to protect it” in the aftermath of Trump’s unilateral withdrawal from the Iran nuclear accord, stating that “It’s no longer the case that the United States will simply just protect us. Rather, Europe needs to take its fate into its own hands, that’s the task of the future”, the German Chancellor has doubled down, and said President Trump’s decision to scrap the Iran nuclear accord was “not right.”

“It’s not right to unilaterally cancel an accord that was negotiated, that was unanimously approved in the UN Security Council,” Merkel said in a speech at a Catholic religious conference in Muenster, Germany “That damages the trust in the international order.”

“What we’re seeing at the moment, which is probably the most alarming, is that multilateralism is in a real crisis” she added. She then echoed her prior warning: “I’ve said this about the U.S. decision on the Iran accord, I could say the same thing about the climate accord, the WTO – if we always say that something doesn’t suit us, and we don’t get a new international order, and everybody simply does what they want – then that’s bad news for the world.”

Or it could simply be bad news for Europe, or rather everyone but the US, and since Trump’s promise was “America first” it should hardly come as a surprise. Perhaps what Angela should be more worried about is that her disastrous “open door” immigration policy has ushered in not only Brexit but – as of yesterday – laid the groundwork for the first populist, anti-establishment government in Italy where the Five Star and League are about to form a government, which will have immigration as its key talking point.

Alas, none of this was discussed and instead Merkel kept hammering on the Iran situation, questioning whether the Iran Nuclear accord can be saved: “The extent to which we can keep this accord alive when one huge economic power isn’t taking part is something that’ll have to be discussed with Iran,” Merkel said. “We hope so, but many factors are in play and we shouldn’t pretend to be stronger than we are. That can lead to severe miscalculations.”

Nonetheless, Germany confirmed its commitment to the Iranian deal, siding with the EU, France, China, Russia, France and the UK on the issue; Merkel also said that options to save the deal without the United States needed to be discussed with Tehran and added that Trump’s decision to withdraw from the Iran nuclear deal is no reason to call into question relationships between Europe and the US.

Iran’s foreign minister Zarif is scheduled to meet with the EU High Representative for Foreign Affairs and Security Policy, Federica Mogherini, on Tuesday 15 May in Brussels in a meeting which will be attended by E3 Foreign Ministers (Germany, France, U.K.) to discuss Iran nuclear accord. Zarif will also meet with China and Russia on the prior two days.

END

Europe ends on a high note and extends its longest winning streak since 2015 despite poor economic data

(courtesy zerohedge)

European Stocks Surge To Longest Win Streak Since 2015 (As Economic Data Collapses)

European stocks are up seven straight weeks (the longest win streak since March 2015), accelerating into the green for 2018 this week…

All as European economic data surprises crash to their weakest since August 2011.

Once again – bad news is good news…

Draghi gets his excuse to keep doing “whatever it takes” and drone-like investors buy on his coat-tails.

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

Israel

It seems that the USA/Israeli plan is to assassinate Iran’s chief revolutionary guard commander, Soleimani. It seems that Israel had him in their sights but Obama negated the attack

(courtesy zerohedge)

The US-Israeli Plan To Assassinate Iran’s Elite Revolutionary Guard Commander

The United States gave Israel the green light to assassinate Iran’s top military officer, Iranian Revolutionary Guards al-Quds Force commander Maj. Gen. Qassem Soleimani, according to a widely circulated report in Kuwaiti newspaper Al-Jarida published earlier this year. News of the agreement, first published in Arabic in January, is now resurfacing in both Russian and Middle East regional media the day after Syria and Israel engaged in a massive overnight exchange of fire in what constitutes the most sustained Israeli attack on Syria in decades.

In the Arab world Al-Jarida is generally considered to be a platform through which Israel circulates news and its perspective to neighboring countries in the region. The newspaper first published report based on an Israeli government source who was cited as saying, “there is an American-Israeli agreement” that Soleimani is a “threat to the two countries’ interests in the region”—which reportedly led to a Washington green-light for the Israelis to assassinate him.

General Soleimani, as leader of Iran’s most elite force, also coordinates military activity between the Islamic Republic and Syria, Iraq, Hezbollah, and Hamas – a position he’s filled since 1998 – and as Quds Force commander reports directly to the Supreme Leader of Iran, Ali Khamenei, and oversees Iran‘s covert operations in foreign countries.

Israeli officials initially “leaked” the story after days of internal Iranian anti-government protests gridlocked the country in late December and early January, bringing international media attention and discussions in Tel Aviv and Washington of a potential coup attempt in the works. Whether or not there actually ever was such a green-light given by the American side, Al-Jarida report ultimately served the purpose of a semi-official threat issued through the media by the Israelis.

The threat of assassinating Iran’s most elite military commander has taken on new importance and urgency after Israel laid official blame on Gen. Soleimani on Thursday, alleging that he personally ordered a rocket attack against Israeli bases on the Golan Heights from within Syria, which triggered a massive escalation overnight. “It was ordered and commanded by Qassem Soleimani and it has not achieved its purpose,” Israeli military spokesman Lieutenant-General Jonathan Conricus claimed, as cited by Reuters.

Perhaps the most interesting aspect to the report, and worth revisiting, is the revelation that Israel was supposedly “on the verge” of killing Soleimani three years ago in an operation near Damascus; however, the Obama administration was said to have warned the Iranians of the impending Israeli plot which according to Israeli sources was thwarted because of US intervention, resulting in “a sharp disagreement between the Israeli and American security and intelligence apparatuses regarding the issue.”

But the Trump administration now appears to be quite at home with a “gloves off” approach as this week more evidence emerged suggesting the White House is now eyeing regime change in Tehran. As we previously reported, the Washington Free Beacon has obtained a three-page white paper now being circulated among National Security Council officials with drafted plans to spark regime change in Iran, following the US exit from the Obama-era nuclear deal and the re-imposition of tough sanctions aimed at toppling the Iranian government.

The plan, authored by , including – who else – National Security Adviser John Bolton, seeks to reshape longstanding American foreign policy toward Iran by emphasizing an explicit policy of regime change.

“The ordinary people of Iran are suffering under economic stagnation, while the regime ships its wealth abroad to fight its expansionist wars and to pad the bank accounts of the Mullahs and the IRGC command,” writes the Security Studies Group, or SSG, a national security think-tank that has close ties to senior White House national security officials. “This has provoked noteworthy protests across the country in recent months” it further claims as an argument to push a “regime change” policy.

No doubt, a targeted strike or clandestine assassination attempt on Soleimani is likely now very high on the Israeli agenda and perhaps even the US agenda, especially after this week’s military escalation and Israeli claim that the Iranians are firing rockets into Israel (something for which there’s currently not a shred of evidence).

* * *