GOLD: $1292.60 UP $1.05 (COMEX TO COMEX CLOSINGS)

Silver: $16.56 UP 6 CENTS (COMEX TO COMEX CLOSINGS)

Closing access prices:

Gold $1291.50

silver: $16.54

For comex gold:

MAY/

NUMBER OF NOTICES FILED TODAY FOR MAY CONTRACT:35 NOTICE(S) FOR 3500 OZ.

TOTAL NOTICES SO FAR 685 FOR 68500 OZ (2.130 tonnes)

For silver:

MAY

13 NOTICE(S) FILED TODAY FOR

65,000 OZ/

Total number of notices filed so far this month: 6130 for 30,650,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: BID $8183/OFFER $8283: DOWN $160(morning)

Bitcoin: BID/ $8127/offer $8227: UP $213 (CLOSING/5 PM)

end

First Shanghai gold fix comes at 10 pm est

The second Shanghai gold fix: 2:15 pm

First Shanghai gold fix gold: 10 pm est: 1295.17

NY price at the same time: 1290.15

PREMIUM TO NY SPOT: $5.02

ss

Second gold fix early this morning: 1298.83

USA gold at the exact same time:1290.80

PREMIUM TO NY SPOT: $9.03

AGAIN, SHANGHAI REJECTS NEW YORK PRICING.

WE WILL NOT PROVIDE LONDON FIXES AS THEY ARE NOT ACCURATE AS TO WHAT IS GOING ON AT THE SAME TIME FRAME.

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total OPEN INTEREST FELL BY A TINY 368 CONTRACTS FROM 200,100 FALLING TO 199,896 DESPITE YESTERDAY’S 5 CENT GAIN IN SILVER PRICING. WE ARE NOW WITNESSING OUR USUAL AND CUSTOMARY COMEX LONG LIQUIDATION AS WE ENTERED INTO THE ACTIVE DELIVERY MONTH OF MAY AS LONGS PACK THEIR BAGS AND MIGRATE OVER TO LONDON. WE WERE NOTIFIED THAT WE HAD A FAIR SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP : 943 EFP’S FOR JULY AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE OF 943 CONTRACTS. WITH THE TRANSFER OF 943 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 943 EFP CONTRACTS TRANSLATES INTO 4.715 MILLION OZ ACCOMPANYING:

1.THE 5 CENT GAIN IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES STANDING FOR MAY COMEX DELIVERY. (31.445 MILLION OZ)

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF APRIL: (FINAL)

29,464 CONTRACTS (FOR 16 TRADING DAYS TOTAL 29,464 CONTRACTS) OR 147.320 MILLION OZ: (AVERAGE PER DAY: 1841 CONTRACTS OR 9.207 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH: 147.320 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 21.04% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)

ACCUMULATION IN YEAR 2018 TO DATE SILVER EFP’S: 1,292.64 MILLION OZ.

ACCUMULATION FOR JAN 2018: 236.879 MILLION OZ

ACCUMULATION FOR FEB 2018: 244.95 MILLION OZ

ACCUMULATION FOR MARCH 2018: 236.67 MILLION OZ

ACCUMULATION FOR APRIL 2018: 385.75 MILLION OZ

RESULT: WE HAD A TINY SIZED DECREASE IN COMEX OI SILVER COMEX OF 368 DESPITE THE 5 CENT GAIN IN SILVER PRICE. WE HAVE NOW ENTERED THE NEW ACTIVE MONTH OF MAY. THE CME NOTIFIED US THAT IN FACT WE HAD AN STRONG SIZED EFP ISSUANCE OF 943 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) . FROM THE CME DATA: 943 EFP CONTRACTS FOR JULY, AND ZERO FOR ALL OVER MONTHS FOR A DELIVERABLE FORWARD CONTRACT OVER IN LONDON WITH A FIAT BONUS (TOTAL: 943). TODAY WE GAINED 575 TOTAL OI CONTRACTS ON THE TWO EXCHANGES: i.e. 943 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH AN DECREASE OF 368 OI COMEX CONTRACTS. AND ALL OF THIS HAPPENED WITH THE 5 CENT GAIN IN PRICE OF SILVER AND A CLOSING PRICE OF $16.50 WITH RESPECT TO FRIDAY’S TRADING. YET WE STILL HAVE A STRONG AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY IN THIS ACTIVE MAY DELIVERY MONTH. IT SURE LOOKS LIKE A FAILED BANKER SHORT COVERING EXERCISE!!

In ounces AT THE COMEX, the OI is still represented by UNDER 1 BILLION oz i.e. 0.999 MILLION OZ TO BE EXACT or 143% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT MAY MONTH/ THEY FILED AT THE COMEX: 13 NOTICE(S) FOR 65,000 OZ OF SILVER

IN SILVER, WE HAVE NOW SET THE NEW RECORD OF OPEN INTEREST AT 243,411 AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $16.51 ON APRIL 9.2018.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH: 27 MILLION OZ , APRIL: 2.485 MILLION OZ AND MAY: 31.445 MILLION OZ )

- HUGE RECORD OPEN INTEREST IN SILVER 243,411 CONTRACTS (OR 1.217 BILLION OZ/ SET APRIL 9/2018

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017

- RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ (FINAL)

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT). IT ALSO LOOKS LIKE BANKER CAPITULATION IN SILVER AS THEY STRUGGLE TO REMOVE SOME OF THEIR HUGE OBLIGATIONS.

In gold, the open interest FELL BY A CONSIDERABLE SIZED 6679 CONTRACTS DOWN TO 508,558 DESPITE THE TINY LOSS IN THE GOLD PRICE/YESTERDAY’S TRADING (LOSS OF $0.50). WE ARE NOW IN THE NON ACTIVE DELIVERY MONTH OF MAY. THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED AN STRONG SIZED 10,793 CONTRACTS : JUNE SAW THE ISSUANCE OF 9738 CONTRACTS , MAY SAW THE ISSUANCE OF 0 CONTRACTS AND AUGUST SAW THE ISSUANCE OF: 1055 CONTRACTS WITH ALL OTHER MONTHS ZERO. The new OI for the gold complex rests at 506,479. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE A STRONG SIZED OI GAIN IN TOTAL CONTRACTS ON THE TWO EXCHANGES: 6,679 OI CONTRACTS DECREASED AT THE COMEX AND AN STRONG SIZED 10,793 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON.THUS TOTAL OI GAIN: 4114 CONTRACTS OR 411,400 OZ = 12.79 TONNES. AND ALL OF THIS OCCURRED WITH A TINY LOSS OF $0.50

YESTERDAY, WE HAD 8034 EFP’S ISSUED.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF MAY : 153,421 CONTRACTS OR 15,342,100 OZ OR 477.20 TONNES (16 TRADING DAYS AND THUS AVERAGING: 9,588 EFP CONTRACTS PER TRADING DAY OR 958,800 OZ/ TRADING DAY),,

TO GIVE YOU AN IDEA AS TO THE HUGE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 16 TRADING DAYS IN TONNES: 477.20 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2017, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 2555 TONNES

THUS EFP TRANSFERS REPRESENTS 477.20/2550 x 100% TONNES = 18.71% OF GLOBAL ANNUAL PRODUCTION SO FAR IN APRIL ALONE.*** THE ACCUMULATION OF EFP CONTRACTS IS RISING PER MONTH.

ACCUMULATION OF GOLD EFP’S YEAR 2018 TO DATE: 3,234.83* TONNES *SURPASSED ANNUAL PROD’N

ACCUMULATION OF GOLD EFP’S FOR JANUARY 2018: 653.22 TONNES

ACCUMULATION OF GOLD EFP’S FOR FEBRUARY 2018: 649.45 TONNES

ACCUMULATION OF GOLD EFP’S FOR MARCH 2018: 741.89 TONNES (22 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR APRIL 2018: 713.84 TONNES (21 TRADING DAYS)

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A CONSIDERABLE SIZED DECREASE IN OI AT THE COMEX OF 6679 WITH THE $0.50 FALL IN PRICE // GOLD TRADING YESTERDAY ($0.50 LOSS). WE ALSO HAD AN STRONG SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 10,793 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 10,793 EFP CONTRACTS ISSUED, WE HAD A GOOD SIZED NET GAIN OF 4114 CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

10,793 CONTRACTS MOVE TO LONDON AND 6679 CONTRACTS DECREASED AT THE COMEX. (in tonnes, the GAIN in total oi equates to 12.80 TONNES). ..AND BELIEVE IT OR NOT BUT ALL OF THESE OCCURRED AT THE COMEX WITH A TINY LOSS OF $0.50 IN TRADING!!!.

we had: 35 notice(s) filed upon for 3500 oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD…

WITH GOLD UP $1.05 / NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RESTS AT 862.04 TONNES

Inventory rests tonight: 862.04 tonnes.

SLV/

WITH SILVER UP 6 CENTS NO CHANGES IN THE SILVER INVENTORY AT THE SLV INVENTORY/

/INVENTORY RESTS AT 321.003 MILLION OZ/

end

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER FELL BY A TINY SIZED 368 CONTRACTS from 200,264 DOWN TO 199,896 (AND, FURTHER FROM THE NEW COMEX RECORD SET /APRIL 9/2017 AT 243,411/SILVER PRICE AT THAT DAY: $16.53). THE PREVIOUS RECORD OTHER THAN WAS ESTABLISHED AT: 234,787, SET ON APRIL 21.2017 OVER ONE YEAR AGO. THE PRICE OF SILVER ON THAT DAY: $17.89. OUR CUSTOMARY MIGRATION OF COMEX LONGS MORPH INTO LONDON FORWARDS CONTINUES AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE: , 0 EFP CONTRACTS FOR MAY (WE DO NOT GET A LOOK AT THESE CONTRACTS AS IT IS PRIVATE BUT THE CFTC DOES AUDIT THEM), AND 943 EFP’S FOR JULY AND ALL OTHER MONTHS ZERO. TOTAL EFP ISSUANCE: 943 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI LOSS AT THE COMEX OF 368 CONTRACTS TO THE 943 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A FAIR SIZED GAIN OF 575 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES: 2.875 MILLION OZ!!! AND THIS OCCURRED WITH NO GAIN IN PRICE . THE BANKERS ORCHESTRATED THEIR RAID THROUGHOUT LAST WEEK DESPERATELY TRYING TO PARE THEIR GIGANTIC OPEN INTEREST SHORT ON BOTH EXCHANGES BUT TO NO AVAIL. JUDGING BY THE RECORD NUMBER OF EFP ISSUANCE DURING LAST MONTH OF APRIL AT 385.75 MILLION OZ AND THE TOTAL OI GAIN ON THE TWO EXCHANGES, THE CONSTANT RAIDS, LIKE YESTERDAY ARE NOW BEING CALLED UPON BY OUR BANKER FRIENDS IN AN ATTEMPT TO SHAKE AS MANY SILVER LEAVES FROM THE SILVER TREE AS POSSIBLE AND JUDGING BY THE RESULTS TO YESTERDAYS ACTION THEY WERE NOT AT ALL SUCCESSFUL.

RESULT: A SMALL SIZED DECREASE IN SILVER OI AT THE COMEX DESPITE THE 5 CENT GAIN IN SILVER PRICING YESTERDAY. BUT WE ALSO HAD ANOTHER STRONG SIZED 943 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR APRIL, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)TUESDAY MORNING/MONDAY NIGHT: Shanghai closed UP 0.51 points or .02% /Hang Sang CLOSED UP 186.44 points or 0.60% / The Nikkei closed DOWN 42.03 POINTS OR 0.18% /Australia’s all ordinaires CLOSED DOWN .65% /Chinese yuan (ONSHORE) closed UP at 6.3686/Oil UP to 72.42 dollars per barrel for WTI and 79.58 for Brent. Stocks in Europe OPENED ALL GREEN. ONSHORE YUAN CLOSED UP AT 6.3688 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.3523/ONSHORE YUAN TRADING WEAKER AGAINST OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING MUCH STRONGER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW LOOKS LIKE A FULL TRADE WAR IS BEGINNING/

/NORTH KOREA/SOUTH KOREA

i)North Korea/South Korea/USA

b) REPORT ON JAPAN

3 c CHINA

i)Big news overnight: China unexpected slashes auto tariffs to 15% and auto parts to 6%. China now waits for the USA to overturn ZTE penalties

( zerohedge)

ii)Trump back down on learning that ZTE would fail if sanctions continue. If agrees to drop ZTE sanctions if China agrees to a fine and a management shakeup

( zerohedge)

4. EUROPEAN AFFAIRS

i)The most important chart to watch: the 10 yr Italian bond yield:

( zerohedge)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

Iran/Syria/Russia

( zerohedge)

6 .GLOBAL ISSUES

Canada’s Brookfield has not forgot its roots and is now buying assets in Brazil hand over fist as they sense blood in the streets

( zero hedge)

7. OIL ISSUES

8. EMERGING MARKET

After Trump initiated sanctions against Venezuela and Maduro on Friday due to the sham elections, Venezuela returned Trump the favour by expelling its top USA diplomat

( zerohedge)

9. PHYSICAL MARKETS

ii)London’;s financial times, Prasad warns investors that the dollar supremacy is waning( Prasad/London’s financial times)

iii)Bloomberg suggests not to believe that 80 dollar oil is here to stay…the forward price of oil is being bet very heavily and the that price is around the mid 60’s

( Bloomberg/GATA)

( JSKim/GATA)

v)Ronan Manly highlights the movement of gold into China, Russia and Switzerland and concludes that gold demand is high. I can see it through demand at the both of comex and London

( Ronan Manly/Bullionstar)

vi)Lawrie Williams, of Sharp’s Pixley discusses movement of gold into and out of the UK. As expected there is huge movement into Switzerland and Mainland China (Shanghai) but also Turkey and the uAE are big receivers of this UK exportation of gold.

(courtesy Lawrie Williams/Sharp’s Pixley)

10. USA stories which will influence the price of gold/silveri)

i)MARKET DATA

iv)SWAMP STORIES

Trading Volumes on the COMEX

PRELIMINARY COMEX VOLUME FOR TODAY: 318,294 contracts

CONFIRMED COMEX VOL. FOR YESTERDAY: 390,227 contracts

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

And now for the wild silver comex results.

Total silver OI FELL BY A TINY SIZED 368 CONTRACTS FROM 200,264 DOWN TO 199,896 (AND FURTHER FROM THE NEW RECORD OI FOR SILVER SET APRIL 9.2018/ 243,411 CONTRACTS) DESPITE THE 5 CENT GAIN IN SILVER PRICING/ FRIDAY. SINCE WE ARE NOW INTO THE ACTIVE DELIVERY MONTH OF MAY. WE WERE INFORMED THAT WE HAD A GOOD SIZED 943 EFP CONTRACT ISSUANCE FOR JULY AND ZERO FOR ALL OTHER MONTHS. THESE EFPS WERE ISSUED TO COMEX LONGS WHO RECEIVED A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. THE TOTAL EFP’S ISSUED: 943. ON A NET BASIS WE GAINED 779 SILVER OPEN INTEREST CONTRACTS AS WE OBTAINED A 368 CONTRACT LOSS AT THE COMEX COMBINING WITH THE ADDITION OF 943 OI CONTRACTS NAVIGATING OVER TO LONDON.

NET GAIN ON THE TWO EXCHANGES: 575 CONTRACTS

AMOUNT STANDING FOR SILVER AT THE COMEX

We are now in the active delivery month of MAY and here the front month FELL BY 14 contracts FALLING TO 172 contracts. We had 27 notices filed upon yesterday so we SURPRISINGLY GAINED 13 contracts or 65,000 additional ounces will stand for delivery in this active delivery month of May AS SOMEBODY AGAIN WAS DESPERATE FOR PHYSICAL SILVER ON THIS SIDE OF THE POND..

June saw a LOSS of 8 contracts to stand at 720. The next big delivery month for silver is July and here the OI LOST 1089 contracts DOWN to 136,824. The next active delivery month after July for silver is September and here the OI ROSE by 856 contracts UP to 28,397

We had 13 notice(s) filed for 65,000 OZ for the MAY 2018 contract for silver

INITIAL standings for MAY/GOLD

MAY 22/2018.

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz |

nil OZ

|

| Deposits to the Dealer Inventory in oz | NIL oz |

| Deposits to the Customer Inventory, in oz | nil OZ |

| No of oz served (contracts) today |

35 notice(s)

3500 OZ

|

| No of oz to be served (notices) |

57 contracts

(5700 oz)

|

| Total monthly oz gold served (contracts) so far this month |

685 notices

68500 OZ

2.130 TONNES

|

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

For MAY:

Today, 0 notice(s) were issued from JPMorgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equates to 35 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 19 notice(s) was (were) stopped/ Received) by j.P.Morgan customer account.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

To calculate the INITIAL total number of gold ounces standing for the MAY. contract month, we take the total number of notices filed so far for the month (685) x 100 oz or 68500 oz, to which we add the difference between the open interest for the front month of MAY. (92 contracts) minus the number of notices served upon today (35 x 100 oz per contract) equals 74,200 oz, the number of ounces standing in this active month of APRIL (2.307 tonnes)

Thus the INITIAL standings for gold for the MAY contract month:

No of notices served (685 x 100 oz) + {(92)OI for the front month minus the number of notices served upon today (35 x 100 oz )which equals 74,200 oz standing in this active delivery month of MAY . THERE ARE 9.0356 TONNES OF REGISTERED GOLD AVAILABLE FOR DELIVERY SO FAR.

WE GAINED 600 OZ OF GOLD (6 CONTRACTS) STANDING IN THIS NON ACTIVE DELIVERY MONTH OF MAY

IN THE LAST 18 MONTHS 73 NET TONNES HAS LEFT THE COMEX.

end

And now for silver

AND NOW THE APRIL DELIVERY MONTH

MAY INITIAL standings/SILVER

| Silver | Ounces |

| Withdrawals from Dealers Inventory | nil oz |

| Withdrawals from Customer Inventory |

29,901.510 oz

CNT

|

| Deposits to the Dealer Inventory |

nil

oz

|

| Deposits to the Customer Inventory |

1,395,378.741

oz

JPMorgan

CNT

|

| No of oz served today (contracts) |

13

CONTRACT(S)

(65,000 OZ)

|

| No of oz to be served (notices) |

159 contracts

(795,000 oz)

|

| Total monthly oz silver served (contracts) | 6130 contracts

(30,650,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

we had 0 inventory movement at the dealer side of things

i

total dealer deposits: nil oz

we had 2 deposits into the customer account

i) Into JPMorgan: 519,563.748 oz

*** JPMorgan for most of 2017 and in 2018 has adding to its inventory almost every single day.

JPMorgan now has 140 million oz of total silver inventory or 52.3% of all official comex silver. (140 million/268 million)

ii) Into CNT: 871,689.193 oz

total customer deposits today: 1,395,378.741 oz

we had 1 withdrawals from the customer account;

i) out of CNT: 29,901.510 oz

total withdrawals; 29,901.510 oz

we had 0 adjustments

total dealer silver: 69.156 million

total dealer + customer silver: 268.963 million oz

The total number of notices filed today for the MAY. contract month is represented by 13 contract(s) FOR 65,000 oz. To calculate the number of silver ounces that will stand for delivery in MAY., we take the total number of notices filed for the month so far at 6130 x 5,000 oz = 30,650,000 oz to which we add the difference between the open interest for the front month of MAY. (172) and the number of notices served upon today (13 x 5000 oz) equals the number of ounces standing.

.

Thus the INITIAL standings for silver for the MAY contract month: 6130(notices served so far)x 5000 oz + OI for front month of MAY(172) -number of notices served upon today (13)x 5000 oz equals 31,445,000 oz of silver standing for the MAY contract month

WE GAINED 13 CONTRACTS OR AN ADDITIONAL 65,000 OZ WILL STAND AT THE COMEX AS SOMEBODY WAS IN URGENT NEED OF PHYSICAL SILVER ON THIS SIDE OF THE POND.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

ESTIMATED VOLUME FOR TODAY: 74,246 CONTRACTS

CONFIRMED VOLUME FOR YESTERDAY: 69,426 CONTRACTS

YESTERDAY’S CONFIRMED VOLUME OF 69,426 CONTRACTS EQUATES TO 347 MILLION OZ OR 49.43% OF ANNUAL GLOBAL PRODUCTION OF SILVER

COMMODITY LAW SUGGESTS THAT OPEN INTEREST SHOULD NOT BE MORE THAN 3% OF ANNUAL GLOBAL PRODUCTION. THE CROOKS ARE SUPPLYING MASSIVE PAPER TRYING TO KEEP SILVER IN CHECK.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price at that day at $18.42

The previous record was 224,540 contracts with the price at that time of $20.44

end

NPV for Sprott

1. Sprott silver fund (PSLV): NAV FALLS TO -2.04% (MAY22/2018)

2. Sprott gold fund (PHYS): premium to NAV RISES TO -0.39% to NAV (MAY 22/2018 )

Note: Sprott silver trust back into NEGATIVE territory at -2.04%-/Sprott physical gold trust is back into NEGATIVE/ territory at -0.39%/Central fund of Canada’s is still in jail but being rescued by Sprott.

Sprott WINS hostile 3.1 billion bid to take over Central Fund of Canada

(courtesy Sprott/GATA)

3.SPROTT CEF.A FUND (FORMERLY CENTRAL FUND OF CANADA): NAV FALLS TO -2.22%: NAV 13.45/TRADING 13.17//DISCOUNT 2.22.

END

And now the Gold inventory at the GLD/

MAY 22/WITH GOLD UP $1.05/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 862.04 TONNES

MAY 21/WITH GOLD DOWN 50 CENTS/A HUGE CHANGE IN GOLD INVENTORY/A WITHDRAWAL OF 3.24 TONNES FORM GLD INVENTORY/INVENTORY RESTS AT 862.04 TONNES

MAY 18/WITH GOLD UP $1.80/A HUGE CHANGE IN GOLD INVENTORY AT THE GLD/ A DEPOSIT OF 9.11 TONNES INTO GLD INVENTORY/INVENTORY RESTS AT 865.28 TONNES/

GLD WAS ONE MASSIVE FRAUD

May 17/WITH GOLD DOWN $1.75/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 856.17 TONNES

MAY 16./WITH GOLD UP $1.05: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 856.17 TONNES

MAY 15/WITH GOLD DOWN $27.35, THE CROOKS WITHDREW 10 TONNES OF GOLD FROM THE GLD WHICH WAS USED IN THE RAID TODAY/INVENTORY RESTS AT 856.17 TONNES

MAY 14/ WITH GOLD DOWN $2.35: A HUGE DEPOSIT OF 4.68 TONNES OF GOLD INTO THE GLD and then a withdrawal of 1.48 tonnes /INVENTORY RESTS AT 866.17

A net gain of 3.2 tonnes of gold.

MAY 11/WITH GOLD DOWN $1.75/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 862.96 TONNES/

MAY 10/WITH GOLD UP $9.60/A WITHDRAWAL OF 1.17 TONNES FROM THE GLD/INVENTORY RESTS AT 862.96 TONNES/SUCH CROOKS

MAY 9/WITH GOLD DOWN $0.55/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 864.13 TONNES

MAY 8/WITH GOLD DOWN $0.10/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 864.13 TONNES

MAY 7/WITH GOLD DOWN $0.55/ANOTHER WITHDRAWAL OF 1.47 TONNES OF GOLD FROM THE GLD/INVENTORY RESTS AT 864.13 TONNES

MAY 4/WITH GOLD UP $2.05/A WITHDRAWAL OF 1.13 TONNES OF GOLD FROM THE GLD/INVENTORY RESTS AT 865.60 TONNES

MAY 3/WITH GOLD UP $7.05/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 866.77 TONNES

MAY 2/WITH GOLD DOWN $1.15/ A HUGE WITHDRAWAL OF 4.43 TONNES FROM THE GLD/INVENTORY RESTS AT 866.77 TONNES

MAY 1/WITH GOLD DOWN $12.15/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 871.20 TONNES

APRIL 30/WITH GOLD DOWN $4.05/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 871.20 TONNES.

APRIL 27./WITH GOLD UP $5.90/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 871.20 TONNES/

APRIL 26/WITH GOLD DOWN $4.90/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 871.20 TONNES

APRIL 25/AFTER 9 CONSECUTIVE DAYS OF NO MOVEMENT OF GOLD INTO OUT OF THE GLD, WE HAD A HUGE DEPOSIT OF 5.31 TONNES OF GOLD INTO THE GLD/INVENTORY RESTS AT 871.20 TONNES.

APRIL 24./WITH GOLD UP $9.90, WE HAD NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 865.89 TONNES/

APRIL 23.2018/WITH GOLD DOWN $14.00/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 865.89 TONNES.

APRIL 20/WITH GOLD DOWN $10.20: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 865.89 TONNES

APRIL 19/WITH GOLD DOWN $4.25: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 865.89 TONNES/

APRIL 18/WITH GOLD UP $3.65: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 865.89 TONNES

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

MAY 22/2018/ Inventory rests tonight at 862.04 tonnes

*IN LAST 386 TRADING DAYS: 78.97 NET TONNES HAVE BEEN REMOVED FROM THE GLD

*LAST 336 TRADING DAYS: A NET 77.33 TONNES HAVE NOW BEEN ADDED INTO GLD INVENTORY.

end

Now the SLV Inventory/

MAY 22/WITH SILVER UP 6 CENTS/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 321.003 MILLION OZ/

MAY 21/ WITH SILVER UP 5 CENTS/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 321.003 MILLION OZ/

MAY 18/WITH SILVER DOWN 5 CENTS A SMALL CHANGE IN SILVER INVENTORY AT THE SLV/ A WITHDRAWAL OF 942,000 OZ/INVENTORY RESTS AT 321.003 MILLION OZ/

May 17/WITH GOLD UP 6 CENTS/A SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 471,000 OZ//INVENTORY RESTS AT 321.945 MILLION OZ/

MAY 16./WITH SILVER UP 10 CENTS/A HUGE DEPOSIT OF 1.883 MILLION OZ OF SILVER INTO THE SLV/INVENTORY RESTS AT 321.474 MILLION OZ

MAY 15/WITH SILVER DOWN 33 CENTS, NO CHANGES AT THE SLV; THE CROOKS COULD NOT BORROW ANY SILVER BECAUSE THERE IS NONE: INVENTORY RESTS AT 319.591 MILLION OZ

MAY 14/WITH SILVER DOWN 10 CENTS/A SMALL CHANGES IN SILVER INVENTORY AT THE SLV/ A WITHDRAWAL OF 858,000 FROM THE SLV/INVENTORY RESTS AT 319.591 MILLION OZ/

MAY 11/WITH SILVER DOWN 2 CENTS/THE CROOKS WITHDREW A MONSTROUS 2.824 MILLION OZ FROM THE SLV INVENTORY/INVENTORY RESTS AT 320.439 MILLION OZ/

MAY 10/WITH SILVER UP 22 CENTS/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 323.263 MILLION OZ/

MAY 9/WITH SILVER UP 6 CENTS/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 323.263 MILLION OZ/

MAY 8/WITH SILVER DOWN 2 CENTS:NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 323.263 MILLION OZ.

MAY 7/WITH SILVER FLAT: A BIG CHANGE IN SILVER INVENTORY AT THE SLV// A WITHDRAWAL OF 942,000 OZ OF SILVER FROM THE SLV INVENTORY/INVENTORY RESTS AT 323.263 MILLION OZ/

MAY4/WITH SILVER UP 5 CENTS/A BIG CHANGES IN SILVER INVENTORY AT THE SLV/ A DEPOSIT OF 1.224 MILLION OZ/INVENTORY RESTS AT 324.205 MILLION OZ/

MAY 2/WITH SILVER UP 24 CENTS/A HUGE CHANGE IN SILVER INVENTORY AT THE SLV// A DEPOSIT OF 6.082 MILLION OZ INTO THE SLV/INVENTORY RESTS AT 322.981 MILLION OZ/

MAY 1/WITH SILVER DOWN 24 CENTS/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 316.899 MILLION OZ/

APRIL 30/WITH SILVER DOWN 11 CENTS/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 316.899 MILLION OZ/

APRIL 27/WITH SILVER DOWN 5 CENTS/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 316.899 MILLION OZ/

APRIL 26/WITH SILVER DOWN 2 CENT/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 316,899 MILLION OZ/

APRIL 25./WITH SILVER DOWN 18 CENTS/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 316.899 MILLION OZ/

APRIL 24./WITH SILVER UP 8 CENTS/SOMETHING SPOOKED OUR CROOKS TO ADD SOME PAPER SILVER: A DEPOSIT OF 1.601 MILLION OZ/INVENTORY RESTS AT 316.899 MILLION OZ/

APRIL 23.2018/WITH SILVER DOWN 50 CENTS, ANOTHER HUGE WITHDRAWAL FROM THE SLV INVENTORY: A WITHDRAWAL OF 1.413 MILLION OZ/INVENTORY RESTS AT 315.298 MILLION OZ.

APRIL 20/WITH SILVER DOWN 11 CENTS: ANOTHER HUGE CHANGE IN SILVER INVENTORY: A WITHDRAWAL OF 1.13 MILLION OZ//SLV RESTS TONIGHT AT 316.711 MILLION OZ/

APRIL 19/WITH SILVER UP 3 CENTS TODAY: WE HAD A BIG CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.355 MILLION OZ/ MAKES ABSOLUTELY NO SENSE!!/INVENTORY RESTS AT 317.841 MILLION OZ

APRIL 18/WITH SILVER UP 44 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 320.196 MILLION OZ

MAY 22/2018:

Inventory 321.003 million oz

end

6 Month MM GOFO 2.07/ and libor 6 month duration 2.50

Indicative gold forward offer rate for a 6 month duration/calculation:

G0FO+ 2.07%

libor 2.50 FOR 6 MONTHS/

GOLD LENDING RATE: .43%

XXXXXXXX

12 Month MM GOFO

+ 2.77%

LIBOR FOR 12 MONTH DURATION: 2.58

GOFO = LIBOR – GOLD LENDING RATE

GOLD LENDING RATE = +.19

end

end

Major gold/silver trading /commentaries for TUESDAY

GOLDCORE/BLOG/MARK O’BYRNE.

GOLD/SILVER

Gold 2048: The Next 30 Years For Gold

Gold 2048: The Next 30 Years For Gold

Gold 2048 is an interesting and comprehensive new report from the World Gold Councilwhich brings together industry-leading experts from across the globe to analyse how the gold market is set to evolve in the next 30 years.

Key insights from authors such as George Magnus, senior economist; Rick Lacaille, Global Chief Investment Officer of State Street Global Advisors; and Michelle Ash, Chief Innovation Officer at Barrick Gold include:

- What does the future hold for gold?

- “Gold will be a refuge for people in times of crisis as it has always been” – Magnus

- The expanding middle class in China and India, combined with broader economic growth, will have a significant impact on gold demand.

- Use of gold across energy, healthcare and technology is changing rapidly. Gold’s position as a material of choice is expected to continue and evolve over the coming decades.

- Mobile apps for gold investment, which allow individuals to buy, sell, invest and gift gold will develop rapidly in India and China.

- Environmental, social and governance issues will play an increasing role in re-shaping mining production methods.

- The gold mining industry will have to grapple with the challenge of producing similar levels of gold over the next 30 years to match the volume it has historically delivered.

Listen on SoundCloud , Blubrry & iTunes. Watch on YouTube below

Gold 2048 full report and related reports are published by the World Gold Council (May, 2018) and available to subscribers here

News and Commentary

Gold prices steady on weaker dollar (Reuters.com)

Spec Funds Exit Gold Amid Strong Dollar and Lack of Fear (Bloomberg.com)

Gold Prices Drift Lower as Global Trade Remains in Focus (Investing.com)

Stocks and dollar rise as U.S.-China trade war put ‘on hold’ (Reuters.com)

Source: Coinnews.net

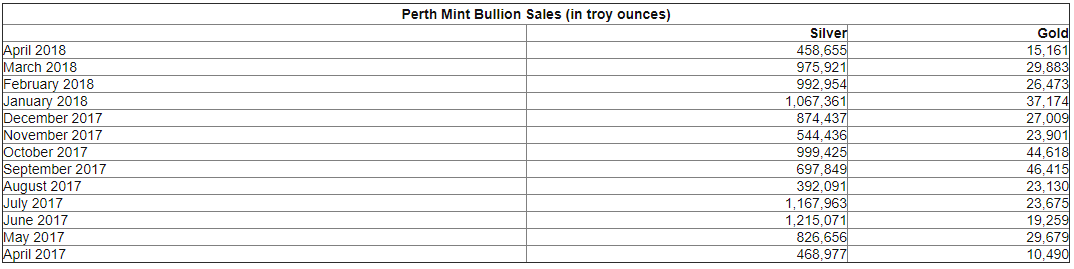

Perth Mint Gold and Silver Bullion Sales Retreat in April (CoinNews.net)

Gold promotions impede exposure of manipulation (SmartKnowledgeu.com)

Corporate Bonds Sink Fast in One of Worst Tumbles Since 2000 (Bloomberg.com)

As Brent Oil Reaches $80. The Big Rally Is in Forward Prices (Bloomberg.com)

Best-case scenario is the U.S. trade gap with China will get worse (MarketWatch.com)

Gold Prices (LBMA AM)

21 May: USD 1,285.85, GBP 959.24 & EUR 1,095.67 per ounce

18 May: USD 1,287.20, GBP 954.20 & EUR 1,091.16 per ounce

17 May: USD 1,288.85, GBP 952.07 & EUR 1,090.50 per ounce

16 May: USD 1,291.75, GBP 958.61 & EUR 1,093.60 per ounce

15 May: USD 1,310.05, GBP 966.42 & EUR 1,098.35 per ounce

14 May: USD 1,320.70, GBP 972.30 & EUR 1,101.86 per ounce

11 May: USD 1,324.80, GBP 978.23 & EUR 1,110.45 per ounce

Silver Prices (LBMA)

21 May: USD 16.34, GBP 12.19 & EUR 13.91 per ounce

18 May: USD 16.39, GBP 12.16 & EUR 13.92 per ounce

17 May: USD 16.39, GBP 12.14 & EUR 13.90 per ounce

16 May: USD 16.26, GBP 12.07 & EUR 13.79 per ounce

15 May: USD 16.41, GBP 12.12 & EUR 13.77 per ounce

14 May: USD 16.65, GBP 12.25 & EUR 13.89 per ounce

11 May: USD 16.76, GBP 12.35 & EUR 14.04 per ounce

Recent Market Updates

– Beware “Snollygosters” and the Empty Promises of Pathological Politicians

– US 10-Year Surges, Emerging Markets Implode…Where Next for Gold?

– Welsh Gold Being Hyped Due To The Royal Wedding?

– Oil Price Is Going To Keep Rising And Inflation Is Coming

– Gold Price Manipulation – A Comprehensive Guide By James Rickards

– EU ‘Nightmare Scenario’ As Popular Anti-Euro and Anti-EU Government Takes Power In Italy

– “Oil price highest in 3 years, gold ready to follow”, by Daniel March

– Gold Mining Supply Globally Looks Set To Decline

– Gold Bullion Demand In Iran May Surge On Trump Sanctions

– “Money Is Gold — and Nothing Else”

– U.K. Home Prices Plunge 3.1% In April – Largest Monthly Drop Since Financial Crisis In 2011

– Weekly Gold Update – Gold In Dollars Lower Despite Poor US Jobs and Other Data

– Own Some Gold and Avoid Overvalued Assets

Andrew Maguire’s Kinesis money which is a “bitcoin” but backed 100% by allocated gold and silver is set to go.

it think it would be a great idea to look at this!

please read at: https://kinesis.money/#/

(Andrew Maguire)

|

2:57 PM (1 hour ago) | ||

|

|||

Harvey

Here It is my friend! https://kinesis.money/#/ Please let everyone know.

Let catch up on Monday if you have time. We have billions in the hopper ready to be allocated on the 1st day of trading. The paper market days are over.

Warm regards

Andy

Gold frequently disappoints Jim Grant, but does he understand why?

Submitted by cpowell on Sat, 2018-05-19 14:24. Section: Daily Dispatches

10:46a ET Saturday, May 19, 2018

Dear Friend of GATA and Gold:

Interviewed this week by the TF Metals Report’s Craig Hemke for the “Ask the Expert” segment at Sprott Money News, James Grant of Grant’s Interest Rate Observer, an advocate of gold, said he doubts that central banks intervene against the price of the monetary metal. Grant’s comments on gold in the interview begin at the 13:20 mark here:

https://www.sprottmoney.com/Blog/ask-the-expert-james-grant-may-2018.htm…

Grant’s comments were disappointing first for their inconsistency and second for indicating ignorance of basic details.

The gold price, Grant said in the interview, is the reciprocal of faith in central banking, and he recalled that former Federal Reserve Chairman Paul Volcker once remarked to him that, for this very reason, he was always rooting for the gold price to go down.

But Grant added that he doesn’t think central banks even care about gold anymore, and that the risk central banks would assume in intervening against gold would be much worse than any benefit they would get from it. He said that as an investor in gold he is always expecting a higher price and is frequently disappointed.

Grant is generally acknowledged to be a brilliant guy, so might there be powerful reasons for the gold price not to be performing up to his expectations?

The interview suggests that Grant’s knowledge of Volcker does not extend to the assertion made by the former Fed chairman in his memoirs in 2004 — that central banks should have intervened against gold during an international currency revaluation in 1973:

Nor does Grant’s knowledge of Volcker seem to extend to the comment he made to the German financial journalist Lars Schall in 2012, defending central bank intervention against gold at “critical” points:

http://www.gata.org/node/10923

But Volcker’s endorsement of central bank intervention against gold is just a small part of the modern history of such intervention.

For example, if, as Grant believes, central banks don’t care about gold, why is their agent, the Bank for International Settlements, maintaining a huge position in gold swaps and derivatives, as recorded, if obscurely, in the bank’s monthly reports, and why does the bank refuse to explain the purposes of its position?:

http://www.gata.org/node/18228

http://www.gata.org/node/17793

If central banks don’t care about gold, why is the Banque de France, according to its director of market operations, secretly trading gold for its own account and the account of other central banks “nearly on a daily basis”?:

http://www.gata.org/node/13373

If central banks don’t care about gold, why does CME Group, operator of the major futures exchanges in the United States, give them discounts of 15 percent in their secret trading of gold and silver futures?:

http://www.gata.org/node/17976

GATA’s documentation file contains much more official acknowledgment of the largely surreptitious involvement of central banks in the gold market. Most of this is not mere “conspiracy theory” but ordinary official public record from government’s own archives and statements from central bankers, even if those statements were made when central bankers thought that only their colleagues were listening:

http://www.gata.org/taxonomy/term/21

A few years ago your secretary/treasurer and Grant both happened to be making presentations in New York at a meeting of the Committee for Monetary Research and Education. Your secretary/treasurer remarked that since Grant is among the exceedingly few gold advocates who is frequently interviewed by mainstream financial news organizations and since central banks had arranged things so that there were hardly any interest rates left for Grant’s newsletter to observe, he might be more helpful to gold’s cause and the cause of free markets if he would study the documentation of central banking’s gold price suppression scheme and then remark on it publicly.

Of course gold price suppression is not a topic that facilitates invitations to appear on financial news programs on television, which seems to be a big part of Grant’s work. (Indeed, your secretary/treasurer doesn’t even get invited to CMRE meetings anymore.) But if Grant continues to be frequently disappointed in the gold price, he might find some consolation in better understanding why gold is disappointing him.

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

London’;s financial times, Prasad warns investors that the dollar supremacy is waning

(courtesy Prasad/London’s financial times)

Eswar Prasad: America, beware — Dollar supremacy is not forever

Submitted by cpowell on Sun, 2018-05-20 15:00. Section: Daily Dispatches

By Eswar Prasad

Financial Times, London

Sunday, May 20, 2018

https://www.ft.com/content/3d4d1190-5931-11e8-806a-808d194ffb75

The dollar reigns supreme in global finance. It accounts for a dominant share of international financial transactions and is the ultimate safe haven currency. But the US currency’s supremacy cannot be taken for granted. President Donald Trump may be sowing the seeds of its demise.

Mr. Trump has often called for a weaker dollar, apparently to counter other countries that he claims are taking unfair advantage of the US by weakening their currencies to boost exports. Talk is cheap, however, and such statements by themselves will hardly derail the dollar. The real damage to its standing is more insidious and comes from policies that are eroding America’s fiscal stability, its trustworthiness and the strength of its institutions.

… …

In times of financial turmoil — including the global financial crisis, which originated in the United States — panicky investors flood into U.S. bond markets. No doubt the sheer size of the American government and corporate bond markets is a key factor. But there is something subtler and more important that accounts for the dollar’s status.

It comes down to trust. Flows into and out of currency and equity markets, where people make consequential financial decisions, show how trust matters even in seemingly cold-hearted and dispassionate decision-making.

The institutions that engender and maintain the trust of both domestic and foreign investors include an open and transparent system of democratic government with checks and balances. This needs to be underpinned by a central bank free from direct political interference and the rule of law administered by an independent judiciary.

Trust in U.S. institutions is why, despite the prospect of rising government debt levels and the economic uncertainty unleashed by Mr. Trump, the dollar remains strong. But this strength could prove fleeting. At present, most international financial transactions are denominated and settled in dollars and often through American financial institutions. This would change rapidly if investors believed that reckless fiscal policies could heighten volatility and erode the dollar’s value.

As it is, the falling cost of transacting in other currencies and the rise of emerging market currencies such as China’s renminbi are already reducing the dollar’s role in denominating and settling cross-border transactions. China and South Korea are conducting trade using their own currencies rather than relying on the dollar as a “vehicle currency.” The logic for denominating in dollars virtually all contracts for oil and other commodities is waning.

Other forces are at work. Under Mr. Trump, the United States is increasingly seen as an unreliable partner in trade, military, and other agreements. This has damaged its international credibility and sown fear that Mr. Trump could wield the dollar as a weapon of control over other countries. Consequently, China and Russia, among others, are setting up their own payment systems and channels that bypass the United States.

Perhaps, even if the dollar wanes as the dominant medium of exchange, it will remain unparalleled as a safe haven. Foreign investors, including central banks, have shown no signs of forsaking their dollar assets.

U.S. institutions have indeed withstood the test of time, but taking them for granted could prove costly. When the American political system has come under severe stress in the past, a free press, backed by an independent judiciary, has functioned as a correcting mechanism. All these institutions are under attack from Mr. Trump, abetted by a Republican-dominated Congress.

The dollar’s supremacy depends not just on America’s economic or military strength, but also on the durability and strength of its institutions. It is precisely these that the Trump administration is eroding — something even his devoted base might one day come to rue.

—–

The writer is a professor at Cornell University and senior fellow at Brookings.

* * *

END

Bloomberg suggests not to believe that 80 dollar oil is here to stay…the forward price of oil is being bet very heavily and the that price is around the mid 60’s

(courtesy Bloomberg/GATA)

Forget about oil at $80, because the big rally is in forward prices

Submitted by cpowell on Mon, 2018-05-21 13:06. Section: Daily Dispatches

By Catherine Ngai, Alex Longley, and Javier Blas

Bloomberg News

Monday, May 21, 2018

Brent crude oil grabbed all the attention after spot prices hit $80 a barrel last week. And yet, almost unnoticed, a perhaps more important rally has occurred in the obscure world of forward prices, with some investors betting the “lower for longer” price mantra is all but over.

The five-year Brent forward price, which has been largely anchored in a tight $55-to-$60 a barrel range for the past year and a half, has jumped over the last month, outpacing the gains in spot prices. It closed at $63.50 on Friday.

“For the first time since December 2015, the back end of the curve has been leading the complex higher,” said Yasser Elguindi, a market strategist at Energy Aspects Ltd. in New York. “It seems that the investor community is finally calling into question the ‘lower for longer’ thesis.” …

… For the remainder of the report:

https://www.bloomberg.com/news/articles/2018-05-21/forget-about-oil-at-8…

END

JS Kim notes the huge manipulation of gold/silver but asks writers not to promote these metals by saying are are imminently about to explode

(courtesy JSKim/GATA)

j.S. Kim: Gold promotions impede exposure of manipulation

Submitted by cpowell on Mon, 2018-05-21 18:18. Section: Daily Dispatches

2:20p ET Monday, May 21, 2018

Dear Friend of GATA and Gold:

Promotions for gold and silver that scream that prices are going to explode imminently are hurting efforts to tell the world the truth about the monetary metals and especially about the manipulation of their markets by central banks, J.S. Kim of Smart Knowledge U writes today.

Such promotions, Kim writes, “perpetually damage the truth movement in gold and silver to the point where one can take GATA-discovered documents whereby bankers make admissions of manipulating gold prices lower, show them to a skeptic, and still have a skeptic dismiss them as rubbish.”

Kim’s commentary is headlined “Why the ‘Gold is Ready to Explode Higher Any Day’ Narrative Hurts the Truth Movement about Gold” and it’s posted at Smart Knowledge U here:

https://smartknowledgeu.com/blog/2018/general-3/why-the-gold-is-ready-to…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

Ronan Manly highlights the movement of gold into China, Russia and Switzerland and concludes that gold demand is high. I can see it through demand at the both of comex and London

(courtesy Ronan Manly/Bullionstar)

Bullion Star’s gold market charts suggest demand remains strong

Submitted by cpowell on Tue, 2018-05-22 00:48. Section: Daily Dispatches

8:50p ET Monday, May 21, 2018

Dear Friend of GATA and Gold:

Bullion Star’s latest gold market charts suggest that despite gold’s recent decline in U.S. dollars, gold demand remains strong in China, Russia, and Switzerland. Bullion Star’s report is headlined “Gold Market Charts — May 2018” and it’s posted here:

https://www.bullionstar.com/blogs/gold-market-charts/gold-market-charts-…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

Lawrie Williams, of Sharp’s Pixley discusses movement of gold into and out of the UK. As expected there is huge movement into Switzerland and Mainland China (Shanghai) but also Turkey and the uAE are big receivers of this UK exportation of gold.

(courtesy Lawrie Williams/Sharp’s Pixley)

LAWRIE WILLIAMS: UK Gold Imports and Exports – Some surprises

With the release of the latest gold import and export figures, the UK demonstrated its importance as a key middle player in global gold trade. While imports of 55.2 tonnes in March (around 21% of world new mined gold output) showed few surprises being largely sourced from major producing nations. The USA, the world’s fourth largest gold producer, accounted for over 40% of the country’s gold imports, while Canada (the World No. 5 nowadays) provided 27.5%. The world’s Nos. 2 and 3 gold miners – Australia and Russia – do not trade much, if any, gold through the UK – the former for geographical reasons and the latter because it takes most of its newly mined gold into its own gold reserves.

But the export distribution is perhaps more interesting. In March the U.K. exported around 10 more tonnes of gold than it imported. Unsurprisingly the lion’s share (just under half) was to Switzerland where the refiners specialise in re-refining London good delivery gold bars into the smaller, and slightly higher tenor, bars and wafers in demand in the world’s largest markets in Asia. Perhaps more interesting however in terms of global gold trade was the export of 16.1 tonnes (24.6%) direct to mainland China (and only 0.5 tonnes to Hong Kong). As we have often pointed out the known gold exports to mainland China (mostly from Hong Kong and Switzerland) tend to be comfortably in excess of the figures assessed by the major precious metals consultancies as Chinese consumption, and the high UK export figure, although well below the amounts from Switzerland and Hong Kong, serves to emphasise this point. The March gold export figures from the U.K. are neatly set out in the bar chart below from Nick Laird’s excellent http://www.goldchartsrus.com service

The other points of particular interest in the U.K.’s gold export figures for March are the relatively high numbers for Turkey (16%) and the United Arab Emirates (9%). Turkey in particular is playing a dangerous geopolitical game in respect of its relationships with Russia and the U.S. and its military incursions into Syria where it has been targeting Kurdish held areas close to the Turkish border. The Kurdish militias have been strong supporters of the U.S. drive against ISIL and the Turkish actions may not be seen as a positive development by the U.S.

Indeed it is now reported that Turkey has been repatriating its gold held in the U.S. which could be a sign of increasing tensions between the nations as Turkey perhaps allies itself closer with Russia. The repatriation has been reported as due to increased geopolitical tensions involving the nation. Turkey’s President Erdogan has also signalled reduced dependence on the dollar in its reserves and has advocated that international loans should be designated in gold rather than dollars.

According to IMF figures, Turkey is the world’s 11th largest holder of gold in its forex reserves.

Your early TUESDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

i) Chinese yuan vs USA dollar/CLOSED UP 6.3686 /shanghai bourse CLOSED UP 0.51 POINTS OR 0.02% / HANG SANG CLOSED UP 42.03 POINTS OR 0.18%

2. Nikkei closed DOWN 42.03 POINTS OR 0.40% / /USA: YEN RISES TO 110.93/

3. Europe stocks OPENED RED /USA dollar index FALLS TO 93.41/Euro RISES TO 1.1805

3b Japan 10 year bond yield: RISES TO . +.06/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 110.64/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD FINALLY IN THE POSITIVE/BANK OF JAPAN LOSING CONTROL OF THEIR YIELD CURVE AS THEY PURCHASE ALL BONDS TO GET TO ZERO RATE!!

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 72.42 and Brent: 79.58

3f Gold UP/Yen UP

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil DOWN for WTI and DOWN FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund FALLS TO +.56%/Italian 10 yr bond yield UP to 2.30% /SPAIN 10 YR BOND YIELD UP TO 1.46%

3j Greek 10 year bond yield RISES TO : 4.39?????????????????

3k Gold at $1294.75 silver at:16.60 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble UP 17/100 in roubles/dollar) 61.39

3m oil into the 71 dollar handle for WTI and 79 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 110.93 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 0.9953 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1754 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now POSITIVE territory with the 10 year RISING to +0.560%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 3.07% early this morning (THIS IS DEADLY TO ALL MARKETS). Thirty year rate at 3.21%

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

(courtesy Jim Reid/Bloomberg/Deutsche bank/zero hedge)

US Futures Jump Amid Easing China Trade War; Dollar, Italian Yields Slide

With much of Europe coming back from Whit Monday holiday, the much more liquid market focused on the latest news in the easing US-China trade war and this morning’s announcement by Beijing to cut import duties on autos to 15%, with the resulting risk-on mood sending U.S. equity futures back to yesterday’s session highs, while Asian and European stocks were mixed.

It wasn’t just China’s auto import tariffs however: as the WSJ reports, US and China also reached a broad outline for settling the lingering ZTE issue, in which the export ban could be removed, while the company would have to make board and management changes. Furthermore, other source reports noted that the side were nearing an agreement that would remove a ban on ZTE and would include China pledge to remove tariffs on, as well as increase imports of

US agricultural products.

Yet despite the good trade news, broader European stocks were mixed, and turned modestly negative, driven by declines in the health care sector and utilities after both were downgraded by Deutsche Bank, pushing the Stoxx Europe 600 Index down 0.1% to session low, erasing earlier gains with 11 of 19 industry groups declining. Earlier, Deutsche Bank downgraded Europe’s energy sector on risks in oil price development in coming months, and also cut utility stocks as further upside to sector’s price relative implied by PMI forecast only marginal. Meanwhile, the European bank sector outperformed as the bund/BTP spread snapped 11bps tighter (see below), while European automakers gapped higher on China’s tariff cut.

Earlier, Asian stocks traded mostly subdued amid holiday closures and a lack of fresh catalysts, which saw sentiment wane from the prior day’s trade-related gains that boosted the DJIA above the 25k level for the first time since March. Australia’s ASX 200 weakened -0.7% amid broad losses across all sectors and with telecoms underperforming on continued woes for Telstra shares, while Healthscope was the worst performer after it flagged impairment charges. Nikkei 225 -0.2% traded indecisive as exporters suffered from a firmer currency and with Sony shares pressured after its 3-year strategy and targets was met with disappointment, while the unchanged Shanghai Composite was subdued following a continued net neutral liquidity position by the PBoC and with market closures in both Hong Kong and South

Korea adding to the humdrum tone, although baby-related stocks were underpinned on prospects China could relax its child-policy restrictions.

After hitting a 5 month high on Monday, the USD continued to weaken across the G-10 space forming a distorted head and shoulders topping formation, even as rangebound 10Y yields rose to session highs of 3.078%.

The second consecutive slide in the USD, at least for now, meant some breathing space for Emerging Markets, which have been crushed over the past month, while the month-long slide in EM local-currency government bonds has widened the yield spread they offer over their developed-market counterparts: “What we see is attractive real yields in the emerging markets, coupled with a good underlying fundamental growth,” said Richard Lawrence, SVP at Brandywine Global. However, it remains to be seen if the recent dollar weakness will translate into an EM buying spree. For now, the EM FX screen is mostly green with the exception of Turkey (thanks Mark Cudmore).

Meanwhile, in Developed Markets, the euro rose a second day as shorts trimmed exposure amid a rebound in Italian bonds while the Dollar Index retreated after it failed to rise Monday above a strong technical resistance level; EURUSD gained as much as 0.3% to touch 1.1830 high, versus 1.1757 day low, although for now it remains in sell-the-rally mode as sizable offers extend all way to 1.1850, a Europe-based trader told Bloomberg.

The pound looked to erase its Monday drop as comments from Bank of England officials during a testimony in front of lawmakers struck a more hawkish tone than investors were positioned for. More notably, Bloomberg notes that as soon as London stepped in, there was a familiar leveraged bid for the dollar that sent its major peers to fresh day lows. However, the market reversed course as Italian bonds rallied after yields touched the highest in more than a year on Monday.

Elsewhere in global macro, GBPUSD rose as much as 0.5% to touch 1.3492 day high, after BOE’s Gertjan Vlieghe, a dove, said he sees one or two rate hikes a year for the next three amid evidence that a tight labor market is boosting wage growth. At the same time, the USDJPY steadied around 111.00 vs day-low of 110.84 as Treasury yields rose; pair snapped its 6-day advance despite comments from BOJ Governor Kuroda the central bank won’t exit its current monetary policy before 2% inflation is reached. In Africa, the USDZAR was heavily offered as EMFX remains highly reactive to USD moves.

In the biggest news out of Europe, one day after a plunge in Italian bonds following the formation of the new 5-star/League government, BTPs bounced, retracing some of Monday’s panicky leg wider versus Germany as markets became somewhat more orderly as Germans returned from holiday. Italy 10-year yield dropped as much as 10bps, after touching 2.40% on Monday, while BTP yields were lower across the curve by 4-8bps.

Italy’s gain was Germany’s and America’s loss as Bunds were under sharp pressure, while also dragging Treasuries and gilts lower, as EGB spreads erased most of the latest spillover move; Bund spreads vs Spain and France also tightened, by 7bps and 3bps, respectively. Monday’s move was the first clear sign of spillover impacting these spreads and has promptly retracted.

Still as Bloomberg’s Heather Burke notes, “Italy’s troubles aren’t all over: credit default swaps have blown out and small caps may continue to face greater pressure. Plus, investors are worried that mini-BOTs could succeed at addressing Italy’s slow growth, undermining the euro project.”

Commodity prices are broadly higher in overnight trade in which crude extended on gains boosted by a softer greenback with geopolitics also remaining at the fore after US Secretary of State Pompeo warned of the severity for Iran sanctions. The US also imposed sanctions on Venezuela following the election last weekend, stirring further fears over supply disruption in the region. Elsewhere, gold prices are buoyed as the dollar retreats from YTD highs. Elsewhere, London copper rise for the second day with prices underpinned as the US-Sino trade war fears fade (for now).

In other trade/geopol overnight news, US Trade Representative Lighthizer said on Monday that he still sees the need of real work to achieve changes in China and noted that intellectual property issues are more important than the trade gap. The US Commerce Department announced it will impose anti-dumping rate of 200% and countervailing rate of 256% on some cold-rolled steel from Vietnam produced using substrate originating from China. Japan and Russia notified the WTO of potential tariff retaliation for US President Trump’s steel and aluminium tariffs. Japan reportedly may impose USD 440mln and Russia may impose USD 538mln in tariffs on US goods.

Italy’s M5S leader Di Maio said that Conte will be premier of the government. In related news, Italy’s President Mattarella reportedly expressed concerns with the 5SM/League fiscal plan and is said to need time to mull the PM choice. Furthermore, Mattarella was reported to demand leaders of Italy’s Lower and Upper House to attend a meeting on Tuesday. There were reports that President Mattarella could pick the new Premier on Wednesday or Thursday.

In overnight central banking news:

- BoJ Governor Kuroda said will take into consideration side effects including impact on financial institutions when guiding monetary policy currently, while he added that he is not seeing conditions rife to study timing of exit and that the BoJ will not exit easy policy prior to reaching 2% price target.

- BoE’s Vlieghe (Neutral) said his central projection will require one or two quarter point rate increases per year over the three-year forecast period. This is a more aggressive path than the BoE’s conditioning path of rates derived from yields in the May QIR which assumes just under three quarter point rate increases over the three-year forecast period.

- BoE’s Carney (Neutral) reiterated that Q1 slowdown is likely due to idiosyncratic and temporary factors, but it is right to with for more data.

- ECB’s Liikanen (Neutral) has expectation of rates to stay low for an extended period after QE ends.

- Fed’s Kashkari (non-voter, dove) said wage growth has not picked up and that there may still be slack in the jobs market, while he also suggested the need to allow the economy to continue strengthening.

- ECB is purchasing the same amount of Italian government bonds under QE programme, as according to traders at primary dealers.

There is little on the calendar today, with the only expected data the Richmond Fed Manufacturing Survey at 10am ET. AutoZone, Eaton Vance, TJX, and Intuit are among companies reporting earnings. Attention will be focused on the ongoing trade talks, the South Korean president’s visit to D.C., and oil’s continued climb amid a new wave of U.S. sanctions on Venezuela.

Bulletin Healdine Summary from RanSquawk

- China confirmed they are to cut car import tariffs to 15% (Prev. 25%) and car part import duty to 6%, which will take effect on July 1st

- TRY suffered an abrupt reversal to plumb fresh record lows against the dollar

- Looking ahead, highlights include UK/EU trade talks and US 2yr Note Auction

Market Snapshot

- S&P 500 futures up 0.2% to 2,737.75

- Brent futures up 0.4% to $79.50/bbl

- Gold spot up 0.1% to $1,293.91

- U.S. Dollar Index down 0.3% to 93.38

- STOXX Europe 600 up 0.07% to 396.16

- MXAP up 0.1% to 174.45

- MXAPJ up 0.2% to 569.13

- Nikkei down 0.2% to 22,960.34

- Topix down 0.2% to 1,809.57

- Hang Seng Index up 0.6% to 31,234.35

- Shanghai Composite up 0.02% to 3,214.35

- Sensex up 0.1% to 34,663.51

- Australia S&P/ASX 200 down 0.7% to 6,041.87

- Kospi up 0.2% to 2,465.57

- German 10Y yield rose 4.2 bps to 0.565%

- Euro up 0.2% to $1.1811

- Italian 10Y yield rose 15.9 bps to 2.127%

- Spanish 10Y yield fell 7.2 bps to 1.436%

Top Overnight News from Bloomberg

- China confirms it is cutting import taxes on autos to 15% from 25%

- WSJ: U.S. and China have agreed outline on a deal to settle dispute over ZTE, according to people familiar

- Dodd-Frank: House Repubicans to vote on Senate compromise as early as today; broader set of House-passed rollbacks will get a vote later this year

- Fed’s Kashkari: yield curve could invert by end of year; paying close attention to long-end of UST curve

- BOE’s Vlieghe: sees one or two 25bps rate hikes a year for the next three years

- President Donald Trump retreated from imposing tariffs on billions of dollars worth of Chinese goods because of White House discord over trade strategy and concern about harming negotiations with North Korea, according to people briefed on the administration’s deliberations

- Britain could be facing another vote in 2018 as Prime Minister Theresa May may be unable to find a way to navigate between those in her party who want Britain to leave the EU’s customs union and the majority in Parliament that wants the opposite

- French President Emmanuel Macron’s trip to Russia this week once threatened to split France from its European allies. Now it’s part of a wider European effort to tie President Vladimir Putin to the Iran nuclear accord

- The Italian government’s borrowing costs have surged to inauspicious territory as the nation is getting punished in the bond market over the incoming populist government coalition. Novice Prime Minister may face rival puppet-masters

- Foreign Secretary Boris Johnson has urged Theresa May not to contemplate calling another early election, after reports that members of parliament are preparing for a snap vote later this year due to Brexit turmoil

- Turkey is paying more than Senegal on its debt, even though it has a higher credit rating and its economy is 60 times bigger

- Fed’s Minneapolis President Kashkari says U.S. job creation despite lack of evidence that inflation is picking up is an argument for allowing the economy to continue to grow. Philadelphia Fed President Patrick Harker says “in general, on average, the economy is just clicking along just fine”

- Confidence about the economic strength of Poland, Hungary and the Czech Republic had helped mute the pain of dollar gains that battered their developing peers. But on Monday, Italy’s plans to embark on a populist fiscal path landed them among the biggest currency decliners in emerging markets

Asian stocks traded mostly subdued amid holiday closures and a lack of fresh catalysts, which saw sentiment wane from the prior day’s trade-related gains that boosted the DJIA above the 25k level for the first time since March. ASX 200 (-0.7%) weakened amid broad losses across all sectors and with telecoms underperforming on continued woes for Telstra shares, while Healthscope was the worst performer after it flagged impairment charges. Nikkei 225 (-0.2%) traded indecisive as exporters suffered from a firmer currency and with Sony shares pressured after its 3-year strategy and targets was met with disappointment, while Shanghai Comp. (flat) was subdued following a continued net neutral liquidity position by the PBoC and with market closures in both Hong Kong and South

Korea adding to the humdrum tone, although baby-related stocks were underpinned on prospects China could relax its child-policy restrictions. Finally, 10yr JGBs were lacklustre alongside an indecisive risk tone in Japan and with participants side-lined ahead of 20yr auction which eventually saw a mixed result, while a deluge of comments from BoJ Governor Kuroda also failed to spur price action as he kept to reiterations and suggested the BoJ is still far from an exit.

Top Asian News

- Singapore Bourse Sued by India Exchange in Futures Dispute

- Hyundai Motor Caves in to Elliott, Scraps $8.8 Billion Deal

- Hyflux Is Said to Weigh Court Protection for Creditor Talks

- Sony to Buy Out EMI Music Publishing for About $2 Billion

- Indonesia’s Stock Rout Claims Another Victim: The IPO Market

- Erdogan Imperils Turkey Rating as Bonds Sink Below Senegal’s

Major European equity bourses are trading flat as German traders return to their desks following a public holiday. The outperforming bourse is currently the IBEX (+0.6%), closely followed by the FTSE MIB (+0.4%) which is benefitting from some much desired political ‘stability’ following the confirmation of the name of the proposed next Premier, Giuseppe Conte; subject to approval from Mattarella. European automotive names have been boosted on the news that China is to cut their car import duties to 15% from 25% (Volkswagen (VOW3 GY) +1.0%, Daimler (DAI GY) +1.2%, BMW (BMW GY) +1.9%). In terms of sector specifics, France’s head of ARCEP saying he could be open to telecom sector consolidation has lead to strength for names such as Orange (ORA FP) +3.5%, Bouygues (EN FP) +3.6% and Iliad (ILD FP) +4.4%. In stock specific news IAG (IAG LN) is set to offer NOK 330/share for Norwegian Air, an acquisition amounting to EUR 1.52bln.

Top European News

- Deutsche Bank Unit Sells $600 Million Seadrill Claim in Days

- Italy Bonds Rise as Yields Retreat From the Highest Since 2017

- French Telecom Regulator Says He’s More Open to Mergers

- Could Britain Have an Election in 2018? It’s Not Impossible

In FX, there was more USD retracement from best levels for the index amidst a broad Usd pull-back vs counterparts that looks more technical than fundamental at this stage overall. The DXY is trying to stabilise after a dip below 93.300, but remains well off the 94.064 ytd peak set on Monday. GBP: Just shading the non-US dollars as top G10 performer after the first session of the BoE’s QIR testimony in front of the TSC featuring MPC member Vlieghe who delivered a more hawkish policy outlook than the mainstream with a preference for 1 to 2 quarter point hikes per annum over the 3 year forecast horizon (largely based on less slack in the UK economy). Cable extended recovery gains above 1.3400 in response and almost reached 1.3500 before losing momentum ahead of Governor Carney’s appearance. NZD/AUD/CAD: As noted, all gleaning more from the general Greenback retreat, with the Kiwi back above 0.6950 and Aud briefly revisiting 0.7600+ territory as the Loonie tested 1.2750 with oil prices providing another boost. EM: Consolidation, short-covering and position paring from arguably oversold levels have combined to lift beleaguered currencies from the depths, with the Zar and Mxn regaining various degrees of composure around 12.20 vs 12.69 and 19.74 vs 19.84 (and even high in some cases at worst). However, after a similar recovery rally the Try suffered an abrupt reversal to plumb fresh record lows vs. the dollar circa 4.63.

In commodities, prices are broadly higher during recent trade in which crude extended on gains boosted by a softer greenback with geopolitics also remaining at the fore after US Secretary of State Pompeo warned of the severity for Iran sanctions. The US also imposed sanctions on Venezuela following the election last weekend, stirring further fears over supply disruption in the region. Elsewhere, gold prices are buoyed as the dollar retreats from YTD highs. Elsewhere, London copper rise for the second day with prices underpinned as the US-Sino trade war fears fade (for now).

Looking at the day ahead, in the US the only release scheduled is the May Richmond Fed PMI. Politics should play a greater role with the next round of Brexit negotiations beginning in Brussels, and South Korean President Moon Jae-in due to visit Washington to meet President Trump, in part to discuss whether next month’s US / North Korea summit is still going ahead.

US Event Calendar

- 10am: Richmond Fed Manufact. Index, est. 10, prior -3

DB’s Jim Reid concludes the overnight wrap

It’s certainly been a 24 hours of split trading with the split depending on whether your assets were more sensitive to hopes of a more positive outcome in the global trade war spat or more sensitive to a worsening Italian risk situation. Indeed Italian debt had what can only be called a “mini-shocker” yesterday after increased speculation about the so called issuance of “mini-BOTs” and warnings from Fitch on their debt path. However neither story was new news and the sell-off just seemed to be a building up of the pressure of these and other related issues over recent days.

2y yields underperformed (+16.8bps) versus 10yr (+15.7bps) and 30y yields (+10.9bps). Remarkably 2y yields are up 59.4bps since May 3rd and now the highest since July 2015. Over the same period 2y Bunds are -3.9bps lower for comparison. The 2y BTP/Bund spread is now at 88.1bps and approaching the 2017 high of 99bps. This was as low as 22bps back in February. 10 year Italian yields (2.371%) are now within a couple of basis points from their highest level since November 2014.

Overnight DB’s Clemente De Lucia and Mark Wall have published an update putting the current Italian risk in some perspective. They note that relative to 2011-2012 Italy has achieved some fundamental improvements. In particular 1) a move from current account deficit to surplus and 2) the terming out of debt. They also note that the Five Star-League final programme for government does not directly question Italy’s membership of the single currency. However, the proposed fiscal and structural policies, including the mini-BOT, are a challenge to EU rules and the Brussels orthodoxy. This means policy clash and uncertainty. If fully implemented, our economists think that Italy’s debt trajectory will no longer be downward sloping. So much depends on the new administration’s policy choices and their ability to pursue them due to the constraints from the President, the constitution, the parliamentary process and of course the markets and the EU. So lots of moving parts. In the report they note that the 2019 Budget is not due to be presented to Parliament until September 20th so plenty of time for markets to go through their whole range of emotions over Italian risk. See the note for more details.

Following on, Italy’s League Party leader Mr Salvini noted in a Facebook video that “we’ve swallowed too many yes sirs” and that Italy must have the freedom to say “no” to Paris, Berlin and Brussels. He added that “…enough is enough, cuts can kill, austerity can kill….and European limits can kill”. Elsewhere, Mr Salvini has confirmed that he has proposed Florence University law professor Giuseppe Conte to be Italy’s new Premier, while President Mattarella is expected to meet the Senate and Lower house speakers today to discuss next steps.

In equities yesterday, Italy’s FTSE MIB (-1.52%) looked as if it materially underperformed peers, but most of this was due to it being a big ex-dividend day for the index. After adjusting for the 20 companies that have gone ex-div, the underlying index change was closer to -0.3%. Nonetheless, the 5y senior CDS for Italian banks did widened 6-8bps vs. iTraxx Senior Financials at +3.8bp. Elsewhere, the Stoxx 600 (+0.30%) and US bourses (S&P +0.74%; Dow +1.21%; Nasdaq +0.54%) were all higher as trade tensions eased following US Secretary Mnuchin’s comments around putting the trade war and tariffs on hold. The S&P closed at a 9 week high with all sectors up and gains led by the industrials and telco. sectors.

Over in government bonds, yields on UST 10y were little changed (+0.4bp) while Gilts (-2.5bp) and Bunds (-5.6bp) seemed to benefit from the flight to safety effect, particularly for Bunds which rallied despite Germany’s markets being off on holiday yesterday. In FX, the US dollar index firmed marginally (+0.04%) while the Euro pared back losses to close up for the first time in six days (+0.16%). Elsewhere, WTI oil rose 1.35% to $72.24/bbl ahead of IEA talks with major oil producers on collapsing Venezuelan output.

This morning in Asia, markets are broadly lower with the Nikkei (-0.07%), Shanghai Comp. (-0.41%) and ASX 200 (-0.84%) all down while the Hang Seng and Kospi are closed for holidays. In Japan, BOJ’s Kuroda told the Parliament that “we’ll patiently pursue powerful monetary easing to achieve 2% inflation” and that we’ll “guide monetary policy taking into account its side effects such as its impact on financial institutions”. Over in China, the State Council is planning to scrap all limits on how many children a family can have, potentially as early as 4Q18. Notably, Bloomberg noted that the number of births in China rose c8% in 2016 after the government shifted the policy from one child to two in 2015, but then births fell 3.5% in 2017. Finally, a group of Western and Chinese journalists are arriving in North Korea today to witness the closure of its nuclear test site.