GOLD: $1304.20 DOWN $0.80 (COMEX TO COMEX CLOSINGS)

Silver: $16.53 DOWN 13 CENTS (COMEX TO COMEX CLOSINGS)

Closing access prices:

Gold $1301.50

silver: $16.53

For comex gold:

For comex gold:

MAY/

TODAY OPTIONS EXPIRE AT THE COMEX/ON MAY 31 THEY EXPIRE AT THE LBMA/OTC CONTRACTS

SO GOLD/SILVER WILL BE WHACKED FROM TODAY UNTIL JUNE 1.

NUMBER OF NOTICES FILED TODAY FOR MAY CONTRACT:1 NOTICE(S) FOR 100 OZ.

TOTAL NOTICES SO FAR 730 FOR 73000 OZ (2.270 tonnes)

For silver:

MAY

813 NOTICE(S) FILED TODAY FOR

4,065,000 OZ/

Total number of notices filed so far this month: 6990 for 34,950,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: BID $7324/OFFER $7425: DOWN $198(morning)

Bitcoin: BID/ $7395/offer $7495: DOWN $127 (CLOSING/5 PM)

end

First Shanghai gold fix comes at 10 pm est

The second Shanghai gold fix: 2:15 pm

First Shanghai gold fix gold: 10 pm est: 1306.00

NY price at the same time: 1302.0

PREMIUM TO NY SPOT: $4.00

Second gold fix early this morning: 1308.80

USA gold at the exact same time:1302.20

PREMIUM TO NY SPOT: $6.60

AGAIN, SHANGHAI REJECTS NEW YORK PRICING.

WE WILL NOT PROVIDE LONDON FIXES AS THEY ARE NOT ACCURATE AS TO WHAT IS GOING ON AT THE SAME TIME FRAME.

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total OPEN INTEREST ROSE BY AN ATMOSPHERIC 6049 CONTRACTS FROM 200,325 RISING TO 206,374 WITH YESTERDAY’S 27CENT GAIN IN SILVER PRICING. WE ARE NOW WITNESSING OUR USUAL AND CUSTOMARY COMEX LONG LIQUIDATION AS WE ENTERED INTO THE ACTIVE DELIVERY MONTH OF MAY AS LONGS PACK THEIR BAGS AND MIGRATE OVER TO LONDON. WE WERE NOTIFIED THAT WE HAD A HUMONGOUS SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP : 3838 EFP’S FOR JULY AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE OF3838 CONTRACTS. WITH THE TRANSFER OF3838CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE3838EFP CONTRACTS TRANSLATES INTO 19.190 MILLION OZ ACCOMPANYING:

1.THE 27 CENT GAIN IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES STANDING FOR MAY COMEX DELIVERY. (35.630 MILLION OZ)

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF MAY: (FINAL)

36,729 CONTRACTS (FOR 19 TRADING DAYS TOTAL 36,729 CONTRACTS) OR 183.645 MILLION OZ: (AVERAGE PER DAY: 1933 CONTRACTS OR 9.665 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH: 183.645MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 26.22% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)

ACCUMULATION IN YEAR 2018 TO DATE SILVER EFP’S: 1,328.9 MILLION OZ.

ACCUMULATION FOR JAN 2018: 236.879 MILLION OZ

ACCUMULATION FOR FEB 2018: 244.95 MILLION OZ

ACCUMULATION FOR MARCH 2018: 236.67 MILLION OZ

ACCUMULATION FOR APRIL 2018: 385.75 MILLION OZ

RESULT: WE HAD A HUMONGOUS SIZED INCREASE IN COMEX OI SILVER COMEX OF 6049 WITH THE 27CENT GAIN IN SILVER PRICE. WE HAVE NOW ENTERED THE NEW ACTIVE MONTH OF MAY. THE CME NOTIFIED US THAT IN FACT WE HAD AN HUMONGOUS SIZED EFP ISSUANCE OF 3838 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) . FROM THE CME DATA: 3838 EFP CONTRACTS FOR JULY, AND ZERO FOR ALL OVER MONTHS FOR A DELIVERABLE FORWARD CONTRACT OVER IN LONDON WITH A FIAT BONUS (TOTAL: 3838). TODAY WE GAINED9887 TOTAL OI CONTRACTS ON THE TWO EXCHANGES: i.e.3838 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH AN INCREASE OF 6049 OI COMEX CONTRACTS. AND ALL OF THIS HAPPENED WITH THE 27 CENT GAIN IN PRICE OF SILVER AND A CLOSING PRICE OF $16.66 WITH RESPECT TO YESTERDAY’S TRADING. YET WE STILL HAVE A GIGANTIC AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY IN THIS ACTIVE MAY DELIVERY MONTH. IT SURE LOOKS LIKE A FAILED BANKER SHORT COVERING EXERCISE!!

In ounces AT THE COMEX, the OI is still represented by OVER 1 BILLION oz i.e. 1.032 MILLION OZ TO BE EXACT or 148% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT MAY MONTH/ THEY FILED AT THE COMEX:813 NOTICE(S) FOR 4,065,000 OZ OF SILVER

IN SILVER, WE HAVE NOW SET THE NEW RECORD OF OPEN INTEREST AT 243,411 AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $16.51 ON APRIL 9.2018.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH: 27 MILLION OZ , APRIL: 2.485 MILLION OZ AND MAY: 35.630 MILLION OZ

- HUGE RECORD OPEN INTEREST IN SILVER 243,411 CONTRACTS (OR 1.217 BILLION OZ/ SET APRIL 9/2018

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017

- RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ (FINAL)

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT). IT ALSO LOOKS LIKE BANKER CAPITULATION IN SILVER AS THEY STRUGGLE TO REMOVE SOME OF THEIR HUGE OBLIGATIONS.

In gold, the open interest DROPPED BY A GIGANTIC SIZED17,559CONTRACTS DOWN TO 478,572WITH THE DESPITE THE GOOD GAIN IN THE GOLD PRICE/YESTERDAY’S TRADING (GAIN OF $12.40). WE ARE NOW IN THE NON ACTIVE DELIVERY MONTH OF MAY. NO DOUBT THE BOYS ARE CASHING IN THEIR COMEX LONGS TO BEGIN THE PROCESS TO MOVE INTO LONDON FORWARDS. THE CME RELEASED THE DATA FOR EFP ISSUANCEAND IT TOTALED A STRONG SIZED 12,839CONTRACTS : JUNE SAW THE ISSUANCE OF 12,491 CONTRACTS , MAY SAW THE ISSUANCE OF 0 CONTRACTS AND AUGUST SAW THE ISSUANCE OF:348 CONTRACTS WITH ALL OTHER MONTHS ZERO. The new OI for the gold complex rests at 478,572. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE A FAIR SIZED OI LOSS IN TOTAL CONTRACTS ON THE TWO EXCHANGES: 17,559 OI CONTRACTS DECREASED AT THE COMEX AND A HUMONGOUS SIZED 12,839 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON.THUS TOTAL OI LOSS: 4720CONTRACTS OR 472,000 OZ = 14.68 TONNES. AND ALL OF THIS OCCURRED WITH A GOOD GAIN OF $12.40

YESTERDAY, WE HAD 10,136 EFP’S ISSUED.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF MAY : 185,596 CONTRACTS OR 18,559,600 OZ OR 577.26 TONNES (19 TRADING DAYS AND THUS AVERAGING: 9,768 EFP CONTRACTS PER TRADING DAY OR 976,800 OZ/ TRADING DAY),,

TO GIVE YOU AN IDEA AS TO THE HUGE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 19 TRADING DAYS IN TONNES: 577.26 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2017, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 2555 TONNES

THUS EFP TRANSFERS REPRESENTS 577.26/2550 x 100% TONNES = 22.63% OF GLOBAL ANNUAL PRODUCTION SO FAR IN APRIL ALONE.*** THE ACCUMULATION OF EFP CONTRACTS IS RISING PER MONTH.

ACCUMULATION OF GOLD EFP’S YEAR 2018 TO DATE: 3,334.90* TONNES *SURPASSED ANNUAL PROD’N

ACCUMULATION OF GOLD EFP’S FOR JANUARY 2018: 653.22 TONNES

ACCUMULATION OF GOLD EFP’S FOR FEBRUARY 2018: 649.45 TONNES

ACCUMULATION OF GOLD EFP’S FOR MARCH 2018: 741.89 TONNES (22 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR APRIL 2018: 713.84 TONNES (21 TRADING DAYS)

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A CONSIDERABLE SIZED DECREASE IN OI AT THE COMEX OF 17,559 DESPITETHE $12.40 GAIN IN PRICE // GOLD TRADING YESTERDAY ($12.40 RISE). WE ALSO HAD AN HUMONGOUS SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 12,839 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 12,839 EFP CONTRACTS ISSUED, WE HAD A GOOD SIZED NET LOSS OF 4720CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

12,839 CONTRACTS MOVE TO LONDON AND 17,559 CONTRACTS DECREASED AT THE COMEX. (in tonnes, the LOSS in total oi equates to 14.68TONNES). ..AND BELIEVE IT OR NOT BUT ALL OF THESE OCCURRED AT THE COMEX WITH A GAIN OF $12.40 IN TRADING!!!.

we had: 1 notice(s) filed upon for 100 oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD...

WITH GOLD UP THIS WEEK BUT DOWN 80 CENTS TODAY: / A HUGE CHANGES IN GOLD INVENTORY AT THE GLD/ A WITHDRAWAL OF 3.54 TONNES/INVENTORY RESTS AT 848.50 TONNES

Inventory rests tonight: 848.50 tonnes.

SLV/

WITH SILVER UP ON THE WEEK BUT DOWN 13 CENTS TODAY A CHANGES IN THE SILVER INVENTORY AT THE SLV INVENTORY/ A WITHDRAWAL OF 1.035 MILLION OZ.

/INVENTORY RESTS AT 319.968 MILLION OZ/ AND WITH A HUGE DEMAND FOR SILVER AT THE COMEX??

end

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER ROSE BY A CONSIDERABLE SIZED 6047 CONTRACTS from 200,325 UP TO 206,374 (AND, CLOSER TO THE NEW COMEX RECORD SET /APRIL 9/2017 AT 243,411/SILVER PRICE AT THAT DAY: $16.53). THE PREVIOUS RECORD OTHER THAN WAS ESTABLISHED AT: 234,787, SET ON APRIL 21.2017 OVER ONE YEAR AGO. THE PRICE OF SILVER ON THAT DAY: $17.89.OUR CUSTOMARY MIGRATION OF COMEX LONGS MORPH INTO LONDON FORWARDS CONTINUES AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE: , 0 EFP CONTRACTS FOR MAY (WE DO NOT GET A LOOK AT THESE CONTRACTS AS IT IS PRIVATE BUT THE CFTC DOES AUDIT THEM), AND3838 EFP’S FOR JULY AND ALL OTHER MONTHS ZERO. TOTAL EFP ISSUANCE: 3838 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI GAIN AT THE COMEX OF 604 9CONTRACTS TO THE 3838 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A FAIR SIZED GAIN OF 9887 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES: 30.75 MILLION OZ!!! AND THIS OCCURRED WITH A 27 CENT GAIN IN PRICE . THE BANKERS ORCHESTRATED THEIR RAID THROUGHOUT LAST WEEK DESPERATELY TRYING TO PARE THEIR GIGANTIC OPEN INTEREST SHORT ON BOTH EXCHANGES BUT TO NO AVAIL. JUDGING BY THE RECORD NUMBER OF EFP ISSUANCE DURING LAST MONTH OF APRIL AT 385.75 MILLION OZ AND THE TOTAL OI GAIN ON THE TWO EXCHANGES, THE CONSTANT RAIDS, LIKE YESTERDAY ARE NOW BEING CALLED UPON BY OUR BANKER FRIENDS IN AN ATTEMPT TO SHAKE AS MANY SILVER LEAVES FROM THE SILVER TREE AS POSSIBLE AND JUDGING BY THE RESULTS TO YESTERDAYS ACTION THEY WERE NOT AT ALL SUCCESSFUL.

RESULT: A GIGANTIC SIZED INCREASE IN SILVER OI AT THE COMEX DESPITE THE 27 CENT GAIN IN SILVER PRICING YESTERDAY. BUT WE ALSO HAD ANOTHER STRONG SIZED 3838EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR APRIL, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)FRIDAY MORNING/THURSDAY NIGHT: Shanghai closed DOWN 13.35 points or 0.42% /Hang Sang CLOSED DOWN 172.37 points or 0.56% / The Nikkei closed UP 13.78 POINTS OR 0.06% /Australia’s all ordinaires CLOSED DOWN .05% /Chinese yuan (ONSHORE) closed UP at 6.3893/Oil DOWN to 69.04 dollars per barrel for WTI and 76.84 for Brent. Stocks in Europe OPENED ALL GREEN/MIXED. ONSHORE YUAN CLOSED DOWN AT 6.3883 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.3812/ONSHORE YUAN TRADING WEAKER AGAINST OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING MUCH WEAKER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW LOOKS LIKE A FULL TRADE WAR IS BEGINNING/

/NORTH KOREA/SOUTH KOREA

i)North Korea/South Korea/USA

That did not take long: North Korea is now crawling trying to desperately convince Trump for the summit

( zerohedge

ii)Trump gloats that Kim wants to come back to the table:

( zerohedge)

iii)Mattis states that the meeting may still be on:

( zerohedge)

b) REPORT ON JAPAN

3 c CHINA

China/USA

Trump will now take a much harder line on China after the summit collapse

( zerohedge)

ii)China/USA

Trump will now take a much harder line on China after the summit collapse

( zerohedge)

4. EUROPEAN AFFAIRS

ITALY

i)The 10 yr Italian bond yield rises to 2.47 this morning triggering contagion problems

( zerohedge)

ii)The European crisis is back: European mid morning trading:

Italian and Spanish bonds crash amid political chaos

( zerohedge)

iii)This is scary: Moody’s has just put Italy on a downgrade review and their current Baa2 rating may be knocked a couple of notches to junk status…that will be a death blow to Italy.

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

( zerohedge)

6 .GLOBAL ISSUES

Moody’s now warns of a huge junk bond default coming as interest rates rise

( Moody’s /zerohedge)

7. OIL ISSUES

The price of oil plunges after the Saudi and Russia state that they will likely boost supply in the second half of the year.

( zerohedge)

8. EMERGING MARKET

9. PHYSICAL MARKETS

10. USA stories which will influence the price of gold/silveri)

i)USA DATA

Soft data, U. of Michigan sentiment slumps near 2018 lows with income expectations faltering

( zerohedge)

ii)SWAMP STORIES

a)An outline of how the genesis of the phony Russian collusion started with the spy Halper the main instigator

( zerohedge)

b)Yesterday the Dept of Justice briefs Congress on the FBI informant

( zerohedge)

Trading Volumes on the COMEX

PRELIMINARY COMEX VOLUME FOR TODAY: 366,712 contracts

CONFIRMED COMEX VOL. FOR YESTERDAY: 549,594 contracts

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

And now for the wild silver comex results.

And now for the wild silver comex results.

Total silver OI ROSE BY A HUMONGOUS SIZED 6049CONTRACTS FROM 200,325 UP TO 206,374 (AND CLOSER TO THE NEW RECORD OI FOR SILVER SET APRIL 9.2018/ 243,411 CONTRACTS) WITH THE 27 CENT GAIN IN SILVER PRICING/ YESTERDAY. SINCE WE ARE NOW INTO THE ACTIVE DELIVERY MONTH OF MAY. WE WERE INFORMED THAT WE HAD A HUMONGOUS SIZED 3838 EFP CONTRACT ISSUANCE FOR JULY AND ZERO FOR ALL OTHER MONTHS. THESE EFPS WERE ISSUED TO COMEX LONGS WHO RECEIVED A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. THE TOTAL EFP’S ISSUED: 3838. ON A NET BASIS WE GAINED9887 SILVER OPEN INTEREST CONTRACTS AS WE OBTAINED A 6049CONTRACT GAIN AT THE COMEX COMBINING WITH THE ADDITION OF 3838OI CONTRACTS NAVIGATING OVER TO LONDON.

NET GAIN ON THE TWO EXCHANGES: 9887 CONTRACTS

AMOUNT STANDING FOR SILVER AT THE COMEX

We are now in the active delivery month of MAY and here the front month ROSE BY 729 contracts RISING TO 949 contracts. We had 25notices filed upon yesterday so we SURPRISINGLY GAINED A MONSTROUS 754 contracts or 3,770,000 additional ounces will stand for delivery in this active delivery month of May AS SOMEBODY AGAIN WAS DESPERATE FOR PHYSICAL SILVER ON THIS SIDE OF THE POND AND A HUGE AMOUNT WAS NEEDED STAT.

June saw a GAIN of 33 contracts to stand at 753. The next big delivery month for silver is July and here the OI GAINED 4746 contracts UP to 140,899. The next active delivery month after July for silver is September and here the OI ROSE by 994 contracts UP to 30,542

We had 813 notice(s) filed for 4,065,000 OZ for the MAY 2018 contract for silver

INITIAL standings for MAY/GOLD

MAY 25/2018.

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz |

nil OZ

|

| Deposits to the Dealer Inventory in oz | NIL oz |

| Deposits to the Customer Inventory, in oz | nil OZ |

| No of oz served (contracts) today |

1 notice(s)

100 OZ

|

| No of oz to be served (notices) |

1 contracts

(100 oz)

|

| Total monthly oz gold served (contracts) so far this month |

730 notices

72900 OZ

2.273 TONNES

|

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

For MAY:

Today, 0 notice(s) were issued from JPMorgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equates to 1 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped/ Received) by j.P.Morgan customer account.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

To calculate the INITIAL total number of gold ounces standing for the MAY. contract month, we take the total number of notices filed so far for the month (730) x 100 oz or 73000 oz, to which we add the difference between the open interest for the front month of MAY. (2 contracts) minus the number of notices served upon today (1 x 100 oz per contract) equals 73,100 oz, the number of ounces standing in this active month of APRIL (2.2737 tonnes)

Thus the INITIAL standings for gold for the MAY contract month:

No of notices served (730 x 100 oz) + {(2)OI for the front month minus the number of notices served upon today (1 x 100 oz )which equals 73,100 ozstanding in this active delivery month of MAY . THERE ARE 8.923 TONNES OF REGISTERED GOLD AVAILABLE FOR DELIVERY SO FAR.

WE LOST 0 OZ OF GOLD (0 CONTRACTS) STANDING IN THIS NON ACTIVE DELIVERY MONTH OF MAY

IN THE LAST 18 MONTHS 74 NET TONNES HAS LEFT THE COMEX.

end

And now for silver

AND NOW THE APRIL DELIVERY MONTH

MAY INITIAL standings/SILVER

| Silver | Ounces |

| Withdrawals from Dealers Inventory | nil oz |

| Withdrawals from Customer Inventory |

nil oz

CNT

|

| Deposits to the Dealer Inventory |

nil

oz

|

| Deposits to the Customer Inventory |

nil

oz

|

| No of oz served today (contracts) |

813

CONTRACT(S)

(4,065,000 OZ)

|

| No of oz to be served (notices) |

136 contracts

(680,000 oz)

|

| Total monthly oz silver served (contracts) | 6990 contracts

(34,950,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

we had 0 inventory movement at the dealer side of things

total dealer deposits: nil oz

we had 0 deposits into the customer account

i) Into JPMorgan: nil oz

*** JPMorgan for most of 2017 and in 2018 has adding to its inventory almost every single day.

JPMorgan now has 140 million oz of total silver inventory or 52.3% of all official comex silver. (140 million/268 million)

ii)everybody else: 0

total customer deposits today: nil oz

we had 0 withdrawals from the customer account;

total withdrawals; nil oz

we had 1

i) adjustments

out of Delaware: 5260 oz was adjusted out of the dealer account and this landed into the customer account of Delaware

total dealer silver: 69.151 million

total dealer + customer silver: 270.040 million oz

The total number of notices filed today for the MAY. contract month is represented by 813 contract(s) FOR 4,065,000 oz. To calculate the number of silver ounces that will stand for delivery in MAY., we take the total number of notices filed for the month so far at 6990 x 5,000 oz = 34,885,000 oz to which we add the difference between the open interest for the front month of MAY. (949) and the number of notices served upon today (813 x 5000 oz) equals the number of ounces standing.

.

Thus the INITIAL standings for silver for the MAY contract month: 6990(notices served so far)x 5000 oz + OI for front month of MAY(949) -number of notices served upon today (813)x 5000 oz equals 35,630,000 ozof silver standing for the MAY contract month

WE GAINED 754 CONTRACTS OR AN ADDITIONAL 3,770,000 OZ WILL STAND AT THE COMEX AS SOMEBODY WAS IN URGENT NEED OF A HUGE QUANTITY OF PHYSICAL SILVER ON THIS SIDE OF THE POND.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

ESTIMATED VOLUME FOR TODAY: 70,480CONTRACTS

CONFIRMED VOLUME FOR YESTERDAY:98,406CONTRACTS

YESTERDAY’S CONFIRMED VOLUME OF 98,406 CONTRACTS EQUATES TO 492 MILLION OZ OR 68.3% OF ANNUAL GLOBAL PRODUCTION OF SILVER

COMMODITY LAW SUGGESTS THAT OPEN INTEREST SHOULD NOT BE MORE THAN 3% OF ANNUAL GLOBAL PRODUCTION. THE CROOKS ARE SUPPLYING MASSIVE PAPER TRYING TO KEEP SILVER IN CHECK.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price at that day at $18.42

The previous record was 224,540 contracts with the price at that time of $20.44

end

NPV for Sprott

1. Sprott silver fund (PSLV): NAV FALLS TO -2.16% (MAY24/2018)

2. Sprott gold fund (PHYS): premium to NAV RISES TO -0.30% to NAV (MAY 24/2018 )

Note: Sprott silver trust back into NEGATIVE territory at -2.16%-/Sprott physical gold trust is back into NEGATIVE/ territory at -0.30%/Central fund of Canada’s is still in jail but being rescued by Sprott.

Sprott WINS hostile 3.1 billion bid to take over Central Fund of Canada

(courtesy Sprott/GATA)

3.SPROTT CEF.A FUND (FORMERLY CENTRAL FUND OF CANADA): NAV FALLS TO -2.22%: NAV 13.51/TRADING 13.23//DISCOUNT 2.12.

END

And now the Gold inventory at the GLD/

May 25/WITH GOLD UP ON THE WEEK BUT DOWN 80 CENTS TODAY: WE HAD A HUGE 3.54 TONNES OF GOLD WITHDRAWAL FROM THE CROOKED GLD/

MAY 24/WITH GOLD UP $12.40/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 852.04

MAY 22/WITH GOLD UP $1.05/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 852.04 TONNES

MAY 21/WITH GOLD DOWN 50 CENTS/A HUGE CHANGE IN GOLD INVENTORY/A WITHDRAWAL OF 3.24 TONNES FORM GLD INVENTORY/INVENTORY RESTS AT 852.04 TONNES

MAY 18/WITH GOLD UP $1.80/A HUGE CHANGE IN GOLD INVENTORY AT THE GLD/ A DEPOSIT OF 9.11 TONNES INTO GLD INVENTORY/INVENTORY RESTS AT 865.28 TONNES/

GLD WAS ONE MASSIVE FRAUD

May 17/WITH GOLD DOWN $1.75/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 856.17 TONNES

MAY 16./WITH GOLD UP $1.05: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 856.17 TONNES

MAY 15/WITH GOLD DOWN $27.35, THE CROOKS WITHDREW 10 TONNES OF GOLD FROM THE GLD WHICH WAS USED IN THE RAID TODAY/INVENTORY RESTS AT 856.17 TONNES

MAY 14/ WITH GOLD DOWN $2.35: A HUGE DEPOSIT OF 4.68 TONNES OF GOLD INTO THE GLD and then a withdrawal of 1.48 tonnes /INVENTORY RESTS AT 866.17

A net gain of 3.2 tonnes of gold.

MAY 11/WITH GOLD DOWN $1.75/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 862.96 TONNES/

MAY 10/WITH GOLD UP $9.60/A WITHDRAWAL OF 1.17 TONNES FROM THE GLD/INVENTORY RESTS AT 862.96 TONNES/SUCH CROOKS

MAY 9/WITH GOLD DOWN $0.55/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 864.13 TONNES

MAY 8/WITH GOLD DOWN $0.10/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 864.13 TONNES

MAY 7/WITH GOLD DOWN $0.55/ANOTHER WITHDRAWAL OF 1.47 TONNES OF GOLD FROM THE GLD/INVENTORY RESTS AT 864.13 TONNES

MAY 4/WITH GOLD UP $2.05/A WITHDRAWAL OF 1.13 TONNES OF GOLD FROM THE GLD/INVENTORY RESTS AT 865.60 TONNES

MAY 3/WITH GOLD UP $7.05/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 866.77 TONNES

MAY 2/WITH GOLD DOWN $1.15/ A HUGE WITHDRAWAL OF 4.43 TONNES FROM THE GLD/INVENTORY RESTS AT 866.77 TONNES

MAY 1/WITH GOLD DOWN $12.15/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 871.20 TONNES

APRIL 30/WITH GOLD DOWN $4.05/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 871.20 TONNES.

APRIL 27./WITH GOLD UP $5.90/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 871.20 TONNES/

APRIL 26/WITH GOLD DOWN $4.90/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 871.20 TONNES

APRIL 25/AFTER 9 CONSECUTIVE DAYS OF NO MOVEMENT OF GOLD INTO OUT OF THE GLD, WE HAD A HUGE DEPOSIT OF 5.31 TONNES OF GOLD INTO THE GLD/INVENTORY RESTS AT 871.20 TONNES.

APRIL 24./WITH GOLD UP $9.90, WE HAD NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 865.89 TONNES/

APRIL 23.2018/WITH GOLD DOWN $14.00/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 865.89 TONNES.

APRIL 20/WITH GOLD DOWN $10.20: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 865.89 TONNES

APRIL 19/WITH GOLD DOWN $4.25: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 865.89 TONNES/

APRIL 18/WITH GOLD UP $3.65: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 865.89 TONNES

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

MAY 25/2018/ Inventory rests tonight at 848.50 tonnes

*IN LAST 388 TRADING DAYS: 82.51 NET TONNES HAVE BEEN REMOVED FROM THE GLD

*LAST 338 TRADING DAYS: A NET 73.79 TONNES HAVE NOW BEEN ADDED INTO GLD INVENTORY.

end

Now the SLV Inventory/

May 25

MAY 24/WITH SILVER UP 27 CENTS/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 321.003 MILLION OZ/

MAY 22/WITH SILVER UP 6 CENTS/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 321.003 MILLION OZ/

MAY 21/ WITH SILVER UP 5 CENTS/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 321.003 MILLION OZ/

MAY 18/WITH SILVER DOWN 5 CENTS A SMALL CHANGE IN SILVER INVENTORY AT THE SLV/ A WITHDRAWAL OF 942,000 OZ/INVENTORY RESTS AT 321.003 MILLION OZ/

May 17/WITH GOLD UP 6 CENTS/A SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 471,000 OZ//INVENTORY RESTS AT 321.945 MILLION OZ/

MAY 16./WITH SILVER UP 10 CENTS/A HUGE DEPOSIT OF 1.883 MILLION OZ OF SILVER INTO THE SLV/INVENTORY RESTS AT 321.474 MILLION OZ

MAY 15/WITH SILVER DOWN 33 CENTS, NO CHANGES AT THE SLV; THE CROOKS COULD NOT BORROW ANY SILVER BECAUSE THERE IS NONE: INVENTORY RESTS AT 319.591 MILLION OZ

MAY 14/WITH SILVER DOWN 10 CENTS/A SMALL CHANGES IN SILVER INVENTORY AT THE SLV/ A WITHDRAWAL OF 858,000 FROM THE SLV/INVENTORY RESTS AT 319.591 MILLION OZ/

MAY 11/WITH SILVER DOWN 2 CENTS/THE CROOKS WITHDREW A MONSTROUS 2.824 MILLION OZ FROM THE SLV INVENTORY/INVENTORY RESTS AT 320.439 MILLION OZ/

MAY 10/WITH SILVER UP 22 CENTS/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 323.263 MILLION OZ/

MAY 9/WITH SILVER UP 6 CENTS/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 323.263 MILLION OZ/

MAY 8/WITH SILVER DOWN 2 CENTS:NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 323.263 MILLION OZ.

MAY 7/WITH SILVER FLAT: A BIG CHANGE IN SILVER INVENTORY AT THE SLV// A WITHDRAWAL OF 942,000 OZ OF SILVER FROM THE SLV INVENTORY/INVENTORY RESTS AT 323.263 MILLION OZ/

MAY4/WITH SILVER UP 5 CENTS/A BIG CHANGES IN SILVER INVENTORY AT THE SLV/ A DEPOSIT OF 1.224 MILLION OZ/INVENTORY RESTS AT 324.205 MILLION OZ/

MAY 2/WITH SILVER UP 24 CENTS/A HUGE CHANGE IN SILVER INVENTORY AT THE SLV// A DEPOSIT OF 6.082 MILLION OZ INTO THE SLV/INVENTORY RESTS AT 322.981 MILLION OZ/

MAY 1/WITH SILVER DOWN 24 CENTS/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 316.899 MILLION OZ/

APRIL 30/WITH SILVER DOWN 11 CENTS/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 316.899 MILLION OZ/

APRIL 27/WITH SILVER DOWN 5 CENTS/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 316.899 MILLION OZ/

APRIL 26/WITH SILVER DOWN 2 CENT/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 316,899 MILLION OZ/

APRIL 25./WITH SILVER DOWN 18 CENTS/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 316.899 MILLION OZ/

APRIL 24./WITH SILVER UP 8 CENTS/SOMETHING SPOOKED OUR CROOKS TO ADD SOME PAPER SILVER: A DEPOSIT OF 1.601 MILLION OZ/INVENTORY RESTS AT 316.899 MILLION OZ/

APRIL 23.2018/WITH SILVER DOWN 50 CENTS, ANOTHER HUGE WITHDRAWAL FROM THE SLV INVENTORY: A WITHDRAWAL OF 1.413 MILLION OZ/INVENTORY RESTS AT 315.298 MILLION OZ.

APRIL 20/WITH SILVER DOWN 11 CENTS: ANOTHER HUGE CHANGE IN SILVER INVENTORY: A WITHDRAWAL OF 1.13 MILLION OZ//SLV RESTS TONIGHT AT 316.711 MILLION OZ/

APRIL 19/WITH SILVER UP 3 CENTS TODAY: WE HAD A BIG CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.355 MILLION OZ/ MAKES ABSOLUTELY NO SENSE!!/INVENTORY RESTS AT 317.841 MILLION OZ

APRIL 18/WITH SILVER UP 44 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 320.196 MILLION OZ

MAY 25/2018:

Inventory 321.003 million oz

end

6 Month MM GOFO 2.12/ and libor 6 month duration 2.49

Indicative gold forward offer rate for a 6 month duration/calculation:

G0FO+ 2.12%

libor 2.49 FOR 6 MONTHS/

GOLD LENDING RATE: .37%

XXXXXXXX

12 Month MM GOFO

+ 2.74%

LIBOR FOR 12 MONTH DURATION: 2.60

GOFO = LIBOR – GOLD LENDING RATE

GOLD LENDING RATE = +.14

end

At 3:30 pm we receive the COT report which gives us position levels of our major players. However due to the fact that all of the major bankers transfer much of their obligations to London as forwards (in conjunction with hedge fund longs) as longs cannot get access to physical metal, this report is absolutely useless for it only deals with the comex;

| Gold COT Report – Futures | ||||||

| Large Speculators | Commercial | Total | ||||

| Long | Short | Spreading | Long | Short | Long | Short |

| 189,677 | 98,720 | 55,606 | 203,101 | 318,676 | 448,384 | 473,002 |

| Change from Prior Reporting Period | ||||||

| -11,791 | -10,305 | -9,713 | 7,176 | 4,662 | -14,328 | -15,356 |

| Traders | ||||||

| 186 | 82 | 85 | 51 | 50 | 277 | 182 |

| Small Speculators | ||||||

| Long | Short | Open Interest | ||||

| 54,558 | 29,940 | 502,942 | ||||

| -2,688 | -1,660 | -17,016 | ||||

| non reportable positions | Change from the previous reporting period | |||||

| COT Gold Report – Positions as of | Tuesday, May 22, 20 | |||||

our large speculators/

those large specs that have been long in gold pitched (transferred) 11,792 contracts from their long side

those large specs that have been short in gold added 10,305 contracts to their short side

our commercials/

those commercials that have been long in gold added 7176 contracts to their long side

those commercials that have been short in gold added 4552 contracts to their short side

our small speculators

our small specs that have been long in gold pitched (transferred) 2668 contracts from their long side

our small specs that have been short in gold covered (transferred) 1680 contracts from their short side.

end

| Silver COT Report: Futures | |||||

| Large Speculators | Commercial | ||||

| Long | Short | Spreading | Long | Short | |

| 78,007 | 62,782 | 14,609 | 76,516 | 107,939 | |

| 5,344 | -9,223 | -1,841 | -1,890 | 11,467 | |

| Traders | |||||

| 108 | 55 | 52 | 36 | 35 | |

| Small Speculators | Open Interest | Total | |||

| Long | Short | 198,248 | Long | Short | |

| 29,116 | 12,918 | 169,132 | 185,330 | ||

| -1,430 | -220 | 183 | 1,613 | 403 | |

| non reportable positions | Positions as of: | ||||

our large speculators/

those large specs that have been long in silver added 5344 contracts to their long side

those large specs that have been short in silver covered (transferred) 9223 contracts from their short side.

our commercials/

those commercials that have been long in silver pitched (transferred) 1890 contracts from their long side

those commercials that have been short in silver added 11,467 contracts to their short side.

our small speculators

those small specs that have been long in silver added 5473 contracts to their long side

those small specs that have been short in silver covered (transferred) 9359 contracts from their short side.

end

Major gold/silver trading /commentaries for FRIDAY

GOLDCORE/BLOG/MARK O’BYRNE.

GOLD/SILVER

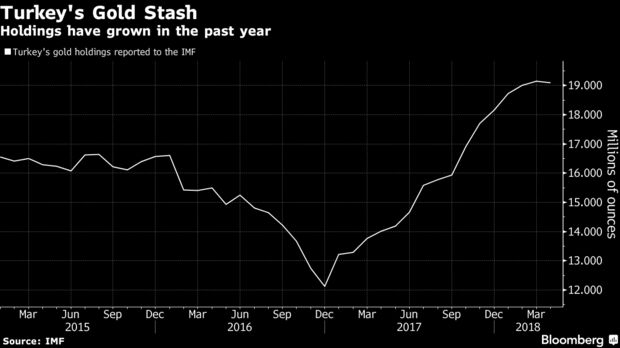

Gold Surges To Record In Turkey and Other Emerging Markets as Currencies Collapse

- Turkey’s election angst, geopolitical risk and collapse of the lira is driving up demand for gold

- Turkish lira has collapsed versus gold and now the lowest on record (see chart)

- Significant demand for gold coins in Turkey and central bank has repatriated gold and added to gold reserves

- “Having the gold physically at home allows countries to feel like they are in control of their reserves” Dr Brian Lucey

- Gold acting as a hedge and has been “expensive” not to own gold in Turkey, Syria, Venezuela, Argentina, Angola, Russia and many other countries in the Middle East, Asia, South America, Africa and Europe (see table of worst performing currencies in 2018 including the Swedish krona)

from Bloomberg:

With just a month until elections, shopkeepers at Turkey’s biggest bazaar say they’re seeing a jump in demand for gold coins.

“Turkish people have an interesting behavior — they buy gold when the prices are rising, they think it’s gonna rise more,” said Gokhan Karakan, 32, who runs a gold exchange office in the heart of Istanbul’s Grand Bazaar. “People think there is a trend here and choose to buy gold until uncertainty is out of the way.”

On Friday afternoon, at the Grand Bazaar — one of the world’s oldest covered markets — shopkeepers said more customers were buying gold, instead of selling it, in hopes that the metal will keep its worth as the value of the lira plunges.

Gold priced in lira is more “expensive” than ever, but that’s not deterring buyers, who are looking for a safe haven.

“Turkish people love gold,” said Tekin Firat, 30, who owns and runs a gold store the bazaar. “People think that it will never lose in the long run.”

Citizens are buying up gold as the lira plunges in latest currency crisis. Recep Tayyip Erdogan, who’s about to launch a re-election campaign that may provide the toughest electoral test of his 15 years in power, is an outspoken advocate of cheap money. He’s up against investors demanding higher returns to fund an economy beset by inflation and a swollen current account deficit.

Gold has a special importance in Turkey. The country is to home the ancient kingdom of Lydia, where the earliest known gold coinage originated in the 7th century B.C.

Turkey imported 118 metric tons of bullion, worth $5 billion at today’s prices, in first four months of this year, the most over that period, according to data going back to 1995 from the Istanbul Gold Exchange. Last year, imports reached a record.

It’s not just consumers that are snapping up gold. Official reserves have also increased over the past year. The central bank doesn’t comment on its gold strategy, but previously said the changes in its holdings are part of an effort to diversify its reserves.

The reported figure may be misleadingly high because the central bank allows commercial banks to deposit gold as part of their reserves. The government last year launched a campaign to get more “under-the-pillow gold” into the formal banking system. About half of the 216 ton inflow since the start of 2017 can be attributed to this alternative source, according to Matthew Turner, a strategist at Macquarie Group Ltd. in London.

Even so, the purchases have happened a year after Erdogan urged Turks to convert their foreign currency savings into liras and gold, and tensions with the U.S. reached a new low.

“The central bank certainly has been more active in the gold market,” said Turner. “It seems the government would like a larger share of its reserves in assets that’s not related to the U.S. dollar.”

In 2017, the central bank withdrew of its 28.7 tons of gold, worth about $1.2 billion, from Federal Reserve vaults. It didn’t say where the gold went, but holdings increased at Borsa Instanbul, the Bank of England and Bank of International Settlements, according to a report released in April.

The decision for any country to withdraw gold from U.S. vaults is rare — happening only a handful of times in the past decade. Since 2011, Germany, the Netherlands, Hungary and Venezuela have repatriated their gold holdings from the U.S.

Turkey’s decision to withdraw gold may have been a reaction to U.S. court cases against Turkish banks for alleged deals struck with Iran, said Cagdas Kucukemiroglu, a Middle Eastern gold analyst at research firm Metals Focus.

“Having the gold physically at home allows countries to feel like they are in control of their reserves,” said Brian Lucey, a professor of finance at Trinity Business School in Dublin.

Related Content

Dollar Squeeze Spells More Pain for World’s Worst Currencies

Gold Is a Safe Haven Asset

Listen on SoundCloud , Blubrry & iTunes. Watch on YouTube above

News and Commentary

Gold prices slip but hold above $1,300 (Reuters.com)

Asian markets cautious after Trump cancels North Korea summit (MarketWatch.com)

Existing-home sales tumble as supply crunch squeezes (MarketWatch.com)

Gold surges and regains 1300 as Kim-Trump meeting is called off (ActionForex.com)

Gold Prices Top $1,300 as Trump Cancels U.S.-North Korea Summit (Investing.com)

Source: Bloomberg.com

Gold is good protection because of Trump and North Korea ‘playing chicken’ – Ray Dalio (CNBC.com)

Turkey’s Election Angst Is Driving Up Demand for Gold (Bloomberg.com)

Simple lesson from Turkey for investors: rising authoritarianism is bearish (MoneyWeek.com)

The great buy-to-let sell up (MoneyWeek.com)

‘American Default’: If gold won’t go up, push the dollar down (Part 3) (Bloomberg.com)

Listen on SoundCloud , Blubrry & iTunes. Watch on YouTube below

Gold Prices (LBMA AM)

24 May: USD 1,296.35, GBP 967.73 & EUR 1,104.88 per ounce

23 May: USD 1,294.00, GBP 967.91 & EUR 1,102.88 per ounce

22 May: USD 1,293.90, GBP 961.24 & EUR 1,095.29 per ounce

21 May: USD 1,285.85, GBP 959.24 & EUR 1,095.67 per ounce

18 May: USD 1,287.20, GBP 954.20 & EUR 1,091.16 per ounce

17 May: USD 1,288.85, GBP 952.07 & EUR 1,090.50 per ounce

Silver Prices (LBMA)

24 May: USD 16.51, GBP 12.32 & EUR 14.09 per ounce

23 May: USD 16.53, GBP 12.38 & EUR 14.11 per ounce

22 May: USD 16.58, GBP 12.32 & EUR 14.04 per ounce

21 May: USD 16.34, GBP 12.19 & EUR 13.91 per ounce

18 May: USD 16.39, GBP 12.16 & EUR 13.92 per ounce

17 May: USD 16.39, GBP 12.14 & EUR 13.90 per ounce

Recent Market Updates

– Gold Price Surges To Record In Turkey and Other Emerging Markets as Currencies Collapse

– Gold Rarity and Value Shown In Stunning Gold Visualisations

– Gold Looks A Better Investment Than UK Property

– Gold 2048: The Next 30 Years For Gold

– Beware “Snollygosters” and the Empty Promises of Pathological Politicians

– US 10-Year Surges, Emerging Markets Implode…Where Next for Gold?

– Welsh Gold Being Hyped Due To The Royal Wedding?

– Oil Price Is Going To Keep Rising And Inflation Is Coming

– Gold Price Manipulation – A Comprehensive Guide By James Rickards

– EU ‘Nightmare Scenario’ As Popular Anti-Euro and Anti-EU Government Takes Power In Italy

– “Oil price highest in 3 years, gold ready to follow”, by Daniel March

– Gold Mining Supply Globally Looks Set To Decline

– Gold Bullion Demand In Iran May Surge On Trump Sanctions

Andrew Maguire’s Kinesis money which is a “bitcoin” but backed 100% by allocated gold and silver is set to go.

it think it would be a great idea to look at this!

please read at: https://kinesis.money/#/

(Andrew Maguire)

|

2:57 PM (1 hour ago) | ||

|

|||

Harvey

Here It is my friend! https://kinesis.money/#/ Please let everyone know.

Let catch up on Monday if you have time. We have billions in the hopper ready to be allocated on the 1st day of trading. The paper market days are over.

Warm regards

Andy

Part 3 from ‘American Default’: If gold won’t go up, push the dollar down

Submitted by cpowell on Fri, 2018-05-25 00:08. Section: Daily Dispatches

8:10p ET Thursday, May 24, 2018

Dear Friend of GATA and Gold:

Part 3 of Bloomberg News’ excerpting of “American Default” by Professor Sebastian Edwards of the University of California at Los Angeles describes President Franklin Roosevelt’s daily effort to figure out the price at which the U.S. government should purchase gold in the hope of raising commodity prices. Part 3 is headlined “The Gamble: If Gold Won’t Go Up, Push the Dollar Down” and it’s posted at Bloomberg here:

https://www.bloomberg.com/view/articles/2018-05-24/fdr-s-gamble-on-gold-…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

Your early FRIDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

i) Chinese yuan vs USA dollar/CLOSED DOWN TO 6.3883 /shanghai bourse CLOSED DOWN 13.35 POINTS OR 0.42% HANG SANG CLOSED DOWN 172.37 POINTS OR 0.56%

2. Nikkei closed UP 13.78 POINTS OR 0.06% / /USA: YEN RISES TO 109.42/

3. Europe stocks OPENED GREEN/MIXED /USA dollar index RISES TO 93.95/Euro FALLS TO 1.1694

3b Japan 10 year bond yield: FALLS TO . +.04/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 109.65/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD FINALLY IN THE POSITIVE/BANK OF JAPAN LOSING CONTROL OF THEIR YIELD CURVE AS THEY PURCHASE ALL BONDS TO GET TO ZERO RATE!!

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 69.04 and Brent: 76.84

3f Gold UP/Yen DOWN

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil DOWN for WTI and DOWN FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund RISES TO +.56%/Italian 10 yr bond yield UP to 2.47% /SPAIN 10 YR BOND YIELD UP TO 1.50%

3j Greek 10 year bond yield RISES TO : 4.32?????????????????

3k Gold at $1305.60 silver at:16.69 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble DOWN 53/100 in roubles/dollar) 62.08

3m oil into the 69 dollar handle for WTI and 76 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 109.42 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 0.9910 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1602 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now POSITIVE territory with the 10 year RISING to +0.560%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.96% early this morning (THIS IS DEADLY TO ALL MARKETS). Thirty year rate at 3.10%

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

(courtesy Jim Reid/Bloomberg/Deutsche bank/zero hedge)

Traders On Edge As Spanish Political Crisis, Oil

Plunge

Threaten Pre-Holiday Market Bliss

For much of the overnight session, the market’s attention was focused on North Korea’s amicable reaction to Trump’s cancellation of the June 12 summit, an indication that yesterday’s selloff may have been overdone as Trump’s gambit was merely a negotiating ploy, and a successful one at that.

For those who missed the latest twist, North Korea expressed regret regarding the US cancellation of the summit and said it is willing to talk with the US anytime. North Korea added it is still willing to resolve issues with US “whenever and however” and that they hoped for issues to be resolved “Trump style”. Furthermore, North Korea stated that the Summit was necessary to resolve current hostile bilateral relationship and that its previous remarks regarding the summit had been in protest against strong US comments, according to reports citing Vice Foreign Minister Kim Kye Gwan.

While some in the markets saw this as a window of opportunity for the summit to be salvaged, and thus a “risk on” catalyst, others twisted the narrative and said nobody had really expected the summit to take place, so yesterday’s diversion was to be expected, and thus also a “risk on” catalyst (and yes, this is an example of how the “market” spins any event as bullish). Which is why for much of the session, bullish sentiment prevailed.

And sure enough, after a mixed Asian session which saw The MSCI Asia Pac close down -0.2%, but up +0.1% ex Japan, Europe’s Stoxx Europe 600 Index rose, with most sectors in the green, and equity-index futures pointed to a higher U.S. open as concerns about an escalation in tensions over North Korea’s nuclear program eased.

However, things rapidly reversed when Saudi energy minister Al-Falih said that OPEC and Russia are now contemplating boosting output in the second half of 2018, sending WTI tumbling below $70, and pressuring energy stocks.

Meanwhile, the plunge in Italy’s bonds continued, with the BTP yield rising above the key resistance level of 2.40%, and the Bund-BTP spread blowing out beyond 200bps, which Goldman said yesterday was the “contagion” threshold beyond which Italy’s crisis becomes Europe’s crisis and is set to hit Portugal next.

Commenting on the move, Nomura said that Italian government bond yields will likely rise toward a four- year high against German bunds, and any relief rally should be short-lived.

Still, for now complacent investors seem to generally be taking a more sanguine view on geopolitical risks, even as things continue to deteriorate, and while North Korea’s apparent willingness to keep talking appeared to soothe markets, other risks remain, most notably the start of what appears to be yet another European political crisis as Spain’s biggest opposition party Ciudadanos said it was ready to push for a no-confidence motion against Prime Minister Mariano Rajoy, while tensions around global trade linger as the following list from Bloomberg’s Garfield Reyonds summarizes:

- Italy’s populists managed to stun markets with their policies more than two months after the election. They are now close to finally taking office

- Erdogan’s determination to use his own, contrarian, monetary policy playbook

- The summit between the mercurial leaders of the U.S. and North Korea was canned, for now

- Fresh outbreaks in trade tensions surrounding China and Nafta

- Argentina seeking an IMF bailout

Still, nearly 10 years of Pavlovian reactions to BTFD have made a dip virtually impossible, and this morning despite the growing storm clouds, US equity futures are well in the green.

In other macro news, the Bloomberg Dollar Spot index rose on the day but was lower on a weekly basis amid fading risk-off sentiment, ahead of a long weekend in the U.S. and the U.K. The euro stayed in close proximity to 1.17 handle while the Swedish krona led gains in G-10. The lira swung between gains and losses of as much as 2%, though still heading for its worst week since in eight years, after the central bank said it would allow exporters to repay dollar-denominated loans in the local currency, while the pound weakened after the European Union dismissed many of the U.K.’s plans for their post-Brexit relationship.

Turkey could certainly contemplate another rate hike next month if the exchange rate continues to come under pressure, says James McCormack, global head of sovereigns at Fitch Ratings.

As noted above, oil is set to close the week in the red for the first time this month as both WTI and Brent are negative for the day at USD 69.31 and USD 76.95 respectively. This comes amid confirmation of a potential easing of supply cuts by OPEC to make up for the lost capacity of Venezuela and Iran with Russian Oil Minister Novak stating that all proposals will be discussed in June when asked about possible oil production increase by 1mln bpd. In addition to this the Saudi Energy Minister said they are certainly prepared to adjust policy in June, and release of supply will be gradual, adding that there is likely to be an oil supply boost in the second half of 2018. Furthermore, SocGen have revised their oil forecast higher for Q4 2018 with Brent revised to USD 78/bbl (+USD 14) and WTI revised to USD 73/bbl (+USD 13).

Gold is currently trading flat as safe haven demand softens the blow of profit taking heading into the weekend. Steel strengthening as concerns over demand diminish alongside declining inventories. Copper and nickel also rising, with nickel hitting near 3 year highs, spurred on by increasing base metals prices

Expected data include durable goods orders and University of Michigan Consumer Sentiment Index. Foot Locker, CAE, and Buckle are among companies reporting earnings.

Bulletin Headline Summary from RanSquawk

- Oil slides as Russian and Saudi energy ministers confirm speculation of possible production increases in June

- Italian/German spread continue widening as markets await news from Italy, party leaders to meet today

- Looking ahead, highlight include, US Durables, Uni. Of Michigan and Coeure, Powell, Kaplan, Weidmann and Carney speaking

Market Snapshot

- S&P 500 futures up 0.2% to 2,733.25

- STOXX Europe 600 up 0.5% to 392.57

- MXAP down 0.2% to 173.32

- MXAPJ up 0.1% to 566.57

- Nikkei up 0.06% to 22,450.79

- Topix down 0.2% to 1,771.70

- Hang Seng Index down 0.6% to 30,588.04

- Shanghai Composite down 0.4% to 3,141.30

- Sensex up 0.8% to 34,930.01

- Australia S&P/ASX 200 down 0.07% to 6,032.82

- Kospi down 0.2% to 2,460.80

- German 10Y yield fell 2.0 bps to 0.452%

- Euro down 0.02% to $1.1718

- Italian 10Y yield fell 0.2 bps to 2.136%

- Spanish 10Y yield rose 1.0 bps to 1.402%

- Brent futures down 1.4% to $77.66/bbl

- Gold spot little changed at $1,304.23

- U.S. Dollar Index little changed at 93.82

Top Overnight News from Bloomberg

- Spain’s Ciudadanos, the centrist party that holds the balance of power in the Parliament, said it’s ready to back a no-confidence vote against Prime Minister Mariano Rajoy unless he calls a snap election; the opposition Socialists registered a no-confidence motion against Rajoy after his former aides were convicted of running a multimillion-euro corruption racket inside the party on his watch

- OPEC and its allies are likely to gradually boost oil output in the second half of the year to ease consumer anxiety as prices trade near $80 a barrel, said Saudi Minister of Energy and Industry Khalid Al-Falih; Oil is set for its first weekly decline this month as OPEC and its allies consider easing supply cuts

- North Korea said it was surprised by President Donald Trump’s decision to cancel a June 12 summit with Kim Jong Un and that the country remains willing to meet with the U.S. at any time

- U.K. consumer spending lost momentum in the first quarter and companies cut investment after severe weather swept the country

- Global finance chiefs urged the Turkish President Recep Tayyip Erdogan to preserve the independence of his country’s central bank after confusion sent the lira plummeting

- Bank of England Governor Mark Carney said Brexit is entering a crucial phase and this means his oft-criticized guidance on monetary policy is more important than ever.

- The European Union dismissed many of the U.K.’s plans for their post-Brexit relationship as little short of “fantasy” as the mood of negotiations deteriorated and progress stalled

- Mexico told the U.S. that it can be flexible on automotive wages and content in exchange for President Donald Trump’s negotiators withdrawing some of their other toughest demands, according to two people familiar with the Nafta talks.

Asian stock markets traded cautiously as the region reacted to US President Trump’s cancellation of the summit with North Korea. However, losses for the regional bourses were contained in a similar fashion to their US counterparts after Trump kept the door open for the summit to take place in the future. ASX 200 (-0.2%), Nikkei 225 (Unch.) and KOSPI (-0.1%) all began weaker due to the summit cancellation with South Korea taking the brunt of the news, although the picture somewhat improved as participants digested a more conciliatory tone from North Korea overnight which stated it was still willing to resolve issues with the US, while US and South Korea officials also agreed to create conditions for talks between US and North Korea. In addition, Japanese stocks found some reprieve from a weaker currency, while Shanghai Comp. (-0.1%) and Hang Seng (-0.2%) were kept subdued amid a lack of drivers and as this week’s PBoC liquidity operations resulted to a net drain of CNY 30bln in contrast to the substantial net injection of CNY 410bln last week. Finally, 10yr JGBs were flat with only minimal support seen amid a cautious-but-improved risk tone in the region, while the BoJ’s Rinban announcement for over JPY 1tln of JGBs in 1yr-10yr maturities also failed to spur demand as the central bank kept all purchase amounts unchanged. US Commerce Secretary Ross will visit China June 2nd-4th for trade discussions.

Top Asian News

- North Korea Says It Remains Willing to Meet With U.S. Any Time

- Chinese Developer Wuzhou Plunges 85% in Hong Kong Trading

- The World’s Most Profitable Banks Can Be Found in India

- China Is Said to Back Private Investment in State Carmakers

- Hon Hai Arm’s $4.3B Chinese IPO More Than 290 Times Subscribed

European equities are mostly positive as the region bucks the trend experienced in Asia and Wall St. FTSE MIB is underperforming against its peers with banks taking a hit as the Italian Banks Index falls to one-month lows. The energy sector underperforms yet again amid the continuing sell-off in oil prices. In terms of stock specifics, Novartis (+1.4%) is buoyed by an upgrade at Credit Suisse, AstraZeneca (+0.9%) is higher following a positive result from Phase 3 trials and Kingfisher (+4%) after Homebase was sold to Hilco Capital and thus marks an exit of Wesfarmers from the UK market. Some negative news for Daimler, as the German motor authority KBA probes suspected emission manipulation in the company with more than 600,000 possibly being recalled. Daimler have refused to comment.

Top European News

- Sweden’s Krona Soars as Debt Office Places Bet on Its Strength

- U.K. Economy Barely Grows as Households Rein in Spending

- BT Is Said to Draw Interest in U.K. Fixed Network Openreac

- The Tories Who Could Force May to Keep Britain Closer to Europe

In FX, the USD resides in modest positive territory (+0.1%) albeit off best levels as the greenback struggles to recoup some of the postFOMC minutes losses. Subsequently EUR/USD was knocked back below 1.1700 in early trade but failed to make a test of the 2018 low at 1.1677 as the recent pullback in the USD moved back onto a 1.1700 handle. In terms of EZ data, this morning’s German IFO release came in slightly ahead of expectations but questions nonetheless remain about the EZ’s economic performance with ABN Amro suggesting ‘The combination of ongoing weakness in underlying inflationary pressures and more uncertainty about the economic growth outlook strengthens the case for the ECB to exit at only a very slow pace’. Elsewhere, GBP/USD remains firmly below 1.3400 with GBP softer against its major counterparts in what’s been a busy week of tier 1 data for the UK after Wednesday’s soft inflation figures and yesterday’s upbeat retail report. Today was the turn of GDP which was a key focus for traders after the prelim reading derailed expectations of a May hike by the BoE. However, the GBP failed to gain any notable traction off the figures with the Q/Q and Y/Y readings both unrevised as expected, albeit coupled with lacklustre business investment metrics. USD/JPY hovers around the 109.50 level and off worst levels as the broadly firmer USD out-muscles the JPY amid touted shortcovering and softer than anticipated inflation metrics overnight. Further direction for the pair will likely come from the broader risktone which has been a guiding force for the pair throughout the week as trade and geopolitical concerns have prompted a FTQ across the space.

In commodities, oil is set to close the week in the red for the first time this month as both WTI and Brent are negative for the day at USD 69.31 and USD 76.95 respectively. This comes amid confirmation of a potential easing of supply cuts by OPEC to make up for the lost capacity of Venezuela and Iran with Russian Oil Minister Novak stating that all proposals will be discussed in June when asked about possible oil production increase by 1mln bpd. In addition to this the Saudi Energy Minister said they are certainly prepared to adjust policy in June, and release of supply will be gradual, adding that there is likely to be an oil supply boost in the second half of 2018. Furthermore, SocGen have revised their oil forecast higher for Q4 2018 with Brent revised to USD 78/bbl (+USD 14) and WTI revised to USD 73/bbl (+USD 13). Gold is currently trading flat as safe haven demand softens the blow of profit taking heading into the weekend. Steel strengthening as concerns over demand diminish alongside declining inventories. Copper and nickel also rising, with nickel hitting near 3 year highs, spurred on by increasing base metals prices.

Looking at today’s calendar, the flash April durable and capital goods orders will likely be the highlight, while the final University of Michigan consumer sentiment survey is also due. Away from that, EU finance ministers are due to discuss the latest on Brexit negotiations, while Russian President Putin, France President Macron, Japan’s Abe and IMF’s Lagarde take part in a panel. Elsewhere, the ECB’s Villeroy and Coeure will speak while the Fed’s Powell and BOE’s Carney will attend a conference in Stockholm.

US Event Calendar

- 8:30am: U.S. Durable Goods Orders, April P, est. -1.3%, prior 2.6%;

- Less Transportation, April P, est. 0.5%, prior 0.1%

- Cap Goods Orders Nondef Ex Air, April P, est. 0.7%, prior -0.4%

- 10am: U. of Mich. Sentiment, est. 98.8, prior 98.8; Current Conditions, est. 98.6, prior 113.3; Expectations, prior 89.5

DB’s Jim Reid concludes the overnight wrap

Ticket to the Champions League final tomorrow? Tick. Accommodation? Tick. Permission to be away from the family for the weekend? A surprising tick. Means of getting to Kiev? Absolutely none! Well not without a 4-legged connection via a couple of different continents that might have kept me away for longer than my marriage could survive. As such I’ll be cracking open a bottle of claret in front of the TV tomorrow night at home and hopefully seeing Liverpool lift one of the biggest trophies in all global sport. I must say I was intimidated by an interview with Ronaldo yesterday who said at 33 he felt he could go on playing until 41 and that he has the body of a 23 year old. I’m 44 in a couple of weeks and feel like I have the body of a 63 year old. Apologies to all the 63 year olds out there reading this.

This week has aged all of us as you can’t look at the screen at the moment without seeing a negative macro headline. Italy, North Korea, China/US trade, wider tariff fears, Turkey, weak PMIs and the usual Brexit shenanigans have all traded blows in an attempt to grab centre stage.

Starting with the US, President Trump has cancelled his planned summit with North Korea’s Kim Jong Un, citing “open hostility” from the regime and warned that the US military “is ready if necessary” and has “massive nuclear” capabilities. Notably, there seems to be some hope that talks may restart further down the track which capped the downside yesterday.

Following on, the S&P initially traded c1% lower but pared back losses to close -0.20%. Within the S&P, the energy (-1.7%) and financials sector were hit the hardest, with the former not helped by WTI oil falling for the third straight day (-1.57% to $70.71/bbl) as Russia’s energy minister noted that OPEC and its partners will discuss phasing out supply curbs at a meeting in June. Over in Europe, all bourses trended lower (Stoxx 600 -0.52%; FTSE -0.92%; DAX -0.94%), with the DAX weighed down auto stocks (-2.5%) as President Trump ordered investigations into whether car imports into the US threaten national security. Conversely, government bonds continued to firm with core 10y bond yields down 2-5bp (UST 10y -1.6bp; OATs -4.9bp) while Bunds (-3.5bp) fell to the lowest since mid-January. Italian BTPs were little changed (-0.4bp) as the news flow somewhat stabilised. The Dutch Finance Minister Hoekstra is withholding judgement on the new Italian government for now, as “we need to judge (them) by its deeds”, while Germany’s Finance Minister Scholz was more positive as he noted that the new Premier “…has expressed himself in a very pro-European way…” and that “the discussion with the President has proven to be very helpful”.

On the other side, Italy’s new Premier-designate Mr Conte is expected to provide the Head of State with a list of candidates for Ministry posts as early as today. Elsewhere, the League’s Mr Salvini noted “we don’t want to destroy, but rather to help Italy to have a say once again at the European and global level”. So lots bubbling along before we find out how rhetoric would translate into policies.

This morning in Asia, markets are paring back losses to be modestly lower, in part as North Korea still seem to be open to talks as the Vice Foreign Minister Kim Kye Gwan released a statement which “express our intent that there is a willingness to sit (with the US) at any time, in any way to resolve issues”. Across the region, the Kospi (-0.22%), Hang Seng (-0.26%), and Shanghai Comp. (-0.07%) are all down while the Nikkei is marginally up as we type.

Now recapping other markets performance from yesterday. The US dollar index weakened -0.24% while the Euro and Sterling rose 0.20% and 0.25% respectively. In Turkey, the support from its emergency rate hike seemed to be short lived as the Lira resumed its decline vs. the USD yesterday (-2.89%). Later on, in his election campaign speech, President Erdogan pledged to support economic growth, keep inflation at single digits and erase the current account deficit, but did not elaborate on the details. This morning, the Lira is down c1% and getting closer to the preintervention intra-day record lows. In commodities, Gold jumped the most in c1 month yesterday with the risk off bias (Gold +0.87%; Silver +1.30%) while other base metal also advanced (Copper +0.49%; Zinc +0.58%; Aluminium +0.85%).

Turning back to oil prices, DB’s Michael Hsueh believes that reports of progress towards an OPEC/non-OPEC unwind of supply discipline should be taken with a grain of salt. His view is that the progression of these talks is more likely to stabilize price rather than start a meaningful downtrend (>5%), given OPEC’s propensity to err on the tighter side. Overall, he expects coalition countries will agree only minimal supply easing which would be consistent with an oil market deficit in 2019 and by implication, prices venturing above Brent US$80+/bbl on a 6-month view.

Now moving onto the US rates outlook, the Fed’s Harker noted that three rate hikes this year continues to be his base case and he has not “moved far from that”. He added that “…we’re getting close to neutral (rates, which is)…say 2.75% to 3%” and that “if we see inflation start to accelerate, then I would be open to a fourth hike this year, but I’d have to see evidence of that first”. Elsewhere, the Fed’s Bostic reiterated that he is comfortable with three rate hikes for this year.

Back in Europe, the ECB has released its latest Financial Stability Review and the “account” of its most recent Governing Council meeting. The FSR noted that systemic risk for the Euro area had remained low over the past six months, with the sovereign sector more resilient due to the improved macroeconomic outlook. On the accounts, it noted “broad agreement” by Council members with Chief economist Mr Praet’s assessment that measures of underlying inflation had moved sideways since the March meeting and had yet to show signs of a sustained upward trend. Earlier yesterday, Mr Praet also reiterated that “economic conditions (in the EU bloc) are good – there are clouds, but economic conditions are good”.

Finally on President Trump’s potential tariffs on imported cars, the Canadian PM Trudeau told Reuters that he is “…trying to figure out where the possible national security connection is” and added that “we know that (the higher tariffs) is very much linked to ongoing negotiations around moving forward on NAFTA”. Elsewhere, a spokesman for Mexico’s President Pena Nieto said “Mexico is not going to negotiate on the basis of pressure”, although unnamed sources have told Reuters that Mexico has made a new NAFTA offer after the US launched its probe on car tariffs.

Before we take a look at today’s calendar, we wrap up with other data releases from yesterday. In the US, the May Kansas City Fed manufacturing index was above market and rose 3pts mom to a fresh record high of 29 (vs. 20 expected).

The production and new orders indices firmed, but the prices received index fell back from last month’s decade-high. The April existing home sales fell -2.5% mom to 5.46m (vs. 5.55m expected), impacted by the lack of available inventory as the number of homes for sale fell 6.2% yoy. Conversely, home prices in 1Q rose 6.9% yoy, the highest start to the year since 2006. Elsewhere, the weekly initial jobless claims rose to a seven week high at 234k (vs. 220k expected) while continuing claims (1,741k vs. 1,746k expected) were broadly in line.

In Europe, the final reading for Germany’s 1Q GDP was confirmed at 0.3% qoq. DB’s Marc Schattenberg expects some rebound in Q2 GDP growth but the decline in the IFO and softer PMIs suggest that the deceleration in Q1 was not just due to one offs but also reflects some moderations in the cycle. The June GfK consumer confidence was marginally below expectations at 10.7 (vs. 10.8).

Elsewhere, France’s May manufacturing confidence (109 vs. 108 expected) and business confidence (106 vs. 108 expected) indicators were mixed but broadly in line. Finally, the April UK retail sales ex-auto rebounded more than expected to 1.3% mom (vs. 0.5% expected), buoyed by shoppers responding to the more conducive Spring weather.

As for today, the May IFO survey in Germany and Q1 GDP report in the UK, including the various growth components is due. In the US flash April durable and capital goods orders will likely be the highlight, while the final University of Michigan consumer sentiment survey is also due. Away from that, EU finance ministers are due to discuss the latest on Brexit negotiations, while Russian President Putin, France President Macron, Japan’s Abe and IMF’s Lagarde take part in a panel. Elsewhere, the ECB’s Villeroy and Coeure will speak while the Fed’s Powell and BOE’s Carney will attend a conference in Stockholm.

3. ASIAN AFFAIRS

i)FRIDAY MORNING/THURSDAY NIGHT: Shanghai closed DOWN 13.35 points or 0.42% /Hang Sang CLOSED DOWN 172.37 points or 0.56% / The Nikkei closed UP 13.78 POINTS OR 0.06% /Australia’s all ordinaires CLOSED DOWN .05% /Chinese yuan (ONSHORE) closed UP at 6.3893/Oil DOWN to 69.04 dollars per barrel for WTI and 76.84 for Brent. Stocks in Europe OPENED ALL GREEN/MIXED. ONSHORE YUAN CLOSED DOWN AT 6.3883 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.3812/ONSHORE YUAN TRADING WEAKER AGAINST OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING MUCH WEAKER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW LOOKS LIKE A FULL TRADE WAR IS BEGINNING/

3 a NORTH KOREA/USA

North Korea/South Korea/usa

That did not take long: North Korea is now crawling trying to desperately convince Trump for the summit

(courtesy zerohedge)

North Korea Comes Crawling Back: Stresses

“Desperate Need” For Summit “Whenever,

However”

Update: As if the earlier begging was not enough, it appears Kim wants to make sure that President Trump is aware of his efforts and desire to meet.

Yonhap reports that North Korea’s state media said Friday the demolition of its only known nuclear test site has demonstrated its “peace-loving” efforts and pursuit of a “total halt” to nuclear tests.

As we detailed yesterday, North Korea officially demolished the test-site overnight, inviting a number of reporters to witness the event.

And today, the Korean Central News Agency (KCNA) said in English.

“The dismantlement of the nuclear test ground is a vivid manifestation of the DPRK government’s fixed peace-loving stand to join in the international aspiration and efforts for total halt to the nuclear test and make positive contribution to building a nuclear free world,”

The KCNA added that the demolition of the tunnels and other surrounding facilities, including a communications center, power systems and observation centers, was carried out “completely” and “with transparency.”

* * *

It appears that Trump “jilted North Korean lover” approach may have been just what the doctor ordered.

Literally minutes after we said that most experts expected a violent, angry outburst from North Korea’s president in response to Trump’s unexpected cancellation of the Singapore June 12 summit, such as this comment from Senator Jack Reed…

Senator Jack Reed

✔@SenJackReed

Spoke w/ @BloombergTV’s @kevcirilli about Pres Trump pulling out of planned nuclear summit w/ North Korea & how if Pres Trump had taken a more considered approach to Mr. Kim’s initial offer for a summit, we wouldn’t be in this position.https://www.bloomberg.com/news/videos/2018-05-24/sen-reed-reacts-to-scrapped-u-s-north-korea-summit-video …

Sen. Reed Reacts to Scrapped U.S.-North Korea Summit

Senator Jack Reed, a Democrat from Rhode Island, gives his thoughts on U.S. President Donald Trump pulling out of the planned summit with North Korean leader Kim Jong Un. He speaks with Bloomberg’s…

… a shocked North Korea is virtually begging for a meeting.

In a statement issued by state-run Korean Central News Agency, citing Vice Foreign Minister Kim Kye Gwan, North Korea announced it was willing to sit with the U.S. “whenever, however” through any method to try to resolve the outstanding issues.

Gwan said that whereas President Trump’s announcement to one-sidedly cancel the planned summit is unexpected and very regrettable, “North Korea’s goal and will to do everything for peace and stability of the Korean peninsula and mankind remains unchanged, and we are always willing to give time and opportunity to the US side with a big and open mind,” according to the statement. He added that “We express our intent that there is a willingness to sit at any time, in any way to resolve issues” and noted that President Trump’s decision to cancel the summit is “not what the world wants” and the summit is necessary to resolve the current hostile bilateral relationship.

Furthermore, North Korea appears to be backtracking on the recent diplomatic escalation and has effectively apologized, stating that “its previous remarks regarding the U.S.-North Korea summit had been in protest against strong US remarks towards North.”

While we await the full KCNA statement, here are the key bullet points courtesy of Reuters and Bloomberg:

- NORTH KOREA SAYS TRUMP’S SUMMIT CANCELLATION IS UNEXPECTED

- NORTH KOREA SAYS IT’S WILLING TO MEET WITH U.S. AT ANY TIME

- NORTH KOREA SAYS IT IS STILL WILLING TO RESOLVE ISSUES WITH UNITED STATES WHENEVER, HOWEVER

- NORTH KOREA SAYS U.S.-N.KOREA SUMMIT IS NECESSARY TO RESOLVE CURRENT HOSTILE BILATERAL RELATIONSHIP

- NORTH KOREA SAYS IT HAD WISHED `TRUMP MODEL’ COULD RESOLVE ISSUES

- NORTH KOREA SAYS IT HAD HOPED FOR ISSUES REGARDING N.KOREA TO BE RESOLVED “TRUMP-STYLE”

- NORTH KOREA SAYS NO CHANGE IN N. KOREA’S WILL TO DO BEST FOR PEACE

- NORTH KOREA SAYS ITS PREVIOUS REMARKS REGARDING U.S.-N.KOREA SUMMIT HAD BEEN IN PROTEST AGAINST STRONG U.S. REMARKS TOWARDS NORTH

- N.KOREA HAS WILLINGNESS TO GIVE CHANCE, TIME TO U.S.

- NORTH KOREA HAS WILLINGNESS TO GIVE CHANCE, TIME TO U.S.

And the punchline:

- NORTH KOREA SAYS CURRENT SITUATION REFLECTS DESPARATE NEED FOR SUMMIT

Or, to summarize North Korea’s response to Trump’s “dear John” letter:

Quoth the Raven@QTRResearchNorth Korea right now

end

Trump gloats that Kim wants to come back to the table:

(courtesy zerohedge)

Trump Gloats Over Kim’s Response: “Very Good” To Receive “Warm And Productive Statement From North Korea”

Crushing the “liberal media’s” early excitement at the failure of Trump’s North Korea Summit (and Nobel Peace Prize) hopes, the president took a moment to gloat Friday morning at getting Kim back to the table, after receiving what he described as a “warm and productive” statement from North Korea less than a day after he canceled a planned summit that was supposed to signal the start of North Korea’s denuclearization.

Donald J. Trump

✔@realDonaldTrump

Very good news to receive the warm and productive statement from North Korea. We will soon see where it will lead, hopefully to long and enduring prosperity and peace. Only time (and talent) will tell!

Trump quickly pivoted to North Korea after discussing the Democrats’ strategy of “so obviously rooting against us” during the US’s ongoing talks with North Korea. Then he compared the Dems’ defense of North Korea to the party’s defense of of the FBI’s decision to plant a mole within the Trump campaign.

Donald J. Trump

✔@realDonaldTrump

Democrats are so obviously rooting against us in our negotiations with North Korea. Just like they are coming to the defense of MS 13 thugs, saying that they are individuals & must be nurtured, or asking to end your big Tax Cuts & raise your taxes instead. Dems have lost touch!

Before moving on to international relations, Trump tweeted a quick congratulations to the Federalist’s Mollie Hemingway, one of the first to publish the “monster story” about the FBI’s operation involving embedding a mole within the Trump campaign – a story that the mainstream media hates (perhaps because their bias stopped them from exposing it first).

Donald J. Trump

✔@realDonaldTrump

“Everyone knows there was a Spy, and in fact the people who were involved in the Spying are admitting that there was a Spy…Widespread Spying involving multiple people.” Mollie Hemingway, The Federalist Senior Editor But the corrupt Mainstream Media hates this monster story!

Donald J. Trump

✔@realDonaldTrump