GOLD: $1295.70 DOWN $5.10 (COMEX TO COMEX CLOSINGS)

Silver: $16.43 DOWN 3 CENTS (COMEX TO COMEX CLOSINGS)

Closing access prices:

Gold $1293.80

silver: $16.42

TODAY IS FIRST DAY NOTICE FOR BOTH THE GOLD AND SILVER COMEX CONTRACTS.

For comex gold:

JUNE/

NUMBER OF NOTICES FILED TODAY FOR JUNE CONTRACT:101 NOTICE(S) FOR 10100 OZ.

TOTAL NOTICES SO FAR 176 FOR 17600 OZ (0.5474 tonnes)

For silver:

JUNE

59 NOTICE(S) FILED TODAY FOR

295,000 OZ/

Total number of notices filed so far this month: 415 for 2,075,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: BID $7495/OFFER $7595: UP $60(morning)

Bitcoin: BID/ $7387/offer $7487: down $52 (CLOSING/5 PM)

end

First Shanghai gold fix comes at 10 pm est

The second Shanghai gold fix: 2:15 pm

First Shanghai gold fix gold: 10 pm est: 1304.45

NY price at the same time: 1299.10

PREMIUM TO NY SPOT: $5.35

Second gold fix early this morning: 1303.93

USA gold at the exact same time:1298.60

PREMIUM TO NY SPOT: $5.33

AGAIN, SHANGHAI REJECTS NEW YORK PRICING.

WE WILL NOT PROVIDE LONDON FIXES AS THEY ARE NOT ACCURATE AS TO WHAT IS GOING ON AT THE SAME TIME FRAME.

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total OPEN INTEREST ROSE BY AN STRONG 1065 CONTRACTS FROM 209,358 UP TO 210,423 ACCOMPANYING YESTERDAY’S 7 CENT FALL IN SILVER PRICING. WE ARE NOW WITNESSING OUR USUAL AND CUSTOMARY COMEX LONG LIQUIDATION AS WE ENTERED INTO THE NON ACTIVE DELIVERY MONTH OF JUNE AS LONGS PACK THEIR BAGS AND MIGRATE OVER TO LONDON. WE WERE NOTIFIED THAT WE HAD A STRONG SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP : 1725 EFP’S FOR JULY AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE OF 1725 CONTRACTS. WITH THE TRANSFER OF 1725 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 1725 EFP CONTRACTS TRANSLATES INTO 8.625 MILLION OZ ACCOMPANYING:

1.THE 7 CENT FALL IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES STANDING FOR JUNE COMEX DELIVERY. (3.630 MILLION OZ) DESPITE IT BEING A NON ACTIVE DELIVERY MONTH.

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF JUNE:

1725 CONTRACTS (FOR 1 TRADING DAYS TOTAL 1725 CONTRACTS) OR 8.625MILLION OZ: (AVERAGE PER DAY: 1725 CONTRACTS OR 8.625 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH: 8.625 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 1.23% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)

ACCUMULATION IN YEAR 2018 TO DATE SILVER EFP’S: 1,322.9 MILLION OZ.

ACCUMULATION FOR JAN 2018: 236.879 MILLION OZ

ACCUMULATION FOR FEB 2018: 244.95 MILLION OZ

ACCUMULATION FOR MARCH 2018: 236.67 MILLION OZ

ACCUMULATION FOR APRIL 2018: 385.75 MILLION OZ

ACCUMULATION FOR MAY 2018: 210.05 MILLION OZ

RESULT: WE HAD A CONSIDERABLE SIZED INCREASE IN COMEX OI SILVER COMEX OF 1065 WITH THE 7 CENT FALL IN SILVER PRICE. WE HAVE NOW ENTERED THE NEW NON ACTIVE MONTH OF JUNE. THE CME NOTIFIED US THAT IN FACT WE HAD AN STRONG SIZED EFP ISSUANCE OF 1725 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) . FROM THE CME DATA: 1725 EFP CONTRACTS FOR JULY, AND ZERO FOR ALL OVER MONTHS FOR A DELIVERABLE FORWARD CONTRACT OVER IN LONDON WITH A FIAT BONUS (TOTAL: 1725). TODAY WE GAINED A HUGE 2790 TOTAL OI CONTRACTS ON THE TWO EXCHANGES: i.e.1725 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH AN INCREASE OF 1065 OI COMEX CONTRACTS. AND ALL OF THIS HAPPENED WITH THE 7 CENT FALL IN PRICE OF SILVER AND A CLOSING PRICE OF $16.46 WITH RESPECT TO YESTERDAY’S TRADING. YET WE STILL HAVE A GIGANTIC AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY IN THIS NON ACTIVE JUNE DELIVERY MONTH. IT SURE LOOKS LIKE A FAILED BANKER SHORT COVERING EXERCISE!!

In ounces AT THE COMEX, the OI is still represented by OVER 1 BILLION oz i.e. 1.052 MILLION OZ TO BE EXACT or 151% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT JUNE MONTH/ THEY FILED AT THE COMEX: 59 NOTICE(S) FOR 295,000 OZ OF SILVER

IN SILVER, WE HAVE NOW SET THE NEW RECORD OF OPEN INTEREST AT 243,411 AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $16.51 ON APRIL 9.2018.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH: 27 MILLION OZ , APRIL: 2.485 MILLION OZ AND MAY: 36.285 MILLION OZ /AND JUNE (3.630 MILLION OZ SO FAR)

- HUGE RECORD OPEN INTEREST IN SILVER 243,411 CONTRACTS (OR 1.217 BILLION OZ/ SET APRIL 9/2018

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017

- RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ (FINAL)

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT). IT ALSO LOOKS LIKE BANKER CAPITULATION IN SILVER AS THEY STRUGGLE TO REMOVE SOME OF THEIR HUGE OBLIGATIONS.

In gold, the open interest FELL BY A FAIR 787 CONTRACTS DOWN TO 459,124 DESPITE THE LOSS IN THE GOLD PRICE/YESTERDAY’S TRADING (LOSS OF $1.60). WE ARE NOW IN THE ACTIVE DELIVERY MONTH OF JUNE. NO DOUBT THE BOYS ARE CASHING IN THEIR COMEX LONGS TO BEGIN THE PROCESS TO MOVE INTO LONDON FORWARDS. THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A GOOD SIZED 7,881 CONTRACTS : JUNE SAW THE ISSUANCE OF 0 CONTRACTS , AND AUGUST SAW THE ISSUANCE OF: 7881 CONTRACTS WITH ALL OTHER MONTHS ZERO. The new OI for the gold complex rests at 459,124. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE A STRONG SIZED OI GAIN IN TOTAL CONTRACTS ON THE TWO EXCHANGES: 787 OI CONTRACTS DECREASED AT THE COMEX AND AN GOOD SIZED 7,881 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON.THUS TOTAL OI GAIN: 7094 CONTRACTS OR 709,400 OZ = 22.06 TONNES. AND ALL OF THIS DEMAND OCCURRED WITH A LOSS OF $1.60

YESTERDAY, WE HAD 17163 EFP’S ISSUED.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF MAY : 7881 CONTRACTS OR 788,100 OZ OR 24.51 TONNES (1 TRADING DAYS AND THUS AVERAGING: 7881 EFP CONTRACTS PER TRADING DAY OR 788,100 OZ/ TRADING DAY),,

TO GIVE YOU AN IDEA AS TO THE HUGE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 1 TRADING DAYS IN TONNES: 24.51 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2017, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 2555 TONNES

THUS EFP TRANSFERS REPRESENTS 24.51/2550 x 100% TONNES = 0.96% OF GLOBAL ANNUAL PRODUCTION SO FAR IN APRIL ALONE.*** THE ACCUMULATION OF EFP CONTRACTS IS RISING PER MONTH.

ACCUMULATION OF GOLD EFP’S YEAR 2018 TO DATE: 3,476.71* TONNES *SURPASSED ANNUAL PROD’N

ACCUMULATION OF GOLD EFP’S FOR JANUARY 2018: 653.22 TONNES

ACCUMULATION OF GOLD EFP’S FOR FEBRUARY 2018: 649.45 TONNES

ACCUMULATION OF GOLD EFP’S FOR MARCH 2018: 741.89 TONNES (22 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR APRIL 2018: 713.84 TONNES (21 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR MAY 2018: 693.80 TONNES ( 22 TRADING DAYS)

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A FAIR SIZED DECREASE IN OI AT THE COMEX OF 787 WITH THE $1.60 LOSS IN PRICE // GOLD TRADING YESTERDAY ($1.60 FALL). WE ALSO HAD AN GOOD SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 7,881 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 7,881 EFP CONTRACTS ISSUED, WE HAD AN STRONG SIZED NET GAIN OF 7094 CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

7,889 CONTRACTS MOVE TO LONDON AND 787 CONTRACTS INCREASED AT THE COMEX. (in tonnes, the GAIN in total oi equates to 22.06 TONNES). ..AND BELIEVE IT OR NOT BUT ALL OF THIS DEMAND OCCURRED AT THE COMEX WITH A LOSS OF $1.60 IN TRADING!!!.

we had: 101 notice(s) filed upon for 10,100 oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD...

WITH GOLD DOWN $5.10 TODAY: / A HUGE CHANGE IN GOLD INVENTORY AT THE GLD/ A WITHDRAWAL OF 4.42 TONNES WHICH NO DOUBT WAS USED IN THE RAID TODAY/ /

Inventory rests tonight: 847.03 tonnes.

SLV/

WITH SILVER DOWN 3 CENTS TODAY NO CHANGES IN THE SILVER INVENTORY AT THE SLV INVENTORY/

/INVENTORY RESTS AT 322.039 MILLION OZ/

end

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER ROSE BY A STRONG SIZED 1065 CONTRACTS from 209,358 UP TO 210,423 (AND, CLOSER TO THE NEW COMEX RECORD SET /APRIL 9/2017 AT 243,411/SILVER PRICE AT THAT DAY: $16.53). THE PREVIOUS RECORD OTHER THAN WAS ESTABLISHED AT: 234,787, SET ON APRIL 21.2017 OVER ONE YEAR AGO. THE PRICE OF SILVER ON THAT DAY: $17.89.OUR CUSTOMARY MIGRATION OF COMEX LONGS MORPH INTO LONDON FORWARDS CONTINUES AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE: (WE DO NOT GET A LOOK AT THESE CONTRACTS AS IT IS PRIVATE BUT THE CFTC DOES AUDIT THEM), 1725 EFP’S FOR JULY AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 1725 CONTRACTS . EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI GAIN AT THE COMEX OF 1343 CONTRACTS TO THE 1725 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A STRONG SIZED GAIN OF 3060 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES: 13.95 MILLION OZ!!! AND THIS HUGE DEMAND OCCURRED WITH A 7 CENT LOSS IN PRICE . THE BANKERS ORCHESTRATED THEIR RAID THROUGHOUT LAST WEEK DESPERATELY TRYING TO PARE THEIR GIGANTIC OPEN INTEREST SHORT ON BOTH EXCHANGES BUT TO NO AVAIL. JUDGING BY THE RECORD NUMBER OF EFP ISSUANCE DURING APRIL AT 385.75 MILLION OZ AND THE CONTINUAL OI GAIN ON THE TWO EXCHANGES, THE CONSTANT RAIDS, (THAT ARE NOW BEING CALLED UPON BY OUR BANKER FRIENDS IN AN ATTEMPT TO SHAKE AS MANY SILVER LEAVES FROM THE SILVER TREE AS POSSIBLE) AND JUDGING BY THE RESULTS FROM YESTERDAYS ACTION, THEY HAVE NOT BEEN AT ALL SUCCESSFUL.

RESULT: A GOOD SIZED INCREASE IN SILVER OI AT THE COMEX WITH THE 7 CENT LOSS IN SILVER PRICING YESTERDAY. BUT WE ALSO HAD ANOTHER STRONG SIZED 1725 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR JUNE, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)FRIDAY MORNING/THURSDAY NIGHT: Shanghai closed DOWN 20.34 points or 0.66% /Hang Sang CLOSED UP 24.35 points or 0.08% / The Nikkei closed DOWN 30.47 POINTS OR 0.14% /Australia’s all ordinaires CLOSED DOWN .32% /Chinese yuan (ONSHORE) closed DOWN at 6.4144/Oil DOWN to 66.66 dollars per barrel for WTI and 77.80 for Brent. Stocks in Europe OPENED ALL GREEN DAX/. ONSHORE YUAN CLOSED DOWN AT 6.4144 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.4077/ONSHORE YUAN TRADING WEAKER AGAINST OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING MUCH WEAKER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW LOOKS LIKE A FULL TRADE WAR IS BEGINNING/

/NORTH KOREA/SOUTH KOREA

i)North Korea/South Korea/USA

b) REPORT ON JAPAN

the yen weakens as the Bank of Japan announces a slight taper to their bond purchases. Basically they are running out of bonds to buy

( zerohedge)

3 c CHINA

A very important read on China. Luongo believes that China’s next move is to devalue their yuan which will provide much needed help to nations that support China, namely Iran, Venezuela and Turkey in order to keep the supply lines open and full

a must read…

( Tom Luongo)

4. EUROPEAN AFFAIRS

i)SPAIN

Spain celebrates with a new Prime Minister, Sanchez who is the leader of the Socialist opposition party. Sanchez now becomes Prime Minister after a coalition of hodge podge parties. They are going to have great difficulty passing anything. The new leader states that he will call an election before 2020

( zerohedge)

iii)I guess Italy is not fixed as bond yields are rising to their session highs. The market has just figured out that the new coalition government is more anti establishment than the one Mattarella rejected

( zerohedge)

iv)what a riot!! Italian yields spike

higher on reports that the now ruling coalition is seeking funds to quit the Euro

( zerohedge)

v)Deutsche bank downgraded by S and P

( zerohedge)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

Despite the huge hike in the interest rate, Turkish stocks and the Lira tumble after Erdogan comments seem to indicate that capital controls may be coming forthwith

( zerohedge)

6 .GLOBAL ISSUES

7. OIL ISSUES

8. EMERGING MARKET

BRAZIL

We are witnessing populist pressures are having on various nations, but it is Brazil that is undergoing huge problems with its huge nationwide trucking and other sector strikes. So far the GDP is down 38% as no commerce is forthcoming. Now we see that the Petrobas CEO, who is 65 years old (Parente)_ quit unexpectedly. He was the stabilizing force and to see him leave on top of the crippling strike could send Brazil into bankruptcy shortly

(courtesy zerohedge)

9. PHYSICAL MARKETS

ii)Mike Kosares pounds the table that for gold ownership you must buy physical and not any of the paper garbage.

( Mike Kosares)

iii)Great commentary from Chris Powell of GATA

( Chris Powell/GATA)

iv)Alasdair Macleod’s latest paper is a must read. You will recall that it is Macleod’s believe (and myself as well) that China has accumulated 20,000 tonnes to its credit. It has allowed its citizens to accumulate approximately 18,000 tonnes. Macleod believes that it is now time for gold to return to real money as China and Russia will finance the next bold infrastructure moves with gold through the use of gold bonds similar to what Britain used to finance the Napoleonic wars.

(a must read..Alasdair Macleod)

v)A great commentary from Nicholas Biezanek as he comes to the conclusion that it is the ESF that is financing these EFP’s/ Is this the end game for the Comex/LBMA and Petro dollar scheme?

a must read…

( Nicholas Biezanek)

10. USA stories which will influence the price of gold/silveri)

i)USA DATA

Official jobs report:

Economy adds 223,000 jobs in May as the unemployment falls to 3.8%

( Needham/the Hill)

ii)Zero hedge: a good jobs report with a surge of 223,000 workers smashing expectations. The jobless rate hits a historic low of 3.8% as more souls join the non labour pool. Hourly earnings increased .3% and that caught the eye of investors as they pulled gold/silver down.

( zerohedge)

iii)The real story: a total of 102 million Americans are not in the labour force;

iv b)The jobs report is one big joke. The number that the BLS gave this morning was 223,000 jobs. It seems that over 100% of this job addition was made up with the fictitious B/D plg. With retail trade in decimation how on earth could this sector we the largest producer of jobs..absolute garbage!!FROM DAVE KRANZLER OF IRD:

v)hard data continues to disappoint. Strange: we have two national manufacturing reports: Markit and ISM. Market has continued to show manufacturing dipping each month while the ISM shows manufacturing rising so take your pick as to the correct one: However prices paid which increases costs to manufacturers hit a 7 yr high on both( zerohedge)

vii)SWAMP STORIES

Trading Volumes on the COMEX

PRELIMINARY COMEX VOLUME FOR TODAY: 305,418 contracts

CONFIRMED COMEX VOL. FOR YESTERDAY: 331,526 contracts

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

And now for the wild silver comex results.

Total silver OI ROSE BY A STRONG SIZED 1065 CONTRACTS FROM 209,358 UP TO 210,423 (AND CLOSER TO THE NEW RECORD OI FOR SILVER SET APRIL 9.2018/ 243,411 CONTRACTS) DESPITE THE 7 CENT LOSS IN SILVER PRICING/ YESTERDAY. SINCE WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF JUNE, WE WERE INFORMED THAT WE HAD A STRONG SIZED 1725 EFP CONTRACT ISSUANCE FOR JULY AND ZERO FOR ALL OTHER MONTHS. THESE EFPS WERE ISSUED TO COMEX LONGS WHO RECEIVED A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. THE TOTAL EFP’S ISSUED: 1725. ON A NET BASIS WE GAINED 2790 SILVER OPEN INTEREST CONTRACTS AS WE OBTAINED A 1065 CONTRACT GAIN AT THE COMEX COMBINING WITH THE ADDITION OF 1725 OI CONTRACTS NAVIGATING OVER TO LONDON.

NET GAIN ON THE TWO EXCHANGES: 2790 CONTRACTS

AMOUNT STANDING FOR SILVER AT THE COMEX

We are now in the NON active delivery month of JUNE and here the front month FELL BY 314 contracts FALLING TO 372 contracts. We had 356 notices filed upon yesterday so we gained 42 contracts or an additional 210,000 oz will stand in this non active delivery month of June AS SOMEBODY IS IN URGENT NEED OF PHYSICAL ON THIS SIDE OF THE POND AND QUEUE JUMPING STARTS IN EARNEST QUITE EARLY.

The next big active delivery month for silver is July and here the OI LOST 1190 contracts DOWN to 139,430. The next delivery month is August and here we gained an initial 4 contracts. The next active delivery month after August for silver is September and here the OI ROSE by 1926 contracts UP to 36,649

We had 59 notice(s) filed for 295,000 OZ for the JUNE 2018 COMEX contract for silver which is extremely large!!

PLEASE NOTE THE FOLLOWING FOR COMPARISON PURPOSES:

ON MAY 31.2017 WE INITIALLY HAD 396 OPEN INTEREST STAND OR A LARGE 1.98 MILLION OZ

STOOD FOR METAL.

AT THE CONCLUSION OF JUNE 2017: 4.92 MILLION OZ FINALLY STOOD AS QUEUE JUMPING STARTED IN EARNEST AND IN THE ENSUING YEAR, IT CONTINUED WITH RECKLESS ABANDON INCLUDING WHAT YOU ARE WITNESSING TODAY

INITIAL standings for JUNE/GOLD

JUNE 1/2018.

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz |

nil OZ

|

| Deposits to the Dealer Inventory in oz | NIL oz |

| Deposits to the Customer Inventory, in oz | 3603.682

OZ Delaware |

| No of oz served (contracts) today |

101 notice(s)

10100 OZ

|

| No of oz to be served (notices) |

7619 contracts

(761,900 oz)

|

| Total monthly oz gold served (contracts) so far this month |

176 notices

17600 OZ

0.5474 TONNES

|

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

For JUNE:

Today, 0 notice(s) were issued from JPMorgan dealer account and 79 notices were issued from their client or customer account. The total of all issuance by all participants equates to 101 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 40 notice(s) was (were) stopped/ Received) by j.P.Morgan customer account.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

To calculate the INITIAL total number of gold ounces standing for the JUNE. contract month, we take the total number of notices filed so far for the month (176) x 100 oz or 17600 oz, to which we add the difference between the open interest for the front month of JUNE. (7720 contracts) minus the number of notices served upon today (101 x 100 oz per contract) equals 778,500 oz, the number of ounces standing in this active month of JUNE (24.214 tonnes)

Thus the INITIAL standings for gold for the JUNE contract month:

No of notices served (176 x 100 oz) + {(7720)OI for the front month minus the number of notices served upon today (101 x 100 oz )which equals 778,500 oz standing in this active delivery month of JUNE .

WE LOST 2542 CONTRACTS OR AN ADDITIONAL 254200 OZ BACKED THEIR BAGS AND HEADED OVER TO LONDON THROUGH THE EFP ROUTE.

THERE ARE ONLY 8.2689 TONNES OF REGISTERED GOLD AVAILABLE FOR DELIVERY WHICH WILL MAKE JUNE AN EXTREMELY INTERESTING MONTH AS WE SEE HOW THIS PLAYS OUT!!!

IN THE LAST 18 MONTHS 74 NET TONNES HAS LEFT THE COMEX.

end

And now for silver

AND NOW THE APRIL DELIVERY MONTH

JUNE INITIAL standings/SILVER

| Silver | Ounces |

| Withdrawals from Dealers Inventory | nil oz |

| Withdrawals from Customer Inventory |

617,721.500 oz

Delaware

jpm

|

| Deposits to the Dealer Inventory |

147,739.900

oz

Brinks

|

| Deposits to the Customer Inventory |

386,980.08

oz

Brinks

|

| No of oz served today (contracts) |

59

CONTRACT(S)

(295,000 OZ)

|

| No of oz to be served (notices) |

313 contracts

(1,565,000 oz)

|

| Total monthly oz silver served (contracts) | 415 contracts

(2,075,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

we had 0 inventory movement at the dealer side of things

total dealer deposits: nil oz

we had 2 deposits into the customer account

i) Into JPMorgan: nil oz

*** JPMorgan for most of 2017 and in 2018 has adding to its inventory almost every single day.

JPMorgan now has 140 million oz of total silver inventory or 52.3% of all official comex silver. (140 million/268 million)

ii) into Delaware: 1021.65 oz

iii) Into Brinks: 385,958.390 oz

total customer deposits today: 386,980.080 oz

we had 2 withdrawals from the customer account;

i) Out of Delaware:: 1005.800 oz

ii) Out of JPM: 616,715.700

total withdrawals; 617,721.500 oz

we had 0 adjustments/ used for delivery purposes

total dealer silver: 65.669 million

total dealer + customer silver: 270.435 million oz

The total number of notices filed today for the JUNE. contract month is represented by 59 contract(s) FOR 295,000 oz. To calculate the number of silver ounces that will stand for delivery in JUNE., we take the total number of notices filed for the month so far at 415 x 5,000 oz = 2,075,000 oz to which we add the difference between the open interest for the front month of JUNE. (372) and the number of notices served upon today (59 x 5000 oz) equals the number of ounces standing.

.

Thus the INITIAL standings for silver for the JUNE contract month: 415(notices served so far)x 5000 oz + OI for front month of JUNE(372) -number of notices served upon today (59)x 5000 oz equals 3,640,000 oz of silver standing for the JUNE contract month

We gained 42 contracts or an additional 210,000 oz will stand in this non active delivery month of June as somebody was in urgent need of silver.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

ESTIMATED VOLUME FOR TODAY: 71,952 CONTRACTS

CONFIRMED VOLUME FOR YESTERDAY:82,109 CONTRACTS

YESTERDAY’S CONFIRMED VOLUME OF 82,109 CONTRACTS EQUATES TO 410 MILLION OZ OR 58.6% OF ANNUAL GLOBAL PRODUCTION OF SILVER

COMMODITY LAW SUGGESTS THAT OPEN INTEREST SHOULD NOT BE MORE THAN 3% OF ANNUAL GLOBAL PRODUCTION. THE CROOKS ARE SUPPLYING MASSIVE PAPER TRYING TO KEEP SILVER IN CHECK.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price at that day at $18.42

The previous record was 224,540 contracts with the price at that time of $20.44

end

NPV for Sprott

1. Sprott silver fund (PSLV): NAV FALLS TO -2.36% (JUNE 1/2018)

2. Sprott gold fund (PHYS): premium to NAV FALLS TO -0.44% to NAV (JUNE 1/2018 )

Note: Sprott silver trust back into NEGATIVE territory at -2.36%-/Sprott physical gold trust is back into NEGATIVE/ territory at -0.38%/Central fund of Canada’s is still in jail but being rescued by Sprott.

Sprott WINS hostile 3.1 billion bid to take over Central Fund of Canada

(courtesy Sprott/GATA)

3.SPROTT CEF.A FUND (FORMERLY CENTRAL FUND OF CANADA): NAV FALLS TO -2.22%: NAV 13.43/TRADING 13.11//DISCOUNT 2.33.

END

And now the Gold inventory at the GLD/

JUNE 1/WITH GOLD DOWN $5.10 TODAY, A HUGE 4.42 TONNES OF GOLD WAS WITHDRAWN FROM THE GLD AND THIS WAS USED IN THE RAID TODAY/INVENTORY RESTS AT 847.03 TONNES

MAY 31/WITH GOLD DOWN 1.60/NO CHANGE IN GOLD INVENTORY/INVENTORY REMAINS AT 851.45 TONNES

MAY 30/WITH GOLD UP $2.70: A HUGE DEPOSIT OF 2.95 TONNES INTO THE GLD/INVENTORY REMAINS AT 851.45 TONNES

MAY 29/2018/WITH GOLD DOWN $4.50/ NO CHANGES IN GLD INVENTORY/INVENTORY REMAINS AT 848.50 TONNES

May 25/WITH GOLD UP ON THE WEEK BUT DOWN 80 CENTS TODAY: WE HAD A HUGE 3.54 TONNES OF GOLD WITHDRAWAL FROM THE CROOKED GLD/

MAY 24/WITH GOLD UP $12.40/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 852.04

MAY 22/WITH GOLD UP $1.05/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 852.04 TONNES

MAY 21/WITH GOLD DOWN 50 CENTS/A HUGE CHANGE IN GOLD INVENTORY/A WITHDRAWAL OF 3.24 TONNES FORM GLD INVENTORY/INVENTORY RESTS AT 852.04 TONNES

MAY 18/WITH GOLD UP $1.80/A HUGE CHANGE IN GOLD INVENTORY AT THE GLD/ A DEPOSIT OF 9.11 TONNES INTO GLD INVENTORY/INVENTORY RESTS AT 865.28 TONNES/

GLD WAS ONE MASSIVE FRAUD

May 17/WITH GOLD DOWN $1.75/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 856.17 TONNES

MAY 16./WITH GOLD UP $1.05: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 856.17 TONNES

MAY 15/WITH GOLD DOWN $27.35, THE CROOKS WITHDREW 10 TONNES OF GOLD FROM THE GLD WHICH WAS USED IN THE RAID TODAY/INVENTORY RESTS AT 856.17 TONNES

MAY 14/ WITH GOLD DOWN $2.35: A HUGE DEPOSIT OF 4.68 TONNES OF GOLD INTO THE GLD and then a withdrawal of 1.48 tonnes /INVENTORY RESTS AT 866.17

A net gain of 3.2 tonnes of gold.

MAY 11/WITH GOLD DOWN $1.75/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 862.96 TONNES/

MAY 10/WITH GOLD UP $9.60/A WITHDRAWAL OF 1.17 TONNES FROM THE GLD/INVENTORY RESTS AT 862.96 TONNES/SUCH CROOKS

MAY 9/WITH GOLD DOWN $0.55/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 864.13 TONNES

MAY 8/WITH GOLD DOWN $0.10/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 864.13 TONNES

MAY 7/WITH GOLD DOWN $0.55/ANOTHER WITHDRAWAL OF 1.47 TONNES OF GOLD FROM THE GLD/INVENTORY RESTS AT 864.13 TONNES

MAY 4/WITH GOLD UP $2.05/A WITHDRAWAL OF 1.13 TONNES OF GOLD FROM THE GLD/INVENTORY RESTS AT 865.60 TONNES

MAY 3/WITH GOLD UP $7.05/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 866.77 TONNES

MAY 2/WITH GOLD DOWN $1.15/ A HUGE WITHDRAWAL OF 4.43 TONNES FROM THE GLD/INVENTORY RESTS AT 866.77 TONNES

MAY 1/WITH GOLD DOWN $12.15/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 871.20 TONNES

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

JUNE 1/2018/ Inventory rests tonight at 851.45 tonnes

*IN LAST 390 TRADING DAYS: 79.56 NET TONNES HAVE BEEN REMOVED FROM THE GLD

*LAST 340 TRADING DAYS: A NET 76.74 TONNES HAVE NOW BEEN ADDED INTO GLD INVENTORY.

end

Now the SLV Inventory/

JUNE 1/WITH SILVER DOWN 3 CENTS/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY REMAINS AT 322.039 MILLION OZ/

MAY 31/WITH SILVER DOWN 7 CENTS/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY REMAINS AT 322.039 MILLION OZ/

MAY 30/WITH SILVER UP 16 CENTS: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV/ A DEPOSIT OF 2.071 MILLION OZ/INVENTORY RESTS AT 322.039 MILLION OZ/

MAY 29.2018/ NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.968 OZ

May 25/INVENTORY LOWERS TO 319.968 AS WE HAD A WITHDRAWAL OF 1.035 MILLION OZ

MAY 24/WITH SILVER UP 27 CENTS/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 321.003 MILLION OZ/

MAY 22/WITH SILVER UP 6 CENTS/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 321.003 MILLION OZ/

MAY 21/ WITH SILVER UP 5 CENTS/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 321.003 MILLION OZ/

MAY 18/WITH SILVER DOWN 5 CENTS A SMALL CHANGE IN SILVER INVENTORY AT THE SLV/ A WITHDRAWAL OF 942,000 OZ/INVENTORY RESTS AT 321.003 MILLION OZ/

May 17/WITH GOLD UP 6 CENTS/A SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 471,000 OZ//INVENTORY RESTS AT 321.945 MILLION OZ/

MAY 16./WITH SILVER UP 10 CENTS/A HUGE DEPOSIT OF 1.883 MILLION OZ OF SILVER INTO THE SLV/INVENTORY RESTS AT 321.474 MILLION OZ

MAY 15/WITH SILVER DOWN 33 CENTS, NO CHANGES AT THE SLV; THE CROOKS COULD NOT BORROW ANY SILVER BECAUSE THERE IS NONE: INVENTORY RESTS AT 319.591 MILLION OZ

MAY 14/WITH SILVER DOWN 10 CENTS/A SMALL CHANGES IN SILVER INVENTORY AT THE SLV/ A WITHDRAWAL OF 858,000 FROM THE SLV/INVENTORY RESTS AT 319.591 MILLION OZ/

MAY 11/WITH SILVER DOWN 2 CENTS/THE CROOKS WITHDREW A MONSTROUS 2.824 MILLION OZ FROM THE SLV INVENTORY/INVENTORY RESTS AT 320.439 MILLION OZ/

MAY 10/WITH SILVER UP 22 CENTS/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 323.263 MILLION OZ/

MAY 9/WITH SILVER UP 6 CENTS/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 323.263 MILLION OZ/

MAY 8/WITH SILVER DOWN 2 CENTS:NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 323.263 MILLION OZ.

MAY 7/WITH SILVER FLAT: A BIG CHANGE IN SILVER INVENTORY AT THE SLV// A WITHDRAWAL OF 942,000 OZ OF SILVER FROM THE SLV INVENTORY/INVENTORY RESTS AT 323.263 MILLION OZ/

MAY4/WITH SILVER UP 5 CENTS/A BIG CHANGES IN SILVER INVENTORY AT THE SLV/ A DEPOSIT OF 1.224 MILLION OZ/INVENTORY RESTS AT 324.205 MILLION OZ/

MAY 2/WITH SILVER UP 24 CENTS/A HUGE CHANGE IN SILVER INVENTORY AT THE SLV// A DEPOSIT OF 6.082 MILLION OZ INTO THE SLV/INVENTORY RESTS AT 322.981 MILLION OZ/

MAY 1/WITH SILVER DOWN 24 CENTS/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 316.899 MILLION OZ/

JUNE 1/2018:

Inventory 322.039 million oz

end

6 Month MM GOFO 2.13/ and libor 6 month duration 2.47

Indicative gold forward offer rate for a 6 month duration/calculation:

G0FO+ 2.13%

libor 2.47 FOR 6 MONTHS/

GOLD LENDING RATE: .34%

XXXXXXXX

12 Month MM GOFO

+ 2.71%

LIBOR FOR 12 MONTH DURATION: 2.57

GOFO = LIBOR – GOLD LENDING RATE

GOLD LENDING RATE = +.14

end

And now for a totally useless report, the COT which gives position levels of our major players.

Due to the fact that we have humongous amounts of transfers to EFP’s this report is of absolutely and unequivocally no value

your gold COT

| Gold COT Report – Futures | ||||||

| Large Speculators | Commercial | Total | ||||

| Long | Short | Spreading | Long | Short | Long | Short |

| 193,652 | 78,522 | 52,942 | 171,361 | 308,050 | 417,955 | 439,514 |

| Change from Prior Reporting Period | ||||||

| 3,975 | -20,198 | -2,664 | -31,740 | -10,626 | -30,429 | -33,488 |

| Traders | ||||||

| 188 | 74 | 73 | 47 | 57 | 268 | 176 |

| Small Speculators | ||||||

| Long | Short | Open Interest | ||||

| 51,427 | 29,868 | 469,382 | ||||

| -3,131 | -72 | -33,560 | ||||

| non reportable positions | Change from the previous reporting period | |||||

our large speculators

those large specs that have been long in gold added 3975 contracts to their long side

those large specs that have been short in gold covered (transferred) a whopping 20,198 contracts

our commercials

those commercials who have been long in gold pitched (transferred) a monstrous net 31,740 contracts from their long side

those commercials who have been short in gold covered (transferred) a net 10,626 contracts from their short side

our small specs

those small specs who have been long in gold added 3131 contracts to their long side

those small specs who have been short in gold transferred (covered) a net 72 contracts from their short side.

and now for our silver cot

| Silver COT Report: Futures | |||||

| Large Speculators | Commercial | ||||

| Long | Short | Spreading | Long | Short | |

| 83,066 | 65,613 | 16,347 | 77,447 | 112,744 | |

| 5,059 | 2,831 | 1,738 | 931 | 4,805 | |

| Traders | |||||

| 107 | 53 | 55 | 36 | 36 | |

| Small Speculators | Open Interest | Total | |||

| Long | Short | 207,610 | Long | Short | |

| 30,750 | 12,906 | 176,860 | 194,704 | ||

| 1,634 | -12 | 9,362 | 7,728 | 9,374 | |

| non reportable positions | Positions as of: | 167 | 130 | ||

our large speculators

those large specs that have been long silver added 5059 contracts to their long side

those large specs that have been short in silver added 107 contracts to their short side

our commercials

those commercials who have been long in silver added 2831 contracts to their long side

those commercials who have been short in silver added 53 contracts to their short side

our small specs

those small specs who have been long in in silver added 1634 contracts to their long side

those small specs who have been short in silver covered (transferred) a net 12 contracts from their short side.

end

Major gold/silver trading /commentaries for FRIDAY

GOLDCORE/BLOG/MARK O’BYRNE.

GOLD/SILVER

Get “Positioned In Gold” Now As “You Will Not Have Time To Get Positioned” Later

Get “Positioned In Gold” Now As “You Will Not Have Time To Get Positioned” In Physical Later

Guest post by Dominic Frisby of Money Week

This year’s “gold standard” of gold-related research has just come out.

Conveniently enough – given gold’s “safe haven” reputation – it’s arrived just in time for another major financial market scare, this time in the form of Italy.

Below, I consider some of the most pertinent points…

The monetary tide is turning – but how far will it wash out?

Every year, Ronald-Peter Stoeferle and Mark Valek at Incrementum AG, a Liechtenstein-based investment and asset-management company, put together an exhaustive report into the state of gold and gold-related markets. It’s known as In gold we trust.

Last year’s edition was downloaded some 1.7 million times. This year’s, some 230 pages long, arrived in my inbox yesterday and I spent yesterday afternoon flicking through it.

In today’s Money Morning I’d like to share some of the thoughts and charts that caught my eye.

The report argues that we are in the early stages of a new bull market for gold. Several factors underpin this thesis, filed under the theme “monetary turns of the tide”.

First, Incrementum notes that central bank monetary policy is changing. What was quantitative easing (QE) is now quantitative tightening (QT). The equivalent of $14.4trn – an almost unfathomably large number – has been created by the world’s five largest central banks over the past decade.

But this year they turn from net buyers into net sellers of securities. It has already begun in the US and the euro area will soon follow (although it’ll be interesting to see what the situation in Italy does to that plan).

There has been a “global debt accumulation orgy”. But now interest rates are starting to go up, and “the tide of global liquidity is beginning to go out”.

However, while I agree with Incrementum that there has been a change in gear, I’m just not sure quite how much QE has affected gold. It’s so hard to monitor. Easy money saw gold rise between 2009 and 2011, but gold then fell for five years. Investors went elsewhere.

So a change from QE to QT might help gold – or it might not. It depends on how much QT there is, I guess, and what its consequences prove to be. The same goes for interest rates. Sometimes, gold rises when rates go up (as happened in 1980), but this is not always the case.

I do not see rates rising by that much. Central banks will be well aware of the consequence of higher rates – not least to government debt servicing costs – and will only put them up by the smallest amount possible.

We remain at what seems an eternal stand-off: so far, all of this debt hasn’t mattered. One day it will, but nobody knows when.

On the debt front, the chart (above) in particular stood out for me.

It shows US tax revenues against the S&P 500. Since 2015, US tax revenues declined, even as the S&P has risen.

The US already runs a deficit (ie the government spends more than it collects in taxes each year). Donald Trump is not going to cut spending; if anything he is going to spend more – at least that’s what he has indicated.

Where’s the money going to come from? More debt. And there will pressure to keep the cost of that debt down.

The only way interest rates are going to go up by any significant amount is if some kind of crisis forces them up. It will not happen voluntarily.

On that note, Incrementum also observes that “in the great tug-of-war between inflationary and deflationary forces, inflationary forces have gained the upper hand in the course of the past year”.

That certainly seems to be so, and it will put some upward pressure on rates. If wages go up, and with high employment they might at last, inflation will self-reinforce. Inflation should be good for gold.

Even so, I remain of the view that rates will be suppressed where possible.

King Dollar will one day be de-throned – but not for some time

Incrementum’s second changing tide is in the global monetary order, what it calls “de-dollarisation”.

According to the report, “the creeping loss of the hegemonic status of the US dollar as the senior global reserve currency could have far-reaching consequences for the US. Declining global demand for the US dollar and Treasury bonds could boost domestic US price inflation and drive interest rates up further.”

Gold will see increasing demand as a substitute. To back up this point, Incrementum presents a chart showing central bank gold reserves, which are clearly rising.

In the ten years since 2008, central banks have increased their gold reserves by about 3,000 tonnes – or 10%.

However, in the context of the global economy this is drop-in-the-ocean stuff, especially given that it came off deeply oversold levels. Yes, the dollar’s absolute status as the global reserve currency is slowly being chipped away – yuan-denominated oil futures are a recent example.

But the dollar is still the global reserve currency. It is currently rising. It remains the world’s default port-of-call in a panic. This time next year and this time in five or, I dare say, even ten years the dollar will still be the world’s reserve currency. That will not change overnight (though it will change).

Gold and cryptocurrencies – allies or mortal enemies?

Incrementum’s third main theme – and this is what presents the biggest threat, in my view, to US dollar hegemony – is the “technological turn of the tide”.

“Epochal technological change is taking place at a breathtaking pace”, says the report – and I could not agree more. As Paypal founder Peter Thiel once noted, technology, not politics, drives change, and we are in the midst of what I have called the Financial Revolution.

Money is changing. From cryptocurrencies to national currencies to something as trivial as reward points, we are moving into a Hayekian era of multiple currencies. “Gold and cryptocurrencies are friends, not foes,” says Incrementum.

That may or may not be so. Crypto has “stolen” the extremely powerful “anti-fiat” narrative from gold and used it to its great advantage. It may be that crypto makes gold even more anachronistic – it may be that gold eventually becomes the backbone of crypto. The jury is still out.

Overall, Incrementum is more bullish on gold than I am, I’d say.

I think I’ve said something along these lines before: it’s like you’re standing up on the cliff tops looking out to sea. Out on the horizon you can see various economic ships sailing about. They are all carrying cargo which will help a gold bull market – inflation, credit crises, monetary panic, and all the rest of it – but they are not yet sailing into harbour. They will one day, but not yet.

When they do, it may be that they move so quickly you will not have time to get positioned in gold – so you need to get positioned now. But gold’s big day in the sun is still a way off.

One day, Rodders – just not yet.

If you want to take a look at Incrementum’s report – and it is full of excellent research, even if our overall conclusions are not in line – you can do so here.

Courtesy of Money Week

News and Commentary

Gold futures end lower, suffer second straight monthly loss (MarketWatch.com)

Gold flat despite weaker dollar as Italy jitters fade (Reuters.com)

Gold surrenders early gains, weighed down by a modest USD (FXStreet.com)

US Silver Scrap prices fall; Silver Futures climb one percent (ScrapeRegister.com)

Italy set for an anti-establishment government after roiling global markets (CNBC.com)

Source: Bloomberg

Italy could be the next Greece — only much worse (CNBC.com)

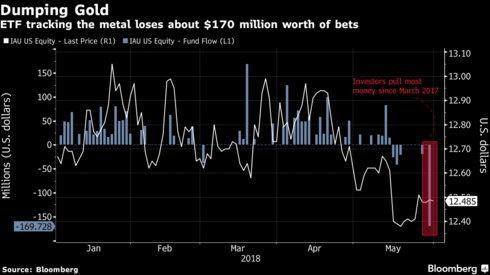

Gold ETF Loses Its Luster for Investors For Now (Bloomberg.com)

Gold Vs Beer Price Since 1950 (Mining.com)

Russian January Gold Output at 15.67 t (MiningWeekly.com)

Dublin Needs To Build Upwards to Keep Rents Down (IrishTimes.com)

Should We Buy This Irish Manor? Bonner Asks (BonnerAndPartners.com)

Listen on SoundCloud , Blubrry & iTunes. Watch on YouTube below

Gold Prices (LBMA AM)

31 May: USD 1,303.50, GBP 978.54 & EUR 1,113.58 per ounce

30 May: USD 1,298.60, GBP 979.27 & EUR 1,119.26 per ounce

29 May: USD 1,302.05, GBP 983.83 & EUR 1,130.57 per ounce

25 May: USD 1,303.95, GBP 976.53 & EUR 1,113.70 per ounce

24 May: USD 1,296.35, GBP 967.73 & EUR 1,104.88 per ounce

23 May: USD 1,294.00, GBP 967.91 & EUR 1,102.88 per ounce

22 May: USD 1,293.90, GBP 961.24 & EUR 1,095.29 per ounce

Silver Prices (LBMA)

31 May: USD 16.55, GBP 12.42 & EUR 14.17 per ounce

30 May: USD 16.37, GBP 12.33 & EUR 14.08 per ounce

29 May: USD 16.48, GBP 12.43 & EUR 14.26 per ounce

25 May: USD 16.67, GBP 12.49 & EUR 14.24 per ounce

24 May: USD 16.51, GBP 12.32 & EUR 14.09 per ounce

23 May: USD 16.53, GBP 12.38 & EUR 14.11 per ounce

22 May: USD 16.58, GBP 12.32 & EUR 14.04 per ounce

Recent Market Updates

– Consequences of Ignoring Economic Reality Are Dangerous

– Are Gold And Silver Bullion Obsolete In The Crypto Age?

– In Gold we Trust: 3 Important Factors Leading to the “Turning of the Monetary Tides”

– Silver Trading in Tight $1 Range As Pressure Builds For A Breakout

– Gold Back Above $1300 – Trump Cancels Historic Summit – Silver “Ready To Breakout”

– Gold Price Surges To Record In Turkey and Other Emerging Markets as Currencies Collapse

– Gold Rarity and Value Shown In Stunning Gold Visualisations

– Gold Looks A Better Investment Than UK Property

– Gold 2048: The Next 30 Years For Gold

– Beware “Snollygosters” and the Empty Promises of Pathological Politicians

– US 10-Year Surges, Emerging Markets Implode…Where Next for Gold?

– Welsh Gold Being Hyped Due To The Royal Wedding?

– Oil Price Is Going To Keep Rising And Inflation Is Coming

Andrew Maguire’s Kinesis money which is a “bitcoin” but backed 100% by allocated gold and silver is set to go.

it think it would be a great idea to look at this!

please read at: https://kinesis.money/#/

(Andrew Maguire)

|

2:57 PM (1 hour ago) | ||

|

|||

Harvey

Here It is my friend! https://kinesis.money/#/ Please let everyone know.

Let catch up on Monday if you have time. We have billions in the hopper ready to be allocated on the 1st day of trading. The paper market days are over.

Warm regards

Andy

Chris Marcus: What the London Gold Pool offers about the current gold market

Submitted by cpowell on Thu, 2018-05-31 14:22. Section: Daily Dispatches

10:22a ET Thursday, May 31, 2018

Dear Friend of GATA and Gold:

Writing for bullion dealer Miles Franklin, financial analyst Chris Marcus calls attention to a couple of fascinating reports about the London Gold Pool of the 1960s by John Paul Koning. They were published in 2009 at the Mises Institute’s internet site.

The London Gold Pool, an operation by Western central banks that sought to hold the gold price at the $35-per-ounce level set by the Bretton Woods agreement of 1944, required a sustained campaign of public and surreptitious government intervention in the financial markets and foreign relations to facilitate the U.S. government’s reckless inflation of the money supply. The pool lasted eight years before collapsing from France’s withdrawal.

Marcus notes the surreptitious intervention in the gold market by central banks since then, credits GATA for helping to expose it, and writes: “Given the recent actions of China and others that continue to build financial infrastructure to eliminate any dependence on or involvement with the petrodollar system, there’s ample reason to believe that it won’t be too much longer before a nation pulls the cord on the current scheme.”

Marcus’ commentary is headlined “What the London Gold Pool Offers about the Current Gold Market” and it’s posted at Miles Franklin’s internet site here:

https://www.milesfranklin.com/what-the-london-gold-pool-offers-about-the…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

Mike Kosares pounds the table that for gold ownership you must buy physical and not any of the paper garbage.

(courtesy Mike Kosares)

Mike Kosares: Gold ownership is a lifestyle decision as much as a portfolio decision

Submitted by cpowell on Thu, 2018-05-31 19:40. Section: Daily Dispatches

3:39p ET Thursday, May 31, 2018

Dear Friend of GATA and Gold:

Gold ownership, USAGold proprietor Mike Kosares writes today, is as much a lifestyle decision as a portfolio decision, more a matter of preserving wealth than making money.

“Don’t buy the paper pretenders,” Kosares writes, “but the real thing in the form of coins and bullion. To do otherwise is to plug into the financial system you are trying to hedge.”

Kosares’ commentary is headlined “Mphm” and it’s posted at USAGold here:

http://www.usagold.com/publications/NewsViewsJune2018-222.html

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

Great commentary from Chris Powell of GATA

(courtesy Chris Powell/GATA)

One of these days, Alice — to the moon!

Submitted by cpowell on Fri, 2018-06-01 01:58. Section: Daily Dispatches

9:58p ET Thursday, May 31, 2018

Dear Friend of GATA and Gold:

At the opening of GATA’s Gold Rush 21 conference in Dawson City, Yukon Territory, back in August 2005, our friend, South Africa’s “Mister Gold,” the late Peter George, was already tired of the brazenness of gold price suppression

“In the last 10 years,” George said, “the central banks have effectively shown that when there is a real crisis, gold actually goes down — and it’s so blatant, it’s a joke”:

Five years ago yesterday your secretary/treasurer wrote:

“If the Northern Hemisphere was destroyed in a nuclear war, the Federal Reserve, JPMorganChase, and HSBC would get some brokers to Sydney, Rio de Janeiro, and Johannesburg to sell gold futures massively and drive the price down by at least 5 percent.

“Kitco market analyst Jon Nadler would crawl out from the rubble and opine to the cockroaches that the gold price had fallen because so many gold buyers had been killed, as he always had predicted would happen.

“CPM Group’s Jeff Christian would telephone New Zealand not to worry because he was flying down with reams of gold-colored paper that would work just as well in Wellington as it did in New York as long as nobody asked what was behind it.

“And the World Gold Council would console itself with whatever high-fashion models could be found wearing nose rings in French Polynesia.

“But with London and New York razed, at least we’d be spared more contrived rationalizations about the strange market action from the Financial Times and Wall Street Journal”:

http://www.gata.org/node/11426

As often said by bus driver Ralph Kramden of “The Honeymooners,” played by Jackie Gleason back in the 1950s, “One of these days, Alice — to the moon!”:

https://www.youtube.com/watch?v=98qw86DsdZ0

But, probably, first the scales will have to fall from the eyes of some of our betters in financial market analysis and journalism or they’ll have to grow backbones and acknowledge the obvious.

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

Alasdair Macleod’s latest paper is a must read. You will recall that it is Macleod’s believe (and myself as well) that China has accumulated 20,000 tonnes to its credit. It has allowed its citizens to accumulate approximately 18,000 tonnes. Macleod believes that it is now time for gold to return to real money as China and Russia will finance the next bold infrastructure moves with gold through the use of gold bonds similar to what Britain used to finance the Napoleonic wars.

(a must read..Alasdair Macleod)

Alasdair Macleod: Gold’s monetary rehabilitation

Submitted by cpowell on Thu, 2018-05-31 19:13. Section: Daily Dispatches

3:14p ET Thursday, May 31, 2018

Dear Friend of GATA and Gold:

In perhaps his most brilliant essay yet, GoldMoney research chief Alasdair Macleod today notes that the U.S. government’s more aggressive use of economic sanctions is pushing the rest of the world away from the U.S. dollar and toward an Asia- and gold-based monetary system.

Macleod then describes the architecture of such a system likely already being constructed by China, leading to the general demise of fiat money throughout the world.

Macleod’s analysis is headlined “Gold’s Monetary Rehabilitation” and it’s posted at GoldMoney here:

https://www.goldmoney.com/research/goldmoney-insights/gold-s-monetary-re…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

Gold’s Monetary Rehabilitation

There is a quiet revolution taking place in the monetary vacuum that’s developing on the back of the erosion of the dollar’s hegemony. It is perhaps too early to call what’s happening to the dollar the beginning of its demise as the world’s reserve currency, but there is certainly a move away from it in Asia. And every time the Americans deploy their control over global trade settlement as a weapon against the regimes they dislike, nations who are neutral observers take note and consider how to protect themselves, “just in case.”

Vide Europe over the Iran issue. And Turkey. These are rifts in NATO. Countries in Africa, and elsewhere are now taking China’s money. And to please the Chinese, Gambia, Burkina Faso, Panama and the Dominican Republic have all recently severed diplomatic relations with Taiwan. Small fry perhaps, but a weathervane showing which way the wind is blowing.

We’ve seen Russia set up an alternative to SWIFT in order to be free from American monetary interference in pan-Asian trade. We’ve seen China take major steps to exclude the dollar from her trade as much as possible and to enhance the role of her own currency. And now we have a schism over Iran between America and the Europe it set up after WW2 through the mechanism of the CIA-controlled American Committee for United Europe in 1948.

It is unprecedented, and today America obviously cares less for her relationship with European allies than she hates Iran. There can be little doubt that America’s undeclared war against the land of Omar Khayyam is intended to undermine its economy and create the conditions for internal revolution. The Iranian rial has continued its collapse, and the theocratic government has played into US hands by shutting down “unauthorised” money-changers, with Grand Ayatollah Nasser Makarem Shirazi calling for the execution of money changers to help end the currency crisis. The black-market rate for rials has rocketed as a result, and according to Professor Steve Hanke whose department at John Hopkins University makes a study of these things, the true rate of price inflation has jumped to 74.8%.[i]

For the ordinary Iranian, gold has always been the ultimate money, while their government’s rials are to be rapidly passed on to someone else. America’s sanctions and the government’s actions merely reinforce that message. Time will tell whether America’s attempt to undermine Iran’s theocracy succeeds, but history suggests it is unlikely. And at a national level, Iran is driven by American actions into accepting anything but dollars in payment for her oil exports. She would like euros, and given the EU is still trying to sell her capital goods, that makes sense. But no commercial bank dares facilitate payment in any currency under the threat of US sanctions and penalties.

That leaves only three possibilities beyond America’s influence: Chinese yuan, Russian roubles, and gold, all independent from the West’s banking system. It is no wonder the new yuan for oil contract in Shanghai, perhaps with a little help from China’s state-owned banks, has got off to a roaring start. We can all understand the desire to lock in oil prices for future delivery, in this case it is in return for yuan issued by the People’s Bank of China. However, in the future Iran will be able to spend the bulk of her yuan on other raw materials, using a range of yuan futures contracts as a bridge to them from her oil.

Essentially, US sanctions are forcing Iran onto a yuan standard for her foreign trade. Furthermore, China is there to pick up the pieces the West abandons because of American sanctions, driving Iran into an increasing dependency on China. The new Silk Road, the Chinese-built 200kph railway between Tehran and the eastern city of Mashad, as well as other Chinese-led rail projects are opening up Iran in a purely Eurasian context, marginalising American power. Iran’s problem with this, if there is one, is international yuan markets are not yet developed enough to make full use of hedging instruments. But Iran’s demand for sophisticated financial tools, as well as from other nations in Asia turning their backs on America, is bound to hasten their development.

I have written several times in the past about the importance of yuan-denominated deliverable gold futures in this context, and the evidence that the two markets offering these contracts, Hong Kong and Dubai, are cooperating in establishing additional vaulting facilities in China, roping in other gold centres in South-east Asia as well. In the case of gold, where physical delivery measured in tonnes is tight, the Chinese are ensuring as far as possible that deliverable liquidity will be there.

Additionally, last week the London Metal Exchange, owned by the Hong Kong Exchange and Clearing (HKEX), admitted it is considering introducing yuan contracts for base metals as well. We can safely assume that while the HKEX is an independent commercial entity, its strategic objectives are closely aligned with and encouraged by the Chinese government. Not only do the Chinese dominate gold markets in Asia, but last year HKEX successfully introduced regulated precious metal contracts in London. There can be little doubt that HKEX will be an important platform for expanding international markets for the Chinese currency. And at some time in the future, a state like Iran will be able to use not only yuan contracts to sell commodities in order to buy other commodities, but to use them as a stepping-stone to mobilise state-owned gold for payments as well.

Our topic is now moving on to gold being actively used as money instead of fiat currencies. While this point is not yet being considered by Western commentators, we can be sure it is by the forward planners in Asian governments. It’s not for nothing India is trying everything to get hold of its citizens gold. To an extent, gold is already used as money by governments, which is why they are still included in monetary reserves. But they are there as a backstop, the money of last resort, no one’s liability. What we could be seeing with the development of international yuan currency markets is a platform that links the use of gold to trade settlement.

This insight means we must look at both the Chinese and Russian policies on gold in a new light. Assumptions in the markets seem to be that China and Russia only see gold as a dollar hedge, or alternatively their accumulation of gold is either to balance the US’s holding of 8,133 tonnes, or alternatively (if you believe the American’s are lying about their reserves) Chinese and Russian gold is there to be used like a sword of Damocles held over the dollar. It would be wrong to dismiss these theories out of hand, but surely, they miss the point. You don’t carefully plan to become a dominant world power, edging out the Americans and their dollars, without careful forward planning of monetary affairs.

There is irrefutable evidence that China has been planning for a post-dollar world since shortly after her leadership threw in the towel on communism and embraced free markets. The regulations appointing the People’s Bank with sole responsibility for gold and silver date all the way back to 1983, since when we can confidently assume the PBOC has quietly accumulated gold on behalf of the state at prices that varied between $250-500 over a nineteen-year period. We know this, because in 2002 the PBOC then permitted private ownership, setting up the Shanghai Gold Exchange to facilitate physical acquisition. This would only have happened after the state had had a clear run at accumulating sufficient physical gold for its future purposes. And, as the largest gold mining nation for many years by far, with state monopolies in refining domestic production, recycling scrap and refining imported doré, there should be no doubt over her policy towards her accumulation of gold bullion.[ii]

Since 2002, the Chinese government has actively encouraged its nationals to accumulate physical gold and judging by net withdrawals from the Shanghai Gold Exchange vaults, the public possesses roughly 18,000 tonnes from more or less a standing start.[iii] My estimate for state ownership of bullion, based on contemporary prices, an analysis of capital inflows in the 1980s, followed by trade surpluses in the 1990s and before the public were permitted to buy in 2002, is approximately 20,000 tonnes. Even so, that may be not be enough gold bullion owned by the state at current prices to operate a simple gold exchange standard, being the equivalent value of ¥5.22 trillion, compared with currency in circulation of ¥7.15 trillion.[iv] For comparison, when President Roosevelt devalued the dollar to $35 in January 1934, the US Treasury held gold worth $7.44bn at the new price against currency in circulation of $5.72bn. Therefore, if the Chinese government has 20,000 tonnes, and if it is to have the same currency cover as America had on 31 January 1934, at current exchange rates gold would have to be priced at $2,317.

Russia began accumulating gold only more recently and is now aggressively building her official reserves. Whether she has accumulated bullion “off balance sheet” is not known but should not be dismissed. Based on her official reserves at 1,910 tonnes worth RUB5.0 trillion, it does not cover M0 yet (RUB8.44 trillion)[v] but a rise in the gold price to $2,200 will do so, and a gold price of $2,860 would be required to match the Americans in 1934. In fact, for both Russia and China if gold is to have a monetary role it would have to be at a far higher price than it is today.

A scheme for linking currency to gold

Comparing the value of bullion held to the narrowest expression of money is likely to prove insufficient upon which to base a future monetary policy. But, given a good base of monetary gold, it is possible to set up arrangements to discourage redemptions of currency for physical gold when a gold exchange standard is fully implemented[vi]. The suggested arrangement that follows is based on the issuance of irredeemable government bonds with a coupon payable in either gold or currency at the owner’s choice (the gold bond). Furthermore, an issue of this sort could be used to improve government finances at the same time.

By issuing the gold bond at a discount to par, early buyers get an enhanced yield. This rewards them for buying a new instrument which has yet to gain its potential market recognition. The market price of the bond will become linked to the yield on physical gold once the conversion rate is set, with an additional margin for issuer risk. And if currency balances invested in such a bond are rewarded with a yield payable in gold, demand for currency redemptions into gold are unlikely to be significant, so long as the public has confidence in the issue and the gold exchange standard. So, a country putting its currency on a gold exchange standard should, with a correctly priced bond, minimise redemptions.

A sinking fund should be established at the same time as the bond is announced to buy physical gold to cover anticipated demand for coupons paid in gold. Some gold from reserves can be allocated for this purpose initially but additional gold should be bought to establish sufficient cover to add conviction to the scheme by winding down existing foreign currency reserves where they are unbacked by gold, immediately.

From here on, we shall assume this scheme to introduce a sound, gold-exchangeable currency is taken up by the Chinese government. Government finances can be expected to improve from the arrangement, to the extent that borrowing costs are reduced. For example, China’s 30-year bond currently yields 4.1% having been as high as 4.4% earlier this year. A gold-linked irredeemable Chinese bond, even allowing for issuer risk would probably yield no more than 3% at the outset, which is slightly less than the current yield on 1-year maturities. If it was issued with, say, a 2.25% coupon, it would be priced at 75.00, giving the attraction of a capital gain to private citizens as the risk premium on Chinese government bonds declines.

This will also lend support to the currency in the foreign exchanges. The gold bond should be listed in Shanghai, Hong Kong, Tokyo, Singapore, Dubai, London and Moscow so that sovereign wealth funds and other conservative long-term investors have ready access to it. New York is not on the list because it is Chinese policy to exclude the American banking system from her monetary affairs as much as possible, and the conflicts that necessarily would arise with the US government. Ultimately, for funds based outside America, the gold bond itself would come to be regarded as a gold substitute for investment purposes, integrating gold into both Chinese-led monetary and investment reforms.

There can be little doubt that if these measures are taken gold convertibility would rapidly promote the yuan to foreigners in Asia and beyond as an acceptable store of value in exchange for trade. In time, all foreign currency held in China’s monetary reserves not backed by gold would have to be disposed for gold or yuan, as being inconsistent with the new monetary policy. As stated above, China’s gold buying using dollars would start immediately and continue until the price of gold has risen to the point where the gold exchange rate is finally established.

Furthermore, with no final redemption on the gold bond, there would be no need to make any repayment provisions. This model is the one that was adopted by the British government for financing the Napoleonic Wars by issuing Consolidated 3% Annuities at a deep discount, so that investors providing war finance not only got an enhanced yield, but also a substantial capital gain when peacetime returned. The fortunes created on the return to peace played an important part in financing the industrial revolution in the early nineteenth century.[vii]

In this sense, there are good parallels between Britain’s war financing two hundred years ago, and China’s current position. In both cases government expenditure exceeded and exceeds respectively tax income by a significant margin, and neither were and are on a gold standard. Britain had temporarily abandoned her gold standard in the 1790s, before reinstating it a few years after Waterloo.

In China’s case, excess government expenditure is due to planned infrastructure spending, which is likely to be ongoing for at least another ten years and extending well beyond her borders. However, Chinese instigated capital expenditure throughout Asia will increasingly be covered by project financing through the Asian Infrastructure Investment Bank, releasing the Chinese government from much of the financing burden.

The British came out of the Napoleonic Wars with an estimated debt to GDP of about 260%. In cash terms it was considerably less, because the debt figure is the total of nominal debt in issue. This was the beauty of irredeemable Consols, because they never need to be repaid, which meant a more accurate debt to GDP figure was 180%. As an historical footnote, it is interesting they were repaid only recently.

China’s government debt is considerably less at just under 50%, but still rising. China is blessed with a savings rate of close to 50% of GDP as well, so further issues of a gold-linked bond into the domestic market should be heavily subscribed. Once the current expansion of infrastructure spending diminishes, the Chinese government will easily return to a budget surplus, paying down its debt more rapidly than the British did in the 1800s.

I would suggest China undertakes the monetarisation of gold in two stages. The first would be to issue the new gold loan outlined above. Proceeds of the new gold bond would be used to finance government expenditure, to purchase existing bonds in the market for cancellation, and to build a sinking fund to provide cover for future coupon demands in gold. The price relationship between coupons paid in gold and yuan will be fixed at a later date and will be the rate for the gold exchange standard once it is set. It cannot be set at the outset, because it is clear that for gold to be rehabilitated into China’s monetary system, and consequently the likelihood it will be elsewhere, will require a far higher gold price than at present. In price theory, it is the introduction of a new use that will set a higher marginal price. That will be the second step, which is announced in advance when the new gold bond is first issued but at a rate yet to be decided.

China is the ideal jurisdiction for the reintroduction of gold into a monetary system by way of a gold exchange standard. To briefly summarise:

- China has been secretly accumulating gold since regulations appointed the PBOC to do so in 1983. Not only has the state accumulated significant quantities of gold, but the citizenry has as well. China and its population is therefore fully attuned to the use of gold as money.

- The Chinese government has no need to resort to the illusory benefits of inflationary financing. Her budget deficits are the consequence of infrastructure spending, which will diminish in time, and her citizens have a savings rate of nearly 50%, which is the real engine behind her economic progress and wealth creation. Furthermore, government debt to GDP is relatively low at about 50%, and she is not burdened by the costs of a Western-style welfare state.

- China’s success is driven by a political requirement to improve the standards of living for everyone in as many as 42 diverse ethnic groups, representing an unwritten contract between the state and its people in lieu of democracy. A gold standard and a savings vehicle that gives ordinary people a yield on gold will increase personal wealth and guarantee the cohesion and economic strength of the Chinese nation, at a time when America’s finances are relying increasingly on the destruction of private wealth through inflation. There has to be a parting of the ways for the two currencies.

- The introduction of sound money by way of a gold exchange scheme will ensure China’s economic dominance will develop and continue for a considerable time, much as it did for Britain in the nineteenth century.

Russia is also manoeuvring towards a gold standard, which given her partnership with China at the head of the Shanghai Cooperation Organisation, will most likely build on the Chinese model. The differences are one positive and one negative. The positive is the Russian government’s finances are in excellent order, the negative is Russia has only relatively recently begun to accumulate significant gold reserves. She is therefore likely to want to accumulate more gold before embarking on a gold exchange standard and may therefore encourage China to delay her plans until she is ready.

The consequences of Asian gold exchange standards

The economic cost of a change to sound money is that the transfer of wealth from lender to borrower, which is the dominant feature of unsound money, ceases. Inevitably, overindebted businesses as likely to experience difficulties. Furthermore, Chinese exporters to countries with pure fiat currencies will have to invest in more efficient production to remain competitive.

This is less of a problem than first appears. In her current five-year plan, China is moving away from relying on competitive export models towards developing high-tech and service industries aimed at satisfying a growing middle class. Furthermore, Asia represents a new semi-captive market for China, where the yuan is likely to become the standard foreign currency.

The effect on the dollar, euro and Japanese yen could be ruinous, depending on how the relevant central banks develop their monetary policies. They would have to realise that the era of pure fiat is over, and currencies which depend entirely on confidence in their value are no longer fit for purpose. The PBOC could smoothen this process by giving the other major central banks advance notice of its intentions, to minimise the risk of bullion banks being badly wrong-footed with undeliverable bullion obligations.

In the wider context, financial markets are themselves completely wedded to neo-Keynesian economics and may take some time to adjust to why a successful gold exchange standard is a threat to unbacked fiat currencies. But by providing a globally-acceptable sound-money alternative to the current fiat money system, those that do adapt will avoid the hyperinflations that are the logical destiny for governments that rely on inflationary finance. The eventual prize will be for the Shanghai Cooperation Organisation to have two gold-backed currencies for cross-border trade for use throughout Asia, Eastern Europe, sub-Saharan Africa and parts of South America. The Middle East as well will find these currencies attractive in payment for oil, and countries that stay purely fiat will be marginalised.

Those countries whose currencies have been recently destabilised by the dollar’s rally should be among the first to realise that being tied to a Chinese-led sound money regime is a better option. In the course of only a year or two, in theory over half the world’s population could have access to a currency exchangeable for gold, or at least tied to it.

If the whole scheme of Asian revival through economic power is to progress and survive long into the future, it will be a precondition that gold is central to monetary policy. Indeed, given the increasingly certain fate for the inflationary dollar, which is likely to drag down the rest of the world with it, it should no longer be a matter of choice, only of timing. And unless the welfare-driven nations, whose governments have waxed on the destruction of their citizens’ wealth through deliberate monetary inflation reform their ways, they will deserve to slide into obscurity.

end

A great commentary from Nicholas Biezanek as he comes to the conclusion that it is the ESF that is financing these EFP’s/ Is this the end game for the Comex/LBMA and Petro dollar scheme?

a must read…

(courtesy Nicholas Biezanek)

THE IMMINENT END GAME re COMEX /LBMA /PETRO DOLLAR HEGEMONY

Nicholas Biezanek

I will start with a very relevant quote copied from Jim Willie’s May 2018 Hat Trick Letter.

‘Many observers do not understand that machines with their complex algorithms use the COMEX contract as a USDollar trading hedge. They do not have to deliver gold. The Fed sees this as a service to enhance the fiat currencies in a hidden support function. It is all part of the sociopath control over a failing system that cannot reform itself’.

The relevance of the above quote has recently been enhanced by the suppression of same day reporting of the two LBMA gold fixes; what we sight now in the West is 100% a COMEX/GLOBEX paper future contract and all transactions involving the eventual delivery of physical gold are totally opaque (opaque is indeed too generous a description, since opaqueness implies some minuscule degree of impaired visibility).Perhaps this iniquitous status quo is about to change .This week the algos, as usual, are working flat out to give the impression that the Italian fiasco means absolutely nothing at all from the perspective of disturbing gold’s extremely limited role in the economic order as dictated by the central planners. Let us examine some recent and evolving events that portend momentous change as paper gold machinations will begin to be overwhelmed by the forthcoming demand for physical delivery of gold. This new daily occurrence of Exchange for Physical contracts inexplicably novated over to the Comex is so egregious as to manifestly portend that the end game is nigh. (A possible explanation is postulated in the body of this paper).

RECENT LBMA VAULT DATA

The LBMA publishes 3 months in arrears the total loco London gold vault holdings. The data as at 28th February 2018 was therefore only released on the morning of 1st June 2018. Why is there a delay of more than 90 days? Even if horse riders are still used to deliver the data returns, loco London implies a very constricted geographic area, so the data should be released within 48 hours if the true intention is to provide meaningful information. The LBMA releases this data under the headline war cry of a move to total transparency, but I believe that this data is complete disinformation, even if accurate. If Deutsche Bank was merely to release the asset side of its balance sheet, how useful would that be in the absence of particulars of all the corresponding liabilities, both on and off balance sheet? The same is true of data in respect of LBMA vault gold. Since all the claims on this gold may be multiples of the physical gold available to meet such claims, then failure to disclose that fact results in merely the dissemination of propaganda, designed to give a false and misleading sense of ‘all is well’. For what it is worth, the table below summarizes loco London vault gold as at 28th February 2018 (the first month of this new LBMA ‘transparency’ was first evidenced in July 2016 and that data is included to assist with contextualization of the figures):

| Data from: | http://www.lbma.org.uk/london- precious-metals-physical-holdings-statistics | |||||

| LBMA data is available per month from July 2016 onwards | LBMA total loco London gold holdings | BOE total vault holdings (included in LBMA data) | Residual gold held with all other LBMA custodians | Residual gold held with all other LBMA custodians in tonnes | GLD holdings with various custodians and sub custodians | Non BOE float, excluding GLD custodial gold, avalable for allocated gold holders etc. |

|

A |

B |

A-B |

A-B |

C |

A-B-C |

|

|

000 |

000 |

000 |

||||