GOLD: $1295.60 DOWN $4.70 (COMEX TO COMEX CLOSINGS)

Silver: $16.86 DOWN 5 CENTS (COMEX TO COMEX CLOSINGS)

Closing access prices:

Gold $1295.60

silver: $16.87

For comex gold:

JUNE/

NUMBER OF NOTICES FILED TODAY FOR JUNE CONTRACT:425 NOTICE(S) FOR 42500 OZ.

TOTAL NOTICES SO FAR 6587 FOR 658,700 OZ (20.488 tonnes)

For silver:

JUNE

16 NOTICE(S) FILED TODAY FOR

80,000 OZ/

Total number of notices filed so far this month: 923 for 4,615,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: BID $6795/OFFER $6895: down $32(morning)

Bitcoin: BID/ $6510/offer $6610: DOWN $317 (CLOSING/5 PM)

end

First Shanghai gold fix comes at 10 pm est

The second Shanghai gold fix: 2:15 pm

First Shanghai gold fix gold: 10 pm est: 1303.34

NY price at the same time: 1298.45

PREMIUM TO NY SPOT: $4.89

Second gold fix early this morning: 1303.52

USA gold at the exact same time:1297.25

PREMIUM TO NY SPOT: $6.28

AGAIN, SHANGHAI REJECTS NEW YORK PRICING.

WE WILL NOT PROVIDE LONDON FIXES AS THEY ARE NOT ACCURATE AS TO WHAT IS GOING ON AT THE SAME TIME FRAME.

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total OPEN INTEREST ROSE BY A STRONG 2208 CONTRACTS FROM 230,413 UP TO 232,621 ACCOMPANYING YESTERDAY’S GOOD 18 CENT GAIN IN SILVER PRICING. WE ARE NOW WITNESSING OUR USUAL AND CUSTOMARY COMEX LONG LIQUIDATION AS WE ENTERED INTO THE NON ACTIVE DELIVERY MONTH OF JUNE AS LONGS PACK THEIR BAGS AND MIGRATE OVER TO LONDON. WE WERE NOTIFIED THAT WE HAD A STRONG SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP: 2473 EFP’S FOR JULY, 153 EFP’S FOR SEPT. AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE: OF 2626 CONTRACTS. WITH THE TRANSFER OF 2626 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 2626 EFP CONTRACTS TRANSLATES INTO 13.13 MILLION OZ ACCOMPANYING:

1.THE 18 CENT FALL IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES STANDING FOR JUNE COMEX DELIVERY. (4.630 MILLION OZ) DESPITE IT BEING A NON ACTIVE DELIVERY MONTH.

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF JUNE:

19,255 CONTRACTS (FOR 8 TRADING DAYS TOTAL 19,255 CONTRACTS) OR 96.28 MILLION OZ: (AVERAGE PER DAY: 2406 CONTRACTS OR 12.034 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH: 96.28 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 13.71% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)

ACCUMULATION IN YEAR 2018 TO DATE SILVER EFP’S: 1,410.47 MILLION OZ.

ACCUMULATION FOR JAN 2018: 236.879 MILLION OZ

ACCUMULATION FOR FEB 2018: 244.95 MILLION OZ

ACCUMULATION FOR MARCH 2018: 236.67 MILLION OZ

ACCUMULATION FOR APRIL 2018: 385.75 MILLION OZ

ACCUMULATION FOR MAY 2018: 210.05 MILLION OZ

RESULT: WE HAD AN STRONG SIZED DECREASE IN COMEX OI SILVER COMEX OF 2208 WITH THE GOOD 18 CENT RISE IN SILVER PRICE. WE HAVE NOW ENTERED THE NEW NON ACTIVE MONTH OF JUNE. THE CME NOTIFIED US THAT IN FACT WE HAD AN SMALL SIZED EFP ISSUANCE OF 2626 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) . FROM THE CME DATA: 2473 EFP CONTRACTS FOR JULY, 153 EFP’S FOR SEPT. AND ZERO FOR ALL OVER MONTHS FOR A DELIVERABLE FORWARD CONTRACT OVER IN LONDON WITH A FIAT BONUS (TOTAL: 2626). TODAY WE GAINED A STRONG: 4834 TOTAL OI CONTRACTS ON THE TWO EXCHANGES: i.e.2626 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH AN INCREASE OF 2208 OI COMEX CONTRACTS. AND ALL OF THIS HAPPENED WITH THE GOOD 18 CENT RISE IN PRICE OF SILVER AND A CLOSING PRICE OF $16.91 WITH RESPECT TO YESTERDAY’S TRADING. YET WE STILL HAVE A GIGANTIC AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY IN THIS NON ACTIVE JUNE DELIVERY MONTH. IT SURE LOOKS LIKE A FAILED BANKER SHORT COVERING EXERCISE!!

In ounces AT THE COMEX, the OI is still represented by OVER 1 BILLION oz i.e. 1.163 MILLION OZ TO BE EXACT or 166% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT JUNE MONTH/ THEY FILED AT THE COMEX: 16 NOTICE(S) FOR 80,000 OZ OF SILVER

IN SILVER, WE HAVE NOW SET THE NEW RECORD OF OPEN INTEREST AT 243,411 AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $16.51 ON APRIL 9.2018. (AND IN LOOKS LIKE WE ARE GOING TO SEE ANOTHER RECORD HIT THIS MONTH)

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ AND MAY: 36.285 MILLION OZ /AND JUNE/2018 (4.630 MILLION OZ SO FAR)

- HUGE RECORD OPEN INTEREST IN SILVER 243,411 CONTRACTS (OR 1.217 BILLION OZ/ SET APRIL 9/2018

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017

- RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ (FINAL)

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT). IT ALSO LOOKS LIKE BANKER CAPITULATION IN SILVER AS THEY STRUGGLE TO REMOVE SOME OF THEIR HUGE OBLIGATIONS.

In gold, the open interest FELL BY A TINY 77 CONTRACTS DOWN TO 446,828 DESPITE THE GAIN IN THE GOLD PRICE/YESTERDAY’S TRADING (RISE OF $0.65). WE ARE NOW IN THE ACTIVE DELIVERY MONTH OF JUNE. NO DOUBT THE BOYS ARE CASHING IN THEIR COMEX LONGS TO BEGIN THE PROCESS TO MOVE INTO LONDON FORWARDS. THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 4685 CONTRACTS : JUNE SAW THE ISSUANCE OF 0 CONTRACTS , AND AUGUST SAW THE ISSUANCE OF: 4685 CONTRACTS WITH ALL OTHER MONTHS ZERO. The new OI for the gold complex rests at 446,828. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE A FAIR SIZED OI GAIN IN TOTAL CONTRACTS ON THE TWO EXCHANGES: 77 OI CONTRACTS DECREASED AT THE COMEX AND A FAIR SIZED 4685 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN: 4,568 CONTRACTS OR 456,800 OZ = 14.208 TONNES. AND ALL OF THIS DEMAND OCCURRED WITH A TINY GAIN OF $0.65

YESTERDAY, WE HAD 5110 EFP’S ISSUED.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF MAY : 76,108 CONTRACTS OR 7,610,800 OZ OR 236.72 TONNES (8 TRADING DAYS AND THUS AVERAGING: 9513 EFP CONTRACTS PER TRADING DAY OR 951,300 OZ/ TRADING DAY),,

TO GIVE YOU AN IDEA AS TO THE HUGE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 7 TRADING DAYS IN TONNES: 236.72 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2017, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 2555 TONNES

THUS EFP TRANSFERS REPRESENTS 236.72/2550 x 100% TONNES = 9.28% OF GLOBAL ANNUAL PRODUCTION SO FAR IN APRIL ALONE.***

ACCUMULATION OF GOLD EFP’S YEAR 2018 TO DATE: 3,688.55* TONNES *SURPASSED ANNUAL PROD’N

ACCUMULATION OF GOLD EFP’S FOR JANUARY 2018: 653.22 TONNES

ACCUMULATION OF GOLD EFP’S FOR FEBRUARY 2018: 649.45 TONNES

ACCUMULATION OF GOLD EFP’S FOR MARCH 2018: 741.89 TONNES (22 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR APRIL 2018: 713.84 TONNES (21 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR MAY 2018: 693.80 TONNES ( 22 TRADING DAYS)

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A TINY SIZED DECREASE IN OI AT THE COMEX OF 77 DESPITE THE TINY $0.65 GAIN IN PRICE // GOLD TRADING YESTERDAY ($0.65 RISE). WE ALSO HAD AN FAIR SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 4685 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 4685 EFP CONTRACTS ISSUED, WE HAD AN NET GAIN OF 4568 CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

4685 CONTRACTS MOVE TO LONDON AND 77 CONTRACTS DECREASED AT THE COMEX. (in tonnes, the GAIN in total oi equates to 14.208 TONNES). ..AND BELIEVE IT OR NOT BUT ALL OF THIS DEMAND OCCURRED AT THE COMEX WITH A TINY GAIN OF $0.65 IN TRADING!!!.

we had: 309 notice(s) filed upon for 30,900 oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD...

WITH GOLD DOWN $4.70 TODAY: / NO CHANGES IN GOLD INVENTORY AT THE GLD/ /GLD INVENTORY 828.76 TONNES

Inventory rests tonight: 828.76 tonnes.

SLV/

WITH SILVER DOWN A TINY 5 CENTS TODAY / A HUGE CHANGES IN THE SILVER INVENTORY AT THE SLV/THE CROOKS RAIDED THE SILVER COOKIE JAR TO THE TUNE OF 1.976 MILLION OZ (WITHDRAWAL)

/INVENTORY RESTS AT 317.290 MILLION OZ/

end

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER ROSE BY AN STRONG SIZED 2208CONTRACTS from 230,413 UP TO 232,621 (AND, FURTHER FROM THE NEW COMEX RECORD SET /APRIL 9/2017 AT 243,411/SILVER PRICE AT THAT DAY: $16.53). THE PREVIOUS RECORD OTHER THAN WAS ESTABLISHED AT: 234,787, SET ON APRIL 21.2017 OVER ONE YEAR AGO. THE PRICE OF SILVER ON THAT DAY: $17.89. OUR CUSTOMARY MIGRATION OF COMEX LONGS MORPH INTO LONDON FORWARDS CONTINUES AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE: (WE DO NOT GET A LOOK AT THESE CONTRACTS AS IT IS PRIVATE BUT THE CFTC DOES AUDIT THEM), 2473 EFP’S FOR JULY, 153 EFP CONTRACTS FOR SEPT. AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 2626 CONTRACTS . EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI GAIN AT THE COMEX OF 2208 CONTRACTS TO THE 2626 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A GAIN OF 4834 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES: 24.17 MILLION OZ!!! AND THIS STRONG SIZED DEMAND OCCURRED WITH A GOOD 18 CENT RISE IN PRICE . THE BANKERS ORCHESTRATED THEIR RAID THROUGHOUT LAST WEEK DESPERATELY TRYING TO PARE THEIR GIGANTIC OPEN INTEREST SHORT ON BOTH EXCHANGES BUT TO NO AVAIL. JUDGING BY THE RECORD NUMBER OF EFP ISSUANCE DURING APRIL AT 385.75 MILLION OZ AND THE CONTINUAL OI GAIN ON THE TWO EXCHANGES, THE CONSTANT RAIDS, (THAT ARE NOW BEING CALLED UPON BY OUR BANKER FRIENDS IN AN ATTEMPT TO SHAKE AS MANY SILVER LEAVES FROM THE SILVER TREE AS POSSIBLE) AND JUDGING BY THE RESULTS FROM YESTERDAYS ACTION, THEY HAVE NOT BEEN AT ALL SUCCESSFUL.

RESULT: A STRONG SIZED INCREASE IN SILVER OI AT THE COMEX WITH THE 18 CENT GAIN IN SILVER PRICING YESTERDAY. BUT WE ALSO HAD ANOTHER STRONG SIZED 2626 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR JUNE, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

)TUESDAY MORNING/MONDAY NIGHT: Shanghai closed UP 27.02 points or 0.89% /Hang Sang CLOSED UP 39.36 points or 0.13% / The Nikkei closed UP 74.31 POINTS OR 0.33% /Australia’s all ordinaires CLOSED UP .13% /Chinese yuan (ONSHORE) closed UP at 6.4043/Oil UP to 66.02 dollars per barrel for WTI and 76.08 for Brent. Stocks in Europe OPENED ALL MIXED//. ONSHORE YUAN CLOSED UP AT 6.4043 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.4005/ONSHORE YUAN TRADING WEAKER AGAINST OFFSHORE YUAN/ONSHORE YUAN TRADING MUCH STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING MUCH WEAKER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW LOOKS LIKE A FULL TRADE WAR IS BEGINNING/

/NORTH KOREA/SOUTH KOREA

i)North Korea/South Korea/USA

The following is the first of many summits, but it seems that Kim is committed to denuclearizaiton

( zerohedge)

b) REPORT ON JAPAN

3 c CHINA

i)Despite his success in North Korea, this morning, China redeploys missiles on the contested South China Sea island of Woody Island part of the Parcel islands

( zero hedge)

ii)the Senate adds a ZTE killing deal amendment to its defense bill..that which will no doubt anger China

( zerohedge)

4. EUROPEAN AFFAIRS

i)ITALY/SPAIN

A stranded migrant ship which was originally headed for Italy, has run out of food as an Italian rescue vessel takes the refugees to Spain

(courtesy zerohedge)

ii)UK

REBELLION IN THE UK MAY GOVERNMENT AHEAD OF A CRITICAL “BREXIT” AMENDMENT VOTE

(courtesy zerohedge)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

( zerohedge)

6 .GLOBAL ISSUES

7. OIL ISSUES

SAUDI ARABIA

oil production jumps considerably in June despite a good drop in oil demand according to a statement by OPEC

( zerohedge)

8. EMERGING MARKET

9. PHYSICAL MARKETS

The worst kind: Bitcoin tumbles below $6500 on no news. The boys seem to be dumping

(courtesy zerohedge)

10. USA stories which will influence the price of gold/silveri)

Naturally the interest component is increasing due to the higher debt held at 21 trilllion dollars

We will no doubt hit 1.2 trillion deficit by next year coupled with 600 billion of bonds that must be purchased due to the Fed rolling off these amounts of bonds. The USA must raise a monstrous 1.8 trillion dollars in bond issuance.

(courtesy zerohedge)

v)SWAMP STORIES

b)Oh this is very funny!! Mueller scrambles to limit evidence after the indicted Russians actually show up in court!!!

Trading Volumes on the COMEX

PRELIMINARY COMEX VOLUME FOR TODAY: 224,437 contracts

CONFIRMED COMEX VOL. FOR YESTERDAY: 219,170 contracts

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

And now for the wild silver comex results.

Total silver OI ROSE BY A CONSIDERABLE SIZED 2208 CONTRACTS FROM 230,413 UP TO 232,621 (AND A GOOD CLOSER TO THE NEW RECORD OI FOR SILVER SET APRIL 9.2018/ 243,411 CONTRACTS) WITH THE GOOD 18 CENT GAIN IN SILVER PRICING/ YESTERDAY. SINCE WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF JUNE, WE WERE INFORMED THAT WE HAD A STRONG SIZED 2473 EFP CONTRACT ISSUANCE FOR JULY, 153 EFP CONTRACTS FOR SEPT. AND ZERO FOR ALL OTHER MONTHS. THESE EFPS WERE ISSUED TO COMEX LONGS WHO RECEIVED A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. THE TOTAL EFP’S ISSUED: 2626. ON A NET BASIS WE GAINED 4834 SILVER OPEN INTEREST CONTRACTS AS WE OBTAINED A 2208 CONTRACT GAIN AT THE COMEX COMBINING WITH THE ADDITION OF 2626 OI CONTRACTS NAVIGATING OVER TO LONDON.

NET GAIN ON THE TWO EXCHANGES: 4834 CONTRACTS

AMOUNT STANDING FOR SILVER AT THE COMEX

We are now in the NON active delivery month of JUNE and here the front month ROSE BY 4 contracts RISING TO 19 contracts. We had 13 notices filed upon yesterday so we gained 17 contracts or an additional 85,000 oz will stand in this non active delivery month of June AS SOMEBODY IS IN URGENT NEED OF PHYSICAL ON THIS SIDE OF THE POND AND QUEUE JUMPING CONTINUES IN EARNEST

The next big active delivery month for silver is July and here the OI LOST 429 contracts DOWN to 133,090. The next delivery month is August and here we GAINED 5 contracts to stand at 46. The next active delivery month after August for silver is September and here the OI ROSE by 2206 contracts UP to 63,602

We had 16 notice(s) filed for 80,000 OZ for the JUNE 2018 COMEX contract for silver

INITIAL standings for JUNE/GOLD

JUNE 12/2018.

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz |

nil OZ

|

| Deposits to the Dealer Inventory in oz | NIL oz |

| Deposits to the Customer Inventory, in oz | nil

oz |

| No of oz served (contracts) today |

425 notice(s)

42,500 OZ

|

| No of oz to be served (notices) |

664 contracts

(66,400 oz)

|

| Total monthly oz gold served (contracts) so far this month |

6587 notices

658,700 OZ

20.488 TONNES

|

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

For JUNE:

Today, 0 notice(s) were issued from JPMorgan dealer account and 369 notices were issued from their client or customer account. The total of all issuance by all participants equates to 425 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 170 notice(s) was (were) stopped/ Received) by j.P.Morgan customer account.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

To calculate the INITIAL total number of gold ounces standing for the JUNE. contract month, we take the total number of notices filed so far for the month (6587) x 100 oz or 658,700 oz, to which we add the difference between the open interest for the front month of JUNE. (1089 contracts) minus the number of notices served upon today (425 x 100 oz per contract) equals 725,100 oz, the number of ounces standing in this active month of JUNE (22.553 tonnes)

Thus the INITIAL standings for gold for the JUNE contract month:

No of notices served (6587 x 100 oz) + {(1089)OI for the front month minus the number of notices served upon today (425 x 100 oz )which equals 725,100 oz standing in this active delivery month of JUNE .

WE GAINED 11 CONTRACTS OR AN ADDITIONAL 1100 OZ WILL STAND FOR DELIVERY AS QUEUE JUMPING IS STARTING TO INTENSIFY AT THE GOLD COMEX SOMETHING THAT WHICH WE HAVE WITNESSED IN SILVER FOR THE PAST YEAR.

“THERE ARE ONLY 15.783 TONNES OF REGISTERED GOLD AVAILABLE FOR DELIVERY AGAINST 22.553 TONNES STANDING WHICH IS MAKING THIS JUNE CONTRACT MONTH AN EXTREMELY INTERESTING ONE TO WATCH (of which probably 5.90 tonnes have already been settled)

IN THE LAST 18 MONTHS 74 NET TONNES HAS LEFT THE COMEX.

end

And now for silver

AND NOW THE APRIL DELIVERY MONTH

JUNE INITIAL standings/SILVER

| Silver | Ounces |

| Withdrawals from Dealers Inventory | nil oz |

| Withdrawals from Customer Inventory |

1,315,787.784 oz

CNT

HSBC

|

| Deposits to the Dealer Inventory |

nil;

oz

|

| Deposits to the Customer Inventory |

1,032,259.960

oz

jpmorgan

Delaware

Brinks

|

| No of oz served today (contracts) |

16

CONTRACT(S)

(80,000 OZ)

|

| No of oz to be served (notices) |

3 contracts

(15,000 oz)

|

| Total monthly oz silver served (contracts) | 923 contracts

(4,615,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

we had 0 inventory movement at the dealer side of things

total dealer deposits: nil oz

we had 3 deposits into the customer account

i) Into JPMorgan: 396,822,600 oz

ii) Into Brinks: 505,747.420 oz

iii) Into Delaware: 129,689.940 oz

*** JPMorgan for most of 2017 and in 2018 has adding to its inventory almost every single day.

JPMorgan now has 140 million oz of total silver inventory or 52.3% of all official comex silver. (140 million/268 million)

total customer deposits today: 1,032,259,960 oz

we had 2 withdrawals from the customer account;

i) Out of CNT: 562,173.862 oz

ii) Out of HSBC: 753,613.922 oz

total withdrawals; 597,642.656 oz

we had 0 adjustment/

total dealer silver: 66.073 million

total dealer + customer silver: 269.798 million oz

The total number of notices filed today for the JUNE. contract month is represented by 16 contract(s) FOR 80,000 oz. To calculate the number of silver ounces that will stand for delivery in JUNE., we take the total number of notices filed for the month so far at 923 x 5,000 oz = 4,615,000 oz to which we add the difference between the open interest for the front month of JUNE. (19) and the number of notices served upon today (16 x 5000 oz) equals the number of ounces standing.

.

Thus the INITIAL standings for silver for the JUNE contract month: 923(notices served so far)x 5000 oz + OI for front month of JUNE(19) -number of notices served upon today (16)x 5000 oz equals 4,630,000 oz of silver standing for the JUNE contract month

PLEASE NOTE THE FOLLOWING FOR COMPARISON PURPOSES:

ON MAY 31.2017 WE INITIALLY HAD 396 OPEN INTEREST STAND OR A LARGE 1.98 MILLION OZ

STOOD FOR METAL.

AT THE CONCLUSION OF JUNE 2017: 4.92 MILLION OZ FINALLY STOOD AS QUEUE JUMPING STARTED IN EARNEST AND IN THE ENSUING YEAR, IT CONTINUED WITH RECKLESS ABANDON INCLUDING WHAT YOU ARE WITNESSING TODAY

We gained 17 contracts or an additional 85,000 oz will stand in this non active delivery month of June as somebody was in urgent need of silver. IN SILVER QUEUE JUMPING HAS BEEN THE NORM FOR OVER A YEAR. IT LOOKS LIKE GOLD WANTS TO JOIN ITS WEAKER SISTER IN THIS SAME PHENOMENON

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

ESTIMATED VOLUME FOR TODAY: 91,707 CONTRACTS

CONFIRMED VOLUME FOR YESTERDAY:85,249 CONTRACTS

YESTERDAY’S CONFIRMED VOLUME OF 85,249 CONTRACTS EQUATES TO 426 MILLION OZ OR 60.8% OF ANNUAL GLOBAL PRODUCTION OF SILVER

COMMODITY LAW SUGGESTS THAT OPEN INTEREST SHOULD NOT BE MORE THAN 3% OF ANNUAL GLOBAL PRODUCTION. THE CROOKS ARE SUPPLYING MASSIVE PAPER TRYING TO KEEP SILVER IN CHECK.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price at that day at $18.42

The previous record was 224,540 contracts with the price at that time of $20.44

end

NPV for Sprott

1. Sprott silver fund (PSLV): NAV FALLS TO -2.96% (JUNE 12/2018)

2. Sprott gold fund (PHYS): premium to NAV RISES TO -0.47% to NAV (JUNE 12/2018 )

Note: Sprott silver trust back into NEGATIVE territory at -2.96%-/Sprott physical gold trust is back into NEGATIVE/ territory at -0.47%/Central fund of Canada’s is still in jail but being rescued by Sprott.

Sprott WINS hostile 3.1 billion bid to take over Central Fund of Canada

(courtesy Sprott/GATA)

3.SPROTT CEF.A FUND (FORMERLY CENTRAL FUND OF CANADA): NAV FALLS TO -2.44%: NAV 13.62/TRADING 13.32//DISCOUNT 2.27.

END

And now the Gold inventory at the GLD/

JUNE 12/WITH GOLD DOWN $4.75:NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 828.76 TONNES

JUNE 11/WITH GOLD UP 65 CENTS/THE CROOKS RAIDED THE COOKIE JAR FOR 3.83 TONNES/INVENTORY RESTS AT 828.76 TONNES

JUNE 8/WITH GOLD DOWN 10 CENTS/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY REMAINS AT 832.59 TONNES./

JUNE 7/WITH GOLD UP $1.45, THE CROOKS DECIDED TO RAID AGAIN THE GLD GOLD COOKIE JAR TO THE TUNE OF 3.54 TONNES/GOLD INVENTORY LOWERS TO 832.59 TONNES

JUNE 6/WITH GOLD UP $1.30 TODAY, WE HAD NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 836.13 TONNES

JUNE 5/WITH GOLD UP $5.30 TODAY, WE HAD A TINY WITHDRAWAL OF .29 TONNES AND THAT NO DOUBT WAS TO PAY FOR FEES/836.13 TONNES

JUNE 4/WITH GOLD DOWN ONLY $2.50, THE CROOKS UNLEASHED A MASSIVE WITHDRAWAL OF 10.61 TONNES OF GOLD FROM THE GLD/INVENTORY RESTS AT 836.42 TONNES

JUNE 1/WITH GOLD DOWN $5.10 TODAY, A HUGE 4.42 TONNES OF GOLD WAS WITHDRAWN FROM THE GLD AND THIS WAS USED IN THE RAID TODAY/INVENTORY RESTS AT 847.03 TONNES

MAY 31/WITH GOLD DOWN 1.60/NO CHANGE IN GOLD INVENTORY/INVENTORY REMAINS AT 851.45 TONNES

MAY 30/WITH GOLD UP $2.70: A HUGE DEPOSIT OF 2.95 TONNES INTO THE GLD/INVENTORY REMAINS AT 851.45 TONNES

MAY 29/2018/WITH GOLD DOWN $4.50/ NO CHANGES IN GLD INVENTORY/INVENTORY REMAINS AT 848.50 TONNES

May 25/WITH GOLD UP ON THE WEEK BUT DOWN 80 CENTS TODAY: WE HAD A HUGE 3.54 TONNES OF GOLD WITHDRAWAL FROM THE CROOKED GLD/

MAY 24/WITH GOLD UP $12.40/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 852.04

MAY 22/WITH GOLD UP $1.05/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 852.04 TONNES

MAY 21/WITH GOLD DOWN 50 CENTS/A HUGE CHANGE IN GOLD INVENTORY/A WITHDRAWAL OF 3.24 TONNES FORM GLD INVENTORY/INVENTORY RESTS AT 852.04 TONNES

MAY 18/WITH GOLD UP $1.80/A HUGE CHANGE IN GOLD INVENTORY AT THE GLD/ A DEPOSIT OF 9.11 TONNES INTO GLD INVENTORY/INVENTORY RESTS AT 865.28 TONNES/

GLD WAS ONE MASSIVE FRAUD

May 17/WITH GOLD DOWN $1.75/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 856.17 TONNES

MAY 16./WITH GOLD UP $1.05: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 856.17 TONNES

MAY 15/WITH GOLD DOWN $27.35, THE CROOKS WITHDREW 10 TONNES OF GOLD FROM THE GLD WHICH WAS USED IN THE RAID TODAY/INVENTORY RESTS AT 856.17 TONNES

MAY 14/ WITH GOLD DOWN $2.35: A HUGE DEPOSIT OF 4.68 TONNES OF GOLD INTO THE GLD and then a withdrawal of 1.48 tonnes /INVENTORY RESTS AT 866.17

A net gain of 3.2 tonnes of gold.

MAY 11/WITH GOLD DOWN $1.75/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 862.96 TONNES/

MAY 10/WITH GOLD UP $9.60/A WITHDRAWAL OF 1.17 TONNES FROM THE GLD/INVENTORY RESTS AT 862.96 TONNES/SUCH CROOKS

MAY 9/WITH GOLD DOWN $0.55/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 864.13 TONNES

MAY 8/WITH GOLD DOWN $0.10/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 864.13 TONNES

MAY 7/WITH GOLD DOWN $0.55/ANOTHER WITHDRAWAL OF 1.47 TONNES OF GOLD FROM THE GLD/INVENTORY RESTS AT 864.13 TONNES

MAY 4/WITH GOLD UP $2.05/A WITHDRAWAL OF 1.13 TONNES OF GOLD FROM THE GLD/INVENTORY RESTS AT 865.60 TONNES

MAY 3/WITH GOLD UP $7.05/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 866.77 TONNES

MAY 2/WITH GOLD DOWN $1.15/ A HUGE WITHDRAWAL OF 4.43 TONNES FROM THE GLD/INVENTORY RESTS AT 866.77 TONNES

MAY 1/WITH GOLD DOWN $12.15/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 871.20 TONNES

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

JUNE 12/2018/ Inventory rests tonight at 828,76 tonnes

*IN LAST 395 TRADING DAYS: 97.83 NET TONNES HAVE BEEN REMOVED FROM THE GLD

*LAST 345 TRADING DAYS: A NET 58.47 TONNES HAVE NOW BEEN ADDED INTO GLD INVENTORY.

end

Now the SLV Inventory/

JUNE 12/WITH SILVER DOWN 5 CENTS/A HUGE CHANGES IN SILVER INVENTORY AT THE SLV/ THE CROOKS RAID THE SILVER COOKIE JAR BY 1.976 MILLION OZ/INVENTORY LOWERS TO 317.290 MILLION OZ/

jUNE 11/NO CHANGE IN SILVER INVENTORY/319.266 MILLION OZ

JUNE 8/WITH SILVER DOWN 5 CENTS/A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.412 MILLION OZ//INVENTORY LOWERS TO 319.266 MILLION OZ/

JUNE 7/WITH SILVER UP ANOTHER 12 CENTS/A HUGE CHANGE IN SILVER INVENTORY AT THE SL: A WITHDRAWAL OF 1.883 MILLION OZ WITH ALL OF THAT SILVER DEMAND//INVENTORY RESTS AT 320.678 MILLION OZ/

JUNE 6/WITH SILVER UP 14 CENTS TODAY/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 322.561 MILLION OZ/

JUNE 5/WITH SILVER UP 10 CENTS NO CHANGE IN SILVER INVENTORY/INVENTORY RESTS AT 322.561 MILLION OZ

JUNE 4/WITH SILVER DOWN 1 CENTA SMALL CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 522,000 OZ INTO THE SLV/.INVENTORY RISES AT 322.561 MILLION OZ/

JUNE 1/WITH SILVER DOWN 3 CENTS/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY REMAINS AT 322.039 MILLION OZ/

MAY 31/WITH SILVER DOWN 7 CENTS/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY REMAINS AT 322.039 MILLION OZ/

MAY 30/WITH SILVER UP 16 CENTS: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV/ A DEPOSIT OF 2.071 MILLION OZ/INVENTORY RESTS AT 322.039 MILLION OZ/

MAY 29.2018/ NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 319.968 OZ

May 25/INVENTORY LOWERS TO 319.968 AS WE HAD A WITHDRAWAL OF 1.035 MILLION OZ

MAY 24/WITH SILVER UP 27 CENTS/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 321.003 MILLION OZ/

MAY 22/WITH SILVER UP 6 CENTS/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 321.003 MILLION OZ/

MAY 21/ WITH SILVER UP 5 CENTS/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 321.003 MILLION OZ/

MAY 18/WITH SILVER DOWN 5 CENTS A SMALL CHANGE IN SILVER INVENTORY AT THE SLV/ A WITHDRAWAL OF 942,000 OZ/INVENTORY RESTS AT 321.003 MILLION OZ/

May 17/WITH GOLD UP 6 CENTS/A SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 471,000 OZ//INVENTORY RESTS AT 321.945 MILLION OZ/

MAY 16./WITH SILVER UP 10 CENTS/A HUGE DEPOSIT OF 1.883 MILLION OZ OF SILVER INTO THE SLV/INVENTORY RESTS AT 321.474 MILLION OZ

MAY 15/WITH SILVER DOWN 33 CENTS, NO CHANGES AT THE SLV; THE CROOKS COULD NOT BORROW ANY SILVER BECAUSE THERE IS NONE: INVENTORY RESTS AT 319.591 MILLION OZ

MAY 14/WITH SILVER DOWN 10 CENTS/A SMALL CHANGES IN SILVER INVENTORY AT THE SLV/ A WITHDRAWAL OF 858,000 FROM THE SLV/INVENTORY RESTS AT 319.591 MILLION OZ/

MAY 11/WITH SILVER DOWN 2 CENTS/THE CROOKS WITHDREW A MONSTROUS 2.824 MILLION OZ FROM THE SLV INVENTORY/INVENTORY RESTS AT 320.439 MILLION OZ/

MAY 10/WITH SILVER UP 22 CENTS/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 323.263 MILLION OZ/

MAY 9/WITH SILVER UP 6 CENTS/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 323.263 MILLION OZ/

MAY 8/WITH SILVER DOWN 2 CENTS:NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 323.263 MILLION OZ.

MAY 7/WITH SILVER FLAT: A BIG CHANGE IN SILVER INVENTORY AT THE SLV// A WITHDRAWAL OF 942,000 OZ OF SILVER FROM THE SLV INVENTORY/INVENTORY RESTS AT 323.263 MILLION OZ/

MAY4/WITH SILVER UP 5 CENTS/A BIG CHANGES IN SILVER INVENTORY AT THE SLV/ A DEPOSIT OF 1.224 MILLION OZ/INVENTORY RESTS AT 324.205 MILLION OZ/

MAY 2/WITH SILVER UP 24 CENTS/A HUGE CHANGE IN SILVER INVENTORY AT THE SLV// A DEPOSIT OF 6.082 MILLION OZ INTO THE SLV/INVENTORY RESTS AT 322.981 MILLION OZ/

MAY 1/WITH SILVER DOWN 24 CENTS/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 316.899 MILLION OZ/

JUNE 12/2018:

Inventory 317.290 million oz

end

6 Month MM GOFO 2.21/ and libor 6 month duration 2.49

Indicative gold forward offer rate for a 6 month duration/calculation:

G0FO+ 2.21%

libor 2.49 FOR 6 MONTHS/

GOLD LENDING RATE: .28%

XXXXXXXX

12 Month MM GOFO

+ 2.76%

LIBOR FOR 12 MONTH DURATION: 2.61

GOFO = LIBOR – GOLD LENDING RATE

GOLD LENDING RATE = +.15

end

end

Major gold/silver trading /commentaries for TUESDAY

GOLDCORE/BLOG/MARK O’BYRNE.

GOLD/SILVER

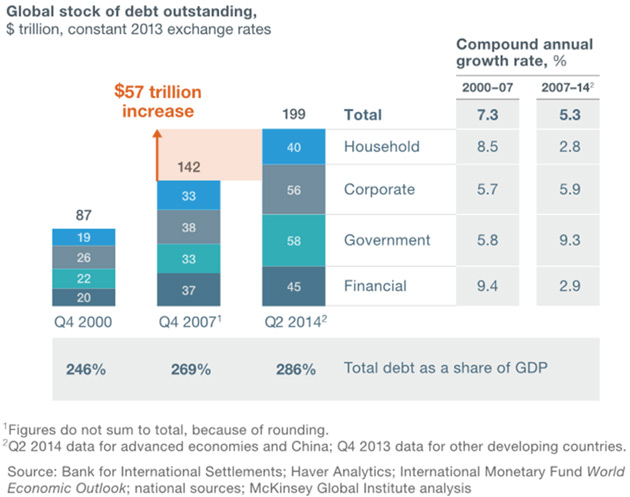

Total US Government Debt Is $200 Trillion – Debt Clock Ticking To Next Crisis

– Too Many Trillions

– Rapid Maturity

– Leverage Plus Leverage

– Circling Vultures

– Total of U.S. Federal, State & City Debt Exceeds $200 Trillion Dollars

Rather go to bed without dinner than to rise in debt.

—Benjamin Franklin

What can be added to the happiness of a man who is in health, out of debt, and has a clear conscience?

—Adam Smith

There are no shortcuts when it comes to getting out of debt.

—Dave Ramsey

Modern slaves are not in chains, they are in debt.

—Anonymous

Debt isn’t always a form of slavery, but those old sayings didn’t come from nowhere. You can find hundreds of quotes on the Internet discussing the problems of debt. Debt traps borrowers, lenders, and innocent bystanders, too. If debt were a drug, we would demand it be outlawed.

The advantage of debt is it lets you bring the future into the present, buying things you couldn’t afford if you had to pay full price now. This can be good or bad, depending on what you buy. Going into debt for education that will raise your income, or for factory equipment that will increase your output, can be positive. Debt for a tropical vacation, probably not.

And that’s our core economic problem. The entire world went into debt for the equivalent of tropical vacations and, having now enjoyed them, realizes it must pay the bill. The resources to do so do not yet exist. So, in the time-honored tradition of lenders everywhere, we extend and pretend. But with our ability to pretend almost gone, we’re heading to the Great Reset.

I’ve been analogizing our fate to a train wreck you know is coming but are powerless to stop. You look away because watching the disaster hurts, but it happens anyway. That’s where we are, like it or not.

And we don’t even really like to talk about it in polite circles. In a private email conversation this week, which must remain anonymous, this pithy line jumped out at me:

The total of Federal (remember they do not use GAAP) debt, state debt, and city debt [unfunded liabilities included] exceeds $200 trillion dollars. There is no set of math that works to pay this off. Let me be sure it’s heard by repeating it: There is no set of math that works to pay this off. Therefore, there has to be some form of remediation. This conversation is uncomfortable, so it is avoided.

This is an excerpt. Full article is a must read and can be read on Mauldin Economics

News and Commentary

Live Blog: Donald Trump-Kim Jong Un Summit in Singapore (Bloomberg)

Gold continues to struggle with $1,300 as key barrier holds action in place (FX Times)

Stocks creep higher, dollar retreats after U.S.- North Korea summit (Reuters)

Gold eases on firmer dollar; US-N.Korea summit, Fed meeting in focus (Economic Times)

Gold coins worth $155,000 discovered in abandoned house(News.com)

Will 2018 Be A Repeat of 2002 Tariffs? (First Macro Capital)

Debt Clock Ticking (Maldin Economics)

CNBC Poll: Gold amid rising geopolitical tensions. Buy or sell gold? (CNBC)

When Will Gold’s “Summer Doldrums” End? History Says Pretty Soon (Dollar Collapse)

Be Your Own Central Banker (Goldseek)

Listen on SoundCloud , Blubrry & iTunes. Watch on YouTube below

Gold Prices (LBMA AM)

11 Jun: USD 1,296.05, GBP 969.32 & EUR 1,099.57 per ounce

08 Jun: USD 1,299.20, GBP 968.68 & EUR 1,103.93 per ounce

07 Jun: USD 1,298.30, GBP 963.86 & EUR 1,097.97 per ounce

06 Jun: USD 1,295.25, GBP 964.57 & EUR 1,101.48 per ounce

05 Jun: USD 1,292.25, GBP 966.73 & EUR 1,105.13 per ounce

04 Jun: USD 1,294.65, GBP 966.46 & EUR 1,103.82 per ounce

01 Jun: USD 1,299.15, GBP 976.83 & EUR 1,111.42 per ounce

Silver Prices (LBMA)

11 Jun: USD 16.76, GBP 12.55 & EUR 14.23 per ounce

08 Jun: USD 16.72, GBP 12.49 & EUR 14.25 per ounce

07 Jun: USD 16.74, GBP 12.44 & EUR 14.15 per ounce

06 Jun: USD 16.55, GBP 12.33 & EUR 14.06 per ounce

05 Jun: USD 16.39, GBP 12.26 & EUR 14.03 per ounce

04 Jun: USD 16.44, GBP 12.29 & EUR 14.03 per ounce

01 Jun: USD 16.42, GBP 12.32 & EUR 14.02 per ounce

Recent Market Updates

– All Gold is Not Equal – Goldnomics Podcast (Episode 4)

– “Without Gold I Would Have Starved To Death” – ECB Governor

– Swiss Government Pension Fund To Buy Gold Bars Worth Some €600 Million

– Turkey Uses Gold Bullion To Stabilise Its Currency And Economy

– Case for Gold in a Diversified Investment Portfolio

– Get “Positioned In Gold” Now As “You Will Not Have Time To Get Positioned” Later

– Consequences of Ignoring Economic Reality Are Dangerous

– Are Gold And Silver Bullion Obsolete In The Crypto Age?

– In Gold we Trust: 3 Important Factors Leading to the “Turning of the Monetary Tides”

– Silver Trading in Tight $1 Range As Pressure Builds For A Breakout

– Gold Back Above $1300 – Trump Cancels Historic Summit – Silver “Ready To Breakout”

– Gold Price Surges To Record In Turkey and Other Emerging Markets as Currencies Collapse

– Gold Rarity and Value Shown In Stunning Gold Visualisations

– Gold Looks A Better Investment Than UK Property

end

ANDREW MAGUIRE’S KINESIS WHICH IS A”BITCOIN’ BACKED 100% BY ALLOCATED GOLD AND SILVER

Andrew Maguire’s Kinesis money which is a “bitcoin” but backed 100% by allocated gold and silver is set to go.

it think it would be a great idea to look at this!

please read at: https://kinesis.money/#/

(Andrew Maguire)

|

|

Dear Harvey Organ,

Thank you for your participation in our webinar on June 7th with our host and CEO of Kinesis, Thomas Coughlin.

The response we received has been incredible, we appreciate you taking the time to join us and hope you found it to be beneficial.

Due to such a high influx of questions we received we were unable to have them all answered. Nevertheless, if there was anything which requires more clarification, or you have a query which needs to be rectified, we invite you to join our telegram group:

We apologize for the technical issues we incurred during the webinar which resulted in it running a little over schedule, we hope that the next one we host will run seamlessly.

A video has been put together and uploaded onto our YouTube channel which can be found here:

Please share and subscribe to our YouTube channel to be notified of all the latest videos as they become available.

The rapid growth that we are currently experiencing has been incredible and with your support, is only going to get better.

We are working behind the scenes very hard to create a better experience for everyone involved! Stay tuned in as we have many more announcements to be released in the upcoming days.

Kind Regards,

|

Kinesis Money

a:C/O ILS Fiduciaries (IOM) Limited, First Floor,Millennium House, Victoria Road, Douglas, Isle of Man IM2 4RW

|

The following is self explanatory

(courtesy GATA/Chris Powell and Harvey Organ)

GATA asks bank regulator to check risks of gold

futures maneuver

Submitted by cpowell on Sun, 2018-06-10 16:17. Section: Daily Dispatches

12:21p ET Sunday, June 10, 2018

Dear Friend of GATA and Gold:

GATA has appealed to the U.S. comptroller of the currency, who has regulatory authority over banks, to review financial risks certain banks may have incurred through derivatives in the monetary metals markets, particularly through the recent heavy use of the “exchange for physicals” mechanism of settling gold and silver futures contracts on the New York Commodities Exchange.

The appeal was made in a letter sent May 5 to the comptroller, Joseph M. Otting, whose office is part of the U.S. Treasury Department, by your secretary/treasurer and GATA futures market consultant Harvey Organ.

“Exchange for physical” settlements of futures contracts long were considered emergency procedures when a seller was not able to deliver metal from an exchange-approved warehouse and wanted to settle with delivery elsewhere. But now such settlements appear to constitute most gold and silver futures settlements on the Comex. It is a strange development that appears to have been necessitated by the increasing difficulties of central banking’s gold and silver price suppression policy.

GATA has received no acknowledgment of the letter. Its text is below and a PDF copy of it is here:

http://www.gata.org/files/ComptrollerOfCurrencyLetter.pdf

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

* * *

May 5, 2018

Joseph M. Otting, Comptroller of the Currency

U.S. Treasury Department

400 7th Street, SW

Washington DC 20219

Dear Comptroller Otting:

Please let us bring to your attention financial risks to major banks involving their possibly unreported exposure to derivatives in the monetary metals markets.

In recent months gold and silver future contracts issued by U.S. banks on the New York Commodities Exchange have been moved off-exchange for delivery through a mechanism known as “exchange for physical” (EFP) contracts. Until recently use of this mechanism was considered an emergency procedure when a seller did not have access to metal for delivery through Comex warehouses. Now the mechanism seems to be in use for a large share of front-month contracts for which delivery is sought.

Here is an example that is happening at the Comex in the front active month of April for gold and the inactive delivery month of April for silver.

In gold, there were 229,436 EFP contracts for 713.64 tonnes, an average of 10,925 contracts and 1,092,500 ounces per trading day.

In silver, there were 77,150 EFP contracts for 385,750,000 ounces, an average of 3,673 contracts and 18,369,000 ounces per trading day.

London Bullion Market Association rules suggest that these contracts may not be reported to regulators. The LBMA’s bylaws say:

“Figures above exclude any contracts not subject to risk-based capital requirements, such as FX contracts with an original maturity of 14 days or less, futures contracts, written options, and basis swaps. Therefore, the total notional amount of derivatives by maturity will not add to the total derivatives figure in this table.”

We are told that these EFP contracts are transferred from the Comex to London as what are called “serial forwards” and their duration is always less than 14 days, which exempts them from being reported.

It is our understanding that in each quarter your office prepares a report detailing risk undertaken by the banks under the comptroller’s supervision.

These risks include derivatives undertaken by U.S. banks and other obligations that may cause a bank to fail. Our concern is that your office may not be aware of large unreported derivative exposure by banks.

Could you review this matter and let us know your conclusions?

Sincerely,

CHRIS POWELL

Secretary/Treasurer

HARVEY ORGAN

Consultant

Gold Anti-Trust Action Committee Inc.

7 Villa Louisa Road

Manchester, Connecticut 06043-7541

END

as a follow up:

Bill, Ed, Harvey:

From: Chris Powell <cxpowell@yahoo.com>

Date: Mon, Jun 11, 2018 at 12:21 AM

Subject: letter to comptroller of the currency

To: Mary Yatrousis <mary.yatrousis@mail.house.gov>Hi, Mary:Here’s a somewhat more substantial request for help from Representative Larson.Attached as a PDF is a letter my organization, the Gold Anti-Trust Action Committee Inc., sent to the U.S. comptroller of the currency more than a month ago. We have gotten no acknowledgment.I realize that the mail can be slow in Washington as it undergoes security checks, but I’d be grateful if the comptroller’s office could be encouraged to respond in the near future.Thanks again.

cp

end

The worst kind: Bitcoin tumbles below $6500 on no news. The boys seem to be dumping

*(courtesy zerohedge)

Bitcoin Tumbles Below $6500 As Cryptos

Suddenly Plunge

No obvious catalysts for now but the crypto space just took another leg lower with Bitcoin now back below $6,500…

Bitcoin is back at its lowest since Feb 2018…which is perhaps the driver of the plunge as it breaks April support lows…

It’s been an ugly few days…

end

Your early TUESDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

i) Chinese yuan vs USA dollar/CLOSED UP TO 6.4043 /shanghai bourse CLOSED UP 27.02 POINTS OR 0.89% HANG SANG CLOSED UP 39.36 POINTS OR 0.13%

2. Nikkei closed UP 74,31 POINTS OR 0.33% / /USA: YEN RISES TO 110.23/

3. Europe stocks OPENED MIXED / /USA dollar index FALLS TO 93.58/Euro RISES TO 1.1786

3b Japan 10 year bond yield: RISES TO . +.05/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 110.00/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD FINALLY IN THE POSITIVE/BANK OF JAPAN LOSING CONTROL OF THEIR YIELD CURVE AS THEY PURCHASE ALL BONDS TO GET TO ZERO RATE!!

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 66.02 and Brent: 76.08

3f Gold UP/Yen DOWN

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil UP for WTI and UP FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund RISES TO +.51%/Italian 10 yr bond yield DOWN to 2.81% /SPAIN 10 YR BOND YIELD UP TO 1.48%

3j Greek 10 year bond yield FALLS TO : 4.47

3k Gold at $1297.25 silver at:16.86 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble DOWN 4/100 in roubles/dollar) 62.58

3m oil into the 64 dollar handle for WTI and 75 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 110.23 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 0.9840 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1598 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now POSITIVE territory with the 10 year RISING to +0.51%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.96% early this morning (THIS IS DEADLY TO ALL MARKETS). Thirty year rate at 3.10%

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

(courtesy Jim Reid/Bloomberg/Deutsche bank/zero hedge)

Stock Rally Fizzles As Korea Summit Fails To

Impress; Market Waiting “For Bigger Things”

Bulletin Headline Summary from RanSquawk

- Summit between Trump and Kim ends

- UK front-bencher resigns ahead of House of Commons EU Withdrawal Bill vote

- Looking ahead, highlights include, US CPI, APIs and UK House of Commons debates EU Withdrawal Bill

Markets shrugged off the the much anticipated historic” Singapore summit, with the global stock rally fading, US futures and Asian currencies falling amid a buoyant dollar, and the S. Korea won reversing an earlier gain after the Trump-Kim summit didn’t result in any major breakthroughs and culminated with a document signed by the two leaders including unspecified security guarantees and a vague, unenforceable denuclearization commitment.

“Despite the historic event, the markets haven’t moved much because they’ve already discounted the risk of military conflict,” Goldman’s co-head of Korea research Goohoon Kwon told Bloomberg Television. What’s more important going forward is the “follow-through, execution, implementation” of any agreements, he said.

There is some doubt about that: none other than Iran was quick to troll the US and warn North Korea that the agreement isn’t worth the paper it was signed on:

- IRAN GOVERNMENT SPOKESMAN WARNS NORTH KOREA THAT TRUMP COULD CANCEL THEIR AGREEMENT BEFORE RETURNING TO WASHINGTON – IRNA

Commenting on the overnight session’s muted trading, Bloomberg notes that “markets are waiting for bigger things” with most asset classes remained within tight ranges. The big surprise was the lack of any real reaction to any of the Trump/Kim summit.

As Bloomberg also notes, there was never much prospect of the U.S.-North Korea summit triggering a large market reaction, except perhaps in the event of a shock outcome. A seemingly certain Federal Reserve rate increase on Wednesday, plus the prospect of a hawkish ECB tilt on Thursday, tease far more concrete developments for traders.

Meanwhile the relief rally in BTPs continues, with the spread against bunds continuing to tighten from blow-out levels seen previously. European equity markets initially open higher before fading back to flat, mining stocks underperform; defensive sectors such as utilities support. Crude and metals markets also relatively flat

Europe’s Stoxx 600 Index opened higher, but pared its advance after modest gains for many Asian gauges failed to ignite the MSCI Asia Pacific Index, with mining stocks underperforming. S&P 500 futures were flat after posting another increase on Monday. Safe-haven assets including the yen and gold slipped in the aftermath of the Singapore agreement.

The pound reversed a decline before Theresa May’s landmark Brexit legislation goes to Parliament, after data showed a surprise moderation in the pace of wage growth.

As a reminder, today the UK faces a historic vote on Brexit, with PM May reportedly heading off a Conservative rebellion ahead of today’s key Brexit vote by reaching out to Remainers in her party according to the Telegraph. Furthermore, UK Brexit Secretary Davis is said to back deal to buy-off Tory rebels on both wings of the party ahead of the EU Withdrawal Bill vote in the UK’s lower house. UK solicitor general Baker that the government is discussing with lawmakers the replacement of an Upper House amendment on EU’s customs union and that it is appropriate to have a customs arrangement with the EU. UK Conservative MP Grieve said to have tabled a compromise amendment on the Brexit deal and would likely rebel if it is rejected. However, UK government sources indicated that they have no intention of backing MP Grieve’s amendment to try to buy off rebels over the meaningful vote. In other words, look for more sterling drama in just a few hours.

Ahead of the Fed announcement tomorrow, today we will get a critical CPI print: the consensus today is for a +0.2% mom core and headline print. The former is also expected to nudge up one-tenth to +2.2% yoy. That +0.2% monthly consensus estimate should be fairly familiar as this is now the 32nd consecutive month that we’ve had such a forecast on the street. For those wondering, only 17 of them have proven to be correct with most missing on the downside. Deutsche economists expect the core to come in at +0.2% as they anticipate some payback from unusual weakness last month in categories such as airfares as well as new and used vehicles. In fact, the German bank expects the annual rate to rise to +2.3% yoy which would be the highest since January 2017. All that to look forward to later.

Putting the Korean drama in the rearview mirror, the dollar was little changed as investors turned their attention toward today’s CPI report and this week’s central bank policy meetings after the deal signed by the U.S. and North Korea was seen as a “sideshow” given the lack of specific commitments. The Bloomberg Dollar Spot Index erased an earlier advance to be steady on the day; Treasury 10-year yields held the gains from the previous two sessions and was at 2.96%

The yen drifted lower against all its Group-of-10 peers as the agreement still was seen as easing global tensions and reducing demand for haven assets. Norway’s krone rallied to a seven-month high against the euro after a survey by the central bank suggested growth outlook remains intact, strengthening the case for a rate hike after the summer

In other geopolitical news, the Russian deputy foreign minister says the nation will retaliate to the latest US sanctions.

In commodities, oil was unable to hold onto initial gains resulting from softer USD coming from the historic US-North Korean summit. WTI currently trading above the USD 66.00 handle, and Brent trading above the USD 76.00 level, with the fossil fuel flat on the day. In the metals scope, Gold is also seeing some follow through from an improved risk tone, with the yellow metal down 0.2% on the day. Steel is positive after two sessions in the red as price increases in large Chinese firms has offered support to the metal. Copper has shed losses earlier in the day and is now up on the day as the metal is benefiting from the improved risk tone.

A handful of companies are set to report earnings, including Oxford Industries and John Wiley. On the macro side, data is expected on NFIB Small Business Optimism and on CPI.

Market Snapshot

- S&P 500 futures down 0.04% to 2,782.00

- STOXX Europe 600 up 0.03% to 388.05

- MXAP up 0.07% to 175.18

- MXAPJ up 0.1% to 574.11

- Nikkei up 0.3% to 22,878.35

- Topix up 0.3% to 1,792.82

- Hang Seng Index up 0.1% to 31,103.06

- Shanghai Composite up 0.9% to 3,079.80

- Sensex up 0.6% to 35,679.14

- Australia S&P/ASX 200 up 0.2% to 6,054.44

- Kospi down 0.05% to 2,468.83

- German 10Y yield rose 2.0 bps to 0.513%

- Euro up 0.2% to $1.1802

- Italian 10Y yield fell 28.9 bps to 2.569%

- Spanish 10Y yield rose 2.2 bps to 1.463%

- Brent Futures up 0.5% to $76.84/bbl

- Gold spot down 0.2% to $1,298.00

- U.S. Dollar Index down 0.1% to 93.50

Top Headline News from Bloomberg

- President Donald Trump and Kim Jong Un expressed optimism that the U.S. and North Korea could find a path toward peace, opening a highly anticipated summit between two adversaries that only last year had seemed on the brink of nuclear war

- The Fed will likely deliver an expected interest-rate increase on Wednesday but still has plenty of topics to dissect — from a falling unemployment rate to emerging-market pain

- Italian Finance Minister Giovanni Tria’s expression of commitment to the euro are “far-sighted and create confidence,” European Union Budget Commissioner Guenther Oettinger said

- German investor confidence tumbled to its lowest level since 2012 as U.S. trade tariffs and Italy’s political turmoil added to concerns that the economy is slowing. German Jun. ZEW Expectations: -16.1 vs -14.0 est; Current Situation 80.6 vs 85.0 est.

- The U.K. economy continued to create jobs faster than forecast, even though basic wage growth unexpectedly slowed. U.K. Apr. Average Weekly Earnings ex-bonus 2.8% vs 2.9% est; Unemployment Rate 4.2% vs 4.2%; Employment Change 146k vs 120k est.

- Brexit: vote today on whether Parliament can direct Brexit negotiations if final deal is rejected by MPs; pro-remain govt. rebels have put forward compromise amendment vs govt’s own compromise agreement; one govt minister resigns to join rebels

- IMF Managing Director Christine Lagarde said the risks to the global economy are rising as major industrial nations sharpen threats of a trade war

- Bond traders have their work cut out for them before they get to the pivotal event for U.S. financial markets this week — Wednesday’s announcement from the Federal Reserve. The Treasury is about to pack $193 billion of debt sales into the next two days. That potentially puts the onus on Wall Street to absorb the deluge if investors are reluctant to choke it down before the central bank’s decision

- Theresa May’s govt is in advanced talks to head off a rebellion by pro-European members of her Conservative Party, edging toward a deal on Brexit that could hold her divided party together through a week of perilous voting

- Irish Prime Minister Leo Varadkar said he won’t accept the return of a hard border on the island of Ireland after Brexit even if Britain crashes out of the European Union without a deal on its future relationship with the bloc

- Oil held gains near $66 a barrel as a divide between OPEC and allies deepened over whether to ease production curbs and sell more crude into global markets

- President Donald Trump’s top economic adviser, Larry Kudlow, was “doing well” on Monday night after suffering a “very mild heart attack,” a White House spokeswoman said

- U.K. Justice Minister Phillip Lee resigns and says he will vote with rebels on an amendment that would give Parliament the power to direct negotiations if lawmakers reject May’s Brexit deal

Asian equity markets mostly traded with modest gains following a similar performance on Wall St. and with focus fully centred on the historical summit between US President Trump and North Korean Leader Kim Jong Un. The meeting between the 2 leaders was seen as amicable in which the leaders shook hands several times and exchanged pleasantries, although the initial face-to-face was somewhat less awe-inspiring than that of the inter-Korean summit in April. In addition, after one-on-one discussions Trump suggested a ‘very very good, good relationship’ and Kim stated there will be challenges ahead but will work with US President Trump, although reports also noted that Kim refrained from answering questions on denuclearisation. ASX 200 (+0.2%) and Nikkei 225 (+0.3%) were positive with early outperformance seen in Japan amid a weaker currency, although some of the gains were pared due to pessimism that a swift agreement could be reached for the Korean peninsula. Elsewhere, Hang Seng (+0.1%) and Shanghai Comp. (+0.9%) have swung between gains and losses alongside a broad tentative tone across the region and after a tepid liquidity effort by the PBoC. Finally, 10yr JGBs were subdued amid a lack of conviction in the region and with an enhanced liquidity auction for longer-dated bonds largely ignored, which showed slight decline in the bid to cover and tighter accepted spreads.

Top Asian News

- TV Maker Blames India’s Modi, Court and Brazil for Bad Debt Pile

European bourses are mixed (Euro Stoxx 50 -0.2%) after failing to hold onto initial gains spurred on by an improved risk sentiment in the wake of the Trump-Kim summit. The underperforming bourse is currently the FTSE (-0.2%) as a stronger GBP is pressuring the index amid reports that UK PM May has struck a compromise with Conservative rebels. Carrefour (+2.5%) is up on the news that Google will begin to sell their products online in France through their platforms. This is offering support to the consumer staples sector, which is the current sector outperformer (+0.44%) Casino (+6%) is leading the gains in Europe after the co. announced an asset sale plan in order to reduce debt. Daimler has recalled 238,000 vehicles in Germany due to illegal emission device concerns; a total of 774,000 vehicles are affected in Europe.

Top European News

- U.K. Employment Rises More Than Forecast But Wage Growth Slows

- Euro Mauled by Political Risk Is Ready to Be Revived by Draghi

- May Seeks to Head off Rebellion With Hours To Go: Brexit Update

- ABB CEO Says U.S. Tariffs Put Jobs at Risk: FT

In currencies, the DXY index and Usd in general has drifted back from peaks seen in wake of the Trump-Kim meeting that climaxed in an historic signing of significant documents to herald a new dawn and more concerted pledge to work towards peace via denuclearisation. The DXY remains supported around 93.500, but off highs just shy of 93.900 as attention shifts to US CPI ahead of the Fed. GBP – A marginal outperformer going in to the latest UK labour/wage data, which was somewhat mixed in the event, and only prompted a knee-jerk retreat in the Pound as the spotlight switches back to the Brexit vote amid reports that PM May has quelled a faction of Tory rebels. Cable currently holding close to 1.3400 and Eur/Gbp pivoting 0.8800 even though the single currency is firmer overall. NZD/CHF/EUR/AUD – All modestly firmer vs the Greenback with the Kiwi consolidating above 0.7000 and Franc still rangebound either side of 0.9850, while Eur/Usd is retesting offers and resistance at 1.1800 just above its 100 HMA (1.1786) and a band of option expiries from 1.1775-90 in 1.5 bn. Note, disappointing ZEW sentiment indicators sapped some of the single currency’s pre- ECB momentum. Aud/Usd has recovered 0.7600+ status after a dip on mixed Aussie data overnight (housing loans not as weak as forecast, but business sentiment and conditions both declined). JPY/CAD – The G10 laggards once again, with Usd/Jpy up through its 200 DMA (110.21) to test offers at 110.50 and Eur/Jpy absorbing residual supply at 130.00 to trip some 130.25 stops in wake of the Summit, while the Loonie is still smarting from the G7 squabble between Trump and Trudeau and just holding off 1.3000+ lows vs its US rival.

In commodities, oil was unable to hold onto initial gains resulting from softer USD coming from the historic US-North Korean summit. WTI currently trading above the USD 66.00 handle, and Brent trading above the USD 76.00 level, with the fossil fuel flat on the day. In the metals scope, Gold is also seeing some follow through from an improved risk tone, with the yellow metal down 0.2% on the day. Steel is positive after two sessions in the red as price increases in large Chinese firms has offered support to the metal. Copper has shed losses earlier in the day and is now up on the day as the metal is benefiting from the improved risk tone.

Looking at the day ahead, the big highlight in terms of data comes with the May CPI report. The May NFIB small business optimism reading and May monthly budget statement will also be out in the US. Prior to this in Europe we’ll get the June ZEW survey in Germany and April/May employment data in the UK including average weekly earnings. Meanwhile, UK Parliament is due to hold a 12-hour session on Brexit legislation with various amendments due.

US Event Calendar

- 6am: NFIB Small Business Optimism, est. 105, prior 104.8

- 8:30am: US CPI MoM, est. 0.2%, prior 0.2%; CPI Ex Food and Energy MoM, est. 0.2%, prior 0.1%

- US CPI YoY, est. 2.8%, prior 2.5%; US CPI Ex Food and Energy YoY, est. 2.2%, prior 2.1%

- 8:30am: Real Avg Weekly Earnings YoY, prior 0.42%; Real Avg Hourly Earning YoY, prior 0.2%

- 2pm: Monthly Budget Statement, est. $139.5b deficit, prior $214.3b

DB’s Jim Reid concludes the overnight wrap

In the decades and centuries to come, will this date go down in history as a big turning point for the history of mankind, a date future generations can celebrate, a new beginning, and a day used to remember that one person can really make a big difference. Yes 44 years ago today I was born. On the more mundane subject of whether world peace gets a step closer today, President Trump and Kim Jong Un’s mission to Singapore seems to be off to a positive start, with Trump noting he had forged a “good relationship” with Kim, while Kim indicated “there will be challenges ahead” but he vowed to work with Trump. As we go to print Trump has declared that the meeting with Kim is “going great ”. We shall find out more at President Trump’s news conference at 4pm local time (9am London time).

Notably, Kim is scheduled to head back home at 2pm today. Meanwhile, earlier yesterday Secretary of State Pompeo reaffirmed that complete and irreversible denuclearisation is the “only outcome that the US will accept”, but unnamed US officials have told Bloomberg that Trump was willing to offer “unique guarantees” to North Korea to consummate a potential deal.

This morning in Asia, markets are trading modestly higher with the Nikkei (+0.42%), Hang Seng (+0.28%) and Shanghai Comp. (+0.46%) all up while the Kospi is broadly flat. Datawise, Japan’s May PPI print was well above consensus at 0.6% mom (vs. 0.2% expected) and 2.7% yoy will be out this afternoon and along with tomorrow’s PPI are the last big data prints that the Fed will have before their meeting. The consensus today is for a +0.2% mom core and headline print. The former is also expected to nudge up one-tenth to +2.2% yoy. That +0.2% monthly consensus estimate should be fairly familiar as this is now the 32nd consecutive month that we’ve had such a forecast on the street. For those wondering, only 17 of them have proven to be correct with most missing on the downside. Our US economists also expect the core to come in at +0.2% as they anticipate some payback from unusual weakness last month in categories such as airfares as well as new and used vehicles. Our colleagues actually expect the annual rate to rise to +2.3% yoy which would be the highest since January 2017. All that to look forward to later.

Also today and tomorrow we have the important parliamentary Brexit votes in the House of Commons. As DB Oli Harvey pointed out yesterday there are three important amendments to look out for. The first, amendment 4, requires the UK government to keep the UK in a customs union with the EU. The government could lose this vote, but as it is quite vaguely drafted, it’s not widely expected that this would prove fatal to May’s Brexit strategy. The second, amendment 7, requires the UK to remain in the EEA. A defeat here would be significant, but the government is less likely to lose as it’s not official Labour Party policy. The third, amendment 49, is probably the most important. This amendment gives more powers to Parliament over the final Brexit outcome. Most importantly, if Parliament rejects the government’s final deal (which it has to put before the Commons by 30th November), Parliament can effectively take over the Brexit negotiations. In these circumstances, the baseline is likely to be that the UK goes straight to a very soft Brexit due to the make-up of MPs being very pro remain. From a market perspective, a government defeat on amendment 49 could therefore either be very bullish or very messy. On the former, if the government loses the amendment and May continues, the tail risk of a hard Brexit would be substantially removed (if Parliament didn’t like the deal, it could instruct the government to go straight to EEA membership). On the latter, by losing the vote, hard Brexit MPs could trigger a vote of no confidence in May. If this was the case, the question is how much of the support of the Conservative Party May would lose. If only 30-odd MPs voted against her, she is likely to survive and be in a stronger position. If it was more like 80, May could resign and things could get very messy. The bottom line is that amendment 49 is the one to look out for. Baseline would be that government offers more concessions today and wins the vote. But if the outcome was more uncertain, the crucial vote is likely to occur on either Tuesday evening or Wednesday morning/lunchtime, based on the parliamentary schedule as it stands. Thanks again to Oli for guidance on the above.

Now recapping other markets performance from yesterday. The focus was on Italian risk assets which rallied after the country’s new Finance Minister noted the coalition was committed to remaining in the Eurozone and wanted to boost growth through structural reforms. The FTSE MIB jumped +3.42% while the banks index posted its biggest one-day gain in 13 months as Intesa (+6.6%) and Unicredit (+6.2%) both rallied. Meanwhile, the yields on 2y and 10y BTPs dropped 61.8bp and 28.9bp respectively, with the former now down to 1.02% vs. its recent peak of 2.64%. The risk on sentiment also lifted the Stoxx 600 (+0.73%) and credit markets (EU Main -3.3bp; iTraxx sub-Financial -13.9bp). Across the pond, the S&P pared back earlier gains to close marginally higher (+0.11%) as utilities and financials stocks.

Elsewhere core European government bonds weakened modestly with the yields on Bunds (+4.5bp) and Gilts (+1.6bp) both higher, while UST 10y were little changed (+0.6bp) after the Treasury Department successfully sold $54bln of 3y and 10y notes with solid investor demand. In FX, the US dollar index and Euro both firmed c0.1% while Sterling weakened -0.19% following softer than expected IP and manufacturing production prints. In commodities, WTI oil rose 0.55% to $66.10/bbl, in part as the Iraqi oil Minister al-Luaibi noted his disagreement with Saudi Arabia’s proposal to unwind oil output caps, while a key pipeline crack was thought to risk oil exports from Nigeria.

Away from the markets and onto some trade rhetoric, President Trump has fired off tweets to his G7 allies yesterday, noting that “fair trade is now to be called fool trade if it’s not reciprocal” and that “sorry, we cannot let our friends, or enemies, take advantage of us on trade anymore”. Meanwhile, IMF Managing Director Ms Lagarde has warned “the clouds on the horizon that we have signalled about six months ago are getting darker by the day” and that “the biggest and darkest cloud” over the global economy is the risk of deterioration of confidence “by attempts to challenge the way in which trade has been conducted….” Meanwhile, a spokesman for Germany’s Ms Merkel noted that EU retaliatory tariffs against the US are ready and can take effect from 1 July, but Germany remains ready to resolve the trade tensions via dialogue.

Before we take a look at today’s calendar, we wrap up with other data releases from yesterday. In the UK, both the April IP and manufacturing production were below consensus, at -0.8% mom (vs. 0.1% expected) and -1.4% mom (vs. 0.3% expected) respectively. The latter represents the largest monthly decline since October 2012. DB’s Harvey noted that manufacturing is a relatively small part of the UK economy (10%) and so stronger demand in services could offset this, but does show that domestic demand needs to pick-up as the windfall from a strong external environment is fading. Elsewhere, the UK’s April trade deficit widened more than expected at -£5.3bln (vs. -£2.5bln expected), with exports down -3.2% mom. Over in France, the May Bank of France industrial sentiment index edged down 2pts mom to 100 (vs. 102 expected), which is the lowest reading since October 2016. Meanwhile, Italy’s April IP also fell more than expected to -1.2% mom (vs. -0.5% expected), slowing annual growth to 1.9% yoy.

Looking at the day ahead, the big highlight in terms of data comes in the afternoon in the US with the May CPI report. The May NFIB small business optimism reading and May monthly budget statement will also be out in the US. Prior to this in Europe we’ll get the June ZEW survey in Germany and April/May employment data in the UK including average weekly earnings. Meanwhile, UK Parliament is due to hold a 12-hour session on Brexit legislation with various amendments due.

3. ASIAN AFFAIRS

i)TUESDAY MORNING/MONDAY NIGHT: Shanghai closed UP 27.02 points or 0.89% /Hang Sang CLOSED UP 39.36 points or 0.13% / The Nikkei closed UP 74.31 POINTS OR 0.33% /Australia’s all ordinaires CLOSED UP .13% /Chinese yuan (ONSHORE) closed UP at 6.4043/Oil UP to 66.02 dollars per barrel for WTI and 76.08 for Brent. Stocks in Europe OPENED ALL MIXED//. ONSHORE YUAN CLOSED UP AT 6.4043 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.4005/ONSHORE YUAN TRADING WEAKER AGAINST OFFSHORE YUAN/ONSHORE YUAN TRADING MUCH STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING MUCH WEAKER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW LOOKS LIKE A FULL TRADE WAR IS BEGINNING/

3 a NORTH KOREA/USA

North Korea/South Korea/usa

The following is the first of many summits, but it seems that Kim is committed to denuclearizaiton

(courtesy zerohedge)

Trump And Kim Sign “Comprehensive” Letter To End Historic Summit, Agree To “Follow-On” Negotiations

Donald Trump and North Korean Leader Kim Jong Un signed what the US president described as a “very important, comprehensive” document following the conclusion of their “really fantastic” whirlwind historic summit in Singapore, the first between a US president and North Korean leader that came after decades of hostility.

“The letter that we are signing is very comprehensive, and I think both sides will be very impressed with the results,” Trump said as he sat alongside the North Korean leader at a large wooden table in front of a bank of U.S. and North Korean flags to endorse the document, which however produced no new specific commitments from Pyongyang to surrender its nuclear weapons aside from broad generalities.

Speaking through an interpreter, Kim said that the two countries “had a historic meeting and decided to leave the past behind and we are about to sign a historic document” adding that “I would like to express gratitude to President Trump for making this meeting happen.”

Trump said more information would come out “in just a little while” and did not say what the agreement entailed, but some had already managed to extract the key contents from the letter Trump held up.

William Craddick@williamcraddickChannel NewsAsia complaining that they haven’t gotten the text of the agreement between Trump and Kim from think tanks – new media already figured out what the four points of agreement were #SingaporeSummit

The letter says that the U.S. and North Korea “will join their efforts to build a lasting and stable peace regime on the Korean Peninsula,” and that North Korea “commits to work toward complete denuclearization of the Korean Peninsula.”

The pair also agree to “establish new U.S.-DPRK relations, and the two leaders “have committed to cooperate for the development of new U.S.-DPRK relations and for the promotion of peace, prosperity and security of the Korean Peninsula and of the world.”

Notably, the U.S. and N. Korea agree to follow-on negotiations led by Sec. of State Mike Pompeo and a DPRK counterpart.

In other words this is just the first of many summits.

* * *

Speaking to reporters, Trump also said the he would “absolutely” invite Kim to the White House to continue their talks, meanwhile Kim called the document “historic” and said it would lead to a new era in the U.S.-North Korea relationship.

“We had a historic meeting and decided to leave the past behind, and we are about to sign a historic document,” he said through a translator. “The world will see a major change.”

Kim also thanked Trump for making “this meeting happen.”

To be sure, analysts had expected both Trump and Kim to sell the summit as a success regardless of outcome since both have much at stake. At the signing ceremony, Trump said he was “very proud” of what happened Tuesday and thanked Kim, reiterating that it was an “honor” to meet.

“I think our whole relationship with North Korea and the Korean peninsula is going to be a very much different situation than it has in the past,” Trump said. “We’ve development a very special bond.”

* * *

The ceremony concluded a summit meeting that appeared impossible just one year ago, when both men’s threats against each other fueled an growing nuclear crisis. Just last summer, Trump mocked the North Korean leader as “Little Rocket Man” as the two exchanged barbs over their weapons programs. Kim responded by dismissing the president as a “mentally deranged dotard” who would “pay dearly” for his threats against Pyongyang.

Trump and Kim, however, appeared to have a friendly rapport during their day together at the Singapore island resort. “The past worked as fetters on our limbs, and the old prejudices and practices worked as obstacles on our way forward. But we overcame all of them, and we are here today,” Kim said through a translator as the two met for the first time.

The pair shook hands and met in a one-on-one setting before conferring with aides. The president even showed the North Korean leader the inside of his limousine after their sessions were over.

“It’s going great. We had a really fantastic meeting. A lot of progress. Really, very positive, I think better than anybody could have expected, top of the line, really good,” Trump said as he stood next to Kim after their meetings.

He then said that “we’re going to take care of a very big and very dangerous problem for the world”.

* * *

The summit marked the first stage in a process that the US, Japan, China and South Korea, and certainly the rest of the wor;d hope will lead to denuclearisation on the Korean peninsula. Trump is scheduled to hold a press conference at 4pm local time to discuss the negotiations.

As the two men walked through the Capello Hotel where the summit was held, Kim said to Trump that “many people in the world will think of this as a . . . form of fantasy . . . from a science fiction movie.”