GOLD: $1246.50 UP $2.30 (COMEX TO COMEX CLOSINGS)

Silver: $15.96 UP 12 CENTS (COMEX TO COMEX CLOSINGS)

Closing access prices:

Gold $1247.40

silver: $15.96

For comex gold:

JULY/

NUMBER OF NOTICES FILED TODAY FOR JULY CONTRACT:8 NOTICE(S) FOR 800

TOTAL NOTICES SO FAR 93 FOR 9300 OZ (0.2892 tonnes)

For silver:

JUNE

35 NOTICE(S) FILED TODAY FOR

175,000 OZ/

Total number of notices filed so far this month: 5148 for 25,740,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: BID $6131/OFFER $6216: DOWN $193(morning)

Bitcoin: BID/ $6130/offer $6215: DOWN $195 (CLOSING/5 PM)

end

First Shanghai gold fix comes at 10 pm est

The second Shanghai gold fix: 2:15 pm

First Shanghai gold fix gold: 10 pm est: 1247.92

NY price at the same time: 1243.65

PREMIUM TO NY SPOT: $4.27

Second gold fix early this morning: 1250.18

USA gold at the exact same time:1243.15

PREMIUM TO NY SPOT: $7.03

AGAIN, SHANGHAI REJECTS NEW YORK PRICING.

WE WILL NOT PROVIDE LONDON FIXES AS THEY ARE NOT ACCURATE AS TO WHAT IS GOING ON AT THE SAME TIME FRAME.

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total OPEN INTEREST ROSE BY A SMALL SIZED 101 CONTRACTS FROM 207,701 UP TO 208,111 DESPITE YESTERDAY’S 22 CENT FALL IN SILVER PRICING. WE HAVE HAD LATELY,SUCH CONSIDERABLE COMEX LIQUIDATION THESE PAST SEVERAL DAYS BUT NOT TODAY. HOWEVER, THIS LIQUIDATION HAS NOT MANIFESTED ITSELF INTO LOWER DEMAND FOR PHYSICAL SILVER..JUST THE OPPOSITE. WE ARE STILL WITNESSING A LARGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY(OVER 29 MILLION OZ) AS WELL AS CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A STRONG SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP: 1917 EFP’S FOR SEPT. , 0 EFP’S FOR DECEMBER AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE: OF 1917 CONTRACTS. WITH THE TRANSFER OF 1917 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 1917 EFP CONTRACTS TRANSLATES INTO 9.585 MILLION OZ ACCOMPANYING:

1.THE 22 CENT FALL IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR THE JUNE/2018 COMEX DELIVERY MONTH. (5.420 MILLION OZ) AND NOW JULY/ 2018 WITH 29.160 MILLION OZ INITIALLY STANDING FOR DELIVERY.

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF JUNE:

14,581 CONTRACTS (FOR 8 TRADING DAYS TOTAL 14,581 CONTRACTS) OR 72.91 MILLION OZ: (AVERAGE PER DAY: 1822 CONTRACTS OR 9.113 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF JULY: 72.91 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 10.41% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* LAST MONTH’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2018 TO DATE SILVER EFP’S: 1,732.6 MILLION OZ.

ACCUMULATION FOR JAN 2018: 236.879 MILLION OZ

ACCUMULATION FOR FEB 2018: 244.95 MILLION OZ

ACCUMULATION FOR MARCH 2018: 236.67 MILLION OZ

ACCUMULATION FOR APRIL 2018: 385.75 MILLION OZ

ACCUMULATION FOR MAY 2018: 210.05 MILLION OZ

ACCUMULATION FOR JUNE 2018: 345.43 MILLION OZ

RESULT: WE HAD A SMALL SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 101 DESPITE THE LARGE 22 CENT FALL IN SILVER PRICE. THE CME NOTIFIED US THAT WE HAD A STRONG SIZED EFP ISSUANCE OF 1917 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) . FROM THE CME DATA: 1917 EFP’S FOR SEPT, 0 EFP’S FOR DECEMBER AND ZERO FOR ALL OVER MONTHS FOR A DELIVERABLE FORWARD CONTRACT OVER IN LONDON WITH A FIAT BONUS (TOTAL: 1917). TODAY WE GAINED A CONSIDERABLE: 2018 TOTAL OI CONTRACTS ON THE TWO EXCHANGES:

i.e 1917 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH AN INCREASE OF 101 OI COMEX CONTRACTS. AND ALL OF THIS DEMAND HAPPENED WITH A 22 CENT FALL IN PRICE OF SILVER AND A CLOSING PRICE OF $15.84 WITH RESPECT TO YESTERDAY’S TRADING. YET WE STILL HAVE A GIGANTIC AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY IN THIS ACTIVE JULY DELIVERY MONTH OF MORE THAN 29 MILLION OZ. IT SURE LOOKS LIKE A FAILED BANKER SHORT COVERING EXERCISE AS BANKERS ARE SCRAMBLING TO COVER THEIR HUGE SHORTFALL.

In ounces AT THE COMEX, the OI is still represented by OVER 1 BILLION oz i.e. 1.022 MILLION OZ TO BE EXACT or 147% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT JULY MONTH/ THEY FILED AT THE COMEX: 35 NOTICE(S) FOR 175,000 OZ OF SILVER

IN SILVER, WE SET THE NEW RECORD OF OPEN INTEREST AT 243,411 CONTRACTS ON APRIL 9.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $16.51

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ / JUNE/2018 (5.420 MILLION OZ) AND NOW JULY 2018 AMOUNT INITIALLY STANDING: 29.160 MILLION OZ )

- HUGE RECORD OPEN INTEREST IN SILVER 243,411 CONTRACTS (OR 1.217 BILLION OZ/ SET APRIL 9/2018

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017

- RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT).

In gold, the open interest ROSE BY A CONSIDERABLE 3754 CONTRACTS UP TO 507,347 DESPITE THE FALL IN THE GOLD PRICE/YESTERDAY’S TRADING (A LOSS IN PRICE OF $10.75). WE ARE NOW IN THE ACTIVE DELIVERY MONTH OF JULY. NO DOUBT THE BOYS ARE CASHING IN THEIR COMEX LONGS TO BEGIN THE PROCESS TO MOVE INTO LONDON FORWARDS. THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 3851 CONTRACTS : AUGUST SAW THE ISSUANCE OF: 3851 CONTRACTS, DECEMBER HAD AN ISSUANCE OF 0 CONTACTS AND THEN ALL OTHER MONTHS ZERO. The new COMEX OI for the gold complex rests at 507,802. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE A SMALL OI GAIN IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 7605 CONTRACTS: 3754 OI CONTRACTS INCREASED AT THE COMEX AND 3851 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN: 7605 CONTRACTS OR 760,500 OZ = 23.65 TONNES. AND STRANGELY ALL OF THIS DEMAND OCCURRED WITH A FALL IN THE PRICE OF GOLD YESTERDAY TO THE TUNE OF $10.75???

YESTERDAY, WE HAD 4830 EFP’S ISSUED.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF JUNE : 66064 CONTRACTS OR 6,606,400 OZ OR 205.48 TONNES (8 TRADING DAYS AND THUS AVERAGING: 8258 EFP CONTRACTS PER TRADING DAY OR 825,800 OZ/ TRADING DAY),,

TO GIVE YOU AN IDEA AS TO THE HUGE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 8 TRADING DAYS IN TONNES: 205.48 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2017, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 2555 TONNES

THUS EFP TRANSFERS REPRESENTS 205.48/2550 x 100% TONNES = 8.05% OF GLOBAL ANNUAL PRODUCTION SO FAR IN JULY ALONE.***

ACCUMULATION OF GOLD EFP’S YEAR 2018 TO DATE: 4,308.38* TONNES *SURPASSED ANNUAL PROD’N

ACCUMULATION OF GOLD EFP’S FOR JANUARY 2018: 653.22 TONNES (21 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR FEBRUARY 2018: 649.45 TONNES (20 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR MARCH 2018: 741.89 TONNES (22 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR APRIL 2018: 713.84 TONNES (21 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR MAY 2018: 693.80 TONNES ( 22 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR JUNE 2018 650.71 TONNES (21 TRADING DAYS)

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A CONSIDERABLE SIZED INCREASE IN OI AT THE COMEX OF 3754 DESPITE THE $10,75 FALL IN PRICING GOLD UNDER TOOK YESTERDAY // . WE ALSO HAD AN FAIR SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 3851 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 3851 EFP CONTRACTS ISSUED, WE HAD A STRONG NET GAIN OF 7605 CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

3851 CONTRACTS MOVE TO LONDON AND 3754 CONTRACTS INCREASED AT THE COMEX. (in tonnes, the GAIN in total oi equates to 23.65 TONNES). ..AND BELIEVE IT OR NOT BUT ALL OF THIS DEMAND OCCURRED WITH A FALL OF $10.75 IN TRADING. AT THE COMEX!!!. THE COMEX IS AN OUTRIGHT FRAUD

we had: 8 notice(s) filed upon for 800 oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD...

WITH GOLD UP $2.30 TODAY: /

NO CHANGE IN GOLD INVENTORY AT THE GLD

/GLD INVENTORY 799.02 TONNES

Inventory rests tonight: 799.02 tonnes.

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

SLV/

WITH SILVER UP 12 CENTS:

ANOTHER BIG CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.035 MILLION OZ

/INVENTORY RESTS AT 326.752 MILLION OZ/

NOTE THE DIFFERENCE BETWEEN THE GLD AND SLV: THE CROOKS CAN RAID GOLD BECAUSE THEY DO HAVE SOME PHYSICAL. THEY DO NOT RAID SILVER PROBABLY BECAUSE THERE IS NO REAL SILVER INVENTORIES BEHIND THEM

end

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER ROSE BY A SMALL SIZED 101 CONTRACTS from 207,701 UP TO 208,111 (AND CLOSER TO THE NEW COMEX RECORD SET /APRIL 9/2017 AT 243,411/SILVER PRICE AT THAT DAY: $16.53). THE PREVIOUS RECORD OTHER THAN WAS ESTABLISHED AT: 234,787, SET ON APRIL 21.2017 OVER ONE YEAR AGO. THE PRICE OF SILVER ON THAT DAY: $17.89. OUR CUSTOMARY MIGRATION OF COMEX LONGS MORPH INTO LONDON FORWARDS CONTINUES AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

1917 EFP CONTRACTS FOR SEPT., 0 EFP CONTRACTS FOR DECEMBER AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 1917 CONTRACTS . EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI GAIN AT THE COMEX OF 101 CONTRACTS TO THE 1917 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A NET GAIN OF 2018 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES: 10.09 MILLION OZ!!! AND YET WE ALSO HAVE A STRONG DEMAND FOR PHYSICAL AS WE WITNESS AN INITIAL STANDING OF OVER 29 MILLION OZ AND YET ALL OF THIS DEMAND OCCURRED DESPITE A LARGE 22 CENT LOSS IN PRICE??? .

IT SURE LOOKS LIKE WE ARE GETTING SOME COVERING FROM THE BANKERS SIDE ESPECIALLY WHEN YOU SEE A GOOD GAIN IN PRICE AND THEN A FALL IN COMEX OI AND A SMALLER THAN EXPECTED EFP ISSUANCE.

RESULT: A SMALL SIZED INCREASE IN SILVER OI AT THE COMEX DESPITE THE 22 CENT LOSS THAT SILVER UNDERTOOK IN PRICING ON TUESDAY. BUT WE ALSO HAD ANOTHER FAIR SIZED 1917 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR JULY, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON AS WELL AS THE STRONG AMOUNT OF PHYSICAL STANDING FOR METAL AT THE COMEX.

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)THURSDAY MORNING/WEDNESDAY NIGHT: Shanghai closed UP 59.89 POINTS OR 2.16% /Hang Sang CLOSED UP 169,14 POINTS OR 0.60%/ / The Nikkei closed UP 255,75 POINTS OR 1.17% /Australia’s all ordinaires CLOSED UP 0.79% /Chinese yuan (ONSHORE) closed UP at 6.6696 AS POBC HALTS ITS HUGE DEVALUATION /Oil DOWN to 70,95 dollars per barrel for WTI and 74.14 for Brent. Stocks in Europe OPENED GREEN //. ONSHORE YUAN CLOSED UP AT 6.6696 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.6931:HUGE DEVALUATION/PAST SEVERAL DAYS HALTS: TARIFF WARS CONTINUE UNABATED AND AT FULL TILT//ONSHORE YUAN TRADING STRONGER AGAINST OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING STRONGER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

/NORTH KOREA/SOUTH KOREA

i)North Korea/South Korea/USA

Kim back into the good graces of Trump: he sends a strong will and sincere efforts formal letter

( zerohedge)

b) REPORT ON JAPAN

3 c CHINA

i)China/USA

Trade talks between China and the USA has collapsed

( zero hedge)

ii)Rare earths are a vital part of the uSA tech industry as the USA imports almost 78% from China. China has included rare earths in the trade war and this could damage the USA economy badly

( zerohedge)

4. EUROPEAN AFFAIRS

i)Europe/USA

This morning, Trump threatens sanctions on European investors who have interests in the Russian pipeline (NordStream 2)

Theresa May’s white paper tries to allow the free movement of goods throughout Europe post a soft Brexit but it is services that are killed and that would be a real blow to UK banks

( zerohedge)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

Turkey

An excellent commentary from Mish Shedlock as he outlines why Turkey is on a clear path towards hyperinflation

( Mish Shedlock/Mishtalk)

6 .GLOBAL ISSUES

( zerohedge)

ii)As we pointed out: when a gun is held to NATO they finally react: NATO countries agreed to increase spending

( zerohedge)

iii)Not so fast: Macron and Merkel deny Trump’s NATO spending claims

7. OIL ISSUES

The Petro yuan for gold scheme is operating beautifully in Shanghai as turnover numbers exceed $1 trillion. Come September, when the oil contracts come due, there will be a huge demand for physical gold as holders of yuan seek the yellow metal in Shanghai

(courtesy Nicholas Bienanek)

8. EMERGING MARKET

9. PHYSICAL MARKETS

i)Almost 75% of all South African mines are unprofitable and now unions ask for higher wages. It is interesting that the unions and the South African government do not care that they are unprofitable

go figure.

( GATA/Business live)

10. USA stories which will influence the price of gold/silver)

i)MARKET TRADING/EARLY MORNING

stocks dip as Mnuchin admits that trade talks with China have broken down

( zerohedge)

a)Income growth in the uSA collapses and for the year remains basically at zero

( zerohedge)

b)The big data report is the CPI and today, consumer prices rose much less than expected at a tiny .1% with expected .2% month /month.

( zerohedge)

iv)SWAMP STORIES

a)What on earth is Rosenstein doing?: he is asking 100 prosecutors to receive the President’s pick, Kavanaugh to go over his court rulings?

( zerohedge

Trading Volumes on the COMEX

PRELIMINARY COMEX VOLUME FOR TODAY: 260,422 contracts

CONFIRMED COMEX VOL. FOR YESTERDAY: 367,586 contracts

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

And now for the wild silver comex results.

Total silver OI ROSE BY A SMALL SIZED 101 CONTRACTS FROM 207,701 UP TO 207,802 (AND A LITTLE CLOSER TO THE THE NEW RECORD OI FOR SILVER SET APRIL 9.2018/ 243,411 CONTRACTS) DESPITE THE LARGE 22 CENT LOSS IN SILVER PRICING/ YESTERDAY. SINCE WE ARE NOW INTO THE ACTIVE DELIVERY MONTH OF JULY, WE WERE INFORMED THAT WE STRONG SIZED 1917 EFP CONTRACTS FOR SEPT., 0 EFP CONTRACTS FOR DECEMBER AND ZERO FOR ALL OTHER MONTHS. THESE EFPS WERE ISSUED TO COMEX LONGS WHO RECEIVED A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. THE TOTAL EFP’S ISSUED: 1917. ON A NET BASIS WE GAINED 2018 SILVER OPEN INTEREST CONTRACTS AS WE OBTAINED A 101 CONTRACT GAIN AT THE COMEX COMBINING WITH THE ADDITION OF 1917 OI CONTRACTS NAVIGATING OVER TO LONDON.

NET GAIN ON THE TWO EXCHANGES: 2018 CONTRACTS

AMOUNT STANDING FOR SILVER AT THE COMEX

We are now in the active delivery month of JULY and here the front month fell by 2 contacts to stand at 719 contracts. We had 37 notices filed yesterday so we continue where we left off yesterday as guys refuse to take any more silver ETF’s and instead seek physical delivery at the comex. We gained 35 contracts or an additional 175,000 oz of silver will stand at the comex.

The next delivery month, after July is the non active delivery month of August and here we gained 84 contracts to stand at 1113. The next active delivery month after August for silver is September and here the OI fell by 1029 contracts DOWN to 155,745

We had 35 notice(s) filed for 175,000 OZ for the JULY 2018 COMEX contract for silver

FROM LAST YEARS DATA, ON FIRST DATE NOTICE FOR THE JULY 2017 SILVER COMEX DELIVERY MONTH WE HAD 12.115 MILLION OZ OF SILVER STANDING FOR DELIVERY. AT MONTH’S END WE HAD 16.435 MILLION OZ EVENTUALLY STAND AS WE ALREADY HAD QUEUE JUMPING BEGIN IN EARNEST FROM APRIL 2017 ONWARD EVEN TO TODAY. SO WITH TODAY’S NUMBERS WE SURPASSED LAST YEAR’S LEVEL BY A WIDE MARGIN.

AND NOW COMPARISON VS AUGUST LAST YR:

ON FIRST DAY NOTICE JULY 31/2017: 1,965,000 OZ STOOD FOR DELIVERY

THE FINAL AMOUNT OF SILVER STANDING: AUGUST 30.2017: 6,245,000 OZ AS WE HAD CONSIDERABLE QUEUE JUMPING.

FOR THE AUGUST CONTRACT MONTH:

LAST YEAR AT THIS TIME JULY 11.2017 WE HAD 768 SILVER COMEX OI OUTSTANDING VS TODAY: 719

SO WE ARE RIGHT ON PAR WITH LAST YR.

INITIAL standings for JULY/GOLD

JULY 12/2018.

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz |

nil OZ

|

| Deposits to the Dealer Inventory in oz | NIL oz |

| Deposits to the Customer Inventory, in oz | nil

oz |

| No of oz served (contracts) today |

8 notice(s)

800 OZ

|

| No of oz to be served (notices) |

144 contracts

(14400 oz)

|

| Total monthly oz gold served (contracts) so far this month |

93 notices

9300 OZ

.2892TONNES

|

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

For JULY:

Today, 0 notice(s) were issued from JPMorgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equates to 8 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped/ Received) by j.P.Morgan customer account.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

To calculate the INITIAL total number of gold ounces standing for the JULY. contract month, we take the total number of notices filed so far for the month (93) x 100 oz or 9300 oz, to which we add the difference between the open interest for the front month of JULY. (152 contracts) minus the number of notices served upon today (8 x 100 oz per contract) equals 23,700 oz,(.7371 tonnes) the number of ounces standing in this non active month of JULY

Thus the INITIAL standings for gold for the JULY contract month:

No of notices served (93 x 100 oz) + {(152)OI for the front month minus the number of notices served upon today (8 x 100 oz )which equals 23,700 oz standing in this NON – active delivery month of JULY .

We lost 5 contracts or an additional 500 oz will not stand for comex delivery.

THERE ARE ONLY 7.4588 TONNES OF REGISTERED COMEX GOLD AVAILABLE FOR DELIVERY AGAINST 0.7371 TONNES STANDING FOR JULY

IN THE LAST 24 MONTHS 85 NET TONNES HAS LEFT THE COMEX.

end

And now for silver

AND NOW THE APRIL DELIVERY MONTH

JULY INITIAL standings/SILVER

| Silver | Ounces |

| Withdrawals from Dealers Inventory | nil oz |

| Withdrawals from Customer Inventory |

nil oz

|

| Deposits to the Dealer Inventory |

nil

oz

|

| Deposits to the Customer Inventory |

1,149,315.400

oz

CNT

JPM

|

| No of oz served today (contracts) |

35

CONTRACT(S)

(175,000 OZ)

|

| No of oz to be served (notices) |

684 contracts

(3,420,000 oz)

|

| Total monthly oz silver served (contracts) | 5148 contracts

(25,740,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

we had 0 inventory movement at the dealer side of things

total dealer deposits: nil oz

total dealer withdrawals: nil oz

we had 2 deposits into the customer account

i) Into JPMorgan: 539,322.200 oz

*** JPMorgan for most of 2017 and in 2018 has adding to its inventory almost every single day.

JPMorgan now has 141 million oz of total silver inventory or 52.0% of all official comex silver. (141 million/270 million)

ii) into CNT; 609,993,200 oz

total customer deposits today: 1,149,315,400 oz

we had 0 withdrawals from the customer account;

total withdrawals: nil oz

we had 0 adjustments/

total dealer silver: 77.696 million

total dealer + customer silver: 280.469 million oz

The total number of notices filed today for the JULY. contract month is represented by 35 contract(s) FOR 175,000 oz. To calculate the number of silver ounces that will stand for delivery in JULY., we take the total number of notices filed for the month so far at 5148 x 5,000 oz = 25,740,000 oz to which we add the difference between the open interest for the front month of JULY. (719) and the number of notices served upon today (35 x 5000 oz) equals the number of ounces standing.

.

Thus the INITIAL standings for silver for the JULY/2018 contract month: 5148(notices served so far)x 5000 oz + OI for front month of JULY(719) -number of notices served upon today (35)x 5000 oz equals 29,160,000 oz of silver standing for the JULY contract month

WE GAINED 35 CONTRACTS OR AN ADDITIONAL 175,000 OZ WILL STAND AS THESE GUYS REFUSE TO MORPH INTO LONDON BASED FORWARDS AND RECEIVE A FIAT SWEETENER FOR THEIR EFFORTS.

PLEASE NOTE THE FOLLOWING FOR COMPARISON PURPOSES:

THE INITIAL STANDING FOR SILVER AT THE COMEX JULY 2017: 12.115 MILLION OZ ALTHOUGH AT MONTH’S END: 16.435 MILLION OZ. THIS COMPARES WITH TODAY’S INITIAL STANDING FOR SILVER OF 29,160 MILLION OZ.

As I stated yesterday:

“WHEN WE WITNESS THE AMOUNT OF PHYSICAL INCREASE IN THE AMOUNT STANDING AT THE COMEX AND ESPECIALLY COMMENCING ON DAY 2 OF THE DELIVERY CYCLE, YOU CAN BET THE FARM THAT THIS AMOUNT WILL INCREASE FROM THIS DAY FORTH UNTIL THE CONCLUSION OF THE MONTH OF JULY. THIS IS KNOWN AS QUEUE JUMPING AND THIS PHENOMENON HAS BEEN FRONT AND CENTRE OF OPERATIONS IN SILVER FOR NOW OVER 14 MONTHS. SILVER IS BEING SOUGHT BY COMMERCIALS OVER ON THIS SIDE OF THE POND AS DWINDLING SUPPLIES VACATE THE GLOBAL ARENA.”

queue jumping continues to intensify to the highest degree in silver as dealers scrounge around for dwindling supplies.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

ESTIMATED VOLUME FOR TODAY: 67,577 CONTRACTS

CONFIRMED VOLUME FOR YESTERDAY: 93,863 CONTRACTS absolutely criminal

YESTERDAY’S CONFIRMED VOLUME OF 93,863 CONTRACTS EQUATES TO 469 million OZ OR 67.0% OF ANNUAL GLOBAL PRODUCTION OF SILVER

COMMODITY LAW SUGGESTS THAT OPEN INTEREST SHOULD NOT BE MORE THAN 3% OF ANNUAL GLOBAL PRODUCTION. THE CROOKS ARE SUPPLYING MASSIVE PAPER TRYING TO KEEP SILVER IN CHECK.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price at that day at $18.42

The previous record was 224,540 contracts with the price at that time of $20.44

end

NPV for Sprott

1. Sprott silver fund (PSLV): NAV FALLS TO -3.29% (JULY 12/2018)

2. Sprott gold fund (PHYS): premium to NAV FALLS TO -0.67% to NAV (JULY 12/2018 )

Note: Sprott silver trust back into NEGATIVE territory at -3.29%-/Sprott physical gold trust is back into NEGATIVE/

(courtesy Sprott/GATA)

3.SPROTT CEF.A FUND (FORMERLY CENTRAL FUND OF CANADA):

NAV 12.97/TRADING 12.46//DISCOUNT 3.91.

END

And now the Gold inventory at the GLD/

JULY 12/WITH GOLD UP $2.30: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 799.02 TONNES

JULY 11/WITH GOLD DOWN $10.75 THE CROOKS RAIDED THE COOKIE JAR AGAIN TO THE TUNE OF 1.75 TONNES/INVENTORY RESTS AT 799.02 TONNES

JULY 10/WITH GOLD DOWN $3.85: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 800.77 TONNES

july 9/WITH GOLD UP $4.00/ANOTHER RAID ON THE GOLD COOKIE JAR: TWO WITHDRAWALS OF 1.18 TONNES THIS MORNING AND 1.47 TONNES THIS AFTERNOON/INVENTORY RESTS AT 800.77 TONNES

JULY 6/WITH GOLD DOWN $2.45: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 803.42 TONNES

JULY 5/WITH GOLD UP ANOTHER $5.15, THE CROOKS RAIDED THE COOKIE JAR AGAIN TO THE TUNE OF 5.89 TONNES/INVENTORY RESTS AT 803.42 TONNES IN THE LAST 10 TRADING DAYS GLD HAS LOST A HUGE 25.34 TONNES WITH A LOSS OF ONLY $15.25 IN PRICE

July 3/WITH GOLD UP $11.15/THE CROOKS RAIDED THE GLD INVENTORY AGAIN TO THE TUNE OF 9.73 TONNES/INVENTORY RESTS AT 809.31 TONNES

JULY 2/WITH GOLD DOWN $12.15, THE CROOKS RAIDED THE GLD INVENTORY AGAIN BY 1.47 TONNES DOWN./INVENTORY RESTS AT 819.04 TONNES

JUNE 29/WITH GOLD UP $3.70/A WITHDRAWAL OF 1.18 TONNES OF GOLD FROM THE GLD/INVENTORY RESTS AT 820.51 TONNES

JUNE 28/WITH GOLD DOWN $5.15/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 821.69 TONNES

June 27/WITH GOLD DOWN $3.60// TWO ENTRIES:/STRANGELY THE CROOKS RETURNED THE WITHDRAWAL OF 4.42 TONNES LAST NIGHT (THUS WE HAD A DEPOSIT OF 4.42 TONNES/INVENTORY RESTS AT 824.63 TONNES. /THEN LATE THIS AFTERNOON A WITHDRAWAL OF 2.94 TONNES

INVENTORY RESTS AT 821.69 TONNES/THIS VEHICLE IS AN OUTRIGHT FRAUD.

june 26/LATE LAST NIGHT, WITH GOLD DOWN $9.10 WE HAD A HUGE WITHDRAWAL OF 4.42 TONNES OF GOLD/INVENTORY RESTS AT 820.21 TONES

JUNE 25/WITH GOLD DOWN $1.45/NO CHANGE IN GOLD INVENTORY AT THE GLD.INVENTORY RESTS AT 824.63 TONNES

JUNE 22/WITH GOLD UP 25 CENTS TODAY, THE CROOKS WITHDREW A MASSIVE 4.13 TONNES OF GOLD/INVENTORY RESTS AT 824.63 TONNES

JUNE 21/WITH GOLD DOWN $4.00/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 828.76 TONNES

JUNE 20/WITH GOLD DOWN $3.55/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 828.76 TONNES

JUNE 19/WITH GOLD DOWN $1.50/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 828.76 TONES

JUNE 18/WITH GOLD UP $1.90/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 828.76 TONNES

JUNE 15/WITH GOLD DOWN $28.90/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 828.76 TONNES

JUNE 14/WITH GOLD UP $7.10/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 828.76 TONNES/

JUNE 13/WITH GOLD UP $2.20/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 828.76 TONNES

JUNE 12/WITH GOLD DOWN $4.75:NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 828.76 TONNES

JUNE 11/WITH GOLD UP 65 CENTS/THE CROOKS RAIDED THE COOKIE JAR FOR 3.83 TONNES/INVENTORY RESTS AT 828.76 TONNES

JUNE 8/WITH GOLD DOWN 10 CENTS/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY REMAINS AT 832.59 TONNES./

JUNE 7/WITH GOLD UP $1.45, THE CROOKS DECIDED TO RAID AGAIN THE GLD GOLD COOKIE JAR TO THE TUNE OF 3.54 TONNES/GOLD INVENTORY LOWERS TO 832.59 TONNES

JUNE 6/WITH GOLD UP $1.30 TODAY, WE HAD NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 836.13 TONNES

JUNE 5/WITH GOLD UP $5.30 TODAY, WE HAD A TINY WITHDRAWAL OF .29 TONNES AND THAT NO DOUBT WAS TO PAY FOR FEES/836.13 TONNES

JUNE 4/WITH GOLD DOWN ONLY $2.50, THE CROOKS UNLEASHED A MASSIVE WITHDRAWAL OF 10.61 TONNES OF GOLD FROM THE GLD/INVENTORY RESTS AT 836.42 TONNES

JUNE 1/WITH GOLD DOWN $5.10 TODAY, A HUGE 4.42 TONNES OF GOLD WAS WITHDRAWN FROM THE GLD AND THIS WAS USED IN THE RAID TODAY/INVENTORY RESTS AT 847.03 TONNES

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

JULY 12/2018/ Inventory rests tonight at 799.02 tonnes

*IN LAST 410 TRADING DAYS: 127.79 NET TONNES HAVE BEEN REMOVED FROM THE GLD

*LAST 360 TRADING DAYS: A NET 28,75 TONNES HAVE NOW BEEN ADDED INTO GLD INVENTORY.

end

Now the SLV Inventory/

JULY 12/WITH SILVER UP 12 CENTS TODAY: ANOTHER BIG CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.035 MILLION OZ/INVENTORY RESTS AT 826.752 MILLION OZ/

JULY 11/WITH SILVER DOWN 22 CENTS TODAY: ANOTHER HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 565,000/INVENTORY RESTS AT 825.717 MILLION OZ

JULY 10/WITH SILVER DOWN 3 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 825.151 MILLION OZ

july 9/WITH SILVER UP 5 CENTS: ANOTHER BIG CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 847,000 OZ ADDED TO INVENTORY/INVENTORY RESTS AT 825.151 MILLION OZ/

JULY 6/WITH SILVER DOWN 2 CENTS/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 824.305 MILLION OZ/

JULY 5/WITH SILVER UP 6 CENTS, A GOOD CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 470,000 OZ/INVENTORY RESTS AT 324.305 MILLION OZ/ FOR THE PAST 10 TRADING DAYS, SILVER INVENTORY HAS ADVANCED BY 4.945 MILLION OZ WITH A LOSS OF 33 CENTS/PLEASE COMPARE THIS WITH THE GLD.

JULY 3/WITH SILVER UP 17 CENTS, A HUGE DEPOSIT OF 1.37 MILLION OZ ADDED TO THE SLV/INVENTORY RESTS AT 323.835 MILLION OZ.

JULY 2/WITH SILVER DOWN 31 CENTS/A HUGE 2.070 MILLION OZ DEPOSIT AT THE SLV/INVENTORY RESTS AT 322.465 MILLION OZ/

JUNE 29/WITH SILVER UP 14 CENTS TODAY, NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS THIS WEEKEND AT 320.395 MILLION OZ/

JUNE 28/WITH SILVER DOWN 18 CENTS, THE CROOKS ADDED 1.035 MILLION OZ OF SILVER INTO THE SLV/INVENTORY RESTS AT 320.395 MILLION OZ

JUNE 27.2018/WITH SILVER DOWN 8 CENTS/NO CHANGE IN SILVER INVENTORY/INVENTORY RESTS AT 819.360 MILLION OZ/

june 26./2018/WITH SILVER DOWN 8 CENTS, THE CROOKS WITHDREW THE DEPOSIT OF TWO DAYS AGO; 941,000 OZ OUT OF INVENTORY/INVENTORY RESTS AT 819.360 OZ

JUNE 25/WITH SILVER DOWN 12 CENTS/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 320.301 MILLION OZ/

JUNE 22/WITH SILVER UP 12 CENTS TODAY,ANOTHER BIG CHANGE IN SILVER INVENTORY AT THE SLV” A DEPOSIT OF 941,000 OZ INTO INVENTORY/INVENTORY RESTS THIS WEEKEND AT 320.301 MILLION OZ/

JUNE 21/WITH SILVER UP ONE CENT/ANOTHER CHANGE IN SILVER INVENTORY AT THE SLV/: A DEPOSIT OF 2.918 MILLION OZ/INVENTORY RESTS AT 319.360 MILLION OZ/ THUS FOR TWO STRAIGHT DAYS A TOTAL OF 5.26 MILLION OZ OF SILVER HAS BEEN ADDED WITH NO CHANGE IN PRICE.

JUNE 20/WITH SILVER DOWN ONE CENT/A HUGE CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY / A DEPOSIT OF 2.35 MILLION OZ/INVENTORY RESTS AT 316.442 MILLION OZ/

JUNE 19/2018/WITH SILVER DOWN 11 CENTS/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 314.090 MILLION OZ/

JUNE 18/WITH SILVER DOWN 6 CENTS TODAY/NO CHANGE IN SILVER INVENTORY/INVENTORY RESTS AT 314.090 MILLION OZ/

JUNE 15/WITH SILVER DOWN 75 CENTS/A BIG CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.788 MILLION OZ//INVENTORY RESTS AT 314.090 MILLION OZ

JUNE 14/WITH SILVER UP 30 CENTS, THE CROOKS DECIDED THAT THEY NEEDED SILVER INVENTORY BADLY SO THEY RAID THE SLV OF 1.412 MILLION OZ/INVENTORY RESTS AT 315.878 MILLION OZ/

JUNE 13/WITH SILVER UP 11 CENTS TODAY/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 317.290 MILLION OZ/

JUNE 12/WITH SILVER DOWN 5 CENTS/A HUGE CHANGES IN SILVER INVENTORY AT THE SLV/ THE CROOKS RAID THE SILVER COOKIE JAR BY 1.976 MILLION OZ/INVENTORY LOWERS TO 317.290 MILLION OZ/

jUNE 11/NO CHANGE IN SILVER INVENTORY/319.266 MILLION OZ

JUNE 8/WITH SILVER DOWN 5 CENTS/A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.412 MILLION OZ//INVENTORY LOWERS TO 319.266 MILLION OZ/

JUNE 7/WITH SILVER UP ANOTHER 12 CENTS/A HUGE CHANGE IN SILVER INVENTORY AT THE SL: A WITHDRAWAL OF 1.883 MILLION OZ WITH ALL OF THAT SILVER DEMAND//INVENTORY RESTS AT 320.678 MILLION OZ/

JUNE 6/WITH SILVER UP 14 CENTS TODAY/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 322.561 MILLION OZ/

JUNE 5/WITH SILVER UP 10 CENTS NO CHANGE IN SILVER INVENTORY/INVENTORY RESTS AT 322.561 MILLION OZ

JUNE 4/WITH SILVER DOWN 1 CENTA SMALL CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 522,000 OZ INTO THE SLV/.INVENTORY RISES AT 322.561 MILLION OZ/

JUNE 1/WITH SILVER DOWN 3 CENTS/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY REMAINS AT 322.039 MILLION OZ/

JULY 12/2018:

Inventory 326.752 MILLION OZ

6 Month MM GOFO 2.08/ and libor 6 month duration 2.51

Indicative gold forward offer rate for a 6 month duration/calculation:

G0FO+ 2.08%

libor 2.51 FOR 6 MONTHS/

GOLD LENDING RATE: .43%

XXXXXXXX

12 Month MM GOFO

+ 2.78%

LIBOR FOR 12 MONTH DURATION: 2.53

GOFO = LIBOR – GOLD LENDING RATE

GOLD LENDING RATE = +.25

end

Major gold/silver trading /commentaries for THURSDAY

GOLDCORE/BLOG/MARK O’BYRNE.

Ponzi Economy Will Lead To Next Crisis

Hallmark of an Economic Ponzi Scheme

News and Commentary

Gold holds steady near 1-wk low as dollar firms against yen (Reuters.com)

Gold falls to 1-week lows, eyes 2018 lows (FXStreet.com)

Dow drops more than 200 points after US unveils new tariffs on Chinese goods (CNBC.com)

U.S. Stocks Drop as Dollar Rallies, Oil Tumbles (Bloomberg.com)

South African Gold Industry in decline as wage talks begin (ScrapRegister.com)

Global Debt Hits A Record $247 Trillion, The IIF Issues A Warning (ZeroHedge.com)

Producer Price Rising Most Since 2011; Yields Spike, Stocks Fall (ZeroHedge.com)

PPI Highest Since 2011 and Rising Inflation Positive For Gold and Silver (KingWorldNews.com)

Dollar Index ‘Rally’ Appeared In the Nick of Time on Monday (GoldSeek.com)

Humane Immigration Will Make America Great Again. (GoldSeek.com)

Listen on SoundCloud , Blubrry & iTunes. Watch on YouTube below

Gold Prices (LBMA AM)

11 Jul: USD 1,250.00, GBP 943.63 & EUR 1,068.38 per ounce

10 Jul: USD 1,253.70, GBP 946.17 & EUR 1,069.41 per ounce

09 Jul: USD 1,262.60, GBP 946.95 & EUR 1,072.70 per ounce

06 Jul: USD 1,254.20, GBP 947.55 & EUR 1,071.09 per ounce

05 Jul: USD 1,252.50, GBP 946.89 & EUR 1,071.64 per ounce

04 Jul: USD 1,256.90, GBP 951.47 & EUR 1,079.80 per ounce

03 Jul: USD 1,245.85, GBP 944.85 & EUR 1,068.81 per ounce

Silver Prices (LBMA)

11 Jul: USD 15.92, GBP 12.02 & EUR 13.59 per ounce

10 Jul: USD 15.93, GBP 12.04 & EUR 13.61 per ounce

09 Jul: USD 16.21, GBP 12.15 & EUR 13.76 per ounce

06 Jul: USD 16.00, GBP 12.09 & EUR 13.66 per ounce

05 Jul: USD 15.95, GBP 12.04 & EUR 13.65 per ounce

04 Jul: USD 16.05, GBP 12.15 & EUR 13.78 per ounce

03 Jul: USD 15.93, GBP 12.08 & EUR 13.68 per ounce

Recent Market Updates

– World Cup Is 200 Ounces Of Gold Worth £140,000 – 30% Less Than Harry Kane’s Weekly Wage

– Chaotic BREXIT More Likely: Risk To London, While Frankfurt, Luxembourg, Paris and Dublin Benefit

– VIDEO: Italy €2.4 Trillion Debt To Create Eurozone Contagion and Global Debt Crisis?

– U.S. China Trade War Escalates as Russia and China Accumulate Gold

– Irish Gold Money Rings Found – Mystery Surrounds What May Be Ancient, Pre-Historic Currency

– Gold $10,000 In Currency Reset? Russia, China Gold Demand To Overwhelm Gold Futures Manipulation (GOLDCORE VIDEO)

– Italian Debt – A Financial Disaster Waiting To Happen

– As The Currency Reset Begins – Get Gold As It Is “Where The Whole World Is Heading”

– Buy Gold Or Bitcoin As The “Liquidity Party” Is Ending?

– Why Russia and Turkey Diversifying Into Gold May Signal A Bigger Global Shift

– London House Prices Fall 1.9% In Quarter – Bubble Bursting?

– Gold Exports To London From U.S. Surge 152% In 2018

– Manipulation of Gold & Silver by Bullion Banks Is “Undeniable”

– “Perfect Environment For Gold” As Fed Will Weaken Dollar and Create Inflation – Rickards

– Russia Buys 600,000 oz Of Gold In May After Dumping Half Of US Treasuries In April

– In Gold, Silver and Bitcoin We Trust? Goldnomics Podcast with Ronald-Peter Stoeferle

– Own A “Bit Of Gold” As We Are Moving Ever Closer To A Trade War

ANDREW MAGUIRE’S KINESIS WHICH IS A”BITCOIN’ BACKED 100% BY ALLOCATED GOLD AND SILVER

Andrew Maguire’s Kinesis money which is a “bitcoin” but backed 100% by allocated gold and silver is set to go.

it think it would be a great idea to look at this!

please read at: https://kinesis.money/#/

(Andrew Maguire)

|

|

Dear Harvey Organ,

Thank you for your participation in our webinar on June 7th with our host and CEO of Kinesis, Thomas Coughlin.

The response we received has been incredible, we appreciate you taking the time to join us and hope you found it to be beneficial.

Due to such a high influx of questions we received we were unable to have them all answered. Nevertheless, if there was anything which requires more clarification, or you have a query which needs to be rectified, we invite you to join our telegram group:

We apologize for the technical issues we incurred during the webinar which resulted in it running a little over schedule, we hope that the next one we host will run seamlessly.

A video has been put together and uploaded onto our YouTube channel which can be found here:

Please share and subscribe to our YouTube channel to be notified of all the latest videos as they become available.

The rapid growth that we are currently experiencing has been incredible and with your support, is only going to get better.

We are working behind the scenes very hard to create a better experience for everyone involved! Stay tuned in as we have many more announcements to be released in the upcoming days.

Kind Regards,

|

Kinesis Money

a:C/O ILS Fiduciaries (IOM) Limited, First Floor,Millennium House, Victoria Road, Douglas, Isle of Man IM2 4RW

|

The following is self explanatory

(courtesy GATA/Chris Powell and Harvey Organ)

GATA asks bank regulator to check risks of gold

futures maneuver

Submitted by cpowell on Sun, 2018-06-10 16:17. Section: Daily Dispatches

12:21p ET Sunday, June 10, 2018

Dear Friend of GATA and Gold:

GATA has appealed to the U.S. comptroller of the currency, who has regulatory authority over banks, to review financial risks certain banks may have incurred through derivatives in the monetary metals markets, particularly through the recent heavy use of the “exchange for physicals” mechanism of settling gold and silver futures contracts on the New York Commodities Exchange.

The appeal was made in a letter sent May 5 to the comptroller, Joseph M. Otting, whose office is part of the U.S. Treasury Department, by your secretary/treasurer and GATA futures market consultant Harvey Organ.

“Exchange for physical” settlements of futures contracts long were considered emergency procedures when a seller was not able to deliver metal from an exchange-approved warehouse and wanted to settle with delivery elsewhere. But now such settlements appear to constitute most gold and silver futures settlements on the Comex. It is a strange development that appears to have been necessitated by the increasing difficulties of central banking’s gold and silver price suppression policy.

GATA has received no acknowledgment of the letter. Its text is below and a PDF copy of it is here:

http://www.gata.org/files/ComptrollerOfCurrencyLetter.pdf

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

* * *

May 5, 2018

Joseph M. Otting, Comptroller of the Currency

U.S. Treasury Department

400 7th Street, SW

Washington DC 20219

Dear Comptroller Otting:

Please let us bring to your attention financial risks to major banks involving their possibly unreported exposure to derivatives in the monetary metals markets.

In recent months gold and silver future contracts issued by U.S. banks on the New York Commodities Exchange have been moved off-exchange for delivery through a mechanism known as “exchange for physical” (EFP) contracts. Until recently use of this mechanism was considered an emergency procedure when a seller did not have access to metal for delivery through Comex warehouses. Now the mechanism seems to be in use for a large share of front-month contracts for which delivery is sought.

Here is an example that is happening at the Comex in the front active month of April for gold and the inactive delivery month of April for silver.

In gold, there were 229,436 EFP contracts for 713.64 tonnes, an average of 10,925 contracts and 1,092,500 ounces per trading day.

In silver, there were 77,150 EFP contracts for 385,750,000 ounces, an average of 3,673 contracts and 18,369,000 ounces per trading day.

London Bullion Market Association rules suggest that these contracts may not be reported to regulators. The LBMA’s bylaws say:

“Figures above exclude any contracts not subject to risk-based capital requirements, such as FX contracts with an original maturity of 14 days or less, futures contracts, written options, and basis swaps. Therefore, the total notional amount of derivatives by maturity will not add to the total derivatives figure in this table.”

We are told that these EFP contracts are transferred from the Comex to London as what are called “serial forwards” and their duration is always less than 14 days, which exempts them from being reported.

It is our understanding that in each quarter your office prepares a report detailing risk undertaken by the banks under the comptroller’s supervision.

These risks include derivatives undertaken by U.S. banks and other obligations that may cause a bank to fail. Our concern is that your office may not be aware of large unreported derivative exposure by banks.

Could you review this matter and let us know your conclusions?

Sincerely,

CHRIS POWELL

Secretary/Treasurer

HARVEY ORGAN

Consultant

Gold Anti-Trust Action Committee Inc.

7 Villa Louisa Road

Manchester, Connecticut 06043-7541

end

Almost 75% of all South African mines are unprofitable and now unions ask for higher wages. It is interesting that the unions and the South African government do not care that they are unprofitable

go figure.

(courtesy GATA/Business live)

Most South African gold mines are unprofitable but owners, unions, government don’t care why

Submitted by cpowell on Wed, 2018-07-11 17:21. Section: Daily Dispatches

Minerals Council Says 75% of South Africa’s Mines Are Unprofitable

By Allan Seccombe

Business Day, Johannesburg, South Africa

Wednesday, July 11, 2018

Three-quarters of South Africa’s gold mines are unprofitable or barely making money, says the Minerals Council SA as the sector enters wage talks that some participants hope will reflect the realities bedevilling the sector.

South Africa’s 140-year-old gold industry, for decades the world’s leading source of the precious metal, is a shadow of itself, barely clinging onto eighth place ahead of Mexico. Its mines are old, deep, with falling grades and productivity, and rising costs.

From more than 392,000 people employed in 1994, the sector now has 111,800 and that decline is showing no signs of slowing, with the weak rand price of gold forcing the closure of Pan African Resources’s Evander gold mine and the shutdown of the Cooke mines owned by Sibanye-Stillwater.

Against this backdrop, the gold sector including Sibanye, AngloGold Ashanti, Harmony, and Village Main Reef, starts wage talks today to set a fresh two-year wage deal.

The opening demands from the two biggest unions, the National Union of Mineworkers, with 51 percent representation of the 79,517 employees at the four companies, and the Association of Mineworkers and Construction Union, with 34 percent, did not reflect an awareness of the difficulties. …

… For the remainder of the report:

https://www.businesslive.co.za/bd/companies/mining/2018-07-11-minerals-c…

END

Holmes states that everybody is hoarding gold as their is a huge shortage due to the huge movement of gold from west to east

(courtesy Frank Holmes)

Peak Gold is Here – Everyone’s Hoarding Gold amidst a Global Gold Shortage

Investment capital is flowing into gold stocks and Frank Holmes, CEO of U.S. Investors, said that this may be due to peak gold. “What we’re witnessing now is money going into gold stock ETFs,” Holmes said. He said that there is currently no breakthrough technology like there was for fracking in the mining industry, so gold production is likely to continue to plateau and eventually decline, according to the theory of peak gold.

He added that investors are likely to see gold stocks move up as more capital continues to flow in, which is usually a precursor to the bullion rallying.

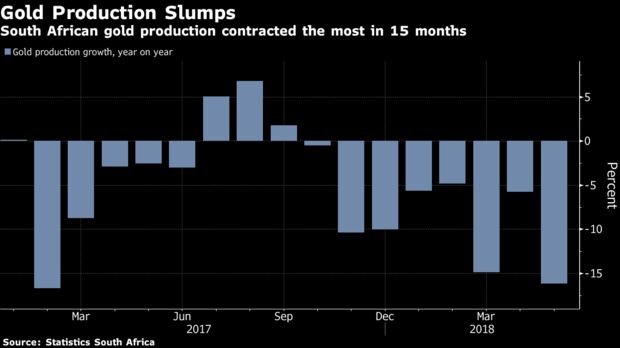

South African Gold Output Falls Most Since February 2017

Gold output in South Africa, once the world’s biggest producer of the metal, declined the most since February 2017 in May.

Production dropped 16.2 percent from a year earlier, compared with a revised 5.8 percent contraction in April, Pretoria-based Statistics South Africa said Thursday in a statement on its website. That’s an eighth straight month of decreases.

Total mining output shrank for a third month, dropping 2.6 percent from a year earlier compared with a revised 4.4 percent retreat in April, it said. Production of platinum-group metals, of which South Africa has the largest known reserves, increased for the first time in six months, expanding 9.6 percent from a revised 6.3 percent contraction a month earlier.

Aging infrastructure, reserve depletion and accidents have raised costs and curbed mines’ output in South Africa. Mining companies came under added pressure late last year and in the start of 2018 from the stronger rand and have responded by closing shafts and cutting thousands of jobs in a labor-intensive industry. Ana Monteiro (Bloomberg)

Peak Gold is Here – Everyone’s Hoarding Gold – A Double Whammy!

Tom Lewis: The tiny nation of Kyrgyzstan has big plans. Caught between its giant trading partners, China and Russia,Kyrgyzstan is stockpiling gold. It wants to increase gold from 16 percent to 50 percent as part of its international reserve.

Tolkunbek Abdygulov of the Kyrgyz Central Bank has stated that any currency, whether dollars, rubles, or yuan, has become too vulnerable. The small mountain nation, with a population of 6 million, relies heavily on Russian and Chinese imports. With the possibility of global trades war on the horizon, Kyrgyzstan prefers to protect its financial stability by amassing gold. It suffered during the ruble devaluation in 2015, and it is turning to gold as a hedge against any renewed economic upheaval.

Kyrgyzstan is merely following in the steps of other, larger nations, such as Russian, India, and Turkey, who are also increasing their gold reserves. The U.S. and Germany both have reserves that are 70 percent of its central bank holdings. If there is a trade war, countries are prepared.

Gold has traded steadily and unspectacularly for the past decade, but looming tariffs and trade sanctions have pushed gold out of the doldrums and into the stoplight.

Kyrgyzstan, one of the few post-Soviet republics with its currency, has been buying gold since 2014. Abdygulov has kept the nation’s currency, the som, relatively steady and recognizes that stockpiling gold will serve as a hedge against inflation.

Kyrgyzstan is smart to worry. Following President Trump’s promise to institute tariffs on imports, Russian has sold off half of its U.S. Treasury bonds, more than $47 billion, in retaliation. At the same time, Russia’s central bank has increased its gold reserves to 62 million ounces, at a value of $80.5 billion, in an effort to diversify its reserves in view of possible geopolitical unrest. Russian is less interested in increasing return on its investments. The U.S. bonds yield a higher return than gold in 2018, but selling off the Treasury bonds lessens Russia’s dependency on the U.S. dollar. Russian’s hoarding of gold has long been viewed as an attempt to devalue the U.S. dollar as the reigning global currency.

China is another country that would like to see the U.S. dollar replaced on the global financial market. If China were to sell off its $1.18 in U.S. Treasury bonds, it could go a long way in accomplishing that goal.

Russia’s increase in gold holdings has made it a global gold powerhouse. It has triple the gold as a percent of GDP, or 5.6 percent of the world’s available precious metal.

This is a thought-out, long-term plan for Russia, and U.S. trade sanctions are only a part of the picture. With large gold reserves and a relatively small international debt, Russia has positioned itself as a strong global financial force. It not only wants to strengthen its own currency, the ruble, but it is preparing itself for the collapse of the U.S. dollar. The future won’t be the dollar vs. the ruble. It may very well be East against West, and East is in an extremely favorable battle position.

Peak Gold – Major suppliers sounding the alarm on a global gold shortage

- The people responsible for supplying the world with gold say we are running out of it.

- Mining companies are no longer finding new deposits of gold to replace their aging mines.

- There’s not a reasonable substitute for gold.

Simon Black : A few months ago I sent you a note explaining that major gold discoveries are shrinking.

Simply put, mining companies are no longer finding vast, new deposits of gold to replace their aging mines.

I quoted Pierre Lassonde, the billionaire founder of gold royalty giant Franco-Nevada and former head of Newmont Mining:

If you look back to the 70s, 80s and 90s, in every one of those decades, the industry found at least one 50+ million-ounce gold deposit, at least ten 30+ million-ounce deposits, and countless 5 to 10 million ounce deposits.

But if you look at the last 15 years, we found no 50-million-ounce deposit, no 30- million-ounce deposit and only very few 15 million ounce deposits.

Pierre Lassonde is one of the most well- respected and knowledgeable mining experts in the world. And he thinks we’re reaching ‘peak gold’.

But he’s not alone.

Last month, Rudy Fronk, Chairman and CEO of Seabridge Gold noted:

“Peak gold is the new reality in the gold business with reserves now being mined much faster than they are being replaced.“

Nick Holland, CEO of South Africa’s largest gold producer Gold Fields: “We were all talking about how production was going to increase every year. I think those days are probably gone. “

Kevin Dushnisky, President of mining giant Barrick Gold: “Falling grades and production levels, a lack of new discoveries, and extended project development timelines are bullish for the medium and long-term gold price outlook.“

But the biggest warning comes from resource legend Ian Telfer, chairman of Goldcorp. In an interview with Financial Post, Telfer said:

“If I could give one sentence about the gold mining business … it’s that in my life, gold produced from mines has gone up pretty steadily for 40 years. Well, either this year it starts to go down, or next year it starts to go down, or it’s already going down… We’re right at peak gold here.”

It’s hard to pinpoint a top or a bottom. But there is an interesting opportunity here since gold has fallen in price over the last several weeks thanks to an inexplicable surge in the US dollar.

The long-term fundamentals seem pretty obvious- the people responsible for supplying the world with gold are saying the world is running out of gold and that supply is declining at an alarming rate.

With a commodity like oil, technology tends to solve the problem of declining supply through more efficient production methods.

When ‘peak oil’ started becoming a problem 10 years ago, the industry developed new fracking and horizontal drilling technologies. And other industries like solar and wind began developing better substitutes for oil.

But there’s not really a substitute for gold. And the biggest players in the space are saying we’re running out.

-END-

Your early THURSDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

i) Chinese yuan vs USA dollar/CLOSED UP TO 6.6696/HUGE DEVALUATION FOR THE PAST TWO WEEKS HALTS/ /shanghai bourse CLOSED UP 59.89 POINTS OR 2,16% /HANG SANG CLOSED UP 169,14 POINTS OR 0.60%

2. Nikkei closed UP 169,14 POINTS OR 0.60% / /USA: YEN RISES TO 112.58/

3. Europe stocks OPENED GREEN / /USA dollar index RISES TO 94.77/Euro FALLS TO 1.1670

3b Japan 10 year bond yield: RISES TO . +.04/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 112.58/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD FINALLY IN THE POSITIVE/BANK OF JAPAN LOSING CONTROL OF THEIR YIELD CURVE AS THEY PURCHASE ALL BONDS TO GET TO ZERO RATE!!

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 70.95 and Brent: 74.14

3f Gold UP/Yen DOWN

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil DOWN for WTI and DOWN FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund RISES TO +.37%/Italian 10 yr bond yield UP to 2.68% /SPAIN 10 YR BOND YIELD UP TO 1.31%

3j Greek 10 year bond yield RISES TO : 3.87

3k Gold at $1243.20 silver at:15.83 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble UP 31/100 in roubles/dollar) 62.11

3m oil into the 70 dollar handle for WTI and 74 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 112.58 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 0.9989 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1642 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now POSITIVE territory with the 10 year RISING to +0.37%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.86% early this morning (THIS IS DEADLY TO ALL MARKETS). Thirty year rate at 2.96%

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

(courtesy Jim Reid/Bloomberg/Deutsche bank/zero hedge)

Global Stocks, US Futures Jump As Trade War

Fears Recede, Commodities Spike

The “trade war on, trade war off” market is back.

One day after global markets tumbled, and commodities suffered the biggest one day drop in 4 years, the risk on mood is back after traders detected a subtle shift in China’s rhetoric, which according to Bloomberg appeared to be toning its responses to Donald Trump’s tariff threats. Evidence of the shift continued Thursday when the Commerce Ministry held off detailing how it plans to retaliate against Trump’s latest threat to impose tariffs on $200 billion worth of Chinese-made goods.

Specifically, commerce Ministry spokesman Gao Feng said the government will take “necessary” steps to hit back, but when pressed he stopped short of repeating a previous pledge to respond with “quantitative” and “qualitative” measures and didn’t outline specifics about which measures China would retaliate with.

Perhaps China simply hasn’t decided yet how to retaliate, or simply did not want to disclose it in public, but to observers, the modest change of tone suggests China could be playing for time with the aim of restarting stalled negotiations for a solution that would limit the need to unleash punitive retaliatory measures. To be sure, for President Xi Jinping, gathering problems at home and abroad may be prompting a less confrontational course. “China may be moving gradually from the current tit-for-tat mode of retaliation toward a controlled, selective retaliation,” said Chang Jian, chief China economist at Barclays Plc in Hong Kong.

Optimism was threatened when Gao Feng rejected an earlier report that Beijing was holding backdoor negotiations with the US and said that China is not in touch with the US right now for renewing trade talks, but that was largely ignored by markets who were desperate for any positive catalyst, and latched on to news of a possible deescalation by Beijing with rabid desperation.

So, as a result of the glimmer of hope of trade war de-escalation, we are having a repeat of the Monday session and a mirror image of Wednesday, as stocks advanced globally, rebounding from yesterday’s sharp selloff, while the dollar steadied while Treasuries edged lower and commodities recovered ground.

The risk on tone started in China where the Shanghai Composite surging 2.2%, recovering the 2800 level and testing the 20-day moving average, while the tech heavy Chinext soared 3.3% to recover 1600. Chinese chipmakers and telecom companies surged after the US said it will remove the ban on Chinese telecom equipment maker ZTE.

A risk on mood sent the Yuan sharply higher, with the USDCNH sliding 0.5% to just below China’s redline of 6.69.

Sentiment from Asian session carried through into European trading. U.S. equity futures joined the broad rally and were close to yesterday’s highs..

… while European equity markets also rebounded sharply, with the Stoxx 600 rising 0.6%.

Still, not everyone was convinced: “There won’t be any winners from the trade war, and the risk is that it will have an impact on global growth, on consumer spending and will end up boosting inflation. All these elements are bad news for the equity market,” said Pictet sr. investment advisor Frederic Rollin, speaking in an interview on Wednesday.

Commodities are bouncing back strongly after yesterday’s historic rout. Brent is advancing after yesterday’s largest one-day drop in five years which was spurred on by trade concerns and increased Libyan production. WTI is up 0.8% and Brent up 1.8% but still well below the levels seen prior to yesterday’s trade, with WTI finding some support at its 100DMA, currently at USD 69.40. IEA maintain their forecast for 2018 global oil demand growth of 1.4mln BPD, say OPEC crude production in June reached a 4-month high of 31.87mln BPD, up 180k BPD (excl. Congo).

Meanwhile, in FX, Bloomberg notes that the low-volume summer trading in the spot market took over from Wednesday’s positioning adjustments, leaving the major currencies confined to relatively narrow ranges. Reports that the U.S. and China may look to resume trade talks helped keep the dollar firmly supported versus the yen following bullish technical breaks. The USD/JPY rose to a fresh 6 month high, continuing to push higher; meanwhile the SEK was weaker on CPIF miss. Emerging Markets were led higher by TRY as new treasury and finance minister – and Erdogan’s son-in-law – said the central bank will be more “active” than ever.

In rates, USTs are close to overnight lows, curve marginally flatter; bunds briefly push higher on reports that Trump is considering pulling out of NATO, however move is quickly faded after Trump announced that NATO had come to an agreement to boost spending.

Market Snapshot

- S&P 500 futures up 0.5% to 2,789.00

- STOXX Europe 600 up 0.2% to 382.25

- MXAP up 0.09% to 164.21

- MXAPJ up 0.4% to 536.58

- Nikkei up 1.2% to 22,187.96

- Topix up 0.5% to 1,709.68

- Hang Seng Index up 0.6% to 28,480.83

- Shanghai Composite up 2.2% to 2,837.66

- Sensex up 1% to 36,611.07

- Australia S&P/ASX 200 up 0.9% to 6,268.31

- Kospi up 0.2% to 2,285.06

- German 10Y yield unchanged at 0.368%

- Euro up 0.1% to $1.1686

- Italian 10Y yield rose 1.7 bps to 2.422%

- Spanish 10Y yield rose 0.6 bps to 1.31%

- Brent futures up 2.1% to $74.91/bbl

- Gold spot up 0.2% to $1,244.73

- U.S. Dollar Index little changed at 94.08

Top Overnight News

- China Ministry of Commerce: U.S. is not in touch with China in regards to renewing trade talks

- Bond traders are calling time on the Federal Reserve’s tightening cycle. The spread between December 2019 and December 2020 eurodollar contracts fell below zero Wednesday for the first time, suggesting short-end traders don’t expect the central bank to raise interest rates at all after next year. In fact, they’re giving slightly better odds that the Fed eases policy over the span instead of tightening it

- NATO: reports from DPA that Trump threatened to pull U.S. out of NATO are later refuted by Reuters citing people familiar

- BOE: 2Q defaults on unsecured lending driven by a significant increase in defaults on credit cards

- Sweden Jun CPIF y/y: 2.2% vs 2.3% est; Riksbank minutes show concerns that moderate inflation raises questions about the development of inflation in the long run

- IEA: OPEC’s Gulf members may need to pump almost as much crude as they can to cover supply losses from Iran and Venezuela

- The U.K. seeks to strike new trade deals for services around the world as part of a Brexit plan that will tie its goods to European Union rules in a bid to preserve open customs borders with the bloc

- In an unexpected twist, NATO leaders are holding an unplanned emergency session on the last day of their two-day summit, which has been upended by U.S. President Donald Trump’s attacks on allies over defense spending.

- Traders will be watching to see what Chinese policymakers do to defend the yuan after it tumbled past a key level against the dollar. The yuan sank as much as 1.1 percent in overnight offshore trading to 6.7249, its biggest loss since January 2016, as a trade conflict with the U.S. worsened

- The market probability of an Aug. 2 Bank of England rate hike stands at about 80 percent, near the levels seen in the run up to May’s meeting when Carney intervened to damp expectations.

Asian equity markets shrugged off the energy-led declines in US and traded higher across the board with short covering in the region seen after the prior day’s trade-related losses. ASX 200 (+0.9%) and Nikkei 225 (+1.2%) were positive in which the latter coat-tailed on upside in USD/JPY and with Softbank among the biggest gainers after US investment fund Tiger Global took a stake of over USD 1bln in the Co., while broad gains were also seen in Australia aside from commodity-related sectors following recent weakness in the complex including a near-5% drop in crude. Elsewhere, Hang Seng (+0.6%) and Shanghai Comp. (+2.1%) conformed to the improved risk tone after the PBoC conducted repo operations for the 1st time in over a week and amid continued positive rhetoric regarding A-shares valuations which were said to be at historic lows. Finally, 10yr JGBs were flat with price action uneventful throughout the session amid focus on riskier assets and with the 20yr auction results largely ignored, despite showing firmer demand and higher accepted prices than previous.

Top Asian News

- Special Effects Maker Plans Hong Kong IPO for China Unit

- China Studies Paying for Kids to Boost Population, Report Says

- Standard Chartered Cuts Yuan Forecasts on Trade War Concerns

- Indonesia to Sign Grasberg Mine Agreement With Freeport

European equities are currently higher with the Euro Stoxx 600 up 0.6%. Equities were slightly choppy amid source reports suggesting that US President Trump was criticising NATO and had threatened to drop out, reports thereafter suggested that pulling out is not on the cards. The IBEX (-0.2%) and FTSE MIB (-0.3%) are in the red, weighed on by bank stocks with exposure to Turkish assets (BBVA -0.7%) alongside broad-based financial underperformance (UniCredit -1.0%, Banca Generali -1.1%, CaixaBank -1.1%) and possible strike action at Fiat’s (-1.0%) Melfi plant over Cristiano Ronaldo’s transfer cost. Telecom Italia (-1.3%) is also underperforming after a price target cut at Barclays, and is weighing on the telecoms sector, which is currently negative for the day. The FTSE is outperforming on the back of betting names such as Paddy Power Betfair (+2.7%) benefitting from England’s exit from the World Cup. Updates on Sky (+1.8%) where Comcast have tabled a GBP 26bln offer to buy the co., moving swiftly to trump Fox’s GBP 24.5bln offer earlier in the week.

Top European News

- Oil Strike Hit on Norway Output Limited to One Field for Now

- U.K. Seeks to Strike Trade Deals for Services in New Brexit Plan

- Asos Plunges, Pulling Down Zalando, as 3Q Disappoints Analysts

- Inmarsat Extends Gains; Berenberg Sees Months of M&A Speculation

In FX, JPY/AUD flanked the G10 list of worst and best performers on less investor angst over a full blown US-China trade war even though the latter (via a Commerce Ministry official) has scotched speculation that the 2 sides have been talking already. Short covering also a factor behind the broad bounce in risk assets and resultant reduced demand for safe-havens like the Jpy that finally yielded to pressure below 111.00 vs the Usd, as the pair broke higher and into a fresh range overnight. Stops are said to have been tripped through 111.50 and major trend-line resistance around 111.57 that had been capping the upside, with more triggered when 112.00 was breached on the way to a circa 112.40 peak. Conversely, the Aud has been able to stem further losses and rebound ahead of 0.7350 vs its US counterpart, although the 0.7400 handle remains elusive. CHF – Mildly softer vs the Usd as the Franc slips through 0.9950, but still not really behaving like a true port in a currency storm given strict SNB intervention to prevent the highly valued Chf getting too strong

In commodities, oil is recovering this morning after the significant losses seen in yesterday’s trade that was spurred on by trade concerns and increased Libyan production. WTI is up 0.8% and Brent up 1.8% but still well below the levels seen prior to yesterday’s trade, with WTI finding some support at its 100DMA, currently at USD 69.40. IEA maintain their forecast for 2018 global oil demand growth of 1.4mln BPD, say OPEC crude production in June reached a 4-month high of 31.87mln BPD, up 180k BPD (excl. Congo) Gold prices are edging up on the back of trade war concerns, with the yellow metal currently at the USD 1,245/oz level. Copper (+0.8%) and nickel (+3.8%) are also seeing some reprieve and have edged up, with copper moving away from year-long lows. Steel has advanced to near 10-month highs as the Chinese Government intensifies efforts to cut pollution is raising supply concerns

Looking at the day ahead, all eyes on will be on the June CPI report in the US in the afternoon. Also out in the US will be the June monthly budget statement along with the latest weekly initial jobless claims data. In terms of central banks, Minneapolis Fed President Neel Kashkari will speak in a panel discussion on immigration issues and Philadelphia Fed President Patrick Harker will speak at the annual Rocky Mountain economic summit. I’ll be singing John Denver all days after hearing of that summit. Meanwhile Euro Area finance ministers are also due to meeting in Brussels to discuss the EMU.

US event calendar

- 8:30am: Initial Jobless Claims, est. 225,000, prior 231,000; Continuing Claims, est. 1.73m, prior 1.74m

- 8:30am: US CPI MoM, est. 0.2%, prior 0.2%; US CPI YoY, est. 2.9%, prior 2.8%

- US CPI Ex Food and Energy MoM, est. 0.2%, prior 0.2%; US CPI Ex Food and Energy YoY, est. 2.3%, prior 2.2%

- 9:45am: Bloomberg Consumer Comfort, prior 57.6

- 2pm: Monthly Budget Statement, est. $80.0b deficit, prior $146.8b deficit

DB’s Jim Reid concludes the overnight wrap

One of the main reasons we’re moving from our wonderful home is that it’s on a busy road and I decided that for our forever family home it was time for a little more peace and quiet. However between 7-10pm last night we had all the windows open and I’ve never known the road so quiet as everyone in the country was at home watching telly. If England could be in a perpetual World Cup semifinal there would be no need to ever move. In fact if I could have got potential buyers to only do a viewing during England games this World Cup, I could have got an extra 50% on the price. Sadly the road will be busy again on Sunday afternoon as England after being on top in the first half and 1-0 up, slowly got outplayed by Croatia. So it’s a France vs Croatia final and to rub in the hurt from last night’s loss I’ll be watching it in France where I leave for holiday tomorrow. I will make sure I barricade myself inside on Sunday afternoon. You may see me on telly next Wednesday though as the Tour de France is going past the place we stay at very close to the mountain finish in La Rosiere. We are planning to put big banners out for the cameras so keep an eye out for the church 8km from the finish as the whole family will be cheering them on up a steep uphill climb. See you in a couple of weeks. Craig and Jeff will be manning the fort until then.

A bit like England’s defence at times last night, risk assets spent most of yesterday waving the white flag following a step-up in the trade war rhetoric on Tuesday night. Indeed equities, metals and EM FX were the markets which bore the brunt of the latest developments with Brent Oil (-6.92%) also seeing the worst day since February 2016, more on Libyan supply increases (see below). In Europe the Stoxx 600 (-1.26%) snapped a run of six consecutive daily gains in style with all sectors ending lower, although metals & mining (-3.64%) and energy (-2.36%) names were particularly hard hit, while the DAX (-1.53%), FTSE MIB (-1.58%) and CAC (-1.48%) were also sharply lower. Last night the S&P 500 (-0.71%) and Dow (-0.88%) also closed in the red albeit not to the extent of those markets in Europe.

Measures of vol also crept higher although to be fair it wasn’t that aggressive with the VIX finishing less than a point higher at 13.63 and the VSTOXX 1.6pts higher at 14.60. It’s worth noting that both measures have been hovering down closer to the lows for the year recently and indeed the VIX is still 3pts or so below its YTD average and the VSTOXX 1.5pts below. So these aren’t particularly stressful times for vol in equities right now.

This morning in Asia, markets are surprisingly rebounding across the board with the Shanghai Comp. (+1.90%), Nikkei (+1.30%) and Hang Seng (+0.71%) all higher. Meanwhile futures on the S&P are c0.4% higher, Brent is up c1.5% while the Yuan is paring back bigger losses to be -0.1% lower as we type.

Back to yesterday in commodities, LME Lead, Copper, Zinc and Aluminium finished -4.89%, -2.96%, -2.55% and -1.44% respectively. The fall for Copper was the biggest since late 2017. Oil was also caught up in the selloff which didn’t help performance for stocks with WTI and Brent falling -5.03% and -6.92% respectively, although it appears that Libya’s National Oil corporation lifting oil export restrictions and boosting the global oil production by c800k barrels per day was a key factor. Finally the big movers in EM FX included the Brazilian Real (-1.61%), Russian Ruble (-1.02%) and Mexican Peso (-0.81%). The Turkish Lira (-3.59%) was the biggest faller though, with a Bloomberg headline quoting President Erdogan as saying that interest rates are to go down in the upcoming period, which heavily weighed on the currency.

By contrast credit and bond markets were a lot more muted. CDX IG for example was just 1.2bps wider while iTraxx Main and Crossover ended 1.3bps and 4.7bps wider respectively. Treasuries actually ended the day unchanged at 2.85% after trading in a smallish 3bp range while yields in core Europe were flat to half a basis lower at best.

Back to the trade spat, there was a fairly constant stream of unsurprising reactions out of China yesterday although it’s worth noting that there is still no official retaliation just yet. A WSJ story did attract some attention in the market though. The story suggested that China was now considering delaying merger approvals involving US companies along with holding up licenses for US firms and increasing inspections of US products at borders. However the story also suggested that behind the scenes, officials were more cautious and “weighing how far to press the retaliation without hurting other national interests”. Meanwhile Bloomberg noted China’s Vice Minister of Commerce Wang Shouwen has called on his US counterparts to resolve conflict through more bilateral negotiations.

Yesterday our China Chief Economist Zhiwei Zhang published a Q&A on the latest developments. Zhiwei believes that if fully implemented, the impact of the tariffs on the real economy would be 0.3% of GDP, which will likely show up mostly in 2019. Zhiwei writes that the list of $200bn of products will go through the same consultation process the $50bn list went through. The US administration’s timeline is (1) receive comments by Aug 17, (2) hold a public hearing on Aug 20, and (3) receive post-hearing comments by Aug 30. Therefore he expects the earliest time some of the products on this list are subject to the 10% tariff would be in early September. That said Zhiwei expects half or more of the products of the list will be challenged in this consultation process. In the previous round of consultation, 16bn out of the 50bn Chinese exports were removed from the list and replaced by other products. Consequently the 16bn new products are still in their consultation process and yet to turn effective. The 200bn list announced will likely be more challenged as it is much more extensive and touches many final products, including consumer goods such as refrigerators and air conditioners. You can find more in Zhiwei’s note here .