GOLD: $1239.60 DOWN $1.55 (COMEX TO COMEX CLOSINGS)

Silver: $15.80 DOWN 0 CENTS (COMEX TO COMEX CLOSINGS)

Closing access prices:

Gold $1241.00

silver: $15.80

For comex gold:

JULY/

NUMBER OF NOTICES FILED TODAY FOR JULY CONTRACT:0 NOTICE(S) FOR nil

TOTAL NOTICES SO FAR 95 FOR 9500 OZ (0.2954 tonnes)

For silver:

JUNE

9 NOTICE(S) FILED TODAY FOR

45,000 OZ/

Total number of notices filed so far this month: 5169 for 25,845,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: BID $6512/OFFER $6597: UP $374(morning)

Bitcoin: BID/ $6621/offer $6706: UP $484 (CLOSING/5 PM)

end

First Shanghai gold fix comes at 10 pm est

The second Shanghai gold fix: 2:15 pm

First Shanghai gold fix gold: 10 pm est: 1245.99

NY price at the same time: 1242.60

PREMIUM TO NY SPOT: $3.39

Second gold fix early this morning: 1245.95

USA gold at the exact same time:1245.30

PREMIUM TO NY SPOT: $0.65???

China is controlling the gold market

WE WILL NOT PROVIDE LONDON FIXES AS THEY ARE NOT ACCURATE AS TO WHAT IS GOING ON AT THE SAME TIME FRAME.

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total OPEN INTEREST ROSE BY A CONSIDERABLE SIZED 2885CONTRACTS FROM 208,079 UP TO 210,964 DESPITE FRIDAY’S RAID AND A STRONG 16 CENT LOSS IN SILVER PRICING. WE HAVE HAD SUCH CONSIDERABLE COMEX LIQUIDATION THESE PAST SEVERAL DAYS BUT NOT TODAY. HOWEVER, THIS HAS NOT MANIFESTED ITSELF INTO LOWER DEMAND FOR PHYSICAL SILVER..JUST THE OPPOSITE. WE ARE STILL WITNESSING A LARGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY(OVER 29 MILLION OZ) AS WELL AS CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A STRONG SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP: 2031EFP’S FOR SEPT. , 0 EFP’S FOR DECEMBER AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE: OF 2031 CONTRACTS. WITH THE TRANSFER OF 2031 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 2031 EFP CONTRACTS TRANSLATES INTO 10.155MILLION OZ ACCOMPANYING:

1.THE 16 CENT LOSS IN SILVER PRICEAT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR THE JUNE/2018 COMEX DELIVERY MONTH. (5.420 MILLION OZ) AND NOW JULY/ 2018 WITH 29.245 MILLION OZ INITIALLY STANDING FOR DELIVERY(SEE DATA BELOW).

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF JUNE:

17,728 CONTRACTS (FOR 10 TRADING DAYS TOTAL 17,728 CONTRACTS) OR 88.64 MILLION OZ: (AVERAGE PER DAY: 1773 CONTRACTS OR 8.865 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF JULY: 88.64 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 12.66% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2018 TO DATE SILVER EFP’S: 1,748.355 MILLION OZ.

ACCUMULATION FOR JAN 2018: 236.879 MILLION OZ

ACCUMULATION FOR FEB 2018: 244.95 MILLION OZ

ACCUMULATION FOR MARCH 2018: 236.67 MILLION OZ

ACCUMULATION FOR APRIL 2018: 385.75 MILLION OZ

ACCUMULATION FOR MAY 2018: 210.05 MILLION OZ

ACCUMULATION FOR JUNE 2018: 345.43 MILLION OZ

RESULT: WE HAD A STRONG SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 2,885 DESPITE THE RAID AND THE CONSIDERABLE 16 CENT FALL IN SILVER PRICE. THE CME NOTIFIED US THAT WE HAD A STRONG SIZED EFP ISSUANCE OF 2031 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) . FROM THE CME DATA: 2031EFP’S FOR SEPT, 0 EFP’S FOR DECEMBER AND ZERO FOR ALL OVER MONTHS FOR A DELIVERABLE FORWARD CONTRACT OVER IN LONDON WITH A FIAT BONUS (TOTAL: 2031). TODAY WE GAINED A STRONG SIZED: 4916TOTAL OI CONTRACTS ON THE TWO EXCHANGES:

i.e 2031 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH AN INCREASE OF 2992 OI COMEX CONTRACTS. AND ALL OF THIS DEMAND HAPPENED WITH A 16 CENT FALL IN PRICE OF SILVER AND A CLOSING PRICE OF $15.80 WITH RESPECT TO FRIDAY’S TRADING. YET WE STILL HAVE A GIGANTIC AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY IN THIS ACTIVE JULY DELIVERY MONTH OF MORE THAN 29 MILLION OZ. IT SURE LOOKS LIKE ANOTHER FAILED BANKER SHORT COVERING EXERCISE AS BANKERS ARE SCRAMBLING TO COVER THEIR HUGE SHORTFALL.

In ounces AT THE COMEX, the OI is still represented by OVER 1 BILLION oz i.e. 1.055 MILLION OZ TO BE EXACT or 151% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT JULY MONTH/ THEY FILED AT THE COMEX: 9 NOTICE(S) FOR 45,000 OZ OF SILVER

IN SILVER, WE SET THE NEW RECORD OF OPEN INTEREST AT 243,411 CONTRACTS ON APRIL 9.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $16.51

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) AND NOW JULY 2018 AMOUNT INITIALLY STANDING: 29.245 MILLION OZ )

- HUGE RECORD OPEN INTEREST IN SILVER 243,411 CONTRACTS (OR 1.217 BILLION OZ/ SET APRIL 9/2018

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017

- RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT).

In gold, the open interest ROSE BY A HUMONGOUS SIZED11,426CONTRACTS UP TO 522,194 DESPITE THE RAID AND FALL IN THE COMEX GOLD PRICE/FRIDAY’S TRADING(A LOSS IN PRICE OF $5.35). WE ARE NOW IN THE ACTIVE DELIVERY MONTH OF JULY. NO DOUBT THE BOYS ARE CASHING IN THEIR COMEX LONGS TO BEGIN THE PROCESS TO MOVE INTO LONDON FORWARDS. THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A CONSIDERABLE SIZED 7546 CONTRACTS : AUGUST SAW THE ISSUANCE OF: 7416 CONTRACTS, DECEMBER HAD AN ISSUANCE OF 130 CONTACTS AND THEN ALL OTHER MONTHS ZERO. The new COMEX OI for the gold complex rests at 522,194. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE AN ATMOSPHERIC OI GAIN IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 21,208 CONTRACTS: 11,426OI CONTRACTS INCREASED AT THE COMEX AND 7546 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN: 18,972 CONTRACTS OR 1,897,200 OZ = 58.38 TONNES. AND THIS IS MIND BOGGLING: ALL OF THIS HUGE DEMAND OCCURRED WITH THE RAID AND FALL IN THE PRICE OF GOLD/ FRIDAY TO THE TUNE OF $5.35???. GIVE ME A BREAK!!

YESTERDAY, WE HAD 4777 EFP’S ISSUED.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF JUNE : 78,393 CONTRACTS OR 7,839,300 OZ OR 243.83 TONNES (10 TRADING DAYS AND THUS AVERAGING: 7839 EFP CONTRACTS PER TRADING DAY OR 783,900 OZ/ TRADING DAY),,

TO GIVE YOU AN IDEA AS TO THE HUGE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 10 TRADING DAYS IN TONNES: 243.83 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2017, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 2555 TONNES

THUS EFP TRANSFERS REPRESENTS 243.83/2550 x 100% TONNES = 9.56% OF GLOBAL ANNUAL PRODUCTION SO FAR IN JULY ALONE.***

ACCUMULATION OF GOLD EFP’S YEAR 2018 TO DATE: 4,346.70* TONNES *SURPASSED ANNUAL PROD’N

ACCUMULATION OF GOLD EFP’S FOR JANUARY 2018: 653.22 TONNES (21 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR FEBRUARY 2018: 649.45 TONNES (20 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR MARCH 2018: 741.89 TONNES (22 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR APRIL 2018: 713.84 TONNES (21 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR MAY 2018: 693.80 TONNES ( 22 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR JUNE 2018 650.71 TONNES (21 TRADING DAYS)

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A HUMONGOUS SIZED INCREASE IN OI AT THE COMEX OF 13,662 DESPITE THE $5,35 LOSS IN PRICING GOLD UNDER UNDERTOOK ON FRIDAY // . WE ALSO HAD AN CONSIDERABLE SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 7546 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 7,546 EFP CONTRACTS ISSUED, WE HAD AN ATMOSPHERIC NET GAIN OF 21,208 CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

7546 CONTRACTS MOVE TO LONDON AND 11,426 CONTRACTS INCREASED AT THE COMEX. (in tonnes, the GAIN in total oi equates to 58.38 TONNES). ..AND BELIEVE IT OR NOT AND THIS IS MIND BOGGLING: ALL OF THIS DEMAND OCCURRED WITH A LOSS OF $5.35 IN FRIDAY TRADING AT THE COMEX!!!. THE COMEX IS AN OUTRIGHT FRAUD

we had: 0notice(s) filed upon for NILoz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD...

WITH GOLD DOWN $1.55 TODAY: /

NO CHANGES IN GOLD INVENTORY AT THE GLD:

/GLD INVENTORY 795.19 TONNES

Inventory rests tonight: 795.19 tonnes.

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

SLV/

WITH SILVER FLAT TODAY :

A HUGE CHANGE IN SILVER INVENTORY AT THE SLV, A DEPOSIT OF 1.128 MILLION OZ

/INVENTORY RESTS AT 327.880 MILLION OZ/

NOTE THE DIFFERENCE BETWEEN THE GLD AND SLV: THE CROOKS CAN RAID GOLD BECAUSE THEY DO HAVE SOME PHYSICAL. THEY DO NOT RAID SILVER PROBABLY BECAUSE THERE IS NO REAL SILVER INVENTORIES BEHIND THEM

end

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER ROSE BY A CONSIDERABLE SIZED 2885CONTRACTS from 208,079 UP TO 210,964 (AND CLOSER TO THE NEW COMEX RECORD SET /APRIL 9/2017 AT 243,411/SILVER PRICE AT THAT DAY: $16.53). THE PREVIOUS RECORD OTHER THAN WAS ESTABLISHED AT: 234,787, SET ON APRIL 21.2017 OVER ONE YEAR AGO. THE PRICE OF SILVER ON THAT DAY: $17.89. OUR CUSTOMARY MIGRATION OF COMEX LONGS MORPH INTO LONDON FORWARDS CONTINUES AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

2031 EFP CONTRACTS FOR SEPT., 0 EFP CONTRACTS FOR DECEMBER AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 2031 CONTRACTS . EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI GAIN AT THE COMEX OF 2992CONTRACTS TO THE 2031 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A NET GAIN OF 4916 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES: 24.58 MILLION OZ!!! AND YET WE ALSO HAVE A STRONG DEMAND FOR PHYSICAL AS WE WITNESS AN INITIAL STANDING OF OVER 29 MILLION OZ AND YET ALL OF THIS DEMAND OCCURRED DESPITE A CONSIDERABLE 16 CENT LOSS IN PRICE???.

IT SURE LOOKS LIKE WE ARE GETTING SOME COVERING FROM THE BANKERS SIDE ESPECIALLY WHEN YOU SEE A GOOD GAIN IN PRICE AND THEN A FALL IN COMEX OI AND A SMALLER THAN EXPECTED EFP ISSUANCE.

RESULT: A STRONG SIZED INCREASE IN SILVER OI AT THE COMEX DESPITE THE 16 CENT LOSSTHAT SILVER UNDERTOOK IN PRICING ON TUESDAY. BUT WE ALSO HAD ANOTHER FAIR SIZED 2031 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR JULY, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON AS WELL AS THE STRONG AMOUNT OF PHYSICAL STANDING FOR METAL AT THE COMEX.

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)MONDAY MORNING/SUNDAY NIGHT: Shanghai closed DOWN 17.14 POINTS OR 0.61% /Hang Sang CLOSED UP 14.22 POINTS OR 0.05%/ / The Nikkei closed HOLIDAY/Australia’s all ordinaires CLOSED DOWN 0.40% /Chinese yuan (ONSHORE) closed UP at 6.6755 AS POBC HALTS ITS HUGE DEVALUATION /Oil DOWN to 69.84 dollars per barrel for WTI and 73.73 for Brent. Stocks in Europe OPENED RED EXCEPT GERMANY //. ONSHORE YUAN CLOSED UP AT 6.6755 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.6889:HUGE DEVALUATION/PAST SEVERAL DAYS HALTS : TARIFF WARS STILL CONTINUE UNABATED AND AT FULL TILT//ONSHORE YUAN TRADING STRONGER AGAINST OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING STRONGER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED/

/NORTH KOREA/SOUTH KOREA

i)North Korea/South Korea/USA/Russia

b) REPORT ON JAPAN

3 c CHINA

i)China is slowing down as evidence shows their huge shadow banking lending unexpectedly plummets. As we have been pointing out to you for quite a while; China is slowing down.

Two commentaries

( zerohedge)

ii)The truth behind what China actually makes in I Phone manufacturing: only $8.46. This should explain why trade wars are futile!

4. EUROPEAN AFFAIRS

i)GREECE

The truth behind the “rescue” of Greece. Engdahl describes how the supposed bailout will no doubt cause tremendous grief to Greek citizens for years to come

( William Engdahl)

ii)UK

The advise of Trump to May: sue the EU

( zerohedge)

Trouble again in Italy as this country blocks the entry of 450 migrants as a new Mediterranean crisis unfolds

( zerohedge)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

i)A good commentary explaining why the Neocons are nervous as Trump may pull out of Syria.

a must read…/

( zerohedge)

( zerohedge)

iii)Turkey

Mish outlines Turkey’s path towards hyperinflation

(courtesy Mish Shedlock/Mishtalk)

6 .GLOBAL ISSUES

i)A good article explaining why NATO is totally useless

( Tom Luongo)_

( zerohedge)

iii)The IMF warns of a sudden repricing of assets due to the trade wars and economic slowdown

(courtesy zerohedge)

7. OIL ISSUES

As we have pointed out to you on several occasions, we are witnessing some events signaling the de- dollarization of the world. Today, Chinese refiners are placing USA imports of oil with Iranian crude. This is a dagger into the heart of USA hegemony

( FinancialTribune.com)

8. EMERGING MARKET

9. PHYSICAL MARKETS

i)The following needs no special introduction: it is self explanatory

a must read..

( Chris Powell/GATA)

ii)As indicated to you on several occasions, it is China that is controlling the gold price, not USA authorities

(courtesy David Brady/Sprott/GATA)

iii)This is good: June sees no change in BIS gold intervention. Whenever we witness raids you can bet the BIS is there lending gold to the criminals

(courtesy Lambourne/GATA)

10. USA stories which will influence the price of gold/silver)

i)MARKET TRADING/EARLY MORNING

This ought to frighten global trading: The USA launches a WTO challenge against 5 nations with respect to the latest tariffs initiated by the following countries:

Canada, Mexico Europe, China and Turkey

( zerohedge)

a)Finally we are witnessing a slowdown in retail sales due to the huge debt overhang on consumers

( zerohedge)

iv)SWAMP STORIES

a)The fun begins: The Republicans are now planning to impeach Rosenstein. They may also hold him in contempt of Congress which is a federal crime. However we still have a long way to go on this. It would be far better for Trump to just declassify the documents and let the public see for themselves

( zerohedge)

b)Saturday: Trump responds to the Russian indictment by correctly asking: where is the DNC server? and why did Obama do nothing

( zerohedge)

c)Wow!! this is surely a biggy! We learn the following:

d)Kim Strassel and the entire Wall Street Journal are now asking that Trump declassify certain documents outlined below. Some suggest that the reason the President does not declassify yet is because the pundits will argue that it will undermine Mueller’s investigation into Russian collusion. However it is important for the American public to understand the truth and it is clear that Justice and the FBI will not hand over documents. Thus in balance, Trump must declassify

e)A great outline of the crime committed by Clinton and family with regard to the Uranium One debacle(courtesy Greg Hunter/USAWatchdog)

f)This is getting totally out of hand: Federal prosecutors charge a Russian national, living in the uSA as being a Russian agent and conspiring to act as an agent of the Russian Federation. She was arrested trying to set up “back channels” of communication between Trump and Putin

Trading Volumes on the COMEX

PRELIMINARY COMEX VOLUME FOR TODAY: 190,678 contracts

CONFIRMED COMEX VOL. FOR YESTERDAY: 313,489 CONTRACTS

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

And now for the wild silver comex results.

Total silver OI ROSE BY A STRONG SIZED 2885 CONTRACTS FROM 208,079 UP TO 210,964 (AND A LITTLE CLOSER TO THE THE NEW RECORD OI FOR SILVER SET APRIL 9.2018/ 243,411 CONTRACTS) DESPITE THE RAID AND CONSIDERABLE 16 CENT FALL IN SILVER PRICING/ FRIDAY. SINCE WE ARE NOW INTO THE ACTIVE DELIVERY MONTH OF JULY, WE WERE INFORMED THAT WE STRONG SIZED 2031 EFP CONTRACTS FOR SEPT., 0 EFP CONTRACTS FOR DECEMBER AND ZERO FOR ALL OTHER MONTHS. THESE EFPS WERE ISSUED TO COMEX LONGS WHO RECEIVED A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. THE TOTAL EFP’S ISSUED: 2031. ON A NET BASIS WE GAINED 4916 SILVER OPEN INTEREST CONTRACTS AS WE OBTAINED A 2885 CONTRACT GAIN AT THE COMEX COMBINING WITH THE ADDITION OF 2031 OI CONTRACTS NAVIGATING OVER TO LONDON.

NET GAIN ON THE TWO EXCHANGES: 4916 CONTRACTS

AMOUNT STANDING FOR SILVER AT THE COMEX

We are now in the active delivery month of JULY and here the front month fell by 5 contacts to stand at 689 contracts. We had 12 notices filed yesterday so we continue where we left off yesterday as guys refuse to take any more silver ETF’s and instead seek physical delivery at the comex. We gained 7 contracts or an additional 35,000 oz of silver will stand at the comex.

The next delivery month, after July is the non active delivery month of August and here we gained 5 contracts to stand at 1183. The next active delivery month after August for silver is September and here the OI ROSE by 262 contracts UP to 154,232

We had 9 notice(s) filed for 45,000 OZ for the JULY 2018 COMEX contract for silver

FROM LAST YEARS DATA, ON FIRST DATE NOTICE FOR THE JULY 2017 SILVER COMEX DELIVERY MONTH WE HAD 12.115 MILLION OZ OF SILVER STANDING FOR DELIVERY. AT MONTH’S END WE HAD 16.435 MILLION OZ EVENTUALLY STAND AS WE ALREADY HAD QUEUE JUMPING BEGIN IN EARNEST FROM APRIL 2017 ONWARD EVEN TO TODAY. SO WITH TODAY’S NUMBERS WE SURPASSED LAST YEAR’S LEVEL BY A WIDE MARGIN.

AND NOW COMPARISON VS AUGUST LAST YR:

ON FIRST DAY NOTICE JULY 31/2017: 1,965,000 OZ STOOD FOR DELIVERY

THE FINAL AMOUNT OF SILVER STANDING: AUGUST 30.2017: 6,245,000 OZ AS WE HAD CONSIDERABLE QUEUE JUMPING.

FOR THE AUGUST CONTRACT MONTH:

LAST YEAR AT THIS TIME JULY 17.2017 WE HAD 494 SILVER COMEX OI OUTSTANDING VS TODAY: 689

SO, AS IN GOLD, WE ARE GOING TO HAVE A CONSIDERABLY LARGER AMOUNT OF SILVER STANDING FOR THE NON ACTIVE CONTRACT MONTH OF AUGUST.

INITIAL standings for JULY/GOLD

JULY 16/2018.

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz |

nil OZ

|

| Deposits to the Dealer Inventory in oz | NIL oz |

| Deposits to the Customer Inventory, in oz | nil

oz |

| No of oz served (contracts) today |

0 notice(s)

NIL OZ

|

| No of oz to be served (notices) |

144 contracts

(14400 oz)

|

| Total monthly oz gold served (contracts) so far this month |

95 notices

9500 OZ

.2954TONNES

|

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

For JULY:

Today, 0 notice(s) were issued from JPMorgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equates to 0 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped/ Received) by j.P.Morgan customer account.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

To calculate the INITIAL total number of gold ounces standing for the JULY. contract month, we take the total number of notices filed so far for the month (95) x 100 oz or 9300 oz, to which we add the difference between the open interest for the front month of JULY. (144 contracts) minus the number of notices served upon today (0 x 100 oz per contract) equals 23,900 oz,(.7433 tonnes) the number of ounces standing in this non active month of JULY

Thus the INITIAL standings for gold for the JULY contract month:

No of notices served (95 x 100 oz) + {(144)OI for the front month minus the number of notices served upon today (0 x 100 oz )which equals 23,900 oz standing in this NON – active delivery month of JULY .

We GAINED 0 contracts or an additional NIL oz will stand for comex delivery.

THERE ARE ONLY 7.4588 TONNES OF REGISTERED COMEX GOLD AVAILABLE FOR DELIVERY AGAINST 0.7433 TONNES STANDING FOR JULY

IN THE LAST 24 MONTHS 85 NET TONNES HAS LEFT THE COMEX.

end

And now for silver

AND NOW THE APRIL DELIVERY MONTH

JULY INITIAL standings/SILVER

| Silver | Ounces |

| Withdrawals from Dealers Inventory | nil oz |

| Withdrawals from Customer Inventory |

120,352,480 oz

Scotia

|

| Deposits to the Dealer Inventory |

nil

oz

|

| Deposits to the Customer Inventory |

nil

oz

|

| No of oz served today (contracts) |

9

CONTRACT(S)

(45,000 OZ)

|

| No of oz to be served (notices) |

680 contracts

(3,400,000 oz)

|

| Total monthly oz silver served (contracts) | 5169 contracts

(25,845,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

we had 0 inventory movement at the dealer side of things

total dealer deposits: nil oz

total dealer withdrawals: nil oz

we had 0 deposit into the customer account

i) Into JPMorgan: nil oz

*** JPMorgan for most of 2017 and in 2018 has adding to its inventory almost every single day.

JPMorgan now has 141 million oz of total silver inventory or 52.0% of all official comex silver. (141 million/270 million)

ii) into everybody else: nil oz

total customer deposits today: nil oz

we had 1 withdrawals from the customer account;

i) Out of Scotia:: 120,352.480 oz

total withdrawals: 120,352.480 oz

we had 0 adjustments/

total dealer silver: 77.712 million

total dealer + customer silver: 280.338 million oz

The total number of notices filed today for the JULY. contract month is represented by 9 contract(s) FOR 45,000 oz. To calculate the number of silver ounces that will stand for delivery in JULY., we take the total number of notices filed for the month so far at 5169 x 5,000 oz = 25,845,000 oz to which we add the difference between the open interest for the front month of JULY. (689) and the number of notices served upon today (9 x 5000 oz) equals the number of ounces standing.

.

Thus the INITIAL standings for silver for the JULY/2018 contract month: 5169(notices served so far)x 5000 oz + OI for front month of JULY(689) -number of notices served upon today (9)x 5000 oz equals 29,245,000 oz of silver standing for the JULY contract month

WE GAINED 7 CONTRACTS OR AN ADDITIONAL 35,000 OZ WILL STAND AS THESE GUYS REFUSE TO MORPH INTO LONDON BASED FORWARDS AND RECEIVE A FIAT SWEETENER FOR THEIR EFFORTS.

PLEASE NOTE THE FOLLOWING FOR COMPARISON PURPOSES:

THE INITIAL STANDING FOR SILVER AT THE COMEX JULY 2017: 12.115 MILLION OZ ALTHOUGH AT MONTH’S END: 16.435 MILLION OZ STOOD FOR DELIVERY. THIS COMPARES WITH TODAY’S INITIAL STANDING FOR SILVER OF 29.245 MILLION OZ.

As I stated all this month of July:

“WHEN WE WITNESS THE AMOUNT OF PHYSICAL INCREASE IN THE AMOUNT STANDING AT THE COMEX AND ESPECIALLY COMMENCING ON DAY 2 OF THE DELIVERY CYCLE, YOU CAN BET THE FARM THAT THIS AMOUNT WILL INCREASE FROM THIS DAY FORTH UNTIL THE CONCLUSION OF THE MONTH OF JULY. THIS IS KNOWN AS QUEUE JUMPING AND THIS PHENOMENON HAS BEEN FRONT AND CENTRE OF OPERATIONS IN SILVER FOR NOW OVER 14 MONTHS. SILVER IS BEING SOUGHT BY COMMERCIALS OVER ON THIS SIDE OF THE POND AS DWINDLING SUPPLIES VACATE THE GLOBAL ARENA.”

queue jumping continues to intensify to the highest degree in silver as dealers scrounge around for dwindling supplies.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

ESTIMATED VOLUME FOR TODAY: 47,036 CONTRACTS

CONFIRMED VOLUME FOR YESTERDAY: 83,891 CONTRACTS absolutely criminal

YESTERDAY’S CONFIRMED VOLUME OF 83,891 CONTRACTS EQUATES TO 419 million OZ OR 59.9% OF ANNUAL GLOBAL PRODUCTION OF SILVER

COMMODITY LAW SUGGESTS THAT OPEN INTEREST SHOULD NOT BE MORE THAN 3% OF ANNUAL GLOBAL PRODUCTION. THE CROOKS ARE SUPPLYING MASSIVE PAPER TRYING TO KEEP SILVER IN CHECK.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price at that day at $18.42

The previous record was 224,540 contracts with the price at that time of $20.44

end

NPV for Sprott

1. Sprott silver fund (PSLV): NAV FALLS TO -3.14% (JULY 16/2018)

2. Sprott gold fund (PHYS): premium to NAV FALLS TO -0.60% to NAV (JULY 16/2018 )

Note: Sprott silver trust back into NEGATIVE territory at -3.14%-/Sprott physical gold trust is back into NEGATIVE/

(courtesy Sprott/GATA)

3.SPROTT CEF.A FUND (FORMERLY CENTRAL FUND OF CANADA):

NAV 12.88/TRADING 12.38//DISCOUNT 3.78.

END

And now the Gold inventory at the GLD/

JULY 16/WITH GOLD DOWN $1.55/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 795.19 TONNES

JULY 13/WITH GOLD DOWN $5.35 THE CROOKS RAID THE COOKIE JAR AGAIN TO THE TUNE OF 3.83 TONNES/INVENTORY RESTS AT 795.19 TONNES

JULY 12/WITH GOLD UP $2.30: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 799.02 TONNES

JULY 11/WITH GOLD DOWN $10.75 THE CROOKS RAIDED THE COOKIE JAR AGAIN TO THE TUNE OF 1.75 TONNES/INVENTORY RESTS AT 799.02 TONNES

JULY 10/WITH GOLD DOWN $3.85: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 800.77 TONNES

july 9/WITH GOLD UP $4.00/ANOTHER RAID ON THE GOLD COOKIE JAR: TWO WITHDRAWALS OF 1.18 TONNES THIS MORNING AND 1.47 TONNES THIS AFTERNOON/INVENTORY RESTS AT 800.77 TONNES

JULY 6/WITH GOLD DOWN $2.45: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 803.42 TONNES

JULY 5/WITH GOLD UP ANOTHER $5.15, THE CROOKS RAIDED THE COOKIE JAR AGAIN TO THE TUNE OF 5.89 TONNES/INVENTORY RESTS AT 803.42 TONNES IN THE LAST 10 TRADING DAYS GLD HAS LOST A HUGE 25.34 TONNES WITH A LOSS OF ONLY $15.25 IN PRICE

July 3/WITH GOLD UP $11.15/THE CROOKS RAIDED THE GLD INVENTORY AGAIN TO THE TUNE OF 9.73 TONNES/INVENTORY RESTS AT 809.31 TONNES

JULY 2/WITH GOLD DOWN $12.15, THE CROOKS RAIDED THE GLD INVENTORY AGAIN BY 1.47 TONNES DOWN./INVENTORY RESTS AT 819.04 TONNES

JUNE 29/WITH GOLD UP $3.70/A WITHDRAWAL OF 1.18 TONNES OF GOLD FROM THE GLD/INVENTORY RESTS AT 820.51 TONNES

JUNE 28/WITH GOLD DOWN $5.15/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 821.69 TONNES

June 27/WITH GOLD DOWN $3.60// TWO ENTRIES:/STRANGELY THE CROOKS RETURNED THE WITHDRAWAL OF 4.42 TONNES LAST NIGHT (THUS WE HAD A DEPOSIT OF 4.42 TONNES/INVENTORY RESTS AT 824.63 TONNES. /THEN LATE THIS AFTERNOON A WITHDRAWAL OF 2.94 TONNES

INVENTORY RESTS AT 821.69 TONNES/THIS VEHICLE IS AN OUTRIGHT FRAUD.

june 26/LATE LAST NIGHT, WITH GOLD DOWN $9.10 WE HAD A HUGE WITHDRAWAL OF 4.42 TONNES OF GOLD/INVENTORY RESTS AT 820.21 TONES

JUNE 25/WITH GOLD DOWN $1.45/NO CHANGE IN GOLD INVENTORY AT THE GLD.INVENTORY RESTS AT 824.63 TONNES

JUNE 22/WITH GOLD UP 25 CENTS TODAY, THE CROOKS WITHDREW A MASSIVE 4.13 TONNES OF GOLD/INVENTORY RESTS AT 824.63 TONNES

JUNE 21/WITH GOLD DOWN $4.00/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 828.76 TONNES

JUNE 20/WITH GOLD DOWN $3.55/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 828.76 TONNES

JUNE 19/WITH GOLD DOWN $1.50/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 828.76 TONES

JUNE 18/WITH GOLD UP $1.90/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 828.76 TONNES

JUNE 15/WITH GOLD DOWN $28.90/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 828.76 TONNES

JUNE 14/WITH GOLD UP $7.10/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 828.76 TONNES/

JUNE 13/WITH GOLD UP $2.20/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 828.76 TONNES

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

JULY 16/2018/ Inventory rests tonight at 795.19 tonnes

*IN LAST 411 TRADING DAYS: 131.62 NET TONNES HAVE BEEN REMOVED FROM THE GLD

*LAST 361 TRADING DAYS: A NET 24,92 TONNES HAVE NOW BEEN ADDED INTO GLD INVENTORY.

end

Now the SLV Inventory/

JULY 16/WITH SILVER FLAT TODAY, A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.128 MILLION OZ//INVENTORY RESTS AT 827.880 MILLION OZ

JULY 13/WITH SILVER DOWN 16 CENTS TODAY/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 826.752 MILLION OZ.

JULY 12/WITH SILVER UP 12 CENTS TODAY: ANOTHER BIG CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.035 MILLION OZ/INVENTORY RESTS AT 826.752 MILLION OZ/

JULY 11/WITH SILVER DOWN 22 CENTS TODAY: ANOTHER HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 565,000/INVENTORY RESTS AT 825.717 MILLION OZ

JULY 10/WITH SILVER DOWN 3 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 825.151 MILLION OZ

july 9/WITH SILVER UP 5 CENTS: ANOTHER BIG CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 847,000 OZ ADDED TO INVENTORY/INVENTORY RESTS AT 825.151 MILLION OZ/

JULY 6/WITH SILVER DOWN 2 CENTS/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 824.305 MILLION OZ/

JULY 5/WITH SILVER UP 6 CENTS, A GOOD CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 470,000 OZ/INVENTORY RESTS AT 324.305 MILLION OZ/ FOR THE PAST 10 TRADING DAYS, SILVER INVENTORY HAS ADVANCED BY 4.945 MILLION OZ WITH A LOSS OF 33 CENTS/PLEASE COMPARE THIS WITH THE GLD.

JULY 3/WITH SILVER UP 17 CENTS, A HUGE DEPOSIT OF 1.37 MILLION OZ ADDED TO THE SLV/INVENTORY RESTS AT 323.835 MILLION OZ.

JULY 2/WITH SILVER DOWN 31 CENTS/A HUGE 2.070 MILLION OZ DEPOSIT AT THE SLV/INVENTORY RESTS AT 322.465 MILLION OZ/

JUNE 29/WITH SILVER UP 14 CENTS TODAY, NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS THIS WEEKEND AT 320.395 MILLION OZ/

JUNE 28/WITH SILVER DOWN 18 CENTS, THE CROOKS ADDED 1.035 MILLION OZ OF SILVER INTO THE SLV/INVENTORY RESTS AT 320.395 MILLION OZ

JUNE 27.2018/WITH SILVER DOWN 8 CENTS/NO CHANGE IN SILVER INVENTORY/INVENTORY RESTS AT 819.360 MILLION OZ/

june 26./2018/WITH SILVER DOWN 8 CENTS, THE CROOKS WITHDREW THE DEPOSIT OF TWO DAYS AGO; 941,000 OZ OUT OF INVENTORY/INVENTORY RESTS AT 819.360 OZ

JUNE 25/WITH SILVER DOWN 12 CENTS/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 320.301 MILLION OZ/

JUNE 22/WITH SILVER UP 12 CENTS TODAY,ANOTHER BIG CHANGE IN SILVER INVENTORY AT THE SLV” A DEPOSIT OF 941,000 OZ INTO INVENTORY/INVENTORY RESTS THIS WEEKEND AT 320.301 MILLION OZ/

JUNE 21/WITH SILVER UP ONE CENT/ANOTHER CHANGE IN SILVER INVENTORY AT THE SLV/: A DEPOSIT OF 2.918 MILLION OZ/INVENTORY RESTS AT 319.360 MILLION OZ/ THUS FOR TWO STRAIGHT DAYS A TOTAL OF 5.26 MILLION OZ OF SILVER HAS BEEN ADDED WITH NO CHANGE IN PRICE.

JUNE 20/WITH SILVER DOWN ONE CENT/A HUGE CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY / A DEPOSIT OF 2.35 MILLION OZ/INVENTORY RESTS AT 316.442 MILLION OZ/

JUNE 19/2018/WITH SILVER DOWN 11 CENTS/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 314.090 MILLION OZ/

JUNE 18/WITH SILVER DOWN 6 CENTS TODAY/NO CHANGE IN SILVER INVENTORY/INVENTORY RESTS AT 314.090 MILLION OZ/

JUNE 15/WITH SILVER DOWN 75 CENTS/A BIG CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.788 MILLION OZ//INVENTORY RESTS AT 314.090 MILLION OZ

JUNE 14/WITH SILVER UP 30 CENTS, THE CROOKS DECIDED THAT THEY NEEDED SILVER INVENTORY BADLY SO THEY RAID THE SLV OF 1.412 MILLION OZ/INVENTORY RESTS AT 315.878 MILLION OZ/

JUNE 13/WITH SILVER UP 11 CENTS TODAY/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 317.290 MILLION OZ/

JULY 16/2018:

Inventory 327.880 MILLION OZ

6 Month MM GOFO 1.99/ and libor 6 month duration 2.52

Indicative gold forward offer rate for a 6 month duration/calculation:

G0FO+ 1.99%

libor 2.52 FOR 6 MONTHS/

GOLD LENDING RATE: .53%

XXXXXXXX

12 Month MM GOFO

+ 2.79%

LIBOR FOR 12 MONTH DURATION: 2.48

GOFO = LIBOR – GOLD LENDING RATE

GOLD LENDING RATE = +.31

end

Major gold/silver trading /commentaries for MONDAY

GOLDCORE/BLOG/MARK O’BYRNE.

Trump and Russian, German, Chinese and Asian

Demand For Gold

Related Content

U.S. China Trade War Escalates as Russia and China Accumulate Gold

Russia Buys 600,000 oz Of Gold In May After Dumping Half Of US Treasuries In April

https://www.youtube.com/watch?v=iBJ3IDVsFT8&t=7s

News and Commentary

Gold prices edge up from 7-month low (Reuters.com)

Gold bid in Asia, attempts break above 50-hour MA (FXStreet.com)

Consumer sentiment hits six-month low on ‘darkening cloud’ of tariffs (CNBC.com)

Gold buying picks up in India on low prices (Reuters.com)

South African Gold Output Falls Most Since February 2017 in May (Bloomberg.com)

India’s Gold Bars Imports Skyrocketed 260% in Q1 (ScrapMonster.com)

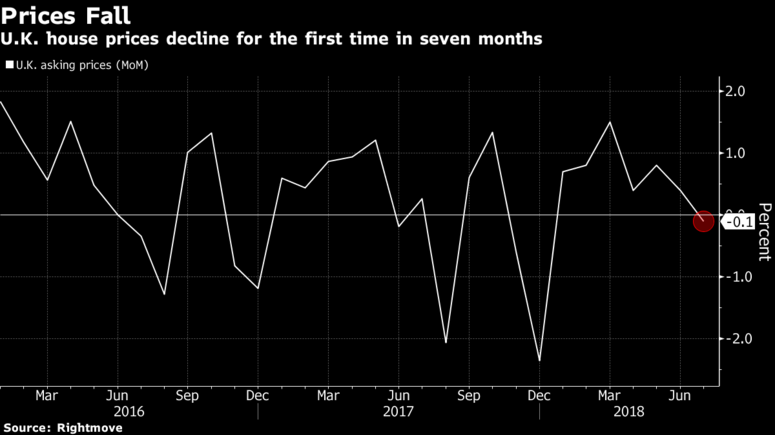

U.K. House Prices Fall as London Decline Intensifies (Bloomberg.com)

Source: Bloomberg

Get ready for a US “wage explosion” (MoneyWeek.com)

Debt Train Will Crash (MauldinEconomics.com)

CHINA takes control of GOLD from the COMEX (GoldSeek.com)

Gold Standard Requirements And Currency Crisis (GoldSeek.com)

US Housing Bubble Enters Stage Two (DollarCollapse.com)

Gold-Stock and Gold Summer Lows (SeekingAlpha.com)

Listen on SoundCloud , Blubrry & iTunes. Watch on YouTube below

Gold Prices (LBMA AM)

13 Jul: USD 1,240.50, GBP 945.14 & EUR 1,066.83 per ounce

12 Jul: USD 1,244.85, GBP 942.10 & EUR 1,065.97 per ounce

11 Jul: USD 1,250.00, GBP 943.63 & EUR 1,068.38 per ounce

10 Jul: USD 1,253.70, GBP 946.17 & EUR 1,069.41 per ounce

09 Jul: USD 1,262.60, GBP 946.95 & EUR 1,072.70 per ounce

06 Jul: USD 1,254.20, GBP 947.55 & EUR 1,071.09 per ounce

05 Jul: USD 1,252.50, GBP 946.89 & EUR 1,071.64 per ounce

Silver Prices (LBMA)

13 Jul: USD 15.81, GBP 12.04 & EUR 13.60 per ounce

12 Jul: USD 15.84, GBP 12.00 & EUR 13.58 per ounce

11 Jul: USD 15.92, GBP 12.02 & EUR 13.59 per ounce

10 Jul: USD 15.93, GBP 12.04 & EUR 13.61 per ounce

09 Jul: USD 16.21, GBP 12.15 & EUR 13.76 per ounce

06 Jul: USD 16.00, GBP 12.09 & EUR 13.66 per ounce

05 Jul: USD 15.95, GBP 12.04 & EUR 13.65 per ounce

Recent Market Updates

– Trump Is Serious About A Global Trade War

– Ponzi Economy Will Lead To Next Global Financial Crisis

– World Cup Is 200 Ounces Of Gold Worth £140,000 – 30% Less Than Harry Kane’s Weekly Wage

– Chaotic BREXIT More Likely: Risk To London, While Frankfurt, Luxembourg, Paris and Dublin Benefit

– VIDEO: Italy €2.4 Trillion Debt To Create Eurozone Contagion and Global Debt Crisis?

– U.S. China Trade War Escalates as Russia and China Accumulate Gold

– Irish Gold Money Rings Found – Mystery Surrounds What May Be Ancient, Pre-Historic Currency

– Gold $10,000 In Currency Reset? Russia, China Gold Demand To Overwhelm Gold Futures Manipulation (GOLDCORE VIDEO)

– Italian Debt – A Financial Disaster Waiting To Happen

– As The Currency Reset Begins – Get Gold As It Is “Where The Whole World Is Heading”

– Buy Gold Or Bitcoin As The “Liquidity Party” Is Ending?

– Why Russia and Turkey Diversifying Into Gold May Signal A Bigger Global Shift

– London House Prices Fall 1.9% In Quarter – Bubble Bursting?

– Gold Exports To London From U.S. Surge 152% In 2018

ANDREW MAGUIRE’S KINESIS WHICH IS A”BITCOIN’ BACKED 100% BY ALLOCATED GOLD AND SILVER

Andrew Maguire’s Kinesis money which is a “bitcoin” but backed 100% by allocated gold and silver is set to go.

it think it would be a great idea to look at this!

please read at: https://kinesis.money/#/

(Andrew Maguire)

|

|

Dear Harvey Organ,

Thank you for your participation in our webinar on June 7th with our host and CEO of Kinesis, Thomas Coughlin.

The response we received has been incredible, we appreciate you taking the time to join us and hope you found it to be beneficial.

Due to such a high influx of questions we received we were unable to have them all answered. Nevertheless, if there was anything which requires more clarification, or you have a query which needs to be rectified, we invite you to join our telegram group:

We apologize for the technical issues we incurred during the webinar which resulted in it running a little over schedule, we hope that the next one we host will run seamlessly.

A video has been put together and uploaded onto our YouTube channel which can be found here:

Please share and subscribe to our YouTube channel to be notified of all the latest videos as they become available.

The rapid growth that we are currently experiencing has been incredible and with your support, is only going to get better.

We are working behind the scenes very hard to create a better experience for everyone involved! Stay tuned in as we have many more announcements to be released in the upcoming days.

Kind Regards,

|

Kinesis Money

a:C/O ILS Fiduciaries (IOM) Limited, First Floor,Millennium House, Victoria Road, Douglas, Isle of Man IM2 4RW

|

The following is self explanatory

(courtesy GATA/Chris Powell and Harvey Organ)

GATA asks bank regulator to check risks of gold

futures maneuver

Submitted by cpowell on Sun, 2018-06-10 16:17. Section: Daily Dispatches

12:21p ET Sunday, June 10, 2018

Dear Friend of GATA and Gold:

GATA has appealed to the U.S. comptroller of the currency, who has regulatory authority over banks, to review financial risks certain banks may have incurred through derivatives in the monetary metals markets, particularly through the recent heavy use of the “exchange for physicals” mechanism of settling gold and silver futures contracts on the New York Commodities Exchange.

The appeal was made in a letter sent May 5 to the comptroller, Joseph M. Otting, whose office is part of the U.S. Treasury Department, by your secretary/treasurer and GATA futures market consultant Harvey Organ.

“Exchange for physical” settlements of futures contracts long were considered emergency procedures when a seller was not able to deliver metal from an exchange-approved warehouse and wanted to settle with delivery elsewhere. But now such settlements appear to constitute most gold and silver futures settlements on the Comex. It is a strange development that appears to have been necessitated by the increasing difficulties of central banking’s gold and silver price suppression policy.

GATA has received no acknowledgment of the letter. Its text is below and a PDF copy of it is here:

http://www.gata.org/files/ComptrollerOfCurrencyLetter.pdf

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

* * *

May 5, 2018

Joseph M. Otting, Comptroller of the Currency

U.S. Treasury Department

400 7th Street, SW

Washington DC 20219

Dear Comptroller Otting:

Please let us bring to your attention financial risks to major banks involving their possibly unreported exposure to derivatives in the monetary metals markets.

In recent months gold and silver future contracts issued by U.S. banks on the New York Commodities Exchange have been moved off-exchange for delivery through a mechanism known as “exchange for physical” (EFP) contracts. Until recently use of this mechanism was considered an emergency procedure when a seller did not have access to metal for delivery through Comex warehouses. Now the mechanism seems to be in use for a large share of front-month contracts for which delivery is sought.

Here is an example that is happening at the Comex in the front active month of April for gold and the inactive delivery month of April for silver.

In gold, there were 229,436 EFP contracts for 713.64 tonnes, an average of 10,925 contracts and 1,092,500 ounces per trading day.

In silver, there were 77,150 EFP contracts for 385,750,000 ounces, an average of 3,673 contracts and 18,369,000 ounces per trading day.

London Bullion Market Association rules suggest that these contracts may not be reported to regulators. The LBMA’s bylaws say:

“Figures above exclude any contracts not subject to risk-based capital requirements, such as FX contracts with an original maturity of 14 days or less, futures contracts, written options, and basis swaps. Therefore, the total notional amount of derivatives by maturity will not add to the total derivatives figure in this table.”

We are told that these EFP contracts are transferred from the Comex to London as what are called “serial forwards” and their duration is always less than 14 days, which exempts them from being reported.

It is our understanding that in each quarter your office prepares a report detailing risk undertaken by the banks under the comptroller’s supervision.

These risks include derivatives undertaken by U.S. banks and other obligations that may cause a bank to fail. Our concern is that your office may not be aware of large unreported derivative exposure by banks.

Could you review this matter and let us know your conclusions?

Sincerely,

CHRIS POWELL

Secretary/Treasurer

HARVEY ORGAN

Consultant

Gold Anti-Trust Action Committee Inc.

7 Villa Louisa Road

Manchester, Connecticut 06043-7541

end

As indicated to you on several occasions, it is China that is controlling the gold price, not USA authorities

(courtesy David Brady/Sprott/GATA)

David Brady at Sprott Money: China robs Comex of control of gold price

Submitted by cpowell on Fri, 2018-07-13 17:45. Section: Daily Dispatches

1:45p ET Friday, July 13, 2018

Dear Friend of GATA and Gold:

The close correlation of the gold price with the valuation of the Chinese yuan and the International Monetary Fund’s Special Drawing Rights shows that China, not the New York Commodities Exchange, is now in control of the price of the monetary metal, money manager David Brady writes today at Sprott Money.

Brady asserts that China’s control over these values is being maintained by coordination with the IMF and that it gives China more options in managing its trade war with the United States.

Brady’s analysis is headlined “China Takes Control of Gold from the Comex” and it’s posted at Sprott Money here:

https://www.sprottmoney.com/Blog/china-takes-control-of-gold.html

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

The following needs no special introduction: it is self explanatory

a must read..

(courtesy Chris Powell/GATA)

The explosive questions the gold riggers won’t answer — and the press won’t ask

Submitted by cpowell on Sun, 2018-07-15 20:06. Section: Documentation

4:34p ET Sunday, July 15, 2018

Dear Friend of GATA and Gold:

How easy it would be for any major financial news organization or trade association to confirm, expose, and combat the rigging of the gold market by governments and central banks.

Such an effort could start with the documentation, most of it from official sources, collected by GATA and compiled here:

http://gata.org/taxonomy/term/21

Everything could be nailed down to the present moment by a few specific questions put to the key participants in the rigging. These questions already have been prepared and posed, just not publicized enough.

— Three months ago U.S. Rep. Alex X. Mooney, R-West Virginia, wrote to the secretary of the treasury and the chairman of the Federal Reserve asking what the U.S. government’s policy on gold is and whether it remains, as government records from years ago establish, to drive the monetary metal out of the world financial system.

Mooney also asked whether the U.S. government, directly or through intermediaries, like the Bank for International Settlements, trades in gold and gold derivatives and what the purposes of any such transactions are.

Mooney’s letter is posted at GATA’s internet site here:

Mooney has received no response.

— Last November GATA put similar questions to the BIS. What, GATA asked, is the purpose of the gold swaps and derivatives purchased and sold by the bank and the purpose of the bank’s involvement in the gold market generally?

The bank replied promptly but only to say it would not answer the question:

— Five weeks ago your secretary/treasurer and GATA consultant Harvey Organ wrote to the comptroller of the currency in the Treasury Department, Joseph M. Otting, whose office regulates the banking industry, calling attention to the recent explosion in use of the emergency procedure of “exchange for physicals” to settle gold and silver contracts issued on the New York Commodities Exchange by government-regulated banks. The financial risks undertaken by the banks in these transactions, GATA wrote, apparently were not being reported to the comptroller.

GATA’s letter concluded: “Could you review this matter and let us know your conclusions?”

The comptroller has not responded.

— On July 2 your secretary/treasurer wrote to the public relations department at JPMorganChase & Co. about the bank’s involvement in the monetary metals market, which occasionally has been controversial. The letter read:

“In April 2012 Blythe Masters, then chief of the bank’s commodities desk, told CNBC that the bank had no position of its own in the monetary metals markets and was trading only for clients:

https://www.youtube.com/watch?v=gc9Me4qFZYo

“Can you tell me if this remains the case and if the bank’s clients in trading the monetary metals markets include governments and central banks?

“Thanks for your help.”

JPMorganChase has not responded.

— Two weeks ago your secretary/treasurer wrote to the public relations department at the International Monetary Fund, calling attention to the recent report by James Rickards’ Gold Speculator newsletter that the price of gold and the valuation of the IMF’s Special Drawing Rights currency seem to have been locked together since the Chinese yuan was incorporated into the SDR currency basket in October 2016. A copy of Rickards’ newsletter was attached to the letter to the IMF. The newsletter is summarized at GATA’s internet site here:

A link to the newsletter’s text as posted at GoldCore can be found there.

“If Rickards’ observation is correct,” your secretary/treasurer wrote, “it implies the IMF’s involvement with governments and central banks in constant surreptitious intervention in the gold and currency markets. Is the IMF aware of or party to such interventions that have not been disclosed officially to the markets and investors?”

After some prodding by GATA to the IMF, an IMF communications officer, Andrew Kanyegirire, replied:

“Please note that the IMF has not engaged in any transactions in gold since the IMF’s strictly limited gold sales (2009-10) were concluded in December 2010. In addition, the IMF’s Articles of Agreement require the IMF, when dealing in gold, to avoid managing or fixing its price, limit the types of operations and transactions in gold that the IMF can conduct, and prescribe that the IMF, when selling gold outright, conduct such sale according to prevailing market prices.

“For more details on these transactions, please refer to the fact sheet on ‘Gold in the IMF,’ which is available on the IMF’s website via the following link:

https://www.imf.org/en/About/Factsheets/Sheets/2016/08/01/14/42/Gold-in-….

“With respect to the SDR, please also note that the daily SDR value is an aggregate of the market value of the five currencies in the basket, based on their relative amounts fixed every five years by the IMF and their daily market exchange rates against the U.S. dollar. See:

https://www.imf.org/external/np/fin/data/rms_sdrv.aspx

“For more background on the SDR, see:

http://www.imf.org/en/About/Factsheets/Sheets/2016/08/01/14/51/Special-D….

“Finally, we would like to emphasize that the IMF’s finances are very transparent and its gold and SDR holdings reported on a quarterly basis on its financial statements are also available via the following link:

http://www.imf.org/external/pubs/ft/quart/index.htm

— IMF Public Affairs”

But of course none of that answered the question GATA posed. So your secretary/treasurer replied to the IMF, noting that it had not really been responsive and posing GATA’s question again:

“Is the IMF aware of or involved with any effort by China to link the SDR’s value to the gold price?

“Since the IMF issues SDRs, does the IMF know at all times how they are allocated among nations, or can they be traded among nations without the IMF’s knowledge?

“Would the IMF notice any scheme involving SDRs such as the one outlined in the Rickards letter? If a nation was controlling the value of SDRs in a way such as the Rickards letter described, would the IMF care — and would the IMF acknowledge it to the public and the markets?”

The IMF has not replied.

* * *

These refusals to answer specific questions about an obviously sensitive point on which the value of all capital, labor, goods, and services in the world depends are as good as admissions that something deceptive and discreditable is going on with governments, central banks, gold, and the financial markets generally.

But GATA is only a small nonprofit educational and civil rights organization. While it can publicize this deception to the approximately 8,000 people on its e-mail list and can make its documentation available to financial news organizations, trade organizations, mining companies, financial houses, and investors, GATA can’t make them care or do what might be presumed to be their jobs.

Even most of the people on GATA’s e-mail list now seem to be too demoralized to act on what GATA has disclosed. That’s understandable enough, since the more that market rigging is exposed, the more of it has to be done to keep working, and the more it that is done, the more obvious it becomes, leading people to think that it can continue forever even in the open.

But it can’t go on forever. That the Treasury Department, Federal Reserve, BIS, JPMorganChase, and IMF refuse to answer the questions spelled out here shows that they fear that exposure can beat them.

While they seem to command all the money in the world, beating them really wouldn’t be that hard. As Jim Sinclair and others have noted, beating them requires mainly that investors take delivery of their monetary metal and vault it outside the banking system. (GATA would define the banking system to include the exchange-traded funds GLD and SLV, operated as they are by big investment banks that can use the EFTs to short the metals: HSBC and JPMorganChase. Unfortunately major fund managers who advocate gold ownership undermine themselves by putting their money in GLD.)

Enough exposure of the gold market rigging policy would push ordinary investors and fund managers in the right direction. It might even embolden the governments of commodity-producing countries, the big victims of gold market rigging, to protest and fight back against this most pernicious form of imperialism. Opposition on the national level might end the rigging policy overnight.

So “say not the struggle naught availeth.” Instead of despairing, help strike a blow against the bad guys.

Send this dispatch to your national elected officials with a request that they obtain and publicize answers to its questions.

Write to financial news organizations to urge them to pursue and publicize the answers too.

If you’re able and have not done so before, support GATA financially:

Even a donation of $5 will be $5 more than GATA has received from most major gold-mining companies.

All the money in the world is indeed powerful, but in the end not as powerful as the truth. That is why the deceivers fear it so. The good guys just have to be clever and courageous.

And David put his hand in his bag, and took thence a stone, and slang it, and smote the Philistine in his forehead, so that the stone sunk into his forehead and he fell upon his face to the earth.

So David prevailed over the Philistine with a sling and with a stone and smote the Philistine and slew him. But there was no sword in the hand of David.

GATA’s got the sling and the stones. Help us put them to good use.

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

This is good: June sees no change in BIS gold intervention. Whenever we witness raids you can bet the BIS is there lending gold to the criminals

(courtesy Lambourne/GATA)

GATA) Robert Lambourne: June shows no change in BIS intervention in gold

Submitted by cpowell on 01:23PM ET Monday, July 16, 2018. Section: Daily Dispatches

By Robert Lambourne

Monday, June 16, 2018

The Bank for International Settlements has published its June statement of account, which gives some information on its use of gold swaps and other gold- related derivatives in the month:

https://www.bis.org/banking/balsheet/statofacc180630.pd f

The information provided in the BIS monthly statements is not sufficient to calculate a precise amount of gold- related derivatives, including swaps, but it appears that the bank’s total exposure as of June 30, 2018, was approximately 413 tonnes of gold, which is essentially unchanged from May.

When it comes to its activities in the gold market, the BIS provides little information on what it is doing, why, and for whom.

—–

Robert Lambourne is a retired business executive in the United Kingdom who consults with GATA about the involvement of the Bank for International Settlements in the gold market.

***

end

I brought this to your attention last week and it is worth repeating. The once mighty South Africa has been reduced to only the 7th highest gold producer, from 5th. During the first part of the twentieth century it produced over 1000 tonnes and this represented almost 90% of the total world production. Now its production is falling continuously

(courtesy Lawrie Williams)

LAWRIE WILLIAMS: How the mighty are fallen. RSA gold on the decline

There is the news this week that South Africa’s gold production volume has been falling for eight months in a row year-on year with a 16.2% decline in May compared with the same month in 2017. South Africa was for many years the World’s No.1 producer of the yellow metal by far hitting around 1,000 tonnes in 1970 before it started to decline. Quite how dominant South African production was then is demonstrated by the fact that China, currently the world’s largest producer, can only manage around less than half this annual production tonnage. South Africa now only ranks 7th in the world gold production league, and could well be struggling to hold this position if a decline of thie May level is repeated throughout the year. Last year it was overtaken by Canada and Peru in terms of total gold output.

Top 10 Gold Producing Nations 2016/2017 (Tonnes)

| Rank | Country | 2017 Output | 20 16 Output | % Change |

| 1 | China | 429 | 464 | -7.9% |

| 2 | Australia | 289 | 288 | +0.5% |

| 3 | Russia | 272 | 253 | +7.6% |

| 4 | USA | 244 | 229 | +6.3% |

| 5 | Canada | 171 | 163 | +5.0% |

| 6 | Peru | 167 | 166 | +0.3% |

| 7 | South Africa | 157 | 163 | -3.6% |

| 8 | Ghana | 130 | 131 | -0.8% |

| 9 | Mexico | 122 | 128 | -4.7% |

| 10 | Indonesia | 114 | 109 | +4.8% |

Source: Metals Focus, lawrieongold

South Africa was thus the world’s leading gold producer for most of the 20thCentury – primarily from gold mined in the Witwatersrand basin centred around Johannesburg, and then from the Carletonville and Orange Free State gold fields from the same geological sequence. The writer worked as a mining engineer in the South African gold mines in the 1960s as production was nearing its peak so has first-hand knowledge of the problems which faced the miners there.

At that time some of the older properties were running out of payable gold ore, while others had to go deeper and deeper (over 2 miles down in some cases) to maintain output and this created both technical and logistical difficulties in terms of high rock stresses, high temperatures (the mere fact of moving ventilation air underground – adiabatic compression – raised the air temperature around 3 degrees celsius (5.38 degrees F) for every 1,000 feet of depth so for say a 10,000 ft deep mine the air temperature just through pumping the air down the temperature would be around 30 degrees C higher than it was on surface, and some mines went even deeper! And rock temperatures also increase with depth.) The excessive depths also added drastically to transportation costs for men, materials and ore hoisting.

Indeed to maintain a workable environment, the deeper operations needed to refrigerate the air being pumped underground, while workers needed to undergo acclimatisation training to prepare them for the high temperatures and humidity they were likely to encounter at the workface.

All this may have put South African mining at the forefront of technology, but despite a huge emphasis on maintaining safety the fatal accident rate still seemed unacceptably high (any fatality is deemed unacceptable) . Miners needed to work at depths where rock stresses and behaviour could be unpredictable leading to unforeseen seismic events – some of which proved fatal to those in the vicinity.

Safety is relative though. In terms of the huge sizes of the mine workforces – some the biggest mines employed perhaps 5,000 people and the industry overall at its peak nearly half a million – per capita fatality rates were no higher than in some Western mining operations, but were still unacceptably elevated and as time progressed and the world overall became more safety conscious work stoppages due to safety investigations following fatalities, made maintaining production ever more precarious. Gold grades still are higher than in many other countries, but the overall costs of mining and milling the gold ore have made most South African mines marginal at best.

South African mining is thus something of a microcosm of the mining industry as a whole. Reserves and resources are finite and mostly depleting. Globally, few major gold deposits have been found in recent years and/or remain undeveloped. Ore grades have been diminishing and while there are a few countries which may still be increasing gold output even these are peaking while others, like South Africa, are in an ever-increasing decline. Whether ‘peak gold is actually with us or not is arguable, but even if it is not it is very close and any global annual increase from now on is likely to be insignificant/ Effectively peak gold is with us and as long as demand in countries like China continues to increase as the middle class expands, then the gold supply/demand balance will come under pressure. In the long term gold has to benefit!

14 Jul 2018

end

Your early MONDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

i) Chinese yuan vs USA dollar/CLOSED UP TO 6.6775/HUGE DEVALUATION FOR THE PAST TWO WEEKS HALTS /shanghai bourse CLOSED DOWN 17,14 POINTS OR 0,61% /HANG SANG CLOSED UP 14,22 POINTS OR 0.05%

2. Nikkei closed HOLIDAY/USA: YEN FALLS TO 112.31/

3. Europe stocks OPENED RED EXCEPT GERMAN DAX / /USA dollar index FALLS TO 94.43/Euro RISES TO 1.1723

3b Japan 10 year bond yield: RISES TO . +.04/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 112.31/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD FINALLY IN THE POSITIVE/BANK OF JAPAN LOSING CONTROL OF THEIR YIELD CURVE AS THEY PURCHASE ALL BONDS TO GET TO ZERO RATE!!

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 69.84 and Brent: 73.73

3f Gold UP/Yen UP

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil DOWN for WTI and DOWN FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund RISES TO +.35%/Italian 10 yr bond yield DOWN to 2.57% /SPAIN 10 YR BOND YIELD UP TO 1.27%

3j Greek 10 year bond yield RISES TO : 3.87

3k Gold at $1243.90 silver at:15.80 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble UP 24/100 in roubles/dollar) 62.19

3m oil into the 69 dollar handle for WTI and 73 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 112.31 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 0.9974 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1693 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now POSITIVE territory with the 10 year RISING to +0.35%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.83% early this morning (THIS IS DEADLY TO ALL MARKETS). Thirty year rate at 2.94%

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

(courtesy Jim Reid/Bloomberg/Deutsche bank/zero hedge)

US Futures, European Stocks Rise Even As

Chinese Data Spooks Asia

U.S. futures are fractionally higher, following European shares in the green as Asian equities retreated ahead of today’s historic Trump-Putin summit and the first big week of earnings for US corporations.

The key economic catalyst overnight was the latest batch of Chinese data, where GDP rose as expected 6.7% – the slowest since 2016 – however Industrial Production missed badly as discussed last night, printing at 6.0%, below the 6.5% expected and the lowest since Dec 2015, pressuring regional equities.

Chinese Economic Data

The data indicates that Chinese economic growth momentum slowed further, but investors are more worried about coming quarters as U.S. tariffs come into effect, says Ben Kwong, executive director at KGI Asia; sentiment remains quite cautious.

As a result, Chinese stocks slumped after data showed GDP grew at the slowest since 2016 in the second quarter, while Xiaomi dropped after being excluded from a list of stocks eligible for trading via connects with mainland as China aims to protect retail investors using HK link from less understood securities. The Shanghai Composite Index closed down 0.6% at 2,814, while the CSI 300 was also 0.6% lower, ChiNext down -0.1%.

Offsetting some of the gloom, the PBoC injected CNY 170bln via 7-day and CNY 130bln via 14-day reverse repos for a net CNY 300bln daily injection.

“Investors will watch for signs of monetary and fiscal policy loosening from the upcoming central economic work conference, and first-half results for stocks with cheap valuations and earnings growth that beat estimates,” said Central China Securities strategist Zhang Gang.

Elsewhere in Asia, shares were lower, the MSCI Asia Pacific index declining -0.3%, with volumes down in most markets while Japan was shut for a public holiday.

Europe bucked the trend with banks rising on the Stoxx Europe 600 Index, after Deutsche Bank said its earnings are likely to be above market expectations, offsetting a drop in miners. The biggest European bank whose stock price recently a new all time low, said it sees net income of about 400 million euros ($468 million) and pretax income of 700 million euros, “considerably” above estimates. The news sent DB stock surging 8% in early trading, its biggest daily gain since April 2017.

In FX, the dollar weakened against most G-10 peers ahead of an expected slowdown in U.S. retail sales data, set to be reported at 830am ET. The Bloomberg Dollar Spot Index fell 0.2%, taking its three-day decline to more than 0.3%; Treasury 10-year yields rose 1bp to 2.84%

“The USD’s sharp turnaround late on Friday may be telling of the currency’s waning bullish momentum –- or the fact that the dollar looks to be running out of positive catalysts,” wrote ING Groep FX strategist Viraj Patel. “We may need a very strong U.S. retail sales print today to see the dollar push higher.”

The pound rose a third day ahead of a vote later Monday on U.K. Prime Minister Theresa May’s Brexit legislation in Parliament, while the euro was stuck in a small range near the $1.17 level, while the yen edged lower, adding to its biggest weekly slide in 10 months.

In rates, US Treasuries inched lower, tracking bond declines across most of Europe: the 10Y TSY yield dipped 1 basis point to 2.84%; German 10Y Bund yields climbed 1bps to 0.35% while Britain’s 10-year yield also climbed 1bp to 1.273%.

Meanwhile, as Bloomberg notes, with no fresh signs of a trade war escalation and President Donald Trump heading to a summit with Vladimir Putin, investors will focus on a barrage of economic data including Monday’s mixed figures from China, and company earnings, with Bank of America Corp. due to report. The big event this week is Federal Reserve Chairman Jerome Powell’s semi-annual testimony where he is expected to lay the groundwork for further tightening.

Commodities traded mixed with WTI and Brent leak lower: Brent flirted around USD 75.00/bbl while WTI hovered near the USD 70.50/bbl level in the aftermath of a pullback from last Friday’s settlement amid reports that the Trump administration was said to be considering tapping into the Strategic Petroleum Reserve to rein in prices. Sentiment also hampered by the weekly Baker Hughes rig count showing an increase of 2 rigs in operation compared to the prior week. Elsewhere, gold (+0.2%) prices are buoyed by the softer USD. London Copper slipped this morning while Chinese Q2 growth printed a slight downtick (yet in-line with expectations), focus continues to remain on China’s response to US tariffs. Steel-linked metals, Nickel and Zinc, are subdued on lower demand expectations amid China’s top steelmaking city ordering steel mills to shut sintering plants for five days due to adverse weather conditions.

Expected data today includes retail sales, which should decline from last month’s 0.8% to 0.5%, and the Empire State Manufacturing Survey. Bank of America, BlackRock, and Netflix are among companies reporting earnings.

Market Snapshot

- S&P 500 futures up 0.1% to 2,805.25

- STOXX Europe 600 up 0.2% to 385.64

- MXAP down 0.3% to 165.20

- MXAPJ down 0.4% to 538.17

- Nikkei up 1.9% to 22,597.35

- Topix up 1.2% to 1,730.07

- Hang Seng Index up 0.05% to 28,539.66

- Shanghai Composite down 0.6% to 2,814.04

- Sensex down 0.2% to 36,455.29

- Australia S&P/ASX 200 down 0.4% to 6,241.52

- Kospi down 0.4% to 2,301.99

- German 10Y yield rose 1.6 bps to 0.356%

- Euro up 0.08% to $1.1694

- Italian 10Y yield fell 7.2 bps to 2.286%

- Spanish 10Y yield rose 0.7 bps to 1.27%

- Brent futures down 0.1% to $75.28/bbl

- Gold spot little changed at $1,244.21

- U.S. Dollar Index down 0.1% to 94.61

Top Overnight News from Bloomberg

- President Donald Trump prepared to meet Vladimir Putin in Helsinki on Monday, under pressure to confront his Russian counterpart over Kremlin meddling in the 2016 election and with concerns rising that the U.S. is abandoning the current international order

- Goldman Sachs Group Inc. bank plans early this week to name company President David Solomon — whom Blankfein has publicly referred to as his successor — as its next CEO, the New York Times reported Sunday, citing people briefed on the plan

- European Union President Donald Tusk called on Donald Trump to reform the world order rather than bring it down, warning that trade wars can lead to “hot conflicts.”

- China’s economic expansion slowed in line with expectations, signaling broadly stable output as the trade conflict with the U.S. intensifies. GDP increased 6.7 percent in the second quarter from a year earlier, slowest since 2016 and down slightly from the 6.8 percent pace in the previous quarter. Investment growth and industrial output also slowed in June.

- Theresa May’s long-running battle with her divided Conservative Party took a potentially more dangerous turn, as one of her former ministers began assembling lawmakers to vote against her Brexit plans. Steve Baker, a former Brexit minister, is coordinating lawmakers on WhatsApp ahead of key parliamentary votes, according to a person familiar with the strategy

- Bank of England policy makers are getting a crucial glimpse of the health of the U.K. economy before their crunch August meeting. A deluge of numbers on wages, inflation, retail sales and public borrowing are coming over the next five days

Asian stocks began the week subdued with the region lacklustre amid the absence of Japanese participants and following a quiet weekend in terms of newsflow, while the region also digested a deluge of mixed Chinese data including a slowdown in Q2 GDP. ASX 200 (-0.4%) was on the backfoot from early trade amid cautiousness prior to the key Chinese releases and with the index dragged by losses in miners and financials. Elsewhere, Shanghai Comp. (-0.6%) and Hang Seng (+0.1%) were initially downbeat after the mixed data in which GDP topped estimates on a Q/Q basis at 1.8% vs. Exp. 1.6%, but GDP Y/Y slowed inline with forecasts to 6.7% vs. Prev. 6.8%. In addition, Retail Sales was better than expected and Industrial Production disappointed, while the lending and money supply data late last week was also varied and added to the uninspired tone. In terms of today’s notable movers, ZTE shares surged after the US confirmed to lift the ban on US sales to the Co. while Xiaomi were on the other side of the spectrum after the Shanghai Stock Exchange banned investors from trading in a dozen of foreign companies and firms with weighted-voting rights via the stock-connect. Chinese Premier Li reiterated China and EU are to uphold multilateralism and free trade during meeting with EU officials, while EU’s Tusk said trade wars can result to hot conflicts and that EU is seeking support for WTO reform.

Top Asian News

- China’s Economy Slows as Expected With Trade War Dimming Outlook

- China Stocks at Record Lows Make Case for $941 Billion Fund

- Bank of Thailand Says 4.5% Growth May Spur More Hawkish Stance

- Malaysia to Propose 10% Sales Tax on Goods, 6% on Services

- Iron Ore’s Top Grade May Hit $100 as China Chases Blue Skies

European equities opened relatively flat and since then have traded in no firm direction (Eurostoxx 50 +0.1%). Financials (+0.7%) outperform as Deutsche Bank (+6.5%) ignited a bid in the sector after announcing better than expected Q2 preliminary results. Banks dominate gains in their respective bourses. Meanwhile, Indivior (+27.1%) shares sky-rocketed after a US court blocked Indian competitors from selling a cut-price version of Indivior’s bestselling opioid addiction treatment in the US. Due to the Farnborough Air Show, it may be worth keeping an eye on BAE Systems (BA/ LN), Rolls-Royce (RR/ LN), Leonardo (LDO IM), Boeing (BA) and Airbus (AIR FP).

Top European News

- Buy Europe’s Defensives as Economic, Earnings Growth Slows: HSBC

- Another Week, Another Brexit Showdown for Theresa May

In FX, the DXY index is meandering within a narrow 94.558-776 band in line with restrained Dollar movement vs its G10 counterparts after last week’s volatile trade and relatively big swings culminated in the Usd netting decent gains, with the DXY briefly over 95.000 at one stage on Friday. Ahead, some data to provide impetus in the form of retail sales. JPY – A marginal underperformer after suffering heaviest losses vs the Usd of late and closing below a key 76.4% Fib (112.33) on Friday, However, the absence of Japanese participants due to the Marine Day holiday has impacted trade overnight between 112.20-55. CHF – Back on a par with the Greenback and still straddling 1.1700 vs the Eur, awaiting the next moves in global trade/tariff wars and anything from Trump’s meeting with Putin. CAD – The Loonie is pretty level vs its US peer and pivoting 1.3150 ahead of some Canadian data that could impact and/or offset any Usd-led moves in the form of existing home sales.

Commodities trade fairly mixed while WTI and Brent continue to leak with losses. Brent has broken below USD 75.00/bbl while WTI has taken out USD 70.00/bbl to the downside in the aftermath of a pullback from last Friday’s settlement amid reports that the Trump administration was said to be considering tapping into the Strategic Petroleum Reserve to rein in prices. Sentiment also hampered by the weekly Baker Hughes rig count showing an increase of 2 rigs in operation compared to the prior week. Meanwhile, in talks with the Saudi’s Energy Minister, Iranian Oil Minister said OPEC decision does not give members the right to raise their production level above targets Elsewhere, gold (+0.2%) prices are buoyed by the softer USD. London Copper slipped this morning while Chinese Q2 growth printed a slight downtick (yet in-line with expectations), focus continues to remain on China’s response to US tariffs. Steel-linked metals, Nickel and Zinc, are subdued on lower demand expectations amid China’s top steelmaking city ordering steel mills to shut sintering plants for five days due to adverse weather conditions. Iran warns OPEC it will be less effective if the production cap slip.