GOLD: $1222.60 DOWN $0.95 (COMEX TO COMEX CLOSINGS)

Silver: $15.51 UP 3 CENTS (COMEX TO COMEX CLOSINGS)

Closing access prices:

Gold $1221.45

silver: $15.49

For comex gold:

JULY/

NUMBER OF NOTICES FILED TODAY FOR JULY CONTRACT:135 NOTICE(S) FOR 13,500 oz

TOTAL NOTICES SO FAR 234 FOR 23400 OZ (0.7278 tonnes)

For silver:

JULY

96 NOTICE(S) FILED TODAY FOR

480,000 OZ/

Total number of notices filed so far this month: 6074 for 30,370,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: BID $8101/OFFER $8186: DOWN $70(morning)

Bitcoin: BID/ $8066/offer $8151: DOWN $105 (CLOSING/5 PM)

end

First Shanghai gold fix comes at 10 pm est

The second Shanghai gold fix: 2:15 pm

First Shanghai gold fix gold: 10 pm est: not provided

NY price at the same time:

PREMIUM TO NY SPOT: $xx

XX

Second gold fix early this morning: not provided

USA gold at the exact same time:xxx

PREMIUM TO NY SPOT: $xx

China is controlling the gold market

WE WILL NOT PROVIDE LONDON FIXES AS THEY ARE NOT ACCURATE AS TO WHAT IS GOING ON AT THE SAME TIME FRAME.

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total OPEN INTEREST ROSE BY A SMALL SIZED 451 CONTRACTS FROM 217,996 UP TO 218,477 DESPITE FRIDAY’S 0 CENT LOSS IN SILVER PRICING AT THE COMEX. WE HAVE NOW WITNESSED A SLOW COMEX ACCUMULATION THESE PAST SEVERAL DAYS. ON TOP OF THIS WE HAVE ALSO WITNESSED A LARGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY(WELL OVER 30 MILLION OZ AT THE COMEX) AS WELL AS CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A SMALL SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP: 800 EFP’S FOR SEPT. , 0 EFP’S FOR DECEMBER AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE: OF 800 CONTRACTS. WITH THE TRANSFER OF 800 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 800 EFP CONTRACTS TRANSLATES INTO 4.000 MILLION OZ AND ACCOMPANYING:

1.THE FLAT SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR THE JUNE/2018 COMEX DELIVERY MONTH. (5.420 MILLION OZ) AND NOW 30.370 MILLION OZ FINALLY STANDING FOR DELIVERY IN JULY (SEE DATA BELOW).

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF JUNE:

33,951 CONTRACTS (FOR 20 TRADING DAYS TOTAL 33,951 CONTRACTS) OR 169.76 MILLION OZ: (AVERAGE PER DAY: 1697 CONTRACTS OR 8.487 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF JULY: 169.76 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 24.25% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2018 TO DATE SILVER EFP’S: 1,824.47 MILLION OZ.

ACCUMULATION FOR JAN 2018: 236.879 MILLION OZ

ACCUMULATION FOR FEB 2018: 244.95 MILLION OZ

ACCUMULATION FOR MARCH 2018: 236.67 MILLION OZ

ACCUMULATION FOR APRIL 2018: 385.75 MILLION OZ

ACCUMULATION FOR MAY 2018: 210.05 MILLION OZ

ACCUMULATION FOR JUNE 2018: 345.43 MILLION OZ

RESULT: WE HAD A SMALL SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 451 DESPITE THE FLAT SILVER PRICING AT THE COMEX YESTERDAY. THE CME NOTIFIED US THAT WE HAD A SMALL SIZED EFP ISSUANCE OF 800 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) . FROM THE CME DATA: 800 EFP’S FOR SEPT, 0 EFP’S FOR DECEMBER AND ZERO FOR ALL OVER MONTHS FOR A DELIVERABLE FORWARD CONTRACT OVER IN LONDON WITH A FIAT BONUS (TOTAL: 800). TODAY WE GAINED A SMALL SIZED: 1251 TOTAL OI CONTRACTS ON THE TWO EXCHANGES:

i.e 800 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH AN INCREASE OF 451 OI COMEX CONTRACTS. AND ALL OF THIS DEMAND HAPPENED WITH A 0 CENT LOSS IN PRICE OF SILVER AND A CLOSING PRICE OF $15.48 WITH RESPECT TO FRIDAY’S TRADING. YET WE STILL HAVE A GIGANTIC AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY IN THIS ACTIVE JULY DELIVERY MONTH OF SLIGHTLY OVER 30 MILLION OZ. IT SURE LOOKS LIKE ANOTHER FAILED BANKER SHORT COVERING EXERCISE AS BANKERS ARE SCRAMBLING TO COVER THEIR HUGE SHORTFALL.

In ounces AT THE COMEX, the OI is still represented by OVER 1 BILLION oz i.e. 1.092 MILLION OZ TO BE EXACT or 156% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT JULY MONTH/ THEY FILED AT THE COMEX: 96 NOTICE(S) FOR 480,000 OZ OF SILVER

IN SILVER, WE SET THE NEW RECORD OF OPEN INTEREST AT 243,411 CONTRACTS ON APRIL 9.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $16.51

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) AND NOW JULY 2018 AMOUNT FINALLY STANDING: 30.370 MILLION OZ )

- HUGE RECORD OPEN INTEREST IN SILVER 243,411 CONTRACTS (OR 1.217 BILLION OZ/ SET APRIL 9/2018

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017

- RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT).

IN GOLD, THE OPEN INTEREST FELL BY A HUMONGOUS SIZED 22,253 CONTRACTS DOWN TO 463,448 DESPITE THE SMALL FALL IN THE COMEX GOLD PRICE/YESTERDAY’S TRADING (A LOSS IN PRICE OF $2.85). GENERALLY WE SEE COMEX LIQUIDATION WHEN WE ARE ENTERING THE LAST DAYS IN THIS ACTIVE DELIVERY MONTH OF JULY AND IT SURELY HAPPENED ON FRIDAY. WE GENERALLY SEE THE BOYS CASHING IN THEIR COMEX LONGS TO BEGIN THE PROCESS TO MOVE INTO LONDON FORWARDS. THIS PROCEDURE HAS BEEN GOING ON NOW FOR OVER 2 AND 1/2 YEARS. THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 11,249 CONTRACTS:

AUGUST SAW THE ISSUANCE OF: 6640 CONTRACTS, OCTOBER SAW THE ISSUANCE OF 0 CONTRACTS AND DECEMBER HAD AN ISSUANCE OF 4609 CONTACTS AND THEN ALL OTHER MONTHS ZERO. The new COMEX OI for the gold complex rests at 463,448. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE A STRONG OI LOSS IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 11,004 CONTRACTS: 22,253 OI CONTRACTS DECREASED AT THE COMEX AND 11,249 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI LOSS: 11004 CONTRACTS OR 1,100,400 OZ = 34.22 TONNES. AND ALL OF THIS LOSS IN DEMAND OCCURRED WITH THE TINY FALL IN THE PRICE OF GOLD/ FRIDAY TO THE TUNE OF $2.85.

FRIDAY, WE HAD 9513 EFP’S ISSUED.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF JUNE : 190,420 CONTRACTS OR 19,042,000 OZ OR 592.28 TONNES (20 TRADING DAYS AND THUS AVERAGING: 9521 EFP CONTRACTS PER TRADING DAY OR 952,100 OZ/ TRADING DAY),,

TO GIVE YOU AN IDEA AS TO THE HUGE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 20 TRADING DAYS IN TONNES: 592.28 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2017, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 2555 TONNES

THUS EFP TRANSFERS REPRESENTS 592.28/2550 x 100% TONNES = 23.22% OF GLOBAL ANNUAL PRODUCTION SO FAR IN JULY ALONE.***

ACCUMULATION OF GOLD EFP’S YEAR 2018 TO DATE: 4,695.09* TONNES *SURPASSED ANNUAL PROD’N

ACCUMULATION OF GOLD EFP’S FOR JANUARY 2018: 653.22 TONNES (21 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR FEBRUARY 2018: 649.45 TONNES (20 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR MARCH 2018: 741.89 TONNES (22 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR APRIL 2018: 713.84 TONNES (21 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR MAY 2018: 693.80 TONNES ( 22 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR JUNE 2018 650.71 TONNES (21 TRADING DAYS)

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A HUMONGOUS SIZED DECREASE IN OI AT THE COMEX OF 22,251 DESPITE THE SMALL LOSS IN PRICING ($2.85 THAT GOLD UNDERTOOK ON FRIDAY) // . WE ALSO HAD A FAIR SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 11,249 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 11,249 EFP CONTRACTS ISSUED, WE HAD A VERY STRONG NET LOSS OF 11004 CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

11,249 CONTRACTS MOVE TO LONDON AND 22,253 CONTRACTS DECREASED AT THE COMEX. (in tonnes, the LOSS in total oi equates to 34.22 TONNES). ..AND THIS LOSS IN DEMAND OCCURRED WITH A TINY LOSS OF $2.85 IN YESTERDAY’S TRADING AT THE COMEX!!!.

we had: 135 notice(s) filed upon for 13,500 oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD...

WITH GOLD DOWN$0.95 TODAY: /

NO CHANGES IN GOLD INVENTORY AT THE GLD

/GLD INVENTORY 800.20 TONNES

Inventory rests tonight: 800.20 tonnes.

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

SLV/

WITH SILVER UP 3 CENTS TODAY :

NO CHANGE IN SILVER INVENTORY TONIGHT

/INVENTORY RESTS AT 329.433 MILLION OZ/

NOTE THE DIFFERENCE BETWEEN THE GLD AND SLV: THE CROOKS CAN RAID GOLD BECAUSE THEY DO HAVE SOME PHYSICAL. THEY DO NOT RAID SILVER PROBABLY BECAUSE THERE IS NO REAL SILVER INVENTORIES BEHIND THEM

end

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER ROSE BY A SMALL SIZED 451 CONTRACTS from 217,996 UP TO 218,477 (AND CLOSER T0 THE NEW COMEX RECORD SET /APRIL 9/2017 AT 243,411/SILVER PRICE AT THAT DAY: $16.53). THE PREVIOUS RECORD OTHER THAN WAS ESTABLISHED AT: 234,787, SET ON APRIL 21.2017 OVER ONE YEAR AGO. THE PRICE OF SILVER ON THAT DAY: $17.89. OUR CUSTOMARY MIGRATION OF COMEX LONGS MORPH INTO LONDON FORWARDS CONTINUES AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

800 EFP CONTRACTS FOR SEPT., 0 EFP CONTRACTS FOR DECEMBER AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 800 CONTRACTS . EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI GAIN AT THE COMEX OF 451 CONTRACTS TO THE 800 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A GOOD NET GAIN OF 1251 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES: 6.255 MILLION OZ!!! AND YET WE ALSO HAVE A STRONG DEMAND FOR PHYSICAL AS WE WITNESS AN FINAL STANDING OF GREATER THAN 30 MILLION OZ AND YET ALL OF THIS DEMAND OCCURRED DESPITE A FLAT PRICING AT THE SILVER COMEX.

RESULT: A SMALL SIZED INCREASE IN SILVER OI AT THE COMEX DESPITE THE FLAT PRICING THAT SILVER UNDERTOOK IN PRICING ON FRIDAY. BUT WE ALSO HAD A SMALL SIZED 800 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR JULY, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON AS WELL AS THE STRONG AMOUNT OF PHYSICAL STANDING FOR METAL AT THE COMEX.

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

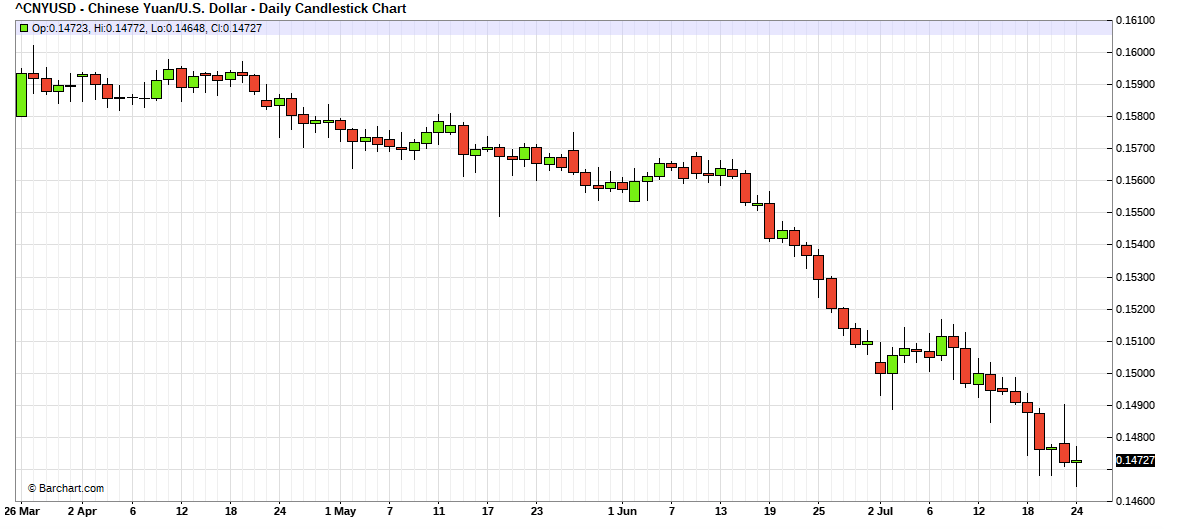

i)MONDAY MORNING/SUNDAY NIGHT: Shanghai closed DOWN 4.54 POINTS OR 0.16% /Hang Sang CLOSED DOWN 71.15 POINTS OR 0.25%/ / The Nikkei closed DOWN 167.91 POINTS OR 0.74%/Australia’s all ordinaires CLOSED DOWN 0.36% /Chinese yuan (ONSHORE) closed DOWN at 6.8218 AS POBC RESUMES ITS HUGE DEVALUATION /Oil UP to 69.71 dollars per barrel for WTI and 74.78 for Brent. Stocks in Europe OPENED RED//. ONSHORE YUAN CLOSED WELL DOWN AT 6.8218 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.8284: HUGE DEVALUATION/PAST SEVERAL DAYS RESUMES : /ONSHORE YUAN TRADING STRONGER AGAINST OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

i

/NORTH KOREA/SOUTH KOREA

i)North Korea/South Korea/USA/Russia

b) REPORT ON JAPAN

Japan has a two day meeting where they will discuss what they are going to do with respect to interest rates. They are tweaking their QE to prevent the 10 yr rate from climbing above 11. However we will probably have to wait until September who news that they will stop their QE altogether

( zero hedge)

3 c CHINA

4. EUROPEAN AFFAIRS

i)Great Britain/Saturday

The UK seems to be in big trouble due to the lackadaisical approach to the Brexit form Theresa May. She should have just left with no deal and orchestrate free trade deals with as many nations as possible. The EU seems to holding the UK for ransom

( zerohedge)

ii)Italy UK/Monday

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

i)Turkey

Trump is demanding the release of Pastor Brunson from Turkish house arrest as his trial on espionage continues. The USA is ready for major sanctions against Turkey as they already stopped the sale of F 35s to Erdogan. There are other major issues such as the Incirlik air base and the housing of a major load of migrants ready to boat across to Greece

( zerohedge)

ii)The Turkish lira is back down to 4.9 to the dollar and will likely exceed 5.00 to one shortly as Erdogan defies the west. To recap, Turkey arrested Pastor Brunson and accused him for espionage (a total phony charge). Turkey wants the USA’s F35 to which Congress blocked as Turkey is also buying SAM 400’s from Russia. Turkey is also a huge customer for Iranian oil another irritant to the USA

iv)Iranian proxies (Houthis) attack Saudi oil tankers at the strategic Bab al Mandeb strait. There are two important straits that we must watch out for:

1. Bab al Mandeb strait linking the Red Sea and the Arabian sea.

2. Strait of Hormuz, on the Gulf side

if these straits are closed it wold be an act of war and I doubt every much if Iran will close them. The currency is already in a free fall.

( TraderStef/Crush the Street)

v)Trump has got it right despite the left’s antics: Trump will meet with Iran’s Rouhani “anytime they want”/with no preconditions

( zerohedge)

vi)Russia/gold

Insiders explain why Russia liquidated its USA treasuries and basically they bought gold with it

( zerohedge)

6 .GLOBAL ISSUES

the Muslimization of Sweden

a must read..

(courtesy Gefira)

7. OIL ISSUES

8. EMERGING MARKET

9. PHYSICAL MARKETS

i)This is our letter to the CFTC it is quite explanatory: is a foreign power controlling the comex gold prices:

(courtesy Chris Powell, Harvey Organ/GATA)

ii)David Brady talks about the gold/yuan valuation and how a steep 25% devaluation by the Chinese government will cause the markets to crash and send gold northbound

( David Brady/Sprott Money)

iii)China is still embracing dollar denominated debt

( Bloomberg/GATA)

10. USA stories which will influence the price of gold/silver)

i)Market trading /GOLD/MARKET MOVERS:

Monday morning

Nasdaq tumbles, the dollar and bonds slump and gold rises

( zerohedge)

a)Incoming data seems to suggest that the USA economy has turned southbound on a dime:

the trifecta of home sales data all indicate a huge slump: today it is pending home sales and the reason is affordability

(courtesy zerohedge)

b)Global Bellwether reports record earnings as well as boosting guidance.

(courtesy zerohedge)

Trump declares a state of emergency in Northern California due to the horrific fires

( zerohedge)

iv)SWAMP STORIES

Guiliani claims that the Trump tapes have been tampered with. He is also pounding the table on the “witch hunt” against Trump

(courtesy zerohedge)

Trading Volumes on the COMEX

PRELIMINARY COMEX VOLUME FOR TODAY: 247,163 contracts

CONFIRMED COMEX VOL. FOR YESTERDAY: 431,997 contracts

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

And now for the wild silver comex results.

Total silver OI ROSE BY A SMALL SIZED 451 CONTRACTS FROM 217,996 UP TO 218,477 (AND A LITTLE CLOSER TO THE THE NEW RECORD OI FOR SILVER SET APRIL 9.2018/ 243,411 CONTRACTS) DESPITE THE 0 CENT LOSS IN PRICING THAT SILVER UNDERTOOK FRIDAY. SINCE WE ARE NOW INTO THE ACTIVE DELIVERY MONTH OF JULY, WE WERE INFORMED THAT WE HAD A SMALL SIZED 800 EFP CONTRACTS FOR SEPT., 0 EFP CONTRACTS FOR DECEMBER AND ZERO FOR ALL OTHER MONTHS. THESE EFPS WERE ISSUED TO COMEX LONGS WHO RECEIVED A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. THE TOTAL EFP’S ISSUED: 800. ON A NET BASIS WE GAINED 1251 SILVER OPEN INTEREST CONTRACTS AS WE OBTAINED 548 CONTRACT GAIN AT THE COMEX COMBINING WITH THE ADDITION OF 800 OI CONTRACTS NAVIGATING OVER TO LONDON.

NET GAIN ON THE TWO EXCHANGES: 1251 CONTRACTS

AMOUNT STANDING FOR SILVER AT THE COMEX

We are now in the active delivery month of JULY and here the front month FELL by 16 contacts to stand at 96 contracts. We had 97 notices filed yesterday so we GAINED 81 contracts or an additional 405,000 oz refused to morph into London based forwards and receive a fiat bonus for their efforts.

The next delivery month, after July is the non active delivery month of August and here we lost 114 contracts to stand at 691. The next active delivery month after August for silver is September and here the OI FELL by 105 contracts UP to 155,445

We had 96 notice(s) filed for 480,000 OZ for the JULY 2018 COMEX contract for silver

AND NOW COMPARISON VS AUGUST LAST YR:

ON FIRST DAY NOTICE JULY 31/2017: 1,965,000 OZ STOOD FOR DELIVERY

THE FINAL AMOUNT OF SILVER STANDING: AUGUST 30.2017: 6,245,000 OZ AS WE HAD CONSIDERABLE QUEUE JUMPING.

FOR THE AUGUST CONTRACT MONTH:

LAST YEAR AT THIS TIME JULY 28.2017 WE HAD 394 SILVER COMEX OI OUTSTANDING VS TODAY: 691

SO, AS IN GOLD, WE ARE GOING TO HAVE A CONSIDERABLY LARGER AMOUNT OF SILVER STANDING FOR THE NON ACTIVE CONTRACT MONTH OF AUGUST THAN LAST YEAR.

FINAL standings for JULY/GOLD

JULY 30/2018.

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz |

NIL OZ

|

| Deposits to the Dealer Inventory in oz | NIL oz |

| Deposits to the Customer Inventory, in oz |

nil oz

|

| No of oz served (contracts) today |

135 notice(s)

13,500 OZ

|

| No of oz to be served (notices) |

0 contracts

(NIL oz)

|

| Total monthly oz gold served (contracts) so far this month |

234 notices

23400 OZ

.7278TONNES

|

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

we have a NO pulse today, AND zero gold enters the comex

For JULY:

Today, 135 notice(s) were issued from JPMorgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equates to 135 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped/ Received) by j.P.Morgan customer account.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

To calculate the INITIAL total number of gold ounces standing for the JULY. contract month, we take the total number of notices filed so far for the month (234) x 100 oz or 23400 oz, to which we add the difference between the open interest for the front month of JULY. (135 contracts) minus the number of notices served upon today (135 x 100 oz per contract) equals 23,400 oz,(.7278 tonnes) the number of ounces standing in this non active month of JULY

Thus the INITIAL standings for gold for the JULY contract month:

No of notices served (234 x 100 oz) + {(135)OI for the front month minus the number of notices served upon today (125 x 100 oz )which equals 23,400 oz standing in this NON – active delivery month of JULY .

We lost 0 contracts or an additional NIL oz will stand for comex delivery

THERE ARE ONLY 7.8648 TONNES OF REGISTERED COMEX GOLD AVAILABLE FOR DELIVERY AGAINST 0.7278 TONNES STANDING FOR JULY

IN THE LAST 24 MONTHS 85 NET TONNES HAS LEFT THE COMEX.

end

And now for silver

AND NOW THE JULY DELIVERY MONTH

JULY FINAL standings/SILVER

| Silver | Ounces |

| Withdrawals from Dealers Inventory | nil oz |

| Withdrawals from Customer Inventory |

NIL oz

|

| Deposits to the Dealer Inventory |

nil oz

|

| Deposits to the Customer Inventory |

1,694,001.520

jpmorgan

Scotia

|

| No of oz served today (contracts) |

96

CONTRACT(S)

(480,000 OZ)

|

| No of oz to be served (notices) |

0 contracts

(NIL oz)

|

| Total monthly oz silver served (contracts) | 6074 contracts

(30,370,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

we had 0 inventory movement at the dealer side of things

total dealer deposits: nil oz

total dealer withdrawals: nil oz

we had 2 deposit into the customer account

i) Into JPMorgan: 584,305.200 oz

*** JPMorgan for most of 2017 and in 2018 has adding to its inventory almost every single day.

JPMorgan now has 144 million oz of total silver inventory or 51.0% of all official comex silver. (144 million/283 million)

ii) into Scotia; 1,109,695.520oz

total customer deposits today: 1,694,001.720 oz

we had 0 withdrawals from the customer account;

total withdrawals: nil oz

we had 1 adjustment/

i) Out of CNT:

70,048.578 oz was adjusted out of the dealer and this landed into the customer account of CNT

total dealer silver: 78.575 million

total dealer + customer silver: 283.556 million oz

The total number of notices filed today for the JULY. contract month is represented by 96 contract(s) FOR 480,000 oz. To calculate the number of silver ounces that will stand for delivery in JULY., we take the total number of notices filed for the month so far at 6074 x 5,000 oz = 30,370,000 oz to which we add the difference between the open interest for the front month of JULY. (96) and the number of notices served upon today (96 x 5000 oz) equals the number of ounces standing.

.

Thus the INITIAL standings for silver for the JULY/2018 contract month: 5074(notices served so far)x 5000 oz + OI for front month of JULY(96) -number of notices served upon today (96)x 5000 oz equals 30,370,000 oz of silver standing for the JULY contract month

WE GAINED 81 CONTRACTS OR AN ADDITIONAL 405,000 OZ WILL STAND AS THESE GUYS REFUSED TO

MORPH INTO LONDON BASED FORWARDS AND RECEIVE A FIAT SWEETENER FOR THEIR EFFORTS.

PLEASE NOTE THE FOLLOWING FOR COMPARISON PURPOSES:

THE INITIAL STANDING FOR SILVER AT THE COMEX JULY 2017: 12.115 MILLION OZ ALTHOUGH AT MONTH’S END: 16.435 MILLION OZ STOOD FOR DELIVERY. THIS COMPARES WITH TODAY’S INITIAL STANDING FOR SILVER OF 30.370 MILLION OZ.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

ESTIMATED VOLUME FOR TODAY:45.191 CONTRACTS

CONFIRMED VOLUME FOR YESTERDAY: 64,114 CONTRACTS absolutely criminal

YESTERDAY’S CONFIRMED VOLUME OF 64,114 CONTRACTS EQUATES TO 320 million OZ OR 45.7% OF ANNUAL GLOBAL PRODUCTION OF SILVER

COMMODITY LAW SUGGESTS THAT OPEN INTEREST SHOULD NOT BE MORE THAN 3% OF ANNUAL GLOBAL PRODUCTION. THE CROOKS ARE SUPPLYING MASSIVE PAPER TRYING TO KEEP SILVER IN CHECK.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price at that day at $18.42

The previous record was 224,540 contracts with the price at that time of $20.44

end

NPV for Sprott

1. Sprott silver fund (PSLV): NAV FALLS TO -3.15% (JULY 30/2018)

2. Sprott gold fund (PHYS): premium to NAV FALLS TO -0.94% to NAV (JULY 30/2018 )

Note: Sprott silver trust back into NEGATIVE territory at -3.15%-/Sprott physical gold trust is back into NEGATIVE/

(courtesy Sprott/GATA)

3.SPROTT CEF.A FUND (FORMERLY CENTRAL FUND OF CANADA):

NAV 12.66/TRADING 12.21//DISCOUNT 3.47.

END

And now the Gold inventory at the GLD/

JULY 30/WITH GOLD DOWN $0.95/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 880.20 TONNES

july 27/WITH GOLD DOWN $2.85 TODAY, NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 800.20 TONNES

JULY 26./WITH GOLD DOWN $5.65: A WITHDRAWAL OF 2.35 TONNES OF GOLD FROM THE GLD/INVENTORY RESTS AT 800.20 TONNES

JULY 25/WITH GOLD UP $6.45; NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 802.55 TONNES

JULY 24/ WITH GOLD DOWN 10 CENTS: A HUGE DEPOSIT OF 4.42 TONNES INTO THE GLD/INVENTORY RESTS AT 802.55 TONNES

JULY 23/WITH GOLD DOWN $5.55: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 798.13 TONNES

JULY 20/WITH GOLD UP $4.15 A HUGE DEPOSIT OF 4.12 TONNES OF GOLD INTO THE GLD.INVENTORY RESTS AT 798.13 TONNES

JULY 19./WITH GOLD DOWN $1.00: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 794.01 TONNES

JULY 18/WITH GOLD UP 0.40: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 794.01 TONNES

JULY 17/WITH GOLD DOWN $12.40, WE HAD A BIG WITHDRAWAL OF 1.18 TONNES FROM THE GLD/INVENTORY RESTS AT 794.01 TONNES

JULY 16/WITH GOLD DOWN $1.55/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 795.19 TONNES

JULY 13/WITH GOLD DOWN $5.35 THE CROOKS RAID THE COOKIE JAR AGAIN TO THE TUNE OF 3.83 TONNES/INVENTORY RESTS AT 795.19 TONNES

JULY 12/WITH GOLD UP $2.30: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 799.02 TONNES

JULY 11/WITH GOLD DOWN $10.75 THE CROOKS RAIDED THE COOKIE JAR AGAIN TO THE TUNE OF 1.75 TONNES/INVENTORY RESTS AT 799.02 TONNES

JULY 10/WITH GOLD DOWN $3.85: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 800.77 TONNES

july 9/WITH GOLD UP $4.00/ANOTHER RAID ON THE GOLD COOKIE JAR: TWO WITHDRAWALS OF 1.18 TONNES THIS MORNING AND 1.47 TONNES THIS AFTERNOON/INVENTORY RESTS AT 800.77 TONNES

JULY 6/WITH GOLD DOWN $2.45: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 803.42 TONNES

JULY 5/WITH GOLD UP ANOTHER $5.15, THE CROOKS RAIDED THE COOKIE JAR AGAIN TO THE TUNE OF 5.89 TONNES/INVENTORY RESTS AT 803.42 TONNES IN THE LAST 10 TRADING DAYS GLD HAS LOST A HUGE 25.34 TONNES WITH A LOSS OF ONLY $15.25 IN PRICE

July 3/WITH GOLD UP $11.15/THE CROOKS RAIDED THE GLD INVENTORY AGAIN TO THE TUNE OF 9.73 TONNES/INVENTORY RESTS AT 809.31 TONNES

JULY 2/WITH GOLD DOWN $12.15, THE CROOKS RAIDED THE GLD INVENTORY AGAIN BY 1.47 TONNES DOWN./INVENTORY RESTS AT 819.04 TONNES

JUNE 29/WITH GOLD UP $3.70/A WITHDRAWAL OF 1.18 TONNES OF GOLD FROM THE GLD/INVENTORY RESTS AT 820.51 TONNES

JUNE 28/WITH GOLD DOWN $5.15/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 821.69 TONNES

June 27/WITH GOLD DOWN $3.60// TWO ENTRIES:/STRANGELY THE CROOKS RETURNED THE WITHDRAWAL OF 4.42 TONNES LAST NIGHT (THUS WE HAD A DEPOSIT OF 4.42 TONNES/INVENTORY RESTS AT 824.63 TONNES. /THEN LATE THIS AFTERNOON A WITHDRAWAL OF 2.94 TONNES

INVENTORY RESTS AT 821.69 TONNES/THIS VEHICLE IS AN OUTRIGHT FRAUD.

june 26/LATE LAST NIGHT, WITH GOLD DOWN $9.10 WE HAD A HUGE WITHDRAWAL OF 4.42 TONNES OF GOLD/INVENTORY RESTS AT 820.21 TONES

JUNE 25/WITH GOLD DOWN $1.45/NO CHANGE IN GOLD INVENTORY AT THE GLD.INVENTORY RESTS AT 824.63 TONNES

JUNE 22/WITH GOLD UP 25 CENTS TODAY, THE CROOKS WITHDREW A MASSIVE 4.13 TONNES OF GOLD/INVENTORY RESTS AT 824.63 TONNES

JUNE 21/WITH GOLD DOWN $4.00/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 828.76 TONNES

JUNE 20/WITH GOLD DOWN $3.55/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 828.76 TONNES

JUNE 19/WITH GOLD DOWN $1.50/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 828.76 TONES

JUNE 18/WITH GOLD UP $1.90/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 828.76 TONNES

JUNE 15/WITH GOLD DOWN $28.90/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 828.76 TONNES

JUNE 14/WITH GOLD UP $7.10/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 828.76 TONNES/

JUNE 13/WITH GOLD UP $2.20/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 828.76 TONNES

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

JULY 30/2018/ Inventory rests tonight at 800.20 tonnes

*IN LAST 419 TRADING DAYS: 130.73 NET TONNES HAVE BEEN REMOVED FROM THE GLD

*LAST 369 TRADING DAYS: A NET 25,81 TONNES HAVE NOW BEEN ADDED INTO GLD INVENTORY.

end

Now the SLV Inventory/

JULY 30/WITH SILVER UP 3 CENTS TODAY; NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 329.433 MILLION OZ.

JULY 27/WITH SILVER FLAT TODAY, NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 329.433 MILLION OZ/

JULY 26/WITH SILVER DOWN 10 CENTS: STRANGE: A BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.046 MILLION OZ OF SILVER/INVENTORY RESTS AT 329.433 MILLION OZ

JULY 25: WITH SILVER UP 8 CENTS TODAY: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV/ A WITHDRAWAL OF 658,000 INVENTORY RESTS AT 328.304 MILLION OZ/

JULY 24/WITH SILVER UP 8 CENTS TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 328.962 MILLION OZ/

JULY 23/WITH SILVER DOWN 11 CENTS/NO CHANGES IN SILVER INVENTORY INTO THE SLV/INVENTORY RESTS AT 328.962 MILLION OZ/

JULY 20/WITH SILVER UP 10 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.411 MILLION OZ INTO THE SLV INVENTORY

INVENTORY RESTS AT 328.962 MILLION OZ

JULY 19/WITH SILVER DOWN 17 CENTS TODAY; A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 752,000 OZ INTO THE SLV INVENTORY/INVENTORY RESTS AT 327.551 MILLION OZ/

JULY 18/WITH SILVER DOWN 3 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 326.799 MILLION OZ/

JULY 17/WITH SILVER DOWN 20 CENTS TODAY: A CHANGE IN SILVER INVENTORY A WITHDRAWAL OF 1.001 MILLION OZ FROM THE SLV: INVENTORY RESTS AT 326.799 MILLION OZ/

JULY 16/WITH SILVER FLAT TODAY, A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.128 MILLION OZ//INVENTORY RESTS AT 327.880 MILLION OZ

JULY 13/WITH SILVER DOWN 16 CENTS TODAY/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 326.752 MILLION OZ.

JULY 12/WITH SILVER UP 12 CENTS TODAY: ANOTHER BIG CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.035 MILLION OZ/INVENTORY RESTS AT 326.752 MILLION OZ/

JULY 11/WITH SILVER DOWN 22 CENTS TODAY: ANOTHER HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 565,000/INVENTORY RESTS AT 325.717 MILLION OZ

JULY 10/WITH SILVER DOWN 3 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 325.151 MILLION OZ

july 9/WITH SILVER UP 5 CENTS: ANOTHER BIG CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 847,000 OZ ADDED TO INVENTORY/INVENTORY RESTS AT 825.151 MILLION OZ/

JULY 6/WITH SILVER DOWN 2 CENTS/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 324.305 MILLION OZ/

JULY 5/WITH SILVER UP 6 CENTS, A GOOD CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 470,000 OZ/INVENTORY RESTS AT 324.305 MILLION OZ/ FOR THE PAST 10 TRADING DAYS, SILVER INVENTORY HAS ADVANCED BY 4.945 MILLION OZ WITH A LOSS OF 33 CENTS/PLEASE COMPARE THIS WITH THE GLD.

JULY 3/WITH SILVER UP 17 CENTS, A HUGE DEPOSIT OF 1.37 MILLION OZ ADDED TO THE SLV/INVENTORY RESTS AT 323.835 MILLION OZ.

JULY 2/WITH SILVER DOWN 31 CENTS/A HUGE 2.070 MILLION OZ DEPOSIT AT THE SLV/INVENTORY RESTS AT 322.465 MILLION OZ/

JUNE 29/WITH SILVER UP 14 CENTS TODAY, NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS THIS WEEKEND AT 320.395 MILLION OZ/

JUNE 28/WITH SILVER DOWN 18 CENTS, THE CROOKS ADDED 1.035 MILLION OZ OF SILVER INTO THE SLV/INVENTORY RESTS AT 320.395 MILLION OZ

JUNE 27.2018/WITH SILVER DOWN 8 CENTS/NO CHANGE IN SILVER INVENTORY/INVENTORY RESTS AT 819.360 MILLION OZ/

june 26./2018/WITH SILVER DOWN 8 CENTS, THE CROOKS WITHDREW THE DEPOSIT OF TWO DAYS AGO; 941,000 OZ OUT OF INVENTORY/INVENTORY RESTS AT 819.360 OZ

JUNE 25/WITH SILVER DOWN 12 CENTS/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 320.301 MILLION OZ/

JUNE 22/WITH SILVER UP 12 CENTS TODAY,ANOTHER BIG CHANGE IN SILVER INVENTORY AT THE SLV” A DEPOSIT OF 941,000 OZ INTO INVENTORY/INVENTORY RESTS THIS WEEKEND AT 320.301 MILLION OZ/

JUNE 21/WITH SILVER UP ONE CENT/ANOTHER CHANGE IN SILVER INVENTORY AT THE SLV/: A DEPOSIT OF 2.918 MILLION OZ/INVENTORY RESTS AT 319.360 MILLION OZ/ THUS FOR TWO STRAIGHT DAYS A TOTAL OF 5.26 MILLION OZ OF SILVER HAS BEEN ADDED WITH NO CHANGE IN PRICE.

JUNE 20/WITH SILVER DOWN ONE CENT/A HUGE CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY / A DEPOSIT OF 2.35 MILLION OZ/INVENTORY RESTS AT 316.442 MILLION OZ/

JUNE 19/2018/WITH SILVER DOWN 11 CENTS/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 314.090 MILLION OZ/

JUNE 18/WITH SILVER DOWN 6 CENTS TODAY/NO CHANGE IN SILVER INVENTORY/INVENTORY RESTS AT 314.090 MILLION OZ/

JUNE 15/WITH SILVER DOWN 75 CENTS/A BIG CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.788 MILLION OZ//INVENTORY RESTS AT 314.090 MILLION OZ

JUNE 14/WITH SILVER UP 30 CENTS, THE CROOKS DECIDED THAT THEY NEEDED SILVER INVENTORY BADLY SO THEY RAID THE SLV OF 1.412 MILLION OZ/INVENTORY RESTS AT 315.878 MILLION OZ/

JUNE 13/WITH SILVER UP 11 CENTS TODAY/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 317.290 MILLION OZ/

JULY 30/2018:

Inventory 329.433 MILLION OZ

6 Month MM GOFO 1.86/ and libor 6 month duration 2.53

Indicative gold forward offer rate for a 6 month duration/calculation:

G0FO+ 1.86%

libor 2.53 FOR 6 MONTHS/

GOLD LENDING RATE: .67%

XXXXXXXX

12 Month MM GOFO

+ 2.82%

LIBOR FOR 12 MONTH DURATION: 2.39

GOFO = LIBOR – GOLD LENDING RATE

GOLD LENDING RATE = +.43

end

Major gold/silver trading /commentaries for MONDAY

GOLDCORE/BLOG/MARK O’BYRNE.

Russia Sells 80% Of Its US Treasuries

Russia Sells 80% Of Its US Treasuries

Description: In just over 2 months Russia has sold-off over 85% of its holdings of U.S. Treasuries, should the U.S. be concerned?

– Russia has liquidated 85% of its US Treasury holdings in just two months

– Russia dumps over $90 billion of Treasuries in April and May as holdings collapse from near $100 billion to just $9 billion

– Deepening geo-political tensions between Russia and U.S. and Russian concerns about the dollar lead to selling

– Trump administration imposed new sanctions on April 6 on seven of Russia’s richest men and 17 top government officials

– Russia continues to accumulate gold bullion and deepening tensions may see this acceleratehttps://www.youtube.com/watch?v=oTZYwMP9dKQ

– Tensions between the U.S. and China are rising and China has been selling Treasuries and this may accelerate if trade wars and currency wars deepen

They sold basically 81 billion in two months, down from just under 100 billion. That’s an 80% reduction in two months!

Meanwhile they’re buying gold, they’re buying up to a million at one point, a million ounces of gold in certain months.

It’s a very important story. I don’t think the potential ramification of the story are being understood.

Tensions are running very, very deep and this appears to be a response by Russia to the sanctions from America……”

Trump Trade and Currency Wars With China – Goldnomics Podcast

Gold prices steady; central bank meetings, US data loom (IndiaTimes.com)

Iran currency extends record fall as U.S. sanctions loom (Reuters.com)

Russia’s gold reserves approaching Stalin-era record, cutting dependence on US dollar (RT.com)

Fed to send clear message that more rate hikes are coming (MarketWatch.com)

Gold Prices Fall Ahead of Central Bank Meetings (Investing.com)

Why Americans Are About To Experience Sharply Higher Prices (ZeroHedge.com)

Gold Technical Analysis: Bears await a break below an important horizontal support (FXStreet.com)

An open letter to the CFTC: Is a foreign power controlling Comex gold prices? (Gata.org)

S&P 500 vs. Gold: A Closer Look At Risk (GLD) (ETFDailyNews.com)

UPDATE 1-Putin says no plans to reject dollar but risks should be stemmed (Reuters.com)

Listen on SoundCloud , Blubrry & iTunes. Watch on YouTube below

Gold Prices (LBMA AM)

27 Jul: USD 1,219.15, GBP 931.06 & EUR 1,048.10 per ounce

26 Jul: USD 1,228.35, GBP 931.46 & EUR 1,049.13 per ounce

25 Jul: USD 1,230.55, GBP 935.09 & EUR 1,051.75 per ounce

24 Jul: USD 1,224.30, GBP 933.77 & EUR 1,047.63 per ounce

23 Jul: USD 1,229.45, GBP 937.21 & EUR 1,050.93 per ounce

20 Jul: USD 1,224.85, GBP 940.56 & EUR 1,050.80 per ounce

Silver Prices (LBMA)

27 Jul: USD 15.36, GBP 11.72 & EUR 13.20 per ounce

26 Jul: USD 15.54, GBP 11.79 & EUR 13.27 per ounce

25 Jul: USD 15.57, GBP 11.83 & EUR 13.31 per ounce

24 Jul: USD 15.51, GBP 11.81 & EUR 13.24 per ounce

23 Jul: USD 15.49, GBP 11.78 & EUR 13.22 per ounce

20 Jul: USD 15.37, GBP 11.79 & EUR 13.19 per ounce

Recent Market Updates

– Are China’s Gold Reserves Slowly Rising?

– Gold Outlook In H2 2018

– Gold Production In South Africa Continues To Collapse – Plummets 85% From Peak In 1970 (VIDEO)

– Physical Gold Is The “Best Defence” Against “Escalating Currency Wars”

– Trump and War With China? Goldnomics Podcast

– Weekly Digest – News, Market Updates and Videos You May Have Missed

– Financial Terrorism In The UK – Collusion between Government, Regulators & Two Bailed-Out UK Banks

– “Biggest Bubble in the History of Mankind” Is “Going To Burst” – Ron Paul

– Global Debt Time Bomb Surges To Nearly $250,000,000,000,000 – GoldCore Video

– Trump, Russia, Brexit and the Demand For Gold and Silver – GoldCore Video Interview

– Trump Is Serious About A Global Trade War

– Ponzi Economy Will Lead To Next Global Financial Crisis

– World Cup Is 200 Ounces Of Gold Worth £140,000 – 30% Less Than Harry Kane’s Weekly Wage

– Chaotic BREXIT More Likely: Risk To London, While Frankfurt, Luxembourg, Paris and Dublin Benefit

– VIDEO: Italy €2.4 Trillion Debt To Create Eurozone Contagion and Global Debt Crisis?

– U.S. China Trade War Escalates as Russia and China Accumulate Gold

Andrew Maguire’s Kinesis money which is a “bitcoin” but backed 100% by allocated gold and silver is set to go.

it think it would be a great idea to look at this!

please read at: https://kinesis.money/#/

(Andrew Maguire)

|

|

Dear Harvey Organ,

Thank you for your participation in our webinar on June 7th with our host and CEO of Kinesis, Thomas Coughlin.

The response we received has been incredible, we appreciate you taking the time to join us and hope you found it to be beneficial.

Due to such a high influx of questions we received we were unable to have them all answered. Nevertheless, if there was anything which requires more clarification, or you have a query which needs to be rectified, we invite you to join our telegram group:

We apologize for the technical issues we incurred during the webinar which resulted in it running a little over schedule, we hope that the next one we host will run seamlessly.

A video has been put together and uploaded onto our YouTube channel which can be found here:

Please share and subscribe to our YouTube channel to be notified of all the latest videos as they become available.

The rapid growth that we are currently experiencing has been incredible and with your support, is only going to get better.

We are working behind the scenes very hard to create a better experience for everyone involved! Stay tuned in as we have many more announcements to be released in the upcoming days.

Kind Regards,

|

Kinesis Money

a:C/O ILS Fiduciaries (IOM) Limited, First Floor,Millennium House, Victoria Road, Douglas, Isle of Man IM2 4RW

|

The following is self explanatory

(courtesy GATA/Chris Powell and Harvey Organ)

GATA asks bank regulator to check risks of gold

futures maneuver

Submitted by cpowell on Sun, 2018-06-10 16:17. Section: Daily Dispatches

12:21p ET Sunday, June 10, 2018

Dear Friend of GATA and Gold:

GATA has appealed to the U.S. comptroller of the currency, who has regulatory authority over banks, to review financial risks certain banks may have incurred through derivatives in the monetary metals markets, particularly through the recent heavy use of the “exchange for physicals” mechanism of settling gold and silver futures contracts on the New York Commodities Exchange.

The appeal was made in a letter sent May 5 to the comptroller, Joseph M. Otting, whose office is part of the U.S. Treasury Department, by your secretary/treasurer and GATA futures market consultant Harvey Organ.

“Exchange for physical” settlements of futures contracts long were considered emergency procedures when a seller was not able to deliver metal from an exchange-approved warehouse and wanted to settle with delivery elsewhere. But now such settlements appear to constitute most gold and silver futures settlements on the Comex. It is a strange development that appears to have been necessitated by the increasing difficulties of central banking’s gold and silver price suppression policy.

GATA has received no acknowledgment of the letter. Its text is below and a PDF copy of it is here:

http://www.gata.org/files/ComptrollerOfCurrencyLetter.pdf

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

* * *

May 5, 2018

Joseph M. Otting, Comptroller of the Currency

U.S. Treasury Department

400 7th Street, SW

Washington DC 20219

Dear Comptroller Otting:

Please let us bring to your attention financial risks to major banks involving their possibly unreported exposure to derivatives in the monetary metals markets.

In recent months gold and silver future contracts issued by U.S. banks on the New York Commodities Exchange have been moved off-exchange for delivery through a mechanism known as “exchange for physical” (EFP) contracts. Until recently use of this mechanism was considered an emergency procedure when a seller did not have access to metal for delivery through Comex warehouses. Now the mechanism seems to be in use for a large share of front-month contracts for which delivery is sought.

Here is an example that is happening at the Comex in the front active month of April for gold and the inactive delivery month of April for silver.

In gold, there were 229,436 EFP contracts for 713.64 tonnes, an average of 10,925 contracts and 1,092,500 ounces per trading day.

In silver, there were 77,150 EFP contracts for 385,750,000 ounces, an average of 3,673 contracts and 18,369,000 ounces per trading day.

London Bullion Market Association rules suggest that these contracts may not be reported to regulators. The LBMA’s bylaws say:

“Figures above exclude any contracts not subject to risk-based capital requirements, such as FX contracts with an original maturity of 14 days or less, futures contracts, written options, and basis swaps. Therefore, the total notional amount of derivatives by maturity will not add to the total derivatives figure in this table.”

We are told that these EFP contracts are transferred from the Comex to London as what are called “serial forwards” and their duration is always less than 14 days, which exempts them from being reported.

It is our understanding that in each quarter your office prepares a report detailing risk undertaken by the banks under the comptroller’s supervision.

These risks include derivatives undertaken by U.S. banks and other obligations that may cause a bank to fail. Our concern is that your office may not be aware of large unreported derivative exposure by banks.

Could you review this matter and let us know your conclusions?

Sincerely,

CHRIS POWELL

Secretary/Treasurer

HARVEY ORGAN

Consultant

Gold Anti-Trust Action Committee Inc.

7 Villa Louisa Road

Manchester, Connecticut 06043-7541

end

This is our letter to the CFTC it is quite explanatory: is a foreign power controlling the comex gold prices:

(courtesy Chris Powell, Harvey Organ)

An open letter to the CFTC: Is a foreign power controlling Comex gold prices?

Submitted by cpowell on Sun, 2018-07-29 02:21. Section: Daily Dispatches

July 28, 2018

J. Christopher Giancarlo, Chairman

Brian Quintenz, Commissioner

Rostin Behnam, Commissioner

U.S. Commodity Futures Trading Commission

3 Lafayette Centre

1155 21st Street, NW

Washington, D.C. 20581

Dear Chairman Giancarlo:

We would like to bring to attention four issues that need to be addressed in gold and silver futures trading.

1. For the second straight month, there has been a huge discrepancy between the preliminary gold open interest and the final number recorded on particular trading days.

Let us examine the one that just happened: July 26.

There was a preliminary Comex gold open interest gain of 3,349 contracts to 503,493. But there was a final Comex gold open interest loss of 14,443 contacts to 485,701 — a discrepancy of 27,792 contracts.

The open interest here is already 24 hours old. Our understanding is that these contracts are canceled for nonpayment. It would be almost impossible for such a large number of voided contracts not to have influenced the price of gold, especially when there was a raid on the Comex by the banks.

2. The huge issuance of “exchange for physical” settlements.

For quite some time we have been told by a CFTC official, Deputy Enforcement Director Matthew Hunter, that this was quite legal as these settlements were deliverable. But in our last email exchange with Hunter he wrote that these EFPs were not deliverable. The CFTC really should provide a thorough accounting of EFPs and explain how they settle contracts.

3. The gold Comex shows a huge open interest of 43,000 contracts remaining with one day before first notice day. So there likely will be a huge amount of gold contracts standing for deliver for the August contract month — probably 31 to 62 tonnes — with only 7.8 tonnes of registered gold at the Comex and with no gold having entered the Comex for some time. How could the banks throughout the last month have depressed the price of gold amid such huge physical demand and a tiny registered gold inventory available to settle?

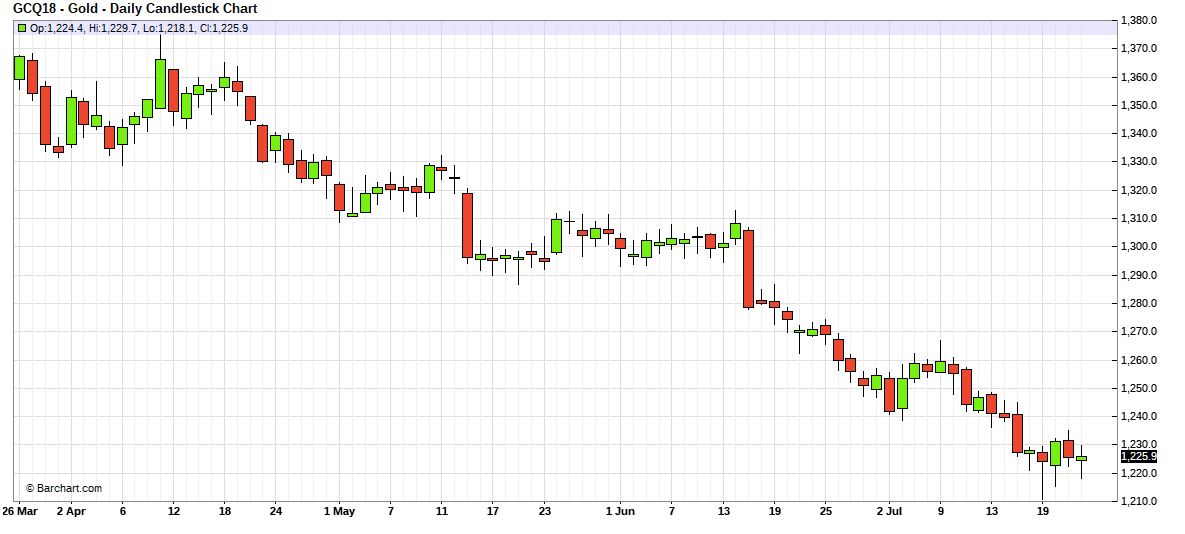

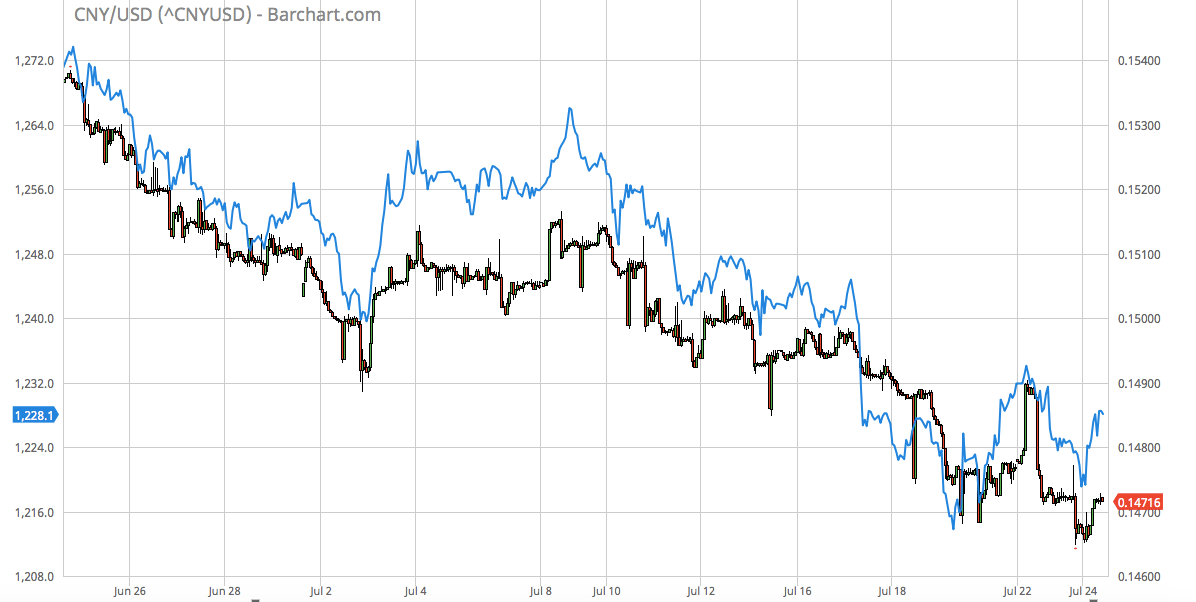

4. For the past month there has been a direct correlation between the value of the Chinese yuan and the price of gold. That is, the higher the yuan, the higher the price of gold and especially vice-versa.

The value of the Chinese yuan is essentially controlled by China’s central bank.

The Comex is generally considered the primary authority in pricing gold.

Here is recent commentary by monetary metals market analyst Craig Hemke on the recent perfect correlation between the yuan and gold:

https://www.sprottmoney.com/Blog/potential-impacts-of-the-yuan-gold-peg-…

* * *

Hemke writes:

“Though the People’s Bank of China has long maintained a ‘peg’ in the relative valuation of the yuan versus the dollar, the past 90 days have seen a steady devaluation of this peg to the tune of nearly 8 percent. See this chart:

“Over the period in this chart the price of Comex gold has fallen by more than 10 percent:

“To make this correlation clearer, let’s plot the two prices together. This correlation has become extraordinarily tight over the past month, as you can see below where the CNY/USD exchange rate is displayed in candlesticks and Comex gold is a blue line:

“And when you draw it down to just the past five days, the two prices react to each other almost simultaneously:

“This is not a correlation searching for a cause, nor is it a simple act of ‘traders’ reacting to a falling yuan by selling digital gold. No, in a market the size of global gold, this immediate correlation can be accomplished only through massive interventions, the size and scope of which are possible only at the state/sovereign level. And which state/sovereign would have a direct interest in linking the dollar price of gold to the yuan? China, of course.”

* * *

So how does the CFTC allow a foreign government or entity to control the price of this important commodity and currency by trading in U.S. markets?

Or is market manipulation by a foreign power happening with the authorization of the U.S. government?

HARVEY B. ORGAN, Consultant

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

Manchester, Connecticut

CPowell@GATA.org

end

David Brady talks about the gold/yuan valuation and how a steep 25% devaluation by the Chinese government will cause the markets to crash and send gold northbound

(courtesy David Brady/Sprott Money)

David Brady: Gold, the yuan, devaluation, and crash

Submitted by cpowell on Fri, 2018-07-27 19:09. Section: Daily Dispatches

3:10p ET Friday, July 27, 2018

Dear Friend of GATA and Gold:

Now that China is rigging the gold market, tying the gold price and the value of the International Monetary Fund’s Special Drawing Rights to the value of the Chinese yuan, money manager David Brady speculates today on gold’s course under a sharp, single devaluation of the yuan and under the yuan’s continued gradual devaluation.

A single, sharp devaluation of the yuan, Brady believes, would send gold soaring.

Brady’s analysis is headlined “Gold, CNY, Devaulation, and Crash” and it’s posted at Sprott Money here:

https://www.sprottmoney.com/Blog/gold-cny-devaluation-and-crash.html

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

China is still embracing dollar denominated debt

(courtesy Bloomberg)

The $500 billion market the world never thought it would see

Submitted by cpowell on Mon, 2018-07-30 01:43. Section: Daily Dispatches

By Chris Anstey and Narae Kim

Bloomberg News

Sunday, July 29, 2018

China used to rail against the outsize role of the U.S. dollar. But in a major turnaround, the world’s second-biggest economy has started embracing the currency of its larger rival.

Chinese companies and banks — and even the government — sold bonds denominated in dollars at a record pace last year, and underwriters expect that growth to continue for years. The roughly half-trillion-dollar market has two key attractions for China’s borrowers. For some, it’s an easier place to raise cash than at home — where regulators are cracking down on leverage. For others, dollars are simply easier to use to fund acquisitions and investments abroad.

The upshot: There’s a large and growing supply of dollar securities that offer exposure to Chinese companies for investors wary of diving into the country’s increasingly accessible yuan — denominated domestic debt. The offshore bond market is also set to provide a stake in President Xi Jinping’s “Belt and Road” initiative (BRI) — a grand plan that envisions deepening trade and investment ties with countries across the Eurasian landmass and beyond. Bankers see the BRI as a key source of growth in Chinese dollar bonds. …

… For the remainder of the report:

https://www.bloomberg.com/news/articles/2018-07-29/china-s-huge-u-s-curr…

Your early MONDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

i) Chinese yuan vs USA dollar/CLOSED DOWN TO 6.8218/HUGE DEVALUATION FOR THE PAST TWO WEEKS RESUMES /shanghai bourse CLOSED DOWN 4.54 POINTS OR 0,16% /HANG SANG CLOSED DOWN 71,15 POINTS OR 0.25%

2. Nikkei closed DOWN 167.91 POINTS OR 0.74%/USA: YEN RISES TO 111.07/

3. Europe stocks OPENED RED /

USA dollar index FALLS TO 94.53/Euro RISES TO 1.1686

3b Japan 10 year bond yield: RISES TO . +.010/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 111.07/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD IS NOW TARGETED AT .11%/JAPAN LOSING CONTROL OF THEIR BOND MARKET

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 69.71 and Brent: 74.78

3f Gold UP/Yen DOWN

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil UP for WTI and UP FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund RISES TO +.440%/Italian 10 yr bond yield DOWN to 2.75% /SPAIN 10 YR BOND YIELD UP TO 1.40%

3j Greek 10 year bond yield RISES TO : 3.88

3k Gold at $1223.20 silver at:15.52 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble UP 9/100 in roubles/dollar) 62.62

3m oil into the 69 dollar handle for WTI and 74 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 111.07 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 0.9924 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1595 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now POSITIVE territory with the 10 year RISING to +0.44%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.98% early this morning (THIS IS DEADLY TO ALL MARKETS). Thirty year rate at 3.11%

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

(courtesy Jim Reid/Bloomberg/Deutsche bank/zero hedge)

Futures Flat As Global Stocks Slump To Start

Torrid Week

A “storm of news” may be coming this week ahead of the start of summer vacation season, but the overnight session has been surprisingly quiet, with the BOJ’s bond market intervention – the 3rd in the past week – the most notable event so far.

“It’s been a somewhat slow start, but not surprising given the action-packed week that lies ahead which includes the BOJ, BOE, Fed, global PMI data, NFP,” said Oanda’s head of APAC trading, Stephen Innes. “Indeed, central bank policy is back at the forefront of market discussions and particularly the BOJ rate decision and outlook report July 31.”

Among the most notable overnight moves, the JGB curve steepened again leading core rates markets, even as the BOJ’s latest YCC operation saw heavy offers accepted as BOJ buys above market price. Sparked by fears the BOJ may tweak its QE program, large futures blocks in gilts, USTs and bunds through early trading accelerated the selloff. Meanwhile, the USD slowly weakened across G-10; SEK spiked higher on strong domestic GDP data while TRY tumbled as Erdogan showed little concern for potential U.S. sanctions; the Chinese yuan initially slumped but is now broadly unchanged. European equity markets hold small losses with Heineken (-5.0%) sliding and dragging the food and beverage sector lower after poor earnings guidance; U.S. equity futures bounced from overnight lows however still at bottom end of Friday’s range.

World stocks fell modestly, US equity futures were flat, the dollar dropped on Monday, 10Y yield rose as high as 2.985%, JGBs sold off before possible BOJ monetary policy tweaks, and most metals fell on continued concern over global trade and China’s economy as a busy week of central bank meetings and company updates started.

Disappointing updates from U.S. tech heavyweights soured the mood across stock markets, knocking European shares off their six-week highs at the open and dragging down by 0.11% the MSCI world index.

As we discussed in “A Record Number Of Companies Are Beating Estimates… And It’s Not Enough“, JCI Capital’s strategist Alessandro Balsotti said that “quarterly results continue to be more than good overall, but markets appear to be particularly sensitive to the sporadic negative updates, especially from tech stocks.”

JPMorgan reported relatively aggressive moves into “value” stocks – in particular banks – and away from shares leveraged to economic growth: “Tech really began cracking on Tuesday before the floodgates opened on Friday,” JPM analysts wrote. “The rotation will likely continue, benefiting value categories at the expense of momentum/tech as rates are biased higher. Europe’s higher weighting to banks/resource will help it vs the U.S.”

Miners and food and beverage makers were among the top losers in the Stoxx Europe 600 Index. Equity specific news is supporting the FTSE MIB and IBEX with Mediaset (+3.0%) reporting positive earnings. The AEX (-0.4%) is currently the underperforming bourse as index heavy-weights Heineken (-4.1%) and Altice (-2.4%) are both in the red on the back of negatively revised guidance and a branch sale.

Earlier, Asian stock markets similarly began the week on the back foot after the tech-led declines last Friday on Wall Street and amid cautiousness ahead of this week’s slew of risk events, while further CNH weakness also dampened sentiment. ASX 200 (-0.4%) and Nikkei 225 (-0.7%) were in the red with the worst performing stocks pressured by corporate updates including Syrah Resources and Dainippon Sumitomo Pharma. Elsewhere, Hang Seng (-0.6%) and Shanghai Comp. (-0.2%) were initially choppy after the PBoC refrained from reverse repo operations for a 7th consecutive occasion but noted that month-end fiscal spending will increase bank liquidity, while further CNH weakness eventually weighed on sentiment and proved to be the deciding factor.

Futures on the S&P 500, Dow and Nasdaq all pointed to a softer open following declines across most Asian markets.

In FX, after starting off strong, the dollar slipped against most G-10 peers at the start of a busy week which sees decisions from the Fed, BOJ and BOE. The Bloomberg Dollar Spot index edges lower by 0.1% with the greenback down against seven of G-10 peers.

The Japanese yen erased initial gains and Japanese 10-year yields retreated from an almost 18-month high after the the BOJ offered to buy an unlimited amount of bonds to stem fears the bank will tweak their ultra-loose policy this week and unleash a rout. The euro rose after German regional inflation data. Sweden’s krona strengthened the most in four weeks against the euro after data showed the nation’s economic growth accelerated more than forecast in the second quarter.

Helped by the weaker dollar, emerging-market shares slipped while their currencies were stable, with a few notable exceptions: the Yuan and Lira have picked up where they left off last week, on the back foot, with USDCNY, USDCNH and USDTRY all higher. The PBOC yuan fixing dropped by 0.28% to 6.8131 per USD, the weakest level since June 2017 while the Turkish Lira continues to suffer after last week’s shock CBRT decision to leave key rates unchanged, with the focus now switching to the latest Inflation Report on Tuesday. The offshore yuan declined as much as 0.5% to 6.8497 per dollar, as China’s central bank weakened its daily reference rate and the dollar advanced.

“The EM FX will remain under weakening pressure in the days and months ahead,” says Prakash Sakpal, a Singapore-based economist at ING Groep NV.

Overnight Bloomberg reported that analysts say China may cut RRR in 3Q, according to a China Securities Journal commentary. In separate comments, China’s Foreign Minister Wang Yi said at a press conference in Beijing that Chinese self-defense is justifiable in the face of an aggressive U.S.

Treasuries fell with euro-area debt, with the curve bear- steepening, matching moves across most of Europe.

In commodities, oil prices rose but gains were limited as the fallout from trade tensions weighed on markets: WTI (+0.9%) and Brent Crude (+0.2%) recovered losses seen at the back end of last week following an uptick in the Baker Hughes rig count while Mexican President Obrador stated his administration will hike crude production by 600K BPD.

Looking at the week ahead (read our full preview here), core central-bank policy decisions and 145 S&P company earnings reports, including from Apple and Tesla, are set to dominate news. Tonight, traders will focus whether the BOJ will fine tune its policy and later in the week will look for any indications the Federal Reserve is shying away from two more interest-rate hikes before the end of this year.

Expected data on deck includes pending home sales and Dallas Fed Manufacturing Activity. Caterpillar, Loews, and Seagate are among companies reporting earnings

Market Snapshot

- S&P 500 futures little changed at 2,815.25

- STOXX Europe 600 down 0.2% to 391.13

- MXAP down 0.4% to 168.14

- MXAPJ down 0.3% to 543.78

- Nikkei down 0.7% to 22,544.84

- Topix down 0.4% to 1,768.15

- Hang Seng Index down 0.3% to 28,733.13

- Shanghai Composite down 0.2% to 2,869.05

- Sensex up 0.4% to 37,496.31

- Australia S&P/ASX 200 down 0.4% to 6,278.39

- Kospi down 0.06% to 2,293.51

- German 10Y yield rose 2.1 bps to 0.424%

- Euro up 0.09% to $1.1668

- Italian 10Y yield rose 3.9 bps to 2.476%

- Spanish 10Y yield rose 2.7 bps to 1.402%

- Brent futures up 0.4% to $74.56/bbl

- Gold spot down 0.2% to $1,222.26

- U.S. Dollar Index down 0.2% to 94.51

Top Overnight News from Bloomberg

- The Bank of Japan bought 1.6t yen worth of 10-year bonds at its fixed-rate operation on Monday, the third offer to buy an unlimited amount of debt for in a week amid speculation the central bank may adjust its ultra-loose monetary policy

- Confidence in the euro-area economy dropped to its lowest level in a year, suggesting that the global trade conflict can weigh down growth momentum. The European Commission’s measure of corporate and household sentiment index fell for a seventh straight month in July. Among executives, their view of the business climate dropped to an 11-month low

- No increase in interest rates is expected when Federal Reserve officials gather on Tuesday and Wednesday in Washington, according to pricing in federal funds futures and all but one of the 57 economists polled by Bloomberg

- China Foreign Minister: U.S. did not fulfill its obligations during the trade negotiations; China has a right of self-defense

- Italy’s Prime Minister Giuseppe Conte is set to burnish his government’s ties with the Trump administration, after his deputy premiers stoked tensions with the European Union

- President Trump floated the idea shutting down the government if he doesn’t get his way on immigration measures, including funding for a wall on the U.S. border with Mexico

- Second-quarter surge shows the U.S. economy is “well on the path” for four or five years of sustained annual growth of 3 percent, Treasury Secretary Steven Mnuchin said

- Billionaire industrialist Charles Koch said he worries President Trump’s actions on trade and tariffs put the U.S. economy at risk of recession

- Theresa May was given fresh hope of getting a post-Brexit trade deal from outside the U.K., even as members of her Conservative Party back home vented their anger at her proposals

- Greece is planning a return to the debt markets in a bid to regain its status as a “normal” country

- Italy’s Deputy Premier Luigi Di Maio said the government will go ahead with its plan to introduce a flat tax and an assured basic income, while scraping a landmark pension reform

- German Jul. Regional CPIs y/y (National est. 2.1%): Saxony 2.2%, Baden Wuert. 2.2%, Brandenburg 2.2%, Hesse 1.8%, Bavaria 2.2%, NRW 2.0%

- Sweden 2Q GDP q/q: 1.0% vs 0.5% est; consumer spending +0.9%, inventories add 0.3pps to overall growth

Asian equity markets began the week lacklustre after the tech-led declines last Friday on Wall Street and amid cautiousness ahead of this week’s slew of risk events, while further CNH weakness also dampened sentiment. ASX 200 (-0.4%) and Nikkei 225 (-0.7%) were in the red with the worst performing stocks pressured by corporate updates including Syrah Resources and Dainippon Sumitomo Pharma. Elsewhere, Hang Seng (-0.6%) and Shanghai Comp. (-0.2%) were initially choppy after the PBoC refrained from reverse repo operations for a 7th consecutive occasion but noted that month-end fiscal spending will increase bank liquidity, while further CNH weakness eventually weighed on sentiment and proved to be the deciding factor. Finally, 10yr JGBs were marginally lower in a continuation of the losses triggered by ongoing BoJ speculation ahead of tomorrow’s policy announcement, while T-notes were uneventful amid tentativeness ahead of the looming risk events. Heading into EU trade, the BoJ once again announced a fixed-rate JGB operation which was met with a muted reaction by the market.

Top Asian News

- China’s IPO Frenzy Is Starting to Fade as Issuers Slash Prices

- JPMorgan Leads Charge as India Logs Record $98 Billion in Deals

- China Human Vaccine Scare Wipes $483 Million From Pig Drug Stock

- No Profit? No Problem. Another Billionaire Rises in China

- July’s Been Good But Emerging Assets Aren’t Out of the Woods

Major European equity bourses are largely lower, with the FTSE MIB (+0.1%) the only bourse in the green, breaking though its 50 DMA of 21,913. Equity specific news is supporting the FTSE MIB and IBEX with Mediaset (+2.0%) reporting positive earnings and Sabadell (+2.7%) upgraded at KBW to outperform from underperform. The AEX (-0.3%) is currently the underperforming bourse as index heavy-weights Heineken (-5.0%) and Altice are both in the red on the back of negatively revised guidance and a branch sale. Taking a look at sectors, broad based losses are being seen with slight underperformance noted in the IT sector, following on from uninspiring performance in US counterparts on Friday. GVC Holdings (+5.0%) has assured a USD 200mln tie-up with the MGM group. Both the GEA Group (+6.0%) and Air Liquide (-2.6%) reported earnings, with GEA beating expectations and Air Liquide operating income falling short of expectations.

Top European News

- Swedish Economy Heats Up in Second Quarter on Consumer Spending

- Domino’s Pizza Group Falls After Media Report on Franchisees

- Italy Offers May Brexit Olive Branch as Grassroots Tories Revolt

- U.K. Ministers Fear Bloody Last Chapter in May’s Brexit Thriller

- Pound Optimism Ebbs as Brexit Gloom Overwhelms BOE Hike Prospect

- Greece’s Plan to Return to Markets While Viable Faces Risks

In currency markets, the chance of a BoJ shift has sent the yen higher in the last week or so, leaving the dollar around 111.05 yen from a peak of 113.18 earlier in the month. Against a basket of currencies the dollar was hovering at 94.606 having repeatedly failed to clear resistance around 95.652 this month. The euro edged up to $1.1664 against the dollar in early European trading, after the European Central Bank reaffirmed last week that rates would remain low through the summer. In Asia, eyes were on China’s yuan after it suffered the longest weekly losing streak since November 2015. It duly weakened further, slipping past 6.8400 per dollar for the first time since June last year.

In commodities, WTI (+0.9%) and Brent Crude (+0.2%) recuperate losses (with the latter breaching USD 74.50/bbl to the upside) seen at the back end of last week following an uptick in the Baker Hughes rig count while Mexican President Obrador stated his administration will hike crude production by 600K BPD. Though news flow remains relatively light, a 12-hour strike is to start at Total’s UK offshore platforms at 12:00BST. Metals trade mostly lower with spot gold marginally easing, yet still rangebound, moving with an uneventful greenback ahead of key risk events this week (FOMC interest rate decision on Wednesday, US jobs data on Friday). Copper continues to trade lower while reports stated that workers at the world’s largest copper mine, Escondida mine in Chile, have rejected the final contract offer over wages and are voting whether to go on strike.

US Event Calendar

- 10am: Pending Home Sales MoM, est. 0.2%, prior -0.5%

- 10am: Pending Home Sales NSA YoY, prior -2.8%

- 10:30am: Dallas Fed Manf. Activity, est. 31, prior 36.5

DB’s Craig Nicol concludes the overnight wrap

A quick glance at our screens this morning shows that markets in Asia have started the week fairly sluggish. The Nikkei (-0.68%), Hang Seng (-0.69%), Shanghai Comp (-0.16%) and Kospi (-0.12%) are all in the red, seemingly playing catch up to Friday’s weaker session on Wall Street. Futures on the S&P are also weaker (-0.27%) while the focus in bonds is on JGBs once more where 10y yields are testing that upper limit again, having broken through 0.10%. In fairness there was very little in the way of new news for markets over the weekend to change the narrative. US Treasury Secretary Steven Mnuchin said on Fox News yesterday that the US is “well on the path” for sustained growth of 3% a year for “several years”, while White House Economic Director Larry Kudlow said that President Trump “deserves the victory lap” following Friday’s solid Q2 GDP print.

Back to those central bank meetings this week, which of the three, the BoJ on Tuesday might be the most hotly anticipated given the various stories related to a possible yield curve tweaking over the last week. That said our Japan economists do expect the BoJ to maintain its current policy stance. In consideration of the side effects of its policy, the team believe that the BoJ will declare at the end of its statement that, based on its analysis in its quarterly Outlook Report, that it will maintain its easing policy for an extended period but will conduct financial market operations and asset purchasing operations to address the mounting cumulative side effects. Our colleagues believe one measure to deal with such side effects will include an overhaul of its ETF purchasing operations (a shift from Nikkei 225-linked ETF to Topix-linked ETF). An increase in the JGB yield target appears unlikely at a time when it is expected to revise downward its inflation forecast.

For the Fed on Wednesday, no change in policy is expected and given that this is not a meeting that includes a post-meeting conference or a fresh summary of economic projections, it’s likely that this will be less of a market mover. Our economists expect any changes to be perfunctory and cosmetic, though they note that the Fed could acknowledge some recent softness in the housing data. As a complement to June’s removal of forward guidance language, the statement could also include some language, such as the phrase “for now” featured in Powell’s recent monetary policy testimony. In the view of our economists, such verbiage would have the effect of including uncertainty into their gradual rate hike mantra. In our colleagues view this would de-emphasise forward guidance and reiterate that their actions are data dependent. More from our economists preview on the Fed here.

As for the third central bank this week, the consensus expectation is that the BoE will deliver a 25bp hike on Thursday, something that the market is currently assigning a 85% chance of happening. Should they hike, which our economists expect the BoE to do albeit dovishly, then this would mark the first time since 2009 that the bank rate would be above 0.5%. It’s worth noting that the latest BoE economic projections will also be released alongside the policy decision, including new forecasts for growth and inflation. It’s also expected that BoE Governor Carney will offer an updated view on the neutral rate. On that our UK economists published a preview note (link) where they argue that the UK’s current neutral rate is between 0.25% to 0.50% with the risk being that the BoE’s estimate is at the higher end of this range. This would translate into a nominal rate of between 1.75% to 2.50%.

If that wasn’t enough, as noted at the top there’s also another employment report to get through in the US on Friday – the highlight of this week’s data. Expectations are for a 193k July payrolls reading, an unemployment rate of 3.9% (down one-tenth from June) and an average weekly earnings reading of +0.3% mom. Our US economists also expect a +0.3% earnings print while their forecast for payrolls is 180k.

Other than that, we’ve also got the June PCE and Q2 ECI data out in the US on Tuesday. Our economists are forecasting +0.7% qoq for ECI and a core PCE reading of +0.1% mom reflecting the weakness in the core CPI print in June. If the latter comes in as our economists expect then the annual reading will round down one-tenth to +1.9%, however this should be taken with a grain of salt given the BEA benchmark revisions with recent quarters’ inflation data revised upwards. In actual fact we’ll get a decent opportunity to test the global inflation pulse this the Eurozone, France and Italy on Tuesday. The Eurozone core reading is expected to come in at +1.0% yoy and up one-tenth from June.

Last but by no means least, it’s another big week for earnings with 145 S&P 500 companies due to report. The big highlights are Caterpillar on Monday – which is always a good barometer for global growth – Apple, Procter & Gamble and Pfizer on Tuesday, Metlife on Wednesday, Dupont on Thursday, and Berkshire Hathaway on Friday. In Europe we’ll also get releases from the likes of Volkswagen, Siemens, BP, Barclays and Credit Suisse.

Earnings certainly dictated much of how equity markets performed last week and it was no different on Friday with disappointing Twitter (-20.54%) and Intel results (-8.59%) contributing to the Nasdaq’s decline (-1.46%), while the S&P 500 (-0.66%) also finished lower. The Nasdaq was actually the only US equity markets that fell last week (-1.06%), while the S&P (+0.61%) and Dow (+1.57%) both advanced. In Europe, equities were all higher on Friday, with the focus also on earnings. The Stoxx 600 closed up +0.40% on Friday and posted its highest weekly gain since early March (+1.68%). Meanwhile core European government bonds were little changed on Friday while 10y Treasury yields dipped -2.2bp following the Q2 GDP data.