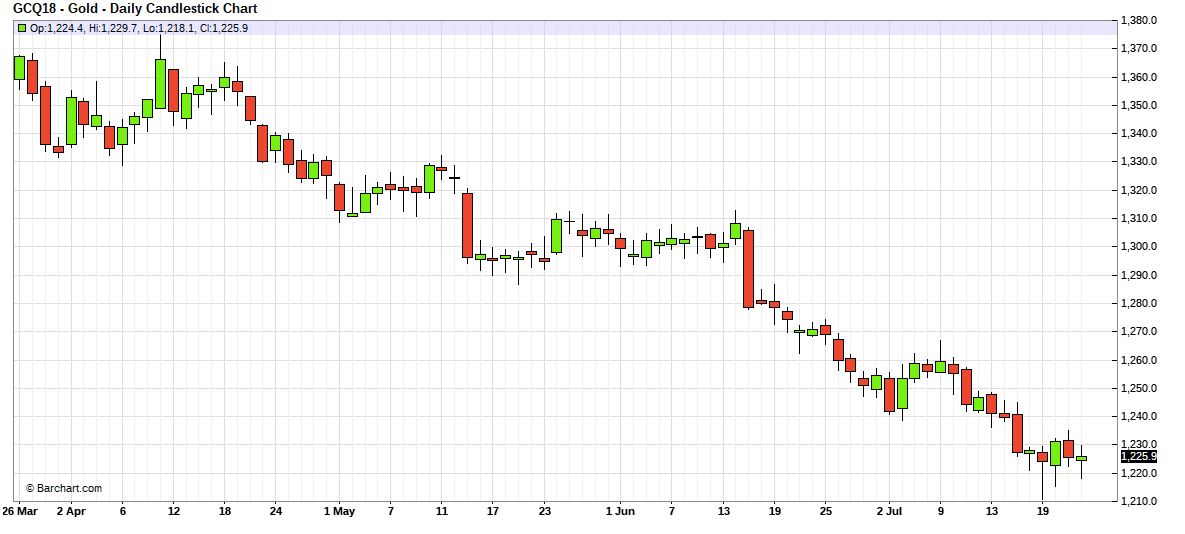

GOLD: $1224.65 UP $2.05 (COMEX TO COMEX CLOSINGS)

Silver: $15.56 UP 5 CENTS (COMEX TO COMEX CLOSINGS)

Closing access prices:

Gold $1224.10

silver: $15.53

For comex gold:

JULY/

NUMBER OF NOTICES FILED TODAY FOR AUGUST CONTRACT:37 NOTICE(S) FOR 3700 oz

TOTAL NOTICES SO FAR 37 FOR 3700 OZ (0.1150 tonnes)

For silver:

JULY

255 NOTICE(S) FILED TODAY FOR

1,275,000 OZ/

Total number of notices filed so far this month: 255 for 1,275,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: BID $7919/OFFER $8003: DOWN $198(morning)

Bitcoin: BID/ $7661/offer $7746: DOWN $457 (CLOSING/5 PM)

end

First Shanghai gold fix comes at 10 pm est

The second Shanghai gold fix: 2:15 pm

First Shanghai gold fix gold: 10 pm est: $1225.59

NY price at the same time:1220.70

PREMIUM TO NY SPOT: $4,89

XX

Second gold fix early this morning: $1225.69

USA gold at the exact same time:$1221.95

PREMIUM TO NY SPOT: $3.74

China is controlling the gold market

WE WILL NOT PROVIDE LONDON FIXES AS THEY ARE NOT ACCURATE AS TO WHAT IS GOING ON AT THE SAME TIME FRAME.

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total OPEN INTEREST ROSE BY A CONSIDERABLE SIZED 2461 CONTRACTS FROM 218,477 UP TO 220,908 DESPITE YESTERDAY’S TINY 3 CENT GAIN IN SILVER PRICING AT THE COMEX. WE HAVE NOW WITNESSED A SLOW COMEX ACCUMULATION THESE PAST SEVERAL DAYS. ON TOP OF THIS WE HAVE ALSO WITNESSED A LARGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY(WELL OVER 30 MILLION OZ AT THE COMEX) AS WELL AS CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A SMALL SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP: 617 EFP’S FOR SEPT. , 0 EFP’S FOR DECEMBER AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE: OF 617 CONTRACTS. WITH THE TRANSFER OF 800 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 617 EFP CONTRACTS TRANSLATES INTO 3.085 MILLION OZ AND ACCOMPANYING:

1.THE 3 CENT GAIN IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR THE JUNE/2018 COMEX DELIVERY MONTH. (5.420 MILLION OZ) 30.370 MILLION OZ FINALLY STANDING FOR DELIVERY IN JULY, AND NOW 3.260 MILLION OZ FOR AUGUST.

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF JULY:

34,568 CONTRACTS (FOR 21 TRADING DAYS TOTAL 34,568 CONTRACTS) OR 172.84 MILLION OZ: (AVERAGE PER DAY: 1646 CONTRACTS OR 8.230 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF JULY: 172.84 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 24.25% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2018 TO DATE SILVER EFP’S: 1,832.57 MILLION OZ.

ACCUMULATION FOR JAN 2018: 236.879 MILLION OZ

ACCUMULATION FOR FEB 2018: 244.95 MILLION OZ

ACCUMULATION FOR MARCH 2018: 236.67 MILLION OZ

ACCUMULATION FOR APRIL 2018: 385.75 MILLION OZ

ACCUMULATION FOR MAY 2018: 210.05 MILLION OZ

ACCUMULATION FOR JUNE 2018: 345.43 MILLION OZ

ACCUMULATION FOR JULY 2018: 172.84 MILLION OZ

RESULT: WE HAD A CONSIDERABLE SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 2461 DESPITE THE TINY 3 CENT GAIN IN SILVER PRICING AT THE COMEX YESTERDAY. THE CME NOTIFIED US THAT WE HAD A SMALL SIZED EFP ISSUANCE OF 617 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) . FROM THE CME DATA: 617 EFP’S FOR SEPT, 0 EFP’S FOR DECEMBER AND ZERO FOR ALL OVER MONTHS FOR A DELIVERABLE FORWARD CONTRACT OVER IN LONDON WITH A FIAT BONUS (TOTAL: 617). TODAY WE GAINED A GOOD SIZED: 3078 TOTAL OI CONTRACTS ON THE TWO EXCHANGES:

i.e 617 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH AN INCREASE OF 2461 OI COMEX CONTRACTS. AND ALL OF THIS DEMAND HAPPENED WITH A 3 CENT GAIN IN PRICE OF SILVER AND A CLOSING PRICE OF $15.51 WITH RESPECT TO YESTERDAY’S TRADING. YET WE HAD A GIGANTIC AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY IN THE BIG JULY DELIVERY MONTH OF SLIGHTLY OVER 30 MILLION OZ AND NOW IN AUGUST ANOTHER BIG 3.620 MILLION OZ IN A NON ACTIVE MONTH. IT SURE LOOKS LIKE ANOTHER FAILED BANKER SHORT COVERING EXERCISE AS BANKERS ARE SCRAMBLING TO COVER THEIR HUGE SHORTFALL.

In ounces AT THE COMEX, the OI is still represented by OVER 1 BILLION oz i.e. 1.106 MILLION OZ TO BE EXACT or 157% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT JULY MONTH/ THEY FILED AT THE COMEX: 255 NOTICE(S) FOR 1,275,000 OZ OF SILVER

IN SILVER, WE SET THE NEW RECORD OF OPEN INTEREST AT 243,411 CONTRACTS ON APRIL 9.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $16.51

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) AND JULY 2018 AMOUNT FINALLY STANDING: 30.370 MILLION OZ ) AND NOW FOR AUGUST 3.260 MILLION OZ.

- HUGE RECORD OPEN INTEREST IN SILVER 243,411 CONTRACTS (OR 1.217 BILLION OZ/ SET APRIL 9/2018

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017

- RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT).

IN GOLD, THE OPEN INTEREST FELL BY ANOTHER HUMONGOUS SIZED 13,577 CONTRACTS DOWN TO 449,871 DESPITE THE SMALL FALL IN THE COMEX GOLD PRICE/YESTERDAY’S TRADING (A LOSS IN PRICE OF $0.95). GENERALLY WE SEE COMEX LIQUIDATION WHEN WE ARE ENTERING THE LAST DAYS IN THIS ACTIVE DELIVERY MONTH OF JULY AND IT SURELY HAPPENED ON FRIDAY. WE GENERALLY SEE THE BOYS CASHING IN THEIR COMEX LONGS TO BEGIN THE PROCESS TO MOVE INTO LONDON FORWARDS. THIS PROCEDURE HAS BEEN GOING ON NOW FOR OVER 2 AND 1/2 YEARS. THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 4,238 CONTRACTS:

AUGUST SAW THE ISSUANCE OF: 0 CONTRACTS, OCTOBER SAW THE ISSUANCE OF 0 CONTRACTS AND DECEMBER HAD AN ISSUANCE OF 4238 CONTACTS AND THEN ALL OTHER MONTHS ZERO. The new COMEX OI for the gold complex rests at 449,871. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE ANOTHER STRONG OI LOSS IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 9339 CONTRACTS: 13,577 OI CONTRACTS DECREASED AT THE COMEX AND 4,238 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI LOSS: 9339 CONTRACTS OR 933900 OZ = 29.04 TONNES. AND ALL OF THIS MONSTROUS LOSS IN DEMAND OCCURRED WITH THE TINY FALL IN THE PRICE OF GOLD/ YESTERDAY TO THE TUNE OF $0.95.

YESTERDAY, WE HAD 11,249 EFP’S ISSUED.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF JUNE : 194,658 CONTRACTS OR 19,465,800 OZ OR 605.468 TONNES (21 TRADING DAYS AND THUS AVERAGING: 9269 EFP CONTRACTS PER TRADING DAY OR 926,900 OZ/ TRADING DAY),,

TO GIVE YOU AN IDEA AS TO THE HUGE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 21 TRADING DAYS IN TONNES: 605.468 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2017, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 2555 TONNES

THUS EFP TRANSFERS REPRESENTS 605.468/2550 x 100% TONNES = 23.74% OF GLOBAL ANNUAL PRODUCTION SO FAR IN JULY ALONE.***

ACCUMULATION OF GOLD EFP’S YEAR 2018 TO DATE: 4,708.41* TONNES *SURPASSED ANNUAL PROD’N

ACCUMULATION OF GOLD EFP’S FOR JANUARY 2018: 653.22 TONNES (21 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR FEBRUARY 2018: 649.45 TONNES (20 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR MARCH 2018: 741.89 TONNES (22 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR APRIL 2018: 713.84 TONNES (21 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR MAY 2018: 693.80 TONNES ( 22 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR JUNE 2018 650.71 TONNES (21 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR JULY 2018 605.5 TONNES (21 TRADING DAYS)

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A HUMONGOUS SIZED DECREASE IN OI AT THE COMEX OF 13,577 DESPITE THE SMALL LOSS IN PRICING ($0.95 THAT GOLD UNDERTOOK ON YESTERDAY) // . WE ALSO HAD A FAIR SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 4238 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 4,238 EFP CONTRACTS ISSUED, WE HAD A VERY STRONG NET LOSS OF 9339 CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

4238 CONTRACTS MOVE TO LONDON AND 13,577 CONTRACTS DECREASED AT THE COMEX. (in tonnes, the LOSS in total oi equates to 26.80 TONNES). ..AND THIS LOSS IN DEMAND OCCURRED WITH A TINY LOSS OF $0.95 IN YESTERDAY’S TRADING AT THE COMEX!!!.

we had: 37 notice(s) filed upon for 3700 oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD...

WITH GOLD UP $2.05 TODAY: /

NO CHANGES IN GOLD INVENTORY AT THE GLD

/GLD INVENTORY 800.20 TONNES

Inventory rests tonight: 800.20 tonnes.

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

SLV/

WITH SILVER UP 5 CENTS TODAY :

NO CHANGE IN SILVER INVENTORY TONIGHT

/INVENTORY RESTS AT 329.433 MILLION OZ/

NOTE THE DIFFERENCE BETWEEN THE GLD AND SLV: THE CROOKS CAN RAID GOLD BECAUSE THEY DO HAVE SOME PHYSICAL. THEY DO NOT RAID SILVER PROBABLY BECAUSE THERE IS NO REAL SILVER INVENTORIES BEHIND THEM

end

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER ROSE BY A CONSIDERABLE SIZED 2461 CONTRACTS from 218,477 UP TO 220,908 (AND CLOSER T0 THE NEW COMEX RECORD SET /APRIL 9/2017 AT 243,411/SILVER PRICE AT THAT DAY: $16.53). THE PREVIOUS RECORD OTHER THAN WAS ESTABLISHED AT: 234,787, SET ON APRIL 21.2017 OVER ONE YEAR AGO. THE PRICE OF SILVER ON THAT DAY: $17.89. OUR CUSTOMARY MIGRATION OF COMEX LONGS MORPH INTO LONDON FORWARDS CONTINUES AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

617 EFP CONTRACTS FOR SEPT., 0 EFP CONTRACTS FOR DECEMBER AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 617 CONTRACTS . EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI GAIN AT THE COMEX OF 2461 CONTRACTS TO THE 617 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A GOOD NET GAIN OF 3197OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES: 15.39 MILLION OZ!!! AND YET WE ALSO HAVE A STRONG DEMAND FOR PHYSICAL AS WE WITNESSED A FINAL STANDING OF GREATER THAN 30 MILLION OZ FOR JULY AND NOW ANOTHER STRONG 3,260 MILLION OZ FOR AUGUST... AND YET ALL OF THIS DEMAND OCCURRED DESPITE A 3 CENT PRICING GAIN AT THE SILVER COMEX.

RESULT: A SMALL SIZED INCREASE IN SILVER OI AT THE COMEX DESPITE THE 3 CENT PRICING GAIN THAT SILVER UNDERTOOK IN PRICING YESTERDAY. BUT WE ALSO HAD A SMALL SIZED 652EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR JULY, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON AS WELL AS THE STRONG AMOUNT OF PHYSICAL STANDING FOR METAL AT THE COMEX.

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

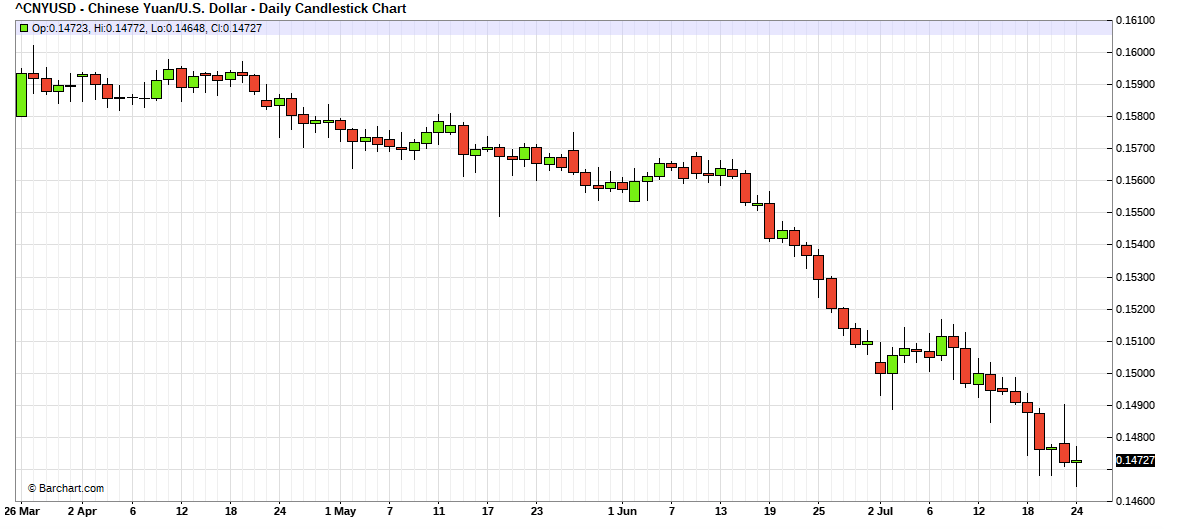

i)TUESDAY MORNING/MONDAY NIGHT: Shanghai closed UP 7.35 POINTS OR 0.26% /Hang Sang CLOSED DOWN 150.12 POINTS OR 0.52%/ / The Nikkei closed UP 8.88 POINTS OR 0.04%/Australia’s all ordinaires CLOSED DOWN 0.04% /Chinese yuan (ONSHORE) closed DOWN at 6.8329 AS POBC RESUMES ITS HUGE DEVALUATION /Oil UP to 69.69 dollars per barrel for WTI and 75.33 for Brent. Stocks in Europe OPENED GREEN//. ONSHORE YUAN CLOSED WELL DOWN AT 6.8329 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.8391: HUGE DEVALUATION/PAST SEVERAL DAYS RESUMES : /ONSHORE YUAN TRADING STRONGER AGAINST OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

/NORTH KOREA/SOUTH KOREA

i)North Korea/South Korea/USA/Russia

b) REPORT ON JAPAN

i)As expected, Japan’s economy is shrinking because it is aging. The bank of Japan shifts to a more flexible bond buying plan trying to steepen the yield curve. Japan will continue with its stealth tapering and if need be, they will increase purchases of bonds to keep the yield below .11% It did not work

( zerohedge)

b)Discussion of the latest Kuroda policy: Kuroda tried to steepen the curve but he failed. Deflation is still ripping Japan apart and Kuroda’s attempt to help the banks was off themark

( zerohedge)

c)The following is an excerpt from Graham Summers’ weekly investment service, Private Wealth Advisory.

Is Japan about to blow up?

( Graham Summers)

3 c CHINA

Stocks and the yuan rise as it was stated that trade talks are resuming. This will not last.

( zero hedge)

4. EUROPEAN AFFAIRS

i)Salvini is accused of creating a climate of hate because of his refusal to allow any more migrants into Italy

( zerohedge)

ii)GREECE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

i)Russia/Syria/USA

We have highlighted to you on several occasions, the fact that Russia can engage in electronic warfare against USA troops by jamming their equipment. There has been a few reports of naval ships being disabled with the Russian jamming equipment. It is now entering a dangerous phase in Syria

( zerohedge)

ii)The Turkish lira plunges to 4.92%, inflation is running rampant at almost 14% and the 10 yr Turkish bond is yielding close to 19%. The court rejects an appeal to release USA Pastor Brunson..trouble ahead on this one…

6 .GLOBAL ISSUES

My goodness!! The loonie tumbles after Canada is excluded from NAFTA talks. All Canada has to do is refuse to sell fresh water to the States as this will become a big issue

( zerohedge)

7. OIL ISSUES

Nicholas to me on the huge volume of Shanghai oil priced in yuan.

As you know these contacts can be converted into gold once the seller of that oil receives his yuan.

(courtesy Nicholas Biezanek)

8. EMERGING MARKET

9. PHYSICAL MARKETS

i)The following is a must read. Rep Mooney asks some tough questions to the Fed and Treasury with respect to the surreptitious trading in gold

( Chris Powell/GATA Stef. Gleeson)

ii)I promised you that gold imports into India would approach 1000 tonnes. I am close

( scrapregister.com)

10. USA stories which will influence the price of gold/silver)

i)Market trading /GOLD/MARKET MOVERS:

Spending outpaces income for the 5th straight month

( zerohedge)

a)uSA home appreciation records its slowest pace since January as the big affordability issue looms

( zerohedge)

b)Your most important passage of the year!! As we have been pounding the table following David Stockman’s lead, we can now state that everything that we told you is coming to fruition. We warned you that the USA budget deficit will climb to just over 800 billion dollars. It is now pegged for 833 billion dollars. However you must also include student loans and auto loans which are not part of the deficit. So the true funding needs exceeds 1.33 trillion dollars. Also remember that the Fed’s balance sheet roll offs will also add to the treasuries huge borrowings. By mid 2019, the total amount of borrowing will be in excess of 1.8 trillion dollars and that will cause the 10 yr yield to skyrocket.

(courtesy zerohedge)

a)The left is going to be very upset with this: Trump is considering a 100 billion USA tax cut for the very wealthy

( zerohedge)

b)Trump declares war on Republican Koch brothers saying they are a total “joke”

(courtesy zerohedge)

c)the trade war will force Americans to pay 4% more for diapers, tissues and toilet paper

(courtesy zerohedge)

iv)SWAMP STORIES

Trading Volumes on the COMEX

PRELIMINARY COMEX VOLUME FOR TODAY: 293,231 contracts

CONFIRMED COMEX VOL. FOR YESTERDAY: 272,396 contracts

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

And now for the wild silver comex results.

Total silver OI ROSE BY A CONSIDERABLE SIZED 2461CONTRACTS FROM 218,477 UP TO 220,908 (AND A LITTLE CLOSER TO THE THE NEW RECORD OI FOR SILVER SET APRIL 9.2018/ 243,411 CONTRACTS)DESPITE THE TINY 3 CENT GAIN IN PRICING THAT SILVER UNDERTOOK YESTERDAY. SINCE WE ARE NOW INTO THE ACTIVE DELIVERY MONTH OF JULY, WE WERE INFORMED THAT WE HAD A SMALL SIZED 617 EFP CONTRACTS FOR SEPT., 0 EFP CONTRACTS FOR DECEMBER AND ZERO FOR ALL OTHER MONTHS. THESE EFPS WERE ISSUED TO COMEX LONGS WHO RECEIVED A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. THE TOTAL EFP’S ISSUED: 617. ON A NET BASIS WE GAINED 3078 SILVER OPEN INTEREST CONTRACTS AS WE OBTAINED 2461 CONTRACT GAINAT THE COMEX COMBINING WITH THE ADDITION OF 617 OI CONTRACTS NAVIGATING OVER TO LONDON.

NET GAIN ON THE TWO EXCHANGES: 3078CONTRACTS

AMOUNT STANDING FOR SILVER AT THE COMEX

We had 652 open interest contracts stand for delivery and thus by definition the amount standing for delivery in August for silver is as follows:

652 contracts x 5000 oz per contract = 3,260,000 oz

The next active delivery month after August for silver is September and here the OI ROSE by 565 contracts UP to 156,010

After September, the next big delivery month is December and here the OI rose by 1780 contracts up to 53,420 contracts.

We had 255 notice(s) filed for 1,275,000 OZ for the AUGUST 2018 COMEX contract for silver

AND NOW COMPARISON VS AUGUST LAST YR:

ON FIRST DAY NOTICE JULY 31/2017: 1,965,000 OZ STOOD FOR DELIVERY

THE FINAL AMOUNT OF SILVER STANDING: AUGUST 30.2017: 6,245,000 OZ AS WE HAD CONSIDERABLE QUEUE JUMPING.

INITIAL standings for AUGUST/GOLD

JULY 31/2018.

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz |

NIL OZ

|

| Deposits to the Dealer Inventory in oz | NIL oz |

| Deposits to the Customer Inventory, in oz |

nil oz

|

| No of oz served (contracts) today |

37 notice(s)

3.700 OZ

|

| No of oz to be served (notices) |

4728 contracts

(472,800 oz)

|

| Total monthly oz gold served (contracts) so far this month |

37 notices

3700 OZ

.1150TONNES

|

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

we have a NO pulse today, AND zero gold enters the comex

For AUGUST:

Today, 0 notice(s) were issued from JPMorgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equates to 37 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped/ Received) by j.P.Morgan customer account.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

To calculate the INITIAL total number of gold ounces standing for the AUGUST. contract month, we take the total number of notices filed so far for the month (37) x 100 oz or 3700 oz, to which we add the difference between the open interest for the front month of AUGUST. (4765 contracts) minus the number of notices served upon today (37 x 100 oz per contract) equals 476,500 OZ OR 14.82 TONNES) the number of ounces standing in this non active month of AUGUST

Thus the INITIAL standings for gold for the AUGUST contract month:

No of notices served (37 x 100 oz) + {(4765)OI for the front month minus the number of notices served upon today (37 x 100 oz )which equals 476,500 oz standing OR 14.82 TONNES in this active delivery month of AUGUST.

We generally see liquidation on the final day equal to around 60-75% of total oi.

For example, last year at this time, on the day prior to first day notice: 33,000 contracts.

Final OI = 8700 contracts. Liquidation percentage; loss of contracts: 24,300 contracts /33000 = 73%

I have never seen it exceed 75%

Today: loss of OI contracts : 33,938

total oi prior to reading: 38,703

percentage loss: 87.8%

We will no doubt see many EFP issuance as these guys will morph into London forwards and receive a huge fiat bonus.

THERE ARE ONLY 7.8648 TONNES OF REGISTERED COMEX GOLD AVAILABLE FOR DELIVERY AGAINST 14.82 TONNES STANDING FOR JULY

IN THE LAST 24 MONTHS 85 NET TONNES HAS LEFT THE COMEX.

end

And now for silver

AND NOW THE AUGUST DELIVERY MONTH

AUGUST INITIAL standings/SILVER

| Silver | Ounces |

| Withdrawals from Dealers Inventory | nil oz |

| Withdrawals from Customer Inventory |

168,649.506 oz

brinks

CNT

HSBC

Scotia

|

| Deposits to the Dealer Inventory |

nil oz

|

| Deposits to the Customer Inventory |

1,391,745.936

Brinks

Scotia

CNT

|

| No of oz served today (contracts) |

255

CONTRACT(S)

(1,250,000 OZ)

|

| No of oz to be served (notices) |

397 contracts

(1,985,000 oz)

|

| Total monthly oz silver served (contracts) | 255 contracts

(1,250,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

we had 0 inventory movement at the dealer side of things

total dealer deposits: nil oz

total dealer withdrawals: nil oz

we had 3 deposit into the customer account

i) Into JPMorgan: nil oz

*** JPMorgan for most of 2017 and in 2018 has adding to its inventory almost every single day.

JPMorgan now has 144 million oz of total silver inventory or 51.0% of all official comex silver. (144 million/283 million)

iii) into Brinks: 328,000.38 oz

iv) Into CNT: 870,554.856 oz

v) Into Scotia: 193,190.700 oz

total customer deposits today: 1,391,745.936 oz

we had 4 withdrawals from the customer account;

i) out of Scotia; 25,240,630 oz

ii) out of Brinks: 2087.610 oz

iii) out of CNT: 121,179.086 oz

iv) out of HSBC: 20,192.180 oz

total withdrawals: 168,649.506 oz

we had 2 adjustment/

i) Out of CNT:

768,030.054 oz was adjusted out of the dealer and this landed into the customer account of CNT

and this most likely is a settlement

ii) Out of Brinks:

646,132.150 oz was adjusted out of the customer and this landed into the dealer account of Brinks

total dealer silver: 79.453 million

total dealer + customer silver: 284.779 million oz

The total number of notices filed today for the AUGUST. contract month is represented by 255 contract(s) FOR 1,275,000 oz. To calculate the number of silver ounces that will stand for delivery in AUGUST., we take the total number of notices filed for the month so far at 255 x 5,000 oz = 1,275,000 oz to which we add the difference between the open interest for the front month of AUGUST. (652) and the number of notices served upon today (255 x 5000 oz) equals the number of ounces standing.

.

Thus the INITIAL standings for silver for the AUGUST/2018 contract month: 255(notices served so far)x 5000 oz + OI for front month of AUGUST(652) -number of notices served upon today (255)x 5000 oz equals 3,260,000 oz of silver standing for the AUGUST contract month

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

ESTIMATED VOLUME FOR TODAY:80,183 CONTRACTS

CONFIRMED VOLUME FOR YESTERDAY: 48,095 CONTRACTS absolutely criminal

YESTERDAY’S CONFIRMED VOLUME OF 48,095 CONTRACTS EQUATES TO 140 million OZ OR 34.3% OF ANNUAL GLOBAL PRODUCTION OF SILVER

COMMODITY LAW SUGGESTS THAT OPEN INTEREST SHOULD NOT BE MORE THAN 3% OF ANNUAL GLOBAL PRODUCTION. THE CROOKS ARE SUPPLYING MASSIVE PAPER TRYING TO KEEP SILVER IN CHECK.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price at that day at $18.42

The previous record was 224,540 contracts with the price at that time of $20.44

end

NPV for Sprott

1. Sprott silver fund (PSLV): NAV FALLS TO -2.66% (JULY 31/2018)

2. Sprott gold fund (PHYS): premium to NAV FALLS TO -0.86% to NAV (JULY 31/2018 )

Note: Sprott silver trust back into NEGATIVE territory at -2.66%-/Sprott physical gold trust is back into NEGATIVE/

(courtesy Sprott/GATA)

3.SPROTT CEF.A FUND (FORMERLY CENTRAL FUND OF CANADA):

NAV 12.69/TRADING 12.25//DISCOUNT 3.48.

END

And now the Gold inventory at the GLD/

JULY 31/WITH GOLD UP $2.05/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 800.20

JULY 30/WITH GOLD DOWN $0.95/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 800.20 TONNES

july 27/WITH GOLD DOWN $2.85 TODAY, NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 800.20 TONNES

JULY 26./WITH GOLD DOWN $5.65: A WITHDRAWAL OF 2.35 TONNES OF GOLD FROM THE GLD/INVENTORY RESTS AT 800.20 TONNES

JULY 25/WITH GOLD UP $6.45; NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 802.55 TONNES

JULY 24/ WITH GOLD DOWN 10 CENTS: A HUGE DEPOSIT OF 4.42 TONNES INTO THE GLD/INVENTORY RESTS AT 802.55 TONNES

JULY 23/WITH GOLD DOWN $5.55: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 798.13 TONNES

JULY 20/WITH GOLD UP $4.15 A HUGE DEPOSIT OF 4.12 TONNES OF GOLD INTO THE GLD.INVENTORY RESTS AT 798.13 TONNES

JULY 19./WITH GOLD DOWN $1.00: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 794.01 TONNES

JULY 18/WITH GOLD UP 0.40: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 794.01 TONNES

JULY 17/WITH GOLD DOWN $12.40, WE HAD A BIG WITHDRAWAL OF 1.18 TONNES FROM THE GLD/INVENTORY RESTS AT 794.01 TONNES

JULY 16/WITH GOLD DOWN $1.55/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 795.19 TONNES

JULY 13/WITH GOLD DOWN $5.35 THE CROOKS RAID THE COOKIE JAR AGAIN TO THE TUNE OF 3.83 TONNES/INVENTORY RESTS AT 795.19 TONNES

JULY 12/WITH GOLD UP $2.30: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 799.02 TONNES

JULY 11/WITH GOLD DOWN $10.75 THE CROOKS RAIDED THE COOKIE JAR AGAIN TO THE TUNE OF 1.75 TONNES/INVENTORY RESTS AT 799.02 TONNES

JULY 10/WITH GOLD DOWN $3.85: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 800.77 TONNES

july 9/WITH GOLD UP $4.00/ANOTHER RAID ON THE GOLD COOKIE JAR: TWO WITHDRAWALS OF 1.18 TONNES THIS MORNING AND 1.47 TONNES THIS AFTERNOON/INVENTORY RESTS AT 800.77 TONNES

JULY 6/WITH GOLD DOWN $2.45: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 803.42 TONNES

JULY 5/WITH GOLD UP ANOTHER $5.15, THE CROOKS RAIDED THE COOKIE JAR AGAIN TO THE TUNE OF 5.89 TONNES/INVENTORY RESTS AT 803.42 TONNES IN THE LAST 10 TRADING DAYS GLD HAS LOST A HUGE 25.34 TONNES WITH A LOSS OF ONLY $15.25 IN PRICE

July 3/WITH GOLD UP $11.15/THE CROOKS RAIDED THE GLD INVENTORY AGAIN TO THE TUNE OF 9.73 TONNES/INVENTORY RESTS AT 809.31 TONNES

JULY 2/WITH GOLD DOWN $12.15, THE CROOKS RAIDED THE GLD INVENTORY AGAIN BY 1.47 TONNES DOWN./INVENTORY RESTS AT 819.04 TONNES

JUNE 29/WITH GOLD UP $3.70/A WITHDRAWAL OF 1.18 TONNES OF GOLD FROM THE GLD/INVENTORY RESTS AT 820.51 TONNES

JUNE 28/WITH GOLD DOWN $5.15/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 821.69 TONNES

June 27/WITH GOLD DOWN $3.60// TWO ENTRIES:/STRANGELY THE CROOKS RETURNED THE WITHDRAWAL OF 4.42 TONNES LAST NIGHT (THUS WE HAD A DEPOSIT OF 4.42 TONNES/INVENTORY RESTS AT 824.63 TONNES. /THEN LATE THIS AFTERNOON A WITHDRAWAL OF 2.94 TONNES

INVENTORY RESTS AT 821.69 TONNES/THIS VEHICLE IS AN OUTRIGHT FRAUD.

june 26/LATE LAST NIGHT, WITH GOLD DOWN $9.10 WE HAD A HUGE WITHDRAWAL OF 4.42 TONNES OF GOLD/INVENTORY RESTS AT 820.21 TONES

JUNE 25/WITH GOLD DOWN $1.45/NO CHANGE IN GOLD INVENTORY AT THE GLD.INVENTORY RESTS AT 824.63 TONNES

JUNE 22/WITH GOLD UP 25 CENTS TODAY, THE CROOKS WITHDREW A MASSIVE 4.13 TONNES OF GOLD/INVENTORY RESTS AT 824.63 TONNES

JUNE 21/WITH GOLD DOWN $4.00/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 828.76 TONNES

JUNE 20/WITH GOLD DOWN $3.55/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 828.76 TONNES

JUNE 19/WITH GOLD DOWN $1.50/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 828.76 TONES

JUNE 18/WITH GOLD UP $1.90/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 828.76 TONNES

JUNE 15/WITH GOLD DOWN $28.90/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 828.76 TONNES

JUNE 14/WITH GOLD UP $7.10/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 828.76 TONNES/

JUNE 13/WITH GOLD UP $2.20/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 828.76 TONNES

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

JULY 31/2018/ Inventory rests tonight at 800.20 tonnes

*IN LAST 420 TRADING DAYS: 130.73 NET TONNES HAVE BEEN REMOVED FROM THE GLD

*LAST 370 TRADING DAYS: A NET 25,81 TONNES HAVE NOW BEEN ADDED INTO GLD INVENTORY.

end

Now the SLV Inventory/

JULY 31/WITH SILVER UP 5 CENTS/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 329.433 MILLION OZ/

JULY 30/WITH SILVER UP 3 CENTS TODAY; NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 329.433 MILLION OZ.

JULY 27/WITH SILVER FLAT TODAY, NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 329.433 MILLION OZ/

JULY 26/WITH SILVER DOWN 10 CENTS: STRANGE: A BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.046 MILLION OZ OF SILVER/INVENTORY RESTS AT 329.433 MILLION OZ

JULY 25: WITH SILVER UP 8 CENTS TODAY: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV/ A WITHDRAWAL OF 658,000 INVENTORY RESTS AT 328.304 MILLION OZ/

JULY 24/WITH SILVER UP 8 CENTS TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 328.962 MILLION OZ/

JULY 23/WITH SILVER DOWN 11 CENTS/NO CHANGES IN SILVER INVENTORY INTO THE SLV/INVENTORY RESTS AT 328.962 MILLION OZ/

JULY 20/WITH SILVER UP 10 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.411 MILLION OZ INTO THE SLV INVENTORY

INVENTORY RESTS AT 328.962 MILLION OZ

JULY 19/WITH SILVER DOWN 17 CENTS TODAY; A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 752,000 OZ INTO THE SLV INVENTORY/INVENTORY RESTS AT 327.551 MILLION OZ/

JULY 18/WITH SILVER DOWN 3 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 326.799 MILLION OZ/

JULY 17/WITH SILVER DOWN 20 CENTS TODAY: A CHANGE IN SILVER INVENTORY A WITHDRAWAL OF 1.001 MILLION OZ FROM THE SLV: INVENTORY RESTS AT 326.799 MILLION OZ/

JULY 16/WITH SILVER FLAT TODAY, A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.128 MILLION OZ//INVENTORY RESTS AT 327.880 MILLION OZ

JULY 13/WITH SILVER DOWN 16 CENTS TODAY/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 326.752 MILLION OZ.

JULY 12/WITH SILVER UP 12 CENTS TODAY: ANOTHER BIG CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.035 MILLION OZ/INVENTORY RESTS AT 326.752 MILLION OZ/

JULY 11/WITH SILVER DOWN 22 CENTS TODAY: ANOTHER HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 565,000/INVENTORY RESTS AT 325.717 MILLION OZ

JULY 10/WITH SILVER DOWN 3 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 325.151 MILLION OZ

july 9/WITH SILVER UP 5 CENTS: ANOTHER BIG CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 847,000 OZ ADDED TO INVENTORY/INVENTORY RESTS AT 825.151 MILLION OZ/

JULY 6/WITH SILVER DOWN 2 CENTS/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 324.305 MILLION OZ/

JULY 5/WITH SILVER UP 6 CENTS, A GOOD CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 470,000 OZ/INVENTORY RESTS AT 324.305 MILLION OZ/ FOR THE PAST 10 TRADING DAYS, SILVER INVENTORY HAS ADVANCED BY 4.945 MILLION OZ WITH A LOSS OF 33 CENTS/PLEASE COMPARE THIS WITH THE GLD.

JULY 3/WITH SILVER UP 17 CENTS, A HUGE DEPOSIT OF 1.37 MILLION OZ ADDED TO THE SLV/INVENTORY RESTS AT 323.835 MILLION OZ.

JULY 2/WITH SILVER DOWN 31 CENTS/A HUGE 2.070 MILLION OZ DEPOSIT AT THE SLV/INVENTORY RESTS AT 322.465 MILLION OZ/

JUNE 29/WITH SILVER UP 14 CENTS TODAY, NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS THIS WEEKEND AT 320.395 MILLION OZ/

JUNE 28/WITH SILVER DOWN 18 CENTS, THE CROOKS ADDED 1.035 MILLION OZ OF SILVER INTO THE SLV/INVENTORY RESTS AT 320.395 MILLION OZ

JUNE 27.2018/WITH SILVER DOWN 8 CENTS/NO CHANGE IN SILVER INVENTORY/INVENTORY RESTS AT 819.360 MILLION OZ/

june 26./2018/WITH SILVER DOWN 8 CENTS, THE CROOKS WITHDREW THE DEPOSIT OF TWO DAYS AGO; 941,000 OZ OUT OF INVENTORY/INVENTORY RESTS AT 819.360 OZ

JUNE 25/WITH SILVER DOWN 12 CENTS/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 320.301 MILLION OZ/

JUNE 22/WITH SILVER UP 12 CENTS TODAY,ANOTHER BIG CHANGE IN SILVER INVENTORY AT THE SLV” A DEPOSIT OF 941,000 OZ INTO INVENTORY/INVENTORY RESTS THIS WEEKEND AT 320.301 MILLION OZ/

JUNE 21/WITH SILVER UP ONE CENT/ANOTHER CHANGE IN SILVER INVENTORY AT THE SLV/: A DEPOSIT OF 2.918 MILLION OZ/INVENTORY RESTS AT 319.360 MILLION OZ/ THUS FOR TWO STRAIGHT DAYS A TOTAL OF 5.26 MILLION OZ OF SILVER HAS BEEN ADDED WITH NO CHANGE IN PRICE.

JUNE 20/WITH SILVER DOWN ONE CENT/A HUGE CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY / A DEPOSIT OF 2.35 MILLION OZ/INVENTORY RESTS AT 316.442 MILLION OZ/

JUNE 19/2018/WITH SILVER DOWN 11 CENTS/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 314.090 MILLION OZ/

JUNE 18/WITH SILVER DOWN 6 CENTS TODAY/NO CHANGE IN SILVER INVENTORY/INVENTORY RESTS AT 314.090 MILLION OZ/

JUNE 15/WITH SILVER DOWN 75 CENTS/A BIG CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.788 MILLION OZ//INVENTORY RESTS AT 314.090 MILLION OZ

JUNE 14/WITH SILVER UP 30 CENTS, THE CROOKS DECIDED THAT THEY NEEDED SILVER INVENTORY BADLY SO THEY RAID THE SLV OF 1.412 MILLION OZ/INVENTORY RESTS AT 315.878 MILLION OZ/

JUNE 13/WITH SILVER UP 11 CENTS TODAY/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 317.290 MILLION OZ/

JULY 31/2018:

Inventory 329.433 MILLION OZ

6 Month MM GOFO 1.93/ and libor 6 month duration 2.53

Indicative gold forward offer rate for a 6 month duration/calculation:

G0FO+ 1.93%

libor 2.53 FOR 6 MONTHS/

GOLD LENDING RATE: .60%

XXXXXXXX

12 Month MM GOFO

+ 2.82%

LIBOR FOR 12 MONTH DURATION: 2.40

GOFO = LIBOR – GOLD LENDING RATE

GOLD LENDING RATE = +.42

end

Major gold/silver trading /commentaries for TUESDAY

GOLDCORE/BLOG/MARK O’BYRNE.

House prices aren’t just slipping in the UK – this is global

It’s very easy to become parochial when it comes to thinking about property markets.

We focus on the slowdown in the UK market and we ponder what’s causing it. Could it be new rules on landlords? Could it be the crackdown on overseas investors? Could it be Brexit?

But this really is less than half the picture.

Because the residential property slowdown isn’t just happening in the UK – it’s happening pretty much everywhere.

Why residential property matters

We talk about property a fair bit in Money Morning. There are a few reasons for that. Firstly, everyone’s obsessed with it. So it’s fair game as a topic.

Secondly, it’s an important asset class. Stockmarket crashes grab headlines, but the truth is the market can slide hard without ever really scratching the sides of the economy. But if the housing market crashes, you tend to know about it, because typically there’s a lot of debt involved.

Thirdly, it’s usually a pretty big item on the household balance sheet. I think it’s fair to say that the majority of us aspire to owning a home and clearing the mortgage. And those who already have might be keen to use it to fund other things – retirement, deposits for offspring, or even an inheritance (although my advice on this latter point is spend the lot, your kids want you to have fun – and if they don’t, they don’t deserve it anyway).

Anyway – so that’s why we go on about property. But as I said in the intro, it’s easy to get a bit too fixated with what’s going on locally. That can lead you to the wrong conclusions. After all, there are a lot of legislative changes that are affecting the UK housing market right now, for example.

But it’s not just the UK. House prices are hitting a wall almost everywhere.

Take Australia. The land down under has long had one of the most expensive property markets in the world. It barely winced during the 2008 financial crisis, despite carnage everywhere else.

And yet now, it finally appears to be losing steam. Prices in Sydney fell by 4.5% in the second quarter, while prices in Melbourne slipped too.

Australia is far from alone. Hot global markets everywhere are slowing down. Canada is another good example.

And now we’re seeing it happen in the US as well. As Bloomberg reports: “The US housing market – particularly in cutthroat areas like Seattle, Silicon Valley and Austin, Texas – appears to be headed for the broadest slowdown in years.”

The number of home sales (of existing homes as opposed to new builds) fell in June for the third month in a row. New builds are selling at the slowest pace in eight months.

Meanwhile, the inventory of unsold homes – the amount of supply on the sidelines – is rising again. Prices in May were up by 6.4% year-on-year (so a lot stronger than in the UK, for example), but that’s the smallest annual gain since 2017 – and over the last three months, prices have risen at their slowest rate since 2012.

What’s interesting about the US housing market is that historically, despite the fact that it bore so much responsibility for the 2008 crash, it has been a relatively well-behaved property market. Over the very long run, US house prices have only risen in line with inflation. You can’t say the same for the UK.

So the fact that it, too, is starting to struggle, suggests that this isn’t purely a bubble market phenomenon.

Why are housing markets around the world slowing down?

Why is this? What do all of these markets have in common? Because clearly, it’s not Brexit. Nor is it cracking down on buy-to-let landlords. And while most countries have grown a little more hostile to foreign investors (most Canadian cities have imposed strict rules, for example), it’s not the most obvious answer.

Let’s go back to basics for a moment. You buy property with debt. Usually a fair chunk of it. Property can be very lucrative as an investment precisely because of this debt (or “leverage”).

Put down £25,000 deposit. Buy a £100,000 house, using a £75,000 mortgage. Sell it in two years’ time for £125,000. Pay the £75,000 back to the bank. Pocket £50,000. The price went up by 25%, but you’ve doubled your money. Rinse and repeat until you’re a millionaire.

But what makes prices go up in the first place? The rational value of a property (as opposed to the “bubble” value) is dependent on the expected rental income it will generate, and what other people are willing to pay for that income stream. It’s just like a bond in many ways, only riskier, and with plumbing involved.

So if you can get 5% from your bank account, you’ll want a lot more from your property – say 10%. But if you can only get 1% from your bank account, you’ll take a lower yield on your property – say 5%.

Let’s assume that the annual rental is £10,000 and it stays there. So with interest rates at 5%, you’ll happily pay £100,000 for that rental income. But with rates at 1%, you’ll happily pay £200,000. (I’m keeping the examples simple here).

You see what’s happened? The price of the property is basically contingent on interest rates.

And what’s happening around the world now? That’s right. Interest rates have stopped going down. And in some cases (notably the US) they are rising. As a result, there’s not much fuel for prices to go higher (rents are as high as they can go without a real boost in wages), and if borrowing costs rise, that will drive prices down.

As Bloomberg notes of the US, affordability is a huge issue in many of these areas, while prices nationwide are still rising “twice as fast as incomes”. Yet the bigger issues is that “buyers are getting squeezed by rising mortgage rates.”

In short, property (alongside bonds) is one of the asset classes that has benefited most from the decline of interest rates in recent decades. And now that’s reversing.

For “normal” people, that has imposed a ceiling on the amount of borrowing they can arrange – they simply can’t afford to buy at the prices sellers still hope to get. For global investors, they’ve realised not only that the world is becoming more hostile to the free flow of footloose capital, but that, quite simply, in a rising rate environment, property is not a good investment.

What happens next? That all depends on rates.

• From free daily investment email Money Morning

Trump Trade and Currency Wars With China – Goldnomics Podcast

Hedge Funds’ Big Short Could Be Fool’s Gold (Bloomerg.com)

PRECIOUS-Gold prices buoyed by weaker dollar vs yen (Reuters.com)

A third straight bludgeoning for tech stocks drives Nasdaq to 3-week closing low (MarketWatch.com)

Gold is having an ugly year, but ‘this bloodbath is leading to a buying opportunity’ (CNBC.com)

Gold Prices Slip Despite Slightly Weaker Dollar (Investing.com)

Source: Bloomberg

Source: Bloomberg

Gold Review: Flirts with an important horizontal support, near $1218 level (FXStreet.com)

Commodities Weekly: No traction for commodities as the dollar softens (MarketPulse.com)

Gold Prices May Fall on Hawkish Fed, US Bond Supply Boost (DailyFX.com)

Ed Steer: When JP Morgan Decides to Stop Shorting Silver, Prices Will Shock You (SilverSeek.com)

Listen on SoundCloud , Blubrry & iTunes. Watch on YouTube below

Gold Prices (LBMA AM)

30 Jul: USD 1,222.05, GBP 931.20 & EUR 1,045.95 per ounce

27 Jul: USD 1,219.15, GBP 931.06 & EUR 1,048.10 per ounce

26 Jul: USD 1,228.35, GBP 931.46 & EUR 1,049.13 per ounce

25 Jul: USD 1,230.55, GBP 935.09 & EUR 1,051.75 per ounce

24 Jul: USD 1,224.30, GBP 933.77 & EUR 1,047.63 per ounce

23 Jul: USD 1,229.45, GBP 937.21 & EUR 1,050.93 per ounce

20 Jul: USD 1,224.85, GBP 940.56 & EUR 1,050.80 per ounce

Silver Prices (LBMA)

30 Jul: USD 15.49, GBP 11.81 & EUR 13.25 per ounce

27 Jul: USD 15.36, GBP 11.72 & EUR 13.20 per ounce

26 Jul: USD 15.54, GBP 11.79 & EUR 13.27 per ounce

25 Jul: USD 15.57, GBP 11.83 & EUR 13.31 per ounce

24 Jul: USD 15.51, GBP 11.81 & EUR 13.24 per ounce

23 Jul: USD 15.49, GBP 11.78 & EUR 13.22 per ounce

20 Jul: USD 15.37, GBP 11.79 & EUR 13.19 per ounce

Recent Market Updates

– Russia Sells 80% Of Its US Treasuries

– Are China’s Gold Reserves Slowly Rising?

– Gold Outlook In H2 2018

– Gold Production In South Africa Continues To Collapse – Plummets 85% From Peak In 1970 (VIDEO)

– Physical Gold Is The “Best Defence” Against “Escalating Currency Wars”

– Trump and War With China? Goldnomics Podcast

– Weekly Digest – News, Market Updates and Videos You May Have Missed

– Financial Terrorism In The UK – Collusion between Government, Regulators & Two Bailed-Out UK Banks

– “Biggest Bubble in the History of Mankind” Is “Going To Burst” – Ron Paul

– Global Debt Time Bomb Surges To Nearly $250,000,000,000,000 – GoldCore Video

– Trump, Russia, Brexit and the Demand For Gold and Silver – GoldCore Video Interview

– Trump Is Serious About A Global Trade War

– Ponzi Economy Will Lead To Next Global Financial Crisis

– World Cup Is 200 Ounces Of Gold Worth £140,000 – 30% Less Than Harry Kane’s Weekly Wage

– Chaotic BREXIT More Likely: Risk To London, While Frankfurt, Luxembourg, Paris and Dublin Benefit

– VIDEO: Italy €2.4 Trillion Debt To Create Eurozone Contagion and Global Debt Crisis?

– U.S. China Trade War Escalates as Russia and China Accumulate Gold

Andrew Maguire’s Kinesis money which is a “bitcoin” but backed 100% by allocated gold and silver is set to go.

it think it would be a great idea to look at this!

please read at: https://kinesis.money/#/

(Andrew Maguire)

|

|

Dear Harvey Organ,

Thank you for your participation in our webinar on June 7th with our host and CEO of Kinesis, Thomas Coughlin.

The response we received has been incredible, we appreciate you taking the time to join us and hope you found it to be beneficial.

Due to such a high influx of questions we received we were unable to have them all answered. Nevertheless, if there was anything which requires more clarification, or you have a query which needs to be rectified, we invite you to join our telegram group:

We apologize for the technical issues we incurred during the webinar which resulted in it running a little over schedule, we hope that the next one we host will run seamlessly.

A video has been put together and uploaded onto our YouTube channel which can be found here:

Please share and subscribe to our YouTube channel to be notified of all the latest videos as they become available.

The rapid growth that we are currently experiencing has been incredible and with your support, is only going to get better.

We are working behind the scenes very hard to create a better experience for everyone involved! Stay tuned in as we have many more announcements to be released in the upcoming days.

Kind Regards,

|

Kinesis Money

a:C/O ILS Fiduciaries (IOM) Limited, First Floor,Millennium House, Victoria Road, Douglas, Isle of Man IM2 4RW

|

The following is self explanatory

(courtesy GATA/Chris Powell and Harvey Organ)

GATA asks bank regulator to check risks of gold

futures maneuver

Submitted by cpowell on Sun, 2018-06-10 16:17. Section: Daily Dispatches

12:21p ET Sunday, June 10, 2018

Dear Friend of GATA and Gold:

GATA has appealed to the U.S. comptroller of the currency, who has regulatory authority over banks, to review financial risks certain banks may have incurred through derivatives in the monetary metals markets, particularly through the recent heavy use of the “exchange for physicals” mechanism of settling gold and silver futures contracts on the New York Commodities Exchange.

The appeal was made in a letter sent May 5 to the comptroller, Joseph M. Otting, whose office is part of the U.S. Treasury Department, by your secretary/treasurer and GATA futures market consultant Harvey Organ.

“Exchange for physical” settlements of futures contracts long were considered emergency procedures when a seller was not able to deliver metal from an exchange-approved warehouse and wanted to settle with delivery elsewhere. But now such settlements appear to constitute most gold and silver futures settlements on the Comex. It is a strange development that appears to have been necessitated by the increasing difficulties of central banking’s gold and silver price suppression policy.

GATA has received no acknowledgment of the letter. Its text is below and a PDF copy of it is here:

http://www.gata.org/files/ComptrollerOfCurrencyLetter.pdf

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

* * *

May 5, 2018

Joseph M. Otting, Comptroller of the Currency

U.S. Treasury Department

400 7th Street, SW

Washington DC 20219

Dear Comptroller Otting:

Please let us bring to your attention financial risks to major banks involving their possibly unreported exposure to derivatives in the monetary metals markets.

In recent months gold and silver future contracts issued by U.S. banks on the New York Commodities Exchange have been moved off-exchange for delivery through a mechanism known as “exchange for physical” (EFP) contracts. Until recently use of this mechanism was considered an emergency procedure when a seller did not have access to metal for delivery through Comex warehouses. Now the mechanism seems to be in use for a large share of front-month contracts for which delivery is sought.

Here is an example that is happening at the Comex in the front active month of April for gold and the inactive delivery month of April for silver.

In gold, there were 229,436 EFP contracts for 713.64 tonnes, an average of 10,925 contracts and 1,092,500 ounces per trading day.

In silver, there were 77,150 EFP contracts for 385,750,000 ounces, an average of 3,673 contracts and 18,369,000 ounces per trading day.

London Bullion Market Association rules suggest that these contracts may not be reported to regulators. The LBMA’s bylaws say:

“Figures above exclude any contracts not subject to risk-based capital requirements, such as FX contracts with an original maturity of 14 days or less, futures contracts, written options, and basis swaps. Therefore, the total notional amount of derivatives by maturity will not add to the total derivatives figure in this table.”

We are told that these EFP contracts are transferred from the Comex to London as what are called “serial forwards” and their duration is always less than 14 days, which exempts them from being reported.

It is our understanding that in each quarter your office prepares a report detailing risk undertaken by the banks under the comptroller’s supervision.

These risks include derivatives undertaken by U.S. banks and other obligations that may cause a bank to fail. Our concern is that your office may not be aware of large unreported derivative exposure by banks.

Could you review this matter and let us know your conclusions?

Sincerely,

CHRIS POWELL

Secretary/Treasurer

HARVEY ORGAN

Consultant

Gold Anti-Trust Action Committee Inc.

7 Villa Louisa Road

Manchester, Connecticut 06043-7541

end

This is our letter to the CFTC it is quite explanatory: is a foreign power controlling the comex gold prices:

(courtesy Chris Powell, Harvey Organ)

An open letter to the CFTC: Is a foreign power controlling Comex gold prices?

Submitted by cpowell on Sun, 2018-07-29 02:21. Section: Daily Dispatches

July 28, 2018

J. Christopher Giancarlo, Chairman

Brian Quintenz, Commissioner

Rostin Behnam, Commissioner

U.S. Commodity Futures Trading Commission

3 Lafayette Centre

1155 21st Street, NW

Washington, D.C. 20581

Dear Chairman Giancarlo:

We would like to bring to attention four issues that need to be addressed in gold and silver futures trading.

1. For the second straight month, there has been a huge discrepancy between the preliminary gold open interest and the final number recorded on particular trading days.

Let us examine the one that just happened: July 26.

There was a preliminary Comex gold open interest gain of 3,349 contracts to 503,493. But there was a final Comex gold open interest loss of 14,443 contacts to 485,701 — a discrepancy of 27,792 contracts.

The open interest here is already 24 hours old. Our understanding is that these contracts are canceled for nonpayment. It would be almost impossible for such a large number of voided contracts not to have influenced the price of gold, especially when there was a raid on the Comex by the banks.

2. The huge issuance of “exchange for physical” settlements.

For quite some time we have been told by a CFTC official, Deputy Enforcement Director Matthew Hunter, that this was quite legal as these settlements were deliverable. But in our last email exchange with Hunter he wrote that these EFPs were not deliverable. The CFTC really should provide a thorough accounting of EFPs and explain how they settle contracts.

3. The gold Comex shows a huge open interest of 43,000 contracts remaining with one day before first notice day. So there likely will be a huge amount of gold contracts standing for deliver for the August contract month — probably 31 to 62 tonnes — with only 7.8 tonnes of registered gold at the Comex and with no gold having entered the Comex for some time. How could the banks throughout the last month have depressed the price of gold amid such huge physical demand and a tiny registered gold inventory available to settle?

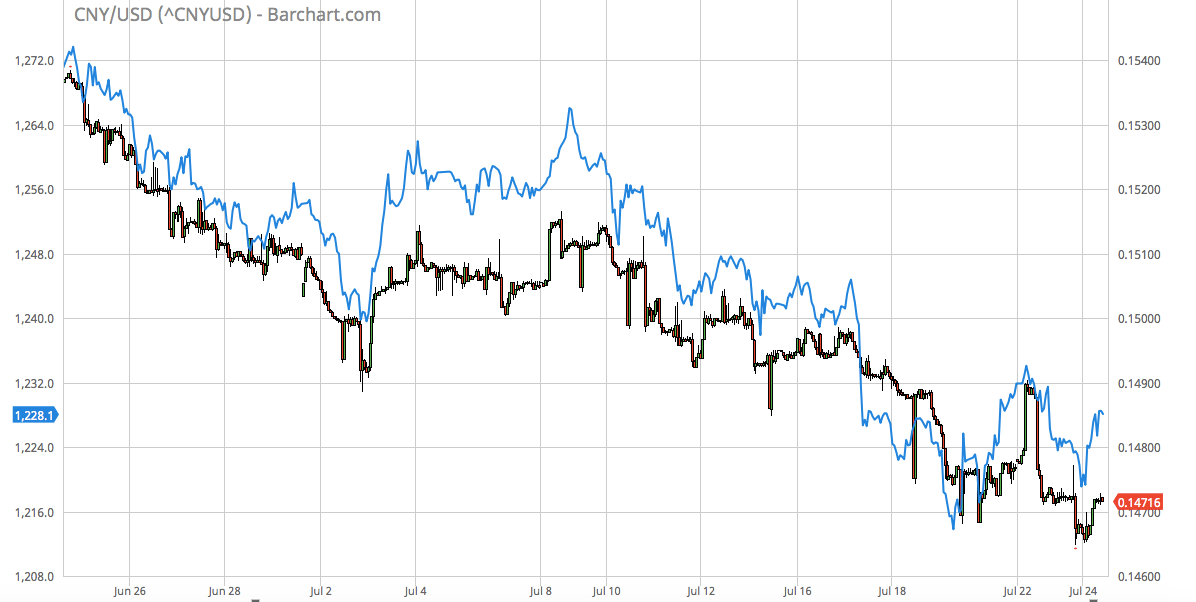

4. For the past month there has been a direct correlation between the value of the Chinese yuan and the price of gold. That is, the higher the yuan, the higher the price of gold and especially vice-versa.

The value of the Chinese yuan is essentially controlled by China’s central bank.

The Comex is generally considered the primary authority in pricing gold.

Here is recent commentary by monetary metals market analyst Craig Hemke on the recent perfect correlation between the yuan and gold:

https://www.sprottmoney.com/Blog/potential-impacts-of-the-yuan-gold-peg-…

* * *

Hemke writes:

“Though the People’s Bank of China has long maintained a ‘peg’ in the relative valuation of the yuan versus the dollar, the past 90 days have seen a steady devaluation of this peg to the tune of nearly 8 percent. See this chart:

“Over the period in this chart the price of Comex gold has fallen by more than 10 percent:

“To make this correlation clearer, let’s plot the two prices together. This correlation has become extraordinarily tight over the past month, as you can see below where the CNY/USD exchange rate is displayed in candlesticks and Comex gold is a blue line:

“And when you draw it down to just the past five days, the two prices react to each other almost simultaneously:

“This is not a correlation searching for a cause, nor is it a simple act of ‘traders’ reacting to a falling yuan by selling digital gold. No, in a market the size of global gold, this immediate correlation can be accomplished only through massive interventions, the size and scope of which are possible only at the state/sovereign level. And which state/sovereign would have a direct interest in linking the dollar price of gold to the yuan? China, of course.”

* * *

So how does the CFTC allow a foreign government or entity to control the price of this important commodity and currency by trading in U.S. markets?

Or is market manipulation by a foreign power happening with the authorization of the U.S. government?

HARVEY B. ORGAN, Consultant

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

Manchester, Connecticut

CPowell@GATA.org

end

The following is a must read. Rep Mooney asks some tough questions to the Fed and Treasury with respect to the surreptitious trading in gold

(courtesy Chris Powell/GATA Stef. Gleeson)

Treasury, Fed evade congressman’s gold questions so he presses them again, and more

Submitted by cpowell on Tue, 2018-07-31 15:53. Section: Daily Dispatches

12:05p ET Tuesday, July 31, 2018

Dear Friend of GATA and Gold:

The U.S. Treasury Department and Federal Reserve responded incompletely and evasively this month to the questions about their involvement in the gold market that were posed in April by U.S. Rep. Alex X. Mooney, R-West Virginia.

So Mooney last week wrote back to Treasury Secretary Steven Mnuchin and Federal Reserve Board Chairman Jerome Powell, repeating his questions and adding a few others about surreptitious U.S. government intervention in financial markets.

..

In doing so Mooney has drawn from GATA’s documentation of such intervention.

Mooney’s first inquiries to the Treasury and the Fed are described in a GATA dispatch here:

http://www.gata.org/node/18210

Mooney’s letter containing those inquiries is here:

http://gata.org/files/MooneyLetter-04-24-2018.pdf

Mooney originally asked Mnuchin and Powell to describe the U.S. government’s policy on gold and cited documentation from the U.S. State Department archive showing that this policy has been to drive gold out of the world financial system.

Mnuchin, whose response was written by Treasury’s acting assistant secretary, Brad Bailey, and Powell did not address this question at all. Mooney has posed it again.

The Treasury’s reply denied that the department trades gold through the Bank for International Settlements, Bank of England, and other central banks or governments. But Mooney now asks if the Treasury trades gold through its Exchange Stabilization Fund or through any other government agency or through commercial banks and brokers.

Powell’s reply denied any involvement by the Fed with gold swaps. (Harvey: a lie) But Mooney’s new inquiry calls attention to minutes of the Fed’s Federal Open Market Committee from 1995, wherein Fed General Counsel Virgil Mattingly says the Exchange Stabilization Fund has engaged in gold swaps.

Mooney also calls attention to the 2009 admission to GATA by Fed Governor Kevin M. Warsh that the Fed has gold swap arrangements with foreign banks and will not disclose them.

Mooney asks Powell for an explanation of what seem like contradictions of his denial.

In his new letter Mooney notes that the auditing of the U.S. gold reserve that is described in Bailey’s letter on behalf of the Treasury is not really auditing at all, and the congressman asks: “When was the last time, if ever, that there was a complete inventory conducted of U.S. government-owned gold? What were the results of the most recent inventory?”

Mooney adds: “A true audit would also review any encumbrances placed upon the metals owned by the United States.Has there been an accounting for any such encumbrances, as part of any audit, inventory, or other review? If so, when did this last occur and what were the results?”

Mooney’s new letter notes the recent close correlation of the gold price with the price of the Chinese yuan and the valuation of the International Monetary Fund’s Special Drawing Rights, and he asks, “Do these correlations reflect surreptitious intervention in U.S. currency markets by China and currency manipulation by China? What do the Fed and Treasury think of these correlations?”

GATA’s open letter to the U.S. Commodity Futures Trading Commission, published Sunday, pressed that issue as well:

http://www.gata.org/node/18405

Perhaps most satisfying for believers in free markets and limited and transparent government, Mooney now asks the Treasury and Fed to come clean about everything. He writes: “What markets, if any, are the Federal Reserve and Treasury trading in, and through what mechanisms? If the Federal Reserve and Treasury are engaged in trading, what is the objective?”

Stefan Gleason, president of the Sound Money Defense League and coin and bullion dealer Money Metals Exchange, who has supported Mooney’s inquiries, today welcomed the congressmen’s persistence.

“This obfuscation by the Fed and the Treasury is unacceptable,” Gleason said, “and we are encouraged Congressman Mooney is calling them out on their game playing. The American people are entitled to transparency and accountability when it comes to the status and use of America’s gold reserves.”

Gleason’s statement is posted at the Money Metals Exchange internet site here:

https://www.moneymetals.com/news/2018/07/31/china-gold-market-interventi…

The replies to Mooney from the Treasury and Fed are posted at GATA’s internet site here:

http://www.gata.org/files/Treasury&FedResponsesToMooney-07-2018.pdf

Mooney’s new letters of inquiry to the Treasury and Fed are posted at GATA’s internet site here:

http://www.gata.org/files/MooneyToTreasury&Fed-07-27-2018.pdf

With his detailed questioning of the Treasury and Fed and his persistence, the congressmen is essentially conducting both the sort of serious policy review Congress seldom does anymore as well as investigative journalism that most mainstream financial news organizations prohibit about gold and market rigging by government.

On the whole the monetary metals mining industry and metals market analysts are too timid to pursue these questions. But ordinary U.S. citizens and investors can help immensely here simply by calling Mooney’s inquiries to the attention of their U.S. senators and representatives and asking them to make and publicize their own similar inquiries.

It’s easily done: Just print this dispatch and send it with a covering note to your members of Congress. If enough members of Congress support Mooney’s inquiries, market rigging will get much more difficult for the government.

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

I promised you that gold imports into India would approach 1000 tonnes. I am close

(courtesy scrapregister.com)

India Gold imports shoot up to 955.16 tons during FY 2018

NEW DELHI (Scrap Register): As per the information passed to the parliament, Gold import in volume terms has increased by 22.43 per cent to 955.16 tons during the fiscal year 2017-18.

In 2016-17, the imports stood at 780.14 tons, according to the data shared by Minister of State for Commerce and Industry.

The demand of gold in the country in 2017-18 has increased during first and second quarters and declined in third and fourth quarters as compared to corresponding period in 2016-17.

The overall import of gold in 2017-18 has increased by 22.43 per cent as compared with imports in 2016-17.

https://www.scrapregister.com/news/44939/india-gold- imports-shoot-up-to-955.16-tons-during-fy-2018

-END-

Your early TUESDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

i) Chinese yuan vs USA dollar/CLOSED DOWN TO 6.8329/HUGE DEVALUATION FOR THE PAST TWO WEEKS RESUMES /shanghai bourse CLOSED UP 7.35 POINTS OR 0,26% /HANG SANG CLOSED DOWN 150,12 POINTS OR 0.52%

2. Nikkei closed UP 8.88 POINTS OR 0.04%/USA: YEN RISES TO 111.54/

3. Europe stocks OPENED GREEN /

USA dollar index FALLS TO 94.29/Euro RISES TO 1.1737

3b Japan 10 year bond yield: FALLS TO . +.06/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 111.54/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD IS NOW TARGETED AT .11%/JAPAN LOSING CONTROL OF THEIR BOND MARKET

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 69.69 and Brent: 75.33

3f Gold DOWN/Yen DOWN

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil UP for WTI and UP FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund RISES TO +.450%/Italian 10 yr bond yield DOWN to 2.77% /SPAIN 10 YR BOND YIELD UP TO 1.41%

3j Greek 10 year bond yield RISES TO : 3.96

3k Gold at $1220.30 silver at:15.47 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble DOWN 19/100 in roubles/dollar) 62.42

3m oil into the 69 dollar handle for WTI and 74 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 111.54 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 0.9877 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1594 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now POSITIVE territory with the 10 year RISING to +0.45%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.95% early this morning (THIS IS DEADLY TO ALL MARKETS). Thirty year rate at 3.08%

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

(courtesy Jim Reid/Bloomberg/Deutsche bank/zero hedge)

Futures Rise As Traders Digest Data Deluge After

Tech Rout; Fed Looms

It has been another relatively quiet session, as traders remain on the sidelines spooked by the sudden reversal in the growth/value trade following a sharp drop in tech stocks while keeping an eye on yields and currencies in the aftermath of the BOJ’s half-hearted attempt to steepen the JGB yield curve even as the central bank “forward guided” to years of easy policy to come as it slashed inflation expectations for FY19 (1.5% from 1.8%) and FY20 (1.6% from 1.8%). Meanwhile, the Eurozone added even more confusion after it reported that GDP unexpectedly slowed coming below expectations while inflation beat consensus, printing above 2.0% for the first time since 2012.

As a result, markets and futures are largely in the green, if only modestly so.

It all started with the BOJ, which took its time to announce just after 1pm local time that it is introducing forward guidance signaling that interest rates will stay low for an “extended period of time”, even as it tweaked Yield Curve Control parameters, which however were not adjusted in same manner as sources had previously hinted, disappointing markets and leading to a sharp drop in JGB yields.

As discussed earlier, in his best attempt to imitate Draghi, BOJ governor Kuroda left the key interest rates unchanged, saying he sees no need for additional easing for now while announcing policy tweaks, including reducing the amount of bank reserves subject to its negative interest rate and forward guidance for policy rates. The BoJ said the decision on asset purchases was unanimous and decision on YCC was made by 7-2 vote with Kataoka and Harada the dissenters, while it added it will permit upward and downward moves in 10yr yields but will buy JGBs promptly in the event of a rapid increase in yields. Furthermore, the BoJ adjusted its ETF allocation to include more TOPIX inclusion and lowered the balance of reserves for which NIRP is applied.

Kuroda also kept YCC mostly unchanged, reiterating that the BOJ will keep the 10-year yield at about zero percent even as the “tolerance band” of the 10Y around 0% would be doubled from 0.1% to 0.2%. For the market, this was not enough.

In sympathy, treasuries advanced and most European government debt nudged upward, although the JGB driven rally was faded through the European morning with respective curves off the flattest levels, in part after above consensus Eurozone CPI pressured bunds and euribors further.

Meanwhile, concerns about the ongoing tech rout kept equities under pressure, with Europe’s Stoxx 600 Index drifting lower even after BP and Credit Suisse reported positive earnings.

Futures on the S&P 500 and Nasdaq pointed to a slightly higher open before Apple’s results. Meanwhile, the euro climbed on positive inflation data from France and Germany, even as European GDP unexpectedly slowed and missed expectations.

- EU HICP Flash YY Jul 2.1% vs. Exp. 2.0% (Prev. 2.0%)

- EU CPI ex-Food, Energy, Alcohol & Tobacco Flash YY 1.1% vs. Exp. 1.0% (Prev. 0.9%)

Europe’s softer economic data was the latest to confirm that global uncertainty over the threat of a trade war is starting to weigh on sentiment and the economy; ECB President Mario Draghi last week singled out protectionism as a key risk to the region’s otherwise encouraging outlook. Europe’s GDP numbers followed data earlier showing Spain’s economy expanded 0.6 percent in the second quarter, slightly below forecasts. In France, growth also fell short of predictions.

There was more economic weakness, this time from China, whose manufacturing PMI dropped again in July, with slower credit growth this year denting demand and the imposition of the first round of U.S. tariffs taking a toll, and pressuring most commodities lower.

In FX, aside from a sharp move in the Yen as longs unwound positions, it was also relatively quiet: the Bloomberg Dollar Spot Index was little changed, set for its first monthly decline (-0.7%) since March, before the Fed starts its own 2-day policy meeting later Tuesday. The euro rose a third day as inflation accelerated further in July, despite a miss in GDP. Treasuries advanced along with euro-area bonds, while the yen weakened, after the Bank of Japan kept its 10-year yield target unchanged and introduced forward guidance to keep rates very low for an “extended period of time.”

Emerging-market shares slipped, while their currencies were steady even as Turkey’s lira extended losses.

Hungry for more? You won’t have long to wait as the next big monetary policy events this week include decisions from the Federal Reserve and Bank of England. After last week’s whopper of a GDP report, Markets are looking for confirmation of at least two more interest-rate hikes before the end of the year, while their British counterparts are also widely expected to increase borrowing costs, although some wonder if this may be a “one and done” affair.

WTI (-0.5%) and Brent (-0.6%) prices are ebbing lower in early European trade with oil prices set for their biggest monthly loss in 2 years. News flow remains light for the complex while Iranian President Rouhani continues to defend the nation’s “rights” to export oil. Meanwhile, spot gold (-0.2%) prices are relatively uneventful in recent trade while the DXY remains rangebound ahead of a few key risk events this week. Elsewhere, Shanghai rebar steel posted its best month in eight amid output curbs in China tightening supply.

Economic data include personal income and spending. Pfizer, P&G, Apple, and Cheesecake Factory are among companies reporting earnings.

Market Snapshot

- S&P 500 futures up 0.1% to 2,806.75

- STOXX Europe 600 down 0.1% to 390.51

- MXAP down 0.6% to 167.15

- MXAPJ down 0.2% to 541.91

- Nikkei up 0.04% to 22,553.72

- Topix down 0.8% to 1,753.29

- Hang Seng Index down 0.5% to 28,583.01

- Shanghai Composite up 0.3% to 2,876.40

- Sensex down 0.2% to 37,425.19

- Australia S&P/ASX 200 up 0.03% to 6,280.20

- Kospi up 0.08% to 2,295.26

- German 10Y yield fell 1.2 bps to 0.434%

- Euro up 0.2% to $1.1725

- Italian 10Y yield rose 19.6 bps to 2.672%

- Spanish 10Y yield fell 0.9 bps to 1.417%

- Brent futures down 0.3% to $74.78/bbl

- Gold spot down 0.2% to $1,219.15

- U.S. Dollar Index little changed 94.28

Top Overnight News

- Bank of Japan Governor Haruhiko Kuroda pushed through changes to his radical monetary stimulus program as the central bank prepares for a longer struggle to stoke inflation. While keeping unchanged its two major benchmarks — the negative interest rate and 10-year yield target — the BOJ took a number of steps to alleviate the strain on banks and the market distortions stemming from its policy

- A bumper day of euro-area economic releases showed the region’s vital signs remain good, but are slowing:

- Eurozone July CPI Estimate y/y: 2.1% vs 2.0% est (unrounded 2.149%); Core CPI 1.1% vs 1.0% est.

- While the region’s economic expansion entered a sixth year in the second quarter, growth unexpectedly slowed to just 0.3 percent, the weakest in two years

- WSJ: Trump has privately agreed to delay a potential shutdown or a fight over border wall funding until after the midterm elections, according to people familiar

- Canada’s bid to take part in senior-level NAFTA talks between the U.S. & Mexico later this week has been rejected, according to people familiar: National Post

- NYT: Trump administration is considering going around Congress and granting a $100b tax cut via tweaking capital gains calculations, according to people familiar

- Inflation accelerated further above the European Central Bank’s goal in July, though that was largely driven by stronger energy prices

- Unemployment in the euro region remained at the lowest since 2008

- Iran’s Revolutionary Guards, in unusually pointed language, called on President Hassan Rouhani to do more to prop up the rial after the currency fell to a historic low this week in anticipation of renewed U.S. sanctions.

Asian equity markets traded mostly subdued after the continued tech sell-off in US where all majors declined and the Nasdaq posted its worst 3-day performance in 4 months, while disappointing Chinese PMI data and tightening concerns heading into the BoJ policy announcement added to the cautiousness. ASX 200 (+0.1%) and Nikkei 225 (-0.1%) were mixed with Australia just about kept afloat amid outperformance in telecoms and gains in commodity-related sectors, while the Japanese benchmark was weighed alongside widespread uncertainty regarding potential BoJ policy tweaks which proved to be less hawkish than some had feared as the central bank maintained its long-term yield target at 0% and provided forward guidance that rates will be maintained at very low levels for an extended period. Elsewhere, Hang Seng (-0.5%) and Shanghai Comp. (+0.3%.) were downbeat after the PBoC skipped repo operations for an 8th consecutive occasion and as participants digested Chinese Official Manufacturing and Non-Manufacturing PMI missed expectations in which the latter fell to its weakest in nearly a year. The Shanghai Comp., however, rebounded into positive territory before the close. Finally, 10yr JGBs initially began on the back-foot as yields continued to gain heading into the BoJ but then recovered after the central bank kept its long-term yield at 0.0% and although it announced more flexibility in allowing yields to move higher and lower, it also signalled to act if there is a rapid increase in yields

Top Asian News

- BOJ to Allow Flexibility in Bond Operations, Adjusts ETF Buying

- China Sovereign Bonds Head for First Monthly Decline in Six

- Coal Goes From Summer Boom to Bust on Ample Supply in China

- Mizuho Profit Rises 36%, Led by Share Sale Gains and Fee Income