GOLD: $1219.00 DOWN $4.65 (COMEX TO COMEX CLOSINGS)

Silver: $15.44 DOWN 12 CENTS (COMEX TO COMEX CLOSINGS)

Closing access prices:

Gold $1216.30

silver: $15.38

For comex gold:

JULY/

NUMBER OF NOTICES FILED TODAY FOR AUGUST CONTRACT:34 NOTICE(S) FOR 3400 oz

TOTAL NOTICES SO FAR 71 FOR 7100 OZ (0.2208 tonnes)

For silver:

JULY

281 NOTICE(S) FILED TODAY FOR

1,405,000 OZ/

Total number of notices filed so far this month: 255 for 2,680,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: BID $7498/OFFER $7583: DOWN $153(morning)

Bitcoin: BID/ $7583/offer $7668: DOWN $71 (CLOSING/5 PM)

end

First Shanghai gold fix comes at 10 pm est

The second Shanghai gold fix: 2:15 pm

First Shanghai gold fix gold: 10 pm est: $1226.38

NY price at the same time:1223.50

PREMIUM TO NY SPOT: $2,88

XX

Second gold fix early this morning: $1226.38

USA gold at the exact same time:$1221.00

PREMIUM TO NY SPOT: $5.38

China is controlling the gold market

WE WILL NOT PROVIDE LONDON FIXES AS THEY ARE NOT ACCURATE AS TO WHAT IS GOING ON AT THE SAME TIME FRAME.

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total OPEN INTEREST ROSE BY A HUMONGOUS SIZED 5604 CONTRACTS FROM 220,908 UP TO 226,512 DESPITE YESTERDAY’S TINY 5 CENT GAIN IN SILVER PRICING AT THE COMEX. WE HAVE NOW WITNESSED A SLOW COMEX ACCUMULATION THESE PAST SEVERAL DAYS. ON TOP OF THIS WE HAVE ALSO WITNESSED A LARGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY(WELL OVER 30 MILLION OZ AT THE COMEX FOR JULY AND OVER 4 MILLION OZ FOR AUGUST) AS WELL AS CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A STRONG SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP: 1034 EFP’S FOR SEPT. , 0 EFP’S FOR DECEMBER AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE: OF 1034 CONTRACTS. WITH THE TRANSFER OF 1034 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 1034 EFP CONTRACTS TRANSLATES INTO 5.170 MILLION OZ AND ACCOMPANYING:

1.THE 5 CENT GAIN IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR THE JUNE/2018 COMEX DELIVERY MONTH. (5.420 MILLION OZ) 30.370 MILLION OZ FINALLY STANDING FOR DELIVERY IN JULY, AND NOW 4.085 MILLION OZ FOR AUGUST.

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF JULY:

1034 CONTRACTS (FOR 1 TRADING DAYS TOTAL 1034 CONTRACTS) OR 5.170 MILLION OZ: (AVERAGE PER DAY: 1034 CONTRACTS OR 5.170 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF JULY: 5.170 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 0.73% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2018 TO DATE SILVER EFP’S: 1,837.74 MILLION OZ.

ACCUMULATION FOR JAN 2018: 236.879 MILLION OZ

ACCUMULATION FOR FEB 2018: 244.95 MILLION OZ

ACCUMULATION FOR MARCH 2018: 236.67 MILLION OZ

ACCUMULATION FOR APRIL 2018: 385.75 MILLION OZ

ACCUMULATION FOR MAY 2018: 210.05 MILLION OZ

ACCUMULATION FOR JUNE 2018: 345.43 MILLION OZ

ACCUMULATION FOR JULY 2018: 172.84 MILLION OZ

RESULT: WE HAD A HUMONGOUS SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 6507 DESPITE THE TINY 5 CENT GAIN IN SILVER PRICING AT THE COMEX YESTERDAY. THE CME NOTIFIED US THAT WE HAD A SMALL SIZED EFP ISSUANCE OF 1034 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) . FROM THE CME DATA: 1034 EFP’S FOR SEPT, 0 EFP’S FOR DECEMBER AND ZERO FOR ALL OVER MONTHS FOR A DELIVERABLE FORWARD CONTRACT OVER IN LONDON WITH A FIAT BONUS (TOTAL: 1034). TODAY WE GAINED AN ATMOSPHERIC SIZED: 6638 TOTAL OI CONTRACTS ON THE TWO EXCHANGES:

i.e 1034 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH AN INCREASE OF 5604 OI COMEX CONTRACTS. AND ALL OF THIS DEMAND HAPPENED WITH A 5 CENT GAIN IN PRICE OF SILVER AND A CLOSING PRICE OF $15.56 WITH RESPECT TO YESTERDAY’S TRADING. YET WE HAD A GIGANTIC AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY IN THE BIG JULY DELIVERY MONTH OF SLIGHTLY OVER 30 MILLION OZ AND NOW IN AUGUST ANOTHER BIG 4.085 MILLION OZ IN A NON ACTIVE MONTH. IT SURE LOOKS LIKE ANOTHER FAILED BANKER SHORT COVERING EXERCISE AS BANKERS ARE SCRAMBLING TO COVER THEIR HUGE SHORTFALL.

In ounces AT THE COMEX, the OI is still represented by OVER 1 BILLION oz i.e. 1.137 MILLION OZ TO BE EXACT or 157% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT JULY MONTH/ THEY FILED AT THE COMEX: 255 NOTICE(S) FOR 1,275,000 OZ OF SILVER

IN SILVER, WE SET THE NEW RECORD OF OPEN INTEREST AT 243,411 CONTRACTS ON APRIL 9.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $16.51

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) AND JULY 2018 AMOUNT FINALLY STANDING: 30.370 MILLION OZ ) AND NOW FOR AUGUST 4.085 MILLION OZ.

- HUGE RECORD OPEN INTEREST IN SILVER 243,411 CONTRACTS (OR 1.217 BILLION OZ/ SET APRIL 9/2018

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017

- RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT).

IN GOLD, THE OPEN INTEREST FINALLY ROSE BY A CONSIDERABLE SIZED 2784 CONTRACTS UP TO 452,655 WITH THE SMALL RISE IN THE COMEX GOLD PRICE/YESTERDAY’S TRADING (A GAIN IN PRICE OF $2.05). THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A GOOD SIZED 8,486 CONTRACTS:

DECEMBER HAD AN ISSUANCE OF 4238 CONTACTS AND THEN ALL OTHER MONTHS ZERO. The new COMEX OI for the gold complex rests at 452,655. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE A STRONG OI GAIN IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 11,270 CONTRACTS: 2784 OI CONTRACTS INCREASED AT THE COMEX AND 8486 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN: 11,270 CONTRACTS OR 1,350,600 OZ = 35.05 TONNES. AND ALL OF THIS STRONG DEMAND OCCURRED WITH THE SMALL RISE IN THE PRICE OF GOLD/ YESTERDAY TO THE TUNE OF $2.05.

YESTERDAY, WE HAD 4238 EFP’S ISSUED.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF JUNE : 8486 CONTRACTS OR 848,600 OZ OR 28.39 TONNES (1 TRADING DAYS AND THUS AVERAGING: 8486 EFP CONTRACTS PER TRADING DAY OR 848,600 OZ/ TRADING DAY),,

TO GIVE YOU AN IDEA AS TO THE HUGE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 1 TRADING DAYS IN TONNES: 28.39 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2017, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 2555 TONNES

THUS EFP TRANSFERS REPRESENTS 28.39/2550 x 100% TONNES = 1.11% OF GLOBAL ANNUAL PRODUCTION SO FAR IN JULY ALONE.***

ACCUMULATION OF GOLD EFP’S YEAR 2018 TO DATE: 4,736.80* TONNES *SURPASSED ANNUAL PROD’N

ACCUMULATION OF GOLD EFP’S FOR JANUARY 2018: 653.22 TONNES (21 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR FEBRUARY 2018: 649.45 TONNES (20 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR MARCH 2018: 741.89 TONNES (22 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR APRIL 2018: 713.84 TONNES (21 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR MAY 2018: 693.80 TONNES ( 22 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR JUNE 2018 650.71 TONNES (21 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR JULY 2018 605.5 TONNES (21 TRADING DAYS)

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A CONSIDERABLE SIZED INCREASE IN OI AT THE COMEX OF 2784 WITH THE SMALL GAIN IN PRICING ($2.05 THAT GOLD UNDERTOOK ON YESTERDAY) // . WE ALSO HAD A STRONG SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 8486 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 8,486 EFP CONTRACTS ISSUED, WE HAD A VERY STRONG NET GAIN OF 11,270 CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

8486 CONTRACTS MOVE TO LONDON AND 2784 CONTRACTS INCREASED AT THE COMEX. (in tonnes, the GAIN in total oi equates to 35.05 TONNES). ..AND THIS STRONG DEMAND OCCURRED WITH A TINY GAIN OF $2.05 IN YESTERDAY’S TRADING AT THE COMEX!!!.

we had: 37 notice(s) filed upon for 3700 oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD...

WITH GOLD DOWN $4.65 TODAY: /

NO CHANGES IN GOLD INVENTORY AT THE GLD

/GLD INVENTORY 800.20 TONNES

Inventory rests tonight: 800.20 tonnes.

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

SLV/

WITH SILVER DOWN 12 CENTS TODAY :

NO CHANGE IN SILVER INVENTORY TONIGHT

/INVENTORY RESTS AT 329.433 MILLION OZ/

NOTE THE DIFFERENCE BETWEEN THE GLD AND SLV: THE CROOKS CAN RAID GOLD BECAUSE THEY DO HAVE SOME PHYSICAL. THEY DO NOT RAID SILVER PROBABLY BECAUSE THERE IS NO REAL SILVER INVENTORIES BEHIND THEM

end

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER ROSE BY A HUMONGOUS SIZED 5604 CONTRACTS from 220,908 UP TO 226,512 (AND MUCH CLOSER T0 THE NEW COMEX RECORD SET /APRIL 9/2017 AT 243,411/SILVER PRICE AT THAT DAY: $16.53). THE PREVIOUS RECORD OTHER THAN WAS ESTABLISHED AT: 234,787, SET ON APRIL 21.2017 OVER ONE YEAR AGO. THE PRICE OF SILVER ON THAT DAY: $17.89. OUR CUSTOMARY MIGRATION OF COMEX LONGS MORPH INTO LONDON FORWARDS CONTINUES AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

1034 EFP CONTRACTS FOR SEPT., 0 EFP CONTRACTS FOR DECEMBER AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 1034 CONTRACTS . EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI GAIN AT THE COMEX OF 6507 CONTRACTS TO THE 1034 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN AN ATMOSPHERIC NET GAIN OF 6638 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES: 33.19 MILLION OZ!!! AND YET WE ALSO HAVE A STRONG DEMAND FOR PHYSICAL AS WE WITNESSED A FINAL STANDING OF GREATER THAN 30 MILLION OZ FOR JULY AND NOW ANOTHER STRONG 4.085 MILLION OZ FOR AUGUST... AND YET ALL OF THIS HUGE DEMAND OCCURRED DESPITE A SMALL 5 CENT PRICING GAIN AT THE SILVER COMEX.

RESULT: A HUMONGOUS SIZED INCREASE IN SILVER OI AT THE COMEX DESPITE THE 5 CENT PRICING GAIN THAT SILVER UNDERTOOK IN PRICING YESTERDAY. BUT WE ALSO HAD A STRONG SIZED 1034 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR JULY, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON AS WELL AS THE STRONG AMOUNT OF PHYSICAL STANDING FOR METAL AT THE COMEX.

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

)WEDNESDAY MORNING/TUESDAY NIGHT: Shanghai closed DOWN 51.87 POINTS OR 1.80% /Hang Sang CLOSED DOWN 242.27 POINTS OR 0.85%/ / The Nikkei closed UP 192,98 POINTS OR 0.86%/Australia’s all ordinaires CLOSED DOWN 0.07% /Chinese yuan (ONSHORE) closed UP at 6.7981 AS POBC STOPS ITS HUGE DEVALUATION /Oil UP to 67.97 dollars per barrel for WTI and 73.25 for Brent. Stocks in Europe OPENED RED//. ONSHORE YUAN CLOSED WELL UP AT 6.7981 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.8072: HUGE DEVALUATION/PAST SEVERAL DAYS STOPS : /ONSHORE YUAN TRADING STRONGER AGAINST OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING STRONGER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

/NORTH KOREA/SOUTH KOREA

i)North Korea/South Korea/USA/Russia

b) REPORT ON JAPAN

Turmoil in Japan as margin calls are galore as bond prices plummeted with the 10 yr yield rising to.13%

( zerohedge)

3 c CHINA

i)Last night

scant progress, but later that has been refuted

( zerohedge)

ii)Trade wars resume as China vows retaliation to the USA. China states that it does not want the USA to engage in blackmail if Trump hikes tariffs. Initially the off shore yuan hit 6.86 and then the POBC intervened

( zerohedge)

iib)The value of yuan and futures rise as Trump extends implementation of China’s tariff deadline by one week

( zerohedge)

iii)A great commentary: we now know that a huge 18% of Chinese debt is interest paid on their massive amount of debt

( zerohedge)

4. EUROPEAN AFFAIRS

i)Spain

They never learn: Spain overtakes Italy for migrant arrivals into their country

( zerohedge)

( Raul Meijer)

( zerohedge)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

6 .GLOBAL ISSUES

( Graham Summers)

7. OIL ISSUES

8. EMERGING MARKET

9. PHYSICAL MARKETS

i)A terrific commentary from Nicholas Bienzanek who proves that zero gold is actually settled upon in England through our EFP’s. These paper contracts just get bigger and bigger and continually rotate like a Ferris wheel…when they pass go they collect $200.00 dollars and continue for another 13 day journey.

( Nicholas Biezanek)

ii)They seem to agree with me that the pricing of gold is being transferred over to China from London and NY

( the daily economist)

10. USA stories which will influence the price of gold/silver)

i)Market trading /GOLD/MARKET MOVERS:

A good Bellwether for the USA economy: lumber prices dump big time as construction spending slumps and this is the worst seen in over 18 years

(courtesy zerohedge)

Wow!! we now have both Markit and ISM reporting huge slumps in PMI and both show big price surges and tumbling orders.

The USA economy is turning on a dime

( zerohedge)

a)My goodness, it this latest commentary we find that the state and local pension accounts have a shortfall of 5 trillion dollars. This has no chance of being financed

( zerohedge)

b)My bride of 47 years is not going to be happy on hearing the following: her favourite store Cheeesecake factory is tumbling the most since 1999 due to a surge in labour costs

(courtesy zerohedge)

c)OH!! how could this happen to such fine and upstanding citizens of the uSA: they were fined again for $2.09 billion in mortgage loan abuses

(zerohedge)

d)heartbreaking: the number of people living in their vehicles explodes.

iv)SWAMP STORIES

a)Trump has had enough as he now urges the Sessions to drop the rigged witch hunt

( zerohedge)

b)Good victory for Trump as they throw out a nationwide injunction as Trump limits funding for them not co-operating

Trading Volumes on the COMEX

PRELIMINARY COMEX VOLUME FOR TODAY: 194,606 contracts

CONFIRMED COMEX VOL. FOR YESTERDAY: 314,005 contracts

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

And now for the wild silver comex results.

Total silver OI ROSE BY A HUMONGOUS SIZED 5604 CONTRACTS FROM 220,908 UP TO 226,512 (AND A LOT CLOSER TO THE THE NEW RECORD OI FOR SILVER SET APRIL 9.2018/ 243,411 CONTRACTS)DESPITE THE TINY 5 CENT GAIN IN PRICING THAT SILVER UNDERTOOK YESTERDAY. SINCE WE ARE NOW INTO THE ACTIVE DELIVERY MONTH OF JULY, WE WERE INFORMED THAT WE HAD A STRONG SIZED 1034 EFP CONTRACTS FOR SEPT., 0 EFP CONTRACTS FOR DECEMBER AND ZERO FOR ALL OTHER MONTHS. THESE EFPS WERE ISSUED TO COMEX LONGS WHO RECEIVED A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. THE TOTAL EFP’S ISSUED: 1034. ON A NET BASIS WE GAINED 6638 SILVER OPEN INTEREST CONTRACTS AS WE OBTAINED 5604 CONTRACT GAIN AT THE COMEX COMBINING WITH THE ADDITION OF 1034 OI CONTRACTS NAVIGATING OVER TO LONDON.

NET GAIN ON THE TWO EXCHANGES: 6638 CONTRACTS

FOR THE FRONT MONTH OF AUGUST WE HAD A NET LOSS OF 100 CONTRACTS. WE HAD 255 NOTICES FILED YESTERDAY SO WE CONTINUE WHERE WE LEFT OFF LAST MONTH IN THAT WE GAINED 155 CONTRACTS STANDING OR AN ADDITIONAL 775,000 OZ WILL STAND AT THE COMEX AS THESE GUYS REFUSED TO MORPH INTO LONDON BASED FORWARDS AND RECEIVE A FIAT BONUS. QUEUE JUMPING AT THE SILVER COMEX IS THE NORM AS THERE IS CONSIDERABLE AMOUNT OF PHYSICAL LOCATED HERE. THERE IS NO QUEUE JUMPING AT THE GOLD COMEX FOR THE SIMPLE REASON THAT THERE IS NO GOLD THERE.

The next active delivery month after August for silver is September and here the OI ROSE by 2696 contracts UP to 158,609. October received its first two contracts to stand at 2

After October, the next big delivery month is December and here the OI rose by 3592 contracts up to 56,990 contracts.

We had 281 notice(s) filed for 1,405,000 OZ for the AUGUST 2018 COMEX contract for silver

AND NOW COMPARISON VS AUGUST LAST YR:

ON FIRST DAY NOTICE JULY 31/2017: 1,965,000 OZ STOOD FOR DELIVERY

THE FINAL AMOUNT OF SILVER STANDING: AUGUST 30.2017: 6,245,000 OZ AS WE HAD CONSIDERABLE QUEUE JUMPING.

INITIAL standings for AUGUST/GOLD

AUGUST 1/2018.

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz |

NIL OZ

|

| Deposits to the Dealer Inventory in oz | NIL oz |

| Deposits to the Customer Inventory, in oz |

nil oz

|

| No of oz served (contracts) today |

34 notice(s)

3,400 OZ

|

| No of oz to be served (notices) |

3816 contracts

(381,600 oz)

|

| Total monthly oz gold served (contracts) so far this month |

71 notices

7100 OZ

.2208TONNES

|

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

we have a NO pulse today, AND zero gold enters the comex

For AUGUST:

Today, 0 notice(s) were issued from JPMorgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equates to 34 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 21 notice(s) was (were) stopped/ Received) by j.P.Morgan customer account.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

To calculate the INITIAL total number of gold ounces standing for the AUGUST. contract month, we take the total number of notices filed so far for the month (71) x 100 oz or 7100 oz, to which we add the difference between the open interest for the front month of AUGUST. (3850 contracts) minus the number of notices served upon today (34 x 100 oz per contract) equals 388,700 OZ OR 12.09 TONNES) the number of ounces standing in this non active month of AUGUST

Thus the INITIAL standings for gold for the AUGUST contract month:

No of notices served (71 x 100 oz) + {(3850)OI for the front month minus the number of notices served upon today (34 x 100 oz )which equals 388,700 oz standing OR 12.09 TONNES in this active delivery month of AUGUST.

WE LOST 875 COMEX CONTRACTS OR AN ADDITIONAL 87500 OZ WILL NOT STAND AND THESE GUYS MORPHED INTO LONDON BASED FORWARDS. THERE WAS NO REASON TO HANG AROUND THE COMEX AS THERE IS NO GOLD THERE TO SETTLE UPON.

THERE ARE ONLY 7.8648 TONNES OF REGISTERED COMEX GOLD AVAILABLE FOR DELIVERY AGAINST 12.09 TONNES STANDING FOR JULY

IN THE LAST 24 MONTHS 85 NET TONNES HAS LEFT THE COMEX.

end

And now for silver

AND NOW THE AUGUST DELIVERY MONTH

AUGUST INITIAL standings/SILVER

| Silver | Ounces |

| Withdrawals from Dealers Inventory | nil oz |

| Withdrawals from Customer Inventory |

1,111,078.660 oz

DELAWARE

HSBC

Scotia

|

| Deposits to the Dealer Inventory |

nil oz

|

| Deposits to the Customer Inventory |

nil oz

|

| No of oz served today (contracts) |

281

CONTRACT(S)

(1,405,000 OZ)

|

| No of oz to be served (notices) |

271 contracts

(1,355,000 oz)

|

| Total monthly oz silver served (contracts) | 536 contracts

(2,680,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

we had 0 inventory movement at the dealer side of things

total dealer deposits: nil oz

total dealer withdrawals: nil oz

we had 0 deposit into the customer account

i) Into JPMorgan: nil oz

*** JPMorgan for most of 2017 and in 2018 has adding to its inventory almost every single day.

JPMorgan now has 144 million oz of total silver inventory or 51.0% of all official comex silver. (144 million/283 million)

iii) into everybody else; 0 oz

total customer deposits today: nil oz

we had 3 withdrawals from the customer account;

i) out of Scotia; 250,488.110 oz

ii) out of Delaware: 7898.900 oz

iii) out of HSBC: 852,691.65 oz

total withdrawals: 1,111,078.820 oz

we had 2 adjustment/

i) Out of CNT:

624,200.820 oz was adjusted out of the customer and this landed into the dealer account of CNT

ii) Out of CNTs:

10,4600.231 oz was adjusted out of the customer and this landed into the dealer account of CNT

total dealer silver: 80 million

total dealer + customer silver: 283.668 million oz

The total number of notices filed today for the AUGUST. contract month is represented by 281 contract(s) FOR 1,405,000 oz. To calculate the number of silver ounces that will stand for delivery in AUGUST., we take the total number of notices filed for the month so far at 536 x 5,000 oz = 2,680,000 oz to which we add the difference between the open interest for the front month of AUGUST. (552) and the number of notices served upon today (281 x 5000 oz) equals the number of ounces standing.

.

Thus the INITIAL standings for silver for the AUGUST/2018 contract month: 536(notices served so far)x 5000 oz + OI for front month of AUGUST(552) -number of notices served upon today (281)x 5000 oz equals 4,085,000 oz of silver standing for the AUGUST contract month

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

ESTIMATED VOLUME FOR TODAY:59,146 CONTRACTS

CONFIRMED VOLUME FOR YESTERDAY: 85,301 CONTRACTS absolutely criminal

YESTERDAY’S CONFIRMED VOLUME OF 85,301 CONTRACTS EQUATES TO 426 million OZ OR 60.9% OF ANNUAL GLOBAL PRODUCTION OF SILVER

COMMODITY LAW SUGGESTS THAT OPEN INTEREST SHOULD NOT BE MORE THAN 3% OF ANNUAL GLOBAL PRODUCTION. THE CROOKS ARE SUPPLYING MASSIVE PAPER TRYING TO KEEP SILVER IN CHECK.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price at that day at $18.42

The previous record was 224,540 contracts with the price at that time of $20.44

end

NPV for Sprott

1. Sprott silver fund (PSLV): NAV FALLS TO -2.80% (AUGUST 1/2018)

2. Sprott gold fund (PHYS): premium to NAV FALLS TO -1.00% to NAV (AUGUST 1/2018 )

Note: Sprott silver trust back into NEGATIVE territory at -2.80%-/Sprott physical gold trust is back into NEGATIVE/

(courtesy Sprott/GATA)

3.SPROTT CEF.A FUND (FORMERLY CENTRAL FUND OF CANADA):

NAV 12.59/TRADING 12.15//DISCOUNT 3.50.

END

And now the Gold inventory at the GLD/

AUGUST 1/WITH GOLD DOWN $4.65/NO CHANGE IN GOLD INVENTORY AT THE GLD.INVENTORY RESTS AT 800.20 TONNES

JULY 31/WITH GOLD UP $2.05/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 800.20

JULY 30/WITH GOLD DOWN $0.95/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 800.20 TONNES

july 27/WITH GOLD DOWN $2.85 TODAY, NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 800.20 TONNES

JULY 26./WITH GOLD DOWN $5.65: A WITHDRAWAL OF 2.35 TONNES OF GOLD FROM THE GLD/INVENTORY RESTS AT 800.20 TONNES

JULY 25/WITH GOLD UP $6.45; NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 802.55 TONNES

JULY 24/ WITH GOLD DOWN 10 CENTS: A HUGE DEPOSIT OF 4.42 TONNES INTO THE GLD/INVENTORY RESTS AT 802.55 TONNES

JULY 23/WITH GOLD DOWN $5.55: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 798.13 TONNES

JULY 20/WITH GOLD UP $4.15 A HUGE DEPOSIT OF 4.12 TONNES OF GOLD INTO THE GLD.INVENTORY RESTS AT 798.13 TONNES

JULY 19./WITH GOLD DOWN $1.00: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 794.01 TONNES

JULY 18/WITH GOLD UP 0.40: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 794.01 TONNES

JULY 17/WITH GOLD DOWN $12.40, WE HAD A BIG WITHDRAWAL OF 1.18 TONNES FROM THE GLD/INVENTORY RESTS AT 794.01 TONNES

JULY 16/WITH GOLD DOWN $1.55/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 795.19 TONNES

JULY 13/WITH GOLD DOWN $5.35 THE CROOKS RAID THE COOKIE JAR AGAIN TO THE TUNE OF 3.83 TONNES/INVENTORY RESTS AT 795.19 TONNES

JULY 12/WITH GOLD UP $2.30: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 799.02 TONNES

JULY 11/WITH GOLD DOWN $10.75 THE CROOKS RAIDED THE COOKIE JAR AGAIN TO THE TUNE OF 1.75 TONNES/INVENTORY RESTS AT 799.02 TONNES

JULY 10/WITH GOLD DOWN $3.85: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 800.77 TONNES

july 9/WITH GOLD UP $4.00/ANOTHER RAID ON THE GOLD COOKIE JAR: TWO WITHDRAWALS OF 1.18 TONNES THIS MORNING AND 1.47 TONNES THIS AFTERNOON/INVENTORY RESTS AT 800.77 TONNES

JULY 6/WITH GOLD DOWN $2.45: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 803.42 TONNES

JULY 5/WITH GOLD UP ANOTHER $5.15, THE CROOKS RAIDED THE COOKIE JAR AGAIN TO THE TUNE OF 5.89 TONNES/INVENTORY RESTS AT 803.42 TONNES IN THE LAST 10 TRADING DAYS GLD HAS LOST A HUGE 25.34 TONNES WITH A LOSS OF ONLY $15.25 IN PRICE

July 3/WITH GOLD UP $11.15/THE CROOKS RAIDED THE GLD INVENTORY AGAIN TO THE TUNE OF 9.73 TONNES/INVENTORY RESTS AT 809.31 TONNES

JULY 2/WITH GOLD DOWN $12.15, THE CROOKS RAIDED THE GLD INVENTORY AGAIN BY 1.47 TONNES DOWN./INVENTORY RESTS AT 819.04 TONNES

JUNE 29/WITH GOLD UP $3.70/A WITHDRAWAL OF 1.18 TONNES OF GOLD FROM THE GLD/INVENTORY RESTS AT 820.51 TONNES

JUNE 28/WITH GOLD DOWN $5.15/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 821.69 TONNES

June 27/WITH GOLD DOWN $3.60// TWO ENTRIES:/STRANGELY THE CROOKS RETURNED THE WITHDRAWAL OF 4.42 TONNES LAST NIGHT (THUS WE HAD A DEPOSIT OF 4.42 TONNES/INVENTORY RESTS AT 824.63 TONNES. /THEN LATE THIS AFTERNOON A WITHDRAWAL OF 2.94 TONNES

INVENTORY RESTS AT 821.69 TONNES/THIS VEHICLE IS AN OUTRIGHT FRAUD.

june 26/LATE LAST NIGHT, WITH GOLD DOWN $9.10 WE HAD A HUGE WITHDRAWAL OF 4.42 TONNES OF GOLD/INVENTORY RESTS AT 820.21 TONES

JUNE 25/WITH GOLD DOWN $1.45/NO CHANGE IN GOLD INVENTORY AT THE GLD.INVENTORY RESTS AT 824.63 TONNES

JUNE 22/WITH GOLD UP 25 CENTS TODAY, THE CROOKS WITHDREW A MASSIVE 4.13 TONNES OF GOLD/INVENTORY RESTS AT 824.63 TONNES

JUNE 21/WITH GOLD DOWN $4.00/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 828.76 TONNES

JUNE 20/WITH GOLD DOWN $3.55/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 828.76 TONNES

JUNE 19/WITH GOLD DOWN $1.50/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 828.76 TONES

JUNE 18/WITH GOLD UP $1.90/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 828.76 TONNES

JUNE 15/WITH GOLD DOWN $28.90/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 828.76 TONNES

JUNE 14/WITH GOLD UP $7.10/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 828.76 TONNES/

JUNE 13/WITH GOLD UP $2.20/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 828.76 TONNES

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

AUGUST1/2018/ Inventory rests tonight at 800.20 tonnes

*IN LAST 421 TRADING DAYS: 130.73 NET TONNES HAVE BEEN REMOVED FROM THE GLD

*LAST 371 TRADING DAYS: A NET 25,81 TONNES HAVE NOW BEEN ADDED INTO GLD INVENTORY.

end

Now the SLV Inventory/

AUGUST 1/WITH SILVER DOWN 12 CENTS TODAY, NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 329.433 MILLION OZ/

JULY 31/WITH SILVER UP 5 CENTS/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 329.433 MILLION OZ/

JULY 30/WITH SILVER UP 3 CENTS TODAY; NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 329.433 MILLION OZ.

JULY 27/WITH SILVER FLAT TODAY, NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 329.433 MILLION OZ/

JULY 26/WITH SILVER DOWN 10 CENTS: STRANGE: A BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.046 MILLION OZ OF SILVER/INVENTORY RESTS AT 329.433 MILLION OZ

JULY 25: WITH SILVER UP 8 CENTS TODAY: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV/ A WITHDRAWAL OF 658,000 INVENTORY RESTS AT 328.304 MILLION OZ/

JULY 24/WITH SILVER UP 8 CENTS TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 328.962 MILLION OZ/

JULY 23/WITH SILVER DOWN 11 CENTS/NO CHANGES IN SILVER INVENTORY INTO THE SLV/INVENTORY RESTS AT 328.962 MILLION OZ/

JULY 20/WITH SILVER UP 10 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.411 MILLION OZ INTO THE SLV INVENTORY

INVENTORY RESTS AT 328.962 MILLION OZ

JULY 19/WITH SILVER DOWN 17 CENTS TODAY; A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 752,000 OZ INTO THE SLV INVENTORY/INVENTORY RESTS AT 327.551 MILLION OZ/

JULY 18/WITH SILVER DOWN 3 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 326.799 MILLION OZ/

JULY 17/WITH SILVER DOWN 20 CENTS TODAY: A CHANGE IN SILVER INVENTORY A WITHDRAWAL OF 1.001 MILLION OZ FROM THE SLV: INVENTORY RESTS AT 326.799 MILLION OZ/

JULY 16/WITH SILVER FLAT TODAY, A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.128 MILLION OZ//INVENTORY RESTS AT 327.880 MILLION OZ

JULY 13/WITH SILVER DOWN 16 CENTS TODAY/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 326.752 MILLION OZ.

JULY 12/WITH SILVER UP 12 CENTS TODAY: ANOTHER BIG CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.035 MILLION OZ/INVENTORY RESTS AT 326.752 MILLION OZ/

JULY 11/WITH SILVER DOWN 22 CENTS TODAY: ANOTHER HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 565,000/INVENTORY RESTS AT 325.717 MILLION OZ

JULY 10/WITH SILVER DOWN 3 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 325.151 MILLION OZ

july 9/WITH SILVER UP 5 CENTS: ANOTHER BIG CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 847,000 OZ ADDED TO INVENTORY/INVENTORY RESTS AT 825.151 MILLION OZ/

JULY 6/WITH SILVER DOWN 2 CENTS/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 324.305 MILLION OZ/

JULY 5/WITH SILVER UP 6 CENTS, A GOOD CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 470,000 OZ/INVENTORY RESTS AT 324.305 MILLION OZ/ FOR THE PAST 10 TRADING DAYS, SILVER INVENTORY HAS ADVANCED BY 4.945 MILLION OZ WITH A LOSS OF 33 CENTS/PLEASE COMPARE THIS WITH THE GLD.

JULY 3/WITH SILVER UP 17 CENTS, A HUGE DEPOSIT OF 1.37 MILLION OZ ADDED TO THE SLV/INVENTORY RESTS AT 323.835 MILLION OZ.

JULY 2/WITH SILVER DOWN 31 CENTS/A HUGE 2.070 MILLION OZ DEPOSIT AT THE SLV/INVENTORY RESTS AT 322.465 MILLION OZ/

JUNE 29/WITH SILVER UP 14 CENTS TODAY, NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS THIS WEEKEND AT 320.395 MILLION OZ/

JUNE 28/WITH SILVER DOWN 18 CENTS, THE CROOKS ADDED 1.035 MILLION OZ OF SILVER INTO THE SLV/INVENTORY RESTS AT 320.395 MILLION OZ

JUNE 27.2018/WITH SILVER DOWN 8 CENTS/NO CHANGE IN SILVER INVENTORY/INVENTORY RESTS AT 819.360 MILLION OZ/

june 26./2018/WITH SILVER DOWN 8 CENTS, THE CROOKS WITHDREW THE DEPOSIT OF TWO DAYS AGO; 941,000 OZ OUT OF INVENTORY/INVENTORY RESTS AT 819.360 OZ

JUNE 25/WITH SILVER DOWN 12 CENTS/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 320.301 MILLION OZ/

JUNE 22/WITH SILVER UP 12 CENTS TODAY,ANOTHER BIG CHANGE IN SILVER INVENTORY AT THE SLV” A DEPOSIT OF 941,000 OZ INTO INVENTORY/INVENTORY RESTS THIS WEEKEND AT 320.301 MILLION OZ/

JUNE 21/WITH SILVER UP ONE CENT/ANOTHER CHANGE IN SILVER INVENTORY AT THE SLV/: A DEPOSIT OF 2.918 MILLION OZ/INVENTORY RESTS AT 319.360 MILLION OZ/ THUS FOR TWO STRAIGHT DAYS A TOTAL OF 5.26 MILLION OZ OF SILVER HAS BEEN ADDED WITH NO CHANGE IN PRICE.

JUNE 20/WITH SILVER DOWN ONE CENT/A HUGE CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY / A DEPOSIT OF 2.35 MILLION OZ/INVENTORY RESTS AT 316.442 MILLION OZ/

JUNE 19/2018/WITH SILVER DOWN 11 CENTS/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 314.090 MILLION OZ/

JUNE 18/WITH SILVER DOWN 6 CENTS TODAY/NO CHANGE IN SILVER INVENTORY/INVENTORY RESTS AT 314.090 MILLION OZ/

JUNE 15/WITH SILVER DOWN 75 CENTS/A BIG CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.788 MILLION OZ//INVENTORY RESTS AT 314.090 MILLION OZ

JUNE 14/WITH SILVER UP 30 CENTS, THE CROOKS DECIDED THAT THEY NEEDED SILVER INVENTORY BADLY SO THEY RAID THE SLV OF 1.412 MILLION OZ/INVENTORY RESTS AT 315.878 MILLION OZ/

JUNE 13/WITH SILVER UP 11 CENTS TODAY/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 317.290 MILLION OZ/

AUGUST 1/2018:

Inventory 329.433 MILLION OZ

6 Month MM GOFO 1.93/ and libor 6 month duration 2.53

Indicative gold forward offer rate for a 6 month duration/calculation:

G0FO+ 1.93%

libor 2.53 FOR 6 MONTHS/

GOLD LENDING RATE: .60%

XXXXXXXX

12 Month MM GOFO

+ 2.83%

LIBOR FOR 12 MONTH DURATION: 2.42

GOFO = LIBOR – GOLD LENDING RATE

GOLD LENDING RATE = +.41

end

Major gold/silver trading /commentaries for WEDNESDAY

GOLDCORE/BLOG/MARK O’BYRNE.

Here’s Where the Next Crisis Starts

By Jim Rickards courtesy of the Daily Reckoning

So many credit crises are brewing, it’s hard to keep track without a scorecard.

The mother of all credit crises is coming to China with over a quarter-trillion dollars owed by insolvent banks and state-owned enterprises, not to mention off-the-books liabilities of provincial governments, wealth management products and developers of white elephant infrastructure projects.

Then there’s the emerging-markets credit crisis, with Turkey and Argentina leading a parade of potentially bankrupt borrowers vulnerable to hot money capital outflows and a slowdown of growth in developing economies.

Close on their heels is the U.S. student loan debacle, with over $1.5 trillion in outstanding debts and default rates approaching 20%.

Now we’re facing a devastating wave of junk bond defaults. The next financial collapse, already on our radar screen, will quite possibly come from junk bonds.

Let’s unpack this…

Since the great financial crisis, extremely low interest rates allowed the total number of highly speculative corporate bonds, or “junk bonds,” to rise 58% — a record high.

Many businesses became highly leveraged as a result. There’s currently a total of about $3.7 trillion of junk bonds outstanding.

And when the next downturn comes, many corporations will be unable to service their debt. Defaults will spread throughout the system like a deadly contagion, and the damage will be enormous.

This is from a report by Mariarosa Verde, Moody’s senior credit officer:

This extended period of benign credit conditions has helped many weak, highly leveraged companies to avoid default… A number of very weak issuers are living on borrowed time while benign conditions last… These companies are poised to default when credit conditions eventually become more difficult… The record number of highly leveraged companies has set the stage for a particularly large wave of defaults when the next period of broad economic stress eventually arrives.

Many investors will be caught completely unprepared.

Each credit and liquidity crisis starts out differently and ends up the same. Each crisis begins with distress in a particular overborrowed sector and then spreads from sector to sector until the whole world is screaming, “I want my money back!”

The problem is that regulators are like generals fighting the last war. In 2008, the global financial crisis started in the U.S. mortgage market and spread quickly to the overleveraged banking sector.

Since then, mortgage lending standards have been tightened considerably and bank capital requirements have been raised steeply. Banks and mortgage lenders may be safer today, but the system is not.

Meanwhile the Fed is raising interest. It’s undertaking QE in reverse by reducing its balance sheet and contracting the base money supply. This is called quantitative tightening, or QT.

Credit conditions are already starting to affect the real economy. New cracks are appearing in emerging markets, as I mentioned. I also mentioned that student loan losses are skyrocketing. That stands in the way of household formation and geographic mobility for recent graduates.

Losses are also soaring on subprime auto loans, which has put a lid on new car sales. As these losses ripple through the economy, mortgages and credit cards will be the next to feel the pinch.

It doesn’t matter where the crisis begins. Once the tsunami hits, no one will be spared.

The stock market is going to correct in the face of rising credit losses and tightening credit conditions.

No one knows exactly when it’ll happen, but the time to prepare is now. Once the market corrects, it’ll be too late to act.

That’s why the time to buy gold is now, while it’s cheap. When you need it most, once the crisis hits, it’ll cost a fortune.

Regards,

Jim Rickards

for The Daily Reckoning

News and Commentary

PRECIOUS-Gold steady ahead of Fed statement (Reuters.com)

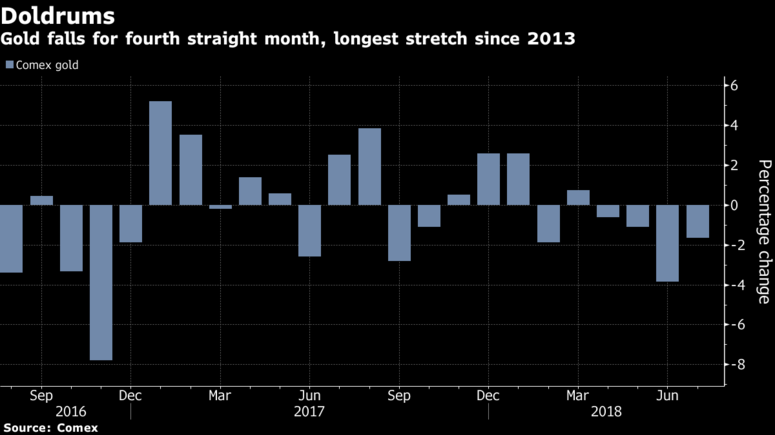

Gold Posts Longest Losing Streak Since 2013 as Bears Crush Bulls (Bloomberg.com)

U.S. consumer spending rises; wage growth slows in second-quarter (Reuters.com)

Futures, Yuan Slammed As US Plans Higher Tariffs On $200 Billion In Chinese Imports (ZeroHedge.com)

Source: Bloomberg

How High Will The Market Rally Before The Economic Collapse Begins? (GoldSeek.com)

What Happens When a Central Bank Loses Control? (ZeroHedge.com)

Treasury, Fed evade congressman’s gold questions so he presses them again, and more (Gata.org)

Ira Epstein’s Metals Video 7 31 2018 (GoldSeek.com)

Listen on SoundCloud , Blubrry & iTunes. Watch on YouTube below

Gold Prices (LBMA AM)

31 Jul: USD 1,219.20, GBP 926.71 & EUR 1,039.86 per ounce

30 Jul: USD 1,222.05, GBP 931.20 & EUR 1,045.95 per ounce

27 Jul: USD 1,219.15, GBP 931.06 & EUR 1,048.10 per ounce

26 Jul: USD 1,228.35, GBP 931.46 & EUR 1,049.13 per ounce

25 Jul: USD 1,230.55, GBP 935.09 & EUR 1,051.75 per ounce

24 Jul: USD 1,224.30, GBP 933.77 & EUR 1,047.63 per ounce

Silver Prices (LBMA)

31 Jul: USD 15.43, GBP 11.72 & EUR 13.15 per ounce

30 Jul: USD 15.49, GBP 11.81 & EUR 13.25 per ounce

27 Jul: USD 15.36, GBP 11.72 & EUR 13.20 per ounce

26 Jul: USD 15.54, GBP 11.79 & EUR 13.27 per ounce

25 Jul: USD 15.57, GBP 11.83 & EUR 13.31 per ounce

24 Jul: USD 15.51, GBP 11.81 & EUR 13.24 per ounce

Recent Market Updates

– House prices aren’t just slipping in the UK – this is global

– Russia Sells 80% Of Its US Treasuries

– Are China’s Gold Reserves Slowly Rising?

– Gold Outlook In H2 2018

– Gold Production In South Africa Continues To Collapse – Plummets 85% From Peak In 1970 (VIDEO)

– Physical Gold Is The “Best Defence” Against “Escalating Currency Wars”

– Trump and War With China? Goldnomics Podcast

– Weekly Digest – News, Market Updates and Videos You May Have Missed

– Financial Terrorism In The UK – Collusion between Government, Regulators & Two Bailed-Out UK Banks

– “Biggest Bubble in the History of Mankind” Is “Going To Burst” – Ron Paul

– Global Debt Time Bomb Surges To Nearly $250,000,000,000,000 – GoldCore Video

– Trump, Russia, Brexit and the Demand For Gold and Silver – GoldCore Video Interview

– Trump Is Serious About A Global Trade War

– Ponzi Economy Will Lead To Next Global Financial Crisis

– World Cup Is 200 Ounces Of Gold Worth £140,000 – 30% Less Than Harry Kane’s Weekly Wage

– Chaotic BREXIT More Likely: Risk To London, While Frankfurt, Luxembourg, Paris and Dublin Benefit

– VIDEO: Italy €2.4 Trillion Debt To Create Eurozone Contagion and Global Debt Crisis?

Andrew Maguire’s Kinesis money which is a “bitcoin” but backed 100% by allocated gold and silver is set to go.

it think it would be a great idea to look at this!

please read at: https://kinesis.money/#/

(Andrew Maguire)

|

|

Dear Harvey Organ,

Thank you for your participation in our webinar on June 7th with our host and CEO of Kinesis, Thomas Coughlin.

The response we received has been incredible, we appreciate you taking the time to join us and hope you found it to be beneficial.

Due to such a high influx of questions we received we were unable to have them all answered. Nevertheless, if there was anything which requires more clarification, or you have a query which needs to be rectified, we invite you to join our telegram group:

We apologize for the technical issues we incurred during the webinar which resulted in it running a little over schedule, we hope that the next one we host will run seamlessly.

A video has been put together and uploaded onto our YouTube channel which can be found here:

Please share and subscribe to our YouTube channel to be notified of all the latest videos as they become available.

The rapid growth that we are currently experiencing has been incredible and with your support, is only going to get better.

We are working behind the scenes very hard to create a better experience for everyone involved! Stay tuned in as we have many more announcements to be released in the upcoming days.

Kind Regards,

|

Kinesis Money

a:C/O ILS Fiduciaries (IOM) Limited, First Floor,Millennium House, Victoria Road, Douglas, Isle of Man IM2 4RW

|

The following is self explanatory

(courtesy GATA/Chris Powell and Harvey Organ)

GATA asks bank regulator to check risks of gold

futures maneuver

Submitted by cpowell on Sun, 2018-06-10 16:17. Section: Daily Dispatches

12:21p ET Sunday, June 10, 2018

Dear Friend of GATA and Gold:

GATA has appealed to the U.S. comptroller of the currency, who has regulatory authority over banks, to review financial risks certain banks may have incurred through derivatives in the monetary metals markets, particularly through the recent heavy use of the “exchange for physicals” mechanism of settling gold and silver futures contracts on the New York Commodities Exchange.

The appeal was made in a letter sent May 5 to the comptroller, Joseph M. Otting, whose office is part of the U.S. Treasury Department, by your secretary/treasurer and GATA futures market consultant Harvey Organ.

“Exchange for physical” settlements of futures contracts long were considered emergency procedures when a seller was not able to deliver metal from an exchange-approved warehouse and wanted to settle with delivery elsewhere. But now such settlements appear to constitute most gold and silver futures settlements on the Comex. It is a strange development that appears to have been necessitated by the increasing difficulties of central banking’s gold and silver price suppression policy.

GATA has received no acknowledgment of the letter. Its text is below and a PDF copy of it is here:

http://www.gata.org/files/ComptrollerOfCurrencyLetter.pdf

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

* * *

May 5, 2018

Joseph M. Otting, Comptroller of the Currency

U.S. Treasury Department

400 7th Street, SW

Washington DC 20219

Dear Comptroller Otting:

Please let us bring to your attention financial risks to major banks involving their possibly unreported exposure to derivatives in the monetary metals markets.

In recent months gold and silver future contracts issued by U.S. banks on the New York Commodities Exchange have been moved off-exchange for delivery through a mechanism known as “exchange for physical” (EFP) contracts. Until recently use of this mechanism was considered an emergency procedure when a seller did not have access to metal for delivery through Comex warehouses. Now the mechanism seems to be in use for a large share of front-month contracts for which delivery is sought.

Here is an example that is happening at the Comex in the front active month of April for gold and the inactive delivery month of April for silver.

In gold, there were 229,436 EFP contracts for 713.64 tonnes, an average of 10,925 contracts and 1,092,500 ounces per trading day.

In silver, there were 77,150 EFP contracts for 385,750,000 ounces, an average of 3,673 contracts and 18,369,000 ounces per trading day.

London Bullion Market Association rules suggest that these contracts may not be reported to regulators. The LBMA’s bylaws say:

“Figures above exclude any contracts not subject to risk-based capital requirements, such as FX contracts with an original maturity of 14 days or less, futures contracts, written options, and basis swaps. Therefore, the total notional amount of derivatives by maturity will not add to the total derivatives figure in this table.”

We are told that these EFP contracts are transferred from the Comex to London as what are called “serial forwards” and their duration is always less than 14 days, which exempts them from being reported.

It is our understanding that in each quarter your office prepares a report detailing risk undertaken by the banks under the comptroller’s supervision.

These risks include derivatives undertaken by U.S. banks and other obligations that may cause a bank to fail. Our concern is that your office may not be aware of large unreported derivative exposure by banks.

Could you review this matter and let us know your conclusions?

Sincerely,

CHRIS POWELL

Secretary/Treasurer

HARVEY ORGAN

Consultant

Gold Anti-Trust Action Committee Inc.

7 Villa Louisa Road

Manchester, Connecticut 06043-7541

end

This is our letter to the CFTC it is quite explanatory: is a foreign power controlling the comex gold prices:

(courtesy Chris Powell, Harvey Organ)

An open letter to the CFTC: Is a foreign power controlling Comex gold prices?

Submitted by cpowell on Sun, 2018-07-29 02:21. Section: Daily Dispatches

July 28, 2018

J. Christopher Giancarlo, Chairman

Brian Quintenz, Commissioner

Rostin Behnam, Commissioner

U.S. Commodity Futures Trading Commission

3 Lafayette Centre

1155 21st Street, NW

Washington, D.C. 20581

Dear Chairman Giancarlo:

We would like to bring to attention four issues that need to be addressed in gold and silver futures trading.

1. For the second straight month, there has been a huge discrepancy between the preliminary gold open interest and the final number recorded on particular trading days.

Let us examine the one that just happened: July 26.

There was a preliminary Comex gold open interest gain of 3,349 contracts to 503,493. But there was a final Comex gold open interest loss of 14,443 contacts to 485,701 — a discrepancy of 27,792 contracts.

The open interest here is already 24 hours old. Our understanding is that these contracts are canceled for nonpayment. It would be almost impossible for such a large number of voided contracts not to have influenced the price of gold, especially when there was a raid on the Comex by the banks.

2. The huge issuance of “exchange for physical” settlements.

For quite some time we have been told by a CFTC official, Deputy Enforcement Director Matthew Hunter, that this was quite legal as these settlements were deliverable. But in our last email exchange with Hunter he wrote that these EFPs were not deliverable. The CFTC really should provide a thorough accounting of EFPs and explain how they settle contracts.

3. The gold Comex shows a huge open interest of 43,000 contracts remaining with one day before first notice day. So there likely will be a huge amount of gold contracts standing for deliver for the August contract month — probably 31 to 62 tonnes — with only 7.8 tonnes of registered gold at the Comex and with no gold having entered the Comex for some time. How could the banks throughout the last month have depressed the price of gold amid such huge physical demand and a tiny registered gold inventory available to settle?

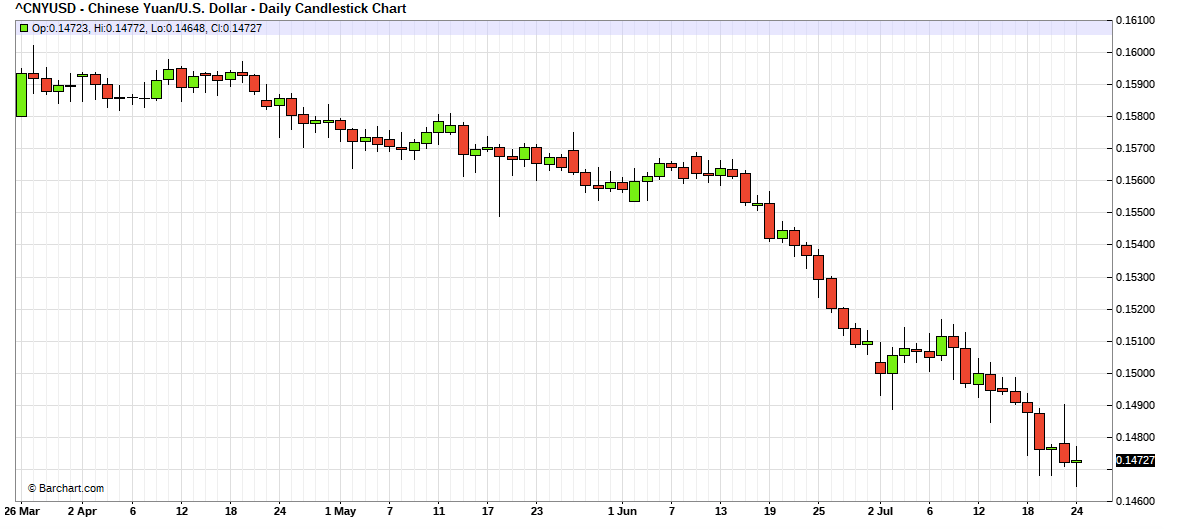

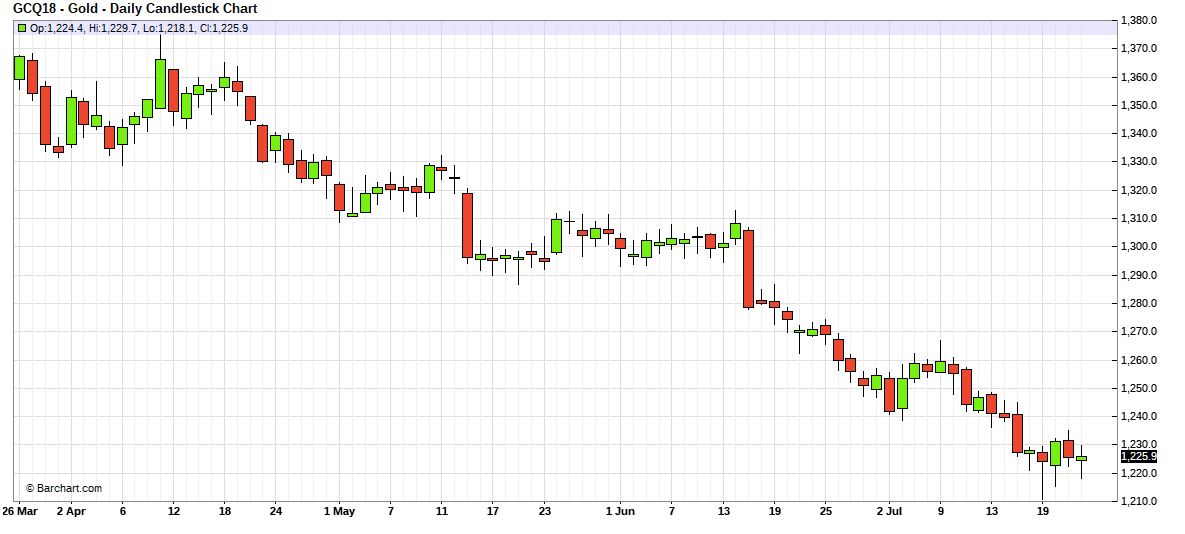

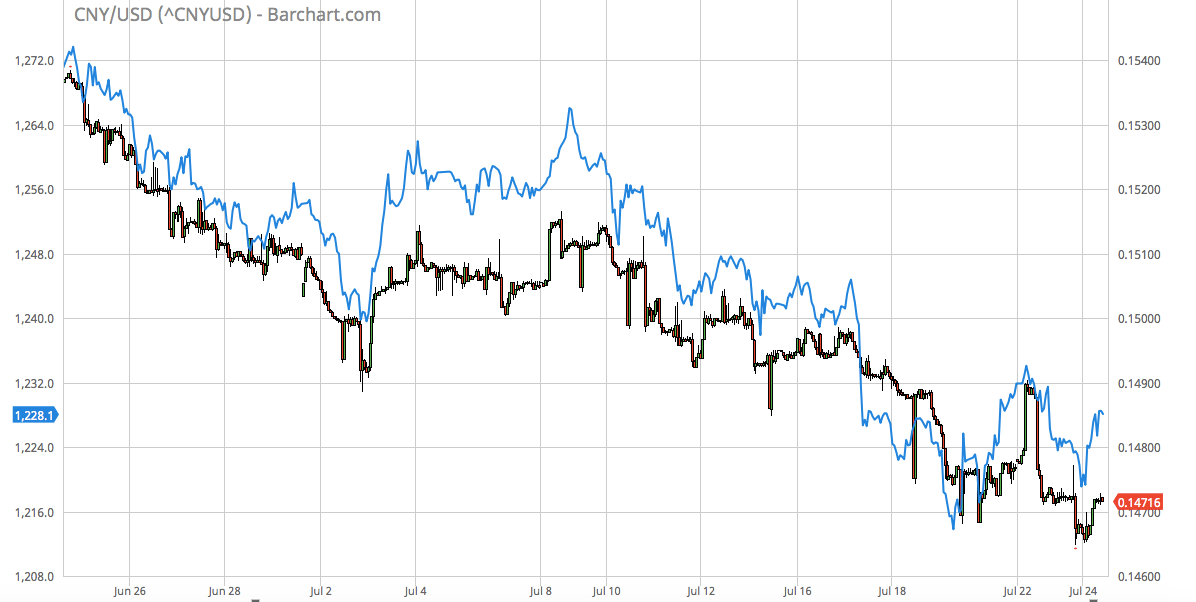

4. For the past month there has been a direct correlation between the value of the Chinese yuan and the price of gold. That is, the higher the yuan, the higher the price of gold and especially vice-versa.

The value of the Chinese yuan is essentially controlled by China’s central bank.

The Comex is generally considered the primary authority in pricing gold.

Here is recent commentary by monetary metals market analyst Craig Hemke on the recent perfect correlation between the yuan and gold:

https://www.sprottmoney.com/Blog/potential-impacts-of-the-yuan-gold-peg-…

* * *

Hemke writes:

“Though the People’s Bank of China has long maintained a ‘peg’ in the relative valuation of the yuan versus the dollar, the past 90 days have seen a steady devaluation of this peg to the tune of nearly 8 percent. See this chart:

“Over the period in this chart the price of Comex gold has fallen by more than 10 percent:

“To make this correlation clearer, let’s plot the two prices together. This correlation has become extraordinarily tight over the past month, as you can see below where the CNY/USD exchange rate is displayed in candlesticks and Comex gold is a blue line:

“And when you draw it down to just the past five days, the two prices react to each other almost simultaneously:

“This is not a correlation searching for a cause, nor is it a simple act of ‘traders’ reacting to a falling yuan by selling digital gold. No, in a market the size of global gold, this immediate correlation can be accomplished only through massive interventions, the size and scope of which are possible only at the state/sovereign level. And which state/sovereign would have a direct interest in linking the dollar price of gold to the yuan? China, of course.”

* * *

So how does the CFTC allow a foreign government or entity to control the price of this important commodity and currency by trading in U.S. markets?

Or is market manipulation by a foreign power happening with the authorization of the U.S. government?

HARVEY B. ORGAN, Consultant

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

Manchester, Connecticut

CPowell@GATA.org

end

I AM REPEATING THIS IN CASE SOME OF YOU MISSED THIS IMPORTANT COMMENTARY FROM CHRIS POWELL:

The following is a must read. Rep Mooney asks some tough questions to the Fed and Treasury with respect to the surreptitious trading in gold

(courtesy Chris Powell/GATA Stef. Gleeson)

Treasury, Fed evade congressman’s gold questions so he presses them again, and more

Submitted by cpowell on Tue, 2018-07-31 15:53. Section: Daily Dispatches

12:05p ET Tuesday, July 31, 2018

Dear Friend of GATA and Gold:

The U.S. Treasury Department and Federal Reserve responded incompletely and evasively this month to the questions about their involvement in the gold market that were posed in April by U.S. Rep. Alex X. Mooney, R-West Virginia.

So Mooney last week wrote back to Treasury Secretary Steven Mnuchin and Federal Reserve Board Chairman Jerome Powell, repeating his questions and adding a few others about surreptitious U.S. government intervention in financial markets.

..

In doing so Mooney has drawn from GATA’s documentation of such intervention.

Mooney’s first inquiries to the Treasury and the Fed are described in a GATA dispatch here:

http://www.gata.org/node/18210

Mooney’s letter containing those inquiries is here:

http://gata.org/files/MooneyLetter-04-24-2018.pdf

Mooney originally asked Mnuchin and Powell to describe the U.S. government’s policy on gold and cited documentation from the U.S. State Department archive showing that this policy has been to drive gold out of the world financial system.

Mnuchin, whose response was written by Treasury’s acting assistant secretary, Brad Bailey, and Powell did not address this question at all. Mooney has posed it again.

The Treasury’s reply denied that the department trades gold through the Bank for International Settlements, Bank of England, and other central banks or governments. But Mooney now asks if the Treasury trades gold through its Exchange Stabilization Fund or through any other government agency or through commercial banks and brokers.

Powell’s reply denied any involvement by the Fed with gold swaps. (Harvey: a lie) But Mooney’s new inquiry calls attention to minutes of the Fed’s Federal Open Market Committee from 1995, wherein Fed General Counsel Virgil Mattingly says the Exchange Stabilization Fund has engaged in gold swaps.

Mooney also calls attention to the 2009 admission to GATA by Fed Governor Kevin M. Warsh that the Fed has gold swap arrangements with foreign banks and will not disclose them.

Mooney asks Powell for an explanation of what seem like contradictions of his denial.

In his new letter Mooney notes that the auditing of the U.S. gold reserve that is described in Bailey’s letter on behalf of the Treasury is not really auditing at all, and the congressman asks: “When was the last time, if ever, that there was a complete inventory conducted of U.S. government-owned gold? What were the results of the most recent inventory?”

Mooney adds: “A true audit would also review any encumbrances placed upon the metals owned by the United States.Has there been an accounting for any such encumbrances, as part of any audit, inventory, or other review? If so, when did this last occur and what were the results?”

Mooney’s new letter notes the recent close correlation of the gold price with the price of the Chinese yuan and the valuation of the International Monetary Fund’s Special Drawing Rights, and he asks, “Do these correlations reflect surreptitious intervention in U.S. currency markets by China and currency manipulation by China? What do the Fed and Treasury think of these correlations?”

GATA’s open letter to the U.S. Commodity Futures Trading Commission, published Sunday, pressed that issue as well:

http://www.gata.org/node/18405

Perhaps most satisfying for believers in free markets and limited and transparent government, Mooney now asks the Treasury and Fed to come clean about everything. He writes: “What markets, if any, are the Federal Reserve and Treasury trading in, and through what mechanisms? If the Federal Reserve and Treasury are engaged in trading, what is the objective?”

Stefan Gleason, president of the Sound Money Defense League and coin and bullion dealer Money Metals Exchange, who has supported Mooney’s inquiries, today welcomed the congressmen’s persistence.

“This obfuscation by the Fed and the Treasury is unacceptable,” Gleason said, “and we are encouraged Congressman Mooney is calling them out on their game playing. The American people are entitled to transparency and accountability when it comes to the status and use of America’s gold reserves.”

Gleason’s statement is posted at the Money Metals Exchange internet site here:

https://www.moneymetals.com/news/2018/07/31/china-gold-market-interventi…

The replies to Mooney from the Treasury and Fed are posted at GATA’s internet site here:

http://www.gata.org/files/Treasury&FedResponsesToMooney-07-2018.pdf

Mooney’s new letters of inquiry to the Treasury and Fed are posted at GATA’s internet site here:

http://www.gata.org/files/MooneyToTreasury&Fed-07-27-2018.pdf

With his detailed questioning of the Treasury and Fed and his persistence, the congressmen is essentially conducting both the sort of serious policy review Congress seldom does anymore as well as investigative journalism that most mainstream financial news organizations prohibit about gold and market rigging by government.

On the whole the monetary metals mining industry and metals market analysts are too timid to pursue these questions. But ordinary U.S. citizens and investors can help immensely here simply by calling Mooney’s inquiries to the attention of their U.S. senators and representatives and asking them to make and publicize their own similar inquiries.

It’s easily done: Just print this dispatch and send it with a covering note to your members of Congress. If enough members of Congress support Mooney’s inquiries, market rigging will get much more difficult for the government.

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

A terrific commentary from Nicholas Bienzanek who proves that zero gold is actually settled upon in England through our EFP’s. These paper contracts just get bigger and bigger and continually rotate like a Ferris wheel…when they pass go they collect $200.00 dollars and continue for another 13 day journey.

(courtesy Nicholas Biezanek)

EFP Contracts-Too Stupid to be Stupid

Nicholas Biezanek

‘Too stupid to be stupid’, is a phrase sometimes coined by Greg Hunter. I believe that its application to the current fiasco in respect of EFP contracts is more than justified. The only propaganda that is leaked to the masses is that somehow these EFP contracts transfer liability from the COMEX to the LBMA in respect of physical delivery, but the CFTC is inconsistent and evasive, even duplicitous on this point; note that there is a massive chasm between ‘liability for delivery’ and the capacity (certainly NIL), willingness (certainly NIL) or even a remotely abstract intention to deliver. In fact let us give a citation here to the universe of all the ‘regulators’ who potentially could be in play, the CFTC, the Comptroller of the Currency, BOE, PRA, FCA and LBMA (the LBMA is a not a regulator, per se, but surely this controlling body should have more than a keen interest in all this deception, fraud and manipulation that will ultimately trash whatever vestige of integrity that is still attached to its name).Whilst the physical vault holdings of loco London precious metals are disclosed (refer below),the criminal fractional reserving in respect of total allocated gold/silver claims on these vaulted metals is never disclosed-never, ever.(Does anybody still cling to the tragic, demented belief that unallocated claims are anything other than insubstantial paper ?) So many potential regulators and not even a microscopic smidgeon of regulation in sight! A review of mere summaries of the salient data leads to the inevitable conclusion that the adjective ‘farcical’ does not come close to doing justice to this ongoing blatant, fraudulent manipulation. Here is the updated table of Harvey Organ’s detailed daily chronicling of EFP ‘transfers’:

-

Data from Harvey Organ

EFP gold

EFP silver

Tonnes

000 Ounces

Jan

2018

653

236,879

Feb

2018

649

244,950

March

2018

742

236,670

April

2018

714

385,750

May

2018

694

210,055

June

2018

651

345,430

July

2018

606

172,840

Total EFPs

4,708

1,832,574

% of annual production (ex Russia /China)

196%

262%

Now follows a table of the most recently disclosed loco London precious metal holdings, issued three months in arrears on 1st August 2018.This is an absurd (too stupid to be stupid) delay in this era of real time information systems:

|

LBMA data is available per month from July 2016 onwards |

LBMA total loco London gold holdings |

BOE total vault holdings (included in LBMA data) |

Residual gold held with all other LBMA custodians |

Residual gold held with all other LBMA custodians in tonnes |

GLD holdings with various custodians and sub custodians |

Non BOE float, excluding GLD custodial gold, available for allocated gold holders etc. |

|

A |

B |

A-B |

A-B |

C |

A-B-C |

|

|

000 |

000 |

000 |

||||

|

Troy ozs. |

Troy ozs. |

Troy ozs. |

Tonnes |

Tonnes |

Tonnes |

|

|

July 2016 |

234,144 |

158,939 |

75,205 |

2,339.14 |

958.09 |

1,381.05 |

|

Dec 2017 |

251,622 |

171,086 |

80,536 |

2,504.95 |

837.05 |

1,667.90 |

|

Jan 2018 |

251,678 |

170,979 |

80,699 |

2,510.02 |

841.35 |

1,668.67 |

|

Feb 2018 |

251,356 |

169,590 |

81,766 |

2,543.21 |

831.03 |

1,712.18 |

|

March 2018 |

250,142 |

168,020 |

82,122 |

2,554.28 |

846.12 |

1,708.16 |

|

April 2018 |

250,257 |

166,881 |

83,376 |

2,593.28 |

871.20 |

1,722.08 |

|

LBMA data is available per month from July 2016 onwards |

LBMA total loco London silver holdings |

SLV holdings with JP Morgan as sole custodian. |

Residual holdings of silver in loco London |

|

000 |

000 |

000 |

|

|

Ounces |

Ounces |

Ounces |

|

|

July 2016 |

951,433 |

349,720 |

601,713 |

|

Dec 2017 |

1,106,489 |

323,459 |

783,030 |

|

Jan 2018 |

1,108,613 |

313,896 |

794,717 |

|

Feb 2018 |

1,104,999 |

316,590 |

788,409 |

|

March 2018 |

1,086,259 |

320,395 |

765,864 |

|

April 2018 |

1,090,476 |

316,899 |

773,577 |

Note the metronomic consistency of just about every figure since December 2017 in the above tables. There are clearly NO amounts ,even gossamer driblings, leaving the loco London precious metal vaults to satisfy any obligations in respect of these EFP transfers, so the incorporation of the term ‘physical’ into this fraudulent terminology is clearly intended to engineer a false and misleading interpretation in the minds of the naïve ,uncritical masses. An ETF transfer is merely a brazen and criminally deceptive attempt to keep the precious metal suppression infrastructure from falling apart in full view of anyone with eyes to see. (In the above gold table, the GLD inventory as at 30th April was 871.20 tonnes but this has decreased to just 800 tonnes as of last night).

Finally here is a summary of some COMEX position as at 31st July 2018:

-

silver as at 31st July 2018

gold as at 31st July 2018

000,000 ozs.

tonnes

YTD EFPs

1,833

4,708

Open Interest

1,105

1,399

Registered at COMEX

79

8

JP Morgan Eligible

139

53

All Other Eligible

66

208

Total Comex

285

269

Registered/OI

7.19%

0.56%

There are two ‘too stupid to be stupid’ prizes to be awarded. The first one in respect of the COMEX must go to gold, where the registered inventory is only 0.56% of the 31st July 2018 Open Interest. Perhaps the fact that this absurd situation has prevailed and been uncritically accepted for so long as “just the way things are” has given the cabal courage to proceed with this equally grotesque manipulation in respect of EFP transfers. Here the prize for ‘too stupid to be stupid’ goes to silver where the 2018 YTD EFP total of 1.83 billion ounces is about 260% of global production (in just seven months) whilst the figure for gold of 4,708 tonnes in the same period is a more modest 200% of global production. On the other hand perhaps this prize in respect of EFPs should perhaps be shared since the gold ETF YTD figure is 2.73 times the residual non BOE custodial gold whilst the same figure for silver is a ratio of only 2.36. These EFPs are an additional ‘claim’ on loco London precious metal holdings on top of all the +100 to 1 fractional reserving for allocated (and unallocated) claims. We hear that gold and silver are in backwardation and an additional corroboration of all the above evidence are the recent reports of European Banks’ outright refusal to deliver allocated gold when called upon to so do.

History will not be kind when full disclosure of what is currently transpiring in the precious markets is ultimately revealed. Some time ago I recorded all of Jim Sinclair’s ‘angels’. I noted down the 12 data points (angels) from 1224 to 2025 and it is interesting to observe that the paper gold price is now hovering around the bottom angel of $1,224 as though it has some extra significance as a chart point. Remember those days when there were high hopes that the uppermost angel would be exceeded after the second highest angel of $1,936 was in play! One thing is definite. China and Russia (and many others) are not accumulating gold without a very definite plan, indeed a master plan many years in the making. We don’t have long to wait to ascertain if imminent pertoyaun settlements on the Shanghai Energy Exchange will have a material impact on the pricing of physical gold at the Shanghai gold exchange. Everything I have read indicates that it is most improbable that the Shanghai Gold Exchange will supply copious amounts of physical gold at these current manipulated prices, below production costs in many instances.

In reverting back to Greg Hunter and his ‘too stupid to be stupid’ tag, when I listened to his latest weekly domestic news wrap up, it seemed to me that he is describing an atrophied, vestigial satanic sewer of a country, no longer fit for purpose as a world leader, or even worthy of taking a minor seat amongst other players. (Atrophied = wasted away, especially as a result of the degeneration of cells: Vestigial =forming a very small remnant of something that was once much greater).

Some of the language in this paper is strong and decidedly vitriolic. This stems from deep anger. Here is a table of the population of just 6 countries that have a deep seated faith in gold:

-

Population (2015)

Millions

China

1,376

India

1,311

Indonesia

257

Russia

143

Iran

79

Turkey

78

3,244

These six countries alone account for nearly half the world’s population. Just 8 tonnes of registered gold at the COMEX is at the heart of this massive conspiracy to deny physical gold from discovering its true valuation. Recently we have witnessed the emergence of this EFP farce as a key component in maintaining this conspiracy of physical gold/silver price suppression. For more than a decade there have been massive waterfall dives engineered in nano seconds on the COMEX by the concentrated selling , during the most comatose trading periods, of thousands of naked short paper contracts. Now this farce is perpetuated by a conspiracy of silence as to the identity of the counter parties in respect of these gargantuan EFP transfers, and there is regulatory/institutional refusal even to disclose the contractual nature of an EFP transfer. Indonesia is included in the table above because I have read that the Indonesian Post Office will be a strategic partner in the new kinesis.money 100% gold backed digital currency due to go live next month. This new development might compound the physical gold demand that is anticipated to emanate from the settlement of petroyaun contracts, also next month.(Early this morning there was a strong start to August 2018 trading with Yuan 121 billion recorded on the SC1809 to compliment the already achieved turnover of Yuan 7 trillion). We must await the advent of next month with interest.

end

They seem to agree with me that the pricing of gold is being transferred over to China from London and NY

(courtesy the daily economist)

Momentum continues to grow for global gold and silver pricing to be seized by either Shanghai or Dubai

With the U.S. Commodities Exchange (Comex) having to transfer more and more of their futures contacts to London due to massive manipulation which has made it impossible for them to deliver on their promises, momentum appears to be growing in the East for markets like Shanghai and Dubai to one day soon seize control over how gold and silver is priced in the world markets.

In fact there are already concerns right now that China has taken over a form of control from both London and the U.S. when it comes to the pricing of gold, as seen recently in GATA’s letter to the CFTC demanding an investigation into this very thing.

For the past month there has been a direct correlation between the value of the Chinese yuan and the price of gold. That is, the higher the yuan, the higher the price of gold and especially vice-versa.

The value of the Chinese yuan is essentially controlled by China’s central bank.

The Shanghai Gold Exchange is the largest physical gold market in the world, and has been taking more and more market share from the West as exchanges in London and New York focus primarily on paper contracts over physical deliveries. However there is also another player beginning to infringe on global market share, and it is the Dubai Gold and Commodities Exchange which has seen another 2018 record occur in the month of July.

The Dubai Gold and Commodities Exchange (DGCX) announced today that it experienced its highest average open interest (AOI) in July, surpassing 300,000 contracts. This builds upon a record-breaking first half of the year for trading value and volumes.

In July, the exchange saw solid trading results, with an AOI of 323,477 contracts. This impressive result brings the total volume for 2018 to an all-time high of 304,398 contracts which is an increase of 29% from 2017.

Due to a rising demand for China-centric products, the best performing asset classes for July were the Shanghai Gold Futures and Chinese Yuan Futures. The volume for Shanghai Gold Futures jumped by 71% when compared to the same period last year. Chinese Yuan Futures were also up by 64% year-on-year. – Finance Magnates

Just as China is seizing more and more market share from London and Chicago in the oil industry with the advent of their Yuan-denominated oil futures contract, so too is their commodities market quickly becoming the world’s primary gold and silver exchange. And thus the real question that remains for investors is not if China will permanently take over control for the pricing of gold, but rather when this mechanism is completely removed from their hands.

http://www.thedailyeconomist.com/2018/08/momentum- continues-to-grow-for-global.html

-END-

Your early WEDNESDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

i) Chinese yuan vs USA dollar/CLOSED UP TO 6.7981/HUGE DEVALUATION FOR THE PAST TWO WEEKS STOPS /shanghai bourse CLOSED DOWN 51.87 POINTS OR 1,80% /HANG SANG CLOSED DOWN 242,27 POINTS OR 0.86%

2. Nikkei closed UP 192.98 POINTS OR 0.86%/USA: YEN RISES TO 111.84/

3. Europe stocks OPENED RED /

USA dollar index RISES TO 94.58/Euro FALLS TO 1.1685

3b Japan 10 year bond yield: RISES TO . +.13/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 111.84/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD IS NOW TARGETED AT .11%/JAPAN LOSING CONTROL OF THEIR BOND MARKET

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 67.97 and Brent: 73.25

3f Gold UP/Yen DOWN

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil DOWN for WTI and DOWN FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund RISES TO +.480%/Italian 10 yr bond yield DOWN to 2.76% /SPAIN 10 YR BOND YIELD UP TO 1.44%

3j Greek 10 year bond yield RISES TO : 3.96

3k Gold at $1222.30 silver at:15.45 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble DOWN 16/100 in roubles/dollar) 62.69

3m oil into the 67 dollar handle for WTI and 73 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 111.84 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 0.9908 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1579 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now POSITIVE territory with the 10 year RISING to +0.48%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.98% early this morning (THIS IS DEADLY TO ALL MARKETS). Thirty year rate at 3.11%

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

(courtesy Jim Reid/Bloomberg/Deutsche bank/zero hedge)

Stocks Drop As Trade War Returns; Japanese

Bond Rout Leads To Emergency Margin Call

The latest trade war truce lasted less than a day, and after stocks jumped yesterday following an early report that Mnuchin had resumed trade talks with his Chinese counterpart, a late Tuesday report that the Trump admin is planning to increase the tariff rate on some $200BN of Chinese imports from 10% to 25% led to an immediate slide in risk assets around the globe, and this morning global stocks and futures were a sea of red despite Apple’s stellar results which helped lift the Nasdaq.

In response, China again warned the U.S. against “blackmailing and pressuring” it over trade. China’s Ministry of Foreign Affairs said it will fight back if the U.S. further increases tariffs as it now contemplated. “If the U.S. takes measures to further escalate the situation, we will surely take countermeasures to uphold our legitimate rights and interests,” spokesman Geng Shuang said at a regular press conference on Wednesday.