GOLD: $1211.80 DOWN $7.20 (COMEX TO COMEX CLOSINGS)

Silver: $15.38 DOWN 6 CENTS (COMEX TO COMEX CLOSINGS)

Closing access prices:

Gold $1207.80

silver: $15.31

For comex gold:

AUGUST/

NUMBER OF NOTICES FILED TODAY FOR AUGUST CONTRACT:35 NOTICE(S) FOR 3500 oz

TOTAL NOTICES SO FAR 106 FOR 10600 OZ (0.3297 tonnes)

For silver:

AUGUST

20 NOTICE(S) FILED TODAY FOR

20,000 OZ/

Total number of notices filed so far this month: 556 for 2,780,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: BID $7526/OFFER $7611: DOWN $19(morning)

Bitcoin: BID/ $7583/offer $7668: DOWN $71 (CLOSING/5 PM)

end

First Shanghai gold fix comes at 10 pm est

The second Shanghai gold fix: 2:15 pm

First Shanghai gold fix gold: 10 pm est: $not available

NY price at the same time:xxx

PREMIUM TO NY SPOT: $xxx

XX

Second gold fix early this morning: $not available

USA gold at the exact same time:$xxx

PREMIUM TO NY SPOT: $xx

China is controlling the gold market

WE WILL NOT PROVIDE LONDON FIXES AS THEY ARE NOT ACCURATE AS TO WHAT IS GOING ON AT THE SAME TIME FRAME.

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total OPEN INTEREST FELL BY A CONSIDERABLE SIZED 2081 CONTRACTS FROM 226,512 DOWN TO 224,431 WITH YESTERDAY’S SMALL 12 CENT LOSS IN SILVER PRICING AT THE COMEX. WE HAVE NOW WITNESSED A SLOW COMEX ACCUMULATION THESE PAST SEVERAL DAYS. ON TOP OF THIS WE HAVE ALSO WITNESSED A LARGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY(WELL OVER 30 MILLION OZ AT THE COMEX FOR JULY AND OVER 4 MILLION OZ FOR AUGUST) AS WELL AS CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A SMALL SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP: 401 EFP’S FOR SEPT. , 0 EFP’S FOR DECEMBER AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE: OF 401 CONTRACTS. WITH THE TRANSFER OF 1401 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 401 EFP CONTRACTS TRANSLATES INTO 2.005 MILLION OZ AND ACCOMPANYING:

1.THE 12 CENT LOSS IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR THE JUNE/2018 COMEX DELIVERY MONTH. (5.420 MILLION OZ) 30.370 MILLION OZ FINALLY STANDING FOR DELIVERY IN JULY, AND NOW 4.095 MILLION OZ FOR AUGUST.

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF JULY:

1435 CONTRACTS (FOR 2 TRADING DAYS TOTAL 1435 CONTRACTS) OR 7.175 MILLION OZ: (AVERAGE PER DAY: 718 CONTRACTS OR 3.587 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF JULY: 7.175 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 1.03% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2018 TO DATE SILVER EFP’S: 1,839.74 MILLION OZ.

ACCUMULATION FOR JAN 2018: 236.879 MILLION OZ

ACCUMULATION FOR FEB 2018: 244.95 MILLION OZ

ACCUMULATION FOR MARCH 2018: 236.67 MILLION OZ

ACCUMULATION FOR APRIL 2018: 385.75 MILLION OZ

ACCUMULATION FOR MAY 2018: 210.05 MILLION OZ

ACCUMULATION FOR JUNE 2018: 345.43 MILLION OZ

ACCUMULATION FOR JULY 2018: 172.84 MILLION OZ

RESULT: WE HAD A CONSIDERABLE SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 2081 WITH THE 12 CENT LOSS IN SILVER PRICING AT THE COMEX YESTERDAY. THE CME NOTIFIED US THAT WE HAD A SMALL SIZED EFP ISSUANCE OF 401 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) . FROM THE CME DATA: 401 EFP’S FOR SEPT, 0 EFP’S FOR DECEMBER AND ZERO FOR ALL OVER MONTHS FOR A DELIVERABLE FORWARD CONTRACT OVER IN LONDON WITH A FIAT BONUS (TOTAL: 401). TODAY WE LOST A FAIR SIZED: 1680 TOTAL OI CONTRACTS ON THE TWO EXCHANGES:

i.e 401 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH A DECREASE OF 2081 OI COMEX CONTRACTS. AND ALL OF THIS DEMAND HAPPENED WITH A 12 CENT GAIN IN PRICE OF SILVER AND A CLOSING PRICE OF $15.44 WITH RESPECT TO YESTERDAY’S TRADING. YET WE HAD A GIGANTIC AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY IN THE BIG JULY DELIVERY MONTH OF SLIGHTLY OVER 30 MILLION OZ AND NOW IN AUGUST ANOTHER BIG 4.085 MILLION OZ IN A NON ACTIVE MONTH. IT SURE LOOKS LIKE ANOTHER FAILED BANKER SHORT COVERING EXERCISE AS BANKERS ARE SCRAMBLING TO COVER THEIR HUGE SHORTFALL.

In ounces AT THE COMEX, the OI is still represented by OVER 1 BILLION oz i.e. 1.123 MILLION OZ TO BE EXACT or 160% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT JULY MONTH/ THEY FILED AT THE COMEX: 20 NOTICE(S) FOR 100,000 OZ OF SILVER

IN SILVER, WE SET THE NEW RECORD OF OPEN INTEREST AT 243,411 CONTRACTS ON APRIL 9.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $16.51

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) AND JULY 2018 AMOUNT FINALLY STANDING: 30.370 MILLION OZ ) AND NOW FOR AUGUST 4.095 MILLION OZ.

- HUGE RECORD OPEN INTEREST IN SILVER 243,411 CONTRACTS (OR 1.217 BILLION OZ/ SET APRIL 9/2018

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017

- RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT).

IN GOLD, THE OPEN INTEREST ROSE BY A tiny SIZED 777 CONTRACTS UP TO 453,432 DESPITE THE FALL IN THE COMEX GOLD PRICE/YESTERDAY’S TRADING (A LOSS IN PRICE OF $4.65). THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A GOOD SIZED 7943 CONTRACTS:

AUGUST HAD AN ISSUANCE OF 190 CONTRACTS,DECEMBER HAD AN ISSUANCE OF 7753 CONTACTS AND THEN ALL OTHER MONTHS ZERO. The new COMEX OI for the gold complex rests at 453,432. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE A STRONG OI GAIN IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 8520 CONTRACTS: 2356 OI CONTRACTS INCREASED AT THE COMEX AND 7943 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN: 8520 CONTRACTS OR 852,000 OZ = 26.50 TONNES. AND ALL OF THIS STRONG DEMAND OCCURRED WITH THE FALL IN THE PRICE OF GOLD/ YESTERDAY TO THE TUNE OF $4.65.

YESTERDAY, WE HAD 8486 EFP’S ISSUED.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF JUNE : 16,429 CONTRACTS OR 1,642,900 OZ OR 51.10 TONNES (2 TRADING DAYS AND THUS AVERAGING: 8215 EFP CONTRACTS PER TRADING DAY OR 821,500 OZ/ TRADING DAY),,

TO GIVE YOU AN IDEA AS TO THE HUGE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 2 TRADING DAYS IN TONNES: 51.10 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2017, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 2555 TONNES

THUS EFP TRANSFERS REPRESENTS 51.10/2550 x 100% TONNES = 2.00% OF GLOBAL ANNUAL PRODUCTION SO FAR IN JULY ALONE.***

ACCUMULATION OF GOLD EFP’S YEAR 2018 TO DATE: 4,761.15* TONNES *SURPASSED ANNUAL PROD’N

ACCUMULATION OF GOLD EFP’S FOR JANUARY 2018: 653.22 TONNES (21 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR FEBRUARY 2018: 649.45 TONNES (20 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR MARCH 2018: 741.89 TONNES (22 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR APRIL 2018: 713.84 TONNES (21 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR MAY 2018: 693.80 TONNES ( 22 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR JUNE 2018 650.71 TONNES (21 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR JULY 2018 605.5 TONNES (21 TRADING DAYS)

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A tiny SIZED INCREASE IN OI AT THE COMEX OF 777 DESPITE THE LOSS IN PRICING ($4.65 THAT GOLD UNDERTOOK ON YESTERDAY) // . WE ALSO HAD A GOOD SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 7943 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 7943 EFP CONTRACTS ISSUED, WE HAD A VERY STRONG NET GAIN OF 8520 CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

7943 CONTRACTS MOVE TO LONDON AND 777 CONTRACTS INCREASED AT THE COMEX. (in tonnes, the GAIN in total oi equates to 26.50 TONNES). ..AND THIS STRONG DEMAND OCCURRED WITH LOSS OF $4.65 IN YESTERDAY’S TRADING AT THE COMEX!!!.

we had: 35 notice(s) filed upon for 3500 oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD...

WITH GOLD DOWN $7.20 TODAY: /

A HUGE CHANGE IN GOLD INVENTORY AT THE GLD/ A WITHDRAWAL OF 3,24 TONNES FROM THE GLD.

/GLD INVENTORY 796.96 TONNES

Inventory rests tonight: 796.96 tonnes.

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

SLV/

WITH SILVER DOWN 6 CENTS TODAY :

A SMALL CHANGE IN SILVER INVENTORY TONIGHT: A WITHDRAWAL OF 141,000 OZ AND THAT WOULD BE TO PAY FOR STORAGE AND INSURANCE FEES

/INVENTORY RESTS AT 329.292 MILLION OZ/

NOTE THE DIFFERENCE BETWEEN THE GLD AND SLV: THE CROOKS CAN RAID GOLD BECAUSE THEY DO HAVE SOME PHYSICAL. THEY DO NOT RAID SILVER PROBABLY BECAUSE THERE IS NO REAL SILVER INVENTORIES BEHIND THEM

end

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER FELL BY A FAIR SIZED 2081 CONTRACTS from 226,512 UP TO 224,431 (AND MUCH FURTHER FROM THE NEW COMEX RECORD SET /APRIL 9/2017 AT 243,411/SILVER PRICE AT THAT DAY: $16.53). THE PREVIOUS RECORD OTHER THAN WAS ESTABLISHED AT: 234,787, SET ON APRIL 21.2017 OVER ONE YEAR AGO. THE PRICE OF SILVER ON THAT DAY: $17.89. OUR CUSTOMARY MIGRATION OF COMEX LONGS MORPH INTO LONDON FORWARDS CONTINUES AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

401 EFP CONTRACTS FOR SEPT., 0 EFP CONTRACTS FOR DECEMBER AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 401 CONTRACTS . EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI LOSS AT THE COMEX OF 2081 CONTRACTS TO THE 401 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A NET LOSS OF 1680 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES: 8.40 MILLION OZ!!! AND YET WE ALSO HAVE A STRONG DEMAND FOR PHYSICAL AS WE WITNESSED A FINAL STANDING OF GREATER THAN 30 MILLION OZ FOR JULY AND NOW ANOTHER STRONG 4.095 MILLION OZ FOR AUGUST... AND YET ALL OF THIS HUGE DEMAND OCCURRED DESPITE A A 12 CENT PRICING LOSS AT THE SILVER COMEX.

RESULT: A CONSIDERABLE SIZED DECREASE IN SILVER OI AT THE COMEX DESPITE THE 12 CENT PRICING LOSS THAT SILVER UNDERTOOK IN PRICING YESTERDAY. BUT WE ALSO HAD A FAIR SIZED 401 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR AUGUST, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)THURSDAY MORNING/WEDNESDAY NIGHT: Shanghai closed DOWN 56.51 POINTS OR 2.00% /Hang Sang CLOSED DOWN 626.18 POINTS OR 2.21%/ / The Nikkei closed DOWN 234.17 POINTS OR 1.03%/Australia’s all ordinaires CLOSED DOWN 0.54% /Chinese yuan (ONSHORE) closed DOWN at 6.8401 AS POBC RESUMES ITS HUGE DEVALUATION /Oil DOWN to 67.05 dollars per barrel for WTI and 71.92 for Brent. Stocks in Europe OPENED DEEPLY IN THE RED//. ONSHORE YUAN CLOSED WELL DOWN AT 6.8401 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.8595: HUGE DEVALUATION/PAST SEVERAL DAYS RESUMES : /ONSHORE YUAN TRADING STRONGER AGAINST OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

/NORTH KOREA/SOUTH KOREA

i)North Korea/South Korea/USA/Russia

b) REPORT ON JAPAN

Turmoil at the Central Bank of Japan: with rates climbing to 13.5% and a poor Japanese auction, the central bank did a purchase of bonds which never happens right after an auction. It seems that the pOBC wants to raise the 10 yr rate purchase to .20% but that will have tremendous risks.

a must read.

(courtesy zerohedge)

3 c CHINA

i)A very important commentary. The yuan falters badly as Trump is thinking to raise the next proposed tariffs to 25%. This would cause China to again lower its yuan value. The risk to the Chinese will be if the firewalls for capital controls break. With a debt to GDP of 300% China does have huge financial problems if the debt dam breaks

( zerohedge)

ii)Another important commentary: China is going to report its first ever first half current account deficit. These results do not include any of the tariff wars yet but for the latter part of 2018, 2018 and 2020, they expect that its current account surplus will be zero and thus they must act like the uSA and cause foreigners to finance its debt.. It must have an open economy something that it is loathe to do.

4. EUROPEAN AFFAIRS

UK

As expected (but a surprise unanimous decision) the central bank of England raised its rate by 25 basis points to .75%

( zerohedge)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

6 .GLOBAL ISSUES

7. OIL ISSUES

8. EMERGING MARKET

ii)VENEZUELA

A brilliant observation from Venezuela’s leader Maduro that the socialist model has failed

(courtesy zerohedge)

9. PHYSICAL MARKETS

i)Craig Hemke describes how China may be controlling the gold market through off shore accounts and then they will be using off shore yuan )CNH) to short gold and thus lowering the paper price of gold while picking up physical gold through Switzerland and London. a must read

(Craig Hemke/Sprott Money)

10. USA stories which will influence the price of gold/silver)

i)Market trading /GOLD/MARKET MOVERS:

a)Car sales are tumbling as the big automakers slash discounts for the first time in 5 years. Just like housing affordability is the key issue

(courtesy zerohedge)

iv)SWAMP STORIES

a)Mueller wants to ask Trump about obstruction of justice and that has zero chance of happening

(courtesy zerohedge)

Trading Volumes on the COMEX

PRELIMINARY COMEX VOLUME FOR TODAY: 211,575 contracts

CONFIRMED COMEX VOL. FOR YESTERDAY: 229,852 contracts

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

And now for the wild silver comex results.

Total silver OI FELL BY A CONSIDERABLE SIZED 2080 CONTRACTS FROM 226,512 DOWN TO 224,431 (AND A LITTLE FURTHER FROM THE THE NEW RECORD OI FOR SILVER SET APRIL 9.2018/ 243,411 CONTRACTS)WITH THE 12 CENT GAIN IN PRICING THAT SILVER UNDERTOOK YESTERDAY. SINCE WE ARE NOW INTO THE NON – ACTIVE DELIVERY MONTH OF AUGUST, WE WERE INFORMED THAT WE HAD A SMALL SIZED 401 EFP CONTRACTS FOR SEPT., 0 EFP CONTRACTS FOR DECEMBER AND ZERO FOR ALL OTHER MONTHS. THESE EFPS WERE ISSUED TO COMEX LONGS WHO RECEIVED A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. THE TOTAL EFP’S ISSUED: 401. ON A NET BASIS WE LOST 1680 SILVER OPEN INTEREST CONTRACTS AS WE OBTAINED 2081 CONTRACT LOSS AT THE COMEX COMBINING WITH THE ADDITION OF 401 OI CONTRACTS NAVIGATING OVER TO LONDON.

NET LOSS ON THE TWO EXCHANGES: 1680 CONTRACTS

FOR THE FRONT MONTH OF AUGUST WE HAD A NET LOSS OF 269 CONTRACTS. WE HAD 281 NOTICES FILED YESTERDAY SO WE CONTINUE WHERE WE LEFT OFF LAST MONTH IN THAT WE GAINED 12 CONTRACTS STANDING OR AN ADDITIONAL 60,000 OZ WILL STAND AT THE COMEX AS THESE GUYS REFUSED TO MORPH INTO LONDON BASED FORWARDS AND RECEIVE A FIAT BONUS. QUEUE JUMPING AT THE SILVER COMEX IS THE NORM AS THERE IS CONSIDERABLE AMOUNT OF PHYSICAL LOCATED HERE. THERE IS NO QUEUE JUMPING AT THE GOLD COMEX FOR THE SIMPLE REASON THAT THERE IS NO GOLD THERE.

The next active delivery month after August for silver is September and here the OI FELL by 2283 contracts DOWN to 155,426. October received another 25 contracts to stand at 27

After October, the next big delivery month is December and here the OI rose by 420 contracts up to 57,407 contracts.

We had 20 notice(s) filed for 100,000 OZ for the AUGUST 2018 COMEX contract for silver

AND NOW COMPARISON VS AUGUST LAST YR:

ON FIRST DAY NOTICE JULY 31/2017: 1,965,000 OZ STOOD FOR DELIVERY

THE FINAL AMOUNT OF SILVER STANDING: AUGUST 30.2017: 6,245,000 OZ AS WE HAD CONSIDERABLE QUEUE JUMPING.

INITIAL standings for AUGUST/GOLD

AUGUST 2/2018.

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil oz |

| Withdrawals from Customer Inventory in oz |

NIL OZ

|

| Deposits to the Dealer Inventory in oz | NIL oz |

| Deposits to the Customer Inventory, in oz |

nil oz

|

| No of oz served (contracts) today |

35 notice(s)

3,500 OZ

|

| No of oz to be served (notices) |

3347 contracts

(334,700 oz)

|

| Total monthly oz gold served (contracts) so far this month |

106 notices

10600 OZ

.3287 TONNES

|

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | xxx oz |

we have a NO pulse today, AND zero gold enters the comex

For AUGUST:

Today, 0 notice(s) were issued from JPMorgan dealer account and 0 notices were issued from their client or customer account. The total of all issuance by all participants equates to 35 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 24 notice(s) was (were) stopped/ Received) by j.P.Morgan customer account.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

To calculate the INITIAL total number of gold ounces standing for the AUGUST. contract month, we take the total number of notices filed so far for the month (106) x 100 oz or 10600 oz, to which we add the difference between the open interest for the front month of AUGUST. (3382 contracts) minus the number of notices served upon today (35 x 100 oz per contract) equals 345,300 OZ OR 10.740 TONNES) the number of ounces standing in this non active month of AUGUST

Thus the INITIAL standings for gold for the AUGUST contract month:

No of notices served (106 x 100 oz) + {(3382)OI for the front month minus the number of notices served upon today (35 x 100 oz )which equals 345,300 oz standing OR 10.740 TONNES in this active delivery month of AUGUST.

WE LOST 433 COMEX CONTRACTS OR AN ADDITIONAL 43300 OZ WILL NOT STAND AND THESE GUYS MORPHED INTO LONDON BASED FORWARDS. THERE WAS NO REASON TO HANG AROUND THE COMEX AS THERE IS NO GOLD THERE TO SETTLE UPON.

THERE ARE ONLY 7.8648 TONNES OF REGISTERED COMEX GOLD AVAILABLE FOR DELIVERY AGAINST 10.740 TONNES STANDING FOR JULY

IN THE LAST 24 MONTHS 85 NET TONNES HAS LEFT THE COMEX.

end

And now for silver

AND NOW THE AUGUST DELIVERY MONTH

AUGUST INITIAL standings/SILVER

| Silver | Ounces |

| Withdrawals from Dealers Inventory | nil oz |

| Withdrawals from Customer Inventory |

60,030.600 oz

BRINKS

|

| Deposits to the Dealer Inventory |

nil oz

|

| Deposits to the Customer Inventory |

nil oz

|

| No of oz served today (contracts) |

20

CONTRACT(S)

(100,000 OZ)

|

| No of oz to be served (notices) |

263 contracts

(1,315,000 oz)

|

| Total monthly oz silver served (contracts) | 556 contracts

(2,780,000 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

we had 0 inventory movement at the dealer side of things

total dealer deposits: nil oz

total dealer withdrawals: nil oz

we had 0 deposit into the customer account

i) Into JPMorgan: nil oz

*** JPMorgan for most of 2017 and in 2018 has adding to its inventory almost every single day.

JPMorgan now has 144 million oz of total silver inventory or 51.0% of all official comex silver. (144 million/283 million)

iii) into everybody else; 0 oz

total customer deposits today: nil oz

we had 1 withdrawals from the customer account;

i) out of BRINKS: 60,030.800 OZ

total withdrawals: 60,030.800 oz

we had 1 adjustment/

i) Out of CNT:

29,588.400 oz was adjusted out of the customer and this landed into the dealer account of CNT

total dealer silver: 80.109 million

total dealer + customer silver: 283.608 million oz

The total number of notices filed today for the AUGUST. contract month is represented by 20 contract(s) FOR 100,000 oz. To calculate the number of silver ounces that will stand for delivery in AUGUST., we take the total number of notices filed for the month so far at 556 x 5,000 oz = 2,780,000 oz to which we add the difference between the open interest for the front month of AUGUST. (283) and the number of notices served upon today (20 x 5000 oz) equals the number of ounces standing.

.

Thus the INITIAL standings for silver for the AUGUST/2018 contract month: 556(notices served so far)x 5000 oz + OI for front month of AUGUST(283) -number of notices served upon today (20)x 5000 oz equals 4,095,000 oz of silver standing for the AUGUST contract month

WE GAINED 12 CONTRACTS OR AN ADDITIONAL 60,000 OZ WILL STAND FOR DELIVERY AT THE COMEX AND THESE GUYS REFUSED TO MORPH INTO A LONDON BASED FORWARDS AND THUS THEY WILL NOT TAKE THE FIAT BONUS.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

ESTIMATED VOLUME FOR TODAY:61,549 CONTRACTS

CONFIRMED VOLUME FOR YESTERDAY: 65,976 CONTRACTS absolutely criminal

YESTERDAY’S CONFIRMED VOLUME OF 65,976 CONTRACTS EQUATES TO 299 million OZ OR 42.68% OF ANNUAL GLOBAL PRODUCTION OF SILVER

COMMODITY LAW SUGGESTS THAT OPEN INTEREST SHOULD NOT BE MORE THAN 3% OF ANNUAL GLOBAL PRODUCTION. THE CROOKS ARE SUPPLYING MASSIVE PAPER TRYING TO KEEP SILVER IN CHECK.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price at that day at $18.42

The previous record was 224,540 contracts with the price at that time of $20.44

end

NPV for Sprott

1. Sprott silver fund (PSLV): NAV RISES TO -2.80% (AUGUST 2/2018)

2. Sprott gold fund (PHYS): premium to NAV FALLS TO -1.00% to NAV (AUGUST 2/2018 )

Note: Sprott silver trust back into NEGATIVE territory at -2.80%-/Sprott physical gold trust is back into NEGATIVE/

(courtesy Sprott/GATA)

3.SPROTT CEF.A FUND (FORMERLY CENTRAL FUND OF CANADA):

NAV 12.59/TRADING 12.15//DISCOUNT 3.50.

END

And now the Gold inventory at the GLD/

AUGUST 2/WITH GOLD DOWN $7.20/A HUGE WITHDRAWAL OF 3.24 TONNES FROM THE GLD WHICH NO DOUBT WAS USED IN THE RAID TODAY/INVENTORY RESTS AT 796.96 TONNES

AUGUST 1/WITH GOLD DOWN $4.65/NO CHANGE IN GOLD INVENTORY AT THE GLD.INVENTORY RESTS AT 800.20 TONNES

JULY 31/WITH GOLD UP $2.05/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 800.20

JULY 30/WITH GOLD DOWN $0.95/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 800.20 TONNES

july 27/WITH GOLD DOWN $2.85 TODAY, NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 800.20 TONNES

JULY 26./WITH GOLD DOWN $5.65: A WITHDRAWAL OF 2.35 TONNES OF GOLD FROM THE GLD/INVENTORY RESTS AT 800.20 TONNES

JULY 25/WITH GOLD UP $6.45; NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 802.55 TONNES

JULY 24/ WITH GOLD DOWN 10 CENTS: A HUGE DEPOSIT OF 4.42 TONNES INTO THE GLD/INVENTORY RESTS AT 802.55 TONNES

JULY 23/WITH GOLD DOWN $5.55: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 798.13 TONNES

JULY 20/WITH GOLD UP $4.15 A HUGE DEPOSIT OF 4.12 TONNES OF GOLD INTO THE GLD.INVENTORY RESTS AT 798.13 TONNES

JULY 19./WITH GOLD DOWN $1.00: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 794.01 TONNES

JULY 18/WITH GOLD UP 0.40: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 794.01 TONNES

JULY 17/WITH GOLD DOWN $12.40, WE HAD A BIG WITHDRAWAL OF 1.18 TONNES FROM THE GLD/INVENTORY RESTS AT 794.01 TONNES

JULY 16/WITH GOLD DOWN $1.55/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 795.19 TONNES

JULY 13/WITH GOLD DOWN $5.35 THE CROOKS RAID THE COOKIE JAR AGAIN TO THE TUNE OF 3.83 TONNES/INVENTORY RESTS AT 795.19 TONNES

JULY 12/WITH GOLD UP $2.30: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 799.02 TONNES

JULY 11/WITH GOLD DOWN $10.75 THE CROOKS RAIDED THE COOKIE JAR AGAIN TO THE TUNE OF 1.75 TONNES/INVENTORY RESTS AT 799.02 TONNES

JULY 10/WITH GOLD DOWN $3.85: NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 800.77 TONNES

july 9/WITH GOLD UP $4.00/ANOTHER RAID ON THE GOLD COOKIE JAR: TWO WITHDRAWALS OF 1.18 TONNES THIS MORNING AND 1.47 TONNES THIS AFTERNOON/INVENTORY RESTS AT 800.77 TONNES

JULY 6/WITH GOLD DOWN $2.45: NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 803.42 TONNES

JULY 5/WITH GOLD UP ANOTHER $5.15, THE CROOKS RAIDED THE COOKIE JAR AGAIN TO THE TUNE OF 5.89 TONNES/INVENTORY RESTS AT 803.42 TONNES IN THE LAST 10 TRADING DAYS GLD HAS LOST A HUGE 25.34 TONNES WITH A LOSS OF ONLY $15.25 IN PRICE

July 3/WITH GOLD UP $11.15/THE CROOKS RAIDED THE GLD INVENTORY AGAIN TO THE TUNE OF 9.73 TONNES/INVENTORY RESTS AT 809.31 TONNES

JULY 2/WITH GOLD DOWN $12.15, THE CROOKS RAIDED THE GLD INVENTORY AGAIN BY 1.47 TONNES DOWN./INVENTORY RESTS AT 819.04 TONNES

JUNE 29/WITH GOLD UP $3.70/A WITHDRAWAL OF 1.18 TONNES OF GOLD FROM THE GLD/INVENTORY RESTS AT 820.51 TONNES

JUNE 28/WITH GOLD DOWN $5.15/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 821.69 TONNES

June 27/WITH GOLD DOWN $3.60// TWO ENTRIES:/STRANGELY THE CROOKS RETURNED THE WITHDRAWAL OF 4.42 TONNES LAST NIGHT (THUS WE HAD A DEPOSIT OF 4.42 TONNES/INVENTORY RESTS AT 824.63 TONNES. /THEN LATE THIS AFTERNOON A WITHDRAWAL OF 2.94 TONNES

INVENTORY RESTS AT 821.69 TONNES/THIS VEHICLE IS AN OUTRIGHT FRAUD.

june 26/LATE LAST NIGHT, WITH GOLD DOWN $9.10 WE HAD A HUGE WITHDRAWAL OF 4.42 TONNES OF GOLD/INVENTORY RESTS AT 820.21 TONES

JUNE 25/WITH GOLD DOWN $1.45/NO CHANGE IN GOLD INVENTORY AT THE GLD.INVENTORY RESTS AT 824.63 TONNES

JUNE 22/WITH GOLD UP 25 CENTS TODAY, THE CROOKS WITHDREW A MASSIVE 4.13 TONNES OF GOLD/INVENTORY RESTS AT 824.63 TONNES

JUNE 21/WITH GOLD DOWN $4.00/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 828.76 TONNES

JUNE 20/WITH GOLD DOWN $3.55/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 828.76 TONNES

JUNE 19/WITH GOLD DOWN $1.50/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 828.76 TONES

JUNE 18/WITH GOLD UP $1.90/NO CHANGES IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 828.76 TONNES

JUNE 15/WITH GOLD DOWN $28.90/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 828.76 TONNES

JUNE 14/WITH GOLD UP $7.10/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 828.76 TONNES/

JUNE 13/WITH GOLD UP $2.20/NO CHANGE IN GOLD INVENTORY AT THE GLD/INVENTORY RESTS AT 828.76 TONNES

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

AUGUST 2/2018/ Inventory rests tonight at 796.96 tonnes

*IN LAST 423 TRADING DAYS: 133.97 NET TONNES HAVE BEEN REMOVED FROM THE GLD

*LAST 373 TRADING DAYS: A NET 22.57 TONNES HAVE NOW BEEN ADDED INTO GLD INVENTORY.

end

Now the SLV Inventory/

AUGUST 2 WITH SILVER DOWN 6 CENTS TODAY/A SMALL CHANGE IN SILVER INVENTORY AT THE SLV/ A WITHDRAWAL OF 141,000 OZ FOR THEIR MONTHLY STORAGE AND INSURANCE FEES:INVENTORY RESTS AT 329.292 MILLION OZ/

AUGUST 1/WITH SILVER DOWN 12 CENTS TODAY, NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 329.433 MILLION OZ/

JULY 31/WITH SILVER UP 5 CENTS/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 329.433 MILLION OZ/

JULY 30/WITH SILVER UP 3 CENTS TODAY; NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 329.433 MILLION OZ.

JULY 27/WITH SILVER FLAT TODAY, NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 329.433 MILLION OZ/

JULY 26/WITH SILVER DOWN 10 CENTS: STRANGE: A BIG CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.046 MILLION OZ OF SILVER/INVENTORY RESTS AT 329.433 MILLION OZ

JULY 25: WITH SILVER UP 8 CENTS TODAY: A SMALL CHANGE IN SILVER INVENTORY AT THE SLV/ A WITHDRAWAL OF 658,000 INVENTORY RESTS AT 328.304 MILLION OZ/

JULY 24/WITH SILVER UP 8 CENTS TODAY: NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 328.962 MILLION OZ/

JULY 23/WITH SILVER DOWN 11 CENTS/NO CHANGES IN SILVER INVENTORY INTO THE SLV/INVENTORY RESTS AT 328.962 MILLION OZ/

JULY 20/WITH SILVER UP 10 CENTS TODAY: A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.411 MILLION OZ INTO THE SLV INVENTORY

INVENTORY RESTS AT 328.962 MILLION OZ

JULY 19/WITH SILVER DOWN 17 CENTS TODAY; A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 752,000 OZ INTO THE SLV INVENTORY/INVENTORY RESTS AT 327.551 MILLION OZ/

JULY 18/WITH SILVER DOWN 3 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 326.799 MILLION OZ/

JULY 17/WITH SILVER DOWN 20 CENTS TODAY: A CHANGE IN SILVER INVENTORY A WITHDRAWAL OF 1.001 MILLION OZ FROM THE SLV: INVENTORY RESTS AT 326.799 MILLION OZ/

JULY 16/WITH SILVER FLAT TODAY, A HUGE CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.128 MILLION OZ//INVENTORY RESTS AT 327.880 MILLION OZ

JULY 13/WITH SILVER DOWN 16 CENTS TODAY/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 326.752 MILLION OZ.

JULY 12/WITH SILVER UP 12 CENTS TODAY: ANOTHER BIG CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.035 MILLION OZ/INVENTORY RESTS AT 326.752 MILLION OZ/

JULY 11/WITH SILVER DOWN 22 CENTS TODAY: ANOTHER HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 565,000/INVENTORY RESTS AT 325.717 MILLION OZ

JULY 10/WITH SILVER DOWN 3 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 325.151 MILLION OZ

july 9/WITH SILVER UP 5 CENTS: ANOTHER BIG CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 847,000 OZ ADDED TO INVENTORY/INVENTORY RESTS AT 825.151 MILLION OZ/

JULY 6/WITH SILVER DOWN 2 CENTS/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 324.305 MILLION OZ/

JULY 5/WITH SILVER UP 6 CENTS, A GOOD CHANGE IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 470,000 OZ/INVENTORY RESTS AT 324.305 MILLION OZ/ FOR THE PAST 10 TRADING DAYS, SILVER INVENTORY HAS ADVANCED BY 4.945 MILLION OZ WITH A LOSS OF 33 CENTS/PLEASE COMPARE THIS WITH THE GLD.

JULY 3/WITH SILVER UP 17 CENTS, A HUGE DEPOSIT OF 1.37 MILLION OZ ADDED TO THE SLV/INVENTORY RESTS AT 323.835 MILLION OZ.

JULY 2/WITH SILVER DOWN 31 CENTS/A HUGE 2.070 MILLION OZ DEPOSIT AT THE SLV/INVENTORY RESTS AT 322.465 MILLION OZ/

JUNE 29/WITH SILVER UP 14 CENTS TODAY, NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS THIS WEEKEND AT 320.395 MILLION OZ/

JUNE 28/WITH SILVER DOWN 18 CENTS, THE CROOKS ADDED 1.035 MILLION OZ OF SILVER INTO THE SLV/INVENTORY RESTS AT 320.395 MILLION OZ

JUNE 27.2018/WITH SILVER DOWN 8 CENTS/NO CHANGE IN SILVER INVENTORY/INVENTORY RESTS AT 819.360 MILLION OZ/

june 26./2018/WITH SILVER DOWN 8 CENTS, THE CROOKS WITHDREW THE DEPOSIT OF TWO DAYS AGO; 941,000 OZ OUT OF INVENTORY/INVENTORY RESTS AT 819.360 OZ

JUNE 25/WITH SILVER DOWN 12 CENTS/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 320.301 MILLION OZ/

JUNE 22/WITH SILVER UP 12 CENTS TODAY,ANOTHER BIG CHANGE IN SILVER INVENTORY AT THE SLV” A DEPOSIT OF 941,000 OZ INTO INVENTORY/INVENTORY RESTS THIS WEEKEND AT 320.301 MILLION OZ/

JUNE 21/WITH SILVER UP ONE CENT/ANOTHER CHANGE IN SILVER INVENTORY AT THE SLV/: A DEPOSIT OF 2.918 MILLION OZ/INVENTORY RESTS AT 319.360 MILLION OZ/ THUS FOR TWO STRAIGHT DAYS A TOTAL OF 5.26 MILLION OZ OF SILVER HAS BEEN ADDED WITH NO CHANGE IN PRICE.

JUNE 20/WITH SILVER DOWN ONE CENT/A HUGE CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY / A DEPOSIT OF 2.35 MILLION OZ/INVENTORY RESTS AT 316.442 MILLION OZ/

JUNE 19/2018/WITH SILVER DOWN 11 CENTS/NO CHANGE IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 314.090 MILLION OZ/

JUNE 18/WITH SILVER DOWN 6 CENTS TODAY/NO CHANGE IN SILVER INVENTORY/INVENTORY RESTS AT 314.090 MILLION OZ/

JUNE 15/WITH SILVER DOWN 75 CENTS/A BIG CHANGE IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.788 MILLION OZ//INVENTORY RESTS AT 314.090 MILLION OZ

JUNE 14/WITH SILVER UP 30 CENTS, THE CROOKS DECIDED THAT THEY NEEDED SILVER INVENTORY BADLY SO THEY RAID THE SLV OF 1.412 MILLION OZ/INVENTORY RESTS AT 315.878 MILLION OZ/

JUNE 13/WITH SILVER UP 11 CENTS TODAY/NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 317.290 MILLION OZ/

AUGUST 2/2018:

Inventory 329.292 MILLION OZ

6 Month MM GOFO 1.96/ and libor 6 month duration 2.53

Indicative gold forward offer rate for a 6 month duration/calculation:

G0FO+ 1.96%

libor 2.53 FOR 6 MONTHS/

GOLD LENDING RATE: .57%

XXXXXXXX

12 Month MM GOFO

+ 2.83%

LIBOR FOR 12 MONTH DURATION: 2.43

GOFO = LIBOR – GOLD LENDING RATE

GOLD LENDING RATE = +.40

end

Major gold/silver trading /commentaries for THURSDAY

GOLDCORE/BLOG/MARK O’BYRNE.

Gold to Enter New Bull Market – Charles Nenner

Gold to Enter New Bull Market – Charles Nenner

- “Gold is going to enter a new bull market”

- “The first cycle will bottom after the summer”

- “$1,212 per ounce is our downside target”

- “It’s going to top $2,500 per ounce . . . in about two years or so”

- “Gold is in a bull market even though it came down from $1,900 per ounce”

In our featured video today, Greg Hunter interviews Charles Nenner, President of The Charles Nenner Research Centre. Previously of Goldman Sachs Nenner has since become one of the world’s leading researchers of market cycles.

Trump Trade and Currency Wars With China – Goldnomics Podcast

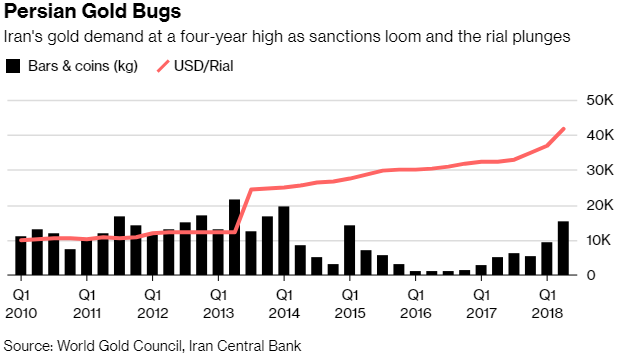

Iran’s Gold Demand at Four-Year High Days Before Sanctions (Bloomberg.com)

PRECIOUS-Gold holds losses after Fed keeps interest rates unchanged (Reuters.com)

Source: Bloomberg

Top Gold Miners Production Declined 15% While Costs Escalate (SRSRoccoReport.com)

The Crash of the Bank of the United States (24HGold.com)

Listen on SoundCloud , Blubrry & iTunes. Watch on YouTube below

Gold Prices (LBMA AM)

01 Aug: USD 1,222.75, GBP 932.47 & EUR 1,046.55 per ounce

31 Jul: USD 1,219.20, GBP 926.71 & EUR 1,039.86 per ounce

30 Jul: USD 1,222.05, GBP 931.20 & EUR 1,045.95 per ounce

27 Jul: USD 1,219.15, GBP 931.06 & EUR 1,048.10 per ounce

26 Jul: USD 1,228.35, GBP 931.46 & EUR 1,049.13 per ounce

25 Jul: USD 1,230.55, GBP 935.09 & EUR 1,051.75 per ounce

Silver Prices (LBMA)

01 Aug: USD 15.48, GBP 11.79 & EUR 13.24 per ounce

31 Jul: USD 15.43, GBP 11.72 & EUR 13.15 per ounce

30 Jul: USD 15.49, GBP 11.81 & EUR 13.25 per ounce

27 Jul: USD 15.36, GBP 11.72 & EUR 13.20 per ounce

26 Jul: USD 15.54, GBP 11.79 & EUR 13.27 per ounce

25 Jul: USD 15.57, GBP 11.83 & EUR 13.31 per ounce

Recent Market Updates

– Here’s Where the Next Crisis Starts

– House prices aren’t just slipping in the UK – this is global

– Russia Sells 80% Of Its US Treasuries

– Are China’s Gold Reserves Slowly Rising?

– Gold Outlook In H2 2018

– Gold Production In South Africa Continues To Collapse – Plummets 85% From Peak In 1970 (VIDEO)

– Physical Gold Is The “Best Defence” Against “Escalating Currency Wars”

– Trump and War With China? Goldnomics Podcast

– Weekly Digest – News, Market Updates and Videos You May Have Missed

– Financial Terrorism In The UK – Collusion between Government, Regulators & Two Bailed-Out UK Banks

– “Biggest Bubble in the History of Mankind” Is “Going To Burst” – Ron Paul

– Global Debt Time Bomb Surges To Nearly $250,000,000,000,000 – GoldCore Video

– Trump, Russia, Brexit and the Demand For Gold and Silver – GoldCore Video Interview

– Trump Is Serious About A Global Trade War

– Ponzi Economy Will Lead To Next Global Financial Crisis

– World Cup Is 200 Ounces Of Gold Worth £140,000 – 30% Less Than Harry Kane’s Weekly Wage

– Chaotic BREXIT More Likely: Risk To London, While Frankfurt, Luxembourg, Paris and Dublin Benefit

Andrew Maguire’s Kinesis money which is a “bitcoin” but backed 100% by allocated gold and silver is set to go.

it think it would be a great idea to look at this!

please read at: https://kinesis.money/#/

(Andrew Maguire)

|

|

Dear Harvey Organ,

Thank you for your participation in our webinar on June 7th with our host and CEO of Kinesis, Thomas Coughlin.

The response we received has been incredible, we appreciate you taking the time to join us and hope you found it to be beneficial.

Due to such a high influx of questions we received we were unable to have them all answered. Nevertheless, if there was anything which requires more clarification, or you have a query which needs to be rectified, we invite you to join our telegram group:

We apologize for the technical issues we incurred during the webinar which resulted in it running a little over schedule, we hope that the next one we host will run seamlessly.

A video has been put together and uploaded onto our YouTube channel which can be found here:

Please share and subscribe to our YouTube channel to be notified of all the latest videos as they become available.

The rapid growth that we are currently experiencing has been incredible and with your support, is only going to get better.

We are working behind the scenes very hard to create a better experience for everyone involved! Stay tuned in as we have many more announcements to be released in the upcoming days.

Kind Regards,

|

Kinesis Money

a:C/O ILS Fiduciaries (IOM) Limited, First Floor,Millennium House, Victoria Road, Douglas, Isle of Man IM2 4RW

|

The following is self explanatory

(courtesy GATA/Chris Powell and Harvey Organ)

GATA asks bank regulator to check risks of gold

futures maneuver

Submitted by cpowell on Sun, 2018-06-10 16:17. Section: Daily Dispatches

12:21p ET Sunday, June 10, 2018

Dear Friend of GATA and Gold:

GATA has appealed to the U.S. comptroller of the currency, who has regulatory authority over banks, to review financial risks certain banks may have incurred through derivatives in the monetary metals markets, particularly through the recent heavy use of the “exchange for physicals” mechanism of settling gold and silver futures contracts on the New York Commodities Exchange.

The appeal was made in a letter sent May 5 to the comptroller, Joseph M. Otting, whose office is part of the U.S. Treasury Department, by your secretary/treasurer and GATA futures market consultant Harvey Organ.

“Exchange for physical” settlements of futures contracts long were considered emergency procedures when a seller was not able to deliver metal from an exchange-approved warehouse and wanted to settle with delivery elsewhere. But now such settlements appear to constitute most gold and silver futures settlements on the Comex. It is a strange development that appears to have been necessitated by the increasing difficulties of central banking’s gold and silver price suppression policy.

GATA has received no acknowledgment of the letter. Its text is below and a PDF copy of it is here:

http://www.gata.org/files/ComptrollerOfCurrencyLetter.pdf

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

* * *

May 5, 2018

Joseph M. Otting, Comptroller of the Currency

U.S. Treasury Department

400 7th Street, SW

Washington DC 20219

Dear Comptroller Otting:

Please let us bring to your attention financial risks to major banks involving their possibly unreported exposure to derivatives in the monetary metals markets.

In recent months gold and silver future contracts issued by U.S. banks on the New York Commodities Exchange have been moved off-exchange for delivery through a mechanism known as “exchange for physical” (EFP) contracts. Until recently use of this mechanism was considered an emergency procedure when a seller did not have access to metal for delivery through Comex warehouses. Now the mechanism seems to be in use for a large share of front-month contracts for which delivery is sought.

Here is an example that is happening at the Comex in the front active month of April for gold and the inactive delivery month of April for silver.

In gold, there were 229,436 EFP contracts for 713.64 tonnes, an average of 10,925 contracts and 1,092,500 ounces per trading day.

In silver, there were 77,150 EFP contracts for 385,750,000 ounces, an average of 3,673 contracts and 18,369,000 ounces per trading day.

London Bullion Market Association rules suggest that these contracts may not be reported to regulators. The LBMA’s bylaws say:

“Figures above exclude any contracts not subject to risk-based capital requirements, such as FX contracts with an original maturity of 14 days or less, futures contracts, written options, and basis swaps. Therefore, the total notional amount of derivatives by maturity will not add to the total derivatives figure in this table.”

We are told that these EFP contracts are transferred from the Comex to London as what are called “serial forwards” and their duration is always less than 14 days, which exempts them from being reported.

It is our understanding that in each quarter your office prepares a report detailing risk undertaken by the banks under the comptroller’s supervision.

These risks include derivatives undertaken by U.S. banks and other obligations that may cause a bank to fail. Our concern is that your office may not be aware of large unreported derivative exposure by banks.

Could you review this matter and let us know your conclusions?

Sincerely,

CHRIS POWELL

Secretary/Treasurer

HARVEY ORGAN

Consultant

Gold Anti-Trust Action Committee Inc.

7 Villa Louisa Road

Manchester, Connecticut 06043-7541

end

Craig Hemke describes how China may be controlling the gold market through off shore accounts and then they will be using off shore yuan )CNH) to short gold and thus lowering the paper price of gold while picking up physical gold through Switzerland and London.

(a must read

Craig Hemke/Sprott Money)

Craig Hemke at Sprott Money: Is China hiding its

gold shorts among the speculators?

Submitted by cpowell on Wed, 2018-08-01 17:47. Section: Daily Dispatches

1:49p ET Wednesday, August 1, 2018

Dear Friend of GATA and Gold:

While trader positioning in the gold futures markets seems extremely bullish, market analyst Craig Hemke of the TF Metals Report today notes the recent tight correlation of gold prices with the valuation of the Chinese yuan and wonders whether the Chinese government is hiding its short positions among those listed as belonging to speculators.

Hemke’s analysis is headlined “The Yuan-Gold Peg and the Commitment of Traders Report” and it’s posted at Sprott Money here:

https://www.sprottmoney.com/Blog/the-yuan-gold-peg-and-the-commitment-of…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

Your early THURSDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

i) Chinese yuan vs USA dollar/CLOSED DOWN TO 6.8401/HUGE DEVALUATION FOR THE PAST TWO WEEKS RESUMES FULLY /shanghai bourse CLOSED DOWN 56.51 POINTS OR 2,00% /HANG SANG CLOSED DOWN 626.18 POINTS OR 2.21%

2. Nikkei closed DOWN 234.17 POINTS OR 1.03%/USA: YEN FALLS TO 111.45/

3. Europe stocks OPENED DEEP INTO THE RED /

USA dollar index RISES TO 94.91/Euro FALLS TO 1.1617

3b Japan 10 year bond yield: RISES TO . +.13/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 111.45/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD IS NOW TARGETED AT .11%/JAPAN LOSING CONTROL OF THEIR BOND MARKET

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 67.05 and Brent: 71.92

3f Gold UP/Yen UP

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil DOWN for WTI and DOWN FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund FALLS TO +.450%/Italian 10 yr bond yield UP to 2.91% /SPAIN 10 YR BOND YIELD UP TO 1.46%

3j Greek 10 year bond yield RISES TO : 4.04

3k Gold at $1215.25 silver at:15.43 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble DOWN 34/100 in roubles/dollar) 63.29

3m oil into the 67 dollar handle for WTI and 71 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 111.45 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 0.9937 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1548 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now POSITIVE territory with the 10 year FALLING to +0.45%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.98% early this morning (THIS IS DEADLY TO ALL MARKETS). Thirty year rate at 3.11%

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

(courtesy Jim Reid/Bloomberg/Deutsche bank/zero hedge)

S&P Futures, Global Stock Tumble As Trade War

Fears Return; Yuan Plummets

It has been the case that every single day for months, the market’s mood is determined by whether trade tensions are better or worse (however subjectively this is determined). And judging by the bloodbath in the market snapshot below, today they are much worse.

For those who missed it, this is the key driver of overnight’s risk off: President Trump asked Lighthizer to consider 25% tariffs on USD 200bln of Chinese goods, while officials also commented that stronger actions are needed on China but added that President Trump is open to negotiating with the Chinese President. China Commerce Ministry said China will immediately retaliate to defend its dignity and people’s interests.

The resulting market hot takes were familiar: “fears of an escalating trade dispute between the United States and China” blasted numerous sellside notes and financial websites. And sure enough, following Trump’s threat to hike tariff rates from 10% to 25% on $200BN in Chinese imports – which incidentally was first reported on Tuesday – stocks from Asia to Europe tumbled, with S&P500 futures joining and sliding to session lows, dragging the S&P back under 2,800. The dollar climbed and bonds were mixed with central bank policy high on the agenda.

Germany’s DAX index, which is seen by as trade war proxy, fell 1.1% about an hour after the open while the broader Europe STOXX 600 was down about 0.5%, dropping for a second day, tracking sharp declines in China and Hong Kong share indexes which were triggered by Trump telling the US trade representative to consider hiking tariffs on $200 billion worth of Chinese goods as early as next month. MSCI’s index of Asia-Pacific shares ex-Japan closed 1.6% down, dragged down by a 1.8 percent fall in Chinese H-shares and a 2% plunge in the Shanghai Composite whose 2-day selloff has taken it back under 2,800.

Then shortly before 6am EDT, Beijing responded that it was ready to retaliate, sending China’s onshore yuan tumbling to 6.8676 per dollar, the weakest level in more than a year.

There was more turbulence, when as reported earlier, 10Y JGB yields touched the highest since February 2017 before paring gains as the Bank of Japan made an unscheduled offer to buy 400 billion yen in bonds.

Following the “risk off” sentiment, and thanks to the BOJ intervention, US Treasuries climbed and were trading near session lows of 2.98% after falling on Wednesday when the Fed decided to leave rates unchanged while making it clear borrowing costs are heading higher. In sympathy, Euro zone government bond yields edged down with borrowing costs in Germany and France pulling back from seven-week highs as demand for safe-haven debt grew.

The Bloomberg Dollar Spot Index extended its advance into a third day as heightened trade tensions and the Federal Reserve’s commitment Wednesday to gradual tightening helped buoy the U.S. currency. The yen pared an earlier gain, while the pound weakened even as BOE policy makers were forecast to raise rates for only the second time since the financial crisis. Turkey’s lira tumbled to a record low after the U.S. imposed sanctions on two ministers. Core euro-area bonds edged higher with Treasuries, while gilts slipped.

In commodities, oil steadied around a two-week low after a surprise gain in American crude inventories exacerbated supply concerns. Gold rose and copper extended a decline. Emerging-market currencies sold off, with South Africa’s rand dropping.

Market Snapshot

- STOXX Europe 600 down 0.5% to 387.86

- MXAP down 1.2% to 165.30

- MXAPJ down 1.6% to 532.97

- Nikkei down 1% to 22,512.53

- Topix down 1% to 1,752.09

- Hang Seng Index down 2.2% to 27,714.56

- Shanghai Composite down 2% to 2,768.02

- Sensex down 0.7% to 37,277.64

- Australia S&P/ASX 200 down 0.6% to 6,240.86

- Kospi down 1.6% to 2,270.20

- German 10Y yield fell 0.2 bps to 0.476%

- Euro down 0.3% to $1.1625

- Brent Futures down 0.1% to $72.31/bbl

- Italian 10Y yield rose 6.9 bps to 2.521%

- Spanish 10Y yield fell 0.8 bps to 1.446%

Top overnight news

- The Trump administration said it’s weighing whether to increase the proposed tariff on $200 billion of Chinese goods to 25 percent from 10 percent, stepping up pressure on Beijing to change its trade practices. China said it was ready to retaliate after latest U.S. tariff threat

- Turkish markets are plunging deeper into the wild. Unprecedented sanctions imposed by the U.S., its NATO ally, have added to the cross-currents buffeting investors. They’ve already been despairing at policy makers’ failure to contain inflation and stem the slide in the lira under pressure from President Recep Tayyip Erdogan to bolster growth

- The Bank of England is set to raise interest rates for only the second time since the financial crisis, even though Brexit threatens to prove a rough ride for the U.K. economy

- The Bank of Japan is showing just what it means by being flexible with bond purchases. The central bank unexpectedly offered to buy 400 billion yen ($3.6 billion) of five- to 10-year bonds Thursday to stem a selloff that saw the 10-year yield touch an 18-month high of 0.145 percent

- Federal Reserve officials left the benchmark interest rate unchanged while reiterating their plan to gradually lift borrowing costs to keep the economy expanding at a healthy pace

- The aim of the latest steps taken by Japan’s central bank is to strengthen the sustainability of its current easing policy, taking into account its side-effects, Bank of Japan Deputy Governor Masayoshi Amamiya tells business leaders in Kyoto

- The lira slumped to a record low as the U.S. imposed sanctions on two Turkish ministers over the continued detention of an American pastor

- OPEC’s crude output increased last month as Saudi Arabia pumped near-record volumes to make good on a pledge to consumers that demand would be met

Asian equity markets were weaker across the board with sentiment weighed by increased global trade tensions after officials confirmed US President Trump instructed Trade Representative Lighthizer to consider a higher tariff of 25% on USD 200bln of goods from China which had earlier warned of retaliation. ASX 200 (-0.5%) and Nikkei 225 (-1.1%) were lower with the mining sector the worst performer in Australia amid losses in Rio Tinto following a miss on earnings, while a firmer currency, various corporate updates and weak US sales among automakers dampened Tokyo trade. Elsewhere, Hang Seng (-2.2%) and Shanghai Comp. (-2.0%) took the brunt of the increased US tariff threats as well as further inaction by the PBoC which refrained from conducting reverse repos for a 10th consecutive occasion. 10yr JGBs were choppy and initially continued on from yesterday’s slump at the open as the 10yr yield rose to its highest since February last year of 0.145%. However, yields then pulled back to provide much needed reprieve for JGBs which were also supported amid safe-haven flows. In addition, the latest securities flows data showed foreign investors upped their purchases of Japanese bonds by around 9-fold from the prior week, while Daiwa also suggested there should be good demand for 10yr JGBs at yields between 0.15%-0.20% at least until next BoJ policy meeting. Today’s 10yr year auction was another catalyst for price action with all metrics pointing to a weaker result which saw 10yr JGBs decline nearly 30 ticks, before bouncing back towards 150.00.

Top Asian News

- Trump’s Tariff Threats Erase $220 Billion From Asia Stock Values

- Citi Sees Sensex Doing Pretty Much Nothing From Now Until March

- House of Fraser Seeks Lifeline After C.Banner Ends Buyout Talks

- Metro Pacific Buys 12% of Air21; to Expand Warehouse Capacity

European equities trade firmly in the red (Eurostoxx 50 -1.3%) as sentiment is soured amid the rise in global trade tensions after officials confirmed US President Trump instructed Trade Representative Lighthizer to consider a higher tariff of 25% on USD 200bln of goods from China which had earlier warned of retaliation. China’s MOFCOM replied that China will fight back to defend its people’s interests and dignity. Germany’s DAX 30 is heavily underperforming, dragged down by heavyweight Siemens (-4.8%) following earnings, while Commerzbank (-4.5%), Deutsche Bank (-3.3%) and the German auto names also pressure the index. Material names continue to underperform, on the back of softer base metal prices. As such, we see UK miners resting at the bottom of the FTSE. Other notable post-earning movers include: LSE (+2.6%), Altice (-14.5%), Hugo Boss (-6.0%) and Inmarsat (-4.9%)

Top European News

- BOE Rate Hike Seen Despite Brexit on Horizon: Decision Day Guide

- U.K. Construction Growth Unexpectedly Jumps to Highest in a Year

- ECB’s Rimsevics Says Can’t Name Substitute for Governing Council

- Dialog Semi Stock Gives Up Gains as Apple Concerns Persist

In FX, The Greenback is broadly firmer in wake of the latest FOMC statement that saw growth, inflation and labour market assessments all upgraded to underpin September rate hike expectations and keep the Fed on track to deliver another ¼ point tightening by year end. Heightened trade and other global tensions have also boosted the Buck as the DXY nudges back up to95.000 having hit lows very close to the big figure below just 2 days ago. EUR – The single currency has lost more traction vs the Usd on the downturn in risk sentiment, and retreated further from 1.1700 towards 1.1600 having breached Fib support near 1.1616 and a daily cloud base at 1.1648 on the way down. However, more layered expiry interest in decent size between 1.1600-10 and 1.1625-35 (both in 1.1 bn) could exert some directional influence ahead of and into the NY cut. EM -Broad losses vs the generally bid Usd, but the Lira’s almost inevitable further depreciation on latest US sanction proposals down through 5.0000 is eye-catching as the Try tumbles to fresh all time lows (circa 5.0900 at one stage).

In commodities, WTI and Brent slip lower with the complex pressured by USD strength following the latest tariff news. Energy news flow remains light, however, sources reported that Russia, the largest oil producer, is forecasting an output around 11.2mln bpd to the yearend. Of note: Russia’s July oil production stood at 11.2mln bpd (vs. June output of 10.93mln bpd). Meanwhile, the Shanghai International Energy Exchange are looking into the possibility of setting up a market maker scheme for crude oil futures after the exchange asked brokers to help boost trading volumes and liquidity. Spot gold is flat as USD strength outweighs safe-haven flows. Copper continues its decline amid demand concerns fuelled by the rise in trade tensions.

US Event Calendar

- 7:30am: Challenger Job Cuts YoY, prior 19.6%

- 8:30am: Initial Jobless Claims, est. 220,000, prior 217,000

- 8:30am: Continuing Claims, est. 1.75m, prior 1.75m

- 9:45am: Bloomberg Consumer Comfort, prior 59

- 10am: Factory Orders, est. 0.7%, prior 0.4%; Factory Orders Ex Trans, prior 0.7%

- 10am: Durable Goods Orders, prior 1.0%; Durables Ex Transportation, prior 0.4%

- 10am: Cap Goods Orders Nondef Ex Air, prior 0.6%; 10am: Cap Goods Ship Nondef Ex Air, prior 1.0%

3. ASIAN AFFAIRS

i)THURSDAY MORNING/WEDNESDAY NIGHT: Shanghai closed DOWN 56.51 POINTS OR 2.00% /Hang Sang CLOSED DOWN 626.18 POINTS OR 2.21%/ / The Nikkei closed DOWN 234.17 POINTS OR 1.03%/Australia’s all ordinaires CLOSED DOWN 0.54% /Chinese yuan (ONSHORE) closed DOWN at 6.8401 AS POBC RESUMES ITS HUGE DEVALUATION /Oil DOWN to 67.05 dollars per barrel for WTI and 71.92 for Brent. Stocks in Europe OPENED DEEPLY IN THE RED//. ONSHORE YUAN CLOSED WELL DOWN AT 6.8401 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.8595: HUGE DEVALUATION/PAST SEVERAL DAYS RESUMES : /ONSHORE YUAN TRADING STRONGER AGAINST OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

3 a NORTH KOREA/USA

North Korea/South Korea/USA/China

3 b JAPAN AFFAIRS

Turmoil at the Central Bank of Japan: with rates climbing to 13.5% and a poor Japanese auction, the central bank did a purchase of bonds which never happens right after an auction. It seems that the pOBC wants to raise the 10 yr rate purchase to .20% but that will have tremendous risks.

a must read.

(courtesy zerohedge)

“Too Much Risk”: Rollercoaster Session For JGBs Ends With Bizarre Central Bank Intervention

Traders expected another rollercoaster session for what has become the “fulcrum security” in the global bond market, Japanese Government Bonds, whose every move reverberates around the globe and has been responsible for much of the global steepening action in the past two weeks… and they were not disappointed.

It started off well enough: when yesterday’s dramatic selloff in JGBs failed to resume off the bat, there was a brief short squeeze, followed by a few hours of stability which kept the yield around 0.12%.

Then just before midnight EDT, Japanese JGB futures tumbled and yields jumped following a 10Y JGB auction which was badly received by the market, and which despite a bid/cover in line with recent auctions, saw poor pricing with a tail of 0.12, which is the longest in two years; the market reaction was to send the yield sharply higher back to session highs of 0.135% around the level when yesterday Japanese market regulators called for a margin call.

At this point questions started swirling: will the BOJ let 10Y JGB yields continue rising, letting them reach the 0.20% (the level Kuroda hinted at in his press conference) or maybe above, or would he launch another fixed-rate “unlimited buying” operation?

The answer turned out to be neither, because just after 1am EDT, the Bank of Japan surprised the market by offering to buy 400BN yen of 5-10 year bonds in a Rinban open market operation, i.e. the Japanese equivalent of POMO, that was outside its regular schedule, as the benchmark 10-year yield continued its advance. Immediately, the 10-year yield erased its advance and slumped back to unchanged.

Needless to say, the demand was more than enough, and the BOJ announced that the operation to purchase 400BN yen received bids worth 1.27t yen. The BOJ also told Bloomberg after the operation that its offer to buy 5-10 year bonds outside its regular schedule on Thursday “was meant to meet its policy objective of keeping the 10-year yield at around zero percent.”

Ok, fine, but why the flip-flop by the BOJ, and why did Kuroda pick to do an unscheduled “POMO” instead of calming the market with the far more forceful “fixed rate” operation?

According to Nomura, the central bank was faxed with two distinct issues: i) the BOJ wanted to wait until 10-year yields climbed to 0.2% before announcing a fixed-rate operation but ii) it needed to slow the pace of the increase so it held an unscheduled debt-purchase operation.

Had the BOJ held a fixed-rate operation at current yield levels, traditionally seen as a yield “red line” for the central bank, it would have risked narrowing the trading range again and undoing all the verbal guidance from the latest policy meeting, while waiting for the yield to reach 0.2% “may have been a bit reckless”, said Nomura’s Takenobu Nakashima.

In other words, Thursday’s move suggests the BOJ will avoid using fixed-rate operations until the yield reaches 0.2%, and until it reaches that level it may continue to use this auction-style buying.

Others agreed, and Daisuke Uno, chief strategist at Sumitomo Mitsui said that the Bank of Japan’s unusual bond buying is aimed at removing the fixed idea about operations.

“What the BOJ sees as side-effects of its policy include a decline in market function,” he says by phone. “Today’s operation is probably meant to be like a rehabilitation to help the market regain its function given it has been in doldrums.”

“The BOJ signals to the market that it still keeps the yield curve under its control but its grip has loosened a little bit” he added.

The last part was spot on, because while the BOJ managed to preserve control, it now has the market guessing not only as to the magnitude of the yield move it will allow, but the form of intervention it will launch: what happens if the BOJ reveals there are far more bids for its rinban than clear? Would it set off an avalanche of selling? Alternatively, what happens when the BOJ has to do a constant fixed-rate operation at 0.20% should panic selling emerge as Kuroda’s control “loosens” a little more?

* * *

But what was most notable about Kuroda’s intervention is that the BOJ purchased JGBs just over an hour after they were issued, and as Mizuho observed, “the BOJ is taking too much risk,” as buying bonds on the day of an auction is usually seen as problematic: “Because the BOJ has said, in principle, it refrains from conducting purchase operations on the day of an auction, most people have thought the central bank wouldn’t do it” said Mizuho’s senior market economic Toru Suehiro… and yet that’s precisely what the BOJ did.

“Today’s operation leaves a question mark on the central bank’s communication with the market” he added.

Concluding ominous, he said that tonight’s intervention “also brings the BOJ a step closer to financing fiscal deficits even though the central bank doesn’t directly buy bonds from the government.”

Of course, monetization of fiscal deficits is how all of this ends, not just in Japan but everywhere.

For now, the good news is that the Japanese bond market remained under control -a bond market which now determines the bond yields from France to the US. But what about next time, and the time after that?

And finally, if this is the kind of drama that a simply move from 0.1% to 0.2% entails, what will happen if the BOJ truly normalizes and lets yields move freely?

c) REPORT ON CHINA/HONG KONG

A very important commentary. The yuan falters badly as Trump is thinking to raise the next proposed tariffs to 25%. This would cause China to again lower its yuan value. The risk to the Chinese will be if the firewalls for capital controls break. With a debt to GDP of 300% China does have huge financial problems if the debt dam breaks

(courtesy zerohedge)

Here’s Why Trump Is Hiking Chinese Tariffs To 25%

One of the cited reasons behind today’s market slide which started in Asia and promptly swept the rest of the globe, is a belated appreciation of Tuesday’s news that the Trump administration is now considering more than doubling proposed tariffs on a further $200 billion worth of Chinese goods to 25%, up from an original 10%.

But what exactly prompted Trump to push for the sharp reset in Chinese tariffs?

The answer was actually first given by Trump himself three weeks ago, when in a candid CNBC interview the president said that he was not only watching the US trade deficit with China, but also its currency, which was “dropping like a rock”, suggesting that trade war was morphing into currency war after he berated the Fed for hiking rates and pushing the dollar higher (when, as we explain below, Trump should be commending Powell for doing just that).

Fast forward to today, when the WSJ gives some further color, noting that while “the administration didn’t spell out a particular rationale for increasing the tariff…. the reasons include anger over the Chinese government’s failure to approve the merger of U.S.-based Qualcomm Inc. and Dutch chip maker NXP Semiconductors, which forced the companies to scrap a deal aimed at boosting Qualcomm’s reach into new markets.”

The WSJ also cites “industry officials who have discussed the move with the White House” and who said that another, perhaps far more important reason for the tariff increase “is to compensate for the decline in the value of the yuan by about 6% over the past two months.“

“It’s important countries refrain from devaluing currencies for competitive purposes,” a senior administration official said, and although he didn’t accuse China of acting in that fashion, the implication was clear.

Yet another reason that forced Trump’s hand is that as several banks have recently pointed out, the Yuan devaluation to date has effectively offset the adverse impact to Beijing from the $34 billion in tariffs enacted on Chinese goods, mainly machinery and components (to which China retaliated with tariffs on the same amount of U.S. exports, especially farm products).

But whatever the reason, the longer the trade war continues, the more Trump will find himself in a bind: on one hand he wants lower rates and a weaker dollar, on the other he keeps escalating by enacting ever bigger (and higher) tariffs on China, which are sure to prompt a broad inflationary response in the US economy requiring even higher rates, as we discussed previously. Here is the WSJ:

The proposed tariff increase poses big risks for both the U.S. and global economy. A 25% tariff would boost the cost of a range of U.S. imports at a time when inflation has begun to pick up. It would become another factor for the Federal Reserve to consider as it decides how quickly to raise interest rates.

“This gets you nothing,” said Fred Bergsten, founder of the Peterson Institute for International Economics, a Washington, D.C., free-trade think tank. “It adds to inflation pressure and interest rates and [would] strengthen the dollar, which makes trade situation even worse” for the U.S., he said.

Worse, not only are US farmers getting crushed by Trump’s tariffs, but domestic companies are starting to feel the burn:

Keith Weinberger, chief executive of Empire Today, a flooring company in Northlake, Ill., said he “might be able to offset” a 10% tariff on his purchases of Chinese vinyl flooring. “But there’s nothing you can do about 25.”

Meanwhile, in corporate America, it appears that there is just one thing executives are talking about: tariffs.

As for China’s response, there are two angles: what it says, what it does and what it could do.

Starting with the latter, and continuing the tit-for-tat retaliation in the trade/currency war, higher-than-anticipated tariffs will encourage Beijing to let the yuan slide even more, exacerbating the currency war and potentially making Trump dictate monetary policy to the Fed.

In fact, China can keep devaluing the Yuan until its capital controls “firewall” finally cracks: recall that this was the trigger that prompted a global bear market (from which the US was spared) in 2015/2016 when China lost a total of $1 trillion in reserves to defend its currency against an onslaught of capital flight.

Then there is what China says and on Thursday, Beijing urged the United States to “calm down” and return to reason after news that Trump may hike the tariffs from 10% to 25%.

Wang Yi, the Chinese government’s top diplomat, said U.S. efforts to pressure China would be in vain, urging its trade policymakers to “calm down”.

“We hope that those directly involved in the United States’ trade policies can calm down, carefully listen to the voices of U.S. consumers…and hear the collective call of the international community,” Wang, a member of the country’s state council, or cabinet, said in Singapore. “The United States’ method of adding pressure will not, I’m afraid, have any effect,”Wang told reporters on the sidelines of a regional forum.

Finally, when it comes to what China does, look no further than the Yuan, whose sharp devaluation started in mid-June, when Trump formally launched the trade war, announcing that new tariffs on $50BN in Chinese products will come into effect, followed just days later with the launch of the next, $200BN round of tariffs.

This is how China has responded so far.

And with the Yuan hitting the lowest level against the dollar in a year overnight, the ball is now in Trump’s court. Any further escalation will only accelerate the Yuan devaluation, strengthen the dollar, and – eventually – breach China’s capital control firewall at which point 2018 will finally become 2015 all over again.

And the biggest irony: it Trump really wants to defeat China, instead of criticizing the Fed for hiking, he has to encourage Powell to do precisely what he has been doing so far, as Eric Peters explained over the weekend:

“The best way to bring Beijing to its knees is by running a tight monetary policy in the US. China has the world’s most overleveraged, fragile financial system.” In 2008, China’s total debt-to-GDP was 140%. It is now roughly 300%, while GDP is slowing.

“The economy is held together by capital controls. If those fail, the whole system fails.” The capital flight in 2015/16 cost the government $1trln in reserves, and that was with ultra-dove Yellen in charge. Imagine what would have happened with Volcker at the helm. “The Chinese are dying to get their money out.”

All Trump has to do, is help them do it and watch as China’s economy crumbles from the inside.

China Is About To Report Its First Ever H1 Current Account Deficit: Why It Matters

In what may represent a historic change to China’s mercantilist economy, recently we noted that in the first quarter of 2018, China had recorded its first current account deficit this century.

Now, in a note from Deutsche Bank that explains the bank’s justification to revise its USDCNH forecast higher (now expecting the Yuan to drop to 7.40 against the dollar versus 6.90 previously), the bank picks up on this observation and as chief China economist Zhiwei Zhang writes, China had a current account deficit of US$ 34bn in Q1, the first quarterly current account deficit since 2001 Q2.

He then goes on to preview that the current account balance for Q2 will be released on Aug 6, and while the monthly balance of payments data suggest that China likely has a surplus in Q2, it will be much smaller than the past years.

“Consequently the current account balance in H1 has likely turned into a deficit”, Deutsche Bank predicts.

Here are the details:

the monthly data release shows China’s balance of goods and service trade recorded a surplus of US$ 31 bn in Q2 after a large deficit of US$21 bn in Q1 ( Figure 1 ). Growth of goods exports slowed in H1 to 11% while import growth surged to 20%. The service trade deficit widened to US$149 bn in H1 from the five year average of US$90 bn ( Figure 2 ).

The Q2 income balance in the current account has not been released. To turn the current account in H1 into surplus the income balance needs to show a surplus of at least 3bn in Q2 which is quite unlikely, as it has been in deficit for most of the past three years ( Figure 3 ).

As a result, DB expects China’s current account balance to show a small deficit around US$15bn in H1 (a deficit of US$34bn in Q1 and a surplus of US$19bn in Q2), assuming the income balance in Q2 to be the average of past two years (- US$12bn).

It would be the first time China had a current account deficit on half year basis since China started to publish quarterly data in 1998.

Why is this important? As Zhivei explains, the decline of current account surplus is a structural trend which is driven by

- consumption upgrade due to a strong wealth effect from the booming property market, particularly in tier 3 cities

- slower growth of exports as China loses competitiveness in labor intensive products to other low income countries. The trade tension will likely put further pressure on the current account in coming years, as China tries to promote imports to avoid trade war.

He goes on to note that while the trade war has not affected China’s current account visibly yet in H1, it will certainly reinforce the downward pressure in H2 and 2019 as pressure on exports increases, especially if Trump imposes more tariffs than are already in place (which he will). Adding to the downward pressure, China is trying to promote imports to mitigate the trade tension. As a result, “the trade surplus will likely shrink in the next few years.”

Extrapolating a few years out, DB forecasts that China’s current account balance will drop to 0.6%, 0.3% and 0% of GDP in 2018, 2019 and 2020 (2017: 1.3%).