GOLD: $1177.25 UP $0.20 (COMEX TO COMEX CLOSINGS)

Silver: $14.65 DOWN 4 CENTS (COMEX TO COMEX CLOSINGS)

Closing access prices:

Gold $1184.70

silver: $14.83

For comex gold:

AUGUST/

NUMBER OF NOTICES FILED TODAY FOR AUGUST CONTRACT: 17 NOTICE(S) FOR 1700

TOTAL NOTICES SO FAR 2197 FOR 219,700 OZ (6.8335 tonnes)

For silver:

AUGUST

96 NOTICE(S) FILED TODAY FOR

480,000 OZ/

Total number of notices filed so far this month: 1149 for 5,745,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: BID $6378/OFFER $6463: UP $78(morning)

Bitcoin: BID/ $6454/offer $6539: UP $220 (CLOSING/5 PM)

end

First Shanghai gold fix comes at 10 pm est

The second Shanghai gold fix: 2:15 pm

First Shanghai gold fix gold: 10 pm est: $1182.90

NY price at the same time:$1177.50

PREMIUM TO NY SPOT: $5.40

XX

Second gold fix early this morning: $ 1180.84

USA gold at the exact same time:$1174.15

PREMIUM TO NY SPOT: $5.49

China is controlling the gold market

WE WILL NOT PROVIDE LONDON FIXES AS THEY ARE NOT ACCURATE AS TO WHAT IS GOING ON AT THE SAME TIME FRAME.

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total OPEN INTEREST FELL BY 1011 CONTRACTS FROM 240,621 DOWN TO 235,287 DESPITE YESTERDAY’S GOOD 14 CENT ADVANCE IN SILVER PRICING AT THE COMEX. WE HAVE GENERALLY BEEN WITNESSING A SLOW COMEX ACCUMULATION THESE PAST SEVERAL DAYS BUT THAT STOPPED ABRUPTLY THE LAST FEW DAYS. HOWEVER, WE HAVE ALSO WITNESSED A LARGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY(WELL OVER 30 MILLION OZ AT THE COMEX FOR JULY AND OVER 5 MILLION OZ FOR AUGUST) AS WELL AS CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A LARGE SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP:

1451 EFP’S FOR SEPT. , 0 EFP’S FOR DECEMBER AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE: OF 1451 CONTRACTS. WITH THE TRANSFER OF 1451 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 1451 EFP CONTRACTS TRANSLATES INTO 23.665MILLION OZ AND ACCOMPANYING:

1.THE 14 CENT RISE IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR THE JUNE/2018 COMEX DELIVERY MONTH. (5.420 MILLION OZ) 30.370 MILLION OZ STANDING FOR DELIVERY IN JULY, AND NOW 5.950 MILLION OZ FOR AUGUST.

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF JULY:

19,021 CONTRACTS (FOR 13 TRADING DAYS TOTAL 19,021 CONTRACTS) OR 95.105 MILLION OZ: (AVERAGE PER DAY: 1463 CONTRACTS OR 7.315 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF JULY: 95.105 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 13.58% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2018 TO DATE SILVER EFP’S: 1,924.77 MILLION OZ.

ACCUMULATION FOR JAN 2018: 236.879 MILLION OZ

ACCUMULATION FOR FEB 2018: 244.95 MILLION OZ

ACCUMULATION FOR MARCH 2018: 236.67 MILLION OZ

ACCUMULATION FOR APRIL 2018: 385.75 MILLION OZ

ACCUMULATION FOR MAY 2018: 210.05 MILLION OZ

ACCUMULATION FOR JUNE 2018: 345.43 MILLION OZ

ACCUMULATION FOR JULY 2018: 172.84 MILLION OZ

RESULT: WE HAD A SMALL SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 1011 DESPITE THE GOOD 14 CENT GAIN IN SILVER PRICING AT THE COMEX YESTERDAY. THE CME NOTIFIED US THAT WE HAD A STRONG SIZED EFP ISSUANCE OF 1451 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) .

TODAY WE GAINED A SMALL SIZED: 440 TOTAL OI CONTRACTS ON THE TWO EXCHANGES:

i.e 1451 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH A DECREASE OF 1011 OI COMEX CONTRACTS. AND ALL OF THIS DEMAND HAPPENED WITH A 14 CENT RISE IN PRICE OF SILVER AND A CLOSING PRICE OF $14.64 WITH RESPECT TO YESTERDAY’S TRADING. YET WE HAD A GIGANTIC AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY IN THE BIG JULY DELIVERY MONTH OF SLIGHTLY OVER 30 MILLION OZ AND NOW IN AUGUST ANOTHER BIG 5.955 MILLION OZ IN A NON ACTIVE MONTH. IT SURE LOOKS LIKE ANOTHER FAILED BANKER SHORT COVERING EXERCISE AS BANKERS ARE SCRAMBLING TO COVER THEIR HUGE SHORTFALL IN SILVER.

In ounces AT THE COMEX, the OI is still represented by OVER 1 BILLION oz i.e. 1.176 MILLION OZ TO BE EXACT or 168% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT AUGUST MONTH/ THEY FILED AT THE COMEX: 96 NOTICE(S) FOR 480,000 OZ OF SILVER

IN SILVER, WE SET THE NEW RECORD OF OPEN INTEREST AT 243,411 CONTRACTS ON APRIL 9.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $16.51

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) AND JULY 2018 AMOUNT STANDING: 30.370 MILLION OZ ) AND NOW FOR AUGUST 5.950 MILLION OZ.

- HUGE RECORD OPEN INTEREST IN SILVER 243,411 CONTRACTS (OR 1.217 BILLION OZ/ SET APRIL 9/2018

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017

- RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT).

IN GOLD, THE OPEN INTEREST FELL BY A CONSIDERABLE SIZED 2509 CONTRACTS DOWN TO 477,460 WITH THE LOSS IN THE COMEX GOLD PRICE/YESTERDAY’S TRADING (A FALL IN PRICE OF $1.05). THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A GOOD SIZED 7166 CONTRACTS:

AUGUST HAD AN ISSUANCE OF 0 CONTRACTS, OCTOBER HAD 0EFP’S ISSUED AND, DECEMBER HAD AN ISSUANCE OF 7166 CONTACTS AND ALL OTHER MONTHS ZERO. The NEW COMEX OI for the gold complex rests at 477,460. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE AN A GOOD OI GAIN IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 4657 CONTRACTS: 2509 OI CONTRACTS DECREASED AT THE COMEX AND 7166 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN: 4657 CONTRACTS OR 465,700 OZ = 14.48 TONNES. AND ALL OF THIS GOOD DEMAND OCCURRED WITH A LOSS IN THE PRICE OF GOLD/ YESTERDAY TO THE TUNE OF $1.05.???..

YESTERDAY, WE HAD 11,389 EFP’S ISSUED.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF JUNE : 97,337 CONTRACTS OR 9,733,700 OZ OR 302.75 TONNES (13 TRADING DAYS AND THUS AVERAGING: 7487 EFP CONTRACTS PER TRADING DAY OR 748,700 OZ/ TRADING DAY),,

TO GIVE YOU AN IDEA AS TO THE HUGE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 13 TRADING DAYS IN TONNES: 302.75 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2017, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 2555 TONNES

THUS EFP TRANSFERS REPRESENTS 302.75/2550 x 100% TONNES = 11.87% OF GLOBAL ANNUAL PRODUCTION SO FAR IN JULY ALONE.***

ACCUMULATION OF GOLD EFP’S YEAR 2018 TO DATE: 5,021.38* TONNES *SURPASSED ANNUAL PROD’N

ACCUMULATION OF GOLD EFP’S FOR JANUARY 2018: 653.22 TONNES (21 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR FEBRUARY 2018: 649.45 TONNES (20 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR MARCH 2018: 741.89 TONNES (22 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR APRIL 2018: 713.84 TONNES (21 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR MAY 2018: 693.80 TONNES ( 22 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR JUNE 2018 650.71 TONNES (21 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR JULY 2018 605.5 TONNES (21 TRADING DAYS)

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A CONSIDERABLE SIZED DECREASE IN OI AT THE COMEX OF 2509 WITH THE LOSS IN PRICING ($1.05 THAT GOLD UNDERTOOK YESTERDAY) // . WE ALSO HAD A STRONG SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 7166 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 7166 EFP CONTRACTS ISSUED, WE HAD A GOOD GAIN OF 4657 CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

7166 CONTRACTS MOVE TO LONDON AND 2509 CONTRACTS DECREASED AT THE COMEX. (in tonnes, the GAIN in total oi equates to 14.48 TONNES). ..AND THIS GOOD DEMAND OCCURRED DESPITE A LOSS OF $1.05 IN YESTERDAY’S TRADING AT THE COMEX!!!. ????

we had: 17 notice(s) filed upon for 1700 oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD...

WITH GOLD UP $0.20 TODAY: /

NO CHANGE IN GOLD INVENTORY AT THE GLD

/GLD INVENTORY 773.41 TONNES

Inventory rests tonight: 773.41 tonnes.

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

SLV/

WITH SILVER DOWN 4 CENTS TODAY

NO CHANGE IN SILVER INVENTORY AT THE SLV

/INVENTORY RISES AT 329.104 MILLION OZ.

NOTE THE DIFFERENCE BETWEEN THE GLD AND SLV: THE CROOKS CAN RAID GOLD BECAUSE THEY DO HAVE SOME PHYSICAL. THEY DO NOT RAID SILVER PROBABLY BECAUSE THERE IS NO REAL SILVER INVENTORIES BEHIND THEM

end

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER FELL BY A SMALL SIZED 1011 CONTRACTS from 240,038 DOWN TO 235,287 (BUT STILL WITHIN SPITTING DISTANCE TO A NEW COMEX RECORD. THE LAST RECORD WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). THE PREVIOUS RECORD TO THAT WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 1 1/4 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89. AS YOU CAN SEE, WE HAVE RECORD HIGH OPEN INTERESTS IN SILVER ACCOMPANIED BY A CONTINUAL LOWER PRICE WHEN THAT RECORD WAS SET…..VERY STRANGE INDEED AND IT WILL COME TO FRUITION AGAIN VERY SHORTLY

.

OUR CUSTOMARY MIGRATION OF COMEX LONGS MORPH INTO LONDON FORWARDS CONTINUES AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

0 EFP CONTRACTS FOR AUGUST., 1451 EFP CONTRACTS FOR SEPTEMBER, 0 CONTRACTS FOR DECEMBER AND AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 1451 CONTRACTS . EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI LOSS AT THE COMEX OF 1011 CONTRACTS TO THE 1451 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A NET GAIN OF 440 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES: 2.200 MILLION OZ!!! AND YET WE ALSO HAVE A STRONG DEMAND FOR PHYSICAL AS WE WITNESSED A FINAL STANDING OF GREATER THAN 30 MILLION OZ FOR JULY AND NOW ANOTHER STRONG 5.950 MILLION OZ FOR AUGUST... AND YET ALL OF THIS HUGE PHYSICAL DEMAND OCCURRED DESPITE A SMALLISH 14 CENT PRICING ADVANCE AT THE SILVER COMEX!!!!????.

RESULT: A FAIR SIZED DECREASE IN SILVER OI AT THE COMEX DESPITE THE 14 CENT PRICING GAIN THAT SILVER UNDERTOOK IN PRICING YESTERDAY.BUT WE ALSO HAD A STRONG SIZED 1451 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR AUGUST, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)FRIDAY MORNING/THURSDAY NIGHT: Shanghai closed DOWN 36.23 POINTS OR 1.34% /Hang Sang CLOSED UP 113.35 POINTS OR 0.42%/ / The Nikkei closed UP 78.34 POINTS OR 0.35%/Australia’s all ordinaires CLOSED UP 0.21% /Chinese yuan (ONSHORE) closed UP at 6.8826 AS POBC HALTS ITS HUGE DEVALUATION /DELEGATION COMING TO THE USA TO SEE TRUMP/Oil UP to 65.80 dollars per barrel for WTI and 72.05 for Brent. Stocks in Europe OPENED DEEPLY IN THE RED //. ONSHORE YUAN CLOSED UP AT 6.8826 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.8613: HUGE DEVALUATION/PAST SEVERAL DAYS STOPS TRADE TALKS WILL RESUME IN THE USA : /ONSHORE YUAN TRADING STRONGER AGAINST OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING STRONGER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

/NORTH KOREA/SOUTH KOREA

i)North Korea/South Korea/USA/Russia

b) REPORT ON JAPAN

3 c CHINA

The pentagon warns that China with its long range bombers are training for a strike against the uSA. And the USA is facilitating gold purchases by China onto their soil?…

( zerohedge)

4. EUROPEAN AFFAIRS

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

6 .GLOBAL ISSUES

( Mac Slavo/SHTFPlan.com)

ii)Canada

Canada reports a huge rise in consumer prices of 3.% year over year and these numbers are really higher as they disguise the true inflation rate. Strangely the loonie spiked higher on the news because the Bank of Canada governor mist raise rates fast against a slowing economy

( zerohedge)

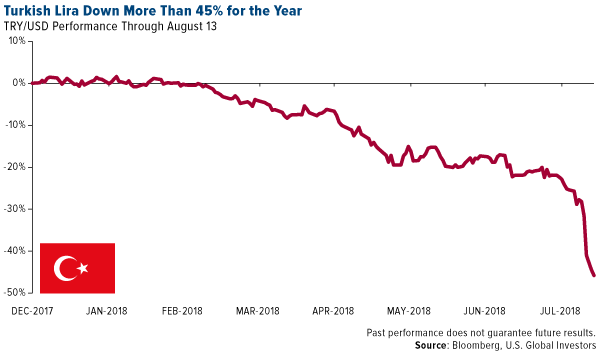

iii)Richard Breslow, is one smart cookie: he points out the huge problems facing the globe this morning which is basically totally ignored e.g. the German bund at .30%, the huge fall in the Turkish lira and other emerging nation currencies

( Richard Breslow/zerohedge)

7. OIL ISSUES

8. EMERGING MARKET

9. PHYSICAL MARKETS

i)Goldcore notes that gold’s fall in price may be official invention by the bankers and the world’s financial system may be showing signs of cracking up

( Chris Powell/Goldcore)

ii)This has zero chance of happening: Keith Weiner is advocating a bond issuance where interest is paid in gold

(Keith Weiner/GATA)

10. USA stories which will influence the price of gold/silver)

i)Market trading /GOLD/MARKET MOVERS:

MARKET TRADING

We are now seeing soft data reports showing that the USA is rolling over: today it is U. of Michigan sentiment and it slumped to an 11 month low. The all important spending category plunged

( zerohedge)

iv)SWAMP STORIES

a)What corruption: A Pentagon whistleblower, Adam Lovinger has been stripped of his security clearance and demoted after complaining about questionable government contracts to Stefan Halper and a company headed by Chelsea Clinton

( zerohedge)

b)The Wall Street journal is the only main stream media reporting on the misdeeds of Bruce Ohr, the Dept of Justice and the FBI. Kim Strassel has done a great job reporting on this although she has been receiving a lot of abuse.

She correctly states that all the information on this is located on the 302 forms…but strangely they are all classified. Once they are revealed to congress and once declassified, we will know the truth

( Kim Strassel, Wall Street Journal/zero hedge)

Let us head over to the comex:

FOR THOSE THAT WISH TO FOLLOW TODAY’S SILVER OI VS LAST YR

AUGUST 16.2017: 95,493 OPEN INTEREST CONTACTS STILL OPEN FOR THE UPCOMING SEPT ACTIVE CONTRACT MONTH VS TODAY AUG 15.2018: 127,871 CONTRACTS.(DEMAND REMAINS EXTREMELY STRONG DESPITE THE LOWER PRICE)

Major gold/silver trading /commentaries for FRIDAY

GOLDCORE/BLOG/MARK O’BYRNE.

This Week’s Golden Nuggets

News, Market Updates and Videos You May Have Missed

As it’s Friday we are bringing you our weekly digest of the news, market updates, charts and videos that caught our eye this week.

We are also giving you a link to our most recent episode of the Goldnomics Podcast – Jim Rogers on Gold, Silver & Surviving the Coming Crash (Episode 7). We have been getting some great feedback on this and our previous episodes of our podcast, so why not check out one or two episodes this weekend.

Market Updates This Week

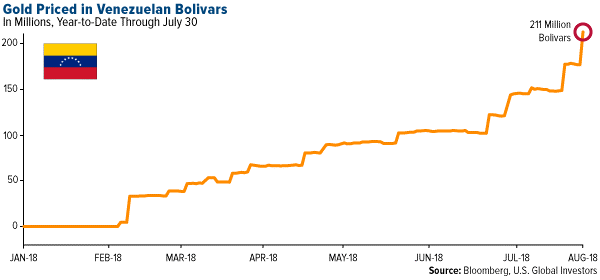

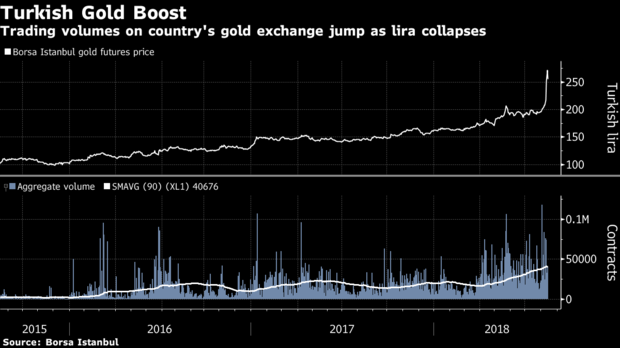

Gold And Silver Prices Fall Sharply To Near 2 Year Lows Despite Strong Demand In Turkey

London House Prices Fall At Fastest Rate Since Height Of Financial Crisis

Financial Crisis In Turkey To Trigger “Wider Calamity In Global Markets”

Videos of the Week

Source: Bloomberg and US Global Investors via GoldSeek

Source: Bloomberg and US Global Investors via GoldSeek

Source: Bloomberg

Source: Bloomberg

Gold and Silver Bullion – News and Commentary

Gold inches up, but set for biggest weekly fall in 15 months (Reuters.com)

Gold recovers early lost ground to fresh 19-month low, lacks follow-through (FXStreet.com)

Paulson keeps stake in gold investments during second-quarter: filing (Reuters.com)

Russia Leaves U.S. Debt Hoard Intact After $81 Billion Retreat (Bloomberg.com)

RBS was selling ‘total garbage’ in lead-up to financial crisis, documents show (IrishExaminer.com)

George Washington gold coin sells for $1.7 million | August 16, 2018 (Reuters.com)

Source: Bloomberg and US Global Investors

It’s Time for Contrarians to Get Bullish on Gold (GoldSeek.com)

How much lower can bitcoin and the crypto sector fall? (MoneyWeek.com)

Trump’s funny math on tariffs and the debt (MarketWatch.com)

Trump’s report card: Good marks for jobs, but other subjects need improvement (MarketWatch.com)

Four simple things you should do to succeed in stock markets (StansBerryChurcHouse.com)

Listen on SoundCloud , Blubrry & iTunes. Watch on YouTube below

Gold Prices (LBMA AM)

16 Aug: USD 1,179.65, GBP 928.38 & EUR 1,037.74 per ounce

15 Aug: USD 1,186.70, GBP 933.10 & EUR 1,047.74 per ounce

14 Aug: USD 1,195.30, GBP 935.32 & EUR 1,049.11 per ounce

13 Aug: USD 1,204.40, GBP 944.85 & EUR 1,058.19 per ounce

10 Aug: USD 1,211.65, GBP 947.87 & EUR 1,056.44 per ounce

09 Aug: USD 1,215.50, GBP 944.08 & EUR 1,048.13 per ounce

Silver Prices (LBMA)

16 Aug: USD 14.61, GBP 11.51 & EUR 12.85 per ounce

15 Aug: USD 14.83, GBP 11.66 & EUR 13.10 per ounce

14 Aug: USD 15.04, GBP 11.77 & EUR 13.18 per ounce

13 Aug: USD 15.18, GBP 11.91 & EUR 13.35 per ounce

10 Aug: USD 15.37, GBP 12.04 & EUR 13.41 per ounce

09 Aug: USD 15.48, GBP 12.01 & EUR 13.35 per ounce

Recent Market Updates

– Gold And Silver Prices Fall 1.6% and 4.3% To Near 2 Year Lows

– London House Prices Fall At Fastest Annual Rate Since Height Of Financial Crisis

– Jim Rogers on Gold, Silver, Bitcoin and Blockchain’s “Spectacular Future”

– This Week’s Golden Nuggets

– The Stock Market is Stretched to Double Tech-Bubble Extremes

– Jim Rogers and the World’s New Reserve Currency

– Gold—Even at its Lowest Levels in 2018—is Behaving Just as Prescribed

– Jim Rogers – Making China Great Again! (Video)

– This Week’s Golden Nuggets

– Gold to Enter New Bull Market – Charles Nenner

– Here’s Where the Next Crisis Starts

Andrew Maguire’s Kinesis money which is a “bitcoin” but backed 100% by allocated gold and silver is set to go.

it think it would be a great idea to look at this!

please read at: https://kinesis.money/#/

(Andrew Maguire)

|

|

Dear Harvey Organ,

Thank you for your participation in our webinar on June 7th with our host and CEO of Kinesis, Thomas Coughlin.

The response we received has been incredible, we appreciate you taking the time to join us and hope you found it to be beneficial.

Due to such a high influx of questions we received we were unable to have them all answered. Nevertheless, if there was anything which requires more clarification, or you have a query which needs to be rectified, we invite you to join our telegram group:

We apologize for the technical issues we incurred during the webinar which resulted in it running a little over schedule, we hope that the next one we host will run seamlessly.

A video has been put together and uploaded onto our YouTube channel which can be found here:

Please share and subscribe to our YouTube channel to be notified of all the latest videos as they become available.

The rapid growth that we are currently experiencing has been incredible and with your support, is only going to get better.

We are working behind the scenes very hard to create a better experience for everyone involved! Stay tuned in as we have many more announcements to be released in the upcoming days.

Kind Regards,

|

Kinesis Money

a:C/O ILS Fiduciaries (IOM) Limited, First Floor,Millennium House, Victoria Road, Douglas, Isle of Man IM2 4RW

|

The following is self explanatory

(courtesy GATA/Chris Powell and Harvey Organ)

GATA asks bank regulator to check risks of gold

futures maneuver

Submitted by cpowell on Sun, 2018-06-10 16:17. Section: Daily Dispatches

12:21p ET Sunday, June 10, 2018

Dear Friend of GATA and Gold:

GATA has appealed to the U.S. comptroller of the currency, who has regulatory authority over banks, to review financial risks certain banks may have incurred through derivatives in the monetary metals markets, particularly through the recent heavy use of the “exchange for physicals” mechanism of settling gold and silver futures contracts on the New York Commodities Exchange.

The appeal was made in a letter sent May 5 to the comptroller, Joseph M. Otting, whose office is part of the U.S. Treasury Department, by your secretary/treasurer and GATA futures market consultant Harvey Organ.

“Exchange for physical” settlements of futures contracts long were considered emergency procedures when a seller was not able to deliver metal from an exchange-approved warehouse and wanted to settle with delivery elsewhere. But now such settlements appear to constitute most gold and silver futures settlements on the Comex. It is a strange development that appears to have been necessitated by the increasing difficulties of central banking’s gold and silver price suppression policy.

GATA has received no acknowledgment of the letter. Its text is below and a PDF copy of it is here:

http://www.gata.org/files/ComptrollerOfCurrencyLetter.pdf

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

* * *

May 5, 2018

Joseph M. Otting, Comptroller of the Currency

U.S. Treasury Department

400 7th Street, SW

Washington DC 20219

Dear Comptroller Otting:

Please let us bring to your attention financial risks to major banks involving their possibly unreported exposure to derivatives in the monetary metals markets.

In recent months gold and silver future contracts issued by U.S. banks on the New York Commodities Exchange have been moved off-exchange for delivery through a mechanism known as “exchange for physical” (EFP) contracts. Until recently use of this mechanism was considered an emergency procedure when a seller did not have access to metal for delivery through Comex warehouses. Now the mechanism seems to be in use for a large share of front-month contracts for which delivery is sought.

Here is an example that is happening at the Comex in the front active month of April for gold and the inactive delivery month of April for silver.

In gold, there were 229,436 EFP contracts for 713.64 tonnes, an average of 10,925 contracts and 1,092,500 ounces per trading day.

In silver, there were 77,150 EFP contracts for 385,750,000 ounces, an average of 3,673 contracts and 18,369,000 ounces per trading day.

London Bullion Market Association rules suggest that these contracts may not be reported to regulators. The LBMA’s bylaws say:

“Figures above exclude any contracts not subject to risk-based capital requirements, such as FX contracts with an original maturity of 14 days or less, futures contracts, written options, and basis swaps. Therefore, the total notional amount of derivatives by maturity will not add to the total derivatives figure in this table.”

We are told that these EFP contracts are transferred from the Comex to London as what are called “serial forwards” and their duration is always less than 14 days, which exempts them from being reported.

It is our understanding that in each quarter your office prepares a report detailing risk undertaken by the banks under the comptroller’s supervision.

These risks include derivatives undertaken by U.S. banks and other obligations that may cause a bank to fail. Our concern is that your office may not be aware of large unreported derivative exposure by banks.

Could you review this matter and let us know your conclusions?

Sincerely,

CHRIS POWELL

Secretary/Treasurer

HARVEY ORGAN

Consultant

Gold Anti-Trust Action Committee Inc.

7 Villa Louisa Road

Manchester, Connecticut 06043-7541

end

Finally, they replied and it was a complete brush off

(courtesy zerohedge)

Currency comptroller brushes off GATA’s inquiry on

gold, silver EFPs

Submitted by cpowell on Fri, 2018-08-10 15:37. Section: Daily Dispatches

11:35a ET Friday, August 10, 2018

Dear Friend of GATA and Gold:

The U.S. comptroller of the currency, a bank regulator, has declined GATA’s request to inquire into the strange explosion of the use of the emergency procedure of “exchange for physicals” in the settlement by banks of the gold and silver futures contracts they have sold on the New York Commodities Exchange.

Your secretary/treasurer and GATA’s consultant about the Comex, Harvey Organ, wrote to the comptroller, James M. Otting, on May 5, calling attention to the recent enormous use of EFPs, which implies derivatives risks being undertaken by U.S. banks that could cause the banks to fail:

http://www.gata.org/node/18303

“Our concern is that your office may not be aware of large unreported derivative exposure by banks,” GATA wrote.

As months passed without any acknowledgment from the comptroller’s office, your secretary/treasurer appealed to his U.S. representative, John B. Larson, D-Connecticut, to ask the comptroller’s office to reply. The congressman’s office made a second inquiry on Monday this week and today the comptroller’s office provided Larson with a copy of a reply written and mailed Wednesday.

The comptroller’s reply, signed by the deputy comptroller for public affairs, Bryan Hubbard, said only that the comptroller’s office has “dedicated examiners” at the largest banks who “continuously evaluate the credit, market, operational, reputation, and compliance risks of bank trading and derivative activities.”

The reply did not say anything about the use of the “exchange for physicals” procedure for settling futures contracts. That is, the reply was a begrudged brushoff and GATA’s letter would have been ignored completely if not for Representative Larson’s repeated intervention.

Of course GATA hardly expected a conscientious reply to its letter, the comptroller’s office being not an independent regulator but part of the Treasury Department, whose mandate includes administration of the Gold Reserve Act of 1934, which, as amended in the 1970s, authorizes the department’s Exchange Stabilization Fund to secretly intervene in and rig any market in the world, directly or through intermediaries:

https://www.treasury.gov/resource-center/international/ESF/Pages/esf-ind…

But there’s always value in demonstrating government’s lack of candor about what it is doing, especially in regard to the monetary metals.

A PDF copy of the reply from the comptroller’s office is posted at GATA’s internet site here:

http://www.gata.org/files/ComptrollerOfCurrencyReply-08-08-2018.pdf

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

Goldcore notes that gold’s fall in price may be official invention by the bankers and the world’s financial system may be showing signs of cracking up

(courtesy Chris Powell/Goldcore)

GoldCore: Gold’s counterintuitive fall may be official intervention

Submitted by cpowell on Thu, 2018-08-16 22:11. Section: Daily Dispatches

6:14p ET Thursday, August 16, 2018

Dear Friend of GATA and Gold:

GoldCore’s daily market analysis today cites GATA in acknowledging the possibility that gold’s counterintuitive crash as the world financial system shows signs of cracking up has been caused by surreptitious intervention in the gold futures market by central banks struggling to save the system against market forces. GoldCore’s analysis is headlined “Gold and Silver Prices Fall Sharply to Near 2-Year Lows Despite Strong Demand In Turkey” and it’s posted here:

https://news.goldcore.com/us/gold-blog/gold-and-silver-prices-fall-1-6-a…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

This has zero chance of happening: Keith Weiner is advocating a bond issuance where interest is paid in gold

(Keith Weiner/GATA)

Keith Weiner: Bond paying interest in gold would confirm metal’s role as money

Submitted by cpowell on Thu, 2018-08-16 22:41. Section: Daily Dispatches

6:44p ET Thursday, August 16, 2018

Dear Friend of GATA and Gold:

Keith Weiner, CEO of Monetary Metals in Scottsdale, Arizona, a sort of gold banking house that seeks to increase gold’s use in finance, today appeals for signatures on a petition to Nevada’s legislature in support of a proposal to authorize state government to issue bonds with interest payable in gold.

Such a state-issued bond, Weiner notes, would confirm gold’s role as money even as respectable people don’t want to think of it that way anymore.

It’s hard to see why state government would object to the idea now that the gold price is getting smashed every day, reducing the burden of gold-denominated debt. Of course a rising gold price might do a lot more to reiterate gold’s ancient function as money. But for that to happen the world may have to wait for surreptitious intervention in the gold market by the Bank for International Settlements to diminish. Instead it increased 17 percent in July:

Weiner’s appeal is headlined “Who Would Invest in a Gold Bond?” and it’s posted at the Monetary Metals internet site here:

https://monetary-metals.com/who-would-invest-in-a-gold-bond/

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org\

END

At 3;30 pm the CME releases its COT which gives position levels of our major players

It does not give levels of obligations held by the longs and shorts via the EFP;s

for that reason, the value of this report is very limited at best

| Gold COT Report – Futures | ||||||

| Large Speculators | Commercial | Total | ||||

| Long | Short | Spreading | Long | Short | Long | Short |

| 211,779 | 215,467 | 54,392 | 164,195 | 171,545 | 430,366 | 441,404 |

| Change from Prior Reporting Period | ||||||

| 3,487 | 19,863 | 5,815 | 9,992 | -8,267 | 19,294 | 17,411 |

| Traders | ||||||

| 162 | 115 | 87 | 50 | 44 | 254 | 206 |

| Small Speculators | © GoldSeek.com | |||||

| Long | Short | Open Interest | ||||

| 46,373 | 35,335 | 476,739 | ||||

| -2,029 | -146 | 17,265 | ||||

| non reportable positions | Change from the previous reporting period | |||||

| COT Gold Report – Positions as of | Tuesday, August 14, 2018 | |||||

our large speculators

those large speculators who have been long in gold added 3487 contracts to their long side

those large speculators who have been short in gold added 19,863 contracts to their short side

and the longs almost equal the shorts for the first time in quite some time.

Our commercials

those commercials who are long in gold added 9992 contracts to their long side

those commercials who are short in gold covered (transferred) 8267 contracts from their short side

Our small speculators

those small specs who have been long in gold pitched (transferred) 2029 contracts from their long side

those small specs who have been short in gold covered (transferred) 146 contracts from their short side

and now the silver cot

| Silver COT Report: Futures | |||||

| Large Speculators | Commercial | ||||

| Long | Short | Spreading | Long | Short | |

| 93,346 | 96,182 | 28,512 | 84,657 | 97,033 | |

| 330 | 7,507 | -569 | 5,167 | -4,575 | |

| Traders | |||||

| 105 | 72 | 55 | 45 | 37 | |

| Small Speculators | Open Interest | Total | |||

| Long | Short | 240,038 | Long | Short | |

| 33,523 | 18,311 | 206,515 | 221,727 | ||

| -330 | 2,235 | 4,598 | 4,928 | 2,363 | |

| non reportable positions | Positions as of: | 179 | 142 | ||

| Tuesday, August 14, 2018 | © SilverSeek.com | ||||

our large speculators

those large speculators who have been long in silver added 330 contracts to their long side

those large speculators who have been short in silver added 7507 contracts to their short side.

Our commercials

those commercials who have been long in silver added 5167 contracts to their long side

those commercials who have been short in silver covered (pitched) 4575 contacts from their short side

Our small speculators

those small specs who have been long in silver pitched (transferred) 330 contracts from their long side

those small specs who have been short in silver added 2235 contracts to its short side.

Conclusions:

it is very unusual to see the large specs having almost an identical long and short in both gold and silver

what a manipulation.

end

Your early FRIDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

i) Chinese yuan vs USA dollar/CLOSED UP TO 6.8826/HUGE DEVALUATION FOR THE PAST FOUR WEEKS STOPS/CHINESE COMING TO USA FOR TRADE TALKS //OFFSHORE YUAN: 6.8613 /shanghai bourse CLOSED DOWN 36.23 POINTS OR 1.34% /HANG SANG CLOSED UP 113.35 POINTS OR 0.42%

2. Nikkei closed UP 113.35 POINTS OR 0.42%/USA: YEN FALLS TO 110.45/

3. Europe stocks OPENED ALL RED

//USA dollar index FALLS TO 96.44/Euro RISES TO 1.1393

3b Japan 10 year bond yield: REMAINS AT . +.10/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 110.87/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD IS NOW TARGETED AT .11%/JAPAN LOSING CONTROL OF THEIR BOND MARKET

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 65.80 and Brent: 72.05

3f Gold UP/JAPANESE Yen DOWN/ CHINESE YUAN UP

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil UP for WTI and UP FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund FALLS TO +.300%/Italian 10 yr bond yield UP to 3.14% /SPAIN 10 YR BOND YIELD UP TO 1.44%

3j Greek 10 year bond yield RISES TO : 4.34

3k Gold at $1177.40silver at:14.64 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble UP 27 /100 in roubles/dollar) 67.03

3m oil into the 65 dollar handle for WTI and 72 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 110.45 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 0.9956 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1343 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now POSITIVE territory with the 10 year FALLING to +0.30%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.85% early this morning (THIS IS DEADLY TO ALL MARKETS). Thirty year rate at 3.01%

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

Relief rally in the Turkish lira…no developments at all…

(courtesy Jim Reid/Bloomberg/Deutsche bank/zero hedge)

Selling Returns As Turkish Lira Suddenly

Tumbles, China Stocks Slide To New 2 Year Low

A sense of “risk off” has returned to the the market, with 10Y yields sliding, the dollar rebounding from session lows and the Turkish Lira resuming its plunge, renewing concerns about emerging market contagion, leading to a “red return” across global market monitors, following yesterday’s torrid surge in the S&P500.

The USDTRY surged over 8% on Friday, infecting risk sentiment in a generally subdued and low volume session.

There wasn’t one specific catalyst for the latest sharp selloff, although some cited the latest credit measures to help domestic corporates as potentially increasing pressure on banking system.

In its latest steps to shield the economy and mitigate the impact of “economic attacks on our country”, Albayrak’s finance ministry on Friday said that non-financial companies’ credit worthiness wouldn’t be affected by failure to service debt amid the recent rout. Credit lines to firms would remain open, and pricing and repayment periods would be kept flexible, it said. The finance ministry also said that:

- It would limit breaches due to lira decline in loans won’t be taken into consideration; banks won’t demand loan closings in such instances

- Banks won’t demand additional collateral for corporate loans whose collateral value have declined due to lira depreciation

- Force majeure may be declared on loan repayment delays, dud cheques and protested bills. Thus, companies’ access to credit won’t be impaired

In other words, the government is giving banks a blank slate to continue business as usual even if they are on the verge of collapse, not only intensifying the deterioration of the economy, but breaking down traditional risk signaling pathways.

Another reason behind today’s slide was potential risk-shedding before week long Turkish public holiday and upcoming S&P comments on Turkish rating.

Overnight, President Trump stated that Turkey has taken advantage of US for many years and are now holding US pastor, while he added the US will not pay anything for the release an innocent man but are cutting back on Turkey. Separately, a report in Middle East Eye said that Turkey is ready to release Pastor Brunson but the US is offering nothing in return.

TRY traders are also spooked as we may see the the outcome of the appeal court’s consideration of Pastor Brunson’s release request today: it is expected some time this week after the second criminal court rejected the request on Wednesday. On Thursday, Treasury Secretary Mnuchin also threatened more sanctions overnight over Brunson’s ongoing detention, suggesting further headline risk for US-Turkey tensions. “It still looks like we’re headed to more conflict,” Kathy Jones, chief fixed-income strategist at Charles Schwab Inc. “Neither side seems to be backing down yet.”

Meanwhile, that other closely watched FX pair, the USDCNH briefly pushed lower on reports that the U.S. will pressure for a stronger yuan, however the move was s not sustained given similar reports from WSJ yesterday; and as a result the offshore Yuan was trading around 6.87, just fractionally lower than the Thursday close. Also notable, the offshore yuan interbank rates (Hibors) rose sharply in delayed response to yesterday’s liquidity move via forwards.

European and U.S. equity futures grind lower, in cash equities the bank and auto sectors underperform in typical risk-off manner. S&P index futures were little changed as investors await further developments in the renewed dialog between the U.S. and China. Attention will shift later to leading indicators and University of Michigan Confidence Index, while the only big company to report earnings is Deere & Co. According to Bloomberg, Department-store stocks will be in focus after Nordstrom boosted forecasts and surged after hours, as well as chip stocks after Nvidia and Applied Materials disappointed investors with their outlook.

In Europe, tech shares weighed on the Stoxx Europe 600 Index after disappointing results from U.S. chipmakers including Nvidia and Applied Materials. And while most Asian stocks advanced, Chinese shares slid again as U.S. President Donald Trump prodded Beijing to offer more at the bargaining table in their first major negotiation planned in more than two months. The Shanghai Composite tumbled to a new two year low.

Emerging-market stocks were relatively steady following a seven-session sell-off that brought them to the brink of a bear market, although if the TRY plunge continues contagion may re-emerge: as noted above, the market convulsions were again on show on Friday, as the lira slid to as low as 6.32 per dollar, bringing its losses for the year to more than 40%.

Today’s instability followed news of a possible breakthrough in the U.S.-China trade dispute which brought some calm to markets whipsawed by the brewing financial crisis in Turkey and renewed angst over technology stocks. Traders are catching their breath after a sell-off in commodities and emerging-market stocks, which are on the brink of their worst weekly performance since the February volatility blow-up, signaling the trade war remains the wildcard for many markets.

“I don’t think we’re quite out of the woods yet,” Marcus Miholich, a managing director at State Street Global Advisors Ltd., told Bloomberg TV in Sydney. “Investors have definitely taken note of these tensions and have reallocated into more defensive sectors and defensive names. Given we don’t seem to have the light at the end of the tunnel just yet, that will continue.”

In other geopolitical news, US administration official said President Trump and Russian President Putin agreed in principle that Iran should exit Syria, although the official added that Russia sees this as a difficult task. US Pentagon report stated China has been expanding fleet of long-range bombers during last 3 years and are ‘likely’ training for missions which target the US.

The Bloomberg Dollar Spot Index headed for a third straight week of gains, and rebounded from session lows on Friday as the Turkish Lira slumped. The euro hit a one-week high versus the Swiss franc as risk sentiment keeps improving and filled option-related supply above 1.14 versus the greenback.

The euro extended its advance and gained as much as 0.4% to touch 1.1419 high as stops above 1.14 were triggered, before falling back below that handle. Yen and New Zealand dollars led gains against the greenback, with many short-term accounts citing yuan performance as a driver for the moves; USD/JPY fell as much as 0.4% to 110.49 low with the pair continuing to consolidate between 110-111. The pound erased gains as leveraged supply near highs absorbed buying pressure; the currency headed for its sixth weekly loss.

Treasuries extend gains as the lira weakens, with the UST curve led by 10-year. The yield on 10-year TSYs dropped 1 bp to 2.85%, the lowest in more than four weeks. Italy’s 10-year yield rose less than one basis point to 3.12%.

Elsewhere, oil climbed despite a surprise gain in U.S. crude stockpiles, while zinc fell, heading for its worst weekly performance since 2011. Oil prices are up this Friday but are still set to end the week in the red for the third week in a row. WTI and Brent are both up ~0.25% on the day as energy specific news flow remains light. In the metals scope, Gold is up marginally off the back of USD weakness and testing the USD1180/OZ level to the upside, but is still set for its largest weekly fall in 15 months. Precious metals are slightly in the green with all of silver (+0.2%), platinum (+0.4%)and palladium (+0.1%) up on the day.

Expected data include Conference Board U.S. Leading Index and University of Michigan Consumer Sentiment Index. Deere reports earnings.

Market Snapshot

- S&P 500 futures down 0.1% to 2,841.25

- STOXX Europe 600 up 0.06% to 381.65

- MXAP up 0.5% to 161.95

- MXAPJ up 0.5% to 521.93

- Nikkei up 0.4% to 22,270.38

- Topix up 0.6% to 1,697.53

- Hang Seng Index up 0.4% to 27,213.41

- Shanghai Composite down 1.3% to 2,668.97

- Sensex up 0.8% to 37,952.37

- Australia S&P/ASX 200 up 0.2% to 6,339.23

- Kospi up 0.3% to 2,247.05

- German 10Y yield fell 1.5 bps to 0.305%

- Euro up 0.3% to $1.1412

- Italian 10Y yield fell 5.1 bps to 2.844%

- Spanish 10Y yield fell 0.5 bps to 1.44%

- Brent futures up 0.5% to $71.80/bbl

- Gold spot up 0.3% to $1,177.61

- U.S. Dollar Index down 0.3% to 96.33

Top Headlines from Bloomberg

- President Donald Trump prodded China to offer more at the bargaining table as the two countries prepared for their first major negotiation in more than two months in an effort to head off an all-out trade war

- U.S. Treasury Department will seek to pressure China to lift the value of yuan in coming trade talks, NYT reports, citing unidentified person briefed on the plans

- In government offices and think tanks, universities and state-run newsrooms, there is an urgent debate underway about what many in Beijing see as the hidden motive for Washington’s escalating trade war against President Xi Jinping’s government: A grand strategy, devised and led by Trump, to thwart China’s rise as a global power

- Australian central bank chief Philip Lowe said he’d still like to see the nation’s currency weaken further and sees interest rates remaining at a record low “for a while yet”

- Oil headed for the longest run of weekly declines in three years, dragged down by everything from an emerging-market rout to rising global supplies and lingering concerns over a spat between the world’s biggest economies

- Investors withdrew money from a range of asset classes over the past week analysts at Jefferies write in research note, citing EPFR Global data for week ended Aug. 16.

- NYT: U.S. Treasury will seek to pressure China to lift the value of yuan in coming trade talks, according to people familiar

- Fed’s Powell speech on monetary policy at Jackson Hole confirmed for 10 a.m. New York time on Aug. 24; full agenda to be released at 8 p.m. New York time on Aug. 23.

- Eurozone July CPI unrevised y/y at 2.1%; Core CPI unrevised at 1.1%

- China People’s Daily: China has ‘big room’ for macro-economic control; will take more proactive policies to stabilize trade, including pushing forward signing of free-trade agreements

- Mnuchin says Turkey faces more sanctions if pastor not released

Asian equity markets were mostly higher as the region tracked the performance on Wall St where all majors gained as sentiment was buoyed by trade optimism from the announcement of upcoming US-China trade talks. ASX 200 (+0.1%) and Nikkei 225 (+0.4%) were both higher although the former somewhat lagged after having stalled at fresh highs last seen in over a decade, while gains in Japanese exporters were contained by a stable currency. Hang Seng (+0.4%) and Shanghai Comp. (-1.3%) both initially conformed to the positive risk tone amid the trade-related hopes, continued PBoC liquidity efforts and as Hong Kong-heavyweight Tencent also rebounded from post-earnings losses, although the Shanghai Comp. eventually gave back its gains and then some, as sentiment deteriorated across the mainland. Finally, 10yr JGBs saw mild gains as prices rebounded from the prior day’s weakness and with the BoJ also in the market under its bond buying programme. PBoC injected CNY 90bln via 7-day reverse repos for a net weekly injection of CNY 130bln vs. neutral last week.

Top Asian News

- Turkey-Exposed Cos. May Be Back in Focus After Mnuchin Comments

- U.S. Said to Seek to Pressure China to Lift Yuan in Talks: NYT

- Interest Rates in China Below the U.S. Level Risks Outflows

- Apple Supplier Luxshare Said to Plan Camera Module IPO: Nikkei

European equities have started the day marginally lower (Euro Stoxx 50 -0.3%) as we approach the week’s end. The AEX is currently the underperforming bourse, with losses lead by Vopak (-7.0%) (whom are also at the foot of the Stoxx 600) after missing expectations on all of net profit, EBITDA and revenue. AP Moeller Maersk (+4.7%) also reported earnings, wherein revenues came in above least years results. The co. also confirmed source reports it is looking to spin-off it’s drilling unit and list it on the NASDAQ so as to focus on their transport business. Air France appointed the Ex-COO of Air Canada last night, Ben Smith, as CEO. Despite opening higher Air France shares reversed course amid protests from French unions about the Canadian’s appointment, and are currently down 4.0%.

Top European News

- Tycoon Deripaska Weighs Moving Sanctioned Companies to Russia

- Barclays Scraps Long Stance on Italy Bonds After Latest Selloff

- Draghi’s Richer Toolbox Keeps ECB Calm as Turkey and Italy Rage

- Air France-KLM’s New CEO Faces Immediate Union Threat of Strike

- Atlantia Gains on Report of Talks to Pay Fine on Bridge Collapse

In FX, the dollar index saw some downside deviation from the relatively tight range around 96.500 that has been prevalent since the Try-led EM exodus subsided amidst reports (albeit dated) that the US will urge China to revalue the Yuan during trade negotiations scheduled for next week. The index dipped just under 96.300 amidst broad Usd declines, but still restrained trade overall. TRY/YUAN – The Lira maintained enough recovery momentum to trade a fraction above 5.7500 vs the Dollar, but stopped short of Thursday’s circa 5.7000 high that is very close to a key Fib level and in volatile conditions reversed to hit 6.0000+ levels. Meanwhile, the PBoC halted a run of daily Cny depreciations via the official mid-point fix to leave the offshore Cnh off recent lows and also bolstered by the provision of 7 day liquidity. NZD/AUD – Highlighting the considerably improved risk tone, the Kiwi is making a more concerted effort to form a base at 0.6600 vs its US counterpart, while the Aud has extended above 0.7250 again, though still unable to reach 0.7300 with technical resistance just a head of the big figure and the RBA reiterating no rush or rationale to raise rates anytime soon (Governor Low overnight and message rammed home by Ellis earlier today). EUR/JPY – The next best G10s, as the single currency revisits 1.1400 vs the Greenback where big option expiries run off today (1.9 bn from the big figure to 1.1410) and Usd/Jpy retreats from 111.00 again and also eyes hefty expiry interest, with 2.2 bn at the110.50 strike.

In commodities, oil prices are up this Friday but are still set to end the week in the red for the third week in a row. WTI and Brent are both up ~0.25% on the day as energy specific news flow remains light. In the metals scope, Gold is up marginally off the back of USD weakness and testing the USD1180/OZ level to the upside, but is still set for its largest weekly fall in 15 months. Precious metals are slightly in the green with all of silver (+0.2%), platinum (+0.4%) and palladium (+0.1%) up on the day.

Looking at the day ahead, we end the week with the July leading index and the preliminary August University of Michigan survey.

US Event Calendar

- 10am: Leading Index, est. 0.4%, prior 0.5%

- 10am: U. of Mich. Sentiment, est. 98, prior 97.9; Current Conditions, prior 114.4; Expectations, prior 87.3

DB’s Jim Reid concludes the overnight wrap

Every time it gets a knock it has tended to wobble a little, find its feet, shake off the blow and then power ahead. After the weakness on Wednesday the S&P 500 rallied +0.79% yesterday and is now back to only 1.1% off the record highs again. Meanwhile the VIX – which spiked to 16.86 late morning on Wednesday – closed at 13.45 last night. We’ve had quite a few spikes in equity vol this year and whilst we’ve never returned fully back to the lowest end of the range we saw prior to the early February VIX melt down period, we have repeatedly retraced back most of the way prior to each fresh spike coming along.

In a world of much higher macro uncertainty, earnings have perhaps played a big part in keeping the S&P 500 in good health (perhaps a similar trend to marriage). Yesterday it was the turn of US retail to shine with Walmart up +9.33% after earnings showed that comparable sales rose 4.5% in the three months ending in July, more than double the consensus forecasts. Grocery sales rose the most in 9 years and they also boosted their full-year forecasts for comparable sales and adjusted profit.

From groceries to Turkey and in this ongoing story the highlights over the last 24 hours has been a continued rally in the Lira (+1.89%) yesterday, an investor call from the finance minister and comments from treasury secretary Mnuchin that Turkey faces fresh sanctions if they don’t release pastor Brunson soon. The sanctions headlines took the shine off the Lira and showed that the saga still has a long way to go. This came after the call with investors that reiterated there are no plans for capital controls or to call on the IMF. The ministry talked up the banking sector and an acknowledgement of the need for fiscal discipline. There was a small rally in the Lira during the call which indicated that there were no nasty surprises.

Meanwhile on trade, President Trump told his cabinet members yesterday that “we’re talking to China….they just are not able to give us an agreement that is acceptable, so we’re not going to do any deal until we get one that’s fair to our country” (per Bloomberg). So lots bubbling along before the formal trade talks resume from 22 August. Elsewhere Reuters noted the US trade representative Lighthizer expressed hope that a revised NAFTA trade deal with Mexico could be reached in the next few days.

This morning in Asia, equities are trading modestly higher following the positive leads from the US. Across the region, the Nikkei (+0.44%), Kospi (+0.32%) and Hang Seng (+0.50%) are all up while Chinese bourses are down c0.5% as we type. Meanwhile futures on the S&P are pointing to a marginally positive start while the Yuan and Lira are both little changed.

Now turning back to yesterday, where equities started on a positive footing as trade tensions eased on news of further trade talks between the US and China. Then the improved sentiment gathered pace with a rebound in commodities and sound corporate earnings as noted earlier. In the US, the DOW rallied +1.58% with the help of trade bellwethers such as Caterpillar (+3.2%) and Boeing (+4.3%), while the S&P (+0.79%) and Nasdaq (+0.42%) also advanced. Back in Europe, the Stoxx 600 firmed for the first time in five days (+0.52%) with all sectors in the black while the DAX (+0.61%) and FTSE (+0.78%) also rose. The exception was Italy’s FTSE MIB which fell -1.83% to the lowest since April 2017, in part playing catch up as trading resumed post a holiday Wednesday while the motorway operator (Atlantia) for the recently collapsed bridge tumbled -22.3%.

Meanwhile core government bonds softened along with the risk on tone, with 10y bond yields up 1-2bp (UST +0.4bp; Bunds & Gilts +1.5bp) while Italian BTPs outperformed (-5bp). Domestic Turkish bonds yields remained volatile with 5y and 10y yields up 63bp and 66bp respectively. Turning to currencies, the US dollar index softened for the second day (-0.05%) while the Euro and Sterling gained +0.28% and +0.15% respectively. Meanwhile commodities staged a broad based recovery to recoup most of Wednesday’s losses, with LME lead (+5.86%), Zinc (+4.0%) and Copper (+2.36%) all up. Elsewhere WTI oil nudged up for the first time in four days to $65.46/bbl (+0.69%).

Before we look at the data our US economists have published a detailed update on the inflation outlook. In the near-term, they expect goods inflation to rise further, supporting the broader core inflation gauge. In the medium-term, the macro backdrop supports modestly higher inflation as Phillips curve effects should dominate some dollar headwinds even without accounting for potential non-linearities in the former. Overall the team continues to forecast core PCE and core CPI inflation at 2.3% and 2.5% for end-2019, respectively. If the data evolve as they anticipate, more Fed officials should support taking a restrictive stance. Refer to their note for details

Yesterday’s economic data was a bit mixed. In the US, initial and continuing jobless claims both ticked lower to 212k and 1,721k respectively. Both series remain extremely healthy around their lowest levels in 35 years. While July building permits rose, actual housing starts surprisingly fell, probably reflecting reduced activity in the western US amid ongoing wildfires. The August Philadelphia Fed Business Outlook surprisingly dropped to 11.9 (a positive value indicates expansion), its weakest level since 2016. After yesterday’s strong Empire State manufacturing survey, the picture for this month’s ISM Manufacturing PMI is somewhat muddled. Despite the headline softness however, forward looking subsections looked strong, especially capital expenditure expectations. Wage and inflation expectations remained healthy as well, supporting our economists’ view for further robust US growth and continued Fed rate hikes. In Europe, the June trade balance printed at a seasonally adjusted €16.7 billion, its lowest level since January last year, potentially signalling less robust global demand. In the UK, July retail sales rose 0.7% mom, a more robust pace than expected,though possibly attributable to warm weather and the World Cup rather than stronger fundamentals.

Looking at the day ahead, in Europe, we get June current account data and the final July CPI prints for the Euro area (1.1% yoy expected). In the US, we end the week with the July leading index and the preliminary August University of Michigan survey.

END

3. ASIAN AFFAIRS

i)FRIDAY MORNING/THURSDAY NIGHT: Shanghai closed DOWN 36.23 POINTS OR 1.34% /Hang Sang CLOSED UP 113.35 POINTS OR 0.42%/ / The Nikkei closed UP 78.34 POINTS OR 0.35%/Australia’s all ordinaires CLOSED UP 0.21% /Chinese yuan (ONSHORE) closed UP at 6.8826 AS POBC HALTS ITS HUGE DEVALUATION /DELEGATION COMING TO THE USA TO SEE TRUMP/Oil UP to 65.80 dollars per barrel for WTI and 72.05 for Brent. Stocks in Europe OPENED DEEPLY IN THE RED //. ONSHORE YUAN CLOSED UP AT 6.8826 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.8613: HUGE DEVALUATION/PAST SEVERAL DAYS STOPS TRADE TALKS WILL RESUME IN THE USA : /ONSHORE YUAN TRADING STRONGER AGAINST OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING STRONGER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

3 a NORTH KOREA/USA

North Korea/South Korea/USA/China

3 b JAPAN AFFAIRS

c) REPORT ON CHINA/HONG KONG

The pentagon warns that China with its long range bombers are training for a strike against the uSA. And the USA is facilitating gold purchases by China onto their soil?…

(courtesy zerohedge)

China’s Long Range Bombers “Likely Training For

Strikes” Against The US, Pentagon Warns

A new Pentagon report has sounded the alarm over China’s expanding military reach and says the rival to American power is increasing its ability to send bombers further afield while “likely training for strikes” against the United States and its allies.

The warning is contained in an annual Pentagon report prepared for Congress called Military and Security Developments Involving The People’s Republic of China 2018, which further notes a defense spending estimate of $190 billion — a third that of the United States — which has in part gone toward the People’s Liberation Army (PLA) “undergoing the most comprehensive restructure in its history”.

The report comes amidst heightened trade tensions and concerns that China is attempting to gobble up territory in international waters through its militarizing artificial islands in the South China Sea.

“Over the last three years, the PLA has rapidly expanded its overwater bomber operating areas, gaining experience in critical maritime regions and likely training for strikes against U.S. and allied targets,” the report reads.

In terms of potential targeting, this may demonstrate the “capability to strike US and allied forces and military bases in the western Pacific Ocean, including Guam,” the report adds.

However while generally outlining ways that China is establishing itself as an unrivaled regional power, such as through its Belt and Road Initiative (BRI), the report notes that it’s not clear what message Beijing is projecting by carrying out the flights “beyond a demonstration of improved capabilities.”

The report projects that China’s military budget is likely to expand to $240 billion over the next decade, adding that “The purpose of these reforms is to create a more mobile, modular, lethal ground force capable of being the core of joint operations” that can “fight and win” against a major military power.

Notably the Pentagon’s annual report also highlights China’s growing space program “despite its public stance against the militarization of space” — something which likely factored into President Trump’s mid-June announcement that he would “immediately” establish a “space force” as an independent service branch of the Department of Defense.

The report says of the contentious issue of Taiwan, which is claimed by China but maintains de facto independent security ties with the US, that China “is likely preparing for a contingency to unify Taiwan with China by force”.

The assessment spells out China is ready to go to war to protect its claim over the island: “Should the United States intervene, China would try to delay effective intervention and seek victory in a high-intensity, limited war of short duration.”

Acknowledging the potential for rapid and worrisome escalation between the global powers, the Pentagon report stresses that the US “seeks a constructive and results-oriented relationship with China”.

As Reuters points out, “While Washington and Beijing maintain a military-to-military relationship aimed at containing tensions, this has been tested in recent months, notably in May when the Pentagon withdrew an invitation to China to join a multinational naval exercise.”

However, Washington and Beijing have kept communication channels open, despite a growing trade war, as a Chinese trade delegation is set to visit the US this month to initiate a new round of talks.

The Chinese delegation, reportedly to be led by vice-commerce minister Wang Shouwen plans to meet a group led by US Treasury undersecretary David Malpass amidst aggressive US tariffs on $50 billion worth of Chinese goods, and after Trump threatened tariffs on a further $200 billion worth of imports.

end

4. EUROPEAN AFFAIRS

6 .GLOBAL ISSUES

The total debt of all nations has risen to 238 trillion dollars a huge 30 trillion rise from 2016. The looming economic collapse will be upon us in short order

(courtesy Mac Slavo/SHTFPlan.com)

The Looming Economic Collapse: The $250 Trillion Dollar Worldwide Debt Crisis

Authored by Mac Slavo via SHTFplan.com,

As governments raise taxes to cope with their unending spending habits, people are increasingly being forced to supplement their own income with loans. And according to most financial experts, this debt problem is so big that it will usher in a global economic collapse of epic proportions.

According to the Institute of International Finance’s latest Global Debt Monitor, the amount of debt held in the world rose by the biggest amount in two years during the first quarter of 2018.It grew by $8 trillion to hit a new all-time high of $247 trillion, up from $238 trillion as of December 31, 2017. And that’s up by $30 trillion from the end of 2016.

Global debt is staggering to the point most of it will never be repaid and as governments continue their spending sprees and the debts keep mounting, the future of the economy looks bleak. There is more than enough economic data out there to show there could be an economic collapse and stock market crash in 2018. Bill Gross stated in 2017 that “our highly levered financial system is like a truckload of nitroglycerin on a bumpy road”. One wrong move and the whole thing could blow sky high, wrote the Epic Economist. Once this bubble pops, it will fling the globe into a financial crisis of epic proportions never before seen.

According to Financial Times, it is becoming clear that the global monetary policy is now caught in a debt trap of its own making. Continuing on the current monetary path is ineffective and increasingly dangerous. But any reversal also involves great risks. It stands to reason that the odds of another crisis blowing up will continue to rise. –Ready Nutrition

The Epic Economist also has a video out detailing how all of this came to pass. It’s easy enough to understand, yet most still can’t get past their own preconceived notions and biases to comprehend that this will be the fault of governments and those who continue to look to rulers or masters to solve their problems.

“It is all about taking money from us and transferring it into government pockets.And then, taking money from government pockets, and transferring it into the hands of the elite. It’s a game that’s been going on for generations and its time for the humanity to say that ‘enough is enough’.” -Epic Economist

The future of the global economy doesn’t look promising based on the vast amount of debt and wealth being transferred from people to their masters. We are living in economic slavery and until humanity understands that, the only other option is an economic crisis.

It comes as a bit of a surprise the infamous Keynesian economist Bernanke would express concerns over the government’s inability to decrease spending. But now that he has, will Americans heed the warning and protect themselves against the next financial crisis? –SHTFPlan

There are ways to prepare for a financial crisis, although an ongoing and global crash could complicate things for preppers. But there are still ways to prepare and an open and educated mind is step one. If you still believe the government and global elites have your best interests in mind, you probably also don’t anticipate a global economic crash, and therefore, are not going to prepare. For the rest of us, taking on a “prepper’s mindset” will give you the upper hand in any financial crisis.

“If we have learned one thing studying the history of disasters, it is this: those who are prepared have a better chance at survival than those who are not.” -Tess Pennington, author of The Prepper’s Blueprint

end

Canada

Canada reports a huge rise in consumer prices of 3.% year over year and these numbers are really higher as they disguise the true inflation rate. Strangely the loonie spiked higher on the news because the Bank of Canada governor mist raise rates fast against a slowing economy

(courtesy zerohedge)

Loonie Spikes As Canadian Consumer Prices Soar Most Since 2011

Canadian Consumer Prices soared 3.0% YoY in July – well above 2.5% expectations – and the highest inflation rate since 2011.

- Inflation for services in July was 3.2%, the fastest pace since 2008.

- Goods inflation was 2.8%.

Gasoline prices – up 0.8% in July and 25.4% from a year earlier – have also been a main contributor to the recent acceleration in prices. Excluding gasoline, inflation would be 2.2 percent in July.

Monthly inflation was up 0.5 percent in July, versus analyst expectations for a 0.1 percent gain. On a seasonally adjusted basis, inflation was also up 0.5 percent, the biggest increase since January.

As Bloomberg notes, the faster-than-expected gains will test Bank of Canada Governor Stephen Poloz’s resolve to raise interest rates gradually over the next year to avoid a disruption to the economy. Price gains have now reached the upper end of the central bank’s 1 percent to 3 percent inflation range.

And that has prompted an immediate reaction in the loonie – instant buying…

Finally, we note that there was little discernable effect of higher tariffs on consumer prices in July. Statistics Canada released a report on the estimated impacts of Canada’s tariffs on U.S. metal and consumer products and found there would only be a small overall increase — with no more than a decimal point increase to inflation over a limited period of time.

end

Richard Breslow, is one smart cookie: he points out the huge problems facing the globe this morning which is basically totally ignored e.g. the German bund at .30%, the huge fall in the Turkish lira and other emerging nation currencies

(courtesy Richard Breslow/zerohedge)

One Trader Rages “If Your Blood Isn’t Boiling” You’re Not Paying Attention

“If your blood is not boiling,” begins former fund manager and FX trader Richard Breslow, “it’s fine to cut out” he threatens as it seems market participant ‘centrally-planned conditioning-biased’ ignorance or perhaps just blind faith in BTFD because of PPT and Midterms has left the US equity market the lone pretender in a world of de-risking.

Via Bloomberg,

Or perhaps we just sleep-walk until a proper blow-up forces some sort of response.

Of course, if we are confronted with the accusation that we should have acted differently, we can always claim

I understand it’s a Friday in August. I get that people are claiming they’ve had a hard week and want to call it a day. It’s no surprise that weekend-position-aversion remains a problem for risk takers. But with so much going on, if traders can’t be inspired to trade and challenge the status quo, it is safe to conclude that markets remain well and truly broken…Maybe forever.

- the Turkish lira dropped as much as 7%,

- the Shanghai Composite closed at its lowest level since January 2016

- and German bunds are trading back below 30 basis points.

- The Governor of the RBA just said what every central banker wishes they could — that he encourages a weaker currency.

- The Malaysian ringgit is the latest Asian currency to experience the effects of slowing growth, sliding to the lowest in nine months.

- BTPs remain at levels the Italian government can’t afford as their equity markets continue to noticeably underperform their brethren.

- And U.S. equities are impervious to it all.

There’s a lot going on and traders need to ditch their base case that monetary policy will, at the end of the day, save all.

And the really dumb one, that calmer heads will ultimately prevail causing geopolitical and trade tensions to ease.

Did you ever think there would be such a systemic need for a new generation of aggressive hedge funds?

Another fatality of quantitative easing. Why stay up at night selling currency when you can just roll into the office at a decent hour and buy whatever the sovereign wealth funds are currently feasting on?

Incidentally, “base case” is now joining my list of banned expressions and words. It’s just commentator speak for I could be totally wrong but hope to be right somewhere down the line. And I’ll get back to you when it happens. While I’m at it, Purchasing Power Parity and the ground meat version of it are also out. It’s just a useless way into a misguided mean-reversion argument.

How appropriate as next week brings the 20th anniversary of when LTCM went hat-in-hand to banks. Make money, make money, lose it all. Sadly, another word in exile, “existential”, is due to return with great fanfare when the Italian government negotiates its budget with the EU.

Strictly off the record, bullies get their way until someone proves they can be stood up to. It may turn out that Erdogan is the unlikely bearer of that message.

end

Turkey

Fitch states that Turkey’s action are insufficient to restore their credibility. In essence they want the country to raise rates, something that they will not do

(courtesy zerohedge)

Fitch: Turkey’s Actions Are Insufficient To Restore Policy Credibility

To contain the historic plunge of its currency, this week Turkey unleashed an unprecedented barrage of interventions in its market, if not the economy, mostly focusing on crushing short sellers and making shorting the Lira by speculators prohibitively expensive. In fact just moments ago, the Turkish banking regulator launched yet another intervention:

- *TURKEY EXPANDS LIMITS ON FX SWAPS TO SOME LIRA FORWARDS

The one thing Turkey did not do, is despite vague promises of fiscal reform and monetary stabilization, it continues to refuse to do the one thing investors across the globe demand: raise rates and tighten financial conditions.

Confirming that this is the missing link, in a report this morning, Fitch said that Turkey’s incomplete policy response to the lira’s depreciation “is unlikely on its own to sustainably stabilize the currency and the economy.”

The rating agency, which one month ago downgraded Turkey to BB outlook “negative’ with more downgrades set to come, said that it believes “this would require an increase in the policy credibility and independence of the central bank, tolerance of weaker growth by policymakers, and a reduction in macroeconomic and financial imbalances.”

None of those are forthcoming as a result of Erdogan’s stongman tactics.

Meanwhile, in further pain for the Turkish economy, today the lira resumed its slide after a Turkish court rejected an American pastor’s appeal for release, drawing a stiff rebuke from President Donald Trump who said the United States would not take the detention “sitting down”.

“They should have given him back a long time ago, and Turkey has in my opinion acted very, very badly,” Trump told reporters at the White House, referring to Brunson. “So, we haven’t seen the last of that. We are not going to take it sitting down. They can’t take our people.”

It was not immediately clear what additional measures, if any, Trump could be considering. U.S. Treasury Secretary Steven Mnuchin told Trump at a cabinet meeting on Thursday that more sanctions were ready to be put in place if Brunson were not freed.

And as traders once again sold off the Lira, they pushed the return on the Turkish currency down to 37%, making it tied with the Argentine Peso for worst performing currency of 2018.

What happens next? Well, as Fitch explained in its detailed note, absent Erdogan folding and conceding his “new economics” have been wrong, the Lira will continue to suffer until eventually Fitch – as well as S&P and Moody’s – all downgrade Turkey to junk and below as its economic unraveling becomes unfixable.

Below is the full Fitch text (link):

Turkey Moves Insufficient to Restore Policy Credibility