GOLD: $1196.75 UP $3.45 (COMEX TO COMEX CLOSINGS)

Silver: $14.77 DOWN 1 CENT (COMEX TO COMEX CLOSINGS)

Closing access prices:

Gold $1195.60

silver: $14.75

For comex gold:

AUGUST/

NUMBER OF NOTICES FILED TODAY FOR AUGUST CONTRACT: 16 NOTICE(S) FOR 1600

TOTAL NOTICES SO FAR 2286 FOR 228,600 OZ (7.110 tonnes)

For silver:

AUGUST

0 NOTICE(S) FILED TODAY FOR

nil OZ/

Total number of notices filed so far this month: 1178 for 5,890,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: BID $6604/OFFER $6689: UP $175(morning)

Bitcoin: BID/ $6386/offer $6471: UP $126 (CLOSING/5 PM)

end

First Shanghai gold fix comes at 10 pm est

The second Shanghai gold fix: 2:15 pm

First Shanghai gold fix gold: 10 pm est: $1201.54

NY price at the same time:$1196.20

PREMIUM TO NY SPOT: $5.34

XX

Second gold fix early this morning: $ 1200.16

USA gold at the exact same time:$1194.15

PREMIUM TO NY SPOT: $6.01

China is controlling the gold market

WE WILL NOT PROVIDE LONDON FIXES AS THEY ARE NOT ACCURATE AS TO WHAT IS GOING ON AT THE SAME TIME FRAME.

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total OPEN INTEREST ROSE BY A VERY STRONG 5583 CONTRACTS FROM 238,613 UP TO 244,196 ACCOMPANYING YESTERDAY’S 12 CENT RISE IN SILVER PRICING AT THE COMEX. WE HAVE GENERALLY BEEN WITNESSING A SLOW COMEX ACCUMULATION THESE PAST SEVERAL DAYS AND AFTER A ONE DAY HIATUS LAST WEEK, IT CONTINUES ONWARD. YESTERDAY I WROTE: “TUESDAY’S OI SHOULD BE A WHOPPER”. ACTUALLY IT WAS TODAY AS WE NOW HAVE AN ALL TIME RECORD FOR COMEX OPEN INTEREST.

WE HAVE ALSO WITNESSED A LARGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY(WELL OVER 30 MILLION OZ AT THE COMEX FOR JULY AND OVER 6 MILLION OZ FOR AUGUST) AS WELL AS CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A RATHER SMALL SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP:

571 EFP’S FOR SEPT. , 0 EFP’S FOR DECEMBER AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE: OF 664 CONTRACTS. WITH THE TRANSFER OF 571 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 571 EFP CONTRACTS TRANSLATES INTO 2.885MILLION OZ AND ACCOMPANYING:

1.THE 12 CENT RISE IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR THE JUNE/2018 COMEX DELIVERY MONTH. (5.420 MILLION OZ) 30.370 MILLION OZ STANDING FOR DELIVERY IN JULY, AND NOW 6.000 MILLION OZ FOR AUGUST.

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF JULY:

20,716 CONTRACTS (FOR 16 TRADING DAYS TOTAL 20,716 CONTRACTS) OR 103.580 MILLION OZ: (AVERAGE PER DAY: 1294 CONTRACTS OR 6.473 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF JULY: 103.580 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 14.8% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2018 TO DATE SILVER EFP’S: 1,933.24 MILLION OZ.

ACCUMULATION FOR JAN 2018: 236.879 MILLION OZ

ACCUMULATION FOR FEB 2018: 244.95 MILLION OZ

ACCUMULATION FOR MARCH 2018: 236.67 MILLION OZ

ACCUMULATION FOR APRIL 2018: 385.75 MILLION OZ

ACCUMULATION FOR MAY 2018: 210.05 MILLION OZ

ACCUMULATION FOR JUNE 2018: 345.43 MILLION OZ

ACCUMULATION FOR JULY 2018: 172.84 MILLION OZ

RESULT: WE HAD A VERY STRONG SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 5583 WITH THE 12 CENT RISE IN SILVER PRICING AT THE COMEX YESTERDAY. THE CME NOTIFIED US THAT WE HAD A SMALL SIZED EFP ISSUANCE OF 571 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) .

TODAY WE GAINED A VERY STRONG SIZED: 6154 TOTAL OI CONTRACTS ON THE TWO EXCHANGES:

i.e 571 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH A INCREASE OF 5583 OI COMEX CONTRACTS. AND ALL OF THIS DEMAND HAPPENED WITH A 12 CENT RISE IN PRICE OF SILVER AND A CLOSING PRICE OF $14.78 WITH RESPECT TO YESTERDAY’S TRADING. YET WE HAD A GIGANTIC AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY IN THE BIG JULY DELIVERY MONTH OF SLIGHTLY OVER 30 MILLION OZ AND NOW IN AUGUST ANOTHER BIG 6.000 MILLION OZ IN A NON ACTIVE MONTH. IT SURE LOOKS LIKE ANOTHER FAILED BANKER SHORT COVERING EXERCISE AS BANKERS ARE SCRAMBLING TO COVER THEIR HUGE SHORTFALL IN SILVER.

In ounces AT THE COMEX, the OI is still represented by OVER 1 BILLION oz i.e. 1.221 MILLION OZ TO BE EXACT or 175% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT AUGUST MONTH/ THEY FILED AT THE COMEX: 0 NOTICE(S) FOR NIL OZ OF SILVER

IN SILVER,PRIOR TO TODAY, WE SET THE NEW RECORD OF OPEN INTEREST AT 243,411 CONTRACTS ON APRIL 9.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $16.51.

AND NOW WE RECORD FOR POSTERITY ANOTHER ALL TIME RECORD OPEN INTEREST AT THE COMEX OF 244,196 CONTRACTS AND AGAIN WHEN THE RECORD IS SET, THE PRICE OF SILVER IS LOWER THAT THE PREVIOUS ONE. TODAY’S LOW PRICE IS 14.78.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) AND JULY 2018 AMOUNT STANDING: 30.370 MILLION OZ ) AND NOW FOR AUGUST 6.000 MILLION OZ.

- HUGE RECORD OPEN INTEREST IN SILVER 243,411 CONTRACTS (OR 1.217 BILLION OZ/ SET APRIL 9/2018) AND NOW AGAIN TODAY: 244,196 CONTRACTS, AUGUST 22.2018 WITH A SILVER PRICE OF $14.78

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017

- RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT).

IN GOLD, THE OPEN INTEREST ROSE BY A GOOD SIZED 2262 CONTRACTS UP TO 483,730 WITH THE STRONG GAIN IN THE COMEX GOLD PRICE/YESTERDAY’S TRADING (A RISE IN PRICE OF $5.75). THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A GOOD SIZED 6154 CONTRACTS:

AUGUST HAD AN ISSUANCE OF 0 CONTRACTS, OCTOBER HAD 0EFP’S ISSUED AND, DECEMBER HAD AN ISSUANCE OF 6471 CONTACTS AND ALL OTHER MONTHS ZERO. The NEW COMEX OI for the gold complex rests at 483,730. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE AN A VERY STRONG OI GAIN IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 8733 CONTRACTS: 2262 OI CONTRACTS INCREASED AT THE COMEX AND 6471 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN: 8733 CONTRACTS OR 873,300 OZ = 27.16 TONNES. AND ALL OF THIS HUGE DEMAND OCCURRED WITH A SMALLISH GAIN IN THE PRICE OF GOLD/ YESTERDAY TO THE TUNE OF $5.75.???..

YESTERDAY, WE HAD 4594 EFP’S ISSUED.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF JUNE : 113,424 CONTRACTS OR 11,324,000 OZ OR 352.22 TONNES (16 TRADING DAYS AND THUS AVERAGING: 7089 EFP CONTRACTS PER TRADING DAY OR 708,900 OZ/ TRADING DAY),,

TO GIVE YOU AN IDEA AS TO THE HUGE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 16 TRADING DAYS IN TONNES: 352.22 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2017, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 2555 TONNES

THUS EFP TRANSFERS REPRESENTS 352.22/2550 x 100% TONNES = 13.81% OF GLOBAL ANNUAL PRODUCTION SO FAR IN JULY ALONE.***

ACCUMULATION OF GOLD EFP’S YEAR 2018 TO DATE: 5,071.51* TONNES *SURPASSED ANNUAL PROD’N

ACCUMULATION OF GOLD EFP’S FOR JANUARY 2018: 653.22 TONNES (21 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR FEBRUARY 2018: 649.45 TONNES (20 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR MARCH 2018: 741.89 TONNES (22 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR APRIL 2018: 713.84 TONNES (21 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR MAY 2018: 693.80 TONNES ( 22 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR JUNE 2018 650.71 TONNES (21 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR JULY 2018 605.5 TONNES (21 TRADING DAYS)

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A GOOD SIZED INCREASE IN OI AT THE COMEX OF 2262 WITH THE GOOD GAIN IN PRICING ($5.75 THAT GOLD UNDERTOOK YESTERDAY) // . WE ALSO HAD A GOOD SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 6471 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 6471 EFP CONTRACTS ISSUED, WE HAD A VERY STRONG GAIN OF 8733 CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

6471 CONTRACTS MOVE TO LONDON AND 2262 CONTRACTS INCREASED AT THE COMEX. (in tonnes, the GAIN in total oi equates to 27.16 TONNES). ..AND THIS VERY STRONG DEMAND OCCURRED WITH THE SMALLISH GAIN OF $5.75 IN YESTERDAY’S TRADING AT THE COMEX!!!. ????

we had: 16 notice(s) filed upon for 1600 oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD...

WITH GOLD UP $3.45 TODAY: /

A NO CHANGES IN GOLD INVENTORY AT THE GLD:

/GLD INVENTORY 768.70 TONNES

Inventory rests tonight: 768.70 tonnes.

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

SLV/

WITH SILVER DOWN 1 CENT TODAY

NO CHANGE IN SILVER INVENTORY AT THE SLV

/INVENTORY RESTS AT 329.104 MILLION OZ.

NOTE THE DIFFERENCE BETWEEN THE GLD AND SLV: THE CROOKS CAN RAID GOLD BECAUSE THEY DO HAVE SOME PHYSICAL. THEY DO NOT RAID SILVER PROBABLY BECAUSE THERE IS NO REAL SILVER INVENTORIES BEHIND THEM

end

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER ROSE BY A VERY STRONG SIZED 5583 CONTRACTS from 238,613 UP TO 244,196 AND A NEW COMEX RECORD WITH A SILVER PRICE OF $14.78/AUGUST 22/2018.. THE PREVIOUS RECORD WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 1 1/4 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89. AS YOU CAN SEE, WE HAVE RECORD HIGH OPEN INTERESTS IN SILVER ACCOMPANIED BY A CONTINUAL LOWER PRICE WHEN THAT RECORD WAS SET…..

.

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

0 EFP CONTRACTS FOR AUGUST., 571 EFP CONTRACTS FOR SEPTEMBER, 0 CONTRACTS FOR DECEMBER AND AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 571 CONTRACTS . EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI GAIN AT THE COMEX OF 5583 CONTRACTS TO THE 571 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A NET GAIN OF 6268 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES: 30.77 MILLION OZ!!! AND YET WE ALSO HAVE A STRONG DEMAND FOR PHYSICAL AS WE WITNESSED A FINAL STANDING OF GREATER THAN 30 MILLION OZ FOR JULY AND NOW ANOTHER STRONG 6.00 MILLION OZ FOR AUGUST... AND YET ALL OF THIS HUGE PHYSICAL DEMAND OCCURRED DESPITE A SMALLISH 12 CENT PRICING GAIN AT THE SILVER COMEX!!!!????.

RESULT: A VERY STRONG SIZED INCREASE IN SILVER OI AT THE COMEX WITH THE 12 CENT PRICING GAIN THAT SILVER UNDERTOOK IN PRICING YESTERDAY. BUT WE ALSO HAD A STRONG SIZED 571 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR AUGUST, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

) WEDNESDAY MORNING/ TUESDAY NIGHT: Shanghai closed DOWN 19.22 POINTS OR 0.70% /Hang Sang CLOSED UP 174.79 POINTS OR 0.63%/ / The Nikkei closed UP 142.82 POINTS OR 0.64%/Australia’s all ordinaires CLOSED DOWN 0.14% /Chinese yuan (ONSHORE) closed UP at 6.8412 AS POBC HALTS ITS HUGE DEVALUATION /DELEGATION COMING TO THE USA TO SEE TRUMP/Oil UP to 67.18 dollars per barrel for WTI and 72.70 for Brent. Stocks in Europe OPENED DEEPLY IN THE GREEN //. ONSHORE YUAN CLOSED UP AT 6.8412 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.8386: HUGE DEVALUATION/PAST SEVERAL DAYS STOPS// TRADE TALKS WILL RESUME IN THE USA : /ONSHORE YUAN TRADING STRONGER AGAINST OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING MUCH STRONGER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

/NORTH KOREA/SOUTH KOREA

i)North Korea/South Korea/USA/

b) REPORT ON JAPAN

3 c CHINA

This is a good one:

Rating agency Dagong.. suspended for selling AA and AAA ratings to Chinese companies who did not deserve them

(courtesy Robert H)

4. EUROPEAN AFFAIRS

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

6 .GLOBAL ISSUES

iii)Michael Snyder states that the lines and the global leaders are telling us exactly what is coming

(courtesy Michael Snyder/Economic Collapse Blog)

7. OIL ISSUES

SAUDI ARABIA/ARAMCO

We promised that this would happen: Saudi Arabia calls off its huge Aramco IPO. The valuation was no doubt much too high and the reserves just were not there.

(courtesy zerohedge)

8. EMERGING MARKET

ii)Brazil

brazilian real falters to 4.09 and that will certainly cause some major problems with respect to contagion

(courtesy zerohedge)

9. PHYSICAL MARKETS

i)Craig Hemke reports that the banks are now long in gold and short on the dollar

( Craig Hemke/Sprott)

ii)We brought this story to you yesterday but it is worth repeating: Germany, an ally of the USA is calling for a global payment system independent of the uSA i.e. another SWIFT system

(courtesy Chazan/London’s Financial Times/GATA)

iii)Chris Powell offers a 6th way the USA could reverse strong dollar trends: stop shorting gold futures and buying the real physical metal

(courtesy Chris Powell/GATA)

iv) Turkey did not sell any of its official gold

(WGC letter/Harvey Organ)

10. USA stories which will influence the price of gold/silver)

i)Market trading /GOLD/MARKET MOVERS:

MARKET TRADING

this does not look like a healthy uSA economy: existing home sales tumble as the home buying sentiment hits Lehman lows

( zerohedge)

iv)SWAMP STORIES

a)Last night

Futures tumble after Cohen pleads guilty to campaign finance violations as he states that Trump directed him to do so. I will go into this in commentaries below

(zerohedge)

b)TRADERS REACTION TO THE COHEN GUILTY PLEA

the markets do not like this at all

( zerohedge)

c)You must watch Mark Levin a constitutional scholar (he was on Hannity last night). He says point blank that hush money or money to silence an individual is not a campaign violation. Trump will escape this legally but he may still face an angry Democrat house if he do take the House in November

( zerohedge)

e)Cohen willing to tell Mueller about Trump’s ‘conspiracy to collude” as he knew of the “Russian hacking of the DNC”. Maybe Cohen did not read the report that Julian Assange’s mother accidentally tweeted that Seth Rich was the person who provided the information to Wikileaks. It is time for Trump to pardon Assange and let him testify in Washington

f)Cohen to launch a 500,000 GoFundMe Campaign to expose the truth about truthgive me a break..

( zerohedge)

g)Trump hits back at Cohen strongly suggesting that anyone looking for a good lawyer turn elsewhere. Generally any lawyer convicted of tax fraud will be disbarred.

( zerohedge)

h)This is nuts: Lanny Davis tells Congress to investigate Trump and calls for his impeachment. The problem is the payment of hush money in not a crime and does not constitute violation of election laws

i)Nothing new here: Trump tells Fox news that he learned later on about the Cohen hush money payments to the two women: Stormy Daniels and Karen McDougal

k)Let us conclude tonight’s commentary with this offering from Greg Hunter and CIA whistleblower Kevin Shipp. Kevin believes and he probably is quite right, that the Trump Dossier was written by Bruce Ohr,no 4 official of the Dept of Justice.

Let us head over to the comex:

FOR THOSE THAT WISH TO FOLLOW TODAY’S SILVER OI VS LAST YR

AUGUST 22.2017: 80,314 OPEN INTEREST CONTACTS STILL OPEN FOR THE UPCOMING SEPT ACTIVE CONTRACT MONTH VS TODAY AUG 22.2018: 110,373 CONTRACTS.(DEMAND REMAINS EXTREMELY STRONG DESPITE THE LOWER PRICE)

Major gold/silver trading /commentaries for WEDNESDAY

GOLDCORE/BLOG/MARK O’BYRNE.

This is huge: Russia buys 24 tonnes of gold in July. They mine about 20 tonnes so they took in 4 tonnes from the west

Video: Gold Speculators Are Least Bullish in Years

Today we bring you two video interviews about the current state of the gold market:

Gold Speculators Are Least Bullish in Years and What If Gold Breaks $1200?

In this video we look at what the charts are suggesting. While gold speculators are almost always long the charts are showing that they are the least long that they have been in a while. Historically, when this has happened, gold has rallied.

Are we on the verge of the next move higher for gold?

Gold is technically still in an uptrend with higher lows still being achieved. The strong support level at $1,200 has been breached since this video was recorded.

So what is next for the price of gold? Are we going to see a further leg down in the price or will it rally from here?

Stephen Flood CEO of GoldCore.com talks to Carley Garner of DeCarleyTrading.com and gets her interpretation of what the charts are suggesting.

Watch these videos and more on our YouTube channel here

News and Commentary

Gold hits 1-wk high as dollar sags on Trump’s Fed attack (Reuters.com)

U.S. Futures Slip on Trump Legal Woes; Euro Rises: Markets Wrap (Bloomberg.com)

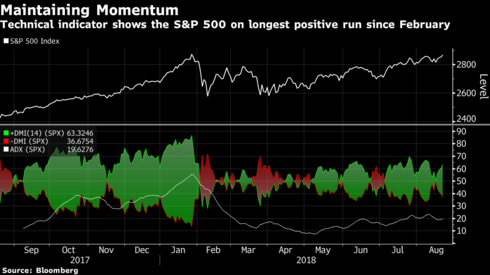

S&P 500 touches record high, equals longest-ever bull run (Reuters.com)

S&P 500 sets record high, dollar slips after Trump attacks Fed (Reuters.com)

Source: Bloomberg.com

German Foreign Minister Calls For Global Payments System Free Of U.S. (GATA.com)

Banks Now Long Gold, Short Dollar. What Do They Know?(Zerohedge.com)

BOJ Issues “Red Hot” Warning: Stocks May Drop And We Won’t Be There (Zerohedge.com)

Are We Entering an “Everything Bubble”? (ETFTrends.com)

Listen on SoundCloud , Blubrry & iTunes. Watch on YouTube below

Gold Prices (LBMA AM)

21 Aug: USD 1,194.10, GBP 931.28 & EUR 1,036.12 per ounce

20 Aug: USD 1,188.75, GBP 933.29 & EUR 1,042.41 per ounce

17 Aug: USD 1,176.70, GBP 925.59 & EUR 1,032.79 per ounce

16 Aug: USD 1,179.65, GBP 928.38 & EUR 1,037.74 per ounce

15 Aug: USD 1,186.70, GBP 933.10 & EUR 1,047.74 per ounce

14 Aug: USD 1,195.30, GBP 935.32 & EUR 1,049.11 per ounce

13 Aug: USD 1,204.40, GBP 944.85 & EUR 1,058.19 per ounce

Silver Prices (LBMA)

21 Aug: USD 14.78, GBP 11.52 & EUR 12.83 per ounce

20 Aug: USD 14.76, GBP 11.57 & EUR 12.93 per ounce

17 Aug: USD 14.66, GBP 11.54 & EUR 12.87 per ounce

16 Aug: USD 14.61, GBP 11.51 & EUR 12.85 per ounce

15 Aug: USD 14.83, GBP 11.66 & EUR 13.10 per ounce

14 Aug: USD 15.04, GBP 11.77 & EUR 13.18 per ounce

13 Aug: USD 15.18, GBP 11.91 & EUR 13.35 per ounce

Recent Market Updates

– Russia Buys 800,000 Ounces Of Gold In July

– Gold Season – Is This It?

– This Week’s Golden Nuggets

– Gold And Silver Prices Fall 1.6% and 4.3% To Near 2 Year Lows

– London House Prices Fall At Fastest Annual Rate Since Height Of Financial Crisis

– Jim Rogers on Gold, Silver, Bitcoin and Blockchain’s “Spectacular Future”

– This Week’s Golden Nuggets

– The Stock Market is Stretched to Double Tech-Bubble Extremes

– Jim Rogers and the World’s New Reserve Currency

– Gold—Even at its Lowest Levels in 2018—is Behaving Just as Prescribed

– Jim Rogers – Making China Great Again! (Video)

Andrew Maguire’s Kinesis money which is a “bitcoin” but backed 100% by allocated gold and silver is set to go.

it think it would be a great idea to look at this!

please read at: https://kinesis.money/#/

(Andrew Maguire)

|

|

Dear Harvey Organ,

Thank you for your participation in our webinar on June 7th with our host and CEO of Kinesis, Thomas Coughlin.

The response we received has been incredible, we appreciate you taking the time to join us and hope you found it to be beneficial.

Due to such a high influx of questions we received we were unable to have them all answered. Nevertheless, if there was anything which requires more clarification, or you have a query which needs to be rectified, we invite you to join our telegram group:

We apologize for the technical issues we incurred during the webinar which resulted in it running a little over schedule, we hope that the next one we host will run seamlessly.

A video has been put together and uploaded onto our YouTube channel which can be found here:

Please share and subscribe to our YouTube channel to be notified of all the latest videos as they become available.

The rapid growth that we are currently experiencing has been incredible and with your support, is only going to get better.

We are working behind the scenes very hard to create a better experience for everyone involved! Stay tuned in as we have many more announcements to be released in the upcoming days.

Kind Regards,

|

Kinesis Money

a:C/O ILS Fiduciaries (IOM) Limited, First Floor,Millennium House, Victoria Road, Douglas, Isle of Man IM2 4RW

|

The following is self explanatory

(courtesy GATA/Chris Powell and Harvey Organ)

GATA asks bank regulator to check risks of gold

futures maneuver

Submitted by cpowell on Sun, 2018-06-10 16:17. Section: Daily Dispatches

12:21p ET Sunday, June 10, 2018

Dear Friend of GATA and Gold:

GATA has appealed to the U.S. comptroller of the currency, who has regulatory authority over banks, to review financial risks certain banks may have incurred through derivatives in the monetary metals markets, particularly through the recent heavy use of the “exchange for physicals” mechanism of settling gold and silver futures contracts on the New York Commodities Exchange.

The appeal was made in a letter sent May 5 to the comptroller, Joseph M. Otting, whose office is part of the U.S. Treasury Department, by your secretary/treasurer and GATA futures market consultant Harvey Organ.

“Exchange for physical” settlements of futures contracts long were considered emergency procedures when a seller was not able to deliver metal from an exchange-approved warehouse and wanted to settle with delivery elsewhere. But now such settlements appear to constitute most gold and silver futures settlements on the Comex. It is a strange development that appears to have been necessitated by the increasing difficulties of central banking’s gold and silver price suppression policy.

GATA has received no acknowledgment of the letter. Its text is below and a PDF copy of it is here:

http://www.gata.org/files/ComptrollerOfCurrencyLetter.pdf

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

* * *

May 5, 2018

Joseph M. Otting, Comptroller of the Currency

U.S. Treasury Department

400 7th Street, SW

Washington DC 20219

Dear Comptroller Otting:

Please let us bring to your attention financial risks to major banks involving their possibly unreported exposure to derivatives in the monetary metals markets.

In recent months gold and silver future contracts issued by U.S. banks on the New York Commodities Exchange have been moved off-exchange for delivery through a mechanism known as “exchange for physical” (EFP) contracts. Until recently use of this mechanism was considered an emergency procedure when a seller did not have access to metal for delivery through Comex warehouses. Now the mechanism seems to be in use for a large share of front-month contracts for which delivery is sought.

Here is an example that is happening at the Comex in the front active month of April for gold and the inactive delivery month of April for silver.

In gold, there were 229,436 EFP contracts for 713.64 tonnes, an average of 10,925 contracts and 1,092,500 ounces per trading day.

In silver, there were 77,150 EFP contracts for 385,750,000 ounces, an average of 3,673 contracts and 18,369,000 ounces per trading day.

London Bullion Market Association rules suggest that these contracts may not be reported to regulators. The LBMA’s bylaws say:

“Figures above exclude any contracts not subject to risk-based capital requirements, such as FX contracts with an original maturity of 14 days or less, futures contracts, written options, and basis swaps. Therefore, the total notional amount of derivatives by maturity will not add to the total derivatives figure in this table.”

We are told that these EFP contracts are transferred from the Comex to London as what are called “serial forwards” and their duration is always less than 14 days, which exempts them from being reported.

It is our understanding that in each quarter your office prepares a report detailing risk undertaken by the banks under the comptroller’s supervision.

These risks include derivatives undertaken by U.S. banks and other obligations that may cause a bank to fail. Our concern is that your office may not be aware of large unreported derivative exposure by banks.

Could you review this matter and let us know your conclusions?

Sincerely,

CHRIS POWELL

Secretary/Treasurer

HARVEY ORGAN

Consultant

Gold Anti-Trust Action Committee Inc.

7 Villa Louisa Road

Manchester, Connecticut 06043-7541

end

Finally, they replied and it was a complete brush off

(courtesy zerohedge)

Currency comptroller brushes off GATA’s inquiry on

gold, silver EFPs

Submitted by cpowell on Fri, 2018-08-10 15:37. Section: Daily Dispatches

11:35a ET Friday, August 10, 2018

Dear Friend of GATA and Gold:

The U.S. comptroller of the currency, a bank regulator, has declined GATA’s request to inquire into the strange explosion of the use of the emergency procedure of “exchange for physicals” in the settlement by banks of the gold and silver futures contracts they have sold on the New York Commodities Exchange.

Your secretary/treasurer and GATA’s consultant about the Comex, Harvey Organ, wrote to the comptroller, James M. Otting, on May 5, calling attention to the recent enormous use of EFPs, which implies derivatives risks being undertaken by U.S. banks that could cause the banks to fail:

http://www.gata.org/node/18303

“Our concern is that your office may not be aware of large unreported derivative exposure by banks,” GATA wrote.

As months passed without any acknowledgment from the comptroller’s office, your secretary/treasurer appealed to his U.S. representative, John B. Larson, D-Connecticut, to ask the comptroller’s office to reply. The congressman’s office made a second inquiry on Monday this week and today the comptroller’s office provided Larson with a copy of a reply written and mailed Wednesday.

The comptroller’s reply, signed by the deputy comptroller for public affairs, Bryan Hubbard, said only that the comptroller’s office has “dedicated examiners” at the largest banks who “continuously evaluate the credit, market, operational, reputation, and compliance risks of bank trading and derivative activities.”

The reply did not say anything about the use of the “exchange for physicals” procedure for settling futures contracts. That is, the reply was a begrudged brushoff and GATA’s letter would have been ignored completely if not for Representative Larson’s repeated intervention.

Of course GATA hardly expected a conscientious reply to its letter, the comptroller’s office being not an independent regulator but part of the Treasury Department, whose mandate includes administration of the Gold Reserve Act of 1934, which, as amended in the 1970s, authorizes the department’s Exchange Stabilization Fund to secretly intervene in and rig any market in the world, directly or through intermediaries:

https://www.treasury.gov/resource-center/international/ESF/Pages/esf-ind…

But there’s always value in demonstrating government’s lack of candor about what it is doing, especially in regard to the monetary metals.

A PDF copy of the reply from the comptroller’s office is posted at GATA’s internet site here:

http://www.gata.org/files/ComptrollerOfCurrencyReply-08-08-2018.pdf

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

Craig Hemke reports that the banks are now long in gold and short on the dollar

(courtesy Craig Hemke/Sprott)

Craig Hemke at Sprott Money: Banks now long gold, short dollar

Submitted by cpowell on Tue, 2018-08-21 14:29. Section: Daily Dispatches

10:30a ET Tuesday, August 21, 2018

Dear Friend of GATA and Gold:

Futures market positioning data shows that commercial banks that are largely agents of the Federal Reserve now appear to be long gold, short the U.S. dollar, short bonds, and long volatility, Craig Hemke of the TF Metals Report writes today at Sprott Money.

The banks, Hemke notes, usually fleece futures market speculators with great skill. Maybe it’s because they are the agents of the U.S. government in rigging markets.

Hemke’s analysis is headlined “What Do the Banks Know?” and it’s posted at Sprott Money here:

https://www.sprottmoney.com/Blog/what-do-the-banks-know-craig-hemke-21-0…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

We brought this story to you yesterday but it is worth repeating: Germany, an ally of the USA is calling for a global payment system independent of the uSA i.e. another SWIFT system

(courtesy Chazan/London’s Financial Times/GATA)

Germany calls for global payments system free of U.S.

Submitted by cpowell on Tue, 2018-08-21 23:26. Section: Daily Dispatches

By Guy Chazan

Financial Times, London

Tuesday, August 21, 2018

Germany’s foreign minister has called for the creation of a new payments system independent of the United States as a means of rescuing the nuclear deal between Iran and the west that Donald Trump withdrew from in May.

Writing in the German daily Handelsblatt, Heiko Maas said Europe should not allow the United States to act “over our heads and at our expense.”

“For that reason it’s essential that we strengthen European autonomy by establishing payment channels that are independent of the U.S., creating a European Monetary Fund and building up an independent Swift system,” he wrote.

Maas’ intervention was the “strongest call yet for European Union financial and monetary autonomy vis-a-vis U.S.,” said Thorsten Benner, director of the Global Public Policy Institute, a Berlin-based think-tank. …

… For the remainder of the report:

https://www.ft.com/content/23ca2986-a569-11e8-8ecf-a7ae1beff35b

END

Chris Powell offers a 6th way the USA could reverse strong dollar trends: stop shorting gold futures and buying the real physical metal

(courtesy Chris Powell/GATA)

Bank currency strategists offer 5 ways U.S. could reverse

strong dollar trend

Submitted by cpowell on Wed, 2018-08-22 00:59. Section: Daily Dispatches

Option 6: Stop shorting gold futures and starting buying real metal instead.

* * *

By Anneken Tappe

MarketWatch, New York

Tuesday, August 21, 2018

President Donald Trump’s recent rhetoric has been fixated on the dollar’s strength against rivals. The U.S. commander in chief doesn’t traditionally jawbone the dollar, but Trump has dispensed with convention and stepped up his assault on currencies and central banks, leaving strategists now speculating on all the ways in which he could seek to influence the buck.

“Can President Trump instruct the U.S. Treasury to intervene in FX markets and weaken the dollar? Twelve months ago, we wouldn’t have even considered this question,” wrote currency strategists Viraj Patel and Chris Turner of ING Group, a banking house in Amsterdam.

Trump has made clear that he is no fan of a strong U.S. dollar, and with a popular gauge for the buck hovering near a 14-month high, it seems the government’s tolerance may have run out. Generally speaking, the president has advocated a weaker-buck policy as a way to make the U.S. more competitive on the global stage.

“Overall, more active steps from the White House to weaken the dollar could serve to knock the top off of an emerging dollar bull trend,” Patel and Turner said. “We think the U.S. administration’s implicit desire for a weaker dollar that is consistent with its mercantilist U.S. trade policy will inevitably be self-fulfilling over the medium-term—and is one of the reasons why we remain strategically bearish on the U.S. dollar.”

Here are five ways the strategists believe such dollar weakening could theoretically be achieved. …

… For the remainder of the report:

https://www.marketwatch.com/story/5-ways-trump-could-upend-the-strong-do…

end

The legendary Jim Sinclair:

My Dear Friends,

We will keep this short and to the point. As time goes by, you will come to know all the ingredients to the fact that economic law lives and is in the process of reasserting itself like a hot solar storm on the surface of the sun.

MOPE has failed and the world is about to implode economically and socially because of it. Your question to all of us has been when will all this happen. The answer is now. The means to this occurrence is accelerating uncontrollable volatility in the world fiat currency markets. The rise in the dollar here and now is due to Richard Russell’s thesis of the synthetic dollar short. This can be easily understood by remembering that the currency you borrow will fluctuate. If that movement is up, then you are at a loss considering where it was trading when your borrowed it.

The Titanic Forces of Economic Sin in the Theory of Management of Perspective Economics (MOPE), which was identified by us only and no one else more than a decade ago, is the most ignorant concept. If markets could be controlled globally, the laws of economic could be cancelled and depressions, plus serious recessions, eliminated forever. They cannot be! You will witness this very soon.

The equity markets around the world have been celebrating the cancellation of economic law, the Austrian School of Economics and all the teachings of Ricardo and Smith, have been declared dead. The assent of the Devil of Artificial Intelligence operated by the most advanced computers has resulted in market manipulation so huge that there is no historical precedent for the volatility that the end of MOPE will produce.

The only way to win in the Game Theory computer manipulation of market of markets is don’t play. The economic insanity of the big players is now clearly behind the reduction of one of the major international financial houses of their trading department from 500 people to 1 person only. They simultaneously hired 9000 computer engineers to build the strongest computer system in order to own all the world of trading and manipulating markets. They are convinced they are right by their own creation, with the huge climb in equity prices regardless of the lack of true internal economic strength. They, therefore, in making the switch between traders and computer engineers confirm their view of MOPE and the Death of Monetary Science. They see their choice of manipulated stocks reaching into the 1000s that contribute nothing fundamental to the world systems such as social networks and movie purveyors. At the same time a major flagship (i.e. GE) of the internal US economy falls from the mid $40s to $12. General Electric is one of the real engines of US economics that now falls price wise therefore capital value wise.

Finally according to the laws of economics the US Fed, having extended its balance sheet insanely, has lost control of its internal and therefore external monetary policy. The run up now in the dollar because of the technical dollar short is the Death Knell of the fiat system. It is the product of a spreading panic in the non – reserve emerging market currencies. It is the currency of Turkey and Venezuela, Brazil and Argentina that have fallen hard and fast with Asia to follow that is the pending Weapon of Mass Economic Destruction. The only way to stop it is for the US Federal Reserve to go ballistic in global QE followed by all the developed world’s central banks in unison to provide the dollars demanded by the debt instruments of this unwind. You will witness the move to hyperinflation in the useless attempt to continue the ignorant game of MOPE and hold economies and fiat system together.

There is no answer other than GOLD to save yourself.

The price of gold will be a product of the size of US debt now outstanding. Gold always balances the balance sheet of the USA as it did in 1980 at $887.50. If we really had the gold at Fort Knox then the price of gold would rise to slightly under $17,000. Since we do not, $50,000 or more is a probability.

This timing is a cause of the scent of the advent of a major trade war between China and the USA confirmed last week.

A tariff war at this time is most unwelcome.

Today, President Trump made it clear that he is a president of lower, not higher interest rates.

Connect all these dots and the return to the long term bull market in gold is at hand.

I have spent 14 years in the attempt to build one of the largest piles of gold possible free of any margin at all. You must know you have to be your own central banks as they are going to fall not one by one but rather all at once. Now you see that the major world’s gold buying nations that are China and Russia are operating on a Policy, not investment motivated.

Thank God you know this now and do the necessary.

Gold will be the last man standing . After June of 2019 there will be an entire new system monetarily only known to the early advocates of the theory of “Free Gold”.

Today the fist system has broken and all the king’s men cannot put it back together again.

Gold will have a market of “$50,000 bid to $50,000 offered” as this new system, by the true law of economic reveals itself. There is no force on Earth that can stop the consequences of greed and mass hysteria of the years 1968 to present. This is also the end of the rule of this planet by what you call the deep state. This is the war of light versus darkness that had to come.

Bill and I have been invited to be interviewed together on this unique connection of the dots by Greg Hunter this coming Friday for weekend presentation.

You need to hear this week’s discussion between Bill, David and myself to connect the dots to your full understanding of the unusual grouping of events taking place.

This answers the when you ask so often about the timing of the resumption of the long term gold bull market.

Jim Sinclair

Executive Chairman

j.sinclair@tanzanianroyalty.com

end

I have just received the letter from the world gold council:

turkey did not sell any gold..the 328 tonnes of gold is held by banks and this is not to be included in their official reserves.

it looks like Turkey has the following:

242.2 tonnes official:

328 tonnes held by banks

total: 570 tonnes.

RE: Turkey

| Trash | x |

|

4:02 AM (3 hours ago) | |||

|

||||

Dear Mr Organ,

Thank you for your email.

The figure we now publish for Turkey’s official gold reserves excludes gold owned by commercial banks held at the central bank under the Reserve Option Mechanism (ROM) policy. You can read more about this policy in the article ‘Maximising gold’s monetary value’ which featured in our Gold Investor publication: https://www.gold.org/research/gold-investor/gold-investor-february-2017. As of end-June ROM holdings amounted to around 328 tonnes.

Our data previously included these ROM holdings in Turkey’s central bank holdings, however since May 2017 Turkey’s central bank has been increasing its gold reserves by purchasing gold outright. We therefore decided to publish the figure for Turkey’s official gold reserves exclusive of ROM holdings, to better reflect true central bank holdings.

Hope this helps.

Kind regards,

Krishan

Krishan Gopaul

Market Intelligence

World Gold Council

WGC (UK) Limited

10 Old Bailey, London EC4M 7NG

United Kingdom

Registered in England and Wales with company number 07867682

| D | +44 20 7826 4704 | ||||||||||||||||||

| M | +44 7889 174 000 | ||||||||||||||||||

| T | +44 20 7826 4700 | ||||||||||||||||||

| F | +44 20 7826 4799 | ||||||||||||||||||

| W | www.gold.org |

END

________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________________

Your early WEDNESDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

i) Chinese yuan vs USA dollar/CLOSED UP TO 6.8412/HUGE DEVALUATION FOR THE PAST FOUR WEEKS STOPS/CHINESE COMING TO USA FOR TRADE TALKS //OFFSHORE YUAN: 6.8386 /shanghai bourse CLOSED DOWN 19.22 POINTS OR 0.70% /HANG SANG CLOSED UP174.79 POINTS OR 0.63%

2. Nikkei closed UP 142.82 POINTS OR 0.64%/USA: YEN RISES TO 110.27/

3. Europe stocks OPENED ALL GREEN

//USA dollar index FALLS TO 94.97/Euro RISES TO 1.1504

3b Japan 10 year bond yield: RISES TO . +.10/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 110.27/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD IS NOW TARGETED AT .11%/JAPAN LOSING CONTROL OF THEIR BOND MARKET

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 66.88 and Brent: 74.03

3f Gold UP/JAPANESE Yen DOWN/ CHINESE YUAN UP

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil UP for WTI and UP FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund RISES TO +.340%/Italian 10 yr bond yield UP to 2.99% /SPAIN 10 YR BOND YIELD UP TO 1.36%

3j Greek 10 year bond yield FALLS TO : 4.20

3k Gold at $1199.40silver at:14.85 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble DOWN 81 /100 in roubles/dollar) 67.97

3m oil into the 67 dollar handle for WTI and 74 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 110.29 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 0.9820 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1401 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now POSITIVE territory with the 10 year RISING to +0.34%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.83% early this morning (THIS IS DEADLY TO ALL MARKETS). Thirty year rate at 2.99%

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

Relief rally in the Turkish lira…no developments at all…

(courtesy Jim Reid/Bloomberg/Deutsche bank/zero hedge)

Futures Slide On Trump Legal Fallout As S&P Bull Run

Hits Record

It’s official: today the S&P 500’s bull run turns 3,453 days old, which makes it the longest such streak in history, surpassing the prior record of 3,452 days between October 1990 and March 2000, which culminated with the bursting of the dot com bubble.

The anniversary was certainly not without fireworks, and followed what some have said was the worst day in Donald Trump’s presidency which saw a guilty plea by Trump’s former attorney, Michael Cohen to illegal campaign-finance charges as well as a conviction of Trump’s former campaign manager, Paul Manafort to 8 different counts of financial wrongdoing, news of which sent U.S. equity futures and global markets modestly lower after the S&P hit a new intraday all time high on Tuesday, and initially sparked mild demand for haven assets, though many moves pared and there was little sign of a pronounced impact in markets beyond America.

Trump’s latest legal troubles added to a complex picture across global markets. U.S. stocks are trading near record highs while 10-year Treasury yields remain well below 3%, as investors grappled with the evolving dynamics of the American tax cut, an escalating trade war and turmoil in emerging markets. Fed minutes released on Wednesday may give more insight into monetary policy after Trump decried interest-rate increases. Later in the week a gathering of central bankers at the Jackson Hole retreat in Wyoming may offer further clues on rates.

“This market will focus on a couple of factors: does this change the math for the mid-term elections, does this cause polls to shift in a material way?” said Morgan Stanley’s Andrew Sheets, in a Bloomberg TV interview. “The market’s going to be watching very closely Friday in Jackson Hole. Does the Fed continue to sound like they are going to continue to tighten policy?”

Indeed, as shown below, while US index futures traded mildly in the red, they bounced from the lowest levels in Asian trading as stocks in Europe and Asia were mixed as traders tried to gauge the fallout from the Trump legal drama.

While the immediate market reaction was not large, the developments represented further uncertainty over Trump’s leadership for investors to navigate. “Trump has weathered quite a few allegations before this, where many people were quick with the `I’ word (impeachment), so we need to see whether this could open a new chapter or if it will calm down again and markets move on,” said Commerzbank rates strategist Christoph Rieger.

Besides the fallout from the Trump political scandal, investors were also looking to Wednesday’s release of FOMC minutes from the August meeting and a speech by Fed Chairman Jerome Powell on Friday for clues on future rate hikes.

“This could present the opportunity for the Fed to discuss longer-term issues, potentially including discussion around the balance sheet and the implementation of monetary policy,” said Jim Reid, strategist at Deutsche Bank.

Treasuries held steady, and the dollar fluctuated, initially spiking with the European open, then sliding to session lows while the euro advanced after Eurozone wages rose 2.2% in 2Q vs 1.7% in Q1, the highest since 2012.

Stocks around the global did not appear too concerned with the Trump turmoil, with the MSCI all-country world index unchanged by the uncertainty, rising 0.1% after the S&P 500 hit a record intraday high of 2,873.23, topping the 2,872.87 set on Jan. 26, before sliding on the Cohen news.

European shares were muted as the market awaited U.S.-China trade talks, set to resume under the cloud of Trump’s prediction that they would make no real progress.

“The key point is these are mid-level officials,” said Donough Kilmurray, managing director and head of the Investment Strategy Group for EMEA at Goldman Sachs. “It’s good they are talking, but at that level of engagement we doubt anything significant will come out of it.”

Stocks were mixed in Asia, with the record high in the S&P followed by another soggy session for Chinese equities, again, which saw the Shanghai Composite drop 0.5%, after the country’s central bank said it would not resort to strong stimulus to support growth, and refrained from liquidity operations and with both US and China said to be pessimistic heading into trade discussions starting today.

Emerging-market stocks climbed 0.3%, leaving 13-month lows further behind as the dollar’s losses helped ease pressure on EM assets, which entered bear territory last week. “If you look at the transmission from economic growth to earnings growth to shareholder returns, it’s strongest in the U.S., it’s ok in Europe and pretty weak in EM,” said Donough Kilmurray, managing director and head of the Investment Strategy Group for EMEA at Goldman Sachs. “The question we’re getting asked now by investors is whether what we see in EM is a sign that something bigger is going wrong in the global economy. Our answer to that is no, these issues have been local issues,” he said.

Stocks were also little changed in Europe in another low volume summer trading session, although Germany’s DAX Index erased gains after tiremaker Continental AG cut its guidance (sees 2018 revenue now €46BN from €47BN, EBIT margin of 9%, from 10%, free cash flow of €1.6BN, was €2BN), sending its stock plunging over 14%, the most since June 2016. The news sent other European automakers sliding: France’s Faurecia (-4.7%), Michelin (-3.9%) and Valeo (-3.4%) were among the biggest decliners.

European markets were muted as they awaited the outcome of the latest round of U.S.-China trade talks, set to resume under the cloud of Trump’s prediction that they would make no real progress. “The key point is these are mid-level officials,” said Goldman’s Kilmurray: “It’s good they are talking, but at that level of engagement we doubt anything significant will come out of it.”

In FX, the U.S. dollar initially inched up after heavy selling following Trump’s criticism of the Federal Reserve’s rate rises in a Reuters interview. However, shortly after the European aopen, the USD eventually weakened against most of G-10, while the AUD underperformed as PM Turnbull was under pressure from own party. The threat of more U.S. sanctions on Russia hit the rouble and backed the market’s view that Russian sanctions would increase in severity regardless of the Trump administration.

The Mexican peso jumped on Tuesday night after the US was said to announce ‘handshake’ NAFTA agreement related to Mexico on Thursday, according to reports in Politico. However, there were later comments from the Canadian government that it has no notification of a NAFTA agreement being imminent, while Mexico was also said to have denied the existence of a NAFTA handshake deal.

As SocGen’s Kit Juckes writes, the top currency this week is ZAR, followed by GBP. The bottom two are BRL and TRY, though a 1% USD/TRY rise doesn’t really count as a move any more. The dollar is the week’s G10FX loser, correcting some of its recent strengths.

US Treasury yields dropped as investors sought safety in Treasuries: 10-year yields were trading at 2.824%, 2bps below Tuesday’s close of 2.844 percent. In Europe, Bund futures edged lower as the curve flattens;

In commodity markets, following a larger than expected decline in API crude inventories last night (-5.170M vs. Exp.-1.500M) , WTI (+1.3%) and Brent (+1.1%) trade on the front foot while concerns continue to linger over the potential repercussions of US oil related sanctions against Iran due to come into effect in November. Elsewhere, spot gold (+0.1%) is relatively uneventful, while copper retreated ahead of US-China trade talks taking place today and tomorrow.

Home sales and mortgage applications figures are due. Scheduled earnings include RBC, Lowe’s, Target and Analog Devices.

Market Snapshot

- S&P 500 futures down 0.3% to 2,854.00

- STOXX Europe 600 down 0.04% to 383.99

- MXAP up 0.4% to 164.03

- MXAPJ up 0.2% to 531.34

- Nikkei up 0.6% to 22,362.55

- Topix up 0.8% to 1,698.37

- Hang Seng Index up 0.6% to 27,927.58

- Shanghai Composite down 0.7% to 2,714.61

- Sensex up 0.02% to 38,285.75

- Australia S&P/ASX 200 down 0.3% to 6,265.98

- Kospi up 0.1% to 2,273.33

- German 10Y yield fell 0.7 bps to 0.324%

- Euro down 0.1% to $1.1555

- Brent Futures up 0.9% to $73.30/bbl

- Italian 10Y yield fell 2.6 bps to 2.717%

- Spanish 10Y yield fell 1.4 bps to 1.354%

- Brent Futures up 0.9% to $73.30/bbl

- Gold spot down 0.2% to $1,193.66

- U.S. Dollar Index up 0.1% to 95.36

Top Overnight News from Bloomberg

- Some Wall Street observers say the possibility that Trump himself will launch a sustained campaign to weaken the dollar as a way to reduce the U.S. trade deficit can’t be dismissed

- Trump could forgive Paul Manafort’s crimes and grant a pardon that allows him to escape all punishment. Or Trump could make a less politically risky move, like waiting and eventually commuting Manafort’s sentence, which would free him from prison but leave his conviction intact

- Progress has been made during five weeks of discussions between the U.S. and Mexico on issues including rules for cars, but there’s no broader agreement on reshaping Nafta, two U.S. administration officials said Tuesday night

- This month’s trading volume in Italian bond futures has already exceeded that of any August since the futures market opened in 2009 amid heightened volatility in the country’s debt assets ahead of the new government’s much-anticipated budget next month

- On Friday, Norway’s government will get a report from an expert committee mapping out the case for divesting the fund’s more than $40 billion in petroleum holdings. The administration will then make a recommendation to parliament later this year, based on the expert committee’s report

- A Barclays Plc foreign exchange trader must face criminal charges he manipulated currency option markets, a U.S. judge ruled

- Russia added more gold reserves in July than any other month this year as it continues to buy up the metal in the face of U.S. sanctions

- Euro- area wages are on the rise, giving another boost to the European Central Bank’s view that it’s the right time to change policy tack. Collective wages rose 2.2 percent in the second quarter, the most since 2012, according to updated data

European equities are trading mostly higher (Eurostoxx 50 +0.3%) with underperformance in Switzerland’s SMI (-0.2%), weighed on by heavyweights Nestle (-0.3%) and Roche (-0.5%). The consumer discretionary sector underperforms amid Germanlisted Continental downgrading guidance. Company shares fell 13.8% following the announcement, dragging the DAX 30 and the likes of Michelin (-5.3%), Pirelli (-3.8%) and Valeo (-5.8%) in sympathy.

Top European News

- Avast Rises After First Post-IPO Earnings Reassure Investors

- Continental Plunges After Cutting 2018 Sales Guidance

Asian equity markets traded mixed with the region indecisive due to the events stateside where the elated mood from the fresh record highs in the S&P 500 eventually deteriorated on political concerns due to legal troubles for President Trump’s former inner circle. This was after Trump’s former campaign manager Manafort was found guilty on 8 counts including tax fraud, while former Trump lawyer Cohen also pleaded guilty at a court hearing and stated he violated campaign financing laws at the direction of a ‘candidate’ which his lawyer further elaborated on and alleged that Trump directed Cohen to commit a crime. ASX 200 (-0.3%) declined from the open with the index weighed by financials although telecoms outperformed on M&A news with TPG in merger discussions with Vodafone Hutchison Australia, while Nikkei 225 (+0.6%) was also initially pressured but then recovered as auto names cheered recent reports that US auto tariffs could be delayed. Elsewhere, Hang Seng (+0.6%) and Shanghai Comp. (- 0.7%) were mixed in which the mainland underperformed after the PBoC refrained from liquidity operations and with both US and China said to be pessimistic heading into trade discussions. Finally, 10yr JGBs saw initial gains as prices tracked the overnight rebound in T-notes and with the BoJ also in the market for JGBs in the belly to super-long end, but then gradually pared throughout the session.

Top Asian News

- Crypto Trading Firm Rents World’s Priciest Offices, Paper Says

- Japanese Stocks Rise as Nafta Development Spurs Trade Optimism

- Santos to Buy Quadrant Energy for $2.15B

- Ping An, Betting Big on Tech, Says Investors Aren’t Won Over Yet

In FX, the DXY held above the 95.000 level as Dollar/majors consolidate post-Trump. The index has pulled up just shy of 95.400 from almost 95.000 when the fall-out from US President’s tirade vs Fed tightening and Usd strength (partly due to FOMC hikes, but also Chinese/EU currency manipulation) was more pronounced. In EM, domestic and geopolitical factors still plaguing several nations in the region and currencies, like the Try, Zar, Rub, Brl. Indeed, the Rand only derived fleeting support from SA inflation data that topped estimates on the headline front, albeit with a more benign core. FX pairs as much as 0.7% firmer. AUD – The clear G10 underperformer as political uncertainty combines with RBA stability on the policy front and the aforementioned general Greenback rebound. Aud/Usd is back below 0.7350 after topping out around 0.7380 on Tuesday, and eying decent option expiry interest at the 0.7375 strike (circa 800 mn) on Thursday. Back to the RBA, Deputy Governor Labelle sees downward pressure on inflation subsiding eventually, but would like to be more confident that CPI will be sustained at target, adding that current accommodative policy will support this outcome, while returning to politics latest reports suggest that Liberal Party members are calling for a leadership meeting later tonight. CHF/EUR/CAD – Bucking the overall trend and holding gains vs the Dollar as the Franc remains at the upper end of 0.9855-25 parameters, the single currency hovers just under 1.1600 and firmly above its 21 DMA (1.1547) after finding a base just ahead of 1.1500, and the Loonie maintains NAFTA/oil price momentum within a 1.3045-15 range, even though Canada denies knowledge of any official notification that a deal is imminent (in response to response about a handshake agreement between the US and Mexico tomorrow).

In commodities, following a larger than expected decline in API crude inventories last night (-5.170M vs. Exp.-1.500M) , WTI (+1.3%) and Brent (+1.1%) trade on the front foot while concerns continue to linger over the potential repercussions of US oil related sanctions against Iran due to come into effect in November. US National Security Advisor Bolton, in an press conference, stated the US will do “other things” beyond economic sanctions to pressure Iran. Meanwhile, the Kuwaiti Oil Minister said he expects the oil market to remain stable until year-end, adding he expects oil exporters to reach an agreement on the mechanism to monitor oil supply by the end of the year. Elsewhere, spot gold (+0.1%) is relatively uneventful, while copper retreated ahead of US-China trade talks taking place today and tomorrow.

Looking at the day ahead, there is little of note in Europe. In the US, we get July existing home sales data for the US along with minutes from the latest FOMC monetary policy meeting. Away from data, Lowe’s and Target will report their earnings.

US Event Calendar

- 7am: MBA Mortgage Applications, prior -2.0%

- 10am: Existing Home Sales, est. 5.4m, prior 5.38m

- 2pm: FOMC Meeting Minutes

DB’s Jim Reid concludes the overnight wrap

Markets were feasting again yesterday and it feels somewhat apt that with the S&P 500 (+0.21%) last night hitting all-time intra-day highs again, today marks the longest ever run without a ‘bear market’ (defined as a 20% drop). The record will stretch back an amazing 3,453 days assuming we don’t see a dramatic oncein-a-lifetime crash today. The all-time intraday high is the first since January 26 earlier this year, though the market did pare gains through the afternoon to close 0.19% off its peak. The DOW (+0.25%) and NASDAQ (+0.49%) were also higher yesterday and the Russell 2000 (+1.14%) closed at a new all-time high.

However if you wanted to maximise your local currency returns yesterday you would have been best served in the Caracas stock exchange in Venezuela where the index climbed 53.69% after the long (but traumatic) weekend. However as we discussed yesterday, given that the Bolivar was devalued by 95% over the weekend, such a return means you would have lost around 40% in dollar terms. As an interesting aside the local stock market is up 277% in August and 26,590% YTD. Shame about the -97% and -99.9998% fall in the currency over the same period. Nevertheless it’s a reminder that if you do see high inflation/hyperinflation and huge FX devaluations, the usual story through history is that bonds and cash get wiped out. Although real assets are likely to underperform initially in inflation adjusted terms, they can offer you some protection if you’re relatively diversified and not too exposed to individual investments that may get wiped out along the way with the economic destruction.

Anyway from the most volatile market in the financial world currently to discussing how much less volatile DM markets are looking now relative to this time last week. Volatility is all of all sudden back to testing the lower end of the range and the direction of travel is certainly a lot more positive for risk. Indeed the VIX touched an intraday low of 12.09 yesterday (intraday highs of 16.86 last week) which is the lowest in seven sessions while currency vol (based on the CVIX) is at the lowest in eight sessions. The European V2X index touched an eight-session low of 13.38 yesterday as well.

Staying with Europe, markets were firmer yesterday amid positive news that low-level trade talks between the US and China are proceeding positively. The Euro Stoxx index closed 0.24% higher, led by financials and energy stocks. Credit also tightened with Main down -2.7bp with Crossover -11.6bp. Meanwhile Atlantia’s 3y CDS tightened -25.7bp to 263.3bp yesterday after widening +184bp since the recent bridge tragedy in Italy.

Elsewhere the softer USD – partly a function of Trump’s comments on Monday about the Fed and foreign currency manipulation – helped EM currencies to broad based gains including the likes of the Polish Zloty (+1.14%), South African Rand (+0.92%) and Turkish Lira (+0.09%). The Brazilian Real underperformed (-1.97%) to its weakest level in 2.5 years after Bloomberg reported that polling showed that electoral support for the Workers Party of ex-President Lula da Silva increased by 5 percentage points to a field-leading 37.3%. Oil (+0.64%) appeared to act as bit of a tailwind for markets while the relative risk on tone was also evident across rates with Treasury (+1.1bps) and Bund (+2.8bps) yields edging higher. At the other end of the spectrum 10yr BTPs (-2.7 bps) fell to 2.98%, closing below 3.00% for the first time since August 10, and a 23 bps rally from the intraday highs of last week.

After the bell in the US, Bloomberg reported that President Trump’s former lawyer – Michael Cohen admitted to the Federal Court that he committed campaign finance violations ahead of the 2016 election. Elsewhere the president’s former campaign chairman Paul Manafort was convicted on eight counts of tax and bank fraud charges. In Asia this morning markets are trading mixed with the Nikkei (+0.56%), Kospi (+0.30%) and Hang Seng (+0.51%) all up while the Shanghai Comp. (-0.51%) and futures on the S&P (-0.2%) are down as we type. Meanwhile treasuries pared back gains to trade broadly flat while the Yen is slightly down. Elsewhere the CNY is also relatively stable which follows the theme of the last 24 hours or so after the PBoC announced that China would not use the CNY as a tool in the trade war, and instead keep the rate “basically stable at a reasonable equilibrium level”. Back in the US, the Politico cited unnamed sources that noted the US plans to announce a “handshake” deal with Mexico on Thursday after reaching a breakthrough in the NAFTA talks.

Moving on now and while yesterday may have been fairly quiet for headlines, the good news for those of us that have to write about something for a living is that we’re now approaching the business end of the week for some of the more potentially market sensitive events. Today we should get news about the US placing new sanctions on Russia related to the UK nerve agent attack. In a report published last week, DB’s Peter Sidorov noted that the first round due today should only have a muted impact but the potential prospect of a second round of sanctions in three months’ time, which could range from mild to severe, brings greater uncertainty through to the US mid-term elections on 6 November. What should be worth watching though is the Russia response which could come as soon as today. As well as this the US and China will also attempt to revive trade talks today, although as we know President Trump has already said that he has “low expectations” for the talks this week and appears to be in no rush to resolve the dispute.

Also on the cards today are the latest FOMC minutes from the Fed meeting earlier this month. Given that it was a meeting with almost nothing material to come from it, the minutes are unlikely to throw up much of interest, although our US economists noted that this could present the opportunity for the Fed to discuss longer-term issues, potentially including discussion around the balance sheet and the implementation of monetary policy (e.g. floor v corridor system), especially given the speech from NY Fed Markets Group chief Simon Potter immediately following the FOMC meeting earlier this month. We may also get more info on how policymakers are thinking about the counter-cyclical capital buffer or the monetary policy framework (e.g. price level targeting).

Ahead of that, the Fed’s Kaplan published an essay yesterday which broadly reiterated the Fed’s progressive path of getting back to neutral rates. In his view, rates can increase 3 to 4 times before it hits the neutral level, but from there, he is “inclined to step back and assess the outlook of the economy….before deciding further actions” while adding that he does not “discount the significance of an inverted yield curve”. Notably Mr Kaplan next votes on monetary policy in 2020.

As for yesterday, the highlight of another incredibly quiet day for data was the July public finances stats in the UK. The July budget surplus came in at a better than expected £2bn (vs. £1.1bn expected). That meant it was also the biggest July surplus since 2000, and with the overall borrowing numbers slightly below the OBR estimates, there might be a bit more fiscal wiggle room for the UK Chancellor than previously thought. Speaking of surpluses, the latest IFO institute forecasts which came out on Monday in Germany are worth flagging. The institute expects Germany’s current account surplus to remain the largest in the world this year – the third year running – and a near $100bn bigger than the next largest, Japan. This certainly got people talking in markets early yesterday and could yet become a political hot potato for Germany.

Coming back to the UK, Brexit was also back in the spotlight yesterday with technical discussions between the UK and EU resuming. At a press conference in the late afternoon, the EU’s Barnier and UK’s Raab sounded relatively positive. Barnier said we must “de-dramatize the issue” of Northern Ireland, potentially signaling a pragmatic resolution to one of the thorniest outstanding issues. Further, he also added that the two sides will negotiate on Brexit “continuously” from now on and that “we can find common ground”, although it does require Britain to “respect the single market”. Sterling rallied 0.82% versus the dollar, though closed flat versus the Euro.

Looking at the day ahead, there is little of note in Europe. In the US, we get July existing home sales data for the US along with minutes from the latest FOMC monetary policy meeting. Away from data, Lowe’s and Target will report their earnings.

3. ASIAN AFFAIRS

i) WEDNESDAY MORNING/ TUESDAY NIGHT: Shanghai closed DOWN 19.22 POINTS OR 0.70% /Hang Sang CLOSED UP 174.79 POINTS OR 0.63%/ / The Nikkei closed UP 142.82 POINTS OR 0.64%/Australia’s all ordinaires CLOSED DOWN 0.14% /Chinese yuan (ONSHORE) closed UP at 6.8412 AS POBC HALTS ITS HUGE DEVALUATION /DELEGATION COMING TO THE USA TO SEE TRUMP/Oil UP to 67.18 dollars per barrel for WTI and 72.70 for Brent. Stocks in Europe OPENED DEEPLY IN THE GREEN //. ONSHORE YUAN CLOSED UP AT 6.8412 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.8386: HUGE DEVALUATION/PAST SEVERAL DAYS STOPS// TRADE TALKS WILL RESUME IN THE USA : /ONSHORE YUAN TRADING STRONGER AGAINST OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING MUCH STRONGER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

3 a NORTH KOREA/USA

North Korea/South Korea/USA/China

3 b JAPAN AFFAIRS

c) REPORT ON CHINA/HONG KONG

This is a good one:

Rating agency Dagong.. suspended for selling AA and AAA ratings to Chinese companies who did not deserve them

(courtesy Robert H)

Dagong, which Slashed the US to BBB+,

Suspended in China for Selling Fake AA and

AAA Ratings to Chinese Outfits

Maybe the US government refused to pay China’s Dagong Global Credit Rating for an AA or AAA rating. And in January 2018, Dagong let the US know how things worked in China: It downgraded US Treasury debt from A- to BBB+ though there is near-zero credit risk since the Fed can always print the US government out of trouble.

At about the same time, Dagong gave Sunshine Kaidi New Energy Group, a privately-held Chinese company, an AA rating though there were already reports about the difficulties the company had with its debt. In June, the company defaulted on 18 billion yuan ($2.6 billion) in bonds. In July, the Shenzhen Stock Exchange warned that a publicly traded subsidiary – Kaidi Ecological and Environmental Technology Co. – may be delisted after its auditor refused to sign off on its financial statements.

Since the default, Dagong slashed Kaidi New Energy’s rating four times to C.

Despite the government’s struggle to contain the growing corporate-debt meltdown in China, Dagong upgraded about a fifth of its clients’ credit ratings since the start of 2017, according to the South China Morning Post.

It’s a broader problem. Dagong isn’t the only credit rating agency in China. There is a whole industry, of which Dagong has about a 20% market share, though the three major US rating agencies – Standard & Poor’s, Moody’s, and Fitch – have been locked out of the market. Of the 1,744 Chinese companies that have issued bonds, 97% were rated AA or higher by Chinese rating agencies, with 27% (464 companies) being AAA-rated. In the US, only a handful of companies are still AAA-rated.

And now two Chinese regulators have disclosed why rating agencies issue these AA and AAA ratings even as corporate debt meltdown becomes difficult to contain: Dagong had effectively sold high credit ratings to bond issuers.

And as punishment, the regulators decided to suspend Dagong’s credit rating services in China for one year, according to the South China Morning Post:

NAFMII, an agency under the People’s Bank of China, said in a statement on Friday that Dagong had been found to have “directly provided consulting services to rated companies,” which is prohibited, and “charged high fees” that compromised its independence between November 2017 and March 2018.

In also said Dagong had provided false statements and untrue information to the watchdog during its investigation, adding that its actions had a “very negative” impact on the market.

The Chinese Securities Regulatory Commission said in a separate statement cited by the SCMP that a site inspection had found serious problems at Dagong, including:

- “Chaotic internal governance”

- “Charging consulting fees from those being rated”

- “Hiring executives without professional qualifications”

- “Loss of original documents for some rating services.”

Dagong released its own statement, apologizing for its actions.

Investors in China’s corporate bond market have to navigate the Wild West of bond markets where debt creation is opaque, where companies, often with inscrutable ownership structures, have loaded up on enormous piles of debt to fund acquisitions, overcapacity, and foreign adventures, but where outright defaults are rare only because the government, via its state-owned megabanks, keeps bailing out troubled borrowers. This includes measures like telling those state-owned banks to convert some defaulting debt into equity.

No investor can trust anything Chinese companies – or Chinese rating agencies for that matter – disclose about their debts, and the only hope is the history of corporate bailouts by the Chinese government. But Chinese authorities are trying to wean investors ever so gradually off these assurances and have allowed a few bond defaults here and there to proceed to the great astonishment of befuddled investors.

The punishment handed to Dagong – effectively not being able to do business for one year – shows that the government is getting more serious about trying to tamp down on the corporate bond morass and bring some glimmers of sunshine to its opacity. But categorically allowing corporate debt to default, and allowing market participants to restructure this debt on the backs of shareholders and creditors, would accomplish a heck of a lot more in that department.

end

4. EUROPEAN AFFAIRS

6 .GLOBAL ISSUES

Supposedly there has been a handshake deal on NAFTA and that was between Mexico and the USA. If so that will clear the way for Canada to join in. Both the Peso and Cdn dollar rose

(courtesy zerohedge)

Peso, Loonie Jump On Reports US-Mexico NAFTA “Handshake Deal” To Be Announced Thursday

One could be forgiven for thinking this sudden ‘coming to the table’ could be related to today’s Trump-related tumult, but away from that cynicism, Politico reports that the Trump administration is planning to announce Thursday that it has reached a breakthrough in NAFTA talks with Mexico.