GOLD: $1195.90 UP $2.30 (COMEX TO COMEX CLOSINGS)

Silver: $14.20 UP 4 CENTS (COMEX TO COMEX CLOSING)

Closing access prices:

Gold $1196.75

silver: $14.19

For comex gold:

AUGUST/

And now Sept:

NUMBER OF NOTICES FILED TODAY FOR SEPT CONTRACT: 10 NOTICE(S) FOR 1000 oz

Total number of notices filed so far for Sept: 430 for 44,000 (1.337 tonnes)

For silver:

Sept

593 NOTICE(S) FILED TODAY FOR

2,965,000 OZ/

Total number of notices filed so far this month: 4668 for 23,340,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: BID $6964/OFFER $7048: DOWN $352(morning)

Bitcoin: BID/ $6898/offer $6983: DOWN $415(CLOSING/5 PM)

end

First Shanghai gold fix comes at 10 pm est

The second Shanghai gold fix: 2:15 pm

First Shanghai gold fix gold: 10 pm est: $1199.44

NY price at the same time:$1193.85

PREMIUM TO NY SPOT: $5.59

XX

Second gold fix early this morning: $ 1200.47

USA gold at the exact same time:$1193.10

PREMIUM TO NY SPOT: $7.37

XXXX

China is controlling the gold market

WE WILL NOT PROVIDE LONDON FIXES AS THEY ARE NOT ACCURATE AS TO WHAT IS GOING ON AT THE SAME TIME FRAME.

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total OPEN INTEREST ROSE BY A CONSIDERABLE 551 CONTRACTS FROM 211,840 UP TO 212,391 DESPITE YESTERDAY’S HUGE 37 CENT FALL IN SILVER PRICING AT THE COMEX.

TODAY WE MOVED CONSIDERABLY CLOSER TO LAST MONTH’S RECORD SETTING OPEN INTEREST OF 244,196 CONTRACTS.

WE HAVE ALSO WITNESSED A LARGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY(WELL OVER 30 MILLION OZ AT THE COMEX FOR JULY , 6 MILLION OZ FOR AUGUST AND NOW OVER 31 MILLION OZ STANDING IN SEPTEMBER. AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD HUMONGOUS SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP:

0 EFP’S FOR SEPT. 6151 EFP’S FOR DECEMBER AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE: OF 6151 CONTRACTS. WITH THE TRANSFER OF 6151 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 6151 EFP CONTRACTS TRANSLATES INTO 30.75MILLION OZ ACCOMPANYING:

1.THE 37 CENT FALL IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR THE JUNE/2018 COMEX DELIVERY MONTH. (5.420 MILLION OZ); 30.370 MILLION OZ STANDING FOR DELIVERY IN JULY, FOR AUGUST: 6.065 MILLION OZ AND NOW 30.330 MILLION OZ STANDING SO FAR IN SEPT.

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF SEPT:

8825 CONTRACTS (FOR 2 TRADING DAYS TOTAL 8825 CONTRACTS) OR 44.125 MILLION OZ: (AVERAGE PER DAY: 4413 CONTRACTS OR 22.06 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF SEPT: 144.125 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 6.30% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2018 TO DATE SILVER EFP’S: 2,081.95 MILLION OZ.

ACCUMULATION FOR JAN 2018: 236.879 MILLION OZ

ACCUMULATION FOR FEB 2018: 244.95 MILLION OZ

ACCUMULATION FOR MARCH 2018: 236.67 MILLION OZ

ACCUMULATION FOR APRIL 2018: 385.75 MILLION OZ

ACCUMULATION FOR MAY 2018: 210.05 MILLION OZ

ACCUMULATION FOR JUNE 2018: 345.43 MILLION OZ

ACCUMULATION FOR JULY 2018: 172.84 MILLION OZ

ACCUMULATION FOR AUGUST 2018: 205.23 MILLION OZ.

RESULT: WE HAD A CONSIDERABLE SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 551 DESPITE THE 37 CENT FALL IN SILVER PRICING AT THE COMEX YESTERDAY. THE CME NOTIFIED US THAT WE HAD A HUMONGOUS SIZED EFP ISSUANCE OF 6151 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) .

TODAY WE GAINED A MONSTER SIZED: 6702 TOTAL OI CONTRACTS ON THE TWO EXCHANGES:

i.e 6151 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH A INCREASE OF 551 OI COMEX CONTRACTS. AND ALL OF THIS HUGE GAIN IN DEMAND HAPPENED WITH A GIGANTIC 37 CENT LOSS IN PRICE OF SILVER AND A CLOSING PRICE OF $14.16 WITH RESPECT TO YESTERDAY’S TRADING. YET WE HAD A GIGANTIC AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY IN THE BIG JULY DELIVERY MONTH OF SLIGHTLY OVER 30 MILLION OZ, IN AUGUST ANOTHER BIG 6.065 MILLION OZ IN A NON ACTIVE MONTH AND NOW IN SEPTEMBER AN INITIAL MONSTROUS 30.330 MILLION OZ AMOUNT OF SILVER STANDING FOR DELIVERY IN SEPTEMBER.. NOBODY IS PAYING ATTENTION TO THE HUGE NUMBER OF PHYSICAL OUNCES STANDING FOR SILVER THESE PAST SEVERAL MONTHS.

In ounces AT THE COMEX, the OI is still represented by OVER 1 BILLION oz i.e. 1.062 MILLION OZ TO BE EXACT or 152% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT AUGUST MONTH/ THEY FILED AT THE COMEX: 593 NOTICE(S) FOR 2,965,000 OZ OF SILVER

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 243,411 CONTRACTS ON APRIL 9.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $16.51.

AND NOW WE RECORD FOR POSTERITY ANOTHER ALL TIME RECORD OPEN INTEREST AT THE COMEX OF 244.,196 CONTRACTS ON AUGUST 22/2018 AND AGAIN WHEN THIS RECORD WAS SET, THE PRICE OF SILVER WAS $14.78 AND LOWER IN PRICE THAN PREVIOUS RECORDS.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. AND NOW SEPT: AN INITIAL HUGE 30.330 MILLION OZ.

- HUGE RECORD OPEN INTEREST IN SILVER 243,411 CONTRACTS (OR 1.217 BILLION OZ/ SET APRIL 9/2018) AND NOW AUGUST 22/2018: 244,196 CONTRACTS, WITH A SILVER PRICE OF $14.78.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017

- RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT).

IN GOLD, THE OPEN INTEREST ROSE BY A VERY STRONG SIZED 6,534 CONTRACTS UP TO 473,118 DESPITE THE DROP IN THE COMEX GOLD PRICE/YESTERDAY’S TRADING (A FALL IN PRICE OF $7.55). THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED AN UNBELIEVABLE SIZED 15.652 CONTRACTS:

OCTOBER HAD 0 EFP’S ISSUED AND, DECEMBER HAD AN ISSUANCE OF 15,652 CONTACTS AND ALL OTHER MONTHS ZERO. The NEW COMEX OI for the gold complex rests at 473,118. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE AN AN ATMOSPHERIC AND AN UNBELIEVABLE SIZED OI GAIN IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 22,186 CONTRACTS: 6534 OI CONTRACTS INCREASED AT THE COMEX AND 15,652 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN: 22,186 CONTRACTS OR 2,218,800 OZ = 69.00 TONNES. AND ALL OF THIS ATMOSPHERIC AND UNBELIEVABLE DEMAND OCCURRED WITH A GIGANTIC FALL IN THE PRICE OF GOLD/ YESTERDAY TO THE TUNE OF $7.55?????????????????????????????.

YESTERDAY, WE HAD 4330 EFP’S ISSUED.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF SEPT : 19982 CONTRACTS OR 1,998,200 OZ OR 62.15 TONNES (2 TRADING DAYS AND THUS AVERAGING: 9991 EFP CONTRACTS PER TRADING DAY OR 999,100 OZ/ TRADING DAY),,

TO GIVE YOU AN IDEA AS TO THE HUGE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 12 TRADING DAYS IN TONNES: 62.15 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2017, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 2555 TONNES

THUS EFP TRANSFERS REPRESENTS 62.15/2550 x 100% TONNES = 2.43% OF GLOBAL ANNUAL PRODUCTION SO FAR IN JULY ALONE.***

ACCUMULATION OF GOLD EFP’S YEAR 2018 TO DATE: 5,259.10* TONNES *SURPASSED ANNUAL PROD’N

ACCUMULATION OF GOLD EFP’S FOR JANUARY 2018: 653.22 TONNES (21 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR FEBRUARY 2018: 649.45 TONNES (20 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR MARCH 2018: 741.89 TONNES (22 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR APRIL 2018: 713.84 TONNES (21 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR MAY 2018: 693.80 TONNES ( 22 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR JUNE 2018 650.71 TONNES (21 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR JULY 2018 605.5 TONNES (21 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR AUG. 2018 488.54 TONNES (23 TRADING DAYS)

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A VERY STRONG SIZED INCREASE IN OI AT THE COMEX OF 6534 DESPITE THE LOSS IN PRICING ($7.55 THAT GOLD UNDERTOOK YESTERDAY) // . WE ALSO HAD AN ATMOSPHERIC NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 15652 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 15652 EFP CONTRACTS ISSUED, WE HAD A GAIN OF 27,105 CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

15652 CONTRACTS MOVE TO LONDON AND 6534 CONTRACTS INCREASED AT THE COMEX. (in tonnes, the GAIN in total oi equates to 69.00 TONNES). ..AND THIS GAIN IN DEMAND OCCURRED WITH THE LOSS OF $7.75 IN YESTERDAY’S TRADING AT THE COMEX.

we had: 10 notice(s) filed upon for 1000 oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD...

WITH GOLD UP $2.30 TODAY: /

THE COMEX BLEEDS GOLD AGAIN AS WE HAVE ANOTHER BIG CHANGE IN GOLD INVENTORY AT THE GLD

A WITHDRAWAL OF 6.24 TONNES

/GLD INVENTORY 746.92 TONNES

Inventory rests tonight: 746.92 tonnes.

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

SLV/

WITH SILVER UP 4 CENTS TODAY

NO CHANGES IN SILVER INVENTORY AT THE SLV;

/INVENTORY RESTS AT 329.856 MILLION OZ.

NOTE THE DIFFERENCE BETWEEN THE GLD AND SLV: THE CROOKS CAN RAID GOLD BECAUSE THEY DO HAVE SOME PHYSICAL. THEY DO NOT RAID SILVER PROBABLY BECAUSE THERE IS NO REAL SILVER INVENTORIES BEHIND THEM

end

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER ROSE BY A CONSIDERABLE SIZED 551 CONTRACTS from 211,804 UP TO 212,291 AND MOVING A LITTLE CLOSER TO THE NEW COMEX RECORD SET LAST MONTH AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 1 1/3 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89. AS YOU CAN SEE, WE HAVE RECORD HIGH OPEN INTERESTS IN SILVER ACCOMPANIED BY A CONTINUAL LOWER PRICE WHEN THAT RECORD WAS SET…..

.

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

0 EFP CONTRACTS FOR SEPTEMBER, 6151 CONTRACTS FOR DECEMBER AND AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 6151 CONTRACTS . EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI GAIN AT THE COMEX OF 551 CONTRACTS TO THE 6151 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A NET GAIN OF 6702 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES: 33.51 MILLION OZ!!! AND YET WE ALSO HAVE A STRONG DEMAND FOR PHYSICAL AS WE WITNESSED A FINAL STANDING OF GREATER THAN 30 MILLION OZ FOR JULY, A STRONG 6.065 MILLION OZ FOR AUGUST.. AND NOW A HUGE 30.330 MILLION OZ INITIALLY STAND FOR SILVER IN SEPTEMBER….

RESULT: A CONSIDERABLE SIZED INCREASE IN SILVER OI AT THE COMEX DESPITE THE 37 CENT PRICING LOSS THAT SILVER UNDERTOOK IN PRICING YESTERDAY. BUT WE ALSO HAD A GOOD SIZED 6151 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR SEPTEMBER, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i) WEDNESDAY MORNING/ TUESDAY NIGHT: Shanghai closed DOWN 46.24 POINTS OR 1.68% /Hang Sang CLOSED DOWN 729.49 POINTS OR 2.61%/ / The Nikkei closed DOWN 116.07 POINTS OR 0.51%/Australia’s all ordinaires CLOSED DOWN 0.93% /Chinese yuan (ONSHORE) closed UP at 6.8313 AS POBC HALTS ITS HUGE DEVALUATION /DELEGATION COMING TO THE USA TO SEE TRUMP IN NOVEMBER/Oil DOWN to 68.95 dollars per barrel for WTI and 77.36 for Brent. Stocks in Europe OPENED RED //. ONSHORE YUAN CLOSED UP AT 6.8313 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.8519: HUGE DEVALUATION/PAST SEVERAL DAYS STOPS// TRADE TALKS NOT DOING TOO GOOD : /ONSHORE YUAN TRADING STRONGER AGAINST OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING MUCH STRONGER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

3A/NORTH KOREA/SOUTH KOREA

i)North Korea/South Korea/USA/

b) REPORT ON JAPAN

3 C/ CHINA

4/EUROPEAN AFFAIRS

i)Germany/UK/Brexit

Germany’s government have softened their key demands on a Brexit and this will ease the path for the UK to strike a deal with the European union

( zerohedge)

ii)UK/RUSSIA

I can assure you that Putin will not be too happy with these charges against two Russian nationals; Petrov and Boshirov

( zerohedge)

iib)Just one small problem with this arrest: both cannot occupy the same space at exactly the same time

have fun with this one;

( zerohedge)

Italy

A good commentary explaining the problems facing Italy as for 20 years, they experienced no growth in their GDP. The new government no doubt will ask Brussels for a bigger increase in their budget spending..probably north of 3% of their GDP. Also the migrant issue is also of extreme importance

( Chris Wood/Grizzle.com)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

Iran/Lebanon/Hezbollah

Intelligence sources now accuse Iran of supplying missiles to Hezbollah via civilian airlines

( zerohedge)

6. GLOBAL ISSUES

This is why it would be foolish for Trump to attack Canada in their NAFTA discussions. The USA will need Canada’s water

(courtesy Michael Snyder)

7. OIL ISSUES

Oil drifted further south despite smaller than expected crude draw down

( zerohedge)

8 EMERGING MARKET ISSUES

the rout across emerging markets continues unabated. The definition of contagion: “catching falling knives inside emerging markets:”

( zerohedge)

9. PHYSICAL MARKETS

i)With the consumption tax set to rise to 10% Japan is bracing itself for another rush of gold smuggling as gold is taxed in Japan but not Hong Kong

( Nikkei/Asian Review/GATA)

ii)Chris Powell and Craig Hemke talk about the lows of gold and silver equal to the cost of production. If the Bozos knock the price further down, then mining companies mothball their properties…supplies dwindle to nothing..and then China buys up the mines at distressed prices while our mining CEO’s gleefully applaud.

10. USA stories which will influence the price of gold/silver)

i)Market trading /GOLD/MARKET MOVERS:

MARKET TRADING

Markets do not like the latest: tech regulations looms from Congress. Amazing, they seem to turn their heads on emerging market turmoil, on tumbling hard USA data and tightening global central bank policies but regulate technology companies..not good

( zerohedge)

a)Trump will not be happy as the trade deficit with the world came in at a huge $50.1 billion dollars. The deficit with China was about 36.$ billion of that. Trump no doubt just received his signal to initiate the 200 billion dollars worth of tariffs on the next lot of Chinese goods

( zerohedge)

b)BERNIE introduces the “stop Bezos Act” as the new bill will require all retailers like Amazon and Walmart to pay back the government for food stamps, and public housing, Medicaid and other federal assistance received by their workers. He will introduce a 100% tax on those employees to be paid by the corporation. Lots of fun.

(courtesy zerohedge)

iv)SWAMP STORIES

a)Trump is visibly upset with the “terrible message’ sent by Nike in its latest ad campaign with Colin Kaepernick

( zerohedge)

b)Looks like Mueller is giving in: He will accept written answers from Trump on Russian collusion

c)Trump is willing to shut down government as he wants funding for his wall

( zerohedge)

Let us head over to the comex:

The next active delivery month after August for silver is September and here the OI FELL by 551 contracts DOWN to 1991.

We had 316 notices filed on yesterday so we lost 235 number of contracts or 1,175,000 oz will not stand at the comex as these guys accepted a fiat bonus and morphed into London based forwards. For the past 17 months starting in April 2017, we have been witnessing on a constant basis queue jumping as the commercials seek physical silver immediately after first day notice. Today they took a little holiday from this exercise.

October LOST 48 contracts to stand at 664. November saw its gain of 11 contracts to stand at 14.

ON FIRST DAY NOTICE FOR THE SEPT/2017 SILVER CONTRACT MONTH: 20.515 MILLION OZ STOOD FOR DELIVERY AND BY MONTH’S END: A HUGE 32.875 MILLION OZ WAS THE FINAL STANDING AS WE WERE WELL INTO THE PHENOMENON OF QUEUE JUMPING IN SILVER. THUS WE ARE WAY AHEAD OF LAST YEAR AS ALREADY WE HAVE 30.330 MILLION OZ OF SILVER INITIALLY STAND. WE WILL NO DOUBT PASS LAST YEAR’S TOTAL OF 32.875 MILLION OZ ONCE SEPTEMBER ENDS AS THE BANKS SCRAMBLE FOR PHYSICAL SILVER.

Major gold/silver trading /commentaries for WEDNESDAY

GOLDCORE/BLOG/MARK O’BYRNE.

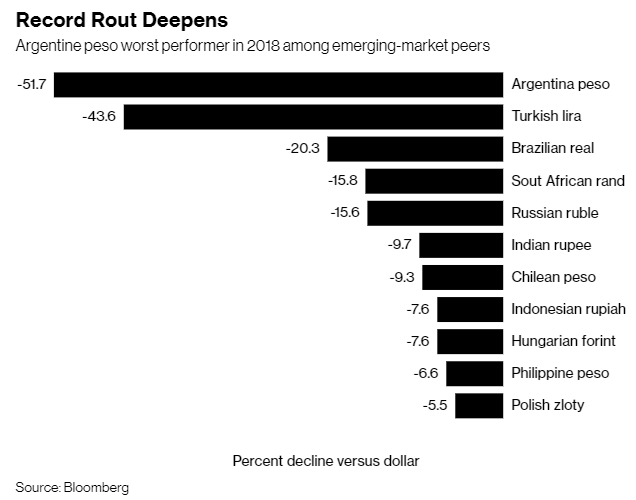

Video: Gold Surges To Record Highs In Emerging Market Currencies – New Highs In USD, EUR, GBP In the Coming Months?

– As emerging market currencies internationally collapse in value, there is a real risk of contagion in bond and currency markets

– Turkish lira falls 43.6% and Argentine peso falls 51% and are respectively the 2nd worst and worst internationally traded and non pegged performing currencies in 2018

– Venezuelan bolivar has completely collapsed

– Inflation is going to take off as wheat has surged 28% and oil is up 16% year to date in dollar terms

– Emerging-market crisis is driving safe-haven demand for German Bunds and soon gold

– Important not to think of gold solely in US dollar terms and realise that gold is again acting as a safe haven for those who need a currency hedge

Source: Goldprice.org

Source: Goldprice.org

Market Performance YTD in USD (Finviz.com)

News and Commentary

Gold nudges up as dollar eases; Sino-U.S. trade tensions in focus (CNBC.com)

Mighty Dollar and Trade Fears Drag Silver Down to Two-Year Low (Bloomberg.com)

Gold near 1-wk lows as trade, emerging market concerns boost dollar (Reuters.com)

Bullard says Fed should hold off on raising rates (MarketWatch.com)

EU Looking to Sidestep U.S. Sanctions With Payments System Plan (Bloomberg.com)

Source: Bloomberg.com

COMEX Silver To Test 2015 Lows (SilverSeek.com)

Winter is coming to the markets says Edwards – Gold will benefit (MoneyWeek.com)

Emerging-market selloff has all the hallmarks of contagion (Bloomberg.com)

Dublin’s housing market not yet ripe for a crash (DavidMCWilliams.ie)

Gold Prices (LBMA AM)

04 Sep: USD 1,195.75, GBP 932.57 & EUR 1,034.20 per ounce

03 Sep: USD 1,201.70, GBP 933.00 & EUR 1,035.75 per ounce

31 Aug: USD 1,206.85, GBP 927.58 & EUR 1,034.03 per ounce

30 Aug: USD 1,202.35, GBP 924.25 & EUR 1,028.49 per ounce

29 Aug: USD 1,204.30, GBP 935.14 & EUR 1,032.33 per ounce

28 Aug: USD 1,212.75, GBP 939.88 & EUR 1,037.02 per ounce

Silver Prices (LBMA)

04 Sep: USD 14.25, GBP 11.11 & EUR 12.33 per ounce

03 Sep: USD 14.53, GBP 11.27 & EUR 12.50 per ounce

31 Aug: USD 14.66, GBP 11.27 & EUR 12.56 per ounce

30 Aug: USD 14.67, GBP 11.27 & EUR 12.54 per ounce

29 Aug: USD 14.69, GBP 11.40 & EUR 12.60 per ounce

28 Aug: USD 14.90, GBP 11.56 & EUR 12.74 per ounce

Recent Market Updates

– September Is The Best Month For Gold and Worst Month For Stocks

– Pound Investors Face Months of Volatility Into Brexit Endgame

– This Week’s Golden Nuggets

– Video: “Financial War” Deepens as Russia Buys Gold and Dollar Hegemony At Risk – Rickards on CNN

– Will Indebted Nations Globally Follow Venezuela Into Hyperinflation?

– End Of Dollar Hegemony May Happen Soon and Badly Impact Indebted America

– 10 Incredible Photos From Venezuela Show The Disastrous Risks Of Currency Devaluation

– This Week’s Golden Nuggets

– Video: Is Silver Set for a Massive Breakout?

– Banks Now Long Gold, Short Dollar. What Do They Know?

– Russia Buys 800,000 Ounces Of Gold In July

– Gold Season – Is This It?

– This Week’s Golden Nuggets

– Gold And Silver Prices Fall 1.6% and 4.3% To Near 2 Year Lows

– London House Prices Fall At Fastest Annual Rate Since Height Of Financial Crisis

Listen on SoundCloud , Blubrry & iTunes. Watch on YouTube below

Andrew Maguire’s Kinesis money which is a “bitcoin” but backed 100% by allocated gold and silver is set to go.

it think it would be a great idea to look at this!

please read at: https://kinesis.money/#/

(Andrew Maguire)

|

|

Dear Harvey Organ,

Thank you for your participation in our webinar on June 7th with our host and CEO of Kinesis, Thomas Coughlin.

The response we received has been incredible, we appreciate you taking the time to join us and hope you found it to be beneficial.

Due to such a high influx of questions we received we were unable to have them all answered. Nevertheless, if there was anything which requires more clarification, or you have a query which needs to be rectified, we invite you to join our telegram group:

We apologize for the technical issues we incurred during the webinar which resulted in it running a little over schedule, we hope that the next one we host will run seamlessly.

A video has been put together and uploaded onto our YouTube channel which can be found here:

Please share and subscribe to our YouTube channel to be notified of all the latest videos as they become available.

The rapid growth that we are currently experiencing has been incredible and with your support, is only going to get better.

We are working behind the scenes very hard to create a better experience for everyone involved! Stay tuned in as we have many more announcements to be released in the upcoming days.

Kind Regards,

|

Kinesis Money

a:C/O ILS Fiduciaries (IOM) Limited, First Floor,Millennium House, Victoria Road, Douglas, Isle of Man IM2 4RW

|

The following is self explanatory

(courtesy GATA/Chris Powell and Harvey Organ)

GATA asks bank regulator to check risks of gold

futures maneuver

Submitted by cpowell on Sun, 2018-06-10 16:17. Section: Daily Dispatches

12:21p ET Sunday, June 10, 2018

Dear Friend of GATA and Gold:

GATA has appealed to the U.S. comptroller of the currency, who has regulatory authority over banks, to review financial risks certain banks may have incurred through derivatives in the monetary metals markets, particularly through the recent heavy use of the “exchange for physicals” mechanism of settling gold and silver futures contracts on the New York Commodities Exchange.

The appeal was made in a letter sent May 5 to the comptroller, Joseph M. Otting, whose office is part of the U.S. Treasury Department, by your secretary/treasurer and GATA futures market consultant Harvey Organ.

“Exchange for physical” settlements of futures contracts long were considered emergency procedures when a seller was not able to deliver metal from an exchange-approved warehouse and wanted to settle with delivery elsewhere. But now such settlements appear to constitute most gold and silver futures settlements on the Comex. It is a strange development that appears to have been necessitated by the increasing difficulties of central banking’s gold and silver price suppression policy.

GATA has received no acknowledgment of the letter. Its text is below and a PDF copy of it is here:

http://www.gata.org/files/ComptrollerOfCurrencyLetter.pdf

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

* * *

May 5, 2018

Joseph M. Otting, Comptroller of the Currency

U.S. Treasury Department

400 7th Street, SW

Washington DC 20219

Dear Comptroller Otting:

Please let us bring to your attention financial risks to major banks involving their possibly unreported exposure to derivatives in the monetary metals markets.

In recent months gold and silver future contracts issued by U.S. banks on the New York Commodities Exchange have been moved off-exchange for delivery through a mechanism known as “exchange for physical” (EFP) contracts. Until recently use of this mechanism was considered an emergency procedure when a seller did not have access to metal for delivery through Comex warehouses. Now the mechanism seems to be in use for a large share of front-month contracts for which delivery is sought.

Here is an example that is happening at the Comex in the front active month of April for gold and the inactive delivery month of April for silver.

In gold, there were 229,436 EFP contracts for 713.64 tonnes, an average of 10,925 contracts and 1,092,500 ounces per trading day.

In silver, there were 77,150 EFP contracts for 385,750,000 ounces, an average of 3,673 contracts and 18,369,000 ounces per trading day.

London Bullion Market Association rules suggest that these contracts may not be reported to regulators. The LBMA’s bylaws say:

“Figures above exclude any contracts not subject to risk-based capital requirements, such as FX contracts with an original maturity of 14 days or less, futures contracts, written options, and basis swaps. Therefore, the total notional amount of derivatives by maturity will not add to the total derivatives figure in this table.”

We are told that these EFP contracts are transferred from the Comex to London as what are called “serial forwards” and their duration is always less than 14 days, which exempts them from being reported.

It is our understanding that in each quarter your office prepares a report detailing risk undertaken by the banks under the comptroller’s supervision.

These risks include derivatives undertaken by U.S. banks and other obligations that may cause a bank to fail. Our concern is that your office may not be aware of large unreported derivative exposure by banks.

Could you review this matter and let us know your conclusions?

Sincerely,

CHRIS POWELL

Secretary/Treasurer

HARVEY ORGAN

Consultant

Gold Anti-Trust Action Committee Inc.

7 Villa Louisa Road

Manchester, Connecticut 06043-7541

end

Finally, they replied and it was a complete brush off

(courtesy zerohedge)

Currency comptroller brushes off GATA’s inquiry on

gold, silver EFPs

Submitted by cpowell on Fri, 2018-08-10 15:37. Section: Daily Dispatches

11:35a ET Friday, August 10, 2018

Dear Friend of GATA and Gold:

The U.S. comptroller of the currency, a bank regulator, has declined GATA’s request to inquire into the strange explosion of the use of the emergency procedure of “exchange for physicals” in the settlement by banks of the gold and silver futures contracts they have sold on the New York Commodities Exchange.

Your secretary/treasurer and GATA’s consultant about the Comex, Harvey Organ, wrote to the comptroller, James M. Otting, on May 5, calling attention to the recent enormous use of EFPs, which implies derivatives risks being undertaken by U.S. banks that could cause the banks to fail:

http://www.gata.org/node/18303

“Our concern is that your office may not be aware of large unreported derivative exposure by banks,” GATA wrote.

As months passed without any acknowledgment from the comptroller’s office, your secretary/treasurer appealed to his U.S. representative, John B. Larson, D-Connecticut, to ask the comptroller’s office to reply. The congressman’s office made a second inquiry on Monday this week and today the comptroller’s office provided Larson with a copy of a reply written and mailed Wednesday.

The comptroller’s reply, signed by the deputy comptroller for public affairs, Bryan Hubbard, said only that the comptroller’s office has “dedicated examiners” at the largest banks who “continuously evaluate the credit, market, operational, reputation, and compliance risks of bank trading and derivative activities.”

The reply did not say anything about the use of the “exchange for physicals” procedure for settling futures contracts. That is, the reply was a begrudged brushoff and GATA’s letter would have been ignored completely if not for Representative Larson’s repeated intervention.

Of course GATA hardly expected a conscientious reply to its letter, the comptroller’s office being not an independent regulator but part of the Treasury Department, whose mandate includes administration of the Gold Reserve Act of 1934, which, as amended in the 1970s, authorizes the department’s Exchange Stabilization Fund to secretly intervene in and rig any market in the world, directly or through intermediaries:

https://www.treasury.gov/resource-center/international/ESF/Pages/esf-ind…

But there’s always value in demonstrating government’s lack of candor about what it is doing, especially in regard to the monetary metals.

A PDF copy of the reply from the comptroller’s office is posted at GATA’s internet site here:

http://www.gata.org/files/ComptrollerOfCurrencyReply-08-08-2018.pdf

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

With the consumption tax set to rise to 10% Japan is bracing itself for another rush of gold smuggling as gold is taxed in Japan but not Hong Kong

(courtesy Nikkei/Asian Review/GATA)

Japan braces for gold smuggling rush in shadow of tax

hike

Submitted by cpowell on Tue, 2018-09-04 11:37. Section: Daily Dispatches

By Aiko Munakata

Nikkei Asian Review, Tokyo

Tuesday, September 4, 2018

TOKYO — As Japan prepares to raise the consumption tax for the first time in half a decade next year, the Ministry of Finance worries that gold smuggling will also get a boost.

When the tax was last increased in 2014, to 8 percent to 5 percent, smuggling of the precious metal jumped as criminal organizations quickly realized how to game the system for their own enrichment.

The scheme works like this: Procure gold in places like Hong Kong, which does not tax it. Have mules hide it in their luggage and blend in with tourists, traveling to Japan to sell to stores that buy gold from the public. The stores pay for both the gold itself and the consumption tax. The tax component becomes pure profit.

And with the consumption tax set to rise to 10% in October 2019, margins will grow even fatter.

Japan has an unflattering reputation as a “go-to place” for gold smugglers. In 2017, there were 1,347 cases discovered by law enforcement — 112 times the tally from 2013, the year before the last tax hike. Seized gold last year amounted to 6,236 kg, a 47-fold increase.

“It looks like the break-even point for smugglers is between 5 and 8%,” a government source said of the sudden spike.

Japan even “exported” 215 tons of gold in 2017, despite being a producer of only tens of tons domestically. That was almost double the 114 tons exported in 2014.

Official gold imports, meanwhile, dropped to 5 tons in 2017 from 16 tons in 2014. The scale of smuggling is said to exceed 150 tons. …

… For the remainder of the report:

https://asia.nikkei.com/Economy/Japan-braces-for-gold-smuggling-rush-in-…

Craig Hemke at Sprott Money: Comex silver to test

2015 lows

Submitted by cpowell on Tue, 2018-09-04 23:05. Section: Daily Dispatches

7:12p ET Tuesday, September 4, 2018

Dear Friend of GATA and Gold:

Craig Hemke of the TF Metals Report, writing at Sprott Money today, argues that futures trader positioning in the monetary metals, by traditional measures enormously bullish at the moment, may mean nothing if central banks and particularly the People’s Bank of China and the Bank for International Settlements aim to keep selling to keep commodity prices down in tandem with the devaluation of the Chinese yuan

The price-positive aspect of this policy, Hemke writes, is that it may push metal prices below their cost of production and cause mines to suspend operations, resulting in the ultimate strain on supply, whereupon China (and maybe other governments) would acquire the mining industry at distress prices before driving metals prices way up to reliquefy themselves.

In any case most gold and silver mining company executives won’t mind more suppression of the price of their products, as with a few exceptions they mine their shareholders more than their properties. For all the sense they make when they talk about the monetary metals “markets,” they already might as well be speaking Chinese.

Hemke’s analysis is headlined “Comex Silver to Test 2015 Lows” and it’s posted at Sprott Money here:

https://www.sprottmoney.com/Blog/comex-silver-to-test-2015-lows-craig-he…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

Alasdair Macleod was the first to comment that China has already accumulated 20,000 tonnes of gold from 1984 onward.I am also in his camp on that one.

(courtesy Macleod/Max Keiser/Keiser report)

GoldMoney’s Macleod, interviewed on ‘Keiser Report,’ envisions a gold-backed yuan

Submitted by cpowell on Wed, 2018-09-05 00:58. Section: Daily Dispatches

9p ET Tuesday, September 4, 2018

Dear Friend of GATA and Gold:

GoldMoney research director Alasdair Macleod, interviewed this week by Max Keiser on Russia Today’s “Keiser Report,” discusses the possibility that China’s gold reserves are far greater than officially reported and possibly as much as 20,000 tonnes, potentially enabling a gold-backed yuan in a world as yet without a practical alternative to the U.S. dollar as the main reserve currency.

Macleod’s interview begins at the 13-minute mark and continues for about 13 minutes at RT here:

https://www.rt.com/business/437595-post-us-dollar-world/

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

Cryptocurrencies flash crash on new news:

(courtesy zerohedge)

Cryptocurrencies Flash Crash; Bitcoin, Ethereum Plummet

On No News

Just before 6am ET, cryptocurrencies suddenly flash crashed, tumbling on no news with some plunging as much as 12%, after a largely unchanged overnight session.

Bitcoin, the world’s biggest digital asset, erased gains and fell more than 3% in about minutes, tumbling back under $7000 after trading in the mid-$7300 range earlier. Litecoin, Ethereum and Ripple followed, with Ethereum crashing by as much as 12%, while litecoin and ripple sank over 8%. There was no catalyst or news behind the selloff, although as Bloomberg’s Andrew Cinko notes, “perhaps its just part of the risk-off mentality gripping all markets amid the latest round of weakness in emerging markets.”

The selloff appears to have stabilized, but so far there is little buying impetus as traders scramble to find what the cause of the selling was.

_____________________________________________________________________________________________________________________________________________________________________________________

Your early WEDNESDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

i) Chinese yuan vs USA dollar/CLOSED UP TO 6.8313/HUGE DEVALUATION FOR THE PAST FOUR WEEKS STOPS/CHINESE COMING TO USA FOR TRADE TALKS IN NOVEMBER //OFFSHORE YUAN: 6.8519 /shanghai bourse CLOSED DOWN 46.24 POINTS OR 1.68% /HANG SANG CLOSED DOWN 729.49 POINTS OR 2.61%

2. Nikkei closed DOWN 116.07 POINTS OR 0.51%/USA: YEN RISES TO 111.58/

3. Europe stocks OPENED DEEPLY IN THE RED

/USA dollar index FALLS TO 95.41/Euro RISES TO 1.1589

3b Japan 10 year bond yield: RISES TO . +.12/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 111.32/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD IS NOW TARGETED AT .11%/JAPAN LOSING CONTROL OF THEIR BOND MARKET

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 68.95 and Brent: 77.36

3f Gold UP/JAPANESE Yen DOWN/ CHINESE YUAN UP ON SHORE/OFF- SHORE UP

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil DOWN for WTI and DOWN FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund RISES TO +.370%/Italian 10 yr bond yield DOWN to 2.89% /SPAIN 10 YR BOND YIELD UP TO 1.44%

3j Greek 10 year bond yield RISES TO : 4.65

3k Gold at $1194.65 silver at:14.16 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble DOWN 17 /100 in roubles/dollar) 68.36

3m oil into the 68 dollar handle for WTI and 77 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 111.58 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 0.9741 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1285 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now POSITIVE territory with the 10 year RISING to +0.37%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.89% early this morning (THIS IS DEADLY TO ALL MARKETS). Thirty year rate at 3.06%

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

TURKISH LIRA: UP TO 6.6788

“It Will Get A Lot Worse”: Global Stocks Tumble As EM

Contagion Roils Markets

Global stocks tumbled on Wednesday, as a drop in European markets followed a broad sell-off across Asia, as rising pressure on emerging markets intensified concerns of contagion and spillover into developed markets, leading to a sea of red in world stocks.

A day after emerging market currencies tumbled, it was the stock market’s turn in the hot seat, with shares sliding from Japan to Australia, and were crushed in Indonesia, where the nation’s benchmark lost almost 4%. Meanwhile, with no let-up in trade tensions near and new $200bn in US tariffs against China likely to be slapped as soon as tomorrow, the dollar strengthened for a fifth session and commodities slipped, led by oil, while the 10-year Treasury yield eased back to 2.89%.

At the same time, with the Fed showing no signs of slowing its rate hikes, investors are turning ever more cautious on emerging markets. Traders were focused on turmoil in developing nations wondering just how high rates will reach to contain the currency selloff, how acute the resulting economic slowdown will be and whether the volatility will spill into developed markets. Overnight, inflation in the Philippines exceeded 6% for the first time in nine years, joining Turkey and Argentina as another developing economy with soaring prices.

Predictably, the ongoing rout in emerging markets has not only not showed any signs of letting up, but accelerated overnight, with most currencies around the globe sliding against the soaring dollar, while the MSCI index of emerging market stocks heading toward a bear market.

Of the 24 most traded EM currencies only the Mexican Peso (+1.44%) is up YTD. In fact 4 have weakened between 10-20% (Indian Rupee, Chilean Peso, Russian Ruble and South African Rand), one between 20-40% (Brazilian Real) and two more than 40% (Turkish Lira, Argentine Peso).

What was initially an “idiosyncratic” rout in Turkey and Argentina, has since spilled to Brazil, Russia, and overnight slammed South Africa, Indonesia and the Philippines.

The negative tone was set Tuesday by the US ISM report, which showed an unexpected surge in US production that boosted the odds of more rate hikes and a strengthening dollar, while South African entered into a recession in the second quarter. As a result, South African bonds led the sell-off in fixed income as the rand slid to its lowest level in more than two years.

The EM selloff shifted from FX to equities, and the MSCI Emerging Markets Index of shares dropped for a sixth day, set for its steepest slide in three weeks. The emerging-market currency index fell to the lowest level in 16 month, led for a second day by South Africa’s rand.

Worst-hit was Indonesia, where shares tumbled the most in three years amid concern the depreciating rupiah will lead to more rate hikes and higher corporate borrowing costs. Indonesian stocks sank for a fifth day as central bankers attempted to support the rupiah through measures including interest-rate hikes that threaten to slow Southeast Asia’s biggest economy. Meanwhile, the Indonesia Rupee hit another record low against the dollar.

Shares in the Philippines extended losses after a report showed inflation prompted by the sliding currency, surged past 6% last month, foreshadowing further rate hikes.

Elsewhere in Asia, markets traded lower across the board amid ongoing trade uncertainty and ahead of the looming risk events. ASX 200 (-1.0%) declined from the open with broad weakness across its sectors and with firm Q2 GDP data failing to underpin sentiment as the damage had already been done, while Nikkei 225 (-0.5%) was subdued following a destructive and deadly Typhoon which was the strongest to hit Japan in 25 years. Hang Seng (-2.6%) and Shanghai Comp. (-1.7%) were also negative on trade-related jitters as the deadline regarding potential US tariffs on USD 200bln of Chinese goods approaches and following disappointing Chinese Caixin Services and Composite PMI data in which the former posted a 10-month low.

Meanwhile, worries remain that Turkey’s central bank may not do enough at its policy meeting next week to shore up the weakening lira, although for the time being at least the TRY’s volatility has been contained. At the same time, Argentina’s economic outlook has deteriorated even as its officials negotiate with the IMF for accelerated aid. And Russia’s central bank Governor Elvira Nabiullina has begun talking of reasons to raise rates at a meeting next week.

“King dollar” was the main theme in currencies for another day with demand for long exposure in spot and options markets alike. The yen and the Swiss franc stayed in a tighter range than Tuesday as risk-off gained traction with Treasuries bid and a commodity gauge at a three-week low. The pound stayed near day lows even after a slight beat in PMI data while the loonie was little changed before the Bank of Canada rate decision.

The EM contagion has started to make headway into European markets, with the Stoxx 600 dropping as much as 0.9%, flirting with the lowest level in three months. The drop lead by Technology (SX8P -1.8%), Food & Beverages (SX3P -1.6%) and Personal Goods (SXQP -1.5%), while Banks (SX7E little changed) outperformed the broader market. Europe’s mining stocks – the Stoxx 600 basic resources index – dropped as much as 1.3%, flirting with the year lows hit on Aug. 17.

According to Bloomberg, two separate market drivers set the European session, on one hand the rising EM pressure continues to drive cross asset risk-off moves while Italian assets are well supported by further positive budget related comments as the ruling coalition vowed not to take the budget deficit above 2%, a number which changes by the day if not the hour. Italy’s Deputy PM Di Maio said budget will keep accounts in order but will be courageous, adding the government has every intention to last a long time. Di Maio added he cannot say if the 2019 budget deficit will be about 2% of GDP adding the deficit level is not part of today’s talks.

“It has to get a lot worse before it gets better,” Kay Van-Petersen, global macro strategist at Saxo Capital Markets in Singapore, told Bloomberg Television. “Before people talk about structurally buying EM you need to get some kind of comfort on the end of U.S. dollar strength and the end of the Fed tightening and I still think that plays out for a lot longer.”

“This has become now increasingly an issue which is no longer just about EM fundamentals,” Sameer Goel, head of macro strategy for Asia at Deutsche Bank AG in Singapore, said in a Bloomberg TV interview with David Ingles. It’s “increasingly about contagion, which largely happens because of cross-holdings and the pressure of redemptions.”

“Investors have become more selective, and countries with negative news such as weak economic growth, weak external balances and high inflation face stronger sell-offs, ”said Koji Fukaya, chief executive officer at FPG Securities Co. in Tokyo.

In Brexit-related news, EU’s Barnier reportedly deemed PM May’s Chequers plan as unacceptable in a meeting with the Brexit select committee. Instead the EU has urged PM May to adopt a Canada-style deal favoured by former Foreign Minister Johnson. UK’s Cabinet Office Minister Lidington says the Irish border is the only outstanding Brexit issue; adding UK PM May is very committed to a Chequers deal. Merkel’s CSU allies say in a draft document they want a close partnership with the UK post-Brexit; adding they reject a hard Brexit.

In other markets, gold climbed – somewhat surprisingly alongside the stronger dollar – while WTI oil futures dropped in the context of a strong dollar and a potential build at the Cushing, Oklahoma, storage hub.

Expected data include mortgage applications and trade balance. HD Supply, Couche-Tard, and DocuSign are among companies reporting earnings.

Market Snapshot

- S&P 500 futures down 0.4% to 2,888.00

- STOXX Europe 600 down 0.7% to 377.28

- MXAP down 1.4% to 161.55

- MXAPJ down 1.8% to 521.12

- Nikkei down 0.5% to 22,580.83

- Topix down 0.8% to 1,704.96

- Hang Seng Index down 2.6% to 27,243.85

- Shanghai Composite down 1.7% to 2,704.34

- Sensex down 1% to 37,780.71

- Australia S&P/ASX 200 down 1% to 6,230.45

- Kospi down 1% to 2,291.77

- German 10Y yield rose 0.6 bps to 0.363%

- Euro down 0.1% to $1.1567

- Italian 10Y yield fell 14.2 bps to 2.746%

- Spanish 10Y yield fell 0.6 bps to 1.423%

- Brent futures down 0.7% to $77.60/bbl

- Gold spot up 0.3% to $1,195.03

- U.S. Dollar Index little changed at 95.48

Top Overnight News from Bloomberg

- President Donald Trump is asking advisers whether it would be good politics to provoke an October government shutdown fight over money for his border wall, even though Republicans in Congress say a closure before the midterm elections in November would backfire

- European Union officials are exploring how to unlock a wider Brexit deal by making the so-called Irish border backstop more palatable to the U.K., according to a person familiar with the deliberations

- Austria’s new government said it’ll bid for a seat at the European Central Bank’s top table next year as euro-area nations jostle for roles in a shake-up of key monetary and political posts

- Manfred Weber, head of the European People’s Party caucus in the European Parliament, announced Wednesday he is running to replace Jean-Claude Juncker as European Commission president in elections next year

- IMF Managing Director Christine Lagarde said Tuesday evening that IMF officials “made progress” with Argentine leaders seeking to reform the $50 billion credit line agreed upon in June following a sharp selloff in the peso last month

- Europe’s high-yield market is braced for a post-summer rush of new bond sales just as talk of a downturn in the credit cycle gathers pace

- Corporate issuers may start turning to the green-bond market in search of something more than environmental kudos — volatility-proof funding

- Italian Deputy PM Salvini reiterates promise to respect all EU restrictions on budget; working on three-year time frame and will not enact all promises immediately; reports that 2019 budget deficit is seen “around” 2% and proposed flat tax will be postponed

- European Aug. Service PMIs: Spain 52.7 vs 52.0 est; Italy 52.6 vs 53.1 est; France 55.4 vs 55.7 est; Germany 55.0 vs 55.2 est; Eurozone 54.4 vs 54.4 est; U.K. 54.3 vs 53.9 est; Markit note worryingly unbalanced growth with Germany and France solid but Italy and Spain growing sharply slower

- Fed’s Kashkari: various threats to U.S. expansion such as EM weakness, trade battles and Fed hiking too quickly; does not see any indication that U.S. is running above potential

- Politico: U.S. Trade Representative Lighthizer and EU Commissioner Malmstrom will discuss scope of a transatlantic trade deal on Monday Sept. 10, according to people familiar

- BOJ judges its recent YYC adjustments to be working well; not ruling out another change if 10y tests 0.2% and the market function fails to improve, according to people familiar

- China Aug. Caixin Services PMI 51.5 vs 52.6 est.

Asian equity markets traded lower across the board after the Labor Day hangover on Wall St amid ongoing trade uncertainty and ahead of the looming risk events, although the US majors finished off worst levels and Amazon briefly entered the USD 1tln club. ASX 200 (-1.0%) declined from the open with broad weakness across its sectors and with firm Q2 GDP data failing to underpin sentiment as the damage had already been done, while Nikkei 225 (-0.5%) was subdued following a destructive and deadly Typhoon which was the strongest to hit Japan in 25 years. Hang Seng (-2.6%) and Shanghai Comp. (-1.7%) were also negative on trade-related jitters as the deadline regarding potential US tariffs on USD 200bln of Chinese goods approaches and following disappointing Chinese Caixin Services and Composite PMI data in which the former posted a 10-month low. Finally, 10yr JGBs saw mild gains amid the backdrop of the widespread risk-averse tone, although price action was relatively muted and stuck within a tight range despite stronger results at this month’s 10yr JGB auction.

Top Asian News

- BOJ Is Said to See Adjustments Working, Content With Yield Range

- Bank Indonesia to Take Pre-emptive Steps, Warjiyo Says

- Iyer Goes Bollywood to Appeal to Central Bank on Yield Surge

- Indonesia’s Markets Get Hammered by Emerging-Market Contagion

European equities trade on the backfoot (with the exception of the FTSE MIB) as the Euro stoxx 50 index falls over 1%. Sectors are mostly experiencing broad-based losses while financial names are outperforming its peers as Italian banks provide some support to the sector on the back of BTP price action (Italian Banking Index +2.6%). In terms of individual stocks, JC Decaux (+6.6%) rose to the top if the Stoxx 600 on the back of an upgrade, while heavyweight Bayer (-1.7%) pressures Germany’s DAX 30 following uninspiring earnings.

Top European News

- Euro Businesses Show Warning Signs Amid Solid Economic Expansion

- Bahrain Investment Firm Buys Swiss Bank Stake in Europe Push

- Ex-BOE Governor King Attacks Government’s Brexit ‘Incompetence’

- EU Said to Explore Irish Backstop Options to Help May on Brexit

In FX, the focus again was on EM, where amidst more widespread depreciation across the region (and not just contained to currencies), the Zar continues to underperform and extend losses in wake of the ‘unexpected’ Q2 GDP contraction that consigned SA to a first half 2018 recession. Moreover, August’s PMI sank further below the 50.0 threshold to flag ongoing negative economic activity, and the Rand still has next month’s budget update to contend with. Usd/Zar has been just over 15.6900, but currently off worst levels around 15.6000, while the Rub, Mxn and Try also remain on the back foot, with the Cnh retreating as well after recent relative stability and no doubt eyeing the looming threat of additional US import tariffs. DXY -The index remains firmly above recent near 95.000 lows and mainly towards the top of a 95.275-675 range, with broad gains vs almost all rivals, as noted above. GBP – The Pound is lagging G10 counterparts even though the UK services PMI broke the run of disappointing surveys with an unexpected beat vs consensus, with Cable down through 1.2800 again and Eur/Gbp firmly over 0.9000 to retest key chart resistance. The rationale, more reports that chief EU Brexit negotiator Barnier flatly rejects the Chequers White Paper that UK PM May and Raab are resolutely sticking to.

In commodities, WTI and Brent futures retreated to below 69.00/bbl and USD 77.50/bbl levels respectively following yesterday’s bull run. The Gulf of Mexico has been very much in theme recently, in terms of the latest updates, the NHC stated Storm Gordan is moving farther inland but is likely to weaken to a tropical depression later this morning, as a result WTI and Brent may be unwinding some risk premium accumulated from the past couple of days. Hurricane Florance is a little stronger and moving over the open Atlantic, while Hurricane Olivia has weakened slightly, ableit remains a category 3 hurricane. OPEC Secretary General Barkindo emerged this morning, noting the world will attain 100mln BPD of consumption this later this year; adding this is “much sooner” than expected. Furthermore, Lukoil VP Fundun stated Russian oil production has nearly peaked. Traders will be keeping a close eye on any development at the Gulf of Mexico, also of note: the API crude inventories numbers are to be released later today. In the metals complex, gold has found mild reprieve after losing the USD 1200/oz level yesterday while copper is relatively uneventful. Elsewhere, according to the City Environmental Watchdog, China’s top steel-making city, Tangshan will extend summer output cuts across the steel, coke and power sectors into September.

On today’s calendar there will be a bit of focus on the July trade balance reading. Meanwhile NY Fed President John Williams, Minneapolis Fed President Neel Kashkari, and Atlanta Fed President Raphael Bostic are all due to speak at separate events. Also potentially worth keeping an eye on will be the Congressional testimony by executives from Twitter, Facebook and Google on Russia’s involvement in the US election.

US Event Calendar

- 7am: MBA Mortgage Applications, prior -1.7%

- 8:30am: Trade Balance, est. $50.2b deficit, prior $46.3b deficit

DB’s Jim Reid concludes the overnight wrap

EM investors could be excused for having tears in their eyes at the moment with September carrying on the trends of August. The other main story of August – namely Italy – did see positive price action yesterday though, as the endless budget second guessing edged towards the less extreme side. On the EM front, we saw another turbulent day for currencies with South Africa adding to the long list of issues following a second negative quarterly GDP print (-0.7% qoq vs. +0.6% expected) pushing the country into its first recession since 2009.

More on that shortly but the end story for EM FX (-0.65%) was a tenth decline in the last twelve sessions. The South African Rand (-3.16%) led losses and fell to the weakest since June 2016. The Argentine Peso (-1.20%) hit a new all-time low while the Turkish Lira (-0.53%) was weaker for the sixth time in the last seven sessions. Of the 24 most traded EM currencies only the Mexican Peso (+1.44%) is up YTD. In fact 4 have weakened between 10-20% (Indian Rupee, Chilean Peso, Russian Ruble and South African Rand), one between 20-40% (Brazilian Real) and two more than 40% (Turkish Lira, Argentine Peso).

European markets seemed to get swept up in the risk-off emanating from the EM moves. The Stoxx 600 (-0.70%), DAX (-1.10%) and CAC (-1.31%) all fell sharply. The exception was Italy though where the FTSE MIB (+1.01%) climbed for the second successive session along with 10 year BTPs rallying 14.7bps. Headlines trickled in all day with party leaders from the League meeting in Rome with Ansa reporting that they repeated a pledge to “respect EU rules”. However late in the day headlines hit the wires suggesting that Salvini was considering implementing a government programme for the budget over 5 years which, if true, would imply a lot more time for fiscal manoeuvring. At the same time Reuters also reported that the League was targeting a deficit “slightly above 2%”. We’ve lost count of the number of ‘targets’ that now must be out there, but our Italy economists put out this helpful overview of the situation last night

Anyway, as we have come to expect, the US equity market largely ignored most of the above – despite a dip at the open – and in the end although slightly lower it outperformed all other markets (with the exception of Italy). The S&P 500 finished last night -0.17% and NASDAQ -0.23%. Possibly the higher rates and stronger dollar (more below) weighed a little on equities, though this combination was positive for US banks which led gains and closed +0.54%. Amazon also joined Apple in briefly passing the $1tn market cap mark, though with a slightly different price-to-earnings ratio of approximately 200x compared to Apple’s 20x.

Asia appears to be following Europe and EM rather than the US overnight with heavy falls across most bourses. Indeed the Hang Seng (-1.65%), ASX (-0.94%) and Shanghai Comp (-0.92%) have seen the biggest moves while the Nikkei (-0.34%) and Kospi (-0.21%) are also lower. The main stock market in Indonesia is also -3.25% with the Indonesian Rupiah now at the weakest since 1991. It’s hard to ignore the EM data which is coming out at the moment either with the most notable overnight print being Philippines CPI for August which printed at a much higher than expected 6.4% (vs. 5.9% expected) and the highest since 2009. Meanwhile China’s Caixin services PMI also surprised but this time to the downside with the August reading falling 1.3pts to 51.5 (vs. 52.6 expected).

Back to yesterday, if EM FX wasn’t already on the ropes then the knockout blow appeared to come in the afternoon in the form of a bumper ISM manufacturing report across the pond which seemingly helped to contribute to concerns for EM that the Fed and the Dollar strength wouldn’t stop soon. The 61.3 print for August smashed expectations for 57.6 and also represented a jump of 3.2pts from July. That’s the highest reading since 2004, near the highest in 35 years and the biggest one month jump since 2010. New orders (65.1) was the highest since January, employment (58.5) the highest since February and production (63.3) the highest since January. So broad-based strength. Prices paid (72.1) also came in above expectations. Prior to this the manufacturing PMI was also revised up, albeit modestly, by 0.2pts to 54.7, though we certainly put more emphasis on the ISM given its stronger historical track record at predicting growth. Qualitatively, the report said “almost two-thirds (64%) of companies reporting higher input prices explicitly blamed tariffs,” and with the US set to impose another round of tariffs on $200bn of Chinese imports as soon as this week, this issue will continue to dominate headlines. The Atlanta Fed’s Q3 GDP tracker ticked up 0.6pp to 4.7%, largely due to a higher forecast for business fixed investment. DB’s survey tracker ticked up to 3.4%, but we maintain our official forecast for 3.1% GDP growth this quarter.

Treasuries, which in fairness were already a bit weak going into the data, soldoff a bit more post the report and by the close last night 10y yields had ended 3.8bps higher at 2.899%. The 2s10s curve also steepened 1bp and at 24bps is about 5.5bps off the lows from last month. Bond markets across Europe – with the exception of the periphery – were also a bit weaker with Bunds 2.3bps higher in yield. Meanwhile the Dollar index ended up last night +0.31%.

Coming back to currencies it was another weaker day for Sterling yesterday with the Pound edging down another -0.11% versus the Dollar to take the twoday loss to -0.80%. After the fallout from the Brexit rhetoric over the weekend, a Guardian article from Monday night quoting Tory MP Jacob Rees-Mogg and EU Chief Brexit Negotiator Michel Barnier as bonding over a shared assessment that the Chequers plan is “complete rubbish” gained a bit of early attention. Adding to the pain was a much softer than expected August construction PMI (52.9 vs. 54.9 expected). Later in the day BoE Governor Carney’s testimony was more of a nonevent for markets but the main takeaways were that that Carney may well be open to staying on beyond his current term, more rate hikes are likely needed if the UK economy stays on the current path and the BoE is, unsurprisingly, making preparations for a no-deal Brexit but this is not the BoE’s base case.

In terms of what to look forward to today, this morning we’ll also get the remaining August services and composite PMIs in Europe and the UK as well as July retail sales data for the Euro area. In the US there will be a bit of focus on the July trade balance reading. Meanwhile NY Fed President John Williams, Minneapolis Fed President Neel Kashkari, and Atlanta Fed President Raphael Bostic are all due to speak at separate events. Also potentially worth keeping an eye on will be the Congressional testimony by executives from Twitter, Facebook and Google on Russia’s involvement in the US election.

3. ASIAN AFFAIRS

i) WEDNESDAY MORNING/ TUESDAY NIGHT: Shanghai closed DOWN 46.24 POINTS OR 1.68% /Hang Sang CLOSED DOWN 729.49 POINTS OR 2.61%/ / The Nikkei closed DOWN 116.07 POINTS OR 0.51%/Australia’s all ordinaires CLOSED DOWN 0.93% /Chinese yuan (ONSHORE) closed UP at 6.8313 AS POBC HALTS ITS HUGE DEVALUATION /DELEGATION COMING TO THE USA TO SEE TRUMP IN NOVEMBER/Oil DOWN to 68.95 dollars per barrel for WTI and 77.36 for Brent. Stocks in Europe OPENED RED //. ONSHORE YUAN CLOSED UP AT 6.8313 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.8519: HUGE DEVALUATION/PAST SEVERAL DAYS STOPS// TRADE TALKS NOT DOING TOO GOOD : /ONSHORE YUAN TRADING STRONGER AGAINST OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING MUCH STRONGER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

3 a NORTH KOREA/USA

North Korea/South Korea/USA/China

3 b JAPAN AFFAIRS

3C CHINA

4.EUROPEAN AFFAIRS

Germany/UK/Brexit

Germany’s government have softened their key demands on a Brexit and this will ease the path for the UK to strike a deal with the European union

(courtesy zerohedge)

Futures, Cable Spikes On Reports Germany, UK Drop

Key Brexit Demands

As critical dates loom for the Brexit process, Bloomberg reports that the British and German governments have abandoned key Brexit demands, potentially easing the path for the U.K. to strike a deal with the European Union, people familiar with the matter said.

As Bloomberg details, Germany is ready to accept a less detailed agreement on the U.K.’s future economic and trade ties with the EU in a bid to get a Brexit deal done, according to people speaking on condition of anonymity because the discussions are private.

The U.K. side is also willing to settle for a vaguer statement of intent on the future relationship, postponing some decisions until after Brexit day, according to an official who declined to be named.

The shift means that widespread opposition to U.K. Prime Minister Theresa May’s proposal for the future relationship – known as the Chequers plan – isn’t necessarily an obstacle to getting a divorce deal.

A fudged political declaration on the future relationship may also make it easier for May to approve the backstop, according to Mujtaba Rahman, managing director at Eurasia Group, in a note on Wednesday.

“EU negotiators are now calculating that the British prime minister will be able to sign off on the EU’s backstop in the Withdrawal Agreement because she will be able to argue –pointing explicitly to the political declaration — that it will never need to be implemented,” Rahman wrote.

Negotiators in the U.K. and EU were once planning a document of up to 100 pages; now it could be just a tenth of that, officials say.

The reaction to this headline was immediate buying in cable…

And US Equity Futures also jumped…

Still, German Chancellor Angela Merkel warned on Tuesday that “we don’t want these negotiations to fail, but we can’t rule it out completely.”

end

UK/RUSSIA

I can assure you that Putin will not be too happy with these charges against two Russian nationals; Petrov and Boshirov

(courtesy zerohedge)

UK Charges 2 Russian Nationals With Attempted

Murder In Skripal Case

In what appears to be the latest escalation in the UK government’s campaign to blame Russia for the poisoning of former double agent Sergei Skripal, his daughter Yulia Skripal and three other seemingly random Britons (one of whom succumbed to the deadly Novichok nerve agent used in the attacks), British prosecutors are saying they have “sufficient evidence” to charge Alexander Petrov and Ruslan Boshirov, both Russian nationals, with conspiracy to murder Skripal, as well as the attempted murder of his daughter and police detective Nick Bailey, according to Reuters.

Reuters UK

✔@ReutersUK

JUST IN: British prosecutors say they have sufficient evidence to charge two Russian nationals with conspiracy to murder Sergei and Yulia Skripal

The news comes nearly two months after investigators said they had identified the suspected perpetrators of the Novichok attack by crossing referencing CCTV feeds with records of people who entered the country around that time.

Per the BBC, the Crown Prosecution Service said both men, who were identified by the suspected aliases they used to enter the country, flew in from Moscow two days before the poisoning. Both are also around the age of 40. In a statement released after the charges were announced, a spokesperson for the Russian government said the names “don’t mean anything to us.” UK Prime Minister is expected to give a statement later today.

Of course, Russia has denied any involvement in the poisoning, though Russian officials aren’t the only ones who have been skeptical of the UK government’s claims. Tory MP and UK Security Minister Ben Wallace declared that “I think this story belongs in the ‘ill informed and wild speculation’ folder”after investigators said they had identified the suspects.While the Skripals survived the poisoning, Dawn Sturgess, who fell ill around the same time as her boyfriend, Charlie Rowley, eventually died. Police say the latter two victims encountered residue from the Novichok used in the Skripal attack. Bailey, who purportedly encountered the nerve agent during the investigation, eventually recovered.

We imagine Russia will not be pleased if two of its citizen are arrested for a crime considering the serious doubts that have been raised about the evidence. Allies of the UK, including the US, expelled dozens of diplomats following the accusations, which emerged just before Russia hosted the World Cup – an inopportune time to instigate a global diplomatic crisis. While the UK has been content with jumping to conclusions, Russian involvement in the operation would mean they targeted a former MI6 spy, who they released from prison eight years ago, using an ineffective, slow-operating, “military grade” nerve agent, which could be easily traced back to them.

But none of this has deterred the UK so far. However, assuming the men are no longer in the UK, we imagine prosecutors will likely have a difficult time extraditing them to face these charges.

end

Just one small problem with this arrest: both cannot occupy the same space at exactly the same time

have fun with this one;

(courtesy zerohedge)

Russia’s Alleged Skripal ‘Assassins’ Caught Breaking The

Laws Of Physics

As we detailed earlier, in what appears to be the latest escalation in the UK government’s campaign to blame Russia for the poisoning of former double agent Sergei Skripal, his daughter Yulia Skripal and three other seemingly random Britons (one of whom succumbed to the deadly Novichok nerve agent used in the attacks), British prosecutors are saying they have “sufficient evidence” to charge Alexander Petrov and Ruslan Boshirov, both Russian nationals, with conspiracy to murder Skripal, as well as the attempted murder of his daughter and police detective Nick Bailey, according to Reuters.

The news comes nearly two months after investigators said they had identified the suspected perpetrators of the Novichok attack by crossing referencing CCTV feeds with records of people who entered the country around that time.

There’s just one thing… About that CCTV feed!

Russia has apparently developed an astonishing new technology enabling its secret agents to occupy precisely the same space at precisely the same time.

These CCTV images released by Scotland yard today allegedly show Alexander Petrov and Ruslan Borishov both occupying exactly the same space at Gatwick airport at precisely the same second. 16.22.43 on 2 March 2018. Note neither photo shows the other following less than a second behind.

There is no physically possible explanation for this. You can see ten yards behind each of them, and neither has anybody behind for at least ten yards. Yet they were both photographed in the same spot at the same second.

The only possible explanations are:

1) One of the two is traveling faster than Usain Bolt can sprint

2) Scotland Yard has issued doctored CCTV images/timeline.

Will any mainstream media organizations question this publicly?

italy

A good commentary explaining the problems facing Italy as for 20 years, they experienced no growth in their GDP. The new government no doubt will ask Brussels for a bigger increase in their budget spending..probably north of 3% of their GDP. Also the migrant issue is also of extreme importance

(courtesy Chris Wood/Grizzle.com)

Italy’s Stagnant Economy The Most Likely Trigger To

Europe’s Existential Crisis

Authored by Christopher Wood via Grizzle.com,

With the focus on Turkey and the potential related fallout in other emerging markets in recent weeks, it is easy to forget about the Eurozone. Yet the current Italian government is likely to trigger a renewed existential crisis in the Eurozone once the Europeans return from the beach and the Italian Government comes up with a budget for 2019 which is likely to put it in direct conflict with the Maastricht Treaty.

BROKEN BRIDGES UNDER THE EURO

The collapse of a motorway bridge in Genoa last month resulting in 43 deaths, and Italian Interior Minister Matteo Salvini’s exploitation of that event by blaming Brussels-imposed austerity, is a reminder of what is coming.

Having driven over that particularly rickety bridge on more than one occasion, this writer is not surprised to hear about what happened. Similarly, driving through Italy in recent years always serves as a reminder just how poor Italy has become under the euro. Remember, Italy has recorded almost no growth since the formation of the euro at the beginning of 1999, nearly 20 years ago. Italian real GDP has risen by only an annualized 0.4% since 1Q99 and is up only an annualized 0.1% in real GDP per capita terms over the same period (see following chart).

ITALY REAL GDP AND REAL GDP PER CAPITA

Source: CLSA, Datastream

The Italian issue is raised again in part because it is timely with the end of the summer holiday season. The view here remains that a systemic event in financial markets is more likely to be triggered by Italy and the Eurozone than other candidates currently discussed by pundits, be it a Donald Trump-triggered trade war, a much anticipated (by talking heads) Chinese currency collapse or overvalued Wall Street FANG stocks.

Still, they are all interconnected phenomena since, for example, a renewed focus on the existential risks in the Eurozone is likely to put renewed downward pressure on the euro which, if what happened in the second quarter is any guide, will then lead to broader US dollar strength against emerging market currencies. This will in turn make it more challenging for China to manage the capital outflow issue.

BURNING THE BRIDGE TO EUROPE, BUILDING A BRIDGE TO THE US

Returning to the Eurozone issue it is also important to remember what is easily forgotten in the financial markets. That is that the anti-euro, anti-immigration populists in Europe now have a supporter in the White House who is openly encouraging them to pursue their agendas. This is, of course, the exact opposite of what was the case under Barack Obama who, unfortunately, intervened in the Brexit debate in Britain with negative consequences for the ‘Remain’ cause he was supporting.

Donald Trump could not have made it clearer that he supports the cause of those in Italy wanting to leave the euro – just as he could not have made it clearer that he supports Brexit. This is not unimportant since a potential future decision by, say, Italy to walk out of the euro looks a lot less risky politically and economically if it has the support of the American president. This will be particularly the case if that particular American president’s political position has been strengthened by the outcome of the November mid-term elections. This is one reason, among many others, why those elections are becoming rather important. The base case here remains that the Republicans will maintain control of the Congress. But, clearly, that is not consensus.

It is also important to remember that Europe has its own upcoming election cycle. Grizzle refers again to the potentially hugely important May 2019 European parliamentary elections. While the focus of financial markets in the coming quarter will likely be on the Italian Government’s budget, and how Brussels and Berlin will respond, next May’s parliamentary elections are likely to be by far the most significant ever.