GOLD: $1192.40 UP $8.70 (COMEX TO COMEX CLOSINGS)

Silver: $14.68 UP 41 CENTS (COMEX TO COMEX CLOSING)

Closing access prices:

Gold $1192.50

silver: $14.66

OPTIONS EXPIRY IS NOW OVER AT LBMA/LONDON /OTC MARKETS

For comex gold and silver:

SEPT/ and OCT

NUMBER OF NOTICES FILED TODAY FOR SEPT CONTRACT: 0 NOTICE(S) FOR nil OZ

Total number of notices filed so far for Sept: 627 for 62700 (1.9502 tonnes) and this is final

NUMBER OF NOTICES FILED TODAY FOR OCT CONTRACT: 1 NOTICE(S) FOR 100 OZ

Total number of notices filed so far for OCT: 1 for 100 OZ (.003 TONNES)

VERY STRANGE..13.69 TONNES OF GOLD STANDING AND ONLY ONE NOTICE FILED?

For silver:

Sept

490 NOTICE(S) FILED TODAY FOR

2,450,000 OZ/

Total number of notices filed so far this month: 7901 for 39,505,000 oz

AND THIS IS FINAL

FOR OCTOBER

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

30 NOTICE(S) FILED TODAY FOR

150,000 OZ/

Total number of notices filed so far this month: 30 for 150,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: OPENING MORNING TRADE $6664: DOWN $34

Bitcoin: FINAL EVENING TRADE: $6630 DOWN $68

end

First Shanghai gold fix comes at 10 pm est

The second Shanghai gold fix: 2:15 pm

First Shanghai gold fix gold: 10 pm est: $1192.26

NY price at the same time:$1184.50

PREMIUM TO NY SPOT: $7.76

XX

Second gold fix early this morning: $ 1192.72

USA gold at the exact same time:$1183.00

PREMIUM TO NY SPOT: $9.72

XXXX

China is controlling the gold market

WE WILL NOT PROVIDE LONDON FIXES AS THEY ARE NOT ACCURATE AS TO WHAT IS GOING ON AT THE SAME TIME FRAME.

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total OPEN INTEREST FELL BY A TINY SIZED 840 CONTRACTS FROM 204,196 DOWN TO 203,356 WITH YESTERDAY’S 10 CENT FALL IN SILVER PRICING AT THE COMEX. TODAY WE MOVED A LITTLE FURTHER FROM LAST MONTH’S RECORD SETTING OPEN INTEREST OF 244,196 CONTRACTS.

WE HAVE ALSO WITNESSED A LARGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY(WELL OVER 30 MILLION OZ AT THE COMEX FOR JULY , 6 MILLION OZ FOR AUGUST AND NOW JUST LESS THAN 31 MILLION OZ STANDING IN SEPTEMBER. AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A STRONG SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP:

0 EFP’S FOR OCT. 1552 EFP’S FOR DECEMBER AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE: OF 1552 CONTRACTS. WITH THE TRANSFER OF 1552 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 1552 EFP CONTRACTS TRANSLATES INTO 7.76 MILLION OZ ACCOMPANYING:

1.THE 10 CENT FALL IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR THE JUNE/2018 COMEX DELIVERY MONTH. (5.420 MILLION OZ); 30.370 MILLION OZ STANDING FOR DELIVERY IN JULY, FOR AUGUST: 6.065 MILLION OZ AND 39.505 MILLION OZ STANDING IN SEPT. AND 1,105,000 OZ STANDING IN OCTOBER.

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF SEPT:

33,410 CONTRACTS (FOR 19 TRADING DAYS TOTAL 33,410 CONTRACTS) OR 167.050 MILLION OZ: (AVERAGE PER DAY: 1758 CONTRACTS OR 8.792 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF SEPT: 167.05 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 23.86% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2018 TO DATE SILVER EFP’S: 2,204.84 MILLION OZ.

ACCUMULATION FOR JAN 2018: 236.879 MILLION OZ

ACCUMULATION FOR FEB 2018: 244.95 MILLION OZ

ACCUMULATION FOR MARCH 2018: 236.67 MILLION OZ

ACCUMULATION FOR APRIL 2018: 385.75 MILLION OZ

ACCUMULATION FOR MAY 2018: 210.05 MILLION OZ

ACCUMULATION FOR JUNE 2018: 345.43 MILLION OZ

ACCUMULATION FOR JULY 2018: 172.84 MILLION OZ

ACCUMULATION FOR AUGUST 2018: 205.23 MILLION OZ.

ACCUMULATION FOR SEPTEMBER 2018: 167,05 MILLION OZ

RESULT: WE HAD A TINY SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 840 WITH THE 10 CENT FALL IN SILVER PRICING AT THE COMEX YESTERDAY. THE CME NOTIFIED US THAT WE HAD A GOOD SIZED EFP ISSUANCE OF 1552 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) .

TODAY WE GAINED A FAIR SIZED: 712 TOTAL OI CONTRACTS ON THE TWO EXCHANGES:

i.e 1552 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH DECREASE OF 840 OI COMEX CONTRACTS. AND ALL OF THIS DEMAND HAPPENED WITH A 10 CENT FALL IN PRICE OF SILVER AND A CLOSING PRICE OF $14.27 WITH RESPECT TO YESTERDAY’S TRADING. YET WE HAD A GIGANTIC AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY IN THE BIG JULY DELIVERY MONTH OF SLIGHTLY OVER 30 MILLION OZ, IN AUGUST ANOTHER BIG 6.065 MILLION OZ IN A NON ACTIVE MONTH AND NOW IN SEPTEMBER AN INITIAL MONSTROUS 39.505 MILLION OZ OF SILVER STANDING FOR DELIVERY… NOBODY IS PAYING ATTENTION TO THE HUGE NUMBER OF PHYSICAL OUNCES STANDING FOR SILVER THESE PAST SEVERAL MONTHS.

In ounces AT THE COMEX, the OI is still represented by OVER 1 BILLION oz i.e. 1.017 MILLION OZ TO BE EXACT or 145% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT AUGUST MONTH/ THEY FILED AT THE COMEX: 30 NOTICE(S) FOR 150,000 OZ OF SILVER

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 243,411 CONTRACTS ON APRIL 9.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $16.51.

AND NOW WE RECORD FOR POSTERITY ANOTHER ALL TIME RECORD OPEN INTEREST AT THE COMEX OF 244,196 CONTRACTS ON AUGUST 22/2018 AND AGAIN WHEN THIS RECORD WAS SET, THE PRICE OF SILVER WAS $14.78 AND LOWER IN PRICE THAN PREVIOUS RECORDS.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: AN INITIAL HUGE 39.505 MILLION OZ./AND NOW OCTOBER:1,105,000 oz

- HUGE RECORD OPEN INTEREST IN SILVER 243,411 CONTRACTS (OR 1.217 BILLION OZ/ SET APRIL 9/2018) AND NOW AUGUST 22/2018: 244,196 CONTRACTS, WITH A SILVER PRICE OF $14.78.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017

- RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT).

IN GOLD, THE OPEN INTEREST ROSE BY A HUMONGOUS SIZED 7491 CONTRACTS UP TO 460,678 DESPITE THE DROP IN THE COMEX GOLD PRICE/YESTERDAY’S TRADING (A FALL IN PRICE OF $10.90). THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED AN ATMOSPHERIC SIZED 16,786 CONTRACTS: ALWAYS, ON THE WEEK PRIOR TO FIRST DAY NOTICE IN ANY ACTIVE MONTH WHETHER GOLD OR SILVER THE OI COLLAPSES. IT IS HERE THAT THE MIGRANTS RECEIVE THEIR FIAT BONUS FOR ENGAGING IN THIS EXERCISE. THE OPEN INTEREST BEGINS TO RISE ON THAT FIRST DAY NOTICE AND THEY DID NOT DISAPPOINT US TONIGHT.

OCTOBER HAD 0 EFP’S ISSUED AND, DECEMBER HAD AN ISSUANCE OF 16,786 CONTACTS AND ALL OTHER MONTHS ZERO. The NEW COMEX OI for the gold complex rests at 460,678. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE AN ATMOSPHERIC SIZED OI GAIN IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 24,277 CONTRACTS: 7491 OI CONTRACTS INCREASED AT THE COMEX AND 16,786 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN: 24,277 CONTRACTS OR 2,427,700 OZ = 75.51 TONNES. AND ALL OF THIS HUGE DEMAND OCCURRED WITH A FALL IN THE PRICE OF GOLD/ YESTERDAY TO THE TUNE OF $10.90???

YESTERDAY, WE HAD 10993 EFP’S ISSUED.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF SEPT : 151,312 CONTRACTS OR 15,131,200 OZ OR 470.64 TONNES (19 TRADING DAYS AND THUS AVERAGING: 7963 EFP CONTRACTS PER TRADING DAY OR 796,300 OZ/ TRADING DAY),,

TO GIVE YOU AN IDEA AS TO THE HUGE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 19 TRADING DAYS IN TONNES: 470.64 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2017, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 2555 TONNES

THUS EFP TRANSFERS REPRESENTS 470.64/2550 x 100% TONNES = 18.45% OF GLOBAL ANNUAL PRODUCTION SO FAR IN JULY ALONE.***

ACCUMULATION OF GOLD EFP’S YEAR 2018 TO DATE: 5,667.57* TONNES *SURPASSED ANNUAL PROD’N

ACCUMULATION OF GOLD EFP’S FOR JANUARY 2018: 653.22 TONNES (21 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR FEBRUARY 2018: 649.45 TONNES (20 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR MARCH 2018: 741.89 TONNES (22 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR APRIL 2018: 713.84 TONNES (21 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR MAY 2018: 693.80 TONNES ( 22 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR JUNE 2018 650.71 TONNES (21 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR JULY 2018 605.5 TONNES (21 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR AUG. 2018 488.54 TONNES (23 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR SEPT 2018 470.64 TONNES (19 TRADING DAYS)

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A HUMONGOUS SIZED INCREASE IN OI AT THE COMEX OF 7491 DESPITE THE LOSS IN PRICING ($10.90 THAT GOLD UNDERTOOK YESTERDAY) // . WE ALSO HAD AN ATMOSPHERIC SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 16,786 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 16,786 EFP CONTRACTS ISSUED, WE HAD AN OUT OF THIS WORLD GAIN OF 24,277 CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

16786 CONTRACTS MOVE TO LONDON AND 7491 CONTRACTS INCREASED AT THE COMEX. (in tonnes, the GAIN in total oi equates to 75.51 TONNES). ..AND ALL OF HUGE DEMAND OCCURRED WITH A LOSS OF $10.90 IN YESTERDAY’S TRADING AT THE COMEX.???

we had: 1 notice(s) filed upon for 100 oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD...

WITH GOLD UP $8.70 TODAY: /

NO CHANGE IN GOLD INVENTORY AT THE GLD:

/GLD INVENTORY 742.23 TONNES

Inventory rests tonight: 742.23 tonnes.

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

SLV/

WITH SILVER UP A HUGE 41 CENTS TODAY

STRANGE. WE HAD A HUGE CHANGES FOR SILVER : A WITHDRAWAL OF 0.517 MILLION OZ

/INVENTORY RESTS AT 333.046 MILLION OZ.

NOTE THE DIFFERENCE BETWEEN THE GLD AND SLV: THE CROOKS CAN RAID GOLD BECAUSE THEY DO HAVE SOME PHYSICAL. THEY DO NOT RAID SILVER PROBABLY BECAUSE THERE IS NO REAL SILVER INVENTORIES BEHIND THEM

end

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER FELL BY A TINY SIZED 840 CONTRACTS from 204,196 DOWN TO 203,356 AND MOVING A LITTLE FURTHER FROM THE NEW COMEX RECORD SET LAST MONTH AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 1 1/3 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89. AS YOU CAN SEE, WE HAVE RECORD HIGH OPEN INTERESTS IN SILVER ACCOMPANIED BY A CONTINUAL LOWER PRICE WHEN THAT RECORD WAS SET…..

.

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

1552 CONTRACTS FOR DECEMBER AND AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 1552 CONTRACTS . EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI LOSS AT THE COMEX OF 840 CONTRACTS TO THE 1552 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A GOOD NET GAIN OF 712 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES: 3.560 MILLION OZ!!! AND YET WE ALSO HAVE A STRONG DEMAND FOR PHYSICAL AS WE WITNESSED A FINAL STANDING OF GREATER THAN 30 MILLION OZ FOR JULY, A STRONG 6.065 MILLION OZ FOR AUGUST.. A HUGE 39.505 MILLION OZ STANDING FOR SILVER IN SEPTEMBER…AND NOW 1.105 million OZ STANDING FOR THE NON ACTIVE MONTH OF OCTOBER.

RESULT: A SMALL SIZED DECREASE IN SILVER OI AT THE COMEX WITH THE 10 CENT PRICING LOSS THAT SILVER UNDERTOOK IN PRICING YESTERDAY.BUT WE ALSO HAD A GOOD SIZED 1552 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR SEPTEMBER, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i) FRIDAY MORNING/ THURSDAY NIGHT: Shanghai closed UP 29.57 POINTS OR 1.06% //Hang Sang CLOSED UP 72.85 POINTS OR 0.26%//The Nikkei closed UP 323.30 POINTS OR 1.36%/ Australia’s all ordinaires CLOSED UP 0.42% /Chinese yuan (ONSHORE) closed DOWN at 6.8829 AS POBC RESUMES ITS HUGE DEVALUATION /DELEGATION COMING TO THE USA TO SEE TRUMP IN NOVEMBER CANCELLED/Oil UP to 72.11dollars per barrel for WTI and 81.64 for Brent. Stocks in Europe OPENED RED EXCEPT//. ONSHORE YUAN CLOSED DOWN AT 6.8829 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.8771: HUGE DEVALUATION/PAST SEVERAL DAYS RESUMES// TRADE TALKS STOPPED : /ONSHORE YUAN TRADING WEAKER AGAINST OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING STRONGER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

3A/NORTH KOREA/SOUTH KOREA

i)North Korea/South Korea/USA/

b) REPORT ON JAPAN

3 C/ CHINA

4/EUROPEAN AFFAIRS

a)Italy in chaos today as the Italian government is taking on Brussels. Italian stocks crashed the most in two years while the 10 yr Italian bond yield soared to 3.21%

( zerohedge)

b)Europe launches war on Italy’s fiscal plans as they will probably sanction Italy. They are extremely worried about their debt explosion and they also warn Italy that the ECB is the only buyer of Italian debt

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

IRAN.ISRAEL, USA, SAUDI ARABIA ,UAE//

More war of warns from Iran after 25 were killed in a military parade last week. Iran has now threatened Saudi Arabia, UAE Israel and the USA

(courtesy zerohedge/)

6. GLOBAL ISSUES

this could be deadly: a 7.7 earthquake just off the coast of Indonesia setting off tsunami warnings

( zerohedge)

7. OIL ISSUES

8 EMERGING MARKET ISSUES

i)ARGENTINA

As the Argentinian Peso plummets to 41.54, the Central Bank of Argentina skyrockets to 65% which should kill the country.

( zerohedge)

9. PHYSICAL MARKETS

i)Simon Black outlines how gold has retained its value even from 1000 years ago. He explains why we should have gold (physical) backing our wealth.

( Simon Black/SovereignMan)

ii)Peter Hambro is now returning to the Russian gold mine; Petropavlovsk

( Sanderson/London’s Financial times/GATA)

10. USA stories which will influence the price of gold/silver)

MARKET TRADING

a)Another favourite indicator of the Fed shows disappointment as spending is growing faster than incomes for the 7th straight month. It means that spending is occurring because of credit card financing to spend for things they need

( zerohedge)

b)Soft data PMI disappoints and its value is the lowest since April

iv)SWAMP STORIES

a)Last night:

after a powerful opening remarks and after an extremely emotional day, Kavanaugh secures the committee votes. It will now go to the full senate where he should be confirmed.

( zerohedge)

b)This ought to be good: The house Oversight Committee chairman subpoenas the documents detailing Rosenstein’s attempted “palace coup” . Also requested are the Fisa court warrants initiating the whole farce on Carter Page and the genesis of the Russian/Trump election collusion Mueller probe

( zerohedge)

b 2.

Not only have the House Judiciary Committee issued a subpoena for the McCabe Rosenstein “palace coup”

but now they wish to talk to him and he refuses, that they will subpoena him

( zerohedge)_

c)The Democrats game plan is already set: they are plotting to impeach not only Trump but also Kavanaugh

( zerohedge)

d)MORE SWAM STORIES FOR YOUR TONIGHT COURTESY OF THE KING REPORT

Let us head over to the comex:

We are now in the non active delivery month of October and here we had surprisingly a drop of only 20 contracts to stand at 221 contracts. Thus by definition the amount of silver standing in this non active delivery month of October is as follows:

221 contracts x 5000 oz per contract = 1,105,000 oz which is a pretty good showing for a very weak delivery month.

November saw a GAIN of 27 contracts to stand at 468.

AND NOW COMPARISON FOR OCTOBER:

those small specs that have been long in gold added 3670 contracts to their long side

those small specs that have been short in gold added 2255 contracts to their short side.

Conclusions: commercials remove some of their net long positions

end

silver cot

| Silver COT Report: Futures | |||||

| Large Speculators | Commercial | ||||

| Long | Short | Spreading | Long | Short | |

| 79,198 | 102,453 | 15,976 | 76,039 | 70,653 | |

| -826 | -3,087 | 605 | -1,108 | 2,340 | |

| Traders | |||||

| 113 | 71 | 48 | 42 | 39 | |

| Small Speculators | Open Interest | Total | |||

| Long | Short | 204,508 | Long | Short | |

| 33,295 | 15,426 | 171,213 | 189,082 | ||

| 368 | -819 | -961 | -1,329 | -142 | |

| non reportable positions | Positions as of: | 177 | 140 | ||

OUR LARGE SPECULATORS

those large specs that have been long in silver pitched (transferred) 826 contracts from their long side

those large specs that have been short in silver covered (transferred) 3087 contracts from their short side.

OUR COMMERCIALS

those commercials that have been long in silver added 1108 contracts to its long side.

those commercials that have been short in silver added 2340 contracts from its short side

OUR SMALL SPECS

those small specs that have been long in silver added 368 contracts to its long side

those small specs that have been short in silver covered (transferred) 819 contracts from its short side.

Major gold/silver trading /commentaries for FRIDAY

GOLDCORE/BLOG/MARK O’BYRNE.

This Week’s Golden Nuggets – Central Banks, Goldman, Bank of America Positive On Undervalued Gold

News, Commentary, Charts and Videos You May Have Missed

Here is our Friday digest of the important news, commentary, charts and videos we were informed by this week.

We released the Goldnomics Podcast and interviewed the ‘Silver Guru’, David Morgan about how silver and gold have been manipulated lower in the short term, are undervalued and will protect and grow wealth in the coming currency collapse.

Gold and silver prices have fallen again this week and this month and sentiment remains very poor. However, the ‘smart money’ is increasingly positive on gold – including central banks such as the People’s Bank of China and Wall Street banks such as Goldman Sachs and Bank of America (see below).

Contrarian investors continue to buy cheap financial insurance and are accumulating gold and silver coins and bars on this price dip. Precious metal prices can go lower in the short term but falls to the downside are likely to be mild while the potential upside is very substantial.

At these depressed prices, canny contrarian investors are adopting the investment adage – buy low and sell high.

Enjoy and have a nice weekend!

Market Updates and News This Week

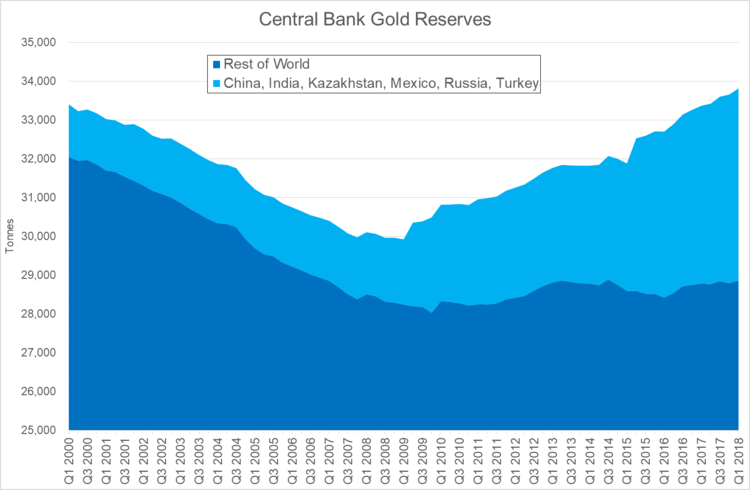

Central Banks Positivity Towards Gold Will Provide Long Term “Support To Gold Prices”

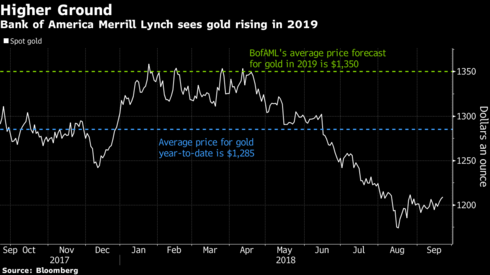

Gold Set to Soar Above $1,300 – Goldman and Bank of America

Charts This Week

Source: Gold Industry Group

Source: Gold Industry Group

Source: Bloomberg

Source: Bloomberg

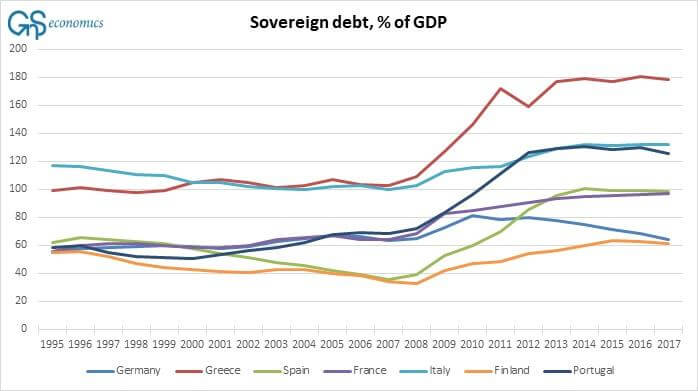

Source: GnS Economics via ZeroHedge

Source: GnS Economics via ZeroHedge

Videos This Week

Gold Prices (LBMA AM)

27 Sep: USD 1,196.00, GBP 911.59 & EUR 1,020.91 per ounce

26 Sep: USD 1,198.80, GBP 910.49 & EUR 1,018.86 per ounce

25 Sep: USD 1,199.45, GBP 912.30 & EUR 1,019.77 per ounce

24 Sep: USD 1,198.75, GBP 913.69 & EUR 1,018.70 per ounce

21 Sep: USD 1,207.60, GBP 914.88 & EUR 1,025.25 per ounce

20 Sep: USD 1,203.00, GBP 910.55 & EUR 1,027.72 per ounce

19 Sep: USD 1,203.00, GBP 912.48 & EUR 1,028.44 per ounce

Silver Prices (LBMA)

27 Sep: USD 14.42, GBP 10.98 & EUR 12.31 per ounce

26 Sep: USD 14.48, GBP 11.01 & EUR 12.32 per ounce

25 Sep: USD 14.29, GBP 10.86 & EUR 12.15 per ounce

24 Sep: USD 14.32, GBP 10.90 & EUR 12.17 per ounce

21 Sep: USD 14.33, GBP 10.87 & EUR 12.18 per ounce

20 Sep: USD 14.23, GBP 10.75 & EUR 12.14 per ounce

19 Sep: USD 14.18, GBP 10.76 & EUR 12.13 per ounce

Recent Market Updates

– Central Banks Positivity Towards Gold Will Provide Long Term “Support To Gold Prices”

– Europe Unveils “Special Purpose Vehicle” With Russia and China To Bypass SWIFT, Jeopardizing Dollar’s Reserve Status

– Gold Set to Soar Above $1,300 – Goldman and Bank of America

– Goldnomics Podcast: Silver Guru – David Morgan – Silver and Gold Will Protect in the Coming Currency Collapse

– This Week’s Golden Nuggets – Dalio’s Dollar Crisis, Fitt’s U.S. Government “Missing” $21 Trillion and Silver Guru’s End of Empire

– Dalio Warns Of Dollar Crisis – “History Is Doomed To Repeat Itself”

– Silver Guru Video: “The End of Empire and End of Fiat Currencies”

– Silver Is ‘Undervalued’ Relative to Stocks, Bonds, Gold – GoldCore

– We Are In “Never Never Land” Accounting As U.S. Government Is “Missing” $21 Trillion

– This Week’s Golden Nuggets – BOE Warns Of UK House Price Crash

END

Andrew Maguire’s Kinesis money which is a “bitcoin” but backed 100% by allocated gold and silver is set to go.

it think it would be a great idea to look at this!

please read at: https://kinesis.money/#/

(Andrew Maguire)

|

|

Dear Harvey Organ,

Thank you for your participation in our webinar on June 7th with our host and CEO of Kinesis, Thomas Coughlin.

The response we received has been incredible, we appreciate you taking the time to join us and hope you found it to be beneficial.

Due to such a high influx of questions we received we were unable to have them all answered. Nevertheless, if there was anything which requires more clarification, or you have a query which needs to be rectified, we invite you to join our telegram group:

We apologize for the technical issues we incurred during the webinar which resulted in it running a little over schedule, we hope that the next one we host will run seamlessly.

A video has been put together and uploaded onto our YouTube channel which can be found here:

Please share and subscribe to our YouTube channel to be notified of all the latest videos as they become available.

The rapid growth that we are currently experiencing has been incredible and with your support, is only going to get better.

We are working behind the scenes very hard to create a better experience for everyone involved! Stay tuned in as we have many more announcements to be released in the upcoming days.

Kind Regards,

|

Kinesis Money

a:C/O ILS Fiduciaries (IOM) Limited, First Floor,Millennium House, Victoria Road, Douglas, Isle of Man IM2 4RW

|

The following is self explanatory

(courtesy GATA/Chris Powell and Harvey Organ)

GATA asks bank regulator to check risks of gold

futures maneuver

Submitted by cpowell on Sun, 2018-06-10 16:17. Section: Daily Dispatches

12:21p ET Sunday, June 10, 2018

Dear Friend of GATA and Gold:

GATA has appealed to the U.S. comptroller of the currency, who has regulatory authority over banks, to review financial risks certain banks may have incurred through derivatives in the monetary metals markets, particularly through the recent heavy use of the “exchange for physicals” mechanism of settling gold and silver futures contracts on the New York Commodities Exchange.

The appeal was made in a letter sent May 5 to the comptroller, Joseph M. Otting, whose office is part of the U.S. Treasury Department, by your secretary/treasurer and GATA futures market consultant Harvey Organ.

“Exchange for physical” settlements of futures contracts long were considered emergency procedures when a seller was not able to deliver metal from an exchange-approved warehouse and wanted to settle with delivery elsewhere. But now such settlements appear to constitute most gold and silver futures settlements on the Comex. It is a strange development that appears to have been necessitated by the increasing difficulties of central banking’s gold and silver price suppression policy.

GATA has received no acknowledgment of the letter. Its text is below and a PDF copy of it is here:

http://www.gata.org/files/ComptrollerOfCurrencyLetter.pdf

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

* * *

May 5, 2018

Joseph M. Otting, Comptroller of the Currency

U.S. Treasury Department

400 7th Street, SW

Washington DC 20219

Dear Comptroller Otting:

Please let us bring to your attention financial risks to major banks involving their possibly unreported exposure to derivatives in the monetary metals markets.

In recent months gold and silver future contracts issued by U.S. banks on the New York Commodities Exchange have been moved off-exchange for delivery through a mechanism known as “exchange for physical” (EFP) contracts. Until recently use of this mechanism was considered an emergency procedure when a seller did not have access to metal for delivery through Comex warehouses. Now the mechanism seems to be in use for a large share of front-month contracts for which delivery is sought.

Here is an example that is happening at the Comex in the front active month of April for gold and the inactive delivery month of April for silver.

In gold, there were 229,436 EFP contracts for 713.64 tonnes, an average of 10,925 contracts and 1,092,500 ounces per trading day.

In silver, there were 77,150 EFP contracts for 385,750,000 ounces, an average of 3,673 contracts and 18,369,000 ounces per trading day.

London Bullion Market Association rules suggest that these contracts may not be reported to regulators. The LBMA’s bylaws say:

“Figures above exclude any contracts not subject to risk-based capital requirements, such as FX contracts with an original maturity of 14 days or less, futures contracts, written options, and basis swaps. Therefore, the total notional amount of derivatives by maturity will not add to the total derivatives figure in this table.”

We are told that these EFP contracts are transferred from the Comex to London as what are called “serial forwards” and their duration is always less than 14 days, which exempts them from being reported.

It is our understanding that in each quarter your office prepares a report detailing risk undertaken by the banks under the comptroller’s supervision.

These risks include derivatives undertaken by U.S. banks and other obligations that may cause a bank to fail. Our concern is that your office may not be aware of large unreported derivative exposure by banks.

Could you review this matter and let us know your conclusions?

Sincerely,

CHRIS POWELL

Secretary/Treasurer

HARVEY ORGAN

Consultant

Gold Anti-Trust Action Committee Inc.

7 Villa Louisa Road

Manchester, Connecticut 06043-7541

end

Finally, they replied and it was a complete brush off

(courtesy zerohedge)

Currency comptroller brushes off GATA’s inquiry on

gold, silver EFPs

Submitted by cpowell on Fri, 2018-08-10 15:37. Section: Daily Dispatches

11:35a ET Friday, August 10, 2018

Dear Friend of GATA and Gold:

The U.S. comptroller of the currency, a bank regulator, has declined GATA’s request to inquire into the strange explosion of the use of the emergency procedure of “exchange for physicals” in the settlement by banks of the gold and silver futures contracts they have sold on the New York Commodities Exchange.

Your secretary/treasurer and GATA’s consultant about the Comex, Harvey Organ, wrote to the comptroller, James M. Otting, on May 5, calling attention to the recent enormous use of EFPs, which implies derivatives risks being undertaken by U.S. banks that could cause the banks to fail:

http://www.gata.org/node/18303

“Our concern is that your office may not be aware of large unreported derivative exposure by banks,” GATA wrote.

As months passed without any acknowledgment from the comptroller’s office, your secretary/treasurer appealed to his U.S. representative, John B. Larson, D-Connecticut, to ask the comptroller’s office to reply. The congressman’s office made a second inquiry on Monday this week and today the comptroller’s office provided Larson with a copy of a reply written and mailed Wednesday.

The comptroller’s reply, signed by the deputy comptroller for public affairs, Bryan Hubbard, said only that the comptroller’s office has “dedicated examiners” at the largest banks who “continuously evaluate the credit, market, operational, reputation, and compliance risks of bank trading and derivative activities.”

The reply did not say anything about the use of the “exchange for physicals” procedure for settling futures contracts. That is, the reply was a begrudged brushoff and GATA’s letter would have been ignored completely if not for Representative Larson’s repeated intervention.

Of course GATA hardly expected a conscientious reply to its letter, the comptroller’s office being not an independent regulator but part of the Treasury Department, whose mandate includes administration of the Gold Reserve Act of 1934, which, as amended in the 1970s, authorizes the department’s Exchange Stabilization Fund to secretly intervene in and rig any market in the world, directly or through intermediaries:

https://www.treasury.gov/resource-center/international/ESF/Pages/esf-ind…

But there’s always value in demonstrating government’s lack of candor about what it is doing, especially in regard to the monetary metals.

A PDF copy of the reply from the comptroller’s office is posted at GATA’s internet site here:

http://www.gata.org/files/ComptrollerOfCurrencyReply-08-08-2018.pdf

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

Simon Black outlines how gold has retained its value even from 1000 years ago. He explains why we should have gold (physical) backing our wealth.

(courtesy Simon Black/SovereignMan)

Look How Well Gold Has Retained Its Value From

1,000 Years Ago

Authored by Simon Black via SovereignMan.com,

On October 12, 929, roughly 1100 years ago, Abd-er Rahman III of the Umayyad Dynasty was proclaimed ruler of Cordova – the Islamic kingdom that comprised most of Spain at the time.

Rahman was just 21 when he ascended to power, and he remained there for nearly 50 years as one of the wealthiest and most powerful monarchs in Europe.

Historians Denis Cardonne and Edward Gibbon calculate his annual tax revenue at approximately 12 million gold dinars… which was a LOT.

The dinar contained 4.25 grams of gold, so 12 million of them would be worth about $2 billion today.

With Cordova’s population estimated at around 500,000 people back in the early 10th century, that works out to be the modern day equivalent of $4,000 in tax per person.

That’s an eerily similar number to modern day tax figures.

The most recent data from the Internal Revenue Service, for example, shows that the average individual income tax is just over $4,000 for every man, woman, and child in the Land of the Free.

(Most of the country, of course, pays nothing.)

It’s an interesting data point that shows just how well gold retains its value over long periods of time.

Records from the same period in Islamic history show that the homes of wealthy individuals were worth between 10,000 and 30,000 dinars, and much higher among the ultra-rich.

That’s roughly $1.7 million to $5 million in today’s money– again, eerily similar to what high-end homes cost today.

Day-to-day, month-to-month, and year-to-year, the price of gold can fluctuate inexplicably.

But over the long term, whether you’re comparing loaves of bread, home prices, or government tax revenue, it REALLY holds its value.

This is one of the things that makes gold such an excellent hedge against political uncertainty, macroeconomic challenges, financial crises, inflation, etc.

Said another way, gold is a great insurance policy for all the “I don’t knows.”

Global debt, for example, recently hit an unfathomable level at nearly $250 TRILLION.

Total US national debt is $21.5 trillion; that exceeds 100% of US GDP, and it’s growing rapidly.

Uncle Sam is burning through cash so quickly that even the Treasury Department expects trillion+ dollar annual budget deficits from now on.

Literally just THREE major line items from the federal budget– Social Security / Medicare, Defense spending, and interest payments on the debt– cost more than ALL the tax revenue that the government collects.

They have to go deeper and deeper into debt to fund EVERYTHING ELSE in the federal government– from Homeland Security to national parks to the light bill at the White House.

That’s not good, considering these ballooning deficits are coming at a time when interest rates are RISING.

So the more debt the government accumulates, their interest payments are growing even more rapidly.

Debt is rising so fast that the Congressional Budget Office estimates interest payments will exceed DEFENSE spending within a few years.

Historically speaking, that’s usually the kiss of death for any empire… when it costs more to service the debt than to defend the nation.

And, not to be a downer, but most of these problems are getting much worse.

10,000 Baby Boomers are retiring every day. And that means ballooning Medicare and Social Security payments.

Meanwhile, there are fewer and fewer young people entering the work force to pay into America’s broken pension system.

In 1960, for example, there was an average of 5.1 workers in the US paying tax into the Social Security system to support every single retiree drawing benefits.

By 2000 that ratio had fallen to 3.4 workers per retiree. Today it’s just 2.6.

Pension funds rely on a steady, growing population and work force to remain stable. So this is pretty much a disaster for Social Security.

The US fertility rate, by the way, is at a record low. So this problem is worsening by the year.

(And the pension / demographic fundamentals in Europe and Japan are even WORSE than they are in the US. . .)

And, remember, all of this is happening at a time when the economy is doing well.

What happens when there’s a major market correction (and people’s retirement savings get wiped out again)? Or there’s a major recession?

Across the water, Europe is drowning in debt with radical political parties taking hold.

Japan, the world’s third-largest economy, has a debt-to-GDP ratio of 236% – more than double that in the US.

Japan’s debt is so huge that the government has to spend nearly 25% of tax revenue just to pay INTEREST!

So let’s just take a step back and summarize–

The world’s largest economy (the US) has a ballooning debt and an unsolvable pension problem, yet is starting a trade war with the world’s second largest economy (China).

Meanwhile the third largest economy in the world (Japan) has to spend nearly one quarter of its tax revenue just to pay interest…

And most of the other top economies in the world (Italy, France, etc.) are drowning in debt and economic stagnation.

It’s impossible to predict EXACTLY how this is going to play out. Or when.

But it certainly seems sensible to have some insurance.

Gold has been around for thousands of years. And, as we discussed earlier, it has a great track record of maintaining value.

But with nearly every other asset in the world trading at / near record high prices today, gold is on sale.

You can buy an ounce of gold today for less than $1,200– 38% below its 2011 high.

(In addition to a low price, there are supply constraints in the gold sector, which could be a major catalyst for higher prices.)

The time to buy insurance is when it’s cheap. . . and when you don’t need it. Because when your house is on fire, it’s already too late.

END

Peter Hambro is now returning to the Russian gold mine; Petropavlovsk

(courtesy Sanderson/London’s Financial times/GATA)

Peter Hambro returns to Russian gold miner

Petropavlovsk

Submitted by cpowell on Thu, 2018-09-27 13:20. Section: Daily Dispatches

By Henry Sanderson

Financial Times, London

Thursday, September 27, 2018

City veteran Peter Hambro has returned to the Russian gold miner he co-founded, Petropavlovsk, following his ousting after a shareholder revolt.

Mr. Hambro will be president of the company and a senior adviser to the board, the company said today.

Mr. Hambro was ousted as an executive in June 2017 by shareholders, following a motion called by Russia’s Renova Group, which is led by billionaire Viktor Vekselberg. He founded the gold miner with Pavel Maslovskiy, current chief executive, in 1994.

Mr. Maslovskiy as well as Roderic Lyne, a former British ambassador to Russia, and Robert Jenkins were all reappointed to the board of Petropavlovsk in June after a second shareholder revolt led by two offshore funds. They were backed by the company’s biggest shareholder, Kenes Rakishev, who launched his own cryptocurrency last year.

Shares in the group rose 2.5 percent this morning. …

… For the remainder of the report:

https://www.ft.com/content/49b81b64-c227-11e8-95b1-d36dfef1b89a

END

Quant specialist pens an article telling us what we have been highlighting to you for the past year: the dollar hegemony is now at risk

(courtesy zerohedge)

JPMorgan’s Marko Kolanovic says dollar hegemony is now at risk

Submitted by cpowell on Thu, 2018-09-27 17:51. Section: Daily Dispatches

By Cecile Gutscher

Bloomberg News

Thursday, September 27, 2018

A backlash against the world’s reserve currency may be brewing as rivals to America look to weaken the dollar’s hold over the global financial system, says Marko Kolanovic, macro-market wiz at JPMorgan Chase & Co.

President Donald Trump’s isolationist foreign policy is a “catalyst for long-term de-dollarization” among countries from Europe and Asia to the Middle East that have long lamented the hegemony of the U.S. currency, he wrote in a note co-authored with Bram Kaplan

“With the current U.S. administration policies of unilateralism, trade wars, and sanctions increasingly affecting both friends and foes, the question arises whether the rest of the world should diversify away from the risks of the U.S. dollar and dollar-centric finance,” said the quantitative and derivatives strategists. …

Gold, which tends to benefit from a weaker greenback, also offers a hedge for any tentative push to de-dollarize. And it’s looking decidedly cheap right now, according to JPMorgan. …

… For the remainder of the report:

https://www.bloomberg.com/news/articles/2018-09-27/jpmorgan-s-marko-kola…

* * *

end

A good commentary from Maria Yavuz of CoinTelegraph.com as she discusses how price stability will be brought to the Crypto world with the introduction of Andrew’s Kinesis

(courtesy zerohedge)

Gold-Based Monetary System To Bring Price Stability

To Crypto

Authored by Maria Yavuz via CoinTelegraph.com,

Gold-based monetary system Kinesis aims to bring price stability to the world of cryptocurrency and to prevent the decrease of its value. The company says it has already attracted interest from key players in the gold industry, which is estimated at $6.8 trillion only on London’s gold market (70 percent of the global trading volume).

image courtesy of CoinTelegraph

After the gold standard that once defined the value of currencies was abandoned in the 20th century, the monetary system became dependent on central banking policies. The Kinesis team decided to create its own “efficient, secure and fair monetary system” based on two of the most stable commodities in the world — gold and silver.

“There is [approximately] $15 trillion in gold traded every year, creating exceptional but untapped potential for investment and exchange if gold can be remonetized. Adding a yield to this exchange multiplies this potential exponentially,” says Thomas Coughlin, CEO of Kinesis.

Kinesis offers digital currencies based 1:1 on allocated physical gold (KAU coins) and silver (KAG coins). When users purchase Kinesis currencies, they actually purchase real metal. The ownership of the gold is digitized with blockchain technology, which allows the user to hold or transfer currency from their Kinesis e-Wallet.

The Kinesis debit card allows the owner to make the instant conversion of KAU and KAG into fiat currency and spend cryptocurrency all around the world. The company states that, unlike other cryptocurrencies, the transactions through the Kinesis system will take just two to three seconds as a result of their bespoke fork of the Stellar network, which is able to withstand over 3,000 transactions per second. Kinesis believes KAU and KAG currencies could be used in day-to-day purchases like buying a cup of coffee or even buying a car. Besides paying the bills, the Kinesis Monetary System can be used for managing international payments with lower transfer rates offered by banks and other international payment services.

Another option offered by the network is the ability to trade holdings on the Kinesis Blockchain Exchange. The cryptocurrencies can be transferred back to physical gold or silver as the system generates a 0.45 percent fee when these are transferred between the holders, accumulating in a pool to be distributed back to users of the system in the form of a yield.

Kinesis was founded by the Allocated Bullion Exchange (ABX), the world’s first electronic, institutional bullion exchange for physical precious metal. Which gave the new blockchain-based fintech company an exceptional start: extensive infrastructure and a fully operational exchange built for the trade and storage of physical bullion in seven locations around the world. The new — but experienced — startup is able to “bring back a truly decentralized, [digitized] stable asset, based on blockchain technology,” Kinesis says.

ITO Launch

Kinesis is currently in the public sale phase of their Initial Token Offering (ITO) of its Velocity Token (KVT), which will be the first cryptocurrency made available by the startup’s team. KVT is a utility token and is not backed by a physical asset but rather a whole monetary system.

With KVT, investors can get a share of the transaction fees generated by the system (maximum 20 percent). This income is distributed to holders of 300,000 KVT, and company promises there will be no future dilution.

According to Kinesis, there is a high demand of its first tokens. Kinesis says it raised over $50 million just in their presale period by selling over 55,000 KVT.

end

______________________________________________________________________________________________________________________________________________________

Your early FRIDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

i) Chinese yuan vs USA dollar/CLOSED DOWN TO 6.8829/HUGE DEVALUATION FOR THE PAST FOUR WEEKS RESUMES/CHINESE COMING TO USA FOR TRADE TALKS IN NOVEMBER CANCELLED //OFFSHORE YUAN: 6.8771 /shanghai bourse CLOSED UP 29.57 POINTS OR 1.06%/HANG SANG CLOSED UP 72.85 POINTS OR 0.26%

2. Nikkei closed UP 323.30 POINTS OR 1.36%/USA: YEN RISES TO 113.42/

3. Europe stocks OPENED IN THE RED

/USA dollar index RISES TO 95.32/Euro FALLS TO 1.1582

3b Japan 10 year bond yield: RISES TO. +.13/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 113.42/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD IS NOW TARGETED AT .11%/JAPAN LOSING CONTROL OF THEIR BOND MARKET

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 72.11 and Brent: 81.64

3f Gold DOWN/JAPANESE Yen DOWN/ CHINESE YUAN: ON SHORE DOWN/OFF- SHORE: UP

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil UP for WTI and UP FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund FALLS TO +.470%/Italian 10 yr bond yield UP to 3.21% /SPAIN 10 YR BOND YIELD UP TO 1.51%

3j Greek 10 year bond yield RISES TO : 4.21

3k Gold at $1182.75 silver at:14.29 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble DOWN 20/100 in roubles/dollar) 65.82

3m oil into the 72 dollar handle for WTI and 81 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 113.42DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 0.9768 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1314 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now POSITIVE territory with the 10 year FALLING to +0.47%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 3.03% early this morning. Thirty year rate at 3.16%

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

6. TURKISH LIRA: UP TO 6.0185

US Futures, Global Markets Slide As Italian Chaos Returns

What started off as a sleepy session after a day in which US traders ignored the market and focused their attention on the Kavanaugh confirmation hearing, resulting in a 50% drop in Thursday trading volumes, quickly escalated with risk-off and a sea of red dominating the board in reaction to Italy settling on a 2.4% deficit/GDP target, which in turn led to a bloodbath for Italian assets over fears that the Italian government is now on collision course with Europe.

Amid the Italian budget chaos, reports initially suggested that President Mattarella had asked Economy Minister to not resign; Tria then followed up these reports by stating that he will stay in the position to avoid ‘chaos’. Italy’s new budget sees debt/GDP to fall in 2019 as according to League lawmaker Bagnai. Italian Deputy PM Di Maio said that the new budget includes €15BN in investments, and he is not worried about the market reaction and spread. When asked about the EU rejecting their budget Italian Deputy PM Salvini said that “they will press ahead”

Observing Italy’s defiance, Europe’s Stoxx 600 Index dropped, led lower by the Italian FTSE MIB which tumbled -3.8%, the biggest one day drop since June 2016, led by the Italian bank index which plunged by 6.8%.

Italian BTP futures gapped lower, with cash 10y yields higher by ~36bps, the biggest jump in 4 months, with the BTP curve bear flattening.

Italy’s planned fiscal deficit of 2.4% for 2019 is “a much more expansionary budget that not only risks some push-back by the European Commission, but also may risk seeing both ratings agencies and investors question the Italian government’s debt sustainability,” said ING Bank’s Viraj Patel.

While no sharp activity was observed in FRA/OIS to indicate acute risk, and no large widening of credit spreads either, the action in Italy today is certainly concerning and unless the ruling populist coalition finds a way to soothe markets, it will likely continue into October.

Safe haven bunds rallied from the open and accelerate higher after a surprisingly low core euro-zone CPI, while US Treasury futures dragged towards yesterday’s high.

Amid growing fears that Italy could once again jeopardise the future of the common currency, the Euro accelerated its 2-day selloff, pushing below 1.16, a 3-week low.

Meanwhile in Asia, there was a brief spike higher in yuan due to activity in front-end of the forward curve, with quarter-end and upcoming week-long China market closure cited as drivers.

S&P futures fell to session lows as US traders walked in to their trading desks greeted by a sea of red, and observing the chaos in Italy and certainly the dramatic declines in Italian banks, such as the 7.3% beating Intesa Sanpaolo is taking.

Meanwhile, treasuries and the dollar jumped to the highest level since September 12. The Bloomberg Dollar Spot Index was set to post a second straight quarterly increase for the first time since 2015 as month-end flows supported the U.S. currency.

The pound touched a two-week low after U.K. yearly GDP data missed estimates and the current-account deficit widened more than economists forecast.

There was more cheer in Asia, where the yen’s slide to the weakest level this year amid quarter-end portfolio rebalancing weighed on the currency and helped stoke Japanese stocks as Asian equities advanced from Sydney to Shanghai; Mrs Watanabe was happy as the Nikkei hit a fresh 27 year high, if still 38% below its 38,916 all time high in 1989.

Japanese yields rose after the Bank of Japan paved the way to reduce purchases of super-long bonds. Oil remained on course for the longest run of weekly gains in four months as energy giants to Wall Street banks predicted the return of $100 crude on an impending supply crunch.

In Brexit news, former UK Foreign Minister Johnson called on PM May to scrap her Brexit proposals in which he stated it would leave UK “half in and half out” of the EU and proposed a six-part alternative plan for Brexit. Separately, teports in the Times suggests that Conservative policymakers are struggling to figure out how to counter Jeremy Corbyn’s populist message at their upcoming party conference.

In geopolitical news, a senior Iranian Cleric says US regional bases would not be safe if Washington does something wrong.

As Bloomberg summarizes, political risks have returned to the top of investors’ agenda at the end of a quarter dominated by central banks and emerging-market crises. In Italy, populists won their battle to fund costly campaign promises, while infighting over Brexit is embroiling the U.K.’s Conservative Party ahead of a conference next week. In the U.S., the confirmation of President Donald Trump’s Supreme Court pick, Brett Kavanaugh, has turned toxic amid allegations of sexual assault. Data on consumer spending, income and inflation may return the focus to the American economy later Friday.

Commodity markets were less exciting, with oil trading within a thin range heading into the week’s end, with Brent and WTI hanging just below the USD 82/bbl and USD 72.50/bbl areas. The gold market is also lacking any major catalysts, with the yellow metal languishing around the 6 week lows set in Thursday’s session. The most significant moves in commodities markets has been seen in steel and coke, where Shanghai rebar fell by over 2% and both materials hit 2 month lows amid speculation that China has shelved blanket production cuts for winter, stoking the flame for more expected output.

Vail Resorts, BlackBerry are due to report earnings. Economic data include U. of Michigan survey, personal spending

Market Snapshot

- S&P 500 futures up 0.02% to 2,920.50

- STOXX Europe 600 down 0.3% to 385.31

- MXAP up 0.3% to 165.37

- MXAPJ down 0.02% to 525.73

- Nikkei up 1.4% to 24,120.04

- Topix up 1% to 1,817.25

- Hang Seng Index up 0.3% to 27,788.52

- Shanghai Composite up 1.1% to 2,821.35

- Sensex down 0.5% to 36,133.04

- Australia S&P/ASX 200 up 0.4% to 6,207.56

- Kospi down 0.5% to 2,343.07

- German 10Y yield fell 2.8 bps to 0.501%

- Euro down 0.2% to $1.1621

- Brent Futures up 0.2% to $81.87/bbl

- Italian 10Y yield rose 2.8 bps to 2.527%

- Spanish 10Y yield rose 1.4 bps to 1.519%

- Brent Futures up 0.2% to $81.87/bbl

- Gold spot up 0.08% to $1,183.81

- U.S. Dollar Index up 0.2% to 95.09

Top Overnight News

- China is preparing to issue a sovereign dollar-denominated bond next month, its first in almost a year, according to people familiar with the matter

- Italy’s bonds may fall at the start of Friday’s trading after the government set next year’s budget deficit target at 2.4 percent, wider than the market originally envisaged.

- Leading indicators for China’s economy show growth continued slowing in September amid the escalating trade war with the U.S. The data suggest the dispute was weighing on economic activity even before the latest round of tariffs, which took effect this week

- Nicky Morgan, who chairs Parliament’s Treasury Committee, threatens to explore new regulations for “market-sensitive polling” unless pollsters overhaul their own standards as lucrative polls conducted in secret for hedge funds, revealed by a Bloomberg investigation into the 2016 Brexit vote, “risk damaging the reputation of U.K. financial markets”

- The U.K. current-account deficit widened more than economists forecast in the second quarter, raising fresh questions about the sustainability of the shortfall as Britain prepares for Brexit

- Swiss asset manager and commodities trader Tiberius Group AG is stepping into the $215 billion digital coin market by offering a new token backed by seven metals in a sale set for Oct. 1

Asian stocks traded mostly higher following a spur in risk-appetite and an upbeat lead on Wall St where bourses ended the day in the green, and Nasdaq outperformed its peers amid the strength in the IT sector, after Apple rallied on the news that JP Morgan sees a 23% upside in their shares. ASX 200 (+0.4%) was lifted by resources and IT names, while Nikkei 225 (+1.4%) outperformed its peers and breached YTD highs to print levels last seen in 1991 amid currency effects and optimistic retail sales. Elsewhere, Hang Seng (+0.3%) and Shanghai Comp. (+1.0%) also gained as trade concerns faded and the positive sentiment dominated the region ahead of next week’s National Day Golden Week holiday. Finally, 10yr JGBs were lower amid the heightened risk appetite although found support ahead of 150.00 while the 2yr JGB auction was uninspiring.

Top Asian News

- How Indian Credit Raters Missed an Epic Fail at a Financier

- BOJ Paves Way to Cut Purchases of Super-Long Bonds in October

- China Prepares for $3 Billion Dollar Bond Sale in October

- Hong Kong Property Shares Decline on Sales Slowdown Concerns

European equities are once again being guided by updates from Italy, where the Government agreed to a 2.4% debt/GDP ratio. Italian stocks are leading the losses, with Italian bank stocks (Ubi Banca -6.0%, UniCredit -6.3%, Intesa Sanpaolo -6.3% and BPER Banca -8.0%) dominating the bottom of the Stoxx 600, as Italian 10 year bond yields continue rising above 3%. This weakness is spreading to banking names in Europe with all of Commerzbank, Credit Agricole and SocGen shares trading at a loss of over 3%, and the financial sector the marked sector underperformer. RSA (-10%) is at the foot of the index as the insurer provided poor Q3 underwriting results. the FTSE is the index outperformer for the second straight session, and is being aided by a weaker GBP.

Top European News

- U.K. Current-Account Deficit Widens; Business Investment Falls

- Knorr-Bremse Plans IPO Valuing Brake Maker Up to $16 Billion

- Buy Europe Value Stocks as Italy Concerns Will Subside, MS Says

- Germany: U.S. Sanctions on Nord Stream May Come in Early Nov.

In FX, the USD index has extended post-FOMC gains to just over 95.000, but the Greenback is not bid across the board by any means even though some rebalancing models for the end of September are pointing to a mild bid. EUR/GBP/JPY/NZD – The major laggards, as the single currency continues to bear the brunt of Italian budget concerns that have intensified following the coalitions Government’s decision to test the EU boundaries with a 2.4% deficit for 2019. Eur/Usd is only just holding around 1.1600 having breached a series of chart supports and the 30 DMA at 1.1646. Cable is also looking precarious close to its 21 DMA and double bottoms all around 1.3055 following a brief dip below on the back of weaker than forecast UK GDP data. Usd/Jpy has broken higher again, and more convincingly through a tech level at 113.24, which could be pivotal on a closing basis given month, quarter and Japanese half year end. The Kiwi looks hampered by ongoing RBNZ policy neutrality and also anchored by a big option expiry at the 0.6600 strike.

In commodities, the oil market is uneventful and trading within a thin range heading in to the week’s end, with Brent and WTI hanging just below the USD 82/bbl and USD 72.50/bbl areas. The gold market is also lacking any major catalysts, with the yellow metal languishing around the 6 week lows set in Thursday’s session. The most significant moves in commodities markets has been seen in steel and coke, where Shanghai rebar fell by over 2% and both materials hit 2 month lows amid speculation that China has shelved blanket production cuts for winter, stoking the flame for more expected output.

US Event Calendar

- 8:30am: Personal Income, est. 0.4%, prior 0.3%; Personal Spending, est. 0.3%, prior 0.4%

- 8:30am: PCE Deflator MoM, est. 0.1%, prior 0.1%; PCE Deflator YoY, est. 2.2%, prior 2.3%

- 8:30am: PCE Core MoM, est. 0.1%, prior 0.2%; PCE Core YoY, est. 2.0%, prior 2.0%

- 9:45am: Chicago Purchasing Manager, est. 62, prior 63.6

- 10am: U. of Mich. Sentiment, est. 100.6, prior 100.8; Current Conditions, prior 116.1; Expectations, prior 91.1

3. ASIAN AFFAIRS

i) FRIDAY MORNING/ THURSDAY NIGHT: Shanghai closed UP 29.57 POINTS OR 1.06% //Hang Sang CLOSED UP 72.85 POINTS OR 0.26%//The Nikkei closed UP 323.30 POINTS OR 1.36%/ Australia’s all ordinaires CLOSED UP 0.42% /Chinese yuan (ONSHORE) closed DOWN at 6.8829 AS POBC RESUMES ITS HUGE DEVALUATION /DELEGATION COMING TO THE USA TO SEE TRUMP IN NOVEMBER CANCELLED/Oil UP to 72.11dollars per barrel for WTI and 81.64 for Brent. Stocks inEurope OPENED RED EXCEPT//. ONSHORE YUAN CLOSED DOWN AT 6.8829 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.8771: HUGE DEVALUATION/PAST SEVERAL DAYS RESUMES// TRADE TALKS STOPPED : /ONSHORE YUAN TRADING WEAKER AGAINST OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING STRONGER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

3 a NORTH KOREA/USA

North Korea/South Korea/USA/China

3 b JAPAN AFFAIRS

3C CHINA

4.EUROPEAN AFFAIRS

Italy in chaos today as the Italian government is taking on Brussels. Italian stocks crashed the most in two years while the 10 yr Italian bond yield soared to 3.21%

(courtesy zerohedge)

Italian Stocks Crash Most In 2 Years, Bond Yields Soar

Amid Budget Deficit Liquidation Panic

After yesterday’s last minute decision by Italy’s ruling coalition to boost the country’s 2019 deficit to 2.4% of GDP, a number that challenged Brussels and its demands for a deficit no greater than 2.0% and made a mockery of the finance minister’s insistence on a funding hole no greater than 1.6% of GDP, we said that it was only a matter of time before the market freaked out as Italy is now on collision course with Europe, and that time came this morning when traders dumped Italian assets with the bathwater, as Italian equities, bank stocks and bonds all tumbled in unison after deputy premier Matteo Salvini vowed to “press ahead” with the controversial budget plan including a deficit that would be three times larger than the deficit under the previous administration.

Italy’s FTSE MIB stock index tumbled to session lows, down 3.7%, after opening sharply lower and failing to find a floor so far; this was the biggest intraday drop for Italian stocks since June 2016, with several banking stocks halted limit down.

The worst performing sector were Italian banks, with the FTSE Italia All-Share Banks Index falling as much as 5.3%, most since May; the biggest decliners were Banco BPM -6%, UBI -4.7%, UniCredit -3.9%, Intesa -3.5%, with most of them being halted, limit down amid the selling chaos.

The bond market was not spared, and Italy’s 10Y bond was taken to the cleaners as the relentless selling sent the yield some 36bps higher to 3.25%…

… surpassing the peaks hit during the recent two Italian liquidation panics.

Italian debt had been volatile in recent days,but rallied for much of September in anticipation economy minister Giovanni Tria would reel in the government’s spending plans. That failed to happen last night when Tria capitulated to demands by Salvini and Di Maio to boost the deficit to support populist promises for basic income which would cost some €10 billion.

Aberdeen Investments’ James Athey said he did not believe the Italian sell-off would necessarily start to “feed on itself” just yet. Nonetheless, he said investors would need greater compensation for holding Italian debt given the higher borrowing levels implied by the new budget, adding that the mood has clearly changed.

“It’s interesting that the first couple of pieces I read from the sell side today are from people who were bullish Italy and are now looking for bearish Italian trades,” he said. “The next three to six months are clearly going to be challenging. We are short and we’re staying short.”

Alternatively, the next 3 to 6 hours may be just as challenger, because the accelerating Italian selloff sent shockwaves around Europe, and led to an acceleration in the selling of the Euro which hit session lows, down over 200 pips in the past two days.

The key driver behind the market’s panicked response is the unknown of how a furious Europe will respond to the Italian defiance, in which the newly elected populist government is now in open confrontation that could ultimately threaten the existence of the euro.

As the FT notes, with the Continent still reeling from a debt crisis that saw the collapse of the Cypriot banking system and nearly led to rebellious Greeks to abandon the Euro, the European Commission fears that an explosion of debt ushered in by Italy’s ruling coalition – which includes the far-right, anti-immigrant League and anti-establishment Five Star Movement – could lead to international investors losing confidence in the eurozone and – more importantly – its debt.

Meanwhile, far from expressing concern, the budget agreement was celebrated by leaders in the coalition Italian government. Luigi Di Maio, the 32-year-old leader of the anti-establishment Five Star Movement, the largest party in the populist coalition, was greeted by a crowd of cheering party members waving flags after emerging from a cabinet meeting on Thursday night.

Di Maio hailed the agreement as a “historic day”. “We made it!” he said, as he emerged from a balcony at Rome’s Palazzo Chigi, where the meeting took place.

“Today we have changed Italy! For the first time the state is on the side of the citizens,” he added, as ministers and members of parliament from his party hugged each other on the square outside.

Matteo Salvini, leader of the hard-right League, part of the coalition and deputy prime minister alongside Mr Di Maio, also welcomed the agreement on spending, saying he was “fully satisfied with the objectives achieved”, which would include his party’s pledges for tax cuts and a reversal of unpopular pension reforms dating back to 2011.

All eyes were on technocratic finmin Giovanni Tria, who had been pressing for a deficit number as low as 1.6% of GDP going into the meeting. On Thursday night, Tria said that he would not resign, and instead would stay according to newspaper la Repubblica reports: “I won’t quit, just for the good of the country, I will do it for patriotism. Otherwise there would be the risk of a financial storm. We would throw the country into chaos,” Tria said.

Still, “the fact that the final agreement sees spending plans three times the initial projections for 2019 . . . very much suggests that Tria does not command the level of influence he was thought to have had,” wrote analysts at Rabobank.

At the same time, strategists at Commerzbank cautioned that while a 2.4% budget deficit need not trigger a new “escalation” for Italian bonds, the reality is that Tria, a former academic who is widely seen as a moderating force in the government, has been weakened and that the “risk and reward” has shifted for investors.

For now the Italian contagion has been limited, and while yields on Spanish and Portuguese government debt also rose on Friday, the moves were far more muted. The yield on 10-year Spanish bonds edged up 2 basis points to 1.52 per cent as that on the equivalent Portuguese bond rose 2bp to 1.87 per cent. However, should the Italian selling accelerate, it is unlikely that the selling panic will remain within Italy’s borders.

Europe Launches War On Italy’s Fiscal Plans: Warns Of Debt “Explosion”, Threatens Savers

In the aftermath of Italy’s defiant announcement that it would expand its 2019 budget deficit to 2.4% of GDP, above both the initial proposal from finmin Tria which was 1.6%, and also higher than the European “redline” of 2.0%, the question was how would Europe respond to this open mutiny by Italy.

The answers started to emerge on Friday, when European Parliament head Antonio Tajani said that fiscal targets set by Italy’s eurosceptic government were “against the people” and could hit savers without creating jobs.

“I am very concerned for what is happening in Italy,” said Tajani, who is a center-right opposition politician in Italy and close ally to former Prime Minister Silvio Berlusconi. The budgetary plans “will not raise employment but will cause trouble to the savings of the Italians,” Tajani said.

“This budget is not for the people, it is against the people,” Tajani said, adding that the planned measures “will create many problems in the north (of Italy) without solving problems in the south,” which is the least developed part of the country.

Separately, Pierre Moscovici, EU Economic Affairs Commissioner, said in an interview with BFM television that “Italy, which has debt at 132 percent, chooses expansion and stimulus. It’s “a budget that looks like jaywalking, and out of line with our rules.”

As a reminder, Italy has the most public debt of any European country, surpassing both France and Germany, and its debt/GDP is the second highest in the EU after bailed-out Greece; until recently, Italy had committed for next year to a deficit three times smaller.

The verbal fireworks continued, with Moscovici reminding Italy that the only reason its “explosive” debt hasn’t collapsed is due to the ECB’s purchases, which has been actively monetizing it for the past few years.

“We have no interest in a crisis between the Commission and Italy,” Moscovici said. “But it’s also not in our interest for Italy to not respect the rules and not reduce its public debt, which remains explosive.”

In turn, Italy’s Di Maio swiftly brushed away Moscovici, with Bloomberg quoting him as telling reporters at a Rome event that “the concerns are legitimate but the government has committed itself to maintaining the deficit-GDP at 2.4 percent and we want to repay the debt.” Salvini was similarly confident. “Markets will come to terms with the budget,” he said in a Facebook video.

The verbal spat took place amid a broad-based liquidation of Italian assets which saw 10Y Italian yields rise as much as 35 basis points to 3.24%, the biggest increase since a rout in May during the government’s formation. The yield spread over Germany reached a three-week high.

Christoph Rieger, Commerzbank’s head of fixed-rate strategy chimed in, saying that investors are right to be nervous with the budget compromise at the high end of the range that had been talked about before.

“And what weighs more, it has demolished Tria’s credibility,” Rieger said. “This underlines the balance of power within the government, and having a lame duck finance minister in this situation will require a higher risk premium.”

For now, the European response to Italy’s defiance has been confined to verbal escalation. As Bloomberg notes, Italy has to submit its 2019 budget for approval to the Commission by Oct. 15, at which point Brussels has the power to impose fines of up to 0.2% of GDP on countries that persistently break the bloc’s fiscal rules. What would complicate a crackdown on Italy is that when “push came to shove” in 2016, the Commission opted to not penalize Spain and Portugal – the culprits at the time – and instead imposed symbolic zero sanctions.

The decision was seen at the time as an effort by the EU’s executive arm to not alienate its members amid rising populism and discontent with austerity. But for many EU officials, it tarnished the credibility of the bloc’s fiscal rules.

As such, any sanctioning of Italy will be seen as a personal vendetta against the Mediterranean country.

Additionally, the loosened budget target is seen as a setback for finance minister Tria and President Mattarella, who had “sought to moderate the more extreme instincts of the government” formed in June by Di Maio’s anti-establishment Five Star Movement and Salvini’s anti-migrant League according to Bloomberg. On the other hand, it shouldn’t be surprising that a country which has demanded populist policies ends up with just that.

As for the technocratic Tria, who initially brought a sense of calm among investors due to his moderate approach, and whose budget recommendations were trampled, he said said he’ll stay in his job because he has a responsibility to help maintain stability, La Repubblica newspaper reported. One look at the turmoil in Italian markets this morning would suggest that he has failed at that job as well…

5.RUSSIAN AND MIDDLE EASTERN AFFAIRS

IRAN.ISRAEL, USA, SAUDI ARABIA ,UAE//

More war of warns from Iran after 25 were killed in a military parade last week. Iran has now threatened Saudi Arabia, UAE Israel and the USA

(courtesy zerohedge/)

Iran Warns Saudis Of “Red Lines” And Threatens US Bases “Will Not Be Safe”

Iran has issued a number of threats on Friday following official charges made by leaders in Tehran that Saudi Arabia and the UAE funded a terrorist attack on a military parade in a southwest district last Saturday which killed 25 people, including members of the elite Iran’s Revolutionary Guards (IRGC).

Iranian military officials declared “red lines” against the two Gulf countries, threatening war, while in a separate statement a senior cleric said US regional bases will not be safe if “America does anything wrong”.

“If America does anything wrong, their bases around Iran would not remain secure,” Ayatollah Mohammadali Movahedi Kermani was quoted as saying by Mizan news agency while leading Friday prayers in Tehran.

And simultaneously the Fars news agency quoted Brigadier General Hossein Salami, deputy head of the IRGC, as saying in reference to the Saudis and Emirates: “If you cross our red lines, we will surely cross yours. You know the storm the Iranian nation can create.”

IRGC Gen. Salami was also addressing the crowd during Friday prayers in Tehran: “Stop creating plots and tensions. You are not invincible. You are sitting in a glass house and cannot tolerate the revenge of the Iranian nation…We have shown self-restraint,” he said in a fiery speech.

Salami didn’t stop at Saudi Arabia and the UAE, but told the United States to “stop supporting the terrorists or they will pay the price”. The elite IRGC has collectively vowed to exact “deadly and unforgettable” vengeance after some of its members were killed in the Ahvaz attack. During the large funeral ceremony for victims of the attack on Monday, Salami had vowed to strike back against the “triangle” of Saudi Arabia, Israel and the United States.

Iran had previously also accused the US of providing support to the gunmen that carried out last weekend’s attack despite Washington’s firm denials that it has any links to the incident. This follows years of Tehran blaming Washington and its Gulf allies for the rise of ISIS and other radical Sunni terror groups.

There’s been some level of confusion and contradictory claims of responsibility after the incident, however, with both a regional Ahvaz separatist group and ISIS claiming responsibility. Iran now says it has members of those involved in the plot in custody.

The bellicose words on Friday further come after Israeli PM Netanyahu spoke before the UN General Assembly the day before, claiming a new atomic weapons development facility in Tehran; something which US intelligence officials have already publicly doubted, according to statements made to Reuters.

END

6. GLOBAL ISSUES

this could be deadly: a 7.7 earthquake just off the coast of Indonesia setting off tsunami warnings

(courtesy zerohedge)

Massive 7.7 Magnitude Earthquake Recorded Off Coast Of Indonesia

A massive magnitude 7.7 earthquake struck off the Indonesia island of Sumatra, prompting tsunami warnings across the Pacific ring of fire, according to USGS. The quake followed a smaller quake killed one person and damaged some homes.

Zach Covey

✔@ZachWPDE

#BREAKING: A magnitude 7.5 earthquake struck just minutes ago 48 miles North of Palu, Indonesia. A tsunami alert, meaning watch for updates and be ready to evacuate, is in effect for the island chain. No Tsunami Warning is in effect for the United States.