GOLD: $1201.60 UP $3.75 (COMEX TO COMEX CLOSINGS)

Silver: $14.63 UP 5 CENTS (COMEX TO COMEX CLOSING)

Closing access prices:

Gold : 1203.00

silver: $14.65

For comex gold and silver:

OCT

NUMBER OF NOTICES FILED TODAY FOR OCT CONTRACT: 0 NOTICE(S) FOR NIL OZ

Total number of notices filed so far for OCT: 850 for 100 OZ (2.6438 TONNES)

FOR OCTOBER

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

0 NOTICE(S) FILED TODAY FOR

NIL OZ/

Total number of notices filed so far this month: 295 for 1,475,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: OPENING MORNING TRADE $6593: UP $2

Bitcoin: FINAL EVENING TRADE: $6595 UP $4

end

First Shanghai gold fix comes at 10 pm est

The second Shanghai gold fix: 2:15 pm

First Shanghai gold fix gold: 10 pm est: $not available

NY price at the same time:$xxx

PREMIUM TO NY SPOT: $xxx

XX

Second gold fix early this morning: $ NOT AVAILABLE

USA gold at the exact same time:$XXX

PREMIUM TO NY SPOT: $XXX

XXXX

China is controlling the gold market

WE WILL NOT PROVIDE LONDON FIXES AS THEY ARE NOT ACCURATE AS TO WHAT IS GOING ON AT THE SAME TIME FRAME.

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total OPEN INTEREST ROSE BY A CONSIDERABLE SIZED 1185 CONTRACTS FROM 201,173UP TO 201,343 DESPITE YESTERDAY’S 9 CENT FALL IN SILVER PRICING AT THE COMEX. TODAY WE MOVED A LITTLE CLOSER TO AUGUST’S RECORD SETTING OPEN INTEREST OF 244,196 CONTRACTS.

WE HAVE ALSO WITNESSED A LARGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY(WELL OVER 30 MILLION OZ AT THE COMEX FOR JULY , 6 MILLION OZ FOR AUGUST AND NOW JUST LESS THAN 31 MILLION OZ STANDING IN SEPTEMBER. AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A STRONG SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP:

0 EFP’S FOR OCT. 2166 EFP’S FOR DECEMBER AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE: OF 2166 CONTRACTS. WITH THE TRANSFER OF 592 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 2166 EFP CONTRACTS TRANSLATES INTO 10.83 MILLION OZ ACCOMPANYING:

1.THE 9 CENT FALL IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR THE JUNE/2018 COMEX DELIVERY MONTH. (5.420 MILLION OZ); 30.370 MILLION OZ STANDING FOR DELIVERY IN JULY, FOR AUGUST: 6.065 MILLION OZ AND 39.505 MILLION OZ STANDING IN SEPT. AND 1,590,000 OZ STANDING IN OCTOBER.

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF SEPT:

9793 CONTRACTS (FOR 5 TRADING DAYS TOTAL 9793 CONTRACTS) OR 48.96 MILLION OZ: (AVERAGE PER DAY: 1959 CONTRACTS OR 48.96 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF SEPT: 48.135 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 6.87% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2018 TO DATE SILVER EFP’S: 2,264.48 MILLION OZ.

ACCUMULATION FOR JAN 2018: 236.879 MILLION OZ

ACCUMULATION FOR FEB 2018: 244.95 MILLION OZ

ACCUMULATION FOR MARCH 2018: 236.67 MILLION OZ

ACCUMULATION FOR APRIL 2018: 385.75 MILLION OZ

ACCUMULATION FOR MAY 2018: 210.05 MILLION OZ

ACCUMULATION FOR JUNE 2018: 345.43 MILLION OZ

ACCUMULATION FOR JULY 2018: 172.84 MILLION OZ

ACCUMULATION FOR AUGUST 2018: 205.23 MILLION OZ.

ACCUMULATION FOR SEPTEMBER 2018: 167,05 MILLION OZ

RESULT: WE HAD A GOOD SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 1185 DESPITE THE 9 CENT FALL IN SILVER PRICING AT THE COMEX //YESTERDAY. THE CME NOTIFIED US THAT WE HAD A STRONG SIZED EFP ISSUANCE OF 2166 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) .

TODAY WE GAINED A STRONG SIZED:3351TOTAL OI CONTRACTS ON THE TWO EXCHANGES:

i.e 2166 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH INCREASE OF 1185 OI COMEX CONTRACTS. AND ALL OF THIS DEMAND HAPPENED WITH A 9 CENT FALL IN PRICE OF SILVER AND A CLOSING PRICE OF $14.69 WITH RESPECT TO YESTERDAY’S TRADING. YET WE HAD A GIGANTIC AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY IN THE BIG JULY DELIVERY MONTH OF SLIGHTLY OVER 30 MILLION OZ, IN AUGUST ANOTHER BIG 6.065 MILLION OZ IN A NON ACTIVE MONTH AND IN SEPTEMBER AN FINAL MONSTROUS 39.505 MILLION OZ OF SILVER STANDING FOR DELIVERY… NOBODY IS PAYING ATTENTION TO THE HUGE NUMBER OF PHYSICAL OUNCES STANDING FOR SILVER THESE PAST SEVERAL MONTHS.

In ounces AT THE COMEX, the OI is still represented by OVER 1 BILLION oz i.e. 1.007 MILLION OZ TO BE EXACT or 144% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT AUGUST MONTH/ THEY FILED AT THE COMEX: 0NOTICE(S) FOR NIL OZ OF SILVER

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 243,411 CONTRACTS ON APRIL 9.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $16.51.

AND NOW WE RECORD FOR POSTERITY ANOTHER ALL TIME RECORD OPEN INTEREST AT THE COMEX OF 244,196CONTRACTS ON AUGUST 22/2018 AND AGAIN WHEN THIS RECORD WAS SET, THE PRICE OF SILVER WAS $14.78 AND LOWER IN PRICE THAN PREVIOUS RECORDS.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: AN INITIAL HUGE 39.505 MILLION OZ./AND NOW OCTOBER:1,590,000 oz

- HUGE RECORD OPEN INTEREST IN SILVER 243,411 CONTRACTS (OR 1.217 BILLION OZ/ SET APRIL 9/2018) AND NOW AUGUST 22/2018: 244,196 CONTRACTS, WITH A SILVER PRICE OF $14.78.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017

- RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT).

IN GOLD, THE OPEN INTEREST ROSE BY A CONSIDERABLE SIZED 6476CONTRACTS UP TO 462,976 DESPITE THE FALL IN THE COMEX GOLD PRICE/YESTERDAY’S TRADING (A LOSS IN PRICE OF $1.20).THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED AN STRONG SIZED 9374CONTRACTS: ALWAYS, ON THE WEEK PRIOR TO FIRST DAY NOTICE IN ANY ACTIVE MONTH WHETHER GOLD OR SILVER THE OI COLLAPSES. IT IS HERE THAT THE MIGRANTS RECEIVE THEIR FIAT BONUS FOR ENGAGING IN THIS EXERCISE. WE HAD THE FOLLOWING EFP ISSUANCE FOR TODAY:

OCTOBER HAD 0 EFP’S ISSUED AND, DECEMBER HAD AN ISSUANCE OF 9374 CONTACTS AND ALL OTHER MONTHS ZERO. The NEW COMEX OI for the gold complex rests at 462,976. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE A HUMONGOUS SIZED OI GAIN IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 15,850 CONTRACTS: 6476 OI CONTRACTS INCREASED AT THE COMEX AND 9374 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN: 15850 CONTRACTS OR 1,585,000 OZ = 49.30 TONNES. AND ALL OF THIS HUGE DEMAND OCCURRED WITH A FALL IN THE PRICE OF GOLD/ YESTERDAY TO THE TUNE OF $1.20???

YESTERDAY, WE HAD 7314 EFP’S ISSUED.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF SEPT : 41,428CONTRACTS OR 4,142,800 OZ OR 128.85TONNES (5 TRADING DAYS AND THUS AVERAGING: 8285 EFP CONTRACTS PER TRADING DAY OR 801,400 OZ/ TRADING DAY),,

TO GIVE YOU AN IDEA AS TO THE HUGE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 5 TRADING DAYS IN TONNES: 128.85 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2017, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 2555 TONNES

THUS EFP TRANSFERS REPRESENTS 128.85/2550 x 100% TONNES = 5.05% OF GLOBAL ANNUAL PRODUCTION SO FAR IN JULY ALONE.***

ACCUMULATION OF GOLD EFP’S YEAR 2018 TO DATE: 5,796.43* TONNES *SURPASSED ANNUAL PROD’N

ACCUMULATION OF GOLD EFP’S FOR JANUARY 2018: 653.22 TONNES (21 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR FEBRUARY 2018: 649.45 TONNES (20 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR MARCH 2018: 741.89 TONNES (22 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR APRIL 2018: 713.84 TONNES (21 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR MAY 2018: 693.80 TONNES ( 22 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR JUNE 2018 650.71 TONNES (21 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR JULY 2018 605.5 TONNES (21 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR AUG. 2018 488.54 TONNES (23 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR SEPT 2018 470.64 TONNES (19 TRADING DAYS)

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A CONSIDERABLE SIZED INCREASE IN OI AT THE COMEX OF 6476 DESPITE THE LOSS IN PRICING ($1.20 THAT GOLD UNDERTOOK YESTERDAY) //. WE ALSO HAD AN GOOD SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 9374 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 9374 EFP CONTRACTS ISSUED, WE HAD A HUMONGOUS GAIN OF 15,850CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

9374 CONTRACTS MOVE TO LONDON AND 6476 CONTRACTS INCREASED AT THE COMEX. (in tonnes, the GAIN in total oi equates to 49.30 TONNES). ..AND ALL OF GOOD DEMAND OCCURRED WITH A LOSS OF $1.20 IN YESTERDAY’S TRADING AT THE COMEX.???

we had: 0 notice(s) filed upon for NIL oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD...

WITH GOLD UP $3,75 TODAY: /

ANOTHER BIG CHANGE IN INVENTOR TODAY

A WITHDRAWAL OF 1.47 TONNES DESPITE THE RISE…

/GLD INVENTORY 730.17 TONNES

Inventory rests tonight: 730.17 tonnes.

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

SLV/

WITH SILVER UP 5 CENTS TODAY

NO CHANGES IN SILVER INVENTORY AT THE SLV.

/INVENTORY RESTS AT 333.475 MILLION OZ.

NOTE THE DIFFERENCE BETWEEN THE GLD AND SLV: THE CROOKS CAN RAID GOLD BECAUSE THEY DO HAVE SOME PHYSICAL. THEY DO NOT RAID SILVER PROBABLY BECAUSE THERE IS NO REAL SILVER INVENTORIES BEHIND THEM

end

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER ROSE BY A CONSIDERABLE SIZED 1185 CONTRACTS from 200,160 UP TO 201,345 AND MOVING A LITTLE CLOSER TO THE NEW COMEX RECORD SET LAST IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 1 1/3 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89. AS YOU CAN SEE, WE HAVE RECORD HIGH OPEN INTERESTS IN SILVER ACCOMPANIED BY A CONTINUAL LOWER PRICE WHEN THAT RECORD WAS SET…..

.

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

2166 CONTRACTS FOR DECEMBER AND AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 2166 CONTRACTS . EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI LOSS AT THE COMEX OF13CONTRACTS TO THE 2166 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A STRONG NET GAIN OF 3351 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES: 16.76MILLION OZ!!! AND YET WE ALSO HAVE A STRONG DEMAND FOR PHYSICAL AS WE WITNESSED A FINAL STANDING OF GREATER THAN 30 MILLION OZ FOR JULY, A STRONG 6.065 MILLION OZ FOR AUGUST.. A HUGE 39.505 MILLION OZ STANDING FOR SILVER IN SEPTEMBER…AND NOW 1.590 million OZ STANDING FOR THE NON ACTIVE MONTH OF OCTOBER.

RESULT: A SMALL SIZED INCREASE IN SILVER OI AT THE COMEX DESPITE THE 9 CENT PRICING LOSS THAT SILVER UNDERTOOK IN PRICING YESTERDAY.BUT WE ALSO HAD A STRONG SIZED 2166 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR SEPTEMBER, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

) FRIDAY MORNING/ THURSDAY NIGHT:

SHANGHAI CLOSED FOR A HOLIDAY

/Hang Sang CLOSED DOWN 51.30 POINTS OR 0.19% //The Nikkei closed DOWN 135.34 POINTS OR 0.56%/ Australia’s all ordinaires CLOSED UP 0.12% /Chinese yuan (ONSHORE) closed UP at 6.8689 AS POBC STOPS ITS HUGE DEVALUATION /DELEGATION COMING TO THE USA TO SEE TRUMP IN NOVEMBER CANCELLED/Oil DOWN to 74.23 dollars per barrel for WTI and 84.74 for Brent. Stocks in Europe OPENED RED//. ONSHORE YUAN CLOSED DOWN AT 6.8686 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.8689: HUGE DEVALUATION/PAST SEVERAL DAYS STOPS// TRADE TALKS STOPPED : /ONSHORE YUAN TRADING STRONGER AGAINST OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING STRONGER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

3A/NORTH KOREA/SOUTH KOREA

i)North Korea/South Korea/USA/

b) REPORT ON JAPAN

3 C/ CHINA

4/EUROPEAN AFFAIRS

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

6. GLOBAL ISSUES

7. OIL ISSUES

8 EMERGING MARKET ISSUES

i)ARGENTINA

9. PHYSICAL MARKETS

10. USA stories which will influence the price of gold/silver)

MARKET TRADING

iv)SWAMP STORIES

Let us head over to the comex:

We are now in the non active delivery month of October and here we had a loss of 19 contracts to stand at 4 contracts. We had 19 notices filed YESTERDAY so we gained 0 contracts or NIL oz will stand for delivery at the comex as these guys refused to accept a London based forward plus as well as a fiat bonus

After October, is the non active delivery month of November and here we lost 3 contracts down to 435 contracts. After November, we have a December contract and here we lost 385 contracts down to 167,851

AND NOW COMPARISON FOR OCTOBER:

OUR LARGE SPECULATORS

those large speculators who are long in gold pitched (transferred) 450 contracts

those large speculators who are short in gold added 3724 contracts

OUR COMMERCIALS/

those commercials who have been long in gold added 1467 contracts to their long side

those commercials who have been short in gold covered (transferred) 328 contracts

OUR SMALL SPECS..

those small specs who have been long in gold added 1748 contracts to their long side

those large specs who have been short in gold covered (transferred) 631 contracts from their short side.

OUR SILVER COT

OUR LARGE SPECULATORS

those large speculators who have been long in silver pitched (transferred) 3261 contracts.

those large speculators who have been short in silver covered (transferred) 9018 contracts/

OUR COMMERCIALS

those commercials who have been long in silver added 695 contracts to the long side

those commercials who have been short in silver added 7093 contracts to the short side

OUR SMALL SPECS..

those small specs who have been long in silver pitched (transferred) 917 contracts

those small specs who have been short in silver covered (transferred) 1390 contracts

Conclusions on both gold and silver:

With the use of EFP’s this data is totally useless!!

Major gold/silver trading /commentaries for THURSDAY

GOLDCORE/BLOG/MARK O’BYRNE.

Poland and Australia Buy Gold As Global Property Bubble Bursts – This Week’s Golden Nuggets

News, Commentary, Charts and Videos You May Have Missed

Here is our Friday digest of the important news, commentary, charts and videos we were informed by this week.

We released our latest short video update in which we explored whether the global property bubble was beginning to burst?

Positive developments in the gold market included a surge in demand for gold and silver bullion coins ‘Down Under’ with our friends at the Perth Mint of Western Australia (we have been an Approved Dealer since 2005). As the Aussie property bubble continues to burst, risk-averse investors are accumulating physical gold and silver as hedges and insurance.

Another important development was an EU central bank buying gold for the first time since 1998. Poland’s central bank added to its gold reserves in August, buying more than seven tons of gold, which followed its purchase of two tons in July.

The prudent are advocating reducing allocations to overvalued risk assets – especially bonds. We featured an excellent article by Money Week editor John Stepek in which he made the case for owning equities and gold, rather than bonds.

Stepek’s article was prescient as bond markets, especially the US bond market, have seen serious sell-offs and a marked rise in yields yesterday. The serious ramifications of this for stock markets and the wider market is now being digested.

Enjoy and have a nice weekend!

Market Updates and News This Week

Are Global Property Bubbles Starting To Burst? GoldCore Video

Interest Rates Are Spiking Again: Why This Is A Huge Deal

Perth Mint’s Gold and Silver Bullion Coin Sales Soar In September

“I’m Favouring Equities and Gold Over Bonds” – Stepek

Poland Buys Gold For First Time In 20 years

“Gold Is Very Oversold And Due A Bounce” said GoldCore

Silver and Platinum Are Both Very Cheap

Charts This Week

Source: Bloomberg

Source: Bloomberg

Source: Bloomberg

Source: Bloomberg

Source: Bloomberg

Source: ZeroHedge

Source: ZeroHedge

Period Gold (oz) Silver (oz)

(year-month)

2018-September 62,552 1,305,600

2018-August 38,904 520,245

2018-July 29,921 486,821

2018-June 16,847 229,280

2018-May 14,800 557,120

2018-April 15,161 458,655

2018-March 29,883 975,921

2018-Feb 26,473 992,954

2018-Jan 37,174 1,067,361

2017-Dec 27,009 874,437

2017-Nov 23,901 544,436

2017-Oct 44,618 999,425

2017-Sept 46,415 697,849

2017-Aug 23,130 392,091

2017-July 23,675 1,167,963

2017-June 19,259 1,215,071

2017-May 29,679 826,656

2017-April 10,490 468,977

2017-March 22,232 716,283

2017-Feb 25,257 502,353

2017-Jan 72,745 1,230,867

2016-Dec 63,420 430,009

2016-Nov 54,747 984,622

2016-Oct 79,048 1,084,213

2016-Sept 58,811 1,031,858

2016-Aug 14,684 376,461

2016-July 16,870 693,447

2016-June 31,368 1,220,817

2016-May 21,035 974,865

2016-April 47,542 1,161,766

2016-March 47,948 1,756,238

2016-Feb 37,063 1,049,062

2016-Jan 47,759 1,473,408

Perth Mint Gold and Silver Sales (Monthly via Reuters)

Videos This Week

Gold Prices (LBMA AM)

04 Oct: USD 1,199.45, GBP 925.02 & EUR 1,043.28 per ounce

03 Oct: USD 1,203.50, GBP 925.73 & EUR 1,040.55 per ounce

02 Oct: USD 1,192.65, GBP 919.77 & EUR 1,035.46 per ounce

01 Oct: USD 1,185.30, GBP 907.94 & EUR 1,021.02 per ounce

28 Sep: USD 1,183.50, GBP 906.44 & EUR 1,020.41 per ounce

27 Sep: USD 1,196.00, GBP 911.59 & EUR 1,020.91 per ounce

Silver Prices (LBMA)

04 Oct: USD 14.63, GBP 11.27 & EUR 12.72 per ounce

03 Oct: USD 14.74, GBP 11.36 & EUR 12.75 per ounce

02 Oct: USD 14.51, GBP 11.20 & EUR 12.59 per ounce

01 Oct: USD 14.55, GBP 11.16 & EUR 12.53 per ounce

28 Sep: USD 14.31, GBP 10.97 & EUR 12.35 per ounce

27 Sep: USD 14.42, GBP 10.98 & EUR 12.31 per ounce

Recent Market Updates

– Brexit To Burst Dublin and London Property Bubbles? GoldCore Video

– Perth Mint’s Gold and Silver Bullion Coin Sales Soar In September

– “I’m Favouring Equities and Gold Over Bonds” – Stepek

– Poland Buys Gold For First Time In 20 years

– This Week’s Golden Nuggets – Central Banks, Goldman, Bank of America Positive On Undervalued Gold

– Central Banks Positivity Towards Gold Will Provide Long Term “Support To Gold Prices”

– Europe Unveils “Special Purpose Vehicle” With Russia and China To Bypass SWIFT, Jeopardizing Dollar’s Reserve Status

– Gold Set to Soar Above $1,300 – Goldman and Bank of America

– Goldnomics Podcast: Silver Guru – David Morgan – Silver and Gold Will Protect in the Coming Currency Collapse

– This Week’s Golden Nuggets – Dalio’s Dollar Crisis, Fitt’s U.S. Government “Missing” $21 Trillion and Silver Guru’s End of Empire

– Dalio Warns Of Dollar Crisis – “History Is Doomed To Repeat Itself”

– Silver Guru Video: “The End of Empire and End of Fiat Currencies”

Andrew Maguire’s Kinesis money which is a “bitcoin” but backed 100% by allocated gold and silver is set to go.

it think it would be a great idea to look at this!

please read at: https://kinesis.money/#/

(Andrew Maguire)

|

|

Dear Harvey Organ,

Thank you for your participation in our webinar on June 7th with our host and CEO of Kinesis, Thomas Coughlin.

The response we received has been incredible, we appreciate you taking the time to join us and hope you found it to be beneficial.

Due to such a high influx of questions we received we were unable to have them all answered. Nevertheless, if there was anything which requires more clarification, or you have a query which needs to be rectified, we invite you to join our telegram group:

We apologize for the technical issues we incurred during the webinar which resulted in it running a little over schedule, we hope that the next one we host will run seamlessly.

A video has been put together and uploaded onto our YouTube channel which can be found here:

Please share and subscribe to our YouTube channel to be notified of all the latest videos as they become available.

The rapid growth that we are currently experiencing has been incredible and with your support, is only going to get better.

We are working behind the scenes very hard to create a better experience for everyone involved! Stay tuned in as we have many more announcements to be released in the upcoming days.

Kind Regards,

|

Kinesis Money

a:C/O ILS Fiduciaries (IOM) Limited, First Floor,Millennium House, Victoria Road, Douglas, Isle of Man IM2 4RW

|

The following is self explanatory

(courtesy GATA/Chris Powell and Harvey Organ)

GATA asks bank regulator to check risks of gold futures maneuver

Submitted by cpowell on Sun, 2018-06-10 16:17. Section: Daily Dispatches

12:21p ET Sunday, June 10, 2018

Dear Friend of GATA and Gold:

GATA has appealed to the U.S. comptroller of the currency, who has regulatory authority over banks, to review financial risks certain banks may have incurred through derivatives in the monetary metals markets, particularly through the recent heavy use of the “exchange for physicals” mechanism of settling gold and silver futures contracts on the New York Commodities Exchange.

The appeal was made in a letter sent May 5 to the comptroller, Joseph M. Otting, whose office is part of the U.S. Treasury Department, by your secretary/treasurer and GATA futures market consultant Harvey Organ.

“Exchange for physical” settlements of futures contracts long were considered emergency procedures when a seller was not able to deliver metal from an exchange-approved warehouse and wanted to settle with delivery elsewhere. But now such settlements appear to constitute most gold and silver futures settlements on the Comex. It is a strange development that appears to have been necessitated by the increasing difficulties of central banking’s gold and silver price suppression policy.

GATA has received no acknowledgment of the letter. Its text is below and a PDF copy of it is here:

http://www.gata.org/files/ComptrollerOfCurrencyLetter.pdf

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

* * *

May 5, 2018

Joseph M. Otting, Comptroller of the Currency

U.S. Treasury Department

400 7th Street, SW

Washington DC 20219

Dear Comptroller Otting:

Please let us bring to your attention financial risks to major banks involving their possibly unreported exposure to derivatives in the monetary metals markets.

In recent months gold and silver future contracts issued by U.S. banks on the New York Commodities Exchange have been moved off-exchange for delivery through a mechanism known as “exchange for physical” (EFP) contracts. Until recently use of this mechanism was considered an emergency procedure when a seller did not have access to metal for delivery through Comex warehouses. Now the mechanism seems to be in use for a large share of front-month contracts for which delivery is sought.

Here is an example that is happening at the Comex in the front active month of April for gold and the inactive delivery month of April for silver.

In gold, there were 229,436 EFP contracts for 713.64 tonnes, an average of 10,925 contracts and 1,092,500 ounces per trading day.

In silver, there were 77,150 EFP contracts for 385,750,000 ounces, an average of 3,673 contracts and 18,369,000 ounces per trading day.

London Bullion Market Association rules suggest that these contracts may not be reported to regulators. The LBMA’s bylaws say:

“Figures above exclude any contracts not subject to risk-based capital requirements, such as FX contracts with an original maturity of 14 days or less, futures contracts, written options, and basis swaps. Therefore, the total notional amount of derivatives by maturity will not add to the total derivatives figure in this table.”

We are told that these EFP contracts are transferred from the Comex to London as what are called “serial forwards” and their duration is always less than 14 days, which exempts them from being reported.

It is our understanding that in each quarter your office prepares a report detailing risk undertaken by the banks under the comptroller’s supervision.

These risks include derivatives undertaken by U.S. banks and other obligations that may cause a bank to fail. Our concern is that your office may not be aware of large unreported derivative exposure by banks.

Could you review this matter and let us know your conclusions?

Sincerely,

CHRIS POWELL

Secretary/Treasurer

HARVEY ORGAN

Consultant

Gold Anti-Trust Action Committee Inc.

7 Villa Louisa Road

Manchester, Connecticut 06043-7541

end

Finally, they replied and it was a complete brush off

(courtesy zerohedge)

Currency comptroller brushes off GATA’s inquiry on gold, silver EFPs

Submitted by cpowell on Fri, 2018-08-10 15:37. Section: Daily Dispatches

11:35a ET Friday, August 10, 2018

Dear Friend of GATA and Gold:

The U.S. comptroller of the currency, a bank regulator, has declined GATA’s request to inquire into the strange explosion of the use of the emergency procedure of “exchange for physicals” in the settlement by banks of the gold and silver futures contracts they have sold on the New York Commodities Exchange.

Your secretary/treasurer and GATA’s consultant about the Comex, Harvey Organ, wrote to the comptroller, James M. Otting, on May 5, calling attention to the recent enormous use of EFPs, which implies derivatives risks being undertaken by U.S. banks that could cause the banks to fail:

http://www.gata.org/node/18303

“Our concern is that your office may not be aware of large unreported derivative exposure by banks,” GATA wrote.

As months passed without any acknowledgment from the comptroller’s office, your secretary/treasurer appealed to his U.S. representative, John B. Larson, D-Connecticut, to ask the comptroller’s office to reply. The congressman’s office made a second inquiry on Monday this week and today the comptroller’s office provided Larson with a copy of a reply written and mailed Wednesday.

The comptroller’s reply, signed by the deputy comptroller for public affairs, Bryan Hubbard, said only that the comptroller’s office has “dedicated examiners” at the largest banks who “continuously evaluate the credit, market, operational, reputation, and compliance risks of bank trading and derivative activities.”

The reply did not say anything about the use of the “exchange for physicals” procedure for settling futures contracts. That is, the reply was a begrudged brushoff and GATA’s letter would have been ignored completely if not for Representative Larson’s repeated intervention.

Of course GATA hardly expected a conscientious reply to its letter, the comptroller’s office being not an independent regulator but part of the Treasury Department, whose mandate includes administration of the Gold Reserve Act of 1934, which, as amended in the 1970s, authorizes the department’s Exchange Stabilization Fund to secretly intervene in and rig any market in the world, directly or through intermediaries:

https://www.treasury.gov/resource-center/international/ESF/Pages/esf-ind…

But there’s always value in demonstrating government’s lack of candor about what it is doing, especially in regard to the monetary metals.

A PDF copy of the reply from the comptroller’s office is posted at GATA’s internet site here:

http://www.gata.org/files/ComptrollerOfCurrencyReply-08-08-2018.pdf

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

Unbelievable!! Scotia Macotta admits rigging of gold and silver on their own

(courtesy GATA/Goldstein/Market Watch)

Key metals player Bank of Nova Scotia admits

rigging gold and silver futures

11:09a ET Tuesday, October 2, 2018

Dear Friend of GATA and Gold:

Few players in the gold and silver markets are bigger than the Bank of Nova Scotia, whose metals trading division, Scotia Mocatta, is world-renowned. The Bank of Nova Scotia is a member of the London Bullion Market Association and has had a seat at the daily London gold price fixing.

And this week the bank admitted to the U.S. Commodity Futures Trading Commission that its traders manipulated the gold and silver futures markets through “spoofing” from June 2013 through June 2016.Rory Hall of The Daily Coin, who brought the CFTC’s action to GATA’s attention today, notes that the developed has been grossly underreported:

https://thedailycoin.org/2018/10/02/another-bank-fined-for-rigging-the-g…

Indeed, at this hour your secretary/treasurer can find only one news story about it, from Marketwatch, which is very brief:

* * *

Bank of Nova Scotia Charged with Spoofing in Gold, Silver Futures

By Steve Goldstein

MarketWatch, New York

Monday, October 1, 2018

https://www.marketwatch.com/story/bank-of-nova-scotia-charged-by-cftc-wi…

The Bank of Nova Scotia was charged by the Commodity Futures Trading Commission with multiple acts of spoofing in gold and silver futures between June 2013 and June 2016. Traders placed orders to buy or sell precious metals futures contracts with the intent to cancel the orders before execution, the CFTC said.

The CFTC fine was $800,000, as the CFTC said the penalty was substantially reduced because the bank reported the conduct to the agency.

* * *

Far from criticizing the bank, the CFTC’s announcement yesterday about the misconduct actually praises the bank for having reported the misconduct itself:

https://cftc.gov/PressRoom/PressReleases/7818-18

The CFTC’s enforcement director, James McDonald, says:

“This case is another great example of the significant benefits of self-reporting and cooperation. We expect market participants to take proactive steps to prevent this sort of misconduct before it starts. But, as this case shows, there is a strong incentive for market participants to quickly and voluntarily report wrongdoing when it is discovered and cooperate with our investigation, as the Bank of Nova Scotia did here. In recognition of its self-reporting and cooperation, the commission imposed a substantially-reduced penalty.”

* * *

Wikipedia notes Scotia Mocatta’s key position in the monetary metals markets throughout history:

https://en.wikipedia.org/wiki/ScotiaMocatta

“The Mocatta firm has historically acted for central banks, notably the Bank of England and the United States Treasury in market stabilizations, notably the 1913 run on the Indian Specie Bank and the 1980 attempt by the Hunt brothers to corner the silver market.”

Of course spoofing the monetary metals futures markets might be considered a mechanism of “stabilization” as well.

In any case market rigging now has been acknowledged to have been perpetrated at the very center of the international gold and silver business.

Not that anyone but the tireless researcher of silver market rigging, Ted Butler, will catch the significance of the dates in yesterday’s announcement from the CFTC, but the regulatory agency closed without result its long-running investigation of silver market rigging in September 2013. That is, the CFTC closed its investigation of silver market rigging three months after the Bank of Nova Scotia’s rigging of gold and silver futures began.

Maybe the CFTC’s chronic blindness to the rigging of the monetary metals markets gave the bank the impression that they were fair game.

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

Eric Sprott, is very angry at gold forecasters due to the continued whacking of paper gold and paper silver

(courtesy GATA/stockhead.com)

In Perth, Eric Sprott scorns gold forecasters

and paper gold and silver

‘No Friggin’ Idea’: Billionaire Investor Eric Sprott Doesn’t Hold Back on Gold Forecasters

By Angela East

Stockhead.com.au, Sydney, Australia

Friday, October 5, 2018

PERTH, Australia — Eric Sprott knows just a bit about how to make money in mining, so when the Canadian billionaire investor gets up to address a crowd people listen.

It was no different when Mr Sprott took the stage on the second day of the Precious Metals Investment in Symposium in Perth to provide his thoughts on the gold space.The 73-year-old — described by Bloomberg as “one of the world’s premiere gold and silver investors” — kicked off an hour-long presentation by expressing his disgust at the underwhelming forecasts for gold. …

… For the remainder of the report:

https://stockhead.com.au/resources/words-of-wisdom-from-canadian-billion…

* * *

end

______________________________________________________________________________________________________________________________________________________

Your early FRIDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

i) Chinese yuan vs USA dollar/CLOSED UP TO 6.8689/HUGE DEVALUATION FOR THE PAST FOUR WEEKS STOPS/CHINESE COMING TO USA FOR TRADE TALKS IN NOVEMBER CANCELLED //OFFSHORE YUAN: 6.8841 /shanghai bourse CLOSED HOLIDAY

. HANG SANG CLOSED DOWN 51.30 POINTS OR 0.19%

2. Nikkei closed DOWN 191.90 POINTS OR 0.80%/USA: YEN RISES TO 113.71/

3. Europe stocks OPENED IN THE RED

/USA dollar index RISES TO 95.58/Euro RISES TO 1.1526

3b Japan 10 year bond yield: FALLS TO. +.15/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 113.71/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD IS NOW TARGETED AT .11%/JAPAN LOSING CONTROL OF THEIR BOND MARKET

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 74.23 and Brent: 84.74

3f Gold UP/JAPANESE Yen DOWN/ CHINESE YUAN: ON SHORE UP/OFF- SHORE: UP

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil DOWN for WTI and DOWN FOR Brent this morning

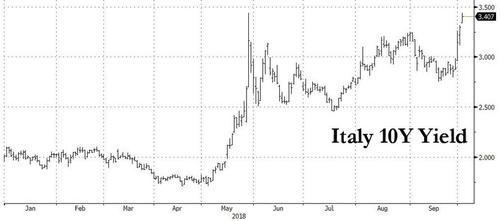

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund RISES TO +.55%/Italian 10 yr bond yield UP to 3.40% /SPAIN 10 YR BOND YIELD UP TO 1.57%

3j Greek 10 year bond yield RISES TO : 4.51

3k Gold at $1204.40 silver at:14.67 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble UP 34/100 in roubles/dollar) 66.58

3m oil into the 74 dollar handle for WTI and 84 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 113.71DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 0.9881 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1397 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now POSITIVE territory with the 10 year RISING to +0.55%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 3.21% early this morning. Thirty year rate at 3.37%

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

6. TURKISH LIRA: UP TO 6.1255

Global Stocks Slide, Asian Techs Hammered As

Rate Rout Continues

Traders were greeted with another sea of red from overnight equity markets, and even as Thursday’s vicious rout slowed ahead of today’s all important jobs report, Asian tech stocks were hammered following Bloomberg’s report that Beijing had hacked American computer networks using a microchip built by its spies.

“Stocks are firmly in the red as investors are worried about rising U.S. government bond yields, emerging-market economies, and Italy’s political situation,” said David Madden, market analyst at CMC Markets. To that he can also now add the tech rout amid Asian stocks following yesterday’s Bloomberg spying report.

Markets remain on edge about the sharp jump in US and global interest rates, although after the surge earlier this week US 10Y Treasury yields have remained relatively flat for the second consecutive day. Benchmark U.S. Treasury yields were at a seven-year top and on their way to their biggest weekly yield rise since February while European yields were adding to their biggest rise in months as well.

And with talk of plenty more U.S. interest rate hikes growing louder, it put all the more focus on the U.S. jobs data later. Eaton Vance portfolio manager Justin Bourgette said though there was too much hype around the payrolls figures, whichever way you approach it, the U.S. labor market is currently super strong. The latest Bloomberg consensus sees 185,000 new jobs and average hourly earnings increasing 0.3 percent in September after leaping 0.4 percent in August.

“Whatever the Fed’s concept of the neutral interest rate is, it must be rising,” Bourgette said. “And it is going to be trial and error to some degree (on how high rates go), because you just don’t know where the choking point is.”

Looking at today’s jobs report, DB’s Jim Reid said it best:

Given the rout in markets that started with Treasuries on Wednesday and has since reverberated throughout risk assets over the last 24 hours you’d be hard-pressed to find a more conveniently timed payrolls Friday than today. Indeed, with 10y Treasury yields up nearly 13bps from Friday’s close to 3.191% as of this morning, the S&P 500 (-0.82%) and NASDAQ (-1.81%) falling by the most since June 25th yesterday with FANG stocks (-2.89%) at the heart of it, the VIX (+2.61pts to 14.22) at one stage surging past 15 again yesterday, EM currencies lower across the board and EM equities (-2.38%) down by the most since February yesterday, the stakes have certainly been raised.

The sell-off in Treasuries led to contagion in Europe, where Germany’s 30-year security is poised for its biggest one-week yield increase since April and the 10Y Bund yield rose to 5 month highs, while Italian bonds slipped, as GDP forecasts failed to convince investors the country will be able to meet fiscal targets.

An interesting observation by Bloomberg, is that unlike in the US where higher yields have traditionally helped bank stocks, in Europe there has been a notable and concerning decoupling between the 10Y Bund yield and bank stocks. If not even a steepening in the yield curve can help Europe’s bank stocks, then Mario Draghi may be fresh out of luck.

Stocks in Europe followed Asia into the red rounding out a tough week in which a rout in technology shares roiled Asian equity markets while the stronger dollar, which slammed emerging markets, resumed rising ahead of the September payrolls report.

Europe’s Stoxx 600 index fell, led lower by miners as metal prices fell, while tech and banking shares also slipped. Lingering worries about Italy’s finances and an overoptimistic budget proposal pushed Milan down 0.9% making it the worst performer among major European markets on Friday. Deutsche Bank said the government’s budget plan, including growth of 1.5%, 1.6%, and 1.4% over the next three years, “is much more optimistic than forecasts from DB’s economists, the Bank of Italy, the ECB, the IMF, or the private sector consensus.”

London’s FTSE, Frankfurt’s DAX and the CAC in Paris were off 0.6-0.8% and Wall Street futures were modestly weaker. Danske Bank A/S headed for the biggest drop in seven years after Denmark’s regulator said it should hold more capital to prepare for potential fines.

Earlier, benchmark stock indexes fell across Asia, led by tech stocks with the MSCI AC Asia Pacific Infotech Index dropping to the lowest since July 2017. Taiwan’s Taiex index fell 1.9% in Taipei for its lowest close since May. The broader MSCI Asia Pacific Index headed for its worst week since March.

Tech stocks led declines after Bloomberg reported that China infiltrated U.S. companies with hardware hacks. The story came the same day Vice President Mike Pence criticized China across economic, commercial and diplomatic fronts in a keynote speech. As a result, Chinese PC maker Lenovo Group plunged as much as 23% in Hong Kong, its biggest loss in almost a decade before paring some of its decline by the close on Friday. In a statement, Lenovo said Super Micro Computer Inc., the company at the center of the hacking chip investigation, is “not a supplier to Lenovo in any capacity” and the company will take steps to protect the ongoing integrity of its supply chain, however that was not enough for traders who sold first and asked questions later.

In a note to clients, JPMorgan recommended shorting Lenovo with a six-month time horizon given the company’s PC and server sales to the U.S. “Whilst Lenovo isn’t directly implicated in the expose, it is hard not to see U.S. slow down their procurement of servers near term,” the note said and added that investors may also consider shorting Taiwanese computer companies including Quanta Computer, Inventec, Wiwynn and Wistron Corp which gets about 20% of its enterprise server business from Super Micro.

Other semiconductor names were similarly crushed: ZTE, a Chinese communications-gear maker that’s been hit by American sanctions, fell 11% in Hong Kong, the most since June. Walsin Technology, the top emerging-market stock through the first half of the year before becoming the worst since mid-July, dropped 9.9% in Taiwan. Taiwan lens maker Largan Precision, an Apple supplier, fell 7.3%. Realtek Semiconductor was down 8.3% to a July low.

“Electronics produced in China may be viewed unsafe due to this news, and tech shares are falling in general because of that,” Ray K W Kwok, an analyst at CGS-CIMB Securities Hong Kong Ltd., said of the Bloomberg story.

Losses in Asia followed Thursday declines in the U.S. where the Nasdaq saw its worst one-day drop since June, as Amazon and Apple – companies named as being affected by the China hack – dropped at least 1.8%. The tech rout has added to the pain suffered by Asian stocks which have so far taken the brunt of the US-China trade war.

The tech rout was the latest blow for global stocks in a week that saw 10-year U.S. Treasury yields climb to to seven-year highs, reducing demand for riskier assets. Fed Chair Jerome Powell stoked the rates surge when he said the central bank could eventually boost its benchmark “past the neutral level“, after data that underscored the strength of the U.S. economy. Investors’ focus is now squarely on Friday’s monthly U.S. payrolls report for further clues on the policy outlook.

The painful combination of rising oil prices, higher interest rates and a climbing dollar have also been rocking emerging markets which tend to be vulnerable to all three. MSCI’s 24-country emerging market equity index was down 0.7 percent and headed for its worst week since February and plenty of currencies were carrying heavy losses too. The slump in Chinese tech stocks, Indian refiners and South African blue chips led to the fifth loss in six days for emerging-market equities, sending them toward the worst week in eight months.

Earlier on Friday, India’s rupee feel to a new record low and bonds rallied after the country’s central bank unexpectedly kept its policy rate unchanged. The country’s Sensex benchmark stock index slumped 2.3%, the most since February, taking its slide from an August high to 12%, falling for a third straight session, dragged down by energy firms one day after the government announced a cut in fuel prices.

In the latest Brexit news, former UK Foreign Minister Boris Johnson welcomed EU Council President Tusk’s offer of a Canada type deal, he added it shows there is a “superb” way forward. Separately, EU Diplomatic Sources says that a divorce deal on Brexit is “very close” with Britain according to Reuters. However, Irish Foreign Minister Coveney says it is “hard to know” if the backstop proposal would work.

Elsewhere, Brent crude futures gained 0.5 percent to $85.03 barrel, and U.S. crude rose 0.7 percent to $74.88 barrel. That kept both just under 4-year highs. They have also risen an staggering 15-20 percent since mid-August. “Iranian exports could fall below 1 million barrels per day in November,” U.S. bank Jefferies said, referring to looming U.S. sanctions on Tehran. The investment bank said there was enough oil to meet demand, but “global spare capacity is dwindling to the lowest level that we can document … meaning any further supply disruptions would be difficult for the market to manage – and could lead to spiking crude oil prices”.

Today’s expected data include trade balance, non-farm payrolls, and unemployment. No major companies are reporting earnings.

Market Snapshot

- S&P 500 futures down 0.1% to 2,904.50

- STOXX Europe 600 down 0.6% to 377.50

- MXAP down 0.6% to 159.80

- MXAPJ down 0.7% to 501.90

- Nikkei down 0.8% to 23,783.72

- Topix down 0.5% to 1,792.65

- Hang Seng Index down 0.2% to 26,572.57

- Shanghai Composite up 1.1% to 2,821.35

- Sensex down 1.1% to 34,781.80

- Australia S&P/ASX 200 up 0.2% to 6,185.49

- Kospi down 0.3% to 2,267.52

- German 10Y yield rose 2.7 bps to 0.558%

- Euro down 0.2% to $1.1494

- Italian 10Y yield rose 1.5 bps to 2.959%

- Spanish 10Y yield rose 0.9 bps to 1.572%

- Brent futures up 0.3% to $84.81/bbl

- Gold spot little changed at $1,199.98

- U.S. Dollar Index up 0.1% to 95.88

Top Overnight News from Bloomberg

- The U.S. Senate is closing in on sending Brett Kavanaugh to the Supreme Court, which would seal a conservative majority and close a bitterly fought confirmation process that hinged on allegations of sexual misconduct. The Senate on Friday morning will take a procedural vote that will determine if he has enough support for approval

- European Central Bank President Mario Draghi met with Italian President Sergio Mattarella on Wednesday and may have discussed the country’s budget and bond spreads in the context of the winding down of the ECB’s QE program, La Stampa reported

- Britain’s International Trade Secretary said he will back an imperfect Brexit deal with the EU, on the basis it can be revised and improved after the U.K. has left the bloc

- India’s central bank kept interest rates unchanged in a surprise decision, opting to assess the impact of previous increases and contain the fallout of defaults from a systemically important lender. Indian bonds rallied

- Oil dropped from the highest price in almost four year amid signs of a growing crude surplus in the world’s biggest economy. An additional 1.7 million barrels of oil were stowed in tanks at a key U.S. pipeline hub in Oklahoma in the five days to Oct. 2, data provider Genscape Inc. was said to have reported

- The controversial budget plans of Italy’s populist government are hanging on an economic premise that looks too optimistic. It sees growth of 1.5 percent in 2019, followed 1.6 percent and 1.4 percent in subsequent years. By comparison, the median in Bloomberg’s latest survey is for expansion of no more 1.2 percent

- The Trump administration warned that too much of the U.S. defense industry is dependent on China or vulnerable to hacking directed by Beijing, part of a mounting campaign to pressure the Chinese government

- Japan’s base pay and household spending both rose by the most in years in August, adding to signs that consumers are beginning to feel the nation’s economic recovery

- For investors in the curve-steepener trade, the updraft in Treasury yields of the past 48 hours is more than just a welcome reprieve — it also signals a long-awaited regime shift

Asia-Pac stocks are traded mixed following a negative lead from Wall St. where tech names led the sell-off amid US-China trade concerns and as the US 10-year yield hit the highest since 2011. ASX 200 (+0.2%) bucked the trend and recuperated initial losses as financial and precious metal names supported the index, while Nikkei 225 (-0.8%) was subdued due to a recovery in the currency and weakness in tech names. Elsewhere, Hang Seng (-0.2%) struggled after opening in bear-market territory as a result of US headwinds and weakness in the energy sector, while tech names also sold off following reports that U.S. tech companies’ systems had been infiltrated by malicious chips inserted by Chinese intelligence agents. Meanwhile, mainland China remained closed due to the Golden Week holiday.

Top Asian News

- Hong Kong Stocks Signal Pain for World’s Priciest Properties

- IMF Says Pakistan Policies Not Enough to Stabilize Economy

European equities are down again, with traders mindful of Italian updates, the current yield environment, US-China trade tensions and the upcoming US job report. Comments from EU sources that a divorce deal for Britain is close has lifted the GBP and pressured the FTSE 100 into negative territory. The IT sector is underperforming amidst the technology supply line infiltration, and comments from Trump that he thinks China is not ready to make a deal creating additional strain on US-China relations. INTU Properties are up by over 28% following murmurs of privatisation led by a consortium including their deputy chairman. Danske Bank are at the bottom of the Stoxx 600 following yesterday’s share buyback discontinuation and being downgraded today to Neutral at Credit Suisse.

Top European News

- Ryanair Calls Off Talks With German Cabin Crew Union

- Rallye Repays Bondholders as Questions Loom About New Loan

- Brexit Financial-Market Threat Leads EU Watchdogs to Step Up

- U.K. Inflation Hawks May Be Missing the Big Picture on Brexit

In FX, GBP extended gains above the 1.3000 mark, and briefly through some stops at the next psychological level around 1.3050 on the back of more constructive Brexit news in the form of EU diplomatic sources suggesting a UK divorce agreement is ‘very close’. Eur/Gbp breached its 200 DMA circa 0.8840 in response and tested bids below 0.8820 before the Pound broadly ran out of steam. JPY was the other relative G10 outperformer, albeit marginal in the pre-NFP amble, as the headline pair remains hemmed in either side of 114.00, but some way above decent support and option expiry interest at the 113.50 strike where 1.1 bn runs off at the NY cut. EUR/CAD – Also softer vs the Greenback, with the single currency unable to sustain momentum on advances beyond 1.1500 and technically weak while under 1.1550 and a 1.1546 Fib, while the Loonie remains contained within a 1.2915-40 range vs its US counterpart awaiting Canadian jobs data due at the same time as NFP. EM – Some consolidation after widespread depreciation vs the Dollar for the most part this week, but not for the Inr that hit fresh all time lows following the RBI’s decision to stand pat on rates against consensus for a 25 bp hike, although it did switch policy stance to ‘calibrated’ tightening from neutral. Elsewhere, more intervention from the Indonesian Central Bank, while the Real may see some upside ahead of Sunday’s Brazilian election after the latest poll put Bolsonaro a bit further ahead of his main rival.

In commodities, the oil market is uneventful heading into the weekend with trade tentative ahead of the US labour market data later in the day, and the fossil fuel essentially flat for the day. The crude complex is set for its fourth consecutive weekly gain, as supply-driven gains have pushed the commodity to 4 year highs this week. The latest plats survey revealed OPEC compliance stands at 110% in September for members with quotas, alongside stating that Saudi output rose by 100k BPD, and that they have exceeded their targeted 1mln BPD increase. In metals markets, gold is also essentially unchanged as traders hold off ahead of a US jobs report that could tempt the Fed to implement a tighter monetary policy should signs of wage growth be seen. Aluminium is also steady, with the construction material set for its biggest weekly rise since April as supply concerns have lifted prices.

US Event Calendar

- 8:30am: Trade Balance, est. $53.6b deficit, prior $50.1b deficit

- 8:30am: Change in Nonfarm Payrolls, est. 185,000, prior 201,000

- Unemployment Rate, est. 3.8%, prior 3.9%

- Average Hourly Earnings MoM, est. 0.3%, prior 0.4%

- Average Hourly Earnings YoY, est. 2.8%, prior 2.9%

- Average Weekly Hours All Employees, est. 34.5, prior 34.5

- 12:30pm: Fed’s Kaplan Speaks in Waco

- 12:40pm: Fed’s Bostic Speaks at Financial Literacy Conference

- 3pm: Consumer Credit, est. $15.0b, prior $16.6b

DB’s Jim Reid concludes the overnight wrap

Given the rout in markets that started with Treasuries on Wednesday and has since reverberated throughout risk assets over the last 24 hours you’d be hard-pressed to find a more conveniently timed payrolls Friday than today. Indeed, with 10y Treasury yields up nearly 13bps from Friday’s close to 3.191% as of this morning, the S&P 500 (-0.82%) and NASDAQ (-1.81%) falling by the most since June 25th yesterday with FANG stocks (-2.89%) at the heart of it, the VIX (+2.61pts to 14.22) at one stage surging past 15 again yesterday, EM currencies lower across the board and EM equities (-2.38%) down by the most since February yesterday, the stakes have certainly been raised.

Indeed, it’s definitely one of the more anticipated employment reports this year and the consensus for payrolls today is for a 185k reading for September which follows that stronger than expected 201k in August. Average hourly earnings are expected to print at +0.3% mom, however base effects are expected to result in a one-tenth of a percent fall for the yearly figure to +2.8% yoy. With this week’s ADP (230k vs. 184k expected) and the employment components of both the manufacturing (58.8) and non-manufacturing (62.4) ISMs hitting seven-month and all-time highs, respectively, too this week, it certainly feels like the risk is to the upside. Indeed, our US economists yesterday revised up their payrolls forecast to 225k in light of the data, which in their view should push the unemployment rate down to 3.8%. Our colleagues also expect a +0.3% mom/+2.8% yoy earnings print but note the risk to the annual rate is a fall of two-tenths due to the base effects from last year’s September surge due to hurricane effects. However, earnings should rebound strongly in October as these base effects unwind.

Back in markets, one of the ironic takeaways from the moves yesterday was that Treasuries actually ended up little changed which seemed to partly be a function of the flight to quality bid in light of the moves for risk assets. Indeed, while the 10y did hit an intraday high of 3.231% early in the day – more than 18bps higher than the yield lows from Wednesday – it ended last night at 3.188% and +0.5bps on the day. 2y and 30y yields ended -0.4bps and +1.3bps respectively so it was at least a day of consolidation after breaking some key technical levels. Meanwhile, the DOW (-0.75%) and Russell 2000 (-1.46%) also joined the equity selloff along with the STOXX 600 (-1.08%) while the only sector which really benefited was Banks with the S&P 500 Banks index ending +0.80% and European Banks (+0.65%). EM FX (-0.58%) fell sharply for the second consecutive day while hard currency 10y yields in the likes of Brazil and Argentina finished +9.5bps and +36.9bps higher respectively. In Europe Bunds ended +5.6bps but in fairness were playing catch-up. Elsewhere in commodity markets WTI (-2.72%) and Brent (-1.98%) Oil tumbled yesterday while base metals were also hit hard (Aluminium -1.65%, Nickel -2.19%).

There’s no doubt that the Treasury move on Wednesday played its part in the selloff for risk assets especially with real yields also marching higher. However, the Bloomberg story which hit yesterday morning about China hacking 30 US companies including Amazon and Apple, and US Vice President Mike Pence saying that there “can be no doubt” that “China is meddling in America’s democracy” and specifically accusing the nation of a “whole-of-government approach” to sway US public opinion, also played just as big or had an even bigger impact on markets yesterday.

Overnight that risk off tone has continued into Asia however losses aren’t quite to the extent of those seen on Wall Street. The Nikkei (-0.71%), Hang Seng (-0.42%) and Kospi (-0.34%) are all in the red which puts those bourses down 1% to 4% this week alone. As a reminder, markets in China are still closed due to national holidays so it could be an interesting open on Monday given the moves this week. Meanwhile futures in the US are broadly flat along with bonds for the most part. Indeed, 10y JGBs are -0.6bps lower at 0.143% and 30y JGBs are -1.1bps lower at 0.934%. Notably there was no change to the BoJ’s outright bond purchase programme this morning and the moves also come following headlines yesterday on Reuters about the BoJ seen as “tolerating higher yields”.

In other news, yesterday there was some debate about an MNI article suggesting that the ECB might consider a “twist-like” operation of reinvestments of maturing debt next year. It’s worth noting that this isn’t the first time we’ve heard such a story and the rationale is certainly nothing new insofar as the ECB may just consider potentially extending maturities with the same capital keys. There wasn’t a great deal of reaction in the market to the story with the euro up a fairly modest +0.31%.

Staying with Europe, Greek assets had another turbulent day yesterday with increasing concern about the country’s banks which feels all a bit déjà vu. Bloomberg ran a story yesterday suggesting that Greece was considering a proposal to help lenders offload bad loans into an SPV, which in turn would issue bonds backed by the state. After falling -8.78% on Wednesday Greek banks rallied back +8.31% yesterday however 5y and 10y Greek yields did rise +7.2bps and +8.8bps respectively.

On Italy, the news flow calmed a bit yesterday which was probably a relief given the volatility in markets elsewhere, though later in the evening we did get the government’s budget plans which include growth of 1.5%, 1.6%, and 1.4% over the next three years. This is much more optimistic than forecasts from DB’s economists, the Bank of Italy, the ECB, the IMF, or the private sector consensus Debt to GDP is also to be targeted at 130.0% in 2019, 128.1% in 2020 and 126.7% in 2021 while the deficit, as we already knew, was confirmed at 2.4% for next year, 2.1% in 2020 and 1.8% in 2021. It’ll be interesting to hear any comments from the European side today.

Elsewhere, yesterday’s data certainly had less of an impact on markets but it did support the consistent message of strong US growth. Initial jobless claims fell to 207,000 from 214,000, close to the 50-year low. August durable goods orders were revised 0.1pp lower to +4.4% mom, though upward revisions to July mostly offset this. August factory orders beat expectations by 0.2pp at +2.3% mom. For now, we maintain our third quarter GDP growth forecast at +3.3% saar.

Finally, while the day ahead will likely be dominated by the US employment report this afternoon, there are various other data releases to be aware of. This morning in Europe we’ve got August factory orders and PPI in Germany followed by the August trade balance reading for France. In the UK we’ll also get Q2 labour costs while in the US this evening we’ll get August consumer credit data. Away from that we’ve got central bank meetings due in India and Argentina while the ECB’s Luis de Guindos and Klaas Knot are due to speak, followed by the Fed’s Robert Kaplan and Raphael Bostic this afternoon.

3. ASIAN AFFAIRS

i) FRIDAY MORNING/ THURSDAY NIGHT:

SHANGHAI CLOSED FOR A HOLIDAY

/Hang Sang CLOSED DOWN 51.30 POINTS OR 0.19% //The Nikkei closed DOWN 135.34 POINTS OR 0.56%/ Australia’s all ordinaires CLOSED UP 0.12% /Chinese yuan (ONSHORE) closed UP at 6.8689 AS POBC STOPS ITS HUGE DEVALUATION /DELEGATION COMING TO THE USA TO SEE TRUMP IN NOVEMBER CANCELLED/Oil DOWN to 74.23 dollars per barrel for WTI and 84.74 for Brent. Stocks in Europe OPENED RED//. ONSHORE YUAN CLOSED DOWN AT 6.8686 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.8689: HUGE DEVALUATION/PAST SEVERAL DAYS STOPS// TRADE TALKS STOPPED : /ONSHORE YUAN TRADING STRONGER AGAINST OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING STRONGER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

3 a NORTH KOREA/USA

North Korea/South Korea/USA/China

3 b JAPAN AFFAIRS

3C CHINA

Trump will not be happy with the latest release of trade data with China. The deficit rose despite tariffs to an all time high of 53.2 billion dollars.

(courtesy zerohedge)

US Trade Deficit With China Hits New All Time

High

The August trade deficit – a closed watched number in a time of trade wars – came in at $53.2BN, fractionally better than the $53.6BN expected, but 6.4% worse than last month’s revised print of $50.0BN ($46.8BN excluding petroleum), and just shy of a new all time high.

The deficit deteriorated as a result of less exports (-0.8%) and more imports (+0.6%). Broken down, August exports were $209.4 billion, $1.7 billion less than July exports, while July imports were $262.7 billion, $1.6 billion more than July. August imports of goods (excluding services) of $215.6 billion were the highest on record

The August increase in the goods and services deficit reflected an increase in the goods deficit of $3.6 billion to $76.7 billion and an increase in the services surplus of $0.4 billion to $23.5 billion. Year-to-date, the goods and services deficit increased $31.0 billion, or 8.6 percent, from the same period in 2017. Exports increased $129.6 billion or 8.4 percent. Imports increased $160.6 billion or 8.4 percent.

Some notable highlights from the report:

- August exports of services ($70.5 billion) were the highest on record.

- August imports of goods and services ($262.7 billion) were the highest on record.

- August imports of goods ($215.6 billion) were the highest on record.

Digging into the numbers, even more records were revealed:

- August imports of industrial supplies and materials ($49.7 billion) were the highest since December 2014 ($51.8 billion).

- August imports of automotive vehicles, parts, and engines ($31.7 billion) were the highest on record.

- August imports of other goods ($9.1 billion) were the highest on record.

- August petroleum imports ($20.5 billion) were the highest since December 2014 ($23.6 billion).

But what was most important is the geographic distribution of trade, and this is where Trump will be displeased because in July the trade deficit with both China ($36.8 billion)…

… and while the trade deficit with the EU rebounded from last month’s record high ($17.6 billion), to $15.7BN, the US also posted a record trade deficit with Mexico ($8.7BN) and Ireland ($4.3BN).

While this number will not have much of an impact on Q3 GDP, it could have a major impact on future trade because if Trump wanted one more “reason” to expand China’s tariffs to all Chinese imports, he just got it.

end

China is very angry with Vice President Pence’s latest speech stating that he is “fanning fires” and escalating tensions

(courtesy zerohedge)

China Slams Pence For “Fanning Fires” And

“Escalating Tensions” After Aggressive Speech

One day after US Vice President Mike Pence all but declared China to be the US’s new “enemy No. 1”, a status previously enjoyed by Russia and its president, during a speech at the Hudson Institute that outlined allegations of Chinese election-hacking, while blasting President Xi Jinping and the Communist Party for illegally asserting territorial dominance over the South China Sea and Taiwan (while at the same time promising that the US will impose its military will across the Indo-Pacific), the Chinese Foreign Ministry has issued a statement warning the US to stop “fanning fires” and “escalating tensions” between the world’s two largest economies, claiming that the US has no right to “irresponsibly” question the One China Policy that has long labeled Taiwan as an inalienable part of China, according to Bloomberg.

Chinese Foreign Minister Wang Yi

The ministry insisted that building necessary defense facilities has nothing to do with militarization, that China attaches “high importance” to safeguarding human rights and that “all ethnic groups have freedom of religion” – a claim that runs contrary to the deluge of reporting by US media outlets regarding China’s repression of its ethnic Uyghur minority. Instead of lobbing accusations at China, the US should “focus on its own domestic human rights issues instead of interfering with China’s internal affairs.”

Pence sought to expand on President Trump accusations, made before the UN Security Council last week, that China had been trying to undermine Republicans by interfering in US elections. While neither Trump nor Pence cited any evidence to justify their claims, Pence said China’s election-hacking efforts were “sophisticated” and vowed to expose Beijing’s “malign influence and interference.”

Here’s more on Pence’s speech from Reuters:

Pence said Beijing, with an eye not only to the congressional elections but also to Trump’s 2020 re-election bid, had “mobilized covert actors, front groups, and propaganda outlets to shift Americans’ perception of Chinese policies” and was targeting its tariffs to hurt states where Trump has strong support.

“China wants a different American president,” Pence said.

Shortly before Pence took the stag (but hours after excerpts of his expected remarks had been released) Bloomberg Businessweek published an explosive report on a top-secret multiyear US investigation into China’s successful infiltration of hardware used by 30 US companies – including Apple and Amazon – and the US intelligence and defense industries.

China and the US have blamed one another for the cancellation of a planned security conference that was expected to involve high ranking officials from both countries. And with the US still planning to expand its tariffs to cover virtually all the Chinese goods flowing into the US market, and China recently partaking in a massive joint military exercise with Russia, the deterioration in the relationship between the US and China has been nothing short of alarming.

4.EUROPEAN AFFAIRS

ITALY

Italy’s government loses credibility with its budget submitted to Brussels. Salvini blasts Juncker after EU mock the Italian budget

(courtesy zerohedge)

Italian Rout Returns As Salvini Blasts Juncker,

Moscovici After Europe Mocks Budget

The selloff across Italian assets returned on Friday, with stocks and bonds sliding as traders had a chance to go over the additional budget details released on Thursday evening and consensus quickly forming that the controversial budget plans of Italy’s populist government are hanging on an economic premise that looks too optimistic.

Italy’s GDP projections now include growth of 1.5%, 1.6%, and 1.4% over the next three years. By comparison, the median in Bloomberg’s latest survey is for expansion of no more than 1.2 percent. According to Deutsche Bank, “this is much more optimistic than forecasts from DB’s economists, the Bank of Italy, the ECB, the IMF, or the private sector consensus.” Rome also said that with the current legislation, GDP growth would be 1.2% for 2018.

Debt to GDP is also to be targeted at 130.0% in 2019, 128.1% in 2020 and 126.7% in 2021 while the deficit, as we already knew, was confirmed at 2.4% for next year, 2.1% in 2020 and 1.8% in 2021.

The “growth targets are ambitious, but not unrealistic and could be exceeded for at least two reasons,” Finance Minister Giovanni Tria said in the foreword to the report including the new estimates and targets. The finance chief mentioned the impact of planned investments and the elimination of legal and bureaucratic obstacles to their full implementation as well as a gradual reduction of public debt financing costs after tensions on financial markets subside.

“Whilst government forecasts always fall on the optimistic side, this particular assumption hints at significant fiscal slippage risk ahead in case of an economic slowdown,” said Axel Botte, a strategist at Ostrum Asset Management.

La Stampa also reported that ECB’s Draghi met with Italy President Mattarella on Wednesday, and may have warned about the budget and discussed the government “undervaluation” of effect on market. Draghi is also said to have warned about the trend of the Italian bond spread in the context of the winding down of the ECB’s quantitative-easing program.

In any case, with Italy’s highly unrealistic budget now public, traders resumed selling Italian stocks on fears it will be summarily rejected by Europe, and the FTSE MIB benchmark index dropped over 1%, the worst performer among major European markets on Friday.

Meanwhile, Italian BTPs breached yesterday’s worst levels after Ansa reported that Deputy Premier and Interior Minister Matteo Salvini blasted European Commission President Jean-Claude Juncker and Economic Affairs Commissioner Pierre Moscovici after they criticised the Italian government’s budget plans.

“The EU said yes to (past) budgets that impoverished Italy and made its situation precarious,” Salvini told a fair staged by agriculture association Coldiretti in Rome. “So I don’t get up in the morning thinking about the judgement that people like Juncker and Moscovici, who have ruined Europe and Italy, have of the government and of Italy.”

“They can say what they want. We’ll keep going straight on with peace of mind”.

On Wednesday, Salvini said that debt will decline “because more people will go back to work.” But short-term fiscal stimulus won’t solve longer-term issues that have left Italy as the slowest-growing economy in the euro area.

“The reality is that Italy’s problems are not about whether it meets its budget deficit next year or the year after,” Talib Sheikh of Jupiter Asset Management told Bloomberg Television. “It’s about can they undergo some deep-seated structural change. Italy’s ultimate problem is a lack of structural growth and it’s not clear to me that many of the populist agendas make any step toward that.”

The renewed war of words between Italy and Brussels after a few days of detente, is not what the market wanted to see, and the result was a prompt selloff in Italian bonds, with the 10Y yield rising as high as 3.422%, just shy of Wednesday’s highs which were the highest going back to early 2014. The drop was led by the front end, with 2y yields climbing as much as 21bps to 1.42% as the Italian budget crisis is nowhere close to getting resolved.

Danske Bank Shares Plummet As More Details

On $234 Billion Money Laundering Scandal

Emerge

Shares of Danske bank tumbled on Friday, adding to an already sizable decline so far this year, following a Financial Times report which revealed that the bank – which has become embroiled in one of the largest money laundering scandals in European history – also executed “mirror trades” for Russian clients, raising the possibility that the bank is facing even more serious fines and sanctions.

Danske Bank executed up to €8.5 billion ($9.8 billion) in mirror trades for Russian customers in a single year, according to an internal memo cited by the FT. The memo raises “new insight into the scale and tactics behind its €200 billion money-laundering scandal.” Deutsche Bank’s Moscow desk also used mirror trades – wherein the same party takes both sides of a trade, selling in rubles then buying in dollars – to help criminals move money out of Russia, an activity for which it was fined more than $600 million. The bank earned some 10 million euros from the trades, it said.

Danske is already facing investigations in six countries, including the US, where the DOJ is investigating revelations of rampant money laundering through Danske’s Estonian branch, which handled capital flows from non-resident clients that amount to multiples of the tiny Baltic nation’s GDP.

The Danske memo, seen by the FT, estimated that Danske made €10m in 2013 from the mirror trades, which used Russian government bonds to allow customers to make international payments in a “faster, cheaper and more reliable way.”

“There is potential reputational risk in being seen to be assisting ‘capital flight’ from Russia,” the memo said, before adding: “This is anyway a risk we run in other parts of our non-resident business, where the natural currency flow is always out of Russia. [ . . .] Given the strong income from the solution, the risk-return is seen as very attractive.”