GOLD: $1221.80 DOWN $3.90 (COMEX TO COMEX CLOSINGS)

Silver: $14.56 DOWN 8 CENTS (COMEX TO COMEX CLOSING)

Closing access prices:

Gold : 1222.50

silver: $14.57

For comex gold and silver:

OCT

NUMBER OF NOTICES FILED TODAY FOR OCT CONTRACT: 55 NOTICE(S) FOR 5500 OZ

Total number of notices filed so far for OCT: 1736 for 173,600 OZ (5.3996 TONNES)

FOR OCTOBER

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

0 NOTICE(S) FILED TODAY FOR

NIL OZ/

Total number of notices filed so far this month: 340 for 1,700,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: OPENING MORNING TRADE $6592: DOWN $4

Bitcoin: FINAL EVENING TRADE: $6577 DOWN 20

end

XXXX

China is controlling the gold market

WE WILL NOT PROVIDE LONDON FIXES AS THEY ARE NOT ACCURATE AS TO WHAT IS GOING ON AT THE SAME TIME FRAME.

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total OPEN INTEREST FELL BY 1475 CONTRACTS FROM 199,051 DOWN TO 197,576 DESPITE FRIDAY’S 6 CENT RISE IN SILVER PRICING AT THE COMEX. TODAY WE MOVED FURTHER FROM AUGUST’S RECORD SETTING OPEN INTEREST OF 244,196 CONTRACTS.

WE HAVE ALSO WITNESSED A LARGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY(WELL OVER 30 MILLION OZ AT THE COMEX FOR JULY , 6 MILLION OZ FOR AUGUST AND NOW JUST LESS THAN 31 MILLION OZ STANDING IN SEPTEMBER. AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A SMALL SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP:

0 EFP’S FOR NOV. 733 EFP’S FOR DECEMBER AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE: OF 733 CONTRACTS. WITH THE TRANSFER OF 733 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 733 EFP CONTRACTS TRANSLATES INTO 3.6665 MILLION OZ ACCOMPANYING:

1.THE 6 CENT RISE IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR THE JUNE/2018 COMEX DELIVERY MONTH. (5.420 MILLION OZ); 30.370 MILLION OZ STANDING FOR DELIVERY IN JULY, FOR AUGUST: 6.065 MILLION OZ AND 39.505 MILLION OZ STANDING IN SEPT. AND 2,050,000 OZ STANDING IN OCTOBER.

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF SEPT:

30,783 CONTRACTS (FOR 16 TRADING DAYS TOTAL 30,783 CONTRACTS) OR 153.91 MILLION OZ: (AVERAGE PER DAY: 1924 CONTRACTS OR 9.619 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF SEPT: 153.91 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 22.00% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2018 TO DATE SILVER EFP’S: 2,373.43 MILLION OZ.

ACCUMULATION FOR JAN 2018: 236.879 MILLION OZ

ACCUMULATION FOR FEB 2018: 244.95 MILLION OZ

ACCUMULATION FOR MARCH 2018: 236.67 MILLION OZ

ACCUMULATION FOR APRIL 2018: 385.75 MILLION OZ

ACCUMULATION FOR MAY 2018: 210.05 MILLION OZ

ACCUMULATION FOR JUNE 2018: 345.43 MILLION OZ

ACCUMULATION FOR JULY 2018: 172.84 MILLION OZ

ACCUMULATION FOR AUGUST 2018: 205.23 MILLION OZ.

ACCUMULATION FOR SEPTEMBER 2018: 167,05 MILLION OZ

RESULT: WE HAD A DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 1389 DESPITE THE 6 CENT GAIN IN SILVER PRICING AT THE COMEX //FRIDAY. THE CME NOTIFIED US THAT WE HAD A STRONG SIZED EFP ISSUANCE OF 1264 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) .

TODAY WE LOST A SMALL SIZED: 742 TOTAL OI CONTRACTS ON THE TWO EXCHANGES:

i.e 733 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH DECREASE OF 1475 OI COMEX CONTRACTS. AND ALL OF DEMAND HAPPENED WITH A 6 CENT RISE IN PRICE OF SILVER AND A CLOSING PRICE OF $14.64 WITH RESPECT TO FRIDAY’S TRADING. YET WE HAD A GIGANTIC AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY IN THE BIG JULY DELIVERY MONTH OF SLIGHTLY OVER 30 MILLION OZ, IN AUGUST ANOTHER BIG 6.065 MILLION OZ IN A NON ACTIVE MONTH AND IN SEPTEMBER AN FINAL MONSTROUS 39.505 MILLION OZ OF SILVER STANDING FOR DELIVERY… NOBODY IS PAYING ATTENTION TO THE HUGE NUMBER OF PHYSICAL OUNCES STANDING FOR SILVER THESE PAST SEVERAL MONTHS.

In ounces AT THE COMEX, the OI is still represented by JUST UNDER 1 BILLION oz i.e. 0.997 BILLION OZ TO BE EXACT or 144% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT AUGUST MONTH/ THEY FILED AT THE COMEX: 0 NOTICE(S) FOR NIL OZ OF SILVER

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 243,411 CONTRACTS ON APRIL 9.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $16.51.

AND NOW WE RECORD FOR POSTERITY ANOTHER ALL TIME RECORD OPEN INTEREST AT THE COMEX OF 244,196 CONTRACTS ON AUGUST 22/2018 AND AGAIN WHEN THIS RECORD WAS SET, THE PRICE OF SILVER WAS $14.78 AND LOWER IN PRICE THAN PREVIOUS RECORDS.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: AN INITIAL HUGE 39.505 MILLION OZ./AND NOW OCTOBER: 2,050,000 oz

- HUGE RECORD OPEN INTEREST IN SILVER 243,411 CONTRACTS (OR 1.217 BILLION OZ/ SET APRIL 9/2018) AND NOW AUGUST 22/2018: 244,196 CONTRACTS, WITH A SILVER PRICE OF $14.78.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017

- RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT).

IN GOLD, THE OPEN INTEREST ROSE BY A CONSIDERABLE SIZED 2174 CONTRACTS UP TO 475,077 DESPITE THE LOSS IN THE COMEX GOLD PRICE/FRIDAY’S TRADING (A FALL IN PRICE OF $1.70).THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 2545 CONTRACTS: ALWAYS, ON THE WEEK PRIOR TO FIRST DAY NOTICE IN ANY ACTIVE MONTH WHETHER GOLD OR SILVER THE OI COLLAPSES. IT IS HERE THAT THE MIGRANTS RECEIVE THEIR FIAT BONUS FOR ENGAGING IN THIS EXERCISE. WE HAD THE FOLLOWING EFP ISSUANCE FOR TODAY:

NOVEMBER HAD 0 EFP’S ISSUED AND, DECEMBER HAD AN ISSUANCE OF 2545 CONTACTS AND ALL OTHER MONTHS ZERO. The NEW COMEX OI for the gold complex rests at 475,077. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE A GOOD OI GAIN IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 4719 CONTRACTS: 2174 OI CONTRACTS INCREASED AT THE COMEX AND 2545 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN: 4719 CONTRACTS OR 471900 OZ = 14.6 TONNES. AND ALL OF THIS DEMAND OCCURRED WITH A FALL IN THE PRICE OF GOLD/ FRIDAY TO THE TUNE OF $1.70.

YESTERDAY, WE HAD 2767 EFP’S ISSUED.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF SEPT : 125,337 CONTRACTS OR 12,533,700 OZ OR 389.85 TONNES (16 TRADING DAYS AND THUS AVERAGING: 7783 EFP CONTRACTS PER TRADING DAY OR 778,300 OZ/ TRADING DAY),,

TO GIVE YOU AN IDEA AS TO THE HUGE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 16 TRADING DAYS IN TONNES: 389.85 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2017, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 2555 TONNES

THUS EFP TRANSFERS REPRESENTS 389.85/2550 x 100% TONNES = 15.28% OF GLOBAL ANNUAL PRODUCTION SO FAR IN JULY ALONE.***

ACCUMULATION OF GOLD EFP’S YEAR 2018 TO DATE: 6,065.65* TONNES *SURPASSED ANNUAL PROD’N

ACCUMULATION OF GOLD EFP’S FOR JANUARY 2018: 653.22 TONNES (21 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR FEBRUARY 2018: 649.45 TONNES (20 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR MARCH 2018: 741.89 TONNES (22 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR APRIL 2018: 713.84 TONNES (21 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR MAY 2018: 693.80 TONNES ( 22 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR JUNE 2018 650.71 TONNES (21 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR JULY 2018 605.5 TONNES (21 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR AUG. 2018 488.54 TONNES (23 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR SEPT 2018 470.64 TONNES (19 TRADING DAYS)

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A CONSIDERABLE SIZED INCREASE IN OI AT THE COMEX OF 2174 DESPITE THE LOSS IN PRICING ($1.70) THAT GOLD UNDERTOOK FRIDAY) //. WE ALSO HAD A GOOD SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 2545 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 2545 EFP CONTRACTS ISSUED, WE HAD A GOOD GAIN OF 4719 CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

2545 CONTRACTS MOVE TO LONDON AND 2174 CONTRACTS INCREASED AT THE COMEX. (in tonnes, the GAIN in total oi equates to 14.6 TONNES). ..AND ALL OF THIS GOOD DEMAND OCCURRED WITH A SMALL LOSS OF $1.70 IN FRIDAY’S TRADING AT THE COMEX.

we had: 55 notice(s) filed upon for 5500 oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD...

WITH GOLD DOWN $3.90 TODAY: /

A HUGE CHANGES IN GOLD INVENTORY: SOMETHING IS GOING ON!!

EARLY MORNING:

A WITHDRAWAL OF 2.97 TONNES OF PAPER GOLD BUT THIS GOLD WAS USED IN THE RAID TODAY.

B) A RAPID DEPOSIT OF 2.06 TONNES OF PAPER GOLD ADDED. THESE GUYS CANNOT FIND AN OZ AT THE COMEX AND YET THEY WITHDRAW AND DEPOSIT WITH RECKLESS ABANDON.

/GLD INVENTORY 747.88 TONNES

Inventory rests tonight: 747.88 tonnes.

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

SLV/

WITH SILVER DOWN 8 CENTS TODAY

A SMALL CHANGE IN SILVER INVENTORY AT THE SLV

A DEPOSIT OF 470,000

/INVENTORY RESTS AT 334.509 MILLION OZ.

NOTE THE DIFFERENCE BETWEEN THE GLD AND SLV: THE CROOKS CAN RAID GOLD BECAUSE THEY DO HAVE SOME PHYSICAL. THEY DO NOT RAID SILVER PROBABLY BECAUSE THERE IS NO REAL SILVER INVENTORIES BEHIND THEM

end

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER FELL BY 1475 CONTRACTS from 199,051 DOWN TO 197,576 AND MOVING A LITTLE FURTHER FROM THE NEW COMEX RECORD SET LAST IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 1 1/3 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89. AS YOU CAN SEE, WE HAVE RECORD HIGH OPEN INTERESTS IN SILVER ACCOMPANIED BY A CONTINUAL LOWER PRICE WHEN THAT RECORD WAS SET…..

.

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

i) 0 EFP’s for November… and

733 CONTRACTS FOR DECEMBER AND AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 733 CONTRACTS . EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI LOSS AT THE COMEX OF 1389 CONTRACTS TO THE 733 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A NET LOSS OF 656 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES: 3.28 MILLION OZ!!! AND YET WE ALSO HAVE A STRONG DEMAND FOR PHYSICAL AS WE WITNESSED A FINAL STANDING OF GREATER THAN 30 MILLION OZ FOR JULY, A STRONG 6.065 MILLION OZ FOR AUGUST.. A HUGE 39.505 MILLION OZ STANDING FOR SILVER IN SEPTEMBER…AND NOW OVER 2 million OZ STANDING FOR THE NON ACTIVE MONTH OF OCTOBER.

RESULT: A DECREASE IN SILVER OI AT THE COMEX DESPITE THE 6 CENT PRICING GAIN THAT SILVER UNDERTOOK IN PRICING// FRIDAY.BUT WE ALSO HAD A GOOD SIZED 733 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR SEPTEMBER, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i) MONDAY MORNING/ SUNDAY NIGHT:

SHANGHAI CLOSED UP 104.41 POINTS OR 4.09% //Hang Sang CLOSED UP 591.75 POINTS OR 2.32% //The Nikkei closed UP 82.74 OR 0.37%/ Australia’s all ordinaires CLOSED DOWN 0.61% /Chinese yuan (ONSHORE) closed DOWN at 6.9422 AS POBC RESUMES ITS HUGE DEVALUATION /DELEGATION COMING TO THE USA TO SEE TRUMP IN NOVEMBER CANCELLED/Oil DOWN to 69.14 dollars per barrel for WTI and 79.93 for Brent. Stocks in Europe OPENED RED MIXED///. ONSHORE YUAN CLOSED SLIGHTLY DOWN AT 6.9422 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED SLIGHTLY DOWN ON THE DOLLAR AT 6.9454: HUGE DEVALUATION/PAST SEVERAL DAYS RESUMES// TRADE TALKS STOPPED : /ONSHORE YUAN TRADING STRONGER AGAINST OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

3A/NORTH KOREA/SOUTH KOREA

i)North Korea/South Korea/USA/

b) REPORT ON JAPAN

3 C/ CHINA

China’s economy is not crashing and as Snider points out: it is worse than that because there is no growth coming from this nation. This would be very scary for the rest of the world as China is the engine for global growth

(Jeffrey Snider/Alhambra Investments partners)

4/EUROPEAN AFFAIRS

i)ITALY/EU

Quite a commentary today from GEFIRA, our resident experts on European affairs especially on Italy. Today, the European Financial establishment just declared war on Italy as Dijsselbloem on the CNBC interview suggested to Italy that there will not be a bailout and that Italy needs a bail in and knock off a huge number of mom and pop depositors. This would be act of war in Italy

( GEFIRA)

Monday morning: ITALY

Italy admits to the deficit breach but refuses to budge

(courtesy zerohedge)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

ii)Anger is spreading throughout the globe on the Saudi response. Turkey responds that they will never allow a cover up of the Khashoggi murder.

iii)This is a biggy!! It seems that the Saudi Crown Prince MbS spoke by phone of Khashoggi moments before he was killed. He looks like he refused to come back to Saudi Arabia and once he refused, he was murdered

( zerohedge)

iv)Russia/USA

Russia is angry at the USA pullout of the INF nuclear deal. They term the situation as “blackmail”

(courtesy zerohedge)

v)ISRAEL/JORDAN

Jordan cancels key part of the historic treaty with Israel, by refusing to renew land annex in the area called Naharayim and Zofar

(courtesy zerohedge)

6. GLOBAL ISSUES

Mexico/Central America/USA

President Trump has threatened to cut Central American aid as Mexico loses control of the migrant situation

(courtesy zerohedge)

7. OIL ISSUES

8 EMERGING MARKET ISSUES

9. PHYSICAL MARKETS

i)Lepard comments that he sees a reversion to the mean and this will send our precious metals rising

10. USA stories which will influence the price of gold/silver)

MARKET TRADING

iv)SWAMP STORIES

This latest commentary is a dandy. The judge hearing the Russian collusion case is Judge Dabney Friedrich a Republican who also has the distinction of dating Supreme Court Justice Kavanaugh. No doubt she is well tuned on the Russian collusion saga. She has ordered Mueller to bring her evidence of that collusion..

(zerohedge)

Let us head over to the comex:

We are now in the non active delivery month of October and here we had a LOSS of 0 contracts to stand at 1 contracts. We had 0 notices filed YESTERDAY so we gained 0 contracts or AN ADDITIONAL nil oz will stand for delivery at the comex as these guys refused to accept a London based forward plus as well as a fiat bonus

After October, is the non active delivery month of November and here we gained 1 contracts up to 1271 contracts. After November, we have a December contract and here we LOST 1407 contracts DOWN to 156,354

AND NOW COMPARISON FOR OCTOBER:

_________________________________________________________________________________________________

End Of The World?

by Gary Christenson of Deviant Investor

Predicting the end of the world, physical or financial, is seldom helpful.

If the prediction is correct, how do you profit from the insight? If the prediction is wrong and the “end of the world” is delayed (typical), you lose credibility.

An estimate of risk versus reward based on an analysis of current information is more useful.

Assessment: The 2018-2020 risk for most asset classes, such as stocks, bonds, corporate debt, and real estate is high while the potential reward in those asset classes is low. Gold and silver are opposite. Their long-term risk is low (September 2018) and their long-term potential reward is huge.

From Goldman Sachs:

OPINIONS AND FACTS SUPPORTING RISK/REWARD ASSESSMENT:

The central banks and the financial world created an “everything bubble.” This includes the stock market, bond market, housing, student loans, sub-prime auto loans, emerging markets, fiat currencies, and central bank credibility.

Low interest rates enable bubbles!

Bubbles always burst or implode. People want to believe “this time is different,” but it usually isn’t. Bubbles will implode and cause huge damage, especially to the middle and lower classes in the United States. Remember the crashes of 1987, 2000 and 2008. Each one seemed more destructive and broader in its reach than the previous crash. What will the crash of 2018 – 202? create?

If it can’t continue, it will stop – someday. Total debt – national, household, corporate, sovereign and more – has increased exponentially since 1913 when the Federal Reserve… you know the drill.

Use national debt for example. Begin the calculations in 1913, 1971, 1980, 2000 or whenever. The rate of increase in the official national debt varies but on average the debt increased by 8% to 9% every year and doubles every eight to nine years. Consider the implications of runaway debt, out of control spending, and no political will to manage spending, debt, or expansion of government, Medicare, military expenditures etc.

Year Official National Debt Projected

2018 $21 trillion doubling every 8.5 years

2027? $42 trillion

2035? $84 trillion

2044? $168 trillion

2052? $336 trillion

Outrageous! Of course, these projections are only based on 100+ years of debt history and could change. Congress might become fiscally responsible, global powers could “make nice,” greed and fear might take a vacation, the Tooth Fairy…

The banking cartel (commercial banks and central banks) will create trillions of dollars of debt in the coming years and will feed it into the economy. However, debt creation cannot continue forever. Either the dollar crashes (think Venezuela, Argentina, Turkey, and others) or the financial world resets.

From Jim Sinclair:

“Federal Reserve Gov. the Hon. Powell has only one of two moves he can make. Flood the world with dollars by active debt monetization (QE) internationally, or have the experience of presiding over the greatest depression in the history of man as his legacy. What would his boss have him do? The debt clock is ticking towards the reset by June of 2019.”

Predicting the “End of the World” is, financially speaking, predicting the reset. Yes, something must occur, but what, why and when?

WHAT IS THE RESET?

Debt must be paid or defaulted. Much of global debt can’t be paid so it will default. That debt is someone’s liability and another person’s asset. Default reduces or destroys both the liability and the value of the asset. Imagine $100,000 of thirty-year bonds being repaid in full, except the $100,000 buys 100 gallons of gasoline in thirty years.

It can’t happen here… It can! Argentina lopped 13 zeros from their pesos since 1945. Interest rates in Argentina reached 60% in 2018. Venezuela and Zimbabwe created recent hyperinflations by central bank printing. It can happen in the U.S., in Europe, in Japan and elsewhere.

When massive defaults occur, will global central banks sit on their hands and watch the collapse, or “do something?” What will they do? It is likely they will print currencies, or as Jim Sinclair says, “flood the world with dollars by active debt monetization.”

WHY WILL A RESET OCCUR?

There are many reasons. Some are:

The $20 trillion in created central bank monetization has made the financial world less stable. Which snowflake causes the avalanche (Jim Rickards) or which grain of sand initiates the collapse (John Mauldin) or which bank collapse will force the global reset? The condition of instability is more important than the apparent cause of the collapse.

The yield curve is declining. Recessions are consequences of excess credit issued by the fractional reserve banking system and central banks. A recession has not occurred for years, but the yield curve indicates a recession is close. Government revenues will collapse, marginal borrowers—corporations and individuals—will go bankrupt and the financial world could reset to a 2008 crisis during the next recession.

Stock markets have been too high for years. Apple and Amazon are trillion dollar companies. The NASDAQ 100 fell over 80% after the 2000 crash. Could it repeat? Yes, but crazy can become crazier to suck in more speculative dollars. Fundamentals are irrelevant compared to central bank liquidity pumps.

The “everything bubble” and excess debt will weaken currencies. Interest rates must remain low so debtors can afford the interest payments, which will weaken currencies. Or interest rates will reset higher and the bankruptcies will weaken currencies. Our central banks and governments have led the world into an ugly currency trap. Rig for stormy weather!

Quantitative Easing (QE) or “currency printing” or monetization is like an anti-anxiety drug or cocaine or hard liquor. Use it enough and you create addiction. Central banks created over $20 trillion in QE, enough to produce a substantial addiction. Chairman Powell of the Fed may attempt to “kick the habit” by taking baby steps to reduce the addiction. Based on 100+ years of history, the Fed will monetize more, not less, and probably soon.

WHEN WILL THE RESET OCCUR?

Read part two in a few days!

CONCLUSIONS FROM PART ONE:

- A risk/reward analysis for 2018 – 202? points toward gold and silver, not stocks, bonds, corporate debt, student loans or most asset classes.

- The “everything bubble” will burst. Consequences will be dire for many individuals, businesses and governments.

- Debt and spending are “out of control.” Fiat currencies will devalue, particularly if they are needed to “paper over” massive defaults.

- Hyperinflation, defaults and resets occurred in many countries and could (will) happen in developed countries such as the U.S.

- Rig for stormy weather! Gold and silver bullion and coins are “insurance” against the inevitable currency devaluations that must occur in our debt based fiat currency systems.

Courtesy of Gary Christenson of Deviant Investor

News and Commentary

Gold inches higher as Asian stocks slip (Reuters.com)

Gold Prices Advance on Rise in Dollar (Investing.com)

Govt sets up $100m gold sector fund (Herald.co.zw)

India’s gold imports rise on new duty concerns (Mubasher.info)

Gold markets: Asian stocks, Saudi Arabia, Italy, Brexit in focus (CNBC.com)

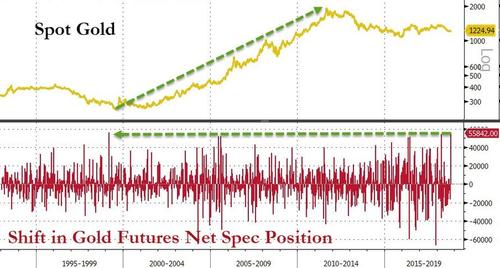

The last time gold speculators went from that short with a huge cover was March 1999. Source: ZeroHedge

Gold Shorts Suffer Biggest Squeeze Since 1999 As Specs Abandon VIX-Selling Spree (ZeroHedge.com)

This Is What A Paper Gold Short Squeeze Looks Like (DollarCollapse.com)

Dollar Libor at a 10-Year High Adds to Global Funding Headwinds (Bloomberg.com)

Italian Bonds Don’t Have History on Their Side (Bloomberg.com)

Italy’s Banks at Risk From Widening Spread, League Official Says (Bloomberg.com)

Listen on SoundCloud , Blubrry & iTunes. Watch on YouTube below

Gold Prices (LBMA AM)

19 Oct: USD 1,228.25, GBP 942.44 & EUR 1,073.12 per ounce

18 Oct: USD 1,224.60, GBP 933.76 & EUR 1,062.83 per ounce

17 Oct: USD 1,226.75, GBP 933.68 & EUR 1,061.38 per ounce

16 Oct: USD 1,228.85, GBP 931.35 & EUR 1,061.73 per ounce

15 Oct: USD 1,233.00, GBP 937.70 & EUR 1,064.45 per ounce

12 Oct: USD 1,218.75, GBP 922.11 & EUR 1,052.15 per ounce

Silver Prices (LBMA)

19 Oct: USD 14.61, GBP 11.21 & EUR 12.75 per ounce

18 Oct: USD 14.52, GBP 11.06 & EUR 12.60 per ounce

17 Oct: USD 14.65, GBP 11.16 & EUR 12.69 per ounce

16 Oct: USD 14.76, GBP 11.16 & EUR 12.74 per ounce

15 Oct: USD 14.74, GBP 11.19 & EUR 12.71 per ounce

12 Oct: USD 14.60, GBP 11.04 & EUR 12.60 per ounce

Recent Market Updates

– Gold Reserves Surge 1,000% In Hungary As It Joins Poland, Russia, China and Other Central Banks Buying Gold

– How Do You Sell Your Digital Gold When the Internet Goes Down?

– IMF Issues Dire Warning – ‘Great Depression’ Ahead?

– Poland Raises Gold Holdings to Record High in September – IMF

– Why It’s Worth Holding Gold Bullion in Your Portfolio

– Gold’s Best Day In 2 Years Sees 2.5 Percent Gain As Global Stocks Sell Off – This Week’s Golden Nuggets

– Gold Up 2.5 Percent As Global Stock Rout Spreads To Europe

– “Gold Is On The Cusp” Of An “Explosion Higher” As Stock and Tech “Crash Is Coming”

– Gold Bottoms As Gold Industry Consolidates and Weak Hands Capitulate

Equity Management Associates: Reversion to mean would send monetary metals soaring

Submitted by cpowell on Sat, 2018-10-20 13:42. Section: Daily Dispatches

9:44a ET Saturday, October 20, 2018

Dear Friend of GATA and Gold:

Our friend Lawrence Lepard, managing partner of Equity Management Associates in Wellesley, Massachusetts, whose investments have been concentrated in the monetary metals mining industry, has just sent a letter to his investors outlining the case for an upward reversal in the industry’s fortunes.

Lepard’s letter may be most interesting for showing that the monetary metals are now priced far below traditional valuations and for arguing that any reversion to the mean would be explosive.

Perhaps most telling is the letter’s chart showing the sharp break in 2011 in the historic correlation between the gold price and the U.S. national debt — a break that powerfully implies urgent official intervention against a rising gold price.

Lepard has kindly allowed GATA to share the letter with you and so it is posted in PDF format here:

http://www.gata.org/files/EMA-GARP-Fund-Letter-10-2018.pdf

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

Russia adds a whopping 37.3 tonnes of gold into its inventory.

(courtesy Lawrie Williams)

LAWRIE WILLIAMS: Russia accelerates gold purchases

The Russian central bank has announced yet another increase in its gold reserves in September – this time it has added a massive 1.2 million troy ounces (37.3 tonnes) to the gold in its forex holdings. This brings the overall total to 65.5 million ounces (2,037.3 tonnes) and means it has added just short of 200 tonnes of gold to its reserves in the first 9 months of the current year which represents an increased acceleration in its reserve increases over the prior few years. While it remains in fifth place among nationally reported holders of gold to the IMF (we think China in sixth place on its official reporting may actually hold more) it is ever moving closer to the big European holders – Italy and France – in the global gold reserve table which respectively report holdings of 2,451.8 tonnes and 2,436 tonnes.

A month ago we noted that the World Gold Council reported that Central Bank gold purchases rose in the first half of the current year compared with 2017, although once again the biggest reported increases were from Russia, Kazakhstan and Turkey which allseemed to be increasing their gold accumulations. The former two are both significant gold producers in their own right – Russia lying third in the global gold producer table and Kazakhstan 15th (see Top 20 World Gold Producers 2017)and Turkey also mines gold but falls outside the top 20. And now, since then, we have learnt of some significant purchases from countries with little or no gold production – namely India, Poland and, most recently Hungary which increased its gold holdings tenfold by adding 28.4 tonnes of gold in the first two weeks of the current month (see: Central Bank gold buying – New kids on the block). Whether Hungary has continued to purchase any gold since then is so far unreported.

The timings of the seeming acceleration of gold reserve increases is interesting. It coincides with the U.S.’s more aggressive attitude to trade and imposition of sanctions against countries like Russia which it deems to be opposed to it.. It also seems to impact those countries which wish to trade with the sanctions-hit economies in case they also become the victims of U.S. trade sanctions and imposed tariffs. This seems to be leading to countries attempting to reduce the dollar components of their reserves and perhaps replacing them with gold. The EU too seems to be taking a strong line against member states(Poland and Hungary are examples) which diverge politically from the consensus policies and rules. There is perhaps a fear here that the EU might break up if too many member states fall out with the EU hierarchy, which is probably why such a hard line is being taken on Brexit. A consensus deal is in both sides’ interests, but intransigence may well win the day, with adverse economic consequences for the U.K. and the EU as a whole.

The U.S.’s increasingly belligerent attitude to trade with China is yet another reason for our view that China is trying to reduce its dependence on dollar holdings in its reserves and perhaps using this money to buy more gold, but without reporting it to the IMF.Chinese officials and academics have intimated in the past that they would like to at least reduce the dollar’s dominant position in world trade and as a global reserve currency. It is already taking measures towards this by negotiating oil and other contracts in yuan (convertible into gold if wanted) rather than in dollars, which is another reason why it may be building its gold reserves as well.

Central Bank reserve increases are but one element in global gold demand, but an important one. With global production at the least plateauing (we’re not sure if it is actually reducing yet) and consumer demand likely to rise if only from population growth and general increases in personal incomes around the world, any continuing growth in global gold reserves will have a positive impact on supply/demand fundamentals. As we have mentioned before gold may be facing short term headwinds, but longer term prospects look to be ever increasingly positive.

20 Oct 2018

Your early MONDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

i) Chinese yuan vs USA dollar/CLOSED DOWN TO 6.9422/HUGE DEVALUATION FOR THE PAST FOUR WEEKS RESUMES/CHINESE COMING TO USA FOR TRADE TALKS IN NOVEMBER CANCELLED //OFFSHORE YUAN: 6.9454 /shanghai bourse CLOSED UP 104.41 POINTS OR 4.09%

. HANG SANG CLOSED UP 591.75 POINTS OR 2.32%

2. Nikkei closed UP 82.74 POINTS OR 0.37%

3. Europe stocks OPENED GREEN

/USA dollar index RISES TO 95.80/Euro FALLS TO 1.1502

3b Japan 10 year bond yield: RISES TO. +.15/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 112.82/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD IS NOW TARGETED AT .11%/JAPAN LOSING CONTROL OF THEIR BOND MARKET

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 69.14 and Brent: 79.93

3f Gold DOWN/JAPANESE Yen DOWN/ CHINESE YUAN: ON SHORE DOWN/OFF- SHORE: DOWN

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil DOWN for WTI and DOWN FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund RISES TO +.47%/Italian 10 yr bond yield UP to 3.42% /SPAIN 10 YR BOND YIELD DOWN TO 1.69%

3j Greek 10 year bond yield FALLS TO : 4.42

3k Gold at $1222.25 silver at:14.61 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble UP 19/100 in roubles/dollar) 65.27

3m oil into the 69 dollar handle for WTI and 79 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 112.82DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 0.9965 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1461 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now POSITIVE territory with the 10 year RISING to +0.47%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 3.19% early this morning. Thirty year rate at 3.37%

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

6. TURKISH LIRA: UP TO 5.6647

US Futures Rise After Chinese Stocks Soar; Italian

Bonds Boosted By Moody’s

After some initial weakness early in the Monday session which pushed S&P futures as low as 2,750 on Sunday night, below their Thursday lows, animal spirits were rekindled and S&P futures rebounded by almost 30 points from session lows…

… with global stocks and futures generally a sea of green…

… after Chinese stocks extended the torrid Friday rally, soaring by 4.1% and jumping the most in three years after Beijing doubled down its pledge of support for the economy and companies which included promises of tax cuts and coordinated official statements of support for stock markets.

A barrage of verbal interventions on Friday from authorities culminated with Chinese President Xi Jinping vowing “unwavering” support for the country’s private sector, which sent the Shanghai Composite back over 2,600 after the index touched a 4 year low below 2,500 late last week.

Chinese consumer stocks were among the best performers after the government released a detailed draft plan for personal income tax cuts over the weekend. China’s draft plan for sweeping personal tax cuts, together with a recent rise in the tax threshold, is a big positive for growth, writes Chang Shu, the Chief Asia Economist for Bloomberg Economics, adding that the move could buttress an economy suffering from tight funding conditions and provide a boost as a trade war intensifies. The news sent consumer staples surging with Yonghui Superstores jumping as much as 7.7%, most this year; Jiangsu Yanghe Brewery gains as much as 6.7%; Inner Mongolia Yili +5.8%; Moutai +2.5%, and so on.

Renewed Chinese optimism helped other Asian markets enjoy healthy gains, with Japan’s Nikkei rising 0.4%, while the MSCI Asia ex Japan rose 0.8%.

European stocks also opened higher after Moody’s kept Italy’s sovereign rating stable on Friday instead of cutting it to negative. The decision fueled a rally in Italian government bonds and boosted shares in the country’s banks. “Moody’s opens the door for a euro bounce, while Chinese verbal support for the economy and markets has given us a risk-friendly mood to start the week,” Societe Generale said in a note to clients.

Optimism over the avoidance of an imminent downgrade to junk also sent Italian 10Y yields to two week lows, at least temporarily, before fading all gains after Italy submitted its response to the EU’s criticism of its 2019 budget proposal.

Specifically, Italy’s Treasury said the government is conscious its budget policy is not in line with EU’s stability pact and the decision was hard but necessary; adding it is committed to reducing structural deficit in direction of medium term objective from 2020. Rome said it would go off path of structural deficit adjustment in 2019 but does not intend to further expand deficit in the 2020-21 period, and added that its recognises different views with EU but will continue to have constructive and loyal talks with EU. Ultimately, if debt/GDP and deficit/GDP dies not evolve as planned, government is committed to take all intervene adopting all necessary measures; the response concluded that strengthening Italian economy is in the interest of the EU

Following the release of Italy’s response to the EU, BTPs pared gains in choppy trade prompting Bunds to touch a new session high. BTP futures drop to the low of the day at 120.77 before rallying after Italy says it’s ready to intervene to ensure that objectives are respected, while Finance Minister Tria says Italy is ready to act if debt and deficit ratios are not in line with goals.

Meanwhile, in European equities, the Stoxx Europe 600 was up only 0.1% after gaining as much as 0.7% in early trade, while Italy’s FTSE MIB pared gains to 0.6% after gaining as much as 2%. The FTSE Italia All-Share Banks Index was up 0.4% after surging 3.6%; as a reminder, the sector index hit its lowest since late 2016 on Friday, and is down about 35% since mid-May

Amid concerns of a renewed standoff between Italy and the EU, the euro gave up a gain and the dollar erased a drop, while the pound retreated as the U.K. blurred more red lines in the Brexit negotiations, heightening the danger to Prime Minister Theresa May.

Meanwhile, as Bloomberg notes, risks still abound across global markets, from tension surrounding the death of a Saudi journalist and the ongoing trade showdown between some of the world’s biggest economies to Italian budget fears and President Donald Trump’s ad hoc actions ahead of American midterm elections. Still, equities are attempting to bounce back after a miserable couple of weeks, and company results from the likes of Amazon, Alphabet, Microsoft and Intel as well as U.S. growth data may provide a welcome distraction in the coming days.

Indeed, this will be the busiest week for corporate profits this earnings season with Amazon, Alphabet, Microsoft and Caterpillar among the companies reporting. Helped by a strong economy and deep corporate tax cuts, S&P 500 earnings per share are expected to grow 22% in the third quarter, according to consensus data.

“The season on an absolute basis will likely wind up being ‘strong’ and the vast majority of companies will exceed consensus expectations,” said analysts at JPMorgan in a note. “However, headwinds are building at the margin in the form of U.S. dollar strength, supply chain disruptions owing to all the trade uncertainty, and rising costs. Even the mere hint of a turn in profit fundamentals would have severe ramifications.” The outlook for global growth in 2019 has dimmed for the first time, according to Reuters polls of economists, who cautioned that the U.S.-China trade war and tightening financial conditions would trigger the next downturn.

In the latest Brexit news, Prime Minister Theresa May will tell parliament that 95% of Britain’s divorce deal has now been settled. But she will repeat her opposition to the EU’s proposal for the land border with Northern Ireland and many see the risk of a leadership challenge being mounted.

In FX markets, an early advance in the euro lost steam as Italian bonds pared gains. Euro-area periphery debt was still bid after Moody’s kept Italy’s rating above junk with stable outlook, while the pound fell before U.K. Prime Minister May’s speech to parliament. The dollar was little changed, as were Treasuries; U.S. bonds traded choppy through Asian hours, initially gaining on Donald Trump’s plan to exit an arms control treaty with Russia, only to pare gains as a rally in Chinese stocks supported a swing in risk sentiment. The yen swung to a loss as the risk-off move was curbed while the Australia’s dollar fell to a one-week low after a by- election on the weekend looked set to deprive the federal government of its one-seat majority in parliament

In rate, the yield on 10-year Treasuries climbed one basis point to 3.20%. Germany’s 10-year yield also increased one basis point to 0.47 percent. Britain’s 10-year yield rose less than one basis point to 1.577 percent, while the spread of Italy’s 10-year bonds over Germany’s declined seven basis points to 2.9583%, the smallest premium in more than a week.

Saudi Arabia has remained in the spotlight after Riyadh called the killing of journalist Jamal Khashoggi a “huge and grave mistake” but sought to shield its powerful crown prince from the crisis. U.S. President Donald Trump and European leaders are pushing Saudi Arabia for more answers.

With concerns about the Saudi response to the Khashoggi murder lingering, most commodities advanced. Brent crude climbed to about $80 per barrel and WTI edged close to $70 with U.S. sanctions against Iran’s crude exports due to be implemented next month. Gold slipped. Emerging-market stocks jumped. The South African rand rallied before the country’s budget.

Market Snapshot

- S&P 500 futures up 0.2% to 2,771.75

- STOXX Europe 600 up 0.2% to 361.98

- MXAP up 0.4% to 153.69

- MXAPJ up 0.8% to 484.84

- Nikkei up 0.4% to 22,614.82

- Topix up 0.2% to 1,695.31

- Hang Seng Index up 2.3% to 26,153.15

- Shanghai Composite up 4.1% to 2,654.88

- Sensex up 0.3% to 34,412.26

- Australia S&P/ASX 200 down 0.6% to 5,904.94

- Kospi up 0.3% to 2,161.71

- German 10Y yield unchanged at 0.461%

- Euro up 0.03% to $1.1517

- Brent Futures up 0.6% to $80.29/bbl

- Italian 10Y yield fell 19.8 bps to 3.111%

- Spanish 10Y yield fell 4.5 bps to 1.69%

- Brent Futures up 0.6% to $80.29/bbl

- Gold spot down 0.3% to $1,223.23

- U.S. Dollar Index down 0.03% to 95.68

Top Overnight News from Bloomberg

- White House economic adviser Larry Kudlow accused China of doing “nothing” to defuse trade tensions ahead of a likely meeting between President Trump and President Xi Jinping at the G-20 in Argentina next month, the Financial Times reported

- Trump has promised a new middle-income tax cut plan to land days before the mid-term election, a move aimed at boosting his party’s chances of holding its Congressional majorities — yet Republican tax policy-makers know nothing about it

- Treasury Secretary Steven Mnuchin is open to changing how the U.S. determines which nations are gaming their currencies, a move that could give Trump the chance to officially brand China an exchange-rate manipulator

- Italy’s populist coalition hinted that it may eventually be prepared to temper its budget for next year as the European Union demands an explanation of its deficit plans

- As impending U.S. sanctions curb Iranian exports, Iraq has quietly increased shipments to Asia, Europe and the Mediterranean region to offset Iran’s missing barrels

- Hedge funds cut bets on rising West Texas Intermediate crude prices for a sixth straight week, to the lowest since October 2017

- Saudi Arabia’s evolving account of the death of journalist Jamal Khashoggi elicited skepticism from officials in the U.S. and its allies weighing how to respond. France demanded more information, while Germany put arms sales to the oil-rich nation on hold

Asian equity markets traded mostly higher as a rally in Chinese stocks helped most the regional bourses shrug-off the

cautious open. ASX 200 (-0.58%) and Nikkei 225 (+0.37%) were both initially lower with Australia dampened by political

uncertainty as PM Morrison’s governing coalition is on track to lose its 1-seat parliamentary majority following a by election in

eastern Sydney, while the early downbeat tone was also attributed to geopolitical concerns after Trump announced the US would

leave the Intermediate-Range Nuclear Forces Treaty. However, most of the losses in the region were later pared as the Shanghai

Comp. (+4.09%) surged on a rebound from 4-year lows which inspired the Hang Seng (+2.32%), while officials were also

conducive to the risk sentiment in which President Xi reiterated unwavering commitment to the private sector, China released its

draft of tax cuts and the PBoC announced a liquidity injection of CNY 120bln. Finally, 10yr JGBs were amid the turnaround in

sentiment for the region and lack of BoJ presence in the market today. China released draft of tax cuts which include lower cost of housing, education and health to boost consumption effective from start.

of 2019.

Top Asian News

- A Big Secret in Japan Debt Market Is Getting Harder to Keep

- China’s $195 Billion Debt Splurge Has Less Bang Than You Think

- BOJ Signals Financial System Able to Withstand Easing for Now

- Thanks to the Trade War, Southeast Asia Has an Investment Boom

Major European indices are all in the green, with the exception of the AEX (-0.1%) which has been dragged down by Phillips (-5.5%) amid a miss on their earnings. The FTSE MIB leads the gains following a Moody’s Italy downgrade to one level above junk, which was less than some had anticipated. Italian banks, such as Intesa Sanpaolo (+1.0%) are supported a result of this; however, the index is being led by gains in Fiat Chrysler (+5.0%) after the confirmation of their Magnetti Marelli unit sale to KKR for EUR 6.2bln. Sectors are mostly in positive territory, with the exception of healthcare and energy. Consumer discretionary and financials are some of the best performers with the former supported by car names moving sympathy to Fiat Chrysler, while the latter is buoyed by Italian banks after the FTSE MIB Banking Index opened higher by over 3%. In terms of individual equities the aforementioned Phillips are at the foot of the Stoxx 600. Danone (-1.3%) are lower after the CEO stated that they are not going to bid for Horlicks. Lloyds Banking Group (+2.0%) are in the green following the Co’s plans to buy back around GDP 2bln of shares in 2019.

Top European News

- U.K. Softens Brexit Red Line as May Faces Lawmaker Backlash

- Philips Tumbles on Disappointing Profit, Growth at Health Unit

- Sweden’s Government Talks Reach a Record With No End in Sight

- Euro Front-End Demand for Wings Drops on Italy Before ECB Meet

- Investors Aren’t Eager to Short-Sell Mining Equities, Citi Says

In FX, the Euro has been encouraged by events in Rome, and specifically the fact that Italy escaped a deeper ratings cut by Moody’s to stay one rung above junk. BTPs and Italian stocks have rallied in response or rather in relief, and Eur/Usd is back above 1.1500 as a result, albeit off best levels having faded around 1.1550 and clearing its 10 DMA at 1.1527 along the way. CAD/CHF/GBP/NZD – All narrowly mixed vs the Greenback, as the DXY pivots 95.500 within a relatively tight 95.756-469 range, and the Loonie straddles 1.3100 ahead of Canadian wholesale trade data and then the BoC policy meeting on Thursday with a 25 bp hike pretty much factored in. The Franc is also anchored and confined around 0.9950, while Cable nudged higher alongside Eur/Usd earlier, but topped out ahead of 1.3100 and last Friday’s 1.3105 high to sit just above 1.3050, awaiting more from UK PM May on Brexit. The Kiwi has drifted back below 0.6600 having lost some pre-weekend event risk premium. AUD/JPY – Both underperforming vs G10 counterparts, the former on domestic political developments as the Government lost its slender majority by virtue of failing to retain its seat at the Sydney by-election. However, Aud/Usd is just holding above 0.7100 in wake of a short squeeze in Chinese equities overnight, which in contrast has weighed on the Jpy as a safe-haven proxy, with Usd/Jpy climbing above a key 112.74 Fib towards 112.90 vs sub-112.50 at the low. EM – Early Monday/week outperformance for the Rand, as Usd/Zar trade under 14.3000 ahead of Wednesday’s MTBS amidst press reports noting improved budget revenues relative to 2017 and more on track with forecasts. Elsewhere, the Rouble is outpacing the Lira in the run up to this week’s CBR and CBT meetings, with the Rub deriving some support from a rebound in Brent to just over Usd 80/brl.

In commodities, both WTI and Brent are easing off intra-day highs with the former hovering around USD 69.50/bbl while the latter retests USD 80.00/bbl to the downside. Early in the session, Saudi Energy Minister Al-Falih emerged stating the kingdom has no intentions to use oil as a weapon, while he added he cannot guarantee prices won’t rise above USD 100/bbl. Elsewhere, on Friday the Baker Hughes rig count showed an additional 4 oil rigs in operations, rising to the highest figure since March 2015, applying downward pressure on prices. Gold trades lower as the yellow metal mirrors moves in the dollar, albeit still at levels close to it’s 2 month peak. In terms of metals China’s winter anti-pollution restrictions are beginning to take an effect with this expected to boost the demand for high grade iron ore as producers priorities the best quality iron, lowering the overall market supply of iron ore, with prices currently at USD 71/tonne. Separately, China has introduced a system which allows for faster customs clearance for some imported ores, including iron ore which China are the world’s biggest importer of. Copper prices have continued to rise following a pledge from China’s central bank that it would support firms which have liquidity problems.

Iranian Energy Minister Zenganeh said that Saudi Arabia and Russia’s crude output are near their highest ever levels and added that Saudi Arabia and Russia have no spare oil capacity. Saudi Energy Minister Al-Falih said he cannot guarantee oil prices will not rise above USD 100/bbl and Saudi production is likely to increase in the near future to 11mln BPD, adding new OPEC+ oil agreement might be signed on Dec 7th . He added if 3mln BPD of oil supplies disappear in 2019, Saudi cannot cover this volume and will have to use reserves.

It’s a very quiet start to the week: in Europe, we get the Euro-area’s 2017 government debt to GDP ratio. In the US, we get the September Chicago Fed National activity index.

US Event Calendar

- 8:30am: Chicago Fed Nat Activity Index, est. 0.2, prior 0.2

DB’s Jim Reid concludes the overnight wrap

By the time you read this I’ll be in my surgical gown ready for another knee operation – my third in 3 and a half years. This time it’s on my “good” knee due to a torn meniscus. My advice to all readers is if you take up skiing in your 30s please make sure you’re not an overconfident, speed hungry person who doesn’t listen to anyone when they tell you skiing is dangerous and to slow down. Markets are also unlikely to slow down much this week even if it is half-term here in the UK but let’s hope they don’t end up in the operating theatre by the end of the week. Indeed it’s another busy week full of interesting events including an ECB meeting (Thu) , S&P’s review of Italy’s sovereign ratings (Fri) after Moody’s completed theirs late on Friday (see below), the advance Q3 GDP release in the US (Fri), and the preliminary October PMIs in Europe and the US (Wed).

In addition, Saudi Arabia will hold its troubled “Davos in the Desert” conference (Tue) with global political tensions high. Earnings releases also pick up pace during the week on both sides of the pond. Given that Q3 saw Turkey and Italy in some turmoil, European banks may be the earnings highlight this week, especially as they start the season at 2-year lows not helped by the Spanish banking woes from last week (see below).

Staying in Europe, the ECB meet on Thursday. Although policy rates are expected to be left unchanged, the meeting is likely to be closely watched for more colour on how the ECB will reinvest maturing QE proceeds post the likely end of QE in December this year. Focus will also be on Draghi’s comments on Italy. It’s hard to imagine the ECB will lower the pressure on Italy but they are also unlikely to want to escalate tension further so expect some element of diplomacy.

Interestingly late on Friday Moody’s decided to leave Italy’s rating at stable after a 1-notch downgrade to Baa3. If there’s one thing the outlook isn’t for Italy at the moment it’s stable but rating agencies are unlikely to want to create a vicious circle. With S&P opining on Friday it’s possible we’ll see a similar response for a similar reason. Italy rallied strongly on Friday (10yr BTPs -20bps, 24.6bps tighter to Bunds) before Moody’s decision which came after the US close. There was some talk late in the session on Friday (via the Italian newspaper Foglio) that the deficit could be lowered to 2.1% for 2019, which would be a substantial de- escalation. However the weekend mood music from the Government doesn’t suggest this is about to happen. Indeed the Government are expected to respond to the EC today in a letter confirming the 2.4% deficit target but according to the weekend press in Italy explain that its a temporary measure to kick start the economy. Interestingly over the weekend an Ipsos survey published by the Corriere della Sera newspaper indicated that 59% of Italians back the Government’s deficit target. The survey also found that 55% believe that higher government debt is needed to stimulate the economy. After years of very weak growth and continued austerity you can’t blame the voters for wanting something different whether it eventually works or not. Europe needs to tread very carefully as it responds.

This morning in Asia, markets are off to a positive start with China’s Shanghai Comp (+4.17%; highest daily gain since March 2016), CSI 300 (+4.40%) and Shenzhen Comp (+4.96%) leading the way after China’s government announced tax cuts over weekend (more on this below). In the meantime, the Nikkei (+0.53%), Hang Seng (+2.40%) and Kospi (+0.18%) are also up along with most Asian markets.

So as discussed above the Chinese government announced details of a personal income tax cut on Saturday. This comes as a positive surprise for our economists. They estimate the size of the tax cut may be RMB 500-600bn (0.5% of GDP) in 2019, including RMB 320bn from the changes of tax brackets and RMB 200-300bn from new tax allowances. It could boost retail sales by about 1% if people spend 70% of tax savings on consumption. DB believe this is the beginning of a series of tax cuts, with VAT and corporate income tax potentially the next targets. These measures would help to offset the downside risks from the trade war, and keep growth in 2019 above 6%. It reinforces DB’s view that China’s current account surplus will turn into a deficit and the RMB will depreciate to 7.4 against the US dollar in 2019. See the link here for more.

On Brexit, the UK PM May is likely to tell the British lawmakers today that “95% of the Withdrawal Agreement and its protocols are now settled,” according to remarks mailed by her office highlighting that headway’s been made over the past three weeks on topics including military bases in Cyprus, arrangements for Gibraltar, and dispute resolution with the EU after Brexit. In the meantime, Brexit Secretary Dominic Raab hinted on Sunday that the UK could provide an alternative to fixed time limited Irish “backstop” arrangements and showing some signs of flexibility over the issue as the EU wants the “backstop” arrangement to be open ended. This could pose fresh leadership challenges for UK PM May with the weekend press suggesting a potential challenge continues to bubble up in the background.

Tomorrow could be an interesting day in geopolitics as Mr Erdogan has suggested he will reveal Turkey’s interpretation of the events surrounding journalist Khashoggi death. This coincides with the start of the Saudi investment conference which is going to be plagued by mass international absenteeism. So all eyes on Turkey tomorrow as the current Saudi explanation for the death has not been particularly well received by the world’s media and politicians.

Reviewing last week now before we look at the week ahead. The S&P 500 eked out a +0.02% gain last week (-0.04% on Friday), but under the surface, investors continued to rotate into defensive sectors. The best performing sectors on the week were consumer staples, real estate, and utilities, while tech continued to be pressured. The FANGs shed -1.81% (-0.96% Friday), despite very strong earnings from Netflix and positive headlines about a potential IPO by Uber, which briefly supported the sector. The DOW gained +0.41% (+0.26% Friday) and the NASDAQ retreated -0.70% (-0.12% Friday). Chinese equities saw a wild ride with the Shanghai Comp falling -2.17% on the week but rising +2.58% on Friday as verbal intervention started before the weekend’s tax cuts added to this. Bonds sold off again, with two-year Treasury yields touching a new decade high, rising +5.1bps (+3.0bps Friday) to 2.90%. Ten-year Treasury yields rose +3.1bps (+1.4bps Friday), while Bunds rallied -5.7bps (+4.4bps Friday) amid the volatility in Italy (see below). The STOXX 600 gained +0.64% (-0.12% Friday), with German equities outperforming (DAX +0.26% on the week, -0.31% Friday), though Euro banks fell to a new two-year low, trading -2.29% on the week (-0.57% Friday), with Spanish banks leading losses (more below). Emerging markets were mixed, as equities lost -1.54% (+0.94% Friday) but currencies gained +0.45% (+0.02% Friday), and the VIX fell 1.4pts on the week (-0.17pts Friday) but remains elevated relative to the recent past at 19.89.

Spanish bonds underperformed last week, with 10-year yields rising +5.9bps (+0.7bps Friday) despite the 20bps rally in Italy. Spanish banks shed -2.91% (+0.38% Friday). A court ruling will shift a mortgage tax away from consumers, who used to pay it, onto banks, who will now have to pay it. The court may revisit the decisions, but for now it represents a significant surprise and a downside risk for the sector, since borrowers would be entitled to seek claims on up to 1.2 trillion euros of mortgages sold over the last 15 years, which could cost the system up to 24 billion euros.

Corporate earnings were mixed on the week, though they remain strong overall this season as we expected. With 17% of S&P 500 companies having reported, sales have grown +7.4% yoy and earnings are up +21.3% yoy. That’s 0.5% and 4.6% better than consensus for revenue and profits, respectively. Last week, Goldman Sachs and Morgan Stanley beat expectations and saw their share prices rally +6.09% and +6.91%, while Bank of America was a bit soft and fell -0.53% on the week. Shipping firm CSX reported healthy volumes, signaling strong macro momentum.

It’s a very quiet start to the week. In Europe, we get the Euro-area’s 2017 government debt to GDP ratio. In the US, we get the September Chicago Fed National activity index.

3. ASIAN AFFAIRS

i) MONDAY MORNING/ SUNDAY NIGHT:

SHANGHAI CLOSED UP 104.41 POINTS OR 4.09% //Hang Sang CLOSED UP 591.75 POINTS OR 2.32% //The Nikkei closed UP 82.74 OR 0.37%/ Australia’s all ordinaires CLOSED DOWN 0.61% /Chinese yuan (ONSHORE) closed DOWN at 6.9422 AS POBC RESUMES ITS HUGE DEVALUATION /DELEGATION COMING TO THE USA TO SEE TRUMP IN NOVEMBER CANCELLED/Oil DOWN to 69.14 dollars per barrel for WTI and 79.93 for Brent. Stocks in Europe OPENED RED MIXED///. ONSHORE YUAN CLOSED SLIGHTLY DOWN AT 6.9422 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED SLIGHTLY DOWN ON THE DOLLAR AT 6.9454: HUGE DEVALUATION/PAST SEVERAL DAYS RESUMES// TRADE TALKS STOPPED : /ONSHORE YUAN TRADING STRONGER AGAINST OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING WEAKER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

3 a NORTH KOREA/USA

North Korea/South Korea/USA/China

3 b JAPAN AFFAIRS

3C CHINA

China’s economy is not crashing and as Snider points out: it is worse than that because there is no growth coming from this nation. This would be very scary for the rest of the world as China is the engine for global growth

(Jeffrey Snider/Alhambra Investments partners)

Alhambra: China’s Economy Is Not Crashing, It’s Worse Than That

Authored by Jeffrey Snider via Alhambra Investment Partners,

China’s economy is not crashing. Hyperbole works both ways. Last year and this, the smallest increment above a prior number was broadcast out as the greatest thing ever (US wage growth in particular), irrefutable proof of globally synchronized growth. Now that that’s over with, largely, there will be a tendency toward the other extreme.

The latest Chinese economic statistics are for several of them the lowest in some time. Starting with real GDP, at just 6.5% in Q3 2018 it’s the slowest pace since the first quarter of 2009. That’s not good especially for a statistic of such dubious practices often specifically crafted to be the best it can be.

What that suggests is not immediate catastrophe, offering instead more complete confirmation that this major economy is slowing. Again. This is the real story in China and therefore for everywhere else.

In other words, the real danger presented by these statistics is not imminent crash but rather the total disappearance of any upside potential. Even during 2017, the narrative about globally synchronized growth continued as a future property. The global economy in that year was clearly better than it was during the worldwide downturn 2015-16, easy comparison, and that was expected only as the first step toward meaningful acceleration and then recovery.

Where Economists and central bankers jumped the gun was in assuming that 2017’s improvement was the only evidence they needed for those complete expectations. As it has turned out, as it always turns out, changing from minus to plus signs is a necessary condition for better days but not by itself a sufficient one.

Acceleration requires momentum among other factors, and momentum is derived from conviction. The best days of 2017 never really had that, the absence perhaps clearest in China (particularly the hollow rebound of CNY which “somehow” lacked “capital inflows”).

Everyone kept waiting for the Chinese to zoom on ahead and bring the whole up with them. Meanwhile, in China they kept waiting for the rest of the world to take the lead so as to pull them up out of their funk. That’s been the thing about “global growth” since 2011, everyone expects that someone else will solve their economic problems for them. Momentum will arrive, you see, it’ll come from somewhere else.

Without a clear path to that next step toward recovery, doubts multiply rather than abate. What was for a time mild opportunity, reflation, sinks back toward the malaise of liquidity risks that over time can only return to self-reinforcing.

This is what’s significant about China’s numbers today. They practically declare reflation dead and gone. There is no upside left, what you saw in 2017 was the best of it – and it wasn’t very good. It was, in honest analysis, not really that much better than 2016 at all; certainly less than the prior peak.

The rest of the statistics bear this out. Nominal GDP, perhaps a more appropriate measure of China’s economic conditions, decelerated yet again in Q3. Year-over-year, it rose just 9.6%, down from 9.8% in Q2 and a peak of 11.7% set way back in Q1 2017. The more time passes without clear acceleration, the more it has to sink in (everywhere but Washington DC) that this really is a rising dollar “L.”

The world economy has never recovered from the 2011 eurodollar crisis (squeeze). The system broke in August 2007, and created all sorts of devastation immediately thereafter. But for a time in 2010 and the first half of 2011 it looked like recovery was at least possible if unusually weak.

Economists, incapable of appreciating the global monetary system for their modern practice of neglect, mistook 2011 for a lack of sufficient time; they crafted monetary policies (with no money in them) so as to buy the financial system enough of it thinking that would be the magic elixir.

Instead, time has proven beyond all doubt that 2011 was the last stand for recovery. It just isn’t possible so long as the global reserve currency, the eurodollar not dollar, remains dysfunctional. There can never be enough momentum to escape, opportunity surrendered by this neglect.

The more Chinese statistics in particular show this to be true the more it will spread and eventually become self-reinforcing (again). In certain places, it may have already.

The rest of the data follows along this way; not crashing but what may be worse as the end of any upside.

Chinese Industrial Production rose just 5.8% year-over-year in September, the first month below 6% in two and a half years going all the way back to the trough of the last downturn in February 2016. As noted at the outset, there can be an inclination to make more out of that comparison when, for now, it simply confirms there just isn’t any recovery.

Along those lines, it stands in sharp contrast to sentiment which even in China had gotten way ahead of economic reality. It’s another element of 2017 and globally synchronized growth that is being slowly, steadily undone in 2018. Sentiment has proved a worthless indicator, and well beyond the other side of the Pacific Ocean.

Retail sales was practically the lone bright spot, which merely means there wasn’t as much slowing as there had been. Rising 9.2% in September, it was the fastest pace in five months, but still materially less than the 10%+ rate that prevailed 2015 forward.

Fixed asset investment managed to tick a little higher last month as private capex remained steady while government investment rebounded slightly. Overall, FAI was up 5.4% on an accumulated basis (YTD) compared to August’s record low 5.3%. Private FAI also on an accumulated basis stayed at 8.7%. State-owned FAI gained 1.2% last month compared to 1.1% the month before.

China’s economy is not crashing. However, it is slowing and from an already weakened level. The Chinese system did not actually recover from the last downturn despite now three years distance. What these numbers show is that, like the eurodollar system, there is now very little chance that it ever will. It may not seem like much compared to a full-blown breakdown, but pretty conclusive evidence for a worldwide, multi-year (decade?) “L” should be terrifying.

A world without opportunity is a far more dangerous one than a world only temporarily stripped of it. The V can be scary but only on the way down. The L is, well, I think we’re going to find out.

4.EUROPEAN AFFAIRS

The European Financial Establishment Just Declared War On Italy

This week in a CNBC interview Jeroen Dijsselbloem, the former Dutch minister of finance who served as the President of the Eurogroup, declared war on the Italian government.

The European financial establishment is prepared to destroy the banking system and cause the Italian economy to implode. Like a Mafia boss, Dijsselbloem warned that Italy could run into trouble if it does not comply with Brussels’ directives. Of course, his statement was cloaked in diplomatic language:

“If the Italian crisis becomes a major crisis, it will mainly implode into the Italian economy … as opposed to spreading around Europe,” he said.

“Because of the way that the Italian economy and the Italian banks are financed, it’s going to be an implosion rather than an explosion.”

For a man of this format it is unusual to publicly expose Italy as a state in a weak negotiating position or try to act as a scaremonger. We have never seen anything remotely like that, so we think that the utterance could only serve the purpose of giving the green light to the financial markets to orchestrate an attack on Italian bonds so as to drive Italian yield up.

“And there is gonna be a role for the markets, I mean if you look at what Italy needs in funding next year alone we are talking about over 250 billion Euro, refinancing part of the stock of their debt and also, of course, these new spending plans. So markets will really have to look at that very critically.”

He reminded the Italian government that Italian banks are a sitting target for the European financial authorities. In order to destabilize a country’s economy, one must break its backbone i.e. banks.

“There will also have to be a role for the Banking authority, banking supervisor to look what this does to the Italian banks. We have already seen their stock valuation are going down” Mr Dijsselbloem said with a smile.

Under the leadership of Jeroen Dijsselbleom, Greece was cut off from TARGET 2, the European payment system, so that not a single euro could be transferred abroad for a long time . Italy is not comparable to Greece, though. The state has had a trade balance surplus for years and is in better shape than France. Because Italy’s exports exceed its imports, the country is not dependent on foreign financing for its needs. The former President of the Eurogroup does not want his Brussels colleagues to have second thoughts, so he used the CBNC interview to let them know they have to proceed.

“Looking at what (Italian officials) have put on the table, the commission really has no option than to send it back, which — by the way — is not the end of the process, but the start of the process,”

“It’s pretty worrisome, there’s going to be confrontation and I think the commission has no choice then to accept that confrontation and to take it,”

This declaration of war was triggered by the Italian budget proposal. The Italian budget deficit is structural, and the state debt amounts to 130% of GDP. The Italian economy is comparable to that of Japan. Both are characterised by shrinking internal consumption and an export surplus. Just like Japan, Italy has a declining population. Demand for real estate and consumer goods is falling, so industrial production will have to eventually decelerate.

The Italian government, supported by the population, refuses to submit to the European financial masters. A shrinking population and increasing public debt are inevitable and need not be a problem as long as the country produces enough to pay for its imports. It is only because the Italians do not have their currency that they are forced to obey their masters in Brussels and the bankers in Frankfurt. The introduction of a parallel currency and a withdrawal from the euro seems a logical solution and is not historically unique. Czechnia and Slovakia, the former Russian and Yugoslav republics each had once a currency union, and as these countries went their separate ways, so did separate currencies emerge and replaced the old ones.

Jeroen Dijsselbloem told CNBC that the only conceivable solution for Italy is money from the European support fund, although it is clear that this fund cannot solve the problems. In the end, Jeroen Dijsselbloem ventured a prediction that there won’t be any bailout for Italy because “politically and financially it won’t happen.

“I don’t see support around the euro zone to say, ‘These guys are completely off track — let’s help them,’” he said, adding thata bailout of Italy would also “wipe out” the European Stability Mechanism fund within two years.”

By mentioning only one possible solution, the European banker is sending a signal to Rome that no alternative, such as the return to the lira, will be discussed.

Dijsselbloem’s statement on CNBC is an ultimatum delivered to his Italian colleagues. In Cyprus, hundreds of retail investors lost their money under Dijselbloem’s authority. Much the same seems to be the case now. The ECB wants Rome to use the money of little retail investors such as pensioners to save the Italian banks. Jeroen Dijselbloem is known for such bail-in templates and he even has the nerve to warn the Italian citizens:

“The only way to get out of this is for Italy to realize that (the destruction of the Italian economy), the Italian retail customers and the voters to understand that (the collapse of the banks), and then the correction will hopefully start coming from inside.”

We wonder what correction he has in mind. Democracy has run its course, the voters have already decided, and according to the polls they are perfectly happy with the Italian deputy minister Mateo Salvini, whose popularity is only growing.

Was the former Dutch minister signalling that the European authorities would not have anything against a coup d’état in Rome? Or was he suggesting that somebody do away with Mateo Salvini?

END

Monday morning: ITALY

Italy admits to the deficit breach but refuses to budge

(courtesy zerohedge)

Italy Responds To EU Commission, Admits Deficit Breach But Refuses To Budge

Initial relief over a favorable Moody’s downgrade of Italy, which pushed the rating just one notch above junk but kept the outlook stable (which in turn prompted the following sarcastic remark from Deutsche Bank’s Jim Reid “If there’s one thing the outlook isn’t for Italy at the moment it’s stable but rating agencies are unlikely to want to create a vicious circle”) faded after Italy’s populist government promised it won’t let its budget deficit widen further than currently planned and called for dialogue with the European Union to address their differences.

In its letter response to the European Commission published Monday and seen by Bloomberg, Italy acknowledged Europe’s concerns about the budget, but refused to change the proposed plan.

Finance Minister Giovanni Tria said the government is ready to act to ensure it doesn’t exceed the 2.4% target for 2019, noting that he’s aware that his spending plans don’t comply with EU rules and he wants “constructive” talks with officials in Brussels.

The decision to increase spending was “difficult though necessary,” Tria said in his letter. He cited slow economic growth and the “difficult economic situation the poorest segments of the Italian society are facing.”

Seeking to placate Brussels, Prime Minister Giuseppe Conte, speaking in Rome, said the deficit target should be seen as an upper limit and it could still be narrower.

“We can still reassess during the budget implementation whether to contain the target so we don’t necessarily need to reach that 2.4%, for sure we won’t exceed it” Cointe said even as he refused to budge from the controversial target which assures that Italy remains on collision course with the EU.