GOLD: $1227.45 UP $6.70 (COMEX TO COMEX CLOSINGS)

Silver: $14.52 UP 23 CENTS (COMEX TO COMEX CLOSING)

Closing access prices:

Gold : 1226.00

silver: $14.49

For comex gold and silver:

NOV

NUMBER OF NOTICES FILED TODAY FOR NOV CONTRACT:3 NOTICE(S) FOR 300 OZ

Total number of notices filed so far for NOV: 209 for 20900 OZ (0.6500 TONNES)

FOR NOVEMBER

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

51 NOTICE(S) FILED TODAY FOR

255,000 OZ/

Total number of notices filed so far this month: 1459 for 7,295,000 oz

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: OPENING MORNING TRADE $4641: up $78

Bitcoin: FINAL EVENING TRADE: $4560 down $2.00

end

XXXX

China is controlling the gold market

WE WILL NOT PROVIDE LONDON FIXES AS THEY ARE NOT ACCURATE AS TO WHAT IS GOING ON AT THE SAME TIME FRAME.

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total OPEN INTEREST ROSE BY A TINY 96 CONTRACTS FROM 222,953 UP TO 223,049 DESPITE YESTERDAY’S 14 CENT FALL IN SILVER PRICING AT THE COMEX. TODAY WE ARRIVED CLOSER TO AUGUST’S RECORD SETTING OPEN INTEREST OF 244,196 CONTRACTS.

WE HAVE ALSO WITNESSED A LARGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY(WELL OVER 30 MILLION OZ AT THE COMEX FOR JULY , 6 MILLION OZ FOR AUGUST AND NOW JUST LESS THAN 31 MILLION OZ STANDING IN SEPTEMBER. AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A STRONG SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP:

0 EFP’S FOR NOV. 1335 EFP’S FOR DECEMBER AND 0 FOR MARCH AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE: OF 1335 CONTRACTS. WITH THE TRANSFER OF 1335 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 1335 EFP CONTRACTS TRANSLATES INTO 7.78 MILLION OZ ACCOMPANYING:

1.THE 14 CENT FALL IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR THE JUNE/2018 COMEX DELIVERY MONTH. (5.420 MILLION OZ); 30.370 MILLION OZ STANDING FOR DELIVERY IN JULY, FOR AUGUST: 6.065 MILLION OZ AND 39.505 MILLION OZ STANDING IN SEPT. 2,520,000 OZ STANDING IN OCTOBER. AND NOW SO FAR A HUGE 7,430,000 OZ STANDING FOR NOVEMBER

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF NOV: 38,733 CONTRACTS (FOR 15 TRADING DAYS TOTAL 38,733 CONTRACTS) OR 193.665 MILLION OZ: (AVERAGE PER DAY: 2582 CONTRACTS OR 12.91 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF NOV: 193.665 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 27.57% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2018 TO DATE SILVER EFP’S: 2,619.74 MILLION OZ.

ACCUMULATION FOR JAN 2018: 236.879 MILLION OZ

ACCUMULATION FOR FEB 2018: 244.95 MILLION OZ

ACCUMULATION FOR MARCH 2018: 236.67 MILLION OZ

ACCUMULATION FOR APRIL 2018: 385.75 MILLION OZ

ACCUMULATION FOR MAY 2018: 210.05 MILLION OZ

ACCUMULATION FOR JUNE 2018: 345.43 MILLION OZ

ACCUMULATION FOR JULY 2018: 172.84 MILLION OZ

ACCUMULATION FOR AUGUST 2018: 205.23 MILLION OZ.

ACCUMULATION FOR SEPTEMBER 2018: 167,05 MILLION OZ

ACCUMULATION FOR OCTOBER 2018: 224.875 MILLION OZ

RESULT: WE HAD A TINY SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 96 DESPITE THE 14 CENT FALL IN SILVER PRICING AT THE COMEX //YESTERDAY. THE CME NOTIFIED US THAT WE HAD A VERY GOOD SIZED EFP ISSUANCE OF 1335 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) .

TODAY WE GAINED A GOOD SIZED: 1436 TOTAL OI CONTRACTS ON THE TWO EXCHANGES:

i.e 1335 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH INCREASE OF 96 OI COMEX CONTRACTS. AND ALL OF THUS DEMAND HAPPENED WITH A 14 CENT FALL IN PRICE OF SILVER AND A CLOSING PRICE OF $14.29 WITH RESPECT TO YESTERDAY’S TRADING. YET WE HAD A GIGANTIC AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY IN THE BIG JULY DELIVERY MONTH OF SLIGHTLY OVER 30 MILLION OZ, IN AUGUST ANOTHER BIG 6.065 MILLION OZ IN A NON ACTIVE MONTH IN SEPTEMBER A FINAL MONSTROUS 39.05 MILLION OZ OF SILVER STANDING FOR DELIVERY, WITH HUGE DELIVERIES OF OVER 2 MILLION OZ IN OCTOBER (A NON DELIVERY MONTH) AND NOW 7.430 MILLION OZ IN NOVEMBER….... NOBODY IS PAYING ATTENTION TO THE HUGE NUMBER OF PHYSICAL OUNCES STANDING FOR SILVER THESE PAST SEVERAL MONTHS.

In ounces AT THE COMEX, the OI is still represented by JUST OVER 1 BILLION oz i.e. 1.115 BILLION OZ TO BE EXACT or 151% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT AUGUST MONTH/ THEY FILED AT THE COMEX: 51 NOTICE(S) FOR 255,000 OZ OF SILVER

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 243,411 CONTRACTS ON APRIL 9.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $16.51.

AND NOW WE RECORD FOR POSTERITY ANOTHER ALL TIME RECORD OPEN INTEREST AT THE COMEX OF 244,196 CONTRACTS ON AUGUST 22/2018 AND AGAIN WHEN THIS RECORD WAS SET, THE PRICE OF SILVER WAS $14.78 AND LOWER IN PRICE THAN PREVIOUS RECORDS.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: AN INITIAL HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz AND NOW NOV AT 7.430 MILLION OZ.

- HUGE RECORD OPEN INTEREST IN SILVER 243,411 CONTRACTS (OR 1.217 BILLION OZ/ SET APRIL 9/2018) AND NOW AUGUST 22/2018: 244,196 CONTRACTS, WITH A SILVER PRICE OF $14.78.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017

- RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT).

IN GOLD, THE OPEN INTEREST ROSE BY A CONSIDERABLE SIZED 2450 CONTRACTS DOWN TO 525,940 DESPITE THE LOSS IN THE COMEX GOLD PRICE/YESTERDAY’S TRADING (A FALL IN PRICE OF $3.95).THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 8268 CONTRACTS:

NOVEMBER HAD 0 EFP’S ISSUED AND, DECEMBER HAD AN ISSUANCE OF 8268 CONTACTS AND ALL OTHER MONTHS ZERO. The NEW COMEX OI for the gold complex rests at 525,940. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE A VERY STRONG SIZED GAIN IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 10,718 CONTRACTS: 2450 OI CONTRACTS INCREASED AT THE COMEX AND 8268 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN: 10,718 CONTRACTS OR 1,071,800 OZ = 33.33 TONNES. AND ALL OF THIS DEMAND OCCURRED WITH A FALL IN THE PRICE OF GOLD/ YESTERDAY TO THE TUNE OF $3.95.

YESTERDAY, WE HAD 5789 EFP’S ISSUED.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF NOV : 110,447 CONTRACTS OR 11,044,700 OZ OR 343.51 TONNES (15 TRADING DAYS AND THUS AVERAGING: 7363 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE HUGE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 15 TRADING DAY IN TONNES: 343.51 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2017, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 2555 TONNES

THUS EFP TRANSFERS REPRESENTS 343.51/2550 x 100% TONNES = 13,47% OF GLOBAL ANNUAL PRODUCTION SO FAR IN JULY ALONE.***

ACCUMULATION OF GOLD EFP’S YEAR 2018 TO DATE: 6,560.34 TONNES *SURPASSED ANNUAL PROD’N

ACCUMULATION OF GOLD EFP’S FOR JANUARY 2018: 653.22 TONNES (21 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR FEBRUARY 2018: 649.45 TONNES (20 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR MARCH 2018: 741.89 TONNES (22 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR APRIL 2018: 713.84 TONNES (21 TRADING DAYS)

ACCUMULATION OF GOLD EFP’S FOR MAY 2018: 693.80 TONNES ( 22 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR JUNE 2018 650.71 TONNES (21 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR JULY 2018 605.5 TONNES (21 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR AUG. 2018 488.54 TONNES (23 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR SEPT 2018 470.64 TONNES (19 TRADING DAYS)

ACCUMULATION OF GOLD EFP FOR OCT. 2018 543.92 TONNES (23 TRADING DAYS)

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A CONSIDERABLE SIZED INCREASE IN OI AT THE COMEX OF 2450 DESPITE THE LOSS IN PRICING ($3.95) THAT GOLD UNDERTOOK YESTERDAY) //.WE ALSO HAD A STRONG SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 8268 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 8268 EFP CONTRACTS ISSUED, WE HAD AN VERY STRONG GAIN OF 10,718 CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

8268 CONTRACTS MOVE TO LONDON AND 2450 CONTRACTS INCREASED AT THE COMEX. (in tonnes, the GAIN in total oi equates to 33.33 TONNES). ..AND ALL OF THIS HUGE DEMAND OCCURRED WITH A LOSS OF $3.95 IN YESTERDAY’S TRADING AT THE COMEX???

we had: 3 notice(s) filed upon for 300 oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD...

WITH GOLD UP $6.70 TODAY: /

NO CHANGE IN GOLD INVENTORY AT THE GLD/

/GLD INVENTORY 760.86 TONNES

Inventory rests tonight: 760.86 tonnes.

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

SLV/

WITH SILVER UP 23 CENTS TODAY

NO CHANGE IN SILVER INVENTORY AT THE SLV

/INVENTORY RESTS AT 325.019 MILLION OZ.

end

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER ROSE BY A TINY 96 CONTRACTS from 222,953 DOWN TO 223,049 AND MOVING A LITTLE CLOSER TO THE NEW COMEX RECORD SET LAST IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 1 1/3 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89. AS YOU CAN SEE, WE HAVE RECORD HIGH OPEN INTERESTS IN SILVER ACCOMPANIED BY A CONTINUAL LOWER PRICE WHEN THAT RECORD WAS SET…..

.

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

i) 0 EFP’s for November… and

1335 CONTRACTS FOR DECEMBER. 0 CONTRACTS FOR MARCH AND AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 1335 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI GAIN AT THE COMEX OF 96 CONTRACTS TO THE 1335 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A GOOD NET GAIN OF 1431 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES: 7.155 MILLION OZ!!! AND YET WE ALSO HAVE A STRONG DEMAND FOR PHYSICAL AS WE WITNESSED A FINAL STANDING OF GREATER THAN 30 MILLION OZ FOR JULY, A STRONG 6.065 MILLION OZ FOR AUGUST.. A HUGE 39.505 MILLION OZ STANDING FOR SILVER IN SEPTEMBER… OVER 2 million OZ STANDING FOR THE NON ACTIVE MONTH OF OCTOBER., AND NOW 7.430 MILLION OZ STANDING IN NOVEMBER.

RESULT: A TINY INCREASE IN SILVER OI AT THE COMEX DESPITE THE 14 CENT PRICING LOSS THAT SILVER UNDERTOOK IN PRICING// YESTERDAY.BUT WE ALSO HAD ANOTHER GOOD SIZED 1335 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR SEPTEMBER, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)WEDNESDAY MORNING/ TUESDAY NIGHT:

SHANGHAI CLOSED UP 5.65 POINTS OR 0.21% //Hang Sang CLOSED UP 131.13 POINTS OR 0.51% //The Nikkei closed DOWN 75.58 OR 0/35%/ Australia’s all ordinaires CLOSED DOWN 0.51% /Chinese yuan (ONSHORE) closed UP at 6.9370 AS POBC RESUMES ITS HUGE DEVALUATION /DELEGATION COMING TO THE USA TO SEE TRUMP IN NOVEMBER /Oil DOWN to 54.27 dollars per barrel for WTI and 63.63 for Brent. Stocks in Europe OPENED GREEN//. ONSHORE YUAN CLOSED UP AT 6.9370AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.9323: HUGE DEVALUATION/PAST SEVERAL DAYS RESUMES// TRADE TALKS NOW ON : /ONSHORE YUAN TRADING WEAKER AGAINST OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING STRONGER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

3A/NORTH KOREA/SOUTH KOREA

i)North Korea/South Korea/USA/

b) REPORT ON JAPAN

3 C/ CHINA

4/EUROPEAN AFFAIRS

i)Italy

Conditions getting hotter inside Italy and the EU. The EU formally reject Italy’s budget which paves the way for sanctions. This will probably be the out that Italy needs to vacate the Euro

( zerohedge)

ii)Bill Blain discusses events of yesterday and the Italian budgetary deficit affair. He states: who will buy the 275 billion euros of debt issued by Italy. He is correct that it will be the Italian banks who will buy this garbage and they are already saturated up to their gills with this stuff. He also states that the ECB will quietly offer the Italians long repo money at zero percent to help them if they reduce their budgetary defict.

( Bill Blain)

iii)GERMANY/DEUTSCHE BANK

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

Russia/Interpol

Interpol defies Russia and backs Bill Browder as they by-pass the Russian candidate and go with a South Korean as President

( zerohedge)

6. GLOBAL ISSUES

7. OIL ISSUES

Crude oil is telling us that demand around the globe is crumbling

( zerohedge)

8 EMERGING MARKET ISSUES

9. PHYSICAL MARKETS

ii)Bart Chilton on Russia Today is hosting a broadcast on the economy. He had Schiff on and here the former CFTC commissioner found much evidence of silver rigging even though he stated that there was not enough to prosecute. However two weeks ago a JPMorgan trader confessed to rigging the gold and silver markets and that he was taught by his superiors.

There is going to be big news coming from future broadcasts from Bart Chilton and guests..stay tune.d

( GATA/Boom or Bust/Bart Chilton)

iii)Today is the day whereby the LBMA is suppose to be transparent. It is not as big as thought

( Bloomberg/GATA)

iv)Craig comments on the LBMA “transparency”

(courtesy Craig Hemke/GATA)

vii)Here are a few things which could precipitate the next crisis( James Rickards/Daily Reckoning)

10. USA stories which will influence the price of gold/silver)

MARKET TRADING

ii)Market data/

a)Again more data to suggest that the USA economy is cooling off: durable good orders plunge including defense spending

( zerohedge)

b)Realtors are urging the Fed to stop hiking as existing home sales slump the most since 2014. All of the 3 major housing data is slumping: new starts, permits and now existing home sales

c)Soft data, U. of Michigan confidence data drops on rate hike expectations.( zerohedge)

a)The situation inside Illinois is pretty bad as Millennials leave.

an excellent presentation as to their huge deficits

( Ted Dabrowski/WirePoints.com)

b)Tom Luongo believes that it is Bill Browder who is behind the anti Russia Interpol propaganda. He is no doubt correct and he explains why

(courtesy Tom Luongo)

c)Five huge American derivative players along with the French bank Paribas have considerable problem with the mess at GE. I would also like to point out that BNP Paribas also has a huge problem with respect to the huge amount of sovereign Italian debt that they have purchased.

(courtesy zerohedge)

d)Two events caused the market to rise: MNI feels that the Fed may end rate hikes and the second was a report that peter Navarro will be “excluded’ form the Trump Xi summit

iv)SWAMP STORIES

Let us head over to the comex:

We are now in the non active delivery month of NOVEMBER and here we now have 78 notices standing for a gain of 74 contacts. We had 1 notice served upon yesterday so we gained 75 contracts or an additional 375,000 oz will stand for delivery as these longs refused to morph into London based forwards as well as not accepting a fiat bonus for their efforts. SOMEBODY TODAY WAS IN GREAT NEED OF PHYSICAL SILVER

After November, we have a December contract and here we LOST 15,303 contracts DOWN to 100,100. January saw a GAIN of 8 contracts up to 1280 contracts. March, the next big delivery month after December saw a gain of 151913 contracts up to 99,272

FOR COMPARISON TO THE COMEX 2017 CONTRACT MONTH:

ON NOV 21. 2017 WE HAD STILL 75,364 OPEN INTEREST CONTRACTS LEFT TO BE SERVED UPON AND THIS COMPARES TO TODAY: 100,100 CONTRACTS

ON FIRST DAY NOTICE DEC 1.2017 WE HAD A RATHER LARGE: 19.47 MILLION OZ STAND FOR DELIVERY

BY THE END OF DECEMBER: 33.295 MILLION OZ AS QUEUE JUMPING WAS THE NAME OF THE GAME IN SILVER.

.

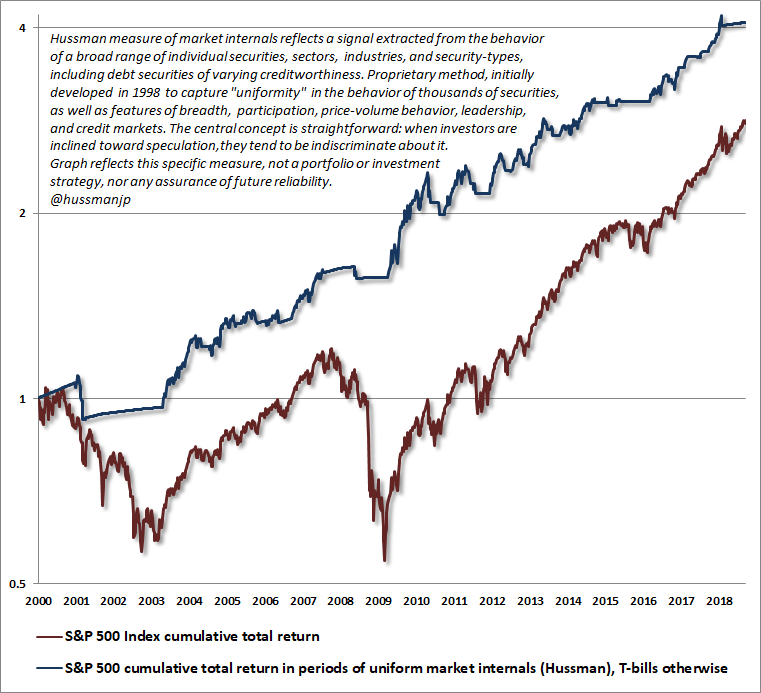

Stock Markets Remains Extremely Overvalued – Hussman

The Heart of the Matter

by John Hussman of Hussman Funds

Let’s be clear. October’s market decline was a rather mild warning shot. At its lowest close, the S&P 500 lost -9.9% from its September peak, before rebounding in recent sessions. As I noted during the 2000-2002 and 2007-2009 collapses, intermittent “fast, furious, prone-to-failure” rebounds are among the factors that encourage investors to hold on through the entirety of major declines. After particularly severe down-legs in the market (which we have not yet observed), these rebounds can extend for weeks, and sometimes approach gains of as much as 19% before the market plunges again.

Get used to that kind of volatility. Though it will be essential to monitor market internals for periodic shifts in investor psychology, by the completion of the current market cycle, I continue to expect the S&P 500 to lose nearly two-thirds of its value.

It’s been nearly a year now since we finally identified and fully addressed the core of our difficulty in the half-cycle advance since 2009. In my view, this is such a critical moment in the markets that a careful understanding of that core issue is essential. Though portions will (hopefully) be familiar, I can presently think of no other topic in finance for which the time spent reviewing and understanding will be as valuable.

The heart of the matter, and the key to navigating this brave new world of extraordinary monetary and fiscal interventions, is to recognize that while 1) valuations still inform us about long-term and full-cycle market prospects, and; 2) market internals still inform us about the inclination of investors toward speculation or risk-aversion, the fact is that; 3) we can no longer rely on well-defined limits to speculation, as we could in previous market cycles across history.

Read the full article on AdvisorPerspectives.com

News and Commentary

Dow plunges more than 500 points, erases gain for 2018 (CNBC.com)

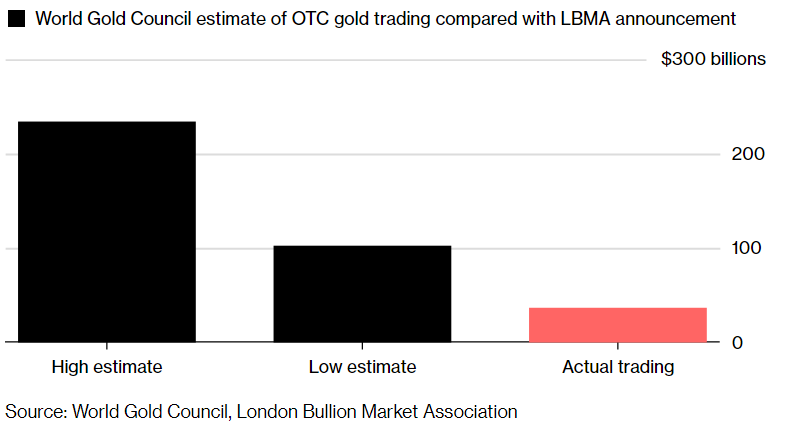

London reveals size of centuries-old gold market for first time (MarketWatch.com)

Gold dips as investors opt for safe-haven dollar, bonds (Reuters.ocm)

Gold reverses and drops to test $1220 (FXStreet.com)

Brexit: May heading to Brussels amid scramble to finalise deal (BBC.com)

Powell and Gold between Inflation and Global Slowdown (24HGold.com)

Another Great Oxymoron: “LBMA Transparency”-Craig Hemke (20/11/2018) (SprottMoney.com)

London Gold Market Comes Clean: It’s Not as Big as Thought (Bloomberg.com)

The Never-Ending Wars of the United States of America (24HGold.com)

Listen on SoundCloud , Blubrry & iTunes. Watch on YouTube below

Gold Prices (LBMA AM)

20 Nov: USD 1,223.10, GBP 951.45 & EUR 1,069.97 per ounce

19 Nov: USD 1,223.55, GBP 951.07 & EUR 1,070.97 per ounce

16 Nov: USD 1,215.80, GBP 948.93 & EUR 1,073.07 per ounce

15 Nov: USD 1,210.60, GBP 948.26 & EUR 1,072.71 per ounce

14 Nov: USD 1,201.45, GBP 927.04 & EUR 1,066.05 per ounce

13 Nov: USD 1,197.55, GBP 928.70 & EUR 1,066.18 per ounce

Silver Prices (LBMA)

20 Nov: USD 14.44, GBP 11.24 & EUR 12.63 per ounce

19 Nov: USD 14.36, GBP 11.21 & EUR 12.57 per ounce

16 Nov: USD 14.29, GBP 11.15 & EUR 12.61 per ounce

15 Nov: USD 14.13, GBP 11.02 & EUR 12.49 per ounce

14 Nov: USD 13.97, GBP 10.80 & EUR 12.39 per ounce

13 Nov: USD 14.02, GBP 10.85 & EUR 12.46 per ounce

Recent Market Updates

– Stocks are Now in ‘Complete Bitcoin Territory,’ Asset Manager Says

– Brexit’s Safe Haven Is a Dangerous Place

– Gold and Silver Rise As Stocks Fall On Valuation Concerns, Italy and Brexit Risks

– Pound Falls 2.5% Against Gold as UK Government in Turmoil Over Brexit

– GoldCore Capitalising On Brexit With Dublin Gold Vault

– Store Gold In The Safest Vaults In Ireland

– Investors Set To Store Gold In Dublin Due To Brexit Risks

– Investors Start Buying Gold ETFs In October In Bullish Shift

– As Brexit Looms and Stocks Plunge In October – Now May Be The Time to Invest in Gold

– AMERICAN ELECTIONS FARCE AS POLITICIANS IGNORE THE LOOMING $121.7 TRILLION DEBT CRISIS

– Gold ETFs See Strong Demand In Volatile October After Robust Global Gold Demand In Q3

NOV 21

Bitcoin-rigging criminal probe focused on tie to Tether

Submitted by cpowell on Tue, 2018-11-20 15:10. Section: Daily Dispatches

By Matt Robinson and Tom Schoenberg

Bloomberg News

Tuesday, November 20, 2018

As Bitcoin plunges, the U.S. Justice Department is investigating whether last year’s epic rally was fueled in part by manipulation, with traders driving it up with Tether — a popular but controversial digital token.

While federal prosecutors opened a broad criminal probe into cryptocurrencies months ago, they have recently homed in on suspicions that a tangled web involving Bitcoin, Tether, and crypto exchange Bitfinex might have been used to illegally move prices, said three people familiar with the matter. …

… For the remainder of the report:

https://www.bloomberg.com/news/articles/2018-11-20/bitcoin-rigging-crimi…

end

Bart Chilton on Russia Today is hosting a broadcast on the economy. He had Schiff on and here the former CFTC commissioner found much evidence of silver rigging even though he stated that there was not enough to prosecute. However two weeks ago a JPMorgan trader confessed to rigging the gold and silver markets and that he was taught by his superiors.

There is going to be big news coming from future broadcasts from Bart Chilton and guests..stay tune.d

(courtesy GATA/Boom or Bust/Bart Chilton)

Chilton says CFTC found much evidence of silver

rigging; Schiff calls rigging’rumor’

Submitted by cpowell on Tue, 2018-11-20 15:58. Section: Daily Dispatches

11:03a ET Tuesday, November 20, 2018

Dear Friend of GATA and Gold:

Bart Chilton, the former member of the U.S. Commodity Futures Trading Commission who pushed his agency to hold in a March 2010 public hearing that addressed manipulation of the monetary metals markets and called GATA leaders as witnesses, this year has been hosting Russia Today’s daily “Boom/Bust” program, and last Thursday he interviewed fund manager and gold advocate Peter Schiff about market manipulation.

On the program Chilton revealed that during his service on the CFTC the commission found “all sorts of evidence of attempted manipulation and manipulation” of the silver market “but not enough to actually prosecute.”

…

Of course two weeks ago a former JPMorganChase trader confessed in federal court to manipulating the silver market with the knowledge of his superiors even while the CFTC was investigating:

http://www.gata.org/node/18596

In his comments to Chilton, Schiff remained dismissive of what he called “rumors” of manipulation of the monetary metals markets, while acknowledging that “some of the rumors are probably true.” Manipulation, Schiff argued, is not the big reason for the poor performance of the monetary metals in recent years. Rather, Schiff said, investors are just too stupid to understand what is going on in the world financial system — not that Schiff himself ever has done much to help them understand how governments long have been intervening in the monetary metals markets to support their currencies and bond prices.

Last Thursday’s edition of “Boom/Bust” is can be viewed at Russia Today here —

https://www.rt.com/shows/boom-bust/444025-amazon-gold-prices-plane/

— and the interview with Schiff is four minutes long, extending from the 5:44 to 9:48 marks.

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

Today is the day whereby the LBMA is suppose to be transparent. It is not as big as thought

(courtesy Bloomberg/GATA)

London gold market comes clean: It’s not as big as

thought

Submitted by cpowell on Wed, 2018-11-21 01:13. Section: Daily Dispatches

By Eddie van der Walt, Rupert Rowling, and Anna Edwards

Bloomberg News

Tuesday, November 20, 2108

London’s gold market owned up to the biggest secret in bullion: It’s not as big as some thought and, for last week at least, smaller than New York’s.

An average of $36.9 billion of gold and $5.2 billion of silver changed hands each day in the city’s over-the-counter market, including metal for delivery in Zurich, according to figures released for the first time today by the London Bullion Market Association. Previous World Gold Council estimates, based on 2016 data, were between three and six times higher. …

… For the remainder of the report:

https://www.bloomberg.com/news/articles/2018-11-20/london-gold-market-co…

end

Craig comments on the LBMA “transparency”

(courtesy Craig Hemke/GATA)

Craig Hemke at Sprott Money: Another great

oxymoron — LBMA ‘transparency’

Submitted by cpowell on Wed, 2018-11-21 01:38. Section: Daily Dispatches

8:38p ET Tuesday, November 20, 2018

Dear Friend of GATA and Gold:

London gold market data published today by the London Bullion Market Association, the TF Metal Report’s Craig Hemke writes at Sprott Money, demonstrates what a fraud the market is, as it purports to trade every day more than a third of the world’s annual gold production and 42 percent of annual silver production.

Hemke writes: “The prices of gold and silver are currently determined by the trading of digital derivatives, which have next-to-zero connection to the physical metal. The price that is discovered is the price of the digital derivative itself and not the physical commodity. And the supply of the digital derivative is nearly endless, as the banks have a monopolistic ability to create a nearly infinite amount.”

Being so fraudulent, Hemke writes, the system inevitably will collapse, and those who thought they had gold in it will find they have none.

Hemke’s analysis is headlined “Another Great Oxymoron: LBMA ‘Transparency'” and it’s posted at Sprott Money here:

https://www.sprottmoney.com/Blog/another-great-oxymoron-lbma-transparenc…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

JPMorgan Metals Probe Spurs U.S. to Ask for Delay in Civil Suit

By Chris Dolmetsch

November 20, 2018, 6:41 PM EST

Prosecutors ask for temporary halt to trader’s antitrust case

U.S. says aim is to protect ‘integrity’ of its investigation

The Justice Department’s investigation of manipulation in the precious-metals markets at JPMorgan Chase & Co. spurred prosecutors to ask a judge to delay a civil lawsuit focusing on similar misconduct.

Former trader John Edmonds pleaded guilty last month to federal charges that he placed hundreds of orders in the futures market he never intended to execute, in a six-year spoofing scheme. On Monday, the Justice Department asked the judge overseeing an antitrust lawsuit against JPMorgan to delay the case for six months to “protect the integrity” of its ongoing criminal probe.

JPMorgan didn’t immediately respond to an email seeking comment.

The request signals that the government is aggressively moving ahead with its inquiry. The charges are part of a broad U.S. crackdown on techniques such as spoofing, a trading practice designed to create fake demand that pushes prices up or down to generate profits. Long considered disreputable but rarely dangerous, spoofing has emerged in an era of computerized trading as a deeper threat to markets.

In his plea to conspiracy and commodities fraud in federal court in Connecticut, Edmonds admitted that he and other traders sought to manipulate futures markets for gold, silver, platinum and palladium on the Nymex and Comex exchanges, prosecutors said.

The Justice Department request for a delay came after lawyers for the plaintiffs in the civil antitrust suit asked a judge to allow them to re-interview Edmonds’s immediate supervisors, saying their testimony will “demonstrate a pattern and practice of intimidation” consistent with the view that JPMorgan created barriers to entry in the “thinly traded” market.

The case is U.S. v. Edmonds, 18-cr-239, U.S. District Court, District of Connecticut (Hartford).

-END-

Manly contends and he is probably correct that the gold/silver trading is predominately unallocated plus fractionally backed synthetic (unallocated) and very little physical gold and silver.

(courtesy Ronan Manly)

GATA) Ronan Manly: LBMA ‘trading data’ is empty, suggests removal of central bank activity

Submitted by cpowell on 03:24PM ET Wednesday, November 21, 2018. Section: Daily Dispatches

10:23a ET Wednesday, November 21, 2018

Dear Friend of GATA and Gold:

Indispensable gold market analyst Ronan Manly, writing for Bullion Star today, writes that the London Bullion Market’s new trading data report contains no trading data at all but does contain an anomaly suggesting that central bank trading has been erased from the data.

Manly writes: “While the LBMA’s new data is very high- level and aggregated and does not do anything to lift the veil of secrecy lying over these markets, the magnitude of the trade volumes does prove what has been widely believed: that the over-the-counter gold and silver markets operating mainly out of London by mainly LBMA bullion banks are trading predominantly unallocated and fractionally-backed synthetic positions on gold and silver and a lot less in the way of physical gold and silver.”

Manly’s analysis is headlined “LBMA Trading Volume Data Confirms the Paper Gold Casino in London” and it’s posted at Bullion Star here:

https://www.bullionstar.com/blogs/ronan-manly/lbma- trading-volume-data-c..

CHRIS POWELL, Secretary/Treasurer/gata

end

Here are a few things which could precipitate the next crisis

(courtesy James Rickards/Daily Reckoning)

Rickards: Multiple Risks Are Converging On Markets

Authored by James Rickards via The Daily Reckoning,

One of the questions I am asked most frequently in my global travels is what will be the cause of the next financial crisis. This question is asked by those who understand that this crisis is coming but want to pin down the date or a specific turn of events that will help them know when to react.

My answer is always the same: We can be certain the crisis is coming and can estimate its magnitude, but no one knows exactly when it will happen or what the specific catalyst will be.

The second part of my answer is to prepare for the crisis now. When it happens, it could unfold very quickly. If you’ve been paying attention to the stock market lately, you know how quickly selling fever can spread once it starts. Just look at these past two days alone.

We’ve had multiple days since October when the Dow loses several hundred points, with the other major indexes posting similar losses on a percentage basis.

There may not be time or opportunity in the middle of the crisis to take defensive measures. That’s why I keep reminding my readers thatthe time to prepare by increasing allocations to cash and gold is now.

With that said, it is useful to consider the most likely flash points for the next crisis and to monitor events as a way to improve one’s chances of seeing a crisis at the early stages.

In yesterday’s Daily Reckoning, I made the case that the next crisis could begin in the junk bond market. But there are a number of other possibilities.

You recall that the financial panic of 2008 actually started in 2007 with massive loan losses in subprime mortgages. Those losses caused certain hedge funds and money market funds to close their doors. Investors scrambled for liquidity to cover their mortgage loan losses. This led them to sell equities, bonds and gold to raise cash to meet margin calls.

The panic was subdued in late 2007 but came back to life in 2008 with the collapse of Bear Stearns, Lehman Bros., AIG and others. The Fed and Treasury intervened to provide guarantees and liquidity, but not before everyday investors saw half their net worth wiped out. The crisis was not confined to the U.S., but spread worldwide to Europe, China and Japan.

Now a new loan loss crisis is unfolding. The new crisis is not in mortgages but in student loans.

Total student loans today at $1.6 trillion are larger than the amount of junk mortgages in late 2007 of about $1.0 trillion. Default rates on student loans are already higher than mortgage default rates in 2007. This time the loan losses are falling not on the banks and hedge funds but on the Treasury itself because of government guarantees.

Not only are student loan defaults soaring, but household debt has hit another all-time high. Student loans and household debt are just the tip of the debt iceberg that also includes junk bonds (again, as I explained yesterday), corporate debt and even sovereign debt, all at or near record highs around the world.

Meanwhile, the trade war remains a great risk to markets.

When the trade wars erupted in early 2018 I said that the trade wars would be long-lasting and difficult to resolve and would have significant negative economic impacts.

Wall Street took the opposite view and estimated that the trade war threats were mostly for show, the impact would be minimal and that Trump and China’s President Xi Jinping would resolve their differences quickly. As usual, Wall Street was wrong.

Trump’s top trade adviser Peter Navarro recently delivered a speech making it clear the trade wars will not be resolved soon. He also tells Wall Street to “get out” of the policy process.

He said, “If there is a deal, if and when there is a deal, it will be on President Donald J. Trump’s terms, not Wall Street terms.”

Navarro warns that prominent Americans such as Hank Paulson, former secretary of the Treasury, and Blackstone chief Stephen Schwarzman may be acting as “unregistered foreign agents” as a result of their lobbying activities on behalf of China.

This could subject these principals to criminal prosecution. Investors should expect lower earnings per share from Apple, Sony and entertainment companies dependent on the Chinese market or Chinese manufacturing to make their profits.

Companies such as Caterpillar are also caught in the crossfire. Get ready for a long and costly trade war. It has already started and won’t be over soon.

But I’ve been warning for months about an even more disturbing possibility: that currency wars and trade wars can easily spill over into shooting wars. This happened in the 1930s and it seems to be happening again.

One of the most dangerous hot spots in the world today is the South China Sea. There are six countries with recognized claims to parts of the South China Sea. Yet China itself claims the entire sea except for small coastal strips and claims all of the oil, natural gas and fish that can be taken from the sea.

China has ignored international tribunal rulings against it. The U.S. is backing up the other national claims including those of the Philippines, which is a treaty ally of the U.S. China has built small reefs into large artificial islands with airstrips and sea bases to support its claims.

The U.S. has increased naval vessels in the area to enforce rights of passage and the equitable sharing of resources. Both sides are escalating and the risk of a shooting war or even an accident at sea is increasing. The South China Sea is mostly out of the headlines at the moment, but it bears watching as a possible catalyst for the next international crisis with global financial implications.

We should look for slower growth and possibly a recession as the trade and currency wars play out. Let’s hope that history does not repeat and that we don’t end up in a Third World War, as the currency/trade wars of the 1930s helped lead to WWII.

Warnings of economic collapse are no longer confined to the fringes of economic analysis but are now coming from major financial institutions and prominent economists, academics and wealth managers. Leading financial elites have been warning of coming collapses and dangers.

These warnings range from the IMF’s Christine Lagarde, Bridgewater’s Ray Dalio, the Bank for International Settlements (known as the “central banker’s central bank”) and many other highly regarded sources.

Just when we think we’ve seen enough of these, another one arrives. This time it’s the legendary Paul Tudor Jones, who manages Tudor Investment.

I’ve met Jones; he’s a cerebral yet polite and mild-mannered manager from Tennessee who has not lost his Southern accent despite decades in Connecticut and an estate on Maryland’s Eastern Shore.

What gives Jones’ voice added authority is his longevity in the fund investment world. He’s managed through the 1987 stock crash, the 1994 Mexican crisis, the 1998 Long Term Capital meltdown, the 2000 dot-com crash and, of course, the 2008 financial panic.

Jones knows that panics happen, but he also knows they don’t happen all the time. Panics take years to build and usually have specific triggers (even though endpoints can spin wildly out of control).

Jones does not treat the possibility of a financial crisis lightly, so his warning deserves close consideration.

Jones warns that the next crisis is likely to be triggered by excessive debt, specifically corporate debt, which can be more difficult to manage or bail out than sovereign debt.

At the same time, other gurus are warning that the next panic will emerge from the foreign exchange market, overvalued equities or commercial real estate. Perhaps the real message is that all of these areas are vulnerable and the next crisis will seem to come from everywhere at once.

That’s the danger. We’re looking at another debt crisis and global financial panic. Only this time it won’t come from mortgages alone but from all directions at once.

So let me repeat what I said earlier: the time to prepare by increasing allocations to cash and gold is now.

__________________________________________

Your early WEDNESDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

i) Chinese yuan vs USA dollar/CLOSED UP TO 6.9370/HUGE DEVALUATION FOR THE PAST FOUR WEEKS RESUMES/CHINESE COMING TO USA FOR TRADE TALKS IN NOVEMBER NOW ON //OFFSHORE YUAN: 6.9323 /shanghai bourse CLOSED UP 5.65 POINTS OR 0.21%

. HANG SANG CLOSED UP 131.13 POINTS OR 0.51%

2. Nikkei closed DOWN 75.58 POINTS OR 0.35%

3. Europe stocks OPENED ALL GREEN

/USA dollar index RISES TO 96.37/Euro FALLS TO 1.1420

3b Japan 10 year bond yield: FALLS TO. +.10/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 112.35/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD IS NOW TARGETED AT .11%/JAPAN LOSING CONTROL OF THEIR BOND MARKET

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 54.27 and Brent: 63.63

3f Gold UP/JAPANESE Yen down/ CHINESE YUAN: ON SHORE UP/OFF- SHORE: UP

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil DOWN for WTI and DOWN FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund RISES TO +.37%/Italian 10 yr bond yield UP to 3.59% /SPAIN 10 YR BOND YIELD UP TO 1.62%…ITALIAN 10 YR BOND YIELD/GERMAN BUND: 3.14: DANGEROUS FOR THE ITALIAN BANKING SYSTEM

3j Greek 10 year bond yield RISES TO : 4.65

3k Gold at $1223.55 silver at:14.43 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble UP 26/100 in roubles/dollar) 65.93

3m oil into the 54 dollar handle for WTI and 63 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 113.03DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 0.9942 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1336 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now POSITIVE territory with the 10 year FALLING to +0.35%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 3.08% early this morning. Thirty year rate at 3.33%

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

6. TURKISH LIRA: UP TO 5.3458

Futures Jump, Dollar Slides After Report Fed May End

Hikes As Early As Spring

After yesterday’s historic rout in the market, there were signs of stabilization in overnight trading with most markets trading higher, with the key catalyst a report from MNI that the Fed may end its rate hikes as soon as this coming spring.

US stocks were set to open sharply firmer after two days of losses that wiped out the S&P500’s gains for the year and left the tech-heavy Nasdaq index teetering on the brink of falling into the red. Losses were concentrated in the technology sector, as investors dumped their holdings of FAANG shares and pushed the Nasdaq index to seven-month lows and energy shares too had dropped in line with a 6 percent oil price slump S&P 500.

“High-flying momentum stocks have come off in a fairly spectacular fashion. At one point Apple and Amazon accounted for 40 percent of U.S. equity gains and people were just recycling money into the winners,” said David Vickers, senior portfolio manager at Russell Investments. “That’s come off the boil and set the cat among the pigeons… We’ve seen a lot of reflexivity, when selling begets selling, the market starts to turn over, people take profits, it leads to another leg down and so on.”

That fed through to Asia on Wednesday, taking MSCI’s index of ex-Japan Asia-Pacific shares almost half a percent lower, but it clawed most of the losses to trade flat, with MSCI’s all-country benchmark was flat too, attempting to snap two days of falls.

Chinese stocks closed in the green and near session highs, rebounding from Tuesday’s drop as Asia closed mixed, but it was Europe that showed the most promise with the Stoxx600 solidly in the green, led by Italy where BTPs rallied from the open, after a report that Deputy PM Salvini may be open to budget revisions; Salvini then denied the report, clarifying that he’s only open to tweaks and won’t compromise on the main issues.

Italians bond yields fell up to 16 basis points initially, putting 10-year yields on track for their biggest daily drop in almost a month but the market gave up some of its gains after the denials. Sentiment was then dented again, and the EUR snapped lower after Ansa reported that the European Union has rejected Italy’s 2019 budget – as expected – and that the Excessive Deficit Procedure would be warranted on Italy. Still, despite the expected escalation in the standoff between Italy and Europe, the Estoxx and DAX pushed higher but were off best levels with banks and telecoms leading gains as Italy’s FTSE MIB outperformed peers with local banks +1.5%.

However, it was a report from wire service MNI just after 6am that caught the market’s attention, when Market News International reported that the Federal Reserve is starting to consider at least a pause to its gradual monetary tightening and could end its cycle of interest rate hikes as early as the spring, citing senior people at the Fed they didn’t identify.

While a Dec. rate hike is all but assured, the debate will become more lively beginning at the central bank’s March meeting and certainly by June, MNI says. The paradox, of course, is that according to the Fed’s own dot plot there will be at least 3 hikes in 2019, so for one or more Fed presidents to engage in such an ECB-esque trial balloon of defiance of Chairman Powell must mean that the disagreements within the FOMC over the future of monetary policy are truly boiling over.

While it is still very much unlikely that the Fed will halt its rate hikes in the spring absent a rout in stocks and bonds, the MNI trial balloon sent futures back to session highs…

… and slammed the Bloomberg dollar index back to session lows.

US Treasuries and the Eurodollar strip also pared losses and faded Wednesday’s bear steepening after the MNI report; that said, Fed rate hike expectations are steady on Wednesday morning with December 2018 pricing in 19bps, and the next 25bps increase expected in March 2019. The U.S. 10Y TSY yield is 1bp to 3.07% with December T-Note futures -20 ticks to 119-04+; U.S. 2/10s +1bp to 26bps; U.S. 5/30s steady at 43bps.

Today’s modest gains immediately sparked positive commentary: “We view the sell-off as overdone and a bull-market correction, with valuations that have become more compelling,” Jason Draho, head of asset allocation, Americas, at UBS Global Wealth Management wrote in a note. “We recently increased our overweight to global equities on the view that the markets are already pricing in growth and trade risks.”

Still, while the Fed trial balloon helped preserve upside momentum in risk assets, investor sentiment remains susceptible to minute to minute volatility that’s rocked markets since October as traders have to contend with President Trump tape bomb unpredictability and demands for lower rates as corporate credit spreads at two-year highs reflect investor angst about borrowing costs.

In FX, the euro got an early boost and Italian bonds rallied after the abovementioned La Stampa report that Italy’s Deputy Prime Minister Matteo Salvini may be open to budget revisions; it trimmed gains after his League party denied the report, and as the EU was said see Rome’s budget at serious non-compliance risk. The pound was little changed against the dollar, after earlier rising on the back of broader weakness in the greenback; Britain’s budget deficit widened in October as spending rose at the fastest pace in 11 years. Australian dollar rebounds from a one-week low hit very early in Asia as a recovery in oil prices combined with exporter demand to trigger short-covering ahead of U.S. Thanksgiving holiday.

In commodities, WTI also halted yesterday’s dramatic rout near $54 a barrel after API showed that U.S. crude inventories unexpectedly fell last week against doubts over OPEC’s plans to cut output. Emerging-market shares and currencies were stable. Bitcoin advanced after a recent sell-off

Expected data include mortgage applications, durable goods orders, jobless claims and existing home sales. Deere and Metro are among companies reporting earnings

Market Snapshot

- S&P 500 futures up 0.5% to 2,653.75

- STOXX Europe 600 up 0.5% to 352.66

- MXAP down 0.4% to 149.96

- MXAPJ down 0.1% to 480.09

- Nikkei down 0.4% to 21,507.54

- Topix down 0.6% to 1,615.89

- Hang Seng Index up 0.5% to 25,971.47

- Shanghai Composite up 0.2% to 2,651.51

- Sensex down 0.7% to 35,212.54

- Australia S&P/ASX 200 down 0.5% to 5,642.77

- Kospi down 0.3% to 2,076.55

- German 10Y yield rose 1.6 bps to 0.366%

- Euro up 0.1% to $1.1381

- Italian 10Y yield rose 1.8 bps to 3.241%

- Spanish 10Y yield fell 0.9 bps to 1.638%

- Brent futures up 1.8% to $63.63/bbl

- Gold spot up 0.2% to $1,224.29

- U.S. Dollar Index down 0.1% to 96.77

Top Overnight News

- German Chancellor Angela Merkel warned the U.K. it can’t set unilateral terms for leaving the European Union as Prime Minister Theresa May heads to Brussels to try to complete a contentious Brexit deal

- The Brexit divorce deal can’t be improved, and EU governments have made that clear, said Northern Ireland Secretary Karen Bradley

- Saudi Arabian oil production surged to a record near 11 million barrels a day this month after the kingdom received stronger-than-usual demand from clients preparing for a disruption in Iranian supplies, according to industry executives who track Saudi output

- Oil at one point slumped more than 7 percent in London and New York on Tuesday. The selloff — just like the previous Tuesday — was exacerbated by banks selling futures to rebalance their positions as prices fell, said people active in the market who are familiar with the matter

- OPEC’s bad dream only deepens next year, when Permian producers expect to iron out distribution snags that will add three pipelines and as much as 2 million barrels of oil a day

- The U.S. on Tuesday accused China of continuing a state-backed campaign of intellectual property and technology theft even as the world’s two largest economies have descended into a tit-for-tat tariff war

Asian stocks mostly weakened as the global stock rout continued into the region following the losses in US, where the DJIA dropped over 500 points to turn negative YTD and in which energy names were pressured as oil slumped nearly 7%. ASX 200 (-0.5%) and Nikkei 225 (-0.3%) were led lower by spill-over selling seen across the commodity-related sectors, while Wesfarmers shares plummeted nearly 30% after the spin-off of its Coles unit which had its stock market debut today. Hang Seng (+0.5%) and Shanghai Comp. (+0.2%) opened with firm losses but then rebounded off their lows with price action choppy amid ongoing trade uncertainty and after criticism from USTR Lighthizer’s report that China has not altered its unfair practices and appears to have conducted further unreasonable actions in recent months. Finally, 10yr JGBs failed to benefit from the widespread risk averse tone with price action subdued amid a lack of BoJ presence in the bond market and after the weakness in T-notes as US investors closed positions heading in to Thanksgiving.

Top Asian News

- The American Carnage Isn’t Tanking Stock Markets in Asia

- China Refrains From Injecting Cash for Longest Time Since August

- Beijing to Judge Every Resident Based on Behavior by End of 2020

- China Said to Eye Steel Mega-Deal as Baowu Chief Joins Rival

- Yuan Debt in the Bag for Philippines as Xi-Duterte Ties Grow

European equities are higher across the board (Eurostoxx 50 +0.8%) as the region stemmed the stock rout seen in Asia and Wall Street. Italy’s FTSE MIB (+0.6%) was initially outperforming with Italian banks higher amid initial reports from Italian press that Deputy PM Salvini could potentially be open to budget revisions, which were later dismissed by League sources ahead of the budget ultimately being rejected. In terms of sectors, financial names lost the top spot to telecom names, who are outperforming after French telecoms jumped following comments from Orange (+1.7%) CEO which renewed M&A gossip. Elsewhere, Indivior (-13.6%) fell to the foot of the Stoxx600 (+0.4%) after the Co. lost a US court ruling that had prevented Dr. Reddy’s from selling a generic version of a treatment for opioid addiction.

Top European News

- Merkel Warns U.K. It Can’t Dictate Brexit Terms for EU Summit

- Rudd Says Parliament Would Block No Deal: Brexit Update

- Laundromat Whistle-Blower Testifies in Brussels: Danske Update

- Nyrstar Wins Lifeline From Trafigura With $650 Million Deal

- Airbus Names New CFO, COO to Replace Wave of Exiting Execs

In FX, the DXY index has maintained its recovery momentum into the midweek session, but is off best levels amidst a welcome reprieve in riskier assets and broad sentiment ahead of Thanksgiving. The DXY has drifted back from another uptick towards 97.000, though remains underpinned ahead of 96.500 and recent lows. The Greenback also retains an underlying bid as G10 and EM counterparts struggle to recoup losses beyond round number/psychological/technical resistance against the backdrop of heavy option expiries at strikes within close proximity to prevailing prices (and with major fundamental issues still prescient of course).

- EUR/CAD – The single currency is holding up relatively well given more toing and froing on the Italian budget, but ultimately ongoing recalcitrant stance from Rome after reports about potential revisions were renounced in advance of the EU’s official rejection and potential if not probable EDP implementation (scheduled release time 11.00GMT, but appears to have been preannounced). However, 1.1400 is proving almost as obstinate and a decent 1 bn option expiry could well be keeping the headline pair in check. Meanwhile, the Loonie is off worst levels after sliding through 1.3300 and could be gleaning some encouragement from a partial recovery in oil prices in the run up to Canadian wholesale trade data.

- GBP/CHF/JPY – All bucking the overall trend, albeit barely in terms of the Pound and Franc, as Cable pivots 1.2800 and Eur/Gbp straddles 0.8900 on Parliament approval aspirations as UK PM May heads to Brussels for more discussions on the Brexit draft and the coup to oust her seems to have fizzled out. Meanwhile, Usd/Chf has only tentatively bounced from near 0.9900 lows within a 0.9935-55 range vs Usd/Jpy back on the 113.00 handle vs a base around 112.30 at one stage on Tuesday when risk-off flows were rife, but bidding interest prevented further downside. Note, a raft of option expiries could be key into the NY cut, stretching from 111.90-112.00 to 114.00 and totalling some 11 bn.

- EM – Rand in focus for several reasons, as Usd/Zar hovers near 14.0000 ahead of Thursday’s SARP policy meeting and following softer than expected SA inflation data, with a decent 1.1+ bn options expiring between 13.9000-14.0000 along with speculation about more strike action.

In commodities, WTI (+1.6%) and Brent (+1.4%) took a breather from yesterday’s selloff, where prices fell almost 7% with the decline attributed to supply concerns, negative risk sentiment and Trump’s protective approach to Saudi relations. Prices are underpinned by the latest API inventory data which printed a surprise drawdown in headline crude stockpiles. Traders will be keeping an eye on today’s DoE release for any hints of increased US shale production. Today will also see the release of the EIA natural gas storage data, which has been rescheduled due to the US Thanksgiving Holiday. Elsewhere, the metals complex is in positive territory with gold (+0.2%), silver (+0.7%) and copper (+0.5%) all supported by the pullback in the USD. Goldman Sachs said slump in oil reflects over supply concerns for 2019 and that technical position factors have exacerbated the volatility, while it also cited low liquidity heading into Thanksgiving as well as broader selling in commodities and cross-assets amid rising growth concerns.

In terms of the day ahead, we’re due to get a first look at October durable and capital goods orders data along with the latest weekly initial jobless claims data, October leading index, October existing home sales and final November University of Michigan consumer sentiment survey revisions. Away from that, Italy’s Finance Minister Tria is due face questions in the Lower House and as highlighted earlier, today is the day that the European Commission is due to publish opinions on the budget plans of Euro Area countries, including possibly Italy.

US Event Calendar

- 8:30am: U.S. Durable Goods Orders, Oct. P, est. -2.6%, prior 0.7%; Durable Goods Orders Less Transportation, Oct. P, est. 0.4%, prior 0.0%

- 8:30am: U.S. Initial Jobless Claims, Nov. 17, est. 215k, prior 216k; Continuing Claims, Nov. 10, est. 1650k, prior 1676k

- 10am: U.S. U. of Mich. Sentiment, Nov. F, est. 98.3, prior 98.3

DB’s Jim Reid concludes the overnight wrap

I suspect they’ll be a lot of market participants in the US relieved that they only have to make it through today to get to Thanksgiving. I suspect they’ll also be a lot of market participants outside of the US relieved that the US market won’t be open tomorrow and we’ll have a circuit breaker for now and a chance to take stock after a very difficult few days.

The sell-off baton has been passed from asset class to asset class of late and yesterday it was oil’s turn to pick it back up again with Brent and WTI crude shedding -6.69% and -6.84% respectively taking losses close to -30% in only around 7 weeks from its 4-year highs. A remarkable run. These moves dominated price action across other markets, with the energy sector (-3.29%) leading US equity declines and inflation breakevens trending lower. US 10-year TIPS-implied breakeven inflation rates are now down to 1.98%, taking their year-to-date change into negative territory for the first time. Somewhat worryingly, there are signs that the oil drop is a negative demand story, rather than a positive supply shock. Oil-importing countries, who would theoretically see an improvement in their terms-of-trade, did not see their currencies gain, e.g. the Turkish Lira the worst performer of the day, falling -1.37%.

There didn’t appear to be one particular event which triggered the oil move although our commodity strategy team did note that recent commentary is foreshadowing possible disappointments at the OPEC meeting on December 6th. They believe that Libya and Russia are unlikely to support a renewed push from Saudi Arabia for discipline and therefore fear an underwhelming meeting outcome. Anyway that weakness for oil did spread to the US HY energy sector which widened +13bps, meaning it is now 169bps wide of the October and YTD tights.

As for equities, well the NASDAQ closed down -1.70% but was as much as -2.81% lower at one stage, while the S&P 500 and DOW closed down -1.82% and -2.21% respectively – both marginally off their lows. The NYSE FANG index also recovered to finish -1.55% from its intraday low of -4.48%, though Apple did fall another -4.78% meaning it’s now -23.74 % off the October peaks and therefore in the definition of a bear market amid concerns over demand for products. That move is also equivalent to a loss of value of $265bn, or roughly the annual GDP of Bangladesh a country with 165 million people. Meanwhile, the VIX touched 23.81 intraday yesterday (highest since October 31st) before closing at 22.48. Apart from the oil sector, which led losses, consumer discretionary also fell -2.18% after profit outlooks for the likes of Target (-10.53%), TJX (-4.39%) and Kohl’s (-9.24%) all disappointed ahead of the busy holiday shopping period.

Back to credit, cash spreads for Euro IG and HY finished +4bps and +13bps wider yesterday while in the US, spreads outperformed a bit but were still +2bps and +7bps wider respectively. It’s worth noting that this is now the eighth day in a row that Euro HY spreads have widened, for a cumulative move of +72bps. In fairness, spreads moved wider eight days in a row back in September, but the total size of that widening was a rather mild +17bps. In May, they actually widened for 10 days in a row when BTP yields were soaring, however the size of that move was +59bps so the current run really stands out. In fact, the biggest eight-day move in recent years came during January 2016, when spreads blew out +79bps amid similar conditions to today: plummeting oil prices.

Considering the sizeable risk-off that we’re seeing at the moment we’re hardly witnessing the flock to safe haven assets that one might expect. Treasury yields were only down -0.7bps yesterday while Bunds rallied -2.2bps and the USD index gained +0.67%. Gold and the Japanese yen both actually sold off -0.17% and -0.14%, respectively, and both have traded in a fairly benign +/-3% range for November to date.

This morning in Asia, sentiment continues to be remain negative but markets have rallied off the opening lows where the likes of the Nikkei began trading down around -1.5%. As we type this has recovered to -0.32%. Elsewhere the same pattern has emerged with the Hang Seng (-0.10%), Shanghai Comp (-0.13%) and Kospi (-0.51%) all down but off their session lows. Oil has bounced a bit from yesterday and is up +1.75% as we go to print. S&P 500 futures (+0.37%) are also pointing towards a slight improvement in market mood.

Sentiment remains nervous though and not helped by the overnight release of a report on China from the US Trade Representative Robert Lighthizer’s office which accuses China of continuing a state-backed campaign of intellectual property and technology theft. The report said, “China fundamentally has not altered its acts, policies, and practices related to technology transfer, intellectual property, and innovation, and indeed appears to have taken further unreasonable actions in recent months.” This ramp up in rhetoric just 10 days ahead of the upcoming G20 meeting overshadowed earlier comments from the White House economic advisor Larry Kudlow about President Trump injecting “a note of optimism” into trade talks with China.

Back to more selling off markets from yesterday now. BTP yields spiked to an intraday high of 3.714% yesterday (+12bps) and the highest since last month before paring much of that to finish at 3.617%. That wild ride for BTPs comes prior to the European Commission today opining on the budget plans of the Euro Area nations. For Italy, under EU fiscal rules the European Commission had three weeks to issue an opinion on Italy from November 13th – when Italy left unchanged its 2019 draft budget plan. The suggestion however is that the Commission will opine on Italy at the same time as other Euro Area nations so we’re likely to hear today. Assuming the Commission pushes ahead with launching an EDP, the process involves the Commission informing the Eurogroup first. The next meeting of the Eurogroup is December 3rd so it’s possible that the process gets aggressively accelerated to meet that deadline.

Our economists have previously highlighted that the decision to launch an EDP remains a political one – the Commission proposes the action but the Eurogroup has the option to overrule. However, it could be difficult to reverse the decision of the Commission. The Eurogroup votes on a double majority of countries representing 65% of the population (the country under procedure does not vote). As long as Germany and France support an EDP, the remaining countries do not have enough weight in the qualified majority vote to overturn the decision. Anyway expect the BTP market to be focused on this today.

The Brexit front was relatively quiet again, though the DUP did abstain again on a procedural vote on the UK budget, forcing the Conservatives to accept several amendments from Labour in order to secure enough votes. The DUP are effectively on strike until they get things more their way on the Irish border thus making the running of government very challenging. Separately, BoE Governor Carney and Chief Economist Haldane testified to Parliament’s Treasury Committee and said they welcome the negotiated Withdrawal Agreement. Haldane noted that uncertainty may be weighing on business investment and could negatively impact fourth quarter economic growth, while Carney said that the risk of a no-deal Brexit outcome is “uncomfortably high.” The BoE policymakers plan to send new Brexit analysis to the Committee next week on November 29. Elsewhere, UK PM May is all set to travel to meet the EC President Juncker this evening in an effort to make progress on an outline of the future trade deal the two sides want to strike. She is likely to ask for further concessions from the EU given the backlash she is facing at home from euroskeptic Tories. However, it seems unlikely that the EU will give further headroom to the UK PM ahead of the upcoming Sunday summit where the two are expected to sign off on the 585-page exit agreement as well as the future partnership paper.

On the data front yesterday, US housing starts and building permits mostly met expectations. New starts came in at 1.23 million, up 1.5% mom but down over the last 12 months, while building permits were at 1.126 million, down -0.6% mom and also down over the last year. In Europe, French unemployment stayed at 9.1%, marginally better than consensus expectations which had called for a rate of 9.2%. German PPI inflation printed at 3.3% yoy as expected.

In terms of the day ahead, this morning we’ll get October public finances data in the UK along with the OECD’s latest economic forecasts. Across the pond this afternoon we’re due to get a first look at October durable and capital goods orders data along with the latest weekly initial jobless claims data, October leading index, October existing home sales and final November University of Michigan consumer sentiment survey revisions. Away from that, Italy’s Finance Minister Tria is due face questions in the Lower House and as highlighted earlier, today is the day that the European Commission is due to publish opinions on the budget plans of Euro Area countries, including possibly Italy.

3. ASIAN AFFAIRS

i)WEDNESDAY MORNING/ TUESDAY NIGHT:

SHANGHAI CLOSED UP 5.65 POINTS OR 0.21% //Hang Sang CLOSED UP 131.13 POINTS OR 0.51% //The Nikkei closed DOWN 75.58 OR 0/35%/ Australia’s all ordinaires CLOSED DOWN 0.51% /Chinese yuan (ONSHORE) closed UP at 6.9370 AS POBC RESUMES ITS HUGE DEVALUATION /DELEGATION COMING TO THE USA TO SEE TRUMP IN NOVEMBER /Oil DOWN to 54.27 dollars per barrel for WTI and 63.63 for Brent. Stocks in Europe OPENED GREEN//. ONSHORE YUAN CLOSED UP AT 6.9370AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.9323: HUGE DEVALUATION/PAST SEVERAL DAYS RESUMES// TRADE TALKS NOW ON : /ONSHORE YUAN TRADING WEAKER AGAINST OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING STRONGER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

3 a NORTH KOREA/USA

North Korea/South Korea/USA/China

3 b JAPAN AFFAIRS

3 C CHINA

4.EUROPEAN AFFAIRS

Italy

Conditions getting hotter inside Italy and the EU. The EU formally reject Italy’s budget which paves the way for sanctions. This will probably be the out that Italy needs to vacate the Euro

(courtesy zerohedge)

In Unprecedented Clash, EU Rejects Italy’s Budget, Paves Way For Sanctions

Yields on Italian government bonds fell on Wednesday morning as the euro climbed following reports that Italy’s ruling coalition might be open to reviewing its budget plan. Though the Italian government swiftly denied the reports about being open to changes in its plan, the moves in the euro and yields persisted, as analysts said they didn’t appear to be news driven.

The spread between the 10-year BTP and 10-year German bund tightened to tightening as much as 16 basis points to 309 basis points.

Italian bank shares also eased off their highs of the session after the denials, but remained 2% higher on the day after sinking to two-year lows on Tuesday.

And in the most significant sign yet that the confrontation between Italy and Europe is heading toward the point of no return, the European Union confirmed Wednesday morning that it would officially reject Italy’s budget plan, an unprecedented move that will likely lead to billions of euros in fines being levied against Rome for violating the bloc’s budget rules. Furthermore, the EC said it would call for the opening of an Excessive Debt Proceeding against the Italian government, which could lead to billions of euros in fines.

In its draft budget, the Italian government called for an expansion of the country’s budget deficit to 2.4% of GDP to finance tax cuts, expanded pension benefits and other handouts to unemployed and desperate Italians.

“Our analysis today suggests that the debt doesn’t respect our budget rules. We conclude that opening a proceeding against excessive spending based n the debt is then justified,” the EU said, according to ANSA.

But EU bureaucrats have long maintained that this expansion will do nothing to boost stagnant Italian growth; instead, it will hurt Italians by inevitably leading to more austerity. The Italian plan represents a “particularly grave disrespect” of EU budget rules, particularly the recommendation from the meeting of EU ecofin ministers last July 13. The statement confirms Brussels’ previous analysis.

European Commission Vice President Valdis Dombrovskis said Italy’s aggressive spending would eventually have a negative impact on growth.

“Despite already having very high debt, Italy is essentially planning significant additional spending, instead of the necessary budgetary prudence, and I want to say that the impact of this maneuver on growth will probably be negative from our point of view,” Dombrovskis said.

Following its opining on the plan, the Commission revealed that it would be calling for an Excessive Debt Procedure against the Italians because their spending for 2019 didn’t comply with EU rules. However, this plan must be put to the Eurogroup (which next meets Dec. 3), which must decide whether to approve the proceedings before they can move forward, as CNBC explained. If Italy doesn’t change course, the Commission said it would push to fine the Italian government.

“There are doubts and questions about growth” forecast in the Italian plan and, despite the clarifications requested, these persist,” said EU Commissioner for economic affairs Pierre Moscovici. “We have no answers to these questions: where does this growth come from nor who will pay the bill,” apart from how the plan will increase the “risks to Italian citizens, banks and businesses” by increasing the deficit and debt.

Moscovici added that the EU would give member states a chance to comment before opening its excessive debt proceedings, but he said he doubts that anybody would agree with the Commission’s analysis.

“Today we are not opening the excessive deficit procedure. However, it is undeniable that we see this is the path which is opening up ahead of us,” EU Economic and Monetary Commissioner Pierre Moscovici told reporters in Brussels. “It is now up to the member states to give their feelings and their views on the basis of our report over the coming two weeks.”

“To be quite frank, I have no reason to believe that they would disagree with what the commission has done by way of analysis,” Moscovici said.

Prime Minister Giuseppe Conte responded that the Italian government is convinced that the plan is “excellent” and in the best interest of the Italian people and Europe. Conte said he hopes to convince European Commission President Jean Claude Juncker during a Saturday meeting. Deputy Prime Minister Matteo Salvini said he expects a letter from the EU announcing its punitive measures to arrive around Christmas.

Analysts at ING believe that, as the proceedings unfold over several months, Italian bank stocks will remain under pressure.

“This procedure will take several months, but stands to keep (government bonds) and the Italian banking sector under pressure. Favor euro underperformance in Europe and probably further choppy euro-dollar trading in a $1.1350-$1.1450 range,” ING Bank analysts told clients.

The relief from tightening financial conditions was a surprising but not unwelcome development for investors, but with neither side showing any indication of backing down – and the Brexit threat still looming for the euro – they could prove short-lived as Conte prepares to travel to the Lions Den this weekend for what looks to be an epic confrontation with Juncker.

end

Bill Blain discusses events of yesterday and the Italian budgetary deficit affair. He states: who will buy the 275 billion euros of debt issued by Italy. He is correct that it will be the Italian banks who will buy this garbage and they are already saturated up to their gills with this stuff. He also states that the ECB will quietly offer the Italians long repo money at zero percent to help them if they reduce their budgetary defict.

(courtesy Bill Blain)

Blain: “Who Will Purchase The €275 Billion Of Debt Italy Expects To Issue In 2019?”

Blain’s Morning Porridge from Bill Blain

Gamma Ray Bursts, El-Erian on market disruption, Tech Stocks and Italy Bonds.

“I’ve always admired Capital Mainwaring.” [I don’t!]

I must stop reading newspapers. They are scary. Why worry about stocks and bonds when we’ve apparently got a pinwheel Nebula spinning at 12mm km/hour, named after the Egyptian God of Chaos (Apep), about to go Nova and its practically right next door – only 8000 light years away! That’s like the desk next to me in galactic terms! If a Gamma Ray Burst from such an event hit we are all literally toast. Global Crash or Supernova? You choose. (https://www.thetimes.co.uk/article/dying-star-could-be-a-time-bomb-rgrw2mvkq)

Rather puts things in perspective….

But, let’s assume a Supernova is not going to happen before I collect my pension.. so back to the day job.

Another bad day in stocks and still it’s the Tech companies that are leading the downside. Oil is taking a spanking, and if there was anything positive to say about the bond markets, bless me, but I can’t find it.

The papers today are full of fear… “buy-the-dip no longer working”, “short-sellers squeezed”, or “Tech Skid Becoming a Full-Blown Crash”. The extraordinarily cold weather in the US, and the threat it raises to the masses going Black Friday shopping, is being touted as yet another nail in the stock-market coffin.

However, relax. It all makes sense. Kind of.

In the FT there is a rather good article by Mo-the-Tash (sorry if anyone is offended by the nickname we’ve given Mohammed El-Arian – but its affectionate!) Let me give you a random sprinkling of phrases from his article “Risks rise for investors as developed economies falter”