GOLD: $1304.10 UP $5.30 (COMEX TO COMEX CLOSING)

Silver: $15.75 UP 5 CENTS (COMEX TO COMEX CLOSING)

Closing access prices:

Gold : 1303.50

silver: $15.76

For comex gold and silver:

JANUARY

NUMBER OF NOTICES FILED TODAY FOR JAN CONTRACT: 0 NOTICE(S) FOR NIL OZ (0.0000 tonnes)

TOTAL NUMBER OF NOTICES FILED SO FAR: 555 NOTICES FOR 55100 OZ (1.7262 TONNES)

SILVER

FOR JANUARY

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

5 NOTICE(S) FILED TODAY FOR 25,000 OZ/

total number of notices filed so far this month: 819 for 4,095,000

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: OPENING MORNING TRADE $3426: DOWN 124

Bitcoin: FINAL EVENING TRADE: $3429 DOWN $122

end

XXXX

JPMorgan or Goldman Sachs are taking a huge issuance (stopping) of gold at the comex.

today 0/0

I wrote the following Friday night:

“Starting Monday we generally see a contraction in open interest once we approach first day notice in an active month. This usually begins 4 days prior to first day notice. The fall is due to spreaders who generally must liquidate. The contraction in OI never effects price because each trade has a buy and a sell of gold at the exact same price..i.e. a buy order and a sell order.

However while this is going on, we had a huge gain in gold price today and that should have caused our bankers to supply endless paper. It will be interesting to see the OI for comex gold for Monday.

Also remember that we are 4 days away from options expiry from London/OTC gold/silver. These expire at around 12 noon on the 31 st of January. So expect the crooks to take advantage of the higher price as they continue to supply unlimited non backed paper.”

Since the inception of the EFP’s we have always seen the contraction of OI begin 4 days prior to first day notice. Somehow this did not happen today. Let us see if it begins tomorrow. We did however see a huge gain in OI in gold. Remember we have 3 days left before first day notice and you know the crooks always raid prior to expiry.

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total OPEN INTEREST ROSE BY A HUGE SIZED 4776 CONTRACTS FROM 186,697 UP TO 191,473 ACCOMPANYING YESTERDAY’S 40 CENT GAIN IN SILVER PRICING AT THE COMEX. TODAY WE ARRIVED CLOSER TO AUGUST’S 2018 RECORD SETTING OPEN INTEREST OF 244,196 CONTRACTS.

WE HAVE ALSO WITNESSED A LARGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY AS WE NOW HAVE JUST LESS THAN 22 MILLION OZ STANDING IN DECEMBER. AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A FAIR SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP:

1100 EFP’S FOR MARCH, 0 FOR APRIL, 200 FOR DECEMBER AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE: OF 1300 CONTRACTS. WITH THE TRANSFER OF 1300 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 1300 EFP CONTRACTS TRANSLATES INTO 6.50 MILLION OZ ACCOMPANYING:

1.THE 40 CENT GAIN IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR DELIVERY IN THE LAST SIX MONTHS:

JUNE/2018. (5.420 MILLION OZ);

FOR JULY: 30.370 MILLION OZ

FOR AUG., 6.065 MILLION OZ

FOR SEPT. 39.505 MILLION OZ S

FOR OCT.2.525 MILLION OZ.

FOR NOV: A HUGE 7.440 MILLION OZ STANDING FOR NOVEMBER AND

21.925 MILLION OZ FINALLY STAND FOR DECEMBER.

AND NOW: INITIALLY 5.805 MILLION OZ STAND IN JANUARY.

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF JANUARY: 40,032 CONTRACTS (FOR 18 TRADING DAYS TOTAL 40,032 CONTRACTS) OR 200.01 MILLION OZ: (AVERAGE PER DAY: 2224 CONTRACTS OR 11.120 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF JAN: 200.01 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 28.57% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2019 TO DATE SILVER EFP’S: 200.01 MILLION OZ.

RESULT: WE HAD A FAIR SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 4776 WITH THE 40 CENT GAIN IN SILVER PRICING AT THE COMEX //YESTERDAY..THE CME NOTIFIED US THAT WE HAD A GOOD SIZED EFP ISSUANCE OF 1300 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) .

TODAY WE GAINED A GIGANTIC SIZED: 6076 TOTAL OI CONTRACTS ON THE TWO EXCHANGES:

i.e 1300 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH INCREASE OF 4887 OI COMEX CONTRACTS. AND ALL OF THIS DEMAND HAPPENED WITH A 40 CENT GAIN IN PRICE OF SILVER AND A CLOSING PRICE OF $15.70 WITH RESPECT TO YESTERDAY’S TRADING. YET WE HAD A GIGANTIC AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY

In ounces AT THE COMEX, the OI is still represented by JUST UNDER 1 BILLION oz i.e. .896 BILLION OZ TO BE EXACT or 128% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT JANUARY MONTH/ THEY FILED AT THE COMEX: 5 NOTICE(S) FOR 25,000 OZ OF SILVER

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 243,411 CONTRACTS ON APRIL 9.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $16.51.

AND NOW WE RECORD FOR POSTERITY ANOTHER ALL TIME RECORD OPEN INTEREST AT THE COMEX OF 244,196 CONTRACTS ON AUGUST 22/2018 AND AGAIN WHEN THIS RECORD WAS SET, THE PRICE OF SILVER WAS $14.78 AND LOWER IN PRICE THAN PREVIOUS RECORDS.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: A HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz NOV AT 7.440 MILLION OZ./ DEC. AT 21.925 MILLION OZ AND NOW JANUARY AT 5.825 MILLION OZ.

- HUGE RECORD OPEN INTEREST IN SILVER 243,411 CONTRACTS (OR 1.217 BILLION OZ/ SET APRIL 9/2018) AND NOW AUGUST 22/2018: 244,196 CONTRACTS, WITH A SILVER PRICE OF $14.78.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017

- RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT).

IN GOLD, THE OPEN INTEREST ROSE BY A HUMONGOUS SIZED 14,377 CONTRACTS UP TO 537,605 WITH THE RISE IN THE COMEX GOLD PRICE/(A GAIN IN PRICE OF $17.90//YESTERDAY’S TRADING)

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 7727 CONTRACTS:

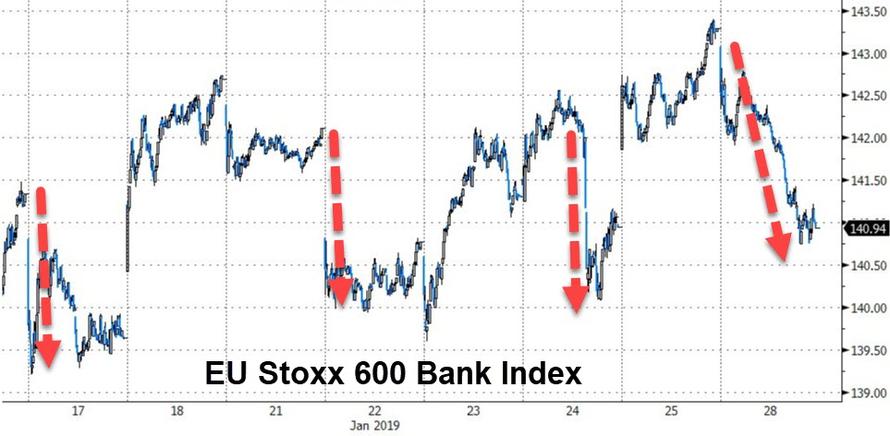

FEBRUARY HAD AN ISSUANCE OF 7585 CONTACTS APRIL 142 CONTRACTS AND ALL OTHER MONTHS ZERO. The NEW COMEX OI for the gold complex rests at 537,605. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE AN ATMOSPHERIC SIZED GAIN IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 22,104 CONTRACTS: 14,377 OI CONTRACTS INCREASED AT THE COMEX AND 7727 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN: 22,104 CONTRACTS OR 2,210,400 OZ = 68.75 TONNES. AND ALL OF THIS HUMONGOUS DEMAND OCCURRED WITH A RISE IN THE PRICE OF GOLD/ FRIDAY TO THE TUNE OF $17.90

FRIDAY, WE HAD 7069 EFP’S ISSUED.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF JANUARY : 140,464 CONTRACTS OR 14,046,400 OZ OR 436.88 TONNES (18 TRADING DAYS AND THUS AVERAGING: 7803 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE HUGE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 18 TRADING DAYS IN TONNES: 436/88 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2017, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 2555 TONNES

THUS EFP TRANSFERS REPRESENTS 436.88/2550 x 100% TONNES = 17.13% OF GLOBAL ANNUAL PRODUCTION SO FAR IN DECEMBER ALONE.***

ACCUMULATION OF GOLD EFP’S YEAR 2019 TO DATE: 436.88 TONNES

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A HUMONGOUS SIZED INCREASE IN OI AT THE COMEX OF 14,377 WITH THE GAIN IN PRICING ($17.90) THAT GOLD UNDERTOOK YESTERDAY) //.WE ALSO HAD A STRONG SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 7727 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 7727 EFP CONTRACTS ISSUED, WE HAD ANOTHER HUMONGOUS GAIN OF 22,104 CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

7727 CONTRACTS MOVE TO LONDON AND 14,377 CONTRACTS INCREASED AT THE COMEX. (IN TONNES, THE GAIN IN TOTAL OI EQUATES TO 68.75 TONNES). ..AND ALL OF THIS DEMAND OCCURRED WITH THE GAIN OF $17.90 IN YESTERDAY’S TRADING AT THE COMEX??????????. THIS IS THE 9TH STRAIGHT DAY THAT WE RECORDED STRONG RISES IN OI ON BOTH EXCHANGES!

we had: 0 notice(s) filed upon for NIL oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD...

WITH GOLD UP $5.30 TODAY

NO CHANGES IN GOLD INVENTORY AT THE GLD

/GLD INVENTORY 809.76 TONNES

Inventory rests tonight: 809.76 tonnes.

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

SLV/

WITH SILVER UP 5 CENTS IN PRICE TODAY:

NO CHANGES IN SILVER INVENTORY/

/INVENTORY RESTS AT 307.251 MILLION OZ.

end

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER ROSE BY A GIGANTIC SIZED 4776 CONTRACTS from 186,697 UP TO 191,473 AND MOVING CLOSER TO THE NEW COMEX RECORD SET LAST IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 1 1/3 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89. AS YOU CAN SEE, WE HAVE RECORD HIGH OPEN INTERESTS IN SILVER ACCOMPANIED BY A CONTINUAL LOWER PRICE WHEN THAT RECORD WAS SET…..

.

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

1100 CONTRACTS FOR MARCH. 0 CONTRACTS FOR APRIL., 200 FOR DECEMBER AND AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 1300 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI GAIN AT THE COMEX OF 4776 CONTRACTS TO THE 1300 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A GIGANTIC GAIN OF 6076 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES: 30.38 MILLION OZ!!! AND YET WE ALSO HAVE A STRONG DEMAND FOR PHYSICAL AS WE WITNESSED A FINAL STANDING OF GREATER THAN 30 MILLION OZ FOR JULY, A STRONG 6.065 MILLION OZ FOR AUGUST.. A HUGE 39.505 MILLION OZ STANDING FOR SILVER IN SEPTEMBER… OVER 2 million OZ STANDING FOR THE NON ACTIVE MONTH OF OCTOBER., 7.440 MILLION OZ FINALLY STANDING IN NOVEMBER. 21.925 MILLION OZ STANDING IN DECEMBER AND 5.825 MILLION OZ STANDING IN JANUARY..

RESULT: A HUMONGOUS SIZED INCREASE IN SILVER OI AT THE COMEX DESPITE THE 40 CENT PRICING GAIN THAT SILVER UNDERTOOK IN PRICING// FRIDAY.BUT WE ALSO HAD A GOOD SIZED 1300 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR SEPTEMBER, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)MONDAY MORNING/ SUNDAY NIGHT:

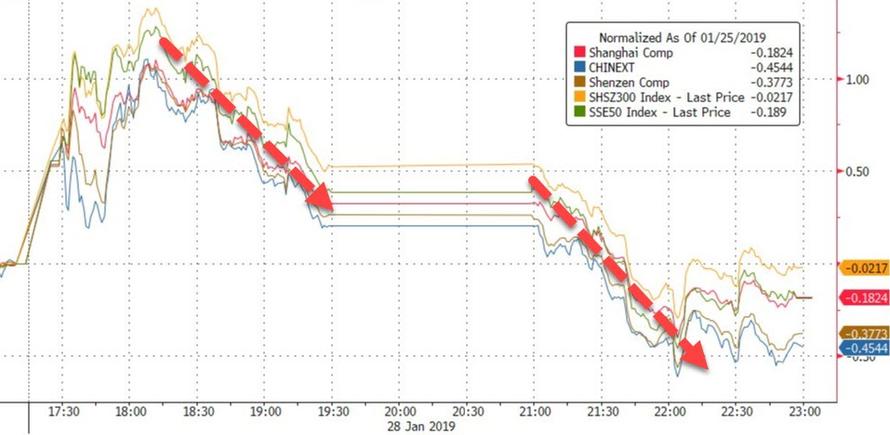

SHANGHAI CLOSED DOWN 4.75 PTS OR 0.18% //Hang Sang CLOSED UP 7.77 POINTS OR 0.03% /The Nikkei closed DOWN 124.56 PTS OR 0.60%/ Australia’s all ordinaires CLOSED UP 0.68%

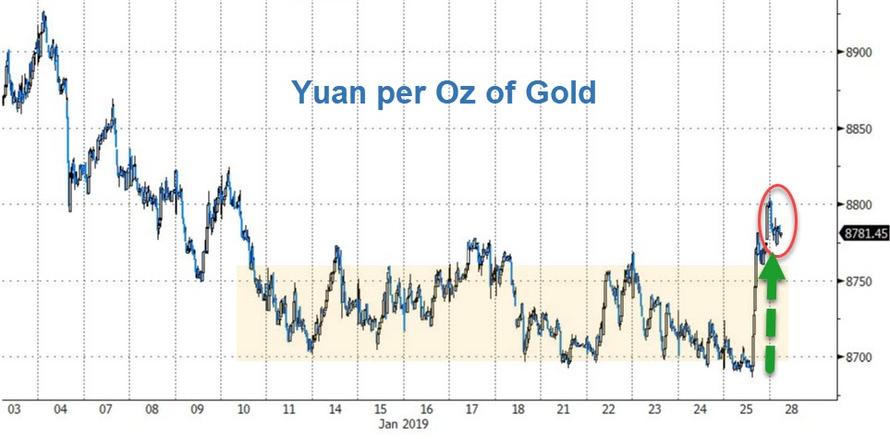

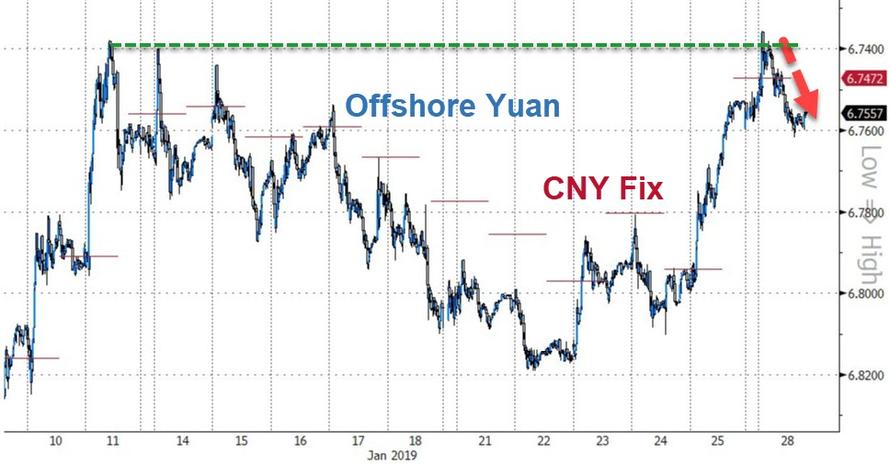

/Chinese yuan (ONSHORE) closed UP at 6.7432 AS TRUCE DECLARED FOR 3 MONTHS /Oil UP to 52.70 dollars per barrel for WTI and 60.66 for Brent. Stocks in Europe OPENED RED

//. ONSHORE YUAN CLOSED UP AT 6.7432 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED DOWN ON THE DOLLAR AT 6.7566: / TRADE TALKS NOW ON/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING STRONGER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

3A/NORTH KOREA/SOUTH KOREA

i)North Korea//USA/Sweden

b) REPORT ON JAPAN

This is not good: Japan has another scandal on its hands as they now admit that over 40% of its economic data is fake. On Wednesday night that reported that labour costs were wrong by at least .7% and that has been going on for several years. Japan has a problem..nobody believes their data.

( zerohedge)

3 C/ CHINA

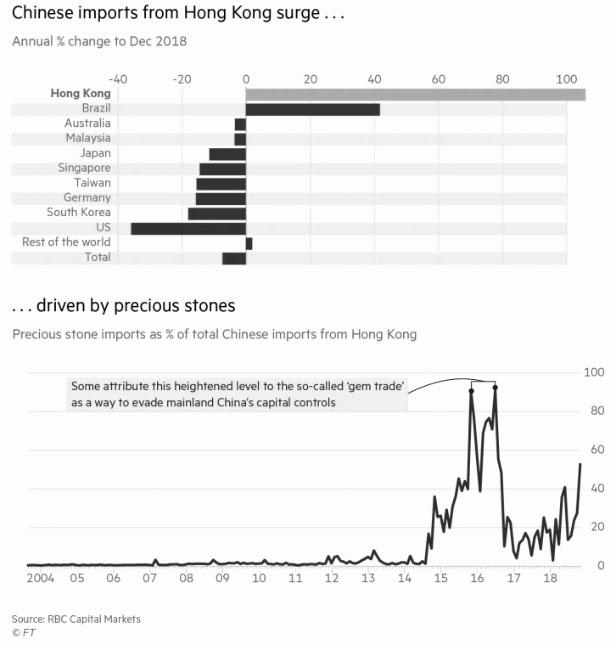

i) CHINA/HONG KONG

Very important…The Chinese are very clever as they find a great way to get around capital controls…fake invoices for gems. China has a big problem as dollars are fleeing their country

(courtesy zerohedge)

iii)At 3 pm this afternoon: as I promised you, criminal charges will be laid against Huawei and that will just about do it with respect to any hope for a USA/China trade deal

4/EUROPEAN AFFAIRS

i)FRANCE/

The Yellow vest movement rages on for its 11th straight week. Macron increases tensions with the red scarf movement that supports his carbon tax due to his assessment of global warming.

( zerohedge)

ii)UK

It looks like Theresa May is nearing a BREXIT deal by the elimination of the Irish backstop with “other arrangements”

( zerohedge)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

i)/Russia

6. GLOBAL ISSUES

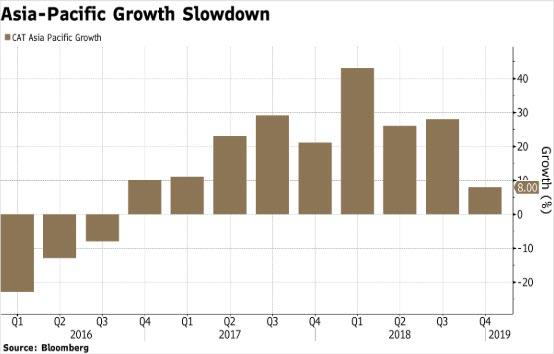

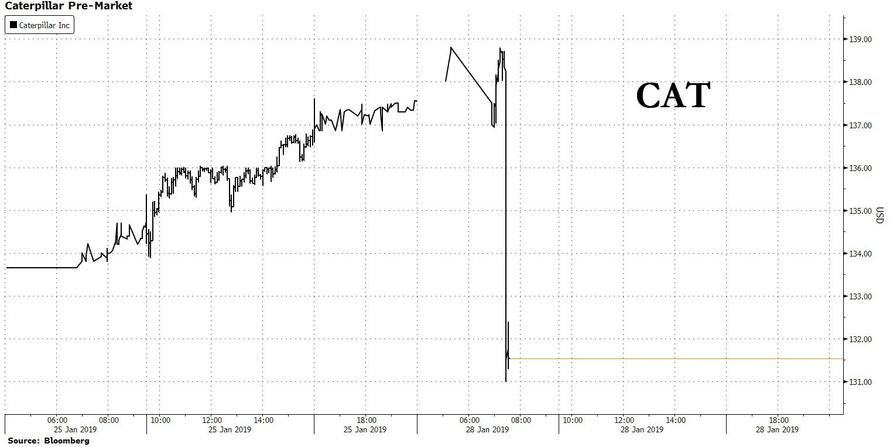

Caterpillar is such a good Bellwether as he good look on global growth. The company blames the fight with the USA as the reason for its poor forward guidance.

( zerohedge)

7. OIL ISSUES

8 EMERGING MARKET ISSUES

i)VENEZUELA

Slowly Maduro is losing his grip on Venezuela

( zerohedge)

9. PHYSICAL MARKETS

iii)The following was the big story on Friday where the Fed is considering to stop selling their bond portfolio. This is what ignited the price of gold.

( Timiraos/Wall Street journal/GATA)

iv)It has been our contention that the gold at Fort Knox has been gone for quite some time. Now Von Greyerz reports that reliable sources told Von Greyerz that DeGaulle was sure 50 yrs ago that the USA had already exhausted its gold reserve to suppress the price of gold. It has been reported that on March 1/1968 through to March 31.1968 huge number of trucks were loading something at Fort Knox. Interestingly enough on March 31, Lyndon Johnston stated that he would not run for another term as President, opposite to what he stated a few months earlier…

a must read…

( Von Greyerz/Kingworldnews)

v)The official release of the Bank of England’s refusal to return 1.2 billion dollars worth of gold to Venezuela

vi)This is the reason why we own gold( John Rubino)

vii)Huge commodity trader Vale crashes 20% and suspends its dividend as it was the owner of the mine that built the dam that collapsed in Brazil. They are a huge derivative player.

10. USA stories which will influence the price of gold/silver)

MARKET TRADING

ii)Market data/

a)Vodafone whacks Hauwei over its head as the halt purchases. Mainland China is not happy

( zerohedge)

b)Trump states that he did not cave: He will move forward on the wall in 21 days, deal or not

c) i)This is getting really bad; Pelosi set to block Trump’s state of the Union speech in Congress chambers.

d)Trump will build the wall with our without Congress: Mick Mulvaney.

e)Monday morning: Trump doubts Congress will strike an acceptable border deal as stocks slump( zerohedge)

f)The CBO’s projection has always been way off. First of all, the announce that this year’s budget deficit will be only 897 billion, but it is already heading for 1 billion dollars. We should also note that 400 billion dollars worth of debt is not included in the figures as these are student and auto loans as they are also an asset on the books so supposedly it did not count as official debt. This is why the 12 month running debt to the penny is running over 1.4 trillion dollars …the real real true deficit.. It should also be noted that there is going to be a 250 billion debt runoff from the Fed. This amount is an additional amount of debt that must be funded.

iv)SWAMP STORIES

How the Democrat hopefuls for President will begin eating themselves up preparing for2020

a good one..

Tom Luongo

@gatewaypundit: The more @realDonaldTrump continues to talk right now after handing over power to @SpeakerPelosi the more I want to throw up

@paulsperry_: Speaker Pelosi in presser just boasted that President Trump “underestimated” her and her Democrat caucus’ “power” in resisting pressure to fund the border wall. Your move, Mr. President

@RealSaavedra: Chuck Schumer mocks President Trump: “Hopefully now the president has learned his lesson… Democrats are firmly against the wall.”

@AnnCoulter: Good news for George Herbert Walker Bush: As of today, he is no longer the biggest wimp ever to serve as President of the United States.

Trump was unnerved by the avalanche of erstwhile supporters’ criticism and venom.

@realDonaldTrump [on Friday night]: I wish people would read or listen to my words on the Border Wall. This was in no way a concession. It was taking care of millions of people who were getting badly hurt by the Shutdown with the understanding that in 21 days, if no deal is done, it’s off to the races!

Reports on Friday night and Saturday averred that DJT was livid with the GOP leadership [McConnell & Graham] that advised him to do the short-term deal. DJT stupidly keeps embracing Swamp creatures. Most of Trump’s problems are self-inflicted, the result of hiring the wrong people.

@fisheri: Most interesting to me after big news day, from @mikeallen quoting republican official. “The Senate Rs were about to cut and run. He had no exit ramp.”

DJT’s cave to Pelosi unleashed grousing from Trump supporters that had been suffering silently while Trump hired, coddled and embraced establishment figures, NeverTrumpers and Swamp creatures.

@kausmickey: If it’s going to be 21 days of the Jared Kushner Show, with your out-of-league son-in-law offering up increasingly large & awful amnesty plans in exchange for some wall money, please PULL THE PLUG NOW.

end

Let us head over to the comex:

THE NEXT NON ACTIVE DELIVERY MONTH IS FEBRUARY AND HERE THE OI FELL BY 17 CONTRACTS DOWN TO 428. AFTER FEBRUARY IS THE VERY BIG AND ACTIVE DELIVERY MONTH OF MARCH AND HERE THE OI GAINED BY 2407 CONTRACTS UP TO 138,159 CONTRACTS.

COMPARISON VS LAST YR:

AS A COMPARISON TO LAST YEAR WITH 2 DAYS TO GO BEFORE FIRST DAY NOTICE WE HAD 148 CONTRACTS STANDING FOR DELIVERY (VS 428 TODAY/3 DAYS BEFORE FIRST DAY NOTICE).

FOR COMPARISON TO THE COMEX 2017 CONTRACT MONTH AND JANUARY 2018 CONTRACT MONTH AND FEB 2018

ON FIRST DAY NOTICE JAN 1/2018 CONTRACT MONTH WE HAD A GOOD 2.695 MILLION OZ STAND FOR DELIVERY’

AT THE CONCLUSION OF JAN/2018 WE HAD 3.650 MILLION OZ STAND AS QUEUE JUMPING WAS THE NORM FOR SILVER

.

ON FIRST DAY NOTICE FEB 1 CONTRACT MONTH WE HAD 670,000 OZ. AT THE MONTH’S CONCLUSION WE HAD 2.035 MILLION OZ STAND AS WE WITNESSED QUEUE JUMPING ON A REGULAR BASIS AT THE SILVER COMEX.

i) Out of Int Delaware: 96.45 oz

(3 kilobars)

Gold Consolidates Above $1,300 After 1.2% Gain Last Week

Gold futures settled above $1,300 an ounce on Friday, with prices for the yellow metal at their highest since June as the U.S. dollar pulled back and investors eyed geopolitical turmoil and global growth worries.

Rising gold prices reflect “political uncertainty” in the U.S., Eurozone, Venezuela and pockets of South America, as well as China-U.S. trade talks, said George Gero, managing director in RBC.

Rising gold prices reflect “political uncertainty” in the U.S., Eurozone, Venezuela and pockets of South America, as well as China-U.S. trade talks, said George Gero, managing director in RBC.

Gold for February delivery added $18.30, or 1.4%, to settle at $1,304.20 an ounce after trading as high as $1,305.80. The April contract notched its highest finish since June and climbed by 1.2% for the week, according to FactSet data.

March silver rose 39.9 cents, or 2.6%, to $15.699 an ounce—settling 2% higher for the week.

Gold Note

The strong gains seen in gold and silver last week and gold’s close above $1,300 per ounce are bullish technically. It suggests that gold has broken out of its recent range and could move higher in the coming days.

Possibly what will determine gold’s short term price outlook is how equity markets perform. If risk appetite continues and stocks make further gains, gold may see some selling again. However, if stocks resume their declines then gold will likely catch a safe haven bid again.

We have seen an increase in safe haven demand from UK and Irish clients in recent days. It is nothing major though and nothing compared to the increase in demand we saw after the Brexit vote, the Northern Rock bank run or indeed the global financial crisis in 2008.

We are seeing little or no selling and nearly all buying. Bullion buyers tend to be risk averse and motivated by wealth preservation and therefore focus on owning gold (and silver) for the long term.

News and Commentary

Parliament to Challenge May for Brexit Power in Crucial Votes (Bloomberg.com)

U.K. Military Stockpiles Food, Fuel, Ammo Ahead of Brexit: Sky (Bloomberg.com)

Gold firm near 7-month peak on U.S. rate pause hopes (Reuters.com)

Asia shares pare gains as focus turns to crucial Sino-U.S. trade talks (Reuters.com)

Trump doubts border security deal, another government shutdown looms (Reuters.com)

Oil falls on increased U.S. rig count, China industrial slowdown (Reuters.com)

Source: Bloomberg

Bitcoin Investors Are Running From Crypto To Invest In Gold This Year (CNBC.com)

Why This Billionaire Just Bought Gold for the First Time in His Life (GoldSeek.com)

U.S. is behind Bank of England’s freeze of Venezuela’s gold (Bloomberg.com)

How Should We Then Invest? (GoldSeek.com)

Tumbling Asian Exports Confirm Global Earnings Recession (ZeroHedge.com)

How the U.K. Parliament Is Trying to Seize Control of Brexit (Bloomberg.com)

Chemical elements which make up mobile phones placed on ‘endangered list’ (St-Andrews.Ac.UK)

Listen on iTunes,Blubrry & SoundCloud & watch on YouTube above

Gold Prices (LBMA PM)

25 Jan: USD 1,282.95, GBP 981.33 & EUR 1,132.08 per ounce

24 Jan: USD 1,279.75, GBP 981.70 & EUR 1,128.36 per ounce

23 Jan: USD 1,284.90, GBP 990.14 & EUR 1,131.74 per ounce

22 Jan: USD 1,284.75, GBP 994.14 & EUR 1,130.58 per ounce

21 Jan: USD 1,278.70, GBP 995.08 & EUR 1,124.11 per ounce

18 Jan: USD 1,285.05, GBP 993.34 & EUR 1,126.86 per ounce

17 Jan: USD 1,294.00, GBP 1,004.92 & EUR 1,135.87 per ounce

Silver Prices (LBMA)

25 Jan: USD 15.37, GBP 11.74 & EUR 13.55 per ounce

24 Jan: USD 15.30, GBP 11.75 & EUR 13.48 per ounce

23 Jan: USD 15.38, GBP 11.80 & EUR 13.54 per ounce

22 Jan: USD 15.26, GBP 11.84 & EUR 13.44 per ounce

21 Jan: USD 15.26, GBP 11.86 & EUR 13.42 per ounce

18 Jan: USD 15.47, GBP 11.96 & EUR 13.56 per ounce

17 Jan: USD 15.57, GBP 12.08 & EUR 13.66 per ounce

Recent Market Updates

– Gold Bullion Will Protect From Politicians, Brexit and Increasing Market Volatility In 2019

– Brexit – The Pin That Bursts London Property Bubble

– Davos: David Attenborough Warns We Are Damaging The World ‘Beyond Repair’

– Gold May Return 25% In 2019 Given Brexit, Trump and Other Risks – IG TV Interview GoldCore

– Brexit, EU, Germany, China and Yellow Vests In 2019 – Something Wicked This Way Comes

– Three Reasons Gold May Embark On An Extended Rally

– Political Turmoil in UK & US Sees Gold Hit 2 Week High

– Gold Holds Steady Over €1,100/oz – Increased Possibility Of A Disorderly Brexit

– Turbulence and Brexit Make Safer Options Like Gold and Cash Essential

– Where Will The “Pending” Financial Crisis Originate?

– Gold and Silver Prices To Rise To $1,650 and $30 By 2020? Video Update

– Gold Outlook 2019: Uncertainty Makes Gold A “Valuable Strategic Asset” – WGC

– Blackrock Say Gold Will Be A “Valuable Portfolio Hedge” In 2019

Physical gold and silver markets tightest since 1971, Maguire tells KWN

Submitted by cpowell on Fri, 2019-01-25 16:23. Section: Daily Dispatches

11:25a ET Friday, January 25, 2019

Dear Friend of GATA and Gold:

London metals trader Andrew Maguire tells King World News today that the physical monetary metals market is tighter than it has ever been since 1971 and much disinformation is being distributed to discourage buyers. The interview is excerpted at KWN here:

https://kingworldnews.com/andrew-maguire-gold-silver-in-massive-coiling-…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

Chris Waltzek interviews Gata chairman Bill Murphy

(courtesy GATA/Goldseek)

GoldSeek Radio interviews GATA Chairman Murphy

Submitted by cpowell on Sat, 2019-01-26 02:44. Section: Daily Dispatches

9:45p ET Friday, January 25, 2019

Dear Friend of GATA and Gold:

GATA Chairman Bill Murphy, interviewed this week by GoldSeek Radio’s Chris Waltzek, says physical silver easily could be cornered on the long side, triggering an explosion in price. The rise in the stock market has curbed interest in gold and silver and curtailed exploration for the metals, making both metals vulnerable to supply shortages, Murphy adds. The interview is 11 minutes long and can be heard at Goldseek Radio here:

http://news.goldseek.com/radio/1548451700.php

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

Bloomberg reports that it is the USA that is behind the freeze on Venezuela’s gold. This is probably true but the other reason for the freeze is the lack of physical gold at the B. of E. I am sure that the B. of E would have paid in dollars what is owed but that request was also stymied.

(courtesy GATA/Bloomberg)

U.S. is behind Bank of England’s freeze of Venezuela’s gold

Submitted by cpowell on Sat, 2019-01-26 14:53. Section: Daily Dispatches

By Patricia Laya and Ethan Bronner

Bloomberg News

Friday, January 25, 2019

Nicolas Maduro’s embattled Venezuelan regime, desperate to hold onto the dwindling cash pile it has abroad, was stymied in its bid to pull $1.2 billion worth of gold out of the Bank of England, according to people familiar with the matter.

The Bank of England’s decision to deny Maduro officials’ withdrawal request comes after top U.S. officials, including Secretary of State Michael Pompeo and National Security Adviser John Bolton, lobbied their U.K. counterparts to help cut off the regime from its overseas assets, according to one of the people, who asked not to be identified.

…

The U.K. followed the U.S. and other countries on Wednesday in recognizing Juan Guaido, the National Assembly leader, as the legitimate president of Venezuela. Maduro, an authoritarian ruler who has overseen the country’s collapse into economic chaos, refuses to give up power, though, and has the backing of the military. The European Union threatened to recognize Guaido unless a “credible” presidential election is called with eight days, according to a draft statement seen by Bloomberg.

The U.S. officials are trying to steer Venezuela’s overseas assets to Guaido to help bolster his chances of effectively taking control of the government. The $1.2 billion of gold is a big chunk of the $8 billion in foreign reserves held by the Venezuelan central bank. The whereabouts of the rest of them is largely unknown. Turkey, though, has emerged recently as a destination for freshly mined Venezuelan gold.

The U.S. is leading an international effort to persuade Turkey — a key Maduro backer, along with Russia and China — to stop being a conduit for these gold shipments. Europe’s shift of position clarifies the international battles lines over Venezuela and aligns key powers such as Germany, France, and Spain more closely with the Trump administration ..

… For the remainder of the report:

https://www.bloomberg.com/news/articles/2019-01-25/u-k-said-to-deny-madu…

END

The following was the big story on Friday where the Fed is considering to stop selling their bond portfolio. This is what ignited the price of gold.

(courtesy Timiraos/Wall Street journal/GATA)

Fed considers earlier stop to sale of bond portfolio

Submitted by cpowell on Sat, 2019-01-26 22:17. Section: Daily Dispatches

Fed Officials Weigh Earlier-Than-Expected End to Bond Portfolio Runoff

By Nick Timiraos

The Wall Street Journal

Friday, January 25, 2019

Federal Reserve officials are close to deciding they will maintain a larger portfolio of Treasury securities than they’d expected when they began shrinking those holdings two years ago, putting an end to the central bank’s portfolio wind-down closer into sight.

Officials are still resolving details of their strategy and how to communicate it to the public, according to their recent public comments and interviews. With interest rate increases on hold for now, planning for the bond portfolio could take center stage at a two-day policy meeting of the central bank’s Federal Open Market Committee next week. …

…

Fed officials led markets to expect the process would take several years to play out. When the runoff began in October 2017, various officials estimated the portfolio — then around $4.5 trillion — could shrink to anywhere between $1.5 trillion and $3 trillion. New York Fed President John Williams said in April 2017, when he was the San Francisco Fed’s president, that runoff could last five years.

“In about three or four years, we’ll be down to a new normal,” said Fed Chairman Jerome Powell at his Senate confirmation hearing in November 2017.

The latest discussions indicate the runoff could end much sooner. …

… For the remainder of the report:

https://www.wsj.com/articles/fed-officials-weigh-earlier-than-expected-e…

END

It has been our contention that the gold at Fort Knox has been gone for quite some time. Now Von Greyerz reports that reliable sources told Von Greyerz that DeGaulle was sure 50 yrs ago that the USA had already exhausted its gold reserve to suppress the price of gold. It has been reported that on March 1/1968 through to March 31.1968 huge number of trucks were loading something at Fort Knox. Interestingly enough on March 31, Lyndon Johnston stated that he would not run for another term as President, opposite to what he stated a few months earlier…

a must read

(courtesy Von Greyerz/Kingworldnews)

De Gaulle was sure U.S. gold was gone 50 years ago, von Greyerz says

Submitted by cpowell on Mon, 2019-01-28 00:01. Section: Daily Dispatches

7p ET Sunday, January 27, 2019

Dear Friend of GATA and Gold:

At this distance in time it’s just hearsay but Swiss gold fund manager Egon von Greyerz tells King World News tonight that reliable sources tell him that French President Charles de Gaulle was sure a half century ago that the United States had already exhausted its gold reserve through its price-suppression policy.

At least no one is likely to argue that President Nixon’s terminating the U.S. dollar’s convertibility into gold for foreign sovereigns suggested a great surplus of the monetary metal in U.S. government vaults.

Von Greyerz’s comments are posted at KWN here:

https://kingworldnews.com/greyerz-sources-close-to-de-gaulle-have-inform…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

Bank of England refused to return $1.2bn in gold to Venezuela – reports

The Bank of England blocked Venezuela’s attempts to retrieve $1.2 billion worth of gold stored as the nation’s foreign reserves in Britain, sources told Bloomberg on Friday.

According to the media outlet, officials in Caracas have for weeks been trying to withdraw the gold, with Calixto Ortega, the head of Venezuela’s central bank, traveling to London in mid-December to seek access to the nation’s assets.

The talks were “unsuccessful,” as US Secretary of State Mike Pompeo and the national security advisor to President Donald Trump, John Bolton, pressured their British counterparts to freeze the Venezuelan assets, Bloomberg reported, citing people familiar with the matter.

By some estimates, Venezuela holds more than $8 billion in foreign reserves. According to earlier reports, the amount of Venezuelan gold kept in the Bank of England doubled in recent months, growing from 14 to 31 tons.

The South American nation has reportedly experienced problems in extracting its own gold from the Bank of England in the past. Bankers in Britain were allegedly concerned that Venezuelan officials would sell the state-owned gold “for personal gain.”

The Bank of England, along with press officials for Pompeo and Venezuelan leader Nicolas Maduro, declined to comment.

Despite the fact that the story was not confirmed, the alleged move of the British bank was swiftly praised by the self-proclaimed ‘interim president’ of Venezuela. “The process of protecting the assets of Venezuela has begun,” Juan Guaido tweeted.

“We will not allow more abuse and theft of money intended for food, medicine and the future of our children.”

Guaido, the speaker of the national parliament, declared himself ‘interim president’ of the state earlier with week in opposition to Maduro. He was subsequently recognized as the “legitimate” leader of Venezuela by the US, Canada, and the majority of South American nations.

Maduro was backed by states like Mexico, Russia, China, and Turkey. He slammed the US for endorsing Guaido, ordering its diplomats to leave the county.

Moscow said it will continue to recognize Maduro as the sole democratically-elected leader of the country and called on others to not allow “destructive foreign interference” in Venezuelan affairs.

ALSO ON RT.COMFrance, Germany & Spain issue ‘identical’ threats to recognize Venezuela’s self-appointed presidentVenezuela has seen a series of large-scale anti-government protests in recent years. Some of them spiraled into riots and clashes with police. Nicolas Maduro blasted “foreign interference” as a source behind the unrest, while in particular accusing US officials of endorsing the rallies and Washington of planning to overthrow him. The anti-government protests were met with counter-demonstrations by Maduro supporters.

Like this story? Share it with a friend!

end

This is the reason why we own gold

(courtesy John Rubino)

If You Could Design A Perfect World For Gold…

Authored by John Rubino via DollarCollapse.com,

Are you sick of your gold just sitting there when it was supposed to have long since made you rich? Have you been fantasizing about a world in which your gold really does make you rich?

If so you’re in good – or at least numerous – company.

So let’s sketch out such a world.

Start by envisioning an America in which a handful of oligopolies have captured banking, media, healthcare and several other important industries, while a tiny group of super-rich neo-aristocrats control as much wealth as the 200 million least-rich citizens.

Toss in a US president who goes out of his way to pick fights which he then proceeds to lose, leading to both falling poll numbers and derisive headlines around the world.

That’s a good start but probably not enough to take gold to its rightful price of $10,000. So let’s add a US opposition party – which, given the above president’s declining popularity, has at least a 50-50 shot at taking power in the next election – that is skewing madly, unprecedentedly to the left. For more on the three most popular Democrats:

- Elizabeth Warren proposes ‘wealth tax’ on Americans with more than $50 million in assets

- Ocasio-Cortez buzz hits Davos with talk of 70% tax-rate plan

- [Socialist frontrunner] Bernie Sanders set to announce 2020 presidential run

Meanwhile, imagine that that same opposition party recently gained control of the branch of Congress that can investigate the President, leading to an escalating battle between legislature and executive that adds an element of legal chaos to what would already have been a presidential campaign of off-the-charts vitriol.

Now that’s a crazy country where gold should be in demand.

But it’s just one place. There’s a whole big world out there where gold and silver can trade. For precious metals to truly go to the moon everyone, not just traumatized Americans, has to desperately crave sound money.

So let’s imagine France roiled by violent street protesters with numerous but nebulous aims, forcing a rattled government to ramp up deficit spending on pretty much everything that anyone seems to want. And let’s have misguided but at least emotionally stable German Chancellor Angela Merkel be pushed out of office in favor of no one knows what.

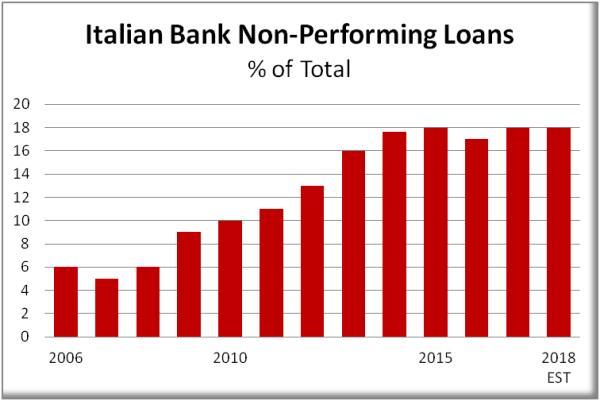

Italy has to be in there somewhere, of course. So let’s pretend its banking system has some insane amount of nonperforming loans. Maybe 18% of total loans – three times what would normally be considered extremely dangerous. We can’t even call that banking system a zombie. Instead let’s go with “persistent vegetative state.”

To sum up our hypothetical Europe, all its current problems require extremely easy money from both governments and the central bank for as far as the eye can see. Negative interest rates and an inflation target of 5% or more will soon be proposed by formerly-rational cabinet ministers and headline writers, and agreed-to by voters.

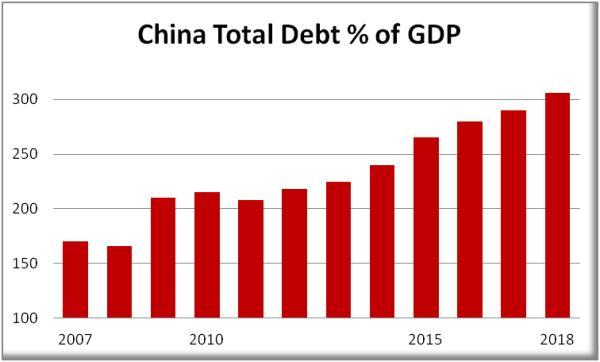

The required level of global chaos is getting close. We just need a dash of…China. Let’s pretend that it has quintupled its debt since 2008, in the course of which it recapitulated three generations of Western financial bubbles in one cycle, apparently without a sense of how those previous bubbles ended. And now it’s running out of new bubbles to inflate even as its growth slows to dangerously low levels.

That should just about do it. So let’s step back and consider our precious metals paradise:

- A US run by a trillion-dollar-deficit spender with an ever-lengthening list enemies at home and abroad, to be followed in 2020 by either more of the same or a bunch of literal, not-trying-to-hide-it socialists who institute wealth taxes, marginal income tax rates reminiscent of 1970s Great Britain and cradle-to-grave free entitlements with only “the rich” expected to cover all the bills — and who love the idea of Modern Monetary Theory, which states that governments should dispense with the whole taxing and borrowing thing and just create as much money as they need. (Can you spot this theory’s fatal flaw in the previous sentence?)

- A Europe spinning apart as the unworkability of a single monetary system housing both Germany and Italy is finally revealed.

- A China with multiple bubbles popping at the same time and no historical or theoretical framework for understanding what, why, or how.

Just in case you missed the rhetorical device, none of the above is actually hypothetical. It’s all real, and heading this way fast.

Where will everyone hide in the dysfunctional world of 2019? In the old kinds of money that the Fed, ECB, and Peoples Bank of China can’t manufacture out of thin air when their debts finally come due. Of course.

In that world the demand for real money will rise to levels that are hard to imagine (since the human mind apparently can’t visualize the concept of “trillions”). It won’t be a fun world, or a safe world. But at least your gold will soften the blow.

Vale Crashes 20%, Suspends Dividend After Deadly Dam Breach

Vale SA, the world’s largest iron ore miner, suspended its planned shareholder dividends, share buybacks and executive bonuses as it braces for the financial fallout from a Friday catastrophe in which a dam breach left at least 58 people dead and more than 300 missing. Vale’s board of directors also created independent committees to investigate the causes of the Friday dam burst in the state of Minas Gerais and monitor relief efforts in the devastated town of Brumadinho and surrounding area.

As Bloomberg notes, the collapse of a tailings dam at the Feijao mine in the rural state of Minas Gerais is Vale’s second fatal disaster since 2015, when the Samarco mine spewed billions of gallons of waste. More importantly for investors, Mayor Avimar de Melo of the city of Brumadinho, which was partly leveled by the spill, is seeking millions in damages and blamed Vale’s “incompetence” for the incident.

Flood waters in Brumadinho, Brazil, on Jan. 27

And, as many expected, the response from the market was instant, with Vale stock plunging 20% on Monday morning.

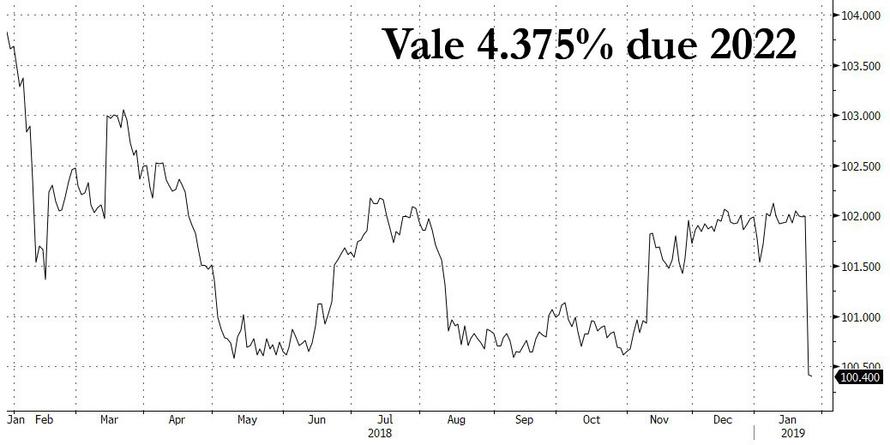

Worse, this may just the beginning of pain for investors, given that this is the second dam burst linked to Vale, we would expect more stringent remediation requirements and tougher penalties,” Macquarie Capital Ltd. analysts including Grant Sporre wrote on Monday. The company’s 750 million euro bond due in January 2022 dropped the most on record, tumbling 10 cents on euro to about 100 cents.

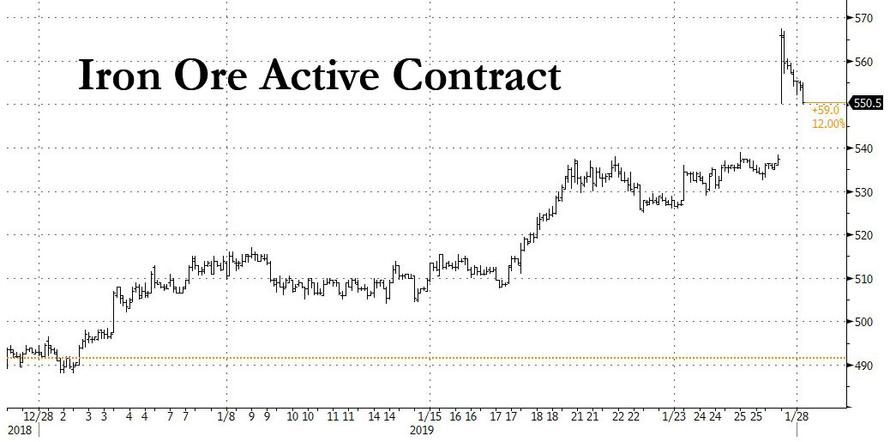

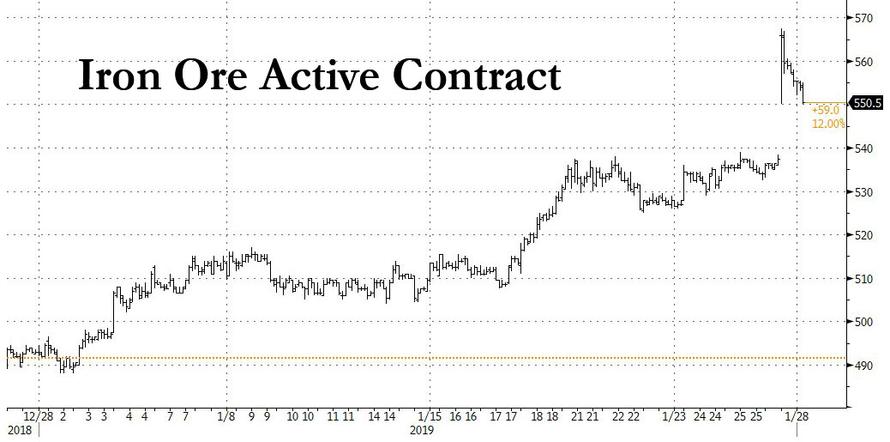

Meanwhile, as noted earlier, iron ore futures in China surged to the highest in more than a year on concern that global supplies will be interrupted.

As Bloomberg adds, the disaster will be the first major test of Vale Chief Executive Officer Fabio Schvartsman, who took the job less than two years ago. His predecessor, then-CEO Murilo Ferreira, was heavily criticized for his early reaction to the Samarco disaster. The seemingly lackluster response was later used against him by rivals eager to replace him.

Schvartsman said the latest disaster must spur the company to raise safety standards to a level “far superior to what we have today.” The Feijao project is one of its smaller operations, producing 7.8 million tons of ore in 2017.

Adding to the uncertainty facing the company, on Sunday, Renan Calheiros, a candidate for Senate president, tweeted that Vale’s top management should resign. Meanwhile, S&P Global Ratings put Vale’s bonds on CreditWatch on Friday, warning that it may be forced to shut some operations. Three judges have already frozen almost $3 billion of the miner’s funds to ensure it will be able to compensate victims and pay for the clean-up. Vale has also agreed to set up committees to probe the disaster and support the victims.

The disaster also comes less than a month after the inauguration of Brazil President Jair Bolsonaro and may upend his plans to ease environmental restrictions and boost mining production through reforms in Congress.

Following this perfect storm for the company, late on Sunday, Vale’s board decided to halt dividends after an extraordinary meeting. It was initially unclear whether dividends had been suspended or the board had just debated the possibility because an English-language statement on the company’s website said it “deliberated” over the matter. But a spokesperson for Vale in Beijing later directed Bloomberg toward the Portuguese statement.

Analysts at Macquarie estimated that the earnings hit would be limited because of the company’s balance sheet strength and robust cash generation.

“The company can cover the remediation cost with ease,” Macquarie said. “However, Vale’s equity re-rating story was in part a reputational one which has now been dealt a body blow.”

Your early MONDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

i) Chinese yuan vs USA dollar/CLOSED UP TO 6.7432/

//OFFSHORE YUAN: 6.7560 /shanghai bourse CLOSED DOWN 4.75 PTS OR 0.18%

HANG SANG CLOSED UP 7.77 POINTS OR 0.03%

2. Nikkei closed DOWN 124.56 POINTS OR 0.60%

3. Europe stocks OPENED ALL RED

/USA dollar index RISES TO 95.85/Euro RISES TO 1.1345

3b Japan 10 year bond yield: FALLS TO. +.00/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 109.46/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD IS NOW TARGETED AT .11%/JAPAN LOSING CONTROL OF THEIR BOND MARKET

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 52.70 and Brent: 60.66

3f Gold UP/JAPANESE Yen UP CHINESE YUAN: ON -SHORE UP/OFF- SHORE: UP

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil DOWN for WTI and DOWN FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund RISES TO +.22%/Italian 10 yr bond yield DOWN to 2.69% /SPAIN 10 YR BOND YIELD UP TO 1.25%…ITALIAN 10 YR BOND YIELD/GERMAN BUND: 2.57: DANGEROUS FOR THE ITALIAN BANKING SYSTEM

3j Greek 10 year bond yield FALLS TO : 4.07

3k Gold at $1299.40 silver at:15.69 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble DOWN 5/100 in roubles/dollar) 66.05

3m oil into the 52 dollar handle for WTI and 60 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 109.46 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 0.9952 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1326 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now POSITIVE territory with the 10 year RISING to +0.22%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.76% early this morning. Thirty year rate at 3.07%

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

6. TURKISH LIRA: UP TO 5.300

Global Stocks Slide Ahead Of Crazy Week; Iron Ore Soars

It’s a sea of red in global equity markets as Friday’s euphoria fizzled after President Donald Trump made clear he won’t take no for an answer in his effort to construct a border wall while investors are hunkering down ahead of an action-packed week which includes the UK Parliament’s Brexit “Plan B” vote, a Fed meeting, a new round of US-China trade talks, the deadline for the Huawei CFO extradition notice, a potential Venezuela showdown, January US payrolls report and the busiest week of earnings season.

While stocks jumped on Friday after Trump “caved” and agreed to reopen the government, the party mood was dented after Trump tweeted “Does anybody really think I won’t build the WALL?” late on Sunday as the committee of lawmakers crafting a plan for the southern U.S. border is expected to start meeting this week. On Sunday, Trump told the WSJ he’ll get the funding even if he has to use emergency powers while Trump’s acting chief of staff said he’s prepared to shutter the government again or declare an emergency if needed to get the wall money.

The dollar was flat as were 10Y TSY yields, while iron ore prices soared following a deadly dam collapse at a mine in Brazil which killed at least 58 people in a huge blow to Brazil mining giant Vale, the world’s biggest producer iron ore, which announced overnight it would suspend its dividend as it shores up liquidity ahead of what could be a crushing legal penalty.

Asian markets started off the week mixed, as bourses in Shanghai, Hong Kong, Tokyo and Seoul all losing ground: Japanese shares retreated along Chinese peers due to trade tensions, while stocks in Hong Kong pared gains to close little changed. The yuan appreciated to its strongest against the dollar since July, the CNH rising some 400 pips tracking the weaker dollar, before Vice Premier Liu He’s trip to Washington for trade talks, and as the People’s Bank of China freed up a potential $37 billion for bank lending and a new chief was named to lead the country’s main securities regulator.

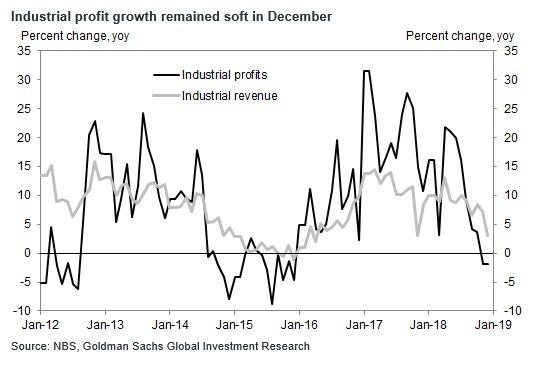

Overnight concerns about China’s slowing economy re-emerged after earnings at China’s industrial firms shrank for the second straight month, suggesting trouble ahead for manufacturers struggling with falling orders, job layoffs and factory closures amid a protracted trade war with the United States.

“A slowdown in the Chinese economy could be sometimes taken as an idiosyncratic event which would be dealt with by Beijing,” said Philip Shaw, chief economist at Investec. “It’s pretty clear that the current situation is more global, in terms of the tariff tension between the U.S. and China and the threat of that dispute spilling over more widely.”

Investors are now waiting for Chinese Vice Premier Liu He’s visit to the United States on Jan. 30-31, for the next round of trade negotiations with Washington. But with the sides still far from resolving trade issues, the dollar stood firm as traders sought a safe haven as they await news from U.S.-China talks on Tuesday and Wednesday.

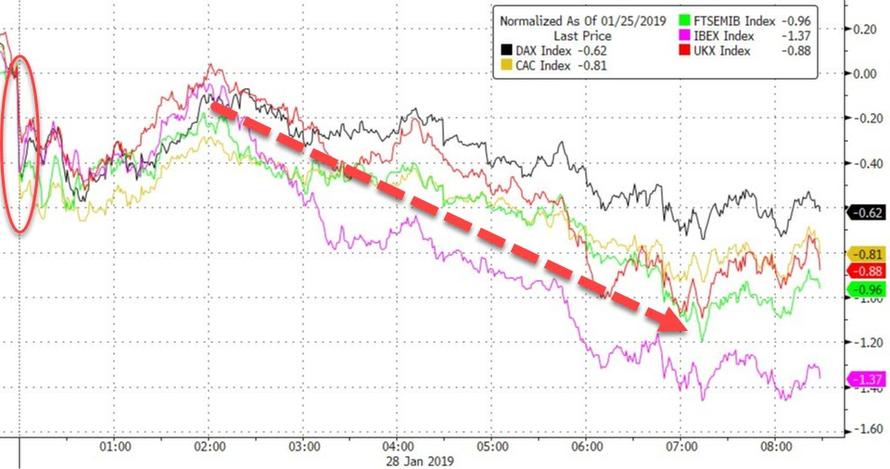

The MSCI world equity index, which tracks shares in 47 countries, fell 0.1 percent, while MSCI’s main European Index dropped 0.5 percent. The broader Euro STOXX 600 index also fell 0.5%, failing to rebound from a slide at the open after two days of gains, with most sectors falling except miners which followed the rising price of iron ore. West Texas oil fell below $53 a barrel after America’s rig count rose for the first time this year.

In addition to Trump’s border wall crusade, traders will focus on negotiations between the US and China which are set to resume in a very busy week which also include: Fed chair Jerome Powell will host a press briefing after the U.S. central bank’s policy decision, some of the biggest technology companies including Apple, Microsoft, Facebook are reporting Q4 results, and there will be another series of potentially key votes in the U.K. Parliament about Brexit. To cap it all, a flurry of American economic figures including GDP and jobs data are also set for release.

Elsewhere, Bitcoin fell again, putting the biggest cryptocurrency on track for its lowest close since December. Emerging-market stocks edged lower while their currencies climbed. Gold retreated. Russia’s MOEX stock index touched an intraday record high after sanctions were lifted on Rusal, before reversing gains to trade lower as oil prices slumped.

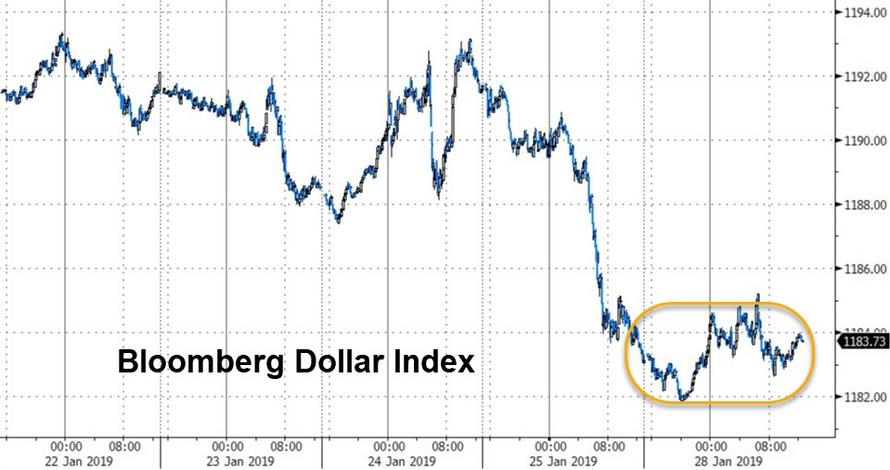

The dollar index, a gauge of its value versus six major peers, was flat at 95.801 as the dollar recovered following the Tokyo fix and Treasuries gained as global stocks started the week on a defensive note. “In this environment the dollar was holding up well,” said Thu Lan Nguyen, a forex strategist at Commerzbank. “I assume that this will continue to be the case, even as the conflict intensifies at the end of the week.”

The dollar will also get a strong steer from this week’s Fed meeting, where the central bank is expected to signal a pause in its tightening cycle and to acknowledge growing risks to the world’s biggest economy. Though the Fed has forecast two more interest rate hikes for 2019, a darkening global economic outlook and highly volatile stock markets have clouded the policy picture.

Elsewhere in currencies, sterling drifted lower as investors consolidated positions ahead of crucial votes in the British parliament designed aim to break the Brexit deadlock. The British currency edged down a quarter of a percent lower to $1.3164. Lawmakers earlier this month rejected Prime Minister Theresa May’s EU withdrawal agreement, which included a nearly two-year transition period to help minimize economic disruption. That defeat set up a series of votes on Tuesday through which lawmakers and the government will try to find a way forward.

Emerging-market currencies rose to the strongest level since June before the rally lost steam, while oil prices consolidated.

In commodities, Brent crude futures were down 1.8 percent, at $61.01 a barrel. Oil prices fell amid signals that crude output may rise further, and worries grew over the signs of economic slowdown in China, the world’s second-largest oil user. Gold was slightly down. Spot gold was down 0.2 percent at $1,300.56 per ounce, hovering just below a more than 7-month high of $1,304.40 reached earlier in the session.

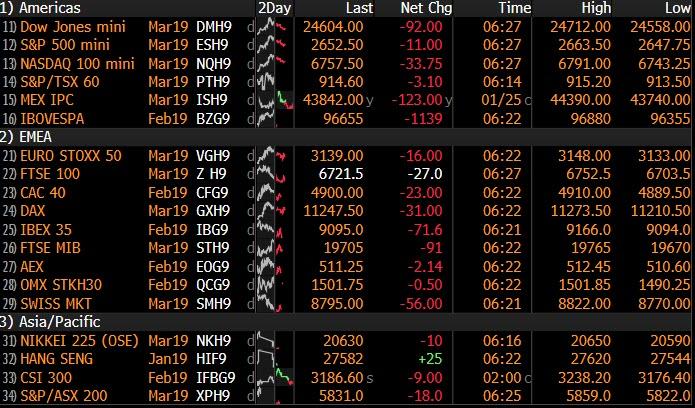

Market Snapshot

- S&P 500 futures down 0.4% to 2,652.00

- STOXX Europe 600 down 0.3% to 356.69

- MXAP down 0.1% to 154.68

- MXAPJ up 0.01% to 504.86

- Nikkei down 0.6% to 20,649.00

- Topix down 0.7% to 1,555.51

- Hang Seng Index up 0.03% to 27,576.96

- Shanghai Composite down 0.2% to 2,596.98

- Sensex down 1% to 35,665.99

- Australia S&P/ASX 200 up 0.7% to 5,905.61

- Kospi down 0.02% to 2,177.30

- German 10Y yield rose 0.4 bps to 0.197%

- Euro unchanged at $1.1406

- Brent Futures down 1.8% to $60.51/bbl

- Italian 10Y yield fell 1.0 bps to 2.293%

- Spanish 10Y yield rose 0.4 bps to 1.235%

- Brent Futures down 1.8% to $60.51/bbl

- Gold spot down 0.3% to $1,301.52

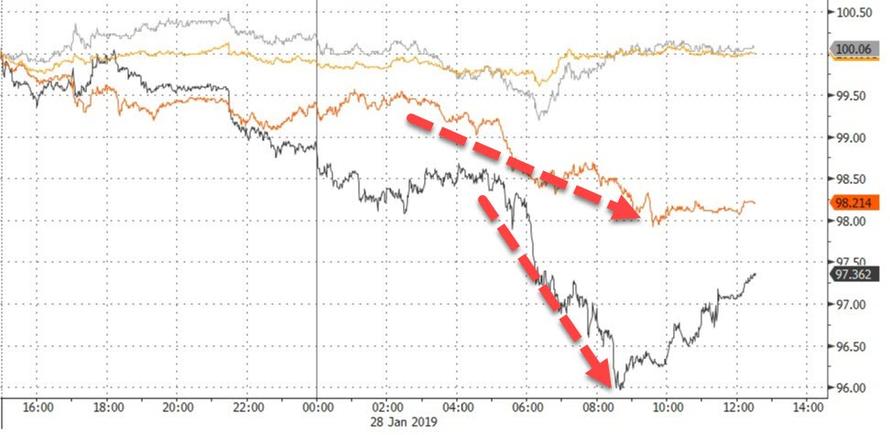

- U.S. Dollar Index up 0.04% to 95.83

Top Overnight News

- Trump said in an interview Sunday with the Wall Street Journal that he doubted whether a group of 17 lawmakers could strike a deal before the next lapse in government funding in less than three weeks and vowed to build a wall anyway, even if he has to use emergency powers

- Prime Minister Theresa May risks losing control of Brexit in a series of votes in Parliament this week that could see her forced to suspend the entire divorce or sent back to Brussels to negotiate the impossible.

- According to weekend news reports, European Commission President Jean-Claude Juncker told Theresa May in a private phone call that the price for the EU revising the Irish backstop would be a permanent customs union for the U.K.

- U.K. Prime Minister Theresa May has told cabinet ministers she won’t take the country out of the EU without a deal, the Sun reported, citing people familiar with meetings between May and her ministers over the past week

- Trump is prepared to close the federal government again if he and congressional leaders are unable to strike a budget deal that includes funding for a U.S.-Mexico border wall, acting White House Chief of Staff Mick Mulvaney said

- One Bank of Japan board member said it would be very difficult to make out the underlying price trend in the year starting in April because of a sales tax hike, softening oil prices and a reduction in cell- phone related fees, Dec. minutes show

- Europe’s retail crisis deepened as companies in the U.K. and Germany are set to cut thousands of jobs as online shopping accelerates the erosion of sales from traditional stores

- U.S. and China will hold a pivotal round of talks this week in an attempt to end their trade war. Interpreting if they’d made real progress toward a truce won’t be an easy matter

Asian equity markets initially began the week mostly higher as the region resumed the positive momentum seen on Friday in the US, where all majors gained and President Trump agreed with lawmakers to end the record-long government shutdown. This lifted sentiment across the Asia-Pac bourses in early trade with ASX 200 and Nikkei 225 (-0.7%) the exceptions as Australia remained closed for holiday and Japanese stocks were hampered by recent currency flows, with Japan Display among the worst hit after it flagged a severe situation regarding its FY net. Elsewhere, Hang Seng (U/C) and Shanghai Comp. (-0.2%) positive for most the session as corporate updates also provided a catalyst in which Sinopec were underpinned by an increase in preliminary FY net and revenue. However, the region later failed to hold on to early gains amid several factors including PBoC liquidity inaction, a consecutive monthly decline in Chinese Industrial Profits and looming risk events including US-China trade discussions. Finally, 10yr JGBs were relatively uneventful with only brief support despite the underperformance of Tokyo stocks and BoJ presence in the market for JPY 1tln of JGBs, while the BoJ minutes from the December meeting also failed to garner a reaction as it provided no surprises and considering there was also a more recent meeting held last week.

Top Asian News

- Here Are Three Scenarios for U.S.-China Trade Talks This Week

- India Stocks Extend Drop as Company Share Pledges Sour Sentiment

- How Low Can China Bond Yield Go? 10-Year Rate Flirts With 3%

- Morgan Stanley’s Quant Signals Say to Stay Long Emerging Markets

Major European equities are in the red [Euro Stoxx 50 -0.5%] following on from a negative end to Asia ahead of key risk events US-China talks and the Brexit ‘Plan B’ vote. Sectors are similarly in the red, energy names are underperforming (amid the price action in the complex) with some outperformance seen in telecom names; with the likes of Dixons Carphone (+3.1%) in the green after being upgraded at Morgan Stanley. Other notable movers include, Telecom Italia (+1.4%) who were initially at bottom of the Stoxx 600, though the company pared losses amid reports suggesting that Enel’s (-0.3%) open fibre unit are said to be seeking a pact with the Co. Elsewhere, London-listed Ocado (+2.7%) are towards the top of the Stoxx 600 following reports that the Co. have held talks with Marks and Spencer (+0.4%) concerning the launch of a food delivery service. Finally, miners are initially outperformed (Rio Tinto +1.6%) amid hopes of rising iron ore prices following the dam collapse at the Vale mine in Brazil.

Top European News

- U.K. PM Told Cabinet Ministers She Will Rule Out ‘No Deal’: Sun

- Poland Vows to Stop ‘Speculators’ as Soros Bids for Radio Zet

- Scottish Investors See CPI-Linked Gilts as ‘Unrealistic’: DMO

- Kering Drops on $1.6 Billion Tax Fine From Italy Over Gucci

In FX, GBP – The main G10 underperformer ahead of Tuesday’s Brexit vote, as Cable recoils from 1.3200+ overnight peaks and Eur/Gbp bounces off circa 0.8637 lows to trade around 1.3150 and 0.8670 respectively. Consolidation, profit-taking and/or position paring has stemmed the latest advance in Sterling, along with a broader stabilisation in the Dollar and relative resilience in the single currency (holding above 1.1400 vs the Usd) following firmer than forecast Eurozone M3 data. Note, decent Eur/Usd option expiry interest between 1.1400-15 as 1.4 bn rolls off at the NY cut. Back to the Pound, some chance of additional impetus via BoE members today including Governor Carney, Broadbent and Ramsden, but in truth tomorrow’s Plan B Parliament judgement will likely be the next major driver.

- NZD – The Kiwi tops the major league, albeit helped by external factors, like a firmer Yuan and Aud cross flows, as Australia’s national day celebrations spilled over to Monday. Nzd/Usd is pivoting 0.6850 and Aud/Nzd has dipped below 1.0500, while Aud/Usd hovers just under 0.7200. Back to the Kiwi, NZ trade data looms and could be key.

- DXY – As noted, the Buck appears to have gleaned some traction in the run up to the FOMC, US-China trade talks and NFP, with perhaps a degree of support coming via the deal to re-open Government. However, the index still looks vulnerable sub-96.00 within a 95.920-671 range, and as the Greenback remains softer vs the Jpy and Chf circa 109.50 and 0.9915.

In commodities, Brent (-1.6%) and WTI (-1.7%) are both firmly in the red, weighed on by risk sentiment, ahead of this week’s key events including US-China trade talks in Washington. Furthermore, Friday’s Baker Hughes rig count showed the number of active oil rigs increased by 10 (first increase this year); adding additional downward pressure to the complex.

Gold (-0.2%) is marginally in negative territory, weighed on by dollar strength despite of the negative risk sentiment, as the yellow metal detaches itself from its safe-haven status (again). Elsewhere, the US has removed sanctions on Rusal and two other firms connected with Russian billionaire Deripaska; with the move returning some certainty to the aluminium markets supply. Separately, iron ore prices have moved higher as markets react to news of a dam collapse at the Corrego do Feijao iron ore mine in Brazil; for reference the mine has an approximate capacity of 7.8mln tonnes.

The focus today will be central banks, with the ECB’s Draghi speaking at a European parliament hearing in Brussels, while the BoE’s Carney, Broadbent, Ramsden, Place and Woods will also be speaking. In terms of data, there is the Chicago Fed National Activity Index for December and the Dallas Fed Manufacturing activity for January. We also have earnings from Caterpillar and the US Congressional Budget Office will be releasing its Budget and Economic outlook.

US event calendar and backlogged econ data:

- Jan. 28-Feb. 4: Advance Goods Trade Balance, est. $76.1b deficit, prior $77.2b deficit, revised $77.0b deficit

- Jan. 28- Feb. 4: Retail Inventories MoM, prior 0.9%, revised 0.8%

- Jan. 28- Feb. 4: Wholesale Inventories MoM, est. 0.45%, prior 0.8%

- Jan. 28-Feb. 4: New Home Sales, est. 567,000, prior 544,000

- Jan. 28- Feb. 4: New Home Sales MoM, est. 4.22%, prior -8.9%

- Jan. 28-Feb. 4: Construction Spending MoM, est. 0.2%, prior -0.1%

- Jan. 28-Feb. 4: Factory Orders, est. 0.3%, prior -2.1%

- Jan. 28-Feb. 4: Factory Orders Ex Trans, prior 0.3%

- Jan. 28-Feb. 4: Durable Goods Orders, est. 0.8%, prior 0.8%

- Jan. 28-Feb. 4: Durables Ex Transportation, prior -0.3%

- Jan. 28-Feb. 4: Cap Goods Orders Nondef Ex Air, prior -0.6%

- Jan. 28-Feb. 4: Cap Goods Ship Nondef Ex Air, prior -0.1%

- Jan. 28-Feb. 4: Trade Balance, est. $54.0b deficit, prior $55.5b deficit

- Jan. 28-Feb. 4: Monthly Budget Statement, est. $10.0b deficit, prior $204.9b deficit

- Jan. 28-Feb. 4: Retail Sales Advance MoM, est. 0.1%, prior 0.2%

- Jan. 28-Feb. 4: Retail Sales Ex Auto MoM, est. 0.0%, prior 0.2%

- Jan. 28-Feb. 4: Retail Sales Ex Auto and Gas, est. 0.4%, prior 0.5%

- Jan. 28-Feb. 4: Retail Sales Control Group, est. 0.4%, prior 0.9%

- Jan. 28-Feb. 4: Business Inventories, est. 0.3%, prior 0.6%

- Jan. 28-Feb. 4: Net Long-term TIC Flows, prior $31.3b

- Jan. 28-Feb. 4: Total Net TIC Flows, prior $42.0b

- Jan. 28-Feb. 4: Housing Starts, est. 1.25m, prior 1.26m

- Jan. 28-Feb. 4: Building Permits MoM, est. -2.93%, prior 5.0%

- Jan. 28-Feb. 4: Housing Starts MoM, est. -0.48%, prior 3.2%

- Jan. 28-Feb. 4: Building Permits, est. 1.29m, prior 1.33m

- 8:30am: Chicago Fed Nat Activity Index, prior 0.2

- 10:30am: Dallas Fed Manf. Activity, est. -2.7, prior -5.1

DB’s Jim Reid concludes the overnight wrap

Here we go again. It’s January, yesterday was bitterly cold with wind and hail in equal measure, I played a miserable round of golf not helped by being battered by the elements and what happens when I get home? Yes a bout of golf club foliage related hay fever kicked in. I spent much of the evening sneezing and rubbing my itchy eyes. Good job my new house (when it’s ready in April) isn’t opposite the entrance to the golf club!! Oh wait it is. Time for my annual ingesting of daily anti-histamines, nasal sprays, local honey and eye drops.

This always happens to me at the golf club from January onwards and how time has flied since last year’s bout. In markets, with only 4 days of January left we are fast coming up to the first anniversary of the vol shock we had after a surprisingly high average hourly earnings print in the January 2018 US payroll report. As you’ll remember the VIX traded over 50 at the intra-day peak in the first week of February as ETF vol products saw a massive unwind. One year on, this Friday will see the latest payroll report with very few people worried about inflation. That surprise print a year ago was +2.8% YoY. Last month we again surprised on the upside at +3.2%. So US inflation has still been building up over the last 12 months, and if you want a curveball for 2019 it’s that inflation continues to edge up and the Fed has to choose between controlling it on one hand and appeasing financial markets on the other, with the latter making it quite clear that it doesn’t want tighter policy. Indeed hopes of the Fed ending its balance sheet wind down early and positive thoughts about China’s latest stimulus (see Zhiwei Zheng’s note on how this moves them closer to QE here ) helped markets end last week on a high.

Updating our screens this morning, Asia has opened the week on a mixed note following Friday’s rally. Although the Hang Seng (+0.42%), the Shanghai Composite (+0.32%) and the KOSPI (+0.44%) have opened higher, the Nikkei (-0.38%) and other Japanese markets are trading lower as investors await the outcome of US-China trade talks and the latest batch of earnings reports. Ahead of those trade talks, the Chinese yuan appreciated to its highest level against the dollar in six months, while in commodity markets WTI oil is trading lower (-0.63%) as investors assess the implications of the current political turmoil in Venezuela.

Back to the week ahead now. Outside of payroll Friday the highlights are the FOMC on Wednesday, fresh Brexit votes from Tuesday, Chinese Vice Premier Liu He arriving in Washington for 2-days of trade talks on Wednesday, the very important global manufacturing PMIs on Friday and 123 S&P 500 companies reporting with Europe’s earnings season also kicking into gear.

Going through these in a little more detail, Wednesday’s Federal Reserve meeting is the first to be followed by a press conference as they all now will. No change is expected to interest rates, but investors will be closely watching Powell’s comments as they aim to discern the future path of monetary policy this year. With no change expected the focus might be on questions on an early end to balance sheet reduction. For a full discussion of DB’s expectations see “January FOMC preview: See you in June” (link here ).

On an approximate basis as I’ve lost count, Brexit reaches pivotal week number 25 with the other 24 or so not in the end proving that pivotal. The UK parliament votes on the possible next steps on Tuesday. MPs will be further debating the government’s Brexit plan, and have the opportunity to vote on a variety of different amendments, which have been proposed by MPs from across the political spectrum. These could include one that says parliament should be able to hold indicative votes on different Brexit outcomes, one that requires the Prime Minister to extend Article 50 if the House of Commons has not approved a Brexit deal by February 26, another simply that the UK should not leave without a deal, and another calls for an expiry date on the backstop. The Speaker of the House of Commons will decide which are to be debated by MPs. The one regarding having an expiry date on the Irish backstop seems to be one both the PM and Tory party Brexiters are gravitating towards at the moment so it will be interesting to watch the support for this. However the Irish and the EU have both suggested there is no wiggle room on renegotiating the backstop. So we will see!!

Last night the Sun reported that Prime Minister May has privately told cabinet ministers that she wouldn’t leave the EU without a deal, with reports suggesting it is being kept on the table as a negotiating tactic. Sterling rallied on the news, trading above $1.3200 for the first time since October as investors priced in the decreasing likelihood of a no-deal outcome. This continues a trend (the pound has gained against the dollar for the last six consecutive weeks) of sterling gains, and comes after a majority in the House of Commons, including a number of Conservative ministers and backbenchers, have made clear their opposition to a no-deal outcome.

The other major political event for markets this week comes as Chinese Vice Premier Liu He visits Washington for trade talks on Wednesday, meeting with Treasury Secretary Mnuchin and US Trade Representative Lighthizer. Last week saw a host conflicting headlines on how much progress has been made so expect more of the same.

Earnings season continues, with 123 companies in the S&P 500 reporting this week and the European season building. Those reporting globally include Caterpillar today (always lots of snippets on how they see global activity), Apple, Pfizer and SAP on Tuesday, Microsoft, Facebook, Boeing and Alibaba on Wednesday, Amazon and Samsung on Thursday, and on Friday, we have Exxon Mobil, Chevron, Merck and Sony. With 109 companies in the S&P 500 having reported, 75% have beaten earnings expectations and 59% have beaten sales expectations.

For payrolls DB is forecasting a gain of 165k jobs which is around the same as consensus. The aforementioned average hourly earnings is expected to remain at 3.2%, the joint highest since the GFC. Other releases of note will be the Q4 GDP data on Wednesday and the Core PCE Price Index on Thursday. With the shutdown now over – for at least the next three weeks – also expect to see the backlog of data slowly come out. Finally, keep an eye out today for the US Congressional Budget Office who will be releasing its Budget and Economic Outlook, including ten-year economic budget projections. These were quite shocking this time last year in terms of the debt and deficit projections. On a rounded up basis the US wasn’t expected to see a deficit below 5% of GDP over the next decade and indeed out to the end of their forecasting period 30 years ahead. Pretty stunning stuff.

Turning to Europe, there are number of data highlights. On Thursday, we have the first release of Q4 GDP for the Euro Area, which will give an indication of whether the slowdown of the European economy continued through the end of the year. Markets are expecting quarter on quarter growth of 0.2%, as in Q3. Elsewhere, Wednesday will see the European Commission release its consumer confidence indicator for January, while Friday will see the release of manufacturing PMIs for January as well as the flash estimate of January’s CPI for the Euro Area. The full week ahead is at the end.