GOLD: $1310.60 UP $2.20 (COMEX TO COMEX CLOSING)

Silver: $15.72 UP 3 CENTS (COMEX TO COMEX CLOSING)

Closing access prices:

Gold : 1310.80

silver: $15.71

For comex gold and silver:

FEBRUARY

NUMBER OF NOTICES FILED TODAY FOR FEB CONTRACT: 73 NOTICE(S) FOR 7300 OZ (0.227 tonnes)

TOTAL NUMBER OF NOTICES FILED SO FAR: 9209 NOTICES FOR 920900 OZ (28.643 TONNES)

SILVER

FOR FEBRUARY

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

0 NOTICE(S) FILED TODAY FOR nil OZ/

total number of notices filed so far this month: 535 for 2,675,000

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

Bitcoin: OPENING MORNING TRADE $3621:DOWN $10

Bitcoin: FINAL EVENING TRADE: $3650 up $17.

end

XXXX

JPMorgan or Goldman Sachs are taking a huge issuance (stopping) of gold at the comex.

today 36/73

EXCHANGE: COMEX

CONTRACT: FEBRUARY 2019 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,307.000000000 USD

INTENT DATE: 02/11/2019 DELIVERY DATE: 02/13/2019

FIRM ORG FIRM NAME ISSUED STOPPED

____________________________________________________________________________________________

657 C MORGAN STANLEY 3

661 C JP MORGAN 7

661 H JP MORGAN 29

690 C ABN AMRO 50

737 C ADVANTAGE 23 19

880 H CITIGROUP 15

____________________________________________________________________________________________

TOTAL: 73 73

MONTH TO DATE: 9,209

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total OPEN INTEREST ROSE BY A GOOD SIZED 2150 CONTRACTS FROM 213,055 UP TO 215,205 WITH YESTERDAY’S 13 CENT LOSS IN SILVER PRICING AT THE COMEX. TODAY WE ARRIVED CLOSER TO AUGUST’S 2018 RECORD SETTING OPEN INTEREST OF 244,196 CONTRACTS.

WE HAVE ALSO WITNESSED A LARGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY AS WE NOW HAVE JUST LESS THAN 22 MILLION OZ STANDING IN DECEMBER. AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A SMALL SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP:

217 EFP’S FOR MARCH, 0 FOR APRIL, 49 FOR MAY, 0 FOR DECEMBER AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE: OF 266 CONTRACTS. WITH THE TRANSFER OF 266 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 6266 EFP CONTRACTS TRANSLATES INTO 1.330 MILLION OZ ACCOMPANYING:

1.THE 13 CENT LOSS IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR DELIVERY IN THE LAST SIX MONTHS:

JUNE/2018. (5.420 MILLION OZ);

FOR JULY: 30.370 MILLION OZ

FOR AUG., 6.065 MILLION OZ

FOR SEPT. 39.505 MILLION OZ S

FOR OCT.2.525 MILLION OZ.

FOR NOV: A HUGE 7.440 MILLION OZ STANDING AND

21.925 MILLION OZ FINALLY STAND FOR DECEMBER.

5.845 MILLION OZ STAND IN JANUARY.

AND NOW 2.690 MILLION OZ STANDING FOR FEBRUARY.

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF FEBRUARY: 6476 CONTRACTS (FOR 8 TRADING DAYS TOTAL 6476 CONTRACTS) OR 32.380 MILLION OZ: (AVERAGE PER DAY: 810 CONTRACTS OR 4.048 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF FEB: 32.38 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 4.62% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2019 TO DATE SILVER EFP’S: 249.84 MILLION OZ. (CORRECTED)

JANUARY 2019 EFP TOTALS: 217.455. MILLION OZ.

RESULT: WE HAD A STRONG SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 2308 DESPITE THE 13 CENT LOSS IN SILVER PRICING AT THE COMEX //YESTERDAY..THE CME NOTIFIED US THAT WE HAD SMALL SIZED EFP ISSUANCE OF 266 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) .

TODAY WE GAINED A STRONG SIZED: 2416 TOTAL OI CONTRACTS ON THE TWO EXCHANGES:

i.e 266 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH INCREASE OF 2150 OI COMEX CONTRACTS. AND ALL OF THIS DEMAND HAPPENED WITH A 13 CENT LOSS IN PRICE OF SILVER AND A CLOSING PRICE OF $15.69 WITH RESPECT TO YESTERDAY’S TRADING. YET WE HAD A GIGANTIC AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY

In ounces AT THE COMEX, the OI is still represented by JUST OVER 1 BILLION oz i.e. 1.075 BILLION OZ TO BE EXACT or 150% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT FEBRUARY MONTH/ THEY FILED AT THE COMEX: 0 NOTICE(S) FOR nil OZ OF SILVER

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 243,411 CONTRACTS ON APRIL 9.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $16.51.

AND NOW WE RECORD FOR POSTERITY ANOTHER ALL TIME RECORD OPEN INTEREST AT THE COMEX OF 244,196 CONTRACTS ON AUGUST 22/2018 AND AGAIN WHEN THIS RECORD WAS SET, THE PRICE OF SILVER WAS $14.78 AND LOWER IN PRICE THAN PREVIOUS RECORDS.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: A HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz NOV AT 7.440 MILLION OZ./ DEC. AT 21.925 MILLION OZ JANUARY AT 5.825 MILLION OZ.AND NOW FEB 2019: 2.690 MILLION OZ/

- HUGE RECORD OPEN INTEREST IN SILVER 243,411 CONTRACTS (OR 1.217 BILLION OZ/ SET APRIL 9/2018) AND NOW AUGUST 22/2018: 244,196 CONTRACTS, WITH A SILVER PRICE OF $14.78.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017

- RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT).

IN GOLD, THE OPEN INTEREST FELL BY A CONSIDERABLE SIZED 3167 CONTRACTS DOWN TO 476,170 WITH THE LOSS IN THE COMEX GOLD PRICE/(A DROP IN PRICE OF $6.25//YESTERDAY’S TRADING).

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A GOOD SIZED 4052 CONTRACTS:

MARCH HAD AN ISSUANCE OF 0 CONTACTS APRIL 3702 CONTRACTS, DECEMBER: 350 CONTRACTS AND ALL OTHER MONTHS ZERO. The NEW COMEX OI for the gold complex rests at 476,170. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE AN A SMALL SIZED GAIN IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 885 CONTRACTS: 3167 OI CONTRACTS DECREASED AT THE COMEX AND 4052 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN: 885 CONTRACTS OR 88,500 OZ = 2.75 TONNES. AND ALL OF THIS DEMAND OCCURRED WITH A LOSS IN THE PRICE OF GOLD/ YESTERDAY TO THE TUNE OF $6.25.

YESTERDAY, WE HAD 2549 EFP’S ISSUED.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF FEBRUARY : 42,912 CONTRACTS OR 4,291,200 OZ OR 133.47 TONNES (8 TRADING DAYS AND THUS AVERAGING: 5551 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE HUGE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 8 TRADING DAYS IN TONNES: 133.47 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2018, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 2555 TONNES

THUS EFP TRANSFERS REPRESENTS 133.47/2550 x 100% TONNES = 5.23% OF GLOBAL ANNUAL PRODUCTION SO FAR IN DECEMBER ALONE.***

ACCUMULATION OF GOLD EFP’S YEAR 2019 TO DATE: 653.62 TONNES (CORRECTED)

JANUARY 2019 TOTAL EFP ISSUANCE; 531.20 TONNES

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A CONSIDERABLE SIZED DECREASE IN OI AT THE COMEX OF 3167 WITH THE LOSS IN PRICING ($6.25) THAT GOLD UNDERTOOK YESTERDAY) //.WE ALSO HAD A GOOD SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 4052 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 4052 EFP CONTRACTS ISSUED, WE HAD A GOOD GAIN OF 885 CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

4052 CONTRACTS MOVE TO LONDON AND 3167 CONTRACTS DECREASED AT THE COMEX. (IN TONNES, THE GAIN IN TOTAL OI EQUATES TO 3.496 TONNES). ..AND ALL OF THIS DEMAND OCCURRED WITH THE LOSS OF $6.25 IN YESTERDAY’S TRADING AT THE COMEX

we had: 73 notice(s) filed upon for 7300 oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD...

WITH GOLD UP $2.20 TODAY

NO CHANGE IN GOLD INVENTORY

/GLD INVENTORY 802.12 TONNES

Inventory rests tonight: 802.12 tonnes.

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

SLV/

WITH SILVER UP 3 CENTS IN PRICE TODAY:

NO CHANGE IN SILVER INVENTORY AT THE SLV

/INVENTORY RESTS AT 307.873 MILLION OZ.

end

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER ROSE BY A STRONG SIZED 2150 CONTRACTS from 213,055 UP TO 215,205 AND MOVING CLOSER TO THE NEW COMEX RECORD SET LAST IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 1 1/3 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89. AS YOU CAN SEE, WE HAVE RECORD HIGH OPEN INTERESTS IN SILVER ACCOMPANIED BY A CONTINUAL LOWER PRICE WHEN THAT RECORD WAS SET…..

.

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

217 CONTRACTS FOR MARCH. 49 CONTRACTS FOR MAY., 0 FOR DECEMBER AND AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 266 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI GAIN AT THE COMEX OF 2150 CONTRACTS TO THE 266 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A GOOD GAIN OF 2416 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES: 12.08 MILLION OZ!!! AND YET WE ALSO HAVE A STRONG DEMAND FOR PHYSICAL AS WE WITNESSED A FINAL STANDING OF GREATER THAN 30 MILLION OZ FOR JULY, A STRONG 6.065 MILLION OZ FOR AUGUST.. A HUGE 39.505 MILLION OZ STANDING FOR SILVER IN SEPTEMBER… OVER 2 million OZ STANDING FOR THE NON ACTIVE MONTH OF OCTOBER., 7.440 MILLION OZ FINALLY STANDING IN NOVEMBER. 21.925 MILLION OZ STANDING IN DECEMBER , 5.845 MILLION OZ STANDING IN JANUARY..AND NOW 2.690 MILLION OZ STANDING IN FEBRUARY.

RESULT: A STRONG SIZED INCREASE IN SILVER OI AT THE COMEX WITH THE 13 CENT PRICING GAIN THAT SILVER UNDERTOOK IN PRICING// YESTERDAY.BUT WE ALSO HAD A GOOD SIZED 266 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR SEPTEMBER, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

)TUESDAY MORNING/ MONDAY NIGHT:

SHANGHAI CLOSED UP 18.00 POINTS OR 0.68% //Hang Sang CLOSED UP 27.49 POINTS OR .10% /The Nikkei closed UP 531.94 POINTS OR 2.61%/ Australia’s all ordinaires CLOSED UP 0.33%

/Chinese yuan (ONSHORE) closed UP at 6.7704 AS TRUCE DECLARED FOR 3 MONTHS /Oil UP to 53.42 dollars per barrel for WTI and 62.91 for Brent. Stocks in Europe OPENED GREEN //.

ONSHORE YUAN CLOSED UP // LAST AT 6.7704 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.7788: / TRADE TALKS NOW ON/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING STRONGER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

3A/NORTH KOREA/SOUTH KOREA

i)North Korea//USA

Trump states that North Korea could become an economic power if talks succeed

( zerohedge)

b) REPORT ON JAPAN

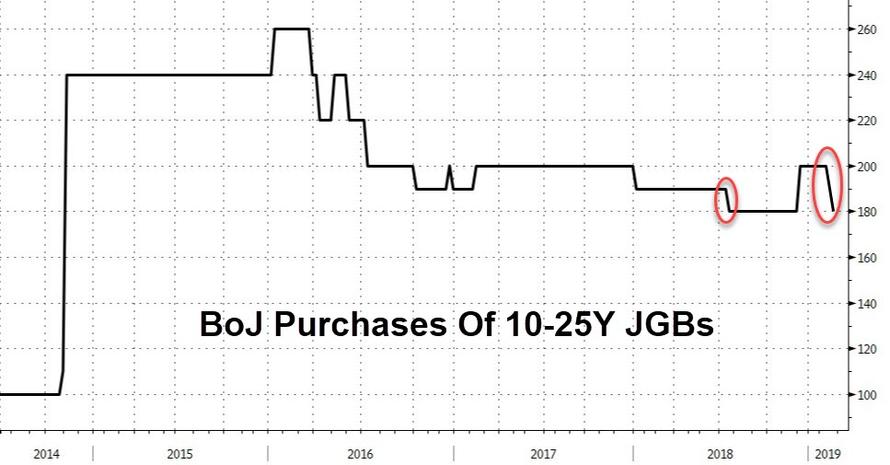

i)Quite clear: The Bank of Japan is running out of assets to purchase as they taper their JGB by another 20 billion yen.

( zerohedge)

ii)Today is the 20 yr anniversary of the Bank of Japan cutting rates to zero. Prices are basically the same as 20 years ago.

( zerohedge)

3 C/ CHINA

i) CHINA/USA

The China/USA trade deal deadline will likely be extended

( zerohedge)

4/EUROPEAN AFFAIRS

i)UK

A Jaguar bankruptcy is only a matter of time and the key development is its poor showing in China

(courtesy zerohedge)

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

So what else is new: the USA and the EU are going to slap new sanctions on Russia for their incursion into the Kerch strait which they had a right to do.

(courtesy zero hedge)

Turkey

Food prices escalate dramatically for two reasons: the lower Lira and then price gouging. Erdogan then began attacking food vendors as terrorists and traders. Is Erdogan losing touch with his people?

(courtesy zerohedge)

Russia/Ukraine/USA

Russia to the USA:

not a very good idea to hold drills in the Black Sea;

( zerohedge)

6. GLOBAL ISSUES

7. OIL ISSUES

8 EMERGING MARKET ISSUES

i)VENEZUELA/USA

9. PHYSICAL MARKETS

(Craig Hemke/Sprott)

iii)the Canadian Law firm Sotos agrees to have Deutsche bank settle on only 5.5 million dollars to settle gold/silver market rigging

( zerohedge)

iv)Despite the fact that the law firm does not communicate with us, the Canadian class action suit continues against 8 other banks

( GATA/Chris Powell)

v)No doubt about it; China is signalling gold buying “to diversify its reserves” against the dollar. When the world’s economies crack, it will be the yuan that survives due to gold backing

10. USA stories which will influence the price of gold/silver)

MARKET TRADING

ii)Market data/

a)Small business optimism plunges to the lowest level of Trump’s presidency

( zerohedge)

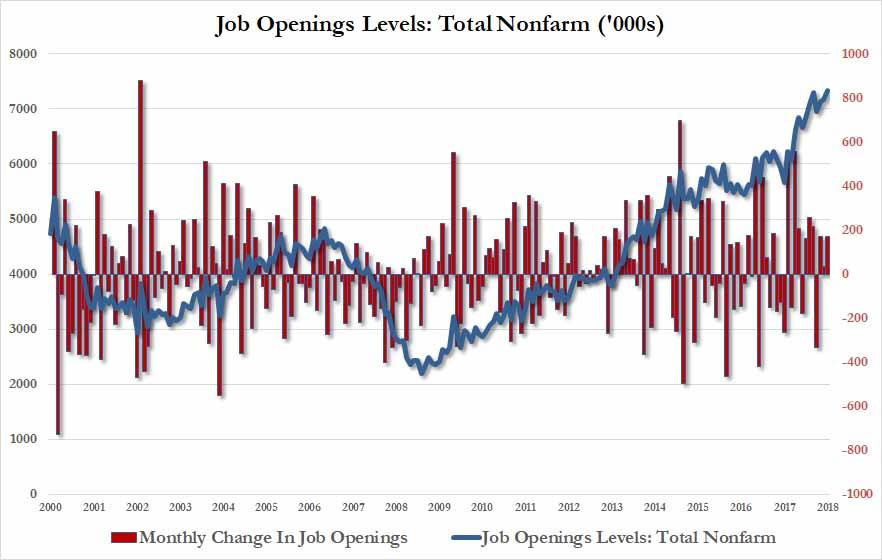

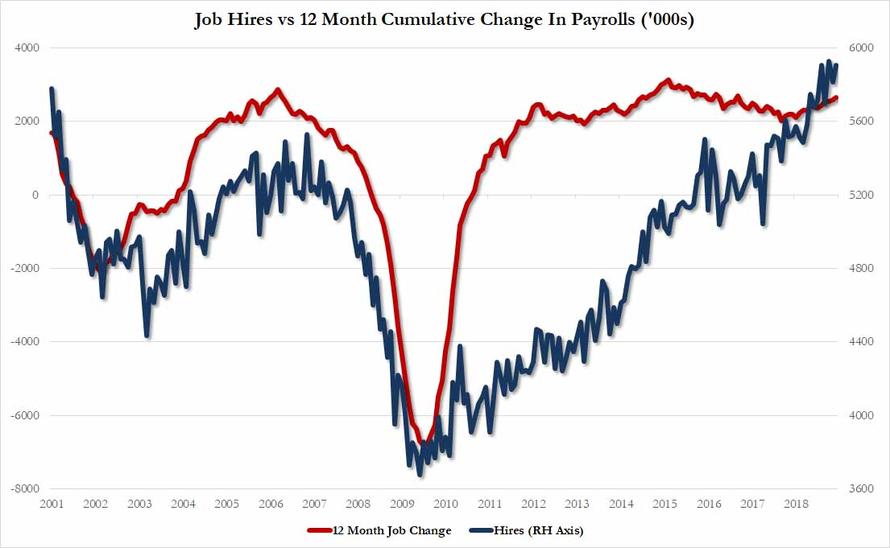

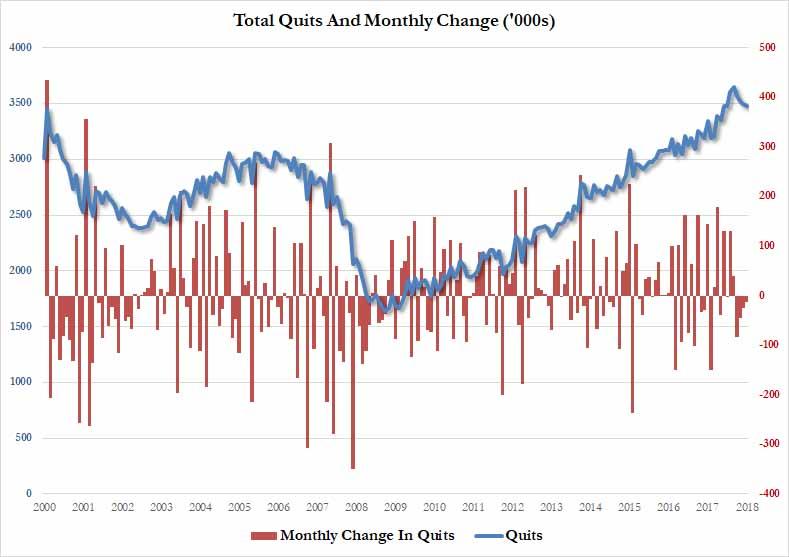

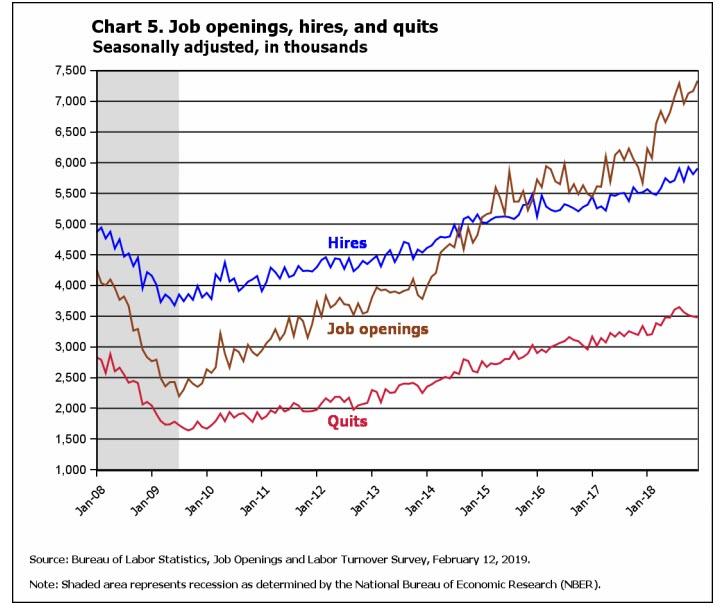

b)A good JOLTS report showing USA job openings soaring to an all time high and 800,000 more than the fake “unemployed workers”

( zerohedge)

iv)SWAMP STORIES

a)John Solomon of the Hill gives mounting evidence that it was the Democrats that colluded with Russia and not Trump

important…

( zerohedge)

b)Justin Fairfax had two staffers resign following the second accusation of sexual assault

( zerohedge)

Trump calls for Rep Omar to resign as conservatives fume over democrat double standards. They should put Stephen King back in and then fight it out.

(courtesy zerohedge)

end

Let us head over to the comex:

THE NEXT NON ACTIVE DELIVERY MONTH AFTER FEBRUARY IS THE VERY BIG AND ACTIVE DELIVERY MONTH OF MARCH AND HERE THE OI FELL BY 3557 CONTRACTS DOWN TO 122,349 CONTRACTS. AFTER MARCH, APRIL FELL TO 58 CONTRACTS FOR A LOSS OF 1 CONTRACT. AFTER APRIL, THE NEXT BIG ACTIVE DELIVERY MONTH IS MAY AND HERE THE OI ADVANCED BY 4718 CONTRACTS UP TO 57,339 CONTRACTS.

comex gold volumes are getting extremely low as players just do not want to play in this casino.

i) out of Brinks: 96.45 oz 3 kilobars

ii) Out of HSBC; 132,321.846 oz

iii) Out of Scotia: 64.300 oz (2 kilobars)

Investors Move To Store Their Gold Bullion In Ireland

More Irish Investors Storing Their Gold In Ireland

via RTE News, Radio and TV

GoldCore has recently transported gold bullion coins and bars weighing nearly 2,000 troy ounces (over 60 kilos) and worth more than €2m into the country from the UK.

This is believed to be the largest legitimate movement of gold bullion into Ireland in decades.

The company said the movement of gold reflected a growing demand from UK and Irish investors to relocate tangible assets out of the UK and “closer to home”.

It added that it expects ongoing consignments of gold bullion to be transported and securely stored in its new vaults in the run up to the Brexit deadline on March 29.

As Brexit comes to a head, GoldCore said it is seeing a growing preference amongst Irish investors to store their gold domestically here rather than Perth, Zurich, Singapore, Hong Kong, Singapore and especially London.

“To date, the demand for gold storage in Dublin has been strong,” GoldCore’s Research Director Mark O’Byrne said.

“However, in the run up to Brexit, we expect this demand to strengthen even further and Dublin may surpass London in terms of the amount of gold assets in the vaults in the coming months,” he said.

“There is strong interest from retail investors, pension owners and high net worth clients, all of whom are expressing a preference for having their assets closer to home,” he added.

He said that while the amount of gold held in the company’s Dublin vaults is a fraction of GoldCore’s client holdings in other jurisdictions, it has already surpassed Hong Kong as a favoured jurisdiction for storing gold with clients.

Zurich remains the favourite location with client bullion holdings there worth nearly €40 million. Zurich is followed by Singapore, then London, Dublin and Hong Kong.

Listen to RTE Radio One Drivetime Interview

Watch TV segment on RTE TV News

Click Here to Access 7 Key Gold and Silver Storage Must-Haves

News and Commentary

More Irish investors storing their gold here (RTE.ie)

One of largest gold shipment moves to Dublin amid Brexit concerns (Breakingnews.ie)

UK’s 2018 economic growth weakest since 2012 due to Brexit (RTE.ie)

China joins global central bank gold rush as foreign exchange reserves stabilise (SCMP.com)

Italian Populists Target Huge Gold Reserves and Some Cry Foul (Bloomberg.com)

How Venezuela turns its useless bank notes into gold (Reuters.com)

British and U.S. Banks Are Deeply Divided on Brexit Ties (Bloomberg.com)

The vast majority of reported company earnings are not fully audited (MarketWatch.com)

“Insane” Deutsche Bank Drowning Under Soaring Funding Costs (Zerohedge.com)

Living Paycheck-To-Paycheck: The New Crisis And Normal For The American Middle Class (Zerohedge.com)

Position this guide please (GoldCore.com)

Listen on iTunes,Blubrry & SoundCloud & watch on YouTube above

Gold Prices (LBMA PM)

11 Feb: USD 1,306.40, GBP 1014.81 & EUR 1,157.08 per ounce

08 Feb: USD 1,311.10, GBP 1012.04 & EUR 1,156.65 per ounce

07 Feb: USD 1,310.00, GBP 1009.49 & EUR 1,154.11 per ounce

06 Feb: USD 1,313.35, GBP 1013.51 & EUR 1,152.86 per ounce

05 Feb: USD 1,314.00, GBP 1009.15 & EUR 1,150.67 per ounce

04 Feb: USD 1,311.00, GBP 1004.36 & EUR 1,145.55 per ounce

Silver Prices (LBMA)

11 Feb: USD 15.70, GBP 12.16 & EUR 13.88 per ounce

08 Feb: USD 15.78, GBP 12.18 & EUR 13.92 per ounce

07 Feb: USD 15.71, GBP 12.20 & EUR 13.87 per ounce

06 Feb: USD 15.73, GBP 12.15 & EUR 13.82 per ounce

05 Feb: USD 15.86, GBP 12.19 & EUR 13.89 per ounce

04 Feb: USD 15.74, GBP 12.05 & EUR 13.75 per ounce

Recent Market Updates

– Large Gold Bullion Shipment Moves From London to Dublin Gold Vaults As Brexit Concerns Deepen

– Gold Surges In Aussie Dollars as Aussie Property Market Declines Sharply

– “Right” Trump and “Left” Ocasio-Cortez Will Join Forces And Debase The Dollar

– 7 Financial Truths In An Uncertain 2019

– Central Banks Buy More Gold In 2018 Than Any Year Since 1967

– Gold Breaks Out of Range After Dovish Fed – Further 1% Gain to $1,321/oz

– U.S.-China War May Be “Just A Shot Away”

– Buy Bitcoin or Gold? Bitcoin Buyers Investing In Gold In 2019

– Gold Consolidates Above $1,300 After 1.2% Gain Last Week

– Gold Bullion Will Protect From Politicians, Brexit and Increasing Market Volatility In 2019

– Brexit – The Pin That Bursts London Property Bubble

– Davos: David Attenborough Warns We Are Damaging The World ‘Beyond Repair’

– Gold May Return 25% In 2019 Given Brexit, Trump and Other Risks – IG TV Interview GoldCore

What if Italy’s locusts try seizing the gold reserves to spend them …

… and find only a moth-eaten promissory note from the Bank for International Settlements or JPMorganChase & Co.?

* * *

Matteo Salvini Talks Up Seizing Control of Italy’s Gold Reserves

By Miles Johnson

Financial Times, London

Monday, February 11, 2019

ROME — Matteo Salvini has raised the possibility of wresting control of Italy’s sizeable gold reserves away from the country’s central bank in the latest in a series of threats to the independence of the Bank of Italy by Rome’s populist coalition.

“The gold is the property of the Italian people, not of anyone else,” Mr Salvini, deputy prime minister and leader of the League party, said in comments to reporters today.

The comments came after he called for the removal of the leadership of the Bank of Italy for failing to prevent the country’s banking crisis, prompting Giovanni Tria, economy minister, to defend the independence of the central bank.

Italian media reports have suggested that the coalition government, formed of Mr Salvini’s anti-migration League and the anti-establishment Five Star Movement, were considering using part of the central bank’s gold to fund their spending plans.

Mr. Salvini said he had not studied the notion of selling Bank of Italy reserves to fund additional government spending in detail, but that “it may be an interesting idea.”

Claudio Borghi, a Eurosceptic League member of parliament and close economic adviser of Mr Salvini, has proposed a law to ensure that the Italian state was recognised as the ultimate owner of Italy’s gold reserves rather than the Bank of Italy.

“Nobody wants to sell the ingots, in fact, quite the opposite, we want to prevent others from having their hands on it,” Mr. Borghi wrote on Twitter after Mr. Salvini’s comments.

Beppe Grillo, the comedian and co-founder of Five Star, last September suggested that Italy could sell off gold to fund higher state spending.

“It would allow us to finally put an end to this annoying story about the fact that ‘there is no money,'” Mr Grillo wrote then. “Why do citizens have to sell their necklaces and not the state?” …

… For the remainder of the report:

https://www.ft.com/content/f16d0aec-2e04-11e9-ba00-0251022932c8

end

Technical analysis for gold/silver by Craig Hemke

(Craig Hemke/Sprott)

Craig Hemke at Sprott Money: The next goals for gold and silver prices

9:20p ET Monday, February 11, 2019

Dear Friend of GATA and Gold:

Craig Hemke of the TF Metals Report, writing for Sprott Money tonight, applies technical analysis to the gold and silver charts and predicts that while the bullion banks will be selling heavily at key points, the monetary metals are firmly on an ascending path again and will be supported by computer programs calculating that the winning formula now is to buy the dips.

Hemke’s analysis is headlined “The Next Goals for Gold and Silver Prices” and it’s posted at Sprott Money here:

https://www.sprottmoney.com/Blog/the-next-goals-for-gold-and-silver-pric…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

From Normalization To NIRP – Reason #437 To Own Gold

Authored by Simon Black via SovereignMan.com,

And just like that, it seems we’re headed back to quantitative easing…

After cutting interest rates to nearly zero following the 2008 crisis, the Federal Reserve starting raising rates near the end of 2015 (from 0.25% to 2.5% today).

Following the most recent hike in December 2018, Chairman Powell seemed hell bent on further tightening, saying “some further gradual increases” were in the cards.

Then the stock market promptly fell nearly 20%.

Investors were in panic mode and calling for the end of the world.

The pain was too much…

Last month, the Fed left rates unchanged… and Powell removed any language about further hikes.

Already Powell is capitulating.

The new chief economist for the International Monetary Fund praised the move, saying she sees “considerable and rising risks” to the global economy.

And no surprise here, but Paul Krugman also supported the Fed’s policy. He’s also worried about a possible recession… but more worried the Fed won’t be able to cut rates low enough.

Central banks tried raising interest rates, but the market wouldn’t take it.

Now, the market is putting the likelihood of a rate hike this year at ZERO… and it’s expecting a rate cut next year.

Both the European Central Bank and the Bank of Japan were supposed to start tightening policy and raising rates… now, they are both considering cutting interest rates even deeper into negative territory.

And after a 20% drop in US stocks, the Fed has taken its foot off the pedal. But the people still want more…

The President of the Federal Reserve Bank of St. Louis thinks current interest rates are “too restrictive.” He too wants lower rates.

The San Francisco Fed agrees – they were singing the praises of negative interest rates in a recent research paper, saying they would have helped the economy recover even faster after 2008.

And SocGen economist Albert Edwards thinks the US will see negative interest rates and helicopter money (meaning central banks will print money and give it directly to the people) during the next recession.

When you’ve got Fed banks publicly praising negative interest rates, get ready… because it means they’re considering bringing negative rates to the US.

And that’s incredibly bullish for gold.

We’re not the only ones who think so…

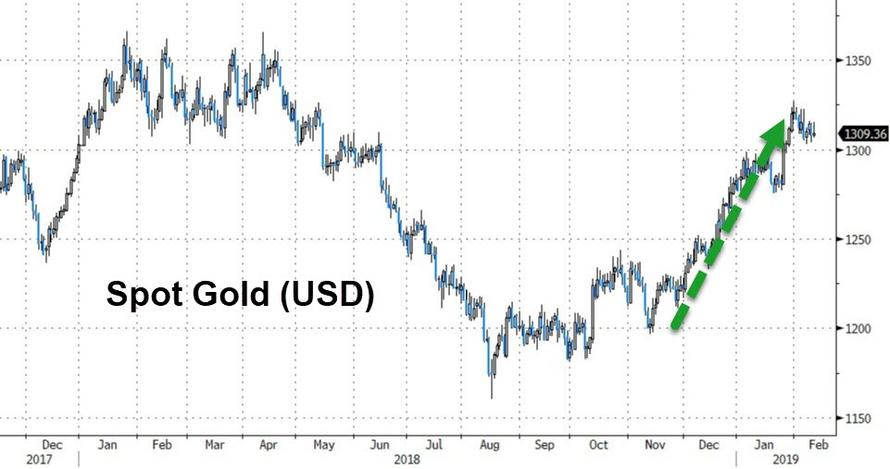

The price of the yellow metal is trading at an eight-month high above $1,300 an ounce.

And central banks are buying hand over first. In fact, the folks that control the world’s money supply, are buying gold at the fastest pace since World War II.

Oh, and they’re lightening up on Treasurys at the same time (foreign purchases of Treasurys through October of last year were down by 50%).

The controllers of the printing press are trading their fiat for gold – and its 5,000 year history as the risk-free asset.

I guess people no longer want to lend money to a government that has no chance of ever paying it back.

But that’s just one reason (albeit a big one) that we’re bullish on gold today…

Another is that we’re not finding any new gold.

Gold and gold stocks have been out of favor for years, so mining companies slashed exploration budgets to 11-year lows to tighten their belts.

As a result, they’re finding less and less gold. So when demand really starts to heat up, the gold probably won’t be there…

Lots of the biggest players in the gold space have been warning about this set up.

This lack of new deposits is no doubt partly responsible for the mega gold mergers we’ve recently seen…

Just a month ago, Newmont Mining, one of the biggest players in the industry, acquired Goldcorp for $10 billion.

And in September of last year, Barrick Gold bought Rangold Resouces for $6 billion.

I wouldn’t be surprised to see a lot more deals in the sector (especially if the Fed does cut rates again, making money cheaper).

So we may see negative interest rates in the US, meaning you earn more holding gold (nothing) than you do losing money in cash.

And some of the biggest players in the gold sector are warning we’ve seen peak gold production.

Also, the biggest pools of money on the planet – central banks – are loading up on gold.

Dwindling supply met with tons of demand means higher prices.

Historically, gold has been a fantastic leading indicator of central bank policy…

The metal ran from under $1,200 an ounce to nearly $1,300 an ounce prior to the Fed’s reversal in January.

And if it runs higher from here, which we fully expect, it means all hell is about to break loose.

I’d recommend adding to your position while you still can.

You can buy physical gold, gold stocks, an ETF… or you can issue loans backed by gold with Silver Bullion.

But here’s one of my favorite ways to buy gold today (it’s almost never been this cheap).

China Accelerates Renewed Gold-Buying Spree “To Diversify Its Reserves”

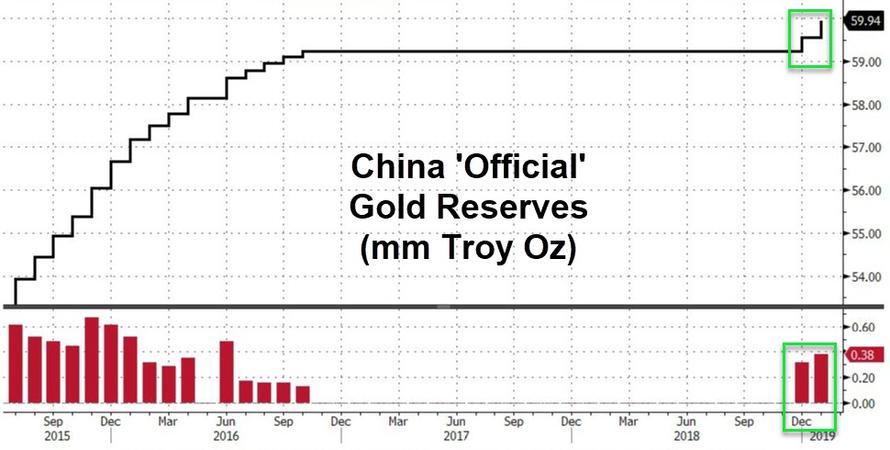

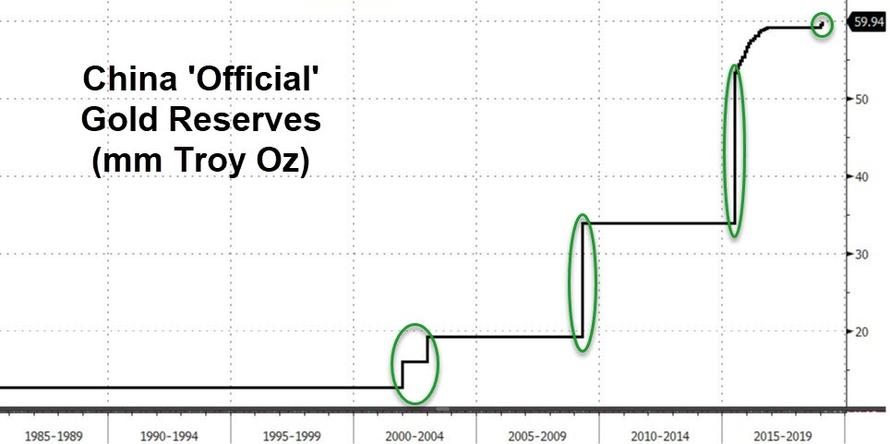

After China’s official gold reserves rose for the first time in around two years (since Oct 2016) in December, Beijing appears to have joined the global gold rush, increasing its gold reserves for the second month in a row in January to 59.94 million ounces.

As we previously noted, China has long been silent on its holdings of gold as many countries are turning away from the greenback.

The value the country’s holdings of the precious metal reached US$79.319 billion, increasing by more than $3 billion compared to the end of last year.

China is also trying “to diversify its reserves” away from the greenback, according to Jeffrey Halley, senior market analyst at currency broker OANDA. The analyst told the South China Morning Post that the state of affairs in global politics, including a trade war with the US, are driving China’s interest to buy gold as a “safe haven hedge.”

In January, China dropped to sixth place among the world’s largest holders of the yellow metal behind Russia. With its 67.6 million ounces of gold, Russia now stands in fifth place behind the US, Germany, France, and Italy.

Crucially, the size of the gold addition are far less important than the signaling effect – why did China decide now was the right time to publicly admit its gold reserves are rising?

After months of seeming stability in the yuan relative to gold, Q4 2018/Q1 2019 saw China seemingly allow gold to appreciate relative to the yuan

One wonders if Alasdair Macleod is on to something when he notes that if the yuan is to replace the dollar for China’s trade, officials will have to back it with gold…

It is hard to see how the US can match a sound-money plan from China. Furthermore, the US Government’s finances are already in very poor shape and a return to sound money would require a reduction in government spending that all observers can agree is politically impossible.This is not a problem the Chinese government faces, and the purpose of a gold-linked jumbo bond is not so much to raise funds; rather it is to seal a price relationship between the yuan and gold.

Whether China implements the plan suggested herein or not, one thing is for sure: the next credit crisis will happen, and it will have a major impact on all nations operating with fiat money systems. The interest rate question, because of the mountains of debt owed by governments and consumers, will have to be addressed, with nearly all Western economies irretrievably ensnared in a debt trap. The hurdles faced in moving to a sound monetary policy appear to be simply too daunting to be addressed.

Ultimately, a return to sound money is a solution that will do less damage than fiat currencies losing their purchasing power at an accelerating pace. Think Venezuela, and how sound money would solve her problems. But that path is blocked by a sink-hole that threatens to swallow up whole governments. Trying to buy time by throwing yet more money at an economy suffering a credit crisis will only destroy the currency. The tactic worked during the Lehman crisis, but it was a close-run thing. It is unlikely to work again.

Because China’s economy has had its debt expansion of the last ten years mostly aimed at production, if she fails to act soon she faces an old-fashioned slump with industries going bust and unemployment rocketing. China offers very limited welfare, and without Maoist-style suppression, faces the prospect of not only the state’s plans going awry, but discontent and rebellion developing among the masses.

For China, a gold-exchange yuan standard is now the only way out. She will also need to firmly deny what Western universities have been teaching her brightest students. But if she acts early and decisively, China will be the one left standing when the dust settles, and the rest of us in our fiat-financed welfare states will left chewing the dirt of our unsound currencies.

Is China’s “signal” an explicit warning of the end to the dollar era that has existed since August 1971, when gold as the ultimate money was driven out of the monetary system.

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

Federal judge tells traders they can combine cases accusing JP Morgan of rigging metals market

- Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

- Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

CNBC.com

A group of traders from across the U.S. who allege that J. P. Morgan Chase manipulated precious metals markets for years are one step closer to bringing a class action suit against the nation’s largest bank.

Earlier this month, a federal judge said five separate lawsuits making similar allegations against the bank could be combined, potentially including thousands of people who traded in the precious metals market from Jan. 2009 through Dec. 2015.

Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

J. P. Morgan declined to comment on this story.

Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

Vincent Briganti, a partner at the firm, filed the first suit seeking class action status in November on behalf of Dominick Cognata, a trader who alleges he suffered losses due to J.P. Morgan’s illegal trading conduct in the silver and gold futures and options markets.

That was after the federal court in Connecticut unsealed a criminal plea agreement by John Edmonds, a former J.P. Morgan metals trader. In his guilty plea, Edmonds, who is 36-years old, admitted that he and other “unnamed co-conspirators” fraudulently manipulated the precious metals markets while they were employed at J. P. Morgan from 2009 to 2015.

Edmonds said he had learned the illegal trading tactics from senior traders, and then used them hundreds of times with the knowledge of and consent of his immediate supervisors.

Briganti’s lawsuit also names John Edmonds and a group of yet-to-be-identified precious metals traders and the bank as defendants.

On Wednesday, the lawyers sent a letter to Judge Koeltl saying they were having difficulty locating Edmonds to serve him legal papers and requested a 30-day extension to do so, which the judge granted on Thursday. Briganti noted that they have been in contact with Edmonds’ attorney in the criminal case. Edmonds’ attorney and Briganti could not be reached for comment.

“We are hopeful that this extension will result in completing service on Mr. Edmonds without formal motion practice and a request for alternative means of service,” Briganti said in the letter.

The next step in the civil case is for the plaintiffs to file an amended class action complaint and set a schedule for defendants to respond.

In addition to the proposed class action, J. P. Morgan also faces a separate civil suit which also accuses the bank of rigging precious metals markets.

end

Your early MONDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

i) Chinese yuan vs USA dollar/CLOSED/ LAST AT: 6.7704/

//OFFSHORE YUAN: 6.7788 /shanghai bourse CLOSED UP 18.00 POINTS OR 0.68% /

HANG SANG CLOSED UP 27.49 POINTS OR .10%

2. Nikkei closed UP 531.94 POINTS OR 2.61%

3. Europe stocks OPENED GREEN

/USA dollar index FALLS TO 96.96/Euro FALLS TO 1.1306

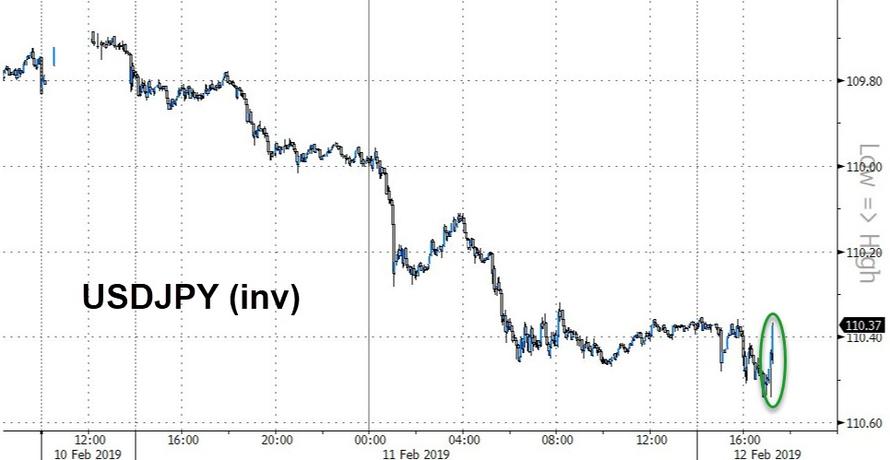

3b Japan 10 year bond yield: RISES TO. –.01/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 110.42/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD IS NOW TARGETED AT .11%/JAPAN LOSING CONTROL OF THEIR BOND MARKET

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 53.42 and Brent: 62.91

3f Gold UP/JAPANESE Yen DOWN CHINESE YUAN: ON -SHORE UP /OFF- SHORE:UP

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil UP for WTI and UP FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund RISES TO +.14%/Italian 10 yr bond yield DOWN to 2.86% /SPAIN 10 YR BOND YIELD DOWN TO 1.24%…ITALIAN 10 YR BOND YIELD/GERMAN BUND: 2.72: DANGEROUS FOR THE ITALIAN BANKING SYSTEM

3j Greek 10 year bond yield RISES TO : 3.95

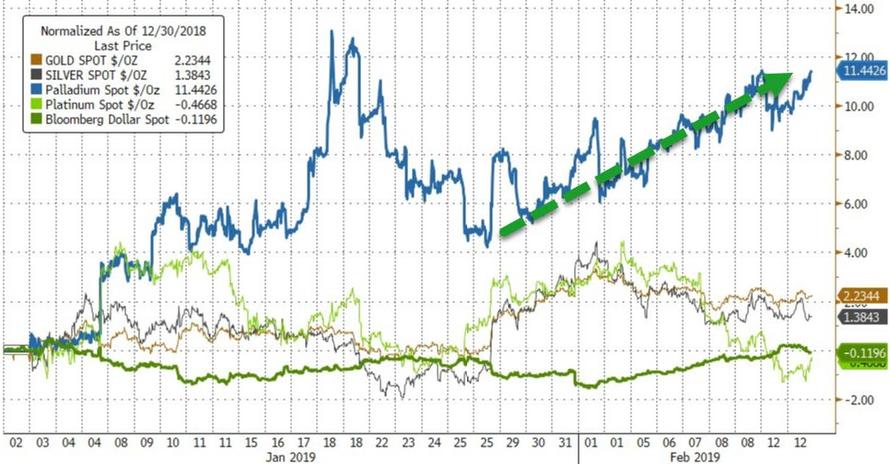

3k Gold at $1312.80 silver at:15.77 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble UP 26/100 in roubles/dollar) 65.54

3m oil into the 53 dollar handle for WTI and 62 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 110.42 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 1.0077 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1382 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now POSITIVE territory with the 10 year RISING to +0.14%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

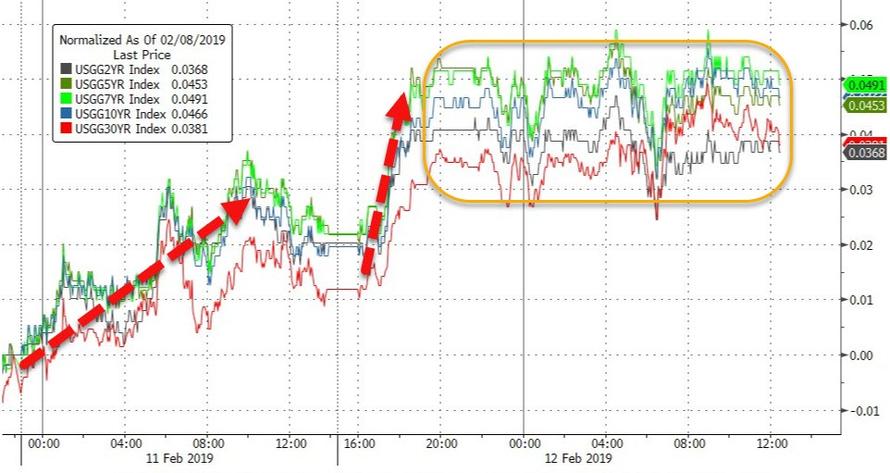

4. USA 10 year treasury bond at 2.66% early this morning. Thirty year rate at 3.02%

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

6. TURKISH LIRA: UP TO 5.2371

Markets Jump, Wall Of Worry Crumbles As Tentative Wall Deal Reached

It’s a sea of green in equity markets from Asia to Europe, with U.S. futures sharply higher following late Monday news of a tentative deal among American lawmakers to avert another government shutdown, while optimism about US-China trade talks rose after administration officials hinted at a meeting between Trump and Chinese President Xi “soon”.

In the key overnight news, US Senator Shelby said an agreement in principle was reached on shutdown talks and that staff will work on the deal. Senator Shelby also commented that he hopes the White House will back the deal and that the border bill will have some money for a barrier, while US Rep. Lowey said staff could work out the full details of border security deal by Wednesday. US congressional aides said the tentative US border security deal provides $1.375bln to build 55 miles of border fence but does not contain any funds for a border wall and does not include Democrats’ demand for capping number of immigrant detention beds

Meanwhile, President Trump said “we are going to make great deals on trade” and don’t want China to have a hard time. President Trump also commented that we probably have some good news regarding border deal but added he didn’t know what they meant regarding progress and affirmed the US would build the wall anyway.

All this was taken quite well by traders, and Tokyo’s Nikkei set the tone with its best day of the year so far, surging 2.6% as the yen tumbled to 2018 lows, while Europe wasted little time in trying to lift the STOXX 600 back to the two-month high it set last week, led by carmakers. Germany’s DAX jumped more than 1.2% after rising 1% on Monday, and Paris and Milan were up 0.8%, while London’s FTSE approached a four-month peak despite ongoing Brexit uncertainty.

Earlier in Asia, MSCI’s broadest index of Asia-Pacific shares outside Japan edged up 0.3%. Shanghai rose 0.7% South Korea’s KOSPI climbed 0.5 percent and Australian shares gained 0.3 percent. The Nikkei rallied though, shooting up 2.6% after closing on Friday at its lowest level since early January after a market holiday on Monday. With the yen sliding again, shares of exporters such as automakers and machinery makers led the charge. Separately, Deutsche Bank noted it was 20 years since Japan cut interest rates to zero, something now standard in large parts of Europe.

Japan’s 10-year bond yields remained in negative territory even after the central bank cut purchases of some longer-dated bonds for the first time since July in a regular operation. The BOJ has sought to taper its purchases while focusing on yield targets rather than quantitative easing. Nissan reported worse-than-expected results.

The dollar hovered at a two-month high and was fractionally higher on the day, its 9th consecutive daily increase, and the Australian dollar also gained (more below). The yen and Swiss franc dipped while U.S. Treasury and German bund yields edged up as investors jettisoned safe havens after U.S. lawmakers said they reached an “agreement in principle” on border security funding that would avert a second government shutdown. The Trump administration said the president still wants to meet China’s Xi Jinping in an effort to end the trade war.

“We have had two bits of relatively good news overnight – optimism about the U.S. shutdown not resuming and optimism about a trade deal,” said Societe Generale strategist Kit Juckes. “Equities are higher, bond yields are a little bit higher, yen and Swiss franc weakest overnight of the major currencies so it’s sort of risk-on rules OK!”

According to Juckes there was now a 75% chance that a hike of U.S. tariffs on Chinese goods at the start of March will be avoided and a 95% chance that another U.S. government shutdown will be dodged. Those odds were boosted late on Monday when as we reported U.S. lawmakers reached a tentative deal on border security funding, though aides cautioned that it did not contain the $5.7 billion President Donald Trump wants to build a wall on the Mexican border, and the president has yet to opine on whether the deal is agreeable.

“The trade talks are key,” Putnam’s Jason Vaillancourt told Bloomberg TV. “If we can get a little bit of those growth engines starting to level out around the world, whether it be Japan or Europe, and just bottom out, then I think that will go a long ways to putting a base under risky assets.”

The developments were good enough for S&P 500 e-mini futures to rise 0.7%, however, pointing to a solid start on Wall Street later after a choppy day on Monday.

Meanwhile, U.S. and Chinese officials expressed hopes the new round of talks, which began in Beijing on Monday, would bring them closer to easing their months-long trade war which would see the tariffs on $200 BN worth of Chinese goods rise from 10% to 25%. “There will be no winner in a trade war. So at some point they will likely strike a deal,” said Mutsumi Kagawa, chief global strategist at Rakuten Securities in Tokyo.

In fx, the dollar was mixed but held on to recent gains, having risen for eight straight sessions against a basket of six major currencies until Monday, its longest rally in two years. Although the Fed’s dovish turn dented the dollar earlier this month, analysts – who were generally expecting a slump in the dollar only to be wrongfooted once again – noted the U.S. currency still has the highest yield among major peers and that the Fed continues to shrink its balance sheet.

“The dollar is the market’s pet currency at present regardless of whether concerns about the global economy are on the rise,” currency strategists at Commerzbank said in a note.

Elsewhere, the Swiss franc was the worst performer; the yen fell to the lowest this year and Treasuries declined across the curve in the wake of the tentative deal on border security funding; the news that President Trump still wants to meet China’s Xi Jinping to help end the trade war also added to the moves. The euro dropped as much as 0.2% to 1.1258, a three-month low, before erasing losses; offers extend to 1.1350 and are part of fresh short interest, according to traders. The Swedish krona led Group- of-10 gains while the Norwegian krone and the Canadian dollar got some tailwind from rising oil prices.

Elsewhere, Brent crude rose after its lowest close in more than a week. Emerging markets shares climbed and their currencies edged higher. The pound held steady as U.K. Prime Minister Theresa May prepared to update lawmakers on the progress — or lack thereof — of Brexit talks with the EU. The offshore yuan strengthened for the first time in five days.

Market Snapshot

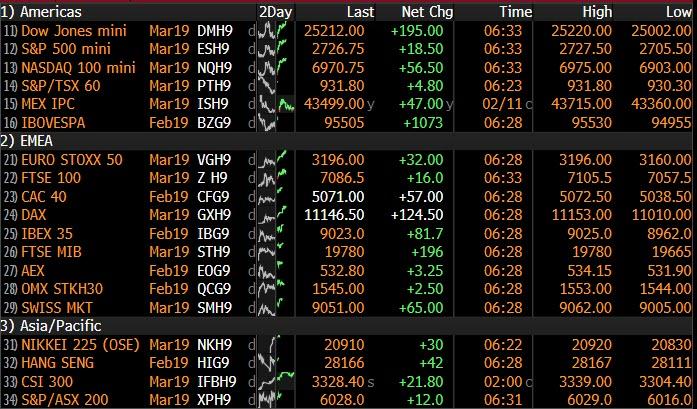

- S&P 500 futures up 0.7% to 2,727.50

- STOXX Europe 600 up 0.6% to 363.16

- MXAP up 0.9% to 156.07

- MXAPJ up 0.3% to 513.09

- Nikkei up 2.6% to 20,864.21

- Topix up 2.2% to 1,572.60

- Hang Seng Index up 0.1% to 28,171.33

- Shanghai Composite up 0.7% to 2,671.89

- Sensex down 0.7% to 36,144.54

- Australia S&P/ASX 200 up 0.3% to 6,079.08

- Kospi up 0.5% to 2,190.47

- German 10Y yield rose 0.8 bps to 0.128%

- Euro down 0.04% to $1.1272

- Italian 10Y yield fell 5.7 bps to 2.539%

- Spanish 10Y yield fell 1.0 bps to 1.232%

- Brent futures up 0.8% to $62.01/bbl

- Gold spot up 0.4% to $1,312.82

- U.S. Dollar Index little changed at 97.08

Top overnight news

- The Trump administration said the U.S. president still wants to meet China’s Xi Jinping in an effort to end the trade war, a sign of optimism as negotiators from the world’s two-biggest economies start their latest round of talks this week

- Congressional negotiators reached a tentative deal on border security that would give President Donald Trump far less money than he’d demanded for new barriers and would avert another government shutdown

- Mark Carney may give some color Tuesday on what lies ahead after enduring the worst year of growth since he arrived at the Bank of England

- U.K. Prime Minister Theresa May will address lawmakers in the House of Commons on Tuesday as she seeks more time to renegotiate her Brexit deal with the European Union

- The Bank of Japan offered to buy 180 billion yen ($1.6 billion) of securities maturing in 10-to-25 years, versus 200 billion yen at its previous operation. The last reduction in this zone was in July

- After raising interest rates late last year, Sweden’s central bank now has little choice other than to wait for a better economic outlook before pushing ahead with its long-awaited tightening cycle.

- European Union member states are considering a possible joint response to cyber attacks allegedly conducted by a Chinese state-linked hacker group after the U.K. presented evidence last month about network infiltration, according to people familiar with the matter

- ECB officials shouldn’t overreact to individual points of incoming data when setting monetary policy as the current environment is highly uncertain, Executive Board candidate Philip Lane said

- Qatar is weighing plans to tap international bond markets as the gas-rich nation seeks to cement its status as a regular issuer, according to three people with knowledge of the matter

Asian equity markets traded mostly higher amid growing optimism regarding US-China trade talks and hopes of averting a government shutdown, as negotiators were said to have reached an agreement in principle in which the border bill will include some funds for a barrier. ASX 200 (+0.3%) and Nikkei 225 (+2.6%) were positive with outperformance in the Japanese benchmark on return from the extended weekend as exporters were underpinned by favourable currency moves, although Toshiba was the notable laggard after it confirmed reports it could reduce FY profit guidance by half. Elsewhere, Shanghai Comp. (+0.7%) and Hang Seng (Unch.) were kept afloat but with upside limited by indecision as participants await the outcome of trade discussions and after the PBoC refrained from open market operations which resulted to a daily net drain of CNY 100bln. Finally, 10yr JGBs were lower amid outperformance of Tokyo stock markets and following a reduction of the BoJ’s Rinban amounts in which it lowered its purchases of 10yr-25yr JGBs by JPY 20bln. PBoC skipped open market operations for a net daily drain of CNY 100bln.

Top Asian News

- BOJ Cuts Purchases of 10-to-25 Year Bonds First Time Since July

- Abe Says Japan Wants Apology for South Korean Remarks on Emperor

- Court Freezes China Minsheng Stake in Valuable Shanghai Land

- Xiaomi, Meituan Among Dual-Class Stocks to Join MSCI Indexes

All major European indices are in the green [Euro Stoxx 50 +1.0%], continuing from the optimism seen in Asia overnight on US-China trade and the potential for averting a US government shutdown. Sectors are also all in the green, with some slight outperformance in material names. The Dax (+1.2%) is marginally outperforming its peers, in spite of being weighed upon by index heavyweight Thyssenkrupp (-1.9%) who are down following earnings where the Co. confirmed their outlook, but stated that economic and political uncertainties are increasing. Other notable movers include, Michelin (+11.6%) who are at the top of the Stoxx 600 following their earnings, with Continental (+4.1%) higher in sympathy. Towards the bottom of the Stoxx 600 are Tui (-3.1%) following their earnings. Separately, Kering (+2.4%) were in the red following their earnings, in spite of Gucci’s operating margin reaching a record 39.5% by end of 2018; although Co. shares have now drifted higher into positive territory.

Top European News

- Thyssenkrupp Profit Plunge Adds to German Industrial Blues

- Michelin Jumps as Outgoing CEO Strikes Optimistic Tone on Profit

In FX, the dollar remains bid in wake of reports that a deal has been struck in principle to avoid another US Government shutdown ahead of Friday’s funding deadline, while the US trade envoy has arrived in Beijing amidst heightened prospects of forging an agreement in time for the next tranche of import tariffs due on March 1st. The index just off a marginal new multi-week peak of 97.209, with the Dollar extending gains vs most G10 rivals.

- CHF/JPY – Another broad upturn in risk appetite has hit the safe havens hardest, understandably, with the Franc slipping closer towards yesterday’s overnight flash crash lows at 1.0091 vs 1.0095, and Usd/Jpy climbing to fresh 2019 highs circa 110.65 having breached 110.50 and the peak from 31st December last year just a pip or so below. Rebounding US Treasury yields are also impacting, and with no Japanese exporter supply anticipated before 111.00 where barrier defence offers are also expected, technical impulses could be more influential in the short term given a key Fib level and the 55 DMA in close proximity (110.54 and 110.59 respectively).

- NZD/GBP/EUR – Also conceding further ground to the Usd, with the Kiwi retesting support around the 100 DMA (0.6725) ahead of Wednesday’s RBNZ policy meeting that is widely forecast to culminate in a dovish hold (see our headline feed and/or research suite for a full preview of the event. Meanwhile, the Pound remains blighted by Brexit risk and related economic repercussions, as Cable teeters just above 1.2800 and a slightly deeper post-UK data low around 1.2834, with bids seen at 1.2820 and the 55 DMA at 1.2810. The single currency is consolidating off a fresh ytd base of 1.1258, but looking more prone to heavier losses while under 1.1300 and given little in the way of chart support ahead of the 2018 low (1.1216) apart from 1.1234.

- AUD/CAD – Defying the overall trend and both firmer vs their US counterpart, the Aud has rebounded firmly above 0.7050 and 1.0500 vs the Nzd with the aid of a more encouraging NAB business survey vs much weaker than forecast housing loans data. Meanwhile, the Loonie has drawn support from a rebound in crude prices and pared losses from 1.3300+ to circa 1.3270.

- EM – Some respite for regional currencies against the backdrop of improved risk sentiment, and with the Rand also relieved to hear that Eskom is hoping to end power cuts by the end of the week – Usd/Zar back down below 13.8000.

In commodities, Brent (+1.7%) and WTI (+1.5%) prices are comfortably in the green and above USD 62/bbl and USD 53/bbl respectively after Saudi Arabia posited that crude production in March is set to be 500k below their OPEC+ cut target at 9.8mln BPD. Support has also been offered by the optimistic risk tone after positive comments pertaining to US-China trade and a deal to prevent the US Government from shutting down again; as USTR Lighthizer arrived in Beijing this morning. OPEC are to publish their monthly oil market report today, where 2019 world oil demand was forecast to grow at 1.29mln BPD. In addition, the EIA are to release their Short-Term Energy Outlook; which previously forecast US oil output to average 12.1mln BBL and 12.9mln BBL in 2019 and 2020 respectively. Gold (+0.4%) has strengthened somewhat this morning, breaking from the subdued price action seen overnight as the dollar remained firm; the yellow metal is now trading towards the top of its USD 10/oz range. Elsewhere, reports indicate that Vale knew the Brazil dam which collapsed last month was more than twice as likely to fail than the maximum allowed risk level from internal guidelines.

Looking at the day ahead, there are no releases of note in Europe this morning while the only data due in the US is the January NFIB small business optimism reading and December JOLTS survey. Revisions to the PPI data will also likely warrant attention. Away from all that it is a busier day for central bank speak with the ECB’s Lane, Weidmann and Nowotny all speaking at separate events this morning. The BoE’s Carney is then speaking shortly after lunchtime in London at an event on the global economy and risks to the outlook. Later this evening the Fed’s Powell is due to speak at 5.45pm GMT albeit about economic development and rural poverty, so an unlikely venue for monetary policy guidance. The Fed’s Mester does however speak on the topic of the economic outlook and monetary policy at 11.30pm GMT while the ECB’s Lautenschlaeger speaks at the same time, albeit at a different event. Away from that Euro Area finance ministers are due to gather in Brussels and the monthly OPEC report is due.

US Event Calendar

- 6am: NFIB Small Business Optimism, actual 101.2, est. 103, prior 104.4

- 10am: JOLTS Job Openings, est. 6,846, prior 6,888

- Revisions: Producer Price Index

DB’s Jim Reid concludes the overnight wrap

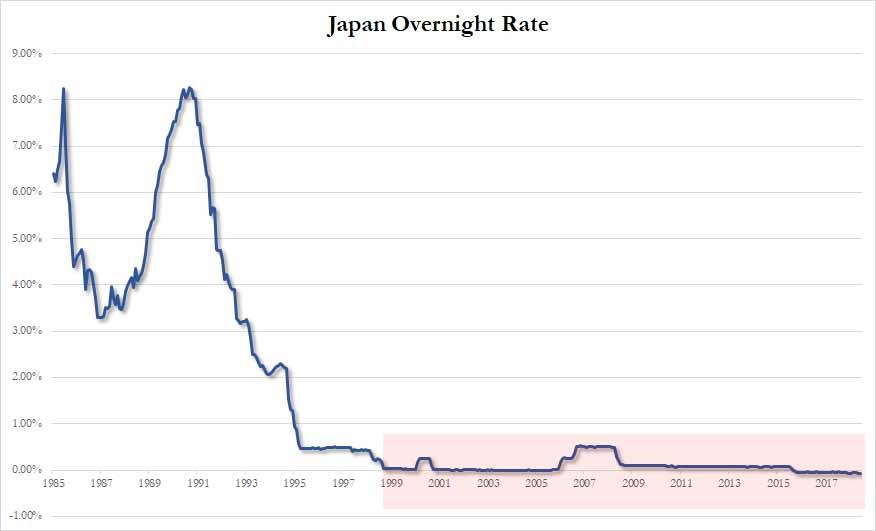

It might go under the radar but today is a bit of a landmark anniversary of sorts for financial markets. It’s the 20-year anniversary of the Bank of Japan cutting rates to 0% and the start of two decades of extreme monetary policy which the country has never been able to sustainably lift out from. A sobering template for Europe to worry about. Japan also kick started what became a more mainstream form of monetary policy post the GFC around the world. For economic historians Japan is really a fascinating case. If you took a snapshot of the nation’s finances and demographics today with no previous knowledge of the country’s journey over the last 30 years since its asset bubble burst, you would wonder how the country isn’t in a constant crisis. Debt to GDP is the highest in the developed world at 236%. The BoJ holds around 43% of all JGBs. Core prices in Japan are also virtually identical to where they were 20 years ago and 10yr JGBs have fallen from 2.21% to -0.03% over this period. Nevertheless, Japan is an example of how long a crisis can be averted for under extreme measures. It also highlights how perceptions can be turned on their heads. Yesterday we found this quote from The Economist 20-years ago: “Without fiscal discipline, say Bank of Japan officials, the government risks losing control of public spending, inviting hyperinflation in the world’s second-biggest economy.” So, an unhappy anniversary today in many respects but it’s also noticeable that after 20 years of high fiscal spending the Japanese don’t have populism. Maybe that’s a message for Europe.

To the present where the last 24 hours hasn’t been anywhere near as exciting as the BoJ that historic day 20 years ago. Case in point, the intraday range on the S&P 500 yesterday for example was just 0.53%, the third smallest of the year, and trading volumes were 20% below their 100-day average. The good news is that there are a number of potential catalysts to make things more interesting bubbling away in the background, however just not quite in danger of spilling over right now. That of course includes the US-China trade meetings this week, another Brexit session in Parliament, and some potentially significant data which really kick starts from tomorrow with US CPI.

Anyway back to markets where the S&P 500 closed a fairly uninspiring +0.07% yesterday. The NASDAQ (+0.13%) was a touch stronger if you’re looking for a shining light while the DOW (-0.21%) lagged behind. It wasn’t a lot more interesting in Europe prior to this where the STOXX 600 may have closed +0.85% but the reality was that it was just catching up to the late Friday rally on Wall Street last week. High yield credit wasn’t all that different where spreads in the US finished -2bps tighter while in bond land, Bund yields backed up +3.3bps to close at 0.117% – and therefore partially undoing some of last week’s rally which saw Bunds fall to as low as 0.076% at one stage and the lowest since October 2016. Treasuries (+1.9bps) were similarly weak (and are up another +2.7bps overnight – more on that below) while the curve – which has remained firmly rooted in a 14-20bps range all year – was flat at 16.6bps.

Meanwhile, in oil markets both WTI (-0.59%) and Brent (-0.95%) sold-off after Reuters reported that a draft document for a OPEC and non-OPEC cooperation charter avoided any mention of prices, market share and production cuts.The document also suggested that OPEC and Russia will discuss creating a mechanism (i.e. no formal body) rather than an organization when they meet in April. Not helping oil was the stronger Greenback with the Dollar index rallying another +0.43%. That means the Dollar has now strengthened for 8 consecutive sessions which is the longest run since February 2017.

In terms of actual news flow yesterday, the latest on the standoff in Washington is that a tentative deal has been reached by congressional negotiators, albeit for far less funding than Trump had sought and without confirmation from Trump yet that he will support it. Bloomberg reported that the lawmakers have agreed on all seven bills with the plan including $1.375bn for new border fencing. That compares to $5.7bn that Trump had wanted. Trump later commented at a political rally that “just so you know, we’re building the wall anyway”.

Nevertheless, the tentative agreement has lifted markets overnight with the Hang Seng (+0.16%), Shanghai Comp (+0.72%) and Kospi (+0.55%) all higher while the Nikkei (+2.64%) has really taken off after markets re-opened and post a couple of weak days for the Yen. The CNY (+0.07%) is stable following the big slide yesterday while S&P 500 futures are up +0.51%. In other news, the BoJ trimmed its purchases of JGBs in the 10-25y bucket to JPY180 bn (vs. JPY200 bn previously) at today’s regular operation. They did a similar thing in July and the move comes after yields on super-long bonds fell to lowest since late 2016 on Friday.

Meanwhile there’s really nothing material to report from the US-China trade talks so far with meetings continuing overnight in Beijing. At the margin the tone remains positive though with White House adviser Kellyanne Conway saying yesterday that “President Trump wants to meet with President Xi very soon” and that “this President wants a deal”. On a related note, it was interesting to read that the Commerce Department is likely to release a final report over the coming days (on the investigation under Section 232) which declares that imported vehicles and auto parts are a threat to national security. Tariffs are said to be an option for the President to consider under the investigation, and there will be a 90 day window for him to decide whether and how to implement them. One to watch.

In Europe, Germany’s SPD party approved pension and labour law reform proposals, which would boost social spending. The proposals included an extension to unemployment benefits, a higher minimum wage, and enhanced pensions. The plan will not be implemented in the current coalition, but it could function as part of an electoral platform if the SPD decides to abandon the government and push for new elections after its planned review later this year. Over at the ECB, Ireland’s Philip Lane was officially nominated to be the ECB’s next Chief Economist which was as expected.

In other news, there was some brief volatility in Spanish assets yesterday however it turned out to be more noise than substance. The IBEX sold-off as much as 0.80% from the highs and 10y Spanish Bonds were nearly 4bps off the lows at one stage after Efe news agency reported that PM Sanchez was considering calling snap elections for April 14th. The story was later rebuffed and Spanish assets quickly reversed the moves however this does come in a week when the government needs to get its budget passed when it goes to a vote in parliament tomorrow and the trial of the Catalan separatists who led the 2017 push for independence begins today. Spanish bond yields closed +0.7bps higher yesterday and the IBEX +0.90%.

Elsewhere, there wasn’t much in the way of new Brexit news yesterday – aside from comments from Barnier which didn’t offer anything that we didn’t already know – however we did get confirmation that PM May will present a “neutral” motion to parliament today, having previously been scheduled for tomorrow.It’s expected that May will be asking for more time over negotiations with the EU. The suggestion is that she will offer parliament the right to vote on other Brexit options by the end of February but will not commit to bringing her deal back before then. Labour in return is expected to push for an amendment that requires any final vote on the deal by February. The vote on May’s motion and any amendments will likely be on Thursday.

Staying with the UK, yesterday’s preliminary Q4 GDP print was even more disappointing than feared, coming in at just +0.2% qoq (vs. +0.3% expected). That means the annual rate has now fallen two-tenths to +1.3% yoy and so matching the six-year lows of Q1 last year. The December monthly reading actually dropped -0.4% mom compared to expectations for no change. It’s worth noting that the breakdown of the Q4 reading revealed that business investment contracted again, and therefore meaning it has contracted for a fourth consecutive quarter – the longest since the financial crisis. Sterling closed -0.69% yesterday, albeit wasn’t the worst performing G10 currency which went to the Norwegian Krone (-0.91%), as it sold off in tandem with oil.

There wasn’t any data out in the US yesterday however we did receive the CPI revisions. Importantly though there was no change to core CPI on a year-on-year basis at 2.21%.Our US economists did however make the point that the January 2018 reading was downgraded from 0.35% mom to 0.30%. Importantly this makes for easier base effects and a lower hurdle for keeping the annual rate near recent levels. A reminder that we get the January CPI report in the US tomorrow.

Finally to the day ahead,which is incredibly sparse for data. Indeed there are no releases of note in Europe this morning while the only data due in the US is the January NFIB small business optimism reading and December JOLTS survey. Revisions to the PPI data will also likely warrant attention. Away from all that it is a busier day for central bank speak with the ECB’s Lane, Weidmann and Nowotny all speaking at separate events this morning. The BoE’s Carney is then speaking shortly after lunchtime in London at an event on the global economy and risks to the outlook. Later this evening the Fed’s Powell is due to speak at 5.45pm GMT albeit about economic development and rural poverty, so an unlikely venue for monetary policy guidance. The Fed’s Mester does however speak on the topic of the economic outlook and monetary policy at 11.30pm GMT while the ECB’s Lautenschlaeger speaks at the same time, albeit at a different event. Away from that Euro Area finance ministers are due to gather in Brussels and the monthly OPEC report is due.

3. ASIAN AFFAIRS

i)TUESDAY MORNING/ MONDAY NIGHT:

SHANGHAI CLOSED UP 18.00 POINTS OR 0.68% //Hang Sang CLOSED UP 27.49 POINTS OR .10% /The Nikkei closed UP 531.94 POINTS OR 2.61%/ Australia’s all ordinaires CLOSED UP 0.33%

/Chinese yuan (ONSHORE) closed UP at 6.7704 AS TRUCE DECLARED FOR 3 MONTHS /Oil UP to 53.42 dollars per barrel for WTI and 62.91 for Brent. Stocks in Europe OPENED GREEN //.

ONSHORE YUAN CLOSED UP // LAST AT 6.7704 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.7788: / TRADE TALKS NOW ON/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING STRONGER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

3 a NORTH KOREA/USA

3 b JAPAN AFFAIRS

Quite clear: The Bank of Japan is running out of assets to purchase as they taper their JGB by another 20 billion yen.

(courtesy zerohedge)

Yen Strengthens After BoJ Tapers JGB Purchases To 5-Year Lows

For the first time since July, The Bank of Japan tapered its 10-to-25-year JGB purchases by 20 billion yen at Tuesday’s regular operation.

BoJ purchased 180 billion yen of 10-25 year bonds vs 200b yen on Feb. 4. The last taper was in July 2018 and this reduction drops the purchase amount to its equal lowest since 2014 (when Abenomics was unleashed on the world)…

The kneejerk reaction was yen buying (after being dumped against the dollar all day long)…

The message is loud and clear – The Bank of Japan is running out of ‘assets’ to monetize

end

Today is the 20 yr anniversary of the Bank of Japan cutting rates to zero. Prices are basically the same as 20 years ago.

(courtesy zerohedge)

Today Is The 20 Year Anniversary Of The Bank Of Japan Cutting Rates To 0%

In the annals of modern central (bank) planning, today is a tragic day, or as DB’s Jim Reid puts it, “it is a bit of a landmark anniversary of sorts for financial markets” – it’s the 20-year anniversary of the Bank of Japan cutting rates to 0% and the start of two decades of extreme monetary policy which neither Japan, nor any other country, has ever been able to escape from.

As Reid notes, this is a “sobering template for Europe to worry about” and adds that Japan also kick started what became a more mainstream form of monetary policy post the GFC around the world.

For economic historians Japan is really a fascinating case. If you took a snapshot of the nation’s finances and demographics today with no previous knowledge of the country’s journey over the last 30 years since its asset bubble burst, you would wonder how the country isn’t in a constant crisis. Debt to GDP is the highest in the developed world at 236%. The BoJ holds around 43% of all JGBs.

Core prices in Japan are also virtually identical to where they were 20 years ago and 10yr JGBs have fallen from 2.21% to -0.03% over this period. Nevertheless,

Japan is an example of how long a crisis can be averted for under extreme measures. It also highlights how perceptions can be turned on their heads.

Yesterday we found this quote from The Economist 20-years ago: “Without fiscal discipline, say Bank of Japan officials, the government risks losing control of public spending, inviting hyperinflation in the world’s second-biggest economy.”

Reid’s conclusion: “an unhappy anniversary today in many respects but it’s also noticeable that after 20 years of high fiscal spending the Japanese don’t have populism. Maybe that’s a message for Europe.“

end

3 C CHINA

The China/USA trade deal deadline will likely be extended

(courtesy zerohedge)

China Trade-Deal Deadline Will Likely Be Extended, Trump Aides Say

More than two months after President Trump and President Xi agreed to the trade truce over a steak dinner in Buenos Aires, a second meeting between the two leaders – one that Trump insists would be essential to striking a final trade deal – remains in doubt. But according to several Trump advisors quoted by Bloomberg, China is still pushing for a meeting (though, given that the Trump administration needs to keep the deal talk alive to buoy stocks in the face of growing calls for an earnings recession, these assurances should be taken with a grain of salt).

During a Monday appearance on Fox News, Kellyanne Conway insisted that Trump “wants to meet with Xi very soon” and that “this president wants a deal.“

“He has forged a mutually respectful relationship with President Xi,” Conway said. “They will meet again soon.”

And it would appear the Chinese, already struggling with sagging domestic markets and a softening economy, want the same thing. With negotiators meeting again this week in Beijing, it’s unclear exactly how much progress has been made. According to Bloomberg, the two sides have only just started the work of drafting a common document and are still negotiating over how a deal may be enforced – which has long been touted as a crucial factor for US officials. The US is also pressuring China to commit to more substantive reforms to its state-driven economic system, which Trump has argued disadvantages American companies trying to compete in China’s domestic market.

Because so much uncertainty remains, Trump’s aides have privately acknowledged that the most likely outcome, at this point, is that the March 1 deadline will be extended (an outcome that Wall Street strategists have identified as the best possible scenario for markets, given that a comprehensive deal remains extremely unlikely). It’s still possible that Trump and Xi might meet at Mar-a-Lago next month, Conway said.

The bigger question, at this point, is whether the Chinese will agree to a new hard deadline, because US officials are “keen for any extension not to be open-ended.”