GOLD: $1319.60 DOWN $6.80 (COMEX TO COMEX CLOSING)

Silver: $15.73 DOWN 14 CENTS (COMEX TO COMEX CLOSING)

Closing access prices:

Gold : 1319.75

silver: $15.74

/LBMA options will expire on Thursday, the 28th of February..

Expect extreme volatility until first day notice.

For comex gold and silver:

FEBRUARY

NUMBER OF NOTICES FILED TODAY FOR FEB CONTRACT: 152 NOTICE(S) FOR 15200 OZ (0.4727 tonnes)

TOTAL NUMBER OF NOTICES FILED SO FAR: 12,352 NOTICES FOR 1,235,200 OZ (38.419TONNES)

SILVER

FOR FEBRUARY

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

19 NOTICE(S) FILED TODAY FOR 95,000 OZ/

total number of notices filed so far this month: 591 for 2,955,000

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

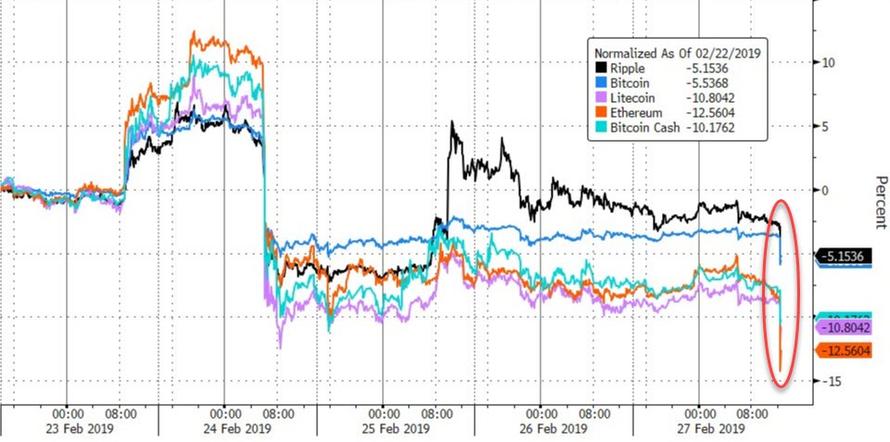

Bitcoin: OPENING MORNING TRADE $3820:UP $10

Bitcoin: FINAL EVENING TRADE: $3803 DOWN 77

end

XXXX

JPMorgan or Goldman Sachs are taking a huge issuance (stopping) of gold at the comex.

today 100/152

EXCHANGE: COMEX

CONTRACT: FEBRUARY 2019 COMEX 100 GOLD FUTURES

SETTLEMENT: 1,325.100000000 USD

INTENT DATE: 02/26/2019 DELIVERY DATE: 02/28/2019

FIRM ORG FIRM NAME ISSUED STOPPED

____________________________________________________________________________________________

661 C JP MORGAN 59

661 H JP MORGAN 100

737 C ADVANTAGE 53

880 H CITIGROUP 40

991 H CME 52

____________________________________________________________________________________________

TOTAL: 152 152

MONTH TO DATE: 12,352

Let us have a look at the data for today

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

In silver, the total OPEN INTEREST FELL BY A HUGE SIZED 7899 CONTRACTS FROM 214,346 DOWN TO 206,447 DESPITE YESTERDAY’S TINY 1 CENT LOSS IN SILVER PRICING AT THE COMEX. TODAY WE ARRIVED FURTHER FROM AUGUST’S 2018 RECORD SETTING OPEN INTEREST OF 244,196 CONTRACTS. WE ALWAYS WITNESS A CONTRACTION IN TOTAL OI AS WE APPROACH FIRST DAY NOTICE AND IT SEEMS THE CULPRIT IS THE FORCED LIQUIDATION OF SPREADERS.

WE HAVE ALSO WITNESSED A LARGE AMOUNT OF PHYSICAL METAL STAND FOR COMEX DELIVERY AS WELL WE ARE WITNESSING CONSIDERABLE LONGS PACKING THEIR BAGS AND MIGRATING OVER TO LONDON IN GREATER NUMBERS IN THE FORM OF EFP’S. WE WERE NOTIFIED THAT WE HAD A SMALL SIZED NUMBER OF COMEX LONGS TRANSFERRING THEIR CONTRACTS TO LONDON THROUGH THE EFP:

250 EFP’S FOR MARCH, 0 FOR APRIL, 450 FOR MAY, 0 FOR DECEMBER AND ZERO FOR ALL OTHER MONTHS AND THEREFORE TOTAL ISSUANCE: OF 730 CONTRACTS. WITH THE TRANSFER OF 730 CONTRACTS, WHAT THE CME IS STATING IS THAT THERE IS NO SILVER (OR GOLD) TO BE DELIVERED UPON AT THE COMEX AS THEY MUST EXPORT THEIR OBLIGATION TO LONDON. ALSO KEEP IN MIND THAT THERE CAN BE A DELAY OF 24-48 HRS IN THE ISSUING OF EFP’S. THE 730 EFP CONTRACTS TRANSLATES INTO 3.6510MILLION OZ ACCOMPANYING:

1.THE 1 CENT LOSS IN SILVER PRICE AT THE COMEX AND

2. THE STRONG AMOUNT OF SILVER OUNCES WHICH STOOD FOR DELIVERY IN THE LAST NINE MONTHS:

JUNE/2018. (5.420 MILLION OZ);

FOR JULY: 30.370 MILLION OZ

FOR AUG., 6.065 MILLION OZ

FOR SEPT. 39.505 MILLION OZ S

FOR OCT.2.525 MILLION OZ.

FOR NOV: A HUGE 7.440 MILLION OZ STANDING AND

21.925 MILLION OZ FINALLY STAND FOR DECEMBER.

5.845 MILLION OZ STAND IN JANUARY.

AND NOW 2.860 MILLION OZ STANDING FOR FEBRUARY.

ACCUMULATION FOR EFP’S/SILVER/J.P.MORGAN’S HOUSE OF BRIBES, / STARTING FROM FIRST DAY NOTICE/FOR MONTH OF FEBRUARY: 26,637 CONTRACTS (FOR 18 TRADING DAYS TOTAL 26,637 CONTRACTS) OR 133.185 MILLION OZ: (AVERAGE PER DAY: 1479 CONTRACTS OR 7.399 MILLION OZ/DAY)

TO GIVE YOU AN IDEA AS TO THE HUGE SUPPLY THIS MONTH IN SILVER: SO FAR THIS MONTH OF FEB: 133.185 MILLION PAPER OZ HAVE MORPHED OVER TO LONDON. THIS REPRESENTS AROUND 19.00% OF ANNUAL GLOBAL PRODUCTION (EX CHINA EX RUSSIA)* JUNE’S 345.43 MILLION OZ IS THE SECOND HIGHEST RECORDED ISSUANCE OF EFP’S AND IT FOLLOWED THE RECORD SET IN APRIL 2018 OF 385.75 MILLION OZ.

ACCUMULATION IN YEAR 2019 TO DATE SILVER EFP’S: 338.20 MILLION OZ. (CORRECTED)

JANUARY 2019 EFP TOTALS: 217.455. MILLION OZ.

RESULT: WE HAD A HUGE SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 7899 WITH THE 1 CENT LOSS IN SILVER PRICING AT THE COMEX /YESTERDAY..THE CME NOTIFIED US THAT WE HAD SMALL SIZED EFP ISSUANCE OF 730 CONTRACTS WHICH EXITED OUT OF THE SILVER COMEX AND TRANSFERRED THEIR OI TO LONDON AS FORWARDS. SPECULATORS CONTINUED THEIR INTEREST IN ATTACKING THE SILVER COMEX FOR PHYSICAL SILVER (SEE COMEX DATA) .

TODAY WE LOST A CONSIDERABLE SIZED: 7169 TOTAL OI CONTRACTS ON THE TWO EXCHANGES:

i.e 730 OPEN INTEREST CONTRACTS HEADED FOR LONDON (EFP’s) TOGETHER WITH DECREASE OF 7899 OI COMEX CONTRACTS. AND ALL OF THIS DEMAND HAPPENED WITH A 1 CENT LOSS IN PRICE OF SILVER AND A CLOSING PRICE OF $15.87 WITH RESPECT TO YESTERDAY’S TRADING. YET WE HAD A GIGANTIC AMOUNT OF SILVER STANDING AT THE COMEX FOR DELIVERY

In ounces AT THE COMEX, the OI is still represented by JUST OVER 1 BILLION oz i.e. 1.099 BILLION OZ TO BE EXACT or 157% of annual global silver production (ex Russia & ex China).

FOR THE NEW FRONT FEBRUARY MONTH/ THEY FILED AT THE COMEX: 19 NOTICE(S) FOR 95,000 OZ OF SILVER

IN SILVER,PRIOR TO TODAY, WE SET THE NEW COMEX RECORD OF OPEN INTEREST AT 243,411 CONTRACTS ON APRIL 9.2018. AND AGAIN THIS HAS BEEN SET WITH A LOW PRICE OF $16.51.

AND NOW WE RECORD FOR POSTERITY ANOTHER ALL TIME RECORD OPEN INTEREST AT THE COMEX OF 244,196 CONTRACTS ON AUGUST 22/2018 AND AGAIN WHEN THIS RECORD WAS SET, THE PRICE OF SILVER WAS $14.78 AND LOWER IN PRICE THAN PREVIOUS RECORDS.

ON THE DEMAND SIDE WE HAVE THE FOLLOWING:

- HUGE AMOUNTS OF SILVER STANDING FOR DELIVERY (MARCH/2018: 27 MILLION OZ , APRIL/2018 : 2.485 MILLION OZ MAY: 36.285 MILLION OZ ; JUNE/2018 (5.420 MILLION OZ) , JULY 2018 FINAL AMOUNT STANDING: 30.370 MILLION OZ ) FOR AUGUST 6.065 MILLION OZ. , SEPT: A HUGE 39.505 MILLION OZ./ OCTOBER: 2,520,000 oz NOV AT 7.440 MILLION OZ./ DEC. AT 21.925 MILLION OZ JANUARY AT 5.825 MILLION OZ.AND NOW FEB 2019: 2.860 MILLION OZ/

- HUGE RECORD OPEN INTEREST IN SILVER 243,411 CONTRACTS (OR 1.217 BILLION OZ/ SET APRIL 9/2018) AND NOW AUGUST 22/2018: 244,196 CONTRACTS, WITH A SILVER PRICE OF $14.78.

- HUGE ANNUAL EFP’S ISSUANCE EQUAL TO 2.9 BILLION OZ OR 400% OF SILVER ANNUAL PRODUCTION/2017

- RECORD SETTING EFP ISSUANCE FOR ANY MONTH IN SILVER; APRIL/2018/ 385.75 MILLION OZ/ AND THE SECOND HIGHEST RECORDED EFP ISSUANCE JUNE 2018 345.43 MILLION OZ

AND YET, WITH THE EXTREMELY HIGH EFP ISSUANCE, WE HAVE A CONTINUAL LOW PRICE OF SILVER DESPITE THE ABOVE HUGE DEMAND. TO ME THE ONLY ANSWER IS THAT WE HAVE SOVEREIGN (CHINA) WHO IS ENDEAVOURING TO GOBBLE UP ALL AVAILABLE PHYSICAL SILVER NO MATTER WHERE, EXACTLY WHAT J.P.MORGAN IS DOING. AND IT IS MY BELIEF THAT J.P.MORGAN IS HOLDING ITS SILVER FOR ITS BENEFICIAL OWNER..THE USA GOVERNMENT WHO IN TURN IS HOLDING THAT SILVER FOR CHINA.(FOR A SILVER LOAN REPAYMENT).

IN GOLD, THE OPEN INTEREST ROSE BY A CONSIDERABLE SIZED 3695 CONTRACTS UP TO 502,543 DESPITE THE FALL IN THE COMEX GOLD PRICE/(A LOSS IN PRICE OF $1.10//YESTERDAY’S TRADING).

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A GOOD SIZED 4593 CONTRACTS:

MARCH HAD AN ISSUANCE OF 0 CONTACTS APRIL 4593 CONTRACTS,JUNE: 0 CONTRACTS DECEMBER: 0 CONTRACTS AND ALL OTHER MONTHS ZERO. The NEW COMEX OI for the gold complex rests at 501,286. ALSO REMEMBER THAT THERE WILL BE A DELAY IN THE ISSUANCE OF EFP’S. THE BANKERS REMOVE LONG POSITIONS OF COMEX GOLD IMMEDIATELY. THEN THEY ORCHESTRATE THEIR PRIVATE EFP DEAL WITH THE LONGS AND THAT COULD TAKE AN ADDITIONAL, 48 HRS SO WE GENERALLY DO NOT GET A MATCH WITH RESPECT TO DEPARTING COMEX LONGS AND NEW EFP LONG TRANSFERS. . EVEN THOUGH THE BANKERS ISSUED THESE MONSTROUS EFPS, THE OBLIGATION STILL RESTS WITH THE BANKERS TO SUPPLY METAL BUT IT TRANSFERS THE RISK TO A LONDON BANKER OBLIGATION AND NOT A NEW YORK COMEX OBLIGATION. LONGS RECEIVE A FIAT BONUS TOGETHER WITH A LONG LONDON FORWARD. THUS, BY THESE ACTIONS, THE BANKERS AT THE COMEX HAVE JUST STATED THAT THEY HAVE NO APPRECIABLE METAL!! THIS IS A MASSIVE FRAUD: THEY CANNOT SUPPLY ANY METAL TO OUR COMEX LONGS BUT THEY ARE QUITE WILLING TO SUPPLY MASSIVE NON BACKED GOLD (AND SILVER) PAPER KNOWING THAT THEY HAVE NO METAL TO SATISFY OUR LONGS. LONDON IS NOW SEVERELY BACKWARD IN BOTH GOLD AND SILVER AND WE ARE WITNESSING DELAYS IN ACTUAL DELIVERIES.

IN ESSENCE WE HAVE A STRONG SIZED GAIN IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 8286 CONTRACTS: 3695 OI CONTRACTS INCREASED AT THE COMEX AND 4593 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN 8286 CONTRACTS OR 828,600 = 25.77 TONNES. AND ALL OF THIS DEMAND OCCURRED WITH A LOSS IN THE PRICE OF GOLD/ YESTERDAY TO THE TUNE OF $1.10.

YESTERDAY, WE HAD 3323 EFP’S ISSUED.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF FEBRUARY : 100,661 CONTRACTS OR 10,055100 OZ OR 313.09 TONNES (18 TRADING DAYS AND THUS AVERAGING: 5,592 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE STRONG SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 18 TRADING DAYS IN TONNES: 313.09 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2018, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 2555 TONNES

THUS EFP TRANSFERS REPRESENTS 313.09/2550 x 100% TONNES = 12.277% OF GLOBAL ANNUAL PRODUCTION SO FAR IN DECEMBER ALONE.***

ACCUMULATION OF GOLD EFP’S YEAR 2019 TO DATE: 832.16 TONNES

JANUARY 2019 TOTAL EFP ISSUANCE; 531.20 TONNES

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

Result: A CONSIDERABLE SIZED INCREASE IN OI AT THE COMEX OF 3695 DESPITE THE LOSS IN PRICING ($1.10) THAT GOLD UNDERTOOK YESTERDAY) //.WE ALSO HAD A CONSIDERABLE SIZED NUMBER OF COMEX LONG TRANSFERRING TO LONDON THROUGH THE EFP ROUTE: 4593 CONTRACTS AS THESE HAVE ALREADY BEEN NEGOTIATED AND CONFIRMED. THERE OBVIOUSLY DOES NOT SEEM TO BE MUCH PHYSICAL GOLD AT THE COMEX. I GUESS IT EXPLAINS THE HUGE ISSUANCE OF EFP’S…THERE IS HARDLY ANY GOLD PRESENT AT THE GOLD COMEX FOR DELIVERY PURPOSES. IF YOU TAKE INTO ACCOUNT THE 4593 EFP CONTRACTS ISSUED, WE HAD A STRONG GAIN OF 9563 CONTRACTS IN TOTAL OPEN INTEREST ON THE TWO EXCHANGES:

4593 CONTRACTS MOVE TO LONDON AND 3695 CONTRACTS INCREASED AT THE COMEX. (IN TONNES, THE GAIN IN TOTAL OI EQUATES TO 25.77TONNES). ..AND ALL OF THIS DEMAND OCCURRED WITH THE LOSS OF $1.10 IN YESTERDAY’S TRADING AT THE COMEX??

we had: 152 notice(s) filed upon for 15200 oz of gold at the comex.

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

With respect to our two criminal funds, the GLD and the SLV:

GLD...

WITH GOLD DOWN $6.80 TODAY

NO CHANGES IN INVENTORY AT THE GLD:

/GLD INVENTORY 788.33 TONNES

Inventory rests tonight: 788.31 tonnes.

TO ALL INVESTORS THINKING OF BUYING GOLD THROUGH THE GLD ROUTE: YOU ARE MAKING A TERRIBLE MISTAKE AS THE CROOKS ARE USING WHATEVER GOLD COMES IN TO ATTACK BY SELLING THAT GOLD. IT SURE SEEMS TO ME THAT THE GOLD OBLIGATIONS AT THE GLD EXCEED THEIR INVENTORY

SLV/

WITH SILVER DOWN 14 CENTS IN PRICE TODAY:

NO CHANGE IN SILVER INVENTORY AT THE SLV..///

/INVENTORY RESTS AT 309.374 MILLION OZ.

end

First, here is an outline of what will be discussed tonight:

1. Today, we had the open interest in SILVER FELL BY A HUGE SIZED 7899 CONTRACTS from 214,346 DOWN TO 206447 AND FURTHER FROM THE NEW COMEX RECORD SET LAST IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 1 1/3 YEARS AGO. THE PRICE OF SILVER ON THAT DAY: $17.89. AS YOU CAN SEE, WE HAVE RECORD HIGH OPEN INTERESTS IN SILVER ACCOMPANIED BY A CONTINUAL LOWER PRICE WHEN THAT RECORD WAS SET…..

.

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

250 CONTRACTS FOR MARCH. 0 CONTRACTS FOR APRIL., 450 FOR MAY AND AND ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 730 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE OI LOSS AT THE COMEX OF 7899 CONTRACTS TO THE 730 OI TRANSFERRED TO LONDON THROUGH EFP’S, WE OBTAIN A LOSS OF 7169 OPEN INTEREST CONTRACTS. THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES: 35.85 MILLION OZ!!! AND YET WE ALSO HAVE A STRONG DEMAND FOR PHYSICAL AS WE WITNESSED A FINAL STANDING OF GREATER THAN 30 MILLION OZ FOR JULY, A STRONG 6.065 MILLION OZ FOR AUGUST.. A HUGE 39.505 MILLION OZ STANDING FOR SILVER IN SEPTEMBER… OVER 2 million OZ STANDING FOR THE NON ACTIVE MONTH OF OCTOBER., 7.440 MILLION OZ FINALLY STANDING IN NOVEMBER. 21.925 MILLION OZ STANDING IN DECEMBER , 5.845 MILLION OZ STANDING IN JANUARY..AND NOW 2.955 MILLION OZ STANDING IN FEBRUARY.

RESULT: A FAIR SIZED DECREASE IN SILVER OI AT THE COMEX WITH THE 1 CENT LOSS IN PRICING THAT SILVER UNDERTOOK IN PRICING// YESTERDAY.BUT WE ALSO HAD A FAIR SIZED 730 EFP’S ISSUED TRANSFERRING COMEX LONGS OVER TO LONDON. THE LOSS IN OPEN INTEREST CONTRACTS IN SILVER WAS CAUSED BY THE FORCED LIQUIDATION OF SPREADERS…IT HAD NO EFFECT ON PRICE..TOGETHER WITH THE STRONG SIZED AMOUNT OF SILVER OUNCES STANDING FOR SEPTEMBER, DEMAND FOR PHYSICAL SILVER CONTINUES TO INTENSIFY AS WE WITNESS SEVERE BACKWARDATION IN SILVER IN LONDON.

(report Harvey)

.

2.a) The Shanghai and London gold fix report

(Harvey)

2 b) Gold/silver trading overnight Europe, Goldcore

(Mark O’Byrne/zerohedge

and in NY: Bloomberg

3. ASIAN AFFAIRS

i)WEDNESDAY MORNING/ TUESDAY NIGHT:

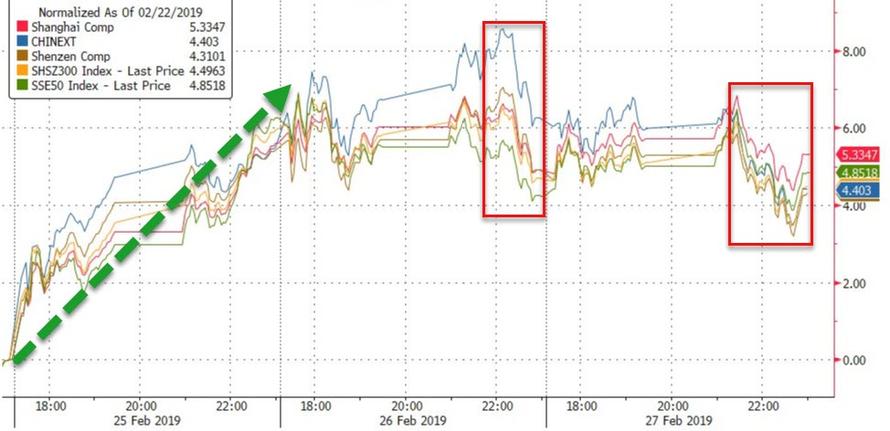

SHANGHAI CLOSED UP 12.31 POINTS OR 0.42% //Hang Sang CLOSED DOWN 14.42 POINTS OR 0.05% /The Nikkei closed UP 107.12 POINTS OR 0.50%/ Australia’s all ordinaires CLOSED UP 0.40%

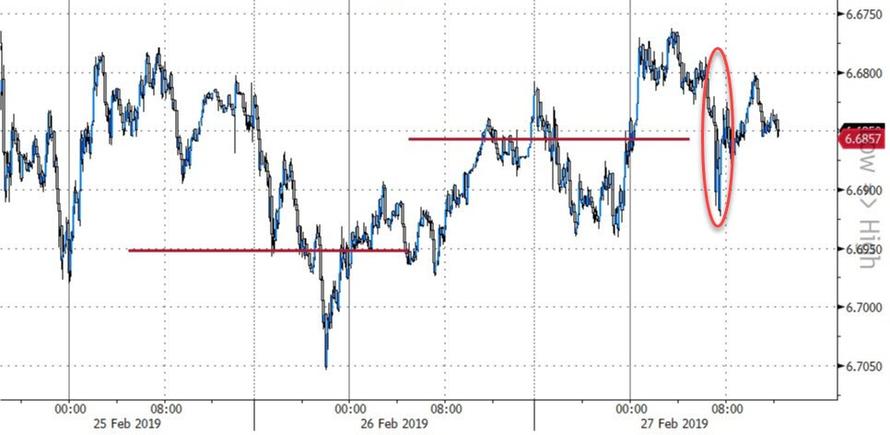

/Chinese yuan (ONSHORE) closed UP at 6.6786 AS TRUCE DECLARED FOR 3 MONTHS /Oil DOWN to 55.56 dollars per barrel for WTI and 66.00 for Brent. Stocks in Europe OPENED GREEN//.

ONSHORE YUAN CLOSED UP // LAST AT 6.6786 AGAINST THE DOLLAR. OFFSHORE YUAN CLOSED UP ON THE DOLLAR AT 6.6781: / TRADE TALKS NOW ON/MAJOR PROBLEMS AT HUAWEI /CFO ARRESTED : /ONSHORE YUAN TRADING BELOW LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST USA DOLLAR/OFFSHORE YUAN TRADING STRONGER AGAINST THE DOLLAR /CHINA RETALIATES WITH TARIFFS/ TRUMP RESPONDS TO NEW TARIFFS AND IT NOW A FULL TRADE WAR COMMENCED

3A/NORTH KOREA/SOUTH KOREA

i)North Korea//USA

b) REPORT ON JAPAN

3 C/ CHINA

i) CHINA/

Wolf Richter describes the huge plunge in imports coming from China and the emerging nations..the most since 2008. )He explains that this is the steepest two month plunge in 11 years). This portends danger to the world’s economic growth

( Wolf Richter/WolfStreet)

ii)Huawei chairman mocks the USA “security threat” as the USA is doing the same

( zerohedge)

4/EUROPEAN AFFAIRS

i)UK

UK banks Hezbollah and other terrorist organizations

( Sara Carter)_

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

DUBAI/UAE

Properties values are imploding in that mecca paradise of Dubai

( zerohedge)

6. GLOBAL ISSUES

Pakistan shoots down 2 Indian fighters jets

( zerohedge)

7. OIL ISSUES

8 EMERGING MARKET ISSUES

i)VENEZUELA/

9. PHYSICAL MARKETS

c)Goldberg is probably correct: Barrick’s move to takeover Newmont is a desperate move:

( Hammond/Bloomberg)

d)Simon Black believes that the Barrick deal means a rise in the price of gold

He explains why.

( Simon Black/SovereignMan)

10. USA stories which will influence the price of gold/silver)

MARKET TRADING

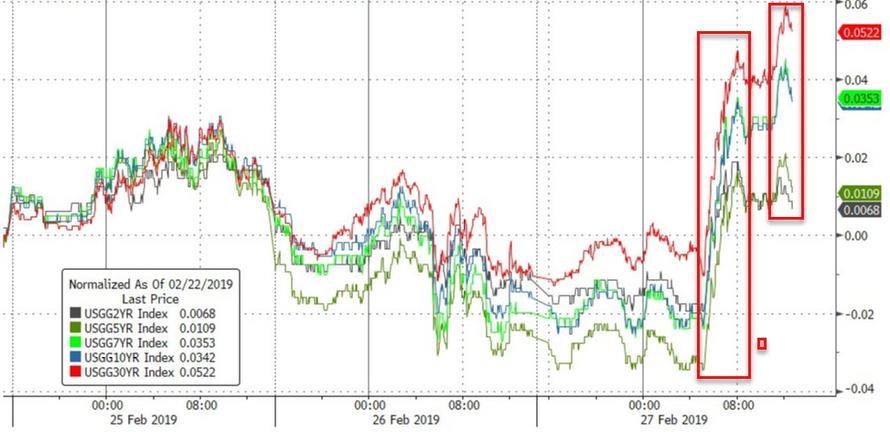

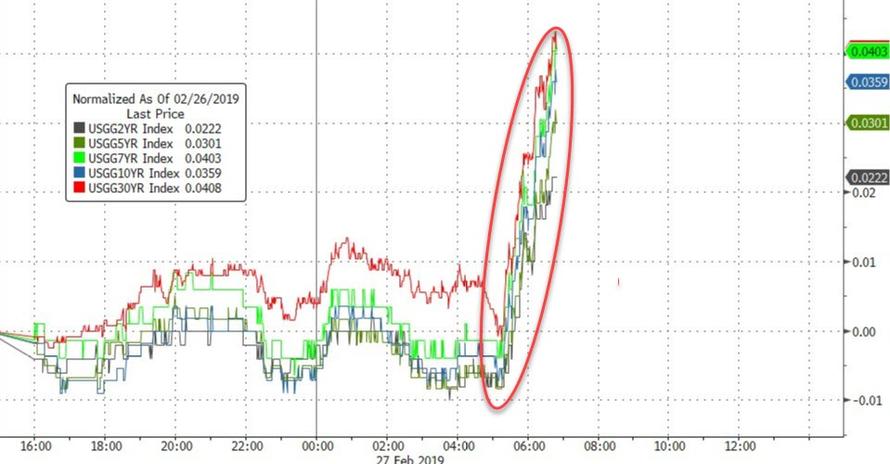

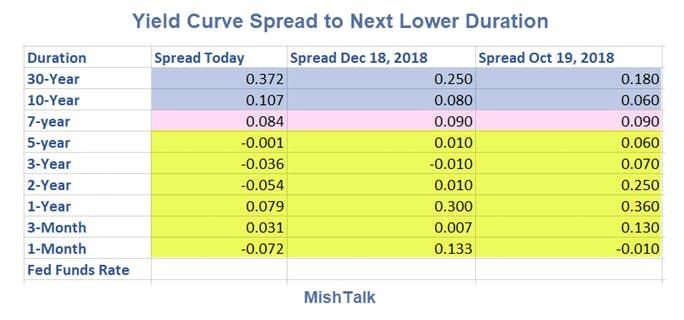

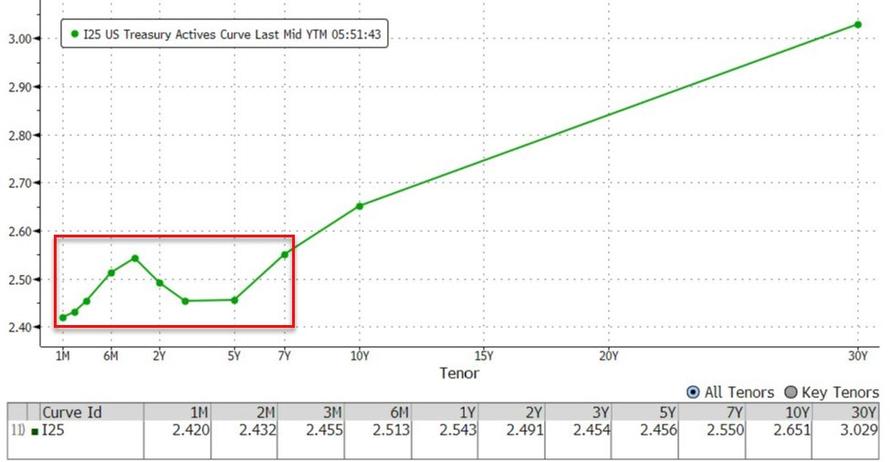

a)Suddenly, the 10 yr treasury yield rises by a huge 4 basis points coupled with a loss on USA markets..not good!

(zerohedge)

b)Signals getting louder and louder: the 5 year inverts with the 3 month yield…funny looking yield curve

ii)Market data

a)WOW!!! The USA trade deficit widened to a whopping 79.5 billion dollars from November’s 70.5 billion. Exports fell 2.8% which is bad and imports rose 2.4%. Not very good. Does not seem that Trump is winning this battle.

( zerohedge)

b)USA pending home sales tumble for the 13th consecutive month

(courtesy zerohedge)-

iv)SWAMP STORIES

Cohen states that Trump is a racist, a conman and a cheat…

(zerohedge)

end

Let us head over to the comex:

THE NEXT NON ACTIVE DELIVERY MONTH AFTER FEBRUARY IS THE VERY BIG AND ACTIVE DELIVERY MONTH OF MARCH AND HERE THE OI FELL BY 14,419 CONTRACTS DOWN TO 15,317 CONTRACTS. AFTER MARCH, APRIL ADVANCES TO 662 CONTRACTS FOR A GAIN OF 86 CONTRACTS. AFTER APRIL, THE NEXT BIG ACTIVE DELIVERY MONTH IS MAY AND HERE THE OI ADVANCED BY 2252 CONTRACTS UP TO 143291 CONTRACTS.

FIRST DAY NOTICE IS THURSDAY FEB 28.2019

comex gold volumes are getting extremely low as players just do not want to play in this casino.

i

MMT: Modern Monetary Madness Will Lead To Higher Taxes and Inflation

– Can this really be a thing? Actually printing money as an economic policy?

– Begin structuring portfolios and lives to avoid being in a tunnel with an oncoming train

by John Mauldin via Mauldin Economics

More than 10 years ago some Australian readers begin regaling me with the ideas of economist Bill Mitchell of the University of Newcastle in New South Wales. He was teaching about something he called (and he coined the term) Modern Monetary Theory. I looked into it and fairly quickly dismissed it as silly.

Actually printing money as an economic policy? Get serious.

MMT is a revival of an early 1900s idea called chartalism. Now it is influencing the thinking of new socialist-like movements in the US and other places and cited by politicians. MMT is increasingly appearing in mainstream media like this sobering Financial Times article.

Since it is increasingly discussed in more public venues, you should know more about it and that will be today’s topic.

Modern Monetary Madness

Essentially, MMT espouses that the public through the government owns the process of money creation, and that in addition to borrowing and taxing, should simply issue currency as payment for its obligations. This is not the sleight-of-hand that quantitative easing was. This is direct monetization in lieu of borrowing.

If that sounds like printing money, that’s because it is. Upfront and in-your-face as a serious economic proposal. Most of the time when I am talking with my fellow writers and economists, when somebody mentions MMT, everybody smiles, maybe chuckles, and shakes their heads. The problem is, what seems like a joke is actually getting traction.

Let’s get the official definition of MMT from Wikipedia. My comments inserted are in brackets.

In MMT, “vertical” money (money created by the government and spent in the private sector) enters circulation through government spending. Taxation and its legal tender enable power to discharge debt and establish the fiat money as currency, giving it value by creating demand for it in the form of a private tax obligation that must be met. [And thus higher taxes create more demand for the currency and help to maintain the value thereof.]

In addition, fines, fees and licenses create demand for the currency. An ongoing tax obligation, in concert with private confidence and acceptance of the currency, maintains its value. Because the government can issue its own currency at will, MMT maintains that the level of taxation relative to government spending (the government’s deficit spending or budget surplus) is in reality a policy tool that regulates inflation and unemployment, and not a means of funding the government’s activities by itself. [The more you want the government to spend, the higher the taxes have to be in order to keep from creating inflation, or so the theory goes.]

Proponents argue that unemployment is caused by lack of demand and lack of demand is caused by insufficient money entering the private sector, a problem the government can solve by creating money and spending it in the private sector. Voilà, demand is created and unemployment goes down. Inflation? That can be controlled by higher taxes. Hey, it’s their theory. Don’t ask me to explain it.

Economists advising major presidential and congressional candidates on the progressive and even “moderate” left are more and more openly talking about MMT and its practical applications.

Free Registration (including Research Reports) for 2019 Gold Summit here

Pet Economists

I have said before that economists are the modern-day equivalent of shamans and priests. Rather than looking at sheep entrails, economists look at “data” and tell the politician (king, emperor, or chief…) what they want to hear. I have been in more than one meeting where a politician is clearly shopping for a rationale for something that they would like to propose and do. Any serious politician is going to have more than a few economic advisors attached in one form or another to their campaign.

Let me quickly state that I am not disparaging the role of economists when they act as political advisors. I have done that myself. It is actually one of the rationales for the discipline. Indeed, it would be strange if that were not the case.

Can This Really Be a Thing?

90% of readers may wonder why we are even talking about this in a serious letter. The rest of you may tell me how I’m wrong and it really will work. Let me hasten to say that 10 years ago it was much less than 1%. And it is beginning to come from readers that I recognize to be fairly serious.

There are multiple and growing motivations and rationales for adopting MMT into your own philosophical base.

Why should this be on your radar? Let me give you just a few scenarios…

Politicians are increasingly talking about “free stuff.” Free college, guaranteed basic income, more total healthcare paid for by the public, basic housing, and more. It is almost like there will be an auction to see who can promise the most free benefits, paid for by taxes on the rich. They will cite economic advisors who say it is completely doable and even necessary for the general welfare.

“The richest country in the history of rich countries can easily afford to spend more on its citizens ensuring basic income and wealth equality.” More or less a direct quote from several interviews. Forget mere income taxes. The new political ante will be a wealth tax.

That means these ideas will be increasingly promoted in the public space. More politicians will argue for increased spending and/or at least different spending priorities. Guns and butter.

Over the next few years this will enter the national mindset. An increasingly large group of voters, especially younger voters, will feel a natural affinity with the idealism. Why shouldn’t a rich nation help those who are less advantaged?

Then somewhere, while we are having this conversation, there will be a recession. Unemployment will rise and deficits increase until we are on our way to a $30-trillion debt in just a few years. This will crowd out private investment, slowing whatever recovery there might be and making us vulnerable to a quick second recession, not unlike the recessions of 1980 and 1982.

But it will also produce the potential for a true “change” election. The frustration noted among Trump voters will still be there, but it will also be shared by many on the left who will see the promises as a way to change things. It is hard to argue in the middle of financial crisis and recession that we don’t need change.

There won’t be a President Warren Harding who essentially decided to do nothing in one of the deepest recessions/depressions in American history in the early 1920s. In that case, severe austerity allowed markets to clear but the recovery gave us the Roaring 1920s. Cause and effect? Numerous scholarly books have been written to suggest that.

But that will not be the case 100 years later as we face the 2020s. There will be an increasing drumbeat for “doing something.” Change will be the mantra.

It is not far-fetched to imagine a White House and Congress beginning to work around the principles of MMT, if not adopt it outright with sharply higher taxes and spending.

Now here’s where it gets a little bit murkier. The Federal Reserve, even if a new president could pack the board with members philosophically attuned to a new president’s desire to increase public spending through monetary creation, does not have the legal authority to directly create money. That is a right reserved strictly for the federal government and specifically the US Treasury. The Treasury can issue all the debt into the private sector it wants. The Federal Reserve can then go into the private market and buy all the debt it wants, adding that debt to its balance sheet. This is called quantitative easing. It is technically not the same thing.

Congress has tried to create agencies which would use the Federal Reserve to directly create money. These agencies and methods have all been ruled overwhelmingly unconstitutional by the Supreme Court. For the Federal Reserve to create money as MMT advocates want, you would have to amend the Federal Reserve Act. Certainly a possibility, but not easy.

Sound Bite Economics

Proponents of MMT point to how successful Japan has been in implementing what essentially looks to be the same policy. They have moved 140% of their GDP under the balance sheet of the Bank of Japan—essentially buying every bond available in the private markets. Their balance sheet is growing because they are buying stocks and carrying Japan’s entire annual deficit, which is large.

Why can’t we do the same? Japan and the US are both modern countries and economies. Europe, though not to the extent of Japan, also engaged in a large amount of quantitative easing. If it didn’t cause problems the last time, why not try it again on a larger scale? Especially if there is a crisis?

The explanation for Japan not having inflation or hyperinflation doesn’t fit into a sound bite and MMT proponents can answer it with dismissive sound bites that will be readily consumed and believed by a public wanting change, coupled with automation increasingly taking jobs and depressing wages. It will be a firestorm of political backlash and calls for change.

Do Deficits Matter?

The only way to really tackle the increasing deficits is to:

- Reduce Medicare and Medicaid benefits, means-test Social Security and at the same time raise the age of eligibility. But few politicians will run on a platform of cutting Medicare and Social Security, because no matter how they propose it, that will be what it means.

- Raise Medicare and Social Security taxes, or simply increase taxes on everyone or at least “the rich.” A lot. The definition of “the rich” would have to be lower than you might think. Most of my readers will be seen as the rich. Whether you feel rich is beside the point. That will still not balance the budget but there’s a high probability that it will send us into yet another recession, bringing calls for more direct spending and some form of money creation as the answer. That’s what MMT says we should do.

Any politician who proposes to limit entitlement spending to balance the budget will be accused of forcing austerity on those least able to afford it. That is not a winning platform. There will be no Clinton/Gingrich compromise. Austerity has no fun and simple sound bites. It requires a certain amount of pain, which is generally not politically popular.

Oh, a segment of the population will embrace such, but we must remember that elections are won on the margin. President Trump won by razor-thin margins in a few Midwest states. A change election in the middle of a recession or its aftermath could not only see those margins evaporate, but bring a wave of progressive and socialist politicians to join AOC and her friends.

Think 1932. The country was in true turmoil and there was a huge shift to the left. FDR didn’t get every policy he wanted, but he got a lot of them. It was truly transformational and has impacted the US for the last 100 years.

What would this look like? How do we get there? We are going to have several sessions at the Strategic Investment Conference to specifically address these issues. Is all this going to happen next year? No, but something along the above line is my base case for the 1920s. That means you need to begin structuring your life and your portfolios to avoid being in a tunnel with an oncoming train.

These are not simple changes, like simple buy and sell instructions, but will require much deeper structural change in not just your portfolios but perhaps your lives. It is something you want to think very seriously about while you have the luxury of time and not wait to the last minute. Waiting too long may mean you won’t be as prepared as you will wish.

Think about how you would deal with taxes 20 or 30% higher (or more!) than today’s, and potentially more. How would that change your lifestyle? What can you do today to deal with whatever may come? It may mean adjusting your lifestyle, saving more and getting out of debt, which takes time. For most families these are not quick decisions. But I think they will become necessary ones, especially if the first wave of a change election happens in 2020. Bluntly, Shane and I have already begun our own changes.

If somehow there is eventually a change back to austerity? Or a crisis forces it? That will mean even more change you need to be prepared for. And unfortunately, it’s not clear what will happen. We will have to get much closer to the actual events and elections to get a feel for the way actual events may develop.

Gold and silver are resisting options expiration smashes, Turk says

Submitted by cpowell on Tue, 2019-02-26 00:54. Section: Daily Dispatches

7:55p ET Monday, February 25, 2019

Dear Friend of GATA and Gold:

GoldMoney founder and GATA consultant James Turk, interviewed today by King World News, says the monetary metals are fending off pretty well the usual smashes tied to options expiration.

“The central planners are having a hard time pushing gold and silver around as they have often done in the past,” Turk says. “That’s good news, but it looks like 2019 is a year in which the precious metals are going to face some very important tests, which I expect them to pass.”

The interview is excerpted at KWN here:

https://kingworldnews.com/james-turk-expect-rocket-launch-off-huge-gold-…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

Goldberg is probably correct: Barrick’s move to takeover Newmont is a desperate move:

(courtesy Hammond/Bloomberg)

Newmont CEO calls Barrick move ‘desperate’

Submitted by cpowell on Tue, 2019-02-26 02:29. Section: Daily Dispatches

By Ed Hammond

Bloomberg News

Sunday, February 24, 2019

The chief executive officer of Newmont Mining Corp. labeled a potential takeover attempt by rival gold miner Barrick Gold Corp. as a “desperate” and “bizarre” move aimed at complicating his company’s pending deal to acquire Goldcorp Inc.

In his first interview since Barrick confirmed Friday it has considered a bid for Newmont, Gary Goldberg said he is focused on completing the Goldcorp takeover and questioned whether Barrick’s management is equipped to run a combined Newmont-Barrick.

…

“They haven’t delivered,” Goldberg said.

“It’s a desperate and bizarre attempt to muddle up our deal,” he said, “And it’s certainly not the sort of behavior that will appeal to investors who want to invest in serious, well-run companies.” …

… For the remainder of the report:

https://www.bloomberg.com/news/articles/2019-02-25/newmont-ceo-calls-bar…

* * *

Help keep GATA going:

GATA is a civil rights and educational organization based in the United States and tax-exempt under the U.S. Internal Revenue Code. Its e-mail dispatches are free, and you can subscribe at:

To contribute to GATA, please visit:

end

Craig Hemke at Sprott Money: Gold and silver 2019 status report

Submitted by cpowell on Wed, 2019-02-27 03:56. Section: Daily Dispatches

10:55p ET Tuesday, February 26, 2019

Dear Friend of GATA and Gold:

Writing for Sprott Money, the TF Metals Report’s Craig Hemke predicts tonight that 2019 will be good for gold and silver but that the investment banks that control the monetary metals futures markets will not be dislodged, at least not as long as speculators seek exposure to the monetary metals by purchasing paper claims to imaginary metal.

Hemke’s analysis is headlined “Gold and Silver 2019 Status Report” and it’s posted at Sprott Money here:

https://www.sprottmoney.com/Blog/gold-and-silver-2019-status-report-crai…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

Do not pay any attention to this man

(courtesy Market Watch/GATA)

If gold doesn’t correlate as it should, how about inquiring why?

Submitted by cpowell on Tue, 2019-02-26 15:18. Section: Daily Dispatches

10:22a ET Tuesday, February 26, 2019

Dear Friend of GATA and Gold:

Financial letter writer Mark Hulbert never offers a good word about gold, which is fine, but then never offers a relevant one either. This practice has turned him into a mere propagandist.

In his essay today at MarketWatch, headlined “Why Gold Won’t Save Your Portfolio from Inflation’s Bite” —

https://www.marketwatch.com/story/why-gold-wont-save-your-portfolio-from…

— Hulbert notes that gold often fails to correlate with inflation, though it is widely supposed to. Indeed, gold’s underperformance of inflation in recent decades has been a major disparagement of the monetary metal.

…

But Hulbert fails to inquire into this anomaly, though possible explanations are obvious.

After all, even some mainstrem financial analysts now acknowledge that government’s official inflation metrics are constantly revised and rigged to underreport inflation. Does anyone who buys his own groceries or pays medical insurance premiums or taxes still believe that, as officials long have been proclaiming, there is no inflation?

And what about surreptitious intervention by government in the gold market? Hulbert hasn’t denied it but then he hasn’t ever mentioned it. Documentation and admissions of it abound —

http://www.gata.org/taxonomy/term/21

— but Hulbert never gets past the supposed sentiment of retail investors as the primary determinant of the gold price.

“For gold to justify its current price in terms of inflation,” Hulbert writes today, “the Consumer Price Index either needs to be 47 percent higher or gold needs to trade for $902.”

But what if the CPI itself is completely invalid? And what if central banks have surreptitiously supplied or underwritten vast amounts of imaginary “paper gold” in the futures markets?

Those questions invite financial journalism. Hulbert’s propaganda only deflects them.

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

US seeks halt in civil lawsuit accusing JP Morgan of manipulating metals market, citing criminal case

- The U.S. wants a federal judge to halt a civil lawsuit accusing J. P. Morgan of manipulating precious metals markets. The Justice Department cited an ongoing criminal case as its reason for the request.

- A former J. P. Morgan trader pleaded guilty in Connecticut last month to manipulation charges.

- In the guilty plea, the trader said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors.

CNBC.com

The Justice Department is asking a judge to put the brakes on a civil lawsuit against J. P. Morgan Chase, citing an ongoing probe into a “related criminal case” that involves alleged manipulation of precious metals markets.

The department wants a six-month postponement in the proceedings of the civil lawsuit, which was filed in 2015 by hedge fund manager Daniel Shak and two commodity traders. The government also says it could ask for a longer delay in the case, according to a court filing on Monday.

The move comes days after Shak’s lawyer, David Kovel, sought permission to reopen questioning of two former J. P. Morgan traders and the bank’s current global head of base and precious metals trading.

Kovel, in making the request with the Manhattan federal judge in the civil case, cited last month’s guilty plea by one of those former traders, John Edmonds, in federal court in Connecticut.

Edmonds admitted making bogus bids on precious metals contracts while working at the bank from 2009 to 2015.

Neither J. P. Morgan Chase nor Kovel’s clients have opposed the Justice Department’s request.

In arguing for a delay, the Justice Department said Shak’s lawsuit is “related” to Edmonds’ criminal case and that Edmonds has “pleaded guilty and acknowledged his own participation in such conduct, as well as that of other traders.”

“Edmonds awaits sentencing, but the broader investigation is ongoing,” the Justice Department said. The U.S. wants to delay the civil case “to protect the integrity of its ongoing criminal investigation,” it said.

J. P. Morgan did not respond to a request for comment by CNBC. Kovel declined to comment.

Tuesday night, after this story first was published, Judge Paul Engelmayer ordered the federal prosecutors to explain in detail by Monday why postponing proceedings in the civil lawsuit would not harm those involved, and why reopening questioning “would be detrimental to the Government’s ongoing criminal investigation.”

Englemayer also wrote that he regards Edmonds’ guilty plea “as potentially highly consequential” to the civil case.

In his guilty plea, the 36-year-old Edmonds said he had learned to make bogus trade orders from senior traders at the bank and that he used the strategy hundreds of times with the knowledge and consent of his immediate supervisors. He admitted to working with “unnamed co-conspirators” at J. P. Morgan, according to the Justice Department.

Kovel wants to question Edmonds again as well as Michael Nowak, the bank’s global head of base and precious metal trading, and former J. P. Morgan Chase Managing Director Robert Gottlieb. The three had previously answered questions under oath in the civil case.

Kovel said in court filings that Nowak was the immediate supervisor of Edmonds, while Gottlieb was Edmonds’ mentor.

In his prior deposition, Edmonds said that Gottlieb sat only a “couple feet” away from him for about five years, and that he was “somebody [he] looked up to in the business,” who helped guide and train him.

Nowak is described by Edmonds as his direct supervisor, with whom he would sometimes discuss trading strategies. Nowak was also the person responsible for overseeing the performance and risk of Edmonds’ portfolio, according to the deposition.

Edmonds also stated in his prior deposition that he would enter precious metals trades for both Nowak and Gottlieb, among others.

The civil lawsuit claims Shak and his fellow plaintiffs lost tens of millions of dollars as a result of actions by J. P. Morgan’s traders.

Federal judge tells traders they can combine cases accusing JP Morgan of rigging metals market

- Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

- Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

A group of traders from across the U.S. who allege that J. P. Morgan Chase manipulated precious metals markets for years are one step closer to bringing a class action suit against the nation’s largest bank.

Earlier this month, a federal judge said five separate lawsuits making similar allegations against the bank could be combined, potentially including thousands of people who traded in the precious metals market from Jan. 2009 through Dec. 2015.

Litigation in a separate civil case has been put on hold until at least May at the behest of the Justice Department, which is investigating a “related criminal case” that involves alleged market manipulation by precious metals traders at J. P. Morgan.

J. P. Morgan declined to comment on this story.

Judge John Koeltl of the Southern District of New York appointed the White Plains, N.Y., law firm Lowey Dannenberg as interim lead counsel for the proposed class action.

Vincent Briganti, a partner at the firm, filed the first suit seeking class action status in November on behalf of Dominick Cognata, a trader who alleges he suffered losses due to J.P. Morgan’s illegal trading conduct in the silver and gold futures and options markets.

That was after the federal court in Connecticut unsealed a criminal plea agreement by John Edmonds, a former J.P. Morgan metals trader. In his guilty plea, Edmonds, who is 36-years old, admitted that he and other “unnamed co-conspirators” fraudulently manipulated the precious metals markets while they were employed at J. P. Morgan from 2009 to 2015.

Edmonds said he had learned the illegal trading tactics from senior traders, and then used them hundreds of times with the knowledge of and consent of his immediate supervisors.

Briganti’s lawsuit also names John Edmonds and a group of yet-to-be-identified precious metals traders and the bank as defendants.

On Wednesday, the lawyers sent a letter to Judge Koeltl saying they were having difficulty locating Edmonds to serve him legal papers and requested a 30-day extension to do so, which the judge granted on Thursday. Briganti noted that they have been in contact with Edmonds’ attorney in the criminal case. Edmonds’ attorney and Briganti could not be reached for comment.

“We are hopeful that this extension will result in completing service on Mr. Edmonds without formal motion practice and a request for alternative means of service,” Briganti said in the letter.

The next step in the civil case is for the plaintiffs to file an amended class action complaint and set a schedule for defendants to respond.

In addition to the proposed class action, J. P. Morgan also faces a separate civil suit which also accuses the bank of rigging precious metals markets.

end

Simon Black believes that the Barrick deal means a rise in the price of gold

He explains why.

(courtesy Simon Black/SovereignMan)

Why The Barrick Deal Could Mean The Mega-Melt-Up Is Here For Gold

Authored by Simon Black via SovereignMan.com,

In 1986, Peter Munk bought a gold mine in northeastern Nevada for $62 million.

The mine was only producing 40,000 ounces of gold a year back then (around $16 million annually) … and the sellers believed the land held 600,000 ounces easily minable gold.

But those estimates were woefully short.

By 1992, the mine yielded 1.1 million ounces of gold. Today, the mine, known as Goldstrike, is the richest mine in North America – producing over two million ounces per year. And it has reserves of over 21 million ounces of gold.

Although the Goldstrike acquisition proved to be his best, Munk bought many other successful gold mines.

He was the founder of the world’s largest gold producer, Barrick Gold. And his company earned the top spot through deal making…

Before buying Goldstrike, Munk bought half the Renabie mine in Ontario… then the Camflo mine in Quebec.

But it was Barrick’s 2005 acquisition of Placer Dome that gave the company its title as the world’s largest gold producer and cemented its place at the top of the food chain.

It’s been over a decade since Barrick’s blockbuster deal. And the gold sector has gone quiet. Low prices for both the metal and mining stocks caused investors to completely ignore the sector.

But the commodities markets are cyclical… As our friend Rick Rule says, “the cure for low prices is low prices.”

And we’re starting to see signs of life.

We’ve been writing about a number of tailwinds for the yellow metal, including a lack of major discoveries, which we argued would lead to higher gold prices and frenzied takeover activity as gold demand increased.

Well, the gold price has increased from a 2018 low of $1,175 to $1,340 – a ten month high.

And we’ve started to see M&A (merger & acquisition) activity among the largest miners…

Barrick made headlines late last year when it announced it would acquire Randgold Resources in a $6 billion deal. It was a major sign of life in a sector that was left for dead.

Then, in January, another mining giant, Newmont, announced it would buy Goldcorp for $10 billion.

But last week, we got a sign that merger mania in the gold sector is officially on…

Barrick announced its intention to make its largest acquisition yet – a $17.8 billion deal for Newmont Mining.

Newmont rejected Barrick’s offer and intends to pursue its merger with Goldcorp. Barrick is turning its bid hostile.

And the miners are publicly trashing each other, with Barrick calling Newmont “desperate” and Newmont in turn calling Barrick “inferior.”

But despite the theatrics, this deal tells us one thing – the gold sector is gearing up for a spate of M&A activity.

We’re seeing the largest companies consolidate first. They’re merging to try to further cut redundant costs and bolster reserves (gold companies have been slashing costs for years to improve margins in a down market).

But these mergers don’t solve the problem of no major new gold discoveries in the past 15 years.

Next, we should see the gold giants start acquiring the junior mining companies. As the name implies, these companies are much smaller. And they raise equity capital to find new gold deposits. These juniors take the big risks to find new deposits. And the successful ones see their share prices soar or get acquired by a larger miner – or both.

It’s not just the economics of the gold sector that make an M&A boom likely. We saw record M&A activity across the board last year, as cheap money and record profits sent companies on a buying spree.

And we’ve got the same backdrop today. The Fed and other central banks around the world have already backed off their plans to tighten monetary policy.

We’re even seeing some very powerful people calling for negative interest rates in the US.

On its own, monetary easing (the continued destruction of fiat money) and record debt around the globe make gold an incredibly attractive asset class.

But in this, coming gold bull market… low rates and an excessive appetite for debt will also continue fueling the gold company merger frenzy.

The stage is being set for a mega melt-up in gold and gold stocks right now.

And we continue to be quite bullish on the sector.

And to continue learning how to ensure you thrive no matter what happens next in the world, I encourage you to download our free Perfect Plan B Guide.

end

Your early MONDAY morning currency, Asian stock market results, important USA/Asian currency crosses, gold/silver pricing overnight along with the price of oil Major stories overnight/9 AM EST

i) Chinese yuan vs USA dollar/CLOSED/ LAST AT: 6.6786/

//OFFSHORE YUAN: 6.6781 /shanghai bourse CLOSED UP 12.31 POINTS OR 0.42% /

HANG SANG CLOSED DOWN 14.62 POINTS OR 0.05%

2. Nikkei closed UP 107.12 POINTS OR 0.50%

3. Europe stocks OPENED RED

/USA dollar index FALLS TO 95.91/Euro RISES TO 1.1392

3b Japan 10 year bond yield: FALLS TO. –.03/ !!!!(Japan buying 100% of bond issuance)/Japanese yen vs usa cross now at 110.51/ THIS IS TROUBLESOME AS BANK OF JAPAN IS RUNNING OUT OF BONDS TO BUY./JAPAN 10 YR YIELD IS NOW TARGETED AT .11%/JAPAN LOSING CONTROL OF THEIR BOND MARKET

3c Nikkei now JUST BELOW 17,000

3d USA/Yen rate now well below the important 120 barrier this morning

3e WTI:: 56.55 and Brent: 66.14

3f Gold DOWN/JAPANESE Yen DOWN CHINESE YUAN: ON -SHORE UP /OFF- SHORE: UP

3g Japan is to buy the equivalent of 108 billion uSA dollars worth of bond per month or $1.3 trillion. Japan’s GDP equals 5 trillion usa./“HELICOPTER MONEY” OFF THE TABLE FOR NOW /REVERSE OPERATION TWIST ON THE BONDS: PURCHASE OF LONG BONDS AND SELLING THE SHORT END

Japan to buy 100% of all new Japanese debt and by 2018 they will have 25% of all Japanese debt. Fifty percent of Japanese budget financed with debt.

3h Oil UP for WTI and UP FOR Brent this morning

3i European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund RISES TO +.11%/Italian 10 yr bond yield UP to 2.74% /SPAIN 10 YR BOND YIELD DOWN TO 1.15%…ITALIAN 10 YR BOND YIELD/GERMAN BUND: 2.68: DANGEROUS FOR THE ITALIAN BANKING SYSTEM

3j Greek 10 year bond yield FALLS TO : 3.72

3k Gold at $1326.75 silver at:15.85 7 am est) SILVER NEXT RESISTANCE LEVEL AT $18.50

3l USA vs Russian rouble; (Russian rouble DOWN 1/100 in roubles/dollar) 65.32

3m oil into the 56 dollar handle for WTI and 66 handle for Brent/

3n Higher foreign deposits out of China sees huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 INITIATES NIRP. THIS MORNING THEY SIGNAL THEY MAY END NIRP. TODAY THE USA/YEN TRADES TO 110.51 DESTROYING JAPANESE CITIZENS WITH HIGHER FOOD INFLATION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the SF. It is not working: USA/SF this morning 0.9970 as the Swiss Franc is still rising against most currencies. Euro vs SF is 1.1353 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

3p BRITAIN VOTES AFFIRMATIVE BREXIT/LOWER PARLIAMENT APPROVES BREXIT COMMENCEMENT/ARTICLE 50 COMMENCES MARCH 29/2017

3r the 10 Year German bund now POSITIVE territory with the 10 year RISING to +0.11%

The bank withdrawals were causing massive hardship to the Greek bank. the Greek referendum voted overwhelming “NO”. Next step for Greece will be the recapitalization of the banks and that will be difficult.

4. USA 10 year treasury bond at 2.63% early this morning. Thirty year rate at 3.01%

5. Details Ransquawk, Bloomberg, Deutsche bank/Jim Reid.

6. TURKISH LIRA: UP TO 5.2922

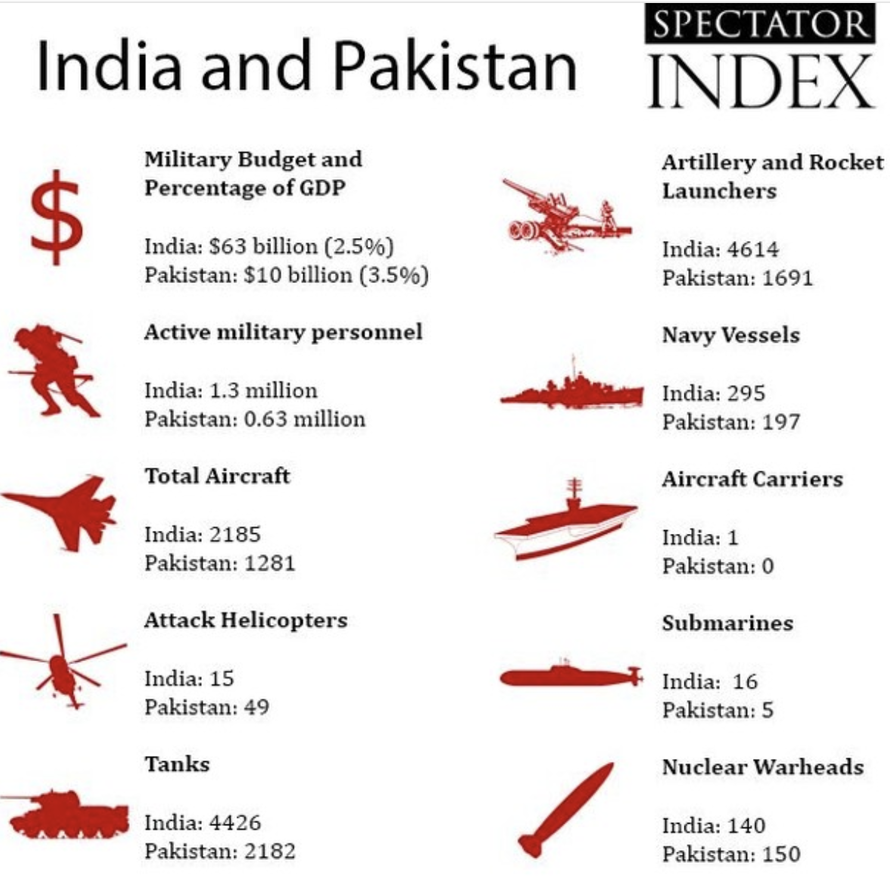

Stocks Slide On India-Pakistan Hostilities As Traders Brace For Day Of Fireworks

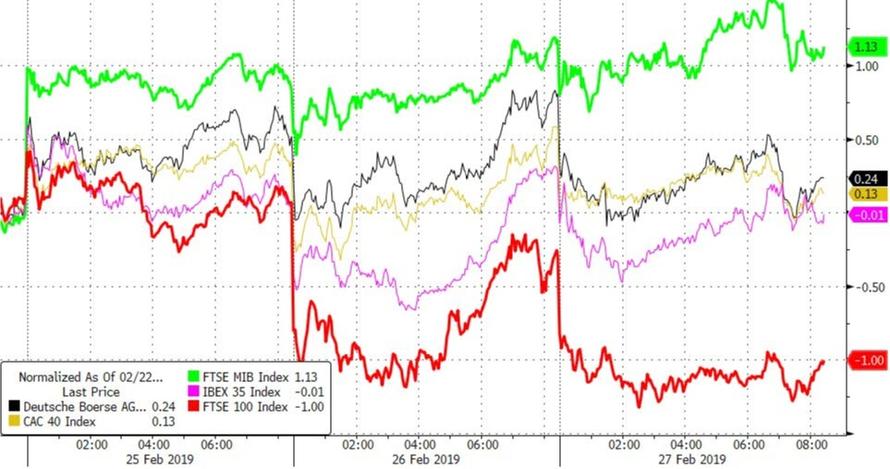

After two days of surprising weakness in US cash stocks in the last hour of trading, and following an overnight session in which S&P futures were offline for two hours following a “glitch” at the CME Globex exchange, world markets are a sea of red as stocks fell in Europe alongside US equity futures pressured by disappointing corporate earnings and a dramatic escalation in India-Pakistan hostilities after Pakistan reportedly shot down two Indian fighter jets even as traders brace for a barrage of news including the latest Trump-Kim summit, the Congressional testimony by Trump’s former lawyer Michael Cohen, and the second day of Powell’s testimony on the hill this time before Maxine Waters and AOC. Treasuries yields dropped, as did the dollar.

The European Stoxx 600 index was down about 0.5%, with all the main regional indexes were in the red as Air France-KLM dropped the most ever and Nivea hand-cream maker Beiersdorf cut guidance, sparking a selloff in consumer stocks.

Earlier, all eyes were on the latest Asian geopolitical conflict: S&P futures fell, Japan equities came off their highs, Hong Kong faded an advance after Pakistan said it had downed two Indian jets, sending Indian and Pakistan bonds and currencies lower and MSCI’s index of Asia-Pacific shares ex-Japan sliding 0.1% as the threat of conflict between the nuclear-armed neighbors grew. Australia’s ASX 200 (+0.4%) gains were led by energy names following the rebound in the complex after sources stated that OPEC are to stick to their output curb agreement coupled with bullish API inventory data, while Nikkei 225 (+0.5%) benefitted from the strength in the healthcare sector. Elsewhere, Shanghai Comp (+0.4%) benefited from gains in IT names whilst the latter profited from the strong performance in heavyweight energy and financial names.

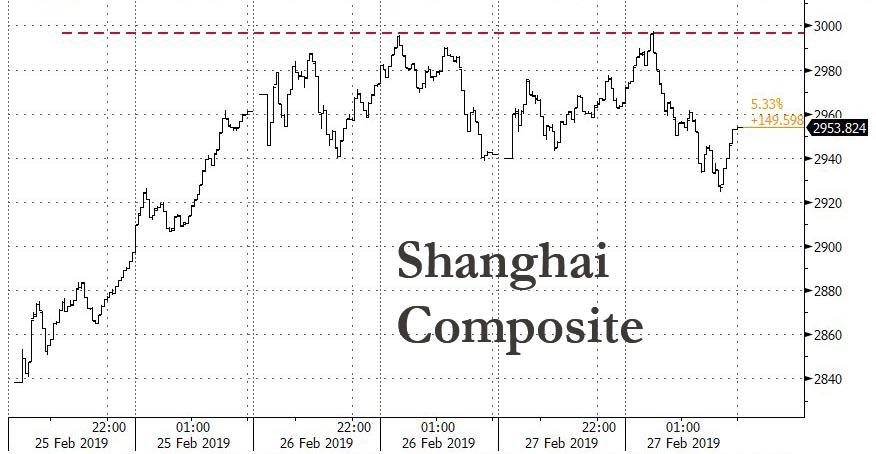

Meanwhile, just as 2800 has emerged as an uncrossable resistance line for the S&P, China is having the same issue with the 3000 level on the Shanghai Composite as Chinese stocks erased a gain in the afternoon, with the Composite again failing to cross the 3,000-point level after climbing into bull market earlier in week. The Shanghai benchmark climbed as much as 1.9% earlier in day before seeing much of its gains fade and close up just 0.4%.

“It was purely a liquidity-driven rebound without the support of fundamentals, so nobody expected the market to embark on another bull run to hit 5,000 points,” said Yin Ming, vice president of Shanghai- based investment firm Baptized Capital. “When the index nears the technically important 3,000-point level, investors will choose to exit first and wait for bargains after the correction. With gains in recent sessions, shareholders of firms are finally able to close out their share-pledge positions to repay loans.”

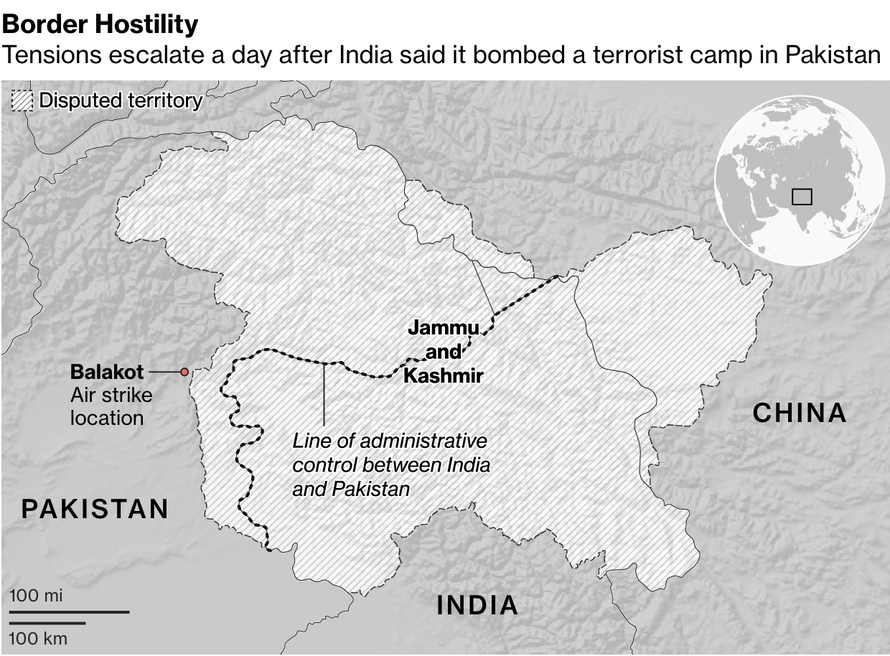

India’s rupee reversed gains and Pakistan’s benchmark stock index plunged more than 3 percent in Karachi before recovering after the latest escalation in tensions. The Pakistani action came a day after India’s Air Force jets bombed what it said was a terrorist training camp inside Pakistan.

“This adds another layer of risks for investors”, said Charles St-Arnaud, a strategist at Lombard Odier, although he noted the market moves remained limited for now.

US Secretary of State Pompeo spoke to the Indian and Pakistani Foreign Minister separately according to the US State Department. The Secretary of State urged Pakistan to avoid military action against India following the previously reported Indian air strike on a terrorist camp on Pakistan. Furthermore, at least three Pakistan fighter jets have entered the Indian side of Kashmir, Indian Air Forces intercepted the Pakistani planes; according to an Indian Official. It was later reported that an Indian Air Force jet has crashed in Jammu & Kashmir, according to PTI. Pakistan Foreign Ministry confirms they have shot down two Indian planes and arrested a pilot, states that we have no intention of escalation, but are prepared to do so if forced into that situation.

As Bloomberg notes, investors have added the India-Pakistan conflict to a host of other uncertainties from China trade talks to Brexit, that could rein in a recovery in global equities from December lows. U.S. President Donald Trump is in Hanoi for a second summit with North Korean leader Kim Jong Un, with the outcome uncertain. Powell’s testimony on Tuesday helped steady the ship, though, as he gave no indication that the Fed is ready to alter policy any time soon.

S&P500 futures were down 0.2%, after earlier a Globex malfunction around 740pm ET halted trading in ES, Treasury and commodity futures, prompting trader anguish for nearly two hours before the “glitch” was eventually resolved.

Markets are also watching the U.S.-North Korean summit, which began shortly after 6am ET in Hanoi. President Trump is meeting North Korean leader Kim Jong Un for their second summit, with the United States pushing North Korea to dismantle its nuclear weapons program.

The heightened geopolitical risks helped assets considered safer than stocks, such as the Japanese yen, which gained against the dollar. Paradoxically, while news of the worst escalation between the two nations since the 1971 war moved the yen higher and India’s rupee lower, volatility across currencies continued on its downward trend as traders continue to sell vol in droves.

In political news, overnight the US House voted to block President Trump’s national emergency declaration regarding a Mexican border wall, as expected. The bill will now be passed onto Senate before eventually being vetoed by the president.

Of note, also today Trumps’s former lawyer Michael Cohen will testify publicly that Trump is a racist, conman & cheat, and that Trump knew ahead of time that Wikeleaks were to release Democratic Committee emails hurting Hilary Clinton’s election campaign; draft statement.

In the latest Brexit news, UK PM May said she is close to winning concessions from the EU that could persuade Eurosceptic MPs to back her deal. More notably, Brexiteer Jacob Rees-Mogg has softened his stance on PM May’s Brexit deal; he is no longer insisting the Irish backstop be scrapped and he is prepared to consider other legal fixes to make sure it does not become permanent. Cabinet Ministers warned PM May that Brexit could be delayed by up to two years after she announced a series of votes on her deal, no deal and a Brexit delay to be held in a fortnight. Meanwhile, the newly-formed Independent Group has tabled an amendment demanding the government to commence preparations for a second EU referendum. The amendment reportedly has support from the SNP, LibDems, and Plaid Cymru and is said to be aimed at provoking a fresh split in the Labour party by tempting MPs who are seeking a new vote.

In FX, the dollar hovered around a three-week low after Federal Reserve Chairman Jerome Powell reiterated on Tuesday the Fed had shifted to a more “patient” policy approach regarding changes to interest rates. “We didn’t learn much new,” St-Arnaud said. The new dovish stance of U.S. monetary policy had not weakened the dollar much, notably against the euro.

Elsewhere, the British pound continued to rise after Prime Minister Theresa May offered lawmakers a chance to vote on delaying Brexit. The pound approached $1.3300 as leveraged accounts bought the currency as it dipped earlier in the day, while gilts declined. The euro recovered from a loss as the dollar erased an Asian session advance; the pound was up a fourth day, its longest winning streak since September amid continued Brexit optimism after Prime Minister Theresa May bought herself more time to secure a Brexit agreement. Scandinavian currencies led the advance after better- than-forecast data; unemployment unexpectedly fell in Norway and retail sales beat estimates, while a Swedish economic tendency survey rose. Australia’s dollar surrendered early gains on disappointing building data.

In rates, bunds were little changed, Treasuries were steady after earlier whipsawing and U.S. equity futures drifted lower; the previously noted technical error at CME Group Inc. disrupted trading of contracts tied to Treasuries and commodities.

Today’s Data include factory orders, pending home sales and mortgage applications. Lowe’s, Square and American Tower are due to report earnings

Market Snapshot

- S&P 500 futures down 0.3% to 2,782.50

- STOXX Europe 600 down 0.5% to 371.76

- MXAP up 0.1% to 160.43

- MXAPJ down 0.1% to 526.18

- Nikkei up 0.5% to 21,556.51

- Topix up 0.2% to 1,620.42

- Hang Seng Index down 0.05% to 28,757.44

- Shanghai Composite up 0.4% to 2,953.82

- Sensex down 0.1% to 35,927.20

- Australia S&P/ASX 200 up 0.4% to 6,150.27

- Kospi up 0.4% to 2,234.79

- German 10Y yield rose 0.4 bps to 0.122%

- Euro up 0.02% to $1.1391

- Brent Futures up 0.8% to $65.70/bbl

- Italian 10Y yield fell 6.8 bps to 2.346%

- Spanish 10Y yield rose 0.5 bps to 1.143%

- Brent Futures up 0.8% to $65.70/bbl

- Gold spot down 0.2% to $1,326.29

- U.S. Dollar Index down 0.01% to 96.00

Top Overnight News from Bloomberg

- U.S. President Donald Trump plans to hold a one-on-one meeting with North Korean leader Kim Jong Un on Wednesday before the two leaders dine together with aides as they kick off their second summit aimed at a deal for Pyongyang to surrender its nuclear arsenal

- Donald Trump’s administration regularly denounces Nicolas Maduro as an autocratic Cuban puppet and may hit the Caribbean island with new sanctions over its support for the Venezuelan leader

- Leading Brexit purist Jacob Rees-Mogg, who has opposed Theresa May’s exit deal, appears to be softening his stance, making it more likely that the divorce agreement could win Parliamentary approval next month

- The European Union is unlikely to offer concessions to the U.K. on its Brexit deal until just before the British Parliament votes on it, triggering a frantic two-week period that culminates in a critical summit of leaders

- U.K. financial firms were dealt a blow after EU policy makers agreed to tighten the rules governing the City of London’s access to the bloc after Brexit

- Bank of Japan board member Goushi Kataoka says the central bank should try to widen the gap between supply and demand by ramping up its easing measures in pursuit of 2% inflation. BOJ may resort to more QE if yen jumps, according to Takahide Kiuchi, a former policy board member

- A Bloomberg Economics gauge indicates that China’s economy is showing the first signs of recovery after months of slowdown, as stock and commodity rallies lift confidence

- A technical error at CME Group Inc. prompted a lengthy trading halt at the world’s largest exchange operator, preventing the buying and selling of contracts tied to U.S. Treasuries, stock-futures and commodities

- The House voted to block President Donald Trump’s declaration of a national emergency on the U.S.-Mexico border, sending the measure to the Senate where the GOP majority will be forced to take a stand on whether to defy their president

- Greece’s foot-dragging on some key economic reforms is raising creditor concern, putting at risk a planned debt relief measure next month and a rebound in its stock and bond markets

- Italian business and economic confidence fell, signaling a possible continuation of the recession that started late last year

Asian equities were higher across the board following a subdued lead from Wall Street where the Dow dipped into the red following disappointing earnings from Home Depot and the S&P retreated further below the 2800 level. ASX 200 (+0.4%) gains were led by energy names following the rebound in the complex after sources stated that OPEC are to stick to their output curb agreement coupled with bullish API inventory data, while Nikkei 225 (+0.5%) benefitted from the strength in the healthcare sector. Elsewhere, Shanghai Comp (+0.4%) and Hang Seng (U/C) extended on gains from the open with the former supported by IT names whilst the latter profited from the strong performance in heavyweight energy and financial names. Furthermore, Morgan Stanley raised its targets for Chinese equities, citing policy stimulus alongside positive trade developments. BoJ Governor Kuroda said the chance of Japanese inflation to hit the 2% target during FY 2020 is low and any exit from the BoJ’s ultra-easy policy will be very gradual. BoJ Board Member Kataoka disagrees with the BoJ’s view of persistently easing policy to reach price goal and added that longer monetary easing will bring more side effects. Kataoka also added that the BoJ is still far from ending its ultra-easy policy. He expects any sales-tax hike driven pickup in Japan’s economy to be moderate and said Japan’s inflation expectations remain weak whilst also acknowledging that global growth has slowed compared to the prior year.

Top Asian News

- China Is Studying Plan to Restructure Vaccine Sector: CSJ

- H.K. Govt ‘Gravely Concerned’ Over Claims Against H.K. Airlines

- Here’s What You Need to Know About Asia’s Stock Markets Today

Major European equities are in the red [Euro Stoxx 50 -0.5%], following a subdued lead from Wall Street and modest gains in Asia overnight, as traders are mindful of growing tensions between India and Pakistan. There is some mild underperformance in the Dax (-0.7%) where only 3 companies are in the green; although losses are limited by strong performance in Bayer (+4.5%) after the Co. posted a beat on their Q4 sales. Sectors are similarly broadly in the red, with underperformance seen in consumer staples. Other notable movers include, Marks & Spencer (-9.5%) who are at the bottom of the Stoxx 600 after the Co. are considering a rights offering to fund their joint venture with Ocado (+4.7%). Air France (-11.7%) are down as the Dutch government has taken a 12.7% shareholding in the Co. in an attempt to protect their interests; which may lead to tensions with France who hold a 14.3% stake in the Co. Rio Tinto (+0.4%) are in the green after posting a significant increase in FY net earnings of USD 13.64bln vs. Prev. USD 8.76bln alongside the announcement of a special dividend.

Top European News

- Air France-KLM Tumbles After Dutch State Builds Surprise Stake

- Britain’s Winter Heat Wave Means Wildfires and Chronic Pollution

- Ted Baker Plunges After Profit Warning Adds to Clothier’s Woes

- Brexiteer Rees-Mogg Softens Stance on May’s Deal: Brexit Update

In FX, the Dollar continues to sag in wake of Fed chair Powell’s reinforcement of the new patient policy stance and on portfolio rebalancing for the turn of the month. The DXY has retreated below 96.000 as a result, and with additional downside pressure coming from the escalation in tensions between India and Pakistan that has prompted greater demand for safer currency havens relative to the Greenback.

- CHF/GBP The Franc and Pound are vying for pole position within the G10 ranks, as the former benefits from defensive positioning amidst the aforementioned rise in Indian-Pakistani hostilities, with Usd/Chf reversing more definitively from par-plus levels to around 0.9970. Meanwhile, Sterling has extended gains on the back of Tuesday’s marked turnaround on Brexit from UK PM May that raises the prospect of a delay to Article 50 and odds on a no deal or cliff edge conclusion to the already protracted withdrawal process. Cable is now probing 1.3300 after eclipsing resistance just shy of the big figure (1.3298 high from September 2018), while Eur/Gbp is hovering around 0.8570 and eyeing chart support a few pips below, like a Fib at 0.8548.

- CAD/JPY The next best majors, with the Loonie drawing comfort/support from a rebound in crude prices and the more pronounced downturn in the Usd, to rebound firmly over 1.3200 again and pivot 1.3150, while Usd/Jpy has now breached its 100 DMA more convincingly to trade under 110.40. Note, 110.00 should be well supported given the 30 DMA at 110.02, and with hefty expiries looming at the strike on Thursday (2 bn), and next up for the CAD top-tier Canadian CPI data and avg. earnings.

- AUD/NZD/NOK/SEK Contrasting fortunes for the more high-beta and risk sensitive Antipodean Dollars and Scandi Crowns, as the Aussie and Kiwi underperform in wake of disappointing data overnight (Q4 construction and January trade respectively), but the Nok and Sek glean protection from the overall risk averse environment with the aid of upbeat macro releases (retail sales, manufacturing and overall industry sentiment, plus trade). Aud/Usd is currently near the bottom of a 0.7198-65 range, Nzd/Usd close to 0.6874 vs 0.6901 at one stage, while Eur/Nok is under 9.7200 and Eur/Sek around 10.5500.

- EUR The single currency is also gaining at the expense of the Greenback, with one prominent bank flagging strongest month end Usd sell signals against the Eur. However, technical obstacles around 1.1400 are proving tough to overcome and the decline in Eur/Gbp noted above is also hampering the single currency to a degree

In commodities, Brent (+1.3%) and WTI (+1.6%) prices are higher and trading towards the top of the sessions range, after yesterday’s unexpected -4.2mln draw in API Weekly Crude Inventories compared with the expectations for a +2.8mln build. Recent newsflow has seen comments from Saudi Energy Minister Al Falih saying that he sees a likelihood of an output cuts extension in H2 and are aiming for March oil exports of 7mln BPD. Separately, the Russian Energy ministry is reportedly planning to meet with Russian oil companies on March 1st in order to discuss the OPEC+ deal. Elsewhere, Nigerian President Buhari has won the re-election, which is to be contested in court and oil prices were little affected by the CME group’s technical issues which resulted in WTI live prices being unavailable for a time. Gold is flat as it follows the dollar after the first testimony by Fed’s Chair Powell yesterday to the Senate and ahead of his testimony to the house today at GMT 15:00. Elsewhere, Freeport’s CEO has instructed his employees to immediately report any safety concerns regarding dams the Co. operate; following January’s Vale mine disaster. Separately, Copper has slipped slightly from it’s 7-month high which was spurred by falling supply and dollar weakness.

In terms of the day ahead, we’re due to get the December advance goods trade balance, and final revisions to December wholesale inventories, durable goods and capital goods orders. Away from that, Powell will speak again, this time testifying to the House Financial Services Committee Panel, while the ECB’s Coeure and Weidmann are due to speak. In the UK the House of Commons will be voting today however it’s unlikely to be significant in light of yesterday’s developments, The other potentially important event to watch is US Trade Representative Lighthizer testifying to the House Ways and Mean Committee’s hearing on the US-China trade talks.

US Event Calendar

- 8:30am: Advance Goods Trade Balance, est. $73.9b deficit, prior $70.5b deficit

- 8:30am: Retail Inventories MoM, est. 0.2%, prior -0.4%; Wholesale Inventories MoM, est. 0.4%, prior 1.1%

- 10am: Pending Home Sales MoM, est. 1.0%, prior -2.2%; Pending Home Sales NSA YoY, est. -4.55%, prior -9.5%

- 10am: Factory Orders, est. 0.6%, prior -0.6%; Factory Orders Ex Trans, prior -1.3%

- 10am: Durable Goods Orders, prior 1.2%; Durables Ex Transportation, prior 0.1%

- 10am: Cap Goods Orders Nondef Ex Air, prior -0.7%; Cap Goods Ship Nondef Ex Air, prior 0.5%

DB’s Jim Reid concludes the overnight wrap

If you’re looking for the next box set to binge on and are happy to suspend any semblance of belief then I can give a wholehearted recommendation to watch Ozark (Netflix). It’s in the mould of Breaking Bad for the uninitiated. Over the last month we have watched the two available series back to back and are now at a loss as to what to do with our evenings again. More time for stressing about kitchens, bathrooms, carpets, new windows, boilers, guttering and the like.

After watching last night’s tense finale, markets seem positively mundane at the moment. Mr Powell might have ignited the flame for positive sentiment at the start of the year but 8 weeks on markets weren’t particularly fussed by the first of his semi-annual testimonies yesterday in front of the Senate. We’ll touch on what he said shortly however 10y Treasuries traded in a range of just a few of basis points as Powell spoke, before ending the day down -2.5bps at 2.638%. We went back and looked at the range since Powell spoke in early January and found that on a closing basis, the range has been just 15.5bps which is the smallest since June last year, and the second smallest since October 2017. The MOVE index (implied vol of 1-month treasury options) is back down slightly above the all time lows (data back to 1988) so central banks have killed vol again for now. As for the response in equites yesterday, reaction to the testimony was mixed as US stocks oscillated between losses and gains with the S&P 500 and NASDAQ indexes retreating -0.08% and -0.09%, respectively, at the close. They do remain +14.13% and +16.80% off their Jan 3 levels before Powell’s initial policy U-turn sparked a rebound in markets. US HY spreads are -122bps tighter over the same period, having tightened -3bps yesterday.

So the change in message has worked for markets in 2019 but there wasn’t much more to give yesterday as it was mostly a repeat of the recent mantra in favour of patience before any further rate hikes are seen. Powell repeated that “our policy decisions will continue to be data dependent” and that “we’re in no rush to make a judgment about changes in policy.” So the Fed continues to be on the sidelines for now. Powell justified his position by citing “muted” inflation pressures and the fact that “growth has slowed in some major foreign economies, particularly China and Europe.” Finally, he also noted that “uncertainty is elevated around several unresolved government policy issues, including Brexit and ongoing trade negotiations.”

Before that, European markets had closed mostly higher, with the STOXX 600 gaining +0.39%, and indexes across the continent advancing as well. The main exception was the FTSE 100, which retreated -0.45% amid a large rally in the pound on positive Brexit developments (details below). Bund yields rose +0.8bps, while peripheral spreads tightened with Italian BTPs yields -6.9bps lower. European HY credit spreads tightened -4.9bps to their tightest level since November.

The other main piece of news yesterday surrounded Brexit with a few more dates for your diaries. PM May confirmed that should her deal be rejected by March 12, then the PM will put forward the choice to MPs of a no-deal Brexit vote on March 13 and should that be rejected, then a vote on extending Article 50 will be put forward on March 14. We know that May would ask for a short and one-off extension (not beyond June) but we don’t know what the EU will agree to and we won’t know for sure until the EU engage on the issue. Bloomberg has previously reported some EU officials as saying they would back an extension of as much as 21 months but the truth is we won’t really know until closer to the above dates. GBP/USD rallied throughout the session yesterday, ending +1.21% stronger, its best performance since last November. We’re reading at $1.3248 overnight which is the highest since last July. EUR/GBP is now at 0.857 and the strongest since May 2017. We should add that our FX strategists yesterday reinstated their Sterling long trade in light of recent developments and target 0.84 in EUR/GBP. More in their note here . Overnight the FT has carried interesting quotes from the de facto leader of the eurosceptic Tory wing Jacob Rees-Mogg. He is suggesting that he is no longer looking to scrap the Irish backstop and will instead consider other legal fixes to it. So the mood music continues to move in favour of Mrs May’s deal albeit without yet having the necessary legal concessions from the EU.

Overnight markets are heading higher with the Nikkei (+0.49%), Hang Seng (+0.60%), Shanghai Comp (+0.79%) and Kospi (+0.24%) all up. Elsewhere, futures on the S&P 500 are trading flat (-0.02%). President Trump and North Korea leader Kim Jong Un are meeting today and tomorrow, with President Trump set to meet North Korea’s Kim at 11:40am GMT. In the meantime, S&P has said that even if the US and North Korea make a formal declaration of an end to the Korean War, it is unlikely to impact South Korea’s rating as the security posed by North Korea will continue to weigh on South Korea’s ratings for the foreseeable future.

In other news, after Italy’s ruling coalition partner M5S lost c. 75% of its vote share in Sardinia (11.18% in 2019 down from 42.5% previously), it’s leader Luigi Di Maio is facing fresh dissent from party members with majority of them calling on him to return the party to its roots and give more power back to the rank-and-file members. M5S trails its other coalition partner League by more than 10% in the most recent polls as the two leaders gear up for May’s European parliamentary elections. In the meantime, Di Maio appeared to recognise the internal dissent yesterday by signaling that he is ready to give some concessions to the party dissenters but added that “we need to have better structure, but my political leadership will only be up for discussion four years from now” (per Bloomberg). This could lead to renewed turbulence in Italian politics but Italian PM Conte and both the ruling coalition leaders have played down the risk of regional and European parliament elections impacting the sustainability of the Italian government by saying that Italy’s current coalition government will govern for its complete term. 91 governments in around the last 117 years might suggest otherwise. One to continue to watch.

Also interesting yesterday was the US data. The most headline grabbing were the February surveys where the Richmond Fed manufacturing index rose 18pts to +16 (vs. +5 expected) – and included a big jump in new orders – and the Conference Board consumer confidence reading jumped 9.7pts to 131.4 (vs. 124.9 expected) and the highest since November last year. Both the expectations and present situations components ticked up and it was noticeable again that the chart highlighting the gap between the two (expectations minus present situations) did the rounds again yesterday- albeit with the gap narrowing slightly to -70 from -82. A negative numbers has been billed as a leading indicator of recessions in the past and the only time it’s been more negative than now was in 2001 when it hit -96 just before the recession. Given that the thought was the government shutdown may have impacted the data the fact that there hasn’t been a huge change in the latest reading is certainly noteworthy.